Engineering & Construction - Credit Suisse | PLUS

105

Engineering & Construction FY’17 Outlook & Q4’16 Earnings Preview January 31, 2017 Team Contacts Jamie L. Cook, CFA +212-538-6098 [email protected] Jamie Anderson +212-538-3418 [email protected] Themis Davis [email protected] +212-538-8443 DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Engineering & Construction - Credit Suisse | PLUS

Engineering & Construction FY’17 Outlook & Q4’16 Earnings Preview

January 31, 2017

Team Contacts

Jamie L. Cook, CFA

+212-538-6098

Jamie Anderson

+212-538-3418

Themis Davis

+212-538-8443

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

US Engineering & Construction

A Year of Transition: For 2017, we see the Engineering and Construction group as a year of transition. We agree the 2018 and beyond

outlook has improved for the group, reflecting the run in commodity prices and what that implies for energy and mining. Also while the timing

and magnitude remain unclear, the Trump administration on multiple levels (assuming execution and commitment to initiatives outlined

during the campaign) should be a positive for the group broadly. However for 2017, we still see some challenges ahead. We believe the

award front will still be challenged on the energy side, leading investors to question whether 2017 or 2018 is the trough for earnings.

Traditionally, E&C is very late cycle business and projects on the drawing board will have to be revisited to price-in current economics and

will go out for rebid delaying awards. Also, bellwethers like FLR and CBI, and to a lesser degree KBR, still need to work through problem

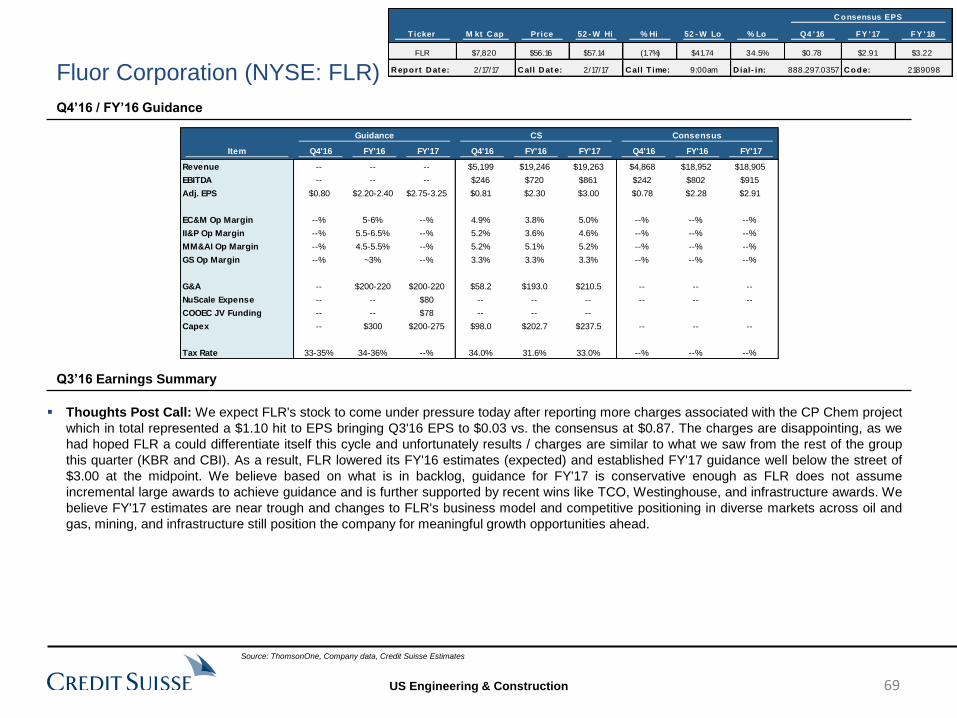

projects associated with taking fixed price work on the Gulf Coast. While third quarter issues were largely attributed to weather, there have

been rumblings that Gulf Coast labor in terms of skill set and productivity remains an issues. So in the absence of new awards, lack of

clarity on when earnings trough, and assuming execution issues are not behind us, will the market look past the news? We suspect we still

have at least a couple of challenged quarters ahead.

Potential for a Cycle of Base Hits Across Multiple Markets vs. Energy Supercycle: As we look to 2018 and beyond, we see

opportunity for E&C backlog to inflect higher although we expect this cycle to be different. Relative to super cycles in the past driven by

energy, we believe it is more realistic to see multiple markets to improve in tandem (energy, mining, infrastructure and gov’t) however more

muted in terms of dollars spend and overall project size. Within energy and mining, we believe it is reasonable to assume a more muted

cycle. In the short term, and in particular for 2017, we remain constructive on the pipeline outlook. This is obviously helped by Trump’s more

recent comments on Keystone and Dakota Access. Obviously, any type of infrastructure renaissance would benefit the group broadly, but

timing, shovel readiness, and funding of projects needs to be worked through. Furthermore, the infrastructure market tends to be more

competitive with private and local mouths to feed versus energy and/or power, where there are limited players with a resume to take on

multi-billion complex projects. Also, assuming the US economy improves and red tape associated with regulatory hurdles are lifted, we

could finally a see a power new gen cycle in the US but still likely gas. In summary, relative to previous super or mega cycles reliant on

elephant projects in energy, we see the potential end market growth across multiple markets at one time (oil and gas, mining, infrastructure

and power). However, the awards are likely more base hit in nature (vs. previous cycles) and diversified across markets. This should be a

positive longer term for the broader group.

Staying a Little More Defensive for Now: Given the run in the group, we believe it still makes sense to stay more defensive on names

with self-help vs. the higher beta names. We continue to favor PWR as one of the biggest players in pipeline, the absence of problem

projects and continued spend in electric transmission. We also favor JEC, with fewer energy headwinds and a compelling self-help story.

Key Themes for 2017 & Beyond

E&C 2017 Outlook

2

US Engineering & Construction

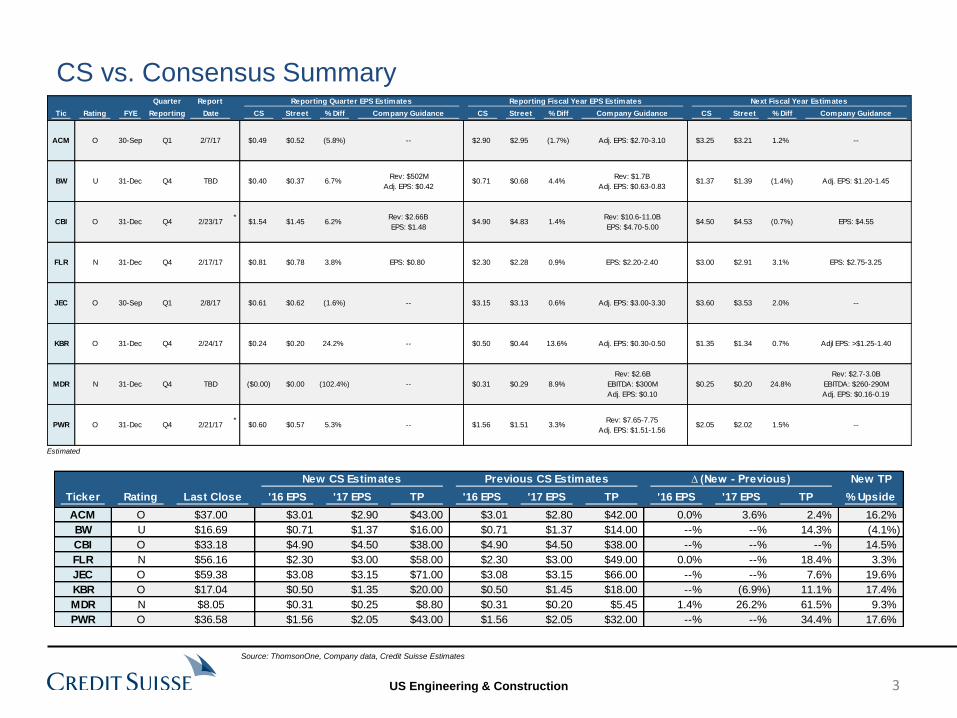

CS vs. Consensus Summary

3

Source: ThomsonOne, Company data, Credit Suisse Estimates

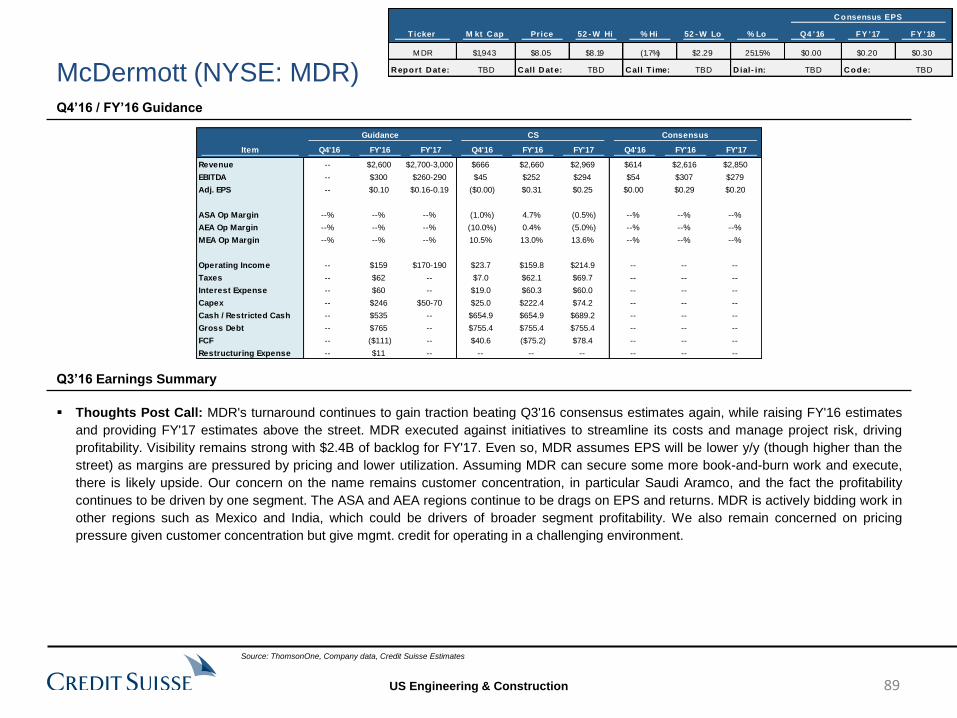

Quarter Report Reporting Quarter EPS Estimates Reporting Fiscal Year EPS Estimates Next Fiscal Year Estimates

Tic Rating FYE Reporting Date CS Street % Diff Company Guidance CS Street % Diff Company Guidance CS Street % Diff Company Guidance

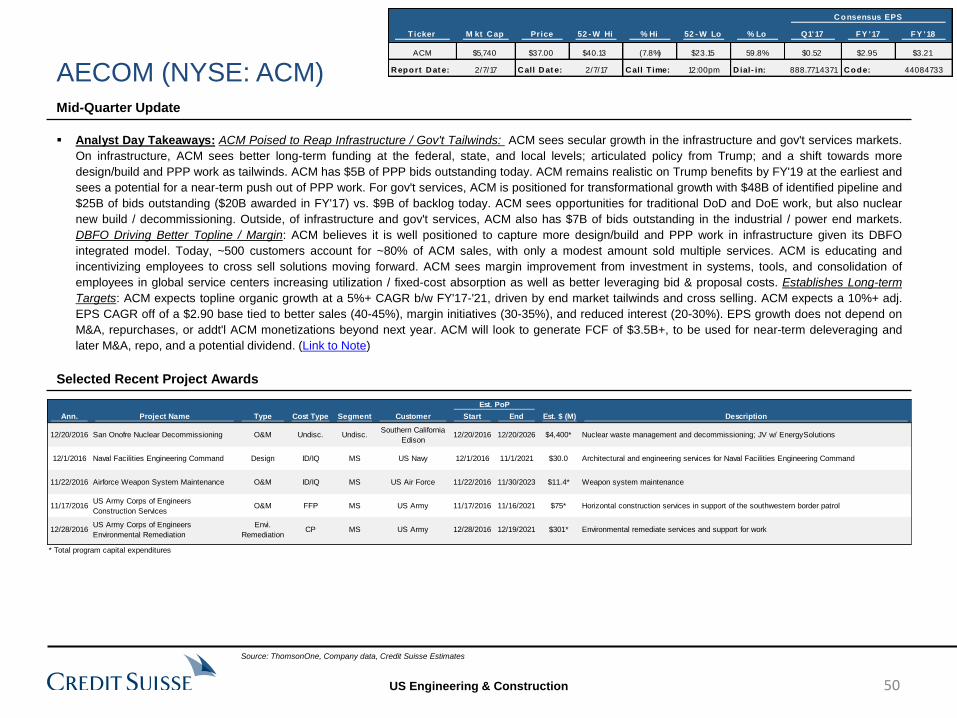

ACM O 30-Sep Q1 2/7/17 $0.49 $0.52 (5.8%) -- $2.90 $2.95 (1.7%) Adj. EPS: $2.70-3.10 $3.25 $3.21 1.2% --

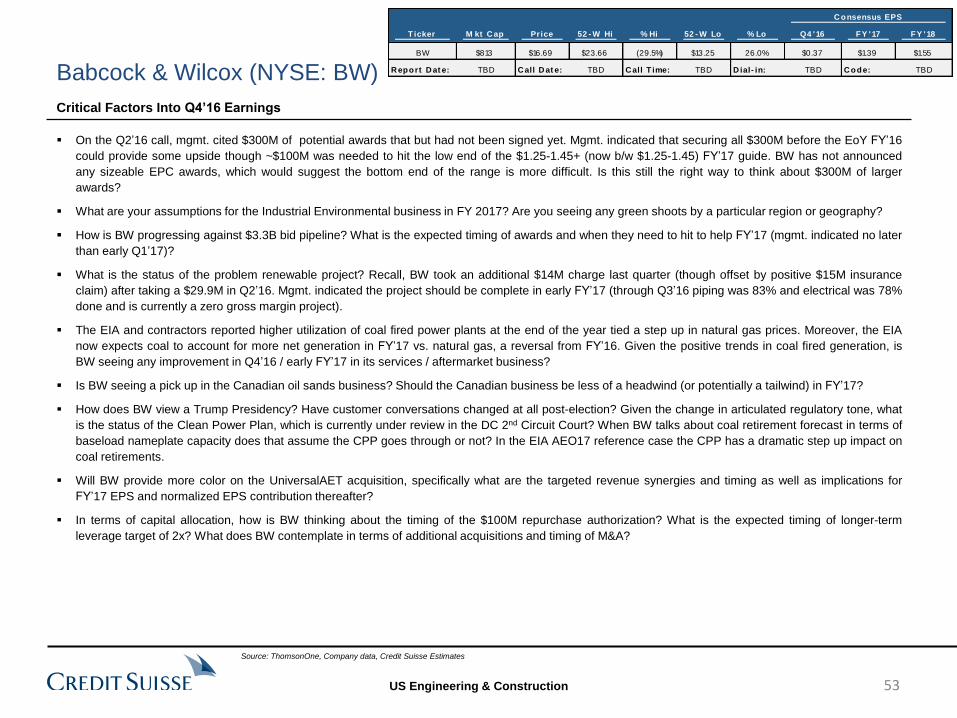

BW U 31-Dec Q4 TBD $0.40 $0.37 6.7%Rev: $502M

Adj. EPS: $0.42 $0.71 $0.68 4.4%

Rev: $1.7B

Adj. EPS: $0.63-0.83 $1.37 $1.39 (1.4%) Adj. EPS: $1.20-1.45

CBI O 31-Dec Q4 2/23/17*

$1.54 $1.45 6.2%Rev: $2.66B

EPS: $1.48 $4.90 $4.83 1.4%

Rev: $10.6-11.0B

EPS: $4.70-5.00 $4.50 $4.53 (0.7%) EPS: $4.55

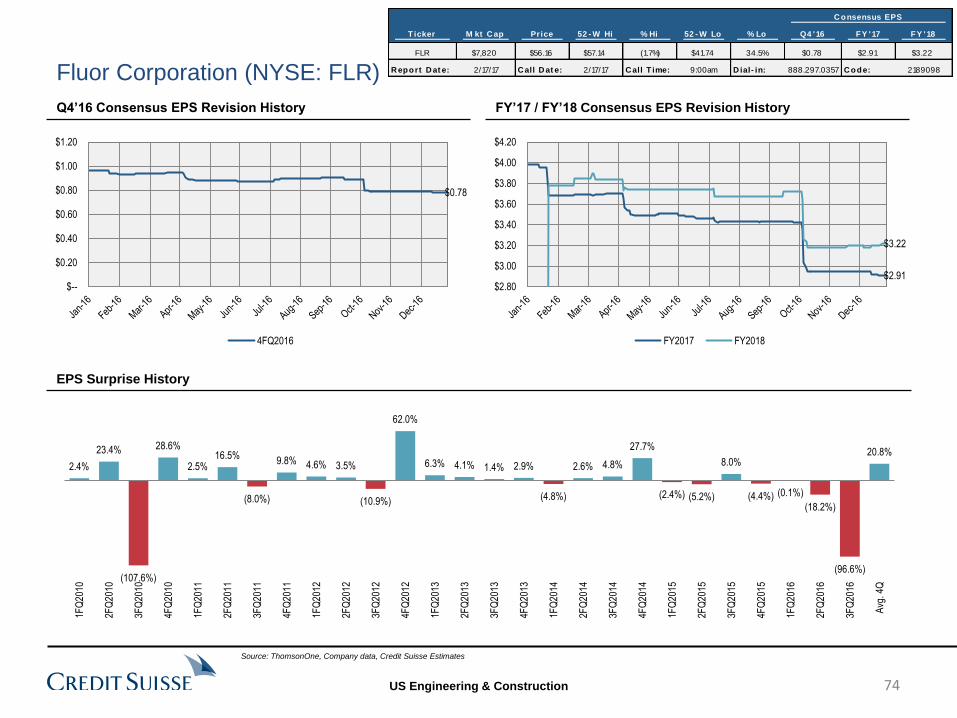

FLR N 31-Dec Q4 2/17/17 $0.81 $0.78 3.8% EPS: $0.80 $2.30 $2.28 0.9% EPS: $2.20-2.40 $3.00 $2.91 3.1% EPS: $2.75-3.25

JEC O 30-Sep Q1 2/8/17 $0.61 $0.62 (1.6%) -- $3.15 $3.13 0.6% Adj. EPS: $3.00-3.30 $3.60 $3.53 2.0% --

KBR O 31-Dec Q4 2/24/17 $0.24 $0.20 24.2% -- $0.50 $0.44 13.6% Adj. EPS: $0.30-0.50 $1.35 $1.34 0.7% Adjl EPS: >$1.25-1.40

MDR N 31-Dec Q4 TBD ($0.00) $0.00 (102.4%) -- $0.31 $0.29 8.9%

Rev: $2.6B

EBITDA: $300M

Adj. EPS: $0.10

$0.25 $0.20 24.8%

Rev: $2.7-3.0B

EBITDA: $260-290M

Adj. EPS: $0.16-0.19

PWR O 31-Dec Q4 2/21/17*

$0.60 $0.57 5.3% -- $1.56 $1.51 3.3%Rev: $7.65-7.75

Adj. EPS: $1.51-1.56 $2.05 $2.02 1.5% --

* Estimated

New CS Estimates Previous CS Estimates ∆ (New - Previous) New TP

Ticker Rating Last Close '16 EPS '17 EPS TP '16 EPS '17 EPS TP '16 EPS '17 EPS TP % Upside

ACM O $37.00 $3.01 $2.90 $43.00 $3.01 $2.80 $42.00 0.0% 3.6% 2.4% 16.2%

BW U $16.69 $0.71 $1.37 $16.00 $0.71 $1.37 $14.00 --% --% 14.3% (4.1%)

CBI O $33.18 $4.90 $4.50 $38.00 $4.90 $4.50 $38.00 --% --% --% 14.5%

FLR N $56.16 $2.30 $3.00 $58.00 $2.30 $3.00 $49.00 0.0% --% 18.4% 3.3%

JEC O $59.38 $3.08 $3.15 $71.00 $3.08 $3.15 $66.00 --% --% 7.6% 19.6%

KBR O $17.04 $0.50 $1.35 $20.00 $0.50 $1.45 $18.00 --% (6.9%) 11.1% 17.4%

MDR N $8.05 $0.31 $0.25 $8.80 $0.31 $0.20 $5.45 1.4% 26.2% 61.5% 9.3%

PWR O $36.58 $1.56 $2.05 $43.00 $1.56 $2.05 $32.00 --% --% 34.4% 17.6%

US Engineering & Construction

Infrastructure

4

US Engineering & Construction

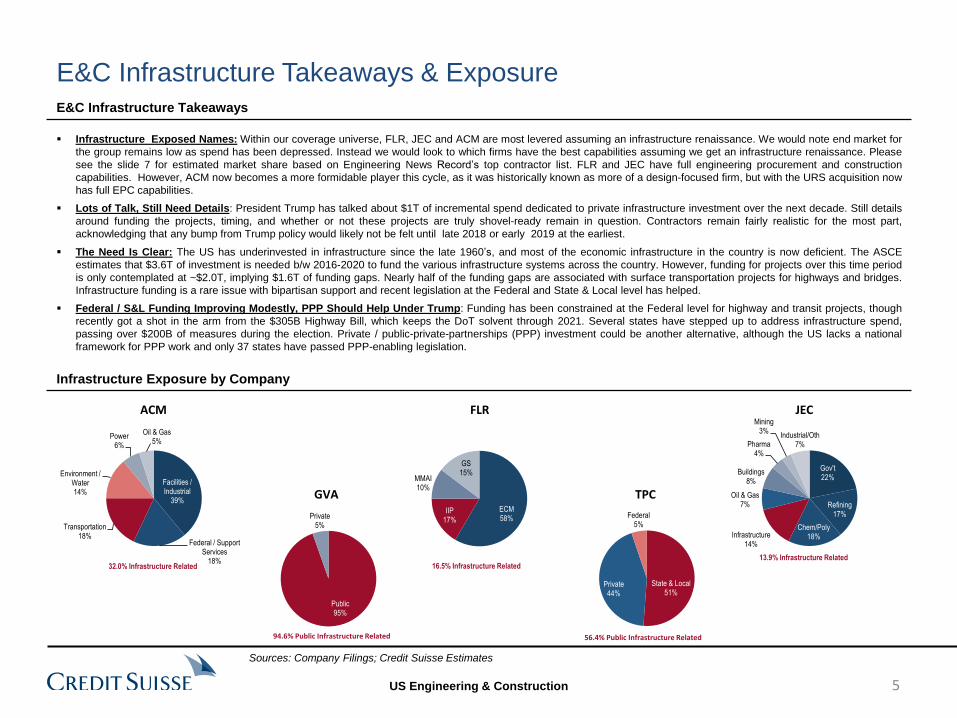

Infrastructure Exposed Names: Within our coverage universe, FLR, JEC and ACM are most levered assuming an infrastructure renaissance. We would note end market for

the group remains low as spend has been depressed. Instead we would look to which firms have the best capabilities assuming we get an infrastructure renaissance. Please

see the slide 7 for estimated market share based on Engineering News Record’s top contractor list. FLR and JEC have full engineering procurement and construction

capabilities. However, ACM now becomes a more formidable player this cycle, as it was historically known as more of a design-focused firm, but with the URS acquisition now

has full EPC capabilities.

Lots of Talk, Still Need Details: President Trump has talked about $1T of incremental spend dedicated to private infrastructure investment over the next decade. Still details

around funding the projects, timing, and whether or not these projects are truly shovel-ready remain in question. Contractors remain fairly realistic for the most part,

acknowledging that any bump from Trump policy would likely not be felt until late 2018 or early 2019 at the earliest.

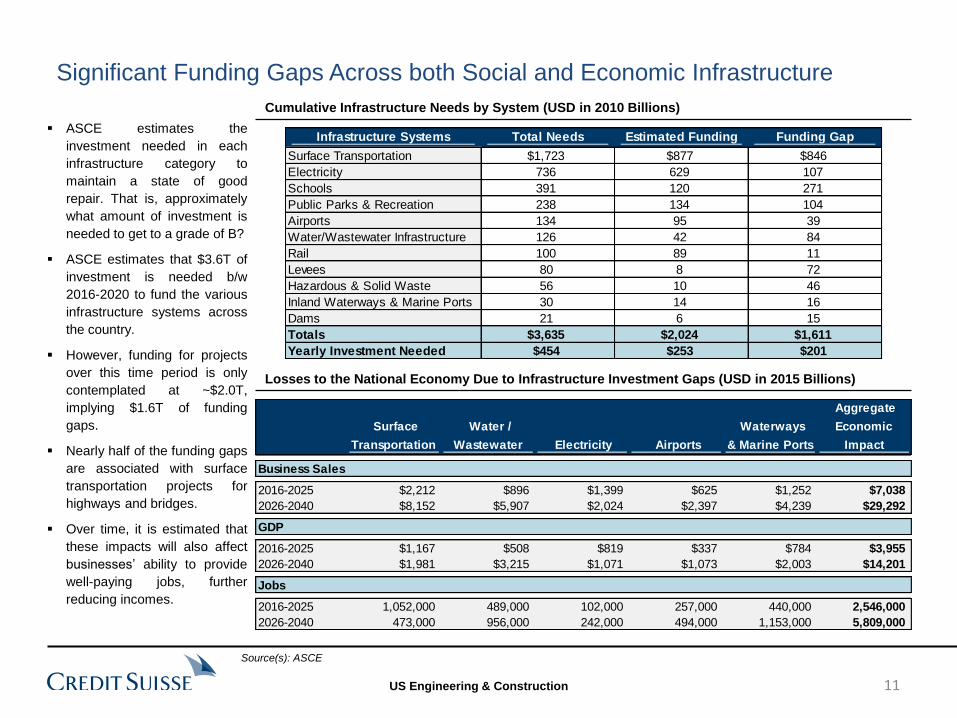

The Need Is Clear: The US has underinvested in infrastructure since the late 1960’s, and most of the economic infrastructure in the country is now deficient. The ASCE

estimates that $3.6T of investment is needed b/w 2016-2020 to fund the various infrastructure systems across the country. However, funding for projects over this time period

is only contemplated at ~$2.0T, implying $1.6T of funding gaps. Nearly half of the funding gaps are associated with surface transportation projects for highways and bridges.

Infrastructure funding is a rare issue with bipartisan support and recent legislation at the Federal and State & Local level has helped.

Federal / S&L Funding Improving Modestly, PPP Should Help Under Trump: Funding has been constrained at the Federal level for highway and transit projects, though

recently got a shot in the arm from the $305B Highway Bill, which keeps the DoT solvent through 2021. Several states have stepped up to address infrastructure spend,

passing over $200B of measures during the election. Private / public-private-partnerships (PPP) investment could be another alternative, although the US lacks a national

framework for PPP work and only 37 states have passed PPP-enabling legislation.

E&C Infrastructure Takeaways

Infrastructure Exposure by Company

E&C Infrastructure Takeaways & Exposure

Facilities / Industrial

39%

Federal / Support Services

18%

Transportation18%

Environment / Water14%

Power6%

Oil & Gas5%

32.0% Infrastructure Related

Gov't22%

Refining17%

Chem/Poly18%Infrastructure

14%

Oil & Gas7%

Buildings8%

Pharma4%

Mining3%

Industrial/Oth7%

13.9% Infrastructure Related

ECM58%

IIP17%

MMAI10%

GS15%

16.5% Infrastructure Related

State & Local51%

Private44%

Federal5%

56.4% Public Infrastructure Related

Public95%

Private5%

94.6% Public Infrastructure Related

ACM FLR

GVA

JEC

TPC

Sources: Company Filings; Credit Suisse Estimates

5

US Engineering & Construction

Engineering News Record (ENR) publishes an annual “Top 400” contractors list,

where it details contractor performance in the U.S. by selected end markets. We

highlight relevant contractors by infrastructure end market in the following tables.

Transportation includes airports, bridges, roads, canals, locks, dredging, marine

facilities, piers, railroads, tunnels, etc.. Publically traded E&C companies with

favorable transportation exposure include TPC, GVA, FLR, and ACM.

General Building includes commercial buildings, offices, stores, educational

facilities, government buildings, hospitals, medical facilities, hotels, apartments,

housing, etc.. Publically traded E&C companies with favorable general building

exposure include TPC and ACM.

Sewer & Water includes dams, reservoirs, transmission pipelines, distribution

mains, irrigation canals, desalination and potability treatment plants, pumping

stations, etc., as well as sanitary and storm sewers, treatment plants, pumping

plants, incinerators, industrial waste facilities, etc. Publically traded E&C

companies with favorable general building exposure include ACM and GVA.

Selected Infrastructure E&C Contractors by End Market Summary by End Market

Top 25 General Building Firms

Top 25 Transportation Focused Firms

Top 25 Water, Sewer, & Wastewater Firms

Sales

Rank Firm Total Transport % Total

1 BECHTEL 23,372.0 4,440.7 19.0%

2 KIEWIT CORP. 8,718.8 2,790.0 32.0%

3 THE WALSH GROUP 4,950.6 2,722.8 55.0%

4 TUTOR PERINI CORP. 5,661.9 2,208.1 39.0%

5 SKANSKA 6,797.9 2,107.3 31.0%

6 GRANITE CONSTRUCTION INC. 2,371.0 1,636.0 69.0%

7 LANE INDUSTRIES INC. 1,354.9 1,246.5 92.0%

8 FLATIRON CONSTRUCTION CORP. 1,283.4 1,155.1 90.0%

9 COLAS USA 1,248.0 1,148.2 92.0%

10 FERROVIAL US CONSTRUCTION CORP. 1,140.0 1,140.0 100.0%

11 CLARK GROUP 4,100.0 1,107.0 27.0%

12 FLUOR CORP. 14,295.1 857.7 6.0%

13 BALFOUR BEATTY US 4,730.1 804.1 17.0%

14 OHL USA INC. 1,409.3 803.3 57.0%

15 AMES CONSTRUCTION INC. 1,068.0 779.6 73.0%

16 RAILWORKS CORP. 687.0 687.0 100.0%

17 GREAT LAKES DREDGE & DOCK 856.9 685.5 80.0%

18 HENSEL PHELPS 3,103.0 651.6 21.0%

19 AUSTIN INDUSTRIES 1,668.3 650.6 39.0%

20 HERZOG FAMILY OF COS. 628.8 628.8 100.0%

21 ALLAN MYERS INC. 629.8 554.2 88.0%

22 WEEKS MARINE INC. 732.9 542.3 74.0%

23 THE TURNER CORP. 10,566.6 528.3 5.0%

24 LAS VEGAS PAVING CORP. 510.0 510.0 100.0%

25 AECOM 7,011.7 490.8 7.0%

Sales

Rank Firm Total

Sewer &

Waste % Total

1 THE WALSH GROUP 4,950.6 792.1 16.0%

2 GARNEY HOLDING CO. 610.7 610.7 100.0%

3 KIEWIT CORP. 8,718.8 610.3 7.0%

4 LAYNE CHRISTENSEN CO. 683.5 587.8 86.0%

5 MWH GLOBAL 491.2 412.6 84.0%

6 AEGION CORP. 973.0 398.9 41.0%

7 SOUTHLAND/RENDA/JBROS 568.0 363.5 64.0%

8 PCL CONSTRUCTION ENTERPRISES 6,785.0 339.3 5.0%

9 CDM SMITH 437.9 267.1 61.0%

10 PC CONSTRUCTION CO. 500.7 250.4 50.0%

11 LYLES CONSTRUCTION GROUP 266.8 234.8 88.0%

12 AECOM 7,011.7 210.4 3.0%

13 KOKOSING INC. 1,049.8 210.0 20.0%

14 SKANSKA 6,797.9 203.9 3.0%

15 GRANITE CONSTRUCTION INC. 2,371.0 189.7 8.0%

16 OHL USA INC. 1,409.3 183.2 13.0%

17 BLACK & VEATCH 1,473.8 176.9 12.0%

18 ALBERICI-FLINTCO 2,100.4 168.0 8.0%

19 BARNARD CONSTRUCTION CO. INC. 511.4 163.6 32.0%

20 RICE LAKE CONSTRUCTION GROUP 218.7 159.7 73.0%

21 WHARTON-SMITH INC. 222.3 140.0 63.0%

22 BOWEN ENGINEERING CORP. 221.7 139.7 63.0%

23 C. OVERAA & CO. 249.9 122.5 49.0%

24 J. FLETCHER CREAMER & SON INC. 482.1 120.5 25.0%

25 BOH BROS. CONSTRUCTION CO. LLC 288.6 115.4 40.0%

Sales

Rank Firm Total

General

Building % Total

1 THE TURNER CORP. 10,566.6 8,664.6 82.0%

2 THE WHITING-TURNER CONTRACTING 5,721.8 4,005.3 70.0%

3 PCL CONSTRUCTION ENTERPRISES 6,785.0 3,867.5 57.0%

4 BALFOUR BEATTY US 4,730.1 3,831.4 81.0%

5 GILBANE BUILDING CO. 4,480.1 3,808.1 85.0%

6 TUTOR PERINI CORP. 5,661.9 3,453.8 61.0%

7 SKANSKA 6,797.9 3,331.0 49.0%

8 AECOM 7,011.7 3,295.5 47.0%

9 STRUCTURE TONE 3,865.6 3,208.4 83.0%

10 CLARK GROUP 4,100.0 2,870.0 70.0%

11 LENDLEASE 3,067.3 2,852.6 93.0%

12 SUFFOLK CONSTRUCTION CO. 2,502.0 2,502.0 100.0%

13 MORTENSON CONSTRUCTION 3,670.7 2,312.5 63.0%

14 SWINERTON INC. 2,934.0 2,200.5 75.0%

15 JE DUNN CONSTRUCTION 2,810.4 2,164.0 77.0%

16 DPR CONSTRUCTION 3,086.0 2,098.5 68.0%

17 MCCARTHY HOLDINGS INC. 2,821.0 2,031.1 72.0%

18 BRASFIELD & GORRIE LLC 2,297.7 1,999.0 87.0%

19 HENSEL PHELPS 3,103.0 1,954.9 63.0%

20 DAVID E. HARVEY BUILDERS 1,991.0 1,791.9 90.0%

21 THE WALSH GROUP 4,950.6 1,386.2 28.0%

22 HOLDER CONSTRUCTION CO. 2,113.0 1,352.3 64.0%

23 CHINA CONSTRUCTION AMERICA/PLAZA CONSTR. 1,430.0 1,258.4 88.0%

24 RYAN COS. US INC. 1,283.0 1,257.3 98.0%

25 CLAYCO INC. 1,350.0 1,242.0 92.0%

Sources: Engineering News Record

6

US Engineering & Construction

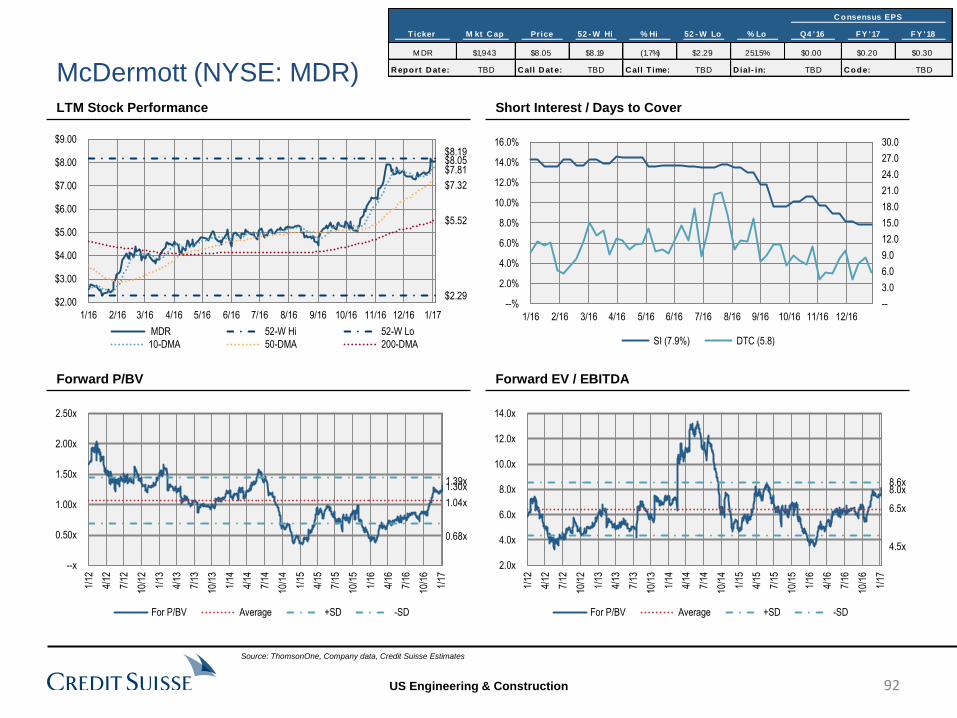

10.9 1.1

0.6 4.8

2.5

20142013201220112010

Australia

3.6 5.7

3.3 0.2

8.0

20142013201220112010

Canada

0.9 1.3 1.4

0.3 1.4

20142013201220112010

United States

15.0 14.6

13.1 5.0

6.5

20142013201220112010

United Kingdom

Summary of Trump Infrastructure Policy Proposals

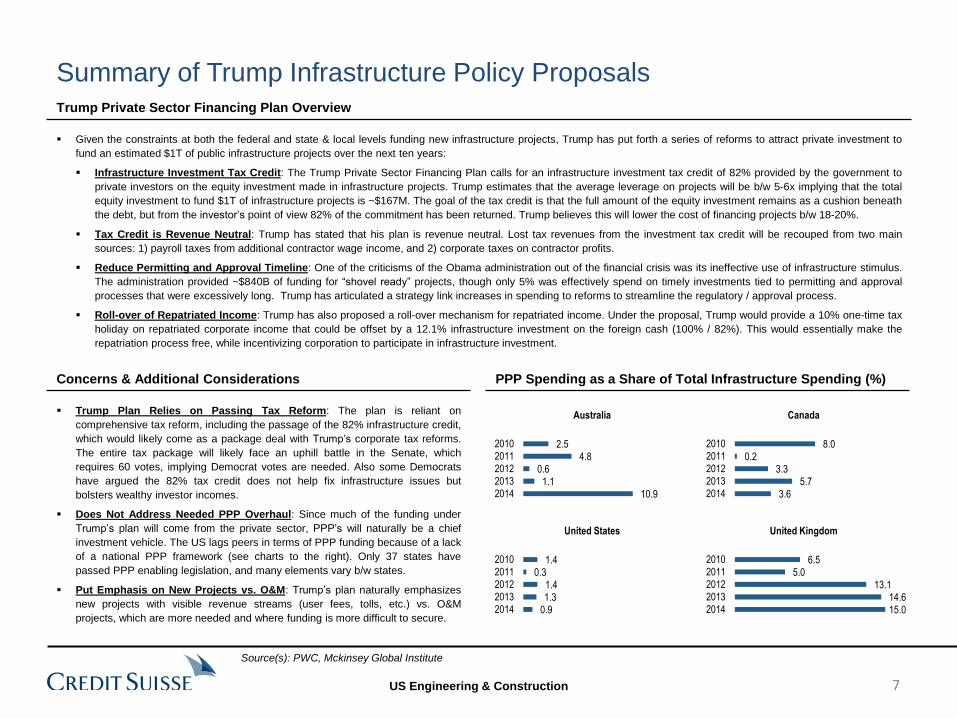

Trump Plan Relies on Passing Tax Reform: The plan is reliant on

comprehensive tax reform, including the passage of the 82% infrastructure credit,

which would likely come as a package deal with Trump’s corporate tax reforms.

The entire tax package will likely face an uphill battle in the Senate, which

requires 60 votes, implying Democrat votes are needed. Also some Democrats

have argued the 82% tax credit does not help fix infrastructure issues but

bolsters wealthy investor incomes.

Does Not Address Needed PPP Overhaul: Since much of the funding under

Trump’s plan will come from the private sector, PPP’s will naturally be a chief

investment vehicle. The US lags peers in terms of PPP funding because of a lack

of a national PPP framework (see charts to the right). Only 37 states have

passed PPP enabling legislation, and many elements vary b/w states.

Put Emphasis on New Projects vs. O&M: Trump’s plan naturally emphasizes

new projects with visible revenue streams (user fees, tolls, etc.) vs. O&M

projects, which are more needed and where funding is more difficult to secure.

Concerns & Additional Considerations PPP Spending as a Share of Total Infrastructure Spending (%)

Given the constraints at both the federal and state & local levels funding new infrastructure projects, Trump has put forth a series of reforms to attract private investment to

fund an estimated $1T of public infrastructure projects over the next ten years:

Infrastructure Investment Tax Credit: The Trump Private Sector Financing Plan calls for an infrastructure investment tax credit of 82% provided by the government to

private investors on the equity investment made in infrastructure projects. Trump estimates that the average leverage on projects will be b/w 5-6x implying that the total

equity investment to fund $1T of infrastructure projects is ~$167M. The goal of the tax credit is that the full amount of the equity investment remains as a cushion beneath

the debt, but from the investor’s point of view 82% of the commitment has been returned. Trump believes this will lower the cost of financing projects b/w 18-20%.

Tax Credit is Revenue Neutral: Trump has stated that his plan is revenue neutral. Lost tax revenues from the investment tax credit will be recouped from two main

sources: 1) payroll taxes from additional contractor wage income, and 2) corporate taxes on contractor profits.

Reduce Permitting and Approval Timeline: One of the criticisms of the Obama administration out of the financial crisis was its ineffective use of infrastructure stimulus.

The administration provided ~$840B of funding for “shovel ready” projects, though only 5% was effectively spend on timely investments tied to permitting and approval

processes that were excessively long. Trump has articulated a strategy link increases in spending to reforms to streamline the regulatory / approval process.

Roll-over of Repatriated Income: Trump has also proposed a roll-over mechanism for repatriated income. Under the proposal, Trump would provide a 10% one-time tax

holiday on repatriated corporate income that could be offset by a 12.1% infrastructure investment on the foreign cash (100% / 82%). This would essentially make the

repatriation process free, while incentivizing corporation to participate in infrastructure investment.

Trump Private Sector Financing Plan Overview

7

Source(s): PWC, Mckinsey Global Institute

US Engineering & Construction

Infrastructure Spending in the U.S.

Gross Investment (% GDP) Average Age of Federal Fixed Assets (Years)

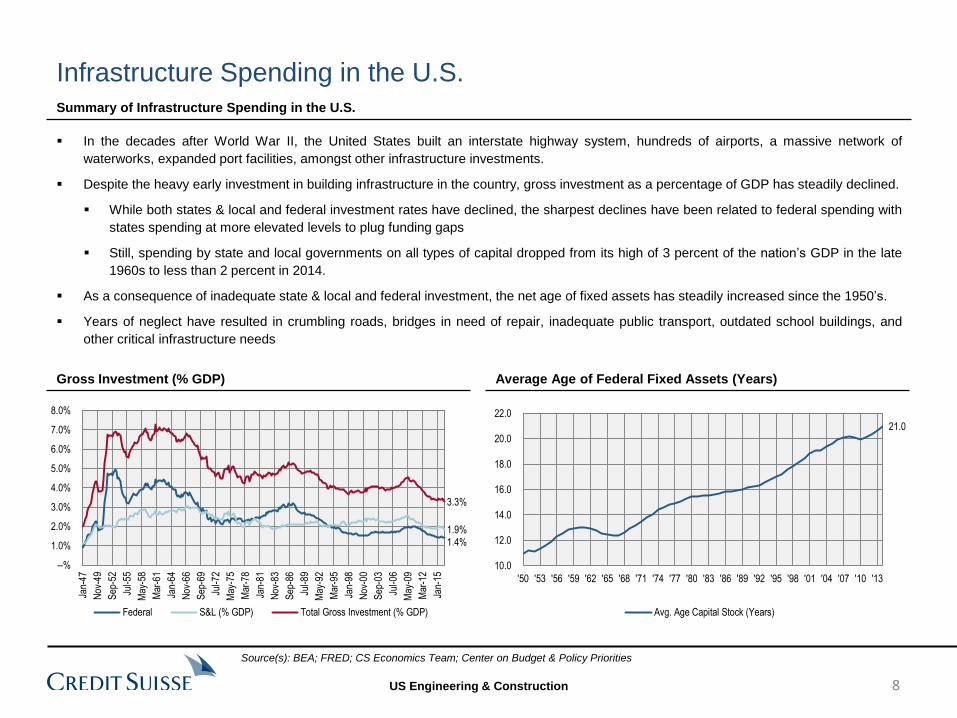

In the decades after World War II, the United States built an interstate highway system, hundreds of airports, a massive network of

waterworks, expanded port facilities, amongst other infrastructure investments.

Despite the heavy early investment in building infrastructure in the country, gross investment as a percentage of GDP has steadily declined.

While both states & local and federal investment rates have declined, the sharpest declines have been related to federal spending with

states spending at more elevated levels to plug funding gaps

Still, spending by state and local governments on all types of capital dropped from its high of 3 percent of the nation’s GDP in the late

1960s to less than 2 percent in 2014.

As a consequence of inadequate state & local and federal investment, the net age of fixed assets has steadily increased since the 1950’s.

Years of neglect have resulted in crumbling roads, bridges in need of repair, inadequate public transport, outdated school buildings, and

other critical infrastructure needs

Summary of Infrastructure Spending in the U.S.

1.4% 1.9%

3.3%

--%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Jan-

47

Nov

-49

Sep

-52

Jul-5

5

May

-58

Mar

-61

Jan-

64

Nov

-66

Sep

-69

Jul-7

2

May

-75

Mar

-78

Jan-

81

Nov

-83

Sep

-86

Jul-8

9

May

-92

Mar

-95

Jan-

98

Nov

-00

Sep

-03

Jul-0

6

May

-09

Mar

-12

Jan-

15

Federal S&L (% GDP) Total Gross Investment (% GDP)

21.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

'50 '53 '56 '59 '62 '65 '68 '71 '74 '77 '80 '83 '86 '89 '92 '95 '98 '01 '04 '07 '10 '13

Avg. Age Capital Stock (Years)

Source(s): BEA; FRED; CS Economics Team; Center on Budget & Policy Priorities

8

US Engineering & Construction

American Society of Civil Engineers Scorecard for America’s Infrastructure

Scorecard of U.S. Infrastructure

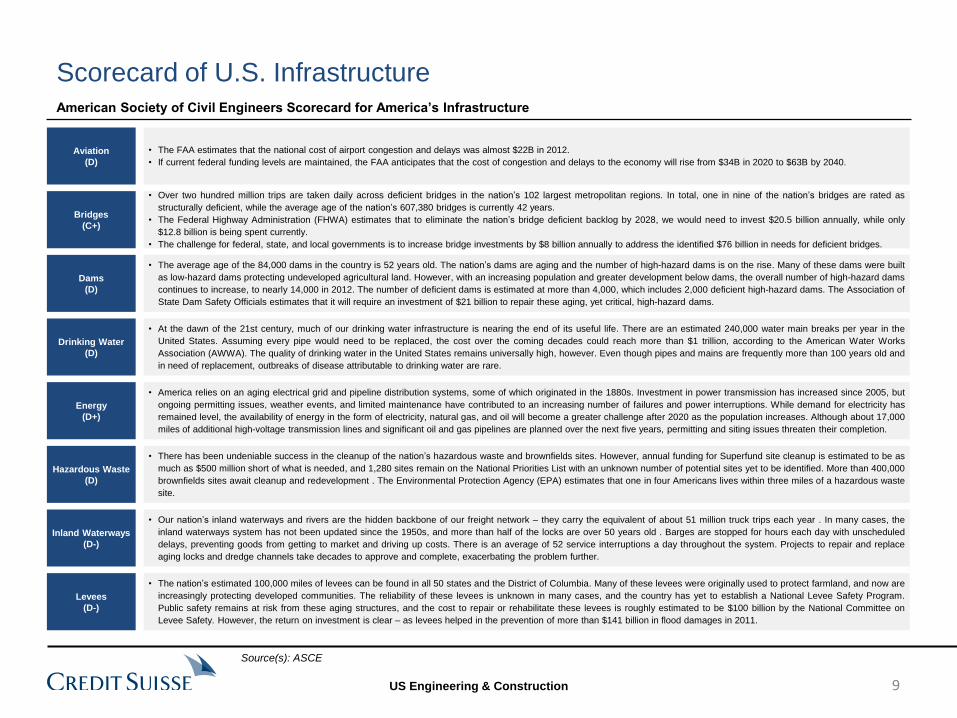

Aviation

(D)

• The FAA estimates that the national cost of airport congestion and delays was almost $22B in 2012.

• If current federal funding levels are maintained, the FAA anticipates that the cost of congestion and delays to the economy will rise from $34B in 2020 to $63B by 2040.

Bridges

(C+)

• Over two hundred million trips are taken daily across deficient bridges in the nation’s 102 largest metropolitan regions. In total, one in nine of the nation’s bridges are rated as

structurally deficient, while the average age of the nation’s 607,380 bridges is currently 42 years.

• The Federal Highway Administration (FHWA) estimates that to eliminate the nation’s bridge deficient backlog by 2028, we would need to invest $20.5 billion annually, while only

$12.8 billion is being spent currently.

• The challenge for federal, state, and local governments is to increase bridge investments by $8 billion annually to address the identified $76 billion in needs for deficient bridges.

Dams

(D)

• The average age of the 84,000 dams in the country is 52 years old. The nation’s dams are aging and the number of high-hazard dams is on the rise. Many of these dams were built

as low-hazard dams protecting undeveloped agricultural land. However, with an increasing population and greater development below dams, the overall number of high-hazard dams

continues to increase, to nearly 14,000 in 2012. The number of deficient dams is estimated at more than 4,000, which includes 2,000 deficient high-hazard dams. The Association of

State Dam Safety Officials estimates that it will require an investment of $21 billion to repair these aging, yet critical, high-hazard dams.

Drinking Water

(D)

• At the dawn of the 21st century, much of our drinking water infrastructure is nearing the end of its useful life. There are an estimated 240,000 water main breaks per year in the

United States. Assuming every pipe would need to be replaced, the cost over the coming decades could reach more than $1 trillion, according to the American Water Works

Association (AWWA). The quality of drinking water in the United States remains universally high, however. Even though pipes and mains are frequently more than 100 years old and

in need of replacement, outbreaks of disease attributable to drinking water are rare.

Energy

(D+)

• America relies on an aging electrical grid and pipeline distribution systems, some of which originated in the 1880s. Investment in power transmission has increased since 2005, but

ongoing permitting issues, weather events, and limited maintenance have contributed to an increasing number of failures and power interruptions. While demand for electricity has

remained level, the availability of energy in the form of electricity, natural gas, and oil will become a greater challenge after 2020 as the population increases. Although about 17,000

miles of additional high-voltage transmission lines and significant oil and gas pipelines are planned over the next five years, permitting and siting issues threaten their completion.

Hazardous Waste

(D)

• There has been undeniable success in the cleanup of the nation’s hazardous waste and brownfields sites. However, annual funding for Superfund site cleanup is estimated to be as

much as $500 million short of what is needed, and 1,280 sites remain on the National Priorities List with an unknown number of potential sites yet to be identified. More than 400,000

brownfields sites await cleanup and redevelopment . The Environmental Protection Agency (EPA) estimates that one in four Americans lives within three miles of a hazardous waste

site.

Inland Waterways

(D-)

• Our nation’s inland waterways and rivers are the hidden backbone of our freight network – they carry the equivalent of about 51 million truck trips each year . In many cases, the

inland waterways system has not been updated since the 1950s, and more than half of the locks are over 50 years old . Barges are stopped for hours each day with unscheduled

delays, preventing goods from getting to market and driving up costs. There is an average of 52 service interruptions a day throughout the system. Projects to repair and replace

aging locks and dredge channels take decades to approve and complete, exacerbating the problem further.

Levees

(D-)

• The nation’s estimated 100,000 miles of levees can be found in all 50 states and the District of Columbia. Many of these levees were originally used to protect farmland, and now are

increasingly protecting developed communities. The reliability of these levees is unknown in many cases, and the country has yet to establish a National Levee Safety Program.

Public safety remains at risk from these aging structures, and the cost to repair or rehabilitate these levees is roughly estimated to be $100 billion by the National Committee on

Levee Safety. However, the return on investment is clear – as levees helped in the prevention of more than $141 billion in flood damages in 2011.

9

Source(s): ASCE

US Engineering & Construction

American Society of Civil Engineers Scorecard for America’s Infrastructure (Continued)

Scorecard of U.S. Infrastructure

Ports

(C)

• The U.S. Army Corps of Engineers estimates that more than 95% (by volume) of overseas trade produced or consumed by the United States moves through our ports. To sustain

and serve a growing economy and compete internationally, our nation’s ports need to be maintained, modernized, and expanded. While port authorities and their private sector

partners have planned over $46 billion in capital improvements from now until 2016, federal funding has declined for navigable waterways and landside freight connections needed to

move goods to and from the ports.

Parks & Recreation

(C-)

• The popularity of parks and outdoor recreation areas in the United States continues to grow, with over 140 million Americans making use of these facilities a part of their daily lives.

These activities contribute $646 billion to the nation’s economy, supporting 6.1 million jobs. Yet states and localities struggle to provide these benefits for parks amid flat and

declining budgets, reporting an estimated $18.5 billion in unmet needs in 2011. The federal government is also facing a serious challenge as well since the National Park Service

estimates its maintenance backlog at approximately $11 billion.

Rail

(C+)

• Railroads are experiencing a competitive resurgence as both an energy-efficient freight transportation option and a viable city-to-city passenger service. In 2012, Amtrak recorded its

highest year of ridership with 31.2 million passengers, almost doubling ridership since 2000, with growth anticipated to continue. Both freight and passenger rail have been investing

heavily in their tracks, bridges, and tunnels as well as adding new capacity for freight and passengers. In 2010 alone, freight railroads renewed the rails on more than 3,100 miles of

railroad track, equivalent to going coast to coast. Since 2009, capital investment from both freight and passenger railroads has exceeded $75 billion, actually increasing investment

during the recession when materials prices were lower and trains ran less frequently.

Roads

(D)

• Forty-two percent of America’s major urban highways remain congested, costing the economy an estimated $101 billion in wasted time and fuel annually. While the conditions have

improved in the near term, and Federal, state, and local capital investments increased to $91 billion annually, that level of investment is insufficient and still projected to result in a

decline in conditions and performance in the long term. Currently, the Federal Highway Administration estimates that $170 billion in capital investment would be needed on an annual

basis to significantly improve conditions and performance.

Schools

(D)

• Almost half of America’s public school buildings were built to educate the baby boomers – a generation that is now retiring from the workforce. Public school enrollment is projected

to gradually increase through 2019, yet state and local school construction funding continues to decline. National spending on school construction has diminished to approximately

$10 billion in 2012, about half the level spent prior to the recession, while the condition of school facilities continues to be a significant concern for communities. Experts now estimate

the investment needed to modernize and maintain our nation’s school facilities is at least $270 billion or more. However, due to the absence of national data on school facilities for

more than a decade, a complete picture of the condition of our nation’s schools remains mostly unknown.

Solid Waste

(B-)

• In 2010, Americans generated 250 million tons of trash. Of that, 85 million tons were recycled or composted. This represents a 34% recycling rate, more than double the 14.5% in

1980. Per capita generation rates of waste have been steady over the past 20 years and have even begun to show signs of decline in the past several years.

Transit

(D)

• America’s public transit infrastructure plays a vital role in our economy, connecting millions of people with jobs, medical facilities, schools, shopping, and recreation, and it is critical to

the one-third of Americans who do not drive cars. Unlike many U.S. infrastructure systems, the transit system is not comprehensive, as 45% of American households lack any

access to transit, and millions more have inadequate service levels. Americans who do have access have increased their ridership 9.1% in the past decade, and that trend is

expected to continue. Although investment in transit has also increased, deficient and deteriorating transit systems cost the U.S. economy $90 billion in 2010, as many transit

agencies are struggling to maintain aging and obsolete fleets and facilities amid an economic downturn that has reduced their funding, forcing service cuts and fare increases.

Wastewater

(D)

• Capital investment needs for the nation’s wastewater and stormwater systems are estimated to total $298 billion over the next twenty years. Pipes represent the largest capital need,

comprising three quarters of total needs. Fixing and expanding the pipes will address sanitary sewer overflows, combined sewer overflows, and other pipe-related issues. In recent

years, capital needs for the treatment plants comprise about 15%-20% of total needs, but will likely increase due to new regulatory requirements. Stormwater needs, while growing,

are still small compared with sanitary pipes and treatment plants. Since 2007, the federal government has required cities to invest more than $15 billion in new pipes, plants, and

equipment to eliminate combined sewer overflows.

10

Source(s): ASCE

US Engineering & Construction

Infrastructure Systems Total Needs Estimated Funding Funding Gap

Surface Transportation $1,723 $877 $846

Electricity 736 629 107

Schools 391 120 271

Public Parks & Recreation 238 134 104

Airports 134 95 39

Water/Wastewater Infrastructure 126 42 84

Rail 100 89 11

Levees 80 8 72

Hazardous & Solid Waste 56 10 46

Inland Waterways & Marine Ports 30 14 16

Dams 21 6 15

Totals $3,635 $2,024 $1,611

Yearly Investment Needed $454 $253 $201

Cumulative Infrastructure Needs by System (USD in 2010 Billions)

Losses to the National Economy Due to Infrastructure Investment Gaps (USD in 2015 Billions)

ASCE estimates the

investment needed in each

infrastructure category to

maintain a state of good

repair. That is, approximately

what amount of investment is

needed to get to a grade of B?

ASCE estimates that $3.6T of

investment is needed b/w

2016-2020 to fund the various

infrastructure systems across

the country.

However, funding for projects

over this time period is only

contemplated at ~$2.0T,

implying $1.6T of funding

gaps.

Nearly half of the funding gaps

are associated with surface

transportation projects for

highways and bridges.

Over time, it is estimated that

these impacts will also affect

businesses’ ability to provide

well-paying jobs, further

reducing incomes.

Significant Funding Gaps Across both Social and Economic Infrastructure

Surface

Transportation

Water /

Wastewater Electricity Airports

Waterways

& Marine Ports

Aggregate

Economic

Impact

Business Sales

2016-2025 $2,212 $896 $1,399 $625 $1,252 $7,038

2026-2040 $8,152 $5,907 $2,024 $2,397 $4,239 $29,292

GDP

2016-2025 $1,167 $508 $819 $337 $784 $3,955

2026-2040 $1,981 $3,215 $1,071 $1,073 $2,003 $14,201

Jobs

2016-2025 1,052,000 489,000 102,000 257,000 440,000 2,546,000

2026-2040 473,000 956,000 242,000 494,000 1,153,000 5,809,000

11

Source(s): ASCE

US Engineering & Construction

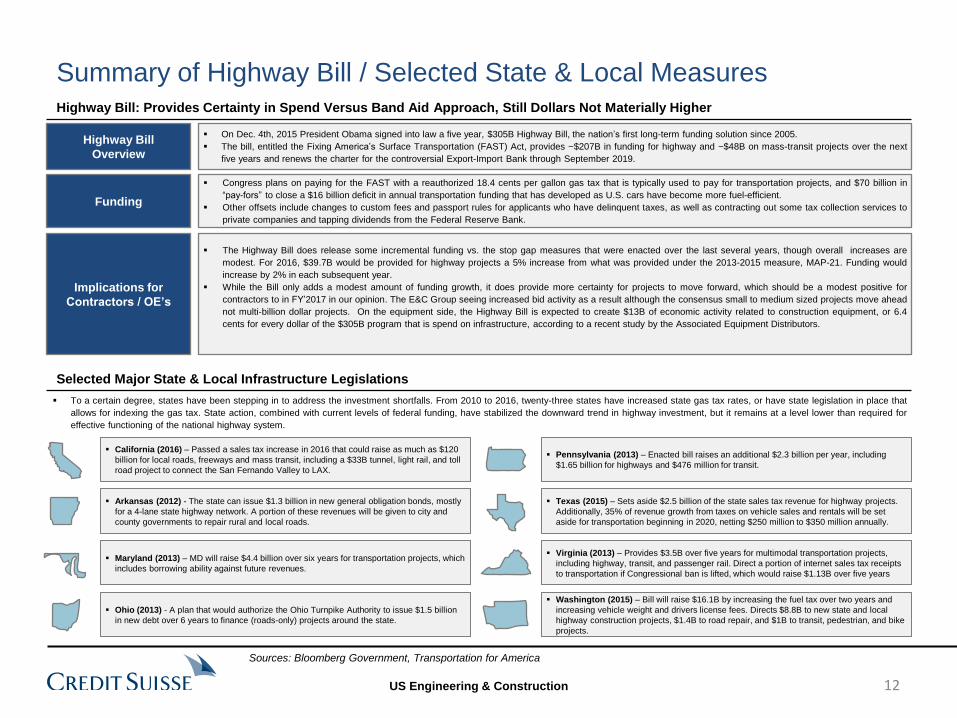

Highway Bill

Overview

On Dec. 4th, 2015 President Obama signed into law a five year, $305B Highway Bill, the nation’s first long-term funding solution since 2005.

The bill, entitled the Fixing America’s Surface Transportation (FAST) Act, provides ~$207B in funding for highway and ~$48B on mass-transit projects over the next

five years and renews the charter for the controversial Export-Import Bank through September 2019.

Funding

Congress plans on paying for the FAST with a reauthorized 18.4 cents per gallon gas tax that is typically used to pay for transportation projects, and $70 billion in

“pay-fors” to close a $16 billion deficit in annual transportation funding that has developed as U.S. cars have become more fuel-efficient.

Other offsets include changes to custom fees and passport rules for applicants who have delinquent taxes, as well as contracting out some tax collection services to

private companies and tapping dividends from the Federal Reserve Bank.

Implications for

Contractors / OE’s

The Highway Bill does release some incremental funding vs. the stop gap measures that were enacted over the last several years, though overall increases are

modest. For 2016, $39.7B would be provided for highway projects a 5% increase from what was provided under the 2013-2015 measure, MAP-21. Funding would

increase by 2% in each subsequent year.

While the Bill only adds a modest amount of funding growth, it does provide more certainty for projects to move forward, which should be a modest positive for

contractors to in FY’2017 in our opinion. The E&C Group seeing increased bid activity as a result although the consensus small to medium sized projects move ahead

not multi-billion dollar projects. On the equipment side, the Highway Bill is expected to create $13B of economic activity related to construction equipment, or 6.4

cents for every dollar of the $305B program that is spend on infrastructure, according to a recent study by the Associated Equipment Distributors.

Summary of Highway Bill / Selected State & Local Measures Highway Bill: Provides Certainty in Spend Versus Band Aid Approach, Still Dollars Not Materially Higher

Selected Major State & Local Infrastructure Legislations

California (2016) – Passed a sales tax increase in 2016 that could raise as much as $120

billion for local roads, freeways and mass transit, including a $33B tunnel, light rail, and toll

road project to connect the San Fernando Valley to LAX.

Pennsylvania (2013) – Enacted bill raises an additional $2.3 billion per year, including

$1.65 billion for highways and $476 million for transit.

Arkansas (2012) - The state can issue $1.3 billion in new general obligation bonds, mostly

for a 4-lane state highway network. A portion of these revenues will be given to city and

county governments to repair rural and local roads.

Texas (2015) – Sets aside $2.5 billion of the state sales tax revenue for highway projects.

Additionally, 35% of revenue growth from taxes on vehicle sales and rentals will be set

aside for transportation beginning in 2020, netting $250 million to $350 million annually.

Maryland (2013) – MD will raise $4.4 billion over six years for transportation projects, which

includes borrowing ability against future revenues.

Virginia (2013) – Provides $3.5B over five years for multimodal transportation projects,

including highway, transit, and passenger rail. Direct a portion of internet sales tax receipts

to transportation if Congressional ban is lifted, which would raise $1.13B over five years

Ohio (2013) - A plan that would authorize the Ohio Turnpike Authority to issue $1.5 billion

in new debt over 6 years to finance (roads-only) projects around the state.

Washington (2015) – Bill will raise $16.1B by increasing the fuel tax over two years and

increasing vehicle weight and drivers license fees. Directs $8.8B to new state and local

highway construction projects, $1.4B to road repair, and $1B to transit, pedestrian, and bike

projects.

Sources: Bloomberg Government, Transportation for America

To a certain degree, states have been stepping in to address the investment shortfalls. From 2010 to 2016, twenty-three states have increased state gas tax rates, or have state legislation in place that

allows for indexing the gas tax. State action, combined with current levels of federal funding, have stabilized the downward trend in highway investment, but it remains at a level lower than required for

effective functioning of the national highway system.

12

US Engineering & Construction

Oil & Gas

13

US Engineering & Construction

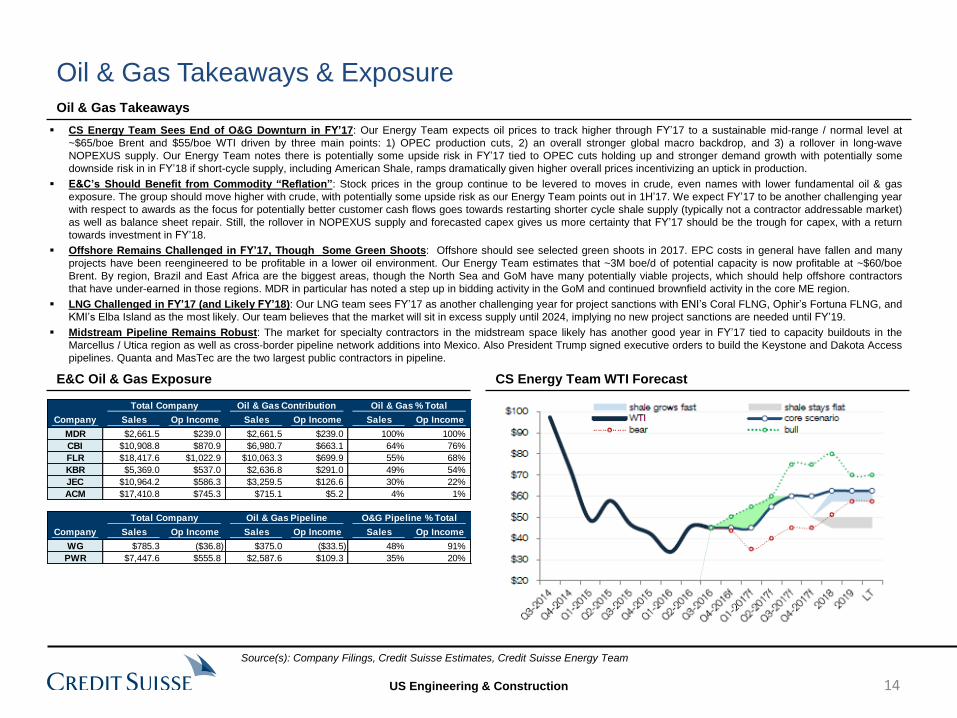

Oil & Gas Takeaways & Exposure

E&C Oil & Gas Exposure CS Energy Team WTI Forecast

CS Energy Team Sees End of O&G Downturn in FY’17: Our Energy Team expects oil prices to track higher through FY’17 to a sustainable mid-range / normal level at

~$65/boe Brent and $55/boe WTI driven by three main points: 1) OPEC production cuts, 2) an overall stronger global macro backdrop, and 3) a rollover in long-wave

NOPEXUS supply. Our Energy Team notes there is potentially some upside risk in FY’17 tied to OPEC cuts holding up and stronger demand growth with potentially some

downside risk in in FY’18 if short-cycle supply, including American Shale, ramps dramatically given higher overall prices incentivizing an uptick in production.

E&C’s Should Benefit from Commodity “Reflation”: Stock prices in the group continue to be levered to moves in crude, even names with lower fundamental oil & gas

exposure. The group should move higher with crude, with potentially some upside risk as our Energy Team points out in 1H’17. We expect FY’17 to be another challenging year

with respect to awards as the focus for potentially better customer cash flows goes towards restarting shorter cycle shale supply (typically not a contractor addressable market)

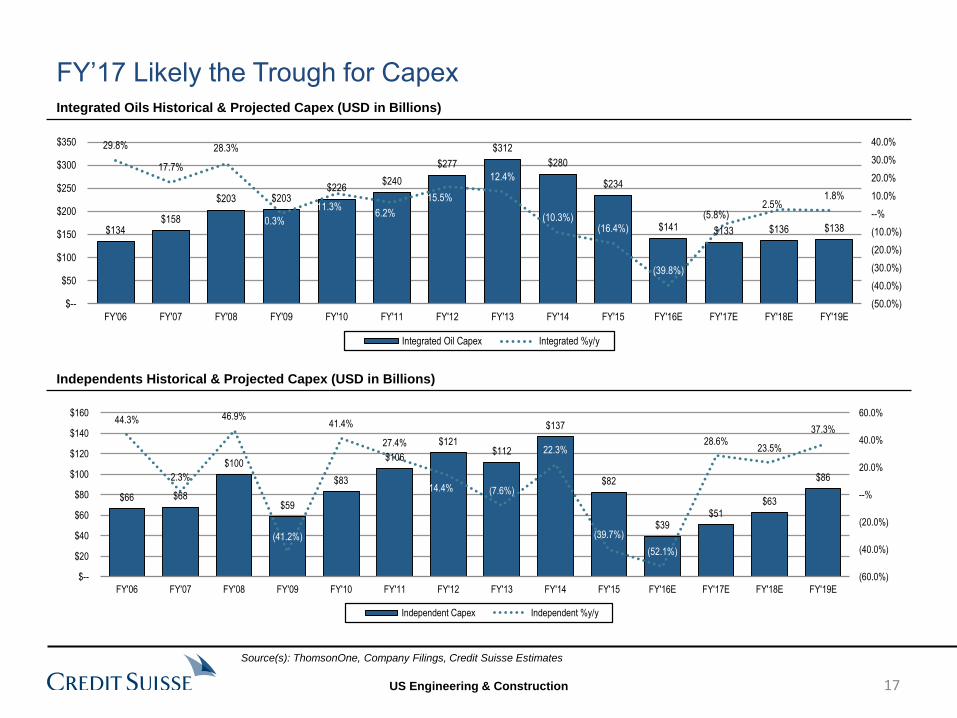

as well as balance sheet repair. Still, the rollover in NOPEXUS supply and forecasted capex gives us more certainty that FY’17 should be the trough for capex, with a return

towards investment in FY’18.

Offshore Remains Challenged in FY’17, Though Some Green Shoots: Offshore should see selected green shoots in 2017. EPC costs in general have fallen and many

projects have been reengineered to be profitable in a lower oil environment. Our Energy Team estimates that ~3M boe/d of potential capacity is now profitable at ~$60/boe

Brent. By region, Brazil and East Africa are the biggest areas, though the North Sea and GoM have many potentially viable projects, which should help offshore contractors

that have under-earned in those regions. MDR in particular has noted a step up in bidding activity in the GoM and continued brownfield activity in the core ME region.

LNG Challenged in FY’17 (and Likely FY’18): Our LNG team sees FY’17 as another challenging year for project sanctions with ENI’s Coral FLNG, Ophir’s Fortuna FLNG, and

KMI’s Elba Island as the most likely. Our team believes that the market will sit in excess supply until 2024, implying no new project sanctions are needed until FY’19.

Midstream Pipeline Remains Robust: The market for specialty contractors in the midstream space likely has another good year in FY’17 tied to capacity buildouts in the

Marcellus / Utica region as well as cross-border pipeline network additions into Mexico. Also President Trump signed executive orders to build the Keystone and Dakota Access

pipelines. Quanta and MasTec are the two largest public contractors in pipeline.

Oil & Gas Takeaways

Total Company Oil & Gas Contribution Oil & Gas % Total

Company Sales Op Income Sales Op Income Sales Op Income

MDR $2,661.5 $239.0 $2,661.5 $239.0 100% 100%

CBI $10,908.8 $870.9 $6,980.7 $663.1 64% 76%

FLR $18,417.6 $1,022.9 $10,063.3 $699.9 55% 68%

KBR $5,369.0 $537.0 $2,636.8 $291.0 49% 54%

JEC $10,964.2 $586.3 $3,259.5 $126.6 30% 22%

ACM $17,410.8 $745.3 $715.1 $5.2 4% 1%

Total Company Oil & Gas Pipeline O&G Pipeline % Total

Company Sales Op Income Sales Op Income Sales Op Income

WG $785.3 ($36.8) $375.0 ($33.5) 48% 91%

PWR $7,447.6 $555.8 $2,587.6 $109.3 35% 20%

14

Source(s): Company Filings, Credit Suisse Estimates, Credit Suisse Energy Team

US Engineering & Construction

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

Q1'

01

Q1'

02

Q1'

03

Q1'

04

Q1'

05

Q1'

06

Q1'

07

Q1'

08

Q1'

09

Q1'

10

Q1'

11

Q1'

12

Q1'

13

Q1'

14

Q1'

15

Q1'

16

Orders Avg Brent

7 Q's for Orders to Recover

History Implies Awards Should Inflect Higher Late 2017 or Early 2018 CBI Orders ($B) vs. Avg. Brent Price ($/boe)

FLR Orders ($M) vs. Avg. Brent Price ($/boe)

CBI Backlog ($B) vs. Avg. Brent Price ($/boe)

FLR Backlog ($M) vs. Avg. Brent Price ($/boe)

Energy awards have largely

disappointed over the past

year and likely remain

challenged in 2017 despite

more favorable commodity

prices. Still, we believe this is

a backward look as 2017 likely

marks the bottom for capex.

Assuming prices stay at

forecasted levels, 2018 capex

should inflect higher.

What remains unclear at this

point as energy capex inflects

higher is where spend will be

concentrated. We would also

customers are more frugal

with larger projects and cost

inflation related to projects.

Still, sustained Brent

recoveries proceed orders and

backlog by b/w 5-7 quarters.

Given Brent likely bottomed in

February of FY’16, we should

see a pickup in orders and

backlog towards the back of

FY’17 / early FY’18.

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Q1'

01

Q1'

02

Q1'

03

Q1'

04

Q1'

05

Q1'

06

Q1'

07

Q1'

08

Q1'

09

Q1'

10

Q1'

11

Q1'

12

Q1'

13

Q1'

14

Q1'

15

Q1'

16

Backlog Avg Brent

5 Q's for Backlog to Recover

$--

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$--

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

Feb

-07

Nov

-07

Aug

-08

May

-09

Feb

-10

Nov

-10

Aug

-11

May

-12

Feb

-13

Nov

-13

Aug

-14

May

-15

Feb

-16

Nov

-16

Avg. 3Q Orders Avg. Brent

5 Quarters for Orders to

Recover

$--

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$--

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

Feb

-07

Nov

-07

Aug

-08

May

-09

Feb

-10

Nov

-10

Aug

-11

May

-12

Feb

-13

Nov

-13

Aug

-14

May

-15

Feb

-16

Nov

-16

Backlog Avg. Brent

5 Quarters for Backlog to Recover

15

Source(s): ThomsonOne, Company Filings, Credit Suisse Estimates

US Engineering & Construction

In their December Report, our Energy Team expects oil prices to track higher

through FY’17 to a sustainable mid-range / normal level at ~$65/boe Brent and

$55/boe WTI from three drivers:

OPEC Production Cuts: In November, OPEC agreed to reduce by a nominal 1.2

Mb/d to a 32.5 Mb/d group total, with non-OPEC producers also contributing 600

kb/d. The move likely tips the market into a supply deficit for much of the year,

implying inventory draws and supporting prices.

Strong Global Demand: Our Economics Team continues to note that global IP is

strengthening, with generally positive PMI's and broad talk of fiscal stimulus. CS

forecasts Global GDP growth to be 3.0% in 2017 from 2.5% in 2016, with Global

PMI new orders at a 19-month high, consistent with ~3% GDP growth.

NOPEXUS Supply Rollover: NOPEXUS production had already rolled over given

declines in places like China and Mexico. Without new project sanctions,

NOPEXUS volumes would start to decline meaningfully from 2018 onward. It is

this decline, together with demand growth, that creates the space for new

investments across the industry.

CS Energy Team Sees Three Drivers to “Energy Renaissance” in 2017 Closer to the End of the Downturn

Stronger Macro Backdrop

CS Oil Supply and Demand Post OPEC Cuts

Rollover of NOPEXUS Supply Creates 2018 Investment Window

16

Source(s): Company Filings, Credit Suisse Estimates, Credit Suisse Energy Team

US Engineering & Construction

Integrated Oils Historical & Projected Capex (USD in Billions)

Independents Historical & Projected Capex (USD in Billions)

FY’17 Likely the Trough for Capex

$134 $158

$203 $203 $226

$240

$277

$312

$280

$234

$141 $133 $136 $138

29.8%

17.7%

28.3%

0.3%

11.3% 6.2%

15.5%

12.4%

(10.3%)(16.4%)

(39.8%)

(5.8%)2.5%

1.8%

(50.0%)

(40.0%)

(30.0%)

(20.0%)

(10.0%)

--%

10.0%

20.0%

30.0%

40.0%

$--

$50

$100

$150

$200

$250

$300

$350

FY'06 FY'07 FY'08 FY'09 FY'10 FY'11 FY'12 FY'13 FY'14 FY'15 FY'16E FY'17E FY'18E FY'19E

Integrated Oil Capex Integrated %y/y

$66 $68

$100

$59

$83

$106

$121 $112

$137

$82

$39 $51

$63

$86

44.3%

2.3%

46.9%

(41.2%)

41.4%

27.4%

14.4% (7.6%)

22.3%

(39.7%)

(52.1%)

28.6% 23.5%

37.3%

(60.0%)

(40.0%)

(20.0%)

--%

20.0%

40.0%

60.0%

$--

$20

$40

$60

$80

$100

$120

$140

$160

FY'06 FY'07 FY'08 FY'09 FY'10 FY'11 FY'12 FY'13 FY'14 FY'15 FY'16E FY'17E FY'18E FY'19E

Independent Capex Independent %y/y

17

Source(s): ThomsonOne, Company Filings, Credit Suisse Estimates

US Engineering & Construction

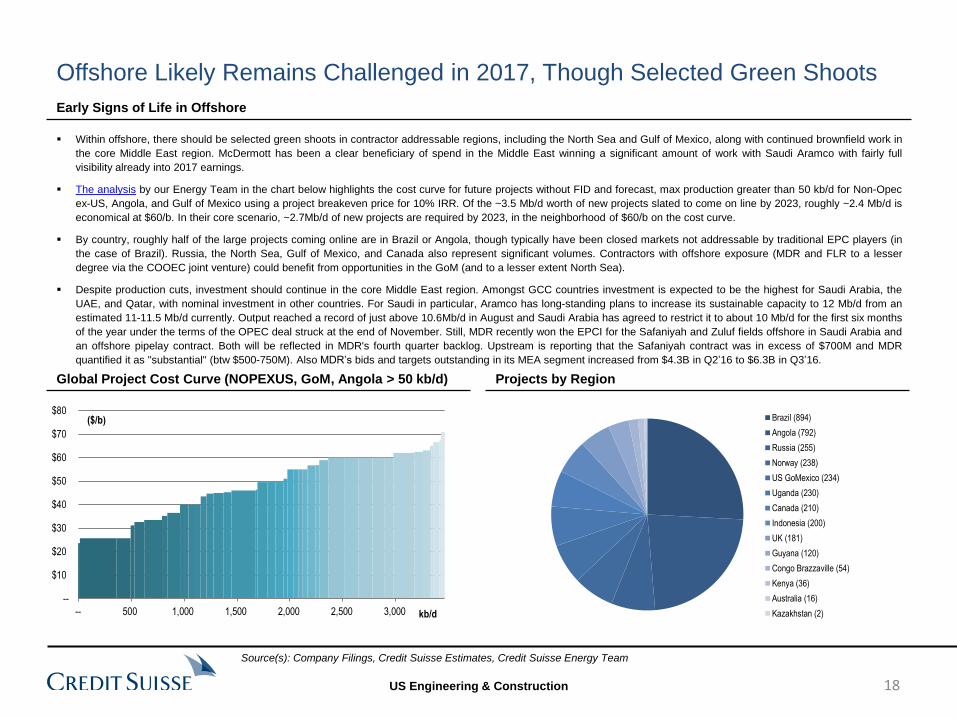

Offshore Likely Remains Challenged in 2017, Though Selected Green Shoots

Global Project Cost Curve (NOPEXUS, GoM, Angola > 50 kb/d) Projects by Region

Within offshore, there should be selected green shoots in contractor addressable regions, including the North Sea and Gulf of Mexico, along with continued brownfield work in

the core Middle East region. McDermott has been a clear beneficiary of spend in the Middle East winning a significant amount of work with Saudi Aramco with fairly full

visibility already into 2017 earnings.

The analysis by our Energy Team in the chart below highlights the cost curve for future projects without FID and forecast, max production greater than 50 kb/d for Non-Opec

ex-US, Angola, and Gulf of Mexico using a project breakeven price for 10% IRR. Of the ~3.5 Mb/d worth of new projects slated to come on line by 2023, roughly ~2.4 Mb/d is

economical at $60/b. In their core scenario, ~2.7Mb/d of new projects are required by 2023, in the neighborhood of $60/b on the cost curve.

By country, roughly half of the large projects coming online are in Brazil or Angola, though typically have been closed markets not addressable by traditional EPC players (in

the case of Brazil). Russia, the North Sea, Gulf of Mexico, and Canada also represent significant volumes. Contractors with offshore exposure (MDR and FLR to a lesser

degree via the COOEC joint venture) could benefit from opportunities in the GoM (and to a lesser extent North Sea).

Despite production cuts, investment should continue in the core Middle East region. Amongst GCC countries investment is expected to be the highest for Saudi Arabia, the

UAE, and Qatar, with nominal investment in other countries. For Saudi in particular, Aramco has long-standing plans to increase its sustainable capacity to 12 Mb/d from an

estimated 11-11.5 Mb/d currently. Output reached a record of just above 10.6Mb/d in August and Saudi Arabia has agreed to restrict it to about 10 Mb/d for the first six months

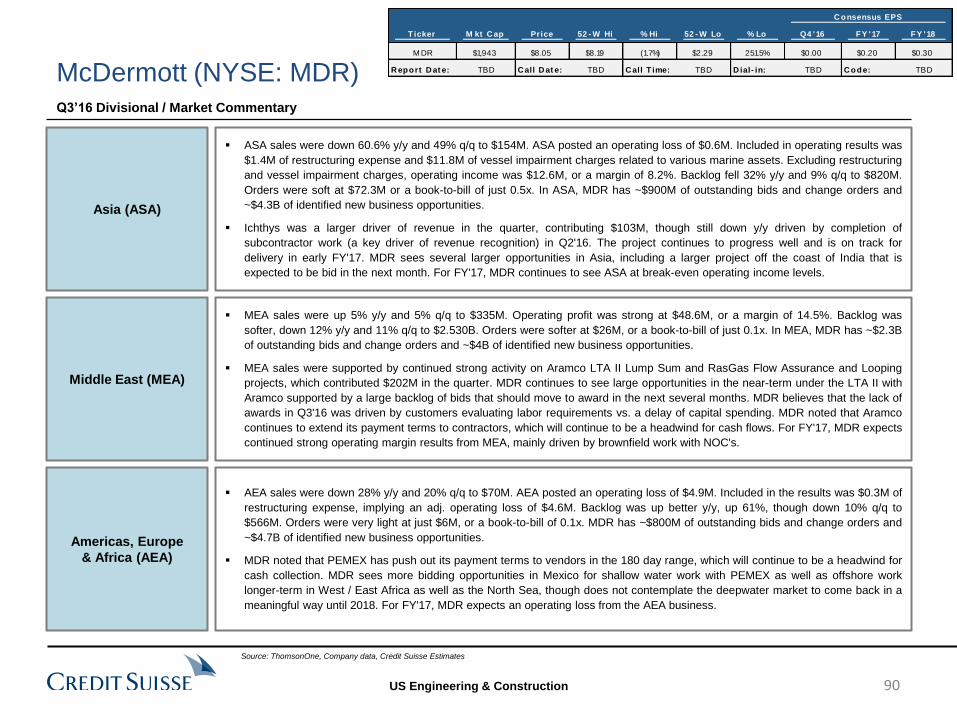

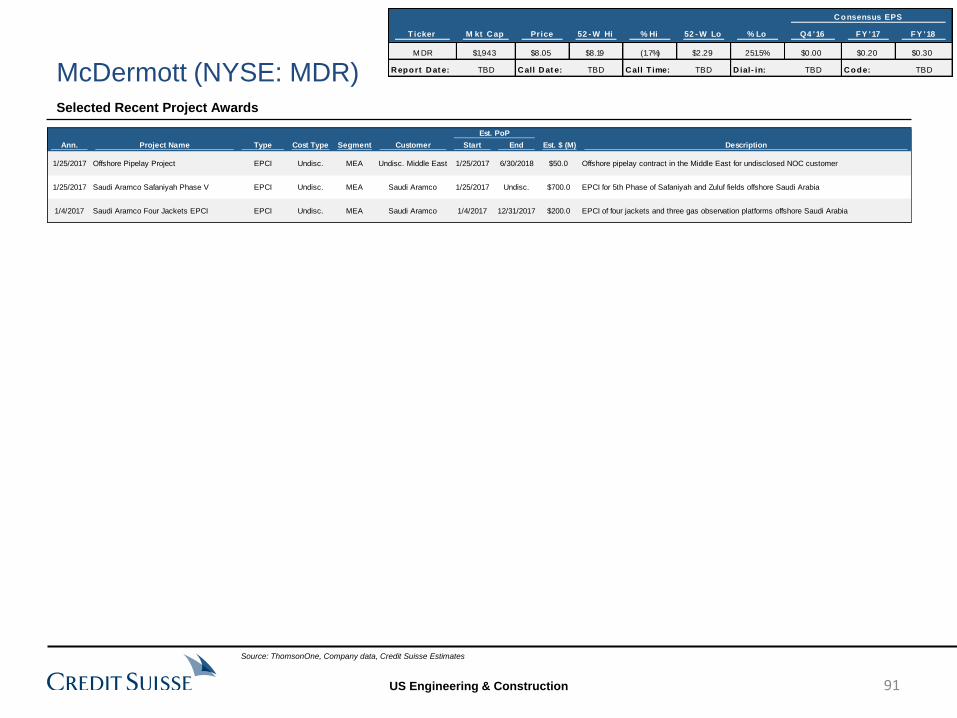

of the year under the terms of the OPEC deal struck at the end of November. Still, MDR recently won the EPCI for the Safaniyah and Zuluf fields offshore in Saudi Arabia and

an offshore pipelay contract. Both will be reflected in MDR's fourth quarter backlog. Upstream is reporting that the Safaniyah contract was in excess of $700M and MDR

quantified it as "substantial" (btw $500-750M). Also MDR’s bids and targets outstanding in its MEA segment increased from $4.3B in Q2’16 to $6.3B in Q3’16.

Early Signs of Life in Offshore

Brazil (894)

Angola (792)

Russia (255)

Norway (238)

US GoMexico (234)

Uganda (230)

Canada (210)

Indonesia (200)

UK (181)

Guyana (120)

Congo Brazzaville (54)

Kenya (36)

Australia (16)

Kazakhstan (2)

--

$10

$20

$30

$40

$50

$60

$70

$80

-- 500 1,000 1,500 2,000 2,500 3,000

($/b)

kb/d

18

Source(s): Company Filings, Credit Suisse Estimates, Credit Suisse Energy Team

US Engineering & Construction

CS LNG Team Project Tracker

Our LNG Team sees the next

demand window not until the

FY’23/24 time frame, with the market

in a persistent oversupply from FY’18

until that time.

If an average greenfield project takes

about five years to construct (from

FID to 1st LNG) and brownfield

expansions less, no projects are

required to sanction in 2017 to meet

that demand window, and in reality no

new sanctions are required until 2019.

Three projects are possible in FY’17,

namely ENI Coral FLNG and Fortuna

FLNG likely move forward. Elba

Island could also move forward based

on Kinder Morgan’s comments,

though there has been no formal FID

announcement. Despite receiving

approvals, Woodfibre LNG will likely

work through the FEED in FY’17

before taking a formal FID in FY’18.

Contractors are still positive longer

term. CBI is optimistic on

Mozambique LNG and ENI

Mozambique although we suspect

they push awards to late 2017. Also

Golden Pass recently received FERC

approval which is on CBI’s prospect

list. KBR could see Woodfibre

sanctions in FY’18 and renewed big

validity for Magnolia. FLR remains

relatively downbeat with regards to

LNG prospects and recently took out

Kitimat from its backlog in Q3’16.

LNG Oversupply Persists in Medium-term CS LNG Team Project Cost Curve

LNG FID’s Likely Delayed to Beyond 2017

$--

$5

$10

$15

$20

Papua LN

G

Mozam

bique 1

Fortuna F

LNG

Sabine P

ass

Golden P

ass

Tanzania LN

G

Cove P

oint

Elba Island

Corpus C

hristi LNG

LNG

Canada

PacN

West LN

G

Brow

se

Prelude F

LNG

Ichthys

AP

LNG

GLN

G

Gorgon

QC

LNG

$40 JCC, 11.25 slope $60 JCC 11.25 slope

US$/mmBtu

(4.5)(1.8)

14.9

21.3 19.9

27.3

11.0

3.0

(10.0)

(19.4)

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Excess (shortfall)

Mtpa

Country 'Possible' projects Start-up Mtpa FEED status Comments

Equatorial Guinea Fortuna FLNG 2022 2.2 In upstream FEED, Golar is midstream McDermott & GE, Subsea 7 & Aker

US Elba Island 2020 2.5 EPC aw arded (IHI) Shell set to be captiv e off-taker. Modular dev elopment (10 modules)

Papua New Guinea De bottlenecking T1 / 2 2017 1.6 NA

Mozambique Mozambique FLNG 2022 2.5 In FEED - KBR / Daew oo Ship FID target w ithin 12 months. Binding HoA for full offtake signed w ith BP.

Papua New Guinea Elk Antelope 2022 5.0 No Dev elopment plan to be clarified post XOM's InterOil acquisition

Country 'Speculative' projects Start-up Mtpa FEED status Comments

Russia Sakhalin 2 T3 2020 4.8 Design contract aw arded to RDS Plan to use Sak III as feed gas

Canada Pacific Northw est LNG 2021 12.0 Presume complete - Bechtel, KBR, JGC, Technip, Samsung, China Huangiu Receiv ed final Gov t approv al, aw aiting FID decision by partners

Mozambique Onshore Area 1 2023 12.0 In FEED; Technip, Subsea 7, Saipem, JGC, Fluor, CBI, Chiy oda Presumably aw aiting super-major farm-in onshore Mozambique

US Sabine Pass T6 2021 4.5 N/K CVX concurrence likely required

US Golden Pass 2021 15.6 In FEED (July 2014) - Chiy oda / CBI

Australia Brow se LNG 2022 10.8 In FEED (July 15) - Technip / Samsung Project defer

Australia Gorgon LNG T4 2022 5.0 No Project focused on T1/3 start-up

Australia Sunrise LNG 2022 4.3 No Little progress

Canada Kitimat LNG 2022 10.0 Complete Doesn't appear on the front burner for CVX

Indonesia Abadi FLNG 2022 7.5 Not for an onshore Basis of Design Large gas resource, multiple dev elopmental challenges

Russia Far East LNG 2022 5.0 Presume complete (2013 aw ard) - Foster Wheeler

Canada Shell LNG Canada 2022 12.0 In FEED; Chiy oda, FW, Saipem, WP Project defer

Construction Lag

(FID to 1st LNG)

19

Source(s): Company Filings, Credit Suisse Estimates, Credit Suisse Energy Team

US Engineering & Construction

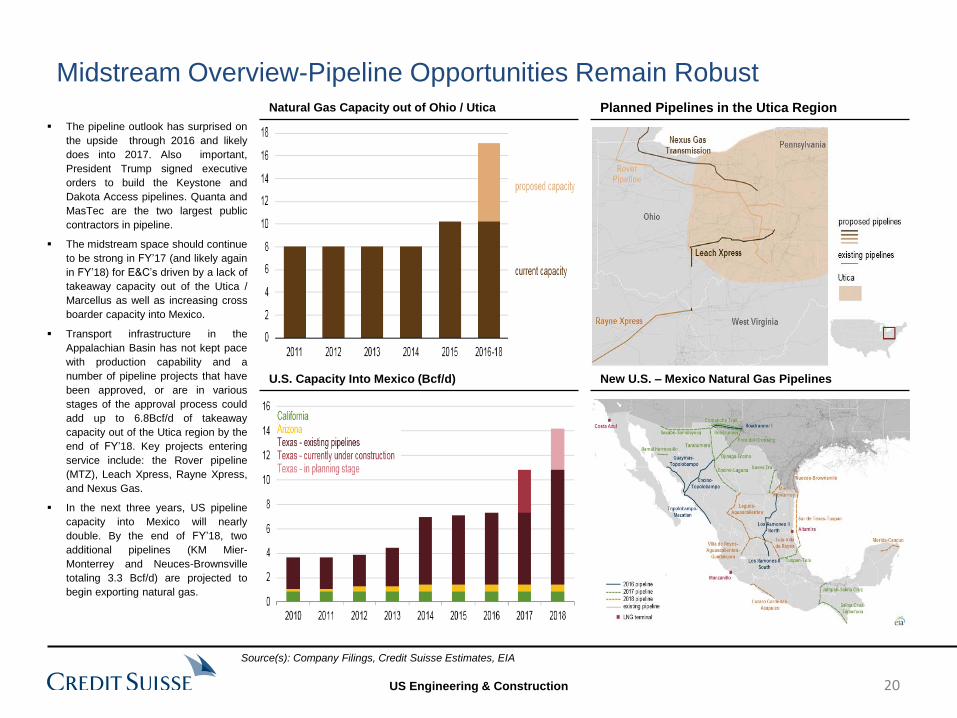

Midstream Overview-Pipeline Opportunities Remain Robust Natural Gas Capacity out of Ohio / Utica

U.S. Capacity Into Mexico (Bcf/d)

Planned Pipelines in the Utica Region

New U.S. – Mexico Natural Gas Pipelines

The pipeline outlook has surprised on

the upside through 2016 and likely

does into 2017. Also important,

President Trump signed executive

orders to build the Keystone and

Dakota Access pipelines. Quanta and

MasTec are the two largest public

contractors in pipeline.

The midstream space should continue

to be strong in FY’17 (and likely again

in FY’18) for E&C’s driven by a lack of

takeaway capacity out of the Utica /

Marcellus as well as increasing cross

boarder capacity into Mexico.

Transport infrastructure in the

Appalachian Basin has not kept pace

with production capability and a

number of pipeline projects that have

been approved, or are in various

stages of the approval process could

add up to 6.8Bcf/d of takeaway

capacity out of the Utica region by the

end of FY’18. Key projects entering

service include: the Rover pipeline

(MTZ), Leach Xpress, Rayne Xpress,

and Nexus Gas.

In the next three years, US pipeline

capacity into Mexico will nearly

double. By the end of FY’18, two

additional pipelines (KM Mier-

Monterrey and Neuces-Brownsville

totaling 3.3 Bcf/d) are projected to

begin exporting natural gas.

20

Source(s): Company Filings, Credit Suisse Estimates, EIA

US Engineering & Construction

Government Services

21

US Engineering & Construction

Government Takeaways

E&C Government Exposure

Government Outlook

Sources: Company filings, Credit Suisse Estimates

*KBR Operating Income is actually Gross Profit & Equity in Earnings and shows annualized pro forma figures to include the Wyle and HTSI acquisitions

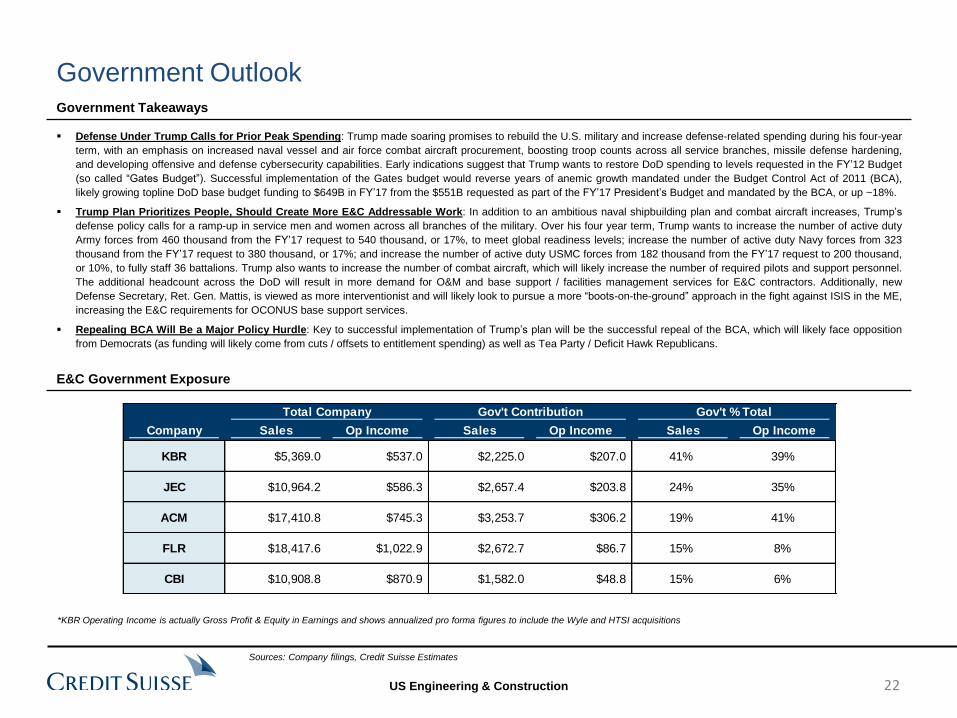

Defense Under Trump Calls for Prior Peak Spending: Trump made soaring promises to rebuild the U.S. military and increase defense-related spending during his four-year

term, with an emphasis on increased naval vessel and air force combat aircraft procurement, boosting troop counts across all service branches, missile defense hardening,

and developing offensive and defense cybersecurity capabilities. Early indications suggest that Trump wants to restore DoD spending to levels requested in the FY’12 Budget

(so called “Gates Budget”). Successful implementation of the Gates budget would reverse years of anemic growth mandated under the Budget Control Act of 2011 (BCA),

likely growing topline DoD base budget funding to $649B in FY’17 from the $551B requested as part of the FY’17 President’s Budget and mandated by the BCA, or up ~18%.

Trump Plan Prioritizes People, Should Create More E&C Addressable Work: In addition to an ambitious naval shipbuilding plan and combat aircraft increases, Trump’s

defense policy calls for a ramp-up in service men and women across all branches of the military. Over his four year term, Trump wants to increase the number of active duty

Army forces from 460 thousand from the FY’17 request to 540 thousand, or 17%, to meet global readiness levels; increase the number of active duty Navy forces from 323

thousand from the FY’17 request to 380 thousand, or 17%; and increase the number of active duty USMC forces from 182 thousand from the FY’17 request to 200 thousand,

or 10%, to fully staff 36 battalions. Trump also wants to increase the number of combat aircraft, which will likely increase the number of required pilots and support personnel.

The additional headcount across the DoD will result in more demand for O&M and base support / facilities management services for E&C contractors. Additionally, new

Defense Secretary, Ret. Gen. Mattis, is viewed as more interventionist and will likely look to pursue a more “boots-on-the-ground” approach in the fight against ISIS in the ME,

increasing the E&C requirements for OCONUS base support services.

Repealing BCA Will Be a Major Policy Hurdle: Key to successful implementation of Trump’s plan will be the successful repeal of the BCA, which will likely face opposition

from Democrats (as funding will likely come from cuts / offsets to entitlement spending) as well as Tea Party / Deficit Hawk Republicans.

Total Company Gov't Contribution Gov't % Total

Company Sales Op Income Sales Op Income Sales Op Income

KBR $5,369.0 $537.0 $2,225.0 $207.0 41% 39%

JEC $10,964.2 $586.3 $2,657.4 $203.8 24% 35%

ACM $17,410.8 $745.3 $3,253.7 $306.2 19% 41%

FLR $18,417.6 $1,022.9 $2,672.7 $86.7 15% 8%

CBI $10,908.8 $870.9 $1,582.0 $48.8 15% 6%

22

US Engineering & Construction

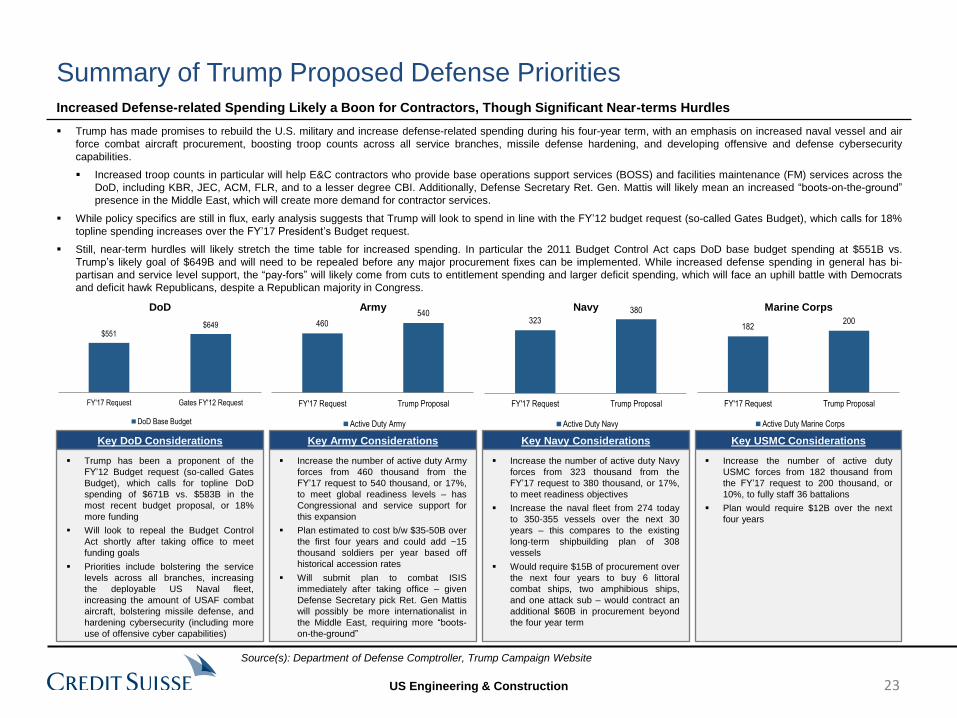

Key DoD Considerations

Trump has been a proponent of the

FY’12 Budget request (so-called Gates

Budget), which calls for topline DoD

spending of $671B vs. $583B in the

most recent budget proposal, or 18%

more funding

Will look to repeal the Budget Control

Act shortly after taking office to meet

funding goals

Priorities include bolstering the service

levels across all branches, increasing

the deployable US Naval fleet,

increasing the amount of USAF combat

aircraft, bolstering missile defense, and

hardening cybersecurity (including more

use of offensive cyber capabilities)

Key Army Considerations

Increase the number of active duty Army

forces from 460 thousand from the

FY’17 request to 540 thousand, or 17%,

to meet global readiness levels – has

Congressional and service support for

this expansion

Plan estimated to cost b/w $35-50B over

the first four years and could add ~15

thousand soldiers per year based off

historical accession rates

Will submit plan to combat ISIS

immediately after taking office – given

Defense Secretary pick Ret. Gen Mattis

will possibly be more internationalist in

the Middle East, requiring more “boots-

on-the-ground”

Key Navy Considerations

Increase the number of active duty Navy

forces from 323 thousand from the

FY’17 request to 380 thousand, or 17%,

to meet readiness objectives

Increase the naval fleet from 274 today

to 350-355 vessels over the next 30

years – this compares to the existing

long-term shipbuilding plan of 308

vessels

Would require $15B of procurement over

the next four years to buy 6 littoral

combat ships, two amphibious ships,

and one attack sub – would contract an

additional $60B in procurement beyond

the four year term

Key USMC Considerations

Increase the number of active duty

USMC forces from 182 thousand from

the FY’17 request to 200 thousand, or

10%, to fully staff 36 battalions

Plan would require $12B over the next

four years

Trump has made promises to rebuild the U.S. military and increase defense-related spending during his four-year term, with an emphasis on increased naval vessel and air

force combat aircraft procurement, boosting troop counts across all service branches, missile defense hardening, and developing offensive and defense cybersecurity

capabilities.

Increased troop counts in particular will help E&C contractors who provide base operations support services (BOSS) and facilities maintenance (FM) services across the

DoD, including KBR, JEC, ACM, FLR, and to a lesser degree CBI. Additionally, Defense Secretary Ret. Gen. Mattis will likely mean an increased “boots-on-the-ground”

presence in the Middle East, which will create more demand for contractor services.

While policy specifics are still in flux, early analysis suggests that Trump will look to spend in line with the FY’12 budget request (so-called Gates Budget), which calls for 18%

topline spending increases over the FY’17 President’s Budget request.

Still, near-term hurdles will likely stretch the time table for increased spending. In particular the 2011 Budget Control Act caps DoD base budget spending at $551B vs.

Trump’s likely goal of $649B and will need to be repealed before any major procurement fixes can be implemented. While increased defense spending in general has bi-

partisan and service level support, the “pay-fors” will likely come from cuts to entitlement spending and larger deficit spending, which will face an uphill battle with Democrats

and deficit hawk Republicans, despite a Republican majority in Congress.

Increased Defense-related Spending Likely a Boon for Contractors, Though Significant Near-terms Hurdles

Summary of Trump Proposed Defense Priorities

$551 $649

FY'17 Request Gates FY'12 Request

DoD Base Budget

DoD

460540

FY'17 Request Trump Proposal

Active Duty Army

Army

323380

FY'17 Request Trump Proposal

Active Duty Navy

Navy

182200

FY'17 Request Trump Proposal

Active Duty Marine Corps

Marine Corps

23

Source(s): Department of Defense Comptroller, Trump Campaign Website

US Engineering & Construction

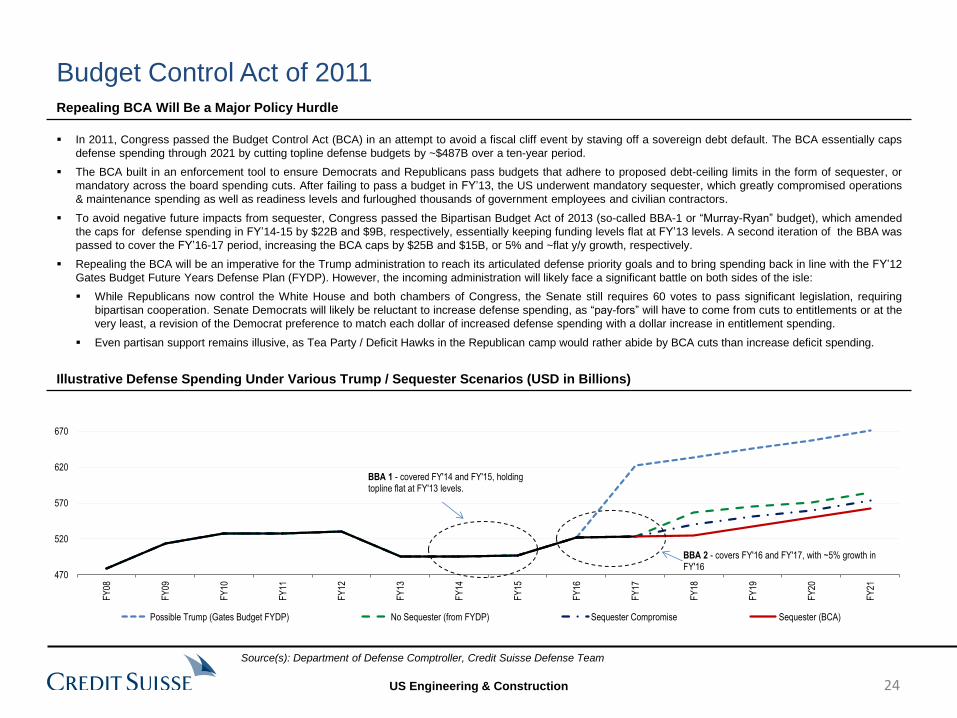

In 2011, Congress passed the Budget Control Act (BCA) in an attempt to avoid a fiscal cliff event by staving off a sovereign debt default. The BCA essentially caps

defense spending through 2021 by cutting topline defense budgets by ~$487B over a ten-year period.

The BCA built in an enforcement tool to ensure Democrats and Republicans pass budgets that adhere to proposed debt-ceiling limits in the form of sequester, or

mandatory across the board spending cuts. After failing to pass a budget in FY’13, the US underwent mandatory sequester, which greatly compromised operations

& maintenance spending as well as readiness levels and furloughed thousands of government employees and civilian contractors.

To avoid negative future impacts from sequester, Congress passed the Bipartisan Budget Act of 2013 (so-called BBA-1 or “Murray-Ryan” budget), which amended

the caps for defense spending in FY’14-15 by $22B and $9B, respectively, essentially keeping funding levels flat at FY’13 levels. A second iteration of the BBA was

passed to cover the FY’16-17 period, increasing the BCA caps by $25B and $15B, or 5% and ~flat y/y growth, respectively.

Repealing the BCA will be an imperative for the Trump administration to reach its articulated defense priority goals and to bring spending back in line with the FY’12

Gates Budget Future Years Defense Plan (FYDP). However, the incoming administration will likely face a significant battle on both sides of the isle:

While Republicans now control the White House and both chambers of Congress, the Senate still requires 60 votes to pass significant legislation, requiring

bipartisan cooperation. Senate Democrats will likely be reluctant to increase defense spending, as “pay-fors” will have to come from cuts to entitlements or at the

very least, a revision of the Democrat preference to match each dollar of increased defense spending with a dollar increase in entitlement spending.

Even partisan support remains illusive, as Tea Party / Deficit Hawks in the Republican camp would rather abide by BCA cuts than increase deficit spending.

Repealing BCA Will Be a Major Policy Hurdle

Illustrative Defense Spending Under Various Trump / Sequester Scenarios (USD in Billions)

Budget Control Act of 2011

470

520

570

620

670

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

Possible Trump (Gates Budget FYDP) No Sequester (from FYDP) Sequester Compromise Sequester (BCA)

BBA 1 - covered FY'14 and FY'15, holding topline flat at FY'13 levels.

BBA 2 - covers FY'16 and FY'17, with ~5% growth in FY'16

24

Source(s): Department of Defense Comptroller, Credit Suisse Defense Team

US Engineering & Construction

Trump Army Implications FY’17 U.S. Army President Budget and FYDP (FY’17 Constant USD in Billions)

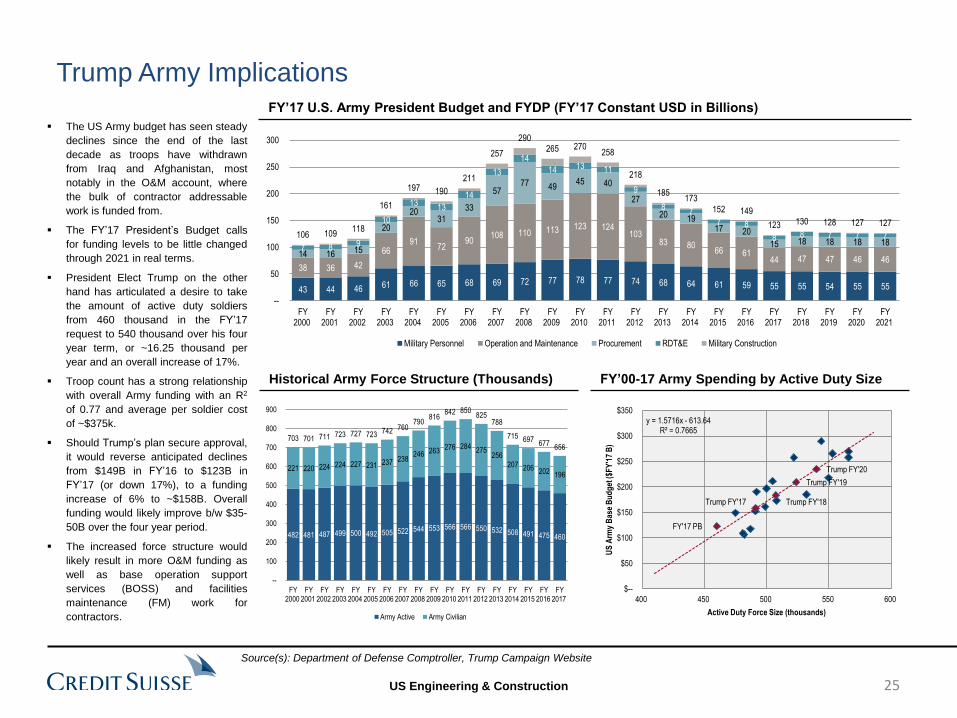

The US Army budget has seen steady

declines since the end of the last

decade as troops have withdrawn

from Iraq and Afghanistan, most

notably in the O&M account, where

the bulk of contractor addressable

work is funded from.

The FY’17 President’s Budget calls

for funding levels to be little changed

through 2021 in real terms.

President Elect Trump on the other

hand has articulated a desire to take

the amount of active duty soldiers

from 460 thousand in the FY’17

request to 540 thousand over his four

year term, or ~16.25 thousand per

year and an overall increase of 17%.

Troop count has a strong relationship

with overall Army funding with an R2

of 0.77 and average per soldier cost

of ~$375k.

Should Trump’s plan secure approval,

it would reverse anticipated declines

from $149B in FY’16 to $123B in

FY’17 (or down 17%), to a funding

increase of 6% to ~$158B. Overall

funding would likely improve b/w $35-

50B over the four year period.

The increased force structure would

likely result in more O&M funding as

well as base operation support

services (BOSS) and facilities

maintenance (FM) work for

contractors.

Historical Army Force Structure (Thousands) FY’00-17 Army Spending by Active Duty Size

43 44 46 61 66 65 68 69 72 77 78 77 74 68 64 61 59 55 55 54 55 55

38 36 42

66 91

72 90

108 110 113 123 124 103

83 80 66 61

44 47 47 46 46 14 16 15

20

20 31

33

57 77 49

45 40

27

20 19 17 20

15 18 18 18 18 7 8 9

10

13 13

14

13

14

14 13 11

9

8 7

7 8

8 8 7 7 7 106 109 118

161

197 190

211

257

290 265 270

258

218

185 173

152 149

123 130 128 127 127

--

50

100

150

200

250

300

FY2000

FY2001

FY2002

FY2003

FY2004

FY2005

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016

FY2017

FY2018

FY2019

FY2020

FY2021

Military Personnel Operation and Maintenance Procurement RDT&E Military Construction

FY'17 PB

Trump FY'17 Trump FY'18

Trump FY'19

Trump FY'20

y = 1.5716x - 613.64R² = 0.7665

$--

$50

$100

$150

$200

$250

$300

$350

400 450 500 550 600U

S A

rmy

Bas

e B

ud

get

($F

Y'1

7 B

)Active Duty Force Size (thousands)

482 481 487 499 500 492 505 522 544 553 566 566 550 532 508 491 475 460

221 220 224 224 227 231 237 238 246 263 276 284

275 256

207 206 202 196

703 701 711 723 727 723 742 760 790

816 842 850

825 788

715 697 677

656

--

100

200

300

400

500

600

700

800

900

FY2000

FY2001

FY2002

FY2003

FY2004

FY2005

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016

FY2017

Army Active Army Civilian

25

Source(s): Department of Defense Comptroller, Trump Campaign Website

US Engineering & Construction

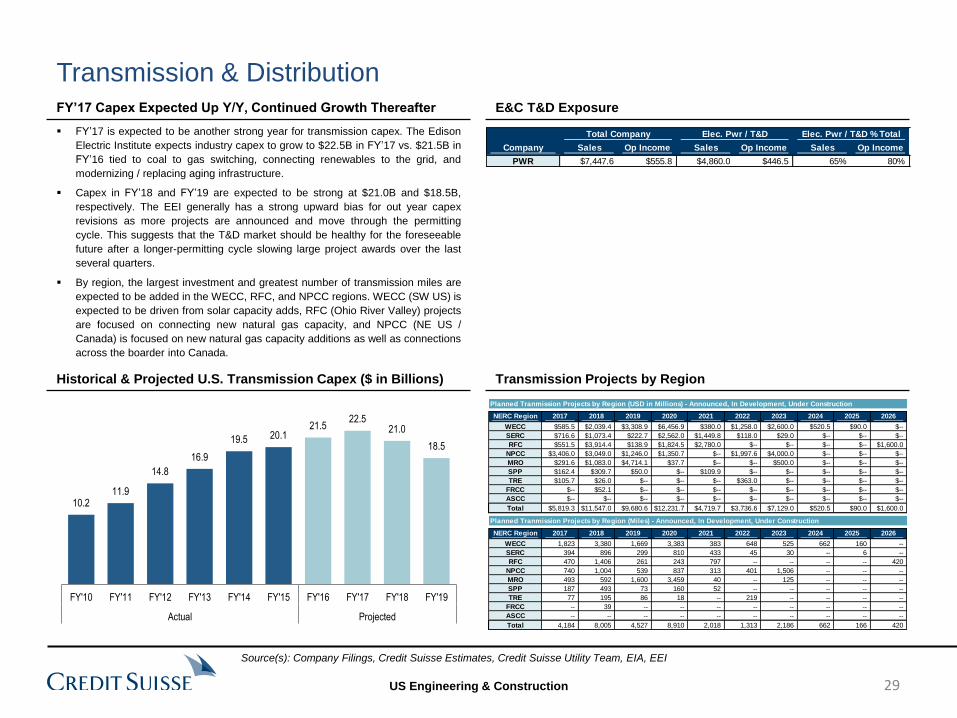

Electric Power

26

US Engineering & Construction

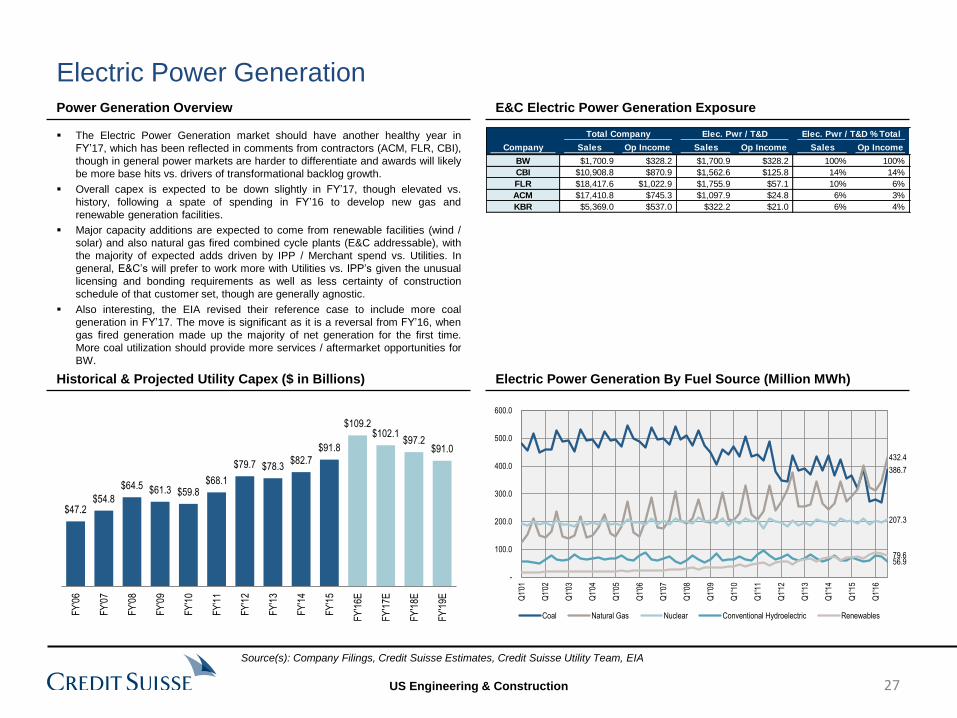

The Electric Power Generation market should have another healthy year in

FY’17, which has been reflected in comments from contractors (ACM, FLR, CBI),

though in general power markets are harder to differentiate and awards will likely

be more base hits vs. drivers of transformational backlog growth.

Overall capex is expected to be down slightly in FY’17, though elevated vs.

history, following a spate of spending in FY’16 to develop new gas and

renewable generation facilities.

Major capacity additions are expected to come from renewable facilities (wind /

solar) and also natural gas fired combined cycle plants (E&C addressable), with

the majority of expected adds driven by IPP / Merchant spend vs. Utilities. In

general, E&C’s will prefer to work more with Utilities vs. IPP’s given the unusual

licensing and bonding requirements as well as less certainty of construction

schedule of that customer set, though are generally agnostic.

Also interesting, the EIA revised their reference case to include more coal

generation in FY’17. The move is significant as it is a reversal from FY’16, when

gas fired generation made up the majority of net generation for the first time.

More coal utilization should provide more services / aftermarket opportunities for

BW.

Electric Power Generation Power Generation Overview

Historical & Projected Utility Capex ($ in Billions)

E&C Electric Power Generation Exposure

Electric Power Generation By Fuel Source (Million MWh)

Total Company Elec. Pwr / T&D Elec. Pwr / T&D % Total

Company Sales Op Income Sales Op Income Sales Op Income

BW $1,700.9 $328.2 $1,700.9 $328.2 100% 100%

CBI $10,908.8 $870.9 $1,562.6 $125.8 14% 14%

FLR $18,417.6 $1,022.9 $1,755.9 $57.1 10% 6%

ACM $17,410.8 $745.3 $1,097.9 $24.8 6% 3%

KBR $5,369.0 $537.0 $322.2 $21.0 6% 4%

386.7

432.4

207.3

56.9 79.6

-

100.0

200.0

300.0

400.0

500.0

600.0

Q1'

01

Q1'

02

Q1'

03

Q1'

04

Q1'

05

Q1'

06

Q1'

07

Q1'

08

Q1'

09

Q1'

10

Q1'

11

Q1'

12

Q1'

13

Q1'

14

Q1'

15

Q1'

16

Coal Natural Gas Nuclear Conventional Hydroelectric Renewables

$47.2 $54.8

$64.5 $61.3 $59.8 $68.1

$79.7 $78.3 $82.7

$91.8

$109.2 $102.1

$97.2 $91.0

FY

'06

FY

'07

FY

'08

FY

'09

FY

'10

FY

'11

FY

'12

FY

'13

FY

'14

FY

'15

FY

'16E

FY

'17E

FY

'18E

FY

'19E

27

Source(s): Company Filings, Credit Suisse Estimates, Credit Suisse Utility Team, EIA

US Engineering & Construction

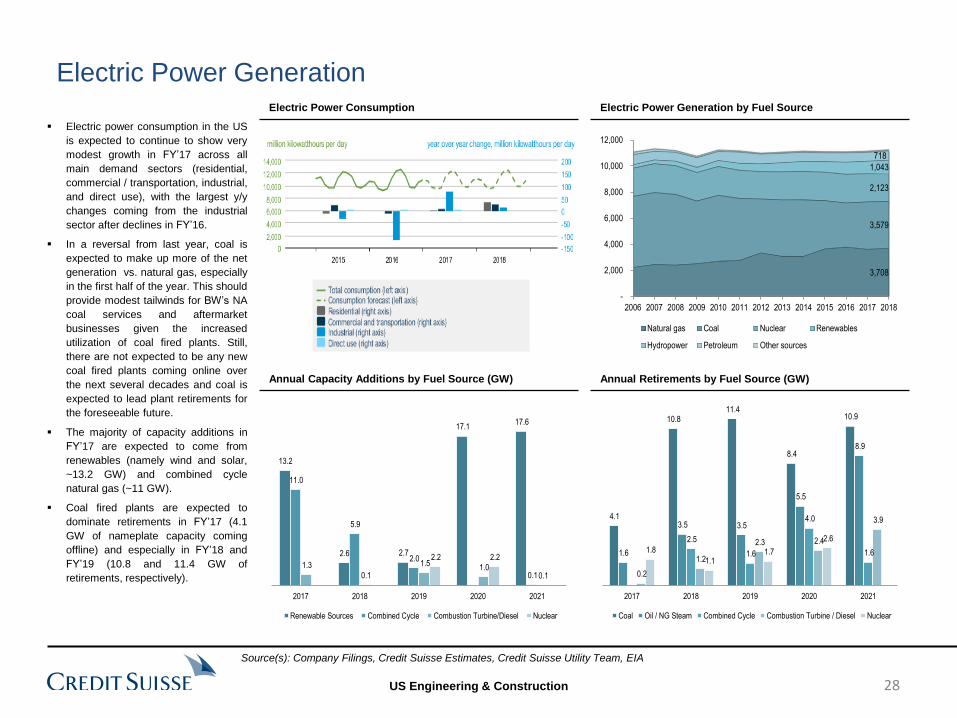

Electric Power Generation Electric Power Consumption

Annual Capacity Additions by Fuel Source (GW)

Electric Power Generation by Fuel Source

Annual Retirements by Fuel Source (GW)

Electric power consumption in the US

is expected to continue to show very

modest growth in FY’17 across all

main demand sectors (residential,

commercial / transportation, industrial,

and direct use), with the largest y/y

changes coming from the industrial

sector after declines in FY’16.

In a reversal from last year, coal is

expected to make up more of the net

generation vs. natural gas, especially