Credit Suisse Global Steel & Mining Conference - Klöckner ...

Upload

khangminh22Category

view

2download

0

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

22 November 2011 Asia Pacific/Taiwan

Equity Research Strategy

Taiwan Market Strategy STRATEGY

Earnings stabilisation and upcycle in 2012 Figure 1: Market trough 3 months ahead of FY2 earnings with 78% correlation

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan-

00

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Oct-0

8

Oct-0

9

Oct-1

0

Oct-1

1

-

5

10

15

20

25

30

35

TWSE (LHS) EPS FY2(Index) (NT$)

Source: TEJ, Datastream, Bloomberg, Credit Suisse Research

■ Expect earnings stabilisation in 1Q 2012. After nine consecutive months of consensus earnings cuts, we expect to see earnings stabilisation in 1Q12. This is based on our finding that in the last 20 years, the average duration of each cycle is ten months with a range of 4.5-14.5 months. By end-1Q12, Taiwan will have completed 14 months of cuts, though the pace of rebound may be moderate. YTD the earnings cut is 32% for 2011 and 27% for 2012.

■ Rotating into tech. We adjust our model portfolio to reflect our view of a sector rotation back to tech with many factors that drove rotation from tech to non-tech reversing. Most notably, tech has led this earnings cut cycle (-42% versus -21% non-tech) and is trading at a discount to non-tech despite better profit growth seen in 2012. Both QFII and ITC are relatively underweight tech, which accounted for 78% of QFII net selling YTD.

■ Elections a risk, not a catalyst. The 14 January 2012 election is expected to be a much closer race; latest polls suggest the KMT has a small lead that is within the margin of error. There is also the legislative election where KMT could see weaker control (65% now) or neither KMT nor DPP will control 50%. Hence, investors should stay cautious into the election, especially for non-tech (airline, tourism, banks and asset plays) that is perceived to benefit from cross strait ties if KMT wins both the Presidential and Legislative Yuan.

■ Stock picks. In an environment of low rate and low growth, stocks that can provide consistent good dividend yields with some growth should outperform the market. Hence, we screen our coverage universe of 95 stocks using the criteria of (1) 5%+ dividend yield; (2) positive earnings growth; (3) net cash and; (4) positive FCF. Using these criteria to choose a basket of stocks has outperformed the market every year in the last nine years. For 2012, we highlight eight stocks: HTC, Novatek, Asustek, TSMC, MStar, E Ink, Taiwan Cement and FET. Our top sell are PCSC, China Airlines and China Steel.

Research Analysts

Chung Hsu, CFA 8862 2715 6362

Randy Abrams, CFA 886 2 2715 6366

Michelle Chou, CFA 886 2 2715 6363

Josette Chang 886 2 2715 6367

Taiwan Research Analyst Team

Randy Abrams (Head of Taiwan Research) (Regional Semiconductors)

Chate Benchvitvilai

(Telecoms)

Pauline Chen (Hardware Components)

Darryl Cheng (LED, Solar, Networking)

Chung Hsu (Financials)

Sam Lee (Transportation)

Jerry Su

(TFT LCD)

Christiaan Tuntono (Economics)

Thompson Wu (Tech hardware)

Sidney Yeh (Basic Materials, Property, Consumer, Chemicals)

Research Assistants Josette Chang

Kevin Chen Jimmy Huang

David Liao Michelle Chou

Grace LI

22 November 2011

Taiwan Market Strategy 2

Focus charts and tables Figure 2: Valuation matrix for the eight top high-yield picks in Taiwan Price EPS (NT$) P/E (x) P/B (x) ROE (%) Earnings growth (%)

Ticker Company (NT$) Rating 2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E

2330.TW TSMC 74.2 O 5.1 5.6 14.4 13.2 3.1 2.8 22.2% 22.0% -17.5% 8.9%

2498.TW HTC 660.0 O 76.8 78.4 8.6 8.4 5.4 4.3 73.3% 56.4% 66.7% 2.1%

4904.TW Far EasTone 56.9 O 2.6 3.1 21.7 18.1 2.6 2.5 11.9% 14.1% -3.3% 19.6%

2357.TW Asustek 202.5 O 22.1 25.5 9.2 7.9 1.3 1.1 14.5% 15.5% -16.0% 15.4%

1101.TW Taiwan Cement 33.0 O 2.5 3.2 13.0 10.4 1.3 1.2 9.8% 11.8% 17.1% 24.9%

3697.TW MStar 170.5 O 11.9 14.9 14.3 11.5 2.8 2.5 19.8% 22.9% -11.2% 24.9%

8069.TWO E Ink 59.2 O 6.7 7.0 8.9 8.4 2.5 2.2 28.9% 28.2% 74.8% 5.4%

3034.TW Novatek Micro 77.1 O 6.4 7.6 12.1 10.1 2.1 1.9 17.4% 19.8% -16.9% 19.0%

Note: O = Outperform. Source: Company data, Credit Suisse estimates

Figure 3: CS 2012E (FY2) earnings revision YTD Figure 4: Market usually peaks and troughs three months

ahead of FY2 earnings with 78% correlation

1% 1% 1% 0%

0%-2%

-7%

-12%-13%

-21%

-27%-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11

CS estimates 2012E earning rev ision YTD

Non-recession earning revision average :-16%

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan-

00

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

-

5

10

15

20

25

30

35

TWSE (LHS) EPS FY2(Index) (NT$)

Source: Credit Suisse estimates Source: Datastream, Reuters, Credit Suisse Research

Figure 5: Summary table earnings revisions and growth expectation (market, tech and non-tech) CS estimates Consensus estimates Valuation (2012E)

Earnings revision YTD Earnings growth Earnings revision YTD Earnings growth P/B P/E ROE

2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E (x) (x)

CS coverage all

All sectors -32% -27% -22% 22% -32% -26% -22% 25% 1.61 13.7 12.1%

Total tech -42% -27% -35% 53% -52% -38% -42% 53% 1.63 12.3 13.8%

Total non-tech -21% -27% -8% 0% -9% -10% -2% 7% 1.60 15.2 10.7%

Excluding DRAM, TFT and transportation sectors

All sectors -16% -18% -6% 8% -12% -12% -4% 12% 1.69 12.9 13.6%

Total tech -20% -16% -14% 17% -23% -19% -16% 18% 1.76 11.0 16.9%

Total non-tech -12% -21% 3% -2% 1% -2% 11% 5% 1.64 15.2 11.0%

Source: Bloomberg, Reuters, Credit Suisse estimates

Figure 6: Comparison between Taiwan model portfolio and CS Taiwan coverage P/E (x) P/B (x) ROE (%) Earnings growth (%) Dividend yield (%) Beta

2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E

Taiwan model portfolio 11.6 11.0 2.2 2.0 20.1% 18.8% 14.7% 6.3% 4.8% 4.8% 0.9 CS Taiwan coverage 16.8 13.7 1.7 1.6 10.3% 12.1% -21.7% 22.4% 4.3% 4.2% 1.1

Source: Company data, Bloomberg, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 3

Earnings stabilisation and upcycle in 2012 The Taiwan market peaked on 28 January 2011 (TAIEX: 9,145) and spent most of 2011 digesting the negative news flow from Europe, the US and even China’s slowdown. In fact, corporate guidance turned cautious earlier in the year and led to consensus earnings cuts of 32%/26% YTD for 2011/2012, respectively. As a result, the TAIEX declined 19% YTD.

Expect earnings stabilisation in 1Q 2012 Yet, we believe after nine consecutive months of consensus earnings cuts, this earnings cut cycle is in its final stage and likely to see stabilisation in 1Q 2012. This is based on our finding that in the last 20 years (and eight cut cycles), the average duration of each cut cycle is about ten months with a range of 4.5-14.5 months. By end-1Q 2012, consensus earnings estimate for the Taiwan market will have completed 14 months of cuts. This also coincides with our economist’s view for quarterly GDP growth to bottom in 1Q12 (+2.5% YoY), though the pace of rebound may be moderate. So far, earnings revisions for the market have reached 32% and are likely to finish at 35-40% by 1Q 2012, which is roughly at par with the average cut of 41% in the previous cycles (including crisis and recessions) but notably higher than the average of 25% for non-recessionary cut cycles.

Rotating out of non-tech into tech We adjust our Taiwan model portfolio to OVERWEIGHT tech (from a slight Underweight) as we believe there will be a sector rotation back to tech with many of the factors that drove rotation from tech to non-tech during May-2010 to Oct-2011 reversing. Notably, tech has led this earnings cut cycle (-42% versus -21%) and is trading at a discount to non-tech (12.3x versus 15.2x P/E) despite better earnings growth (53% vs 0%) in 2012. Both QFII and ITC’s portfolio weighting in tech are one standard deviation below historical average and 78% of QFII net selling YTD is in tech. We have an index target of 8,500.

Elections are a near-term risk, not catalyst The elections on 14 January 2012 are widely expected to be a close race, especially with the People First Party (PFP)’s James Soong running a separate campaign that will split some pan-blue’s support. The experience in 2006’s Taipei city mayor election (James Soong contested but only got 4% of the vote) may provide some hope that pan-blue support may consolidate again but it is too early to tell and it may not happen,. While much of the focus is on the presidential election, the legislative election is also critical as KMT could end up with much less control (versus 65% now) or neither KMT nor DPP may control 50% of the Legislative Yuan. Hence, we believe investors will likely stay cautious as the election is perceived to be more a risk than a catalyst. The concern over a potential KMT loss could facilitate sector rotation out of non-tech as we approach year-end.

Choosing a basket of yield stocks for next year The Taiwan market is one of the highest dividend yield markets (4.3%) in the region and is even more attractive given that interest rates are expected to stay low (sub-1.5%) through 2012. This, together with our view of moderate growth in 2012, suggests that stocks that can provide consistent good dividend with some growth will outperform the market.

Thus, we screen our coverage universe of 95 stocks using the criteria of: (1) at least 5% dividend yield; (2) positive earnings growth into the following fiscal year; (3) net cash on balance sheet; (4) positive free cash flow and; (5) market cap of US$1 bn+. Such a basket of yield stocks has outperformed the market every year since 2003 (nine years). For 2012, we shortlist eight stocks: HTC, Novatek, Asustek, TSMC, MStar, E Ink, Taiwan Cement and FET. Our top sell are PCSC, China Airline and China Steel.

Expect earnings stabilisation in 1Q 2012 with earnings cuts being 14 months into the cycle

Prefer tech over non-tech on cheaper valuation, better growth and underowned by institutions

The elections will, at best, maintain status quo and the latest poll rankings are too close to suggest if KMT has a lead

Quality yield stocks have beat the market every year in the last nine years

Top picks for 2012: HTC, Novatek, Asustek, TSMC, MStar, E Ink, Taiwan Cement and FET

22 November 2011

Taiwan Market Strategy 4

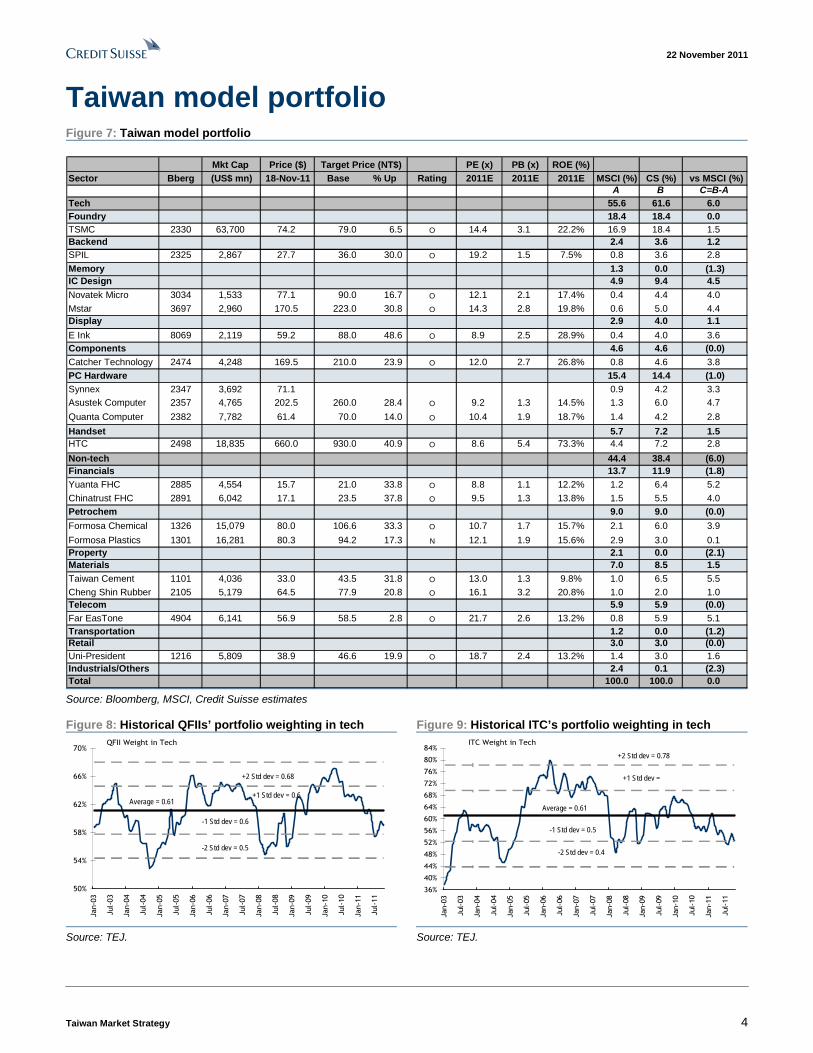

Taiwan model portfolio Figure 7: Taiwan model portfolio

Mkt Cap Price ($) PE (x) PB (x) ROE (%)

Sector Bberg (US$ mn) 18-Nov-11 Base % Up Rating 2011E 2011E 2011E MSCI (%) CS (%) vs MSCI (%)A B C=B-A

Tech 55.6 61.6 6.0Foundry 18.4 18.4 0.0TSMC 2330 63,700 74.2 79.0 6.5 O 14.4 3.1 22.2% 16.9 18.4 1.5Backend 2.4 3.6 1.2SPIL 2325 2,867 27.7 36.0 30.0 O 19.2 1.5 7.5% 0.8 3.6 2.8

Memory 1.3 0.0 (1.3)IC Design 4.9 9.4 4.5Novatek Micro 3034 1,533 77.1 90.0 16.7 O 12.1 2.1 17.4% 0.4 4.4 4.0

Mstar 3697 2,960 170.5 223.0 30.8 O 14.3 2.8 19.8% 0.6 5.0 4.4Display 2.9 4.0 1.1

E Ink 8069 2,119 59.2 88.0 48.6 O 8.9 2.5 28.9% 0.4 4.0 3.6Components 4.6 4.6 (0.0)Catcher Technology 2474 4,248 169.5 210.0 23.9 O 12.0 2.7 26.8% 0.8 4.6 3.8PC Hardware 15.4 14.4 (1.0)Synnex 2347 3,692 71.1 0.9 4.2 3.3Asustek Computer 2357 4,765 202.5 260.0 28.4 O 9.2 1.3 14.5% 1.3 6.0 4.7

Quanta Computer 2382 7,782 61.4 70.0 14.0 O 10.4 1.9 18.7% 1.4 4.2 2.8

Handset 5.7 7.2 1.5HTC 2498 18,835 660.0 930.0 40.9 O 8.6 5.4 73.3% 4.4 7.2 2.8

Non-tech 44.4 38.4 (6.0)Financials 13.7 11.9 (1.8)Yuanta FHC 2885 4,554 15.7 21.0 33.8 O 8.8 1.1 12.2% 1.2 6.4 5.2

Chinatrust FHC 2891 6,042 17.1 23.5 37.8 O 9.5 1.3 13.8% 1.5 5.5 4.0Petrochem 9.0 9.0 (0.0)

Formosa Chemical 1326 15,079 80.0 106.6 33.3 O 10.7 1.7 15.7% 2.1 6.0 3.9

Formosa Plastics 1301 16,281 80.3 94.2 17.3 N 12.1 1.9 15.6% 2.9 3.0 0.1Property 2.1 0.0 (2.1)Materials 7.0 8.5 1.5Taiwan Cement 1101 4,036 33.0 43.5 31.8 O 13.0 1.3 9.8% 1.0 6.5 5.5Cheng Shin Rubber 2105 5,179 64.5 77.9 20.8 O 16.1 3.2 20.8% 1.0 2.0 1.0Telecom 5.9 5.9 (0.0)Far EasTone 4904 6,141 56.9 58.5 2.8 O 21.7 2.6 13.2% 0.8 5.9 5.1Transportation 1.2 0.0 (1.2)Retail 3.0 3.0 (0.0)Uni-President 1216 5,809 38.9 46.6 19.9 O 18.7 2.4 13.2% 1.4 3.0 1.6Industrials/Others 2.4 0.1 (2.3)Total 100.0 100.0 0.0

Target Price (NT$)

Source: Bloomberg, MSCI, Credit Suisse estimates

Figure 8: Historical QFIIs’ portfolio weighting in tech Figure 9: Historical ITC’s portfolio weighting in tech

50%

54%

58%

62%

66%

70%

Jan-

03

Jul-

03

Jan-

04

Jul-

04

Jan-

05

Jul-

05

Jan-

06

Jul-

06

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

QFII Weight in Tech

+2 Std dev = 0.68

+1 Std dev = 0.6Average = 0.61

-1 Std dev = 0.6

-2 Std dev = 0.5

36%

40%

44%

48%

52%

56%

60%

64%

68%

72%

76%

80%

84%

Jan-

03

Jul-

03

Jan-

04

Jul-

04

Jan-

05

Jul-

05

Jan-

06

Jul-

06

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

ITC Weight in Tech

+2 Std dev = 0.78

+1 Std dev = 0.7

Average = 0.61

-1 Std dev = 0.5

-2 Std dev = 0.4

Source: TEJ. Source: TEJ.

22 November 2011

Taiwan Market Strategy 5

Earnings stabilisation in 1Q 2012 After nine consecutive months of consensus earnings cuts, we believe the earning revision cycle for the Taiwan market is in its final stage and likely to see stabilisation in 1Q 2012. This is based on our finding that in the last 20 years (and eight cut cycles), the average duration of each cut cycle is about ten months with a range 4.5-14.5 months (Figure 12). By end of 1Q 2012, consensus earnings estimates for the Taiwan market would have completed a 14-month cut cycle. This also coincides with our economist’s view for quarterly GDP growth to bottom in 1Q12 (+2.5% YoY), though the pace of rebound may be moderate. So far, earnings revisions for the market have reached 32% and are likely to finish at 35-40% by 1Q 2012, which is roughly at par with the average cut of 41% in the previous cycle (include crisis and recessions) but notably higher than the average of 25% in non-recessionary cut cycles.

Figure 10:CS 2011E (FY1) earnings cut (-32%) YTD Figure 11: CS 2012E (FY2) earnings cut (-27%) YTD

0% 1%

-1% -2% -4%-6%

-14%

-21% -21%

-27%

-32%-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11

CS estimates 2011E profit revision since the beginning of the year

Non-recession earning revision average :-25%

1% 1% 1% 0%

0%-2%

-7%

-12%-13%

-21%

-27%-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11

CS estimates 2012E earning rev ision YTD

Non-recession earning revision average :-16%

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 12: There were eight meaningful earnings cut cycle in Taiwan since 1990

Source: Bloomberg, Credit Suisse estimates

Market typically troughs three months before consensus earnings While we believe earnings revisions could last into 1Q next year, the market usually troughs three months ahead of consensus with a 70% correlation (Figure 13). This implies that unless this current earnings cut cycle sets a new record for the longest duration in Taiwan’s history, the equity market may have already discounted the bulk of negative earnings expectations. In fact, the final months of earnings cuts usually have little impact on share prices and we believe earnings revisions for the next few months could continue to skew to non-tech sectors that have historically lagged in earnings cut cycles. Year-to-date, tech has seen 52% of consensus cuts (or -23% ex-TFT and DRAM) while non-tech has seen 9% cuts of which most came in 4Q and concentrated on the transportation and steel sectors.

Expect earning stabilisation in 1Q12 with the earnings cut cycle reaching 14 months

Historically, the market troughs three months ahead of earnings, which has seen the largest cut in 3Q11

22 November 2011

Taiwan Market Strategy 6

Figure 13: Market usually peaks and troughs three

months ahead of FY1 earnings with 70% correlation

Figure 14: Market usually peaks and troughs three

months ahead of FY2 earnings with 78% correlation

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan-

00

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

-

5

10

15

20

25

30

TWSE (LHS) EPS FY1(Index ) (NT$)

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan-

00

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Oct

-08

Oct

-09

Oct

-10

Oct

-11

-

5

10

15

20

25

30

35

TWSE (LHS) EPS FY2(Index) (NT$)

Source: TEJ, Datastream, Bloomberg, Credit Suisse research Source: TEJ, Datastream, Bloomberg, Credit Suisse research

Tech has led the cycle but non-tech is catching up We have learned from the previous (eight) cycles that earnings revisions usually start in upstream tech and are followed by downstream tech. Non-tech (including financials) has historically lagged and only starts to see more significant cuts at the latter part of the cycle.

We find a similar trend this time as well with upstream tech’s 24% earnings cut YTD (ex-TFT and DRAM) largely done in early 3Q11 while non-tech’s 21% earnings cut was only done in the past month (Figure 15). We note that consensus has only cut non-tech earnings by 9% YTD, which suggests there are likely more consensus cuts on the way.

Figure 15: CS estimates revision YTD by sector (2011) Figure 16: CS estimates revision YTD by sector (2012)

-24%

-15%

-21%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Total Upstream tech (ex. TFT, DRAM) Total Downstream Tech AverageNon tech (incl financial)

bulk of tech cut tookplace in early 3Q

non-tech cutcatch up in 4Q

-21%

-11%

-27%-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Total Upstream tech (ex. TFT, DRAM) Total Downstream Tech AverageNon tech (incl financial)

bulk of tech cut tookplace in early 3Q

non-tech cutcatch up in 4Q

Source: Credit Suisse estimates Source: Credit Suisse estimates

Figure 17: Consensus revision changes YTD by sector

(2011)

Figure 18: Consensus revision changes YTD by sector

(2012)

-24%

-9%

-22%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Total Upstream tech (ex. TFT, DRAM) Total non techTotal Downstream Tech Average

Consensus estimates

-21%

-17%

-10%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Total Upstream tech (ex. TFT, DRAM) Total Downstream Tech AverageNon tech (incl financial)

Source: Reuters, Credit Suisse research Source: Reuters, Credit Suisse research

Tech has led earnings cuts this time with non-tech just starting to see bigger cuts

22 November 2011

Taiwan Market Strategy 7

Figure 19: Earnings revisions YTD by sub-sector 2011 Figure 20: Earnings revisions YTD by sub-sector 2012

-29 -27 -27-21 -17 -12 -9 -7

-2

- -

21 23

-286 -100 -91 -67

-38

-60

-40

-20

-

20

40

TFT

LCD

Sola

r

Tran

spor

tatio

n

LED

IC d

esig

n

Stee

l

Com

pone

nts

Petro

chem

icals

PC/N

B

Foun

dry

Back

end

Con

sum

er

Dev

elop

ers

Fina

ncia

ls

Mem

ory

Mem

ory

Han

dset

Cem

ent

(% ) 2011E CS earnings revision YTD

-33 -32 -29 -25 -21-14 -13 -10

- - 4

2329

-39-50

-73-77-120-60

-40

-20

-

20

40

TFT

LCD

Tran

spor

tatio

n

Sola

r

LED

IC d

esig

n

Petro

chem

icals

Com

pone

nts

Dev

elop

ers

Stee

l

Fina

ncia

ls

Foun

dry

PC/N

B

Back

end

Mem

ory

Mem

ory

Con

sum

er

Han

dset

Cem

ent(%)

2012E CS earnings revision YTD

Source: Credit Suisse estimates Source: Credit Suisse estimates

Moderate growth expectation for 2012 We acknowledge that while earnings estimates are likely to stabilise in 1Q 2012, the pace of earnings rebound may be moderate for next year without a meaningful recovery in the European and US economies. Based on CS estimates, we are currently expecting a 22% profit decline for 2011 followed by a 22% profit rebound in 2012, partly due to a lower base in 2011. Yet, this earnings growth is heavily skewed by the DRAM, TFT and transportation sectors; if we strip these out, we are looking at a more moderate 6% profit decline this year and then an 8% profit rebound in 2012.

Within Taiwan, the tech sector has again demonstrated higher cyclicality with 35% profit decline in 2011 (-14% ex-DRAM and TFT) but will post a 53% rebound next year (+17% ex-DRAM and TFT). Non-tech is expected to deliver 8% profit decline this year (+3% ex-transportation) but 0% growth in 2012 (-2% ex-transportation).

Figure 21: Summary table earnings revisions and growth expectation (market, tech and non-tech) CS estimates Consensus estimates Valuation (2012E)

Earnings revision YTD Earnings growth Earnings revision YTD Earnings growth P/B P/E ROE

2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E (x) (x)

CS coverage all

All sectors -32% -27% -22% 22% -32% -26% -22% 25% 1.61 13.7 12.1%

Total tech -42% -27% -35% 53% -52% -38% -42% 53% 1.63 12.3 13.8%

Total non-tech -21% -27% -8% 0% -9% -10% -2% 7% 1.60 15.2 10.7%

Excluding DRAM, TFT and transportation sectors

All sectors -16% -18% -6% 8% -12% -12% -4% 12% 1.69 12.9 13.6%

Total tech -20% -16% -14% 17% -23% -19% -16% 18% 1.76 11.0 16.9%

Total non-tech -12% -21% 3% -2% 1% -2% 11% 5% 1.64 15.2 11.0%

Source: TEJ, Credit Suisse estimates

Figure 22: CS earnings estimates for Taiwan, tech and

non-tech

Figure 23: CS earnings estimates for Taiwan, tech and

non-tech, ex-DRAM, TFT and transportation

-35%

-8%

-22%

53%

0%

22%

-40%

-20%

0%

20%

40%

60%

Total Tech average Total Non-Tech average Total Taiwan average

2011E 2012E

-14%

3%

-6%

17%

-2%

8%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Total Tech ex. DRAM andTFT

Total Non-Tech ex.Transportation

CS coverage ex. DRAM, TFTand Transportation

2011E 2012E

Source: Credit Suisse estimates Source: Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 8

Rotating out of non-tech into tech If we look at both QFII and local ITC’s portfolio allocation, there has been 18 months of sector rotation from tech into non-tech during May-2010 to Oct-2011. During this period, the USD has depreciated (negative for tech earnings) and most tech sub-sectors have seen significant earnings cuts that resulted in a negative earnings growth for 2011 versus a modest positive growth for non-tech. Yet, we believe most of these trends are reversing going into 2012 and will sustain a sector rotation back to tech. Both QFII and ITC’s portfolio weightings in tech are currently one standard deviation below their historical average (Figures 24 and 25) and this will provide tailwinds when fundamentals turn. Tech also accounted for 78% of QFII net selling YTD.

Figure 24: Historical QFIIs’ portfolio weighting in tech Figure 25: Historical ITC’s portfolio weighting in tech

50%

54%

58%

62%

66%

70%

Jan-

03

Jul-

03

Jan-

04

Jul-

04

Jan-

05

Jul-

05

Jan-

06

Jul-

06

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

QFII Weight in Tech

+2 Std dev = 0.68

+1 Std dev = 0.6Average = 0.61

-1 Std dev = 0.6

-2 Std dev = 0.5

36%

40%

44%

48%

52%

56%

60%

64%

68%

72%

76%

80%

84%

Jan-

03

Jul-

03

Jan-

04

Jul-

04

Jan-

05

Jul-

05

Jan-

06

Jul-

06

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

ITC Weight in Tech

+2 Std dev = 0.78

+1 Std dev = 0.7

Average = 0.61

-1 Std dev = 0.5

-2 Std dev = 0.4

Source: TEJ. Source: TEJ.

Tech will show better earnings growth in 2012… Based on consensus estimates in 2011, non-tech has a better earnings profile of -2% profit decline (or +11% ex-transportation). This is attributed to a larger earnings cut for tech till end-3Q11 while non-tech only started to see larger earnings cuts in recent weeks, which should last into early 2012. In 2012, we expect this trend to reverse with tech’s earnings cuts stabilising ahead of non-tech (includes financials) and given tech’s early cycle nature, it is likely to see earlier positive earnings revisions than non-tech. Currently, we estimate an earnings growth of 17% for tech (ex-DRAM and TFT) for 2012 but a 2% decline for non-tech (ex-transportation).

Figure 26: Tech (ex-DRAM/TFT) forward earnings growth Figure 27: Non-tech forward earnings growth

-40%

-20%

0%

20%

40%

60%

80%

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Average = 0.16

+1 Std dev = 0.4

-1 Std dev = -0.1

+2 Std dev = 0.65

-2 Std dev = -0.3

Taiwan Tech Forward YoY EPS growth (%)

9.8%

-130%

-80%

-30%

20%

70%

120%

170%

220%

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Average = 0.20

+1 Std dev = 0.7

-1 Std dev = -0.3

+2 Std dev = 1.13

-2 Std dev = -0.7

Taiwan Non-Tech Forward YoY EPS growth (%)

-0.1%

Source: TEJ, Credit Suisse estimates Source: TEJ, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 9

Figure 28: Earnings growth/valuation summary table CS estimates Consensus estimates Valuation (2012E)

Earnings Earnings Earnings Earnings

revisions YTD growth revisions YTD growth P/B P/E ROE

2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E (x) (x)

CS coverage all

All sector -32% -27% -22% 22% -32% -26% -22% 25% 1.61 13.7 12.1%

Total tech -42% -27% -35% 53% -52% -38% -42% 53% 1.63 12.3 13.8%

Total non-tech -21% -27% -8% 0% -9% -10% -2% 7% 1.60 15.2 10.7%

Excluding DRAM, TFT and transportation sectors

All sector -16% -18% -6% 8% -12% -12% -4% 12% 1.69 12.9 13.6%

Total tech -20% -16% -14% 17% -23% -19% -16% 18% 1.76 11.0 16.9%

Total non-tech -12% -21% 3% -2% 1% -2% 11% 5% 1.64 15.2 11.0%

Breakdown by sector

Foundry -17% -14% -23% 8% -15% -11% -22% 9% 2.27 13.5 17.4%

Packaging & testing -12% -10% -21% 11% -23% -23% -17% 12% 1.51 11.7 13.4%

Memory 0% 0% n.m n.m 353% -471% -106% 40% 0.74 13.8 5.9%

IC design -38% -39% -36% 21% -40% -38% -40% 24% 2.38 14.6 16.9%

TFT LCD -286% -120% n.m n.m -236% -130% -1174% 67% 0.84 n.m -2.7%

Upstream tech -72% -42% -69% 165% -83% -59% -79% 189% 1.73 16.5 10.7%

Components -27% -32% -10% 10% -31% -33% -11% 12% 1.50 11.0 14.2%

PC / NB -21% -13% -14% 27% -31% -22% -22% 34% 1.26 9.3 14.5%

Handset 21% 23% 63% 3% 26% 22% 67% 8% 4.07 8.7 51.8%

Downstream tech -15% -11% -2% 19% -22% -17% -7% 24% 1.52 9.4 17.2%

Financials -2% -21% 59% -9% 13% -4% 53% -3% 0.95 12.5 8.0%

Petrochemicals -27% -33% -18% -4% -2% 7% 1% 14% 2.19 16.9 13.1%

Developers -7% -29% 1% -22% -10% -25% 9% -10% 1.46 13.0 11.3%

Cement 23% 29% 26% 17% 27% 17% 22% 8% 1.18 9.6 12.6%

Steel -29% -25% -34% 15% -22% -28% -27% 12% 1.43 14.4 10.2%

Transportation -91% -77% -90% 183% -91% -76% -92% 189% 0.99 16.8 6.0%

Consumer -9% 4% -6% 21% -5% -6% -1% 11% 3.12 15.7 20.8%

Telecom 0% 0% -2% 8% -1% 2% 0% 6% 2.62 17.1 15.5%

Non-tech -21% -27% -8% 0% -9% -10% -2% 7% 1.60 15.2 10.7%

Source: Company data, Credit Suisse estimates

…and is trading at cheaper valuations… If we exclude DRAM and TFT, we estimate tech is trading at 11.0x FY12E P/E while non-tech is trading at 15.2x against a 17% and 0% profit growth for 2012, respectively.

Figure 29: Historical tech vs non-tech’s P/E gap Figure 30: Historical tech vs non-tech’s P/B gap

(25.0)

(20.0)

(15.0)

(10.0)

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan-

00

Dec

-00

Oct

-01

Sep-

02

Jul-03

Jun-

04

May

-05

Mar

-06

Feb-

07

Dec

-07

Nov

-08

Oct

-09

Sep-

10

Jul-11

Average = 2.47

+1 Std dev = 9.0

-1 Std dev = -4.0

+2 Std dev = 15.46

-2 Std dev = -10.5

Tech vs. Non Tech PE Gap (x)

(1.0)

0.0

1.0

2.0

3.0

4.0

5.0

Jan-

00

Dec

-00

Oct

-01

Sep-

02

Jul-03

Jun-

04

May

-05

Mar

-06

Feb-

07

Dec

-07

Nov

-08

Oct

-09

Sep-

10

Jul-11

Average = 1.11

+1 Std dev = 2.0

-1 Std dev = 0.3

+2 Std dev = 2.83

-2 Std dev = -0.6

Tech vs. Non Tech PB Gap (x)

Source: TEJ, Credit Suisse estimates Source: TEJ, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 10

…and 78% of QFII net selling YTD is in tech Year-to-date, QFIIs have net sold US$9 bn worth of Taiwanese stocks and 78% of this net selling was in the tech sector (Figure 31). Within tech, PC/NB saw the largest net selling of US$3.6 bn and this sub-sector alone accounted for 40% of QFII total net selling in Taiwan. Within tech, TFT and handsets were the two other sub-sectors that saw the largest selling.

Within non-tech, steel and property were the largest net sold sectors YTD while banks have actually seen small net buying YTD due to a stronger start at the beginning of the year.

Figure 31: YTD QFIIs net selling by sub-sector (US$ mn) Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 YTD 2011

Upstream tech 158 -1,095 -1,158 474 282 -584 -631 -1,055 549 703 171 -2,186 Foundry 252 -770 -483 442 487 -33 31 -380 232 655 451 882 IC design -22 -228 -120 -53 -107 -113 -395 29 407 3 -175 -774 Backend 403 122 -101 33 78 -219 -172 -343 -25 68 -24 -180 Memory 58 -38 -43 7 -37 -29 -14 -47 -20 2 -30 -190 TFT -493 -215 -420 89 -112 -168 -42 -288 -17 -18 -31 -1,718 Solar -40 34 10 -44 -28 -21 -39 -26 -27 -7 -20 -207 Downstream tech 1,061 -929 -990 885 -367 -799 -719 -2,348 -1,410 714 -35 -4,937 Handset 286 260 237 -18 -503 -193 -424 -552 -569 144 -286 -1,618 Component 376 -268 -132 623 15 -173 533 -511 -467 55 -36 15 PC/NB/MB/EMS 279 -992 -1,082 97 111 -405 -784 -1,319 -336 551 246 -3,634 Networking 9 -22 -17 10 -3 -1 13 13 2 -3 2 3 LED 110 92 4 173 13 -26 -57 22 -40 -33 40 297 Financial 1,231 -459 238 394 -203 318 40 -1,171 -797 -146 -393 -949 Bank 679 -91 247 382 -88 76 81 -586 -269 -74 -225 131 Insurance 371 -221 -2 117 -58 227 -80 -389 -468 -121 -163 -786 Brokerage 181 -146 -6 -105 -57 15 39 -196 -60 48 -5 -294 Materials 24 -424 186 528 -63 95 -671 -917 -354 232 -173 -1,536 Cement -7 -92 88 211 -12 33 -25 -121 -83 57 -36 13 Steel 0 -139 49 59 -157 -102 -816 -495 -195 11 -102 -1,885 Other material 31 -192 49 258 106 163 170 -301 -76 164 -35 337 Petrochem 904 466 505 679 -146 280 45 -621 -517 103 -165 1,533 Property -42 -198 -127 74 -34 -120 -104 -359 -111 -17 17 -1,021 Retail -24 -80 28 72 30 81 110 -124 -80 39 -72 -19 Others 17 -5 55 71 42 -8 7 -39 -16 29 2 155 Telecom -72 -339 -105 109 -77 -151 -256 109 232 -25 57 -518 Transportation 110 -202 -133 -54 14 -18 -29 -70 7 100 -27 -300 Total 3,411 -3,078 -1,436 3,251 -472 -849 -2,188 -6,512 -2,472 1,785 -603 -9,161

Source: TEJ, Credit Suisse Research

22 November 2011

Taiwan Market Strategy 11

Elections are a near-term risk, not a catalyst The elections on 14 January 2012 are widely expected to be a much closer race, especially with People First Party (PFP)’s James Soong running a separate campaign that will split some pan-blue support and further narrow the gap between the incumbent Kuomintang (KMT) and Democratic Progressive Party (DPP). The experience in 2006’s Taipei city mayor election (James Soong also contested there but only got only 4% of the vote versus 7% in the poll) may provide some hope that pan-blue supporters may consolidate again but it is too early to tell and it may not happen, for various reasons.

Figure 32: 2006’s Taipei city mayor election Figure 33: 2006’s Taipei city mayor election poll

Taipei municipal elections, 2006

DPP41%

KMT54%

Others1%

James Soong 4%

Before Election Poll (TVBS)

James Soong 7%

Others20%

KMT52%

DPP21%

Source: Central Election Commission Source: TVBS poll

Figure 34: 2012 presidential candidate preference (TVBS) Figure 35: 2012 presidential candidate preference (ERA)

2012 Presidential Candidate Preference (TVBS)

0

10

20

30

40

50

60

Jan-

11

Feb-

11

Mar

-11

Apr-1

1

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Ying-jeou Ma Ing-wen Tsai James Soong

2012 Presidential Candidate Preference (ERA)

05

1015202530354045

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Ying-jeou Ma Ing-wen Tsai James Soong

Source: TVBS poll Source: ERA

Figure 36: 2012 presidential candidate poll (United Daily) Figure 37: 2012 presidential candidate poll (Liberty Time)

2012 Presidential Candidate Preference (United Daily)

05

101520253035404550

Mar

-11

Apr-1

1

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Ying-jeou Ma Ing-wen Tsai James Soong

2012 Presidential Candidate Preference (Liberty Times)

05

10152025303540

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Ying-jeou Ma Ing-wen Tsai James Soong

Source: United Daily poll Source: Liberty Times

22 November 2011

Taiwan Market Strategy 12

Do not forget about the legislative election While most of the focus will be on the presidential election, the outcome of the legislative election will also dictate Taiwan’s political landscape over the next four years. We still believe that the outcome of the presidential election is firmer (i.e., a 0.1% win is still a win) while the legislative election is less direct. Currently, KMT holds 65% of total seats (was 75% at the beginning of 2008) but there is risk that KMT could end up with much less control or that neither KMT nor DPP will end up controlling 50% of the Legislative Yuan, which makes it more difficult for President Ma to push through more a controversial agenda even if re-elected for the second term. Hence, we believe investors will likely stay cautious into the election as it is perceived to be more of a risk than a catalyst. This concern over a potential KMT loss could facilitate sector rotation out of non-tech as we head into year-end.

Figure 38: KMT currently has 65% control in the

Legislative Yuan (down from 75%)

Figure 39: xFuture Expects less KMT control on the

upcoming Legislative Yuan election

Legislative Yuan Party Breakdown

Kuomintang65%

Democratic Progressive

Party30%

Non-Partisan 5%

xFuture Expectation of Legislative Yuan Election

Kuomintang54%

Democratic Progressive

Party42%

Non-Partisan 4%

Source: Central Election Commission Source: The Exchange of Future Events

The outcome is, at best, status quo As we noted in our previous Taiwan Market Strategy report (Reading the cycles…, published on 29 August), unlike in the 2004 and 2008 elections where the market hoped for a change (i.e., the hope that at least the political gridlock of one party controlling the presidency and the other controlling the legislature would be removed), in this election the hope is for no change. It almost appears that the best outcome for the election would be maintaining status quo, or a neutral. In our view, the worst outcome would be if one party ends up controlling the presidency and the other the Legislative Yuan, as this would take Taiwan back to the political gridlock seen between 2000 and 2008.

Figure 40: The political landscape in Taiwan 2000-2004 2004-2008 2008-2012 2012-2016 President Chen Shui-Bian (DPP) Chen Shui-Bian (DPP) Ma Ying-Jeou (KMT) ??

Legislative Yuan

KMT 30.7% 35.6% 64.6% ??

PFP 20.4% 15.1% 8.0% ??

DPP 44.4% 44.9% 23.9% ??

Others 4.4% 4.4% 3.5% ??

Source: Central Election Commission

What makes investors more uneasy is that, historically, pre-election polls usually end up favouring KMT candidates as there tend to be more “undecided” voters who end up voting for the DPP candidate. If we look at the last three presidential elections (Figure 41), the KMT candidate’s actual votes were less than what pre-election polls indicated, if we re-base the poll only to those expressed a view. Conversely, DPP’s actual votes have consistently been higher than pre-election polls. We believe this phenomenon may be

22 November 2011

Taiwan Market Strategy 13

attributed to the way polls are carried out in Taiwan. However, this track record does suggest that the current close race between KMT and DPP could end up being a slight advantage for the DPP.

Figure 41: Historical presidential election results versus pre-election poll Election Date KMT Candidate DPP Candidate PFP Candidate

2000 18-Mar-00 Lien Chan Chen Shui-Bian James Soong

Outcome 23.1% 39.3% 36.8%

Pre-Poll 27.0% 37.8% 35.1%

2004 20-Mar-04 Lien Chan Chen Shui-Bian n.a.

Outcome 49.9% 50.1% n.a.

Pre-Poll 54.5% 45.5% n.a.

2008 22-Mar-08 Ma Ying-Jeou Frank Hsieh n.a.

Outcome 58.5% 41.6% n.a.

Pre-Poll 64.6% 35.4% n.a.

Note: Pre-poll data were re-based by number of people who expressed their political inclination toward the

election. In the 2000 pre-poll, 74% of those interviewed expressed an opinion, in the 2004 pre-poll, 77% did

and in the 2008 pre-poll, 82% of those interviewed expressed an opinion.

Source: Central Election Commission, TVBS poll, United Daily poll

While sentiment about the election can have a material impact on the equity market in the near term, it has affected non-tech to a much greater degree than tech in the past. This is mainly because non-tech sectors (i.e., airlines, tourism and asset plays) are perceived to be the major beneficiaries if KMT wins and Taiwan enters into an expedited economic (but not necessarily political) cooperation or integration with China. We believe that even if a DPP candidate is elected president, Taiwan will continue to develop its economic ties with China but at a much moderate pace compared to that under a KMT government.

Figure 42: Selective sector performance pre and post

2000 presidential election

Figure 43: Selective sector performance pre and post

2004 presidential election 2000 Presidential Election (DPP Victory)

80

85

90

95

100

105

110

115

Feb-00 Mar-00 Apr-00

Index price

Electronics, 2000 Developer, 2000 Transportation, 2000 Tourism, 2000

DPP won the presidentaiol election. Developer/Transportation/Tourism stocks were sold off.

2004 Presidential Election (DPP Victory)

80

85

90

95

100

105

110

115

120

Feb-04 Mar-04 Apr-04

Index price

Electronics, 2004 Developer, 2004 Transportation, 2004 Tourism, 2004

Poll suggested KMT would win.

DPP won the election and Developer/Transportation/Tourismstocks were sold off.

Source: Central Election Commission Source: United Daily poll

Market supported ahead of election? It is widely believed (especially among domestic investors) that the market will see some form of government support (either through policy stimulus or real intervention) ahead of the elections in the hope of fostering positive market sentiment. In the last four presidential elections we have seen that the Taiwan market outperformed regional markets by almost 8% three months ahead of the election, though we feel this has become almost self-fulfilling as we estimate government related funds account for less than 5% of Taiwan’s total market cap. In other words, the so-called election rally is really driven by stronger retail confidence that leads to higher market participation and turnover.

However, if retail investors fear that the election outcome is too uncertain and could turn out to be negative, then it would be very difficult for the government to foster an election rally. If we look at fund flow in the last six months, it seems to suggest there could be

22 November 2011

Taiwan Market Strategy 14

some level of government support already in place to prevent a bigger market decline year-to-date. The amount of QFII (20-30% of market) net selling in the last six months is significant and equivalent to 61% of total QFII selling during the financial crisis back in late 2008-2009. At the same time, retail’s (50-60% of market) long margin is also at one of the lowest levels in history (ex-crisis). Hence, one of the key buyers in the market is likely the government or its affiliates (we have seen consistent net buying by local ITC, which gets part of its mandate from the government’s pension funds).

Figure 44: QFII net sold NT$341 bn since May Figure 45: ITC net bought NT$13.6 bn since August

-300

-200

-100

0

100

200

300

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

(NT$ bn)

QFII net sold NT$341bnsince May

QFII net sold NT$531bnin financial crisis

QFII

-40

-20

0

20

40

60

80

100

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

ITC(NT$ bn)

ITC net bought NT$13.6bnsince August

Source: TEJ, Credit Suisse research Source: TEJ, Credit Suisse research

Figure 46: Retail’s long margin balance is near the low of

its historical range (ex-previous crisis)

Figure 47: The implied TAIEX (calculated based on retail

long margin) is noticeably lower than the actual

-

100

200

300

400

500

600

700

Jan-

97

Oct

-97

Aug-

98

Jun-

99

Apr-

00

Jan-

01

Nov

-01

Sep-

02

Jul-0

3

Apr-

04

Feb-

05

Dec

-05

Oct

-06

Aug-

07

May

-08

Mar

-09

Jan-

10

Nov

-10

Sep-

11

Long Balance Average(NT$ bn)

Current margin balance nearrecession level

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

TAIEX (RHS) Margin implied TAIEX (Index)

Techbubble

Asian financialcrisis

Globalfinancial crisis

Source: TEJ, Credit Suisse research Source: TEJ, Credit Suisse research

22 November 2011

Taiwan Market Strategy 15

Figure 48: Major cross strait policies and regulatory changes Effective time Cross-strait development Details

Jun-08 to Jun-11 Direct flights Jun-08: Agreement reached on 13 June 2008 to begin charter flights on weekends starting 4

July 2008. A total of 18 flights per weekend (Friday to Monday) were allowed. According to

the agreement, anyone with legal traveling documents, regardless of nationality, was allowed

to travel on these charter flights.

Jun-11: In November 2008, flights became daily instead of only for the weekends. 108

weekly flights were established and planes no longer had to travel through Hong Kong

airspace, cutting travel times by two-thirds in some cases (flying from Taipei to Shanghai).

Aug-09: In April 2009, a new agreement was reached to allow cross-strait flights to become

regularly scheduled instead of chartered. The cap on flights was also raised to 270 per week,

effective 31 August 2009.

May-10: On 22 May 2010, another 100 weekly flights were permitted (370 flights in

total), effective 14 June 2010, and added Shanghai Hongqiao International Airport and

Shijiazhuang Airport to the list of allowed destinations.

Jun-11: Increased direct flights to 558 per week (from 370). In addition, Taiwan was to kick

off a trial programme on 28 June to allow individual tourists from three mainland Chinese

cities—namely Shanghai, Beijing and Xiamen—to visit the island.

Jul-08 to Jun-11 Chinese tourists Jul-08: Under the agreement reached on 13 June 2008, Taiwan was opened to 3,000

Mainland tourists per day.

May-10: Both sides have agreed to ramp up efforts to boost cross-straits tourism by opening

tourism offices in each other’s regions with 5,000 tourists a day.

Jun-11: Taiwan to start a trial programme on 28 June to allow individual tourists from three

mainland Chinese cities (Shanghai, Beijing and Xiamen) to visit the island (up to 500

individuals per day). Currently, there are 1.6 mn mainland tourists a year and the

government targets reaching 2 mn-plus with individual tourists.

Aug-08 Loosening outbound

investment restrictions

Investment threshold up to 60% NAV. MNC subsidiaries will be exempt from any

investment limits. SMEs will have two options in terms of mainland Chinese investment cap.

First is the maximum investment cap of NT$80 mn, and the other is 60% of their company net

worth. As for large-sized enterprises, they will be allowed to invest 60% of their net worth or

their group combined net worth in China, up from the existing maximum percentage of 40%.

Nov-09 Financial MOU China/Taiwan have signed three MOUs on banking, insurance, and securities. The MOUs,

took effect in Jan-10, establish the financial supervisory framework and opening discussions

on financial market access for both sides.

Jan-10 Loosening inbound

investment restrictions Under the financial MOU agreement reached on 16 November 2009, Taiwan allows up to 5%

direct investment from China and another 5% through QDII with an aggregate amount of no

more than US$500 mn. Separate approval is required from MOEA for investments over 10%.

Jun-10 ECFA The two sides signed the cross-straits Economic Cooperation Framework Agreement (ECFA),

in which: (1) China will cut tariff on 539 items while Taiwan will cut tariff on 267 items (2011-

2013) and; (2) Taiwan banks can do RMB business with Taiwanese corporates in China one

year after branch upgrade (vs two years under CEPA and three years under WTO).

20-Dec-2010 to

1H12

Cross-Strait Agreement on

Investment Protection

Dec-10: China/Taiwan reached consensus on the "Cross-Strait Agreement on Investment

Protection". Both sides agreed to establish a contact platform and dispute settlement

mechanism featuring a transparent investment process and full communication.

Feb-11: Taiwan hoped within six months to first create cross-straits investment protection

accord and dispute resolution mechanisms within one year to complete negotiations on tax

cuts for the panel and automobile sectors.

Scheduled to be signed in the 8th round cross-strait talks.

Source: Commercial Times, MoEA, SEF

22 November 2011

Taiwan Market Strategy 16

Choosing a basket of yield stocks for next year The Taiwan market is one of the highest dividend yield markets (4.3%) in the region and this is even more attractive give that the interest rate is expected to stay extremely low (sub-1.5%) through 2012. This, together with our view of moderate growth for 2012, suggests that stocks that can provide consistent good dividends with some growth should outperform the market.

Therefore, we screened our coverage universe of 95 stocks using the criteria of: (1) at least 5% dividend yield for next year; (2) positive earnings growth into the following fiscal year so once can expect dividend to grow; (3) net cash on balance sheet; (4) positive free cash flow and; (5) market cap of US$1 bn-plus. Using these criteria to choose a basket of yield stocks each year, has outperformed the market every year in the past nine years (2003-YTD 2011, Figure 51). For 2012, we highlight a list of eight stocks: HTC, Novatek, Asustek, TSMC, MStar, E Ink, Taiwan Cement and FET.

Figure 49: Valuation matrix for the eight top high yield picks in Taiwan Price EPS (NT$) P/E (x) P/B (x) ROE (%) Earnings growth (%)

Ticker Company (NT$) Rating 2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E

2330.TW TSMC 74.2 O 5.1 5.6 14.4 13.2 3.1 2.8 22.2% 22.0% -17.5% 8.9%

2498.TW HTC 660.0 O 76.8 78.4 8.6 8.4 5.4 4.3 73.3% 56.4% 66.7% 2.1%

4904.TW Far EasTone 56.9 O 2.6 3.1 21.7 18.1 2.6 2.5 11.9% 14.1% -3.3% 19.6%

2357.TW Asustek 202.5 O 22.1 25.5 9.2 7.9 1.3 1.1 14.5% 15.5% -16.0% 15.4%

1101.TW Taiwan Cement 33.0 O 2.5 3.2 13.0 10.4 1.3 1.2 9.8% 11.8% 17.1% 24.9%

3697.TW MStar 170.5 O 11.9 14.9 14.3 11.5 2.8 2.5 19.8% 22.9% -11.2% 24.9%

8069.TWO E Ink 59.2 O 6.7 7.0 8.9 8.4 2.5 2.2 28.9% 28.2% 74.8% 5.4%

3034.TW Novatek Micro 77.1 O 6.4 7.6 12.1 10.1 2.1 1.9 17.4% 19.8% -16.9% 19.0%

Source: Company data, Credit Suisse estimates

Figure 50: Taiwan’s high dividend yield is even more

attractive with ten-year bond yield falling

Figure 51: The high yield basket has outperformed the

market in 2003-2011

Taiwan dividend yield vs. 10-yr bond rate

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Feb-

06

Jun-

06

Oct

-06

Feb-

07

Jun-

07

Oct

-07

Feb-

08

Jun-

08

Oct

-08

Feb-

09

Jun-

09

Oct

-09

Feb-

10

Jun-

10

Oct

-10

Feb-

11

Jun-

11

%

Taiwan dividend yield vs. 10-yr bond rate

Basket relative performance

33%

2%14%

25%

3%

36%

4%

86%

28%

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011

Basket relative performance

Hitosical average outperformance of 26%

Source: TEJ, Credit Suisse estimates * Relative performance is based on simple average of the basket

against TAIEX.

Source: Bloomberg, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 17

Figure 52: Historical dividend high yield basket

2012 CompanyTarget price

(NT$)Rating Div Yld (%)

Net debt (cash) to equity (%)

Free cash flow yield

(%)

Earning growth (%)

P/B (x) P/E (x) ROE (%)

8069.TWO E Ink 88.0 O 9.5% -12.2% 10.7% 5.5% 2.2 8.4 28.2%3034.TW Novatek Micro 90.0 O 7.3% -39.7% 8.1% 19.1% 1.9 10.1 19.8%2498.TW HTC 930.0 O 7.1% -89.0% 10.8% 2.1% 4.3 8.4 56.4%1101.TW Taiwan Cement 43.5 O 6.7% -6.0% 7.6% 24.9% 1.2 10.4 11.8%3697.TW Mstar 223.0 O 6.5% -75.6% 8.6% 24.8% 2.5 11.5 22.9%2330.TW TSMC 79.0 O 5.4% -17.2% 4.7% 8.9% 2.8 13.2 22.0%2357.TW Asustek Computer 260.0 O 5.1% -50.7% 13.4% 20.4% 1.1 7.9 15.5%4904.TW Far East Tone 58.5 O 5.0% -17.8% 6.9% 19.6% 2.5 18.1 15.4%

2011 CompanyTarget price

(NT$)Rating Div Yld (%)

Net debt (cash) to equity (%)

Free cash flow yield

(%)

Earning growth (%)

P/B (x) P/E (x) ROE (%)

8069.TWO E Ink 88.0 O 8.3% -6.3% 15.0% 78.8% 2.5 8.9 28.9%2015.TW Feng Hsin 54.8 N 5.7% -26.5% 12.7% 12.4% 1.9 12.2 16.3%1101.TW Taiwan Cement 43.5 O 5.4% -3.9% 7.4% 17.1% 1.2 12.9 9.8%2498.TW HTC 930.0 O 5.4% -91.9% 9.2% 67.4% 7.0 11.2 73.3%

2010 CompanyTarget price

(NT$)Rating Div Yld (%)

Net debt (cash) to equity (%)

Free cash flow yield

(%)

Earning growth (%)

P/B (x) P/E (x) ROE (%)

2498.TW HTC 930.0 O 11.1% -100.8% 14.7% 74.9% 3.8 7.2 56.3%2412.TW ChungHwa Telecom 100.0 N 11.1% -24.8% 7.2% 8.8% 1.9 14.7 12.9%1326.TW Formosa Chemical 106.6 O 10.8% -4.5% 12.7% 60.6% 1.5 8.4 18.8%1301.TW Formosa Plastics 94.2 N 10.1% -12.7% 11.4% 65.4% 1.6 9.0 18.7%5371.TWO Coretronic Corp 26.0 N 7.5% -48.5% 16.3% 32.0% 1.6 9.5 18.0%1101.TW Taiwan Cement 43.5 O 6.0% -2.3% 8.0% 8.2% 1.3 15.4 9.2%2357.TW Asustek Computer 260.0 O 5.9% -39.0% 9.0% 32.1% 1.4 9.0 11.8%2324.TW Compal Electronics 26.0 N 5.4% -20.3% 8.7% 21.2% 1.6 8.1 20.4%

2009 CompanyTarget price

(NT$)Rating Div Yld (%)

Net debt (cash) to equity (%)

Free cash flow yield

(%)

Earning growth (%)

P/B (x) P/E (x) ROE (%)

2382.TW Quanta Computer 70.0 O 10.4% -32.4% 12.6% 10.3% 1.1 5.6 21.6%1301.TW Formosa Plastics 94.2 N 9.8% -1.5% 11.3% 39.7% 1.1 9.1 13.6%2881.TW Fubon FHC 36.0 N 9.0% -- -- 83.3% 0.8 9.0 11.3%2885.TW Yuanta FHC 21.0 O 6.1% -- -- 340.5% 0.9 16.4 6.5%

2008 CompanyTarget price

(NT$)Rating Div Yld (%)

Net debt (cash) to equity (%)

Free cash flow yield

(%)

Earning growth (%)

P/B (x) P/E (x) ROE (%)

2382.TW Quanta Computer 70.0 O 7.9% -54.0% 21.2% -12.6% 1.7 7.9 21.6%2498.TW HTC 930.0 O 6.7% -105.6% 9.5% -1.0% 5.7 12.1 49.0%4904.TW Far East Tone 58.5 O 5.8% -9.1% 9.8% -12.6% 2.2 15.7 14.6%2412.TW ChungHwa Telecom 100.0 N 5.6% -25.3% 7.9% -6.7% 1.8 14.8 11.7%

2007 CompanyTarget price

(NT$)Rating Div Yld (%)

Net debt (cash) to equity (%)

Free cash flow yield

(%)

Earning growth (%)

P/B (x) P/E (x) ROE (%)

1301.TW Formosa Plastics 94.2 N 13.3% -7.4% 10.9% 54.8% 1.2 6.0 21.6%2002.TW China Steel Corp. 31.1 N 12.1% -0.8% 10.9% 30.9% 1.5 6.5 24.1%2498.TW HTC 930.0 O 10.3% -100.4% 13.4% 14.6% 5.1 9.8 58.5%2325.TW SPIL 36.0 O 9.1% -26.3% 8.3% 31.2% 2.2 8.6 26.5%2324.TW Compal Electronics 26.0 N 8.6% -59.8% 13.2% 56.4% 1.2 7.8 16.8%2892.TW First FHC 20.0 N 8.0% -- -- 17.7% 1.2 11.4 12.2%2412.TW ChungHwa Telecom 100.0 N 6.7% -23.9% 9.9% 14.7% 1.6 12.8 12.1%2382.TW Quanta Computer 70.0 O 6.3% -22.8% 8.4% 42.9% 2.2 10.4 22.8%1722.TW Taiwan Fertilizer 104.1 O 5.5% -26.2% 4.0% 3.6% 1.2 16.2 7.4% Note: O = Outperform; N = Neutral.

* We exclude earnings growth criteria for 2008 given most companies faced earnings decline on YoY basis in that year.

Source: TEJ, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 18

CS Taiwan model portfolio adjustment We adjust our Taiwan model portfolio to OVERWEIGHT tech (from a slight underweight) as we believe there will be a sector rotation back to tech with many of the factors that drove rotation from tech to non-tech during May-2010 to Oct-2011 reversing. Most notably, tech has led this earnings cut cycle (-42% versus -21%) and is trading at a discount to non-tech (12.3x versus 15.2x P/E) despite better earnings growth in 2012 (53% versus 0%, or 17% versus -2% ex-DRAM, TFT and transportation sectors). Both the QFII and local ITC’s portfolio weighting in tech are one standard deviation below their historical average and 78% of total QFII net selling of US$9 bn YTD is in tech. Hence, there will be tailwinds for the sector rotation when it kicks off.

We have funded our Overweight in tech by lowering our weighting in financials (from 1% Overweight to 1.8% UNDERWEIGHT), property (from Neutral to 2.1% UNDERWEIGHT) and transportation (from 1.6% Overweight to 1.2% UNDERWEIGHT).

Figure 53: Taiwan model portfolio Mkt Cap Price ($) PE (x) PB (x) ROE (%)

Sector Bberg (US$ mn) 18-Nov-11 Base % Up Rating 2011E 2011E 2011E MSCI (%) CS (%) vs MSCI (%)A B C=B-A

Tech 55.6 61.6 6.0Foundry 18.4 18.4 0.0TSMC 2330 63,700 74.2 79.0 6.5 O 14.4 3.1 22.2% 16.9 18.4 1.5Backend 2.4 3.6 1.2SPIL 2325 2,867 27.7 36.0 30.0 O 19.2 1.5 7.5% 0.8 3.6 2.8

Memory 1.3 0.0 (1.3)IC Design 4.9 9.4 4.5Novatek Micro 3034 1,533 77.1 90.0 16.7 O 12.1 2.1 17.4% 0.4 4.4 4.0

Mstar 3697 2,960 170.5 223.0 30.8 O 14.3 2.8 19.8% 0.6 5.0 4.4Display 2.9 4.0 1.1

E Ink 8069 2,119 59.2 88.0 48.6 O 8.9 2.5 28.9% 0.4 4.0 3.6Components 4.6 4.6 (0.0)Catcher Technology 2474 4,248 169.5 210.0 23.9 O 12.0 2.7 26.8% 0.8 4.6 3.8PC Hardware 15.4 14.4 (1.0)Synnex 2347 3,692 71.1 0.9 4.2 3.3Asustek Computer 2357 4,765 202.5 260.0 28.4 O 9.2 1.3 14.5% 1.3 6.0 4.7

Quanta Computer 2382 7,782 61.4 70.0 14.0 O 10.4 1.9 18.7% 1.4 4.2 2.8

Handset 5.7 7.2 1.5HTC 2498 18,835 660.0 930.0 40.9 O 8.6 5.4 73.3% 4.4 7.2 2.8

Non-tech 44.4 38.4 (6.0)Financials 13.7 11.9 (1.8)Yuanta FHC 2885 4,554 15.7 21.0 33.8 O 8.8 1.1 12.2% 1.2 6.4 5.2

Chinatrust FHC 2891 6,042 17.1 23.5 37.8 O 9.5 1.3 13.8% 1.5 5.5 4.0Petrochem 9.0 9.0 (0.0)

Formosa Chemical 1326 15,079 80.0 106.6 33.3 O 10.7 1.7 15.7% 2.1 6.0 3.9

Formosa Plastics 1301 16,281 80.3 94.2 17.3 N 12.1 1.9 15.6% 2.9 3.0 0.1Property 2.1 0.0 (2.1)Materials 7.0 8.5 1.5Taiwan Cement 1101 4,036 33.0 43.5 31.8 O 13.0 1.3 9.8% 1.0 6.5 5.5Cheng Shin Rubber 2105 5,179 64.5 77.9 20.8 O 16.1 3.2 20.8% 1.0 2.0 1.0Telecom 5.9 5.9 (0.0)Far EasTone 4904 6,141 56.9 58.5 2.8 O 21.7 2.6 13.2% 0.8 5.9 5.1Transportation 1.2 0.0 (1.2)Retail 3.0 3.0 (0.0)Uni-President 1216 5,809 38.9 46.6 19.9 O 18.7 2.4 13.2% 1.4 3.0 1.6Industrials/Others 2.4 0.1 (2.3)Total 100.0 100.0 0.0

Target Price (NT$)

Note: O = Outperform.

Source: Company data, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 19

Figure 54: Comparison between Taiwan model portfolio and CS Taiwan coverage P/E (x) P/B (x) ROE (%) Earnings growth (%) Dividend yield (%) Beta

2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E 2011E 2012E

Taiwan model portfolio 11.6 11.0 2.2 2.0 20.1% 18.8% 14.7% 6.3% 4.8% 4.8% 0.9 CS Taiwan coverage 16.8 13.7 1.7 1.6 10.3% 12.1% -21.7% 22.4% 4.3% 4.2% 1.1

Source: Company data, Bloomberg, Credit Suisse estimates

Maintain index target of 8,500 We have year-end 2012 index target of 8,500 (18% implied upside), which is based on 1.8x forward P/B, or the mid-point of Taiwan’s historical P/B range. Our current estimate of 12.1% ROE for 2012 is higher than its historical average of 11%, though it should be roughly at par if we also take into account 5-10% further earnings revision into 1Q 2012.

Figure 55: P/E of Taiwan market Figure 56: P/B of Taiwan market

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Average = 17.33

+1 Std dev = 23.2

-1 Std dev = 11.5

+2 Std dev = 29.10

-2 Std dev = 5.6

Market PE (x)Current Forward PE @ 14.4 x

1.0

1.5

2.0

2.5

3.0

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Average = 1.80

+1 Std dev = 2.1

-1 Std dev = 1.5

+2 Std dev = 2.43

-2 Std dev = 1.2

Market PB (x)Current Forward PB @ 1.7 x

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

22 November 2011

Taiwan Market Strategy 20

Taiwan valuation summary Figure 57: Credit Suisse P/B vs ROE analysis—

(upstream tech)

Figure 58: Credit Suisse P/B vs ROE analysis—

(downstream tech)

TSMC

UMCVanguard

ASE

PowertechSPIL

InoteraNanya Tech

Elan

MediaTek

Mstar

Novatek

Pixart

RealtekWPG

AUO

Coretronic

GiantplusCMI

E InkTPK

Wintek Young Fast

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

5.0% 7.5% 10.0% 12.5% 15.0% 17.5% 20.0% 22.5% 25.0%Return on Equity (% EPS / BV)

Price

/ B

ook

Valu

e (P

/ BV

)

Inex pensiv e

Ex pensiv e

P P E - = - / -

E BV BV

GEM TEKD-Link

CyberTAN

Silitech

Largan

HTC

Wistron

Quanta

Pegatron

Hon Hai

Foxcon

Compal

Catcher

AustekAcer

I-Chiun

Everlight

Epistar

Unimicron

Tripot

Topoint

Nan Ya PCB

Kinsus

Delta

Chicony

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

5.0% 7.5% 10.0% 12.5% 15.0% 17.5% 20.0% 22.5% 25.0%Return on Equity (% EPS / BV)

Price

/ B

ook

Valu

e (P

/ BV

)

Inex pensiv e

Ex pensiv e

P P E - = - / -

E BV BV

Source: TEJ, Credit Suisse estimates Source: TEJ, Credit Suisse estimates

Figure 59: Credit Suisse P/B vs ROE analysis—

(financials)

Figure 60: Credit Suisse P/B vs ROE analysis—

(non-tech)

Yuanta Mega

Hua Nan

FirstCHB

Taishin

Ta ChongSinoPac

E. Sun

Chinatrust

Shin Kong

Fubon

Cathay

0.8x

1.0x

1.2x

1.4x

1.6x

1.8x

2.0x

6.0% 8.0% 10.0% 12.0% 14.0% 16.0%Return on Equity (% EPS / BV)

Pric

e /

Boo

k Va

lue

(P /

BV)

Inexpensive

Expensive

P P E - = - / -

E BV BV

Cheng Shin Rubber

Uni-President

President Chain Store

Yang Ming M arine Wan Hai Lines

U-M ing Marine

Sincere Navigation

Evergreen Marine

EVA AirChina Airlines

Feng Hsin

Tung Ho Steel

China Steel

Asia Cement

Taiwan Cement

Sinyi Realty

Taiwan FertilizerFar Eastern Textiles

Chong Hong

FargloryHuaku

Hung Poo

Prince Housing

Nan Ya Plastics

Formosa Plastics

Formosa Petrochemical

Formosa Chemical

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

5.0% 7.5% 10.0% 12.5% 15.0% 17.5% 20.0% 22.5% 25.0%Return on Equity (% EPS / BV)

Pric

e /

Boo

k Va

lue

(P /

BV)

Inexpensive

Expensive

P P E - = - / -

E BV BV

Source: TEJ, Credit Suisse estimates Source: TEJ, Credit Suisse estimates

22 N

ovem

ber 2011

Taiw

an M

arket Strateg

y 21

Figure 61: Credit Suisse Taiwan coverage universe key valuation matrix 12-mth EPS Earnings P/E P/B ROAE Div Mkt cap Price 12-mth Invst. return (NT$) Growth (%) (x) (x) (%) yield (%) Analyst Company US$ mn 18-Nov target rating (%) 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012

2330.TW TSMC 63,700 74.2 79.0 O 10.5 5.15 5.60 -17.5 8.9 14.4 13.2 3.1 2.8 22.2 22.0 4.0 4.0 Randy Abrams 2303.TW UMC 5,249 12.6 12.6 N 3.0 0.80 0.78 -57.9 -1.4 15.7 16.2 0.8 0.8 4.7 4.7 0.0 3.4 Randy Abrams 5347.TWO Vanguard 618 11.2 12.0 N 10.4 0.38 0.47 -67.5 24.2 29.3 23.7 0.9 0.9 3.1 3.8 5.4 2.4 Randy Abrams Foundry 69,567 -23.1 8.2 14.6 13.5 2.4 2.3 17.1 17.4 3.7 4.0 2311.TW ASE 6,131 27.6 34.0 O 25.7 2.10 2.40 -23.9 14.0 13.1 11.5 1.8 1.6 14.8 14.9 2.4 2.3 Randy Abrams 6239.TW Powertech 1,849 70.0 88.0 O 30.6 8.19 8.01 -14.4 -2.2 8.5 8.7 1.6 1.4 18.8 17.0 5.7 4.7 Randy Abrams 2325.TW SPIL 2,867 27.7 36.0 O 34.8 1.45 1.75 -19.8 20.7 19.2 15.8 1.5 1.4 7.5 9.1 5.8 4.7 Randy Abrams Backend 10,846 -20.9 11.0 13.0 11.7 1.6 1.5 13.0 13.4 3.8 3.3 3474.TW Inotera 665 4.4 17.0 N 290.8 -1.98 0.51 n.m n.m n.m 8.5 0.5 0.4 -18.9 5.3 0.0 0.0 MS Hwang 2408.TW Nanya Tech 357 2.7 10.0 U 274.5 -5.20 0.33 n.m n.m n.m 8.1 0.9 0.5 -95.0 7.7 0.0 0.0 MS Hwang Memory 1,022 n.m n.m n.m 13.8 0.9 0.7 -42.7 5.9 0.0 0.0 2458.TW Elan 402 29.2 25.0 U -11.5 1.12 0.98 -33.4 -12.5 25.9 29.6 1.9 1.9 7.6 6.5 2.7 2.6 Jimmy Huang 2454.TW MediaTek 11,237 308.0 306.0 U 2.8 13.06 15.30 -53.5 21.9 23.6 20.1 3.3 3.2 13.3 16.3 6.4 3.1 Randy Abrams 3034.TW Novatek 1,533 77.1 90.0 U 23.1 6.39 7.61 -16.3 19.1 12.1 10.1 2.1 1.9 17.4 19.8 6.4 7.3 Jerry Su 3227.TWO Pixart 344 80.1 78.0 N 1.2 2.96 4.32 -52.6 47.6 27.0 18.5 1.7 1.7 6.2 9.0 4.0 4.0 Jimmy Huang 2379.TW Realtek 775 48.5 50.0 U 3.2 3.42 3.85 -1.3 12.6 14.2 12.6 1.5 1.4 10.0 11.4 0.0 0.0 Randy Abrams 3702.TW WPG 1,672 32.8 44.0 O 39.1 3.38 4.00 7.9 18.3 9.7 8.2 1.5 1.3 15.6 17.2 0.0 5.7 Randy Abrams IC design 18,923 -35.5 20.9 17.6 14.6 2.5 2.4 14.3 16.9 5.3 3.9 2409.TW AUO 4,020 13.8 16.0 O 16.7 -6.00 -1.40 n.m n.m n.m n.m 0.5 0.6 -20.8 -5.6 0.0 0.0 Jerry Su 5371.TWO Coretronic 590 24.6 26.0 N 12.2 2.07 2.99 -57.6 44.7 11.9 8.2 1.1 1.0 8.1 12.5 5.5 7.9 Jerry Su 8105.TW Giantplus 144 9.9 11.0 N 11.6 -1.22 -0.71 n.m n.m n.m n.m 0.5 0.6 -6.5 -4.0 0.0 0.0 Jimmy Huang 3481.TW CMI 3,165 13.3 13.0 N -1.9 -8.16 -4.29 n.m n.m n.m n.m 0.5 0.6 -26.1 -17.1 0.0 0.0 Jerry Su 8069.TWO E Ink 2,119 59.2 88.0 O 56.8 6.67 7.02 78.8 5.5 8.9 8.4 2.5 2.2 28.9 28.2 8.3 9.5 Jerry Su 3673.TW TPK 3,703 442.0 800.0 O 82.5 51.58 57.09 174.3 20.4 8.6 7.7 2.8 2.1 46.9 33.3 1.7 4.2 Jerry Su 2384.TW Wintek 1,078 20.3 18.0 U -10.7 0.22 1.50 -83.6 634.4 93.0 13.5 0.9 0.8 1.0 6.3 0.5 0.6 Jerry Su 3622.TW Young Fast 398 79.9 84.0 N 9.1 4.84 8.00 -72.8 65.7 16.5 10.0 1.1 1.0 6.7 10.9 4.2 4.8 Jerry Su TFT LCD 15,217 n.m n.m n.m n.m 0.8 0.8 -14.7 -2.7 1.9 2.8 3514.TW Gintech 320 28.6 36.0 N 29.7 -1.05 2.70 n.m n.m n.m 10.6 0.7 0.7 -2.2 6.7 0.0 4.1 Darryl Cheng 6244.TWO Motech 723 50.0 49.0 U 0.0 -2.28 2.30 n.m n.m n.m 21.8 1.2 1.1 -4.8 5.4 0.0 2.3 Darryl Cheng 5483.TWO Sino-American 585 42.4 48.0 N 17.4 3.14 3.29 -62.7 9.4 13.5 12.9 1.0 1.0 7.2 7.7 4.0 4.2 Darryl Cheng Solar 1,628 n.m n.m n.m 14.6 1.0 0.9 0.0 6.6 1.5 3.4 2385.TW Chicony 1,033 48.4 58.0 N 28.1 6.96 6.06 22.9 -12.9 6.9 8.0 1.6 1.5 25.7 19.1 9.2 8.0 Pauline Chen 2308.TW Delta 5,618 70.6 60.0 U -9.6 4.66 5.18 -28.9 11.2 15.1 13.6 1.8 1.8 12.5 13.2 5.1 5.5 Pauline Chen 3189.TW Kinsus 1,448 98.0 110.0 N 16.3 6.67 8.43 21.2 26.5 14.7 11.6 1.8 1.6 12.7 14.6 4.1 4.1 Pauline Chen 8046.TW Nan Ya PCB 1,623 75.6 100.0 N 33.4 5.74 7.75 81.0 35.5 13.2 9.8 1.4 1.2 10.9 13.4 0.9 1.2 Pauline Chen 8021.TW Topoint 101 20.3 26.0 N 32.5 2.06 2.40 14.3 16.1 9.8 8.4 0.8 0.8 9.0 9.4 4.1 4.1 Pauline Chen 3044.TW Tripod 1,381 79.3 90.0 N 17.5 7.99 7.95 -17.3 -0.5 9.9 10.0 1.9 1.7 19.9 17.8 4.0 4.0 Pauline Chen 3037.TW Unimicron 1,800 35.3 43.0 N 27.6 3.69 3.95 -20.3 7.2 9.6 8.9 1.2 1.1 13.0 14.0 7.4 5.6 Pauline Chen Components 13,003 -10.5 9.9 12.1 11.0 1.6 1.5 13.8 14.2 5.0 4.9

22 N

ovem

ber 2011

Taiw

an M

arket Strateg

y 22

Figure 61: Credit Suisse Taiwan coverage universe key valuation matrix (continued) 12-mth EPS Earnings P/E P/B ROAE Div Mkt cap Price 12-mth Invst. return (NT$) Growth (%) (x) (x) (%) yield (%) Analyst Company US$ mn 18-Nov target rating (%) 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012

2448.TW Epistar 1,635 58.1 65.0 N 15.8 1.48 3.79 -78.1 157.3 39.3 15.3 1.2 1.1 2.9 7.7 1.6 4.2 Darryl Cheng 2393.TW Everlight 716 51.6 54.0 N 9.9 3.40 4.31 -38.3 26.8 15.2 12.0 1.6 1.5 10.4 12.9 4.3 5.4 Darryl Cheng 2486.TW I-Chiun 100 14.6 51.0 O 268.5 4.22 4.74 24.1 12.4 3.5 3.1 0.6 0.6 18.3 19.1 20.4 19.1 Darryl Cheng LED 2,451 -59.4 69.6 20.8 12.2 1.2 1.2 5.7 9.8 3.2 5.2 2353.TW Acer Inc. 2,959 34.2 26.0 U -22.7 -2.73 2.15 n.m n.m n.m 15.9 1.2 1.1 -8.3 7.0 10.9 n.a. Thompson Wu 2357.TW Asustek 4,765 202.5 260.0 O 28.4 22.10 25.50 -3.3 20.4 9.2 7.9 1.3 1.1 14.5 15.5 6.1 5.1 Thompson Wu 2474.TW Catcher 4,248 169.5 210.0 O 26.6 14.11 16.18 144.9 14.7 12.0 10.5 2.7 2.3 26.8 23.6 2.4 2.7 Pauline Chen 2324.TW Compal 4,123 28.8 26.0 N -4.9 3.19 3.54 -40.8 11.1 9.0 8.1 1.1 1.0 11.7 12.5 7.5 4.4 Thompson Wu 2354.TW Foxconn Tech 3,852 99.5 89.5 N -2.2 6.50 7.25 8.8 11.6 15.3 13.7 1.9 1.7 13.3 13.3 1.3 8.7 Thompson Wu 2317.TW Hon Hai 28,094 80.1 102.7 N 30.9 7.92 9.24 9.4 16.7 10.1 8.7 1.5 1.3 15.9 16.4 2.3 2.7 Thompson Wu 4938.TW Pegatron 2,303 31.0 30.0 N -2.5 -0.36 1.70 n.m n.m n.m 18.2 0.8 0.7 -0.9 4.1 4.7 n.a. Thompson Wu 2382.TW Quanta 7,782 61.4 70.0 O 19.0 5.90 6.35 21.6 7.6 10.4 9.7 1.9 1.6 18.7 18.0 6.6 4.8 Thompson Wu 3231.TW Wistron 2,435 36.5 46.0 O 31.8 4.35 5.10 -27.0 20.3 8.4 7.2 1.2 1.1 14.8 16.2 8.5 5.5 Thompson Wu PC / NB 60,559 -13.5 27.0 11.8 9.3 1.4 1.3 12.5 14.5 3.7 3.1 2498.TW HTC 18,835 660.0 930.0 O 48.0 76.78 78.42 67.4 2.1 8.6 8.4 5.4 4.3 73.3 56.4 7.0 7.1 Pauline Chen 3008.TW Largan 2,542 572.0 700.0 N 26.2 42.06 49.30 39.5 17.2 13.6 11.6 4.2 3.4 32.4 32.3 3.3 3.9 Pauline Chen 3311.TW Silitech 501 82.7 84.0 N 9.0 7.74 8.08 -3.5 4.4 10.7 10.2 2.7 2.6 24.8 25.9 7.4 7.4 Pauline Chen Handset 21,878 62.6 3.3 9.0 8.7 5.1 4.1 64.6 51.8 6.6 6.8 3062.TW CyberTAN 356 32.9 39.0 O 24.2 1.95 3.11 72.6 59.1 16.9 10.6 2.0 1.8 12.5 18.1 3.7 6.0 Darryl Cheng 2332.TW D-Link 478 22.3 31.0 O 46.2 1.72 2.58 -9.0 50.2 13.0 8.7 1.1 1.0 7.9 11.9 5.0 7.5 Darryl Cheng 4906.TW Gemtek 257 25.3 27.0 N 11.2 0.29 1.83 -77.6 532.8 87.0 13.8 0.9 0.9 2.3 6.6 0.7 4.7 Darryl Cheng Networking 1,092 -7.7 76.8 17.9 10.1 1.2 1.1 6.8 11.4 3.6 6.3 2882.TW Cathay FHC 10,730 31.4 36.5 N 17.3 1.53 1.73 243.5 13.1 20.6 18.2 1.7 1.5 7.7 8.8 1.0 1.1 Chung Hsu 2881.TW Fubon FHC 9,207 31.2 36.0 N 19.6 4.35 3.14 91.7 -25.9 7.2 9.9 1.1 1.1 16.4 11.0 3.8 4.0 Chung Hsu 2888.TW Shin Kong 2,421 8.7 8.8 N 1.4 0.86 0.89 184.7 3.2 10.1 9.8 0.8 0.8 8.3 8.2 0.0 0.0 Chung Hsu 2891.TW Chinatrust 6,031 17.1 23.5 O 41.5 1.79 1.69 46.1 -5.3 9.5 10.1 1.3 1.2 13.8 12.0 3.9 3.7 Chung Hsu 2884.TW E.Sun FHC 2,024 13.7 19.0 O 41.3 0.93 1.49 -3.9 80.7 14.7 9.2 1.0 0.9 6.2 9.9 1.4 2.2 Chung Hsu 2887.TW Taishin 2,408 11.6 16.5 O 44.9 1.40 1.29 40.7 -7.6 8.3 9.0 1.0 0.9 12.0 10.2 2.0 2.8 Chung Hsu 2890.TW Sinopac 2,108 8.8 9.5 N 11.7 0.61 0.72 -16.0 21.9 14.3 12.2 0.7 0.7 4.9 5.7 2.7 3.3 Chung Hsu 2801.TW CHB 3,804 17.0 19.0 N 13.9 1.50 1.19 24.2 -16.9 11.3 14.2 1.0 1.0 9.8 7.0 2.5 2.1 Chung Hsu 2892.TW First FHC 4,372 17.6 20.0 N 15.9 1.25 1.23 25.9 6.7 14.0 14.2 1.0 1.0 7.5 7.0 2.0 2.0 Chung Hsu 2880.TW Hua Nan FHC 4,559 17.2 16.0 U -5.2 1.17 0.98 43.0 -7.1 14.6 17.4 1.3 1.2 8.4 7.3 1.7 1.4 Chung Hsu 2886.TW Mega FHC 7,332 19.7 21.0 N 11.9 1.60 1.62 18.3 2.1 12.3 12.2 1.1 1.0 8.7 8.6 5.3 5.3 Chung Hsu 2885.TW Yuanta FHC 4,549 15.7 21.0 O 36.8 1.78 0.93 84.8 -45.7 8.8 16.9 1.1 1.0 12.2 6.2 4.0 3.0 Chung Hsu Financials 60,158 58.8 -8.7 11.4 12.5 1.0 1.0 9.3 8.0 2.8 2.8 1326.TW FCFC 15,079 80.0 106.6 O 40.9 7.50 7.18 -9.7 -4.2 10.7 11.1 1.7 1.7 15.7 14.9 8.0 7.6 Sidney Yeh 6505.TW FPCC 29,597 93.8 75.8 U -16.1 3.15 3.24 -26.7 3.0 29.8 28.9 3.8 3.7 12.5 12.9 3.0 3.1 Sidney Yeh 1301.TW FPC 16,281 80.3 94.2 N 23.1 6.62 5.72 -11.1 -13.6 12.1 14.0 1.9 1.9 15.6 13.4 6.6 5.7 Sidney Yeh 1303.TW Nan Ya Plastic 15,892 61.1 64.4 N 10.8 3.85 3.89 -26.3 1.1 15.9 15.7 1.7 1.7 10.8 11.0 5.4 5.4 Sidney Yeh Petrochemical 76,849 -17.9 -4.2 16.2 16.9 2.2 2.2 13.6 13.1 5.2 5.0

22 N

ovem

ber 2011

Taiw

an M

arket Strateg

y 23

Figure 61: Credit Suisse Taiwan coverage universe key valuation matrix (continued) 12-mth EPS Earnings P/E P/B ROAE Div

Mkt cap Price 12-mth Invst. return (NT$) Growth (%) (x) (x) (%) yield (%) Analyst

Company US$ mn 18-Nov target rating (%) 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012 2011 2012

2511.TW Prince Housing 646 18.2 25.8 N 48.1 2.38 2.13 21.1 -10.4 7.6 8.5 1.3 1.3 18.6 15.2 6.5 5.9 Sidney Yeh

2536.TW Hung Poo 250 23.8 36.7 O 62.2 2.23 3.41 -28.1 52.9 10.7 7.0 0.8 0.7 7.7 11.0 3.8 8.6 Sidney Yeh

2548.TW Huaku 607 67.8 95.4 O 52.4 11.14 11.40 3.3 2.3 6.1 5.9 1.5 1.4 27.0 25.1 11.5 11.8 Sidney Yeh

5522.TW Farglory 1,293 51.1 57.8 N 19.2 8.36 5.98 -3.6 -28.5 6.1 8.5 1.4 1.3 24.1 16.1 8.2 5.9 Sidney Yeh