Crompton Greaves - Credit Suisse

27

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 13 June 2012 Asia Pacific/India Equity Research Engineering & Construction Crompton Greaves (CROM.BO / CRG IN) INITIATION Losing steam We initiate coverage on Crompton Greaves with an Underperform rating and price target of Rs92, implying a potential downside of 23%. View: We believe that the power generation capex has peaked, as lack of clarity on fuel supply is expected to delay 125-GW capacity addition. This should impact domestic power T&D capex, which represents 25% of sales. We expect a moderate 15-20% growth in overseas T&D orders (42% of sales) from FY12-15, given our expectation of continued weakness in T&D capex in Europe and the US and global over-capacity issues. While Crompton’s diversification into new products & geographies for industrial & consumer (13/19% of sales) business segments is positive, we believe these initiatives would take time to drive meaningful growth. We believe that the company’s guidance of 450bps margin expansion over FY12-15 is aggressive and expect the margin to expand by only 171bps, mostly led by the overseas power business and impacted by the domestic power business. Falling realisations led by the expectation of a sharp decline in domestic order flows from FY14 (PGCIL ordering to peak in FY13) and the inability to meet the top-end of its FY13 margin guidance, are key negative catalysts. Valuation: Our key concerns are Crompton’s (a) decelerating EPS CAGR of 19% over FY13-15 (versus FY13 EPS growth at 44% on low base of FY12), (b) subdued RoE of 14-16% (vs >30% in past), led by lower margins & continued capex impacting asset turns, (c) working capital pressures and (d) unrelated diversification into power generation/distribution business. Given Crompton’s disappointing earnings for four consequtive quarters, we believe investors would turn positive on the stock only on visibility of it meeting its 3- year margin guidance, which is aggressive. Key upside risks: Power/coal sector reforms in India and improvement in global macro conditions. Share price performance 40 90 140 0 100 200 300 400 Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12 Price (LHS) Rebased Rel (RHS) The price relative chart measures performance against the BSE SENSEX IDX which closed at 16862.8 on 12/06/12 On 12/06/12 the spot exchange rate was Rs56.04/US$1 Performance Over 1M 3M 12M Absolute (%) 1.8 -18.6 -55.7 Relative (%) -1.7 -12.7 -48.1 Financial and valuation metrics Year 3/12A 3/13E 3/14E 3/15E Revenue (Rs mn) 112,485.8 127,457.7 141,289.9 153,173.7 EBITDA (Rs mn) 8,036.4 10,135.8 11,848.5 13,569.5 EBIT (Rs mn) 5,436.8 7,450.2 8,890.5 10,528.4 Net profit (Rs mn) 3,735.9 5,392.3 6,576.9 7,638.0 EPS (CS adj.) (Rs) 5.82 8.41 10.25 11.91 Change from previous EPS (%) n.a. Consensus EPS (Rs) n.a. 8.9 11.0 13.2 EPS growth (%) -59.7 44.3 22.0 16.1 P/E (x) 20.5 14.2 11.6 10.0 Dividend yield (%) 1.2 1.4 1.5 1.6 EV/EBITDA (x) 9.7 7.5 6.1 4.9 P/B (x) 2.1 1.9 1.7 1.5 ROE (%) 10.9 14.1 15.4 15.7 Net debt/equity (%) 4.3 net cash net cash net cash Source: Company data, Thomson Reuters, Credit Suisse estimates. Rating UNDERPERFORM* Price (12 Jun 12, Rs) 119.30 Target price (Rs) 92.00¹ Upside/downside (%) -22.9 Mkt cap (Rs mn) 76,530 (US$ 1,366) Enterprise value (Rs mn) 75,894 Number of shares (mn) 641.49 Free float (%) 60.0 52-week price range 274.2 - 106.1 *Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months. Research Analysts Amish Shah, CFA 91 22 6777 3743 [email protected] Abhishek Bansal 91 22 6777 3968 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Crompton Greaves - Credit Suisse

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

13 June 2012 Asia Pacific/India Equity Research

Engineering & Construction

Crompton Greaves (CROM.BO / CRG IN)

INITIATION

Losing steam ■ We initiate coverage on Crompton Greaves with an Underperform rating

and price target of Rs92, implying a potential downside of 23%.

■ View: We believe that the power generation capex has peaked, as lack of clarity on fuel supply is expected to delay 125-GW capacity addition. This should impact domestic power T&D capex, which represents 25% of sales. We expect a moderate 15-20% growth in overseas T&D orders (42% of sales) from FY12-15, given our expectation of continued weakness in T&D capex in Europe and the US and global over-capacity issues. While Crompton’s diversification into new products & geographies for industrial & consumer (13/19% of sales) business segments is positive, we believe these initiatives would take time to drive meaningful growth. We believe that the company’s guidance of 450bps margin expansion over FY12-15 is aggressive and expect the margin to expand by only 171bps, mostly led by the overseas power business and impacted by the domestic power business.

■ Falling realisations led by the expectation of a sharp decline in domestic order flows from FY14 (PGCIL ordering to peak in FY13) and the inability to meet the top-end of its FY13 margin guidance, are key negative catalysts.

■ Valuation: Our key concerns are Crompton’s (a) decelerating EPS CAGR of 19% over FY13-15 (versus FY13 EPS growth at 44% on low base of FY12), (b) subdued RoE of 14-16% (vs >30% in past), led by lower margins & continued capex impacting asset turns, (c) working capital pressures and (d) unrelated diversification into power generation/distribution business. Given Crompton’s disappointing earnings for four consequtive quarters, we believe investors would turn positive on the stock only on visibility of it meeting its 3-year margin guidance, which is aggressive. Key upside risks: Power/coal sector reforms in India and improvement in global macro conditions.

Share price performance

40

90

140

0100200300400

Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the BSE SENSEX IDX which closed at 16862.8 on 12/06/12 On 12/06/12 the spot exchange rate was Rs56.04/US$1

Performance Over 1M 3M 12M Absolute (%) 1.8 -18.6 -55.7 Relative (%) -1.7 -12.7 -48.1

Financial and valuation metrics

Year 3/12A 3/13E 3/14E 3/15E Revenue (Rs mn) 112,485.8 127,457.7 141,289.9 153,173.7 EBITDA (Rs mn) 8,036.4 10,135.8 11,848.5 13,569.5 EBIT (Rs mn) 5,436.8 7,450.2 8,890.5 10,528.4 Net profit (Rs mn) 3,735.9 5,392.3 6,576.9 7,638.0 EPS (CS adj.) (Rs) 5.82 8.41 10.25 11.91 Change from previous EPS (%) n.a. Consensus EPS (Rs) n.a. 8.9 11.0 13.2 EPS growth (%) -59.7 44.3 22.0 16.1 P/E (x) 20.5 14.2 11.6 10.0 Dividend yield (%) 1.2 1.4 1.5 1.6 EV/EBITDA (x) 9.7 7.5 6.1 4.9 P/B (x) 2.1 1.9 1.7 1.5 ROE (%) 10.9 14.1 15.4 15.7 Net debt/equity (%) 4.3 net cash net cash net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating UNDERPERFORM* Price (12 Jun 12, Rs) 119.30 Target price (Rs) 92.00¹ Upside/downside (%) -22.9 Mkt cap (Rs mn) 76,530 (US$ 1,366) Enterprise value (Rs mn) 75,894 Number of shares (mn) 641.49 Free float (%) 60.0 52-week price range 274.2 - 106.1 *Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months.

Research Analysts

Amish Shah, CFA 91 22 6777 3743

Abhishek Bansal 91 22 6777 3968

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 2

Focus charts Figure 1:Expect 125GW power generation capacity to be

delayed pending fuel supply clarity…

Figure 2: …implies power generation capex has peaked

and could impact T&D capex…

-

2 5

5 0

7 5

1 0 0

1 2 5

L in k a g e c o a l I m p o r t e d c o a l G a s P r o je c t s o nh o l d

T o t a l d e la y e dc a p a c i t y

G W

P r o je c t s u n d e r c o n s t r u c t io n

-

200

400

600

800

1,000

1,200

1,400

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

FY15

E

FY16

E

FY17

E

Power generation capex (Rs bn)

Source: Ministry of Power, Credit Suisse estimates Source: Ministry of Power, Credit Suisse estimates

Figure 3: …even discarding our concern, planned T&D

capex in XIIth & XIIIth plans offer tepid growth

Figure 4: We believe PGCIL capex has peaked

20%

25%

30%

35%

40%

45%

50%

55%

-

1,500

3,000

4,500

6,000

IX Plan X Plan XI Plan XII Plan (E) XII Plan (E)

T&D T&D as % of total

(Rs bn)

30

60

90

120

150

180

210

240

270

FY09 FY10 FY11 FY12 FY13 FY14 FY15

PGCIL ordering (Rs bn)

Assuming most of remaining Rs330bnorders to be placed in FY13

Limited ordering in FY15 as XIII Plan ordering would commence only from FY16

Source: PGCIL, Credit Suisse estimates Source: PGCIL, Credit Suisse estimates

Figure 5: Foreign players have picked up 30-40% share… Figure 6: …while Crompton’s share has halved

0%

10%

20%

30%

40%

50%

60%

FY09 FY10 FY11 FY12

Mkt share of Chinese/Koreans in PGCIL orders for transformers & reactors

15%

20%

25%

30%

35%

40%

FY09 FY10 FY11 FY12

Crompton's market share in transformers & reactors

Source: PGCIL, Credit Suisse estimates Source: PGCIL, Company data, Credit Suisse estimates

Figure 7: Expect jump in FY13 EPS on low base, but FY13-

15 earnings growth trajectory to decelerate

Figure 8: Expect RoE to remain subdued on relatively low

margins & capex continuing to impactasset turnover

-80%

-60%

-40%

-20%

0%

20%

40%

60%

4

6

8

10

12

14

16

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Consolidated EPS (Rs/ share) YoY growth (%)

5%

10%

15%

20%

25%

30%

35%

40%

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

RoE (%)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 3

Losing steam Declining order visibility across businesses We expect 125-GW of power generation capacity to be delayed led by lack of clarity on fuel supply. This implies that power generation capex has peaked and should impact the T&D capex, albeit with a lag. Contrary to the general perception, about 88% of transmission capex is linked to generation capex, despite India’s under-investment in T&D infrastructure in the past. Even after discarding these concerns, we see muted growth in planned T&D capex during the XIIth (FY12-17) and the XIIIth (FY17-22) Plans over the XIth Plan (FY07-12).

PGCIL has already ordered 67% of its Rs1 tn investments planned during the XIIth Plan. Given that ordering for most of its balance Rs330 bn is expected to be completed in FY13 and ordering for the XIIIth Plan is unlikely to start before FY16, we expect PGCIL ordering to peak in FY13. On the other hand, SEBs’ transmission capex is expected to decline by 15% in the XIIth Plan, IPPs’ transmission capex would be impacted by a slowdown in their power generation capex and the build-own-operate model is yet to pick up meaningfully.

Overall, we expect its domestic power systems’ (25% of sales) order flows to grow by 20% in FY13, but decline by 15-25% during FY15/16. We expect a moderate 15-20% growth in overseas power systems (constituting 42% of sales) order flows over FY12-15 as we expect continued weakness in T&D capex in Europe & the US and global over-capacity issues.

We reckon that Crompton has been diversifying into new geographies, products and business segments, for its industrial (13% of sales) as well as consumer businesses (19% of sales). However, we believe these initiatives would take time to drive meaningful growth. We expect growth in industrial order inflows to remain muted at 10% over FY12-15 and expect consumer segment sales to grow at 13% CAGR over FY12-15.

Pricing pressures are intensifying The transformer industry is witnessing intense competition with the entry of foreign as well as new domestic players. Domestic-only capacity utilisation is at 65-75%. During FY09-12, Chinese & Korean players captured 30-40% share in PGCIL transformer & reactor orders, while Crompton’s share has halved to 19%. TBEA (Chinese player) is planning to set up a domestic capacity. We are surprised with Crompton’s 50K MVA capacity addition plan.

On the pricing front, realisations for its key product (765KV 500MVA transformer) have fallen by 55% since September 2008. Overall, transformer & reactor realisations for Crompton seems to have fallen by 25-40% over FY09-12. However, as per our discussions with industry experts, pricing has now stabilised or is marginally improving.

We expect domestic power margin to improve by 70bps in FY13 but fall by 100bps over FY13-15 on peaking order flows. We expect a sharp 323 bps increase in overseas power margin over FY12-15 from its lows of 1.7% in FY12. We believe Crompton would achieve an increase of 171bps in its consolidated margin over FY12-15 (guidance of 450bps).

Initiate with Underperform, 23% potential downside We initiate coverage on Crompton Greaves with an Underperform rating and target price of Rs92. Decelerating EPS growth of 19% over FY13-15 (versus FY13 EPS growth of 44% on a low base of FY12), subdued RoE at 14-16% (vs >30% in past) led by relatively lower margins & and capex continuing to impact asset turnover, working capital pressures and unrelated diversifications into power generation & distribution business are our concerns.

Given that Crompton has disappointed on earnings for four consequtive quarters, we believe that investors would turn positive only on visibility of it meeting its 3-year margin guidance, which seems aggressive. However, for FY13, we expect Crompton to meet its sales and order inflow growth guidance and the lower end of its margin guidance. Power sector reforms in India and improvement in global macro conditions are key positive risks.

Power generation capex appears to have peaked, which should impact T&D capex, although with a lag

PGCIL/T&D capex likely to peak by FY13; expect Crompton’s domestic power systems inflows to decline 15-25% during FY15/16

Transformer industry seeing intense competition with entry of foreign and new domestic players

Against 450bps margin improvement guidance over FY12-15, expect Crompton to achieve 171bps

Key concerns: decelerating earnings growth, subdued RoE led by relatively lower margins & high capex, working capital pressures & unrelated diversifications

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 4

Financial summary Figure 9: Crompton - Financial summary (consolidated) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

Net sales 91,409 100,051 112,486 127,458 141,290 153,174

Total operating expenses 78,639 86,613 104,449 117,322 129,441 139,604

EBITDA 12,770 13,438 8,036 10,136 11,848 13,570

EBITDA margin (%) 14.0% 13.4% 7.1% 8.0% 8.4% 8.9%

Depreciation 1,551 1,936 2,600 2,686 2,958 3,041

EBIT 11,219 11,502 5,437 7,450 8,890 10,528

Interest 428 201 463 583 620 658

Other income 1,100 990 524 732 636 871

Tax 3,650 3,100 1,821 2,275 2,403 3,182

Tax rate (%) 30.7% 25.2% 33.1% 29.9% 27.0% 29.6%

Minority interest/ Asssociates 57 84 47 55 61 66

Recurring PAT 8,247 9,268 3,736 5,392 6,577 7,638

Exceptionals 352 (381) - - - -

Reported PAT 8,599 8,887 3,736 5,392 6,577 7,638

Share capital 1,283 1,283 1,283 1,283 1,283 1,283

Reserves and surplus 23,760 31,464 34,826 38,931 44,145 50,325

Networth 25,043 32,747 36,109 40,214 45,428 51,608

Loan funds 5,010 4,703 11,555 11,555 13,055 13,055

Minority interest 43 157 157 150 144 137

Total liabilities 30,095 37,607 47,821 51,919 58,627 64,800

Net fixed assets 13,760 19,417 16,693 20,008 22,550 23,508

Investments 5,536 6,747 7,864 7,864 7,864 7,864

Goodwill - - 5,882 5,882 5,882 5,882

Deferred tax asset (net) (49) (160) 513 513 513 513

Net current assets 10,849 11,604 16,869 17,653 21,818 27,032

Total assets 30,095 37,607 47,821 51,919 58,627 64,800

Cash Flow from Operations 10,229 6,860 2,383 9,491 10,009 11,321

Cash Flow from Investing Activities (5,037) (9,185) (6,875) (6,000) (5,500) (4,000)

Cash Flow from Financing Activities (4,160) (1,379) 6,484 (1,287) 137 (1,459)

Increase/ (Decrease) in Cash 1,032 (3,704) 1,992 2,203 4,646 5,863

Closing cash and cash equivalents 6,688 2,984 4,976 7,179 11,825 17,688

Net Debt /Equity (x) (0.2) (0.1) 0.0 (0.0) (0.1) (0.2)

EPS (Rs) 12.9 14.4 5.8 8.4 10.3 11.9

DPS (Rs) 1.3 1.3 1.4 1.7 1.8 1.9

BPS (Rs) 39 51 56 63 71 80

P/E (x) 9.3 8.3 20.5 14.2 11.6 10.0

Yield (%) 1.1% 1.1% 1.2% 1.4% 1.5% 1.6%

P/BV (x) 3.1 2.3 2.1 1.9 1.7 1.5

EV/EBITDA (x) 5.6 5.5 9.7 7.5 6.1 4.9

EV/Sales (x) 0.8 0.7 0.7 0.6 0.5 0.4

EPS Growth % 47.3% 12.4% -59.7% 44.3% 22.0% 16.1%

RoCE (%) 29.6% 27.4% 8.7% 10.8% 11.9% 12.4%

RoE (%) 38.0% 32.1% 10.9% 14.1% 15.4% 15.7%

Source: Company data, Credit Suisse estimates

13 Ju

ne 2012

Cro

mp

ton

Greaves

(CR

OM

.BO

/ CR

G IN

) 5

Relative valuation summary Figure 10: India capital goods relative valuation Company Price Shares Mkt Cap PER (x) P/BV (x) EPS growth (%) Div. yield (%) RoE (%)

(Rs) o/s (mn) (US$ mn) FY12 FY13E FY14E FY12 FY13E FY14E FY13E FY14E FY12 FY13E FY12 FY13E FY14E

Larsen & Toubro * 1,316 613 14,463 18 17 15 3.1 2.8 2.5 8% 12% 1.2% 1.5% 17 17 16

Punj Lloyd 48 332 286 14 14 9 0.5 0.5 0.5 5% 50% 0.3% 0.5% (2) 3 5

BGR Energy Systems 294 72 380 9 10 9 1.9 1.6 1.3 -4% 13% 3.4% 2.5% 22 17 17

Bharat Heavy Electricals * 219 2,448 9,632 8 9 10 2.1 1.8 1.6 -12% -10% 2.9% 2.5% 27 20 16

Thermax 461 119 986 14 15 14 4.2 2.9 2.6 -10% 6% 2.0% 1.8% 32 21 19

Cummins India * 422 277 2,100 22 20 17 5.7 5.3 4.8 10% 19% 2.6% 3.0% 26 27 29

Greaves Cotton 69 244 303 9 10 9 2.7 2.2 2.0 -15% 13% 2.2% 2.7% 29 24 23

Kirloskar Oil Engines 152 146 396 12 12 11 2.5 1.8 1.6 -7% 17% 2.6% 0.9% 22 16 16

Blue Star 162 90 262 9 21 11 2.9 3.4 2.8 -56% 83% 4.3% 3.0% 31 18 27

Voltas * 107 331 636 10 12 12 2.4 2.1 1.8 -18% 4% 1.5% 1.7% 24 17 16

ABB India 765 212 2,908 n.a. 46 35 6.4 5.7 5.0 89% 34% 0.4% 0.4% 7 13 15

Alstom T&D India 181 239 776 23 23 18 4.3 4.3 4.0 0% 25% 1.0% 0.9% 29 17 18

Crompton Greaves * 119 641 1,374 21 14 12 2.1 1.9 1.7 44% 22% 1.2% 1.4% 10 13 14

Emco 27 65 32 n.a 9 n.a. 0.3 0.3 n.a. n.m n.a. 0.7% 0.7% (10) 4 n.a.

Siemens 683 340 4,171 27 29 24 6.1 5.3 4.6 -6% 19% 0.9% 0.9% 24 20 21

Voltamp Transformers 480 10 87 15 12 12 1.2 1.1 1.1 22% 3% 1.9% 1.3% 9 9 9

Jyoti Structures 41 82 60 4 4 3 0.5 0.5 0.5 -5% 23% 2.7% 3.0% 15 13 15

Kalpataru Power Transmission 81 153 223 7 6 5 0.7 0.6 0.5 15% 11% 1.9% 2.2% 11 11 12

KEC International India 52 257 238 6 6 5 1.2 1.1 0.9 1% 15% 2.3% 2.4% 20 18 18

Shriram EPC 57 44 45 6 6 9 0.4 0.3 0.3 1% -35% 2.1% 2.1% 7 6 n.a.

Suzlon Energy 18 1,777 568 n.a. 9 6 0.6 0.5 0.4 n.m 53% 0.0% 0.3% (8) 5 8

Elecon Engineering 55 93 92 8 6 6 1.1 1.0 0.9 42% -4% 3.3% 3.5% 14 16 15

McNally Bharat Engineering 88 31 49 4 4 3 0.8 0.7 0.6 7% 15% 2.3% 1.4% 22 16 16

BEML 384 42 287 28 17 n.a. 0.7 0.7 n.a. n.m n.a. 2.6% 2.6% 3 4 n.a.

Havells India 553 125 1,237 19 15 13 7.2 5.2 3.9 24% 16% 0.5% 1.0% 46 39 34

Titagarh Wagons 306 20 110 7 7 7 1.0 0.9 0.8 0% 5% 2.6% 2.6% 14 14 13

Average 13 14 11 2.4 2.1 2.0 6% 17% 1.9% 1.8% 17 15 17

Prices as on 12 June 2012. * CS estimates, rest are consensus estimates.

Source: Company data, Bloomberg, Credit Suisse estimates

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 6

Declining order visibility across businesses We expect 125-GW of power generation capacity to be delayed led by lack of fuel supply clarity. This implies that power generation capex has peaked and should impact the T&D capex, albeit with a lag. Contrary to general perception, about 88% of transmission capex is linked to generation capex, despite India’s under-investment in T&D infrastructure in the past. Even after discarding these concerns, we see muted growth in planned T&D capex during the XIIth (FY12-17) and the XIIIth (FY17-22) Plans over the XIth Plan (FY07-12).

PGCIL has already ordered 67% of its Rs1 tn investments planned during the XIIth Plan. Given that ordering for most of its balance of Rs330 bn is expected to be completed in FY13 and ordering for the XIIIth Plan is unlikely to start before FY16, we expect PGCIL ordering to peak in FY13. On the other hand, SEBs’ transmission capex is expected to decline by 15% in the XIIth Plan, IPPs’ transmission capex would be impacted by a slowdown in their power generation capex and the build-own-operate model is yet to pick up meaningfully.

Overall, we expect its domestic power systems’ (25% of sales) order flows to grow by 20% in FY13, but decline by 15-25% during FY15/16. We expect a moderate 15-20% growth in overseas power systems (42% of sales) order flows over FY12-15 as we expect continued weakness in T&D capex in Europe & the US and global over-capacity issues.

We reckon that Crompton has been diversifying into new geographies, products and business segments, for its industrial (13% of sales) as well as consumer businesses (19% of sales). However, we believe these initiatives would take time to drive meaningful growth. We expect growth in industrial order inflows to remain muted at 10% over FY12-15 and expect consumer segment sales to grow at 13% CAGR over FY12-15.

Figure 11: Snapshot of Crompton’s key business segments Segment % of FY12 consol.

revenues Key issues / growth outlook

Domestic Power 25% PGCIL / T&D ordering is close to its peak; order inflows to grow by 20% in FY13 but decline by 15-25% during FY14-15

International Power 42% T&D capex in Europe/ US to remain weak led by global over-capacity issues; expect moderate 15-20% growth in inflows over FY12-15

Industrials 13% Diversifying into new segments & geographies, however new initiatives would take time to drive meaningful growth; expect 5% inflow growth in FY13 and 10-15% over FY14-15

Consumer 19% Leader in fans segment, however, high competition and & weak macro to limit growth prospects; expect 13% revenue CAGR over FY12-15

Source: Company data, Credit Suisse estimates

Expect India T&D capex to mirror generation capex As highlighted in our detailed India utilities sector report, “Coal deficit issue really resolved?”, dated 13 March, 2012, we argue that of the 122GW linkage coal-based capacity currently under construction, we expect only 60-GW projects to be allocated coal. In order to be eligible to get coal allocation, the developer would have to meet the following three criteria (a) having a LoA, (b) project commissioning till Mar 2015 and (c) power sales tied up through long-term PPAs.

This implies that 62GW of back-ended capacity under construction, which was expected to commission during FY15-17, would now be delayed as these projects are unlikely to be allocated coal at least till Mar 2017. This trend has already started to play out with NTPC recently guiding to add only 14GW capacity over FY12-17 vs over 23GW earlier. Similarly, the Ministry of Power has advised IPPs to go slow/defer gas-based capacity addition plans, given poor visibility of gas supplies at least till FY16.

Power generation capex appears to have peaked, which should impact T&D capex, although with a lag

PGCIL/T&D capex likely to peak by FY13; expect Crompton’s domestic power systems inflows to decline 15-25% during FY15/16

Out of 122GW capacity under construction, only 60GW to be allocated coal

Overall 125GW capacity adds likely to be delayed; slowing generation capex would impact T&D capex

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 7

Figure 12: Extract from Ministry of Power urging gas based power developers to go slow on capacity adds until FY16

Source: Ministry of Power

Besides, developers have now put on hold 54GW projects that are still seeking regulatory approvals. Overall, we estimate about 125GW capacity adds likely to be delayed or put on hold pending fuel supply clarity.

Figure 13: 62GW under construction linkage coal projects

likely to be delayed given no coal allocation till Mar 2017...

Figure 14: …overall we expect about 125GW capacity to

be delayed or put on hold pending fuel supply clarity

40

60

80

100

120

140

160

180

200

Upto

FY09

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17Targetted

till FY17

Capacity to be delayed

Capacity adds over FY09-17 capped at 60GW

75

GW

196

-

25

50

75

100

125

Linkage coal Imported coal Gas Projects onhold

Total delayedcapacity

GW

Projects under construction

Source: Ministry of Power, Company data, Credit Suisse estimates Source: Ministry of Power, Company data, Credit Suisse estimates

For an optimum T&D infrastructure, T&D capex should be equal to the generation capex. Though we reckon that India has historically under-invested in T&D infrastructure, the mix of generation vs T&D capex now appears reasonable. Despite that, we see limited growth in planned T&D capex during the XIIth and the XIIIth Plans in comparison to the XIth Plan.

However, as explained above, we expect power generation capex to slow down materially, which should impact T&D capex spends.

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 8

Figure 15: XIIth & XIIIth Plans to see tepid T&D capex

growth despite optimum mix of T&D vs generation capex..

Figure 16: …and is at a risk of slowdown led by expected

slowdown in generation capex

20%

25%

30%

35%

40%

45%

50%

55%

-

1,500

3,000

4,500

6,000

IX Plan X Plan XI Plan XII Plan (E) XII Plan (E)

T&D T&D as % of total

(Rs bn)

-

200

400

600

800

1,000

1,200

1,400

FY07

FY08

FY09

FY10

FY11

FY12

FY13

E

FY14

E

FY15

E

FY16

E

FY17

E

Power generation capex (Rs bn)

Source: PGCIL, Credit Suisse estimates Source: Ministry of Power, Credit Suisse estimates

Typically, T&D capex follows generation capex with a lag as it takes less than two years to execute a T&D project as against the four years it takes to implement a coal-based power generation project. An analysis of PGCIL’s XIIth Plan capex highlights that most of its transmission capex is aimed at meeting the evacuation requirements of generation projects, while the share of grid strengthening capex is relatively small, implying a high risk of slippages in capex as generation capex slows down.

Figure 17: PGCIL’s XIIth Plan capex is mainly linked to generation capex

For central govt. generation projects

22%

For UMPPs generation projects

14%

For Private sector genertion projects

52%

Grid strengthening12%

Source: PGCIL, Credit Suisse

We believe PGCIL/T&D ordering is close to its peak Of the Rs1,000 bn that PGCIL plans to spend during the XIIth Plan, it has already awarded orders worth Rs670 bn. During FY12 itself, it has awarded orders worth Rs250 bn (up 39% YoY). Powergrid plans to order the remaining Rs330bn projects over FY13-14, indicating decline in order flow growth during FY13/14 over FY12 (assuming evenly spreadout orders over FY13/14), or orders peaking by FY13 (assuming most of the Rs330bn would be ordered in FY13 – the most likely scenario, in our view). This is even after assuming that our concerns about a slowdown in T&D capex are ill-founded.

Typically, T&D capex follows generation capex with a lag

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 9

As highlighted earlier, T&D spends during the XIIIth Plan are likely to offer no growth as compared to the XIIth Plan. Also, when compared to the peak ordering of PGCIL during FY12/13, the industry would observe a decline in ordering activity from PGCIL. Besides, PGCIL’s XIIIth Plan ordering is unlikely to start before FY16, implying significant dip in order flows during FY15.

An analysis of T&D capex plans from SEBs suggests a) decline in intra-state transmission spends in XIIth Plan, b) growth from intra-state transmission spends would materialise only from FY16/17 c) limited growth from distribution capex in the XIIth and XIIIth Plans and d) intense competition in the distribution segment compared to transmission segment.

Figure 18: PGCIL ordering has peaked Figure 19: SEB’s XIIth Plan T&D spends suggests limited

growth and is highly competitive

30

60

90

120

150

180

210

240

270

FY09 FY10 FY11 FY12 FY13 FY14 FY15

PGCIL ordering (Rs bn)

Assuming most of remaining Rs330bnorders to be placed in FY13

Limited ordering in FY15 as XIII Plan ordering would commence only from FY16

-

500

1,000

1,500

2,000

2,500

3,000

3,500

XI Plan XII Plan (E) XIII Plan (E)

Intra-State transmission (Rs bn) Distribution (Rs bn)

Source: PGCIL, Credit Suisse estimates Source: PGCIL, Credit Suisse estimates

We believe transmission capex from IPPs would certainly be impacted by a slowdown in generation capex, while transmission capex spends through the build-own-operate model is yet to pick up meaningfully.

Expect moderate power system order flow growth from overseas Crompton derives about 50-60% of its power systems orders from overseas markets. However, the visibility of growth in T&D orders from international geographies is weak currently, led by excess global capacity prompting high competition and weak capex on account of financial stress in Europe and strife in the Middle East.

However, the management is optimistic on revival of growth from international markets driven by (a) offshore wind orders from EMEA (expected 20GW implementation), (b) revival of orders from renewable segment in US (expected 20GW implementation) also driving growth for distribution transformers, (c) ageing or old grid structure in the US, and (d) bouyancy in the oil and gas sector expected to drive growth for Crompton’s power and industrial business segments.

We expect Crompton’s domestic power systems order inflows to grow by 20% in FY13, but decline by 15% and 25% respecitively during FY15 and FY16. However, we expect growth in the overseas order inflows to continue over FY12-15 at 15-20%.

PGCIL ordering to decline materially in FY14-15; XIII Plan ordering unlikely to start before FY16

Global over-capacity, financial stress in Europe and unrest in Middle East impacting global T&D ordering

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 10

Figure 20: Expect domestic power system order inflows

to peak in FY13…

Figure 21: …but we expect growth in international power

systems order inflows to continue

20,000

22,500

25,000

27,500

30,000

32,500

35,000

37,500

40,000

FY11 FY12 FY13E FY14E FY15E

Power systems order inflows - domestic (Rs mn)

40,000

50,000

60,000

70,000

80,000

90,000

FY11 FY12 FY13E FY14E FY15E

Power systems order inflows - international (Rs mn)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

New intiatives in industrial segment would take time to drive meaningful growth Crompton’s industrial business was predominantly driven by motors and alternators business segments until recently. It also entered into the drives business with its acquisition of Sweden-based Emotron (specialising in design, engineering & manufacturing of high-end drive solutions) in May 2011 for €57.8 mn. Crompton now plans to ramp up its drives business (2% of consolidated revenues currently) with the commencement of drives production from India (expected from October 2012) and packaging it with the sale of its motors.

These products have application in varied industries. However, industrial capex has been weak and we do not expect any substantial pick-up in the industrial capex cycle at least over the next few quarters due to (a) over-capacity in industries such as metals, cement etc., (b) lack of gas supply visibility impacting fertiliser capex, (c) lack of new gas discoveries impacting hydrocarbons capex and (d) overall industrial capex being impacted by expectations of continued high interest rates and liquidity stress in the near term.

In order to boost its industrial segment growth, Crompton is diversifying in new business segment and geogrpahies:

■ In India, it has received initial orders from Indian Railways and is aiming to win orders from metro rail projects

■ Diversifing into international geographies, especially in the Eastern Europe

■ Adding capacity to manufacture synchronous generators in Hungary which has high demand in the Eastern Europe.

■ Start of drives manufacturing in India expected from Oct 2012.

Crompton has met with some success in the industrial segment from foreign goegraphies. So far, it has won a 6.7MW HT motors order from a German cement manufacturer, a 2.5MW HT motor & 6.6KV drives order from a steel plant in Central Asia and a 4MW motors order for a nuclear plant in Russia. Crompton believes its industrial products have better pricing and higher acceptability in the international markets, and would allow it to earn better margins, given its low-cost structure.

Expect inflow growth from industrials to remain muted at 5% and improve to 10-15% over FY14-15

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 11

However, we believe that its new initiatives would take time to drive meaningful growth. Overall, we expect order inflow growth from industrial segment to remain muted at 5% and improve to 10-15 over FY14-15.

Figure 22: Expect muted order inflow growth from

industrial segment near-term, to pick up from FY14-15…

Figure 23: …consumer segment growth would also take

time to pick-up

15,000

17,000

19,000

21,000

23,000

25,000

FY11 FY12 FY13E FY14E FY15E

Industrial order inflows (Rs mn)

15,000

17,500

20,000

22,500

25,000

27,500

30,000

32,500

FY11 FY12 FY13E FY14E FY15E

Consumer business sales (Rs mn)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Consumer business would take time to pick up

Crompton is one of the leaders in the fans business in India. It recently introduced a new premium range of fans and sold about 972k fans in FY12, gaining 24% market share. It plans to introduce new products in the consumer segment including kitchen appliances, coolers, geysers, solar fans, etc. Besides, the company is in the process of improving its already strong distribution reach in India of 4,000 distributors and 240,000 retailers (plans to scale up to 400,000 during FY13).

However, we believe that growth in this segment would take time to pick up and is likely to be impacted by high competitive intensity in the segment. Besides, the slowdown in real estate sector on account of high mortgage rates would continue to impact growth in this sector over the next few quarters. We expect Crompton’s consumer business sales to grow at 13% CAGR over FY12-15.

High competition, slowdown in real estate sector impacting consumer segment growth

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 12

Pricing pressures are intensifying The transformer industry is witnessing intense competition with the entry of foreign as well as new domestic players. Domestic-only capacity utilisation is at 65-75%. During FY09-12, Chinese & Korean players captured 30-40% share in PGCIL transformer & reactor orders, while Crompton’s share has halved to 19%. TBEA (Chinese player) is planning to set up a domestic capacity. We are surprised with Crompton’s 50K MVA capacity addition plan.

On the pricing front, realisations for its key product (765KV 500MVA transformer) have fallen by 55% since September 2008. Overall, transformer & reactor realisations for Crompton seems to have fallen by 25-40% over FY09-12. However, as per our discussions with industry experts, pricing has now stabilised or is marginally improving.

We expect domestic power margin to improve by 70bps in FY13 but fall by 100bps over FY13-15 on peaking order flows. We expect a sharp 323 bps increase in overseas power margin over FY12-15 from its lows of 1.7% in FY12. We believe Crompton would achieve an increase of 171bps in its consolidated margin over FY12-15 (guidance of 450bps).

Intense competition, over-capacity in T&D segment Competition in the transformer industry has intensified over time with the entry of new domestic as well as foreign players as can be seen from the table below.

Figure 24: Competition in the transformer space has intensified over time Transformers Reactors

Company 132KV 220KV 400KV 765KV 400KV 765KV

Crompton Yes Yes Yes Since FY09. Earlier through JV

with Toshiba

Yes In JV with ZTR since FY10

BHEL Yes Yes Yes Since FY12 Yes Since FY12

Bharat Bijlee Yes Yes x x x x

Alstom India (Areva earlier) Yes Yes Yes Since FY09 Since FY09 Yes

IMP Power Yes Yes x x x x

TELK Yes Yes Yes x x x

TRIL Since FY07 Since FY07 Since FY07 Since FY12 x x

EMCO Since FY07 Since FY07 Since FY07 x x x

ABB India Since FY07 Since FY07 Since FY07 Since FY09. Earlier through

ABB parent

Since FY09 Yes

Indotech Since FY08 Since FY08 Since FY08 x x x

ECE Yes Yes x x x x

Kanohar Since FY09 Since FY09 Yes x x x

Siemens India Since FY09 Since FY09 Since FY09 Since FY09 Since FY09 Yes

Vijai Electricals Since FY09 Since FY09 Since FY09 Yes Yes x

Voltamp Yes Yes x x x x

Victory Transformers Yes Yes x x x x

Hyosung (Korea)* x x Since FY11 Since FY09 x Since FY10 TBEA (China)* x x Since FY11 Since FY11 x Since FY10 ZTR (Ukraine)* x x x Yes x Since FY10 Baoding (China)* x x x Since FY10 x Since FY11 Hyundai (Korea)* x x x Since FY10 x x Xian (China)* x x x x x Since FY11

* These players do have manufacturing capabilities in lower KV segments as well, however, orders wins in India restricted to 400-765KV so far.

Source: Company data, Credit Suisse

Along with the entry of Chinese & Korean competitors such as Hyosung, Hyundai, TBEA, Baoding, Xian etc., domestic players like Vijai Electricals, TRIL & BHEL have now developed capabilities to manufacture 765KV/1200KV transformers. As per the IEEMA, total imports of 765 KV transformers & reactors in FY12 went up to Rs12.3 bn.

Transformer industry seeing intense competition with entry of foreign and new domestic players

Against 450bps margin improvement guidance over FY12-15, expect Crompton to achieve 171bps

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 13

As can be seen from the charts below, Chinese & Korean players have captured 30-40% market share in PGCIL’s transformer & reactor orders, while the share of Crompton has halved during FY09-12.

Figure 25: Chinese & Koreans have picked up major share

of PGCIL’s transformer & reactor orders…

Figure 26: …while Crompton’s market share has halved

over FY09-12

0%

10%

20%

30%

40%

50%

60%

FY09 FY10 FY11 FY12

Mkt share of Chinese/Koreans in PGCIL orders for transformers & reactors

15%

20%

25%

30%

35%

40%

FY09 FY10 FY11 FY12

Crompton's market share in transformers & reactors

Source: PGCIL, Credit Suisse Source: PGCIL, Company data, Credit Suisse

Currently, even after excluding competition from Chinese and Korean players, power transformer industry has a huge domestic manufacturing over-capacity. As per industry estimates, currently the transformer industry capacity utilisation is at 65-75%. We expect this situation to deteriorate from FY14, given our expectation of peaking of orders in FY13. However, in that context, we note that Crompton is currently in the process of increasing its installed capacity in India by 50,000MVA.

Besides, some foreign players are also planning to set up manufacturing capacities in India. As per media reports, TBEA plans to set up transformer manufacturing capacity in Gujarat at a capex of Rs2.5 bn.

Transformer prices have touched new lows Due to high competitive intensity and low capacity utilisation, transformer pricing has become very aggressive. As per the data presented by the management, prices for the 765KV 500MVA transformers have fallen by over 65% from September 2008 to December 2010. From the lows of December 2010, the prices seem to have recovered by about 30% by January 2012 and since then have mostly remained flat. However, from the September 2008 levels, current prices seem to be lower by over 55%.

Our calculations suggests that during FY09-12, Crompton’s transformers and reactors realisations have fallen between 25-40%. However, as per our discussions with industry experts, pricing has now remained flat or is marginally improving.

We, thus, expect domestic power business margins to improve by 70bps during FY13. However, we expect the domestic power business margins to fall by 100bps during FY13-15 as order inflows are likely to deteriorate after peaking in FY13. However, we expect overseas margins to improve by 323bps over FY12-15 from its lows of 1.7% in FY12 to 5% by FY15.

765KV 500MVA transformer current prices lower by 55% from Sep-08 levels

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 14

Figure 27: 765KV 500MVA transformer pricing have fallen

~55% during FY09-FY12

Figure 28: Crompton’s transformers & reactors

realisations between 25-40%

0

50

100

150

200

250

300

Sept

-08

Dec-

08

Jul-0

9

Aug-

09

Dec-

10

Jan-

11

May

-11

Aug-

11

Nov-

11

Jan-

12

Feb-

12500MVA 765KV transformers (Rs mn)

0%

5%

10%

15%

20%

25%

30%

FY09 FY10 FY11 FY12

MVA volume growth YoY (%)

Power systems sales growth YoY (%)

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

Localisation norms do not help contain margin erosion In CY10, for high-voltage transformers & reactor tenders, Powergrid relaxed its criteria that mandated to source at least 50% transformers (versus 66% earlier) from a manufacturing facility whose transformers have been operating for at least two years. Crompton was one of the few domestic manufacturers meeting these guidelines.

Since CY11, Powergrid introduced certain domestic manufacturing clauses which requires a bidder to have a subsidiary or a JV in India, to qualify bidding for its transformer & reactor tenders.

It was expected that Crompton would be able to benefit from new qualification requirement by gaining market share until foreign players (especially Chinese & Korean competitors), managed to set up JVs/subsidiaries in India. However, foreign competition has remained high despite the localisation norms, impacting margins.

Fixed price industrial & overseas power orders pose margin risk Power orders received from PGCIL as well as from SEBs have price variation clauses, while most of orders received from international geographies are fixed priced contracts. Similarly, given Crompton’s industrial orders have short delivery cycles (about 3 months), it does not get a price variation clause in these contracts. Industrial and overseas power orders thus exposes Crompton to margin risk.

CRGO steel used for the core of transformer and copper used for winding are the key commodities required for its transformers business. As a strategy, Crompton takes a forward hedge for copper and covers it when they receive an order to mitigate margin pressures. However, there are a very few CRGO producers globally and, hence, its price and availability is a key concern for margins.

Strategic plan for margin expansion is aggressive Crompton has devised a three year strategic plan to increase its consolidated EBITDA margin by 450bps. The plan is dependent on four drivers as below:

Industrial and overseas power orders exposes Crompton to margin risk

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 15

■ Improved offering: Crompton aims to move to high value-added product offerings such as the 1200KV transformers, CVT & surge arrestors, in line with the market requirements and manufacture energy efficient motors for global markets. It also plans to offer engineering services to utilities and enter new geographies such as the Middle East and Brazil. It expects 150bps EBITDA margin improvement to be contributed from these initiatives.

■ Sourcing: Crompton plans to increase its material sourcing from low cost countries. It has already established its sourcing office in Shanghai in July 2011. Crompton expects 150bps EBITDA margin improvement from its global sourcing initiatives.

■ Manufacturing footprint: Crompton plans to consolidate its manufacturing operations in Europe for optimum utilisation at each of the factories. Crompton also plans to augment capacity by over 50,000 MVA in India. It expects to improve its EBITDA margin by 100bps through these initiatives.

■ Cost efficiencies: Crompton plans to continue its efforts to optimise costs through the implementation of Six Sigma at its worldwide operations and expects these efforts to help improve its EBITDA margin by 50bps.

Figure 29: Segment-wise margin outlook for Crompton Segment % of FY12 consol.

EBITDA Key issues / margin outlook

Domestic Power 35% Pricing pressures intensifying, key product realisation down 55% since Sep-08; expect margin to improve by 70bps in FY13 but fall by 100bps over FY13-15 on peaking order flows

International Power 10% EBITDA margin deteriorated to 1.7% in FY12; expect margins to improve by 323bps over FY12-15

Industrials 25% Mostly fixed priced orders, thus risks margins; expect 210bps margin improvement over FY12-15 led by pick-up in industrial growth and penetration in high margin foreign markets

Consumer 30% Margins to marginally improve (55bps) over FY12-15

Source: Company data, Credit Suisse estimates

Expect 171bps margin improvement over FY12-15

We believe the management guidance for 450bps margin improvement is aggressive. We expect 171bps improvement in consolidated margin for the company over FY12-15. We expect most of the margin improvement to be driven by its international subsidiaires (contributes over 42-46% of sales), followed by industrial (14-15% of sales) and consumer (18-20% of sales) business segments.

Figure 30: Crompton – Consolidated sales mix Figure 31: Margin improvement to be mainly driven by

international subsidiaries

-

20

40

60

80

100

120

140

160

FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Power systems Consumer Products Industrial Systems International subs

6%

7%

8%

9%

10%

11%

12%

13%

14%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

FY11 FY12 FY13E FY14E FY15E

Power systems Consumer Products

Industrial Systems International subs

Consol. EBITDA margin

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Against 450bps margin improvement guidance over FY12-15, expect Crompton to achieve 171bps

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 16

Initiate with Underperform, 23% potential downside We initiate coverage on Crompton Greaves with an Underperform rating and target price of Rs92. Decelerating EPS growth of 19% over FY13-15 (versus FY13 EPS growth of 44% on a low base of FY12), subdued RoE at 14-16% (vs >30% in past) led by relatively lower margins & and capex continuing to impact asset turnover, working capital pressures and unrelated diversifications into power generation & distribution business are our concerns.

Given that Crompton has disappointed on earnings for four consequtive quarters, we believe that investors would turn positive only on visibility of it meeting its 3-year margin guidance, which seems aggressive. However, for FY13, we expect Crompton to meet its sales and order inflow growth guidance and the lower end of its margin guidance.

Power sector reforms in India and improvement in global macro conditions are key positive risks.

Expect earnings trajectory to decelerate Crompton’s earnings growth declined by 60% YoY during FY12. Given expected pick-up in power sector order flows as well as margins both from the domestic as well as the international market, we expect FY13 earnings growth to rebound to 44% in FY13. However, we do not see this as a continuing trend for the company, going forward.

During FY13-15, we expect industrial and consumer business diversification to improve sales growth as well as margins. We also expect a significant 193bps margin improvement in its international power segment. However, with peaking domestic power sector order flows in FY13, we expect sales growth and margins for this segment to deteriorate. Overall, we expect the earnings growth to slow to 19% over FY13-15.

This is despite our assumption of a significant improvement in working capital cycle for its domestic business & marginal improvement in its international business led by improvement in pick-up of deliveries by clients & increasing share of industrial business. However, its move towards undertaking EPC jobs (versus only products & services) in 765KV segment should inflate working capital.

We have also assumed the continuaton of tax benefits in India on R&D spends (entitled to a tax rebate for 2x the R&D capex) over FY13-14, resulting in standalone business tax rate at 27%. International subsidiaries are, however, subject to 11-39% tax rates depending on their locations and benefits from carry forward of losses. We expect a tax rate of 26% for its international business.

Key concerns: decelerating earnings growth, subdued RoE led by relatively lower margins & high capex, working capital pressures & unrelated diversifications

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 17

Figure 32: Expect a jump in FY13 EPS on low base, FY13-

15 EPS growth trajectory to decelerate

Figure 33: Expect improvement in working capital cycle

-80%

-60%

-40%

-20%

0%

20%

40%

60%

4

6

8

10

12

14

16

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Consolidated EPS (Rs/ share) YoY growth (%)

-

4

8

12

16

20

24

28

32

36

FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Working capital net of cash (Standalone)

Working capital net of cash (International subs)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Guidance for FY13 seems achievable; medium-term margin guidance is aggressive Crompton has guided for FY13 order inflow growth of 15%, sales growth of 12-14% and consolidated EBITDA margin improvement of 8-9% (vs 7.1% in FY12). We expect Crompton to meet the lower end of its margin guidance for FY13 and achieve its guidance for order inflow and sales growth.

We estimate 14.7% order inflow growth in FY13 for Crompton, mainly led by domestic as well as international power sector orders, though we expect muted growth in the industrial segment. We expect consolidated sales to increase by 13.3% (close to the high-end of its guidance) mainly led by 17% order book growth in FY12 and strong FY13 order inflows.

We expect FY13 margins to improve by 81bps to 8%, mainly led by a sharp 130bps YoY improvement in international subsidiaries’ margins and 70bps YoY improvement in margins for domestic power business due to increased ordering activity combined with stable to marginally increasing transfomer pricing.

We note that during FY12, while Crompton achieved its sales growth guidance and exceeded its order inflow growth guidance, it missed its EBITDA margin guidance.

Figure 34: Crompton – Guidance summary FY12 FY13

Guidance Actual Guidance CSe

Order inflow growth (%) 12.0 14.8 15.0 14.7

Sales growth (%) 10-12 12.4 12-14 13.3

Margin (%) 8-10 7.1 8-9 8.0

Source: Company data, Credit Suisse estimates

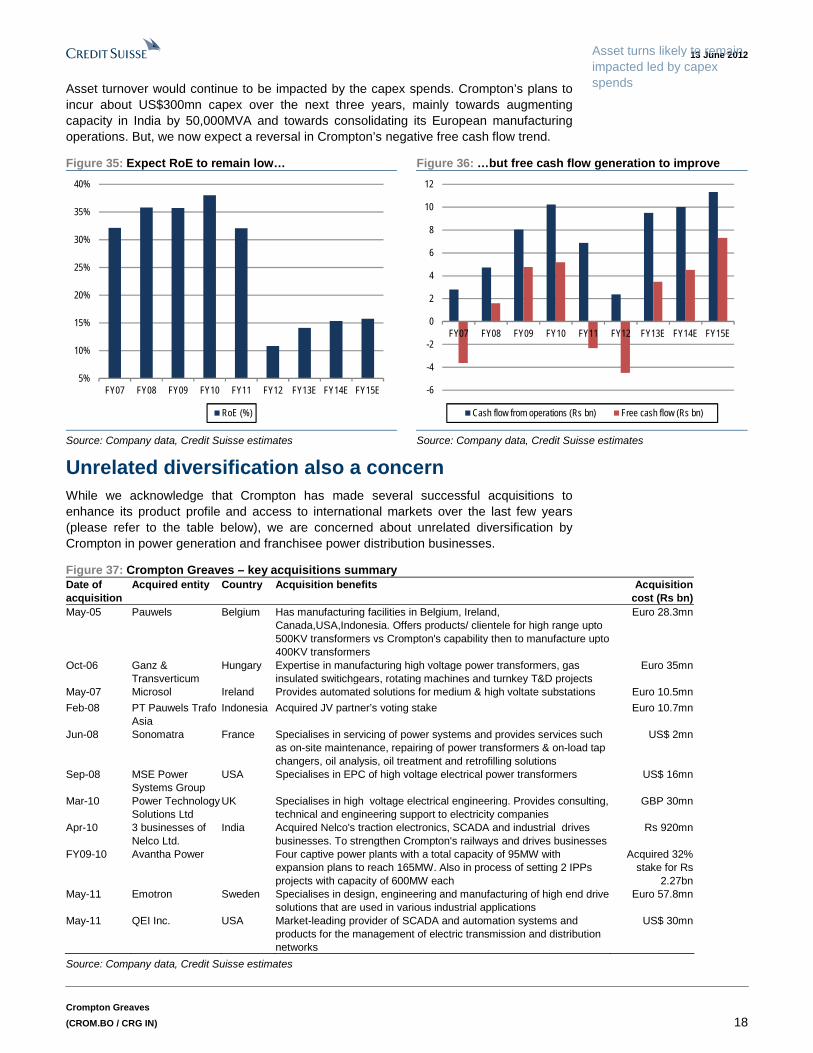

RoE to remain low on lower asset turnover & margins Though we expect improvement in Crompton’s RoE from its low of 11% observed in FY12 to about 16% by FY15 mainly led by our expectation of improving margins, compared to its history of over 30% RoE since FY05, we expect Crompton’s RoE to remain low led by relatively lower margins and asset turnover.

Expect 14.7% inflow growth, 13.3% revenue growth and 8% margins in FY13

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 18

Asset turnover would continue to be impacted by the capex spends. Crompton’s plans to incur about US$300mn capex over the next three years, mainly towards augmenting capacity in India by 50,000MVA and towards consolidating its European manufacturing operations. But, we now expect a reversal in Crompton’s negative free cash flow trend.

Figure 35: Expect RoE to remain low… Figure 36: …but free cash flow generation to improve

5%

10%

15%

20%

25%

30%

35%

40%

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

RoE (%)

-6

-4

-2

0

2

4

6

8

10

12

FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Cash flow from operations (Rs bn) Free cash flow (Rs bn)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Unrelated diversification also a concern While we acknowledge that Crompton has made several successful acquisitions to enhance its product profile and access to international markets over the last few years (please refer to the table below), we are concerned about unrelated diversification by Crompton in power generation and franchisee power distribution businesses.

Figure 37: Crompton Greaves – key acquisitions summary Date of acquisition

Acquired entity Country Acquisition benefits Acquisition cost (Rs bn)

May-05 Pauwels Belgium Has manufacturing facilities in Belgium, Ireland, Canada,USA,Indonesia. Offers products/ clientele for high range upto 500KV transformers vs Crompton's capability then to manufacture upto 400KV transformers

Euro 28.3mn

Oct-06 Ganz & Transverticum

Hungary Expertise in manufacturing high voltage power transformers, gas insulated switichgears, rotating machines and turnkey T&D projects

Euro 35mn

May-07 Microsol Ireland Provides automated solutions for medium & high voltate substations Euro 10.5mn

Feb-08 PT Pauwels Trafo Asia

Indonesia Acquired JV partner’s voting stake Euro 10.7mn

Jun-08 Sonomatra France Specialises in servicing of power systems and provides services such as on-site maintenance, repairing of power transformers & on-load tap changers, oil analysis, oil treatment and retrofilling solutions

US$ 2mn

Sep-08 MSE Power Systems Group

USA Specialises in EPC of high voltage electrical power transformers US$ 16mn

Mar-10 Power Technology Solutions Ltd

UK Specialises in high voltage electrical engineering. Provides consulting, technical and engineering support to electricity companies

GBP 30mn

Apr-10 3 businesses of Nelco Ltd.

India Acquired Nelco's traction electronics, SCADA and industrial drives businesses. To strengthen Crompton's railways and drives businesses

Rs 920mn

FY09-10 Avantha Power Four captive power plants with a total capacity of 95MW with expansion plans to reach 165MW. Also in process of setting 2 IPPs projects with capacity of 600MW each

Acquired 32% stake for Rs

2.27bn May-11 Emotron Sweden Specialises in design, engineering and manufacturing of high end drive

solutions that are used in various industrial applications Euro 57.8mn

May-11 QEI Inc. USA Market-leading provider of SCADA and automation systems and products for the management of electric transmission and distribution networks

US$ 30mn

Source: Company data, Credit Suisse estimates

Asset turns likely to remain impacted led by capex spends

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 19

Crompton plans to diversify into power generation business through its investments in its Avantha Group company. Avantha Power operates four captive power plants totaling 95MW, with plans to increase the capacity at these projects to 165MW. Besides, it also plans to set up IPP projects of 1.2GW each in Korba (Chattisgarh) and Jhabua (MP). Crompton had earlier also acquired a 59% stake in Malanpur captive power plant, which it sold in FY10 to the Avantha group company.

Crompton has has earlier tried to venture into power distribution franchisee business. It was selected as the lowest bidder for the Nagpur power distribution franchisee. However, it later withdrew from this bid. In FY11, it again participated and won the power distribution franchisee license for 10 years at Jalgaon, Maharashtra.

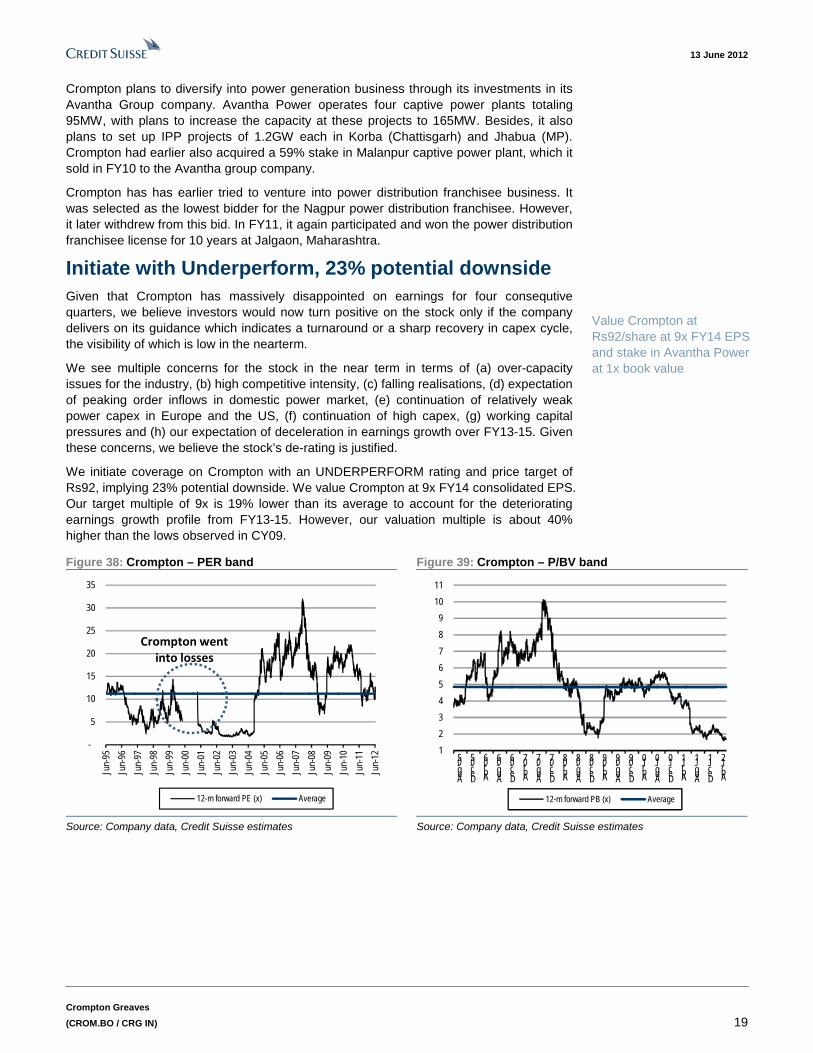

Initiate with Underperform, 23% potential downside Given that Crompton has massively disappointed on earnings for four consequtive quarters, we believe investors would now turn positive on the stock only if the company delivers on its guidance which indicates a turnaround or a sharp recovery in capex cycle, the visibility of which is low in the nearterm.

We see multiple concerns for the stock in the near term in terms of (a) over-capacity issues for the industry, (b) high competitive intensity, (c) falling realisations, (d) expectation of peaking order inflows in domestic power market, (e) continuation of relatively weak power capex in Europe and the US, (f) continuation of high capex, (g) working capital pressures and (h) our expectation of deceleration in earnings growth over FY13-15. Given these concerns, we believe the stock’s de-rating is justified.

We initiate coverage on Crompton with an UNDERPERFORM rating and price target of Rs92, implying 23% potential downside. We value Crompton at 9x FY14 consolidated EPS. Our target multiple of 9x is 19% lower than its average to account for the deteriorating earnings growth profile from FY13-15. However, our valuation multiple is about 40% higher than the lows observed in CY09.

Figure 38: Crompton – PER band Figure 39: Crompton – P/BV band

-

5

10

15

20

25

30

35

Jun-

95

Jun-

96

Jun-

97

Jun-

98

Jun-

99

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

12-m forward PE (x) Average

Crompton went into losses

1

2

3

4

5

6

7

8

9

10

11

Aug-05

Dec-05

Apr-06

Aug-06

Dec-06

Apr-07

Aug-07

Dec-07

Apr-08

Aug-08

Dec-08

Apr-09

Aug-09

Dec-09

Apr-10

Aug-10

Dec-10

Apr-11

Aug-11

Dec-11

Apr-12

12-m forward PB (x) Average

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Value Crompton at Rs92/share at 9x FY14 EPS and stake in Avantha Power at 1x book value

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 20

Financial snapshot – Standalone Figure 40: Crompton – Profit and Loss statement summary (Standalone Financials) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

Net sales 52,840 59,514 64,854 73,611 79,709 82,794

Total operating expenses 44,262 50,190 57,647 65,114 70,503 72,727

EBITDA 8,578 9,324 7,207 8,497 9,206 10,067

EBITDA margin (%) 16.2% 15.7% 11.1% 11.5% 11.5% 12.2%

Depreciation 519 809 907 925 1,071 1,143

EBIT 8,059 8,516 6,300 7,572 8,135 8,925

EBIT margin (%) 15.3% 14.3% 9.7% 10.3% 10.2% 10.8%

Interest 200 41 37 10 10 10

Other income 844 795 504 678 600 824

PBT 8,703 9,269 6,767 8,240 8,724 9,739

Tax 2,933 2,327 1,718 2,225 2,355 2,922

Tax rate (%) 33.7% 25.1% 25.4% 27.0% 27.0% 30.0%

Recurring PAT 5,770 6,943 5,049 6,015 6,369 6,817

Exceptionals 403 - - - - -

Reported PAT 6,173 6,943 5,049 6,015 6,369 6,817

Source: Company data, Credit Suisse estimates

Figure 41: Crompton - Balance Sheet summary (standalone financials) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

Share capital 1,283 1,283 1,283 1,283 1,283 1,283

Reserves and surplus 16,364 21,758 25,726 30,454 35,459 40,817

Networth 17,647 23,041 27,009 31,737 36,742 42,100

Loan funds 268 134 104 104 104 104

Deferred tax liability 834 735 432 432 432 432

Total liabilities 18,749 23,910 27,545 32,273 37,279 42,637

Gross block 11,714 16,042 14,474 17,974 20,974 22,974

Less: Depreciation 6,376 7,288 8,195 9,120 10,191 11,333

Net block 5,338 8,754 6,279 8,854 10,783 11,640

CWIP 330 476 476 476 476 476

Net fixed assets 5,668 9,230 6,755 9,330 11,259 12,116

Investments 6,881 7,816 10,525 10,525 10,525 10,525

Inventory 3,035 4,057 4,496 4,840 5,233 5,383

Debtors 12,128 15,102 17,356 17,412 17,763 17,316

Cash and bank 5,485 1,509 3,211 6,242 10,927 16,229

Loans and advances 1,554 3,182 3,362 3,816 4,132 4,292

Total current assets 22,202 23,850 28,425 32,310 38,055 43,220

Current liabilities 14,466 15,293 16,657 18,078 20,597 21,185

Provisions 1,536 1,693 1,503 1,814 1,964 2,040

Total current liabilities 16,002 16,986 18,160 19,892 22,561 23,224

Net current assets 6,200 6,864 10,265 12,418 15,495 19,995

Misc. expenditure written off - - - - - -

Total assets 18,749 23,910 27,545 32,273 37,279 42,637

Source: Company data, Credit Suisse estimates

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 21

Figure 42: Crompton – Cash flow statement summary (standalone financials) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

PBT 8,703 9,269 6,767 8,240 8,724 9,739

Tax Paid (2,933) (2,327) (1,718) (2,225) (2,355) (2,922)

Change in net DTL 195 (99) (303) - - -

Add: Depreciation 519 809 907 925 1,071 1,143

Change in Working Capital 263 (4,640) (1,700) 879 1,608 801

Cash Flow from Operations 6,747 3,013 3,953 7,819 9,048 8,761

Extrordinary Income/ (Expenses) 403 - - - - -

Capex (951) (4,370) 1,568 (3,500) (3,000) (2,000)

Change in Investments (4,225) (936) (2,709) - - -

Cash Flow from Investing (4,773) (5,306) (1,141) (3,500) (3,000) (2,000)

Change in Debt (269) (134) (30) - - -

Change in Share capital 550 - - - - -

Change in Reserves (414) 93 - - - -

Dividend and Dividend Tax (1,080) (1,642) (1,081) (1,287) (1,363) (1,459)

Cash Flow from Financing (1,213) (1,683) (1,111) (1,287) (1,363) (1,459)

Increase/ (Decrease) in Cash 760 (3,976) 1,702 3,031 4,685 5,302

Opening cash and cash equivalents 4,725 5,485 1,509 3,211 6,242 10,927

Closing cash and cash equivalents 5,485 1,509 3,211 6,242 10,927 16,229

Source: Company data, Credit Suisse estimates

Figure 43: Crompton – Key ratios and valuation summary (standalone financials) FY10 FY11 FY12 FY13E FY14E FY15E

Share Price (Rs) 119 119 119 119 119 119

Shares Outstanding (mn) 642 642 642 642 642 642

Market Cap (Rs mn) 76,531 76,531 76,531 76,531 76,531 76,531

Net Debt (Rs mn) (8,216) (5,402) (8,116) (11,147) (15,832) (21,134)

EV (Rs mn) 68,315 71,129 68,415 65,383 60,699 55,397

Net Debt /Equity (x) (0.5) (0.2) (0.3) (0.4) (0.4) (0.5)

Gross Debt/ Equity (x) 0.0 0.0 0.0 0.0 0.0 0.0

EPS (Rs) 9 11 8 9 10 11

CEPS (Rs) 10 12 9 11 12 12

DPS (Rs) 1 2 1 2 2 2

BPS (Rs) 28 36 42 49 57 66

P/E (x) 13.3 11.0 15.2 12.7 12.0 11.2

P/CEPS (x) 12.2 9.9 12.9 11.0 10.3 9.6

Yield (%) 1.2% 1.8% 1.2% 1.4% 1.5% 1.6%

P/BV (x) 4.3 3.3 2.8 2.4 2.1 1.8

EV/EBITDA (x) 8.0 7.6 9.5 7.7 6.6 5.5

EV/Sales (x) 1.3 1.2 1.1 0.9 0.8 0.7

EPS Growth % -17.0% 20.3% -27.3% 19.1% 5.9% 7.0%

RoCE (%) 35.7% 32.5% 19.6% 20.1% 18.3% 17.1%

RoE (%) 38.4% 34.1% 20.2% 20.5% 18.6% 17.3%

EBITDA Margin (%) 16.2% 15.7% 11.1% 11.5% 11.5% 12.2%

EBIT Margin (%) 15.3% 14.3% 9.7% 10.3% 10.2% 10.8%

PBT Margin (%) 16.5% 15.6% 10.4% 11.2% 10.9% 11.8%

PAT Margin (%) 10.9% 11.7% 7.8% 8.2% 8.0% 8.2%

Source: Company data, Credit Suisse estimates

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 22

Financial snapshot – Consolidated Figure 44: Crompton – Profit and Loss statement summary (consolidated financials) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

Net sales 91,409 100,051 112,486 127,458 141,290 153,174

Total operating expenses 78,639 86,613 104,449 117,322 129,441 139,604

EBITDA 12,770 13,438 8,036 10,136 11,848 13,570

EBITDA margin (%) 14.0% 13.4% 7.1% 8.0% 8.4% 8.9%

Depreciation 1,551 1,936 2,600 2,686 2,958 3,041

EBIT 11,219 11,502 5,437 7,450 8,890 10,528

EBIT margin (%) 12.3% 11.5% 4.8% 5.8% 6.3% 6.9%

Interest 428 201 463 583 620 658

Other income 1,100 990 524 732 636 871

PBT 11,891 12,291 5,497 7,600 8,906 10,742

Tax 3,650 3,100 1,821 2,275 2,403 3,182

Tax rate (%) 30.7% 25.2% 33.1% 29.9% 27.0% 29.6%

Minority interest/ Asssociates 57 84 47 55 61 66

Recurring PAT 8,247 9,268 3,736 5,392 6,577 7,638

Exceptionals 352 (381) - - - -

Reported PAT 8,599 8,887 3,736 5,392 6,577 7,638

Source: Company data, Credit Suisse estimates

Figure 45: Crompton - Balance Sheet summary (Consolidated financials) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

Share capital 1,283 1,283 1,283 1,283 1,283 1,283

Reserves and surplus 23,760 31,464 34,826 38,931 44,145 50,325

Networth 25,043 32,747 36,109 40,214 45,428 51,608

Loan funds 5,010 4,703 11,555 11,555 13,055 13,055

Minority interest 43 157 157 150 144 137

Total liabilities 30,095 37,607 47,821 51,919 58,627 64,800

Gross block 29,858 37,804 37,681 43,681 49,181 53,181

Less: Depreciation 17,234 19,490 22,090 24,775 27,733 30,774

Net block 12,623 18,314 15,591 18,905 21,447 22,406

CWIP 1,137 1,102 1,102 1,102 1,102 1,102

Net fixed assets 13,760 19,417 16,693 20,008 22,550 23,508

Investments 5,536 6,747 7,864 7,864 7,864 7,864

Goodwill - - 5,882 5,882 5,882 5,882

Deferred tax asset (net) (49) (160) 513 513 513 513

Inventory 10,194 11,893 12,233 13,595 15,402 16,767

Debtors 21,463 25,427 31,433 31,205 33,790 35,248

Cash and bank 6,688 2,984 4,976 7,179 11,825 17,688

Loans and advances 2,674 5,192 6,703 6,508 7,211 7,811

Total current assets 41,018 45,496 55,344 58,487 68,229 77,514

Current liabilities 26,567 29,595 34,688 36,258 41,286 44,830

Provisions 3,603 4,298 3,787 4,577 5,124 5,652

Total current liabilities 30,170 33,892 38,475 40,835 46,410 50,482

Net current assets 10,849 11,604 16,869 17,653 21,818 27,032

Misc. expenditure written off - - - - - -

Total assets 30,095 37,607 47,821 51,919 58,627 64,800

Source: Company data, Credit Suisse estimates

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 23

Figure 46: Crompton – Cash flow statement summary (Consolidated Financials) (Rs mn) FY10 FY11 FY12 FY13E FY14E FY15E

Recurring PAT (pre-minority) 8,272 9,272 3,729 5,386 6,570 7,631

Change in net DTL 531 111 (673) - - -

Add: Depreciation 1,551 1,936 2,600 2,686 2,958 3,041

Change in Working Capital (125) (4,459) (3,273) 1,419 480 649

Cash Flow from Operations 10,229 6,860 2,383 9,491 10,009 11,321

Extrordinary Income/ (Expenses) 352 (381) (5,882) - - -

Capex (1,526) (7,593) 124 (6,000) (5,500) (4,000)

Change in Investments (3,864) (1,211) (1,117) - - -

Cash Flow from Investing (5,037) (9,185) (6,875) (6,000) (5,500) (4,000)

Change in Debt (2,173) (306) 6,852 - 1,500 -

Change in Share capital 550 - - - - -

Change in Reserves / Minority (1,591) (126) 713 - - -

Dividend and Dividend Tax (946) (946) (1,081) (1,287) (1,363) (1,459)

Cash Flow from Financing (4,160) (1,379) 6,484 (1,287) 137 (1,459)

Increase/ (Decrease) in Cash 1,032 (3,704) 1,992 2,203 4,646 5,863

Opening cash and cash equivalents 5,656 6,688 2,984 4,976 7,179 11,825

Closing cash and cash equivalents 6,688 2,984 4,976 7,179 11,825 17,688

Source: Company data, Credit Suisse estimates

Figure 47: Crompton – key ratios and valuation summary (Consolidated Financials) FY10 FY11 FY12 FY13E FY14E FY15E

Share Price (Rs) 119 119 119 119 119 119

Shares Outstanding (mn) 642 642 642 642 642 642

Market Cap (Rs mn) 76,531 76,531 76,531 76,531 76,531 76,531

Net Debt (Rs mn) (4,678) (2,308) 1,568 (636) (3,782) (9,644)

EV (Rs mn) 71,853 74,223 78,098 75,895 72,749 66,887

Net Debt /Equity (x) (0.2) (0.1) 0.0 (0.0) (0.1) (0.2)

Gross Debt/ Equity (x) 0.2 0.1 0.3 0.3 0.3 0.3

EPS (Rs) 12.9 14.4 5.8 8.4 10.3 11.9

CEPS (Rs) 15.3 17.5 9.9 12.6 14.9 16.6

DPS (Rs) 1.3 1.3 1.4 1.7 1.8 1.9

BPS (Rs) 39 51 56 63 71 80

P/E (x) 9.3 8.3 20.5 14.2 11.6 10.0

P/CEPS (x) 7.8 6.8 12.1 9.5 8.0 7.2

Yield (%) 1.1% 1.1% 1.2% 1.4% 1.5% 1.6%

P/BV (x) 3.1 2.3 2.1 1.9 1.7 1.5

EV/EBITDA (x) 5.6 5.5 9.7 7.5 6.1 4.9

EV/Sales (x) 0.8 0.7 0.7 0.6 0.5 0.4

EPS Growth % 47.3% 12.4% -59.7% 44.3% 22.0% 16.1%

RoCE (%) 29.6% 27.4% 8.7% 10.8% 11.9% 12.4%

RoE (%) 38.0% 32.1% 10.9% 14.1% 15.4% 15.7%

EBITDA Margin (%) 14.0% 13.4% 7.1% 8.0% 8.4% 8.9%

EBIT Margin (%) 12.3% 11.5% 4.8% 5.8% 6.3% 6.9%

PBT Margin (%) 13.0% 12.3% 4.9% 6.0% 6.3% 7.0%

PAT Margin (%) 9.0% 9.3% 3.3% 4.2% 4.7% 5.0%

Source: Company data, Credit Suisse estimates

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 24

Companies Mentioned (Price as of 12 Jun 12) ABB Ltd. (ABB.BO, Rs 771.40) BEML Ltd (BEML.BO, Rs 384.45) BGR Energy (BGRE.BO, Rs 293.95) Bharat Heavy Electricals (BHEL.BO, Rs 219.35, UNDERPERFORM, TP Rs 182.00) Blue Star Limited (BLUS.BO, Rs 161.35) Crompton Greaves (CROM.BO, Rs 119.30, UNDERPERFORM [V], TP Rs 92.00) Cummins India (CUMM.BO, Rs 422.95, OUTPERFORM, TP Rs 506.00) Havells India Ltd. (HVEL.BO, Rs 551.85) Jyoti Structures Ltd (JYTS.BO, Rs 40.60) KEC International Ltd (KECL.BO, Rs 51.80) Larsen & Toubro (LART.BO, Rs 1,315.50, NEUTRAL, TP Rs 1,091.00) Mahindra & Mahindra (MAHM.BO, Rs 695.30, OUTPERFORM, TP Rs 820.00) Maruti Suzuki India Ltd (MRTI.BO, Rs 1,146.30, OUTPERFORM, TP Rs 1,422.00) Powergrid (PGCIL) (PGRD.BO, Rs 108, NOT RATED) Punj Lloyd Ltd (PUJL.BO, Rs 48.00) Siemens India (SIEM.BO, Rs 683.45) Suzlon Energy Ltd (SUZL.BO, Rs 17.75) Tata Steel Ltd (TISC.BO, Rs 412.60, NEUTRAL, TP Rs 340.00) TBEA Co Ltd (600089.SS, Rmb 7.38, UNDERPERFORM, TP Rmb 7.90) Thermax (THMX.BO, Rs 459.10) Voltas Ltd (VOLT.BO, Rs 107.15, UNDERPERFORM, TP Rs 83.00)

Disclosure Appendix

Important Global Disclosures Amish Shah, CFA & Abhishek Bansal each certify, with respect to the companies or securities that he or she analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

See the Companies Mentioned section for full company names. 3-Year Price, Target Price and Rating Change History Chart for CROM.BO CROM.BO Closing

Price Target

Price

Initiation/ Date (Rs) (Rs) Rating Assumption 6-Nov-09 219.515 274.275 O X 19-Feb-10 230.315 306.367 16-Mar-10 245.15 306.37 24-May-10 233.1 306.78 21-Jul-10 282.5 309.843 26-Oct-10 325.45 310 12-Jan-11 291.8 354.292 1-Apr-11 272.9 337.762 24-May-11 251 337.8 21-Jul-11 181.3 217 27-Oct-11 139.35 NC

274

306306 307 310 310

354338 338

217

6-Nov-09NC

O

106

156

206

256

306

356

13-Ju

n-09

13-A

ug-09

13-O

ct-09

13-D

ec-09

13-Feb-10

13-Apr-1

0

13-Ju

n-10

13-Aug-1

0

13-O

ct-10

13-D

ec-10

13-Feb

-11

13-Apr-1

1

13-Ju

n-11

13-Aug-1

1

13-O

ct-11

13-D

ec-11

13-Feb

-12

13-A

pr-12

Closing Price Target Price Initiation/Assumption Rating

Rs

O=Outperform; N=Neutral; U=Underperform; R=Restricted; NR=Not Rated; NC=Not Covered

The analyst(s) responsible for preparing this research report received compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities. Analysts’ stock ratings are defined as follows: Outperform (O): The stock’s total return is expected to outperform the relevant benchmark* by at least 10-15% (or more, depending on perceived risk) over the next 12 months. Neutral (N): The stock’s total return is expected to be in line with the relevant benchmark* (range of ±10-15%) over the next 12 months. Underperform (U): The stock’s total return is expected to underperform the relevant benchmark* by 10-15% or more over the next 12 months. *Relevant benchmark by region: As of 29th May 2009, Australia, New Zealand, U.S. and Canadian ratings are based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe**, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. Some U.S. and Canadian ratings may fall outside the absolute total return ranges defined above, depending on market conditions and industry factors. For Latin American, Japanese, and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of

13 June 2012

Crompton Greaves

(CROM.BO / CRG IN) 25

the relevant country or regional benchmark; for European stocks, ratings are based on a stock’s total return relative to the analyst's coverage universe**. For Australian and New Zealand stocks, 12-month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10-15% and -10-15% levels in the Neutral stock rating definition, respectively. **An analyst's coverage universe consists of all companies covered by the analyst within the relevant sector. Restricted (R): In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances. Volatility Indicator [V]: A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ coverage universe weightings are distinct from analysts’ stock ratings and are based on the expected performance of an analyst’s coverage universe* versus the relevant broad market benchmark**: Overweight: Industry expected to outperform the relevant broad market benchmark over the next 12 months. Market Weight: Industry expected to perform in-line with the relevant broad market benchmark over the next 12 months. Underweight: Industry expected to underperform the relevant broad market benchmark over the next 12 months. *An analyst’s coverage universe consists of all companies covered by the analyst within the relevant sector. **The broad market benchmark is based on the expected return of the local market index (e.g., the S&P 500 in the U.S.) over the next 12 months. Credit Suisse’s distribution of stock ratings (and banking clients) is: