Chipotle Mexican Grill, Inc. (CMG) - Credit Suisse | PLUS

31

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 25 June 2019 Americas/United States Equity Research Restaurants Chipotle Mexican Grill, Inc. (CMG) Rating OUTPERFORM Price (21-Jun-19, US$) 726.85 Target price (US$) 870.00 52-week price range (US$) 740.59 - 385.84 Market cap(US$ m) 20,144 Enterprise value (US$ m) 19,732 Target price is for 12 months. Research Analysts Lauren Silberman 212 325 2720 [email protected] INITIATION Guac is Worth the Extra Charge and So Is Growth; Initiate Outperform ■ We initiate coverage of Chipotle (CMG) with an Outperform rating and $870 target price. CMG has returned to a narrative of growth rather than recovery, with on-trend initiatives that well position the company to appeal to its target base and outperform peers. Contributions from traffic and average check growth should support mid-single-digit SSS longer-term and generate margin leverage to drive an EPS CAGR of ~33% over the next four years. ■ Confidence in Top-Line Performance: CMG’s comprehensive sales plan and omni-channel strategy should generate SSS of ~8% in 2019 and ~5.0- 5.5% longer-term. Digital/delivery make up ~15% of sales, with CMG well positioned with a younger consumer base, transportable food, and best-in- class operations. New menu innovation through recipes with existing ingredients and new menu items/processes could be a meaningful driver of growth. An improved social media and marketing strategy, new loyalty program, and increased analytical capabilities should drive more effective engagement. Improving new-unit productivity and the potential for alternative formats support mid-single-digit unit growth, with modest step-ups likely. ■ Power of the Economic Model: CMG is the only publicly traded restaurant company in quick serve/fast casual with a 100% company-owned model, supporting attractive upside potential. A return to $2.4MM average unit volumes (AUVs, $2MM currently) should enable restaurant-level margins expansion to ~23.5% by 2022 (18.7% in 2018) and new-unit returns of 70- 80%. We estimate each $100K in AUVs should translate to ~100bps of margin and ~10-15% in EPS. ■ Valuation: Our $870 target price is based on ~25x our NTM EBITDA in 12 months and implies ~46x our NTM EPS in 12 months, slightly below current multiples. Key risks: food safety headlines, consumer spending, inflation. Share price performance On 21-Jun-2019 the S&P 500 INDEX closed at 2950.46 Daily Jun22, 2018 - Jun21, 2019, 06/22/18 = US$469.94 Quarterly EPS Q1 Q2 Q3 Q4 2018A 2.13 2.87 2.16 1.72 2019E 3.40 3.80 3.26 3.15 2020E 4.19 5.13 4.20 4.36 Financial and valuation metrics Year 12/18A 12/19E 12/20E 12/21E EPS (CS adj.) (US$) 8.88 13.60 17.89 22.42 Prev. EPS (US$) - - - - P/E rel. (%) 458.0 309.5 261.6 228.8 Revenue (US$ m) 4,865.0 5,435.4 6,052.6 6,712.4 EBITDA (US$ m) 543.8 713.9 899.6 1,083.2 OCFPS (US$) 22.23 25.39 29.91 35.55 P/OCF (x) 19.4 28.6 24.3 20.4 EV/EBITDA (current) 36.5 27.8 22.1 18.3 Net debt (US$ m) -250 -412 -632 -889 ROIC (%) 20.26 29.20 36.63 44.24 Number of shares (m) 27.71 IC (current, US$ m) 1,191.39 BV/share (Next Qtr., US$) 151.1 Dividend (current, US$) - Net debt (Next Qtr., US$ m) -333.7 Net debt/tot eq (Next Qtr.,%) -21.4 Source: Company data, Refinitiv, Credit Suisse estimates

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Chipotle Mexican Grill, Inc. (CMG) - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

25 June 2019 Americas/United States

Equity Research

Restaurants

Chipotle Mexican Grill, Inc. (CMG) Rating OUTPERFORM Price (21-Jun-19, US$) 726.85 Target price (US$) 870.00 52-week price range (US$) 740.59 - 385.84 Market cap(US$ m) 20,144 Enterprise value (US$ m) 19,732 Target price is for 12 months.

Research Analysts

Lauren Silberman

212 325 2720

INITIATION

Guac is Worth the Extra Charge and So Is

Growth; Initiate Outperform

■ We initiate coverage of Chipotle (CMG) with an Outperform rating and

$870 target price. CMG has returned to a narrative of growth rather than

recovery, with on-trend initiatives that well position the company to appeal to

its target base and outperform peers. Contributions from traffic and average

check growth should support mid-single-digit SSS longer-term and generate

margin leverage to drive an EPS CAGR of ~33% over the next four years.

■ Confidence in Top-Line Performance: CMG’s comprehensive sales plan

and omni-channel strategy should generate SSS of ~8% in 2019 and ~5.0-

5.5% longer-term. Digital/delivery make up ~15% of sales, with CMG well

positioned with a younger consumer base, transportable food, and best-in-

class operations. New menu innovation through recipes with existing

ingredients and new menu items/processes could be a meaningful driver of

growth. An improved social media and marketing strategy, new loyalty

program, and increased analytical capabilities should drive more effective

engagement. Improving new-unit productivity and the potential for alternative

formats support mid-single-digit unit growth, with modest step-ups likely.

■ Power of the Economic Model: CMG is the only publicly traded restaurant

company in quick serve/fast casual with a 100% company-owned model,

supporting attractive upside potential. A return to $2.4MM average unit

volumes (AUVs, $2MM currently) should enable restaurant-level margins

expansion to ~23.5% by 2022 (18.7% in 2018) and new-unit returns of 70-

80%. We estimate each $100K in AUVs should translate to ~100bps of

margin and ~10-15% in EPS.

■ Valuation: Our $870 target price is based on ~25x our NTM EBITDA in 12

months and implies ~46x our NTM EPS in 12 months, slightly below current

multiples. Key risks: food safety headlines, consumer spending, inflation.

Share price performance

On 21-Jun-2019 the S&P 500 INDEX closed at 2950.46

Daily Jun22, 2018 - Jun21, 2019, 06/22/18 = US$469.94

Quarterly EPS Q1 Q2 Q3 Q4 2018A 2.13 2.87 2.16 1.72 2019E 3.40 3.80 3.26 3.15 2020E 4.19 5.13 4.20 4.36

Financial and valuation metrics

Year 12/18A 12/19E 12/20E 12/21E EPS (CS adj.) (US$) 8.88 13.60 17.89 22.42 Prev. EPS (US$) - - - - P/E rel. (%) 458.0 309.5 261.6 228.8 Revenue (US$ m) 4,865.0 5,435.4 6,052.6 6,712.4 EBITDA (US$ m) 543.8 713.9 899.6 1,083.2 OCFPS (US$) 22.23 25.39 29.91 35.55 P/OCF (x) 19.4 28.6 24.3 20.4 EV/EBITDA (current) 36.5 27.8 22.1 18.3 Net debt (US$ m) -250 -412 -632 -889 ROIC (%) 20.26 29.20 36.63 44.24

Number of shares (m) 27.71 IC (current, US$ m) 1,191.39 BV/share (Next Qtr., US$) 151.1 Dividend (current, US$) - Net debt (Next Qtr., US$ m) -333.7 Net debt/tot eq (Next Qtr.,%) -21.4 Source: Company data, Refinitiv, Credit Suisse estimates

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 2

Chipotle Mexican Grill, Inc. (CMG)

Price (21 Jun 2019): US$726.85; Rating: OUTPERFORM; Target Price: 870.00; Analyst: Lauren Silberman

Income Statement 12/18A 12/19E 12/20E 12/21E

Revenue (US$ m) 4,865.0 5,435.4 6,052.6 6,712.4 EBITDA (US$ m) 544 714 900 1,083 Depr. & amort. (195) (215) (233) (252) EBIT (US$) 349 499 666 831 Net interest exp -0 -0 -0 -0 PBT (US$) 359 511 677 838 Income taxes (111) (133) (186) (235) Profit after tax 248 379 490 604 Net profit (US$) 248 379 490 604 Other NPAT adjustments 0 0 0 0

Cash Flow 12/18A 12/19E 12/20E 12/21E

Cash flow from operations 622 707 820 957 CAPEX (287) (304) (300) (300) Free cashflow to the firm 334 403 520 657 Cash flow from investments (388) (333) (300) (300) Net share issue(/repurchase) (161) (203) (300) (400) Dividends paid 0 0 0 0 Changes in Net Cash/Debt 65 162 220 257

Balance Sheet (US$) 12/18A 12/19E 12/20E 12/21E

Cash & cash equivalents 250 412 632 889 Account receivables 62 50 55 62 Other current assets 481 492 492 492 Total fixed assets 1,379 1,445 1,512 1,560 Investment securities 0 0 0 0 Total assets 2,266 4,843 5,138 5,451 Total current liabilities 450 606 627 650 Shareholder equity 1,441 1,677 1,951 2,241 Total liabilities and equity 2,266 4,843 5,138 5,451 Net debt (250) (412) (632) (889)

Per share 12/18A 12/19E 12/20E 12/21E

No. of shares (wtd avg) 28 28 27 27 CS adj. EPS 8.88 13.60 17.89 22.42 Prev. EPS (US$) Dividend (US$) 0.00 0.00 0.00 0.00 Free cash flow per share 11.95 14.46 18.96 24.40

Earnings 12/18A 12/19E 12/20E 12/21E

Sales growth (%) 8.7 11.7 11.4 10.9 EBIT growth (%) 16.1 42.9 33.5 24.7 Net profit growth (%) 31.8 52.5 29.5 23.1 EPS growth (%) 34.6 53.1 31.5 25.3 EBITDA margin (%) 11.2 13.1 14.9 16.1 EBIT margin (%) 7.2 9.2 11.0 12.4 Pretax margin (%) 7.4 9.4 11.2 12.5 Net margin (%) 5.1 7.0 8.1 9.0

Valuation 12/18A 12/19E 12/20E 12/21E

EV/EBITDA (x) 36.5 27.8 22.1 18.3 P/E (x) 81.8 53.4 40.6 32.4

Returns 12/18A 12/19E 12/20E 12/21E

ROIC (%) 20.3 29.2 36.6 44.2

Gearing 12/18A 12/19E 12/20E 12/21E

Net debt/equity (%) (17.3) (24.6) (32.4) (39.7)

Quarterly EPS Q1 Q2 Q3 Q4 2018A 2.13 2.87 2.16 1.72 2019E 3.40 3.80 3.26 3.15 2020E 4.19 5.13 4.20 4.36

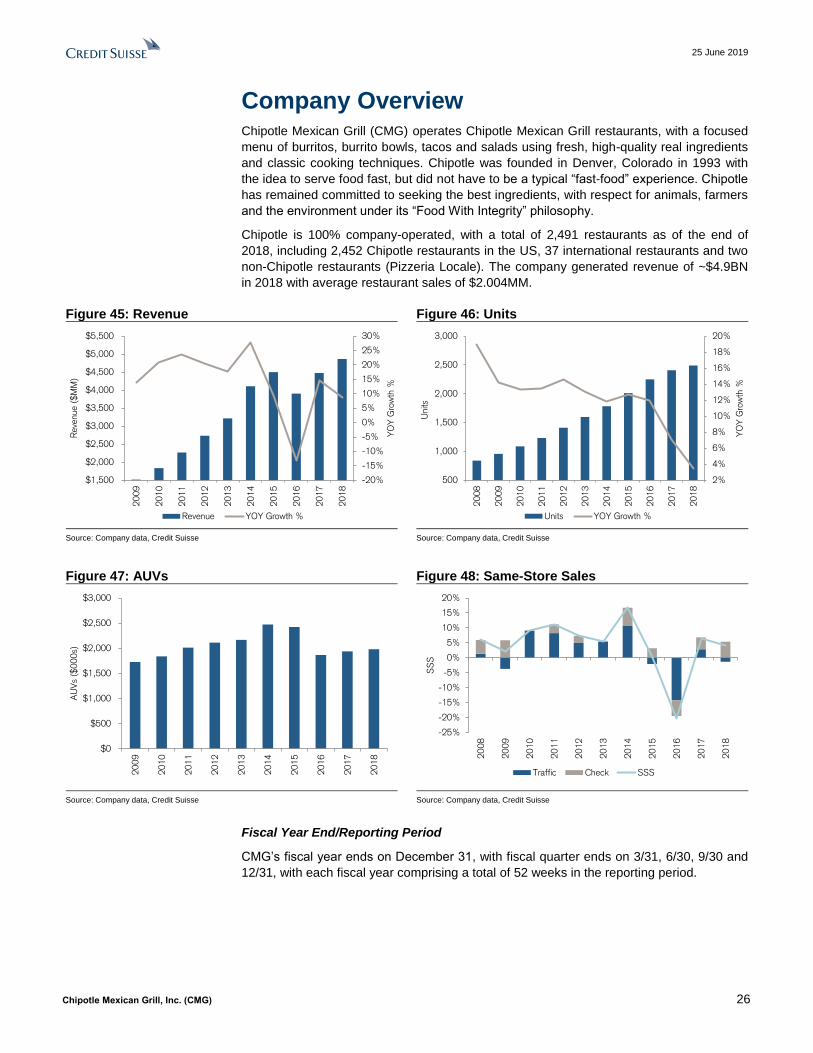

Company Background

Chipotle Mexican Grill operates fast casual restaurants with a focused menu of burritos, tacos, burrito bowls and salads, made using fresh ingredients.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 1000.00

Our $1,000 one-year valuation in a blue sky scenario is based on an EV/EBITDA of ~26x our blue sky FY20 EBITDA. Our blue sky FY20 EBITDA is based on: 1) SSS of 7%; 2) unit growth of 8%; and 3) restaurant-level margins of ~23%.

Our Grey Sky Scenario (US$) 550.00

Our $550 one-year valuation in a grey sky scenario is based on an EV/EBITDA of ~19x our grey sky FY20 EBITDA. Our grey sky FY20 EBITDA is based on: 1) SSS of 3%; 2) unit growth of ~5%; and 3) restaurant-level margins of ~20.7%.

Share price performance

On 21-Jun-2019 the S&P 500 INDEX closed at 2950.46

Daily Jun22, 2018 - Jun21, 2019, 06/22/18 = US$469.94

Source: Company data, Refinitiv, Credit Suisse estimates

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 3

Executive Summary We initiate coverage of Chipotle (CMG) with an Outperform rating and $870 target price.

CMG has returned to a narrative of growth rather than recovery, with on-trend initiatives

that well position the company to appeal to its target base and outperform peers. Mid-

single-digit SSS should enable margins to support an EPS CAGR of ~33% over the next

four years.

Please refer to our views summarizing the Restaurants industry: Phone to Table: Digitizing

Restaurants.

■ Implementing Slate of On-Trend Sales Initiatives: CMG should maintain mid-single-

digit SSS fueled by a slate of on-trend sales initiatives resonating with customers. Our

confidence in ongoing momentum includes contributions from: 1) digital initiatives; 2)

delivery growth; 3) the loyalty program; 4) new menu innovation; 5) social media

strategy; and 6) customer data analytics. More consistent price increases, improved

operations and potential benefits from catering growth should also contribute to SSS.

■ Long Runway for Growth: Chipotle has historically generated best-in-class cash-on-

cash returns, driven by strong average unit volumes (AUVs), favorable labor leverage

and attractive new-unit investment costs. Cash-on-cash returns are still above average at

~40%+, but far below peak levels of 70-80%. Stronger new-unit productivity, a multi-layer

sales plan to increase AUVs, and efforts to generate cost efficiencies should continue to

drive returns higher from more recent troughs. We expect Chipotle to step up unit growth

each year over the next few years, including the exploration of alternative formats such

as Chipotlanes, which should unlock additional real estate opportunities.

■ Sales Leverage to Enable Restaurant Margin Expansion: AUV growth is the

primary driver of margin expansion, and we estimate every $100K in AUV translates to

~100bps of restaurant-level margin expansion excluding inflation. We expect

restaurant margins to continue to expand, largely driven by sales leverage, with

ongoing opportunities for cost efficiencies. We model 20.4% restaurant-level margins in

2019 (+170bps) and ~100bps of expansion per year, reaching ~23.5% by 2022, behind

system AUVs of ~$2.4MM and prime costs of ~57.5% (from ~60% in 2018 and ~55-

56.5% historically).

Upside to our margin expectations exists if Chipotle is able to leverage labor costs

closer to historical levels. We model sustainably higher marketing and promo costs

(~3% vs ~1.5% historically) and overall other operating costs, largely due to delivery

fees, which represent incremental costs. Downside to expectations exists should AUV

growth be below our expectations, and Chipotle generates lower sales leverage.

Should Chipotle require marketing and promo costs above our estimate of ~3% of

sales (which implies ~10% dollar growth per year), margins could be further pressured.

■ Valuation: Our $870 target price is based on ~25x our NTM EBITDA in 12 months,

implying a P/E of ~46x our NTM EPS in 12 months. Our ~25x multiple is in line with

CMG’s multiple in recent weeks, and a slight discount to its current multiple (~26x).

CMG’s three-year average P/E multiple is ~42x, slightly below the P/E implied by our

target price.

■ Risks: Primary risks include: (1) food safety headlines, with consumer perceptions

more sensitive regarding Chipotle following food safety incidents (2009-2015); (2)

trends in consumer spending, with Chipotle’s more premium offering priced higher than

traditional QSR competitors; and (3) inflation, with every 100bps of margin translating

to ~10-15% in EPS.

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 4

Key Charts

Figure 1: We estimate SSS of 8% in 2019 and ~5%

long term, relative to consensus’ ~5.5% in 2019 and

~4-5% longer-term.

Figure 2: SSS leverage and cost efficiencies should

support ongoing margin improvement; we estimate

every $100K in AUVs translates to ~100bps of

margin improvement (excl inflation).

Source: Company data, Consensus Metrix, Credit Suisse estimates Source: Company data, Consensus Metrix, Credit Suisse estimates

Figure 3: Top-line growth of ~11% and margin

expansion should support an EPS CAGR of ~33%

over the next several years (consensus ~27%).

Figure 4: CMG currently trades at ~26x EV/EBITDA,

with a strong growth outlook supportive of an

above-average valuation multiple.

Source: Company data, Consensus Metrix, Credit Suisse estimates Source: FactSet, Credit Suisse estimates

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

SS

S

CSe Traffic CSe Check Consensus Traffic Consensus Check

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

$2,400

$2,600

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Rest

aura

nt

Mar

gin

s

AU

Vs

($00

0s)

AUVs CSe Restaurant Margins Consensus Restaurant Margins

5%

15%

25%

35%

45%

55%

65%

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

2019E 2020E 2021E 2022E

EP

S G

row

th

EP

S

CSe EPS Consensus EPS CSe EPS Growth Consensus EPS Growth

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Jun-1

6

Aug-1

6

Oct

-16

Dec-

16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Dec-

17

Feb-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct

-18

Dec-

18

Feb-1

9

Apr-

19

Jun-1

9

EV

/EB

ITD

A

NTM EV/EBITDA 3-yr Avg +1 Std Dev -1 Std Dev

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 5

Can Chipotle maintain mid-single-digit SSS long term? Credit Suisse View

Yes, we believe Chipotle can sustain SSS of ~5.0-5.5% over the next four years, with

contribution from both traffic and average check. The implementation of on-trend initiatives

should support ongoing sales growth, while better new-unit performance and the closing of

55-65 underperforming restaurants should optimize the health of the asset base. We

model SSS of 8% in 2019 (guide: mid- to high-single-digits), comprised of ~4% traffic and

~4% average check growth. Longer term, we model SSS of ~5.0-5.5%, with ~2-2.5%

contribution from traffic and ~3% from average check.

Chipotle has transitioned to a more focused organization with a methodical approach to

developing, testing and modifying new initiatives. Chipotle’s 100% company-operated

model and relatively small asset base allows it to be more agile and to roll out new

initiatives from concept to execution at a much faster pace than larger, heavily franchised

companies. As Chipotle builds a more robust database of customer information, we expect

the company to further enhance its processes.

Chipotle appeals to a prime demographic of younger consumers, and we are encouraged

the brand is implementing initiatives to enhance engagement and improve positioning.

Sales drivers contributing to our positive outlook include: 1) digital; 2) delivery; 3) loyalty

program; 4) innovation; 5) marketing; 6) social media; and 7) customer data analytics. We

also believe Chipotle maintains healthy pricing power and expect the brand to implement

lower and more consistent increases of ~2% per year. An increasing digital sales mix

drives our expectation of positive mix over the next few years.

Consensus Expectations

Consensus Metrix estimates SSS of 7.6% in 2019 (guide: mid- to high-single-digits),

including traffic of ~4% and average check of ~3.5%. Expectations include decelerating

SSS averaging ~4.5% over the next few years, including 5.3% in 2020, 4.7% in 2021 and

3.7% in 2022. Consensus models positive but declining traffic, with price of ~2% and

positive mix of ~1%.

Healthy SSS expectations in 2019

SSS is the primary driver of CMG’s stock, and healthy expectations in 2019 could leave

some on the sidelines. But AUVs are still down ~20% from 2014 peaks, and we believe

the company is as well positioned as ever to generate outperformance relative to the

group. In 1Q19, CMG raised its 2019 guidance for SSS to mid- to high-single-digit, from

mid-single-digit initially, driven by 1Q19 outperformance (SSS ~10%).

Traffic has improved sequentially over the last four quarters, including 2% in 4Q18 and

5.8% in 1Q19, reflective of initiatives gaining traction and a more sustainable trend. We

expect SSS to decelerate through 2019 against tougher compares and a drag from

deferred revenue related to the loyalty program. While 2020 will be up against the

toughest compares CMG has faced in several years, execution against early-stage

initiatives should continue to yield benefits.

While the consensus expectations for SSS of 7.6% in 2019 and 4-5% long-term are rich

relative to recent history, Chipotle has exhibited average SSS of ~4.5% over the last 10

years and ~8.5% in the seven years prior to the initial food safety incidents (2009-2015).

We believe Chipotle could outperform current expectations as it works to return to prior

peak AUVs of $2.5MM.

We model SSS of ~8% in 2019 and

~5.0-5.5% longer-term

Consensus models SSS of 7.6% in 2019

and ~4-5% longer-term

SSS average of 4.5% over last 10 years and

~8.5% prior to food safety incidents

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 6

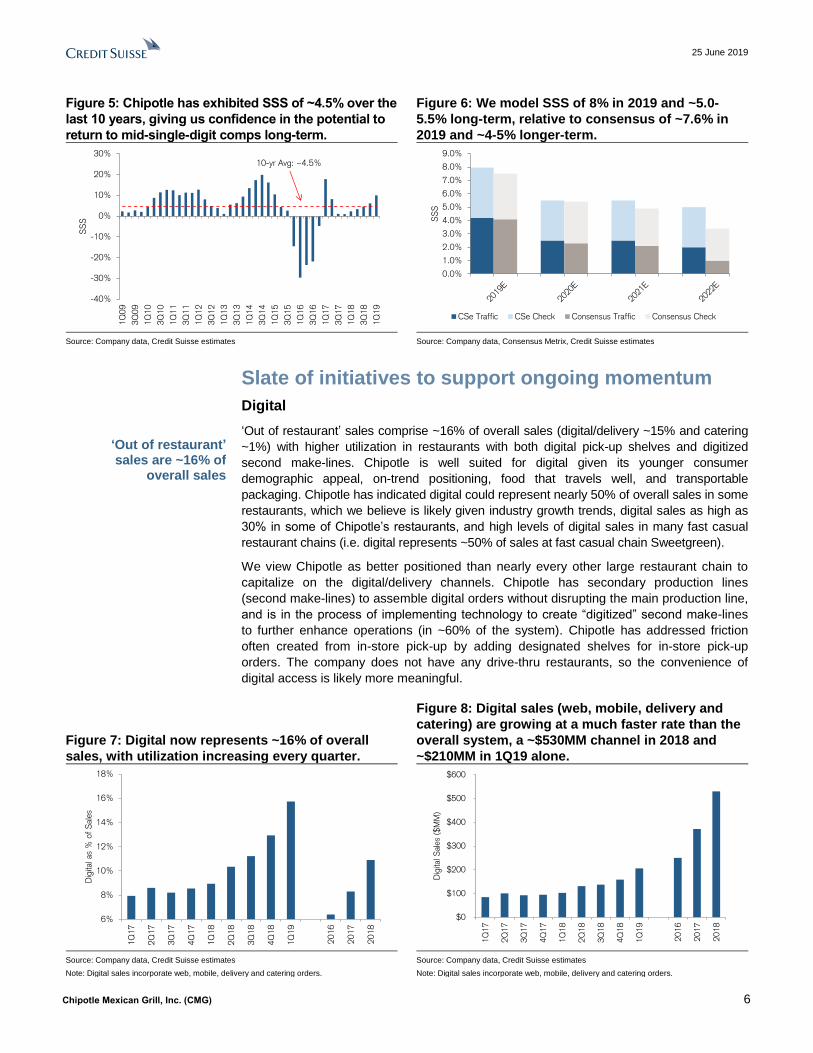

Figure 5: Chipotle has exhibited SSS of ~4.5% over the

last 10 years, giving us confidence in the potential to

return to mid-single-digit comps long-term.

Figure 6: We model SSS of 8% in 2019 and ~5.0-

5.5% long-term, relative to consensus of ~7.6% in

2019 and ~4-5% longer-term.

Source: Company data, Credit Suisse estimates Source: Company data, Consensus Metrix, Credit Suisse estimates

Slate of initiatives to support ongoing momentum

Digital

‘Out of restaurant’ sales comprise ~16% of overall sales (digital/delivery ~15% and catering

~1%) with higher utilization in restaurants with both digital pick-up shelves and digitized

second make-lines. Chipotle is well suited for digital given its younger consumer

demographic appeal, on-trend positioning, food that travels well, and transportable

packaging. Chipotle has indicated digital could represent nearly 50% of overall sales in some

restaurants, which we believe is likely given industry growth trends, digital sales as high as

30% in some of Chipotle’s restaurants, and high levels of digital sales in many fast casual

restaurant chains (i.e. digital represents ~50% of sales at fast casual chain Sweetgreen).

We view Chipotle as better positioned than nearly every other large restaurant chain to

capitalize on the digital/delivery channels. Chipotle has secondary production lines

(second make-lines) to assemble digital orders without disrupting the main production line,

and is in the process of implementing technology to create “digitized” second make-lines

to further enhance operations (in ~60% of the system). Chipotle has addressed friction

often created from in-store pick-up by adding designated shelves for in-store pick-up

orders. The company does not have any drive-thru restaurants, so the convenience of

digital access is likely more meaningful.

Figure 7: Digital now represents ~16% of overall

sales, with utilization increasing every quarter.

Figure 8: Digital sales (web, mobile, delivery and

catering) are growing at a much faster rate than the

overall system, a ~$530MM channel in 2018 and

~$210MM in 1Q19 alone.

Source: Company data, Credit Suisse estimates

Note: Digital sales incorporate web, mobile, delivery and catering orders.

Source: Company data, Credit Suisse estimates

Note: Digital sales incorporate web, mobile, delivery and catering orders.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

SS

S

10-yr Avg: ~4.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

SS

S

CSe Traffic CSe Check Consensus Traffic Consensus Check

6%

8%

10%

12%

14%

16%

18%

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

20

16

20

17

20

18

Dig

ital a

s %

of

Sale

s

$0

$100

$200

$300

$400

$500

$600

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

20

16

20

17

20

18

Dig

ital S

ale

s ($

MM

)

‘Out of restaurant’ sales are ~16% of

overall sales

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 7

Digitized Second Make-Lines and Digital Pick-Up Shelves

Chipotle has secondary production lines across its store base to assemble out-of-store

orders, including web, mobile, delivery and catering orders. Chipotle is in the process of

“digitizing” these secondary production lines to incorporate digital screens, improving

accuracy, throughput (~40% increase in throughput) and capacity.

The second make-lines well position Chipotle to increase capacity without disrupting

operations, with Chipotle noting orders from the second make-lines are more profitable

than a traditional in-store order. Digitized second make-lines are in ~60% of the system

(~1,500 restaurants), with expectations to be rolled out across the rest of the system by

the end of 2019. The integration of secondary production lines highlights Chipotle’s best-

in-class approach to operations and should serve as the operational foundation for

Chipotle to successfully execute against accelerating digital sales.

To further improve the digital experience, Chipotle has rolled out in-store pick-up shelves

for digital orders. The designated section for out-of-store orders creates a more convenient

and seamless experience for the customer, helps limit congestion and provides in-store

marketing for digital orders. The shelves also improve the delivery experience, as delivery

drivers know where to pick up the food and do not disrupt in-store operations.

Figure 9: Chipotle’s digitized make-lines improve

accuracy, throughput and increase capacity without

disrupting operations. The digitized make-lines are

expected to be rolled out to the entire system by the

end of 2019.

Figure 10: Chipotle has recently rolled out in-store

pick-up shelves for out-of-store orders across its

store base.

Source: Chipotle Presentation Source: Chipotle Presentation

Chipotlanes

Chipotle is testing digital drive-thru lanes, branded “Chipotlanes,” which are drive-up

windows for customers to pick up digital orders. Early feedback has been very positive, with

the ~10 restaurants with Chipotlanes generating digital sales above the national average

(~30% sales) and higher overall sales. Chipotle expects to expand this test to another few

dozen stores in 2019. While Chipotle does not build drive-thru lanes as part of its current

store layout, we can see Chipotle opportunistically building digital drive-up lanes where

appropriate, benefitting operations by shifting more orders to the second make-lines, without

significant investment and additional labor as required with a traditional drive-thru.

Across the restaurant industry, restaurants that add a drive-thru tend to see sales lifts of

~20-30%. We assume the addition of drive-up lanes will benefit from a similar lift, and new

restaurants with these drive-up lanes will likely generate AUVs above average new opens.

We do not expect Chipotle to focus on remodeling restaurants with drive-up lanes, but

rather to unlock sites that may not have been appropriate for a traditional restaurant.

Digital App

Out-of-restaurant sales make up ~16% of Chipotle sales, with digital and delivery

comprising ~15% of sales and ~1% sales mix from catering. We believe Chipotle’s skew

towards younger and more affluent cohorts should help drive higher digital sales relative to

Digitized second make-lines are expected to be

rolled out to the entire system by the end of

2019 (~60% currently)

Digital pick-up shelves are now rolled out across the system

Chipotlanes generate higher sales and digital mix, with opportunities

to unlock additional sites and unit potential

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 8

the industry. We would not be surprised if Chipotle approached a ~50% digital sales mix

long-term, with a digital sales mix that has nearly doubled over the last several quarters

and some restaurants exhibiting a digital sales mix as high as 25-30% of sales.

Chipotle has indicated the digital ecosystem is attracting light and medium users, which is

a best-case scenario to drive increased frequency and influence behavior. We would have

expected heavy users to adopt digital more quickly given the inherent loyalty implied from

customers downloading an app or joining a rewards program.

Delivery

Chipotle has partnered with DoorDash and Postmates, and delivery is seamlessly

integrated into Chipotle’s back-of-house system, avoiding operational disruptions. We

suspect Chipotle has negotiated extremely favorable rates from its partners, making

delivery a surprisingly margin-accretive channel (assuming incrementality). These

partnerships represent an opportunity for dual marketing, with delivery providers

selectively offering free delivery for Chipotle orders, and in return for these customer

acquisition costs, Chipotle marketing the channel to its customers, increasing awareness

of the third-party delivery providers.

Importantly, Chipotle is the first large restaurant chain to offer delivery directly through its

app, which should help enable digital sales, drive awareness of the channel, lower delivery

costs and support increasing delivery sales. One of the challenges restaurant brands are

faced with is the opportunity cost of shifting customers to a third-party platform. By offering

delivery directly on the app, delivery becomes an unlock for digital as customers must

download the app, Chipotle maintains its customers without transferring them to a different

platform and has full access to the customer data. Based on commentary from Chipotle,

there has been minimal customer overlap between its in-app delivery and third-party

delivery apps, highlighting the benefit of utilizing both channels.

Based on our analysis of Chipotle digital app users, ~10% use Postmates and ~25% use

DoorDash, suggesting there is overlap between customers and the benefits of Chipotle

offering delivery through its app to reduce fees paid to third parties. More importantly, just

~5% of Postmates and DoorDash users also use Chipotle, in-line with company commentary

suggesting minimal cannibalization and unlocking opportunities to increase awareness of

delivery and attract new customers. We believe Chipotle’s approach to integrate delivery in

its app and also separately through third-party platforms optimizes the potential.

Figure 11: ~10% of Chipotle digital app users also

use Postmates and ~25% of Chipotle digital app

users also use DoorDash.

Figure 12: Importantly, just ~5% of Postmates and

DoorDash users also use Chipotle digitally,

highlighting the potential incrementality from

presence on the platforms and limited cannibalization.

Source: comScore Credit Suisse estimates Source: comScore, Credit Suisse estimates

To increase awareness of the delivery feature in its app, Chipotle periodically offers free

delivery exclusively through its app. Delivery is generating order sizes ~1.5x that of an in-

store order ($16-17 vs $12-13 average in-store order), with commentary suggesting

incrementality of at least ~65-70%. Chipotle is well positioned for delivery with food that

travels well and is already in an easily transportable container. Execution appears strong,

with an average delivery time of less than 30 minutes.

14%

4%1% 2%

10%

21% 22%25%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Tac

o B

ell

Moe's

Del T

aco

Qdoba

Post

mate

s

Uber

Eat

s

Gru

bH

ub

DoorD

ash

Mexican Restaurant Peers Delivery

% C

hip

otle

Use

rs -

Cro

ss-V

isiti

ng

8%12%

4%

16%

5%8%

5% 6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Tac

o B

ell

Moe's

Del T

aco

Qdoba

Post

mat

es

Uber

Eat

s

Gru

bH

ub

DoorD

ash

Mexican Restaurant Peers Delivery

% P

eers

/Deliv

ery

Use

rs -

Cro

ss-V

isiti

ng

Delivery is a margin- accretive channel for

Chipotle given high incrementality

Chipotle is optimizing its delivery channel, with app integration

and presence on platforms

Delivery is generating order sizes ~1.5x an in-

store order and incrementality of

65-70%

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 9

We expect delivery to contribute ~130bps to 2019, assuming delivery makes up ~4% of

sales and is ~70% incremental. In 2020, we estimate a delivery contribution of ~130bps to

SSS based on a ~5% sales mix and ~65% incrementality.

Figure 13: 2019 Delivery SSS Contribution Figure 14: 2020 Delivery SSS Contribution

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Loyalty

Chipotle Rewards launched nationally in March 2019 following an initial test in 3Q18. The

spend-based program rewards customers with a free entrée for every $125 spent (or ~10

visits), translating to a ~10% discount.

Chipotle has indicated a loyalty/rewards program has been a top consumer request, and

we believe the program could incentivize both new and existing customers. Within one

month, Chipotle amassed 3MM loyalty members, with March and April together generating

~1MM app downloads, representing the highest monthly downloads in the company’s

history. Chipotle has indicated the loyalty program has a higher incidence of light and

medium users enrolling (best case scenario), unlocking opportunities to increase

frequency and incentivize behavior.

In 1Q19, Chipotle deferred ~$3.5MM of revenue related to earned, unredeemed loyalty

points, translating to a ~30bps drag on revenue in the quarter. As reward points expire

within 60 days, Chipotle will recognize the full value of the deferral, though 2Q revenue

deferral should fully offset the benefit given a full quarter of the loyalty program being

implemented and greater awareness driving sign-up. Chipotle highlighted expectations for

an ongoing drag from the loyalty program deferral until it reaches ~100bps in magnitude

before reversing to a net neutral or positive impact.

Innovation

Chipotle is taking a more strategic approach to menu innovation, with opportunities to

market a combination of existing ingredients, add new ingredients and invest in new

processes/equipment.

In January, Chipotle added Lifestyle Bowls, which combined Chipotle’s existing ingredients

into marketable meals/recipes that increased customer convenience and generated new

news. Chipotle is taking a page out of the Taco Bell playbook by leveraging its existing

ingredients to create new innovation without affecting operations.

Chipotle is currently testing new menu items that are easy to implement by adding them

to the traditional line. Carne Asada, for example, is being tested in select markets.

Salads could also be added as a new menu category relatively simplistically (salad

dressings have been tested for a while in the NYC NEXT Kitchen). New products

requiring new processes are more difficult, with concerns around throughput and

operational disruption. Quesadillas, the most frequently requested item at Chipotle, are

in test with new pressers reducing cook time to ~30 seconds (from ~3 minutes

currently). Nachos similarly are more difficult to execute. Chipotle has also highlighted

an opportunity to enhance its beverage line-up.

2019 Scenario Analysis 2020 Scenario Analysis

1.3% 3.0% 3.5% 4.0% 5.0% 6.0%

50% 0.4% 0.7% 0.9% 1.4% 1.9%

60% 0.5% 0.8% 1.1% 1.7% 2.3%

70% 0.6% 0.9% 1.3% 2.0% 2.7%

80% 0.7% 1.1% 1.5% 2.3% 3.1%

90% 0.7% 1.2% 1.6% 2.6% 3.5%

Sales Mix

Incre

men

tali

ty

2020 Scenario Analysis

1.3% 4.0% 4.5% 5.0% 6.0% 7.0%

55% 0.5% 0.8% 1.1% 1.7% 2.3%

60% 0.5% 0.8% 1.2% 1.8% 2.5%

65% 0.6% 0.9% 1.3% 2.0% 2.7%

70% 0.6% 1.0% 1.4% 2.2% 2.9%

75% 0.6% 1.1% 1.5% 2.3% 3.1%

Sales Mix

Incre

men

tali

tyLoyalty program is attracting light and

medium users – key unlock to increase

frequency and influence behavior

Menu innovation 1) market recipe of

existing ingredients; 2) add new ingredients;

3) invest in new equipment

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 10

We expect Chipotle could selectively incorporate new innovation through digital channels

only, limiting the potential disruption from new products and processes. This would also

help increase digital utilization.

Previous efforts around menu expansion in recent years have been lackluster, with queso

receiving mixed reviews after an accelerated roll-out and chorizo removed from the menu

less than a year after roll-out. In 3Q17, Chipotle opened the NEXT restaurant in NYC as a

test kitchen to introduce, test and modify new menu items, though it seems the company is

taking a larger-scale approach to testing across different markets. We would not be

surprised to see a larger-scale test kitchen closer to its HQ to develop an innovative

pipeline that can be well tested through customer feedback and restaurant operations,

resulting in a more streamlined approach to national scale and commercialization.

Social Media

Chipotle has made a noticeable change in its social media strategy over the last 12-18

months, transitioning to a more engaging, humorous personality from a more food-centric

approach previously. Chipotle often features tweets from customers or non-food posts

unique to Chipotle. Engagement with followers appears to have increased, and the team

makes it more personal by signing their names with each response. We are encouraged

Chipotle has a more distinct personality and believe it is well positioned to drive increased

loyalty and affinity with its followers given the brand’s younger target demographic.

Figure 15: Chipotle has historically engaged a food-

centric social media approach, largely featuring its

menu items and ingredients (September/October

2017 posts).

Figure 16: More recently, Chipotle has been more

diversified in its posts, creating a more distinct

brand personality through humor and fun.

Source: Chipotle Instagram Source: Chipotle Instagram

Shift in strategy to personality-driven

content rather than food-centric content

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 11

Analytics

Overarching Chipotle’s new strategy is the utilization of customer data analytics to drive

decision making and implementation of initiatives. Over the past few years, Chipotle has

made several attempts to rebound traffic and sales primarily though new innovation and

marketing, but did not have the infrastructure in place to robustly test, evaluate and iterate

before full-scale roll-out. Prior to the food safety incidents, Chipotle was able to organically

drive sales growth based on its commitment to food, quality ingredients and grass-roots

marketing. Against a backdrop of heightened competition, the emergence of other fast

casual chains with mission driven strategies and digital penetration helping smaller chains

better compete, the timing of the food safety incident created somewhat of a “perfect

storm”. While Chipotle attempted to launch initiatives to compete in a more traditional way,

the brand was not prepared and operational execution suffered.

We believe that an organization’s ability to collect and utilize data is paramount to

understanding initiatives that will resonate with consumers. We expect these insights will

be relevant for generating marketing campaigns that appeal to new and existing

customers, as well as in building the innovation pipeline. Chipotle has already highlighted

strength among Millennials and Gen Z customers, and we believe initiatives geared

towards engaging marketing campaigns, new menu innovation, value and digital should

resonate with these customer segments.

Catering

Catering represents just ~1% of sales, a potentially significant and largely untapped

opportunity. Chipotle has amended the platform in recent years to lower the minimum

order size and offer catering delivery. Customers can also earn loyalty points through

catering transactions. Taken together, increased access through lower group order sizes,

lower pricing tiers, ability to earn loyalty points and delivery availability should help drive

channel growth.

Chipotle’s catering business has some seasonality, with catering sales higher in 2Q and

4Q from graduations and holidays, respectively, and generally skews at-home vs office.

We believe catering delivery could be a significant unlock to gain share among

businesses/offices, with the convenience of delivery a potentially meaningful factor in

restaurant catering choices and offices being relatively inelastic to delivery fees.

Over the last several years, different companies have emerged targeting the catering

channel, particularly focused on office buildings and through marketplace platforms. Fast

casual competitor, Sweetgreen, is testing a hybrid delivery-catering model, where the

company will deliver customized orders to office buildings with designated pick-up shelves.

We would not be surprised to see restaurants engaging in these types of opportunities

given the benefits of higher volume orders on delivery profitability.

Operations

Initiatives implemented to address operational execution thus far appear to be generating

results, with Chipotle experiencing improvements in restaurant AB scores, lower hourly

turnover, declines in guest complaints and improved guest satisfaction scores. Going

forward, improved throughput, consistent execution of food and consistent delivery of a

great atmosphere remain opportunities.

To evaluate employee satisfaction for Chipotle and select peers, we utilized self-reported

employee satisfaction scores through ratings on Glassdoor, which are rated on a scale of

1-5 (5 being the best). Over the last 11 years, employee satisfaction scores have largely

trended upward, with employee satisfaction ratings in 2018 at the highest level in the

history of our data set. Chipotle’s overall employee satisfaction score in 2018 is 3.77

representing an increase of 0.42 since 2013. Employee satisfaction with compensation

and benefits has increased 0.46 points since 2013 to 3.67 in 2018.

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 12

Figure 17: Chipotle employee satisfaction has

increased 0.42 over the last several years to 3.77 in

2018, the highest satisfaction ratings employees

have reported in the history of our data set.

Figure 18: In part, increasing satisfaction with

compensation and benefits has supported overall

employee satisfaction, highlighting the importance

of investments.

Source: Thinknum, Glassdoor, Credit Suisse Source: Thinknum, Glassdoor, Credit Suisse

Pricing

Chipotle has historically been conservative with its pricing strategy, enacting menu price

increases every 2-3 years to offset rising food costs. Following three to four years of flat

pricing, Chipotle rolled out price increases in tranches averaging ~5% across markets

starting in 2Q17 through early 2018. There appeared to be minimal resistance to the price

increase, with the majority flowing through to comp.

Chipotle implemented a price increase of ~1.7% in late December, which will carry through

2019. We expect Chipotle will enact more regular, but lower, price increases each year to

offset margin pressures. To maintain margins in a mid-single-digit inflationary cost

environment, transaction-growth must be approximately mid-single-digit, so prudent

pricing will likely be used to better leverage the economic model.

Figure 19: CMG has historically enacted price

increases every 2-3 years. CMG rolled out average

price increases ~5% system-wide for the first time in

3-4 years in 2017 and 2018, and another increase in

December 2018.

Figure 20: We expect CMG to implement lower and

more consistent price increases to better leverage

the economic model while limiting resistance.

Source: Company data, Credit Suisse Source: Company data, Consensus Metrix, Credit Suisse estimates

3.00

3.10

3.20

3.30

3.40

3.50

3.60

3.70

3.80

3.90

2013 2014 2015 2016 2017 2018

Ove

rall

Sat

isfa

ctio

n R

atin

g

3.00

3.10

3.20

3.30

3.40

3.50

3.60

3.70

3.80

2013 2014 2015 2016 2017 2018

Com

p &

Benefits

Satis

fact

ion R

atin

g

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

1Q

06

4Q

06

3Q

07

2Q

08

1Q

09

4Q

09

3Q

10

2Q

11

1Q

12

4Q

12

3Q

13

2Q

14

1Q

15

4Q

15

3Q

16

2Q

17

1Q

18

4Q

18

Price

4Q06: Select menu price

increases

2007/2008: Menu price

increases (market by

market)

1H11:

Menu price

increases

2Q14: Menu price

increase

2017/2018: Menu price

increases (market by

market)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Price

CSe Consensus Actual

We expect more consistent price

increases of ~2% per year

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 13

Will unit growth accelerate from current levels? Credit Suisse View

Yes, we expect unit growth to reaccelerate, though likely remaining below historical levels

over the near to medium-term. We model 144 net new units in 2019, and an incremental 10 units per year over the next several years.

Strong new unit opens in 2018 and the closing of 55-65 underperforming stores give us confidence Chipotle will continue to develop and optimize the health of its portfolio. 2018’s

137 new unit opens was the lowest in eight years, with guidance of 140-155 new opens in

2019 still reflecting multi-year lows. We believe Chipotle will further step up growth over time, including the exploration of alternative prototypes such as Chipotlanes.

Chipotle has historically generated best-in-class cash-on-cash returns, driven by strong AUVs, favorable labor leverage and attractive new-unit investment costs. Cash-on-cash

returns are still above average at ~40%+, but far below peak levels of 70-80%. Stronger

new-unit productivity, a multi-layer sales plan to increase AUVs and efforts to generate cost efficiencies should continue to drive returns higher from more recent troughs.

Consensus Expectations

Consensus models 142 net new units in 2019 and a step up each year for an average of

~165 units in 2020-2022.

Unit growth expectations appear achievable

Chipotle has been one of the fastest growing large chains in the restaurants space, generating consistent double-digit unit growth prior to brand challenges following food safety

incidents. Over the past two years, CMG has tempered unit growth in the US behind lower

sales volumes, soft unit productivity and a challenging growth environment with heightened

competition. Over the near to medium term, unit growth will likely remain lower than historical

levels as CMG prioritizes its existing asset base. We expect a slow and steady build will be more likely than a more immediate step up, especially with a tight labor market.

We model net unit growth of ~6% over the next few years, averaging ~165 units per year. We estimate 144 net new units in 2019 and an incremental step up of ~10 units each year

over the next few years. Consensus models 142 net new units in 2019, ~160 in 2020 and

2021, and 175 in 2022.

2018 was the first year CMG opened fewer than ~150 units since 2011, an intentional

reduction to focus on the existing base. Guidance for 2019 is gross new unit growth of 140-155 and continued planned closures of ~55-65 underperforming restaurants, with expectations for

improved sales and unit economics supporting acceleration from these levels.

Figure 21: Chipotle has generated average unit growth

of ~12% over the last several years, with tempered unit

growth over the past two as the company has focused

on improving the existing asset base.

Figure 22: We model 144 new units in 2019, and a

slow step up going forward, relatively in line with

the consensus.

Source: Company data, Credit Suisse Source: Consensus Metrix, Credit Suisse estimates

2%

4%

6%

8%

10%

12%

14%

16%

500

1,000

1,500

2,000

2,500

3,000

2012 2013 2014 2015 2016 2017 2018

YO

Y G

row

th %

Units

Units YOY Growth %

40

60

80

100

120

140

160

180

200

2019E 2020E 2021E 2022E

Unit

Gro

wth

CSe Consensus

We expect modest step ups in unit growth

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 14

Best-in-class returns supportive of development story

Chipotle has historically demonstrated best-in-class unit economics given its simplistic

operating structure, high AUVs, strong new unit productivity and labor leverage. At peak,

Chipotle was exhibiting cash-on-cash returns of 70-80%, which have come down to ~40%.

Chipotle has indicated its new classes of restaurants are opening at ~80%+ of the existing

base, reflecting historical new unit productivity highs (though on a lower AUV). We believe

confidence in strong new unit opens is required to accelerate unit growth from recently

tempered levels.

Chipotle has recently started testing Chipotlanes, a new format prototype with a digital pick-up

lane similar to a drive-thru. While only in ~10 restaurants, these units are generating higher

overall sales and a higher digital mix (~25-30% of sales). We believe the new format could

unlock new opportunities to open restaurants in trade areas that require higher volumes, or in

smaller footprints. We estimate the Chipotlanes could add ~20-30% to the volume of a

traditional restaurant. We expect the company to open a few dozen Chipotlane prototypes in

2019, with higher AUV openings that could boost net unit productivity levels.

Figure 23: Chipotle has generated best-in-class

returns, and while well off its 70-80% peak, is still

driving ~40%+ cash-on-cash returns.

Figure 24: Even at current levels, Chipotle’s cash-

on-cash returns are above nearly all restaurant

peers in our data set.

Source: Company data, Credit Suisse

Note: Calculated using system AUVs and restaurant level margins. New class opens likely lower than the system average.

Source: Company data, Restaurant Research Journal, Credit Suisse estimates

Note: Reflects 2018 AUVs, investment costs and EBITDAR margins.

Net new unit demographic trends mixed

New opens likely in established markets

~80% of Chipotle’s US system is concentrated in 15 markets, with the greatest exposure

in California (~17%), Texas (~8.5%), Ohio (~7.5%), Florida (~6.5%) and New York (~6%).

We expect growth to be largely concentrated in Chipotle’s core and established markets,

providing increased visibility into the economics of the restaurants, creating efficiencies for

marketing campaigns and making it easier to establish procedures to test, scale and

commercialize new initiatives. As Chipotle stabilizes its existing base, improves economics

in established markets and has a well-developed strategy, we expect the company to

return to greater expansion in newer markets.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Cash

-on-C

ash

Retu

rn %

0%

10%

20%

30%

40%

50%

60%

70%

Dom

ino's

Chip

otle

Moe's

McD

onal

d's

Pizza

Hut

Fiv

e G

uys

Dunkin

'

Tac

o B

ell

Pan

era

Jack

in t

he B

ox

Qdoba

Sonic

Burg

er

Kin

g

Wendy'

s

KF

C

Cash

-on-C

ash

Retu

rns

(Exc

l Rent

& G

&A

)

Chipotle is generating cash-on-cash returns

of ~40%, below 70-80% at peak, but still above

peers

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 15

Figure 25: ~80% of CMG’s units are concentrated in

15 markets.

Figure 26: We expect new unit growth to largely be

concentrated in more established markets.

Source: Company data, Credit Suisse Source: Company data, Thinknum, Credit Suisse

Demographics around new opens could be a factor affecting trends

Our analysis of new-unit opens suggests Chipotle has opened new units in less affluent

and less dense markets over the last few years, which could be a factor weighing on new-

unit trends. In 2017, new units were opened in markets with median incomes ~less than

that of the existing base. Given Chipotle’s more expensive pricing and appeal to a higher-

end consumer, moving into less affluent markets could represent a drag on sales. In 2016

and 2017, Chipotle opened units in less densely populated markets, which could affect

potential foot traffic. 2018 new opens appear to be located in areas with more favorable

demographics and closer to those of prior years, which could be a positive for new-unit

productivity and the health of the new classes, at least at the margin.

Figure 27: Over the past few years, new units have

opened in markets with lower median income

relative to the base, which could represent a drag

on sales volumes, though 2018 units were open in

more affluent areas.

Figure 28: In 2018, Chipotle opened units in more

densely populated markets relative to the existing

base, which we view as a potential positive for foot

traffic.

Source: Company data, Thinknum, Credit Suisse estimates

Note: (1) Existing Base Median Income represents average median income of Chipotle’s system for the year ended 12/31/15. (2) New Units Median Income vs Base represents the average median income of the new units opened in each respective year relative to the average median income of Chipotle’s 2015 existing base.

Source: Company data, Thinknum, Credit Suisse estimates

Note: (1) Existing Base Population represents average population by postal code of Chipotle’s system for the year ended 12/31/15. (2) New Units Population vs Base represents the average population by postal code of the new units opened in each respective year relative to the average population by postal code of Chipotle’s 2015 existing base.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

CA TX OH FL NY IL VA MD PA AZ CO NJ MN NC MA

% U

S S

yste

m E

xposu

re

47% 46% 46%

73% 75%81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2016 2017 2018

% U

nit

Gro

wth

Contr

ibutio

n

Top 5 States Top 10 States Top 15 States

$68.4K $68.5K

$66.2K

$70.4K

-4%

-2%

0%

2%

4%

6%

8%

10%

$64K

$65K

$66K

$67K

$68K

$69K

$70K

$71K

2015 Existing

Base

2016 New

Opens

2017 New

Opens

2018 New

Opens

New

Units

Media

n Inco

me v

s B

ase

Media

n Inco

me (

$00

0s)

Median Income New Units Median Income vs Base

35.4K

33.8K 33.8K

35.4K

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

30K

31K

32K

33K

34K

35K

36K

2015 Existing

Base

2016 New

Opens

2017 New

Opens

2018 New

Opens

New

Units

Popula

tion v

s B

ase

Popula

tion b

y P

ost

al C

ode (

000s)

Population New Units Population vs Base

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 16

What is the opportunity for restaurant margin expansion? Credit Suisse View

We expect restaurant margins to continue to expand, largely driven by sales leverage, with

ongoing opportunities for cost efficiencies. We model 20.4% in 2019 (+170bps) and

~100bps of expansion per year, to ~23.5% by 2022, behind system AUVs of ~$2.4MM and

prime costs of ~57.5% (from ~60% in 2018 and ~55-56.5% historically). We believe AUV

growth will be the key driver of margin expansion potential. We model AUVs of ~$2.2MM

in 2020 and ~$2.4MM in 2022, with every $100K in AUV translating to ~100bps of

restaurant margin excluding inflation.

Upside to our margin expectations exists if Chipotle is able to leverage labor costs closer

to historical levels. We are modeling sustainably higher marketing and promo costs (~3%

vs ~1.5% historically) and overall other operating costs, largely due to delivery fees, which

could be pressuring margins. Downside to expectations exists should AUV growth be

below our expectations, and Chipotle generates lower sales leverage. Should Chipotle

require marketing and promo costs above our estimated ~3% of sales (which implies

~10% dollar growth per year), margins could be further pressured.

Consensus Expectations

Consensus models margin improvement to ~20.2% in 2019 and ~22% by 2022.

Estimates include leverage across all cost buckets, including ~50bps from food and

packaging, ~110bps from labor, ~90bps from occupancy, and ~65bps from other

restaurant expenses.

AUV growth to support margin leverage and

profitability

We expect average unit volumes (AUVs) to continue to recover from current levels of

~$2MM. We estimate SSS of ~5.0-5.5% over the next four years, comprised of

contribution from digital initiatives, delivery, new menu innovation, and enhanced analytics.

We model AUV growth of ~$100K per year to ~$2.1MM in 2019 growing to ~$2.4MM by

2022. Top-line revenue growth represents the most significant factor driving margin

leverage and profitability. At current AUVs of ~$2MM, the economic model should

generate a ~20% restaurant-level margin, with expansion to mid-20% margins as AUVs

get closer to ~$2.4MM.

Figure 29: Top-line revenue growth is the most

significant factor driving restaurant-level margins.

Figure 30: We expect sales leverage to be the

primary driver of restaurant margin improvement.

Source: Company data, Credit Suisse Source: Company data, Consensus Metrix, Credit Suisse estimates

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

$2,400

$2,600

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Rest

aura

nt

Mar

gin

s

AU

Vs

($00

0s)

AUVs Restaurant Margins

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

$2,400

$2,600

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Rest

aura

nt

Marg

ins

AU

Vs

($00

0s)

AUVs CSe Restaurant Margins Consensus Restaurant Margins

Sales leverage and cost efficiencies should

support a return to mid-20% margins

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 17

We estimate SSS of ~8% in 2019 to drive AUVs of ~$2.1MM. There appear to be

opportunities for efficiencies in the food and labor lines, including contract negotiations,

waste savings, and better labor management. In our view, Chipotle has done well to

manage food margins with lower AUVs and structurally higher costs from food safety

related procedures. Better sales forecasting and labor scheduling, and an increase in the

digital mix should positively benefit labor margins. We expect prime costs to improve

~280bps, relative to consensus’ ~160bps of improvement, through 2022.

While there could be additional opportunities to reduce costs, we expect Chipotle to

prioritize top-line revenue. As new initiatives are rolled out, requiring crew training and

some inefficiencies, we do not expect the company to approach peak margins over the

near to medium term. Efficiencies in the labor line will likely be somewhat offset by

elevated marketing and promo costs and delivery expenses. We estimate marketing and

promo costs of ~3% of sales going forward.

We model restaurant-level margins of 20.4% in 2019, an increase of 170bps, reaching

23.5% by 2022. This compares to consensus for restaurant-level margins of 20.2% in

2019, expanding to 21.9% by 2022.

Figure 31: Strong AUVs and relatively low labor

margins have supported strong restaurant level

margins and best-in-class returns.

Figure 32: We expect restaurant-level margins to

expand to 23.5% by 2022, behind improving AUVs

and efficiency gains. Consensus estimates margin

improvement to ~22% by 2022.

Source: Company data, Credit Suisse

Note: Red line represents average over period shown.

Source: Company data, Consensus Metrix, Credit Suisse estimates

Figure 33: Sales leverage is a meaningful factor in driving margin expansion,

with opportunities for efficiencies supporting further benefits.

Source: Company data, Credit Suisse estimates

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

26.0%

28.0%

30.0%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Rest

aura

nt

Leve

l Mar

gin

s

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

2019E 2020E 2021E 2022E

Rest

aura

nt

Leve

l M

arg

ins

CSe Restaurant Margins Consensus Restaurant Margins

Low double-

digits

Mid-to-high

teensLow 20%

Mid 20%

0%

5%

10%

15%

20%

25%

30%

$1.9MM $2.0MM $2.2MM $2.4-2.5MM

Rest

aura

nt

Leve

l M

arg

ins

AUVs ($MM)

Sales leverage is the primary driver of

margin expansion, with ~$2.4-2.5MM AUVs

supportive of mid-20% margins

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 18

What is the EPS growth opportunity? Credit Suisse View

We model EPS growth of ~33% over the next four years. Top-line growth of ~11%,

including SSS of ~5.0-5.5%, should enable margin expansion to support operating profit

growth of ~31% over the next few years.

For 2019, we model EPS growth of ~53%, including top-line growth of 11.7%, restaurant

margin expansion of ~170bps, G&A leverage and accretion from share repurchases.

Consensus Expectations

Consensus models EPS growth of ~27% over the next four years, including 47% in 2019.

For 2019, consensus estimates top-line growth of 11.4%, restaurant margin expansion of

~140bps, G&A leverage and benefits from share repurchases for EPS growth of ~47%.

Figure 34: In the seven years prior to food safety

challenges at the end of 2015, EPS growth averaged

~31.5%.

Figure 35: We model EPS growth of ~33% over the

next four years, above consensus’ ~27%.

Source: Company data, Credit Suisse Source: Consensus Metrix, Credit Suisse estimates

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

EP

S G

row

th

EP

S

EPS EPS Growth

5%

15%

25%

35%

45%

55%

65%

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

2019E 2020E 2021E 2022E

EP

S G

row

th

EP

S

CSe EPS Consensus EPS CSe EPS Growth Consensus EPS Growth

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 19

Valuation $870 Target Price

Our $870 target price is based on ~25x our NTM EBITDA in 12 months, implying a P/E of

~46x our NTM EPS in 12 months. Our ~25x multiple is in line with where CMG has been

trading, above its three-year average of ~19.5x. Our ~46x P/E multiple reflects a premium

to CMG’s three-year average of ~42x, and is lower than its current ~49x multiple.

Peer Group EV/EBITDA Analysis

CMG currently trades at ~26x consensus NTM EBITDA estimates, above its three-year

average EV/EBITDA multiple of ~19.5x. CMG has historically traded at a ~75% premium

to restaurant peers, but is currently trading at a ~115% premium, with the three-year

historical valuation premium implying CMG could trade at ~20.5x EBITDA. CMG has

maintained an average EV/EBITDA multiple of ~21x since Brian Niccol was appointed

CEO in March 2018 and ~24x year to date.

Figure 36: CMG NTM EV/EBITDA Figure 37: CMG EV/EBITDA vs Peers

Source: FactSet, Credit Suisse estimates Source: FactSet, Credit Suisse estimates

Note: Peers include average of publicly traded restaurant companies.

Peer Group P/E Analysis

CMG currently trades at ~49x consensus NTM EPS estimates, above its three-year

average P/E multiple of ~42x. CMG has historically traded at a ~100% premium to

restaurant peers. At current levels, CMG trades at a ~130% premium to peers, with its

historical premium implying a multiple of ~42x NTM EPS.

Figure 38: CMG NTM P/E Figure 39: CMG P/E vs Peers

Source: FactSet, Credit Suisse estimates Source: FactSet, Credit Suisse estimates

Note: Peers include average of publicly traded restaurant companies.

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Jun-1

6

Aug-1

6

Oct

-16

Dec-

16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Dec-

17

Feb-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct

-18

Dec-

18

Feb-1

9

Apr-

19

Jun-1

9

EV

/EB

ITD

A

NTM EV/EBITDA 3-yr Avg +1 Std Dev -1 Std Dev

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Jun-1

6

Aug-1

6

Oct

-16

Dec-

16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Dec-

17

Feb-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct

-18

Dec-

18

Feb-1

9

Apr-

19

Jun-1

9

EV

/EB

ITD

A

CMG Peers Implied Multiple on Avg. Premium

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

40.0x

45.0x

50.0x

55.0x

60.0x

Jun-1

6

Aug-1

6

Oct

-16

Dec-

16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Dec-

17

Feb-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct

-18

Dec-

18

Feb-1

9

Apr-

19

Jun-1

9

P/E

NTM P/E 3-yr Avg +1 Std Dev -1 Std Dev

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

40.0x

45.0x

50.0x

55.0x

60.0x

Jun-1

6

Aug-1

6

Oct

-16

Dec-

16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Dec-

17

Feb-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct

-18

Dec-

18

Feb-1

9

Apr-

19

Jun-1

9

P/E

CMG Peers Implied Multiple on Avg. Premium

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 20

Figure 40: Credit Suisse US Restaurants Coverage

Source: Company data, FactSet, Consensus Metrix

Note: (1) FCF, system sales and EBITDA growth calculated based on 3-yr forward CAGR using consensus estimates. (2) % Franchised/ Licensed reflects 2018 franchise mix. (3) Averages exclude SHAK.

Scenario Analysis

Blue Sky: $1,000 One-Year Valuation

Our $1,000 one-year valuation in a blue sky scenario is based on an EV/EBITDA of ~26x

our blue sky FY20 EBITDA. Our blue sky FY20 EBITDA is based on: 1) SSS of 7%; 2) unit

growth of 8%; and 3) restaurant-level margins of ~23%.

Grey Sky: $550 One-Year Valuation

Our $550 one-year valuation in a grey sky scenario is based on an EV/EBITDA of ~19x

our grey sky FY20 EBITDA. Our grey sky FY20 EBITDA is based on: 1) SSS of 3%; 2) unit

growth of ~5%; and 3) restaurant-level margins of ~20.7%.

NTM

EV/EBITDANTM P/E

System Sales

Growth% Unit Growth EBITDA Growth

% Franchised/

Licensed

SHAK 28.2x 113.8x 22.2% 22.8% 17.5% 40%

CMG 25.6x 53.0x 11.0% 5.9% 22.6% 0%

DPZ 20.4x 29.0x 9.7% 6.8% 10.5% 98%

YUM 20.1x 28.3x 6.8% 4.1% 7.3% 98%

DNKN 18.3x 26.4x 3.5% 1.5% 5.0% 100%

MCD 18.0x 24.8x 5.0% 2.1% 4.4% 93%

QSR 17.5x 25.5x 6.5% 5.4% 5.8% 100%

SBUX 17.4x 29.0x 7.1% 6.9% 7.5% 48%

PZZA 15.7x 36.8x 1.3% 2.8% 3.1% 88%

WEN 15.0x 30.3x 3.3% 1.9% 5.3% 95%

JACK 12.1x 19.1x 2.3% 0.9% 2.6% 94%

Average 18.0x 30.2x 5.7% 3.8% 7.4% 81.3%

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 21

Investment Risks

■ Headline risk related to food safety incidents: Chipotle headline risk is still elevated as

multiple food safety incidents have emerged over the last few years, damaging brand

perceptions which are likely still sensitive. While Chipotle has elevated its food safety

protocols since the initial food safety incident in 2015, the company has since faced

multiple and unrelated outbreaks, related to sourcing and in-store restaurant preparation

(i.e. food at unsafe temperatures, ill employees). While Chipotle has implemented robust

food safety procedures, continuous outbreaks likely have a compounding effect on

consumer perceptions and brand trust, and as a result of so many recent incidents,

Chipotle is under increased scrutiny by the market and consumers.

■ Competition: In recent years, there has been an emergence of smaller competitors

delivering on attributes that have differentiated Chipotle for many years, offering high-

quality food at reasonable prices, many of which are similarly mission-driven and

locally sourced. Given restaurant saturation, high levels of competitive activity and a

challenging consumer/retail environment, fast casual trends have been pressured in

recent years, highlighting a potentially challenging backdrop. Traditional QSRs are also

enhancing their menu and commitments, and while not perceived in the same way as

Chipotle, could be sufficient alternatives, particularly for price sensitive consumers.

■ Consumer Spending: CMG’s success in part depends on consumer confidence,

which is influenced by economic conditions and discretionary income levels. CMG’s

average restaurant sales could decline during economic downturns or periods of

uncertainty caused by higher unemployment, increased taxes, lower home prices or

other economic factors.

■ Food and Supply Costs: The prices of ingredients used in CMG products are

susceptible to increases from factors beyond CMG’s control such as weather, disease,

product recalls, government regulations and others. CMG also sources a significant

amount of its ingredients from Mexico and other countries outside the US. Increased

tariffs, taxes, political uncertainty or economic problems in these countries could

increase CMG’s food and supply costs and adversely affect its financial results.

More premium ingredients result in higher costs, increased production times and a limited

number of suppliers meeting the criteria. Food costs could increase and margins could

be adversely affected due to supplier shortage of ingredients or other events.

25 June 2019

Chipotle Mexican Grill, Inc. (CMG) 22

Financials

Figure 41: CMG Income Statement

Source: Company data, Credit Suisse estimates

Chipotle (CMG) Fiscal Yr Fiscal Yr 2018 Fiscal Yr 2019 Fiscal Yr 2020 Fiscal Yr Fiscal Yr Fiscal Yr

($ in millions) 2016 2017 1Q18 2Q18 3Q18 4Q18 2018 1Q19 2Q19E 3Q19E 4Q19E 2019E 1Q20E 2Q20E 3Q20E 4Q20E 2020E 2021E 2022E

2016 2017 Mar-18 Jun-18 Sep-18 Dec-18 2018 Mar-19 Jun-19 Sep-19 Dec-19 2019E Mar-20 Jun-20 Sep-20 Dec-20 2020E 2021E 2022E

Income Statement