Philippines Market Strategy - Credit Suisse | PLUS

25

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 1 November 2016 Asia Pacific/Philippines Credit Suisse Research Philippines Market Strategy The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients. Economic Research: Michael Wan 65 6212 3418 [email protected] Santitarn Sathirathai 65 6212 5675 [email protected] Equity Research: Dan Fineman 66 2 614 6218 [email protected] Chate Benchavitvilai 65 6212 3241 [email protected] Danielo Picache 632 858 7758 [email protected] Patricia Palanca 63 2 858 7752 [email protected] Varun Ahuja, CFA 65 6212 3017 [email protected] Muzhafar Mukhtar, CFA 60 3 2723 2084 [email protected] Kathi Go 63 2 858 7756 [email protected] Sofia Cabral 63 2 858 7757 [email protected] CONNECTIONS SERIES Pivot towards China: Impact and implications Figure 1: China tourists sensitive to politics—positive this time? Source: CEIC, Credit Suisse ■ "Pivot towards China". While there are a lot of moving parts regarding the Philippines’ government new foreign policy, Credit Suisse Economic Research Team and Credit Suisse Philippine Equity research team provide our initial assessment of the impact from ‘pivot towards China’ stance on both the economy and equities based on what we have observed so far. ■ Economic benefits outweigh costs, support above-consensus GDP view. The shift in foreign policy is likely to bring in more FDI and tourists as gains in both flows from China outweigh the potential decline in flows from the US, at least in the near term. This lends further support to our already above-consensus views on Philippines GDP growth of 6.4% (vs consensus' 6.1%) in 2017, and also consumption (CS: 6.4% vs consensus: 6.1%). ■ Mixed equities implications. The equities implications of Duterte's policy shift are mixed. Gaming stocks—especially BLOOM and MEL—and Cebu Pacific are clear beneficiaries of a potential increase in Chinese tourism, but power could suffer from increased competition from Chinese firms. The impact for most other sectors will be mixed but likely slight. 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Person Philippine Visitor Arrivals from China seasonally adjusted March 2014: Philippines submit case to UN April 2012: Scarborough Shoal standoff

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Philippines Market Strategy - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

1 November 2016 Asia Pacific/Philippines

Credit Suisse Research

Philippines Market Strategy The Credit Suisse Connections Series leverages our

exceptional breadth of macro and micro research to deliver

incisive cross-sector and cross-border thematic insights for

our clients.

Economic Research: Michael Wan

65 6212 3418

Santitarn Sathirathai

65 6212 5675

Equity Research: Dan Fineman

66 2 614 6218

Chate Benchavitvilai

65 6212 3241

Danielo Picache

632 858 7758

Patricia Palanca

63 2 858 7752

Varun Ahuja, CFA

65 6212 3017

Muzhafar Mukhtar, CFA

60 3 2723 2084

Kathi Go

63 2 858 7756

Sofia Cabral

63 2 858 7757

CONNECTIONS SERIES

Pivot towards China: Impact and implications

Figure 1: China tourists sensitive to politics—positive this time?

Source: CEIC, Credit Suisse

■ "Pivot towards China". While there are a lot of moving parts regarding the

Philippines’ government new foreign policy, Credit Suisse Economic

Research Team and Credit Suisse Philippine Equity research team provide

our initial assessment of the impact from ‘pivot towards China’ stance on

both the economy and equities based on what we have observed so far.

■ Economic benefits outweigh costs, support above-consensus GDP

view. The shift in foreign policy is likely to bring in more FDI and tourists as

gains in both flows from China outweigh the potential decline in flows from

the US, at least in the near term. This lends further support to our already

above-consensus views on Philippines GDP growth of 6.4% (vs consensus'

6.1%) in 2017, and also consumption (CS: 6.4% vs consensus: 6.1%).

■ Mixed equities implications. The equities implications of Duterte's policy

shift are mixed. Gaming stocks—especially BLOOM and MEL—and Cebu

Pacific are clear beneficiaries of a potential increase in Chinese tourism,

but power could suffer from increased competition from Chinese firms. The

impact for most other sectors will be mixed but likely slight.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

200

0

200

1

200

2

2003

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

PersonPhilippine Visitor Arrivals from China seasonally adjusted

March 2014: Philippines submit case to UN

April 2012: Scarborough Shoal standoff

1 November 2016

Philippines Market Strategy 2

Pivot towards China: Impact & implications

"Pivot towards China"

While there are a lot of moving parts regarding the Philippines government's new foreign

policy, Credit Suisse Economic Research Team and Credit Suisse Philippine Equity

research team provide our initial assessment of the impact from ‘pivot towards China’

stance on both the economy and equities based on what we have observed so far.

Economic: Benefits outweigh costs in the short-run

On the macro side, the shift in foreign policy is likely to bring in more FDI and tourists as

the gains in both flows from China outweigh the potential decline in flows from the US, at

least in the near term. This lends further support to our already above-consensus views on

the Philippines GDP growth of 6.4% (vs consensus' 6.1%) in 2017, and also consumption

(CS: 6.4% vs consensus: 6.1%). We think that around US$1 bn to US$4 bn (0.3% to 1.2%

of GDP) out of a total of US$15 bn investment pledges (4.6% of GDP) could have the

potential to start in 2017. This implies a two- to six-fold increase in current investments

from China, and compares with the Philippines' typical annual total FDI inflows of US$6-8

bn. Importantly, our analysis suggests that Chinese tourists have been sensitive to political

tensions between China and the Philippines. With these political drags on tourism

removed, the Philippines should benefit more from the boom in outbound Chinese tourism,

which currently accounts for around 11% of total visitor arrivals in the country. While direct

tourism revenue only accounts for around 2% of GDP in the Philippines, the indirect

benefits could be two times larger, with the gains likely accrued to employment and

consumer spending.

Equities: Gaming and airline the winners

Although Duterte's foreign policy shift should prove a moderate net positive for the

economy, the implications for the equities market are mixed. Gaming and airlines are

clear winners from an expected boost in Chinese tourist arrivals, but power and possibly

banks could suffer from competition from Chinese firms. It is unclear whether a Chinese

bank would seek a stake in a smaller local bank, but interest among Chinese firms in

power seems fairly high. In property, residential could suffer if US investment in BPO

weakens, while hospitality could gain from higher Chinese tourist arrivals. Telcos might

gain on the margin from more preferential financing terms from Chinese network vendors.

The consumer sector should broadly benefit if we are right that consumption would gain

on a net basis, though increased Chinese investment in the sector might raise competitive

pressures. Outside of gaming, airlines and possibly power, we do not see the China effect

as being great. For most of the market, other factors will predominate.

Within our top picks, SMPH and RLC should benefit from malls and hospitality exposure.

JFC and URC could also benefit as higher tourists' spending and employment boost

consumption. For EDC, we have not built in any potential adverse impact, but noted that

this is only a longer-term risk while attractive valuation and near-term catalysts remain

intact. For gaming, we also have an OUTPERFORM rating on BLOOM.

More FDI and tourists from China could

outweigh decline in flows from the US

Boost in Chinese tourists to benefit

gaming (BLOOM, MCP) and airline (CEBU)

1 November 2016

FOR IMPORTANT DISCLOSURES AND DISCLAIMERS, PLEASE SEE THE ECONOMIC RESEARCH DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT.

Economic Research

1 November 2016

Philippines Market Strategy 4

Assessing potential economic impact of foreign policy shift towards China

Potential economic benefits could outweigh costs in the short-run

While there are a lot of moving parts regarding the Philippines government's new foreign

policy, we provide below an initial economic assessment of the ‘pivot towards China’

based on what we have observed so far.

■ Net positive for 2017 GDP and balance of payments. The shift in foreign policy is

likely to bring in more FDI and tourists as the gains in both flows from China outweigh

the potential decline in flows from the US, at least in the near term. This lends further

support to our already above-consensus views on the Philippines GDP growth of 6.4%

vs the consensus of 6.1% in 2017, and also consumption (CS: 6.4% vs consensus:

6.1%).

■ External funding of investment – a lot more from China, a little less from the US.

We think that around US$1 bn to US$4 bn (0.3% to 1.2% of GDP) out of a total of

US$15 bn investment pledges (4.6% of GDP) could have the potential to start in 2017.

This implies a two- to six-fold increase in current investments from China, and

compares with the Philippines' typical annual total FDI inflows of US$6-8 bn. While the

US is still the most important source of FDI in the Philippines, we found that US FDI is

driven by structural economic considerations rather than just solely from political noise.

Availability of concessional financing from China will also help finance the rise in

investment.

■ Real investment boost to GDP will take time to realise. Although the potential

Chinese FDI is large compared to existing FDI flows, it is still quite small relative to the

overall size of the economy, which is heavily geared towards private consumption. We

also found that some of these investment projects would probably have happened

anyway even without Chinese collaboration, while other large scale ones will at best

take time to materialise, as they are still in the initial planning stages.

■ Tourism – getting larger slice of the Chinese tourist boom. Our analysis suggests

that the Philippines has been losing market share in Chinese tourists to other Asian

economies and that these tourists are also sensitive to political tensions between

China and the Philippines. With these political drags on tourism removed, the

Philippines should benefit more from the boom in outbound Chinese tourism, which

currently accounts for around 11% of total visitor arrivals in the country. While direct

tourism revenue only accounts for around 2% of GDP in the Philippines, the indirect

benefits could be two times larger, with the gains likely accrued to employment and

consumer spending.

More investments from China, but full pledges will

take time to realise

We estimate that around US$1 bn to US$4 bn (0.3% to 1.2% of GDP) out of the total

US$15 bn investment pledges (4.6% of GDP) could have the potential to start in 2017.

This implies a two- to six-fold increase in investments from China (currently ~US$0.5 bn),

and compares with the Philippines' typical annual FDI inflows of US$6-8 bn.

Our analysis suggests that the majority of the investment agreements are in the initial

planning stages and will take time to sort out details. As such, we doubt companies and

the government are able to start executing the full US$15 bn list of projects in 2017 (see

Figure 3 and Appendix for full list of projects).

Economic Research:

Michael Wan

65 6212 3418

Santitarn Sathirathai

65 6212 5675

1 November 2016

Philippines Market Strategy 5

There are nonetheless some infrastructure projects which have already received initial

approvals from local governments and would therefore be more advanced in the process.

These include the Davao coastline and port development project (US$0.8 bn) and the

Manila Harbour reclamation project (US$0.15 bn). These are, however, not new projects

and would probably have happened anyway regardless of Chinese collaboration (see

Figure 2).

We are also sanguine on the agreement between MVP Global and Tianjin Suli to build a

cable manufacturing facility worth US$3 bn, given that there are far more details on the

financing and equity arrangements compared with the other projects1. This project will

likely be counted officially as FDI in the balance of payments.

Not all will be pure investment, but Chinese companies can take equity stake in infrastructure projects based on experience of other countries

To be clear, not all of the committed projects are for "pure" investment. We estimate that

projects with equity stakes involved account for around US$5 bn of the total US$15 bn

pledged projects, with most of these in the manufacturing, utilities or agriculture space.

It's still uncertain whether the US$7.5 bn worth of infrastructure projects involve just paying

for construction services done or actual investment by Chinese companies (see Figure 3).

Nonetheless, the experience of other countries such as Indonesia and Malaysia suggests

that the Chinese companies are typically part of a joint venture putting in equity (e.g.,

Jakarta High Speed Rail and also Bandar Malaysia project), with the Chinese state also

providing concessional financing as part of the deal (see section below).

Figure 2: Announced size of deals with China

Figure 3: Infrastructure makes up the bulk of

investment deals with China

Value (US$ bn) Remarks

Total Investment and Loan

Facilities with China

24.0

Total Investment agreements 15.0 …Planned infrastructure investment by local governments 0.9

These investments would likely have happened anyway

… Manufacturing 3.0 Potential to be counted as new

FDI in 2017

… Others 11.1 Mostly in planning stage

Loan Facilities 9.0

… $3bn credit line from Bank of

China

3.0 Non-binding with eight

Philippines conglomerates

… Concessional loans 6.0 With China Government

Source: Credit Suisse

Source: Various News Reports, Credit Suisse Economic Research Source: Various News Reports, Credit Suisse Economic Research

External funding of investment likely to improve

Attractiveness will also depend on terms of the loans from China

The change at the margin from President Duterte's visit is also the loan commitments, i.e.,

the US$3 bn credit line from Bank of China and US$6 bn soft loans from the government.

Based on past experience, China will likely provide these concessional loans for specific

1 http://bilyonaryo.com.ph/2016/10/20/mvp-forges-jv-with-chinas-tianjin-for-high-end-cable-production-in-ph/

Under the agreement, the Suli Group will have a 70 percent share in the new joint venture while MVP will hold the remaining 30 percent. The Chinese group will finance the business and run the operations, while MVP will serve as the local partner.

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

USD bn Announced investment deals between the Philippines and China by sector

1 November 2016

Philippines Market Strategy 6

projects and tie them in with conditions to use Chinese companies for construction-related

services. The planned investments mentioned above (~US$1 bn) have not yet officially

decided on financing options yet, and could eventually tap the Chinese instead of

domestic banks or capital markets, depending on the terms.

The experience of Indonesia and Thailand suggests that interest rates could range from 2%

to 4%, and will likely be FX denominated, while loan tenures could stretch as long as 40

years, with a five- to ten-year grace period. The willingness of Philippines' corporates and

local governments to tap into these financing arrangements from China will as such depend

on the relative attractiveness of the terms and tenor versus the domestic market (see Figure

5). The availability of these loans could help finance the rise in investment rate and

associated increase in import needs as we move into 2017, providing some support to the

PHP.

Figure 4: Examples of financing terms from China for major projects

Country Financed by Terms Project Progress

Indonesia China Development

Bank

25% equity, 75% loans from China

Development Bank;

Loan terms: 40-year, 10-year grace period

60% US$, 2% interest per year

40% RMB, 3.46% interest per year

Jakarta-Bandung

High Speed Rail

Delays due to land

acquisition

Thailand Export Import Bank of

China

15 year loan payment period, five year grace

period

2.5% interest or higher under discussion.

Either USD or RMB denominated

Thailand High

Speed Rail

Thailand government

rejected the financing

proposal as interest rates

were deemed too high

Source: Institute of Southeast Asian Studies, Bangkok Post, Various News Websites, Credit Suisse Economic Research

Figure 5: Comparison of interest rates in the Philippines

Source: CEIC, Credit Suisse Economic Research

A little less investment from the US

Improvement in China investment to outweigh US slowdown

The US is currently a more important source of FDI compared with China, accounting for

around 30% of total FDI, compared with 5% for China (see Figure 6). Nonetheless, our

assessment is that any potential slowdown in 2017 is likely to be mild, for two reasons.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

10 year PH USD govtbond yield

25 year PH USD govtbond yield

Commercial Bankaverage lending rate(Peso denominated )

Soft loan from China(likely FX

denominated)

Comparison of Philippines Interest rates (%)

At what rate and

tenor?

1 November 2016

Philippines Market Strategy 7

First, feedback from our recent research trip suggests that while some foreign investors in

the BPO, manufacturing and agriculture sectors are holding back on expansion plans due

to the political environment, these are still small as a percentage of total investments. We

also have not heard of existing US companies pulling out of the country because of the

political environment.

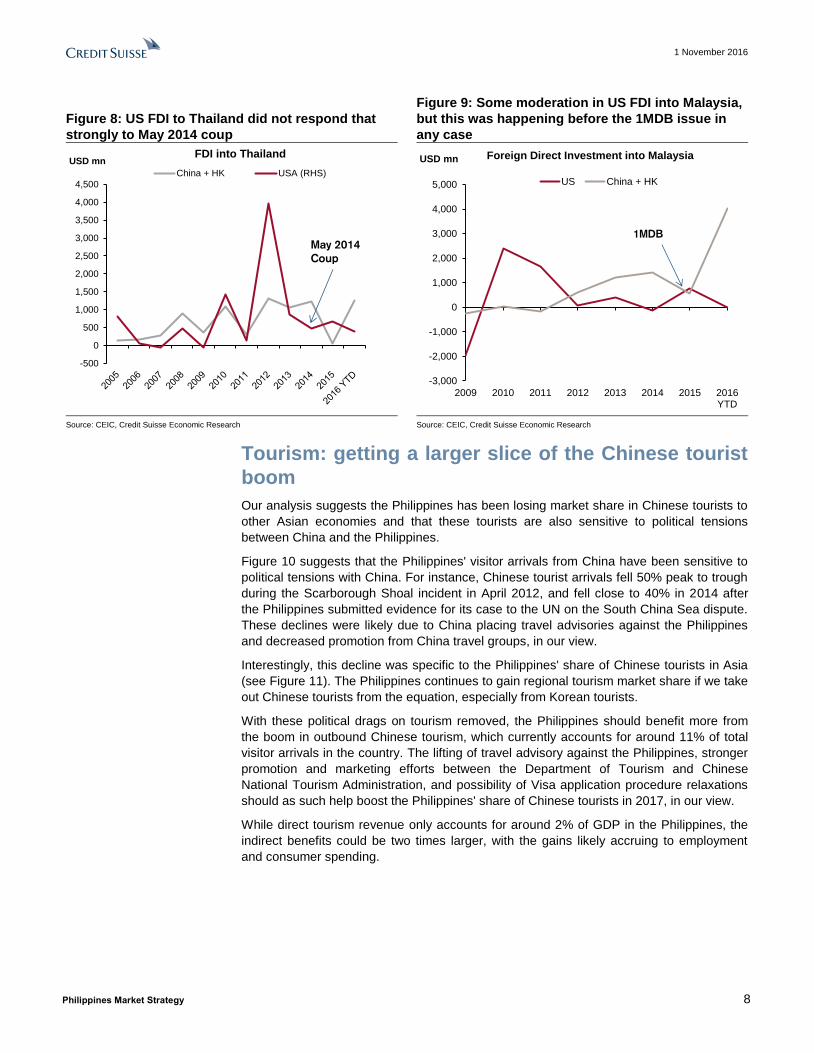

Second, and more importantly, US FDI tends not to respond too much to political tensions,

unlike what we see in China (see Figure 7). We believe that US FDI is driven more by

structural economic considerations rather than just solely from politics. For instance, US

FDI hardly moved in Thailand post the coup in May 2014, as seen in Figure 8. In Malaysia,

post the 1MDB saga, we saw some moderation in FDI from the US, but this decline was

already happening way before 2015 (see Figure 9).

Figure 6: US FDI far more important than China-

related FDI at the moment

Figure 7: FDI from China could have been affected

by political tensions in 2012

Source: CEIC, Credit Suisse Economic Research Source: CEIC, Credit Suisse Economic Research

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%% share of the Philippines FDI accumulated since

2014

-800

-600

-400

-200

0

200

400

600

800

1,000

1,200

USD mn Philippines FDI (Equity)

China + HK US

Scarborough Shoal

?

1 November 2016

Philippines Market Strategy 8

Figure 8: US FDI to Thailand did not respond that

strongly to May 2014 coup

Figure 9: Some moderation in US FDI into Malaysia,

but this was happening before the 1MDB issue in

any case

Source: CEIC, Credit Suisse Economic Research Source: CEIC, Credit Suisse Economic Research

Tourism: getting a larger slice of the Chinese tourist

boom

Our analysis suggests the Philippines has been losing market share in Chinese tourists to

other Asian economies and that these tourists are also sensitive to political tensions

between China and the Philippines.

Figure 10 suggests that the Philippines' visitor arrivals from China have been sensitive to

political tensions with China. For instance, Chinese tourist arrivals fell 50% peak to trough

during the Scarborough Shoal incident in April 2012, and fell close to 40% in 2014 after

the Philippines submitted evidence for its case to the UN on the South China Sea dispute.

These declines were likely due to China placing travel advisories against the Philippines

and decreased promotion from China travel groups, in our view.

Interestingly, this decline was specific to the Philippines' share of Chinese tourists in Asia

(see Figure 11). The Philippines continues to gain regional tourism market share if we take

out Chinese tourists from the equation, especially from Korean tourists.

With these political drags on tourism removed, the Philippines should benefit more from

the boom in outbound Chinese tourism, which currently accounts for around 11% of total

visitor arrivals in the country. The lifting of travel advisory against the Philippines, stronger

promotion and marketing efforts between the Department of Tourism and Chinese

National Tourism Administration, and possibility of Visa application procedure relaxations

should as such help boost the Philippines' share of Chinese tourists in 2017, in our view.

While direct tourism revenue only accounts for around 2% of GDP in the Philippines, the

indirect benefits could be two times larger, with the gains likely accruing to employment

and consumer spending.

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

USD mnFDI into Thailand

China + HK USA (RHS)

May 2014

Coup

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

2009 2010 2011 2012 2013 2014 2015 2016YTD

USD mn Foreign Direct Investment into Malaysia

US China + HK

1MDB

1 November 2016

Philippines Market Strategy 9

Figure 10: Philippines visitor arrivals from China

have been sensitive to political tensions

Figure 11: This is drop is also specific to the

Philippines' share of China tourists

Source: CEIC, Credit Suisse Economic Research Source: CEIC, Credit Suisse Economic Research

Meanwhile, US tourist arrival slowdown should be limited

While the US is still more important as a source of tourist arrivals (14% for the US vs 11%

for China in 2016 YTD), and is a larger spender than the average Chinese tourist, we

believe that US tourists tend to be less sensitive to political noise.

For instance, the experience of Thailand tourist arrivals post political shocks suggests that

US tourist arrivals, while still slowing, tend to be less volatile and sensitive to shocks than

Chinese tourist arrivals (see Figure 13). Admittedly, this still is a second best comparison

to the Philippines' situation, as the Thailand experience is a slowdown across the whole

sector due to security concerns and not specific to US tourists.

Figure 12: US tourists still more important than

China tourists at the moment

Figure 13: US tourists appear less sensitive to

political developments

Source: CEIC, Credit Suisse Economic Research Source: CEIC, Credit Suisse Economic Research

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Person Philippine Visitor Arrivals from Chinaseasonally adjusted

March 2014: Philippines submit

case to UN

April 2012: Scarborough

Shoal standoff

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Philippines market share of Asia regional tourist arrivals (%)

from China from Asia ex China

-0.3%-0.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

% share of Tourist Arrivals in the Philippines by country

2010 2016 YTD

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Thailand Tourist Arrivals from US vs China %yoy

US China

2011 floods

2010 clashes

2014coup

2008Airport Closure

1 November 2016

Philippines Market Strategy 10

Potential disinflation through rising competition

The Philippines' pivot towards China could also increase competitive pressure from

Chinese companies in key sectors such as power, consumer goods and also

telecommunications, helping to put downward pressure on inflation in these areas. While

this may be undesirable for listed firms, it should overall benefit consumers, and in turn

help the economy (see equity research section below). In addition, a potential pick up in

infrastructure could also help the Philippines address its supply-side logistics bottlenecks,

and hence bring down inflation rates over the longer-run, increasing consumers'

purchasing power.

Figure 14: Greater competition from China could

help bring down inflation at least for some sectors

Figure 15: Improving infrastructure can help

address the Philippines' supply-side bottlenecks

Source: CEIC, Credit Suisse Economic Research Source: World Bank Logistics Performance Index, Credit Suisse Economic Research

The key uncertainty – further shift in foreign policy

We continue to monitor closely President Duterte's shift in foreign policies as there are still

many moving parts and our assessment here is based on what we have seen so far.

Should further pivot towards China and away from the US accelerate significantly, then the

negative impact on inward FDI from the US could rise to the point that the net impact on

total FDI turns negative, for example. The recent remarks by the President and also the

Speaker of the House to require visas for Americans visiting the Philippines, if

implemented, might also have a negative impact on tourism and FDI if the new

requirements prove onerous enough.

These developments also have to be balanced against the wide range of domestic reforms

the government is undertaking at the moment, for instance the tax reform package and

also the push to improve infrastructure, both of which are credit positive according to both

Moody's and S&P.

Food36%

Electricity4%Telephone

services2%

Others58%

The Philippines' CPI weights

0

10

20

30

40

50

60

70

80

2007 2010 2012 2014 2016

The Philippines Logistics Performance Index Rank

The lower the rank the better

1 November 2016

Philippines Market Strategy 11

Figure 16: A potential rethink of BPO investments?

Figure 17: The US remains the largest source of

remittances for the Philippines

Source: CEIC, Credit Suisse Economic Research The likely overstates the importance of US as a source of remittances as it includes remittances coursed through US banks. Source: CEIC, Credit Suisse Economic Research

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013

BPO Export Revenue to USA (% share of total)

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015

The Philippines' Remittances from USA (% share)

1 November 2016

Philippines Market Strategy 12

Appendix

Figure 18: The Philippines' investment deals with China

No. China investment into Philippines Value (US$ bn) Time Period

1 Globe Signs $750 mn Pacts With Huawei, Others for Wider Use of LTE - Globe Telecom says it signed several agreements with Huawei Technologies, Nokia and Wuhan Fiberhome worth ~$750 mn over a five-year period to accelerate use of new LTE technologies to enhance data services.

0.750 Telecoms

2 Baiyin Nonferrous Group to evaluate trade financing for Global Ferronickel’s Palawan mine and study building a stainless steel plant with annual capacity of 1mn t nickel ore sourced in the Philippines, Global Ferronickel said in a stock exchange filing.

0.700 Steel/Mining

3 China Railway Engineering Corp. signed a memorandum of understanding for a $2.5 bn project with MVP Global Infrastructure Group.

2.500 Infrastructure (Railway)

4 Davao coastline and port development project by Mega Harbor Port and Development and China Harbour Engineering 0.780 Infrastructure (Port)

5 Agreement between MVP Global and Tianjin Suli Cable Group to build a $3 bn cabling manufacturing facility 3.000 Manufacturing

6 $148 mn Manila Harbour Centre reclamation project with R-II Builders and China Harbour Engineering 0.148 Infrastructure (Reclamation)

7 CCCC Dredging (China Communications Construction Company) to sign $328 mn Cebu bulk terminal project with Mega Harbour Port

0.328 Infrastructure (Port)

8 DoubleDragon Properties Corp. and its subsidiary Hotel of Asia Inc. signed a P6.6 bn deal with China's JinJiang Inn to expand their accommodations business in the Philippines.

0.140 Tourism

9 Subic-Clark railway project by Bases Conversion and Development Authority (BCDA) and China Harbour Engineering Co 1.900 Infrastructure (Railway)

10 A rapid transit bus link between Bonifacio Global City and Ninoy Aquino International Airport. This will be carried out by the BCDA and China Road and Bridge Corp

Infrastructure (Transport)

11 BCDA-China Fortune Land Real Estate project (memorandum of understanding) Real Estate

12 Safe and smart city projects for BCDA by BCDA and Huawei Technologies Infrastructure

13 Joint venture agreement of Jimei Group of China and Expedition Construction Corp. for infrastructure projects Infrastructure

14 North Negros biomass and South Negros biomass project by North Negros Biopower and Wuxi Huaguang Electric Power Engineering Utilities

15 Joint development project on renewable energy by Columbus Capitana and China CAMC Engineering Utilities

16 New Generation Steel Manufacturing Plant by Mannage Resources and SIIC Shanghai International Trade HK; 0.200 Manufacturing

17 Renewable energy projects by Xinjiang TBEA Sunoasis Utilities

18 Manila EDSA Bus Transportation program by Phil State Group and Yangtse Motor group and Minmetals International 0.100 Infrastructure (Transport)

19 Hybrid rice production by SL Agritech and Jiangsu Hongqi Seed Inc. 0.160 Agriculture

20 Bus manufacturing facility by Zhuhai Bus and Coach Co. 0.300 Manufacturing

21 Banana plantation project by AVLB Asia Pacific and Shanghai Xinwo Agriculture Development Co. 0.100 Agriculture

22 300MW Pulangi-5 Hydro Project by Greenergy Co. and Power China Guizhou Engineering Corp. 1.000 Utilities

23 Pasig River, Marikina River and Manggahan Floodway bridges construction project by Zonar Construct and SinoHydro; 0.600 Infrastructure (Bridge)

24 Ambal Simuay sub-river basin flood control project by One Whitebeach Land Development and Sino Hydro; 0.325 Infrastructure (Flood Control)

25 Nationwide island provinces link bridges by Zonarsystems and PowerChina Sino Hydro 0.800 Infrastructure (Bridge)

Source: Various News Reports, Credit Suisse Economic Research

1 November 2016

FOR IMPORTANT DISCLOSURES AND DISCLAIMERS, PLEASE SEE THE EQUITY RESEARCH DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Equity Research

1 November 2016

Philippines Market Strategy 14

Equities: Gaming and airline the winners Although Duterte's foreign policy shift should prove a moderate net positive for the

economy, the implications for the equities market are mixed.

Gaming and airlines are clear winners from an expected boost in Chinese tourists, but

power and possibly banks could suffer from competition from Chinese firms. It is unclear

whether a Chinese bank would seek a stake in a smaller local bank, but interest among

Chinese firms in power seems fairly high.

In property, residential could suffer if US investment in BPO weakens, while hospitality

could gain from higher Chinese tourist arrivals. Telcos might gain on the margin from

more preferential financing terms from Chinese network vendors. The consumer sector

should broadly benefit if we are right that consumption would gain on a net basis, though

increased Chinese investment in the sector might raise competitive pressures.

Outside of gaming, airlines and possibly power, we do not see the China effect as being

great. For most of the market, other factors will predominate.

Within our top picks, SMPH and RLC should benefit from malls and hospitality exposure.

JFC and URC could also benefit as higher tourists' spending and employment boost

consumption. For EDC, we have not built in potential adverse impact, but noted that this is

only a longer-term risk while attractive valuation and near-term catalyst remain intact.

Gaming: Positive

− Potential relaxation of visa regulations for Chinese visitors will be a huge positive for

tourist arrivals for gaming given that player demand is largely spontaneous.

− We estimate that Chinese account for 23% of total, and 63% of foreign VIP, gaming

revenues. On the other hand, gaming revenues from US tourists is insignificant.

− Companies that could benefit more from the theme are BLOOM and MCP given their

higher exposure to Chinese players.

Figure 19: China/HK/Macau accounts for 60-100%

of foreign VIP revenues…

Figure 20: …and thus as much as 24%-38% of total

revenue, much higher exposure than RWM

Source: Company data, Credit Suisse Equity Research estimates Source: Company data, Credit Suisse Equity Research estimates

16%

60%

100%

63%

42%

20% 19%30%

20% 16%

12%3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

RWM BLOOM MCP Industry

China/HK/Macau Korea SEA Others

5%

24%

38%

23%12%

8% 7%

9%

8%6%

72%

60% 62% 63%

3% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

RWM BLOOM MCP Industry

China/HK/Macau Korea SEA Local Others

Equity Research Analyst Team

Dan Fineman

66 2 614 6218

Chate Benchavitvilai

65 6212 3241

chate.benchavitvilai@credit-

suisse.com

Danielo Picache

632 858 7758

Patricia Palanca

63 2 858 7752

Varun Ahuja, CFA

65 6212 3017

Muzhafar Mukhtar, CFA

60 3 2723 2084

muzhafar.mukhtar@credit-

suisse.com

Kathi Go

63 2 858 7756

1 November 2016

Philippines Market Strategy 15

Airline: Positive

− Cebu Pacific would be a beneficiary of any surge in Chinese tourist demand for the

Philippines.

− We do note that as Thailand's experience has shown, a rapid rise in Chinese

outbound tourist could trigger a greater competitive response from Chinese airlines

themselves. However, Cebu Pacific would still benefit from an increase in demand

for domestic connecting flights.

Figure 21: Thailand experienced surge in

capacity/traffic as Chine relationship improved

Figure 22: CEBU dominates domestic market share,

will benefit from more domestic connecting flights

Source: Company data, Credit Suisse Equity Research estimates Source: Company data, Credit Suisse Equity Research estimates

Telco: Positive (assuming no new entrant)

− The Philippine telecom operators are likely to make significant investment in the

data network over the next 3-5 years, and potentially be buying more Chinese

equipment for their network. An improvement in diplomatic and business

relationship could lead these Chinese equipment manufacturers to provide more

lucrative financing deals to Philippine operators. Both PLDT and Globe might

benefit from this.

− Currently, PLDT is using three vendors: Huawei, NSN and Ericsson, and will

maintain this strategy for pricing power/diversification. Globe on the other hand is

sourcing equipment primarily from Huawei.

− We do note that there could be a negative risk in the case that Chinese operators

decide to launch cellular services in the Philippines as the third player. This

however is very unlikely. While Chinese operators are well-capitalised, we do not

see the possibility of a new entrant in the market over the next three years given the

limited availability of spectrum. Please see our sector report “Philippines Telecoms

Sector - Quick Take: Introduction of a third operator faces many hurdles” for more

details.

− Our negative thesis on the sector is based on the telcos’ high contribution from

structurally declining SMS/ILD services while data monetisation continues to be

poor due to competition and customers’ tendency to use WiFi. We see further

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2010 2011 2012 2013 2014 2015

ASK(mn) China-Thailand airline capacity

Chinese airlines Other airlines

59% 59%

29% 29%

11% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1H15 1H16

Domestic market share (Philippines)

Cebu PAL AirAsia

1 November 2016

Philippines Market Strategy 16

downside for PLDT as it is still in the early phase of restructuring but maintain

OUTPERFORM rating on Globe on valuation ground.

Property: Negative on developers, Positive on hospitality

− Property values specifically in underdeveloped markets outside of Metro Manila

may receive a boost given the potential for infrastructure projects in the

aforementioned new provincial growth centers.

− On the residential segment we think there will be pockets of developments that

Chinese developers can commit to such as economic and socialised housing. The

huge housing backlog is an area of frustration for past administrations and it can be

an addressable market that the government in partnership with a new foreign

investor can tap. On the flipside, any new investment into saturated segments like

middle-income residential condos can only exacerbate the oversupply situation,

which is a negative for the rental market.

− The boost in tourism is a positive for the hospitality industry, in general. The

contribution of hotel operations is still small, though, on the back of the robust

expansion pipeline of almost all the major property developers we think this can be

a potential driver for growth.

− Overall we believe this could be positive for property names with hospitality

exposure: RLC, AL but negative for developers like MEG and FLI.

Figure 23: Housing backlog shows need for

socialized/economic housing…

Figure 24: ALI and RLC highest exposure to

hospitality

Source: Company data, Credit Suisse Equity Research estimates Source: Company data, Credit Suisse Equity Research estimates

Power: Negative

− China as a new source of capital could lower entry barriers, either for Chinese

investor or JV with local new entrant, which could lead to increased competition and

lower generation ASPs.

− We note that except for renewables, there is no foreign ownership cap on power

generation.

− We note that during the President’s visit to China, Alfredo Yao of the Zest-O group

has signed a partnership deal with Energy China to invest more than $2 bn in a

1,200-megawatt coal-fired power plant in Luzon in the Philippines.

1,449,854

1,582,497

2,588,897

605,692

0

0

- 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

Can't afford/needs subsidy

Socialized housing

Economic housing

Affordable/low cost housing

Mid cost housing

High-end/luxury

Government estimates a total of 6.2mnhousing backlog till 2030, 67% of which

is in the socialized and economic segment

47%55%

41%

18% 16%

30%18%

24%

55%

75%

15% 27%

33%21%

6%8%3% 6%

2%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

ALI FLI MEG RLC SMPH

Residential Malls Office Hotels

1 November 2016

Philippines Market Strategy 17

− An increase in supply / competition in the sector would negatively affect pretty much

all names; AP, EDC, FGEN, Seminara, Meralco and conglomerates with power

exposure / aspirations including Ayala, MPIC, AEV, JGS, SMC.

Banks: Negative

− Potential for M&A can be ripe especially if we take into account the entry of any

Chinese bank on the back of the relaxation of the foreign ownership limit in the

sector.

− An aggressive new player (i.e., Chinese financial institutions that will initially offer

credit lines) or an existing domestic bank but with new capital is disruptive for

margins given the potential for more intense competition for pricing on big-ticket

investment deals.

Figure 25: Phils Banks sector is highly

fragmented… Figure 26: …and competition has driven down NIMs

Source: Company data, Credit Suisse Equity Research estimates Source: Company data, Credit Suisse Equity Research estimates

Consumers: Tourism positive on consumption, but competition to rise

− Stronger tourism positive on consumption, assuming BPO remains…

Consumption could benefit from an increase in tourist arrival from China through

both tourists’ spending and higher employment (tourism is relatively labour-

intensive).

While the recent rhetoric against the US creates some concern on the BPO

sector (~7% of GDP) given that the US is a major source of BPO investment,

we believe this will only have limited impact in 2017. We understand that some

companies might be holding back their investments, but do not plan for a broad-

based reduction in BPO investment. We note that regional evidences suggest

that US FDI didn’t seem to be that sensitive to political shocks, and is driven

more by economic considerations.

Overall, our base case is that an improvement in relationship with China would

be net positive on consumption, as the positive impact from a rise in tourism

outweigh the limited decline in BPO investment.

− …but risk for more intense competition also rises

Packaged foods and beverage – Closer ties could encourage more Chinese

companies to either set up a manufacturing facility here, and/or bring their

products to the Philippines market.

Retail (Food and non-food) – A possible influx of Chinese companies bringing

their products or brands to the Philippine market (as a result of closer ties) could

add additional pressure to an already competitive segment.

BDO19%

BPI13%

MBT13%

LBP6%

PNB5%

CHIB5%

RCB5%

SECB4%

UBP3%

DBP2%

Others25%

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Earning Asset Yield Funding Cost Interest Spread NIM

1 November 2016

Philippines Market Strategy 18

− Potential to penetrate China market is small

URC – entered the Chinese market back in 2000 but has been unable to scale

up the business. It is currently only contributing 1% of consolidated sales in

FY15.

JFC – Already in Chinese market (business about 11% of system-wide sales),

where business is currently seeing some SSSG weakness.

EMP – news reports saying that it is planning to export Emperador Brandy to

China; however the Chinese alcoholic drinks market is dominated by Chinese

spirits and beer…hence unlikely that Emperador Brandy will be able to

penetrate the market there. Better opportunity with the whisky business with

Dalmore & Jura brands but this could be limited by competition from bigger and

more known brands.

− Net positive impact on consumption could benefit JFC and in turn DNL (supplier of

ingredients to JFC). RRHI (food and non-food retails) could also benefit.

1 N

ovem

be

r 201

6

CS Philippines coverage: Valuation summary

Figure 27: CS Philippines coverage–valuation summary

CS Current Target Up/down ADTO-6M Mkt cap P/E (x) EPS (%YoY) P/B (x) ROE (%) Div (%)

Company RIC rating price price side (%) (US$mn) (US$mn) FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY16E

Banks

Asia United Bank AUB.PS N 47.75 44.94 (6) 0.0 477 14.3 12.7 6.8 12.7 0.9 0.9 6.8 -

BDO Unibank Inc BDO.PS U 112.80 94.80 (16) 5.2 8,479 15.5 13.4 6.2 16.0 1.9 1.7 12.6 1.1

Bank of Philippine Islands BPI.PS U 101.10 77.90 (23) 3.6 8,183 20.4 18.1 7.0 12.7 2.3 2.1 12.0 1.4

Metrobank MBT.PS O 81.30 109.20 34 6.8 5,317 12.5 10.5 6.6 18.7 1.2 1.1 10.2 1.2

Security Bank SECB.PS N 220.40 205.30 (7) 8.2 3,421 16.9 15.8 2.1 6.8 1.5 1.6 11.7 0.8

Weighted average 16.6 14.6 6.0 14.2 1.8 1.7 11.7 1.2

Consumer

Jollibee Foods Corporation JFC.PS O 238.0 296.0 24 3.2 5,244 39.2 33.0 11.9 19.0 7.0 6.1 19.5 0.9

Universal Robina Corporation URC.PS O 182.0 226.3 24 8.1 8,179 29.3 24.1 7.4 21.6 5.3 4.5 19.1 1.7

Emperador Inc. EMP.PS N 7.25 7.60 5 0.3 2,407 17.3 15.9 (2.7) 8.7 2.1 1.9 12.7 2.4

D&L Industries, Inc. DNL.PS O 10.98 13.60 24 1.1 1,616 29.8 25.0 19.7 19.1 5.7 5.0 20.0 1.8

Robinsons Retail Holdings, Inc. RRHI.PS N 77.30 80.10 4 1.9 2,205 22.2 19.2 11.0 15.9 2.3 2.1 10.7 0.8

SSI Group, Inc. SSI.PS N 2.76 3.10 12 0.4 188 16.3 13.4 (38.0) 22.1 0.9 0.9 5.7 -

Weighted average 29.6 24.9 8.4 18.5 5.0 4.4 17.4 1.5

Telecom

Globe Telecom GLO.PS O 1,780 2,250 26 3.9 4,867 15.7 15.5 3.5 1.3 3.8 3.6 24.7 4.9

PLDT TEL.PS U 1,530 1,400 (8) 7.0 6,808 11.8 17.5 (20.0) (33.0) 2.7 2.5 23.9 5.1

Weighted average 13.4 16.7 (10.2) (18.7) 3.1 3.0 24.2 5.0

Note: Highlighted stocks are included in the Top Longs Source: Thomson Reuters DataStream, Credit Suisse Equity Research estimates

1 N

ovem

be

r 201

6

CS Philippines coverage: Valuation summary (continued)

Figure 28: CS Philippines coverage–valuation summary

CS Current Target Up/down ADTO-6M Mkt cap P/E EPS (%YoY) P/B (x) ROE (%) Div (%)

Company RIC rating price price side (%) (US$mn) (US$mn) FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY16E

Gaming

Belle Corporation BEL.PS N 2.92 3.24 11 0.1 631 16.8 11.6 49.7 44.7 1.2 1.1 7.2 3.3

Bloomberry Resorts BLOOM.PS O 5.92 7.07 19 1.6 1,342 377.1 61.8 n.m. 510.3 3.0 2.8 0.8 -

Melco Crown MCP.PS U 4.30 3.28 (24) 1.0 501 n.m. n.m. n.m. n.m. 8.3 29.4 (77.9) -

Premium Leisure Corp PLC.PS N 1.13 1.02 (9) 0.5 736 57.7 33.6 n.m. 71.7 2.2 2.1 3.9 1.9

Travellers International RWM.PS N 3.35 3.80 14 0.1 1,087 14.3 17.5 (8.6) (18.4) 1.2 1.1 8.5 1.5

Weighted average 133.7 31.2 5.1 173.5 2.7 5.1 (5.0) 1.2

Property

Ayala Land ALI.PS N 36.25 40.70 12 10.8 10,986 25.9 23.4 16.0 11.1 3.6 3.3 14.6 1.4

Filinvest Land FLI.PS U 1.77 1.60 (10) 0.7 884 7.9 7.1 7.4 11.3 0.7 0.7 9.4 3.2

Megaworld Corp MEG.PS U 4.02 4.00 (0) 4.4 2,669 11.7 10.5 6.9 11.7 1.0 0.9 8.9 0.9

Robinsons Land RLC.PS O 30.95 36.30 17 1.5 2,610 18.8 15.9 17.7 18.0 2.0 1.8 11.3 1.2

SM Prime Holdings SMPH.PS O 26.90 31.90 19 9.6 16,003 30.8 26.9 20.4 14.5 3.7 3.3 12.4 1.0

Weighted average 26.1 23.0 17.3 13.3 3.2 2.9 12.7 1.2

Utilities

Aboitiz Power Corp AP.PS O 45.95 52.50 14 1.9 6,965 17.5 15.5 9.6 13.4 3.3 3.0 19.2 3.6

Energy Development Corp EDC.PS O 5.90 7.50 27 1.6 2,277 11.7 11.1 18.3 5.5 2.1 1.9 19.2 3.6

First Gen FGEN.PS O 22.95 28.70 25 1.6 1,731 10.3 9.3 29.7 14.1 1.0 0.9 10.3 1.6

Manila Electric (Meralco) MER.PS N 276.00 320.00 16 1.7 6,408 16.3 15.8 (0.3) 3.5 4.4 4.4 25.2 9.1

Manila Water MWC.PS U 30.25 21.80 (28) 1.4 1,256 12.1 11.5 3.7 4.9 1.5 1.3 12.7 2.8

Semirara Mining SCC.PS O 125.90 165.00 31 1.8 2,763 11.8 10.0 34.4 17.7 4.0 3.2 37.4 3.2

Weighted average 14.9 13.7 12.0 9.7 3.3 3.1 22.2 5.0

Others

Cebu Air Inc CEB.PS N 105.00 130.00 24 1.8 1,311 5.7 7.6 62.6 (24.6) 1.9 1.5 37.7 3.0

Int'l Container Terminal Inc. ICT.PS O 77.80 112.00 44 3.1 3,258 31.2 29.0 n.m. 7.5 3.7 3.4 20.0 1.2

Note: Highlighted stocks are included in the Top Longs Source: Thomson Reuters DataStream, Credit Suisse Equity Research estimates

1 November 2016

Philippines Market Strategy 21

Economic Research Disclosure Appendix

Analyst Certification Michael Wan and Santitarn Sathirathaieach certify that (1) the views expressed in this report accurately reflect their personal views about all of the subject companies and securities and (2) no part of their compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. This report is produced by subsidiaries and affiliates of Credit Suisse operating under its Global Markets Division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who-we-are This report may contain material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse or its affiliates ("CS") to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates.The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in this report. Those communications reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other communications are brought to the attention of any recipient of this report. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR's, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk.

This report is issued and distributed in European Union (except Switzerland): by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Germany: Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). United States and Canada: Credit Suisse Securities (USA) LLC; Switzerland: Credit Suisse AG; Brazil: Banco de Investimentos Credit Suisse (Brasil) S.A or its affiliates; Mexico: Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); Japan: by Credit Suisse Securities (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau ( Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Investment Advisers Association, Type II Financial Instruments Firms Association; Hong Kong: Credit Suisse (Hong Kong) Limited; Australia: Credit Suisse Equities (Australia) Limited; Thailand: Credit Suisse Securities (Thailand) Limited, regulated by the Office of the Securities and Exchange Commission, Thailand, having registered address at 990 Abdulrahim Place, 27th Floor, Unit 2701, Rama IV Road, Silom, Bangrak, Bangkok10500, Thailand, Tel. +66 2614 6000; Malaysia: Credit Suisse Securities (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch; India: Credit Suisse Securities (India) Private Limited (CIN no.U67120MH1996PTC104392) regulated by the Securities and Exchange Board of India as Research Analyst (registration no. INH 000001030) and as Stock Broker (registration no. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th Floor, Ceejay House, Dr.A.B. Road, Worli, Mumbai - 18, India, T- +91-22 6777 3777; South Korea: Credit Suisse Securities (Europe) Limited, Seoul Branch;

Taiwan: Credit Suisse AG Taipei Securities Branch; Indonesia: PT Credit Suisse Securities Indonesia; Philippines: Credit Suisse Securities (Philippines ) Inc., and elsewhere in the world by the relevant authorised affiliate of the above. Additional Regional Disclaimers Hong Kong: Credit Suisse (Hong Kong) Limited ("CSHK") is licensed and regulated by the Securities and Futures Commission of Hong Kong under the laws of Hong Kong, which differ from Australian laws. CSHKL does not hold an Australian financial services licence (AFSL) and is exempt from the requirement to hold an AFSL under the Corporations Act 2001 (the Act) under Class Order 03/1103 published by the ASIC in respect of financial services provided to Australian wholesale clients (within the meaning of section 761G of the Act). Research on Taiwanese securities produced by Credit Suisse AG, Taipei Securities Branch has been prepared by a registered Senior Business Person. Malaysia: Research provided to residents of Malaysia is authorised by the Head of Research for Credit Suisse Securities (Malaysia) Sdn Bhd, to whom they should direct any queries on +603 2723 2020. Singapore: This report has been prepared and issued for distribution in Singapore to institutional investors, accredited investors and expert investors (each as defined under the Financial Advisers Regulations) only, and is also distributed by Credit Suisse AG, Singapore branch to overseas investors (as defined under the Financial Advisers Regulations). By virtue of your status as an institutional investor, accredited investor, expert investor or overseas investor, Credit Suisse AG, Singapore branch is exempted from complying with certain compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the "FAA"), the Financial Advisers Regulations and the relevant Notices and Guidelines issued thereunder, in respect of any financial advisory service which Credit Suisse AG, Singapore branch may provide to you. UAE: This information is being distributed by Credit Suisse AG (DIFC Branch), duly licensed and regulated by the Dubai Financial Services Authority (“DFSA”). Related financial services or products are only made available to Professional Clients or Market Counterparties, as defined by the DFSA, and are not intended for any other persons. Credit Suisse AG (DIFC Branch) is located on Level 9 East, The Gate Building, DIFC, Dubai, United Arab Emirates. EU: This report has been produced by subsidiaries and affiliates of Credit Suisse operating under its Global Markets Division This research may not conform to Canadian disclosure requirements. In jurisdictions where CS is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements. Non-US customers wishing to effect a transaction should contact a CS entity in their local jurisdiction unless governing law permits otherwise. US customers wishing to effect a transaction should do so only by contacting a representative at Credit Suisse Securities (USA) LLC in the US. Please note that this research was originally prepared and issued by CS for distribution to their market professional and institutional investor customers. Recipients who are not market professional or institutional investor customers of CS should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK or to other matters which are not authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority or in respect of which the protections of the Prudential Regulation Authority and Financial Conduct Authority for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available upon request in respect of this report. CS may provide various services to US municipal entities or obligated persons ("municipalities"), including suggesting individual transactions or trades and entering into such transactions. Any services CS provides to municipalities are not viewed as "advice" within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. CS is providing any such services and related information solely on an arm's length basis and not as an advisor or fiduciary to the municipality. In connection with the provision of the any such services, there is no agreement, direct or indirect, between any municipality (including the officials,management, employees or agents thereof) and CS for CS to provide advice to the municipality. Municipalities should consult with their financial, accounting and legal advisors regarding any such services provided by CS. In addition, CS is not acting for direct or indirect compensation to solicit the municipality on behalf of an unaffiliated broker, dealer, municipal securities dealer, municipal advisor, or investment adviser for the purpose of obtaining or retaining an engagement by the municipality for or in connection with Municipal Financial Products, the issuance of municipal securities, or of an investment adviser to provide investment advisory services to or on behalf of the municipality. If this report is being distributed by a financial institution other than Credit Suisse AG, or its affiliates, that financial institution is solely responsible for distribution. Clients of that institution should contact that institution to effect a transaction in the securities mentioned in this report or require further information. This report does not constitute investment advice by Credit Suisse to the clients of the distributing financial institution, and neither Credit Suisse AG, its affiliates, and their respective officers, directors and employees accept any liability whatsoever for any direct or consequential loss arising from their use of this report or its content. Principal is not guaranteed. Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that. Copyright © 2016 CREDIT SUISSE AG and/or its affiliates. All rights reserved.

Investment principal on bonds can be eroded depending on sale price or market price. In addition, there are bonds on which investment principal can be eroded due to changes in redemption amounts. Care is required when investing in such instruments. When you purchase non-listed Japanese fixed income securities (Japanese government bonds, Japanese municipal bonds, Japanese government guaranteed bonds, Japanese corporate bonds) from CS as a seller, you will be requested to pay the purchase price only.

1 November 2016

Philippines Market Strategy 22

Companies Mentioned (Price as of 01-Nov-2016) Aboitiz Power Corp (AP.PS, P45.95) Asia United Bank (AUB.PS, P47.75) Ayala Land (ALI.PS, P36.25) BDO Unibank Inc (BDO.PS, P112.8) Bank of Philippine Islands (BPI.PS, P101.1) Belle Corporation (BEL.PS, P2.92) Bloomberry Resorts Corporation (BLOOM.PS, P5.92) Cebu Air Inc (CEB.PS, P105.0) D&L Industries, Inc. (DNL.PS, P10.98) Emperador Inc. (EMP.PS, P7.25) Energy Development Corporation (EDC.PS, P5.9) Filinvest Land (FLI.PS, P1.77) First Gen Corporation (FGEN.PS, P22.95) Globe Telecom (GLO.PS, P1780.0) Int'l Container Terminal Inc. (ICT.PS, P77.8) Jollibee Foods Corporation (JFC.PS, P238.0) Manila Electric (Meralco) (MER.PS, P276.0) Manila Water Company (MWC.PS, P30.25) Megaworld Corp (MEG.PS, P4.02) Melco Crown (Phils) Resorts Corporation (MCP.PS, P4.3) Metropolitan Bank & Trust Co (MBT.PS, P81.3) Philippine Long Distance Telephone Company (TEL.PS, P1530.0) Premium Leisure Corp (PLC.PS, P1.13) Robinsons Land Corporation (RLC.PS, P30.95) Robinsons Retail Holdings, Inc. (RRHI.PS, P77.3) SM Prime Holdings (SMPH.PS, P26.9) SSI Group, Inc. (SSI.PS, P2.76) Security Bank Corp (SECB.PS, P220.4) Semirara Mining Corporation (SCC.PS, P125.9) Travellers International Hotel Group, Inc. (RWM.PS, P3.35) Universal Robina Corporation (URC.PS, P182.0)

Disclosure Appendix

Important Global Disclosures Dan Fineman, Chate Benchavitvilai, Danielo Picache, Patricia Palanca, Varun Ahuja, CFA, Muzhafar Mukhtar, CFA, Kathi Go and Sofia Cabral each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows: Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months. Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months. Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months. *Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s tota l return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin Ame rican and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiv eness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 1 2-month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011. Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances. Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the company at this time. Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or investment view on the equity security of the company or related products.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation: Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months. Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months. Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

1 November 2016

Philippines Market Strategy 23

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%) Outperform/Buy* 43% (63% banking clients) Neutral/Hold* 39% (61% banking clients) Underperform/Sell* 15% (56% banking clients) Restricted 3% *For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please re fer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein. Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties. See the Companies Mentioned section for full company names The subject company (AUB.PS, MEG.PS, URC.PS, MER.PS, EDC.PS, SMPH.PS, BEL.PS, MBT.PS, RLC.PS, BDO.PS, GLO.PS, ALI.PS, PLC.PS, CEB.PS, AP.PS, MWC.PS, RWM.PS, FGEN.PS, RRHI.PS, TEL.PS) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse. Credit Suisse provided investment banking services to the subject company (GLO.PS, TEL.PS) within the past 12 months. Credit Suisse provided non-investment banking services to the subject company (MBT.PS) within the past 12 months Credit Suisse has received investment banking related compensation from the subject company (GLO.PS, TEL.PS) within the past 12 months Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (AUB.PS, MEG.PS, URC.PS, MER.PS, MCP.PS, SECB.PS, SMPH.PS, BEL.PS, SCC.PS, MBT.PS, SSI.PS, RLC.PS, BDO.PS, GLO.PS, ALI.PS, PLC.PS, CEB.PS, AP.PS, MWC.PS, RWM.PS, FGEN.PS, RRHI.PS, EMP.PS, TEL.PS, FLI.PS) within the next 3 months. Credit Suisse has received compensation for products and services other than investment banking services from the subject company (MBT.PS) within the past 12 months Credit Suisse has a material conflict of interest with the subject company (MER.PS) . Credit Suisse is acting as a financial advisor to San Miguel Corporation regarding the proposed sale of its 27% stake in Manila Electric Company (Meralco) to JG Summit Holdings.