Cisco Systems Inc. (CSCO) - Credit Suisse | PLUS

121

DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 18 September 2013 Americas/United States Equity Research Networking Equipment Cisco Systems Inc. (CSCO) INITIATION Software Defined Disruption ■ Initiate with Underperform—Now for the Hard Part: Over the past year, Cisco has seen the benefits of improving execution, gross margin stability, and increased capital redeployment, all of which are to be applauded. However, the impact on the networking market from Software Defined Networking (SDN) architectures should be very real and accelerate over time, leading to further margin compression. We initiate with an Underperform rating and a target price of $21. ■ SDN to Threaten the Most Profitable Part of the Stack: Currently, on the hardware side, networking stands as one of the least competitive and highest margin industries in the IT stack. SDN, by allowing software to be separate from the physical infrastructure, will allow competition at multiple points in the network, which was not previously possible. While the impact will take time, the threat will be very real, shrinking gross profit dollars for the industry. Irrespective of whether Cisco executes well in SDN environments, the company is in a vulnerable position amidst this transition. ■ Margins to Continue Their Long-Term Trend Downward: Based on five factors, we estimate that gross margins will decrease to ~60% and operating margins to 26% over the long term, with limited growth in organic operating income. We note the following: (1) our proprietary segmentation analysis shows gross margins by business line; within that UCS is materially dilutive at ~30% GMs; (2) while software and services can offset some of the headwinds, gaps in Cisco's IT stack mean that success in wider IT environments cannot be guaranteed; (3) SDN has the potential to shrink gross profit dollars available to vendors by as much as 70%; (4) Huawei will have an effect on the service provider market and internationally; and (5) the opex base is quite lean and further optimization will likely prove challenging. ■ Valuation—Target Price of $21: While we do not see significant downside risk on Cisco, we also do not see significant upside potential. Our TP of $21 is a blended average of P/E, DCF, and Credit Suisse HOLT ® valuation. Share price performance 16 21 26 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Daily Sep 17, 2012 - Sep 17, 2013, 9/17/12 = US$19.16 Price Indexed S&P 500 INDEX On 09/17/13 the S&P 500 INDEX closed at 1704.76 Quarterly EPS Q1 Q2 Q3 Q4 2012A 0.43 0.47 0.48 0.47 2013A 0.48 0.51 0.51 0.52 2014E 0.51 0.51 0.53 0.55 Financial and valuation metrics Year 07/12A 07/13A 07/14E 07/15E EPS - (Excl. ESO) (US$) 1.85 2.02 2.10 2.13 EPS (CS adj.) (US$) 1.85 2.02 2.10 2.13 Prev. EPS (CS adj.) (US$) — — — — P/E (CS adj., x) 13.1 12.0 11.6 11.4 P/E rel. (CS adj., %) — 73.7 75.4 82.4 Revenue (US$ m) 46,061.0 48,607.0 50,822.9 53,655.8 EBITDA (US$ m) 15,338.0 16,033.0 16,289.8 16,322.9 Net debt (US$ m) 6,529 8,286 2,833 -2,316 OCFPS (US$) 2.13 2.40 2.47 2.47 P/OCF (x) 7.5 10.6 9.9 9.9 Number of shares (m) 5,361.55 Price/sales(x) 2.62 BV/share (Next Qtr., US$) — P/BVPS (x) 2.2 Net debt (Next Qtr., US$ m) — Dividend (current, US$) — Dividend yield (%) — Source: Company data, Credit Suisse estimates. Rating UNDERPERFORM* Price (17 Sep 13, US$) 24.37 Target price (US$) 21.00¹ 52-week price range 26.37 - 16.82 Market cap. (US$ m) 130,660.97 *Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months. Research Analysts Kulbinder Garcha 212 325 4795 [email protected] Andrew Ruben 212 325 4798 [email protected] Vlad Rom 212 325 5442 [email protected] Matthew Cabral 212 538 6260 [email protected] Talal Khan, CFA 212 325 8603 [email protected] Ray Bao 212 325 1227 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Cisco Systems Inc. (CSCO) - Credit Suisse | PLUS

DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

18 September 2013

Americas/United States

Equity Research

Networking Equipment

Cisco Systems Inc. (CSCO) INITIATION

Software Defined Disruption ■ Initiate with Underperform—Now for the Hard Part: Over the past year,

Cisco has seen the benefits of improving execution, gross margin stability, and increased capital redeployment, all of which are to be applauded. However, the impact on the networking market from Software Defined Networking (SDN) architectures should be very real and accelerate over time, leading to further margin compression. We initiate with an Underperform rating and a target price of $21.

■ SDN to Threaten the Most Profitable Part of the Stack: Currently, on the hardware side, networking stands as one of the least competitive and highest margin industries in the IT stack. SDN, by allowing software to be separate from the physical infrastructure, will allow competition at multiple points in the network, which was not previously possible. While the impact will take time, the threat will be very real, shrinking gross profit dollars for the industry. Irrespective of whether Cisco executes well in SDN environments, the company is in a vulnerable position amidst this transition.

■ Margins to Continue Their Long-Term Trend Downward: Based on five factors, we estimate that gross margins will decrease to ~60% and operating margins to 26% over the long term, with limited growth in organic operating income. We note the following: (1) our proprietary segmentation analysis shows gross margins by business line; within that UCS is materially dilutive at ~30% GMs; (2) while software and services can offset some of the headwinds, gaps in Cisco's IT stack mean that success in wider IT environments cannot be guaranteed; (3) SDN has the potential to shrink gross profit dollars available to vendors by as much as 70%; (4) Huawei will have an effect on the service provider market and internationally; and (5) the opex base is quite lean and further optimization will likely prove challenging.

■ Valuation—Target Price of $21: While we do not see significant downside risk on Cisco, we also do not see significant upside potential. Our TP of $21 is a blended average of P/E, DCF, and Credit Suisse HOLT

® valuation.

Share price performance

16

21

26

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

Daily Sep 17, 2012 - Sep 17, 2013, 9/17/12 = US$19.16

Price Indexed S&P 500 INDEX

On 09/17/13 the S&P 500 INDEX closed at 1704.76

Quarterly EPS Q1 Q2 Q3 Q4 2012A 0.43 0.47 0.48 0.47 2013A 0.48 0.51 0.51 0.52 2014E 0.51 0.51 0.53 0.55

Financial and valuation metrics

Year 07/12A 07/13A 07/14E 07/15E EPS - (Excl. ESO) (US$) 1.85 2.02 2.10 2.13 EPS (CS adj.) (US$) 1.85 2.02 2.10 2.13 Prev. EPS (CS adj.) (US$) — — — — P/E (CS adj., x) 13.1 12.0 11.6 11.4 P/E rel. (CS adj., %) — 73.7 75.4 82.4 Revenue (US$ m) 46,061.0 48,607.0 50,822.9 53,655.8 EBITDA (US$ m) 15,338.0 16,033.0 16,289.8 16,322.9 Net debt (US$ m) 6,529 8,286 2,833 -2,316 OCFPS (US$) 2.13 2.40 2.47 2.47 P/OCF (x) 7.5 10.6 9.9 9.9

Number of shares (m) 5,361.55 Price/sales(x) 2.62 BV/share (Next Qtr., US$) — P/BVPS (x) 2.2 Net debt (Next Qtr., US$ m) — Dividend (current, US$) — Dividend yield (%) —

Source: Company data, Credit Suisse estimates.

Rating UNDERPERFORM* Price (17 Sep 13, US$) 24.37 Target price (US$) 21.00¹ 52-week price range 26.37 - 16.82 Market cap. (US$ m) 130,660.97

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Kulbinder Garcha

212 325 4795

Andrew Ruben

212 325 4798

Vlad Rom

212 325 5442

Matthew Cabral

212 538 6260

Talal Khan, CFA

212 325 8603

Ray Bao

212 325 1227

18 September 2013

Cisco Systems Inc. (CSCO) 2

Table of Contents Proprietary Profits: How Long? 3 Networking to See Moderate Growth 5

A Nexus of Forces at Play for Networking 5 Carrier—Capex Moderate Growth 9 Enterprise Switching and Routing: +3.5% CAGR 17 Service Provider Switching & Routing: +5.5% CAGR 21

Scorecard—Cisco wins 26 What Makes a Networking Vendor Successful? 30

Wireless LAN—Secular Growth 33 Competitive Dynamics—Cisco Dominates 35

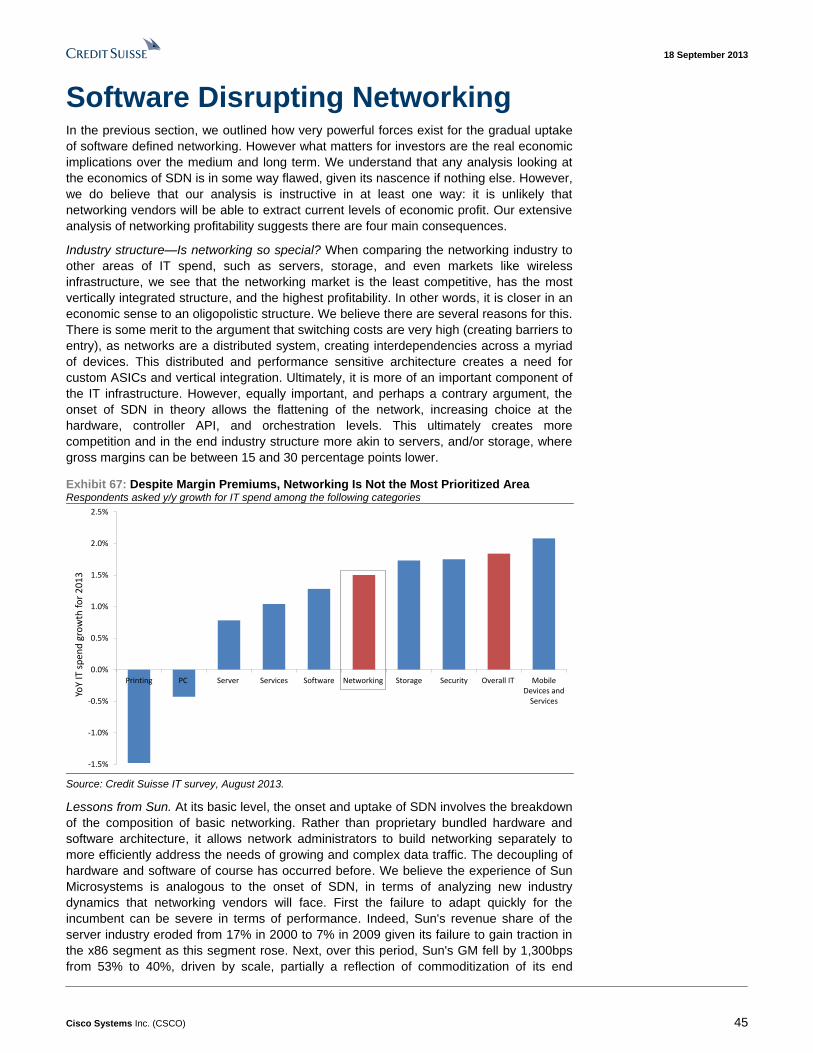

SDN—Reorienting Networking 39 SDN—Gradual but real adoption 42 Software Disrupting Networking 45

Networking—Is It So Special? SDN May Change That 46 Hardware and Software Decouple—Lessons from Sun 49 SDN Drives a Major Headwind on Profit Dollars 52 Mean Reversion on Margins 55

UCS—Gaining Share in Servers 57 x86 Server Outlook—Pockets of Strength 58 x86 Server Market—Positioning Critical 60 Cisco Gaining Share with UCS 63

Aiming for the IT Stack 68 Chasing TAM Expansion Is the Norm 68

IT Strategies in Evolution 72 The Industry Says…Cisco, IBM, and MSFT 73

Major Headwinds on Margins 76 Segmentation Analysis—UCS Dilutive 79 Building Software and Services Some Challenges 80 Mean Reversion on Margins 84 SDN Drives a Major Headwind on Profit Dollars 85 ASIC Strategy a Differentiator in an SDN World? 89 Huawei a Threat Not to Be Underestimated 90 Cost Management Has Been Strong of Late 94

Portfolio Refresh Helping Share 97 Switching Portfolio Refresh 97

Capital Distributions Could Move Higher 100 Could Cisco Do More? 100

Valuation—FV of $21 Per Share 104 Risks: Where Could We Be Wrong? 110 Management Team 113 Financial Statements 114

18 September 2013

Cisco Systems Inc. (CSCO) 3

Proprietary Profits: How Long? If there has been one constant in networking over the past 15 years, it has been Cisco.

Through multiple waves of technologies and competitors, Cisco has been able to

out-execute its rivals. At the same time, the company, along with Juniper, has benefited

from a highly vertically integrated structure in networking, where hardware, software, and

services are bundled. Combining this with the perceived value of networking within the IT

space and its impact on other areas has shown that network administrators are loathed to

disrupt it too rapidly. All these factors have led to an oligopolistic industry structure, where

vendors have been able to extract margins that resemble more of a monopoly. One

example of this is the gross margins in switching, which are estimated at 65-70%, notably

higher than other IT hardware categories such as servers and storage.

Exhibit 1: Cisco Summary Income Statement in US millions, unless otherwise stated

Revenue by segment FY12 FY13 FY14E FY15E FY16E

Switching 14,531 14,741 15,239 15,734 16,049

Routing 8,425 8,230 8,522 9,136 9,501

SP Video 3,858 4,852 4,836 4,806 4,857

DC 1,298 2,073 2,516 2,893 3,182

Wireless 1,669 2,166 2,708 3,077 3,385

Security 1,344 1,347 1,374 1,429 1,472

Collaboration 4,182 3,956 3,963 4,083 4,207

Other 1,019 664 398 359 323

Services 9,735 10,578 11,267 12,139 12,989

Revenue 46,061 48,607 50,823 53,656 55,965

yoy 6.6% 5.5% 4.6% 5.6% 4.3%

Consensus 50,944 53,895 57,639

Gross Profit 28,763 30,400 31,563 32,867 33,700

Gross Margin (%) 62.4% 62.5% 62.1% 61.3% 60.2%

Operating Income 12,736 13,682 14,431 14,654 14,727

Operating Margin (%) 27.7% 28.1% 28.4% 27.3% 26.3%

Net Income 10,017 10,866 11,485 11,714 11,815

Share Count 5,405 5,369 5,462 5,502 5,542

EPS ($) 1.85 2.02 2.10 2.13 2.13

yoy 14.4% 9.2% 3.9% 1.3% 0.1%

Consensus 2.11 2.29 2.49

Source: Factset, Company data, Credit Suisse estimates.

Simply put, we believe that the gradual onset of Software Defined Networking (SDN) will

radically change networking economics, driving a more competitive structure and

sustaining the long-term downward trend on gross margins. This implies that, while Cisco's

operating margin shrinks over time, EPS can remain flat driven by capital distribution.

Given this, we initiate coverage on Cisco with an Underperform rating and target price of

$21.

SDN—Some real drivers. The onset of SDN is driven by a very real and genuine

phenomena, which mainly includes changing and rapidly growing datacenter traffic and

the need for more flexible and automated application-specific networks. At its basic level,

the onset and uptake of SDN means that, while previous networking architectures

consisted of bundled hardware and software, these can now be separated effectively into

multiple planes, with functionality being increasingly abstracted away from hardware to

enable aggregation and management, functionality, and automation. To be clear, we

believe that the shift will be gradual, as our survey shows most enterprises currently are in

the proof-of-concept stage, with initial deployments over 18 months away, and production

18 September 2013

Cisco Systems Inc. (CSCO) 4

in scale to be a 2-5 years away. However, this new way of operating will bring with it new

competition at multiple levels, including at the hardware/data plane, the controller,

applications, and orchestration levels. The end result, in our view, is a much more

competitive structure for the networking markets, and consequently, lower margins.

Margins—Downward pressure. We reviewed the outlook for margins through five different

approaches, and the bias to profitability remains to the downside. As shown in Exhibit 104,

we project 26% long-term operating margins, given several factors:

Segmentation analysis—Negative UCS mix shift against the software and services upsell.

Our proprietary segmentation analysis for Cisco’s gross margins by business segment

reveals several major conclusions. First, and not surprisingly, UCS is materially gross

margin dilutive; we believe margins are around 30%, half of corporate levels, given that

growth will increasingly come from gaining share and, given the company's server

exposure, higher scale seems unlikely. Second, approximately 44% of incremental gross

profit dollars that Cisco targets in the medium-term come from the ability to sell additional

services. This strategy centers around both creating software-based solutions and

upselling incremental software functionality, which may prove difficult, especially given the

historically bundled nature of networking spend. Third, we forecast that there will be a

disruption to networking gross margins over time from SDN, which will result in profit

compression.

SDN could make networking look more like other areas of IT spend. Over a five-year view,

we believe SDN will alter the dynamics of the networking market, whereby at its most

basic level, hardware, software, and services may be delivered in a far less integrated

manner. Although it remains to be seen how the traditional networking vendors adapt to

this change, based on our analysis, we believe that SDN will present a major change and

headwind to gross profit dollars. Indeed, the networking industry structure in the longer

term could more closely resemble the server or storage industry which are more

competitive, with gross margins between 15 and 30 percentage points lower. We

compared the cost and total cost of ownership, ex-labor, running costs, etc. for a basic

Cisco datacenter switch (Nexus 3064) to an alternative in an SDN world (Cumulus Linux

software and top-of-line rack bare metal switch). We demonstrate that the Cumulus option

is some 70% cheaper per year, and as a result, gross profits of hardware and software are

a combined 74% lower. In other words, even if Cisco were to embrace SDN, the gross

profit dollars available would significantly shrink. While this is simplistic in many ways, it

highlights the headwinds facing the traditional margin structure of Cisco and something

that the software and services upsell may not easily offset. To be clear, we do not assume

such drastic declines in gross margins, but equally we do believe the pressure over time is

downwards.

Cost management has been solid but in danger of perennial restructuring. Cisco has been

continuously focused on managing its operating costs, highlighted by the recent 4,000

employee workforce rebalancing. Given these efforts, we assume a long-term opex to

sales ratio of 34% is sustainable. We would also note that on a revenue-per-head basis,

compared with other major IT companies, Cisco looks lean.

In traditional networking, Cisco should continue to dominate. In the traditional enterprise

networking, especially in switching, Cisco’s strategy is by far the most robust. Cisco has

continued to out execute its rivals consistently in the networking over time. Our scorecard

also shows that customers have long favored Cisco, with the company ranked first on our

overall scorecard, including number one positions on six metrics, such as roadmap,

salesforce, service offering, and IT portfolio. This level of dominance, though, is arguably

already reflected in its market share. Equally interestingly, on the most important metrics

of price and performance and reliability, Cisco is essentially on par with Juniper and

Huawei. This suggests Cisco’s incumbency, rather than technology, is the key

differentiator for the company. The real concern, as we discuss in detail, is that SDN

threatens the very structure of the industry in which Cisco operates.

18 September 2013

Cisco Systems Inc. (CSCO) 5

Networking to See Moderate Growth Within the context of a cyclical spending recovery, our bottom-up model suggests that the

networking industry, in aggregate, will grow at a rate of 4.2% per year. Given the different

purchasing patterns and products, we segment the market into enterprise and service

provider, and within each of these, look at three distinct product lines: Switching, Routing,

and WLAN. In aggregate, these three markets have an addressable opportunity of some

$53bn in the long term. Within this market we several important growth drivers:

A nexus of forces at play. Fundamentally, both service provider and enterprise networks

have a significant number of forces to drive revenue growth over time. These include: (1)

smartphone and tablet driven data traffic; (2) growth of internet based video; (3) elastic

cloud computing and business analytics; and (4 aggregate trends in carrier capex. We do

believe that through cycle these will produce a networking segment (defined as enterprise

and service provider switching and routing) growth rate of 4.2% per year, modestly higher

that aggregate IT. We note that IDC expects IT spending growth of approximately 5% per

annum going forward; however, as detailed in our May 30, 2013 report, titled "IT

Hardware: "Un"clouding Storage – EMC Shines," we expect this to be significantly less

given the compression effects of cloud.

Enterprise Ethernet switching, multiple mix changes. In 2012, the enterprise switching

market amounted to $19.8 billion in sales and has grown at a rate of 3% per annum over

the past five years, something which we believe will continue in the long term. Within this

we see 10GbE adoption driving both port and revenue growth, stimulated by Intel's Xeon

server chip release code-named "Romley" as well as server virtualization. Among Layer 2,

Layer 3, and chassis, we see 10GbE port adoption to rise to 25% in 2017, up from 6%

currently and only 0.3% five years ago. Additionally, we see Layer 3 switches continuing to

gain wallet share at the expense of Layer 2. We believe the added intelligence of Layer 3

switches removes the need for the manual configuration historically required within

enterprise networks, which is especially important in virtualized infrastructures, as L3

switches are able to abstract away a myriad of VLANs. Finally, we see chassis switches

under macro and secular pressure.

Service provider routing. In examining trends within the service provider (SP) market, we

begin by focusing on routers that accounted $11.3 billion out of $14.2 billion in total service

provider spend in 2012. In revenue terms, the market has shown significant growth over

the past five years, expanding at a pace of 7.9% per annum, which is far faster than

growth on the enterprise side. Within this segment, we see core routers losing wallet share

within spend, as spending within the core of the network tends to be a function of capacity,

and recently service providers have been trying to prolong spend within the area as long

as possible. We see edge routing as the primary source of growth, rising 6.3% in the long

term. The tailwind to edge routing spend has been the tremendous growth in smartphones

and the resulting growth in mobile data consumption. We believe a key driver here will be

LTE that enables both voice and data to travel across IP networks, leading to converged

IP solutions across service providers' networks.

A Nexus of Forces at Play for Networking

We see several fundamental drivers at play for the networking market, as the major

secular trends of social, mobile, cloud, and big data analytics place considerable strains

on today’s networking infrastructure. These forces are playing out on both the carrier side

and enterprise side, essentially creating what Gartner describes as a nexus of forces. This

suggests that there remains healthy underlying growth ultimately driven by IP traffic growth

Global IP traffic growing at the rate of 23%. The Cisco Visual Networking Index highlights

that growth of aggregate IP traffic in the long term should be at a rate of 23% per year,

rising to 120 EB in 2017. Of this traffic, 68% will still reside on the fixed internet, whereas

23% will be on managed IP networks, and finally 9% will be driven from mobile data.

18 September 2013

Cisco Systems Inc. (CSCO) 6

Exhibit 2: Global IP Traffic Distribution... Exhibit 3: ...A Skew Towards Consumer Use

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2012 2013 2014 2015 2016 2017Fixed Internet Managed IP Mobile data

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2012 2013 2014 2015 2016 2017Consumer Business

Source: Cisco Visual Networking Index. Source: Cisco Visual Networking Index.

Smartphone and tablet adoption will be key. Long-term (2012-17) mobile data is expected

to grow at a CAGR of some 66%. Of this segment, 72% of this traffic will come from

smartphones with a further 13% from tablets. Here, the driver is not only the impact of user

growth of the installed base, but also the impact of the multiplier effect. For example,

compared with a non-smartphone user, a typical smartphone user may use 50 times as

much traffic, whereas a tablet user may use 120 times as much. (See Exhibit 5.)

Exhibit 4: Smartphones Lead Traffic Growth Exabytes per month

Exhibit 5: Summary of Per Device Usage Growth in MB per Month

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2012 2013E 2014E 2015E 2016E 2017E

Exab

yte

s p

er

mo

nth

Smartphones Tablets Other Portables Laptops M2M Non-Smartphones

Device Type 2012

2012*

Multiple2017

2017*

Multiple

Non-Smartphones 7 1.0x 31 1.0x

M2M Module 64 9.4x 330 10.6x

Smartphone 342 50.3x 2,660 85.8x

4G Smartphone 1,302 191.5x 5,114 165.0x

Tablet 820 120.6x 5,387 173.8x

Laptop 2,503 368.1x 5,731 184.9x

* Multiple of non-smartphone device usage Source: Cisco Visual Networking Index. Source: Cisco Visual Networking Index.

Video highlights. It is expected that by 2017 consumer internet video traffic will be 69% of

all consumer internet traffic, up from 57% in 2012. If one were to include video exchanged

through P2P sharing, VoD, and TV, the range would be 80-90% of all global consumer

traffic by 2017. Within this, internet video to TV is expected to increase 5 times by 2017

and VoD traffic in 2017 is expected to be equivalent to 6bn DVDs per month. By 2017 65%

of all Internet video traffic is expected to cross content delivery networks in 2017, up from

53% in 2012.

18 September 2013

Cisco Systems Inc. (CSCO) 7

Exhibit 6: Internet Video Growing to ~70% of All Consumer Internet Traffic by 2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 2017

Internet video Web, Email and Data File Sharing Online Gaming

Source: Cisco Visual Networking Index.

Networking lifecycle. Like all IT hardware, appliances have an essential useful life. Several

factors determine the useful life of an asset including replacement costs, ongoing

operating costs, industry innovation, and vendor support. Based on Gartner data,

highlighted in Exhibit 7, the useful life for edge LAN switching is the longest at seven to ten

years, with core switching and routing coming in at a useful life of five to seven years.

Datacenter networking has a modestly lower useful life of four to seven years, which

makes sense given more disruptive changes.

Exhibit 7: Core Switching and Routing Product Life Is Somewhat Longer Than

Datacenter Networking Product

-

2.0

4.0

6.0

8.0

10.0

12.0

Useful Life Depreciation

Source: Gartner.

This corresponds with our own survey work that suggests that the average installed base

of enterprise switching equipment is 3.5 years. (See Exhibit 8.) As the age of the installed

base continues to move toward the useful life, in a normalized environment, we would

expect to see a replacement cycle across both switching and routing spend. However, it is

important to keep in mind that across the various end markets within IT hardware

18 September 2013

Cisco Systems Inc. (CSCO) 8

(Servers, Storage, PCs, Printers, etc.), organizations are choosing to run their existing

equipment longer, which prolongs the upgrade cycle.

Exhibit 8: On Average, the Installed Base of Ethernet Switches Is ~3.5 Years

Respondents asked the average life of an Ethernet switch

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Less than 1year

1-2 years 3-5 years 5-7 years 7-9 years 10 years ormore

Year

s

Perc

en

tage

of

resp

on

den

ts

Source: Credit Suisse Networking Survey August 2013.

Credit Suisse CIO Survey supportive of networking growth into 2014. Our proprietary

survey of 40 enterprise CIOs suggests that overall IT spending growth in 2014 will likely

mirror that of 2013. (See Exhibit 9).

Exhibit 9: IT Spending Growth in 2014 to Equal 2013

Respondents asked for y/y growth rates for IT spending

1.71% 1.78%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2013 (vs. 2012) 2014 (vs. 2013)

YoY

gro

wth

in IT

sp

end

Source: Credit Suisse IT Spending Survey August 2013.

While not the highest priority item within enterprise budgets, networking spend continues

to stand out relative to other hardware markets and falls roughly in the middle of overall

priorities. (See Exhibit 10 and Exhibit 11.)

18 September 2013

Cisco Systems Inc. (CSCO) 9

Exhibit 10: Networking in the Middle of Priorities… % of respondents ranking IT segments as top spending areas

Exhibit 11: …as Reflected in Growth Expectations 2013 annual revenue growth for IT spending by category

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Printing PC Server Services Software Networking Storage Security Overall IT MobileDevices and

Services

YoY

IT s

pen

d g

row

th f

or

20

13

Source: Credit Suisse CIO Survey August 2013. Source: Credit Suisse CIO Survey August 2013.

Carrier—Capex Moderate Growth

With 38% of the networking market coming from the service provider market, capital

expenditure trends and fundamentals remain important to the outlook for switching and

routing. Following our detailed analysis of wireless capex, for which we have updated our

proprietary model (which tracks spend at over 100 leading carriers globally), we see

accelerating growth ahead driven by a recovery with Western Europe, continued high

levels of spending in the United States, and a strong roll out in China for LTE.

Europe Weak Capex Trends So Far, Are Things about to Change?

Vodafone has been gradually increasing its capex investments in Europe recently.

Vodafone has been maintaining flat capex spend for its European operations similar to its

group level trend over the past two to three years. However, in its FY13 (ending March

2013), it is worth noting that although group capex was roughly flat, its capex spend in

Europe actually grew 7% yoy, mainly driven by investments in Germany and the UK.

Figure 12: Vodafone Capex Spend in Europe Has Already Seen Some Pick Up in Early 2013 in GBP millions, unless otherwise stated; Vodafone financial year ending March

Vodafone capex (£ mn) H1 10/11 H2 10/11 H1 11/12 H2 11/12 H1 12/13 H2 12/13 FY 09/10 FY 10/11 FY 11/12 FY 12/13

Vodafone Germany 342 482 410 470 445 628 766 824 880 1,073

% change yoy 3% 11% 20% -2% 9% 34% 8% 7% 22%

Vodafone UK 178 338 219 356 231 370 494 516 575 601

% change yoy 26% -4% 23% 5% 5% 4% 4% 11% 5%

Vodafone Italy 260 330 269 352 239 328 610 590 621 567

% change yoy -13% 6% 3% 7% -11% -7% -3% 5% -9%

Vodafone Spain 220 297 147 282 152 225 543 517 429 377

% change yoy 29% -20% -33% -5% 3% -20% -5% -17% -12%

Vodafone Other Europe 521 709 497 595 417 823 1,282 1,230 1,092 1,240

% change yoy 11% -13% -5% -16% -16% 38% -4% -11% 14%

Total Vodafone Europe 1,521 2,156 1,542 2,055 1,484 2,374 3,695 3,677 3,597 3,858

% change yoy 8% -6% 1% -5% -4% 16% 0% -2% 7%

Source: Company data, Credit Suisse research

But now Vodafone is looking to break the vicious circle with £6bn investment over three

years? At the time of the Verizon deal (September 2013), Vodafone also unveiled its plan

to increase investments significantly over the next three years to enhance network quality

and drive service leadership. As a reminder, Vodafone has maintained capex at around

£6.3bn over the past couple of years, but under its new Project Spring, the carrier plans to

invest £6bnof incremental investment over the next three years with the majority of spend

directed towards capex. This would imply a capex increase of slightly over 30% yoy from

the current level. In fact, as per Vodafone, it plans to spend 45-50% of the £6bn on the

18 September 2013

Cisco Systems Inc. (CSCO) 10

mobile network, with an additional 20-25% likely spent in the area of NGN, VDSL, and

selective fiber rollouts.

Figure 13: 65-75% of Incremental Investment under Vodafone's Project Spring Will Be Directed Towards Networks

Source: Vodafone.

"Capex arms race is better than a subsidy race" as per Vodafone CEO. While it is still

early days to see how other carriers in Europe react to this aggressive stance from

Vodafone in terms of increasing investment to improve upon the quality of the network, we

would note that this is the first time in years that we have seen some real intent from a

European carrier to focus on network quality as a form of creating differentiation among

the consumer base. Judging by comments from the CEO of Vodafone, it seems that this

shift in strategy from the company may eventually force other bigger players in Europe

(such as DT, Telefonica, and France Telecom) to follow suit, which could then lead to a

situation similar to that which we saw in the United States over the past two to three years.

"I don't know what a capex arms race is. If that's the case then it's better than a

subsidy race because it requires real long-term orientation. It requires taking

money out of some commercial costs, which could be good because at the end of the

day it's a positive for the industry if everybody focuses on quality and investment as

opposed to promotion and short-term. I don't think it will happen. I think some other

competitors, the ones with bigger shoulders, will follow and I think in the end it

will help the industry structure." – Vittorio Colao, CEO of Vodafone Group

(September 3, 2013)

Vodafone represents ~25% of Western European capex. What if others follow with capex

upgrades? We estimate Vodafone represents around 25% of overall wireless capex in

Western Europe. Given Vodafone has decided to increase its capex from £6.3bn to

around £8.3bn per annum over the next three years (implies around 30% increase), we

believe this may put pressure on other operators in the region to follow suit. On the other

hand, our European Telecoms team (Justin Funnell) notes that some of the challenger

operators in Europe continue to struggle owing to declining revenues and a lack of share

gains, for example Yoigo in Spain, Wind in Italy, Everything Everywhere and 3 in the UK,

and may lack the financial resources to increase capex investments. However, we believe

this decision from Vodafone is at least likely to put pressure on bigger operators in Europe

(Deutsche Telekom, Telefonica, and France Telecom) to respond by increasing

investments to improve network quality.

18 September 2013

Cisco Systems Inc. (CSCO) 11

Figure 14: Can the Capex to Sales Ratio in W. Europe Rise Similar to the United States?

13.3%12.4%

14.2%14.8%

16.2%

18.3%

10.0% 9.6% 9.9%

11.3%12.4% 12.1%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012 1H13

Wir

ele

ss

-C

ap

ex t

o S

erv

ice

Re

ve

nu

e (

%)

US W Europe

Source: Company data, Credit Suisse research, EU Telecoms Research team (Justin Funnell).

Capex to sales significantly behind in WE when compared with the United States. Capex

trends within Europe have been lackluster over the past few years with most carriers

looking to maintain flat investment levels. Further, with service revenues having been

under pressure, the capex to sales ratio has seen a slight improvement in spite of flat

capex. When comparing this with the United States, what is striking is that service

revenues have grown at around 5% pa, but wireless capex has grown significantly faster

resulting in the capex to sales ratio rising from nearly 12.5% in 2009 to slightly over 18% in

1H13. When comparing this with Western Europe, we see that the capex to sales ratio has

only picked up from around 10% in 2009 to 12% in 1H13.

United States to Continue to See High Levels of Capex Activity

What is worth noting is that wireless capex in the United States has seen strong growth

over the past few years. In fact, based on our estimates, we believe that wireless capex is

likely to have grown from $20bn in 2009 to around $34bn in 2013 (CAGR of 15%) driven

by a move from carriers to improve the quality of their networks in order to drive

differentiation and roll out of 4G/LTE networks. (See Exhibit 15.) Looking at guidance from

carriers, we believe that wireless capex spend may remain flat in 2014. We would equally

note that it is already running at a high level of slightly over $34bn per annum. In addition,

we believe there may be risks to the upside to 2014 guidance as carriers continue to look

for ways to differentiate by improving the quality of their 4G networks.

Exhibit 15: Wireless Capex in the United States Likely to Grow to $34bn in 2013, and Remain at There for 2014 in US$ millions, unless otherwise stated

Wireless Capex (US$ mn) Q112 Q212 Q312 Q412 Q113 Q213 2009 2010 2011 2012 2013E 2014E

Verizon 1,885 2,048 2,133 2,791 1,992 2,278 7,152 8,438 8,973 8,857 9,675 9,650

AT&T 2,324 2,345 2,709 3,422 2,500 3,450 6,066 9,171 9,759 10,800 12,750 13,000

Sprint 710 1,012 1,376 1,786 1,706 1,728 1,161 1,444 2,416 4,884 7,425 7,475

T-Mobile US 747 539 717 898 1,230 1,111 3,687 2,819 2,729 2,901 4,300 4,100

Leap 146 119 106 63 26 23 680 399 442 434 150 200

MetroPCS 144 182 262 258 832 790 890 846

Total (US$ mn) 5,956 6,245 7,303 9,217 7,454 8,590 19,578 23,061 25,208 28,722 34,300 34,425

% change yoy -2% -8% 21% 46% 25% 38% 0% 18% 9% 14% 19% 0%

Source: Company data, Credit Suisse estimates.

Wireless capex to sales ratio also rose by around 4pp in the past three years. One of the

factors that has helped this continued increase in capex investment across all U.S. carriers

18 September 2013

Cisco Systems Inc. (CSCO) 12

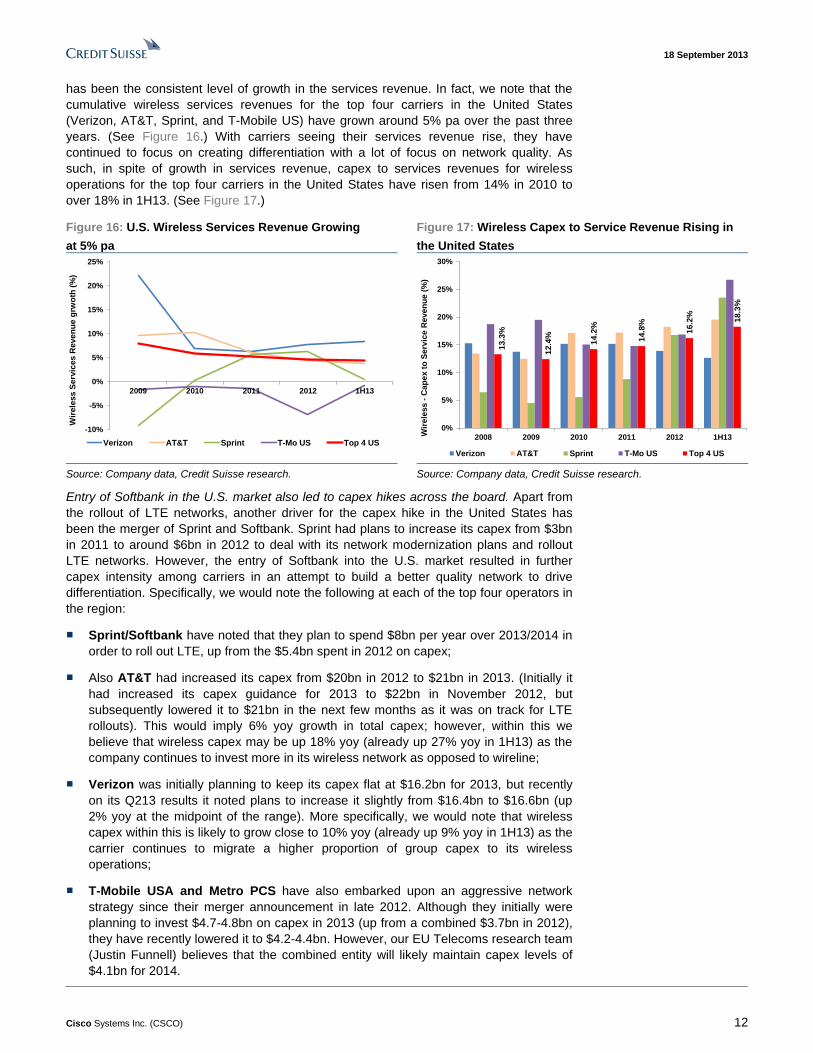

has been the consistent level of growth in the services revenue. In fact, we note that the

cumulative wireless services revenues for the top four carriers in the United States

(Verizon, AT&T, Sprint, and T-Mobile US) have grown around 5% pa over the past three

years. (See Figure 16.) With carriers seeing their services revenue rise, they have

continued to focus on creating differentiation with a lot of focus on network quality. As

such, in spite of growth in services revenue, capex to services revenues for wireless

operations for the top four carriers in the United States have risen from 14% in 2010 to

over 18% in 1H13. (See Figure 17.)

Figure 16: U.S. Wireless Services Revenue Growing

at 5% pa

Figure 17: Wireless Capex to Service Revenue Rising in

the United States

-10%

-5%

0%

5%

10%

15%

20%

25%

2009 2010 2011 2012 1H13

Wir

ele

ss

Serv

ices

Reve

nu

e g

rwo

th (

%)

Verizon AT&T Sprint T-Mo US Top 4 US

13.3

%

12.4

%

14.2

%

14.8

%

16.2

%

18.3

%

0%

5%

10%

15%

20%

25%

30%

2008 2009 2010 2011 2012 1H13Wir

ele

ss

-C

ap

ex t

o S

erv

ice R

eve

nu

e (

%)

Verizon AT&T Sprint T-Mo US Top 4 US

Source: Company data, Credit Suisse research. Source: Company data, Credit Suisse research.

Entry of Softbank in the U.S. market also led to capex hikes across the board. Apart from

the rollout of LTE networks, another driver for the capex hike in the United States has

been the merger of Sprint and Softbank. Sprint had plans to increase its capex from $3bn

in 2011 to around $6bn in 2012 to deal with its network modernization plans and rollout

LTE networks. However, the entry of Softbank into the U.S. market resulted in further

capex intensity among carriers in an attempt to build a better quality network to drive

differentiation. Specifically, we would note the following at each of the top four operators in

the region:

■ Sprint/Softbank have noted that they plan to spend $8bn per year over 2013/2014 in

order to roll out LTE, up from the $5.4bn spent in 2012 on capex;

■ Also AT&T had increased its capex from $20bn in 2012 to $21bn in 2013. (Initially it

had increased its capex guidance for 2013 to $22bn in November 2012, but

subsequently lowered it to $21bn in the next few months as it was on track for LTE

rollouts). This would imply 6% yoy growth in total capex; however, within this we

believe that wireless capex may be up 18% yoy (already up 27% yoy in 1H13) as the

company continues to invest more in its wireless network as opposed to wireline;

■ Verizon was initially planning to keep its capex flat at $16.2bn for 2013, but recently

on its Q213 results it noted plans to increase it slightly from $16.4bn to $16.6bn (up

2% yoy at the midpoint of the range). More specifically, we would note that wireless

capex within this is likely to grow close to 10% yoy (already up 9% yoy in 1H13) as the

carrier continues to migrate a higher proportion of group capex to its wireless

operations;

■ T-Mobile USA and Metro PCS have also embarked upon an aggressive network

strategy since their merger announcement in late 2012. Although they initially were

planning to invest $4.7-4.8bn on capex in 2013 (up from a combined $3.7bn in 2012),

they have recently lowered it to $4.2-4.4bn. However, our EU Telecoms research team

(Justin Funnell) believes that the combined entity will likely maintain capex levels of

$4.1bn for 2014.

18 September 2013

Cisco Systems Inc. (CSCO) 13

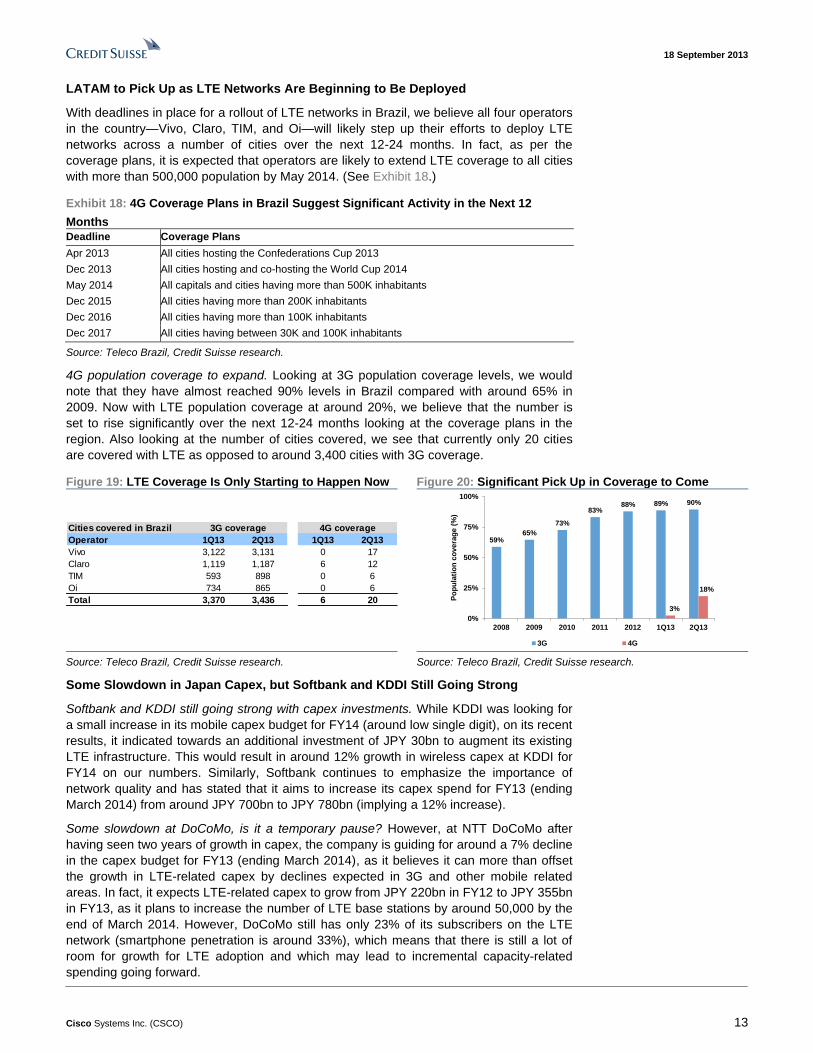

LATAM to Pick Up as LTE Networks Are Beginning to Be Deployed

With deadlines in place for a rollout of LTE networks in Brazil, we believe all four operators

in the country—Vivo, Claro, TIM, and Oi—will likely step up their efforts to deploy LTE

networks across a number of cities over the next 12-24 months. In fact, as per the

coverage plans, it is expected that operators are likely to extend LTE coverage to all cities

with more than 500,000 population by May 2014. (See Exhibit 18.)

Exhibit 18: 4G Coverage Plans in Brazil Suggest Significant Activity in the Next 12

Months

Deadline Coverage Plans

Apr 2013 All cities hosting the Confederations Cup 2013

Dec 2013 All cities hosting and co-hosting the World Cup 2014

May 2014 All capitals and cities having more than 500K inhabitants

Dec 2015 All cities having more than 200K inhabitants

Dec 2016 All cities having more than 100K inhabitants

Dec 2017 All cities having between 30K and 100K inhabitants

Source: Teleco Brazil, Credit Suisse research.

4G population coverage to expand. Looking at 3G population coverage levels, we would

note that they have almost reached 90% levels in Brazil compared with around 65% in

2009. Now with LTE population coverage at around 20%, we believe that the number is

set to rise significantly over the next 12-24 months looking at the coverage plans in the

region. Also looking at the number of cities covered, we see that currently only 20 cities

are covered with LTE as opposed to around 3,400 cities with 3G coverage.

Figure 19: LTE Coverage Is Only Starting to Happen Now Figure 20: Significant Pick Up in Coverage to Come

Cities covered in Brazil

Operator 1Q13 2Q13 1Q13 2Q13

Vivo 3,122 3,131 0 17

Claro 1,119 1,187 6 12

TIM 593 898 0 6

Oi 734 865 0 6

Total 3,370 3,436 6 20

3G coverage 4G coverage

59%65%

73%

83%88% 89% 90%

3%

18%

0%

25%

50%

75%

100%

2008 2009 2010 2011 2012 1Q13 2Q13

Po

pu

lati

on

co

vera

ge (

%)

3G 4G Source: Teleco Brazil, Credit Suisse research. Source: Teleco Brazil, Credit Suisse research.

Some Slowdown in Japan Capex, but Softbank and KDDI Still Going Strong

Softbank and KDDI still going strong with capex investments. While KDDI was looking for

a small increase in its mobile capex budget for FY14 (around low single digit), on its recent

results, it indicated towards an additional investment of JPY 30bn to augment its existing

LTE infrastructure. This would result in around 12% growth in wireless capex at KDDI for

FY14 on our numbers. Similarly, Softbank continues to emphasize the importance of

network quality and has stated that it aims to increase its capex spend for FY13 (ending

March 2014) from around JPY 700bn to JPY 780bn (implying a 12% increase).

Some slowdown at DoCoMo, is it a temporary pause? However, at NTT DoCoMo after

having seen two years of growth in capex, the company is guiding for around a 7% decline

in the capex budget for FY13 (ending March 2014), as it believes it can more than offset

the growth in LTE-related capex by declines expected in 3G and other mobile related

areas. In fact, it expects LTE-related capex to grow from JPY 220bn in FY12 to JPY 355bn

in FY13, as it plans to increase the number of LTE base stations by around 50,000 by the

end of March 2014. However, DoCoMo still has only 23% of its subscribers on the LTE

network (smartphone penetration is around 33%), which means that there is still a lot of

room for growth for LTE adoption and which may lead to incremental capacity-related

spending going forward.

18 September 2013

Cisco Systems Inc. (CSCO) 14

Figure 21: Japan Capex to Continue to Grow Mid-Single Digit in Spite of Expected Slowdown at DoCoMo

Wireless Capex (JPY bn) Mar

2011

Jun

2011

Sep

2011

Dec

2011

Mar

2012

Jun

2012

Sep

2012

Dec

2012

Mar

2013

Jun

2012

Mar

2011

Mar

2012

Mar

2013

Mar

2014E

NTT DoCoMo 200 137 175 190 225 177 184 180 213 146 668 727 754 700

Softbank 170 101 120 115 180 106 152 190 250 181 421 516 698 780

KDDI 96 49 64 79 112 68 83 85 103 69 339 304 338 380

Total 466 287 360 384 517 352 419 454 565 395 1,428 1,547 1,790 1,860

% change 11% 9% 3% 11% 23% 16% 18% 9% 12% 8% 16% 4%

Source: Company data, Credit Suisse estimates.

Capex Spend to Pick Up in Korea after Weak 1H13 Post Spectrum Auctions

Wireless capex spend in Korea has grown from KRW 2.9tn in 2010 to KRW 5.9tn in 2012

due to increased levels of investment on existing 3G capacity and preparing for the rollout

of LTE services. In addition, within total capex we also saw a significant shift towards

wireless operations, especially at KT Corp and LG U+. However, with the impending

spectrum auctions during Q313, capex spend in Korea took a significant pause in 1H13. In

fact, total capex spend in 1H13 in Korea was down 34% yoy but more importantly

wireless-related capex was down 46% yoy.

Figure 22: Korean Capex under Pressure in 1H due to Spectrum Auctions, Expect Strong Pick Up in 2H13

Wireless Capex (KRW bn) Q111 Q211 Q311 Q411 Q112 Q212 Q312 Q412 Q113 Q213 2010 2011 2012 2013E

SK Telecom 243 472 419 708 424 555 708 867 322 223 1,390 1,842 2,554 1,600

KT Corp 363 457 394 393 661 560 262 622 247 182 1,086 1,608 2,105 1,600

LG U+ 44 93 285 424 275 309 292 322 265 256 401 846 1,198 1,100

Total 650 1,022 1,098 1,525 1,360 1,424 1,262 1,811 834 661 2,876 4,296 5,857 4,300

% change 204% 70% 51% 14% 109% 39% 15% 19% -39% -54% 49% 36% -27%

Source: Company data, Credit Suisse estimates.

However, guidance suggests 65% of FY capex to be spent in 2H13. The spectrum auction

results in Korea were determined in the last week of August, and our Korea Telecom

analyst (Taewon Kim) views these results to be a positive for the overall telecom sector in

Korea, given reasonable levels of cost involved in spectrum purchase. While overall

wireless capex for 2013 will be down around 25% yoy given the weak spend in 1H, we still

expect a material uptick in capex spend in 2H13. In fact, we estimate that carriers have

only spent 35% of their FY capex in 1H; we believe that 2H capex spend could be around

KRW 2.8tn (up around 88% hoh).

Figure 23: LTE Penetration in Korea Now Stands at over 40%; But Still Lots to Go

7%

13%

22%

29

%

36%

42%

0%

10%

20%

30%

40%

50%

60%

Q112 Q212 Q312 Q412 Q113 Q213

LT

E p

en

etr

ati

on

(%

)

SK Telecom KT Corp LG U+ Korea Market

Source: Company data, Credit Suisse research.

18 September 2013

Cisco Systems Inc. (CSCO) 15

LTE penetration continues to rise. Korea has been one of the most advanced markets

when it comes to LTE rollouts and levels of consumer adoption. While Korea has already

seen strong LTE penetration over the past few quarters (with 42% of mobile subscribers

now on LTE networks as opposed to only 13% a year ago, as we show in Figure 23);

however, we would note that it still stands at less than 45%. This in our view could result in

continued levels of investment from Korean operators as they prepare to deal with a

growing level of LTE subscribers on their network along with rising usage patterns.

China Pushing on LTE

At its recent 1H results, China Mobile (CM) reiterated its full-year capex plans of

Rmb190bn for 2013, up from Rmb127bn in 2012. Note these numbers do not include

TD-SCDMA (3G) related capex as, it is done at the parent company level, but does

include TD-LTE related capex, which is being planned at the listed company level. If we

were to include around Rmb20bn of TD-SCDMA related capex in our numbers for both

2012 and 2013, we estimate that the total capex at China Mobile may be around

Rmb210bn, up from close to Rmb150bn in 2012.

Exhibit 24: CM Has Retained Rmb190bn of Capex

Guidance Breakdown of capex at listed company and parent company levels

Exhibit 25: Significant Capex Budget for 2H due to LTE Breakdown of listed company capex at China Mobile (1H/2H)

136.3 129.4 124.3 128.5 127.4

190.2

30.0 40.023.0 21.0 20.7

22.0

166.3 169.4

147.3 149.5 148.1

212.2

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013E

Cap

ex

at

Ch

ina

Mo

bile

(R

mb

bn

)

TD-SCDMA GSM, TD-LTE and Others

6671

6367

62 63 6267

59

69

57

133

0

20

40

60

80

100

120

140

1H

08

2H

08

1H

09

2H

09

1H

10

2H

10

1H

11

2H

11

1H

12

2H

12

1H

13

2H

13EC

hin

a M

ob

ile

lis

tco

ca

pex

1H

/2H

(R

mb

bn

)

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse research estimates

This planned increase in capex is mainly driven by aggressive TD-LTE network

deployment plans at China Mobile given weak subscriber uptake of its TD-SCDMA (3G)

services, as opposed to other players in the market such as China Telecom and China

Unicom.

Figure 26: Increase in Mobile Comm Capex Due to LTE Planned breakdown of capex by area of spend

Figure 27: TD-LTE Related Capex of Rmb41.5bn for 2013 Breakdown of capex for 2013 in detail

54.773.2

56.1

79.9

28.6

23.135.7

59.0

124.3 128.5 127.4

190.2

0

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013E

Ca

pe

x a

t C

hin

a M

ob

ile

lis

tco

(R

mb

bn

)

Others

Buildings &Infrastructure

SupportSystems

BusinessDevelopment

Transmission

MobileCommunicationNetworks

44%57%

44% 42%

23%

18%

28% 31%

13%6%

6% 6%

7% 6% 8% 6%

9% 9% 11% 13%4% 4% 3% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013E

Others Buildings & Infrastructure

Support Systems Business Development

Transmission Mobile Communication Networks

TD-LTE52%

GSM + WLAN + Core48%

Source: Company data, Credit Suisse research estimates Source: Company data, Credit Suisse research estimates

1H spending has been weak, so pick-up expected in 2H. Out of the Rmb190bn of FY

capex guidance from China Mobile at the listed company level, it has only spent Rmb57bn

18 September 2013

Cisco Systems Inc. (CSCO) 16

in 1H13, which implies around Rmb133bn to be spent in 2H13. This is surprisingly high in

our view, given the company has not spent this level of capex in any six-month period over

the past five years. So the question remains whether the company will spend all of the

Rmb41.5bn on TD-LTE in 2H13, or some of that spending may potentially get pushed in to

2014 as we see these networks being rolled out.

TD-LTE contracts seem to have been awarded to vendors by China Mobile. Over the past

few weeks, China Mobile has been in the process of attracting bids from various domestic

and international vendors for participating in the rollout of TD-LTE networks. According to

press reports in China, it seems that the carrier recently decided on its suppliers for

procuring TD-LTE equipment, and it has awarded 65% share of contracts to China-based

suppliers (such as Huawei, ZTE, and Datang), with the remaining 35% split between

European suppliers (Alcatel-Lucent, Ericsson, and Nokia Solutions Networks), with shares

split as shown below in Exhibit 28.

Exhibit 28: Share of China Mobile's TD-LTE Network for Rollout of 207K Base Stations

Vendor Contract Share (%)

International Alcatel-Lucent Shanghai Bell 13%

Ericsson 11%

Nokia Solutions Networks 11%

China-based Huawei 25%

ZTE 20%

Datang Mobile Communications Equipment 10%

FiberHouse Technologies, Nanjing Putian, New Postcom combined 10%

Source: DigiTimes.

18 September 2013

Cisco Systems Inc. (CSCO) 17

Enterprise Switching and Routing: +3.5% CAGR

Enterprise Ethernet Switching

Diving into specific segments of networking spend, we begin by exploring the enterprise

Ethernet switch market. In 2012, in aggregate, the market was $19.8 billion and has grown

at a rate of 3.0% per annum over the past five years. Within this, shifts are underway that

have important implications for the trajectory of the industry going forward, including

broader adoption of 10GbE ports and the preference for Layer 3 over Layer 2 switches.

10GbE adoption drives both port and revenue growth. While 10 gigabit Ethernet ports

have been available for nearly ten years, Intel's Xeon server chip release code-named

"Romley" paved the way for rampant adoption as it standardized 10GbE

"LAN-on-Motherboard" across both blade and rack-mounted servers. Further, server

virtualization is a secular driver of 10GbE adoption as increased utilization of the physical

compute hardware results in higher data traffic. While many enterprises continue to

operate with a mix of legacy and modern technologies, replacement cycles coupled with

new datacenter build-outs should continue to drive adoption within the enterprise switching

market. Further, while use cases for 10GbE outside the datacenter are somewhat nascent

now, increasing use of end-user video and voice over traditional enterprise networks

should over time drive adoption within campus environments as well. As seen in Exhibit 29,

Exhibit 30, and Exhibit 31, we expect 10GbE adoption to rise to 25% in 2017, up from 6%

now and only 0.3% five years ago.

Exhibit 29: 10GbE Non-Existent in 2007 Exhibit 30: 6% of the Market Now Exhibit 31: Growing to 25% in 2017

Enterprise switch ports by port speed. Note: excludes web-managed and un-managed ports

40GbE+, 0.0%

10GbE, 0.3%

1GbE and below,

99.7%

40GbE+, 0.1%

10GbE, 6.4%

1GbE and below,

93.6%

40GbE+,

0.6%

10GbE,

24.6%

1GbE and

below,

74.8%

Source: Infonetics. Source: Infonetics. Source: Infonetics, Credit Suisse estimates

Layer 3 switches to continue gaining wallet share at the expense of Layer 2. Another

growing trend within datacenters has been an increasing use of Layer 3 (L3) switches,

often at the expense of Layer 2 (L2) switches. The added intelligence of Layer 3 switches

removes a lot of the manual configuration historically required within enterprise networks,

which is especially important within virtualized infrastructures, as L3 switches are able to

abstract away distinct, proliferating, and difficult-to-manage VLANs. Legacy datacenter

networks were built with a three-tier model with L2 switches at the top of the server rack,

the end of the server row, and then at the aggregation layer before connecting to a router.

However, in many cases the added functionality of Layer 3 switches removes the need for

one of the tiers, whether through the use of fabric extenders or otherwise. Looking forward,

we expect these growth trajectories to continue as the modest incremental cost (only 5%

for a 10GbE port) of Layer 3 switches is offset by the ease of management and ability to

utilize less hardware. Outside of datacenter environments, we expect Layer 2 switches to

continue to prevail and port growth to be a function of device growth, although it is

18 September 2013

Cisco Systems Inc. (CSCO) 18

important to keep in mind that general campus switches tend to be at a lower ASP than

their datacenter equivalents, which pressures revenue trends. Further, Layer 2 switches

are most at risk from wireless cannibalization, as they have the highest attach to end

devices.

Exhibit 32: Layer 3 Spend Continues to Grow Faster Than Layer 2 Revenue

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Y/Y

reve

nue gro

wth

Total Layer 2 Revenue Total Layer 3 Revenue

Source: Infonetics.

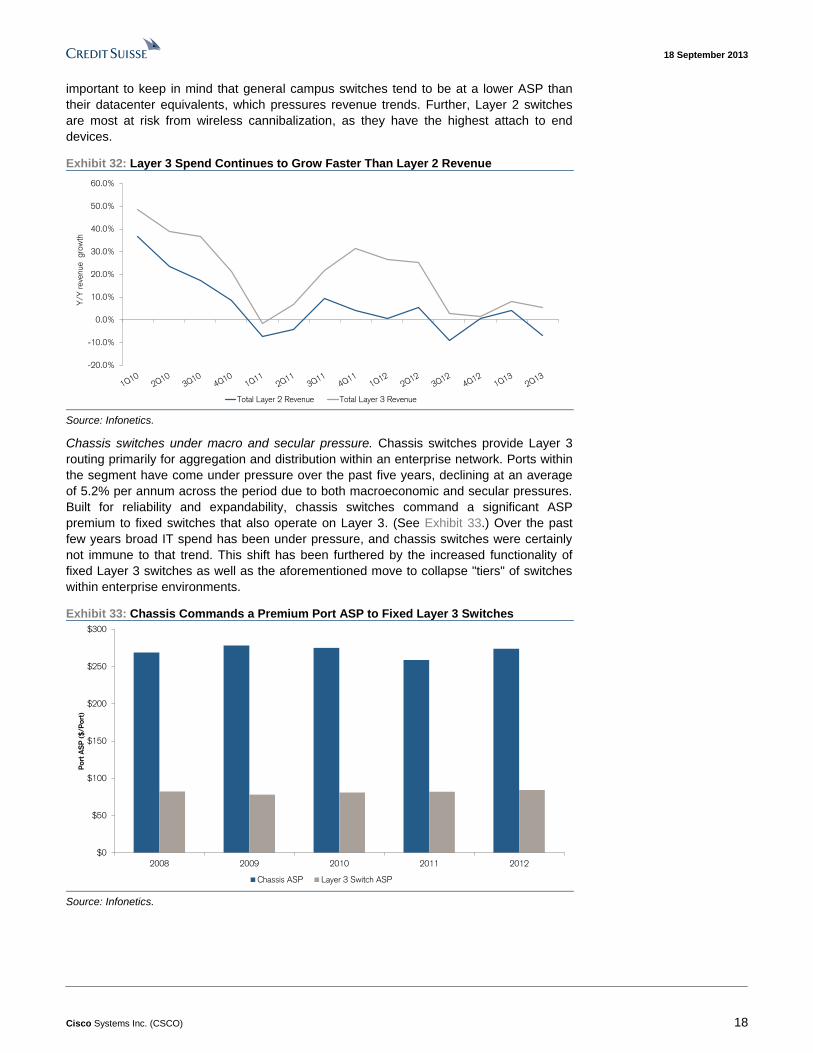

Chassis switches under macro and secular pressure. Chassis switches provide Layer 3

routing primarily for aggregation and distribution within an enterprise network. Ports within

the segment have come under pressure over the past five years, declining at an average

of 5.2% per annum across the period due to both macroeconomic and secular pressures.

Built for reliability and expandability, chassis switches command a significant ASP

premium to fixed switches that also operate on Layer 3. (See Exhibit 33.) Over the past

few years broad IT spend has been under pressure, and chassis switches were certainly

not immune to that trend. This shift has been furthered by the increased functionality of

fixed Layer 3 switches as well as the aforementioned move to collapse "tiers" of switches

within enterprise environments.

Exhibit 33: Chassis Commands a Premium Port ASP to Fixed Layer 3 Switches

$0

$50

$100

$150

$200

$250

$300

2008 2009 2010 2011 2012

Po

rt A

SP

($

/P

ort

)

Chassis ASP Layer 3 Switch ASP

Source: Infonetics.

18 September 2013

Cisco Systems Inc. (CSCO) 19

Enterprise Routing

We turn now to the enterprise routing market, which is far smaller than the switching

market at $3.5 billion in 2012. In modeling this segment, we look at the market across

high-end (listed unit ASP >$30,000), midrange (between $5,000 and $30,000), branch

(between $490 and $5,000), and low-end / SOHO (<$490). WAN bandwidth consumption

continues to be a driver of the enterprise routing market, as seen in a November 2012

Infonetics survey, in which North American respondents expect their bandwidth needs to

grow 30% annually. We expect an improving macroeconomic environment to provide a

tailwind into 2014. However, we expect more modest revenue growth of 3.2% in the long

term out of the enterprise routing market.

Exhibit 34: We Expected Low-Single-Digit Revenue Growth in Enterprise Routing

0

200

400

600

800

1,000

1,200

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

Quar

terly

reve

nue (

US

D m

n)

High-end Mid-Range Branch Office Low-end / SOHO

Source: Infonetics.

Total Enterprise Switching and Routing

In modeling aggregate enterprise spend for switching and routing, we combine the secular

trends with indications from our survey work on how industry participants view the overall

spending environment. Specifically, we model both switches and routers by ports and

ASPs ($/port) by port speed across the various sub-segments identified in Exhibit 42. We

expect total enterprise spend on switching and routing to grow at a 3.4% CAGR in the long

term, with port growth of 4.8% offset by 1.3% declines in $/port.

With respect to the overall demand environment, in our survey of 40 enterprise CIOs we

posed the question of "Why are you investing in Networking?" and found that nearly 50%

of respondents view increased business demand as the most important factor. (See

Exhibit 35.) Indeed, such a response indicates to us that the overall economic backdrop is

improving, which will likely propel networking spend into 2014.

18 September 2013

Cisco Systems Inc. (CSCO) 20

Exhibit 35: Credit Suisse CIO Survey: Why Are You Investing in Networking? % of responses identified as "Most Important"

Increased business demand, 47.2%

Cost savings (OpEx), 22.2%

Application performance, 22.2%

Remain competitive, 5.6%

Regulation, 2.8%

Maintenance, 0.0%Drive new revenues,

0.0%

Source: Credit Suisse CIO Survey August 2013.

Factoring in the aforementioned secular trends at play within the enterprise market

including 10GbE adoption and a preference for fixed Layer 3 switches over Layer 2 and

chassis switches, we expect the market to grow at a CAGR of 3.4% in the long term.

Interestingly, while we expect port growth to slow versus the previous five years to 4.8%

per annum from 5.7% previously, the ASP uplift due to the shift toward 10GbE will offset

the decline and drive a modest reacceleration in the near term in revenue growth.

Exhibit 36: Enterprise Switching and Routing Revenue to Grow at a 3.4% CAGR in the Long Term US$ in millions, unless otherwise stated

Enterprise ($mn) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

Unmanaged / Web managed 726.6 772.8 790.3 856.8 902.8 937.1 963.6 981.4 5.3% 4.4%

Total Layer 2 2,736.5 2,748.4 2,726.0 2,642.5 2,565.4 2,536.4 2,517.0 2,511.5 -12.4% -1.6%

Total Layer 3 7,702.0 8,843.8 9,961.8 10,892.6 11,407.3 11,961.1 12,446.7 12,898.0 20.4% 5.3%

Total Chassis 7,487.4 6,500.0 6,291.7 6,075.8 6,321.8 6,526.5 6,788.0 7,051.6 -2.8% 2.3%

Total Switching $18,652.5 $18,865.0 $19,769.8 $20,467.7 $21,197.4 $21,961.2 $22,715.3 $23,442.5 3.0% 3.5%

y/y % Change 30.4% 1.1% 4.8% 3.5% 3.6% 3.6% 3.4% 3.2%

Total 1GbE & Below 14,243.4 13,057.2 12,677.7 12,003.3 11,168.0 10,318.8 9,484.4 8,694.3 -4.1% -7.3%

Total 10GbE 4,409.1 5,786.1 6,865.4 7,814.7 9,118.4 10,607.4 12,071.4 13,491.7 36.9% 14.5%

Total 40GbE & 100GbE - 21.7 226.7 649.8 910.9 1,035.1 1,159.4 1,256.5 NA 40.8%

High-end 482.8 580.9 566.0 604.6 618.9 636.4 655.8 675.7 -2.2% 3.6%

Mid-Range 1,290.0 1,232.6 1,122.4 1,182.3 1,232.0 1,266.7 1,290.2 1,314.0 -7.8% 3.2%

Branch Office 1,565.3 1,529.7 1,492.9 1,537.5 1,538.3 1,549.9 1,619.6 1,692.5 -4.4% 2.5%

Low-end / SOHO 133.6 273.8 327.5 338.0 356.5 373.5 395.3 422.7 19.6% 5.2%

Total Routing $3,471.7 $3,617.0 $3,508.8 $3,662.3 $3,745.6 $3,826.6 $3,960.9 $4,105.0 -4.1% 3.2%

y/y % Change 13.0% 4.2% -3.0% 4.4% 2.3% 2.2% 3.5% 3.6%

Total Enterprise $22,124.2 $22,482.0 $23,278.6 $24,130.1 $24,943.0 $25,787.8 $26,676.2 $27,547.5 1.7% 3.4%

y/y % Change 27.3% 1.6% 3.5% 3.7% 3.4% 3.4% 3.4% 3.3%

Source: Infonetics, Credit Suisse estimates.

18 September 2013

Cisco Systems Inc. (CSCO) 21

Service Provider Switching & Routing: +5.5% CAGR

Service Provider Routing

In examining trends within the service provider (SP) market, we begin by focusing on

routers which totaled $11.3 billion in 2012 out of $14.2 billion in total service provider

spend. In revenue terms, the market has shown significant growth over the past five years,

expanding at a pace of 7.9% per annum, which is far faster than growth on the enterprise

side. Digging one layer deeper, there are significant divergences between the growth

within core (0.8% 2007-2012 CAGR) and edge (10.7% 2007-2012 CAGR) routers, as

service providers continue to focus on adding capacity and intelligence to the edge of their

networks at the expense of the core.

Exhibit 37: The Hierarchy of Service Provider Network Design

Edge - the boundary between the service-

provider’s premises and the customer’s

location. The concentration point where large

numbers of customer connections will be

terminated.

Aggregation - a concentration point where

data from multiple Edge locations will be

funneled. Functionally another tier of the “Edge.”

Core - the heart of the network. The major

switching locations that form the center of the

network, where data from multiple

Aggregation sites will be funneled

This is typically where one sees the

highest volume of data present in the

network.

Source: Juniper Networks, Credit Suisse research.

Core routers losing wallet share within spend. Core routers are robust, high-speed routers

built for reliability that sit in the center of a service provider's network. These routers are

critical to a network's operations and carriers pay quite a premium for that reliability as a

result. Indeed, in 2012 the average unit price of a core router was $129,000, although only

slightly more than 20,000 were sold. In aggregate, the core routing market totaled $2.7bn

in 2012 and has come under pressure, as it grew only 0.8% per annum over the past five

years and declined 10.3% y/y in 2012. Deployments tend to be 'lumpy' with large

fluctuations depending on individual service provider rollouts. (See Exhibit 38.)

Spending within the core of the network tends to be a function of capacity, and recently

service providers have been trying to prolong spend within the area as long as possible.

Indeed, recent commentary from Juniper indicates that core networks continue to be run

'hotter' i.e., closer to their capacity with an expectation of a coming upgrade cycle. On the

2Q13 conference call, Juniper CEO Kevin Johnson noted that "[Juniper] has seen the core

of the network in our analysis has been running hotter and hotter, and we're just now

starting to see the signs that investment will, in addition to being on the edge, will start to

kick in for the core and we expect to see that start to unfold later this year." We expect a

18 September 2013

Cisco Systems Inc. (CSCO) 22

cyclical uptick over the coming quarters; however, we do not see a structural shift back to

the core on a long-term basis. We model 3.5% growth through 2017 with a significant

deceleration beyond 2014.

Exhibit 38: Core Router Revenue Can be Lumpy from Quarter to Quarter y/y % change in core router revenue

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

Source: Company data, Infonetics

Increased focus on investment at the edge likely to continue. While core investment has

been stagnant in the aggregate over the past five years, edge routing has seen substantial

growth over the same period, rising 10.7% on average per year in revenue terms. In 2012,

the market totaled $8.6bn amid secular tailwinds of added capacity and services within

service provider networks. One such example of expanded services is the "triple play"

offerings (i.e., cable, phone, and internet) of many traditional voice or cable service

providers, as they look to drive additional ARPU from their installed base and as a result

are forced to add capacity to the edge of their networks. Additionally, overall bandwidth

consumption per subscriber driven by, for example, internet video coupled with broad

subscriber growth, has resulted in increased demand for edge routing capabilities.

A second secular tailwind to edge routing spend has been the tremendous growth in

smartphones and the resulting growth in mobile data consumption. Indeed, within North

America, smartphone penetration (defined as smartphones as a percentage of mobile

shipments) rose from 4.0% in 2006 to 49.5% in 2012, driving massive amounts of mobile

data. Globally, penetration stood at only 4.2% in 2006. Further, the move toward LTE from

2G/3G technologies within mobile networks is causing a renewed focus on a converged IP

network driving an upgrade cycle across service provider networks. Historically, 2G/3G

technologies parsed between voice and data transmissions, sending the former over

legacy circuit-switched networks while routing the data packets across IP networks.

However, LTE enables both voice and data to travel across IP networks, leading to

converged IP solutions across service providers' networks. As seen in Exhibit 39, we

expect tremendous growth in LTE smartphone units through 2017 driving a continued

focus on edge routers.

18 September 2013

Cisco Systems Inc. (CSCO) 23

Exhibit 39: LTE to See Tremendous Growth over the Next Five Years on Our Estimates Number of LTE devices sold in millions

7

86

219

298

460

604

789

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

100

200

300

400

500

600

700

800

900

2011 2012E 2013E 2014E 2015E 2016E 2017E

Asia Pacific North America Western Europe Africa

CEE Latin America Middle East % of the handset market

Source: Company data, Credit Suisse estimates.

Combining these factors, we continue to expect edge routers to outperform core within the

service provider space. We forecast 6.3% long-term revenue growth within the edge

routing market.

Service Provider Switching

In contrast to the enterprise market, the switching market is dwarfed by the routing market

within service provider spend. In 2012 the market totaled $2.9bn and has grown at an

average annual rate of 6.0% over the past five years, although last year spend was down

11.0%. As switches are primarily deployed at the edge of networks, we expect the same

secular drivers of edge routing discussed above to propel carrier switches, as we model a

5.1% growth rate in the long term.

Exhibit 40: Total Service Provider Switching and Routing to Grow 5.5% Per Year Long Term US$ in millions, unless otherwise stated

Service Provider 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

Core 2,838.8 2,975.0 2,668.8 2,840.1 3,058.4 3,089.3 3,126.3 3,163.8 0.8% 3.5%

Edge 7,683.1 8,544.0 8,639.6 9,118.8 9,957.7 10,575.1 11,183.2 11,725.6 10.7% 6.3%

Total Routing $10,521.9 $11,519.0 $11,308.4 $11,958.9 $13,016.1 $13,664.4 $14,309.5 $14,889.4 7.9% 5.7%

y/y % Change 17.2% 9.5% -1.8% 5.8% 8.8% 5.0% 4.7% 4.1%

Total Switching $3,176.1 $3,257.3 $2,900.8 $2,897.3 $3,110.8 $3,323.0 $3,517.0 $3,722.4 6.0% 5.1%

y/y % Change 57.7% 2.6% -10.9% -0.1% 7.4% 6.8% 5.8% 5.8%

Total Service Provider $13,698.0 $14,776.3 $14,209.3 $14,856.2 $16,126.9 $16,987.3 $17,826.5 $18,611.8 7.5% 5.5%

y/y % Change 24.6% 7.9% -3.8% 4.6% 8.6% 5.3% 4.9% 4.4%

Source: Company data, Credit Suisse estimates.

1

8 S

ep

tem

ber 2

013

Cis

co

Sy

ste

ms In

c. (C

SC

O)

24

Exhibit 41: Aggregate Networking: 4.2% LT Growth Driven by Edge Routers and 10GbE Adoption in Enterprise Switching

Enterprise Switching Revenue ($mn) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

Unmanaged / Web managed $726.6 $772.8 $790.3 $856.8 $902.8 $937.1 $963.6 $981.4 5.3% 4.4%

Total Layer 2 $2,736.5 $2,748.4 $2,726.0 $2,642.5 $2,565.4 $2,536.4 $2,517.0 $2,511.5 -12.4% -1.6%

Total Layer 3 $7,702.0 $8,843.8 $9,961.8 $10,892.6 $11,407.3 $11,961.1 $12,446.7 $12,898.0 20.4% 5.3%

Total Chassis $7,487.4 $6,500.0 $6,291.7 $6,075.8 $6,321.8 $6,526.5 $6,788.0 $7,051.6 -2.8% 2.3%

Total 1GbE & Below 14,243.4 13,057.2 12,677.7 12,003.3 11,168.0 10,318.8 9,484.4 8,694.3 -4.1% -7.3%

Total 10GbE 4,409.1 5,786.1 6,865.4 7,814.7 9,118.4 10,607.4 12,071.4 13,491.7 36.9% 14.5%

Total 40GbE & 100GbE - 21.7 226.7 649.8 910.9 1,035.1 1,159.4 1,256.5 NA 40.8%

Total Enterprise Switching $18,652.5 $18,865.0 $19,769.8 $20,467.7 $21,197.4 $21,961.2 $22,715.3 $23,442.5 3.0% 3.5%

y/y % Change 30.4% 1.1% 4.8% 3.5% 3.6% 3.6% 3.4% 3.2%

Carrier Ethernet Switching Revenue ($mn) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

Total Carrier Ethernet Switching $3,176.1 $3,257.3 $2,900.8 $2,897.3 $3,110.8 $3,323.0 $3,517.0 $3,722.4 6.0% 5.1%

y/y % Change 57.7% 2.6% -10.9% -0.1% 7.4% 6.8% 5.8% 5.8%

Enterprise Routing Revenue ($mn) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

High-end 482.8 580.9 566.0 604.6 618.9 636.4 655.8 675.7 -2.2% 3.6%

Mid-Range 1,290.0 1,232.6 1,122.4 1,182.3 1,232.0 1,266.7 1,290.2 1,314.0 -7.8% 3.2%

Branch Office 1,565.3 1,529.7 1,492.9 1,537.5 1,538.3 1,549.9 1,619.6 1,692.5 -4.4% 2.5%

Low-end / SOHO 133.6 273.8 327.5 338.0 356.5 373.5 395.3 422.7 19.6% 5.2%

Total Enterprise Routing $3,471.7 $3,617.0 $3,508.8 $3,662.3 $3,745.6 $3,826.6 $3,960.9 $4,105.0 -4.1% 3.2%

y/y % Change 13.0% 4.2% -3.0% 4.4% 2.3% 2.2% 3.5% 3.6%

Service Provider Routing Revenue ($mn) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

Core 2,838.8 2,975.0 2,668.8 2,840.1 3,058.4 3,089.3 3,126.3 3,163.8 0.8% 3.5%

Edge 7,683.1 8,544.0 8,639.6 9,118.8 9,957.7 10,575.1 11,183.2 11,725.6 10.7% 6.3%

Total Service Provider Routing $10,521.9 $11,519.0 $11,308.4 $11,958.9 $13,016.1 $13,664.4 $14,309.5 $14,889.4 7.9% 5.7%

y/y % Change 17.2% 9.5% -1.8% 5.8% 8.8% 5.0% 4.7% 4.1%

Total Enterprise vs. Service Provider ($mn) 2010 2011 2012 2013E 2014E 2015E 2016E 2017E '07 - '12 '12 - '17E

Total Enterprise 22,124.2 22,482.0 23,278.6 24,130.1 24,943.0 25,787.8 26,676.2 27,547.5 1.7% 3.4%

Total Service Provider 13,698.0 14,776.3 14,209.3 14,856.2 16,126.9 16,987.3 17,826.5 18,611.8 7.5% 5.5%

Total Revenue $35,822.2 $37,258.2 $37,487.9 $38,986.3 $41,069.9 $42,775.1 $44,502.7 $46,159.3 3.7% 4.2%

y/y % Change 26.3% 4.0% 0.6% 4.0% 5.3% 4.2% 4.0% 3.7%

1) Expect 4.2% LT revenue growth in aggregate Ethernet Switching & Routing. Looking at combined Ethernet Switching and Routing, we expect the market to grow at