Pan-European Capital Goods - 2014 - Credit Suisse | PLUS

204

Pan-European Capital Goods 2014: Re-rating is done. Must deliver on earnings growth – Stock Ideas & 7 Themes for 2014 – Sector Valuation & Outlook – End Markets & Companies Analysis Dec 2013 CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION® Client-Driven Solutions, Insights, and Access DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit https://rave.credit- suisse.com/disclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Research team Andre Kukhnin, CFA 44 20 7888 0350 [email protected] Jonathan Hurn, CFA 44 20 7883 4532 [email protected] Simon Toennessen 44 20 7883 6893 [email protected] Max Yates 44 20 7883 8501 [email protected] Tiantian Li 44 20 7883 1552 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Pan-European Capital Goods - 2014 - Credit Suisse | PLUS

Pan-European Capital Goods 2014: Re-rating is done. Must deliver on earnings growth – Stock Ideas & 7 Themes for 2014 – Sector Valuation & Outlook – End Markets & Companies Analysis Dec 2013

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION® Client-Driven Solutions, Insights, and Access

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit https://rave.credit-

suisse.com/disclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result,

investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor

in making their investment decision.

Research team

Andre Kukhnin, CFA 44 20 7888 0350 [email protected]

Jonathan Hurn, CFA 44 20 7883 4532 [email protected]

Simon Toennessen 44 20 7883 6893 [email protected]

Max Yates 44 20 7883 8501 [email protected]

Tiantian Li 44 20 7883 1552 [email protected]

2

What’s inside & Our key recent research

I. Summary of Key Stock Ideas and Sector Themes Slides 3-7

II. 7 Sector Themes for 2014 Slides 8-23

III. Sector Performance & Valuation Slides 24-36

IV. End-Markets Outlook Slides 37-59

V. Companies Bull & Bear case & Summaries Slides 60-196

Sector / Themes:

02/12/2013 UK Capital Goods – Spotlight on Valuation / Global peer analysis

18/11/2013 CS Industrials China Trip – Steady, higher-quality growth ahead

04/11/2013 Gas turbine demand / market share

31/10/2013 Global Mining Equipment – Q3 reality check

11/09/2013 Pan-Euro Cap Goods – Searching for through-cycle value creation

16/07/2013 Global Industrials – Automation Software Deep-Dive

03/07/2013 Global Mining Equipment – Between a rock and a hard place

01/05/2013 Industrials Insight – In search for quality growth

12/02/2013 European Cables – Initiation – Follow the leader

Stock-specific:

02/12/2013 Metso – Rock, Paper, Spin-off

06/11/2013 SKF – China becoming more of a threat than opportunity

30/10/2013 ABB – Pace of early-cycle recovery could surprise

28/10/2013 Assa Abloy – Relentless progress. TP to SEK 350

22/10/2013 IMI – We see further upside from here

21/10/2013 Sandvik – Rising risks while expectations remain full

30/09/2013 Prysmian – Under-appreciated growth & returns profile

11/09/2013 Alstom – Structural issues to persist – Downgrade to U/P

11/09/2013 Geberit – High quality deserves the premium

19/09/2013 Fenner – Time to get involved – Upgrade to O/P

05/08/2013 Siemens – Potential CEO action points

20/08/2013 Senior – Four reasons to buy - TP up to 315p

11/07/2013 Melrose – Counting the potential cash return

20/02/2013 ABB – Initiation – A transforming business

Key recent research:

3

Key Conclusions

In 2013, the sector moved up 17% on an 8% EPS downgrade resulting in a 25% re-rating to 2014E 12x

EV/EBITA and 15.5x P/E. For 2014, we expect a year of relatively slow growth with self-help themes of

cost-cutting and acquired growth continue to work. With limited scope for further re-rating, we have

a Neutral view on the sector with c8-10% expected performance for 2014.

Top line. Expect some growth acceleration in 2014-15 from near-zero in 2013 but overall slow

growth environment to continue. Expect a gradual recovery in short-cycle but later-cycle to continue to

drag, especially in 2014.

Profitability. Expect margins to expand by c50bps pa in 2014-15 driven by combination of operational

gearing, cost-cutting, benign raw materials environment and broadly flat pricing.

Quality vs Cyclical. With Quality Growth premium vs Cyclical Growth at all time high for both Europe

and UK, we believe the overall theme has played out but we continue to see selective growth

opportunities within quality.

Electricals vs Mechanicals vs UK. We continue to have a preference for Electricals vs Mechanicals

for 2014 but acknowledge that c3-5% of the relative rerating already took place in 2013. We continue

to see UK space attractive given the M&A angle.

Key stock ideas. We favour ABB and Prysmian in Electricals, Assa Abloy and Metso in Mechanicals

and Spectris and IMI in the UK. We remain cautious on Alstom, SKF and Sandvik.

Please see next 4 slides for detailed summaries of our key stock ideas and sector themes.

4

Key Stock Ideas with Cyclical, Secular & Structural framework

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2006-2008 2009 2010-2012 2013E-2015E

Cyclical Average Secular average Structural (ex Assa & Legrand) average

Organic growth performance by category

2004-2012 avg. cash conversion performance

0%

20%

40%

60%

80%

100%

120%

140%

Legr

and

Pry

smia

n

Spe

ctris

Sch

indl

er

Ass

a A

bloy

Kon

e

Geb

erit

Hal

ma

Sch

neid

er

Alfa

Lav

al

Sen

ior

IMI

AB

B

Bod

ycot

e

Rot

ork

Sie

men

s

Nex

ans

SK

F

Met

so

Laird

Atla

s C

opco

Sm

iths

Fen

ner

Wei

r

Ren

isha

w

Mel

rose

Spi

rax

Ele

ctro

lux

Ves

uviu

s

San

dvik

Als

tom

Phi

lips

Mor

gan

Adv

. Mat

s

GK

N

Sector average

Source: Company data, Credit Suisse estimates

Rating CCY TP Rating CCY TP Rating CCY TP

Prysmian OP € 21 1.2% 115% ABB OP CHF 26 7.1% 91% Assa Abloy OP SEK 360 1.9% 106%

Metso OP € 35 4.3% 69% Atlas Copco OP SEK 210 9.7% 68% Halma OP £ 6.2 4.8% 97%

GKN OP £ 4.30 3.6% 19% Fenner OP £ 4.9 8.7% 67% Schindler OP CHF 150 5.7% 106%

Bodycote OP £ 7.6 3.6% 89% Spectris OP £ 25.6 4.5% 111% Rotork OP £ 32.3 11.5% 85%

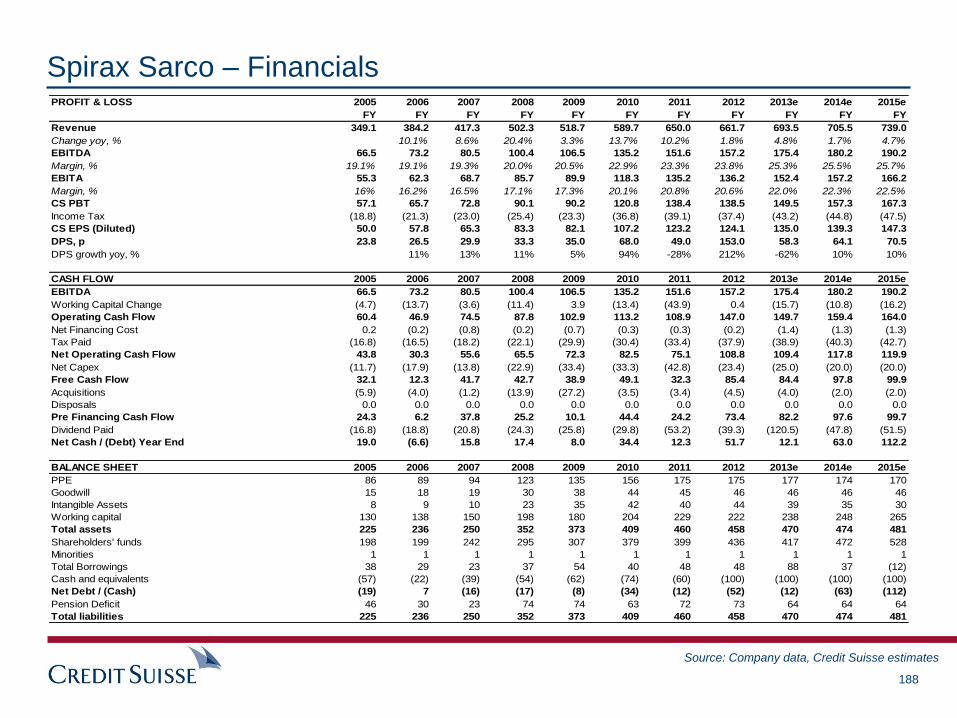

Electrolux OP SEK 190 1.3% 60% IMI OP £ 16.4 3.3% 94% Spirax Sarco N £ 30.3 6.0% 63%

Philips N € 26 1.5% 47% Siemens OP € 105 5.3% 77% Geberit N CHF 240 5.9% 102%

Nexans N € 31 0.4% 73% Senior OP £ 3.15 5.2% 94% Renishaw N £ 17.15 9.6% 66%

Sandvik UP SEK 75 7.4% 56% Smiths OP £ 14.6 1.6% 68% Kone N € 34 9.1% 104%

Morgan AM UP £ 2.70 1.6% 40% Schneider N € 58 4.6% 97% Legrand UP € 38 1.6% 126%

Laird UP £ 2.15 3.2% 69% Weir N £ 22.1 12.2% 66%

Vesuvius UP £ 4.05 2.6% 60% Alfa Laval N SEK 145 5.9% 94%

SKF UP SEK 150 3.7% 72% Melrose N £ 2.75 6.4% 64%

Alstom UP € 24 3.9% 55%

2005-12

organic

growth

2006-12

FCF

conv.

2005-12

organic

growth

2006-12

FCF

conv.

CYCLICAL SECULAR STRUCTURAL

2005-12

organic

growth

2006-12

FCF

conv.

5

Summary of Key Stock Ideas OUTPERFORM

Electricals

ABB – TP CHF 26 – Automation growth potential, Margin recovery in Power Products, Acquisitions potential, Quality returns profile.

Prysmian – TP €21 – Under-appreciated growth and returns profile. Attractive valuation.

Siemens – TP €105 – Self-help & Balance sheet use in near-term, EM Automation & US Gas longer-term themes.

Mechanicals

Assa Abloy – TP SEK 360 – Proven high quality ‘Acquire & Restructure’ model with several organic growth & margin levers.

Metso – TP €35 – >15% discount to SOTP ahead of Valmet spin off, strong €200m cost-cutting effort.

Atlas Copco – TP SEK 210 – High quality play in GI recovery, mining aftermarket exposure, further balance sheet potential.

UK

Spectris – TP 2560p – Attractive valuation vs. peers, strong cash conversion, automation play, B/S optionality, potential M&A target.

IMI – TP 1640p – Portfolio focus on better growth, margin, improving ROIC, high cash conversion, B/S optionality, potential M&A target.

GKN – TP 430p – Valuation re-rating potential, self-help (Driveline, Volvo Aero), business mix improvement (towards Aero).

Fenner – TP 490p – Attractive mining aftermarket exposure, valuation discount vs. peer group, healthy EPS growth through 2016.

Bodycote – TP 760p – Cyclical turn-around story, Margin resilience under-estimated, Un-geared balance sheet.

UNDERPERFORM

Alstom – TP €24 – Risk to Thermal Service margins, Challenging Power Gen Equipment outlook, On-going weak cash conversion

SKF – TP SEK 150 – Japanese and Chinese competition risks, full valuation, balance sheet capacity now used up.

Sandvik – TP SEK 75 – Further earnings risk in Mining and Construction from volume declines and potential pricing offsetting self-help.

NEUTRALS (that are generating client debate)

Alfa Laval – TP SEK 145 – High quality late-cyclical arriving at the bottom of its end-markets but expectations appear already full

Geberit – TP CHF 240 – Best in class growth, returns and cash conversion vs near-term end-markets

Schneider – TP €58 – High quality and Growth attractions VS M&A risk & Relatively full valuation.

6

7 themes for the sector in 2014

Theme #1: How to play a short cycle recovery

CS GDP and IP forecasts indicate a European recovery in 2014 but we remain

cautious on names where consensus expectations and valuations are already

relatively full (we forecast 6% organic growth for SKF with 35% operational gearing).

We prefer names with scope for positive surprises including GKN (OP), Bodycote

(OP) and Prysmian (OP).

Theme #2: Structural growth – Need to be selective in 2014

Structural growth as a theme has worked in 2013 and the relative valuation (32%

premium) of high quality European names (Assa Abloy, Geberit, Kone, Legrand &

Schindler) is now at its highest for ten years. Among these names we favour those

names where we see clear levers to generate best in class growth: Assa Abloy

(OP), and Schindler (OP).

Theme #3: Opportunity in mining aftermarket exposed names

There remains a consensus negative view in the market toward mining capex, but

we continue to see an opportunity in names with higher aftermarket exposure (Atlas

Copco (OP) & Fenner (OP). On new equipment we discount a cautious scenario (-

16% in 2014 and -21% in 2015) but expect aftermarket to grow in 2014/15 as mine

production continues to rise.

Theme #4: Stabilization of weaker businesses should allow Electricals to re-

rate further

In the last two quarters underperforming businesses in Electricals that have

received attention in the last 12mths have shown signs of stabilization. We believe

this can shift the market focus away from ABB Power, Siemens I&C and Prysmian

T&I and to the remainder of the businesses which ultimately drive group profitability.

In our view this can lead to further re-rating with, for example, ABB’s automation

business clearly trading at a discount to global peers.

-20%

-10%

0%

10%

20%

30%

40%

Nov-03 Nov-04 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11 Nov-12 Nov-13

EU High quality stocks EV/EBIT premium / discount vs sector Average premium / discount

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fenner Weir Atlas CAT Metso Sandvik FLS Outotec

New Equipment A/market

7.2%

6.4%

13.4%

11.4%

5.9%

-12.7%

6.4%

11.6%

3.5%

0.4%

4.0% 4.5%

10.0%

11.1%

12.2%

13.1%

11.1%

13.8%

14.6%

14.4%14.3%14.8%15.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-18.0%

-14.0%

-10.0%

-6.0%

-2.0%

2.0%

6.0%

10.0%

14.0%

18.0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013E

2014E

2015E

Sector EBIT margin, % Sector organic growth, %

Sector Organic Growth vs Margin

European Quality Growth vs Sector

Mining Players OE vs Aftermarket exposure

Source: Thomson Reuters, Company data, Credit Suisse estimates

7

7 themes for the sector in 2014

Theme #5: Balance sheet re-leverage

Across the sector we believe there is opportunity for balance sheet

re-leverage. We see the greatest acquisition opportunity as being

for Assa Abloy in Entrance systems while Siemens is likely to focus

on Process Automation. In our view, buybacks are most likely at

Atlas Copco and Alfa Laval (both have a history of buybacks and

currently have low leverage)

Theme #6: Competitive risk

We continue to believe Alstom (UP) bears the greatest medium

term structural risk from competition. We also believe the risk for

SKF (UP) (from Chinese and Japanese competitors) is rising and in

Mining Equipment see risk in the crushing and grinding segment.

We remain cautious on Sandvik (UP).

Theme #7: Potential M&A

We have re-run our HOLT® CFROI® M&A Screen for the Pan

European Capital Goods universe with analysis over 6 criteria. We

would highlight the following names from the Screen:

Met 5 criteria: Alfa Laval, Fenner, Legrand, Rotork

Met 4 criteria: Smiths Group, Spectris, Weir

Met 3 criteria: IMI

0%

1%

2%

3%

4%

5%

6%

7%

8%

Prys

mia

n

Assa

Abl

oy

ABB

Alfa

Lav

al

Atla

s C

opco

Schn

eide

r

Legr

and

Met

so

Nex

ans

SKF

Sand

vik

Kone

Siem

ens

Elec

trolu

x

Philip

s

Alst

om

Schi

ndle

r

Geb

erit

Average acquisition impact on sales (2007-12)

Acquired Growth Track Record

Emerging Markets Competition Risk Assessment

Risk Rating 1 2 3 4 5

High Power Gen.(Coal)

Appliances, T&D

Bearings

Trucks

Mining Equipment - Crushers & Grinders

Medium Drive systems

Transport

O&G (Fracking)

Heat exchangers

Elevator

Low

Heat Treatment

Timeframe in years

Automation

Construction Equipment

Low Voltage equipment

Auto components

Mining Equipment

Source: Company data, Credit Suisse research

8

Sector Themes

9

Theme #1: How to play a short-cycle recovery

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

AB

B

Legr

and

Nex

ans

Pry

smia

n

Sch

neid

er

Sie

men

s

Atla

s C

opco

Met

so

San

dvik

SK

F

Q3 13 2014

Q313 organic growth and 2014 CS forecast CS economists’ EU GDP (+1.3%) and IP (4.5%) forecasts imply a

recovery for in shorter-cycle demand in 2014.

We acknowledge Sandvik and SKF have good gearing to a EU short

cycle recovery but believe this is already discounted in consensus –

CS forecasts 6% organic growth for their relevant businesses. We

also believe valuations on both of these stocks are relatively full.

In Europe we would rather gain exposure to this theme through Atlas

Copco in Europe where the CT and IT businesses give good

exposure to this theme and multiples are not at a level that we

believe is likely to absorb further earnings upgrades

In the UK we believe there is scope for positive surprises on growth

for Bodycote and Spectris in 2014.

Source: Company data, Credit Suisse estimates, IBES consensus, Thomson Reuters

% of group 2014 EV/EBIT CS EBITA vs Consensus

SKF Group 85% 5.9% 35% 11.2 0.3%

GKN Group ex Aerospace 74% 4.0% 30% 11.9 4.0%

Spectris Group 60% 3.2% 30% 14.6 1.7%

Bodycote AGI 56% 2.6% 35% 9.6 1.5%

ABB Low voltage & DAM 41% 7.0% 30% 11.0 9.3%

Nexans Distributors & Installers 51% 1.0% 15% 12.0 11.3%

Atlas Copco CT & IT 49% 5.5% 35% 12.6 2.8%

IMI Fluid Power 42% 4.0% 30% 15.2 0.0%

Sandvik Machine Solutions 30% 6.0% 35% 11.4 -0.6%

Prysmian Trade & Installers 28% 2.5% 15% 10.0 7.0%

Siemens Industry 24% 2.7% 30% 12.9 2.8%

Schneider Industry 19% 5.0% 30% 10.7 4.5%

Average 47% 4.1% 29% 11.9 3.7%

2014 organic

growth for these

divisions

Op. Leverage for these

divisions

Key short cycle

divisions

Group

10

Theme #2: Structural Growth – Need to be selective in 2014

Prefer Assa & Schindler in EU structural growth

In 2013 the high quality names (Assa, Geberit, Kone,

Legrand & Schindler) premium to the sector has

extended from 17% to 26%.

In our view this is justified by our expectation of on

average organic sales growth of 4.8% in 2013 for

structural growth names vs a sector average of 0.4%.

However, based on this re-rating we believe in 2014

there is less scope for structural growth to outperform

as a theme. We favour a more selective approach and

based on their clear growth drivers in 2014 we see

scope for outperformance at Assa & Schindler

0%

20%

40%

60%

80%

100%

120%

Nov-03 Nov-04 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11 Nov-12 Nov-13

UK High quality names PE premium / discount vs the sector Average

-20%

-10%

0%

10%

20%

30%

40%

Nov-03 Nov-04 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11 Nov-12 Nov-13

EU High quality stocks EV/EBIT premium / discount vs sector Average premium / discount

Prefer Halma among UK structural growth names

In 2013 the PE premium for high quality stocks

(Halma, Renishaw, Rotork and Spirax Sarco) has also

increased to 109% from 85%.

Among these names we favour Halma based on the

continued success of its business model focusing on

safety and legislative driven end markets with high

barriers to entry.

Relative to its structural peer group Halma trades at a

more attractive relative valuation.

Source: Thomson Reuters, Credit Suisse research

11

#2: Structural growth: More to go at Assa Abloy, Halma & Schindler

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Pedestrian doors Gate & Windowautomation

Industrial doors Assa Abloy ESsales

Europe Rest of world

60

70

80

90

100

110

120

130

Dec-08 Jul-09 Feb-10 Sep-10 Apr-11 Nov-11 Jun-12 Jan-13 Aug-13

KONE Schindler Thyssen OTIS

Assa Abloy (OP) remains a top pick in to 2014 as we see scope

for a positive surprise in the Entrance systems market. Assa’s

sales in this market (SEK12bn) imply a c7% global market share

but we see opportunity for Assa to execute on its acquire and

restructure strategy in this fragmented SEK c180bn market.

Halma (OP) in the medium term can benefit from increasing

safety and regulation in Industry and buildings but in the near-

term we believe its acquisition pipeline remains full which should

support strong organic growth over the next 12 months (in Q3

Halma grew organically at 6% which was 2x the UK average).

Schindler (OP) is our preferred way to play the attractive

Elevator market. Schindler is now growing broadly in-line with

best in class Kone, is well positioned to increase its share with

investment in new capacity (listed above) yet continues to trade

at an attractive 13% discount vs high quality peers.

New factories ramp up at Schindler

Source: Company data

Country City Type Start target Purpose

Europe (Slovakia) Dunajská Streda Elevators Q4 2013 Replacement - cost reduction

US Pennsylvania Elevators Q4 2013 Replacement - change of technology

China Shanghai Escalators Q1 2014 Replacement and Expansion

China Shanghai Elevators 2015 Replacement and Expansion

India Pune Elevators Q1 2014 Expansion

India Pune Escalators 2014 Expansion

Organic growth of lift manufacturers

Market size estimates & Assa ES sales (bn SEK)

12

Theme #2: Cyclical vs Secular vs Structural Framework

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2006-2008 2009 2010-2012 2013E-2015E

Cyclical Average Secular average Structural (ex Assa & Legrand) average

Cyclical Secular Structural

Alstom ABB Assa Abloy

Bodycote >>> Alfa Laval Geberit

Electrolux Atlas Copco >>> Halma

GKN >>> Fenner <<< Kone

Laird IMI Legrand

Metso Melrose Renishaw

Morgan Adv. Mats Schneider Rotork

Nexans Siemens Schindler

Philips >>> Senior Spirax Sarco

Prysmian >>> Smiths Group

Sandvik Spectris

SKF Weir

Vesuvius

European Cyclical

UK Secular

European Structural

UK Cyclical European Secular

UK Structural

7

8

9

10

11

12

13

14

15

5% 7% 9% 11% 13% 15% 17% 19%

2013-2014 Average ROIC vs 2014E EV/EBIT Here we show our cyclical vs secular vs structural

company framework and those shaded companies we

believe have potential to move between categories:

GKN (OP), Bodycote (OP), Prysmian (OP) & Atlas (OP)

being our key picks.

Between 2006-08 the secular growth companies (largely

mining capex driven) outgrew structural names but the

structural names proved more resilient in 2009.

Structural growth companies tend to trade on a EV/EBIT

multiple 2 points higher than secular and therefore we

see scope for re-rating if companies are perceived to

move between categories.

N.B. We classify secular growth companies as those companies that may be exposed to a c2 year growth theme (eg Automation)

vs structural growth which may be driven by a theme (aging populations) or a businesses model (acquire and restructure).

Organic growth performance by category

Source: Company data, Credit Suisse research

13

Theme #3: Opportunity in Mining Aftermarket names

CAT Atlas Copco Fenner Sandvik Metso Weir FLSmidth Outotec

New equipment

More decline in end-

user demand in 2014

than 2013, but less

destocking by dealers.

Overall more than 20%

decline.

Surface - remains soft;

Underground -

reasonable

N.A.

Satisfactory with

volatility expected to

continue

Some macro positive

signs but not

necessarily leading to

improved mining

business. Copprt good

but outlook for coal

deteriorated.

Continued slowness in

mining capex spending

Service Flat in 2014 Good

Customer sentiment is

gradually improving -

US coal recovering,

Australia stablizing

Good & expect

aftermarket destock to

finish by end 2013

See aftermarket growth

at around 5%+ through

cycle going forward.

Relatively good shape

except coal. Difficult to

cut opex with mines

running at full capacity.

Remain solid due to the

need to optimize

operations

Demand OutlookUPSTREAM DOWNSTREAM

First time saw

stabilisation of demand

Stable

Sentiment towards mining equipment players remains low: We believe against a backdrop of low sentiment

to mining equipment players there is opportunity among those names with greater exposure to aftermarket; Atlas

Copco (60% aftermarket) and Fenner (85% aftermarket). At Sandvik we see relatively higher volume risk due to

its greater exposure to new equipment and on pricing in the more competitive crushing and grinders market.

We have a -21% mining OE decline in our forecasts in 2015: For the mining equipment players we forecast

new equipment to decline by -16% and -21% in 2014 and 2015. We believe this is also supported by comments at

3Q13 results for Sandvik (demand in mining showed signs of stabilization at low levels in 3Q) and Atlas Copco

(sequentially orders for underground mining were stable). Taking 3Q order levels as a run rate in to 2014 would

imply order declines broadly in line with our -16% 2014 forecast.

Mine Production should grow in 2014: In mining aftermarket we forecast 2014 and 2015 to grow by 5% based

on continued increases in mine production. Despite mine production growing in 2013 we believe that aftermarket

demand in 2013 is broadly flat due to destocking that took place across the 1H13.

Retain positive view on Atlas Copco (OP) & Fenner (OP), cautious on Sandvik: We see greater risk to

consensus at Sandvik and see scope for Atlas to re-rate relatively vs Sandvik as it currently is only at a 10%

premium on 2014E EV/EBITA. We believe this under-appreciates remaining Compressors and Industrial

Technique businesses. Fenner trades at a 28% discount to the UK sector on 2014E, which we also view as

attractive.

Source: Company data, Credit Suisse research

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fenner Weir Atlas CAT Metso Sandvik FLS Outotec

New Equipment A/market

Theme#3 Mining aftermarket: Mine production growing in 2014/15

-

20,000

40,000

60,000

80,000

100,000

120,000

2008 2009 2010 2011 2012 2013E 2014E 2015E

Large Diversified Miners Smaller Focused Players

Total- June forecast

60

80

100

120

140

160

180

2011 2012 2013E 2014E 2015E

COAL- Oct COPPER- Oct IRON ORE- Oct

PRECIOUS- Oct COPPER- June IRON ORE- June

COAL- June PRECIOUS- June

2012 2013E 2014E 2015E 2013-15

Iron Ore 1.8% 7.3% 12.9% 7.6% 9.3%

Met Coal 6.4% 6.4% 6.2% 6.7% 6.4%

Therm Coal 10.2% 5.1% 2.4% 3.9% 3.8%

Copper 3.5% 4.5% 4.4% 4.2% 4.4%

Aluminium 4.8% 5.0% 6.4% 5.4% 5.6%

Zinc 11.1% 5.7% 3.2% 3.6% 4.2%

Silver -2.5% -2.8% -0.1% 0.4% -0.8%

Platinum -7.8% 1.3% 2.3% 0.9% 1.5%

Total Average 3.4% 4.1% 4.7% 4.1% 4.3%

Our forecasts of -16% and -21% declines in NE in 2014/15 are based on the capex forecasts of 90 miners covered by CS.

According to CS mining analysts, mine production is expected to continue to rise in 2014/15 supporting aftermarket growth.

Fenner and Atlas have the largest exposure to mining aftermarket, which we view as favorable.

Coal in the US was the first commodity to see declines and it is now stabilizing at an earlier stage, which we view as positive

for Fenner.

Source: Company data, Credit Suisse estimates for aftermarket exposure

15

#3: Mining aftermarket: Equipment players valuations

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Nov-

04

Nov-

05

Nov-

06

Nov-

07

Nov-

08

Nov-

09

Nov-

10

Nov-

11

Nov-

12

Nov-

13

Atlas EV/EBIT vs Mechanicals

Through-cycle Average (2004-07)

-20%

-10%

0%

10%

20%

30%

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Nov

-08

Nov

-09

Nov

-10

Nov

-11

Nov

-12

Nov

-13

Sandvik EV/EBIT vs Mechanicals

Through-cycle Average (2004-07)

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Nov-

04

Nov-

05

Nov-

06

Nov-

07

Nov-

08

Nov-

09

Nov-

10

Nov-

11

Nov-

12

Nov-

13

Metso EV/EBIT vs Mechanicals

Through cycle average (2004-07)

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Nov

-04

Nov

-05

Nov

-06

Nov

-07

Nov

-08

Nov

-09

Nov

-10

Nov

-11

Nov

-12

Nov

-13

Fenner EV/EBIT vs UK industrials

Through-cycle average (2004-07)

Relative Atlas Copco 2014E EV/EBITA: We view the broadly

in-line with the sector valuation as attractive

Relative Sandvik 2014E EV/EBITA: Despite de-rating we

continue to see a risk to consensus forecasts

Fenner 201E4 EV/EBITA: We are 5% ahead of consensus and

believe upgrades can drive further a further re-rating for Fenner

Relative Metso 2014E EV/EBITA: The focus currently is on

the value of the individual segments due to the group splitting

Source: Thomson Reuters

16

Theme #4: Stabilization should allow Electricals to re-rate

Prysmian T&I 10%

Rest of group90%

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

ABB Power Products Siemens I&C Prysmian T&I

Siemens Infrastructure &

Cities14%

Rest of group86%

ABB Power Products + Systems

34%

Rest of group66%

ABB 2012 EBITDA split Prysmian 2012 profit split

We believe that, given the share of profits ABB Power

(particularly Systems), Siemens I&C and Prysmian’s T&I

divisions account for, they are given undue focus by the

market.

Increasingly at ABB’s, Siemens’ and Prysmian’s

underperforming businesses there are signs of stabilization and

even of improving profitability. Also at Siemens a new CEO

may result in a refreshed strategy for I&C.

We believe this stabilization can drive a re-rating for the overall

groups. In our view, the higher quality businesses of the group,

for example, ABB’s Automation business, are currently being

undervalued relative to its peers.

Siemens 2012 profit split

4Q MAV margins of underperforming Electricals divisions

Source: Company data, Credit Suisse estimates of profit split

17

#4: Electricals’ acquisitions should further improve business mix

0%

4%

8%

12%

16%

0

2000

4000

6000

8000

10000

ABB (to 1x) Siemens (1x Ind net debt) Prysmian (to 1.5x)

Acquisition firepower (€mn) Earning accretion scenario (RHS)

Date Company acquired End market

Sep-13 ELIBI Elektrik Low Voltage

Aug-13 Newron System Building Automation software

Jul-13 Alstom's Ring Motor Business Process Automation motors

May-13 Los Gatos Research Gas measurement

Apr-13 Power-One Solar Power Invertors

Feb-13 APS Technology Group Shipyard automation

Sep-12 Amarcon BV Shipping software

Aug-12 Newave Energy Holding SA Uninterruptible Power Supply

Jun-12 Tropos Networks Inc Wireless communications

May-12 Thomas & Betts Low Voltage

Date Company acquired End market

Jul-13 Service Guide Inc Metals and Mining

Jun-13 Preactor Group Industry Software

Nov-12 Invensys rail Rail signalling

Nov-12 LMS International Industry Software

Oct-12 Kineo CAM Industry Software

Sep-12 Perfect Costing Solutions GmbH Industry Software

Aug-12 Penrith Corporation Healthcare

Aug-12 Kaon Holdings Pty Ltd Power Transmission

Jul-12 Senergy Sistemas de Medição S.A Smart Metering

Apr-12 FCE Metals and Mining

Mar-12 Expro Measurements Division Subsea Oil & Gas

ABB

Siemens

Recent acquisitions by ABB and Siemens Based on re-leveraging below we show ABB, Siemens & Prysmian’s fire

power and an earnings accretion scenario based on this firepower

The recent strategy for ABB and Siemens has been to acquire in

end markets away from their underperforming divisions (excluding

Invensys rail which improved the business mix of I&C).

In our view this active acquisition strategy, particularly in Industry

automation software, improves their competitive offering and

therefore the medium term growth prospects and is supportive of

an overall re-rating for the groups.

We believe that, based on re-leveraging, acquisitions can drive

15% and 8% EPS accretion at ABB and Siemens, respectively. We

expect ABB to continue to acquire across the Automation end

market and Siemens’ focus to be on Process Automation

Source: Company data, Credit Suisse estimates

18

Theme #5: Balance sheet re-leveraging

0%

1%

2%

3%

4%

5%

6%

7%

8%

Prys

mia

n

Assa

Abl

oy

ABB

Alfa

Lav

al

Atla

s C

opco

Schn

eide

r

Legr

and

Met

so

Nex

ans

SKF

Sand

vik

Kone

Siem

ens

Elec

trolu

x

Philip

s

Alst

om

Schi

ndle

r

Geb

erit

Average acquisition impact on sales (2007-12)

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

Sch

indl

er

Geb

erit

Ren

isha

w

Kon

e

Rot

ork

Bod

ycot

e

Spi

rax

Sar

co

Alfa

Lav

al

AB

B

Sen

ior

Spe

ctris

Hal

ma

Phi

lips

IMI

GK

N

Ele

ctro

lux

Met

so

Fenn

er

Legr

and

Atla

s C

opco

Mor

gan

Adv

. Mat

s.

Sie

men

s

Ves

uviu

s

Sch

neid

er

Laird

SK

F

San

dvik

Pry

smia

n

Wei

r G

roup

Ass

a A

bloy

Sm

iths

Als

tom

Nex

ans

Mel

rose

2014 net Debt/EBITDA 2007-12 average net debt/EBITDA

Average 2007-12 acquisition impact on sales

Companies with low leverage vs history are GKN, Fenner, Legrand, Sandvik, Bodycote, GKN, Senior, Spectris & Vesuvius

Source: Company data, Credit Suisse estimates

We would expect Legrand and Assa to continue on

their bolt on strategy.

We see scope for Siemens to acquire in the Process

Automation space.

We believe ABB may focus on expanding their

offering in valves through acquisitions.

We believe share buybacks are most likely at Atlas

Copco, Alfa Laval.

UK names most likely to acquire include Spectris,

Rotork, Bodycote, Melrose and Senior.

19

#5: Balance sheet re-leveraging – where is the potential

Source: Company data, Credit Suisse estimates

2014 Net Debt /

EBITDA

5 year

averageManagement comments / Previous corporate action

ABB 0.10x -0.32xTarget 3-4% inorganic sales CAGR. Recent acquisition focus in automation including Baldor ($4.2bn, Motors) and Thomas & Betts ($3.9bn,

Low Voltage). Buybacks less of a focus

Legrand 0.66x 1.26xStrategy of bolt on acquisitions predominantly in emerging markets. Added on average 5% to sales in 2011 and 2012 but this will fall to

c2.5% in 2013.

Siemens 0.92x 1.00xAnnounced a €3bn buyback in 2012 and a €4bn buyback in 2013. Recent acquisitions included Invensys rail for €2bn and also in Automation

software. An end market targeted for further expansion is Process Automation

Alfa Laval -0.17x 0.31xThe company has a track record of returning cash to shareholders and targets c4% growth from acquisitions per annum. We see a fair

probability of a special distribution in 2014.

Assa Abloy 1.33x 1.65xOne of the best quality 'Acquire & Restructure' models in the sector with a healthy pipeline of further deals. We expect acquired growth of

8.6% for 2014 and 8.2% for 2015.

Atlas Copco 0.74x 0.78xA very consistent track record of returning excess cash to shareholders in absence of acquisitions combined with a stream of successful bolt-

on deals. We do not discount further acquisitions beyond Edwards but expect a cSEK 5bn cash return.

Electrolux 0.49x 0.51xHistorically the company has returned cash to shareholders but the more recent focus has been on investment in growth internally and on

building up an acquisitions pipeline.

Kone -0.80x -0.74xConsistently has returned excess cash to shareholders. With special dividend announced at Q3 2013 results, we see a small probability of

an extra distribution over the next 6-9 months. Continue to target small bolt on service acquisitions.

Schindler -1.34x -1.62xHas returned some excess cash to shareholders in the past. The recent fixed price buyback offer would have amounted to c7% of share

capital but was only c30% taken up.

Bodycote -0.37x 0.54xHas returned cash to shareholders in the past but the recent focus has been more on bolt-on acquisitions. In absence of sizable deals over

the next 6 months, we would expect a cash distribution.

Halma 0.17x 0.33xStrategy of bolt on acquisitions and in FY12/13 Halma made six acquisitions. We believe their focus going forward will be on Health &

Analysis and estimate an average deal multiple of 9x EV/EBIT. We estimate at 2x net debt / EBITDA Halma has c£300m of firepower.

IMI 0.48x 0.52xIMI's acquisition strategy is to expand in to Process with the last three acquisitions including in Fluid Power and Severe Service. We

estimate IMI have £600m of firepower assuming releveraging to 2x net debt / EBITDA

Melrose 2.15x 1.42xMelrose have disposed of Crosby / Acco, Truth & Marelli in 2013. Bridon likely to go in 2014 and Energy in 2015. Management have stated

they are on the look out for the next deal. We believe the target size would be £3bn EV which would result in a rights issue.

Spectris 0.00x 1.12x

We estimate Spectris has c£470m of firepower upon releveraging to 2x net debt / EBITDA. We think acquisition focus will include Industrial

controls while maintaining their current global sales exposure. In 2012 their acquired Omega (now rolled out to China) for £290m implying an

12x EBIT acquisition multiple.

20

Theme #6: Competitive Risk

We believe competitive risk will become a more prominent theme in 2014 than it has been in 2013.

Key end markets where we see the risks increasing are bearings due to Japanese competitors benefitting from a

weakening Yen and also because of Chinese bearings makers increasingly focusing on higher end bearings. SKF in 2Q

and 3Q reported negative price mix and we believe with increasing competition this is unlikely to change in 2014.

We also believe the risks are increasing in the Crushing and Grinders segment (Sandvik, Weir & Metso) in mining

equipment with large Chinese players, such as Citic Heavy, gaining prominence and also gaining their first systems

contract in Europe in 2014.

Risk Rating 1 2 3 4 5

High Power Gen.(Coal)

Appliances, T&D

Bearings

Trucks

Mining Equipment - Crushers & Grinders

Medium Drive systems

Transport

O&G (Fracking)

Heat exchangers

Elevator

Low

Heat Treatment

Timeframe in years

Automation

Construction Equipment

Low Voltage equipment

Auto components

Mining Equipment

Risk Rating 1 2 3 4 5

High Alstom

Electrolux

ABB

Medium Philips

Sandvik

Atlas Copco

Low

Volvo, Man, Scania

SKF

Metso

Timeframe in years

Alfa Laval

Kone, Schindler

Legrand

Geberit

Schneider

Source: Credit Suisse research

21

#6: Charting the competitive risk

-15%

-10%

-5%

0%

5%

10%

15%

20%

SKF Qianchao(QC)

Wafangdian(ZWZ)

Tianma(TMB)

Longxi (LS) Xiangyang(ZXY)

Zhouyan Keji(ZYS)

Xibei (NXZ) Nanfang(NF)

ZhonghangHazhou(ZHHZ)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Total Revenue (RMB m) Bearing revenue (RMB m) Total EBIT margin

COMMUNITION

Crushing Grinding Screening Pumps Cyclones Concentration Refining

Atlas Copco Y

Sandvik Y Y

Astec Y Y Y

FL Smidth Y Y Y Y Y Y Y

Metso Y Y Y Y Y

Thyssen Krupp Y Y Y

TENOVA Y Y Y Y

FAM Y Y

Weir Y Y Y Y Y

CITIC HEAVY Y Y

SLURRY PROCESSING

European

Companies

Japanese

CompetitorsArea of Business

Relevance for

European

competitor

ABB Yokogawa Process Automation Low

Fanuc Discreet Automation (Robots) Low

Alstom Mitsubishi Heavy Thermal Power Division Medium

Atlas Copco Furukawa MRET and Construction Low

Furukawa Low

Komatsu Low

Kawasaki Low

SumitomoSandvik Tooling and Material

Technology Low

Kyocera Sandvik Tooling Medium

Mitsubishi Sandvik Tooling Medium

Furukawa Mining and Construction Low

Hitachi Material Technology Low

Mitsubishi Heavy Power Transmission & Fossil Power Medium

Toshiba Healthcare, Turbines Low

Hitachi Healthcare Low

Fanuc Drive Technology Low

NSK High

NTN High

JTEKT High

THK Actuation Motion Control Low

Metso Construction

Sandvik

Siemens

SKFBearing & Units

Chinese players are taking share from SKF and focusing on high end bearings

(rectangles indicate companies focused on export and rectangles on high end bearings)

Crushing & Grinding is a competitive mining sub-segment with prominent Chinese players

We also see risk for SKF from Japanese players in a sustained weak

Japanese Yen environment

100

110

120

130

140

150

Dec-12

Dec-12

Jan-13

Jan-13

Feb-13

Feb-13

Mar-13

Mar-13

Apr-13

Apr-13

Apr-13

May-13

May-13

Jun-13

Jun-13

Jul-13

Jul-13

Aug-13

Aug-13

Sep-13

Sep-13

Sep-13

Oct-13

Oct-13

Nov-13

Nov-13

Dec-13

EUR/JPY

xCS forecasts (next 12m): 148.8

Source: Company data, Bloomberg, Credit Suisse research

22

#6: Greatest structural competition risk continues to be for Alstom

0%

20%

40%

60%

80%

100%

2008 2013

General Electric Siemens Mitsubishi Alstom Other

We continue to see the greatest medium term structural risk for Alstom. This is primarily due to its sub-scale gas turbine

business and greatly reduced market share in steam turbines. In Rail Alstom has a c15% global market share but has

two large Chinese competitors in China Southern Rail and China Northern Rail.

In Gas Turbines Alstom had 4% market share in 2013 vs 5% in 2012. However, in that time Mitsubishi has increased its

share to 22% from 12% meaning there are now three established players in this market (GE, Siemens & Mitsubishi)

with combined 85% market share.

In Steam turbines (even excluding Chinese players which dominate China – the world’s largest market) Alstom’s share

fell to 5% in 2011 having been 9% between 2002-11.

We also remain concerned that an emerging threat for Alstom on the Power services side is the risk of Utilities trying to

offset weak earnings by potentially taking part of Power Plant servicing in-house to reduce their costs. This would

primarily negatively impact Alstom due to its large European Installed base.

0%

20%

40%

60%

80%

100%

2002-11 2011

BHEL Siemens Toshiba GE MHI Alstom Other

Global Gas Turbine market shares (2013 vs 2008) Steam turbine market shares (ex China) in 2011 vs shares between 2002-11

Source: McCoys, Company data, Credit Suisse research

23

Theme #7: Sector M&A

In 2013, we have seen further M&A within the

sector with Invensys taken out by Schneider

post Siemens acquiring the Rail segment.

We have re-run our HOLT CFROI M&A Screen

for the Pan European Capital Goods universe

with analysis over 6 criteria. We would highlight

the following names from the Screen:

From companies that met 5 criteria

Alfa Laval

Fenner

Legrand

Rotork

From companies that met 4 criteria

Smiths Group

Spectris

Weir

From companies that met 3 criteria

IMI

Score Company

Mkt Implied

CFROI below

1Fail and 5

year

median

CFROI FY1

above 8%

hurdle WACC

CFROI

improvement

expected in

FY1 over

FYFail

Consensus

estimates not

greater than

the median

FY1 Net

Debt/EBITDA

less than

2.Failx

Sustainable

Growth Rate

is greater

than 5%

6 ABB LIMITED Pass Pass Pass Pass Pass Pass

5 ALFA LAVAL AB Pass Pass Pass Fail Pass Pass

5 ASSA ABLOY AB Fail Pass Pass Pass Pass Pass

5 FENNER PLC Fail Pass Pass Pass Pass Pass

5 HALMA P.L.C. Pass Pass Pass Fail Pass Pass

5 KABA HOLDINGS AG Pass Pass Pass Pass Pass Fail

5 KONINKLIJKE PHILIPS NV Fail Pass Pass Pass Pass Pass

5 LEGRAND S.A. Pass Pass Pass Fail Pass Pass

5 ROTORK P.L.C. Pass Pass Pass Fail Pass Pass

4 ALSTOM SA Pass Pass Fail Fail Pass Pass

4 GEBERIT AG Fail Pass Pass Pass Pass Fail

4 KONE OYJ Fail Pass Pass Pass Pass Fail

4 SANDVIK AB Pass Pass Pass Fail Pass Fail

4 SCHINDLER HOLDING AG Pass Pass Fail Fail Pass Pass

4 SCHNEIDER Pass Pass Fail Fail Pass Pass

4 SMITHS GROUP PLC Pass Pass Fail Fail Pass Pass

4 SPECTRIS PLC Pass Pass Fail Fail Pass Pass

4 VESUVIUS PLC Fail Pass Pass Pass Pass Fail

4 WEIR GROUP PLC (THE) Pass Pass Fail Fail Pass Pass

3 ATLAS COPCO AB Pass Pass Fail Fail Pass Fail

3 IMI PLC Fail Pass Fail Fail Pass Pass

3 LAIRD PLC Fail Pass Pass Fail Pass Fail

3 MELROSE INDUSTRIES PLC Pass Pass Fail Fail Fail Pass

3 METSO OYJ Pass Pass Fail Fail Pass Fail

3 PRYSMIAN SPA Pass Pass Fail Fail Fail Pass

3 RENISHAW PLC Fail Pass Fail Fail Pass Pass

3 SENIOR PLC Fail Pass Fail Fail Pass Pass

3 SIEMENS AG Pass Pass Fail Fail Pass Fail

3 SKF AB Fail Pass Pass Fail Pass Fail

3 SPIRAX-SARCO ENGINEERING PLC Fail Pass Fail Fail Pass Pass

2 MORGAN ADVANCED MATERIALS PLC Fail Pass Fail Fail Pass Fail

1 BODYCOTE PLC Fail Fail Fail Fail Pass Fail

1 ELECTROLUX AB Fail Fail Fail Fail Pass Fail

1 GKN PLC Fail Fail Fail Fail Pass Fail

0 NEXANS SA Fail Fail Fail Fail Fail Fail

Criteria

Source: Credit Suisse HOLT®

24

Sector Performance

25

Growth and margin expectations for 2014

2.7%

1.4%

0.7%

0.4%

5.0%

4.4%4.2%

4.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

post 1Q13 post 2Q13 post 3Q13 Current

2013 organic growth forecast 2014 organic growth forecast

7.2%

6.4%

13.4%

11.4%

5.9%

-12.7%

6.4%

11.6%

3.5%

0.4%

4.0% 4.5%

10.0%

11.1%

12.2%

13.1%

11.1%

13.8%

14.6%

14.4%14.3%14.8%15.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-18.0%

-14.0%

-10.0%

-6.0%

-2.0%

2.0%

6.0%

10.0%

14.0%

18.0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013E

2014E

2015E

Sector EBIT margin, % Sector organic growth, %

Sector organic growth and margin forecast CS revisions to 2013 and 2014 organic growth forecasts YTD

We forecast 4% organic growth for the sector in 2014 and 40bps of margins expansion. The key drivers of margin expansion

in 2014 are 1) on-going cost cutting programmes across the sector (we assume c50% retention), 2) benign raw material

environment.

In 2013 organic growth disappointed with our expectations having declined by 230bps YTD. In that time expectations for

2014 have moderated by 100bps.

In our view, despite improvements in lead indicators, we find it moderately concerning that this has not filtered through to

demand in Europe for some of the shorter-cycle companies in the sector – SKF guides for sequentially flat demand in Q4.

Therefore, we believe the risk on 2014 consensus organic growth is somewhat to the downside, in particular as Q3

destocking in Europe continued to negatively impact volumes for Legrand and Schneider. In our view, this continues to be a

risk to the assumption of an strong European volume recovery in early 2014, most notably in France.

Source: Company data, Credit Suisse estimates

26

Lead indicators are supportive of a gradual 2014 recovery

Q1 Q2 Q3E Q4E Q1 Q2 Q3 Q4 12 13E 14E 15E

Global Real GDP (y/y) 2.4 2.7 2.9 3.2 3.6 3.6 3.7 3.8 3.1 2.9 3.7 3.9

US Real GDP (q/q ann) 1.1 2.5 2.8 1.9 2.5 2.7 3.0 3.0 2.8 1.7 2.6 2.8

Euro Area Real GDP (q/q ann) -0.9 1.1 0.4 1.3 1.3 1.4 1.8 1.5 -0.6 -0.4 1.3 1.7

China Real GDP (y/y) 7.7 7.5 7.8 7.7 7.7 7.7 7.8 7.7 7.7 7.6 7.7 8.2

India Real GDP (y/y) 4.8 4.4 5.2 5.9 6.2 6.7 6.8 6.7 5.0 5.4 6.6 6.9

Annual Average2013 2014E

-4%

0%

4%

8%

12%

16%

2011 2012 2013 2014

Global IP Euro area IP US IP China IP

In Europe the PMI has remained marginally above the 50 level for four months indicating growth, but at a moderate

level. The US ISM has indicated a stronger environment with its third consecutive reading >60 in Oct.

The CS Economics team forecasts global GDP growth of 3.7% in 2014 and Global IP growth of 4.4% (1.7% in EU).

20.00

30.00

40.00

50.00

60.00

70.00

Nov-04 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11 Nov-12 Nov-13

EU PMI new orders US ISM new orders China PMI new orders

Source: Company data, Credit Suisse research

27

Pricing: Broadly similar trends in 2014 as in 2013

Automotive3%

General industrial14%

Construction Res6%

Construction non Res16%

Oil & Gas4%

Mining6%

Power T & D10%

Power Gen 12%

Transport 7%

Medical9%

Consumer/ Appliances

10%

Other3%

Sector exposure by geography

West Europe

38%

US20%

Emerging Mkt39%

Others3%

CS estimate of pricing as a % of sales per year by end market

We believe pricing trends will remain broadly similar in 2014 to 2013 but we

believe the end markets where there is the greatest risk of pricing taking a more

negative step-down is the bearings market.

We believe the end markets seeing the greatest pricing pressure are Healthcare

equipment (due to Japanese players lowering prices) and Gas turbines (due to

low demand levels) which are running at -4% to 5% of sales per year.

Our current assumption is that bearings are not seeing negative pricing pressure.

However, we believe this is the end market where pricing is most likely to worsen

in 2014/15 with the Chinese market being most vulnerable, followed by Emerging

markets where Chinese players have greatest scope to accelerate the exporting

of locally produced bearings (EM is 40% of SKF’s revenues).

Sector exposure by end-market

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

Gas Turbines Healthcare LargeTransformers

Constructioncables

Appliances Miningaftermarket

Bearings Low Voltage

Pricing pressure as a % of sales

Source: Company data, Credit Suisse estimates

28

Margin driver #1: Cost cutting

Those companies we believe have potential to surprise

positively on cost savings are Prysmian and Assa Abloy.

The Electricals cost savings in 2014E are relatively

higher than the Mechanicals but the Electricals end

markets (Healthcare, Power Gen) are also those seeing

greatest pricing pressure.

A driver of share price outperformance in 2012 and

1H13 was cost cutting (Philips & Electrolux), but we

believe programmes across the sector are now well

understood by the market.

Broadly across the sector we assume a 50% retention

rate for cost savings in our models.

For SKF we currently discount the full SEK3bn of

savings by 2015 and therefore see limited scope for

surprise.

Finally, c50% of cost savings targeting in the sector

relate to reduced sourcing cost reduction (eg using lower

cost component suppliers). We believe this trend may

pose a risk to companies such as SKF that sell higher

quality parts (bearings) in to larger products.

Source: Credit Suisse estimates

Cost savings as a % of sales 2013E 2014E 2015E

Electricals

ABB 2.6% 2.5% 2.4%

Alstom nm 2.4% 2.3%

Legrand nm

Nexans 0.5% 1.1% 1.6%

Philips 0.2% 0.2% 0.1%

Prysmian 0.5% 0.6% 0.3%

Schneider 1.3% 0.0%

Siemens 2.6% 4.7%

Electrical Average 1.3% 1.5% 1.1%

Mechanical

Alfa Laval 0.3%

Assa Abloy 0.7% 0.6%

Atlas Copco nm 0.2%

Electrolux 1.2% 0.9% 0.8%

Geberit nm

Kone 0.4%

Metso 0.8% 2.2%

Sandvik 1.2% 0.8% 0.8%

Schindler 0.0% 0.3% 0.2%

SKF 0.3% 1.4% 1.6%

Mechanical Average 0.6% 1.0% 0.9%

29

Margin Driver #2: Raw materials as a small tailwind

0

20

40

60

80

100

120

140

160

180

200

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Iron Ore Credit Suisse forecasts

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Copper Credit Suisse forecasts

1000

1500

2000

2500

3000

3500

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Aluminium Credit Suisse forecasts

The raw material environment was benign in 2013 and our CS

commodities team remains cautious on prices going in to 2014.

Their expectations are for copper prices at the end of 2014 to

have fallen by -14% from current levels and iron ore by -32%.

Most companies in the sector are relatively well hedged but we

believe a declining raw material price environment would be most

positive for Legrand, Schneider, Electrolux and SKF.

Current Electrolux guidance is for flat raw material impact on

EBIT in 2014, but it agrees the 2014 hedging price for steel in

4Q13. Therefore, a decline in steel prices is unlikely to benefit

Electrolux until 2015 (having hedged at a lower price in 4Q14).

Source: Thomson Reuters, Credit Suisse research

30

Sector Valuations

31

Valuation: We are currently at Mid-cycle multiples

8%

9%

10%

11%

12%

13%

14%

15%

16%

17%

0.50

0.70

0.90

1.10

1.30

1.50

1.70

1.90

Nov-0

3

Ma

y-0

4

Nov-0

4

May-0

5

Nov-0

5

Ma

y-0

6

Nov-0

6

Ma

y-0

7

Nov-0

7

Ma

y-0

8

Nov-0

8

Ma

y-0

9

Nov-0

9

Ma

y-1

0

Nov-1

0

Ma

y-1

1

Nov-1

1

Ma

y-1

2

Nov-1

2

Ma

y-1

3

Nov-1

3

Sector EV/Sales Sector underlying EBIT margin

6

7

8

9

10

11

12

13

14

Nov-03 Nov-05 Nov-07 Nov-09 Nov-11 Nov-13

European Cap Goods EV/EBIT Average

On balance we have a neutral view on the sector as, with 12mth FWD EV/EBIT for the sector at 11.8x earnings,

earnings upgrades are needed to drive further share-price performance in 2014.

The sector has re-rated through 2013 and is now trading above its mid-cycle multiple. In our view, based on the

sector margin having reached a new peak, a higher through cycle average than 2004-2007 is justified. However, we

still believe there is 6% downside in the event of a return to mid-cycle multiples.

In our view earnings upgrades in the medium term will be driven by the top-line (volume and price) rather than by

margin improvements driven by cost savings. The sector is already at peak margins and with competition in areas

such as bearings and mining equipment increasing, we believe the scope for a further margin step up is limited.

We believe those companies that can surprise positively on the topline in 2014 are ABB, Assa Abloy, Prysmian,

Bodycote, Fenner, GKN & Spectris.

Source: Thomson Reuters, Credit Suisse research

32

Valuation: Preference for sub-sectors

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Nov-0

6

Ma

y-0

7

Nov-0

7

Ma

y-0

8

Nov-0

8

Ma

y-0

9

Nov-0

9

Ma

y-1

0

Nov-1

0

Ma

y-1

1

Nov-1

1

Ma

y-1

2

Nov-1

2

Ma

y-1

3

Nov-1

3

EV/EBIT (Elec vs Mech premium (discount))

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Nov-0

6

Ma

y-0

7

Nov-0

7

Ma

y-0

8

Nov-0

8

Ma

y-0

9

Nov-0

9

May-1

0

Nov-1

0

Ma

y-1

1

Nov-1

1

Ma

y-1

2

Nov-1

2

Ma

y-1

3

Nov-1

3

EV/EBIT (UK vs European premium(discount))

Looking at the performance of sub-sectors into the year end, the Electricals have rallied relative to the Mechanicals with

their share prices outperforming by 5% over the last three months. In terms of sector positioning we believe that in

Electricals, Siemens remains the best owned name, with short mining capex (and particularly Atlas Copco) being the

most common trade in Mechanicals.

Into 2014 we do not have a strong preference for Electricals vs Mechanicals but based only on valuation downside we

see greater scope for de-rating based on our valuation framework (on the next page) in Electricals (-8% potential

downside in a return to mid-cycle) vs the Mechanicals (-3%).

We believe the UK sector has 6% downside in a return to mid-cycle multiples but there has been the clear trend in 2013

of the higher quality names re-rating vs the UK industrial average. Among the high quality names, we prefer Halma and

also those names with secular growth drivers including Spectris (Automation) and Bodycote & GKN (Aerospace).

Source: Thomson Reuters

33

Valuation: 6% potential downside on mid-cycle multiples

L. Growth Mid-cycle L. Growth Mid-cycle L. Growth Mid-cycle

Electricals

ABB SFR 9.0 10.0 21.6 24.0 -7% 4%

Alstom EUR 7.5 8.5 18.7 23.0 -30% -14%

Legrand EUR 9.5 11.0 29.7 33.1 -25% -17%

Philips EUR 8.0 9.5 20.3 24.7 -22% -6%

Prysmian EUR 8.5 9.5 16.4 19.0 -14% -1%

Schneider EUR 8.5 10.0 45.5 55.2 -26% -10%

Siemens EUR 8.5 10.0 68.3 83.6 -30% -14%

Average Electricals 8.4 9.7 -22% -8%

Mechanicals

Alfa Laval SEK 9.0 11.0 114.6 139.5 -25% -9%

Assa Abloy SEK 10.0 12.0 210.2 259.7 -37% -22%

Atlas Copco SEK 9.0 11.0 128.7 160.2 -31% -14%

Electrolux SEK 7.5 9.5 154.1 200.0 -3% 26%

Geberit CHF 10.5 13.0 171.6 208.5 -36% -22%

Kone EUR 10.0 12.0 44.9 53.1 -35% -23%

Metso EUR 7.5 9.5 27.0 34.8 -10% 16%

Sandvik SEK 8.5 10.0 96.8 111.3 6% 21%

Schindler CHF 10.0 12.0 104.7 122.8 -17% -3%

SKF SEK 7.5 9.5 126.7 168.1 -29% -5%

Average Mechanicals 9.0 11.0 -22% -3%

UK

Bodycote GBP 8.0 9.5 5.3 6.2 -14% 1%

Fenner GBP 8.5 10.5 5.2 6.4 20% 46%

GKN GBP 7.0 8.5 2.8 3.5 -25% -7%

Halma GBP 9.0 11.5 3.6 4.7 -39% -21%

IMI GBP 8.0 10.0 9.5 12.1 -36% -19%

Laird GBP 7.5 9.0 1.6 2.0 -39% -24%

Melrose GBP 9.0 10.0 2.3 2.5 -23% -15%

Morgan Adv. Mats. GBP 7.0 8.0 2.7 3.1 -8% 7%

Renishaw GBP 10.0 12.0 12.0 14.2 -35% -23%

Rotork GBP 10.5 13.0 21.0 25.7 -27% -10%

Senior GBP 8.0 9.5 2.2 2.6 -22% -7%

Smiths GBP 8.0 10.5 13.7 17.3 0% 26%

Spectris GBP 8.7 10.5 16.3 19.7 -31% -17%

Spirax Sarco GBP 9.0 11.5 18.9 23.9 -35% -18%

Vesuvius GBP 7.5 9.0 3.3 4.1 -33% -17%

Weir Group GBP 9.0 11.0 16.9 21.3 -21% -1%

Average UK 8.4 10.3 -23% -6%

Pan-Euro Sector Average 8.6 10.4 -22% -6%

Target EV/EBITA (2014)Scenario Valuation using

Target EV/EBITA (2014)

Upside / (Downside) vs

current share price

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

Ele

ctric

al A

v.

Mec

hani

cal A

v.

UK

Av.

Sec

tor

Av.

Cyc

lical

Av.

Str

uctu

ral A

v.

Upside/ (Downside) vs current share price

Using target mid-cycle multiples for

companies and backing out the implied

share price using our forecasts, the

sector has -6% potential downside on a

return to these target multiples.

Having re-rated the structural growth

names show -18% potential downside

using this methodology and while

companies in our cyclicals category are

showing -3% potential downside.

Source: Credit Suisse estimates

34

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Nex

ans

Pry

smia

n

Sch

indl

er

Ass

a A

bloy

Ele

ctro

lux

Sie

men

s

San

dvik

Met

so

Gkn

Ves

uviu

s

Inve

nsys

Alfa

Lav

al

AB

B

Kon

e

SK

F

Sch

neid

er

Als

tom

Mor

gan

Cru

cibl

e

Bod

ycot

e

Spe

ctris

Sen

ior

Phi

lips

Laird IM

I

Ren

isha

w

Geb

erit

Hal

ma

Rot

ork

Spi

rax

Sar

co

Atla

s C

opco

Sm

iths

Gro

up

Wei

r

Legr

and

Fen

ner

2014 EV/EBIT premium / discount vs sector

2015 EV/EBIT premium / discount vs sector

Difference between 2015 and 2014 premium / discount (stocks on LHS look relatively cheapest on 2015 multiples vs 2014)

Valuation: Too early to look at the sector on 2015 multiples? Difference between 2015 and 2014 premium / discount to the sector –

Companies on the LHS of the chart look relatively cheaper vs the sector on 2015 EV/EBITA than on 2014.

We continue to believe that it is too early to start looking at companies on 2015 multiples. Currently, companies are indicating

broadly flat sequential demand in Q4 while consensus organic growth for the sector is c4% in 2014.

In our view the market will start looking at 2015 multiples at the end of 1Q14 and in this scenario we believe Schindler (OP)

(11% premium in 2015E) and Prysmian (OP) (-24% discount in 2015E) look relatively cheaper as compared to 2014 multiples.

On the above chart the higher quality names (IMI, Halma, Atlas Copco, Rotork & Spirax Sarco) look less attractive but clearly

the valuation focus for these stocks is the sustainability of longer term growth rather than a 2015 recovery in profitability.

Source: Company data, Credit Suisse research

35

ROIC – higher asset turns should be the future driver

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E

Sector average Mechanicals average Electricals average UK average

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E2014E2015E

Sector average Mechanicals average

Electricals average UK average

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E2014E2015E

Sector average Mechanicals average

Electricals average UK average

Since 2008/09 the sector has returned to 2008 ROICs driven by the

sector NOPAT margin achieving a new peak while asset turns have

declined (led by the Electricals sub-sector as they have invested in

working capital and R&D)

Current share prices are discounting ROICs to increase for the sector

on average and we believe for this to occur, given peak margin levels,

asset turns need to improve from current levels.

We believe companies positioned to deliver on this are Siemens (OP)

under a new CEO as it continues to take out cost following three years

of investing in the business. We also believe there is an opportunity for

improving asset turns at IMI (OP) across their remaining flow control

businesses

Source: Company data, Credit Suisse estimates

36

Cash conversion – we remain cautious on companies at the low end FCF conversion from clean net income 2004-2012

Companies that look attractive based on their

cash adjusted ROIC (cash conversion

multiplied by ROIC) are Prysmian, Senior and

Bodycote.

In the sector Legrand, Prysmian, Schindler

and Assa have the highest cash conversion

ratios driven by good working capital

management and limited restructuring

charges.

We remain cautious on those companies with

relatively weak cash conversion: Sandvik (UP),

Alstom (UP) and Morgan Adv. Mats (UP).

0%

20%

40%

60%

80%

100%

120%

140%

Legr

and

Pry

smia

n

Spe

ctris

Sch

indl

er

Ass

a A

bloy

Kon

e

Geb

erit

Hal

ma

Sch

neid

er

Alfa

Lav

al

Sen

ior

IMI

AB

B

Bod

ycot

e

Rot

ork

Sie

men

s

Nex

ans

SK

F

Met

so

Laird

Atla

s C

opco

Sm

iths

Fenn

er

Wei

r

Ren

isha

w

Mel

rose

Spi

rax

Ele

ctro

lux

Ves

uviu

s

San

dvik

Als

tom

Phi

lips

Mor

gan

Adv

. Mat

s

GK

N

Sector average

Alfa Laval

Assa Abloy

Atlas Copco

Electrolux

Kone

Metso

Sandvik

Schindler

SKF ABB

Alstom

LegrandNexans

PhilipsPrysmian

Schneider

Siemens

Bodycote

Fenner

GKN

Halma

IMI

Laird

Melrose

Morgan Adv. Mats

Renishaw

Senior Smiths Group

Spectris

Spirax

VesuviusWeir

Sector average

7

8

9

10

11

12

13

14

15

16

2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22% 24% 26% 28%

2014E

EV

/EB

IT

Cash Adjusted 2013-2014E ROIC

Geberit(ROIC 30.8%, EV/EBIT 16.7)

Rotork(ROIC 29.8%, EV/EBIT 14.1)

Source: Company data, Credit Suisse research

37

Key End Markets Outlook

38

End market forecasts

Source: Credit Suisse estimates

Key End Market Forecasts 2013E 2014E 2015E 2013E 2014E 2015E 2013E 2014E 2015E 2013E 2014E 2015E

Automotive -5% 3% 4% 5% 2% 4% 7% 7% 7% 2% 4% 5%

Automotive Aftermarket 2% 3% 3% 4% 3% 3% 7% 7% 7% 4% 4% 4%

Aerospace 7% 7% 6% 7% 7% 6% 7% 7% 6% 7% 7% 6%

Construction Residential -3% 2% 5% 15% 12% 10% 7% 8% 7% 6% 7% 7%

Construction Commercial -6% 0% 3% 5% 7% 7% 6% 8% 7% 2% 5% 6%

Construction Government -6% -2% 0% -2% 1% 5% 5% 5% 5% -1% 1% 3%

Consumer/ Appliances 1% 3% 5% 7% 10% 8% 8% 8% 7% 5% 7% 7%

Gen. Ind. Production 0% 2% 4% 2% 4% 5% 8% 10% 8% 3% 5% 6%

Gen. Ind. Capex -6% 0% 3% 3% 6% 6% 5% 5% 5% 1% 4% 5%

Gen. Ind. Aftermarket 3% 3% 4% 5% 5% 5% 7% 7% 7% 5% 5% 5%

Medical -4% -1% 4% -3% 3% 5% 10% 10% 8% 1% 4% 6%

Mining OE -30% -15% -5% -30% -15% -5% -30% -15% -5% -30% -15% -5%

Mining Aftermarket -7% 5% 5% -7% 5% 5% -7% 5% 5% -7% 5% 5%

Oil & Gas 3% 2% 3% 5% 4% 5% 8% 7% 7% 5% 4% 5%

Pulp & Paper OEM -10% -5% 0% -7% -3% 0% -5% 2% 3% -7% -2% 1%

Pulp & Paper Aftermarket -3% 0% 3% -3% 0% 3% 5% 5% 5% 0% 2% 4%

Power T&D -5% 5% 4% -3% 1% 3% 6% 6% 5% -1% 4% 4%

Power Generation -10% -6% 0% -3% 2% 4% 6% 6% 5% -2% 1% 3%

Transportation 4% 2% 2% 2% 3% 3% 8% 7% 7% 5% 4% 4%

Truck -3% -1% 2% 2% 9% 5% 8% 4% 5% 2% 4% 4%

Average -3.9% 0.4% 2.8% 0.2% 3.3% 4.4% 3.8% 5.4% 5.6% 0.0% 3.0% 4.2%

Europe North America Emerging Markets GLOBAL

39

Aerospace – strong growth expected in 2014 Airbus and Boeing production forecast

12 month rolling average aircraft orders

In Aerospace, we forecast growth of 7% in 2014.

Airbus and Boeing are seeing orders recovering

from a small trough in 2012, leading to higher

production volumes next year.

Long term demand for aircraft production is driven

by increasing demand for air travel worldwide and

growing international trade volume. Air passenger

traffic growth is geared on GDP around 2-3x.

Source: Company data, Credit Suisse research, KMT

40

Appliances – Emerging markets to drive growth, US recovery

Medium term growth expectation for appliances by Electrolux

Emerging markets are an important driver of European

companies’ performance in the appliances market.

US appliance market is expected to recover following the

housing recovery, while outlook for Europe is stable.

Online presence is becoming increasingly important with

85% of consumers looking at products on-line before

purchasing.

Consumers expect higher quality products for the same

price, as cost of appliances falling greatly for the past few

years – new product will be the main driver of

profitability.

Early stage of US Housing Recovery

US Appliance unit shipment outlook by Whirlpool

Source: Electrolux, Whirlpool

41

Automation – Value chain

Major players

PLM: Autodesk, Dassault, Siemens

ERP: Oracle, SAP

MES: Aspen, CDC Software, Invensys, Siemens

SCADA: ABB, Invensys, Siemens

DCS: ABB, Honeywell, Siemens, Yokogawa

PLC: ABB, Omron, Mitsubishi, Rockwell,

Schneider, Siemens

V ^ V ^

Computerized Numerical

Control (CNC)CNC: Fanuc, Siemens

V ^ V ^ V

V ^ V ^ Human Machine Interface (HMI)

Drives Sensors

Robots

MotorsMachine

Vision

Enterprise Level

Controls

Product Lifecycle Management (PLM)

Enterprise Resource Planning (ERP)

Manufacturing Execution System (MES)

Plant Level

Controls

Supervisory Control and Data Analysis (SCADA)

Process Factory

Distributed Control

System (DCS)

Programmable Logic

Controller (PLC)

HMI: ABB, Invensys, Mitsubishi, Siemens,

Schneider

Plant

InstrumentationValves Sensors Machine Tools

Sensors: ABB, Eaton, Honeywell, Omron

Machine Vision: Cognex, Teledyne

Drives: ABB, Danaher Mitsubishi

Robots: ABB, Fanuc, Kuka

Machine Tools: Gildemeister, Mori Seiki

Motors: ABB, Emerson, GE, Regal Beloit,

Rockwell, Schneider, Siemens, Weg,

Yaskawa

Source: Credit Suisse research

42

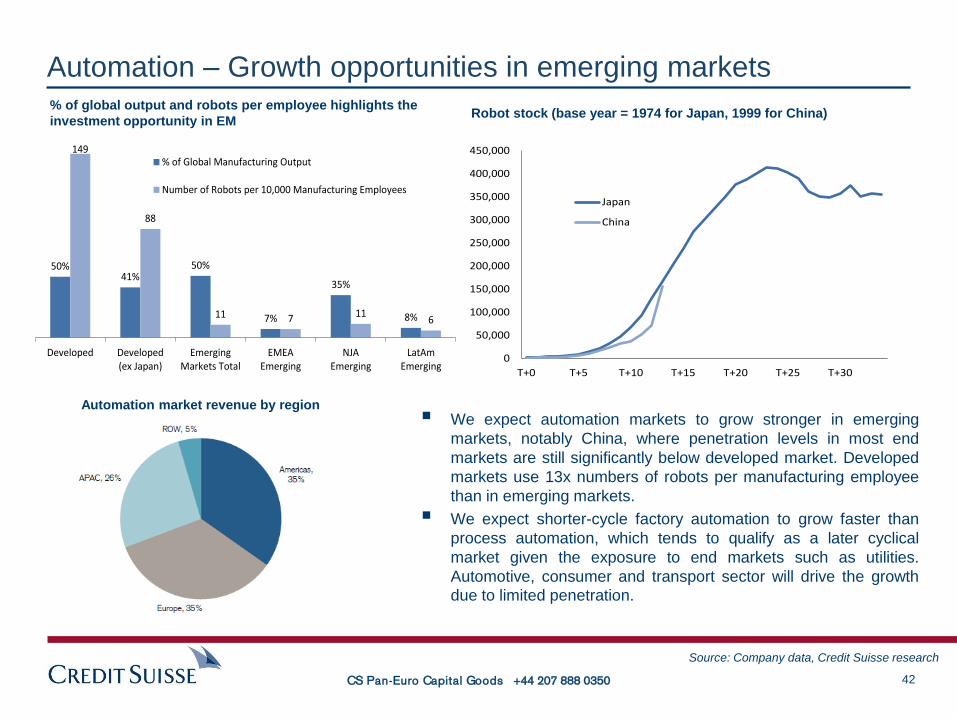

Automation – Growth opportunities in emerging markets

We expect automation markets to grow stronger in emerging

markets, notably China, where penetration levels in most end

markets are still significantly below developed market. Developed

markets use 13x numbers of robots per manufacturing employee

than in emerging markets.

We expect shorter-cycle factory automation to grow faster than

process automation, which tends to qualify as a later cyclical

market given the exposure to end markets such as utilities.

Automotive, consumer and transport sector will drive the growth

due to limited penetration.

% of global output and robots per employee highlights the

investment opportunity in EM Robot stock (base year = 1974 for Japan, 1999 for China)

50%41%

50%

7%

35%

8%

149

88

11 7 116

Developed Developed(ex Japan)

EmergingMarkets Total

EMEAEmerging

NJAEmerging

LatAmEmerging

% of Global Manufacturing Output

Number of Robots per 10,000 Manufacturing Employees

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

T+0 T+5 T+10 T+15 T+20 T+25 T+30

Japan

China

CS Pan-Euro Capital Goods +44 207 888 0350

Automation market revenue by region

Source: Company data, Credit Suisse research

43

Automotive – Sustained recovery into 2014

Global automotive production forecast by IHS

19.4 19.3 19.1 19.4

20.2 20.220.7

22.0

20.8

16.5

19.0

20.2

19.3 19.119.7

20.5

14.0

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

23.0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

E

20

14

E

20

15

E

Pro

du

ctio

n (

Mil.

Un

its)

Europe

17.2

15.516.4

15.9 15.8 15.815.3 15.1

12.6

8.6

11.9

13.1

15.416.2

16.817.5

7.0

9.0

11.0

13.0

15.0

17.0

19.0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08