Taiwan LED Sector - Credit Suisse | PLUS

52

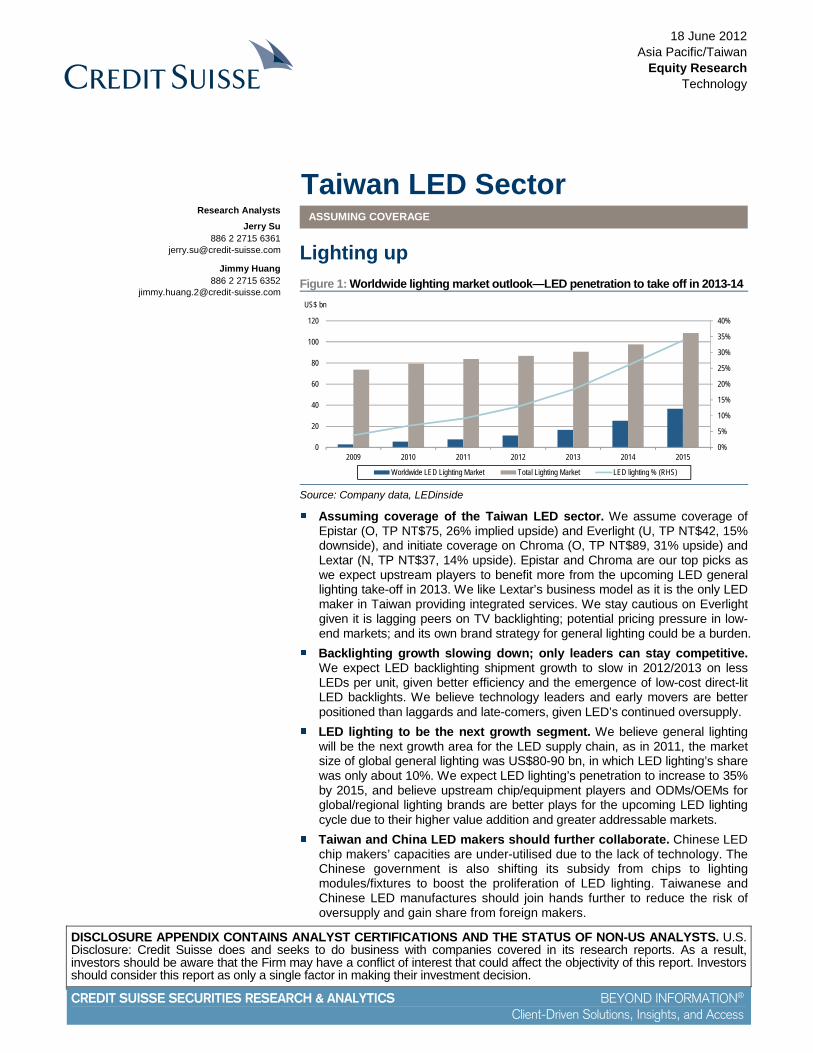

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 18 June 2012 Asia Pacific/Taiwan Equity Research Technology Taiwan LED Sector ASSUMING COVERAGE Lighting up Figure 1: Worldwide lighting market outlook—LED penetration to take off in 2013-14 0% 5% 10% 15% 20% 25% 30% 35% 40% 0 20 40 60 80 100 120 2009 2010 2011 2012 2013 2014 2015 US$ bn Worldwide LED Lighting Market Total Lighting Market LED lighting % (RHS) Source: Company data, LEDinside Assuming coverage of the Taiwan LED sector. We assume coverage of Epistar (O, TP NT$75, 26% implied upside) and Everlight (U, TP NT$42, 15% downside), and initiate coverage on Chroma (O, TP NT$89, 31% upside) and Lextar (N, TP NT$37, 14% upside). Epistar and Chroma are our top picks as we expect upstream players to benefit more from the upcoming LED general lighting take-off in 2013. We like Lextar’s business model as it is the only LED maker in Taiwan providing integrated services. We stay cautious on Everlight given it is lagging peers on TV backlighting; potential pricing pressure in low- end markets; and its own brand strategy for general lighting could be a burden. Backlighting growth slowing down; only leaders can stay competitive. We expect LED backlighting shipment growth to slow in 2012/2013 on less LEDs per unit, given better efficiency and the emergence of low-cost direct-lit LED backlights. We believe technology leaders and early movers are better positioned than laggards and late-comers, given LED’s continued oversupply. LED lighting to be the next growth segment. We believe general lighting will be the next growth area for the LED supply chain, as in 2011, the market size of global general lighting was US$80-90 bn, in which LED lighting’s share was only about 10%. We expect LED lighting’s penetration to increase to 35% by 2015, and believe upstream chip/equipment players and ODMs/OEMs for global/regional lighting brands are better plays for the upcoming LED lighting cycle due to their higher value addition and greater addressable markets. Taiwan and China LED makers should further collaborate. Chinese LED chip makers’ capacities are under-utilised due to the lack of technology. The Chinese government is also shifting its subsidy from chips to lighting modules/fixtures to boost the proliferation of LED lighting. Taiwanese and Chinese LED manufactures should join hands further to reduce the risk of oversupply and gain share from foreign makers. Research Analysts Jerry Su 886 2 2715 6361 [email protected] Jimmy Huang 886 2 2715 6352 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Taiwan LED Sector - Credit Suisse | PLUS

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

18 June 2012 Asia Pacific/Taiwan

Equity Research Technology

Taiwan LED Sector ASSUMING COVERAGE

Lighting up Figure 1: Worldwide lighting market outlook—LED penetration to take off in 2013-14

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014 2015

US$ bn

Worldwide LED Lighting Market Total Lighting Market LED lighting % (RHS)

Source: Company data, LEDinside

■ Assuming coverage of the Taiwan LED sector. We assume coverage of Epistar (O, TP NT$75, 26% implied upside) and Everlight (U, TP NT$42, 15% downside), and initiate coverage on Chroma (O, TP NT$89, 31% upside) and Lextar (N, TP NT$37, 14% upside). Epistar and Chroma are our top picks as we expect upstream players to benefit more from the upcoming LED general lighting take-off in 2013. We like Lextar’s business model as it is the only LED maker in Taiwan providing integrated services. We stay cautious on Everlight given it is lagging peers on TV backlighting; potential pricing pressure in low-end markets; and its own brand strategy for general lighting could be a burden.

■ Backlighting growth slowing down; only leaders can stay competitive. We expect LED backlighting shipment growth to slow in 2012/2013 on less LEDs per unit, given better efficiency and the emergence of low-cost direct-lit LED backlights. We believe technology leaders and early movers are better positioned than laggards and late-comers, given LED’s continued oversupply.

■ LED lighting to be the next growth segment. We believe general lighting will be the next growth area for the LED supply chain, as in 2011, the market size of global general lighting was US$80-90 bn, in which LED lighting’s share was only about 10%. We expect LED lighting’s penetration to increase to 35% by 2015, and believe upstream chip/equipment players and ODMs/OEMs for global/regional lighting brands are better plays for the upcoming LED lighting cycle due to their higher value addition and greater addressable markets.

■ Taiwan and China LED makers should further collaborate. Chinese LED chip makers’ capacities are under-utilised due to the lack of technology. The Chinese government is also shifting its subsidy from chips to lighting modules/fixtures to boost the proliferation of LED lighting. Taiwanese and Chinese LED manufactures should join hands further to reduce the risk of oversupply and gain share from foreign makers.

Research Analysts

Jerry Su 886 2 2715 6361

Jimmy Huang 886 2 2715 6352

18 June 2012

Taiwan LED Sector 2

Focus charts Figure 2: Worldwide high brightness LED market revenue

by application (2011)—backlighting leads

Figure 3: Worldwide high brightness LED market revenue

by application (2015E)—general lighting leads

Large size display BLU, 28%

Lighting, 24%Automotiv e, 12%

Sign & Signal, 10%

Others, 9%

Mobile application, 17%

Large size display BLU, 14%

Lighting, 52%

Automotiv e, 13%

Sign & Signal, 8%

Others, 6%

Mobile application, 7%

Source: Company data, LEDinside Source: Company data, LEDinside, Credit Suisse estimates

Figure 4: LED backlighting penetration will likely reach its

peak in 2013-14E

Figure 5: Mainstream TVs are shifting to low-cost direct

LED BLU starting 2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012E 2013E 2014E

Mobile PC LCD TV LCD Monitor Large Area Total

0%

10%

20%

30%

40%

50%

60%

25"-29" 30"-34" 35"-39" 40"-44" 45"-49" 50"-54" 55"-59"

Low cost direct LED BLU %

2011 2012 2013 2014

Source: Company data, DisplaySearch, Credit Suisse estimates Source: Company data, DisplaySearch, Credit Suisse estimates

Figure 6: Worldwide lighting market outlook—LED

penetration is still low but should take-off in 2013–14E

Figure 7: Architectural and indoor lighting are the main

drivers for LED lighting demand

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014 2015

US$ bn

Worldwide LED Lighting Market Total Lighting Market LED lighting % (RHS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015

US$ bn Architectural Outdoor Area/Grid LED Indoor Others YoY (RHS)

Source: Company data, LEDinside, Credit Suisse estimates Source: Company data, LEDinside, Credit Suisse estimates

18 June 2012

Taiwan LED Sector 3

Lighting up Backlighting: Only leaders can stay competitive LED backlighting is the main growth driver of the LED industry since 2009/2010 due to LED backlight TV proliferation. We expect LED shipment growth for display backlighting to slow down in 2012 and 2013 given less LEDs per unit as a result of better efficiency and the emergence of low-cost direct-lit LED backlight TVs. This is despite the likely improvement of LED penetration for monitors and TVs from 40-45% in 2011 to ~70% in 2012E and 85-90% in 2013E.

Given the continued oversupply in the LED industry, we think technology leaders and early movers are better positioned than laggards and late-comers. LED chips for TV applications have tighter specifications than that for smartphones or lighting, given concerns about display uniformity. We also think it will be difficult for late comers (i.e., Chinese LED makers) to penetrate into global leading panel makers given the supply chain is already crowded and it takes at least 6-12 months to pass the qualification.

LED general lighting: The next growth area We believe general lighting will be the next growth area for the LED supply chain as in 2011, the market size of global general lighting was US$80-90 bn, in which LED lighting’s share was only ~10%. We forecast LED lighting demand will grow from US$7.6 bn in 2011 to US$37 bn by 2015 (~35% penetration), representing a 48% CAGR over 2011-15. We think architectural and indoor lighting are the main drivers for LED lighting demand, given LED has the advantages of lower power consumption and longer life, and is more environment friendly than incandescent and fluorescent lamps.

We think upstream chip/equipment players and ODM/OEMs for global/regional lighting brands are better plays for the upcoming LED lighting cycle, given their higher value addition and greater addressable markets. The Taiwanese LED supply chain should have more opportunities in the fixtures market rather than in the retrofit market as global Tier 1 players only account for ~25% share of the fixtures market, while the remaining ~75% share is split between regional brands and new entrants. The fixtures market is also less price sensitive versus retrofit market given fixtures’ designs and functionality can be highly customised.

Taiwanese and Chinese LEDs should further tie-up Taiwanese LED makers are moving towards downstream, to increase their revenue/profit, and to build relationships with channels to secure their orders. We view the virtual alliance via vertical integration as a positive for Taiwanese LED makers, especially to capture the growing lighting demand. We think Chinese LED supply chain will witness another round of consolidation in the next few years given (1) a lack of core technology, (2) intense competition, (3) government policy change and (4) global economic slowdown.

Chinese LED chip makers’ capacities are under-utilised due to the lack of technology. The Chinese government is also shifting its subsidy from chips to lighting modules/fixtures to boost the proliferation of LED lighting. The Taiwan-China tie-up for LED should help Chinese lighting brands secure LED chips/packages and reduce the risk of oversupply for Taiwan LED makers; this should also help them gain share from foreign makers.

Assuming coverage of the Taiwan LED sector We assume coverage of the Taiwan LED sector. Our top pick in the sector are Epistar (O, TP NT$75) and Chroma (O, TP NT$89), as we expect upstream players to benefit more from the upcoming LED lighting take-off in 2013. We like Lextar’s (N, TP NT$37) business model as it has been qualified by global Tier 1 general lighting brands for providing ODM business. Moreover, AUO (major shareholder of Lextar with a 46% holding) will absorb Lextar’s output for TFT backlighting. We stay cautious on Everlight (U, TP NT$42) as it has been lagging peers in entering the LED monitor/TV backlighting space, and its strategy to capture the LED general lighting market via own brands could face intense competition from global Tier 1 brands as well as regional lighting brands.

Backlighting growth is slowing down, only leaders can stay competitive

LED lighting’s penetration to grow from ~10% of the market in 2011 to ~35% by 2015E

Taiwanese and Chinese LEDs should further tie-up to reduce oversupply risk and gain share from foreign brands

Epistar and Chroma are our top picks in the Taiwan LED supply chain

18 Ju

ne 2012

Taiw

an L

ED

Secto

r 4

Sector valuation Figure 8: LED supply chain—valuation comparison

Reporting Price Marketcap CS 12mthCompany Currency 6/14/2012 US$ mn Rating Target 2012 2013 2012 2013 2012 2013 2012 2013 2012 2013Taiwan LED upstream2448.TW Epistar TWD 59.6 1,714 O 75.0 0.88 2.73 67.9 21.8 51.4 53.3 1.2 1.1 1.7 5.2 3061.TW ForeEpi* TWD 20.6 331 NC NA NA NA NA NA NA NA NA NA NA NA3339.TWO Tekcore* TWD 15.7 144 NC NA (1.29) NA NM NA 16 NA 1.0 NA NA NA3383.TW Genesis Photonics* TWD 27.7 253 NC NA NA NA NA NA NA NA NA NA NA NA2340.TW Opto Tech* TWD 11.9 217 NC NA NA NA NA NA NA NA NA NA NA NA8199.TW Huga* TWD 12.7 220 NC NA NA NA NA NA NA NA NA NA NA NA3698.TW Lextar TWD 32.4 454 N 37.0 1.02 2.05 31.8 15.8 19.8 21.4 1.6 1.5 9.5 11.1 Taiwan LED downstream2393.TW Everlight TWD 49.2 689 U 42.0 2.77 3.39 17.8 14.5 35.9 37.1 1.4 1.3 7.2 8.5 2301.TW Lite-on* TWD 36.5 2,778 NC NA 3.58 3.74 10.2 9.8 33 33 1.1 1.1 11.2 11.9 3591.TW Edison* TWD 50.4 186 NC NA 2.20 2.84 22.9 17.7 30.2 28.1 1.7 1.8 6.5 8.4 2499.TW Unity Opto* TWD 29.1 327 NC NA NA NA NA NA NA NA NA NA NA NATaiwan LED component/equipment6271.TW Tong Hsing* TWD 91.8 499 NC NA 6.34 6.77 14.5 13.6 38.4 40.1 2.4 2.3 12.5 12.8 2360.TW Chroma TWD 68.0 856 O 89.0 4.09 5.55 16.6 12.3 21.7 24.0 3.1 2.8 23.1 23.7 China peers600703.SS Sanan Opto* CNY 14.3 3,231 NC NA 0.75 0.95 19.0 15.0 4.8 5.8 3.0 2.5 16.1 18.2 600100.SS Tsinghua Tofang* CNY 8.7 2,725 NC NA 0.49 0.82 17.8 10.7 4.7 5.2 1.8 1.7 8.8 9.7 002005.SZ Elec-tech Int'l* CNY 8.3 1,520 NC NA 0.57 0.68 14.6 12.2 3.7 4.4 2.2 1.9 13.6 15.5 600261.SS Zhejiang Yankon* CNY 12.4 1,255 NC NA 0.50 0.65 24.7 19.2 3.1 3.6 4.0 3.4 15.5 16.9 600460.SS Hangzhou Silan* CNY 4.9 668 NC NA 0.31 0.36 15.6 13.5 2.2 2.4 2.2 2.0 14.0 11.0 300102.SZ Xiamen Changelight* CNY 13.1 605 NC NA 1.33 1.00 9.8 13.1 7.3 7.8 1.8 1.7 14.4 13.6 Global peers009150.KS SEMCO KRW 108,500 6,946 N 97,000 4,569 4,791 23.7 22.6 43,628 47,607 2.5 2.3 11.0 10.6 011070.KS LG Innotek KRW 87,300 1,509 U 58,000 (463) 1,203 NM 72.5 62,920 63,623 1.4 1.4 (0.7) 1.9 038060.KQ Lumens* KRW 5,220 180 NC NA 587 733 8.9 7.1 3,610 4,342 1.4 1.2 18.0 18.3 046890.KQ Seoul Semi KRW 21,400 1,069 U 13,000 338 588 63.4 36.4 10,927 11,315 2.0 1.9 3.2 5.3 7282 Toyoda Gosei JPY 1,613 2,630 N 1,650 69 124 23.3 13.0 1,708 1,793 0.9 0.9 4.1 7.1 CREE Cree USD 23.05 2,677 N 32 0.93 1.33 24.7 17.4 22 24 1.0 1.0 4.4 5.7 Global equipmentAIXGn.DE Axitron* EUR 11.6 1,482 NC NA 0.06 0.55 183.8 21.0 6.0 6.4 1.9 1.8 NA NAVECO Veeco USD 33.0 1,282 N 32.0 1.58 2.42 20.8 13.6 NA NA NA NA 7.9 11.1 0522.HK ASM Pacific HKD 93.0 4,766 N 89.5 4.99 6.64 18.7 14.0 18.9 22.5 4.9 4.1 28.7 32.0

ROAE (%)EPS P/E (X) P/B (X)BVPS

Source: Company data, Credit Suisse estimates, *IBES consensus estimates for NR stocks.

18 June 2012

Taiwan LED Sector 5

Backlighting growth is slowing down: Only leaders can stay competitive We expect LED shipment growth for display backlighting to slow down in 2012 and 2013 due to less LEDs per unit as a result of better efficiency and the emergence of low-cost direct-lit LED backlight TVs. This is despite the likely improvement of LED penetration for monitors and TVs from 40-45% in 2011 to ~70% in 2012E and 85-90% in 2013E. Given the continued oversupply in the LED industry, we think technology leaders and early movers are better positioned than laggards and late- comers.

Backlighting LED growth is decelerating We expect IT shipment growth to slow down in the next two years given gloomy demand on concerns about the global economy. TV has been an important growth driver to support LED consumption (~35% of backlighting demand), but we think its growth will start to decelerate in 2012-13 as a result of (1) the slower growth of the TV market, (2) an already high penetration of LED backlight and (3) share gain of low-cost LED backlight for low-end models. Figure 11 shows that despite LED TV unit growth being likely maintained at 67% YoY in 2012 and 33% YoY in 2013, the total LED chip demand for TV backlight will slow down to 19% YoY and 4% YoY for 2012 and 2013, respectively.

Figure 9: IT product shipment growth is slowing down,

especially for LCD TVs

Figure 10: LED backlighting penetration will likely reach

its peak in 2013-14

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2008 2009 2010 2011 2012E 2013E 2014E 2015E

Handsets NB/Tablet LCD Monitor LCD TV

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012E 2013E 2014E

Mobile PC LCD TV LCD Monitor Large Area Total

Source: IDC, Gartner, DisplaySearch, Credit Suisse estimates Source: Company data, DisplaySearch, Credit Suisse estimates

Figure 11: LED TV backlighting growth is slowing down (mn units) 2010 2011 2012E 2013E

LCD TV 192 205 220 242

LED backlight penetration 24% 45% 70% 85%

LED backlight TV 46 92 154 205

Edge-lit LED 98% 98% 86% 80%

Direct-lit LED 2% 2% 2% 2%

Low cost direct-lit LED 0% 0% 12% 18%

Total LED demand for TV 10,619 12,117 14,369 14,969

YoY

Total LCD TV 32% 7% 7% 10%

LED backlight TV 1481% 101% 67% 33%

Total LED demand for TV 721% 14% 19% 4%

Source: Company data, DisplaySearch, Credit Suisse estimates

Backlighting growth is decelerating

18 June 2012

Taiwan LED Sector 6

We think the main reasons for decelerating of LED chip growth for TV backlighting are: (1) market share gain of low-cost direct-lit LED TVs and (2) improving efficiency of LED backlight on high power chips and new designs. Consumer expenditure behaviour is moving towards two extremes given the slowing macroeconomic condition and we believe consumers are paying less premium for TVs. Tier 1 TV brands have launched low-cost direct-lit LED TVs since 1Q12 to meet consumers’ needs for low-cost but high-energy efficient products, using the CCFL mechanical structure (thicker design). According to DisplaySearch, the price gap of CCFL and low-cost direct backlight could narrow to 1.2-1.3x by 2H12 from 1.4-1.5x currently on better LED efficiency and new designs. We think the low-cost direct-lit LED TV will quickly penetrate into mainstream sizes such as 32", 39" and 50" over 2012-14.

We forecast overall low-cost direct-lit LED TV penetration will increase from 7% in 1Q12 to 18% in 4Q12 and reach 25% in 4Q13. Although overall LED penetration could be pushed to ~70% in 2012 and reach ~85% in 2013, we believe the adoption of low-cost direct-lit LED TV and the new backlighting designs for edge-lit with less lightbar (as shown in Figure 14) will reduce total LED chips being used per TV set, leading to slow LED chip growth for TV backlighting.

Nevertheless, notebook PC and tablets could be a new growth area in 2012-13 on Windows 8 product launch, as well as the fast growth of Apple’s new iPad and iPad mini. High-end notebook PCs with higher resolution will adopt high-power LEDs. Being equipped with more LED chips per unit should essentially help the Taiwanese LED supply-chain. For Apple’s products, we expect Taiwanese LED suppliers to have limited exposure in the new iPad and iPad mini, given this is mostly dominated by Japanese LED makers, and panel makers have no decision-making power over LED suppliers.

Figure 12: 2012 LED TV proliferation is driven by low-cost

direct-lit LED backlight

Figure 13: Mainstream TV sizes are shifting to low-cost

direct LED BLU starting 2012

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

000' sets

LED-Direct (T) LED-Edge CCFL LED-Direct (L) Low-cost direct % (RHS)

0%

10%

20%

30%

40%

50%

60%

25"-29" 30"-34" 35"-39" 40"-44" 45"-49" 50"-54" 55"-59"

Low cost direct LED BLU %

2011 2012 2013 2014

Source: Company data, DisplaySearch, Credit Suisse estimates Source: Company data, DisplaySearch, Credit Suisse estimates

Figure 14: Less LED chips being used per TV set on luminous improvement and cost reduction 4 sides 2 sides 2 sides 1 sides6 LED lightbars 4 LED lightbars 2 LED lightbars 1 LED lightbar

2H09 2H09 1H10 2H10

or or

37" TV

2H09 1H10 2011 201242" TV

Source: DisplaySearch, Witsview, Credit Suisse estimates

Low-cost direct-lit LED TV penetration is growing fast

18 June 2012

Taiwan LED Sector 7

Figure 15: Roadmap of backlights for direct LED-backlit TVs—less LEDs… 1H12 2H12 2H12 (Ultra low cost)

Specification

2nd LensLED

LED structure 3228/3528 PKG, 32ea 3228/3528 PKG, 20ea 3228/3528 PKG, 20ea

Optical sheet

PrismDiffuserDiffuser

PrismDiffuserPatterened Diffuser Film

PrismDiffuserPatterened Diffuser Film

Light source MCPCB FR4 FR4Bezel & Frame SECC SECC PlasticBLU cost vs CCFL 1.4x 1.3x 1.17x

LED structure32" HD Direct LED Backlight

Source: DisplaySearch

Only leaders can stay competitive Given the continued oversupply in the LED industry, we think technology leaders and early movers are in a better position than laggards and late-comers. LED chips for TV applications have tighter specifications than that for smartphones or LED general lighting given concerns about display uniformity. We also think it will be difficult for late-comers (i.e., Chinese LED makers) to penetrate into global leading panel makers, since the supply chain is already crowded and it takes at least 6-12 months to pass the qualification. In Taiwan, we prefer Epistar among other Taiwanese LED chip makers given its technology leadership and broad customer base. Epistar has penetrated into global top panel makers (Samsung, LGD, AUO, CMI, Sharp) and also supplies LED chips through its packaging partners for Chinese panel makers. We estimate TV and IT backlighting to account for ~30% of Epistar’s revenue in 1H12.

Figure 16: LED backlight TV supply chain—more challenges ahead for independent suppliers

LED Chip LED Package Panel Set/Brand

Samsung LED Samsung LED Samsung

Epistar, ForeEPI Lumens Open cell TFT

LG Innotek

Wooree ETI

LG Innotek

Wooree ETI

Epistar, ForeEPI Wooree, Everlight

Nichia Nichia/Sharp, Stanley Sharp Sharp

Nichia/CMLT AOT CMI Sony

Epistar, ForeEPI Harvatek

Lextar/Osram Lextar/Wellypower

Epistar Liteon

CMLT GIO, Harvatek

Epistar Everlight/Liteon

AUO Multiple TV brands

CMI Multiple TV brands

Samsung

LGD LGE

Source: Company data, Credit Suisse

Only leaders and early movers can stay competitive

18 June 2012

Taiwan LED Sector 8

LED lighting: The next growth segment We believe general lighting will be the next growth area for the LED supply-chain given in 2011, the market size of global general lighting was US$80-90 bn, in which LED lighting’s share was only ~10%. We forecast LED lighting demand will grow from US$7.6 bn in 2011 to US$37 bn by 2015 (~35% penetration), representing a 48% CAGR over 2011-15. We think architectural and indoor lighting are the main drivers for the LED lighting demand, since LED has the advantages of lower power consumption and longer life, and is more environmental friendly than incandescent and fluorescent lamps. We think upstream players and ODM/OEMs for global/regional lighting brands are better plays for the upcoming LED lighting cycle given their higher value addition and greater addressable markets.

Figure 17: Worldwide high brightness LED market

revenue by application (2011)—backlighting leads

Figure 18: Worldwide high brightness LED market

revenue by application (2015E)—general lighting leads

Large size display BLU, 28%

Lighting, 24%Automotiv e, 12%

Sign & Signal, 10%

Others, 9%

Mobile application, 17%

Large size display BLU, 14%

Lighting, 52%

Automotiv e, 13%

Sign & Signal, 8%

Others, 6%

Mobile application, 7%

Source: Company data, LEDinside Source: Company data, LEDinside, Credit Suisse estimates

Figure 19: Worldwide lighting market outlook—LED

penetration is still low but should take off in 2013-14

Figure 20: Architectural and indoor lighting are main

drivers for LED lighting demand

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014 2015

US$ bn

Worldwide LED Lighting Market Total Lighting Market LED lighting % (RHS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015

US$ bn Architectural Outdoor Area/Grid LED Indoor Others YoY (RHS)

Source: Company data, LEDinside Source: Company data, LEDinside

LED lighting is propelled by government initiatives The initial adoption of LED lighting is propelled by government policies and subsidies, given high fixture costs. Various countries have announced phasing out of or regulatory bans on incandescent light bulbs by setting up new energy efficiency standards, as well as prohibiting the use of hazardous materials such as mercury. Japan and Europe are the two fastest-growing markets for LED lighting, as both banned selling of incandescent light bulbs in 2011 and 2012, respectively. The US has set minimum efficiency standards for

LED lighting’s penetration should increase from ~10% in 2011 to ~35% by 2015

Government initiatives and subsidies drive LED lighting demand

18 June 2012

Taiwan LED Sector 9

lighting to be implemented between 2012 and 2014, instead of directly banning incandescent light bulbs. China will ban imports and sales of certain incandescent light bulbs starting from October 2012 and has launched subsidy programmes for LED lighting. The opportunity in China’s street lighting space has been perceived to likely create the largest market on the government’s push.

Figure 21: Incandescent phase-out plans in Europe, the US and Japan

Started phasing out traditional light bulbs from 2009 onwards in favor of a new generation of energy-efficient lighting.

Under the rule which came into force in September 2009, manufacturers and importers can no longer sell clear incandescent light bulbs (general-purpose, non-directional incandescent bulbs) of 100 watts or above in the EU.The ban will be expanded in September 2011 and 2012 to include lower wattages of clear incandescent bulbs. Frosted bulbs and high-energy halogen lights are also being phased out.Under the Energy Independence and Security Act of 2007 (EISA), USA has set minimum efficiency standards for lighting which would be implemented in phases between 2012 and 2014.

Minimum lighting wattages required to meet the criteria are: 100W in 2012, 75W in 2013, followed by 60W and 40W bulbs in 2014.

By 2020, a second tier of restrictions would become effective, which requires all generalpurpose bulbs to produce at least 45 lumens per watt (similar to current CFLs).

Japan Japan will stop producing and selling high-wattage incandescent bulbs in 2012.

EU

USA

Source: IEA, Credit Suisse

Is fluorescent lighting a threat? We think fluorescent lighting could be a transition technology, given the mercury content would cause environmental issues, accompanied with higher disposal costs. LED lighting should replace fluorescent lighting in 2013-14 given its falling retail price on the back of cost reduction resulting from better LED efficiency, improved design and greater scale. Nevertheless, fluorescent lamps could be a threat to LED lighting in the residential retrofit market if LED retail prices continue to remain at current levels as (1) LED lighting has a longer payback period and (2) fluorescent lighting is at ~6x of an equivalent incandescent light bulb, much cheaper than an equivalent LED light bulb (~10x of incandescent). Despite the continued decline in LED retrofit lamp cost on better efficiency and cost reduction, fluorescent lamps could still be a threat for LED retrofit lamps in the residential market in the near term, given the high upfront cost.

Figure 22: Fluorescent light bulb looks cheaper than LED LED Fluorescent Incandescent LED vs Fluorescent vs LED vs

(US$) (12W) (14W) (60W) incandescent (x) incandescent (x) fluorescent (x)

Amazon 15.95 8.50 1.99 8.0 4.3 1.9

Home depot 15.97 8.97 1.47 10.9 6.1 1.8

Lowes 19.98 9.01 1.62 12.4 5.6 2.2

Walmart 17.99 9.00 1.41 12.8 6.4 2.0

Average 17.47 8.87 1.62 10.8 5.5 2.0

Source: Company data

Figure 23: Assumptions for residential lighting retrofit under current pricing LED (12W) Fluorescent (14W) Incandescent (60W)

Electricity cost (US$/kWh) 0.15 0.15 0.15

Wattage 12 14 60

Lumens 800 800 860

Lm/W 67 57 14

Life time (hrs) 30,000 8,000 1,000

Lamp cost (US$) 17.47 8.87 1.62

Annual electricity cost (US$) 3.9 4.6 19.7

Source: Company data, Credit Suisse estimates

Fluorescent is a transitional technology but could be a threat for LED residential retrofit market if LED bulb pricing does not fall

18 June 2012

Taiwan LED Sector 10

Figure 24: Payback period for LED and fluorescent retrofit bulbs are both within a year, but LED retrofit light bulb has

higher upfront cost (assume six hours a day, 365 days a year for residential usage)

0

20

40

60

80

100

120

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

US$ LED (12W) Fluorescent (14W) Incandescent (60W)

Source: Company data, DOE, Credit Suisse

Is LED lighting really going to take off this time? LED lighting demand has been lukewarm for the past two years (2010-11) given the significant price gap between LED and fluorescent light bulbs. However, on aggressive ASP erosion, government subsidy and cost reduction of peripheral material through new design, 8W LED light bulb (for 40W retrofit) retail price has steadily declined by 6-8% QoQ and should hit US$10 in 3Q12.

The 12W LED light bulb (for 60W retrofit) retail price is still in the range of US$15-20 in 2Q12 but we expect more pricing erosion ahead on ~10% quarterly decline and expect 12W LED light bulb ASP to reach the tipping point of US$10 by 2H13, driving higher LED lighting demand.

Figure 25: LED light bulb retail price continues to fall and will likely be near the tipping

point by 2013

0

5

10

15

20

25

30

35

40

45

US$

8W 12W

Source: LEDinside, Credit Suisse estimates

18 June 2012

Taiwan LED Sector 11

Newly installed fixtures market is much bigger than the retrofit market We estimate LED lighting retrofit market (US$1.3 bn in 2011) will reach US$7.7 bn by 2015 with a 56% CAGR in 2011-2015. However, the newly installed fixture market has much greater potential, as its market size could reach US$29 bn by 2015, up from US$6.3 bn in 2011, given that the total addressable market includes LED module, LED lighting fixtures, and system control. We believe the household retrofit market is smaller than industrial/commercial retrofit and fixtures markets, given industrial and commercial users are more sensitive to electricity pricing; hence, they are more willing to adopt LED lighting as replacement or new fixture.

We believe ODM makers (such as Lextar and Edison) that provide integrated solutions and ODM/OEM services to global/regional lighting brands are better positioned to capture the potential growth of the LED fixtures market, given their fixture and system design capabilities offer more value addition to brands, instead of LED packaging. We also think mid- to high- power LED chip makers are in a better position in the LED fixtures market given their less price sensitivity and shorter payback time, as LED fixture lighting is mostly for industrial and commercial applications.

Figure 26: New installed fixtures market is much bigger

than the retrofit market

Figure 27: Household retrofit market is small compared to

industrial/commercial retrofit and fixture markets

0

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013 2014 2015

US$ bn New installed fixture Retrofit lamp

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

0.20

0.40

0.60

0.80

1.00

1.20

2009 2010 2011 2012 2013 2014 2015

US$ bn Household retrofit Household retrofit % of total LED lighting (RHS)

Source: Company data, LEDinside, MIC, Credit Suisse estimates Source: Company data, LEDinside, MIC, Credit Suisse estimates

Upstream and ODMs are better plays for LED lighting We think upstream and ODMs are in a better position to capture the rapidly growing LED lighting market. We estimate the LED retrofit market will account for 20-25% of the total LED lighting market during 2011-15, while the remaining 75-80% is for the fixtures market. We think the fixtures market is less price sensitive than the retrofit market and has more customisation requirement; this offers more outsourcing opportunities for the Taiwanese LED supply-chain.

The LED retrofit market has been dominated by international brands with ~80% market share. We expect this trend to continue, given that the retrofit market is more price sensitive and the new entrants lack scale, technology, channel and brand image to compete with well-established players. We noticed several Taiwanese brands (Everlight, Delta, Nan Ya, Tatung, China Electronics, Wintek, etc) have entered the retrofit market, but we highlight the retrofit market is already crowded with international brands (Philips, OSRAM, Panasonic, etc) and the price competition between local brands seems inevitable.

We think the Taiwanese LED supply-chain should have more opportunity in the fixtures market given global Tier 1 players only account for about 25% share of the fixtures market, while the remaining ~75% share is split between regional brands and new entrants. The

Fixture market has a bigger TAM than retrofit market

Upstream and ODMs are in a better position to capture the rapidly growing LED lighting market

18 June 2012

Taiwan LED Sector 12

fixtures market is also less price sensitive versus the retrofit market given fixture designs and functionality can be highly customised. Integrated solution providers for global/regional lighting brands and high power LED chip makers are in a better position to capture this market, in our view. Street lighting could also be an attractive area, but this is mostly price sensitive with lower value-adds given the nature of government tenders. China is the most aggressive country pushing street lighting, but we think it will be difficult for Taiwanese brands to benefit, given government projects normally compete on relationship and pricing. Upstream chip makers (such as Epistar) could have a better position given its alliance with local lighting makers.

Figure 28: Taiwanese LED maker’s own brand strategy on LED lighting—crowded area Brand Everlight (2393 TT) Delta (2308 TT) Nan Ya Photonics TK3C (2430 TT) China Electronic (1611 TT)

ProductSupply chain Epistar, Everlight Epistar, Delta Nan Ya Photonics Formosa Epitaxy, Unity Opto Formosa Epitaxy, Unity Opto

Brand BenQ TESS (5226 TT) Neo-Neon (911868 TT) Tatung (2371 TT) Genesis Photonics (3383 TT)

ProductSupply chain Lextar CREE Neo-Neon Formosa Epitaxy, Unity Opto Genesis Photonics Source: Company data

Figure 29: LED lighting retrofit market—dominated by international and regional brands Product diversifity Pricing sensitive Key criteria Competition Traditional player

Low High Brand & PricesMarketing skill

Basic quality, low cost

Dominated by int'l brands

Medium Medium QualityBetter quality, low costLocal connections for

new projects

Regional brandsFixture brands

High Low Design

Fixture design capability,

customization for customers

Regional brandsFixture brands

Low Low Cost and security Basic quality, low cost Regional Fixture brands

B2C B2B B2G

HouseholdRetrofit Commercial/

IndustrialRetrofit

Commercial/ Industrial

Fixture

Street lightingFixture

Residental/Commercial

Fixture

Source: Company data, MIC, Credit Suisse

Figure 30: Strategies for LED lighting fixture market—outsourcing is the trend Market segment

Existing lighting players New comers

Intl. brandsRegional

Fixture brandsLED

Fixture brandsLED component

makersRegional Fixture brands LED Fixture brands

Mainstream business model

OBM, partially outsourcing

OEM

OBM, outsource optical engine and assembly on their

own

Own production line and outsource optical

engine

Own production line and outsource optical

engine

Mostly only provide lamps and fixtures; have not

develop integrated LED luminaire

Own production line OBM

Industrial LED Fixture

LED Fixture player

Existing lighting players New comers

Residental/Commercial LED Fixture

Source: Company data, MIC, Credit Suisse

18 June 2012

Taiwan LED Sector 13

In the Taiwanese LED supply-chain, we think upstream chip makers such as Epistar and Forepi, equipment suppliers such as Chroma, and integrated solutions providers, including Lextar and Edison, look more interesting in the upcoming LED lighting cycle. We acknowledge Everlight’s efforts in building its brand business for LED lighting, but remain concerned about the intense competition from global/regional brands and new entrants, which could trigger inventory loss due to rapid retail price decline. We estimate Everlight will have the lowest LED general lighting exposure among Taiwanese LED players in 2012-13.

Figure 31: Everlight has lower exposure to LED general lighting in the Taiwan LED supply chain Company Name Marketcap (US$ mn) 2011 Revenue

(US$ mn) 2011 2012E 2013EEpistar 1,714 600 20% 26% 33%Everlight 689 550 9% 18% 25%Lextar 454 309 28% 35% 45%Forepi 331 139 20% 36% 50%Unity Opto 327 195 21% 25% 30%Genesis 253 152 30% 45% 60%Edison 186 84 85% 90% 90%

Lighting % of sales

Source: Company data, Credit Suisse estimates

18 June 2012

Taiwan LED Sector 14

More consolidation or alliance to happen for Taiwan/China LEDs The Taiwanese LED supply-chain has already experienced several rounds of M&A and alliance in the last few years, especially for Epistar. Recent trend for Taiwan LED makers are to move toward downstream, i.e. packaging, module, and lighting, to increase their revenue/profit, as well as to build their relationships with channels to secure its orders. We view the virtual alliance via vertical integration as a positive for Taiwanese LED makers, especially to capture the growing lighting demand.

However, we think the Chinese LED supply-chain will witness another round of consolidation in the next few years given (1) lack of core technology, (2) intense competition, (3) government policy change, and (4) global economy slowdown. We think the high inventory could be a burden for Chinese LED makers after the Chinese government concludes the MOCVD procurement subsidy in 2011, given industry wide oversupply.

Based on our industry checks, ~100 LED lighting makers in Shenzhen and Foshan went bankrupt in 2011 given intense pricing pressure and high inventory. The Chinese government also raised the bar for companies participating in the lighting bidding by requesting bidders to pass energy saving certifications.

Figure 32: China LED leader Sanan seems to have a better

ROE vs Taiwan LED makers on government subsidy

Figure 33: …but the bubble may burst on high inventory

days

(5)

0

5

10

15

20

25

2008 2009 2010 2011

ROE (%) Epistar Lextar Everlight Sanan Opto

0

50

100

150

200

250

300

350

400

2008 2009 2010 2011

Inventory Days Epistar Lextar Everlight Sanan Opto

Source: Company data, TEJ Source: Company data, TEJ

Taiwan and China LEDs should further tie-up China has installed ~400 sets of MOCVD in 2011 (~60% of global shipments), ahead of the end of MOCVD subsidy by Chinese government, but ~50% of the MOCVD tools installed in China remain idle given lack of technology and lower production yield, according to our industry checks. We think LED supply and demand sufficiency for high-power and mid-power application could improve in 2H12 on new lighting applications and low utilisation for Chinese LED makers, but low-power LEDs will still remain oversupplied.

According industry and government data as end of 2011, China has ~70 companies focusing on LED wafers manufacturing, ~1,000 companies on packaging, and more than 4,000 companies are involved in lighting fixtures, but most of the Chinese LED companies are facing declining revenue, high inventory on lack of technology, resulting in worsen balance sheets given the oversupply.

We believe the Taiwan/China tie-up for LED will help Chinese lighting brands in securing LED chip/package, reduce the risk of oversupply for Taiwanese LED makers, and benefit Chinese local lighting brands to gain share from foreign makers. The Chinese government is also shifting the subsidy from chip manufacturing to lighting module/fixture to boost the proliferation of LED lighting. We would expect more consolidation/alliance in 2012-2014.

More alliance or consolidation to happen for Taiwan/China LEDs

18 June 2012

Taiwan LED Sector 15

Figure 34: LED supply/demand: Mid- and high-power

application are improving, but low-power still oversupply

Figure 35: China LED makers are focusing on lower-end

applications

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012E

LED supply/demand sufficiency

Low Power Mid Power High Power

NichiaCreeOSRAM

Korean LEDsTaiwan LEDs

China LEDs

High Power (>1W)

Niche application

Mid Power (0.5-1W)

Display backlighting

High brightness lighting, outdoor display

Low Power (<0.5W)

Lower power lighting, consumer electronics, mobile devices

Source: Company data, LEDinside, Credit Suisse estimates Source: Credit Suisse

Figure 36: Vertical integration of Taiwan LED makers Vertical integration Epistar (2448 TT) Everlight (2393 TT) Unity (2499 TT) Formosa Epitaxy (3061 TT)Chip Huga (51%) Epistar (5%) Formosa Epitaxy (4%) Wafer Works Optronics (1%)

Tekcore (24%) Tekcore (10%) Huga (1%)

Crystalwise Technology (9%) Huga (6%)

Nan Ya Photonics (41%)

Package Prolight (15%)

Lighting Feng Optoelectronics (40%) LumenMax Opto. (2%)

Kaistar (43%)

BLU Global Lighting Technology (1%)

Others I-Chiun (3%) Source: Company data

Figure 37: Taiwan LED maker’s JV and alliance in China

Company name Ticker China JV China Alliance

Epistar 2448.TW Epi-sky, ULED, Epicrystal, Kaistar, Crystalrich NVC lighting, Yankon

Formosa Epitaxy 3061.TW CanYang Opto

Genesis Photonics 3383.TW Genesis Phtonic Kunshan Potevio

Lextar 3698.TW Lextar Yangzhou

Everlight 2393.TW Evertop

Unity Opto 2499.TW Unity Opto Beijing Hongyar Electrical

Edison 3591.TW Edison Yangzhou Source: Company data

18 June 2012

Taiwan LED Sector 16

Assuming coverage of the Taiwan LED: Prefer Epistar and Chroma We assume coverage of the Taiwan LED sector and with Epistar and Chroma being our top picks, as we expect upstream players to benefit more from the upcoming general lighting take off in 2013. We like Lextar’s business model as it has been qualified by global Tier-one general lighting brands for providing ODM business. Moreover, AUO (major shareholder of Lextar with 46% holding) will absorb Lextar’s output for TFT backlighting. We remain cautious on Everlight as it has been lagging behind to enter the LED monitor/TV backlighting and its strategy to capture general lighting market via own brand could face intense competition from global Tier-one brands, as well as regional lighting brands.

Figure 38: EBITDA—LED upstream is ahead over the

cycle

Figure 39: Net debt/equity comparison—Epistar is having

net cash position

0%

5%

10%

15%

20%

25%

30%

35%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

EBITDA margin

Upstream Downstream

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Net debt to equity

Epistar Lextar Everlight

Source: Company data, TEJ Source: Company data, TEJ

Assume coverage of Epistar with OUTPERFORM: Well positioned for the next LED cycle We assume coverage of Epistar with an OUTPERFORM rating and a target price of NT$75 (26% upside potential), based on 1.4x 12-month forward P/B. Epistar’s solid technology on improving LED performance, strong customer base, and investments in China should benefit from the general lighting take-off. Epistar’s capacity has been fully utilised since late April and should continue into July. It has also taken full control of Huga (51% holding) starting 1Q12 and will help Huga to improve the production yield and fill the capacity by leasing Huga’s equipment.

TV application accounts for ~25% of Epistar’s sales. We think the recent slowdown witnessed by Korean panel makers on weak China May holiday sales and European economic crisis is temporary and should have limited impact to Epistar, given solid demand from Taiwanese and Chinese panel makers for holiday season. Upside surprise could come from better-than-expected LED TV demand in China from new energy efficient subsidy and conclusion of rural subsidy by end 2012, and additional street lighting projects announced by China government.

Epistar and Chroma are our top picks in Taiwan LED

Epistar is well positioned for next LED cycle

18 June 2012

Taiwan LED Sector 17

UNDERPERFORM on Everlight: Own brand strategy could be a burden We assume coverage of Everlight with an UNDERPERFORM rating and a target price of NT$42 (15% downside potential), based on 15x FY12 P/E. We remain cautious on Everlight, as it has been lagging behind its peers to enter the LED TV backlighting and could face price competition from existing players. According to our industry checks, Everlight’s LED monitor/TV backlighting business has been struggling on lower efficiency, despite it having large exposure to mobile and consumer applications. Although Everlight intends to increase its TFT backlighting sales mix from ~16% in 2011 to more than 20% in 2012, we think this will be at the expense of price competition, as it aims to focus on the low-cost direct-lit LED TV market.

Everlight claims it has more than 50% market share in the Taiwanese LED light bulb retail market via its own brand, and intends to enter the global market with dual brands strategy (Everlight for greater China, Zenano for Europe and the US). We think Everlight’s strategy to capture the general lighting market via own brand could lead to lower returns given (1) intense competition from global Tier-one brands and regional lighting players, (2) higher marketing expense is required to build brand image, and (3) total available market for retrofit is much smaller than new fixture on a long-term basis.

We forecast Everlight’s FY12 and FY13 EPS of NT$2.77 and NT$3.39, 8-14% lower than consensus estimate. The stock is trading at 18x FY12 P/E versus the historical 12x-22x range, while the company intend to issue 85 mn shares of GDR (17% dilution) in 2012. We think Everlight’s stock is overpriced and could de-rate on intense competition and lower return for building its own LED lighting brand.

Figure 40: Everlight OPEX is increasing on own brand

strategy

Figure 41: Everlight employee bonus trend—payout and

absolute dollar both decline….

10%

12%

14%

16%

18%

20%

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012E 2013E

NT$ mn ex Bonus OPEX Ex-bonus OPEX/Sales (RHS)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

50

100

150

200

250

300

2008 2009 2010 2011

NT$ mn Employee bonus Employee bonus/Net profit (RHS)

Source: Company data, TEJ, Credit Suisse estimates Source: Company data, Credit Suisse

Initiate coverage on Chroma with OUTPERFORM: Innovator in LED testing We initiate coverage on Chroma with an OUTPERFORM rating and a target price of NT$89 (31% upside potential), based on 17x 12-month forward P/E and NT$2.5 cash dividend. We think Chroma has been undervalued as it is trading at 13.5x FY12 P/E, at the lower end of historical 13x-21x range. We also believe street has underestimated Chroma’s opportunity in LED and visual inspection given its proprietary testing and equipment design know-how has resulted in several new project wins from global Tier-one general lighting, consumer electronics and CIS (CMOS image sensor) makers. We think

Own brand strategy could be a burden to Everlight

Undervalued

18 June 2012

Taiwan LED Sector 18

these new project wins could turn into actual orders in 2H12 and estimate Chroma’s 2H12 standalone revenue of NT$3.3 bn, above consensus estimate of less than NT$3.0 bn.

Chroma’s technology leadership in power testing, visual inspection, and automation has provided the company with strong bargaining power on pricing and margin. Chroma has maintained a 50-55% gross margin since 2006 and we expect it to continue in the next few years. Thus, our FY13E EPS of NT$5.55 is 8% above consensus estimates on higher revenue assumption from new project wins, as well as solid margin profile.

Unique business model, initiate Lextar with NEUTRL We initiate coverage on Lextar with a NEUTRAL rating and a target price of NT$37 (14% upside potential), based on 1.7x 12-month forward P/B. Lextar is the only LED maker in Taiwan that provides vertical integration service from LED wafer manufacturing, packaging, light module, light source, and fixtures. We like its business model as it has been qualified by global tier one general lighting brands (i.e. Philip, OSRAM, etc) for providing lighting ODM business (30-35% of sales). Moreover, its TFT backlighting (60-65% of sales) output is guaranteed by its major shareholder AUO and also penetrated into other panel makers (CMI, Korean, Chinese panel makers).

Lextar is also the first Taiwanese LED maker to mass produce 6” LED wafer. It obtains key manufacturing IPs through cross-licensing and ODM for global Tier-one makers to avoid patent infringement. We think Lextar’s strategy of working with global Tier-ones and regional general lighting brands, and its R&D effort regarding cost reduction should support the growth of its general lighting business. Nevertheless, we initiate coverage on Lextar with a NEUTRAL rating as our target price of NT$37 only leaves 14% upside potential from current levels. We are also concerned on potential major shareholder sell down and domestic CB issuance could cap the stock. We could turn more optimistic on the stock on faster-than-expected growth of its general lighting business or recovery of global economy for better LED TV shipments.

Figure 42: Lextar provides total solution to capture LED lighting ODM market

Source: Company data

Figure 43: Epistar and Chroma offers more upside

Price Marketcap CS 12mthHistorical valuation

Ticker Company 6/14/2012 US$ mn Rating Target Multiple range 2012 2013 2012 20132448.TW Epistar 59.6 1,714 O 75.0 26% 1.5x forward P/B 1.0-2.0x P/B nm 21.8 1.2 1.12360.TW Chroma 68.0 856 O 89.0 31% 17x forward P/E 13-21x P/E 16.6 12.3 3.1 2.82393.TW Everlight 49.2 689 N 42.0 -15% 15x 2012 P/E 12-22x P/E 17.8 14.5 1.4 1.33698.TW Lextar 32.4 454 U 37.0 14% 1.7x forward P/B 1.0-2.1x P/B 31.8 15.8 1.6 1.5

P/E (x) P/B (x)Upside/

downside to PT

Source: TEJ, Credit Suisse estimates

Stable gross margin profile of 50-55% since 2006

Lextar is the only LED turnkey provider in Taiwan

18 June 2012

Taiwan LED Sector 19

Asia Pacific / Taiwan Electronic Components & Connectors

Epistar Corporation (2448.TW / 2448 TT)

Well positioned for the next LED cycle ■ Assume coverage with OUTPERFORM. We assume coverage of Epistar

with an OUTPERFORM rating and a target price of NT$75 (from NT$65), based on 1.4x 12-month forward P/B. We believe Epistar is well positioned for the next LED cycle driven by general lighting, given its solid technology for improving LED performance, strong customer base and China investments.

■ LED backlighting demand remains solid. TV backlighting accounts for ~25% of Epistar’s sales, while IT (monitor and NB) is around 5-10%. We think the recent slowdown witnessed by Korean panel makers on weak China May holiday sales and European economy crisis is temporary and should have limited impact on Epistar, given solid demand from Taiwanese and Chinese panel makers for 2H holiday season demand. Upside surprise could come from better-than-expected LED TV demand in China from new energy efficient subsidy and conclusion of rural subsidy by end-2012.

■ Capacity remains tight in 2012. Epistar’s capacity has been fully utilised since late April and should continue into July. Epistar does not intend to add new capacity in 2012 but will de-bottleneck some legacy equipment in 2H12 for 10% increase in capacity. We estimate its 2012 capex to be halved from NT$10 bn in 2011. We think the growing general lighting demand in 2H12 should help Epistar in maintaining high utilisation and improve its margins. Epistar has also formed a tighter alliance with Huga (51% holding) since 4Q11 and will help Huga in improving the production yield by transferring process recipe and fill the capacity by leasing Huga’s equipment.

■ Valuation is attractive. Epistar stock is trading at 1.2x FY12 P/B, at the lower end of historical of 1.0-2.0x range. Our target price of NT$75 is based on 1.4x 12-month forward P/B, mid-cycle average multiple. We expect Epistar’s revenue momentum to improve sequentially in 2Q12 and 3Q12 on improving LED demand for backlighting and general lighting take off in 2H12. Key risks will be new capacity additions, weak LED TV demand, and slower-than-expected take off for LED general lighting.

Share price performance

406080100120

406080

100120

Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the TAIWAN SE WEIGHTED INDEX which closed at 7075.1 on 14/06/12 On 14/06/12 the spot exchange rate was NT$29.95/US$1

Performance Over 1M 3M 12M Absolute (%) -14.9 -27.8 -35.5 Relative (%) -10.5 -15.6 -15.6

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (NT$ mn) 21,963.6 22,061.9 23,526.3 28,323.1 EBITDA (NT$ mn) 3,964.0 4,703.7 7,414.5 8,835.1 EBIT (NT$ mn) 22.8 271.1 2,591.8 3,877.5 Net profit (NT$ mn) 480.3 755.3 2,349.9 3,481.1 EPS (CS adj.) (NT$) 0.56 0.88 2.73 4.04 Change from previous EPS (%) n.a. n.a. n.a. Consensus EPS (NT$) n.a. 0.89 2.44 3.01 EPS growth (%) -92.2 56.4 211.1 48.1 P/E (x) 106.2 67.9 21.8 14.7 Dividend yield (%) 7.5 1.8 1.0 3.2 EV/EBITDA (x) 12.2 11.1 6.7 5.5 P/B (x) 1.1 1.2 1.1 1.1 ROE (%) 1.1 1.7 5.2 7.5 Net debt/equity (%) net cash 1.3 net cash net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates.

*Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months.

Research Analysts

Jerry Su 886 2 2715 6361

Jimmy Huang 886 2 2715 6352

Rating (from Neutral) OUTPERFORM* Price (14 Jun 12, NT$) 59.60 Target price (NT$) (from 65.00) 75.00¹ Upside/downside (%) 25.8 Mkt cap (NT$ mn) 51,316 (US$ 1,714) Enterprise value (NT$ mn) 51,992 Number of shares (mn) 861.01 Free float (%) 91.0 52-week price range 92.4 - 51.1

18 June 2012

Taiwan LED Sector 20

Well positioned for the next LED cycle Margin improving on better utilisation; limited capacity addition in 2012

We think Epistar’s margin troughed in 4Q11-1Q12 and will recover on better utilisation. We estimate Epistar will run at full utilisation in June/July, up from ~90% in April and ~70% in 1Q12. Epistar currently has 360,000 pieces of 2" equivalent capacity for Nitride LED and will de-bottleneck some of its old equipment with Veeco E300 in 2Q12 for 10% additional capacity starting to ramp in 3Q12. We estimate its utilisation should be maintained at ~90% levels in 3Q12, after the ~10% capacity increase on debottlenecking.

We forecast Epistar’s gross margin to recover sequentially on better utilisation and product mix. Four-element LED (25-30% sales) gross margin should improve from 20% to 30%+ in 2H12 on seasonality and lower depreciation. Gross margin of high power Nitrid LED (~15% of sales) should also improve to ~30% from mid-teens on new product ramp and higher utilisation. We also estimate gross margin for its TV and smartphone applications (40%+ of sales) will improve from breakeven to ~10% in 2H12 on more shipments and better product mix.

Figure 44: Epistar—1Q12 revenue breakdown Figure 45: Epistar—gross margin vs utilisation

TV23%

Monitor4%

NB3%

Mobile15%Lighting

23%

Outdoor / Indoor Display

15%

Automotive5%

Others12%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1Q2010 3Q2010 1Q2011 3Q2011 1Q2012 3Q2012E

Gross margin (parent only) Utilisation (RHS)

Source: Company data Source: Company data, Credit Suisse estimates

Huga to turn around on Epistar’s help; leveraging JVs for China market

Epistar invested in Huga (51% holding) in 2010 and only assigned two senior management personnel to run the company. Given lower yield and quality, Epistar started to transfer know-how and process recipes since 4Q11 to help Huga improve its production efficiency and yield. Epistar will also help fill Huga’s capacity by leasing its equipment starting 2H12 given its own capacity is already fully utilised.

We also think Epistar’s alliance and JVs in China for chip processing (Epicrystal), packaging (Prolight), and general lighting (Kaistar) should help the company to form virtual integration in China to capture general lighting opportunity. The upcoming announcement of street lighting bidding results could be a catalyst for Epistar’s 2H12 growth if its Chinese partners successfully win the biddings.

2Q12 recovery remains on track, 3Q12 should be better

Epistar reported May standalone sales of NT$1.66 bn, up 10% MoM but down 16% YoY. We estimate its 2Q12 standalone sales of NT$4.8 bn, up 34% QoQ but down 9% YoY. On a consolidated basis, we estimate Epistar’s 2Q12 consolidated revenue of NT$5.7 bn, up 35% QoQ but down 16% YoY. We forecast Epistar’s 2Q12 consolidated gross margin to improve by 14.7 pp from 1Q11 (3.9%) on better utilisation (700 bp contribution) and improving product mix. We estimate Epistar to report 2Q12 EPS of NT$0.38, versus 1Q12

Margin troughed in 4Q11-1Q12

Epistar is helping Huga to improve quality and yield

2Q12 recovery is on track

18 June 2012

Taiwan LED Sector 21

LPS of NT$0.60. We expect its revenue and gross margin recovery to continue into 3Q12 on better backlighting demand, lighting demand pick up, narrower loss from Huga, and turnaround of its investments.

Figure 46: Epistar—EBITDA margin trend Figure 47: Epistar—capex/sales is trending down after

2011 peak

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1Q2008 4Q2008 3Q2009 2Q2010 1Q2011 4Q2011 3Q2012E

EBITDA margin

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012E

Capex/Sales

Source: Company data, Credit Suisse estimates Source: Company data, , Credit Suisse estimates

Assuming coverage with OUTPERFORM and NT$75 TP

We assume coverage of Epistar with an OUTPERFORM rating and a target price of NT$75, based on 1.4x 12-months forward P/B. Our target price of NT$75 implies 26% potential upside from current levels as we believe Epistar is well positioned for the next LED cycle driven by general lighting given its solid technology for improving LED performance, strong customer base, and China investments. Epistar has been working with various global lighting makers given its superior processing yield and has less IP concerns than Korean and Chinese peers given its early mover position and IP cross-licensing with Toyoda Gosei and Philips. We also believe its technology leadership could offer potential opportunity to break into Japan LED supply chain.

We think 4Q11-1Q12 is the worst period for Epistar and fundamentals should improve sequentially from 2Q12 on better demand from both display backlighting and LED general lighting. We also expect LED ASPs to remain relatively stable comparing with 2011 on supply tightness for high-end and niche products, while low-end LEDs for China market continues on a downward trend.

Downside risks are: (1) More new capacity additions in China; (2) weak LED TV demand; (3) slower-than-expected take off for LED general lighting; (4) dilution from private placement, and (5) market share loss to competitors.

Figure 48: Epistar – One year forward P/B Figure 49: Epistar – Share price vs monthly sales YoY

0

20

40

60

80

100

120

140

160

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Apr-12

NT$ Stock Price vs. One-Year Forward PB

Stock Price 0.5x 0.8x 1.0x 1.5x 2.0x

0

20

40

60

80

100

120

140

160

-50%

0%

50%

100%

150%

200%

250%

300%

350%

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

(NT$)YoY Monthly sales YoY Stock Price (RHS)

Source: Company data, TEJ, Credit Suisse estimates Source: Company data, TEJ

Assume coverage with OUTPERFORM

18 June 2012

Taiwan LED Sector 22

Figure 50: Epistar’s financial summary Year-end 31 Dec (NT$ mn) 2008 2009 2010 2011 2012E 2013E 2014ERevenue 10,321 12,849 20,888 21,964 22,062 23,526 28,323 COGS 9,013 9,607 13,044 19,260 19,268 18,373 21,695 Gross profit 1,308 3,242 7,844 2,704 2,794 5,153 6,628 Operating expense 1,381 1,462 2,337 2,681 2,523 2,561 2,751 EBIT (74) 1,780 5,507 23 271 2,592 3,878 EBITDA 1,867 3,921 7,902 3,964 4,704 7,415 8,835 Total non-op 159 164 829 (323) (122) 215 324 Pre-tax profit 85 1,944 6,336 (300) 149 2,807 4,202 Tax expense 44 116 512 (14) (88) 309 462 Net profit 42 1,732 5,766 480 755 2,350 3,481 EPS (NT$) 0.06 2.26 7.17 0.56 0.88 2.73 4.04Gross margin (%) 12.7 25.2 37.6 12.3 12.7 21.9 23.4Operating margin (%) (0.7) 13.9 26.4 0.1 1.2 11.0 13.7EBITDA margin (%) 18.1 30.5 37.8 18.0 21.3 31.5 31.2Net margin (%) 0.4 13.5 27.6 2.2 3.4 10.0 12.3

Balance sheet (NT$ mn) 2008 2009 2010 2011 2012E 2013E 2014ECash & ST investments 4,491 18,187 22,525 17,274 14,900 17,048 18,370 Receivables 3,120 4,644 7,864 7,402 9,538 10,581 12,159 Inventory 2,470 1,974 3,842 4,292 4,561 4,698 5,357 Other current assets 2,640 4,586 2,662 1,930 4,069 4,514 5,188 Current assets 12,720 29,390 36,892 30,898 33,068 36,841 41,074 Long-term investment 28 1,356 3,442 3,844 3,980 3,980 3,980 Total fixed assets 12,722 14,150 27,200 32,634 31,952 30,908 29,729 Total other assests 652 677 4,325 5,082 5,513 5,257 5,152 Total assets 26,122 45,573 71,860 72,458 74,513 76,986 79,934 Short-term debt 555 6,168 6,322 3,014 3,653 3,609 3,624 Payables 509 989 1,993 2,037 2,781 3,184 3,750 Other current liabilities 1,232 2,484 5,901 4,188 5,084 5,641 6,482 Total current liabilities 2,296 9,641 14,215 9,239 11,519 12,433 13,856 Long-term debt 1,717 - 4,434 11,601 11,923 11,776 11,827 Other long term liabilities 15 132 321 592 673 673 673 Total liabilities 4,028 9,773 18,970 21,432 24,115 24,883 26,356 Minority Interest 2 98 6,421 6,547 6,204 6,204 6,204Common stock 6,331 7,690 8,475 8,589 8,606 8,606 8,606 Retained earnings 132 1,784 5,993 1,947 2,924 4,628 6,104 Others 15,630 26,229 32,000 33,943 32,664 32,664 32,664 Total equity 22,094 35,800 52,890 51,026 50,398 52,103 53,578 Total liabilities & equity 26,122 45,573 71,860 72,458 74,513 76,986 79,934

Cash flow (NT$ mn) 2008 2009 2010 2011 2012E 2013E 2014ENet profit 42 1,732 5,766 480 755 2,350 3,481 Depreciation and Amortization 1,941 2,140 2,395 3,941 4,433 4,823 4,958 Change in working capital (587) 467 (2,059) (1,218) (3,355) (666) (1,503) Others (1) 3 (269) 328 40 - - Operating cash flow 1,395 4,342 5,834 3,531 1,873 6,507 6,936 Capital expenditure (2,652) (2,816) (5,725) (10,030) (4,617) (3,600) (3,600) Long term investments 393 (1,330) (1,818) (729) (176) - - Others 848 (778) (13,369) (102) 434 78 (74) Investment cash flow (1,411) (4,923) (20,911) (10,861) (4,358) (3,522) (3,674) Dividends paid (1,489) (75) (1,384) (3,842) (947) (529) (1,645) Equity financing (172) 11,529 7,014 339 1,423 (0) - Change in debt financing 167 4,013 4,777 4,130 1,042 (191) 66 Others 60 520 5,693 1,158 (1,859) (117) (361) Financing cash flow (1,434) 15,987 16,100 1,786 (340) (837) (1,940) Other adjustments 0 (0) - 0 (0) 0 (0) Total cash flow (1,450) 15,406 1,023 (5,544) (2,825) 2,148 1,323

Ratios 2008 2009 2010 2011 2012E 2013E 2014EYoY growth (%)Sales 1 24 63 5 0 7 20 Gross profit (58) 148 142 (66) 3 84 29 EBIT (104) (2,518) 209 (100) 1,091 856 50 EBITDA (49) 110 102 (50) 19 58 19 Net income (98) 3,981 233 (92) 57 211 48 Balance sheet ratios (%)ROE 0.2 6.0 14.0 1.1 1.7 5.2 7.5 Net debt/ equity (10.0) (33.6) (22.3) (5.2) 1.3 (3.2) (5.4) Source: Company data, Credit Suisse estimates

18 Ju

ne 2012

Taiw

an L

ED

Secto

r 23

Figure 51: Epistar quarterly income statement and forecasts Year-end 31 Dec (NT$mn) 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12E 3Q12E 4Q12E 1Q13E 2Q13E 3Q13E 4Q13E 2011 2012E 2013E 2014ESales 5,618 6,804 4,863 4,679 4,248 5,735 6,194 5,884 4,884 5,714 6,400 6,528 21,964 22,062 23,526 28,323COGS 4,680 5,187 4,467 4,925 4,413 4,894 5,073 4,888 4,085 4,471 4,782 5,035 19,260 19,268 18,373 21,695Depreciation 861 902 932 981 1,053 1,035 1,065 1,101 1,135 1,161 1,179 1,170 3,676 4,254 4,644 4,779COGS ex D&A 3,795 4,237 3,500 3,788 3,315 3,814 3,964 3,742 2,905 3,266 3,559 3,821 15,318 14,836 13,551 16,737

Gross profits 938 1,616 396 (246) (165) 841 1,121 996 799 1,243 1,618 1,493 2,704 2,794 5,153 6,628 Total operating exp. 566 676 687 752 632 614 607 670 578 648 673 661 2,681 2,523 2,561 2,751

Operating exp. promotion 83 97 87 76 82 86 87 97 85 92 96 100 344 351 373 405 Operating exp. administrative 255 326 344 413 284 287 279 292 261 294 302 307 1,337 1,141 1,163 1,241 Operating expense R&D 228 253 255 263 266 241 242 282 232 263 276 255 1,000 1,030 1,025 1,105

EBIT 372 940 (291) (998) (796) 228 514 326 221 594 944 832 23 271 2,592 3,878 Non-oper. income (Loss) 42 (139) (75) (151) (84) (12) (28) 2 7 48 66 95 (323) (122) 215 324

Interest expenses (73) (87) (97) (90) (96) (98) (101) (101) (98) (97) (99) (99) (346) (396) (394) (397) Interest income 43 53 49 37 47 47 43 38 40 45 45 44 182 175 174 191 Other non-op. income/(loss) 71 (105) (27) (97) (36) 40 30 65 65 100 120 150 (158) 99 435 530

Pre-tax Income 414 801 (366) (1,149) (880) 216 486 328 228 642 1,010 926 (300) 149 2,807 4,202 Income taxes exp./(gains) 64 83 (66) (94) (48) (32) (24) 16 25 71 111 102 (14) (88) 309 462 Net income before extraord. 350 719 (299) (1,055) (832) 248 510 311 203 571 899 824 (286) 237 2,498 3,739

Net income 349 738 12 (619) (515) 328 587 355 198 558 845 749 480 755 2,350 3,481 EPS (NT$) 0.41 0.86 0.01 (0.72) (0.60) 0.38 0.68 0.41 0.23 0.65 0.98 0.87 0.56 0.88 2.73 4.04 Aveage shares 851 857 857 858 859 861 861 861 861 861 861 861 856 860 861 861

EBITDA 1,257 1,891 677 139 301 1,308 1,623 1,472 1,401 1,800 2,168 2,046 3,964 4,704 7,415 8,835

Margins (%)EBITDA margin 22.4 27.8 13.9 3.0 7.1 22.8 26.2 25.0 28.7 31.5 33.9 31.3 18.0 21.3 31.5 31.2 Gross margin 16.7 23.8 8.1 (5.3) (3.9) 14.7 18.1 16.9 16.4 21.7 25.3 22.9 12.3 12.7 21.9 23.4 Operating margin 6.6 13.8 (6.0) (21.3) (18.7) 4.0 8.3 5.5 4.5 10.4 14.8 12.7 0.1 1.2 11.0 13.7 Tax rate 15.5 10.3 18.2 8.2 5.5 (15.0) (5.0) 5.0 11.0 11.0 11.0 11.0 4.6 (59.2) 11.0 11.0 Net margin 6.2 10.8 0.3 (13.2) (12.1) 5.7 9.5 6.0 4.1 9.8 13.2 11.5 2.2 3.4 10.0 12.3

QoQ (%)Sales 13 21 (29) (4) (9.2) 35 8 (5) (17) 17 12 2 COGS 37 11 (14) 10 (10) 11 4 (4) (16) 9 7 5 Gross profit (40) 72 (76) (162) NM NM 33 (11) (20) 55 30 (8) Operating profit (58) 153 (131) NM NM NM 126 (37) (32) 169 59 (12) Net profit (70) 112 (98) (5,052) NM NM 79 (39) (44) 181 52 (11)

YoY (%)Sales 34 20 (20) (6) (24) (16) 27 26 15 (0) 3 11 5 0 7 20 COGS 77 52 26 44 (6) (6) 14 (1) (7) (9) (6) 3 48 0 (5) 18 Gross profit (39) (28) (84) (116) (118) (48) 183 NM NM 48 44 50 (66) 3 84 29 Operating profit (66) (44) (116) (214) (314) (76) NM NM NM 161 84 155 (100) 1,091 856 50 Net profit (65) (56) (99) (153) (248) (56) 4,597 NM NM 70 44 111 (92) 57 211 48 Source: Company data, Credit Suisse estimates

18 June 2012

Taiwan LED Sector 24

Asia Pacific / Taiwan Electronic Equipment & Instruments

Everlight Electronics Co Ltd (2393.TW / 2393 TT)

Own brand could be a burden ■ Assume coverage with UNDERPERFORM. We assume coverage of

Everlight with an UNDERPERFORM rating and a target price of NT$42 (from NT$54), based on 15x 2012 P/E. We remain cautious on Everlight as it has been lagging in entering LED-TV backlighting and could face price competition from existing players. We also think its strategy to capture the LED lighting via own brand could lead to lower return on high competition and could potentially harm its relationships with existing customers.

■ Own brand could be a burden. Everlight claims it has more than 50% market share in Taiwan LED light bulb retail market via its own brand, and intends to enter global market with dual brands strategy (Everlight for greater China, Zenano for Europe and US). We think Everlight’s strategy to capture the general lighting market via own brand could lead to lower return given: 1) intense competition from global tier one brands and regional lighting players, 2) higher marketing expense is required to build brand image, and 3) total available market for retrofit is much smaller than new fixture on a long-term basis. We are also concerned that building its own brand could potentially harm its relationships with existing customers.

■ Lagging on backlighting. Everlight’s LED monitor/TV backlighting business has been struggling on lower efficiency, although it has large exposure in mobile and consumer applications. Despite Everlight intending to increase its TFT backlighting sales mix from ~16% in 2011 to 20%+ in 2012, we think this will be at the expense of price competition as it aims to focus on the low-cost direct-lit LED TV market.

■ Looks overpriced. We forecast Everlight’s 2012/2013 EPS of NT$2.77/NT$3.39, 8-14% lower than consensus estimates. The stock is trading at 18x 2012 P/E versus historical 12x-22x range, while the company intend to issue 85 mn shares of GDR (17% dilution) in 2012. We think Everlight stock is overpriced and could de-rate on intense competition and lower return for building own LED lighting brand.

Share price performance

406080100120

40

60

80

100

Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the TAIWAN SE WEIGHTED INDEX which closed at 7075.1 on 14/06/12 On 14/06/12 the spot exchange rate was NT$29.95/US$1

Performance Over 1M 3M 12M Absolute (%) -16.3 -24.3 -38.0 Relative (%) -12.0 -12.1 -18.1

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (NT$ mn) 18,642.3 20,241.2 21,998.7 22,772.5 EBITDA (NT$ mn) 3,368.3 3,410.1 3,837.6 3,912.5 EBIT (NT$ mn) 1,482.4 1,326.2 1,771.0 1,677.0 Net profit (NT$ mn) 1,316.3 1,159.3 1,419.6 1,327.2 EPS (CS adj.) (NT$) 3.14 2.77 3.39 3.17 Change from previous EPS (%) n.a. n.a. n.a. Consensus EPS (NT$) n.a. 3.20 3.66 3.57 EPS growth (%) -43.2 -11.9 22.5 -6.5 P/E (x) 15.7 17.8 14.5 15.5 Dividend yield (%) 7.3 5.1 3.9 5.0 EV/EBITDA (x) 6.9 6.9 6.1 5.9 P/B (x) 1.4 1.4 1.3 1.3 ROE (%) 8.7 7.6 9.3 8.5 Net debt/equity (%) 15.4 18.0 16.1 15.2

Source: Company data, Thomson Reuters, Credit Suisse estimates.

*Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months.

Research Analysts

Jerry Su 886 2 2715 6361

Jimmy Huang 886 2 2715 6352

Rating (from Neutral) UNDERPERFORM* Price (14 Jun 12, NT$) 49.20 Target price (NT$) (from 54.00) 42.00¹ Upside/downside (%) -14.6 Mkt cap (NT$ mn) 20,624.7 (US$ 688.7) Enterprise value (NT$ mn) 23,535 Number of shares (mn) 419.20 Free float (%) 73.0 52-week price range 79.3 - 45.7

18 June 2012

Taiwan LED Sector 25

Own brand could be a burden The majority of Everlight’s revenue and profit was from handset, consumer products, and infrared, with only 16% from backlighting and 9% from lighting in 2011. We acknowledge Everlight’s effort to build its own brand to capture the LED general lighting growth. However, we remain concerned on Everlight as it will be competing with global lighting giants, namely Philips, OSRAM, Panasonic, etc, and these global Tier-one brands dominate the LED retrofit market with ~80% share.

Everlight claims it has more than 50% market share in the Taiwanese LED light bulb retail market. However, we are worried that it will face more pricing pressure from new entrants including Delta, Nan Ya, Tatung, China Electronics, TESS, BenQ, Wintek, etc, and price competition seems inevitable. Based on our survey from retail channels in Taiwan, Everlight’s 8W LED light bulb’s retail price has come down to NT$299 in May from NT$399 in January and NT$499 in September 2011.

Figure 52: Taiwanese LED maker’s own brand strategy on LED lighting—crowded area Brand Everlight (2393 TT) Delta (2308 TT) Nan Ya Photonics TK3C (2430 TT) China Electronic (1611 TT)

ProductSupply chain Epistar, Everlight Epistar, Delta Nan Ya Photonics Formosa Epitaxy, Unity Opto Formosa Epitaxy, Unity Opto

Brand BenQ TESS (5226 TT) Neo-Neon (911868 TT) Tatung (2371 TT) Genesis Photonics (3383 TT)

ProductSupply chain Lextar CREE Neo-Neon Formosa Epitaxy, Unity Opto Genesis Photonics Source: Company data

We also noticed Everlight has been cutting its employee bonus payout ratio since 2008 despite its earnings being on an upward trend. We understand Everlight might need to spend more on marketing campaign to build its brand image, but we still view lowering bonus payout as a negative for its long-term competitiveness, since it will be more difficult to retain R&D talent amid competition from Chinese LED makers.

Figure 53: Everlight 8W LED light bulb retail price fell 40%

in eight months

Figure 54: Everlight employee bonus trend—payout and

absolute dollar both declining….

0

100

200

300

400

500

600

Sep-11 Jan-12 May-12

NT$ Everlight 8W LED light bulb retail price

Down 40% in 8 months

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

50

100

150

200

250

300

2008 2009 2010 2011

NT$ mn Employee bonus Employee bonus/Net profit (RHS)

Source: Company data Source: Company data, Credit Suisse

LED retrofit market is a crowded in Taiwan

18 June 2012

Taiwan LED Sector 26

Lagging behind on backlighting

Everlight’s LED monitor/TV backlighting business has been struggling on lower efficiency, despite it having a large exposure in mobile and consumer applications. Everlight intends to increase its TFT backlighting sales mix from ~16% in 2011 to more than 20% in 2012, but we think this will be at the expense of price competition, as it aims to focus on the low-cost direct-lit LED TV market. We think the value addition for backlighting will shift from LED packager to chip provider, given 80% of lighting efficiency improvement is from LED chip, not packaging. For example, the high resolution trend for mobile devices (smartphone, tablet, NB) has offered chip makers a better position to communicate with panel makers directly, which lowers the value for LED packagers.

Figure 55: Everlight—2011 revenue by product line, by different regions, and by applications

SMD57%

Lamp & Display

18%

Infrared24%

Others1%

Taiwan23%

US & Europe

20%

China & Asia57%

Handset & consumer products

51%

Infrared24%

BLU16%

Lighting9%