David & Goliath - Credit Suisse

67

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 10 September 2010 Asia Pacific Equity Research Small Cap Companies David & Goliath WEEKLY ANALYSIS Low rates, high prices Apart from Hong Kong, the domestic recovery theme is also working well in other Asian markets. With an anticipated prolonged low interest rate cycle on the weakened macro data from the West, Asian asset-based stocks, such as small-cap properties and REITs, have been outperforming since June 2010. Trading at low estimated 2011 P/Es of 4.9-8.8x and yields of 3.1-13.2%, the Taiwan, Thailand and Singapore small-cap property stocks look attractive. Recovery among Thai property stocks has been under way since the end of the Red Shirt protest in mid-May 2010. CS Thailand property and small-cap analyst Chai Techakumpuch sees new launches remaining active for the rest of the year. He likes Asia Property, Quality Houses and LPN in Thailand. Like the Hong Kong government’s measures to “prevent an overheating property market”, tightening measures on property have been issued recently by the Singapore government and Taiwan’s Central Bank. Property price hikes on strong monetary liquidity amid low interest rates is a common phenomenon across the Asian markets. Both CS Taiwan property analyst Sidney Yeh and Singapore property analyst Tricia Song believe that the government’s tightening measures have only minimal impact and should not alter the property market uptrend. Their view is supported by the short-lived pullback in share prices of these property stocks on the measures – there ain’t no measures without a strong physical real estate market. Sidney likes the small-cap property plays Huaku, Prince, Chong Hong, Hung Poo and Sinyi (for transaction volume) in Taiwan, while Tricia likes Wing Tai and Allgreen in Singapore. Charts of the week SC properties outperforming MSCI AxJ Taiwan, Thailand and SG ppt plays 75 100 125 150 175 Jun-10 Jul-10 Aug-10 Sep-10 MSCI AxJ Prince Housing Asian Property Wing Tai Ticker Stock 11E P/E (x) 3M px chg (%) 2511.TW Prince Housing 5.6 52.3 AP.BK Asian Property 8.3 47.9 9940.TW Sinyi Realty 8.6 31.9 LPN.BK L.P.N. 6.7 31.1 QH.BK Quality Houses 7.8 30.3 5534.TW Chong Hong 4.9 27.8 2536.TW Hung Poo 7.9 11.8 WTHS.SI Wing Tai 6.0 10.5 AGRN.SI Allgreen 8.8 9.6 2548.TW Huaku 5.8 9.6 Source: Datastream, Credit Suisse estimates Davids of the week: India: BEML – we initiate coverage of India’s largest mining equipment maker, benefiting from coal reform; 17.5x FY3/12E P/E, 14% potential upside (p. 24) Taiwan: Prince – we raise our NAV estimate by 28% on value appreciation of two commercial properties; 42% discount to NAV, 20% potential upside (p. 50) Research Analysts Kenny Lau, CFA 852 2101 7914 [email protected] Adrian Chan 852 2101 6469 [email protected] Eva Wang 852 2101 7365 [email protected] Sunil Tirumalai 9122 6777 3714 [email protected] Teddy Oetomo 6221 2553 7911 [email protected] Minseok Sinn 822 3707 8898 [email protected] Loke Foong Wai 603 2723 2082 [email protected] Su Tye Chua 65 6212 3014 [email protected] Sidney Yeh 8862 2715 6368 [email protected] Chai Techakumpuch 662 614 6211 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of David & Goliath - Credit Suisse

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

10 September 2010Asia Pacific

Equity ResearchSmall Cap Companies

David & Goliath WEEKLY ANALYSIS

Low rates, high prices Apart from Hong Kong, the domestic recovery theme is also working well in other Asian markets. With an anticipated prolonged low interest rate cycle on the weakened macro data from the West, Asian asset-based stocks, such as small-cap properties and REITs, have been outperforming since June 2010. Trading at low estimated 2011 P/Es of 4.9-8.8x and yields of 3.1-13.2%, the Taiwan, Thailand and Singapore small-cap property stocks look attractive.

Recovery among Thai property stocks has been under way since the end of the Red Shirt protest in mid-May 2010. CS Thailand property and small-cap analyst Chai Techakumpuch sees new launches remaining active for the rest of the year. He likes Asia Property, Quality Houses and LPN in Thailand.

Like the Hong Kong government’s measures to “prevent an overheating property market”, tightening measures on property have been issued recently by the Singapore government and Taiwan’s Central Bank. Property price hikes on strong monetary liquidity amid low interest rates is a common phenomenon across the Asian markets. Both CS Taiwan property analyst Sidney Yeh and Singapore property analyst Tricia Song believe that the government’s tightening measures have only minimal impact and should not alter the property market uptrend. Their view is supported by the short-lived pullback in share prices of these property stocks on the measures – there ain’t no measures without a strong physical real estate market. Sidney likes the small-cap property plays Huaku, Prince, Chong Hong, Hung Poo and Sinyi (for transaction volume) in Taiwan, while Tricia likes Wing Tai and Allgreen in Singapore.

Charts of the week SC properties outperforming MSCI AxJ Taiwan, Thailand and SG ppt plays

75

100

125

150

175

Jun-10 Jul-10 Aug-10 Sep-10

MSCI AxJ Prince HousingAsian Property Wing Tai

Ticker

Stock

11E P/E (x)

3M px chg (%)

2511.TW Prince Housing 5.6 52.3 AP.BK Asian Property 8.3 47.9 9940.TW Sinyi Realty 8.6 31.9 LPN.BK L.P.N. 6.7 31.1 QH.BK Quality Houses 7.8 30.3 5534.TW Chong Hong 4.9 27.8 2536.TW Hung Poo 7.9 11.8 WTHS.SI Wing Tai 6.0 10.5 AGRN.SI Allgreen 8.8 9.6 2548.TW Huaku 5.8 9.6

Source: Datastream, Credit Suisse estimates

Davids of the week: India: BEML – we initiate coverage of India’s largest mining equipment maker, benefiting from coal reform; 17.5x FY3/12E P/E, 14% potential upside (p. 24) Taiwan: Prince – we raise our NAV estimate by 28% on value appreciation of two commercial properties; 42% discount to NAV, 20% potential upside (p. 50)

Research Analysts Kenny Lau, CFA

852 2101 7914 [email protected]

Adrian Chan 852 2101 6469

Eva Wang 852 2101 7365

Sunil Tirumalai 9122 6777 3714

Teddy Oetomo 6221 2553 7911

Minseok Sinn 822 3707 8898

Loke Foong Wai 603 2723 2082

Su Tye Chua 65 6212 3014

Sidney Yeh 8862 2715 6368

Chai Techakumpuch 662 614 6211

10 September 2010

David & Goliath 2

The tales of Davids Hong Kong I.T – Company visit – an expanding business along with rising valuations 10

China BYD – Disappointing August auto sales adds gravity to EPS forecasts 17

Geely – Surprising MoM rebound in August sales; achieving FY target still a big challenge 17

India BEML – New report: Thematic play on likely acceleration in coal capex 24

KEC – New report: Valuations price in a weak near term; contra pick in the sector 24

Voltas – Play on recovery in industrial and infra capex 25

Havells – New report: Risk-adjusted returns do not appear attractive 25

BGR Energy – New report: Strong earnings momentum expected; valuations appear rich though 26

Punj Lloyd – Crisis of confidence 26

Malaysia Ta Ann – Plywood prices +25% YTD YoY but Tasmania is still loss-making 38

Singapore OUE – New report: Scaling new peaks 44

Taiwan Prince Housing – The undervalued commercial properties 50

Cyberlink – Softer 2H10 PC momentum already priced in; Looking into positive 2011 outlook 50

Hung Poo – Still a value play 51

Wintek – A winner in the tablet revolution 51

EVA Airways – August operating numbers flat sequentially due to seasonality 52

Taishin Financial – August monthly earnings remain strong 52

Thailand LPN Development – Newly acquired land plot has a very good profit potential 59

10 September 2010

David & Goliath 3

Small-cap index performance Figure 1: Non-Japan Asia Figure 2: China

90

100

110

120

130

09/09 12/09 03/10 06/10 09/10

MSCI AxJ Small Caps MSCI Asia Ex-Japan

85

100

115

130

145

09/09 12/09 03/10 06/10 09/10

MSCI HK Small Caps MSCI AxJ Small Caps MSCI HK

Figure 3: Hong Kong Figure 4: India

85

100

115

130

145

09/09 12/09 03/10 06/10 09/10

MSCI HK Small Caps MSCI AxJ Small Caps MSCI HK

85

100

115

130

145

09/09 12/09 03/10 06/10 09/10

MSCI India Small Caps MSCI AxJ Small Caps MSCI India

Figure 5: Indonesia Figure 6: South Korea

70

85

100

115

130

09/09 12/09 03/10 06/10 09/10

MSCI Indonesia Small Caps MSCI AxJ Small Caps MSCI Indonesia

85

100

115

130

09/09 12/09 03/10 06/10 09/10

MSCI Korea Small Caps MSCI AxJ Small Caps MSCI Korea

Figure 7: Malaysia Figure 8: Singapore

90

100

110

120

130

09/09 12/09 03/10 06/10 09/10

MSCI Malaysia Small Caps MSCI AxJ Small Caps MSCI Malaysia

90

100

110

120

130

09/09 12/09 03/10 06/10 09/10

MSCI Singapore Small Caps MSCI AxJ Small Caps MSCI Singapore

Figure 9: Taiwan Figure 10: Thailand

90

100

110

120

130

09/09 12/09 03/10 06/10 09/10

MSCI Taiwan Small Caps MSCI AxJ Small Caps MSCI Taiwan

75

100

125

150

175

09/09 12/09 03/10 06/10 09/10

MSCI Thailand Small Caps MSCI AxJ Small Caps MSCI Thailand

Source: MSCI, Credit Suisse estimates Source: MSCI, Credit Suisse estimates

10 September 2010

David & Goliath 4

Take a real (estate) look at these… Figure 11: Some small cap property plays in Singapore, Taiwan and Thailand Price TP Mkt cap Last FY1 FY1 FY1 3MCompany Ticker (local) (local) (US$ mn) Rating reported P/E (x) Yield (%) P/B (x) perf.Wing Tai WTHS.SI 1.69 2.06 999 OUTPERFORM Jun 10 5.9 4.3 0.7 10.5Allgreen Properties AGRN.SI 1.14 1.53 1,350 OUTPERFORM Dec 09 11.4 3.5 0.7 9.6Chong Hong 5534.TW 72.20 72.74 547 OUTPERFORM Dec 09 7.4 8.8 2.1 27.8Prince Housing 2511.TW 20.10 24.20 604 OUTPERFORM Dec 09 7.4 6.7 1.4 52.3Huaku 2548.TW 84.20 102.00 684 OUTPERFORM Dec 09 7.8 8.8 2.0 9.6Hung Poo 2536.TW 43.50 51.00 396 OUTPERFORM Dec 09 13.1 5.4 1.4 11.8Sinyi Realty 9940.TW 52.40 66.76 601 OUTPERFORM Dec 09 11.0 4.5 3.0 31.9L.P.N. Development LPN.BK 9.90 12.10 473 OUTPERFORM Dec 09 8.8 5.4 2.4 31.1Quality Houses QH.BK 2.54 3.35 698 OUTPERFORM Dec 09 10.1 4.7 1.6 30.3Asian Property AP.BK 7.10 8.60 538 OUTPERFORM Dec 09 9.4 3.5 1.8 47.9Source: Company data, Credit Suisse estimates

10 September 2010

David & Goliath 5

Small-cap index valuation and sector performance Figure 12: Valuation

Index Net profit Book value Trailing Index performance Country/ weighting (US$ mn) (US$ mn) P/E (x) P/B (x) Yield (local currency term) region (%) 2009 2010 2009 2010 2009 2010 2009 2010 (%) 1W 1M 3M 6M 1Y 2YChina 18.9 8,193 11,414 78,273 86,006 16.6 11.9 1.7 1.6 1.7 3.2 2.8 16.6 (0.3) 22.1 78.5 Hong Kong 9.3 4,447 5,069 42,018 43,888 15.1 13.2 1.6 1.5 2.8 1.9 2.9 15.2 14.6 30.3 50.2 Indonesia 10.8 2,723 4,495 26,751 29,833 28.4 17.2 2.9 2.6 1.7 4.0 7.9 22.5 28.9 54.6 90.8 Korea 15.1 5,583 10,879 80,830 89,224 19.4 10.0 1.3 1.2 1.4 0.3 3.5 12.0 13.9 13.5 22.1 Malaysia 9.9 4,336 5,134 45,068 47,566 16.4 13.8 1.6 1.5 2.6 0.6 2.1 11.7 11.2 21.9 31.7 Singapore 12.8 3,996 6,069 60,253 60,894 23.0 15.2 1.5 1.5 3.3 2.2 0.8 10.9 7.7 18.8 32.2 Taiwan 12.4 1,813 7,177 50,996 54,631 49.0 12.4 1.7 1.6 2.9 0.9 (2.5) 12.1 3.9 11.9 24.4 Thailand 10.8 5,270 5,180 44,115 46,162 14.7 15.0 1.8 1.7 2.9 (0.8) 5.8 25.5 32.9 40.2 59.6 NJA 100.0 36,361 55,417 428,303 458,205 19.7 13.0 1.7 1.6 1.8 2.0 2.9 19.5 13.1 29.6 49.5 Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Non-Japan Asia weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 14.0 4,924 6,652 47,851 51,732 20.5 15.2 2.1 1.9 2.4 6.2 20.8 16.5 40.9 45.6 Consumer Staples 9.5 4,501 5,448 34,492 37,773 15.2 12.6 2.0 1.8 1.6 4.0 23.3 22.2 53.1 93.2 Energy 4.7 2,544 2,208 14,479 15,372 13.1 15.1 2.3 2.2 3.3 3.7 17.1 16.2 29.9 55.3 Financials 22.0 10,518 12,350 124,912 128,676 15.0 12.8 1.3 1.2 1.5 2.5 20.9 15.2 23.9 59.9 Health Care 4.1 1,383 1,708 8,815 9,906 21.1 17.1 3.3 2.9 1.1 1.7 13.0 20.6 54.6 64.3 Industrials 16.4 3,179 9,604 71,683 78,797 37.0 12.2 1.6 1.5 1.0 2.6 23.0 12.8 24.0 31.3 Information Technology 11.7 2,598 6,343 44,295 48,074 32.3 13.2 1.9 1.7 3.1 (2.3) 6.9 (3.1) 14.1 39.0 Materials 11.3 3,764 7,607 54,593 59,586 21.6 10.7 1.5 1.4 3.3 4.5 24.9 14.2 27.1 67.0 Telecommunication Services 3.6 1,329 1,933 13,298 14,275 19.3 13.3 1.9 1.8 2.8 4.9 19.8 21.3 44.2 5.6 Utilities 2.7 1,620 1,565 13,884 14,015 12.1 12.6 1.4 1.4 0.6 4.4 20.4 4.0 24.2 18.3 Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance China weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 25.0 1,402 1,939 10,765 11,896 24.2 17.5 3.2 2.9 4.3 9.1 23.1 12.7 61.7 104.4 Consumer Staples 10.4 1,114 1,348 7,841 8,572 12.7 10.5 1.8 1.7 0.7 (3.4) 11.2 (5.3) 22.9 64.3 Energy 0.5 44 146 947 1,036 16.3 4.9 0.8 0.7 6.1 (6.4) (6.7) (16.3) (29.9) (30.9)Financials 11.6 1,548 1,723 19,975 20,843 10.2 9.2 0.8 0.8 3.4 0.4 13.7 (7.5) (13.8) 34.2 Health Care 6.2 430 501 2,269 2,574 19.5 16.7 3.7 3.3 3.4 1.8 6.7 31.8 109.8 213.7 Industrials 15.2 1,634 2,440 13,254 15,305 12.6 8.4 1.6 1.3 3.1 4.5 24.4 1.3 16.1 65.6 Information Technology 7.3 222 589 6,052 6,461 44.4 16.7 1.6 1.5 2.9 (4.6) 4.7 (18.7) 22.4 75.5 Materials 15.8 1,129 2,057 10,620 12,997 19.0 10.4 2.0 1.7 2.7 0.8 14.3 (5.7) 5.2 103.1 Telecommunication Services 0.6 48 49 266 291 15.9 15.5 2.9 2.6 23.5 13.8 14.9 (4.3) 21.1 53.4 Utilities 7.4 621 623 6,283 6,030 16.2 16.2 1.6 1.7 1.8 7.4 26.8 (1.2) 30.9 40.3 Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Hong Kong weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 32.0 1,209 1,530 10,202 11,217 17.7 14.0 2.1 1.9 1.2 6.3 14.3 21.4 44.4 52.3 Consumer Staples 0.3 16 26 227 247 12.7 7.7 0.9 0.8 8.8 9.1 25.2 39.1 25.3 76.8 Financials 36.6 1,692 1,799 18,754 18,551 14.5 13.6 1.3 1.3 0.8 5.7 24.4 24.7 28.3 33.9 Industrials 10.1 678 479 6,133 6,481 9.9 14.1 1.1 1.0 2.7 (3.2) 10.3 (7.6) 4.3 22.1 Information Technology 12.3 590 831 3,076 3,524 14.0 9.9 2.7 2.3 2.4 (2.6) 4.8 5.5 32.7 104.0 Materials 5.9 183 274 2,015 2,237 21.5 14.4 2.0 1.8 3.0 (2.7) 4.8 (3.0) 45.8 202.2 Telecommunication Services 2.8 79 129 1,609 1,630 24.1 14.8 1.2 1.2 (0.6) (1.1) 21.0 45.3 45.7 (3.9)Source: DataStream, Credit Suisse estimates

10 September 2010

David & Goliath 6

Index Net profit Book value Index performance Indonesia weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 2.1 81 92 854 916 20.4 18.0 1.9 1.8 5.3 4.9 1.9 (0.5) 25.6 25.8 Consumer Staples 23.8 870 941 4,917 5,391 21.2 19.6 3.7 3.4 4.9 19.7 35.2 41.5 106.5 225.7 Energy 20.6 756 854 3,142 3,448 21.0 18.6 5.1 4.6 3.0 4.0 17.3 25.8 46.2 63.4 Financials 25.4 822 1,248 7,800 8,847 23.9 15.7 2.5 2.2 4.1 3.8 19.6 35.2 39.5 85.6 Health Care 3.5 103 147 479 582 26.5 18.6 5.7 4.7 3.2 1.0 32.5 45.1 97.7 202.6 Industrials 4.6 (354) 225 2,283 2,632 (10.1) 15.9 1.6 1.4 3.1 7.7 40.3 39.6 39.4 58.7 Materials 9.0 43 528 3,741 4,017 161.8 13.2 1.9 1.7 3.0 3.2 15.8 7.4 17.9 17.0 Telecommunication Services 10.9 402 461 3,535 4,000 21.0 18.3 2.4 2.1 4.7 9.2 16.3 15.9 84.3 (18.5)Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Korea weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 14.6 618 1,254 11,039 12,200 25.6 12.6 1.4 1.3 0.7 6.4 15.7 21.5 23.7 25.6 Consumer Staples 7.8 696 1,122 8,753 9,873 12.2 7.6 1.0 0.9 (2.0) (1.7) (0.6) 3.2 8.1 2.3 Financials 12.4 1,367 1,771 11,939 13,715 9.8 7.6 1.1 1.0 (0.1) (4.5) 1.2 1.1 (1.9) 41.9 Health Care 7.7 422 538 3,091 3,457 19.7 15.5 2.7 2.4 (1.1) 6.4 8.3 2.2 (6.7) (6.0)Industrials 18.8 324 1,500 12,675 13,884 62.9 13.6 1.6 1.5 (0.2) 6.5 19.6 13.2 10.4 (2.5)Information Technology 7.9 444 755 4,789 5,440 19.3 11.3 1.8 1.6 3.3 0.3 (5.6) 8.4 8.9 90.6 Materials 25.8 1,306 3,109 21,718 23,307 21.4 9.0 1.3 1.2 1.1 7.0 27.7 30.3 34.5 63.0 Telecommunication Services 4.2 209 686 4,725 5,120 21.7 6.6 1.0 0.9 (2.2) (5.9) (10.6) (4.0) (11.7) (28.3)Utilities 1.0 195 144 2,101 2,229 5.3 7.2 0.5 0.5 0.9 1.4 1.4 (0.6) (9.5) (26.6)Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Malaysia weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 12.3 682 807 5,889 6,069 12.8 10.8 1.5 1.4 3.5 4.5 11.7 19.1 36.7 49.8 Consumer Staples 15.2 628 759 5,992 6,403 17.2 14.2 1.8 1.7 1.5 1.4 15.2 16.7 22.4 33.0 Energy 10.1 547 466 4,174 4,065 13.1 15.4 1.7 1.8 (1.5) 0.9 11.8 2.4 9.0 6.1 Financials 18.9 1,059 1,045 10,126 10,574 12.6 12.8 1.3 1.3 (0.4) 1.0 7.3 3.6 21.6 32.2 Health Care 3.7 168 213 801 901 15.5 12.2 3.3 2.9 (3.3) (5.9) (2.3) 3.5 62.5 131.1 Industrials 29.4 889 1,254 11,147 12,477 23.5 16.7 1.9 1.7 0.4 4.3 13.7 14.7 17.8 34.2 Information Technology 0.8 (5) 23 291 299 (110.8) 23.8 1.9 1.9 (1.0) 0.1 (4.0) (7.5) 0.2 (19.5)Materials 8.8 310 497 6,049 6,172 20.2 12.6 1.0 1.0 2.1 1.3 20.2 15.1 25.1 31.8 Utilities 0.7 59 69 598 606 9.0 7.7 0.9 0.9 (2.2) (5.8) (1.3) (4.6) 0.8 (0.1)Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Singapore weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 4.4 230 189 3,669 3,646 17.4 21.2 1.1 1.1 1.9 0.3 5.0 1.8 (10.7) (26.8)Consumer Staples 7.2 559 528 3,699 3,984 11.8 12.5 1.8 1.7 0.4 (4.7) 9.6 6.1 20.2 99.7 Energy 3.7 259 241 1,252 1,706 13.1 14.1 2.7 2.0 1.4 (2.5) 7.9 (7.7) 0.7 17.0 Financials 43.7 1,916 2,516 36,769 35,475 21.0 16.0 1.1 1.1 2.8 0.9 11.1 5.3 15.3 29.1 Health Care 5.2 141 182 1,463 1,606 34.0 26.3 3.3 3.0 1.8 0.7 6.1 27.9 75.6 76.9 Industrials 24.5 349 1,729 9,851 10,877 64.6 13.0 2.3 2.1 2.7 3.2 15.6 15.4 30.8 40.3 Information Technology 3.0 43 189 2,270 2,288 65.1 14.8 1.2 1.2 1.2 (3.3) 5.6 3.6 5.0 30.2 Materials 1.2 48 71 464 496 22.4 15.2 2.3 2.2 3.8 0.9 10.1 (4.4) 9.5 (31.5)Telecommunication Services 5.0 350 312 284 235 13.1 14.7 16.1 19.5 (1.8) 4.9 8.5 10.4 21.4 12.7 Utilities 2.2 102 112 531 582 20.0 18.0 3.8 3.5 4.1 (2.9) 4.4 (13.8) 8.0 (16.7)Source: DataStream, Credit Suisse estimates

10 September 2010

David & Goliath 7

Index Net profit Book value Index performance Taiwan weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 7.7 311 384 3,125 3,344 22.1 17.8 2.2 2.0 0.8 (0.6) 24.3 13.3 11.3 20.0 Financials 12.1 850 988 8,664 9,106 12.6 10.9 1.2 1.2 (1.0) (1.1) 26.1 19.1 17.4 49.7 Industrials 18.6 (596) 1,786 10,549 11,356 (27.7) 9.2 1.6 1.5 (4.6) (7.5) 17.1 15.3 20.4 10.8 Information Technology 58.2 1,121 3,706 26,290 28,410 46.1 13.9 2.0 1.8 3.3 (1.3) 6.0 (3.6) 7.7 27.2 Materials 3.5 127 311 2,368 2,416 24.1 9.9 1.3 1.3 1.7 (1.1) 22.5 14.0 22.7 53.8 Source: DataStream, Credit Suisse estimates

Index Net profit Book value Index performance Thailand weighting (US$ mn) (US$ mn) P/E (x) P/B (x) (US$ term) Sector (%) 2009 2010 2009 2010 2009 2010 2009 2010 1W 1M 3M 6M 1Y 2YConsumer Discretionary 10.7 392 455 2,308 2,444 21.2 18.2 3.6 3.4 (4.7) 4.9 25.7 30.2 43.8 27.2 Consumer Staples 12.6 618 724 3,063 3,303 15.8 13.5 3.2 3.0 (4.0) 0.1 33.3 74.3 146.5 253.2 Energy 8.0 938 502 4,964 5,116 6.6 12.4 1.3 1.2 9.1 9.2 6.0 10.0 0.9 66.0 Financials 26.2 1,264 1,261 10,885 11,566 16.1 16.1 1.9 1.8 (3.2) 7.4 32.5 29.9 42.9 85.0 Health Care 3.0 118 127 713 786 19.4 18.1 3.2 2.9 (5.2) (0.5) 15.1 15.7 26.0 (7.4)Industrials 8.2 255 191 5,792 5,786 24.9 33.2 1.1 1.1 (2.4) 9.4 25.6 28.7 30.7 37.6 Information Technology 2.8 182 248 1,527 1,652 11.9 8.7 1.4 1.3 (7.1) (8.7) 14.2 28.9 30.9 26.1 Materials 13.8 618 759 7,617 7,943 17.3 14.1 1.4 1.3 7.4 11.5 20.5 34.2 28.0 55.7 Telecommunication Services 7.1 242 296 2,878 2,998 22.7 18.6 1.9 1.8 4.6 7.7 52.7 67.8 58.1 106.9 Utilities 7.7 643 616 4,370 4,567 9.3 9.7 1.4 1.3 (3.1) 1.3 13.5 13.8 13.8 27.2 Source: DataStream, Credit Suisse estimates

D&G15 portfolio – the small-cap picks in the region Mkt Cap Price Year P/E (x) Potential CS

Company Ticker (US$ mn) Cncy Price End FY1 FY2 TP Gain (%) Rating China/Hong Kong Nine Dragons 2689.HK 6,799 HKD 11.36 Jun 18.9 15.4 10.85 (4.5) U Skyworth 0751.HK 1,553 HKD 4.75 Mar 8.3 6.5 7.50 57.9 O Great Eagle 0041.HK 1,767 HKD 22.05 Dec 12.6 11.8 27.95 26.8 O Varotronix 0710.HK 119 HKD 2.86 Dec 5.6 4.5 3.75 31.1 O Korea LIG Insurance 002550.KS 1,182 KRW 23,000 Mar 7.0 5.9 31,300 36.1 O Samsung Securities 016360.KS 3,463 KRW 60,500 Mar 0.0 0.0 47,000 (22.3) U Malaysia AirAsia AIRA.KL 1,617 MYR 1.82 Dec 8.1 7.8 2.05 12.6 O Singapore Cosco (Singapore) COSC.SI 2,734 MYR 1.64 Dec 21.8 19.4 1.20 (26.8) U Taiwan Nanya PCB 2408.TW 2,140 SGD 19.90 Dec (3.2) 22.3 18.00 (9.5) U Prince Housing 2511.TW 604 TWD 20.10 Dec 7.4 5.6 24.20 20.4 O Thailand Quality Houses QH.BK 698 THB 2.54 Dec 10.1 7.8 3.35 31.9 O Source: Company data, Credit Suisse estimates

10 September 2010

David & Goliath 8

Hong Kong – Street talk * SmarTone (0315.HK, HK$8.52, U, TP HK$7.00) full-year profit up 5.9x. SmarTone posted a 5.9x increase in net earnings to HK$294 mn for the year ended June 2010. EPS came in at HK$0.55 and an interim DPS of HK$0.35 was recommended. Handset subsidy amortisation in the period rose by 10% to HK$280 mn. (8-Sep)

80

100

120

140

160

09/09 12/09 03/10 06/10 09/10

SmarTone MSCI Hong Kong

Johnson Electric (0179.HK, HK$3.79, O [V], TP HK$4.40) appoints Joseph Yam. Yam Chi Kwong Joseph, the former head of the Hong Kong Monetary Authority, has been appointed by Johnson Electric as an independent non-executive director for a term of two years with effect from September 30. Johnson Electric’s shares rose more than 3% on Wednesday on the back of the news. (9-Sep)

75

100

125

150

175

09/09 12/09 03/10 06/10 09/10

Johnson Electric MSCI Hong Kong

Kong Sun (0295.HK, HK$0.33, NR) to raise at least HK$59.91 mn via rights issue. Kong Sun plans to issue not less than 240 mn offer shares at HK$0.25 each on the basis of one offer share for every two shares held. The company intends to utilize the net proceeds for general working capital and future business development. (9-Sep)

25

50

75

100

125

09/09 12/09 03/10 06/10 09/10

Kong Sun MSCI Hong Kong

North Asia Resources (0061.HK, HK$1.41, NR) issues unlisted CBs. North Asia Resources has issued convertible bonds in the aggregate principal amount of US$33 mn in two tranches. Proceeds from the issue is around HK$243 mn, which will be used for general working capital or acquisition of iron concession in Mongolia. (9-Sep)

40

60

80

100

120

09/09 12/09 03/10 06/10 09/10

North Asia Resources MSCI Hong Kong

10 September 2010

David & Goliath 9

Sunlight REIT (0435.HK, HK$2.29, NR) distributable income down 31%. Sunlight REIT’s distributable income went down almost 31% to HK$187 mn for the year ended June 2010. DPU for the year was HK$0.144, down 41% YoY. Final DPU fell almost 50% to HK$0.0751. (10-Sep)

90

100

110

120

130

09/09 12/09 03/10 06/10 09/10

Sunlight REIT MSCI Hong Kong

*Source: China Press Digest, CIS, DataStream

10 September 2010

David & Goliath 10

Who’s saying what? I.T (0999.HK, HK$4.19, NR) Company visit – an expanding business along with risingvaluations

■ We met with I.T management last week.

■ Hong Kong operations are more mature – management expectsgrowth to be more in line with market growth, but with limited market share gain. According to the company, for March-July 2010, its HK sales were + 20% YoY and SSS growth +13%, in line14.9% market growth during the same period.

■ I.T expects the China platform to be its growth driver. It targets 30% sales area expansion in FY2/11. China sales were +20%YoY in March-July, with SSS +6%, according to I.T.

■ I.T expects operating margin upside from the continued shift ofsales mix to more in-house brand sales and increasing salesefficiency of staff through training. It expects rentals to be themajor source of margin pressure, as around 30% its rentalagreements are renewed each year.

■ I.T’s valuation is catching up with its peers. It currently trades at 13.5x CY11, at a 10.4% discount to Giordano and a 29.1% discount to the average of HK/China retail plays.

I.T is a multi-brand mid- to high-end retailer

I.T is a multi-brand mid- to high-end retailer selling apparel, footwearand accessories. Its FY2/10 net profit was HK$262.7 mn on sales ofHK$3.0 bn, 60.7% gross margin and 10.3% operating margin.According to I.T, its HK business (71.0% sales) is more mature, whileits mainland China business (25.5% sales) would be the growth driver;it has 3.5% sales from franchised operations in other countries. I.Tsells in-house brands (49.6% sales) and over 300 international brands(47.0% sales), and generates royalty revenues from licensed brands.These are sold in the high-end I.T stores, the mid-end i.t store, the street fashion store doublepark and standalone shops. The multi-brand strategy allows it to have 187 stores in HK alone.

I.T expects its HK segment to grow in line with the market

I.T is well established in HK (around 6% market share in 2009) andexpects further market share gain to be limited. However, it sees roomfor further expansion in the HK market and plans 10% retail spacegrowth in 2010. According to I.T, for March-July 2010, its HK saleswere +20% YoY; its SSS growth was +13%, in line with HK’s 14.9%growth in apparel/footwear/allied product sales. Management seesincreasing sales in HK from mainland consumers – it estimates that30% sales from its Times Square Causeway Bay and its Festive Walk Kowloon Tong shops come from mainland Chinese shoppers.

I.T sees significant room for expansion in mainland China

I.T sees significant room for expansion in mainland China from its 134 self-managed and 44 franchised stores. Growth is expected to bemore driven by floor space expansion – I.T targets 30% sales areaexpansion in FY2/11. It plans to expand in main cities on its own and

to lower tier cities through franchise partners. The strategy in China is to expand through department stores and shopping malls. According to the company, I.T’s China sales were up around 20% during March-July, with SSS up 6%.

I.T hopes for margin improvements

I.T hopes to: 1) improve its China front-line employee’s product knowledge to increase efficiency, and thus increase the number of items purchased per transaction – the company figures show that HK generates (on average) 2.5 items per transaction, while China generates 1.5 items per transaction, and 2) shift sales mix toward the higher-margin in-house brands (with gross margins of around 70%). I.T targets 75% in-house brand sales in five years, raising gross margin up to 65%.

The major source of margin pressure would come from rentals

Around 30% of its rental agreements need to be extended each year. Management expects rental increases of 15-25% for HK rental renewals and around 15% for China. However, I.T noted that it aims to cap rental expenses at 25% of sales.

I.T’s valuation is catching up, but is still at a discount to peers

I.T now trades at 13.5x CY2011 P/E, at a 10.4% discount to its closest peer Giordano and at a 29.1% discount to the 19.0x average of HK/China retail plays.

Gabriel Chan, CFA / Research Analyst / 852 2101 6523 /

[email protected] Extracted from The Asian Daily 09 Sep 2010

10 Septem

ber 2010

David &

Goliath

11

Valuations of Credit Suisse HK small-cap watch list* Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MAeon Credit 0900.HK 366 6.80 5.38 (20.9) Not rated Feb n.a. 10.4 1.6 1.4 12.3 4.9 1.5 0.7 7.6Aeon Stores 0984.HK 478 14.30 3.73 (73.9) Not rated Dec 22.2 19.2 3.3 2.9 5.5 (1.7) 1.3 22.2 24.3Arts Optical 1120.HK 180 3.65 3.38 (7.4) Not rated Dec 11.4 13.2 1.3 1.2 9.7 3.0 (1.9) (4.5) 10.6Asia Financial 0662.HK 397 3.03 4.41 45.4 Not rated Dec 9.4 7.8 0.6 0.6 4.6 (2.8) 0.0 (2.6) 5.6Asia Sat. Telecom 1135.HK 653 12.98 20.29 56.3 Not rated Dec 9.6 9.8 0.9 0.9 6.3 0.3 2.9 6.0 10.6Café De Coral 0341.HK 1,548 21.40 12.37 (42.2) Not rated Mar 23.9 22.3 4.4 4.0 8.6 2.5 2.9 12.6 14.8Champion REIT 2778.HK 2,430 3.83 4.34 13.3 Not rated Dec 4.7 24.7 0.7 0.7 3.5 (3.2) 2.1 (2.5) 7.6Chen Hsong 0057.HK 243 3.00 4.00 33.3 OUTPERFORM Mar 13.8 7.9 0.8 0.7 4.4 (2.1) 3.4 (6.3) 11.1Chong Hing Bank 1111.HK 948 16.94 12.68 (25.2) Not rated Dec 32.0 17.1 1.2 1.2 4.2 (3.0) 2.7 (5.9) 14.5Chow Sang Sang 0116.HK 1,368 15.70 14.42 (8.2) Not rated Dec 16.5 14.1 2.4 2.1 11.9 5.3 0.8 (0.9) 14.9Comba Telecom Sys. 2342.HK 1,402 9.16 13.50 47.4 OUTPERFORM Dec 16.9 14.1 4.2 3.5 20.1 14.1 11.7 15.2 0.0Dachan Food 3999.HK 202 1.55 2.45 58.0 Not rated Dec 12.7 7.7 0.9 0.8 8.1 1.3 0.6 (7.2) 11.5Dah Chong Hong 1828.HK 1,660 7.17 6.13 (14.5) Not rated Dec 18.2 11.6 2.4 2.2 9.0 2.1 9.3 24.9 53.9Dah Sing Banking 2356.HK 1,826 12.76 11.59 (9.2) Not rated Dec 21.3 13.1 1.3 1.2 3.2 (3.9) 2.9 8.5 27.6Dah Sing Financial 0440.HK 1,708 51.00 49.05 (3.8) Not rated Dec 21.2 12.6 1.2 1.1 3.9 (3.2) 2.6 3.9 17.5Daphne 0210.HK 1,849 8.77 4.96 (43.5) Not rated Dec 36.4 20.7 6.5 5.5 9.6 3.0 1.3 11.4 7.3Dickson Concepts 0113.HK 268 5.59 6.50 16.3 Not rated Mar n.a. 6.5 n.a. 1.0 7.3 (0.8) 2.8 (6.5) 27.0Fairw ood 0052.HK 134 8.25 3.81 (53.8) Not rated Mar 11.6 9.8 2.6 2.5 4.9 (3.2) (1.1) (0.6) 7.0First Pacific 0142.HK 3,204 6.40 8.02 25.3 Not rated Dec 7.0 9.5 1.7 1.8 12.3 5.8 9.4 10.3 26.2Fubon Bank 0636.HK 564 3.74 3.58 (4.3) Not rated Dec (71.9) 16.3 1.1 1.0 4.0 (3.2) 1.1 4.8 15.1Galax y Entertainment 0027.HK 3,016 5.94 6.45 8.6 NEUTRAL Dec 20.3 24.6 2.9 2.8 7.3 1.0 1.4 8.6 63.2Giordano 0709.HK 845 4.40 2.81 (36.3) Not rated Dec 22.8 14.8 3.1 2.9 5.8 (1.3) (2.4) 10.3 36.2Glorious Sun 0393.HK 393 2.88 1.81 (37.0) Not rated Dec 11.8 10.0 1.5 1.4 6.0 (1.4) (3.4) (4.3) (3.0)Great Eagle 0041.HK 1,767 22.05 27.95 26.7 OUTPERFORM Dec 12.0 12.6 0.6 0.6 3.7 (2.6) 3.8 3.3 10.4HKC 0190.HK 681 0.51 0.88 73.3 Not rated Dec 3.5 25.5 0.4 0.4 (1.7) (8.4) 6.3 (3.8) 3.0HKR 0480.HK 537 3.09 23.37 656.4 Not rated Mar 3.2 1.6 n.a. 0.4 0.8 (6.2) 0.3 (4.0) 29.8Hong Kong & S'hai Hotels 0045.HK 2,454 12.92 13.36 3.4 Not rated Dec 8.2 35.2 0.8 0.8 1.5 (5.0) (0.8) 1.4 0.8Hutchison Telecom HK 0215.HK 1,332 2.15 1.50 (30.2) NEUTRAL Dec 22.2 14.2 1.0 1.0 5.0 (2.2) (2.7) (2.3) 30.3

Share price performanceHK$ term (%)P/B (x)P/E (x)

CalendarizedCalendarized

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

10 Septem

ber 2010

David &

Goliath

12

Valuations of Credit Suisse HK small-cap watch list* Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3Mi-Cable 1097.HK 254 0.98 1.34 37.1 Not rated Dec (49.0) 163.3 1.0 1.0 (0.2) (7.0) 1.0 (4.9) (17.6)I.T. 0999.HK 643 4.19 2.67 (36.4) Not rated Feb 20.3 16.4 3.4 3.2 10.8 3.0 2.9 54.6 129.0ICBC Asia 0349.HK 4,968 28.55 21.61 (24.3) Not rated Dec 14.6 15.8 2.1 2.1 16.2 9.3 (1.0) 23.9 49.5IDS 2387.HK 1,021 24.45 0.29 (98.8) Not rated Dec 33.6 n.a. 6.3 5.6 5.0 (2.1) 3.8 58.6 91.0Johnson Electric 0179.HK 1,792 3.79 4.40 16.1 OUTPERFORM Mar 31.0 14.8 1.7 1.5 8.8 2.7 9.2 0.8 (2.8)Ju Teng 3336.HK 601 4.18 9.30 122.4 Not rated Dec 6.3 5.3 1.2 0.9 12.7 6.3 0.7 (21.7) (27.3)Kingboard Chemical 0148.HK 3,967 36.30 38.20 5.2 NEUTRAL Dec 12.8 9.3 1.4 1.3 8.9 3.0 (1.4) 1.7 8.4Kingboard Laminates 1888.HK 2,938 7.61 10.19 33.9 Not rated Dec 13.9 8.8 2.7 2.5 14.5 8.6 0.8 (4.4) 13.6Kowloon Dev. 0034.HK 1,231 8.31 13.71 65.0 Not rated Dec 7.9 n.a. 0.6 0.6 5.9 (0.5) 1.7 (4.9) 9.1Lee & Man Paper 2314.HK 3,409 5.82 5.05 (13.2) NEUTRAL Mar 18.3 13.6 2.7 2.4 13.5 7.4 3.0 (1.0) 8.0Luk Fook 0590.HK 986 15.56 13.80 (11.3) Not rated Mar 16.4 12.3 n.a. 4.0 20.2 13.2 (3.4) 22.5 73.1Luks 0366.HK 194 2.95 3.83 29.8 Not rated Dec 14.1 11.4 0.7 0.6 4.7 (2.1) 1.4 (11.9) (8.1)Lung Kee 0255.HK 350 4.33 5.15 18.9 OUTPERFORM Dec 12.2 9.8 1.4 1.3 9.2 2.9 (5.0) (2.7) 8.3Midland 1200.HK 638 6.84 8.60 25.8 OUTPERFORM Dec 6.9 9.1 2.8 2.8 19.7 13.1 8.7 (14.8) 15.0Nagacorp 3918.HK 343 1.28 1.60 24.8 Not rated Dec 13.3 10.2 1.2 1.1 9.5 3.0 6.7 39.1 42.2Natural Beauty 0157.HK 397 1.54 0.87 (43.6) Not rated Dec 20.5 n.a. 3.5 3.5 13.4 7.0 2.7 6.9 10.0Neo-Neon 1868.HK 587 4.98 3.58 (28.2) Not rated Dec 25.5 21.7 1.3 1.2 3.4 (3.0) 0.4 11.2 16.9Nex t Media 0282.HK 326 1.05 1.32 26.1 Not rated Mar 8.4 10.7 n.a. 0.7 7.8 1.3 5.0 (6.3) (12.5)OOIL 0316.HK 4,715 58.55 76.80 31.2 OUTPERFORM Dec (12.6) 6.7 1.2 0.9 (3.4) (10.2) 1.6 (5.4) 17.8Oriental Press 0018.HK 352 1.14 1.32 15.8 Not rated Mar 8.4 10.2 n.a. 0.9 9.1 2.8 0.9 (3.4) 9.6Pacific Basin 2343.HK 1,404 5.65 6.20 9.7 NEUTRAL Dec 12.3 15.1 1.0 0.9 3.4 (3.7) 0.0 (1.6) 15.3Pacific Textiles 1382.HK 787 4.27 4.80 12.4 OUTPERFORM Mar 8.8 7.1 1.9 1.7 21.1 15.1 5.4 (5.1) 16.7Pico Far East 0752.HK 214 1.38 1.61 16.6 Not rated Oct 12.4 8.9 1.7 1.6 9.6 2.8 1.5 2.2 6.2Poly (HK) 0119.HK 4,081 8.80 9.90 12.5 OUTPERFORM Dec 30.4 24.0 1.8 1.4 3.3 (2.6) 4.0 (3.8) 18.8Pou Sheng 3813.HK 613 1.11 1.17 5.2 Not rated Sep 6.4 57.7 n.a. 0.7 0.1 (6.4) 1.8 2.8 22.0Public Financial 0626.HK 639 4.52 3.04 (32.7) Not rated Dec 18.0 n.a. 0.9 0.8 10.9 3.7 2.7 4.1 13.6Sa Sa 0178.HK 1,049 5.84 7.10 21.6 OUTPERFORM Mar 22.2 18.6 6.9 6.4 14.3 8.0 0.9 (4.4) 3.2Samling Global 3938.HK 338 0.61 0.90 47.5 OUTPERFORM Jun (19.6) 52.3 0.5 0.7 (2.1) (9.4) 3.4 (12.9) (14.1)Samson 0531.HK 549 1.40 1.73 23.3 Not rated Dec 13.9 9.2 1.0 0.9 6.7 0.6 2.9 2.9 21.7

P/E (x) P/B (x)Share price performance

HK$ term (%)Calendarized Calendarized

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

10 Septem

ber 2010

David &

Goliath

13

Valuations of Credit Suisse HK small-cap watch list* Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MSCMP 0583.HK 283 1.41 1.15 (18.5) Not rated Dec 15.8 n.a. 1.1 1.0 1.7 (4.5) 6.0 (0.7) 4.4Shun Tak 0242.HK 1,120 4.30 6.68 55.3 OUTPERFORM Dec 3.2 14.1 0.6 0.6 1.7 (4.7) (0.9) (13.5) 7.0SIM Technology 2000.HK 353 1.75 1.24 (28.9) Not rated Dec 20.6 n.a. 1.8 1.4 15.3 8.6 5.4 (1.7) 12.9SJM 0880.HK 4,915 7.37 9.00 22.1 OUTPERFORM Dec 40.7 11.7 4.4 3.5 7.3 1.2 0.0 7.6 29.8SmarTone 0315.HK 576 8.52 7.00 (17.8) UNDERPERFORM Jun 30.1 16.2 1.7 1.7 4.5 (2.9) 4.5 1.5 3.9Stella 1836.HK 1,495 14.62 15.47 5.8 Not rated Dec 14.6 13.4 1.9 1.8 12.8 7.2 0.3 0.0 (0.7)Sun Hung Kai & Co. 0086.HK 1,179 5.24 7.57 44.4 Not rated Dec 7.2 5.7 0.7 0.7 12.3 5.2 2.1 (4.9) 30.6Sunlight REIT 0435.HK 461 2.29 2.08 (9.2) Not rated Jun 27.9 (27.6) 0.8 0.8 2.5 (4.9) 1.8 9.0 18.0Taifook Securities 0665.HK 518 5.68 2.23 (60.8) Not rated Jun n.a. 28.2 2.0 2.0 7.5 0.1 18.6 11.4 28.2Techtronic 0669.HK 1,468 7.10 7.00 (1.4) NEUTRAL Dec 22.3 13.5 1.4 1.3 7.9 1.0 0.6 9.4 0.6Texwinca 0321.HK 1,362 7.93 8.78 10.7 NEUTRAL Mar 10.9 9.2 2.4 2.1 8.4 1.6 0.3 0.9 3.8TPV 0903.HK 1,428 4.73 8.30 75.5 Not rated Dec 9.1 8.7 0.9 0.8 12.1 6.0 3.7 (4.6) 3.1Transport Int'l 0062.HK 1,244 23.95 27.08 13.1 Not rated Dec 14.3 13.4 1.4 1.4 3.9 (2.0) (0.2) (3.4) 5.0Truly 0732.HK 657 10.14 11.70 15.4 NEUTRAL Dec 15.6 10.1 1.4 1.2 7.4 0.5 0.6 (9.1) 15.9Varitronix 0710.HK 119 2.86 3.75 31.1 OUTPERFORM Dec (3.4) 5.6 0.7 0.7 2.6 (4.8) 1.4 12.6 24.3Victory City 0539.HK 249 1.82 2.18 19.8 OUTPERFORM Mar 6.0 5.1 n.a. 0.6 8.5 0.7 4.6 7.7 25.5Vitasoy 0345.HK 812 6.19 3.79 (38.8) Not rated Mar 25.2 21.9 n.a. 4.6 12.0 6.0 1.5 (1.1) 4.0VTech 0303.HK 2,531 79.25 101.00 27.4 OUTPERFORM Mar 13.1 11.1 5.1 4.6 20.8 15.4 (0.1) (3.7) 8.6Win Hanv erky 3322.HK 198 1.21 1.30 7.7 Not rated Dec 12.6 n.a. 0.8 0.8 7.5 0.4 7.1 15.2 6.1Wing Hang Bank 0302.HK 3,165 83.35 62.11 (25.5) Not rated Dec 20.4 15.0 2.0 1.8 9.5 2.6 (2.6) 0.4 18.1Yip's Chemical 0408.HK 558 7.87 10.65 35.3 Not rated Mar n.a. 9.8 n.a. 1.8 13.6 6.8 3.4 (0.6) 9.0Yue Yuen 0551.HK 5,241 24.70 27.50 11.3 NEUTRAL Sep 11.4 11.4 1.9 1.6 9.9 4.2 (2.4) (2.9) 7.9

Calendarized Calendarized Share price performanceP/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse Hong Kong Small Cap Index

10 Septem

ber 2010

David &

Goliath

14

Hong Kong – Screening Absolute price performance - top & bottom 10 companies Absolute price performance - top & bottom 10 companies Absolute price performance - top & bottom 10 companies Price 1W return Price 1M return Price 3M returnCompany RIC (HK$) (%) Company RIC (HK$) (%) Company RIC (HK$) (%)Winners Winners Winners Taifook Securities 0665.HK 5.68 18.6 IDS 2387.HK 24.45 58.6 I.T. 0999.HK 4.19 129.0 Comba Telecom Sys. 2342.HK 9.16 11.7 I.T. 0999.HK 4.19 54.6 IDS 2387.HK 24.45 91.0 First Pacific 0142.HK 6.40 9.4 Nagacorp 3918.HK 1.28 39.1 Luk Fook 0590.HK 15.56 73.1 Dah Chong Hong 1828.HK 7.17 9.3 Dah Chong Hong 1828.HK 7.17 24.9 Galaxy Entertainment 0027.HK 5.94 63.2 Johnson Electric 0179.HK 3.79 9.2 ICBC Asia 0349.HK 28.55 23.9 Dah Chong Hong 1828.HK 7.17 53.9 Midland 1200.HK 6.84 8.7 Luk Fook 0590.HK 15.56 22.5 ICBC Asia 0349.HK 28.55 49.5 Win Hanverky 3322.HK 1.21 7.1 Aeon Stores 0984.HK 14.30 22.2 Nagacorp 3918.HK 1.28 42.2 Nagacorp 3918.HK 1.28 6.7 Win Hanverky 3322.HK 1.21 15.2 Giordano 0709.HK 4.40 36.2 Melco 0200.HK 3.30 6.5 Comba Telecom Sys. 2342.HK 9.16 15.2 Sun Hung Kai & Co. 0086.HK 5.24 30.6 HKC 0190.HK 0.51 6.3 Café De Coral 0341.HK 21.40 12.6 Hutchison Telecom HK 0215.HK 2.15 30.3 Losers Losers Losers Lung Kee 0255.HK 4.33 (5.0) Ju Teng 3336.HK 4.18 (21.7) Ju Teng 3336.HK 4.18 (27.3)Glorious Sun 0393.HK 2.88 (3.4) Midland 1200.HK 6.84 (14.8) i-Cable 1097.HK 0.98 (17.6)Luk Fook 0590.HK 15.56 (3.4) Shun Tak 0242.HK 4.30 (13.5) Samling Global 3938.HK 0.61 (14.1)Hutchison Telecom HK 0215.HK 2.15 (2.7) Samling Global 3938.HK 0.61 (12.9) Next Media 0282.HK 1.05 (12.5)Giordano 0709.HK 4.40 (2.4) Luks 0366.HK 2.95 (11.9) Luks 0366.HK 2.95 (8.1)Arts Optical 1120.HK 3.65 (1.9) Truly 0732.HK 10.14 (9.1) Glorious Sun 0393.HK 2.88 (3.0)Kingboard Chemical 0148.HK 36.30 (1.4) ASM Pacific 0522.HK 65.00 (8.6) Johnson Electric 0179.HK 3.79 (2.8)Fairwood 0052.HK 8.25 (1.1) Dachan Food 3999.HK 1.55 (7.2) Stella 1836.HK 14.62 (0.7)ICBC Asia 0349.HK 28.55 (1.0) Dickson Concepts 0113.HK 5.59 (6.5) Shun Tak 0242.HK 4.30 (0.9) Chen Hsong 0057.HK 3.00 (6.3) Price-to-earnings - most & least expensive 10 companies Price-to-book - most & least expensive 10 companies CFROI® Spread - top & bottom 10 companies Price 10 P/E Price 10 P/B Price CFROI® SpreadCompany RIC (HK$) (x) Company RIC (HK$) (x) Company RIC (HK$) (%)Winners Winners Winners HKR 0480.HK 3.09 1.6 HKR 0480.HK 3.09 0.4 VTech 0303.HK 79.25 15.4Victory City 0539.HK 1.82 5.1 HKC 0190.HK 0.51 0.4 Pacific Textiles 1382.HK 4.27 15.1Ju Teng 3336.HK 4.18 5.3 Melco 0200.HK 3.30 0.6 Comba Telecom Sys. 2342.HK 9.16 14.1Varitronix 0710.HK 2.86 5.6 Kowloon Dev. 0034.HK 8.31 0.6 Luk Fook 0590.HK 15.56 13.2Sun Hung Kai & Co. 0086.HK 5.24 5.7 Victory City 0539.HK 1.82 0.6 Midland 1200.HK 6.84 13.1Dickson Concepts 0113.HK 5.59 6.5 Asia Financial 0662.HK 3.03 0.6 ICBC Asia 0349.HK 28.55 9.3Pacific Textiles 1382.HK 4.27 7.1 Great Eagle 0041.HK 22.05 0.6 Kingboard Laminates 1888.HK 7.61 8.6Dachan Food 3999.HK 1.55 7.7 Shun Tak 0242.HK 4.30 0.6 SIM Technology 2000.HK 1.75 8.6Asia Financial 0662.HK 3.03 7.8 Luks 0366.HK 2.95 0.6 Sa Sa 0178.HK 5.84 8.0Chen Hsong 0057.HK 3.00 7.9 Champion REIT 2778.HK 3.83 0.7 Lee & Man Paper 2314.HK 5.82 7.4 Losers Losers Losers i-Cable 1097.HK 0.98 163.3 Sa Sa 0178.HK 5.84 6.4 OOIL 0316.HK 58.55 (10.2)Pou Sheng 3813.HK 1.11 57.7 IDS 2387.HK 24.45 5.6 Samling Global 3938.HK 0.61 (9.4)Samling Global 3938.HK 0.61 52.3 Daphne 0210.HK 8.77 5.5 Melco 0200.HK 3.30 (8.8)Hong Kong & S'hai Hotels 0045.HK 12.92 35.2 Vitasoy 0345.HK 6.19 4.6 HKC 0190.HK 0.51 (8.4)Taifook Securities 0665.HK 5.68 28.2 VTech 0303.HK 79.25 4.6 i-Cable 1097.HK 0.98 (7.0)HKC 0190.HK 0.51 25.5 Café De Coral 0341.HK 21.40 4.0 Pou Sheng 3813.HK 1.11 (6.4)Champion REIT 2778.HK 3.83 24.7 Luk Fook 0590.HK 15.56 4.0 HKR 0480.HK 3.09 (6.2)Galaxy Entertainment 0027.HK 5.94 24.6 SJM 0880.HK 7.37 3.5 Hong Kong & S'hai Hotels 0045.HK 12.92 (5.0)Poly (HK) 0119.HK 8.80 24.0 Natural Beauty 0157.HK 1.54 3.5 Sunlight REIT 0435.HK 2.29 (4.9)Café De Coral 0341.HK 21.40 22.3 Comba Telecom Sys. 2342.HK 9.16 3.5 Varitronix 0710.HK 2.86 (4.8)

* For stocks that are not rated, I/B/E/S consensus forecast numbers are used. CFROI® Spread is the difference between CFROI® and market implied discount rate. A larger number indicates that more value is created by a company

10 September 2010

David & Goliath 15

China – Street talk * Zhaojin Mining (1818.HK, HK$20.75, NR) to construct a gold production plant. Zhaojin Mining plans to construct a gold production plant with a processing capacity of 2,000 tons per day for about Rmb500 mn within the next three years. The gold mining firm has partnered with the Government of Qinghe County, Xingjiang, to construct the plant located in Qinghe County. (6-Sep)

60

100

140

180

220

09/09 12/09 03/10 06/10 09/10

Zhaojin Mining MSCI China

Longrun Tea (2898.HK, HK$0.54, NR) to acquire teahouses in China. Longrun Tea is planning to acquire Tea Story (not listed), a chain of trendy teahouses in the mainland for Rmb5 mn. Major products served in Tea Story trendy teahouses include bubble tea, cocoa drinks, fruity drinks, shakes and Taiwanese snacks and light refreshments. There are over 400 Tea Story trendy teahouses in China, mainly located in Hunan, Yunnan, Guangdong and Zhejiang Provinces. (7-Sep)

40

60

80

100

120

09/09 12/09 03/10 06/10 09/10

Longrun Tea MSCI China

361 Degrees (1361.HK, HK$6.40, NR) contracted sales up. 361 Degrees announced that 2011 contracted sales for spring and summer rose 20% YoY. Also, the number of “361 Towns” stores has been increased to five. (8-Sep)

60

100

140

180

220

09/09 12/09 03/10 06/10 09/10

361 Degrees MSCI China

China Grand Forestry (0910.HK, HK$0.255, NR) to place 1 bn shares. China Grand Forestry intends to place 1 bn shares at a price of HK$0.21 per share. The net proceeds from the placing is expected to amount to around HK$205 mn. The company plans to use the proceeds for future business investment. (9-Sep)

60

80

100

120

09/09 12/09 03/10 06/10 09/10

China Grand Forestry MSCI China

10 September 2010

David & Goliath 16

Haier Electronics (1169.HK, HK$5.76, NR) to build logistics centres in tier 3 and 4 cities. Haier Electronics aims to develop an integrated channel service business, focusing on tier 3 and tier 4 cities in the mainland. The electronics group is planning to construct 91 logistics centers throughout China, of which 11 will be operated by Haier and the remainder will be franchised. (10-Sep)

0

100

200

300

400

09/09 12/09 03/10 06/10 09/10

Haier Electronics MSCI China

*Source: China Press Digest, CIS, DataStream

10 September 2010

David & Goliath 17

China – Company updates BYD (1211.HK, HK$48.60, U [V], TP HK$40.00) Geely (0175.HK, HK$2.81, U [V], TP HK$1.92) Disappointing August auto sales adds gravity to EPS forecasts

■ According to various media sources (Bloomberg, Dow Jones and WSJ, among others) citing BYD, the company’s auto salesdeclined 6% MoM and 19% YoY to 31,069 units for August. Thiswould take its total YTD sales to around 350,000 units.

■ YTD sales represent only 58% of BYD management’s guidanceand 61% of our 2010 forecast of 570,000. Given the currentsales run-rate, we believe BYD is unlikely to achieve its ownguidance as well as our full-year estimates.

■ Besides the lacklustre performances of its three core businesses,we expect BYD to face numerous challenges in the mediumterm, including: 1) the potential foray into home appliances; and2) investigation by the Ministry of Land and Resources.

■ BYD has underperformed significantly since June; however, thede-rating is not yet complete, in our view. We see furtherdownside risks to consensus and our earnings forecasts. Weadvise investors to avoid the stock in the near term. We maintainour UNDERPERFORM rating.

Surprising MoM rebound in August sales; achieving FY target still a big challenge

■ Geely’s August sales surprisingly rebounded 10% YoY and 17% MoM to 25,303 units, versus management’s initial guidance two weeks ago for flat-to-down monthly sales, due to annual summer plant maintenance, during the interim results.

■ Key models contributing to the strong MoM rebound included Free Cruiser, Kingkong and EC718, which rose 24-49% MoM. Exports were stable MoM at around 1,500 units but stayed well below the 4,250 monthly units required to meet management’s target of 20,000 units for 2H10. Despite the MoM sales rebound, Geely has achieved only 61% of its full-year sales target of 400,000 units for 8M10, suggesting near-record monthly sales of 40,000 units for the remaining months to meet the target; we believe the company is unlikely to achieve the target.

■ While we believe in Geely’s medium-term potential with improving brand transformation, quality and ASP, we think the stock could continue to underperform the sector in the near term on weaker-than-expected sales, potential consensus earnings downgrade and expensive valuation at 13x FY11E P/E vs peers at 9-10x.

Bbg/RIC 48.4040.00 (40.00)

2,275.10 (17)6.6

59.3Free float (%) 40.4 Performance 1M 3M 12M

Absolute (%) (7.0) (24.3) (14.2)Relativ e (%) (6.7) (31.2) (18.7)

Year 12/08A 12/09A 12/10E 12/11E 12/12E26,788 39,469 51,541 66,035 80,1492,831 6,548 7,822 10,040 12,2001,021 3,794 4,194 5,451 6,6910.50 1.77 1.84 2.40 2.94n.a. n.a. 0 0 0n.a. n.a. 2.25 2.64 3.06

(36.6) 255.0 4.2 30.0 22.784.9 23.9 23.0 17.7 14.4

0 0.8 0.9 1.3 1.736.6 14.9 13.2 10.2 8.2

7.7 5.4 4.8 3.9 3.29.1 22.7 20.8 22.0 22.2

55.9 6.9 30.6 21.4 11.1

85.50 - 44.50

Rev enues (Rmb mn)

Major shareholders

110.1/ 14.2Mkt cap (HK$/US$ bn)Daily trad v al - 6m av g (US$ mn)

EBITDA (Rmb mn)Net profit (Rmb mn)

ROE (%)Net debt (net cash)/equity (%)

EPS (Rmb)

Note1:Ord/ADR=10.0000.Note2:BYD manufactures and sells batteries, handset components and automobiles. Besides, it also provides handset assembly services..

P/E (x )Div idend y ield (%)EV/EBITDA (x )

1211 HK / 1211.HKU (U) [V]

P/B (x )

Daily trad v ol - 6m av g (mn)

- Consensus EPS (Rmb)EPS grow th (%)

Rating (prev. rating)

- Change from prev . EPS (%)

Shares outstanding (mn)

Wang Chuan-fu

Price (07 Sep 10, HK$)TP (Prev. TP W)Est. pot. % chg. to TP52-w k range (W)

Bbg/RIC 2.851.92 (1.92)

7,389.66 (33)56.226.8

Free float (%) 48.5 Performance 1M 3M 12MAbsolute (%) 0.4 7.5 37.7 Relativ e (%) 2.3 (0.5) 34.8

Year 12/08A 12/09A 12/10E 12/11E 12/12E4,289 14,069 17,307 20,766 25,828

994 2,032 2,656 3,174 3,896 879 1,183 1,362 1,642 2,063

0.14 0.17 0.16 0.19 0.23 n.a. n.a. 0 0 0n.a. n.a. 0.20 0.24 0.28

136.6 16.7 (6.3) 19.3 24.317.5 15.0 16.0 13.4 10.80.6 0.8 0.9 1.1 1.4

18.7 8.9 6.7 5.2 3.83.9 2.9 2.4 2.0 1.7

20.9 18.6 18.0 18.2 19.13.6 (3.2) (7.8) (19.3) (31.3)

4.61 - 1.79

Rev enues (Rmb mn)

Major shareholders

21,060.5/ 2,710.4Mkt cap (HK$/US$ mn)Daily trad v al - 6m av g (US$ mn)

EBITDA (Rmb mn)Net profit (Rmb mn)

ROE (%)Net debt (net cash)/equity (%)

EPS (Rmb)

Note1:Ord/ADR=20.0000.Note2:Geely Automobile is involved in the sales and manufacture o f passenger cars in China. The company also exports its automobiles overseas.

P/E (x )Div idend y ield (%)EV/EBITDA (x )

175 HK / 0175.HKU (U) [V]

P/B (x )

Daily trad v ol - 6m av g (mn)

- Consensus EPS (Rmb)EPS grow th (%)

Rating (prev. rating)

- Change from prev . EPS (%)

Shares outstanding (mn)

Proper Glory - 51%

Price (08 Sep 10, HK$)TP (Prev. TP W)Est. pot. % chg. to TP52-w k range (W)

Price performance vs. MSCI China Price performance vs. MSCI China

70

100

130

160

190

09/09 11/09 01/10 03/10 05/10 07/10 09/10

BYD MSCI China

40

100

160

220

280

09/09 11/09 01/10 03/10 05/10 07/10 09/10

Geely MSCI China

Adrian Chan / Research Analyst / 852 2101 6469 / [email protected] Extracted from The Asian Daily 08 Sep 2010

HungBin Toh / Research Analyst / 852 2101 7481 / [email protected] Extracted from The Asian Daily 10 Sep 2010

10 September 2010

David &

Goliath

18

Valuations of Credit Suisse China small-cap watch list* Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MAjisen 0538.HK 1,567 11.38 5.48 (51.8) Not Rated Dec 38.6 29.6 5.1 4.4 9.2 3.0 (10.0) 23.0 44.1AMVIG 2300.HK 628 5.29 6.20 17.2 OUTPERFORM Dec 15.8 8.4 4.0 3.6 12.6 6.4 (3.5) 23.0 11.4Anhui Expressway 0995.HK 324 5.10 4.66 (8.7) Not Rated Dec 11.1 10.4 1.4 1.3 8.1 1.7 (1.2) 0.6 14.1Anhui Tianda Oil Pipe 0839.HK 113 2.92 4.51 54.5 Not Rated Dec 9.8 5.7 1.3 1.2 8.2 1.5 6.6 (11.5) (1.0)Anton Oilfield 3337.HK 207 0.77 1.12 45.5 NEUTRAL Dec 6.6 5.1 0.8 0.7 5.5 (0.9) (1.3) (2.5) 8.5Asia Cement (China) 0743.HK 697 3.48 2.46 (29.2) Not Rated Dec 7.8 11.5 0.7 0.6 5.9 (0.6) 3.0 (9.4) (2.8)Beijing Capital Land 2868.HK 336 2.56 2.97 16.1 Not Rated Dec 8.4 6.2 1.0 1.0 8.3 1.4 2.4 3.6 18.0Beijing Jingkelong 0814.HK 224 9.55 4.43 (53.6) Not Rated Dec 23.2 17.4 2.5 2.2 8.1 0.6 (1.5) 5.6 21.8Beijing North Star 0588.HK 190 2.09 1.58 (24.6) Not Rated Dec 4.1 n.a. 0.5 0.5 3.9 (3.0) 1.0 (3.2) 11.2Bosideng 3998.HK 2,911 2.91 2.06 (29.3) Not Rated Mar 22.0 17.5 2.9 2.9 14.8 9.2 4.7 24.4 50.8Brilliance China Auto. 1114.HK 2,404 3.74 2.14 (42.8) Not Rated Dec (18.1) 25.6 3.3 3.2 (7.6) (13.8) 11.0 21.8 53.3BYD 1211.HK 4,960 48.60 40.00 (17.7) UNDERPERFORM Dec 24.2 23.2 5.5 4.8 19.7 15.2 2.5 (10.0) (21.6)BYD Electronic 0285.HK 1,142 3.94 4.80 21.8 NEUTRAL Dec 10.3 8.9 1.2 1.1 14.4 8.9 1.0 (11.7) (13.0)Chaoda Modern 0682.HK 2,694 6.26 22.16 254.0 Not Rated Jun 4.3 3.9 1.1 0.9 16.6 11.0 (2.6) (27.7) (17.0)China Aerospace 0031.HK 417 1.05 1.80 71.0 Not Rated Dec 6.9 10.3 1.0 1.2 4.3 (2.0) 9.4 1.9 29.6China Aoyuan 3883.HK 417 1.24 1.71 37.9 NEUTRAL Dec 12.0 11.0 0.5 0.5 2.9 (4.0) 4.2 (0.8) 8.8China Automation 0569.HK 691 5.27 4.61 (12.5) Not Rated Dec 21.0 17.1 3.6 2.5 20.6 14.5 8.7 (3.8) (0.6)China Everbright Int'l. 0257.HK 1,692 3.61 2.06 (43.1) Not Rated Dec 31.7 24.7 2.9 2.4 7.4 1.4 3.1 0.3 19.9China Fire Safety 0445.HK 94 0.26 0.31 20.4 Not Rated Dec (6.1) n.a. 0.5 0.5 (6.8) (13.7) 3.7 10.4 3.7China Foods 0506.HK 2,048 5.70 2.83 (50.3) Not Rated Dec 27.9 30.0 2.9 2.8 12.0 6.5 (0.2) 3.4 35.1China Gas 0384.HK 1,910 4.12 4.52 9.7 OUTPERFORM Mar 24.7 21.4 4.3 3.6 8.0 1.3 1.0 5.1 15.1China Grand Forestry 0910.HK 339 0.26 0.55 114.9 Not Rated Mar (0.9) (1.8) n.a. 0.4 (50.9) (57.2) 10.4 18.1 9.9China Green 0904.HK 826 7.26 12.51 72.3 Not Rated Apr 11.2 9.4 1.9 1.6 17.0 10.8 (5.3) (19.0) 8.4China Haisheng 0359.HK 140 0.89 1.37 54.4 Not Rated Dec 9.7 4.0 1.1 1.1 8.6 0.9 (2.2) (8.2) 4.7China Huiyuan 1886.HK 1,121 5.93 2.76 (53.5) Not Rated Dec 32.6 34.5 1.6 1.4 0.1 (5.7) 3.7 (0.3) 7.8China LotSynergy 8161.HK 286 0.30 0.22 (26.3) Not Rated Dec (27.3) 16.7 2.8 2.6 (7.0) (13.8) 5.3 (7.7) (10.4)China Mengniu 2319.HK 5,299 23.70 28.00 18.1 OUTPERFORM Dec 30.6 27.3 4.2 3.8 12.3 7.1 0.4 0.0 3.7China Metal 0319.HK 243 1.88 2.81 49.3 Not Rated Dec 12.1 8.1 1.1 1.0 6.8 0.4 2.7 (4.1) (6.0)China Metal Recycling 0773.HK 1,126 8.37 12.52 49.6 Not Rated Dec 15.4 9.7 2.9 1.8 16.9 11.2 4.6 7.0 29.6

CalendarizedCalendarized Share price performanceHK$ term (%)P/B (x)P/E (x)

* Include the China Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse China Small Cap Index.

10 September 2010

David &

Goliath

19

Valuations of Credit Suisse China small-cap watch list * Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MChina Nickel 2889.HK 375 1.28 0.74 (42.5) Not Rated Dec (7.0) n.a. 0.6 0.6 (15.8) (22.9) 4.1 (0.8) 5.8China Pharma. 1093.HK 816 4.13 5.55 34.4 Not Rated Dec 6.5 8.4 1.2 1.1 16.5 10.2 (0.2) (4.8) (5.7)China Power Int'l. 2380.HK 1,111 1.69 2.25 33.1 OUTPERFORM Dec 10.5 13.9 0.4 0.6 1.6 (5.5) 0.6 (3.4) 7.6China Pow er New Energy 0735.HK 742 0.81 0.62 (23.0) Not Rated Dec 36.8 21.9 1.2 1.2 5.7 (1.2) 1.3 (8.0) 8.0China Resources Gas 1193.HK 2,028 11.14 14.20 27.5 OUTPERFORM Dec 37.4 25.1 3.1 2.8 8.0 2.0 (2.1) 2.4 15.4China Shanshui Cement 0691.HK 1,771 4.91 5.70 16.1 OUTPERFORM Dec 17.1 12.8 2.3 2.2 8.2 1.9 11.3 11.1 33.8China Shineway Pharma. 2877.HK 2,198 20.65 18.44 (10.7) Not Rated Dec 19.4 18.8 5.5 5.2 27.5 21.9 (2.1) (8.6) (11.4)China State Construction 3311.HK 1,653 4.34 2.40 (44.7) Not Rated Dec 19.1 15.9 3.0 2.2 7.7 1.4 3.8 18.9 89.5China Travel 0308.HK 1,319 1.80 1.36 (24.7) Not Rated Dec 360.0 n.a. 0.9 0.9 1.7 (4.1) 2.3 (4.3) 9.1China Water 0855.HK 488 2.80 2.25 (19.6) Not Rated Mar 14.1 10.3 1.8 1.5 8.6 1.6 0.7 0.7 15.7China Windpow er 0182.HK 806 0.86 0.82 (4.9) Not Rated Dec 25.3 21.0 1.9 1.7 17.6 11.7 4.9 7.5 22.9Chongqing Iron 1053.HK 141 2.03 0.26 (87.0) Not Rated Dec 35.6 12.3 0.6 0.5 1.1 (6.0) 4.1 (6.9) 16.7Chongqing Mch. & Elec. 2722.HK 311 2.20 1.30 (40.9) OUTPERFORM Dec 14.7 12.9 2.0 1.5 9.3 2.9 11.1 12.8 18.3Chu Kong Shipping Dev. 0560.HK 217 1.87 0.80 (57.4) Not Rated Dec 22.3 12.7 0.9 0.9 1.8 (5.8) (3.1) (4.6) 10.7CITIC 1616 1883.HK 758 2.47 2.42 (1.9) Not Rated Dec 13.1 12.8 2.8 2.6 19.0 12.9 23.5 13.8 14.9CITIC Resources 1205.HK 1,433 1.84 2.56 38.9 Not Rated Dec 96.8 14.2 1.3 1.0 2.5 (4.2) 7.6 6.4 34.3Clear Media 0100.HK 289 4.25 7.51 76.6 Not Rated Dec 70.8 14.3 0.9 0.8 14.9 7.5 (1.6) (8.8) (2.1)COSCO Int'l. 0517.HK 863 4.44 4.53 2.0 Not Rated Dec 7.9 9.6 1.0 1.0 11.5 5.6 0.0 0.5 19.0Dalian Port 2880.HK 429 3.14 3.85 22.6 OUTPERFORM Dec 13.3 12.9 1.2 1.1 6.0 (0.4) 1.0 (6.8) 1.0Digital China 0861.HK 1,545 11.76 12.97 10.3 Not Rated Mar 14.9 13.5 3.0 2.7 12.7 6.5 (1.3) (3.1) 0.3Dynasty Fine Wines 0828.HK 577 3.60 1.81 (49.8) Not Rated Dec 28.8 25.0 2.5 2.3 8.5 2.3 5.6 7.8 13.2First Tractor 0038.HK 317 6.12 6.33 3.4 Not Rated Dec 18.5 15.2 1.8 1.6 7.1 0.7 3.2 12.9 37.2Franshion Properties 0817.HK 2,735 2.32 1.11 (52.2) Not Rated Dec 16.9 16.2 1.3 1.0 6.3 0.3 2.2 2.2 4.0Fufeng 0546.HK 1,130 5.29 7.95 50.2 Not Rated Dec 8.3 8.1 3.2 2.6 29.4 23.3 (0.4) (9.0) (1.5)Fushan Int'l Energy 0639.HK 3,026 4.37 5.83 33.3 Not Rated Dec 18.6 11.6 1.5 1.1 11.6 6.4 0.5 (7.4) 2.1Geely 0175.HK 2,672 2.81 1.92 (31.7) UNDERPERFORM Dec 14.8 15.9 2.8 2.4 14.8 9.1 5.2 0.7 8.5Global Bio-chem 0809.HK 556 1.33 1.49 12.3 Not Rated Dec (266.0) 7.1 0.5 0.5 2.7 (4.6) 11.8 4.7 1.0Global Sweeteners 3889.HK 214 1.45 1.52 4.6 Not Rated Dec 17.7 8.2 0.9 0.9 7.5 0.2 3.6 (7.1) 9.8Golden Eagle 3308.HK 5,287 21.15 9.23 (56.3) Not Rated Dec 134.7 37.3 12.4 11.4 14.9 9.6 5.2 11.2 30.9

Share price performanceHK$ term (%)

Calendarized CalendarizedP/E (x) P/B (x)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse China Small Cap Index.

10 September 2010

David &

Goliath

20

Valuations of Credit Suisse China small-cap watch list * Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MGolden Meditech 0801.HK 307 1.41 1.31 (7.3) Not Rated Mar 16.9 15.0 n.a. 0.7 9.4 2.6 (4.1) (4.7) (9.6)Great Wall Motor 2333.HK 974 18.32 23.66 29.1 Not Rated Dec 17.2 12.1 2.3 2.1 13.0 7.1 10.4 21.6 50.4Greentown China 3900.HK 1,837 8.72 8.30 (4.8) UNDERPERFORM Dec 16.3 9.5 1.3 1.3 2.5 (4.2) 1.8 (6.5) 5.7Guangzhou Pharma. 0874.HK 238 8.41 5.46 (35.1) Not Rated Dec 27.8 21.5 1.7 1.7 3.1 (3.1) 6.7 22.1 18.5Guangzhou Ship 0317.HK 296 14.60 11.67 (20.1) Not Rated Dec 12.3 11.0 2.0 1.9 12.3 6.1 15.1 14.2 33.2GZI REIT 0405.HK 542 3.95 2.99 (24.3) Not Rated Dec 14.0 14.9 1.0 1.0 5.7 (1.4) 4.2 7.3 23.1GZI Transport 1052.HK 896 4.16 5.44 30.8 Not Rated Dec 16.0 10.4 0.8 0.8 24.4 18.0 1.7 (1.4) 6.4Hainan Meilian 0357.HK 255 8.74 6.23 (28.7) Not Rated Dec 20.1 16.6 1.9 1.8 8.8 2.8 4.0 0.6 8.6Haitian 1882.HK 1,280 6.23 6.05 (2.9) Not Rated Dec 19.5 11.7 2.6 2.5 12.7 6.6 3.5 5.6 11.3Harbin Power 1133.HK 696 8.01 6.20 (22.6) UNDERPERFORM Dec 16.0 14.4 1.1 1.1 2.4 (4.3) 8.0 11.1 50.8Hidili 1393.HK 1,782 6.72 7.60 13.2 Not Rated Dec 30.0 12.2 1.9 1.8 3.8 (2.1) 0.1 (4.5) 15.9Honghua 0196.HK 398 0.96 1.64 70.8 UNDERPERFORM Dec (21.7) 7.8 0.7 0.6 0.0 (6.3) 10.3 (6.8) (14.3)Hopson Dev. 0754.HK 2,091 9.27 9.90 6.8 NEUTRAL Dec 6.3 5.6 0.5 0.5 3.6 (3.0) 0.4 (13.7) 4.3Huabao 0336.HK 4,655 11.50 11.30 (1.7) NEUTRAL Mar 27.8 23.2 10.1 7.7 48.8 43.6 0.0 0.9 22.6Huadian Power 1071.HK 346 1.88 0.52 (72.2) Not Rated Dec 8.7 14.9 0.7 0.6 3.4 (3.6) 2.2 (3.1) 10.6Hunan Nonferrous 2626.HK 607 2.89 0.91 (68.4) Not Rated Dec (25.8) 28.1 2.2 2.0 0.9 (5.8) 19.9 14.2 11.2Inspur 0596.HK 315 0.65 0.86 32.5 Not Rated Dec 8.8 8.9 1.7 1.3 21.3 15.3 (3.0) (15.6) (3.0)Intime Dept. Store 1833.HK 2,366 10.44 4.70 (54.9) Not Rated Dec 35.2 31.5 4.7 4.1 7.7 1.7 1.4 23.1 33.8Kingdee 0268.HK 848 3.16 2.16 (31.8) Not Rated Dec 25.9 24.9 4.6 3.9 16.6 10.2 3.3 (8.7) 20.6Kingsoft 3888.HK 568 3.96 7.65 93.2 Not Rated Dec 9.5 9.0 2.4 2.0 22.5 16.8 4.8 (9.6) (3.4)Kingw ay Brew ery 0124.HK 485 2.20 1.50 (31.9) Not Rated Dec 275.0 n.a. 1.3 1.3 3.0 (3.4) 0.0 21.5 48.6KWG Property 1813.HK 2,290 6.15 6.30 2.4 OUTPERFORM Dec 20.3 11.8 1.5 1.4 3.3 (3.2) 9.2 12.6 39.1Lianhua Supermarket 0980.HK 823 30.90 10.96 (64.5) Not Rated Dec 33.3 26.9 6.9 6.8 4.2 (2.1) (1.3) (1.1) 10.4Lingbao Gold 3330.HK 114 2.97 1.47 (50.4) Not Rated Dec 17.3 6.0 1.1 1.0 8.9 1.4 1.4 4.9 10.0Little Sheep 0968.HK 730 5.50 2.40 (56.5) Not Rated Dec 31.8 26.7 4.8 4.4 11.5 5.1 12.7 22.2 31.0Lonking 3339.HK 1,991 7.23 9.08 25.6 OUTPERFORM Dec 17.0 10.4 4.3 3.6 14.7 8.5 4.2 21.3 65.4Lumena 0067.HK 677 2.70 3.95 46.3 OUTPERFORM Dec 9.2 6.7 2.7 2.1 16.7 10.4 8.0 6.3 44.4Mingyuan Medicare 0233.HK 423 0.88 1.15 31.1 Not Rated Dec 35.2 14.7 2.1 2.0 16.0 9.7 8.6 (2.2) 6.0Minmetals Resources 1208.HK 1,080 4.14 2.64 (36.2) Not Rated Dec 46.5 28.0 1.4 1.4 3.0 (3.4) 17.6 29.4 56.8

Calendarized Calendarized Share price performanceP/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse China Small Cap Index.Valuations of Credit Suisse China small-cap watch list *

10 September 2010

David &

Goliath

21

Valuations of Credit Suisse China small-cap watch list * Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MMinth 0425.HK 1,740 12.64 13.07 3.4 Not Rated Dec 17.0 15.0 2.8 2.5 15.9 10.2 (0.2) 4.3 33.6Nanjing Panda 0553.HK 59 1.91 1.80 (5.6) Not Rated Dec 70.7 17.4 0.8 0.7 (11.6) (18.7) 1.6 (4.0) 1.6New World China 0917.HK 2,008 2.71 3.15 16.3 Not Rated Jun 6.9 10.3 0.4 0.4 0.5 (5.8) 4.2 (1.1) 13.4New World Dept. St. China 0825.HK 1,584 7.30 5.38 (26.3) Not Rated Jun 23.9 22.1 3.2 2.7 8.3 2.3 3.0 7.7 13.9Nine Dragons 2689.HK 6,799 11.36 10.85 (4.5) UNDERPERFORM Jun 22.0 17.1 2.6 2.2 5.2 (0.4) 5.6 (1.4) 10.5Phoenix Satellite 2008.HK 1,598 2.49 1.13 (54.6) Not Rated Dec 41.5 29.0 6.8 6.1 12.7 6.9 12.7 18.0 39.1Ports Design 0589.HK 1,441 19.78 16.14 (18.4) Not Rated Dec 20.8 18.2 7.2 6.0 16.9 11.0 2.5 (3.5) 8.8Qingling Motors 1122.HK 340 2.13 2.62 22.8 Not Rated Dec 18.7 15.9 0.7 0.7 3.0 (3.0) 2.9 6.5 22.4Qunxing Paper 3868.HK 396 2.91 4.76 63.5 Not Rated Dec 8.2 7.0 1.1 1.0 10.7 4.7 2.1 (4.9) 12.4Real Gold 0246.HK 1,419 12.18 13.19 8.3 Not Rated Dec 13.5 11.0 3.3 2.0 20.3 14.5 (0.2) 3.6 (5.0)RexLot 0555.HK 735 0.74 1.03 39.6 Not Rated Dec 13.0 8.9 1.7 1.6 19.8 13.8 1.4 4.2 0.0Shandong Weigao 1066.HK 2,397 21.75 19.00 (12.6) OUTPERFORM Dec 65.0 49.4 14.0 10.3 19.7 14.5 10.7 21.7 31.8Shanghai Forte 2337.HK 326 2.40 0.49 (79.4) Not Rated Dec 10.7 6.9 0.9 0.8 3.8 (3.5) 6.7 4.8 17.1Shanghai Jin Jiang 2006.HK 378 2.11 1.80 (14.7) Not Rated Dec 70.3 65.9 1.1 1.1 (0.3) (6.4) 8.8 1.9 31.9Shanghai Prime 2345.HK 153 1.56 1.60 2.6 NEUTRAL Dec 13.1 11.7 0.7 0.7 5.6 (1.1) 8.3 5.4 13.9Shenji Group Kumato 0300.HK 85 4.69 5.21 11.2 Not Rated Dec 8.1 9.3 1.5 1.6 13.7 7.4 3.1 (9.6) 1.1Shenyin Wanguo (HK) 0218.HK 242 3.55 1.54 (56.5) Not Rated Dec 25.2 19.3 1.9 1.8 7.8 0.3 16.8 11.6 20.3Shenzhen Expressway 0548.HK 378 3.93 4.14 5.4 Not Rated Dec 13.8 11.8 0.9 0.9 1.6 (5.4) 1.8 3.4 15.6Shenzhen Int'l. 0152.HK 984 0.54 0.58 7.2 Not Rated Dec 8.7 5.7 1.1 0.7 5.5 (1.4) 3.8 5.9 11.3Shenzhen Invest. 0604.HK 1,306 2.87 1.75 (39.2) Not Rated Dec 9.7 9.8 0.8 0.8 4.2 (2.5) 1.1 11.7 32.3Shenzhou 2313.HK 1,442 9.00 11.00 22.2 OUTPERFORM Dec 7.9 6.7 2.5 2.0 25.2 19.3 (2.6) (9.1) 18.1Shougang Concord Int'l 0697.HK 1,410 1.34 0.92 (31.3) Not Rated Dec 148.9 9.6 1.3 1.2 (15.0) (21.5) 11.7 3.9 12.6Sichuan Expressway 0107.HK 635 5.51 4.43 (19.6) Not Rated Dec 16.1 14.8 2.0 2.0 5.8 (0.4) 0.4 14.3 34.7Sino Biopharm. 1177.HK 1,850 2.90 3.00 3.4 Not Rated Dec 33.0 26.4 5.3 3.9 23.1 17.5 (0.3) (2.7) (10.8)Sinocom Software 0299.HK 145 1.01 1.39 37.1 Not Rated Dec 10.9 8.8 1.9 1.7 16.0 9.3 0.0 (17.2) (4.7)Sinopec Kantons 0934.HK 479 3.59 1.72 (52.2) Not Rated Dec 18.9 n.a. 1.6 1.5 6.1 (1.1) (1.9) (7.0) (18.4)Sinotrans 0598.HK 446 1.94 1.59 (18.0) Not Rated Dec 17.0 11.1 0.8 0.8 1.9 (5.1) (0.5) (0.5) 11.5Sinotrans Shipping 0368.HK 1,644 3.20 4.12 28.9 Not Rated Dec 15.2 13.7 0.8 0.8 3.5 (2.1) 1.3 (5.3) 6.0Skyworth Digital 0751.HK 1,553 4.75 7.50 57.9 OUTPERFORM Mar 10.7 8.5 2.1 1.8 10.7 4.4 14.7 (16.2) (28.5)

Calendarized Calendarized Share price performanceP/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse China Small Cap Index.

10 September 2010

David &

Goliath

22

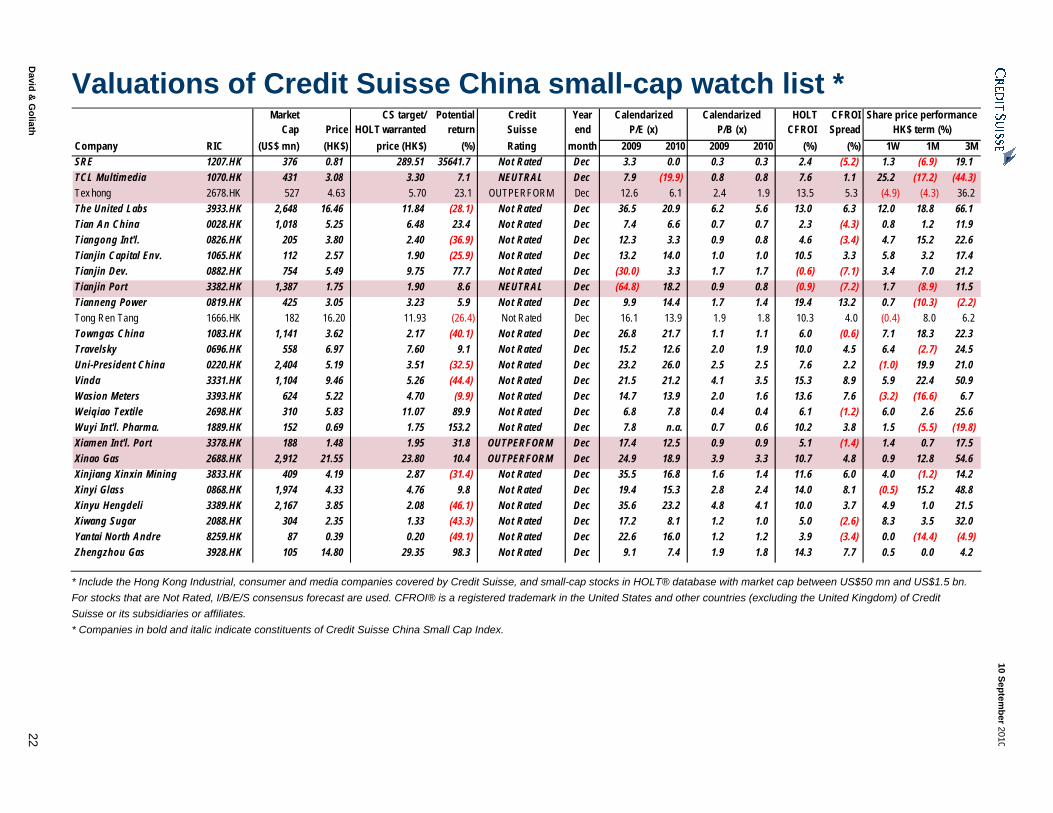

Valuations of Credit Suisse China small-cap watch list * Market CS target/ Potential Credit Year HOLT CFROI

Cap Price HOLT warranted return Suisse end CFROI SpreadCompany RIC (US$ mn) (HK$) price (HK$) (%) Rating month 2009 2010 2009 2010 (%) (%) 1W 1M 3MSRE 1207.HK 376 0.81 289.51 35641.7 Not Rated Dec 3.3 0.0 0.3 0.3 2.4 (5.2) 1.3 (6.9) 19.1TCL Multimedia 1070.HK 431 3.08 3.30 7.1 NEUTRAL Dec 7.9 (19.9) 0.8 0.8 7.6 1.1 25.2 (17.2) (44.3)Tex hong 2678.HK 527 4.63 5.70 23.1 OUTPERFORM Dec 12.6 6.1 2.4 1.9 13.5 5.3 (4.9) (4.3) 36.2The United Labs 3933.HK 2,648 16.46 11.84 (28.1) Not Rated Dec 36.5 20.9 6.2 5.6 13.0 6.3 12.0 18.8 66.1Tian An China 0028.HK 1,018 5.25 6.48 23.4 Not Rated Dec 7.4 6.6 0.7 0.7 2.3 (4.3) 0.8 1.2 11.9Tiangong Int'l. 0826.HK 205 3.80 2.40 (36.9) Not Rated Dec 12.3 3.3 0.9 0.8 4.6 (3.4) 4.7 15.2 22.6Tianjin Capital Env. 1065.HK 112 2.57 1.90 (25.9) Not Rated Dec 13.2 14.0 1.0 1.0 10.5 3.3 5.8 3.2 17.4Tianjin Dev. 0882.HK 754 5.49 9.75 77.7 Not Rated Dec (30.0) 3.3 1.7 1.7 (0.6) (7.1) 3.4 7.0 21.2Tianjin Port 3382.HK 1,387 1.75 1.90 8.6 NEUTRAL Dec (64.8) 18.2 0.9 0.8 (0.9) (7.2) 1.7 (8.9) 11.5Tianneng Power 0819.HK 425 3.05 3.23 5.9 Not Rated Dec 9.9 14.4 1.7 1.4 19.4 13.2 0.7 (10.3) (2.2)Tong Ren Tang 1666.HK 182 16.20 11.93 (26.4) Not Rated Dec 16.1 13.9 1.9 1.8 10.3 4.0 (0.4) 8.0 6.2Towngas China 1083.HK 1,141 3.62 2.17 (40.1) Not Rated Dec 26.8 21.7 1.1 1.1 6.0 (0.6) 7.1 18.3 22.3Travelsky 0696.HK 558 6.97 7.60 9.1 Not Rated Dec 15.2 12.6 2.0 1.9 10.0 4.5 6.4 (2.7) 24.5Uni-President China 0220.HK 2,404 5.19 3.51 (32.5) Not Rated Dec 23.2 26.0 2.5 2.5 7.6 2.2 (1.0) 19.9 21.0Vinda 3331.HK 1,104 9.46 5.26 (44.4) Not Rated Dec 21.5 21.2 4.1 3.5 15.3 8.9 5.9 22.4 50.9Wasion Meters 3393.HK 624 5.22 4.70 (9.9) Not Rated Dec 14.7 13.9 2.0 1.6 13.6 7.6 (3.2) (16.6) 6.7Weiqiao Textile 2698.HK 310 5.83 11.07 89.9 Not Rated Dec 6.8 7.8 0.4 0.4 6.1 (1.2) 6.0 2.6 25.6Wuyi Int'l. Pharma. 1889.HK 152 0.69 1.75 153.2 Not Rated Dec 7.8 n.a. 0.7 0.6 10.2 3.8 1.5 (5.5) (19.8)Xiamen Int'l. Port 3378.HK 188 1.48 1.95 31.8 OUTPERFORM Dec 17.4 12.5 0.9 0.9 5.1 (1.4) 1.4 0.7 17.5Xinao Gas 2688.HK 2,912 21.55 23.80 10.4 OUTPERFORM Dec 24.9 18.9 3.9 3.3 10.7 4.8 0.9 12.8 54.6Xinjiang Xinxin Mining 3833.HK 409 4.19 2.87 (31.4) Not Rated Dec 35.5 16.8 1.6 1.4 11.6 6.0 4.0 (1.2) 14.2Xinyi Glass 0868.HK 1,974 4.33 4.76 9.8 Not Rated Dec 19.4 15.3 2.8 2.4 14.0 8.1 (0.5) 15.2 48.8Xinyu Hengdeli 3389.HK 2,167 3.85 2.08 (46.1) Not Rated Dec 35.6 23.2 4.8 4.1 10.0 3.7 4.9 1.0 21.5Xiwang Sugar 2088.HK 304 2.35 1.33 (43.3) Not Rated Dec 17.2 8.1 1.2 1.0 5.0 (2.6) 8.3 3.5 32.0Yantai North Andre 8259.HK 87 0.39 0.20 (49.1) Not Rated Dec 22.6 16.0 1.2 1.2 3.9 (3.4) 0.0 (14.4) (4.9)Zhengzhou Gas 3928.HK 105 14.80 29.35 98.3 Not Rated Dec 9.1 7.4 1.9 1.8 14.3 7.7 0.5 0.0 4.2

Calendarized Calendarized Share price performanceP/E (x) P/B (x) HK$ term (%)

* Include the Hong Kong Industrial, consumer and media companies covered by Credit Suisse, and small-cap stocks in HOLT® database with market cap between US$50 mn and US$1.5 bn. For stocks that are Not Rated, I/B/E/S consensus forecast are used. CFROI® is a registered trademark in the United States and other countries (excluding the United Kingdom) of Credit Suisse or its subsidiaries or affiliates. * Companies in bold and italic indicate constituents of Credit Suisse China Small Cap Index.

10 September 2010

David &

Goliath

23

China – Screening Absolute price performance - top & bottom 10 companies Absolute price performance - top & bottom 10 companies Absolute price performance - top & bottom 10 companies Price 1W return Price 1M return Price 3M returnCompany RIC (HK$) (%) Company RIC (HK$) (%) Company RIC (HK$) (%)Winners Winners Winners TCL Multimedia 1070.HK 3.08 25.2 Minmetals Resources 1208.HK 4.14 29.4 China State Construction 3311.HK 4.34 89.5 CITIC 1616 1883.HK 2.47 23.5 Bosideng 3998.HK 2.91 24.4 The United Labs 3933.HK 16.46 66.1 Hunan Nonferrous 2626.HK 2.89 19.9 Intime Dept. Store 1833.HK 10.44 23.1 Lonking 3339.HK 7.23 65.4 Minmetals Resources 1208.HK 4.14 17.6 Ajisen 0538.HK 11.38 23.0 Minmetals Resources 1208.HK 4.14 56.8 Shenyin Wanguo (HK) 0218.HK 3.55 16.8 AMVIG 2300.HK 5.29 23.0 Brilliance China Auto. 1114.HK 3.74 53.3 Guangzhou Ship 0317.HK 14.60 15.1 Vinda 3331.HK 9.46 22.4 Vinda 3331.HK 9.46 50.9 Skyworth Digital 0751.HK 4.75 14.7 Little Sheep 0968.HK 5.50 22.2 Harbin Power 1133.HK 8.01 50.8 Little Sheep 0968.HK 5.50 12.7 Guangzhou Pharma. 0874.HK 8.41 22.1 Bosideng 3998.HK 2.91 50.8 Phoenix Satellite 2008.HK 2.49 12.7 Brilliance China Auto. 1114.HK 3.74 21.8 Great Wall Motor 2333.HK 18.32 50.4 The United Labs 3933.HK 16.46 12.0 Shandong Weigao 1066.HK 21.75 21.7 Kingway Brewery 0124.HK 2.20 48.6 Losers Losers Losers Ajisen 0538.HK 11.38 (10.0) Chaoda Modern 0682.HK 6.26 (27.7) TCL Multimedia 1070.HK 3.08 (44.3)China Green 0904.HK 7.26 (5.3) China Green 0904.HK 7.26 (19.0) Skyworth Digital 0751.HK 4.75 (28.5)Texhong 2678.HK 4.63 (4.9) Sinocom Software 0299.HK 1.01 (17.2) BYD 1211.HK 48.60 (21.6)Golden Meditech 0801.HK 1.41 (4.1) TCL Multimedia 1070.HK 3.08 (17.2) SMIC 0981.HK 0.52 (18.8)AMVIG 2300.HK 5.29 (3.5) Skyworth Digital 0751.HK 4.75 (16.2) Sinopec Kantons 0934.HK 3.59 (18.4)Chu Kong Shipping Dev. 0560.HK 1.87 (3.1) Inspur 0596.HK 0.65 (15.6) Chaoda Modern 0682.HK 6.26 (17.0)Inspur 0596.HK 0.65 (3.0) Hopson Dev. 0754.HK 9.27 (13.7) Honghua 0196.HK 0.96 (14.3)Chaoda Modern 0682.HK 6.26 (2.6) BYD Electronic 0285.HK 3.94 (11.7) BYD Electronic 0285.HK 3.94 (13.0)Shenzhou 2313.HK 9.00 (2.6) Anhui Tianda Oil Pipe 0839.HK 2.92 (11.5) China Shineway Pharma. 2877.HK 20.65 (11.4)China Haisheng 0359.HK 0.89 (2.2) Tianneng Power 0819.HK 3.05 (10.3) Sino Biopharm. 1177.HK 2.90 (10.8)

Price-to-earnings - most & least expensive 10 companies Price-to-book - most & least expensive 10 companies CFROI® Spread - top & bottom 10 companies Price 10 P/E Price 10 P/B Price CFROI® SpreadCompany RIC (HK$) (x) Company RIC (HK$) (x) Company RIC (HK$) (%)Winners Winners Winners Tianjin Dev. 0882.HK 5.49 3.3 SRE 1207.HK 0.81 0.3 Huabao 0336.HK 11.50 43.6Tiangong Int'l. 0826.HK 3.80 3.3 China Grand Forestry 0910.HK 0.26 0.4 Fufeng 0546.HK 5.29 23.3Chaoda Modern 0682.HK 6.26 3.9 New World China 0917.HK 2.71 0.4 China Shineway Pharma. 2877.HK 20.65 21.9China Haisheng 0359.HK 0.89 4.0 Beijing North Star 0588.HK 2.09 0.5 Shenzhou 2313.HK 9.00 19.3Anton Oilfield 3337.HK 0.77 5.1 China Fire Safety 0445.HK 0.26 0.5 GZI Transport 1052.HK 4.16 18.0Hopson Dev. 0754.HK 9.27 5.6 Chongqing Iron 1053.HK 2.03 0.5 Sino Biopharm. 1177.HK 2.90 17.5Anhui Tianda Oil Pipe 0839.HK 2.92 5.7 China Aoyuan 3883.HK 1.24 0.5 Kingsoft 3888.HK 3.96 16.8Shenzhen Int'l. 0152.HK 0.54 5.7 Hopson Dev. 0754.HK 9.27 0.5 Inspur 0596.HK 0.65 15.3TCC Int'l. 1136.HK 2.86 5.8 Global Bio-chem 0809.HK 1.33 0.5 BYD 1211.HK 48.60 15.2Lingbao Gold 3330.HK 2.97 6.0 China Power Int'l. 2380.HK 1.69 0.6 Real Gold 0246.HK 12.18 14.5 Losers Losers Losers Shanghai Jin Jiang 2006.HK 2.11 65.9 Golden Eagle 3308.HK 21.15 11.4 China Nickel 2889.HK 1.28 (22.9)Shandong Weigao 1066.HK 21.75 49.4 Shandong Weigao 1066.HK 21.75 10.3 Shougang Concord Int'l 0697.HK 1.34 (21.5)Golden Eagle 3308.HK 21.15 37.3 Huabao 0336.HK 11.50 7.7 SMIC 0981.HK 0.52 (21.1)China Huiyuan 1886.HK 5.93 34.5 Lianhua Supermarket 0980.HK 30.90 6.8 Nanjing Panda 0553.HK 1.91 (18.7)Intime Dept. Store 1833.HK 10.44 31.5 Phoenix Satellite 2008.HK 2.49 6.1 Brilliance China Auto. 1114.HK 3.74 (13.8)China Foods 0506.HK 5.70 30.0 Ports Design 0589.HK 19.78 6.0 China LotSynergy 8161.HK 0.30 (13.8)Ajisen 0538.HK 11.38 29.6 The United Labs 3933.HK 16.46 5.6 China Fire Safety 0445.HK 0.26 (13.7)Phoenix Satellite 2008.HK 2.49 29.0 China Shineway Pharma. 2877.HK 20.65 5.2 Tianjin Port 3382.HK 1.75 (7.2)Hunan Nonferrous 2626.HK 2.89 28.1 BYD 1211.HK 48.60 4.8 Tianjin Dev. 0882.HK 5.49 (7.1)Minmetals Resources 1208.HK 4.14 28.0 Little Sheep 0968.HK 5.50 4.4 Shanghai Jin Jiang 2006.HK 2.11 (6.4)

* For stocks that are not rated, I/B/E/S consensus forecast numbers are used. CFROI® Spread is the difference between CFROI® and market implied discount rate. A larger number indicates that more value is created by a company

10 September 2010

David & Goliath 24

India – Company updates BEML (BEML.BO, Rs1211.45, O, TP Rs1383.53) KEC (KECL.BO, Rs521.45, O [V], TP Rs611.46) New report: Thematic play on likely acceleration in coal capex

■ We initiate coverage of BEML with an OUTPERFORM rating anda target price of Rs1,384 (20x FY12E). BEML is our contra pickin the sector, as near-term fundamentals stay muted. Coalconstraints are now well documented and it is likely that policyaction could accelerate extraction of coal in India. BEML hasabout 70% market share in Coal India’s (not listed) capex andthus benefits from any such acceleration.

■ If there are no coal reforms, we expect BEML’s revenue from themining equipment business to see only 10% CAGR (FY10-17E) while reforms could double it over the next 10 years.Management also expects the railway business to turn profitablethis year.

■ We believe margins might have troughed, as the impact of lowermargins in the metro rail segment might have been alreadycaptured in the mix. Management comments support thatargument and as such BEML expects to achieve gross turnoverof Rs42 bn in FY11. BEML currently has an order book of Rs52bn and we expect a 20% adjusted earnings CAGR (FY10-13). Key risk to our target price in our view is delay in coal reforms.

New report: Valuations price in weak near term; contra pick in the sector

■ We initiate coverage of KEC international, with an OUTPERFORM rating and a target price of Rs611 (13.5x FY12E). KEC is our contra pick in the sector and appears favourable on valuations relative to peers suggesting that the weak near-term fundamentals are captured in its stock pri.

■ We expect an order recovery to commence in FY12, when spend for the next plan commences. Competition is fragmenting the industry, pressuring margins, but KEC’s international footprint helps. The recent acquisition of SAE Towers (not listed) is a positive, as it is EPS accretive and expands geographic footprint.

■ Diversification into railway EPC and capabilities in telecom tower, cable business should help drive order inflow growth over the long term, in our view. On the margin front, despite competitive pressures, we expect KEC to maintain margins at FY10 levels, as over 50% of business stems from international geographies where they may benefit from a favourable RM pricing environment. Key risk to our view is a continued weakness in tower capex.

Bbg/RIC 1,174.001,384 (NA)

41.65 18 0.12.2

Free float (%) 46 Performance 1M 3M 12MAbsolute (%) 15.6 19.7 9.2 Relativ e (%) 12.5 7.7 (6.2)

Year 3/09A 3/10A 3/11E 3/12E 3/13E27,972 28,382 32,800 39,829 46,662 3,393 2,634 3,342 4,631 5,378 2,641 2,229 2,273 2,890 3,313 57.60 46.10 54.40 69.20 79.30

n.a. n.a. (11) 0 0n.a. n.a. 0 0 011.1 (20.0) 18.0 27.1 14.620.4 25.5 21.6 17.0 14.8

1.0 0.8 1.4 1.8 2.015.3 19.9 16.1 12.3 11.1

2.6 2.4 2.2 2.0 1.914.0 10.9 10.3 12.0 12.615.9 16.8 22.6 34.4 41.9

1235.75 - 923.80

Rev enues (Rs mn)

Major shareholders

48,891.2/ 1,043.9Mkt cap (Rs/US$ mn)Daily trad v al - 6m av g (US$ mn)

EBITDA (Rs mn)Net profit (Rs mn)

ROE (%)Net debt (net cash)/equity (%)

EPS (Rs)

Note1:BEM L Limited produces and sells earthmoving equipment, including railway ro lling stock, heavy duty vehicles, wheel loaders, trailers, excavators and heavy recovery vehicles..

P/E (x )Div idend y ield (%)EV/EBITDA (x )

BEML IN / BEML.BOO (NA)

P/B (x )

Daily trad v ol - 6m av g (mn)

- Consensus EPS (Rs)EPS grow th (%)

Rating (prev. rating)

- Change from prev . EPS (%)

Shares outstanding (mn)

Gov t of India:54%