The Kroger Co. (KR) - Credit Suisse

49

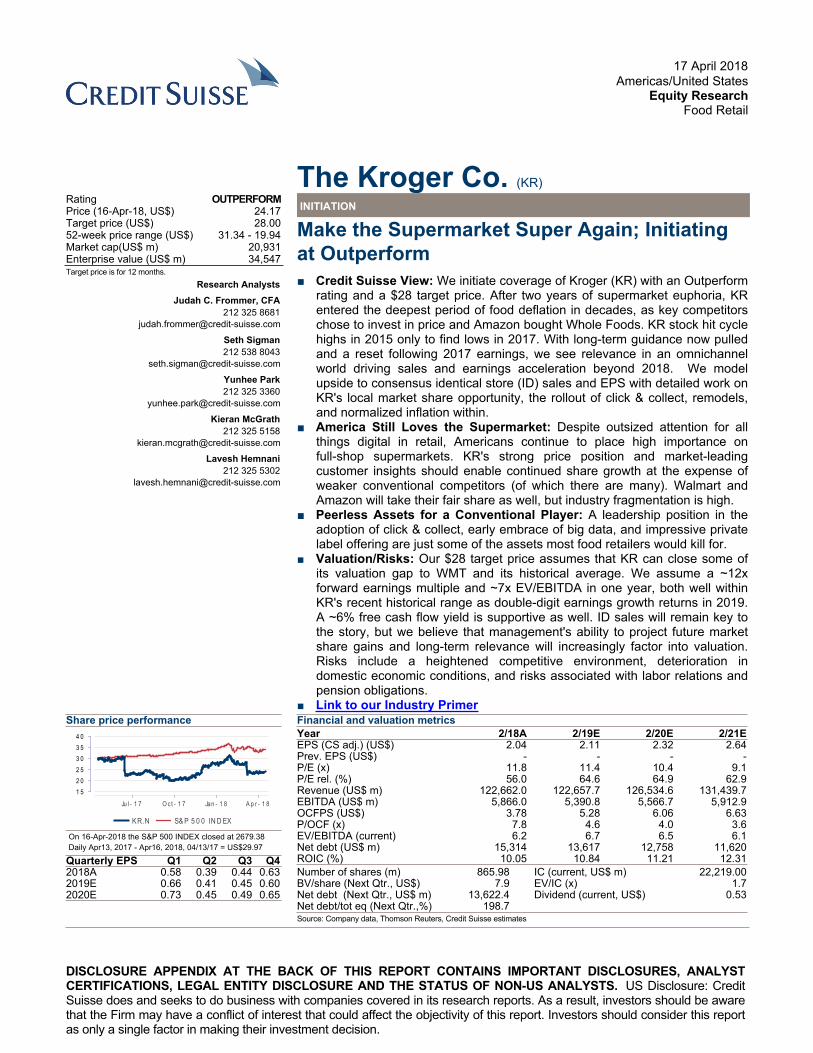

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 17 April 2018 Americas/United States Equity Research Food Retail The Kroger Co. (KR) INITIATION Rating OUTPERFORM Price (16-Apr-18, US$) 24.17 Target price (US$) 28.00 52-week price range (US$) 31.34 - 19.94 Market cap(US$ m) 20,931 Enterprise value (US$ m) 34,547 Target price is for 12 months. Research Analysts Judah C. Frommer, CFA 212 325 8681 [email protected] Seth Sigman 212 538 8043 [email protected] Yunhee Park 212 325 3360 [email protected] Kieran McGrath 212 325 5158 [email protected] Lavesh Hemnani 212 325 5302 [email protected] Make the Supermarket Super Again; Initiating at Outperform ■ Credit Suisse View: We initiate coverage of Kroger (KR) with an Outperform rating and a $28 target price. After two years of supermarket euphoria, KR entered the deepest period of food deflation in decades, as key competitors chose to invest in price and Amazon bought Whole Foods. KR stock hit cycle highs in 2015 only to find lows in 2017. With long-term guidance now pulled and a reset following 2017 earnings, we see relevance in an omnichannel world driving sales and earnings acceleration beyond 2018. We model upside to consensus identical store (ID) sales and EPS with detailed work on KR's local market share opportunity, the rollout of click & collect, remodels, and normalized inflation within. ■ America Still Loves the Supermarket: Despite outsized attention for all things digital in retail, Americans continue to place high importance on full-shop supermarkets. KR's strong price position and market-leading customer insights should enable continued share growth at the expense of weaker conventional competitors (of which there are many). Walmart and Amazon will take their fair share as well, but industry fragmentation is high. ■ Peerless Assets for a Conventional Player: A leadership position in the adoption of click & collect, early embrace of big data, and impressive private label offering are just some of the assets most food retailers would kill for. ■ Valuation/Risks: Our $28 target price assumes that KR can close some of its valuation gap to WMT and its historical average. We assume a ~12x forward earnings multiple and ~7x EV/EBITDA in one year, both well within KR's recent historical range as double-digit earnings growth returns in 2019. A ~6% free cash flow yield is supportive as well. ID sales will remain key to the story, but we believe that management's ability to project future market share gains and long-term relevance will increasingly factor into valuation. Risks include a heightened competitive environment, deterioration in domestic economic conditions, and risks associated with labor relations and pension obligations. ■ Link to our Industry Primer Share price performance KR.N S&P 500 INDEX Ju l- 1 7 Oct-17 Jan - 1 8 Apr-18 15 20 25 30 35 40 On 16-Apr-2018 the S&P 500 INDEX closed at 2679.38 Daily Apr13, 2017 - Apr16, 2018, 04/13/17 = US$29.97 Quarterly EPS Q1 Q2 Q3 Q4 2018A 0.58 0.39 0.44 0.63 2019E 0.66 0.41 0.45 0.60 2020E 0.73 0.45 0.49 0.65 Financial and valuation metrics Year 2/18A 2/19E 2/20E 2/21E EPS (CS adj.) (US$) 2.04 2.11 2.32 2.64 Prev. EPS (US$) - - - - P/E (x) 11.8 11.4 10.4 9.1 P/E rel. (%) 56.0 64.6 64.9 62.9 Revenue (US$ m) 122,662.0 122,657.7 126,534.6 131,439.7 EBITDA (US$ m) 5,866.0 5,390.8 5,566.7 5,912.9 OCFPS (US$) 3.78 5.28 6.06 6.63 P/OCF (x) 7.8 4.6 4.0 3.6 EV/EBITDA (current) 6.2 6.7 6.5 6.1 Net debt (US$ m) 15,314 13,617 12,758 11,620 ROIC (%) 10.05 10.84 11.21 12.31 Number of shares (m) 865.98 IC (current, US$ m) 22,219.00 BV/share (Next Qtr., US$) 7.9 EV/IC (x) 1.7 Net debt (Next Qtr., US$ m) 13,622.4 Dividend (current, US$) 0.53 Net debt/tot eq (Next Qtr.,%) 198.7 Source: Company data, Thomson Reuters, Credit Suisse estimates

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of The Kroger Co. (KR) - Credit Suisse

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

17 April 2018Americas/United States

Equity ResearchFood Retail

The Kroger Co. (KR)

INITIATION Rating OUTPERFORMPrice (16-Apr-18, US$) 24.17Target price (US$) 28.0052-week price range (US$) 31.34 - 19.94Market cap(US$ m) 20,931Enterprise value (US$ m) 34,547Target price is for 12 months.

Research AnalystsJudah C. Frommer, CFA

212 325 [email protected]

Seth Sigman212 538 8043

Yunhee Park212 325 3360

Kieran McGrath212 325 5158

Lavesh Hemnani212 325 5302

Make the Supermarket Super Again; Initiating at Outperform■ Credit Suisse View: We initiate coverage of Kroger (KR) with an Outperform

rating and a $28 target price. After two years of supermarket euphoria, KR entered the deepest period of food deflation in decades, as key competitors chose to invest in price and Amazon bought Whole Foods. KR stock hit cycle highs in 2015 only to find lows in 2017. With long-term guidance now pulled and a reset following 2017 earnings, we see relevance in an omnichannel world driving sales and earnings acceleration beyond 2018. We model upside to consensus identical store (ID) sales and EPS with detailed work on KR's local market share opportunity, the rollout of click & collect, remodels, and normalized inflation within.

■ America Still Loves the Supermarket: Despite outsized attention for all things digital in retail, Americans continue to place high importance on full-shop supermarkets. KR's strong price position and market-leading customer insights should enable continued share growth at the expense of weaker conventional competitors (of which there are many). Walmart and Amazon will take their fair share as well, but industry fragmentation is high.

■ Peerless Assets for a Conventional Player: A leadership position in the adoption of click & collect, early embrace of big data, and impressive private label offering are just some of the assets most food retailers would kill for.

■ Valuation/Risks: Our $28 target price assumes that KR can close some of its valuation gap to WMT and its historical average. We assume a ~12x forward earnings multiple and ~7x EV/EBITDA in one year, both well within KR's recent historical range as double-digit earnings growth returns in 2019. A ~6% free cash flow yield is supportive as well. ID sales will remain key to the story, but we believe that management's ability to project future market share gains and long-term relevance will increasingly factor into valuation. Risks include a heightened competitive environment, deterioration in domestic economic conditions, and risks associated with labor relations and pension obligations.

■ Link to our Industry Primer Share price performance

KR.N S& P 5 0 0 IN D EX

Ju l - 1 7 O ct - 1 7 Jan - 1 8 A p r - 1 81 52 02 53 03 54 0

On 16-Apr-2018 the S&P 500 INDEX closed at 2679.38Daily Apr13, 2017 - Apr16, 2018, 04/13/17 = US$29.97

Quarterly EPS Q1 Q2 Q3 Q42018A 0.58 0.39 0.44 0.632019E 0.66 0.41 0.45 0.602020E 0.73 0.45 0.49 0.65

Financial and valuation metricsYear 2/18A 2/19E 2/20E 2/21EEPS (CS adj.) (US$) 2.04 2.11 2.32 2.64Prev. EPS (US$) - - - -P/E (x) 11.8 11.4 10.4 9.1P/E rel. (%) 56.0 64.6 64.9 62.9Revenue (US$ m) 122,662.0 122,657.7 126,534.6 131,439.7EBITDA (US$ m) 5,866.0 5,390.8 5,566.7 5,912.9OCFPS (US$) 3.78 5.28 6.06 6.63P/OCF (x) 7.8 4.6 4.0 3.6EV/EBITDA (current) 6.2 6.7 6.5 6.1Net debt (US$ m) 15,314 13,617 12,758 11,620ROIC (%) 10.05 10.84 11.21 12.31

Number of shares (m) 865.98 IC (current, US$ m) 22,219.00BV/share (Next Qtr., US$) 7.9 EV/IC (x) 1.7Net debt (Next Qtr., US$ m) 13,622.4 Dividend (current, US$) 0.53Net debt/tot eq (Next Qtr.,%) 198.7Source: Company data, Thomson Reuters, Credit Suisse estimates

17 April 2018

The Kroger Co. (KR) 2

The Kroger Co. (KR)Price (16 Apr 2018): US$24.17; Rating: OUTPERFORM; Target Price: US$28.00; Analyst: Judah FrommerIncome Statement 2/18A 2/19E 2/20E 2/21ERevenue (US$ m) 122,662.0 122,657.7 126,534.6 131,439.7EBITDA 5,866 5,391 5,567 5,913Depr. & amort. (2,455) (2,565) (2,655) (2,748)EBIT (US$) 3,411 2,825 2,911 3,165Net interest exp (599) (558) (538) (535)PBT (US$) 2,812 2,267 2,373 2,630Income taxes (971) (499) (522) (579)Profit after tax 1,841 1,768 1,851 2,051Other NPAT adjustments 31 (17) (17) (17)Cash Flow 2/18A 2/19E 2/20E 2/21ECash flow from operations 3,413 4,457 4,876 5,188CAPEX (2,809) (3,000) (3,000) (3,000)Free cashflow to the firm 604 1,457 1,876 2,188Cash flow from investments (2,707) (805) (2,940) (2,940)Net share issue(/repurchase) 51 0 0 0Dividends paid (443) (455) (477) (510)Cashflow from financing activities (2,193) (1,955) (1,077) (1,110)Changes in Net Cash/Debt (1,487) 1,697 859 1,138Balance Sheet (US$) 2/18A 2/19E 2/20E 2/21ECash & cash equivalents 347 774 1,133 1,470Account receivables 1,637 1,621 1,671 1,723Total fixed assets 21,071 19,311 19,595 19,787Investment securities - - - -Total assets 37,228 35,553 36,345 37,029Total current liabilities 14,229 14,632 16,650 18,593Shareholder equity 6,905 6,718 7,492 8,433Total liabilities and equity 37,228 35,553 36,345 37,029Net debt 15,314 13,617 12,758 11,620Per share 2/18A 2/19E 2/20E 2/21ENo. of shares (wtd avg) 902 845 805 782CS adj. EPS 2.04 2.11 2.32 2.64Prev. EPS (US$)Dividend (US$) 0.49 0.54 0.59 0.65Free cash flow per share 0.67 1.73 2.33 2.80Earnings 2/18A 2/19E 2/20E 2/21ESales growth (%) 6.4 (0.0) 3.2 3.9EBIT growth (%) (3.6) (17.2) 3.0 8.7Net profit growth (%) (8.5) (3.9) 4.6 10.7EPS growth (%) (4.0) 3.6 9.9 13.9EBITDA margin (%) 4.8 4.4 4.4 4.5EBIT margin (%) 2.8 2.3 2.3 2.4Pretax margin (%) 2.3 1.8 1.9 2.0Net margin (%) 1.5 1.5 1.5 1.6Valuation 2/18A 2/19E 2/20E 2/21EEV/EBITDA (x) 6.2 6.7 6.5 6.1P/E (x) 11.8 11.4 10.4 9.1Returns 2/18A 2/19E 2/20E 2/21EROIC (%) 10.1 10.8 11.2 12.3Gearing 2/18A 2/19E 2/20E 2/21ENet debt/equity (%) 221.8 202.7 170.3 137.8Quarterly EPS Q1 Q2 Q3 Q42018A 0.58 0.39 0.44 0.632019E 0.66 0.41 0.45 0.602020E 0.73 0.45 0.49 0.65

Company BackgroundKroger is one of the world's largest food retailers. Kroger operates multiple banners with various store formats including grocery and multi-department stores, convenience, and jewelry stores. Kroger was founded in 1883 and headquartered in Cincinnati, OH

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 32.00Our $32 Blue Sky scenario for KR is based on improved top-line momentum through our modeling period with non-fuel IDs in the 3% range, offset to some extent by incremental gross margin pressure, which could translate to earnings and EBITDA upside of ~5% versus our base case in 2019. The improved earnings trajectory would likely garner a ~7.5x EBITDA multiple relative to the ~7x we use in our base case scenario.

Our Grey Sky Scenario (US$) 21.00Our $21 Grey Sky scenario for KR represents a ~6.5x multiple applied to reduced 2019 EBITDA that is ~6% below our base case. A return to ~2% non-fuel IDs, coupled with further operating expense deleverage would likely pressure both earnings and valuation.

Share price performance

KR.N S& P 5 0 0 IN D EX

Ju l - 1 7 O ct - 1 7 Jan - 1 8 A p r - 1 81 52 02 53 03 54 0

On 16-Apr-2018 the S&P 500 INDEX closed at 2679.38Daily Apr13, 2017 - Apr16, 2018, 04/13/17 = US$29.97

Source: Company data, Thomson Reuters, Credit Suisse estimates

17 April 2018

The Kroger Co. (KR) 3

Table of ContentsKey Charts 4

Investment Thesis 5

Groceries Aren't Books; Local Share Trumps All .....................................................5

Broad Toolbox Underappreciated ..........................................................................11

Kroger's Attempt at a Walmart Moment .................................................................19

Valuation 30

The Blue Sky Scenario...........................................................................................31

The Grey Sky Scenario ..........................................................................................31

Key Drivers and Credit Suisse Estimates ..............................................................33

HOLT® Analysis 34

Investment Risks 35

Company Overview 36

Management and Board of Directors 38

Appendix 40

PEERs....................................................................................................................41

Financial Models 42

Operating Results Summary & Financial Analysis.................................................42

17 April 2018

The Kroger Co. (KR) 4

Key ChartsFigure 1: Above-Consensus ID Sales Supported by Bottoms-Up Build

Figure 2: Bull Case on Market Share Gains Even More Compelling

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2018E 2019E 2020E

KR ID Sales Composition

Gap to Total ID

Click & Collect

KR local B&M food channelshare gains of 10-20bps

Space Optimization

Inflation

Cons

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2018E 2019E 2020E

KR ID Sales Composition: Market Share Bull Case

Gap to Total ID

Click & Collect

KR local B&M food channel sharegains of 40bps

Space Optimization

Inflation

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 3: Plenty of Weaker Players Left to Donate Share

18.8% 20.0% 20.3% 20.7% 20.9% 20.9% 20.9% 20.9% 21.0% 20.9% 21.1%

8.2% 8.3% 8.3% 8.6% 9.1% 9.4% 9.4% 9.9% 9.8% 9.9% 10.3%3.2% 3.3% 3.4% 3.5% 3.7% 3.7% 3.6% 3.4% 3.4% 2.9% 2.8%4.2% 4.4% 4.4% 4.6% 4.7% 5.0% 5.1% 5.2% 4.8% 4.8% 4.9%4.8% 4.9% 5.0% 5.2% 5.3% 5.3% 5.2% 5.1% 4.9% 4.7% 4.5%2.3% 2.4% 2.2% 2.5% 2.7%3.0% 3.0%

19.3% 18.6% 18.2% 19.4% 19.1% 15.9% 17.4% 17.9% 16.7% 16.0% 16.1%

37.0% 35.6% 35.4% 33.3% 32.2% 34.3% 32.6% 30.9% 32.7% 33.5% 32.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Regionals, Independents & Other

Traditional (Ahold Delhaize, HEB,Publix, Meijer)Hard Discounting (ALDI, SAL)

Specialty Formats (WFM, SFM)

Dollar Stores (DG, DLTR)

Drugstores (Front-end)

Warehouse Clubs (COST, BJ's)

Discounters (TGT, Kmart)

Kroger

WMT (US+Sam's)

Source: Euromonitor, Supermarket News, Company data, Credit Suisse estimates.

Figure 4: KR Share Price Could Inflect With IDs… Figure 5: …Driven In Part by Improved Valuation

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

$50.0

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

4Q18

1Q19

2Q19

3Q19

4Q19

1Q20

2Q20

3Q20

4Q20

Non-Fuel IDs Non-Fuel IDs CS Est Price

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

4Q18

1Q19

2Q19

3Q19

4Q19

1Q20

2Q20

3Q20

4Q20

Non-Fuel IDs Non-Fuel IDs CS Est NTM Fwd PE

Source: Company data, Thomson Reuters, Credit Suisse estimates. Source: Company data, Thomson Reuters, Credit Suisse estimates.

17 April 2018

The Kroger Co. (KR) 5

Investment ThesisKroger is the second largest traditional food retailer in the United States, behind Walmart, but finds itself in the throes of a rapidly evolving consumer staples retail landscape. Supermarket stocks have long been trading vehicles, subject to cyclical pressures and tailwinds such as inflation, gas prices, and the overall macroeconomic environment. With valuation back in KR's historical reasonable range and an underappreciated stable of long-term market share building assets, we believe top-line drivers are evident and credit for the investment is due.

Well-managed supermarkets have a material market share growth opportunity as consumers likely look to consolidate trips toward those with the broadest offering and omnichannel options proliferate; why not buy as much as you can when potentially paying a fixed fee for pick-up or delivery? At the same time, weaker conventional players continue to fall by the wayside and those sales should disproportionately transfer to stronger, local traditional operators, we believe.

Figure 6: KR Stock Chart 2000–Present (04/16/2018)

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Source: Thomson Reuters, Company data, Credit Suisse estimates.

Groceries Aren't Books; Local Share Trumps AllAmazon's entry into the supermarket fray has diverted investor attention away from the importance of local market share in this industry. The high fixed cost structure of the grocery business and limited shelf life of fresh product benefits those can amortize expense across multiple locations. Advertising, promotion, distribution, and even labor costs can be leveraged by many or all stores in a given area.

Competition has increased over the past decade, as the United States has embraced Walmart, club stores, discounters, and small-format natural/organic players. These operators have attacked KR in its core markets, but KR has maintained top-tier share across the board (inclusive of acquired chains).

The supermarket channel still represents >30% of food at home spend in this country, per our estimates, and a well-run traditional supermarket still provides a compelling offering. We firmly believe that strong supermarkets will continue to play a meaningful role in U.S. food retail as shoppers look to consolidate trips to operators with full shopability - a broad SKU offering, prepared foods, online capabilities, and inviting stores.

17 April 2018

The Kroger Co. (KR) 6

Figure 7: Supermarkets Deliver Unparalleled In-Store Experience

Source: Temkin; n=10,000

Industry data support the supermarket's importance in the food channel, with 47% of Americans surveyed saying a supermarket is their primary grocery store format. This level has come down, even in recent years, but the full-service supermarket remains the most frequently visited format in the industry. As weaker players continue to close doors, we believe stronger traditional operators, of which KR is one, will benefit disproportionately.

Figure 8: Channels of Primary Store

67%

22%

7%2% 1% 1%

56%

27%

6%2%

7%2%

<1%

52%

23%

6%2% 4% 3%

9%

49%

25%

5%2%

7%3% 2%

7%

47%

24%

5% 3% 5%2%

5%8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Supermarket Supercenter Warehouse Discount Limited Assortment Organic/Specialty Other Channels No Primary Store

2005 2010 2015 2016 2017

Source: FMI, Credit Suisse estimates.

17 April 2018

The Kroger Co. (KR) 7

Americans continue to make multiple grocery shopping trips every week, despite the rising popularity of e-commerce options. Average spend per trip has been rising, which is consistent with commentary out of KR, and frequency of shop appears to have bottomed at ~1.5-1.6 trips per week.

Figure 9: Average Weekly Shopping Trips Figure 10: Average Weekly Spend on Grocery

2.22.1

1.9 1.92.0

2.1

1.7

2.2

1.71.6

1.51.6

1.2

1.4

1.6

1.8

2

2.2

2.4

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Average Weekly Shopping Trips to Grocery Store

93.2

97.8 98.499.9

97.3

104.9 105.5102.9

100.8

107.3109.7

$80.0

$85.0

$90.0

$95.0

$100.0

$105.0

$110.0

$115.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Weekly Spending on Grocery

Source: FMI, Credit Suisse estimates. Source: FMI, Credit Suisse estimates.

The Easy Way to Grow Market Share: Pick on the Weaklings

KR has had to contend with Walmart, clubs, discounters, specialty stores and the advent of online grocery over the past decade, but remains a top-three player in virtually all of its most stored areas. The share takers in most of these markets have been mass merchants, clubs, or specialty players, while primary share donors have been weaker conventional players - evidence of KR's ability to grow share among traditional supermarket players. KR must defend its market share against all grocery competition, but the rapidly evolving U.S. market is presenting a rare market share growth opportunity; simply take the share from weaker conventional operators.

Figure 11: KR’s Market Share Position Change 2016 vs. 2013Kroger Market Share Position Note Kroger Stores

MSA 2016 2013 ∆ Takers DonorsLos Angeles-Orange, CA 1 1 - WMT, WFM, TJ's, SFS COST, ABS, TGT, Stater Bro's

Atlanta, GA 3 3 - WMT, COST, Aldi Publix , Ingles, TGT, WFMHouston, TX 3 2 (1) WMT, HEB, COST, WFM ABS, TGTPhoenix , AZ 1 1 - WMT, SFM, TJ's ABS, Basha's, COST, TGT

Dallas-Fort Worth, TX 2 3 1 WMT, WFM, Aldi ABS, TGT, COSTDetroit, MI 1 1 - Meijer, WFM, TJ's WMT, COST, GFS

Seattle, WA 1 2 1 COST, WMT, TJ's ABS, WinCo, HaagenDenver, CO 1 1 - WMT, SFM, TJ's, NGVC ABS, COST, TGT

Cincinnati, OH 1 1 - COST, WFM,Houchen's WMT, Meijer, Remke, TGTColumbus, OH 1 1 - WMT, COST, WFM Meijer, TGT

Chicago, IL 3 4 1 WMT, WFM, TJ's ABS, SVT, TGTCharlotte, NC 2 1 (1) WMT, WFM, BJ's, TFM Southeastern, Ahold, TGT, COST

Milwaukee, WI 1 1 - WMT, COST, WFM Piggly Wiggly , Woodman's, TGTNashville, TN 2 2 - WMT, WFM, SFM Ahold, Publix , COST

Indianapolis-Carmel-Anderson, IN 1 2 1 Meijer, COST, WFM Marsh, TGT, GFSRiverside-San Bernardino, CA 4 3 (1) WMT, SFS, SFM Stater Bro's, ABS, Winco

Portland, OR-WA 2 2 - WMT, WFM, TJ's ABS, WinCo, COSTRaleigh-Cary, NC 1 2 1 COST, SFM WMT, Ahold, Lowe's

Memphis, TN 2 1 (1) WMT, WFM, TFM, Associated COST, TGT, S-A-LWashington, DC 5 6 1 WMT, Weis, WFM, Wegman's Ahold, ABSLas Vegas, NV 2 3 1 WMT, COST, TJ's, SFS, SFM ABS, TescoSan Diego, CA 3 3 - WMT, SFS, SFM, TJ's ABS, COST

Salt Lake City , UT 2 2 - COST, SFM, TJ's, ABS Harmon's, WinCo, Ream'sVirginia Beach-Norfolk-Newport News, VA 3 4 1 WMT, WFM, TFM Ahold, SVU,BJ's

Wichita, KS 2 2 - COST, Aldi, SFM, NGVC WMT, TGT, Leeker's FamDayton, OH 1 1 - COST, TJ's WMT, Meijer,GFS, MarshTucson, AZ 2 1 (1) WMT, SFM ABS, COST, Basha's

Little Rock, AR 2 2 - GES, WFM WMT, Harp's, Knight's

Source: Metro Market Studies 2017 & 2014, Credit Suisse estimates; note: ABS = Albertsons, TJ's = Trader Joe's, SAL = Save-A-Lot , GES= Edwards Food Giant, GFS = Gordon Food Service

17 April 2018

The Kroger Co. (KR) 8

The outlook for independent grocers being put forward by industry consultants is not pretty; Euromonitor sees this cohort as the only one ceding sales in the near-term and Willard Bishop is exceedingly negative on traditional supermarkets. Herein lies KR's continued opportunity to gain share. Channel checks indicate that shuttered supermarket sales are most often transferred to another full-shop format, namely another supermarket or WMT.

Figure 12: Historical and Projected Growth by Channel (2016-2021 CAGR)

Discounters$17B

Forecourt Retailer$143B

Hypermarket$316B

Convenience$27B

Supermarket$371B

Food/Drink/TobaccoSpec$68B

Independent Small Grocers

$73B

Other$5.3B

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

-1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

2003

-20

16 C

AGR

2016 - 2021E CAGR

Source: Euromonitor, Credit Suisse estimates

Figure 13: Projected Annual Growth by Channel (2016-2021E Sales CAGR) Figure 14: Store Count by Channel 2016 vs. 2021E

8.0%

4.8% 4.5%

3.1% 3.0% 3.0% 2.6%2.0%

1.0% 0.9%-0.3%

-5.2%-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Limite

d Ass

ortm

ent

Fres

h For

mat

Supe

r war

ehou

se

Supe

rcente

r

Dolla

r

Who

lesale

Club

Othe

r sma

ll gro

cery

Conv

enien

ce S

tore

Drug

Millit

ary

Trad

itiona

l

Mass

2016 Store Counts 2021 Store Counts % ∆ in Store CountsTraditional Supermarkets 25,380 19,132 -24.6%Fresh Format 1,547 2,290 48.0%Limited Assortment 4,093 4,963 21.3%Super Warehouse 730 947 29.7%Other (Small Grocery) 8,748 8,878 1.5%Convenience (w/gas) 130,755 132,203 1.1%Convenience (w/o gas) 30,297 30,633 1.1%Wholesale club 1,472 1,613 9.6%Supercenter 4,106 4,560 11.1%Dollar 30,496 37,964 24.5%Drug 23,607 24,202 2.5%Mass 2,775 1,904 -31.4%Millitary 178 164 -7.9%

Source: Inmar Willard Bishop, Credit Suisse estimates Source: Inmar Willard Bishop, Credit Suisse estimates

Impressive Track Record of Local Market Share Gains Underlies Opportunity Take the recently announced bankruptcies of Tops Markets and Southeastern Grocers (Winn-Dixie parent), and even SVU's sale of its former Albertsons stores back to Albertsons; not to mention the shuttering of its Farm Fresh banner (with most stores going to KR) - stronger supermarkets are the winners when weaker competition closes. At its October 2017 Analyst Day, management cited $120 billion as the magnitude of competitors' brick-and-mortar food channel sales that KR could chip away at, roughly the size of total KR company sales today. There is also the $150 billion non-food channel opportunity that KR is increasingly focused on.

17 April 2018

The Kroger Co. (KR) 9

Figure 15: Very Long Runway for Local Market Share Growth for KR

KR Market Share Opportunity Within Local Markets (ex-fuel, Rx, most gen merch)

KR 2017 Sales ex-Fuel, Pharmacy, some GM

Non-Food Channel in KR Markets ($150bn)

Food Channel in KR Markets ($120bn)

Source: Company data, Credit Suisse estimates

Our bottom-up build of market share in U.S. food retail further underscores the market share opportunity available to stronger players, as weaker operators continue to cede share. Similar to the story shown in Figure 16, unconventional formats have grown store counts and share at the expense of traditional players over the past decade. Among traditional players, however, there are those top-tier operators that have maintained or grown share, and we estimate >20% of the market is still in the hands of longer-term share donors. A trip to a supermarket is most easily replaced by a trip to another supermarket, in our view.

Figure 16: Plenty of Weaker Players Left to Donate Share

18.8% 20.0% 20.3% 20.7% 20.9% 20.9% 20.9% 20.9% 21.0% 20.9% 21.1%

8.2% 8.3% 8.3% 8.6% 9.1% 9.4% 9.4% 9.9% 9.8% 9.9% 10.3%3.2% 3.3% 3.4% 3.5% 3.7% 3.7% 3.6% 3.4% 3.4% 2.9% 2.8%4.2% 4.4% 4.4% 4.6% 4.7% 5.0% 5.1% 5.2% 4.8% 4.8% 4.9%4.8% 4.9% 5.0% 5.2% 5.3% 5.3% 5.2% 5.1% 4.9% 4.7% 4.5%

2.3% 2.4% 2.2% 2.5% 2.7%3.0% 3.0%

19.3% 18.6% 18.2% 19.4% 19.1% 15.9% 17.4% 17.9% 16.7% 16.0% 16.1%

37.0% 35.6% 35.4% 33.3% 32.2% 34.3% 32.6% 30.9% 32.7% 33.5% 32.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Regionals, Independents & Other

Traditional (Ahold Delhaize, HEB,Publix, Meijer)

Hard Discounting (ALDI, SAL)

Specialty Formats (WFM, SFM)

Dollar Stores (DG, DLTR)

Drugstores (Front-end)

Warehouse Clubs (COST, BJ's)

Discounters (TGT, Kmart)

Kroger

WMT (US+Sam's)

Source: Euromonitor, Supermarket News, Company data, Credit Suisse estimates.

17 April 2018

The Kroger Co. (KR) 10

Figure 17: Food and Consumables Market Share, 2017

21.2%

10.3%

5.2% 4.3%2.9% 2.6% 2.2% 2.2% 1.9% 1.6% 1.6% 1.5% 1.5% 1.4% 1.3% 1.2% 1.1% 0.7% 0.5% 0.4% 0.4% 0.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%W

MT+

Sam'

s

Krog

er

Albe

rtson

s

Costc

o

Publi

x

Targ

et

Walg

reen

s

Ahold

(US)

HEB

Meije

r

CVS DG

Delha

ize (U

S)

ALDI

Who

le Fo

ods

Dolla

r Tre

e

Trad

er Jo

e's

Rite

Aid BJ

Save

-A-L

ot

Spro

uts

Supe

rvalu

Source: Euromonitor, Supermarket News, Company data, Credit Suisse estimates.

Figure 18: Food and Consumables Market Share, 2004–2017 Food Retailing Market Share 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Total Grocery Market (CS Estimate) 722,981 768,561 809,392 859,258 913,148 928,538 950,752 988,717 1,029,525 1,051,209 1,095,100 1,124,815 1,164,781 1,187,643

Discounters 15.4% 16.1% 17.9% 18.8% 20.0% 20.5% 21.0% 21.3% 21.3% 21.1% 21.1% 21.2% 20.6% 20.7%Wal-Mart stores 12.7% 13.4% 14.8% 15.6% 16.7% 17.1% 17.5% 17.6% 17.6% 17.5% 17.6% 17.8% 17.7% 18.0%Target stores 1.8% 2.0% 2.4% 2.5% 2.6% 2.7% 2.9% 3.1% 3.2% 3.1% 3.1% 3.1% 2.6% 2.6%Kmart (4) 0.8% 0.7% 0.7% 0.7% 0.7% 0.7% 0.6% 0.6% 0.5% 0.5% 0.4% 0.3% 0.3% 0.2%

Warehouse Clubs 7.7% 7.8% 7.3% 7.4% 7.7% 7.7% 7.8% 7.9% 8.3% 8.4% 8.5% 8.1% 8.0% 8.1%Costco 3.9% 4.0% 3.5% 3.6% 3.7% 3.7% 3.8% 3.9% 4.3% 4.4% 4.5% 4.3% 4.2% 4.3%BJ 0.6% 0.6% 0.6% 0.6% 0.7% 0.7% 0.7% 0.7% 0.7% 0.7% 0.7% 0.6% 0.5% 0.5%Sam's Club 3.2% 3.2% 3.1% 3.1% 3.3% 3.2% 3.2% 3.3% 3.3% 3.3% 3.3% 3.2% 3.2% 3.2%

Drugstores (Front-end) 4.0% 4.1% 4.4% 4.8% 4.9% 5.0% 5.2% 5.3% 5.3% 5.2% 5.1% 4.9% 4.7% 4.5%CVS 1.3% 1.3% 1.5% 1.7% 1.7% 1.8% 1.9% 1.9% 1.9% 1.9% 1.8% 1.7% 1.6% 1.6%Walgreens 1.9% 2.0% 2.1% 2.2% 2.3% 2.4% 2.5% 2.6% 2.6% 2.5% 2.5% 2.4% 2.4% 2.2%Rite Aid 0.8% 0.8% 0.8% 0.9% 0.9% 0.9% 0.8% 0.8% 0.8% 0.8% 0.8% 0.7% 0.7% 0.7%

Dollar Stores 1.4% 1.5% 1.6% 1.6% 1.6% 1.8% 1.9% 2.1% 2.2% 2.3% 2.4% 2.2% 2.5% 2.7%Family Dollar (1) 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.7% 0.7% 0.7% 0.7% Acq by DLTRDollar General (2) 0.7% 0.7% 0.7% 0.7% 0.8% 0.9% 1.0% 1.1% 1.2% 1.3% 1.3% 1.4% 1.4% 1.5%Dollar Tree (3) 0.2% 0.2% 0.2% 0.2% 0.2% 0.3% 0.3% 0.3% 0.4% 0.4% 0.4% 0.9% 1.1% 1.2%

Specialty Formats 1.1% 1.3% 1.4% 1.5% 1.7% 1.8% 1.9% 2.2% 2.4% 2.6% 2.8% 3.0% 3.0% 3.0%Whole Foods 0.5% 0.6% 0.7% 0.8% 0.9% 0.9% 0.9% 1.0% 1.1% 1.2% 1.3% 1.4% 1.3% 1.3%Trader Joe's (4) 0.4% 0.5% 0.5% 0.6% 0.6% 0.7% 0.7% 0.9% 0.9% 1.0% 1.1% 1.2% 1.1% 1.1%Sprouts -- -- -- -- 0.1% 0.1% 0.2% 0.2% 0.2% 0.2% 0.3% 0.3% 0.3% 0.4%The Fresh Market -- 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.2% 0.2% 0.2% 0.1%

Hard Discounting 1.4% 1.4% 1.4% 1.4% 1.5% 1.4% 0.7% 0.7% 0.9% 0.8% 1.4% 1.5% 1.7% 1.9%ALDI (4) 0.6% 0.6% 0.6% 0.7% 0.7% 0.7% 0.7% 0.7% 0.8% 0.8% 0.9% 1.0% 1.2% 1.4%Save-A-Lot (4) 0.9% 0.8% 0.7% 0.7% 0.7% 0.6% 0.0% 0.0% 0.0% 0.0% 0.4% 0.4% 0.4% 0.4%

Total - Major Non-Traditional Retailers 31.0% 32.3% 34.0% 35.5% 37.4% 38.1% 38.6% 39.6% 40.4% 40.6% 41.3% 40.9% 40.6% 40.9%

Traditional - Big Three 19.0% 18.5% 17.6% 17.8% 17.5% 16.5% 16.4% 16.3% 13.6% 15.1% 16.2% 15.4% 15.4% 15.9%Kroger 7.8% 7.9% 8.2% 8.2% 8.3% 8.3% 8.6% 9.1% 9.4% 9.4% 9.9% 9.8% 9.9% 10.3%Supervalu 1.5% 1.4% 3.5% 4.0% 3.8% 3.4% 3.0% 2.4% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4%Albertsons 4.8% 4.5% 1.0% 0.7% 0.5% 0.5% 0.4% 0.4% 0.4% 1.9% 2.5% 5.2% 5.1% 5.2%Safeway 5.0% 4.7% 5.0% 4.9% 4.8% 4.4% 4.3% 4.4% 3.4% 3.3% 3.3% Acq by ABS

Traditional - Other 10.3% 10.2% 9.7% 9.7% 9.5% 10.0% 11.7% 11.9% 11.7% 11.7% 11.6% 11.0% 10.5% 10.6%Ahold (US sales) 3.1% 2.9% 2.5% 2.4% 2.4% 2.5% 2.5% 2.5% 2.5% 2.5% 2.4% 2.3% 2.2% 2.2%Delhaize (US sales) 2.2% 2.2% 2.1% 2.1% 2.1% 2.0% 2.0% 1.9% 1.8% 1.6% 1.6% 1.5% 1.5% 1.5%Harris Teeter 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.5% 0.4% 0.4% 0.4% Acq by KRHEB 1.4% 1.4% 1.4% 1.4% 1.4% 1.4% 1.7% 1.8% 1.9% 2.0% 2.1% 2.0% 1.9% 1.9%Meijer 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 1.5% 1.5% 1.4% 1.4% 1.4% 1.5% 1.5% 1.6%Publix 2.6% 2.7% 2.7% 2.7% 2.6% 2.6% 2.7% 2.7% 2.7% 2.8% 2.8% 2.9% 2.9% 2.9%Roundy's -- -- -- -- -- 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% Acq by KRSpartan Stores 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.7% 0.2% 0.2% 0.2%Weis Markets 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%

Total - Traditional Grocery 29.3% 28.6% 27.3% 27.4% 27.0% 26.5% 28.1% 28.2% 25.3% 26.8% 27.8% 26.4% 25.9% 26.4%Regionals, Independents & Other 39.7% 39.1% 38.7% 37.0% 35.6% 35.4% 33.3% 32.2% 34.3% 32.6% 30.9% 32.7% 33.5% 32.7%

Source: Euromonitor, Supermarket News, Company data, Credit Suisse estimates.

Market share data presented by KR underscores the company's consistent track record of taking market share, a trend we expect to continue and to support our above-consensus ID sales in 2019-2020. Assuming 15 bps of local market share gains annually (the low end of the trend over the last 3 years) within just the ~$120 billion brick-and-mortar food channel market opportunity gets KR within 40 bps of our total ex-fuel ID level. An upside scenario of 40 bps of market share gains (closer to the prior 3-year average) leaves just a 10 bps gap to the total ID. The gap can be closed by incremental delivery sales, non-food channel share gains (a $150 billion opportunity), improved merchandising, etc.

17 April 2018

The Kroger Co. (KR) 11

Figure 19: Conservative Market Share Gains Still Worth ~20 bps of ID Sales Growth

Figure 20: Market Share Gains Closer to 3-Yr Average Worth ~50 bps

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2018E 2019E 2020E

KR ID Sales Composition

Gap to Total ID

Click & Collect

KR local B&M food channelshare gains of 10-20bps

Space Optimization

Inflation

Cons

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2018E 2019E 2020E

KR ID Sales Composition: Market Share Bull Case

Gap to Total ID

Click & Collect

KR local B&M food channel sharegains of 40bps

Space Optimization

Inflation

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 21: KR has Consistently Grown Market Share in its Local Markets

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3* Q4*

2014 2015 2016 2017

%

YoY Change in Market Share DollarsMarket Share (LHS) Non-Fuel IDs (RHS)

Source: Company data per IRI, Credit Suisse estimates | Q317 market share is KR estimates and Q417 market share is not available

Broad Toolbox UnderappreciatedKroger is often lumped in with other conventional or traditional supermarket players, a group that, as a whole, has been and will likely continue to be a long-term market share donor to competing retail concepts. At the same time, KR has a suite of assets and capabilities that nearly all brick-and-mortar retailers would envy. Click & collect capability is being rolled out rapidly, and learnings from Harris Teeter are a material advantage. Technology is the cornerstone of an industry-leading targeted promotion and rewards program that incorporates direct mail, digital offerings, and fuel rewards. KR's price gap to WMT is at the low end of supermarket players, but on-the-shelf pricing is often irrelevant at KR, as pricing and promotion can be tailored to loyal households.

Click & Collect Leads Digital Offering, but Delivery Offered As WellKroger is leaning into its physical assets and choosing click & collect as its primary online grocery offering. Delivery is an option in at least 45 markets, primarily via third-party services such as Instacart (KR handles delivery in Denver.) The Amazon-Whole Foods combination has further piqued investor interest in grocery delivery, but we see this as a legitimate two-horse race (delivery vs. click & collect) for at least the coming five to ten years. AMZN's decision to invest in physical stores and prune its AmazonFresh offering is telling, in our view.

17 April 2018

The Kroger Co. (KR) 12

Industry feedback implies that KR is going about its online investment the right way for the near term, as satisfaction scores are notably higher for click & collect offerings at WMT and KR than those for delivery services such as AmazonFresh and Peapod. The convenience of delivery is attractive, but delivery windows and damaged produce are often cited as offsets.

Figure 22: Overall Satisfaction with Online Grocery Service

69%75%

69%59% 62% 64%

23%20%

24%

29%31% 25%

0%

20%

40%

60%

80%

100%

Average ofall Services

Other

Extremely Satisfied Somewhat Satisfied Neutral Dissatisfed

Source: Kantar Consulting, Credit Suisse estimates.

Offering Delivery, but Owning Click & CollectWith KR's 2014 acquisition of Harris Teeter came a crash course in click & collect grocery retail. Harris Teeter launched its click & collect service, ExpressLane, in 2000 and touted its availability as a differentiator. Per company commentary, it was profitable as well. KR is now leaning into the buy-online-pick-up-in-store medium and choosing to leave delivery to third parties (for the most part). Across KR's store base of ~2,800 supermarkets, approximately 40% have ClickList or ExpressLane infrastructure in place today with plans to expand to the vast majority of stores.

Figure 23: Ramp in Click & Collect Locations

0

200

400

600

800

1,000

1,200

Dec 12 Aug 15 Oct 15 May16 Jun16 Aug16 Sep16 Nov16 Dec16 May17 Jun17 Sep17 Nov 17 Dec 17 Mar 18

ClickList ExpressLane (Harris Teeter)

Source: Company data, Credit Suisse estimates

17 April 2018

The Kroger Co. (KR) 13

Figure 24: Click & Collect Offerings at Competitors

1,200 1,100

115 80 4

+1,000

+500

+420

-

500

1,000

1,500

2,000

2,500

Walmart Kroger HEB Albertsons Loblaw's Smart & Final Publix

Number of Locations Today Plan for 2018

Source: Company data, Credit Suisse estimates

The ultimate impact of click & collect is difficult to calculate given little pointed commentary from industry participants. Our sense is that, if done well, this can be a comp, margin, and profit dollar driver, but the path to profitability is uncertain at best. The size of each click & collect basket, its product mix, and the particular trip that basket is cannibalizing are all fundamental variables that can determine ultimate returns. Key factors to consider include the following:

■ Base Basket: Average supermarket industry baskets are in the $30-40 range, and given KR's full shopability, we utilize $40. For gross margin, we assume a rate slightly higher than the company's prior three-year average, as the program is likely being rolled out at stores that can handle the investment first. Our assumption for direct store expenses is between the levels reported by Sprouts and Whole Foods historically.

■ Cannibalization: Industry commentary indicates that a click & collect basket is typically larger than one purchased in-store, but the question of where those incremental sales come from is more difficult. Our bear case assumes a click & collect basket cannibalizes a trip to KR, while our base and bull cases assume these incremental sales dollars are taken from other retailers.

■ Margin Impact: The incremental net cost for a click & collect basket must be considered as well. Key factors in this bucket include the service fee charged to the customer, the cost to pick the customer's order, incremental direct store expense (which we believe achieves some overall leverage despite related upfront capital investment), and the expense saved at the checkout. While others have pointed to improved gross margins on click & collect baskets, KR is not pushing this narrative.

It is easy to see how quickly click & collect can become materially dilutive to overall profitability, as is demonstrated in our bear case. That said, the company indicates there is little pushback to KR's current fee structure, a crucial element in achieving profitability, albeit at a lower margin, in the program at this time, despite WMT's decision to provide the service for free. Offsets to the fee, possibly with promotional dollars from vendors, are a likely avenue to go down as well.

17 April 2018

The Kroger Co. (KR) 14

Figure 25: Click & Collect Model Store EconomicsClick & Collect

Scenario Bear Case Base Case Bull Case

Standard Trip

Basket Size $40 $40 $40

Gross Margin Per Basket 24.5% 24.5% 24.5%

Picking Cost / Fee to 3rd Party 0.0% 0.0% 0.0%

Direct Store Expense 21.0% 21.0% 21.0%

Operating Profit Per Basket $1.40 $1.40 $1.40

Operating Profit % (ex-corporate) 3.5% 3.5% 3.5%

Impact from C&C / Delivery

Trip Cannibalization 2nd Trip to Same Store Discounter/Specialty Club/Warehouse

+ Bump in Basket Size 100.0% 200.0% 300.0%

- Impact from Lost Trip -50.0% -10.0% -10.0%

= Adjusted Basket Size $60 $116 $156

+ Fee Charged $0.0 $4.0 $6.0

Gross Margin Impact +0% +0% +0%

DSE on Incremental Sales 18.0% 18.0% 18.0%

Net Picking Cost / Fee to 3rd Party $8 $8 $10

Adj. Operating Profit Per Basket ($5.30) $2.34 $4.94

Operating Profit % -8.8% 2.0% 3.2%

Source: Company data, Credit Suisse estimates.

Add in a Little Inflation and Out-Year IDs Look Easily AchievableIn Figure 26 we demonstrate the achievability of our above-consensus ID sales estimates in 2019 and 2020. Based on historical achievement at Harris Teeter and anecdotal industry commentary that even the most productive click & collect stores do just a mid-single-digit percentage of their business this way, we estimate that the average comp impact to KR's 2018 IDs will be in the range of 10-30 basis points. The take-away here, however, is not near-term comp impact but the long-term build toward industry norms (and related sales growth) and relevance in what we anticipate will be a U.S. online grocery market that equitably splits share between delivery and pickup.

As click & collect locations ramp, and the service matures within each box toward the ~3% penetration range we believe Harris Teeter enjoys, we can very easily model a scenario where up to 20% of annual identical store sales are being fueled by the program (which we show in 2019-2020). A return to normalized inflation of ~2% would then require <100 bps ID sales generation from avenues other than click & collect or inflation over the next couple years. We see this as easily achievable from a combination of population growth, beating up on weaker competitors (discussed above), remodels, increased sales via delivery, etc. 2018 is likely lacks material inflation, but competitor closings (Southeastern Grocers and SVU's Farm Fresh, the latest) seem to be increasing.

17 April 2018

The Kroger Co. (KR) 15

Figure 26: Math on Click & Collect Impact Supports Acceleration in ID SalesImpact to 2018E KR IDs Impact to 2019E Impact to 2020E

Bear Case Base Case Bull Case Base Case Base Case

FY Est. Retail Sales ($M) $107,022 $107,022 $107,022 $110,886 $115,322

Total Stores 2,789 2,789 2,789 2,796 2,803

Total Stores w/ Click & Collect 1,600 1,600 1,600 2,100 2,400

Avg. Per Store Sales Penetration 0.8% 1.0% 1.2% 1.3% 1.6%

Total Click & Collect Sales ($M) $491 $614 $706 $1,083 $1,580

Incremental from Click & Collect ($M) 155 277 370 $469 $497

Est. ID Contribution from C&C 0.1% 0.3% 0.3% 0.4% 0.4%

Total ID Ex-Fuel (CS est.) 1.9% 1.9% 1.9% 2.7% 3.1%

Assumed Inflation 1.0% 1.0% 1.0% 1.7% 2.0%

Inflation Competed Away (0.2% ) (0.2% ) (0.2% ) (0.2% ) (0.2% )

Gap to Total ID 0.9% 0.8% 0.7% 0.8% 0.9%

Source: Company data, Credit Suisse estimates

Figure 27: Gap to Total ID Smaller When Consider Market Share Gains and Remodels

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2018E 2019E 2020E

KR ID Sales Composition

Gap to Total ID

Click & Collect

KR local B&M food channelshare gains of 10-20bps

Space Optimization

Inflation

Cons

Source: Company data, Credit Suisse estimates

Delivery Is Instacart's ProblemWith Amazon firmly planted in the supermarket fray, rapidly expanding Whole Foods delivery, and even WMT expanding its delivery options, the likes of KR and Albertsons can ill-afford to stand still on grocery delivery to home. In the past few months, each has announced a partnership with Instacart, electing to let someone else worry about profiting from delivery. KR has offered delivery via owned vehicles in Denver for years but is not particularly pleased with returns there, calling the format "cumbersome to pull off." Tests with various service providers including Uber, Shipt, deliv, and Roadie have taken place as well. KR is building the tools to effectively compete in online grocery, but it is worth noting that overlaps with Whole Foods are toward the low end of companies within our coverage universe. Our base case assumption is that AMZN will lead grocery delivery, and insulation from its Whole Foods store base may be an advantage for KR.

17 April 2018

The Kroger Co. (KR) 16

Figure 28: KR and Other Retailers' Overlap with WFMOverlap with WFM

1 Mile 5 Mile 10 Mile

KR 4.0% 30.0% 51.1%

SFM 7.3% 44.6% 68.3%

SFS 7.0% 42.0% 60.8%

WMT 1.3% 13.8% 29.4%

TGT 7.3% 31.0% 53.6%

COST 6.4% 37.5% 63.3%

Source: Company data, Credit Suisse estimates.

Figure 29: Delivery Margin Lost in Third-Party FeesThird Party Delivery

Scenario Base Case

Standard TripBasket Size $40

Basket Size $40.0

Gross Margin Per Basket 24.5%

Picking Cost / Fee to 3rd Party 0.0%

Direct Store Expense 21.0%

Operating Profit Per Basket $1.40

Operating Profit % (ex-corporate) 3.5%

Impact from C&C / DeliveryTrip Cannibalization Discounter/Specialty

+ Bump in Basket Size 200.0%

- Impact from Lost Trip -10.0%

= Adjusted Basket Size $116

+ Fee Charged $0.0

Gross Margin Impact +0%

DSE on Incremental Sales 12.0%

Net Picking Cost / Fee to 3rd Party Mid-High Single Digit % of Sales

Picking Cost / Fee to 3rd Party 7%

Adj. Operating Profit Per Basket $2.78

Operating Profit % 2.4%

Source: Company data, Credit Suisse estimates.

We see this dual-pronged strategy for KR's online grocery offering as reasonable in the near to medium term, as it leverages existing infrastructure and avoids the investment and logistics headaches of delivery. KR could transition select locations to dark stores if the pick-up-in-store offering is proven highly successful. In many ways, this would represent a best-case scenario, as stores could be fully optimized for in-store shopping or pickup, with delivery services running out of both. If we assume that AMZN will establish itself as the market leader in grocery delivery, we see no reason why KR (and WMT) can't play the same role in click & collect. Car ownership levels, commute times, and population densities in the United States all point to grocery pickup playing a large role in the evolving food retail landscape.

17 April 2018

The Kroger Co. (KR) 17

Figure 30: Scorecard of Countries Ranks Global Markets for Online Grocery Delivery

CountryGDP per capita(Current US $)

% of Urban Population

Population of Top 5 Metro

Areas as % of Total Population

# Metro Areas >1m

# Metro Areas >3m

Population Density

(people per sq. km of land area)

Vehicle Ownership

(Vehicles per Capita

(/1000 inh.)

Smartphone Penetration

U.S. 1 2 4 2 2 5 5 3 Overall Rank

U.K. 3 1 1 3 3 1 3 1 U.S. 4

Germany 2 4 3 4 3 2 4 2 U.K. 1

France 4 3 2 4 3 4 2 4 Germany 2

China 5 5 5 1 1 3 1 5 France 3

China 5

Country% of Individuals

Using Internet

Fixed broadband subscriptions (per

100 people)

Wireless broadband

subscriptions (per 100 people)

# of B&M Channels with 25%+ Shares

Selling Sq Meter per 1 Million

Inhabitant

# of B&M Competitors with

10%+ Share

Online Share of Retail Spend

Online Share of Grocery Spend

U.S. 4 4 1 3 1 4 4 5

U.K. 1 2 2 3 4 2 2 1

Germany 2 3 4 1 2 1 3 4

France 3 1 3 1 3 2 5 3

China 5 5 5 3 5 5 1 2

Source: Company data, Credit Suisse estimates.

Online Sales Immaterial Today but Long-Term Potential is HUGEKR has multiple avenues for online sales, but we believe the relative contribution to sales is rapidly evolving. Press reports regarding conversations with Alibaba and Target (regarding Shipt) are likely 2-way, we believe, as KR has plenty of experience to bring to the table. Recent commentary indicates that digital sales grew 90% in 2017, but remain immaterial to total sales. We estimate that digital sales in 2017 were around $950 million based on prior disclosures as well as industry sources, but this is a ballpark range given little company commentary on hard dollars. We know that Vitacost represented ~$400 million in sales at its time of acquisition in 2014, but the other pie pieces are derived.

More important, however, is the potential for ClickList to grow to the levels enjoyed by Harris Teeter with ExpressLane, where we believe the best performing stores have high-single-digit sales penetration and the average is around 3%. 3% of non-fuel sales at KR today is >$3 billion. If we assume ClickList did <$200 million in sales in 2017, it would take 11+ years of 30% annualized click & collect growth to get this medium to the level of penetration Harris Teeter enjoys today, a meaningful ID tailwind for an extended period.

Figure 31: Road to 3% Penetration of Click & Collect Represents Very Long ID Sales Contribution Runway

Vitacost.com

Express Lane

ClickList, $175

Delivery & other

Estimated Breakdown of 2017 Digital SalesVitacost.com

ExpressLane

ClickList, $2,957

Delivery & other

2017 Digital Sales BreakdownPROFORMA

for Click & Collect Representing

3% of Total Co. Sales

Source: Company data, Credit Suisse estimates

17 April 2018

The Kroger Co. (KR) 18

Data WMT Would Die ForIn 2015, Kroger made the decision to dissolve a ten-year-old industry-exclusive joint venture with data science firm dunnhumby and effectively bring the majority of dunnhumby USA operations in house under the name 84.51°. This enabled Kroger the flexibility to apply the firm's proprietary analytics to other partners, whereas it had initially been restricted to working with dunnhumby alone. KR retains a perpetual license to use dunnhumby analytical tools.

Kroger and 84.51° work as cross-functional teams across operations and merchandizing with certain teams being co-located. 84.51° recently announced Kroger Precision Marketing, a cross-channel media solution focused on precise personalized communication to customers “at the right time with the right message in the right way.” This marketing program taps into purchase data from 60 million households to produce holistic targeted advertising and content campaigns across an expanded digital ecosystem. Loyal households are provided with a tailored digital experience online and by mobile as well as custom coupons and a print magazine (MyMagazine) that includes targeted product content and recipes.

Meal Kits and Restaurants Covered as WellManagement is increasingly using the term share of stomach for how it views KR's market share opportunity, a reasonable position with Food at Home and Food Away from Home sales approximately even in the United States today. Americans appear to be approaching indifference as to whether a meal is prepared at home or away, instead focusing more on how convenient, fresh, healthy, or local that food is.

Prepared foods are one of the fastest growing areas of KR's overall offering, a nod to the consumer's propensity to purchase high-quality food wherever it's available in a convenient format and at a competitive price point. There is no doubt AMZN recognized the strength of Whole Foods' prepared foods business and its mixed grocery store-restaurant, or Groceraunt, appeal. KR is focused on this theme as well, recognizing the importance of all things food to all people. Whereas Albertsons chose to acquire an established meal kit player in Plated, KR is going it alone with its Prep+Pared offering. These kits come at a notable discount to shipped offerings with a near-identical experience. Figure 32 represents management's long-term goal to compete across the entire fresh-prepared food spectrum.

Figure 32: Kroger’s Prepared Food/Meal Kit Offerings Run the Gamut

Source: Company data, Credit Suisse estimates.

Private Label Portfolio to Compete with DiscountersThe rising popularity of hard discounters with elevated private label sales mix in the U.S. points to the consumer's evolving relationship with large brands and the rising importance

17 April 2018

The Kroger Co. (KR) 19

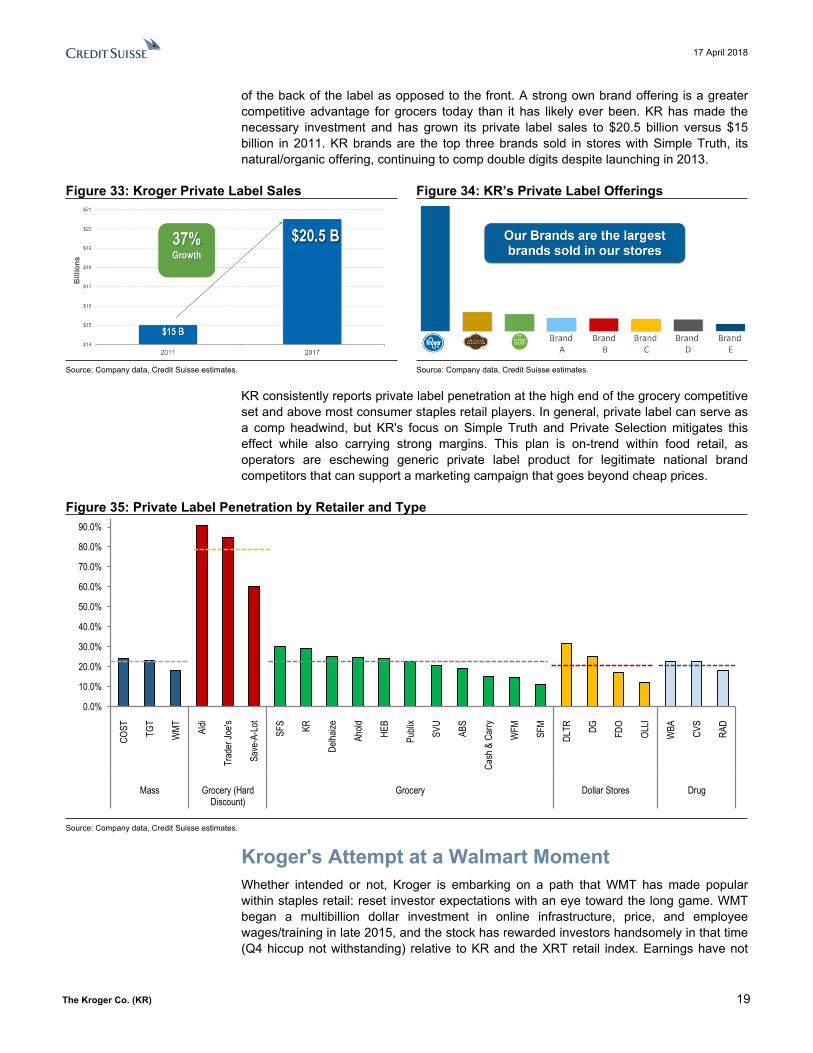

of the back of the label as opposed to the front. A strong own brand offering is a greater competitive advantage for grocers today than it has likely ever been. KR has made the necessary investment and has grown its private label sales to $20.5 billion versus $15 billion in 2011. KR brands are the top three brands sold in stores with Simple Truth, its natural/organic offering, continuing to comp double digits despite launching in 2013.

Figure 33: Kroger Private Label Sales Figure 34: KR’s Private Label Offerings

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

KR consistently reports private label penetration at the high end of the grocery competitive set and above most consumer staples retail players. In general, private label can serve as a comp headwind, but KR's focus on Simple Truth and Private Selection mitigates this effect while also carrying strong margins. This plan is on-trend within food retail, as operators are eschewing generic private label product for legitimate national brand competitors that can support a marketing campaign that goes beyond cheap prices.

Figure 35: Private Label Penetration by Retailer and Type

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

COST TG

T

WMT Al

di

Trad

er Jo

e's

Save

-A-L

ot

SFS KR

Delha

ize

Ahold HE

B

Publi

x

SVU

ABS

Cash

& C

arry

WFM SF

M

DLTR DG FDO

OLLI

WBA CV

S

RAD

Mass Grocery (HardDiscount)

Grocery Dollar Stores Drug

Source: Company data, Credit Suisse estimates.

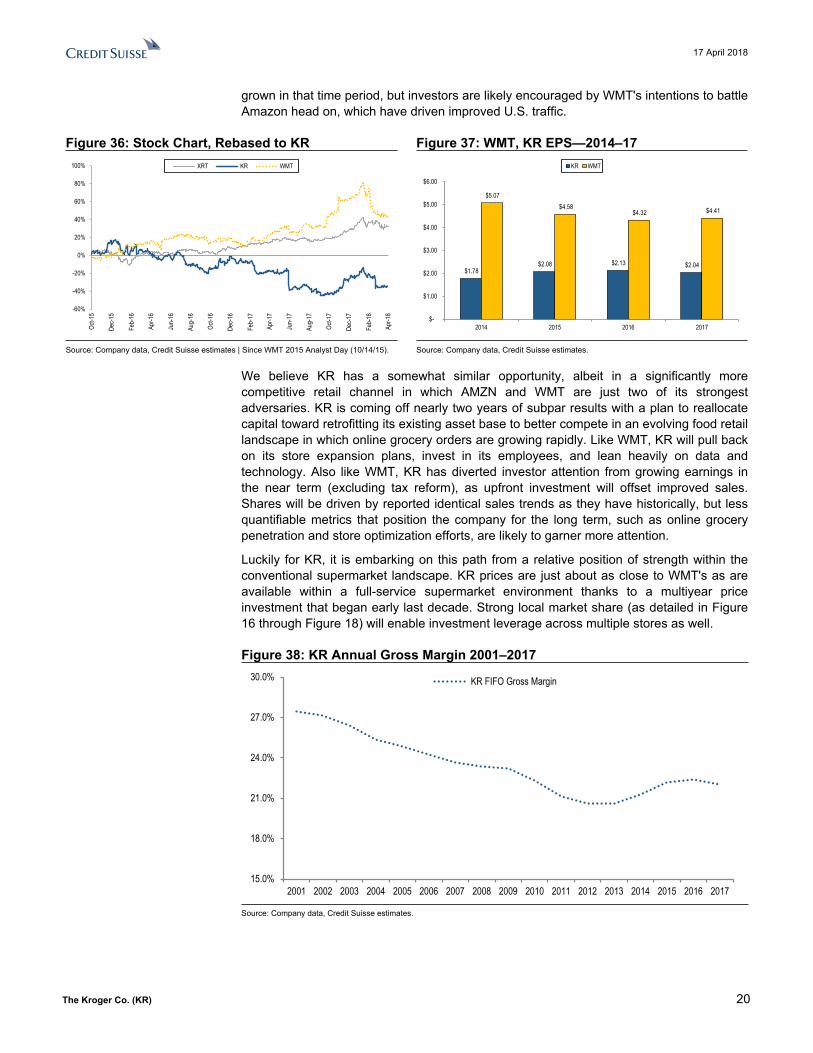

Kroger's Attempt at a Walmart MomentWhether intended or not, Kroger is embarking on a path that WMT has made popular within staples retail: reset investor expectations with an eye toward the long game. WMT began a multibillion dollar investment in online infrastructure, price, and employee wages/training in late 2015, and the stock has rewarded investors handsomely in that time (Q4 hiccup not withstanding) relative to KR and the XRT retail index. Earnings have not

17 April 2018

The Kroger Co. (KR) 20

grown in that time period, but investors are likely encouraged by WMT's intentions to battle Amazon head on, which have driven improved U.S. traffic.

Figure 36: Stock Chart, Rebased to KR Figure 37: WMT, KR EPS—2014–17

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Oct-1

5

Dec-1

5

Feb-

16

Apr-1

6

Jun-

16

Aug-

16

Oct-1

6

Dec-1

6

Feb-

17

Apr-1

7

Jun-

17

Aug-

17

Oct-1

7

Dec-1

7

Feb-

18

Apr-1

8

XRT KR WMT

$1.78 $2.08 $2.13 $2.04

$5.07 $4.58

$4.32 $4.41

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

2014 2015 2016 2017

KR WMT

Source: Company data, Credit Suisse estimates | Since WMT 2015 Analyst Day (10/14/15). Source: Company data, Credit Suisse estimates.

We believe KR has a somewhat similar opportunity, albeit in a significantly more competitive retail channel in which AMZN and WMT are just two of its strongest adversaries. KR is coming off nearly two years of subpar results with a plan to reallocate capital toward retrofitting its existing asset base to better compete in an evolving food retail landscape in which online grocery orders are growing rapidly. Like WMT, KR will pull back on its store expansion plans, invest in its employees, and lean heavily on data and technology. Also like WMT, KR has diverted investor attention from growing earnings in the near term (excluding tax reform), as upfront investment will offset improved sales. Shares will be driven by reported identical sales trends as they have historically, but less quantifiable metrics that position the company for the long term, such as online grocery penetration and store optimization efforts, are likely to garner more attention.

Luckily for KR, it is embarking on this path from a relative position of strength within the conventional supermarket landscape. KR prices are just about as close to WMT's as are available within a full-service supermarket environment thanks to a multiyear price investment that began early last decade. Strong local market share (as detailed in Figure 16 through Figure 18) will enable investment leverage across multiple stores as well.

Figure 38: KR Annual Gross Margin 2001–2017

15.0%

18.0%

21.0%

24.0%

27.0%

30.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

KR FIFO Gross Margin

Source: Company data, Credit Suisse estimates.

17 April 2018

The Kroger Co. (KR) 21

Figure 39: L.A. Pricing Survey: KR's Price Gap to WMT Relatively Low

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

8/30/1

79/6

/179/1

3/17

9/20/1

79/2

7/17

10/4/

1710

/11/17

10/18

/1710

/25/17

11/1/

1711

/8/17

11/15

/1711

/22/17

11/29

/1712

/6/17

12/13

/1712

/20/17

12/27

/171/3

/181/1

0/18

1/17/1

81/2

4/18

1/31/1

82/7

/182/1

4/18

2/21/1

82/2

8/18

3/7/18

3/14/1

83/2

1/18

3/28/1

84/4

/18

Index

ed to

WMT

Survey Basket Price Gap to WMT

WFM

AMZN

ABSSWY

KR

SFM

SFS

Source: Company data, Credit Suisse estimates | In select Los Angeles Zip Codes.

Figure 40: KR Pricing Survey Against Competitors (Average of Periods 8/30/2017–4/5/2018) # Item Name Unit SFM WMT ABS/SWY Ralph's (Kroger) WFM SFS Amazon1 Bread White Bread 20 ounces $ 2.49 $ 2.33 $ 2.54 $ 2.72 $ 2.99 $ 2.58 $ 3.07 2 Cereal Kashi GOLEAN Cereal Original 13.1 ounces $ 3.80 $ 3.28 $ 4.01 $ 3.52 $ 3.71 $ 3.00 $ 3.77 3 Cereal bars Kind Healthy Grains Clusters 11 ounces $ 5.42 $ 4.53 $ 6.11 $ 5.25 $ 5.99 $ 4.45 $ 4.73 4 Oliv e Oil Pompeian Ex tra Virgin Oliv e Oil 16 ounces $ 5.99 $ 4.89 $ 5.86 $ 5.43 $ 5.99 $ 5.90 $ 5.07 5 Peanut Butter Jif Creamy Peanut Butter 16 ounces $ 2.75 $ 2.50 $ 4.29 $ 3.01 $ 2.49 $ 2.69 $ 2.67 6 Chips Stacy 's Pita Chips Simply Naked 7.33 ounces $ 3.52 $ 2.82 $ 3.73 $ 3.32 $ 3.29 $ 2.83 $ 2.67 7 Water Smartw ater 1 liter $ 2.38 $ 1.48 $ 2.21 $ 1.76 $ 2.19 $ 1.91 $ 1.61 8 Juice Orange juice - original 59 ounces $ 3.53 $ 3.59 $ 3.98 $ 3.94 $ 3.99 $ 3.63 $ 3.86 9 Pasta Sauce Marinara Pasta Sauce 24 ounces $ 3.49 $ 1.98 $ 2.80 $ 3.78 $ 3.49 $ 3.00 $ 2.76

Center of Store $ 33.35 $ 27.40 $ 35.52 $ 32.72 $ 34.13 $ 29.99 $ 30.22 10 Eggs Cage Free Eggs Grade A Large Brow n Eggs 1 dozen $ 3.95 $ 4.17 $ 5.18 $ 4.63 $ 3.50 $ 4.42 $ 3.41 11 Milk Horizon Organic Whole Milk 0.5 Gallon $ 4.45 $ 4.46 $ 5.30 $ 4.70 $ 5.63 $ 4.69 $ 4.61 12 Milk Almond Breeze Original Almond Milk 0.5 Gallon $ 3.30 $ 2.97 $ 3.12 $ 3.05 $ 3.49 $ 3.06 $ 3.13 13 Ice Cream Haagen Dazs Ice Cream - any flav or 14 ounces $ 5.25 $ 4.21 $ 4.45 $ 4.23 $ 4.99 $ 4.23 $ 4.35 14 Yogurt Fage Total Greek Strained Yogurt - any flav or 5.3 ounces $ 1.36 $ 1.26 $ 1.60 $ 1.18 $ 1.55 $ 1.38 $ 1.41 15 Butter Salted Butter 16 ounces $ 3.45 $ 4.26 $ 4.75 $ 3.94 $ 3.49 $ 3.58 $ 4.56

Dairy/Refrigerated $ 21.77 $ 21.33 $ 24.40 $ 21.73 $ 22.65 $ 21.36 $ 21.46 16 Straw berry Fresh Straw berries 1 lbs $ 2.45 $ 3.19 $ 3.94 $ 3.21 $ 2.94 $ 2.99 $ 3.45 17 Banana Yellow Banana 1 lbs $ 0.50 $ 0.53 $ 0.74 $ 0.59 $ 0.77 $ 0.57 $ 0.98 18 Apple Gala Apples 1 lbs $ 1.14 $ 1.04 $ 2.60 $ 1.79 $ 1.87 $ 1.28 $ 1.64 19 Apple Fuji Apples 1 lbs $ 1.31 $ 1.44 $ 1.98 $ 1.08 $ 2.49 $ 1.35 $ 1.42 20 Broccoli Broccoli Crow ns 1 lbs $ 1.70 $ 1.52 $ 2.03 $ 1.96 $ 2.35 $ 1.83 $ 2.05 21 Onions Yellow Onions 1 lbs $ 0.79 $ 0.65 $ 1.16 $ 0.65 $ 1.09 $ 0.99 $ 0.70 22 Tomato Roma Tomato 1 lbs $ 1.11 $ 0.98 $ 2.02 $ 1.15 $ 2.07 $ 1.78 $ 1.39 23 Orange Nav el Orange 1 each $ 1.29 $ 0.59 $ 0.99 $ 0.55 $ 0.44 $ 0.31 $ 0.81 24 Av ocado Large Hass Av ocado 1 each $ 2.33 $ 1.04 $ 1.67 $ 1.21 $ 1.73 $ 1.34 $ 1.84 25 Carrots Carrots 1 lbs $ 0.77 $ 0.74 $ 1.09 $ 0.85 $ 1.08 $ 0.69 $ 0.94

Fresh Produce $ 13.39 $ 11.71 $ 18.20 $ 13.03 $ 16.83 $ 13.14 $ 15.22 26 Chicken Whole Chicken 1 lbs $ 1.66 $ 1.07 $ 1.54 $ 1.49 $ 2.88 $ 1.44 $ 2.42 27 Salmon Atlantic Salmon Fillet 1 lbs $ 10.79 $ 11.16 $ 8.78 $ 9.23 $ 13.12 $ 8.67 $ 12.28 28 Pork Boneless Center Cut Thin Pork Chops 1 lbs $ 3.42 $ 4.45 $ 4.84 $ 4.36 $ 5.99 $ 3.89 $ 5.79 29 Beef Ground Beef ~80% Lean 1 lbs $ 4.80 $ 4.08 $ 3.76 $ 5.62 $ 6.48 $ 3.99 $ 4.51 30 Beef Beef Top Boneless Sirloin Steak 1 lbs $ 7.99 $ 6.46 $ 7.41 $ 9.31 $ 10.81 $ 6.99 $ 17.22

Protein $ 28.66 $ 27.23 $ 26.32 $ 30.01 $ 39.29 $ 24.98 $ 42.22 Total $ 97.17 $ 87.67 $ 104.45 $ 97.49 $ 112.90 $ 89.47 $ 109.13

Source: Company data, Credit Suisse estimates In Select Los Angeles Zip codes; *Substitute: SFM: Peanut Butter (Private Label), Bread (Market Corner); WMT: Salted butter (Darigold), ABS: Salted Butter (Lucern), WFM: Orange juice (Simply Beverages), Bread, Olive Oil, Peanut Butter, Eggs (Private Label). SFS: Olive Oil (Star) , AMZN: Bread (Oroweat).

Two Years of Feast Followed by Famine Prompt Restock Food retail is one of the least elastic areas of consumer demand available to investors, but stock prices are another story altogether. The year 2014 began an epic two-year run in Kroger shares fueled by strong IDs, cratering gas prices, the integration of Harris Teeter, and competitor bankruptcies, among other things. Management beat and raised EPS guidance in each of the first three quarters of 2014 and 2015, even electing to split its stock in July 2015, a move last made in 1999.

The year 2016 reversed the prior two-year trend, as an extended period of food deflation roiled the industry and KR began a string of guidance reductions. The first half of 2017 played out much the same way. At the company's Investor Day in October, management

17 April 2018

The Kroger Co. (KR) 22

voiced regret over the missed opportunity to further leverage expenses when IDs were running at the 5%+ level in 2014-15, a move that may have been able to pull forward some of the SG&A spend recorded in 2016-1H17.

Figure 41: KR Stock Chart, 1/1/2014–4/16/2018

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

5

Jul-1

5

Oct-1

5

Jan-

16

Apr-1

6

Jul-1

6

Oct-1

6

Jan-

17

Apr-1

7

Jul-1

7

Oct-1

7

Jan-

18

Apr-1

8

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Removal of LT Guidance Evokes Pre-2012 Kroger ComparisonAt its October 2012 Investor Day, KR instituted long-term EPS guidance of 8-11%, effectively signaling to investors that stock performance was a real consideration for management. Prior to this move, KR was in the habit of periodically surprising on the gross margin line, as the company's product price gap versus competitors was top of mind. The year 2012 seemed to signal relative comfort with the company's overall price position and price perception, not to say that KR wouldn't remain vigilant on pricing.

With 2Q17 earnings, management removed its 8-11% EPS growth guidance, garnering greater leeway in its corporate planning process as the food landscape evolves. Whereas 2012-216 may have been a harvest period in which KR basked in the decision to invest in price long before other conventional supermarkets, management now finds itself back in investment mode, trying to ensure that it can skate to where the puck is going, not where it's been. Renewed focus on food at WMT, AMZN's purchase of Whole Foods, and constant price competition at the hands of discounters and others will require the freedom to invest accordingly.

Figure 42: SSS and EPS Surprise and Price Reaction

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

EPS Surprise (LHS) SSS (ex-fuel) Surprise (LHS) Price Reaction (RHS)

Source: Company data, Thomson Reuters, Credit Suisse estimates.

17 April 2018

The Kroger Co. (KR) 23

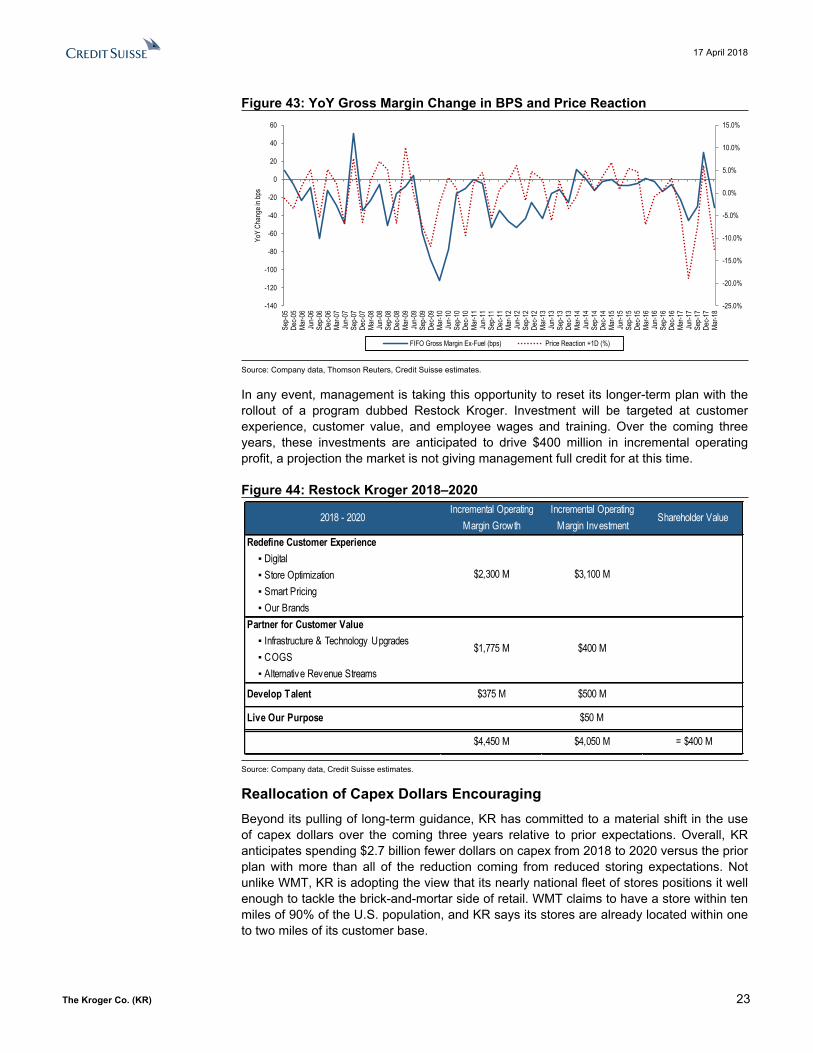

Figure 43: YoY Gross Margin Change in BPS and Price Reaction

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

-140

-120

-100

-80

-60

-40

-20

0

20

40

60

Sep-

05De

c-05

Mar-0

6Ju

n-06

Sep-

06De

c-06

Mar-0

7Ju

n-07

Sep-

07De

c-07

Mar-0

8Ju

n-08

Sep-

08De

c-08

Mar-0

9Ju

n-09

Sep-

09De

c-09

Mar-1

0Ju

n-10

Sep-

10De

c-10

Mar-1

1Ju

n-11

Sep-

11De

c-11

Mar-1

2Ju

n-12

Sep-

12De

c-12

Mar-1

3Ju

n-13

Sep-

13De

c-13

Mar-1

4Ju

n-14

Sep-

14De

c-14

Mar-1

5Ju

n-15

Sep-

15De

c-15

Mar-1

6Ju

n-16

Sep-

16De

c-16

Mar-1

7Ju

n-17

Sep-

17De

c-17

Mar-1

8

YoY

Chan

ge in

bps

FIFO Gross Margin Ex-Fuel (bps) Price Reaction +1D (%)

Source: Company data, Thomson Reuters, Credit Suisse estimates.

In any event, management is taking this opportunity to reset its longer-term plan with the rollout of a program dubbed Restock Kroger. Investment will be targeted at customer experience, customer value, and employee wages and training. Over the coming three years, these investments are anticipated to drive $400 million in incremental operating profit, a projection the market is not giving management full credit for at this time.

Figure 44: Restock Kroger 2018–2020

2018 - 2020Incremental Operating

Margin GrowthIncremental Operating

Margin InvestmentShareholder Value

Redefine Customer Experience▪ Digital▪ Store Optimization▪ Smart Pricing▪ Our Brands

Partner for Customer Value▪ Infrastructure & Technology Upgrades▪ COGS▪ Alternative Revenue Streams

Develop Talent $375 M $500 M

Live Our Purpose $50 M

$4,450 M $4,050 M = $400 M

$2,300 M $3,100 M

$1,775 M $400 M

Source: Company data, Credit Suisse estimates.

Reallocation of Capex Dollars Encouraging Beyond its pulling of long-term guidance, KR has committed to a material shift in the use of capex dollars over the coming three years relative to prior expectations. Overall, KR anticipates spending $2.7 billion fewer dollars on capex from 2018 to 2020 versus the prior plan with more than all of the reduction coming from reduced storing expectations. Not unlike WMT, KR is adopting the view that its nearly national fleet of stores positions it well enough to tackle the brick-and-mortar side of retail. WMT claims to have a store within ten miles of 90% of the U.S. population, and KR says its stores are already located within one to two miles of its customer base.

17 April 2018

The Kroger Co. (KR) 24

Management will focus on retrofitting its existing physical assets to better compete in the evolving food retail landscape. Major project counts, inclusive of remodels, will decline in favor of Space Optimization, a program informed by 84.51° analysis that will tailor individual store layouts to the needs and wants of the local customer base. If successful, this effort alone will demonstrate a competitive advantage for KR among traditional players, in our view.

Figure 45: Restock Kroger Current Expectation vs. Previous Expectation2018-2020E

Current Expectation Previous Expectation ∆Capital to Support Restock Plan $3,045 $1,700 $1,345Store Remodels $3,675 $3,800 ($125)Storing $1,150 $5,000 ($3,850)Major Project Counts 65-75 <300 (230)Infrastructure Maintenance $1,130 $1,200 ($70)Total $9,000 $11,700 ($2,700)$ in millions

Source: Company data, Credit Suisse estimates.

Get Used to the Term Space OptimizationThe store refresh program at KR has seen modest evolution over the past decade, but the utilization of 84.51° learnings could kick returns into overdrive. Historically, stores were bucketed by type (value, mainstream, and upscale), and a one-size-fits-most renovation was implemented at that location. Over the past year, approximately 6-7% of stores were touched using the bucket approach. Space Optimization will look at each store individually, analyzing internal store trends as well as specific competition affecting that store. The company believes this more targeted approach will allow for 20-30% of the 2018 store base to be touched under the new program.

Areas of focus will include expanded natural foods in the center store, expansion of high-growth categories (beverage, snacking, pet, etc.), and further implementation of fresh food elements such as grab-n-go items. Square footage will be reallocated toward ClickList, self-checkout, and other efficiency initiatives. Renovations and remodels should be more effective given projects will be tailored to each store. If a particular market over-indexes for carbonated soft drinks, that store could see expanded CSD square footage, a departure from conventional supermarket wisdom today. The pasta example in Figure 46 illustrates expanded private label shelf space, a decision driven by customer spend analytics and representative of how targeted these efforts are.

Figure 46: Pasta Shelf Optimization Example

Source: Company data, Credit Suisse estimates.

One could argue that Space Optimization is the holy grail of retail or the supermarket equivalent of money ball, a national chain with store-by-store offerings that differ according

17 April 2018

The Kroger Co. (KR) 25

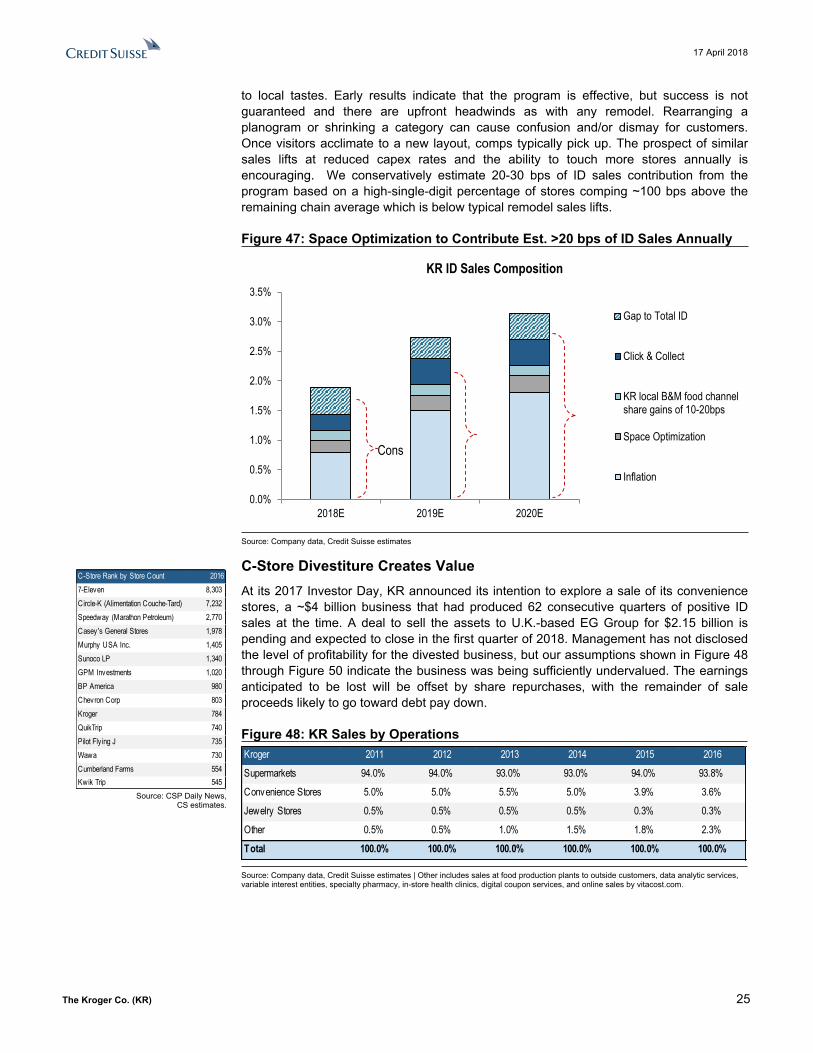

to local tastes. Early results indicate that the program is effective, but success is not guaranteed and there are upfront headwinds as with any remodel. Rearranging a planogram or shrinking a category can cause confusion and/or dismay for customers. Once visitors acclimate to a new layout, comps typically pick up. The prospect of similar sales lifts at reduced capex rates and the ability to touch more stores annually is encouraging. We conservatively estimate 20-30 bps of ID sales contribution from the program based on a high-single-digit percentage of stores comping ~100 bps above the remaining chain average which is below typical remodel sales lifts.

Figure 47: Space Optimization to Contribute Est. >20 bps of ID Sales Annually

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2018E 2019E 2020E

KR ID Sales Composition

Gap to Total ID

Click & Collect

KR local B&M food channelshare gains of 10-20bps

Space Optimization

Inflation

Cons

Source: Company data, Credit Suisse estimates

C-Store Divestiture Creates ValueAt its 2017 Investor Day, KR announced its intention to explore a sale of its convenience stores, a ~$4 billion business that had produced 62 consecutive quarters of positive ID sales at the time. A deal to sell the assets to U.K.-based EG Group for $2.15 billion is pending and expected to close in the first quarter of 2018. Management has not disclosed the level of profitability for the divested business, but our assumptions shown in Figure 48 through Figure 50 indicate the business was being sufficiently undervalued. The earnings anticipated to be lost will be offset by share repurchases, with the remainder of sale proceeds likely to go toward debt pay down.

Figure 48: KR Sales by Operations Kroger 2011 2012 2013 2014 2015 2016

Supermarkets 94.0% 94.0% 93.0% 93.0% 94.0% 93.8%

Convenience Stores 5.0% 5.0% 5.5% 5.0% 3.9% 3.6%

Jewelry Stores 0.5% 0.5% 0.5% 0.5% 0.3% 0.3%

Other 0.5% 0.5% 1.0% 1.5% 1.8% 2.3%

Total 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Source: Company data, Credit Suisse estimates | Other includes sales at food production plants to outside customers, data analytic services, variable interest entities, specialty pharmacy, in-store health clinics, digital coupon services, and online sales by vitacost.com.

C-Store Rank by Store Count 20167-Eleven 8,303Circle-K (Alimentation Couche-Tard) 7,232Speedway (Marathon Petroleum) 2,770Casey 's General Stores 1,978Murphy USA Inc. 1,405Sunoco LP 1,340GPM Investments 1,020BP America 980Chevron Corp 803Kroger 784QuikTrip 740Pilot Fly ing J 735Wawa 730Cumberland Farms 554Kwik Trip 545

Source: CSP Daily News, CS estimates.

17 April 2018

The Kroger Co. (KR) 26

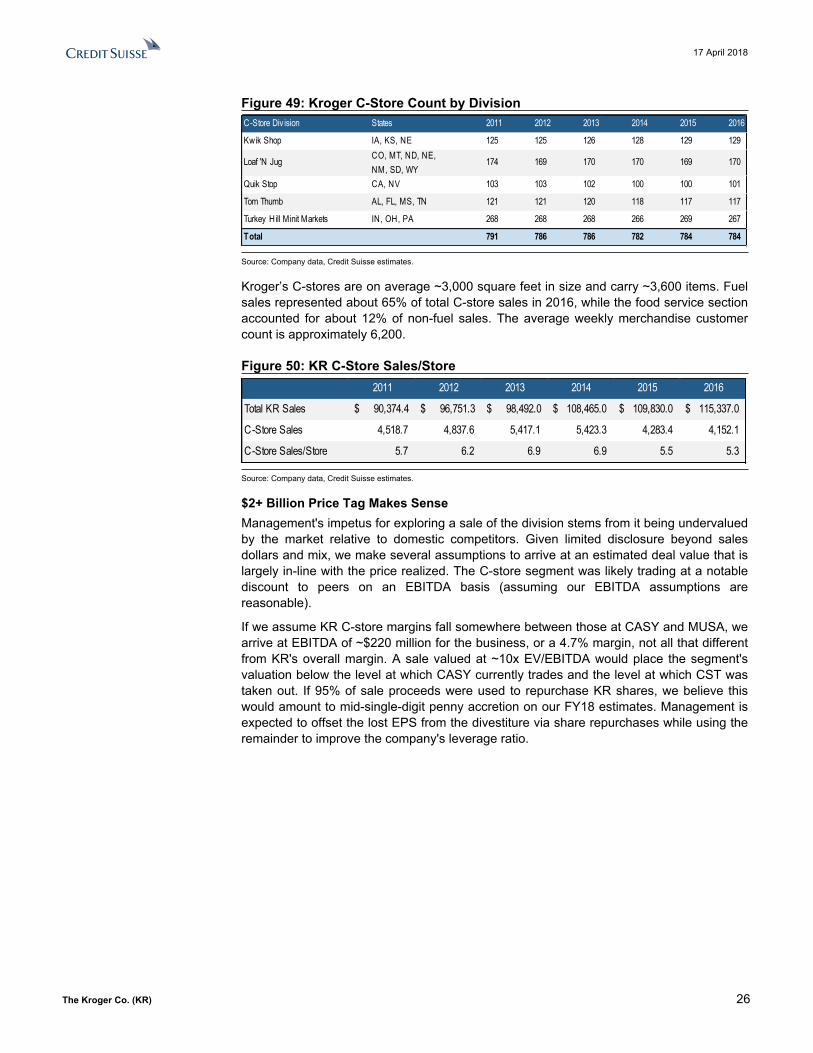

Figure 49: Kroger C-Store Count by Division C-Store Div ision States 2011 2012 2013 2014 2015 2016

Kwik Shop IA, KS, NE 125 125 126 128 129 129

Loaf 'N Jug CO, MT, ND, NE, NM, SD, WY

174 169 170 170 169 170

Quik Stop CA, NV 103 103 102 100 100 101

Tom Thumb AL, FL, MS, TN 121 121 120 118 117 117

Turkey Hill Minit Markets IN, OH, PA 268 268 268 266 269 267

Total 791 786 786 782 784 784

Source: Company data, Credit Suisse estimates.

Kroger’s C-stores are on average ~3,000 square feet in size and carry ~3,600 items. Fuel sales represented about 65% of total C-store sales in 2016, while the food service section accounted for about 12% of non-fuel sales. The average weekly merchandise customer count is approximately 6,200.

Figure 50: KR C-Store Sales/Store 2011 2012 2013 2014 2015 2016

Total KR Sales $ 90,374.4 $ 96,751.3 $ 98,492.0 $ 108,465.0 $ 109,830.0 $ 115,337.0

C-Store Sales 4,518.7 4,837.6 5,417.1 5,423.3 4,283.4 4,152.1

C-Store Sales/Store 5.7 6.2 6.9 6.9 5.5 5.3

Source: Company data, Credit Suisse estimates.

$2+ Billion Price Tag Makes SenseManagement's impetus for exploring a sale of the division stems from it being undervalued by the market relative to domestic competitors. Given limited disclosure beyond sales dollars and mix, we make several assumptions to arrive at an estimated deal value that is largely in-line with the price realized. The C-store segment was likely trading at a notable discount to peers on an EBITDA basis (assuming our EBITDA assumptions are reasonable).