Emerging Consumer Survey 2012 - Credit Suisse | PLUS

49

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 16 January 2012 Emerging Consumer Survey 2012 Global Equities Research Credit Suisse, in conjunction with Nielsen, launch the second edition of the Emerging Market Consumer survey Credit Suisse Research Institute Thought leadership from Credit Suisse Research and the world’s foremost experts

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Emerging Consumer Survey 2012 - Credit Suisse | PLUS

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

16 January 2012

Emerging Consumer Survey 2012

Global Equities Research Credit Suisse, in conjunction with Nielsen, launch the second edition of the Emerging Market Consumer survey

Mary Curtis +44 20 7883 8885

Richard Kersley 44 20 7888 0313

Mujtaba Rana 44 20 7883 3773

Andrew Garthwaite 44 20 7883 6477

Credit Suisse Research Institute Thought leadership from Credit Suisse Research and the world’s foremost experts

16 January 2012

2

Table of contents Introduction 3 Executive Summary 4

Key Themes 4 Country Highlights 5

Stock Recommendations – Emerging Markets 7 Stock Recommendations – Developed Markets 9 The Credit Suisse emerging consumer survey map 11 The Emerging consumer in 2012 13

Optimism varies across the emerging world 13 Cyclical headwinds interrupt the shift towards discretionary spending 17 The appetite for technology 20 The role of brands 22

Brazil 28 China 30 Egypt 32 India 34 Indonesia 36 Russia 38 Saudi Arabia 40 Turkey 42 About the survey 44

Also published today in conjunction with our global analysts:

China Consumer Survey – “The best of youth” (Vincent Chan / Peggy Chan)

India Consumer Survey – “Building a strong base” (Neelkanth Mishra / Jatin Chawla)

Indonesia Consumer Survey (Teddy Oetomo / Ella Nusantoro / Agus Sandianto)

Consumer Survey – “Healthcare Conclusions” (Global Pharmaceuticals Team)

Consumer Survey – “Automotive Consumer Survey” (Ellinghorst / Hauser / Galliers)

16 January 2012

3

Introduction We are delighted to publish the second edition of the Credit Suisse Global Emerging Consumer Survey. The 2012 survey goes further than last year’s inaugural edition in extending our survey to eight countries – Brazil, China, Egypt, India, Indonesia, Russia, Saudi Arabia and Turkey. To undertake this project, the Credit Suisse Research Institute has again engaged the leading global market research firm AC Nielsen to conduct primary research on its behalf, this year interviewing over 14,000 consumers across countries that together account for 3.5 billion people.

At a time when investors are debating how sensitive emerging economies are to broader market and political turmoil, especially within Europe, this survey provides the investor a unique perspective on consumer behaviour at ground level. More broadly, the survey highlights the major income and demographic differences, and cultural and social drivers within the emerging world, a key consideration for spending preferences and also for the brand positioning of companies.

The analysis delivered in the report and the accompanying Databook provides insights not available from public sources of information. This underlines Credit Suisse’s commitment to provide our clients unique and proprietary insights to support their investment process. It also builds on prior detailed research of trends in emerging markets, notably the recent Credit Suisse Global Wealth Report that underlined the rapid wealth accumulation and consumption potential in the emerging world.

Analysts from across the breadth of Credit Suisse’s global research team have drawn out the key trends and investment conclusions for stocks both in the emerging and developed world. These are detailed in the pages that follow.

Research analyst Telephone Email

Mary Curtis +44 20 7883 8885 [email protected]

Richard Kersley +44 20 7888 0313 [email protected]

Mujtaba Rana +44 20 7883 3773 [email protected]

Jahanzeb Naseer +852 2101 6554 [email protected]

Istvan Mate-Toth +44 20 7888 1598 [email protected]

Daisuke Takato +81 3 4550 9671 [email protected] Michael Kassab +1 212 538 6307 [email protected] Ashley Van Der Waag +1 212 538 2908 [email protected] Andrew Garthwaite +44 20 7883 6477 [email protected] Sakhti Siva +65 6212 3027 [email protected] Alex Redman +44 20 7883 6896 [email protected] Contributors

Brazil Andrew Campbell +55 11 3841 6313 [email protected]

Daniel Federle +55 11 3841 6311 [email protected]

Gustavo Wigman +55 11 3841 6302 [email protected]

China Vincent Chan +852 2101 6568 [email protected]

Peggy Chan +852 2101 6305 [email protected]

Egypt Ahmed Badr +971 4 362 0223 [email protected]

Vincent Resillot +44 20 7883 5550 [email protected]

India Neelkanth Mishra +91 22 6777 3716 [email protected] Jatin Chawla +91 22 6777 3719 [email protected]

Indonesia Teddy Oetomo +62 21 255 37911 [email protected]

Ella Nusantoro +62 21 255 37917 [email protected]

Agus Sandianto +62 21 255 37916 [email protected]

Saudi Digvijay Singh +971 4 362 0311 [email protected]

Russia Victoria Petrova +7 495 967 8393 [email protected] Turkey Onur Muminoglu +90 212 349 0454 [email protected] Atinc Ozkan +90 212 349 0453 [email protected]

Stefano Natella Head of Global Equity Research

16 January 2012

4

Executive Summary Key Themes Greater emerging market consumption remains a key long-term trend for investors. It is a theme that has already been apparent for much of the past 10 years but one that we think investors need to continue to be positioned to exploit. Various similarities in pent-up demand from emerging consumers can be identified at a macro level. However, our survey highlights that this consumption is far from uniform in direction or scope and that important distinctions can be identified between both sectors, stocks and markets. From this year’s survey data, we highlight four key themes:

(1) Confidence still strong but not as strong as last year

Our survey suggests that confidence among emerging consumers is still reasonably strong. Of just over 14,000 adults included in the survey across eight markets, 35% thought their personal finances would improve over the next six months and 9% expected some deterioration. Optimism is highest in Brazil, India and China and lowest in Egypt, Turkey and Russia.

However, compared with last year, consumer confidence has slipped. This is particularly apparent for consumers that allocate a significant proportion of income towards food expenditure. The good news is that the inflation outlook is set to become significantly more supportive as the high food prices of H1 2011 lend a favourable base to H1 2012.

(2) Cyclical headwinds slow discretionary spending

The structural theme underpinning the outlook for the emerging consumer is a shift to a more discretionary bias that typifies spending in the developed world away from the basic essentials of life – a global rebalancing of consumption. However, this structural shift towards greater discretionary spending has stalled, on average, over the past year as slower growth and high food inflation has impacted confidence.

Consequently, when we compare the growth in spending rates between the latest survey and the year before, we can see that household consumption contracted for many of the more discretionary areas of expenditure over the year. This was particularly apparent in spending on sport shoes and fashion apparel, private healthcare and property ownership. However, certain sectors still delivered growth in consumer penetration rates despite the economic concerns. Examples here include mobile phones, smartphones, computers and internet access and education. Interestingly, a significant proportion of respondents in six out of seven markets said they had allocated more money to private education courses this year compared with last (Egypt was the only exception).

(3) The appetite for technology

The survey data indicate the strength of demand for technology varies according to income group as well as market. For example, the data show that the penetration of smartphones is greater in the low income groups in Saudi Arabia than it is for the high income groups in Brazil and Russia. The ownership of computers is higher for the mid-income brackets in China than it is for the high income brackets in Saudi Arabia, Russia or India. Possible explanations for this include (i) the strength and sophistication of the distribution network; (ii) relative prices and (iii) the relative development of broadband infrastructure.

Looking forward, the survey suggests growth in mobile phone penetration looks set to be relatively strong in Indonesia (still 29% of our survey sample said they did not own a mobile), India (6% in total had no mobile rising to 12% at the lower income brackets) and Brazil (where 11% of the lower income groups had no mobile).

16 January 2012

5

Momentum in smartphone penetration is likely to continue to be strong in Brazil and China. Saudi penetration rates also look likely to continue upwards. Supporting factors are (a) growth in real wages, (b) size and affluence of the mid-to-high income groups in each of these markets, (c) existing momentum (smartphone penetration increased by 22%, 11% and 5% for Saudi, Brazil and China respectively over the last year).

(4) The role of brands

In previous research, we have looked at the significance of the brands for investing in consumer related stocks (see Great Brands of Tomorrow, 25 February 2010). The survey continues along this theme and analyses the consumer perception of both unbranded and branded goods across a wide range of consumer products. Three specific topics are apparent from the data:

(i) The scope for greater M&A activity. Global consumer companies have already taken advantage of the growth opportunities in emerging vs. developed markets. It is the sectors, such as dairy and personal products which are more fragmented and where local brands proliferate that look most likely to benefit from greater M&A activity in the future.

(ii) “Trading up” opportunities as consumers shift from unbranded to branded products as incomes improve. Having a well-positioned brand for the improving living standards among low and middle income earners can be just as relevant for growth as the typical focus of investors on luxury brands. The survey identifies retailing, fashion and cosmetics brands that are well-positioned and locally-owned in India, Brazil and China.

(iii) The potential long-term winners. If the long-term story is about the emerging consumer incomes becoming ever more robust, investors need to be aware of the brands that are well-positioned among low and high income consumers. The survey illustrates brands that should succeed, as well as highlights brands that are vulnerable, to strong income improvements. Potential winners include Tsingtao, Natura and Li Ning which all enjoy strong brand acceptance among low and high income consumers within their respective markets. The global players look set to continue to dominate the luxury space but a question mark hangs over the global and Western technology companies, where, Apple aside, there are illustrations of diminishing brand traction. Emerging market technology brands could well become the global standard.

Country Highlights Pages 28 to 43 provide page-by-page findings for each country. Key highlights include:

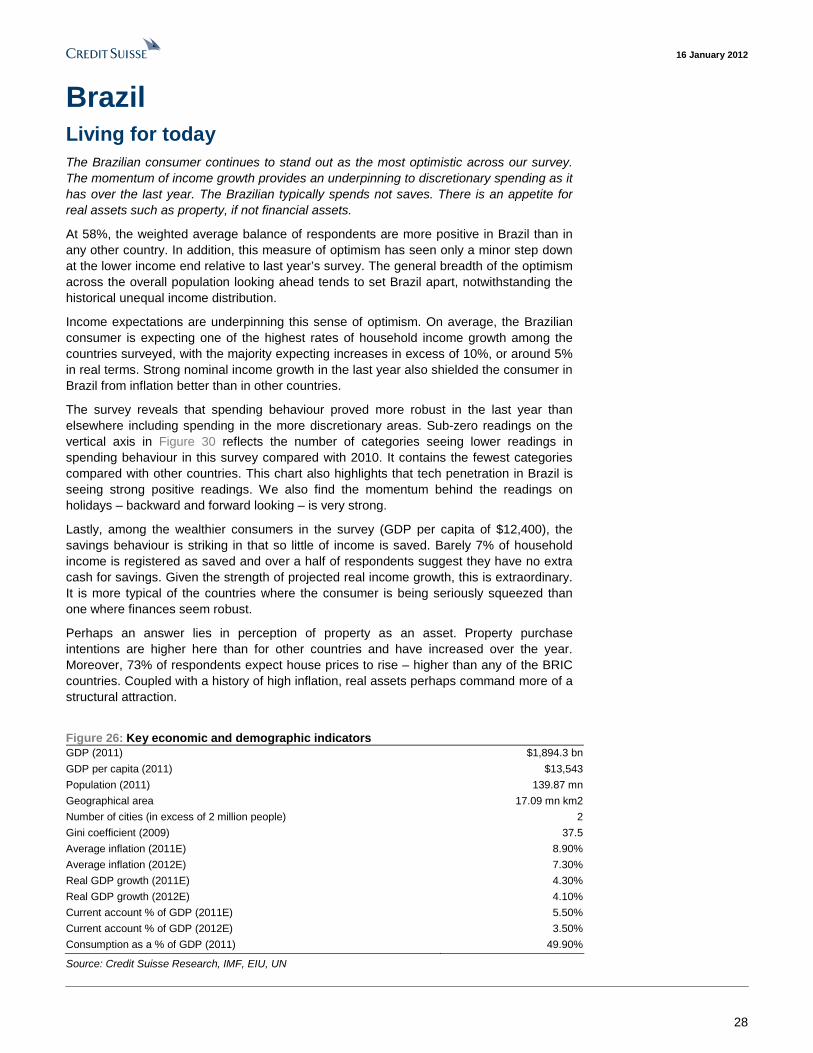

Brazil: Living for today

The Brazilian consumer stands out as the most optimistic across our survey. This confidence is underpinned by expectations of one of the highest rates of income growth among the countries surveyed – nominal increases of over 10%. Given a consumer that typically spends not saves (barely 7% of income is registered as saved), it remains a market for momentum in discretionary spending (smartphones, technology, personal care). It seems real assets such as property command more interest than financial assets.

Key stock recommendations: AmBev, Brasil Foods, Natura, Diagnósticos da América, PDG, Multiplus, MercadoLibre, Procter & Gamble, Diageo, Yakult.

China: A savings culture

The outlook for the Chinese consumer is robust though expectations have softened in the last 12 months and optimism is lower than in Brazil and India. Food prices have provided a squeeze on a range of consumer staples as well as some more discretionary items. The strength of technology spending is a clear bull theme while a prioritisation of healthcare and education also stand out. Given the additional government spending plans in these latter areas, structural growth potential clearly exists.

Key stock recommendations: China Modern Dairy, Belle, 7 Days, BMW, Swatch, Wynn, Tencent.

16 January 2012

6

Egypt: Change but no change

Drawing definitive conclusions from our survey for Egypt this year is clearly challenging given a political backdrop that is fluid. The reality in the data, though, is less has changed than one might have hoped. Optimism is still the lowest in the survey. The structural bullish story that exists for the consumer in Egypt is that spending levels are so low. The key is finding the stability and impetus to unlock it. At present, and politics aside, ongoing real declines in income do not provide long term opportunities.

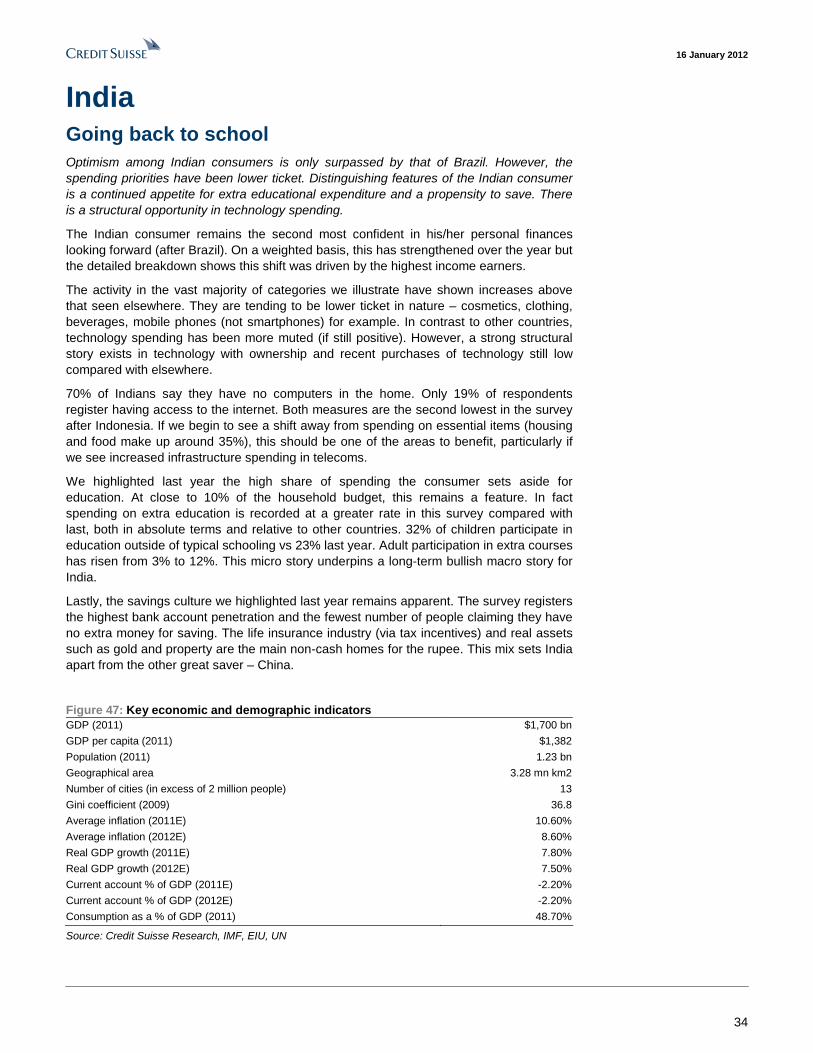

India: Going back to school

The Indian consumer in the survey remains the second most confident in his/her future personal finances. The survey points to spending activity in most consumer categories, particularly low ticket, well above those seen elsewhere in the emerging world. Additional distinguishing features of the Indian consumer is the appetite for extra investment in education and also a propensity to save. A major structural opportunity in technology spending exists with penetration rates still very low in keeping with limited internet rollout.

Key stock recommendations: Educomp, HDFC Bank, Hero, Sun Pharma, Prudential .

Indonesia: On a fast track

The Indonesian consumer displays strong structural growth potential. Its GDP per capita may be one of the lowest in the survey but its optimism is closer to the highest. The risk that always exists for the Indonesian consumer is the sensitivity of food prices as in any of the poorer economies. However, in the absence of this, there is considerable potential to unlock under-penetrated markets such as autos (cars and motor-bikes) and technology.

Key stock recommendations: Mitra Adiperkasa, Indofood CBP, XL Axiata, Daihatsu, BATs

Russia: The weakest BRIC in the wall

Optimism in Russia remains the lowest of the BRICs. The net balance of only 20% viewing an improved financial position in the six months ahead is only a third of that of Brazil. The simple explanation stems from poor income growth but it seems unlikely that this lid on optimism will be removed easily. The outlook for growth may be better in high ticket items due to the severe income inequality and under-penetration of luxury goods and technology.

Key stock recommendations: Magnit, Sberbank, Synergy, Philip Morris, Crown, JTI.

Saudi Arabia: The oil price hedge

Optimism is relatively high across a swathe of the Saudi population. The government’s spending plans and policy announcements have been highly supportive. Optimism goes hand in hand with perceived income growth - the highest in our survey. The upper end of earners expect their incomes to grow by 9% in real terms. The spending outlook should remain discretionary focused - smartphones, computers, property and cars.

Key stock recommendations: Almarai, Etihad Etisalat, Yum! Brands, Nokia, BMW, Apple

Turkey: Feeling the squeeze

Confidence among Turkish consumers is close to the weakest in the survey. Despite GDP per capita in keeping with the middle income bracket, Turkey’s spending patterns are more typical of the low income countries Food and housing costs are squeezing out discretionary spending and leaving limited funds for saving. With the outlook for real incomes still questionable, this does not look a market for high ticket spending.

Key stock recommendations: Efes, Arcelik, Tofas, Reckitt-Benckiser.

Custom Basket Alongside the specific stocks recommendations in this report, Credit Suisse prime financing offers a custom basket (CSGLEMDS Index [GO]) of 30 developed and emerging listed stocks that offer investors diversified exposure to the continued growth in emerging consumption, and remain attractive from a valuation perspective .

16 Jan

uary 2012

7

Stock Recommendations – Emerging Markets Figure 1: Plays on the emerging consumer

Stock Country Investment story

Current Price (local CCY)

Target Price (Local CCY)

EV / Ebitda (2012)

PE (2012)

P/B (2012)

ROE (2012)

3 year EPS

growth

3 year Revenue growth

Rating

Ambev Brazil Fourth largest brewer globally. Portfolio has desirable brands with high penetration across income categories. Revenues should have high resilience to the current low economic growth period in Brazil.

64.00 60.00 13.2x 20.5x 6.8x 33.3% 224% 42.2% Outperform

Brasil Foods Brazil Largest and most diversified Brazilian food company, a leading protein exporter, using global distribution network to access Middle-East, Asia and Europe/Russia.

35.00 38.50 8.4x 17.8x 2.0x 11.1% -38.5% 190% Outperform

Natura Brazil 30% share in the cosmetics and 11% share in the personal care markets. Operates in the Latin American market, selling premium HPC and middle prices cosmetics through its direct sales force.

37.84 42.50 10.8x 17.3x 12.1x 69.9% 185% 226% Neutral

Diagnósticos da América

Brazil Diagnósticos da América is the largest chain of clinical and imaging diagnostic testing laboratories in Latin America, operating in the Brazilian cities of Sao Paulo, Rio de Janeiro and Curitiba.

15.50 21.00 8.9x 18.3x 1.8x 9.6% 151% 237% Outperform

PDG

Brazil Largest homebuilder in Brazil and holding company for subsidiaries Goldfarb, CHL

and Agre. The company is geographically diversified and acts in both low and mid-high income housing.

6.45 10.00 9.1x 6.4x 1.0x 15.5% 140% 379% Outperform

Multiplus Brazil Engaged in the operation and management of customer loyalty programs, the main revenue driver is credit card usage.

33.96 41.00 11.5x 18.2x 20.7x 113.5% n.a. n.a. Outperform

China Modern Dairy

China Largest dairy farm company in China. Well positioned to benefit from fast-growing demand for quality milk and industry consolidation and modernisation. Sales CAGR of 51% for FY2010-15E.

1.74 3.25 11.4x 13.1x 1.3x 10.0% n.a. n.a. Outperform

7 Days Group

China Second largest economy hotel chain operator in China and fast growing; well positioned to benefit from the rapidly-growing domestic travel demand

82.28 153.44 6.3x 15.1x 2.3x 15.3% n.a. 492.9% Outperform

Belle China Belle is China's largest footwear retailer, with nearly 33% market share in China's mid- to high-end women's footwear segment, and China's second sportswear distributor, mainly selling Nike and Adidas.

11.86 14.5 10.8x 16.6x 3.5x 21.2% 64.0% 103.1% Outperform

Tencent China Largest SNS player in China. The company’s investment in new businesses i.e., Ecommerce, search, and payment is getting attention of internet users. Mobile internet is another key strength of Tencent, but not yet reflected in the consumer survey.

170.10 220.00 13.2x 21.1x 5.9x 28.5% 406.4% 414.2% Outperform

Educomp India Play on nascent education industry. Leader in technology-based interactive

learning; vocational training, on-line education potential. 217.95 275.00 5.1x 6.6x 0.9x 13.4% 339.1% 372.4% Neutral

HDFC Bank India Retail banking: rising ROE driven by stronger-than-industry credit growth and falling credit costs. Well placed for rising rates.

469.30 514.00 10.4x 22.1x 3.7x 17.4% 84.1% 102.4% Outperform

16 Jan

uary 2012

8

Stock Country Investment story

Current Price (local CCY)

Target Price (Local CCY)

EV / Ebitda (2012)

PE (2012)

P/B (2012)

ROE (2012)

3 year EPS

growth

3 year Revenue growth

Rating

Hero Motorcorp

India Market brand leader in two-wheeler market. Increased penetration in rural and female market. Among the cheaper plays on Indian consumer

1790.25 2238.00 8.6x 15.5x 10.6x 68.2% 115.7% 87.8% Outperform

Sun Pharma India Market leader in selling medicines for lifestyle diseases in India. We expect chronic drugs to outpace industry growth and grow at 18-20% CAGR over 5 years.

512.95 595.00 18.8x 23.6x 4.7x 20.1% 58.7% 83.1% Outperform

Mitra Adiperkasa

Indonesia Mid to high-end segment retailer, benefits from the rise of its target segments in Indonesia. Well positioned to benefit from the potential re-emergence of Java’s purchasing power.

5100.00 6000.00 8.8x 20.0x 4.0x 19.8% -29.0% 68.1% Outperform

Indofood CBP

Indonesia Leading instant-noodle and dairy producer, well positioned to benefit from the rise in country GDP/Capita. Indomie (instant noodle) is market leader.

5150.00 7300.00 6.8x 13.6x 2.6x 19.0% 2950% 89.4% Outperform

XL Axiata Indonesia Third largest cellular operator in Indonesia. Cost control record has been excellent, and this is being raised to a new level by the launch of a comprehensive network outsourcing deal.

5050.00 7200.00 4.8x 10.7x 2.6x 24.8% 860.8% 121.9% Outperform

Magnit

Russia

Play on food consumption and underpenetration of modern food retail format in Russia with high profitability, excellent track record, and strong organic growth.

$22.96 $25.00 12.1x 18.4x 4.0x 22.0% 128.3% 103.3% Outperform

Sberbank Russia

46% market share of retail deposits, due to its very large branch network. We expect Sberbank to generate a 20% ROTE over the next two years, in part due to high NIM. Major growth opportunity in under-developed Russian loan market.

85.69 129.14 n.a. 6.2x 1.2x 19.9% 66.4% 88.7% Outperform

Synergy Russia

Likely to improve profitability via different sales mix in alcohol segment. Longer term it could be a potential acquisition target for large international producers.

517.62 1060.43 3.5x 5.2x 0.6x 11.0% 41.4% 13.7% Outperform

Almarai Saudi Inequality of income means Middle East will see strong spending in both

essentials and discretionary. Stock offers growth via staples exposure. 99.00 113.00 11.0x 13.8x 2.8x 20.6% 49.7% 83.9% Outperform

Etihad Etisalat

Saudi Leading exponent on mobile data growth in GEM. One of the first operators in GEM to launch an LTE service driving strong growth in data revenues and helping it take further market share from STC in Saudi.

53.50 70.00 5.2x 7.1x 1.9x 26.0% 118.1% 89.7% Outperform

Efes Turkey Turkey’s largest brewer with 90% market share and set to become #2 player in Russia following the recently announced JV with SAB Miller. Very strong pricing power, a highly selective consumer base.

25.10 26.20 9.7x 17.9x 3.3x 18.6% 34.5% 37.6% Outperform

Arcelik Turkey 50% market share in white-goods appliances, powered by strong brand awareness, distribution power, R&D efforts.

7.08 7.70 5.1x 7.5x 1.2x 16.0% 227.8% 4.7% Outperform

Tofas Turkey Young product line-up continues to find new client base, evident from recently awarded export contracts from Opel, Vauxhall and Chrysler. Its export contracts are cost-plus and take-or-pay protected.

6.72 8.65 5.2x 6.5x 1.6x 24.6% 118.5% 75.2% Outperform

Source: Credit Suisse Emerging Market Consumer Survey, Credit Suisse estimates. NOTE: EM Sales exposures refer to 2010.

16 Jan

uary 2012

9

Stock Recommendations – Developed Markets Figure 2: Plays on the developed consumer

Stock Country Investment story

Current Price (local CCY)

Target Price (Local CCY)

EV / Ebitda (2012)

PE (2012)

P/B (2012)

ROE (2012)

3 year EPS

growth

3 year Revenue growth

Rating

Bayer Europe Unjustified decoupling from the pharma sector to the Dax should reverse in 2012 as

positive developments in pipeline and new launches add to the base pharma business which has minimal patent loss. EM accounts for 37% of group revenues.

52.82 56.00 6.0x 10.8x 2.1x 19.4% -72.5% 8.3% Outperform

BMW Europe Best auto play on EM exposure (c.30% of sales), particularly with respect to China, as it represents the closest play to a branded luxury good within the sector. Equity contribution from Chinese venture is expected to grow by 1.7% to €2.1bn in 2011E?.

58.04 76.00 1.2x 7.4x 0.9x 12.4% 14.0% 7.9% Outperform

BATs Europe Best margin visibility in coverage, underpinned by innovation-led premiumisation in emerging markets, untapped savings potential and over 50% EM sales exposure.

29.70 30.80 10.1x 14.1x 5.5x 39.3% 38.2% 52.7% Outperform

Diageo Europe New stretch targets are a welcome addition and a sign of management's confidence in the prospects. We think EM margins have reached an inflection point and should now start to trend up, restructuring in DM should help too. 35% EM sales exposure.

13.90 15.50 11.9x 15.3x 4.7x 31.0% 29.0% 22.8% Outperform

Nokia Europe Recovery story, timing right as last year spent putting the building blocks in place (partnership with Microsoft, integrating the new OS, taking significant cost out of the business, and developing stronger partnerships with carriers). 60% EM sales.

4.09 6.00 4.4x 16.6x 1.2x 7.0% -73.9% -17.3% Outperform

Prudential Europe Breadth and depth across Asia (53% of new business value from Asia). While US macro concerns appear to have come to fore in recent months, we believe that the sustained strength of the Asian franchise remains a key driver of the stock.

6.63 8.80 n.a. 10.4x 1.7x 16.5% 46.3% n.a. Outperform

Reckitt Benckiser

Europe Having been de-rated from 20x to 13.5x shares now fully reflect the slow down in the growth rates. Cheapest of the consumer staple majors. 30% EM sales exposure.

33.10 38.00 9.8x 13.5x 3.6x 26.5% 65.5% 60.4% Outperform

Swatch Europe Established brand awareness, best positioned players structurally and geographically in the luxury sector thanks to its portfolio. We estimate that the group’s current Greater China exposure accounts for about 35% of group sales.

372.10 480.00 8.5x 13.8x 2.1x 15.8% 10.6% 5.0% Outperform

Telenor Europe High exposure to smartphones becoming cheap in emerging markets and driving data growth. 40% of 2010 ebitda is from Asia.

96.50 114.00 5.2x 11.6x 1.6x 14.2% -25.3% 6.1% Outperform

Apple Inc United

States EM classes could add $70bn in sales and $17.50 in EPS. We estimate five countries will account for 63% of this potential –BRICS / Mexico, and with the upside being so focused, we believe that costs could also be manageable. 15% EM sales exposure .

$421.39 $500.00 9.4x 15.3x 5.1x 35.2% 285.5% 165.4% Outperform

Crown Holdings Inc.

United States

World's largest producer of metal packaging and the third largest producer of beverage cans. Nearly 30% of Crown's revenue is derived in emerging markets and the company is benefiting from rapid demand growth in these regions.

$34.40 $44.00 7.3x 12.3x n.a. n.a. n.a. n.a. Outperform

International Flavors & Fragrances

United States

IFF is the third largest player in the Flavor and Fragrance industry. Management is positioning the company’s top-line to benefit from increasing customer innovation despite recent raw material headwinds. Focus on project profitability and pricing.

$55.08 $66.00 9.7x 14.9x 3.6x 24.4% 26.6% 15.2% Outperform

16 Jan

uary 2012

10

Stock Country Investment story

Current Price (local CCY)

Target Price (Local CCY)

EV / Ebitda (2012)

PE (2012)

P/B (2012)

ROE (2012)

3 year EPS

growth

3 year Revenue growth

Rating

Las Vegas Sands Corp.

United States

Large global gaming operator with 90% of 2010A EBITDA generated from Macau and Singapore. LVS has a strong exposure to both VIP and Mass gaming segments

$45.23 $60.00 12.6x 22.4x 3.6x 17.7% 8.8% 132.3% Outperform

Mead Johnson Nutrition Co.

United States

#1 market share in the highly attractive infant formula category in China with exceptionally large profit margins and 10% annual top-line growth. .

$72.48 $82.00 16.9x 26.1x n.a. n.a. n.a. n.a. Outperform

Mercado Libre Inc.

United States

Operates the leading e-commerce marketplaces and online payments platforms which are set to benefit from the ongoing growth of internet penetration as well as online shopping. Brazil is largest operating region.

$86.51 $99.00 33.2x 49.4x 16.7x 33.8% 244.6% 151.9% Neutral

Philip Morris International

United States

Biggest tobacco company in the world. PMI owns what we regard the strongest cigarette brand portfolio in the industry (centred on Marlboro), being well positioned to capture untapped uptrading potential in EM (accounted for 50% of group profits).

$76.45 $79.00 10.6x 15.8x 61.0x 386.9% 38.3% 19.3% Outperform

Procter & Gamble Co.

United States

Global HPC company with 30%+ of sales in EM (5-6% in China). Given weak growth in developed markets, management is aggressively pursuing white space opportunities in growth markets by switching to country level planning.

$65.81 $70.00 11.6x 16.7x n.a. 17.8% 20.7% 3.2% Outperform

Wynn Resorts

United States

Premier global gaming brand catering to high-end, with properties in Las Vegas and Macau, with another Macau property in the pipeline for 2015. 70% China EBITDA.

$109.80 $167.00 9.2x 19.6x 4.4x 22.9% -28.3% 55.7% Outperform

Yum! Brands, Inc.

United States

EM are 58% of 2011E operating profits. Growth beneficiary from unit expansion opportunity and exposure to underdeveloped consumption patterns. >30% EM sales

$60.86 $64.00 11.7x 21.1x 14.2x 69.1% 50.8% 8.9% Outperform

Nissan Motor (7201)

Japan China accounts for 20% operating profit, continues to launch new products to gain market share and grow earnings. Expects China to be the biggest premium market in the future and relocated global headquarters for its premium brand, Infiniti, to HK

689.00 760.00 6.4x 11.0x 1.0x 8.9% -35.0% -18.9% Neutral

Daihatsu (7262)

Japan Operating profit contribution from Asia > 45%. Indonesia is the main driver, where it commands 15% share of sales and 50% of production.

1438.00 1680.00 3.9x 10.7x 1.4x 13.6% 50.6% -8.4% Outperform

Suzuki Motor (7269)

Japan Strong presence in India, poised to benefit from growing demand in the country. Subsidiary Maruti Suzuki is expanding supply of diesel products and production capacity. May be some long-term risk if preference shifts to higher-end cars.

1590.00 1860.00 4.4x 14.1x 0.9x 6.5% -54.7% -25.5% Neutral

Fast Retailing (9983)

Japan The operator of Uniqlo is aggressively expanding in Asia -- esp in China, South Korea, Malaysia, Thailand and Indonesia. The number of stores in China doubled to 105 (Nov ‘11) since mid-2010 and emerging markets account for about 5% of 2011E profits.

14610.00 13500.00 8.2x 21.6x 4.1x 18.8% 24.9% 39.9% Neutral

JT (2914) Japan Russia and CIS account for 30% of sales and is a key driver of profit growth. JT may struggle to increase sales volumes, but has room to raise prices in Russia.

394500 430000 7.3x 25.7x 2.3x 9.2% -39.2% -1.7% Outperform

Yakult (2267)

Japan Asia/Oceania and the Americas (mainly Brazil and Mexico) account for a fifth of the company's sales. China is the third-biggest market with sales growing at 30%+.

2402.00 2350.00 8.9x 30.2x 1.8x 5.9% -22.0% -3.6% Neutral

Shiseido (4911)

Japan With Asia accounting for 38% of operating profit and 18% of sales in 2011E, the region (led by China) has been a key driver of the company's FY3/13 profit growth and future.

1371.00 1660.00 9.3x 27.2x 1.7x 6.3% -63.0% -7.3% Outperform

Unicharm (8113)

Japan The company's focus on low-end baby diapers is contributing to sales growth and margin improvement. Main driver Asia accounts for 39% of OP and 31% of 2011E sales.

3865.00 4200.00 10.7x 22.1x 3.3x 14.8% 106.0% 11.9% Outperform

Source: Credit Suisse Emerging Market Consumer Survey, Credit Suisse estimates. NOTE: EM Sales exposures refer to 2010.

16 Jan

uary 2012

11

The Credit Suisse emerging consumer survey map Figure 3: Countries surveyed

Russia (11%*)GDP: $1,894.3 bn

Consumption: $945.3 bn (50%)GDP Growth (2011E): 4.29%

China (18%*)GDP: $6,476.2 bn

Consumption: $2085.3 bn (32%)GDP growth (2011E): 9.47%

India (18%*)GDP: $1,700 bn

Consumption: $827.9 bn (49%)GDP growth (2011E): 7.84%

Indonesia (11%*)GDP: $813.9 bn

Consumption: $454.2 bn (56%)GDP growth (2011E): 6.4%

Brazil (11%*)GDP: $2447.8 bn

Consumption: $1520.1 bn (62%)GDP growth (2011E): 3.77%

Egypt (11%*)GDP: $248.6 bn

Consumption: $174 bn (70%)GDP growth (2011E): 1.22%

Saudi Arabia (11%*)GDP: $580.7 bn

Consumption: $153.3 bn (26%)GDP growth (2011E): 6.47%

Russia (11%*)GDP: $1,894.3 bn

Consumption: $945.3 bn (50%)GDP Growth (2011E): 4.29%

China (18%*)GDP: $6,476.2 bn

Consumption: $2085.3 bn (32%)GDP growth (2011E): 9.47%

India (18%*)GDP: $1,700 bn

Consumption: $827.9 bn (49%)GDP growth (2011E): 7.84%

Indonesia (11%*)GDP: $813.9 bn

Consumption: $454.2 bn (56%)GDP growth (2011E): 6.4%

Brazil (11%*)GDP: $2447.8 bn

Consumption: $1520.1 bn (62%)GDP growth (2011E): 3.77%

Egypt (11%*)GDP: $248.6 bn

Consumption: $174 bn (70%)GDP growth (2011E): 1.22%

Saudi Arabia (11%*)GDP: $580.7 bn

Consumption: $153.3 bn (26%)GDP growth (2011E): 6.47%

Note: 1.Total GDP for the country shown in nominal US $ (2011E).2.* % of survey sampled from this country3.Country GDP from IMF4.Consumption from UN data

2012 Credit Suisse Emerging Consumer Survey

Number of respondents : 14,232

Across 8 countries

70% in urban areas; 30% in rural areas

2012 Credit Suisse Emerging Consumer Survey

Number of respondents : 14,232

Across 8 countries

70% in urban areas; 30% in rural areas

Turkey (11%*)GDP: $846.5 bn

Consumption: $601 bn (71%)GDP growth (2011E): 6.59%

Source: Credit Suisse Emerging Market Consumer Survey, IMF, EIU, UN

16 January 2012

12

Figure 4: Credit Suisse Emerging Consumer related research

Asia Latin America / EMEA Global

Asian telecom sector. Smartphones - where are the best remaining Asian opportunities?

5 October 2011

2012 Outlook - Smartphones for everyone 6 December 2011

TMT The Emerging Apple 20 September 2011

Brazil Telecoms - Competitive sands are shifting; Vivo launches new initiatives

17 November 2011 2012 Outlook for Global Telecom Equipment 5 January 2012

China Healthcare Sector. 2012 outlook 5 January 2012

China Education Sector. OVERWEIGHT. K12 after-school tutoring market

29 November 2011 Healthcare / Education

India Pharmaceuticals Sector. Stay the course 19 October 2011

Brazilian Healthcare - Health care sector consolidation expected from the bottom up

21 March 2011

PharmaValues: Global analysis - Demographic exposure to ageing 14 September 2011

Global Proteins Industry - 2012: Another Year of Growing Demand 18 October 2011

Food / Beverages / HPC China Consumer Sector. Industry consolidation to

accelerate 20 October 2011 U.S. Protein - Elements in Place for Long-term Export

Growth 18 November 2011

Reloading the matrix - "The real world is not the Western world"

23 September 2011

Hong Kong Retail Sector. Rental cycle is catching up4 January 2012

Wealth Report Analysis - 2011 Wealth Report - Implications for Luxury

27th October 2011 Luxury / Retail / Leisure Macau gaming sector. Growth is normalizing, but not

collapsing 8 December, 2011

PCAR4: Blue Sky Over Cloudy Weather 3 October 2011 Global Hotel Sector - Assessing the GEM opportunity

23 March 2011

Brazilian Homebuilders and Real Estate Brokers - Attractive Valuation but Outlook Still Unclear

27 November 2011 Property

China Property Sector. Short-term gain? Long-term pain

5 December 2011 Russian homebuilders - Maintaining positive 2012 outlook

27 December 2011

Asia Transportation Sector. Captain's Log: Tough macro, but sector also a high beta recovery play

6 December 2011

Automotive - 2012: Two worlds in one sector 9 January 2012

Autos / Transport Asia Airline Sector. Enemies in the backyard

8 September 2011

LatAm Capital Goods Sector - A blend of conundrums and opportunities 1 December 2011 Travel & Leisure 2012 outlook - Rising above the

macro 9 December 2011

Themes Credit Suisse Research Institute: Global Wealth Report 2011,Credit Suisse Research Institute: The power of brand investing,Global Equity Strategy - 2012 Outlook

Source: Credit Suisse research

16 January 2012

13

The Emerging consumer in 2012 Our survey suggests that confidence among emerging market consumers is still reasonably strong. Of just over 14,000 adults included in the survey across eight markets, 35% thought their personal finances would improve over the next six months and 9% expected some deterioration. However, compared with last year, consumer confidence is not as strong as higher inflation and slower growth have taken their toll.

Optimism varies across the emerging world Optimism on the financial outlook is strongest in Brazil, India and China. In Brazil, 58% of respondents to the survey said they expected an improvement in their personal finances over the next six months. The Russian consumer is the most pessimistic of the BRIC countries.

At the other end of the scale, the greatest degree of pessimism in financial prospects was recorded in Egypt and Turkey. Despite the radical change in the political situation, Egyptian consumers remain the most downbeat among the countries included in our survey. Nearly as many Egyptians (24%) predicted a worse financial position as expected some improvement (25%) over the next six months. The picture in Turkey was not much better: 12% of respondents to the survey expected their financial position to worsen vs 16% who expected it to improve.

Figure 5: Do you think the state of your own personal finances over the next 6 months

will be better, worse or about the same?

58

43 40 36 3425 24

16

37

50 51 60 63

51

6772

7 9

24

8 12

0%

20%

40%

60%

80%

100%

Bra

zil

Indi

a

Chi

na

Sau

di

Indo

nesi

a

Egy

pt

Rus

sia

Tur

key

% o

f res

pond

ents

Better About the same Worse

Source: Credit Suisse Emerging Market Consumer Survey

When we compare the aggregate results in our latest survey with last year’s survey, we find that consumers, on average, are less optimistic. In Brazil, the balance of consumers expecting better rather than worse financial prospects over the next six months has fallen from 59% in 2010 to 53% in 2011. In China, the same statistic has slipped from 39% to 31% and in India it has fallen from 40% to 36%. The mood has improved in only two of the markets. In Indonesia, a net 31% now expect personal finances to improve over the next six months compared with 28% last year and in Egypt, the consumer is much more upbeat compared with last year but this is clearly off a very low base and still poor in absolute terms.

16 January 2012

14

Figure 6: Do you think the state of your own personal finances over the next 6 months

will be better, worse or about the same? 2011 vs 2010 results

53

3632 31 31

16

1

59

40

3239

28

17

-26-30

-20

-10

0

10

20

30

40

50

60

Bra

zil

Indi

a

Sau

di

Indo

nesi

a

Chi

na

Rus

sia

Egy

pt% e

xpec

ting

pers

onal

fina

nces

to b

e be

tter

min

us th

ose

expe

ctin

g it

to b

e w

orse

2011 2010

Source: Credit Suisse Emerging Market Consumer Survey

The rationale for the overall decline in optimism looks to be two-fold:

(1) On average, there has been a moderation in future wage expectations compared with last year. As we illustrate in Figure 7, wage expectations for the next 12 months, in the most recent survey compared with last year’s survey, have declined considerably in Brazil and have edged down in China. Wage expectations have picked up in Egypt, but, as with most indicators for Egypt, this comes from a very low base. The one market where there has, however, been a clear rise in wage expectations is Saudi Arabia. Arguably this reflects the increase in social spending programmes and rise in the minimum wage that the authorities have pursued in the wake of the political upheaval in other North African and Middle Eastern markets. This increase in optimism in Saudi Arabia is the obvious bright-spot in what is otherwise a somewhat more subdued consumer story on average.

Figure 7: % expecting better less worse household income in 2011 vs 2010

5855

47

3935

24 22

66

40

58

38 36

1822

0

10

20

30

40

50

60

70

Bra

zil

Sau

di

Indo

nesi

a

Indi

a

Chi

na

Egy

pt

Rus

sia

2011 2010

Source: Credit Suisse Emerging Market Consumer Survey

16 January 2012

15

(2) Food inflation has had a significant impact on consumer sentiment

When we compare the proportion of expenditure that is directed towards food against the optimism embodied in expectations on the state of personal finances, a clear pattern emerges. The least optimistic (consumers in Egypt) allocate over 40% of their total income towards food expenditure, the most optimistic (in Brazil) have the lowest relative expenditure on food.

Figure 8: Weight of food expenditure vs optimism on the outlook for personal finances

Saudi 2010

Russia 2010

Indonesia 2010

India 2010

Egypt 2010

China 2010

Brazil 2010

Turkey 2011

Saudi 2011

Russia 2011

Indonesia 2011India 2011

Egypt 2011

China 2011

Brazil 2011

-30

-20

-10

0

10

20

30

40

50

60

70

10% 15% 20% 25% 30% 35% 40% 45% 50%

Food expenditure as % total income

% re

spon

dent

s w

ith e

xpec

tatio

ns o

f bet

ter l

ess

wor

se

pers

onal

fina

nces

2010 survey 2011 survey

Source: Credit Suisse Emerging Market Consumer Survey

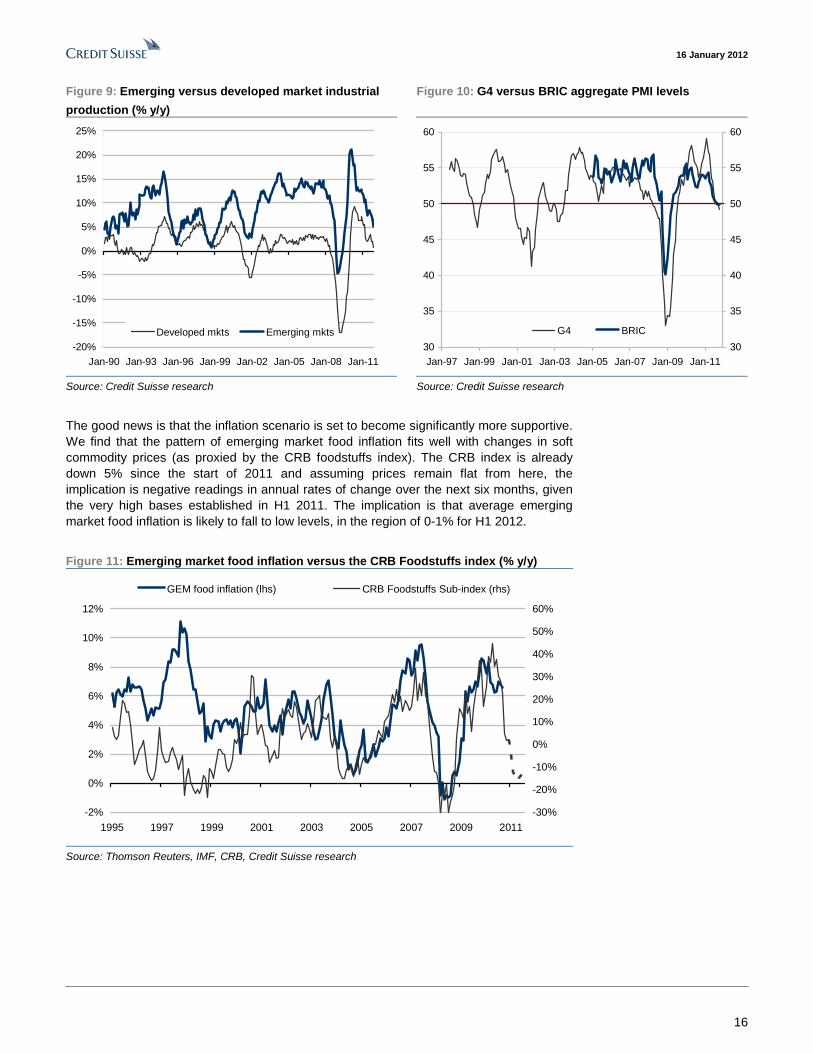

Clearly, food price inflation has negatively impacted consumer sentiment. The extent of the recent food price inflation felt across the emerging economies is illustrated in Figure 11. By our calculation, the annual rate of food price increases for the emerging markets in aggregate was running at 6.6% (in the 12 months ending September 2011) and this comes on top of 8.0% in the year before that. This puts food inflation for the last two years well above the 10-year average of 4.5%.

What next?

Economic momentum, on average, looks likely to continue to slow. Given that the export to GDP ratio for the emerging economies is a relatively high 35%, they are inevitably going to feel the headwinds of the slowdown and contraction in key developed markets. As we illustrate in Figure 9, emerging markets have consistently averaged higher growth rates in industrial production over the past decade but are clearly not independent of developed market trends. The most recent PMI readings are consistent with some contraction in industrial or manufacturing production for both the G4 and the BRIC economies in the months ahead. This suggests there is a risk of further slippage in nominal wage expectations over the next year across our survey markets and thus pressure remaining on confidence.

16 January 2012

16

Figure 9: Emerging versus developed market industrial

production (% y/y)

Figure 10: G4 versus BRIC aggregate PMI levels

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11

Developed mkts Emerging mkts

30

35

40

45

50

55

60

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-1130

35

40

45

50

55

60

G4 BRIC

Source: Credit Suisse research Source: Credit Suisse research

The good news is that the inflation scenario is set to become significantly more supportive. We find that the pattern of emerging market food inflation fits well with changes in soft commodity prices (as proxied by the CRB foodstuffs index). The CRB index is already down 5% since the start of 2011 and assuming prices remain flat from here, the implication is negative readings in annual rates of change over the next six months, given the very high bases established in H1 2011. The implication is that average emerging market food inflation is likely to fall to low levels, in the region of 0-1% for H1 2012.

Figure 11: Emerging market food inflation versus the CRB Foodstuffs index (% y/y)

-2%

0%

2%

4%

6%

8%

10%

12%

1995 1997 1999 2001 2003 2005 2007 2009 2011-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

GEM food inflation (lhs) CRB Foodstuffs Sub-index (rhs)

Source: Thomson Reuters, IMF, CRB, Credit Suisse research

16 January 2012

17

Cyclical headwinds interrupt the shift towards discretionary spending The key structural theme that underpins the outlook for emerging markets is how income and demographic drivers could change the make-up of consumer spending in these economies. Consumer spending, which has been heavily focused around more essential areas of spending, is likely to continue to shift to the more discretionary bias that typifies the developed world. This is the pattern that has typically played out across the developed markets through the last century.

Aggregate emerging market GDP per capita now stands at US$7,600 (in PPP terms). Over the next five years, the IMF forecasts that this will increase to US$10,100. The US, France and Japan saw similar changes in the level of their GDP per capita in the 1930s, the 1950s and the 1960s, respectively. If we look back at the shifts in their spending patterns during this transition, it is clear that growth in spending on the more discretionary items was far stronger than the growth in expenditure on basic essentials.

We can see that growth in volume demand for “essential items” (such as food and beverages and utilities) was, on average, still positive, but it was not as strong as the growth in discretionary spending. Consumption of what we might describe as “useful items” (such as transportation, education, financial services or healthcare) proved to be much more sensitive to the rising income levels. We note that strong growth in household demand for communication services largely reflected the shift in technology that was taking place at the time as well as the substantial decline in prices that took place as the technology gained scale. Indeed, the fall in communication costs to date now means that the pattern of demand for basic mobile services is very much in line with that of other essential utilities.

Figure 12: Average* annual real growth in the volume of consumer expenditure as GDP

per capita rises from US$7,600 to US$10,100

4.6%

10.4%9.7%

7.2% 6.8%6.2% 6.2%

5.4%4.6% 4.3%

3.0%

0%

2%

4%

6%

8%

10%

12%

PC

E

Com

mun

icat

ion

Tra

nspo

rtat

ion

Edu

catio

n

Rec

reat

ion

Hou

sing

Fin

anci

al s

ervs

Hea

lthca

re

Hse

hld

& P

ers

Goo

ds Util

ities

Foo

d &

bevAve

rage

ann

ual g

row

th in

rea

l ter

ms

.

Source: BEA, INSEE, Ministry of Internal Affairs and Communications, Credit Suisse research

* Taking the average of growth in the components of real consumer expenditure in the US (1936 – 1940),

Japan (1961 – 1966) and France (1950 – 1959). These numbers are approximate to some extent:

differences in categorisation in expenditure by sector between these markets limits a more precise

calculation

We noted that the data from the survey last year confirmed that similar patterns of consumer expenditure were visible across the emerging economies. These trends are still clearly visible in the data from the recent survey.

16 January 2012

18

Demand for small-ticket, basic essentials (such as protein consumption or mobile phones) increases rapidly from very low income levels, but beyond average monthly household income of c. US$ 1,000 (PPP adjusted), consumption of essential goods and services tends to stagnate in favour of more discretionary items.

Figure 13: Mobile phone ownership Figure 14: Expenditure on entertainment

50

60

70

80

90

100

110

0 500 1000 1500 2000 2500 3000

Avg mthly household income (PPP, US$)

Brazil China Russia Egypt Indonesia

Mobile phone % ownership

0

100

200

300

400

500

0 1000 2000 3000 4000 5000 6000 7000 8000

Avg mthly household income (PPP, US$)

Brazil China Russia

Monthly spending on entertainment (PPP, US$)

Source: Credit Suisse Emerging Market Consumer Survey Source: Credit Suisse Emerging Market Consumer Survey

However, this long-term structural shift across the emerging economies towards greater discretionary spending has stalled, on average, over the past year as the slowdown in economic momentum and high food inflation has impacted confidence.

Consequently, when we compare the growth in spending rates between 2010 and 2011 for a range of goods and services, we can see that household consumption contracted for many of the more discretionary areas of expenditure over the course of the year. Figure 15 and Figure 16 serve to illustrate these changes. In these charts, we aggregate the survey results from all the markets to show how consumption or ownership of different types of goods and services changed this year compared with last year.

Figure 15: % of respondents that have bought various goods and services in 2011 and

the change vs 2010

Private healthcare

Extra education

Holidays

Perfume

Jewellery

Watches

Sports shoes

Fashion apparel

Cosmetics

Feminine hygiene

Tissues Dairy

Spirits

Bottled waterBeer Carbonated drinks

-8

-6

-4

-2

0

2

4

0 10 20 30 40 50 60 70 80 90 100

2011 % respondents that own or have bought each item

Cha

nge

vs 2

010

Source: Credit Suisse Emerging Market Consumer Survey

16 January 2012

19

Figure 16: % of respondents that own various goods/assets in 2011 and the change vs

2010

Ex Ch Internet accessEx Ch Smartphone Ex Ch Mobile phones

Ex Ch Computers

Ex Ch Cars

Ex Ch Property

Ch Internet access

Ch Smartphone

Ch Mobile phones

Ch Computers

Ch Cars Ch Property

-4

-3

-2

-1

0

1

2

3

4

5

6

7

0 20 40 60 80 100 120

2011 % respondents that own/have aecess to each item

Cha

nge

vs 2

010

Source: Credit Suisse Emerging Market Consumer Survey. NOTE: ‘Ex Ch’ – refers to data excluding China

We note the reduction over the course of the last year in average consumer exposure to:

- sport shoes and fashion apparel – these sectors have borne the brunt of the decline in consumer sentiment and higher average food prices. Both categories were down strongly across nearly all of our survey markets, including Saudi Arabia where consumer sentiment still appears to be relatively strong.

- private healthcare – four out of the seven markets (where we can compare the recent data against last year’s survey) recorded a decline in the number of households who allocated spending to private healthcare. Theoretically, this could simply reflect an improvement in state provision of healthcare services. However, in practice, since the detailed data show the decline was most obvious across the lowest income groups, it suggests that healthcare spend was forfeited to offset high food prices.

- property ownership also declined on aggregate in this survey versus the last survey. At the country level, the data show that ownership remained flat in China and Russia but declined slightly in India and Brazil. In a clear sign of the prevailing economic turmoil,, property ownership levels in Egypt were down significantly compared with last year.

Meanwhile, consumer penetration rates picked up on average for:

- mobile phones – this is predominantly driven by the rise in ownership across the lower income markets (India, Egypt, Indonesia and Brazil). Growth rates continue to hold the greatest potential in Indonesia (29% of our sample still do not have a mobile phone) followed by Egypt (15%) and Turkey (11%).

- smartphones – at the opposite extreme to the basic mobile, the higher income markets have been the key drivers of the rise in ownership of smartphones. Saudi Arabia tops the list with a penetration rate of 68% (a 22% increase on last year). The survey shows that smartphones have also proved popular in Brazil and China.

- computers and internet access – have also enjoyed strong growth in penetration rates over the year. Interestingly, this has not been driven by China (where computer ownership and internet access is already relatively high). Instead, the key drivers over the last year have been Brazil and Saudi Arabia.

- cosmetics – demand appears to have picked up marginally over the last year. Closer inspection of the data shows that the low income groups in Brazil were important drivers of this trend. This follows the well-established spending patterns of the higher income groups in Brazil. The country as a whole has one of the highest recorded spending rates on cosmetics and skincare (86% of our sample said they had spent on this item in the past three months) in contrast to China, with one of the lowest rates (only 43% of our Chinese sample said they had spent money on cosmetics over the same period).

16 January 2012

20

- education – a more significant proportion of respondents in six out of seven markets said they had allocated money to private education courses this year compared with last year. The exception was Egypt where the economic disruption has clearly undermined routines. But, Egypt aside, it is remarkable that the growth in education is so consistent across markets that differ so much in terms of consumer preference in so many other areas. And moreover, that education increased in prioritisation in a year that was far from supportive from a cyclical perspective. There is a substantial weight of historical evidence that suggests this strategy is highly likely to pay economic dividends and deliver sustainably higher GDP per capita in the long run. Thus, this is a strong underpin to the continued outperformance of emerging market economic growth.

The appetite for technology As noted above, the appetite for technology across our consumer universe appears to be very strong. However, we note that the strength of this demand varies according to income group as well as market. As an example, the data show that the penetration of smartphones is greater in the low income groups in Saudi Arabia than it is for the high income groups in Brazil and Russia. The ownership of computers is higher for the mid-income brackets in China than it is for the high income brackets in Saudi Arabia, Russia or India. Figure 17 and Figure 18 illustrate the point.

Figure 17: % of households (according to income bracket)

owning at least 1 computer

Figure 18: % of households (according to income bracket)

owning smartphones

0%

20%

40%

60%

80%

100%

120%

0 2000 4000 6000 8000 10000

Avg mthly household income (PPP, US$)

% h

ouse

hold

s w

ith c

ompu

ters

Brazil China India Russia Saudi Arabia

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0 2000 4000 6000 8000 10000

Av g mthly household income (PPP, US$)

% h

ouse

hold

s w

ith a

Sna

rt ph

one

Brazil China India Russia Saudi Arabia

Source: Credit Suisse Emerging Market Consumer Survey Source: Credit Suisse Emerging Market Consumer Survey

The possible explanations for this are threefold:

(1) Strength and sophistication of the distribution network – the greater this is, the higher the penetration rate. Churn rates are one potential indicator of the scope and reach of the distribution network. Our survey data show that where mobile and smartphone penetration rates are highest, a mobile handset has a relatively short life (only 14 months on average in Saudi Arabia). In markets where phone penetration rates are lowest, the average length of time that a handset is owned is much longer (22 months on average in Russia and 24 months in India).

(2) Relative prices – are an obvious factor to explain relative penetration rates. The prevalence of low-cost smartphones in China and the competitive nature of that market has arguably boosted consumer access to the product.

(3) Relative development of broadband infrastructure – helps explain computer ownership. We find there is a clear correlation between broadband access and household computer penetration: where broadband access is low (notably Egypt, India and Indonesia) the average computer ownership is also low.

16 January 2012

21

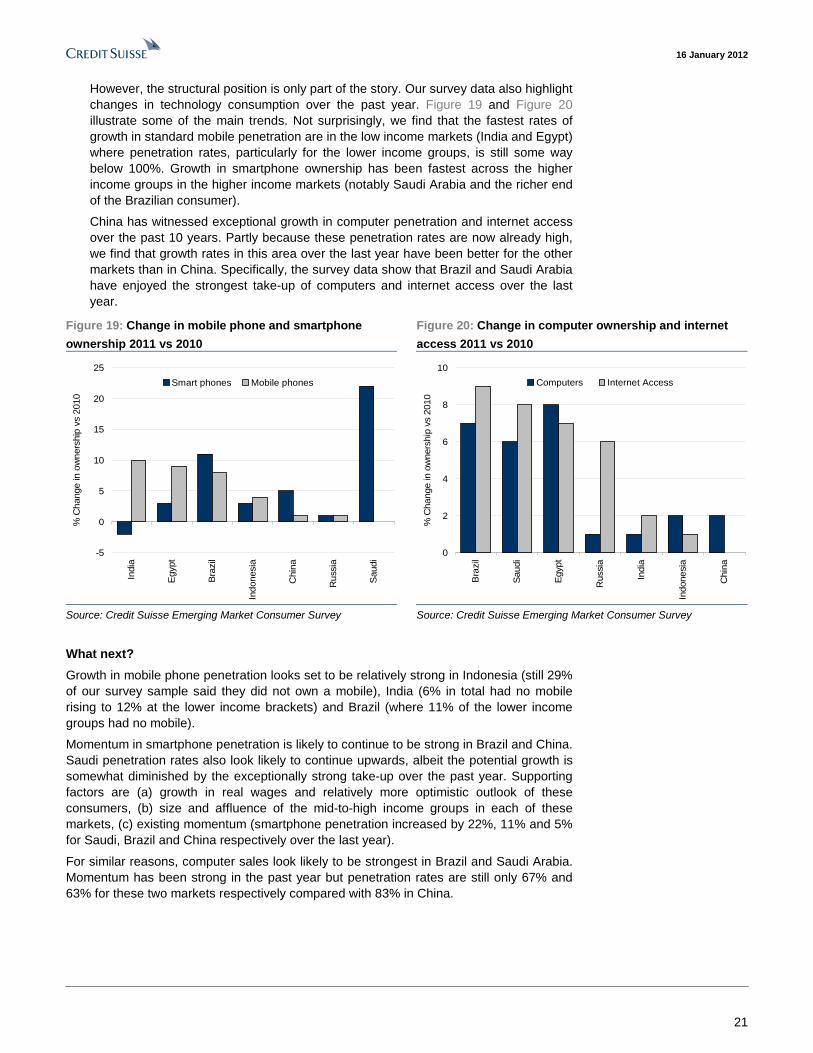

However, the structural position is only part of the story. Our survey data also highlight changes in technology consumption over the past year. Figure 19 and Figure 20 illustrate some of the main trends. Not surprisingly, we find that the fastest rates of growth in standard mobile penetration are in the low income markets (India and Egypt) where penetration rates, particularly for the lower income groups, is still some way below 100%. Growth in smartphone ownership has been fastest across the higher income groups in the higher income markets (notably Saudi Arabia and the richer end of the Brazilian consumer).

China has witnessed exceptional growth in computer penetration and internet access over the past 10 years. Partly because these penetration rates are now already high, we find that growth rates in this area over the last year have been better for the other markets than in China. Specifically, the survey data show that Brazil and Saudi Arabia have enjoyed the strongest take-up of computers and internet access over the last year.

Figure 19: Change in mobile phone and smartphone

ownership 2011 vs 2010

Figure 20: Change in computer ownership and internet

access 2011 vs 2010

-5

0

5

10

15

20

25

Indi

a

Egy

pt

Bra

zil

Indo

nesi

a

Chi

na

Rus

sia

Sau

di

% C

hang

e in

ow

ners

hip

vs 2

010

Smart phones Mobile phones

0

2

4

6

8

10

Bra

zil

Sau

di

Egy

pt

Rus

sia

Indi

a

Indo

nesi

a

Chi

na

% C

hang

e in

ow

ners

hip

vs 2

010

Computers Internet Access

Source: Credit Suisse Emerging Market Consumer Survey Source: Credit Suisse Emerging Market Consumer Survey

What next?

Growth in mobile phone penetration looks set to be relatively strong in Indonesia (still 29% of our survey sample said they did not own a mobile), India (6% in total had no mobile rising to 12% at the lower income brackets) and Brazil (where 11% of the lower income groups had no mobile).

Momentum in smartphone penetration is likely to continue to be strong in Brazil and China. Saudi penetration rates also look likely to continue upwards, albeit the potential growth is somewhat diminished by the exceptionally strong take-up over the past year. Supporting factors are (a) growth in real wages and relatively more optimistic outlook of these consumers, (b) size and affluence of the mid-to-high income groups in each of these markets, (c) existing momentum (smartphone penetration increased by 22%, 11% and 5% for Saudi, Brazil and China respectively over the last year).

For similar reasons, computer sales look likely to be strongest in Brazil and Saudi Arabia. Momentum has been strong in the past year but penetration rates are still only 67% and 63% for these two markets respectively compared with 83% in China.

16 January 2012

22

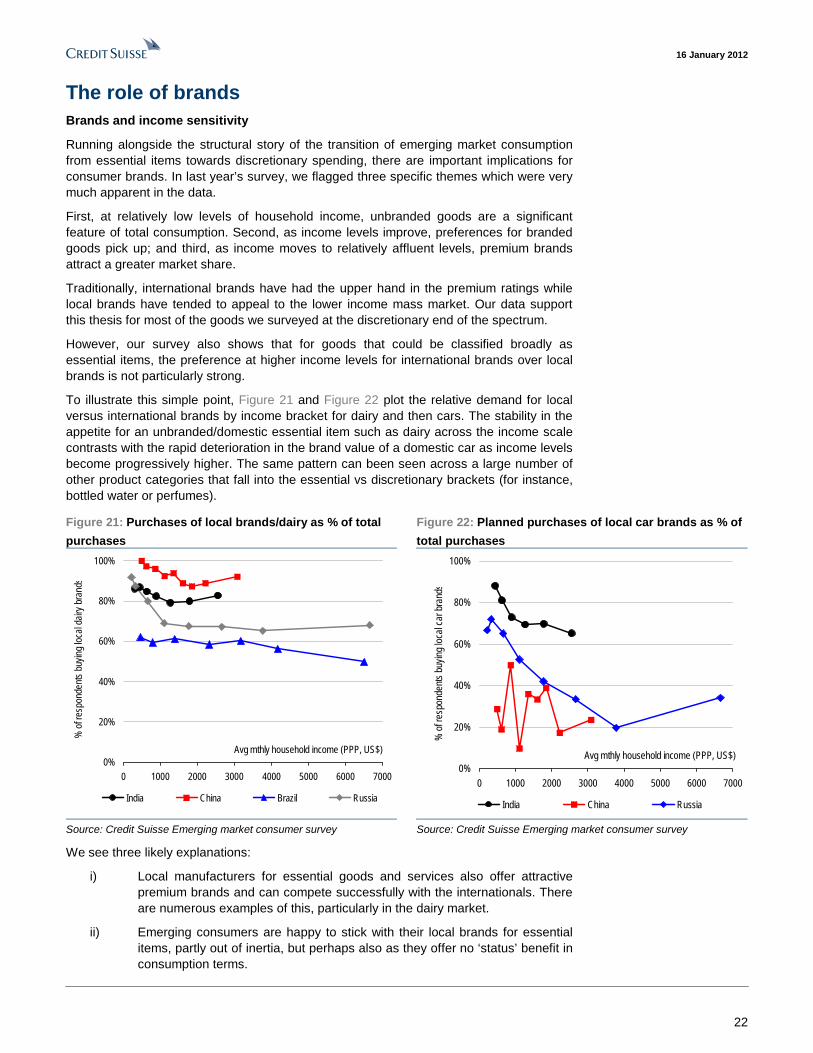

The role of brands Brands and income sensitivity

Running alongside the structural story of the transition of emerging market consumption from essential items towards discretionary spending, there are important implications for consumer brands. In last year’s survey, we flagged three specific themes which were very much apparent in the data.

First, at relatively low levels of household income, unbranded goods are a significant feature of total consumption. Second, as income levels improve, preferences for branded goods pick up; and third, as income moves to relatively affluent levels, premium brands attract a greater market share.

Traditionally, international brands have had the upper hand in the premium ratings while local brands have tended to appeal to the lower income mass market. Our data support this thesis for most of the goods we surveyed at the discretionary end of the spectrum.

However, our survey also shows that for goods that could be classified broadly as essential items, the preference at higher income levels for international brands over local brands is not particularly strong.

To illustrate this simple point, Figure 21 and Figure 22 plot the relative demand for local versus international brands by income bracket for dairy and then cars. The stability in the appetite for an unbranded/domestic essential item such as dairy across the income scale contrasts with the rapid deterioration in the brand value of a domestic car as income levels become progressively higher. The same pattern can been seen across a large number of other product categories that fall into the essential vs discretionary brackets (for instance, bottled water or perfumes).

Figure 21: Purchases of local brands/dairy as % of total

purchases

Figure 22: Planned purchases of local car brands as % of

total purchases

0%

20%

40%

60%

80%

100%

0 1000 2000 3000 4000 5000 6000 7000

Avg mthly household income (PPP, US$)

% o

f res

pond

ents

buy

ing

loca

l dai

ry b

rand

s

India China Brazil Russia

0%

20%

40%

60%

80%

100%

0 1000 2000 3000 4000 5000 6000 7000

Avg mthly household income (PPP, US$)

% o

f res

pond

ents

buy

ing

loca

l car

bra

nds

India China Russia

Source: Credit Suisse Emerging market consumer survey Source: Credit Suisse Emerging market consumer survey

We see three likely explanations:

i) Local manufacturers for essential goods and services also offer attractive premium brands and can compete successfully with the internationals. There are numerous examples of this, particularly in the dairy market.

ii) Emerging consumers are happy to stick with their local brands for essential items, partly out of inertia, but perhaps also as they offer no ‘status’ benefit in consumption terms.

16 January 2012

23

iii) Brand power for essential items is not as strong as it is for discretionary items. Even international brands are often marketed on price and value.

The broad conclusion is that as incomes continue to improve, as we would expect in emerging economies, the growth outlook for local brands should be at least as good as international brands for essential goods and services. International brands offer greater growth potential than their local peers in the discretionary space. However, we would flag that, given the greater growth on offer in essential items in the emerging world, international companies may be moved—indeed in some cases have already been moved—to acquire these local brands.

Who are the winners?

If this is the broad picture, what are the specific illustrations of brand potential or vulnerability? The survey allows us to isolate specific brands at a very granular level by category of spending, by country and by the nature of the consumer concerned, whether by income or a wide range of demographics. The Credit Suisse Research Institute report Great Brands of Tomorrow underlined the significance for investors in understanding the drivers of brand development and positioning.

When taken to the micro level, we see three specific themes already at work and that might develop further:

(i) The scope for industry consolidation and M&A activity.

(ii) “Trading up” opportunities as consumers shift from unbranded to branded products as their incomes improve.

(iii) The potential structural global and local winning brands alongside those that may see their brand status challenged.

To explore these themes, Figure 24 and Figure 25 display a number of key country brands consumers highlighted in the survey. This is a small, but significant, sub-set of the data the hundreds of brands in the survey as a whole. The two tables split the brands by food and beverage, that would include some more lower ticket and essential items, and then the more highly discretionary areas of spending.

Each table shows the category of spending, a key country brand and its penetration in the lowest and highest income groups within the market. We have also shown which company owns the brand, which helps identify whether the brand is local or global in nature.

The brands selected fall into one of three categories and are colour coded accordingly – brands in the survey that see their market penetration among consumers increase as we move from low to high income (blue) that decrease as income rises (orange), and those that hold their own across the income scale (grey).

M&A

M&A is proving a major ongoing theme in emerging markets. Global consumer companies have taken advantage of the growth opportunities in emerging vs. developed markets and also the relaxation of regulatory constraints that permit it. It is the sectors which are more fragmented and where local brands proliferate that look most likely to benefit from greater M&A.

Taking the two tables together, the dairy and cosmetics space provide good illustrations of M&A potential, albeit for different reasons. As our earlier work suggested, global brands such as Nestle, Danone and Kraft gain limited traction in “essential” items. The dominance, and indeed resilience across the income scale, of companies like Mengnui and Yili in China illustrate the strength lies domestically. Unlisted companies and co-operatives (eg. Mother Dairy and Amul in India and Botavo in Brazil) also play a major role. Beyond the likes of the co-operatives, the ownership of local brands by major global companies is still low (in contrast to much of the beverages space). However, Pepsi‘s Wimm-Bill-Dann acquisition in Russia and its ownership of two dairy brands shows that

16 January 2012

24

this need not be the case. The global companies’ own brands meet with limited appetite; they may be better off buying the local brands and perhaps leveraging their superior capabilities in brand awareness and distribution to create value.

Cosmetics is a different story. Global players are present and income sensitivity does impact their attraction. However, as in dairy, there are well-positioned local brands that offer strong market position, growth potential and that are not already in the hands of the global players – Natura in Brazil, Parachute in India and Chistaya Linia in Russia to name a few.

Trading up: Unbranded to branded and beyond

While the process of how consumers shift from low-end brands to premium brands captures plenty of consideration; the reality is that many consumers across the emerging world still buy unbranded products in many categories. In the discretionary areas, this is at its extreme in low income earners but, as we have highlighted, can also be widespread in essential items. Being well-positioned to exploit the shift from unbranded to branded products offers sizeable potential gains for companies.

Figure 23 breaks down by country and by category the proportion of respondents suggesting they bought unbranded products. The relevance of unbranded purchases seems greatest among the discretionary areas and in essentials like dairy.

Figure 23: % of purchases by sector that are “unbranded” Brazil China Egypt India Indonesia Russia Saudi Turkey

Dairy 9 7 68 15 14 32 0 23

Soft drinks 6 1 1 2 2 16 0 4

Beer 1 4 N/A 5 N/A 20 N/A 7

Spirits 13 19 N/A 6 N/A 16 N/A 34

Cosmetics 6 13 38 8 68 14 7 15

Perfumes 9 23 72 45 81 32 31 66

Fashion 46 43 78 53 72 67 38 80

Leather goods 67 43 79 31 46 76 35 68

Sports shoes and wear

24 13 54 19 37 29 10 37

Source: Credit Suisse Emerging market consumer survey

If we consider a scenario where incomes improve at the low end and the appetite for branded products grow, there would be immediate benefits for those well positioned among the lowest income earners. Linking this into specific brands, Figure 24 and Figure 25 would suggest considerable potential in fashion/retailing for brands such as Bata in India, Hering and Marisa in Brazil; in cosmetics, again, for Natura and Parachute; in sportswear Action In India and Li Ning in China. Pepsi’s dairy acquisition in Russia would also look strategically well placed.

We have some scepticism of the quality of the low responses to the questions on unbranded alcohol. Buying unbranded alcohol may be deemed illegal in some areas. (Also note that the question was not asked in Indonesia, Saudi Arabia and Egypt for cultural reasons.) Even taking the data at face value, we can see a clear read through to the attraction of Baltika and Klinskoe in Russia. If you believe that the beer/spirits responses below under-estimate the local non-branded consumption, it is worth noting local brands dominating the low income brackets such as the likes of Snow in China and Skol in Brazil.

Many of these brands that play to the low income consumer, particularly beverages, have been acquired by the global consumer companies such as ABI and SAB Miller. Tsingtao in China is one notable that still rests outside of global ownership. Unilever owns strong low income local brands in India and Indonesia. However, none of the cosmetics and fashion brands is, as yet, owned by global companies.

16 January 2012

25

Structural winners and structurally challenged

While this potential positioning for a “low end” opportunity has an immediate relevance in some areas, the long-term theme in the survey is to consider a multi-year shift to discretionary spending that extends well beyond the lowest of income earners. Consumers who have moved from unbranded to effective low-end or value-branded products are not going to stop there if their incomes improve further. Brands that have critical mass at the low end but sustain it or grow it up the income scale could prove to be major structural winners.

As strong as the appetite may be for Snow and Skol at the low end, it tails off rapidly beyond the low income earners. Snow’s effective penetration halves between low and high income earners. In the cosmetics space in Russia, Oriflame sees its penetration fall from 61% to 20% between low and high income groups. As much as missing out on the potential structural shift up the income scale, they are very dependent on one income segment today. Oriflame has found this a painful experience in the last year given the pressure on the real incomes of low income Russian consumers – a fact borne out in our survey this year and last.

Many of the brands that display the ideal mix of being strong across the board stand within the portfolio of the global companies above – e.g. ABI’s soft drink brand Guarana Antarctica or beer brand Brahma. The global players owning brands such as these will generally continue to benefit. However, a number of the local brands we have mentioned above that stood out for their low income attractions and sitting in unconsolidated sectors emerge here as well.

For example, our survey shows that just as around a quarter of consumers purchase Tsingtao in the low income band, a quarter at the high end do likewise. Natura enjoy shares of 51% and 62% respectively between low and high income bands and Li Ning a stable 20% from top to bottom. Brands that do not enjoy the same income resilience would ultimately have to devise a “rebranding” or “reinvention” or run the risk of being left behind as incomes steadily improve beyond the most basic levels.

A final thought is to what extent can these local brands supplant the global players in the bigger ticket areas? High end luxury seems unlikely. Brands such as Burberry continue to grow apace. Technology though seems an area to watch. We have highlighted the structural growth the sector continues to see even in the currently less helpful cyclical environment. The Western brands are in many areas tiring. Brands such as Dell and HP have a declining appeal in India among higher earners while Lenovo dominates across the board in China. Nokia’s share is declining in most markets as Huawei establishes itself in a number of countries. Only Apple continues to sweep all before it and importantly its still lowly market shares suggests it has plenty of further potential yet. However, there seems every reason to believe that domestic brands can erode the brand value developed companies have enjoyed in this space. The ‘million-dollar’ question is, can these ultimately become the global not just local standard and fully turn the tables on their global counterparts?

16 January 2012

26

Figure 24: Food and Beverages: Brand market penetration according to income group

Sector Country / Brand% penetration at LOWER income

% penetration at HIGHER income

Difference

Parent Company (If applicable) Listed / Private

Juhaina (EGYPT) 35% 73% 38% Juhayna Food Industries JUFO EYDomik v Derevne (RUSSIA) 27% 50% 23% PepsiCo Inc. PEP US

Chudo (RUSSIA) 13% 29% 16% PepsiCo Inc. PEP USBatavo (BRAZIL) 30% 44% 13% Batavo Cooperativa Agroindustrial Prvate

Parmalat (BRAZIL) 39% 48% 9% AEP Investments, Ltd. PrivateNestle (INDIA) 2% 11% 9% Nestlé S.A. NESN VX

Danone (SAUDI) 7% 15% 8% Danone BN FPYili (CHINA) 55% 63% 8% Inner Mongolia Yili Industrial Group Co., Ltd. 600887 CH

Mengniu (CHINA) 63% 68% 4% China Mengniu Dairy Company Limited 2319 HKPinar (TURKEY) 41% 44% 3% Yasar Holding PrivateAnchor (SAUDI) 20% 21% 1% Fonterra Co-operative Group Limited Private

Mother Dairy (INDIA) 26% 25% -1% National Dairy Development Board PrivateKraft (SAUDI) 30% 28% -2% Kraft Foods Inc. KFT US

Thirumala (INDIA) 16% 7% -9% Tirumala Milk Products (P) L PrivateGuaraná Antarctica (BRAZIL) 46% 64% 18% Anheuser-Busch InBev NV ABI BBMirinda Pepsi-Cola (SAUDI) 41% 53% 12% PepsiCo Inc. PEP US

Coca-Cola (INDIA) 25% 33% 8% The Coca-Cola Company KO USLimca (INDIA) 29% 33% 4% The Coca-Cola Company KO US

Guozhiguole (CHINA) 10% 9% -1% China Huiyuan Juice Group Limited 1886 HKChernogolovka (RUSSIA) 10% 9% -1% OST Group Private

Dolly (BRAZIL) 19% 13% -6% Dolly PrivateBudweiser (TURKEY) 6% 23% 17% Anheuser-Busch InBev NV ABI BB