Emerging Markets Quarterly - Credit Suisse | PLUS

242

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ™ Client-Driven Solutions, Insights, and Access Emerging Markets Quarterly Emerging Markets Economics Global Q2 2014 [Picture] Global growth should accelerate moderately to 3.3% in 2014 from 2.9% in 2013. This is lower than our previous forecast of 3.7%, as growth projections for EM in 2014 have been downgraded to 4.7% from 5.3%. We believe that EM growth performance should remain unchanged from 2013 despite an acceleration of activity in DM (2.1% in 2014 versus 1.2% in 2013). The spread between EM and DM growth rates should therefore fall to 2.6pp, the lowest since 2001. Stronger growth in DM should be fairly positive for EM as the outlook for global trade improves moderately. In particular, in some EM countries, internal imbalances (e.g., China) or external imbalances (e.g., Turkey) built as a consequence of falling external demand since the Great Recession could be unwound more smoothly in an environment of better growth elsewhere. However, key structural reforms aimed at increasing the potential growth are taking place in many countries. But fixing the road to accommodate faster traffic for the future often entails disruption and delay in the present. 06 March 2014 Fixed Income Research http://www.credit-suisse.com/researchandanalytics Research Analysts Neal Soss +1 212 325 3335 [email protected] Berna Bayazitoglu +44 20 7883 3431 [email protected] Alonso Cervera +52 55 5283 3845 [email protected] Robert Prior-Wandesforde +65 6212 3707 [email protected] Dong Tao +852 2101 7469 [email protected] Nilson Teixeira +55 11 3701 6288 [email protected] See inside cover for full list of analysts

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Emerging Markets Quarterly - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES AND

ANALYST CERTIFICATIONS.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

Emerging Markets Quarterly Emerging Markets Economics Global

Q2 2014 [Picture]

Global growth should accelerate moderately to 3.3% in 2014 from 2.9% in 2013.

This is lower than our previous forecast of 3.7%, as growth projections for EM in

2014 have been downgraded to 4.7% from 5.3%. We believe that EM growth

performance should remain unchanged from 2013 despite an acceleration of

activity in DM (2.1% in 2014 versus 1.2% in 2013). The spread between EM and

DM growth rates should therefore fall to 2.6pp, the lowest since 2001.

Stronger growth in DM should be fairly positive for EM as the outlook for global

trade improves moderately. In particular, in some EM countries, internal

imbalances (e.g., China) or external imbalances (e.g., Turkey) built as a

consequence of falling external demand since the Great Recession could be

unwound more smoothly in an environment of better growth elsewhere.

However, key structural reforms aimed at increasing the potential growth are

taking place in many countries. But fixing the road to accommodate faster traffic

for the future often entails disruption and delay in the present.

06 March 2014

Fixed Income Research

http://www.credit-suisse.com/researchandanalytics

Research Analysts

Neal Soss

+1 212 325 3335

Berna Bayazitoglu

+44 20 7883 3431

Alonso Cervera

+52 55 5283 3845

Robert Prior-Wandesforde

+65 6212 3707

Dong Tao

+852 2101 7469

Nilson Teixeira

+55 11 3701 6288

See inside cover for full list of analysts

06 March 2014

Emerging Markets Quarterly 2

06 March 2014

Emerging Markets Quarterly 3

Table of Contents

Global Economy: Speeding up to average 5

IP growth momentum slows further in EM as it strengthens notably in DM 14

Core inflation on the rise in EEMEA and Latin America 21

Latin America 47

Latin America: Growing pains 47

Argentina: Bandaged, but not cured 51

Brazil: Some fiscal austerity might mitigate the risks of a downgrade 56

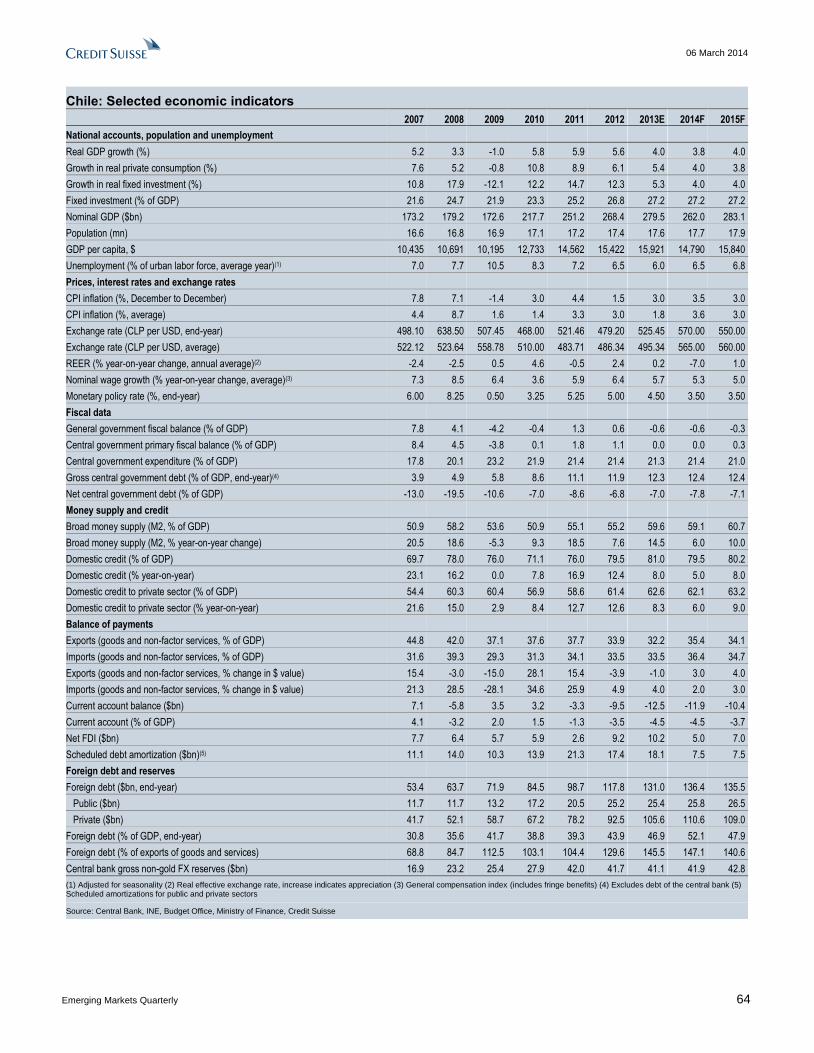

Chile: The slowdown is not over yet 61

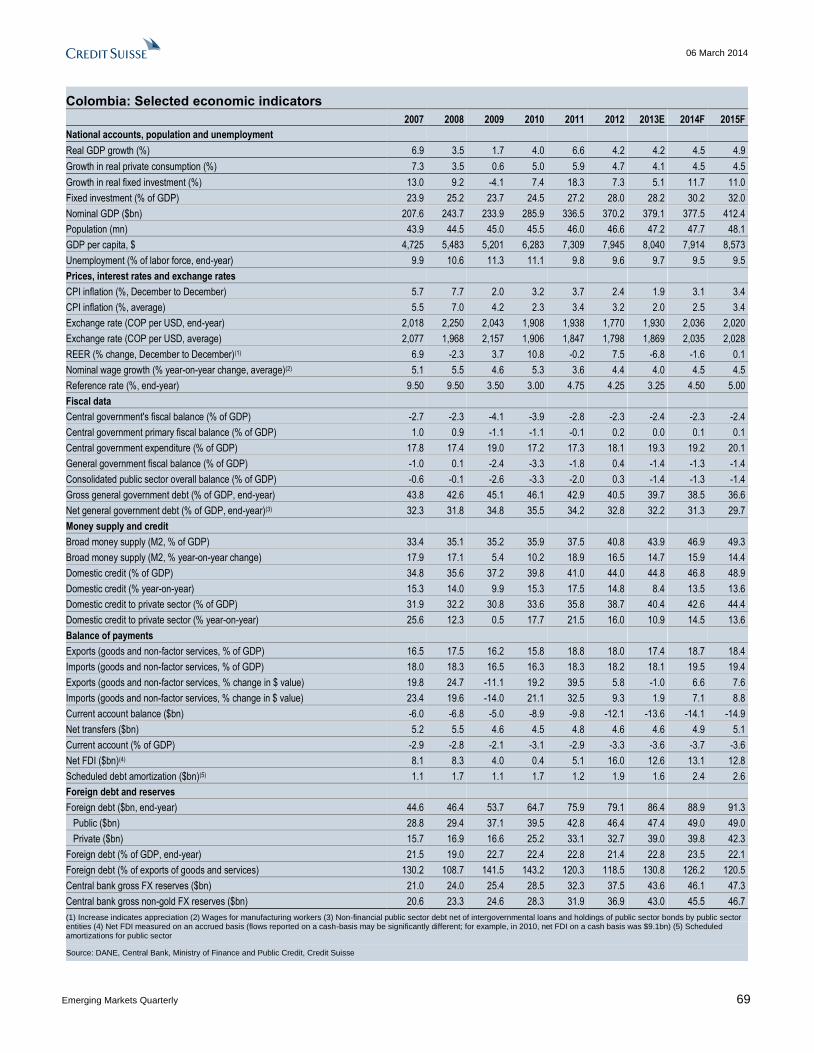

Colombia: Timing the next hiking cycle 65

Mexico: A transition year 70

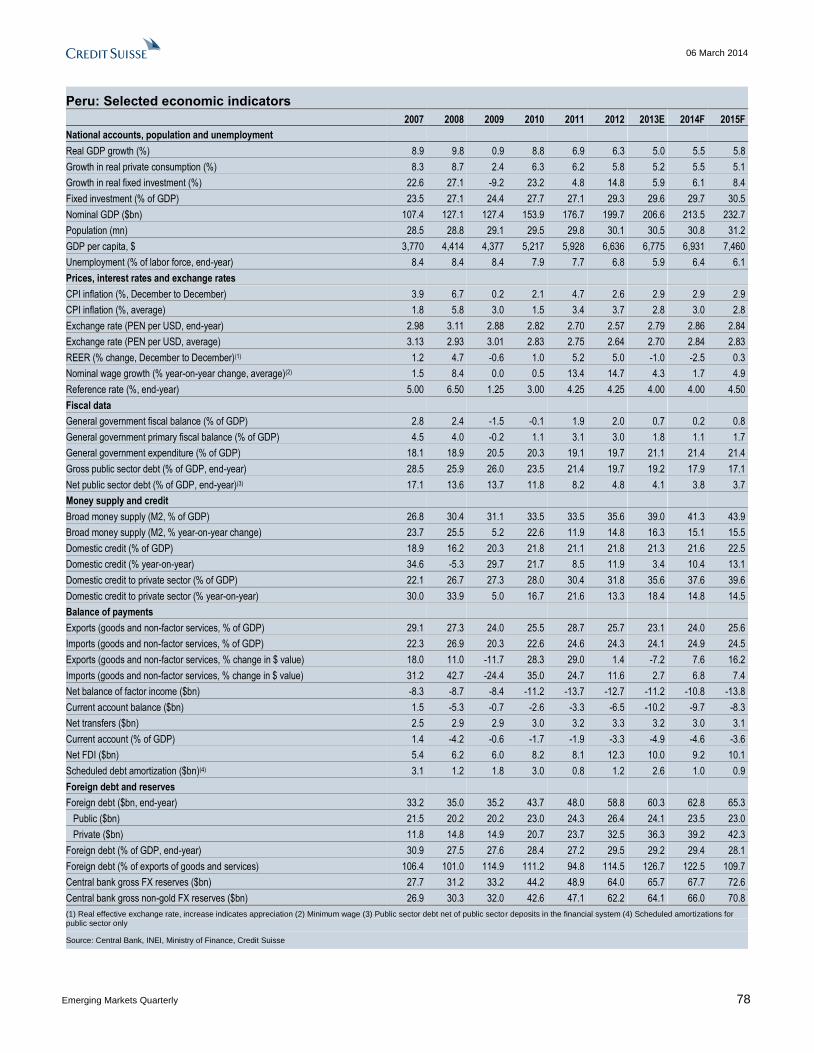

Peru: Marginal improvement thanks to mining 75

Venezuela: The heat is on 79

Europe, Middle East and Africa 85

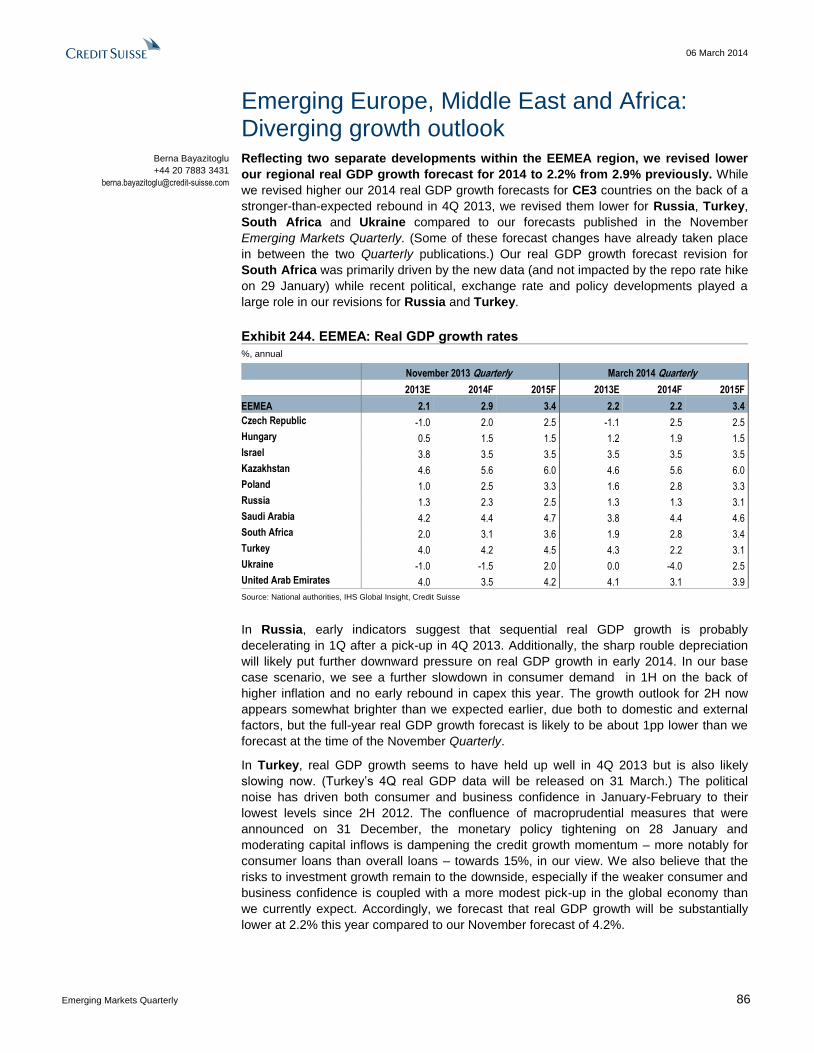

Emerging Europe, Middle East and Africa: Diverging growth outlook 86

Czech Republic: A strong rebound 90

Hungary: Taking it easy in election year 95

Israel: Still in easing mode 100

Poland: A more balanced growth outlook 105

Russia: Ukraine tensions prompt monetary policy action 110

South Africa: Adjusting policies as pressure mounts 115

Turkey: No end in sight for the turf war 120

Ukraine: A chance for comprehensive policy adjustment 126

06 March 2014

Emerging Markets Quarterly 4

Non-Japan Asia 131

Non-Japan Asia: Our high conviction calls 132

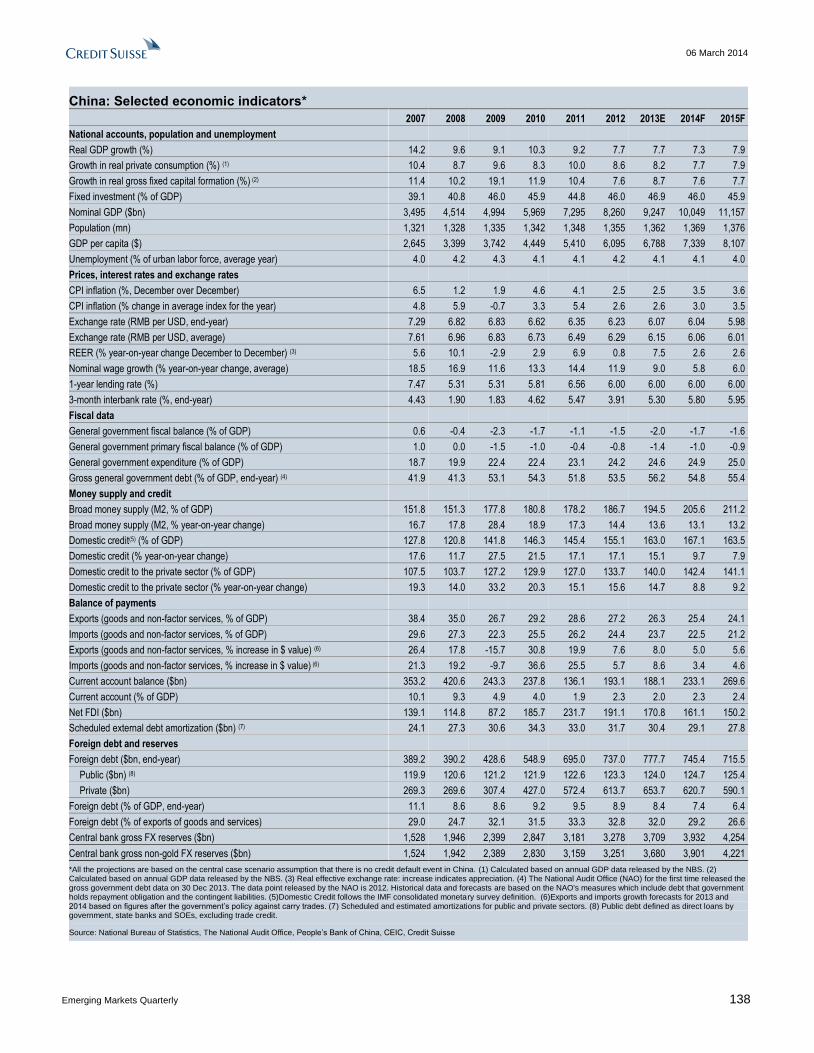

China: Embracing higher risks 134

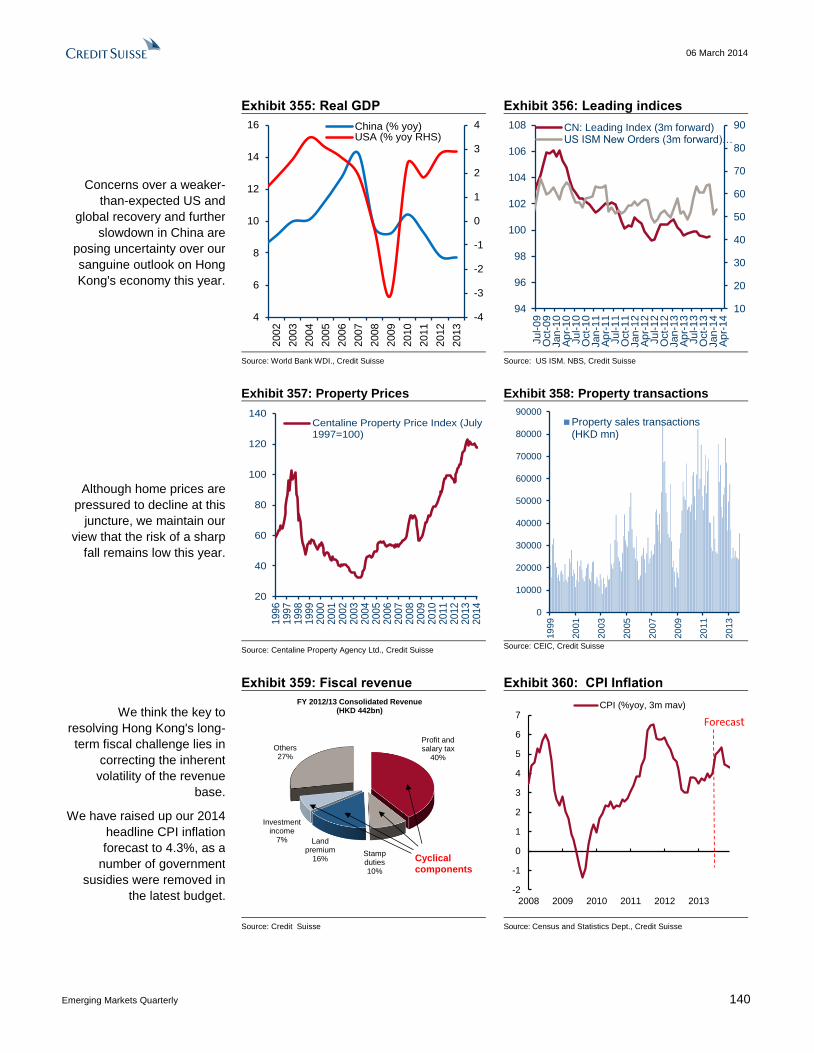

Hong Kong: Looming long-term fiscal challenge 139

India: Inflation fighting, dismal growth & election issues 142

Indonesia: Re-balancing before rate cutting 146

Korea: Entering a soft patch 149

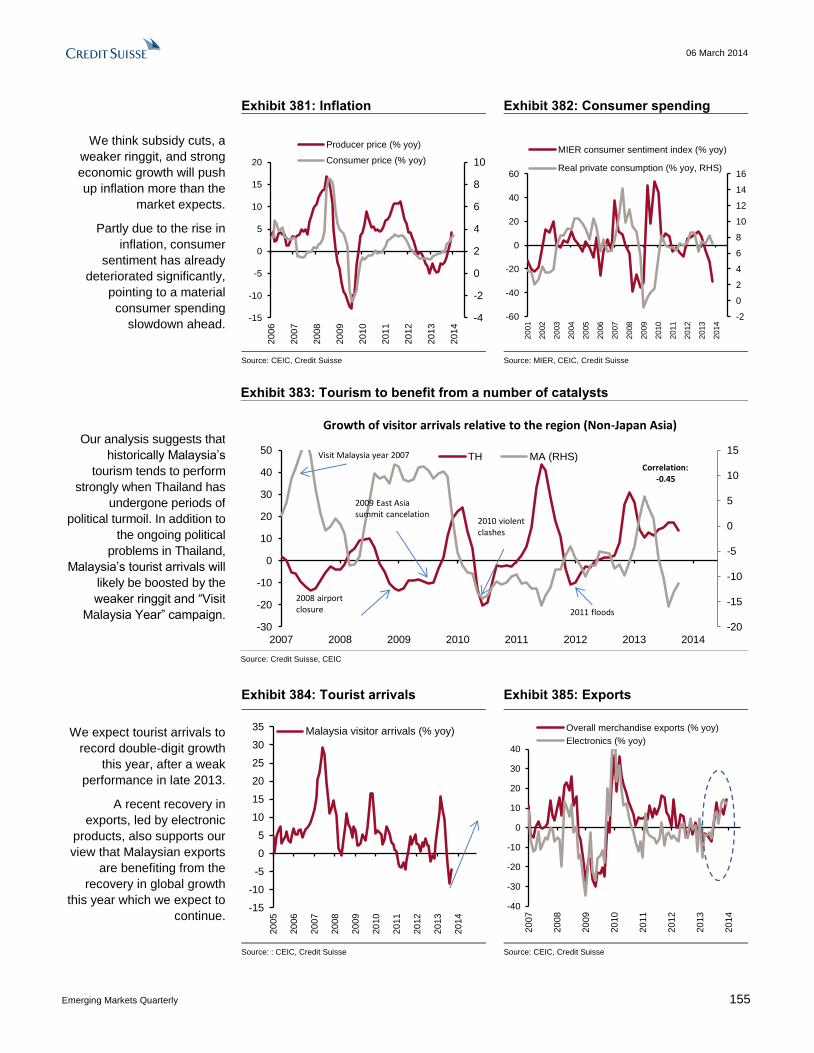

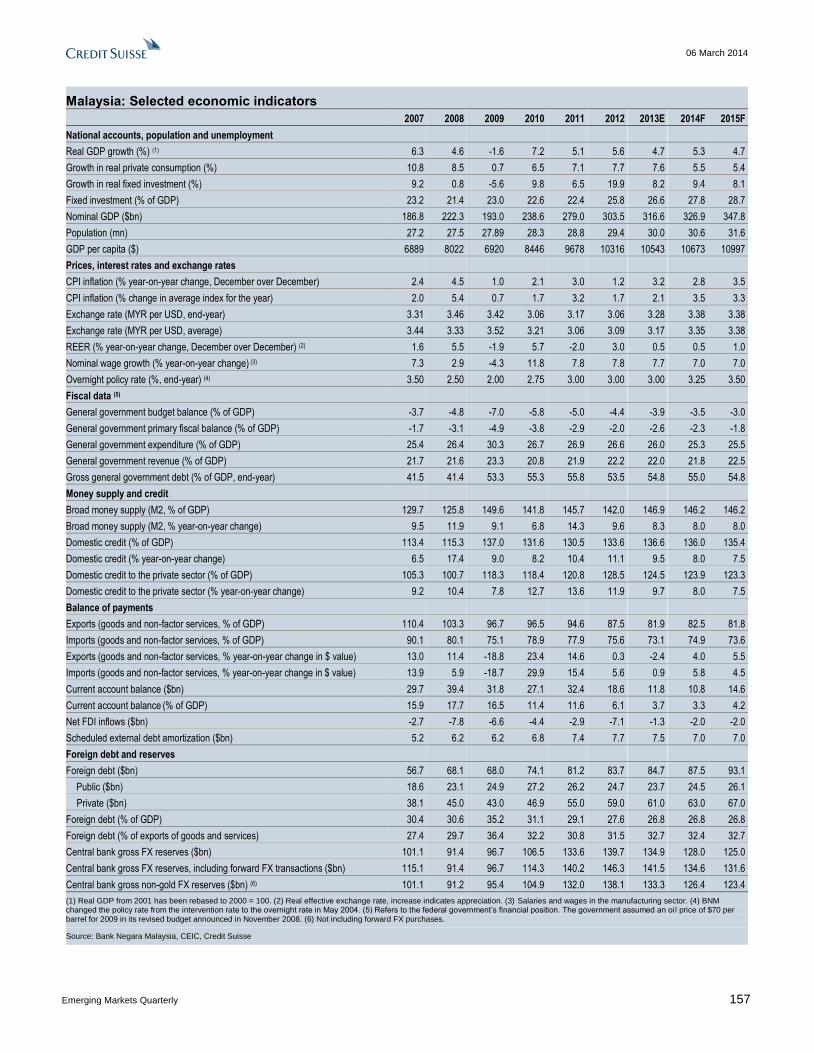

Malaysia: Changing the growth mix 154

Philippines: Against the consensus 158

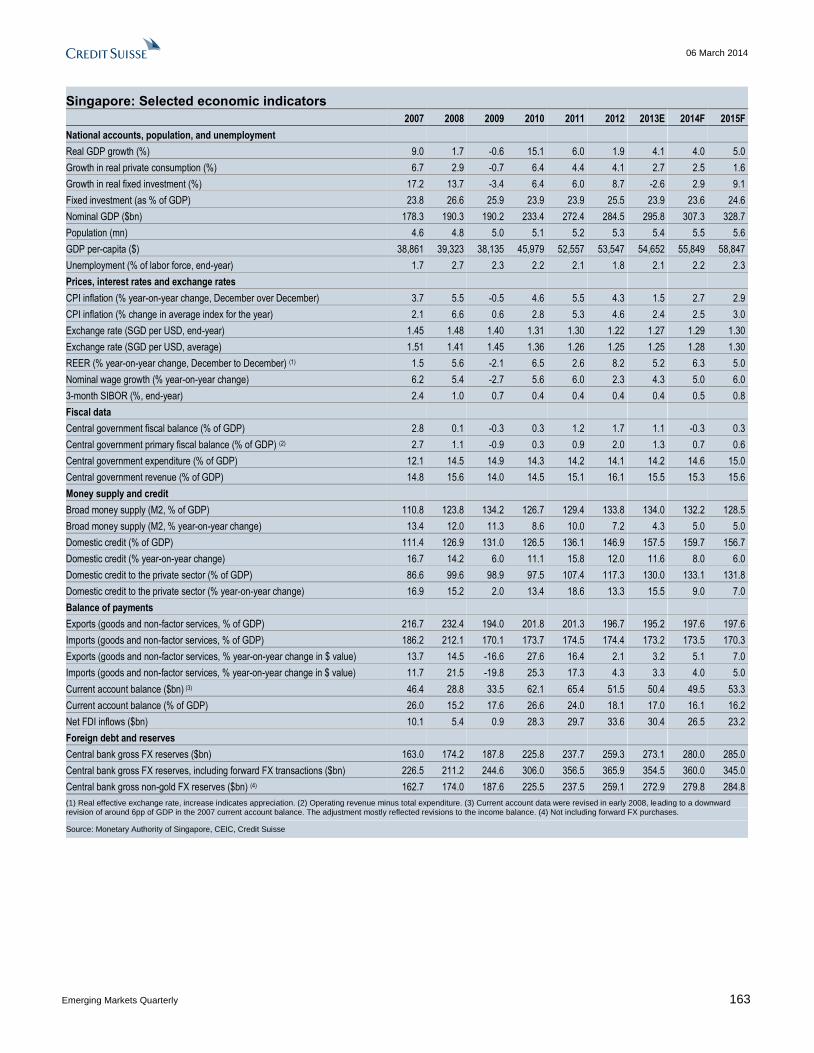

Singapore: The consequences of stronger growth? 161

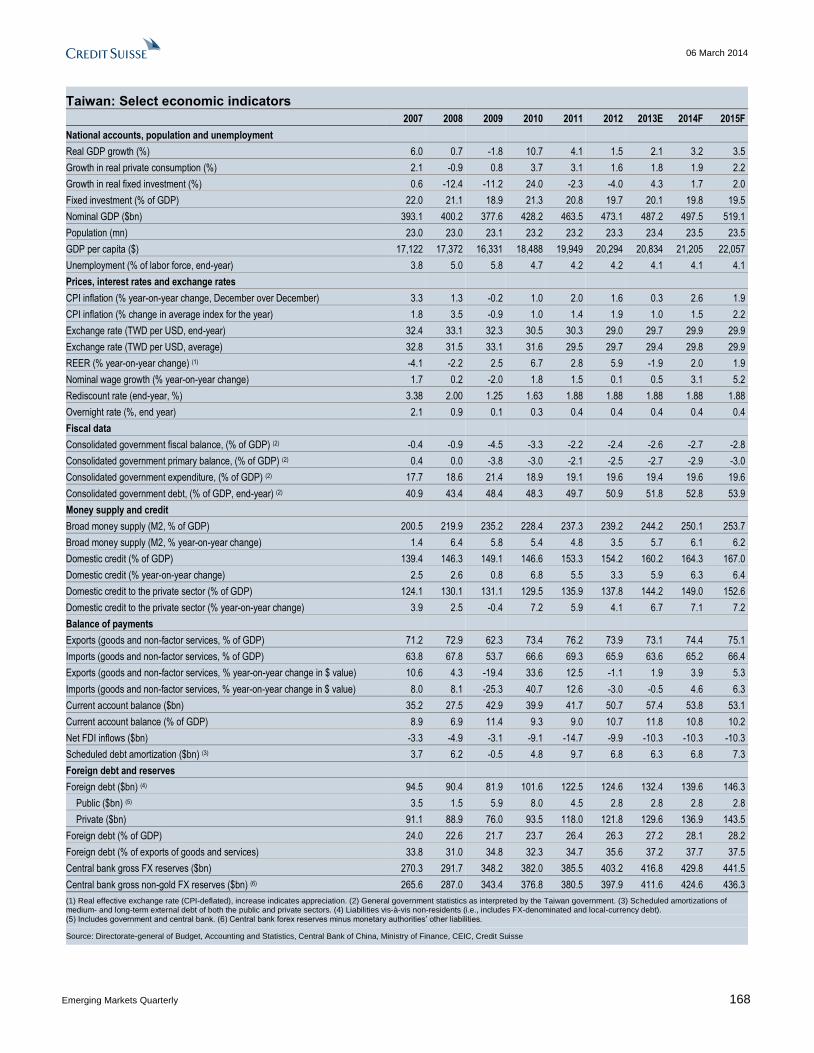

Taiwan: Developed markets' demand holds the key 164

Thailand: Political mess, economic stress 169

Long-term sovereign FX debt ratings 173

Key websites 175

Previous publications 181

Key dates 186

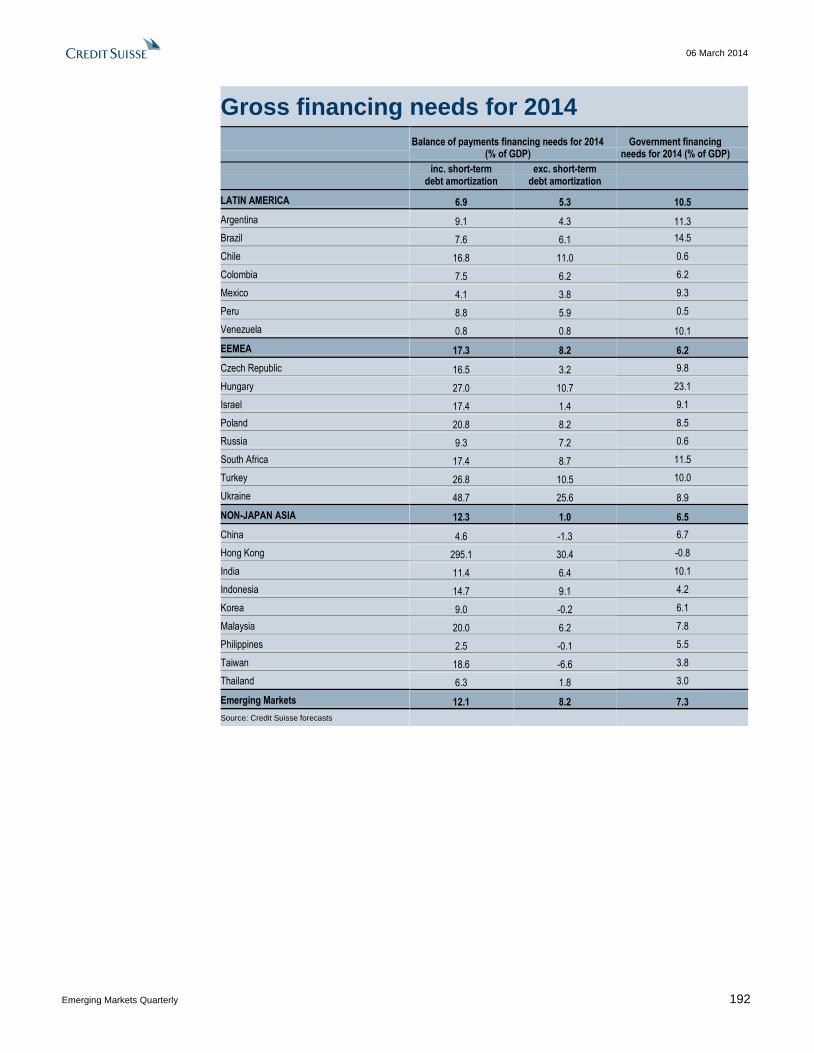

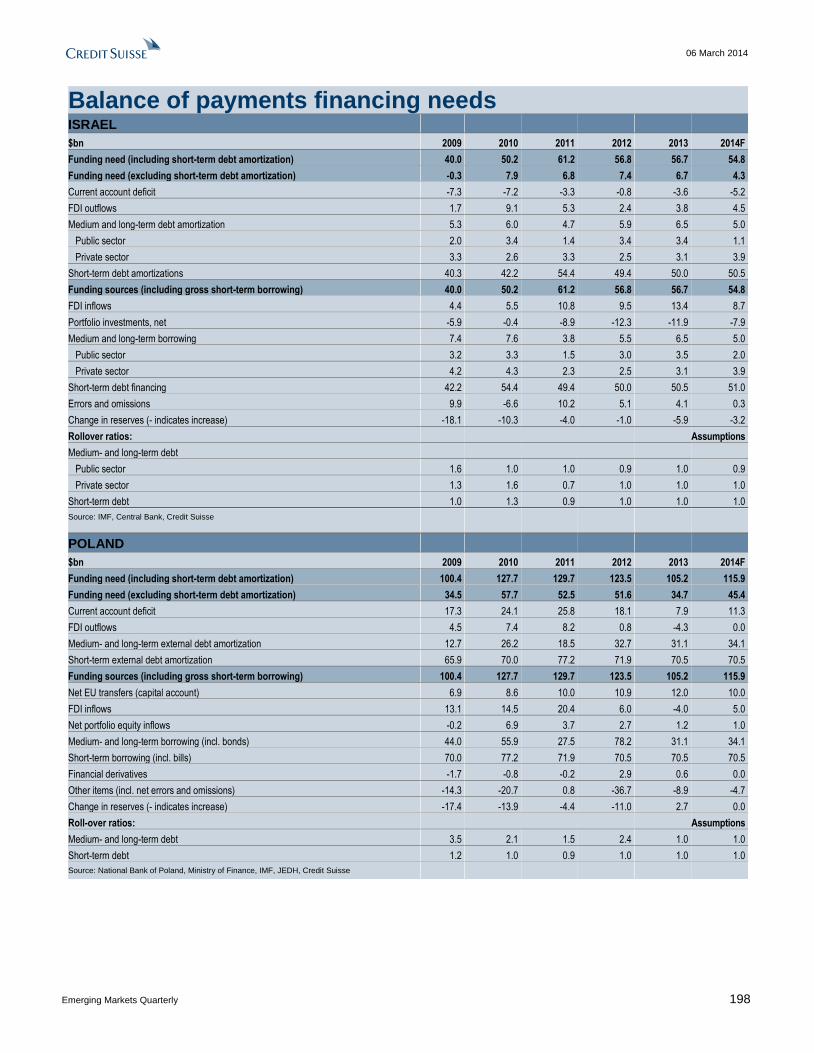

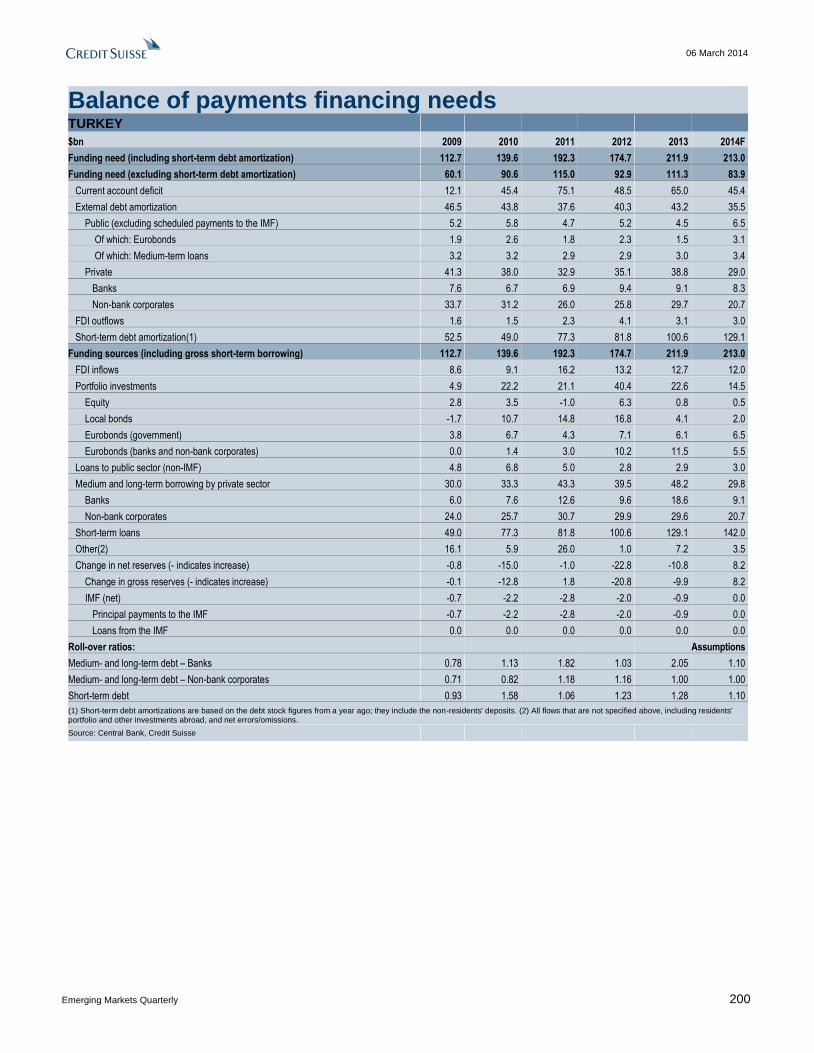

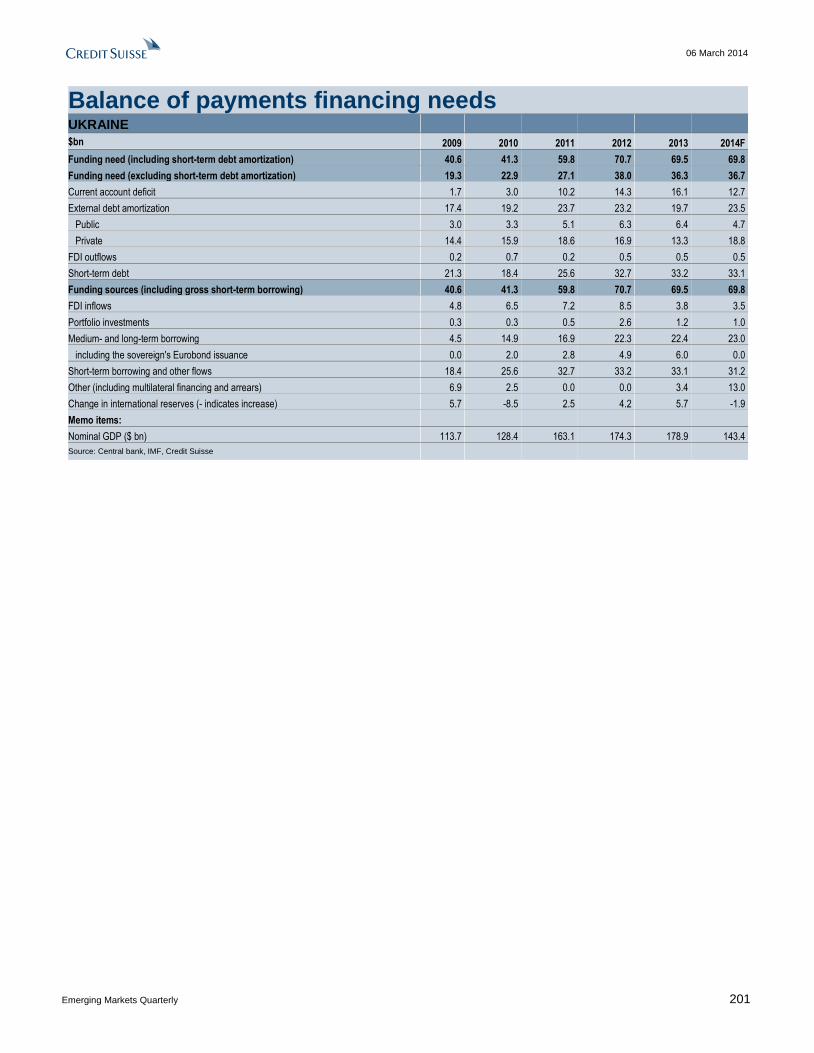

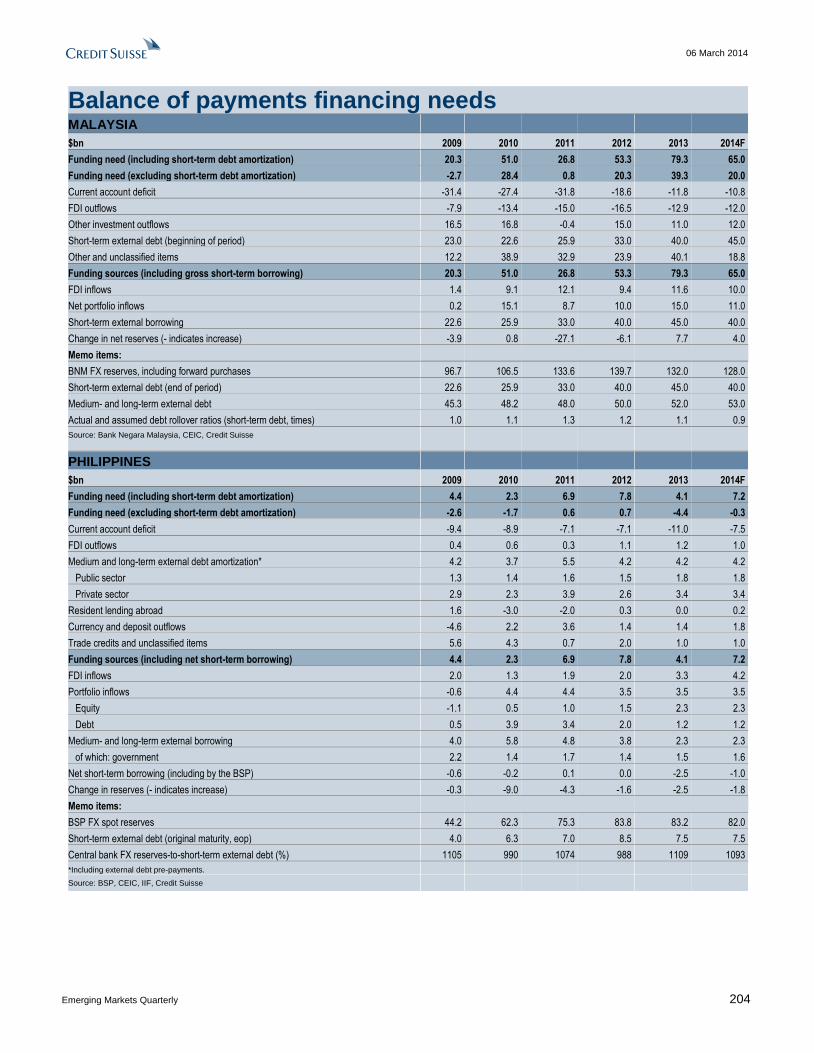

Gross financing needs for 2014 192

Balance of payments financing needs 193

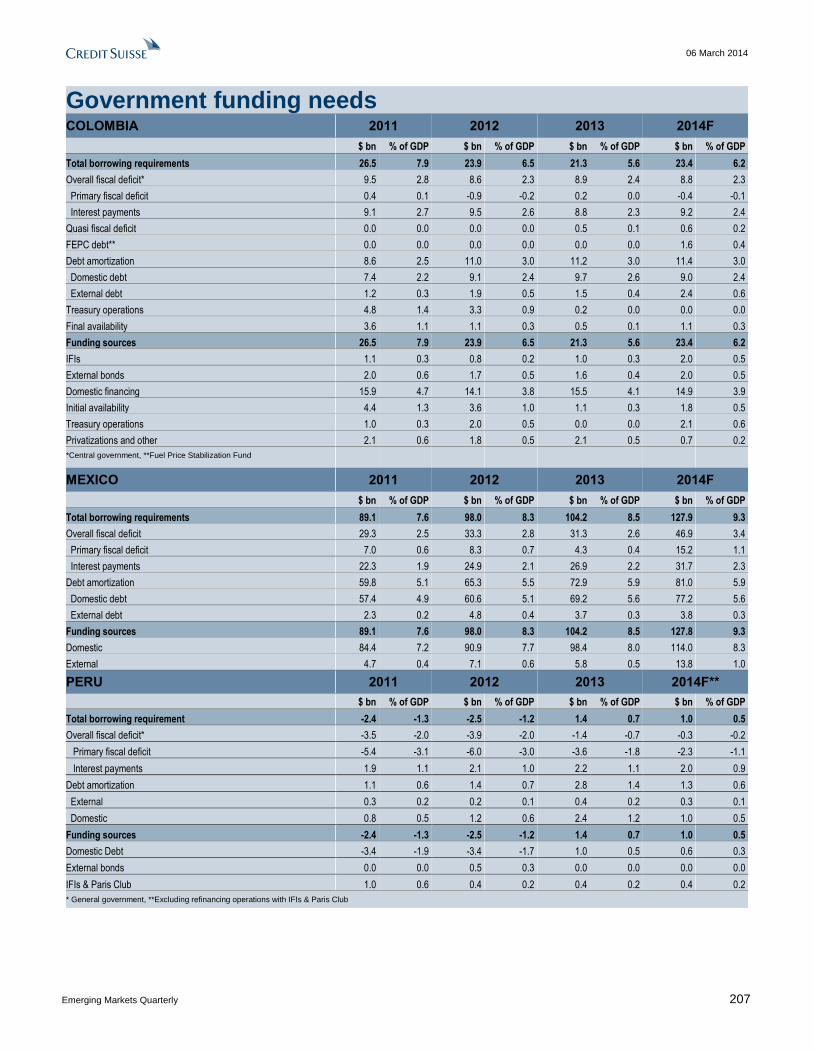

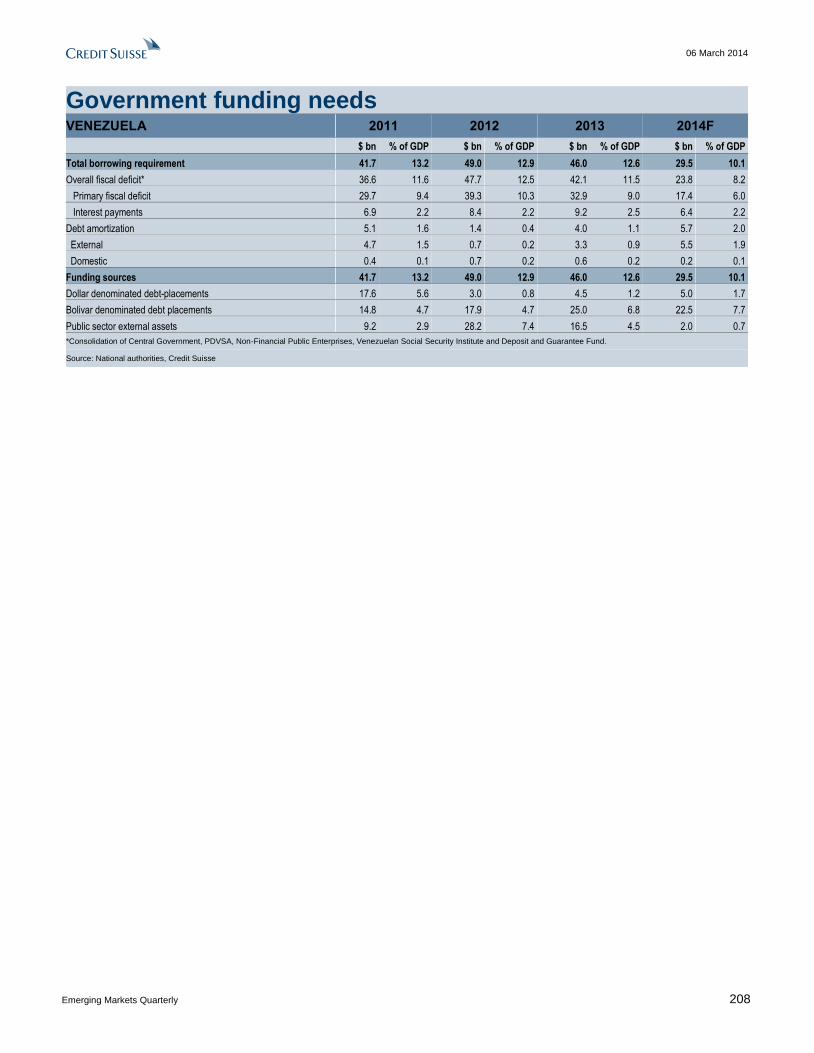

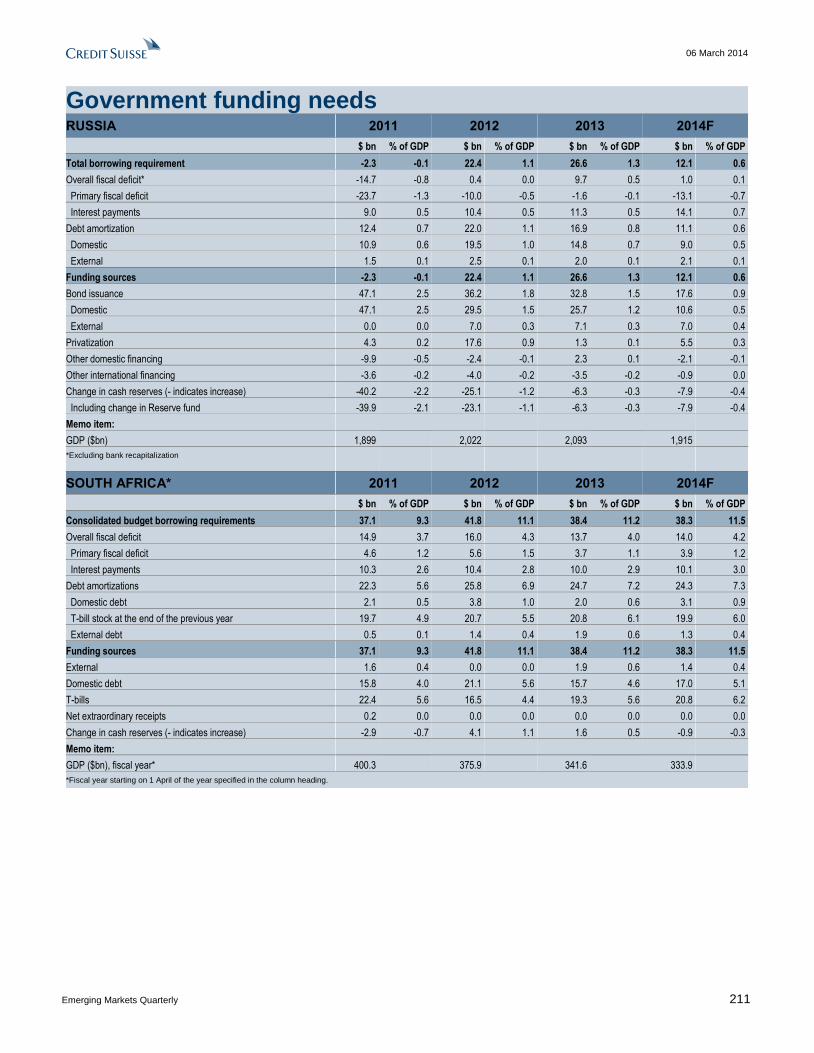

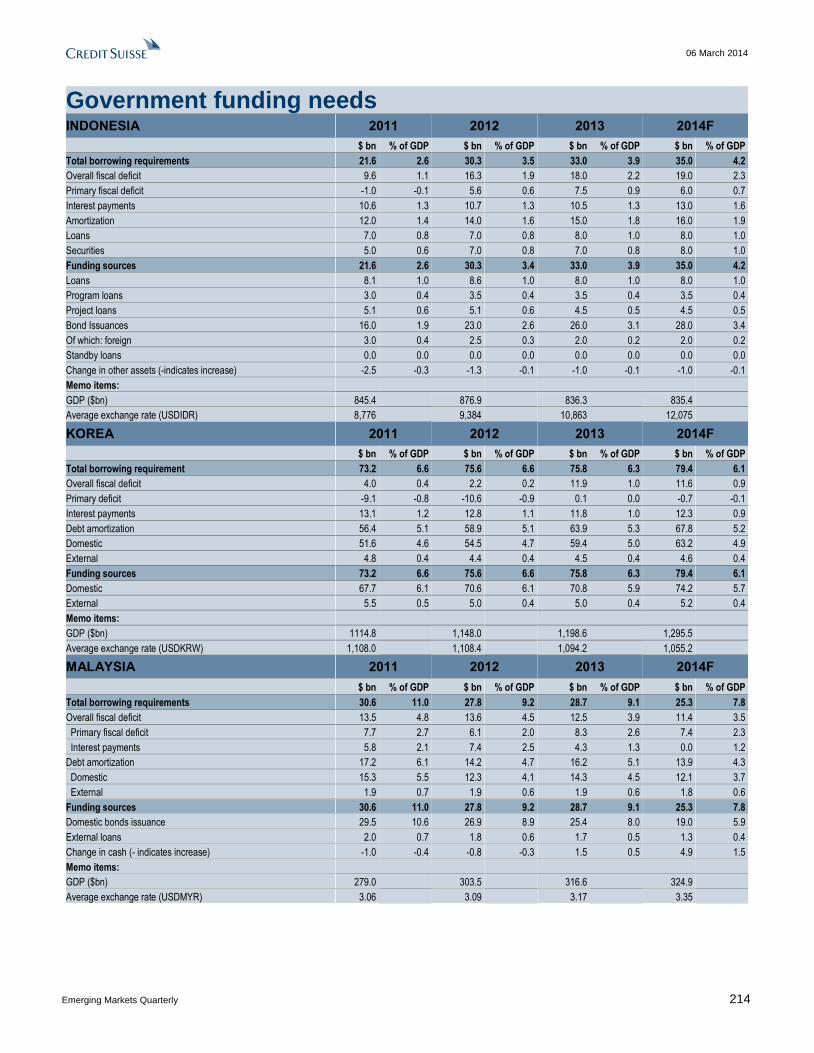

Government funding needs 206

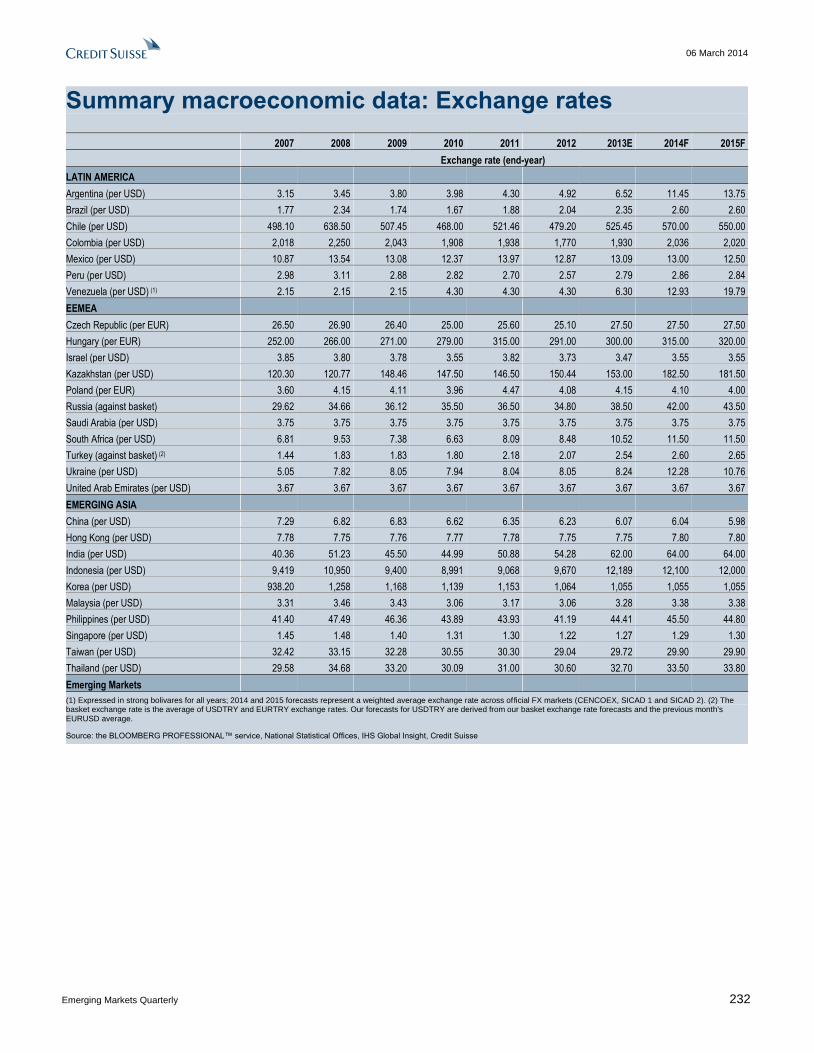

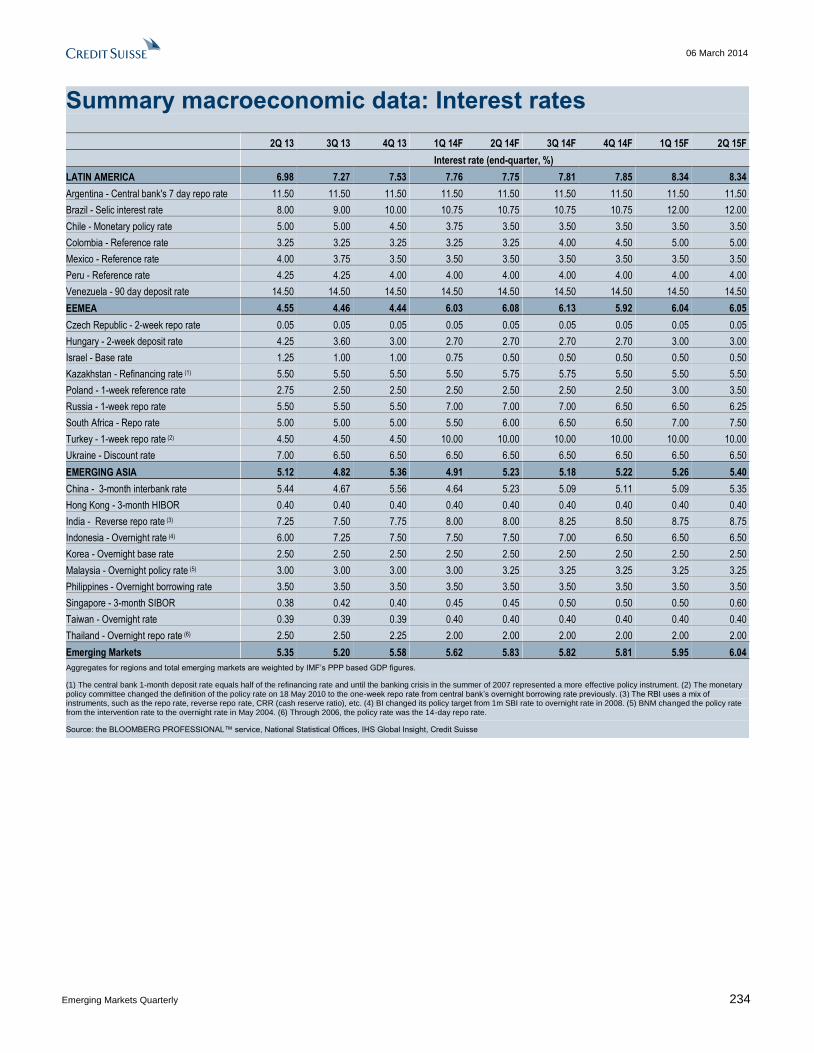

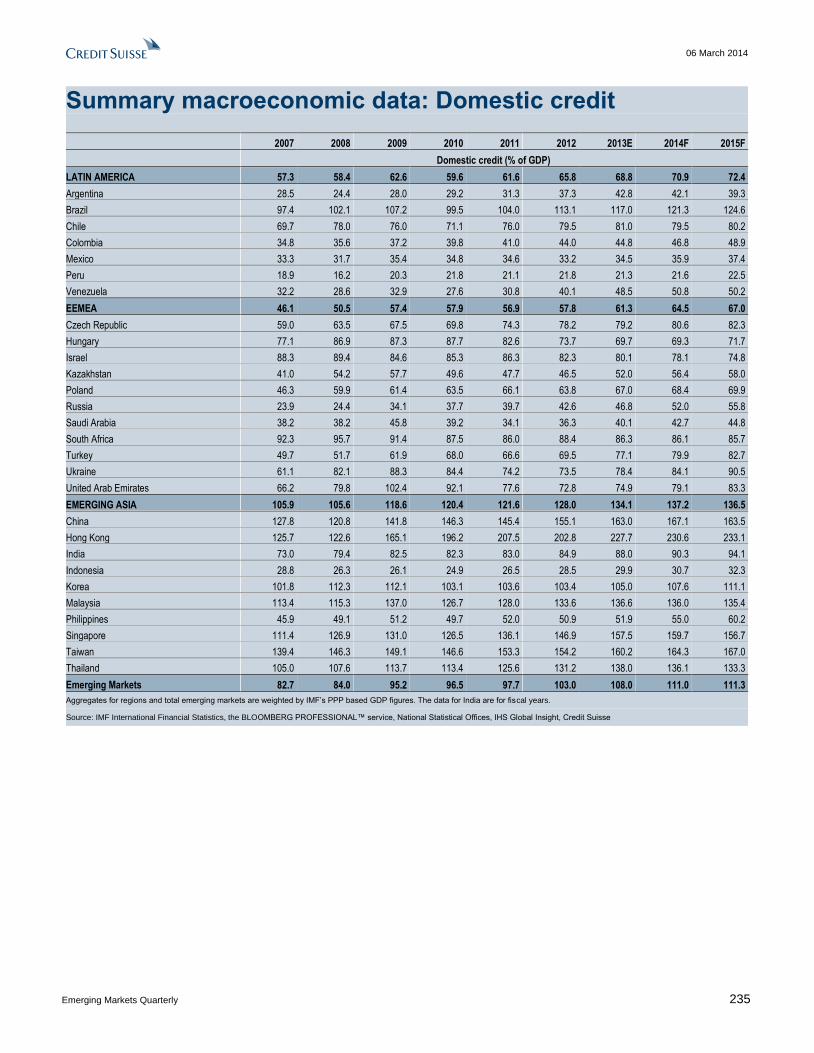

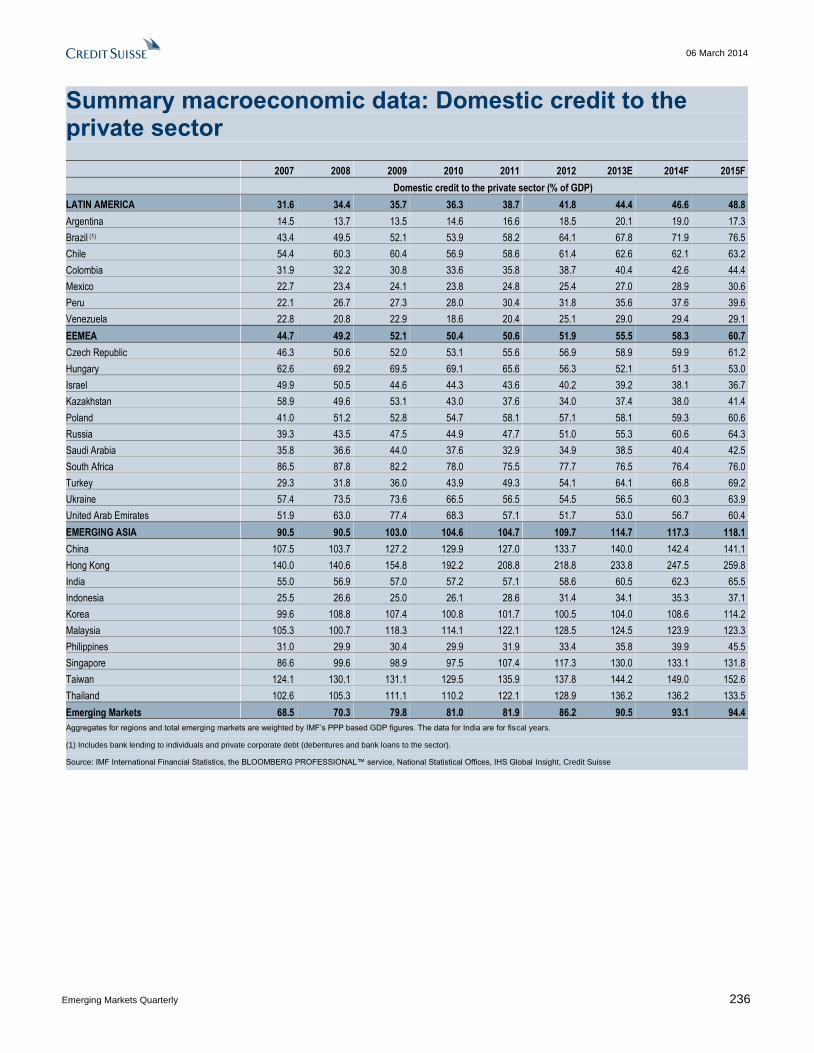

Quarterly and annual forecasts 216

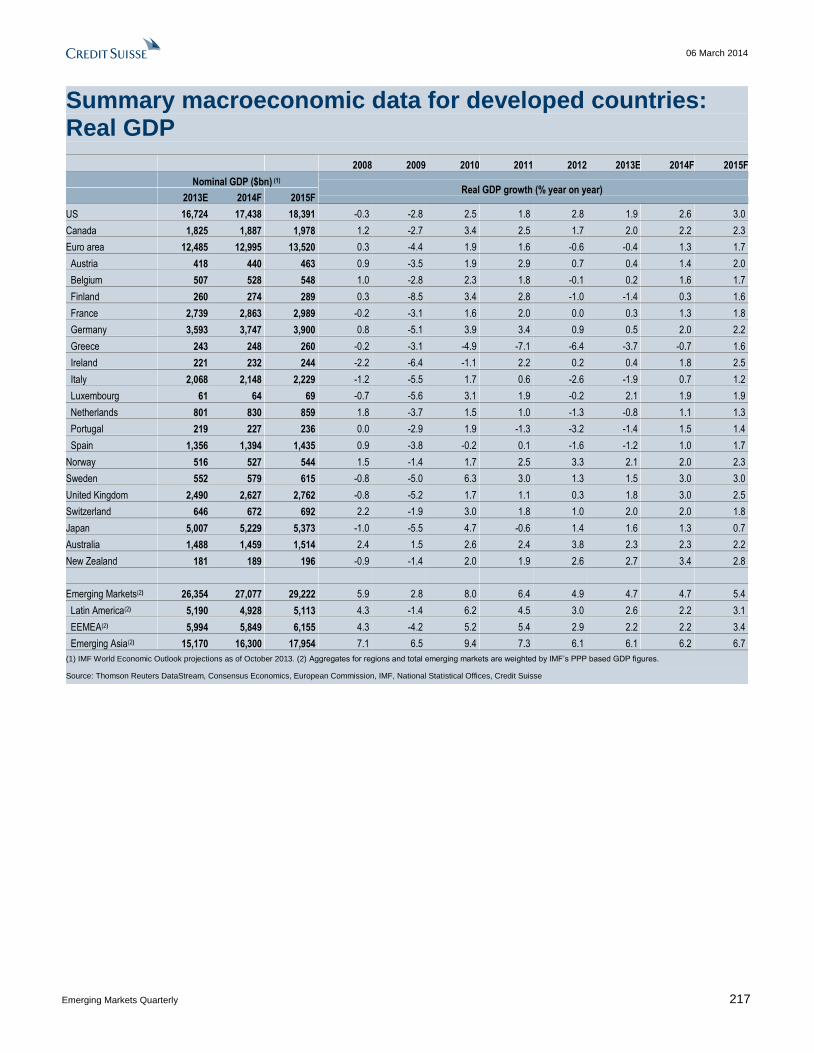

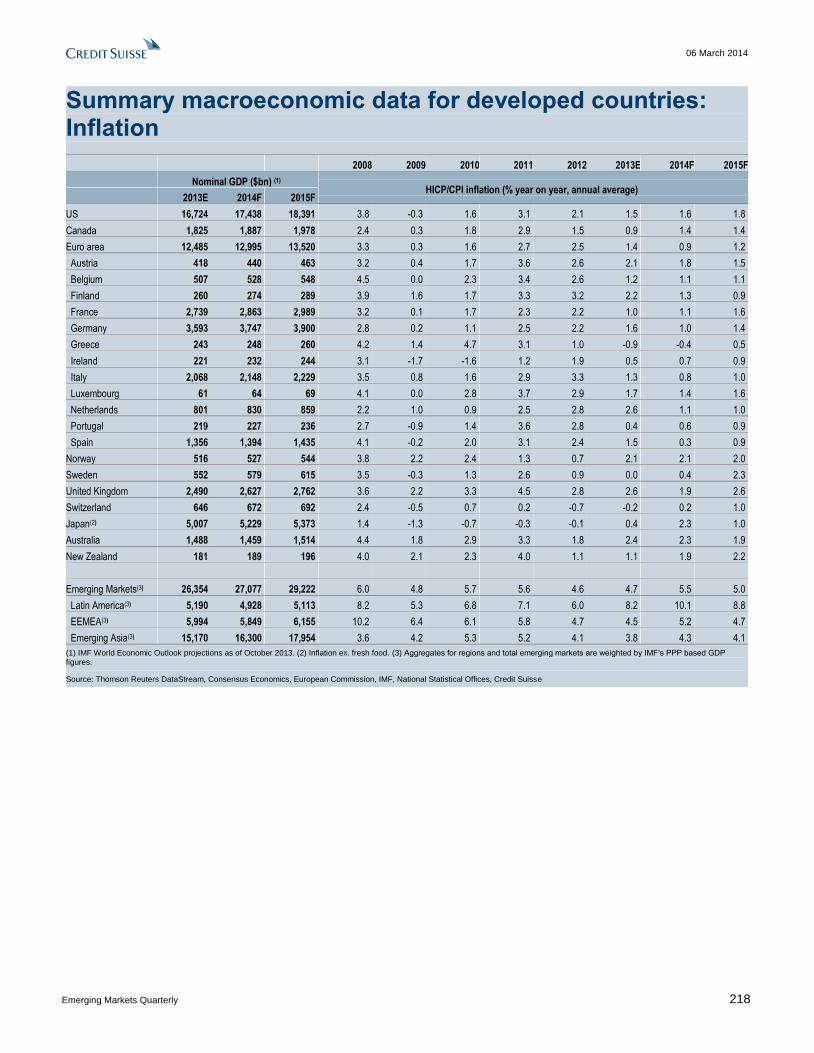

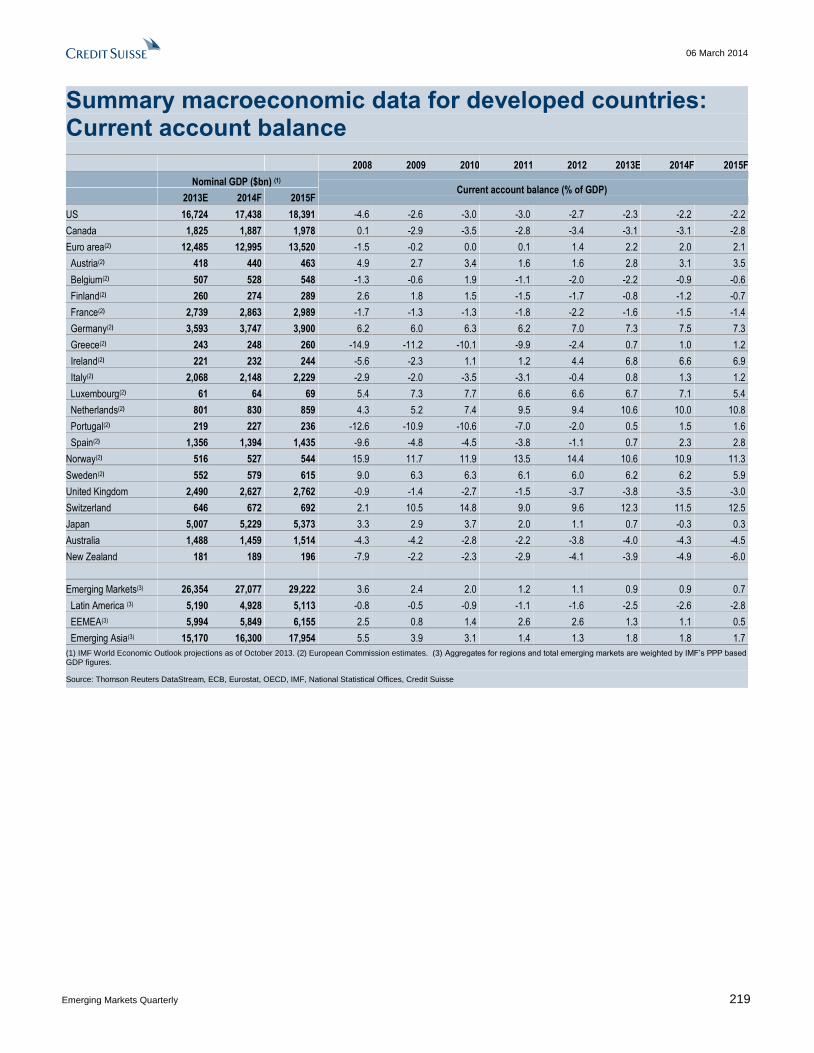

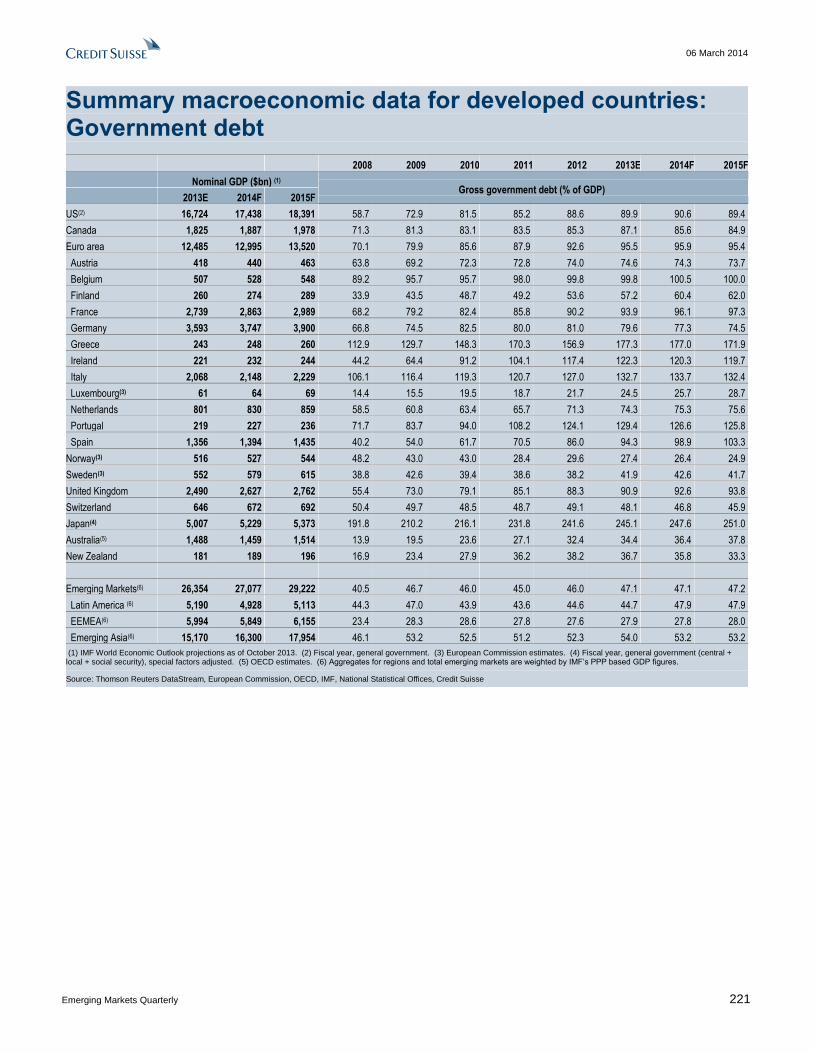

Summary macroeconomic data for developed countries 217

Summary macroeconomic data for emerging countries 222

We would like to acknowledge the contribution made by Pawel Chmielniak, an employee of

CRISIL Global Research and Analytics, a business division of CRISIL Limited, a third-party

provider of research services to Credit Suisse, in compiling the information and data tables

presented at the end of this report.

06 March 2014

Emerging Markets Quarterly 5

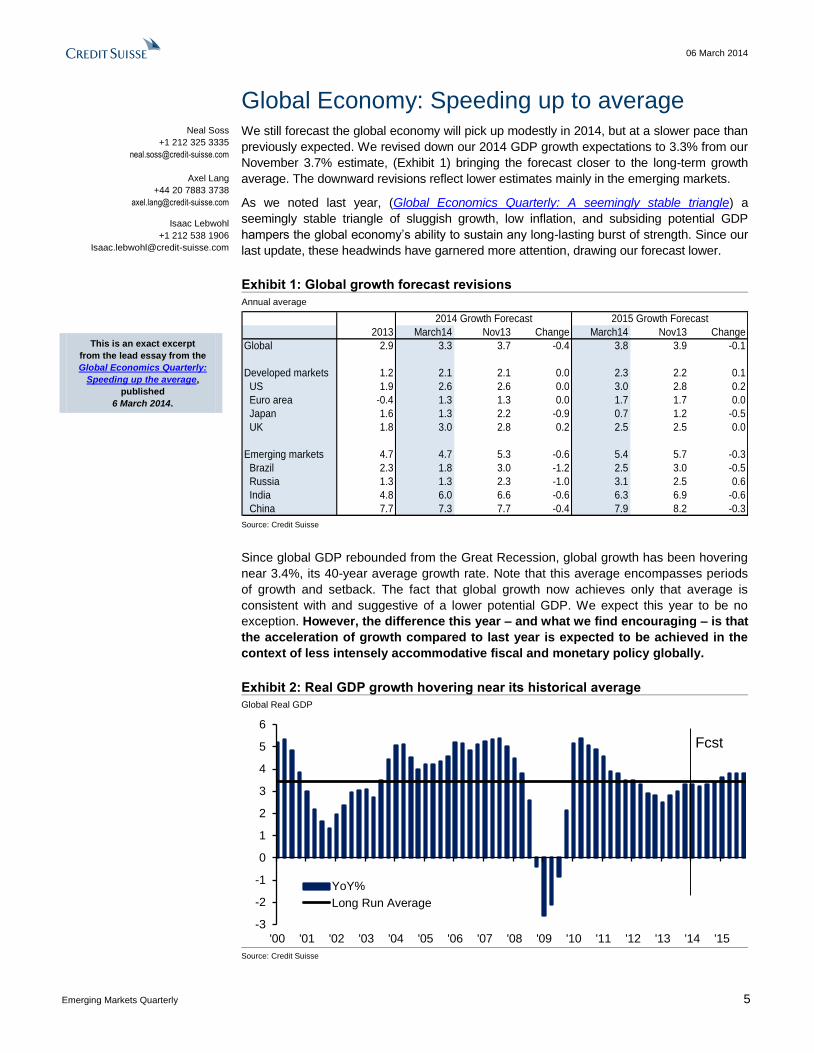

Global Economy: Speeding up to average We still forecast the global economy will pick up modestly in 2014, but at a slower pace than

previously expected. We revised down our 2014 GDP growth expectations to 3.3% from our

November 3.7% estimate, (Exhibit 1) bringing the forecast closer to the long-term growth

average. The downward revisions reflect lower estimates mainly in the emerging markets.

As we noted last year, (Global Economics Quarterly: A seemingly stable triangle) a

seemingly stable triangle of sluggish growth, low inflation, and subsiding potential GDP

hampers the global economy’s ability to sustain any long-lasting burst of strength. Since our

last update, these headwinds have garnered more attention, drawing our forecast lower.

Exhibit 1: Global growth forecast revisions

Annual average

2013 March14 Nov13 Change March14 Nov13 Change

Global 2.9 3.3 3.7 -0.4 3.8 3.9 -0.1

Developed markets 1.2 2.1 2.1 0.0 2.3 2.2 0.1

US 1.9 2.6 2.6 0.0 3.0 2.8 0.2

Euro area -0.4 1.3 1.3 0.0 1.7 1.7 0.0

Japan 1.6 1.3 2.2 -0.9 0.7 1.2 -0.5

UK 1.8 3.0 2.8 0.2 2.5 2.5 0.0

Emerging markets 4.7 4.7 5.3 -0.6 5.4 5.7 -0.3

Brazil 2.3 1.8 3.0 -1.2 2.5 3.0 -0.5

Russia 1.3 1.3 2.3 -1.0 3.1 2.5 0.6

India 4.8 6.0 6.6 -0.6 6.3 6.9 -0.6

China 7.7 7.3 7.7 -0.4 7.9 8.2 -0.3

2015 Growth Forecast2014 Growth Forecast

Source: Credit Suisse

Since global GDP rebounded from the Great Recession, global growth has been hovering

near 3.4%, its 40-year average growth rate. Note that this average encompasses periods

of growth and setback. The fact that global growth now achieves only that average is

consistent with and suggestive of a lower potential GDP. We expect this year to be no

exception. However, the difference this year – and what we find encouraging – is that

the acceleration of growth compared to last year is expected to be achieved in the

context of less intensely accommodative fiscal and monetary policy globally.

Neal Soss

+1 212 325 3335

Axel Lang

+44 20 7883 3738

Isaac Lebwohl

+1 212 538 1906

This is an exact excerpt

from the lead essay from the

Global Economics Quarterly:

Speeding up the average,

published

6 March 2014.

Exhibit 2: Real GDP growth hovering near its historical average

Global Real GDP

-3

-2

-1

0

1

2

3

4

5

6

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

YoY%

Long Run Average

Fcst

Source: Credit Suisse

06 March 2014

Emerging Markets Quarterly 6

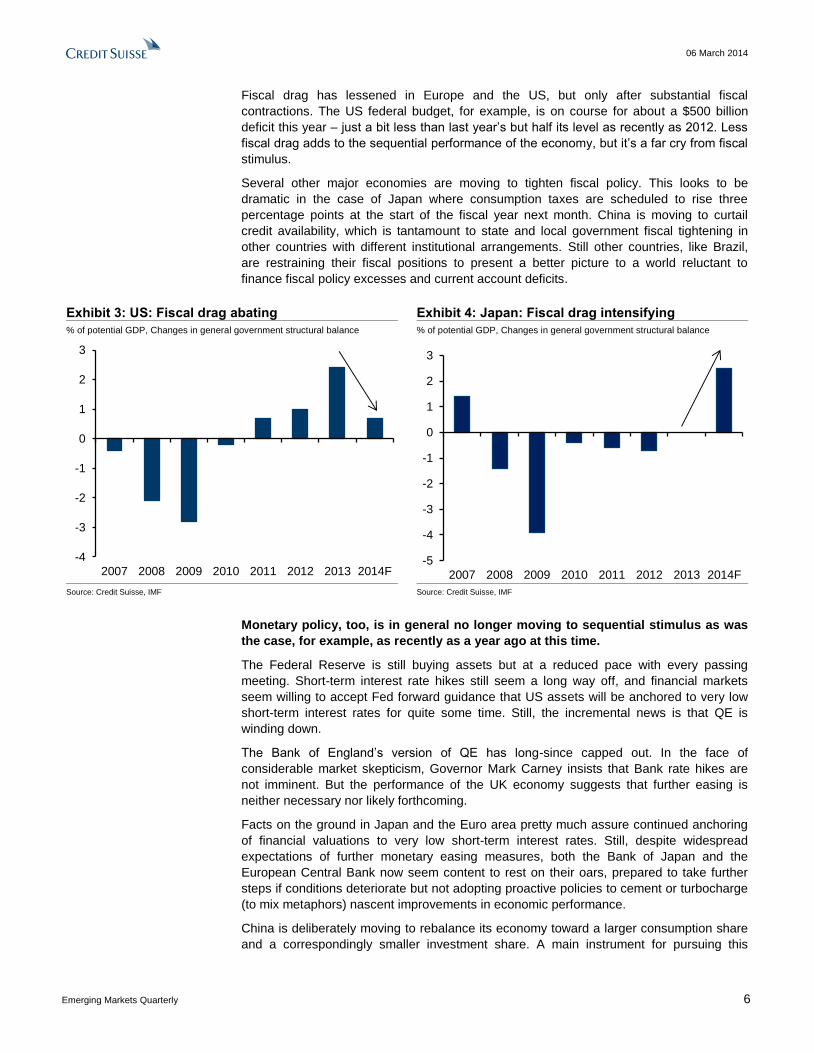

Fiscal drag has lessened in Europe and the US, but only after substantial fiscal

contractions. The US federal budget, for example, is on course for about a $500 billion

deficit this year – just a bit less than last year’s but half its level as recently as 2012. Less

fiscal drag adds to the sequential performance of the economy, but it’s a far cry from fiscal

stimulus.

Several other major economies are moving to tighten fiscal policy. This looks to be

dramatic in the case of Japan where consumption taxes are scheduled to rise three

percentage points at the start of the fiscal year next month. China is moving to curtail

credit availability, which is tantamount to state and local government fiscal tightening in

other countries with different institutional arrangements. Still other countries, like Brazil,

are restraining their fiscal positions to present a better picture to a world reluctant to

finance fiscal policy excesses and current account deficits.

Exhibit 3: US: Fiscal drag abating Exhibit 4: Japan: Fiscal drag intensifying

% of potential GDP, Changes in general government structural balance % of potential GDP, Changes in general government structural balance

-4

-3

-2

-1

0

1

2

3

2007 2008 2009 2010 2011 2012 2013 2014F

-5

-4

-3

-2

-1

0

1

2

3

2007 2008 2009 2010 2011 2012 2013 2014F Source: Credit Suisse, IMF Source: Credit Suisse, IMF

Monetary policy, too, is in general no longer moving to sequential stimulus as was

the case, for example, as recently as a year ago at this time.

The Federal Reserve is still buying assets but at a reduced pace with every passing

meeting. Short-term interest rate hikes still seem a long way off, and financial markets

seem willing to accept Fed forward guidance that US assets will be anchored to very low

short-term interest rates for quite some time. Still, the incremental news is that QE is

winding down.

The Bank of England’s version of QE has long-since capped out. In the face of

considerable market skepticism, Governor Mark Carney insists that Bank rate hikes are

not imminent. But the performance of the UK economy suggests that further easing is

neither necessary nor likely forthcoming.

Facts on the ground in Japan and the Euro area pretty much assure continued anchoring

of financial valuations to very low short-term interest rates. Still, despite widespread

expectations of further monetary easing measures, both the Bank of Japan and the

European Central Bank now seem content to rest on their oars, prepared to take further

steps if conditions deteriorate but not adopting proactive policies to cement or turbocharge

(to mix metaphors) nascent improvements in economic performance.

China is deliberately moving to rebalance its economy toward a larger consumption share

and a correspondingly smaller investment share. A main instrument for pursuing this

06 March 2014

Emerging Markets Quarterly 7

rebalancing is deregulation of the financial sector, which manifests itself in periodic spikes

in short-term interbank interest rates, episodic depreciations of the foreign exchange value

of its currency, and the seeking out of SETF (Small Enough To Fail) links in the financial

system. Among the hoped-for benefits are more efficient allocation of capital, reduced

corruption, and heightened sensitivity to environmental pollution concerns. However real

these long-term benefits turn out to be, the short-term effect is less policy stimulus to the

Chinese economy now.

Remarkably, with no new cyclical policy stimulus being applied, the global economy

seems to be stubbornly and grudgingly improving.

However, our expectations for close-to-average growth should not be confused with

growing at trend. Remember that average growth encompasses periods of expansion and

recession. Growth in periods of expansion should be higher than average growth, which

we are evidently not achieving.

Growth needs “escape velocity” to provide the necessary dynamism to promote a healthy

global economy. The fear is that such a continuous average state of global growth will

cause the world’s economic muscles to atrophy, embodied as lower potential GDP.

Exhibit 5: A declining trend: DM growth Exhibit 6: A declining trend: EM growth

YoY%, Ten-year moving average YoY%, Ten-year moving average

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Fcst.

4.0

4.5

5.0

5.5

6.0

6.5

7.0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Fcst.

Source: Credit Suisse, Markit, Thomson Reuters Datastream, Haver Analytics® Source: Credit Suisse, Markit, Thomson Reuters Datastream, Haver Analytics®

We believe the Communique of the recent G-20 meeting in Sydney, Australia reflects the

recognition of a structurally impaired global economy (see: The CS Macro Playbook:

Growth: on the agenda, but off the menu). Without quite using the words, the most senior

economic policy-makers from the biggest countries in the world pledged themselves to

raising the potential growth rate of the global economy.

The specifics appear in point 3 of the Communique:

We will develop ambitious but realistic policies with the aim to lift our collective GDP by more than 2 percent above the trajectory implied by current policies over the coming 5 years.

In the nature of a G-20 Communique, there are very few specifics, but the laundry list

topics read like the textbook description of growth accounting. Growth comes from people

presenting themselves for work, getting jobs, being equipped with productivity-enhancing

capital, in an institutional context that promotes economic activity. To quote from the

Communique again, point 3 continues.

06 March 2014

Emerging Markets Quarterly 8

To achieve this we will take concrete actions across the G-20, including to increase investment, lift employment and participation, enhance trade and promote competition, in addition to macroeconomic policies.

And, point 7 elaborates:

We are committed to creating a climate that facilitates higher investment, particularly in infrastructure and small and medium enterprises. This is crucial for the global economy’s transition to stronger growth in the short and medium term. We will undertake reforms to remove constraints to private investment by establishing sound and predictable policy and regulatory frameworks and emphasising the role of market incentives and disciplines. These, along with other actions to promote long-term private sector investment, maximise the impact of public sector capital expenditure, and enhance the catalytic role of multilateral development banks will be an important part of our growth strategies and the Brisbane Action Plan.

We would not expect early implementation of specific policies to further the G-20

goal. We would, however, point to the G-20 emphasis. Labor force participation has

been sliding in many countries. Some of this reflects the demographics of aging

populations, and some reflects slack aggregate demand. Business fixed investment has

been poor in nearly all developed economies, and public infrastructure investment has

been weak in a few places.

Exhibit 7: US investment ratio Exhibit 8: Japan investment ratio

% of GDP % of GDP

13

14

15

16

17

18

19

20

50 55 60 65 70 75 80 85 90 95 00 05 10

20

22

24

26

28

30

32

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 Source: Credit Suisse, Thomson Reuters Datastream Source: Credit Suisse, Thomson Reuters Datastream

Inasmuch as most of the world is allergic to explicit fiscal stimulus and the public sector

balance sheet leverage it implies, the burden of macroeconomic policy to spur greater

potential GDP falls on central banks. Although most central banks are refraining from

offering more stimulus, they still proclaim their eagerness to maintain accommodative

monetary stances. The G-20 puts a global umbrella over policies most central banks might

wish to follow for domestic reasons anyway.

However, the ability of central banks to raise potential GDP is uncertain. In a recent

speech by Yves Mersch, member of the executive board of the ECB, monetary policy is

presented as a means of preventing a decay of potential GDP. But the question that

remains is for how long central banks can provide this cushion. According to Mersch, “If

there is no prospect of higher growth in the future, we could fall victim to self-fulfilling

negative expectations”.

06 March 2014

Emerging Markets Quarterly 9

Exhibit 9: Euro area investment ratio Exhibit 10: Euro area participation rate

% of GDP % of working age population

17

18

19

20

21

22

95 97 99 01 03 05 07 09 11 13

54.5

55.0

55.5

56.0

56.5

57.0

57.5

00 01 02 03 04 05 06 07 08 09 10 11 12 13 Source: Credit Suisse, Thomson Reuters Datastream Source: Credit Suisse, Eurostat

Immediate cyclical risks in the global economy appear to have diminished; the

structural risks of slower potential GDP thus come into sharper focus. The

challenges of the future will be much easier to manage with more GDP and much

harder to manage with less. These are medium-and long-term considerations. We would

not necessarily expect to see any near-term specific policy actions.

DM is needed for the heavy lifting. Our expectation for the global economy to achieve close

to average growth in 2014 (3.3%) is supported by a rebound in developed markets. Specifically,

real GDP growth in the developed markets should almost double to 2.1% in 2014 from the

estimated 1.2% in 2013. At the same time, we revised down our emerging market GDP growth

forecast to 4.7% from 5.3%. We therefore expect EM to grow at the same speed as in 2013.

As a result, the spread between EM and DM growth rates is expected to narrow to 2.6pp in

2014, the smallest since 2001 (Exhibit 12). Excluding Chinese growth, the spread between EM

and DM growth follows a similar pattern, suggesting that the slowdown in EM is broad-based

and is not just a China story.

Exhibit 11: Global growth outlook Exhibit 12: Growth gap between EM and DM

YoY% Ppt.

2.6

3.6

4.8 4.55.0 5.2

2.4

-0.8

5.2

3.93.1 2.9 3.3 3.8

1.42.0

3.12.6 2.8

2.4

-0.1

-3.7

2.6

1.5 1.4 1.2

2.1 2.3

4.5

6.1

7.5 7.3

8.38.8

5.5

2.7

8.2

6.4

4.9 4.7 4.75.4

-6

-4

-2

0

2

4

6

8

10

02 04 06 08 10 12 14E

Global

Developed markets

Emerging markets

0

1

2

3

4

5

6

7

00 02 04 06 08 10 12 14E

EM - DM

EM ex. China - DM

Source: Credit Suisse Source: Credit Suisse

06 March 2014

Emerging Markets Quarterly 10

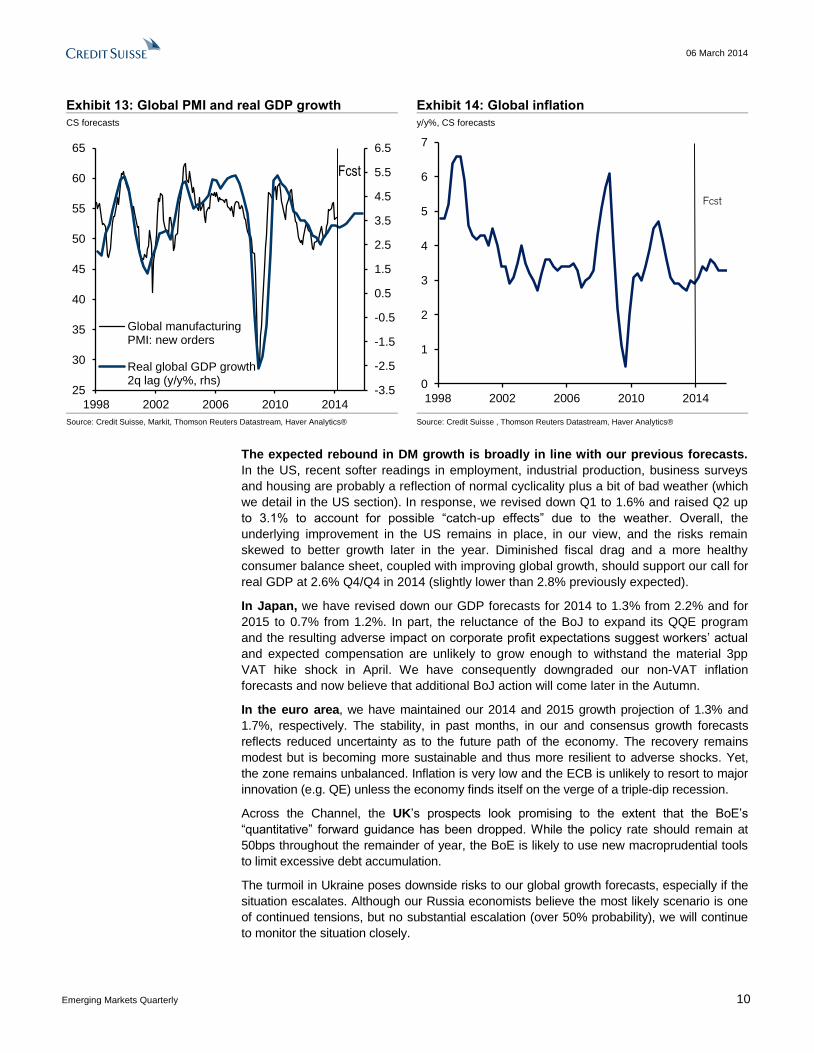

Exhibit 13: Global PMI and real GDP growth Exhibit 14: Global inflation

CS forecasts y/y%, CS forecasts

-3.5

-2.5

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

25

30

35

40

45

50

55

60

65

1998 2002 2006 2010 2014

Global manufacturingPMI: new orders

Real global GDP growth2q lag (y/y%, rhs)

Fcst

0

1

2

3

4

5

6

7

1998 2002 2006 2010 2014

Fcst

Source: Credit Suisse, Markit, Thomson Reuters Datastream, Haver Analytics® Source: Credit Suisse , Thomson Reuters Datastream, Haver Analytics®

The expected rebound in DM growth is broadly in line with our previous forecasts.

In the US, recent softer readings in employment, industrial production, business surveys

and housing are probably a reflection of normal cyclicality plus a bit of bad weather (which

we detail in the US section). In response, we revised down Q1 to 1.6% and raised Q2 up

to 3.1% to account for possible “catch-up effects” due to the weather. Overall, the

underlying improvement in the US remains in place, in our view, and the risks remain

skewed to better growth later in the year. Diminished fiscal drag and a more healthy

consumer balance sheet, coupled with improving global growth, should support our call for

real GDP at 2.6% Q4/Q4 in 2014 (slightly lower than 2.8% previously expected).

In Japan, we have revised down our GDP forecasts for 2014 to 1.3% from 2.2% and for

2015 to 0.7% from 1.2%. In part, the reluctance of the BoJ to expand its QQE program

and the resulting adverse impact on corporate profit expectations suggest workers’ actual

and expected compensation are unlikely to grow enough to withstand the material 3pp

VAT hike shock in April. We have consequently downgraded our non-VAT inflation

forecasts and now believe that additional BoJ action will come later in the Autumn.

In the euro area, we have maintained our 2014 and 2015 growth projection of 1.3% and

1.7%, respectively. The stability, in past months, in our and consensus growth forecasts

reflects reduced uncertainty as to the future path of the economy. The recovery remains

modest but is becoming more sustainable and thus more resilient to adverse shocks. Yet,

the zone remains unbalanced. Inflation is very low and the ECB is unlikely to resort to major

innovation (e.g. QE) unless the economy finds itself on the verge of a triple-dip recession.

Across the Channel, the UK’s prospects look promising to the extent that the BoE’s

“quantitative” forward guidance has been dropped. While the policy rate should remain at

50bps throughout the remainder of year, the BoE is likely to use new macroprudential tools

to limit excessive debt accumulation.

The turmoil in Ukraine poses downside risks to our global growth forecasts, especially if the

situation escalates. Although our Russia economists believe the most likely scenario is one

of continued tensions, but no substantial escalation (over 50% probability), we will continue

to monitor the situation closely.

06 March 2014

Emerging Markets Quarterly 11

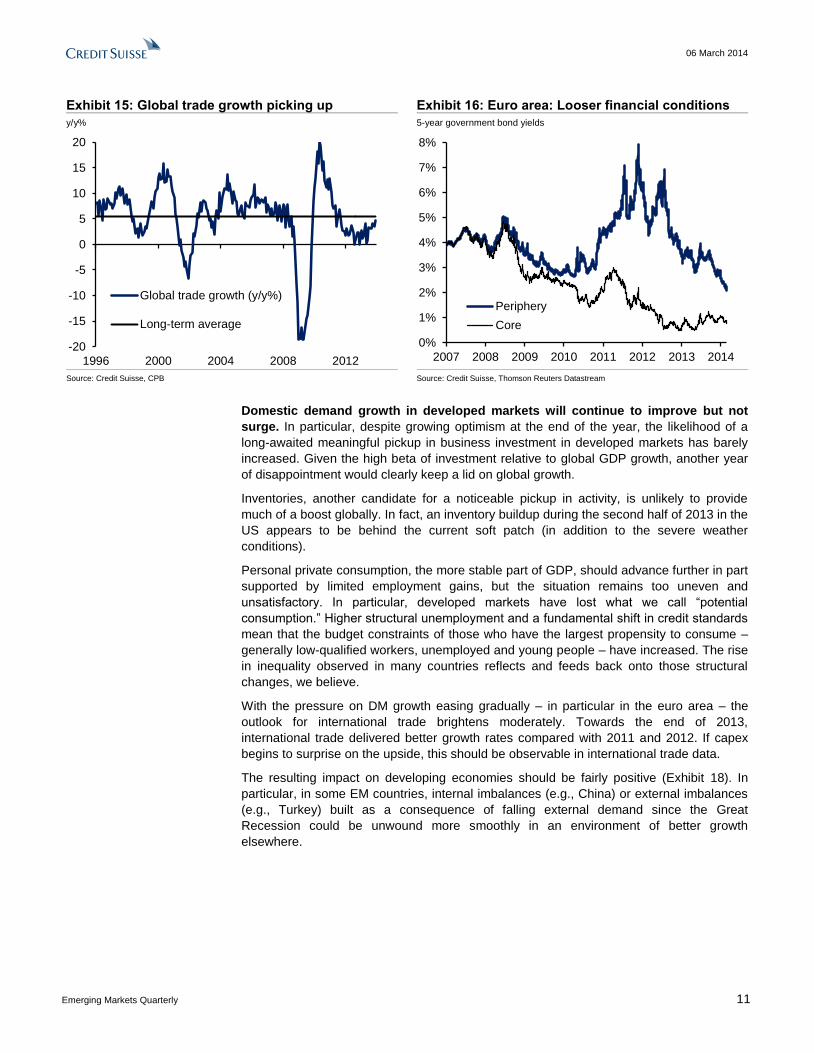

Exhibit 15: Global trade growth picking up Exhibit 16: Euro area: Looser financial conditions

y/y% 5-year government bond yields

-20

-15

-10

-5

0

5

10

15

20

1996 2000 2004 2008 2012

Global trade growth (y/y%)

Long-term average

0%

1%

2%

3%

4%

5%

6%

7%

8%

2007 2008 2009 2010 2011 2012 2013 2014

Periphery

Core

Source: Credit Suisse, CPB Source: Credit Suisse, Thomson Reuters Datastream

Domestic demand growth in developed markets will continue to improve but not

surge. In particular, despite growing optimism at the end of the year, the likelihood of a

long-awaited meaningful pickup in business investment in developed markets has barely

increased. Given the high beta of investment relative to global GDP growth, another year

of disappointment would clearly keep a lid on global growth.

Inventories, another candidate for a noticeable pickup in activity, is unlikely to provide

much of a boost globally. In fact, an inventory buildup during the second half of 2013 in the

US appears to be behind the current soft patch (in addition to the severe weather

conditions).

Personal private consumption, the more stable part of GDP, should advance further in part

supported by limited employment gains, but the situation remains too uneven and

unsatisfactory. In particular, developed markets have lost what we call “potential

consumption.” Higher structural unemployment and a fundamental shift in credit standards

mean that the budget constraints of those who have the largest propensity to consume –

generally low-qualified workers, unemployed and young people – have increased. The rise

in inequality observed in many countries reflects and feeds back onto those structural

changes, we believe.

With the pressure on DM growth easing gradually – in particular in the euro area – the

outlook for international trade brightens moderately. Towards the end of 2013,

international trade delivered better growth rates compared with 2011 and 2012. If capex

begins to surprise on the upside, this should be observable in international trade data.

The resulting impact on developing economies should be fairly positive (Exhibit 18). In

particular, in some EM countries, internal imbalances (e.g., China) or external imbalances

(e.g., Turkey) built as a consequence of falling external demand since the Great

Recession could be unwound more smoothly in an environment of better growth

elsewhere.

06 March 2014

Emerging Markets Quarterly 12

Exhibit 17: G3: Real domestic demand Exhibit 18: G3 demand vs. EM exports

4Q 2007=100 YoY%

94

96

98

100

102

104

4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12 1Q13 4Q13

US

Japan

Euro area

-15

-10

-5

0

5

10

15

20

-5

-4

-3

-2

-1

0

1

2

3

4

5

'00 '02 '04 '06 '08 '10 '12 '14

G3 real demandgrowth (y/y%)

EM ex. China realexports, rhs

Fcst.

Source: Credit Suisse, Thomson Reuters DataStream, Haver Analytics® Source: Credit Suisse, Thomson Reuters DataStream, Haver Analytics®

In China, while the economy performed admirably well in the past, the government’s wide

array of reforms aims at transforming a growth model that is running out of steam (e.g.,

over-investment in production capacities made for a world growing at a faster pace, rising

debt accumulation by the private and public sectors or increasing pollution-related issues

to name a few). To put the economy on a more sustainable footing, the government

intends to further liberalize the economy and incentivize households consumption. In the

medium term, it’s possible that the loss of “potential consumption” mentioned above could

be recouped in China and other EM countries more generally (Exhibit 19).

But that’s not an immediate story. Instead, China’s growth rate is currently decelerating.

Risks of a more significant slowdown have increased, but the authorities may only

intervene in a measured way, favoring a continuation of the rebalancing of the economy.

Exhibit 19: Share of world consumption Exhibit 20: India’s stagflation needs to be addressed

% YoY%

20%

30%

40%

50%

60%

70%

80%

98 00 02 04 06 08 10 12 14E

DM

EM

2

4

6

8

10

12

14

06 07 08 09 10 11 12 13

Real GDP growth

Headline CPI inflation

Source: Credit Suisse, © 2014 Thomson Reuters Limited, Haver Analytics® Source: Credit Suisse, Haver Analytics®

06 March 2014

Emerging Markets Quarterly 13

India is another country where the central bank is willing to introduce key changes to its

operating framework. There, the central bank desires to switch from a dual growth and

inflation mandate to a stricter inflation targeting regime. Given the nature of the inflation

process – food and energy make up around 60% of the total basket – and its stubborn

level – inflation has averaged 8.4% since 2005 – extremely conservative policies will have

to be enacted to bring inflation down to the target of 4% within two years. This should be

negative for economic activity in coming quarters.

In the meantime, commodity exporters, such as Australia and Canada, which benefitted

for several years from China’s and other EM countries’ growing role in the global

production process have lost competitiveness since the resulting financial resources found

their way back into the energy and (non-productive) residential sectors. This phenomenon

was exacerbated by overvalued currencies. This is why their central banks will be content

with cheaper ones.

Behind imbalances reside structural issues that need to be addressed. In the short

term, fundamental changes in the structure of an economy – in both emerging or

developed economies – can be damaging from an economic and social point of view.

Furthermore, modifying the growth model of an economy with the aim of increasing

potential GDP could nonetheless have negative effects that persist for quite some time as

the losing sectors must adjust promptly while the winning sectors can adjust at leisure.

The more dramatic the changes are, the more likely the economy will underperform for a

period of time and the lower the probabilities that an increase in potential GDP will quickly

materialize. This is why central bank policies need to remain exceptionally accommodative

to accompany these reforms. Our concern in 2014 is that major structural changes

continue to take place without the support of more policy stimulus.

06 March 2014

Emerging Markets Quarterly 14

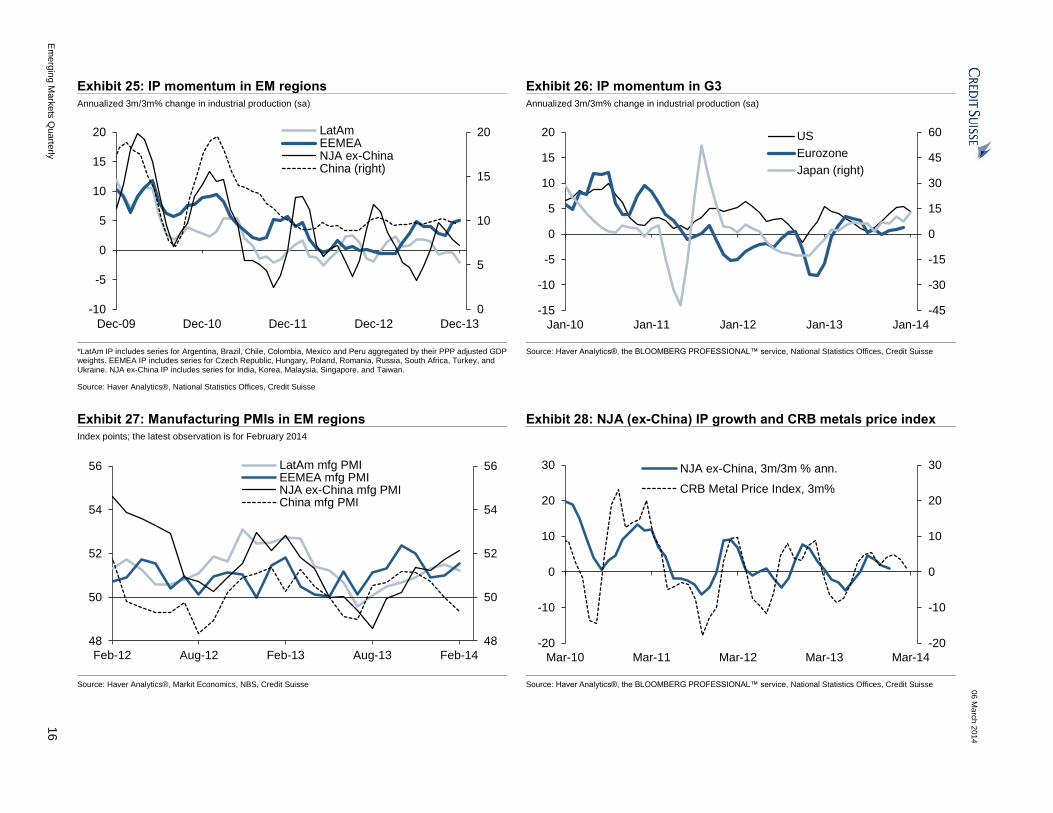

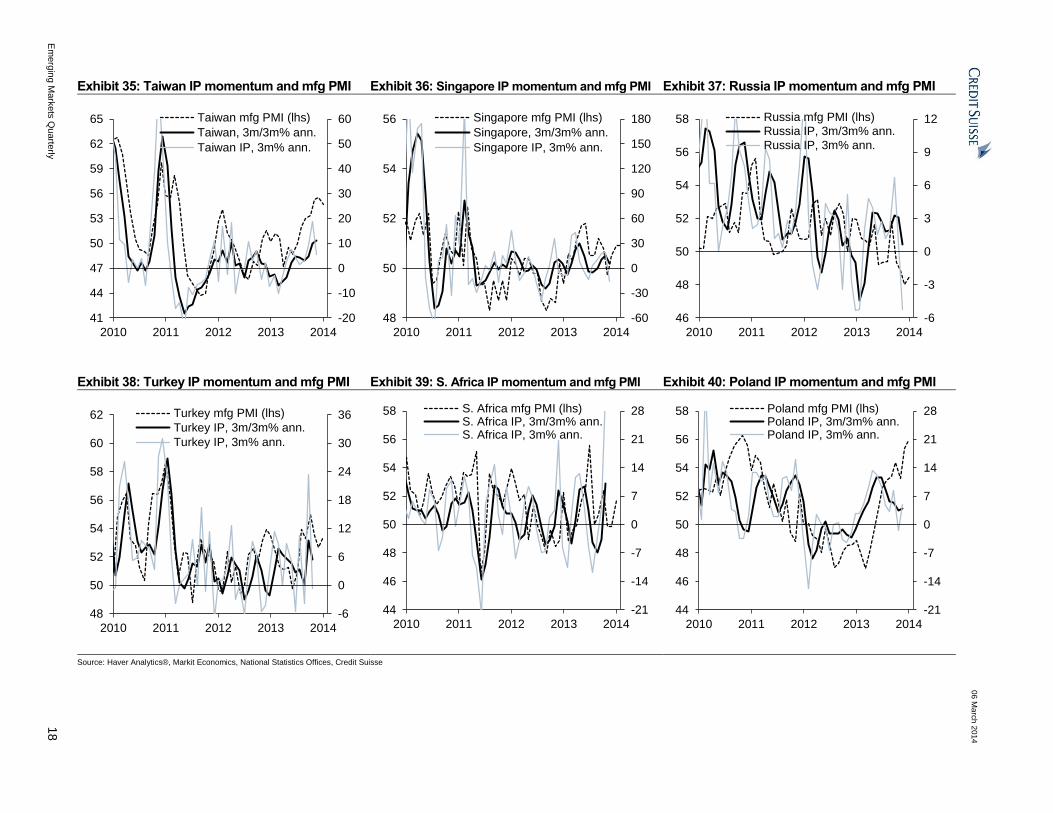

IP growth momentum slows further in EM as it strengthens notably in DM The pace of aggregate EM industrial output growth continued to slow in December,

moving further down from its recent peak in September. The momentum (3m/3m%,

annualized) of EM IP growth slowed to 4.4% in December from its eight-month peak of

5.3% in September (Exhibits 21 and 23). (December is the last month for which we have

data for all EM countries.) This diverges from DM IP growth which has steadily gained

momentum through 2H 2013 and reached its fastest pace in the past two years in January

2014 (Exhibits 24 and 26). IP growth momentum in DM is likely to have rolled over in

February, according to our economists' estimates.

The slowdown in EM's overall IP growth momentum in 4Q 2013 was primarily driven by

India and the LatAm region (Exhibit 25). The EEMEA region's IP growth momentum

rebounded modestly in 4Q 2013 from its recent trough in September and reached its strongest

pace in the past two years. This pick-up was led primarily by Turkey and South Africa

(Exhibits 38-39). Meanwhile, IP growth momentum in CE3 continued to slow for the fourth

consecutive month in December after accelerating rapidly between January and August 2013.

IP growth momentum in the NJA (excluding China) region was on a downtrend trajectory

during 4Q, driven by a notable weakness in India, while it strengthened in the rest of emerging

Asia in late 2013. China's IP growth momentum has also softened modestly since October

2013. LatAm's IP growth momentum slowed for the third consecutive quarter led by a broad-

based deceleration across the region. It is worth highlighting that Brazil's IP contracted in

sequential terms in 4Q for the second consecutive quarter (Exhibit 43). In 4Q 2013, IP growth

momentum improved in Turkey, South Africa, the Czech Republic, Russia, South Korea,

Singapore, Malaysia, and Taiwan (Exhibits 32-46).

The latest leading indicators suggest a further slowdown in EM IP growth

momentum coupled with some weakness in DM IP growth momentum in the coming

months (Exhibit 22). A deceleration in the run-rate (3m%, annualized) of EM IP in

December, which generally catches the turning points in IP growth momentum earlier, is

also suggesting that EM IP momentum should continue to slow in the near term (Exhibit

23). We note that the CSBMI – our leading indicator for global manufacturing activity –

declined (on 3mma basis) in January and December after a brief rebound in December,

pointing to weaker global IP growth momentum in the near term (Exhibit 22).

In NJA (excluding China) IP growth momentum weakened further in December. However,

we expect it to rebound in 1Q as also signaled by the latest three-month change in the

CRB metal price index which increased modestly between November and January before

coming off slightly in February (Exhibit 28). Our economists expect China’s IP growth

momentum to moderate further in 1Q before rebounding in 2Q, while India’s IP growth

momentum is expected to rebound sharply in 1Q.

According to our economists, IP growth momentum in EEMEA has eased during 1Q

despite stronger IP growth momentum in the CE3 countries and is set to bounce in 2Q. IP

growth momentum in CE3 has come down from its peak of 11% in August to about 4% in

December. It is expected to rebound in the near term and remain resilient at about 6.5%

throughout 2014, benefiting from the recovery in the euro area. We note that German Ifo

expectations index reached its multi-year high in January before easing slightly in

February. Russia’s IP growth momentum has been notably weak since late 2012 and this

weakness is likely to persist during 2014, according to our Russia economists.

IP growth momentum in LatAm fell sharply in December, driven mainly by a sharp drop in

Brazil's industrial output growth. However, our LatAm economists expect the region's IP

growth momentum to pick up gradually during 1H 2014, mainly driven by the rebound in

Brazil’s and Mexico's IP growth momentum.

Natig Mustafayev

+44 20 7888 1065

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

15

EM Regional IP and PMIs

Exhibit 21: IP momentum in DM and EM Exhibit 22: DM/EM Manufacturing PMIs and CSBMI

Annualized 3m/3m% change in industrial production (sa); the latest observations for EM and DM are Dec 2013 and Jan 2014 respectively

Index points; the latest observation is for February 2014

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012 2013 2014

Global IP momentum

EM IP* momentum

DM IP momentum

-5

-4

-3

-2

-1

0

1

2

30

35

40

45

50

55

60

2006 2007 2008 2009 2010 2011 2012 2013 2014

DM PMIEM PMI*CSBMI (3mma, right)

*IP data for India, Korea, Malaysia, Singapore, Taiwan, Argentina, Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Hungary, Poland, Romania, Russia, S. Africa, Turkey and Ukraine were aggregated by PPP GDP weights.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

*We aggregate the country PMIs by their PPP adjusted GDP weights. **The EM PMI includes readings for Brazil, Mexico, Czech Republic, Hungary, Poland, Russia, South Africa, Turkey, China, India, South Korea, Singapore and Taiwan.

Source: Haver Analytics®, Markit Economics, NBS, Credit Suisse

Exhibit 23: EM IP momentum and run-rate Exhibit 24: DM IP momentum and run-rate

Annualized % change in industrial production (sa) Annualized % change in industrial production (sa)

09 10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15

0

5

10

15

20

0

5

10

15

20

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

EM IP momentum, 3m/3m% ann.

EM IP run-rate, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14

-8

-4

0

4

8

12

16

-8

-4

0

4

8

12

16

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

DM IP momentum, 3m/3m% ann.

DM IP run-rate, 3m% ann.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse Source: Haver Analytics®, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

16

Exhibit 25: IP momentum in EM regions Exhibit 26: IP momentum in G3

Annualized 3m/3m% change in industrial production (sa) Annualized 3m/3m% change in industrial production (sa)

09 10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14

0

5

10

15

20

-10

-5

0

5

10

15

20

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

LatAmEEMEANJA ex-ChinaChina (right)

-45

-30

-15

0

15

30

45

60

-15

-10

-5

0

5

10

15

20

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

US

Eurozone

Japan (right)

*LatAm IP includes series for Argentina, Brazil, Chile, Colombia, Mexico and Peru aggregated by their PPP adjusted GDP weights. EEMEA IP includes series for Czech Republic, Hungary, Poland, Romania, Russia, South Africa, Turkey, and Ukraine. NJA ex-China IP includes series for India, Korea, Malaysia, Singapore, and Taiwan.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

Source: Haver Analytics®, the BLOOMBERG PROFESSIONAL™ service, National Statistics Offices, Credit Suisse

Exhibit 27: Manufacturing PMIs in EM regions Exhibit 28: NJA (ex-China) IP growth and CRB metals price index

Index points; the latest observation is for February 2014

12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

48

50

52

54

56

48

50

52

54

56

Feb-12 Aug-12 Feb-13 Aug-13 Feb-14

LatAm mfg PMIEEMEA mfg PMINJA ex-China mfg PMIChina mfg PMI

10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14

-20

-10

0

10

20

30

-20

-10

0

10

20

30

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

NJA ex-China, 3m/3m % ann.

CRB Metal Price Index, 3m%

Source: Haver Analytics®, Markit Economics, NBS, Credit Suisse Source: Haver Analytics®, the BLOOMBERG PROFESSIONAL™ service, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

17

Exhibit 29: NJA ex-China IP momentum and mfg PMI Exhibit 30: EEMEA IP momentum and mfg PMI Exhibit 31: LatAm IP momentum and mfg PMI

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-3

0

3

6

9

12

15

48

50

52

54

56

58

60

2010 2011 2012 2013 2014

EEMEA mfg PMI** (lhs)

EEMEA IP, 3m/3m% ann.*

EEMEA IP, 3m% ann.*

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-3

0

3

6

9

12

15

48

50

52

54

56

58

60

2010 2011 2012 2013 2014

EEMEA mfg PMI** (lhs)

EEMEA IP, 3m/3m% ann.*

EEMEA IP, 3m% ann.*

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-8

-4

0

4

8

12

16

46

48

50

52

54

56

58

2010 2011 2012 2013 2014

LatAm mfg PMI** (lhs)

LatAm IP, 3m/3m% ann.*

LatAm IP, 3m% ann.*

Exhibit 32: China IP momentum and mfg PMI Exhibit 33: India IP momentum and mfg PMI Exhibit 34: Korea IP momentum and mfg PMI

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

6

9

12

15

18

21

24

48

50

52

54

56

58

2010 2011 2012 2013 2014

China mfg PMI** (lhs)

China IP, 3m/3m% ann.

China IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-20

-15

-10

-5

0

5

10

15

20

25

48

50

52

54

56

58

60

62

2010 2011 2012 2013 2014

India mfg PMI (lhs)

India IP, 3m/3m% ann.

India IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-18

-12

-6

0

6

12

18

24

30

44

46

48

50

52

54

56

58

60

2010 2011 2012 2013 2014

S. Korea mfg PMI (lhs)

S. Korea IP, 3m/3m% ann.

S. Korea IP, 3m% ann.

*LatAm IP includes series for Argentina, Brazil, Chile, Colombia, Mexico and Peru aggregated by their PPP adjusted GDP weights. EEMEA IP includes series for Czech Republic, Hungary, Poland, Romania, Russia, South Africa, Turkey, and Ukraine. NJA ex-China IP includes series for India, Korea, Malaysia, Singapore, and Taiwan. Country IP series are seasonally and workday-adjusted. The latest observation is for December 2013 or January 2014.

**LatAm PMI includes series for Brazil and Mexico aggregated by their PPP adjusted GDP weights. EEMEA PMI includes series for Czech Republic, Hungary, Poland, Russia, South Africa and Turkey. NJA ex-China PMI includes series for India, Korea, Singapore, and Taiwan. For China, we use the average of NBS and HSBC manufacturing PMIs. The latest observation is for February 2014.

Source: Haver Analytics®, Markit Economics, NBS, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

18

Exhibit 35: Taiwan IP momentum and mfg PMI Exhibit 36: Singapore IP momentum and mfg PMI Exhibit 37: Russia IP momentum and mfg PMI

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-20

-10

0

10

20

30

40

50

60

41

44

47

50

53

56

59

62

65

2010 2011 2012 2013 2014

Taiwan mfg PMI (lhs)

Taiwan, 3m/3m% ann.

Taiwan IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-60

-30

0

30

60

90

120

150

180

48

50

52

54

56

2010 2011 2012 2013 2014

Singapore mfg PMI (lhs)

Singapore, 3m/3m% ann.

Singapore IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-6

-3

0

3

6

9

12

46

48

50

52

54

56

58

2010 2011 2012 2013 2014

Russia mfg PMI (lhs)

Russia IP, 3m/3m% ann.

Russia IP, 3m% ann.

Exhibit 38: Turkey IP momentum and mfg PMI Exhibit 39: S. Africa IP momentum and mfg PMI Exhibit 40: Poland IP momentum and mfg PMI

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-6

0

6

12

18

24

30

36

48

50

52

54

56

58

60

62

2010 2011 2012 2013 2014

Turkey mfg PMI (lhs)

Turkey IP, 3m/3m% ann.

Turkey IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-21

-14

-7

0

7

14

21

28

44

46

48

50

52

54

56

58

2010 2011 2012 2013 2014

S. Africa mfg PMI (lhs)S. Africa IP, 3m/3m% ann.S. Africa IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-21

-14

-7

0

7

14

21

28

44

46

48

50

52

54

56

58

2010 2011 2012 2013 2014

Poland mfg PMI (lhs)Poland IP, 3m/3m% ann.Poland IP, 3m% ann.

Source: Haver Analytics®, Markit Economics, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

19

Exhibit 41: Hungary IP momentum and mfg PMI Exhibit 42: Czech IP momentum and mfg PMI Exhibit 43: Brazil IP momentum and mfg PMI

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-24

-16

-8

0

8

16

24

32

44

46

48

50

52

54

56

58

2010 2011 2012 2013 2014

Hungary mfg PMI (3mma, lhs)Hungary IP, 3m/3m% ann.Hungary IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-18

-12

-6

0

6

12

18

24

30

45

48

51

54

57

60

63

2010 2011 2012 2013 2014

Czech mfg PMI (lhs)Czech IP, 3m/3m% ann.Czech IP, 3m% ann.

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-14

-7

0

7

14

21

44

47

50

53

56

59

2010 2011 2012 2013 2014

Brazil mfg PMI (lhs)Brazil IP, 3m/3m% ann.Brazil IP, 3m% ann.

Exhibit 44: Mexico IP momentum and mfg PMI Exhibit 45: Chile IP momentum Exhibit 46: Colombia IP momentum

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14

-6

-3

0

3

6

9

45

48

51

54

57

60

2010 2011 2012 2013 2014

Mexico INEGI mfg PMI (lhs)Mexico IP, 3m/3m% ann.Mexico IP, 3m% ann.

-30

-20

-10

0

10

20

30

40

50

-30

-20

-10

0

10

20

30

40

50

2010 2011 2012 2013 2014

Chile IP, 3m/3m% ann.

Chile IP, 3m% ann.

-15

-10

-5

0

5

10

15

20

25

-15

-10

-5

0

5

10

15

20

25

2010 2011 2012 2013 2014

Colombia IP, 3m/3m% ann.

Colombia IP, 3m% ann.

Source: Haver Analytics®, Markit Economics, National Statistics Offices, HALPIM, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

20

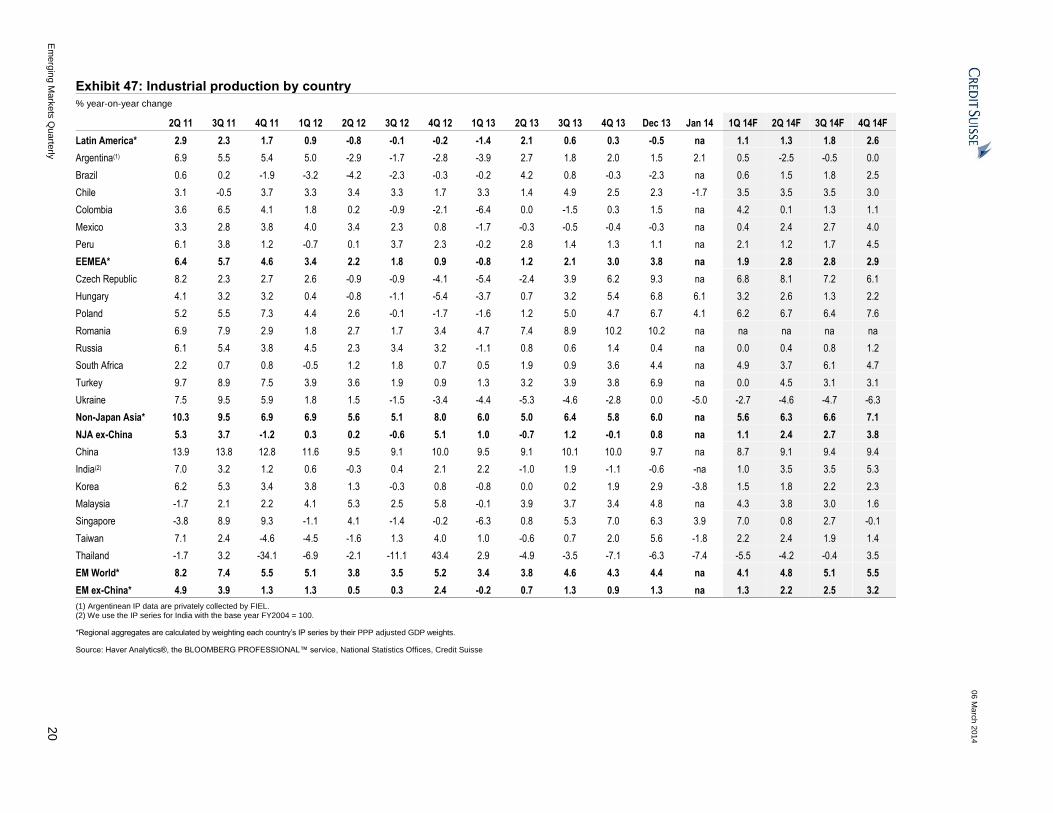

Exhibit 47: Industrial production by country

% year-on-year change

2Q 11 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 1Q 13 2Q 13 3Q 13 4Q 13 Dec 13 Jan 14 1Q 14F 2Q 14F 3Q 14F 4Q 14F

Latin America* 2.9 2.3 1.7 0.9 -0.8 -0.1 -0.2 -1.4 2.1 0.6 0.3 -0.5 na 1.1 1.3 1.8 2.6

Argentina(1) 6.9 5.5 5.4 5.0 -2.9 -1.7 -2.8 -3.9 2.7 1.8 2.0 1.5 2.1 0.5 -2.5 -0.5 0.0

Brazil 0.6 0.2 -1.9 -3.2 -4.2 -2.3 -0.3 -0.2 4.2 0.8 -0.3 -2.3 na 0.6 1.5 1.8 2.5

Chile 3.1 -0.5 3.7 3.3 3.4 3.3 1.7 3.3 1.4 4.9 2.5 2.3 -1.7 3.5 3.5 3.5 3.0

Colombia 3.6 6.5 4.1 1.8 0.2 -0.9 -2.1 -6.4 0.0 -1.5 0.3 1.5 na 4.2 0.1 1.3 1.1

Mexico 3.3 2.8 3.8 4.0 3.4 2.3 0.8 -1.7 -0.3 -0.5 -0.4 -0.3 na 0.4 2.4 2.7 4.0

Peru 6.1 3.8 1.2 -0.7 0.1 3.7 2.3 -0.2 2.8 1.4 1.3 1.1 na 2.1 1.2 1.7 4.5

EEMEA* 6.4 5.7 4.6 3.4 2.2 1.8 0.9 -0.8 1.2 2.1 3.0 3.8 na 1.9 2.8 2.8 2.9

Czech Republic 8.2 2.3 2.7 2.6 -0.9 -0.9 -4.1 -5.4 -2.4 3.9 6.2 9.3 na 6.8 8.1 7.2 6.1

Hungary 4.1 3.2 3.2 0.4 -0.8 -1.1 -5.4 -3.7 0.7 3.2 5.4 6.8 6.1 3.2 2.6 1.3 2.2

Poland 5.2 5.5 7.3 4.4 2.6 -0.1 -1.7 -1.6 1.2 5.0 4.7 6.7 4.1 6.2 6.7 6.4 7.6

Romania 6.9 7.9 2.9 1.8 2.7 1.7 3.4 4.7 7.4 8.9 10.2 10.2 na na na na na

Russia 6.1 5.4 3.8 4.5 2.3 3.4 3.2 -1.1 0.8 0.6 1.4 0.4 na 0.0 0.4 0.8 1.2

South Africa 2.2 0.7 0.8 -0.5 1.2 1.8 0.7 0.5 1.9 0.9 3.6 4.4 na 4.9 3.7 6.1 4.7

Turkey 9.7 8.9 7.5 3.9 3.6 1.9 0.9 1.3 3.2 3.9 3.8 6.9 na 0.0 4.5 3.1 3.1

Ukraine 7.5 9.5 5.9 1.8 1.5 -1.5 -3.4 -4.4 -5.3 -4.6 -2.8 0.0 -5.0 -2.7 -4.6 -4.7 -6.3

Non-Japan Asia* 10.3 9.5 6.9 6.9 5.6 5.1 8.0 6.0 5.0 6.4 5.8 6.0 na 5.6 6.3 6.6 7.1

NJA ex-China 5.3 3.7 -1.2 0.3 0.2 -0.6 5.1 1.0 -0.7 1.2 -0.1 0.8 na 1.1 2.4 2.7 3.8

China 13.9 13.8 12.8 11.6 9.5 9.1 10.0 9.5 9.1 10.1 10.0 9.7 na 8.7 9.1 9.4 9.4

India(2) 7.0 3.2 1.2 0.6 -0.3 0.4 2.1 2.2 -1.0 1.9 -1.1 -0.6 -na 1.0 3.5 3.5 5.3

Korea 6.2 5.3 3.4 3.8 1.3 -0.3 0.8 -0.8 0.0 0.2 1.9 2.9 -3.8 1.5 1.8 2.2 2.3

Malaysia -1.7 2.1 2.2 4.1 5.3 2.5 5.8 -0.1 3.9 3.7 3.4 4.8 na 4.3 3.8 3.0 1.6

Singapore -3.8 8.9 9.3 -1.1 4.1 -1.4 -0.2 -6.3 0.8 5.3 7.0 6.3 3.9 7.0 0.8 2.7 -0.1

Taiwan 7.1 2.4 -4.6 -4.5 -1.6 1.3 4.0 1.0 -0.6 0.7 2.0 5.6 -1.8 2.2 2.4 1.9 1.4

Thailand -1.7 3.2 -34.1 -6.9 -2.1 -11.1 43.4 2.9 -4.9 -3.5 -7.1 -6.3 -7.4 -5.5 -4.2 -0.4 3.5

EM World* 8.2 7.4 5.5 5.1 3.8 3.5 5.2 3.4 3.8 4.6 4.3 4.4 na 4.1 4.8 5.1 5.5

EM ex-China* 4.9 3.9 1.3 1.3 0.5 0.3 2.4 -0.2 0.7 1.3 0.9 1.3 na 1.3 2.2 2.5 3.2

(1) Argentinean IP data are privately collected by FIEL. (2) We use the IP series for India with the base year FY2004 = 100.

*Regional aggregates are calculated by weighting each country’s IP series by their PPP adjusted GDP weights.

Source: Haver Analytics®, the BLOOMBERG PROFESSIONAL™ service, National Statistics Offices, Credit Suisse

06 March 2014

Emerging Markets Quarterly 21

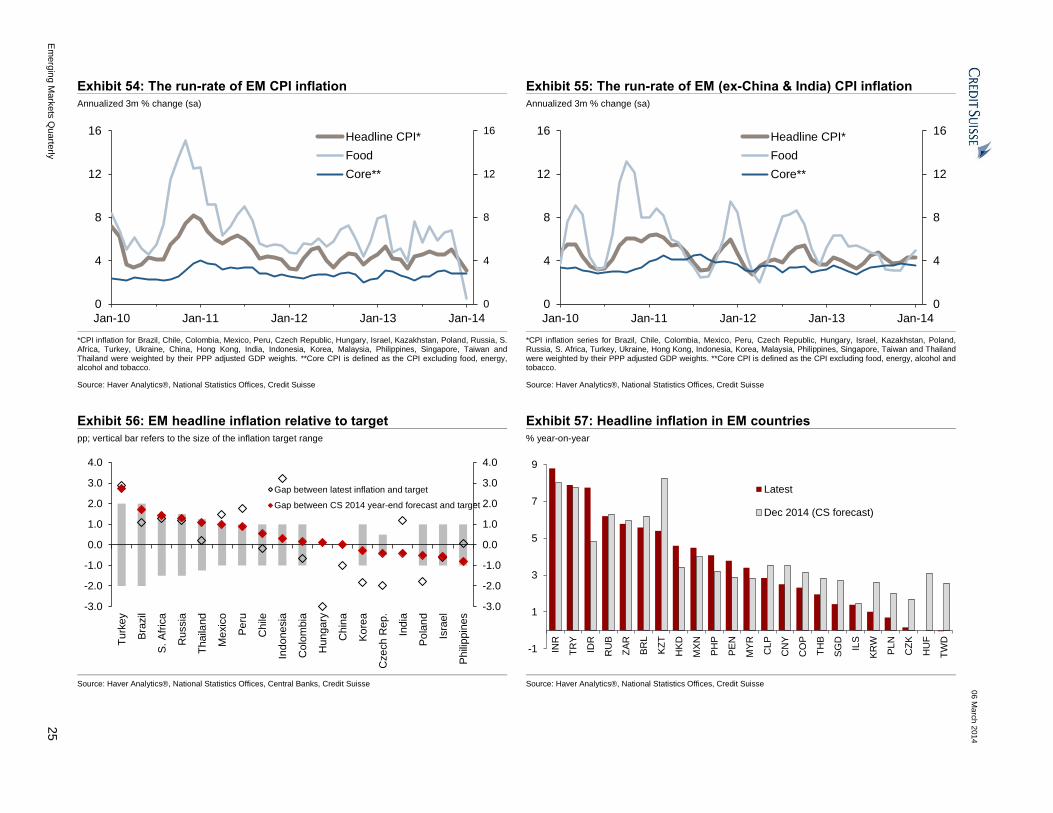

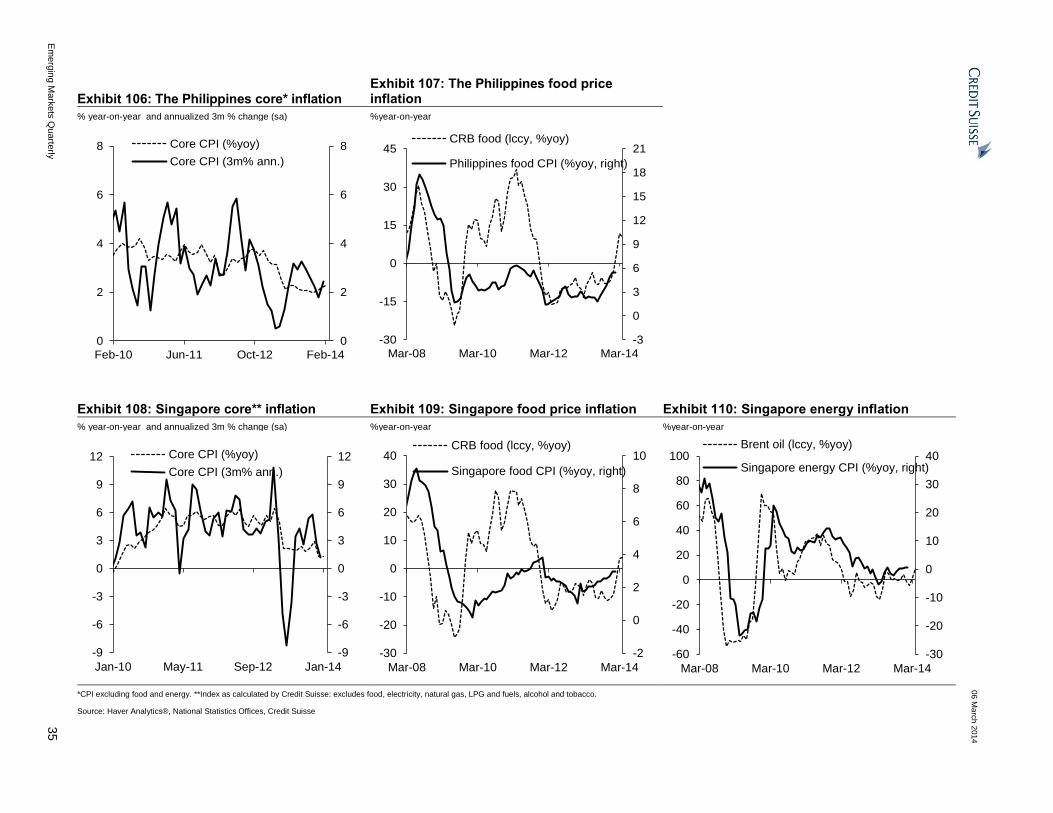

Core inflation on the rise in EEMEA and Latin America This section aims to present the latest inflation developments across the EM world.

In Exhibits 50-55 we provide an overview of headline and core inflation dynamics in EM,

the US and the euro area, and in Exhibits 58-60 and 83-91 we present regional inflation

charts along with medium-term inflation outlooks for EM countries.

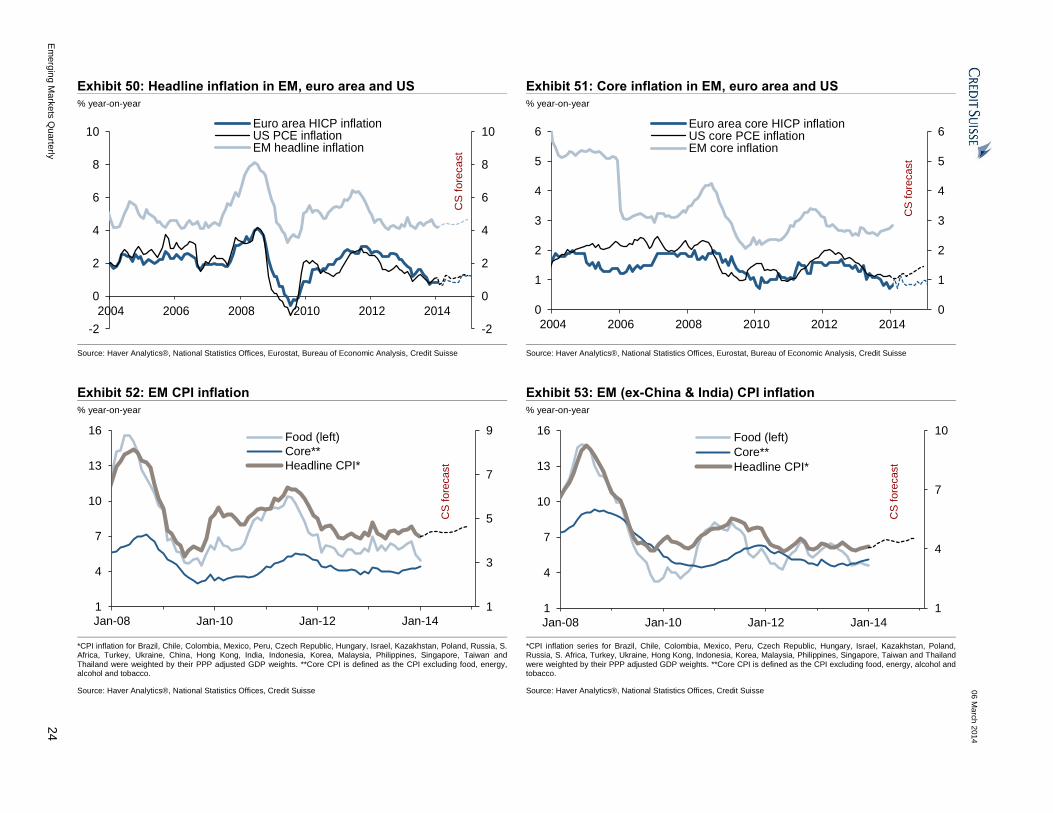

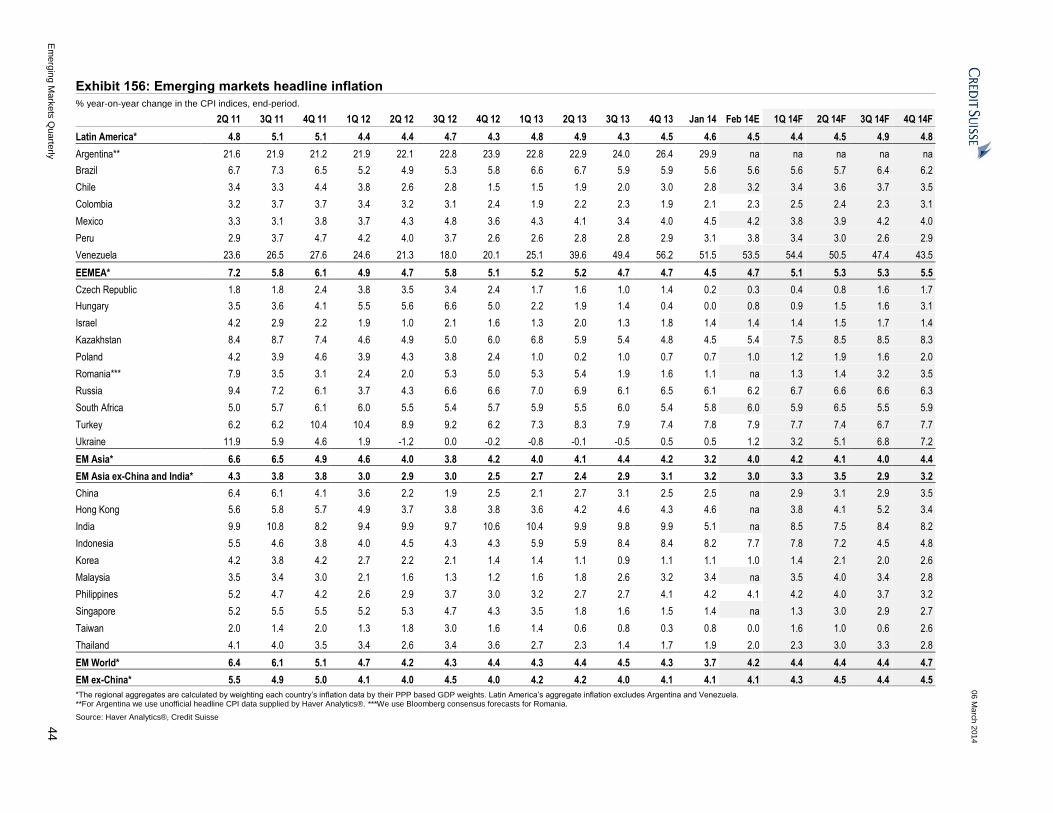

Year-on-year aggregate headline inflation in EM fell to 4.2% in January from its

recent high of 4.6% in November 2013 (Exhibits 52-53). The decline in EM headline

inflation between November 2013 and January 2014 was primarily driven by the sharp fall

in China's and India's food price inflation rates. Overall, we note that EM headline inflation

has been broadly stable since early 2012, while it moderated notably in DM during the

same period (Exhibit 50).

Indonesia, Turkey, Mexico and Peru stand out as the EM countries whose latest year-

on-year headline inflation readings exceed the upper bound of their respective headline

inflation target ranges, while in Poland, Hungary, the Czech Republic and Korea

headline inflation currently remains below the lower bound of their respective headline

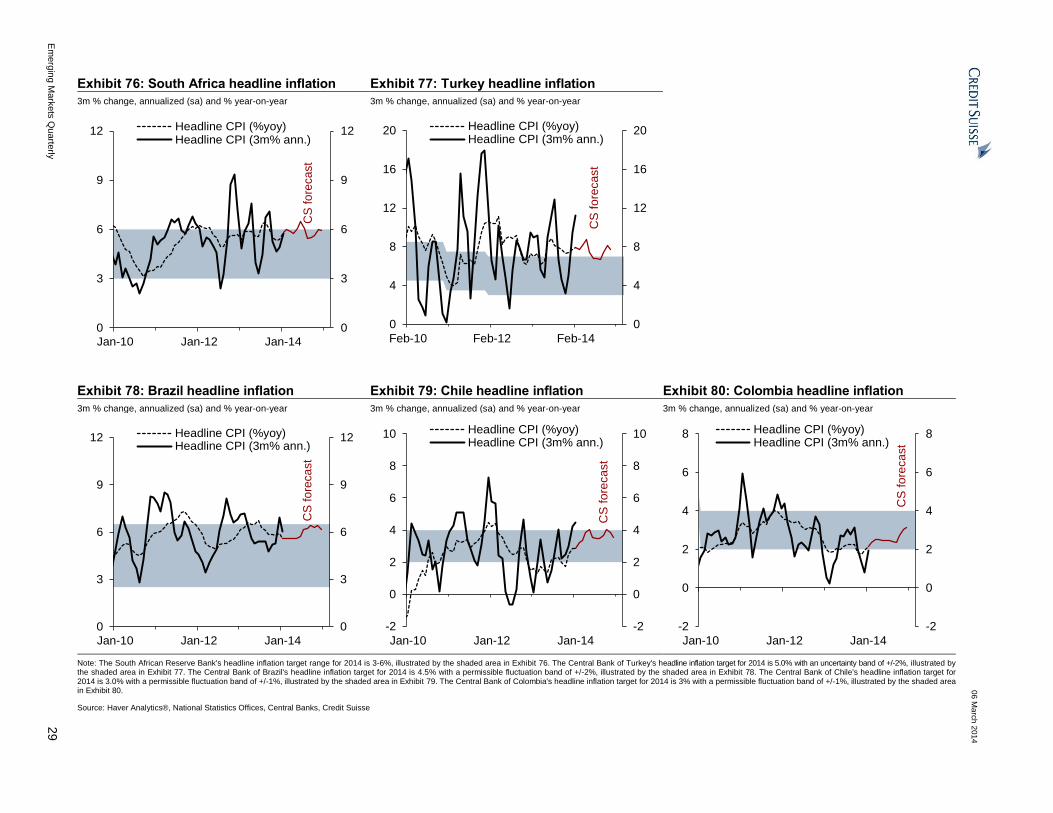

inflation target ranges (Exhibits 56 and 61-82). We expect year-on-year headline inflation to

exceed the upper bound of the target range only in Turkey by end-2014.

The run-rate (annualized three-month % change) of aggregate EM inflation declined

notably to 3.1% in January from a nine-month high of 5.1% in November, driven

mainly by the slowdown in the run-rate of food inflation in recent months in India

and China (Exhibits 54-55). The run-rate of headline inflation has been picking up in

LatAm since September, but it is set to ease modestly in 1Q 2014. The run-rate of the

EEMEA region's headline inflation, however, troughed in November and will continue to

increase in 1Q 2014, according to CS forecasts. In NJA (ex-China and India) the run-rate

of headline inflation has been almost stable since November 2013 and is set to remain soft

in the near term. The latest data for January and February are suggesting that the run-rate

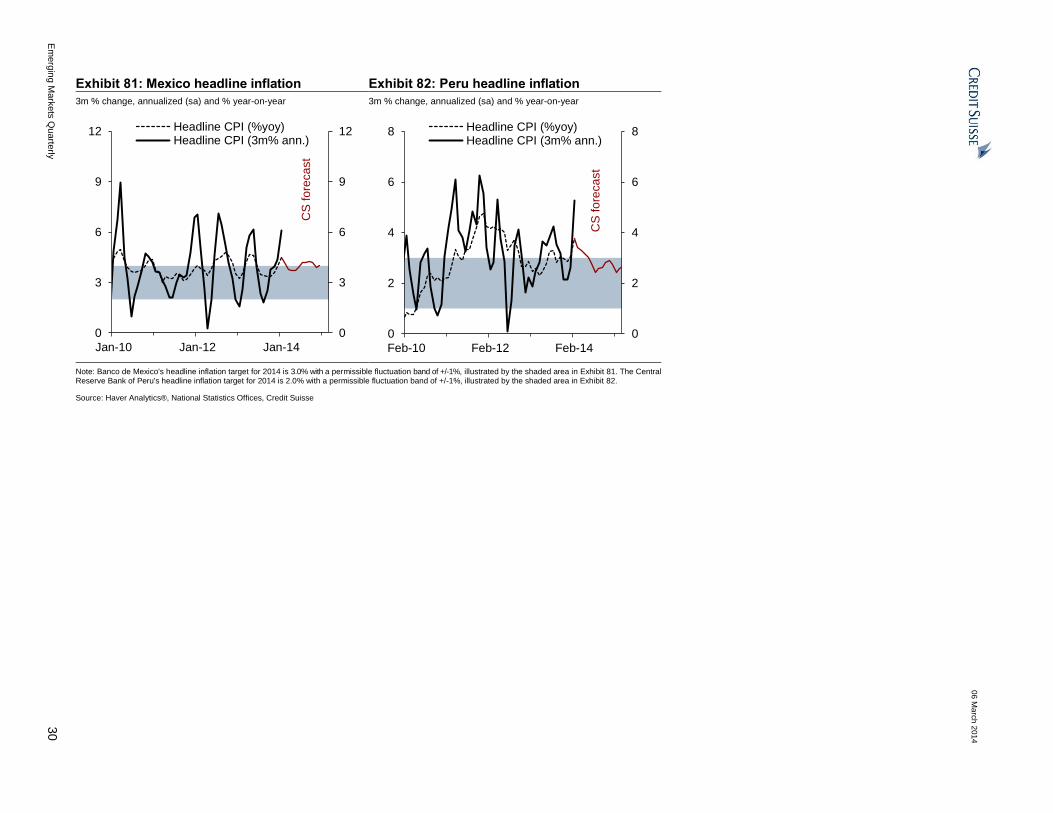

of headline inflation has been picking up in Mexico, Chile, Peru, Turkey, South Africa,

Romania, and the Philippines, while it has been declining in China, India, Singapore,

Taiwan, South Korea, the Czech Republic, Hungary, Israel, Poland and Russia in

recent months (Exhibits 61-82).

EM core1 inflation picked up modestly to 2.8% yoy in January from a 34-month low

of 2.5% yoy in August 2013 (Exhibits 51-53). This deterioration in core inflation dynamics

was driven primarily by sharp depreciation in some EM currencies during the past nine

months. However, we note that most EM economies (with the exception of Indonesia,

Malaysia, Thailand and Turkey) have been operating with notable excess capacities and

we forecast that they will continue to operate below potential in 2014, thus keeping

demand-pull inflationary pressures low, in our view. It is worth highlighting that Turkey and

Peru are the only EM countries that have their latest core inflation prints above the central

banks' target ranges for headline inflation.

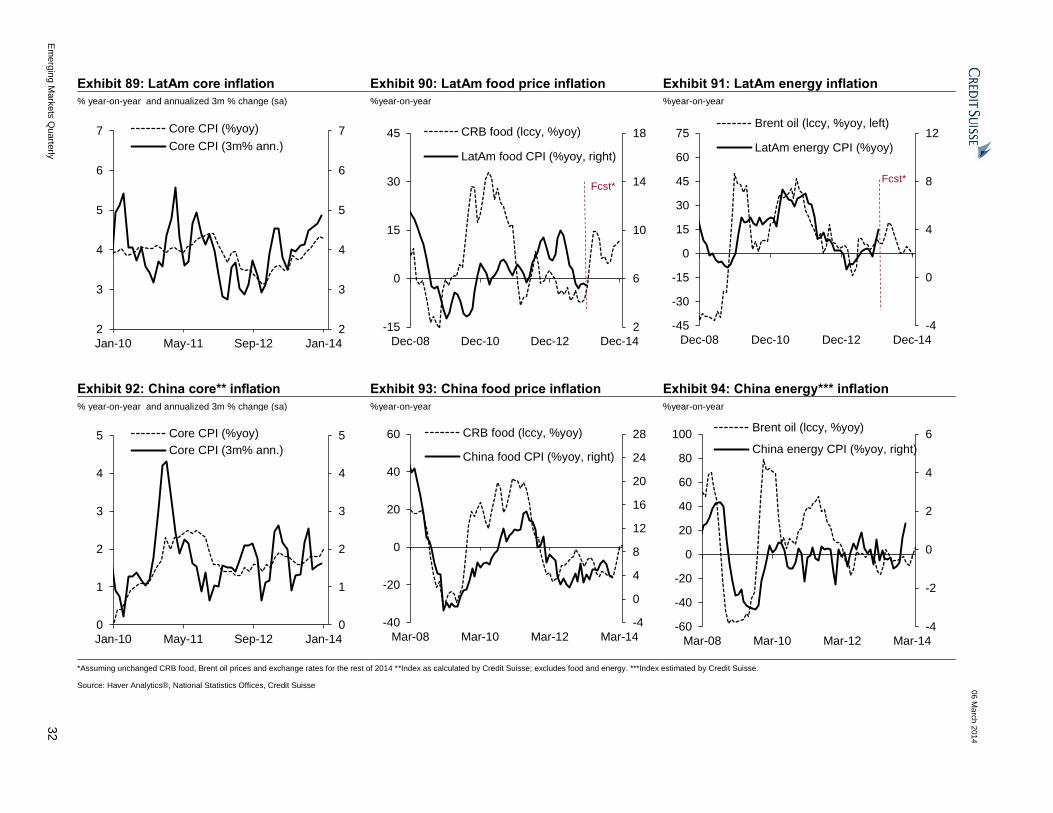

The run-rate of EM’s core inflation remained flat at 2.8% since November 2013 after

increasing from as low as 2.2% in May 2013, driven by the pick-up in LatAm and

EEMEA regions in 2H 2013 (Exhibits 83, 86 and 89). EMFX weakness in early 2014 has

yet to pass through to core inflation, in our view. EEMEA’s core inflation dynamics have

been deteriorating since July 2013 and the run-rate of core inflation reached a 17-month

high of 4.3% in January 2014 (Exhibit 86). In LatAm where the core inflation pressure is

most acute among EM regions, the run-rate of core inflation has been on the uptrend since

May 2013 and reached a 34-month high of 4.9% in January (Exhibit 89). Meanwhile, in the

1 CPI excluding food, energy, alcohol and tobacco for most EM countries. For exceptions, please see Exhibit 157 footnotes.

Natig Mustafayev

+44 20 7888 1065

06 March 2014

Emerging Markets Quarterly 22

NJA region (excluding China and India), the run-rate of core inflation declined to 1.8% in

January from the recent high of 2.7% in September 2013 (Exhibit 83).

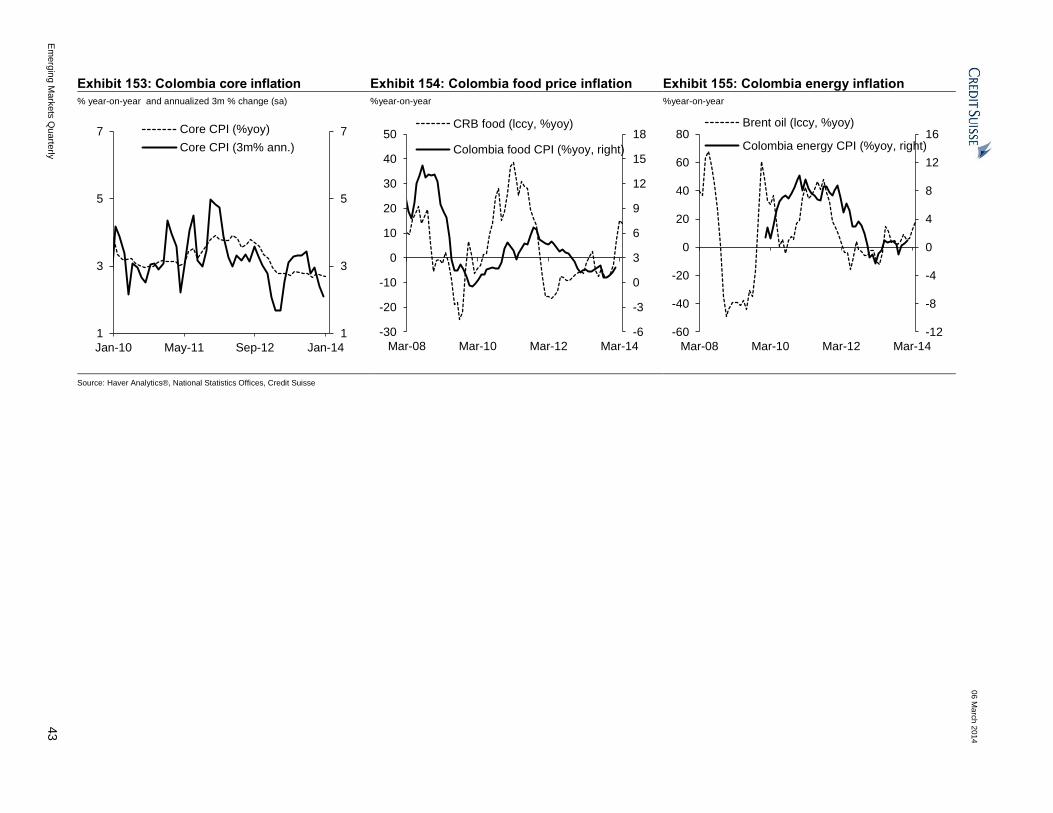

Overall, core inflation dynamics remain well-behaved in most EM countries, as the

run-rate of core inflation has remained within the respective central banks’ headline

inflation target ranges (Exhibits 92-153). The only exceptions are Turkey and Peru,

where the run-rate of core inflation has been above the target range for headline inflation

in recent months. We also note that the run-rate of core inflation remains elevated in

Brazil, Mexico and Russia as well.

EM’s year-on-year food price inflation has declined since November 2013 to a four-

year low of 5.0% in January (Exhibits 52-53). This was mainly driven by the sharp

decline in food price inflation in China and India while it remained broadly flat at record

low levels in the rest of NJA, EEMEA and LatAm in the past several months. However, the

recent sharp pick-up in agricultural commodities prices (Exhibit 48) (CRB food index has

increased by about 15% since late December to an eight-month high) poses upside risk to

EM food price inflation dynamics in the coming months (Exhibits 84, 87 and 90).

Exhibit 48: CRB food prices Exhibit 49: Brent oil price

% year-on-year % year-on-year

08 09 09 09 09 09 09 09 09 09 09 09 09 10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14

-30

-20

-10

0

10

20

30

40

50

-30

-20

-10

0

10

20

30

40

50

Dec-08 Dec-10 Dec-12 Dec-14

stable prices+/-15% shock

08 09 09 09 09 09 09 09 09 09 09 09 09 10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14

-60

-30

0

30

60

90

-60

-30

0

30

60

90

Dec-08 Dec-10 Dec-12 Dec-14

stable prices+/-15% shock

Note: We consider three different scenarios - global food prices remain at their March 2014 levels throughout 2014 and they are 15% higher/lower from their March 2014 levels throughout 2014.

Source: BLOOMBERG PROFESSIONAL™ service, Credit Suisse

Note: We consider three different scenarios - global oil prices remain at their March 2014 levels throughout 2014 and they are 15% higher/lower from their March 2014 levels throughout 2014.

Source: BLOOMBERG PROFESSIONAL™ service, Credit Suisse

If the current global oil price levels are sustained, this would support the benign

inflation dynamics in EM countries during the current year, in our view (Exhibits 85,

88 and 91). Global oil prices rose sharply in late summer 2013 before easing to about

$110/bbl (Brent oil) in early September 2013 and has been range-bound since then

(Exhibit 49). If the oil price remains at current levels, the contribution of energy prices to

EM year-on-year inflation might pick up slightly by mid-2014 due to unfavorable base

effects before coming off by the end of 2014, all else (such as EM nominal exchange rates

against USD and tax/subsidy levels) are unchanged. However, energy prices have a far

lower weight (about 10%) in the CPI baskets in EM countries than food (about 25%), and

the increase in energy prices would have to become very dramatic to generate an inflation

problem in EM countries on its own. We note that local energy inflation in most EEMEA

(South Africa, Poland, Romania, Israel and Turkey) and LatAm countries (Brazil, Chile,

Colombia and Peru), and in some NJA countries (South Korea, Singapore, Thailand

and Taiwan) have high correlation with global oil prices (Exhibits 94-155).

Our economists expect year-on-year aggregate EM headline inflation to pick up

from 4.2% in January to 4.4% by March 2014 and remain broadly stable at that level

until 4Q 2014 before picking up to 4.7% by end-2014 (Exhibit 52). The projected

06 March 2014

Emerging Markets Quarterly 23

gradual pick-up in EM inflation is mainly related to China where our economists expect the

year-on-year headline inflation to pick up from 2.5% in January to 3.5% by end-2014.

In NJA, we expect year-on-year headline inflation to increase from 4.0% in January to

4.4% by end-2014.

In LatAm, we expect year-on-year headline inflation to gradually increase from 4.6% in

January to 4.8% by 4Q 2014 after remaining stable through mid-2014.

In EEMEA, year-on-year headline inflation will increase modestly from 4.5% in January

to 5.5% by end-2014, according to our forecasts.

We expect the most notable increase in year-on-year headline inflation in 2014 to be

recorded in Kazakhstan, Hungary, Taiwan, South Korea and the Czech Republic, while

Indonesia’s and Hong Kong's headline inflation should decline modestly during the rest

of 2014, according to our forecasts (Exhibit 57).

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

24

Exhibit 50: Headline inflation in EM, euro area and US Exhibit 51: Core inflation in EM, euro area and US

% year-on-year % year-on-year

-2

0

2

4

6

8

10

-2

0

2

4

6

8

10

2004 2006 2008 2010 2012 2014

Euro area HICP inflationUS PCE inflationEM headline inflation

CS

fo

reca

st

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2004 2006 2008 2010 2012 2014

Euro area core HICP inflationUS core PCE inflationEM core inflation

CS

fore

cast

Source: Haver Analytics®, National Statistics Offices, Eurostat, Bureau of Economic Analysis, Credit Suisse Source: Haver Analytics®, National Statistics Offices, Eurostat, Bureau of Economic Analysis, Credit Suisse

Exhibit 52: EM CPI inflation Exhibit 53: EM (ex-China & India) CPI inflation

% year-on-year % year-on-year

1

3

5

7

9

1

4

7

10

13

16

Jan-08 Jan-10 Jan-12 Jan-14

Food (left)

Core**

Headline CPI*

CS

fore

cast

1

4

7

10

1

4

7

10

13

16

Jan-08 Jan-10 Jan-12 Jan-14

Food (left)

Core**

Headline CPI*

CS

fore

cast

*CPI inflation for Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Hungary, Israel, Kazakhstan, Poland, Russia, S. Africa, Turkey, Ukraine, China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand were weighted by their PPP adjusted GDP weights. **Core CPI is defined as the CPI excluding food, energy, alcohol and tobacco.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

*CPI inflation series for Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Hungary, Israel, Kazakhstan, Poland, Russia, S. Africa, Turkey, Ukraine, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand were weighted by their PPP adjusted GDP weights. **Core CPI is defined as the CPI excluding food, energy, alcohol and tobacco.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

25

Exhibit 54: The run-rate of EM CPI inflation Exhibit 55: The run-rate of EM (ex-China & India) CPI inflation

Annualized 3m % change (sa) Annualized 3m % change (sa)

0

4

8

12

16

0

4

8

12

16

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Headline CPI*

Food

Core**

0

4

8

12

1610 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14

0

4

8

12

16

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Headline CPI*

Food

Core**

*CPI inflation for Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Hungary, Israel, Kazakhstan, Poland, Russia, S. Africa, Turkey, Ukraine, China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand were weighted by their PPP adjusted GDP weights. **Core CPI is defined as the CPI excluding food, energy, alcohol and tobacco.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

*CPI inflation series for Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Hungary, Israel, Kazakhstan, Poland, Russia, S. Africa, Turkey, Ukraine, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand were weighted by their PPP adjusted GDP weights. **Core CPI is defined as the CPI excluding food, energy, alcohol and tobacco.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

Exhibit 56: EM headline inflation relative to target Exhibit 57: Headline inflation in EM countries

pp; vertical bar refers to the size of the inflation target range % year-on-year

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Turk

ey

Bra

zil

S.

Afr

ica

Russia

Thaila

nd

Mexic

o

Pe

ru

Chile

Indonesia

Colo

mbia

Hungary

Chin

a

Ko

rea

Cze

ch R

ep.

India

Po

lan

d

Isra

el

Ph

ilippin

es

Gap between latest inflation and target

Gap between CS 2014 year-end forecast and target

-1

1

3

5

7

9

INR

TR

Y

IDR

RU

B

ZA

R

BR

L

KZ

T

HK

D

MX

N

PH

P

PE

N

MY

R

CL

P

CN

Y

CO

P

TH

B

SG

D

ILS

KR

W

PL

N

CZ

K

HU

F

TW

D

Latest

Dec 2014 (CS forecast)

Source: Haver Analytics®, National Statistics Offices, Central Banks, Credit Suisse Source: Haver Analytics®, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

26

Exhibit 58: NJA* (ex-Ch & In) headline inflation Exhibit 59: EEMEA* headline inflation Exhibit 60: LatAm* headline inflation

3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

0

2

4

6

8

10

0

2

4

6

8

10

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

0

2

4

6

8

10

0

2

4

6

8

10

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

0

2

4

6

8

10

0

2

4

6

8

10

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

Exhibit 61: China headline inflation Exhibit 62: India headline inflation Exhibit 63: Indonesia headline inflation

3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

0

3

6

9

12

0

3

6

9

12

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

0

5

10

15

20

25

0

5

10

15

20

25

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15 15

0

3

6

9

12

15

18

0

3

6

9

12

15

18

Feb-10 Feb-12 Feb-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

*LatAm CPI includes series for Brazil, Chile, Colombia, Mexico and Peru aggregated by their PPP adjusted GDP weights. EEMEA CPI includes series for Czech Republic, Hungary, Israel, Poland, Romania, Russia, South Africa, Turkey, and Ukraine. NJA CPI includes series for Hong Kong, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand.

Note: Bank Indonesia's headline inflation target for 2014 is 4.5% with a +/-1% permissible fluctuation band, illustrated by the shaded area in Exhibit 63.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

27

Exhibit 64: South Korea headline inflation Exhibit 65: Malaysia headline inflation Exhibit 66: The Philippines headline inflation

3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15 15

-1

2

5

8

-1

2

5

8

Feb-10 Feb-12 Feb-14

Headline CPI (%yoy)Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

0

2

4

6

8

0

2

4

6

8

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15 15

0

2

4

6

8

10

0

2

4

6

8

10

Feb-10 Feb-12 Feb-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

Exhibit 67: Singapore headline inflation Exhibit 68: Taiwan headline inflation Exhibit 69: Thailand headline inflation

3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-8

-4

0

4

8

12

-8

-4

0

4

8

12

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-6

-4

-2

0

2

4

6

8

-6

-4

-2

0

2

4

6

8

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15 15

-2

0

2

4

6

8

-2

0

2

4

6

8

Feb-10 Feb-12 Feb-14

Headline CPI (%yoy)

Headline CPI (3m% ann.)

CS

fo

reca

st

Note: 1. Bank of Korea's headline inflation target range for 2014 is 2.5-3.5%, illustrated by the shaded area in Exhibit 64. The Philippines Central Bank's headline inflation target for 2012-2014 is 4.0% with a +/-1% permissible fluctuation band, illustrated by the shaded area in Exhibit 66.

Source: Haver Analytics®, National Statistics Offices, Credit Suisse

06

Ma

rch

20

14

Em

erg

ing M

ark

ets

Qu

arte

rly

28

Exhibit 70: Czech Republic headline inflation Exhibit 71: Hungary headline inflation Exhibit 72: Israel headline inflation

3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-4

-2

0

2

4

6

8

-4

-2

0

2

4

6

8

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-2

1

4

7

10

13

-2

1

4

7

10

13

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-3

0

3

6

9

-3

0

3

6

9

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)Headline CPI (3m% ann.)

CS

fo

reca

st

Exhibit 73: Poland headline inflation Exhibit 74: Romania headline inflation Exhibit 75: Russia headline inflation

3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year 3m % change, annualized (sa) and % year-on-year

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-3

0

3

6

9

-3

0

3

6

9

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)Headline CPI (3m% ann.)

CS

fo

reca

st

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15

-4

0

4

8

12

16

-4

0

4

8

12

16

Jan-10 Jan-12 Jan-14

Headline CPI (%yoy)Headline CPI (3m% ann.)

fore

ca

st

10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 12 12 12 12 12 13 13 13 13 13 13 13 13 13 13 13 13 14 14 14 14 14 14 14 14 14 14 14 14 15 15 15

0

3

6

9

12

15

0

3

6

9

12