Olympus (7733 / 7733 JP) - Credit Suisse | PLUS

44

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 06 September 2016 Asia Pacific/Japan Equity Research Imaging Technology (Precision (Japan)) / MARKET WEIGHT Olympus (7733 / 7733 JP) INITIATION Opportunity to buy in as medium-term investment ■ Initiate coverage: We initiate coverage of Olympus with an OUTPERFORM rating and a ¥4,100 target price (potential return 22%). We see risk that Olympus may miss FY3/17 guidance due to yen appreciation and protracted business negotiations, and think it lacks share-price catalysts over the near term. However, we think the current share price offers an opportunity to buy in as a medium-term investment, given the potential for growth by the medical business. ■ Product line-up that provides significant benefits for both patients and doctors: Olympus’ mainstay gastrointestinal endoscope, surgical endoscope systems, and endotherapy devices have significant growth potential, as they are a good fit with the current healthcare trends of early diagnosis and minimally invasive therapies. We expect steady growth in the gastrointestinal endoscope segment, as Olympus dominates in terms of market share and technical skills. In the surgical and endotherapy device segments, we expect Olympus to grow its market share as it has a strong sales force and a unique line-up of products that reduce the burden on both patient and doctor. Sales stagnated in both endoscope and surgery fields in 1Q, particularly in the US, as business negotiations dragged on, but we think this may only be a transient trend. We expect Olympus to return to growth as more patients undergo gastroscopic procedures, in line with the trends of demographic aging and early diagnosis, and with the introduction of ultra-high definition (4K) surgical endoscopy systems. ■ Risks/catalysts: Risks include an economic slowdown, yen appreciation, and price competition with rival companies. The market could re-evaluate Olympus if 2Q results show a recovery in endoscope and surgerical sales in the US after these segments stagnated in 1Q. ■ Valuation: We base our valuation on EV/EBITDA to allow global comparisons and to reflect investment in expansion of manufacturing sites to grow the medical business. We apply an EV/EBITDA of 11x, the average multiple since FY3/14 after the company announced a capital tie-up with Sony (6758) and had resolved the loss-concealed issue. Share price performance 80 90 100 110 120 2000 3000 4000 5000 6000 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Price (LHS) Rebased Rel (RHS) The price relative chart measures performance against the TOPIX which closed at 1343.85 on 23/08/16 On 23/08/16 the spot exchange rate was ¥103.47/US$1 Performance over 1M 3M 12M Absolute (%) 5.1 -24.2 -17.7 Relative (%) 0.1 -24.5 -10.7 Financial and valuation metrics Year 3/16A 3/17E 3/18E 3/19E Sales (¥ bn) 804.6 753.0 805.3 843.7 Operating profit (¥ bn) 104.5 72.4 87.2 97.0 Recurring profit (¥ bn) 70.8 58.5 73.2 83.0 Net income (¥ bn) 62.6 49.4 54.9 58.1 EPS (¥) 182.9 144.5 160.5 169.8 Change from previous EPS (%) n.a. IBES Consensus EPS (¥) n.a. 161.4 180.8 194.6 EPS growth (%) n.m. -21.0 11.1 5.8 P/E (x) 23.9 23.4 21.0 19.9 Dividend yield (%) 0.4 0.8 1.0 1.2 EV/EBITDA(x) 10.5 9.6 8.1 7.2 P/B (x) 3.9 2.7 2.5 2.3 ROE(%) 16.9 12.2 12.3 11.9 Net debt/equity (%) 32.4 14.1 6.1 net cash Source: Company data, Thomson Reuters, IFIS, Credit Suisse estimates. Rating OUTPERFORM* Price (05 Sep 16, ¥) 3,375 Target price (¥) 4,100¹ Chg to TP (%) 21.5 Market cap. (¥ bn) 1,155.08 (US$ 11.16) Enterprise value (¥ bn) 1,214.99 Number of shares (mn) 342.25 Free float (%) 70.0 52-week price range 4,945 - 3,195 *Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months. Research Analysts Mika Nishimura 81 3 4550 7369 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Olympus (7733 / 7733 JP) - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit

Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

06 September 2016

Asia Pacific/Japan

Equity Research

Imaging Technology (Precision (Japan)) / MARKET WEIGHT

Olympus (7733 / 7733 JP) INITIATION

Opportunity to buy in as medium-term investment ■ Initiate coverage: We initiate coverage of Olympus with an OUTPERFORM

rating and a ¥4,100 target price (potential return 22%). We see risk that Olympus

may miss FY3/17 guidance due to yen appreciation and protracted business

negotiations, and think it lacks share-price catalysts over the near term. However,

we think the current share price offers an opportunity to buy in as a medium-term

investment, given the potential for growth by the medical business.

■ Product line-up that provides significant benefits for both patients and

doctors: Olympus’ mainstay gastrointestinal endoscope, surgical endoscope

systems, and endotherapy devices have significant growth potential, as they are

a good fit with the current healthcare trends of early diagnosis and minimally

invasive therapies. We expect steady growth in the gastrointestinal endoscope

segment, as Olympus dominates in terms of market share and technical skills. In

the surgical and endotherapy device segments, we expect Olympus to grow its

market share as it has a strong sales force and a unique line-up of products that

reduce the burden on both patient and doctor. Sales stagnated in both

endoscope and surgery fields in 1Q, particularly in the US, as business

negotiations dragged on, but we think this may only be a transient trend. We

expect Olympus to return to growth as more patients undergo gastroscopic

procedures, in line with the trends of demographic aging and early diagnosis,

and with the introduction of ultra-high definition (4K) surgical endoscopy systems.

■ Risks/catalysts: Risks include an economic slowdown, yen appreciation, and

price competition with rival companies. The market could re-evaluate Olympus if

2Q results show a recovery in endoscope and surgerical sales in the US after

these segments stagnated in 1Q.

■ Valuation: We base our valuation on EV/EBITDA to allow global comparisons

and to reflect investment in expansion of manufacturing sites to grow the medical

business. We apply an EV/EBITDA of 11x, the average multiple since FY3/14

after the company announced a capital tie-up with Sony (6758) and had resolved

the loss-concealed issue.

Share price performance

80

90

100

110

120

2000

3000

4000

5000

6000

Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

TOPIX which closed at 1343.85 on 23/08/16

On 23/08/16 the spot exchange rate was ¥103.47/US$1

Performance over 1M 3M 12M Absolute (%) 5.1 -24.2 -17.7 Relative (%) 0.1 -24.5 -10.7

Financial and valuation metrics

Year 3/16A 3/17E 3/18E 3/19E Sales (¥ bn) 804.6 753.0 805.3 843.7 Operating profit (¥ bn) 104.5 72.4 87.2 97.0 Recurring profit (¥ bn) 70.8 58.5 73.2 83.0 Net income (¥ bn) 62.6 49.4 54.9 58.1 EPS (¥) 182.9 144.5 160.5 169.8 Change from previous EPS (%) n.a. IBES Consensus EPS (¥) n.a. 161.4 180.8 194.6 EPS growth (%) n.m. -21.0 11.1 5.8 P/E (x) 23.9 23.4 21.0 19.9 Dividend yield (%) 0.4 0.8 1.0 1.2 EV/EBITDA(x) 10.5 9.6 8.1 7.2 P/B (x) 3.9 2.7 2.5 2.3 ROE(%) 16.9 12.2 12.3 11.9 Net debt/equity (%) 32.4 14.1 6.1 net cash

Source: Company data, Thomson Reuters, IFIS, Credit Suisse estimates.

Rating OUTPERFORM* Price (05 Sep 16, ¥) 3,375 Target price (¥) 4,100¹ Chg to TP (%) 21.5 Market cap. (¥ bn) 1,155.08 (US$ 11.16) Enterprise value (¥ bn) 1,214.99 Number of shares (mn) 342.25 Free float (%) 70.0 52-week price range 4,945 - 3,195

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Mika Nishimura

81 3 4550 7369

06 September 2016

Olympus (7733 / 7733 JP) 2

Table of contents Key charts 3 1. Rating and valuation 4

Initiate at OUTPERFORM with ¥4,100 target price 4 Expect steady growth by endoscopes, higher market share for surgical and

endotherapy devices 5 Current valuation lower than sector peers 5 Risks, catalysts 7

2. Business structure 9 Medical business generates nearly all of the profits 9

3. Focus on early diagnosis and minimally invasive treatment in medical 11 Products contribute to improve patients’ quality of life 11 Help curb medical expenditure, reduce burden on health workers 12

4. Gastrointestinal endoscopes basis for growth 13 Commanding market share, continuous technical innovation should ensure stable

growth 13 Demand for scopes and services growing in line with increase in testing volume 14 Current generation of endoscopes in fourth year of five-to-seven year product cycle 15 North American endoscope sales down YoY in 1Q FY3/17, but protracted decline

unlikely 16 5. Expanding product lineup, promoting development of surgical techniques 18

Wider application of endoscopic surgery expands demand for instruments 18 Steady sales expansion, growth likely to continue 21

6. Expecting share gains in surgery driven by unique products 23 Building up business via M&A activity, gaining share 23 Endoscopic surgery growing, eligible for insurance 23 Expecting steady growth in energy devices excluding special factors 24 4K surgical endoscopy systems: inquiries strong 25 First-quarter earnings off to slow start, but growth expectations unchanged 25

7. Significant growth potential for medical segment in emerging markets 28 Expansion in emerging markets likely to continue 28

8. Earnings outlook 30 Expecting return to profit growth from FY3/18 30 Beefing up production structure to meet medium-term plan 31 Shareholder returns 32

9. Company history 38 Gastroscopy history of more than 60 years 38 Upgrading compliance and governance systems 39

06 September 2016

Olympus (7733 / 7733 JP) 3

Key charts Figure 1: Olympus EV/EBITDA: Our ¥4,100 target price on

FY3/18E EV/EBITDA of 11x

Figure 2: EV/EBITDA of peers: Growing disparity with

sector peer average

6

8

10

12

14

16

18

20

3/9

13

/92

3/9

33

/94

3/9

53

/96

3/9

73

/98

3/9

93

/00

3/0

13

/02

3/0

33

/04

3/0

53

/06

3/0

73

/08

3/0

93

/10

3/1

13

/12

3/1

33

/14

3/1

53

/16

3/1

7E

3/1

8E

3/1

9E

(X)

11X

2 x

4 x

6 x

8 x

10 x

12 x

14 x

16 x

1/2

007

7/2

007

1/2

008

7/2

008

1/2

009

7/2

009

1/2

010

7/2

010

1/2

011

7/2

011

1/2

012

7/2

012

1/2

013

7/2

013

1/2

014

7/2

014

1/2

015

7/2

015

1/2

016

7/2

016

Johnson & Johnson StrykerMedtronic Boston ScientificOlympus AVERAGE

Source: Thomson Reuters, Credit Suisse estimates Source: Thomson Reuters

Figure 3: Medical business sales forecast: Expecting

return to sales growth from FY3/18

Figure 4: Medical business OP forecast: Maintaining a

high margin

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

700

3/0

2

3/0

3

3/0

4

3/0

5

3/0

6

3/0

7

3/0

8

3/0

9

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

3/1

7E

3/1

8E

3/1

9E

((JP

Y b

n)

Endotherapy

Surgical

Endoscopes

YoY

Surgical + Endoscopes

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

1603/0

8

3/0

9

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

3/1

7E

3/1

8E

3/1

9E

(JP

Y b

n)

OP OPM

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates,

Figure 5: Medical sales YoY growth by region: Slowdown

in 1Q only temporary; Olympus still has growth potential

Figure 6: Healthcare expenditure per capita: Growth

potential in China and Asia market

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

FY13 FY14 FY15 FY16

North America

Europe

Asia/Oceania

0

50

100

150

200

250

300

350

400

450

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

(US

$)

China

Asia (excluding Japan and China)

Source: Company data, Credit Suisse Source: World Bank, Credit Suisse

06 September 2016

Olympus (7733 / 7733 JP) 4

1. Rating and valuation Initiate at OUTPERFORM with ¥4,100 target price

Near-term catalysts lacking, but opportunity to buy in as medium-term investment

We initiate coverage of Olympus with an OUTPERFORM rating and a ¥4,100 target price

(potential return 22%).

We see risk that Olympus may miss its FY3/17 guidance, due to the negative effects of

yen appreciation and protracted business negotiations. We believe the 1Q results could

depress the consensus forecast and think Olympus lacks share-price catalysts over the

near term. However, we think the current share price offers an opportunity to buy in as a

medium-term investment, given the potential for growth in the medical business.

Figure 7: Olympus (7733) – Earnings summary

DPS P/E

¥3,375 ¥bn YoY (%) ¥bn YoY (%) ¥bn YoY (%) ¥bn YoY (%) ¥ YoY (%) ¥ (x)

Consolidated FY

Mar-15 A 764.7 7.2% 91.0 23.9% 8.9 -45.6% -8.7 NM -25.5 NM 10.0 NM

Mar-16 A 804.6 5.2% 104.5 14.8% 70.8 692.5% 62.6 NM 182.9 NM 17.0 23.9

Mar-17 CS E (new) 753.0 -6.4% 72.4 -30.6% 58.5 -17.4% 49.4 -21.0% 144.5 -21.0% 28.0 23.4

CoE 775.0 -3.7% 77.0 -26.3% 67.0 -5.4% 57.0 -8.9% 166.6 -8.9% 28.0 20.3

IBES E 767.2 -4.6% 78.5 -24.9% 68.8 -2.8% 55.7 -10.9% 161.4 -11.8% 28.3 20.9

Mar-18 CS E (new) 805.3 6.9% 87.2 20.4% 73.2 25.2% 54.9 11.1% 160.5 11.1% 35.0 21.0

IBES E 796.5 3.8% 92.6 18.0% 83.7 21.6% 62.0 11.2% 180.8 12.0% 33.7 18.7

Mar-19 CS E (new) 843.7 4.8% 97.0 11.2% 83.0 13.4% 58.1 5.8% 169.8 5.8% 40.0 19.9

IBES E 832.0 4.5% 102.2 10.3% 93.0 11.1% 66.3 6.9% 194.6 7.6% 41.8 17.3

Consolidated Half Year

Mar-16 1H A 395.8 11.5% 50.1 30.3% 39.5 41.3% 35.8 60.4% 104.6 60.4% 0.0

2H A 408.8 -0.2% 54.4 3.5% 31.3 NM 26.8 NM 78.3 NM 17.0

Mar-17 1H CS E (new) 357.0 -9.8% 26.6 -46.8% 19.6 -50.2% 18.4 -48.7% 53.7 -48.7% 0.0

CoE 366.0 -7.5% 29.0 -42.1% 25.0 -36.7% 20.0 -44.1% 58.4 -44.1% 0.0

2H CS E (new) 396.1 0.1% 45.8 -8.5% 38.8 -1.6% 31.1 -13.2% 90.8 -13.2% 28.0

CoE 409.0 0.0% 48.0 -11.7% 42.0 34.0% 37.0 38.1% 108.1 38.1% 28.0

Consolidated Quarter

Mar-16 Q1 A 187.6 12.3% 17.2 14.0% 14.3 27.8% 16.7 105.6%

Q2 A 208.2 10.7% 32.9 40.8% 25.2 50.2% 19.1 34.4%

Q3 A 196.8 0.9% 23.6 -0.2% 6.9 -46.5% 7.0 -26.6%

Q4 A 212.0 -1.2% 30.8 6.6% 24.5 NM 19.7 NM

Mar-17 Q1 A 168.4 -10.2% 10.8 -37.0% 7.3 -48.5% 8.5 -49.0%

Q2 CS E (new) 188.5 -9.5% 15.8 -51.9% 12.3 -51.1% 9.9 -48.3%

EPS05-Sep-16 Sales Operating profit Recurring profit Net profit

Source: Company data, I/B/E/S, Credit Suisse estimates

Our ¥4,100 target price is

based on FY3/18E

EV/EBITDA of 11x

06 September 2016

Olympus (7733 / 7733 JP) 5

Expect steady growth by endoscopes, higher market

share for surgical and endotherapy devices

Product portfolio consistent with current medical trends of early diagnosis,

minimally invasive therapies

Endoscopic techniques allow early diagnosis and treatment and improve patient

prognoses (allowing longer survival rates). Endoscopic and gastroscopic treatments

reduce the physical burden on the patient and allow an earlier return to work and other

social activities. Olympus has a product line-up that helps improve patient QOL at every

phase, from diagnosis to treatment.

High barriers to entry in gastroscopy market; potential for higher market share in

endosurgical and therapeutic device segments

Over the past few decades, Olympus has built up close lines of communication with

hospitals and physicians, which has allowed the company to develop various

groundbreaking technologies for gastroscopic systems and build high barriers to entry to

keep out the competition.

In the endosurgery and therapeutic device segments, Olympus has bolstered its sales

force, hiring more sales staff in the largest market in the US. Olympus can differentiate

itself from the competition through its superior line-up of endosurgery products that help to

reduce the burden on the physician; we think the company could grow its market share

further. The Olympus product portfolio includes 3D and 4K endosurgery systems that

make observations easier during surgery and a dual-energy instrument (Thunderbeat) that

combines devices for dissection and vessel sealing in a single unit. We expect Olympus to

benefit from an expanded line-up of therapeutic devices and the development of

technologies that draw on the company’s strengths.

Medical segment slowdown in 1Q only temporary; Olympus still has growth

potential over the medium term

Both the endoscopes and surgical segments stagnated in the US in 1Q, generating market

concerns over structural problems. Olympus attributes the slowdown to slightly protracted

negotiations over capital products and explained that sales have been pushed back into

2Q or beyond. We agree that the slowdown is probably temporary. We expect Olympus to

return to a growth trajectory as more patients undergo gastroscopic procedures, in line

with the trends of demographic aging and early diagnosis, and with the launch of 4K

surgical endoscopy systems.

Current valuation lower than sector peers

Base our ¥4,100 target price on EV/EBITDA of 11x to our FY3/18 estimates

We base our valuation on EV/EBITDA to allow global comparisons and to reflect

investment in expansion of manufacturing sites in order to grow the medical business. We

apply to our FY3/18 estimates an EV/EBITDA of 11x, the average multiple since FY3/14

after the company announced a capital tie-up with Sony and had resolved the loss-

concealed losses issue. The share price has fallen below a multiple of 10x, approaching

the bottom of the range for the past three years; we think it could recover to the average

for the past three years given the ongoing growth by the medical business.

Product lineup that helps

improve patient QOL

High barriers to entry to

keep out the competition by

various groundbreaking

technologies development

Olympus to return to a

growth trajectory as more

patients undergo

gastroscopic procedures

and the launch of 4K

surgical endoscopy

systems.

EV/EBITDA of 11x is the

average multiple since

FY3/14

06 September 2016

Olympus (7733 / 7733 JP) 6

Figure 8: Olympus (7733) – EV/EBITDA

6

8

10

12

14

16

18

20

3/9

1

3/9

2

3/9

3

3/9

4

3/9

5

3/9

6

3/9

7

3/9

8

3/9

9

3/0

0

3/0

1

3/0

2

3/0

3

3/0

4

3/0

5

3/0

6

3/0

7

3/0

8

3/0

9

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

3/1

7E

3/1

8E

3/1

9E

(X)

11X

Source: Thomson Reuters, Credit Suisse estimates

Figure 9: Olympus (7733) – P/E Figure 10: Olympus (7733) – P/B

0

10

20

30

40

50

60

70

80

90

100

3/9

13/9

23/9

33/9

43/9

53/9

63/9

73/9

83/9

93/0

03/0

13/0

23/0

33/0

43/0

53/0

63/0

73/0

83/0

93/1

03/1

13/1

23/1

33/1

43/1

53/1

63/1

7E

3/1

8E

3/1

9E

(X)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

3/9

13/9

23/9

33/9

43/9

53/9

63/9

73/9

83/9

93/0

03/0

13/0

23/0

33/0

43/0

53/0

63/0

73/0

83/0

93/1

03/1

13/1

23/1

33/1

43/1

53/1

63/1

7E

3/1

8E

3/1

9E

(X)

Source: Thomson Reuters, Credit Suisse estimates Source: Thomson Reuters, Credit Suisse estimates

Growing disparity with sector peer average

The difference between the Olympus P/E and the average multiple at other medical device

and equipment makers engaged in endoscopic devices is currently greater than at any

other time over the past ten years. Olympus still dominates the gastroscopy market,

however, and we think this gap will almost certainly narrow as Olympus moves its

unprofitable digital still camera business to the breakeven point. The average P/E for

sector peers is 13x.

The average P/E for sector

peers is 13x

06 September 2016

Olympus (7733 / 7733 JP) 7

Figure 11: EV/EBITDA of peers: Growing disparity with sector peer average

2 x

4 x

6 x

8 x

10 x

12 x

14 x

16 x1/2

007

6/2

007

11/2

007

4/2

008

9/2

008

2/2

009

7/2

009

12/2

009

5/2

010

10/2

010

3/2

011

8/2

011

1/2

012

6/2

012

11/2

012

4/2

013

9/2

013

2/2

014

7/2

014

12/2

014

5/2

015

10/2

015

3/2

016

8/2

016

Johnson &Johnson

Stryker

Medtronic

BostonScientific

Olympus

AVERAGE

Source: Thomson Reuters

Figure 12: Valuations vs. medical device peers

NAME FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E

JOHNSON & JOHNSON 12.5 12.3 11.6 11.3 18.4 17.7 16.7 15.9 4.0 4.1 4.1 4.1

STRYKER CORP 19.1 13.9 12.5 11.7 30.0 19.9 18.0 16.6 5.1 4.3 4.3 4.3

MEDTRONIC PLC 16.0 14.3 13.2 12.1 31.4 18.8 17.1 - 2.1 2.2 2.2 2.2

BOSTON SCIENTIFIC CORP 65.9 16.2 14.7 13.1 - 21.6 18.9 16.7 3.8 4.2 4.2 4.2

OLYMPUS CORP 11.0 10.1 8.9 8.1 24.4 21.3 19.1 17.5 4.0 2.7 2.7 2.7

PER PBREV/EBITDA

Source: Bloomberg

Risks, catalysts

Risks include an economic slowdown, yen appreciation, and competition; catalysts

could include 2Q results

Full-year OP is depressed ¥1.1bn for every ¥1 appreciation versus the dollar and ¥700mn

for every ¥1 appreciation versus the euro. Olympus assumes ¥105/$ and ¥115/€ from 2Q

FY3/17, compared with our estimates of ¥103/$ and ¥114/€.

Investors should watch for signs of an economic slowdown that could further draw out

business negotiations as hospitals work to cut spending. We expect Olympus to secure

orders for a certain level of renewal demand through increased use of the value per

procedure (VPP) system.

The high barriers to entry in the endoscope market mean competition is unlikely to heat up

in this segment. Olympus aims to increase its share of the surgical and endotherapy

device segments, so we think investors need to keep monitoring for any changes in share

due to price competition by rivals.

We see few events capable of catalyzing the share price over the near term, but the

market could re-evaluate Olympus if the 2Q results show a recovery in endoscope and

surgical sales in the US, after these segments stagnated in 1Q.

The market could re-

evaluate Olympus if 2Q

results show a recovery in

endoscope and surgical

sales in the US

06 September 2016

Olympus (7733 / 7733 JP) 8

Figure 13: Olympus share price, OP trend and major history

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0

20

40

60

80

100

120

140

198

0/0

4

198

1/0

4

198

2/0

4

198

3/0

4

198

4/0

4

198

5/0

4

198

6/0

4

198

7/0

4

198

8/0

3

198

9/0

3

199

0/0

3

199

1/0

3

199

2/0

3

199

3/0

3

199

4/0

3

199

5/0

3

199

6/0

3

199

7/0

3

199

8/0

3

199

9/0

3

200

0/0

3

200

1/0

3

200

2/0

3

200

3/0

3

200

4/0

3

200

5/0

3

200

6/0

3

200

7/0

3

200

8/0

3

200

9/0

3

201

0/0

3

201

1/0

3

201

2/0

3

201

3/0

3

201

4/0

3

201

5/0

3

201

6/0

3

OP (LHS)

Share price (RHS)

2001Olympus enters into a

comprehensive alliance agreement with Terumo

in the medical equipment field

2005Olympus and Terumo to

strengthen their business partnership

2008Acquisition of the

Gyrus Group

2009Olympus agrees to divest its analyzer

business to Beckman Coulte

2011Transfer inkjet printer

business to Riso Kagaku

2012Hiroyuki Sasa is

appointed to President

2012Forms a business and capital alliance

with Sony

2013Sony Olympus Medical

Solutions is established

2011The concealment

of losses is revealed

(JP

Yb

n)

(JP

Y)

Source: Company data, Thomson Reuters, Credit Suisse

06 September 2016

Olympus (7733 / 7733 JP) 9

2. Business structure Medical business generates nearly all profit

Medical business focuses on gastroscopes, surgical endoscopes and

attachments/devices; scientific solutions segment profits are stable

The medical business, which centers on gastroscopes, surgical endoscopes and

attachments/devices, accounts for 76% of total company sales. The scientific solutions

segment, comprising mainly microscopes (the company’s original business), accounts for

13% of total company sales, while the imaging solutions segment (mainly digital still

cameras) accounts for 10% (all figures based on FY3/16).

The mainstay medical business generates nearly all of the company’s profits. Excluding

corporate/eliminations, the medical business had a high OPM of 23% in FY3/16

(company-wide OPM of 13%).

The scientific solutions segment handles biological microscopes for research institutes and

universities, industrial videoscopes, industrial microscopes and other such products. With

high market share for each of these products, the segment generates stable earnings.

However, demand is dependent on public sector/government capex trends, so sales are

vulnerable to macro environment swings.

Imaging solutions: stabilizing earnings through restructuring amid shrinking DSC

market

In the imaging solutions segment, nearly 90% of sales come from DSCs, and more than

75% of this comes from mirrorless SLR cameras and interchangeable lens. Hurt by DSC

market contraction, the segment has been unprofitable since FY3/11. However, losses are

narrowing as the company scales back on low-margin compact cameras, cuts costs, and

otherwise restructures the business. We expect a wider loss in FY3/17 due to the recent

earthquakes in Kumamoto, but we believe earnings will improve to around breakeven on

an adjusted basis.

Figure 14: Sales breakdown by segments in FY3/16 Figure 15: OP breakdown by segments in FY3/16

Endoscopes43%

Surgical24%

Endotherapy9%

Life Science5%

Industrials7%

Digital Cameras

9%

Others(imaging)

1%

Others2%

FY16/3 Sales JPY 804.6 bn

Medical 76%

ScientificSoluations 13%

Imaging 10%

Medic

al

Scie

ntific

So

lutions

Imagin

g

Oth

ers

Elim

ina

tions

-60

-40

-20

0

20

40

60

80

100

120

140

160

FY16/3 OP JPY 104.5 bn

(¥bn)

Note: Company does not disclose life science and industrial sub

segments from FY3/17.

Source: Company data, Credit Suisse

Source: Company data, Credit Suisse

The medical business

accounts for 76% of total

company sales

DSC OP is closely to around

breakeven without the

impact of Kumamoto

earthquake

06 September 2016

Olympus (7733 / 7733 JP) 10

Figure 16: Business domain and major products

Gastrointestinal EndoscopesEndoscope systems (videoscopes, video processors, light sources, liquid crystal display(LCD) panels);

Peripheral equipment (image recording device, endoscope cleaning systems, sterilization systems), etc.

Surgical Devices Surgical video endoscopy systems, peripheral devices for endoscope surgery, electrosurgical knives, etc.

Endotherapy Devices

Endoscopic devices for all disciplines of endoscopy (approximately 1,000 different devices for various

diagnostic and treatment procedures, including biopsy forceps, high-frequency polypectomy snares,

grasping forceps, stone retrieval and lithotriptor baskets, hemostasis accessories, etc.)

Life Science

Upright microscopes and polarizing microscopes, inverted microscopes, laser confocal microscopes,

box-type fluorescence macromicroscopes, microscope digital cameras, imaging software, bio-imaging

systems, virtual slide systems

Industrial

Metallurgical microscopes, semiconductor inspection microscope, laser microscopes, measuring

microscopes, microscopic 3D measurement systems, industrial videoscopes, industrial fiberscopes,

industrial rigid scopes, ultrasonic flaw detectors, eddy current flaw detectors, phased array flaw detectors,

X-ray diffraction analyszers, peripheral equipment

Dital CamerasMirrorless interchangeable-lens cameras, compact digital cameras, digital camera-related products,

digital camera lens barrels, optical components

Others IC recorders, binoculars

Medical

Business

Scientific

Solutions

Business

Imaging

Business

Source: Company data, Credit Suisse

06 September 2016

Olympus (7733 / 7733 JP) 11

3. Focus on early diagnosis and minimally invasive treatment in medical Products improve patient quality of life

Core products are gastrointestinal endoscopes, endotherapy, surgical endoscopes,

energy devices

Olympus' core medical segment comprises endoscopes, surgical and endotherapy. The

endoscope segment includes systems and scopes for gastrointestinal endoscopy, while

the surgical segment includes surgical endoscope systems and surgical energy devices.

Endotherapy refers to those used in endoscopic treatment, by being attached to

gastrointestinal endoscopes.

In global share, Olympus has around 70% of the gastrointestinal endoscope system

market, around 20% of the endotherapy market, 20–25% of the surgical endoscope

system market, and 18–20% of the surgical energy devices market (all values are

company estimates; as of FY3/16). Its share of the gastrointestinal endoscope system

market is the largest by far and underpins growth in the medical business.

Figure 17: Medical business sales Figure 18: Medical business sales YoY

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

700

3/0

2

3/0

3

3/0

4

3/0

5

3/0

6

3/0

7

3/0

8

3/0

9

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

3/1

7E

3/1

8E

3/1

9E

((JP

Y b

n)

Endotherapy

Surgical

Endoscopes

YoY

Surgical + Endoscopes

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%3/0

2

3/0

3

3/0

4

3/0

5

3/0

6

3/0

7

3/0

8

3/0

9

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

Endoscopes

Surgical

Endotherapy

YoY

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

Products span range from early diagnostics to minimal invasive treatment

Endoscopic examination enables early diagnosis and treatment, which improves patients'

prognosis and helps to improve survival rates. Treating patients with endoscopes and

laparoscopes reduces the physical burden on patients and enables a quick return to

normal life. Olympus' strength lies in its range of products that help improve patients'

quality of life from diagnosis to treatment.

In global share, Olympus

has around 70% of the

gastrointestinal endoscope

system market

06 September 2016

Olympus (7733 / 7733 JP) 12

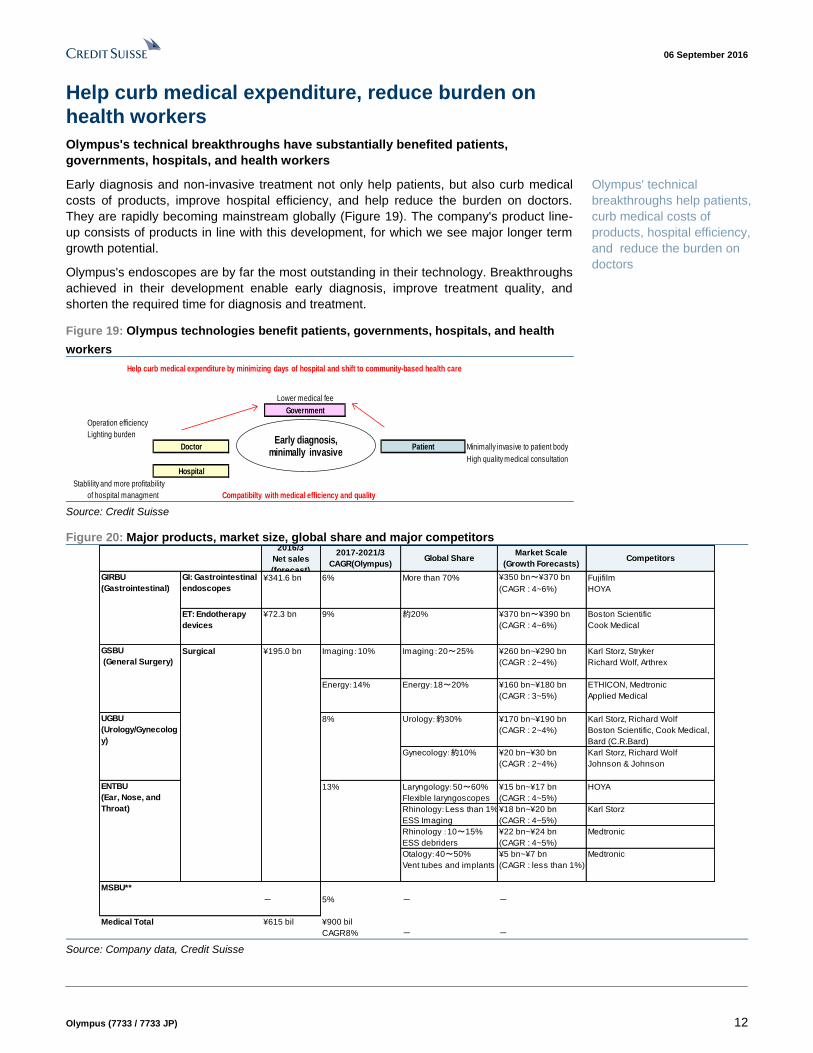

Help curb medical expenditure, reduce burden on

health workers

Olympus's technical breakthroughs have substantially benefited patients,

governments, hospitals, and health workers

Early diagnosis and non-invasive treatment not only help patients, but also curb medical

costs of products, improve hospital efficiency, and help reduce the burden on doctors.

They are rapidly becoming mainstream globally (Figure 19). The company's product line-

up consists of products in line with this development, for which we see major longer term

growth potential.

Olympus's endoscopes are by far the most outstanding in their technology. Breakthroughs

achieved in their development enable early diagnosis, improve treatment quality, and

shorten the required time for diagnosis and treatment.

Figure 19: Olympus technologies benefit patients, governments, hospitals, and health

workers

Lower medical fee

Government

Operation efficiency

Lighting burden

Doctor Patient Minimally invasive to patient body

High quality medical consultation

Hospital

Stablility and more profitability

of hospital managment

Early diagnosis,minimally invasive

Compatibilty with medical efficiency and quality

Help curb medical expenditure by minimizing days of hospital and shift to community-based health care

Source: Credit Suisse

Figure 20: Major products, market size, global share and major competitors 2016/3

Net sales

(forecast)

2017-2021/3

CAGR(Olympus)Global Share

Market Scale

(Growth Forecasts)Competitors

¥341.6 bn 6% More than 70% ¥350 bn〜¥370 bn Fujifilm

(CAGR : 4~6%) HOYA

¥72.3 bn 9% 約20% ¥370 bn〜¥390 bn Boston Scientific

(CAGR : 4~6%) Cook Medical

Surgical ¥195.0 bn Imaging:10% Imaging:20〜25% ¥260 bn~¥290 bn Karl Storz, Stryker

(CAGR : 2~4%) Richard Wolf, Arthrex

Energy:14% Energy:18〜20% ¥160 bn~¥180 bn ETHICON, Medtronic

(CAGR : 3~5%) Applied Medical

8% Urology:約30% ¥170 bn~¥190 bn Karl Storz, Richard Wolf

(CAGR : 2~4%) Boston Scientific, Cook Medical,

Bard (C.R.Bard)

Gynecology:約10% ¥20 bn~¥30 bn Karl Storz, Richard Wolf

(CAGR : 2~4%) Johnson & Johnson

13% Laryngology:50〜60% ¥15 bn~¥17 bn HOYA

Flexible laryngoscopes (CAGR : 4~5%)

Rhinology:Less than 1%¥18 bn~¥20 bn Karl Storz

ESS Imaging (CAGR : 4~5%)

Rhinology :10〜15% ¥22 bn~¥24 bn Medtronic

ESS debriders (CAGR : 4~5%)

Otalogy:40〜50% ¥5 bn~¥7 bn Medtronic

Vent tubes and implants (CAGR : less than 1%)

MSBU**

(Medical Service) - 5% - -

Medical Total ¥615 bil ¥900 bil

CAGR8% - -

GI: Gastrointestinal

endoscopes

GIRBU

(Gastrointestinal)

GSBU

(General Surgery)

UGBU

(Urology/Gynecolog

y)

ENTBU

(Ear, Nose, and

Throat)

ET: Endotherapy

devices

Source: Company data, Credit Suisse

Olympus' technical

breakthroughs help patients,

curb medical costs of

products, hospital efficiency,

and reduce the burden on

doctors

06 September 2016

Olympus (7733 / 7733 JP) 13

4. Gastrointestinal endoscopes basis for growth Commanding market share, continuous technical

innovation should ensure stable growth

Forecast steady growth for gastrointestinal endoscopes, as stock-type business

with income stream

The gastrointestinal (GI) endoscope business forms part of Olympus’ gastrointestinal and

respiratory business unit. It has a stock-type business model, focusing on sales of GI

endoscopy systems while also generating recurring revenues from replacement scopes as

well as maintenance and other services.

In general, GI endoscopy systems comprise the main body (which displays the image),

peripheral equipment, and two scopes (for the upper and lower GI tract). As scopes must

be sterilized after each procedure, it is usually necessary to have spares on hand, in

addition to which scopes need replacing after two or three years due to wear and tear.

Services include system maintenance, scope repair, maintenance of scope cleaning and

disinfection equipment, and replenishment of cleaning and disinfection agents. Olympus

fosters strong relationships with hospitals, resulting in steady flow of contract renewals

Close communication with hospitals contributes to technological advances,

resulting in high barriers to entry

Over several decades now, Olympus has maintained close communication with hospitals

and medical professionals, giving rise to constant innovation in its GI endoscopy systems.

Olympus invented a technology known as narrow band imaging (NBI). NBI provides

enhanced imaging of the capillaries and mucosal patterns on the mucosal surface layers

using two narrow-band wavelengths (characteristic changes when a tumor is growing

include an increase in the number of fine capillaries and a complex texture on the mucosal

surface, and the use of NBI technology makes tumor tissue stand out). By combining NBI

with magnification endoscopy, it is possible to detect small lesions that otherwise would

have been overlooked using standard endoscopy. Technological advances of this kind

have created high barriers to entry.

Also involved in respiratory endoscopy, endoscopic ultrasonography, and capsule

endoscopy, albeit on small scale

Respiratory endoscopy is used in diagnosing, biopsying, and treating bronchial conditions.

Endoscopic ultrasonography is used to determine the depth of lesion penetration into the

submucosal layer, and for closer examination of the pancreas, bile duct and other deep

organs that are difficult to view directly with standard endoscopy. Capsule endoscopy is

used to diagnose problems in the small intestine. It combines low-power consumption

imaging with wireless transmission technology, whereby images from the camera inside

the capsule are sent wirelessly to an antenna unit attached to the patient's body, and

recorded by a receiver. Olympus intends to use cross-selling to boost sales of both GI

endoscopes and these other types of endoscope.

Generating recurring

revenues from replacement

scopes as well as

maintenance and other

services

Olympus invented a

technology known as narrow

band imaging (NBI)

Olympus intends to use

cross-selling to boost sales

of both GI endoscopes and

these other types of

endoscope

06 September 2016

Olympus (7733 / 7733 JP) 14

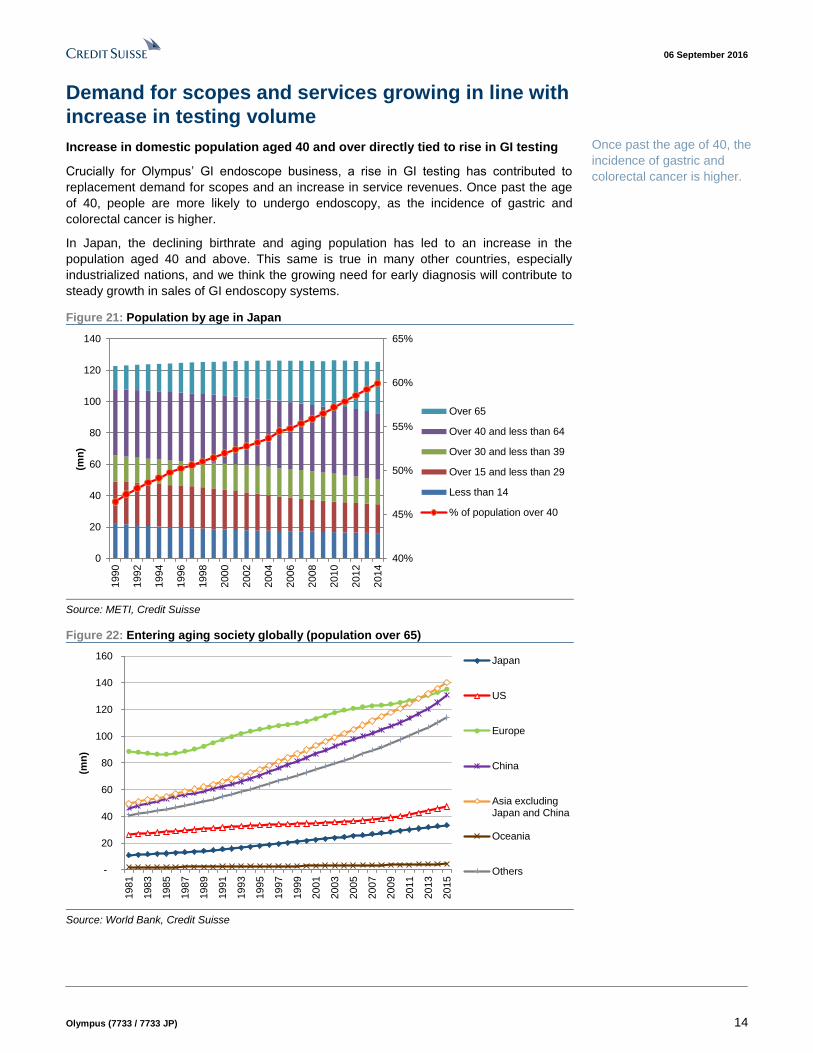

Demand for scopes and services growing in line with

increase in testing volume

Increase in domestic population aged 40 and over directly tied to rise in GI testing

Crucially for Olympus’ GI endoscope business, a rise in GI testing has contributed to

replacement demand for scopes and an increase in service revenues. Once past the age

of 40, people are more likely to undergo endoscopy, as the incidence of gastric and

colorectal cancer is higher.

In Japan, the declining birthrate and aging population has led to an increase in the

population aged 40 and above. This same is true in many other countries, especially

industrialized nations, and we think the growing need for early diagnosis will contribute to

steady growth in sales of GI endoscopy systems.

Figure 21: Population by age in Japan

40%

45%

50%

55%

60%

65%

0

20

40

60

80

100

120

140

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

(mn

)

Over 65

Over 40 and less than 64

Over 30 and less than 39

Over 15 and less than 29

Less than 14

% of population over 40

Source: METI, Credit Suisse

Figure 22: Entering aging society globally (population over 65)

-

20

40

60

80

100

120

140

160

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

(mn

)

Japan

US

Europe

China

Asia excludingJapan and China

Oceania

Others

Source: World Bank, Credit Suisse

Once past the age of 40, the

incidence of gastric and

colorectal cancer is higher.

06 September 2016

Olympus (7733 / 7733 JP) 15

Current generation of endoscopes in fourth year of

five-to-seven year product cycle

Product cycle is around five to seven years; 2018–19 launch likely for next-

generation of GI endoscopes

The new product cycle for GI endoscopes is around five to seven years; the current

generation, comprising the EVIS EXERA III (for the US and European markets) and EVIS

LUCERA ELITE (for the domestic market), came out in 2012. In comparison with the

previous generation launched in 2006, these products feature a dual focus function that

allows physicians to switch from normal-focus mode to near-focus mode with a single

button. It seems 40–45% in case of the US and Europe (50–55% in Japan as of 1Q

FY3/17) of customers have upgraded from the previous generation to the current

generation. Olympus has said the next generation should be out in the latter half of the

five-year period FY3/17–21, based on which we think a launch is likely around 2018–19.

Figure 23: Production cycle of gastrointestinal endoscopes

Name of product Main features

1985 EVIS-1

1990 EVIS100/200

2000 EVIS EXERA (Available in Europe)

2002 EVIS LUCERA The w orld's f irst hi-vision endoscope

2006 EVIS EXERA II NBI (Narrow Band Imaging)

2006 EVIS LUCERA SPECTRUM NBI (Narrow Band Imaging)

2012 EVIS EXERA III (Available in Europe)

2012 EVIS LUCERA ELITE (Available in Japan)

2014 Endoscope with x80 (approx.) Optical Magnification

Advanced NBI and dual focus function, etc.

Source: Company data, Credit Suisse

Accelerating replacements via VPP /CPP system

Under the VPP or value-per-procedure system, the usage contract includes warranty and

maintenance costs in a single package, and charges are made on a per-use basis,

allowing for efficient endoscopic examinations under a payment plan matched to

procedure volume. Generally, endoscopic systems are replaced in about year five (with an

option to acquire the system for its residual value in the final year). In US, this system is

expanded with the name CPP (cost-per procedure system). As VPP and CPP operate

through finance companies, there is no impact on Olympus' balance sheet.

The VPP system enhances operational efficiency by keeping initial investment costs down

and making equipment costs variable. Also, because the hospitals are not purchasing the

equipment, they can turn it in for an upgrade at the end of the VPP term (under normal

arrangements, maintenance costs start to rise from around five years in).

From Olympus’ perspective, the VPP system ensures that equipment is replaced more

often, and because it gives Olympus an accurate picture of procedure volume the system

also helps to further enhance relationships with hospitals, enabling the company to float

suggestions concerning replacement timing and so forth.

In the US, around 40% of GI endoscope sales are under the CPP system, while in Japan

the weighting is about 10-20% (under the VPP system).

It seems 40-45% in case of

US and Europe of

customers have upgraded

from the previous

generation to the current

generation

In the US, around 40% of GI

endoscope sales are under

the CPP system, while in

Japan the weighting is about

10–20%under the VPP

system.

06 September 2016

Olympus (7733 / 7733 JP) 16

North American endoscope sales down YoY in 1Q

FY3/17, but protracted decline unlikely

No change to scenario of continued growth in scope demand over medium term

In 1Q FY3/17, total endoscope sales fell 7% YoY with a 3% YoY increase in Japan and

9% fall overseas. On a local currency basis, total overseas sales were up 3% YoY with a

5% YoY increase in Europe and 32% in Asia/Oceania. In North America, though, sales

dropped 8% YoY. As sales in North American hitherto had been solid, there has been

concern among investors that the decline may be structural in nature.

According to management, though, the fall in sales was primarily due to prolongation of

business negotiations, with those sales now likely to be booked in 2Q or later. As quarterly

growth rates can vary significantly, we also believe that the problem is not structural, and

we look for growth to resume from 2H.

As structural issues that could conceivably arise, we identify among others a loss of

market share (customers switching to rival manufacturers’ equipment), and a decline in the

number of patients. At present, though, the number of patients is actually increasing, in

tandem with the aging population and trend toward early diagnosis. As a general trend, we

think demand will continue to expand.

Figure 24: Domestic and overseas endoscope sales trend (Yen base)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

10

20

30

40

50

60

70

80

90

100

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

((JP

Y b

n)

Overseas Domestic

Domestic YoY Overseas YoY

Source: Company data, Credit Suisse

Figure 25: Domestic and overseas endoscope sales trend

(Local currency base)

Figure 26: Endoscope sales growth by region (Local

currency base)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

FY13 FY14 FY15 FY16

Japan

Overseas

-20%

-10%

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

FY13 FY14 FY15 FY16

North America

Europe

Asia/Oceania

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

The fall in sales was

primarily due to prolongation

of business negotiations, we

look for growth to resume

from 2H

06 September 2016

Olympus (7733 / 7733 JP) 17

New product effect has waned, but CPP system should ensure ongoing

contributions from contract renewals in US

As we are now in FY3/17, four years have passed since the current generation of

endoscopes were rolled out; at this stage of the product cycle, one might assume the new

product effect has now waned. In previous cycles, sales growth has been strongest in the

fiscal year of launch and in the subsequent fiscal year, tending to narrow thereafter (the

sharp decline in FY3/09 can be attributed in large part to the global financial crisis, and the

fall in FY3/10 to the effects of yen appreciation; Figure 27 is yen-based).

However, we think the increasing weighting of CPP contracts in the US should mitigate

against sales slowing with the new product effect lower. Users who signed up when

purchasing the previous (2012) generation of endoscopes will soon be coming up for

contract renewal. From an efficiency standpoint, we think few users will opt to buy the

equipment at residual value. Thus in 2H FY3/17 and FY3/18 we expect replacement

demand to emerge among CPP-contract users in the US.

While we think yen appreciation inevitably will erode yen-based overseas sales in FY3/17,

from FY3/18 we expect growth at least on a par with the 5% or so pace we forecast for the

global medical equipment market, with sales also increasing steadily in Japan.

Figure 27:Domestic and overseas sales forecast of endoscope

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

400

450

500

3/0

2

3/0

3

3/0

4

3/0

5

3/0

6

3/0

7

3/0

8

3/0

9

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

((JP

Y b

n)

Overseas Domestic

Overseas YoY Domestic YoY

EVIS LUCERA

(02/11-)

EVIS EXERA IIEVIS LUCERA SPECTRUM (06/6-)

EVIS EXERA III (12/4-Overseas)EVIS LUCERA ELITE (12/11-Domestic)

Source: Company data, Credit Suisse

In 2H FY3/17 and FY3/18

we expect replacement

demand to emerge among

CPP contract users in the

US.

06 September 2016

Olympus (7733 / 7733 JP) 18

5. Expanding product lineup, promoting development of surgical techniques Wider application of endoscopic surgery expands

demand for instruments

Difference between endoscopic treatment and surgery using endoscopes;

endoscopic treatment is less invasive

Endoscopic surgery is usually an internal procedure performed by a physician by inserting

an endoscope into the patient’s mouth or anus to remove a lesion or other abnormality.

External endoscopic surgery requires only a few small holes be made in the skin of the

abdomen or chest, a less invasive technique that is increasingly replacing the more

invasive laparotomy and thoracotomy procedures. Endoscopic procedures do not require

making large external incisions, which helps to speed up post-surgery recoveries. Various

types of endoscopic instruments are used in procedures ranging from diagnostic biopsies

to lesion resections, as shown in Figures 28–29. The type of instruments used depends on

the location of the lesion, its size and the surgical technique.

Expansion of insurance coverage for and types of lesions removable by endoscopic

surgery

The development of endoscopic instruments and physicians’ improving procedural skills

are making it possible to use endoscopic surgery in a wider range of gastrointestinal tract

procedures, including the resection of larger lesions than previously possible.

Typical endoscopic surgeries for stomach cancer and colorectal cancer include

endoscopic mucosal resections (EMR) and endoscopic submucosal dissections (ESD). In

recent years, ESD is increasingly being used to entirely remove larger lesions in one

procedure. Insurance coverage for ESD procedures was first approved for treatment of

early-stage stomach cancer in 2006 and has since been expanded to include early-stage

esophageal cancer in 2008 and early-stage colorectal cancer and colorectal adenoma in

2012.

ESD is basically used to remove early-stage lesions, which seldom spread to lymph nodes,

with an invasion depth of less than 2cm (i.e., when the cancer has not spread beyond the

submucosal superficial layer). However, technological progress and the examination of

various cases have in recent years expanded the application of endoscopic surgery to

lesions with an invasion depth of more than 2cm (under the condition that lymph node

metastasis is unlikely).

Expanding share of endotherapy device sales, promoting development of surgical

techniques

Whereas Olympus has devoted resources to the development of endoscopic systems and

endoscopes, the main suppliers of endotherapy devices have been medical equipment

makers up until now. The US’s Boston Scientific is the world’s No. 1 supplier of

endoscopic instruments, with an overwhelming global market share of 50–60%. Olympus

and Cook Medical, another US company, are tied for second, with shares of about 20%.

Olympus began developing endotherapy devices years ago and continues to strengthen

its product lineup.

Today’s endotherapy devices can basically be grouped into three categories: (1) ERCP

instruments, (2) hemostatic devices, and (3) EMR/ESD instruments.

Endoscopic procedures do

not require making large

external incisions, which

helps to speed up post-

surgery recoveries

ESD is increasingly being

used to entirely remove

larger lesions in one

procedure

Olympus has around 20%

global share and continues

to strengthen its product

lineup.

06 September 2016

Olympus (7733 / 7733 JP) 19

ERCP involves the insertion of an instrument from the duodenum into the bile duct and is

used to treat biliary tract dysfunction and narrowing of the bile ducts, as well as to remove

gallstones. The procedure requires the use of various instruments, such as an insertion

assist device (guidewire), a knife (papillotome) for making an incision of the papilla (the

opening to the duodenum’s bile duct), and gallstone recovery equipment (basket).

Olympus plans to strengthen its lineup of devices used in ERCP.

Olympus’ hemostatic devices include clips, and its devices for EMR and ESD procedures

include knives and hemostatic forceps. Thanks to its strength in its gastrointestinal

endoscopic systems, Olympus has grabbed a large share of the market for EMR/ESD

devices, and the company is cooperating with physicians to develop surgical techniques

that will expand the use of ESD to the resection of more deeply invasive lesions.

Figure 28: Area of endotherapy usage

E nd o sco p e (exclud ing end o therap y) :Vid eo sco p es、end o sco p e cleaning system s

B iopsy

P olypectom y

H ot biopsy

EM R

ES D

ER C P

ES T

EB D etc.

S urg ery

Endotherapy

Observing・Imaging Display・ Diagnois

Treatment・

Hemostasis

Irrigation・

Disinfection

EndoscopicSurgery (Laparoscopic

surgery)

Laparotomy

Insertion

Source: Company data, Credit Suisse

Figure 29: Main endoscopic procedures used in internal medicine

PolypectomyThe polyp is grasped with forceps and removed by radiofrequency ablation; mostly

used for small polyps <5mm

Hot biopsyA snare is advanced from the tip of the endoscope to around the polyp root and

the polyp is removed by cauterization

EMR (Endoscopic Mucosal

Resection)Endoscopic mucosal resection

A needle is advanced from the endoscope tip and physiological saline is injected

into the submucosa under the polyp -> the physiological saline lifts the

submucosa off the muscle layer and the polyp forms a bleb -> the polyp bleb is

encircled by a snare and removed by radiofrequency ablation, as with

ESD (Endoscopic Submucosal

Dissection)

Endoscopic submucosal

dissection

For early stage gastric cancer or colorectal cancer, physiological saline is

injected between the normal tissue and the diseased tissue to inflate the site and

the lesion is removed using a snare

ERCP (Endoscopic Retrograde

Cholangio Pancreatography)

Endoscopic retrograde cholangio

pancreatographyEndoscopy to test the pancreas and bile duct

EST (Endoscopic

Sphincterotomy)Endoscopic sphincterotomy

Endoscopic method to sever the sphincter muscle at the point where bile enters

the duodenum; used to eliminate gallstones and bile

EBD (Endoscopic Biliary

Drainage)Endoscopic biliary drainage

Therapeutic method that involves the placement of a biliary stent (narrow tube) in

the bile duct using an endoscope to facilitate the flow of bile into the duodenum in

patients with biliary stenosis and poor bile flow. Endoscopic naso-biliary drainage

(ENBD) is performed to drain the bile externally, via a tube that leads externally

via the nasal passage.

Source: Company data, Credit Suisse

06 September 2016

Olympus (7733 / 7733 JP) 20

Figure 30: EMR and ESD EM R (Endoscopic M ucosal Resection) ESD (Endoscopic Subm ucosal D issection)

Lesion

Mucosa

Submucosa

Proper muscular layer

Snare

1. Injection of physiological 2. Invert the snare and encircle

Local

Physiological

3. Electrocautery 4. Retrieve the excised tissue

1. MarkingEndoscope is passed into the stomach to mark out the area surrounding the lesion that is to be excised

Canser

2. Local injectionAgent is injected into the submucosa to inflate the area

4. Separate the submucosaCarefully cut away the lesion little by little using the specialized knife

3. DissectionFollow the marking with the knife to cut the mucosa around the lesion

5. Complete excisionCut completely through using the knife, or complete tissue removal using the snare

6. Hemostasis After removal, treat to stop bleeding on the stomach surface; retrieve the excised lesion to send for pathology testing

7.Pathological testingTissue examination by microscope to examine whether cured completely or not.

Source: Company website

06 September 2016

Olympus (7733 / 7733 JP) 21

Steady sales expansion, growth likely to continue

Successful efforts to strengthen sales system and product lineup

Over the past two years, Olympus' sales of endoscopic systems and devices have been

expanding at a stronger pace than sales of the global No.1 supplier, Boston Scientific. We

think this strong growth reflects Olympus’ efforts to strengthen its sales structure,

especially in the US and Europe, and the broadening of its product lineup. Olympus has

also enjoyed strong sales in product categories where it has particular competitive

advantages, such as its devices used in ESD procedures. In the future, we expect growing

sales of these devices, many of which must be disposed of after use and have high profit

margins, to help improve the overall profitability of Olympus’ medical business. Excluding

the forex impact, we think sales growth is likely to be around the high single digit to 10%

range.

Figure 31: Domestic and overseas endotherapy sales trend (Yen base)

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

2

4

6

8

10

12

14

16

18

20

22

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

FY10 FY11 FY12 FY13 FY14 FY15 FY16

((JP

Y b

n)

Overseas

Domestic

Overseas YoY

Domestic YoY

Source: Company data, Credit Suisse

Figure 32: Sales of endotherapy comparison 1 Figure 33: Sales of endotherapy comparison 2

-5%

0%

5%

10%

15%

20%

25%

30%

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Boston Scientific Endoscopy

Olympus Endotherapy total, yen base

-5%

0%

5%

10%

15%

20%

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Boston Scientific Endoscopy

Olympus domestic yen base

Olympus oversease local currency base

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

Growing sales of these

devices help improve the

overall profitability of

Olympus’ medical business

06 September 2016

Olympus (7733 / 7733 JP) 22

Figure 34: Domestic and overseas endotherapy sales

trend (Local currency base)

Figure 35: Endotherapy sales growth by region (Local

currency base)

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

FY13 FY14 FY15 FY16

Japan

Overseas

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

FY13 FY14 FY15 FY16

North America

Europe

Asia/Oceania

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

Figure 36: Domestic and overseas sales forecast of endotherapy

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

10

20

30

40

50

60

70

80

90

100

3/1

0

3/1

1

3/1

2

3/1

3

3/1

4

3/1

5

3/1

6

3/1

7E

3/1

8E

3/1

9E

(JP

Y b

n)

Overseas

Domestic

Overseas YoY

Domestic YoY

Source: Company data, Credit Suisse estimates

06 September 2016

Olympus (7733 / 7733 JP) 23

6. Expecting share gains in surgery driven by unique products Building up business via M&A activity, gaining share

Building business via M&A activity, implementing strategic investment for long-

term growth

Olympus made a full-fledged entry into surgical endoscopes with the acquisition of

German rigid endoscope maker Winter & Ibe in 1979. In 2008, the company acquired UK

medical equipment maker Gyrus Group, and expanded its business to include energy

equipment such as high-frequency equipment used in minimally invasive treatment. Over

the past few years, the company has made strategic investments aimed at long-term

growth while focusing on strengthening its sales structure in North America and China.

Three units: surgical business, urology & gynecology business, and ENT business

The company's main products in the surgical field include surgical endoscope systems,

videoscopes, rigid endoscopes, forceps, and energy devices. We estimate that the general

surgical business accounts for around 50% of sales at the surgical unit, urology and

gynecology business for around 40%, and ENT for around 10%.

The surgical business unit has main categories with the company's mainstays being in

surgical imaging (surgical endoscope systems, surgical videoscopes) and energy products

(electronic and ultrasonic scalpels to make incisions and stop bleeding).

At the urology and gynecology business unit, the company has major shares of the flexible

ureteroscope and cystoscope markets.

At the ENT business unit, the company has a solid share of the market for flexible

endoscopes used in the ENT field (ear, nose, and throat) and substantial shares of the

markets for eardrum tubes and auditory ossicle implants. However, these markets are

modest in size.

Strengths lie in unique products that help reduce physicians' burden or enable

advanced treatment

The company's strength in surgical imaging is the technology it has accumulated through

the making of gastrointestinal endoscopes. As products that differentiate Olympus from its

rivals, 3D videoscopes enable 3D examination and 4K surgical endoscope systems make

it easy to examine patients during surgery. At the energy business, the company's

Thunderbeat system (a single device that can make incisions and stop bleeding) is a

product with no direct competitor. These unique products shorten the time to perform

surgical procedures and reduce stress, thus easing the burden on doctors.

Endoscopic surgery growing, eligible for insurance

Endoscopic surgery increasing due to growing demand for minimally-invasive

In Japan, endoscopic surgery was first covered by insurance in 1992, for cholecystectomy

(surgical removal of the gall bladder). In 1994, coverage widened to include hernia repair,

pneumonectomy (removal of a lung or part of a lung), and gynecological surgical

procedures. In 1995, gastrectomy was covered, and in 1996, coverage was extended to

splenectomy and liver resection. Coverage has been expanded to more difficult operative

procedures under the recently revised medical fee scheme in Japan (2016).

The expansion in insurance coverage has driven growth in the number of endoscopic

procedures performed (Figure 37). Given the expansion in minimally invasive treatment to

date, we think this trend will continue.

In 2008, the company

acquired UK medical

equipment maker Gyrus

Group

The general surgical

business accounts for 50%

of sales at the surgical unit,

urology and gynecology

business for 40%, and ENT

for 10%

3D videoscopes enable 3D

examination and 4K surgical

endoscope systems make it

easy to examine patients

during surgery

Insurance coverage

currently includes 16

gastrointestinal procedures

06 September 2016

Olympus (7733 / 7733 JP) 24

Figure 37: Number of endoscopic surgeries in Japan

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

(Num

ber

of surg

erie

s)

Plastic surgery

Orthopedic surgery

Urology surgery

Obstetrics andgynecology surgeryThyroid surgery

Mastopathy surgery

Respiratory surgery

Pediatric surgery

Obesity surgery

Abdominal surgery

Source: Japan Society for Endoscopic Surgery data

Figure 38:Propolution of type of endoscopic surgery in Japan

Abdominal surgery, 46%

Obesity surgery, 0%

Pediatric surgery, 3%

Respiratory surgery, 12%

Mastopathy surgery, 0%

Thyroid surgery, 0%

Obstetrics and gynecology surgery,

30%

Urology surgery, 7%

Orthopedic surgery, 1%

Plastic surgery, 0%

Source: Japan Society for Endoscopic Surgery data

Expecting steady growth in energy devices

excluding special factors

Firm sales for Thunderbeat, whose unique technology makes surgery more efficient

Thunderbeat, a fully integrated energy device, is a unique Olympus product that can

simultaneously generate bipolar high-frequency current energy (with its outstanding blood

vessel sealing and hemostatic performance) and ultrasonic vibration energy (with its

outstanding structure sectioning and detachment performance). Previously two

instruments with the respective functionalities had to be used. Integrating them in one

device enables rapid sectioning and stable hemostasis operations. As it also means there

is little changing of devices during surgery, less time is needed to carry out procedures,

and the burden on doctors and patients is reduced.

Sales of Thunderbeat, which was launched in 2012, have been firm. We understand sales

of energy devices have grown by 150% over the past three years (we estimate energy

devices generate around 15% of sales in the surgical field).

Thunderbeat was launched in 2016 for abdominal surgery. Via technology accumulated

through endoscopic surgery, the products helps shorten surgery time and make

We understand sales of

energy devices have grown

by 150% over the past three

years owing to firm sales of

Thunderbeat

06 September 2016

Olympus (7733 / 7733 JP) 25

laparotomy (abdominal surgery) procedures more efficient. The company has also

developed equipment to expand the range of application of endoscopic surgery. Taking

stomach cancer as an example, endoscopic surgery is employed in only around 30% of

surgical operations. We think development of equipment for the remaining 70% will lead to

long-term growth.

FDA alert concerning PK technology devices still affecting maternity field, but

should ease up

Gyrus Group, which Olympus acquired in 2008, is engaged in PK technology devices. In

April 2014, the US Food and Drug Administration (FDA) issued an alert about the use of

energy devices (power morcellators) in endoscopic surgery (laparoscopic surgery) in

gynecology. Power morcellators are medical devices used to remove the uterus

(hysterectomy) or uterine fibroids (myomectomy). The FDA said laparoscopic power

morcellation poses a risk of spreading unsuspected cancerous tissue, notably uterine

sarcomas, beyond the uterus. Demand for energy devices in gynecology subsequently

declined, hitting Olympus's sales in FY3/16 by several billion yen. We think the impact

lingered into 1Q FY3/17, although the YoY decline was less severe. The company has

submitted an application to the FDA regarding a new model that can remove tumors

without morcellation and is awaiting approval.

4K surgical endoscopy systems: inquiries strong

Differentiated products leverage strengths of Olympus and Sony

In September 2012, Olympus and Sony announced an operating alliance and in April 2013,

they launched a joint venture company (51% owned by Sony) called Sony Olympus

Medical Solutions. The first products jointly developed by the three companies (Sony,

Olympus, and Sony Olympus Medical Solutions) are 4K surgical endoscopy systems.

These 4K surgical endoscopy systems have three notable characteristics: (1) high

resolution (4K video from input to output), (2) a wide color gamut (high color

reproducibility), and (3) magnification (owing to the use of a large monitor). The recently

unveiled systems leverage Olympus’s optics technology (e.g., lenses) and medical-

segment expertise, Sony’s imaging technology (e.g., imaging sensors) and 4K video

technology (e.g., monitors and recorders). Utilizing these two companies technologies,

Sony Olympus Medical Solutions was tasked with basic system development and overall

optimization. Olympus will be in charge of sales.

Inquiries from hospitals regarding these 4K surgical endoscopy systems have been strong,

and business negotiations currently under way regarding their adoption are coming at an

increasingly brisk rate. This is because these systems increase visibility and improve

identification of microstructures such as blood vessels during endoscopic surgery, greatly

reducing the burden on the doctor during the procedure. The new systems are evidently

30–40% more expensive than conventional systems, but we expect sales to grow because

of the aforementioned features. Because of the time to close sales agreements, these

systems did not contribute meaningfully to sales until 1Q FY3/17. However, we think the

boost to earnings from the introduction of new products will accelerate from 2H FY3/17

into FY3/18.

First-quarter earnings off to slow start, but growth

expectations unchanged

First-quarter sales weakness due to protracted negotiations, likely temporary

In 1Q, sales were firm in Europe and robust in Asia & Oceania, but decreased in Japan

and the US. This was largely attributable to protracted sales negotiations regarding

surgical endoscopy systems. Another factor was the ongoing stagnation in PK technology

devices (which in the domestic market began in 2H FY3/15). However, the robustness of

orders leads us to believe the negative growth seen in 1Q is only temporary.