Nintendo (7974) - Credit Suisse | PLUS

37

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 15 September 2017 Asia Pacific/Japan Equity Research Entertainment Software (Video Game (Japan)) Nintendo (7974) UPGRADE RATING Rating (from NEUTRAL) OUTPERFORM [V] Price (14 Sep 17, ¥) 37,670 Target price (¥) (from 40,000) 55,000 Change to TP (%) 46 Market cap (¥ bn) 4,523 (US$ 40.9) Enterprise value (¥ bn) 3,776 Number of shares (mn) 120.1 Free float (%) 70.0 52-week price range 39,320–22,520 Target price is for 12 months. [V] = Stock Considered Volatile (see Disclosure Appendix) Research Analysts Keiichi Yoneshima 81 3 4550 9740 [email protected] Hanako Takahashi 81 3 4550 7366 [email protected] Upgrading to OUTPERFORM: Multi-Switch homes to drive high earnings peak ■ Action: We raise our forecasts and lift our target price for Nintendo from ¥40,000 to ¥55,000 (potential return 46%). We also upgrade Nintendo from Neutral to OUTPERFORM. We now forecast Switch sales of 130mn (previously 70mn) units through FY3/22. ■ Including multi-Switch households into demand outlook: We had previously expected the Switch to sell like a traditional console, but now expect it to sell more like a handheld, due to three main reasons: (1) a Famitsu survey released in June indicating that many users are already using the Switch like a handheld (see Figure 1), (2) the comparatively low price, and (3) prospects for a long-tail sales cycle driven by minor changes. We now forecast Switch sales peaking at 31mn units in FY3/20–21 (previously 15mn in FY3/19). ■ Catalysts/risks: Potential upside catalysts include a 2Q earnings report accompanied by upwardly revised guidance and unveiling of a major third- party software title at the Tokyo Game Show (21–24 September). Downside risks include disappointing Switch sales and yen appreciation. ■ Valuation: We set our ¥55,000 target price using a the sum-of-the-parts (SOTP) method, using game consoles, smart devices, and cash. We value the game hardware business at an ex-cash P/E of 18x (previously 20x) to reflect that we now expect Switch sales to peak in FY3/20–21 instead of FY3/19. Share price performance Price (LHS) Rebased Rel (RHS) Jan - 1 6 Ju l- 1 6 Jan - 1 7 Ju l- 1 7 10,000 20,000 30,000 40,000 The price relative chart measures performance against the TOPIX which closed at 1,632.13 on 14-Sep-2017 On 14-Sep-2017 the spot exchange rate was ¥110.46/US$1 Performance 1M 3M 12M Absolute (%) 2.8 4.5 46.3 Relative (%) 1.8 2.3 22.1 Financial and valuation metrics Year 3/17A 3/18E 3/19E 3/20E Sales (¥ bn) 489.1 831.4 1,196.4 1,599.1 Operating profit (¥ bn) 29.4 80.4 258.1 470.1 Recurring profit (¥ bn) 50.4 106.3 284.0 496.0 Net income (¥ bn) 102.6 69.1 184.6 322.4 EPS (¥) 853.9 575.1 1,536.5 2,683.6 IBES Consensus EPS (¥) n.a. 856.0 1,409.0 1,877.9 EPS growth (%) 521.4 (32.6) 167.2 74.7 P/E (x) 30.3 65.5 24.5 14.0 Dividend yield (%) 1.7 0.8 2.0 3.6 EV/EBITDA (x) 65.6 42.6 13.9 7.4 P/B (x) 2.9 4.1 3.9 3.5 ROE(%) 8.5 5.4 13.8 22.0 Net debt/equity (%) Net cash Net cash Net cash Net cash Source: Company data, Thomson Reuters, Credit Suisse estimates

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Nintendo (7974) - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

15 September 2017Asia Pacific/JapanEquity Research

Entertainment Software (Video Game (Japan))

Nintendo (7974)

UPGRADE RATING Rating (from NEUTRAL) OUTPERFORM [V]Price (14 Sep 17, ¥) 37,670Target price (¥) (from 40,000) 55,000Change to TP (%) 46Market cap (¥ bn) 4,523 (US$ 40.9)Enterprise value (¥ bn) 3,776Number of shares (mn) 120.1Free float (%) 70.052-week price range 39,320–22,520Target price is for 12 months.[V] = Stock Considered Volatile (see Disclosure Appendix)

Research AnalystsKeiichi Yoneshima

81 3 4550 [email protected]

Hanako Takahashi81 3 4550 7366

Upgrading to OUTPERFORM: Multi-Switch homes to drive high earnings peak■ Action: We raise our forecasts and lift our target price for Nintendo from

¥40,000 to ¥55,000 (potential return 46%). We also upgrade Nintendo from Neutral to OUTPERFORM. We now forecast Switch sales of 130mn (previously 70mn) units through FY3/22.

■ Including multi-Switch households into demand outlook: We had previously expected the Switch to sell like a traditional console, but now expect it to sell more like a handheld, due to three main reasons: (1) a Famitsu survey released in June indicating that many users are already using the Switch like a handheld (see Figure 1), (2) the comparatively low price, and (3) prospects for a long-tail sales cycle driven by minor changes. We now forecast Switch sales peaking at 31mn units in FY3/20–21 (previously 15mn in FY3/19).

■ Catalysts/risks: Potential upside catalysts include a 2Q earnings report accompanied by upwardly revised guidance and unveiling of a major third-party software title at the Tokyo Game Show (21–24 September). Downside risks include disappointing Switch sales and yen appreciation.

■ Valuation: We set our ¥55,000 target price using a the sum-of-the-parts (SOTP) method, using game consoles, smart devices, and cash. We value the game hardware business at an ex-cash P/E of 18x (previously 20x) to reflect that we now expect Switch sales to peak in FY3/20–21 instead of FY3/19.

Share price performancePr ice (LH S) Reb ased Re l (RH S)

Jan - 1 6 Ju l - 1 6 Jan - 1 7 Ju l - 1 71 0 ,0 0 0

2 0 ,0 0 0

3 0 ,0 0 0

4 0 ,0 0 0

The price relative chart measures performance against the TOPIX which closed at 1,632.13 on 14-Sep-2017On 14-Sep-2017 the spot exchange rate was ¥110.46/US$1

Performance 1M 3M 12MAbsolute (%) 2.8 4.5 46.3Relative (%) 1.8 2.3 22.1

Financial and valuation metricsYear 3/17A 3/18E 3/19E 3/20ESales (¥ bn) 489.1 831.4 1,196.4 1,599.1Operating profit (¥ bn) 29.4 80.4 258.1 470.1Recurring profit (¥ bn) 50.4 106.3 284.0 496.0Net income (¥ bn) 102.6 69.1 184.6 322.4EPS (¥) 853.9 575.1 1,536.5 2,683.6IBES Consensus EPS (¥) n.a. 856.0 1,409.0 1,877.9EPS growth (%) 521.4 (32.6) 167.2 74.7P/E (x) 30.3 65.5 24.5 14.0Dividend yield (%) 1.7 0.8 2.0 3.6EV/EBITDA (x) 65.6 42.6 13.9 7.4P/B (x) 2.9 4.1 3.9 3.5ROE(%) 8.5 5.4 13.8 22.0Net debt/equity (%) Net cash Net cash Net cash Net cash

Source: Company data, Thomson Reuters, Credit Suisse estimates

15 September 2017

Nintendo (7974) 2

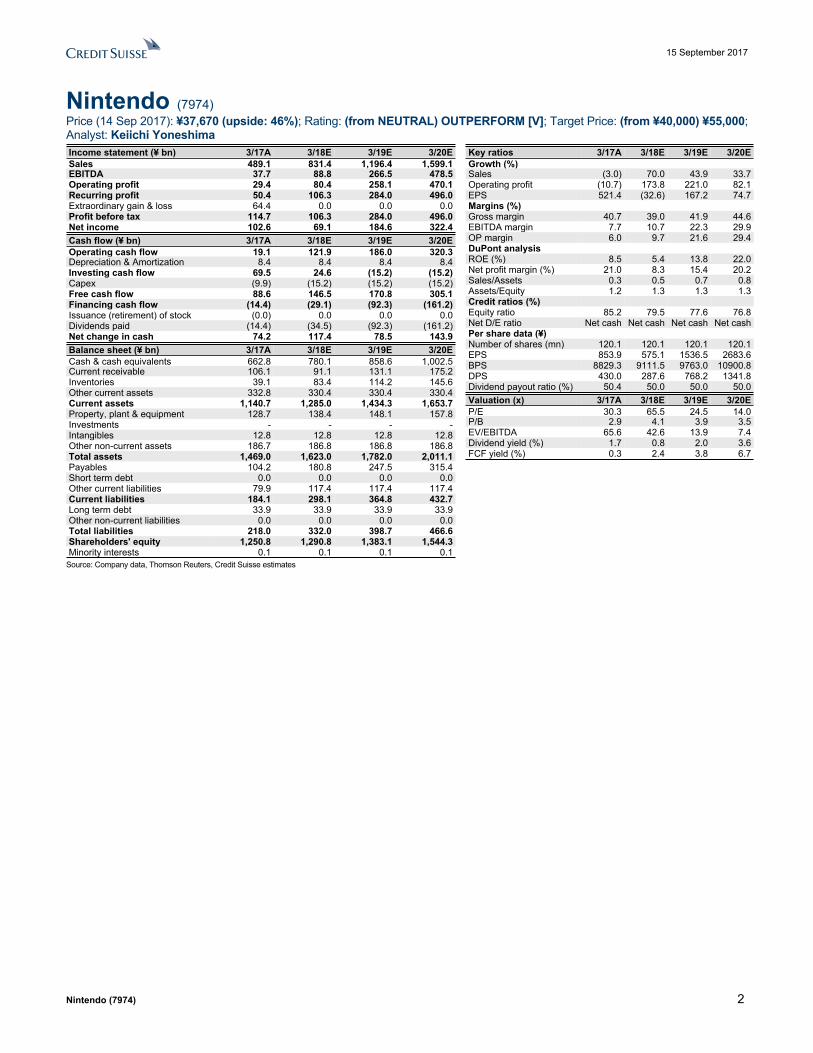

Nintendo (7974)Price (14 Sep 2017): ¥37,670 (upside: 46%); Rating: (from NEUTRAL) OUTPERFORM [V]; Target Price: (from ¥40,000) ¥55,000; Analyst: Keiichi YoneshimaIncome statement (¥ bn) 3/17A 3/18E 3/19E 3/20ESales 489.1 831.4 1,196.4 1,599.1EBITDA 37.7 88.8 266.5 478.5Operating profit 29.4 80.4 258.1 470.1Recurring profit 50.4 106.3 284.0 496.0Extraordinary gain & loss 64.4 0.0 0.0 0.0Profit before tax 114.7 106.3 284.0 496.0Net income 102.6 69.1 184.6 322.4Cash flow (¥ bn) 3/17A 3/18E 3/19E 3/20EOperating cash flow 19.1 121.9 186.0 320.3Depreciation & Amortization 8.4 8.4 8.4 8.4Investing cash flow 69.5 24.6 (15.2) (15.2)Capex (9.9) (15.2) (15.2) (15.2)Free cash flow 88.6 146.5 170.8 305.1Financing cash flow (14.4) (29.1) (92.3) (161.2)Issuance (retirement) of stock (0.0) 0.0 0.0 0.0Dividends paid (14.4) (34.5) (92.3) (161.2)Net change in cash 74.2 117.4 78.5 143.9Balance sheet (¥ bn) 3/17A 3/18E 3/19E 3/20ECash & cash equivalents 662.8 780.1 858.6 1,002.5Current receivable 106.1 91.1 131.1 175.2Inventories 39.1 83.4 114.2 145.6Other current assets 332.8 330.4 330.4 330.4Current assets 1,140.7 1,285.0 1,434.3 1,653.7Property, plant & equipment 128.7 138.4 148.1 157.8Investments - - - -Intangibles 12.8 12.8 12.8 12.8Other non-current assets 186.7 186.8 186.8 186.8Total assets 1,469.0 1,623.0 1,782.0 2,011.1Payables 104.2 180.8 247.5 315.4Short term debt 0.0 0.0 0.0 0.0Other current liabilities 79.9 117.4 117.4 117.4Current liabilities 184.1 298.1 364.8 432.7Long term debt 33.9 33.9 33.9 33.9Other non-current liabilities 0.0 0.0 0.0 0.0Total liabilities 218.0 332.0 398.7 466.6Shareholders' equity 1,250.8 1,290.8 1,383.1 1,544.3Minority interests 0.1 0.1 0.1 0.1

Key ratios 3/17A 3/18E 3/19E 3/20EGrowth (%)Sales (3.0) 70.0 43.9 33.7Operating profit (10.7) 173.8 221.0 82.1EPS 521.4 (32.6) 167.2 74.7Margins (%)Gross margin 40.7 39.0 41.9 44.6EBITDA margin 7.7 10.7 22.3 29.9OP margin 6.0 9.7 21.6 29.4DuPont analysisROE (%) 8.5 5.4 13.8 22.0Net profit margin (%) 21.0 8.3 15.4 20.2Sales/Assets 0.3 0.5 0.7 0.8Assets/Equity 1.2 1.3 1.3 1.3Credit ratios (%)Equity ratio 85.2 79.5 77.6 76.8Net D/E ratio Net cash Net cash Net cash Net cashPer share data (¥)Number of shares (mn) 120.1 120.1 120.1 120.1EPS 853.9 575.1 1536.5 2683.6BPS 8829.3 9111.5 9763.0 10900.8DPS 430.0 287.6 768.2 1341.8Dividend payout ratio (%) 50.4 50.0 50.0 50.0Valuation (x) 3/17A 3/18E 3/19E 3/20EP/E 30.3 65.5 24.5 14.0P/B 2.9 4.1 3.9 3.5EV/EBITDA 65.6 42.6 13.9 7.4Dividend yield (%) 1.7 0.8 2.0 3.6FCF yield (%) 0.3 2.4 3.8 6.7

Source: Company data, Thomson Reuters, Credit Suisse estimates

15 September 2017

Nintendo (7974) 3

Table of contentsUpgrading to OUTPERFORM: Multi-Switch homes to drive high earnings peak 1

Executive summary 4

Upgrading to OUTPERFORM with ¥55,000 TP .......................................................4

Three reasons why Switch will be more like a handheld..........................................4

Valuation ..................................................................................................................7

Upgrading to OUTPERFORM, raising TP to ¥55,000 9

Forecasting Switch sales through FY3/22 at 130mn units, revised from 70mn .......9

Incorporating multi-Switch households into our sales forecast ................................9

Game hardware is relatively inexpensive per CPI data .........................................12

Switch poised for similar uptake as the DS series 14

3DS+NDS constitute a broader “DS series”...........................................................14

Revising attach rate outlook...................................................................................17

Expecting production capacity to rise to 2.5mn units/month; peak FY capacity of

30mn units within reach .........................................................................................18

Prospects for long-tail sales driven by minor changes 19

Switch color variations suggests scope for device personalization........................19

Previous minor changes.........................................................................................21

Minor changes in handheld and stationary consoles differ by an order of magnitude

...............................................................................................................................22

Near-term catalyst: upward revision at 2Q (Jul–Sep) results 23

Profits concentrated in Oct–Dec; expecting lift to full-year guidance if 1H progress

is around 50% ........................................................................................................23

Forecasts for non-Switch products 25

2DS likely to become the core handheld................................................................25

Modest revision to smartphone app forecasts .......................................................25

Valuation: raising value of game console business from ¥2.7tn to ¥4.7tn 26

Focusing on the Switch; smartphone apps also look promising in the long term...26

Earnings forecasts 30

Revising Switch earnings peak from FY3/19 to FY3/20–21; raising peak sales ‒

15mn to 31mn units................................................................................................30

15 September 2017

Nintendo (7974) 4

Executive summaryUpgrading to OUTPERFORM with ¥55,000 TPChanges from our previous report: Now reflecting realization of upside scenario■ 1) We raise our earnings forecasts after lifting our cumulative sales forecast for the

Switch through FY3/22 from 70mn units to 130mn units.

■ 2) We raise our target price from ¥40,000 to ¥55,000. We push back our expected earnings peak from FY3/19 to FY3/20–21 and, given the time value factor, lower our target P/E for the game console business from 20x to 18x.

Raising Switch sales forecast through FY3/22 from 70mn to 130mn units to reflect a handheld-like sales cycleAs Nintendo’s Switch is a unique game platform for use as either a console or handheld, there was initially some uncertainty over whether its sales cycle would more closely resemble that of a console or handheld. Although the Switch is currently categorized as more of a console, we expect it to sell like a handheld. Many users are in fact using the Switch as a portable according to a Famitsu survey of users (Figure 1). We previously projected a sales peak at about three years after launch (i.e., in FY3/19) on the assumption of a console-like sales cycle. Now that the Switch looks more likely to sell like a handheld, we update our sales forecast to reflect a longer sales cycle. We now expect the Switch to achieve peak sales about five years after launch (i.e., around FY3/20–21) like a typical handheld game device. We also raise our peak-year sales forecast from 25mn to 31mn units.

We expect Switch sales to rival combined NDS/3DS salesAssuming the Switch sells like a handheld, we could use the Nintendo DS, or NDS, (sales of 150mn units), or Nintendo 3DS (80mn units) as benchmarks for forecasting sales. In retrospect, however, the NDS and 3DS were ultimately similar to each other and, in our opinion, more aptly grouped together as a single broadly defined DS series. Our updated Switch sales forecast assumes that Switch sales will exhibit an arc similar to this broader DS series.

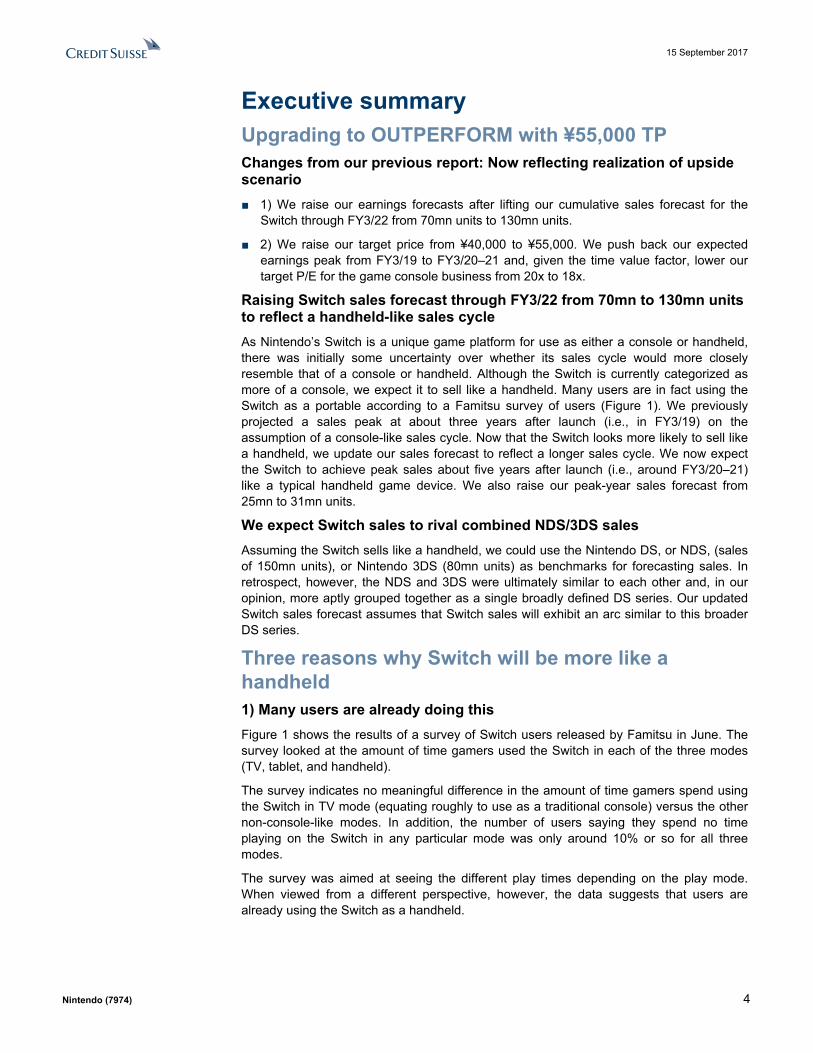

Three reasons why Switch will be more like a handheld1) Many users are already doing thisFigure 1 shows the results of a survey of Switch users released by Famitsu in June. The survey looked at the amount of time gamers used the Switch in each of the three modes (TV, tablet, and handheld).

The survey indicates no meaningful difference in the amount of time gamers spend using the Switch in TV mode (equating roughly to use as a traditional console) versus the other non-console-like modes. In addition, the number of users saying they spend no time playing on the Switch in any particular mode was only around 10% or so for all three modes.

The survey was aimed at seeing the different play times depending on the play mode. When viewed from a different perspective, however, the data suggests that users are already using the Switch as a handheld.

15 September 2017

Nintendo (7974) 5

Figure 1: Switch reportedly often used in tabletop/handheld modes

Figure 2: We expect Switch sales cycle to resemble NDS & 3DS

0%5%

10%15%20%25%30%35%40%

Time spending

TV mode

Tabletop mode

Handheld mode

05

1015202530354045

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

(mn

units

)

Switch (New- CSE) Switch (Old- CSE)

NDS+3DS Wii

Source: Famitsu, Credit Suisse Source: Company data, Credit Suisse estimates

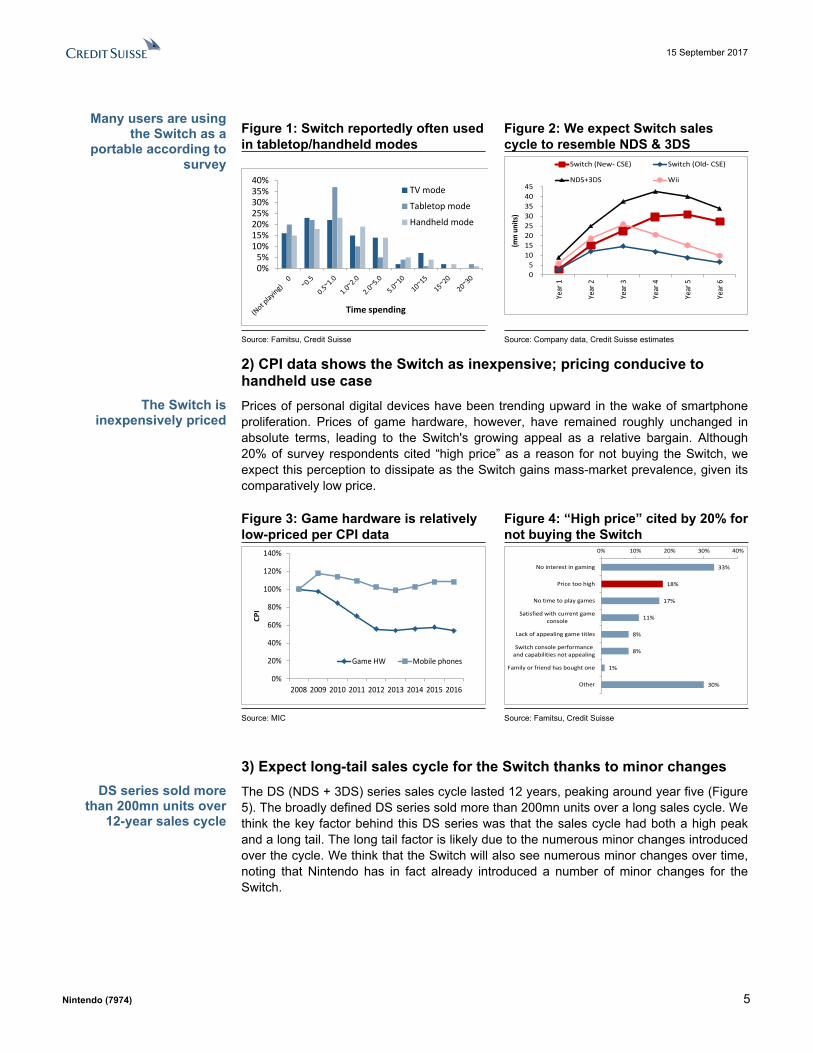

2) CPI data shows the Switch as inexpensive; pricing conducive to handheld use casePrices of personal digital devices have been trending upward in the wake of smartphone proliferation. Prices of game hardware, however, have remained roughly unchanged in absolute terms, leading to the Switch's growing appeal as a relative bargain. Although 20% of survey respondents cited “high price” as a reason for not buying the Switch, we expect this perception to dissipate as the Switch gains mass-market prevalence, given its comparatively low price.

Figure 3: Game hardware is relatively low-priced per CPI data

Figure 4: “High price” cited by 20% for not buying the Switch

0%

20%

40%

60%

80%

100%

120%

140%

2008 2009 2010 2011 2012 2013 2014 2015 2016

CPI

Game HW Mobile phones

33%

18%

17%

11%

8%

8%

1%

30%

0% 10% 20% 30% 40%

No interest in gaming

Price too high

No time to play games

Satisfied with current gameconsole

Lack of appealing game titles

Switch console performanceand capabilities not appealing

Family or friend has bought one

Other

Source: MIC Source: Famitsu, Credit Suisse

3) Expect long-tail sales cycle for the Switch thanks to minor changesThe DS (NDS + 3DS) series sales cycle lasted 12 years, peaking around year five (Figure 5). The broadly defined DS series sold more than 200mn units over a long sales cycle. We think the key factor behind this DS series was that the sales cycle had both a high peak and a long tail. The long tail factor is likely due to the numerous minor changes introduced over the cycle. We think that the Switch will also see numerous minor changes over time, noting that Nintendo has in fact already introduced a number of minor changes for the Switch.

Many users are using the Switch as a

portable according to survey

The Switch is inexpensively priced

DS series sold more than 200mn units over

12-year sales cycle

15 September 2017

Nintendo (7974) 6

Figure 5: DS series had very long-tailed sales cycle

Figure 6: Total market penetration of game hardware

05

101520253035

FY3/

05

FY3/

06

FY3/

07

FY3/

08

FY3/

09

FY3/

10

FY3/

11

FY3/

12

FY3/

13

FY3/

14

FY3/

15

FY3/

16

FY3/

17

(mn

units

)

3DS

NDS12 years

DSi

DS LiteDS i LL

102

14

128 120

81

154

78

201232

0

50

100

150

200

250

Wii

Wii-

U

Switc

h(C

S E)

Gam

e Bo

y

GBA

ND

S

3DS

GB+

GBA

ND

S+3D

S

Console Console?Portable?

Portable CS definition

(mn

units

)

as of end-FY3/22

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

In traditional handhelds, the NDS (150mn units) and 3DS (80mn units) could be viewed as appropriate benchmarks. Looking back over the history of the NDS and 3DS, however, we see the two series as ending up being quite similar. As a result, we include both handhelds in our broad definition of the DS series. We further expect that Switch sales will generally follow those of the broadly defined DS (NDS+3DS) series.

We conservatively assume a lower Switch attach rate than for consoles Game consoles generally tend to have higher attach rates than their handheld counterparts. The Switch, however, is a cross between a console and handheld. We assume the Switch will have a relatively low attach rate, on par with handheld game hardware. Our forecasts therefore have upside potential if the Switch proves to have a higher attach rate more in line with that of a console.

Figure 7: Handheld game devices tend to have lower attach rates than consoles

Figure 8: Switch could benefit from high console-like attach rate and handhelds’ greater mass-market appeal

0 x

2 x

4 x

6 x

8 x

10 x

Year

1

Year

2

Year

3

Year

4

Year

5

NDS

3DS

Wii

Wii-U

Low High

Smaller Conventionalhome console

BiggerConventional

handheldconsole

Positivescenario for

Switch

Attach rate

Inst

all b

ase

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Combined NDS/3DS series achieved

mass-market success with penetration over

200mn units

Broad definition of DS series includes

NDS+3DS; expect Switch to follow broad

DS series cycle

Handheld game devices tend to have

lower attach rates than consoles

15 September 2017

Nintendo (7974) 7

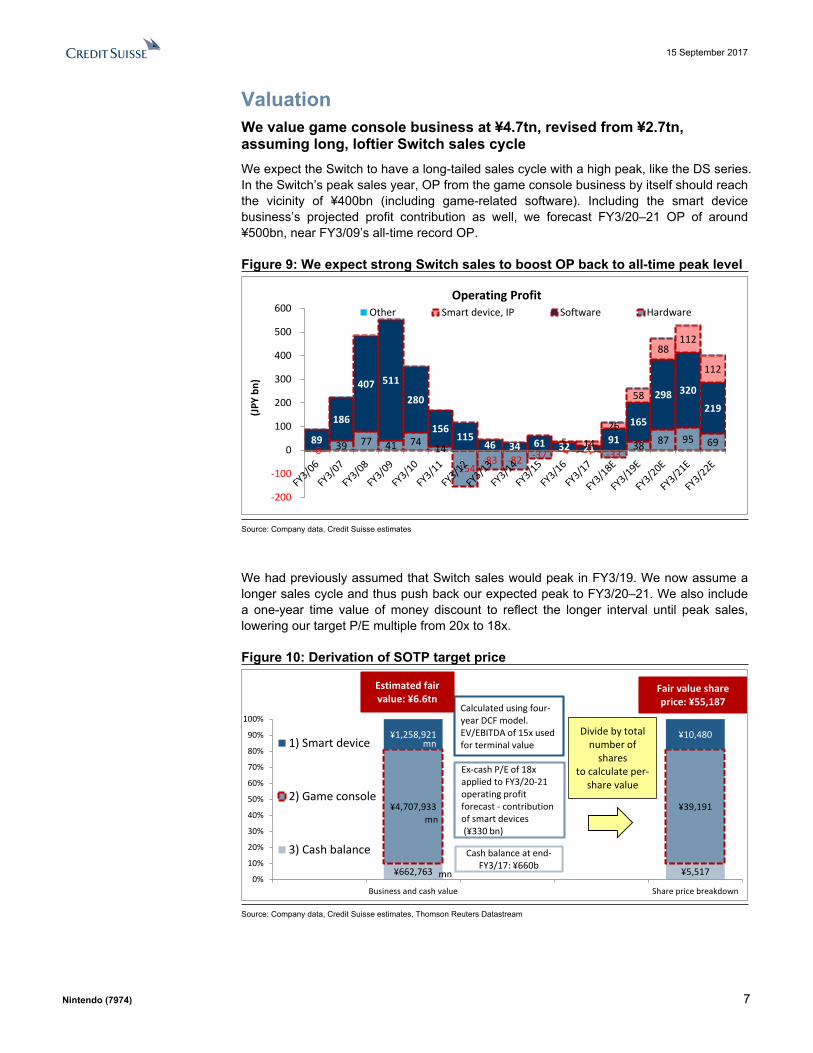

Valuation We value game console business at ¥4.7tn, revised from ¥2.7tn, assuming long, loftier Switch sales cycleWe expect the Switch to have a long-tailed sales cycle with a high peak, like the DS series. In the Switch’s peak sales year, OP from the game console business by itself should reach the vicinity of ¥400bn (including game-related software). Including the smart device business’s projected profit contribution as well, we forecast FY3/20–21 OP of around ¥500bn, near FY3/09’s all-time record OP.

Figure 9: We expect strong Switch sales to boost OP back to all-time peak level

-0 39 77 41 74 14

-154 -83 -82 -37 -4 -7 -33

38 87 95 69 89

186

407 511

280

156 115

46 34 61 32 21 91

165

298 320

219

5 14

26

58

88 112

112

-200

-100

0

100

200

300

400

500

600

(JPY

bn)

Operating ProfitOther Smart device, IP Software Hardware

Source: Company data, Credit Suisse estimates

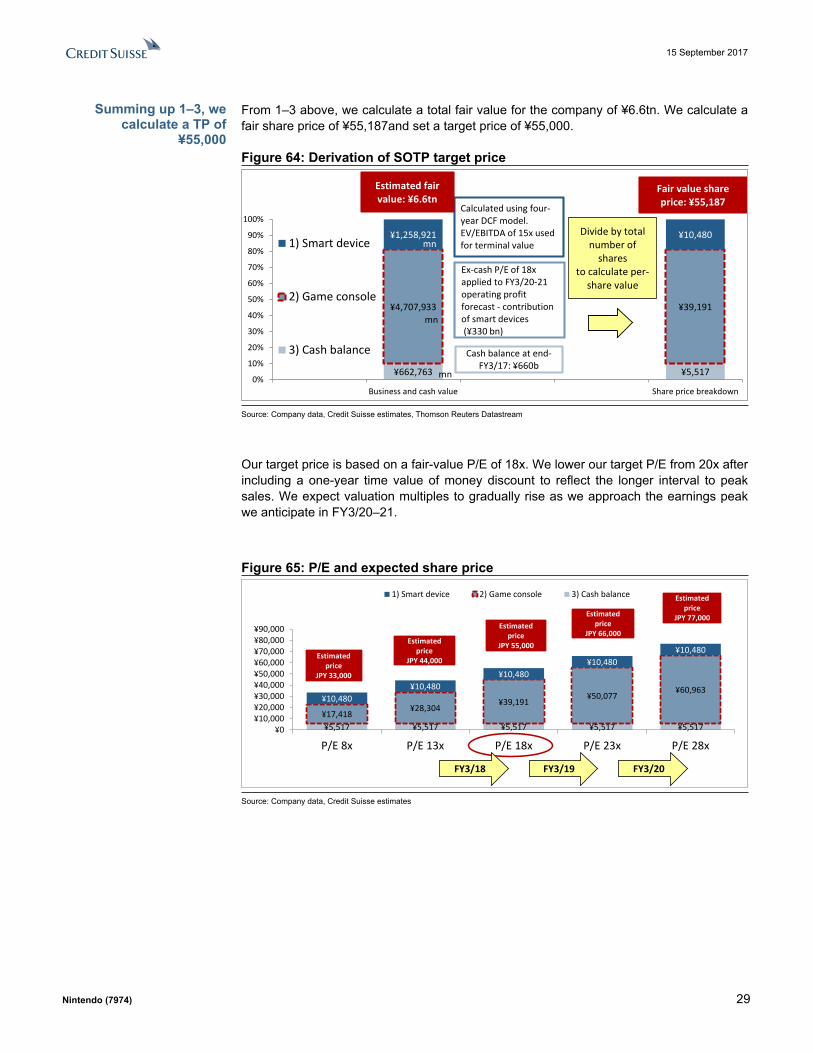

We had previously assumed that Switch sales would peak in FY3/19. We now assume a longer sales cycle and thus push back our expected peak to FY3/20–21. We also include a one-year time value of money discount to reflect the longer interval until peak sales, lowering our target P/E multiple from 20x to 18x.

Figure 10: Derivation of SOTP target price

¥662,763 ¥5,517

¥4,707,933 ¥39,191

¥1,258,921 ¥10,480

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Business and cash value Share price breakdown

1) Smart device

2) Game console

3) Cash balance Cash balance at end-FY3/17: ¥660b

mn

mn

Ex-cash P/E of 18x applied to FY3/20-21operating profit forecast - contribution of smart devices(¥330 bn)

Calculated using four-year DCF model.EV/EBITDA of 15x used for terminal valuemn

Divide by total number of

sharesto calculate per-

share value

Estimated fair value: ¥6.6tn

Fair value share price: ¥55,187

Source: Company data, Credit Suisse estimates, Thomson Reuters Datastream

15 September 2017

Nintendo (7974) 8

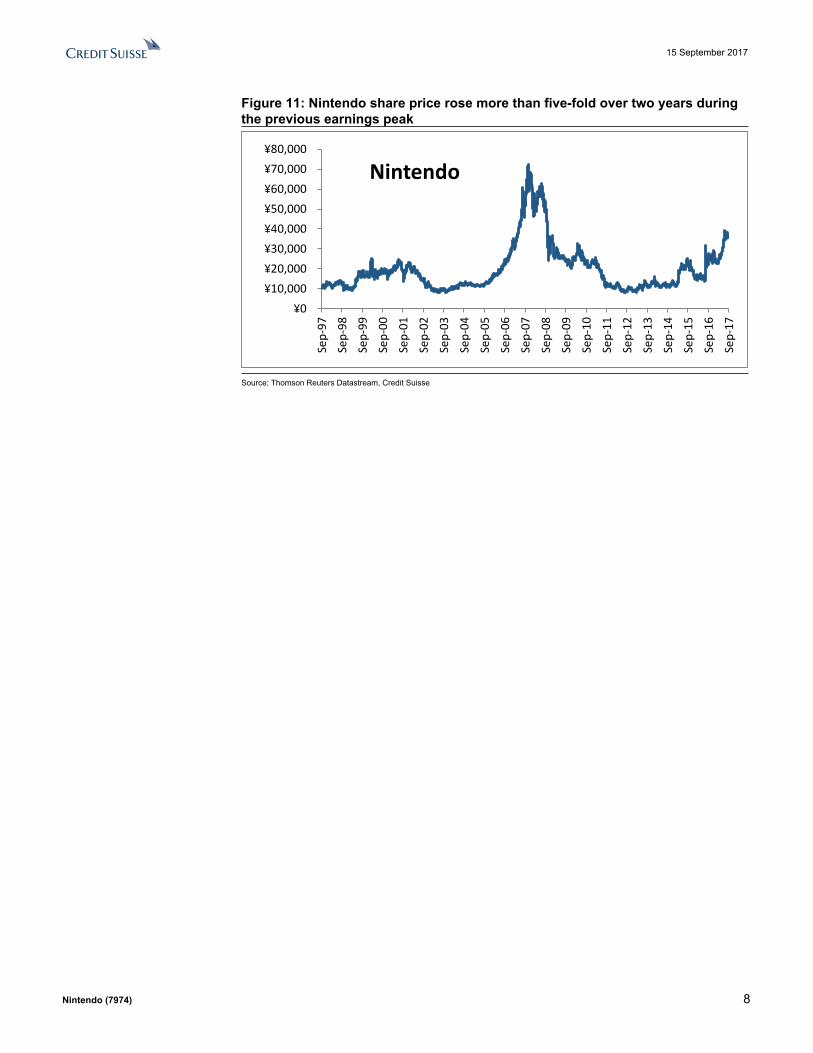

Figure 11: Nintendo share price rose more than five-fold over two years during the previous earnings peak

¥0¥10,000¥20,000¥30,000¥40,000¥50,000¥60,000¥70,000¥80,000

Sep-

97

Sep-

98

Sep-

99

Sep-

00

Sep-

01

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Sep-

06

Sep-

07

Sep-

08

Sep-

09

Sep-

10

Sep-

11

Sep-

12

Sep-

13

Sep-

14

Sep-

15

Sep-

16

Sep-

17

Nintendo

Source: Thomson Reuters Datastream, Credit Suisse

15 September 2017

Nintendo (7974) 9

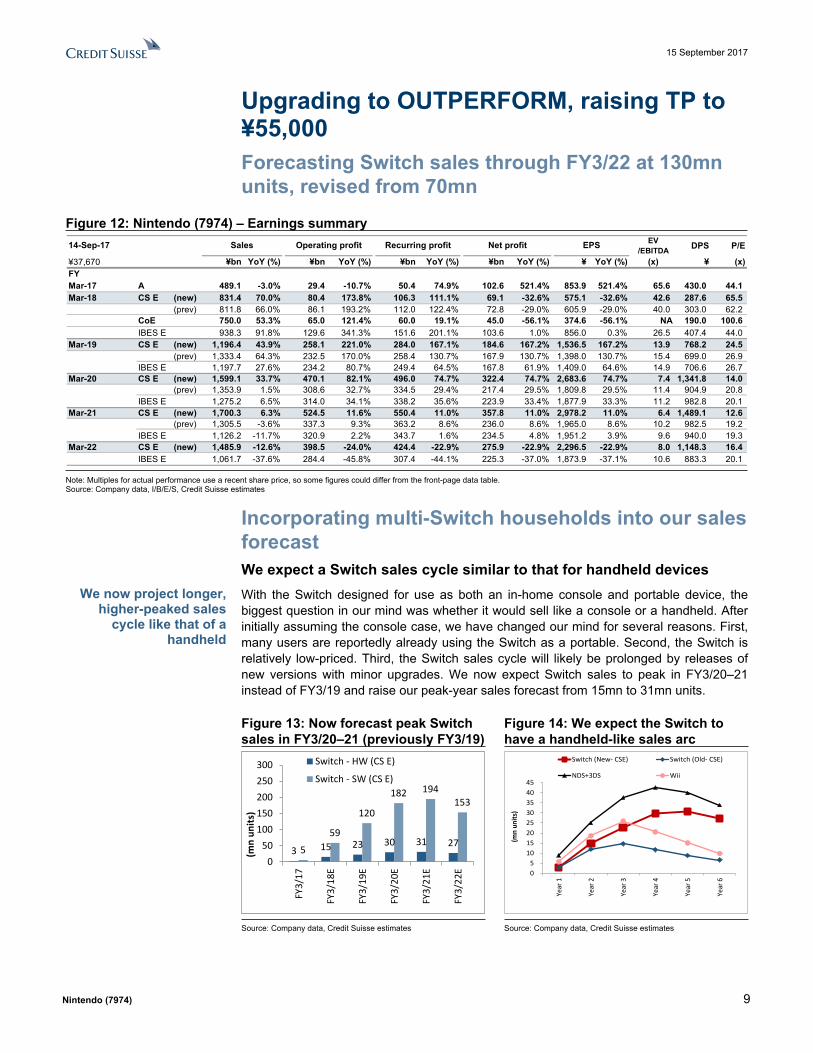

Upgrading to OUTPERFORM, raising TP to ¥55,000Forecasting Switch sales through FY3/22 at 130mn units, revised from 70mn

Figure 12: Nintendo (7974) – Earnings summary EV

/EBITDA DPS P/E

¥37,670 ¥bn YoY (%) ¥bn YoY (%) ¥bn YoY (%) ¥bn YoY (%) ¥ YoY (%) (x) ¥ (x)FYMar-17 A 489.1 -3.0% 29.4 -10.7% 50.4 74.9% 102.6 521.4% 853.9 521.4% 65.6 430.0 44.1Mar-18 CS E (new) 831.4 70.0% 80.4 173.8% 106.3 111.1% 69.1 -32.6% 575.1 -32.6% 42.6 287.6 65.5

(prev) 811.8 66.0% 86.1 193.2% 112.0 122.4% 72.8 -29.0% 605.9 -29.0% 40.0 303.0 62.2CoE 750.0 53.3% 65.0 121.4% 60.0 19.1% 45.0 -56.1% 374.6 -56.1% NA 190.0 100.6IBES E 938.3 91.8% 129.6 341.3% 151.6 201.1% 103.6 1.0% 856.0 0.3% 26.5 407.4 44.0

Mar-19 CS E (new) 1,196.4 43.9% 258.1 221.0% 284.0 167.1% 184.6 167.2% 1,536.5 167.2% 13.9 768.2 24.5(prev) 1,333.4 64.3% 232.5 170.0% 258.4 130.7% 167.9 130.7% 1,398.0 130.7% 15.4 699.0 26.9

IBES E 1,197.7 27.6% 234.2 80.7% 249.4 64.5% 167.8 61.9% 1,409.0 64.6% 14.9 706.6 26.7Mar-20 CS E (new) 1,599.1 33.7% 470.1 82.1% 496.0 74.7% 322.4 74.7% 2,683.6 74.7% 7.4 1,341.8 14.0

(prev) 1,353.9 1.5% 308.6 32.7% 334.5 29.4% 217.4 29.5% 1,809.8 29.5% 11.4 904.9 20.8IBES E 1,275.2 6.5% 314.0 34.1% 338.2 35.6% 223.9 33.4% 1,877.9 33.3% 11.2 982.8 20.1

Mar-21 CS E (new) 1,700.3 6.3% 524.5 11.6% 550.4 11.0% 357.8 11.0% 2,978.2 11.0% 6.4 1,489.1 12.6(prev) 1,305.5 -3.6% 337.3 9.3% 363.2 8.6% 236.0 8.6% 1,965.0 8.6% 10.2 982.5 19.2

IBES E 1,126.2 -11.7% 320.9 2.2% 343.7 1.6% 234.5 4.8% 1,951.2 3.9% 9.6 940.0 19.3Mar-22 CS E (new) 1,485.9 -12.6% 398.5 -24.0% 424.4 -22.9% 275.9 -22.9% 2,296.5 -22.9% 8.0 1,148.3 16.4

IBES E 1,061.7 -37.6% 284.4 -45.8% 307.4 -44.1% 225.3 -37.0% 1,873.9 -37.1% 10.6 883.3 20.1

EPS14-Sep-17 Sales Operating profit Recurring profit Net profit

Note: Multiples for actual performance use a recent share price, so some figures could differ from the front-page data table. Source: Company data, I/B/E/S, Credit Suisse estimates

Incorporating multi-Switch households into our sales forecastWe expect a Switch sales cycle similar to that for handheld devicesWith the Switch designed for use as both an in-home console and portable device, the biggest question in our mind was whether it would sell like a console or a handheld. After initially assuming the console case, we have changed our mind for several reasons. First, many users are reportedly already using the Switch as a portable. Second, the Switch is relatively low-priced. Third, the Switch sales cycle will likely be prolonged by releases of new versions with minor upgrades. We now expect Switch sales to peak in FY3/20–21 instead of FY3/19 and raise our peak-year sales forecast from 15mn to 31mn units.

Figure 13: Now forecast peak Switch sales in FY3/20–21 (previously FY3/19)

Figure 14: We expect the Switch to have a handheld-like sales arc

3 15 23 30 31 275

59

120

182 194153

050

100150200250300

FY3/

17

FY3/

18E

FY3/

19E

FY3/

20E

FY3/

21E

FY3/

22E

(mn

units

)

Switch - HW (CS E)

Switch - SW (CS E)

05

1015202530354045

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

(mn

units

)

Switch (New- CSE) Switch (Old- CSE)

NDS+3DS Wii

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

We now project longer, higher-peaked sales

cycle like that of a handheld

15 September 2017

Nintendo (7974) 10

Figure 15: Game hardware’s cumulative sales (historical)

Figure 16: DS (NDS+3DS) and Gameboy series both sold over 200mn units

GB, 65 GBA, 82

NDS, 154

3DS, 78

N64, 27 NGC, 22

Wii, 102

Wii U, 14

Switch (CSE), 128

020406080

100120140160180

FY19

97FY

1999

FY20

01FY

2003

FY20

05FY

2007

FY20

09FY

2011

FY20

13FY

2015

FY20

17E

FY20

19E

FY20

21E

(mn

units

) 102

14

128 120

81

154

78

201232

0

50

100

150

200

250

Wii

Wii-

U

Switc

h(C

S E)

Gam

e Bo

y

GBA

ND

S

3DS

GB+

GBA

ND

S+3D

S

Console Console?Portable?

Portable CS definition

(mn

unit

s)

as of end-FY3/22

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

We look for a lofty earnings peak coinciding with peak Switch sales in FY3/20–21Assuming that Switch sales peak in line with our forecast, we expect OP from the game console business by itself to reach ¥400bn (including game software). Meanwhile, the smart device business should contribute additional profits. Although we do not expect hardware unit sales to match their FY3/09 all-time high (Figure 19), we believe consolidated OP should peak above ¥500bn like in FY3/09.

Figure 17: Game hardware’s cumulative sales (historical)

Figure 18: DS (NDS+3DS) and Gameboy series both sold over 200mn units

268 257 519 677

851 877 793 230 206

266

409

577 604 473

6 24

49

113

173 221

221

0200400600800

1,0001,2001,4001,6001,800

FY3/16 FY3/17 FY3/18E FY3/19E FY3/20E FY3/21E FY3/22E

(JPY

bn)

Sales

Other

Smart device, IP

Software

Hardware

-4 -7 -33 38 87 95 69 32 21

91

165

298 320

219

5 14

26

58

88 112

112

-100

0

100

200

300

400

500

600

FY3/16 FY3/17 FY3/18E FY3/19E FY3/20E FY3/21E FY3/22E

(JPY

bn)

Operating ProfitOther

Smartdevice, IPSoftware

Hardware

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 19: Hardware unit-sales and OP

-100,000

0

100,000

200,000

300,000

400,000

500,000

600,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

FY3/

90FY

3/91

FY3/

92FY

3/93

FY3/

94FY

3/95

FY3/

96FY

3/97

FY3/

98FY

3/99

FY3/

00FY

3/01

FY3/

02FY

3/03

FY3/

04FY

3/05

FY3/

06FY

3/07

FY3/

08FY

3/09

FY3/

10FY

3/11

FY3/

12FY

3/13

FY3/

14FY

3/15

FY3/

16FY

3/17

FY3/

18E

FY3/

19E

FY3/

20E

FY3/

21E

FY3/

22E

3DS NDSGB total SwitchWii-U WiiGC N64SFC FCOP total (RHS)

('000 units) (JPY mn)

Source: Company data, Credit Suisse estimates

15 September 2017

Nintendo (7974) 11

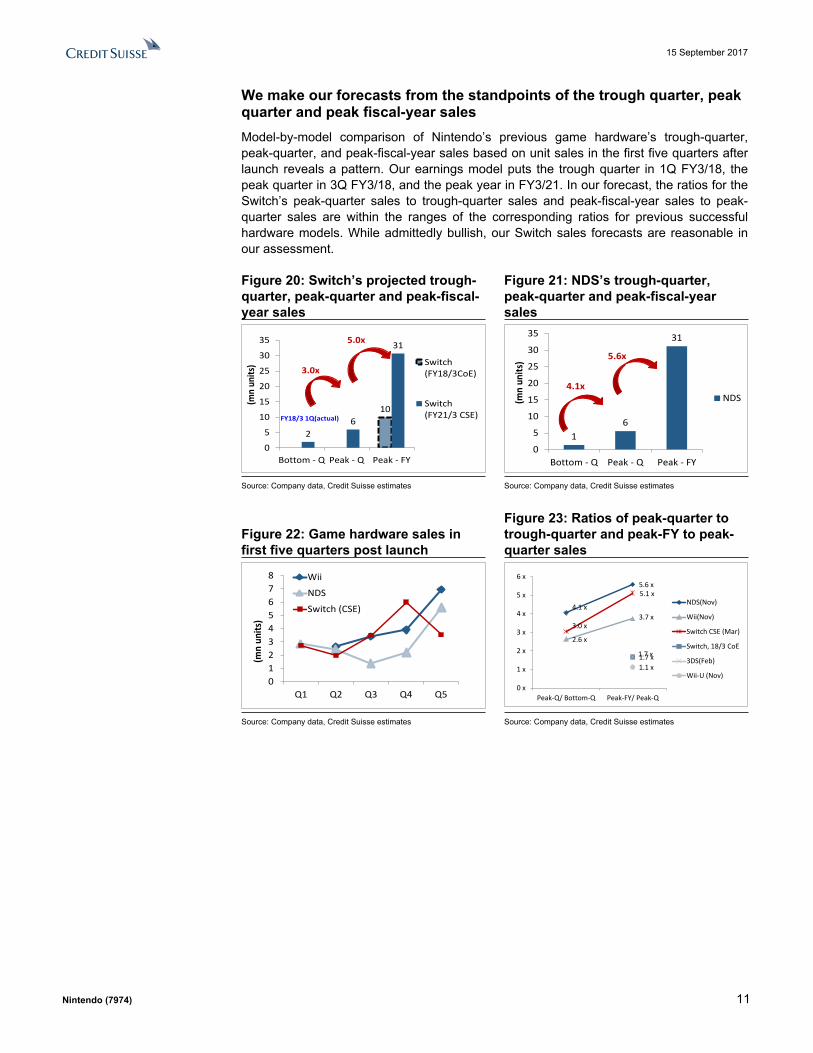

We make our forecasts from the standpoints of the trough quarter, peak quarter and peak fiscal-year salesModel-by-model comparison of Nintendo’s previous game hardware’s trough-quarter, peak-quarter, and peak-fiscal-year sales based on unit sales in the first five quarters after launch reveals a pattern. Our earnings model puts the trough quarter in 1Q FY3/18, the peak quarter in 3Q FY3/18, and the peak year in FY3/21. In our forecast, the ratios for the Switch’s peak-quarter sales to trough-quarter sales and peak-fiscal-year sales to peak-quarter sales are within the ranges of the corresponding ratios for previous successful hardware models. While admittedly bullish, our Switch sales forecasts are reasonable in our assessment.

Figure 20: Switch’s projected trough-quarter, peak-quarter and peak-fiscal-year sales

Figure 21: NDS’s trough-quarter, peak-quarter and peak-fiscal-year sales

10

26

31

0

5

10

15

20

25

30

35

Bottom - Q Peak - Q Peak - FY

(mn

units

) Switch(FY18/3CoE)

Switch(FY21/3 CSE)

3.0x

5.0x

FY18/3 1Q(actual)

16

31

0

5

10

15

20

25

30

35

Bottom - Q Peak - Q Peak - FY

(mn

units

)

NDS4.1x

5.6x

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 22: Game hardware sales in first five quarters post launch

Figure 23: Ratios of peak-quarter to trough-quarter and peak-FY to peak-quarter sales

012345678

Q1 Q2 Q3 Q4 Q5

(mn

units

)

Wii

NDS

Switch (CSE) 4.1 x

5.6 x

2.6 x

3.7 x3.0 x

5.1 x

1.7 x1.7 x1.1 x

0 x

1 x

2 x

3 x

4 x

5 x

6 x

Peak-Q/ Bottom-Q Peak-FY/ Peak-Q

NDS(Nov)

Wii(Nov)

Switch CSE (Mar)

Switch, 18/3 CoE

3DS(Feb)

Wii-U (Nov)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

15 September 2017

Nintendo (7974) 12

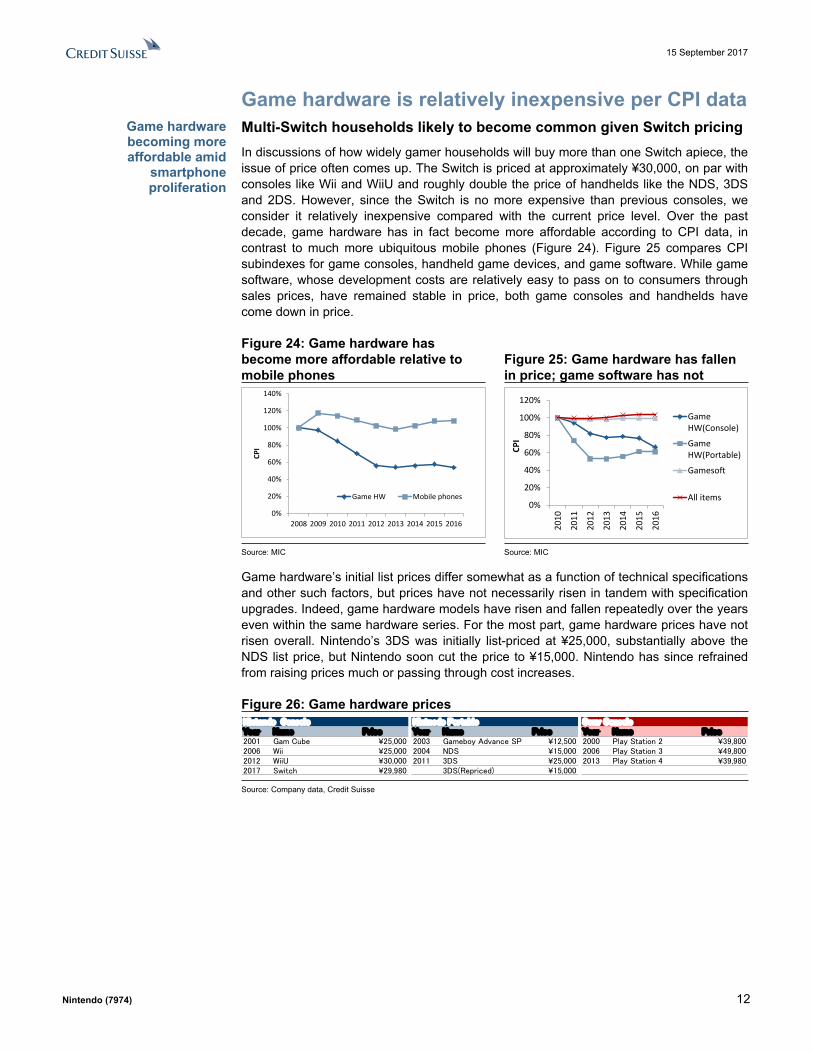

Game hardware is relatively inexpensive per CPI dataMulti-Switch households likely to become common given Switch pricingIn discussions of how widely gamer households will buy more than one Switch apiece, the issue of price often comes up. The Switch is priced at approximately ¥30,000, on par with consoles like Wii and WiiU and roughly double the price of handhelds like the NDS, 3DS and 2DS. However, since the Switch is no more expensive than previous consoles, we consider it relatively inexpensive compared with the current price level. Over the past decade, game hardware has in fact become more affordable according to CPI data, in contrast to much more ubiquitous mobile phones (Figure 24). Figure 25 compares CPI subindexes for game consoles, handheld game devices, and game software. While game software, whose development costs are relatively easy to pass on to consumers through sales prices, have remained stable in price, both game consoles and handhelds have come down in price.

Figure 24: Game hardware has become more affordable relative to mobile phones

Figure 25: Game hardware has fallen in price; game software has not

0%

20%

40%

60%

80%

100%

120%

140%

2008 2009 2010 2011 2012 2013 2014 2015 2016

CPI

Game HW Mobile phones0%

20%

40%

60%

80%

100%

120%

2010

2011

2012

2013

2014

2015

2016

CPI

GameHW(Console)

GameHW(Portable)

Gamesoft

All items

Source: MIC Source: MIC

Game hardware’s initial list prices differ somewhat as a function of technical specifications and other such factors, but prices have not necessarily risen in tandem with specification upgrades. Indeed, game hardware models have risen and fallen repeatedly over the years even within the same hardware series. For the most part, game hardware prices have not risen overall. Nintendo’s 3DS was initially list-priced at ¥25,000, substantially above the NDS list price, but Nintendo soon cut the price to ¥15,000. Nintendo has since refrained from raising prices much or passing through cost increases.

Figure 26: Game hardware pricesNintendo ConsoleYear Name Price Year Name Price Year Name Price2001 Gam Cube ¥25,000 2003 Gameboy Advance SP ¥12,500 2000 Play Station 2 ¥39,8002006 Wii ¥25,000 2004 NDS ¥15,000 2006 Play Station 3 ¥49,8002012 WiiU ¥30,000 2011 3DS ¥25,000 2013 Play Station 4 ¥39,9802017 Switch ¥29,980 3DS(Repriced) ¥15,000

Nintnedo Portable Sony Console

Source: Company data, Credit Suisse

Game hardware becoming more affordable amid

smartphone proliferation

15 September 2017

Nintendo (7974) 13

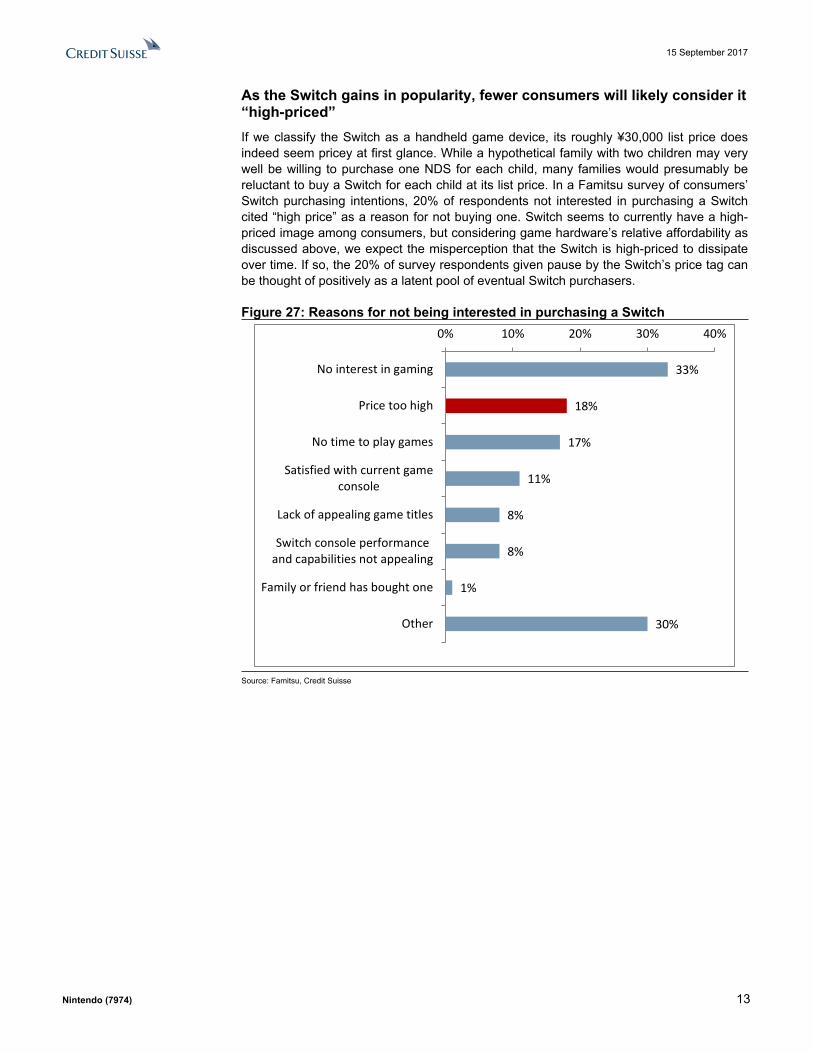

As the Switch gains in popularity, fewer consumers will likely consider it “high-priced” If we classify the Switch as a handheld game device, its roughly ¥30,000 list price does indeed seem pricey at first glance. While a hypothetical family with two children may very well be willing to purchase one NDS for each child, many families would presumably be reluctant to buy a Switch for each child at its list price. In a Famitsu survey of consumers’ Switch purchasing intentions, 20% of respondents not interested in purchasing a Switch cited “high price” as a reason for not buying one. Switch seems to currently have a high-priced image among consumers, but considering game hardware’s relative affordability as discussed above, we expect the misperception that the Switch is high-priced to dissipate over time. If so, the 20% of survey respondents given pause by the Switch’s price tag can be thought of positively as a latent pool of eventual Switch purchasers.

Figure 27: Reasons for not being interested in purchasing a Switch

33%

18%

17%

11%

8%

8%

1%

30%

0% 10% 20% 30% 40%

No interest in gaming

Price too high

No time to play games

Satisfied with current gameconsole

Lack of appealing game titles

Switch console performanceand capabilities not appealing

Family or friend has bought one

Other

Source: Famitsu, Credit Suisse

15 September 2017

Nintendo (7974) 14

Switch poised for similar uptake as the DS series3DS+NDS constitute a broader “DS series” A broader view of the Gameboy and DS seriesNintendo’s post-Gameboy handheld game console sales volume (Figure 28) looks to have repeatedly undergone ups and downs in relatively short sales cycles. However, the sales curve is somewhat more gentle if we adopt the broader view of Gameboy and Gameboy Advance (GB+GBA) constituting the GB series and NDS+3DS constituting the DS series (Figure 29). The sharp sales dip followed by a rebound mid-cycle of the GB series was apparently due to the introduction of the slimmer Gameboy Pocket (GB Pocket) in July 1996 (Figure 30).

Figure 28: High sales volatility if the game consoles are viewed separately…

Figure 29:…but ups and downs are smoother for the broader GB and DS series

05

101520253035

FY3/

90FY

3/92

FY3/

94FY

3/96

FY3/

98FY

3/00

FY3/

02FY

3/04

FY3/

06FY

3/08

FY3/

10FY

3/12

FY3/

14FY

3/16

FY3/

18E

FY3/

20E

FY3/

22E

(mn

units

)

Game Boy GBA NDS 3DS

05

101520253035

FY3/

90FY

3/92

FY3/

94FY

3/96

FY3/

98FY

3/00

FY3/

02FY

3/04

FY3/

06FY

3/08

FY3/

10FY

3/12

FY3/

14FY

3/16

FY3/

18E

FY3/

20E

(mn

units

)

GB+GBA NDS+3DS

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Sales for the broader GB and DS series have proven to be long-tailed. Restricting the former to consoles released after Gameboy Pocket, we note the two broader series’ sales cycles lasted around 12 years, gradually heading for a peak-out after registering stable sales (Figures 30-31).

Figure 30: GB and GBA sales trends Figure 31: NDS and 3DS sales trends

0

5

10

15

20

25

(mn

units

)

GAMEBOY ADVANCE

Game BoyGameboy

PocketRelease

12 years

05

101520253035

FY3/

05

FY3/

06

FY3/

07

FY3/

08

FY3/

09

FY3/

10

FY3/

11

FY3/

12

FY3/

13

FY3/

14

FY3/

15

FY3/

16

FY3/

17

(mn

units

)

3DS

NDS12 years

DSi

DS LiteDS i LL

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

15 September 2017

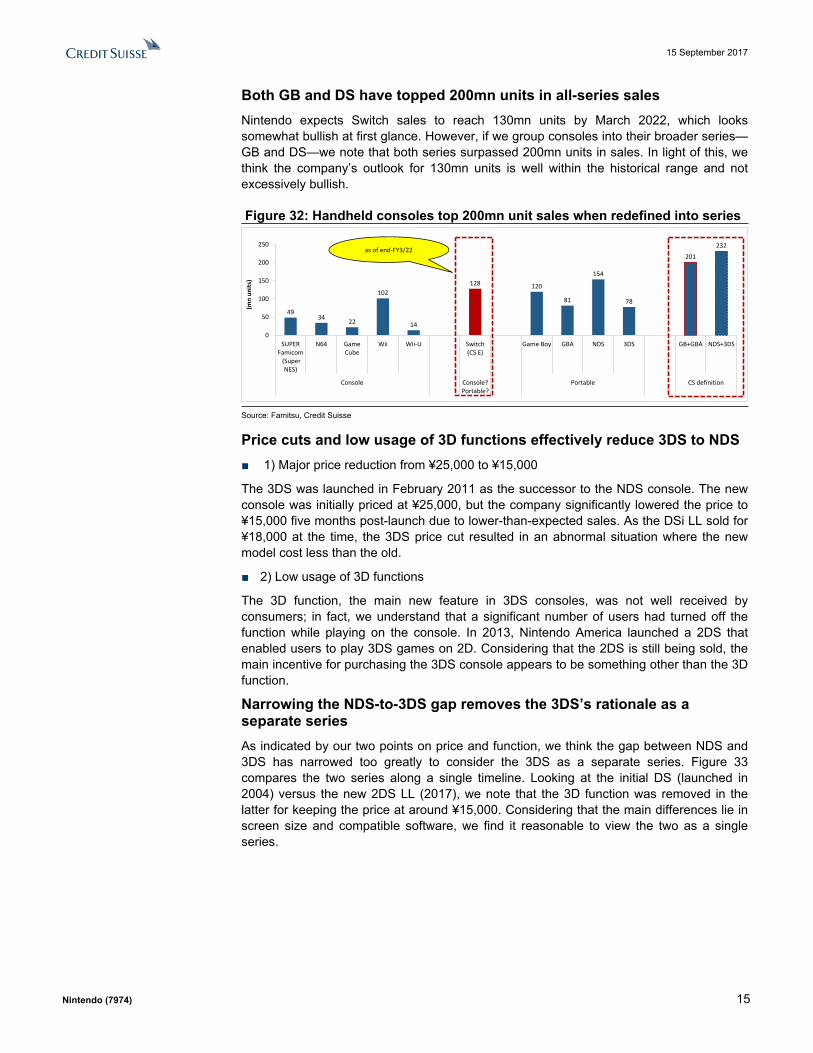

Nintendo (7974) 15

Both GB and DS have topped 200mn units in all-series salesNintendo expects Switch sales to reach 130mn units by March 2022, which looks somewhat bullish at first glance. However, if we group consoles into their broader series—GB and DS—we note that both series surpassed 200mn units in sales. In light of this, we think the company’s outlook for 130mn units is well within the historical range and not excessively bullish.

Figure 32: Handheld consoles top 200mn unit sales when redefined into series

4934

22

102

14

128 120

81

154

78

201

232

0

50

100

150

200

250

SUPERFamicom (Super

NES)

N64 GameCube

Wii Wii-U Switch(CS E)

Game Boy GBA NDS 3DS GB+GBA NDS+3DS

Console Console?Portable?

Portable CS definition

(mn

units

)as of end-FY3/22

Source: Famitsu, Credit Suisse

Price cuts and low usage of 3D functions effectively reduce 3DS to NDS■ 1) Major price reduction from ¥25,000 to ¥15,000

The 3DS was launched in February 2011 as the successor to the NDS console. The new console was initially priced at ¥25,000, but the company significantly lowered the price to ¥15,000 five months post-launch due to lower-than-expected sales. As the DSi LL sold for ¥18,000 at the time, the 3DS price cut resulted in an abnormal situation where the new model cost less than the old.

■ 2) Low usage of 3D functions

The 3D function, the main new feature in 3DS consoles, was not well received by consumers; in fact, we understand that a significant number of users had turned off the function while playing on the console. In 2013, Nintendo America launched a 2DS that enabled users to play 3DS games on 2D. Considering that the 2DS is still being sold, the main incentive for purchasing the 3DS console appears to be something other than the 3D function.

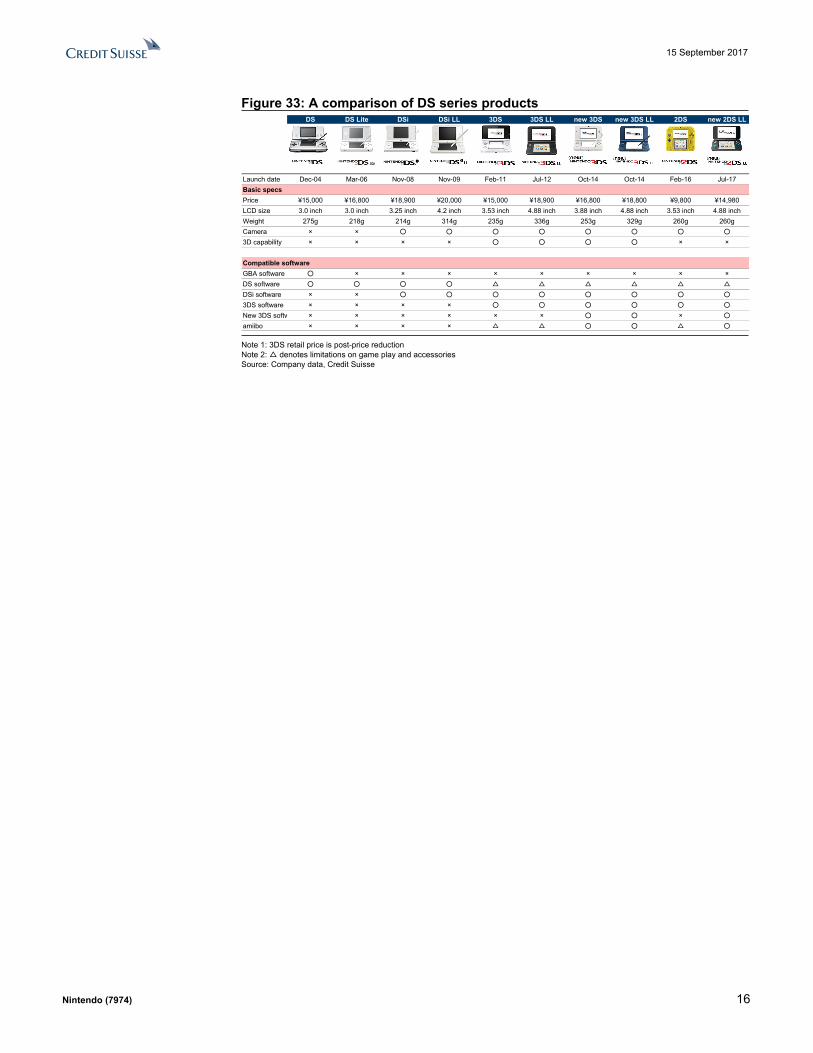

Narrowing the NDS-to-3DS gap removes the 3DS’s rationale as a separate seriesAs indicated by our two points on price and function, we think the gap between NDS and 3DS has narrowed too greatly to consider the 3DS as a separate series. Figure 33 compares the two series along a single timeline. Looking at the initial DS (launched in 2004) versus the new 2DS LL (2017), we note that the 3D function was removed in the latter for keeping the price at around ¥15,000. Considering that the main differences lie in screen size and compatible software, we find it reasonable to view the two as a single series.

15 September 2017

Nintendo (7974) 16

Figure 33: A comparison of DS series products DS DS Lite DSi DSi LL 3DS 3DS LL new 3DS new 3DS LL 2DS new 2DS LL

Launch date Dec-04 Mar-06 Nov-08 Nov-09 Feb-11 Jul-12 Oct-14 Oct-14 Feb-16 Jul-17Basic specs Price ¥15,000 ¥16,800 ¥18,900 ¥20,000 ¥15,000 ¥18,900 ¥16,800 ¥18,800 ¥9,800 ¥14,980LCD size 3.0 inch 3.0 inch 3.25 inch 4.2 inch 3.53 inch 4.88 inch 3.88 inch 4.88 inch 3.53 inch 4.88 inchWeight 275g 218g 214g 314g 235g 336g 253g 329g 260g 260gCamera × × ○ ○ ○ ○ ○ ○ ○ ○

3D capability × × × × ○ ○ ○ ○ × ×

Compatible softwareGBA software ○ × × × × × × × × ×DS software ○ ○ ○ ○ △ △ △ △ △ △

DSi software × × ○ ○ ○ ○ ○ ○ ○ ○

3DS software × × × × ○ ○ ○ ○ ○ ○

New 3DS software × × × × × × ○ ○ × ○

amiibo × × × × △ △ ○ ○ △ ○

Note 1: 3DS retail price is post-price reduction Note 2: △ denotes limitations on game play and accessoriesSource: Company data, Credit Suisse

15 September 2017

Nintendo (7974) 17

Revising attach rate outlookRevising our attach rate outlook to be on a par with handheld consoles, given expectations of comparable uptake ratesHandheld consoles usually have lower software attach rates than stationary game consoles. This is usually attributed to serious gamers favoring the stationary console, while the handheld console is seen as oriented more toward casual users with few hardcore games using handheld devices, but we believe the price of hardware also plays a significant role.

The new 2DS LL is currently priced at ¥14,980, while the Wii, which had a higher attach rate, was priced at ¥25,000. We believe this can also be attributed to the psychological factor that having purchased expensive hardware the user will aim to derive maximum value from the purchase. In fact, as shown in Figure 36, Nintendo’s hardware to software sales ratio has remained constant at roughly 6:4. We believe this highlights consumers’ unconscious efforts to balance their spending on hardware and software.

As for the Switch (retail price ¥29,980), we see prospects for the attach rate becoming a positive. particularly in hardware pricing. However, it remains to be seen how users respond to the new hardware design. We thus incorporate into our outlook relatively modest attach rates closer to those for the previous generation of handheld consoles.

Figure 34: Handheld consoles tend to have lower attach rates

Figure 35: Lowering attach rate outlook to be on par with the historical NDS average

0 x

2 x

4 x

6 x

8 x

10 x

Year

1

Year

2

Year

3

Year

4

Year

5

NDS

3DS

Wii

Wii-U0 x2 x4 x6 x8 x

10 x

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Switch (Old CSE)Switch (New CSE)Switch (CoE)

Source: Company data, Credit Suisse Source: Company data, Credit Suisse estimates

Figure 36: Hardware/software sales ratio constant at around 6:4

Figure 37: Switch could enjoy both the high attach rates of stationary consoles and high market penetration of handhelds

0%10%20%30%40%50%60%70%80%90%

100%

Software

Hardware

Low High

Smaller Conventionalhome console

BiggerConventional

handheldconsole

Positivescenario for

Switch

Attach rate

Inst

all b

ase

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Psychological factor behind the relationship

between attach rates and hardware price

Still upside

15 September 2017

Nintendo (7974) 18

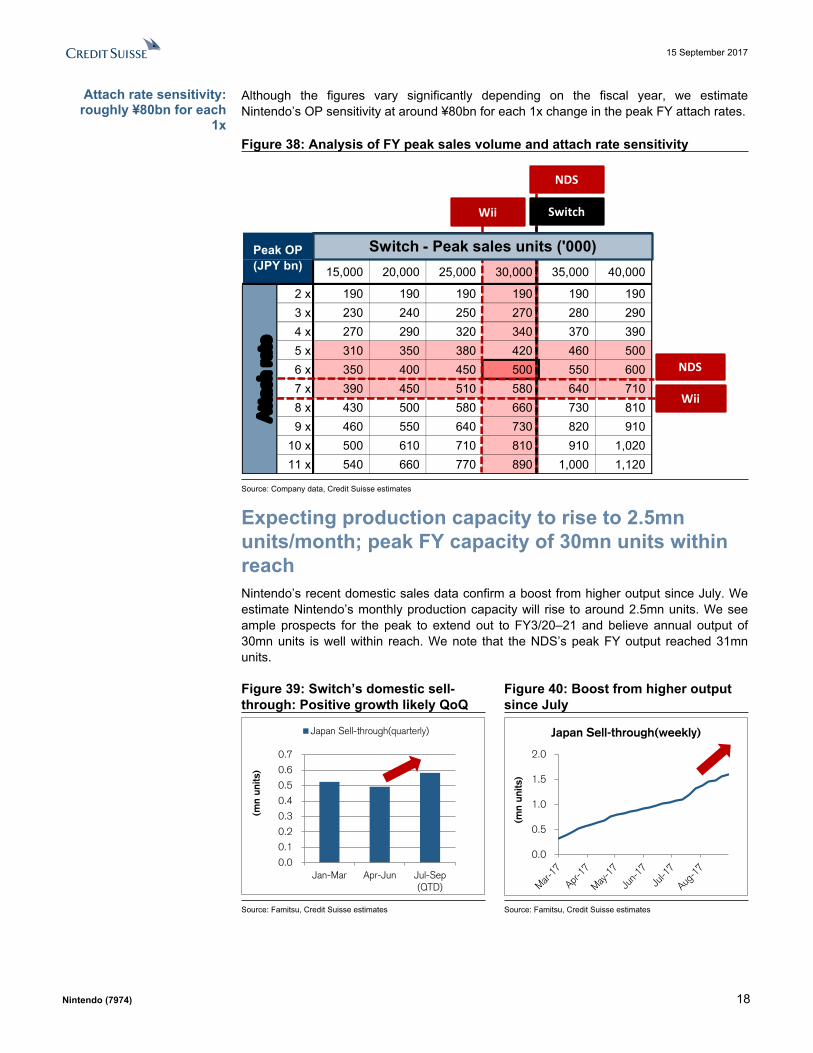

Although the figures vary significantly depending on the fiscal year, we estimate Nintendo’s OP sensitivity at around ¥80bn for each 1x change in the peak FY attach rates.

Figure 38: Analysis of FY peak sales volume and attach rate sensitivity

15,000 20,000 25,000 30,000 35,000 40,000

2 x 190 190 190 190 190 1903 x 230 240 250 270 280 2904 x 270 290 320 340 370 3905 x 310 350 380 420 460 5006 x 350 400 450 500 550 6007 x 390 450 510 580 640 7108 x 430 500 580 660 730 8109 x 460 550 640 730 820 910

10 x 500 610 710 810 910 1,02011 x 540 660 770 890 1,000 1,120

Peak OP(JPY bn)

Switch - Peak sales units ('000)A

ttac

h r

ate

Wii

Wii

NDS

Switch

NDS

Switch - Peak sales units ('000)

Source: Company data, Credit Suisse estimates

Expecting production capacity to rise to 2.5mn units/month; peak FY capacity of 30mn units within reachNintendo’s recent domestic sales data confirm a boost from higher output since July. We estimate Nintendo’s monthly production capacity will rise to around 2.5mn units. We see ample prospects for the peak to extend out to FY3/20–21 and believe annual output of 30mn units is well within reach. We note that the NDS’s peak FY output reached 31mn units.

Figure 39: Switch’s domestic sell-through: Positive growth likely QoQ

Figure 40: Boost from higher output since July

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Jan-Mar Apr-Jun Jul-Sep(QTD)

(mn

units

)

Japan Sell-through(quarterly)

0.0

0.5

1.0

1.5

2.0

(mn

units

)

Japan Sell-through(weekly)

Source: Famitsu, Credit Suisse estimates Source: Famitsu, Credit Suisse estimates

Attach rate sensitivity: roughly ¥80bn for each

1x

15 September 2017

Nintendo (7974) 19

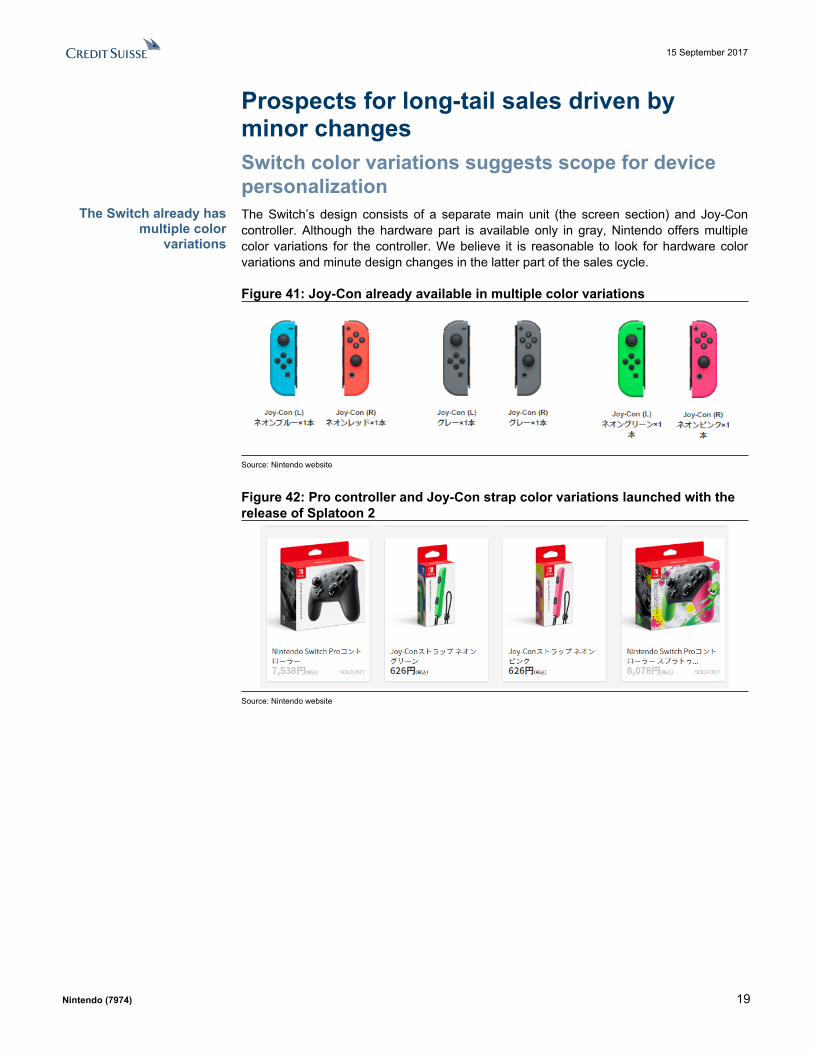

Prospects for long-tail sales driven by minor changesSwitch color variations suggests scope for device personalizationThe Switch’s design consists of a separate main unit (the screen section) and Joy-Con controller. Although the hardware part is available only in gray, Nintendo offers multiple color variations for the controller. We believe it is reasonable to look for hardware color variations and minute design changes in the latter part of the sales cycle.

Figure 41: Joy-Con already available in multiple color variations

Source: Nintendo website

Figure 42: Pro controller and Joy-Con strap color variations launched with the release of Splatoon 2

Source: Nintendo website

The Switch already has multiple color

variations

15 September 2017

Nintendo (7974) 20

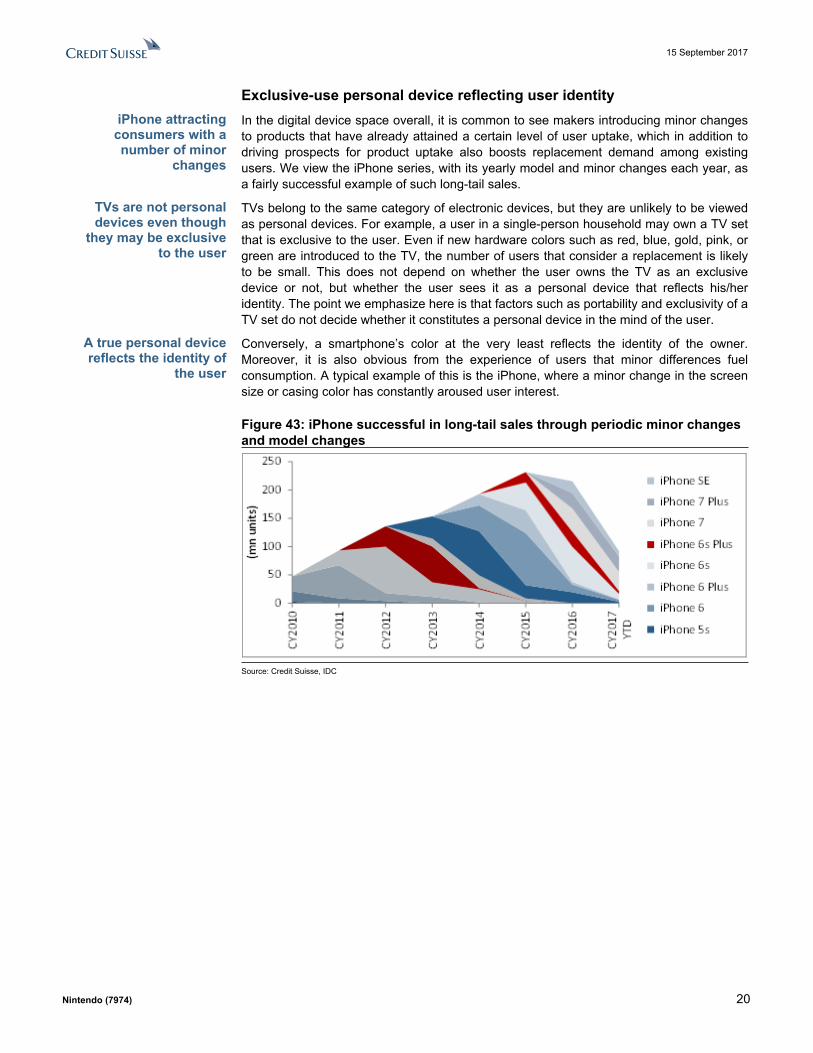

Exclusive-use personal device reflecting user identityIn the digital device space overall, it is common to see makers introducing minor changes to products that have already attained a certain level of user uptake, which in addition to driving prospects for product uptake also boosts replacement demand among existing users. We view the iPhone series, with its yearly model and minor changes each year, as a fairly successful example of such long-tail sales.

TVs belong to the same category of electronic devices, but they are unlikely to be viewed as personal devices. For example, a user in a single-person household may own a TV set that is exclusive to the user. Even if new hardware colors such as red, blue, gold, pink, or green are introduced to the TV, the number of users that consider a replacement is likely to be small. This does not depend on whether the user owns the TV as an exclusive device or not, but whether the user sees it as a personal device that reflects his/her identity. The point we emphasize here is that factors such as portability and exclusivity of a TV set do not decide whether it constitutes a personal device in the mind of the user.

Conversely, a smartphone’s color at the very least reflects the identity of the owner. Moreover, it is also obvious from the experience of users that minor differences fuel consumption. A typical example of this is the iPhone, where a minor change in the screen size or casing color has constantly aroused user interest.

Figure 43: iPhone successful in long-tail sales through periodic minor changes and model changes

Source: Credit Suisse, IDC

iPhone attracting consumers with a number of minor

changes

TVs are not personal devices even though

they may be exclusive to the user

A true personal device reflects the identity of

the user

15 September 2017

Nintendo (7974) 21

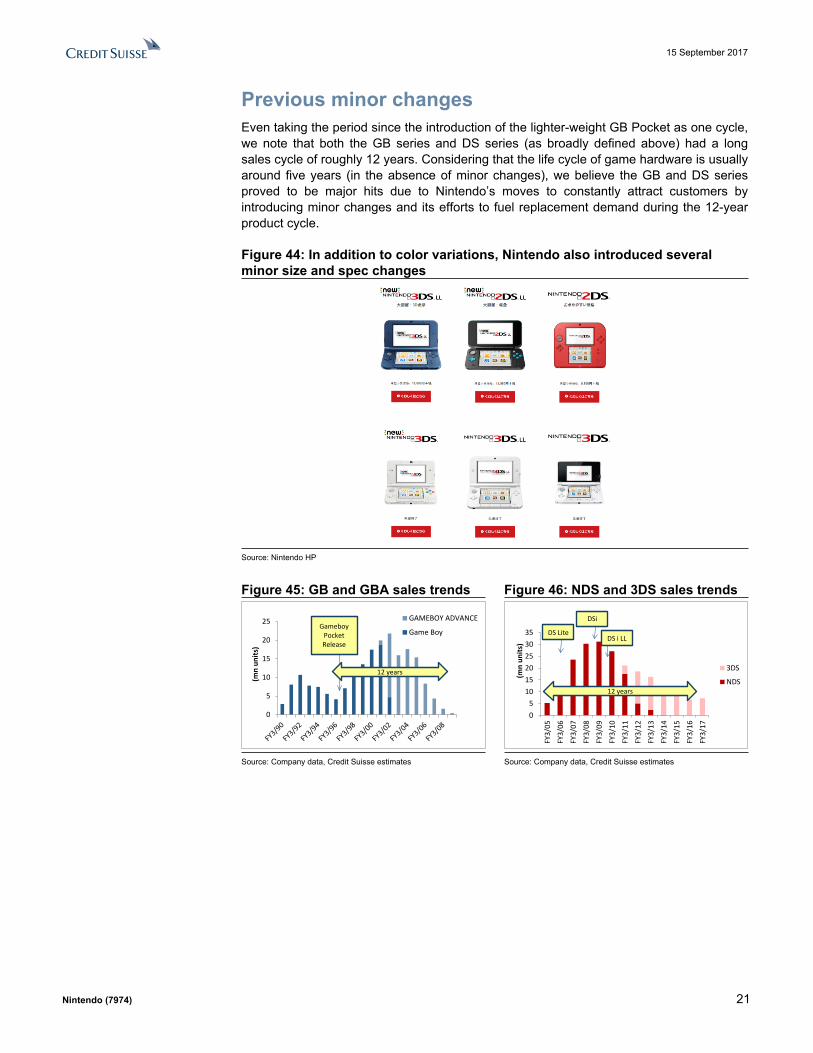

Previous minor changesEven taking the period since the introduction of the lighter-weight GB Pocket as one cycle, we note that both the GB series and DS series (as broadly defined above) had a long sales cycle of roughly 12 years. Considering that the life cycle of game hardware is usually around five years (in the absence of minor changes), we believe the GB and DS series proved to be major hits due to Nintendo’s moves to constantly attract customers by introducing minor changes and its efforts to fuel replacement demand during the 12-year product cycle.

Figure 44: In addition to color variations, Nintendo also introduced several minor size and spec changes

Source: Nintendo HP

Figure 45: GB and GBA sales trends Figure 46: NDS and 3DS sales trends

0

5

10

15

20

25

(mn

units

)

GAMEBOY ADVANCE

Game BoyGameboy

PocketRelease

12 years

05

101520253035

FY3/

05

FY3/

06

FY3/

07

FY3/

08

FY3/

09

FY3/

10

FY3/

11

FY3/

12

FY3/

13

FY3/

14

FY3/

15

FY3/

16

FY3/

17

(mn

units

)

3DS

NDS12 years

DSi

DS LiteDS i LL

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

15 September 2017

Nintendo (7974) 22

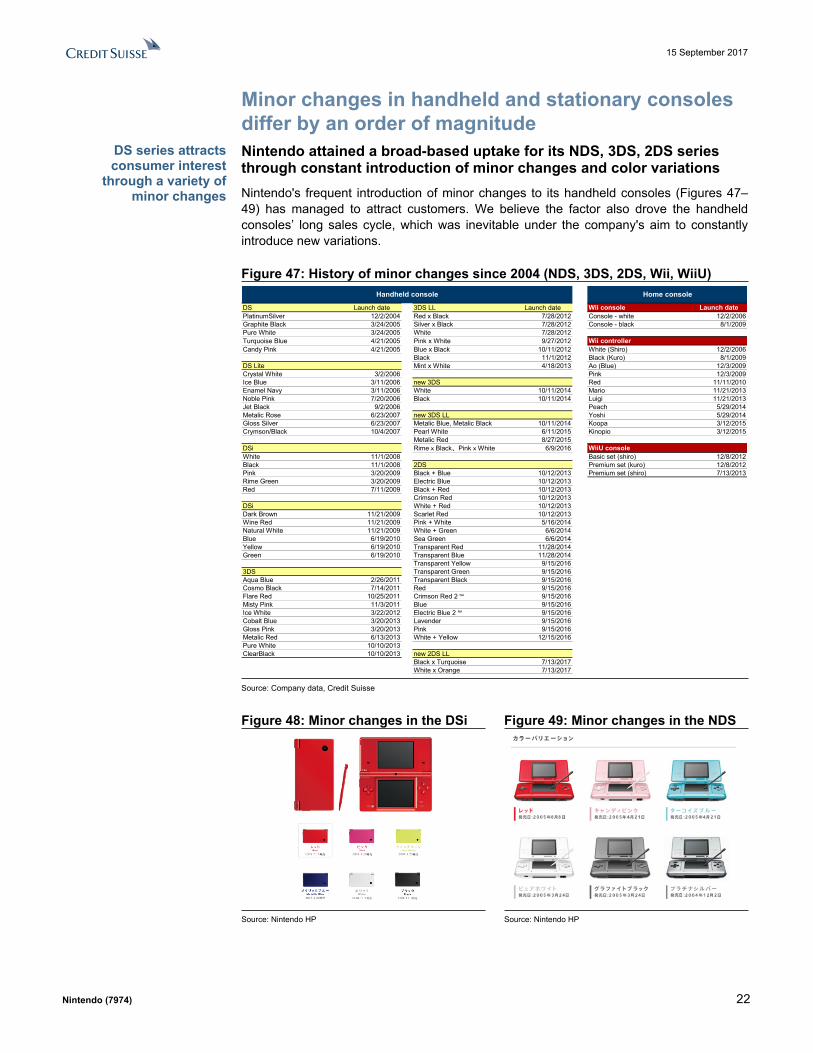

Minor changes in handheld and stationary consoles differ by an order of magnitudeNintendo attained a broad-based uptake for its NDS, 3DS, 2DS series through constant introduction of minor changes and color variationsNintendo's frequent introduction of minor changes to its handheld consoles (Figures 47–49) has managed to attract customers. We believe the factor also drove the handheld consoles’ long sales cycle, which was inevitable under the company's aim to constantly introduce new variations.

Figure 47: History of minor changes since 2004 (NDS, 3DS, 2DS, Wii, WiiU)

DS Launch date 3DS LL Launch date Wii console Launch datePlatinumSilver 12/2/2004 Red x Black 7/28/2012 Console - white 12/2/2006Graphite Black 3/24/2005 Silver x Black 7/28/2012 Console - black 8/1/2009Pure White 3/24/2005 White 7/28/2012Turquoise Blue 4/21/2005 Pink x White 9/27/2012 Wii controller Candy Pink 4/21/2005 Blue x Black 10/11/2012 White (Shiro) 12/2/2006

Black 11/1/2012 Black (Kuro) 8/1/2009DS Lite Mint x White 4/18/2013 Ao (Blue) 12/3/2009Crystal White 3/2/2006 Pink 12/3/2009Ice Blue 3/11/2006 new 3DS Red 11/11/2010Enamel Navy 3/11/2006 White 10/11/2014 Mario 11/21/2013Noble Pink 7/20/2006 Black 10/11/2014 Luigi 11/21/2013Jet Black 9/2/2006 Peach 5/29/2014Metalic Rose 6/23/2007 new 3DS LL Yoshi 5/29/2014Gloss Silver 6/23/2007 Metalic Blue, Metalic Black 10/11/2014 Koopa 3/12/2015Crymson/Black 10/4/2007 Pearl White 6/11/2015 Kinopio 3/12/2015

Metalic Red 8/27/2015DSi RimexBlack、PinkxWhite 6/9/2016 WiiU consoleWhite 11/1/2008 Basic set (shiro) 12/8/2012Black 11/1/2008 2DS Premium set (kuro) 12/8/2012Pink 3/20/2009 Black + Blue 10/12/2013 Premium set (shiro) 7/13/2013Rime Green 3/20/2009 Electric Blue 10/12/2013Red 7/11/2009 Black + Red 10/12/2013

Crimson Red 10/12/2013DSi White + Red 10/12/2013Dark Brown 11/21/2009 Scarlet Red 10/12/2013Wine Red 11/21/2009 Pink + White 5/16/2014Natural White 11/21/2009 White + Green 6/6/2014Blue 6/19/2010 Sea Green 6/6/2014Yellow 6/19/2010 Transparent Red 11/28/2014Green 6/19/2010 Transparent Blue 11/28/2014

Transparent Yellow 9/15/20163DS Transparent Green 9/15/2016Aqua Blue 2/26/2011 Transparent Black 9/15/2016Cosmo Black 7/14/2011 Red 9/15/2016Flare Red 10/25/2011 Crimson Red 2 NA 9/15/2016Misty Pink 11/3/2011 Blue 9/15/2016Ice White 3/22/2012 Electric Blue 2 NA 9/15/2016Cobalt Blue 3/20/2013 Lavender 9/15/2016Gloss Pink 3/20/2013 Pink 9/15/2016Metalic Red 6/13/2013 White + Yellow 12/15/2016Pure White 10/10/2013ClearBlack 10/10/2013 new 2DS LL

Black x Turquoise 7/13/2017White x Orange 7/13/2017

Handheld console Home console

Source: Company data, Credit Suisse

Figure 48: Minor changes in the DSi Figure 49: Minor changes in the NDS

Source: Nintendo HP Source: Nintendo HP

DS series attracts consumer interest

through a variety of minor changes

15 September 2017

Nintendo (7974) 23

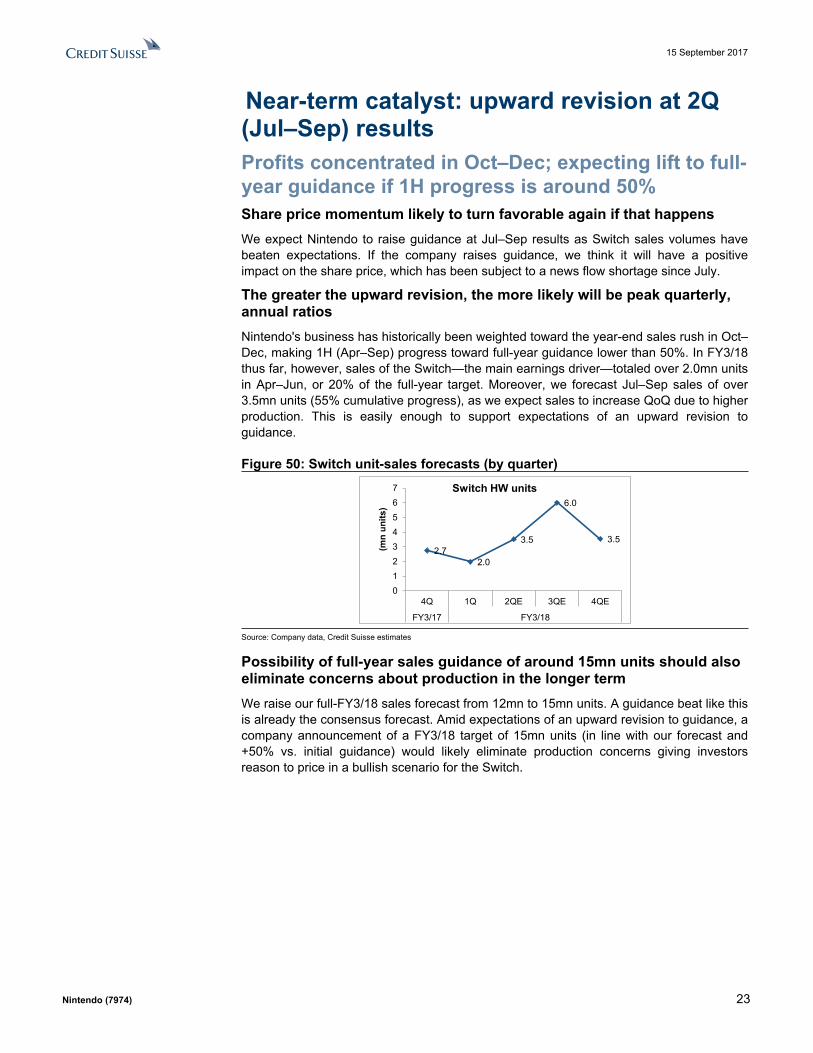

Near-term catalyst: upward revision at 2Q (Jul–Sep) resultsProfits concentrated in Oct–Dec; expecting lift to full-year guidance if 1H progress is around 50%Share price momentum likely to turn favorable again if that happensWe expect Nintendo to raise guidance at Jul–Sep results as Switch sales volumes have beaten expectations. If the company raises guidance, we think it will have a positive impact on the share price, which has been subject to a news flow shortage since July.

The greater the upward revision, the more likely will be peak quarterly, annual ratiosNintendo's business has historically been weighted toward the year-end sales rush in Oct–Dec, making 1H (Apr–Sep) progress toward full-year guidance lower than 50%. In FY3/18 thus far, however, sales of the Switch—the main earnings driver—totaled over 2.0mn units in Apr–Jun, or 20% of the full-year target. Moreover, we forecast Jul–Sep sales of over 3.5mn units (55% cumulative progress), as we expect sales to increase QoQ due to higher production. This is easily enough to support expectations of an upward revision to guidance.

Figure 50: Switch unit-sales forecasts (by quarter)

2.7 2.0

3.5

6.0

3.5

01234567

4Q 1Q 2QE 3QE 4QE

FY3/17 FY3/18

(mn

units

)

Switch HW units

Source: Company data, Credit Suisse estimates

Possibility of full-year sales guidance of around 15mn units should also eliminate concerns about production in the longer termWe raise our full-FY3/18 sales forecast from 12mn to 15mn units. A guidance beat like this is already the consensus forecast. Amid expectations of an upward revision to guidance, a company announcement of a FY3/18 target of 15mn units (in line with our forecast and +50% vs. initial guidance) would likely eliminate production concerns giving investors reason to price in a bullish scenario for the Switch.

15 September 2017

Nintendo (7974) 24

Figure 51: Oct–Dec sales are typically large

Figure 52: We forecast sales of over 6mn units in Oct–Dec, 31mn in FY3/21

Oct-Dec 2007

Oct-Dec 2012

Oct-Dec 2005

Oct-Dec 2011

0123456789

1st Q

2nd

Q

3rd

Q

4th

Q

5th

Q

6th

Q

7th

Q

8th

Q

(mn

unit

s) Wii

Wii-U

NDS

3DS10

26

31

0

5

10

15

20

25

30

35

Bottom - Q Peak - Q Peak - FY

(mn

units

) Switch(FY18/3CoE)

Switch(FY21/3 CSE)

3.0x

5.0x

FY18/3 1Q(actual)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

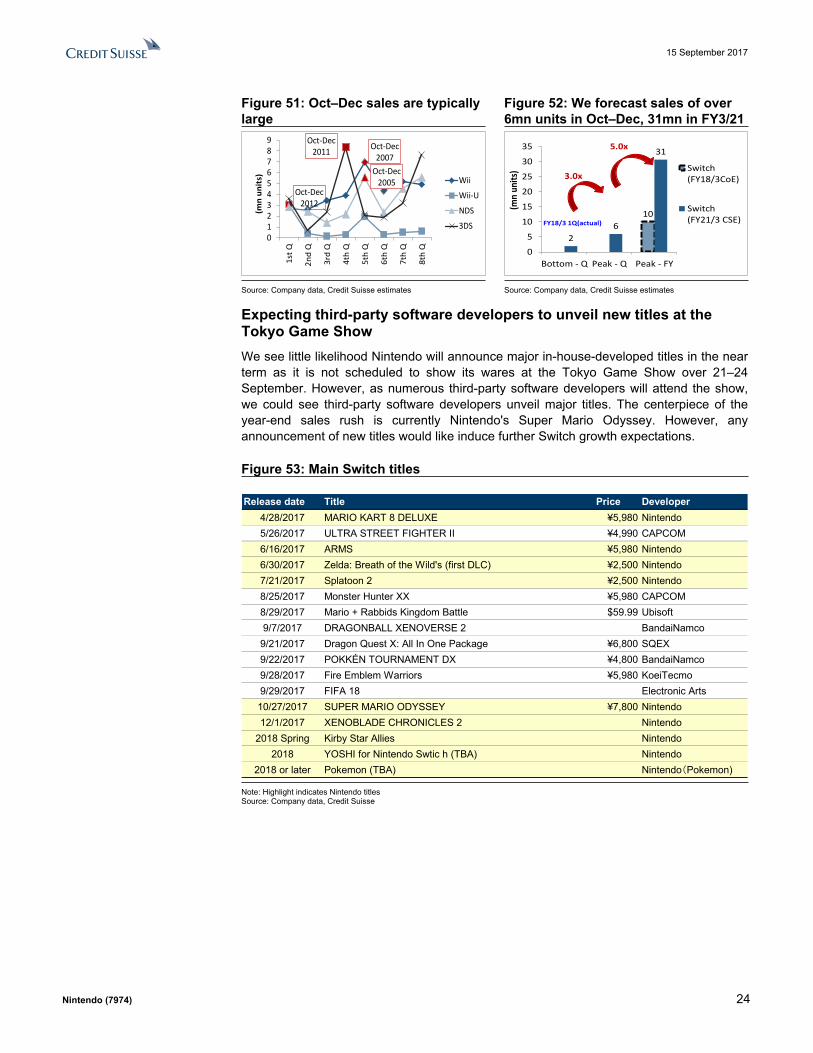

Expecting third-party software developers to unveil new titles at the Tokyo Game ShowWe see little likelihood Nintendo will announce major in-house-developed titles in the near term as it is not scheduled to show its wares at the Tokyo Game Show over 21–24 September. However, as numerous third-party software developers will attend the show, we could see third-party software developers unveil major titles. The centerpiece of the year-end sales rush is currently Nintendo's Super Mario Odyssey. However, any announcement of new titles would like induce further Switch growth expectations.

Figure 53: Main Switch titles

Release date Title Price Developer4/28/2017 MARIO KART 8 DELUXE ¥5,980 Nintendo5/26/2017 ULTRA STREET FIGHTER II ¥4,990 CAPCOM6/16/2017 ARMS ¥5,980 Nintendo6/30/2017 Zelda: Breath of the Wild's (first DLC) ¥2,500 Nintendo7/21/2017 Splatoon 2 ¥2,500 Nintendo8/25/2017 Monster Hunter XX ¥5,980 CAPCOM8/29/2017 Mario + Rabbids Kingdom Battle $59.99 Ubisoft9/7/2017 DRAGONBALL XENOVERSE 2 BandaiNamco

9/21/2017 Dragon Quest X: All In One Package ¥6,800 SQEX9/22/2017 POKKÉN TOURNAMENT DX ¥4,800 BandaiNamco9/28/2017 Fire Emblem Warriors ¥5,980 KoeiTecmo9/29/2017 FIFA 18 Electronic Arts10/27/2017 SUPER MARIO ODYSSEY ¥7,800 Nintendo12/1/2017 XENOBLADE CHRONICLES 2 Nintendo

2018 Spring Kirby Star Allies Nintendo2018 YOSHI for Nintendo Swtic h (TBA) Nintendo

2018 or later Pokemon (TBA) Nintendo(Pokemon)

Note: Highlight indicates Nintendo titles Source: Company data, Credit Suisse

15 September 2017

Nintendo (7974) 25

Forecasts for non-Switch products2DS likely to become the core handheldStepped cut in expected price of handhelds from ¥15,000 to ¥9,000, envisaging shift from 3DS to 2DSNintendo's current handheld is the 3DS series. The 2DS series is currently included within the 3DS numbers released by the company, but we believe this series will effectively become the company's core handheld product from next year. Our expectation for a strategic move from the 3DS to the 2DS is grounded on (1) substantial 3DS market penetration at around 70mn units at end-FY3/17, (2) 3DS users who prefer high-end products replacing their existing units with the Switch, and (3) 3DS users who prefer low-end devices replacing their current handhelds with the 2DS.

Figure 54: 3DS (including 2DS) average unit price

Figure 55: 3DS (including 2DS) sales volume

¥0

¥2,000

¥4,000

¥6,000

¥8,000

¥10,000

¥12,000

¥14,000

¥16,000

FY3/17 FY3/18E FY3/19E FY3/20E

ASP (3DS, 2DS)

0

2

4

6

8

10

12

14

16

(mn

units

)

3DS

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Modest revision to smartphone app forecastsAnimal Crossing appears to be getting off to a slow start. The company has scaled down its take-off expectations to “slow.”

Figure 56: Nintendo lowers its smartphone app sales forecasts

Figure 57: Smart device business forecasts

050

100150200250300

(JPY

bn)

New

Old

1 19

44

108

168

216 216

0 9 21 53

83 107 107

0

50

100

150

200

250

(JPY

bn)

Smart device Sales

Smart device OP

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

15 September 2017

Nintendo (7974) 26

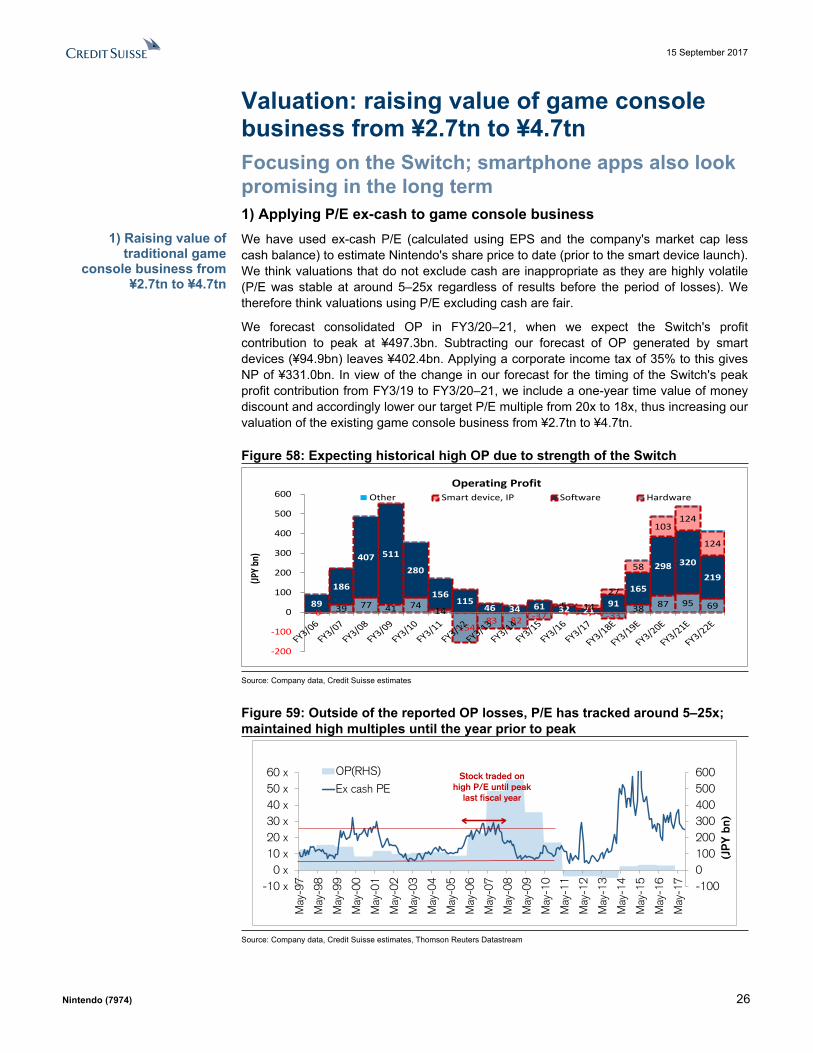

Valuation: raising value of game console business from ¥2.7tn to ¥4.7tnFocusing on the Switch; smartphone apps also look promising in the long term1) Applying P/E ex-cash to game console businessWe have used ex-cash P/E (calculated using EPS and the company's market cap less cash balance) to estimate Nintendo's share price to date (prior to the smart device launch). We think valuations that do not exclude cash are inappropriate as they are highly volatile (P/E was stable at around 5–25x regardless of results before the period of losses). We therefore think valuations using P/E excluding cash are fair.

We forecast consolidated OP in FY3/20–21, when we expect the Switch's profit contribution to peak at ¥497.3bn. Subtracting our forecast of OP generated by smart devices (¥94.9bn) leaves ¥402.4bn. Applying a corporate income tax of 35% to this gives NP of ¥331.0bn. In view of the change in our forecast for the timing of the Switch's peak profit contribution from FY3/19 to FY3/20–21, we include a one-year time value of money discount and accordingly lower our target P/E multiple from 20x to 18x, thus increasing our valuation of the existing game console business from ¥2.7tn to ¥4.7tn.

Figure 58: Expecting historical high OP due to strength of the Switch

-0 39 77 41 74 14

-154 -83 -82 -37 -4 -7 -33

38 87 95 69 89

186

407 511

280

156 115

46 34 61 32 21 91

165

298 320

219

5 14

27

58

103 124

124

-200

-100

0

100

200

300

400

500

600

(JPY b

n)

Operating ProfitOther Smart device, IP Software Hardware

Source: Company data, Credit Suisse estimates

Figure 59: Outside of the reported OP losses, P/E has tracked around 5–25x; maintained high multiples until the year prior to peak

-1000100200300400500600

-10 x0 x

10 x20 x30 x40 x50 x60 x

May

-97

May

-98

May

-99

May

-00

May

-01

May

-02

May

-03

May

-04

May

-05

May

-06

May

-07

May

-08

May

-09

May

-10

May

-11

May

-12

May

-13

May

-14

May

-15

May

-16

May

-17

(JP

Y b

n)

OP(RHS)

Ex cash PEStock traded on

high P/E until peak last fiscal year

Source: Company data, Credit Suisse estimates, Thomson Reuters Datastream

1) Raising value of traditional game

console business from ¥2.7tn to ¥4.7tn

15 September 2017

Nintendo (7974) 27

2) Using DCF to value smart devices businessWe use discounted cash flow to value Nintendo's smart device business as we see it as a growth business that generates stable cash and uses a different business model than the existing game console business.

Under this DCF approach, we apply a market risk premium of 6.65% and a risk-free rate of 0.1%. Based on actual figures, we set a WACC of 8.28%, with debt at zero and beta of 1.23 (past five years, adjusted). We forecast earnings though FY3/21, while for business valuations from FY3/22 we continue to apply a P/E of 15.0x—the average of the three major global handheld game companies (Nintendo, Tencent, and Netease)—to our FY3/21 EBITDA forecasts for the company's smart devices business. Based on the above, we estimate the value of the smart devices business at ¥1.259tn (previously ¥1,461tn).

Figure 60: We estimate the value of the smart devices business at ¥1,259tn DCF Analysis 1.74

(JPY mn)Assumptions FCF estimates# of shares 120,129,323 3/18E 3/19E 3/20E 3/21E 3/22ENet debt (17/3A) (662,763) OP (Smart device business) 20,905 52,905 82,905 106,905 106,905Exit EV/EBITDA Multiple 15.0x Tax rate 35% 35% 35% 35% 35%

EBIAT 13,588 34,388 53,888 69,488 69,488WACC Calculation Depreciation & Amortization - - - - -Risk free rate 0.10% Other non-cash cost - - - - -Beta (5year, adjusted) 1.23 EBITDA 20,905 52,905 82,905 106,905 106,905Mkt. Risk Premium 6.65% Net working capital - - - - -Cost of Equity 8.28% CAPEX - - - - -Interest rate 1.00% FCF 13,588 34,388 53,888 69,488 69,488After-tax cost of debt 0.65% Year 1.00 2.00 3.00 4.00 5.00D/E ratio 0.0x Discount rate 0.92 0.85 0.79 0.73 0.67WACC 8.28% Present Value 12,549 29,331 42,448 50,551 46,685

(a) Present Value Current - 3/22E 181,564

(b) Terminal Value 1,077,357

(c) Enterprise Value (a) + (b) 1,258,921

(d) Net Debt (3/17A Smart device only) -

(e) Market Value (Smart device only) (c) - (d) 1,258,921

Source: Company data, Credit Suisse estimates

Figure 61: EV/EBITDA: Global smart devices and game stocks

17.8 x16.1 x

21.0 x

6.3 x

11.2 x12.0 x

15.2 x

0 x

5 x

10 x

15 x

20 x

25 x

30 x

35 x

EV/E

BITD

A

Activision Blizzard ELECTRONIC ARTS TENCENT HOLDINGS

APPLE ALPHABET 'A' NETEASE

Nintendo

Source: Company data, Credit Suisse estimates, Thomson Reuters Datastream

2) Valuing smart device business at ¥1.259tn

15 September 2017

Nintendo (7974) 28

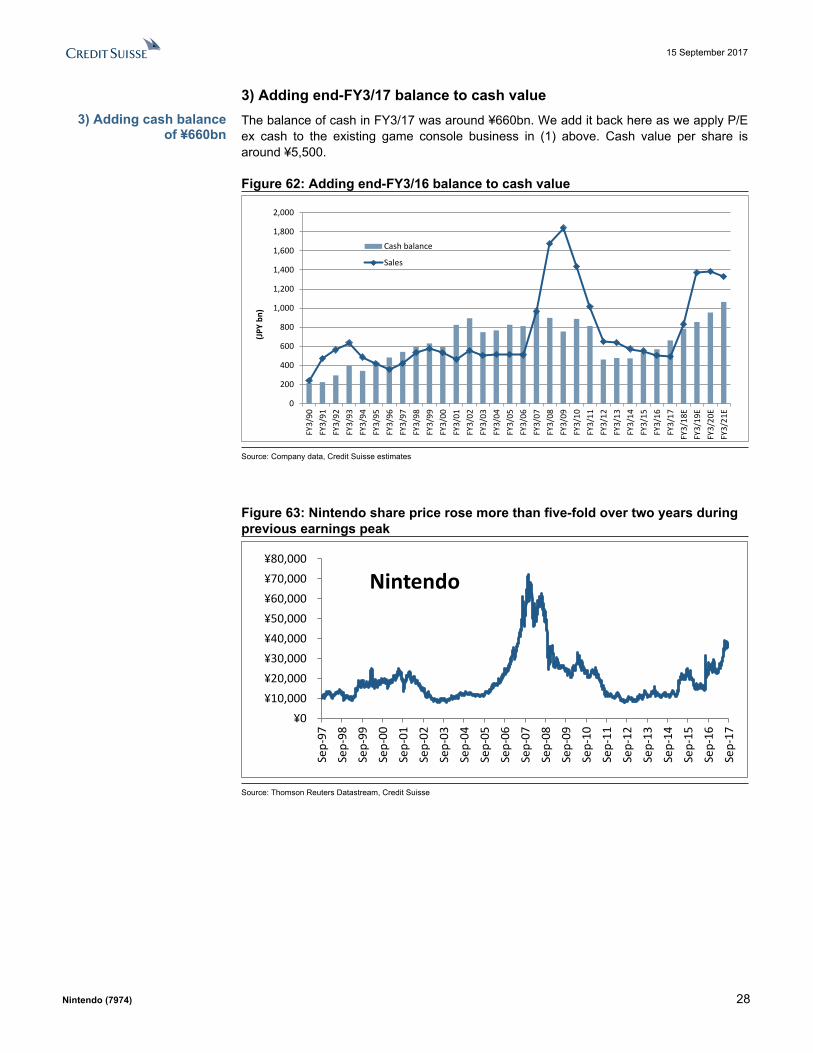

3) Adding end-FY3/17 balance to cash valueThe balance of cash in FY3/17 was around ¥660bn. We add it back here as we apply P/E ex cash to the existing game console business in (1) above. Cash value per share is around ¥5,500.

Figure 62: Adding end-FY3/16 balance to cash value

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

FY3/

90FY

3/91

FY3/

92FY

3/93

FY3/

94FY

3/95

FY3/

96FY

3/97

FY3/

98FY

3/99

FY3/

00FY

3/01

FY3/

02FY

3/03

FY3/

04FY

3/05

FY3/

06FY

3/07

FY3/

08FY

3/09

FY3/

10FY

3/11

FY3/

12FY

3/13

FY3/

14FY

3/15

FY3/

16FY

3/17

FY3/

18E

FY3/

19E

FY3/

20E

FY3/

21E

(JPY

bn)

Cash balance

Sales

Source: Company data, Credit Suisse estimates

Figure 63: Nintendo share price rose more than five-fold over two years during previous earnings peak

¥0¥10,000¥20,000¥30,000¥40,000¥50,000¥60,000¥70,000¥80,000

Sep-

97

Sep-

98

Sep-

99

Sep-

00

Sep-

01

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Sep-

06

Sep-

07

Sep-

08

Sep-

09

Sep-

10

Sep-

11

Sep-

12

Sep-

13

Sep-

14

Sep-

15

Sep-

16

Sep-

17

Nintendo

Source: Thomson Reuters Datastream, Credit Suisse

3) Adding cash balance of ¥660bn

15 September 2017

Nintendo (7974) 29

From 1–3 above, we calculate a total fair value for the company of ¥6.6tn. We calculate a fair share price of ¥55,187and set a target price of ¥55,000.

Figure 64: Derivation of SOTP target price

¥662,763 ¥5,517

¥4,707,933 ¥39,191

¥1,258,921 ¥10,480

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Business and cash value Share price breakdown

1) Smart device

2) Game console

3) Cash balance Cash balance at end-FY3/17: ¥660b

mn

mn

Ex-cash P/E of 18x applied to FY3/20-21operating profit forecast - contribution of smart devices(¥330 bn)

Calculated using four-year DCF model.EV/EBITDA of 15x used for terminal valuemn

Divide by total number of

sharesto calculate per-

share value

Estimated fair value: ¥6.6tn

Fair value share price: ¥55,187

Source: Company data, Credit Suisse estimates, Thomson Reuters Datastream

Our target price is based on a fair-value P/E of 18x. We lower our target P/E from 20x after including a one-year time value of money discount to reflect the longer interval to peak sales. We expect valuation multiples to gradually rise as we approach the earnings peak we anticipate in FY3/20–21.

Figure 65: P/E and expected share price

¥5,517 ¥5,517 ¥5,517 ¥5,517 ¥5,517¥17,418

¥28,304¥39,191

¥50,077¥60,963

¥10,480¥10,480

¥10,480¥10,480

¥10,480

¥0¥10,000¥20,000¥30,000¥40,000¥50,000¥60,000¥70,000¥80,000¥90,000

P/E 8x P/E 13x P/E 18x P/E 23x P/E 28x

1) Smart device 2) Game console 3) Cash balance Estimated price

JPY 77,000Estimated price

JPY 66,000Estimated

price JPY 55,000

Estimated price

JPY 33,000

Estimated price

JPY 44,000

FY3/18 FY3/19 FY3/20

Source: Company data, Credit Suisse estimates

Summing up 1–3, we calculate a TP of

¥55,000

15 September 2017

Nintendo (7974) 30

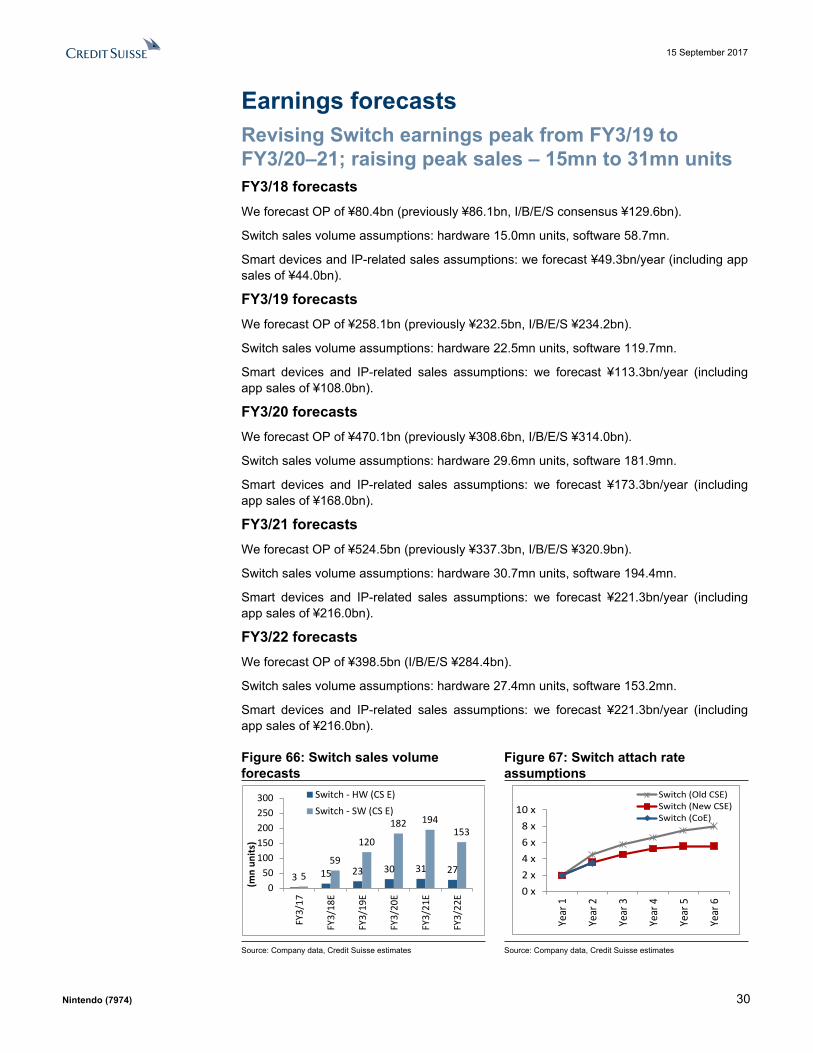

Earnings forecastsRevising Switch earnings peak from FY3/19 to FY3/20–21; raising peak sales ‒ 15mn to 31mn unitsFY3/18 forecasts We forecast OP of ¥80.4bn (previously ¥86.1bn, I/B/E/S consensus ¥129.6bn).

Switch sales volume assumptions: hardware 15.0mn units, software 58.7mn.

Smart devices and IP-related sales assumptions: we forecast ¥49.3bn/year (including app sales of ¥44.0bn).

FY3/19 forecasts We forecast OP of ¥258.1bn (previously ¥232.5bn, I/B/E/S ¥234.2bn).

Switch sales volume assumptions: hardware 22.5mn units, software 119.7mn.

Smart devices and IP-related sales assumptions: we forecast ¥113.3bn/year (including app sales of ¥108.0bn).

FY3/20 forecasts We forecast OP of ¥470.1bn (previously ¥308.6bn, I/B/E/S ¥314.0bn).

Switch sales volume assumptions: hardware 29.6mn units, software 181.9mn.

Smart devices and IP-related sales assumptions: we forecast ¥173.3bn/year (including app sales of ¥168.0bn).

FY3/21 forecasts We forecast OP of ¥524.5bn (previously ¥337.3bn, I/B/E/S ¥320.9bn).

Switch sales volume assumptions: hardware 30.7mn units, software 194.4mn.

Smart devices and IP-related sales assumptions: we forecast ¥221.3bn/year (including app sales of ¥216.0bn).

FY3/22 forecasts We forecast OP of ¥398.5bn (I/B/E/S ¥284.4bn).

Switch sales volume assumptions: hardware 27.4mn units, software 153.2mn.

Smart devices and IP-related sales assumptions: we forecast ¥221.3bn/year (including app sales of ¥216.0bn).

Figure 66: Switch sales volume forecasts

Figure 67: Switch attach rate assumptions

3 15 23 30 31 27559

120

182 194153

050

100150200250300

FY3/

17

FY3/

18E

FY3/

19E

FY3/

20E

FY3/

21E

FY3/

22E

(mn

units

)

Switch - HW (CS E)Switch - SW (CS E)

0 x2 x4 x6 x8 x

10 x

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Switch (Old CSE)Switch (New CSE)Switch (CoE)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

15 September 2017

Nintendo (7974) 31

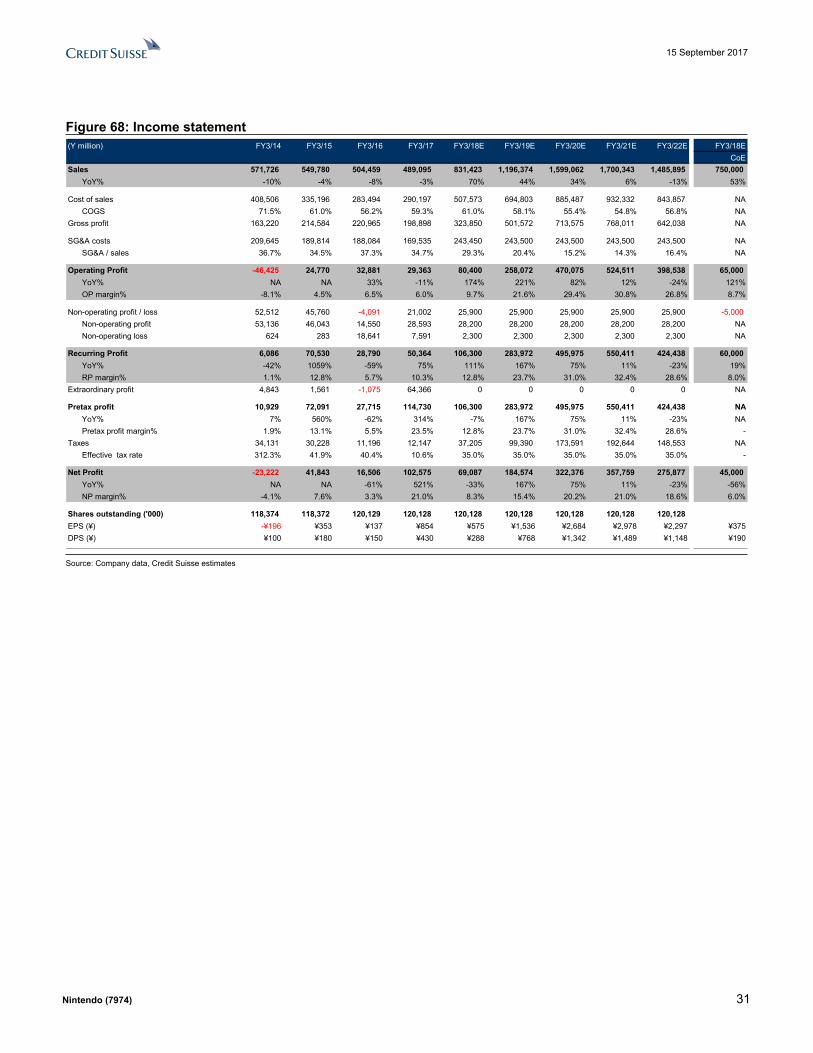

Figure 68: Income statement(Y million) FY3/14 FY3/15 FY3/16 FY3/17 FY3/18E FY3/19E FY3/20E FY3/21E FY3/22E FY3/18E

CoESales 571,726 549,780 504,459 489,095 831,423 1,196,374 1,599,062 1,700,343 1,485,895 750,000

YoY% -10% -4% -8% -3% 70% 44% 34% 6% -13% 53%

Cost of sales 408,506 335,196 283,494 290,197 507,573 694,803 885,487 932,332 843,857 NACOGS 71.5% 61.0% 56.2% 59.3% 61.0% 58.1% 55.4% 54.8% 56.8% NA

Gross profit 163,220 214,584 220,965 198,898 323,850 501,572 713,575 768,011 642,038 NA

SG&A costs 209,645 189,814 188,084 169,535 243,450 243,500 243,500 243,500 243,500 NASG&A / sales 36.7% 34.5% 37.3% 34.7% 29.3% 20.4% 15.2% 14.3% 16.4% NA

Operating Profit -46,425 24,770 32,881 29,363 80,400 258,072 470,075 524,511 398,538 65,000YoY% NA NA 33% -11% 174% 221% 82% 12% -24% 121%OP margin% -8.1% 4.5% 6.5% 6.0% 9.7% 21.6% 29.4% 30.8% 26.8% 8.7%

Non-operating profit / loss 52,512 45,760 -4,091 21,002 25,900 25,900 25,900 25,900 25,900 -5,000 Non-operating profit 53,136 46,043 14,550 28,593 28,200 28,200 28,200 28,200 28,200 NANon-operating loss 624 283 18,641 7,591 2,300 2,300 2,300 2,300 2,300 NA

Recurring Profit 6,086 70,530 28,790 50,364 106,300 283,972 495,975 550,411 424,438 60,000YoY% -42% 1059% -59% 75% 111% 167% 75% 11% -23% 19%RP margin% 1.1% 12.8% 5.7% 10.3% 12.8% 23.7% 31.0% 32.4% 28.6% 8.0%

Extraordinary profit 4,843 1,561 -1,075 64,366 0 0 0 0 0 NA

Pretax profit 10,929 72,091 27,715 114,730 106,300 283,972 495,975 550,411 424,438 NAYoY% 7% 560% -62% 314% -7% 167% 75% 11% -23% NAPretax profit margin% 1.9% 13.1% 5.5% 23.5% 12.8% 23.7% 31.0% 32.4% 28.6% -

Taxes 34,131 30,228 11,196 12,147 37,205 99,390 173,591 192,644 148,553 NAEffective tax rate 312.3% 41.9% 40.4% 10.6% 35.0% 35.0% 35.0% 35.0% 35.0% -

Net Profit -23,222 41,843 16,506 102,575 69,087 184,574 322,376 357,759 275,877 45,000YoY% NA NA -61% 521% -33% 167% 75% 11% -23% -56%NP margin% -4.1% 7.6% 3.3% 21.0% 8.3% 15.4% 20.2% 21.0% 18.6% 6.0%

Shares outstanding ('000) 118,374 118,372 120,129 120,128 120,128 120,128 120,128 120,128 120,128EPS (¥) -¥196 ¥353 ¥137 ¥854 ¥575 ¥1,536 ¥2,684 ¥2,978 ¥2,297 ¥375DPS (¥) ¥100 ¥180 ¥150 ¥430 ¥288 ¥768 ¥1,342 ¥1,489 ¥1,148 ¥190

Source: Company data, Credit Suisse estimates

15 September 2017

Nintendo (7974) 32

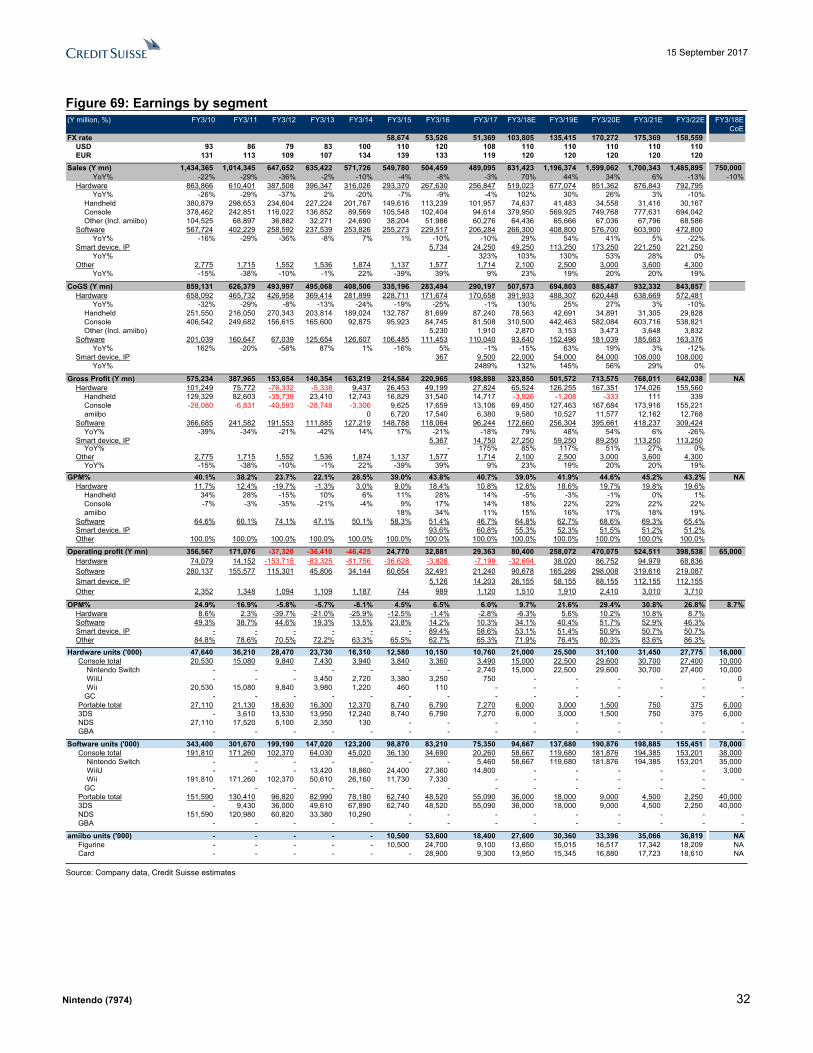

Figure 69: Earnings by segment(Y million, %) FY3/10 FY3/11 FY3/12 FY3/13 FY3/14 FY3/15 FY3/16 FY3/17 FY3/18E FY3/19E FY3/20E FY3/21E FY3/22E FY3/18E

CoEFX rate 58,674 53,526 51,369 103,805 135,415 170,272 175,369 158,559

USD 93 86 79 83 100 110 120 108 110 110 110 110 110EUR 131 113 109 107 134 139 133 119 120 120 120 120 120

Sales (Y mn) 1,434,365 1,014,345 647,652 635,422 571,726 549,780 504,459 489,095 831,423 1,196,374 1,599,062 1,700,343 1,485,895 750,000YoY% -22% -29% -36% -2% -10% -4% -8% -3% 70% 44% 34% 6% -13% -10%

Hardware 863,866 610,401 387,508 396,347 316,026 293,370 267,630 256,847 519,023 677,074 851,362 876,843 792,795YoY% -26% -29% -37% 2% -20% -7% -9% -4% 102% 30% 26% 3% -10%

Handheld 380,879 298,653 234,604 227,224 201,767 149,616 113,239 101,957 74,637 41,483 34,558 31,416 30,167Console 378,462 242,851 116,022 136,852 89,569 105,548 102,404 94,614 379,950 569,925 749,768 777,631 694,042Other (Incl. amiibo) 104,525 68,897 36,882 32,271 24,690 38,204 51,986 60,276 64,436 65,666 67,036 67,796 68,586

Software 567,724 402,229 258,592 237,539 253,826 255,273 229,517 206,284 266,300 408,800 576,700 603,900 472,800YoY% -16% -29% -36% -8% 7% 1% -10% -10% 29% 54% 41% 5% -22%

Smart device, IP 5,734 24,250 49,250 113,250 173,250 221,250 221,250YoY% - 323% 103% 130% 53% 28% 0%

Other 2,775 1,715 1,552 1,536 1,874 1,137 1,577 1,714 2,100 2,500 3,000 3,600 4,300YoY% -15% -38% -10% -1% 22% -39% 39% 9% 23% 19% 20% 20% 19%

CoGS (Y mn) 859,131 626,379 493,997 495,068 408,506 335,196 283,494 290,197 507,573 694,803 885,487 932,332 843,857Hardware 658,092 465,732 426,958 369,414 281,899 228,711 171,674 170,658 391,933 488,307 620,448 638,669 572,481

YoY% -32% -29% -8% -13% -24% -19% -25% -1% 130% 25% 27% 3% -10%Handheld 251,550 216,050 270,343 203,814 189,024 132,787 81,699 87,240 78,563 42,691 34,891 31,305 29,828Console 406,542 249,682 156,615 165,600 92,875 95,923 84,745 81,508 310,500 442,463 582,084 603,716 538,821Other (Incl. amiibo) 5,230 1,910 2,870 3,153 3,473 3,648 3,832

Software 201,039 160,647 67,039 125,654 126,607 106,485 111,453 110,040 93,640 152,496 181,039 185,663 163,376YoY% 162% -20% -58% 87% 1% -16% 5% -1% -15% 63% 19% 3% -12%

Smart device, IP 367 9,500 22,000 54,000 84,000 108,000 108,000YoY% 2489% 132% 145% 56% 29% 0%

Gross Profit (Y mn) 575,234 387,965 153,654 140,354 163,219 214,584 220,965 198,898 323,850 501,572 713,575 768,011 642,038 NAHardware 101,249 75,772 -76,332 -5,338 9,437 26,453 49,199 27,824 65,524 126,255 167,351 174,026 155,560

Handheld 129,329 82,603 -35,739 23,410 12,743 16,829 31,540 14,717 -3,926 -1,208 -333 111 339Console -28,080 -6,831 -40,593 -28,748 -3,306 9,625 17,659 13,106 69,450 127,463 167,684 173,916 155,221amiibo 0 6,720 17,540 6,380 9,580 10,527 11,577 12,162 12,768

Software 366,685 241,582 191,553 111,885 127,219 148,788 118,064 96,244 172,660 256,304 395,661 418,237 309,424YoY% -39% -34% -21% -42% 14% 17% -21% -18% 79% 48% 54% 6% -26%

Smart device, IP 5,367 14,750 27,250 59,250 89,250 113,250 113,250YoY% - 175% 85% 117% 51% 27% 0%

Other 2,775 1,715 1,552 1,536 1,874 1,137 1,577 1,714 2,100 2,500 3,000 3,600 4,300YoY% -15% -38% -10% -1% 22% -39% 39% 9% 23% 19% 20% 20% 19%