Astro Malaysia Holdings Bhd - Credit Suisse

46

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ™ Client-Driven Solutions, Insights, and Access 27 November 2012 Asia Pacific/Malaysia Equity Research Radio & TV Broadcasting Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) INITIATION A media powerhouse ■ Initiating coverage with an OUTPERFORM. Astro is the only satellite pay TV operator in Malaysia, with a subscriber base of over 3 mn. We expect Astro to grow its subscriber base as well as ARPU at the same time. We initiate coverage on Astro with an OUTPERFORM rating and a DCF-based target price of RM3.50, implying c.32% potential upside. ■ Proxy for rising Malay household income. We believe Astro is a potential beneficiary of Malaysia’s attractive demographics: a young and growing population, whereby a growing economy is driving income growth. Malay households, which account for 60% of Astro’s subscribers, have the highest income growth within the Malaysian population. Astro’s wide range of content is suited to Malaysia’s multi -lingual population, whereas free-to-air (FTA) TV has limited capacity to offer dedicated vernacular channels. ■ Growth drivers. Astro’s ARPU grew 8.5% from FY10A to FY12A. Potential ARPU drivers include high definition (30% take-up currently), personal video recorder (PVR), Super Pack and IPTV. We have baked in mid-single-digit ARPU growth for FY14-16E but if management delivers high single-digit ARPU growth, we estimate, 16% further potential upside to our target price. ■ Trading 11% below IPO price. We apply a mid-point 15% discount-to-DCF to arrive at our RM3.50 target price. Historically, Astro has traded at a 3%- 29% discount to DCF valuations—this suggests a share price range of RM2.90-4.00. Key risk factors, in our view, include content cost, satellite transponder capacity, technical/broadcast failure, competition, regulatory risks and currency. While FY13-14E EBITDA is dampened by significant costs related to a box swap, we expect profitability to rebound in FY15E when the bulk of Astro’s subscriber homes will be equipped with an HD-box. Share price performance 80 90 100 110 120 2 3 4 5 6 Oct-12 Price (LHS) Rebased Rel (RHS) The price relative chart measures performance against the FTSE BURSA MALAYSIA KLCI IDX which closed at 1614.32 on 23/11/12 On 23/11/12 the spot exchange rate was RM3.06/US$1 Performance over 1M 3M 12M Absolute (%) -7.0 — — Relative (%) -3.5 — — Financial and valuation metrics Year 1/12A 1/13E 1/14E 1/15E Revenue (RM mn) 3,888.8 4,317.5 4,701.9 5,065.7 EBITDA (RM mn) 1,414.7 1,366.3 1,467.8 1,730.1 EBIT (RM mn) 990.4 755.6 744.2 869.5 Net profit (RM mn) 624.1 420.7 415.4 489.8 EPS (CS adj.) (RM) 0.12 0.08 0.08 0.09 Change from previous EPS (%) n.a. EPS growth (%) -24.2 -32.6 -1.3 17.9 P/E (x) 22.2 32.9 33.3 28.2 Dividend yield (%) 0 1.1 2.3 2.7 EV/EBITDA (x) 12.1 11.3 10.4 8.9 P/B (x) 28.6 24.8 20.9 17.9 ROE (%) 258.5 80.8 68.1 68.3 Net debt/equity (%) 657.6 281.1 207.9 207.5 Source: Company data, Thomson Reuters, Credit Suisse estimates Rating OUTPERFORM* [V] Price (23 Nov 12, RM) 2.66 Target price (RM) 3.50¹ Upside/downside (%) 31.6 Mkt cap (RM mn) 13,827 (US$ 4,522) Enterprise value (RM mn) 15,432 Number of shares (mn) 5,198.30 Free float (%) 30.0 52-week price range 3.00 - 2.61 ADTO - 6M (US$ mn) 31.9 *Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months. [V] = Stock considered volatile (see Disclosure Appendix). Research Analysts Foong Wai Loke 60 3 2723 2082 [email protected] Regional Consumer Research Team Regional Head: Karim P. Salamatian, CFA Gabriel Chan, CFA Kevin Yin Sonia Kim Foong Wai Loke Ella Nusantoro Dian Haryokusumo Chung Hsu, CFA Arnab Mitra Chai Techakumpuch Vivian Zhao Thaniya Kevalee Isis Wong

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Astro Malaysia Holdings Bhd - Credit Suisse

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

27 November 2012

Asia Pacific/Malaysia

Equity Research

Radio & TV Broadcasting

Astro Malaysia Holdings Bhd

(ASTR.KL / ASTRO MK) INITIATION

A media powerhouse

■ Initiating coverage with an OUTPERFORM. Astro is the only satellite pay

TV operator in Malaysia, with a subscriber base of over 3 mn. We expect

Astro to grow its subscriber base as well as ARPU at the same time. We

initiate coverage on Astro with an OUTPERFORM rating and a DCF-based

target price of RM3.50, implying c.32% potential upside.

■ Proxy for rising Malay household income. We believe Astro is a potential

beneficiary of Malaysia’s attractive demographics: a young and growing

population, whereby a growing economy is driving income growth. Malay

households, which account for 60% of Astro’s subscribers, have the highest

income growth within the Malaysian population. Astro’s wide range of

content is suited to Malaysia’s multi-lingual population, whereas free-to-air

(FTA) TV has limited capacity to offer dedicated vernacular channels.

■ Growth drivers. Astro’s ARPU grew 8.5% from FY10A to FY12A. Potential

ARPU drivers include high definition (30% take-up currently), personal video

recorder (PVR), Super Pack and IPTV. We have baked in mid-single-digit

ARPU growth for FY14-16E but if management delivers high single-digit

ARPU growth, we estimate, 16% further potential upside to our target price.

■ Trading 11% below IPO price. We apply a mid-point 15% discount-to-DCF

to arrive at our RM3.50 target price. Historically, Astro has traded at a 3%-

29% discount to DCF valuations—this suggests a share price range of

RM2.90-4.00. Key risk factors, in our view, include content cost, satellite

transponder capacity, technical/broadcast failure, competition, regulatory

risks and currency. While FY13-14E EBITDA is dampened by significant

costs related to a box swap, we expect profitability to rebound in FY15E

when the bulk of Astro’s subscriber homes will be equipped with an HD-box.

Share price performance

80

90

100

110

120

2

3

4

5

6

Oct-12

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

FTSE BURSA MALAYSIA KLCI IDX which closed at 1614.32

on 23/11/12

On 23/11/12 the spot exchange rate was RM3.06/US$1

Performance over 1M 3M 12M Absolute (%) -7.0 — — Relative (%) -3.5 — —

Financial and valuation metrics

Year 1/12A 1/13E 1/14E 1/15E Revenue (RM mn) 3,888.8 4,317.5 4,701.9 5,065.7 EBITDA (RM mn) 1,414.7 1,366.3 1,467.8 1,730.1 EBIT (RM mn) 990.4 755.6 744.2 869.5 Net profit (RM mn) 624.1 420.7 415.4 489.8 EPS (CS adj.) (RM) 0.12 0.08 0.08 0.09 Change from previous EPS (%) n.a. EPS growth (%) -24.2 -32.6 -1.3 17.9 P/E (x) 22.2 32.9 33.3 28.2 Dividend yield (%) 0 1.1 2.3 2.7 EV/EBITDA (x) 12.1 11.3 10.4 8.9 P/B (x) 28.6 24.8 20.9 17.9 ROE (%) 258.5 80.8 68.1 68.3 Net debt/equity (%) 657.6 281.1 207.9 207.5

Source: Company data, Thomson Reuters, Credit Suisse estimates

Rating OUTPERFORM* [V] Price (23 Nov 12, RM) 2.66 Target price (RM) 3.50¹ Upside/downside (%) 31.6 Mkt cap (RM mn) 13,827 (US$ 4,522) Enterprise value (RM mn) 15,432 Number of shares (mn) 5,198.30 Free float (%) 30.0 52-week price range 3.00 - 2.61 ADTO - 6M (US$ mn) 31.9

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts

Foong Wai Loke

60 3 2723 2082

Regional Consumer Research Team

Regional Head: Karim P. Salamatian, CFA

Gabriel Chan, CFA

Kevin Yin

Sonia Kim

Foong Wai Loke

Ella Nusantoro

Dian Haryokusumo

Chung Hsu, CFA

Arnab Mitra

Chai Techakumpuch

Vivian Zhao

Thaniya Kevalee

Isis Wong

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 2

Focus charts Figure 1: FY12A revenue, by segment Figure 2: Monthly ARPU (USD)

TV93%

Radio5%

Others2%

0

10

20

30

40

50

60

70

80

90

100

DirecTV

Austa

r

DIS

H U

S

SK

Y N

Z

BS

kyB

Sta

rhub

Naspers

Astr

o

PC

CW

i-C

able

MN

C S

ky

KT S

kylif

e

DIS

H India

Source: Company data Source: Company data, Credit Suisse estimates

Figure 3: Astro subscriber base, by ethnic group Figure 4: Malay households have the fastest growing

incomes (%)

Malay, 28%

Malay, 60%

Chinese, 55%

Chinese, 22%

Indian, 13% Indian, 11%

Other, 4%Other, 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 Current

Malay Chinese Indian Other

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Malay Indian Chinese

CAGR 07-09

Source: Company data Source: Economic Planning Unit

Figure 5: Global pay TV penetration rates Figure 6: Pay TV penetration trends

0%

20%

40%

60%

80%

100%

120%

140%

Kor

ea

Tai

wan

Hon

g K

ong

Indi

a

Sin

gapo

re

New

Zea

land

Mal

aysi

a

Chi

na

Aus

tral

ia

Japa

n

Vie

tnam

Tha

iland

Phi

lippi

nes

Indo

nesi

a

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1965

1975

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

USA UK Australia

New Zealand Malaysia

Source: Media Partners Asia Source: Value Partners, Screen Digest, Credit Suisse estimates

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 3

A media powerhouse We initiate coverage on Astro with an OUTPERFORM rating and a DCF-based target

price of RM3.50. Astro is the only DTH satellite pay TV operator in Malaysia, with a

subscriber base of over 3 mn. In addition to its leadership in pay TV, Astro is also the

leading radio operator in Malaysia, with 20 channels and a 52% share of radio advertising

expenditure (adex). While its FY13-14E EBITDA is dampened by significant costs related

to a box swap, we expect profitability to rebound in FY15 when the bulk of Astro’s

subscriber homes will be equipped with an HD-enabled box.

Proxy for rising Malay incomes

We expect Astro to grow subscribers and ARPU; it is well-positioned to tap Malaysia’s

attractive demographics: a young and growing population, whereby a growing economy is

driving income growth. The ethnic breakdown of Astro’s subscriber base is a close

reflection of Malaysia’s multi-cultural population (60% of its subscribers are Malays).

Hence, Astro is likely to be a prime beneficiary of rising income growth of the Malay

population, the highest growth for any race in Malaysia. Astro’s monthly ARPU accounts

for a tiny proportion of household incomes (1%-3%); this suggests affordability of its

services is relatively high. The company’s 3 mn-plus subscribers translate into a

household penetration rate of close to 50%, which is low compared to India’s 80% and

Singapore’s 70%; hence, there is potential for Malaysia to catch up, in our view.

Competition is limited

We believe Astro is in a strong competitive position as FTA TV is hampered by structural

issues while IPTV competitors lack scale. Print has historically dominated Malaysia’s adex

pie and this effectively serves to cap FTA TV revenues (effectively limiting its content

budgets). Astro offers 156 TV channels (of which 68 are Astro-created and branded)

compared to six channels for FTA (which are also aired on Astro’s platform) and 71 for

HyppTV (IPTV). As Astro’s subscriber base has grown and viewership has risen, pay TV

adex growth has outstripped FTA adex growth. Meanwhile, IPTV offerings by telcos are

relatively limited as FTH lacks scale (TM’s UniFi has 450,000 subscribers). We believe the

telcos are also keen to avoid margin erosion from overzealous spending on IPTV content

as they have significant dividend commitments to meet.

New growth drivers

HD, PVR, premium content and IPTV services are potential ARPU drivers for Astro in the

longer term. There’s also an opportunity for Astro to tap prepaid revenues via its NJOI

offering, which doesn’t incur any subscriber acquisition cost (the consumer pays for the set

top box and installation). Yet, NJOI could see long-term potential revenue upside if users

buy prepaid content.

Trading 11% below IPO price

We apply a mid-point 15% discount to DCF to arrive at our RM3.50 target price for Astro.

Historically, Astro has traded at a 3%-29% discount to DCF valuations, which suggests a

share price range of RM2.90-4.00 (which spells 9-50% upside from current levels). We

have baked in mid-single-digit ARPU growth for FY14-16E but if management delivers

high single-digit ARPU growth, there is 16% potential upside to our target price. In our

view, the key risk factors for Astro include content costs, satellite transponder capacity,

technical/broadcast failure, competition, regulatory risks and currency.

On the positive side, the senior management comprising CEO, COO, Chief Commercial

Officer and also the Chief Innovation Officer all bought Astro shares after the listing.

Initiating coverage on Astro

with a target price of

RM3.50, which spells 32%

potential upside from current

levels

Pay TV penetration is still

low in Malaysia, in our view

FTA TV has a limited

content budget because

Malaysia’s adex pie is

dominated by print

HD, PVR, premium content

and IPTV services are

potential ARPU drivers for

Astro

We have baked in mid-

single-digit ARPU growth for

FY14-16E but if

management delivers high

single-digit ARPU growth,

there is 16% potential

upside to our target price

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 4

Astro Malaysia Holdings Bhd ASTR.KL / ASTRO MK Price (23 Nov 12): RM2.66, Rating: OUTPERFORM, Target Price: RM3.50, Analyst: Foong Wai Loke

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside 3.90 46.62 5% Discount to DCF Central Case 3.50 31.58 15% Discount to DCF Downside 3.10 16.54 25% Discount to DCF

Key earnings drivers 1/12A 1/13E 1/14E 1/15E

Pay TV residential subs ('000)

3,067 3,257 3,424 3,561 Astro Household penetration (%)

47.4 49.3 51.1 52.3 Residential ARPU (RM/month)

89.0 95.0 99.0 103.0 Net adds ('000) 136.0 190.0 166.9 136.9 MAT Churn (%) 7.00 9.00 9.00 9.00

Income statement (RM mn) 1/12A 1/13E 1/14E 1/15E

Sales revenue 3,889 4,318 4,702 5,066 Cost of goods sold 2,237 2,770 3,069 3,237 SG&A — — — — Other operating exp./(inc.) 237.5 181.7 164.7 98.1 EBITDA 1,415 1,366 1,468 1,730 Depreciation & amortisation 424.3 610.7 723.6 860.6 EBIT 990.4 755.6 744.2 869.5 Net interest expense/(inc.) 126.0 165.3 161.6 183.6 Non-operating inc./(exp.) — — — — Associates/JV — — — — Recurring PBT 864.4 590.3 582.5 685.9 Exceptionals/extraordinaries — — — — Taxes 234.7 165.3 163.1 192.0 Profit after tax 629.7 425.0 419.4 493.9 Other after tax income (0.05) (0.05) (0.05) (0.05) Minority interests 5.5 4.3 4.0 4.0 Preferred dividends — — — — Reported net profit 624.1 420.7 415.4 489.8 Analyst adjustments — — — — Net profit (Credit Suisse) 624.1 420.7 415.4 489.8

Cash flow (RM mn) 1/12A 1/13E 1/14E 1/15E

EBIT 990.4 755.6 744.2 869.5 Net interest — — — — Tax paid (164.2) (165.3) (163.1) (192.0) Working capital (212.5) 336.7 362.0 241.1 Other cash & non-cash items 90.1 610.7 723.6 860.6 Operating cash flow 704 1,538 1,667 1,779 Capex (538.5) (452.0) (725.5) (745.9) Free cash flow to the firm 165 1,086 941 1,033 Disposals of fixed assets — — — — Acquisitions — — — — Divestments — — — — Associate investments — — — — Other investment/(outflows) (1,449) 86 86 73 Investing cash flow (1,988) (366) (639) (673) Equity raised — — — — Dividends paid (1,331) (147) (312) (380) Net borrowings 3,505 (500) (300) (200) Other financing cash flow (912.1) 604.1 (566.6) (587.8) Financing cash flow 1,262 (43) (1,178) (1,167) Total cash flow (22) 1,129 (151) (61) Adjustments — — — — Net change in cash (22) 1,129 (151) (61)

Balance sheet (RM mn) 1/12A 1/13E 1/14E 1/15E

Cash & cash equivalents 478 1,607 1,456 1,395 Current receivables 798.2 847.6 923.1 994.5 Inventories 13.3 22.8 25.2 26.6 Other current assets 116.3 116.3 116.3 116.3 Current assets 1,406 2,594 2,521 2,532 Property, plant & equip. 1,654 1,944 2,220 2,809 Investments 48.1 48.1 48.1 48.1 Intangibles 1,771 1,771 1,771 1,771 Other non-current assets 1,635 135 135 135 Total assets 6,514 6,491 6,694 7,295 Accounts payable 1,581 1,699 1,489 1,753 Short-term debt 43.5 43.5 43.5 43.5 Current provisions 86.5 86.5 86.5 86.5 Other current liabilities 66.2 66.2 66.2 66.2 Current liabilities 1,777 1,895 1,685 1,949 Long-term debt 3,666 3,168 2,824 2,997 Non-current provisions 323 600 1,250 1,300 Other non-current liab. 256.0 256.0 256.0 256.0 Total liabilities 6,022 5,920 6,016 6,502 Shareholders' equity 482.9 558.0 661.9 772.1 Minority interests 8.6 12.9 16.9 20.9 Total liabilities & equity 6,514 6,491 6,694 7,295

Per share data 1/12A 1/13E 1/14E 1/15E

Shares (wtd avg.) (mn) 5,198 5,198 5,198 5,198 EPS (Credit Suisse) (RM)

0.12 0.08 0.08 0.09 DPS (RM) — 0.03 0.06 0.07 BVPS (RM) 0.09 0.11 0.13 0.15 Operating CFPS (RM) 0.14 0.30 0.32 0.34

Key ratios and valuation

1/12A 1/13E 1/14E 1/15E

Growth(%) Sales revenue 6.1 11.0 8.9 7.7 EBIT (7.2) (23.7) (1.5) 16.8 Net profit (24.2) (32.6) (1.3) 17.9 EPS (24.2) (32.6) (1.3) 17.9 Margins (%) EBITDA 36.4 31.6 31.2 34.2 EBIT 25.5 17.5 15.8 17.2 Pre-tax profit 22.2 13.7 12.4 13.5 Net profit 16.0 9.7 8.8 9.7 Valuation metrics (x) P/E 22.2 32.9 33.3 28.2 P/B 28.6 24.8 20.9 17.9 Dividend yield (%) — 1.06 2.25 2.75 P/CF 19.6 9.0 8.3 7.8 EV/sales 4.39 3.57 3.24 3.05 EV/EBITDA 12.1 11.3 10.4 8.9 EV/EBIT 17.2 20.4 20.5 17.8 ROE analysis (%) ROE 258 81 68 68 ROIC 38.8 18.4 25.1 27.6 Asset turnover (x) 0.60 0.67 0.70 0.69 Interest burden (x) 0.87 0.78 0.78 0.79 Tax burden (x) 0.73 0.72 0.72 0.72 Financial leverage (x) 13.3 11.4 9.9 9.2 Credit ratios Net debt/equity (%) 658 281 208 208 Net debt/EBITDA (x) 2.28 1.17 0.96 0.95 Interest cover (x) 7.86 4.57 4.60 4.74

Source: IBES, Credit Suisse estimates

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 5

Proxy for rising Malay incomes We initiate coverage on Astro with an OUTPERFORM rating and a DCF-based target

price of RM3.50. Astro is currently trading 11% below its 19 October, 2012 IPO price of

RM3.00. It is the only DTH pay TV operator in Malaysia, currently offering 156 channels

(of which 22 are HD). In addition to its leadership in pay TV, Astro is also the leading radio

operator in Malaysia, with 20 channels and 52% share of the radio advertising

expenditure.

Figure 7: FY12A revenue, by segment

TV93%

Radio5%

Others2%

Source: Company data

Figure 8: FY12A TV revenue breakdown

Subscription91%

Airtime Sales7%

Others2%

Source: Company data

Even if we were to exclude the FTA channels aired on its platform, Astro still offers a wider

range of TV channels (150) than the FTA (6) and IPTV players (64) combined.

According to Astro’s website, the most basic pack starts at RM37.95 and includes 41 basic

TV channels and 20 radio channels.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 6

Figure 9: Most popular TV content by language

Malay content Description

Maharaja Lawak Mega Comedy reality show across Malaysia, Indonesia and Singapore

Imam Muda Islamic reality show in search of the new Imam

Kilauan Emas Singing competition for senior citizens

Tanah Kubur Tales from grave-diggers

Chinese content Description

Astro Classic Golden Melody Singing competition for senior citizens

Hua Hee Everyday The first locally-produced Hokkien sitcom in Malaysia

Miss Astro Chinese International Pageant Beauty pageant, with its winner representing Malaysia to compete in the Miss Chinese International

Pageant.

My New Village Stories Documentary series of Chinese villages, cultures and heritage in Malaysia

Indian content Description

Vaanavil Super Star Singing competition

Aattam 100 Dance competition

Vagai Thigil Documentary on horror and supernatural stories in Malaysia

Viyarvai Documentary of community involved in dirty jobs such as cleaning toilets and rubbish for a living

Source: Company data

Exclusive channels include National Geographic, Disney channel, Discovery channel,

AXN, ESPN and Fox Movie Premium. Astro also offers key sporting content such as

Barclays Premier League, UEFA Champions League and FIFA World Cup.

Astro’s exclusivity for DTH transmission is due to expire in 2017 while its licence for DTH

transmission is due to expire in 2022. Given that the company has invested heavily in the

business in the past few decades, we expect it to seek a renewal of the exclusivity in due

time.

Astro operates on Ku-band DTH satellite which has the advantage of small dishes (as

opposed to much larger C-band dishes) but is susceptible to rain fade.

Astro is a multi-platform operator

Astro operates on various platforms:

■ DTH satellite,

■ IPTV, and

■ OTT (Astro-On-The-Go).

IPTV: In 2011, Astro launched Astro B.yond IPTV, delivered through fibre optics

broadband as a triple play offering, with high-speed broadband and telephony services.

This currently has an infrastructure tie-up with TIME dotCom which is in the midst of wiring

up multi-dwelling units (condominiums). On 30 August, Maxis announced that it has

entered into a JV for Astro to be its exclusive content service provider for Maxis’ IPTV on

its fibre broadband service for three years.

Astro-On-The-Go: This is an OTT online and mobile application service, offering 11 linear

TV channels and non-linear content.

Astro is part of the Ananda Krishnan group of companies, which include Maxis

(telecommunications) and Bumi Armada (oil & gas).

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 7

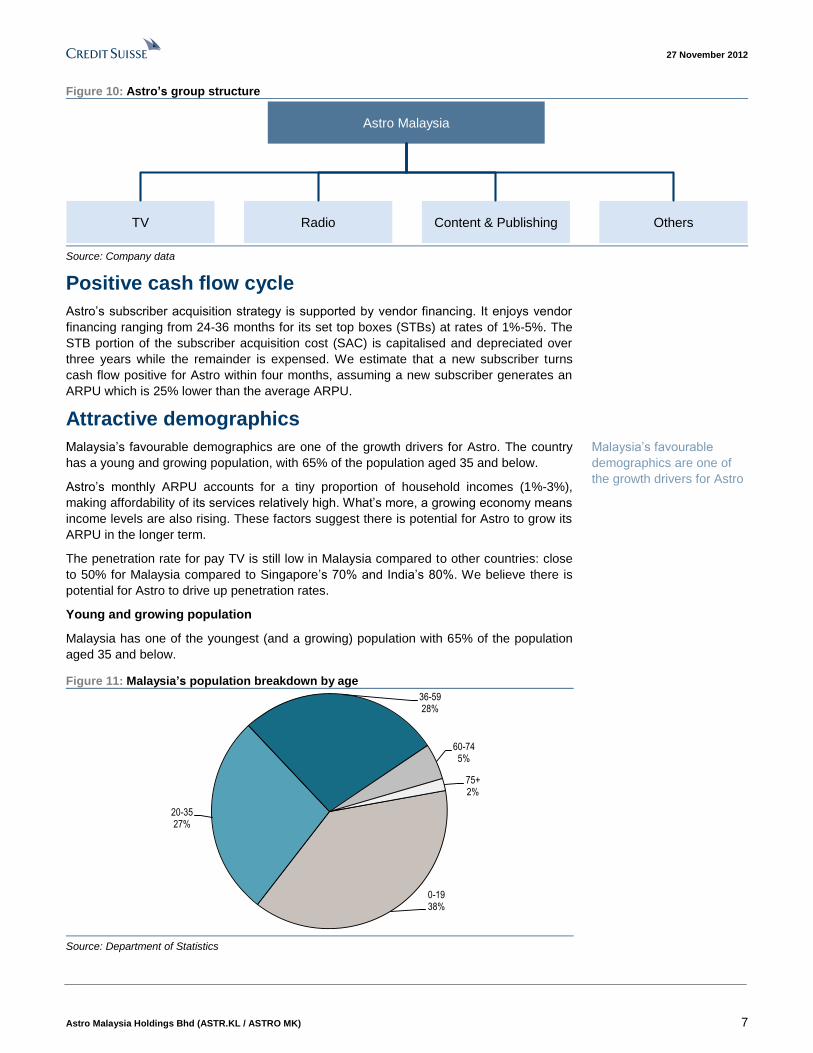

Figure 10: Astro’s group structure

Astro Malaysia

TV Radio Content & Publishing Others

Source: Company data

Positive cash flow cycle

Astro’s subscriber acquisition strategy is supported by vendor financing. It enjoys vendor

financing ranging from 24-36 months for its set top boxes (STBs) at rates of 1%-5%. The

STB portion of the subscriber acquisition cost (SAC) is capitalised and depreciated over

three years while the remainder is expensed. We estimate that a new subscriber turns

cash flow positive for Astro within four months, assuming a new subscriber generates an

ARPU which is 25% lower than the average ARPU.

Attractive demographics

Malaysia’s favourable demographics are one of the growth drivers for Astro. The country

has a young and growing population, with 65% of the population aged 35 and below.

Astro’s monthly ARPU accounts for a tiny proportion of household incomes (1%-3%),

making affordability of its services relatively high. What’s more, a growing economy means

income levels are also rising. These factors suggest there is potential for Astro to grow its

ARPU in the longer term.

The penetration rate for pay TV is still low in Malaysia compared to other countries: close

to 50% for Malaysia compared to Singapore’s 70% and India’s 80%. We believe there is

potential for Astro to drive up penetration rates.

Young and growing population

Malaysia has one of the youngest (and a growing) population with 65% of the population

aged 35 and below.

Figure 11: Malaysia’s population breakdown by age

0-1938%

20-3527%

36-5928%

60-745%

75+2%

Source: Department of Statistics

Malaysia’s favourable

demographics are one of

the growth drivers for Astro

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 8

Affordability is high and growing

Pay TV ARPU is growing, yet it accounts for a tiny proportion of household incomes. The

2Q FY13 monthly ARPU of RM92 is equivalent to 1-2 family visits to a cinema without a

meal (the cost of a cinema ticket ranges from RM12-60). Astro’s ARPU has grown as it

has added more channels and introduced premium services, such as HD, NVOD and PVR,

which indicates a willingness to pay for content.

We measured Astro’s FY12A average monthly ARPU as a proportion of average

household incomes across various parts of Malaysia. Astro’s FY12A average monthly

ARPU of RM89 accounted for less than 2.5% of household incomes in Malaysia (with the

exception of Perlis state where it accounted for 3.1% of income). Perlis accounts for 0.8%

of Malaysia’s total population).

Figure 12: Astro’s FY12A monthly ARPU as a percentage of household incomes

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Joho

r

Ked

ah

Kel

anta

n

Mel

aka

N S

embi

lan

Pah

ang

Per

ak

Per

lis

Pen

ang

Sel

ango

r

Ter

engg

anu

KL

Put

raja

ya

Sab

ah

Labu

an

Sar

awak

2011 Malaysia average

Source: Company data, Economic Planning Unit, Credit Suisse estimates

Figure 13: Malaysia’s middle income population is growing

58%49%

33%

33%

36%

42%

10%15%

24%

-20%

0%

20%

40%

60%

80%

100%

1999 2002 2009

HH Annual Income < RM24,000 RM24,001-59,999 > RM60,000

Source: Department of Statistics

Pay TV ARPU is growing,

yet it accounts for a tiny

proportion of household

incomes

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 9

Astro is aligned to rising Malay household incomes

Figure 14: Astro subscribers by race

Malay, 28%

Malay, 60%

Chinese, 55%

Chinese, 22%

Indian, 13% Indian, 11%

Other, 4%

Other, 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 Current

Malay Chinese Indian Other

Source: Company data

The ethnic breakdown of Astro’s subscriber base is a close reflection of Malaysia’s multi-

racial population. Almost 60% of its subscribers are Malays. Hence, Astro is likely to be a

prime beneficiary of rising income growth of the Malay population, at 7%—the highest

growth for any ethnic group in Malaysia. Chinese and Indians account for 22% and 11% of

the company’s subscriber base, respectively.

Figure 15: Malay households have the fastest growing incomes (%)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Malay Indian Chinese

CAGR 07-09

Source: Department of Statistics

Demographics are attractive: Malaysia has a fast-growing working population, which

suggests a positive household formation rate and this bodes well for Astro. A young

population means this trend will likely continue, in our view. In addition, the Malaysian

economy is growing: Credit Suisse expects 4.7%-4.8% GDP growth for 2012E-13E and

this is likely to translate into rising incomes. Average household incomes for Malaysia

grew at a CAGR of 5.4% over 2007-09.

Almost 60% of Astro’s

subscribers are Malays

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 10

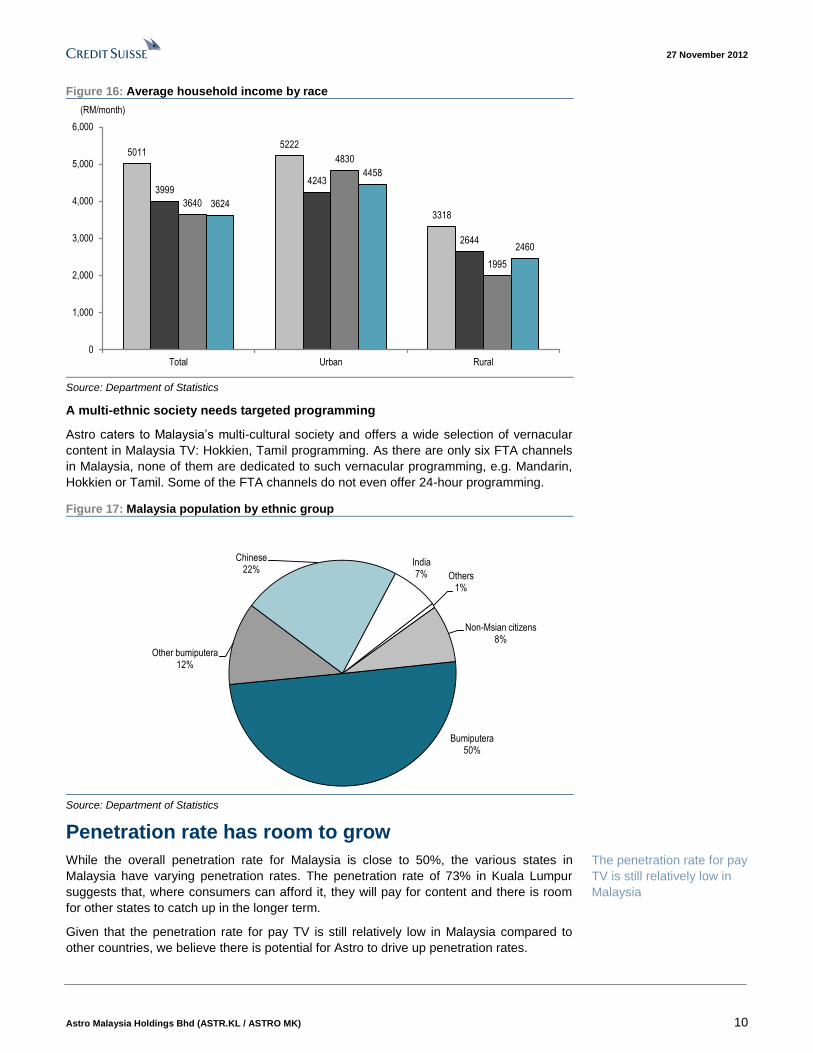

Figure 16: Average household income by race

50115222

3318

39994243

2644

3640

4830

1995

3624

4458

2460

0

1,000

2,000

3,000

4,000

5,000

6,000

Total Urban Rural

(RM/month)

Source: Department of Statistics

A multi-ethnic society needs targeted programming

Astro caters to Malaysia’s multi-cultural society and offers a wide selection of vernacular

content in Malaysia TV: Hokkien, Tamil programming. As there are only six FTA channels

in Malaysia, none of them are dedicated to such vernacular programming, e.g. Mandarin,

Hokkien or Tamil. Some of the FTA channels do not even offer 24-hour programming.

Figure 17: Malaysia population by ethnic group

Bumiputera50%

Other bumiputera12%

Chinese22%

India7% Others

1%

Non-Msian citizens8%

Source: Department of Statistics

Penetration rate has room to grow

While the overall penetration rate for Malaysia is close to 50%, the various states in

Malaysia have varying penetration rates. The penetration rate of 73% in Kuala Lumpur

suggests that, where consumers can afford it, they will pay for content and there is room

for other states to catch up in the longer term.

Given that the penetration rate for pay TV is still relatively low in Malaysia compared to

other countries, we believe there is potential for Astro to drive up penetration rates.

The penetration rate for pay

TV is still relatively low in

Malaysia

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 11

Figure 18: Global pay TV penetration rates

0%

20%

40%

60%

80%

100%

120%

140%K

orea

Tai

wan

Hon

g K

ong

Indi

a

Sin

gapo

re

New

Zea

land

Mal

aysi

a

Chi

na

Aus

tral

ia

Japa

n

Vie

tnam

Tha

iland

Phi

lippi

nes

Indo

nesi

a

Source: Media Partners Asia

ARPU still low versus other markets

Astro’s ARPU of RM91 as of 1Q FY13A is still relatively low versus other markets and has

potential to grow, in our view.

Figure 19: Monthly ARPU (US$)

0

10

20

30

40

50

60

70

80

90

100

Dire

cTV

Aust

ar

DIS

H U

S

SK

Y N

Z

BS

kyB

Sta

rhub

Nas

pers

Ast

ro

PC

CW

i-C

able

MN

C S

ky

KT S

kyl

ife

DIS

H India

(US$/month)

Source: Company data, Credit Suisse estimates

Rising urbanisation

Urbanisation is on the rise in Malaysia, which points to rising income levels and hence,

greater potential to spend on leisure and entertainment.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 12

Figure 20: Rising urbanisation in Malaysia

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

0

5,000

10,000

15,000

20,000

25,000

30,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Rural population (thousands) Urban population (thousands) Percentage urban (%)

Urban (%)('000)

Source: United Nations

Piracy is not a problem

Pay TV piracy in Malaysia is very low compared to other countries. Piracy is estimated to

be 2% in the country compared to 23% in India, 61% in Thailand and 69% in Indonesia.

Figure 21: Piracy rates across Asia (illegal connections as a percentage of total)

68.9%

60.8%

33.7%30.4%

23.2%

10.1%

1.8% 1.1% 1.1% 0.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Indonesia Thailand Vietnam Philippines India Taiwan Malaysia Australia Hong Kong Singapore

Source: Value Partners

In our view, Astro is likely to enjoy economies of scale benefits from its large subscriber

base which exceeds 3 mn (similar in absolute size to the postpaid subscriber base of top

cellular operator, Maxis). We believe this large subscriber base likely gives Astro better

negotiating power when purchasing content, STBs, etc.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 13

Competition is limited FTA TV is hampered by structural issues. Print has historically dominated Malaysia’s adex

pie and this effectively serves to cap FTA revenues. Astro currently offers 156 TV

channels compared to six channels for FTA (which are also aired on Astro’s platform) and

71 for HyppTV (IPTV). As Astro’s subscriber base has grown and viewership has risen,

pay TV adex growth has outstripped FTA adex growth. Meanwhile, IPTV offerings by

telcos are relatively limited as FTH (fibre-to-home) lacks scale. Fixed line incumbent, TM

(Telekom Malaysia), has 450,000-plus HSBB subscribers currently, whereby coverage is

limited to 1.3 mn premises unlike DTH coverage which is likely to be close to 100%.

Telcos are also keen to avoid margin erosion from overzealous spending on IPTV content

as they have significant dividend commitments to meet.

Structural issues

FTA is hampered by structural issues; Malaysia’s adex pie has historically been dominated

by print media. In recent years, pay TV has been eroding the market share of FTA. The

FTA offering is limited compared to Astro’s range of channels. Astro’s content is superior

to FTA, which has a limited purchasing power for content because Malaysia’s adex pie is

unusually dominated by print (50% market share). Within TV adex, pay TV is gaining

share at the expense of FTA. With only six FTA channels, we believe it is difficult for FTA

to fully cater to Malaysia’s multi-lingual population (there are no dedicated vernacular FTA

channels). MediaPrima’s TV revenues were just short of RM700 mn (primarily driven by

advertising) in 2011 versus RM3.6 bn (primarily driven by subscription fees) for Astro in

FYJan12.

Figure 22: Pay TV adex market share has been growing at the expense of FTA TV adex

0

5

10

15

20

25

30

35

2010 2011 9M12

Pay TV FTA TV

Source: Nielsen Media Research

According to Nielsen, pay TV adex grew 12.8% YoY in 2011 and 14% YoY in 9M12

whereas FTA TV adex fell 7% YoY in 2011 and 0.3% in 9M12. The market share for pay

TV adex has risen from 20.3% in 2010 to 24.3% in 9M12 whereas FTA TV’s adex market

share has fallen from 30.1% in 2010 to 27.6% in 9M12, according to Nielsen.

Print has historically

dominated Malaysia’s adex

pie and this effectively

serves to cap FTA revenues

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 14

Other IPTV players lack scale

In the IPTV space, Astro presently has an infrastructure tie-up with TIME dotCom which is

in the process of wiring up multi-dwelling units (condominiums). We believe IPTV offers an

advantage over DTH satellite, e.g., rain fade doesn’t occur for IPTV whereas Ku-band

satellite signals are vulnerable to rain fade.

Maxis announced a much-awaited content tie-up with Astro on 30 August 2012. The ten-

year partnership makes Astro the exclusive content service provider to Maxis’s fibre

broadband service for three years. Maxis and Astro will jointly co-market the service via

their respective distribution channels. We believe this combined offering will be the best

IPTV offering in the market, exceeding TM’s HyppTV in terms of content breadth (number

of channels) while surpassing the Astro-TIME dotCom’s IPTV offering in terms of coverage

(Astro-Maxis’ current coverage will be 1.3 mn compared to 100,000 premises for Astro-

TIME dotCom). In comparison, TM’s UniFi service offers 71 TV channels (including FTA

and VOD channels but excluding interactive channels) and coverage of 1.3 mn premises.

Within the IPTV segment, Astro’s key competitor is HyppTV (owned by Telekom Malaysia),

where the basic channels are built into TM’s HSBB (fibre-to-home) service called UniFi.

UniFi currently has 450,000-plus subscribers (compared to Astro’s 3+mn subscriber base)

but coverage for TM’s HSBB is limited to 1.3 mn premises currently, unlike DTH coverage

which is likely to be close to 100% of Malaysia’s 6.7 mn households. According to TM,

about 20% of its UniFi subscribers subscribe for premium content. TM’s smaller subscriber

base doesn’t warrant significant content spend (we estimate <1% of its revenues) unlike

Astro’s content spend which amounts to 32%-35% of its TV segment revenues each year.

Maxis and Astro plan to roll out IPTV packages in the first quarter of 2013. We believe the

Astro-Maxis IPTV offering could be a credible threat to TM’s HSBB service, particularly

given that a rising proportion of UniFi subscribers will see their contracts mature in 2013.

Maxis currently offers similar coverage of 1.3 mn premises (as the bulk of its fibre

broadband services utilise TM’s HSBB pipe) which is significantly more than TIME

dotCom’s agreement with Astro (100,000 households covered currently).

Are the telcos a long-term threat?

We evaluate the possibility of the telcos becoming more aggressive in their IPTV offerings

but conclude that this is not likely in the next one-two years. The telcos have significant

dividend commitments; hence, we believe cash flow generation is of primary importance

and this could limit their budget for content. Also, relative to Astro’s 100% population

coverage for satellite transmission, TM’s HSBB coverage is relatively limited, at 1.3 mn

premises (for which there are 450,000+ subscribers currently) and about 20% of TM’s

HSBB subscribers pay for premium content currently. Hence, the economics may not

justify TM getting into a full blown war on content with Astro. Given TM’s relatively smaller

base of HSBB subscribers, we believe it may have to incur premium pricing on content,

which suggests significant ‘cash burn’ will become necessary if TM becomes more

ambitious in IPTV.

HyppTV (owned by Telekom Malaysia)

TM’s HyppTV currently offers 71 channels, including premium content costing

RM30/month for 30 channels. HyppTV is bundled together with TM’s HSBB service, UniFi.

Maxis announced a much-

awaited content tie-up with

Astro on 30 August 2012 for

IPTV

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 15

Figure 23: HyppTV platinum pack channels (premium content)

News Kids

Aljazeera Nick Jr

Capital TV Cbeebies

Local & Asian selection Baby First

Star Chinese movies 2 Entertainment

Star Chinese channel Warner TV

TVB8 Universal channel HD

tvN HD Syfy HD

UTV Movies Fox Crime HD

Screen Red Lifestyle

Emas BBC Lifestyle

UTV Bindass Trace sports HD

Jayamax Channel V

MNC International Fashion tv

SETI i-concerts HD

Educational Nat Geo Music

BBC Knowledge MTV Live HD

Nat Geo Adventure MUTV

Source: Company data

Comparing Astro-TIME dotCom IPTV with UniFi:

■ Astro offers a greater range of channels.

■ UniFi has superior coverage currently, of 1.3 mn premises.

■ Astro’s IPTV tie-up with TIME dotCom currently covers 100,000 premises in major

Malaysian cities.

Comparing Astro-TIME dotCom IPTV with Astro DTH:

■ Unlike Astro’s DTH services, Astro IPTV is not susceptible to rain fade.

■ Astro IPTV allows users more interactive options such as VOD (video on demand).

■ Pricing for Astro IPTV is similar to the DTH service (stripping out the broadband cost)

but the Super Packs are slightly cheaper on the IPTV platform.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 16

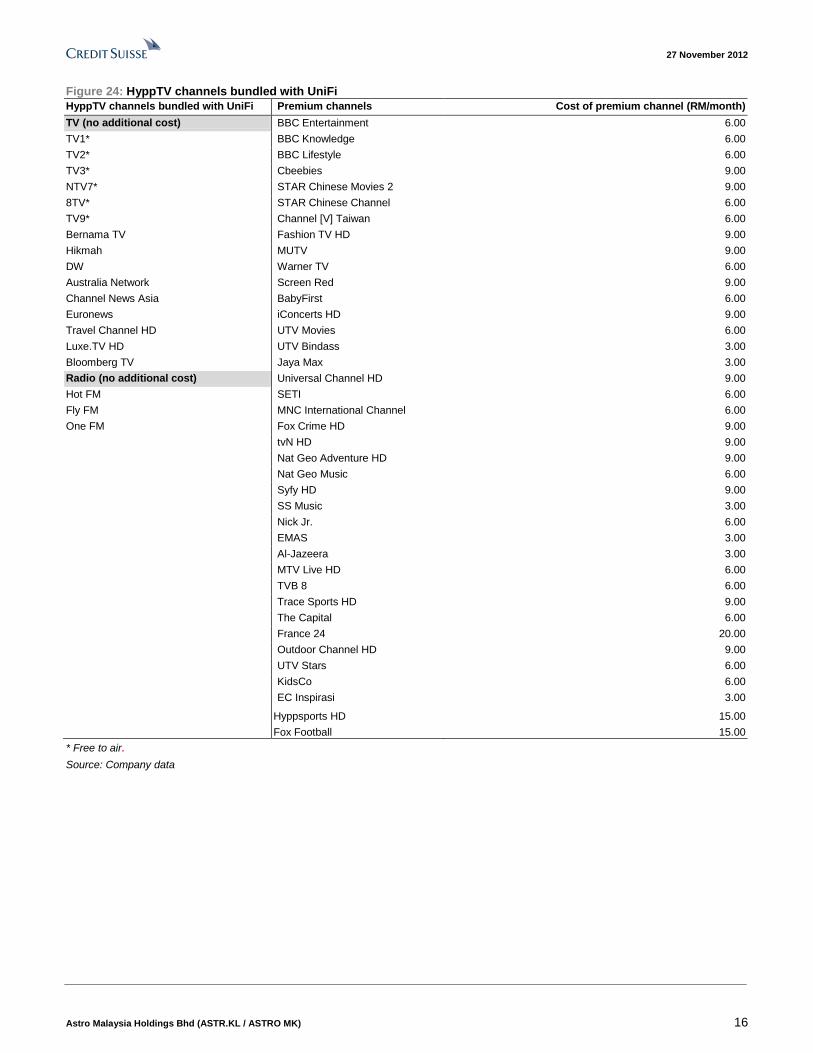

Figure 24: HyppTV channels bundled with UniFi

HyppTV channels bundled with UniFi Premium channels Cost of premium channel (RM/month)

TV (no additional cost) BBC Entertainment 6.00

TV1* BBC Knowledge 6.00

TV2* BBC Lifestyle 6.00

TV3* Cbeebies 9.00

NTV7* STAR Chinese Movies 2 9.00

8TV* STAR Chinese Channel 6.00

TV9* Channel [V] Taiwan 6.00

Bernama TV Fashion TV HD 9.00

Hikmah MUTV 9.00

DW Warner TV 6.00

Australia Network Screen Red 9.00

Channel News Asia BabyFirst 6.00

Euronews iConcerts HD 9.00

Travel Channel HD UTV Movies 6.00

Luxe.TV HD UTV Bindass 3.00

Bloomberg TV Jaya Max 3.00

Radio (no additional cost) Universal Channel HD 9.00

Hot FM SETI 6.00

Fly FM MNC International Channel 6.00

One FM Fox Crime HD 9.00

tvN HD 9.00

Nat Geo Adventure HD 9.00

Nat Geo Music 6.00

Syfy HD 9.00

SS Music 3.00

Nick Jr. 6.00

EMAS 3.00

Al-Jazeera 3.00

MTV Live HD 6.00

TVB 8 6.00

Trace Sports HD 9.00

The Capital 6.00

France 24 20.00

Outdoor Channel HD 9.00

UTV Stars 6.00

KidsCo 6.00

EC Inspirasi 3.00

Hyppsports HD 15.00

Fox Football 15.00

* Free to air.

Source: Company data

27 N

ov

em

ber 2

012

Astro

Mala

ysia

Ho

ldin

gs B

hd

(AS

TR

.KL

/ AS

TR

O M

K)

17

Figure 25: Astro TIME dotCom IPTV versus TM UniFi's packages

Monthly Internet price Astro TIME dotCom Internet TM UniFi

(RM/month) 128 148 198 298 149 199 249

Speed (Mbps) 3 10 12 24 5 10 20

Data volume Unlimited Unlimited Unlimited Unlimited Unlimited Unlimited Unlimited

Voice

Same network Free Free Free

Pay per use 15 sen/min 15 sen/min 15 sen/min 15 sen/min 10 sen/min 10 sen/min 10 sen/min

Value plan monthly RM10 10 sen/min 10 sen/min 10 sen/min 10 sen/min

IDD calls with value plan USA, UK, Canada, Australia, Japan. Hong Kong, South Korea,

Singapore, Taiwan, China

Note RM300 activation fee waived RM200 installation fee waived

Astro pay TV HyppTV

Monthly pay TV price

(RM/month)

37.95 100.00 130.00 182.90 0.0 30.0

TV pack Basic family pack

only

Super pack Super pack (w

new emperor

plus pack)

Super pack (w 1

box office, 1 add-

on item and AOD)

HyppTV HyppTV

Platinum pack

Channels 33 44+ channels 44+ channels 44+ channels 18 30

TV Notes Astro First movies very limited (only 3 Malay movies atm – 15 Aug 2012)

– RM15 for 48 hours

Additional channels are between RM6 and RM10 per

month

Video on demand movies – RM8 SD, RM10 HD for

48 hours

Video on demand series – RM15 for 1 month

Comparable packages

prices test

Astro Note TM Note

Internet speed (Mbps) 3 10 24 5 10 20

w/ most basic pay TV

(RM/month)

165.95 185.95 335.95 Basic family pack

only

149.00 199 249 Basic bundled

HyppTV

w/ mid range pay TV

(RM/month)

228.00 248.00 398.00 Basic super pack 179.00 229.00 279.00 HyppTV platinum

pack pay TV

w/ high-end pay TV

(RM/month)

310.90 330.90 480.90 Super pack (w 1

box office, 1 add

item & AOD)

229.00 279.00 329.00

Assume 5 VOD

movies/1 TV series

Source: Company data, Credit Suisse estimates

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 18

Maxis (sister company to Astro)

Maxis is in the midst of ramping up its home fibre broadband division, while some of the

fibre is the company’s own, the bulk of its home fibre service rides off TM’s HSBB network.

On 30 August, Maxis announced that has entered into a JV for Astro to be its exclusive

content service provider for Maxis’s IPTV on its fibre broadband service for three years.

OTT: Astro-On-The-Go

Astro attempts to address the threat of OTT via Astro-On-The-Go, an authenticated

service accessible via smartphones, PCs and tablets.

Although OTT remains a long-term competitor for consumers’ attention, we believe it is not

likely to be a major issue for Astro for at least several more years because the majority of

the population doesn’t have HSBB (there are only 450,000-plus HSBB subscribers

currently). HSBB coverage is still limited to selected major urban areas whereby total

premises covered amounts to 1.3 mn (whereas total households amount to 6.7 mn). From

2013, TM is no longer bound to any coverage target by the government and the company

says that rollout will be determined by market demand.

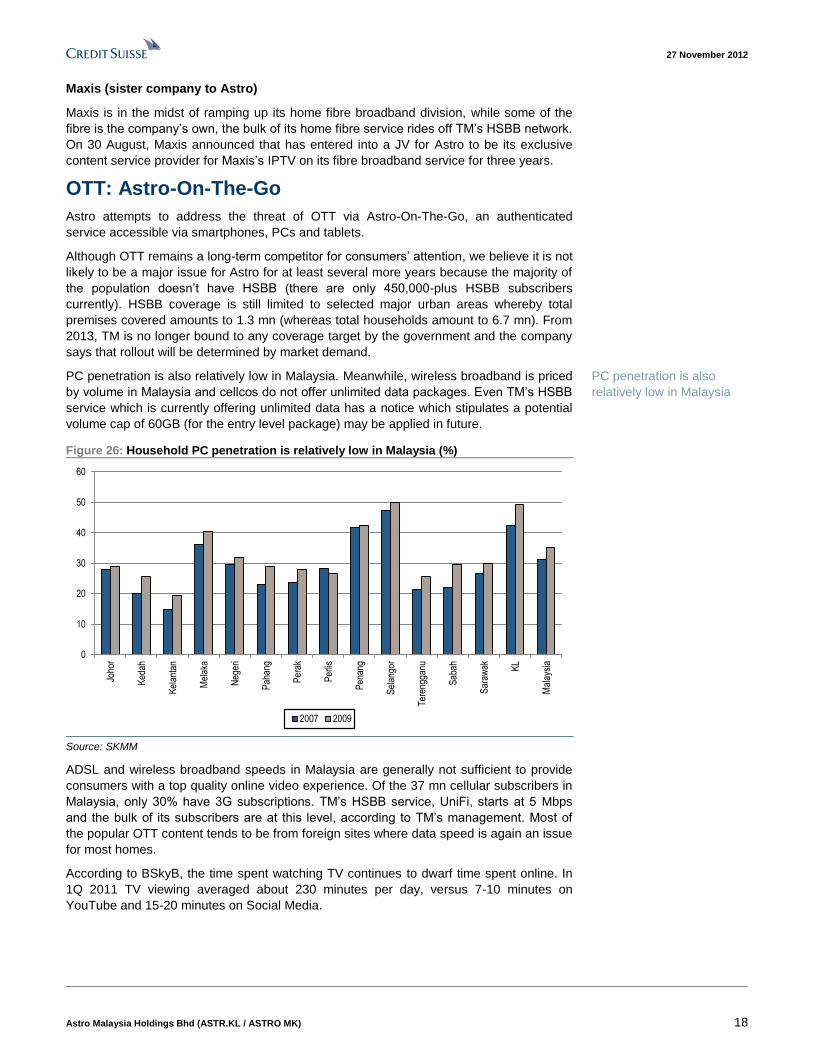

PC penetration is also relatively low in Malaysia. Meanwhile, wireless broadband is priced

by volume in Malaysia and cellcos do not offer unlimited data packages. Even TM’s HSBB

service which is currently offering unlimited data has a notice which stipulates a potential

volume cap of 60GB (for the entry level package) may be applied in future.

Figure 26: Household PC penetration is relatively low in Malaysia (%)

0

10

20

30

40

50

60

Joho

r

Ked

ah

Kel

anta

n

Mel

aka

Neg

eri

Pah

ang

Per

ak

Per

lis

Pen

ang

Sel

ango

r

Ter

engg

anu

Sab

ah

Sar

awak KL

Mal

aysi

a

2007 2009

Source: SKMM

ADSL and wireless broadband speeds in Malaysia are generally not sufficient to provide

consumers with a top quality online video experience. Of the 37 mn cellular subscribers in

Malaysia, only 30% have 3G subscriptions. TM’s HSBB service, UniFi, starts at 5 Mbps

and the bulk of its subscribers are at this level, according to TM’s management. Most of

the popular OTT content tends to be from foreign sites where data speed is again an issue

for most homes.

According to BSkyB, the time spent watching TV continues to dwarf time spent online. In

1Q 2011 TV viewing averaged about 230 minutes per day, versus 7-10 minutes on

YouTube and 15-20 minutes on Social Media.

PC penetration is also

relatively low in Malaysia

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 19

Figure 27: Live TV is as important as ever

Note: Trademarked icons used.

Source: BSkyB, BARB TechEdge, ComScore, Sky Media research

Live TV still represents 85% of total viewing, according to BSkyB’s research of viewing in

BSkyB homes. BSkyB argued that investors should not underestimate how important

viewing of live TV still is in the UK.

Figure 28: On-The-Go services

Channels Selection of 11 linear TV channels across kids, news and entertainment

Live sports Selection of live sport matches and signature events or programmes

Pay per view Offering movies on demand and Astro First content

Catch up “Catch-up” and SVOD services for previously aired signature programmes

Note: 11 linear channels include: Astro AEC, Astro Awani, Astro Ria plus, Astro Shung Xing, Astro Warna,

Astro Xiao Tai Yang, CNN, Disney Channel, Disney Junior, One HD, Astro TVIQ.

Source: Company data

Low churn reflects weak competition

Astro has sustained a relatively low churn rate of 7%-11% for the past three years. The 1Q

FY13 churn rate stood at 8%. We believe Astro’s relatively low churn rate may be

attributable to strong affordability (monthly ARPU is just 1%-3% of household incomes)

and its content portfolio.

Astro has sustained a

relatively low churn rate of

7-11% for the past three

years

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 20

New growth drivers We believe a rising take-up of HD, PVR, premium content and IPTV services bodes well

for Astro. In developed markets, we have seen HD take-up rates of 40%-57% (e.g., 43%

for BSkyB, 40% for DISH, 57% for DirecTV, etc). There’s also an opportunity for Astro to

tap prepaid revenues via its NJOI offering, which does not incur any subscriber acquisition

cost (consumer pays for STB and installation), yet could see potential upside if users buy

prepaid content.

Long-term drivers

We believe a rising take up of HD, PVR, premium content and IPTV services could bode

well for Astro.

HD migration

Having launched HD in 2010, Astro is in the midst of migrating its subscriber base over to

the HD-enabled B.Yond box and plans to have the bulk of its subscriber base fully

converted by FYJan2014. Thereafter, we expect the company to encourage these

subscribers to take up HD services, which entail an extra RM20 a month (a potential 21%

uplift to the current ARPU of RM91). Even though only 1.4 mn Astro subscribers have an

HD-enabled B.Yond box, Astro’s HD take-up rate currently stands at 30%, which is

equivalent to a 66% take-up rate if measured as a proportion of households with a B.Yond

box. This suggests it should see its take-up rate rise beyond 30% once the migration is

completed for its entire 3.1 mn subscriber base.

Figure 29: Astro’s HD channels

Basic HD Movies Variety Learning Sports Local / vernacular / others News

One Fox Premium Star World Discovery World Astro Supersport Astro Zhi Zun (Chinese) Sky News HD

Be HBO Disney XD National Geographic Astro Supersport 2 Astro Mustika

AXN Sundance History ESPN Astro First

FX Astro 'Signature'

KIX

Celestial

Food Network Asia

Life Inspired

Source: Company data

Russia’s largest satellite TV operator, Tricolor just launched HD services in July 2012 and

expects its ARPU to rise from R629 in 2011 to R1,200 next year. Austar in Australia which

launched PVR and HD in 2008-09 saw a 12% increase in ARPU in two years. HD is also

one of the key ARPU drivers for BSkyB in the UK.

We believe a rising take-up

of HD, PVR, premium

content and IPTV services

bodes well for Astro

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 21

Figure 30: HD is a major ARPU growth driver for BSkyB (£)

25

27

29

31

33

35

37

39

41

43

2004 2005 2006 2007 2008 2009 2010 2011 2012E 2013E 2014E

Par TV ARPU excl HD HD ARPU

Source: Company data, Credit Suisse estimates

PVR

PVR allows for time-shifted viewing. PVR currently costs an additional RM10 a month for

Astro subscribers. Its Beyond PVR box is being rolled out across its subscriber base. In

the UK, we expect TiVo subscribers to make up a growing proportion of VMED’s total

subscribers, rising above 50% in 2015E.

Figure 31: TiVo accounts for a growing proportion of VMED’s TV customer base

1.3%4.3%

11.6%

17.9%

23.3%

27.3%29.9%

38.9%

46.1%

53.3%

60.5%

0%

10%

20%

30%

40%

50%

60%

70%

2Q11 3Q11 4Q11 1Q12 2Q12E 3Q12E 4Q12E 2013E 2014E 2015E 2016E

Source: Company data, Credit Suisse estimates

Premium packages

Astro also offers premium packages such as Super Pack. There are currently four Super

Packs available, targeting a different customer segment. Super Pack ARPUs are relatively

high, ranging from RM125 to RM255.

In the UK, TiVo subscribers

are projected to make up a

growing proportion of

VMED’s total subscribers,

rising above 50% in 2015E

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 22

Figure 32: Astro Super Packs

Package Super Pack 1 Super Pack 2 Super Pack 3 Super Pack 4

Price (RM/month) 125 125 255 125

1 Basic Family package Basic Family package Basic Family package Basic Family package

2 Any 3 mini packages Any 3 mini packages Any 3 mini packages Any 3 mini packages

News News News News

Learning Learning Learning Learning

Variety Variety Variety Variety

Kids Kids Kids Kids

3 Prime Packages Prime Packages Prime Packages Prime Packages

Movies Movies Movies Movies

Sports Sports Sports Sports

Dynasty

4 Plus Package Plus Package Plus Package Plus Package

Mustika Maharaja New Emperor Metro

Celestial Movies

5 Astro box office Astro box office Astro box office Astro box office

Tayangan Hebat Thangathirai On Demand Dragon pack

6 HD service HD service HD service HD service

PVR PVR PVR PVR

Source: Company data

NJOI: A prepaid opportunity

Astro has a new pay TV business segment, NJOI, which incurs zero subscriber acquisition

cost, yet, offers long-term upside from prepaid content. While we have only modelled for

minor contributions from NJOI initially, a dominant prepaid telecommunications market

suggests it could become a major growth driver in the longer term. NJOI was launched in

February 2012.

Astro utilises basic set top boxes for the NJOI service. Subscribers pay for the box and

installation fees. In return, Astro provides 37 free TV and radio channels. The upside for

Astro lies with additional prepaid content which users may purchase.

Figure 33: NJOI channels

Entertainment Music Educational News

Astro Prima Tvi Astro Tutor TV SPM Astro Awani

Astro Oasis Astro Tutor TV UPSR CCTV4

Makkal TV Astro Tutor TV PMR Bernama TV

Jia Yu

TV1*

TV2*

Astro Vaanavil

i130

iView

Astro AEC

Source: Company data

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 23

Figure 34: NJOI radio channels

Astro Radio's commercial stations Direct-to-user (DTU) radio stations

ERA India Beat

Sinar FM Golden Oldies

THR.fm Raaga Jazz

THR.fm Gegar Opus

MY FM Rock

Hitz.fm Melody

Mix FM Osai

Lite FM Bayu

XFM(3) Kenyalang

Musiq'a

Source: Company data

There are also some 50,000 NJOI set top boxes, provided free to lower-income

households via the government’s E-kasih programme. We believe NJOI will enable Astro

to widen its penetration of rural households and at the same time, limit the potential

downside risk via a prepaid model.

Experience in Russia: Tricolor

Tricolor (National Satellite Company, JSC) is Russia’s largest satellite TV operator with a

subscriber base in excess of 10 mn households (as of March 2012) of which 7.7 mn are

paying subscribers.

Tricolor began its services in 2005 with a package of 15 free Russian and regional

channels, where hardware was the only cost to subscribers. Subsequently, it launched 12

new pay channels in May 2007 via low-cost packages, by which time, its subscriber base

had reached 800,000. Tricolor has since expanded its portfolio: it currently offers 100

channels for an annual fee of R600 (equivalent to €15).

Pay TV: Malaysia versus global markets

Figure 35: Pay TV market dynamics

Malaysia UK US India

Penetration Low High High High

ARPU Low High High Very low

Competition Low High High High

Threat from IPTV & OTT Low Medium-high High Low

Source: Credit Suisse estimates

We believe the growth prospects for Astro are supported by positive market dynamics and

favourable demographics. In contrast, pay TV operators in developed markets are faced

with mature industry conditions (high penetration and slowing basic ARPU growth),

competition from IPTV and OTT, in our view. Within Asia, India is another market which

has a low penetration rate for pay TV and attractive demographics but competition is

strong and ARPU is very low (US$3).

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 24

Figure 36: Global pay TV—competitive landscape by country

Country No. of operators Pay TV operators

UK 6 BSkyB, Youview, VirginMed, BT, Top up TV, Smallworld Cable

USA >5 Cable: Time Warner, Comcast, Cox communications, Charter communications, Cablevision; Satellite: DISH, DTV

South Korea >5 C&M co, KT Skylife, Tbroad Hanvit, Hyundai HCN, SK Broadband, LG Dacom, Hanaro Telecom

New Zealand 2 Sky Network, Telstra clear (most content offered on behalf of Sky)

India >10 APTV network, Shri Balaji cable, Hathway, Asianet, Dish TV, JAK communications, Barasat Cable TV

Singapore 3 Starhub, Singtel, M1

South Africa 5 Multichoice, Telkom Media, E-Sat, On Digital Media, Walking on Water

Hong Kong 2 PCCW, i-cable

Australia 3 Telstra, Foxtel, Yes Optus

Source: Company data.

Figure 37: Global pay TV penetration rates

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1965

1970

1975

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

USA UK Australia New Zealand Malaysia

Source: Value Partners, Screen Digest, Credit Suisse estimates.

Pay TV penetration in the US reached about 84% in 4Q09/1Q10 and has been falling

since, causing major operators like DirecTV to focus on customer retention as opposed to

new customer acquisition.

Figure 38: Multi-channel video penetration of US households

79.5%

80.4%

81.0%

81.9%

82.5% 82.5%

83.5%

83.2%

82.4%82.5%

79.0%

79.5%

80.0%

80.5%

81.0%

81.5%

82.0%

82.5%

83.0%

83.5%

84.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 1Q12 HH data include occasional use, URE (usual residence elsewhere), and seasonal housing units.

Source: Company data, SNL Kagan, Credit Suisse estimates

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 25

BSkyB in the UK has been facing more competition from the telcos, which are offering

triple-play services. Notably, BT will spend £700 mn for some Premier League matches in

the next season for its IPTV service, BT Vision. Meanwhile, TalkTalk has launched

YouView whose pricing is in between BSkyB (premium) and Freeview (no charge but no

interactive services offered).

Figure 39: BSkyB—net additions are running at substantially lower levels than historical

experience

0

50,000

100,000

150,000

200,000

250,000

300,000

Q1

2002

Q3

2002

Q1

2003

Q3

2003

Q1

2004

Q3

2004

Q1

2005

Q3

2005

Q1

2006

Q3

2006

Q1

2007

Q3

2007

Q1

2008

Q3

2008

Q1

2009

Q3

2009

Q1

2010

Q3

2010

Q1

2011

Q3

2011

Q1

2012

Q3

2012

net adds (subscribers)

Source: Company data.

The Malaysian economy is fine

Unlike its peers in developed markets, Astro is not grappling with weak economic

conditions. The Malaysian economy is growing and unemployment is low, resulting in

favourable indicators, e.g., consumer sentiment is robust and retail sales are growing.

Figure 40: Malaysia’s GDP growth is positive (% YoY) Figure 41: Consumer sentiment is robust

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2007 2008 2009 2010 2011F 2012F 2013F

(%

60

70

80

90

100

110

120

130

Mar-00 Apr-01 May-02 Jun-03 Jul-04 Aug-05 Sep-06 Oct-07 Nov-08 Dec-09 Jan-11 Feb-12

Source: Bank Negara, Credit Suisse estimates Source: MIER

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 26

Figure 42: Unemployment is relatively low, at 3% Figure 43: Retail sales are growing (% YoY)

0%

1%

2%

3%

4%

5%

6%

7%

8%

1982

1984

1986

1988

1990

1993

1996

1998

2000

2002

2004

2006

2008

2010

YT

D 2

012

0%

2%

4%

6%

8%

10%

12%

14%

0

10

20

30

40

50

60

70

80

90

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

(RM bn)

Retail sales (RM mn) Retail sales YoY

Growth (%)

Source: Department of Statistics Source: Malaysia Retailers Association

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 27

Trading 11% below the IPO price We use DCF as the primary valuation methodology for Astro as we believe it is most

suited to give a true representation of Astro's underlying cash flows, in our view. We apply

a mid-point 15% discount to DCF to arrive at our RM3.50 target price for Astro.

Historically, Astro has traded at a 3%-29% discount to DCF valuations, suggesting a share

price range of RM2.90-4.00.

Our key assumptions

Based on DCF valuation methodology, and applying a WACC of 8.4%, we derive an equity

valuation of RM21.5 bn for Astro.

In our view, P/E valuation is not suitable in this case because Astro's earnings will be

prone to fluctuating depreciation and amortisation of STBs, programme rights and satellite

transponder capacity. For example, while Astro is aggressively swapping out old STBs to

HD-enabled ones (which may generate higher ARPUs), we expect near-term net profits to

be depressed by exceptionally high depreciation charges.

Key drivers

Figure 44: Key assumptions

2010 2011 2012 2013E 2014E 2015E

Y/e pay TV subs (’000) 2930.0 2931.0 3067.0 3257.0 3423.9 3560.7

Subscriber growth (%) 0.0 4.6 6.2 5.1 4.0

Net adds (’000) 284.0 1.0 136.0 190.0 166.9 136.9

MAT churn (%) 11.0 10.0 7.0 9.0 9.0 9.0

Total JOI subs (excl NJOI) 2930.0 2931.0 3220.0 3415.0 3586.9 3728.7

Astro household penetration (%) 44.4 45.9 48.1 49.8 51.0

Total Malaysia households (’000) 6220.0 6605.0 6675.0 6775.1 6876.8 6979.9

Astro penetration of TV households (%) 45.7 47.4 49.3 51.1 52.3

Adex/TV revenues (%) 4.9 6.7 7.0 6.9 6.8 6.7

Adex growth (%) 56.6 8.5 10.0 8.0 7.5

Residential ARPU (RM) 82.0 85.0 89.0 95.0 99.0 103.0

ARPU growth (%) 3.7 4.7 6.7 4.2 4.0

Source: Company data, Credit Suisse estimates

Subscriber base: We have imputed 4%-7% growth in residential subscribers a year. This

suggests Astro's household penetration rate could rise to 51% by FY15E. If its FY14 net

adds are 50,000 more than we have assumed, this would imply 6.7% subscriber growth

(versus our forecast of 5%), and there could be 1% potential upside to our FY14E EBITDA

forecast.

ARPU: Over FY10-12, Astro’s ARPU rose from RM82 to RM89, and we have modelled for

it to rise to RM103 in FY15E. For an additional RM2 of ARPU above our current forecast

of RM99 for FY14E, there is 2.6% potential upside to EBITDA.

Content cost: Over FY10-12, Astro’s content cost was 32-35% of TV segment revenues.

We have allowed for content cost to be 32.5-35% of TV revenues from FY13-15E. If

content cost is 32% of TV revenues for FY13E instead of the 35% which we have built in,

there's 7.6% potential upside to EBITDA.

Administrative costs: Over FY10-12, administrative costs were about 8%-9% of revenues.

For FY13-15E, we have assumed administrative costs will be 9.0%-9.5% of revenues.

Marketing/distribution costs: Over FY10-12, distribution costs were 8%-9% of revenues.

For FY13-15E, we have assumed distribution costs will be stable at 10% of revenues.

Historically, Astro has

traded at a 3%-29%

discount to DCF valuations

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 28

Figure 45: FY2012A TV revenue, by segment

Subscription91%

Airtime Sales7%

Others2%

Source: Company data

Figure 46: FY2012A revenue breakdown—subscription versus airtime sales

Subscription84%

Airtime Sales12%

Others4%

Source: Company data

DCF scenario analysis

Using DCF valuation methodology, applying a WACC of 8.4%, we derive an equity

valuation of RM21.5 bn for Astro. We apply a mid-point 15% discount to DCF to arrive at

our RM3.50 target price for Astro. Historically, Astro has traded at a 3%-29% discount to

DCF valuations, suggesting a share price range of RM2.90-4.00.

Our base case scenario is for ARPU growth of 4.0%-6.7% over FY13-16E and this leads

to our DCF-based target price of RM3.50. If Astro’s ARPU growth is high-single digit (from

6.4% to 8.4%) from FY13E to FY16E, we see 16% further potential upside to our target

price. However, if Astro’s ARPU growth is low single digit (from 2.0% to 3.4%) from FY13E

to FY16E, there is 9% potential downside to our target price.

We apply a mid-point 15%

discount to DCF to arrive at

our RM3.50 target price for

Astro.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 29

Figure 47: Target price range (RM) for Astro based on various ARPU growth rates (%)

and terminal growth rates (%)

Annual ARPU growth / terminal growth rates 2.5% 3.0% 3.5%

6-8% 3.80 4.07 4.39

4-6% 3.28 3.50 3.78

2-3% 2.96 3.16 3.41

Source: Credit Suisse estimates

Figure 48: Target price range (RM) for Astro based on various ARPU growth rates (%)

and WACC (%)

Annual ARPU growth / WACC 8.0% 8.4% 9%

6-8% 4.38 4.07 3.60

4-6% 3.77 3.50 3.10

2-3% 3.40 3.16 2.80

Source: Credit Suisse estimates

Figure 49: Key discount rate assumptions

Beta 0.9

Cost of equity 9.8%

Cost of debt 5.0%

Terminal growth 3.0%

WACC 8.4%

Source: Credit Suisse estimates

(1) Base case: Moderate ARPU growth

Our base case scenario is for ARPU growth of 4.0%-6.7% over FY13-16E; ARPU could

reach RM107 by FY16E, and this implies a DCF-based target price of RM3.50 (using a

mid-point 15% discount to DCF).

(2) High ARPU growth

If Astro’s ARPU growth is high-single digit (from 6.4% to 8.4%) over FY13-16E, ARPU

could reach RM117 by FY16E; this implies a DCF-based target price of RM4.07, 16%

above our current target price of RM3.50 (using a mid-point 15% discount to DCF).

(3) Low ARPU growth

If Astro’s ARPU growth is low-single digit (from 2.0% to 3.4%) over FY13-16E, ARPU

could reach RM98 by FY16E; this implies a DCF-based target price of RM3.17, 9.4%

below our current target price of RM3.50 (using a mid-point 15% discount to DCF).

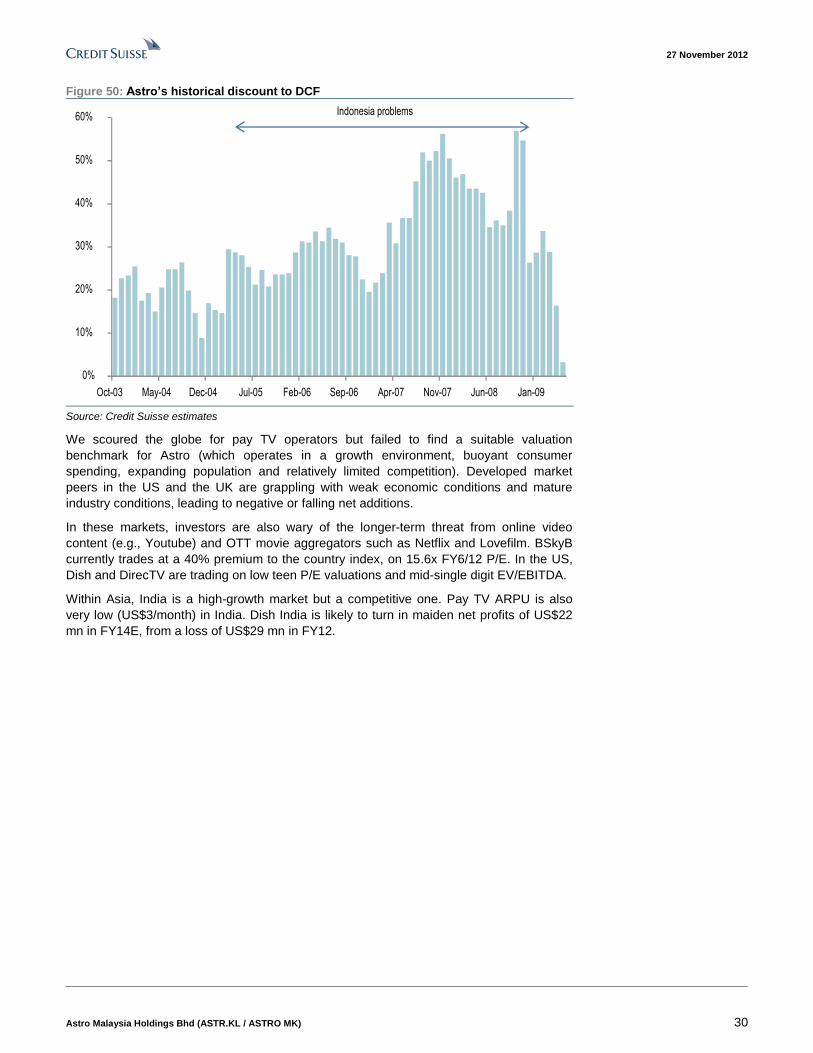

Historical discount to DCF

Historically, Astro has traded at a discount to its DCF valuations, ranging from 3%-29% .

(We have excluded the period during which there was a problematic Indonesian joint

venture in existence.)

If Astro’s ARPU growth is

high-single digit (from 6.4%

to 8.4%) from FY13E to

FY16E, there is 16%

potential upside to our target

price.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 30

Figure 50: Astro’s historical discount to DCF

0%

10%

20%

30%

40%

50%

60%

Oct-03 May-04 Dec-04 Jul-05 Feb-06 Sep-06 Apr-07 Nov-07 Jun-08 Jan-09

Indonesia problems

Source: Credit Suisse estimates

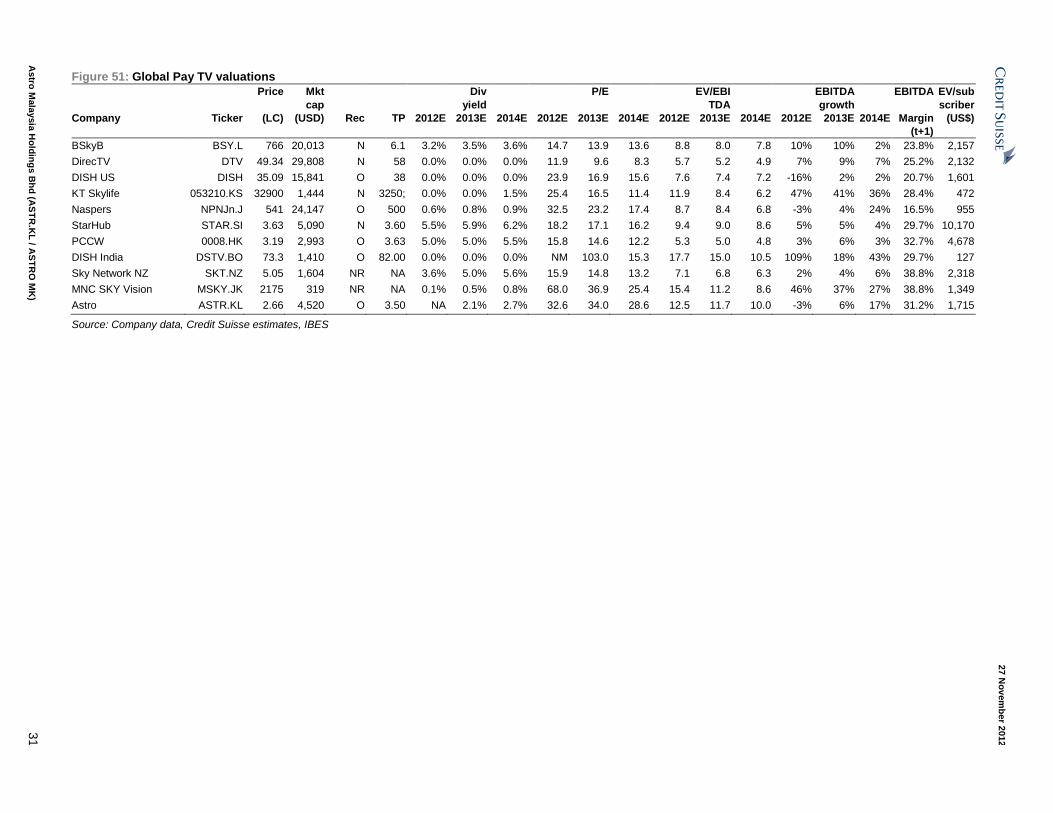

We scoured the globe for pay TV operators but failed to find a suitable valuation

benchmark for Astro (which operates in a growth environment, buoyant consumer

spending, expanding population and relatively limited competition). Developed market

peers in the US and the UK are grappling with weak economic conditions and mature

industry conditions, leading to negative or falling net additions.

In these markets, investors are also wary of the longer-term threat from online video

content (e.g., Youtube) and OTT movie aggregators such as Netflix and Lovefilm. BSkyB

currently trades at a 40% premium to the country index, on 15.6x FY6/12 P/E. In the US,

Dish and DirecTV are trading on low teen P/E valuations and mid-single digit EV/EBITDA.

Within Asia, India is a high-growth market but a competitive one. Pay TV ARPU is also

very low (US$3/month) in India. Dish India is likely to turn in maiden net profits of US$22

mn in FY14E, from a loss of US$29 mn in FY12.

27 N

ov

em

ber 2

012

Astro

Mala

ysia

Ho

ldin

gs B

hd

(AS

TR

.KL

/ AS

TR

O M

K)

31

Figure 51: Global Pay TV valuations

Price Mkt

cap

Div

yield

P/E EV/EBI

TDA

EBITDA

growth

EBITDA EV/sub

scriber

Company Ticker (LC) (USD) Rec TP 2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E Margin

(t+1)

(US$)

BSkyB BSY.L 766 20,013 N 6.1 3.2% 3.5% 3.6% 14.7 13.9 13.6 8.8 8.0 7.8 10% 10% 2% 23.8% 2,157

DirecTV DTV 49.34 29,808 N 58 0.0% 0.0% 0.0% 11.9 9.6 8.3 5.7 5.2 4.9 7% 9% 7% 25.2% 2,132

DISH US DISH 35.09 15,841 O 38 0.0% 0.0% 0.0% 23.9 16.9 15.6 7.6 7.4 7.2 -16% 2% 2% 20.7% 1,601

KT Skylife 053210.KS 32900 1,444 N 3250; 0.0% 0.0% 1.5% 25.4 16.5 11.4 11.9 8.4 6.2 47% 41% 36% 28.4% 472

Naspers NPNJn.J 541 24,147 O 500 0.6% 0.8% 0.9% 32.5 23.2 17.4 8.7 8.4 6.8 -3% 4% 24% 16.5% 955

StarHub STAR.SI 3.63 5,090 N 3.60 5.5% 5.9% 6.2% 18.2 17.1 16.2 9.4 9.0 8.6 5% 5% 4% 29.7% 10,170

PCCW 0008.HK 3.19 2,993 O 3.63 5.0% 5.0% 5.5% 15.8 14.6 12.2 5.3 5.0 4.8 3% 6% 3% 32.7% 4,678

DISH India DSTV.BO 73.3 1,410 O 82.00 0.0% 0.0% 0.0% NM 103.0 15.3 17.7 15.0 10.5 109% 18% 43% 29.7% 127

Sky Network NZ SKT.NZ 5.05 1,604 NR NA 3.6% 5.0% 5.6% 15.9 14.8 13.2 7.1 6.8 6.3 2% 4% 6% 38.8% 2,318

MNC SKY Vision MSKY.JK 2175 319 NR NA 0.1% 0.5% 0.8% 68.0 36.9 25.4 15.4 11.2 8.6 46% 37% 27% 38.8% 1,349

Astro ASTR.KL 2.66 4,520 O 3.50 NA 2.1% 2.7% 32.6 34.0 28.6 12.5 11.7 10.0 -3% 6% 17% 31.2% 1,715

Source: Company data, Credit Suisse estimates, IBES

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 32

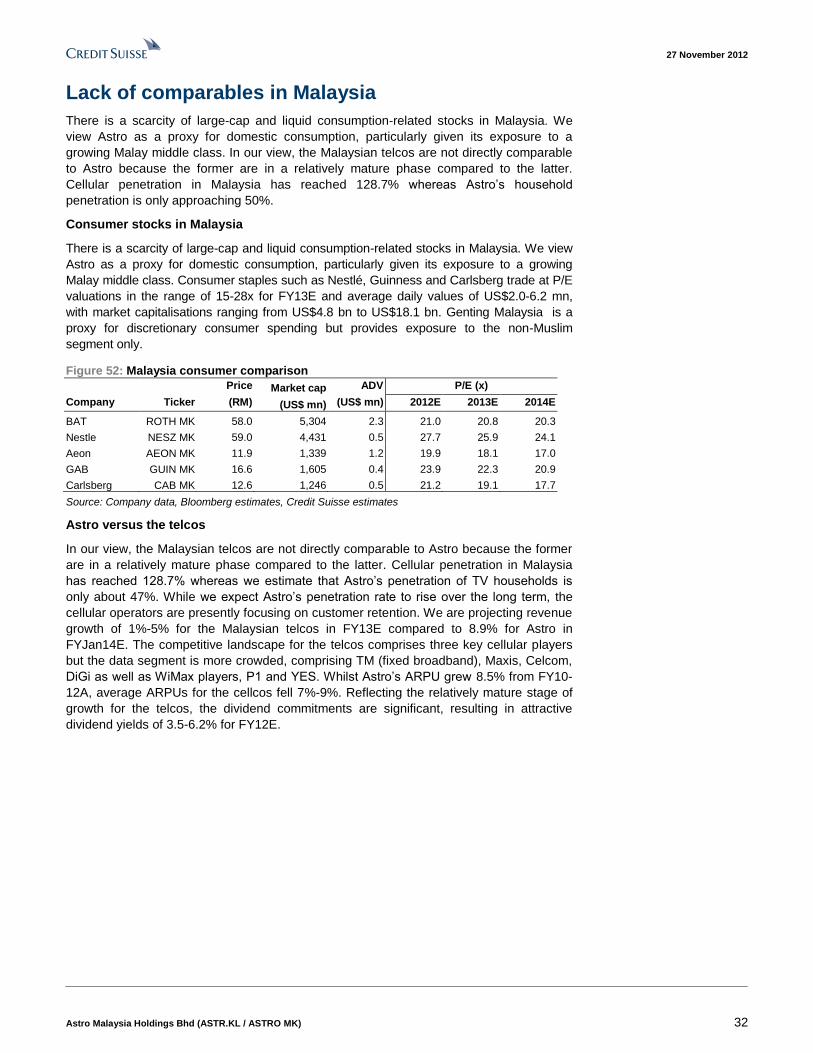

Lack of comparables in Malaysia

There is a scarcity of large-cap and liquid consumption-related stocks in Malaysia. We

view Astro as a proxy for domestic consumption, particularly given its exposure to a

growing Malay middle class. In our view, the Malaysian telcos are not directly comparable

to Astro because the former are in a relatively mature phase compared to the latter.

Cellular penetration in Malaysia has reached 128.7% whereas Astro’s household

penetration is only approaching 50%.

Consumer stocks in Malaysia

There is a scarcity of large-cap and liquid consumption-related stocks in Malaysia. We view

Astro as a proxy for domestic consumption, particularly given its exposure to a growing

Malay middle class. Consumer staples such as Nestlé, Guinness and Carlsberg trade at P/E

valuations in the range of 15-28x for FY13E and average daily values of US$2.0-6.2 mn,

with market capitalisations ranging from US$4.8 bn to US$18.1 bn. Genting Malaysia is a

proxy for discretionary consumer spending but provides exposure to the non-Muslim

segment only.

Figure 52: Malaysia consumer comparison

Price Market cap ADV P/E (x)

Company Ticker (RM) (US$ mn) (US$ mn) 2012E 2013E 2014E

BAT ROTH MK 58.0 5,304 2.3 21.0 20.8 20.3

Nestle NESZ MK 59.0 4,431 0.5 27.7 25.9 24.1

Aeon AEON MK 11.9 1,339 1.2 19.9 18.1 17.0

GAB GUIN MK 16.6 1,605 0.4 23.9 22.3 20.9

Carlsberg CAB MK 12.6 1,246 0.5 21.2 19.1 17.7

Source: Company data, Bloomberg estimates, Credit Suisse estimates

Astro versus the telcos

In our view, the Malaysian telcos are not directly comparable to Astro because the former

are in a relatively mature phase compared to the latter. Cellular penetration in Malaysia

has reached 128.7% whereas we estimate that Astro’s penetration of TV households is

only about 47%. While we expect Astro’s penetration rate to rise over the long term, the

cellular operators are presently focusing on customer retention. We are projecting revenue

growth of 1%-5% for the Malaysian telcos in FY13E compared to 8.9% for Astro in

FYJan14E. The competitive landscape for the telcos comprises three key cellular players

but the data segment is more crowded, comprising TM (fixed broadband), Maxis, Celcom,

DiGi as well as WiMax players, P1 and YES. Whilst Astro’s ARPU grew 8.5% from FY10-

12A, average ARPUs for the cellcos fell 7%-9%. Reflecting the relatively mature stage of

growth for the telcos, the dividend commitments are significant, resulting in attractive

dividend yields of 3.5-6.2% for FY12E.

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 33

Figure 53: 2011A Astro versus Malaysia cellular penetration rates

47%

128%

0%

20%

40%

60%

80%

100%

120%

140%

Astro Cellular

Source: Company data, SKMM

Figure 54: CY13E revenue growth comparison

8.9%

4.7%

2.0%

0.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Astro Digi Celcom Maxis

Source: Credit Suisse estimates

27 November 2012

Astro Malaysia Holdings Bhd (ASTR.KL / ASTRO MK) 34

Investment risks

Content cost

Content cost has accounted for a significant proportion of Astro’s costs and in the past

three years, amounting to 32%-35% of TV segment revenues. If content costs increase

significantly, this could negatively impact Astro's earnings. The Malaysian rights for live

Premier League football matches (for three seasons) have just been awarded to Astro for

the next three years for 2013/14 to 2015/16. If Astro fails to renew this contract in future,

there could be an impact on ARPU.

Satellite transponder capacity

Astro is currently utilising 17 transponders on two satellites, namely Measat 3 and Measat

3A. Another satellite, Measat 3B is currently scheduled for launch in 2014, which should

enable Astro to increase its channels to 180, from 156 currently. If Measat 3B is delayed,

Astro will not be able to expand the number of channels as planned and this could hamper

ARPU growth.

Technical/broadcast failure

In the past 16 years, Astro has not suffered any major outage or interruption to its service,

save for rain-fade. If either of the satellites were to suffer technical difficulties, Astro will not

be able to provide its full range of channels using the one remaining satellite. If there is

prolonged service interference, Astro could potentially lose subscribers.

Regulatory risk

Astro’s licences are subject to renewal and while it can apply to renew them, there is no

guarantee that it can secure the necessary approvals. Astro has a 25-year renewable

broadcasting licence with exclusivity on DTH satellite TV services till 2017 and non-

exclusivity until 2022.