India Telecoms Sector - Credit Suisse

70

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™ Client-Driven Solutions, Insights, and Access 21 August 2012 Asia Pacific Equity Research Telecommunication Services India Telecoms Sector DOWNGRADE RATING LTE in India: Piecing together RIL's strategy Figure 1: Bharti stock looks expensive at 1.1x EV/IC, with RoIC likely to stay significantly below WACC (even after three years) 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% - 1 2 3 4 5 6 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Bharti EV/IC (LHS) Bharti 12M fwd ROIC(RHS) Source: Company data, Credit Suisse estimates ■ We downgrade Bharti to UNDERPERFORM. Despite the recent sharp correction in Bharti’s stock price, we believe that risks from key events over the next 12 months are not fully understood or appreciated by the street. In particular, 2G spectrum auctions over the next four to six months and RIL Infotel’s launch over the next 12 months pose significant risks to the business models of incumbent telcos. ■ Stepping into RIL Infotel’s shoes. Our analysis shows that a data + voice strategy could make a lot more sense for RIL Infotel than just a pure data strategy. In addition, its voice economics (on regular 2G, not VoIP) could be far superior compared to those of other pure voice new entrants (no need for price discounting). The key hurdle for the company is the device ecosystem—manifested in the device price upon launch. In our analysis, at a 12% WACC, RIL Infotel is in the game if it manages to negotiate a TDD- LTE handset price less than US$150 by next year (challenging but not impossible) and potentially stands to gain a significant share of industry revenues (this is not yet built into our telco models). ■ Do not expect easy 2G auction. This raises the possibility of RIL Infotel participating in the upcoming 2G auction. It does not help that the Indian telecoms industry is among the most spectrum-starved in the world. This increases the likelihood of auctions succeeding, and we thus build an additional Rs40 impact from regulatory issues into our Bharti target price (in addition to the Rs25 already in), taking it to Rs220 (16% potential downside). Similarly, our target price for Idea goes down to Rs55 (25% potential downside). Research Analysts Sunil Tirumalai 91 22 6777 3714 [email protected] Chunky Shah 91 22 6777 3872 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of India Telecoms Sector - Credit Suisse

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

21 August 2012

Asia Pacific

Equity Research

Telecommunication Services

India Telecoms Sector DOWNGRADE RATING

LTE in India: Piecing together RIL's strategy

Figure 1: Bharti stock looks expensive at 1.1x EV/IC, with RoIC likely to stay

significantly below WACC (even after three years)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-

1

2

3

4

5

6

Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12

Bharti EV/IC (LHS) Bharti 12M fwd ROIC(RHS) Source: Company data, Credit Suisse estimates

■ We downgrade Bharti to UNDERPERFORM. Despite the recent sharp

correction in Bharti’s stock price, we believe that risks from key events over

the next 12 months are not fully understood or appreciated by the street. In

particular, 2G spectrum auctions over the next four to six months and RIL

Infotel’s launch over the next 12 months pose significant risks to the

business models of incumbent telcos.

■ Stepping into RIL Infotel’s shoes. Our analysis shows that a data + voice

strategy could make a lot more sense for RIL Infotel than just a pure data

strategy. In addition, its voice economics (on regular 2G, not VoIP) could be

far superior compared to those of other pure voice new entrants (no need for

price discounting). The key hurdle for the company is the device

ecosystem—manifested in the device price upon launch. In our analysis, at

a 12% WACC, RIL Infotel is in the game if it manages to negotiate a TDD-

LTE handset price less than US$150 by next year (challenging but not

impossible) and potentially stands to gain a significant share of industry

revenues (this is not yet built into our telco models).

■ Do not expect easy 2G auction. This raises the possibility of RIL Infotel

participating in the upcoming 2G auction. It does not help that the Indian

telecoms industry is among the most spectrum-starved in the world. This

increases the likelihood of auctions succeeding, and we thus build an

additional Rs40 impact from regulatory issues into our Bharti target price (in

addition to the Rs25 already in), taking it to Rs220 (16% potential downside).

Similarly, our target price for Idea goes down to Rs55 (25% potential

downside).

Research Analysts

Sunil Tirumalai

91 22 6777 3714

Chunky Shah

91 22 6777 3872

21 August 2012

India Telecoms Sector 2

Focus charts and table Figure 2: In a spectrum-starved environment, a well-capitalised entrant is bound to push up spectrum prices

Spectrum allocations to telecom industries globally (across all spectrum bands)

-

50

100

150

200

250

300

350

400

450

India Australia UK Singapore Germany China US

MHz of Spectrum

BSNL/MTNL

Note: The stacks in each column represent allocation to different operators (except US –see inside for details);Source: Respective country

regulators, Credit Suisse estimates

Figure 3: RIL Infotel data + voice business—NPV sensitivity to handset price assumption

Base case

Selling price of handset in 2013 (US$) 136 105 115 125 135 145 155 165 175

Cut-off voice ARPU for affordability FY3/14 (Rs) 628 510 549 588 615 656 698 743 773

Addressable revenue market FY3/14 (US$ mn) 7,498 12,202 10,411 8,849 7,926 6,704 5,658 4,767 4,250

Addressable revenue market FY3/20(US$ mn) 27,142 33,017 30,137 28,759 27,142 24,967 23,539 22,437 20,565

RIL Infotel revenues FY3/20 (US$ mn) 7,664 9,552 8,724 8,334 7,664 7,241 6,656 6,347 5,968

RIL Infotel revenue market share FY3/20 (%) 14.7 18.3 16.7 16.0 14.7 13.9 12.8 12.2 11.4

EBITDA margins FY3/20 (%) 29.6 31.3 30.6 30.3 29.6 29.0 28.2 28.2 27.4

NPV (US$ mn) @ 12% WACC 971 3,239 2,317 1,648 965 338 (324) (914) (1,468)

RoCE FY3/20 (%) 21.1 24.4 23.0 22.4 21.0 20.2 18.8 18.6 17.5

Source: Credit Suisse estimates

Figure 4: LTE handset prices for RIL Infotel to have an

NPV +ve business case at various internal hurdle rates

Figure 5: Bharti: P/B of 1.8x looks expensive for RoE of

sub-10%

100

120

140

160

180

200

220

9.0% 9.4% 9.8% 10.2% 10.6% 11.0% 11.4% 11.8% 12.2% 12.6% 13.0% 13.4% 13.8%

RIL Infotel WACC

20

13

T

DD

-L

TE

Ha

nd

set

Pri

ce (

US

$)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

-

2

4

6

8

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Bharti P/B (LHS) Bharti 12-month forward RoE (RHS)

Source: Bloomberg, Company data, Credit Suisse estimates Source: Bloomberg, Company data, Credit Suisse estimates

21 August 2012

India Telecoms Sector 3

LTE in India: Piecing together RIL’s strategy Expect fierce bidding in auctions—and no end to

competition

A key takeaway from our analysis in this report is that the threat from RIL Infotel may not

be restricted to the data business alone, but may even impact core voice businesses of

incumbent telcos. While over the longer term this means the competitive intensity could

remain high with a well-capitalised new entrant in the sector, the short-term impact could

be felt in spectrum auctions, with a likely participation of RIL Infotel. The India telecoms

sector is already in an extremely spectrum-starved situation compared to telcos across the

world. The entry of a large, well-capitalised player with a significant differentiator only

increases the likelihood of auction prices being bid up aggressively. We thus build an

additional Rs40 impact from spectrum-related issues into our target price for Bharti (total

regulatory hit Rs65, taking the target price to Rs220, with 16% potential downside).

In addition, we believe any hopes of a tariff increase post the auctions could prove utopian,

due to the high price elasticity in the subscriber base and given that a large part of the

spectrum burden is going to be felt by incumbents, rather than marginal players, in the

near term. We downgrade Bharti to UNDERPERFORM.

What can RIL Infotel achieve in Indian telecom?

With the technological barriers for RIL Infotel’s entry into the telecoms sector falling one-

by-one, what remains is the commercial barrier (manifested by high device price points).

With the visibility for RIL Infotel’s launch increasing, we try to answer the above question

looking at technical and commercial aspects (in consultation with equipment vendors).

We believe that RIL Infotel’s telecom strategy will be contrary to conventional thinking. A

data-only LTE strategy (as is popularly expected) could lead to a small addressable

market (~US$750 mn revenues)—not enough to build a business case given the

US$2.5 bn paid for spectrum in 2010. However, bundling voice with LTE could help RIL

Infotel achieve the proverbial “2+2>4”. Voice could help expand the addressable market

for LTE manifold (~US$8 bn). At the same time, LTE will offer the voice business a strong

selling point which few other telcos can match—that is, mobile broadband at unmatched

tariffs. In a yet-to-take-off data market, this can be used as a tool to attract customers from

the upper-end of the ARPU ladder, without needing to discount voice tariffs.

In our analysis, RIL Infotel could see an NPV positive business case if it manages to

negotiate LTE handset prices with voice capability (technical details inside) to less than

US$150 by next year (assuming a 12% WACC). At a lower WACC of 10% (likely, given

parent RIL’s strong balance sheet), even a US$190 handset price would suffice.

One ‘G’ to rule them all?

We work with equipment vendors to build network models that can help study the

economics of LTE in India. LTE achieves far greater speeds than any other existing mobile

broadband technology. It is also extremely flexible, in that it can work on a range of

spectrum allocations. However, these feats can be achieved because LTE was designed

from scratch using the best technology—without any historical baggage about being

backward compatible. This means that LTE cannot rely on an existing ecosystem and

customer base in its initial years (leading to high device prices initially). To worsen things

further, Indian LTE networks will be working on a high frequency band (2,300MHz), which

is not as good economically as existing 2G/3G deployments. Thus, a study of the

economics of LTE in India should take a balanced view of all these factors.

RIL Infotel better off and

also targetting voice market;

chances of participation in

auctions high

Bundling voice with LTE

could help RIL Infotel

achieve the proverbial

‘2+2>4’

21 August 2012

India Telecoms Sector 4

Table of contents Focus charts and table 2 LTE in India: Piecing together RIL’s strategy 3

Expect fierce bidding in auctions—and no end to competition 3 What can RIL Infotel achieve in Indian telecom? 3 One ‘G’ to rule them all? 3

Sector valuation summary 5 Chapter I: Expect fierce bidding in auctions—and no end to competition 6

RIL Infotel could potentially disrupt market shares significantly 6 Water is expensive in a desert 6 Chances of passing on spectrum burden to customer are slim 7 Downgrade Bharti to UNDERPERFORM 8 But wait … Bharti’s stock is already at five-year low! 9

Chapter II: What can RIL Infotel achieve in Indian telecom? 11 Data: What advantages does LTE bestow on RIL Infotel? 11 Voice: What can RIL Infotel achieve? 14 Bringing the device price into picture 20 Building a data + voice business case for RIL Infotel 24 Testing the conclusions for key assumptions 29 Could the LTE device ride on the existing phone of the subscriber? 30 Who is investing into the content ecosystem? 31

Chapter III: One ‘G’ to rule them all? 33 Avoiding square plugs and round holes… 33 Telecom world before 3GPP 34 The run-up to LTE: Constantly pushing the speed limits 35 Two roads beyond 3G 37 How does LTE manage higher speeds? 38 1. Cutting through the clutter 39 2. I’m sorry, say that again ... 43 3. Saying a lot more with a few words 44 4. Multiple antennas 50 Performance of LTE vs other data technologies 51 Developing a basic LTE model for the Indian context 53 Microwave as a near-term fix for backhaul? 55 LTE ≠ 4G 57

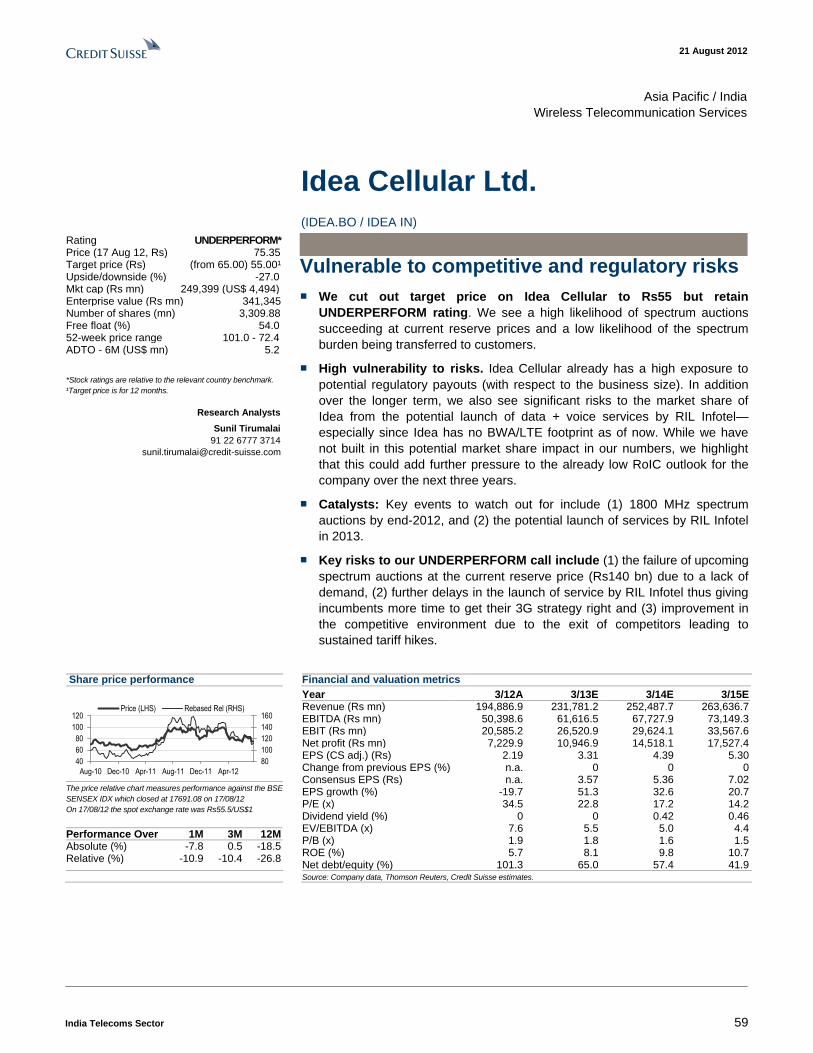

Bharti Airtel Ltd. (BRTI.BO / BHARTI IN) 58 Returns could stay low for long 58

Idea Cellular Ltd. (IDEA.BO / IDEA IN) 59 Vulnerable to competitive and regulatory risks 59

Appendix 1: RIL data + voice business financials 60 Appendix 2: RIL Infotel data-only (dongle) business model 64 Appendix 3: Calculation of rural coverage requirement for RIL Infotel 65

21 August 2012

India Telecoms Sector 5

Sector valuation summary Figure 6: Regional valuation summary

Close Mkt cap Target Normalised PE EV/EBITDA

20-Aug-12 Ticker Ccy price (US$ bn) Rating price FY3/13 FY3/14 FY3/13 FY3/14

12E 13E 12E 13E

AIS ADVANC TB Bt 210.0 19.8 O 220.0 17.3 15.1 9.9 9.5

AXIATA AXIATA MK RM 6.0 16.2 O 6.4 18.3 17.0 8.2 7.7

Bakrie BTEL IJ Rp 149.0 0.4 U 137.0 n.m. n.m. 8.3 8.0

Bharti BHARTI IN Rs 262.1 20.3 U 220.0 19.9 14.6 6.3 5.1

China Mobile 941 HK HK$ 82.4 213.2 O 101.0 10.9 10.6 4.0 3.7

DiGi DIGI MK RM 5.0 12.4 O 5.0 29.5 21.9 13.0 12.3

Excelcom EXCL IJ Rp 6,650.0 6.0 O 7,650.0 15.2 13.5 6.3 5.7

FarEasTone 4904 TT NT$ 73.3 8.0 O 82.4 20.2 17.2 9.0 8.5

Globe GLO PM P 1,125.0 3.5 O 1,330.0 15.0 13.4 5.6 5.0

IDEA IDEA IN Rs 75.4 4.8 U 55.0 22.8 17.2 5.5 5.0

Indosat ISAT IJ Rp 5,350.0 3.1 O 8,150.0 17.3 13.1 4.3 3.9

LGT 032640 KS W 7,450.0 3.4 U 6,000.0 10.4 8.2 3.9 3.4

Maxis MAXIS MK RM 7.0 16.7 O 8.0 23.6 24.2 13.1 13.4

M1 M1 SP S$ 2.6 1.9 O 3.0 14.9 14.0 8.6 8.1

NTT DoCoMo 9437 JP ¥ 134,400.0 70.1 O 150,000.0 9.9 9.6 2.9 2.8

PT Telkom TLKM IJ Rp 9,800 20.2 O 10,300 15.1 13.8 6.7 6.2

Reliance RCOM IN Rs 55.8 2.4 N 75.0 10.1 5.8 5.3 4.0

SKT 017670 KS W 149,500 10.6 O 201,000 6.4 6.1 3.2 3.1

TNZ TEL NZ A$ 2.7 5.4 U 2.2 14.9 12.9 5.4 5.3

SmarTone 315 HK HK$ 17 2.3 N 18 15.5 13.8 9.5 8.5

StarHub STH SP S$ 3.6 4.9 N 3.6 17.9 16.8 9.3 8.8

TAC DTAC TB Bt 82.3 6.2 O 104.0 17.7 16.2 7.8 7.4

Taiwan Mobile 3045 TT NT$ 109.0 12.4 O 115.0 18.2 15.8 13.3 12.2

Telstra TLS AU A$ 3.7 48.1 N 4.0 12.8 12.6 5.7 5.7

Regional average 13.5 12.4 5.6 5.2

Source: Company data, Credit Suisse estimates

How to read this report: Any report on new technology is bound to be full of technical

concepts, but we have tried to put these in simple terms that are relevant from a

business/financial perspective (and enjoyable to read!). Further, we restrict the technical

details to the third (last) chapter, so that the readers who are in a hurry can get the

investment takeaways from the first two chapters. However, we believe a full

understanding of the financial implications can be had only if one has a good

understanding of the technical details. For interested readers, we recommend reversing

the order, i.e., reading the third chapter first followed by the second and first chapters, in

that order.

21 August 2012

India Telecoms Sector 6

Expect fierce bidding in auctions—and no end to competition Two of the key bull arguments on the regulatory spectrum burden in India are that: (1) the

auction will find no takers and will fail, at recommended prices and (2) even if the auction

succeeds, the industry (in particular, the marginal players) will be so burdened with debt

that the incumbents will have enough room to push through tariff hikes. We disagree with

both these ideas.

A key takeaway from the next chapter will be that the threat from RIL Infotel may not be

restricted to the data business alone, but even impact the core voice business of

incumbent telcos. While over the longer term this means competitive intensity could

remain high with a well-capitalised new entrant in the sector, the short-term impact could

be felt in spectrum auctions, with likely participation from RIL Infotel. The Indian telecom

industry is already in an extremely spectrum-starved situation compared to telcos across

the world. While we have always maintained that the likelihood of the auctions succeeding

at the reserve price is high, the entry of a large, well-capitalised player with a significant

advantage (as will be seen in the next chapter) only increases the likelihood. We thus build

in a higher proportion of impact from spectrum-related issues for Bharti, leading to us to

cut our target price to Rs220 (from Rs260).

In addition, we believe any hopes of a tariff increase post the auction could prove utopian,

due to high price elasticity in the subscriber base and the fact that a large part of the

spectrum burden is going to be felt by incumbents in the near term rather than the

marginal players (thanks to the deferred payment rule).

We downgrade our recommendation on Bharti to UNDERPERFORM on the back of this

target price reduction.

RIL Infotel could potentially disrupt market shares

significantly

The entry of RIL Infotel into the telecom sector through a data + voice strategy should

have two levels of impact on Indian telcos:

■ Over the longer term, RIL Infotel could potentially gain a significant share of industry

revenue market share, denting the market share of incumbents. Thus, while the Bharti

bulls are hoping for reduced competitive intensity from one set of challengers in the

market post auctions, another new challenger could enter the fray leading to sustained

competitive pressure. This impact is not yet in our numbers. This also implies that

Bharti could soon lose the tag of having the ‘strongest balance sheet in Indian

telecom’, and the investor comfort that comes with this.

■ In the near term, however, the impact could be felt in the upcoming 2G auctions. RIL

Infotel would prefer to participate in the auction rather than acquire a company, in our

view (waiting for clarity on M&A rules, in particular on spectrum transfer charges, could

take up precious time). This adds a well-capitalised player to an already spectrum-

starved industry, making it more likely that the auction succeeds and spectrum gets

bid upon aggressively. We build this higher probability into our target price.

The next two chapters are devoted to the potential impact from RIL Infotel in the telecom

sector.

Water is expensive in a desert

Indian telcos operate under an extreme shortage of spectrum (Figure 7). Further, whatever

spectrum is given to the industry in India is fragmented (the stacks in each column in the

The entry of a large, well-

capitalised player with a

significant advantage only

increases the likelihood of

auctions succeeding

Bharti could soon lose the

tag of having the ‘strongest

balance sheet in Indian

telecom’

21 August 2012

India Telecoms Sector 7

chart). It is well known that a fragmented spectrum allocation is inefficient from an overall

industry capacity perspective. In addition, nearly 20% of the spectrum is allocated to state-

run telcos, with the private operators having to work with the remaining. The upcoming

spectrum auctions are not going to increase the spectrum allocation, but will only

redistribute spectrum holdings among existing/new operators.

Thus, we believe that all the noise around the reserve price of auctions should become

irrelevant once the auctions begin. The (artificial?) scarcity of spectrum in the country will

ensure this important raw material for the industry is bid for aggressively. In addition, we

also show in this report that RIL Infotel could also benefit from having a 2G spectrum and

running a 2G network.

Figure 7: Spectrum allocations to telecom industries globally (across all spectrum bands)

Note: The stacks in each column represent allocation to different operators

-

50

100

150

200

250

300

350

400

450

India Australia UK Singapore Germany China US

MHz of Spectrum

BSNL/MTNL

Note: (1) Number for India is the average spectrum allocation across 22 circles; (2) Australia: spectrum allocation in Metro regions presented

here; (3) only the total average spectrum across counties presented for the US, since the number of licence holders is high; (4) unpaired

spectrum treated as half paired.

Source: Respective country regulators, Credit Suisse estimates

Chances of passing on spectrum burden to customer

are slim

A lot of hope is being placed on the fact that post the upcoming spectrum auctions, the

industry will be so burdened with debt that the incumbents will have room to push through

tariff hikes. The chart below shows the spectrum-related payouts over the next three years

for the key industry players.

The left part of the chart shows that the payments (as a percentage of current debt) should

be highest for incumbents (Vodafone, Idea, Bharti in that order), while the challengers

(Tata and Aircel) will hardly feel the pinch. This is because incumbents have spectrum

renewals (and the related refarming) coming up in key circles over the next three years,

The entire Indian telecom

industry has less spectrum

than just China Mobile!

21 August 2012

India Telecoms Sector 8

while the challengers are all recent entrants with renewals due over a decade away

[Telenor has already announced it will be bidding in auctions selectively]. Thus, not all

players in the market face the spectrum burden at once—making it difficult for the ones

who do face the burden in the near future (read incumbents) to pass on the cost to

customers.

Further, if the challengers choose not to buy any ‘new’ spectrum in the auctions, there is

no material change to their financial health. We also show the impact on challengers’

gross debt levels if they choose to participate in auctions to pick up additional ‘new’

spectrum blocks in select circles.

Figure 8: Next three years’ spectrum payouts as a % of current debt

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Bharti Idea Vodafone Uninor Tata Aircel RCom MTNL/BSNL Tata Aircel Tata Aircel Tata

Reta

in 9

00

MH

z

Reta

in 9

00 M

Hz

Retain 900 MHz

Rene

wal

Rene

wal

Canc

elle

d

Cancelled

Renewal

2 bl

ocks

in le

adin

g ci

rcle

s

2 blocks in leading circles

2 bl

ocks

in a

ll ci

rcle

s

2 bl

ocks

in a

ll ci

rcle

s

6.8%

8.2%

1.0%

7.9%

1.5%

0.2%

23.7%

4.8%

10.7%

Del

hi C

ircle

(new

)

5.2%

Discretionary biddingMandatory payments

Spectrum payouts as % of current gross debt

0%

Canc

elle

d(9

cir

cles

)

0%

21.9%

Note: Payments calculated based on Cabinet reserve price.

Source: Company data, Credit Suisse estimates

In addition, we have earlier highlighted that the price points of a voice call in India are not

really cheap—considering the low income levels in the country (for details, see our report

What are the risks to growth expectations?, 23 February 2012). Thus, elasticity to voice

tariffs are likely to be high in India, and any increase in tariffs could meet with a drop in

usage, leading to a negligible transfer of the burden to subscribers.

Downgrade Bharti to UNDERPERFORM

We make no changes to our estimates (despite having a reasonable case to cut longer

term forecasts due to RIL Infotel’s threat discussed above), and are thus leaving the DCF

value of the core business unchanged at Rs285 (implying 5.6x FY3/13 EV/EBITDA).

For the past eight months, we have built in only a Rs25 impact from regulatory issues (a

37% probability of the full impact on the cabinet reserve price, 33% on the old TRAI

reserve price), into Bharti’s target price. Following the above discussion, we see the

Not all players in the market

face the spectrum burden at

once

21 August 2012

India Telecoms Sector 9

likelihood of auctions succeeding as being high, and the chances of the burden being

passed onto customers low. We thus take an additional Rs40 impact into our Bharti target

price (implying ~100% impact from regulatory issues on the reserve price). With no other

changes to business estimates, this brings down our target price to Rs220, implying 16%

potential downside to current levels. Similarly, our target price for Idea Cellular goes down

to Rs55 (the Rs85 core business value unchanged, but the regulatory impact increased by

Rs10 to Rs30). We reiterate that these target price changes do not build in the potential

long-term market share disruption from RIL Infotel’s entry, but only the impact on spectrum

auctions. We downgrade our recommendation on Bharti to UNDERPERFORM from

Neutral.

But wait … Bharti’s stock is already at five-year low!

Bharti stock’s recent sharp fall has taken the price close to multi-year lows—making the

stock price appear attractive.

Figure 9: Bharti stock price is at multi-year low Figure 10: Stock trading at lower end of historical

valuations

100

200

300

400

500

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Bharti stock price (Rs)

10

14

18

22

26

30

Jan-05 Nov-05 Sep-06 Jul-07 May-08 Mar-09 Jan-10 Nov-10 Sep-11 Jul-12

Source: Bloomberg Source: Company data, Credit Suisse estimates

However, we believe that the low valuation is for a reason. The returns from the business

have fallen off significantly over the past three years—both in terms of RoE and RoIC as

seen below. Seen this way, the stock does not appear cheap. In fact, we would argue that

with an RoIC of less than 9% even three years from now against a WACC of 12% (used in

our DCF), the EV/IC of 1.1x actually looks expensive! The same holds for a P/B of 1.8x

versus an RoE of sub-10%.

Figure 11: Bharti RoIC is at all-time low— justifying a low

EV/IC

Figure 12: The same holds true for RoE and P/B

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-

1

2

3

4

5

6

Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12

Bharti EV/IC (LHS) Bharti 12M fwd ROIC(RHS)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

-

2

4

6

8

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Bharti P/B (LHS) Bharti 12-month forward RoE (RHS)

Source: Bloomberg, Company data, Credit Suisse estimates Source: Bloomberg, Company data, Credit Suisse estimates

Bharti looks expensive on

EV/IC and P/B given the low

returns

21 August 2012

India Telecoms Sector 10

An important point on the above charts: The RoE and RoIC numbers above do not include

the impact of either spectrum payouts or RIL entry (both of these are only discounts to fair

value in our target price). The real visibility on RoE/RoIC improving near term is thus low,

in our view.

Consensus still bullish?

While consensus estimates have been slashed post poor Jun-12 quarter results for Bharti,

we highlight that the street is still significantly bullish on the stock (with nearly two-thirds

buy-style recommendations). The consensus target price of Rs326 on Bloomberg implies

high EV/EBITDA and P/E multiples of 7x and 25x for Bharti (FY3/13), down to 6.3x and

17x for FY3/14, respectively. We believe there are risks to these valuations due to the

headwinds over the next 12 months as discussed in this report.

Figure 13: Bharti: Street view is still significantly bullish

Buys

66%

Holds

20%

Sells

14%

Source: Bloomberg

Figure 14: Consensus target price implies significantly high multiple for Bharti near-term

FY13 FY14 FY15

Consensus TP (Rs) 326

EV/EBITDA implied by consensus TP and EBITDA estimates 7.2 6.3 5.6

P/E implied by consensus TP and EPS estimates 25 17 14

Source: Bloomberg, Company data

21 August 2012

India Telecoms Sector 11

What can RIL Infotel achieve in Indian telecom? All the technological barriers for RIL Infotel’s entry into the Indian telecom sector are falling

one after another (including multi-mode TDD-LTE handsets this year). What remain are

the commercial barriers of high device price points which will be surpassed with time.

Thus, we believe the time is right to find answers to the above question.

With its 20MHz of BWA spectrum, RIL Infotel’s approach to the Indian telecom market can

be quite different from that of other recent entrants, and also different from what investors

seem to be expecting.

The conventional view is that RIL Infotel will target the data segment and stay away from

the commoditised voice business. However, our calculations show that the addressable

market for such a service could be ~US$750 mn to start with—given current device prices.

Not enough to build a viable business case with the US$2.5 bn paid for spectrum in 2010,

in our view.

However, the situation changes markedly if RIL Infotel also bundles voice along with data.

The key point to note is that this approach for RIL Infotel will be more than just a sum of

disjointed data and voice businesses. Voice will help expand the addressable market for

the data business manifold (to ~US$8 bn according to our estimates). At the same time,

LTE will offer the voice business a strong selling point which few other telcos can match

(in fact, just one other telco in each circle): that is, high speed mobile broadband at

unmatched tariffs. In a nascent data market, this can be used as a tool to attract

customers from the upper-end of the ARPU ladder, without needing to discount voice

tariffs significantly (the opposite of the strategy of recent newcomers in the voice business

who have targeted the bottom end with tariff discounts). Thus, voice economics for RIL

Infotel could be quite different to the economics faced by recent entrants to the sector.

Using a WACC of 12%, we see an NPV positive case for RIL Infotel on voice if it manages

to negotiate LTE handset prices to less than US$150—a level that is challenging, but not

impossible, in our view.

Data: What advantages does LTE bestow on RIL

Infotel?

Conclusion:

LTE can deliver data at a tenth of the cost that 3G can, under Indian conditions.

The key aspiration behind designing LTE, as we shall study later, is to increase the data

capacities of sites with a given amount of spectrum. Our first exercise is to compare the

economics of generating unit data capacity by an Indian LTE operator versus the nearest

competing data technology that is in the market: 3.5G (HSPA). Note that most Indian 3G

operators have already deployed HSPA.

To begin with, we need a comparison of the data-carrying capacities of LTE and HSPA

(under Indian conditions). In the third chapter, we develop concepts which allow us to

compare the results of 3.5G with LTE in Indian settings (see Figure 63), developed in

consultation with equipment vendors (Ericsson, PointRed).

RIL Infotel’s approach to the

telecom sector can be quite

different from current

investor expectations

21 August 2012

India Telecoms Sector 12

Figure 15: LTE can carry 11x more data traffic than 3.5G per site for a similar coverage area

Technology HSPA @ 2,100MHz LTE @ 2,300MHz

Frequency band (MHz) 2,100 2,300

Intersite distance (m) 480 440

Coverage area (sq km) 0.20 0.17

Spectrum allocated (MHz) 5 20

Paired/Unpaired Paired Unpaired

Average throughput per site (Mbps) 6 66

Source: Company data, Credit Suisse estimates

What this implies is that an LTE site of nearly the same coverage area as a 3.5G site has

11x the capacity of a 3.5G site, given Indian spectrum allocations. Next, we consider the

costs of running the site, to get a comparison of running cost-per-unit data capacity

between the two technologies. Note that we consider the recurring network opex as well

as capex depreciation (over 15 years).

Figure 16: LTE can bring down data costs by 90% versus 3.5G

HSPA @ 2,100MHz LTE @ 2,300MHz LTE vs HSPA (x)

Average throughput per site (Mbps) (A) 6 66 11.1

Coverage area (sq km) (B) 0.20 0.17 0.8

Cost of 3-sector site (US$) (including backhaul) 15,000 22,000 1.5

Cost of 3-sector site (Rs) (including backhaul) 825,000 1,210,000

Life of equipment (years) 15 15

Annual depreciation (Rs) (C) 55,000 80,667

Tower rentals + passthrough (Rs/month) 45,000 45,000

Tower rentals + passthrough (Rs/year) (D) 540,000 540,000

Total annual operating cost (Rs) [E = C + D] 595,000 620,667

Annual cost of Mbps capacity (Rs) [F = E / A] 99,167 9,354 0.09

Annual cost of Mbps capacity per sq km (Rs) [G = F / B] 497,719 55,788 0.11

Note: INR/USD = 55; Source: Company data, Credit Suisse estimates

Thus, we note that LTE can beat 3.5G on data costs convincingly, as it can generate unit

capacity at a tenth of the cost required by a 3.5G site. Further, note that the cost of

equipment is a small fraction of the total costs (less than 10%); hence, the results are not

sensitive to variations in equipment prices from what we have assumed in this calculation.

LTE is just too efficient, and Indian LTE spectrum allocation (20MHz unpaired) is far higher

than 3G (5Mhz paired), more than compensating for the small advantage that 3G

operators enjoy on frequency band of operation (2,100MHz versus 2,300MHz).

How do Bharti’s LTE tariffs compare with 3G tariffs?

A look at the LTE (in two cities) and 3G data rates of Bharti shows that the entry-level LTE

plan (999) has half the data tariff per MB of the entry level 3G plans (a similar relationship

holds between the high-end plans on both technologies). This shows that there is

significant scope for the gap between 3G and LTE data tariffs to expand.

21 August 2012

India Telecoms Sector 13

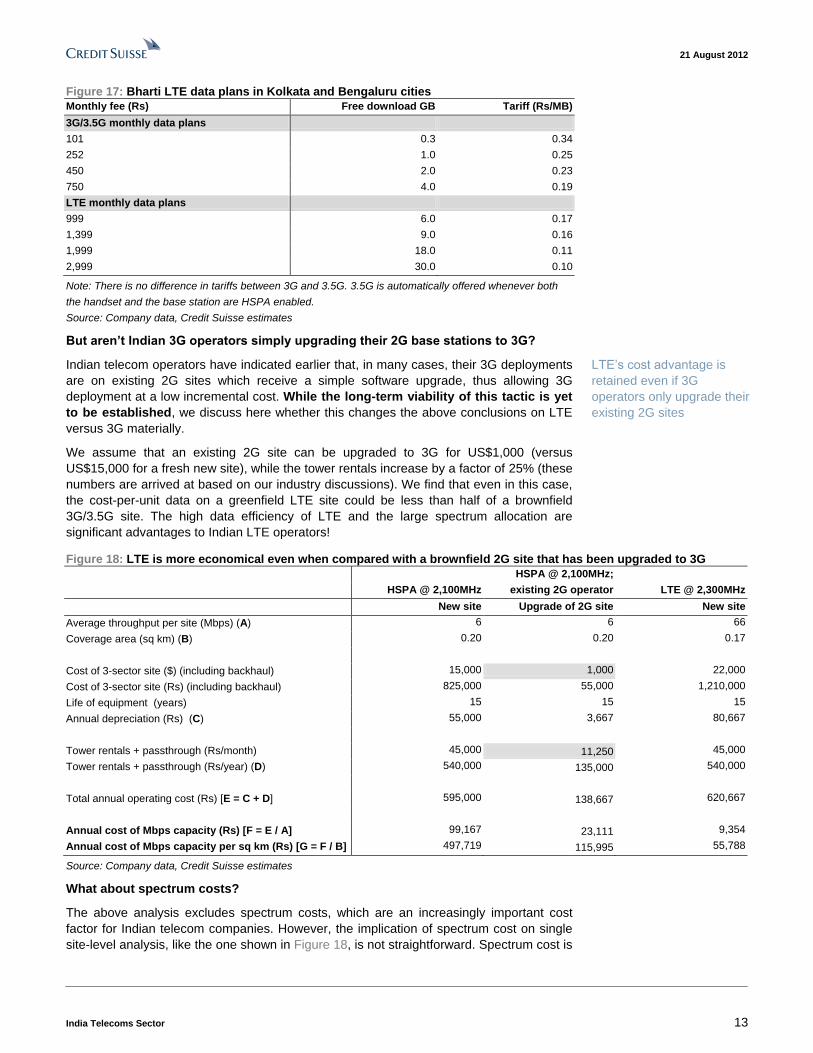

Figure 17: Bharti LTE data plans in Kolkata and Bengaluru cities

Monthly fee (Rs) Free download GB Tariff (Rs/MB)

3G/3.5G monthly data plans

101 0.3 0.34

252 1.0 0.25

450 2.0 0.23

750 4.0 0.19

LTE monthly data plans

999 6.0 0.17

1,399 9.0 0.16

1,999 18.0 0.11

2,999 30.0 0.10

Note: There is no difference in tariffs between 3G and 3.5G. 3.5G is automatically offered whenever both

the handset and the base station are HSPA enabled.

Source: Company data, Credit Suisse estimates

But aren’t Indian 3G operators simply upgrading their 2G base stations to 3G?

Indian telecom operators have indicated earlier that, in many cases, their 3G deployments

are on existing 2G sites which receive a simple software upgrade, thus allowing 3G

deployment at a low incremental cost. While the long-term viability of this tactic is yet

to be established, we discuss here whether this changes the above conclusions on LTE

versus 3G materially.

We assume that an existing 2G site can be upgraded to 3G for US$1,000 (versus

US$15,000 for a fresh new site), while the tower rentals increase by a factor of 25% (these

numbers are arrived at based on our industry discussions). We find that even in this case,

the cost-per-unit data on a greenfield LTE site could be less than half of a brownfield

3G/3.5G site. The high data efficiency of LTE and the large spectrum allocation are

significant advantages to Indian LTE operators!

Figure 18: LTE is more economical even when compared with a brownfield 2G site that has been upgraded to 3G

HSPA @ 2,100MHz;

HSPA @ 2,100MHz existing 2G operator LTE @ 2,300MHz

New site Upgrade of 2G site New site

Average throughput per site (Mbps) (A) 6 6 66

Coverage area (sq km) (B) 0.20 0.20 0.17

Cost of 3-sector site ($) (including backhaul) 15,000 1,000 22,000

Cost of 3-sector site (Rs) (including backhaul) 825,000 55,000 1,210,000

Life of equipment (years) 15 15 15

Annual depreciation (Rs) (C) 55,000 3,667 80,667

Tower rentals + passthrough (Rs/month) 45,000 11,250 45,000

Tower rentals + passthrough (Rs/year) (D) 540,000 135,000 540,000

Total annual operating cost (Rs) [E = C + D] 595,000 138,667 620,667

Annual cost of Mbps capacity (Rs) [F = E / A] 99,167 23,111 9,354

Annual cost of Mbps capacity per sq km (Rs) [G = F / B] 497,719 115,995 55,788

Source: Company data, Credit Suisse estimates

What about spectrum costs?

The above analysis excludes spectrum costs, which are an increasingly important cost

factor for Indian telecom companies. However, the implication of spectrum cost on single

site-level analysis, like the one shown in Figure 18, is not straightforward. Spectrum cost is

LTE’s cost advantage is

retained even if 3G

operators only upgrade their

existing 2G sites

21 August 2012

India Telecoms Sector 14

borne by the entire network and hence we need to assume a network size to arrive at a

spectrum cost allocation at the site level.

In the below table, we assume that, over the long term, a nationwide 3G network will reach

75,000 sites (note: Bharti reported ~18,000 3G sites in June 2012). The LTE site count is

arrived at by matching the coverage area of this 3G network with LTE sites. We find that

the spectrum cost does not make much difference to the relative costs (LTE remains 11%

of 3.5G). While it is true that 3G spectrum was more expensive than BWA (LTE) spectrum

in the 2010 auctions, spectrum cost spread over a large network is too small to move the

needle meaningfully.

In all these calculations, we have not considered spectrum usage charges. The fact that

LTE operators need to pay only 1% of revenues as spectrum fee while the fee for 3G

operators will be the same as their existing 2G operations (3-6% currently) could skew the

calculations further in favour of LTE.

Figure 19: Including spectrum costs does not make much difference to the conclusions

New site deployments HSPA @ 2,100MHz LTE @ 2,300MHz LTE vs. HSPA (x)

Results from Figure 16

Average throughput per site (Mbps) (A) 6 66 11.06

Coverage area (sq km) (B) 0.20 0.17 0.84

Total annual operating cost per site (Rs) (C) 595,000 620,667

Annual cost of Mbps capacity (Rs) 99,167 9,354 0.09

Annual cost of Mbps capacity per sq km (Rs) 497,719 55,788 0.11

No. of sites in network (D) 75,000 89,126

Coverage area of network (sq km) [E = B x D] 14,943 14,943

Nationwide spectrum auction cost (2010 auctions) (Rs mn) (F) 167,506 128,478 0.77

Spectrum licence duration (years) 20 20

Spectrum cost amortised per year per site (Rs) (G) 111,671 72,076 0.65

Total annual operating cost per site (incl. spectrum cost) Rs [H = C + G] 706,671 692,743 0.98

Annual cost (incl. spectrum) of Mbps capacity (Rs) [I = H / A] 117,778 10,440 0.09

Annual cost (incl. spectrum) of Mbps capacity per sq km (Rs) [J = I / B] 591,132 62,267 0.11

Amortised spectrum cost as % of total costs (%) 15.8 10.4

Source: Company data, Credit Suisse estimates

Voice: What can RIL Infotel achieve?

Conclusion:

■ VoIP calls on LTE will be cheaper than regular voice calls for the subscriber, but it is

not economical for the operator to offer ubiquitous VoIP coverage. So, we doubt it will

be a key service offered.

■ VoLTE standards still to be finalised.

■ CSFB (i.e., relying on an underlying 2G/3G network) is definitely possible, and we

explore this further in the report.

The big value and cash flows in the Indian telecom sector remain in the voice business

(and will do so for the foreseeable future). Further, the government’s recent intention to

allow unrestricted VoIP in India raises speculation over the possible actions from RIL

Infotel on this front. [Note that phone-to-phone VoIP is currently banned in India.]

21 August 2012

India Telecoms Sector 15

Thus, it is worthwhile understanding the options available for RIL Infotel to enter the voice

business, in our view.

Before we discuss the various voice options for RIL Infotel, let us understand how

regulations stand with respect to this issue. Regulations allow for BWA(LTE) spectrum

winners to offer voice calls—as can be seen from the clarifications issued by the

Dpeartment of Telecommunications (DoT) below. VoIP (restricted to PCs only) can be

offered with just an ISP (internet service provider) licence; however, circuit switched voice

will require a UASL licence. Note that under the new unified licence regime, a licence to

offer any service can be purchased for Rs200 mn (US$4 mn). Further, the new telecom

policy aims to allow unrestricted (phone-to-phone) VoIP as well.

Figure 20: DoT clarifications on voice being offered by LTE operators

Source: Dept. of Telecom

As we shall see when we study LTE’s design targets, LTE is a fully packet (IP) based

technology and does not support traditional circuit switched voice services. Circuit

switched voice requires the network to reserve (block) network resources for each user

during a call, whereas no such blocking happens in an IP network. LTE networks need to

find workarounds to handle voice calls.

There are mainly three options for LTE operators to provide voice services, and we study

them below.

1. Over the top VoIP (ex-Skype)

OTT VoIP services, like Skype, just require a broadband connection and use their own

techniques to deliver voice calls over a normal Internet connection (i.e., they create a

perception of ‘circuit-switched service’ while working on an IP network). The customer

does not pay specifically for each voice call, but the data usage for each call is deducted

from his monthly data allowance. This is a possible way out for LTE operators in India.

Let us understand the economics further with some numbers. On its website, Skype

recommends a bandwidth of 100 kbps (on both uplink and downlink each) to have a good

quality voice call. Even under current 3G tariffs, calls made using VoIP would be 30%

Regulations allow for LTE

operators to either offer

restricted VoIP, or normal

voice upon purchasing a

unified licence

21 August 2012

India Telecoms Sector 16

cheaper than regular voice calls as seen below (this was not the case a year ago,

however. 3G data tariffs have fallen ~75% over the past 12 months). VoIP calls could be

even cheaper on LTE networks given the lower data costs possible on LTE as we have

seen earlier.

Figure 21: VoIP calls can be significantly cheaper than regular voice calls in the Indian context

VoIP calls—economics Comment

Headline 2G voice tariff in India (Rs/min) 0.72

Bandwidth requirement–uplink (kbps) 100 Skype recommended

Bandwidth requirement–downlink (kbps) 100 Skype recommended

Total bandwidth required (up + down) (kbps) 200 Unpaired spectrum in India

Data used for a 60-second call (MB) 1.5 = (200 x 60) / (8 x 1000)

Data tariff (Rs/MB) 0.34 Entry level 3G tariff of Bharti

Data cost for a one-min Skype call (Rs) 0.51 Would be Rs0.24 if we use the entry level LTE plan of Bharti

Source: Company data, Credit Suisse estimates

However, the migration to a VoIP-based system is not straightforward, and we need to

keep in mind the following issues:

■ GSM is a technology that is tailor-made for voice services, and can work with voice

codecs of 12.2-13 kbps. However, as we have seen above, OTT VoIP requires a lot

more bandwidth in order to create a ‘circuit-switched’ feeling in a packet-based

environment. This is because of additional information that gets added to each voice

packet (overheads).

■ High-speed data services may not be required at all locations; however, voice

coverage needs to be ubiquitous (i.e., should be available even on highways, outskirts

of cities, etc.) where traffic may not be high. In India, LTE suffers from the fact that

spectrum allocated is in a higher frequency band.

We show below the economics of creating voice capacity to cover 70% of the Indian

population (a reasonable long-term objective for any voice player), on 2G and LTE. We

consider two scenarios in 2G: (1) an operator with 5Mhz in a 900MHz band representing

an incumbent and (2) an operator with 5MHz in a 1,800MHz band representing a new

entrant. On LTE, we consider three deployment scenarios as shown (these are the

deployment scenarios we develop in the third chapter of this report).

We see that the costs in the LTE options can be significantly higher than even the

new entrant 2G voice case (even after accounting for 2G spectrum at the Cabinet-

recommended reserve price). The long-range option in LTE (Macro 2) can cover an area

similar to a 2G 900MHz BTS, but the capacity gets spread out so thin over this range that

it can support only a quarter of the traffic that a 2G BTS can. On the other hand, the

shorter range options (Microcell and Macro 1) can provide high capacity but the cost of

covering the required 70% area becomes prohibitive since the range of these cells is too

short.

21 August 2012

India Telecoms Sector 17

Figure 22: Economics of 2G voice vs VoIP by an LTE operator in India

2G @ 900MHz 2G @ 1,800MHz LTE @ 2,300MHz LTE @ 2,300MHz LTE @ 2,300MHz

Microcell Macro 1 Macro 2

Spectrum allocation (MHz) [A] 5 5 20 20 20

Paired / unpaired Paired Paired Unpaired Unpaired Unpaired

Intersite distance (m) 4,508 2,962 200 440 4,000

Coverage area (sq km) [B] 18 8 0.035 0.2 13.9

2G: No. of channels of 200kHz

[C = Ax1000 / 200] 25 25

LTE: Average throughput per site (Mbps)

[see Figure 60 ] 93 66 10

Bandwidth requirement for voice call 7 calls supported per channel of

200kHz1

7 calls supported per channel of

200kHz1

200 kbps 200 kbps 200 kbps

No. of simultaneous calls supported per site2 [D] 175 175 465 332 50

Cost of 3-sector site (US$) 12,000 12,000 17,500 22,000 22,000

Cost of 3-sector site (Rs) 660,000 660,000 962,500 1,210,000 1,210,000

Life of equipment (years) 15 15 15 15 15

Annual depreciation (Rs) 44,000 44,000 64,167 80,667 80,667

Network opex per site (Rs/month) 45,000 45,000 45,000 45,000 45,000

Network opex per site (Rs/year) 540,000 540,000 540,000 540,000 540,000

Total annual operating cost per site (incl.

depreciation) (Rs) [E] 584,000 584,000 604,167 620,667 620,667

Total inhabited land area in India (sq km) 2,159,870 2,159,870 2,159,870 2,159,870 2,159,870

70% of area (sq km) [F] 1,511,909 1,511,909 1,511,909 1,511,909 1,511,909

No. sites required to cover 70% inhabited area [G

= F / B] 85,904 198,935 43,645,053 9,017,573 109,113

Voice capacity of network (mn simultaneous calls)

[H = G x D] 15 35 20,298 2,992 5

Total annual operating cost for network to cover

70% area (Rs mn) [I = E x G] 50,168 116,178 26,368,886 5,596,907 67,723

Spectrum cost per MHz (for 20 yrs) (Rs mn)

[EGoM / 2010 auctions] 60,000 30,000 6,424 6,424 6,424

Amortisation cost for allocated spectrum over 20

yrs (Rs mn) [J] 15,000 7,500 6,424 6,424 6,424

Total annual operating costs including spectrum

amortisation (Rs mn) [K = I + J] 65,168 123,678 26,375,310 5,603,331 74,146

Vs 2G @ 900MHz 100% 190% 40473% 8598% 114%

Total operating cost per unit voice capacity (Rs) [L

= K / H] 4,335 3,553 1,299 1,873 13,591

vs 2G @ 900MHz 100% 82% 30% 43% 314%

Note: (1) Assuming one BCCH slot; (2) If we were designing a network dimensioning strategy then we would have used the Erlang B function to

determine voice capacity for 2% blocking factor in each case. However, we skip this step since we are only comparing the overall capacities of

various technologies in this exercise. Further, we assume no frequency re-use in GSM.

Source: Company data, Credit Suisse estimates

21 August 2012

India Telecoms Sector 18

VoIP could exist in small pockets

The above two conclusions appear contradictory at first, but they aren’t. For the customer,

it will probably be cheaper to make a VoIP call on an LTE network than a regular 2G voice

call given the low data tariffs (thanks to LTE’s superior data capacity). However, it is not

economical for an LTE operator to promise omnipresent VoIP coverage given the high

frequency band of operation. Further, unlike voice operators which can ‘roam’ their

subscribers on other networks where there is no coverage of their own, roaming for a VoIP

customer is not straightforward (roaming onto a regular operator’s network would require

the phone to have circuit-switched capabilities as well !). So customers may have to switch

back to regular 2G/3G networks to make calls when out of an LTE coverage area—which

means that the LTE network will not be the sole service provider for the customer.

So, it is unlikely that LTE operators will offer/promise VoIP as a service. However, some

customers may still make use of the tariff arbitrage in urban areas with good LTE coverage

to make VoIP calls, and use other 2G/3G SIM cards in other areas. So VoIP on an LTE

operator’s network may be one of the voice options used by a customer, but not the sole

voice service.

Further, any new operator in a voice business will find that calls being made by its

subscribers will be to subscribers of other incumbents (same would hold true on incoming

calls). There are no technological limitations for calls made by a VoIP subscriber to land

on a regular 2G number. But the regulatory aspects are not clear. We can be certain that

the voice incumbents will resist opening up their networks to local VoIP calls, and even

when they do, the VoIP operator will have to pay a termination fee (which will put a floor

on the call tariff). Currently the termination charge in India is Rs0.20 per min. As a saving

grace, however, the few calls that come into the VoIP operator’s network from other

networks will generate termination revenue at significantly higher margin than for a regular

2G new entrant.

2. Voice over LTE (VoLTE)

We mentioned earlier that OTT VoIP is an effort to provide a circuit switched experience

over a packet-based network, and leads to a lot of overheads (i.e., lot of bandwidth is

required for a voice call). Efforts are on at 3GPP and outside to device a way to handle

voice calls efficiently on an LTE network and the technology will be called VoLTE. The

idea is to devise a way to handle many of the issues discussed earlier, including: handling

voice calls with few overheads, roaming, automatic fall-back onto a 2G network when

moving out of LTE coverage area (without the user realising it), developing commercial

models for termination of calls from/to regular 2G/3G networks, etc.

At the moment, the standards for VoLTE are still being developed, and the first

commercial deployments globally are expected only in 2013. We would not see this as a

significant near-term possibility in India. Even if the standards get finalised, we still believe

that the higher frequency of operation (and hence more sites per sq km) would continue to

be a disadvantage for Indian LTE operators to match the economics of voice business on

900MHz/1,800Mhz

3. CSFB (Circuit Switched Fall Back)

Under this method, whenever a voice call is made by a handset on an LTE network, the

network immediately transfers the call to an underlying 2G/3G network. From then

onwards, there is no economic difference between a CSFB call and a regular call made on

a 2G/3G network. Technology does not prevent the LTE operator from transferring the

voice call to a 2G/3G network of another operator through roaming arrangements.

RIL Infotel (which does not have any telecom business as of now) could tie up with

existing 2G/3G operators to offer voice calls using CSFB. However, we doubt if a voice

business can run completely on leased capacity (similar to an MVNO model)—especially

in a spectrum-starved situation such as the one in India (see chart in previous chapter).

21 August 2012

India Telecoms Sector 19

The other possibility is that RIL Infotel builds out its own 2G network by acquiring spectrum

in the upcoming auctions (or by acquiring an existing operator). Thus, RIL Infotel could

have an underlying 2G network to drive coverage (essential for voice service) and have an

LTE network as an overlay on this 2G network. We recall that RIL Infotel was an active

participant in TRAI’s spectrum auction consultation process (see our note, RIL could enter

voice before data?, 23 March 2012, for details).

In the following sections, we study how the economics with respect to CSFB work for RIL

Infotel. We assume the cost of spectrum to be as recommended by the cabinet recently

(Rs140 bn for 5MHz pan-India). We believe the results would be no different if RIL Infotel

were to acquire an existing operator—since the government intends to recover the full

spectrum value from any M&A transaction where the underlying spectrum was not

purchased at market price.

CSFB case study: NTT Docomo

Towards the end of 2011, NTT Docomo launched LTE smartphones with voice calls being

handled by an underlying 3G network. The company hopes to completely do away with 3G

once VoLTE is developed and voice calls can be handled on the LTE network itself.

Figure 23: LTE with CSFB—NTT Docomo in Japan

Source: Company data

21 August 2012

India Telecoms Sector 20

Figure 24: NTT Docomo—LTE smartphones recently introduced with CSFB functionality

Source: Company data

Bringing the device price into picture

Conclusion

In a data-only dongle strategy, the addressable market could be restricted to US$750 mn

of industry revenues upon launch in 2013 (versus US$2.5 bn paid for spectrum).

However, a data + voice handset strategy could lead to an addressable market of

US$8 bn upon launch (versus a US$5 bn spectrum cost).

Thus, entering voice makes a lot of sense for RIL Infotel.

As the following sections show, while LTE scores highly on data speeds, it suffers the

drawback of a weak device ecosystem—a significant hurdle to overcome before it can

challenge other, more well-established, technologies. This is more true in the Indian

context, where LTE operators will be working with TDD LTE on 2,300MHz spectrum

(unique on two counts). Thus, we believe that an exercise to determine the addressable

market for LTE in India depends crucially on the device price points that an operator is

able to achieve with its vendor negotiations. The exercise requires two sets of information:

■ a demand supply curve for mobile devices – which basically gives the % of subscriber

base (or population) that can afford devices at a given price point;

■ price points of devices that RIL can ‘achieve’ through its vendor negotiations.

We explore both these aspects in the following sub-sections, before proceeding to build a

business model for RIL Infotel.

Unlike the younger days of the mobile voice industry, we believe that not only cost, but

also the form of the user device, will determine the addressable market for LTE in India in

the near term.

The linkage with cost is pretty straightforward, only the segment of population that can

afford the device will be counted in the addressable market (note: we are not assuming

any upfront cash subsidies here). However, it is possible to offer LTE service in various

21 August 2012

India Telecoms Sector 21

forms: as a data-only service (through a dongle or a tablet) or as a ‘data + voice’ service

through a handset – which could have a bearing on the addressable market as well.

Developing a demand-supply curve for mobile devices in India

The Indian handset industry is quite unorganised with very little reliable data available

(even on annual handset sales, let alone volumes at each price point).

While the traditional voice market sizing models worked with affordability based on GDP

data (since the mass mobile telecom market was without any precedent), an exercise to

estimate the addressable market for data based on device prices can feed off the

experiences from the voice market. Here, we use some data which Bharti had submitted to

TRAI three years ago, giving the distribution of subscribers in its metro circles in various

monthly spend levels. The ARPU/price points have no doubt come down since then, but

we assume that the distribution around the average ARPU would not have changed

materially. We thus assume the same percentage distributions around the current ARPU

of ~Rs130 (TRAI: AGR on VLR subs) for India, as seen below.

Figure 25: Bharti 2009 data giving distribution of

subscribers in various ARPU buckets

Figure 26: Assuming the same distribution to hold

around the current average India ARPU

0%

2%

4%

6%

8%

10%

12%

14%

16%

0-4

0

40

-80

80

-120

12

0-1

60

16

0-2

00

20

0-2

40

24

0-2

80

28

0-3

20

32

0-3

60

36

0-4

00

40

0-4

40

44

0-4

80

48

0-5

20

52

0-5

60

56

0-6

00

60

0-6

40

64

0-6

80

68

0-7

20

72

0-7

60

76

0-8

00

80

0-8

40

84

0-8

80

88

0-9

20

92

0-9

60

96

0-1

00

0

10

00+

Distribution of Bharti subs across various ARPU buckets in metros -

2009. Mean ARPU Rs472

0%

2%

4%

6%

8%

10%

12%

14%

16%

0-1

1

11

-22

22

-33

33

-44

44

-55

55

-66

66

-77

77

-87

87

-98

98

-10

9

10

9-1

20

12

0-1

31

13

1-1

42

14

2-1

53

15

3-1

64

16

4-1

75

17

5-1

86

18

6-1

97

19

7-2

08

20

8-2

19

21

9-2

30

23

0-2

40

24

0-2

51

25

1-2

62

26

2-2

73

27

3+

Distribution of India subs across various ARPU buckets 2012. Mean

ARPU Rs130

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Next, we use this ARPU distribution to estimate the demand-supply curve for the

handset/device market. What we gather from our handset industry discussions is that the

average selling price (ASP) of the Indian mobile device industry is Rs2,300-2,400 (US$42-

44) currently. Along with the current mobile ARPU of Rs130, we conclude that the average

mobile subscriber buys a handset worth 17.5x his monthly telecom spend. We

simplistically assume that this ratio (17.5x) holds at each ARPU level. In other words, the

distribution of subscribers in various ARPU buckets should mirror the distribution of mobile

device demand at various price points with the above ratio holding at each price point

(i.e., the shapes of the curves around the mean should resemble each other).

We use the ARPU distribution function in Figure 26, along with the 17.5x ASP/ARPU ratio

derived earlier, to develop a distribution function for mobile device prices. What this chart

tells us is that a handset priced at Rs5,000 can be afforded by the top 10% of the

subscriber base, who contribute ~35% of industry voice revenues.

21 August 2012

India Telecoms Sector 22

Figure 27: Distribution function for device affordability

0%

10%

20%

30%

40%

50%

60%

70% 3

,100

3,9

00

4,7

00

5,5

00

6,3

00

7,1

00

7,9

00

8,7

00

9,5

00

10,3

00

11,1

00

11,9

00

12,7

00

13,5

00

14,3

00

15,1

00

Addressible market:

share of industry voice

revenues

Addressible market:

share of industry voice

subscribers

Device prices (Rs)

Indian telecom: Addressable market at each device price point

Rs 5000

Source: Company data, Credit Suisse estimates

How low can RIL Infotel price an LTE device?

The best starting point for this analysis is the data we already have from Bharti’s LTE

launch. Bharti’s LTE modem and dongle sell at Rs7,500-8,000 a piece (US$136-145);

these are full prices without any subsidy. We believe that RIL Infotel (launching a year

after Bharti, as we assume in this report) will be able to procure the devices at significantly

lower price points, because:

■ RIL’s scale of purchasing will be far higher than Bharti’s. Bharti launched its service in

just two cities (Kolkata and Bengaluru). We understand from our checks with channel

partners that the number of devices sold by Bharti in these two cities total a few

thousand so far (four months after launch). Lack of spectrum prevented Bharti from

launching in other large cities (notably Mumbai/Delhi, though this could change with

Bharti’s recent acquisition of Qualcomm’s India broadband entity). RIL Infotel, on the

other hand, has spectrum in all circles, and would likely be able to commit higher

volumes (in millions rather than thousands) to drive better scale for the device

vendors, in our view. This should help RIL get a further 20% bargain on the device’s

pricing, in our view.

■ Normal deflation in the technology hardware industry could shave off the device price

by ~15% by the time RIL Infotel launches next year.

Thus, we believe that it is not impossible for RIL Infotel to price an LTE dongle at a 35%

discount to Bharti’s current price or at around Rs5,000 (~US$90, assuming it launches in

2013).

Now, in order to estimate potential LTE handset prices (with voice capability on 2G/3G

with CSFB), we make use of the fact that the cost of entry-level 3G touchscreen

smartphones is higher than that of entry level 3G USB dongles by around Rs2,500-3,000

(Micromax device prices). Using this information, we estimate that RIL Infotel would be

able to launch handsets (with data on LTE, voice on 2G/3G) priced at Rs7,500-8,000

(US$136-145). The price points assumed here have significant bearing on final

results/conclusions, and we will test them for sensitivities later.

Important points to highlight in this discussion:

■ The TD-LTE handset ecosystem is small currently, though FDD-LTE handsets have

been around for some time. Our discussions with chipset vendors indicate that multi-

mode (TDD + FDD) chipsets have been developed. One European chipset vendor we

met recently indicated that TDD-LTE handsets using their chipsets have been

RIL Infotel should be able to

commit to higher volumes

and thus obtain lower device

price points than Bharti so

far

21 August 2012

India Telecoms Sector 23

developed by their China-based handset partners. At the recent Mobile Asia Expo,

ZTE indicated plans to launch TDD-LTE handsets this year.

■ All the device price points mentioned above are based on devices by Chinese vendors

(even Bharti’s LTE devices are of Huawei /ZTE make).

■ Bharti’s LTE devices have multi-mode chipsets so the same device latches onto a

2G/3G network when the user moves out of the LTE coverage area. This is important

from the context of CSFB that we discussed earlier.

Addressable market with a data-only dongle strategy

The important point to note is that a handset is a standalone device and can run all by

itself, while a dongle/tablet is likely to be the second device in addition to the primary voice

device (if the device is a dongle—it is probably even the tertiary device since it needs a

laptop computer to become usable). So, a customer capable of buying a tablet/dongle

device at a given price point must be significantly wealthier than a customer capable of

buying only a handset at the same price point. For our analysis, we assume the

addressable market for a dongle of a given price point would be the same as the

addressable market of a handset at 2.5x the price point. [Note that with cost deflation, the

addressable markets in both cases will only increase with each passing year.]

Our study leads us to conclude that if RIL Infotel launches with a data-only dongle priced

at ~Rs5,000 (US$91), it could target the high-end subscribers who currently contribute 5%

of industry revenues (and hope to win only the data spend of these customers). The total

addressable market for RIL Infotel is restricted to ~US$750 mn upon launch (of which RIL

Infotel can hope to gain some share)—not big enough to build a business case

considering the US$2.5 bn paid for spectrum by the company in 2010. In Appendix 2 we

give a financial model if RIL Infotel were to follow a data-only dongle strategy, and find that

there is no payback even over the entire 20-year licence period (assuming RIL Infotel gets

a 30% share of the addressable market).

It is possible for RIL Infotel to expand the addressable market by selling subsidised

devices on contract; however, given past experience we believe the possibility of such a

strategy is remote.

Figure 28: Addressable telecom market for RIL Infotel at various dongle price points

Selling price of dongle (US$) 50 60 70 80 90 100 110 120

Addressable data revenue market (US$ mn) 3,574 2,559 1,716 1,146 767 518 357 252

Source: Credit Suisse estimates

We thus conclude that a data-only strategy by RIL Infotel may not justify a business case

given the high amount paid for spectrum upfront.

Addressable market with a data + voice handset strategy: Worth a shot?

However, by launching a handset priced at Rs7,500 (US$136), the addressable market

upon launch becomes the subscribers who account for 20% of industry revenues worth

US$8 bn (and the company has a chance at capturing the entire spend of these

customers, including voice). This compares with ~US$5 bn the company may have to

spend on 2G and LTE spectrums combined (at the Cabinet reserve price for 2G auctions

with full upfront payment). While the business case even here is still not readily visible, it is

better than the data-only case above and seems worth a shot (and from our perspective,

worth further analysis).

Importantly, these voice subscribers will be from the higher-end of the market and are

unlikely to be price sensitive. What RIL Infotel can offer to these subscribers will be

something which very few other telcos can (actually, just one other telco in each circle):

mobile Internet at unmatched speeds at extremely low cost compared to other options in

the market. With voice already becoming commoditised, RIL Infotel could use data as a

21 August 2012

India Telecoms Sector 24

bait to target the top-end voice customers of incumbent telcos. The fact that the data

market (mobile or otherwise) has not yet taken off helps RIL Infotel’s case.

Thus, we believe that RIL Infotel’s approach to voice business will be very different from

the approach of recent entrants to the voice market. The pure voice newcomers have

used voice tariff discounting to gain market share. However, RIL Infotel can afford

to match the incumbents on voice tariffs, but use high-speed data as a market share

gaining tool. The corollary of this argument is that the voice economics of RIL Infotel

could be significantly better than that of pure voice newcomers.

Figure 29: Addressable telecom market for RIL Infotel at various handset price points

Selling price of handset (US$) 105 120 135 150 165 180 195 210

Addressable revenue market (US$ mn) 12,202 9,866 7,926 6,337 4,767 3,787 3,006 2,387

Source: Company data, Credit Suisse estimates

Building a data + voice business case for RIL Infotel

We now have the tools to build a financial model for RIL Infotel for its Indian telecom

business—offering data and voice through multi-mode handsets.

RIL Infotel’s financial model: Key takeaways assuming a Rs7,500 (US$136) handset

price in 2013

■ RIL Infotel could require a peak investment in terms of capex and operating losses of

US$8 bn by the fourth year of launch, after which the business would start generating

free cash (EBITDA-capex). This includes US$5 bn of spectrum payments on LTE and

(upfront) 2G.

■ If we had assumed deferred payments for 2G spectrum (with NPV preserved), the

peak investment would be ~US$7.2 bn.

■ The business could become EBITDA positive by the third year of launch, the key

driver being the focus on the higher end segment. The model gives a pay-back period

of ten years from launch of operations (FY23).

■ Assuming a 3% terminal growth and 12% WACC, we get a positive NPV of US$1 bn.

Any new business model depends on a number of assumptions. The broad top-level

assumptions are summarised below, and the detailed model is presented in Appendix 1.

We build our model assuming the start of commercial operations on 1 April 2013 (i.e.,

launch starting FY3/14), with FY3/13 being used to build out the initial network.

Top-level assumptions

■ We assume that RIL Infotel will be able to launch services through handsets priced at

Rs7,500. These would be LTE-capable phones with voice calls using CSFB. We also

assume 10-15% annual price deflation (which would help to expand the addressable

market with each passing year). With these assumptions, the addressable market

becomes 20% of total Indian telecom market revenues upon launch, going up to 45%

by the fifth year and 60% by the tenth year. The blended ARPU of the addressable

market starts at Rs840 upon launch and falls to Rs600 by the fifth year (as the

addressable market expands). [We acknowledge this starting price point is a

significant assumption, and provide a sensitivity analysis of our final conclusions to

handset prices later.]

■ We model RIL to start with a 6% revenue/subscriber market share of the addressable

segment, gradually going up to 30% by the fifth year. Recall that RIL Infotel will

probably face only one other operator as competition as far as the product offering is

concerned, given the current industry structure.

21 August 2012

India Telecoms Sector 25

■ This translates to ~11% overall industry revenue market share by the fifth year and

18% by the tenth year. Before one raises eyebrows at these assumptions, we highlight

that Uninor (not listed) had reached a 3-8% revenue market share in its core eight

circles within two years of launch (with a pure voice strategy). We expect RIL Infotel’s

task to be easier since it has a strong tool other than low-pricing to attract customers

from the top end.

■ In terms of subscribers, this translates to ~45 mn subscribers by the fifth year and

~90 mn by the tenth year of operation. The key point to note is that while subscriber

numbers may be far lower than for incumbent voice operators, these subscribers

would be from the higher ARPU segments of the customer base.

■ We conservatively assume data revenues, as a percentage of total revenues for the

addressable market, at 25% initially, gradually going up to 35-40% longer term. This

assumption implies that the top end of Indian telecom subscribers will only match the

data consumption trends of other emerging markets and stay less than the data

consumption of developed markets (40-50%).

■ We assume that RIL Infotel will follow an asset-light strategy on its network; i.e., it will

not build out its own towers but rent tower space from other towercos.

■ We use the cabinet-recommended reserve price for nationwide spectrum (Rs140 bn

for 5MHz) as the 2G spectrum cost, with one-shot upfront payment (rather than

deferred payment as suggested). The timing of payment should not make any

difference from an NPV perspective.

Data (LTE) assumptions

Before we dive into the LTE assumptions, we would like to highlight a point on capex in

telecoms. The supply-side in telecoms can be broadly divided into ‘coverage’ and

‘capacity’ site deployments. ‘Coverage’ sites help cover large areas to bring large

populations under network coverage. This is the bare minimum investment required before

an operator can offer services in an area. In some of the densely populated areas, the

capacity offered by the coverage sites may not be sufficient, and the need arises for

additional ‘capacity’ top-ups on a case-by-case basis.

In the technical discussion in the next chapter, we develop four deployment scenarios for

LTE in India. For the current discussion, we assume the results which will be developed in

the next section. Of the four deployment scenarios developed, we choose the ‘Macro 2’

option to build coverage requirement and the ‘microcell’ option to build capacity

requirements. ‘Coverage’ sites cover large areas but have low capacity, while ‘capacity’

sites do not cover any meaningful area, but offer high capacity. We reproduce the key

parameters of these two options below (details in the third chapter):

Figure 30: We use ‘microcells’ and ‘Macro 2’ deployment options in our RIL Infotel modelling

Microcell Macro 2

Cell deployment options (used as ‘capacity’ site) (used as ‘coverage’ site)

Inter-site distance (m) 200 4,000

Coverage area (sq km) 0.0 13.9

Average throughput (Mbps) 93 10

Cost per site (including backhaul US$) 17,500 22,000

Source: Company data, Credit Suisse estimates

Tariff strategy