Mobile pricing - Credit Suisse | PLUS

39

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 04 April 2012 Europe/United Kingdom Equity Research Telecommunication Services Mobile pricing THEME Approaching cost in some markets now Figure 1: Some mobile prices below cost – e.g. 3Austria, BiBob (Denmark) 0.0 10.0 20.0 30.0 40.0 50.0 60.0 3Austria BiBob DNA Iliad 3UK Telfort 3 Italia Yoigo e u /m Price Max. cost - today Max cost - long term Source: Company data, Credit Suisse estimates Summary: We highlight how in some European markets—in particular in Austria and Denmark—the cheapest tariffs on offer are now approaching the marginal cost of carrying the traffic on the network plus interconnect costs. Pricing is potentially approaching a floor in these markets, irrespective of the outcome of attempts to consolidate. We see this as bullish. Stock calls: We maintain Telekom Austria as Neutral due to the challenges remaining in its Eastern Europe operations (37% of EBITDA). On TDC (Neutral), Consumer Mobile ARPU still has to adjust to the price cutting of the past nine months. But longer term, the outlook for the stock is now improving in our view. We reiterate our Outperform rating on Elisa. We also update forecasts for Telekom Austria, TDC and Elisa in the company sections of this report after Q4 11 results. Research Analysts Justin Funnell 44 20 7888 0268 [email protected] Paul Sidney 44 20 7888 6015 [email protected] Jakob Bluestone 44 20 7883 0834 [email protected] Henrik Herbst 44 20 7888 0286 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Mobile pricing - Credit Suisse | PLUS

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

04 April 2012 Europe/United Kingdom

Equity Research Telecommunication Services

Mobile pricing THEME

Approaching cost in some markets now Figure 1: Some mobile prices below cost – e.g. 3Austria, BiBob (Denmark)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

3Austria BiBob DNA Iliad 3UK Telfort 3 Italia Yoigo

eu

/m

Price Max. cost - today Max cost - long term

Source: Company data, Credit Suisse estimates

■ Summary: We highlight how in some European markets—in particular in Austria and Denmark—the cheapest tariffs on offer are now approaching the marginal cost of carrying the traffic on the network plus interconnect costs. Pricing is potentially approaching a floor in these markets, irrespective of the outcome of attempts to consolidate. We see this as bullish.

■ Stock calls: We maintain Telekom Austria as Neutral due to the challenges remaining in its Eastern Europe operations (37% of EBITDA). On TDC (Neutral), Consumer Mobile ARPU still has to adjust to the price cutting of the past nine months. But longer term, the outlook for the stock is now improving in our view. We reiterate our Outperform rating on Elisa.

■ We also update forecasts for Telekom Austria, TDC and Elisa in the company sections of this report after Q4 11 results.

Research Analysts

Justin Funnell 44 20 7888 0268

Paul Sidney 44 20 7888 6015

Jakob Bluestone 44 20 7883 0834

Henrik Herbst 44 20 7888 0286

04 April 2012

Mobile pricing 2

MTRs – the results so far

When the European Commission decided to lower European MTRs (mobile termination rates) to eu1c/m investors were left wondering what the impact would be on mobile pricing. There was always the likelihood that by lowering marginal cost, the lower MTRs would lead to mobile voice pricing. During 2010 and for much of 2011 pricing remained quite benign – indeed yield erosion slowed as MTR erosion accelerated. Unfortunately, mobile pricing is starting to fall faster now – see Figure 2.

Figure 2: MTR erosion vs mobile yield erosion

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q112E

Q212E

Q312E

Q412E

MTR y/y Outbound yield Y/Y

Source: Company data, Credit Suisse estimates

Quite how low pricing can go when MTRs fall is a lot clearer to the stock-market following Iliad’s launch in France (where MTRs are now eu1.5c/min). As French regulator Arcep has demonstrated, if you give a new entrant low MTRs to pay, cheap spectrum and put sustained pressure on an existing operator to agree 2G and 3G national roaming rights, the new entrant can even offer mobile for free to some customers – see Figure 3.

Figure 3: The logical end-game – Iliad mobile pricing at launch – all SIM only Monthly fee (inc. VAT)

Voice SMS Data Extra calls Extra SMS Other

eu19.99* Unlimited Unlimited 3GB

eu15.99* Unlimited Unlimited 3GB + subscribe to Iliad fixed broadband

eu2.0* 60 mins per month 60 SMS per month 5c/min 1c/SMS

eu0.0* 60 mins per month 60 SMS per month 5c/min 1c/SMS + subscribe to Iliad fixed broadband

Source: Iliad, Credit Suisse research * Iliad announced at launch that these tariffs are only for the first 3m subscribers that sign

Meanwhile, mobile tariffs in over-crowded markets such as Denmark and Austria have been falling to similar levels:

■ The latest 3 Austria pricing offer 1000 mins, 1000 SMS and 1GB data for eu7 per month, SIM only

■ In Denmark, the SIM-only sub-brands have got as low as DKK119/m (eu16/m) for 360 mins, unlimited SMS and 6GB of data, again SIM only.

■ In Finland, DNA for example offers 500 voice minutes and 400 SMS and unlimited data for eu18.95/m SIM only.

04 April 2012

Mobile pricing 3

Our 2012 sector view

In our 2012 sector outlook piece (2012 Outlook – Smartphones for everyone, 28 November 2011) one point we made was that mobile pricing could converge more; ie that whilst pricing would fall in markets where it was relatively high like Spain and France, price erosion in markets where pricing was cheaper (see Figure 4) could slow – indeed at the time we published, some prices were even rising – see again Figure 4.

The idea that price could slow or stop in markets like Denmark and Austria is anti-consensus - because prices have fallen for so many years in such markets they are seen as broken and therefore at further risk. Rather than buy TDC or Telekom Austria, investors are simply avoiding the sector altogether.

Figure 4: Price of average contract plan by European market – June 2011

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Switzer

land

Spain

Franc

e

Portu

gal

Sweden

German

y

Belgium

Europe

Nether

lands

Norway UK

Italy

Denm

ark

Austria

Finl

andM

ont

hly

co

st o

f av

erag

e co

ntac

t pl

an (

eu)

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Switzer

land

Spain

Franc

e

Portu

gal

Sweden

German

y

Belgium

Europe

Nether

lands

Norway UK

Italy

Denm

ark

Austria

Finl

andM

ont

hly

co

st o

f av

erag

e co

ntac

t pl

an (

eu)

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Switzer

land

Spain

Franc

e

Portu

gal

Sweden

German

y

Belgium

Europe

Nether

lands

Norway UK

Italy

Denm

ark

Austria

Finl

andM

ont

hly

co

st o

f av

erag

e co

ntac

t pl

an (

eu)

Source: Credit Suisse research

As we said in the report…

“We expect mobile price erosion to slow in the markets with the lowest pricing, whilst continue where prices are highest. This would seem obvious but is the opposite trend to how the stockmarket sees things, with Denmark and Austria seen stuck in eternal price wars, and Switzerland an impregnable fortress. This reflects pricing changes of the past. A reversal of this investor sentiment would generate significant alpha for investors in 2012. “

Marginal pricing in Denmark and Austria is now close to cost

■ Austria: BigBob is eu12.8/m for 1GB data, 1000 minutes and 1000 SMS SIM only.

■ Denmark: typical no frills offers are DKK149/m (eu20/m) for 1GB data, 300 minutes and unlimited SMS – SIM only

■ Finland: Saunalahti eu14.90/m for unlimited data and 250mins, SMS at eu9c, SIM only

We have previously calculated the long run cost of data to be usd4/GB. So 1GB of data and 500 minutes (equivalent to 37.5MB, running at 10kbps) would cost around eu4 in net work cost. So prices in Austria are now around 2-3x network cost, implying capex/sales at this price long term of around 33-50%, leaving little for profit once customer service, interconnect and selling costs are considered. Pricing in these markets is approaching total cost.”“

04 April 2012

Mobile pricing 4

Pricing approach cost? Meeting investors in January, with equity markets rallying, telcos dividends and earnings being cut and a big rotation out of the sector, we did not find much interest in a bullish point like this. But given the weakness of sector sentiment currently, and continued attractive sector valuation (12% 2012E equity FCF yield), any good news could lead to significant upside for the stocks concerned. So we revisit this idea, to explain it more.

Cost of increasing network capacity

We first looked at the cost of a GB (gigabyte) of data in a mobile network in 2010. In our note (Mobile CAPEX – 10% not sustainable, 6 January 2010) we calculated the cost of increasing network capacity, as follows:

■ We used detailed US industry data (from 2007) for the cost of building a new cell site (usd250,000) and the cost of running that cell site (around usd80,000 pa).

■ We could also use this data, which broke down the main cost items, to calculate the cost of increasing capacity by adding more spectrum or refarming spectrum (e.g. from 3G to LTE) on to an existing cell site.

■ One key point of the cost breakdown is that only 25% of the cost of a new cell was radio equipment, even in 2007. This will be 20% or lower now, given the ongoing deflation in radio network costs vs inflation in some of the physical costs (e.g. site rental). Price deflation from China on radio equipment is going to have only a small effect on cost per cell and therefore cost per GB going forward.

■ We used projections of how theoretical capacity per cell grows as radio technology continues to evolve – see Figure 5. Between 2002 and 2010, 3G capacity had grown almost 10-fold from a spectral efficiency of 0.125bps/Hz (Release 99) to 1.1bps/Hz (HSPA+ or 3GPP Release 7). The spectral efficiency of LTE was expected at the time of our work in 2010 to start at 1.3bps/Hz and rise to 2.4bps/Hz with 4x4 MiMo. We have recently seen news of a first trial (in Germany) of this 4x4MiMo.

■ One point from this technology roadmap, is that whilst 3G increased spectral efficiency by a factor of 10 over its development (mainly by adopting HSDPA), the gains by moving to LTE do not seem quite so big. A Tele2 CTO told us he expects a long term LTE spectral efficiency of 6bps/Hz, but this seems some way off. Furthermore, a lot of the efficiency gains come from multiple antenna technology (i.e. MiMo), which has a cost in the user device in terms of size and battery life and may therefore not be fully supported. So we do not expect the same size of easy technology gains ahead as we have seen in the past 10 years.

■ Using industry assumptions of average peak hour network utilisation (ie how daily traffic is spread over the 24 hours in a day), one can then calculate the cost of increasing network capacity in that peak hour, the bottleneck which the network capacity is scaled for.

We then back-checked this work, meeting Vodafone, who agreed with the methodology but pointed out that the US industry cost assumptions we had used were 25% higher than Vodafone was seeing in Europe in 2010, partly due to lower technology costs. Adjusting for this, our new costings were broadly supported when discussing our mobile start-up model (which used the same cost assumptions) with Iliad last year (2011).

Adjusting for these 25% lower unit costs, we came to the following conclusions:

■ The cost of increasing network capacity by adding spectrum to an existing cell (or by refarming spectrum on an existing cell) is around usd1.7 (eu1.3) per GB – see Figure 7. This is the short term cost of network capacity expansion.

04 A

pril 2012

Mo

bile p

ricing

5

Figure 5: Radio technology roadmap (c. 2010) Timing Generation Technology Theoretical

maximum downlink speed

Actual downlink speed

Spectral efficiency (bps/Hz)

New technical features

1992 2G GSM 10 kbps 10 kbps Digital, TDMA

GSM-HSCSD 20 kbps 20 kbps

2000-1 2.5G GPRS 128 kbps 64 kbps Packet data, IP core

EDGE 256 kbps 100 kbps

2002+ 3G (Release 99) W-CDMA 384 kbps 100-200 kbps 0.125 CDMA, 5Mhz channels

(IMT-2000)

2005-7 3GPP Release 5 HSDPA (cat 4) 1.8 Mbps down / 384 kbps up

500 kbps 0.5 HS-DSCH, adaptive modulation (QPSK - 2bit/symbol or 16QAM - 4 bit/symbol), IMS

HSDPA (cat 6) 3.6 Mbps down 500 kbps - 1 Mbps 0.6

HSDPA (cat 8) 7.2 Mbps down 700-1.7 Mbps 0.7

HSDPA (cat 10) 14.4 Mbps down 2-3 Mbps 0.9

3GPP Release 6 HSUPA / upto 5.8 Mbps up 1 Mbps uplink Multimedia support (MBMS), initial VoIP capability, IMS enhancements

2009+ 3GPP Release 7 HSPA Evolved (Phase 1)

21 Mbps down / 11 Mbps up

1.5 - 7Mbps 1.1 64QAM downlink, evolved EDGE, beamforming, 2x2 MiMo, Continuous packet connectivity

(HSPA+, I-HSPA)

2010+ 3GPP Release 8 HSPA Evolved (Phase 2)

42 Mbps down / 11Mbps up

1.3 Under development: simultaneous use of MIMO and 64QAM, dual carrier HSPA (ie combine adjacent 5Mhz bands)

2011+ 3GPP Release 9 HSPA Evolved (Phase 3)

84 Mbps down / 23 Mbps up

> 1.3 Under development: will include 10Mhz channels

2010+ LTE Release 8 OFDMA 173 Mbps down / 58 Mbps up

4-24Mbps down (2 x 20MHz)

1.5 Under development: will include OFDMA, 2x2 MiMo, upto 20Mhz channels, system architecture evolution (unified IP core)

2011+ LTE Release 9 OFDMA 326 Mbps down/ 86 Mbps up

2.4 Under development: 4x2 and 4x4 MiMo

? 4G LTE advanced (IMT advanced)

OFDMA 1 Gbps down ? ? Under development: may include 40Mhz channels, 8 layer spatial multiplexing, co-ordinated multi-cell transmission

Source: Company data, Credit Suisse estimates

04 April 2012

Mobile pricing 6

Figure 6: Cost per GB of increasing network capacity by building a new cell site usd UMTS HSDPA (7.2) HSPA+ LTE

Spectrum (Mhz) 2 x 10 2 x 10 2 x 10 2 x 10

Spectral efficiency (bits/s/Hz) 0.15 0.70 1.10 1.50

Full buffer capacity of sector - downlink (Mbps) 1.5 7.0 11.0 15.0

Average load (to avoid excessive latency) 86% 86% 86% 86%

Utilisation rate (5.54 : 1) 0.18 0.18 0.18 0.18

Average sector/site (not all sites have 3 sectors) 2.40 2.40 2.40 2.40

Effective downlink capacity (Mbps) 0.56 2.61 4.10 5.59

Monthly site throughput - downlink (GB/month) 181 845 1328 1811

Full buffer capacity of sector - uplink (Mbps) 0.53 2.47 3.88 5.29

Average load 0.86 0.86 0.86 0.86

Traffic distribution factor 0.18 0.18 0.18 0.18

Average sector/site 2.40 2.40 2.40 2.40

Effective uplink capacity (Mbps) 0.20 0.92 1.45 1.97

Monthly site throughput - uplink (GB/month) 64 298 469 639

Incremental annual cost (usd) 138,127 149,691 154,881 165,424

Cost/month (usd) 11,511 12,474 12,907 13,785

Cost per Gigabyte used (usd) - 2007 US benchmark 47.0 10.9 7.2 5.6

Cost per GB used (usd) - 2010 Europe 30.5 7.1 4.7 3.7

Source: Credit Suisse research

Figure 7: Cost per GB of increasing network capacity by adding spectrum or upgrading from HSDPA to HSPA+ Cost/GB upgrade HSDPA

upgrade (3.6 to 7.2)

HSDPA (7.2 to 14.4)

HSPA+ upgrade

Extra radio carrier (HSPA+)

Extra radio carrier (LTE)

Incremental spectrum (Mhz) 2 x 10 2 x 10 2 x 10 2 x 5 2 x 5

Spectral efficiency (bits/s/Hz) 0.7 0.9 1.1 1.1 1.50

Incremental buffer capacity of sector - downlink (Mbps) 1.5 2.0 4.0 5.5 7.5

Average load (to avoid excessive latency) 86% 86% 86% 86% 86%

Utilisation rate (5.54 : 1) 0.18 0.18 0.18 0.18 0.18

Average sector/site (not all sites have 3 sectors) 2.40 2.40 2.40 2.40 2.40

Effective downlink capacity (Mbps) 0.56 0.75 1.49 2.05 2.79

Incremental site throughput - downlink (GB/month) 181 241 483 664 905

Incremental buffer capacity of sector - uplink (Mbps) 0.53 0.71 1.41 1.94 2.65

Average load 86% 86% 86% 86% 86%

Traffic distribution factor 0.18 0.18 0.18 0.18 0.18

Average sector/site 2.40 2.40 2.40 2.40 2.40

Effective uplink capacity (Mbps) 0.20 0.26 0.53 0.72 0.99

Incremental site throughput - uplink (GB/month) 64 85 170 234 320

Incremental annual cost (usd) 8,758 7,440 20,005 30,883 38,516

Cost/month (usd) 730 620 1,667 2,574 3,210

Cost per Gigabyte used (usd) - 2007 US benchmark 3.0 1.9 2.6 2.9 2.6

Cost per GB used (usd) - 2010 Europe 1.9 1.2 1.7 1.9 1.7

Source: Credit Suisse research

04 April 2012

Mobile pricing 7

■ The cost of increasing network capacity by building a new HSPA+ cell site in Europe was in 2010 an average usd4.7 or eu3.5 per GB. This falls to around usd3.7 or eu2.8 per GB when building LTE (due to higher bps/Hz) – see Figure 6. This is the long term cost of network capacity expansion, once extra spectrum and refarming spectrum to use new technology (e.g. LTE) have been fully exploited.

With mobile voice running at an average 2x10kbps (ie 0.000075 GB/min), this also implies a cost per minute of voice in the network of eu0.02c/min today (ie expanding capacity through spectrum and refarming) and eu0.05c/min in the long term (through more cell sites). This cost would be higher by a factor of 3-4x if a customer uses over the top VOIP services instead (which would typically run at a higher bit rate—a few years ago Skype said it needed a minimum 60kbps to run on mobile).

Key issue is traffic costs not margins

We focus in this report only on direct costs i.e. network costs and termination costs, rather than other costs (such as SAC and overheads). These latter costs will likely be flexed down over time. India shows how much SAC and overheads can be lowered with Bharti and Vodafone India making similar OpFCF margins to Vodafone in Europe and the UK with one tenth the voice yield (rev/min).

Figure 8: Yield vs OpFCF margin (ex regulation) Bharti (Airtel) Vodafone India Vodafone Europe Vodafone UK

Yield (eu'c/min) 0.635 0.842 6.6 7.9

EBITDA margin ex regulatory fees* 43% 35% 34% 24%

OpFCF margin ex regulatory fees* 27.6% 19.7% 24.6% 14.3%

Source: Company data, Credit Suisse estimates *Bharti incurs 10% of revenues on regulatory fees, we assume Vodafone India does too,

numbers relates to 2011 for Bharti and H1 FY3/12 for Vodafone

As we highlight in Figure 9 Vodafone India has similar direct costs (interconnect) to Vodafone UK, with India having a much lower yield but also a much lower MTR. Vodafone India has much higher operating expenses to sales, the result of its higher network costs relative to sales due to the low pricing in the market, as well as revenue taxes. But it makes similar EBITDA margins to Vodafone UK by incurring much lower customer costs (ie SAC and shops). In Europe making lower FCF margins is not sufficient for pricing to bottom whilst the industry is still wasting money on SACs and distribution. Pricing is still falling in plenty of markets where the marginal player is struggling to generate FCF. The floor is reached when pricing does not even cover direct (network and termination) costs.

04 April 2012

Mobile pricing 8

Figure 9: Vodafone India vs Vodafone UK

0%

10%

20%

30%

40%

50%

60%

70%

80%

Vodafone India Vodafone UK

Co

sts/

sal

es

Direct costs Customer costs Operating expenses

Source: Company data, Credit Suisse research, Note: data as of H1 FY3/12

Pricing has reached direct cost in some markets

We can use these our calculation of network costs to compare these direct costs (network plus termination) to current mobile pricing.

In Figure 10 we show the direct cost to the network operator of providing a typical bundle of 1000 mins, 1000 SMS and 1GB (the typical 3x1000 bundle in Austria – Denmark typically offers less voice and more SMS and data but the approach is similar). We break down direct costs as follows:

■ Network cost – this is the cost of expanding the capacity of the network to deal with the traffic generated by the customer, as discussed above. For today’s operator we assume that all the network expansion is through using new spectrum and from technology upgrades (rather than the more expensive route of building new cells sites).

■ Termination cost – this is the termination costs incurred on cross network traffic. We assume 25% of traffic is on-net (typical for a challenger operator), 35% to other mobile (at the eu1c/min target for the current MTR glide path) and 40% to fixed line (current FTRs average 0.5c/min).

On this calculation if a customer were to use all of the 3x1000 bundle, it would cost the network operator around eu12+VAT/month. Separately, based on typical usage today (500MB of data, 200 voice minutes and 120 SMS), a customer using the 3x1000 bundle would cost the network operator eu2.4+VAT/month.

Figure 10: Cost of 3 x 1000 bundle - current Today Unit cost Bundle Max cost per

month Typical usage Typical cost

per month Network Termination*

Voice eu0.02c/min eu0.55c/min 1000 mins 5.7 200 mins 1.14

Data eu1.3/GB eu0.0/GB 1000 MB 1.3 500 MB 0.7

SMS eu0.0c/SMS eu0.5c/SMS 1000 SMS 5.0 120 SMS 0.6

12.0 2.4

Source: Company data, Credit Suisse research * target for current glide path

04 April 2012

Mobile pricing 9

In the longer term (see Figure 11) once spectrum and technology gain has been exhausted, operators have to build new cells to meet capacity. This is more expensive, as previously discussed. On the other hand, in the long term it is possible termination will approach zero, ie bill and keep. Assuming growth in voice and data usage over time, the cost per bundle would be around eu3.0 - 3.3/month, not far from current 3Austria pricing ex VAT.

Figure 11: Cost of 3 x 1000 bundle – long term Long term Unit cost Bundle Max cost per

month Typical usage Typical cost

per month Network Termination*

Voice eu0.05c/min 0 1000 mins 0.5 300 mins 0.15

Data eu2.8/GB 0 1000 MB 2.8 1000 MB 2.8

SMS eu0.0c/SMS 0 1000 SMS 0.0 50 SMS 0.0

3.3 2.95

Source: Company data, Credit Suisse research

In Figure 12, we then compare these costs to the prices being offered by challenger operators in a number of European markets. We summarise the findings in Figure 12 to Figure 16. We highlight:

Austria – 3Austria pricing below direct cost for many users

In Austria, 3Austria is pricing below direct cost on its eu7 plan if customers use all the bundle. If customers use the 1GB allowance, plus the 1000 minutes and texts, this costs 3Austria today in network and interconnect around eu12 vs its eu5.6 price ex VAT. Customers have to use less than half the bundle for 3Austria to break even. We should add that T-Mobile is at eu8 and Telekom Austria (BigBob) at eu9 for a similar product. It is no coincidence the Austrian market is now trying to consolidate.

3Austria only makes money if customers do not use a lot of the bundle. Even if we take average contract smartphone usage in W.Europe of 500MB, only 200 minutes and 120 SMS, this would cost eu2.4 per month. On this average a price of eu5.6 ex VAT generates a gross margin over direct costs (interconnect and network) of around 60% on a typical customer vs a sector average of 77.5% (15pp of interconnect/sales and around 7.5pp of network CAPEX/sales). Furthermore:

■ the 3x1000 bundles are likely to attract higher users

■ whilst average usage is 500MB/200 voice calls, there are typically relatively few average data customers with usage clustered either at low levels or high levels of data usage.

3Austria gross margins on its marginal price point of eu7 are likely to be even lower than 60%. Most importantly, it is tough for 3Austria to cut much below this eu7 (inc VAT) price point currently.

In the longer term, termination rates may fall to zero, lowering cost further. But at this point (which is not on the current EC regulatory horizon), 3Austria will likely be having to build a higher amount of new cells to expand network capacity, as the gains from spectrum and technology are further exhausted. So as we show in Figure 10 and Figure 11, the direct cost of 3Austria for the average customer is unlikely to fall much below this current eu2.4 per GB level, suggesting that this pricing level is close to a long term as well as a near term floor.

So in the case of Austria we can say that price is close to or at the floor. We consider the investment case for Telekom Austria later in this note.

04 April 2012

Mobile pricing 10

Denmark – price is at cost for the heaviest users

In Denmark recent promotions from BiBob (Telenor) and Oister (3) have seen bundle pricing of DKK119 offering 6GB as well as the customary 6 hours of calls and unlimited SMS. We calculate in Figure 12 that such promotional bundles are, like Austria, below the direct cost for many users. VAT in Denmark is 25% so the DKK119 is a real price for the operator of around eu12/m whilst the direct cost of the bundle if fully used is around eu15/m. The customer has to use 80% or less of the bundle for the operator to cover its direct costs. Most customers will use less than 6GB but there will be a significant minority that can use this much, particularly if tethering is allowed.

For the average customer (500MB, 200 voice minutes, 120 SMS) the bundles are still priced well above cost, with a mark up of around 5x close to the current sector average. But again, users are clustered at either low or high levels of usage, so there will be a significant amount of customers that the operators are making little money from, or even losing money on.

So Denmark may also be close to a floor on pricing. We consider the investment case for TDC later in this note.

Finland – some way to go to get to cost, but costs not to fall much more

On the same calculation, in Finland marginal pricing is around 2.4x direct cost if the bundle is fully used (as the voice bundle is again capped), still some way above cost but only around half the 4.4x mark-up for the average established European operator today. The mark up is also low on a long term basis, given the mix of the plans (capped voice, unlimited data) with the benefit of going to bill and keep (ie zero) on MTRs offset by rising data network capacity costs. So the cost of delivering the current bundles isn’t going to change much on our analysis. But marginal pricing could fall more in Finland given the 2.5x mark-up.

France – Iliad selling below current marginal cost

Our analysis suggests Iliad is selling slightly below direct cost if the customer uses the whole bundle (we assume 1000 minutes and 1000 SMS). Iliad’s actual costs in the short term are even greater than this, given a large proportion of traffic will be carried as national roaming on FT’s network at a wholesale price probably above FT’s direct network cost.

The mark-up is more reasonable if we assume Iliad wins only typical customers rather than higher usage customers. On average usage of 500MB and 200 minutes, the mark-up is around 5.4x, although it falls again to well below industry levels once national roaming costs are included as well.

If Iliad were to migrate all its traffic to its own network and gain average rather than high usage customers, its mark-up would be closer to industry average, before overheads. Even then it would need scale (10-15% revenue share) to cover these overheads. And if the bulk of its traffic stays on national roaming, or its customers respond to the price offer by using a lot of the bundle, then Iliad will struggle to make money even with 10-15% share.

The main problem in France now is probably not further price cuts by Iliad, but a repricing of the FT, SFR and Bouygues customer base as they respond to this recent move by Iliad. Market ARPU is still a multiple of marginal price.

04 A

pril 2012

Mo

bile p

ricing

11

Figure 12: Price vs direct cost (network cost plus interconnect) of big bundles Market Austria Denmark Finland France UK Neths Italy Spain

Operator 3Austria BiBoB DNA Iliad 3UK Telfort 3 Italia Yoigo

Bundle 3SuperSIM Comfort

SIM 300 12m TOP SIM La Mega Plana 55

Type of bundle SIM only SIM only SIM only SIM only SIM only SIM only SIM only SIM only

Price local FX 7.0 119 18.95 16.0 * 12.0 24.85 25.0 55

Price (eu) 7.0 16.1 18.95 16.0 * 14.4 24.85 25.0 55

VAT rate 20% 25% 23% 19.6% 20% 19% 23% 18%

Price ex VAT 5.6 12.1 14.6 12.9 11.5 20.1 19.3 55

Voice (mins) 1000 360 500 Unlimited 300 400 800 1200

Data (GB) 1.0 6.0 Unlimited 3.0 1.0 1.0 2.0 1.2

SMS 1000 Unlimited 400 Unlimited 3000 300 200 0

Maximum traffic cost per month*

Cost today 12.00 14.85 6.15 14.60 18.01 5.08 8.16 8.40

Price relative to cost today 0.47 0.81 2.37 0.88 0.64 3.96 2.36 6.55

Cost long term 3.30 16.98 5.85 8.90 2.95 3.00 6.00 3.96

Price relative to cost long term 1.70 0.71 2.49 1.44 3.91 6.71 3.21 13.89

Typical traffic cost per month

Cost today 2.39 2.39 2.39 2.39 2.39 2.39 2.39 2.39

Price relative to cost today 2.34 5.05 6.11 5.38 4.82 8.42 8.05 23.01

Cost long term 2.95 2.95 2.95 2.95 2.95 2.95 2.95 2.95

Price relative to cost long term 1.90 4.09 4.95 4.36 3.91 6.82 6.53 18.64

Source: Company data, Credit Suisse research * for Iliad fixed broadband customers ** for calculating the maximum cost of an unlimited offer we assume 1000 mins, 2GB and 1000 SMS. In

some cases, usage would be even higher. *** interconnect plus network costs divided by monthly fee

04 A

pril 2012

Mo

bile p

ricing

12

Figure 13: Mark-up of customer bill over direct costs if customer uses the

whole bundle (red line is actual average ratio of customer bill to direct costs

for established operators today =4.4x)

Figure 14: Mark-up of customer bill over direct costs based on average

customer usage in W.Europe (red line is actual average ratio of customer bill

to direct costs for established operators today =4.4x)

Based on typical usage of bundle

-

5.0

10.0

15.0

20.0

25.0

3Austria BiBob DNA Iliad 3UK Telfort 3 Italia Yoigo

Cu

sto

mer

bill

/ tr

affi

c co

sts

Current Long term

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

Figure 15: Price vs maximum cost of cheapest big bundles in each market Figure 16: Price vs typical cost of cheapest big bundles in each market*

0.0

10.0

20.0

30.0

40.0

50.0

60.0

3Austria BiBob DNA Iliad 3UK Telfort 3 Italia Yoigo

eu/m

(ex

VA

T)

Price Max. cost - today Max cost - long term

0.0

10.0

20.0

30.0

40.0

50.0

60.0

3Austria BiBob DNA Iliad 3UK Telfort 3 Italia Yoigo

eu p

er m

on

th (

ex V

AT

)

Price Typical cost - today Typical cost - long term

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

Based on maximum usage of bundle

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

3Austria BiBob DNA Iliad 3UK Telfort 3 Italia Yoigo

Cu

stom

er b

ill/t

raff

ic c

ost

s

Current Long term

04 A

pril 2012

Mo

bile p

ricing

13

Figure 17: Cost structure of Bharti India vs Vodafone Europe and UK Bharti (2011) Vodafone Europe (H1, FY3/12e) Vodafone UK (H1, FY3/12e)

ARPM INR 0.43 Outbound yield (eu'c) 6.6 Voice yield (eu'c per min) 7.9

Yield (eu'c/min) 0.635

Regulatory fee 10% Regulatory fee 0% Regulatory fee 0%

Interconnect / sales 12% Direct costs (interconnect, ULL, airtime commission)

23.8% Direct costs (interconnect, airtime commission) 28.3%

Customer costs (subsidies, commission, own shops)

30.5% Customer costs (subsidies, commission, own shops)

37.2%

Network opex 20% Operating expenses 11.6% Operating expenses 10.6%

SG&A 21%

Personnel 4%

EBITDA margin 33% EBITDA margin 34% EBITDA margin 34%

EBITDA margin ex regulatory fees 43% EBITDA margin ex regulatory fees 34% EBITDA margin ex regulatory fees 34%

CAPEX/sales CAPEX/sales 9.4% CAPEX/sales 9.4%

Source: Company data, Credit Suisse estimates

04 April 2012

Mobile pricing 14

Europe / Finland Wireless Telecommunication Services

Elisa Corporation (ELI1V.HE) COMPANY UPDATE

Reiterate Outperform ■ Action: We have raised our revenue forecasts by 1-2% and EBITDA by 3-

5% and are 2-4% ahead of consensus revenue forecasts for 2012-13E. We reiterate our Outperform rating and €20 TP.

■ Finnish mobile outlook improving – After being one of the weaker mobile markets in Europe we now believe the Finnish market is starting to look like one of the stronger as: 1) Headline pricing is no longer falling and the promotional activity has reduced over the last couple of quarters with Elisa ARPU trends improving 420bp the same period; 2) The Finnish market has already implemented bundled price plans reducing the risk of data cannibalising on voice and SMS revenues; and 3) Smartphone penetration has lagged the rest of Europe with Elisa only having 14% smartphone penetration at the end of Q4 11 and penetration could potentially accelerate in 2012 driven by the launch of Nokia’s Windows handsets.

■ We further believe Elisa Vhiide (Elisa’s IPTV product) will continue to drive fixed line revenues and with 91% of call volumes already over mobile we see little risk of FTM substitution.

■ Elisa’s guidance incorporates a deterioration in the Finnish economy in 2012, this has so far not happened and Elisa’s guidance could prove conservative.

■ Catalysts: Elisa reports Q1 12 results on 27 April

■ Valuation: Elisa is trading at 8.2% 2012E FCF yield.

Share price performance

12

17

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11

Price Price relative

The price relative chart measures performance against the HEX25 INDEX. which closed at 2217.66 on 02/04/12 On 02/04/12 the spot exchange rate was Eu .75 /US$1

Performance Over 1M 3M 12M Absolute (%) 3.6 10.3 14.0 Relative (%) 0.7 -9.1 13.7

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (Eu m) 1,530.0 1,571.8 1,602.1 1,622.1 EBITDA (Eu m) 506.00 529.98 548.31 554.20 Net Income (Eu m) 201.4 218.9 226.7 231.5 CS adj. EPS (Eu) 1.30 1.40 1.45 1.49 Prev. EPS (Eu) — 1.30 1.36 1.43 ROIC (%) 13.89 14.82 15.01 15.40 P/E (adj., x) 13.82 12.77 12.33 12.07 P/E rel. (%) 96.3 94.6 105.6 112.4 EV/EBITDA 7.5 7.2 6.9 6.8

Dividend (12/12E, Eu) 1.43 IC (12/12E, Eu m) 1,648.27 Dividend yield (%) 8.0 EV/IC 2.3 Net debt (12/12E, Eu m) 803.1 Current WACC 8.0 Net debt/equity (12/12E, %) 95.0 Free float (%) 87.8 BV/share (12/12E, Eu) 5.4 Number of shares (m) 166.66

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates.

*Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months.

Research Analysts

Henrik Herbst 44 20 7888 0286

Paul Sidney 44 20 7888 6015

Rating OUTPERFORM* Price (02 Apr 12, Eu) 17.93 Target price (Eu) 20.00¹ Market cap. (Eu m) 2,988.26 Enterprise value (Eu m) 3,791.4

04 April 2012

Mobile pricing 15

2-4% ahead of 2012-14E consensus revenues We are 2-4% ahead of consensus revenues and 3-6% ahead of consensus EBITDA for 2012-14E (set out in Figure 18). We believe we are mainly more positive than consensus on the Finnish mobile market which, in our view, has become more benign with fewer price promotions and further upside from Elisa lagging in terms of smartphone penetration. We forecast Elisa’s mobile ARPU trends to further improve from 11.6% decline in 2011 to 6.3% decline in 2012E and 4.5% decline in 2013E.

We believe Elisa’s guidance could be conservative (consensus is broadly in line with 0.8% revenue growth) and we forecast 2.7% revenue growth in 2012 vs guidance of flat revenues. Elisa stated on its Q4 11 conference call it had taken a cautious view on the macro economic development in Finland; however so far we believe the Finnish economy has held up well and we have not seen a deterioration so far.

Figure 18: Credit Suisse versus consensus € in millions, unless otherwise stated 2012E 2013E 2014E

CS est Cons Diff CS est Cons Diff CS est Cons Diff

Revenues 1,572 1,543 1.9% 1,602 1,555 3.0% 1,622 1562 3.8%

EBITDA 530 514 3.1% 548 521 5.3% 554 525.5 5.5%

margin 33.7% 33.3% 34.2% 33.5% 34.2% 33.6%

EBIT 319 308 3.8% 337 317 6.3% 343 319.8 7.4%

Net Income 219 208 5.4% 227 212 6.7% 232 214.4 8.0%

Source: Credit Suisse estimates, the BLOOMBERG PROFESSIONAL™ service

Figure 19: Elisa guidance vs Credit Suisse and consensus Company guidance 2012 CSe Cons

Revenues flat 2.7% 0.8%

EBITDA (ex one-offs) flat 4.7% 1.3%

CAPEX/sales <=12% 12.0%

Net debt/EBITDA 1.5-2x 1.5

Source: Company data, Credit Suisse estimates, the BLOOMBERG PROFESSIONAL™ service

Finnish mobile market improving Mobile price competition has at least temporarily bottomed out. In Q4 11 we saw fewer aggressive Christmas promotions than usual whilst the consensus view among the operators is that the pricing environment is still competitive but not getting worse. ARPU trends for both Elisa and TeliaSonera has improved over the last 3-4 quarters – set out in Figure 20, in our view, further implying that the pricing cuts in Finnish mobile is bottoming out is that y/y.

Talking to Elisa and TeliaSonera, we get the impression that the promotional activity has remained low going into Q1 12 as none of the operators has seen the other launching aggressive promotions. However whether telemarketing sales activity has increased is harder to tell. .

04 April 2012

Mobile pricing 16

Figure 20: Elisa and TeliaSonera ARPU trends improving

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

Q110 Q210 Q310 Q410 Q111 Q211 Q311 Q411

y/y

chag

ne in

AR

PU

Elisa Telia

Source: Company data, Credit Suisse research

A further indication that the Finnish mobile market is turning more rational is churn levels coming down in the last couple of quarters, mainly for TeliaSonera while Elisa churn has stabilised below 15%. We set out TeliaSonera and Elisa churn levels in Figure 21.

Figure 21: Elisa and TeliaSonera churn stabilising

0%

5%

10%

15%

20%

25%

30%

35%

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11

Annu

alis

ed c

hurn

(%)

Elisa TLSN

Source: Company data, Credit Suisse research

Smartphone catch-up effect to continue

In our view future recovery of ARPU is also likely to be driven by a catch up in smartphone penetration in Finland. Finland has lagged the rest of Europe, in our view, partly driven by the absence of a Nokia smartphone. With the launch of the Nokia Lumia (with a Windows operating system) in February this year in Finland, we believe smartphone penetration could further accelerate. The Nokia Lumia 800 was the best selling handset for Elisa, Telia and DNA in February.

By end of Q4 11 smartphone penetration of Elisa’s phone base was still only 14% on a definition containing only handsets with a iOS, Android, Symbian 2 or Windows operating system.

We set out the development in Elisa’s smartphone penetration in Figure 22, and acceleration in smartphone penetration in Q4 11.

04 April 2012

Mobile pricing 17

Figure 22: Elisa smartphone penetration

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11

smar

tpho

ne p

enet

ratio

n

0.0 pp

0.5 pp

1.0 pp

1.5 pp

2.0 pp

2.5 pp

3.0 pp

3.5 pp

4.0 pp

4.5 pp

5.0 pp

incr

emen

tal s

mar

tpho

ne p

enet

ratio

n q/

q

Elisa Smartphone penetration Incrementeal penetration (pp q/q)

Source: Company data, Credit Suisse research, Note: definition of smartphone includes handsets with iOS,

Symbian3, Android and Windows operating systems

Raising 2012-13 forecasts We raise our revenue forecasts for 2012-14E by 1-3% on the back of higher mobile forecasts. We have adjusted our forecasts for a stronger than expected ARPU in Q4 11 and less price promotion and an accelerating smartphone promotion, leading to higher ARPU. In the second half of 2011 Elisa’s mobile ARPU y/y trends improved by 420bp and we now forecast a 310bp improvement in 2012 versus 240bp on previous forecasts.

We have only marginally changed our Finnish fixed revenue forecasts.

Figure 23: Elisa: Credit Suisse changes to forecasts € in millions, unless otherwise stated 2012E 2012E 2013E 2013E 2014E 2014E

Group new old change new old change new old change

Revenues 1,572 1,557 1.0% 1,602 1,566 2.3% 1,622 1,576 3.0%

Underlying EBITDA 530 523 1.4% 548 534 2.8% 554 547 1.4%

EBITDA margin 33.5% 33.5% 0.0pp 33.7% 33.7% 0.0pp 33.7% 33.7% 0.0pp

EBIT 319 305 4.8% 337 317 6.1% 554 332 66.7%

Underlying net income 219 202 8.3% 227 212 7.2% 232 223 3.9%

EPS 1.40 1.30 8.3% 1.45 1.36 7.2% 1.49 1.43 3.9%

CAPEX 189 176 6.9% 192 179 7.4% 195 189 3.0%

FCF 215 225 -4.2% 244 232 5.4% 252 241 4.4%

Net debt 803 788 1.9% 802 788 1.8% 800 785 1.8%

Finnish Mobile

Mobile subscribers (000s) 3,839 3,902 -1.6% 3,999 4,062 -1.6% 4,139 4,062 1.9%

Revenues 888 871 1.9% 892 859 3.8% 893 853 4.8%

Finnish Fixed

Revenues 618 623 -0.7% 636 636 -0.1% 647 645 0.3%

Source: Credit Suisse estimates

04 April 2012

Mobile pricing 18

Figure 24: Elisa financial forecasts € in millions, unless otherwise stated EURm 2009 2010 2011A 2012E 2013E 2014E 2015E 2016E

P&L

Mobile 884 938 979 999 1,011 1,020 1,030 1,037

Finland 800 848 879 888 892 893 898 900

Estonia 84 90 100 111 120 127 132 137

Fixed 591 571 596 618 636 647 654 660

Internal and other (45) (46) (45) (45) (45) (45) (45) (45)

Total Revenue 1,430 1,463 1,530 1,572 1,602 1,622 1,639 1,652

growth y/y -3.7% 2.3% 4.6% 2.7% 1.9% 1.2% 1.0% 0.8%

999

Costs

Materials and services (576) (600) (644) (661) (668) (673) (677) (679)

Employee expenses (189) (208) (223) (231) (237) (244) (251) (259)

Other (181) (170) (157) (150) (149) (151) (152) (154)

Total OPEX (ex one-offs) (946) (978) (1,023) (1,042) (1,054) (1,068) (1,081) (1,092)

One-offs OPEX 0 0 1 0 0 0 0 0

EBITDA 484 485 506 530 548 554 558 561

margin % 33.8% 33.2% 33.1% 33.7% 34.2% 34.2% 34.1% 33.9%

growth y/y 0.2% 4.3% 4.7% 3.5% 1.1% 0.8% 0.4%

EBITDA excl. one-offs 484 485 507 530 548 554 558 561

margin % 34.0% 33.0% 33.1% 33.7% 34.2% 34.2% 34.1% 33.9%

D&A (ex one-offs) (217) (217) (211) (211) (211) (211) (210) (208)

One-offs 0 0 (1) 0 0 0 0 0

EBIT 267 268 296 319 337 343 349 353

EBIT excl. one-offs 267 268 297 319 337 343 349 353

margin % 19% 18% 19% 20% 21% 21% 21% 21%

Net financials (33) (71) (30) (31) (31) (30) (30) (30)

PBT 234 197 266 288 306 313 318 322

Income taxes (58) (47) (64) (69) (80) (81) (83) (84)

Effective tax-rate 25% 24% 24% 24% 26% 26% 26% 26%

Net income 176 151 201 219 227 232 235 238

EPS (€) 1.13 0.96 1.30 1.40 1.45 1.49 1.51 1.53

Average number of shares ('m)

Basic 155.6 155.7 155.9 155.9 155.9 155.9 155.9 155.9

DPS (€)

Ordinary proposed 0.92 0.90 0.90 0.98 1.02 1.04 1.06 1.07

Payout ratio 81.4% 93.8% 69.3% 70% 70% 70% 70% 70%

Special announced 0.50 0.40 0.45 0.45 0.45 0.45 0.45 0.45

Total DPS, € 1.42 1.30 1.35 1.43 1.47 1.49 1.51 1.52

CAPEX (171) (181) (189) (189) (192) (195) (197) (198)

CAPEX/sales 12.0% 12.4% 12.4% 12.0% 12.0% 12.0% 12.0% 12.0%

Net debt 719 776 788 803 802 800 799 801

Net debt / EBITDA 1.5 1.6 1.6 1.5 1.5 1.4 1.4 1.4

Source: Company data, Credit Suisse estimates

04 April 2012

Mobile pricing 19

Europe / Denmark Integrated Telecommunication Services

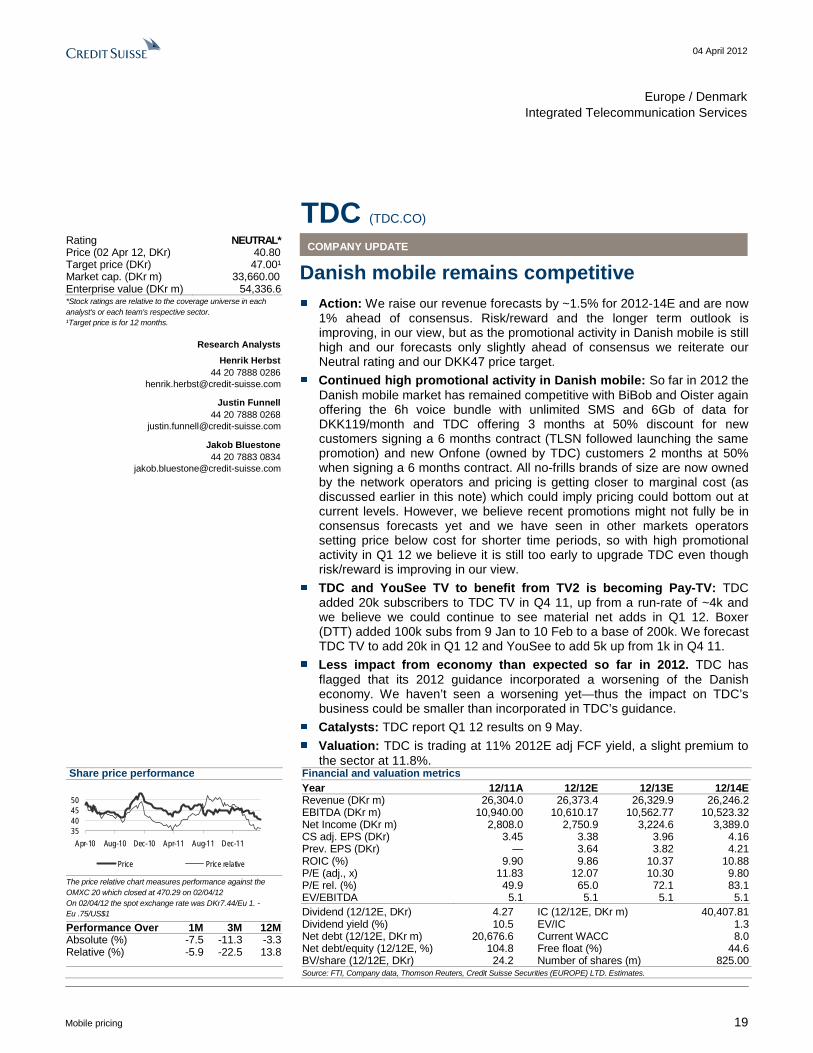

TDC (TDC.CO) COMPANY UPDATE

Danish mobile remains competitive ■ Action: We raise our revenue forecasts by ~1.5% for 2012-14E and are now

1% ahead of consensus. Risk/reward and the longer term outlook is improving, in our view, but as the promotional activity in Danish mobile is still high and our forecasts only slightly ahead of consensus we reiterate our Neutral rating and our DKK47 price target.

■ Continued high promotional activity in Danish mobile: So far in 2012 the Danish mobile market has remained competitive with BiBob and Oister again offering the 6h voice bundle with unlimited SMS and 6Gb of data for DKK119/month and TDC offering 3 months at 50% discount for new customers signing a 6 months contract (TLSN followed launching the same promotion) and new Onfone (owned by TDC) customers 2 months at 50% when signing a 6 months contract. All no-frills brands of size are now owned by the network operators and pricing is getting closer to marginal cost (as discussed earlier in this note) which could imply pricing could bottom out at current levels. However, we believe recent promotions might not fully be in consensus forecasts yet and we have seen in other markets operators setting price below cost for shorter time periods, so with high promotional activity in Q1 12 we believe it is still too early to upgrade TDC even though risk/reward is improving in our view.

■ TDC and YouSee TV to benefit from TV2 is becoming Pay-TV: TDC added 20k subscribers to TDC TV in Q4 11, up from a run-rate of ~4k and we believe we could continue to see material net adds in Q1 12. Boxer (DTT) added 100k subs from 9 Jan to 10 Feb to a base of 200k. We forecast TDC TV to add 20k in Q1 12 and YouSee to add 5k up from 1k in Q4 11.

■ Less impact from economy than expected so far in 2012. TDC has flagged that its 2012 guidance incorporated a worsening of the Danish economy. We haven’t seen a worsening yet—thus the impact on TDC’s business could be smaller than incorporated in TDC’s guidance.

■ Catalysts: TDC report Q1 12 results on 9 May.

■ Valuation: TDC is trading at 11% 2012E adj FCF yield, a slight premium to the sector at 11.8%.

Share price performance

35404550

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11

Price Price relative

The price relative chart measures performance against the OMXC 20 which closed at 470.29 on 02/04/12 On 02/04/12 the spot exchange rate was DKr7.44/Eu 1. - Eu .75/US$1

Performance Over 1M 3M 12M Absolute (%) -7.5 -11.3 -3.3 Relative (%) -5.9 -22.5 13.8

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (DKr m) 26,304.0 26,373.4 26,329.9 26,246.2 EBITDA (DKr m) 10,940.00 10,610.17 10,562.77 10,523.32 Net Income (DKr m) 2,808.0 2,750.9 3,224.6 3,389.0 CS adj. EPS (DKr) 3.45 3.38 3.96 4.16 Prev. EPS (DKr) — 3.64 3.82 4.21 ROIC (%) 9.90 9.86 10.37 10.88 P/E (adj., x) 11.83 12.07 10.30 9.80 P/E rel. (%) 49.9 65.0 72.1 83.1 EV/EBITDA 5.1 5.1 5.1 5.1

Dividend (12/12E, DKr) 4.27 IC (12/12E, DKr m) 40,407.81 Dividend yield (%) 10.5 EV/IC 1.3 Net debt (12/12E, DKr m) 20,676.6 Current WACC 8.0 Net debt/equity (12/12E, %) 104.8 Free float (%) 44.6 BV/share (12/12E, DKr) 24.2 Number of shares (m) 825.00

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates.

*Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months.

Research Analysts

Henrik Herbst 44 20 7888 0286

Justin Funnell 44 20 7888 0268

Jakob Bluestone 44 20 7883 0834

Rating NEUTRAL* Price (02 Apr 12, DKr) 40.80 Target price (DKr) 47.00¹ Market cap. (DKr m) 33,660.00 Enterprise value (DKr m) 54,336.6

04 April 2012

Mobile pricing 20

1% ahead of 2012-13E consensus revenues We are only marginally (~1%) ahead of consensus revenues for 2012-14E and retain our Neutral rating, awaiting further evidence that price promotions in the Danish mobile market are bottoming out after a Q1 12 with high promotional activity and TDC’s promotions being especially aggressive, in our view.

We are >2% ahead of Bloomberg consensus EBITDA for 2012-14E, although we flag that Bloomberg consensus historically has been lower than the consensus provided by TDC and we could be slightly less ahead were we to strip out some outliers. We set out our forecasts vs consensus in Figure 25.

We believe mobile pricing could consolidate near term around current levels as marginal revenue is now close to marginal cost and without any further mobile price cuts we believe consensus forecasts have fallen enough and we could potentially even see increases to forecasts.

We further believe the Danish economy has held up better to date in 2012 than had been allowed for in TDC’s guidance, and we forecast revenues towards the upper end of TDC’s guidance. We set out TDC’s guidance versus our forecasts in Figure 26.

Figure 25: TDC: Credit Suisse versus consensus in millions, unless otherwise stated 2012E 2013E 2014E

CS est Consensus diff CS est Consensus diff CS est Consensus diff

Revenues 26,373 26,121 1.0% 26,330 26,059 1.0% 26,246 26,098 0.6%

EBITDA 10,610 10,384 2.2% 10,563 10,311 2.4% 10,523 10,273 2.4%

EBIT 5,493 5,324 3.2% 5,590 5,313 5.2% 5,674 5,318 6.7%

Net income 2,751 3,145 -12.5% 3,225 2,880 12.0% 3,389 3,163 7.1%

Source: Credit Suisse estimates, the BLOOMBERG PROFESSIONAL™ service

Figure 26: TDC guidance versus Credit Suisse forecasts DKK in billions, unless otherwise stated Guidance 2012 CSe

Revenues 26-26.5 26.4

EBITDA (pre-pension income) 10.3-10.5 10.4

P&L CAPEX 3.4-3.5 3.4

Source: Company data, Credit Suisse estimates

Continued high promotional activity in mobile in Q1 12 TDC initiating another round of promotions in Q1 12

While Telenor was the most aggressive operator in Q4 11 (re-introducing handset subsidies) and TDC staying away from promotional activity TDC, in our view, was the most aggressive in Q1 12.

TDC also launched a new round of promotions when it started to offer new TDC customers 3 months at a 50% discount when signing a 6 months contract and new Onfone customers 2 months at 50% discount when signing a 6 months contract. TeliaSonera immediately responded to the promotion in the TDC brand launching the same offer.

TDC also slightly increased the size of the bundles for Onfone and Telmore, although still including less data than competitors.

BiBob (owned by Telenor) and Oister (owned by 3) also ran promotions in March offering 6h of voice, unlimited SMS and 6Gb of data for DKK119/month (on Oister and BiBob), a level we had in July to September last year as well. The promotions were only available for new customers for about a month (prices went back up to DKK149/month 1 April). Pricing was DKK119/month last July-Sept last year as well, but prices went back up, implying the operators seem unwilling to make the DKK119/month to the permanent pricing. However we do not rule out DKK119/month becoming the new headline price level.

04 April 2012

Mobile pricing 21

In Figure 27 we set out the development of the marginal pricing of a 5h bundle (now 6h) with unlimited SMS and ~1Gb (now ~6Gb) of data against Danish market ARPU since the December 2010, ahead of the start of the Danish price war.

At DKK119/month marginal revenue is close to today’s marginal cost and we believe this could remain a floor to pricing. Especially as after TDC’s acquisition of Onfone all no-frills brands of any material size in the Danish market are now owned by the network operators (Telenor owns BiBob, 3 owns Oister, TDC owns Onfone and Telmore and TeliaSonera owns CallMe), we believe this is likely to further reduce sentiment for price cuts in the no-frills brands as it is likely to cannibalise on the premium brands.

Figure 27: Danish no-frills pricing against market ARPU

0

50

100

150

200

250

Dec-10

Jan-1

1

Feb-11

Mar-11

Apr-11

May-11

Jun-11

Jul-1

1

Aug-11

Sep-11

Oct-11

Nov-11

Dec-11

Jan-1

2

Feb-12

Mar-12

DKK

/mon

th

5h with unlimited SMS Average ARPU (TDC consumer, TLSN and TNOR)

Source: Company data, Credit Suisse research

TDC consumer mobile forecasts

We forecast a broadly flat Danish consumer mobile service revenue trends to -10.2% y/y (excluding Onfone) in 2012 from a 10.4% fall in 2011.

We forecast Q1 and Q2 Consumer mobile revenues (excluding Onfone) to fall by 13% and 15.2% y/y respectively as 1) there are still some customers to migrate to the new lower priced tariffs introduced in July 2011; however with only 6 months contracts lengths in Denmark we expect most customers to have migrated by now; and 2) TDC launched another round of promotions in late Q1 12 both in the TDC and Onfone brand with the majority of the negative impact coming through in Q2.

We set out our full TDC Consumer mobile forecasts in Figure 28.

04 April 2012

Mobile pricing 22

Figure 28: TDC consumer mobile forecasts DKK in millions, unless otherwise stated Mobile Voice 2009 2010 Q111 Q211 Q311 Q411 2011 Q112E Q212E Q312E Q412E 2012E 2013E 2014E

Total TDC mobile revenues 4,312 4,343 1,019 1,042 1,084 1,039 4,164 1,025 997 1,041 1,035 4,098 4,129 4,152

y/y 4.7% 0.7% -8.2% -3.5% 0.5% -3.3% -4.1% 0.6% -4.3% -4.0% -0.4% -1.6% 0.8% 0.5%

Mobile service revenues (incl Onfone)

4,160 4,167 983 1,016 1,030 1,040 4,070 1,000 972 1,015 1,009 3,996 4,027 4,050

% yoy growth 0.4% 0.2% -5.6% -2.5% -1.1% -0.1% -2.3% 1.7% -4.3% -1.5% -3.0% -1.8% 0.8% 0.6%

Other revenues 152 176 36 26 54 -1 94 26 25 26 26 102 101 101

Blended ARPU (DKK) 180 169 161 159 156 157 159 152 148 154 152 151 151 151

% yoy growth -2.2% -6.1% -2.4% -4.8% -10.3% -8.7% -5.9% -5.5% -6.9% -1.5% -3.1% -5.2% 0.2% 0.2%

Total subs 2051 2046 2194 2186 2217 2201 2201 2181 2196 2206 2216 2216 2226 2231

Net adds 134 -5 148 -8 31 -16 155 -20 15 10 10 15 10 5

Mobile Revenue (ex Onfone) 4,312 4,343 1,019 1,003 970 899 3,891 881 853 885 876 3,494 3,483 3,474

y/y 4.7% 0.7% -8.2% -7.1% -10.1% -16.3% -10.4% -13.6% -14.9% -8.8% -2.6% -10.2% -0.3% -0.3%

Service Revenue 4,160 4,167 983 977 916 900 3,777 855 828 859 850 3,393 3,381 3,373

y/y 0.4% 0.2% -5.6% -6.2% -12.1% -13.5% -9.4% -13.0% -15.2% -6.2% -5.6% -10.2% -0.3% -0.3%

Other Revenue 152 176 36 26 54 (1) 114 26 25 26 26 102 101 101

Proportion % 3.6% 4.2% 3.7% 2.6% 5.9% -0.2% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

ARPU ex Onfone 180.0 169.0 161.0 158.7 152.3 150.3 156.4 144.9 141.3 146.2 144.3 144.1 143.4 143.4

growth y/y -2.2% -6.1% -2.4% -5.0% -12.5% -12.6% -7.5% -10.0% -11.0% -4.0% -4.0% -7.8% -0.5% 0.0%

Subscribers, ex Onfone ('000) 2,051 2,046 2,024 1,999 2,013 1,982 1,982 1,952 1,957 1,962 1,967 1,967 1,962 1,957

% yoy growth 7.0% -0.2% -6.2% -0.2% 1.2% -3.1% -3.1% -3.6% -2.1% -2.5% -0.8% -0.8% -0.3% -0.3%

Avg Subs ('000) 1,984 2,049 2,035 2,012 2,006 1,998 2,013 1,967 1,955 1,960 1,965 1,961 1,965 1,960

Net Adds ('000) 134 (5) (22) (25) 14 (31) (64) (30) 5 5 5 (15) (5) (5)

Onfone Revenues 39 114 140 293 144 144 156 159 603 646 678

ARPU (DKK/sub/month) 146 194 221 215 205 215 215 213 210 210

Subscribers (’00) 170 187 204 219 219 229 239 244 249 249 264 274

Net adds (‘000) 17 17 15 49 10 10 5 5 30 15 10

Source: Company data, Credit Suisse estimates

TDC ARPU to fall 9% from levels pre the price cut in the TDC brand

TDC cut pricing in the TDC brand by ~20% in July 2011. We believe some of the ARPU impact from the price cut will be offset by cheaper data pricing and the introduction of TDC rate stimulating growth in smartphone penetration.

We forecast TDC’s ARPU (excluding Onfone) to fall by 9% from Q2 11 (ie before the price cut in the TDC brand).

With TDC’s July 11 price cuts the gap between TDC’s main brand and Onfone has materially reduced (from DKK250/month to DKK150/month) and we believe pricing could now have bottomed out and we forecast ARPU to remain broadly flat for 2013 and 2014.

Customers to continue to migrate to cheaper tariffs

TDC cut the pricing in the TDC brand by 20% (ex VAT) on what we believe is the most common price plan (including 240min of voice, unlimited SMS and 5Gb of data) on 11 July 2011.

The maximum contract length in Denmark is 6 months implying that all customers should have had the opportunity to migrate to the new price plans in January 2012 (6 months from the introduction of the new prices in July 2011) we believe the migration from the TDC brand to both no-frills brands and to the new lower priced tariffs in the TDC brand could continue at least throughout the first half of 2012.

04 April 2012

Mobile pricing 23

In Figure 29 we set out current pricing of a bundle including ~5h of voice, unlimited SMS and >1Gb data.

Figure 29: DKK/month pricing on a 4-7h bundle with unlimited SMS

0 50 100 150 200 250 300 350

Bibob (6h, 6Gb)

Oister (6h, 6Gb)

Onfone (6h, 1Gb)

Telmore (5h, 3Gb)

Call Me (7h , 10Gb)

3 Denmark (5h, 5Gb)

Telenor (5h, 3Gb)

Te lia (6h, 5Gb)

TDC (4h, 5Gb)

DKK/month

Source: Company data, Credit Suisse research

Q1 12 price moves in more detail

After Telenor ran some aggressive promotions in Q4 11 there were relatively few at the beginning of Q1 12. However towards the end of the quarter Oister (owned by 3) and BiBob (owned by Telenor) re-introduced the DKK119/month pricing on a 6h voice bundle with unlimited SMS and 6Gb of data. TDC responded by re-introducing the 2 months at 50% discount promotion in the Onfone brand.

TDC also introduced a promotion in the TDC brand beginning of March offering new customers a 50% discount on the monthly fee for the first 3 months of a 6 months contract. Telia very quickly responded and introduced a promotion offering new customers 50% discount for the first 4 months on a 6 months contract.

We note the following key changes over the last 3 months:

■ 3 Denmark has materially cut its pricing since January, from DKK399/month to DKK179/month. However it has also reduced included voice usage from 360mins to 300mins and the data bundle from 10Gb to 5Gb per month. We believe this is a response to Telenor and TeliaSonera cutting price in Q2 11 and TDC in early Q3 11.

■ BiBob (owned by Telenor) and Oister (owned by 3) has both cut pricing back to DKK119/month (from DKK149/month) without adjusting either the voice or data bundle.

■ TeliaSonera has slightly increased pricing (from DKK240/month to DKK279/month) although also included more data (now 5Gb, up from 1Gb per month) in the bundle.

■ Onfone (owned by TDC) increased the DKK149/month bundle to 360mins (from 300mins) of voice and 1Gb (from 0.5Gb) of voice per month.

04 April 2012

Mobile pricing 24

Figure 30: Headline pricing and change over the last 3 months

0

50

100

150

200

250

300

350

400

450

Bibob (6h,6Gb)

Oister (6h,6Gb)

Onfone (6h,1Gb)

Telmore (5h,3Gb)

Call Me (7h,10Gb)

3 Denm ark(5h, 5Gb)

Te lenor (5h,3Gb)

Telia (6h,5Gb)

TD C (4h,5Gb)

DKK

/mon

th

Jan uary March

Source: Company data, Credit Suisse research

Figure 31: Monthly voice bundle and change over the last 3 months

0

1

2

3

4

5

6

7

8

TDC(DKK2 99/m,

5G b)

Telmore( DK K149 /m,

3Gb)

3 Den ma rk(DKK17 9/m,

5Gb)

Telen or(DKK 230/m,

3 Gb)

B ibob(DKK11 9/m,

6Gb )

O ister(DKK1 19/m,

6G b)

Onfone(DK K149 /m,

1Gb)

Te lia(DKK2 79/m,

5G b)

Call Me(DK K149 /m,

10G b)

h/m

onth

Jan uary March

Source: Company data, Credit Suisse research

Figure 32: Monthly data bundle and change over the last 3 months

0

2

4

6

8

10

12

O nfo ne(DKK1 49/m,

6h)

Telmore(DKK1 49/m,

5h)

Te lenor(DKK2 30/m,

5h)

TDC(DKK29 9/m,

4h)

3 Den ma rk(DKK1 79/m,

5h)

Telia(DKK27 9/m,

6h)

B ibob(DKK11 9/m,

6h)

Oiste r(DK K11 9/m,

6 h)

Call Me(DK K149 /m,

7 h)

Gb/

mon

th

Ja nuar y March

Source: Company data, Credit Suisse research

04 April 2012

Mobile pricing 25

Changes to forecasts We raise our revenue forecasts by 1.3-1.5% and cut our EBITDA including pension income by 1.3-1.6% for 2012-13E. In more detail (set out in Figure 33) we adjust our forecasts for:

TDC TV to benefit from TV2 turning pay-TV

We raise our TDC TV (included in Consumer) estimate by 10% for 2012 as we expect some increased uptake of TV customers coming from TV2 becoming a pay-TV channel and price increases put through from 1 Jan 2012. TDC has also launched a new entry 3-play level bundle called TDC HomeTrio Mini to stimulate uptake of FTA customers; the company also ran some promotions which will have a negative impact on ARPU and offset some of the positive impact from price increases from 1 Jan 2012.

Overall we forecast TV revenue growth to accelerate to 32% in 2012 from 26% in 2011.

2-3% cut to 2012-13E Consumer mobile revenue forecasts

To reflect mainly the above-mentioned price promotions in the Danish market and also weaker than expected Q4 results, we have cut our TDC Consumer mobile revenue forecasts. This mainly comes through as cuts to our ARPU forecasts.

2-3% cut to TDC wholesale revenues

We have materially cut our forecasts for TDC wholesale on the back of weak Q4 11 results across the board mainly on the subscriber side but also in terms of slightly weaker than expected ARPU.

04 April 2012

Mobile pricing 26

Figure 33: TDC: Credit Suisse changes to forecasts DKK in millions, unless otherwise stated 2012E 2013E 2014E

New Old diff New Old diff New Old diff

Summary

Revenues 26,373 26,032 1.3% 26,330 25,933 1.5% 26,246 25,920 1.3%

y/y growth 0.3% -0.5% -0.2% -0.4% -0.3% 0.0%

Revenues ex impact Onfone 25,770 25,626 0.6% 25,684 25,460 0.9% 25,568 25,397 0.7%

EBITDA (incl pension income) 10,610 10,754 -1.3% 10,563 10,731 -1.6% 10,523 10,732 -1.9%

y/y growth -3.0% -1.7% -0.4% -0.2% -0.4% 0.0%

EBITDA margin 40.2% 41.3% -2.6% 40.1% 41.4% -3.1% 40.1% 41.4% -3.2%

D&A and impairment losses (5,118) (4,967) 3.0% (4,973) (4,969) 0.1% (4,849) (4,694) 3.3%

Special items (inc leaver charges)

(600) (600) 0.0% (300) (300) 0.0% (250) (250) 0.0%

Net financial costs (inc JV & associate profits)

(1,072) (1,069) 0.2% (932) (1,255) -25.7% (906) (1,220) -25.8%

Income tax charge (1,070) (1,153) -7.2% (1,133) (1,094) 3.6% (1,130) (1,142) -1.1%

Income from discontinued operations

0 0 0 0 0 0

Net income 2,751 2,965 -7.2% 3,225 3,113 3.6% 3,389 3,426 -1.1%

Cash CAPEX (3,337) (3,364) -0.8% (3,403) (3,351) 1.5% (3,392) (3,350) 1.3%

Equity FCF - Codefinition 4,342 4,576 -5.1% 4,600 4,538 1.4% 4,575 4,483 2.1%

Cashflow related to special items

(465) (700) -33.6% (350) (350) 0.0% (250) (250) 0.0%

Equity FCF - CS definition 3,877 3,876 0.0% 4,250 4,188 1.5% 4,325 4,233 2.2%

Net financial debt (20,677) (22,038) (20,199) (21,571) (19,717) (21,103)

Net debt / EBITDA 1.95 2.05 -4.9% 1.91 2.01 -4.9% 1.87 1.97 -4.7%

Revenues 26,373 26,032 1.3% 26,330 25,933 1.5% 26,246 25,920 1.3%

TDC Consumer 9,058 8,776 3.2% 9,017 8,668 4.0% 8,945 8,574 4.3%

y/y growth 0.6% -1.8% -0.5% -1.2% -0.8% -1.1%

TDC consumer mobile 4,098 4,205 -2.6% 4,129 4,262 -3.1% 4,129 4,322 -4.5%

y/y growth

TDC Business 7,139 7,095 0.6% 6,781 6,842 -0.9% 6,504 6,629 -1.9%

y/y growth -5.0% -4.9% -5.0% -3.6% -4.1% -3.1%

TDC Nordic 4,807 4,673 2.9% 5,001 4,812 3.9% 5,175 4,997 3.6%

y/y growth 7.1% 5.1% 4.0% 3.0% 3.5% 3.8%

Operations & Wholesale 2,003 2,074 -3.4% 1,966 2,008 -2.1% 1,907 1,951 -2.3%

y/y growth -6.9% -3.9% -1.8% -3.2% -3.0% -2.8%

YouSee 4,505 4,527 -0.5% 4,703 4,712 -0.2% 4,850 4,877 -0.6%

y/y growth 5.8% 5.7% 4.4% 4.1% 3.1% 3.5%

Other (1,140) (1,113) 2.4% (1,138) (1,109) 2.6% (1,134) (1,109) 2.3%

EBITDA (including PI) 10,610 10,754 -1.3% 10,563 10,731 -1.6% 10,523 10,732 -1.9%

Source: Credit Suisse estimates

04 April 2012

Mobile pricing 27

Figure 34: TDC: Financial forecast summary DKK in millions, unless otherwise stated 2009 2010 2011 Q112E Q212E Q312E Q412E 2012E 2013E 2014E

Summary

Revenues 26,079 26,167 26,304 6,638 6,549 6,498 6,674 26,373 26,330 26,246

y/y growth -3.1% 0.3% 0.5% 0.4% 0.1% 0.5% -0.2% 0.3% -0.2% -0.3%

EBITDA (incl pension income) 10,536 10,772 10,940 2,627 2,582 2,723 2,677 10,610 10,563 10,523

y/y growth 4.8% 2.2% 1.6% -3.1% -1.9% -3.5% -3.5% -3.0% -0.4% -0.4%

EBITDA margin 40.4% 41.2% 41.6% 39.6% 39.4% 41.9% 40.1% 40.2% 40.1% 40.1%

D&A (4,659) (5,356) (5,227) (1,310) (1,287) (1,268) (1,253) (5,118) (4,973) (4,849)

Special items (1,119) (1,347) (864) (150) (150) (150) (150) (600) (300) (250)

Net financial costs (inc JV & associate profits)

(3,542) (3,074) (905) (284) (276) (265) (247) (1,072) (932) (906)

Income tax charge (809) (782) (1,131) (247) (243) (291) (288) (1,070) (1,133) (1,130)

Income from discontinued operations

422 1,203 (5) 0 0 0 0 0 0 0

Net income 2,383 3,007 2,808 636 626 749 740 2,751 3,225 3,389

Cash CAPEX (3,857) (3,508) (3,376) (839) (828) (823) (847) (3,337) (3,403) (3,392)

Equity FCF - Company definition 4,426 4,515 4,594 698 686 1,303 1,655 4,342 4,600 4,575

Cashflow related to special items (793) (792) (786) (15) (150) (150) (150) (465) (350) (250)

Equity FCF - CS definition 3,633 3,723 3,808 683 536 1,153 1,505 3,877 4,250 4,325

Net financial debt (34,791) (23,381) (21,790) (20,677) (20,199) (19,717)

Net debt / EBITDA 3.30 2.17 1.99 1.95 1.91 1.87

Source: Company data, Credit Suisse estimates

Figure 35: TDC: Breakdown of revenue forecasts DKK in millions, unless otherwise stated 2008 2009 2010 2011 Q112E Q212E Q312E Q412E 2012E 2013E 2014E

Revenues 26,917 26,079 26,167 26,304 6,638 6,549 6,498 6,674 26,373 26,330 26,246

y/y growth -3.7% -3.1% 0.3% 0.5% 0.4% 0.1% 0.5% -0.2% 0.3% -0.2% -0.3%

TDC Consumer 9,662 9,455 9,130 9,004 2,271 2,226 2,258 2,303 9,058 9,017 8,945

y/y growth -4.5% -2.1% -3.4% -1.4% 1.3% 0.3% 1.2% -1.1% 0.6% -0.5% -0.8%

TDC Business 8,785 8,182 7,804 7,517 1,860 1,763 1,731 1,773 7,139 6,781 6,504

y/y growth -0.9% -6.9% -4.6% -3.7% -4.9% -5.7% -5.0% -5.1% -5.0% -5.0% -4.1%

TDC Nordic 3,854 3,515 4,087 4,487 1,183 1,199 1,149 1,277 4,807 5,001 5,175

y/y growth -0.2% -8.8% 16.3% 9.8% 8.3% 7.5% 6.8% 5.9% 7.1% 4.0% 3.5%

Operations & Wholesale 2,334 2,185 2,234 2,153 486 509 500 510 2,003 1,966 1,907

y/y growth -35.2% -6.4% 2.3% -3.6% -8.3% -7.4% -8.0% -4.0% -6.9% -1.8% -3.0%

YouSee 3,189 3,598 4,012 4,259 1,117 1,130 1,129 1,127 4,505 4,703 4,850

y/y growth 12.7% 12.8% 11.5% 6.2% 4.9% 6.1% 6.3% 5.7% 5.8% 4.4% 3.1%

Other (907) (856) (1,100) (1,136) (278) (277) (267) (316) (1,140) (1,138) (1,134)

Source: Company data, Credit Suisse estimates

04 April 2012

Mobile pricing 28

Figure 36: TDC: Breakdown of TDC EBITDA forecasts DKK in millions, unless otherwise stated 2009 2010 2011 Q112E Q212E Q312E Q412E 2012E 2013E 2014E

EBITDA (including pension income) 10,536 10,772 10,940 2,627 2,582 2,723 2,677 10,610 10,563 10,523

y/y growth 4.8% 2.2% 1.6% -3.1% -1.9% -3.5% -3.5% -3.0% -0.4% -0.4%

EBITDA Margin 40.4% 41.2% 41.6% 39.6% 39.4% 41.9% 40.1% 40.2% 40.1% 40.1%

TDC Consumer 3,821 3,864 3,684 874 863 984 962 3,683 3,739 3,752

y/y growth 2.3% 1.1% -4.7% -2.8% -1.1% 5.0% -1.3% 0.0% 1.5% 0.3%

Segment EBITDA Margin 40.4% 42.3% 40.9% 38.5% 38.8% 43.6% 41.8% 40.7% 41.5% 41.9%

TDC Business 3,895 3,821 3,903 958 916 912 904 3,690 3,457 3,314

y/y growth 1.8% -1.9% 2.1% -3.9% -4.3% -8.1% -5.6% -5.5% -6.3% -4.1%

Segment EBITDA Margin 47.6% 49.0% 51.9% 51.5% 52.0% 52.7% 51.0% 51.7% 51.0% 51.0%

TDC Nordic 497 564 649 158 157 181 179 675 728 772

y/y growth 8.5% 13.5% 15.1% 6.3% -0.2% -2.7% 14.2% 4.1% 7.8% 6.1%

Segment EBITDA Margin 14.1% 13.8% 14.5% 13.4% 13.1% 15.8% 14.0% 14.0% 14.6% 14.9%

Operations & Wholesale 988 995 1,031 232 244 244 232 952 935 907

y/y growth -16.6% 0.7% 3.6% -5.9% -5.8% -11.1% -7.5% -7.7% -1.7% -3.0%

Segment EBITDA Margin 45.2% 44.5% 47.9% 47.7% 48.0% 48.9% 45.6% 47.5% 47.6% 47.6%

YouSee 1,141 1,353 1,521 400 397 397 395 1,589 1,684 1,758

y/y growth 19.6% 18.6% 12.4% 6.5% 6.2% 2.0% 3.4% 4.5% 6.0% 4.4%

Segment EBITDA Margin 31.7% 33.7% 35.7% 35.8% 35.2% 35.2% 35.0% 35.3% 35.8% 36.3%

Other 194 175 152 5 5 5 5 20 20 20

Pension income 287 435 439 53 53 53 53 210 210 210

EBITDA (ex pensions income) 10,249 10,337 10,501 2,575 2,530 2,671 2,625 10,400 10,353 10,313

y/y growth 6.0% 0.9% 1.6% -1.0% 0.3% -1.5% -1.5% -1.0% -0.5% -0.4%

EBITDA Margin 39.3% 39.5% 39.9% 38.8% 38.6% 41.1% 39.3% 39.4% 39.3% 39.3%

Source: Company data, Credit Suisse estimates

04 April 2012

Mobile pricing 29

Europe / Austria Wireless Telecommunication Services

Telekom Austria (TELA.VI) COMPANY UPDATE

Mobile prices close to cost ■ Action: We cut 2012E EBITDA 0.4% and are close to consensus estimates.

We reiterate our Neutral rating. We believe Austrian mobile is bottoming out but this is insufficient to outweigh the headwinds in Eastern Europe.

■ Rationality coming back to mobile. Austria has been Europe’s toughest mobile market for several years but as we discuss earlier in this note we believe it is now close to bottoming. 1,000 minutes/1,000 SMS/1GB of data costs as little as €7/month with most no-frills packages around €10-13. The introduction of €10-20 annual SIM charges and TKA’s ending of some no-frills bob tariffs (taking prices from €9.9 to €12.8) suggest some rationality.

■ The market could also consolidate. If the Orange consolidation deal wins regulatory approval then we believe the market could stabilize through market repair. If regulation proves a hurdle (as it did with tele.ring in 2005-6) then some irrationality could come back to the market. However, with price close to cost, we think the scope for further price cutting is much more limited than in the past no matter the outcome of the Orange deal.

■ But CEE challenging and stake holder Ronny Pecik’s intentions main stock drivers. We have become more bullish on Austrian mobile and raise our 2012 service revenue growth estimates 2%, to -3.8%. However, Eastern Europe remains a major headwind (Bulgaria, Croatia and Belarus) and we believe the stock price depends more on Ronny Pecik’s intentions which are uncertain than the fundamental performance of the company.

■ Catalysts: TKA publishes 1Q 11 results on 10 May and hosts its AGM on 23 May. Press reports (e.g., Telecompaper) have suggested Pecik will seek board representation at the AGM, though it is unclear how many board seats he will seek.

■ Valuation: TKA shares trade on a 12.6% 2013E FCFY vs the Incumbent peers trading on 11.9%.

Share price performance

6

8

10

12

Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11

Price Price relative

The price relative chart measures performance against the VIENNA SE AUSTRIAN TRADED IDX which closed at 2158.03 on 02/04/12 On 02/04/12 the spot exchange rate was Eu .75 /US$1

Performance Over 1M 3M 12M Absolute (%) -1.2 -3.3 -14.9 Relative (%) -4.1 -22.7 -15.2

Financial and valuation metrics

Year 12/11A 12/12E 12/13E 12/14E Revenue (Eu m) 4,454.6 4,339.3 4,302.4 4,288.2 EBITDA (Eu m) 1,537.42 1,466.31 1,473.51 1,479.93 Net Income (Eu m) -255.3 131.0 174.5 250.7 CS adj. EPS (Eu) 0.46 0.46 0.50 0.68 Prev. EPS (Eu) — 0.53 0.74 0.95 ROIC (%) 10.66 7.45 9.41 11.40 P/E (adj., x) 18.87 18.84 17.27 12.88 P/E rel. (%) 154.1 189.7 204.2 169.4 EV/EBITDA 4.7 4.7 4.6 4.4

Dividend (12/12E, Eu) 0.38 IC (12/12E, Eu m) 4,015.41 Dividend yield (%) 4.4 EV/IC 1.7 Net debt (12/12E, Eu m) 3,001.3 Current WACC 7.0 Net debt/equity (12/12E, %) 296.0 Free float (%) 71.6 BV/share (12/12E, Eu) 1.9 Number of shares (m) 443.00

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates.

*Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months.

Research Analysts

Jakob Bluestone 44 20 7883 0834

Justin Funnell 44 20 7888 0268

Rating NEUTRAL* Price (02 Apr 12, Eu) 8.72 Target price (Eu) 10.00¹ Market cap. (Eu m) 3,862.96 Enterprise value (Eu m) 6,864.3

04 April 2012

Mobile pricing 30

Change in estimates We raise Austrian mobile numbers but lower CEE – 2013E EBITDA cut 2%

We slightly raise our estimates for Austrian mobile in our Telekom Austria model, following the 4Q 11 results. We now assume service revenue growth in 2012 only falls 3.8% (previously -5.8%), as we believe the Austrian mobile market is slowly bottoming out. We discuss this in further detail below.

However, we have cut estimates for other parts of the business to reflect the fact that Telekom Austria’s international operations remain under significant pressure. In 4Q 11:

■ Bulgarian mobile service revenue growth deteriorated to -17% vs -13% in 3Q 11. This should take another step down in 1Q 12 when MTR cuts resume.

■ Croatia mobile service revenue growth deteriorated to -10% vs -8.2% in 3Q 11. We see continued pressure as Croatia is likely to bring its wholesale rates in line with the EU rules, ahead of EU accession in July 2013. The caveat would be if Tele2 exited the market, though visibility on such a move is low.

■ Belarus growth was strongly impacted by the country’s inflation (inflation is currently running above 100%). Revenues fell 55% in euro in 4Q 11 despite Velcom raising prices 22% (following a previous 20% price hike). Local currency growth slowed from 66% in 3Q 11 to 56% (ie negative 40-50% in real terms).

We show our detailed changes in estimates in Figure 38.

Our estimates are in line with consensus

Overall this puts our EBITDA estimates in line with consensus (2012E 0.7% above, 2013E 0.4% above), suggesting that there is unlikely to be sufficient earnings momentum to justify an outperform rating.

Figure 37: Credit Suisse vs consensus € in millions, unless otherwise stated 2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E

CS CS CS Cons Cons Cons % delta % delta % delta

Revenues 4,294 4,302 4,288 4,325 4,323 4,289 -0.7% -0.5% 0.0%

EBITDA 1,466 1,474 1,480 1,456 1,467 1,456 0.7% 0.4% 1.6%

Operating income 401 488 574 441 482 526 -9.0% 1.2% 9.2%

Net income 205 223 300 195 227 254 5.0% -1.5% 18.0%

Source: Credit Suisse estimates. the BLOOMBERG PROFESSIONAL™ service Revenues and Net income may differ to the databox due to

adjustments for One-offs

We would also note that with Ronny Pecik’s stake building and the continued uncertainty about his intentions, the stock performance is arguably more likely to be driven by this special situation than by fundamentals.

04 April 2012

Mobile pricing 31

Figure 38: Changes to estimates € in millions, unless otherwise stated 2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E

Old Old Old New New New % chge % chge % chge