Domino's Pizza Inc. (DPZ) - Credit Suisse | PLUS

57

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 25 June 2019 Americas/United States Equity Research Restaurants Domino’s Pizza Inc. (DPZ) Rating OUTPERFORM Price (21-Jun-19, US$) 280.33 Target price (US$) 320.00 52-week price range (US$) 300.67 - 234.35 Market cap(US$ m) 11,523 Enterprise value (US$ m) 14,963 Target price is for 12 months. Research Analysts Lauren Silberman 212 325 2720 [email protected] INITIATION Time to Get A Piece of This Pie; Initiate Outperform ■ We initiate coverage of Domino’s (DPZ) with an Outperform rating and $320 target price. DPZ is one of the best growth stories in restaurants, with ~10% revenue growth, margin expansion and benefits from repurchases driving an EPS CAGR of ~15% over the next four years. We believe concerns regarding the impact of third-party delivery could be overdone as the honeymoon phase wears off and carryout could offset pressure, with outperformance against SSS estimates as upside. Confidence in ~7% global unit growth is driven by global brand strength, domestic whitespace opportunities in a fragmented category and international master franchise agreements. ■ US SSS Outperformance: DPZ should maintain SSS momentum and share gains as one of the few companies with contribution from positive traffic, the only company with a frequency-based loyalty program, consistent value messaging, favorable franchisee relations (avg franchisee ~$975K EBITDA) and an industry-leading digital ecosystem supporting best-in-class execution. We estimate US SSS of 5.5% in 2019, with expectations for sequential improvement throughout the year against easing compares and reduced competitive headwinds from 1Q (Points for Pies, QSR chains delivery campaigns). Longer term, we model US SSS of ~5%. ■ Third-Party Delivery as NT Pressure, But Not LT Issue: An increasing number of cross-branded campaigns with national QSR chains, competition for delivery drivers and aggressive promos represent incremental competitive pressure NT. LT, pizza’s stable 10-yr ~$10BN delivery market share should largely hold, with pizza a cuisine that travels well and offers great value. Positioning as a delivery company could be a net positive for DPZ as delivery demand increases, while increased focus on carryout can drive incremental sales and help offset competitive pressures (~2/3 delivery, 1/3 carryout split). ■ Valuation: Our $320 target price is based on ~20.5x our NTM EBITDA in 12 months, implying ~28x our NTM EPS in 12 months (30x avg), in-line with current multiples. Key risks: competition, consumer spending, interest rates. Share price performance On 21-Jun-2019 the S&P 500 INDEX closed at 2950.46 Daily Jun22, 2018 - Jun21, 2019, 06/22/18 = US$292.39 Quarterly EPS Q1 Q2 Q3 Q4 2018A 2.00 1.84 1.95 2.62 2019E 2.20 2.08 2.11 3.07 2020E 2.44 2.43 2.46 3.79 Financial and valuation metrics Year 12/18A 12/19E 12/20E 12/21E EPS (CS adj.) (US$) 8.42 9.44 11.10 12.66 Prev. EPS (US$) - - - - P/E rel. (%) 186.3 172.0 162.6 156.3 Revenue (US$ m) 3,432.9 3,686.0 4,042.2 4,386.1 EBITDA (US$ m) 625.9 694.5 783.2 847.1 OCFPS (US$) 9.10 10.54 12.69 14.52 P/OCF (x) 27.5 26.6 22.1 19.3 EV/EBITDA (current) 24.0 21.6 19.2 17.7 Net debt (US$ m) 3,506 3,440 3,540 3,588 ROIC (%) 103.56 113.41 115.03 117.77 Number of shares (m) 41.10 IC (current, US$ m) 466.22 BV/share (Next Qtr., US$) -72.8 Dividend (current, US$) 2.60 Net debt (Next Qtr., US$ m) 3,400.6 Net debt/tot eq (Next Qtr.,%) -114.3 Source: Company data, Refinitiv, Credit Suisse estimates

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Domino's Pizza Inc. (DPZ) - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

25 June 2019 Americas/United States

Equity Research

Restaurants

Domino’s Pizza Inc. (DPZ)

Rating OUTPERFORM Price (21-Jun-19, US$) 280.33 Target price (US$) 320.00 52-week price range (US$) 300.67 - 234.35 Market cap(US$ m) 11,523 Enterprise value (US$ m) 14,963 Target price is for 12 months.

Research Analysts

Lauren Silberman

212 325 2720

INITIATION

Time to Get A Piece of This Pie; Initiate

Outperform

■ We initiate coverage of Domino’s (DPZ) with an Outperform rating and $320 target price. DPZ is one of the best growth stories in restaurants, with ~10% revenue growth, margin expansion and benefits from repurchases driving an EPS CAGR of ~15% over the next four years. We believe concerns regarding the impact of third-party delivery could be overdone as the honeymoon phase wears off and carryout could offset pressure, with outperformance against SSS estimates as upside. Confidence in ~7% global unit growth is driven by global brand strength, domestic whitespace opportunities in a fragmented category and international master franchise agreements.

■ US SSS Outperformance: DPZ should maintain SSS momentum and share

gains as one of the few companies with contribution from positive traffic, the only company with a frequency-based loyalty program, consistent value messaging, favorable franchisee relations (avg franchisee ~$975K EBITDA) and an industry-leading digital ecosystem supporting best-in-class execution. We estimate US SSS of 5.5% in 2019, with expectations for sequential improvement throughout the year against easing compares and reduced competitive headwinds from 1Q (Points for Pies, QSR chains delivery campaigns). Longer term, we model US SSS of ~5%.

■ Third-Party Delivery as NT Pressure, But Not LT Issue: An increasing number of cross-branded campaigns with national QSR chains, competition for delivery drivers and aggressive promos represent incremental competitive pressure NT. LT, pizza’s stable 10-yr ~$10BN delivery market share should largely hold, with pizza a cuisine that travels well and offers great value. Positioning as a delivery company could be a net positive for DPZ as delivery demand increases, while increased focus on carryout can drive incremental sales and help offset competitive pressures (~2/3 delivery, 1/3 carryout split).

■ Valuation: Our $320 target price is based on ~20.5x our NTM EBITDA in 12

months, implying ~28x our NTM EPS in 12 months (30x avg), in-line with current multiples. Key risks: competition, consumer spending, interest rates.

Share price performance

On 21-Jun-2019 the S&P 500 INDEX closed at 2950.46

Daily Jun22, 2018 - Jun21, 2019, 06/22/18 = US$292.39

Quarterly EPS Q1 Q2 Q3 Q4 2018A 2.00 1.84 1.95 2.62 2019E 2.20 2.08 2.11 3.07 2020E 2.44 2.43 2.46 3.79

Financial and valuation metrics

Year 12/18A 12/19E 12/20E 12/21E EPS (CS adj.) (US$) 8.42 9.44 11.10 12.66 Prev. EPS (US$) - - - - P/E rel. (%) 186.3 172.0 162.6 156.3 Revenue (US$ m) 3,432.9 3,686.0 4,042.2 4,386.1 EBITDA (US$ m) 625.9 694.5 783.2 847.1 OCFPS (US$) 9.10 10.54 12.69 14.52 P/OCF (x) 27.5 26.6 22.1 19.3 EV/EBITDA (current) 24.0 21.6 19.2 17.7 Net debt (US$ m) 3,506 3,440 3,540 3,588 ROIC (%) 103.56 113.41 115.03 117.77

Number of shares (m) 41.10 IC (current, US$ m) 466.22 BV/share (Next Qtr., US$) -72.8 Dividend (current, US$) 2.60 Net debt (Next Qtr., US$ m) 3,400.6 Net debt/tot eq (Next Qtr.,%) -114.3 Source: Company data, Refinitiv, Credit Suisse estimates

25 June 2019

Domino’s Pizza Inc. (DPZ) 2

Domino’s Pizza Inc. (DPZ)

Price (21 Jun 2019): US$280.33; Rating: OUTPERFORM; Target Price: 320.00; Analyst: Lauren Silberman

Income Statement 12/18A 12/19E 12/20E 12/21E

Revenue (US$ m) 3,432.9 3,686.0 4,042.2 4,386.1 EBITDA (US$ m) 626 695 783 847 Depr. & amort. (54) (59) (65) (70) EBIT (US$) 572 635 718 777 Net interest exp (140) (149) (156) (157) PBT (US$) 433 487 562 619 Income taxes (68) (92) (112) (124) Profit after tax 365 395 450 496 Net profit (US$) 365 395 450 496 Other NPAT adjustments 0 0 0 0

Cash Flow 12/18A 12/19E 12/20E 12/21E

Cash flow from operations 394 440 514 568 CAPEX (120) (112) (100) (90) Free cashflow to the firm 274 328 414 478 Cash flow from investments (88) (71) (100) (90) Net share issue(/repurchase) (581) (223) (392) (391) Dividends paid (92) (105) (122) (136) Changes in Net Cash/Debt (388) 66 (100) (49)

Balance Sheet (US$) 12/18A 12/19E 12/20E 12/21E

Cash & cash equivalents 25 17 82 98 Account receivables 190 193 212 230 Other current assets 305 268 268 268 Total fixed assets 233 241 276 296 Investment securities - - - - Total assets 1,124 1,095 1,214 1,268 Total current liabilities 412 396 404 414 Shareholder equity (3,040) (2,986) (3,040) (3,061) Total liabilities and equity 1,124 1,095 1,214 1,268 Net debt 3,506 3,440 3,540 3,588

Per share 12/18A 12/19E 12/20E 12/21E

No. of shares (wtd avg) 43 42 41 39 CS adj. EPS 8.42 9.44 11.10 12.66 Prev. EPS (US$) Dividend (US$) 2.20 2.60 3.12 3.59 Free cash flow per share 6.33 7.85 10.22 12.22

Earnings 12/18A 12/19E 12/20E 12/21E

Sales growth (%) 23.1 7.4 9.7 8.5 EBIT growth (%) 9.7 11.0 13.1 8.1 Net profit growth (%) 29.5 8.1 14.0 10.2 EPS growth (%) 42.4 12.1 17.6 14.1 EBITDA margin (%) 18.2 18.8 19.4 19.3 EBIT margin (%) 16.7 17.2 17.8 17.7 Pretax margin (%) 12.6 13.2 13.9 14.1 Net margin (%) 10.6 10.7 11.1 11.3

Valuation 12/18A 12/19E 12/20E 12/21E

EV/EBITDA (x) 24.0 21.6 19.2 17.7 P/E (x) 33.3 29.7 25.3 22.1

Returns 12/18A 12/19E 12/20E 12/21E

ROIC (%) 103.6 113.4 115.0 117.8

Gearing 12/18A 12/19E 12/20E 12/21E

Net debt/equity (%) (115.3) (115.2) (116.4) (117.2)

Quarterly EPS Q1 Q2 Q3 Q4 2018A 2.00 1.84 1.95 2.62 2019E 2.20 2.08 2.11 3.07 2020E 2.44 2.43 2.46 3.79

Company Background

Domino's Pizza is the one of the world's largest pizza companies, with nearly 15,000 locations in more than 85 markets.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 385.00

Our $385 one-year valuation in a blue sky scenario is based on an EV/EBITDA of ~22.5x our blue sky FY20 EBITDA. Our blue sky FY20 EBITDA is based on: 1) domestic SSS of 8%; 2) domestic unit growth of ~6%; and 3) operating margins of ~19%.

Our Grey Sky Scenario (US$) 235.00

Our $235 one-year valuation in a grey sky scenario is based on an EV/EBITDA of ~18x our grey sky FY20 EBITDA. Our grey sky FY20 EBITDA is based on: 1) domestic SSS of 3.5%; 2) domestic unit growth of ~4.5%; and 3) operating margins of ~16.5%.

Share price performance

On 21-Jun-2019 the S&P 500 INDEX closed at 2950.46

Daily Jun22, 2018 - Jun21, 2019, 06/22/18 = US$292.39

Source: Company data, Refinitiv, Credit Suisse estimates

25 June 2019

Domino’s Pizza Inc. (DPZ) 3

Executive Summary We initiate coverage of Domino’s Pizza (DPZ) with an Outperform rating and $320 target

price. DPZ is one of the best growth stories in restaurants, with ~10% revenue growth,

margin expansion and benefits from repurchases supporting EPS growth of ~15% over the

next four years.

Please refer to our views summarizing the Restaurants industry: US Restaurants Phone

To Table: Digitizing Restaurants.

■ DPZ Well Positioned for Global SSS Outperformance: DPZ has exhibited industry-

leading and consistent global SSS, with domestic SSS averaging ~9% and

international SSS averaging ~5.5% over the last five years. DPZ has consistently met

or exceeded its long-term SSS targets, currently 3-6% globally. While increasing

competitive pressure from third-party delivery companies has pressured SSS more

recently, we believe DPZ’s long-term strategy around value, digital and delivery well

positions the company for market share gains.

For 2019, we estimate domestic SSS of 5.5%, with expectations for sequential

improvement throughout the year as compares ease. We model domestic SSS of 5%

post 2019, toward the higher end of DPZ’s long-term SSS target of 3-6%. Our

confidence in ongoing SSS outperformance and market share gains comes from: 1)

historical precedent, with 32 consecutive quarters of positive US SSS averaging ~7.5%

since 2010 comprised of healthy traffic gains and average check increases; 2)

fragmented pizza market, with opportunities to gain share from independents, regional

chains and large chains; and 3) execution against sales initiatives, including ongoing

evolution of its digital platform, compelling and consistent value offers and benefits

from a greater focus on carryout.

We model international SSS of 3.1% in 2019, including sequential improvement

throughout the year as compares ease. Long term, we model international SSS of

~3.5%, toward the lower end of DPZ’s long-term SSS target of 3-6%, in-line with slower

growth over the last two years.

■ Delivery Concerns Could Be Overdone: Third-party delivery is likely to represent

incremental pressure near term, driven by: 1) increasing demand and supply from

third-party delivery providers fueling higher awareness; 2) aggressive

promotions/discounts; 3) QSR chains offering delivery; 4) cross-branded campaigns

between aggregators and large QSR chains; and 5) competition for delivery drivers.

Long term, we believe the pizza delivery market will largely maintain its delivery market

share, which has been ~$10BN for a decade. We view Domino’s as best positioned to

continue to gain share within the segment given the strength of its digital ecosystem

and long-term strategic approach. We expect Domino’s loyalty program and superior

execution in delivery will allow the company to maintain a competitive advantage even

against increasing competition.

■ Global Growth Opportunity Strong: We believe DPZ can reach 25,000 units by

2025, with contribution from accelerating domestic growth and continued robust

international development. The 25,000 unit growth target implies global growth of ~7%

over the next several years, including ~4.5% domestic unit growth and ~8%

international unit growth. We model global unit growth of ~7% through 2022, including

domestic unit growth of ~5% and international unit growth of ~8%. This compares to a

5-yr global growth CAGR of 7.9%, including 3.3% domestically and 11.2%

internationally.

Our confidence in development expectations comes from: 1) global brand strength,

fundamentals and operating momentum; 2) domestic whitespace opportunities with

fortressing strategy in existing markets; and 3) international development opportunities,

with increased visibility from master franchise agreements.

25 June 2019

Domino’s Pizza Inc. (DPZ) 4

■ Earnings Estimates: We expect top-line growth of ~9% over the next few years to

enable margin leverage for operating profit growth of ~10.5%. Together with accretion

from share repurchases, we model EPS growth of ~15% long term. For 2019, we

model EPS growth of ~12%, including dilution from the refranchising of company-

operated stores in New York. We also note 2020 includes a 53rd

week.

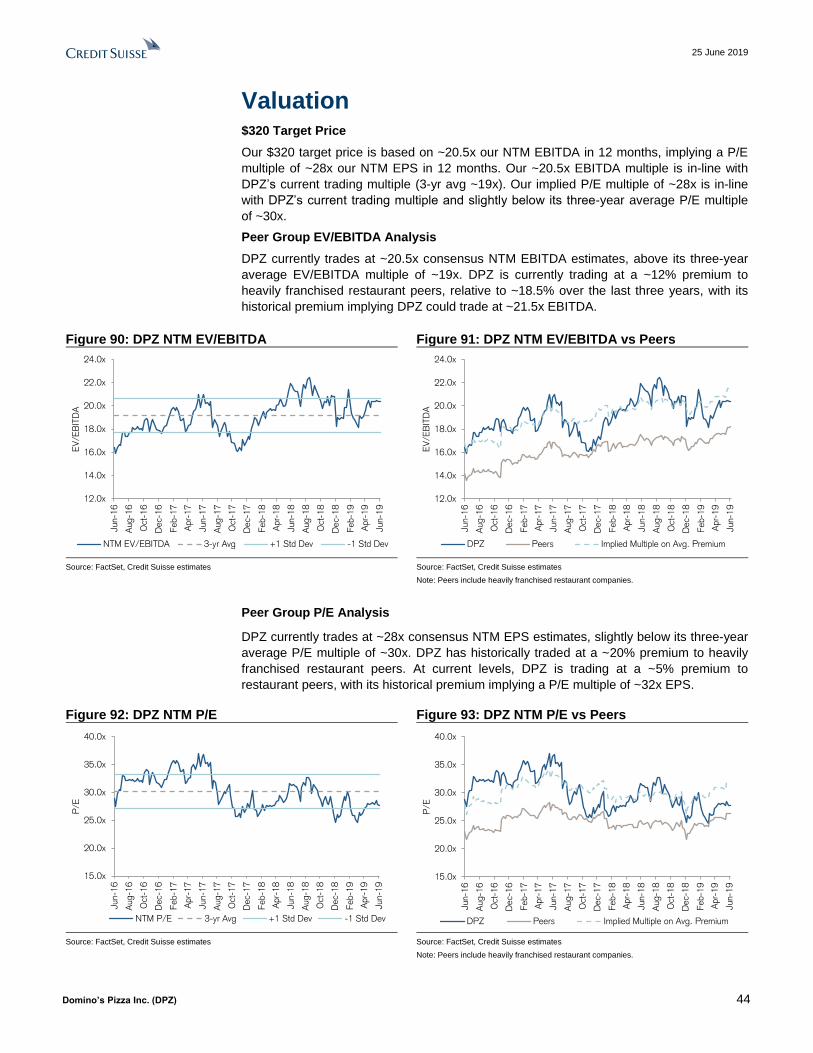

■ Valuation: Our $320 target price is based on ~20.5x our NTM EBITDA in 12 months,

implying a P/E multiple of ~28x our NTM EPS in 12 months. Our ~20.5x EV/EBITDA

multiple is in-line with DPZ’s current multiple and a premium to its 3-year average

multiple of ~19x. Our implied P/E multiple of ~28x is in-line with DPZ’s current trading

multiple and below its three-year average P/E multiple of ~30x.

■ Key risks include: 1) competition from pizza peers, other QSR chains and delivery

aggregators; 2) consumer spending; and 3) interest rates, as DPZ is highly levered at

~6x debt/EBITDA.

25 June 2019

Domino’s Pizza Inc. (DPZ) 5

Key Charts

Figure 1: DPZ has demonstrated system sales

growth of ~11% over the last five years, consistently

beating at least the lower end of long-term

guidance, with expectations to maintain 8-12%

growth over the next 3-5 years.

Figure 2: Execution against digital initiatives,

delivery and consistent value should support

ongoing SSS outperformance, even against

increased competitive pressures from delivery and

fortressing growth strategy.

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 3: Following several years of international

SSS at the high-end of DPZ’s LT range, we model

international SSS toward the low-end of guidance

and in-line with slower growth over the last two

years.

Figure 4: We model global unit growth of 6.9% over

the next four years, relative to 7.9% growth over the

last five years and DPZ’s target of 6-8% growth over

the next three to five years.

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

0%

2%

4%

6%

8%

10%

12%

14%

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Sys

tem

Sale

s G

row

th

Domestic International DPZ LT Target

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Dom

est

ic S

SS

Domestic SSS DPZ Target

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Inte

rnatio

nal S

SS

International SSS DPZ Target

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Glo

bal U

nit

Gro

wth

Domestic International DPZ LT Target (6-8%)

25 June 2019

Domino’s Pizza Inc. (DPZ) 6

Figure 5: Delivery aggregators are growing at a

faster rate than pizza companies, highlighting

increasing competition.

Figure 6: Domino’s is currently trading at ~20.5x

EBITDA and we expect the company will maintain

its valuation premium to peers.

Source: Sensor Tower, Credit Suisse estimates

Note: Pizza Apps include Pizza Hut, Papa John’s, Hungry Howie’s, Domino’s, MyCicis, Little Caesars, Blaze, Papa Murphy’s, PizzaRev, Pieology and Marco’s. Delivery Apps include Grubhub, Seamless, Delviery.com, Postmates, DoorDash, Caviar and Uber Eats.

Source: FactSet, Credit Suisse estimates

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan-1

2

Jun-1

2

Nov-

12

Apr-

13

Sep-1

3

Feb-1

4

Jul-1

4

Dec-

14

May-

15

Oct

-15

Mar-

16

Aug-1

6

Jan-1

7

Jun-1

7

Nov-

17

Apr-

18

Sep-1

8

Feb-1

9

Dig

ital A

pp D

ow

nlo

ad S

hare

Pizza Apps Delivery Apps

12.0x

14.0x

16.0x

18.0x

20.0x

22.0x

24.0x

Jun-1

6

Aug-1

6

Oct

-16

Dec-

16

Feb-1

7

Apr-

17

Jun-1

7

Aug-1

7

Oct

-17

Dec-

17

Feb-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct

-18

Dec-

18

Feb-1

9

Apr-

19

Jun-1

9

EV

/EB

ITD

A

NTM EV/EBITDA 3-yr Avg +1 Std Dev -1 Std Dev

25 June 2019

Domino’s Pizza Inc. (DPZ) 7

What is DPZ’s SSS outlook? Credit Suisse View

DPZ has exhibited industry-leading and consistent global SSS over the last ten years.

Domestic SSS have averaged ~9% over the last 20 quarters and international SSS have

averaged ~5.5%. While increasing competitive pressure from third-party delivery

companies has pressured SSS more recently, we believe Domino’s remains well

positioned for outperformance globally.

For 2019, we estimate domestic SSS of 5.5%, with expectations for sequential

improvement throughout the year as compares ease. Long term, we model domestic SSS

of 5%, toward the higher end of DPZ’s long-term SSS target of 3-6%. Our confidence in

ongoing SSS outperformance and market share gains comes from: 1) historical precedent,

with 32 consecutive quarters of positive US SSS averaging ~7.5% since 2010 and ~9%

over the last five years comprised of healthy traffic gains and average check increases; 2)

fragmented pizza market, with opportunities to gain share from independents, regional

chains and large chains; and 3) execution against sales initiatives, including ongoing

evolution of its digital platform, compelling and consistent value offers and benefits from a

greater focus on carryout.

We model international SSS of 3.1% in 2019, including sequential improvement

throughout the year as compares ease. Long term, we model international SSS of ~3.5%,

toward the lower end of DPZ’s long-term SSS target of 3-6%, in-line with slower growth

over the last two years.

Consensus Expectations

Consensus Metrix estimates domestic SSS of 4.7% in 2019 and ~4.2% longer term. For

international SSS, consensus models 2.8% in 2019 and ~3.4% longer term.

Brand strength supports continued share gains in

the US

Domino’s has demonstrated 32 consecutive quarters of positive US SSS averaging ~7.5%

since 2010 and ~9% over the last five years comprised of healthy traffic gains and

average check increases. Ongoing execution against key sales drivers should continue to

support outperformance relative to peers and capture market share in the fragmented

pizza category.

We model sequential improvement in SSS throughout 2019 as compares ease. We

believe accelerating digital download growth in 1Q19 (~40% vs ~17% in 4Q18) could be a

leading indicator for accelerating SSS growth in 2Q19 (driven by DPZ’s expanded Piece of

the Pie Rewards program). We also expect the impact of Chipotle’s free delivery bowl

promotion in early January and Taco Bell’s co-branded marketing campaign with Grubhub

offering free delivery in February/March were both incremental pressures in 1Q19.

Chipotle and Taco Bell are two of the strongest competitors in the QSR/fast casual space

currently, and we believe advertising around delivery could have had an incremental

impact. We do note a large marketing campaign by McDonald’s would also represent a

more significant competitive pressure point and is likely to come at some point in 2019.

We model domestic SSS of ~5.5% in 2019, which assumes consistent 2-yr SSS trends

through the year, relative to consensus expectations of ~4.7%. Long term, we model 5%

SSS, at the high end of DPZ’s long-term target of 3-6% and relative to consensus’ ~4%.

We model domestic SSS of ~5-5.5% over

the next few years, relative to DPZ’s long-

term target of 3-6%

25 June 2019

Domino’s Pizza Inc. (DPZ) 8

Figure 7: Domino’s is facing easing compares

throughout 2019, noting 2018 represents the easiest

compares over the last three years.

Figure 8: We expect SSS to accelerate throughout

2019 against easier compares.

Source: Company data, Credit Suisse Source: Company data, Consensus Metrix, Credit Suisse estimates

Figure 9: Domino’s has demonstrated SSS strength

in the US since 2010, with average SSS of 7.4%.

Figure 10: We model domestic SSS of 5.5% in 2019

& 5% long-term, relative to consensus expectations

of ~4.7% in 2019 & ~4-4.5% long term.

Source: Company data, Credit Suisse Source: Company data, Consensus Metrix, Credit Suisse estimates

Consistent and impressive SSS offer confidence in long-term share gains

US SSS have averaged ~7.5% since 2010, supporting ~500bps of pizza segment market

share gains. Despite a challenging restaurant industry backdrop and heightened

competitive environment, Domino’s has maintained its long-term strategy to grow market

share profitability with compelling value and innovation through the evolution of its digital

platform and delivery infrastructure.

Over the last several years, DPZ has raised its long-term SSS outlook, currently guided for

3-6%. While the market has gotten accustomed to DPZ outperforming targets, SSS within

the targeted 3-6% range is still well above peers and demonstrates enviable market share

gains. DPZ has consistently met or exceeded targets, adding to our confidence in the

outlook.

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

Dom

est

ic S

SS

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

1Q

19

2Q

19

E

3Q

19

E

4Q

19

E

1Q

20

E

Dom

est

ic S

SS

CSe

Consensus

0%

5%

10%

15%

20%

25%

0%

2%

4%

6%

8%

10%

12%

14%

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

2-y

r D

om

est

ic S

SS

1-y

r D

om

est

ic S

SS

1-yr Domestic SSS 2-yr Domestic SSS

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2019E 2020E 2021E 2022E

Dom

est

ic S

SS

CSe Consensus DPZ Target

Domestic SSS Target +3-6%

US SSS have averaged

~7.5% since 2010, generating ~500bps of

US pizza segment market share gains

25 June 2019

Domino’s Pizza Inc. (DPZ) 9

Figure 11: Domestic SSS have averaged ~7.5%

since 2010, reflecting consistently impressive

performance on a 1-yr and 2-yr basis.

Figure 12: Domino’s has largely outperformed long-

term outlooks set by management, which have

increased over time.

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

Fragmented industry sets an attractive backdrop

The pizza segment is the most fragmented in restaurants, with the five largest chains making

up 45% of segment sales. For comparison, the five largest burger chains comprise nearly

80% of burger sales and the five largest Mexican restaurant chains make up ~70% of sales.

In every other category outside of pizza, the segment leaders maintain at least 30% of the

market share, and on average, comprise ~45% of their respective segment sales.

Figure 13: Pizza is the most fragmented segment in

restaurants, with the top five largest chains making

up less than 50% of category sales.

Figure 14: Across all segments except pizza, the

market leader makes up 30%+ of the category’s

sales.

Source: Technomic, Credit Suisse estimates Source: Technomic, Credit Suisse estimates

Domino’s is the market share leader, with 15%+ of segment sales, representing an

increase of ~560bps over the last ten years. Small chains and independents have lost

~140bps of market share over the same period, while Pizza Hut and other large pizza

chains have together lost ~10% of the segment’s sales. We believe large chains are better

positioned to gain market share over time as the segment consolidates. Structurally higher

cost structures, a shift toward margin-dilutive delivery channels and technological

investment requirements are likely headwinds for the smaller companies.

Domino’s has exhibited average domestic system sales growth of ~12% per year over the

last five years, nearly triple the rate of the US pizza segment’s ~4% average growth. Many

of the larger and regional chains have donated share, highlighting opportunities to capture

share from both larger players as well as regionals/local pizza shops. Domino’s has

indicated a US market share target of at least 25%, consistent with other market share

leaders, driven by a combination of SSS and unit growth.

-10%

-5%

0%

5%

10%

15%

20%

25%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

2-y

r D

om

est

ic S

SS

1-y

r D

om

est

ic S

SS

1-yr SSS 2-yr SSS

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Dom

est

ic S

SS

Domestic SSS DPZ Target

45% 14% 40%

0% 20% 40% 60% 80% 100%

Burgers

Chicken

Coffee

Bakery Café

Mexican

Sandwich

Frozen Desserts

Asian/Noodle

Pizza

Sales Composition by Segment

Sales Other Large Chains Small Chains & Independents

15%

0% 20% 40% 60% 80%

Burgers

Chicken

Coffee

Bakery Café

Mexican

Sandwich

Frozen Desserts

Asian/Noodle

Pizza

Market Leader by Sales

The pizza segment is the most fragmented in

restaurants, with the five largest pizza

chains making up just 45% of sales

25 June 2019

Domino’s Pizza Inc. (DPZ) 10

Figure 15: Small chain, independents and more

regionalized brands have lost ~700bps of market

share since 2009.

Figure 16: Large chains have represented the

majority of segment sales contribution, though

more recently, share losses from larger pizza

players have weighed on segment growth.

Source: Technomic, Credit Suisse estimates Source: Technomic, Credit Suisse estimates

Best-in-class digital ecosystem as a meaningful

growth driver

Domino’s maintains an industry-leading digital platform, which has supported

outperformance relative to pizza peers and the overall industry. The company uses digital

development to lead its innovation strategy and maintain a competitive advantage. For the

first time, Domino’s added “online ordering” as a reason customers purchase from

Domino’s in its 2018 Franchise Disclosure Document (FDD).

Digital represents ~65% of Domino’s sales, with the pizza segment overall generating the

highest levels of digital utilization across the industry. Domino’s digital ecosystem and

compelling loyalty program have supported robust sales growth and a meaningful

outperformance gap relative to peers. While there are increasing concerns that digital

ecosystems will become table stakes as more restaurants invest in technology and service

providers make it more affordable for smaller companies, we still believe DPZ’s proprietary

infrastructure and integrated operations will help the company sustain a competitive

advantage. Domino’s has the potential to transition to an unprecedented nearly 100%

digital ordering business, and we expect the company to continue to evolve to be at the

forefront of innovation.

We expect Domino’s to continue to evolve its digital ecosystem through both consumer

facing and back of house technology. Domino’s already offers a voice ordering channel,

and though not widely used, can potentially be leveraged for phone orders, unlocking

capacity. Phone orders represent ~25% of the business, so greater digital conversion

should meaningfully drive benefits for restaurant operations and profitability. With every

order guaranteed to be answered in any language and automatically offer add-

ons/suggested sell, the digital technology could actually improve the customer experience.

In addition, we expect utilization of in-store technology such as kiosks makes it possible to

generate labor savings and help in the transition to an increasingly digital company.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Mar

ket

Shar

e

Papa Murphy's

Papa John's

Little Caesars

Pizza Hut

Domino's

Other Large Pizza

Chains

Small Chains &

Independents

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2012 2013 2014 2015 2016 2017 2018

Sal

es

Gro

wth

YO

Y %

Large Pizza Chains Small Pizza Chains & Independents

Digital makes up ~65% of sales, with an

opportunity to reach an unprecedented nearly

~100% of sales over time

25 June 2019

Domino’s Pizza Inc. (DPZ) 11

Figure 17: The pizza segment leads the industry in

digital sales mix, with the top three largest pizza

players generating at least 50% of their sales

through digital channels.

Figure 18: More than 65% of sales come from digital

channels, with expectations to approach nearly

100% long term.

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

High digital utilization and a large scale loyalty program offer Domino’s a significant

advantage to analyze, segment and target customers through personalized marketing

efforts and suggestive sell. Domino’s is one of the most aggressive in the industry with

suggestive selling, offering add-ons and upselling at nearly every step of the ordering

process. We expect this has been supportive of average check increases and should

continue to offer a benefit.

Figure 19: Domino’s uses suggestive sell at multiple times during the online

ordering process, likely a factor driving its healthy average mix.

Source: Domino’s Digital App

Mobile:

50%+

Mobile:

~75%

Mobile:

~75%

~65%

~50%+

~60%+

Domino's Pizza Hut Papa John's

Digital Sales Mix

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018 Future

Dig

ital S

ales

Mix

Domino’s app suggests add-ons at each stage

of the ordering process, likely a

meaningful factor driving its average

check growth

25 June 2019

Domino’s Pizza Inc. (DPZ) 12

Figure 20: For comparison, Pizza Hut offers an “Extras” page for add-ons and

Papa John’s features popular add-ons at the top of its checkout screen.

Source: Pizza Hut Digital App, Papa John’s Digital App

Domino’s is arguably a pizza company, technology company and marketing company. The

Domino’s AnyWare platform provides a suite of ordering options, from Facebook

messenger to Amazon Alexa. We largely view the AnyWare platform as a marketing tool

to maintain relevancy and generate new news, with limited sales mix likely generated from

a tweet or Facebook message. The Hotspots program allows customers to order delivery

from nontraditional sites, though we expect minimal sales mix from the channel.

Figure 21: Domino’s offers a suite of fun and

innovative ordering platforms.

Figure 22: Domino’s offers 200K Delivery HotSpots

in the US, expanding delivery available to

nontraditional sites, though utilization is limited.

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

2017 Slack

2016 Google Home

2016 Facebook Messenger

2016 Zero Clicks

2016 Apple Watch

2016 Amazon Alexa

2015 Text

2015 Tweet

2015 Pebble & Android Wear smartwatches

2015 Samsung Smart TV

2014 Voice

2014 Ford Sync AppLink

AnyWare Platform

Pizza Hut and Papa John’s both use

suggestive sell though separate from the

overall ordering process

25 June 2019

Domino’s Pizza Inc. (DPZ) 13

Both Pizza Hut and Papa John’s have increased investments to accelerate digital

development. Pizza Hut is playing a catch-up game to Domino’s, launching its Delivery

Tracker in early 2017, nearly a decade after Domino’s, and digital enhancements were

largely rolled out at once. Papa John’s similarly introduced its Papa Track in March 2017,

and has expanded into additional order channels, including Amazon Alexa, Apple and

Google Pay, evolved its loyalty program and expanded into a delivery partnership with

DoorDash. While pizza peers are beginning to offer similar headline features, we believe

Domino’s will maintain a competitive advantage given its holistic integration.

“Piece of the Pie” Loyalty Program

Domino’s “Piece of the Pie” loyalty program launched in late 2015 and is already one of

the largest in the industry, with ~20MM active users (ordered within last 6 months). The

ease of sign up and integration of the Pizza Profile make it a compelling and frictionless

process.

The loyalty program has consistently contributed meaningfully to SSS growth, with its

simplicity, ease of use and ease for customers to understand the value as sources of

strength. The frequency-based loyalty program rewards consumers 10 points for every

order, and consumers can redeem a free pizza once they reach 60 points. Benefits from

data analytics will likely accelerate over time given the large scale of its program.

Domino’s has created an integrated digital ecosystem built off of simplicity, consistency

and value that should continue to be a meaningful contributor to SSS going forward.

Figure 23: Domino’s frequency-based loyalty

program requires minimum spend of $60, which is

compelling relative to pizza peers.

Figure 24: We believe Domino’s loyalty program has

supported high levels of digital download share,

with Domino’s ~35% download share outpacing its

pizza market share (~15% overall and 26% among

large pizza chains).

Source: Company data, Credit Suisse estimates Source: Sensor Tower, Credit Suisse estimates

Domino’s recently launched a 12-week (February to April 2019) campaign through its

loyalty program by rewarding customers for eating any pizza, a creative attempt to acquire

new customers onto to the platform and capture more customer data. To earn points,

customers use the app to upload a picture of their pizzas, and can earn up to 60 total

points, the redemption value of a free pizza, over the promotional period.

Importantly, Domino’s used the program as an opportunity to inquire about competitors

and customers’ experiences. The company also inquired about other loyalty program

memberships to assess competitive overlap. Questions ranged from where customers

ordered the pizza from, how the pizzas were ordered, the quality of the pizza, the type of

pizza ordered (i.e., crust, sauce, cheese, meat) and reward program membership.

$60

$60

$75

$75

$100

$100

$100

$120

Domino's

Hungry Howie's Pizza

Pizza Hut

Papa John's

Marco's

PizzaRev

Pieology

Blaze Pizza

Spend Required For Reward

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

%D

ow

nlo

ad S

hare Other Large Chains

Papa Murphy's

Little Caesars

Papa John's

Pizza Hut

Domino's

Domino’s frequency-based loyalty program

has meaningfully contributed to SSS

since it launched in late 2015

25 June 2019

Domino’s Pizza Inc. (DPZ) 14

Figure 25: Domino’s Points for Pies Promotion (February to April 2019)

Source: Domino’s App

Consistent value messaging

Execution against value has supported strength, through consistent permanent value

platforms, including a $5.99 Mix & Match deal, $7.99 carryout deal and $19.99 combo

meal deal. Domino’s has maintained its $5.99 deal for nearly a decade, with options

spanning the entire menu, encouraging trial, flexibility and limiting menu fatigue. The $5.99

Mix & Match deal requires the purchase of at least two items, setting a floor for minimum

tickets and supporting margins. Beyond the $5.99 deal, Domino’s has maintained a

permanent $7.99 large three topping carryout deal, which has helped drive growth in that

part of the business, as well as other periodic promos and deals.

Domino’s value strategy is based on consistency. Domino’s sends customers emails daily,

featuring its $5.99 Mix & Match deal in every single communication, and often includes its

$7.99 carryout and $19.99 combo in the majority of its communications. Additionally, its

homepage also features the three national value offers, communicating a consistent

message across channels and across time. For comparison, Pizza Hut also features its $5

Lineup and $7.99 online national price points on its website, though email marketing is

lacking (though has picked up in recent weeks). Papa John’s has relatively inconsistent

value messaging across different platforms.

Execution against consistent value

messaging has supported share gains

25 June 2019

Domino’s Pizza Inc. (DPZ) 15

Figure 26: Domino’s prominently features its three

value deals on its website.

Figure 27: Domino’s maintains a consistent

message by offering the same deal through its

email marketing (and selectively through text).

Source: Domino’s website Source: Domino’s Email – 5/9/19

Menu innovation is limited

Domino’s does not use menu innovation as a driver of growth. The company rarely

introduces new items to the menu. It appears the company’s strategy is to use value deals

as a consistent message, digital innovation as an opportunity to generate new news and

limits operational complexity to optimize operations..

In August 2016, Domino’s rolled out salads nationwide, which are available on the $5.99

meal deal and can help eliminate the veto vote, though unlikely a high volume category.

Bread twists were introduced in mid-2017, a complementary add-on with potential for

suggested sell and supportive of higher average tickets.

Increased focus on driving carryout business

As the rest of the restaurant industry shifts into the food delivery channel, Domino’s has

increased its focus on the carryout side of its business, which represents approximately

1/3 of sales. Domino’s has indicated carryout sales are largely incremental and supportive

of its fortressing strategy as consumers are less willing to travel long distances to pick up a

pizza. We believe this strategy allows the company to remain defensive as delivery

expands into different segments, and also offers added flexibility on value, as carryout

orders eliminate the cost of delivery. Further, in a tight labor market, particularly with

delivery drivers, carryout can help unlock some capacity and drive additional sales.

Carryout represents ~1/3 of Domino’s US sales mix, highlighting opportunity for further

growth. As other restaurants push the delivery message, we believe Domino’s could gain

further share in the carryout segment.

New menu innovation does not appear to be a

meaningful part of the strategy

Carryout sales can help offset increasing

competitive pressure in the delivery segment and unlock capacity

25 June 2019

Domino’s Pizza Inc. (DPZ) 16

Figure 28: Pizza delivery sales have remained

largely stable, while carryout has increased over the

last several years.

Figure 29: Carryout represents ~1/3 of sales for

Domino’s, with opportunities for further share gains

closer to competitors.

Source: Company data, Credit Suisse estimates Source: Company data, Restaurant Research Journal, Credit Suisse estimates

International market strong, but some slowdown

raises concerns

Domino’s has demonstrated 101 consecutive quarters of positive international SSS

averaging ~6% over the last ten years, largely driven by traffic growth. Growth has slowed

more recently, with 1Q19’s 1.8% SSS the lowest comp over the last decade. 2-yr SSS

trends have also decelerated, with 2018 2-yr trends down ~300bps to ~6.9%, relative to

~9.7% in 2017 and ~14.1% in 2016. 2017 and 2018 were the lowest international SSS

over the last 20 years.

We model international SSS of 3.1% in 2019 and ~3.5% longer term, near the low end of

DPZ’s long-term guidance of 3-6%. Our go-forward estimates are below historical

averages given ongoing expectations for an elevated drag from new store cannibalization

given DPZ’s fortressing strategy, more recently lower SSS and the potential impact of

increasing global delivery competition. Consensus models international SSS of 2.8% in

2019 and ~3.5% over the next few years, relatively in-line with the last two years.

Figure 30: International SSS have averaged ~6%,

though have decelerated more recently.

Figure 31: We expect international SSS of ~3.1% in

2019 and ~3.5% over the next several years, in-line

with consensus expectations and DPZ guidance.

Source: Company data, Credit Suisse estimates Source: Company data, Consensus Metrix, Credit Suisse estimates

$0MM

$5MM

$10MM

$15MM

$20MM

$25MM

$30MM

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

US

QS

R P

izza

Segm

ent

Sal

es

Delivery Carryout0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Domino's Pizza Hut Papa John's Little Caesars

Sal

es

Mix

%

Dine-in

Carryout

Delivery

4%

6%

8%

10%

12%

14%

16%

2%

3%

4%

5%

6%

7%

8%

9%

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

2-y

r In

tern

atio

nal S

SS

1-y

r In

tern

atio

nal S

SS

1-yr International SSS 2-yr International SSS

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2019E 2020E 2021E 2022E

Inte

rnat

ional

SS

S

CSe Consensus DPZ Target

International SSS Target +3-6%

We model international SSS of 3.1% in 2019

and ~3.5% LT, near the low end of DPZ’s 3-6%

target

25 June 2019

Domino’s Pizza Inc. (DPZ) 17

New store cannibalization pressuring international SSS

The proliferation of new store growth in existing markets is one factor weighing on

international SSS trends, with territory splits now making up the majority of unit growth in

certain markets.

In the United Kingdom, splits have had a ~200-300bps drag on SSS on the region’s SSS.

Going forward, the majority of new store openings are expected to be splits, which will

continue to pressure SSS. While sales appear to recover over time and the company

benefits from overall market share gains, near-term organic SSS growth will remain

pressured. With the UK one of DPZ’s largest international markets representing ~11% of

international stores, we expect international SSS to see a drag from this strategy.

Figure 32: The majority of new unit growth is

expected to come in the form of splits.

Figure 33: Increased unit growth and greater splits

have weighed on SSS.

Source: Company data, Credit Suisse estimates

Note: 2018 unit growth estimates reflect Domino’s Pizza Group (DOM) guidance for 2/3 split unit composition.

Source: Company data, Credit Suisse estimates

India represents ~12% of international units. SSS performance improved in 2018, though

unit growth has notably decelerated over the last two years. Recently, India’s master

franchisee, Jubliant Foodworks (JUBI), has indicated intent to incorporate the fortressing

strategy in certain areas through some store splits (which the market has done before).

Given the market’s relatively large store base and lower unit growth, the splits should not

have a material impact on the region’s SSS, though could add some pressure relative to

more recent quarters with modest unit growth. JUBI indicated new opens should not affect

SSS by more than 200-300bps, noting existing stores affected by splits return to the same

level within one year.

Figure 34: SSS have been somewhat volatile, with

2018 performance the strongest in several years.

Figure 35: Unit growth in the region has

decelerated, likely alleviating SSS pressure on the

base.

Source: Company data, Credit Suisse estimates

Note: SSS above reflect calendar quarters. Jubilant Foodworks (JUBI) FY end March 31.

Source: Company data, Credit Suisse estimates

Note: Unit growth reflects calendar years.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

10

20

30

40

50

60

70

80

90

100

2014 2015 2016 2017 2018

UK

New

Unit

Gro

wth

YO

Y %

UK

New

Unit

Opens

Splits Non-Split Unit Growth YOY %

-3.5pp

-2.5pp

-1.5pp

-0.5pp

0.5pp

1.5pp

2.5pp

3.5pp

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2013 2014 2015 2016 2017 2018

SS

S D

rag f

rom

Split

s

UK

SS

S

UK SSS excl splits UK SSS incl splits SSS drag from splits

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2013 2014 2015 2016 2017 2018

India

SS

S

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

400

500

600

700

800

900

1,000

1,100

1,200

1,300

2013 2014 2015 2016 2017 2018

Unit

Gro

wth

YO

Y %

India

Units

Units Unit Growth YOY%

25 June 2019

Domino’s Pizza Inc. (DPZ) 18

Increasing penetration of global delivery aggregators

The proliferation of delivery aggregators has been a common theme across geographies

given the potential impact on the pizza segment and DPZ’s digital and delivery strength. In

the US, Domino’s has largely strayed away from delivery aggregators and does not

appear to have plans to add presence on a national scale (though franchisees may

choose to be on a third-party platform). Internationally, master franchisees appear to be

more open to at least testing partnerships with third-party providers as they grow in scale

and customer demand continues to shift toward delivery.

India tested delivery through third-party partners, though has since pulled back and

decided to control the end-to-end experience. The master franchisee, JUBI, has noted the

growth in third-party delivery driven by fundamental consumer changes (greater demand

for convenience, increasing number of women in workforce, more traffic/congestion) and

discounting. The company is working with aggregators from a platform presence

perspective, though not to complete the actual delivery.

The master franchisee, DOM, views delivery aggregators as a potential gateway to

acquire new customers. The company has been on an aggregator platform in Switzerland

for several years and in Norway and Iceland there is minimal if any aggregator presence.

In the UK, DOM recently ran a 20-store trial through Just Eat, indicating overall profit per

order was actually higher than a direct order, with nearly 40% of customers new to

Domino’s. The UK is extending the trial to more than 100 stores in 2019, highlighting

aggregators tend to appeal more to younger cohorts and can be a potential customer

acquisition channel.

DMP in Australia has also indicated it is partnering with aggregators across different

markets, viewing the platforms as a customer acquisition tool and a search engine. Given

lower discounts offered on these platforms, the orders are still profitable transactions.

DMP has also highlighted customers tend to be incremental and are different customers

not specifically entrenched to a brand or cuisine.

ALSEA has also called out the rise of third-party delivery apps pressuring Domino’s

delivery sales in Spain in particular.

25 June 2019

Domino’s Pizza Inc. (DPZ) 19

Will third-party delivery eat into Domino’s US market share? Credit Suisse View

No, we don’t expect the expansion of third-party delivery to meaningfully eat into Domino’s

US market share, though it is likely to represent incremental pressure for the foreseeable

future, driven by: 1) increasing demand and supply from third-party delivery providers

fueling higher awareness; 2) aggressive promotions/discounts; 3) QSR chains offering

delivery; 4) cross-branded campaigns between aggregators and large QSR chains; and 5)

competition for delivery drivers. Long term, we believe the pizza delivery market will

largely maintain its delivery market share, and view Domino’s as best positioned to

continue to gain share within the segment given the strength of its digital ecosystem and

long-term strategic approach. We expect Domino’s loyalty program and superior execution

in delivery will allow the company to maintain a competitive advantage even against

increasing competitive pressure in the delivery channel.

In 1Q19, Domino’s reported its lowest domestic comp in 21 quarters (3.9% in 1Q19 vs 8.7%

avg over 21 qtrs), identifying aggressive promotional activity by delivery aggregators as a

pressure point. While Domino’s has historically indicated limited impact from aggregators, we

believe the 2019 inflection reflects: 1) partnerships and cross-marketing campaigns between

delivery aggregators and QSR chains, and 2) increased advertising by aggregators with

greater access to capital as they grow, particularly at times when the convenience of delivery is

more in demand. We believe the greatest delivery share risk is at the late night daypart, during

at-home events (i.e., major sporting events, elections, etc.) and with inclement weather.

Despite increasing competition, we believe the pizza segment will largely maintain its

delivery market share despite increasing competitive threats given: 1) customers largely

choose the pizza cuisine, limiting the potential share shift; 2) customers prefer individual

brand platforms over third-party aggregators; 3) pizza is a cuisine that maintains its

integrity and travels well; 4) pizza delivers attractive value to the customer based on the

amount of food; and 5) restaurant operators and delivery aggregators still have significant

challenges ahead to improve economics for all parties involved, ensure operational

execution, develop a better system to share data and to limit the customer shift to third-

party platforms. We do believe regional and local chains are facing greater risk given the

aforementioned challenges, as delivery becomes an expectation.

Consensus Expectations

We believe consensus is pricing in pressure from the increasing growth of delivery

aggregators, with domestic SSS estimates of ~4-4.5% over the next several years below

DPZ’s average ~9% over the last five years and lower than prior estimates (albeit in part

related to decelerating comps in recent quarters, also a function of increased competitive

pressure). A significant number of questions in recent quarters have been focused on the

impending impact of third-party delivery, and expectations for delivery market share

growth among other QSR chains to be sourced from the pizza segment.

Domino’s delivery infrastructure is a competitive

advantage…

Domino’s is the number one delivery player in the number one delivery category, uniquely

positioned relative to every other restaurant concept. While many large QSR competitors

have recently partnered with third-party providers, challenges remain, and likely

exacerbate over time as incrementality and the benefit of “newness” declines. Delivery is a

core competency for Domino’s, which we believe has been a meaningful driver of its

success. In contrast, even other pizza chains have failed to execute delivery at the same

level as Domino’s, and we’re unconvinced third-party aggregators will be able to approach

25 June 2019

Domino’s Pizza Inc. (DPZ) 20

Domino’s execution levels any time soon. That said, a flexible work schedule and

potentially higher pay could be a meaningful headwind in attracting delivery drivers for

Domino’s regardless of its proprietary delivery infrastructure.

■ Overall experience – Domino’s has full control of the customer experience, from initial

order to customer delivery. In contrast, restaurants on third-party platforms hand off

control to the third-party provider completing the last mile, though ultimately are

responsible for the end experiences. While customers currently appear more accepting

of lower quality delivery orders in exchange for convenience, we’re not sure they will be

as forgiving longer term.

■ Quality control – Restaurants have limited control over the quality of the food once it

is handed off to a third party. As third-party delivery drivers seek to maximize their

order count, the quality of the food could be secondary (i.e., could wait around for

multiple orders from restaurants before delivering). In contrast, Domino’s has strict

standards regarding food quality and maintains control over the “chain of custody.”

Based on discussions with franchisees from pizza competitors, the quality of the food

delivered by third-party aggregators has been an issue.

■ Economics – Delivery is expensive for all stakeholders, including delivery drivers,

restaurants and customers. Aggressive promotions and discounting have helped drive

customer demand for delivery, though third-party aggregators and restaurants have

borne much of that customer acquisition cost. Over time, we expect costs to largely

shift to customers in the form of inflated delivery menu prices, delivery fees and service

fees. While delivery demand seems relatively inelastic right now, we don’t view that as

sustainable on a larger scale. Additionally, pizza arguably offers one of the best value

propositions for customers, and as newness and aggressive discounting dissipates, we

think the value of pizza will help sustain the segment’s delivery market share.

■ Data – Third-party aggregators own the data transacted through their platforms, giving

minimal information to restaurants about their own customers, while also having

powerful and diversified data. In contrast, customer transactions through restaurants’

own branded platforms captures proprietary data that can be used to better market and

segment customers. Access to data from digital platforms has been a key driver of

success from industry-leading share gainers over the last several years, including

Domino’s, Starbucks and Panera. New up-and-coming restaurant chains are also

leaning into their digital strategies.

■ Customer Shift – Delivery through aggregator platforms alone creates risk that

customers will shift onto the platforms, get introduced to competitors and choose to

start at the platform in the future rather than consider the restaurant from the start.

We do believe presence on a platform could be beneficial should it be incremental to

the business and attract new customers, particularly as third-party aggregators

expand and acquire new customers. Domino’s digital ecosystem is a core tenet of its

success, and risk of customer shift could be high relative to restaurants with nascent

and small digital platforms.

…but not ruling out presence on delivery platforms

Domino’s has been very clear about its unwillingness to allow a third-party to complete the

last-mile of delivery given concerns around the quality of the food and experience.

Franchisees in select markets have signed up with aggregators, which could help offset

some risk of delivery share shift to platforms, while offering an opportunity to enter the

consideration sets of customers.

We do not expect Domino’s to partner with a third-party aggregator of any kind at a

national level, though we do believe franchisees have the decision to partner with

platforms for order aggregation.

25 June 2019

Domino’s Pizza Inc. (DPZ) 21

Domino’s has indicated company-operated delivery is the lower cost option relative to

outsourcing to third-party providers given scale. However, we expect if Domino’s followed

the strategy implemented by many QSR chains and inflated delivery menu prices on

aggregator platforms to cover commission costs and/or do not offer traditional promotions,

the economics could be compelling. However, we also recognize the added potential cost

of poor execution from third parties.

There is some level of overlap between digital Domino’s users and third-party platforms,

suggesting there could be some cannibalization from presence on platforms, but such is

limited. ~10-15% of Domino’s digital users also use the four largest third-party platforms

(Grubhub, DoorDash, Uber Eats, Postmates). Customers using these platforms could

choose to transact through third parties rather than Domino’s directly, which would be a

negative, though it seems to be relatively limited in scope, for now. On the other side, ~15-

20% of customers using third-party platforms also transact through Domino’s digitally. This

suggests Domino’s could access the ~80-85% of customers on these platforms not currently

transacting through Domino’s. This could represent an opportunity to attract new customers,

as well as reduce the impact of the growing popularity of third-party aggregators.

Figure 36: ~10-15% of Domino’s digital users also

use the four largest third-party platforms.

Figure 37: ~15-20% of third-party delivery

customers also transact with Domino’s digitally,

highlighting an opportunity for Domino’s to reach

seemingly incremental 80-85% of third-party

delivery customers.

Source: comScore, Credit Suisse estimates Source: comScore, Credit Suisse estimates

Competition for delivery stomach share is growing

Demand and supply from third-party delivery providers is growing

The exponential growth of third-party delivery providers undoubtedly represents a

competitive threat to the pizza segment, which has largely faced minimal competition in

the delivery channel to-date. Third-party delivery providers have meaningfully expanded

geographic coverage and the number of restaurants on their platforms. Many QSRs have

stepped up their investments and are increasingly engaging with third-party partners,

fueling growth in the delivery channel. Further, these third-party platforms help level the

playing field for smaller companies to engage with consumers on a large scale.

Industry conferences, articles, research and discussions have focused on the delivery

channel as the industry navigates through dynamic changes. This is transforming delivery

into a “need-to-have” channel, and third-party delivery is the fastest way to “turn on”

delivery, driving the growth of the aggregators.

Based on our analysis of digital app downloads over time, third-party delivery platforms

are meaningfully growing download share relative to pizza companies. Over the past

several years, growth in third-party platform downloads have outpaced that of traditional

pizza companies. While this is in part due to the relative newness of these platforms,

such highlights increasing demand for delivery. For reference, Domino’s has ~20MM+

0%

5%

10%

15%

20%

25%

Pizza Hut Papa

John's

GrubHub DoorDash Uber Eats Postmates

Pizza Peers Delivery

% D

om

ino's

Use

rs

Cro

ss V

isiti

ng

0%

5%

10%

15%

20%

25%

30%

Pizza Hut Papa

John's

GrubHub DoorDash Uber Eats Postmates

Pizza Peers Delivery

% P

izza

Peers

/Deliv

ery

Use

rs

Cro

ss V

isiti

ng

25 June 2019

Domino’s Pizza Inc. (DPZ) 22

active users on its digital platform. Grubhub has already amassed 19MM+ active users

as of the end of 1Q19 alone, and together with other aggregators, would meaningfully

top Domino’s users.

Figure 38: Delivery app providers are now growing

digital downloads at a faster rate than the pizza

players.

Figure 39: There is notable overlap among top

digital aggregators, highlighting competition in the

restaurant space overall as well as among delivery

providers.

Note: Read starting from left. Example: 34% of Uber Eats users also visit Grubhub. 19% of Grubhub digital users also use Uber Eats.

Source: SensorTower, Credit Suisse estimates

Note: Pizza Apps include Pizza Hut, Papa John’s, Hungry Howie’s, Domino’s, MyCicis, Little Caesars, Blaze, Papa Murphy’s, PizzaRev, Pieology and Marco’s. Delivery Apps include Grubhub, Seamless, Delviery.com, Postmates, DoorDash, Caviar and Uber Eats.

Source: comScore, Credit Suisse estimates

Figure 40: Based on Google search volumes by metro areas, Domino’s has lost relative volume share

compared to the largest delivery aggregators, highlighting the increasing competitive threat from these

players (we use Grubhub and DoorDash as proxies).

Source: Google Trends, Credit Suisse estimates

Aggressive promos and discounts have recently driven more compelling value proposition

Increasing advertising by the largest third-party delivery aggregator, Grubhub, the launch

of DoorDash’s first TV campaign in January and co-marketing campaigns between QSR

chains and third-party providers suggest increasing competition for share of voice in

delivery. Grubhub spent $170MM in advertising in 2018, a ~60% increase from 2017,

which does not even include free promotions it might offer with select partners (i.e., Taco

Bell). Many other platforms also fund free delivery periodically for select chains to drive

trial as part of the partnership.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan-1

2

Jun-1

2

Nov-

12

Apr-

13

Sep-1

3

Feb-1

4

Jul-1

4

Dec-

14

May-

15

Oct

-15

Mar-

16

Aug-1

6

Jan-1

7

Jun-1

7

Nov-

17

Apr-

18

Sep-1

8

Feb-1

9

Dig

ital A

pp D

ow

nlo

ad S

hare

Pizza Apps Delivery Apps

Uber Eats Grubhub DoorDash Postmates

Uber Eats 34% 35% 19%

Grubhub 19% 27% 12%

DoorDash 22% 30% 15%

Postmates 23% 27% 30%

Cross App Usage

2013 2014 2015

2016 2017 2018

25 June 2019

Domino’s Pizza Inc. (DPZ) 23

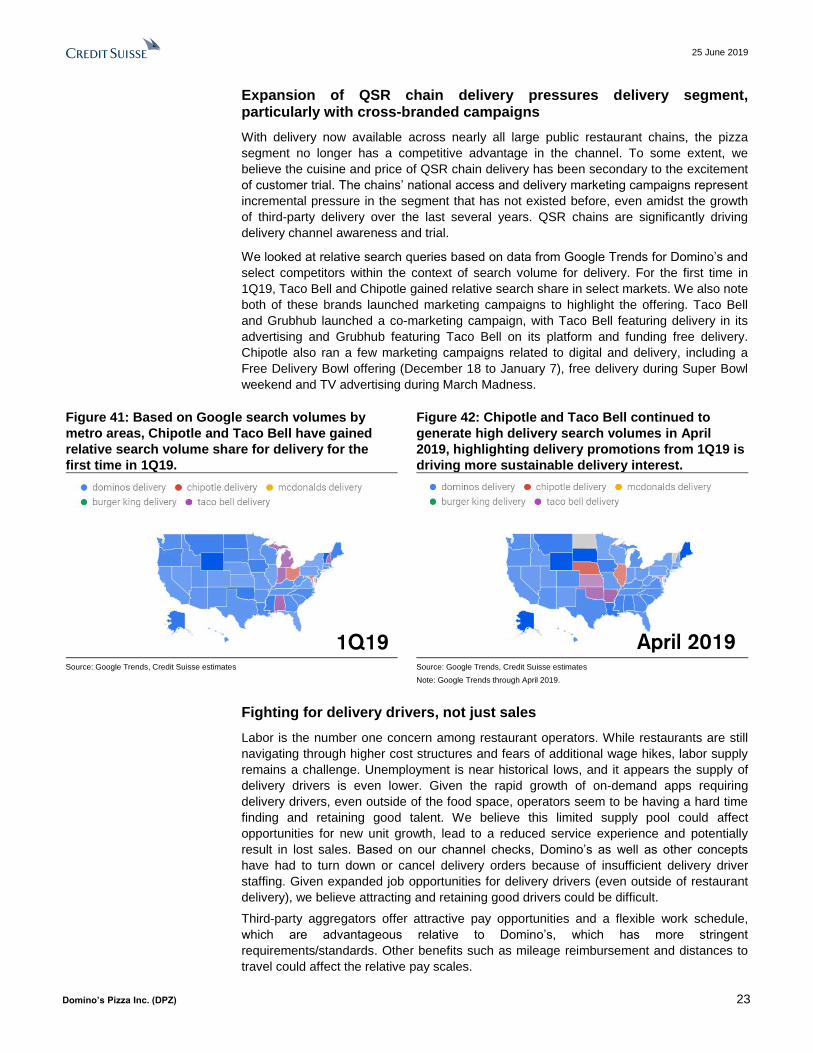

Expansion of QSR chain delivery pressures delivery segment, particularly with cross-branded campaigns

With delivery now available across nearly all large public restaurant chains, the pizza

segment no longer has a competitive advantage in the channel. To some extent, we

believe the cuisine and price of QSR chain delivery has been secondary to the excitement

of customer trial. The chains’ national access and delivery marketing campaigns represent

incremental pressure in the segment that has not existed before, even amidst the growth

of third-party delivery over the last several years. QSR chains are significantly driving

delivery channel awareness and trial.

We looked at relative search queries based on data from Google Trends for Domino’s and

select competitors within the context of search volume for delivery. For the first time in

1Q19, Taco Bell and Chipotle gained relative search share in select markets. We also note

both of these brands launched marketing campaigns to highlight the offering. Taco Bell

and Grubhub launched a co-marketing campaign, with Taco Bell featuring delivery in its

advertising and Grubhub featuring Taco Bell on its platform and funding free delivery.

Chipotle also ran a few marketing campaigns related to digital and delivery, including a

Free Delivery Bowl offering (December 18 to January 7), free delivery during Super Bowl

weekend and TV advertising during March Madness.

Figure 41: Based on Google search volumes by

metro areas, Chipotle and Taco Bell have gained

relative search volume share for delivery for the

first time in 1Q19.

Figure 42: Chipotle and Taco Bell continued to

generate high delivery search volumes in April

2019, highlighting delivery promotions from 1Q19 is

driving more sustainable delivery interest.

Source: Google Trends, Credit Suisse estimates Source: Google Trends, Credit Suisse estimates

Note: Google Trends through April 2019.

Fighting for delivery drivers, not just sales

Labor is the number one concern among restaurant operators. While restaurants are still

navigating through higher cost structures and fears of additional wage hikes, labor supply

remains a challenge. Unemployment is near historical lows, and it appears the supply of

delivery drivers is even lower. Given the rapid growth of on-demand apps requiring

delivery drivers, even outside of the food space, operators seem to be having a hard time

finding and retaining good talent. We believe this limited supply pool could affect

opportunities for new unit growth, lead to a reduced service experience and potentially

result in lost sales. Based on our channel checks, Domino’s as well as other concepts

have had to turn down or cancel delivery orders because of insufficient delivery driver

staffing. Given expanded job opportunities for delivery drivers (even outside of restaurant

delivery), we believe attracting and retaining good drivers could be difficult.

Third-party aggregators offer attractive pay opportunities and a flexible work schedule,

which are advantageous relative to Domino’s, which has more stringent

requirements/standards. Other benefits such as mileage reimbursement and distances to

travel could affect the relative pay scales.

1Q19 April 2019

25 June 2019

Domino’s Pizza Inc. (DPZ) 24

The shift toward aggregators over time

Increasing awareness, geographic coverage and restaurant partnerships are indicative of

the growing demand and supply of delivery aggregators, with share expected to increase

over time. Based on our survey of consumers in March 2019, delivery aggregators are

gaining favor among consumers as a preferred choice for delivery. On average, ~14% of

consumers indicated third-party platforms were their preferred ordering methods, up from

10% in July 2018. Across all age groups and neighborhoods, less consumers indicated

their preferred ordering method was calling the restaurant directly, suggesting digital could

improve the overall customer experience.

~50% of consumers indicated ordering directly through the restaurant website/app was

their favorite ordering method, an increase of ~7% from July 2018 and now the most

preferred ordering method. More than 60% of consumers age 18-29 selected ordering

through restaurant website/app as their preferred method (+13% March 2019 from July

2018), which we believe is in part due to the offering of loyalty/rewards programs, which

seems to be the most important and intent-driving factor relative to other cohorts.

While we do believe third-party aggregators will grab a greater market share over time, the

overall customer experience from branded websites/apps is superior to the platforms and

is a competitive advantage, for now. Domino’s remains well positioned given its digital

ecosystem and compelling loyalty program, and expect the company to defend its share

even in an environment of growing penetration from delivery aggregators.

Figure 43: On average ~14% consumers indicated

third-party platforms as the preferred delivery

method, with some range across cohorts.

Figure 44: Consumers across age groups are

shifting to digital channels, with the greatest

change in delivery aggregator preference among

those ages 30-44, and the greatest move toward

branded websites/apps among those ages 18-29.

Source: Survey data, Credit Suisse estimates Source: Survey data, Credit Suisse estimates

12%22%

12% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

18-29 30-44 45-60 60+

Age

% R

esp

ondents

What is/would be your preferred method to order delivery?

Call the restaurant Restaurant website/mobile app Third-party aggregator

-15%

-10%

-5%

0%

5%

10%

15%

18-29 30-44 45-60 60+

Chan

ge M

arch

201

9 v

s Ju

ne 2

01

8

Call the restaurant Restaurant website/mobile app Third-party aggregator

25 June 2019

Domino’s Pizza Inc. (DPZ) 25

Figure 45: Consumers in urban markets tend to

prefer third-party aggregators, though this is in part

due to the availability and magnitude of restaurants

relative to suburban/rural neighborhoods.

Figure 46: Consumers are increasingly shifting