Themes in Energy Efficiency - Credit Suisse | PLUS

112

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 03 April 2014 Global Equity Research Themes in Energy Efficiency Connections Series Source: Thinkstock As part of our global energy efficiency research, this report reviews building energy efficiency challenges and investment opportunities. Challenges: Buildings are the largest energy consumers, with a c35% share of global energy consumption. Without further efficiency gains, our research indicates that energy consumption and CO² emissions by buildings could increase more than 50% by 2050. This is led by emerging countries, where residential floor space looks set to expand by 50bn m², or more than the current amount for the US and Europe combined. Opportunities: Interest in energy efficiency from property owners is rapidly increasing owing to cost-savings and the positive impact on property values. According to our research, refurbishing the existing building stock across developed countries would require investment of more than $3,000bn. This provides long-term structural growth dynamics to OEMs, property consultants, technical installation companies and construction firms. Stock implications: We identify c170 stocks exposed to this theme, with our Credit Suisse HOLT ® analysis indicating that they have generated above- average through-cycle cash-flow returns. In addition, HOLT indicates the companies have outperformed the MSCI Global Industrials and MSCI World indices on a 1-, 3- and 5-year basis. We highlight 46 companies with significant exposure to the theme: 20 are rated Outperform by our global equity analysts. Credit Suisse has a Delta One basket (CSGLBENF Index) featuring companies exposed to this theme. The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients. Thematic Research Eugene Klerk 44 20 7883 4678 [email protected] Richard Kersley 44 20 7888 0313 [email protected] Ashlee Ramanathan 44 20 7883 9934 [email protected] Stefano Natella 212 325 4217 [email protected] Thematic Research: This report forms part of Credit Suisse's Global Thematic Research offering.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Themes in Energy Efficiency - Credit Suisse | PLUS

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

03 April 2014

Global

Equity Research

Themes in Energy Efficiency Connections Series

Source: Thinkstock

As part of our global energy efficiency research, this report reviews

building energy efficiency challenges and investment opportunities.

Challenges: Buildings are the largest energy consumers, with a c35% share of

global energy consumption. Without further efficiency gains, our research

indicates that energy consumption and CO² emissions by buildings could

increase more than 50% by 2050. This is led by emerging countries, where

residential floor space looks set to expand by 50bn m², or more than the current

amount for the US and Europe combined.

Opportunities: Interest in energy efficiency from property owners is rapidly

increasing owing to cost-savings and the positive impact on property values.

According to our research, refurbishing the existing building stock across

developed countries would require investment of more than $3,000bn. This

provides long-term structural growth dynamics to OEMs, property consultants,

technical installation companies and construction firms.

Stock implications: We identify c170 stocks exposed to this theme, with our

Credit Suisse HOLT® analysis indicating that they have generated above-

average through-cycle cash-flow returns. In addition, HOLT indicates the

companies have outperformed the MSCI Global Industrials and MSCI World

indices on a 1-, 3- and 5-year basis. We highlight 46 companies with significant

exposure to the theme: 20 are rated Outperform by our global equity analysts.

Credit Suisse has a Delta One basket (CSGLBENF Index) featuring companies

exposed to this theme.

The Credit Suisse Connections Series

leverages our exceptional breadth of

macro and micro research to deliver

incisive cross-sector and cross-border

thematic insights for our clients.

Thematic Research

Eugene Klerk

44 20 7883 4678

Richard Kersley

44 20 7888 0313

Ashlee Ramanathan

44 20 7883 9934

Stefano Natella

212 325 4217

Thematic Research:

This report forms part of Credit Suisse's

Global Thematic Research offering.

03 April 2014

Themes in Energy Efficiency 2

Table of contents Credit Suisse research 3 Key macro charts 4 Key stock-related charts 5 Executive summary 6

Global energy demand growth set to continue 6 Buildings drive energy consumption globally 6 The residential building efficiency market 8 The non-residential opportunity 9 Energy efficiency is a strong investment theme 10

Energy demand unlikely to slow down 12 Three key demand drivers 12 Consumption in case efficiency does not improve 15 Rising supply concerns to act as efficiency catalyst 17

Buildings and energy efficiency 18 Environmental concerns in no-change scenario 19 Building efficiency for the residential market 21 Building efficiency for non-residential buildings 31

Legislation plays a key role 34 Building-related policies 34 Component policies 38

Engagement from the private sector 39 Key products and technologies 42

Improving the building envelope 44 Reducing heating and cooling requirements 46 Improving lighting and appliances 47

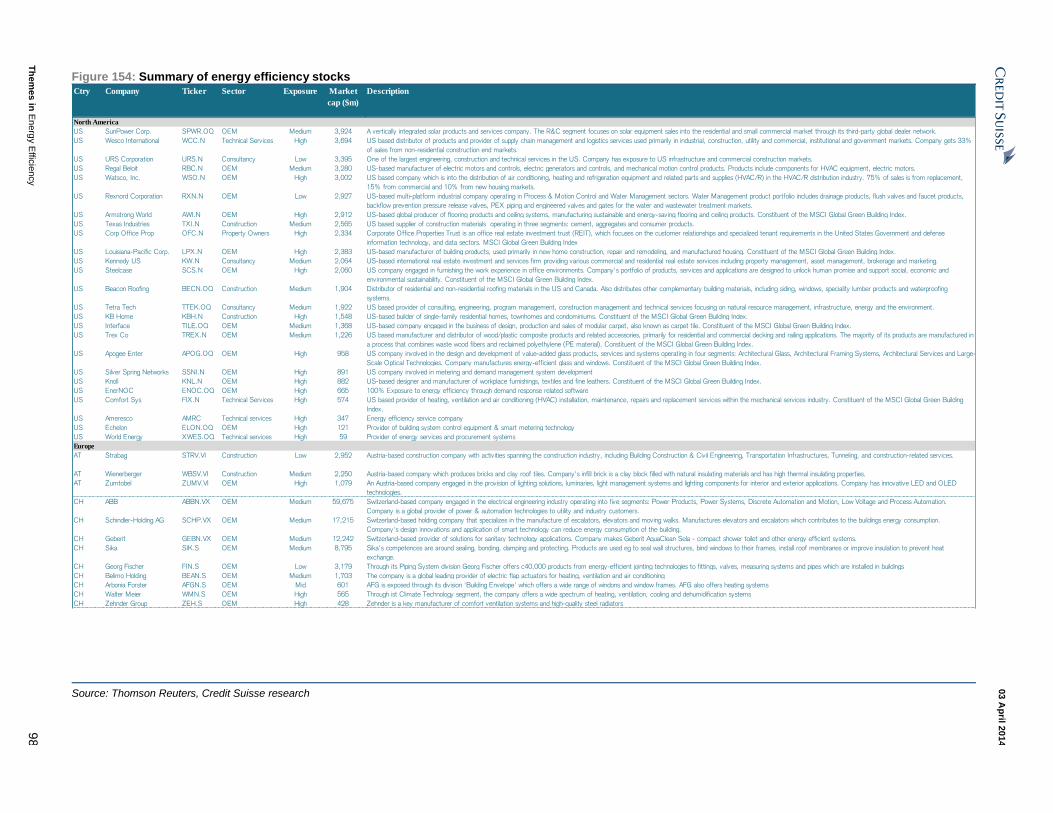

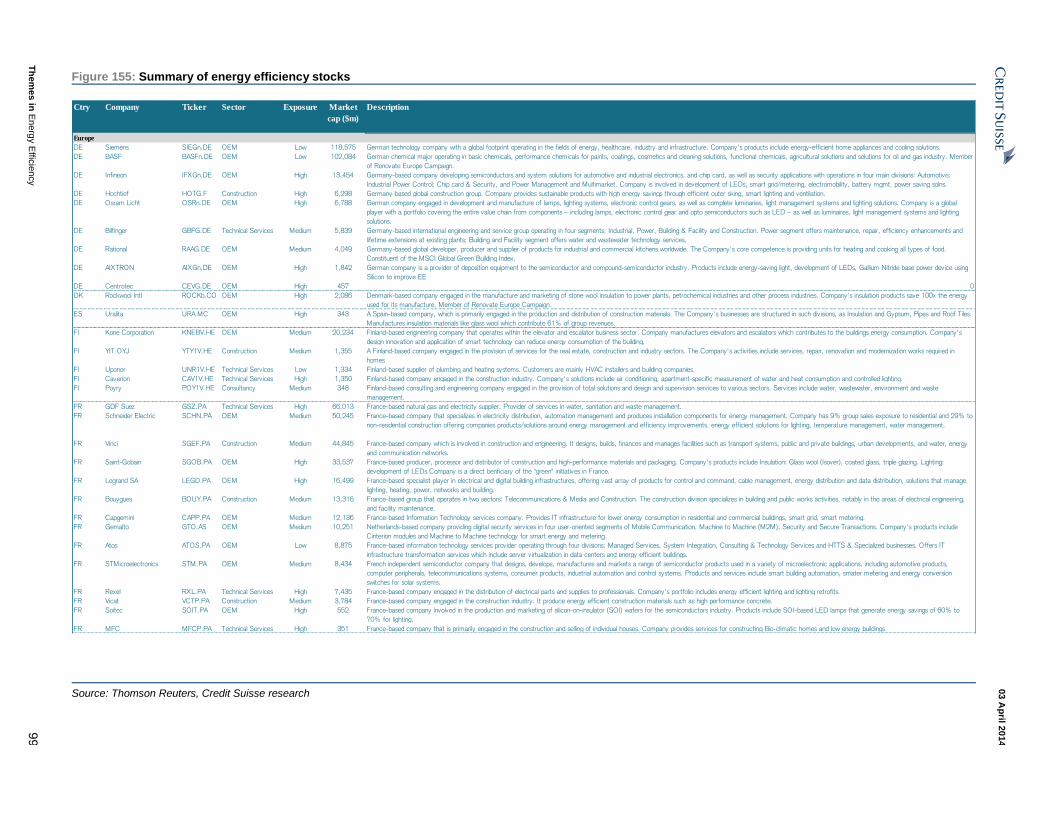

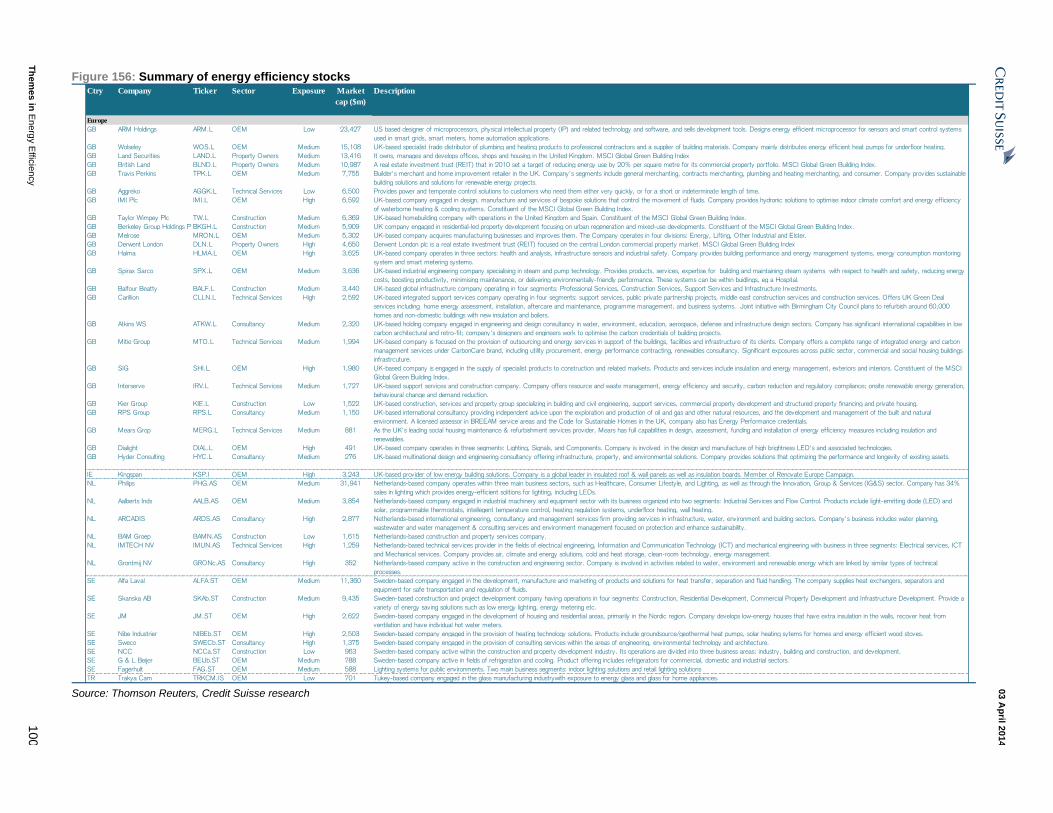

Identifying investment opportunities 50 Who is exposed to building energy efficiency? 50 Building efficiency related stocks 52 Efficiency-related stocks vs. global industrials 53 Efficiency-exposed companies by subsector 55 Global stock ideas using Credit Suisse HOLT 59 Key global stock ideas from our analysts 61

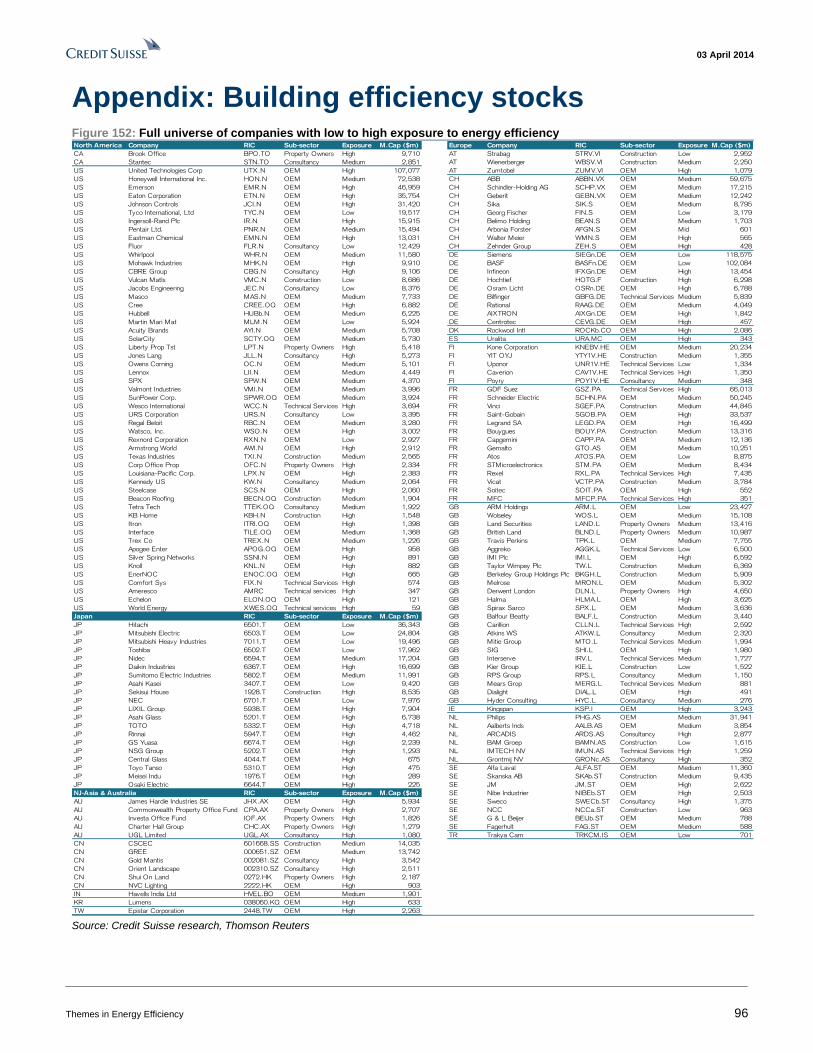

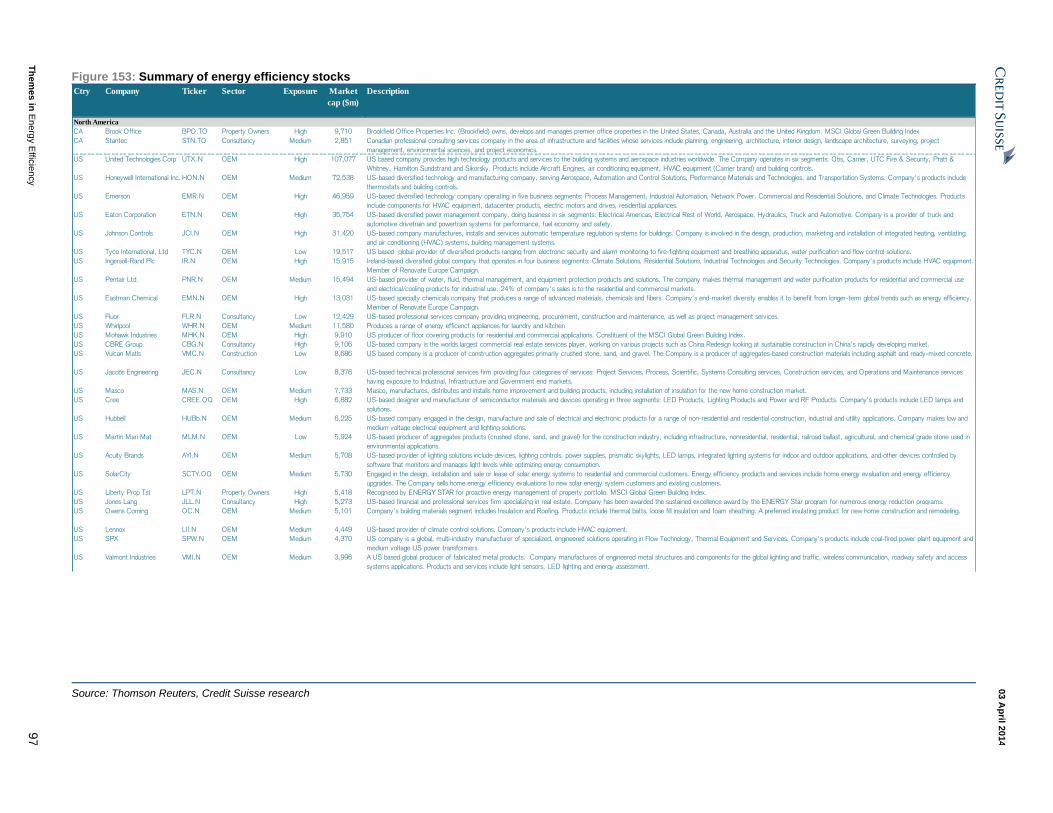

Company profiles 62 Appendix: Building efficiency stocks 96 Appendix: Key technologies 102

03 April 2014

Themes in Energy Efficiency 3

Credit Suisse research Figure 1: Contributing analysts and key teams

Thematic Research Telephone E-mail

Eugène Klerk + 44 20 7883 4678 [email protected]

Richard Kersley + 44 20 7888 0313 [email protected]

Ashlee Ramanathan + 44 20 7883 9934 [email protected]

Stefano Natella + 212 325 4217 [email protected]

North America

Capital Goods

Julian Mitchell + 212 325 6668 [email protected]

Charles Clarke + 212 538 7095 [email protected]

Jonathan Shaffer + 212 325 1259 [email protected]

Clean Technology

Patrick Jobin + 212 325 0843 [email protected]

Brandon Heiken + 212 325 6608 [email protected]

Maheep Mandloi + 212 325 2345 [email protected]

Business Services

Hamzah Mazari + 212 538 7983 [email protected]

Flavio Campos + 212 325 4411 [email protected]

Oil & Gas

Edward Westlake + 212 325 6751 [email protected]

Utilities

Dan Eggers + 212 538 8430 [email protected]

Europe

Capital Goods

Andre Kukhnin + 44 20 7888 0350 [email protected]

Jonathan Hurn + 44 20 7883 4532 [email protected]

Simon Toennessen + 44 20 7883 6893 [email protected]

Utilities

Vincent Gilles + 44 20 7888 1926 [email protected]

Michel Debs + 44 20 7883 9952 [email protected]

Oil & Gas

David Thomas + 44 20 7888 0277 [email protected]

Japan

Machinery

Shinji Kuroda + 81 3 4550 9994 [email protected]

Yunchao Zhao + 81 3 4550 9903 [email protected]

Steel

Shinya Yamada + 81 3 4550 9910 [email protected]

Glass/Ceramics/Battery

Jun Yamaguchi + 81 3 4550 9789 [email protected]

Electronic component

Akinori Kanemoto + 81 3 4550 7363 [email protected]

Construction & real estate

Masahiro Mochizuki + 81 3 4550 7389 [email protected]

Non-Japan Asia

REITs

John Richmond + 61 2 8205 4580 [email protected]

Stephen Rich + 61 2 8205 4617 [email protected]

Mikhail Mohl + 61 2 8205 4413 [email protected]

Construction & Engineering

Emma Alcock + 61 2 8205 4403 [email protected]

Electronics

Derrick Yang + 886 2 2715 6367 [email protected]

Product Management

Katio Iorio + 212 538 6386 [email protected]

Daisuke Takato + 81 3 4550 9671 [email protected] Source: Credit Suisse research

03 April 2014

Themes in Energy Efficiency 4

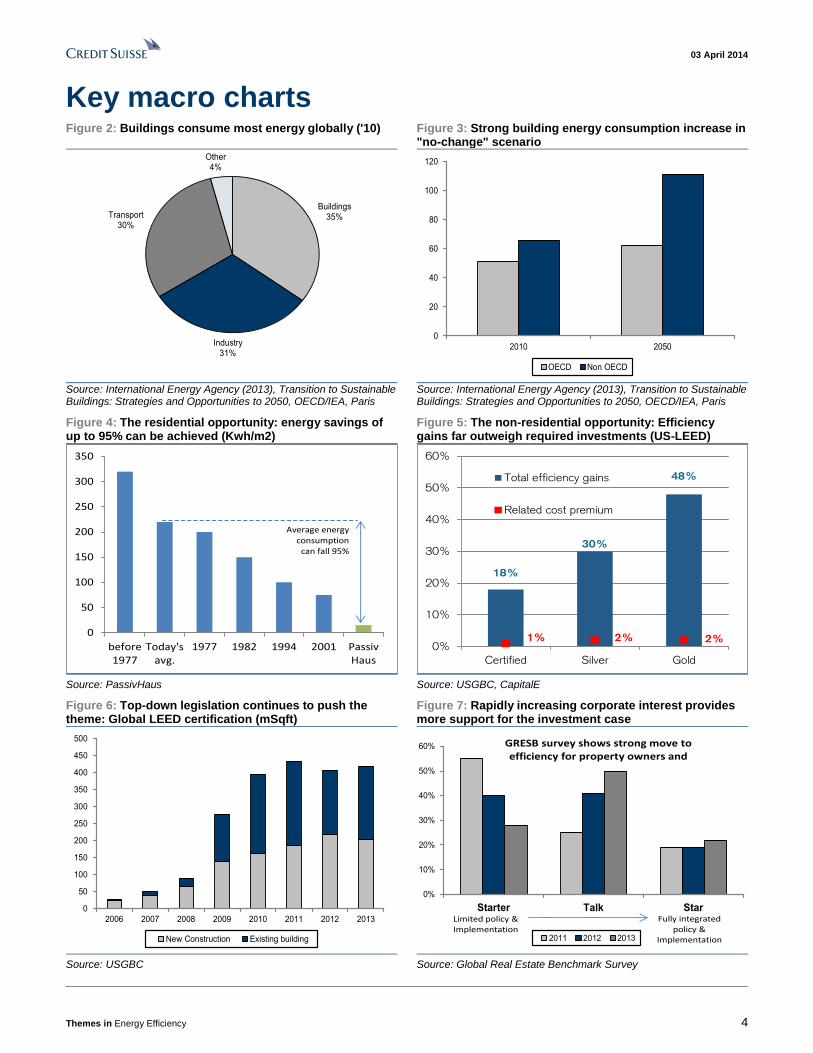

Key macro charts Figure 2: Buildings consume most energy globally ('10) Figure 3: Strong building energy consumption increase in

"no-change" scenario

Buildings35%

Industry31%

Transport30%

Other4%

0

20

40

60

80

100

120

2010 2050

OECD Non OECD

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Figure 4: The residential opportunity: energy savings of up to 95% can be achieved (Kwh/m2)

Figure 5: The non-residential opportunity: Efficiency gains far outweigh required investments (US-LEED)

0

50

100

150

200

250

300

350

before1977

Today'savg.

1977 1982 1994 2001 PassivHaus

Average energyconsumption

can fall 95%

18%

30%

48%

1% 2% 2%0%

10%

20%

30%

40%

50%

60%

Certified Silver Gold

Total efficiency gains

Related cost premium

Source: PassivHaus Source: USGBC, CapitalE

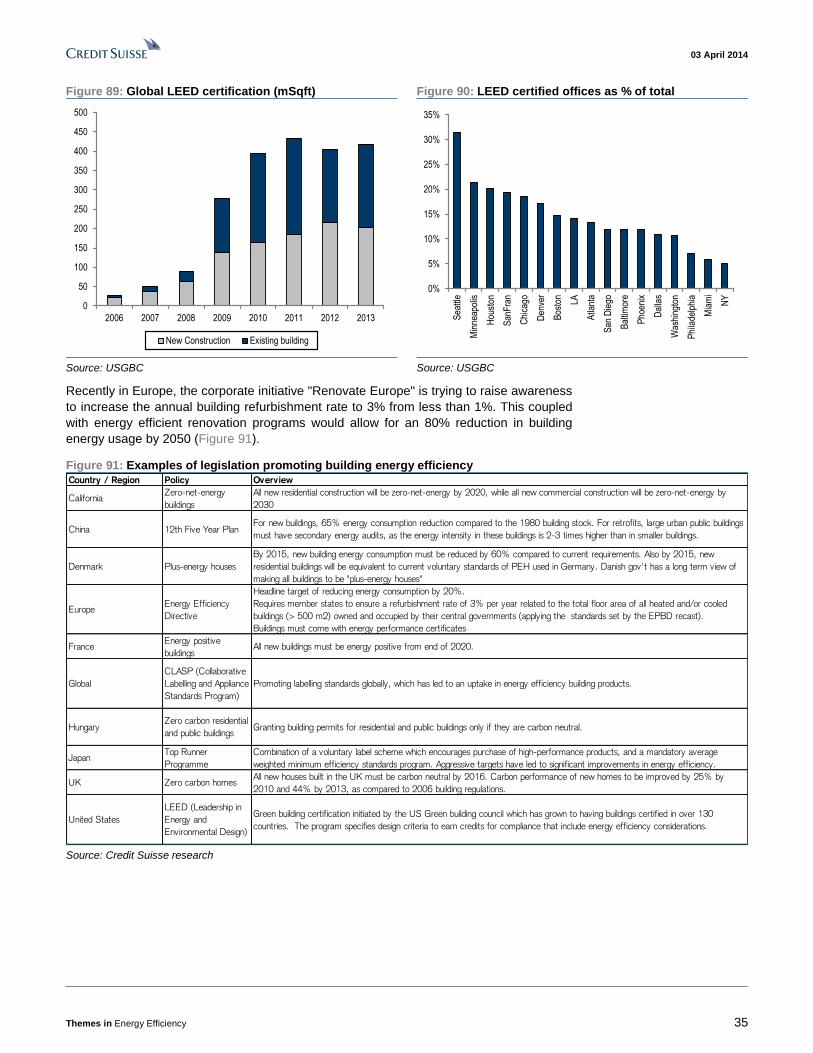

Figure 6: Top-down legislation continues to push the theme: Global LEED certification (mSqft)

Figure 7: Rapidly increasing corporate interest provides more support for the investment case

0

50

100

150

200

250

300

350

400

450

500

2006 2007 2008 2009 2010 2011 2012 2013

New Construction Existing building

0%

10%

20%

30%

40%

50%

60%

Starter Talk Star

2011 2012 2013

Limited policy & Implementation

Fully integrated policy &

Implementation

GRESB survey shows strong move to efficiency for property owners and

Source: USGBC Source: Global Real Estate Benchmark Survey

03 April 2014

Themes in Energy Efficiency 5

Key stock-related charts Figure 8: We see c170 companies with exposure: c75% of stocks have a Mcap of less than $10bn

Figure 9: Building efficiency exposed companies have generated higher cash flow returns than global industrials…

Europe,

82

N.Americ

a, 57

Asia, 17

Japan,

20

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Value creation: CFROI -/- discount rate

Efficiency universe Global industrials

Source: Credit Suisse research Note: Past performance should not be taken as an indication or guarantee of future performance. Source: Credit Suisse HOLT

Figure 10: …and have generated superior returns to global equities and industrials on 1, 3 and 5 years

Figure 11: Undervalued subsectors on Credit Suisse HOLT are cooling, consultancy, appliances and lighting

1.0

1.5

2.0

2.5

3.0

3.5

Feb-09 Jan-10 Dec-10 Nov-11 Oct-12 Sep-13

Universe

MSCI World

MSCI Industrials

Returns 1yr 3yr 5yr

Universe 22% 38% 199% MSCI World 16% 25% 101%

0

2

4

6

8

10

12

14

16

18

10yr Last fiscal year Forecast Market implied CFROI

Undervalued Overvalued

Source: Credit Suisse HOLT Source: Credit Suisse HOLT, Credit Suisse research

Figure 12: Outperform-rated companies highlighted by our analysts, grouped by region and ranked by Mcap

Ctry Company Ticker Sector Exposure

HOLT

score

Mcap

($m) CS Rating

% to

CS TP

P/E '14E

(x) CFROI EG Revenue

North America

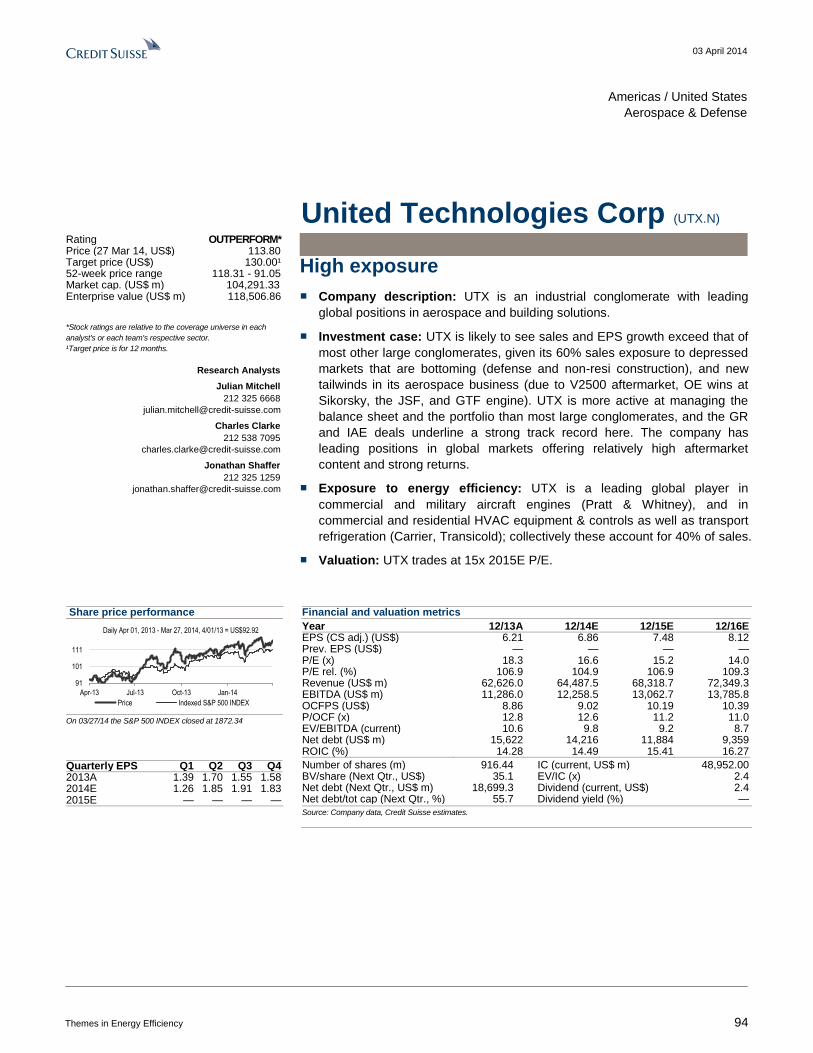

US United Technologies Corp UTX.N OEM High 5 107,077 OUTPERFORM 11% -12% 17.0 19% 10% 4%

US Emerson EMR.N OEM High 5 46,959 OUTPERFORM 14% 33% 17.1 18% 10% 3%

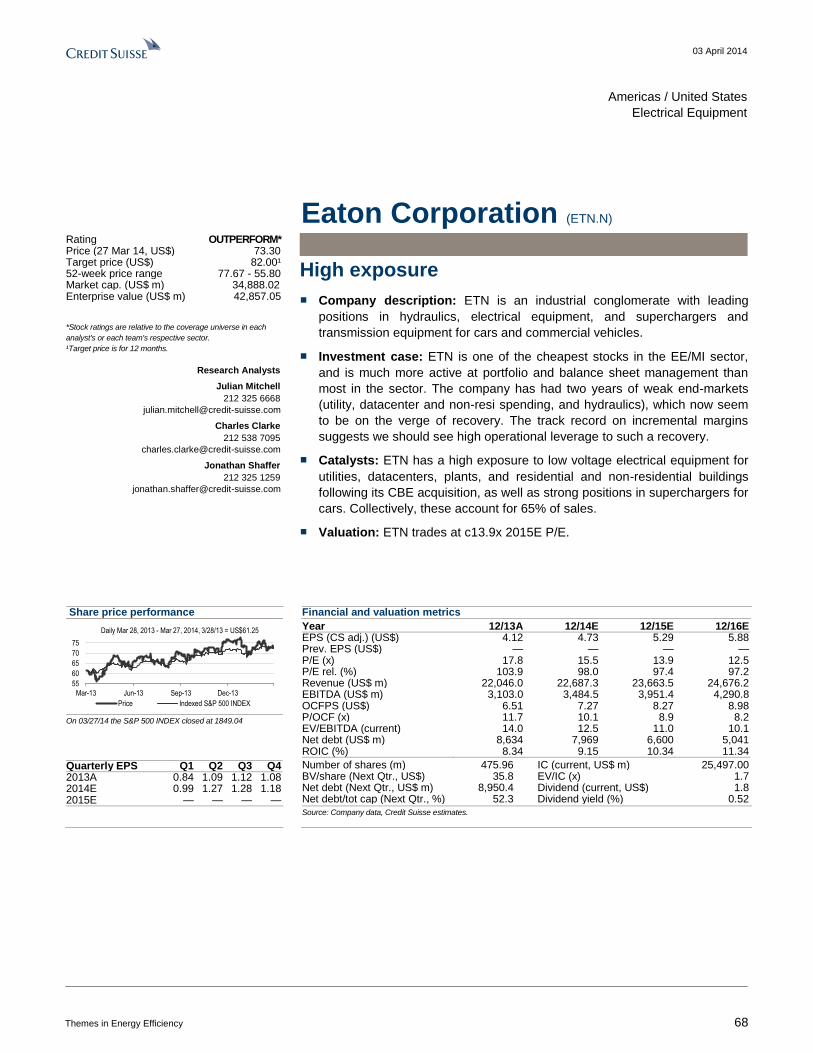

US Eaton Corporation ETN.N OEM High 4 35,754 OUTPERFORM 9% -18% 15.9 19% 13% 4%

US Ingersoll-Rand Plc IR.N OEM High 2 15,915 OUTPERFORM 21% -16% 17.9 20% 22% 5%

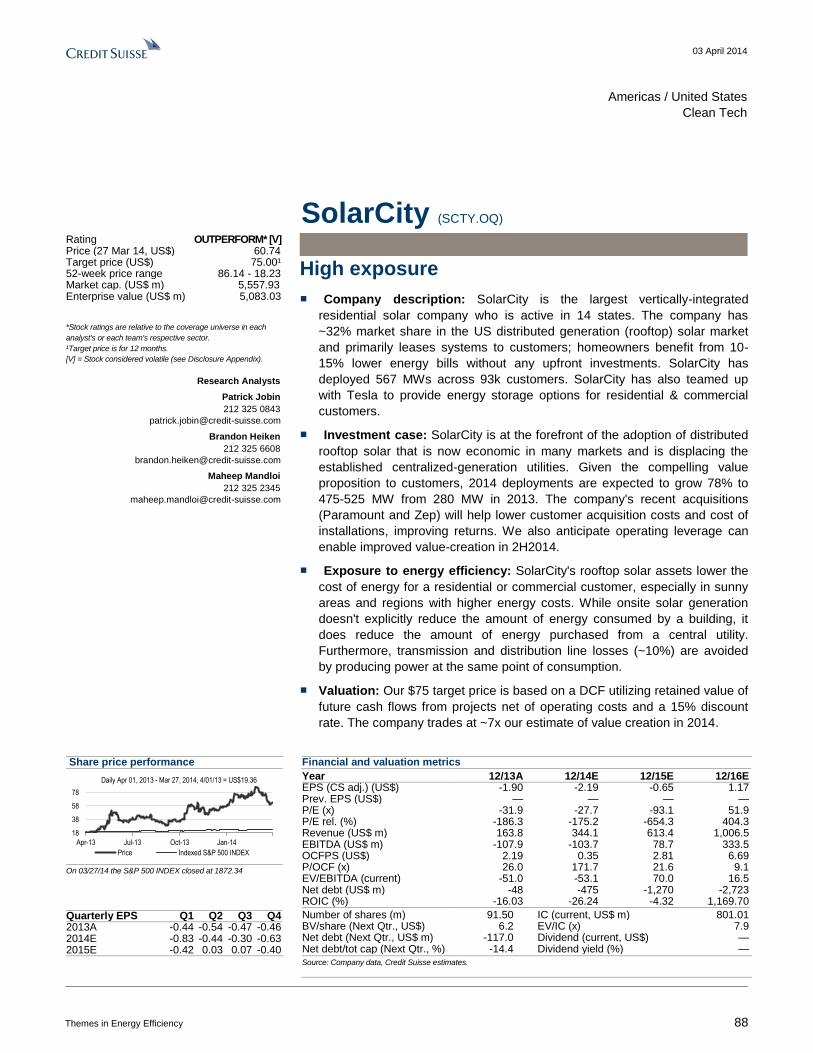

US SolarCity SCTY.OQ OEM Medium 1 5,730 OUTPERFORM 20% -90% -37% 28% 94%

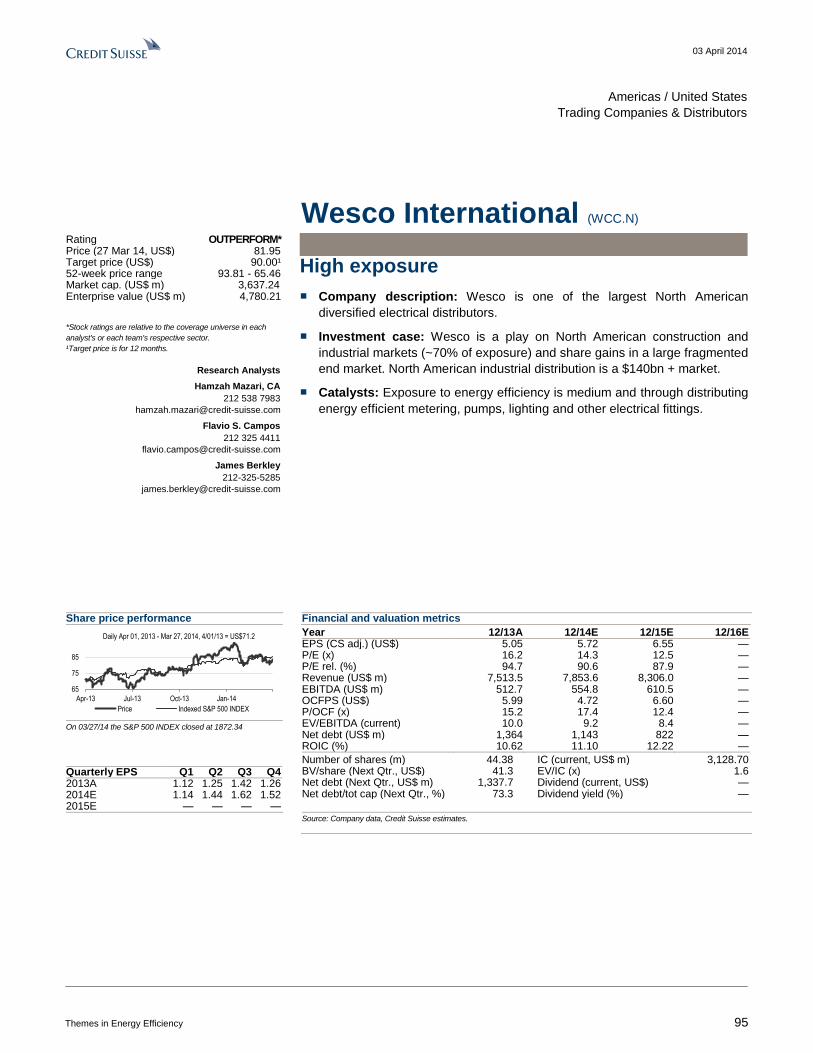

US Wesco International WCC.N Technical Services High 5 3,694 OUTPERFORM 8% 68% 14.6 23% 14% 5%

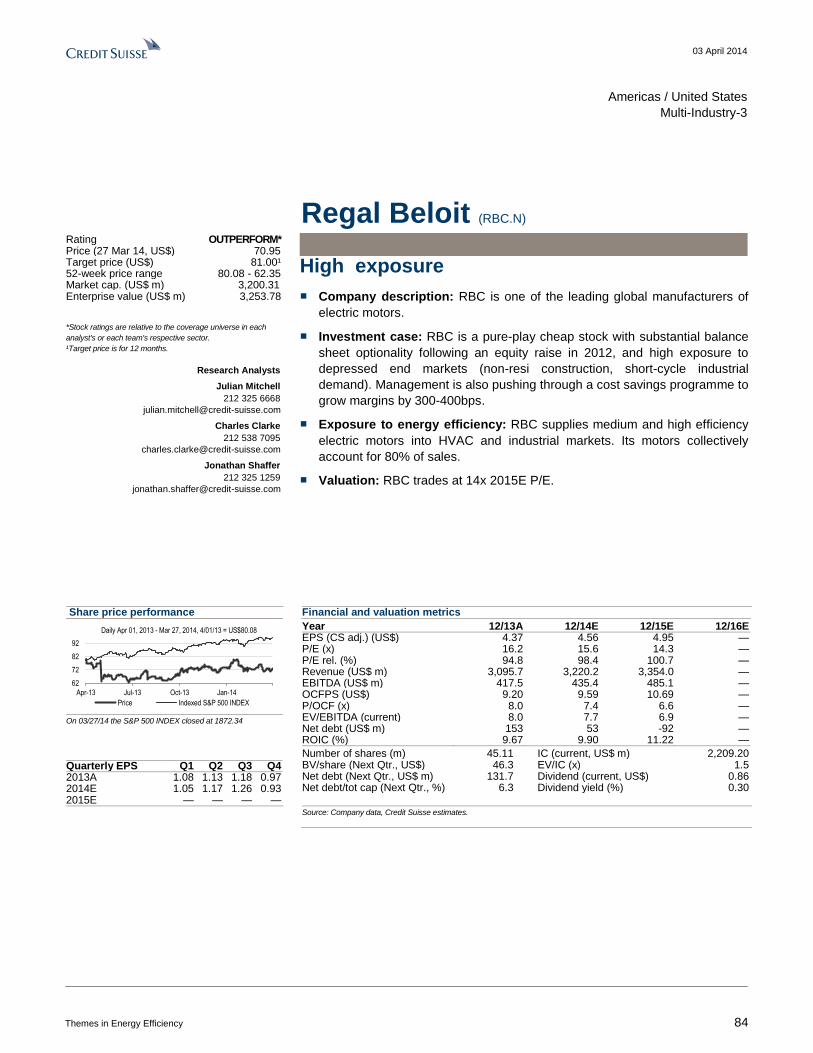

US Regal Beloit RBC.N OEM Medium 5 3,280 OUTPERFORM 11% 67% 16.0 11% 6% 4%

Europe

CH ABB ABBN.VX OEM Medium 4 59,675 OUTPERFORM 14% 40% 13.8 15% 17% 4%

CH Schindler-Holding AG SCHP.VX OEM Medium 2 17,215 OUTPERFORM 15% -1% 20.6 15% 11% 6%

FR GDF Suez GSZ.PA Technical Services High 3 66,013 OUTPERFORM 3% -22% 15.1 4% -2% 3%

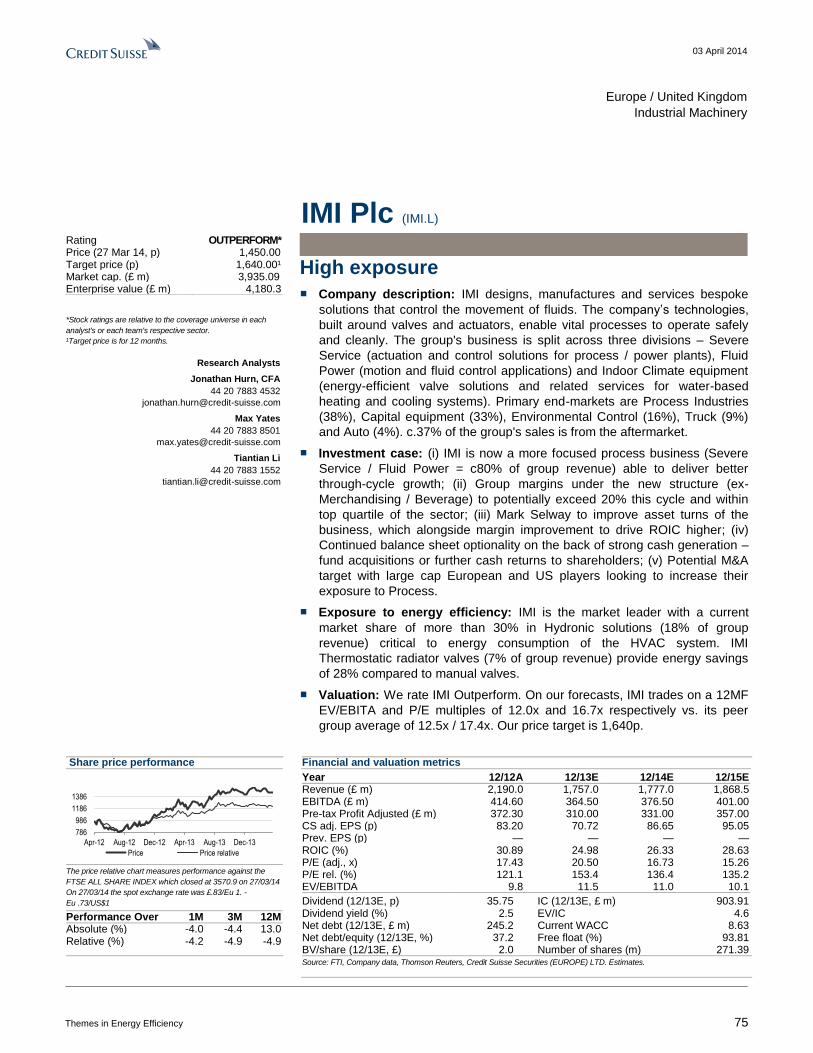

GB IMI Plc IMI.L OEM High 1 6,592 OUTPERFORM 12% -8% 16.8 16% 16% 3%

GB Halma HLMA.L OEM High 4 3,625 OUTPERFORM 8% -7% 19.3 25% 6% 4%

NL ARCADIS ARDS.AS Consultancy High 5 2,877 OUTPERFORM 13% 11% 14.9 18% 10% 4%

Japan

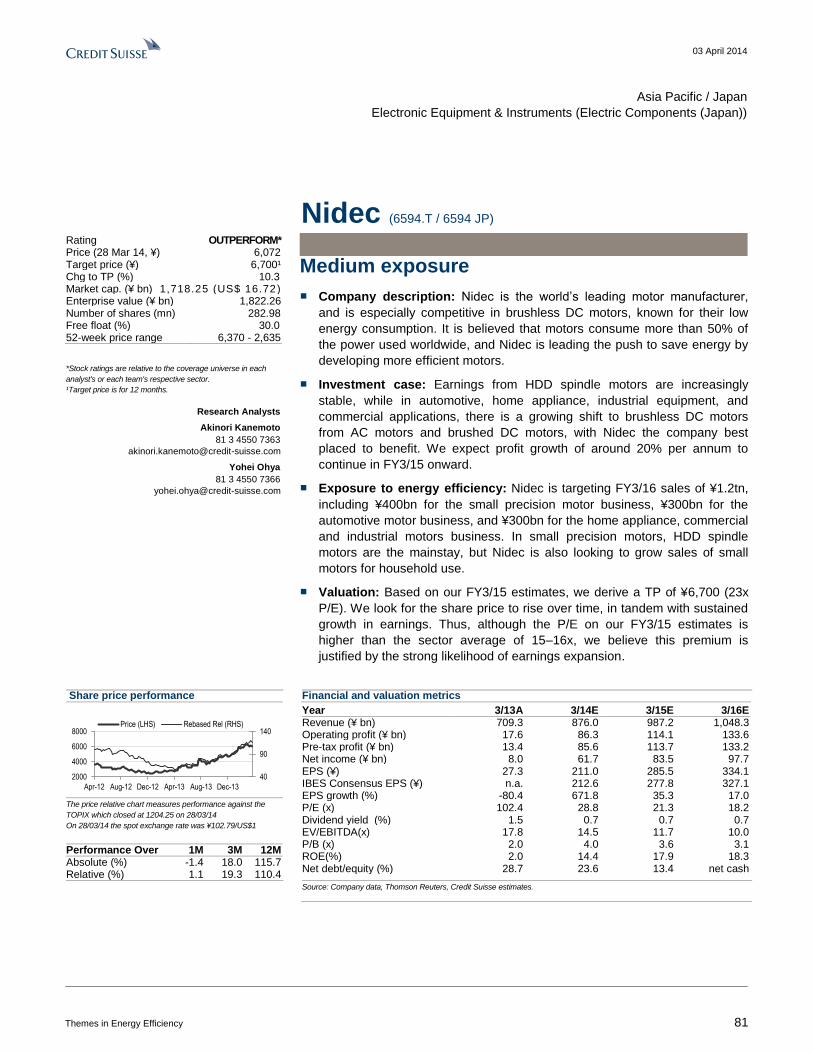

JP Nidec 6594.T OEM Medium 1 17,204 OUTPERFORM 4% -50% 24.1 8% 41% 11%

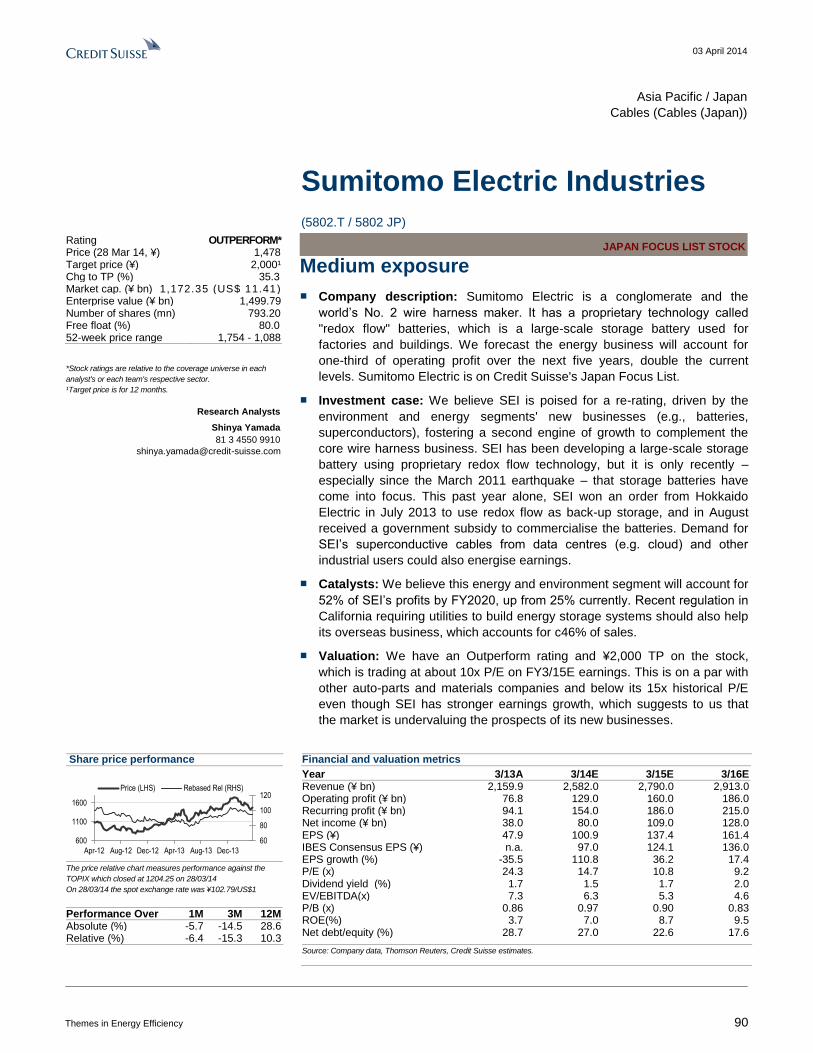

JP Sumitomo Electric Industries 5802.T OEM Medium 3 11,991 OUTPERFORM 28% 23% 12.2 2% 34% 8%

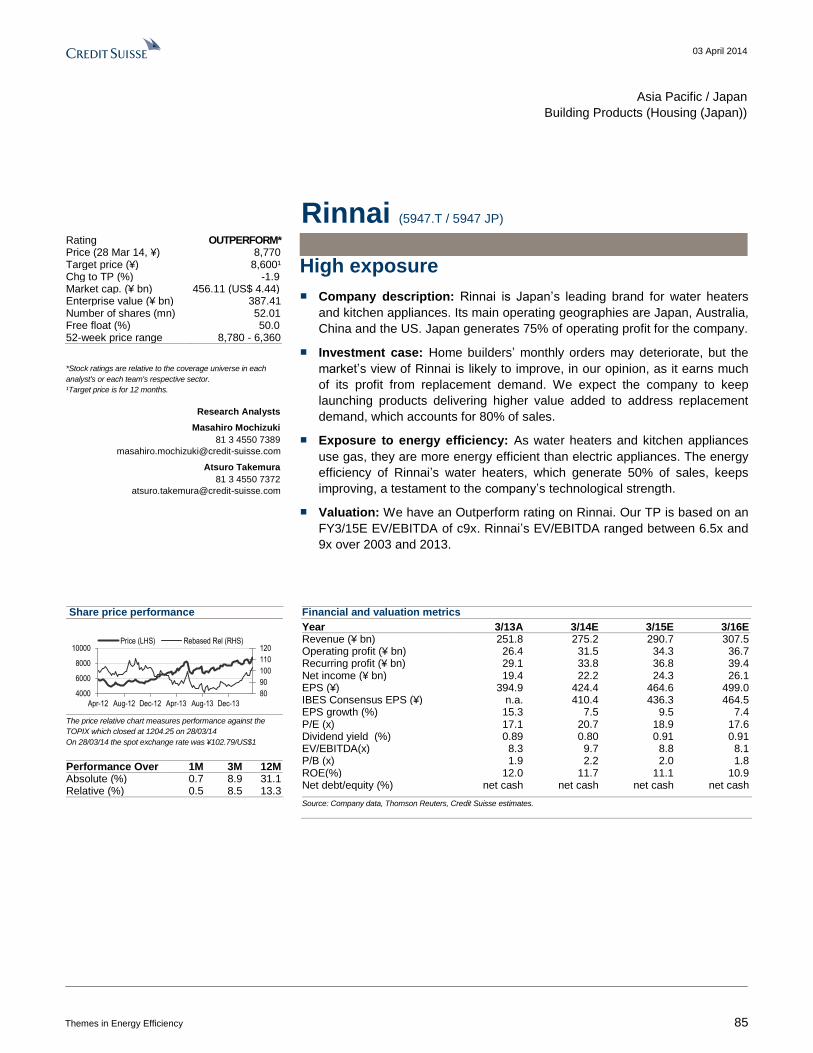

JP Rinnai 5947.T OEM High 4 4,462 OUTPERFORM -3% -19% 19.5 8% 8% 6%

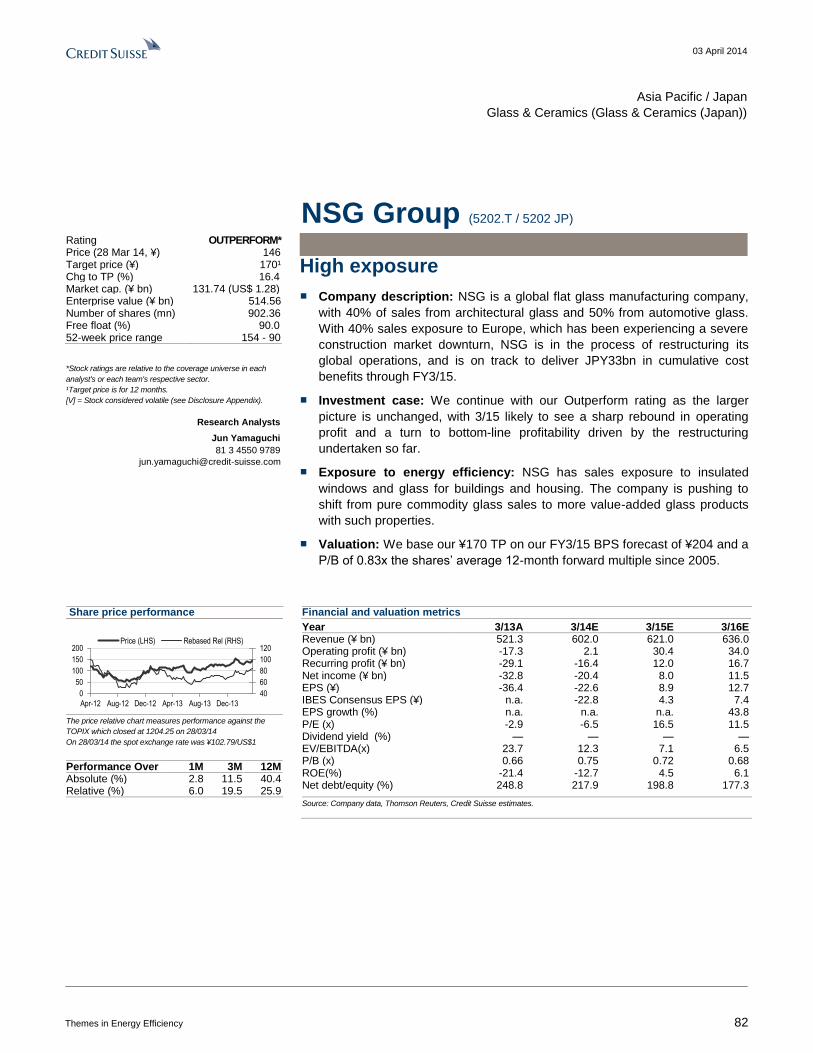

JP NSG Group 5202.T OEM High 1 1,293 OUTPERFORM 15% -104% nm -1% 535% 4%

JP Toyo Tanso 5310.T OEM High 2 475 OUTPERFORM 6% 6% 21.3 -1% 1093% 40%

Non-Japan Asia

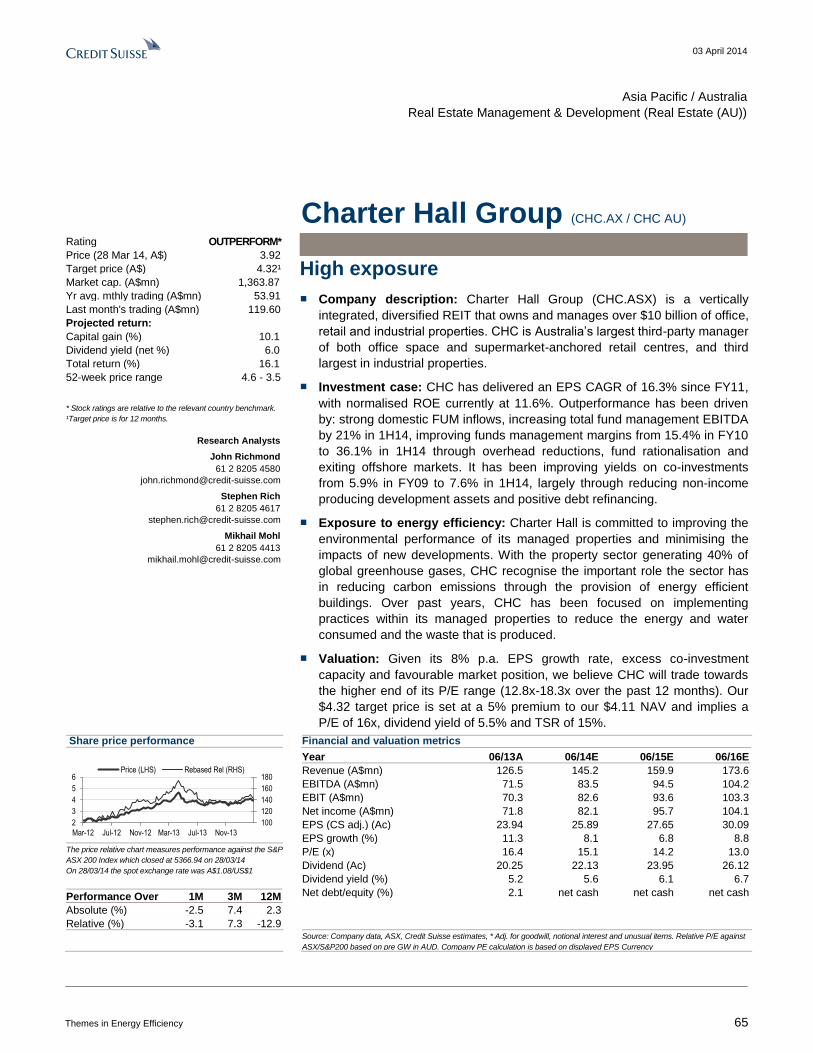

AU Charter Hall Group CHC.AX Property Owners High 5 1,279 OUTPERFORM 9% -20% 14.8 41% 8%

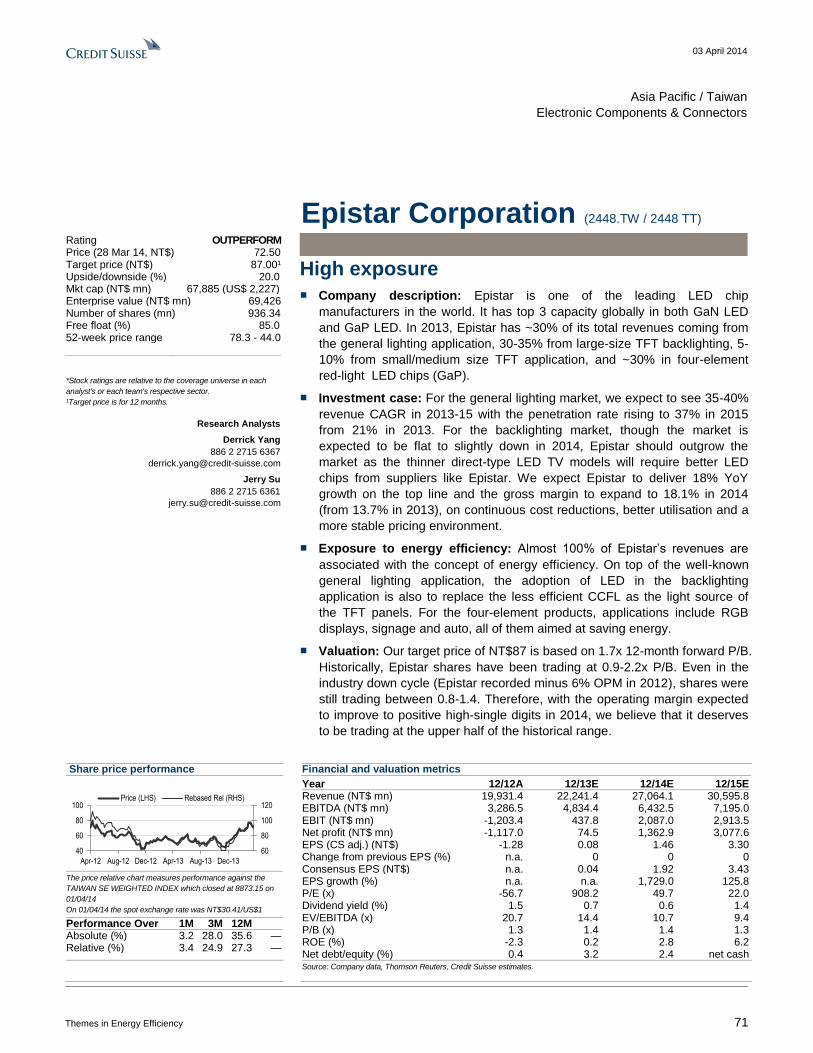

TW Epistar Corporation 2448.TW OEM High 1 2,263 OUTPERFORM 18% -21% 50.3 4% 927% 17%

HOLT Price

to Best

Growth 2013-15E

Source: Credit Suisse research, Thomson Reuters

03 April 2014

Themes in Energy Efficiency 6

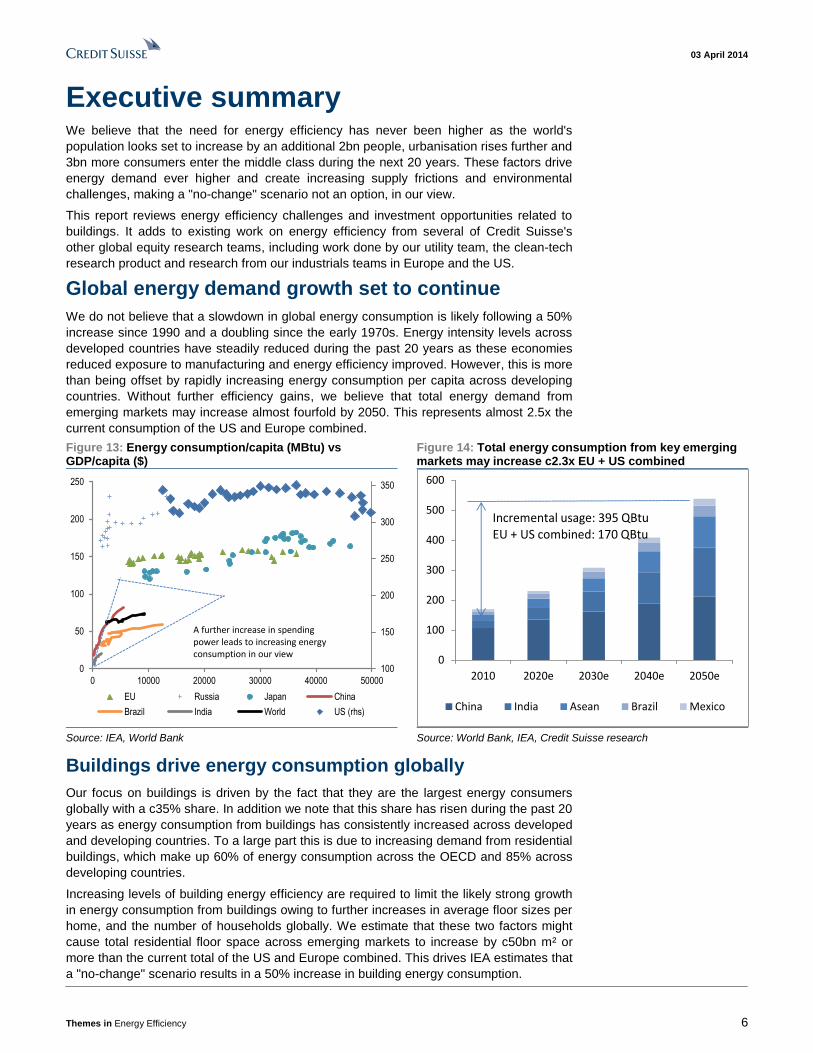

Executive summary We believe that the need for energy efficiency has never been higher as the world's

population looks set to increase by an additional 2bn people, urbanisation rises further and

3bn more consumers enter the middle class during the next 20 years. These factors drive

energy demand ever higher and create increasing supply frictions and environmental

challenges, making a "no-change" scenario not an option, in our view.

This report reviews energy efficiency challenges and investment opportunities related to

buildings. It adds to existing work on energy efficiency from several of Credit Suisse's

other global equity research teams, including work done by our utility team, the clean-tech

research product and research from our industrials teams in Europe and the US.

Global energy demand growth set to continue

We do not believe that a slowdown in global energy consumption is likely following a 50%

increase since 1990 and a doubling since the early 1970s. Energy intensity levels across

developed countries have steadily reduced during the past 20 years as these economies

reduced exposure to manufacturing and energy efficiency improved. However, this is more

than being offset by rapidly increasing energy consumption per capita across developing

countries. Without further efficiency gains, we believe that total energy demand from

emerging markets may increase almost fourfold by 2050. This represents almost 2.5x the

current consumption of the US and Europe combined.

Figure 13: Energy consumption/capita (MBtu) vs GDP/capita ($)

Figure 14: Total energy consumption from key emerging markets may increase c2.3x EU + US combined

100

150

200

250

300

350

0

50

100

150

200

250

0 10000 20000 30000 40000 50000

EU Russia Japan China

Brazil India World US (rhs)

A further increase in spending power leads to increasing energyconsumption in our view

0

100

200

300

400

500

600

2010 2020e 2030e 2040e 2050e

China India Asean Brazil Mexico

Incremental usage: 395 QBtuEU + US combined: 170 QBtu

Source: IEA, World Bank Source: World Bank, IEA, Credit Suisse research

Buildings drive energy consumption globally

Our focus on buildings is driven by the fact that they are the largest energy consumers

globally with a c35% share. In addition we note that this share has risen during the past 20

years as energy consumption from buildings has consistently increased across developed

and developing countries. To a large part this is due to increasing demand from residential

buildings, which make up 60% of energy consumption across the OECD and 85% across

developing countries.

Increasing levels of building energy efficiency are required to limit the likely strong growth

in energy consumption from buildings owing to further increases in average floor sizes per

home, and the number of households globally. We estimate that these two factors might

cause total residential floor space across emerging markets to increase by c50bn m² or

more than the current total of the US and Europe combined. This drives IEA estimates that

a "no-change" scenario results in a 50% increase in building energy consumption.

03 April 2014

Themes in Energy Efficiency 7

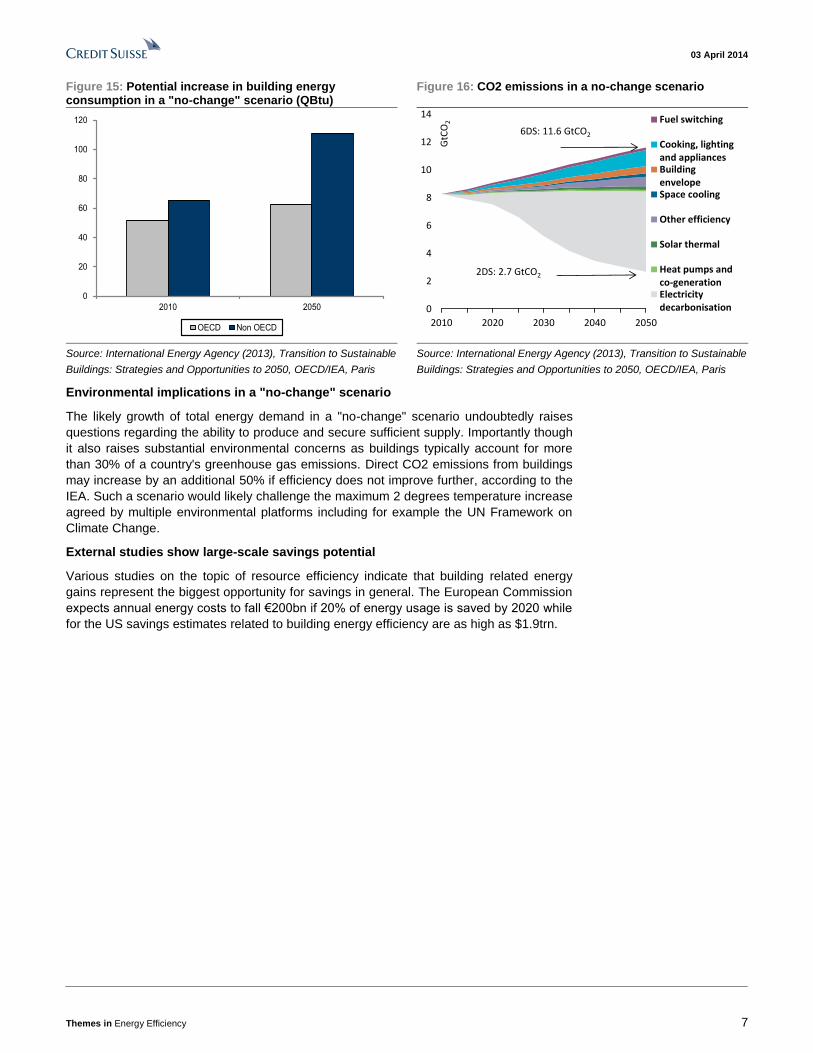

Figure 15: Potential increase in building energy consumption in a "no-change" scenario (QBtu)

Figure 16: CO2 emissions in a no-change scenario

0

20

40

60

80

100

120

2010 2050

OECD Non OECD

0

2

4

6

8

10

12

14

2010 2020 2030 2040 2050

GtC

O2 Fuel switching

Cooking, lightingand appliancesBuildingenvelopeSpace cooling

Other efficiency

Solar thermal

Heat pumps andco-generationElectricitydecarbonisation

2DS: 2.7 GtCO2

6DS: 11.6 GtCO2

Source: International Energy Agency (2013), Transition to Sustainable

Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable

Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Environmental implications in a "no-change" scenario

The likely growth of total energy demand in a "no-change" scenario undoubtedly raises

questions regarding the ability to produce and secure sufficient supply. Importantly though

it also raises substantial environmental concerns as buildings typically account for more

than 30% of a country's greenhouse gas emissions. Direct CO2 emissions from buildings

may increase by an additional 50% if efficiency does not improve further, according to the

IEA. Such a scenario would likely challenge the maximum 2 degrees temperature increase

agreed by multiple environmental platforms including for example the UN Framework on

Climate Change.

External studies show large-scale savings potential

Various studies on the topic of resource efficiency indicate that building related energy

gains represent the biggest opportunity for savings in general. The European Commission

expects annual energy costs to fall €200bn if 20% of energy usage is saved by 2020 while

for the US savings estimates related to building energy efficiency are as high as $1.9trn.

03 April 2014

Themes in Energy Efficiency 8

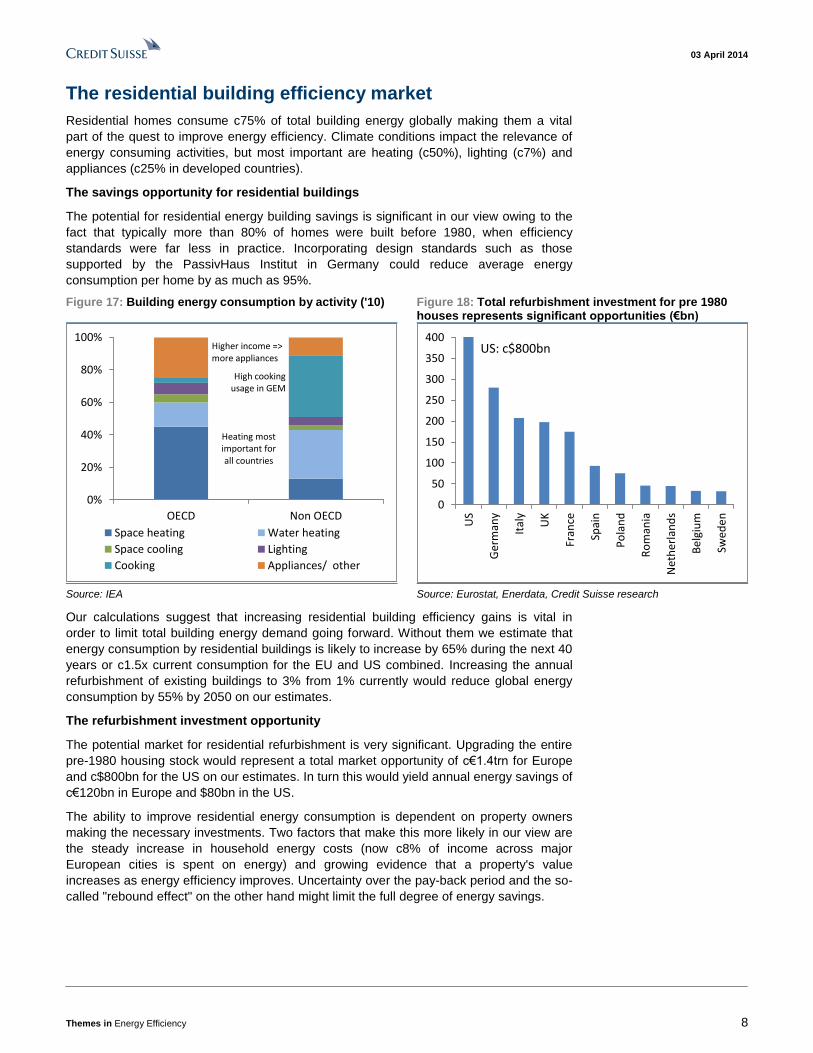

The residential building efficiency market

Residential homes consume c75% of total building energy globally making them a vital

part of the quest to improve energy efficiency. Climate conditions impact the relevance of

energy consuming activities, but most important are heating (c50%), lighting (c7%) and

appliances (c25% in developed countries).

The savings opportunity for residential buildings

The potential for residential energy building savings is significant in our view owing to the

fact that typically more than 80% of homes were built before 1980, when efficiency

standards were far less in practice. Incorporating design standards such as those

supported by the PassivHaus Institut in Germany could reduce average energy

consumption per home by as much as 95%.

Figure 17: Building energy consumption by activity ('10) Figure 18: Total refurbishment investment for pre 1980 houses represents significant opportunities (€bn)

0%

20%

40%

60%

80%

100%

OECD Non OECD

Space heating Water heating

Space cooling Lighting

Cooking Appliances/ other

Higher income => more appliances

High cooking usage in GEM

Heating mostimportant forall countries

0

50

100

150

200

250

300

350

400

US

Ger

man

y

Ital

y

UK

Fran

ce

Spai

n

Po

lan

d

Ro

man

ia

Net

her

lan

ds

Be

lgiu

m

Swed

en

US: c$800bn

Source: IEA Source: Eurostat, Enerdata, Credit Suisse research

Our calculations suggest that increasing residential building efficiency gains is vital in

order to limit total building energy demand going forward. Without them we estimate that

energy consumption by residential buildings is likely to increase by 65% during the next 40

years or c1.5x current consumption for the EU and US combined. Increasing the annual

refurbishment of existing buildings to 3% from 1% currently would reduce global energy

consumption by 55% by 2050 on our estimates.

The refurbishment investment opportunity

The potential market for residential refurbishment is very significant. Upgrading the entire

pre-1980 housing stock would represent a total market opportunity of c€1.4trn for Europe

and c$800bn for the US on our estimates. In turn this would yield annual energy savings of

c€120bn in Europe and $80bn in the US.

The ability to improve residential energy consumption is dependent on property owners

making the necessary investments. Two factors that make this more likely in our view are

the steady increase in household energy costs (now c8% of income across major

European cities is spent on energy) and growing evidence that a property's value

increases as energy efficiency improves. Uncertainty over the pay-back period and the so-

called "rebound effect" on the other hand might limit the full degree of energy savings.

03 April 2014

Themes in Energy Efficiency 9

The non-residential opportunity

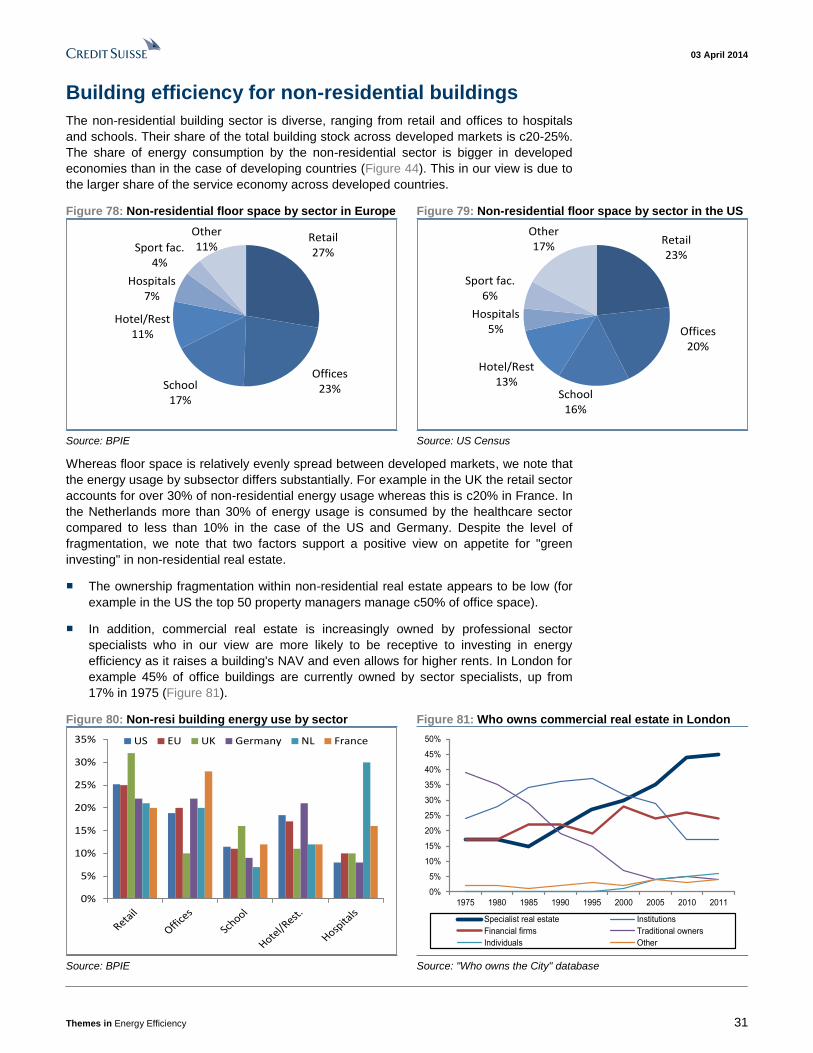

The non-residential building market makes up c25% of the global building market but

consumes c40% of total energy owing to the higher penetration of electricity-consuming

products (for example HVAC, Computers and lighting). We believe that the energy

efficiency investment opportunity for non-residential buildings is significant given that:

■ Ownership is far less fragmented than in the case of residential buildings (in the US

the top 50 property managers manage c50% of the country's office space); and

■ Commercial real estate is increasingly owned by professional investors. In London, for

example, we find that 45% of office buildings are currently owned by specialist real

estate investors, up from 17% in 1975.

These investors are likely to be more receptive to investing in value and rent enhancing

products and services, in our view. We estimate that refurbishing 75% of the commercial

real estate market across Europe and the US at a cost of c$100 per square foot would

provide an investment opportunity of c€475bn in Europe and almost $500bn in the US. At

a 30% saving per refurbishment, this would imply annual energy savings of €35bn and

$38bn for Europe and the US respectively.

Figure 19: Potential efficiency gains for US LEED certification far outweighs cost of achieving this

Figure 20: Non-residential refurbishment opportunity may reach $1.1trn for Europe and US combined

18%

30%

48%

1% 2% 2%0%

10%

20%

30%

40%

50%

60%

Certified Silver Gold

Total efficiency gains

Related cost premium

0

20

40

60

80

100

120

140

160

180

200

US

Ger

man

y

Fran

ce UK

Ital

y

Po

lan

d

Spai

n

NL

Swed

en

Au

stri

a

Gre

ece

US: $490bn

Source: USGBC, CapitalE Source: Eurostat, Enerdata, US DOE, Credit Suisse research

Increasing private sector involvement

Our view that the investment opportunity in energy efficiency is significant is supported by

several leading global surveys among property owners and corporates. These indicate

that 70% of companies now have an energy goal and that the key reason for this is no

longer "doing the right thing" but purely economic: companies want to reduce costs.

Property owners now also believe that the value of a building is positively correlated to the

degree of its energy efficiency. As a result we are not surprised to find that the level of

green building activity is rapidly increasing. More than 50% of construction is expected to

be green-focussed by 2015, up from c10% in 2009 and 30% in 2012 according to

McGraw-Hill.

03 April 2014

Themes in Energy Efficiency 10

Energy efficiency is a strong investment theme

In cooperation with analysts across Credit Suisse's global equity research platform we

have identified c170 companies that have significant revenue exposure to the theme.

These companies can be grouped into consultancy firms, construction/home builders,

technical service companies, equipment manufacturers and property/real estate owners.

Superior value creation translates into long-term outperformance

We believe that the through-cycle cash flow characteristics for energy efficiency exposed

companies are attractive relative to the broader industrials universe. The structural degree

of strong cash flow returns is in our view one reason why the efficiency related group has

outperformed on a 1-, 3- and 5-year basis.

Most value found in Cooling, Consultancy, Appliances and Lighting companies

Credit Suisse HOLT indicates that cooling companies, consultancy firms, appliance

manufacturers and lighting companies are most undervalued at this stage. Insulation,

heating and construction firms on the other hand appear overvalued when comparing cash

flow based valuations to current share prices.

Figure 21: Building efficiency exposed companies have generated higher cash flow returns than global industrials

Figure 22: Undervalued subsectors on Credit Suisse HOLT are those with market-implied CFROI below the "forecast" CFROI

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Value creation: CFROI -/- discount rate

Efficiency universe Global industrials

0

2

4

6

8

10

12

14

16

18

10yr Last fiscal year Forecast Market implied CFROI

Undervalued Overvalued

Global Industrials refers to Credit Suisse HOLT classified industrials.

Past performance should not be taken as an indication or guarantee

of future performance. Source: Credit Suisse HOLT

Source: Credit Suisse HOLT, Credit Suisse research

03 April 2014

Themes in Energy Efficiency 11

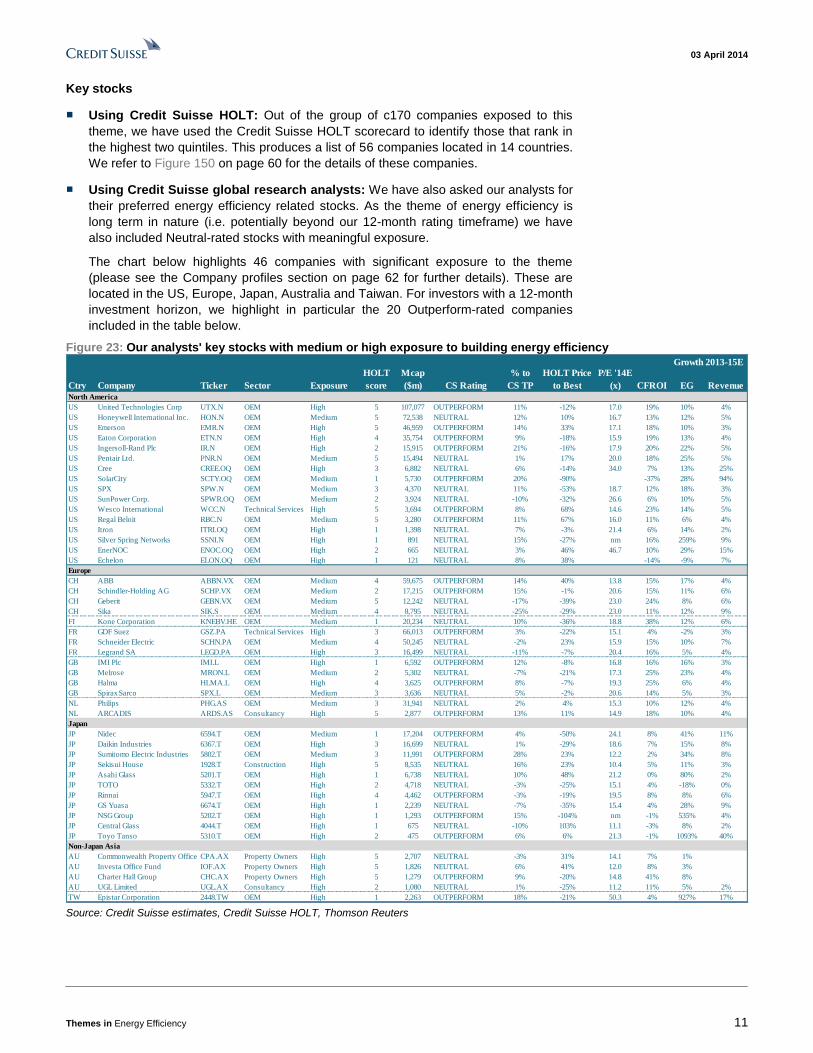

Key stocks

■ Using Credit Suisse HOLT: Out of the group of c170 companies exposed to this

theme, we have used the Credit Suisse HOLT scorecard to identify those that rank in

the highest two quintiles. This produces a list of 56 companies located in 14 countries.

We refer to Figure 150 on page 60 for the details of these companies.

■ Using Credit Suisse global research analysts: We have also asked our analysts for

their preferred energy efficiency related stocks. As the theme of energy efficiency is

long term in nature (i.e. potentially beyond our 12-month rating timeframe) we have

also included Neutral-rated stocks with meaningful exposure.

The chart below highlights 46 companies with significant exposure to the theme

(please see the Company profiles section on page 62 for further details). These are

located in the US, Europe, Japan, Australia and Taiwan. For investors with a 12-month

investment horizon, we highlight in particular the 20 Outperform-rated companies

included in the table below.

Figure 23: Our analysts' key stocks with medium or high exposure to building energy efficiency

Ctry Company Ticker Sector Exposure

HOLT

score

Mcap

($m) CS Rating

% to

CS TP

P/E '14E

(x) CFROI EG Revenue

North America

US United Technologies Corp UTX.N OEM High 5 107,077 OUTPERFORM 11% -12% 17.0 19% 10% 4%

US Honeywell International Inc. HON.N OEM Medium 5 72,538 NEUTRAL 12% 10% 16.7 13% 12% 5%

US Emerson EMR.N OEM High 5 46,959 OUTPERFORM 14% 33% 17.1 18% 10% 3%

US Eaton Corporation ETN.N OEM High 4 35,754 OUTPERFORM 9% -18% 15.9 19% 13% 4%

US Ingersoll-Rand Plc IR.N OEM High 2 15,915 OUTPERFORM 21% -16% 17.9 20% 22% 5%

US Pentair Ltd. PNR.N OEM Medium 5 15,494 NEUTRAL 1% 17% 20.0 18% 25% 5%

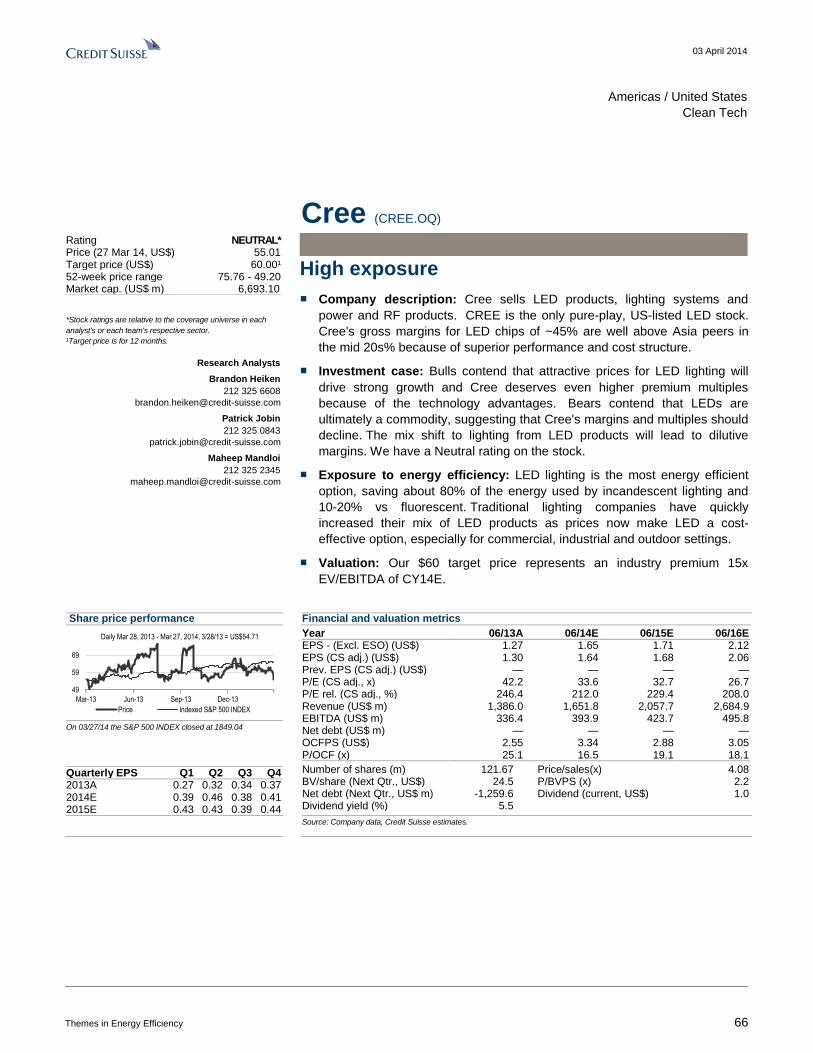

US Cree CREE.OQ OEM High 3 6,882 NEUTRAL 6% -14% 34.0 7% 13% 25%

US SolarCity SCTY.OQ OEM Medium 1 5,730 OUTPERFORM 20% -90% -37% 28% 94%

US SPX SPW.N OEM Medium 3 4,370 NEUTRAL 11% -53% 18.7 12% 18% 3%

US SunPower Corp. SPWR.OQ OEM Medium 2 3,924 NEUTRAL -10% -32% 26.6 6% 10% 5%

US Wesco International WCC.N Technical Services High 5 3,694 OUTPERFORM 8% 68% 14.6 23% 14% 5%

US Regal Beloit RBC.N OEM Medium 5 3,280 OUTPERFORM 11% 67% 16.0 11% 6% 4%

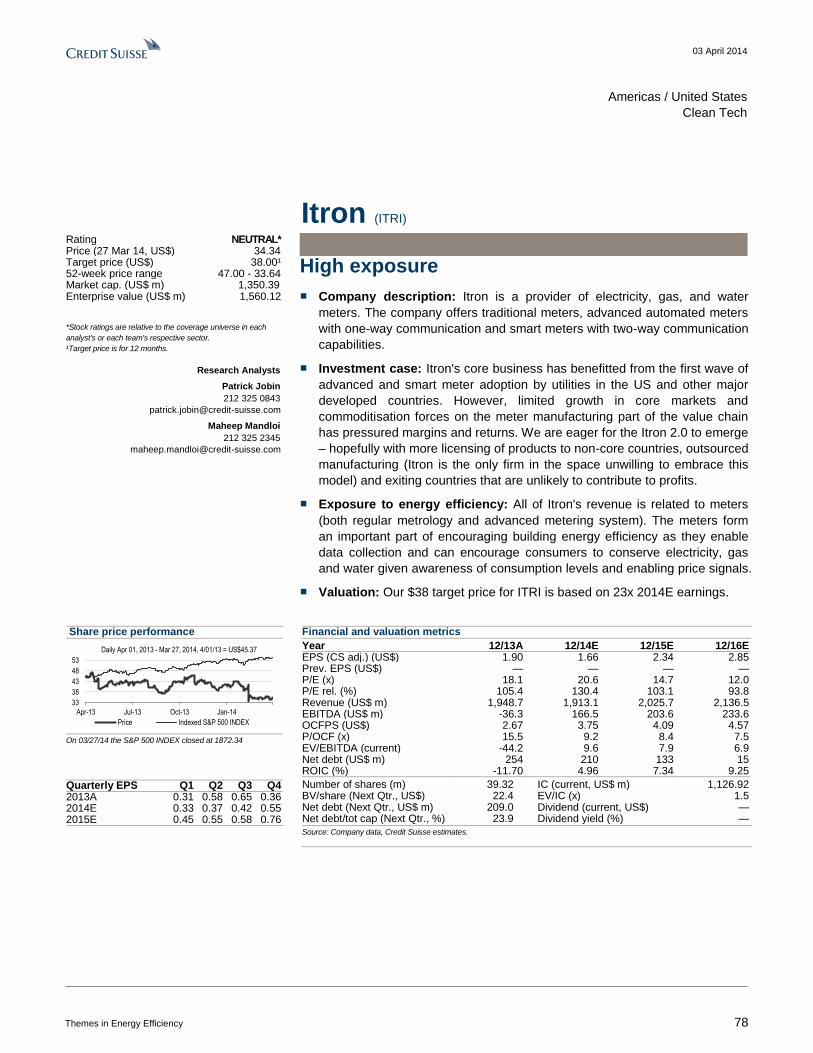

US Itron ITRI.OQ OEM High 1 1,398 NEUTRAL 7% -3% 21.4 6% 14% 2%

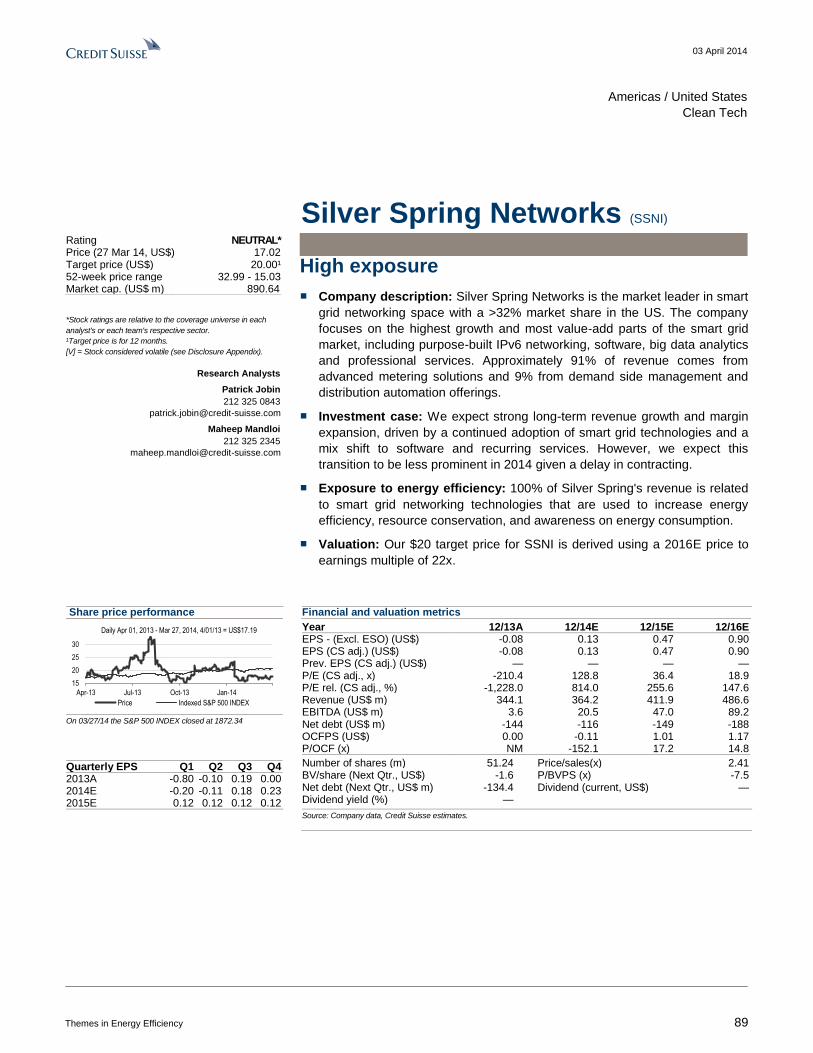

US Silver Spring Networks SSNI.N OEM High 1 891 NEUTRAL 15% -27% nm 16% 259% 9%

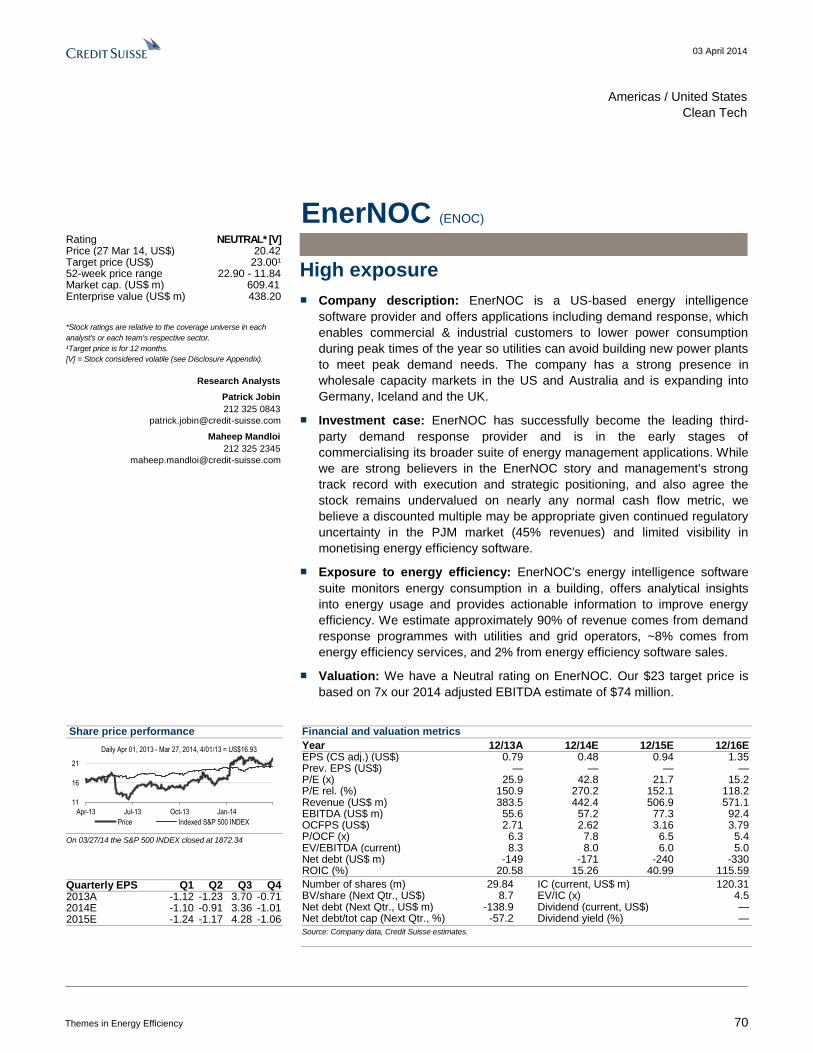

US EnerNOC ENOC.OQ OEM High 2 665 NEUTRAL 3% 46% 46.7 10% 29% 15%

US Echelon ELON.OQ OEM High 1 121 NEUTRAL 8% 38% -14% -9% 7%

Europe

CH ABB ABBN.VX OEM Medium 4 59,675 OUTPERFORM 14% 40% 13.8 15% 17% 4%

CH Schindler-Holding AG SCHP.VX OEM Medium 2 17,215 OUTPERFORM 15% -1% 20.6 15% 11% 6%

CH Geberit GEBN.VX OEM Medium 5 12,242 NEUTRAL -17% -39% 23.0 24% 8% 6%

CH Sika SIK.S OEM Medium 4 8,795 NEUTRAL -25% -29% 23.0 11% 12% 9%

FI Kone Corporation KNEBV.HE OEM Medium 1 20,234 NEUTRAL 10% -36% 18.8 38% 12% 6%

FR GDF Suez GSZ.PA Technical Services High 3 66,013 OUTPERFORM 3% -22% 15.1 4% -2% 3%

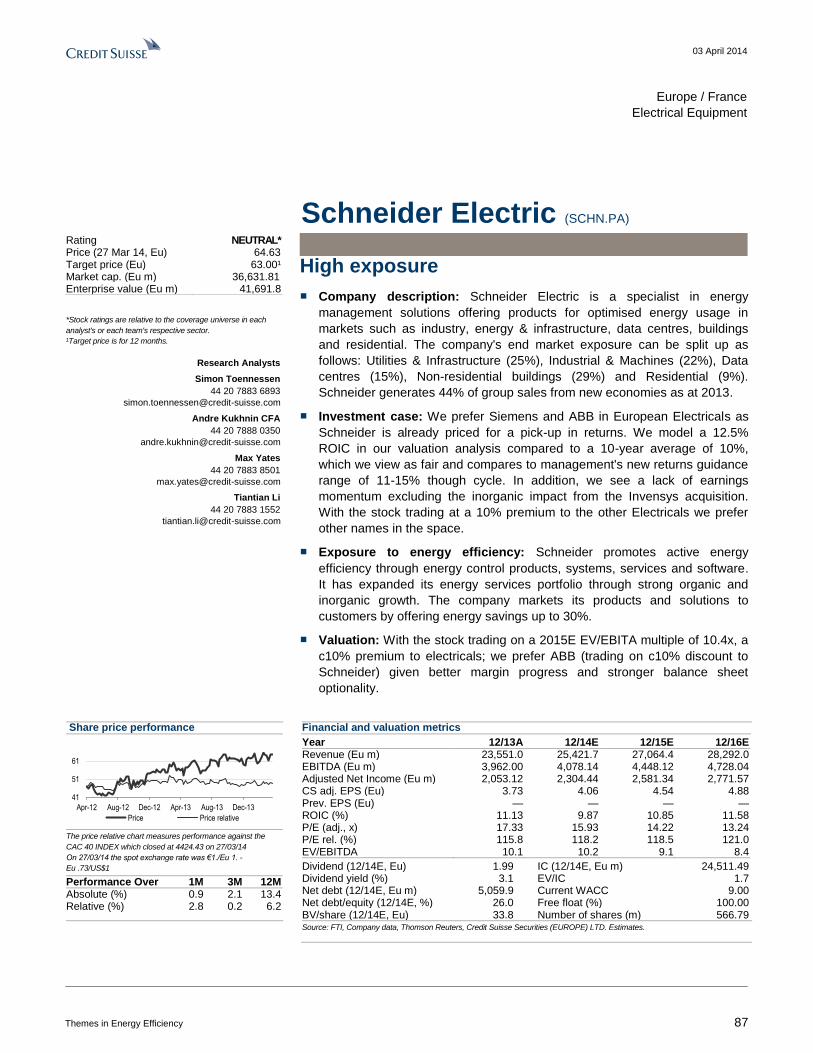

FR Schneider Electric SCHN.PA OEM Medium 4 50,245 NEUTRAL -2% 23% 15.9 15% 10% 7%

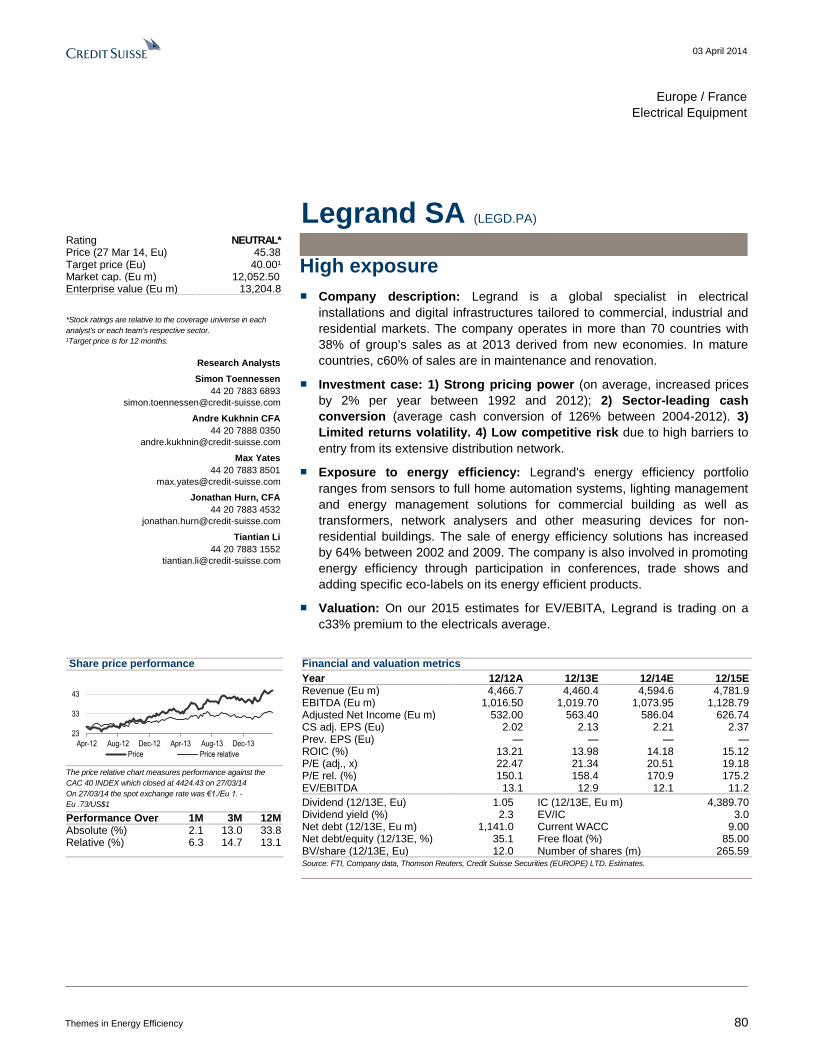

FR Legrand SA LEGD.PA OEM High 3 16,499 NEUTRAL -11% -7% 20.4 16% 5% 4%

GB IMI Plc IMI.L OEM High 1 6,592 OUTPERFORM 12% -8% 16.8 16% 16% 3%

GB Melrose MRON.L OEM Medium 2 5,302 NEUTRAL -7% -21% 17.3 25% 23% 4%

GB Halma HLMA.L OEM High 4 3,625 OUTPERFORM 8% -7% 19.3 25% 6% 4%

GB Spirax Sarco SPX.L OEM Medium 3 3,636 NEUTRAL 5% -2% 20.6 14% 5% 3%

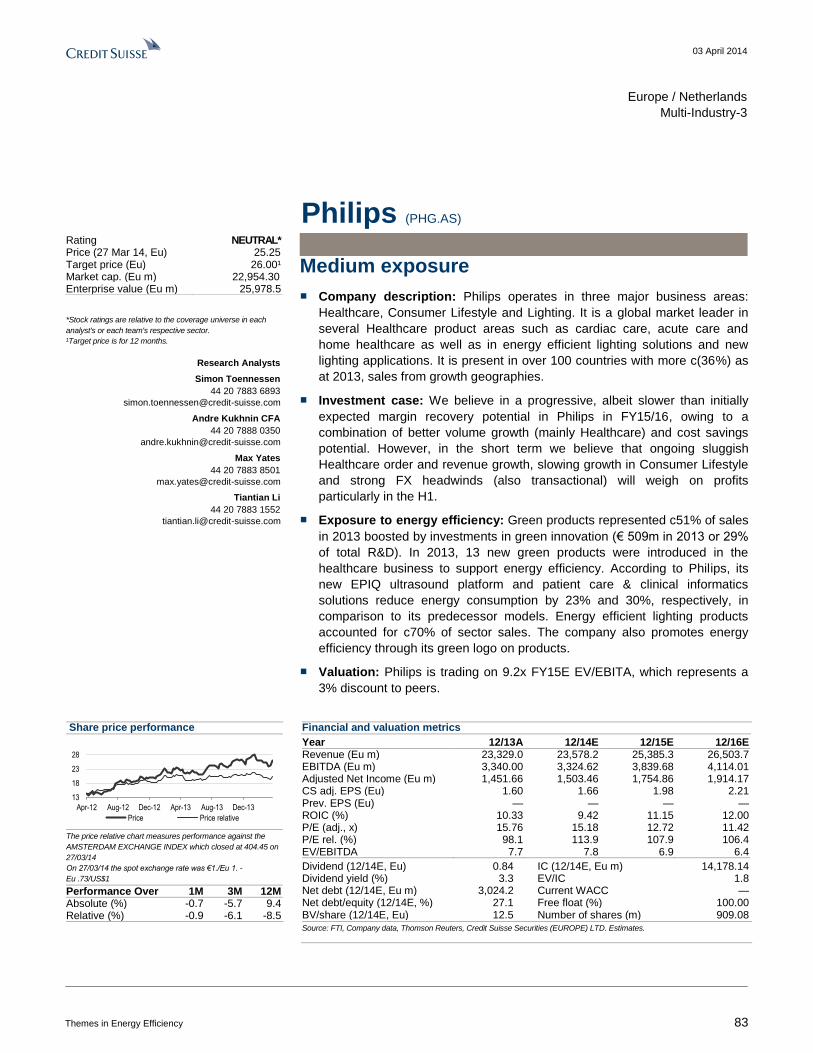

NL Philips PHG.AS OEM Medium 3 31,941 NEUTRAL 2% 4% 15.3 10% 12% 4%

NL ARCADIS ARDS.AS Consultancy High 5 2,877 OUTPERFORM 13% 11% 14.9 18% 10% 4%

Japan

JP Nidec 6594.T OEM Medium 1 17,204 OUTPERFORM 4% -50% 24.1 8% 41% 11%

JP Daikin Industries 6367.T OEM High 3 16,699 NEUTRAL 1% -29% 18.6 7% 15% 8%

JP Sumitomo Electric Industries 5802.T OEM Medium 3 11,991 OUTPERFORM 28% 23% 12.2 2% 34% 8%

JP Sekisui House 1928.T Construction High 5 8,535 NEUTRAL 16% 23% 10.4 5% 11% 3%

JP Asahi Glass 5201.T OEM High 1 6,738 NEUTRAL 10% 48% 21.2 0% 80% 2%

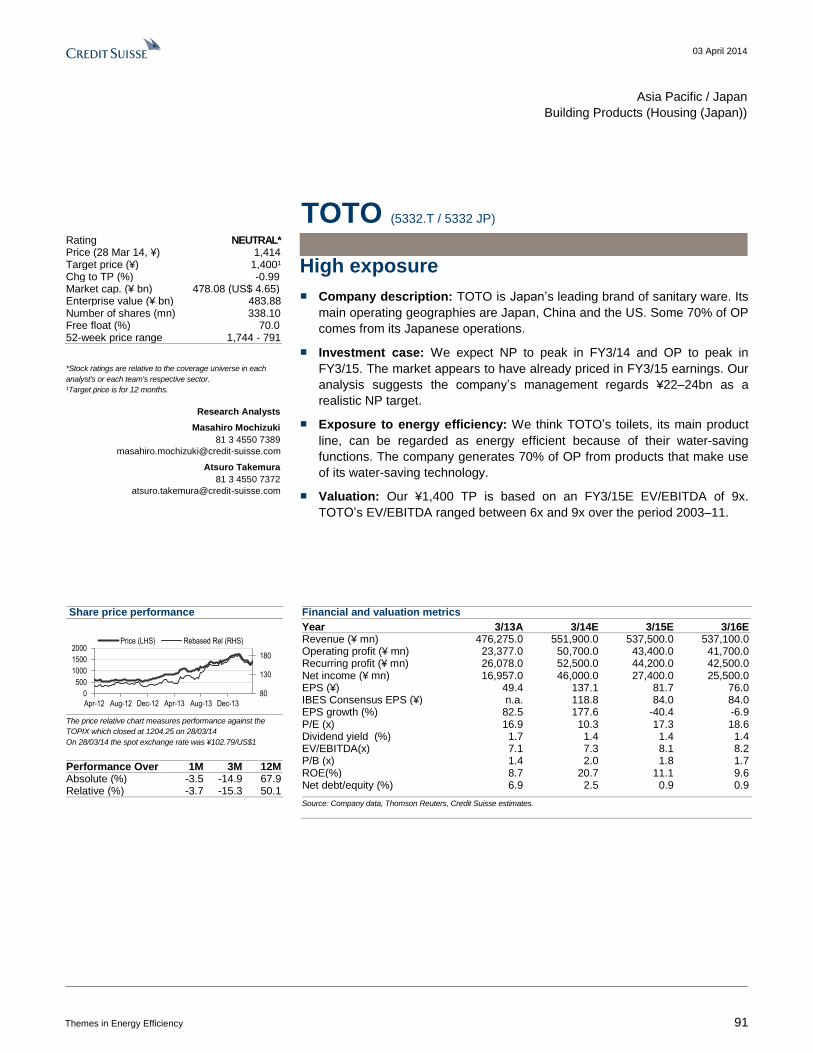

JP TOTO 5332.T OEM High 2 4,718 NEUTRAL -3% -25% 15.1 4% -18% 0%

JP Rinnai 5947.T OEM High 4 4,462 OUTPERFORM -3% -19% 19.5 8% 8% 6%

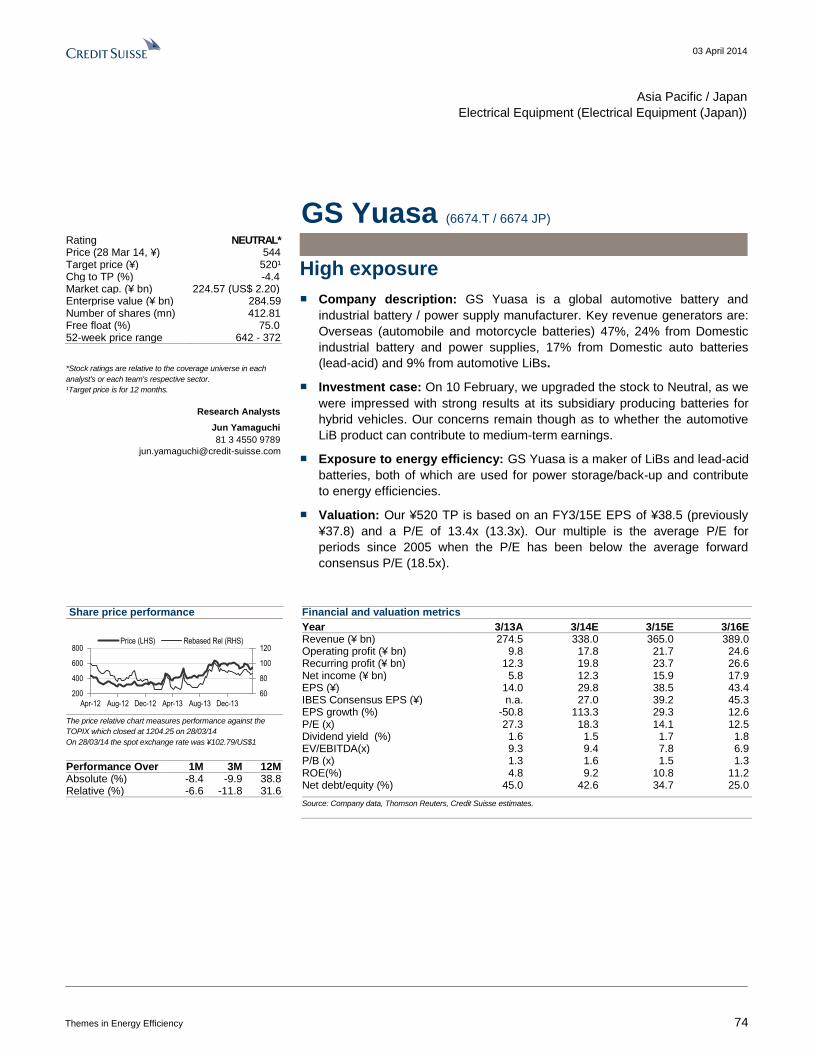

JP GS Yuasa 6674.T OEM High 1 2,239 NEUTRAL -7% -35% 15.4 4% 28% 9%

JP NSG Group 5202.T OEM High 1 1,293 OUTPERFORM 15% -104% nm -1% 535% 4%

JP Central Glass 4044.T OEM High 1 675 NEUTRAL -10% 103% 11.1 -3% 8% 2%

JP Toyo Tanso 5310.T OEM High 2 475 OUTPERFORM 6% 6% 21.3 -1% 1093% 40%

Non-Japan Asia

AU Commonwealth Property Office FundCPA.AX Property Owners High 5 2,707 NEUTRAL -3% 31% 14.1 7% 1%

AU Investa Office Fund IOF.AX Property Owners High 5 1,826 NEUTRAL 6% 41% 12.0 8% 3%

AU Charter Hall Group CHC.AX Property Owners High 5 1,279 OUTPERFORM 9% -20% 14.8 41% 8%

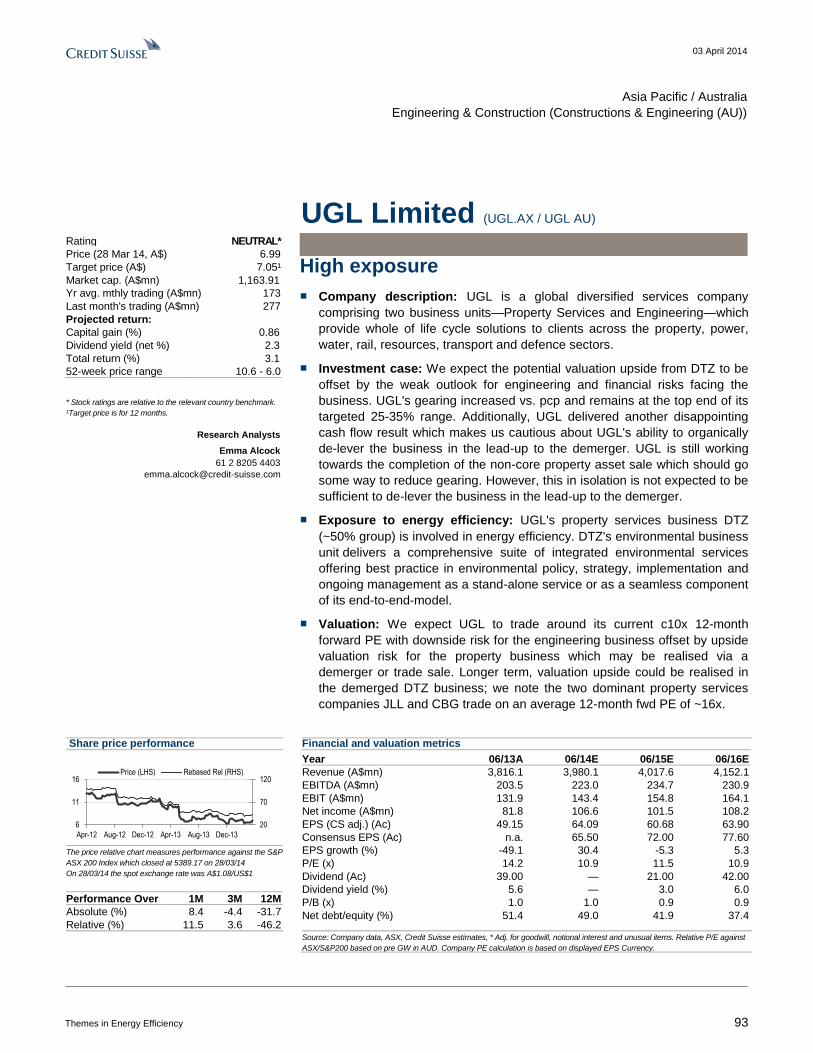

AU UGL Limited UGL.AX Consultancy High 2 1,080 NEUTRAL 1% -25% 11.2 11% 5% 2%

TW Epistar Corporation 2448.TW OEM High 1 2,263 OUTPERFORM 18% -21% 50.3 4% 927% 17%

HOLT Price

to Best

Growth 2013-15E

Source: Credit Suisse estimates, Credit Suisse HOLT, Thomson Reuters

03 April 2014

Themes in Energy Efficiency 12

Energy demand unlikely to slow down In recent decades, worries regarding the long term impact of population growth on

available resources globally started to rise since the "Club of Rome" reported their findings

in the early 1970s. Demand for the world's key resources (energy, water, land and food)

did indeed increase rapidly during the past 40 years, and we believe that the key drivers

for this remain very much in place.

Since the early 1970s global primary energy consumption has more than doubled whereas

it increased by c50% since 1990 (Figure 24). This growth has largely been driven by

developing economies as consumption from non-OECD countries has doubled since 1990

compared to an increase from OECD members of just 20%. The share of energy

consumption from developed countries has fallen to 41% in 2011 from 60% in 1973 while

Asian economies, including China, raised their share to 31% from 14% (Figure 25).

Figure 24: World energy consumption (QBtu) Figure 25: Energy consumption by region

0

100

200

300

400

500

600

1990 2000 2010

Non-OECD: +100%

OECD: +20%

60%41%

8%18%

6%13%

0%

20%

40%

60%

80%

100%

120%

1973 2011

OECD China

Asia Latam

Non-OECD Europe Middle East

Africa Other

Source: IEA Source: IEA

Three key demand drivers

In a global context, we see three key drivers behind the continued increase in demand for

energy. These three drivers are population growth, urbanisation and the developing middle

class.

Population growth

To date productivity improvements, technological progress and expansion into low-cost

sources of supply has allowed the global economy to continue to grow and cope with an

increase in the world's population from less than 3 billion in 1950 to approximately 7 billion

today.

However we believe that the challenges of meeting incremental demand for water, energy,

land and basic materials going forward are likely to remain high as the world's population

is expected to increase further to approximately 9 billion by 2050 with an upper estimate of

as more than 10bn, according to McKinsey.

Most of this expected population growth is set to originate in developing economies. This

in our view makes the resource issue more challenging given incremental logistical

challenges as infrastructure across emerging countries is typically less developed.

03 April 2014

Themes in Energy Efficiency 13

Figure 26: World population projections to 2050: Strong growth expected to continue

Figure 27: Urbanisation in emerging market regions (urban population, % of total)

500

2,500

4,500

6,500

8,500

10,500

1950 1970 1990 2010 2030 2050

World

World upper estimate

World lower estimate

LEDC

MEDC

0

10

20

30

40

50

60

70

80

90

100

1950 1970 1990 2010 2030 2050

Latin America Eastern Europe

MENA Non-Japan Asia

Sub-Saharan Africa

Source: United Nations, Credit Suisse research Source: Population Division of the Department of Economic and

Social Affairs of the UN Secretariat, Credit Suisse research

Urbanisation

Urbanisation is another factor impacting resource challenges in our view. For example

some academic studies show that every 1% increase in the urbanisation rate increases

energy consumption by an additional 0.47% (Jones, 1991). Urbanisation in low income

countries may reduce total energy use as households start to switch to more efficient

heating and cooking practices. However, this changes once countries enter the middle to

higher income levels (Figure 28) and (Figure 29).

Urbanisation also impacts carbon emission generation. For example, carbon emissions

per capita for cities in middle and higher income countries are typically c10x higher than

for cities in low developing countries with underdeveloped infrastructure (Figure 31).

Figure 28: Elasticity between economic growth and energy use and carbon emissions for households

Figure 29: Energy consumption increases with urbanisation and income levels

$ 1,500 $5,500 $20,000Low-income Middle High-income

29% 58% 76%

Urbanisation (mean)

GDP/capita(mean)

Household energytransation

Biomass Biomass/Oil Nat.gas/electr.

Urbanisation elasticityof residential energy use

Urbanisation elasticityof residential emissions

0

10

20

30

40

50

60

70

80

90

0

100

200

300

400

500

600

700

800

900

Low-income Middle-income High-income

Ura

bisa

tion

(%)

kgoe

per

cap

ita

Energy , '75 Energy, '05

Urbanisation, '75 (rhs) Urbanisation, '05 (rhs)

Source: Phetkeo Poumanyvong, Shinji Kaneko, Shobhakar Dhakal,

Impacts of urbanization on national transport and road energy use:

Evidence from low-, middle- and high-income countries, Hiroshima

University, 2012

Source: Phetkeo Poumanyvong, Shinji Kaneko, Shobhakar Dhakal,

Impacts of urbanization on national transport and road energy use:

Evidence from low-, middle- and high-income countries, Hiroshima

University, 2012

03 April 2014

Themes in Energy Efficiency 14

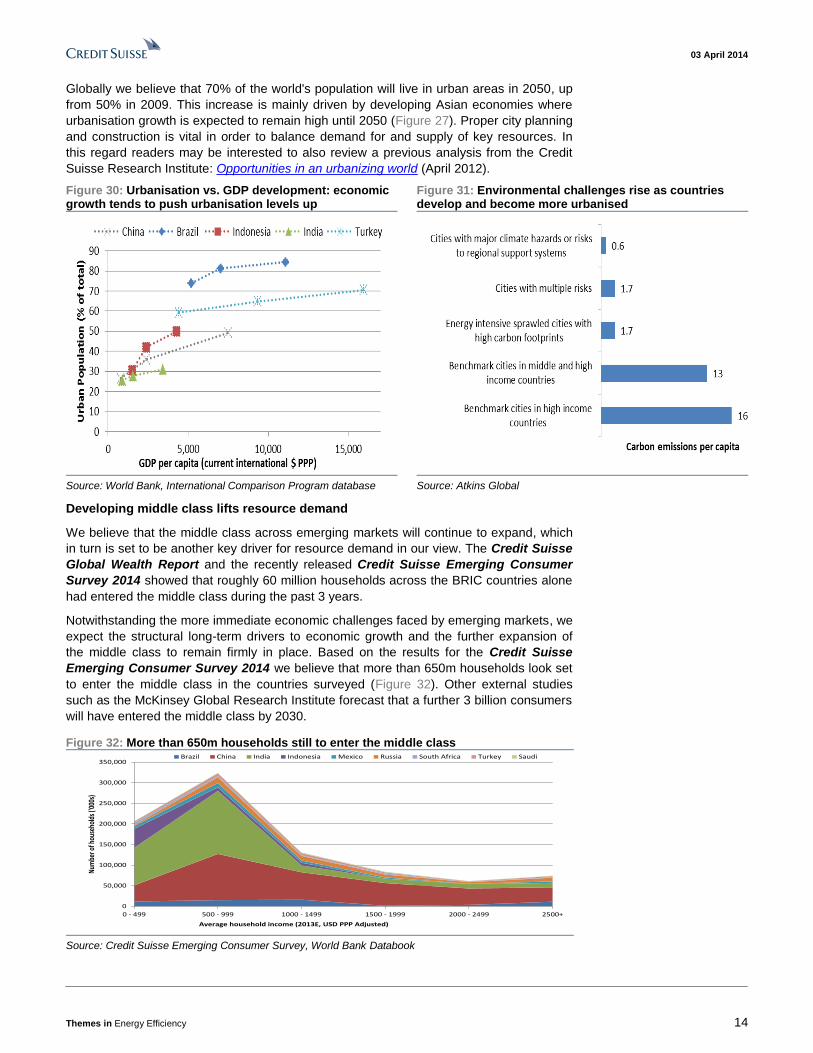

Globally we believe that 70% of the world's population will live in urban areas in 2050, up

from 50% in 2009. This increase is mainly driven by developing Asian economies where

urbanisation growth is expected to remain high until 2050 (Figure 27). Proper city planning

and construction is vital in order to balance demand for and supply of key resources. In

this regard readers may be interested to also review a previous analysis from the Credit

Suisse Research Institute: Opportunities in an urbanizing world (April 2012).

Figure 30: Urbanisation vs. GDP development: economic growth tends to push urbanisation levels up

Figure 31: Environmental challenges rise as countries develop and become more urbanised

Source: World Bank, International Comparison Program database Source: Atkins Global

Developing middle class lifts resource demand

We believe that the middle class across emerging markets will continue to expand, which

in turn is set to be another key driver for resource demand in our view. The Credit Suisse

Global Wealth Report and the recently released Credit Suisse Emerging Consumer

Survey 2014 showed that roughly 60 million households across the BRIC countries alone

had entered the middle class during the past 3 years.

Notwithstanding the more immediate economic challenges faced by emerging markets, we

expect the structural long-term drivers to economic growth and the further expansion of

the middle class to remain firmly in place. Based on the results for the Credit Suisse

Emerging Consumer Survey 2014 we believe that more than 650m households look set

to enter the middle class in the countries surveyed (Figure 32). Other external studies

such as the McKinsey Global Research Institute forecast that a further 3 billion consumers

will have entered the middle class by 2030.

Figure 32: More than 650m households still to enter the middle class

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

0 - 499 500 - 999 1000 - 1499 1500 - 1999 2000 - 2499 2500+

Num

ber o

f hou

seho

lds (

'000

s)

Average household income (2013E, USD PPP Adjusted)

Brazil China India Indonesia Mexico Russia South Africa Turkey Saudi

Source: Credit Suisse Emerging Consumer Survey, World Bank Databook

03 April 2014

Themes in Energy Efficiency 15

We believe that some of the largest emerging economies are at or close to the "sweet

spot" where acceleration in middle class discretionary spending typically accelerates. This

in turn typically leads to significant growth in energy consuming appliances and products.

Consumption in case efficiency does not improve

Energy intensity for developed regions has been declining for years owing to a shift away

from manufacturing and the adoption of energy efficiency measures. This is less the case

for emerging countries (Figure 33). In fact we note that energy consumption per capita in

countries such as China, Brazil, India and Indonesia is rising rapidly owing to population

growth, urbanisation and the developing middle class (Figure 34).

Figure 33: Energy intensity across key geographies Figure 34: Energy consumption/capita (M BTU/year)

0

5000

10000

15000

20000

25000

30000

35000

40000 Energy consumption per dollar of GDP (Btu/year), 2011

0

10

20

30

40

50

60

70

80

90

1980 1985 1990 1995 2000 2005 2010

China Brazil India Indonesia

Source: World Bank Source: World Bank

Energy consumption per capita in developing countries remains substantially below levels

seen in developed markets (Figure 35). However we believe that further economic

expansion will push energy consumption per capita in developing countries higher and

closer to levels seen in developed economies. Continued emerging market growth is

therefore likely to have a profound impact on total energy consumption if no efficiency

gains are achieved.

Figure 35: Energy consumption per capita vs GDP/capita (MBtu/capita/year)

100.0

150.0

200.0

250.0

300.0

350.0

0

50

100

150

200

250

0 5000 10000 15000 20000 25000 30000 35000 40000 45000 50000

EU Russia Japan China Brazil India World US (rhs)

Source: EIA, World Bank

03 April 2014

Themes in Energy Efficiency 16

Assuming that emerging countries converge economically with developed markets by

2050 would suggest a possible increase in average energy consumption levels per capita

to c150 MBtu/capita by 2050 (Figure 36). This together with population expectations

implies that total energy consumption for these emerging economies may increase almost

fourfold by 2050 from 2010. To put this in context, the potential increase between 2010

and 2050 for these countries would be 2.3 times the total energy consumption of the EU

and US combined (Figure 37).

Figure 36: Potential energy consumption/capita for key emerging countries (M Btu)

Figure 37: Total energy demand for key emerging countries could increase c2.3 times the EU/US total

0

20

40

60

80

100

120

140

160

180

200

0 5000 10000 15000 20000 25000 30000 35000

Asean Brazil China India Mexico

0

100

200

300

400

500

600

2010 2020 2030 2040 2050

China India Asean Brazil Mexico

Incremental usage: 395 QBtuEU + US combined: 170 QBtu

Source: World Bank, IEA, Credit Suisse research Source: World Bank, IEA, Credit Suisse research

Our calculations are similar to those from the McKinsey Global Institute which predicts that

between 2010 and 2030 demand for energy may increase by an additional 32% or the

equivalent of the current annual consumption of the US and EU members of the OECD

combined.

Our calculations imply that without further energy efficiency gains, pressure on energy

supply conditions are likely to intensify going forward.

Figure 38: Total global energy supply requirements

340460

130

160

0

100

200

300

400

500

600

700

1990-2010 2010-2030

Primary Energy (QBTU)

Incremental supply Supply replacement (at historical rates)

+32%

Source: McKinsey Global Institute

03 April 2014

Themes in Energy Efficiency 17

Rising supply concerns to act as efficiency catalyst

Our calculations show that energy demand globally is set to increase strongly if no

efficiency gains are achieved. While this report does not have a focus on supply-side

related issues, we do point out that the potentially strong increase in total energy demand

is likely to create supply concerns on multiple levels, which in turn provides support for the

efficiency agenda. We see at least three reasons why supply-side related concerns are

likely to increase and act as a catalyst for the efficiency agenda:

■ Firstly we note that the ability to produce the required level of resources is not a given.

Energy reserves in the case of oil and coal for example appear to be sufficient for at

least another few decades; however, accessing these resources is becoming more

problematic while the marginal cost of extracting them is increasing. In the case of oil

we note higher costs for drilling and oil-field services. The development of shale gas

may help in this regard, especially from a US perspective; however, uncertainty

remains over the impact that this may have on the global energy supply.

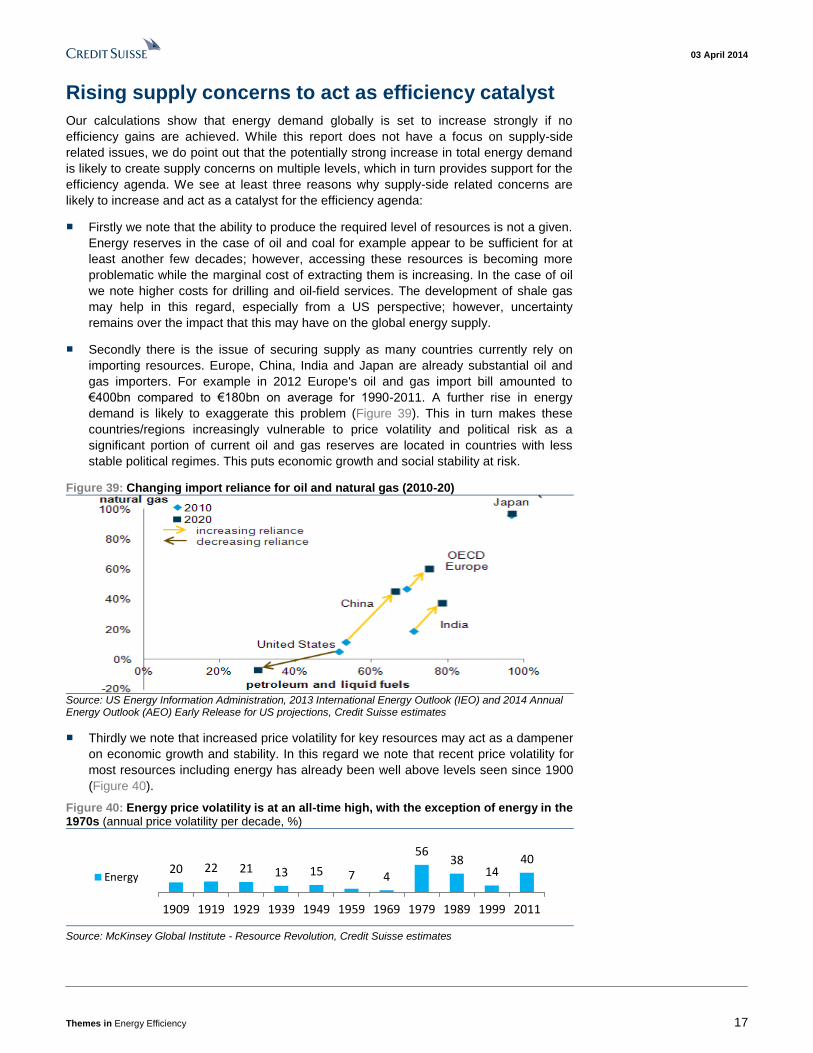

■ Secondly there is the issue of securing supply as many countries currently rely on

importing resources. Europe, China, India and Japan are already substantial oil and

gas importers. For example in 2012 Europe's oil and gas import bill amounted to

€400bn compared to €180bn on average for 1990-2011. A further rise in energy

demand is likely to exaggerate this problem (Figure 39). This in turn makes these

countries/regions increasingly vulnerable to price volatility and political risk as a

significant portion of current oil and gas reserves are located in countries with less

stable political regimes. This puts economic growth and social stability at risk.

Figure 39: Changing import reliance for oil and natural gas (2010-20)

Source: US Energy Information Administration, 2013 International Energy Outlook (IEO) and 2014 Annual Energy Outlook (AEO) Early Release for US projections, Credit Suisse estimates

■ Thirdly we note that increased price volatility for key resources may act as a dampener

on economic growth and stability. In this regard we note that recent price volatility for

most resources including energy has already been well above levels seen since 1900

(Figure 40).

Figure 40: Energy price volatility is at an all-time high, with the exception of energy in the 1970s (annual price volatility per decade, %)

20 22 21 13 15 7 4

5638

1440

1909 1919 1929 1939 1949 1959 1969 1979 1989 1999 2011

Energy

Source: McKinsey Global Institute - Resource Revolution, Credit Suisse estimates

03 April 2014

Themes in Energy Efficiency 18

Buildings and energy efficiency Final energy demand can be broken down into three broad end-user categories: Buildings,

Transport and Industry (Figure 42). For the purpose of this report, we focus primarily on

the area of buildings as it makes up the biggest portion in terms of energy consumption at

c35%. We intend to focus on the other areas of energy consumers in future updates of our

resource efficiency research.

Figure 41: World energy demand set to grow further primarily driven by developing economies (Q-Btu)

Figure 42: Energy end-demand can be broken down into three categories (2010)

0

100

200

300

400

500

600

700

800

900

1990 2000 2010 2020 2030 2040

Non-OECD

OECD

Buildings35%

Industry31%

Transport30%

Other4%

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

The increasing role of buildings in emerging markets

Total building related energy consumption in OECD countries has increased by 1.3% pa

since 1990; however, buildings in emerging countries have shown much stronger growth

at 1.7% per annum. As a result, total building energy consumption in emerging markets is

currently c40% higher than for developed countries (Figure 43).

Figure 43: Building energy consumption increasingly dominated by developing countries (Pj)

Figure 44: Share of energy usage split by residential and commercial buildings (2010)

0

10000

20000

30000

40000

50000

60000

70000

1990 2000 2010

OECD Non-OECD

+1.3% CAGR

+1.7% CAGR

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

OECD Non OECD

Residential Commercial

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

03 April 2014

Themes in Energy Efficiency 19

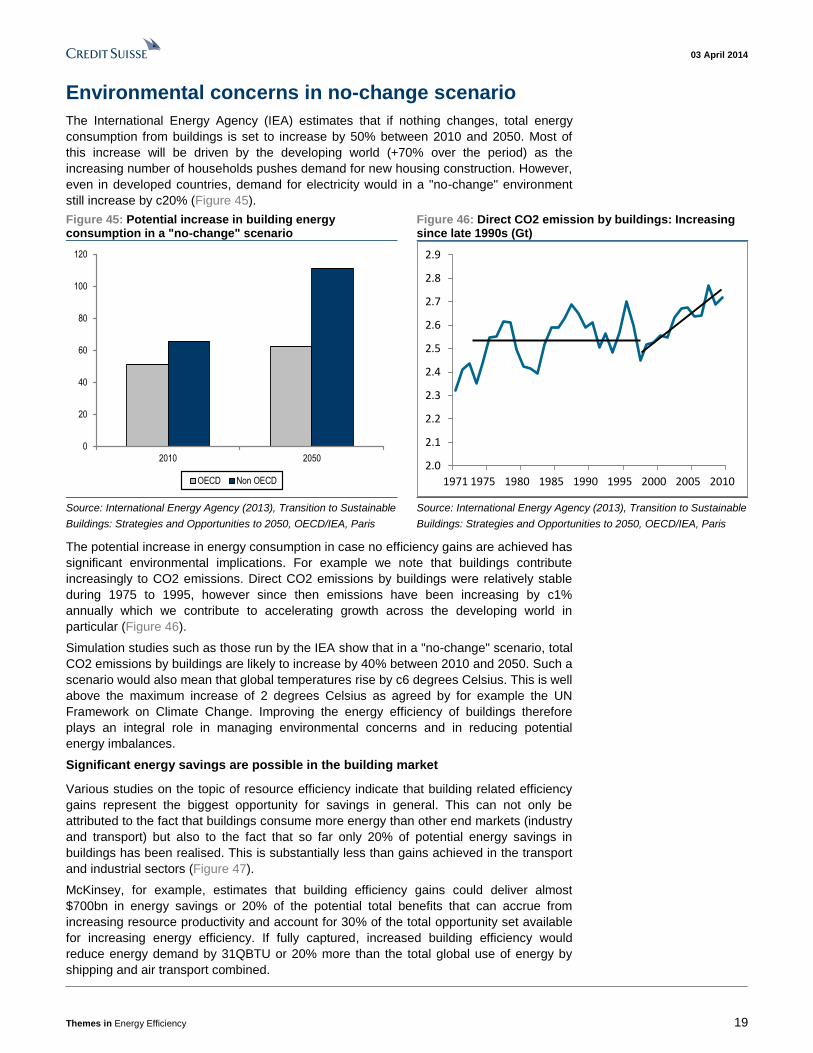

Environmental concerns in no-change scenario

The International Energy Agency (IEA) estimates that if nothing changes, total energy

consumption from buildings is set to increase by 50% between 2010 and 2050. Most of

this increase will be driven by the developing world (+70% over the period) as the

increasing number of households pushes demand for new housing construction. However,

even in developed countries, demand for electricity would in a "no-change" environment

still increase by c20% (Figure 45).

Figure 45: Potential increase in building energy consumption in a "no-change" scenario

Figure 46: Direct CO2 emission by buildings: Increasing since late 1990s (Gt)

0

20

40

60

80

100

120

2010 2050

OECD Non OECD

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

1971 1975 1980 1985 1990 1995 2000 2005 2010

Source: International Energy Agency (2013), Transition to Sustainable

Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable

Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

The potential increase in energy consumption in case no efficiency gains are achieved has

significant environmental implications. For example we note that buildings contribute

increasingly to CO2 emissions. Direct CO2 emissions by buildings were relatively stable

during 1975 to 1995, however since then emissions have been increasing by c1%

annually which we contribute to accelerating growth across the developing world in

particular (Figure 46).

Simulation studies such as those run by the IEA show that in a "no-change" scenario, total

CO2 emissions by buildings are likely to increase by 40% between 2010 and 2050. Such a

scenario would also mean that global temperatures rise by c6 degrees Celsius. This is well

above the maximum increase of 2 degrees Celsius as agreed by for example the UN

Framework on Climate Change. Improving the energy efficiency of buildings therefore

plays an integral role in managing environmental concerns and in reducing potential

energy imbalances.

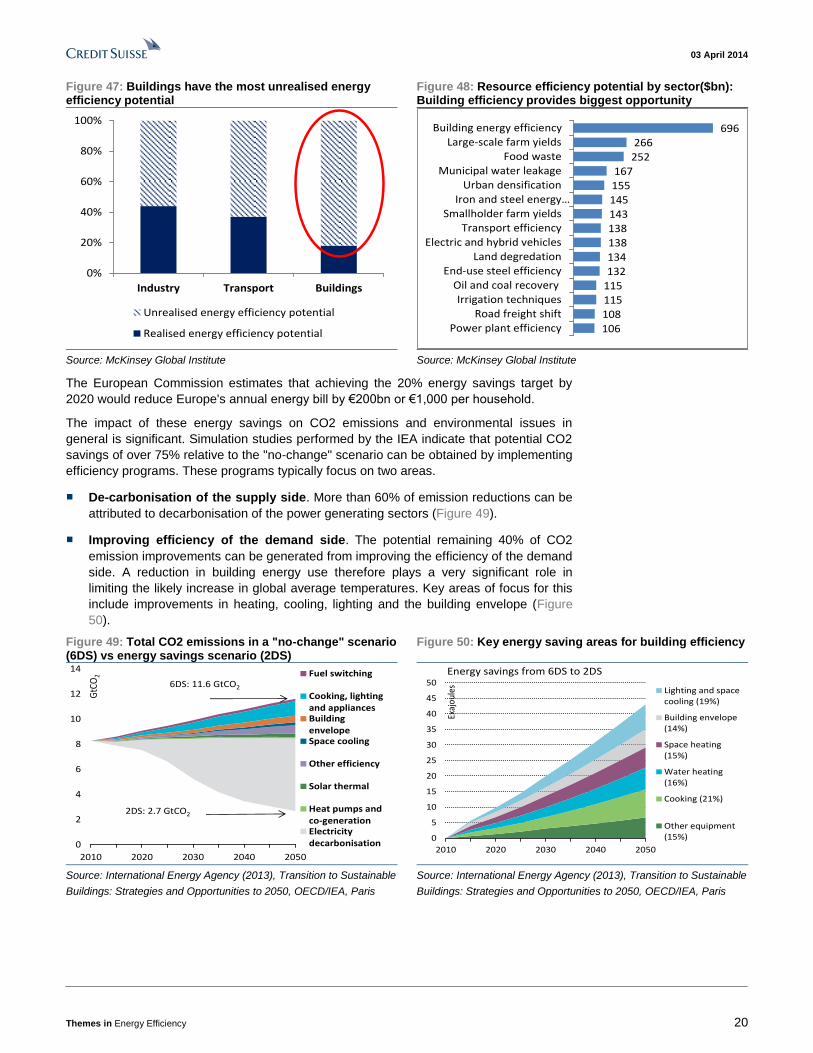

Significant energy savings are possible in the building market

Various studies on the topic of resource efficiency indicate that building related efficiency

gains represent the biggest opportunity for savings in general. This can not only be

attributed to the fact that buildings consume more energy than other end markets (industry

and transport) but also to the fact that so far only 20% of potential energy savings in

buildings has been realised. This is substantially less than gains achieved in the transport

and industrial sectors (Figure 47).

McKinsey, for example, estimates that building efficiency gains could deliver almost

$700bn in energy savings or 20% of the potential total benefits that can accrue from

increasing resource productivity and account for 30% of the total opportunity set available

for increasing energy efficiency. If fully captured, increased building efficiency would

reduce energy demand by 31QBTU or 20% more than the total global use of energy by

shipping and air transport combined.

03 April 2014

Themes in Energy Efficiency 20

Figure 47: Buildings have the most unrealised energy efficiency potential

Figure 48: Resource efficiency potential by sector($bn): Building efficiency provides biggest opportunity

0%

20%

40%

60%

80%

100%

Industry Transport Buildings

Unrealised energy efficiency potential

Realised energy efficiency potential

106

108

115115

132134138

138143145

155167

252

266696

Power plant efficiency

Road freight shiftIrrigation techniques

Oil and coal recovery

End-use steel efficiencyLand degredation

Electric and hybrid vehicles

Transport efficiencySmallholder farm yields

Iron and steel energy…

Urban densificationMunicipal water leakage

Food waste

Large-scale farm yieldsBuilding energy efficiency

Source: McKinsey Global Institute Source: McKinsey Global Institute

The European Commission estimates that achieving the 20% energy savings target by

2020 would reduce Europe's annual energy bill by €200bn or €1,000 per household.

The impact of these energy savings on CO2 emissions and environmental issues in

general is significant. Simulation studies performed by the IEA indicate that potential CO2

savings of over 75% relative to the "no-change" scenario can be obtained by implementing

efficiency programs. These programs typically focus on two areas.

■ De-carbonisation of the supply side. More than 60% of emission reductions can be

attributed to decarbonisation of the power generating sectors (Figure 49).

■ Improving efficiency of the demand side. The potential remaining 40% of CO2

emission improvements can be generated from improving the efficiency of the demand

side. A reduction in building energy use therefore plays a very significant role in

limiting the likely increase in global average temperatures. Key areas of focus for this

include improvements in heating, cooling, lighting and the building envelope (Figure

50).

Figure 49: Total CO2 emissions in a "no-change" scenario (6DS) vs energy savings scenario (2DS)

Figure 50: Key energy saving areas for building efficiency

0

2

4

6

8

10

12

14

2010 2020 2030 2040 2050

GtC

O2 Fuel switching

Cooking, lightingand appliancesBuildingenvelopeSpace cooling

Other efficiency

Solar thermal

Heat pumps andco-generationElectricitydecarbonisation

2DS: 2.7 GtCO2

6DS: 11.6 GtCO2

0

5

10

15

20

25

30

35

40

45

50

2010 2020 2030 2040 2050

Exaj

oule

s

Energy savings from 6DS to 2DS

Lighting and spacecooling (19%)

Building envelope(14%)

Space heating(15%)

Water heating(16%)

Cooking (21%)

Other equipment(15%)

Source: International Energy Agency (2013), Transition to Sustainable

Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable

Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

03 April 2014

Themes in Energy Efficiency 21

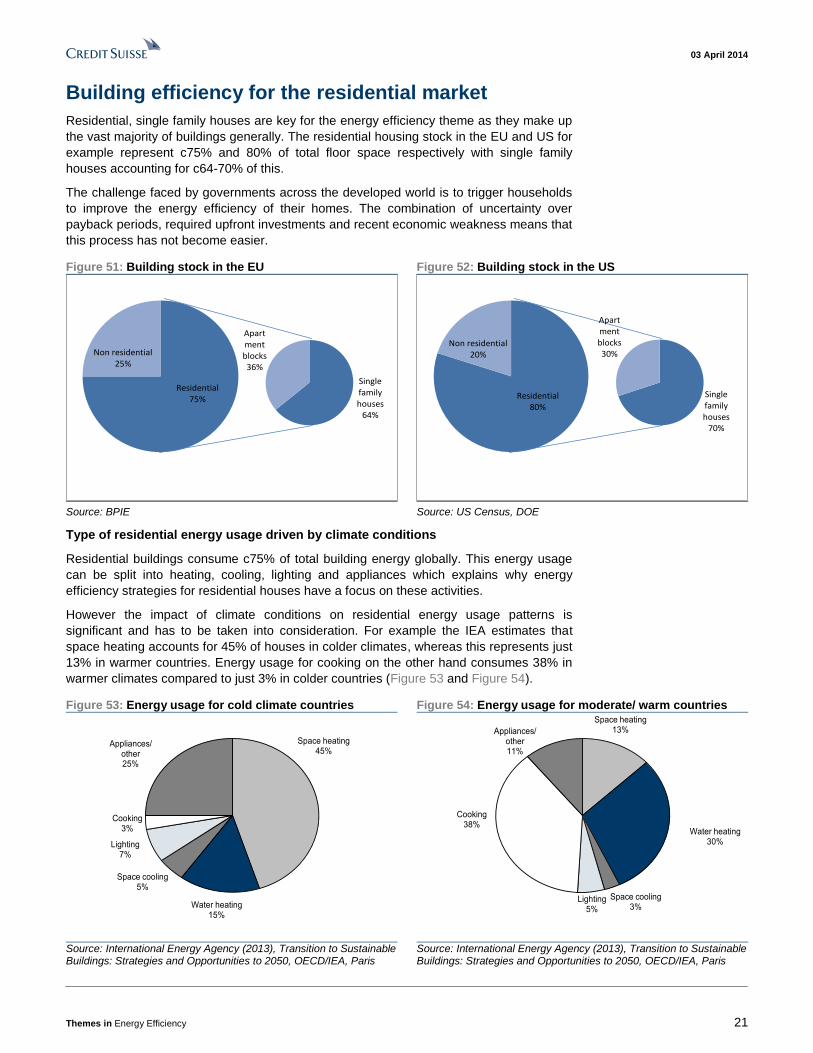

Building efficiency for the residential market

Residential, single family houses are key for the energy efficiency theme as they make up

the vast majority of buildings generally. The residential housing stock in the EU and US for

example represent c75% and 80% of total floor space respectively with single family

houses accounting for c64-70% of this.

The challenge faced by governments across the developed world is to trigger households

to improve the energy efficiency of their homes. The combination of uncertainty over

payback periods, required upfront investments and recent economic weakness means that

this process has not become easier.

Figure 51: Building stock in the EU Figure 52: Building stock in the US

Residential75%

Non residential25%

Single family houses

64%

Apartment blocks36%

Residential80%

Non residential20%

Single family houses

70%

Apartment blocks30%

Source: BPIE Source: US Census, DOE

Type of residential energy usage driven by climate conditions

Residential buildings consume c75% of total building energy globally. This energy usage

can be split into heating, cooling, lighting and appliances which explains why energy

efficiency strategies for residential houses have a focus on these activities.

However the impact of climate conditions on residential energy usage patterns is

significant and has to be taken into consideration. For example the IEA estimates that

space heating accounts for 45% of houses in colder climates, whereas this represents just

13% in warmer countries. Energy usage for cooking on the other hand consumes 38% in

warmer climates compared to just 3% in colder countries (Figure 53 and Figure 54).

Figure 53: Energy usage for cold climate countries Figure 54: Energy usage for moderate/ warm countries

Space heating45%

Water heating15%

Space cooling5%

Lighting7%

Cooking3%

Appliances/ other25%

Space heating13%

Water heating30%

Space cooling3%

Lighting5%

Cooking38%

Appliances/ other11%

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

Source: International Energy Agency (2013), Transition to Sustainable Buildings: Strategies and Opportunities to 2050, OECD/IEA, Paris

03 April 2014

Themes in Energy Efficiency 22

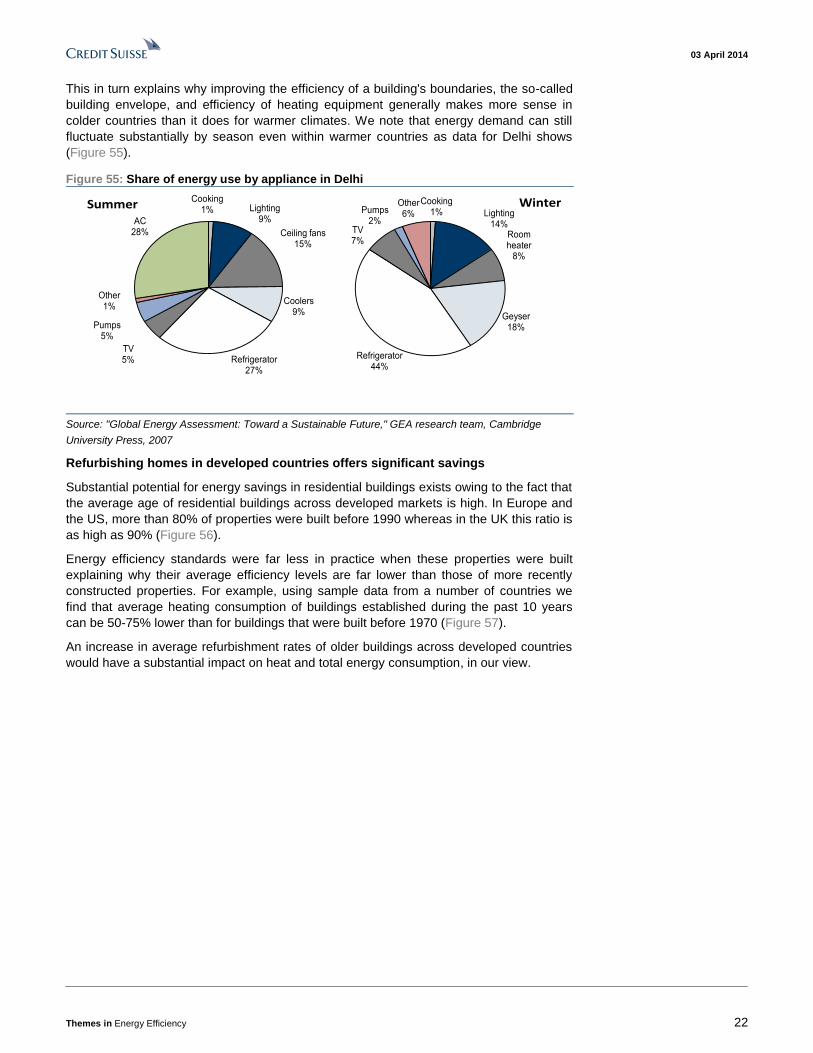

This in turn explains why improving the efficiency of a building's boundaries, the so-called

building envelope, and efficiency of heating equipment generally makes more sense in

colder countries than it does for warmer climates. We note that energy demand can still

fluctuate substantially by season even within warmer countries as data for Delhi shows

(Figure 55).

Figure 55: Share of energy use by appliance in Delhi

Cooking1% Lighting

14%Room heater

8%

Geyser18%

Refrigerator44%

TV7%

Pumps2%

Other6%

WinterCooking1% Lighting

9%

Ceiling fans15%

Coolers9%

Refrigerator27%

TV5%

Pumps5%

Other1%

AC28%

Summer

Source: "Global Energy Assessment: Toward a Sustainable Future," GEA research team, Cambridge

University Press, 2007

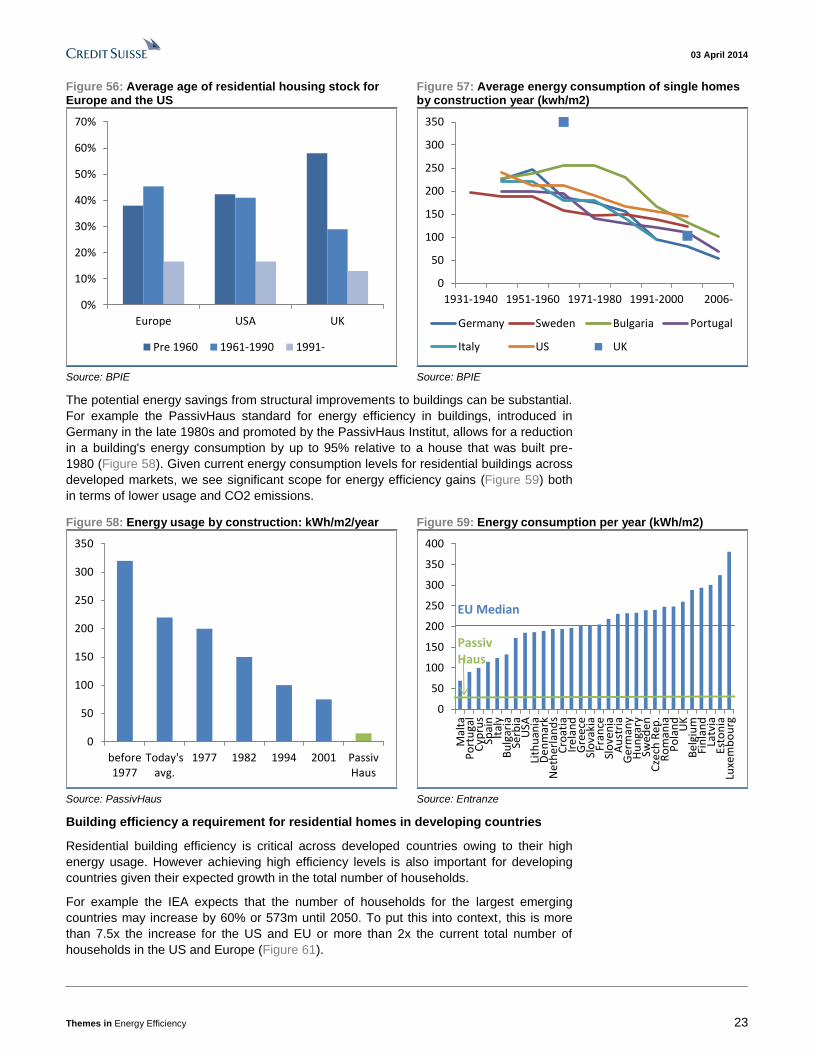

Refurbishing homes in developed countries offers significant savings

Substantial potential for energy savings in residential buildings exists owing to the fact that

the average age of residential buildings across developed markets is high. In Europe and

the US, more than 80% of properties were built before 1990 whereas in the UK this ratio is

as high as 90% (Figure 56).

Energy efficiency standards were far less in practice when these properties were built

explaining why their average efficiency levels are far lower than those of more recently

constructed properties. For example, using sample data from a number of countries we

find that average heating consumption of buildings established during the past 10 years

can be 50-75% lower than for buildings that were built before 1970 (Figure 57).

An increase in average refurbishment rates of older buildings across developed countries

would have a substantial impact on heat and total energy consumption, in our view.

03 April 2014

Themes in Energy Efficiency 23

Figure 56: Average age of residential housing stock for Europe and the US

Figure 57: Average energy consumption of single homes by construction year (kwh/m2)

0%

10%

20%

30%

40%

50%

60%

70%

Europe USA UK

Pre 1960 1961-1990 1991-

0

50

100

150

200

250

300

350

1931-1940 1951-1960 1971-1980 1991-2000 2006-

Germany Sweden Bulgaria Portugal

Italy US UK

Source: BPIE Source: BPIE

The potential energy savings from structural improvements to buildings can be substantial.

For example the PassivHaus standard for energy efficiency in buildings, introduced in

Germany in the late 1980s and promoted by the PassivHaus Institut, allows for a reduction

in a building's energy consumption by up to 95% relative to a house that was built pre-

1980 (Figure 58). Given current energy consumption levels for residential buildings across

developed markets, we see significant scope for energy efficiency gains (Figure 59) both

in terms of lower usage and CO2 emissions.

Figure 58: Energy usage by construction: kWh/m2/year Figure 59: Energy consumption per year (kWh/m2)

0

50

100

150

200

250

300

350

before1977

Today'savg.

1977 1982 1994 2001 PassivHaus

0

50

100

150

200

250

300

350

400

Mal

taP

ort

uga

lC

ypru

sSp

ain

Ital

yB

ulg

aria

Serb

iaU

SALi

thu

ania

De

nm

ark

Net

her

lan

ds

Cro

atia

Ire

lan

dG

ree

ceSl

ova

kia

Fran

ceSl

ove

nia

Au

stri

aG

erm

any

Hu

nga

rySw

ede

nC

zech

Rep

.R

om

ania

Po

lan

dU

KB

elg

ium

Fin

lan

dLa

tvia

Esto

nia

Luxe

mb

ou

rg

EU Median

PassivHaus

Source: PassivHaus Source: Entranze

Building efficiency a requirement for residential homes in developing countries

Residential building efficiency is critical across developed countries owing to their high

energy usage. However achieving high efficiency levels is also important for developing

countries given their expected growth in the total number of households.

For example the IEA expects that the number of households for the largest emerging

countries may increase by 60% or 573m until 2050. To put this into context, this is more

than 7.5x the increase for the US and EU or more than 2x the current total number of

households in the US and Europe (Figure 61).

03 April 2014

Themes in Energy Efficiency 24

Figure 60: Average house size across emerging and developed markets (2010)

0

50

100

150

200

250

Developed: 104m2

Emerging: 58m2

Source: IEA, UN

Future energy consumption from residential houses is not just driven by the expected

increase in the number of houses but also by their size. The average home in developed

markets is almost twice as a big as in developing countries (Figure 60). As wealth

increases, we would generally expect demand for bigger living space to increase also,

which in turn increases energy requirements further.

We estimate that the growth in households and the size per home across developing

countries may increase the total residential floor space that needs heating or cooling by

50bn m2 (Figure 62). This increase is more than the current total residential floor space for

the US and EU-27 combined.

Figure 61: Emerging households set to rise by c573m up to 2050 or 7.5x the increase for the US/EU

Figure 62: Residential emerging floor space may rise by 50bn m2 or more than current US and EU combined

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2010 2020 2030 2040 2050

EU+US Emerging

+60%: +573m

+23%: +75m

0

20

40

60

80

100

120

140

160

2010 2020 2030 2040 2050

EU+US Emerging

+80%: +42bn m2

+32%: +14bn m2

Source: IEA. Emerging = Asean, Brazil, China, India, Mexico, Russia and South Africa

Source: IEA. Emerging = Asean, Brazil, China, India, Mexico, Russia and South Africa

The need for refurbishment: mapping total residential energy consumption

In order to indicate what the impact of the expected growth in households globally might

mean for energy consumption we have run some scenarios. Using forecasts for household

formation across key regions and countries, assuming that average house sizes for

developing countries increase as income levels rise and using existing energy

consumption levels per square meter we can forecast potential total energy consumption.

03 April 2014

Themes in Energy Efficiency 25

We can then estimate what level of annual refurbishment of existing homes is needed to

stabilise total energy consumption from residential buildings.

Based on our data we calculate that without additional efficiency gains, total energy

consumption by residential buildings globally could increase by 71% until 2050 (Figure

63). This is not only driven by emerging markets (+118%) but also by a further 17%

increase from Europe and the US over that period.

To slow down the global growth in residential energy consumption requires energy savings

and therefore investments into refurbishment. We estimate that the current c1%

refurbishment rate in Europe and the US is sufficient to keep developed market growth

flat, however, this is not sufficient for emerging markets.

To keep global residential energy consumption flat, we believe that the annual

refurbishment rate has to increase to c3% per annum. This is in line with suggestions from

the "Renovate Europe" group but we note that it would have only a material impact on a

global basis as of 2030 (Figure 66).

Figure 63: No efficiency improvements implies residential energy consumption increase of 71% on a global basis

Figure 64: 1% refurbishment annually not sufficient to limit global energy consumption

0

10

20

30

40

50

60

70

80

90

2010 2020 2030 2040 2050

EU+US GEM

+118%

+ 17%

0

10

20

30

40

50

60

70

80

2010 2020 2030 2040 2050

EU+US GEM

+84%

+ 2%

Source: IEA, World Bank, Credit Suisse estimates Source: IEA, World Bank, Credit Suisse estimates

Figure 65: A 2% refurbishment stops consumption growth in EMG but only as of 2030

Figure 66: A 3% refurbishment rate would be sufficient to lower global residential energy consumption from 2030

0

10

20

30

40

50

60

70

2010 2020 2030 2040 2050

EU+US GEM

+40% to peak in 2030 then decline in Emg.

- 20%

0

10

20

30

40

50

60

2010 2020 2030 2040 2050

EU+US GEM

-24% global decline

Source: IEA, World Bank, Credit Suisse estimates Source: IEA, World Bank, Credit Suisse estimates

03 April 2014

Themes in Energy Efficiency 26

Our calculations for the "no-change" scenario show that further energy efficiency

improvements for residential buildings are vital in order to address potential energy supply-

demand concerns and related environmental challenges.

The potential size of the residential refurbishment market

We believe that the potential market for residential energy efficiency refurbishments is

significant; however, sizing the market opportunity is difficult owing largely to a lack of

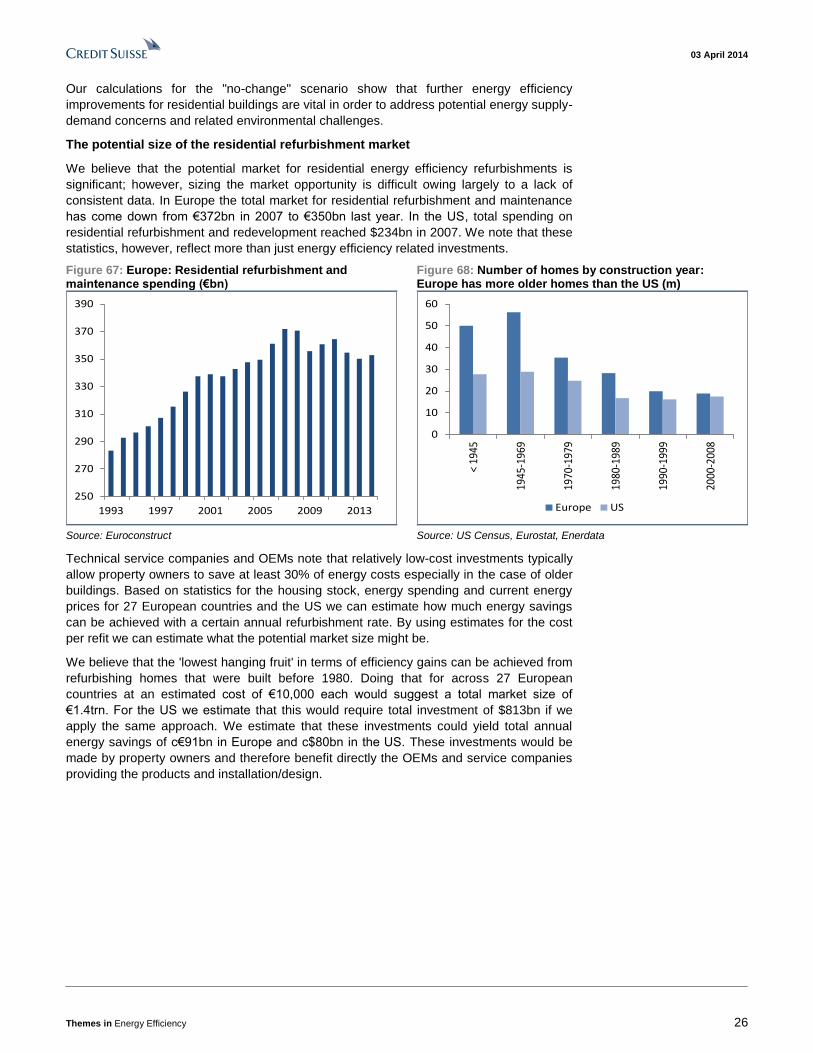

consistent data. In Europe the total market for residential refurbishment and maintenance

has come down from €372bn in 2007 to €350bn last year. In the US, total spending on

residential refurbishment and redevelopment reached $234bn in 2007. We note that these

statistics, however, reflect more than just energy efficiency related investments.

Figure 67: Europe: Residential refurbishment and maintenance spending (€bn)

Figure 68: Number of homes by construction year: Europe has more older homes than the US (m)

250

270

290

310

330

350

370

390

1993 1997 2001 2005 2009 2013

0

10

20

30

40

50

60

< 19

45

1945

-196

9

1970

-197

9

1980

-198

9

1990

-199

9

2000

-200

8

Europe US

Source: Euroconstruct Source: US Census, Eurostat, Enerdata

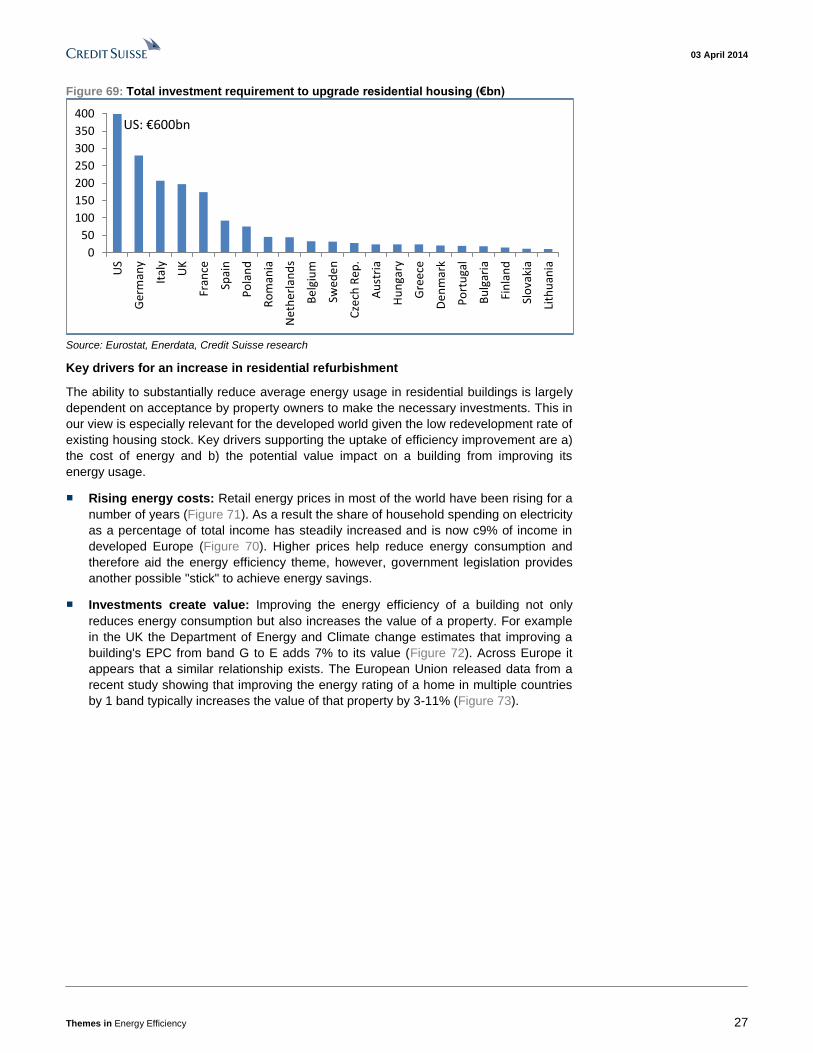

Technical service companies and OEMs note that relatively low-cost investments typically

allow property owners to save at least 30% of energy costs especially in the case of older

buildings. Based on statistics for the housing stock, energy spending and current energy

prices for 27 European countries and the US we can estimate how much energy savings

can be achieved with a certain annual refurbishment rate. By using estimates for the cost

per refit we can estimate what the potential market size might be.

We believe that the 'lowest hanging fruit' in terms of efficiency gains can be achieved from

refurbishing homes that were built before 1980. Doing that for across 27 European

countries at an estimated cost of €10,000 each would suggest a total market size of

€1.4trn. For the US we estimate that this would require total investment of $813bn if we

apply the same approach. We estimate that these investments could yield total annual

energy savings of c€91bn in Europe and c$80bn in the US. These investments would be

made by property owners and therefore benefit directly the OEMs and service companies

providing the products and installation/design.

03 April 2014

Themes in Energy Efficiency 27

Figure 69: Total investment requirement to upgrade residential housing (€bn)

0

50

100

150

200

250

300

350

400U

S

Ger

man

y

Ital

y

UK

Fran

ce

Spai

n

Po

lan

d

Ro

man

ia

Net

her

lan

ds

Be

lgiu

m

Swed

en

Cze

ch R

ep.

Au

stri

a

Hu

nga

ry

Gre

ece

De

nm

ark

Po

rtu

gal

Bu

lgar

ia

Fin

lan

d

Slo

vaki

a

Lith

uan

ia

US: €600bn

Source: Eurostat, Enerdata, Credit Suisse research

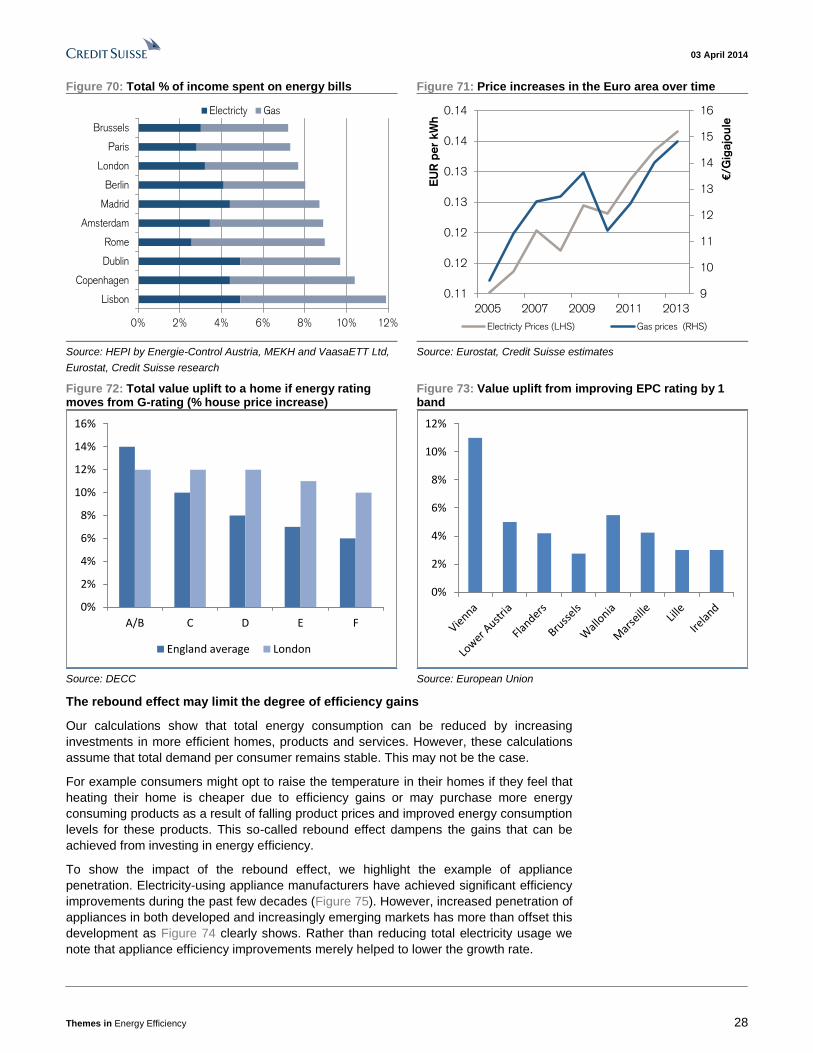

Key drivers for an increase in residential refurbishment

The ability to substantially reduce average energy usage in residential buildings is largely

dependent on acceptance by property owners to make the necessary investments. This in

our view is especially relevant for the developed world given the low redevelopment rate of

existing housing stock. Key drivers supporting the uptake of efficiency improvement are a)

the cost of energy and b) the potential value impact on a building from improving its

energy usage.

■ Rising energy costs: Retail energy prices in most of the world have been rising for a

number of years (Figure 71). As a result the share of household spending on electricity

as a percentage of total income has steadily increased and is now c9% of income in

developed Europe (Figure 70). Higher prices help reduce energy consumption and

therefore aid the energy efficiency theme, however, government legislation provides

another possible "stick" to achieve energy savings.

■ Investments create value: Improving the energy efficiency of a building not only

reduces energy consumption but also increases the value of a property. For example

in the UK the Department of Energy and Climate change estimates that improving a

building's EPC from band G to E adds 7% to its value (Figure 72). Across Europe it

appears that a similar relationship exists. The European Union released data from a

recent study showing that improving the energy rating of a home in multiple countries

by 1 band typically increases the value of that property by 3-11% (Figure 73).

03 April 2014

Themes in Energy Efficiency 28

Figure 70: Total % of income spent on energy bills Figure 71: Price increases in the Euro area over time

0% 2% 4% 6% 8% 10% 12%

Lisbon

Copenhagen

Dublin

Rome

Amsterdam

Madrid

Berlin

London

Paris

Brussels

Electricty Gas

9

10

11

12

13

14

15

16

0.11

0.12

0.12

0.13

0.13

0.14

0.14

2005 2007 2009 2011 2013

€/G

igajo

ule

EU

R p

er

kW

h

Electricty Prices (LHS) Gas prices (RHS)

Source: HEPI by Energie-Control Austria, MEKH and VaasaETT Ltd,

Eurostat, Credit Suisse research

Source: Eurostat, Credit Suisse estimates

Figure 72: Total value uplift to a home if energy rating moves from G-rating (% house price increase)

Figure 73: Value uplift from improving EPC rating by 1 band

0%

2%

4%

6%

8%

10%

12%

14%

16%

A/B C D E F

England average London

0%

2%

4%

6%

8%

10%

12%

Source: DECC Source: European Union

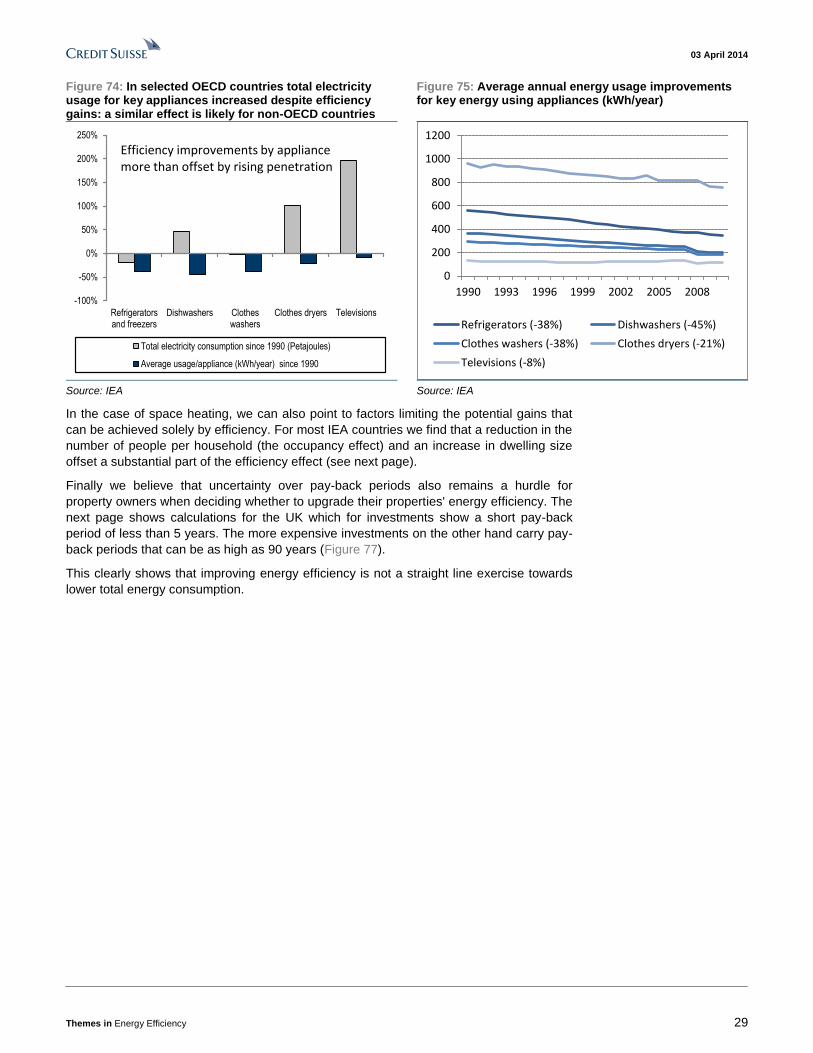

The rebound effect may limit the degree of efficiency gains

Our calculations show that total energy consumption can be reduced by increasing

investments in more efficient homes, products and services. However, these calculations

assume that total demand per consumer remains stable. This may not be the case.

For example consumers might opt to raise the temperature in their homes if they feel that

heating their home is cheaper due to efficiency gains or may purchase more energy

consuming products as a result of falling product prices and improved energy consumption

levels for these products. This so-called rebound effect dampens the gains that can be

achieved from investing in energy efficiency.

To show the impact of the rebound effect, we highlight the example of appliance