Indonesia Consumer Survey 2013 - doc .credit -suisse .com

96

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 25 January 2013 Asia Pacific/Indonesia Equity Research Consumer Discretionary / Consumer Staples Indonesia Consumer Survey 2013 STRATEGY Maintaining confidence and optimism Research Analysts Ella Nusantoro 62 21 255 37917 [email protected] Priscilla Tjitra 62 21 255 37906 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Indonesia Consumer Survey 2013 - doc .credit -suisse .com

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

25 January 2013Asia Pacific/Indonesia

Equity ResearchConsumer Discretionary / Consumer Staples

Indonesia Consumer Survey 2013

STRATEGY

Maintaining confidence and optimism

Research Analysts

Ella Nusantoro 62 21 255 37917

Priscilla Tjitra 62 21 255 37906

25 January 2013

Indonesia Consumer Survey 2013 2

Introduction We are delighted to publish the third edition of the Credit Suisse Global Emerging Consumer Survey and its accompanying Databook. At a time when investor confidence in the outlook for global growth is improving, it is opportune to review the dynamics and drivers of what is a key component of the prospects for global growth—the role played by the consumer in the emerging world. The analysis carried in this report provides insights not available from public sources of economic information.

To undertake this project, the Credit Suisse Research Institute had engaged the leading global market research firm Nielsen to conduct face-to-face interviews with over 14,000 consumers across eight emerging economies posing more than 125 questions to help reflect a granular picture of their spending habits, future intentions and importantly, the factors that influence them.

The 2013 survey has been refreshed to address new issues—social and economic—and alongside Brazil, China, India, Indonesia, Russia, Saudi Arabia and Turkey, we have added South Africa. The detailed analysis of the differing demographic, income and rural/urban characteristics underlines that these emerging consumers cannot be viewed in a generic fashion.

This report is a more granular version of the Credit Suisse Emerging Consumer Survey, focusing specifically on Indonesian consumption. We surveyed 1,531 consumers in the country across ten exclusive geographies, both urban and rural areas.

Telephone Email+44 20 7888 0313 [email protected]+44 20 7883 3773 [email protected]+44 20 7883 9247 [email protected]

Jo Walton (Healthcare) +44 20 7888 0304 [email protected]+852 2101 6554 [email protected]

Felix Rusli +852 2101 6482 [email protected]+1 212 538 6386 [email protected]

Arbin Sherchan +1 212 325 8967 [email protected] Takato +81 3 4550 9671 [email protected]

Brazil Andrew Campbell +55 11 3841 6313 [email protected] Federle +55 11 3841 6311 [email protected] Wigman +55 11 3841 6302 [email protected]

China Vincent Chan +852 2101 6568 [email protected] Salamatian +852 2101 7996 [email protected] Yin +852 2101 7655 [email protected] Chan +852 2101 6523 [email protected]

India Jatin Chawla +91 22 6777 3719 [email protected] Mitra +91 22 6777 3806 [email protected] Saxena +91 22 6777 3825 [email protected]

Indonesia Ella Nusantoro +62 21 255 37917 [email protected] Tjitra +62 21 255 37906 [email protected]

Russia Victoria Petrova +7 495 967 8393 [email protected] Bystrova +7 495 967 8244 [email protected]

South Africa Carlos Teixeira +27 11 012 80 54 [email protected] Bhundia +27 11 012 80 94 [email protected] Ginsberg +27 11 012 80 64 [email protected] Barker +27 11 012 80 51 [email protected]

Turkey Onur Muminoglu +90 212 349 0454 [email protected] Ozkan +90 212 349 0453 [email protected] Buldur +90 212 349 0459 [email protected]

Contributors

Kiranjot Grewal

Research analystRichard KersleyMujtaba Rana

Jahanzeb Naseer

Katie Iorio

Stefano Natella Co-head of Global Securities Research

25 January 2013

Indonesia Consumer Survey 2013 3

Credit Suisse Indonesia research analysts

Research analysts Telephone Email

Ella Nusantoro +62 21 2553 7917 ella.nusantoro@credit suisse.com

Teddy Oetomo +62 21 2553 7911 [email protected]

Ami Tantri +62 21 2553 7976 [email protected]

Dian Haryokusumo +62 21 2553 7974 [email protected]

Agus Sandianto +62 21 2553 7916 [email protected]

Colin McCallum +852 2101 6514 [email protected]

Paworamon Suvarnatemee +66 8 1814 4515 [email protected]

Timothy Ross +65 6212 3337 [email protected]

Robert Prior-Wandesforde +65 6212 3707 [email protected]

25 January 2013

Indonesia Consumer Survey 2013 4

Credit Suisse Indonesia Consumer Survey 2013: Key themes Figure 1: Key themes from Indonesia Consumer Survey 2013

Themes(1) Confidence and optimism continue to remain robust Indonesians are the second most confident people after Brazilians, with 64% of respondents

expecting a better income outlook over the next 12 months and 40% expecting a better personal finace outlook over the next six months.

(2) Higher income growth and expecting further hike This year, more respondents said that their income has increased in the past 12 months. Despite that, they expect to get a higher income in the next 12 months. We view this in line with the increase in minimum wages in 2012 and the expected increase in 2013.

(3) Shift towards higher discretionary spending continues This year spending on discretionaty items increased more than that on essentials, especially on fashion apparel and mobile phones.

(4) Consumer preferences lean towards local brands for essentials We found that indonesians prefer local brands for essential items. However, appetite for foreign brands is higher for discretionary items such as fashion apparel and cosmetics, especially among high income earners.

Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 2: Indonesians are the most confident after Brazilians Figure 3: Outside Java earns more than Java

6764

53

42

26

19

58

47

55

3539

22

66

58

4036 38

22

0

10

20

30

40

50

60

70

80

Brazil Indonesia Saudi China India Russia

Inco

me

Out

look

nex

t 12M

(% o

f res

pond

ents

)

Better less worse 2012 Better less worse 2011 Better less worse 2010

3.2

3.5

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Total Urban Rural Java Non-Java

Avg

mon

thly

inco

me

(Rp

mn/

mon

th)

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 4: Shift towards higher discretionary spending

continues

Figure 5: Consumers preferences lean towards local

brands for essentials

Carbonated drinks

Bottled Water

Dairy products

Instant Noodles

Cigarettes

Tissues Femine hygiene Cosmetics

Basic mobile phone

DVD PlayerTraditional TV

Smartphone

Fashion

Sport shoes & wear

WatchesJewellery

Perfumes

Cars

Internet Access

Property

-15

-10

-5

0

5

10

15

20

25

30

0 20 40 60 80 100

% c

hang

e fro

m la

st y

ear s

urve

y

% of respondent which have bought essentials and discretionary goods

80

85

90

95

100

<Rp1,000k

Rp1,000k -Rp1,500k

Rp1,500k -Rp2,000k

Rp2,000k -Rp3,000k

Rp3,000k -Rp5,000k

Rp5,000k -Rp7,500k

Rp10,000k-Rp15,000k

Rp10,000k -Rp15,000k

>Rp15,000k

% o

f res

pond

ents

buy

ing

loca

l bra

nds

Cigarette Instant noodles Bottled water

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

25 January 2013

Indonesia Consumer Survey 2013 5

Key themes from the eight emerging markets We highlight four key themes:

(1) Consumer confidence improving

The survey suggests that, after stalling in 2012, confidence is strengthening—a feature our macro views would endorse and expect. Some 37% believe their personal finances will improve over the next six months while 9% expect some deterioration. This marks a net expected improvement of 3% points on a like-for-like basis. However, our survey casts a spotlight on the striking contrasts across the emerging world.

Optimism is strongest and improving in Brazil, China and Indonesia. At the other end of the scale, the greatest degree of pessimism in financial prospects was recorded in South Africa, Russia and Turkey (albeit improving). Troubling are the effective “fault lines” that still seem to exist between rich and poor in some countries. For example, our survey revealed that nearly as many South Africans (22%) predicted a worse financial position as those who expected some improvement (28%). We remember—if in a far more extreme manner—how severe disparity in experience for Egypt stood out in our 2010 survey.

(2) Income trends are the key driver—who has it?

The outlook for and the distribution of income has replaced the influence of food prices as the determinant of optimism. The countries with the highest income growth expectations display the greatest optimism—Brazil, Indonesia and Saudi Arabia. Wage expectations remain relatively depressed in Turkey, Russia and South Africa. However, equally notable is the fact that the highest income earners are the most optimistic in every country. In certain countries, that is particularly stark—South Africa and India for example. In contrast, Brazil reflects far greater equality of expectations.

As much as regional contrasts in the income outlook, age profile within the countries is a notable differentiator. In a number of the countries, the high income consumers are clustered in the younger age brackets of the working population. China is a stand out example. Moreover, the incomes are not only higher but are typically growing more rapidly. This picture is in marked contrast to the West. The drivers at work in the emerging world are relative educational attainment, urban/rural migration and the necessity of technology based skill-sets.

(3) Discretionary spending back on track

Understanding what younger, wealthier and typically better educated consumers will spend their money upon is a key investment theme as this is where growth is likely to be strongest. This would structurally point to areas of discretionary spending. Our survey illustrates that this theory is borne out in practice. The survey asks consumers what categories of spending they have been spending most upon and effectively what they expect to prioritise looking forward. Having stalled last year, discretionary spending looks back on track and should maintain its momentum.

In terms of specifics, meat and protein gets a higher profile on the menu. A thirst for technology, smartphones and tablets, is supported by ever greater expansion in internet penetration. This was a theme last year and is if anything an even stronger one. Bigger ticket items such as cars and property also display strong prospects though notably without the typical appetite for borrowing we have historically seen in the West.

Interestingly, the outlook for services such as healthcare and education seems more muted. However, it seems the state is increasingly stepping in to supply the former while private educational spend has simply been exceptionally strong in recent years and seeing

25 January 2013

Indonesia Consumer Survey 2013 6

a moderation from a high base. It remains a structural story in our view, with India still displaying it best of all.

(4) Brand recognition … momentum and critical mass

The track record being built by the survey is allowing us to delve deeper into our analysis of brands. We can analyse with the help of our Databook brands displaying momentum, where local brands hold sway over global rivals and the income sensitivity of brands. Important themes have emerged: (i) the significance of the unbranded segment of spending; (ii) the resilience of domestic brands in the essential areas of spending space and their attractiveness to acquisitive global companies; and (iii) the aspirational quality (or lack thereof) of specific brands in the discretionary space, which plays to the international names.

With improving income trends being the key driver of the emerging consumer structurally, and also a key differentiator of the immediate outlook in the survey as suggested above, we specifically analyse brands with this theme in mind. With high income earners being where income growth expectations and optimism are the highest, we want to identify which brands exhibit momentum or dominance in this category. Equally, at the low income end where a transition from unbranded to branded products is likely, we wish to be positioned to exploit that. We would be concerned about brands that are losing momentum and also those whose attractions peter out markedly higher up the income scale given this is the direction of travel in emerging consumer markets.

Figure 6: Brands dominating their sector or having momentum within an income bracket

Low income High income Low income High income

AAPL US Apple Inc. x x Outperform

BMW.DE BMW x Outperform

BRBY L Burberry x Outperform

2319 HK China Mengniu Dairy Company x x Outperform

1929 HK Chow Tai Fook Jewellery x x x Neutral

HGTX3 BZ Cia. Hering x x x Neutral

DGE LN Diageo plc x x x x Outperform

HUVR IN Hindustan Unilever Limited x x x Outperform

005380 KS Hyundai Motor Co x x Outperform

2331 HK Li Ning x Neutral

LREN3 Lojas Renner x x Neutral

OR FP L'Oreal SA x x Neutral

AMAR3 Marisa Lojas SA x x x x Outperform

MSIL IN Maruti Suzuki India Ltd x x x Neutral

MDLZ Mondelēz International x x Outperform

NKE US Nike, Inc x x x x Neutral

RI FP Pernod Ricard x x Outperform

SAB L SAB Miller x x x x Outperform

005930 KS Samsung Group x x x x Outperform

UHR VX Swatch x x Outperform

ULVR Unilever x x Neutral

Ticker Company

Criteria

Trend DominatingCS Rating

Source: Credit Suisse Emerging Consumer Survey 2013

Country highlights Key highlights include:

Brazil: The beat goes on

The Brazilian consumer remains the most optimistic in our survey, with confidence raised year-on-year despite an economic slowdown. A definitive characteristic of this confidence is its breadth; both low and high income consumers are confident, unlike the findings for many other developing economies. Although an implicit savings ratio seems to have increased, it remains substantially lower than the other larger economies. Momentum

25 January 2013

Indonesia Consumer Survey 2013 7

remains in discretionary products such as technology, fashion and spirits. Education is also a priority. Key stock recommendations: Anhanguera, Brasil Foods, Hypermarcas, Marisa S.A., Qualicorp, SAB Miller, Cinemark, Casino Guichard, Nissan, Intertek

China: An educated consumer

Optimism amongst the Chinese consumer remains relatively robust against a weaker economic background. Much of this increased strength can be attributed to the low income brackets rather than the high. Attitudes surrounding savings remain unhindered, although the routes adopted to achieve this are changing; the increased role of the stock market and life products for savings. The key feature of spending is a heavy focus on technology and education, with the strongest spend in smartphones out of any country surveyed. Key stock recommendations: Belle, Intime, Tingyi, Chow Tai Fook, Naspers, Prada, Yum!, Mead Johnson, TOTO, HSBC, Richemont, Wynn, Las Vegas Sands, MGM resorts, Nissan India: A sum of different parts

Although the optimism of the Indian consumer remains robust, there is an increasing divergence between the confidence levels of rich and poor consumers: poor consumers demonstrate a sharp decline in confidence. Spending momentum in education continues to stride ahead, supported by a number of government initiatives. Discretionary spend categories are the stronger areas within India though appear relatively more mute vs. other countries, with India in fact being the only country surveyed showing a fall in the number of smartphones bought for example. Aggressive promotion of property investment has led to positive expectations for the direction of property prices. Key stock recommendations: ITC, Bajaj Auto, Emami, HDFC Bank, Titan, Shiseido, Tumi

Indonesia: BRIC becomes BIIC

The Indonesian consumer continues to grow increasingly confident, corresponding with the trend growth seen in the Indonesian economy. The increases in minimum wages have contributed to the relatively steeper growth in confidence amongst the lower earners. Rising incomes and lowered food prices have resulted in increased spending on discretionary goods, with fashion and holidays being items of choice. As the vast majority of Indonesia remains offline, technology growth remains concentrated in basic mobile phones rather than internet enabled devices such as smartphones. Key stock recommendations: Astra International, Indofood CBP, Erajaya Swasembada, Mitra Adiperkasa, Bank Central Asia, Unicharm, Daihatsu, Prudential, Sumitomo, Yakult

Russia: The poor BRIC relation

Low optimism, poor income growth and a large disparity between the expectations of rich and poor consumers characterised Russia in 2012. Inflation rates are forecast to be one of the highest out of our survey. With a large proportion of income being devoted to food, Russian consumers have been constrained in spending elsewhere though this should ease. At present, only discretionary spend categories in reach of the rich remain robust, with others on the whole weak. Technology is the strongest feature. Key stock recommendations: Magnit, MegaFon, MTS, Yandex, Mail.Ru, JT, Fast Retailing

Saudi Arabia: Contrasting fortunes

Although the Saudi Arabian consumer remains one of the most optimistic in our survey, optimism has dropped relatively year-on-year post 2011’s boost from the major government initiatives for employment and pay. It remains highly progressive in relation to incomes. There is high growth in highly penetrated markets, in particular, computers, smartphones, fashion apparel and perfumes. There remains considerable structural opportunity for the financial industry to tap into the deep pool of savings which are currently predominantly held in bank accounts. Key stock recommendations: Apple, Marriott, BMW, Accor, Ralph Lauren, Starwood, Saks

25 January 2013

Indonesia Consumer Survey 2013 8

South Africa: Challenges and opportunities

South Africa is a new edition to the Credit Suisse Emerging Consumer Survey for 2013. Consumer optimism levels in South Africa fall toward the lower end of the survey spectrum. The polarity of experience within the population is concerning. Nearly as many South African consumers predicted a worse financial position as those who expected some improvement. Despite broad pay rises for many, it does not appear to have completely assuaged negative perceptions of the financial outlook of low income earners which has impacted the pattern of spending and its relative position vs other countries in the survey. A major distinguishing feature of South Africa is the institutionalised savings and a more developed banking system. Key stock recommendations: Foschini, African Bank, Pick n Pay, Lewis, Medpro, SAB

Turkey: Potential emerging

While optimism is relatively weak compared to other countries in the survey, Turkey has seen an improvement in overall confidence, with greatest improvement amongst the higher earners. They are comparable with Saudi Arabia. Spending patterns more generally are beginning to look like those of a middle-income country, with smartphones, computers, internet access, cars and holidays seeing some of the strongest gains. Growth in alcohol spend has not been deterred by recent tax hikes. Bank penetration remains poor, indicating a structural opportunity. Key stock recommendations: Arcelik Coca Cola Icecek, Migros, Tofas, Telenor, Diageo

25 Janu

ary 2013

Ind

on

esia Co

nsu

mer S

urvey 2013

9

Stock recommendations: Emerging markets Figure 7: Plays on the developing consumer

Stock Country Investment story

Current Price (local CCY)

Target Price (Local CCY)

EV / Ebitda (2012e)

PE (2012e)

P/B (2012e)

ROE (2012e)

3 year EPS

growth

3 year Revenue growth

Rating

Anhanguera BrazilBenefit from recovering profitability and higher earnings visibility. 30% gross margin ramp up expected from integration of acquired assets. Campus maturation & improving intake cycle to expand gross margin.

34.3 40.0 16.9 117.0 2.5 2% 101% 20% Outperform

Brasil Foods BrazilSuperior product portfolio and distribution assets to continue driving market share gains and consensus beats. Expect positive earnings momentum due to normalisation of operations after asset sw ap.

45.1 45.0 15.5 28.7 2.8 10% 21% 10% Outperform

Hypermarcas Brazil#1 in OTC and branded generics drugs, #3 in generics. Capex and w orking capital requirements should start to ease and profitability is expected to be restored in both the pharma and consumer divisions.

16.2 16.0 16.2 33.9 1.8 5% - 12% Outperform

Marisa S.A. BrazilScope for acceleration in store productivity and prof itability as the company benefits from a rapidly maturing sales area, coupled w ith internally-driven initiatives to improve sales f loor eff iciency.

32.5 28.0 16.2 33.8 7.0 21% 27% 9% Outperform

Qualicorp BrazilBelieve there are signif icant opportunities in the aff inity market and in the convergence of health and f inancial services, both in w hich Qualicorp is w ell positioned to benefit.

22.4 22.5 36.3 66.5 3.1 5% 55% 23% Outperform

Belle ChinaRecovery in 1Q13 to be driven by easy comp base, cold w inter and Chinese New Year. Benefit from expected stronger underlying economy as translates into rising discretionary in 2H13 and onw ards.

18.0 19.0 20.0 28.6 6.3 22% 13% 15% Outperform

Chow Tai Fook ChinaMost established sales netw ork - currently w ith 1,700 stores and to increase store counts by 200pa. Strong brand recognition. Better access to new department stores and economies of scale.

13.2 12.1 15.2 19.2 4.2 22% 23% 29% Neutral

Intime ChinaNew ly matured stores are the most effective contributor to earnings grow th. Is developing modern shopping mall formats as a part of a large scale project - gives key advantage in obtaining prime location.

10.5 11.8 18.2 20.0 2.5 11% 15% 23% Outperform

Prada ChinaRising brand aw areness is expected to lead to the highest sales grow th among major luxury brands. Probability of positive earnings surprises in 2013 is high - may lead to consensus upgrades.

71.6 78.0 23.4 40.6 9.6 24% 47% 27% Outperform

Tencent ChinaStronger consumer confidence, higher discretionary spending and demand for brands may benefit Tencent as it is a strong Internet brand. Tencent should have different business cycle as compared to the economy.

269.0 292.0 27.9 39.3 13.8 36% 30% 38% Outperform

Tingyi ChinaLooking into 2013, w e expect Tingyi to deliver strong grow th on the back of (1) core business turnaround and (2) more synergy from Pepsi bottling business to emerge in the next 2-3 years.

21.5 27.0 16.9 39.6 7.4 19% 26% 20% Outperform

Bajaj Auto IndiaTw o w heeler market still has high grow th potential. Positive impact of long term upgradation trend in market as it is strongest in upper segments. Export volumes grow ing at over 15% CAGR.

2061.8 2537.0 14.6 19.6 9.8 50% 4% 15% Outperform

Emami IndiaStrong potential of the current pipeline of ramp ups. Likelihood of margin expansion ahead on low er input costs. Scope for re-rating as one the highest ROE's and dividend ratios but at discount to peers.

579.9 690.0 29.2 33.9 12.4 37% 20% 17% Outperform

HDFC Bank IndiaLeadership in the retail segment to continue to drive stronger than industry grow th. Profitability remains strong on healthy margins and low credit cost. Strong product origination and credit appraisal skills.

653.6 770.0 18.1 29.3 5.2 18% 29% 21% Outperform

ITC IndiaHas absolute pricing pow er as has 75% market share. Expect cigarette EBIT grow th to stay in a range of 15-20pc irrespective of increase in taxation. Built one of India's top 5 FMCG businesses.

288.7 329.0 26.5 36.6 12.0 33% 21% 16% Outperform

Titan IndiaHas very high grow th potential as over 90% of the market is unorganized. Company w ill continue to gain market share w ith aggressive additions in expanding retail space.

269.0 341.0 27.5 39.8 16.5 41% 28% 23% Outperform

Note: Current price as of market close on 21 January 2013. Source: Credit Suisse Emerging Consumer Survey 2013

25 Janu

ary 2013

Ind

on

esia Co

nsu

mer S

urvey 2013

10

Figure 8: Plays on the developing consumer

Stock Country Investment story

Current Price (local CCY)

Target Price (Local CCY)

EV / Ebitda (2012e)

PE (2012e)

P/B (2012e)

ROE (2012e)

3 year EPS

growth

3 year Revenue growth

Rating

Astra Intl. Indonesia Attractive exposure to consumer sector. Expect recovery in earnings grow th. Attractive entry point. 7750 9400 14.9 17.6 5.2 28% 20% 16% Outperform

Bank Central Asia

IndonesiaIndonesia’s largest transaction bank. As of 3Q12, BBCA has one of the low est LDR (68.9%) of the Indonesian banking system, w hich implies that they have one of the highest grow th capacites.

9300 11000 16.5 21.1 5.4 24% 12% 14% Outperform

Erajaya Sw asembada

IndonesiaBeneficiary of rising income. New handset import regulation to be effective by end-Mar. Forex risk w ill be borne by the principal.

2750 3300 20.2 31.2 3.7 18% 41% 40% Outperform

Indofood CBP IndonesiaNoodle is its major contributor and continue to provide healthy profitability. Dairy expansion to come on stream. New JVs to expand product portfolio.

7950 8100 14.2 23.5 4.5 19% 13% 12% Outperform

Mitra Adiperkasa

IndonesiaSpecialty stores continue to be the key driver. Strategic expansion. Limited and manageable impact on current regulation changes.

6400 8100 12.7 29.5 5.9 21% 26% 21% Outperform

Magnit RussiaExceptional grow th (c25% 3Y CAGR); excellent management execution and communication; and upside risks given supportive regulatory environment in the sector.

46.2 42.0 24.5 52.2 9.0 23% 34% 24% Outperform

Mail.Ru RussiaConsumer internet names strong beneficiaries of trends in mobile data as consumer internet stocks are highly geared to increasing mobile internet traff ic via online advertising and consumption spend.

33.7 55.0 14.6 33.7 1.8 6% 24% 29% Outperform

MegaFon Russia#1 position in mobile data position in Russia, better netw orks, strong execution and business concentration on the Russian market. Expect Russian mobile to deliver 20-25% CAGR over next 3ys.

25.9 30.0 4.5 11.1 1.8 37% 3% 8% Outperform

MTS RussiaMTS as a second w inner of the Russian smartphone trend w hich has also show n strong execution in mobile data segment and commitment to infrastructure build.

19.1 22.0 5.1 12.8 5.4 43% 11% 5% Outperform

Yandex RussiaConsumer internet names strong beneficiaries of trends in mobile data as consumer internet stocks are highly geared to increasing mobile internet traff ic via online advertising and consumption spend.

22.9 29.0 23.6 39.3 7.8 22% 34% 36% Outperform

African BankSouth Africa

Market leader in low er-income consumer f inance. It also ow ns a furniture retailer, Ellerines. Recent investor concerns about non-performing loans and slow ing asset grow th are overdone in our view .

31.0 49.5 5.6 9.0 1.7 20% 16% 18% Outperform

Cipla MedproSouth Africa

Grow th is supported by its supply agreement w ith Cipla India w hich gives it access to a large new product pipeline, w hile the low cost of the drugs it sources from Cipla India help to support margins.

8.9 9.5 9.2 15.3 2.0 12% 20% 17% Outperform

Lew is GroupSouth Africa

Valuation is attractive, and cheapest entry into SA retail sector. Dividend yield is attractive at c7%. We believe that risks associated w ith "credit life" revenues are over blow n.

68.9 90.0 6.5 7.9 1.3 16% 12% 8% Outperform

Naspers South Africa

Good balance betw een internet-driven earnings grow th and strong pay-TV cash f low , see strong grow th potential in Tencent from its mobile internet, online advertising and eCommerce investments.

548.0 500.0 9.3 43.7 4.4 10% 32% 17% Outperform

Pick n Pay Holdings

South Africa

32% market share and margins of 1.8%. New CEO w ith strong track record as a retailer should result in the group recovering signif icantly, w e estimate margin to more than double over the next 3yrs

44.6 49.0 10.4 31.1 8.8 26% 16% 10% Outperform

The Foschini Group

South Africa

Offering covers low er, middle and upper end consumers. Well positioned to take advantage of grow th prospects into Africa. Expect group to sell its stake in RCS w hich w ill release value.

125.2 158.0 10.1 16.2 4.1 25% 21% 14% Outperform

Arcelik TurkeyStrong brand aw areness, distribution pow er and R&D efforts. Grow th initiatives - have announced they may buy a premium brand in developed w orld or extend production into new emerging countries.

12.5 12.5 11.2 15.6 2.4 16% 15% 16% Outperform

Coca Cola Icecek

Turkeyc70% market share in Turkish sparkling beverages. CCI has market leading shares in some of the w orld’s least saturated markets. 60% of its 360mn population is below 30 years of age.

41.4 37.2 11.2 19.0 5.0 25% 6% 6% Neutral

Migros TurkeyIts strong brand name and best store locations enable up to 40% shelf price dif ferential. Its attractive store netw ork could mean a lot for a strategic investor looking for inorganic grow th in Turkey.

22.6 23.8 14.9 -14.4 3.0 5% NA 13% Outperform

Tofas TurkeyIts low -to-mid segment models could benefit from the potential car penetration grow th in Turkey in the long-run. c73% of the capacity is locked by take-or-pay export contracts.

11.1 11.4 8.9 10.8 3.1 24% 0% 6% Outperform

Note: Current price as of market close on 21 January 2013. Source: Credit Suisse Emerging Consumer Survey 2013

25 J

an

uary

201

3

Ind

on

esia

Co

ns

um

er S

urv

ey 2

01

3

11

The Credit Suisse Emerging Consumer Survey 2013 Figure 9: Countries surveyed

Source: Credit Suisse Emerging Consumer Survey 2013, IMF, EIU, UN

25 January 2013

Indonesia Consumer Survey 2013 12

Table of contents Key themes from Indonesia 13

The third Credit Suisse Indonesia Consumer Survey 14

Key sector selections 28

Automotive 29

Consumer 33

Telecoms 43

Healthcare 47

Property 51

Banks 53

Key stock selections 56

Astra International (ASII.JK / ASII IJ) 57

Indofood CBP (ICBP.JK / ICBP IJ) 59

Erajaya Swasembada Tbk (ERAA.JK / ERAA IJ) 61

Mitra Adiperkasa (MAPI.JK / MAPI IJ) 63

Bank Central Asia (BBCA.JK / BBCA IJ) 65

Appendix: Respondents’ summary 67

25 January 2013

Indonesia Consumer Survey 2013 13

Key themes from Indonesia ■ Confidence and optimism continue to remain robust. Indonesia is the second-

most confident country, after Brazil, among the eight emerging economies that we surveyed, with 64% consumers expecting better incomes over the next 12 months. Indonesians are also the second-most optimistic consumers within the eight emerging countries that we surveyed, with 40% of the respondents also having a better personal finance outlook over the next six months, in view the surge in minimum wages of an average 20% in 2013 (it ranges by province between 9% and 46%). This is despite Indonesia’s GDP per capita being the second-lowest among the eight countries that we surveyed.

■ Higher income growth and expecting a further hike. In the survey, more respondents said that their income has increased in the past 12 months compared with the previous years’ survey. The hike is observed to be particularly higher for those in the rural areas and in places outside Java. We believe that this is in view of the increase in the minimum wages of an average 10% in 2012 across the provinces (ranging between 3% and 19%). More people in the lower and middle income groups have seen their income increase versus last year, according to this year’s survey.

■ Shift towards higher discretionary spending continues. Overall spending on discretionary items has increased more than on the essentials. This bodes well with our thesis that the purchasing power of the middle income group is rising as the country’s GDP per capita has doubled over the past five years to US$3,680 in 2012.

■ Consumer preferences lean towards local brands for essentials. According to our survey, Indonesian consumers continue to prefer local brands for essential items such as instant noodles, bottled water and cigarettes. However, a different trend is observed in the purchase of discretionary items. We found that appetite for foreign brands is more for purchase of discretionary items such as fashion apparels and cosmetics, especially with the higher income group. This is consistent with the findings from our survey across the emerging countries, where consumers appear to stick with the local brands that they have always used for staples while foreign brands appeal more for discretionary items, especially with the higher income group.

■ Key stock preferences. We identify five stocks that bode well with the findings of this survey. They are: (1) Astra International, (2) Bank Central Asia, (3) Indofood CBP, (4) Mitra Adiperkasa, and (5) Erajaya Swasembada.

Indonesia is the second-most confident country among the eight emerging countries we surveyed

This year, Indonesians are earning a higher income and expect it to increase further

Spending on discretionary items has increased, as Indonesia’s GDP per capita rises

Indonesian consumers continue to prefer local brands for essentials

25 January 2013

Indonesia Consumer Survey 2013 14

The third Credit Suisse Indonesia Consumer Survey This report details the findings of the third Credit Suisse Indonesia Consumer Survey conducted around 3Q12, as part of the survey that Credit Suisse Research Institute conducts in eight emerging countries—Brazil, China, India, Indonesia, Russia, Saudi Arabia, Turkey, and South Africa (new addition). CS Research Institute engaged the leading global market research firm, AC Nielsen to conduct face-to-face interviews with over 14,000 consumers. The survey is a comprehensive and exclusive study of the consumption patterns in each country as well as individuals’ outlook about the future.

The third survey in Indonesia was carried out with 1,531 participants, across ten areas—six located in the Java area (including Jakarta, Botabek, Surabaya, Kab Gresik/Lamongan/Sidoarjo, Bandung, Kab Bandung) and four outside Java (including Medan, Kab Deli Serdang, Makasar, Kab Gowa). Participants from Java accounted for 70% of the total respondents, 66% lived in the urban areas and 49% were male. This composition is similar to our previous two surveys.

There were 125 questions posed to each respondent in 12 categories: (1) general income and wealth, (2) autos, (3) food & beverage, (4) personal care, (5) branded goods, (6) computers & TV, (7) mobile phones, (8) Internet, (9) travel, (10) property, (11) education, and (12) healthcare.

Figure 10: Indonesia survey summary and key economic statistics Statistics

GDP (2012) $894.9 billion

GDP per Capita (2012) $3,660

Population (2012) 244.5 million

Geographical Area 1.90 mn km2

Number of Cities (in excess of 2 million people)

5

Gini Coefficient (2009) 39.4

Average Inflation (2012E) 4.4%

Average Inflation (2013E) 5.1%

Real GDP Growth (2012E) 6.0%

Real GDP Growth (2013E) 6.3%

Real private consumption growth (2012E)

5.39%

Real private consumption growth (2013E)

5.61%

Consumption as a % of GDP (2012)

54.5%

2013 CS Consumer Survey

Number of Respondents : 1,531

Across 10 geographic locations

66% in Urban areas; 34% in Rural areas

Jakarta ( 20% )

GDP: $70.7bn

Botabek ( 10% )

Surabaya ( 13% )

Gresik, Lamongan ,

Sidoarjo ( 9% )

Medan ( 10% )

Deli Serdang ( 5% )

Makasar ( 10% )

Gowa ( 5% )Bandung ( 18% )

Note: 1. All city level GDP figures are 2010 nominal est. (MGI), total GDP for the country shown in nominal US$.2. * % of survey sampled from this area3. Country GDP, GDP per capita, inflation, population data from IMF, Gini from UNDP, area from CIA World

Factbook, city population from CityPopulation4. Real private consumption growth and consumption as a % of GDP from Oxford Economics

Source: Credit Suisse Indonesia Consumer Survey 2013, IMF, EIU, UN

The third Indonesia Consumer Survey …

... was conducted in ten areas—six in Java and four outside Java

25 January 2013

Indonesia Consumer Survey 2013 15

Confidence and optimism continue to remain robust Indonesia is the second-most confident country, after Brazil, among the eight emerging economies that we surveyed, with 64% respondents expecting a better income over the next 12 months. Indonesians are also the second-most optimistic consumers within the eight emerging countries that we surveyed, with 40% having a better personal finance outlook over the next six months, in line with the surge in minimum wages in 2013 of an average 20% (it ranges by province between 9% and 46%). This is despite Indonesia’s GDP per capita being the second-lowest among the eight countries that we surveyed.

Figure 11: Indonesia is most confident after Brazil… Figure 12: …despite the country’s low GDP per capita

6764

53

42

26

19

58

47

55

3539

22

66

58

4036 38

22

0

10

20

30

40

50

60

70

80

Brazil Indonesia Saudi China India Russia

Inco

me

Out

look

nex

t 12M

(% o

f res

pond

ents

)

Better less worse 2012 Better less worse 2011 Better less worse 2010

0

5000

10000

15000

20000

25000

Saudi Arabia

Russia

Brazil

Turkey

South Africa

China

Indonesia

India

2012

E G

DP

per c

apita

(USD

)

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 13: Do you think the state of your own personal finances over the next six months

will be better, worse or about the same?

63

40 39

3128

12

53

31 31 3236

16

59

28

39

32

40

17

0

10

20

30

40

50

60

70

Brazil Indonesia China Saudi India Russia

Pers

onal

Fin

ance

out

look

nex

t 6M

(% o

f res

pond

ents

)

Better less worse 2012 Better less worse 2011 Better less worse 2010

Source: Credit Suisse Indonesia Consumer Survey 2013

Higher income growth and expecting further hike This year’s survey reveals that more respondents saw their income increase in the past 12 months as compared with the previous years’ survey results. The hike is observed to be particularly higher for people living in the rural areas and outside Java. We view that this is in view of the increase in minimum wages of an average 10% in 2012 across the provinces, with the range between 3% and 19%. According to our survey, more people in

Indonesia is the second-most confident country among the eight countries we surveyed

Indonesians earned a higher income in FY12 due to the average 10% rise in the country’s minimum wage…

25 January 2013

Indonesia Consumer Survey 2013 16

the lower and middle income groups have seen their income increase in FY12 compared with the previous year’s survey results.

The respondents were also more optimistic about getting a higher income in the next 12 months, especially the lower and middle income group. We believe that this is on the back of an announcement of an increase in the minimum wage of an average 20% across provinces in 2013 (ranges from 9% to 46%). Our survey also indicated a higher percentage of respondents expecting an increase of more than 10% in their monthly income, as compared with the previous years’ study.

Figure 14: In the past 12 months, respondents’ income has risen ... Age Monthly income

% of respondents Total Urban Rural Java Non-Java 18-29 30-45 46-55 56-65 <Rp1.5mn Rp1.5-7.5mn >Rp7.5mn

2012

Down to flat 10 12 7 10 8 8 11 8 12 13 9 18

Flat to +10% 77 74 85 77 77 78 78 75 78 83 77 56

>+10% 13 14 8 12 15 13 11 16 10 5 14 26

2011

Down to flat 19 18 19 17 21 13 21 22 16 23 17 15

Flat to +10% 72 72 74 74 70 76 70 75 79 74 72 62

>+10% 9 10 7 9 9 11 10 3 5 3 11 23

2010

Down to flat 14 15 12 12 16 11 15 15 11 14 13 -

Flat to +10% 77 76 80 79 72 78 76 76 84 83 75 81

>+10% 9 9 9 9 12 11 9 9 5 4 11 19

Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 15: ... and is expected to continue to rise in the next 12 months Age Monthly income

% of respondents Total Urban Rural Java Non-Java 18-29 30-45 46-55 56-65 <Rp1.5mn Rp1.5-7.5mn >Rp7.5mn

2012

Down to flat 3 3 2 3 2 3 2 4 1 4 2 8

Flat to +10% 57 51 65 55 59 54 57 53 64 71 54 35

>+10% 40 46 33 42 39 42 41 43 35 24 44 57

2011

Down to flat 6 7 5 5 10 4 8 6 6 5 6 15

Flat to +10% 69 67 76 71 67 70 65 79 77 77 69 30

>+10% 24 26 19 24 22 26 27 15 16 18 25 55

2010

Down to flat 4 4 2 3 4 2 4 4 4 6 4 -

Flat to +10% 70 69 77 73 67 72 70 71 81 80 68 57

>+10% 26 27 21 23 28 26 26 25 14 14 28 43

Source: Credit Suisse Indonesia Consumer Survey 2013

And expect higher income with an average 20% minimum wage increase in 2013

25 January 2013

Indonesia Consumer Survey 2013 17

Figure 16: Increase in minimum wages in 2012 Figure 17: Expected increase in minimum wages in 2013

-

2

4

6

8

10

12

14

16

18

20

North Sulaw

esiD

ki JakartaC

entral Kalimantan

North Sum

ateraBengkuluLam

pungSouth Sum

ateraW

est Kalimantan

West Sulaw

esiJam

biSouth East Sulaw

esiR

iauYogyakartaG

orontaloSouth Sulaw

esiW

est Sumatera

East Nusa Tenggara

South Kalimantan

BaliEast Kalim

antanBangka BelitungM

alukuN

orth Maluku

PapuaC

entral Sulawesi

West N

usa TenggaraBantenR

iau IslandsAcehW

est Papua

FY12

incr

ease

in m

in w

age

(%)

Average 10% increase

-

5

10

15

20

25

30

35

40

45

50

East Kalimantan

Jakarta

Riau Islands

Bengkulu

South Sulawesi

West Kalim

antan

West Sum

atera

Central Kalim

antan

Bangka Belitung

Jambi

Aceh

South Kalimantan

North Sulaw

esi

North Sum

atera

Papua

FY13

E in

crea

se in

min

. wag

e (%

)

Average 20% increase

Source: Directorate General for Industrial Relations and Manpower

Social Guarantee

Source: Directorate General for Industrial Relations and Manpower

Social Guarantee

Income of Indonesia-ex. Java population grew at a higher pace than that of Java As a result of the increase in minimum wage in 2012 by around 10%, our respondents’ average monthly income increased to Rp3.2 mn, compared with Rp2.9 mn in the previous survey. The urban area experienced a higher increase in the monthly income, while the rural area had a slightly lower monthly income. People located outside Java also saw their income grow faster than that in Java, and interestingly, it surpassed the figure in Java. The younger generation is earning more, according to this survey, compared with our previous surveys, and their income is rising at a much higher pace than the older generation. However, savings outside Java as a percentage of total income declined—from 15% to 12%—even though it is still higher than those in Java.

Figure 18: Respondents living outside Java earned more

than those in Java in 2012; urban income rising faster

Figure 19: Java-based people earned more in 2011

3.2

3.5

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Total Urban Rural Java Non-Java

Avg

mon

thly

inco

me

(Rp

mn/

mon

th)

2.93.0

2.6

2.9 2.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Total Urban Rural Java Non-Java

Avg

mon

thly

inco

me

(Rp

mn/

mon

th)

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

People living outside Java earned more in 2012

25 January 2013

Indonesia Consumer Survey 2013 18

Figure 20: Savings of respondents outside Java as a

percentage of total income declined ...

Figure 21: ... but still is higher than of Java residents

10.411.0

8.2

10.0

11.612.2

13.0

8.5

11.1

15.1

0

2

4

6

8

10

12

14

16

Total

Urban

Rural

Java

Non-Java

Total

Urban

Rural

Java

Non-Java

Savi

ng (a

s %

of t

otal

inco

me)

2012 2011

3.0

0.3

3.5

0.4

0

0.5

1

1.5

2

2.5

3

3.5

4

Income Saving

Java Non-Java

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 22: Income rising with the younger age group earning more …

2.5

2.6

2.7

2.8

2.9

3.0

3.1

3.2

3.3

3.4

2012 18-29 30-45 46-55 56-65 2011 18-29 30-45 46-55 56-65 2010 18-29 30-45 46-55 56-65

Avg

mon

thly

inco

me

(Rp

mn)

Source: Credit Suisse Indonesia Consumer Survey 2013

Food continues to be the largest component of spending, with the expectation of higher inflation With regard to spending, food continues to be the largest component, accounting for 28% of the total spending. This is followed by savings at 11%, healthcare at 7%, education and auto, each at 6%, housing and public utilities, each at 4%, and entertainment at 3%.

As in the previous years, respondents are expecting inflation to continue to rise. This might be underpinned by the rise in electricity tariffs and the removal of fuel subsidies that eventually did not happen the previous year. While the government has announced increased electricity tariffs for 2013, we will see if fuel subsidies are going to be removed. Potentially, this poses a threat to overall spending, as respondents expect higher inflation than in the past 12 months.

Interestingly, while the contributions of other categories are similar to those of the past two years’ surveys, only healthcare spending has witnessed an increase—4% of household spending on healthcare in 2010 rose to 5% in 2011 and 7% in 2012. We believe this is

Food continues to be the largest component of spending, with the expectation of higher inflation

Higher spending seen for healthcare

25 January 2013

Indonesia Consumer Survey 2013 19

underpinned by the rising wealth of consumers, thus triggering healthier lifestyles, as well as accessibility of state healthcare providers.

Figure 23: Food continues to be the largest component of

spending in 2012

Figure 24: Inflation is expected to rise further

Housing4%

Auto6%

Education6%

Food28%

Home & Personal Care

5%Health Care

7%

Savings11%

Entertainment3%

Public Utilities4%

Others26%

62

17

3

69

12

2

0

10

20

30

40

50

60

70

80

It will be higher than thelast 12 months

It will be the same as thelast 12 months

It will be lower than thelast 12 months

2012 2011

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 25: Monthly spending by category, 2010 Figure 26: Monthly spending by category, 2011

Housing7% Auto

6%Education

6%

Food26%

Home & Personal Care

5%

Health Care4%

Savings11%

Entertainment3%

Public Utilities0%

Others32%

Housing4%

Auto7%

Education7%

Food31%

Home & Personal Care

6%

Health Care5%

Savings12%

Entertainment3%

Public Utilities7%

Others18%

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Better confidence for major purchases Nevertheless, despite the expectation of a higher inflation, respondents have better confidence to make major purchases this time compared with the previous year, even though it was still less confident than in 2010, the period of booming commodity prices. We believe that improving confidence is underpinned by the higher income that the respondents are expecting to receive.

Figure 27: Time to make a major purchase, by area 2012 2011 2010

Total Urban Rural Java Non-Java Total Urban Rural Java Non-Java Total Urban Rural Java Non-Java

Excellent time 3 3 5 4 3 3 3 2 2 5 6 7 5 6 7

Good time 30 27 35 27 36 26 26 27 19 44 50 48 54 56 40

Not such a good time 62 65 55 64 56 62 61 64 69 45 40 40 39 36 49

A bad time 5 5 5 6 4 9 10 8 10 6 4 5 3 4 6

Source: Credit Suisse Indonesia Consumer Survey 2013

This year is a better year to make major purchases compared with the past year, implying rising confidence

25 January 2013

Indonesia Consumer Survey 2013 20

Figure 28: Time to make a major purchase, by age 2012 2011 2010

% of respondents Total 18-29 30-45 46-55 56-65 Total 18-29 30-45 46-55 56-65 Total 18-29 30-45 46-55 56-65

Excellent time 3 3 4 3 3 3 2 3 4 3 6 6 6 6 6

Good time 30 33 26 33 22 26 28 25 27 23 50 53 49 50 45

Not such a good time 62 59 65 58 66 62 60 63 61 68 40 38 40 39 45

A bad time 5 5 5 5 8 9 10 9 8 7 4 3 5 4 4

Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 29: Time to make a major purchase, by income 2012 2011 2010

% of respondents Total <Rp1.5 mn

Rp1.5-7.5 mn

>Rp7.5mn

Total <Rp1.5mn

Rp1.5-7.5mn

>Rp7.5mn

Total <Rp1.5 mn

Rp1.5-7.5mn

>Rp7.5mn

Excellent time 3 2 4 4 3 2 2 7 6 3 7 4

Good time 30 30 30 36 26 16 30 32 50 45 51 68

Not such a good time 62 61 62 58 62 69 59 54 40 46 38 21

A bad time 5 7 5 2 9 13 8 7 4 5 4 7

Source: Credit Suisse Indonesia Consumer Survey 2013

Rising income also leads to property upgrade There were fewer first-time home buyers in this survey versus last year, with more respondents looking to purchase property for an upgrade. Around 39% of the respondents are keen for an upgrade, up from 31% in the previous year, with 37% being first-time buyers, down from 45% last year. We believe this trend is due to property ownership being larger than in previous years, and rise in income coupled with a low interest rate environment.

According to our survey, people outside Java are more keen to purchase property than those in Java, despite them already owning property. According to our survey, people living outside Java are more keen to purchase property than those in Java, despite the previous already owning property. For those outside Java, the number of respondents opting for property upgrades were more than of first-time home buyers.

Figure 30: Property ownership and reason to purchase, by area 2012 2011 2010

% of respondents Total Urban Rural Java Non-Java Total Urban Rural Java Non-Java Total Urban Rural Java Non-Java

Property ownership 74 65 90 74 73 70 63 83 73 63 73 66 86 74 71

Planning to buy in next 2 years? 30 34 22 28 33 25 28 18 25 23 24 30 12 24 22

Reason to buy

Upgrade 39 34 53 36 44 31 32 28 33 26 38 39 35 39 37

First-time home buyer 37 39 30 38 35 45 46 42 43 51 33 32 37 32 35

Investment 15 16 12 14 16 17 16 19 17 16 13 12 18 12 18

Change of location 9 11 5 12 4 7 5 11 7 8 15 17 7 17 11

Source: Credit Suisse Indonesia Consumer Survey 2013

Figure 31: Property ownership and reason to purchase, by age 2012 2011 2010

% of respondents Total 18-29 30-45 46-55 56-65 Total 18-29 30-45 46-55 56-65 Total 18-29 30-45 46-55 56-65

Property ownership 74 70 72 84 86 70 65 68 78 81 73 67 70 86 92

Planning to buy in next 2 years? 30 30 33 29 15 25 27 27 20 11 24 23 27 22 11

Reason to buy

Upgrade 39 38 38 37 59 31 27 29 47 50 38 35 36 48 55

First-time home buyer 37 46 35 28 6 45 53 45 26 17 33 36 40 6 0

Investment 15 8 17 20 29 17 13 19 21 17 13 9 12 22 36

Change of location 9 6 10 14 6 7 7 7 6 17 15 19 9 24 9

Source: Credit Suisse Indonesia Consumer Survey 2013

Some 39% of the respondents are looking to upgrade property in the nexttwo years

25 January 2013

Indonesia Consumer Survey 2013 21

Figure 32: Property ownership and reason to purchase, by income 2012 2011 2010

% of respondents Total <Rp1.5mn

Rp1.5-7.5 mn

>Rp7.5mn

Total <Rp1.5mn

Rp1.5-7.5 mn

>Rp7.5mn

Total <Rp1.5mn

Rp1.5-7.5 mn

>Rp7.5mn

Property ownership 74 77 73 79 70 67 70 85 73 71 74 69

Planning to buy in next 2 years? 30 21 32 43 25 17 27 37 24 15 27 42

Reason to buy

Upgrade 39 51 38 26 31 32 31 10 38 42 37 55

First-time home buyer 37 36 37 39 45 53 44 10 33 48 31 18

Investment 15 2 17 22 17 8 17 80 13 2 15 27

Change of location 9 11 8 13 7 7 7 - 15 8 17 -

Source: Credit Suisse Indonesia Consumer Survey 2013

Shift towards higher discretionary spending continues Comparing the spending of the essentials and discretionaries, overall spending on discretionary items increased more than that on the essentials. This bodes well with our estimate that the middle class’ income is rising along with the country’s GDP/ capita, which has doubled over the last five year to reach US$3,660 in 2012.

Spending on discretionary items in categories such as fashion, smartphones and mobile phones were up, while spending on perfumes, sports shoes and apparels, TV, DVD player was lower. We believe following are the reasons for the rise in discretionary spend on: (1) fashion—changing lifestyles, along with the rising of income as well as higher confidence of better income in the coming months; and (2) mobile phones—low penetration and availability of more affordable handsets.

Consumers continued to spend on essentials such as instant noodles, carbonated drinks, dairy products, and bottled water, which remain popular items. Interestingly, cigarettes were less popular, even though they are still widely consumed.

Figure 33: Spending on fashion, mobile phones and smartphones increasing

Carbonated drinks

Bottled Water

Dairy products

Instant Noodles

Cigarettes

TissuesFemine hygiene

Cosmetics

Basic mobile phone

DVD Player

Traditional TV

Smartphone

Fashion

Sport shoes & apparel

WatchesJewellery

Perfumes

CarsInternet Access

Property

(15)

(10)

(5)

-

5

10

15

20

25

30

0 10 20 30 40 50 60 70 80 90 100

% c

hang

e fro

m la

st y

ear s

urve

y

% of respondent which have bought essentials and discretionary goods

Source: Credit Suisse Indonesia Consumer Survey 2013

We notice an increase in the spending on discretionary items, especially fashion

25 January 2013

Indonesia Consumer Survey 2013 22

Figure 34: Mobile phone penetration remains the lowest... Figure 35: …similarly on computer penetration

Brazil

China

IndiaIndonesiaRussia

Saudi

Turkey

South Africa

0

10

20

30

40

50

60

70

80

90

75 80 85 90 95 100 105

Smar

tpho

ne o

wne

rshi

p (%

)

Mobile phone ownership (%)

89 88

7770

57

33 31

20

0

10

20

30

40

50

60

70

80

90

100

China

Saudi

Russia

Brazil

Turkey

India

South Africa

Indonesia

Com

pute

r ow

ners

hip

(%)

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Consumers prefer local brands for essentials Our survey confirmed that the Indonesian consumers prefer local brands for essential items such as instant noodles, bottled water and cigarettes. However, a different pattern is seen for the discretionary items. We found that appetite for foreign brands is higher in discretionary items such as fashion apparels and cosmetics, especially among higher income earners. This finding is in line with the findings across emerging countries in our survey, where consumers appear to stick with local brands, while foreign brands appeal more in the discretionary item category, especially for higher income consumers.

Figure 36: Local brands are preferred for essential items Figure 37: Appetite for foreign brands is higher in

discretionary items …

80

85

90

95

100

<Rp1,000k

Rp1,000k -

Rp1,500k

Rp1,500k -

Rp2,000k

Rp2,000k -

Rp3,000k

Rp3,000k -

Rp5,000k

Rp5,000k -

Rp7,500k

Rp10,000k-

Rp15,000k

Rp10,000k -

Rp15,000k

>Rp15,000k

% o

f res

pond

ents

buy

ing

loca

l bra

nds

Cigarette Instant noodles Bottled water

-

10

20

30

40

50

60

70

80

90

<Rp1,000k

Rp1,000k -

Rp1,500k

Rp1,500k -

Rp2,000k

Rp2,000k -

Rp3,000k

Rp3,000k -

Rp5,000k

Rp5,000k -

Rp7,500k

Rp10,000k-

Rp15,000k

Rp10,000k -

Rp15,000k

>Rp15,000k

% re

spon

dent

s bu

ying

loca

l bra

nds

Fashion Cosmetic

Source: Credit Suisse Indonesia Consumer Survey 2013 Source: Credit Suisse Indonesia Consumer Survey 2013

Our survey also found that for Indonesian consumers, branded products appeal more for essentials, as they are the basic needs such as dairy and soft drinks, while for discretionary items such as cosmetics, perfumes and fashion, the consumers in Indonesia still prefer “unbranded” products. We believe this is due to affordability, as for the higher income earners, this is on the other way around. Nevertheless, in general, compared to other emerging countries in our survey, Indonesians are still mostly using “unbranded” products.

Indonesians prefer local brands for essentials

Branded products appeal more for essentials while for discretionary items, consumers prefer “unbranded products”, mostly due to affordability

25 January 2013

Indonesia Consumer Survey 2013 23

Figure 38: Percentage of purchases by sector that are "unbranded" % of respondents Brazil China India Indonesia Russia Saudi Arabia Turkey South Africa

Dairy 3 8 19 9 30 2 14 20

Soft Drinks 2 2 4 8 13 1 4 8

Beer 0 5 2 n/a 10 n/a 3 0

Spirits 3 15 3 n/a 13 n/a 30 17

Cosmetics 4 10 11 27 15 13 10 40

Perfumes 7 30 56 71 39 29 57 42

Fashion 27 37 62 64 65 40 69 66

Leather Goods 39 40 36 42 82 38 46 58

Sportswear 19 9 25 29 34 17 31 23

Source: Credit Suisse Indonesia Consumer Survey 2013 Figure 39: Preference for branded goods pick up on higher income group

0

20

40

60

80

100

Less than1,000k

Rp1,000k -Rp1,500k

Rp1,500k-Rp2,000k

Rp2,000k -Rp3,000k

Rp3,000k -Rp 5,000k

Rp5,000k -Rp7,500k

Rp7,500k-Rp10,000k

Rp10,000 -Rp15,000k

More thanRp15,000k%

of p

urch

ases

that

are

"unb

rand

ed"

Fashion Leather goods, bag & shoes Sportswear Watches Perfumes

Source: Credit Suisse Indonesia Consumer Survey 2013

25 January 2013

Indonesia Consumer Survey 2013 24

Figure 40: Brand preference in different income segments Food and Beverages % penetration at

LOWER income % penetration at MIDDLE Income

%penetration at HIGHER income

Difference (LOW & HIGH)

Parent Company (if applicable

Listed Private

Noodles

Indomie 39 41 33 (6) Indofood CBP ICBP.JK

Mie Sedap 35 30 24 (11) Wings Group Private

Cigarettes

Djarum Super 5 4 2 (2) Djarum Private

Dji Sam Soe 9 9 10 1 HM Sampoerna HMSP.JK

Sampoerna Hijau 8 2 5 (3) HM Sampoerna HMSP.JK

Gudang Garam Filter 8 5 2 (6) Gudang Garam GGRM.JK

Gudang Garam Surya 18 7 8 (10) Gudang Garam GGRM.JK

Sampoerna A Mild 11 8 22 10 HM Sampoerna HMSP.JK

Soft drinks -

Coca-Cola 35 31 31 (3) Coca Cola Co Ltd Foreign listed

Fanta 26 28 27 1 Coca Cola Co Ltd Foreign listed

Sprite 25 27 26 0 Coca Cola Co Ltd Foreign listed

Bottled drinks -

Aqua 62 62 56 (6) Danone Company Private

Club 19 13 12 (7) Tirta Bahagia Private

Dairy products

Frissian Flag 34 34 28 (6) Frissian Flag Private

Indomilk 23 19 11 (11) Indomilk ICBP.JK

Milk Ultra 13 14 16 3 Ultrajaya ULTJ.JK

Personal care

Tissue

Paseo 26 33 31 (6) Pindo Deli Private

Mitu 17 18 21 (11) Megasari Makmur Private

Nice 13 15 18 3 Pindo Deli Private

Female hygiene

Laurier 26 29 31 (6) Kao Foreign listed

Charm 28 35 35 (11) Unicharm Foreign listed

Softex 24 15 12 3 Softex Indonesia Private

Hers Protex 8 5 - 4 Wings Group Private

Skin products

Ponds 13 20 18 (6) Unilever Indonesia UNVR.JK

Citra 21 21 21 (11) Unilever Indonesia UNVR.JK

Viva 15 8 5 3 PT Vitapharm Private

Technology

Internet provider

Speedy 36 23 50 14 Telkom Indonesia TLKM.JK

Telkom Flash 45 34 40 (5) Telkom Indonesia TLKM.JK

Mobile phone

Nokia 41 43 36 (5) Nokia Foreign listed

Samsung 7 9 7 1 Samsung Foreign listed

Nexian 8 6 4 (4) Metrotech Private

Blackberry 1 8 21 20 RIM Foreign listed

Mobile operator

Telkomsel 38 42 57 18 Telkom Indonesia TLKM.JK

Indosat 23 22 16 (7) Indosat ISAT.JK

Esia 7 6 4 (3) Bakrie Telecom BTEL.JK

Excel 16 12 6 (10) Excel Axiata EXCL.JK

Telkom Fleksi 7 5 6 (1) Telkom Indonesia TLKM.JK

Automotive

Car

Toyota - 29 31 31 Astra International ASII.JK

Daihatsu - 23 15 15 Astra International ASII.JK

25 January 2013

Indonesia Consumer Survey 2013 25

% Penetration at LOWER income

% penetration at Middle Income

%penetration at HIGHER income

Difference (LOW & HIGH)

Parent Company (if applicable)

Listed Private

Suzuki - 29 31 31 Indomobil IMAS.JK

Motorcycle

Honda 51 51 52 2 Astra International ASII.JK

Yamaha 36 37 45 8 Yamaha Indonesia Private

Suzuki 10 9 - (10) Indomobil IMAS.JK

Source: Credit Suisse Indonesia Consumer Survey 2013

Our stock preferences We identify five stocks that bode well with our findings on this survey. They are:

■ Astra International (ASII.JK, OUTPERFORM, TP Rp9,400.00): We continue to believe the stock remains a beneficiary of growing penetration in Indonesia’s auto segment. Its brands, Toyota in 4-W and Honda in 2-W, continue to lead in each of its segment. The auto segment of Astra should contribute 53% to its 2013E earnings. We believe the company is an attractive option for investors looking for exposure to the Indonesian consumer sector. Currently, Astra’s auto implied valuations exhibit the lowest 2013E multiple among all Indonesian consumer-related names under our coverage. Its auto business is trading at 11.4x 12-month forward P/E, versus historical peak of 17.8x in July 2011.

■ Bank Central Asia (BBCA.JK, OUTPERFORM, TP Rp11,000.00) remains our top pick in the Indonesian banking sector. BBCA has one of the highest growth capacity supported by its low LDR (68.9%). In addition, it also has one of the highest CASA contributions to total deposits (79.5%), allowing the bank to have one of the lowest CoF among Indonesian banks. Given their low LDR and low CoF, BBCA is well positioned to deliver above-industry growth, offering more competitive pricing to borrowers, while at the same time sustaining robust NIM. We believe BBCA exhibits one of the strongest fundamentals among the Indonesian banks under our coverage.

■ Within Indonesia food & beverage, we like Indofood CBP (ICBP.JK, OUTPERFORM, TP Rp8,100), as it is widely exposed to the products that consumers seek, such as instant noodles. It also has strong brand equity and continues to innovate products such as the beef-based noodle (Mie Goreng Rendang) and the recently launched Mie Goreng Cabe Ijo. Noodle is the highest contributor to the company, accounting for 64% of its revenue and 79% operating profit, with operating margin at 16.5% in 2013E. Within its product portfolio, Indofood CBP also includes dairy products. Dairy should be its second largest contributor, accounting for 20% of revenue and 12% of operating profit with margin at 8% in 2013E. The completion of its new factory should help boost volumes this year, with sales volume expected to surge 18% YoY, on a 3% ASP increase.

■ Mitra Adiperkasa (MAPI.JK, OUTPERFORM, TP Rp8,100): With the rise in the middle-class income and higher confidence among Indonesian consumers, this survey found that spending on discretionary items has been rising more than the essentials. Fashion apparel was recorded as having increased by close to 25%, highest among all items we surveyed. We believe this should benefit the mid- to high-end retailer, Mitra Adiperkasa. The company manages more than 100 world class brands across its divisions, with more than half of the revenue contribution coming from speciality stores, followed by department stores, and food & beverage. We expect strong SSG to continue, given the rising middle- and high-income segments, with a consolidated SSG of 14% as of FY12, with specialty stores posting the strongest SSG at 17%, followed by department stores at 13%, F&B at 9% and others at 3%. We expect its SSG to reach 13% this year.

Our stocks preference include: ASII, BBCA, ICBP, MAPI and ERAA

25 January 2013

Indonesia Consumer Survey 2013 26

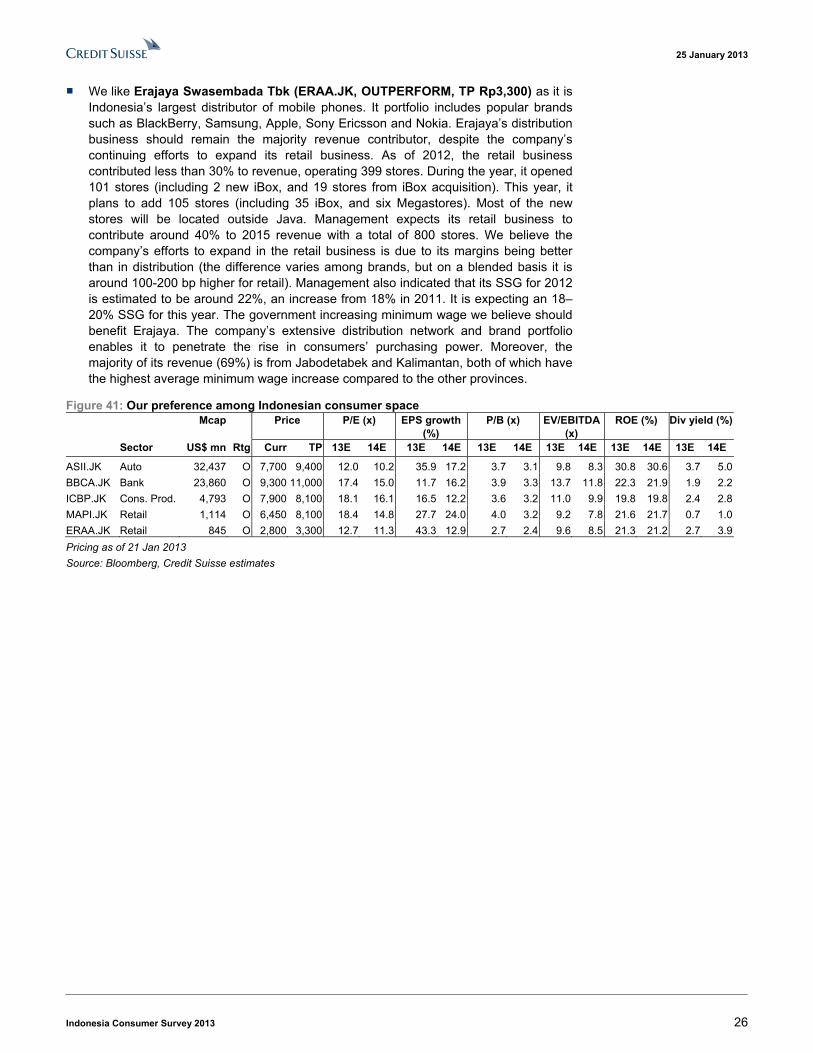

■ We like Erajaya Swasembada Tbk (ERAA.JK, OUTPERFORM, TP Rp3,300) as it is Indonesia’s largest distributor of mobile phones. It portfolio includes popular brands such as BlackBerry, Samsung, Apple, Sony Ericsson and Nokia. Erajaya’s distribution business should remain the majority revenue contributor, despite the company’s continuing efforts to expand its retail business. As of 2012, the retail business contributed less than 30% to revenue, operating 399 stores. During the year, it opened 101 stores (including 2 new iBox, and 19 stores from iBox acquisition). This year, it plans to add 105 stores (including 35 iBox, and six Megastores). Most of the new stores will be located outside Java. Management expects its retail business to contribute around 40% to 2015 revenue with a total of 800 stores. We believe the company’s efforts to expand in the retail business is due to its margins being better than in distribution (the difference varies among brands, but on a blended basis it is around 100-200 bp higher for retail). Management also indicated that its SSG for 2012 is estimated to be around 22%, an increase from 18% in 2011. It is expecting an 18–20% SSG for this year. The government increasing minimum wage we believe should benefit Erajaya. The company’s extensive distribution network and brand portfolio enables it to penetrate the rise in consumers’ purchasing power. Moreover, the majority of its revenue (69%) is from Jabodetabek and Kalimantan, both of which have the highest average minimum wage increase compared to the other provinces.

Figure 41: Our preference among Indonesian consumer space Mcap Price P/E (x) EPS growth

(%) P/B (x) EV/EBITDA

(x) ROE (%) Div yield (%)

Sector US$ mn Rtg Curr TP 13E 14E 13E 14E 13E 14E 13E 14E 13E 14E 13E 14E

ASII.JK Auto 32,437 O 7,700 9,400 12.0 10.2 35.9 17.2 3.7 3.1 9.8 8.3 30.8 30.6 3.7 5.0

BBCA.JK Bank 23,860 O 9,300 11,000 17.4 15.0 11.7 16.2 3.9 3.3 13.7 11.8 22.3 21.9 1.9 2.2

ICBP.JK Cons. Prod. 4,793 O 7,900 8,100 18.1 16.1 16.5 12.2 3.6 3.2 11.0 9.9 19.8 19.8 2.4 2.8

MAPI.JK Retail 1,114 O 6,450 8,100 18.4 14.8 27.7 24.0 4.0 3.2 9.2 7.8 21.6 21.7 0.7 1.0

ERAA.JK Retail 845 O 2,800 3,300 12.7 11.3 43.3 12.9 2.7 2.4 9.6 8.5 21.3 21.2 2.7 3.9

Pricing as of 21 Jan 2013

Source: Bloomberg, Credit Suisse estimates

25 January 2013

Indonesia Consumer Survey 2013 27

Figure 42: Indonesia consumer-related names Code Rtg Price Target Ups Mcap P/E (x) EPS growth

(%) P/B (x) EV/EBITDA

(x) Div yield (%) ROE (%) Ytd perf

US$mn 12E 13E 14E 12E 13E 14E 12E 13E 14E 12E 13E 14E 12E 13E 14E 13E 14E 12E 13E

Automobiles

ASII.JK O 7,700 9,400 22% 32,437 16.3 12.0 10.2 8 36 17 4.5 3.7 3.1 12.8 9.8 8.3 3.4 3.7 5.0 31 31 3% 1%

IMAS.JK U 5,300 4,800 -9% 1,525 14.1 12.3 7.7 8 14 60 2.4 2.2 1.8 17.9 14.5 8.4 1.2 1.3 1.6 18 23 -17% 0%

Banks

BBCA.JK O 9,300 11,000 18% 23,860 19.5 17.4 15.0 8 12 16 4.6 3.9 3.3 15.3 13.7 11.8 1.7 1.9 2.2 22 22 14% 2%

BMRI.JK O 8,550 11,000 29% 20,552 14.1 12.2 10.8 16 15 13 2.7 2.3 1.9 9.9 8.6 7.6 1.4 1.6 1.9 19 18 20% 6%

BBRI.JK O 7,900 9,100 15% 20,280 11.5 11.8 11.0 12 (2) 7 3.1 2.5 2.1 9.1 9.3 8.5 1.7 1.7 1.8 22 20 3%14%

BBNI.JK O 3,850 5,000 30% 7,396 10.5 9.5 8.2 17 11 16 1.8 1.5 1.3 7.9 7.4 6.4 3.3 3.7 4.3 16 16 -3% 4%

BTPN.JK N 5,250 5,800 10% 3,159 15.7 13.5 11.0 35 16 23 4.0 3.1 2.4 12.2 10.5 8.6 0.0 0.0 0.0 23 22 54% 0%

BBTN.JK N 1,540 1,600 4% 1,660 11.7 9.5 8.3 2 23 14 1.7 1.4 1.2 0.4 0.3 0.3 0.0 0.0 0.0 15 14 25% 6%

BJBR.JK O 1,180 1,420 20% 1,179 8.8 8.6 7.1 34 2 21 1.9 1.6 1.3 5.8 5.7 4.8 4.4 5.9 6.1 19 18 16%11%

Consumer

UNVR.JK U 23,000 15,725 -32% 18,261 35.8 33.0 30.8 21 9 7 31.6 29.3 27.6 25.7 23.8 22.1 2.4 2.8 3.0 89 90 11%10%

GGRM.JK U 53,700 44,600 -17% 10,752 25.1 20.5 17.4 (16) 22 18 3.9 3.4 3.1 15.6 13.2 11.5 1.9 1.6 2.0 17 18 -9% -5%

INDF.JK N 6,000 6,700 12% 5,482 15.7 14.8 14.2 9 6 5 2.5 2.3 2.1 5.6 5.2 5.0 2.9 3.2 3.4 15 15 27% 3%

KLBF.JK U 1,040 800 -23% 5,495 31.3 27.3 23.2 14 15 18 7.6 6.7 5.9 20.8 18.2 15.5 1.8 1.9 2.2 25 25 56% -2%

ICBP.JK O 7,900 8,100 3% 4,793 21.1 18.1 16.1 11 17 12 4.0 3.6 3.2 12.5 11.0 9.9 2.1 2.4 2.8 20 20 50% 1%

Retail

MAPI.JK O 6,450 8,100 26% 1,114 23.5 18.4 14.8 26 28 24 4.9 4.0 3.2 10.8 9.2 7.8 0.6 0.7 1.0 22 22 29% -3%

ACES.JK N 860 700 -19% 1,535 39.3 30.0 24.2 32 31 24 9.6 7.5 5.9 26.3 19.9 16.4 0.3 0.4 0.5 25 24 100% 5%

ERAA.JK O 2,800 3,300 18% 845 18.3 12.7 11.3 74 43 13 3.1 2.7 2.4 12.9 9.6 8.5 0.0 2.7 3.9 21 21 195% -5%

Media

MNCN.JK O 2,400 2,700 13% 3,485 21.3 17.8 14.3 46 20 24 4.6 4.0 3.4 13.1 11.3 9.3 1.4 2.1 2.5 22 24 91% -4%

SCMA.JK O 2,300 2,760 20% 2,334 22.2 18.3 15.1 10 21 21 14.0 12.4 10.9 15.8 13.3 11.1 4.5 5.5 6.6 68 72 43% 2%

IDKM.JK O 1,030 1,400 36% 1,086 23.7 15.5 11.8 554 53 31 18.5 8.4 4.9 16.4 11.2 8.8 0.0 0.0 1.0 54 42 78% 0%

Telco

TLKM.JK O 9,600 10,900 14% 20,139 14.8 13.2 12.4 16 12 6 3.7 3.4 3.2 5.1 4.7 4.5 4.4 5.3 6.4 26 26 28% 6%

EXCL.JK O 5,400 8,000 48% 4,791 15.4 12.2 10.9 6 26 11 2.9 2.6 2.4 5.5 4.9 4.5 2.3 4.1 5.5 22 22 26% -5%

ISAT.JK O 6,750 8,300 23% 3,817 24.0 16.5 13.8 83 46 20 1.9 1.8 1.7 5.6 5.2 4.8 2.1 1.7 3.5 11 12 14% 5%

TOWR.JK O 25,000 19,500 -22% 2,654 58.1 40.4 31.1 55 44 30 14.0 11.6 9.8 16.9 13.6 11.4 0.5 1.0 1.6 29 31 127%10%

TBIG.JK N 5,900 3,800 -36% 2,945 29.2 22.5 17.5 94 30 29 6.8 5.7 4.8 22.2 16.0 13.0 1.0 1.8 2.9 25 27 140% 4%

BTEL.JK U 50 50 0% 159 -1.3 -1.4 -1.4 (46) 8 5 0.4 0.6 1.1 7.0 7.5 6.9 0.0 0.0 0.0 -46 -79 -81% 0%

Airline

GIAA.JK O 650 900 38% 1,531 13.3 8.0 16.1 29 65 (50) 1.6 1.4 1.3 5.4 3.7 3.9 0.0 3.1 2.7 18 8 39% -2%

Pricing as of 21 Jan 2013.

Source: Bloomberg, Credit Suisse estimates

25 January 2013

Indonesia Consumer Survey 2013 28

Key sector selections

25 January 2013

Indonesia Consumer Survey 2013 29

Automotive sector Four-wheelers In Indonesia, car penetration is still low (based on our survey, only 6% of the respondents own a car); this suggests the market has more potential to grow with rise in income levels. Most of the car owners in our survey are high income earners and live in Java. Some 92% of those who own a car purchased it 4.7 years ago, even though car ownership turnover has improved slightly—from an average of 6.2 years to 5.9 years.

As confidence improves, there is an increase in the number of respondents who are willing to purchase a car in the next 12 months—from about 7% of respondents in last year’s survey to 11% this year. This could also be due to the availability of cheaper cars (priced as low as US$11,000/unit), thus making it more affordable.

Figure 43: Four-wheeler penetration in Indonesia has ample opportunity to grow Age Monthly income

Total Urban Rural Java Non-Java 18-29 30-45 46-55 56-65 <Rp1.5 mn Rp1.5-7.5 mn >Rp7.5 mn

2012

Four-wheeler ownership % respondents 6 6 4 6 5 5 7 3 6 - 6 29

No of cars per household

1 Car % car owners 92 91 94 91 95 88 92 100 100 - 93 85

>1 Car % car owners 8 9 6 9 5 12 8 - - - 7 15

When was the car purchased?

years ago 5 5 5 5 3 4 5 6 6 - 5 5

Car ownership turnover years 6 6 5 6 5 6 5 7 10 - 6 6

Prob of purchase in 12M

Potentially Yes % respondents 11 13 8 11 10 10 13 13 4 2 12 21

Unsure % respondents 32 34 30 34 28 33 33 32 27 36 31 40

Potentially No % respondents 57 54 62 55 61 57 55 55 69 62 57 40

2011

Four-wheeler ownership % respondents 5 6 3 4 5 5 5 3 4 0 5 50

No of cars per household

1 Car % car owners 89 88 93 86 96 92 86 86 100 100 91 83

>1 Car % car owners 11 12 7 14 4 8 14 14 - - 9 17

When was the car purchased?

years ago 4 5 3 5 4 4 5 5 5 4 5 4

Car ownership turnover years 6 6 6 6 6 5 7 6 2 9 6 7

Prob of purchase in 12M

Potentially Yes % respondents 7 9 3 6 7 7 9 2 5 2 8 30

Unsure % respondents 33 32 34 30 38 32 33 33 34 30 33 10

Potentially No % respondents 60 59 62 63 54 61 59 64 60 68 59 60

2010

Four-wheeler ownership % respondents 6 6 5 6 5 3 7 6 10 1 6 50

No of cars per household

1 Car % car owners 86 81 95 83 92 88 86 75 90 100 90 67

>1 Car % car owners 14 19 5 17 8 12 14 25 10 - 10 33

When was the car purchased?

years ago 4 4 4 4 3 4 3 5 4 5 4 3

Car ownership turnover years 6 7 6 7 6 7 5 9 7 5 7 6

Prob of purchase in 12M

Potentially Yes % respondents 7 8 5 6 9 5 8 10 6 3 8 39

Unsure % respondents 25 26 22 26 22 29 22 24 23 20 26 39

Potentially No % respondents 68 66 72 67 69 66 70 66 71 77 66 21

Source: Credit Suisse Indonesia Consumer Survey 2013