Doc Credit appraisal IB

75

STUDY ON CREDIT APPRAISAL SYSTEM IN INDIAN BANK 1

Transcript of Doc Credit appraisal IB

STUDY ON CREDIT APPRAISAL SYSTEM IN

INDIAN BANK

1

ABSTRACT

This project has been undertaken at the Credit Department of

Indian Bank. Financial requirements for Project Finance and

Working Capital purposes are taken care of at the Credit

Department. Companies that intend to seek credit facilities

approach the bank. Primarily, credit is required for following

purposes:

1. Term loan for master projects

2. Working capital finance

3. Non Fund Based Limits.

Project Financing discipline includes understanding the rationale

for project financing, how to prepare the financial plan, assess

the risks, design the financing mix, and raise the funds. In

addition, one must understand some project financing plans have

succeeded while others have failed. A knowledge-base is required

regarding the design of contractual arrangements to support

project financing; issues for the host government legislative

provisions, public/private infrastructure partnerships,

public/private financing structures; credit requirements of

lenders, and how to determine the project's borrowing capacity;

how to analyze cash flow projections and use them to measure

expected rates of return; tax and accounting considerations; and

analytical techniques to validate the project's feasibility

Project finance is different from traditional forms of finance

because the credit risk associated with the borrower is not as2

important as in an ordinary loan transaction; what most important

is the identification, analysis, allocation and management of

every risk associated with the project.

The purpose of this project is to explain, in a brief and general

way, the manner in which risks are approached by financiers in a

project finance transaction. Such risk minimization lies at the

heart of project finance. Efficient management of credit

portfolio is of utmost importance as it has a tremendous impact

on the Indian Bank’s assets quality & profitability. The ongoing

financial reforms have no doubt provided unparallel opportunities

to banks for growth, but have simultaneously exposed them to

various risks, which need to be effectively managed.

The concept of Credit Appraisal is undergoing radical changes.

Credit Risk in all exposures calls for precise measuring and

monitoring for taking considered credit decisions with suitable

risk mitigants, risk premium, etc. Credit portfolio should be

well diversified in various promising sectors with a cautious

approach to be adopted in risky segments.

Bank has to be competitive without compromising on the basic

integrity of lending. The quality of the Bank’s credit portfolio

has a direct and deep impact on the Bank’s profitability. The

study has been conducted with the purpose of getting in-depth

knowledge about the credit appraisal and credit risk management

procedure in Indian Bank for the above said first two purposes.

3

4

TABLE OF CONTENTS

ABSTRACT ................................................

CHAPTER 1: INTRODUCTION TO CREDIT APPRAISAL..............

CHAPTER 2: REVIEW OF LITERATURE..........................

CHAPTER 3: INDUSTRY PROFILE..............................

CHAPTER 4: COMPANY PROFILE...............................

CHAPTER 5: OBJECTIVES OF THE STUDY.......................

CHAPTER 6: RESEARCH METHODOLOGY..........................

CHAPTER 7: ANALYSIS AND INTERPRETATION...................

CHAPTER 8: RESEARCH FINDINGS AND CONCLUSION..............

REFERENCES...............................................

5

CHAPTER 1

INTRODUCTION TO CREDIT APPRAISAL

1.1 Credit Appraisal

Credit Appraisal is the process by which a lender appraises the

technical feasibility, economic viability and bankability

including creditworthiness of the prospective borrower. Credit

appraisal process of a customer lies in assessing if

that customer is liable to repay the loan amount in the

stipulated time, or not. Here bank has their own methodology to

determine if a borrower is creditworthy or not. It is determined

in terms of the norms and standards set by the banks. Being a

very crucial step in the sanctioning of a loan, the borrower

needs to be very careful in planning his financing modes.

However, the borrower alone doesn’t have to do all the hard work.

The banks need to be cautious, lest they end up increasing their

risk exposure. All banks employ their own unique objective,

subjective, financial and non-financial techniques to evaluate

the creditworthiness of their customers.

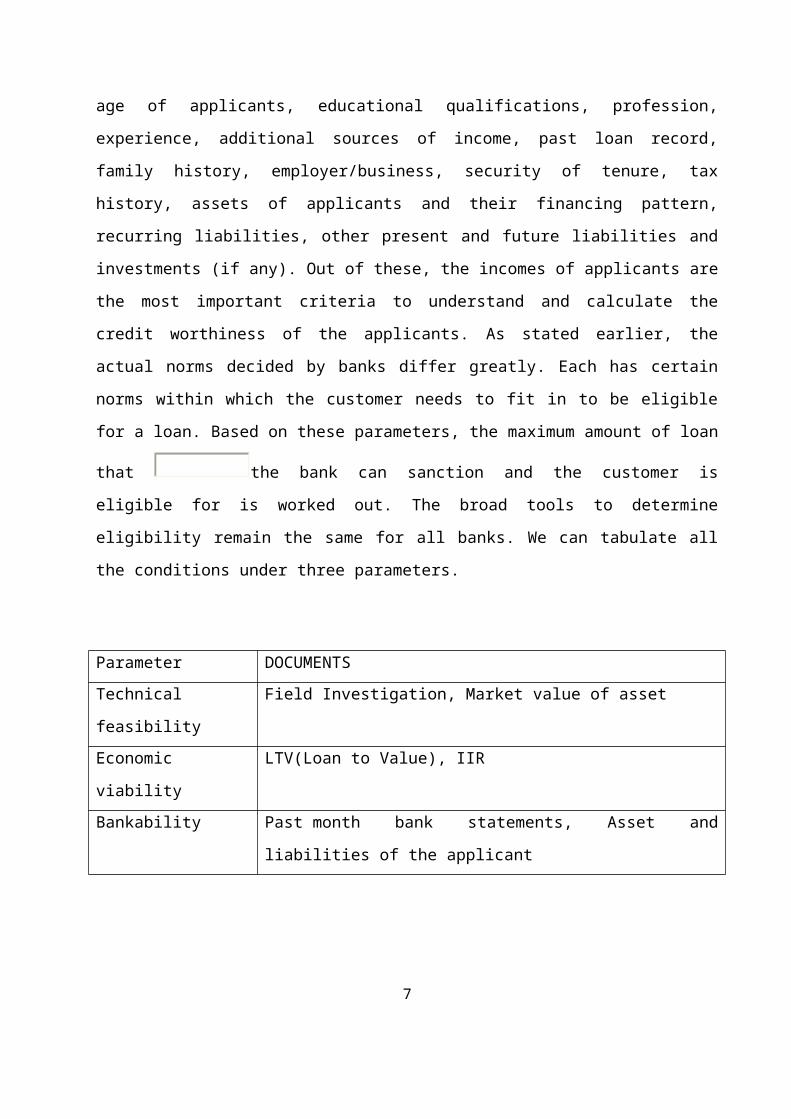

1.2 Components of Credit Appraisal Process

While assessing a customer, the bank needs to know the

following information: Incomes of applicants and co-applicants,

6

age of applicants, educational qualifications, profession,

experience, additional sources of income, past loan record,

family history, employer/business, security of tenure, tax

history, assets of applicants and their financing pattern,

recurring liabilities, other present and future liabilities and

investments (if any). Out of these, the incomes of applicants are

the most important criteria to understand and calculate the

credit worthiness of the applicants. As stated earlier, the

actual norms decided by banks differ greatly. Each has certain

norms within which the customer needs to fit in to be eligible

for a loan. Based on these parameters, the maximum amount of loan

that the bank can sanction and the customer is

eligible for is worked out. The broad tools to determine

eligibility remain the same for all banks. We can tabulate all

the conditions under three parameters.

Parameter DOCUMENTSTechnical

feasibility

Field Investigation, Market value of asset

Economic

viability

LTV(Loan to Value), IIR

Bankability Past month bank statements, Asset and

liabilities of the applicant

7

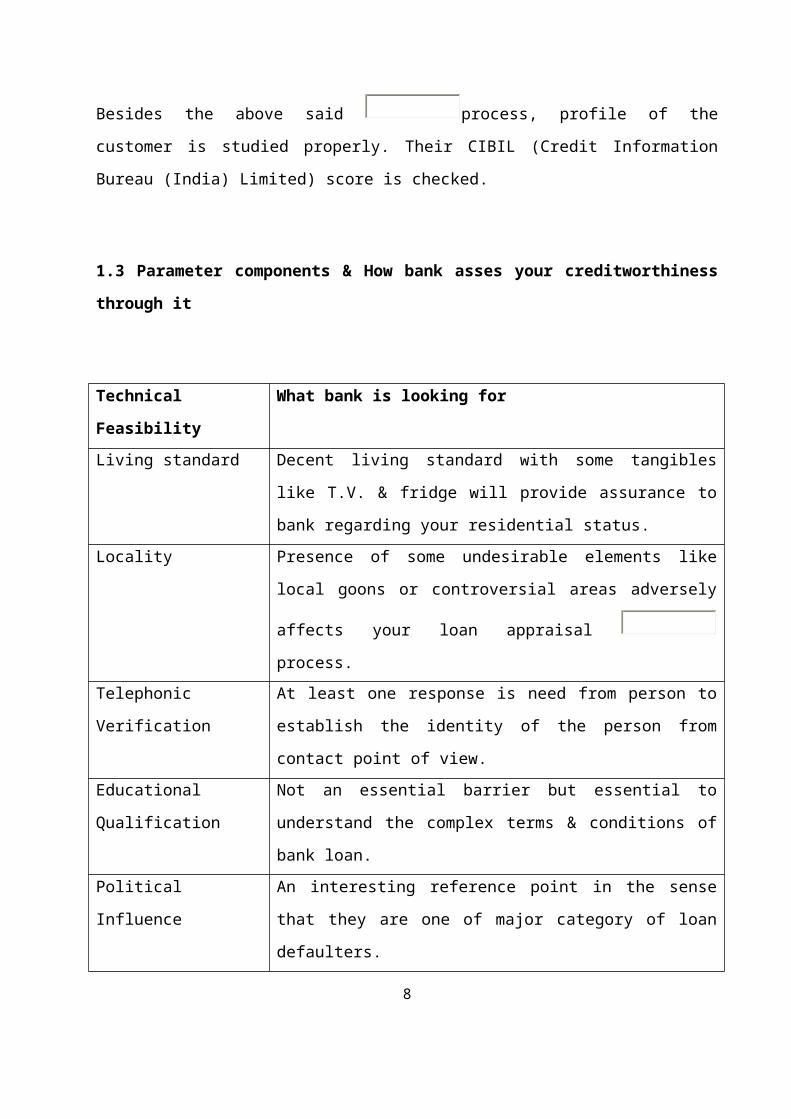

Besides the above said process, profile of the

customer is studied properly. Their CIBIL (Credit Information

Bureau (India) Limited) score is checked.

1.3 Parameter components & How bank asses your creditworthiness

through it

Technical

Feasibility

What bank is looking for

Living standard Decent living standard with some tangibles

like T.V. & fridge will provide assurance to

bank regarding your residential status.Locality Presence of some undesirable elements like

local goons or controversial areas adversely

affects your loan appraisal

process.Telephonic

Verification

At least one response is need from person to

establish the identity of the person from

contact point of view.Educational

Qualification

Not an essential barrier but essential to

understand the complex terms & conditions of

bank loan.Political

Influence

An interesting reference point in the sense

that they are one of major category of loan

defaulters.

8

References To establish the residential identity of

person from human contact point of view &

cross check of their loans.

The 3 methods used to arrive at Eligibility

Installment to income ratio

Fixed obligation to income ratio

Loan to cost ratio

1.4 Installment to income ratio

This ratio is generally expressed as a percentage. This

percentage denotes the portion of the customer's monthly

installment on the home loan taken. Usually, banks use 33.33

percent to 40 percent ratio. This is because it is has been

observed that under normal circumstances, a person can pay an

installment up to 33.33 to 40 per cent of his salary towards a

loan.

Example: if we consider the installment to income ratio equal to

33.33 per cent, and assume the gross income to be Rs. 30,000 per

month, then as per the ratio, the applicant is eligible for a

loan with the maximum installment of Rs. 10,000 per month.

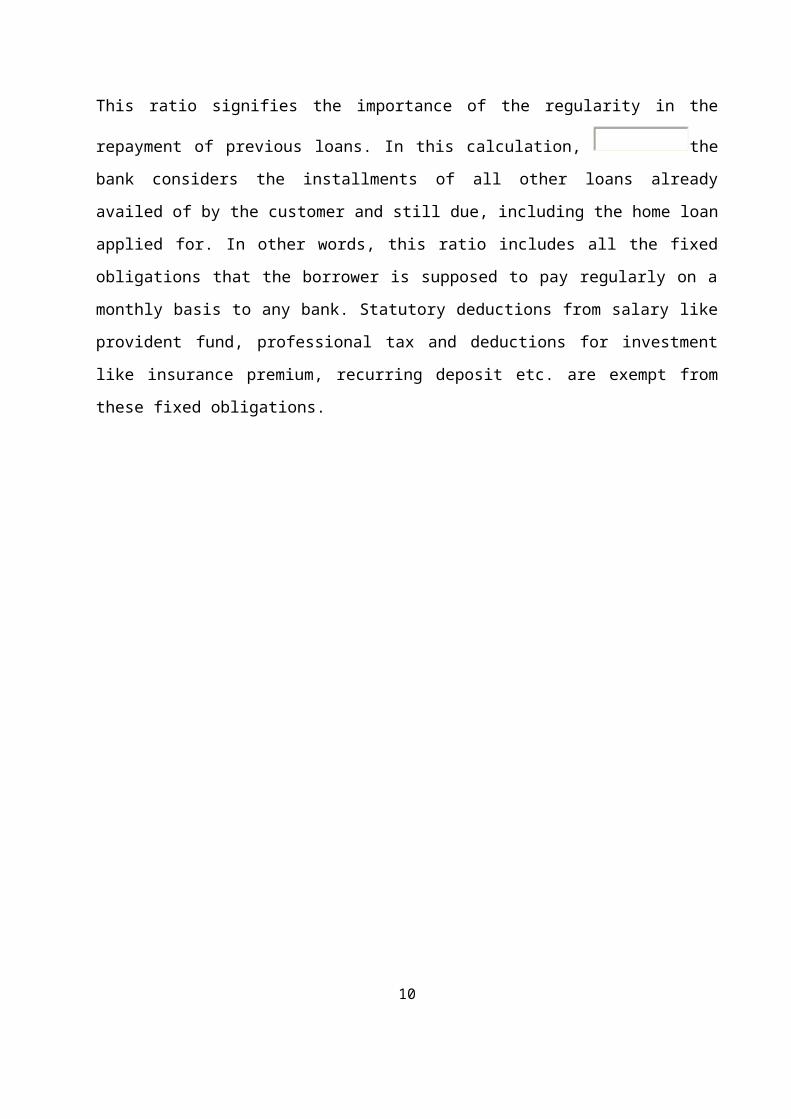

1.5 Fixed obligation to income ratio

9

This ratio signifies the importance of the regularity in the

repayment of previous loans. In this calculation, the

bank considers the installments of all other loans already

availed of by the customer and still due, including the home loan

applied for. In other words, this ratio includes all the fixed

obligations that the borrower is supposed to pay regularly on a

monthly basis to any bank. Statutory deductions from salary like

provident fund, professional tax and deductions for investment

like insurance premium, recurring deposit etc. are exempt from

these fixed obligations.

10

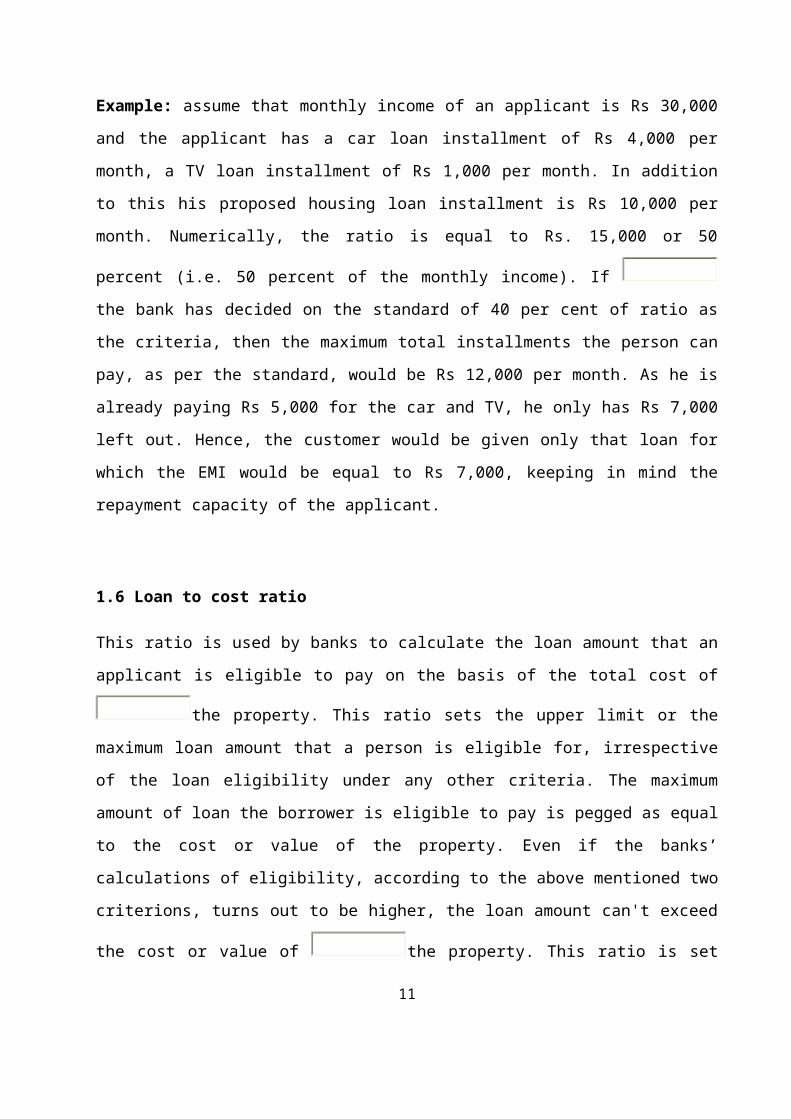

Example: assume that monthly income of an applicant is Rs 30,000

and the applicant has a car loan installment of Rs 4,000 per

month, a TV loan installment of Rs 1,000 per month. In addition

to this his proposed housing loan installment is Rs 10,000 per

month. Numerically, the ratio is equal to Rs. 15,000 or 50

percent (i.e. 50 percent of the monthly income). If

the bank has decided on the standard of 40 per cent of ratio as

the criteria, then the maximum total installments the person can

pay, as per the standard, would be Rs 12,000 per month. As he is

already paying Rs 5,000 for the car and TV, he only has Rs 7,000

left out. Hence, the customer would be given only that loan for

which the EMI would be equal to Rs 7,000, keeping in mind the

repayment capacity of the applicant.

1.6 Loan to cost ratio

This ratio is used by banks to calculate the loan amount that an

applicant is eligible to pay on the basis of the total cost of

the property. This ratio sets the upper limit or the

maximum loan amount that a person is eligible for, irrespective

of the loan eligibility under any other criteria. The maximum

amount of loan the borrower is eligible to pay is pegged as equal

to the cost or value of the property. Even if the banks’

calculations of eligibility, according to the above mentioned two

criterions, turns out to be higher, the loan amount can't exceed

the cost or value of the property. This ratio is set

11

equal to between 70 to 90 per cent of the registered value of

the property.

Hence, while deciding on the maximum amount of loan a customer

can be given, the banks use these three parameters. These

parameters help in computing loan eligibility, which is crucial

in calculating the creditworthiness of a customer. It also acts

as a guide to determine the loan amount.

12

Economic viability Installment to income

ratio

· IIR for salaried cases would be capped

at 60% of Net income in general

· Pension Income cases IIR to be

restricted to 40%aFixed obligation to

income ratio

FIOR kept at 55%

Loan to cost ratio LTV amount to 80%

1.7 Bankability Parameters

Parameter Norms Checkpoints

Bank Statements 6 months bank

statements need to be

furnished

To check the average

amount client is

maintaining in the

account is

sufficient to pay

the installment

amount or not.Business

continuity proof

Two year IT returns

made compulsory

To enquire primary

source of income.Credit interview For the big loan amount

credit interview is

necessary.

To check the general

attitude of customer

along with efforts

are put in to

understand their

13

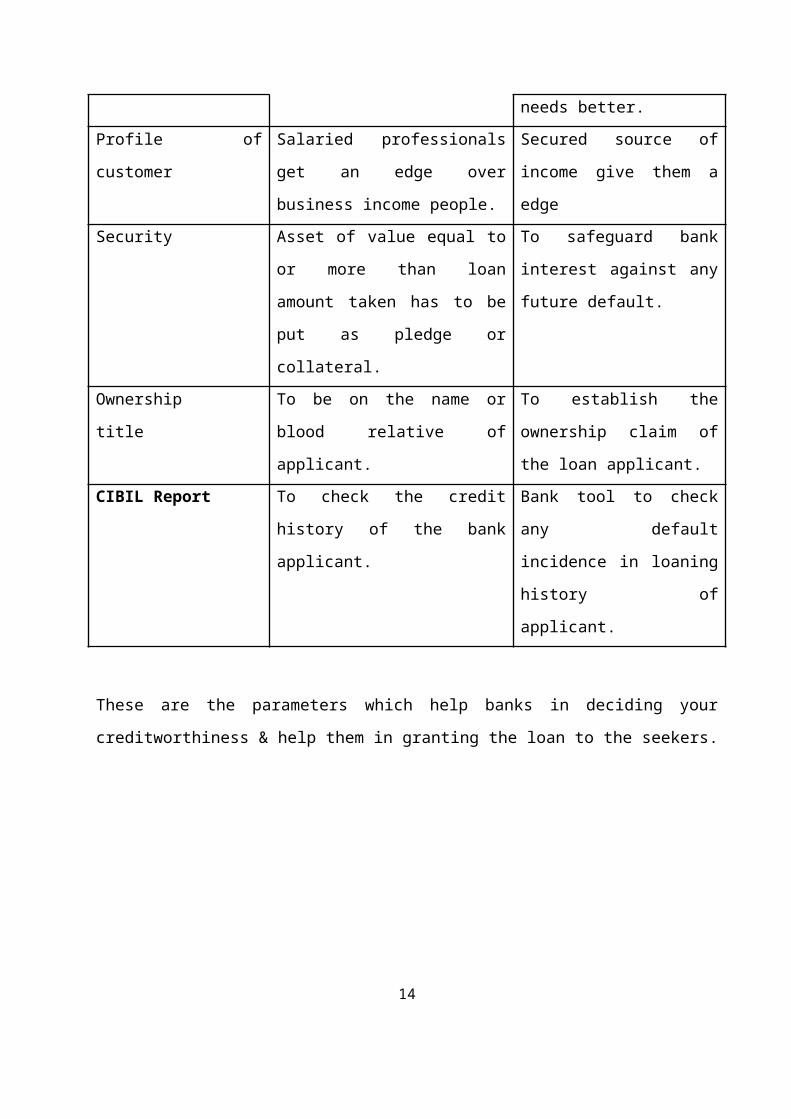

needs better.Profile of

customer

Salaried professionals

get an edge over

business income people.

Secured source of

income give them a

edgeSecurity Asset of value equal to

or more than loan

amount taken has to be

put as pledge or

collateral.

To safeguard bank

interest against any

future default.

Ownership

title

To be on the name or

blood relative of

applicant.

To establish the

ownership claim of

the loan applicant.CIBIL Report To check the credit

history of the bank

applicant.

Bank tool to check

any default

incidence in loaning

history of

applicant.

These are the parameters which help banks in deciding your

creditworthiness & help them in granting the loan to the seekers.

14

15

CHAPTER 2

REVIEW OF LITERATURE

The objective of running any industry is earning profits. An

industry will require funds to acquire “fixed assets” like land

and building, plant and machinery, equipments, vehicles etc… and

also to run the business i.e. its day to day operations.

Working capital is defined, as the funds required for carrying

the required levels of current assets to enable the unit to carry

on its operations at the expected levels uninterruptedly. Thus

working capital required (WCR) is dependent on

i. The volume of activity (viz. level of operations i.e.

Production and Sales)

ii. The activity carried on viz. manufacturing process, product,

production programme, and the materials and marketing mix.

The purpose of assessing the WC requirement of the industry is to

determine how the total requirements of funds will be met. The

two sources for meeting these requirements are the unit’s long-

term sources (like capital and long term borrowings) and the

short-term borrowings from banks. The long-term resources

available to the unit are called the liquid surplus or Net

Working Capital (NWC).

It can be explained by visualizing the process of setting up of

industry. The unit’s starts with a certain amount of capital,

which will not normally be sufficient, even to meet the cost of

fixed assets. The unit, therefore, arranges for a long-term loan16

from a financial institution or a bank towards a part of the cost

of fixed assets. From these two sources after meeting the cost of

fixed assets some funds remain to be used for working capital.

This amount is the Net Working Capital or Liquid Surplus and will

be one of the sources of meeting the working capital

requirements.

The remaining funds for working capital have to be raised from

banks; banks normally provide working capital finance by way of

advantage against stocks and sundry debtors. Banks, however, do

not finance the full amount of funds required for carrying

inventories and receivables: and normally insist on the stake of

the enterprise at every stage, by way of margins. Bank finance is

normally restricted to the amount of funds locked up less a

certain percentage of margins. Margins are imposed with a view to

have adequate stake of the promoter in the business both to

ensure his adequate interest in the business and to act as a

protection against any shocks that the business may sustain. The

margins stipulated will depend on various factors like

salability, quality, durability, price fluctuations in the market

for the commodity etc. taking into account the total working

capital requirements as assessed earlier, the permissible limit,

up to which the bank finance cab be granted is arrived.

While granting working capital advances to a unit, it will be

necessary to ensure that a reasonable proportion of the working

capital is met from the long-term sources viz. liquid surplus.

Normally, liquid surplus or net working capital be at least 25%

17

of the working capital requirement (corresponding to the

benchmark current ratio of 1.33), though this may vary depending

on the nature of industry/ trade and business conditions.

Various methods for assessment of Working Capital are discussed in detail:

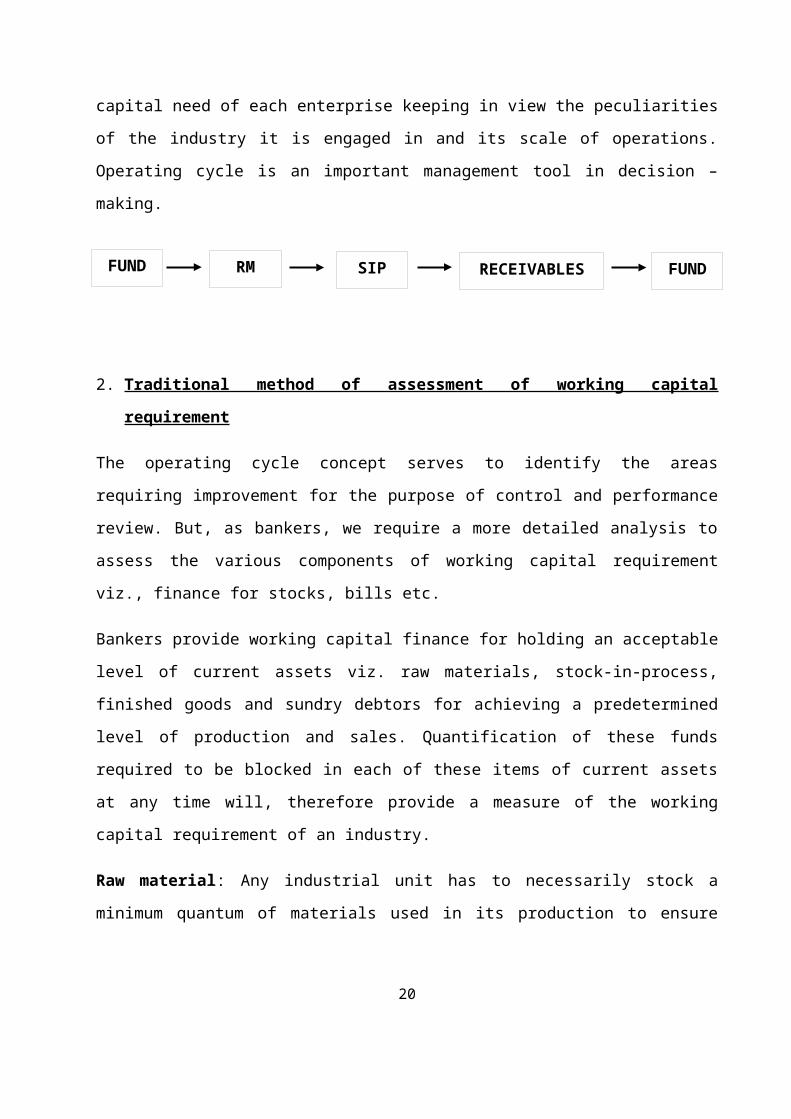

1. Operating cycle method :

Any manufacturing activity is characterized by a cycle of

operations consisting of purchase of raw materials for cash,

converting them into finished goods and realizing cash by sale

of these finished goods. The time that lapses between cash

outlay and cash realization by sale of finished goods and

realization of sundry debtors is known as length of operating

cycle. That is, the operating cycle consists of:

i. Time taken to acquire raw materials and average periodfor which they are in store.

ii. Conversion process time

iii. Average period for which finished goods are in storeand

iv. Average collection period of receivables (sundry

debtors).

Operating Cycle is also called cash-to-cash and indicates how

cash is converted into raw materials, stocks in process, finished

goods, bills (receivables) and finally backs to cash. Working

18

capital is the total cash that is circulating in this cycle.

Therefore, working capital can be turned over or deployed after

completing the cycle. Factors, which influence working capital

requirement, are Level of operating expenses and Length of

operating cycle.

Any reduction in either of the both will mean reduction in

working capital requirement or indicate an efficient working

capital management.

It can thus be concluded that by improving that by improving the

working capital turnover ratio (i.e. by reducing the length of

operating cycle) a better management (utilization) of working

capital results. It is obvious that any reduction in the length

of the operating cycle can be achieved only by better management

only by better management of one or more of the individual phases

of the operating cycle period for which raw materials are in

store, conversion process time, period for which finished goods

are in store and collection period of receivables. Looking at

whole problem from another angle, we find that we can set up

extremely clear guidelines for working capital management viz.

examining the length of each of the phases of the operating cycle

to assess the scope for reduction in one or more of these phases.

The length of the operating cycle is different from industry to

industry and from one firm to another within the same industry.

For instance, the operating cycle of a pharmaceutical unit would

be quite different from one engaged in the manufacture of machine

tools. The operating cycle concept enables to assess working

19

FUND RM SIP RECEIVABLES FUND

capital need of each enterprise keeping in view the peculiarities

of the industry it is engaged in and its scale of operations.

Operating cycle is an important management tool in decision –

making.

2. Traditional method of assessment of working capital

requirement

The operating cycle concept serves to identify the areas

requiring improvement for the purpose of control and performance

review. But, as bankers, we require a more detailed analysis to

assess the various components of working capital requirement

viz., finance for stocks, bills etc.

Bankers provide working capital finance for holding an acceptable

level of current assets viz. raw materials, stock-in-process,

finished goods and sundry debtors for achieving a predetermined

level of production and sales. Quantification of these funds

required to be blocked in each of these items of current assets

at any time will, therefore provide a measure of the working

capital requirement of an industry.

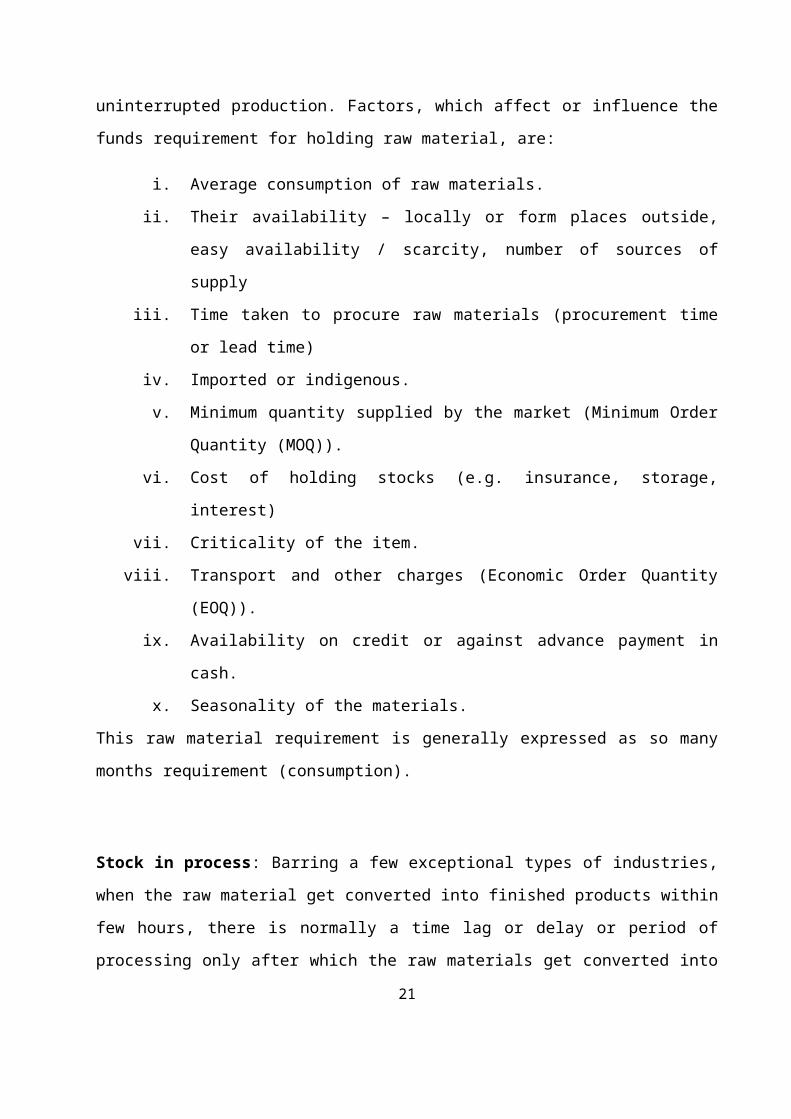

Raw material: Any industrial unit has to necessarily stock a

minimum quantum of materials used in its production to ensure

20

uninterrupted production. Factors, which affect or influence the

funds requirement for holding raw material, are:

i. Average consumption of raw materials.

ii. Their availability – locally or form places outside,

easy availability / scarcity, number of sources of

supply

iii. Time taken to procure raw materials (procurement time

or lead time)

iv. Imported or indigenous.

v. Minimum quantity supplied by the market (Minimum Order

Quantity (MOQ)).

vi. Cost of holding stocks (e.g. insurance, storage,

interest)

vii. Criticality of the item.

viii. Transport and other charges (Economic Order Quantity

(EOQ)).

ix. Availability on credit or against advance payment in

cash.

x. Seasonality of the materials.

This raw material requirement is generally expressed as so many

months requirement (consumption).

Stock in process: Barring a few exceptional types of industries,

when the raw material get converted into finished products within

few hours, there is normally a time lag or delay or period of

processing only after which the raw materials get converted into

21

finished product. During this period of processing, the raw

materials get converted into finished goods and expenses are

being incurred. The period of processing may vary from a few

hours to a number of months and unit will be blocked working

funds in the stock-in-process during this period. Such funds

blocked in SIP depend on:

i.The processing time

ii.Number of products handled at a time in the process

iii.Average quantities of each product, processed at each

time (batch quantity)

iv.The process technology

v.Number of shifts.

Finished goods: All products manufactured by an industry are not

sold immediately. It will be necessary to stock certain amount of

goods pending sale. This stock depends on:

i. Whether the manufacture is against firm order or

against anticipated order

ii. Supply terms

iii. Minimum quantity that can be dispatched

iv. Transport availability and transport cost

v. Pre-dispatch inspection

vi. Seasonality of goods

vii. Variation in demand

viii. Peak level/ low level of operations

22

ix. Marketing arrangement- e.g. direct sale to consumers or

through dealers/ wholesalers.

The requirement of funds against finished goods is expressed so

many months’ cost of production.

Sundry debtors (receivables): Sales may be affected under three

different methods:

i. Against advance payment

ii. Against cash

iii. On credit

A unit grants trade credit because it expects this investment to

be profitable. It would be in the form of sales expansion and

fresh customers or it could be in the form of retention of

existing customers. The extent of credit given by the industry

normally depends upon:

i. Trade practices

ii. Market conditions

iii. Whether it is bulky by the buyer

iv. Seasonality

v. Price advantage

Even in cases where no credit is extended to buyers, the transit

time for the goods to reach the buyer may take some time and till

the cash is received back, the unit will have to be cut out of

funds. The period from the time of sale to receipt of funds will

have to be reckoned for the purpose of quantifying the funds

blocked in sundry debtors. Even though the amount of sundry

23

debtors according to the unit’s books will be on the basis of

Sale Price, the actual amount blocked will be only the cost of

production of the materials against which credit has been

extended- the difference being the unit’s profit margin- (which

the unit does not obviously have to spend). The working capital

requirement against Sundry Debtors will therefore be computed on

the basis of cost of production (whereas the permissible bank

finance will be computed on basis of sale value since profit

margin varies from product to product and buyer to buyer and

cannot be uniformly segregated from the sale value).

The working capital requirement is expressed as so many months’

cost of production.

Expenses: It is customary in assessing the working capital

requirement of industries, to provide for 1 month’s expenses

also. A question might be raised as to why expenses should be

taken separately, whereas at every stage the funds required to be

blocked had been taken into account. This amount is provided

merely as a cushion, to take care of temporary bottlenecks and to

enable the unit to meet expenses when they fall due. Normally 1-

month total expenses, direct and indirect, salaries etc. are

taken into account.

While computing the working capital requirements of a unit, it

will be necessary to take into account 2 other factors,

24

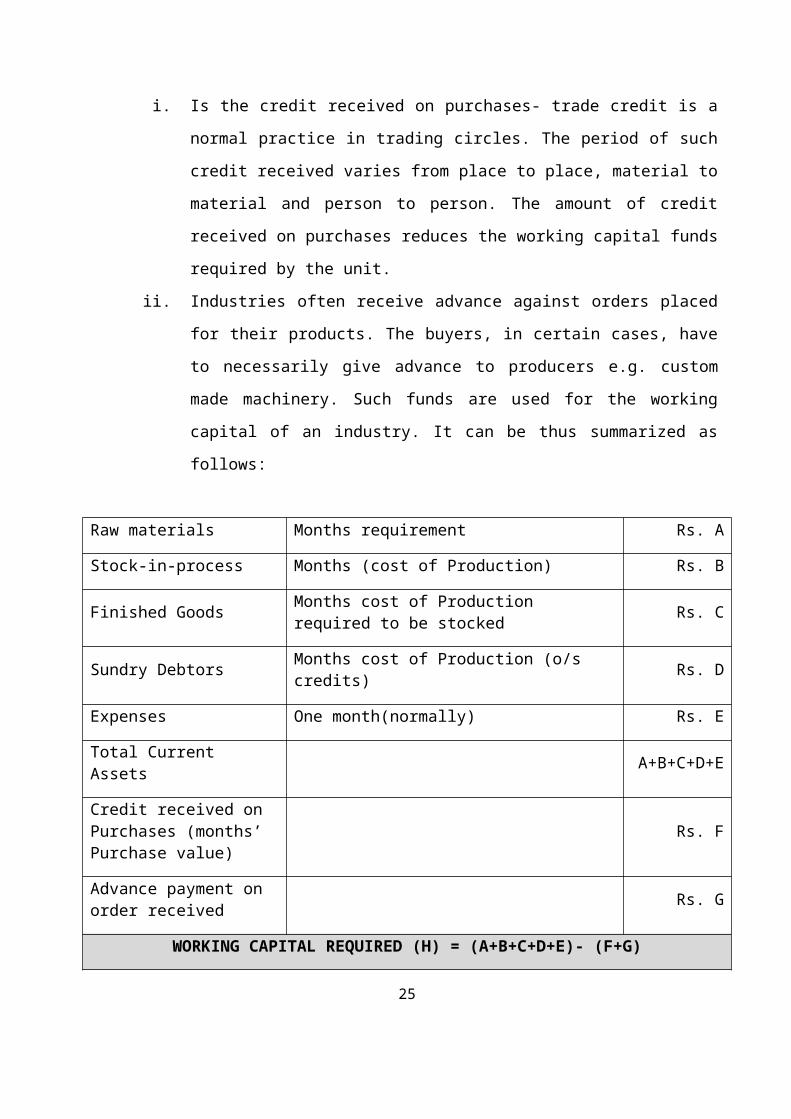

i. Is the credit received on purchases- trade credit is a

normal practice in trading circles. The period of such

credit received varies from place to place, material to

material and person to person. The amount of credit

received on purchases reduces the working capital funds

required by the unit.

ii. Industries often receive advance against orders placed

for their products. The buyers, in certain cases, have

to necessarily give advance to producers e.g. custom

made machinery. Such funds are used for the working

capital of an industry. It can be thus summarized as

follows:

Raw materials Months requirement Rs. A

Stock-in-process Months (cost of Production) Rs. B

Finished Goods Months cost of Production required to be stocked Rs. C

Sundry Debtors Months cost of Production (o/s credits) Rs. D

Expenses One month(normally) Rs. E

Total Current Assets A+B+C+D+E

Credit received on Purchases (months’ Purchase value)

Rs. F

Advance payment on order received Rs. G

WORKING CAPITAL REQUIRED (H) = (A+B+C+D+E)- (F+G)

25

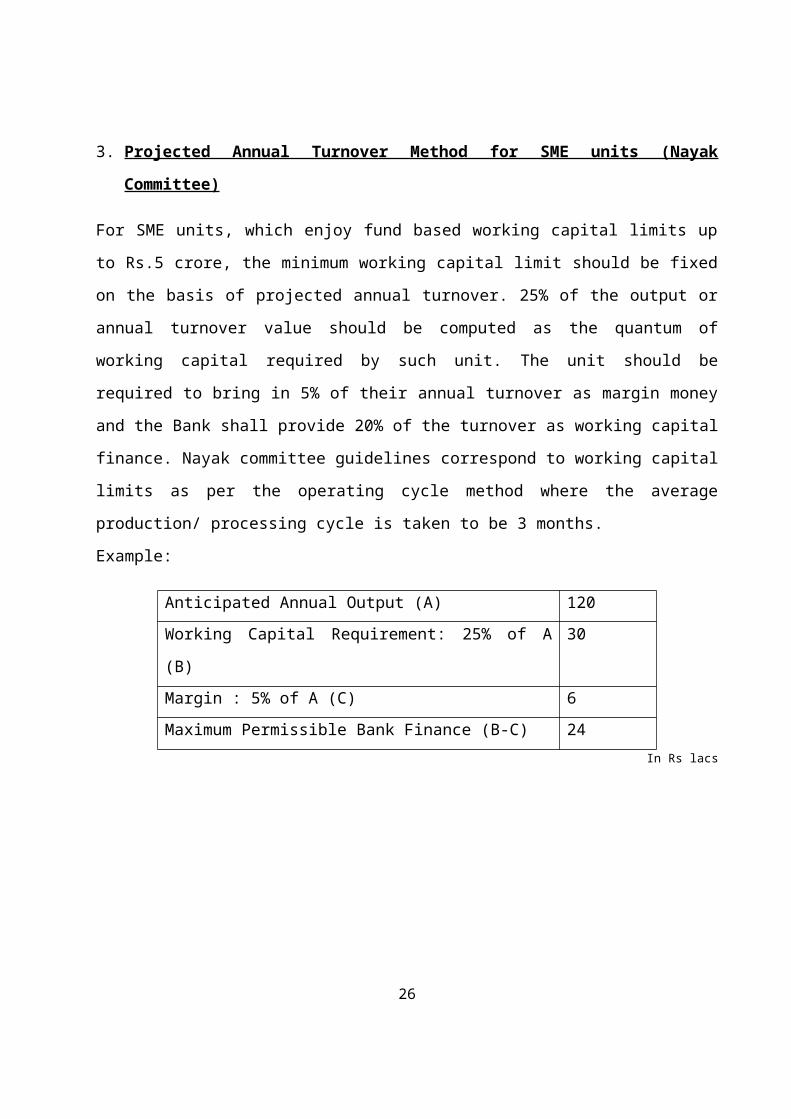

3. Projected Annual Turnover Method for SME units (Nayak

Committee)

For SME units, which enjoy fund based working capital limits up

to Rs.5 crore, the minimum working capital limit should be fixed

on the basis of projected annual turnover. 25% of the output or

annual turnover value should be computed as the quantum of

working capital required by such unit. The unit should be

required to bring in 5% of their annual turnover as margin money

and the Bank shall provide 20% of the turnover as working capital

finance. Nayak committee guidelines correspond to working capital

limits as per the operating cycle method where the average

production/ processing cycle is taken to be 3 months.

Example:

Anticipated Annual Output (A) 120Working Capital Requirement: 25% of A

(B)

30

Margin : 5% of A (C) 6Maximum Permissible Bank Finance (B-C) 24

In Rs lacs

26

Important clarifications:

i. The assessment of WC limits should be done both as per

Projected Turnover Method and Traditional Method; the higher

of the two is to be sanctioned as credit limit. If the

operating cycle is more than 3 months, there is no

restriction on extending finance at more than 20% of the

turnover provided that the borrower should bring n

proportionally higher stake in relation to his requirements

of bank finance.

ii. While the approach of extending need based credit will be

kept in mind, the financial strengths of the unit is also

important, the later aspect assumes greater significance so

as to take care of quality of bank’s assets. The margin

requirement, as a general rule, should not be diluted.

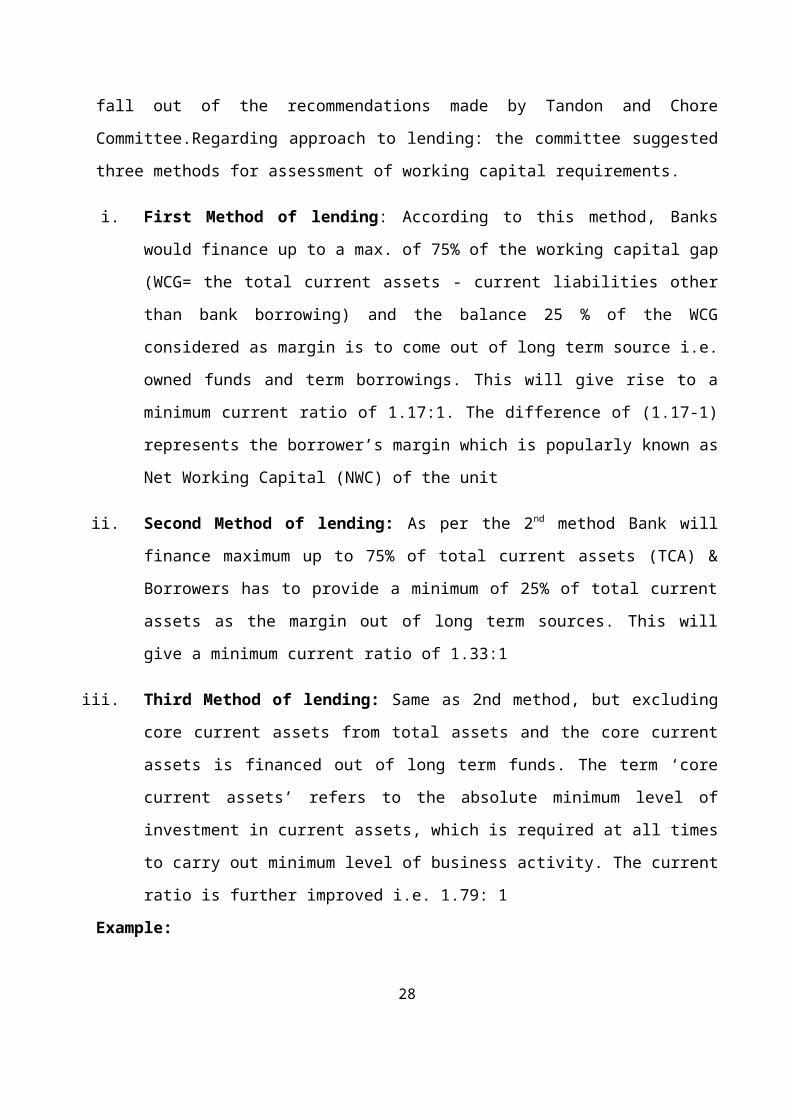

4. MPBF Method (Tandon and Chore Committee Recommendations)

The Tandon Committee was appointed to suggest a method for

assessing the working capital requirements and the quantum of

bank finance. Since at that time, there was scarcity of bank’s

resources, the Committee was also asked to suggest norms for

carrying current assets in different industries so that bank

finance was not drawn more than the minimum required level. The

Committee was also asked to devise an information system that

would provide, periodically, operational data, business

forecasts, production plan and resultant credit needs of units.

Chore Committee, which was appointed later, further refined the

approach to working capital assessment. The MPBF method is the27

fall out of the recommendations made by Tandon and Chore

Committee.Regarding approach to lending: the committee suggested

three methods for assessment of working capital requirements.

i. First Method of lending: According to this method, Banks

would finance up to a max. of 75% of the working capital gap

(WCG= the total current assets - current liabilities other

than bank borrowing) and the balance 25 % of the WCG

considered as margin is to come out of long term source i.e.

owned funds and term borrowings. This will give rise to a

minimum current ratio of 1.17:1. The difference of (1.17-1)

represents the borrower’s margin which is popularly known as

Net Working Capital (NWC) of the unit

ii. Second Method of lending: As per the 2nd method Bank will

finance maximum up to 75% of total current assets (TCA) &

Borrowers has to provide a minimum of 25% of total current

assets as the margin out of long term sources. This will

give a minimum current ratio of 1.33:1

iii. Third Method of lending: Same as 2nd method, but excluding

core current assets from total assets and the core current

assets is financed out of long term funds. The term ‘core

current assets’ refers to the absolute minimum level of

investment in current assets, which is required at all times

to carry out minimum level of business activity. The current

ratio is further improved i.e. 1.79: 1

Example:

28

Current Liabilities Current assets

Creditors for purchase 100 Raw material 200

Other current liability 50 Stock in process 20

Bank borrowings 200 Finished goods 90

Receivables 50

Other current assets 10

Total Current Liabilities 350 Total Current

Assets 370

(In Rs lacs)

29

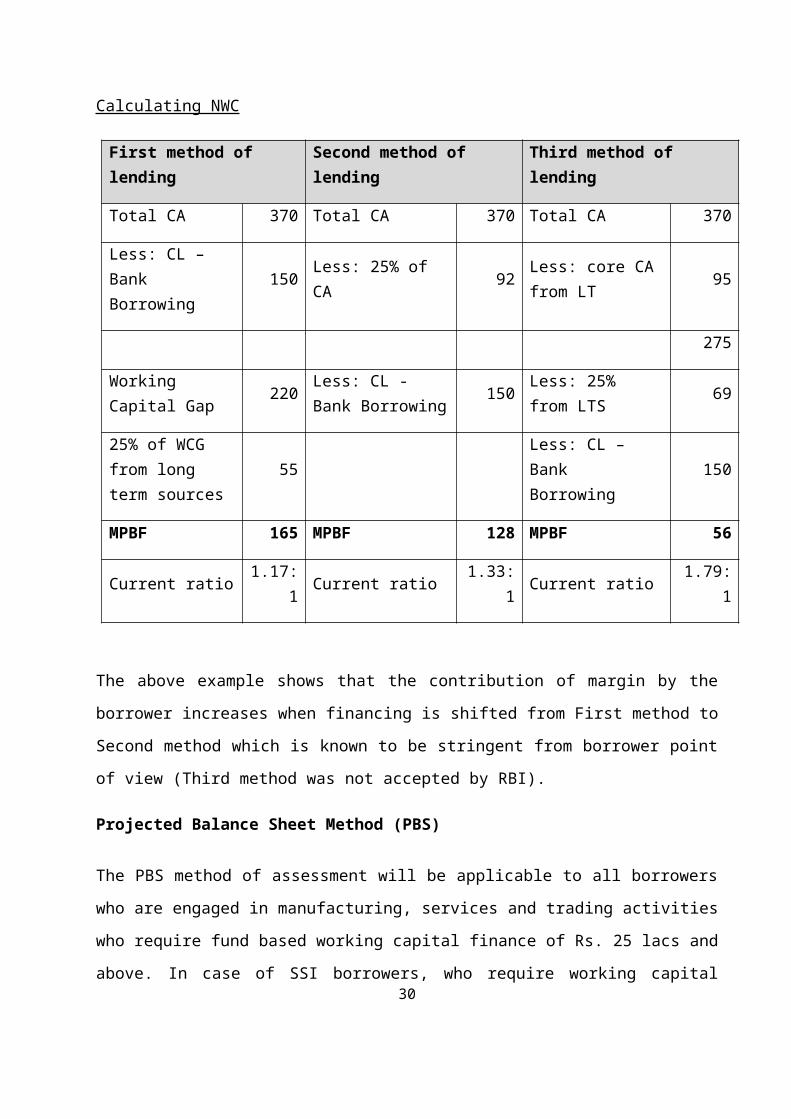

Calculating NWC

First method of lending

Second method of lending

Third method of lending

Total CA 370 Total CA 370 Total CA 370

Less: CL – Bank Borrowing

150 Less: 25% of CA 92 Less: core CA

from LT 95

275

Working Capital Gap 220 Less: CL -

Bank Borrowing 150 Less: 25% from LTS 69

25% of WCG from long term sources

55Less: CL – Bank Borrowing

150

MPBF 165 MPBF 128 MPBF 56

Current ratio 1.17:1 Current ratio 1.33:

1 Current ratio 1.79:1

The above example shows that the contribution of margin by the

borrower increases when financing is shifted from First method to

Second method which is known to be stringent from borrower point

of view (Third method was not accepted by RBI).

Projected Balance Sheet Method (PBS)

The PBS method of assessment will be applicable to all borrowers

who are engaged in manufacturing, services and trading activities

who require fund based working capital finance of Rs. 25 lacs and

above. In case of SSI borrowers, who require working capital30

credit limit up to Rs. 5 cr, the limit shall be computed on the

basis of Nayak Committee formula as well as that based on

production and operating cycle of the unit and the higher of the

two may be sanctioned.. The assessment will be based on the

borrower’s projected balance sheet, the funds flow planned for

current/ next year and examination of the profitability,

financial parameters etc. unlike the MPBF method, it will not be

necessary in this method to fix or compute the working capital

finance on the basis of a stipulated minimum level of liquidity

(Current Ratio).

31

The working capital requirement worked out is based on the

following:

i. CMA assessment method is continued with certain

modifications.

ii. Analysis of the Profit and Loss account, Balance Sheet,

Funds flow etc. for the past periods is done to examine

the profitability, financial position, and financial

management etc of the business.

iii. Scrutiny and validation of the projected income and

expenses in the business and projected changes in the

financial position (sources and uses of funds). This is

carried out to examine whether these parameters are

acceptable from the angle of liquidity, overall gearing,

efficiency of operations etc.

In the PBS method, the borrower’s total business operations,

financial position, management capabilities etc. are analysed in

detail to assess the working capital finance required and to

evaluate the overall risk. The assessment procedure is as

follows:

i. Collection of financial information from the borrower

ii. Classification of current assets / current liabilities

iii. Verification of projected levels of inventory/

receivables/ sundry creditors

iv. Evaluation of liquidity in the business operation

v. Validation of bank finance sought32

7.2 ASSESSMENT OF TERM LOANS

Term Loans are generally granted to finance capital expenditure,

i.e. for acquisition of land, building and plant and machinery,

required for setting up a new industrial undertaking or

expansion/diversification of an existing one and also for

acquisition of movable fixed assets. Term Loans are also given

for modernization, renovation, etc. to improve the product

quality or increase the productivity and profitability.

The basic difference between short-term facilities and term loans

is that short-term facilities are granted to meet the gap in the

working capital and are intended to be liquidated by realization

of assets, whereas term loans are given for acquisition of fixed

assets and have to be liquidated from the surplus cash generated

out of earnings. They are not intended to be paid out of the

sale of the fixed assets given as security for the loan. This

makes it necessary to adopt a different approach in examining the

application of the borrowers for term credits.

For the assessment to Term Loan Techno Economic Feasibility Study

is done. The success of a feasibility study is based on the

careful identification and assessment of all of the important

issues for business success. A detailed Project Report is

submitted by an entrepreneur, prepared by a approved agency or a

consultancy organization. Such report provides in-depth details

of the project requesting finance. It includes the technical

aspects, Managerial Aspect, the Market Condition and Projected

33

performance of the company. It is necessary for the appraising

officer to cross check the information provided in the report for

determining the worthiness of the project.

The feasibility study is a part of Credit Appraisal process and

the same is discussed in the following chapter.

34

7.3 BASEL ACCORD & RISK MANAGEMENT

The Basel accord/accords refer to the banking supervision accords

namely Basel I and Basel II issued by the Basel Committee on

Banking Supervision (BCBS).

Basel I accord

The 1988 Basel Accord primarily addressed banking in the sense of

deposit taking and lending. The main focus was Credit Risk. It

described the strength of the Bank as measured by the Capital

employed. Accordingly it put a minimum level of capital adequacy

(Capital to Credit Risk Weighted Assets ratio) at 8%. Basel I

allocated 4 risk weights i.e. 0%, 20, 50% and 100% to different

exposure types, based on the risk perceived on the exposure types

under the credit portfolio. Basel I provided a set norm for

capital allocation which helped many banks to allocate capital to

counter the risks faced by them.

CRAR = Capital

Risk Weighted Assets (Credit Risk+ Market Risk

+Operational Risk)

CAPITAL Tier I

Capita

l

Paid Up Equity Capital + Statutory Reserves +

Other disclosed free reserves + Capital

Reserves representing surplus arising out of

sale proceeds of Assets + Innovative Perpetual

35

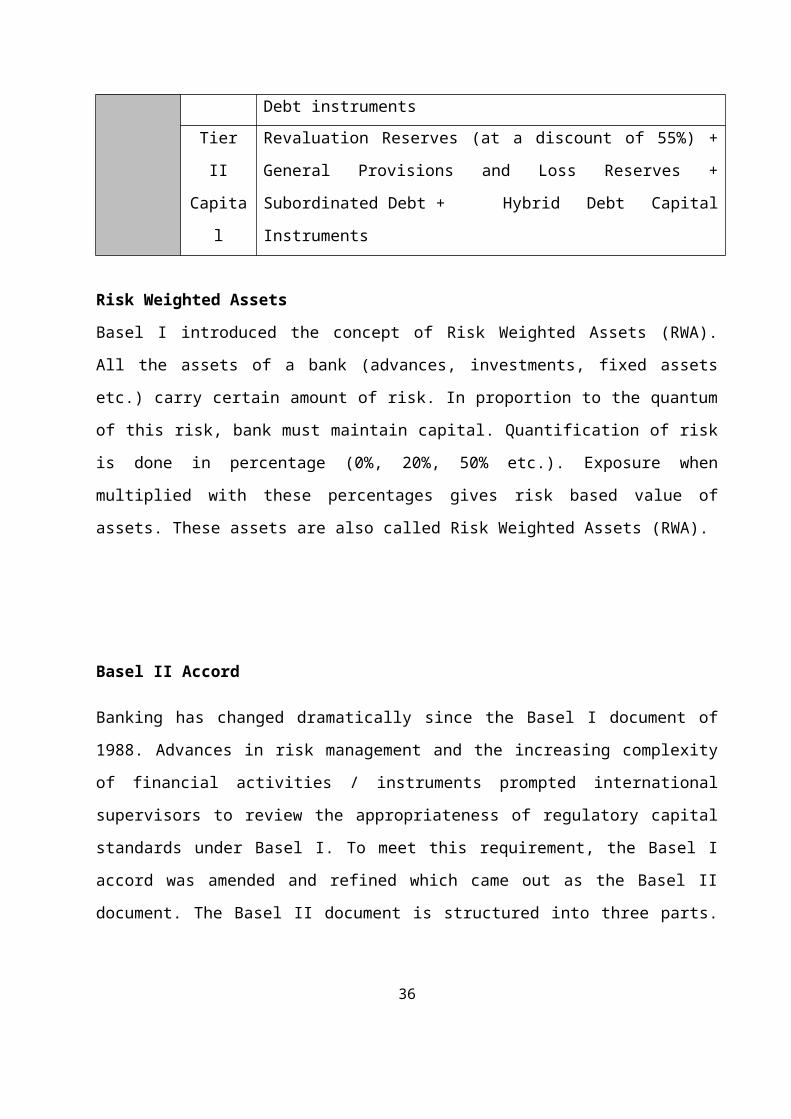

Debt instrumentsTier

II

Capita

l

Revaluation Reserves (at a discount of 55%) +

General Provisions and Loss Reserves +

Subordinated Debt + Hybrid Debt Capital

Instruments

Risk Weighted Assets

Basel I introduced the concept of Risk Weighted Assets (RWA).

All the assets of a bank (advances, investments, fixed assets

etc.) carry certain amount of risk. In proportion to the quantum

of this risk, bank must maintain capital. Quantification of risk

is done in percentage (0%, 20%, 50% etc.). Exposure when

multiplied with these percentages gives risk based value of

assets. These assets are also called Risk Weighted Assets (RWA).

Basel II Accord

Banking has changed dramatically since the Basel I document of

1988. Advances in risk management and the increasing complexity

of financial activities / instruments prompted international

supervisors to review the appropriateness of regulatory capital

standards under Basel I. To meet this requirement, the Basel I

accord was amended and refined which came out as the Basel II

document. The Basel II document is structured into three parts.

36

Each part is called as a pillar. Thus these three parts

constitute three pillars of Basel II.

PILLAR I

This pillar is compatible with the credit risk,

market risk and operational risk. The regulatory

capital will be focused on these three risks

PILLAR II

This pillar gives the bank responsibility to

exercise the best ways to manage the risk specific

to that bank. It also casts responsibility on the

supervisors to review and validate banks’ risk

measurement models.

PILLAR III

This pillar is on market discipline is used to

leverage the influence that other market players

can bring

37

CHAPTER 3

INDUSTRY PROFILE

Banks are the most significant players in the Indian

financial market. They are the biggest purveyors of credit, and

they also attract most of the savings from the population.

Dominated by public sector, the banking industry has so far acted

as an efficient partner in the growth and the development of the

country. Driven by the socialist ideologies and the welfare state

concept, public sector banks have long been the supporters of

agriculture and other priority sectors. They act as crucial

channels of the government in its efforts to ensure equitable

economic development.

The Indian banking can be broadly categorized into

nationalized (government owned), private banks and specialized

banking institutions. The Reserve Bank of India acts a

centralized body monitoring any discrepancies and shortcoming in

the system. Since the nationalization of banks in 1969, the

public sector banks or the nationalized banks have acquired a

place of prominence and has since then seen tremendous progress.

The need to become highly customer focused has forced the slow-

moving public sector banks to adopt a fast track approach. The

unleashing of products and services through the net has

galvanized players at all levels of the banking and financial

institutions market grid to look anew at their existing portfolio38

offering. Conservative banking practices allowed Indian banks to

be insulated partially from the Asian currency crisis. Indian

banks are now quoting a higher valuation when compared to banks

in other Asian countries (viz. Hong Kong, Singapore, Philippines

etc.) that have major problems linked to huge Non Performing

Assets (NPA’s) and payment defaults. Co-operative banks are

nimble footed in approach and armed with efficient branch

networks focus primarily on the ‘high revenue’ niche retail

segments.

The Indian banking has finally worked up to the competitive

dynamics of the ‘new’ Indian market and is addressing the

relevant issues to take on the multifarious challenges of

globalization. Banks that employ IT solutions are perceived to be

‘futuristic’ and proactive players capable of meeting the

multifarious requirements of the large customer’s base. Private

Banks have been fast on the uptake and are reorienting their

strategies using the internet as a medium The Internet has

emerged as the new and challenging frontier of marketing with the

conventional physical world tenets being just as applicable like

in any other marketing medium.

The Indian banking has come from a long way from being a

sleepy business institution to a highly proactive and dynamic

entity. This transformation has been largely brought about by

the large dose of liberalization and economic reforms that

39

allowed banks to explore new business opportunities rather than

generating revenues from conventional streams (i.e. borrowing and

lending). The banking in India is highly fragmented with 30

banking units contributing to almost 50% of deposits and 60% of

advances. Indian nationalized banks (banks owned by the

government) continue to be the major lenders in the economy due

to their sheer size and penetrative networks which assures them

high deposit mobilization. The Indian banking can be broadly

categorized into nationalized, private banks and specialized

banking institutions.

The Reserve Bank of India acts as a centralized body

monitoring any discrepancies and shortcoming in the system. It

is the foremost monitoring body in the Indian financial sector.

The nationalized banks (i.e. government-owned banks) continue to

dominate the Indian banking arena. Industry estimates indicate

that out of 274 commercial banks operating in India, 223 banks

are in the public sector and 51 are in the private sector. The

private sector bank grid also includes 24 foreign banks that have

started their operations here.

The liberalize policy of Government of India permitted entry

to private sector in the banking, the industry has witnessed the

entry of nine new generation private banks. The major

differentiating parameter that distinguishes these banks from all

40

the other banks in the Indian banking is the level of service

that is offered to the customer. Their focus has always centered

around the customer – understanding his needs, preempting him and

consequently delighting him with various configurations of

benefits and a wide portfolio of products and services. These

banks have generally been established by promoters of repute or

by ‘high value’ domestic financial institutions.

The popularity of these banks can be gauged by the fact that

in a short span of time, these banks have gained considerable

customer confidence and consequently have shown impressive growth

rates. Today, the private banks corner almost four per cent

share of the total share of deposits. Most of the banks in this

category are concentrated in the high-growth urban areas in

metros (that account for approximately 70% of the total banking

business). With efficiency being the major focus, these banks

have leveraged on their strengths and competencies viz.

Management, operational efficiency and flexibility, superior

product positioning and higher employee productivity skills.

The private banks with their focused business and service

portfolio have a reputation of being niche players in the

industry. A strategy that has allowed these banks to concentrate

on few reliable high net worth companies and individuals rather

than cater to the mass market. These well-chalked out integrates

strategy plans have allowed most of these banks to deliver

superlative levels of personalized services. With the Reserve

41

Bank of India allowing these banks to operate 70% of their

businesses in urban areas, this statutory requirement has

translated into lower deposit mobilization costs and higher

margins relative to public sector banks.

HISTORY OF BANKING SECTOR IN INDIA

Without a sound and effective banking system in India it

cannot have a healthy economy. The banking system of India should

not only be hassle free but it should be able to meet new

challenges posed by the technology and any other external and

internal factors.

For the past three decades India's banking system has

several outstanding achievements to its credit. The most striking

is its extensive reach. It is no longer confined to only

metropolitans or cosmopolitans in India. In fact, Indian banking

system has reached even to the remote corners of the country.

This is one of the main reasons of India's growth process.

The government's regular policy for Indian bank since 1969

has paid rich dividends with the nationalization of 14 major

private banks of India.

Not long ago, an account holder had to wait for hours at the

bank counters for getting a draft or for withdrawing his own

money. Today, he has a choice. Gone are days when the most42

efficient bank transferred money from one branch to other in two

days. Now it is simple as instant messaging or dial a pizza.

Money has become the order of the day.

There are three different phases in the history of banking in

India.

1) Pre-Nationalization Era.

2) Nationalization Stage.

3) Post Liberalization Era.

1) Pre-Nationalization Era:

In India the business of banking and credit was practices

even in very early times. The remittance of money through

Hundies, an indigenous credit instrument, was very popular. The

hundies were issued by bankers known as Shroffs, Sahukars, Shahus

or Mahajans in different parts of the country.

The modern type of banking, however, was developed by the

Agency Houses of Calcutta and Bombay after the establishment of

Rule by the East India Company in 18th and 19th centuries.

43

During the early part of the 19th Century, ht volume of

foreign trade was relatively small. Later on as the trade

expanded, the need for banks of the European type was felt and

the government of the East India Company took interest in having

its own bank. The government of Bengal took the initiative and

the first presidency bank, the Bank of Calcutta (Bank of Bengal)

was established in 180. In 1840, the Bank of Bombay and in 1843,

the Bank of Madras was also set up.

These three banks are also known as “Presidency Bank”. The

Presidency Banks had their branches in important trading centers

but mostly lacked in uniformity in their operational policies. In

1899, the Government proposed to amalgamate these three banks in

to one so that it could also function as a Central Bank, but the

Presidency Banks did not favor the idea. However, the conditions

obtaining during world war period (1914-1918) emphasized the need

for a unified banking institution, as a result of which the

Imperial Bank was set up in1921. The Imperial Bank of India acted

like a Central bank and as a banker for other banks.

The RBI (Reserve Bank of India) was established in 1935 as

the Central Bank of the Country. In 1949, the Banking Regulation

act was passed and the RBI was nationalized and acquired

extensive regulatory powers over the commercial banks.

44

In 1950, the Indian Banking system comprised of the RBI, the

Imperial Bank of India, Cooperative banks, Exchange banks and

Indian Joint Stock banks.

2) Nationalization Stage:

After Independence, in 1951, the All India Rural Credit

survey, committee of Direction with Shri. A. D. Gorwala as

Chairman recommended amalgamation of the Imperial Bank of India

and ten others banks into a newly established bank called the

State Bank of India (SBI). The Government of India accepted the

recommendations of the committee and introduced the State Bank of

India bill in the Lok Sabha on 16th April 1955 and it was passed

by Parliament and got the president’s assent on 8th May 1955. The

Act came into force on 1st July 1955, and the Imperial Bank of

India was nationalized in 1955 as the State Bank of India.

The main objective of establishing SBI by nationalizing the

Imperial Bank of India was “to extend banking facilities on a

large scale more particularly in the rural and semi-urban areas

and to diverse other public purposes.”

In 1959, the SBI (Subsidiary Bank) act was proposed and the

following eight state-associated banks were taken over by the SBI

as its subsidiaries.

Name of the Bank Subsidiary with effect from

1. State Bank of Hyderabad 1st October 1959

45

2. State Bank of Bikaner 1st January 1960

3. State Bank of Jaipur 1st January 1960

4. State Bank of Saurashtra 1st May 1960

5. State Bank of Patiala 1st April 1960

6. State Bank of Mysore 1st March 1960

7. State Bank of Indore 1st January 1968

8. State Bank of Travancore 1st January 1960

With effect from 1st January 1963, the State Bank of Bikaner

and State Bank of Jaipur with head office located at Jaipur.

Thus, seven subsidiary banks State Bank of India formed the SBI

Group.

The SBI Group under statutory obligations was required to

open new offices in rural and semi-urban areas and modern banking

was taken to these unbanked remote areas.

On 19th July 1969, then the Prime Minister, Mrs. Indira

Gandhi announced the nationalization of 14 major scheduled

Commercial Banks each having deposits worth Rs. 50 crores and

above. This was a turning point in the history of commercial

banking in India.

Central Bank of India

Bank of Maharashtra

Dena Bank

Punjab National Bank

Syndicate Bank

Canara Bank

46

Indian Bank

Indian Overseas Bank

Bank of Baroda

Union Bank

Allahabad Bank

United Bank of India

UCO Bank

Bank of India

Later the Government Nationalized six more commercial private

sector banks with deposit liability of not less than Rs. 200

crores on 15th April 1980, viz.

i) Andhra Bank.

ii) Corporation Bank.

iii) New Bank if India.

iv) Oriental Bank of Commerce.

v) Punjab and Sindh Bank.

vi) Vijaya Bank.

In 1969, the Lead Bank Scheme was introduced to extend

banking facilities to every corner of the country. Later in 1975,

Regional Rural Banks were set up to supplement the activities of

the commercial banks and to especially meet the credit needs of

the weaker sections of the rural society.

Nationalization of banks paved way for retail banking and as

a result there has been an alt round growth in the branch

47

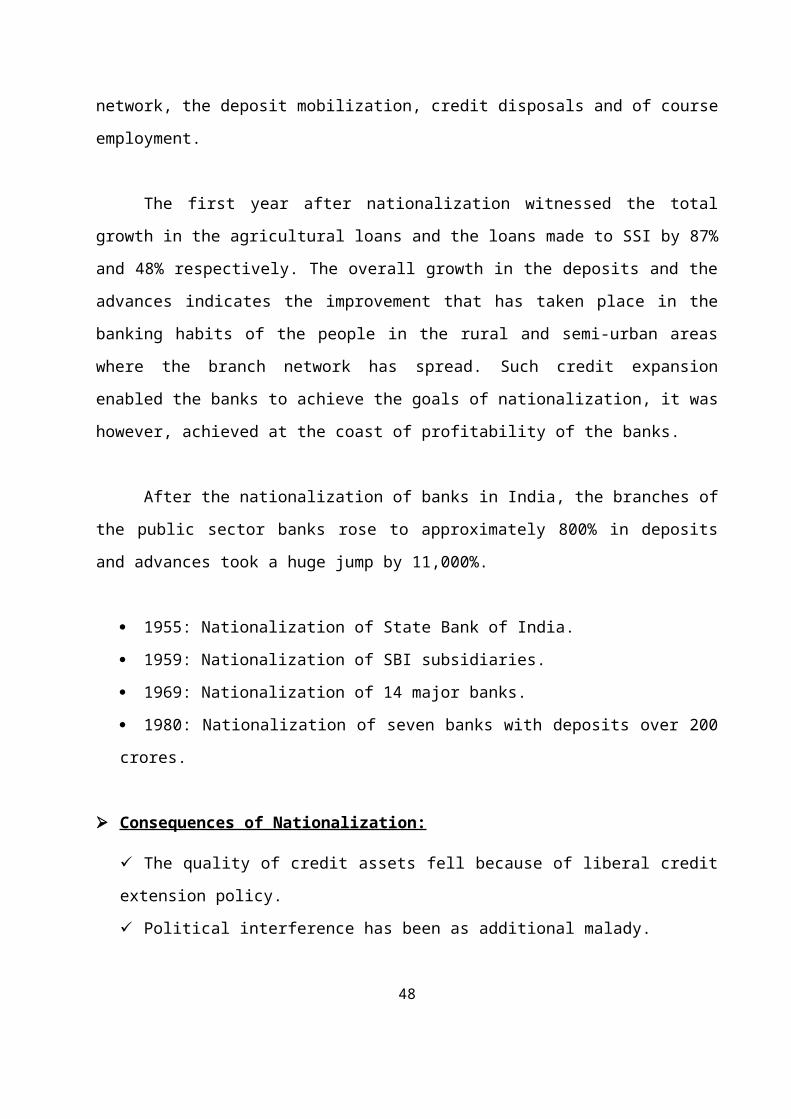

network, the deposit mobilization, credit disposals and of course

employment.

The first year after nationalization witnessed the total

growth in the agricultural loans and the loans made to SSI by 87%

and 48% respectively. The overall growth in the deposits and the

advances indicates the improvement that has taken place in the

banking habits of the people in the rural and semi-urban areas

where the branch network has spread. Such credit expansion

enabled the banks to achieve the goals of nationalization, it was

however, achieved at the coast of profitability of the banks.

After the nationalization of banks in India, the branches of

the public sector banks rose to approximately 800% in deposits

and advances took a huge jump by 11,000%.

1955: Nationalization of State Bank of India.

1959: Nationalization of SBI subsidiaries.

1969: Nationalization of 14 major banks.

1980: Nationalization of seven banks with deposits over 200

crores.

Consequences of Nationalization:

The quality of credit assets fell because of liberal credit

extension policy.

Political interference has been as additional malady.

48

Poor appraisal involved during the loan meals conducted for

credit disbursals.

The credit facilities extended to the priority sector at

concessional rates.

The high level of low yielding SLR investments adversely

affected the profitability of the banks.

The rapid branch expansion has been the squeeze on

profitability of banks emanating primarily due to the

increase in the fixed costs.

There was downward trend in the quality of services and

efficiency of the banks.

3) Post-Liberalization Era---Thrust on Quality and Profitability:

By the beginning of 1990, the social banking goals set for

the banking industry made most of the public sector resulted in

the presumption that there was no need to look at the fundamental

financial strength of this bank. Consequently they remained

undercapitalized. Revamping this structure of the banking

industry was of extreme importance, as the health of the

financial sector in particular and the economy was a whole would

be reflected by its performance.

The need for restructuring the banking industry was felt

greater with the initiation of the real sector reform process in

1992. the reforms have enhanced the opportunities and challenges

for the real sector making them operate in a borderless global

49

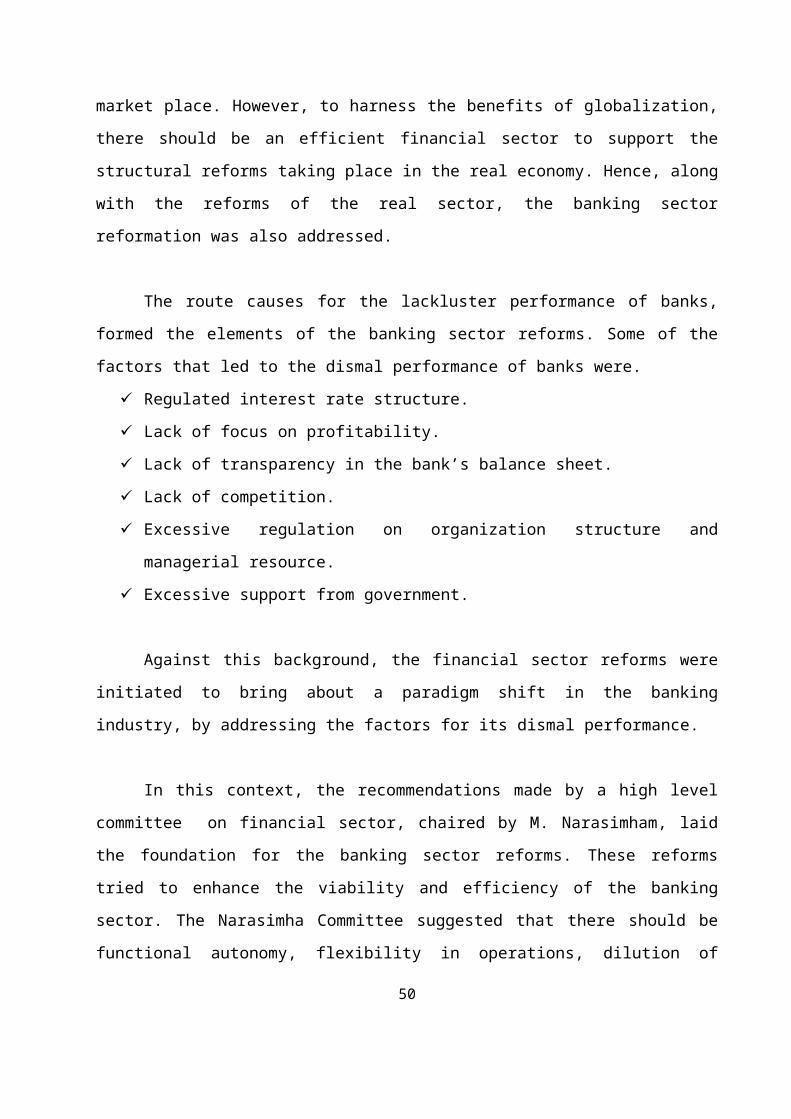

market place. However, to harness the benefits of globalization,

there should be an efficient financial sector to support the

structural reforms taking place in the real economy. Hence, along

with the reforms of the real sector, the banking sector

reformation was also addressed.

The route causes for the lackluster performance of banks,

formed the elements of the banking sector reforms. Some of the

factors that led to the dismal performance of banks were.

Regulated interest rate structure.

Lack of focus on profitability.

Lack of transparency in the bank’s balance sheet.

Lack of competition.

Excessive regulation on organization structure and

managerial resource.

Excessive support from government.

Against this background, the financial sector reforms were

initiated to bring about a paradigm shift in the banking

industry, by addressing the factors for its dismal performance.

In this context, the recommendations made by a high level

committee on financial sector, chaired by M. Narasimham, laid

the foundation for the banking sector reforms. These reforms

tried to enhance the viability and efficiency of the banking

sector. The Narasimha Committee suggested that there should be

functional autonomy, flexibility in operations, dilution of

50

banking strangulations, reduction in reserve requirements and

adequate financial infrastructure in terms of supervision, audit

and technology. The committee further advocated introduction of

prudential forms, transparency in operations and improvement in

productivity, only aimed at liberalizing the regulatory

framework, but also to keep them in time with international

standards. The emphasis shifted to efficient and prudential

banking linked to better customer care and customer services.

PRIVATE SECTOR BANKS

Private banking in India was practiced since the beginning

of banking system in India. The first private bank in India to be

set up in Private Sector Banks in India was IndusInd Bank. It is

one of the fastest growing Private Sector Bank in India. IDBI

ranks the tenth largest development bank in the world as Private

Banks in India and has promoted world class institutions in

India.

The first Private Bank in India to receive an in principle

approval from the Reserve Bank of India was Housing Development

Finance Corporation Limited, to set up a bank in the private

sector banks in India as part of the RBI's liberalization of the

Indian Banking Industry. It was incorporated in August 1994 as

HDFC Bank Limited with registered office in Mumbai and commenced

operations as Scheduled Commercial Bank in January 1995.

51

ING Vaysya, yet another Private Bank of India was

incorporated in the year 1930. Bangalore has a pride of place for

having the first branch inception in the year 1934. With

successive years of patronage and constantly setting new

standards in banking, ING Vaysya Bank has many credits to its

account.

Entry of Private Sector Banks:

There has been a paradigm shift in mindsets both at the

Government level in the banking industry over the years since

Nationalization of Banks in 1969, particularly during the last

decade (1990-2000). Having achieved the objectives of

Nationalization, the most important issue before the industry at

present is survival and growth in the environment generated by

the economic liberalization greater competition with a view to

achieving higher productivity and efficiency in January 1993 for

the entry of Private Sector banks based on the Nationalization

Committee report of 1991, which envisaged a larger role for

Private Sector Banks.

The RBI prescribed a minimum paid up capital of Rs. 100

crores for the new bank and the shares are to be listed at stock

exchange. Also the new bank after being granted license under the

Banking Regulation Act shall be registered as a public limited

company under the companies Act, 1956.

52

Subsequently 9 new commercial banks have been granted

license to start banking operations. The new private sector banks

have been very aggressive in business expansion and is also

reporting higher profile levels taking the advantage of

technology and skilled manpower. In certain areas, these banks

have even our crossed the other group of banks including foreign

banks.

PRESENT SCENARIO OF BANKING SECTOR

The stalwarts of India's financial community nodded their

heads sagaciously when Prime Minister Manmohan Singh said in a

speech: "If there is one aspect in which we can confidentially

assert that India is ahead of China, it is in the robustness and

soundness of our banking system." Indian banks have been rated

higher than Chinese banks by international rating agency Standard

& Poor's.

With the credibility of the Indian banking system on a high,

a number of Indian banks are now leveraging it to expand

overseas. State Bank of India, the country’s largest bank has

acquired 76 per cent stake in a Kenyan bank, Giro Commercial

53

Private Sector BanksOld Pvt. Sector Banks (25)New Pvt. Sector Banks (9)

Bank, for US$ 7 million. Canara Bank is helping Chinese banks

recover their huge non-performing assets (NPA).

To meet the challenges of going global, the Indian banking

sector is implementing internationally followed prudential

accounting norms for classification of assets, income recognition

and loan loss provisioning. The scope of disclosure and

transparency has also been raised in accordance with

international practices.

India has complied with almost all the Core Principles of

Effective Banking Supervision of the Basel Committee. Some Indian

banks are also presenting their accounts as per the U.S. GAAP.

The roadmap for adoption of Basel II is under formulation.

The use of technology has placed Indian banks at par with

their global peers. It has also changed the way banking is done

in India. ‘Anywhere banking’ and ‘Anytime banking’ have become a

reality. The financial sector now operates in a more competitive

environment than before and intermediates relatively large volume

of international financial flows.

BANKING IN INDIA:

Overview of Banking

54

Banking Regulation Act of India, 1949 defines Banking as

“accepting, for the purpose of lending or of investment of

deposits of money from the public, repayable on demand or

otherwise or withdrawable by cheque, draft order or otherwise.”

The Reserve Bank of India Act, 1934 and the Banking Regulation

Act, 1949, govern the banking operations in India.

Classification of Banks

Banks in India can be categorized into non-scheduled banks

and scheduled banks. Scheduled banks constitute of commercial

banks and co-operative banks. There are about 67,000 branches of

Scheduled banks spread across India. During the first phase of

financial reforms, there was a nationalization of 14 major banks

in 1969. This crucial step led to a shift from Class banking to

Mass banking. Since then the growth of the banking industry in

India has been a continuous process.

As far as the present scenario is concerned the banking

industry is in a transition phase. The Public Sector Banks

(PSB’s), which are the foundation of the Indian Banking system

account for more than 78 per cent of total banking industry

assets. Unfortunately they are burdened with excessive Non

Performing assets (NPA’s), massive manpower and lack of modern

technology.

55

On the other hand the Private Sector Banks in India are

witnessing immense progress. They are leaders in Internet

banking, mobile banking, phone banking, ATMs. On the other hand

the Public Sector Banks are still facing the problem of unhappy

employees. There has been a decrease of 20 percent in the

employee strength of the private sector in the wake of the

Voluntary Retirement Schemes (VRS). As far as foreign banks are

concerned they are likely to succeed in India.

Indusland Bank was the first private bank to be set up in

India. IDBI, ING Vyasa Bank, SBI Commercial and International

Bank Ltd, Dhanalakshmi Bank Ltd, Karur Vysya Bank Ltd, Bank of

Rajasthan Ltd etc are some Private Sector Banks. Banks from the

Public Sector include Punjab National bank, Vijaya Bank, UCO

Bank, Oriental Bank, Allahabad Bank, Andhra Bank etc.

ANZ Grindlays Bank, ABN-AMRO Bank, American Express Bank

Ltd, Citibank etc are some foreign banks operating in India.

Commercial Banks

The commercial banking structure in India consists of:

Scheduled Commercial Banks

Unscheduled Banks

56

Scheduled commercial Banks constitute those banks which have been

included in the Second Schedule of Reserve Bank of India(RBI)

Act, 1934.

RBI in turn includes only those banks in this schedule which

satisfy the criteria laid down vide section 42 (60 of the Act.

Some co-operative banks are scheduled commercial banks albeit not

all co-operative banks are. Being a part of the second schedule

confers some benefits to the bank in terms of access to

accomodation by RBI during the times of liquidity constraints. At

the same time, however, this status also subjects the bank

certain conditions and obligation towards the reserve regulations

of RBI.

For the purpose of assessment of performance of banks, the

Reserve Bank of India categorise them as public sector banks, old

private sector banks, new private sector banks and foreign banks.

This sub sector can broadly be classified into:

1. Public sector

2. Private sector

3. Foreign banks

Public sector banks have either the Government of India or

57

Reserve Bank of India as the majority shareholder. This segment

comprises of:

Associate Banks

State Bank of India has the following seven Associate Banks (ABs)

with controlling interest ranging from 75% to 100%.

State Bank of Bikaner and Jaipur (SBBJ)

State Bank of Hyderabad (SBH)

State Bank of Indore (SBIr)

State Bank of Mysore (SBM)

State Bank of Patiala (SBP)

State Bank of Saurashtra (SBS)

State Bank of Travancore (SBT)

Public Sector Banks

Allahabad Bank

Andhra Bank

Bank of Baroda

Bank of India

Bank of Maharashtra

Canara Bank

Central Bank of India

Corporation Bank

Dena Bank

Indian Bank

Indian Overseas Bank

Oriental Bank of Commerce

Punjab and Sind Bank

Punjab National Bank

Syndicate Bank

UCO Bank

Union Bank of India

United Bank of India

58

Vijaya Bank

IDBI and IDBI Bank Ltd. have been merged to form Industrial

Development Bank of India (IDBI) Ltd. IDBI is notified as a

scheduled bank by the Reserve Bank of India (RBI) under the

Reserve Bank of India Act, 1934. RBI has categorized IDBI under a

new sub group "other public sector bank".

Private Sector Banks

Bank of Punjab Ltd. (since merged with Centurion Bank)

Centurion Bank of Punjab (since merged with HDFC Bank)

Development Credit Bank Ltd.

HDFC Bank Ltd.

ICICI Bank Ltd.

IndusInd Bank Ltd.

Kotak Mahindra Bank Ltd.

Axis Bank (earlier UTI Bank)

Yes Bank Ltd.

Foreign Banks in India

ABN-AMRO Bank N.V.

Abu Dhabi Commercial Bank

Ltd.

American Express Bank

Ltd.

Barclays Bank PLC

BNP Paribas

Citibank N.A.

DBS Bank Ltd

Deutsche Bank AG

59

HSBC Ltd.

Standard Chartered Bank

State Bank of Mauritius

Ltd.

60

ROLE OF BANKS

Banks play a positive role in economic development of a

country as repositories of community’s savings and as

purveyors of credit. Indian Banking has aided the economic

development during the last fifty years in an effective way.

The banking sector has shown a remarkable responsiveness to

the needs of planned economy. It has brought about a

considerable progress in its efforts at deposit mobilization

and has taken a number of measures in the recent past for

accelerating the rate of growth of deposits. As recourse to

this, the commercial banks opened branches in urban, semi-

urban and rural areas and have introduced a number of

attractive schemes to foster economic development.

The activities of commercial banking have growth in

multi-directional ways as well as multi-dimensional manner.

Banks have been playing a catalytic role in area development,

backward area development, extended assistance to rural

development all along helping agriculture, industry,

international trade in a significant manner. In a way,

commercial banks have emerged as key financial agencies for

rapid economic development.

By pooling the savings together, banks can make available

funds to specialized institutions which finance different

61

sectors of the economy, needing capital for various purposes,

risks and durations. By contributing to government securities,

bonds and debentures of term-lending institutions in the

fields of agriculture, industries and now housing, banks are

also providing these institutions with an access to the common

pool of savings mobilized by them, to that extent relieving

them of the responsibility of directly approaching the saver.

This intermediation role of banks is particularly important in

the early stages of economic development and financial

specification. A country like India, with different regions at

different stages of development, presents an interesting

spectrum of the evolving role of banks, in the matter of

inter-mediation and beyond.

Mobilization of resources forms an integral part of the

development process in India. In this process of mobilization,

banks are at a great advantage, chiefly because of their

network of branches in the country. And banks have to place

considerable reliance on the mobilization of deposits from the

public to finance development programmes. Further, deposit

mobilization by banks in India acquired greater significance

in their new role in economic development.

Commercial banks provide short-term and medium-term

financial assistance. The short-term credit facilities are

granted for working capital requirements. The medium-term

62

loans are for the acquisition of land, construction of factory

premises and purchase of machinery and equipment. These loans

are generally granted for periods ranging from five to seven

years. They also establish letters of credit on behalf of

their clients favoring suppliers of raw materials/machinery

(both Indian and foreign) which extend the banker’s assurance

for payment and thus help their delivery. Certain transaction,

particularly those in contracts of sale of Government

Departments, may require guarantees being issued in lieu of

security earnest money deposits for release of advance money,

supply of raw materials for processing, full payment of bills

on the assurance of the performance etc. Commercial banks

issue such guarantees also.

63

CHAPTER 4

COMPANY PROFILE

Indian Bank is an India-based bank. The Bank’s business

segments are Treasury, Corporate/Wholesale Banking, Retail

Banking and Other Banking operations. Personal loans offered

by the Bank include home loan, automobile loan, personal loan,

loan against National Savings Certificate/Kisan Vikas

Patra/Life Insurance Corporation policy, mortgage loan,

education loan, jewel loan and others. The Bank offers three

card variants under Global Credit Cards-IB Gold, Classic Card

under Personal Card Segment and IB Visa Business Card for

Business entities.

As of March 31, 2012, the Bank operated 1,955 branches,

comprising 520 Rural, 549 Semi Urban, 500 Urban and 386

Metropolitan branches. The Bank has three foreign branches in

Singapore, Colombo and Jaffna. As of March 31, 2012, the total

number of automated teller machines (ATMs) were 1280, which

included 357 offsite ATMs and customers could access more than

89,000 ATMs in the shared network.

64

A premier bank owned by the Government of India, the Indian

Bank was incorporated in 5th March of the year 1907 as Indian

Bank Limited and commenced operations in 15th August of the

year 1907 as part of the Swadeshi movement. Indian Bank has

many deposit schemes tailored to suit the needs of its

customers, both individuals and organisations.

Credit/Advances/Loan Schemes specifically designed for its

customers. Also offers various novel services to customers,

both individuals and organisations.

The Bank opened its first overseas branch in Colombo, Sri

Lanka during the year 1932 and also opened its Singapore

branch in 1941. In the year 1962, Indian Bank acquired the

businesses of Royalaseema Bank, the Bank of Alagapuri, Salem

Bank, the Mannargudi Bank and the Trichy United Bank. The Bank

was nationalised in 19th July of the year 1969. The Bank name

was changed to Indian Bank after the nationalisation. It was

appointed as the lead bank for nine districts in the States of

Tamil Nadu, Andhra Pradesh and Kerala and the Union Territory

of Pondicherry. The first regional rural bank sponsored by the

Bank, Sri Venkateswara Grameena Bank, was founded in the year

1981. Indbank Merchant Banking Services Ltd was incorporated

as a subsidiary of the Bank during the year 1989.

65

The Bank of Thanjavur Limited (with 157 branches) was

amalgamated with the Bank during the year 1990. Ind Bank

Housing Limited was incorporated in the year 1991 as a

subsidiary. Indfund Management Limited was established in 1994

to manage the operations of Indian Bank Mutual Fund. During

the year 1995, The Bank's own training establishment, Indian

Bank Management Academy for Growth & Excellence (IMAGE) was

established. Indian Bank has launched a scheme called Cash

Management Services' in the year 2001 for speedy collection of

outstation cheques.

The Bank entered into a strategic tie-up with HDFC Standard

Life Insurance Company Ltd., the first in the private sector

to receive the Certificate of Registration for foray into Life

Insurance business for distribution of latter's insurance

products. The Bank with the Insurance Company signed a

Memorandum of understanding in February of the year 2001. In

2002-03, Indian Bank received an award from NABARD for best

performance under Self Help Group (SHG) in Tamil Nadu and

Andhra Pradesh. In 2003, The Bank made association with the M

S Swaminathan Research Foundation (MSSRF), Chennai to sponsor

a programme on agriculturists to be aired on the All India

Radio.

The Bank in two branches implemented the Core Banking Solution

in December of the year 2004. The Bank signed an agreement

with Export Credit Guarantee Corporation of India in the year

2004 to distribute the latter's credit insurance packages for66

exporters and also in the same year the Bank joined hands with

TimesofMoney for remittance solution, introduced 'IB Swarna

Abharana' a new loan product for buying gold jewellery and

made tie-up with Tamil Nadu Newsprint and Papers Ltd (TNPL)

for financing farmers taking up farm forestry project with the

sponsorship of TNPL. During the year 2004-05, The Bank entered

into strategic alliance with Mahindra & Mahindra Limited and

TAFE Limited for pushing up tractor usage among farmers. In

the year 2005, the Bank made tie up with three overseas

companies for money transfer, signed the papers with the

National Exchange Company of Doha, Mussandum Exchange Company

of Oman and Abu Dhabi-based UAE Exchange Company. In 2006,

Indian Bank sets up new branch in Mumbai and also launched the

Bharat Card. During the year 2006-07, The Bank entered into a

strategic alliance with Oriental Bank of Commerce and also

with Corporation Bank. As of March 2007, Indian Bank launched

Ind on-line Doorstep Banking to deliver Banking and Financial

Services at the doorsteps of the common man.

The Bank signed an agreement with Indian Railway Catering and

Tourism Corporation Limited (IRCTC) for offering train ticket

booking services through IRCTC website

http://www.irctc.co.in/. The agreement was signed in 1st

August of the year 2007 at New Delhi and also in December of

the year 2007 Indian Bank entered into a MoU with Indian

Railways to install ATMs in 51 Railway Stations across the67

country. Of these, 34 stations will have e-ticketing kiosks

also along with ATMs. Indian Bank and SME Rating Agency of

India Ltd. (SMERA) formally executed an MOU in January 31st

2008 for extending their co-operation in the arena of

financing of SME sector. Indian Bank won the Financial

Express's Best Bank Award 2008. The network of the bank

comprises 100% Business Computerisation, 168 Centres

throughout the country covered under 'Anywhere Banking', Core

Banking Solution (CBS) in 1557 branches and 66 extension

counters, 618 connected Automated Teller Machines (ATM) in 225

cities/towns and also 24 x 7 Service through 32000 ATMs under

shared network.

68

Indian Bank differentiates itself from other public banks

Indian Bank having a major presence in southern India

witnessed a loan CAGR of 22.7% over FY08-12. In the

aforementioned period, the bank delivered superior RoAs

(average 1.55% over FY08-12) underpinned by robust NIM

(average 3.5%), lean operating structure and sanguine asset

quality. Operating efficiency was driven by reduction in

headcount, improving employee age pyramid and calibrated

branch expansion. Asset quality though has deteriorated in

recent quarters; however, displayed stress has been lower than

peers.

After having shed majority of the short term corporate loans,

Indian Bank’s loan growth is expected to accelerate H2 FY13

onwards. NIM would likely stabilize near 3.2% with the impact

of lending rate cuts being offset by improvement in deposit

franchise, more productive deployment of excess liquidity and

re-pricing of term deposits. With the bank having no or low

exposure to some publicly known stressed companies, slippages

are less likely to surprise negatively in coming quarters.