Bullion and Oreign Exchanges - Forgotten Books

707

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Bullion and Oreign Exchanges - Forgotten Books

BULLION

AND

OREIGN EXCHANGES

THEORETICALLY AND PRACTICALLY

CON S IDERED ;

FOLLOWED BY A DEFENCE

THE DOUBLE VALUATION ,

WITH SPECIAL REFERENCE TO THE PROPOSED SYSTEM

UN IVERSAL COINAGE .

ERNE ST SEYD .

LO N D O N

EFFINGHAM WILSON , ROYAL EXCHANGE.

1868 .

HG

LONDONa'

rnn mv W. W. MORGAN, 232, CunnouuuROAD, N .

TABLE OF CONTENTS .

PART I.

INTRODUCT ION

RAP PER L—Mnmmt or ExaNOt

II.-MxDmuor EXCHANOL (continued)

III.—Cua cr

IV.—BtLLs

V.

VL StLv nn

VIL—BULLION

VIII.—MnLn NO or GOLD AND StLv n

IX—Puu GOLD AND 8 v “, AND ALLOYS or Tmm v rta0m“ Ht mLs

X.—Tr.m NO AND Asun NO BULLION

XI.-Mm ons or En ussmo AND Rt rom NO TB: FINE

use or BULLION

XII.—0N m :aars v sxD ron m : Pn cxous Mn us

XIII—Tn:acns or GOLD AND StLv n

XIV—Pn c ncAL Dtn c'n ONs ron CALCULA‘

H NG m VALUE }or BOLLtON IN ENOLAND

XV. PAlm NO” BULLION

XVI.—GLN1mAL DnscntPe N or m : l NxNO or

EVIL—M in now or AssAn NO

XVIII.—Inwwx , AND BurrrLLas IN BULLxON

XIX—Tm:BULLION oum AT m g BANK or ENGLAND

XX.—BULLION Bnou ns, AND SHIPPING or BULLlON

XXL—Comma

CONTENTS .

PART II.

n I. -PAns or ExcuANos

Monetary Systems, Great BritianFranceBe lgiumSwitze rlandItalyGe rmany

South Ge rmanyHanse Town s

HollandSwedenand NorwayDenmarkRussia

BurmahSiamCochin ChinaDutch Posse ssion s (Java, 369

Philippine Islands 370

SpainPortugalTurkish EmpireEgyptUnited State s ofAm ericaBritish North AmericaMexico

West Indies

Central AmericaSouth Am er ican Re publicsBrazilLaPlataState sAfrica, Barbary State sWest Coast of AfricaEast Coast OfAfr icaAbyssiniaPe rsia

CONTENTS .

C s Ar rn I.-PAas or En su e s—continued .

Monetary System s, ChinaJapanSandwich Islands

Table Of the Value Of the Pr incipal Coins

C s Ar rta IL— SB IPMENTS AND As snrauxONs IN BULLION

Go ld Shipmen ts

From London to ParisFrom Paris to LondonFrom New York to LondonFrom London to New YorkGold from Californ iaHalf Imper ials from St. Petersburg

Si lv er Shipments

Silv er Bars to HamburgSilv er Bars from Hamburg to LondonSilv er Bars to AmsterdamSilv er Bars to IndiaSilv er Bars from Marse illes to CalcuttaFiv e Francs pieces from Marse illes to IndiaSilv er Dollars to ShanghaiSilv er Bars from Californiato Hong Kong

Clum n III.— 'I‘naSs oar EXCHANGE

IV.—Ts n LONO ExcsANe r.

V.—Ts z LONDON Gouasaor ExaNOL

VI.- FoaxxON Couasas or ExaNos

Brussels

Frankfort-ou-the-MaineHamburgBremen

Vienna

v i CONTENTS .

CHAPTER VL—FOIIs ION Counsr s or ExcaANOII—continuad.

Constantinople

NewYork

VII.—CALcIILArION or ExaNens

VIII—ABBITRATION or EXCHANGES

Operations in Direct ExchangeOperations in Indirect ExchangeBaukers’ Arbitrations

IX.—INrLIn ArrncrINe run ExcuANens

Cum “ I.—Cam cxsn ON THE Ban-IsaMINr

IL—BULLION AND Buns or DIscoe

III.—Ts r PAaIs CONrranc ON Im nNA

'r IONAL COINAOL

IVA—Drum : or run DOUDLL VALUATIONV.

-PaOI>OSAL TO EsrAaLIss run DOUDLII VALUATION IN

ENOLAND

VL—UNIv sasAL COINAOL

INTRODUCTION .

BULLION and Foreign Exchanges are subjectsgenerally comprised among the contents of

higher class books on Practical Ar ithmetic ; though ,of course, the consideration given in works of thekind to these in teresting topics is necessarily onlylimited and superficial,at the best . There are severalpublications on Bankin g and Commercial Businesswhich go somewhat more deeply into the matteramong others , Gilbart

’s admirable work, and Laing’s

Theory Of Business and there are, finally, at leastthree well known works specially devoted to the study

of these most important subjects, —Goschen’s Theory

of the Foreign Exchanges ,’ Nicholson ’s Science of

Exchanges ,’ and Tate ’s Cambist, or Manual of Ex

changes . ’

Why then, it might beasked, should the author ofthe present volume ventur e upon a field apparently

already so well cultivated, which would seem to affordno legitimate opening for him P A brief glance at

the nature and scope of the thr ee last-named works

will, he believes, show that, notwithstanding their

2 INTRODUCTION.

confessed excellence, neither of the three can be saidto fully answer and satisfy all requirements, to makeit a completeand perfect guide in all matters relatingto Bullion and the Foreign Exchanges ;and that thereis room left, for another work on the subject, constructed on more comprehensive principles, and more

universally adapted to all classes of readers . Tosupply such a work is the writer’s object . The

financialand commercial public will judge whether hehas brought the necessary qualifications to the taskundertaken by him .

We have then, first, Goschen’

s Theory Of theForeign Exchanges,

’ which may be defin ed as a general

treatise on international commerce, and the effectsproduced by the ordinary and extraordinary v icissi

tudes Of the same on the Exchange transactions

of Foreign coun tries with England. The book iswr itten in plain, clear language . It bears throughout

a stonrg impress of the writer’s personal experience .The views expressed, and the conclusions drawnby him , are lucid and logical, and there are notmany of them open to contestation . It is altogetheran admirable work, and does the fullest justice toits title, The Theory of the Foreign Exchanges . ’

But, for that very reason, it falls necessarily shortOf the requirements Of the ordinary reader. The

author starts upon the supposition that the readerwhom he addresses knows all about the elementarygroun d-work of the subject, and he confin es his teach

ing, accordingly, to the higher and highest branches .There is, for instance, no information given on the

INTRODUCTION . 3

value of Foreign Coinsand Monies ;and thereare onlya few practical examples and illustrations to be foundin the book . These omissions and deficiencies cannotbut detract, in some measur e, from the practical usefulness of the work to that large class Of readers who ,in their study of Exchange operations , have to begin

with the beginning of the subject .Nicholson’s Science of Exchanges’ is conceived

and constructed upon a different principle, -the authorusing the Catechetical form . The book consists

prin cipally Of a series of 289 questions and answers ,r anging over a wide field, from the first question ,What is value P to the last, What shouldwe desire most for the general welfare ofall classes inEngland P” Explanations are given on the subject of

Gold, Silver, and Currency ; also some practical illustrations and calculations . The book forms a mostexcellent Manual, which should be in the hands of

every student of Exchanges . Still, it may be que stion ed whether the Catechetical form , with its inherent

dogmatism, is the best calculated to give the student aclear insight into, and a competent knowledge of, a

subject of such magnitudeand importance, and one soOpen to difference of Opinion on many of the leadingpoints, as the Science of Exchanges . The more so , asthe work is slightly tinged with the author’s somewhat

absolute free-trade views , and bears the impress alsoof his strong bias to look upon all things from anexclusively British point of view .

We now come to the last of the three SpecialWorks

on the Science of Exchanges , v iz .

— Tate ’s Cambist,

4 INTRODUCTION.

or Manual of Exchanges the Banker and Merchant’s

old and trusty friend, ‘ as it is deser v edly called . This

work is, in conception, construction, and treatment,the very opposite to Goschen’s book . Whilst thelatter is nearlyall “Theory,” Tate’s ‘Cambist’ is almostexclusively Practice abounding in figur es and calculation s, practical examples and illustrations of allpossible Exchange transactions , single and compoun d

Arbitrations, conversion of Bullion, &c. A considerableportion of the work is taken up with the Weights,Measures

,Coins , and Monies of every coun try in the

world, with their British equivalents . In short, everything in Tate is dry matter-of-fact ; and the beginnerwho would take him for his guide in the study of the

Science of Exchanges cannot but sadly feel the absence

ofall theoretical explanations, which yet are soabsolutely indispensable to a proper comprehension of the

subject .The purpose of the author of the present volume

then is, to endeavour to give the fullest information

on every branch and detail of Exchanges . The titlewhich he gives to his Work The Foreign ExchangesTheoretically and Practically Considered’ -is in tended

to express the end which he has in v iew .

Before entering upon his task, he deems it neces

sary to explain to the reader how he in tends to dealwith the matter . The term, Science of Exchanges,which has been repeatedly used in the foregoing

Mr . Tate has wr itten other Works on Business Matters. See ,

among others, his Counting-house Guide .

’

INTRODUCTION. 5

observations , might perhaps seem to imply a carefullystudied systematic arrangement and scientific treatmen t of the subject, dressed in suitable elegantlanguage to match . The author begs at once to statehere , that such is not his inten tion . He is simply amerchant, with but few hours of leisure at his com

mand, who does notaspire to a reputation for eleganceof language and gracefulness of style . He means totreat the matter in the plainest and most practicalmanner, and to use the simplest and most fam iliarlanguage, which he deems, in fact, the best suited tothe purpose .

Bankers and Merchants well versed in Exchangeoperations , may, perhaps , feel inclined to object tothe frequent repetitions occurri ng in the book , of

principles, facts , and figures, which may be familiar tothem. They should bear in mind, however, that thework is intended also for the use of those lessadvanced in the knowledge of the business , to whomthe same repetitions may prove beneficial,as remindersand as guides to amore easy comprehension of its

several branches .

A few words will suffice to show and explain theplan followed by the author in the distribution andarrangement of the subject matter of the Book .

The first Chapters are devoted to the consideration

of the so-called Mediums of Exchange .

” Here thereader will find a full exposition of the author’s views

upon this important branch of the subject,and of theprinciples upon which he intends to proceed in his

treatment of the same . These are followed by Chapters

6 INTRODUCTION.

ouGoldand Silver Bullion, giv ing minute and elaborateaccounts and description s of the various processesandmanipulations through which the precious metals have

to pass ,— from their native state down to their ultim ateconversion into Coin .

The author has bestowed particular care and atten

tion upon thi s part of the work,— which he deems of

special importance to the large class of people who ,though quite aware of the practical use and application of Gold and Silver,as Mediums of Exchange andStandards of value , are yet more or less ignorant ofthe why and the wherefore of such uses and applications , and of the manner in , and the means by,which the precious metals are fitted to subserve the

intended purpose . Proper consideration is also givento the technicalities involved in the Bullion business ,which,as a rule, are known only to a few finan ciers

and m en on ’Change, whom the special nature of theirbusin ess obliges to make themselves masters of thisparticular branch of their lin e . Practical experiencehas taught the writer that an intimate acquaintan cewith these technicalities , and with Bullion operationsin general, in all the branches and details of the

busin ess , is indi spensable to a competentunderstandingof the working of Exchanges .

After these Chapters , which form , as it were, theground-work of the book, comes the necessary instruction in the Monetary Systems of Foreign

Countries ,”illustrated by practical example s of

Exchange Operations and Transactions ; succeeded bythe Course of Exchange , and the operations eon

INTRODUCTION. 7

useted generally with Foreign Exchanges,”

trations of Exchange ,” &c . , &c .

In conclusion of these introductory remarks, the

author would observe that he takes the reader, inte re sted in the subject, and willin g to follow him in his

exposition and treatmen t of the same, to be a goodordinary arithm etician .

CHAPTER I .

MEDIUM or EXCHANGE.

HE Employment of a Medium of Exchange is aSocial Necessity . There are only two state s of

Human Society in which no Medium of Exchange isneeded ; and even of these two States the one hasno ac tual existence, and can only be considered as amere matter of theoretic assumption ; whilst the otheris restricted to the lowest and most absolutely nu

civ ilised of the Savage tribes . The untutored Savage

readily supplies his few and simple wants from thegreat store of Natur e ; his limited requirements leavehim independent even of the aid and co-Operation of

his fellow Savages . So long as he finds food andshelter, and the coarsest covering to shield him from

the weather, he is satisfied ; and his benefactressMother Earth— does not call upon him to return heran equivalent for her gifts . The other imaginary Stateof Society which might dispense with the need of a

Medium of Exchange, is represented by the prettytheory of Commun ism . The amiable Philanthropist

may, in his search after a satisfactory solution of the

great Social Problem, propound the question , Why

cannot men live together on a footing of perfect

10 MEDIUM or EXCHANGE.

America, and the Tartars, in Asia, reckon, in their

commercial dealings, by horses and some other articles

highly valued by them . Cowries (the shells of theCyprwaMoneta) are still extensively used as smallchange in Bengal, the Philippines , and on the Coast of

Africa . In Abyssinia, pieces of coarse salt, in size andshape like the sole of a boot, are used as Currency ;thirty to forty of them going to the dollar. Amongst

semi-barbarous nations, Gold and Silver ornamentsare made to subserve the purpose of a purchasingmedium ; whilst the more civ ilised people already know

the use of Coin made of the Precious Metals ; and,finally, the nations most advanced in civ ilisation haveestablishedacomplete system ofMeant/ms of Exchange,which may be considered the highest and most perfect

so far attainable in this scale of progression .

It is in reference to the most civ ilised state of

Society that we call the employment ofaMedium of

ExchangeaSocial Necessity.

Civilisation , so far from beingan artificial state, inthe invidious sense so Often applied to the term ,

mayreally and truly be considered the natural state ofman,on whom it confers so many material and intellectualblessings . This accounts also for the tendency moreor less manifestly shown by savage tribes, whencoming into contact with more advanced nations, toshare in these blessings,and secure the advantages ofsocial improvement . It is not saying too much; then,that the highest state of civ ilisation is also the most

natural state ofman, and thatall the results springingtherefrom

,good or ev il, are simply legitimate, natural,

MEDIUM or EXCHANGE. 1 1

and inev itable consequences thereof. Among these

results figures ,also, the existence of anacknowledgedMedium of Exchange, which may therefore, withoutn eed of further argument, safely be looked upon as

one of the constituent elemen ts of Society.

The existence of an ackn owledged Medium of

Exchange strongly influences the general intercourse

between individuals, communities, and nations ; whilst

the commercial intercour se between them is entirelyregulated by it.

The Value ofaCommodity is dependent upon thereal, or fancied, benefit which its possession confersupon the holder . Upon the means at our command to

secure such possession depends then , n ecessarily, our

enjoyment of the benefit thereby conferred . The lack

of a proper Medium of Exchange lessen s our ability to

procure the necessaries, comforts,and luxuries of life ;whereas the command of it in our hands enables us tosatisfy our wants,and obtain the co-operation of our

n eighbours . A proper Medium of Exchange, therefore, exercisesamost powerful influence on all classesofHuman Society . It is the life-blood of commerce,that great agency by which the blessings of civilisationare carried and disseminatedall over the World ; andthe due actionand scope of this great agen cy may wellbe said to be dependent, not only upon the properquantity, but also upon the healthy movement, or circulation, of such Medium of Exchange .

The fu ction s which a Medium of Exchange iscalled upon to perform in social and comm ercial intercourse are twofold ; it acts as an agent, and as a

12 MEDIUM or EXCHANGE.

principal. In the former capacity, it serv es to effect

the valuation of commodities , and to put a price uponthem ; its div ision in to certain fixed fractional partssupplying us with un its by which to calculate and

express in figur es the value of things . The other

function , that of a principal, is still more important ;for , in that capacity, it has to serve as an actual

guarantee for the correct performance of the valuation

of other commodities based upon its own value , as ithas itself to pass in exchange for such commodities

in accordance with such valuation ; which involves the

necessity of a fixed intrinsic value of its own .

We will now proceed to discuss and establishthe proper nature and form required to constitute

a Medium of Exchange . This can be done bestby following out, by way of illustration, a series of

assumed transactions, such as are constantly occurring

in ordinary life .

A stands possessed of certain goods in excess of

his own wants, but which are required by B , who, on

his part, is again in the same position with another

article required by A . Prov ided the value of bothcommodities be equal, A and B can easily effect an

exchange of them . B , however , may not want A’s

goods ; but may require certain other articles held by

C , who may want the goods of A . If the articles are

of equal value, the exchange can again be as easily

effected,— A taking the goods of B , C those ofA, and Bthose of C . Let us carry the illustration still further,and introduce D , E , F, and all the other letters of thealphabet ; and provided always , of course, the value of

MEDIUM or EXCHANGE. 13

the articles be equal, there will be no practical difficultyin the way of effecting the whole series of Exchanges,without the intervention of a general Medi

But, leav ing out of consideration the patent factthat Society, wi th its thousandfold divisions and rami

fication s, cannot well be represented by the letters of

the alphabet ; and the equally patent fact, that the

assumption here made, of an equal value of all thearticles held by the different parties , is altogetherimprobable, it is quite clear that even in so limited acommunityas the letters of the alphabet might sufficeto embrace and designate, production and consumption ,supply and demand are naturally subject to theordinary variation s ; which, of course , must tend to

upset the mathematical balance of the system,and tolead to lesser or greater difference s in the respectivevalues of the several commodities ; and these differenceswould nece ssarily require some independent method ofequalisation .

The foregoing illustration represents Barter , thesimplest and most primitive form of Commerce

,which

,

it may as well be men tioned here, remains still a

n ecessity among semi-barbarous nations , and in certaincolonies in remote corners of the world .

Let us now carry our alphabetical illustration a step

further . A has supplied B with goods, for which B

cannot give him anything in return at the tim e . B

stands accordingly indebted toA, to whom he promises

to give an equivalent at some future period . C, D , E ,

and the rest of the party, find themselves placed in thesame position with reference to A, who happens to

14 MEDIUM or EXCHANGE.

have no imm ediate need of effecting a further series of

Exchanges to supply his own personal wants . TheAccounts between him and the other parties represent

the benefit derived by him in exchange for the goodshe has supplied to his debtors . Here we have the

positions designated in commercial intercourse asAccountsand Indebtedness.

Let us proceed another step in advance, and con

vert these Accounts in to Certificates of Indebtedness,promising to supply and deliver to A a particular commodity. Give A the right of passing these Certificatesfrom hand to hand, entitling the holder to claim at hispleasure delivery of the goods thereon designated .

Now,although these Certificates are of a specific cha

racter , yet they will afford A a Medium of Exchangepassing current within the limited circle in which heholds the advantageous position of creditor .

Go still one step further, and, instead of specifying

on the Certificates the particular description of goodswhich the debtors severally promise to supply,let all the Certificates express the value of such

goods calculated in fixed corresponding quantities ofone general article in which theyall deal, and whichthey are at any time ready and willing to exchange forother commodities . By this means the sphere of usefulness of the Medium of Exchange afforded by such

Certificates of Indebtedness is considerably enlarged .

Still greater usefuln ess may be imparted to these in

strum ents by expressing the value represented by them

measured by some generally accepted Standard .

In the foregoing illustration, which shows the

MEDIUM or EXCHANGE. 15

difference between Barter Trade and Accounts andIndebtedness, we have assumed the Certificates of In

debtedness to be safe and certain to meet with duesettlement and conversion into positive value for

otherwise there is at once an end again to the mathematical precision of the system .

Now, the fallacy of such an assumption is too palpable to require comment . It cannot stand for amoment . A much firmer and safer basis is requir ed to

secure the proper balancing of the Exchange ofCommodities .

The claim to an equivalent return which one partyderives from the sale and transfer of an article effectedby him to another party, must be properly secured by

the actual possession of something of intr in sic value,which is held in the same high esteem byall parties ,and offers thus all requi site guarantees , independentofall conditions of verbal or written promises ; whichremains unaffected by external influences, and is of aconvenient form and shape to pass readily fi'

om hand

to hand .

As a matter of fact, we know that the Precious

Metalsare the substances used for this purpose . Thequestion whether they hold this high position simply

by general agreement, or by an inherent right of theirown , will be discussed hereafter .Still, Barter and Indebtedness continue, to the pre

sent day, to play an important part in commercial intercourse, both between indiv iduals and nations ; and wemust not, therefore , lose sight of them in connectionwith the subject of this work .

1 6 MEDIUM or EXCHANGE.

Nations , mutually exchanging their produce, may besaid to Barter, in the first instance ; if the balance of

such Barter turns in favour of the one, the other is

placed thereby in a state of Indebtedness, which Indebt

edness may, thr ough the creation of Bills of Exchange,be made to serve for a time as a Medium ofEachange;such Bills serv ing as Economisers of actual money .

But the final balance of the Account must be settled

by a more solid Medium , of the class of which Gold isthe highest representative .

18 MEDIUM or EXCHANGE .

value, and of a convenient form to pass from hand to

hand, is necessary for the purpose of facilitating inter

course in civilised society .

2ndly. That there are certain substances of highintrinsic value wi thin our reach, amongst which Goldholds an elevated rank .

3rdly. That Gold, from a mechan ical point of v iew,

is the material best suited for the purpose .

’

The first proposition we have already endeav oured to demonstrate in the preceding chapter ;but we repeat it here once more, as it cannot be

pointed out too strongly that our estimate of Gold,and all our remarks about its employment in thecapacity of a Medium of Exchange , are meant throughout solely in connection with , and in reference to

ci v ilised society. This consideration will also enable usto dismiss at on ce the popular anecdote of Robinson

Crusoe , who found a lump of Gold on his island, andmade such sorrowful reflections upon the uselessness tohim of this discovery .

In tr insic value , and a convenient form to passreadily from hand to hand, rank among the principal

conditions to constitute the suitableness of a materialto serve as a Medium of Exchange . It is clear that

the substances which possess these qualifications in the

highest degree must be considered first . The term

W eare en titled to claim this high position for Gold, in so farat leastas England is concern ed, where the Gold valuation pre vails,and Silv erand Copper coinsare lookeduponas occupyingasecondaryposition

—asubject to which we shall return hereafte r .

MEDIUM or EXCHANGE. 19

intrinsic value means that the worth of the material towhich it is applied should be actually inherent in it,independent of any addition to itmade by art or labour .

Bearing this in mind, we may accordingly at oncedismiss from consideration many costly portable objects

ofart, which owe their value only partly to the material ofwhich they are made, and in a greater or lesser

measure to the art and labour bestowed upon their

fashion . The same remark applies equally, for obvious

reasons , to all the more perishable productions of

nature , howe v er rare and costly they may otherwise

happen to be .

Am ong the most valuable substances within thereach of man , Pearls , Diamonds , Precious Stones , and

the so-called Noble Metals , may be said to occupy thehighest position . We know as a matter of fact that,with due reference to both weight and size , these substances rank among the m ost costly , and that their

intrinsic value is mainly naturally inherent in them,

art having but a secondary influence in regard to it.

Which of these substances is the most noble and themost durable ? Pearls are deservedly considered of

ver y high value,on account of their rarity and beauty,

and also the peculiar circum stances under which their

formation takes place . They are , however, easily

destroyed, and therefore lack one of the most indi s

pensable qualifications to serve for the purpose whichwe have here in view .

The Diamond" (to which , as the very highest

W e are quite aware , Of course , that the Diam ond is simfiy

20 MEDIUM or EXCHANGE.

representative of Precious Stones, we limit our

attention here), is, next to the Noble Metals , prao

tically the most indestructible of all the substanceson earth .

It is the hardest body in natur e ; it scratches allother bodies, and is itself scratched by none . Though,from its lamellar structur e it is brittle, and will give

way in the line of its cleavage, itwill stand, un scathed,the test of the strongest force that can be brought tobear upon it through the agency of other bodies of asize not considerably exceeding its own ; and, even

where it has to yield to the crushing force of

some other hard body, of relatively much greater bulk,the fragments in to which it is shattered still remain

Diamonds . A Diamond can only be cut or abradedby means of another Diamond, and the powder or dustcom ing ofl

'

in this process alone will serve to effect the

polishing Of its faces . It absolutely resists the dissolving or corroding action of the very strongestchemical agents ; even a mixtur e of the concentratedacids fail to produce the slighest efl

'

ect upon it. As it

consists simply of crystallised carbon, it will, of course,burn in fire with free access ofair , and more readilystill when heated even to ordinary redn ess in a vessel

of oxygen, passing Ofl'

as carbonic acid gas , without

leaving a residue ; yet, so long as access ofair is ex

pure carbon in acondensedand crystallized form ,and cannot, therefore , prope rly be ranked am ong ston es . Still,as it is held in com

m erce the most precious of the gem s, we think we are justified intaking it hereas the highe st repre sentativ e of the class .

MEDIUM or EXCHANGE. 21

eluded, it will bear a very intense heat without fusingor suffering alteration . One of the most marked and

characteristic features of the Diamond is its peculiar

Splendid lustre, which surpasses the highest brilliancyofall other gems , and contributes much to make it athing of such marvellous beauty . Add to all this itsgreat rarity, and there is certainly ample to accoun t,in a great measure at least, for the high esteem in

which mankind holds the Diamond.

Now let us take Gold as the representative of theNoble Metals . Bulk for bulk, and weight for weight,Gold is certam much less costly than the Diamond ;but, in so far as the virtue of indestructibility isconcerned, it may be said to be even superior to thelatter, for although it fuses at about 201 6 degreesFahrenheit, the intensest heat attainable fails to other

wise afl'

ect it in its nature and properties as Gold

whereas the Diamond, as we have just seen, isabsolutely desm'

oged by fire , being converted into a

comparatively alm ost valueless compound, which noart within the sphere of hum an ken can change back

again into a Diamond. All chemical agents, even the

str ongest mineral acids, employed singly,are powerlessagainst Gold,and it requires the combined action of

two of the most powerful acids— nitric and hydr o

chloric— to force it into a chemicalunion with another

body ; but, even in the inferior compound thus formed,the Gold still continues to exist, and may be re-obtainedin its virgin purity. The same remark applies tothe mechanical mixtures or alloys of Gold with other

metals from the amalgam which Mercury form s with

22 MEDIUM or EXCHANGE.

Gold, the former metal is readily separated again by

distillation . In ductibility and malleability Gold sur

passesall other metals . Its beautiful colour, and thehigh polish which it takes, are other qualities addingto its value .

But, although the foregoing considerations might

certainly seem to afford ample grounds for the high

value we set by these precious materials , and although

the fact of the ir be ing held in such high esteem bymankind is a matter of daily practical experience , yet,somehow, to many people all this is not sufficientlyconvincing to preclude constant recurrence to the sameplain question , Why should comparatively small

quantitie s of mere dead matter be este emed of such

high value ? To reply that this estimation is a matter

of common consent , based upon general convenience,is really no satisfactory answer to the que stion ,as italtogether fails to convey to the que stioner’s mind

any positive or direct e v idence of in trin sic value .

There is nothing left, then , but to rest satisfied

with the distinct recognition of the fact that theseprecious substances owe the exalted rank which theyhold among the bodies of nature, independently ofallother considerations , to the peculiar material propertie sinheren t in them . They have , in fact

,always been

held in high esteem from the earliest ages , even longbefore mankind had begun to enter upon the path of a

more advanced civilisation, and when man’s knowledge

of their nature and propertie s remained stillvery imperfeet and defective . W C , with the teachings of science toaid us in the consideration of the subject, are therefore

MEDIUM or EXCHANGE. 23

all the more bound to assign to these bodies the sameexalted position among created matters which they

have always held from time imm emorial. We ‘may

even go so far , at the risk of taking too high ground,to adv ance our belief that Providence has purposelyendowed t hese bodies with exceptional properties tofit them for the uses to which they are turned bycivilised man .

We do not mean by this to assert that Providence

has explicitly pointed out Gold, for instance, asthe only proper materi al for coin ed mon ey but thi s

much is perfectly clear, that a careful comparison of

all known bodies in nature leads in evitably to therecognition of the fact that the Precious Metals ,andmore especially Gold, are the best suited to serve asthe comm on measure of value forall other commodities ,and as the medium through which one kind of goods

may most readily be exchanged for another . An d thisfact is indeed practically adm itted by man, inasmuchas he uses Gold chiefly in the capacity of Coin . But

are we quite sure that this is really and truly the

most useful application of Gold Is it impossiblebut that other applications may be found for it of

still higher importance ?Let us assume, for the sake of argument, that Gold

is no longer used for Coin , but that some other

material performs its present fun ctions in that capacity .

“That would then be the value of Gold as comparedto that of such other material ? Would it be higher orlower ? That must, of course, depend upon the usefulness of Gold for other purposes ; and, with reference

24 MEDIUM or EXCHANGE.

to this , it would be difficult indeed to overlook the

patent fact that the fin e physical and chemicalproperties of Gold must necessarily fit it for a vari ety

of uses and applications . Were it no longer used for

Coin, then there woifld naturally be much fuller scopegiven to turn it perchance to better account in a greatmany different ways .We will endeavour to bring this to a plain , prac

tical illustration . Steam boilers are now made of Iron ,or Copper, which, as weall kn ow, will only last a fewyears . Suppose we were to make a steam boiler of

Gold, suitably alloyed for the purpose . Beingproof against the corroding action of the elements,such a boiler might, within certain limits, andleaving the chance of explosion out of consideration,be practically held fit to last for ev er . True, there would

be the great objection to the loss of interest upon thecapital sunk in the manufacture of the article but,

on the mere question of comparative usefuln ess anddurability, there could hardly be a doubt that the deci

sion would be in favour of the Gold . An d can it besaid that we have actually arrived at the fin al limit Ofallinvention The progress of science may at some futur e

period lead to discoveries necessitating the use of even

so noble a material as Gold for many important ends ,of which we at present have as little notion as our

forefathers had of the use of steam as a motive power .It is, indeed, in this very direction that there may

before long arise a necessity for a new application of

Gold on a large scale . Our age is in active search of

a new motive power of much greater force than

26 MEDIUM or EXCHANGE.

direction in which the peculiar properties of Gold maybefore long necessitate the employm ent of this metalfor a new, most important end . But may we not hopethat, with the continued progress ofmankind, there will,in centuries to come , be di scovered many other, perhapsstill more important uses and applications ofGold ?

In the foregoing remarks we have in some measure

considered the Diamond and Gold jointly, each as thetype of a class .We will now proceed to show that the Diamond,

however,is not a suitable body to serve as a proper

Medium of Exchange , even were it only for certain

mechanical objections . Leaving altogether out of consideration the question of price , which fluctuate s with

the supply of the article and the demand for it (thesupply and demand of Gold, and the supposed effectson the value of this metal, will form a subject for laterinquiry), it is quite clear that the Diamond is disqualified for the purpose of serving as a Medium of

Exchange , for the following reasons : it is found in

most irregular proportions ; it cannot readily be divided

into parts ; it is liable to fairly successful im itation ;and it cannot be stamped or marked with a visiblepatent sign of its exact value ; whereas Gold, onthe other hand, can be manipulated with the greatest

facility it can be melted, alloyed, and tempered ; it canbe hamm ered and drawn out ad libitum

,and it is sus

ceptible of infin ite subdivision , without detraction fromits value . Pieces can be made of it of precisely thesame size and weight ; its real character is very easily

detected by the test of weight, as well as by other

MEDIUM or EXCHANGE. 27

tests , and it can be so impressed with figur es that the

most ignorant may know at a glance its numericalv alue as Coin .

Silver, of which we shall say more in anotherchapter, has certain characteristics which fit it for

the same purpose , as we all kn ow . It serves , therefore, also to a great extent for coinage . But Gold andSilver are not the only Noble Metals . Platinum,

Palladium, Iridium , and several others , belong equallyto the same class . Platinum is even heavier than Gold,and almost as noble a metal, although it is greatlyinferior in lustre, and is in point of colour only a littlewhiter than iron . One of the great drawbacks to theemployment of Platinum for monetary purposes is theextreme difficulty of melting it, as it will fuse onlybefore the oxy-hydrogen blowpipe . Still this difficulty

m ight be considered disposed of in a measure by theproperty of the metal of welding, like iron , at a veryhigh temperature . But there is yet another,and a moreimportant drawback— v iz . , paradoxicalas itmay appear,its co mparativ e scarcity. Whilst we can count Gold byhundreds of millions of ounces , we can count Platinumonly by hundreds of thousands . Gold is, therefore,say a thousand times more plentiful. IfPlatinum werefound in quantities sufficientlyabundant for this pur

pose, itmight be used as money . The Russian Govern

ment tried in fact to introduce a Platinum coinage ;but the experiment failed . Platinum fetches aboutone-sixth ofthe price ofGold in the market . Palladiumis even more rare than Platinum ; and Iridium, which

28 MEDIUM or EXCHANGE.

is scarcely inferi or to the Diamond in hardness, is stillmore refractory than Platinum, and much less weldable

,and there are, moreover, probably no more than

a few hundred ounces of it in existence .Now, it must appear quite clear that the material

intended to beused for monetary purposes should possess the requi site conditionsas perfectlyas is attainable in natur e ; and when, therefore, a material is defi

cient in one or other of these conditions , it is therebynecessarily disqualified for employment as Coin .

These remarks , if they do not exactly demonstrate

with mathematical precision that Gold and Silver arethe right and proper materials for Coinage, must atallevents be held toafl'

ord powerful argum ents in support

of this conclusion, which the undoubted fact of theirholding this position can , of cour se, only tend to confirm and strengthen . Gold appears to possess thesenecessary qualifications in the highest degree ; Silverfollows next in order.

CHAPTER II I .

OLD is then the most perfect of the Mediums of

Exchange in actual use in the civilised world,and its superiority in thi s respect is so absolute that

all other practical substitutes are governed by it, nomatter whether they be of intr insic or of conditionalvalue .The general Mediums of Exchange in use among

civilised nation s may now be givenas consisting of

Gold coin sSilver coinsCopper coins The Currency .

Bank note s, orState notesBills of Exchange .

Gold, Silver, and Copper coins , and Bank notes,pass cur rent from hand to hand without restrictions ;they are therefore called Curre ncy.

Bills of Exchange are not Currerwg their transmission does not take place in the same free andsimple mann er ; but they also serve, under certainrestrictions, as a Medium of Exchange .

The Mediums of Exchange comprised here under

30 CURRENCY .

the general term Currency may be subdivided again

into

Gold coinsSilver coins Metallic CurrencyCopper coinsBank notes andState notes Paper Currency .

and, upon the ground that in England Gold forms the

basis of valuation , into

Gold coin s Free Currency .

Silver coins"

Copper coinsBank notes , andState notes

Conditional Currency.

M ETALLIC CURREN CY .

-There is reason to believe that Gold, Silver, and Copper have generally stood

in pretty much the same relation to each other withregard to their proportionate value as they do now .

In so far as Gold and Silv er are concerned, at least,the fluctuations of the proportionate value of these twometals may be assumed to lie within the narrow lim its

ofa few per cent . But the case is somewhat differentwith Copper . This metal, though not belonging to theclass called noble , holds yet a certain rank among the

inferior metals , on account of its many valuable qualities , and its general usefulness . In some countries ,and in some ages , it has been more extensively usedthan it is now in Europe . In the East and in China

In certain coun tr ies Silv er is fre e currency,and Gold condi

tional cur rency,as will be shown hereafter .

CURRENCY. 31

Copper, Brass , and even Iron coins , still form animportant part of the Currency . In Eur ope , however,we now look upon Copper Coin s simply as tokens , as isclearly proved by the fact, for instance, that a fewyears ago the whole of the old French, and soonafterall the old English Copper Currency, were calledin ,and new coinages of the same denominations, but

of little more than half the weight or size of the formerpieces , were issued . The intrinsic v alue of thesetokens falls accordingly very short of their deno

minational value . In England Silver coins are alsotokens , but their intrinsic metallic value is comparativ ely much higher than that of Copper tokens ,although it falls still below the actual market price of

Silver .But it may be asked, if these Silver or Copper

tokens do not possess their full denominational

metallic value, yet pass as money, would not thisrather seem to militate against the assumed absolutesupremacy of Gold ? Here we have the justification of

our div ision of the Currency into Free Curr ency and

Conditional Curr ency. In England a law exists , calledthe law of legal tender, in accordance with which Gold

coin is legal tender for any amount whilst Silv er coinis legal tender up to for ty shillings, and Copper up to

one shilling on ly. So a creditor, whils t bound to take

all the Gold tendered him in discharge of his claim, canrefuse to receive payment in Silver if the sum tendered

in that coinage exceeds two poun ds , and in Copper if itis more than twelve pence ; and he can accordingly

Compel payment in Gold of any sum exceeding two

32 CURRENCY .

pounds sterling . He may also be paid in Bank of

England note s, which he is equally boun d to take . But

as the Bank itself has the right of refusin g to receivepayment in its own notes , this description of Currencytoo belongs to the conditional. It will at once be

seen that this law of legal tender is an efl'

eetual bar toany attempt to displace the supremacy of Gold in

England, and to use instead the conditional currenciesof Silver and Copper .The values represented in Paper Currency and

Bills of Exchange, are expressed in the denominationsof the metallic Currency andall other securities andvalues— State bonds , shares , lands , houses, and everyother description of property and service— are alsomeasured and expressed among civ ilised nations in the

denominations of the metallic coins of the country .

It is one of the special objects of this book to giveas much information as possible upon everything con

nected with metallic Coinage, as will be seen hereafter

in the chapters on Bullion, Gold, Silver, Mining, Melting, Assaying, Coining, 850. But in this presentchapter we will, in the first place, discuss the description of Curr ency known as Paper Money, as a proper

understanding on this subject is a matter of some

importance in dealing with the Es changes with certainforeign countries .

PAPER CURREN CY .—Thi s description of current

money, in contradistinction to which metallic money

is appropriately called HARD CASH , plays a highlyimportant part in most of the systems of Currency .

34 CURRENCY.

A brief investigation of the prin ciple upon which

Paper Money may properly be issued will therefore be

useful.There are two descriptions of Paper Issue— v iz . ,

RANK NOTES, or Notes issued by banks, under theauthority and with some participation or guarantee of

the Government ; and STATE NOTES, issued by the

Treasuries of the State (these also are fi equentlyissued through the agency of banks) . Both Bank

Notes and State Notes may be regarded on the

same footing in their offices and functions as

part of the Curr ency. Now each such Note carri eson its face the promise to pay to the holder,or bearer, on demand, or upon presentation, a certain amount of Metallic Money. Upon the faith

of this promise the Note becomes current, and is

assumed to stand in the place of Hard Cash . The

simple plain promi se to the bearer that, in exchangefor the piece of paper he holds, he may at any th e ,

at the place designated, receive Gold or Silver (asthe case may he),admits of no qualification. Introduce a qualification on the face of the Note

,pro

mising payment otherwise than on demand, or in anyother value than in Metallic Money, and the worth ofthe Note falls at once . We have, therefore, to dealwiththe plain and dry fact of this promise and the holdersofNotes must have the absolute right, individually andcollectively, of demanding Hard Cash for their Noteswhenever they choose . Now here the question arises

,

— Is this promise to pay in Coin safe to be fulfilledunder all and any cir cum stances ? The respective

CURRENCY . 35

degrees of the certainty that this promise will be keptmay be illustrated by the following classification of

Paper Currency into four descri ption s

l st. Bank Notes made absolutely safe, by beingissued only against an equivalent amount of Bullionheld by the issuer .

2nd. Bank Notes made good for all practical purposes , by being issued partly against Bullion held

by the issuer, and partly against Government and otherv aluable securities .

3rd. Bank or State Notes depreciated in value ,issued again st a small reserve of Bullion, but restingon the Credit of the country generally, and on theStrength and good Faith of the Governm ent .

4th. State Notes issued almost entirely or alto

gether without a Bullion reser v e, and under the bare

Guarantee of a weak or totte ring Government, which

arealr eady valueless, or threaten to become so .

The FIRST CLASS of Notes assum ed here is only

imaginary ; for thereare no Bank Notes issued uponthat system . If there were, the securi ty ofl

'

ered by them

would seem absolute in theory as well as in practice .

A Bank, for instance, might hold ten millions in Gold,and issue ten millions of Notes against them . The

Gold being specially assigned to serve as security forthese Note s , and resting dormant in the vaults of the

Bank,to be paid away only against the production of

the pieces of paper by which it is represented, there

would be a complete balance between the two . Ifall

36 CURRENCY .

the Note s were pre sente d at once , payment could be

made at once,and no question of liability would remain

on either side . So perfect and safe a system of con

vertibility has frequently been suggested in England,and there is much to be said in its fav our .

’li In the

first plac e, on the Bullion deposit there would be thesaving of the expenses of Coinage, and on the Coin

lying inactive in the coffers of the Bank there would

be the sav ing of the usual loss by abrasion or fri ctionand

, in the second place , Bank Note s constitute a farmore convenient and portable kind of Currency, espe

cially for heav y sums, than Coin ; and for all otherpractical purposes such Notes would seem to be asgood as Gold .

But even to thi s apparently so safe basis of con

vertibility at least a few theoretical objections worth

mentioning may be started . Although Bank Note s

are certainly more portable and more convenient, moreespecially for large paym ents , yet they are, on the

other hand, also more liable to destruction than Me

tallic Money . They may also be more or less success

fully imitated by forgery,—arisk which, much as it islessened now-a-days by superior manufacture andengraving, has still to be taken into account . We

must not lose sight either altogether of the expenses

W e may here remark that in Hamburgthe Bank holdsastockof Silv er Bullion on som ething like the pr in ciple here suggested ;

howev er , it issues no Notesagain st the sam e , but in lieuthereof it

keepsaccounts with Merchants , and tran sfers the respectiv e own er

ship in this stock of Bullion from one to the other . (See Hamburgand Mark Banco . )

CURRENCY . 37

entailed by the manufactur e and issue of Bank Notes,which would hardly be balanced altogether by thesaving of the expenses of Coinage on the other hand ;for a certain amount of Coined Money would still be

required under any cir cumstances . Then there arecertain other contingencies which must be taken intoaccount in comparing the respective worth of a Gold

currency and a Note Currency . A war or a revolutionmight break out an enemy might invade the country,and might possess himself of the treasure in the Bank,and carry it away. What would then become of thecertainty of the con v ertibility of the Note In Englandwe may now laugh at the very suggestion of such acontingency but however remote the risk, there is no

blinking the fact that it still really does exist, by

however small a fiaction it may be theoretically expressed. In other countri es, less secure than England,the risk will be more appreciable . It is partly for thisreason that thr eatened war s and revolutions exercise

so great an influence on Paper Currency . As the

danger dr aws near the Note holder becomes alarmed,and presents his Notes for payment, preferring to

have his Gold in his own posse ssion rather than entrust

it to any other custody ; and in Spite ofall principlesof politicaland social economy propoun ded and expounded to him , he prefers to hoard it. The desire

for the actual substance , for the materi al of intr insicvalue itself, as affording the on lyabsolute guarantee inthe end, is too strong ; which again shows the supe

ri ority of Gold over all other Mediums of Exchange .

We refer to thi s natural tendency of the Note holder

8 CURRENCY .

here , in conn ection with our assum ed first-class Bank

Note system,as a mere theoretical objection ofperhapsno great weight under ordinary circumstances but it

becomes intensely practical under actually existingconditions of lesser certainty .

The SECOND cu ss or BANK News in our scale of

gradation, which we have designated as good, is repre

sented by the Paper Currencies of the more prosperous

states , such as England, France, Germany, Holland,and Belgium . It rests upon the basis of a combination

of Precious Metals and other Securities,upon the joint

value ofwhich the issue is made .

The Bank of England, for instance, under the Actcalled Sir Robert Peel’s Act, has the privilege of

issuing Bank Notes against the amount of Bullion in

its vaults , and also against an additional amount offifteen millions sterling, which the British Government

owes to the Bank . Thus if the Bank of England has

(say) twenty millions 1n Bullion in its cellars , it may

issue against thi s Bullion, and against the fifteen millions Government liability, thirty fiv e millions m Notes .The Bank Note promises payment in Gold the Bankhas thus issued thir ty-fiv e millions in Notes for whichonly twenty millions in Gold are in its hands , or about

fifty-seven per cent . If the stock of Bullion should

increase to thirty millions , and forty-fiv e m illions inNotes be thereupon issued, the proportion of the

In this sum of fifte en millions certain other securities held by

the Bankare included.

CURRENCY . 39

Note s actually covered by Gold would be about sixtysix per cent . butwith a decline of the stock of Bullion

to ten millions , the proportion would be only forty per

cent . in an issue of twenty-fiv e millions in Note s andit would fall to twenty-fiv e per cent . if the stock of

Bullion were reduced to fiv e millions , and an issue oftwenty millions were made in Notes . In the face ofthis , the promise to payall Note s in Gold would seemsomewhat paradoxical, and slightly illusory ; and, indeed, the uncompromising Opponents of Sir Robert

Peel’s Act do not scruple to assert that the Bank of

England is generally in a state of insolvency . If the

term insolvency as used by them be meant to expressthe Bank’s inability to pay all its Notes in Gold atonce, they may, strictly speaking, not be altogetherwrong in this extreme assertion of their views ; butthere are other considerations in the case whicheffectually counterbalance this allegation . In the firstplace, the Government has guaranteed the fifteen m illions over-issue which is notactually covered by Gold .

What is the value of that guarantee ? So long as theEnglish Government remains as firm as it is now, it

could easily, by loan or otherwise, raise that amountin Gold, and pay the Bank therewith, thus actually

covering this over-issue of Notes by Gold ; or it couldissue Stock bearing interest, and sell the same, taking

in payment Bank of England Notes , and so withdraw

them fi'

om circulation . Even in times of internalcommotion and foreign complications , the British

Governm ent could raise money on its credit ; and incase of urgent need, as the supreme authority of the

40 CURRENCY .

nation itself, it might even raise money by extrataxation payable in Gold. The question then would be ,Is there— leaving the stock of Bullion at the Bank

out of consideration— sufficient Gold in the country,or can the industry of the people draw enough fromabroad, to produce fifteen millions at the bidding of

the authorities ?” The people must under the cir

cum stances of course be willing to support the

Government ; should they, by revolution or otherwi se,Oppose or resist the call made upon them, or shouldthe country turn out to be too poor in Gold to pay the

demand, the forced taxation fails of necessity. In

England we fortunately have an acknowledged goodGovernm ent, in splendid credit, and the wealth andindustrial power of the nation are undoubted. This

shows how important a bearing the stability of a

Government, and the prosperity of apeople, haveupon the question .

There are other safeguards besides the guarantee

of the British Government . The Bank of England

has a capital of fourteen millions sterling, the securi tiesfor which may be realised and converted into Gold ; sothat, with the aid afforded to the institution by thelaw of legal tender (which compels every body, except

the Bank itself, to receive Bank Notes in paym ent), it

may be looked upon as pretty well secured . And thesupposition that the Note s should be presented all atonce, without giving the Bank timc to realise, is an

extr eme one, which may fair ly be dismissed fi'

om con

sideration here .

We in England have good reason to attach perfect

42 CURRENCY.

be substituted ; for , if we may be permitted to borrow

the term used by its enthusiastic advocates andadmir ers, it is eminently sound.

On looking again, fi'

om another point of view,at

the position of the Bank of England, which, with a

stock of only twenty millions of Bullion in reser v e, andfifteen millions ofGovernment Securities, is empoweredto issue thirty-fiv e millions of Money in Notes, thequestion naturally presents itself Ifwe can createfifteen millions of extra money on such easy terms ,why not make the sum twenty millions, or thirty, orfifty ? Government surely is good enough for the

larger as it is for the smaller issue l” We do not pretend here to appraise and fix the amount for whichthe Government of Great Bri tain may be held to beactually good— in the commercial sense of the word ;but we very much question whether the EnglishGovernment itself could, in times of great pressur e,attended with scarcity of Gold, force from its own

constituents— the people—an amount of fifty millionssterling in Gold, which yet would be absolutelyrequired to enable it to perform its own part of theengagement

,to take up and pay in hard cash the fifty

millions issued in Notes . We cannot say whether itwould, under such circumstances, succeed in squeezing

even thirty millions out of the people ;all we know forcertain is, that at present it undertakes to pay the

fifteen millions over-issue if called upon to do so .

In limiting its liability to this amount, the Govern

ment may certainly be considered to act upon a proper

and prudent principle ; for it may pretty safely be

CURRENCY . 43

taken for granted that, besides the Bullion reser v e inthe Bank, there is always sufficient Gold Currency incirculation to produce, at an extreme pinch, by thepower and the credit of the Governm ent, the fifteen

millions wanted to pay off in Coin all the Notesof the fifte en millions over issue .

This limi t of the over-issue to fifteen millions maysimply be accidental, or it may be the result of acareful consideration and calculation ; but there canbe no doubt that upon the whole it works well. ‘

Whenever a cri sis occur s,and both Gold and Notesare scarce, we hear the cry for mor e Mon ey raised,and Government is urged to sanction a larger issueofNotes to supply the eager demand . Every argument is pressed into the service to prove that ther equirements of theage and the mansion of trade impe

The most conser vativ e of our Financiers regard e v en these

fifteen m illions of Gov ernment Notes in the light ofamischie v oussurplus of currency, and impute to this ov er-issue of Notes the

pe r iodical panics which v isit us in tim es of m ercantile distress,They contend that if we hadaCurren cy founded on Bullion alone .

the exportation of Gold or Silv er would not in v olv e the risk,atallev ents , of disturbing the proper balance of our Curren cy System

whilst, under the present arrangemen t, the exportation of Bullion

in hard tim es cannot but tend to raiseappr ehensions in the public

mind lest the Bank should not be able to pay its own Notes, andthus to create apan ic, in greataggravation of the gen eral distress ;which pan ic, with its disastrous results, cannot justly be imputed,under such circumstances, to ov ertrading and impruden t speen

lation . These Financiers see som ethingarbitraryand unmean ingin the present priv ilege of the Bank of England, and adv ocate thefalling back upon our first class” plan— v iz . issue of Note s basedsolely upon Gold.

44 CURRENCY .

rativ ely call for an increase of Currency . It was so in1866 . Last year, in 1867, not a word was heardabout thi s necessity of an increase of Cur rency, for the

Bank was not only overstocked with Bullion then , butits Notes in reserve were nearly equal in amount to thefifte en millions guaranteed by Government , which certainly shows that the r equir ements of the age and theexpansion of trade should not be judged by the contingen cies of a single year .

Proposals have also been made for a double PaperCurrency to be issued by the Bank— v ia, Bank Note s

based exclusively upon the stock of Bullion (our own

first class plan here), and Bank Note s based expressly

upon the guarantee of Government . It is argued that,supposing this latter description of Paper Money to

sufi'

er depreciation fi'

om distrust, it might still continue

to serve as a Currency, even though it should be at a

discount of fifty per cent . The proposers of this scheme

clearly overlook the disturbing action which the intro

duction of such a system would be sure to exercise

upon the healthy operations of trade, as well as the im

portant fact that no provision is made in their project

for theultimate conversion of their guarante e Notes into

actual value . We, for our part, believe in the wisdom

of the present system of the Bank of England, which

rests the basis of its issue upon the combination of the

Bullion of the country, the substantial mark and token

of its prosperity, with the credit of the Government ;restricting the latter factor, however, within prudent

limitations . We are of Opinion also , that though there

might be room for rational improvement in the present

CURRENCY . 45

system,experiments in matters of this nature are too

hazardous to be lightly attempted unless called for byabsolute necessity. We hope, then, that the English

Government will listen to no plan tending to extendthe Paper Currency of the country at the expense of

lessening the proportion of Bullion which now serves

asafair basis .’The system ofthe Bank of France may be said to be

even more secure than that of the Bank of England, as

the issue of Bank of France Notes has a comparativelymuch larger foundation of Bullion, the French Government owing only four millions to the Bank, instead of

fifteen millions as is the case in England. The other good

Continental Bank Notes which pass upon a par wi th

the Metallic Currency, are also based on systems con

nected with Banks and State Treasuries , and sufficiently

solid to invest the Note s with that character of safetywhich alone can enable them to performall the officesand functions of full-valued money.

The only reallyuseful improv em entwhich may be suggested

in reference to the Bank of England Notes is the issue ofa£1Paper Cur rency. Form erly the Bank issued £1 Note s, but now

the smallestamount is £5 . It may fairly be taken for granted thatthe issue of £1 Notes would hav e the beneficial result of bringingagood deal of the presen t Gold coin back into the cofi

'

ers of the

Bank , prev enting thus the wear of the coin . It m ightalso be more

con v en ient to the public . In other coun tr ies, quite or nearlyassound

” as England, Note sare issued for amounts much less than£1 . Our Bankauthor ities, no doubt,act upon what they consider

apruden t policy ; but it is n ot clear whether analteration of the

system in this respect m ight not serv e to bring out con v incingly

theadvan tages of £1 Notes .

6 CURRENCY .

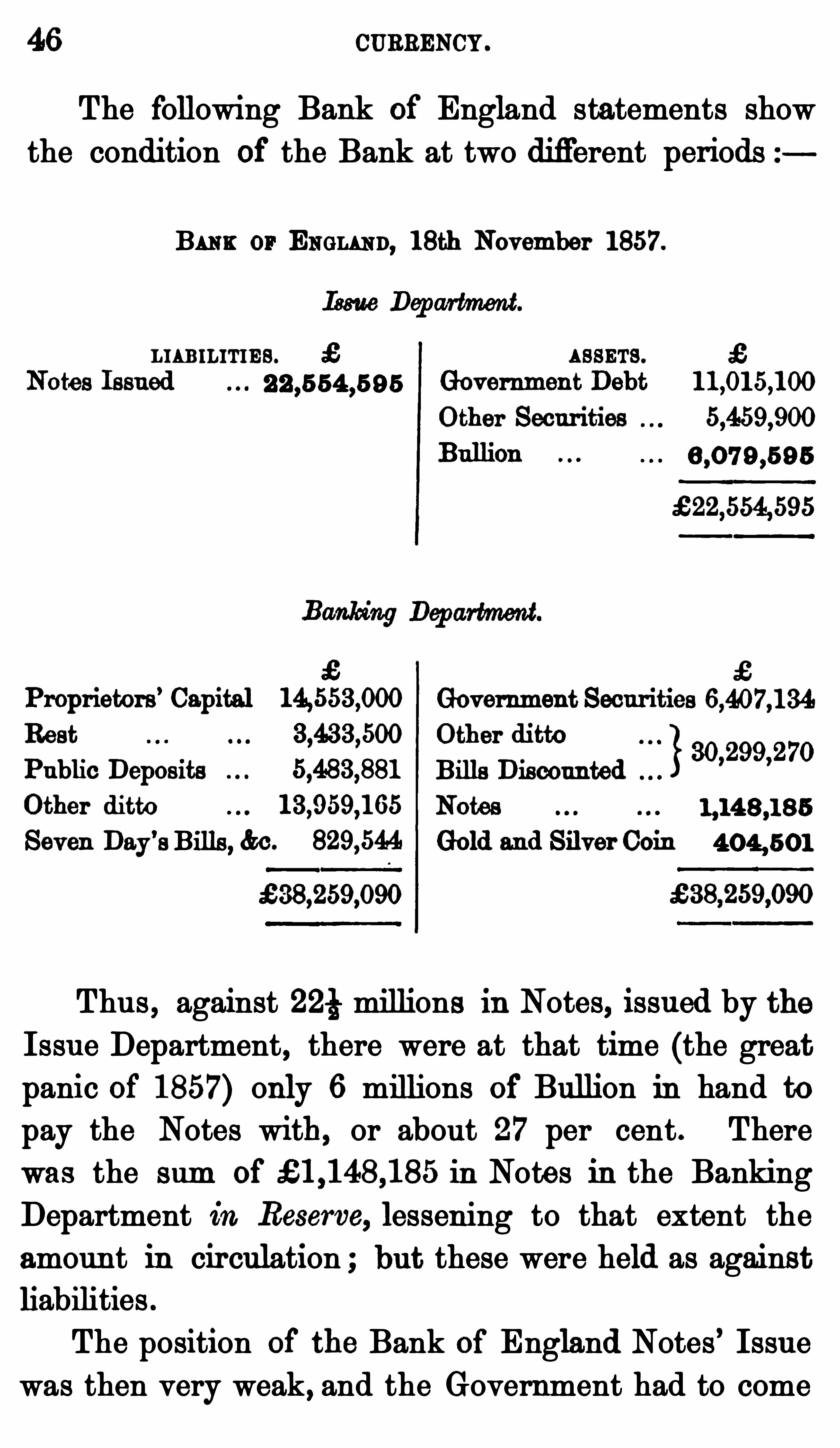

The following Bank of England statements showthe condition of the Bank at two different peri ods

BANK or ENGLAND, 18th Nov ember 1857.

LIABILITIES. 43 ASSETS.

Note s Issued Gov ernment Debt

Other Secur ities

Propri etors’

CapitalRest

Public Deposits

Other ditto

Se v en Day’

s Bills, &c .

Thus , against 22} millions in Notes, issued by the

Issue Department, there were at that time (the great

panic of 1857) only 6 millions of Bullion in hand topay the Notes with, or about 27 per cent . There

was the sum of in Note s in the Banking

Department in Reser v e, lessening to that extent the

amoun t in cir culation ; but these were held as againstliabilities .

The position of the Bank of England Notes’ Issuewas then very weak , and the Government had to come

Gov ernm entSecur ities

Other ditto

Bills Discounted

Notes

Goldand Silv er Coin

CURRENCY . 47

to the rescue by suspending the Bank Act, andauthorising an extra issue of in Note s .

BANK or ENGLAND, 2oth Nov ember 1867.

Issue Depart/ment.LIABILITIES. 16 ASSETS.

Notes Issued Gov ernm ent Debt

Other Secur ities

(Total £15 m illions . )

Banking Departme nt.

Proprietors’

Capital Gov ernm ent Se

Re st

Public Deposits

Other ditto

Se v en Days’ Bills, dtc .

Against 36 millions in Note s issued by the IssueDepartment, the Bank held at the time 21 millions in

Bullion, or about 59 per cent . But, in the Banking

Department, there were in Reserve (lying there idle),in Note s , and in Coin , to

gether not in cir culation, which , deductedfrom the Notes , leaves onlyin actual circulation against 21 millions Bullion, or

about 94 per cent . The position of the Bank wasconsequently very strong at the time .

Other ditto

Bills Discounted

Note s

Goldand Silv er Coin

48 CURRENCY.

The position of the Bank of England is thusalwaysplaced Openly before the Public in the Weekly Statement of the two Departments , the Issue and the Banking. In estimating the position of the Bank fi'

om

these Statements , the Items of Notes and Coin in

Reserve must be taken into account .The following statements of the Bank of France

at the same peri ods , will furni sh a comparison . TheBank of France has no separate Issue Department likethe Bank of England .

BANK or FRANCE, for Week ending 12th Nov ember 1857.

LIABILITIES ASSETS.

Notes Issued Bullion

Post Bills, dtc. Bills Discounted

Deposits Advanceson BullionTreasury BalanceReser v e Advances on PublicProfitand Loss Funds, SharesandCapital Deben ture s

Gov ernm en t Debt

Gov ernm ent Stock

New Bank Stock,

notyet settled

Prem ises

The amoun t of Bullion in the vaults of the Bank

at this time was thus about 33 per cent . of the Issue

of Note s . This was dur ing the commercial panic in

England, which necessarily affected the French Bank .

It is, however, worth rememberi ng that beyond this

adverse influence there was no crisis in France atthat time .

50 CURRENCY .

(towards the close of last year it stood at about thirty

per cent .) in Russia it varies from ten to twenty per

cent . ; in Italy about the same . The fluctuations in

the value of Gold in these countri es are closely con

n ected with the varying phases of their commercial

prosperity, and with the internal and external changesin the political horizon, upon which commerce andwealth, as well as the stability of Governments , ultimately depend . The over-issue of Paper Currency

is either caused by the inferi or industri ous andmercantile condition of the country (frequentlyaggravated by unwise acts of the Government in referenceto the trade of the world), or mainly, and generally in

the first instance, by the actual necessities of the

Government . Requiri ng very large sums ofMoney forWar or other purposes , and finding that the country

cannot, even by forced taxation, be made to yield sufhcient Coin , for the very simple reason that there happensto be in circulation only a fraction of the large amountso suddenly wanted, —and having besides exhausted

its borrowing powers in the Money Market of other

countries , the Government is forced to have recourse to

the issue of Paper Money, either direct from the StateTreasuri es , or through the Medium and Agency of

Banks . State Notes of this kind carry upon their facethe usual dry promise to pay the amount stated in cashto the bearer or holder on presentation or demand .

So long as the credit of the Government remains

pretty good, and prudent arrangements have been

made respecting Bullion reser v es , to secure the conver

sion ofthe Notes into Coin under certain circumstances .

CURRENCY . 51

the system is elastic enough to permit of a compa

rativ ely wider range than is required for good Notes ofour second class . So soon , however, as the issue

breaks these elastic bonds , and the public becomeaware that it is impossible for the issuer to pay at the

time, and that the fulfilment of the promi se to pay has

to be waited for till some future period, the contingency

even of the deferred payment being dependent uponthe future prosperity of the nation , and the stabilityof the political organisation, confidence in the safetyof the Notes is at once destroyed . With an increasingissue ofNotes the Treasuri es and Banks furnish actual

proof of their inability to cash them ; the Governmentforbids the export of Gold,and declares its Notes legaltender; creating thus a so-calledfor ced Paper Cur rency.

The Bullion basis is set aside, and Gold is turned into

simple merchandise , in Spite of the well-recognised

fact that it is the true standard of value .

The degree of faith still reposed in the Government

by the people, and inspired by the hopes of a future

revival or improvement of Industry and Commerce,

is expressed in the marketable sense , by the per cent

age rate of depreciation of the Paper Currency ,andthe prem ium which Hard Cash, or Bullion in all shape s,brings in the market .

Operations of ov er-issue of this kind by State

Governments , or Communities generally, closely re

semble the borrowing of money by individuals upon

promise to repay the loan at some future time . The

charges of Interest —sometimes in both cases of ausur ious character— are in the case of State operations

52 CURRENCY .

of this kind represented by the greater or lesser depr e

ciation of the Paper Money, and the effect which such

depreciation has upon the home and foreign trade of

the country . An over-issue of Paper Money in a

country may apparently create a momentaryflnshn ess

indeed , in the United States , for instance, during the

late civil war, the flood ofGreenbacks pouring into the

Market stimulated the home trade , and afl’

orded an

easy means of amassing wealth to those who knew

how to profit by the circumstances of the times . In the

end, however, a people will find the obligation of re

paying Capital and Interest just as onerous and difficult of fulfilment as an individual may find it ; and ifthe hopes of the future , resting on an improved state

of Trade and Politics , are disappointed, National

Bankruptcy becomes imminent .

An over-issue of Paper Currency, no matter

whether brought about by politicaland financial m is

management, or forced upon the Gov ernment of a Stat eby absolute necessity, is therefore not only detrim entalto the pre sent interests of a country, in so far as itsExchanges with other State s are concern ed , but it

involve s , like a continual discoun tand r enewal, a heavycharge on the future prospe ri ty and resource s of the

State . In Italy the forced Currency is onlyafewyearsOld, but it is continually on the increase . In Spain thestate of things is so uncertain that the relative valuebetween Paper Money and Metallic Money can no longerbe fixed wi thany degree of accuracy . AS regards theRouble Notes in circulation in the Russian Empire , it isstated that the ImperialGovernment itself is not aware

CURRENCY .53

of the actual totals issued , and has thus lost controlover its liabilities in reference to the same ; morever, alarge quantity of successfully forged Notes is in ciren

lation , which the authori ties he sitate to suppress , fearing a further disturbance of credit . If this be true, we

may soon hear of something more serious than a merefurther depreciation of Russian Paper Money .

Austriaoffers one of the most remarkable instancesof the position of an ov er-issuing State . For many

years Bankruptcy has hung over her like the sword

of Damocles yet she still stands erect . Gold and

Silv er Coins have almost entirely disappeared from theland, and Paper Money reigns paramount , in Notes fromthousands of florin s , down to the value of a few pence .

Indeed,the Austrians seem almost to have solved

the problem of di spensing altogether with a Metallic

Currency . Their intercourse with other nations is

limited,and their Industry is Shut out from the markets

of the world . Yet they do not seem to be poor ; they

have a full measure ofall the luxuries and refinementswhich other nations enjoy . The Austrian system of

Paper Money seems to drag on its existence on the

faint hope that , at some future time or other, a suc

cessful movement may be accomplished to regain a

sufficient stock of Bullion . A day of reckoningéhowever, must come , sooner or later, for Austr ia as well

as for other States that are equally in a condition of

almost hopeless financial confusionand embarrassment .It needs only— and with the ever-increasing liabilities

which certain States load upon them selv es in our times

such an event is not unlikely— that one of the se

54 CURRENCY .

States should become Bankrupt, when the whirlwind

of the panic created thereby would be sure to blow

downall the rest . Then we may expect to see revolution , civ il war , and anarchy taking the place of thepeaceful interchange of benefits upon which civilised

society is founded .

The means of averting such a catastrophe are, first

and foremost , the strictest economy on the part of theGovernment . Every effort should be made to reduce

the Expenditure of the State within the narrowest pos

sible limits , and to secure an excess of the Revenue

over it,applying the balance to the gradualwithdrawal

of the fictitious Currency from circulation . In the

second place , Government and People should heartilyun ite in fostering those Industries , more especially, of

which the products can be beneficially exported, thus

attracting Bullion into the State . In this manner,Government , Industry, and Commerce wouldall regainstrength and credit, sufficiently to enable the Stateultimately to command the necessary confidence , eitherfor the Consolidation of its Liabilities into a properly

regulated State Debt, or for the re-establishment of a

proper par between Paper and Metallic Money . Let

us hope that the Austrians will be able to accomplish

this much desirable end . At least they have an

example before them in— England .

During the wars of Napoleon, this country wascalled upon suddenly to raise enormous Sums of

Money ; and so severe was the strain at the tim e, thatfor twenty years Specie paym ents were suspended,andGold stood at a premium of forty per cent . In the

CURRENCY . 55

years of peace which followed,Retrenchment ofExpen

diture— but, aboveall, the indomitable Industry of the

Nation, which commanded the markets of the world ;the insatiable thirst for enterprise which, aided by thisIndustry,and strengthened by the influence gained inthe victorious struggles, dr ew Bullion to the coun try— enabled the Statesmen of England to convert theFloating Liabilities into a National Debt

,and a Bullion

basis was regarned sooner than ev en sanguine peoplehad Cxpected . It is true, that this National Debt— On

which we of the present generation,who have inherited

this bur then from our forefathers , still continue to the

present day to pay the Discount or Interest , and evenare not altogether without some hope of being yet

able some time to pay back the Pri ncipal— is a heav ycharge ; but the fearfirl evils of National Bankruptcy,with its attendant demoralisation, were avoided . If

this proved a hard and diflicult task for England, with

all her extensive means , her great industry, and hervas t power, leaving her still to the present day bearingthe heav y burden thereby entailed upon her, how much

more difficult may such a recovery be expected toprov e to other States of so much less powerand wealthand ability to COpe with the overwhelming difficulties

of their position !

The United States, whose present Floating Debt is

enormous , are likely to follow in the footsteps of