Risk management in the venture capital industry - EconStor

36

econstor Make Your Publications Visible. A Service of zbw Leibniz-Informationszentrum Wirtschaft Leibniz Information Centre for Economics Proksch, Dorian; Stranz, Wiebke; Pinkwart, Andreas; Schefczyk, Michael Article Risk management in the venture capital industry: Managing risk in portfolio companies The Journal of Entrepreneurial Finance (JEF) Provided in Cooperation with: The Academy of Entrepreneurial Finance (AEF), Los Angeles, CA, USA Suggested Citation: Proksch, Dorian; Stranz, Wiebke; Pinkwart, Andreas; Schefczyk, Michael (2016) : Risk management in the venture capital industry: Managing risk in portfolio companies, The Journal of Entrepreneurial Finance (JEF), ISSN 1551-9570, The Academy of Entrepreneurial Finance (AEF), Montrose, CA, Vol. 18, Iss. 2, pp. 1-33 This Version is available at: http://hdl.handle.net/10419/197553 Standard-Nutzungsbedingungen: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Zwecken und zum Privatgebrauch gespeichert und kopiert werden. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich machen, vertreiben oder anderweitig nutzen. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, gelten abweichend von diesen Nutzungsbedingungen die in der dort genannten Lizenz gewährten Nutzungsrechte. Terms of use: Documents in EconStor may be saved and copied for your personal and scholarly purposes. You are not to copy documents for public or commercial purposes, to exhibit the documents publicly, to make them publicly available on the internet, or to distribute or otherwise use the documents in public. If the documents have been made available under an Open Content Licence (especially Creative Commons Licences), you may exercise further usage rights as specified in the indicated licence. https://creativecommons.org/licenses/by-nc/4.0/ www.econstor.eu

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Risk management in the venture capital industry - EconStor

econstorMake Your Publications Visible.

A Service of

zbwLeibniz-InformationszentrumWirtschaftLeibniz Information Centrefor Economics

Proksch, Dorian; Stranz, Wiebke; Pinkwart, Andreas; Schefczyk, Michael

Article

Risk management in the venture capital industry:Managing risk in portfolio companies

The Journal of Entrepreneurial Finance (JEF)

Provided in Cooperation with:The Academy of Entrepreneurial Finance (AEF), Los Angeles, CA, USA

Suggested Citation: Proksch, Dorian; Stranz, Wiebke; Pinkwart, Andreas; Schefczyk,Michael (2016) : Risk management in the venture capital industry: Managing risk in portfoliocompanies, The Journal of Entrepreneurial Finance (JEF), ISSN 1551-9570, The Academy ofEntrepreneurial Finance (AEF), Montrose, CA, Vol. 18, Iss. 2, pp. 1-33

This Version is available at:http://hdl.handle.net/10419/197553

Standard-Nutzungsbedingungen:

Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichenZwecken und zum Privatgebrauch gespeichert und kopiert werden.

Sie dürfen die Dokumente nicht für öffentliche oder kommerzielleZwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglichmachen, vertreiben oder anderweitig nutzen.

Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen(insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten,gelten abweichend von diesen Nutzungsbedingungen die in der dortgenannten Lizenz gewährten Nutzungsrechte.

Terms of use:

Documents in EconStor may be saved and copied for yourpersonal and scholarly purposes.

You are not to copy documents for public or commercialpurposes, to exhibit the documents publicly, to make thempublicly available on the internet, or to distribute or otherwiseuse the documents in public.

If the documents have been made available under an OpenContent Licence (especially Creative Commons Licences), youmay exercise further usage rights as specified in the indicatedlicence.

https://creativecommons.org/licenses/by-nc/4.0/

www.econstor.eu

The Journal of Entrepreneurial FinanceVolume 18Issue 2 Summer 2016 Article 1

1-2016

Risk management in the venture capital industry:Managing risk in portfolio companiesDorian ProkschHHL Leipzig Graduate School of Management

Wiebke StranzHHL Leipzig Graduate School of Management

Andreas PinkwartHHL Leipzig Graduate School of Management

Michael SchefczykTechnical University of Dresden

Follow this and additional works at: https://digitalcommons.pepperdine.edu/jef

Part of the Entrepreneurial and Small Business Operations Commons, and the Finance andFinancial Management Commons

This Article is brought to you for free and open access by the Graziadio School of Business and Management at Pepperdine Digital Commons. It hasbeen accepted for inclusion in The Journal of Entrepreneurial Finance by an authorized editor of Pepperdine Digital Commons. For more information,please contact [email protected] , [email protected].

Recommended CitationProksch, Dorian; Stranz, Wiebke; Pinkwart, Andreas; and Schefczyk, Michael (2016) "Risk management in the venture capitalindustry: Managing risk in portfolio companies," The Journal of Entrepreneurial Finance: Vol. 18: Iss. 2, pp. 1-33.Available at: https://digitalcommons.pepperdine.edu/jef/vol18/iss2/1

Risk management in the venture capital industry: Managing risk inportfolio companies

Cover Page FootnoteWe thank the nine venture capital funds from Germany which supported our research by allowing us toanalyze their documents and interview the investment managers. We are grateful for their trust and support.Further, we thank the ‘Wissenschaftsförderung der Sparkassen-Finanzgruppe e.V.’ as well as the ‘NRW.Bank’for their continuous support of our project. In addition, we would like to thank Arnd Wiedemann and VolkerStein from the University of Siegen for their value feedback at the 3rd Annual Conference on RiskGovernance.

This article is available in The Journal of Entrepreneurial Finance: https://digitalcommons.pepperdine.edu/jef/vol18/iss2/1

THE JOURNAL OF ENTREPRENEURIAL FINANCE VOLUME 18, NO. 2 (SUMMER 2016) 1-33

Copyright © 2016 Pepperdine Digital Commons and the Academy of Entrepreneurial Finance. All rights reserved. ISSN: 2373-1761.

Risk management in the venture capital industry: Managing risk in portfolio companies

Dorian Proksch1

HHL Leipzig Graduate School of Management

Wiebke Stranz HHL Leipzig Graduate School of Management

Andreas Pinkwart

HHL Leipzig Graduate School of Management

Michael Schefczyk Technical University of Dresden

ABSTRACT

Managing risk is one of the main activities of venture capital companies. Despite the fact that this topic is of high practical relevance, only little research was published on risk management performed by venture capital companies in their ventures. Hence, we conducted a structured literature review which was the basis for developing five hypotheses concerning measures to decrease failure risk in venture capital-backed ventures. We tested these hypotheses with an empirical data set of 93 venture capital-backed ventures in Germany using original deal data from nine different venture capital funds using a structural equation model. We showed that the experience and the skills of the corresponding investment manager have a significant negative impact on the failure risk of a venture. Investment manager´s experience and skills were measured by the working and founding experience, the technology expertise and the network size. Hence, the results emphasize the importance of the selection of the investment manager for risk management in venture capital investments. Keywords: Risk management, failure risk, venture capital, new-technology-based firms

1 We thank the nine venture capital funds from Germany which supported our research by allowing us to analyze their documents and interview the investment managers. We are grateful for their trust and support. Further, we thank the ‘Wissenschaftsförderung der Sparkassen-Finanzgruppe e.V.’ as well as the ‘NRW.Bank’ for their continuous support of our project. In addition, we would like to thank Arnd Wiedemann and Volker Stein from the University of Siegen for their value feedback at the 3rd Annual Conference on Risk Governance.

2 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

JEL Codes: G32, G24, L26, M130

I. Introduction Risk management can add value and is necessary in all types of companies to

secure long-term stability (Frooth et al., 1993; Mackay and Moeller, 2007). Nevertheless, the topic of risk management is still in its infancy as articles are mainly published in finance and accounting, but less in management or entrepreneurship journals (Bromiley et al., 2015). Especially venture capital (VC) investments are well known as high risk investments since venture capital companies (VCCs) invest in ventures with a high growth but also high risk potential (LiPuma and Park, 2014). Young entrepreneurial firms face the challenge of “liability of newness” resulting in particular difficulties, e.g. shorter expected life, and a greater risk of failure (Ang, 1992; Coleman, 2004).

In the investment decision making process, VCC are often faced with uncertainty about the future performance of the venture and the adverse selection problem. The reason for that is that VCC have to rely on information about the venture supplied by the entrepreneur (Tourani-Rad and England, 2003). A comparative study by Zacharakis and Meyer (2000) showed that VC investments fail at a rate of 35 to 55 per cent. Young and entrepreneurial firms are an essential part of the German economy and an important source for innovation in order to stay competitive on a global basis. Hence, research on comprehensive risk management for the VC industry is of great practical importance to improve the practices how German VCCs pursue risk management which might reduce the risk of failure of their ventures.

Risk management pursued in VC-backed ventures is only moderately researched in academic literature (Yoshikawa et al., 2004; Tan et al., 2008). Previous studies either focus on single types of risk, e.g. macro-risk (Ning et al., 2015) or liquidity risk (Cumming et al., 2005) or on specific types of risk management measures, e.g. syndication (Wang et al., 2012), (Hopp, 2010) or financial contracting and incentive mechanisms (Tan et al., 2008). Studies analyzing comprehensive sets of risk management measures applied by VCCs ventures are limited (see e.g. Kut et al., 2006; Kut et al., 2007; Kut and Smolarski, 2006 and Smolarski et al., 2005). These studies used comparable methods and similar samples leading to a lack of new findings (Dimov and Murray, 2008; Milavo and Fernhaber, 2009). However, risk management is one of the core competencies of VCC and therefore a highly relevant topic in practice. One reason for the limited amount of studies in this field might be the lack of reliable data. VC-backed ventures are private companies and only limited subject to the

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

3

duty of publishing company data and financial statements (Bygrave, 2006; Neergaard and Ulhoi, 2006).

To analyze risk management measures and their impact on the failure risk of VC-backed ventures we pursued the following research strategy: We conducted a structured literature review to develop five hypotheses on risk management measures applied by VCC in ventures, i.e. the assessment and evaluation of new ventures, contracts, investment manager´s experience and skills, governance mechanisms and management support. These hypotheses were tested with a structural equation model using an empirical data set of 93 VC-backed ventures in Germany from nine different VC funds.

As risk management received relatively little attention in entrepreneurship literature (Pinkwart, 2002) and is an important research topic, but largely unsystematic and not easy to diversify (Manigart et al., 2002), we add to literature and practice as follows:

1. We used a rare data set with in-depth quantitative and qualitative data from nine public and private VC funds combining data obtained from a survey with investment managers and original deal documents like business plans, investment committee papers, reporting and annual statements.

2. We provide an analysis of the Germany VC market which was rather moderately studied in literature before. Thereby, we shed light into the risk management practices of German VC funds.

3. The results from our structural equation model imply that particularly investment manager´s experience and skills have a statistically significant impact to reduce failure risk in VC-backed ventures. This finding supports Hopp and Lukas (2014) who were among the first showing that investment managers can have technological, industry, financial and managerial experience and leadership skills which might be crucial for the success and failure ventures. Furthermore, governance mechanisms, e.g. milestones and reporting, were heavily applied by all VCC. However, contrary to other studies like Bengtsson and Sensoy (2011) and Tan et al. (2008) we cannot show that governance mechanisms have a significant effect on reducing the risk of venture´s failure.

II. Literature review and hypothesis development

Risk can be defined as the probability and severity of adverse effects (Aven,

2011). Therefore, risk management is crucial to manage the uncertainty of risks. A

4 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

sound risk management is characterized as proactive, aligned and economic including the identification, estimation, evaluation, treatment and monitoring of possible negative influences on performance (Hain, 2011). VCC are financial intermediaries investing foremost in ventures bridging the gap created by the shortage of appropriate financing for small and entrepreneurial firms (LiPuma and Park, 2014; Okpala, 2012). By investing in ventures VCC bear high risk due to information asymmetries between the investor and entrepreneur known as the principal agent problem (LiPuma and Park, 2014). Hence, VCC apply different types of risk management measures to reduce the risk of the investment. Risk management in VC-backed ventures was sparsely analyzed in academic literature (Yoshikawa et al., 2004; Tan et al., 2008). The studies of Kut et al. (2006), Kut et al. (2007), Smolarski et al. (2005) investigated how buy-out and VC funds in Europe overall, in India, UK, France and Germany manage risk in the pre-screening phase of the investment, in existing ventures, the portfolio risk and macro risk considering a comprehensive set of risk management measures. These studies showed first attempts to analyze a set of risk management measures. Nevertheless, the studies are subject to several limitations especially due to partially small samples.

We conducted a structured literature review to study the current state of academic literature on the topic of risk management in VC-backed ventures. First, we analyzed all entrepreneurship journals ranked in the 55th edition of the Journal Quality List edited by Prof. Anne-Wil Harzing from 2005 to 2015 regarding the keywords “risk”, “risk management”, “venture capital” and “failure”. We identified thirteen relevant studies. Second, we searched in the EBSCOhost Online Research Databases for the abovementioned keywords in the titles and abstracts of all types of academic journals from 2005 to 2015. Overall, we identified 17 relevant papers (see Appendix A, Table 4). The samples of the different studies vary greatly in size and data collection method. A considerable number of studies are of explorative nature due to partly small sample sizes. This implies that this field of research is relatively unexplored offering room for further research. The majority of papers used data from the US and in some cases parts of Europe or Asia. Only few studies were conducted in Germany.

A. Risk types in VC-backed ventures VC investments are subject to several risks. Our structured literature review

showed that academic scholars investigated agency risk, financial or liquidity risk, technology risk, market risk, human resources risk, internationalization risk and macro risk. In the following, the different types of risks are described.

Agency risk is often stated as the major risk for VCC due potential problems of adverse selection and moral hazard between entrepreneurs and VCC (Bengtsson and

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

5

Sensoy, 2011; Lu et al., 2006; Tan et al., 2008). The theory was developed by William Meckling, Eugene Fama and Michael Jensen depicting the conflict of interest between the principal and the agent, in the case of VC founders or managers of the venture and the VCC (Fama and Jensen, 1983; Jensen and Meckling, 1976). Mechanisms like financial contracting, milestones, gradual provision of capital and active involvement in the board are applied by venture capitalists to overcome the information asymmetry between the VCCs and the entrepreneur (Bengtsson and Sensoy, 2011; Lu et al., 2006; Tan et al., 2008).

Liquidity or financial risks are partially used as synonyms in academic literature. Kut et al. (2006), Kut et al. (2007), Smolarski et al. (2005) classified financial risk in their analysis on the level of the portfolio and macro economy. Contrary, liquidity risk was analyzed by Cumming et al. (2005) indicating that VCC adjust their investment decisions according to liquidity risk. Liquidity risk refers according to Cumming et al. (2005) to the exit risk for the VCC in IPO markets describing the risk of not being able to reach an exit in a proper way. The study showed that VCC prefer to invest in high-tech and early stage ventures to defer the exit and increases the syndication size (Cumming et al., 2005). In our analysis, we define liquidity or financial risk as the risk of the venture to become illiquid or even bankrupt.

Technology risk is often used synonymously as product risk, technological risk or technical risk in academic literature. Assessing the technology or product risk is crucial risk for VCC before investing in ventures due to the fact that technologies and products are often not market-ready. Technology due diligences, syndication and the opinions of investment managers with industry experience are used to overcome the risk associated with technologies and products (Kut et al., 2006; Kut et al., 2007; Smolarski et. al., 2005; Wang et al., 2012).

Market risk is mainly related to the commercialization of a new technology (Wang et al., 2012). Ventures often lack the marketing capabilities necessary to take the technology to market (Wang et al., 2012). VCC apply due diligences to assess the market risk as a central part of the investment decision process (Lu et al., 2006). Furthermore, VCC utilize their network and skills to foster the market introduction. According to Kaplan and Strömberg (2002) major market risks are market size and growth, competition and barriers to entry and the likelihood of customer adoption. However, the results indicated that competition, market size and customer adoption risks mentioned at a moderate rate of 40, 31 and 22 per cent in the investment documents (Kaplan and Strömberg, 2002).

Human resources risks are risks associated with the quality and capabilities of the management of the venture. This was analyzed by the studies of Kut et al. (2006), Kut

6 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

et al. (2007) and Smolarski et al. (2005). In these studies human resources risk was measured by the lack of management performance and the lack of management focus. To mitigate the risk related to the management, VCC can verify the track record of the management team and can invest in management teams which are previously known (Kut et al., 2007). Kaplan and Strömberg (2002) showed that risks associated with the management were mentioned in 61% of the analyses. It was documented that the CEO is a “difficult” person, that the management lacks in financial planning, the management is not able to focus or that the management is young and inexperienced (Kaplan and Strömberg, 2002). In addition, a further risky issue for VCC is an incomplete management team (Kaplan and Strömberg, 2002). Overall, the results indicate that risks associated with human capital are of high relevance for VCC.

LiPuma and Park studied the special topic of internationalization risk using longitudinal data of 962 invested rounds in 334 VC-backed ventures (LiPuma and Park, 2014). Variables for risk management were round size, round interval and round syndication. Compared to solely domestic ventures, VCC use smaller syndicates and provide smaller and less frequent rounds of capital for ventures which internationalize opportunistically (LiPuma and Park, 2014).

Volatility and macroeconomic drivers, namely macro risk, affect VC investments by the total amount, by the number of deals, and by the average amount per deal (Ning et al., 2015). Types of macro risk can be inflation risk, business-cycle risk, interest rate risk and foreign exchange rate risk (Kut et al., 2006). Therefore, in times of high macro risk VCC adapt their risk preferences and investment strategies by investing in fewer deals with a smaller average amount per deal, raising their investments in later investment stages and injecting a lower percent of cash in the first several financing sequences (Ning et al., 2015).

Failure risk as one of the most severe risks for VCC was not contained in the results of our structured literature review. In a further search we explored that only very few researchers studied this topic empirically (Dimov and De Clercq, 2006). Therefore, we focused in our analysis on this type of risk since failure risk consists partially of the above mentioned risk types according to insolvency literature (Carter and van Auken, 2006), (Davila et al., 2003), (Headd, 2003), (Pinkwart et al., 2015), (Pleschak, 2002), (Schilling, 2002), namely liquidity risk, market risk, human resources risk and technology risk. Therefore we include these risk factors as variables in our model to describe failure risk.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

7

B. Risk management in VC-backed firms The literature review has shown that VCC apply the following risk

management measures: 1) assessment and evaluation of new ventures (Kut et al., 2007; Lu et al., 2006), 2) governance (Bengtsson and Sensoy, 2011; Tan et al., 2008) and 3) contracting (Bengtsson and Sensoy, 2011; Kut et al., 2007; Tan et al., 2008). In the course of the interviews with practitioners we identified two further influencing factor to reduce risk in VC investments, investment manager´s experience and skills as well as management support. There might be some interactions between the different risk management measures, e.g. governance mechanisms and management support. In the context of support functions of VCC governance mechanisms are a part of the support functions. However, in this context we separated governance mechanisms from management support due to the fact that governance mechanisms belong to the most important risk management measures in VC deals.

Assessing and evaluating potential new investments are the first steps of risk management VCC can apply in the investment process. Kut et al. (2007) showed that risk management in evaluating new investments is a well-developed area in practice in the VC industry (Kut et al., 2007). VCC have a variety of tools to assess and evaluate potential investment targets regarding risk and return, e.g. performing different types of due diligences like financial, product, market, customer, legal, competitor analysis internally and externally and analyzing audited financial statements (Kut et al., 2007; Kut and Smolarski, 2006; Lu et al., 2006; Smolarski et al., 2005). Information asymmetries can for example be resolved through the overall coherence of the business plan and the VCC’s own due diligence report according to Tourani-Rad and England (2003). VCC can also check the risk associated with the management by verifying the track record of the management team and board members and performing criminal background checks (Kut et al., 2007; Kut and Smolarski, 2006; Smolarski et al., 2005). Further measures to be conducted before an investment decision is made can be the consideration of synergies with existing ventures and the risk preferences of the investors of the fund (Kut et al., 2007; Kut and Smolarski, 2006; Smolarski et al., 2005). We assume that a better assessment of the risk before investing might lead to a lower failure rate of VC-backed venture.

Hypotheses 1: A high effort in assessing and evaluating the investment is negatively related to failure risk of VC-backed ventures.

Financial contracting can be used by VCC as a protection against downside risk (Bengtsson and Sensoy, 2011; Kut et al., 2007; Tan et al., 2008), but also to generate value in portfolio companies by mitigating the agency problem with financial contracts (Kaplan and Strömberg, 2002). Financial contracting is one measure next to active

8 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

involvement (Kut et al., 2007) and direct monitoring to reduce information asymmetry, motivational and financials problems (Bengtsson and Sensoy, 2011). VCC apply financial contracting mechanisms like liquidation preference, anti-dilution rights, cumulative dividends, redemption rights, participation rights and pay-to-play provisions according to Bengtsson and Sensoy (2011) and Tan et al. (2008). Syndication is a common measure in the VC industry to team up for assessing and investing collaboratively ventures to share the risk (Hopp, 2010; Hopp and Lukas, 2014; Smolarski et al., 2005; Wang et al., 2012). Staged financing is a useful control mechanism for VCC to gather information and monitor the progress of the venture having the option to inject further capital when milestones are reached and periodically abandon the venture (Kut and Smolarski, 2006; Tan et al., 2008). Adding to this, Bengtsson and Sensoy (2011) identified that good governance abilities can be a substitute for measures of financial contracting. Therefore, we state that a high use of contracting mechanisms might lower the risk of failure of VC-backed firms:

Hypothesis 2: An extensive use of contracting mechanisms is negatively related to the failure risk of VC-backed ventures.

VCC are known as active investors in their ventures. Risk management mechanisms related to governance like milestones, reporting and an active involvement in the board are applied by VCC to reduce agency risk. This risk type describes the interest conflict in the relationship between the investor and the entrepreneur. A considerable amount of studies investigated how VCC use control and incentive mechanisms to enhance the firm’s performance and receive higher returns. Contrary, only a few studies focused on this topic to reduce downside or failure risk (Bengtsson and Sensoy, 2011; Tan et al., 2008). According to Tan et al. (2008) governance risk management measures can be distinguished in either control mechanisms like monitoring (e.g. reporting, frequency of interaction, convertible securities), staged investments, which we allocated to financial contracting, and the allocation of ownership and control rights or incentive mechanisms (Tan et al., 2008). Shares of stock rights of the entrepreneur and employee stock options are incentive mechanisms to reduce agency risk. The greater VCC´s monitoring abilities, the more effective is the monitoring at constraining the entrepreneur´s behavior (Bengtsson and Sensoy, 2011). From practice, we know that all VCC use control mechanism, hence we assume:

Hypothesis 3: The extensive use of governance mechanisms are negatively related to the failure risk of VC-backed ventures.

Investment managers are responsible for assessing new ventures and investment decisions in the pre-investment phase as well as the management of existing ventures in the post-investment phase, i.e. communication, meetings, controlling and supporting

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

9

the venture. Investment managers can have technological, industry, financial and managerial experience and leadership skills which might be crucial for the success and failure ventures (Hopp and Lukas, 2014). According to Hopp and Lukas (2014) more experienced investment managers control their investments less often than less experiences investors. Furthermore, more industry experience allows less frequent and intense evaluation (Hopp and Lukas, 2014). Yazdipour and Constand (2010) argued that researchers cannot ignore the human/managerial/decision-making side in failure prediction. Hence, they suggest in human decisions about the making or breaking of a private company a shifts from the commerce/operational (effect) side of failure analysis to the human/managerial/decision making (cause) side of it (Yazdipour and Constand, 2010). We assume that an experienced investment manager can be better in assessing risk and using countermeasures which can lead to a lower failure risk of VC-backed firms:

Hypothesis 4: The degree of investment manager´s experience is negatively related to the failure risk of VC-backed ventures.

A variety of studies proved that VCC add value to their portfolio companies (Alperovych and Hübner, 2013; Manigart et al., 2002; Sapienza, 1992; Sapienza et al., 1996) by applying different types of value added services like financials, governance, strategy, operational improvements and human capital improvements (Bottazzi et al., 2002; Cumming et al., 2005; Guo and Jiang, 2013; Tang et al., 2014; Timmons and Bygrave, 1986). We transferred the positive effects from management support to the literature of risk management in the VC industry. Hence, we assume that management support can have an impact on the failure risk of VCC´s portfolio companies:

Hypothesis 5: The extensive use of management support provided by VCC is negatively related to the failure risk of VCC´s portfolio companies.

III. Data and method

A. Sample Our sample consists of 93 VC-backed firms collected from nine different

public and private public partnership VC funds in Germany. Considering the statistics of the Bundesverband Deutscher Kapitalbeteiligungsgesellschaften, which recorded 433 seed investments in Germany from 2005 to 2010, our sample covers 21.5% of the seed investments in this time frame in Germany. We conducted a survey with the corresponding investment managers. In addition, we had access to the original deal documents including the business plans, investment committee papers, reporting and

10 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

annual statements of the investments. That enabled us to collect in-depth quantitative and qualitative data.

Considering our data set, the VC-backed firms are on average 4.6 years old at the time of data collection. In the seed round the firms received on average 784,487 Euros as investment and in the series A round 1,202,948 Euros (see table 1). The firms in our data set are technology-based firms as they operate in the industries information technology and automation (39 %), life science (34%), material science (9 %), energy (5 %), communication (4 %) and others (9 %).

Table 1. Overview of our data set Variable Mean Median Std. Dev

Age of ventures 4.59 years 5 2.09

Size of founders team 2.85 founders 3 1.13

Number of founding rounds

1.98 rounds 2 0.89

Investment sum Seed 784,487 Euro 644,109 Euros 519,577

Investment sum Series A 1,202,948 Euros 816,287 Euros 1,179,085

Number of investors Seed 2.55 2 1.98

Number of investors Series A

3.94 3 2.54

B. Measures and variables We used a structural equation model approach to build and test our model

because failure risk can hardly be measured directly. Hence, we used a set of proxy variables. We built a partial least squares (PLS) model because of its suitability for proxy variables and the lack of existing scales in this field of research (Ainudding et al., 2007; Henseler et al., 2009). Furthermore, the fit of PLS models compared to covariance based methods for sample sizes smaller than 100 also attributed to our choice (Fornell and Bookstein, 1982). Not all of our items follow normal distribution. Hence, they would have been omitted once using a covariance based approach. In PLS models items do not have to follow a certain distribution (Hulland, 1999). In addition, we use variables measured with a 5-point Likert scale in our model. PLS models support the use of nominal, ordinal and interval scaled data (Fornell and Bookstein, 1982, Nitzl, 2010; see also Menzar and Nigh, 1995, Brinckmann et al., 2011). We

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

11

decided to use a reflective measurement model for the outer constructs of the risk management measures, the control variables and the construct of business failure as well as for the inner construct for two reasons. Reflective measurement models have defined reliability test criteria and are well researched (Roy and Tarafdar, 2012). Further, our indicator variables strongly correlate within our construct.

1. Dependent variables

Measuring failure risk of a company is difficult. Therefore, we measure failure risk by proxy variables, namely human resource risk, technology risk, financial risk and market risk based on the literature of bankruptcy and insolvency (Pinkwart et al., 2015). Pinkwart et al. (2005) showed that 80 per cent of the reasons for failure include a lack of management companies or management companies. Other studies confirmed human resources as an important reason for business failure (Carter and van Auken, 2006; Headd, 2003). A further cause of failure is risk related to the technology of a venture (Schilling, 2002). These companies are dependent on developing their technology to a working and marked-proved product. If ventures do not succeed in reaching the market readiness in a timely manner development costs can grow in outstanding way which ventures often cannot afford (Pleschak et al., 2002). Difficulties in getting a follow-up financing, miscalculation for the capital need and bad planning are among the most common reasons for business failure, namely financial risk (Davila et al., 2003; Headd, 2003; Pleschak et al., 2002; Thornhill and Amit, 2003). New ventures often need too long to break even or even fail because of the lack of financial resources. A further reason for the failure of companies can be found in the area of the market. Problems with the market entry or in marketing and sales are among the most common reasons of failure (Wagner, 1994; Dowling and Drumm, 2002; Pleschak, 2002). This can be explained by a lack of experience in marketing and sales as well as an overoptimistic planning (Hall, 1992; Thornhill and Amit, 2003). In addition, new companies often rely on a few key clients leading to a strong dependency from these customers (Brüderl et al., 1996; Guggemoos, 2012). We measured the five above mentioned risk types by the assessment of the supervising investment managers on a scale from 1 to 5 (1: very low risk, 5: very high risk).

2. Independent variables

As mentioned in chapter II. B. we identified five groups of risk management measures applied by VCC, i.e. assessment and evaluation of new ventures, contracting, governance, investment managers’ experience and skills and management support. Each group was measured by different items since VCC use several risk management measures for each group comprehensively in practice.

12 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

We used different items to measure the degree of assessment. We first looked if an external assessment of the company was done. From the VCC documents we knew that often external companies are hired to evaluate e.g. technology, market and legal risks. Further, we looked at the intellectual property protection. If the technology is protected by e.g. patents or registered designs the market and technology risks might be lower. In addition, we measured if the VCC relied on their network in assessing the technology and the competencies of the founders.

Contracts handle different aspects of risks between the entrepreneur and the VCC. An important item is liquidation preference. A high liquidation preference lowers the risk of VCC as it minimizes possible losses. We analyzed how strongly a liquidation preference was used. Further, we measured the number of syndication partners. Syndication is a possibility to share risk with other investors. Further, we looked at the investment sum. If the investment sum is lower it might increase the risk of failure in terms of liquidity. In addition we intended to measure if staged financing was used. However, due to the fact that this was the case for all our cases we did not include this item in our model.

Governance mechanisms like reporting and milestones are useful to assess risks continuously. To measure governance we included five proxy variables in our model. At first we looked if milestones were used and monitored. VCC often use milestones to bind founders to certain goals. If milestones are reached, founders receive the full investment sum. In addition, we looked at reporting. From expert interviews we knew that successful companies report regularly. If the company does not perform as expected, reporting rates might decrease. We therefore measured how heavily VCC rely on reporting. Furthermore, we included personal exchange in our model as it indicates a high interaction between founders and investment managers. Fourthly, we included the variable information through network in our model. According to principal agent theory a conflict exists between founders and VCC due to information asymmetry. Therefore, if VCC use their network to lower information asymmetries risks might be reduced. Lastly, we investigated at the shares of the founders. If the founders still have a high share of equity they might be more motivated financially and incentivized even if they lost decision rights due to the contract with the VCC.

Investment manager´s experience and skills might have a significant influence on the failure risk of ventures. We described the experience and skills of the investment manager by five variables. First, we looked at the working experience. More working experience might make it easier to deal in business environment. Second, we assessed the founding experience. Third, we analyzed the expertise with the field of technology. Forth, we assessed the business skills of the investment manager. An investment

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

13

manager has to have a profound understanding of business to be able to evaluate the development of the ventures. Lastly, we analyzed the network size. With a superior network, the investment manager has more possibilities to get additional knowledge and support for areas he is not an expert on.

We measured the degree of management support by six variables. Firstly, we looked at the support by the VCC using own competencies. Bringing in their experience in the company might lead to better development of the portfolio company. Further, we looked at sales support. Young companies often fail because of a lack of sales activities. A support in the area could possibly lead to a lower risk of failure. Thirdly, we analyzed support with technology. For new ventures technology is a crucial success factor. Fourthly, we examined strategic support. A strong strategy is often an indicator for successful firms. In addition, we looked at support in follow-up financing. For new ventures it is critical to raise additional financing in a timely manner to avoid illiquidity and bankruptcy. Lastly, we measured the use of network in general to lower the risk of the venture after the investment took place. Networks might be useful to get new customers or consultants for solving issues.

3. Control variables

We controlled for age and industry. The risk of failure might be higher when companies are younger. Albach (1987) suggested that for most companies the highly probable chance of failure ends after five years. In addition, some industries might have higher failure rate than others.

IV. Results

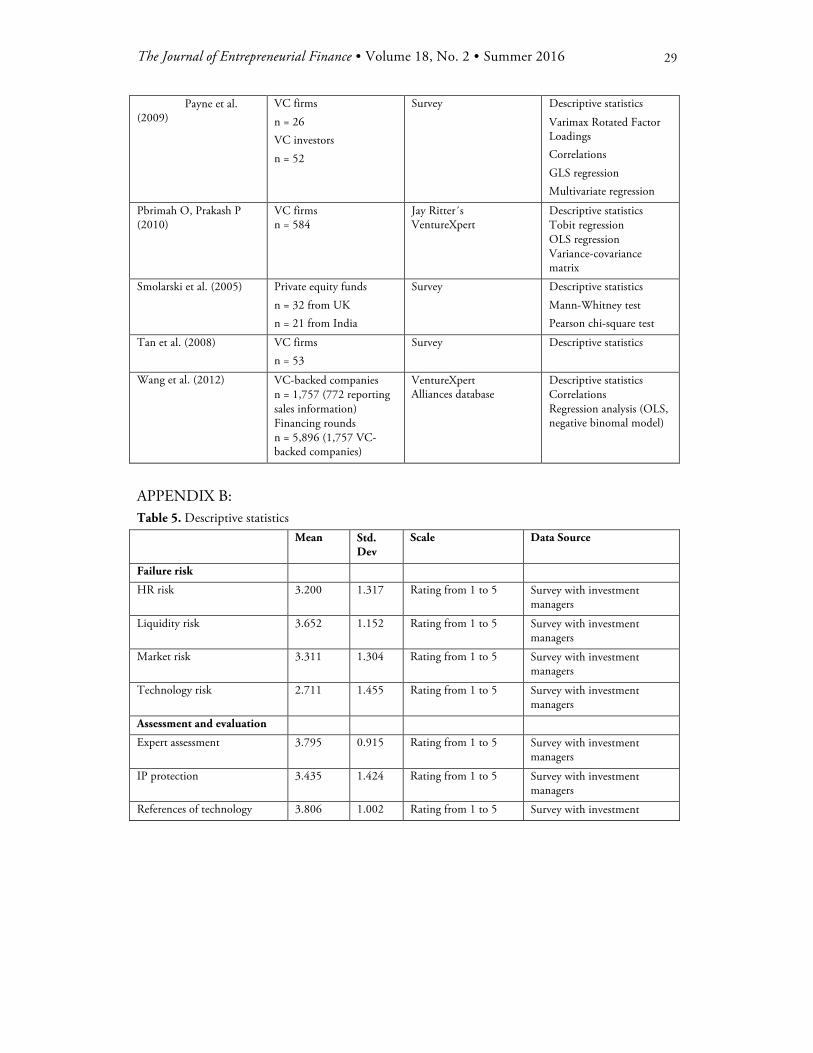

A. Descriptive statistics The results of the descriptive statistics are presented in appendix B (see Table

5). The failure risk was measures on a 5-point Likert scale (1: very low, 5 very high). The statistics show that liquidity risk has the highest value of 3.652 at the lowest standard deviation of 1.152. Technology risk was rated on average at 2.711 depicting the lowest failure of risk measures, but at the highest standard deviation of 1.455.

The descriptive statistics for the five groups of risk management present that governance mechanisms like milestones (mean = 4.247) or reporting (mean= 4.355) at a standard deviation of below 0.8 were deployed consistently high by the VCC in our sample. The same applies for risk management like obtaining references of founders (mean=4.086), liquidation preference (mean= 4.096) or support in follow up financing (mean= 4.065).

14 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

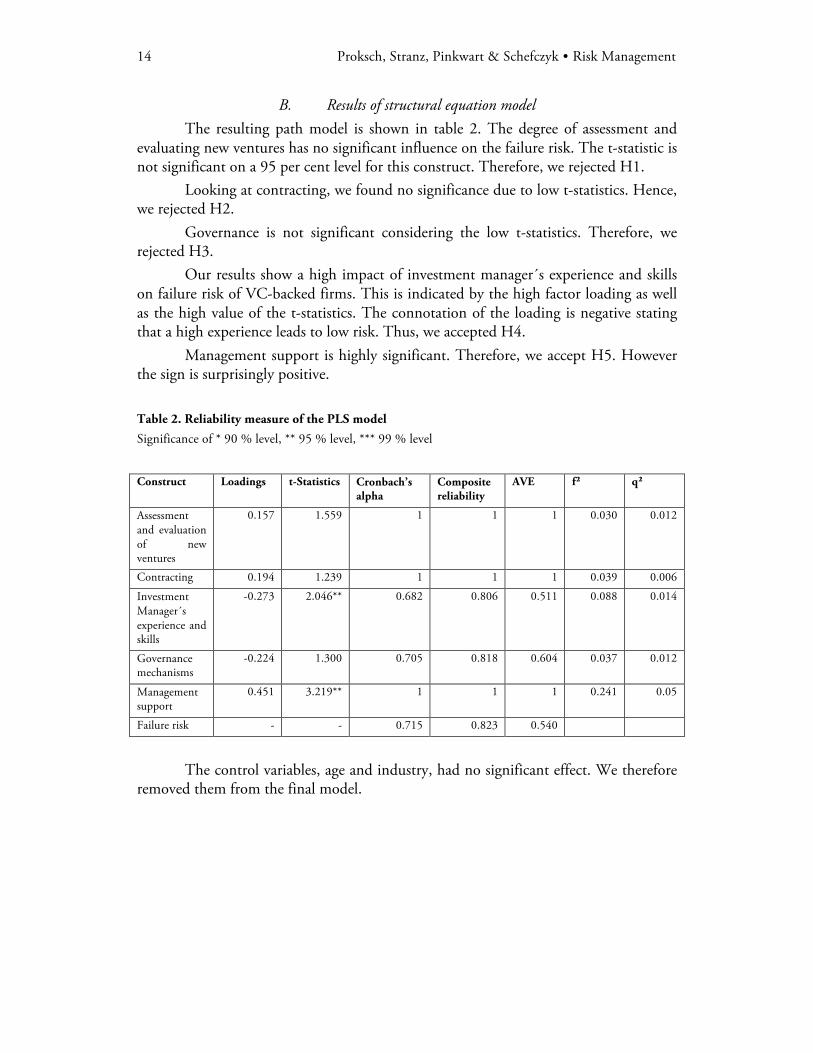

B. Results of structural equation model The resulting path model is shown in table 2. The degree of assessment and

evaluating new ventures has no significant influence on the failure risk. The t-statistic is not significant on a 95 per cent level for this construct. Therefore, we rejected H1.

Looking at contracting, we found no significance due to low t-statistics. Hence, we rejected H2.

Governance is not significant considering the low t-statistics. Therefore, we rejected H3.

Our results show a high impact of investment manager´s experience and skills on failure risk of VC-backed firms. This is indicated by the high factor loading as well as the high value of the t-statistics. The connotation of the loading is negative stating that a high experience leads to low risk. Thus, we accepted H4.

Management support is highly significant. Therefore, we accept H5. However the sign is surprisingly positive.

Table 2. Reliability measure of the PLS model

Significance of * 90 % level, ** 95 % level, *** 99 % level

Construct Loadings t-Statistics Cronbach’s

alpha Composite reliability

AVE f² q²

Assessment and evaluation of new ventures

0.157 1.559 1 1 1 0.030 0.012

Contracting 0.194 1.239 1 1 1 0.039 0.006

Investment Manager´s experience and skills

-0.273 2.046** 0.682 0.806 0.511 0.088 0.014

Governance mechanisms

-0.224 1.300 0.705 0.818 0.604 0.037 0.012

Management support

0.451 3.219** 1 1 1 0.241 0.05

Failure risk - - 0.715 0.823 0.540

The control variables, age and industry, had no significant effect. We therefore

removed them from the final model.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

15

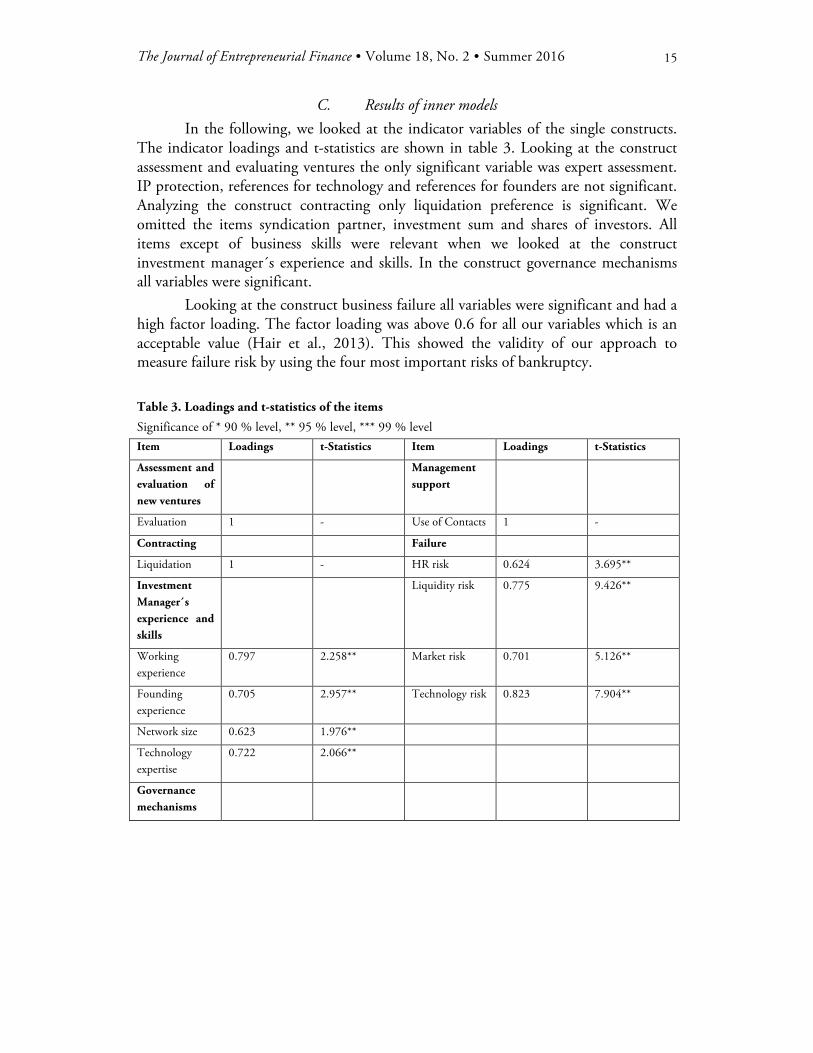

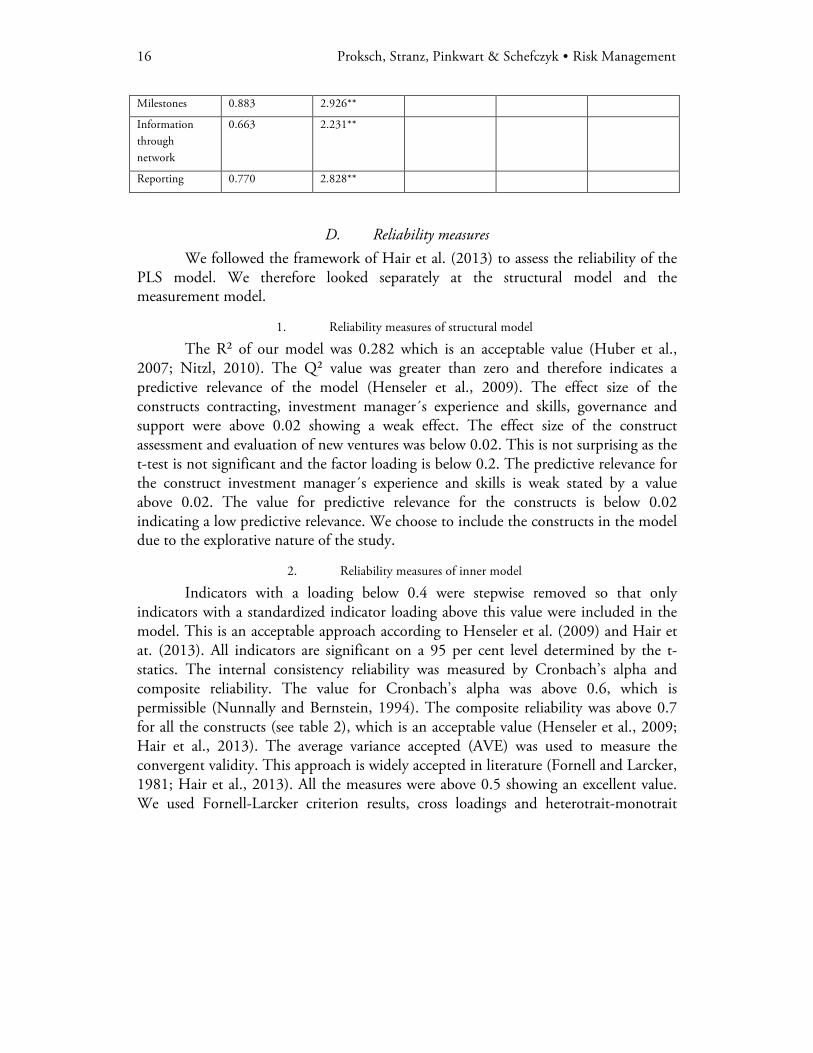

C. Results of inner models In the following, we looked at the indicator variables of the single constructs.

The indicator loadings and t-statistics are shown in table 3. Looking at the construct assessment and evaluating ventures the only significant variable was expert assessment. IP protection, references for technology and references for founders are not significant. Analyzing the construct contracting only liquidation preference is significant. We omitted the items syndication partner, investment sum and shares of investors. All items except of business skills were relevant when we looked at the construct investment manager´s experience and skills. In the construct governance mechanisms all variables were significant.

Looking at the construct business failure all variables were significant and had a high factor loading. The factor loading was above 0.6 for all our variables which is an acceptable value (Hair et al., 2013). This showed the validity of our approach to measure failure risk by using the four most important risks of bankruptcy.

Table 3. Loadings and t-statistics of the items

Significance of * 90 % level, ** 95 % level, *** 99 % level Item Loadings t-Statistics Item Loadings t-Statistics

Assessment and evaluation of new ventures

Management support

Evaluation 1 - Use of Contacts 1 -

Contracting Failure

Liquidation 1 - HR risk 0.624 3.695**

Investment Manager´s experience and skills

Liquidity risk 0.775 9.426**

Working experience

0.797 2.258** Market risk 0.701 5.126**

Founding experience

0.705 2.957** Technology risk 0.823 7.904**

Network size 0.623 1.976**

Technology expertise

0.722 2.066**

Governance mechanisms

16 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

Milestones 0.883 2.926**

Information through network

0.663 2.231**

Reporting 0.770 2.828**

D. Reliability measures We followed the framework of Hair et al. (2013) to assess the reliability of the

PLS model. We therefore looked separately at the structural model and the measurement model.

1. Reliability measures of structural model

The R² of our model was 0.282 which is an acceptable value (Huber et al., 2007; Nitzl, 2010). The Q² value was greater than zero and therefore indicates a predictive relevance of the model (Henseler et al., 2009). The effect size of the constructs contracting, investment manager´s experience and skills, governance and support were above 0.02 showing a weak effect. The effect size of the construct assessment and evaluation of new ventures was below 0.02. This is not surprising as the t-test is not significant and the factor loading is below 0.2. The predictive relevance for the construct investment manager´s experience and skills is weak stated by a value above 0.02. The value for predictive relevance for the constructs is below 0.02 indicating a low predictive relevance. We choose to include the constructs in the model due to the explorative nature of the study.

2. Reliability measures of inner model

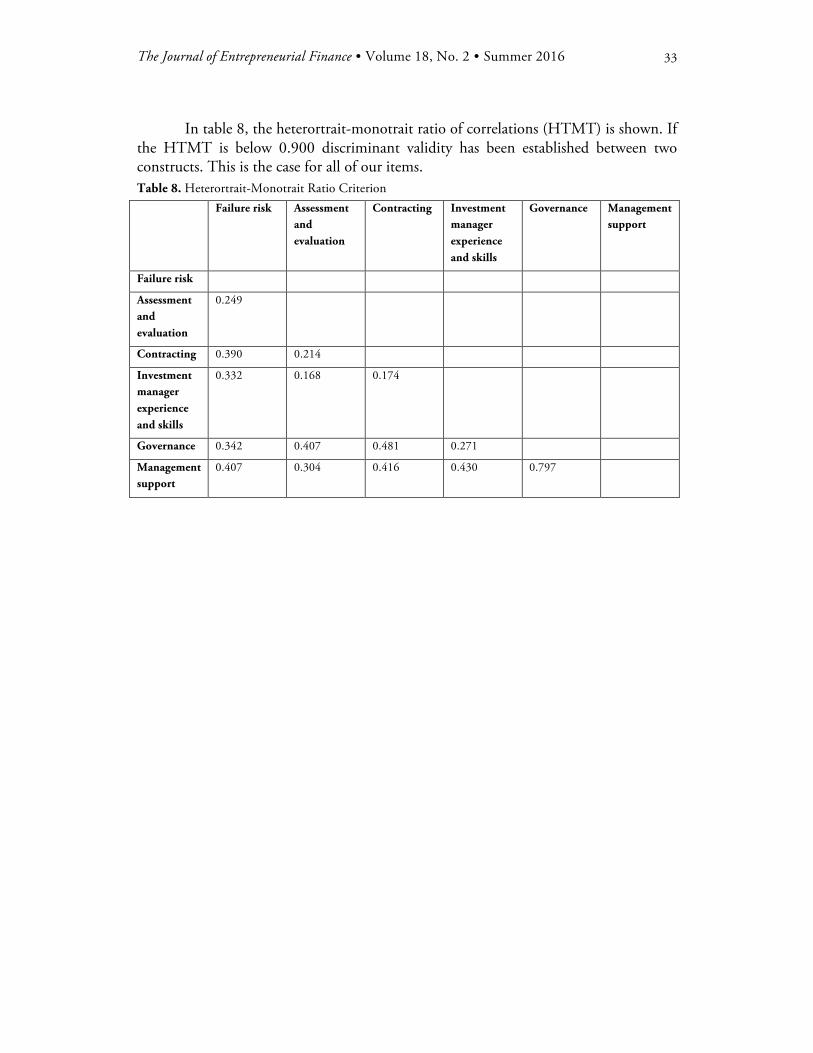

Indicators with a loading below 0.4 were stepwise removed so that only indicators with a standardized indicator loading above this value were included in the model. This is an acceptable approach according to Henseler et al. (2009) and Hair et at. (2013). All indicators are significant on a 95 per cent level determined by the t-statics. The internal consistency reliability was measured by Cronbach’s alpha and composite reliability. The value for Cronbach’s alpha was above 0.6, which is permissible (Nunnally and Bernstein, 1994). The composite reliability was above 0.7 for all the constructs (see table 2), which is an acceptable value (Henseler et al., 2009; Hair et al., 2013). The average variance accepted (AVE) was used to measure the convergent validity. This approach is widely accepted in literature (Fornell and Larcker, 1981; Hair et al., 2013). All the measures were above 0.5 showing an excellent value. We used Fornell-Larcker criterion results, cross loadings and heterotrait-monotrait

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

17

ratio of correlations (HTMT) to test for discriminant validity (Fornell and Larcker, 1981; Ringle et al., 2015). The model passed all three tests as described in the appendix C.

V. Discussion and conclusion Based on a structured literature review, the analysis of qualitative data of nine

VC funds and an empirical analysis using a structural equation model we studied five groups of risk management measures VCCs can partake in their ventures to reduce failure risk. We empirically tested the relevance for each group of risk management measures. As a result, we show which risk management measures have an influence on business failure of VC-backed ventures.

First, the assessment of the investment prior the decision had no significant influence to reduce the failure risk in VCC´s ventures in the model. Therefore, we cannot support the studies of Kut et al. (2007), Kut and Smolarski (2006), Lu et al. (2006), Smolarski et al. (2005) and Tourani-Rad and England (2003) showing the significant relevance of assessment and evaluation in the pre-investment phase. One reason might be that this is often seen as the most important part in the investment decision process. The usage of different assessment methods was high for all cases in the sample (see descriptive statistics in A1), which confirms Kut et al. (2007) that risk management in evaluating new investments is a well-developed area in practice in the VC industry. However, the difference between the usages within the ventures might not be very high resulting in no significant influence.

Second, the construct contracting is not significant. Hence, we cannot support the results of Bengtsson and Sensoy (2011), Kut et al. (2007) and Tan et al. (2008) that financial contracting can be used by VCC as a protection against downside risk. A reason for that could be that VCC use similar formats of contracting, which also can be seen in the descriptive statistics (A1). In addition, all VCC used staged financing, syndication and milestone with each venture. This implies no significant differences across the cases in the sample.

Third, the results show that governance mechanisms are not significant to reduce failure risk in the model. The descriptive statistics showed that governance mechanisms are extensively used in all ventures supporting no significance of the statistical results (see Appendix A). Considering this result, we cannot support Bengtsson and Sensoy (2011) and Tan et al. (2008) who found significant evidence for the importance of governance mechanisms in VC risk management.

18 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

The construct investment manager´s experience and skills as a risk management measure in VC-backed ventures are significant, which was rarely discussed in literature before. This finding continuous the discussion of Hopp and Lukas (2014) who were among the first showing that investment managers have various competencies, skills and experiences which might be crucial for the success and failure ventures. Also, the study of Yazdipour and Constand (2010) highlighted the importance of human capital in failure prediction of private firms. If the investment manager is more experienced the VC-backed ventures have less failure risk as the investment manager might be able to uncover possible problematic issues earlier and use the right countermeasures. In addition, we found that also VC-backed ventures supported by investment managers with founding experience have a lesser risk of failure.

Last, we found that management support is significant. Counter-intuitively, the connotation is negative. The extensive use of management support leads to a higher risk. This might be a chicken-and-egg problem. Possibly, investors only extensively support their portfolio companies when risk is already high which might be too late to save the company. To test this assumption we created a PLS model to analyze the influence of business failure on the degree of management support. We found that a high chance of business failure has a positive impact on the degree of management support as described by the use of VCC´s network and bringing external consultants into the portfolio company. Therefore, we can assume that this result might be explained by a chicken-egg problem. Considering this problem in the study, we recommend further investigation on the use of the risk management measures in the VC industry. It would be interesting to analyze if risk mitigation measures are only used when a risk occurred or also in a preemptive way.

VI. Limitations and implications

A. Limitations Like most empirical studies the research is subject to several limitations. First,

we could not assess all risk management measures identified in literature. A holistic model including further risk management measures could lead to additional results.

Secondly, we used a self-assessment of the investment manager for their experience in a survey. This might introduce a possible bias. However, the survey covered a variety of different areas of VC financing wherefore it was not clear for the investment managers that a connection between their experience and the risk was made.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

19

Thirdly, we focused on German technology start-ups from public and private VC funds. It is unclear if the results can be generalized to other countries and all types of new ventures. Therefore, similar studies, e.g. using data in the US or Asia, might uncover similarities and differences between risk management measures across countries.

The data set consists of a higher share of public as well as public private partnership funds which also could include a possible bias as public funds might pursue a different investment and risk management strategy as private funds.

The quantitative approach does not allow to further study changes in the perceived failure risk over time. A qualitative approach to explicitly study the development of the risks in different investment stages could further yield to new results.

In addition, the use of PLS does not allow to control for endogeneity effects which is also discussed in current literature (Ronko and Evermann, 2013; Henseler et al., 2014).

The results might be partially biased due to the fact that our sample includes VC investments from 2005 - 2010, i.e. during the financial crisis. It might be possible that risks were higher during that time because of the economic downturn and the restricted capital situation.

B. Implications Our research has several implications for the literature and practice. In terms of the literature, the analysis has shown that the research stream of risk

management in VC investments is rather underdeveloped, but nevertheless of great practical importance, for VCCs. We tested the effectiveness of different risk management measures on lowering the risk of business failure in new ventures. Thereby, we showed the importance of risk management on the probability of failure. With this article we aim to encourage discussions on and analyses of this field of literature to shed more light on VCC risk management practices. The results indicate the relevance of the investment manager in risk management in VC investments. Continuing this discussion, a possible research question could be which experiences, skills and knowledge as well as what kind of interaction between founders lowers venture´s failure risk. Another research direction might be a cross-country analysis as there are several differences, e.g. legal, between European and US VCCs. The German law for asset management companies like VCC prohibits active involvement of the VCC in the portfolio firm. VCC are only allowed to provide advice which also impacts their risk management practices. Further one, a mixed method approach including, for

20 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

example, surveys, verbal protocol analysis, and content analysis might be favorable to explore aspects of formal and informal risk assessment in VC investments. Furthermore, since our sample is limited to early stage VC funds, further investigations into different fund stages might be of interest to explore the differences across investment stages.

In terms of practice, we showed that all VCC in our sample pursue comparable risk management measures for the assessment and evaluation of new ventures, in contracting as well as in governance issues. Looking at the descriptive statistics we observed that particularly governance mechanisms, liquidation preferences and partially assessment and evaluation measures are extensively applied by VCC in their ventures in our data set. Nevertheless, there mechanisms do not show a significant influence on failure risk, which might be explained by the fact that they act like hygiene factors. Our study provides empirical evidence for the great importance of investment manager´s experience and skills which could be understand as the motivator of the analyzed risk management. Considering our empirical results, LPs and VC funds should therefore rely on highly experienced employees managing ventures. The results suggest that VCC have to invest in their human capital to improve the skills and knowledge of their investment managers as well as the working environment and conditions to hire the best investment managers. In that course, an exchange between more experienced and younger investment managers triggered by the VCC might be a possibility to achieve a knowledge transfer. REFERENCES

Ainuddin R.A., Beamish P.W., Hulland J.S., Rouse M.J., Resource attributes and firm

performance in international joint ventures, Journal of World Business, 2007, 42, 47–60.

Albach H., Geburt und Tod von Unternehmen, in: Institut für Mittelstandsforschung Bonn (ed) Rückblick auf das Jahr 1987, 1987, Bonn, 91-160.

Alperovych Y. and Hübner G., Incremental impact of venture capital financing, Small Business Economics, 2013, 41, 651–666.

Ang, J. S., On the Theory of Finance for Privately Held Firms, The Journal of Entrepreneurial Finance, 1992, 1(3), 185-203.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

21

Aven T., On Some Recent Definitions and Analysis Frameworks for Risk, Vulnerability, and Resilience, Risk Analysis, 2011, 31, 515-522.

Bengtsson O., Sensoy B.A., Investor abilities and financial contracting: Evidence from venture capital, Journal of Financial Intermediation, 2011, 20, 477–502.

Botazzi, L., Da Rin, M., van Ours, J., Berglöf E., Venture Capital in Europe and the Financing of Innovative Companies, Economic Policy, 2002, 17 (34), 231 – 269.

Brinckmann J., Salomo S., Gemuenden H.G., Financial Management Competence of Founding Teams and Growth of New Technology-Based Firms, Entrepreneurship Theory and Practise, 2011, 35, 217–243.

Bromiley P., McShane M., Nair A., Rustambekov E., Enterprise Risk Management: Review, Critique, and Research Directions, Long Range Planning, 2015, 48, 265–276.

Brüderl J., Preisendörfer P., Ziegler R., Der Erfolg neugegründeter Betriebe. Eine Empirische Studie zu den Chancen und Risiken von Unternehmensgründungen, 1996, Berlin.

Bygrave W.D., The entrepreneurship paradigm revisited. In Neergaard H, Ulhoi JP (ed), Handbook of qualitative research methods in Entrepreneurship, 2006, Cheltenham and Northhampton, 17-48.

Carter R., Van Auken H., Small Firm Bankruptcy. Journal of Small Business Managing, 2006, 44, 493-512.

Coleman, S., The "Liability of Newness" and Small Firm Access to Debt Capital: Is There a Link?, The Journal of Entrepreneurial Finance, 2004, 9(2), 37-60.

Cumming D., Fleming G., Schwienbacher A. (2005) Liquidity Risk and Venture Capital Finance, Financial Management, 2005, 34, 77–105.

Davila A., Foster G., Gupta M., Venture capital financing and the growth of startup firms, Journal of Business Venturing, 2003, 18, 689–716

22 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

Dimov D. and De Clercq D., Venture capital investment strategy and portfolio failure rate: a longitudinal study. Entrepreneurship Theory and Practise, 2006, 30, 207-223.

Dimov D. and Murray G., Determinants of the Incidence and Scale of Seed Capital Investments by Venture Capital Firms, Small Business Economics, 2008, 30, 127–152.

Dowling M. and Drumm H.J., Gründungsmanagement: Vom erfolgreichen Unternehmensstart zu dauerhaftem Wachstum, 2002, Springer Fachmedien Wiesbaden GmbH, Wiesbaden.

Fama E. and Jensen M., Separation of Ownership and Control, Journal of Law and Economics, 1983, 26 (2), 301 – 325.

Fornell C. and Larcker D., Structural equation models with unobservable variables and measurement error: Algebra and statistics, Journal of Marketing Research, 1981, 18, 382–389.

Fornell C. and Bookstein F., Two structural equation models: LISREL and PLS applied to consumer exit-voice theory, Journal of Marketing Research, 1982, 19, 440–453.

Froot K. A., Scharfstein D. A., Stein J. C., Risk Management: Coordinating Corporate Investment and Financing Policies, Journal of Finance, 1993, 48, 1629–1658.

Guggemoos P.G., Unterstützung der Unternehmensentwicklung junger wachstumsorientierter Technologieunternehmen durch Venture Capital-Gesellschaften in der Betreuungsphase: Eine empirische Analyse unter besonderer Berücksichtigung der Kapitalnehmer, 2012, Gabler, Wiesbaden.

Guo D. and Jiang K., Venture capital investment and the performance of entrepreneurial firms: Evidence from China, Journal of Corporate Finance, 2013, 22, 375–395.

Hain S., Risk perception and risk management in the Middle East market: theory and practice of multinational enterprises in Saudi Arabia, Journal of Risk Research, 2011, 14, 819-835.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

23

Hair J.F., Ringle C.M., Sarstedt M., Partial Least Squares Structural Equation Modeling: Rigorous Applications, Better Results and Higher Acceptance, Long Range Planning, 2013, 46, 1–12.

Hall G., Reasons for insolvency amongst small firms - A review and fresh evidence, Small Business Economics, 1992, 4, 237-250.

Headd B., Redefining business success: Distinguishing between closure and failure, Small Business Economics, 2003, 21, 51-61.

Henseler J., Dijkstra T.K., Sarstedt M., Common Beliefs and Reality About PLS: Comments on Ronkko and Evermann (2013), Organizational Research Methods, 2014, 17, 182–209.

Henseler J., Ringle C.M., Sinkovics R.R., The use of partial least square path modeling in international marketing, Advances in International Marketing, 2009, 20, 277–319.

Hopp C., When do venture capitalists collaborate? Evidence on the driving forces of venture capital syndication, Small Business Economics, 2010, 35, 417–431.

Hopp C., Lukas C., Evaluation frequency and evaluator’s experience: the case of venture capital investment firms and monitoring intensity in stage financing, Journal of Management and Governance, 2014, 18, 649–674.

Huber F., Herrmann A., Meyer F., Vogel J., Vollhardt K., Kausalmodellierung mit Partial Least Squares, 2007, Gabler, Wiesbaden.

Hulland J., Use of partial least squares (PLS) in strategic management research: a review of four recent studies, Strategic Management Journal, 1999, 20, 195-204.

Jensen M.C., Meckling W.H., Theory of the firm: Managerial behavior, agency costs and ownership structure, Journal of Financial Economics, 1976, 3, 305-360.

Kaplan S.N., Strömberg P., Financial Contracting Theory Meets the Real World: An Empirical Analysis of Venture Capital Contracts, The Review of Economic Studies, 2002, 70, 281-315.

24 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

Kut C., Pramborg B., Smolarski J., Risk Management in European Private Equity Funds: Survey Evidence, Journal of Private Equity, 2006, 9, 42–54.

Kut C., Pramborg B., Smolarski J., Managing financial risk and uncertainty: The case of venture capital and buy-out funds, Global Business and Organizational Excellence, 2007, 26, 53–64.

Kut C., Smolarski J., Risk Management in Private Equity Funds: A comparative study of Indian and Franco-German Funds, Journal of Developmental Entrepreneurship, 2006, 11, 35–55.

LiPuma J.A. and Park S., Venture Capitalists' Risk Management of Portfolio Company Internationalization, Entrepreneurship Theory and Practise, 2014, 38, 1183–1205.

Lu Q., Hwang P., Wang C.K., Agency risk control through reprisal. Journal of Business Venturing, 2006, 21, 369–384.

Mackay P. and Moeller S. B., The Value of Corporate Risk Management. Journal of Finance, 2007, 62, 1379–1419.

Manigart S., Waele K., Wright M., Robbie K., Desbrières P., Sapienza H.J., Beekman A., Determinants of required return in venture capital investments: a five-country study, Journal of Business Venturing, 2002, 17, 291–312.

Maula M.V., Autio E., Murray G.C., Corporate venture capital and the balance of risks and rewards for portfolio companies Journal of Business Venturing, 2009, 24, 274–286.

Menzar M. B. and Nigh D., Buffer or Bridge? Environmental and Organizational Determinants of Public Affairs Activities in American Firms, The Academy of Management Journal, 1995, 38 (4), 975 – 996.

Milanov, H., and Fernhaber, S. A., The impact of early imprinting on the evolution of new venture networks, Journal of Business Venturing, 2009, 24, 46-61.

Neergaard H. and Ulhoi J.P., Handbook of qualitative research methods in Entrepreneurship, 2006, Edward Elgar Publishing Limited, Cheltenham and Northampton.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

25

Ning Y., Wang W., Bo Y., The driving forces of venture capital investments, Small Business Economics, 2015, 44, 315-344.

Nitzl C., Eine anwenderorientierte Einführung in die Partial Least Square (PLS)-Methode, 2010, Universität Hamburg, Arbeitspapier Nr. 21.

Nunnally J.C. and Bernstein I.H., Psychometrie theory (3rd ed.), 1994, McGraw-Hill, New York.

Okpala K.E., Venture Capital and the Emergence and Development of Entrepreneurship: A Focus on Employment Generation and Poverty Alleviation in Lagos State, Journal of Business Management, 2012, 5, 134–141.

Payne T., Davis J.L., Moore C.B., Bell R.G., The deal structuring stage of the venture capitalist decision-making process: Exploring confidence and control. Journal of Small Business Management, 2009, 47, 154 - 179.

Pbrimah O. and Prakash P., Performance reversals and attitudes towards risk in the venture capital (VC) market, Journal of Economics and Business, 2010, 62, 537-561.

Pinkwart A., Die Unternehmensgründung als Problem der Risikogestaltung. Zeitschrift für Betriebswirtschaftslehre, 2002, Erg.-heft 5/2002, 55-84.

Pinkwart A., Kolb S., Heinemann D., Unternehmen aus der Krise führen. Die Turnaround-Balanced Scorecard als ganzheitliches Konzept zur Wiederherstellung des Unternehmenserfolgs von kleinen und mittleren Unternehmen, 2005, Deutscher Sparkassen Verlag. Stuttgart.

Pinkwart A., Proksch D., Schefczyk M., Fiegler T., Ernst C., Reasons for the Failure of New Technology-Based Firms: A Longitudinal Empirical Study for Germany. Credit and Capital Markets, 2015, 48 (4), 597 – 627.

Pleschak F., Ossenkopf B., Wolf B., Ursachen des Scheiterns von Technologieunternehmen mit Beteiligungskapital aus dem BTU-Programm. 2002, Fraunhofer IRB-Verlag, Stuttgart.

Ringle C.M., Wende S., Becker J.M. (2015) "SmartPLS 3" Boenningstedt: SmartPLS GmbH, 2015, http://www.smartpls.com

26 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

Ronkko M., Evermann J., A critical examination of common beliefs about partial least squares path modeling, Organizational Research Methods, 2013, 16, 425–448.

Roy S. and Tarafdar M., The effect of misspecification of reflective and formative constructs in operations and manufacturing management research, The Electronic Journal of Business Research Methods, 2012, 10, 34–52.

Sapienza H.J., When do venture capitalists add value?, Journal of Business Venturing, 1992, 7, 9–27.

Sapienza H.J., Manigart S., Vermeir W., Venture capitalist governance and value added in four countries, Journal of Business Venturing, 1996, 11, 439–469.

Schilling M., Technology Success and Failure in Winner-Take-All Markets: The Impact of Learning Orientation, Timing, and Network Externalities. Academy of Management Journal, 2002, 45, 387-398.

Smolarski J., Verick H., Foxen S., Kut C., Risk management in Indian venture capital and private equity firms: A comparative study, Thunderbird International Business Review, 2005, 47, 469–488.

Tan J., Zhang W., Jun X., Managing risk in a transitional environment: An exploratory study of control and incentive mechanisms of venture capital firms in China, Journal of Small Business Management, 2012, 46, 263-285.

Tang Y., Wu M., Cao Q., Zhou J., How Venture Capital Institutions Affect the Structure of Startups’ Board of Directors, 2014 In Xu J., Cruz-Machado V.A., Lev B., Nickel S. (ed), Advances in Intelligent Systems and Computing, Proceedings of the Eighth International Conference on Management Science and Engineering Management, 2014, Springer, Berlin and Heidelberg, 871–882.

Thornhill S., Amit R., Learning about failure: bankruptcy, firm age, and the resource-based view, Organization Science, 2003, 14, 497-509.

Timmons J.A. and Bygrave W.D., Venture capital's role in financing innovation for economic growth, Journal of Business Venturing, 1986, 1, 161–176.

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

27

Tourani-Rad A. and England C., Characteristics of Venture Capital Firms and Investment Appraisals: Australian Evidence, The Journal of Entrepreneurial Finance, 2003, 8(2), 71-85.

Wang H., Wuebker R.J., Han S., Ensley M.D., Strategic alliances by venture capital backed firms: an empirical examination, Small Business Economics, 2012, 38, 179–196.

Wagner J., The post-entry performance of new small firms in German manufacturing industries. Journal of Industrial Economics, 1994, 42, 141-154.

Yazdipour R. and Constand R., Predicting Firm Failure: A Behavioral Finance Perspective, The Journal of Entrepreneurial Finance, 2010, 14(3), 90-104.

Yoshikawa T., Phan P.H., Linton J., The relationship between governance structure and risk management approaches in Japanese venture capital firms, Journal of Business Venturing, 2004, 19, 831–849.

Zacharakis A.L. and Meyer G.D., The Potential of Actuarial Decision Models: Can They Improve the Venture Capital Investment Decision, Journal of Business Venturing, 2000, 9026, 323–346.

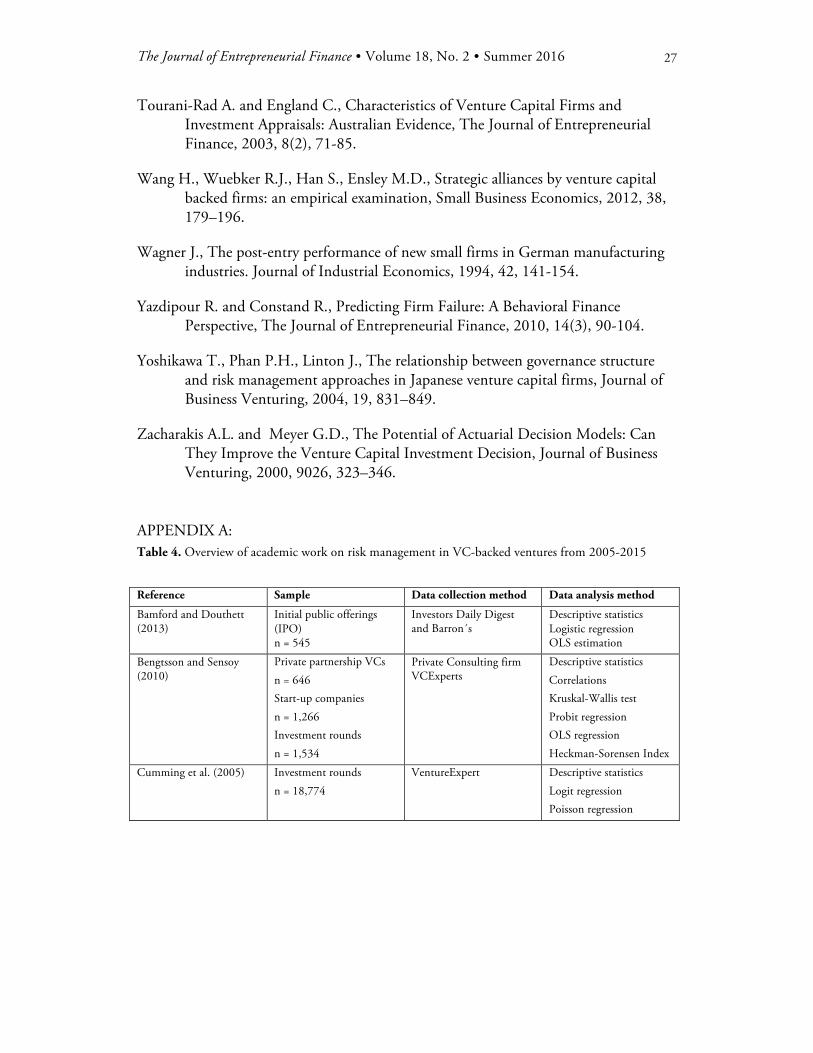

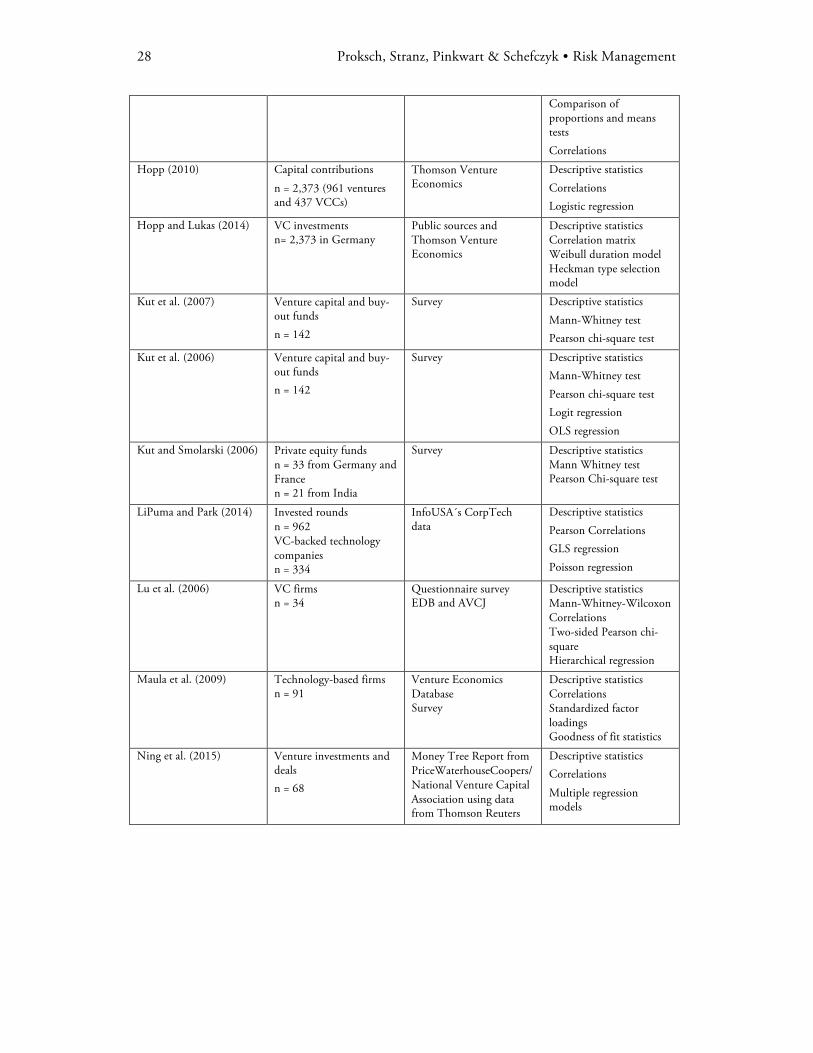

APPENDIX A: Table 4. Overview of academic work on risk management in VC-backed ventures from 2005-2015 Reference Sample Data collection method Data analysis method

Bamford and Douthett (2013)

Initial public offerings (IPO) n = 545

Investors Daily Digest and Barron´s

Descriptive statistics Logistic regression OLS estimation

Bengtsson and Sensoy (2010)

Private partnership VCs n = 646 Start-up companies n = 1,266 Investment rounds n = 1,534

Private Consulting firm VCExperts

Descriptive statistics Correlations Kruskal-Wallis test Probit regression OLS regression Heckman-Sorensen Index

Cumming et al. (2005) Investment rounds n = 18,774

VentureExpert Descriptive statistics Logit regression Poisson regression

28 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

Comparison of proportions and means tests Correlations

Hopp (2010) Capital contributions

n = 2,373 (961 ventures and 437 VCCs)

Thomson Venture Economics

Descriptive statistics Correlations Logistic regression

Hopp and Lukas (2014) VC investments n= 2,373 in Germany

Public sources and Thomson Venture Economics

Descriptive statistics Correlation matrix Weibull duration model Heckman type selection model

Kut et al. (2007) Venture capital and buy-out funds n = 142

Survey Descriptive statistics Mann-Whitney test Pearson chi-square test

Kut et al. (2006) Venture capital and buy-out funds n = 142

Survey Descriptive statistics Mann-Whitney test Pearson chi-square test Logit regression OLS regression

Kut and Smolarski (2006) Private equity funds n = 33 from Germany and France n = 21 from India

Survey Descriptive statistics Mann Whitney test Pearson Chi-square test

LiPuma and Park (2014) Invested rounds n = 962 VC-backed technology companies n = 334

InfoUSA´s CorpTech data

Descriptive statistics Pearson Correlations GLS regression Poisson regression

Lu et al. (2006) VC firms n = 34

Questionnaire survey EDB and AVCJ

Descriptive statistics Mann-Whitney-Wilcoxon Correlations Two-sided Pearson chi-square Hierarchical regression

Maula et al. (2009) Technology-based firms n = 91

Venture Economics Database Survey

Descriptive statistics Correlations Standardized factor loadings Goodness of fit statistics

Ning et al. (2015) Venture investments and deals n = 68

Money Tree Report from PriceWaterhouseCoopers/ National Venture Capital Association using data from Thomson Reuters

Descriptive statistics Correlations

Multiple regression models

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

29

Payne et al. (2009)

VC firms n = 26 VC investors n = 52

Survey Descriptive statistics

Varimax Rotated Factor Loadings Correlations GLS regression Multivariate regression

Pbrimah O, Prakash P (2010)

VC firms n = 584

Jay Ritter´s VentureXpert

Descriptive statistics Tobit regression OLS regression Variance-covariance matrix

Smolarski et al. (2005) Private equity funds n = 32 from UK n = 21 from India

Survey Descriptive statistics Mann-Whitney test Pearson chi-square test

Tan et al. (2008) VC firms n = 53

Survey Descriptive statistics

Wang et al. (2012) VC-backed companies n = 1,757 (772 reporting sales information) Financing rounds n = 5,896 (1,757 VC-backed companies)

VentureXpert Alliances database

Descriptive statistics Correlations Regression analysis (OLS, negative binomal model)

APPENDIX B: Table 5. Descriptive statistics Mean Std.

Dev Scale Data Source

Failure risk

HR risk 3.200 1.317 Rating from 1 to 5 Survey with investment managers

Liquidity risk 3.652 1.152 Rating from 1 to 5 Survey with investment managers

Market risk 3.311 1.304 Rating from 1 to 5 Survey with investment managers

Technology risk 2.711 1.455 Rating from 1 to 5 Survey with investment managers

Assessment and evaluation

Expert assessment 3.795 0.915 Rating from 1 to 5 Survey with investment managers

IP protection 3.435 1.424 Rating from 1 to 5 Survey with investment managers

References of technology 3.806 1.002 Rating from 1 to 5 Survey with investment

30 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

managers

References of founders 4.086 0.686 Rating from 1 to 5 Survey with investment managers

Contracting

Liquidation preference 4.096 0.990 Rating from 1 to 5 Survey with investment managers

Number of syndication partners

2.568 1.975 Metric Term sheet

Investment sum 436,169 206,874 Metric (Euros) Investment committee papers

Investment manager experience and skills

Working experience 3.311 0.932 Rating from 1 to 5 Survey with investment managers

Founding experience 3.237 0.993 Rating from 1 to 5 Survey with investment managers

Technology expertise 3.355 0.842 Rating from 1 to 5 Survey with investment managers

Business skills 3.946 0.578 Rating from 1 to 5 Survey with investment managers

Network size 3.720 0.851 Rating from 1 to 5 Survey with investment managers

Governance

Milestones 4.247 0.789 Rating from 1 to 5 Survey with investment managers

Information through network 4.323 0.710 Rating from 1 to 5 Survey with investment managers

Reporting 4.355 0.653 Rating from 1 to 5 Survey with investment managers

Shares of Founder 83.30 8.830 Per cent Term sheet

Personal exchange 4.323 0.710 Rating from 1 to 5 Survey with investment managers

Management support

Support with competence 3.554 0.881 Rating from 1 to 5 Survey with investment managers

Support with sales 2.681 0.987 Rating from 1 to 5 Survey with investment managers

Support with technology 2.304 1.117 Rating from 1 to 5 Survey with investment managers

Support with strategy 3.839 0.664 Rating from 1 to 5 Survey with investment managers

Support with follow-up financing

4.065 1.046 Rating from 1 to 5 Survey with investment managers

Use of network 3.785 0.900 Rating from 1 to 5 Survey with investment

The Journal of Entrepreneurial Finance • Volume 18, No. 2 • Summer 2016

31

managers

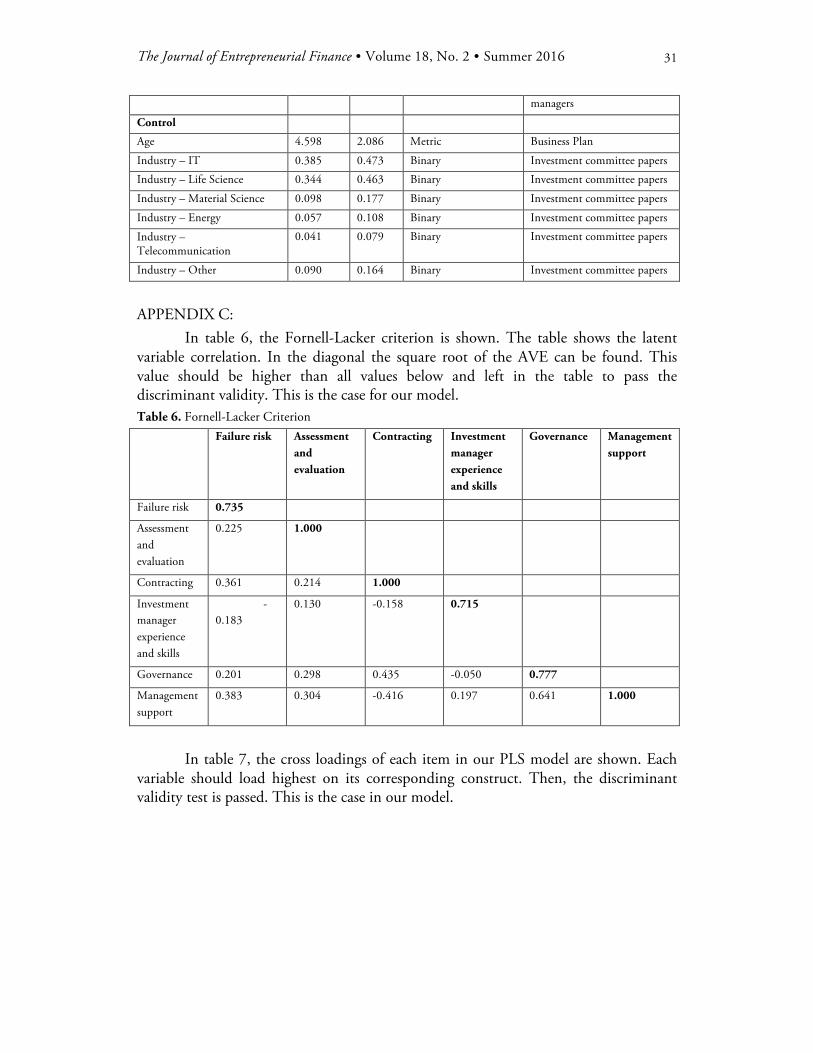

Control

Age 4.598 2.086 Metric Business Plan

Industry – IT 0.385 0.473 Binary Investment committee papers

Industry – Life Science 0.344 0.463 Binary Investment committee papers

Industry – Material Science 0.098 0.177 Binary Investment committee papers

Industry – Energy 0.057 0.108 Binary Investment committee papers

Industry – Telecommunication

0.041 0.079 Binary Investment committee papers

Industry – Other 0.090 0.164 Binary Investment committee papers

APPENDIX C:

In table 6, the Fornell-Lacker criterion is shown. The table shows the latent variable correlation. In the diagonal the square root of the AVE can be found. This value should be higher than all values below and left in the table to pass the discriminant validity. This is the case for our model. Table 6. Fornell-Lacker Criterion Failure risk Assessment

and evaluation

Contracting Investment manager experience and skills

Governance Management support

Failure risk 0.735

Assessment and evaluation

0.225 1.000

Contracting 0.361 0.214 1.000

Investment manager experience and skills

-0.183

0.130 -0.158 0.715

Governance 0.201 0.298 0.435 -0.050 0.777

Management support

0.383 0.304 -0.416 0.197 0.641 1.000

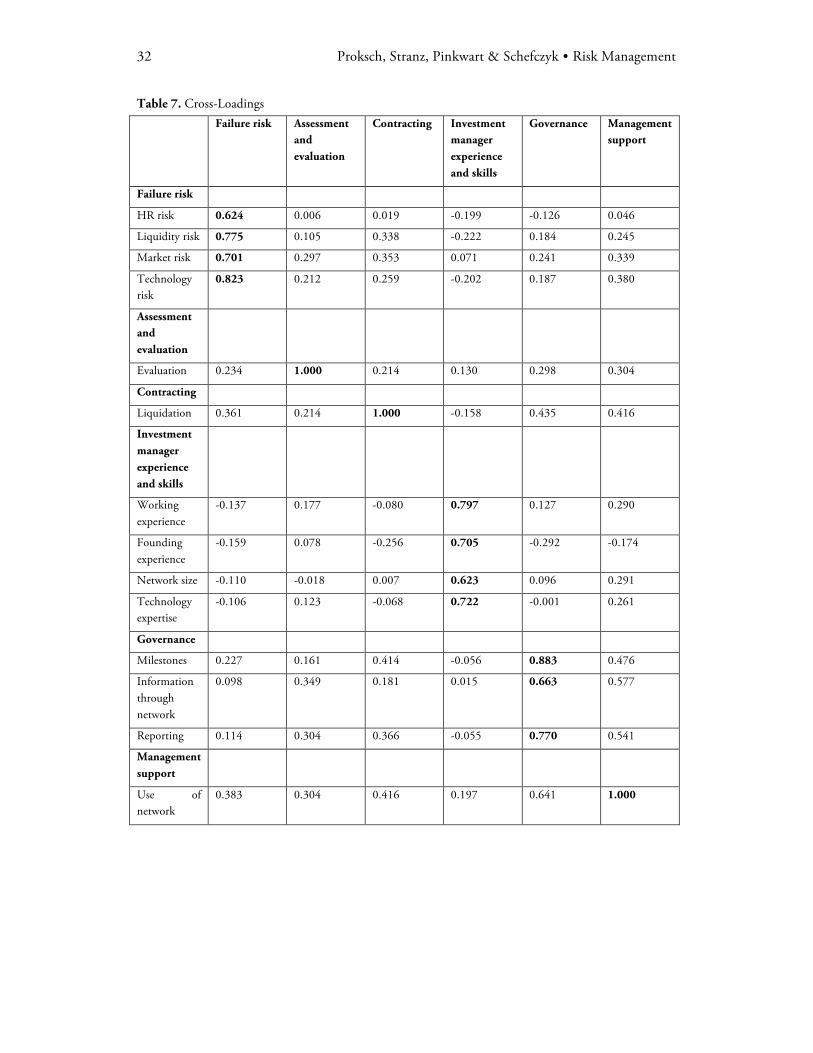

In table 7, the cross loadings of each item in our PLS model are shown. Each

variable should load highest on its corresponding construct. Then, the discriminant validity test is passed. This is the case in our model.

32 Proksch, Stranz, Pinkwart & Schefczyk • Risk Management

Table 7. Cross-Loadings Failure risk Assessment

and evaluation

Contracting Investment manager experience and skills

Governance Management support

Failure risk

HR risk 0.624 0.006 0.019 -0.199 -0.126 0.046

Liquidity risk 0.775 0.105 0.338 -0.222 0.184 0.245

Market risk 0.701 0.297 0.353 0.071 0.241 0.339

Technology risk

0.823 0.212 0.259 -0.202 0.187 0.380

Assessment and evaluation

Evaluation 0.234 1.000 0.214 0.130 0.298 0.304

Contracting

Liquidation 0.361 0.214 1.000 -0.158 0.435 0.416