Update on Private Equity & Venture Capital in Southeast Asia Contents

16

1 Update on Private Equity & Venture Capital in Southeast Asia French Trade Advisors Regional Forum 28 November 2011 ALPANA ADVISORY SERVICES PTE LTD 128 Serangoon North Ave 1 #10-62 Tel/fax : +65 62826795 www.alpana.com.sg Email : [email protected]

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Update on Private Equity & Venture Capital in Southeast Asia Contents

1

Update onPrivate Equity & Venture Capital

in Southeast Asia French Trade Advisors Regional Forum

28 November 2011

ALPANA ADVISORY SERVICES PTE LTD128 Serangoon North Ave 1

#10-62Tel/fax : +65 62826795www.alpana.com.sg

Email : [email protected]

2

Contents

Definitions

Attractiveness

Reality

Alpana Advisory Services Pte Ltd

3

DefinitionsPrivate Equity versus Venture Capital

Alpana Advisory Services Pte Ltd

Private equity consists primarily of acquiring equity investments in unlisted companies at various stages of their development.

French practice uses the term capital investment (capital investissement) to refer generally to investment in unquoted companies and this encompasses venture capital, development, business transfers and buy-outs, and turn-around funds. Venture capital refers to investments in start-up or developing innovative companies with little or no cash flow but strong growth potential. Private equity typically refers to investment in more mature businesses.

Practical Law Handbook – France, 2009

In Asia, principal sources of data are computed by APER, PAI, AVCJ, EMPEA

Private Equity refers to the whole spectrum of investments – Until 2009 the main breakdown was “Buyout/ Non Buy-out”. Since 2010, the main breakdown is “Yuan denominated /Non-Yuan Denominated”.

4

DefinitionsTypical Structure

Alpana Advisory Services Pte Ltd

5

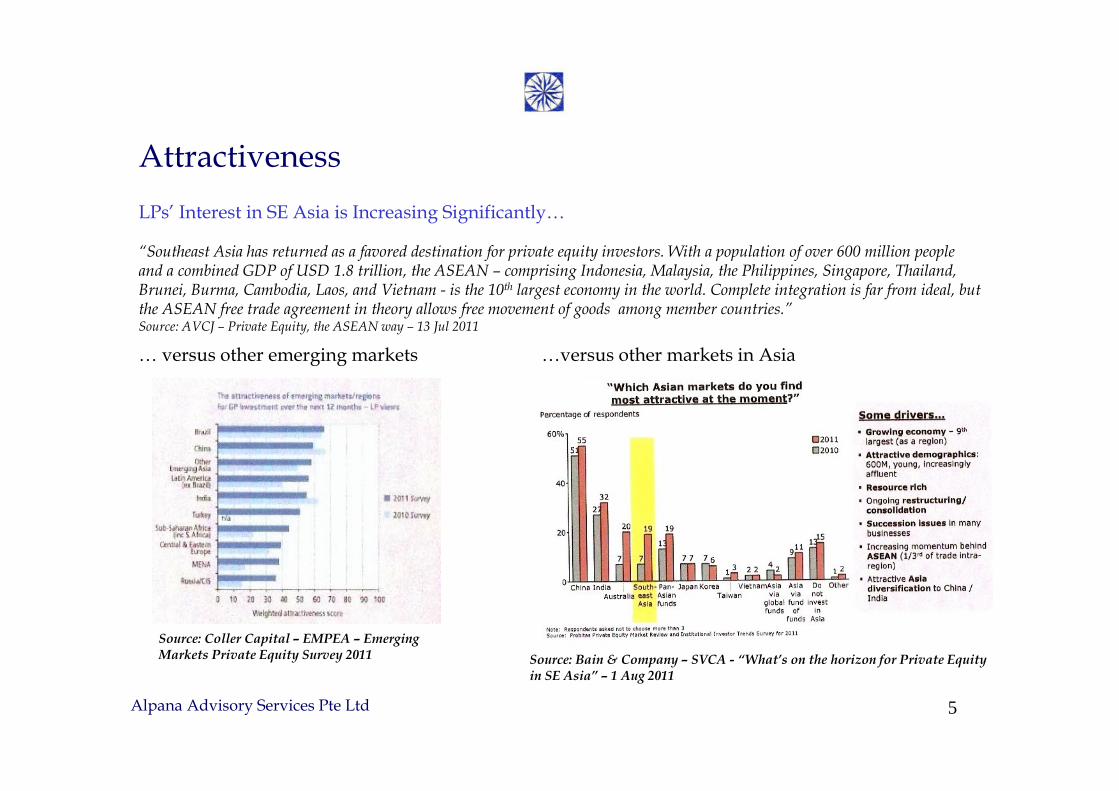

Attractiveness LPs’ Interest in SE Asia is Increasing Significantly…

Alpana Advisory Services Pte Ltd

Source: Coller Capital – EMPEA – Emerging Markets Private Equity Survey 2011

… versus other emerging markets …versus other markets in Asia

Source: Bain & Company – SVCA - “What’s on the horizon for Private Equity in SE Asia” – 1 Aug 2011

“Southeast Asia has returned as a favored destination for private equity investors. With a population of over 600 million peopleand a combined GDP of USD 1.8 trillion, the ASEAN – comprising Indonesia, Malaysia, the Philippines, Singapore, Thailand, Brunei, Burma, Cambodia, Laos, and Vietnam - is the 10th largest economy in the world. Complete integration is far from ideal, but the ASEAN free trade agreement in theory allows free movement of goods among member countries.” Source: AVCJ – Private Equity, the ASEAN way – 13 Jul 2011

6

AttractivenessDrivers & Opportunities

Alpana Advisory Services Pte Ltd

Drivers- Indonesia: surge of interest by the buyout firms, because of the country’s ability

to absorb large amounts of capital + a number of Indonesian conglomerates are now going through a process of rationalization and are looking to sell off some local assets. Global & regional buyout funds (>USD 100 million) are ideal buyers.

- Singapore, Malaysia, Thailand: existing track-record- Vietnam, the Philippines, Cambodia, Myanmar: emerging markets (especially

Vietnam, since all other markets are underinvested) Source: after AVCJ – Private Equity, the ASEAN way – 13 Jul 2011

“Indonesia and Vietnam are excellent consumer growth stories, driven by rising disposable incomes; Singapore, Malaysia and Thailand boast more mature industries that add a level of regulatory clarity other destinations may lack. Natural resources can be found across the region.”Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

Opportunities“This translates into opportunities in areas such as food and beverage, financials, education, retail and healthcare goods and services. The global appetite for resources will also drive growth in commodities, energy, agriculture and infrastructure.”Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

Examples of transactions

- Mar 11: KKR – 10% in Masan Consumer Corporation – USD 159 million (dried noodles and condiments – Vietnam)

- Apr 11: CVC – 15% in Rizal Commercial Banking Corporation – USD 115 million (financial sector – Philippines).

- Jun 11: Carlyle Group – 25% in Garuda Food – USD 200 million (instant food and snacks –Indonesia).

7

AttractivenessSE Asia: a Good Alternative/Diversification to India/China ?

Alpana Advisory Services Pte Ltd

LPs’ Views: High Valuations in China and India are squeezing expected returns

Source: Bain & Company – SVCA - “What’s on the horizon for Private Equity in SE Asia” – 1 Aug 2011

GPs’ View : competition of funds (for example : > 500 funds in India)

Source: Coller Capital – EMPEA – Emerging Markets Private Equity Survey 2011

8

RealitySoutheast Asia : a Small Fraction of the Activity in Asia

Alpana Advisory Services Pte Ltd

Source: APER – 2010 Year-End Issue

Source: AVCJ Private Equity and Venture Capital Report Southeast Asia 2011

Total Capital under Management in Private Equity

Aggregate Asia Fund Pool

“Only a fraction of the money that’s flowing into India and into China is flowing into Southeast Asia.

And that seems an anomaly to us, because actually, when you look at SEA as an aggregate, which I think one can do now because of the ASEAN free trade agreement, where tariffs on 90% of goods and services are down to zero – you have the conditions for cross border growth, cross border M&A across this whole free trade area.

When you aggregate that economy it’s approaching USD 1.8 trillion (with a population of) 60 million people [ vs. Economy of India: USD 1.3 – 1.4 tn] (Nicholas Bloy -Navis)”Source: INSEAD, 21/12/10

9

RealityDeal Value by Destination : SEA Versus Other Markets in Asia

Alpana Advisory Services Pte Ltd

Source: Asia Private Equity Review – October 2011

After peaking at 33%, SE Asia’s share of Asia deals is down to 18% in 2010

Source: Bain & Company – SVCA - “What’s on the horizon for Private Equity in SE Asia” – 1 Aug 2011

10

Reality

Alpana Advisory Services Pte Ltd

As at end of 2010:

1. Singapore : > USD 10 billion (most capital is deployed outside Singapore)2. Malaysia : USD 4.46 billion (the 2nd largest market is less than one third of total Singapore)3. Vietnam: USD 4 billion (fashionable investment destination for years)4. Indonesia: USD 1 billion (USD 192 million in 2009)5. Thailand: USD 642 million (scarcely changed over the past five years)6. Philippines: USD 292 million7. Cambodia: USD 48 million

Source: AVCJ Private Equity and Venture Capital Report Southeast Asia 2011

Capital under Management in Private Equity in Southeast Asia by Countries

11

RealityLPs’ Exposure and GPs’ Views to Southeast Asia Private Equity

Alpana Advisory Services Pte Ltd

Asia-Pacific LPs are less exposed to SEA North than American and European LPs

Source: Coller Capital – Global Private Equity Barometer – Summer 2011

“Of course, Southeast Asia is not without risks. Unstable political situations, corruption, lack of management/corporate governance – the list is not a short one.”Source: AVCJ – Private Equity, the ASEAN way – 13 Jul 2011

“Another obstacle is the region’s apparent inability to absorb capital. For big returns, investors need to deploy at least tens of millions per investment, but these transactions are few and far between.”Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

“Exits are also difficult, especially for GPs that prefer the IPO route”Source: AVCJ – Private Equity, the ASEAN way – 13 Jul 2011

“[PE in this region] is a challenging market and experience and connectivity count for a lot” (Gary Addison, Actis SEA).Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

“A lack of experienced fund managers remain a problem. There are only a handful of domestic GPs in place like in Indonesia and Vietnam, compared to hundreds in China and India”.Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

“It is still a relatively opaque PE market, requiring local knowledge and networks to generate good deal flow” (Gary Ng; CLSA).Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

12

RealityType of Transactions

Alpana Advisory Services Pte Ltd

Source: Asia Private Equity Review – October 2011

Source: Coller Capital – Global Private Equity Barometer – Summer 2011

“Few large-scale transactions have been completed and those that do get done tend not to be buyouts.[…] Small deals dominate. Industry breakdowns for investments made in Southeast Asia as a whole between January 2010 and May 2011 are distorted by one mega-deal Malaysian sovereign wealth fund Khazanah Nasional’sacquisition of Singapore-based Parkway Health for USD 2.3 billion. CVC’s USD 616.3 million investment Indonesia’s Matahari Department Store ranks second, but it is an outlier as far as consumer transactions are concerned.

This doesn‘t indicate a lack of potential targets or a general discomfort with the idea of accepting large portions of foreign capital – the current owners are just unwilling to sell. […] wealthy families account for as much as 70% of economic activity in emerging markets like Indonesia. […] The lack of large buyouts is driven more by the resilience of family businesses. […] The large PE firms have to come to understand that it is easier to work with controlling families – often as minority shareholders – than to try and buy them out.”Source: AVCJ – Private Equity seeks Southeast Asia consumer plays – 15 Jun 2011

“Few large deals: according to AVCJ Research, 3 of the top 5 largest deals in Southeast Asia year-to-date took place in the consumer or financial services area. […] Large-scale transactions are few in number; while 57.4% of funds in SEA are Buy-out vehicles, only 16.6% of deals fall into this category. The majority – at 57.8% - were PIPE transactions”Source: AVCJ – Southeast Asia takes on the neighbors – 3 Nov 2011

13

RealityActive Players

Alpana Advisory Services Pte Ltd

Source: Bain & Company – SVCA - “What’s on the horizon for Private Equity in SE Asia” – 1 Aug 2011

“In terms of Private Equity, this region remains underpenetrated with few firms, most notably Navis, making specialized investments” AVCJ - Private Equity, the ASEAN way- 13 Jul 2011

TPG – US - no 4 worldwide (PEI ranking 2010)CVC, CVC Asia Pacific – UK – no 6 worldwide (PEI ranking 2010)Temasek, SingaporeEmployees Provident Fund, MalaysiaKhazanah Nasional. MalaysiaATIC (Mubadala) – Abu Dhabi (advanced technology)First Reserve Corporation – US (energy sector)Northstar Pacific – Indonesian, partnering with TPG in IndonesiaAncora Capital – US – targeting IndonesiaMubadala – Abu DhabiCitigroupAshmore – UK – specializing in emerging marketsKKR – US – no 3 worldwide (PEI ranking 2010)J&Partner - ? Morgan Stanley - USProvidence Equity – Global media, communications, information,educationBio One – EDBI SingaporeCalyon Financial – (has merged with Societe Generale’s Fimat)->NewedgePinebrook Road – US - energyPrimus Pacific – Asia-based (HK)Actis – Responsible investments in Africa, Asia, Latin AmericaChina-Asean Fund – infrastructure, energy, natural resources (China EximBank)Pamplona – UK – hedge fundsHony Capital – China – sponsored by large Chinese conglomerateApollo – UK Navis - growth-oriented buyouts in South and Southeast AsiaIFC – World BankMirae Assets – Asia-based (HK), investing in emerging countriesJP Morgan - US3i - USEMP – US - emerging markets (founders are ex World Bank executives)Seavi – oldest fund in SingaporeOrix – Japanese financial services Oman Investment Corporation - OmanBaring Asset Management HSBCStandard CharteredAIFSymphony – US (Silicon Valley) - software and servicesGEM – US – emerging markets Vina Capital - Vietnam

14

RealityPerspectives

Alpana Advisory Services Pte Ltd

“[there is a] flowering of an entrepreneurial class across the region. Vietnam, the Philippines, Indonesia and Malaysia are all at different points on the path towards organized retail and commoditized consumerism – and each market presents unique challenges – but there are no shortages of opportunities for growth capital. Backed by investments of anything from USD 5 million to USD 50 million, consumer companies that successfully build out their branch networks and enlarge revenue streams are strong candidates for sale to either larger buyout firms or to multinationals looking for greater Southeast Asian exposure.

With the exception of Vietnam, deal valuations are going up across the region. Given the influx of new investors, this situation isn’t likely to change in the near term. A typical mid-market transaction was USD 20 million ten years ago; it is now USD 50 million today and few are willing to doubt that it will be USD 100 million in ten years time” AVCJ – Private Equity seeks Southeast Asia consumer plays – 15 Jun 2011.

15

Alpana Advisory Services Pte Ltd

Alpana Advisory Services Pte Ltd

Our Services

We are a consultancy company specializing in Corporate and Project Finance Advisory and in Business Development Strategy.

We advise our clients:

- In both strategic and financial aspects of their project in Singapore and Southeast Asia, be it setting up a new business or developing an existing business.- In their decisions whether they should grow internally or externally- In their M&A transactions, especially cross-border acquisitions South & Southeast Asia-France and France-South & Southeast Asia.- In their fund raising with a view to a further expansion of their business in South and Southeast Asia.

16

Alpana Advisory Services Pte Ltd

Thank you for your attention !

Alpana Advisory Services Pte Ltd