An Appraisal of Venture Capital Activity in Ghana

82

UNIVERSITY OF GHANA BUSINESS SCHOOL DEPARTMENT OF ACCOUNTING AN APPRAISAL OF VENTURE CAPITAL ACTIVITY IN GHANA BY OBENG YEBOAH PATRICK (10204175) OSEI-TUTU YAW BRAKO (10205383) AMAMU DAVID (10195666) A DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF BACHELOR OF SCIENCE IN ADMINISTRATION (ACCOUNTING OPTION), DEGREE. MAY 2009.

Transcript of An Appraisal of Venture Capital Activity in Ghana

UNIVERSITY OF GHANA BUSINESS SCHOOL

DEPARTMENT OF ACCOUNTING

AN APPRAISAL OF VENTURE CAPITAL ACTIVITY IN

GHANA

BY

OBENG YEBOAH PATRICK (10204175)

OSEI-TUTU YAW BRAKO (10205383)

AMAMU DAVID (10195666)

A DISSERTATION SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENT FOR THE AWARD

OF BACHELOR OF SCIENCE IN ADMINISTRATION

(ACCOUNTING OPTION), DEGREE.

MAY 2009.

i

DECLARATION

We, the undersigned, hereby declare that except for references to the work of other persons,

which have been duly acknowledged, this dissertation is the product of our own research

completed under the supervision of Mr. R. M. Kuipo. This work has never been presented in

whole or in part for any other degree in this university or elsewhere.

OBENG YEBOAH PATRICK (10204175)

………………………………………………

OSEI-TUTU YAW BRAKO (10205383)

………………………………………………

AMAMU DAVID (10195666)

………………………………………………

MR. R. M. KUIPO (SUPERVISOR)

…..…………………………………..

ii

ACKNOWLEDGEMENT

Our foremost gratitude goes to God for helping us to achieve this feat.

We would also want to acknowledge the following persons and institutions; Fuseini Issah of

Bedrock Venture Capital Finance Company; Isaac Owusu Ansah of Aureos Ghana Advisors;

George of Activity Venture Finance Company; Osei Akuamoah of the Venture Capital Trust

Fund; Fidelity Capital Partners Ltd and the respondents in the various VC SMEs surveyed.

Without you, our study would have been impossible.

We express gratitude to our supervisor, Mr. R.M. Kuipo for his insightful comments and

critique. To all the people who helped us in many small ways but whom we cannot

acknowledge for want of space, we are eternally grateful.

We conclude by saying that we bear sole responsibility for all errors in this dissertation.

iii

DEDICATION

Obeng Yeboah Patrick; This work is dedicated to my parents, Mr and Mrs Yeboah.

Yaw Brako Osei-Tutu; I dedicate this work to my parents, Mr. and Mrs. Osei-Tutu, and to my

whole family. Thanks for your unwavering support.

Amamu David; This work is dedicated to my family and Margaret Adounin

iv

Table of ContentsContent Page

Declaration ........................................................................ i

Acknowledgement ........................................................................ ii

Dedication ……………………………………………… iii

Table of Contents …................................................................... iv

List of Figures ……………………………………………... x

List of Tables ……………………………………………… xi

Abstract ......................................................................... xii

CHAPTER 1: INTRODUCTION...……………………………… 1

1.1 Background to the Study............................................................... 1

1.2 Problem Statement....................................................................... 2

1.3 Research Questions...................................................................... 2

1.4 Significance of the Study............................................................ 2

1.5Overview of Literature................................................................. 3

1.6 Methodology............................................................................... 4

1.6.1 Data Collection............................................................. 5

1.6.2 Data Analysis............................................................... 5

v

1.7 Scope and Limitations................................................................. 5

1.7.1 Scope of the Study...................................................... 5

1.7.2 Limitations of the Study............................................. 5

1.8 Organisation of the Study.......................................................... 5

1.9 References ...................................................................... 6

CHAPTER 2: REVIEW OF LITERATURE ON VENTURE

CAPITAL ACTIVITY................................................................... 7

2.1 Introduction ........................................................................ 7

2.2 Venture Capital – An Overview................................................... 8

2.3 Venture Capital Financing – Nature and Trends.......................... 9

2.3.1 VC Fundraising Process................................................ 11

2.3.2 VC Investment Process................................................. 12

2.4 The Flow of VC – Determinants of VC Investments.................. 13

2.4.1 Factors in the Remote Environment............................. 13

2.4.2 Factors in the Operating Environment......................... 14

2.5 Government Action in Relation to VC....................................... 15

2.5.1 Different Models of Government Intervention........... 16

2.5.2 Policy Initiatives in Ghana – The Venture Capital Trust Fund 16

2.6 Issues in the VC Market – The Equity Gap............................... 17

vi

2.6.1 Assessing VC Return.................................................. 18

2.6.2 Assessing VC Liquidity and Risk............................... 18

2.6.3 Innovation, Growth and Development Prospects for SMEs 19

2.6.4 Bottlenecks in VC Financing..................................... 20

2.6.5 Growth and Development Prospects of VC – Financed SMEs 20

2.7 Conclusion ...................................................................... 21

2.8 References ...................................................................... 21

CHAPTER 3: METHODOLOGY............................................... 27

3.1 Introduction ...................................................................... 27

3.2 Data Collection ...................................................................... 27

3.3 Sampling ....................................................................... 28

3.3.1 Populations................................................................... 28

3.3.2 Sample Size................................................................... 28

3.3.3 Sampling Technique....................................................... 28

3.4 Data Analysis................................................................................. 29

3.5 Limitations of Study Methods....................................................... 30

CHAPTER 4: ANALYSIS AND DISCUSSION OF FINDINGS 31

4.1 Introduction ........................................................................... 31

4.2 State of VC in Ghana. ............................................................... 31

vii

4.2.1 Trends in VC Financing.................................................... 33

4.2.2 Trends in VC Investments................................................ 33

4.2.3 The State of Government Action in Relation to VC......... 38

4.2.3.1Financing Activities – Fundraising..................... 38

4.2.3.2 Investing Activities............................................. 39

4.2.3.2.1 Direct Investment Programme............. 39

4.2.3.2.2 Indirect Investment Programme........... 39

4.2.3.2.3 Programmes Targeted at Demand for

Venture Capital................................................... 40

4.2.3.3 Tax Incentives.................................................... 41

4.3 Factors which Influence the Flow of Funds from VCFCs to VC SMEs 42

4.3.1 Determinants of VC Investments – Initial Investments..... 42

4.3.2 Determinants of Follow-on (Subsequent) Financing.......... 43

4.4 Benefits, Problems and Related Issues in the VC Industry................ 44

4.4.1 Benefits of VC .................................................................. 44

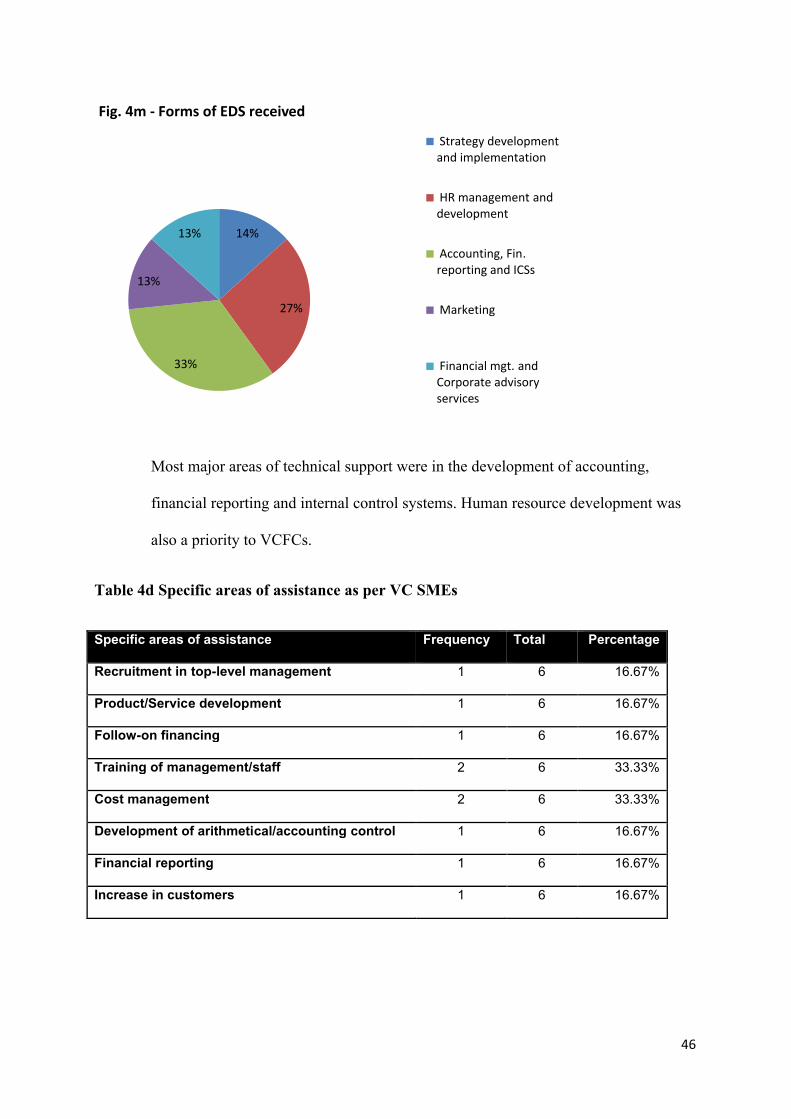

4.4.1.1 Enterprise Development Services......................... 45

4.4.2 Problems in VC ...................................................... 47

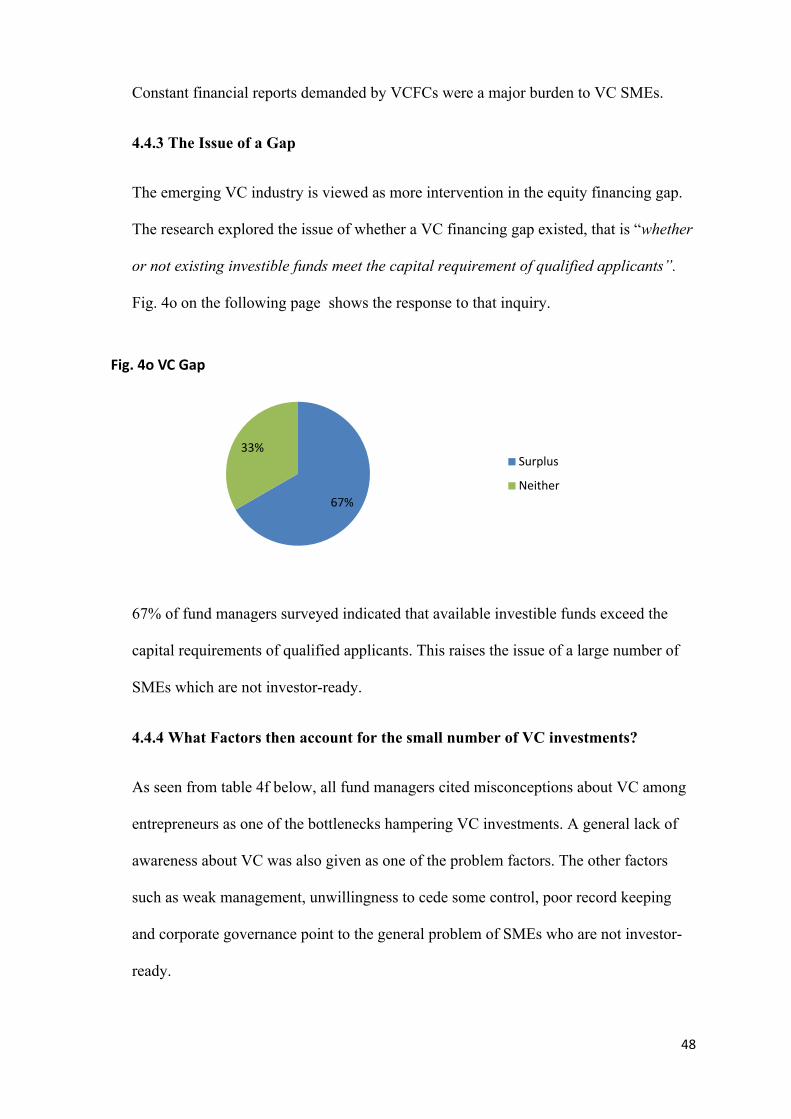

4.4.3 The Issue of a Gap .................................................... 48

viii

4.4.4 What Factors then Account for the Small Number of VC

investments? ..................................................... 48

4.4.5 Regulatory Issues .................................................... 49

4.5 References ............................................................................ 49

CHAPTER 5: SUMMARY, CONCLUSION AND

RECOMMENDATIONS.................................................................... 51

5.1 Introduction ............................................................................ 51

5.2 Summary of Findings ............................................................... 51

5.2.1 Trends in VC Financing.................................................... 51

5.2.2 Trends in VC Investments................................................. 51

5.2.3 State of Government Action.............................................. 52

5.2.4 Benefits, Problems and Issues in VC Financing................ 52

5.2.4.1 Benefits .................................................... 52

5.2.4.2 Problems............................................................. 52

5.2.4.3 Regulatory Issues in VC..................................... 53

5.3 Conclusions ............................................................................ 53

5.4 Recommendations............................................................................ 53

ix

BIBLIOGRAPHY ............................................................................ 54

APPENDIX A ............................................................................. 61

APPENDIX B ............................................................................ 65

x

LIST OF FIGURES

Figures Page

Fig. 4a Source of VC Funds 31

Fig. 4b VC Funders 32

Fig. 4c Trend of Total Capital under Management 32

Fig. 4d Trend of Total VC Investments 33

Fig. 4e Successful Applicants Compared to Total Applicants 34

Fig. 4f Investments by Industry 35

Fig. 4g Investments by Size of enterprise 36

Fig. 4h Type of VC Invested 36

Fig. 4i Trend of Average Deal Size per Year 37

Fig. 4j Investments by Stage of Growth 38

Fig. 4k Approved Investments 39

Fig. 4l VC SMEs Who Receive Enterprise Development Services 45

Fig. 4m Forms of EDS Received 46

Fig. 4n Is Venture Capital Demanding? 47

Fig. 4o VC Gap 48

xi

LIST OF TABLES

Tables Page

Tab. 4a Success Rate (Successful Applicants as a 34

Percentage of Total Applicants)

Tab. 4b Factors Which Determine Initial VC Investments 42

Ranked in Order of Importance

Tab. 4c Benefits of VC as per VC SME Respondents 44

Tab. 4d Specific Areas of Assistance as per VC SMEs 46

Tab. 4e Problems Encountered by VC SMEs 47

Tab. 4f Factors Accounting for the Small Number of VC 49

Investments

xii

ABSTRACT

This exploratory study appraised venture capital (VC) activity, comprising financing

(fundraising) and investing, within the context of SME financing in Ghana. The researchers

set out to identify significant trends in VC financing and investments, including public sector

participation, and determine the critical factors which influence the flow of funds from

finance companies to investee companies. Additionally, the study aimed to isolate key

strengths and weaknesses of the emerging Ghanaian VC industry.

A purposive sampling technique was used to survey the Venture Capital Finance Companies

(VCFCs), SMEs financed by venture capital (VC SMEs) and the Venture Capital Trust Fund

(VCTF). Statistical and financial analysis of the data collected indicated among other things

that over a four year period (2005-2008), most investee companies were those in the larger

scale bracket, and that almost half of investments were made in the real estate and ICT

sectors. Fund managers ranked the business concept of a prospective investee, regardless of

industry, as the most important consideration in making a VC investment decision.

While the survey evidence obtained shows an upward trend in total capital under

management and investments, the study points to a weak regulatory environment and

widespread misconceptions about VC as the major challenges confronting this relatively new

form of entrepreneurial finance.

1

CHAPTER 1

1.0 INTRODUCTION

1.1 Background to the Study

There are limited financing options for SMEs in Ghana. Traditional sources of finance

have consisted mainly of owner’s equity and debt. While a business owner’s savings is

typically inadequate to support business expansion, many find the cost of debt prohibitive

owing to generally high lending rates. Long term finance is essential in the transition

from small business to big business as the investment projects of any growing business

require significant capital commitments. This difficulty in obtaining finance, particularly

long term finance may be the single most important challenge facing small business

owners in Ghana.

Over the past decade, venture capital (VC) has emerged as one more option for

entrepreneurs. In addition to equity financing, venture capital finance companies provide

debt finance and mezzanine (quasi-equity) finance. The VC market although nascent has

widened the spectrum of risk capital options.

The Venture Capital Trust Fund (VCTF) is a scheme established by the Government

through Parliamentary Act 680 passed in November 2004. This fund represents the

greatest public financial intervention in the VC market. The object of the Act is to

establish a venture capital trust fund with the aim of providing investment capital to small

and medium scale enterprises. In addition the Act provides for the development and

promotion of VC financing in the country. A greater percentage of monies from the Trust

Fund will be invested in priority sectors of the economy identified from time to time in

accordance with the Government’s growth strategy.

2

Undoubtedly venture capital will improve SME financing. Improved finance translates

into better prospects for small businesses and ultimately the whole economy.

1.2 Problem Definition

Given the strategic importance of SMEs to national growth and development, the quality

and range of financing options available to them are of prime concern. Because venture

capital is a relatively new source of entrepreneurial finance in Ghana, little is known

about the participants in the VC market. Information on VC financing; the size of funds

raised, amounts invested, the profile of investee companies, how successful the VCTF is

minimal and diffused. In general, the state of VC activity in Ghana is largely

unresearched.

1.3 Research Questions

This exploratory study seeks to undertake a general assessment of venture capital activity

in Ghana through a review of the following questions;

a) What is the state of VC financing in Ghana? What key trends, strengths and

weaknesses characterise the VC industry?

b) What factors influence the flow of VC financing from VC funds to SMEs?

c) Where are the gaps or outstanding issues related to VC market? How do

bottlenecks in the VC industry impair innovation, growth and development of

SMEs?

1.4 Significance of the study

Academically, this study will contribute to the rather limited body of knowledge

concerning the VC environment in general and VC financing in particular. This

contribution could constitute the foundation for additional inquiry.

3

Practically, the findings of this research have policy implications. SMEs form the

majority of business enterprises in Ghana. The success of this economic sector therefore

has important implications for the level of employment, GDP and overall economic

growth and development. Effective policy rests on sound information and analysis, the

results of this research could aid in policy formulation.

1.5 Overview of Literature

Available data from the Registrar General indicates that 90% of companies

registered are micro, small and medium enterprises. This target group has been identified

as the catalyst for the economic growth of the country as they are a major source of

income and employment (Mensah, 2004).

Data on this group is however not readily available. The Ministry of Trade and Industry

(MOTI), in 1998 estimated that the Ghanaian private sector consists of approximately

80,000 registered limited companies and 220,000 registered partnerships.

Generally, this target group in Ghana is defined as:

Micro enterprises: Those employing up to 5 employees with fixed assets

(excluding realty) not exceeding the value of $10,000

Small enterprises: Employ between 6 and 29 employees with fixed assets of

$100,000

Medium enterprises: Employ between 30 and 99 employees with fixed assets

of up to $1million.

Venture capital is a comparatively new source of funding for Ghanaian entrepreneurs.

VC is long-term, hands-on equity investment in privately held, high-growth-potential

companies, initiated and managed by professional investors. Each element of this

4

definition is important.VC investors organize VC firms (through private partnerships or

closely-held corporations) that establish VC funds to raise capital from individual and

institutional investors. Subsequently, VC funds invest in equity-type instruments (such as

shares) issued by SMEs.

VC is usually invested in young, rapidly growing companies that have the potential to

develop into important players in their industry. Venture capitalists evaluate several

hundred investment opportunities each year, but only invest in a few companies that can

offer high returns within five to seven years.

When an SME approaches a Venture Capital financing Company (VCFC), the VCFC is

going to do more than negotiating about the financial terms. Apart from the financial

resources these firms are offering; the VCFC also provides the necessary expertise the

venture is lacking, such as legal or marketing knowledge (Ruhnka and Young, 1987).

There exists an information vacuum with regard to local VC activity.

1.6 Methodology

A detailed outline of the issues on methodology is contained in Chapter 3. The study

adopts a qualitative approach. Purposive sampling, a nonprobability sampling technique

has been adopted. Purposive sampling requires the selection of cases (VCFCs and VC

SMEs) that are especially informative. The cases are then investigated in depth.

Our target populations are;

Venture capital – financed SMEs (VC SMEs)

Venture capital finance companies (VCFCs)

Samples will be chosen from each of the two populations above.

Officials of the VCTF will also be surveyed.

5

1.6.1 Data collection

Although survey questionnaires will be the primary research instrument,

interviews will also be conducted to obtain supplementary information.

1.6.2 Data analysis

Data collected will undergo several dimensions of analysis. Quantitative analysis

will comprise statistical and financial analysis.

1.7 Scope and limitations of the study

1.7.1 Scope of the study

The study will focus on VCFCs and their investee companies in Ghana and the

VCTF.

1.7.2 Limitations of the study

Given the nascence of venture capital activity in Ghana, literature on venture

capital financing in general is limited. There is also the inadequacy of SMEs to

provide comprehensive financial information as a result of simple accounting

systems. These two constraints inhibit exhaustive analysis, evaluation and

interpretation of data.

1.8 Organisation of the study

This study is organized into five chapters;

The first chapter looks at the introduction and general overview of the study.

This gives the background into the study, the problem statement, the

objective of the study and methodology used.

The second chapter discusses the literature review of the study and looks at

an objective view of SME financing schemes in Ghana.

6

The third chapter focuses on the methodology of the research and analysis of

data.

The fourth chapter contains analysis and discussion of our findings

The fifth chapter draws our conclusion to the study, provides

recommendations, and details the contribution of the research findings to the

general body of knowledge.

1.9 References

‘Canadian Venture Capital Activity; An analysis of Trends and Gaps, (1996-

2000)’.

(http://www.pme-prf.gc.ca/eic/site/sme_fdi-prf_pme.nsf/eng/h_01305.html)

Gesellschaft Für Technische Zusammenarbeit (GTZ),(2001) ‘Promotion of

Small and Micro Enterprises Financial Sector Market Study’, Republic Of

Ghana Final Report.

Mensah S. (2004), ‘A review of SME financing schemes in Ghana’, presented

at the UNIDO regional workshop on financing Small and Medium Scale

enterprises, Accra, Ghana.

Ruhnka J.C and Young J.E. (1987), ‘A venture capital model of the

development process for new ventures’, Journal of Business Venturing,

volume: 2, issue: 2, pp: 167-184.

Venture Capital Trust Fund Act, 2004 (Act 680)

‘Venture Capital Financing’ (http://en.wikipedia.org/wiki/venture_capital)

7

CHAPTER 2

2.0 A REVIEW OF LITERATURE ON VENTURE CAPITAL ACTIVITY

2.1 Introduction

SMEs form about 75% of the membership of the Association of Ghanaian Industries (AGI),

(Ablordeppey, 2009). According to some estimates, every 10% of growth by the SME sector

translates in the creation of 45,000 jobs. A major problem that has stymied the growth of

small scale enterprise over the years is the paucity of entrepreneurial finance. Funds managed

by National Board for Small Scale Industries (NBSSI) and the District Industrialisation

Programme (DIP) have been established to aid small businesses. However, for many SME

owners, personal savings (usually inadequate) remain the only option. This problem has

created a situation where many businesses remain small businesses and never make the

transition to large scale operations.

A competitive banking environment has helped to a certain extent. Now many banks have

SME banking divisions and offer financial services dedicated to SMEs. Term loans and trade

financing provided by banks have proved expensive for many entrepreneurs; the high-risk

profile of a high-growth SME is just incompatible with conventional financing arrangements.

So while informal equity (consisting of personal savings, grants from friends and families

etc.) is typically inadequate, bank credit has proved too costly for many growing enterprises.

The emerging venture capital (VC) industry in Ghana fills this equity financing gap – risk

capital options for promising firms have now been increased. This review examines scholarly

literature on the nature, trends and processes of VC financing and investing; public policy

and government action in relation to VC and the factors which impact on the flow of funds

between finance companies and SMEs.

8

2.2 Venture Capital – An Overview

Venture Capital according to the National Venture Capital Association (NVCA) of Canada is

a long-term, hands-on equity investment in privately held, high-growth-potential companies,

initiated and managed by professional investors. Black and Gilson (1998) however define

“venture capital,” consistent with American understanding, as an investment by a specialised

venture capital organisation in high-growth, high-risk, often high-technology firms that need

capital to finance product development or growth and must by the nature of their businesses,

obtain this capital largely in the form .of equity rather than debt. This excludes “buyout”

financing that enables a mature firm’s managers to acquire the firm from its current owners.

Wikipedia’s definition of venture capital is consistent with that given by the NVCA(Canada),

but adds that venture capital investments in these potentially high-growth companies are

undertaken in the interest of generating a return through an eventual realisation event such as

an IPO (Initial Public Offering) or trade sale of the company. It further states that venture

capital investments are generally made as cash in exchange for shares in the invested

company. It should be noted that for the purposes of our study the terms ‘venture capital’ and

‘private equity’ are used interchangeably.

Venture capital typically comes from institutional investors and high net worth individuals

and is pooled together by dedicated investment firms. A venture capitalist (also known as a

VC) is a person or investment firm that makes venture investments, and these venture

capitalists are expected to bring managerial and technical expertise as well as capital to their

investments. Venture capitalists according to Gompers and Lerner (1996) finance these high-

risk, potentially-high reward projects, purchasing equity stakes while the firms are still

privately held. Venture capitalists have backed many high-technology companies including

Microsoft, Intel, Cisco Systems, Lotus and Genentech, as well as a substantial number of

9

service firms. Whether the firm is in a high or low-technology, venture capitalists are active

investors. They monitor the progress of firms, sit on board, and mete out financing. VCs

retain the right to appoint key managers and remove members of the entrepreneurial team. In

addition, venture capitalists provide entrepreneurs with access to consultants, investment

bankers and lawyers.

2.3 Venture Capital Financing – Nature and Trends

First of all, VC investors generally focus on specific industries (see among others Gompers

1995, Amit et al. 1998, Bottazzi and Da Rin 2002). Due to their sectoral specialization, they

allegedly develop context-specific screening capabilities that make them able to judge quite

accurately the commercial value of entrepreneurial projects and the entrepreneurial talent of

the proponents (Chan 1983, Amit et al. 1998). Therefore, they are able to deal effectively

with the adverse selection problems that would otherwise prevent great hidden value firms

from obtaining the financing they need. In turn, relaxation of financial constraints leads to

higher firm growth.

Secondly, VC firms are no silent partners (Gorman and Sahlman 1989, Barry et al. 1990). On

the one hand, they actively monitor portfolio companies. For instance, Kaplan and Strömberg

(2003) show that VC firms control 41.4% of the seats of the board of directors of the US VC-

backed companies that are considered in their study; in 25% of the companies they control

the majority of the board seats. Bottazzi et al. (2004) document that in 66% of the deals of

European VC firms the VC investor obtained one or more seats of the board of the

participated company. Moreover Lerner (1995) highlights that the number of VC investors

who sit in the board of directors is more likely to increase between two financing rounds if

during the same period the top manager of the participated firm is replaced, that is in

situations where monitoring is most important. On the other hand, VC investors make use of

specific financial instruments and contractual clauses (e.g. stage financing) that protect their

investments from opportunistic behaviour on the part of entrepreneurs and create high

10

powered incentives for them (Sahlman 1990, Gompers 1995, Hellmann 1998, Kaplan and

Strömberg 2003).

Thirdly, VC investors allegedly perform a key coaching function to the benefit of portfolio

firms (Gorman and Sahlman 1989, MacMillan et al. 1987, Bygrave and Timmons 1992,

Sapienza 1992, Barney et al. 1996, Sapienza et al. 1996, Kaplan and Strömberg 2003). In

fact, they provide advising services to portfolio companies in fields such as strategic

planning, marketing, finance and accounting, and human resource management, in which

these firms typically lack internal competencies. Accordingly, Hellmann and Puri (2002)

document that VC investors favor the recruitment of external managers, the adoption of stock

option plans, and the revision of human resource policies by portfolio firms, thus contributing

to their managerial “professionalisation”. Bottazzi et al. (2004) show that European VC firms

helped portfolio companies in recruiting outside directors and senior managers in 40.8% and

48.4% of the deals they analyze, respectively. Moreover, portfolio companies take advantage

of the network of social contacts of VC investors with potential customers, suppliers, alliance

partners, and providers of specialized services like legal, accounting, head hunting, and

public relation services (Lindsey 2002, Colombo et al. 2006, Hsu 2004).

Lastly, VC financing signals the good quality of an entrepreneurial business to third parties;

therefore VC-backed companies find it easier to get access to external resources and

competencies that would be out of reach without the endorsement of the VC (Stuart et al.

1999). In accordance with the existence of a “certification effect”, Megginson and Weiss

(1991) found that US VC-backed IPOs exhibit smaller under pricing than non VC-backed

ones that are matched by sector and IPO size. Nonetheless, it is important to acknowledge

that the agency relation between the VC investor and the entrepreneurs of portfolio

companies may engender conflicts, leading to a deterioration of the performance of these

latter companies. In fact, entrepreneurs and external investors may have different strategic

visions; disagreements may absorb the entrepreneurs’ effort and attention to the detriment of

11

the pursuit of business opportunities. Even if no conflict arises, the need of VC investors to

monitor managerial decisions may increase bureaucracy and formalisation of decision

processes, hampering flexibility and the ability of firms to timely grasp business

opportunities.

The VC financing process involves two distinct, sequential steps: fund raising and

investment.

2.3.1 Venture Capital Fundraising Process

Various factors may affect the level of commitments to venture capital organisations.

Poterba (1989b) argues that many of the changes in fundraising could arise from

changes in either the supply of or the demand for venture capital. For example

decreases in capital gains tax rates might increase commitments to venture capital funds

not through increases in the desire for commitments to new funds by taxable investors

but rather through increases in the demand for venture capital investments when

workers have greater incentives to become entrepreneurs. Gompers and Lerner (1997)

found out that most venture organisations raised money either through closed-end funds

or Small Business Investment Companies (SBICs), state-guaranteed risk capital pools

that proliferated during the 1960s. According to them, while the market for SBICs in

the late 1960s and the early 1970s was strong, incentive problems led to the collapse of

the sector. Even so, the annual flow into the venture capital fund during the first three

decades never exceeded a few hundred million dollars and was substantially less.

The sources of capital for VC funds usually establish investment criteria for each fund.

These criteria can be either general or specialized, and tend to reflect the investment

strategies and risk appetites of the providers of capital. In Ghana and other countries,

the main sources of capital are:

Small individual investors, attracted by federal and provincial tax incentives provided

12

through Labour-Sponsored Venture Capital Corporations (LSVCCs), which continue to

play a significant role in the VC industry; Wealthy individual investors, trust and

endowments, diversifying their investment portfolios by funding private independent

VC firms; Chartered banks, which extend their SME financing activities by funding

subsidiary VC firms; Industrial corporations that fund subsidiary VC firms to attract

and develop new technologies in their sectors; Pension funds such as the Social

Security and National Investment Trust (SSNIT) looking for investments to match their

long-term liabilities, either by funding private-independent VC firms or by making

direct investments through their own VC firms; Insurance companies such as SIC

Financial Services Ltd., a subsidiary of the State Insurance Company; Mutual funds

and other money managers that invest modestly in VC to diversify their portfolios.

Other forms of finance provided in addition to venture capitalist equity include:

Clearing banks, Merchant banks, Finance houses and Factoring companies. Mezzanine

firms provide loan finance that is halfway between equity and secured debt. These

facilities require either a second charge on the company's assets or are unsecured.

Because the risk is consequently higher than senior debt, the interest charged by the

mezzanine debt provider will be higher than that from the principal lenders and

sometimes a modest equity will be required through options or warrants. It is generally

most appropriate for larger transactions.

2.3.2 Venture Capital Investment Process

The investment process, from reviewing the business plan to actually investing in a

proposition, can take a venture capitalist anything from one month to one year but

typically it takes between 3 and 6 months. There are always exceptions to the rule and

deals can be done in extremely short time frames. Much depends on the quality of

information provided and made available.

13

2.4 The Flow of Venture Capital – Determinants of Venture Capital Investments

The size of the venture capital investments1 differs from country to country. In Canada for

example, amounts invested have increased by over 139 percent from a little over $1 billion in

1996 to $ 2.5 billion in 2002 (with a peak of 5.8 billion in 2000)2.

As at 2004, the value of investment portfolios held by private equity funds was €20,136.2

million in Germany, €25,539.5 million in France and €59,814 million in the U.K3. There is a

lack of scholarly literature and data on venture capital investments in SMEs in Ghana. Pearce

and Robinson (2009) classified the various environments affecting business, SMEs inclusive,

as the remote, industrial and operating environments. This review will focus on operating-

level factors which affect the flow of venture capital from firms to SMEs.

2.4.1 Factors in the Remote Environment.

The remote environment comprises factors that originate beyond and usually

irrespective of, any single firm’s operating situation; economic, social, political,

technological factors, etc. (Pearce and Robinson, 2009). Economic factors which affect

VC would include the overall savings rate which determines the amount available for

investment within an economy. Examples of Political factors which would affect VC

are government policies and taxation in relation to VC. In OECD (1996), rapid

economic growth in the high-technology industry in South-East Asia was attributed to

government venture capital initiatives.

___________________________________________________________

1 ‘Investment’ here refers to amounts invested in SMEs (investee companies) as opposed to investments in VC funds (funds raised)

2 Data was obtained from the Macdonald & Associates Ltd. – www.canadavc.com

3 Data was obtained from the European Private equity and venture capital association (EVCA) –www.evca.com

14

2.4.2 Factors in the operating environment

The operating environment also referred to as the task or competitive environment

comprises the factors in the competitive situation that affect a firm’s success in

acquiring needed resources or in profitably marketing its goods and services (Pearce

and Robinson, 2009). Factors such as competitive situation, customer profile and a

firm’s human resources are considered operating-level factors and are critically

considered in the VC investment process.

In Hisrich and Jankowicz (1990), three basic constructs are identified as the major

determinants of VC investments; concept, management and returns

Concept entails four main elements. A good concept must; involve a new business idea

(product, service or retail concept); represent a significant earnings potential; offer a

substantial competitive advantage and have reasonable overall capital requirements.

Management is also an essential consideration. VC finance companies want see

managers who exhibit personal integrity and have a convincing track record.

Management is expected to possess the necessary experience and competence to drive

performance while identifying and mitigating risks (Fried and Hisrich, 1994).

Returns comprise three main components. Firstly VCs expect the investment to provide

them with an opportunity for exit as returns are only realised through a public offer, a

sale of the company or a buyback of the investment by the investee company.

Secondly, the investment must offer the potential for a high rate of return. Hurdle rates

internal rates of return are in the 30%-70% range (Fried and Hisrich, 1994). Finally, the

venture must also offer the potential for a high absolute rate of return. In Ljungqvist

and Richardson (2003), VC investments were found to generate returns in excess of 5

to 8 times the initial investment. One interpretation offered this magnitude of returns is

that a return on a VC investment typically represents a compensation for holding a 10

15

year illiquid investment. Venture capital is risk capital, the returns realised must

therefore be commensurate with the inherently risky and illiquid nature of the

investment (Cochrane, 2001). Evidently even though an SME with a unique product or

idea and tremendous market potential can attract VC investment (Gompers, 2001),

finance companies consider several factors before any funds are committed to a

venture.

Some distinctive characteristics of VC-financed SMEs include4;

High-growth orientation that involves rapid potential and demonstrated growth in

sales and market share, based on competitive advantage and dominant market

position.

An International orientation that includes strong potential to penetrate foreign

markets and rapid growth in exports or foreign business operations.

High research and development (R&D) spending to develop unique products

with varied applications, which is required to maintain rapid sales growth and high

profit margins in domestic and foreign markets.

Ownership structures that provide for approximately one-third ownership

holdings by the initial venture capitalists (generally up to a maximum of 50

percent), follow-on venture capitalists and founders.

2.5 Government action in relation to venture capital

According to Lerner (1998), economic analysis identifies informational asymmetries and

social returns as two major reasons for the involvement of government in venture capital.

________________________________________

4. Data was obtained from the Canada Venture Capital and Private equity association (CVCA) – www. cvca.ca

16

Lerner suggests that for some enterprises, social returns exceed private returns and it these

firms that attract funds from government venture finance programmes. It is worthy to note

that public policy responses often tend to focus on engendering sustained economic growth

rather than just profit maximisation in the medium to long term which is the primary

motivation for private venture capitalists. Much of the growth in high-technology firms in

nations such as Israel, Singapore and Taiwan has been attributed to government venture

capital initiatives (OECD, 1996).

2.5.1 Different Models of Government Intervention

Papadimitrious and Mourdoukoutas (2002) identify different public policy approaches

to bridging the start-up equity-financing gap. Three major models or approaches are

defined. The indirect or ‘passive’ approach adopted by the U.S government, the catalyst

approach which is less indirect practiced by Israel and the Irish strategy of government

as an active investor. The three models show the progressive levels of governmental

participation in venture capital financing.

2.5.2 Policy initiatives in Ghana – The Venture Capital Trust Fund

In November 2004, the Venture Capital Trust Fund (VCTF) was established under Act

6805. The only publicly funded VC fund in Ghana presently, it probably represents

government’s largest intervention in bridging the SME equity financing gap. The object

of the fund is to provide financial resources for the promotion of venture capital

financing for small and medium scale enterprises in the economy and also to stimulate

the emergence of a sustainable privately owned venture capital industry in Ghana5.

_________________________________________

5. Data was obtained from the Venture Capital Trust Fund (VCTF) - www.venturecapitalghana.com

17

The fund does not directly finance businesses, instead it forms debt, equity and quasi-

equity partnerships with VCFCs who then build and maintain investment portfolios.

Although any viable enterprise may be considered, the fund’s investment focus is

restricted to certain priority sectors specified by government economic policy. As at the

time of inception, the priority sectors identifies were the pharmaceutical, ICT, tourism

and agro-processing industries. These sectors may benefit from about 55% of the fund.

The remainder is available for other business ventures. The main source of financing

for the fund was 25% the National Reconstruction Levy which was phased out in 2007.

Other sources include monies as earned by the fund in pursuance of its functions and

returns which accrue to the fund from any investment undertaken by the Board (Act

680). The fund is managed by a 9 member board of trustees appointed by the President

in Consultation with the Council of State.

Day-to-day administration of the trust fund is carried out by the Secretariat which is

headed by an administrator who is a full member of the board5. Through the VCTF, the

government has seemingly adopted the ‘catalyst approach’ to the development of

venture financing.

2.6 Issues in the Venture capital market – The Equity gap

According to UNIDO (1999), the provision of equity capital has a place in the financing of

small businesses in Africa but it can only fill a financing 'niche' which might be called 'the

equity gap' to generate an adequate balance between debt and equity. Most venture capitalists

will not invest principally in small enterprises, since high return opportunities are relatively

few; risks are high and 'exits' very difficult. In western countries, such investments take place

in smaller companies, to finance the initial concept of a business, product development,

18

expansion or to prepare a company for a public offering, typically in innovative or 'high-tech

fields’.

In the African context, it is hard to find such cases, though competitive advantages in the

low(er)-technology and service sectors with export potential could provide VC opportunities.

Agro business projects might also offer opportunities. As an indication of the risky nature of

venture capital in smaller firms in developed countries, the statistics usually quoted are that

20-30% of investments end in total losses, around 40% are survivors but with little growth

prospects or hopes of profitable assets sales. Only about 20% (at the most 30%) are successes

in which substantial returns and profits are made, often enough to cover the losses sustained

in the others. There is therefore the need to assess the potential risk (liquidity risk) and

returns of venture capital financing by the VCFC in Ghana, in light of the conditions for

offering and participating in the SMEs capital.

2.6.1 Assessing Venture Capital Return

A natural way to estimate venture capital returns is to examine the returns of venture

capital funds, rather than the underlying projects. This is not easy either. Most venture

capital funds are organized as limited partnerships rather than as continuously traded or

even quoted entities. Thus, one must either deal with missing data during the interim

between investments and payout, or somehow mark the unfinished investments to

market. Bygrave and Timmons (1992) found an average internal rate of return of 13.5%

for 1974-1989. The technique does not allow any risk calculations. This brings into fore

the issues in determining liquidity risk.

2.6.2 Assessing venture capital liquidity risk

The decision to invest in an SME by a VCFC is highly difficult one with adverse

selection risk. Venture capitalists (“VCs”) invest in small private growth companies

19

that typically do not have cash flows to pay interest on debt or dividends on equity.

VCs invest in private companies over a period that generally ranges from 2-7 years

prior to exit. As such, VCs derive their returns through capital gains in exit transactions.

IPO exits typically provide VCs with the greatest returns and reputational benefits to

venture capitalists (Gompers, 1996; Gompers and Lerner, 1999, 2001).

Liquidity risk in the context of venture capital finance therefore refers to exit risk,

particularly IPO exit risk. That is, liquidity risk refers to the risk of not being able to

effectively sell exit and thus being forced either to remain much longer in the venture or

to sell the shares at a high discount. The risk of not being able to effectively exit an

investment is an important reason for why venture capitalists require high returns for

their investments (Lerner, 2002; Lerner and Schoar, 2002). It is therefore natural to

expect that exit market liquidity affects VCs’ incentives to invest in different types of

entrepreneurial firms.

2.6.3 Innovation, Growth and Development prospects for SMEs

Porter (1990) defines innovation as «an attempt to create competitive advantage by

perceiving or discovering new and better ways of competing in an industry and

bringing them to market». Put briefly, innovation is the commercialization of new ideas

(Simmie, 2006). In 1996 little was known about the extent of innovation in SMEs. At

that time most facts and figures covered large firms but not much was known about

SMEs. At that time, ‘innovation’ was not a word used frequently; ‘technology’ and

‘R&D‘(Research & Development) received the most consideration. EIM (Executive

Interim Management) completed a study in 1996 to gain more insight into what

innovation means in small businesses, and how innovativeness can be measured in

practice. The first innovation report was published to present SME innovation figures.

Innovation in industrial sectors was measured using 13 indicators distinguishing

20

between inputs, processes and outputs of innovation. These indicators visualized the

method and organization of innovation in SMEs is better than traditional indicators

such as R&D-expenses and numbers of patents. The foreword in the report makes clear

that the publication of SME-figures was not as straightforward as it might seem to be

nowadays (EIM, 2009).

2.6.4 Bottlenecks in VC Financing

According to Fritsch and Schilder (2006), interviews with 85 German investors,

indicates, however, that the importance of closeness and proximity between investor

and company is widely overestimated in the literature. A conclusion from this survey is

therefore that the absence of venture capital investors in an area does not represent a

bottleneck for innovative entrepreneurs in Germany. Fritsch and Schilder conclude that

from the investors’ point of view the biggest bottleneck is simply the existence of

sufficiently good investment opportunities.

2.6.5 Growth and Development Prospects of VC – financed SMEs

Opinions vary about how successful VCs are in allocating resources. Chan (1983)

argues that the presence of a VC encourages efficient capital allocation. Amit, Glosten,

and Muller (1990a, p.110), though, are more critical, stating: Under the current

institutional structure of the venture capital industry, the most promising entrepreneurs

will not seek venture capital financing, and are likely to make slower progress in the

development and commercialization of emerging technologies. Further, those

entrepreneurs that are backed by venture capital are less likely to succeed in developing

their ventures because of their relatively low ability.

21

2.7 Conclusion

From the literature reviewed, venture capital can be summarised as value-added finance, as

venture capitalists not only provide investment capital but also business development services

such as marketing, strategy development and financial management. While VC financing as a

measure to bridge the entrepreneurial equity financing gap has been extensively researched

and documented in other countries, there is a paucity of information regarding the same in

Ghana. The nature and trends; the major factors which impact on the flow of funds between

VC finance companies and SMEs; and the general bottlenecks in the industry are largely

unknown. This study seeks to reduce this knowledge gap and contribute to the body of

knowledge on SME financing in Ghana.

2.8 References

1. Ablordeppey D. S. (2009), “SME agenda makes progress”, Daily Graphic, issue:

Tuesday, January 13, pp: 33.

2. Black, B. S., and Gilson, R.J.(1998), “Venture capital and the structure of capital

markets: banks versus stock markets”. Journal of Financial Economics 47, 243-277.

3. Amit, R., L. Glosten, and E. Muller (1990a), "Does Venture Capital Foster the Most

Promising Entrepreneurial Firms?" California Management Review (Spring), 102-111.

4. Amit, R., Brander, J., Zott, C., (1998). “Why do venture capital firms exist? Theory

and Canadian evidence”, Journal of Business Venturing 13, 441–466.

5. Barry, C.B., Muscarella, C.J., Peavy, J.W., Vetsuypens, M.R., (1990). “The role of

venture capital in the creation of public companies”, Journal of Financial Economics

27, 447–471.

22

6. Black, Bernard S., and Ronald J. Gilson (1997), “Venture Capital and the Structure of

Capital Markets: Banks versus Stock Markets,” Journal of Financial Economics

forthcoming

7. Bottazzi, L., Da Rin, M.(2002), “Venture capital in Europe and the financing of

innovative companies”, Economic Policy 17, 229-269.

8. Bottazzi, L., Da Rin, M., Hellmann, T. (2004), “Active financial intermediation:

evidence on the role of organizational specialization and human capital”, Finance

working paper No. 49-2004, ECGI.

9. Bygrave, William D. and Jeffrey A. Timmons(1992), “Venture Capital at the Cross-

Roads” Boston, Harvard Business School Press

10. Canadian Venture Capital and Private Equity Association (www.cvca.com)

11. Chan, Y.S., (1983). “On the positive role of financial intermediation in allocation of

venture capital in market with imperfect information”, Journal of Finance 35, 1543-

1568

12. Cochrane J. (2001), "The Risk and Return of Venture Capital", mimeo Chicago

Graduate School of Business.

13. Colombo, M.G., Grilli, L., Piva, E., (2006). “In search for complementary assets: the

determinants of alliance formation of high-tech start-ups”, Research Policy 35,

1166-1199.

14. EIM (2009), “Ten years entrepreneurship policy: a global overview”, January 2009

15. European Private equity and venture capital association (EVCA) (www.evca.com)

16. Fried V. H. and Hisrich R.D (1994), “The Venture Capitalist: A Relationship

Investor”, California Management Review

23

17. Fritsch M. and Schilder D. (2006),“Does Venture Capital Investment Really Require

Spatial Proximity?”, Discussion Papers on Entrepreneurship, Growth and Public

Policy, Technical University of Freiberg.

18. Gompers, P. (1995), “Optimal Investment, Monitoring, and the Staging of Venture

Capital,” Journal of Finance 50 (5), pp. 1461-1489.

19. Gompers, P. (1996), “Grandstanding in the Venture Capital Industry,” Journal of

Financial Economics 42, pp: 133-156

20. Gompers, Paul A., and Lerner, J. (1999), “The Venture Capital Cycle”, MIT Press.

21. Gompers, P. (2001), ‘A Note on the Venture Capital Industry’, Harvard Business

School, Boston.

22. Gompers, Paul A., and Lerner J. (1996), “The use of covenants: An analysis of

venture partnership agreements”, Journal of Law and Economics 39, 463-498.

23. Gompers, Paul A., and Lerner J. (1997), “Risk and Reward in Private Equity

Investments: The Challenge of Performance Assessment”, Journal of Private Equity

(Winter 1997): 5-12.

24. Gompers, P.A., and Lerner J. (2001), “The Money of Invention: How Venture

Capital Creates New Wealth”. Cambridge: Harvard Business School Press

25. Gorman M. and William A. S. (1989), “What do Venture Capitalists Do?,” Journal

of Business Venturing 4, pp. 231-248

26. Hellmann, T. (1998), “The allocation of control rights in venture capital contracts”,

Rand Journal of Economics 29, 57– 76.

27. Hellmann, T., Puri, M. (2002), “Venture capital and the professionalization of start-

up firms: empirical evidence”, Journal of Finance 57, 169-197.

24

28. Hisrich D. and Jankowicz A.D (1990), ‘Intuition in Venture Capital Decisions: An

Exploratory Study’, Journal of Business Venturing , January, pp 49-62

29. Hsu, D. (2004), “What do Entrepreneurs Pay for venture capital Affiliation?”

Journal of Finance 59.

30. Kaplan, S. And Stromberg P. (2003), “Financial contracting theory meets the real

world: an empirical analysis of venture capital contracts”, Review of Economic

Studies 70, pp: 281-315.

31. Lerner, J. (1995), “Venture Capitalists and the Oversight of Private Firms,” Journal

of Finance 50, pp: 301-318

32. Lerner J. (1998), The Long-run Impact of the SBIR Program

33. Lerner, J. (2002), “Boom and Bust in the Venture Capital Industry and the Impact on

Innovation”, Federal Reserve Bank of Atlanta Economic Review 4, pp: 25-39.

34. Lerner, J., and A. Schoar (2002), “The Illiquidity Puzzle: Theory and Evidence from

Private Equity,” forthcoming in the Journal of Financial Economics.

35. Lerner, J. (1995). “Venture Capitalists and the Oversight of Private firms”, Journal

of Finance 50, pp: 301-318.

36. Lindsey, L., (2002). “The venture capital Keiretsu effect: an empirical analysis of

strategic alliances among portfolio firms”, Working paper, Stanford University

37. Ljungqvist, A. and Richardson, Matthew P. (2003), “The Cash Flow, Return and

Risk Characteristics of Private Equity”, Finance Working Paper No. 03-001, NYU.

38. ‘Macdonald & Associates Ltd.’ (www.canadavc.com)

25

39. MacMillan, I.C., Kulow, D.M., Khoylian, R. (1989), “Venture capitalists’

involvement in their investments: extent and performance”, Journal of Business

Venturing 4, pp: 27-47

40. MacMillan, I.C., Zemann L., and Subbanarasimha P.N. (1987), "Criteria

Distinguishing Successful from Unsuccessful Ventures in the Venture Screening

Process," Journal of Business Venturing (Spring), pp: 123-137.

41. Megginson, W., Weiss, K. (1991). “Venture capitalist certification in initial public

offerings”, Journal of Finance 46, pp: 879-903.

42. Organisation for Economic Cooperation and Development (OECD)(1996),

Government Programmes for Venture Capital, OECD, Paris.

43. Papadimitrious S. and Mourdoukoutas P. (2002), Bridging the Start-up Equity

Financing Gap, European Business Review, Volume 14, No. 2, pp: 104-110

44. Pearce J. A. and Robinson R. B. (2009), “Formulation, Implementation and Control

of Competitive Strategy”, 11th ed., McGraw-Hill Irwin Inc. New York, NY

45. Porter, M. (1990), “The Competitive Advantage of Nations”, Macmillan, London

and Basongstoke

46. Poterba, J. (1989), “Venture capital and capital gains taxation” in: Lawrence H.

Summers (ed.), Tax Policy and the Economy 3, Cambridge: MIT Press, pp: 47-67.

47. Sapienza, H., Manigart, S., and Vermeir, W. (1996),“ Venture capital governance

and value-added in four countries”. Journal of Business Venturing, 11, pp: 439-469.

48. Sahlman, W.A., (1990). “The structure and governance of venture-capital

organizations”, Journal of Financial Economics 27, pp: 473-521.

26

49. Simmie, J. (2006). Do Clusters or innovation systems drive competitiveness? In

Asheim, Cooke and Martin, Clusters and Regional Development. London:

Routledge.

50. Stuart, T.E., Hoang, H., Hybels, R. (1999). “Interorganisational endorsements and

the performance of entrepreneurial ventures”, Administrative Science Quarterly 44,

pp: 315-349.

51. Oyen L. V. and Levitsky J. (UNIDO) (March 1999), “Financing of Private Enterprise Development in Africa”, Working Paper No. 2, commissioned by the Small and Medium Industries Branch.

52. ‘Venture Capital Financing’(http://en.wikipedia.org/wiki/venture_capital)

53. ‘Venture Capital Trust Fund’(www.venturecapitalghana.com)

27

CHAPTER 3

3.0 METHODOLOGY

3.1 Introduction

This chapter details the overall strategy employed in the survey dilating on matters such

as the data collection methods, the target population, the sample size and sampling

technique, the method of analysis and the limitations of the study methods. The study

adopts a qualitative sampling approach; however some quantitative tools are used in data

analysis.

3.2 Data Collection

Primary and secondary data were used for data collection. Primary data were obtained

through survey questionnaires and interviews, and secondary data were collected from

sources such as the internet, library search and indexing, magazines and journals.

To avoid problems associated with conducting interviews, interviewees were given prior

notice. The investment coordinator of the Trust Fund was interviewed in this manner.

Questionnaires were used for the VCFCs and the VC SMEs. The respondents consisted

mainly of managers in finance and accounting roles for the SMEs and fund managers for

the Venture Capital Finance Companies and the Trust Fund. While questionnaires were

personally administered to the managers in the SMEs, the questionnaires for the VCFCs

were self-administered. The questionnaires for the VCFCs demanded greater breadth and

depth of information, and therefore the investment managers needed more time. Some

fund managers were interviewed in order to gain supplementary information.

28

3.3 Sampling

3.3.1 Populations

Sample populations were chosen from each of the two target populations below.

The target populations were;

Venture Capital – Financed SMEs (VC SMEs).

Venture Capital Finance companies (VCFCs).

The investment coordinator of the Venture Capital Trust Fund was also

interviewed.

3.3.2 Sample Size

The venture capital industry in Ghana is an emerging one, and as at the time of the

research, 5 finance companies were identified. 4 of them were surveyed, yielding a

sampling ratio of 80%.

The small number of VCFCs gives an indication of the number of VC SMEs. Based

on information gathered from all the VCFCs, the total VC SME population was

estimated at around 22. This list of VC SMEs constituted our sampling frame. Out

of this estimate, 9 VC SMEs were surveyed yielding a sampling ratio of

approximately 41 %.

3.3.3 Sampling Technique

For the purposes of this study, purposive sampling, a non-probability sampling

technique was adopted. Purposive sampling requires the selection of cases (VCFCs

and VC SMEs in our case) that are especially informative. These cases are then

investigated in depth. The respondents were selected with a clear purpose in mind.

The central purpose in our case was to locate VC SMEs which were microcosmic

29

of the venture capital industry in Ghana. To that end, the sample of VC SMEs was

drawn from across all VCFC portfolios and can therefore be considered to be fairly

representative.

3.4 Data Analysis

Two software packages were used; the Statistical Package for the Social Sciences

(SPSS) and Microsoft Excel. Quantitative analysis focused on;

Statistical analysis to ascertain;

The demographics of VC SMEs

The demographics of VCFCs

Distribution of VC SMEs by size, stage of growth, industry etc.

The proportion of successful SME – applicants

A financial analysis was performed to determine;

The types of VC invested

The investment preferences of Fund managers

Qualitative analysis;

Extracted key trends and defining strengths and weaknesses of VC activity

Ghana

Identified gaps and bottlenecks in the financing process

Examined the relevance of the government policy framework for VC financing

within the context of the current data obtained.

30

3.5 Limitations of Study Methods

Non-probability sampling techniques are subject to the biases of the researcher. All the

VC SMEs sampled were in the Greater Accra region of Ghana. Although most VC SMEs

are located in this region, samples from other geographic areas might have yielded a

more comprehensive result.

Besides this geographic limitation, research was constrained by the inadequacy of

disclosure from some VCFCs and VC SMEs. Additionally, the duration of the study

limited extensive data collection and analysis.

31

CHAPTER 4

4.0 ANALYSIS AND DISCUSSION OF FINDINGS

4.1 Introduction

Although secondary data was used, interviews and questionnaires were the major sources of

data for this analysis. The analysis (both quantitative and qualitative) conducted in this

chapter seeks to provide the descriptive statistics and information relevant to the research

questions.

4.2 State of Venture Capital in Ghana.

4.2.1 Trends in VC Financing

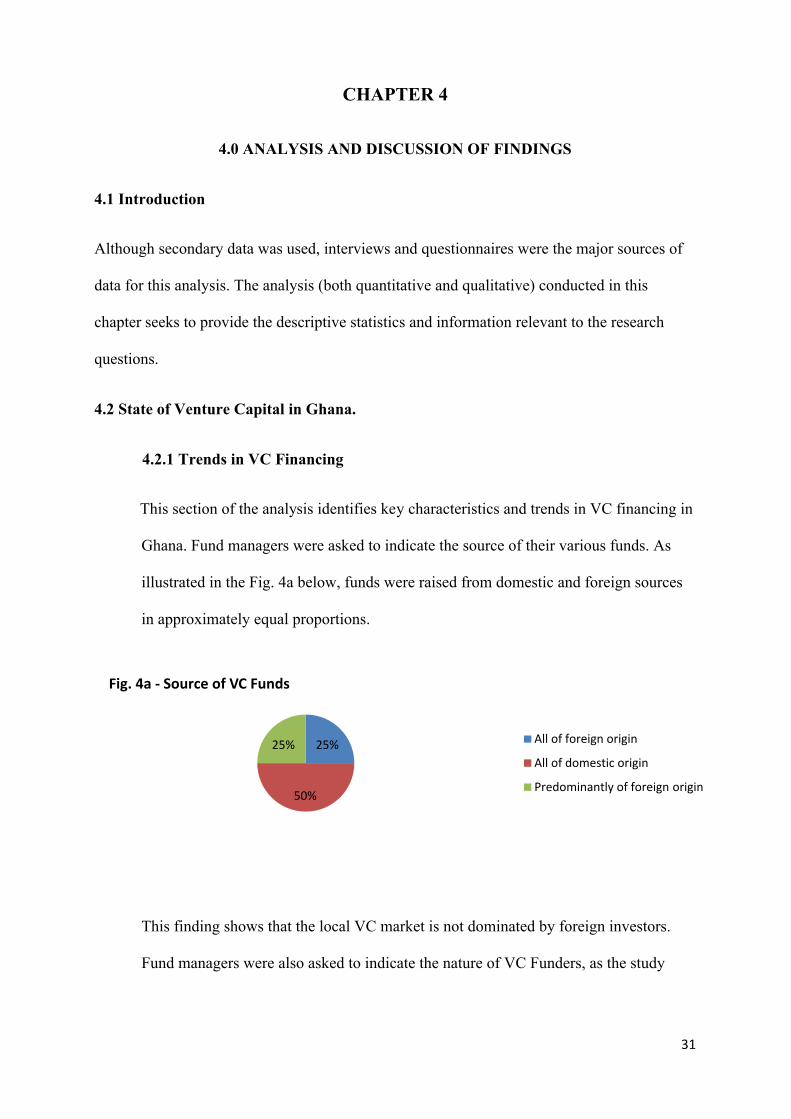

This section of the analysis identifies key characteristics and trends in VC financing in

Ghana. Fund managers were asked to indicate the source of their various funds. As

illustrated in the Fig. 4a below, funds were raised from domestic and foreign sources

in approximately equal proportions.

This finding shows that the local VC market is not dominated by foreign investors.

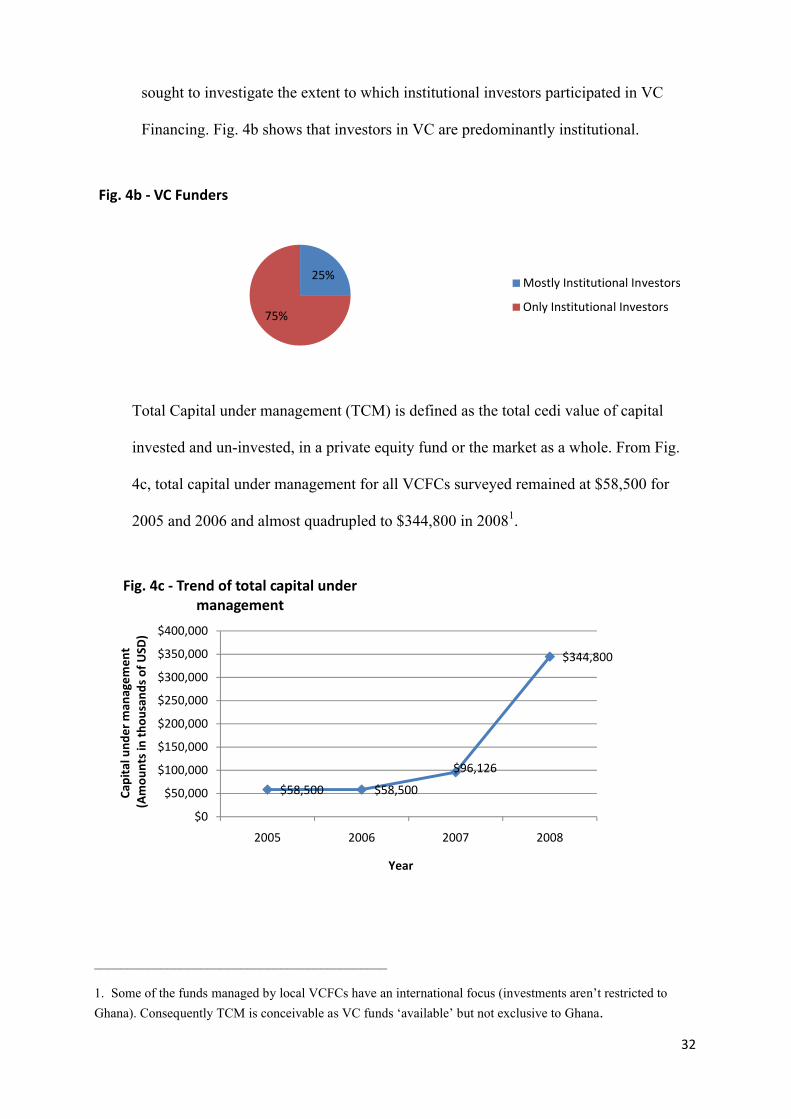

Fund managers were also asked to indicate the nature of VC Funders, as the study

25%

50%

25%

Fig. 4a - Source of VC Funds

All of foreign origin

All of domestic origin

Predominantly of foreign origin

32

sought to investigate the extent to which institutional investors participated in VC

Financing. Fig. 4b shows that investors in VC are predominantly institutional.

Total Capital under management (TCM) is defined as the total cedi value of capital

invested and un-invested, in a private equity fund or the market as a whole. From Fig.

4c, total capital under management for all VCFCs surveyed remained at $58,500 for

2005 and 2006 and almost quadrupled to $344,800 in 20081.

____________________________________________

1. Some of the funds managed by local VCFCs have an international focus (investments aren’t restricted to

Ghana). Consequently TCM is conceivable as VC funds ‘available’ but not exclusive to Ghana.

25%

75%

Fig. 4b - VC Funders

Mostly Institutional Investors

Only Institutional Investors

$58,500 $58,500

$96,126

$344,800

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2005 2006 2007 2008

Capi

tal u

nder

man

agem

ent

(Am

ount

s in

thou

sand

s of

USD

)

Year

Fig. 4c - Trend of total capital undermanagement

33

4.2.2 Trends in VC Investments

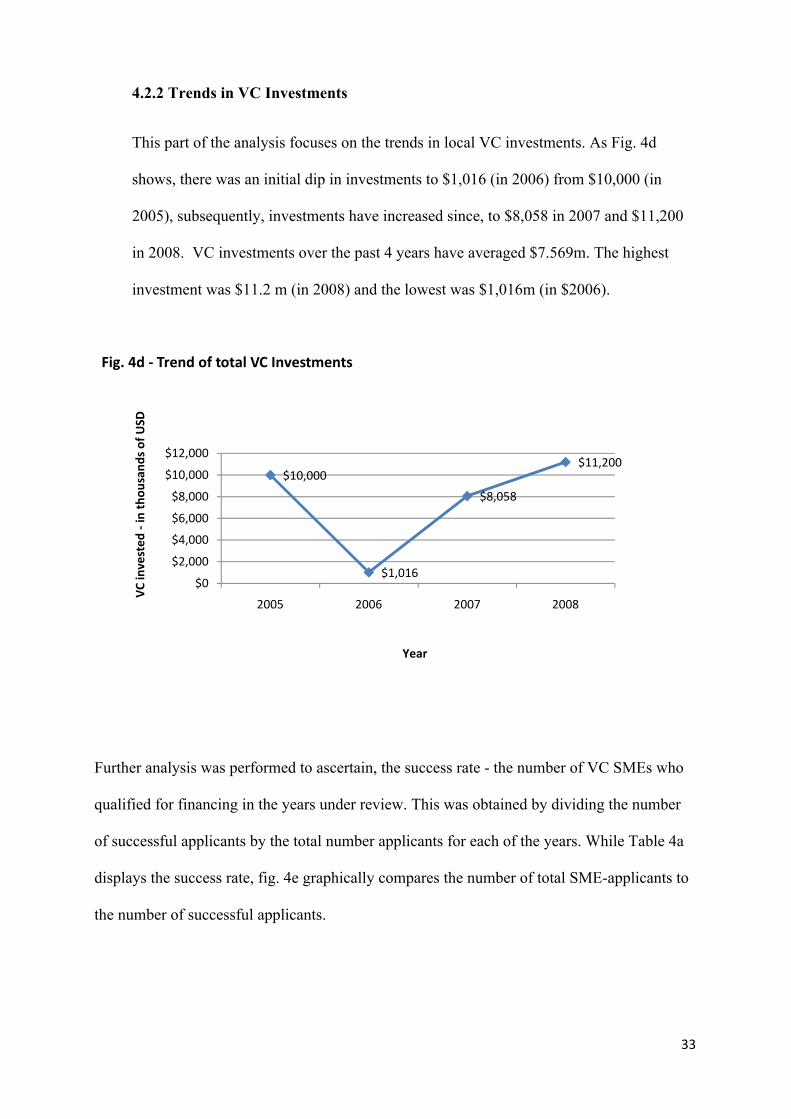

This part of the analysis focuses on the trends in local VC investments. As Fig. 4d

shows, there was an initial dip in investments to $1,016 (in 2006) from $10,000 (in

2005), subsequently, investments have increased since, to $8,058 in 2007 and $11,200

in 2008. VC investments over the past 4 years have averaged $7.569m. The highest

investment was $11.2 m (in 2008) and the lowest was $1,016m (in $2006).

Further analysis was performed to ascertain, the success rate - the number of VC SMEs who

qualified for financing in the years under review. This was obtained by dividing the number

of successful applicants by the total number applicants for each of the years. While Table 4a

displays the success rate, fig. 4e graphically compares the number of total SME-applicants to

the number of successful applicants.

$10,000

$1,016

$8,058

$11,200

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2005 2006 2007 2008

VC in

vest

ed -

in th

ousa

nds

of U

SD

Year

Fig. 4d - Trend of total VC Investments

34

Table 4a - Success rate ( successful applicants as a percentage of total applicants)

Year Success Rate (%)

2005 3.1

2006 1.9

2007 2.1

2008 3.5

Average 2.7

Fig. 4e shows that the proportion of successful applicants to unsuccessful applicants is very low,

an average success rate of 2.7 % (from Table 4a). However, even this success rate is higher than

the Canadian average of less than 1%2.

____________________________________________

2. According to the Statistics Canada Study of Growth SMEs in 1996, only 5 percent of growing SMEs (about 0.04 percent

of all SMEs in Canada) would be considered potential investment targets by venture capitalists.

98 104

387

231

3 2 8 80

50100150200250300350400450

2005 2006 2007 2008

Num

ber o

f app

lican

ts

Year

Fig. 4e - Successful applicants compared to total applicants

Total applicants

Successful applicants

35

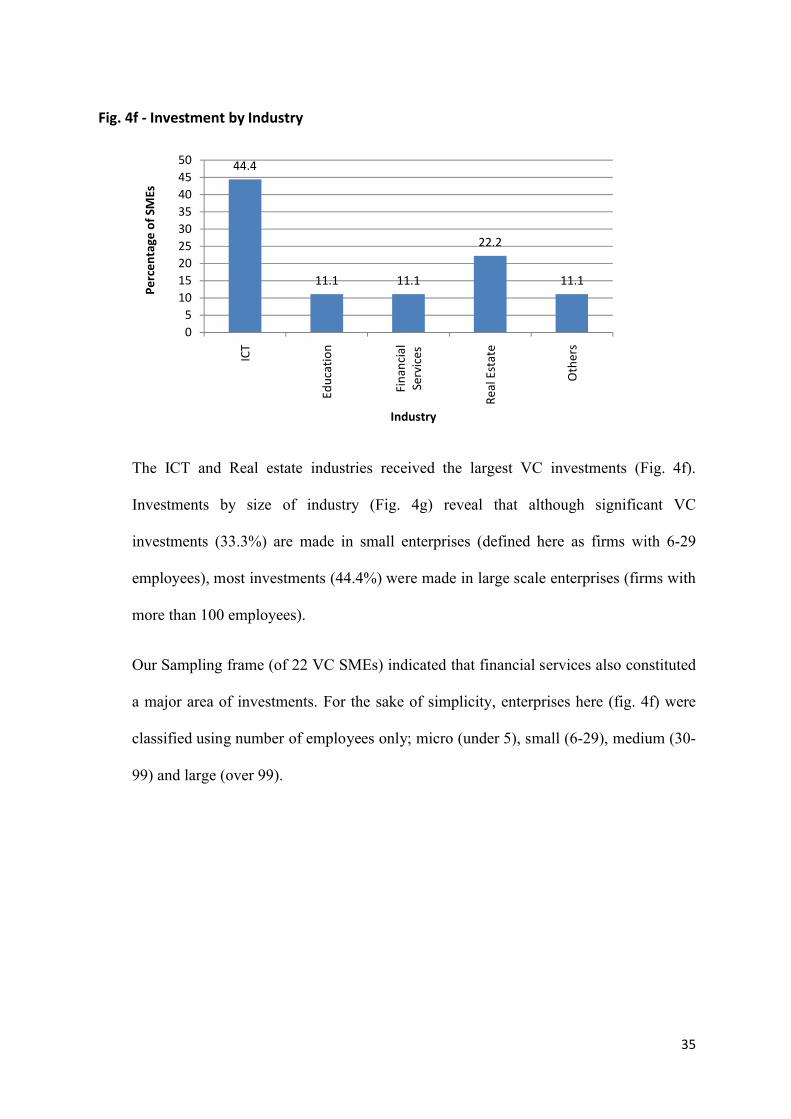

The ICT and Real estate industries received the largest VC investments (Fig. 4f).

Investments by size of industry (Fig. 4g) reveal that although significant VC

investments (33.3%) are made in small enterprises (defined here as firms with 6-29

employees), most investments (44.4%) were made in large scale enterprises (firms with

more than 100 employees).

Our Sampling frame (of 22 VC SMEs) indicated that financial services also constituted

a major area of investments. For the sake of simplicity, enterprises here (fig. 4f) were

classified using number of employees only; micro (under 5), small (6-29), medium (30-

99) and large (over 99).

44.4

11.1 11.1

22.2

11.1

05

101520253035404550

ICT

Educ

atio

n

Fina

ncia

l Se

rvic

es

Real

Est

ate

Oth

ers

Perc

enta

ge o

f SM

Es

Industry

Fig. 4f - Investment by Industry

36

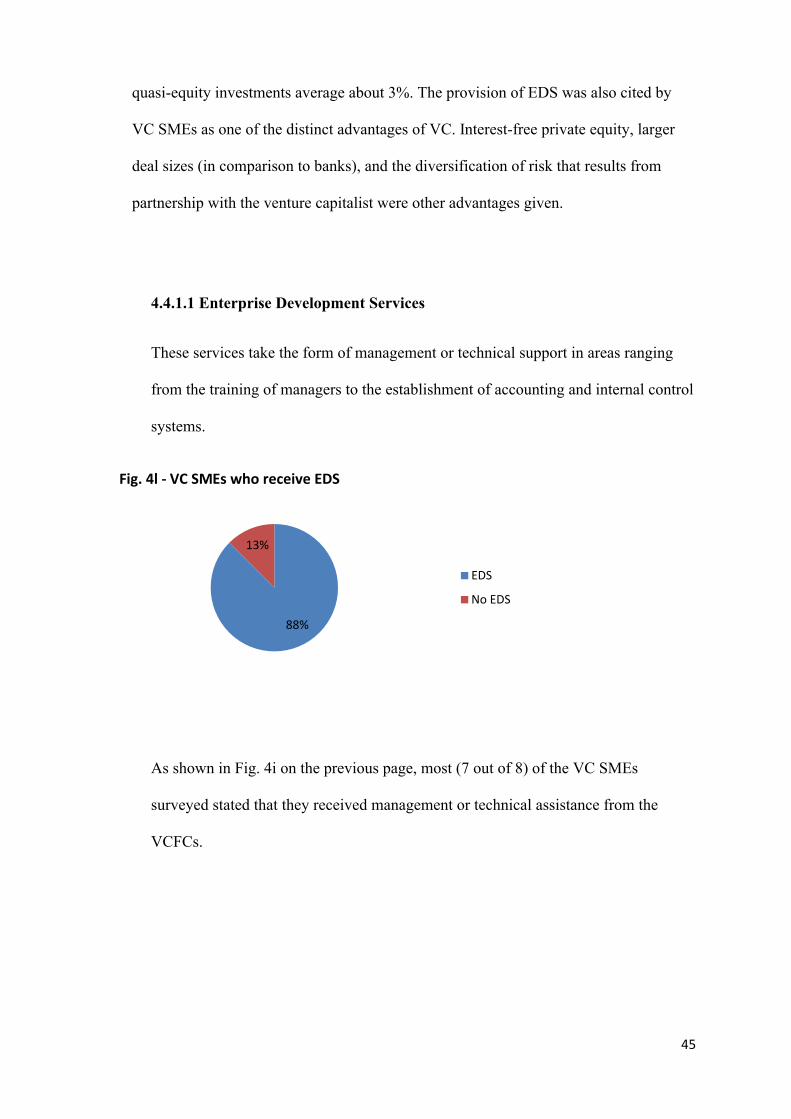

Data collected (as shown in Fig.4h) indicates that VC invested was mostly (56%) in the

form of quasi-equity, which is a combination of debt and equity.

The preference for quasi-equity to pure equity may be because of benefit of the interest

and principal payments. The time horizon for a VC investment is long (usually 5 years

or more). These payments provide interim cash flow to the VC investor, minimising the

risk and duration of the investment.

11.1

33.3

11.1

44.4

05

101520253035404550

Micro Small Medium Large

Perc

enta

ge o

f SM

Es

Size of Enterprise

Fig. 4g - Investments by size of enterprise

44%

56%

Fig. 4h - Type of VC invested

Equity

Quasi-equity

37

Average deal (investment per transaction) sizes ranged from $508,000 in 2006 to $3.3m

in 2005. The average deal size per year was obtained by dividing the total VC

investment per year by the number of successful applicants for the same year. In other

words, total funds invested by the number of investments.

Although Fig. 4i shows funds invested have dropped from a high in 2005, Fig. 4e shows

that the numbers of successful applicants (or the number of investments) have increased

since 2005.

The four year (2005-2008) average for Fig. 4i is $1.562m.

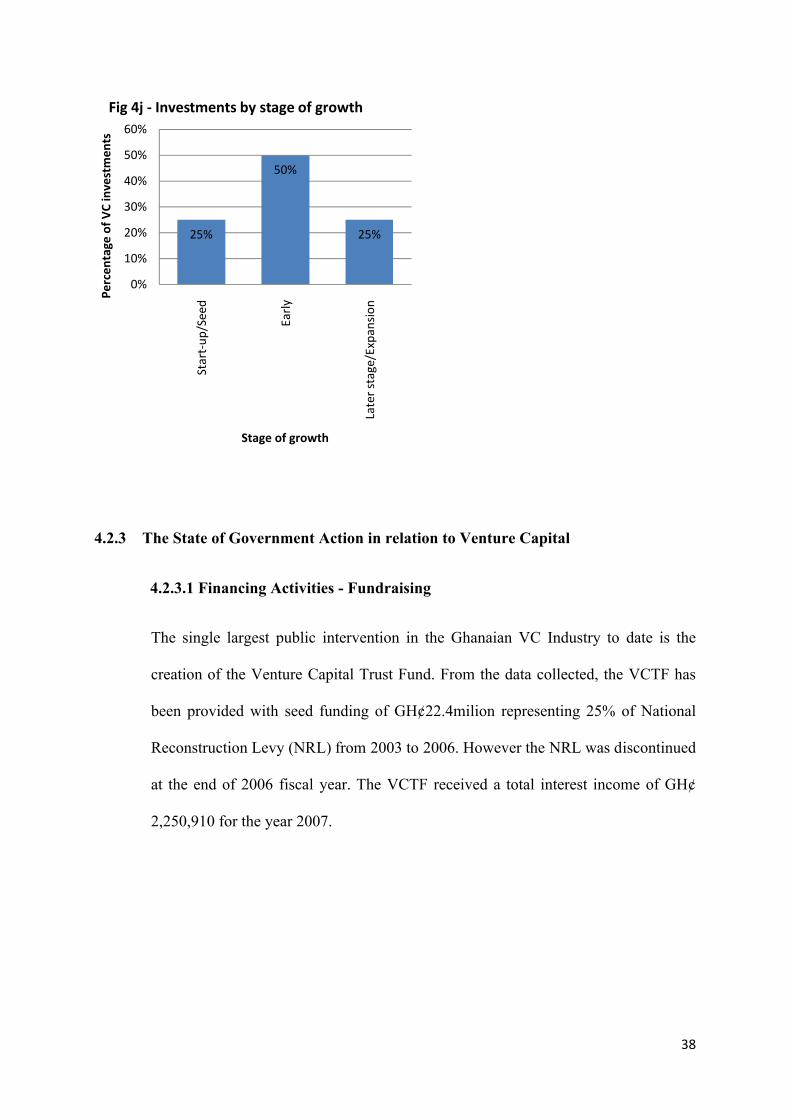

Fund managers were asked to indicate the SME growth stage at which they investments were

usually made. Three categories were provided; the start-up/seed stage (defined as SMEs less

than a year old), Early stage (1 to 3 years) and Later/expansion stage (over 3 years).

As Fig. 4j indicates, most investments take place at the early stage while the expansion and

start-up share equal amounts of investments. It is to be noted that some VCFCs manage more

than one fund. Different funds may therefore be targeted towards different stages of growth.

$3,333

$508$1,007

$1,400

$0$500

$1,000$1,500$2,000$2,500$3,000$3,500$4,000

2005 2006 2007 2008

Aver

age

deal

siz

e ( A

mou

nts

in th

ousa

nds

of U

SD)

Year

Fig. 4i - Trend of Average deal size per year

38

4.2.3 The State of Government Action in relation to Venture Capital

4.2.3.1 Financing Activities - Fundraising

The single largest public intervention in the Ghanaian VC Industry to date is the

creation of the Venture Capital Trust Fund. From the data collected, the VCTF has

been provided with seed funding of GH¢22.4milion representing 25% of National

Reconstruction Levy (NRL) from 2003 to 2006. However the NRL was discontinued

at the end of 2006 fiscal year. The VCTF received a total interest income of GH¢

2,250,910 for the year 2007.

25%

50%

25%

0%

10%

20%

30%

40%

50%

60%

Star

t-up

/See

d

Early

Late

r sta

ge/E

xpan

sion

Perc

enta

ge o

f VC

inve

stm

ents

Stage of growth

Fig 4j - Investments by stage of growth

39

4.2.3.2 Investing Activities

4.2.3.2.1 Direct Investment Programme

Currently, energy is the only addition to the initial priority sectors. The VCFCs

have so far invested approximately GH¢5.8 million in: Agriculture; ICT;

Services; Financial and Manufacturing industries represented by the graph

below:

It is estimated that a cumulative benefit of approximately 858 jobs will be

created with a projected tax revenue of approximately GH¢5.9million within

the next 5years resulting from investment of the venture in those businesses.

4.2.3.2.2 Indirect Investment Program

The Trust Fund in certain circumstances engages in specific purpose financing

where it lends to a finance company or lend exclusively to participants of a

specific project. An example is the Sorghum Value Chain Project where the

VCTF provided GH¢360,000 to farmers in the Upper East, Upper West,

Northern and Brong Ahafo regions for the production of sorghum for Guinness

8%

33%

17%

25%

17%

Fig. 4k- Approved investment

Manufacturing

Agricultural

ICT

Services

Financial

40

Ghana Brewery Limited in replacement of imported barley used by the

company for its brewery processes.

4.2.3.2.3 Programs Targeted At Demand for Venture Capital

Awareness creation

The VCTF Management embarked on a nationwide Road Show in the year

2007 to create public awareness of the Trust Fund’s financing resources. The

impact of this event was immediately evidenced by an increase in business

applications seeking funding from a monthly average of 21 to 34, representing

a 62% increase shortly thereafter.

Technical Assistance Program

Venture Capital Trust Fund has established a Technical Assistance programme

to provide heavily subsidized or free business support to various Small and

Medium Scale Enterprises who have been approved for funding by the venture

finance companies. The program adopts a three-tier strategic approach to

provide services to SMEs through training/capacity building,

mentoring/matching, and contract services by business solutions all aimed at

creating efficiency in the operations of the SMEs for successful investment.

Partnerships with Additional VCFCs

As a result of partnerships with VCFCs (such as Gold Coast Securities and

Fidelity capital partners Ltd.), the Trust Fund leveraged its initial seed money

of GH¢22.4million, to bring on board an additional GH¢27.7 million, making

a total of GH¢50.1 million for investments in SMEs. Currently the total capital

41

under management stands at GH¢56.9million representing an increase of

13.6%.

4.2.3.3 Tax Incentives

Section 18 of the Venture Capital Trust Fund Act, 2004 (Act 680) states that “ a

venture capital financing company shall enjoy such tax incentives as shall be

provided in the Internal Revenue Act, 2000 (Act 592) as amended. Under the

Internal Revenue (Amendment) Act, 2007 VCFCs are allowed the following tax

incentives;

A 5 year tax holiday on corporate income

A 5 year tax holiday on dividends earned

A 5 year tax holiday on capital gains

Losses from the disposal of shares during the 5 year tax holding period can

be carried over for 5 years

For banks and other financial institutions which provide VC finance, they are

allowed;

A full deduction of the VC investment from their total income in the year of

assessment.

All the incentives enjoyed by VCFCs.

According to an investment coordinator of the VCTF interviewed, these incentive

schemes have been quite successful in stimulating partnerships with VCFCs. It is to

be noted that the tax incentives are only available to finance companies which

partner with the Trust Fund.

42

4.3 Factors which influence the flow of funds from VCFCs to VC SMEs

4.3.1 Determinants of VC investments – Initial Investment

Table 4b – Factors which determine initial VC Investment ranked in order of

importance

Percentage of VCFCs

Factor Most

Important

Second Most

Important

Third Most

Important

Fourth Most

Important

Total

Concept 75% 0% 25% 0% 100%

Returns 0% 75% 25% 0% 100%

Management 25% 25% 50% 0% 100%

International

Orientation

0% 0% 0% 100% 100%

Total 100% 100% 100% 100%

Fund managers were asked to rank the following the factors; concept, returns and

management. The foregoing factors were based on the model of Hisrich and Jankowicz

(1990). ‘International orientation’ was included by the researchers.

Given the ranking of factors in Table 4b above, concept is the first consideration,

returns the second, managerial calibre the third, and international orientation the last.

43

4.3.2 Determinants of follow-on (subsequent financing)

Venture capital financing is not a one-time transaction. It entails several rounds of