Sustainable Venture Capital Investments: An Enabler ... - MDPI

Upload

independentCategory

view

2download

0

3rd Venture Capital in the Middle East & North Africa Report

2

Table of Contents

1. Introduction P. 3

2. Contributors P. 6

3. Information on VC in MENA P. 7

4. Definition of VC in MENA P. 7

5. MENA VC Country Overviews P. 8

• GCC: United Arab Emirates, Kingdom of Saudi Arabia

• Egypt

• Levant: Lebanon, Jordan

• Maghreb

6. MENA VC Investment Data P. 32

7. About the MENA Private Equity Association P. 37

8. Appendix 1: Note on Data Criteria P. 40

MENA: For the purpose of this report, MENA refers to the following countries in the Middle East and North Africa: Algeria, Bahrain, Egypt, Iraq, Jordan, KSA, Kuwait, Lebanon, Libya, Morocco, Oman, Palestine, Qatar, Sudan, Syria, Tunisia, UAE and Yemen.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is or will continue to be ac-curate. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

3rd Venture Capital in the Middle East & North Africa Report

3

IntroductionThe SME of SMEsThe Start-up Multiplier Effect of Small and Medium Companies in MENABy Dr. Philip Boigner, Director - Technology Investment at Dubai Silicon Oasis Authority

Silicon Valley began as 65 new companies were born by eight former employ-ees of Shockley Semiconductor. (Gromov, 2011) These 65 companies, among them one called Intel, in turn spawned off most of the enterprises that we associate with Silicon Valley today. One can argue that all it took were these eight employees who left Shockley to form Fairchild Semiconductor in 1957 to create Silicon Valley. Certainly, other factors also contributed to the immense success of the “Valley”. These include acceptance of failure and a liberal em-ployment policy that did not allow for non-competing restrictions when em-ployees left a company. The Silicon Valley success story has shown that with a handful of people and the proper ecosystem, a prosperous cluster of economic and social success can be built.

A 2010 study by the Kauffman Foundation shows that in the United States (US) net job growth occurs only through startups. (Kane, 2010) In addition, according to Enrico Moretti, every additional technology job in the US creates five new jobs in its city. Apple, for example, has 13,000 employees in Cuper-tino, but has created 70,000 indirect jobs in Silicon Valley. (Moretti, 2012) A recent report by the Bay Area Council Economic Institute in San Francisco agrees with Moretti’s findings, yet estimated the multiplier at 4.3. (Bay Area Council, 2012)

In the countries of the MENA region, job creation is of the essence. With steadily increasing population growth, sufficient employment options must be available to satisfy demand from graduates and the unemployed. For years, the International Monetary Fund (IMF) has urged the region’s governments to create new sustainable private-sector jobs. The Norwegian Peace building Resource Centre (NOREF) estimates that of about 100 million young people in MENA, a quarter is unemployed. Hence, over this decade about 40 to 50 mil-lion new jobs need to be created. (NOREF, 2012)

In the UAE, for example, one in five nationals is unemployed. (The National, 2012) Abu Dhabi alone has announced that it plans to create 600,000 jobs for UAE nationals over the next decade. (Gulf News, 2012) Considering the high non-UAE-national population portion of the country, the demand for new em-ployment options becomes apparent. In other GCC countries, the situation is similar and the Levant and the Maghreb need even more local jobs.

While the UAE is a tax-free country, setting up a business is not cheap. Most entrepreneurs are non-UAE nationals and hail from many different countries in the region and internationally. Due to this fact and legal reasons, start-ups elect to set up in one of the many free zones. The results are expensive busi-ness license fees, potential required office space, and restrictions on the num-ber of visas available.

1

3rd Venture Capital in the Middle East & North Africa Report

4

Countries, such as Egypt and Jordan, are much less expensive for setting up and running businesses. However, if young start-ups want to grow, play re-gion wide, and enter markets such as Saudi Arabia, a location such as Dubai or Abu Dhabi is very helpful. Also investment, market intelligence, and net-working is more readily available in such cities.

The obvious solution to create jobs is to support start-up and entrepreneur efforts in the region, especially since a great number of young regional entre-preneurs are already attempting to start new businesses. Start-ups are often supported by business incubators and angels, and lately also by crowd fund-ing initiatives. However, once nascent ventures have managed to survive for several months, received seed funding, and proven their concept, they often find themselves facing the funding gap.

Since no functioning venture capital industry exists, follow-on investment and early-state mentoring and coaching cannot happen. As young start-ups face significant barriers to gain follow-on early- and growth-stage investment, many if not most do not survive long enough to mature and create a sustain-able job base. Due to this funding gap the SME – the Startup job Multiplier Effect – cannot work and the country is left with a static labor market. By nur-turing an emerging venture capital industry that will take the most promising start-up companies to a stage where the business is sustainable, countries can-not create employment and economic development and fail to train an entre-preneurial “elite” that in turn would launch many new follow-on enterprises to employ even more people – just as it happened in Silicon Valley a half of a century ago.

Furthermore, in a no-tax environment, such as the UAE, the government col-lects income from fees on businesses and residents. These include visa fees, water and power charges, SALIK, etc. By creating more new businesses that attract regional and international talent to the UAE, income streams from both groups can contribute to government coffers.

One of the prevailing cultural and legal problems with setting up a start-up busi-ness in the region is the non-acceptance of failure. While many cultures embrace failure as an invaluable learning experience, the Middle East is less comfortable with the topic. The fear of embarrassment, shame, loss of face, and potentially imprisonment discourages many young potentials from becoming entrepre-neurs. The cultural ramification of failure could be substantial to the individual and his or her family. The region’s legal systems are also not build to deal with bankruptcy and liquidations, and company founders could be subject to major legal litigation if their companies are not able to pay their dues in troubled times.

Nevertheless, we have already seen some regional companies that man-aged to complete the full funding cycle, sometimes without the help of venture capital. Maktoob, a company founded in 1998 by two Jordanian entrepreneurs, is one example. It was one of the first Arab Internet services companies. In 2006, it received funding from Abraaj Capital and was even-tually sold to Yahoo! in 2009. In turn, Samih Toukan and Hussam Khoury, the founders of Maktoob, created a number of other successful new com-panies in the Jabbar Internet Group. Samih Toukan estimates that they have created about 1,500 direct job in several companies over the years.

3rd Venture Capital in the Middle East & North Africa Report

5

While the region has started to actively nurture the venture creating environ-ment, successful incubation schemes such as Oasis500 in Jordan, Flat6, and Tahrir2 in Egypt or Honeybee Ventures in the UAE; as well as informal angel investment clubs such as Envestors in the UAE; it fails to ensure that young com-panies have access to the funding and mentoring that will ensure their survival and maturity to become a significant force in private industry net job creation.

Special Thanks to Fadi Gandour and Faysal Sohail.

Bay Area Council Economic Institute, December 2012. “Technology Works: High Tech Employment and Wages in the United States”. Authors: Ian Hathaway and Patrick Kallerman.

Gromov, G. 2011. “Silicon Valley History”. available at www.netvalley.com/silicon_valley_history.html cashed.

Gulf News, 2012. “Tawteen to find 300,000 jobs for Emiratis by 2020“, Author: Samir Salama. Published: January2nd, 2012

Kane, T. July 2010. “The Importance of Startups in Job Creation and Job Destruction”, Kauffman Foundation Research Series: Firm Formation and Economic Growth.

Moretti, E. 2012. “The New Geography of jobs”, Houghton Mifflin Har-court.

NOREF Policy Brief, May 2012. “Youth integration and job creation in the Middle East and North African region”, Norwegian Peace-building Resource Center. Author: Jad Chaaban

The National, 2012. “UAE jobs minister promises a new surge in Emir-atisation.” Author: Ola Salem. Published: December 11th, 2012

3rd Venture Capital in the Middle East & North Africa Report

6

Contributors

This report was a collaboration between the MENA Private Equity Association, the Association’s VC Taskforce, KPMG, Zawya and industry professionals.

Special thanks to Middle East Venture Partners (MEVP) for sponsoring the report:MEVP is Middle East-focused venture capital firm that invests in the early and growth stages of innovative companies run by talented entrepreneurs primarily, but not exclusively, in the UAE, Jordan and Lebanon.MEVP has a unique combination of backgrounds and expertise that allows them to partner with innovative entrepreneurs and help them grow and develop, especially in their early stages.Since inception in 2010, MEVP has invested about $12M in 15 outstanding ICT com-panies. For more information about MEVP and its investment strategy, please visit http://www.mevp.com/

MENA Private Equity Association would also like to thank

VC Taskforce

Ali Arab, Zawya www.zawya.com

Basel Roshdy, IT Ventures/Nile Capital www.nile-capital.com

Dr. Philip Boigner, Dubai Silicon Oasis Authoritywww.dsoa.ae

Salam Saadeh, Y+ Venture Partnerswww.yplusventures.com

Sami Beydoun and Elie Boujaoude, Berytech fundwww.berytechfund.org

Walid Hanna, Middle East Venture Partners www.mevp.com

William Fellows, Managing Principal, Lixia Capsia Gestionis www.lixcap.com

Industry professionals

Aiman Al-Atiqi, Iris Capital MENA, STC Ventureswww.stcventures.com

Brad Whittfield and Zuhaib Khan, KPMGwww.kpmg.ae

Salwa Katkhuda, Oasis 500www.oasis500.com

2

3rd Venture Capital in the Middle East & North Africa Report

7

Information on Venture Capital in MENAThis report is the third in the series of the Venture Capital (VC) Reports issued by the MENA Private Equity Association on yearly basis. For further details on venture capital in MENA, including a guide to MENA VC for entrepre-neurs and a directory of Venture Capital Firms in MENA and related entities in the Middle East, please see:

MENA PE Association Website: www.menapea.com

VC Ecosystem Directory: www.menapea.com/vcecosystem

Definition of Venture Capital (VC) in MENA

Key criteria used to define VC investments also include:

• Investments are in non-listed companies (private companies)

• Investment commitment over the life of the deal can average USD 3 to 5M but can also reach up to USD 15 million

• A typical plan exit through IPO, mergers & acquisition, man- agement buy-out or trade sale

• Above average returns expected

• Seed/angel or investments by non-financial shareholders do not count as VC

• VC is not confined solely to technology investments, but technology is often a core factor that creates the level of scalability required in a VC deal.

3

4VC is defined as the provision of long-term equity investment and strategic support by financial investors to innovative, scalable companies at the early growth stage.

3rd Venture Capital in the Middle East & North Africa Report

8

MENA VC Country OverviewsOverviews of VC and VC type activity, and the entrepreneurial environment in a selection of countries across MENA, based on experience of our task-force team members and availability of information.

Gulf Cooperation Council

United Arab Emirates by • Salam Saadeh, Yplus Ventures and

Dr. Philip Boigner, Dubai Silicon Oasis

Kingdom of Saudi Arabia by • Aiman Atiqi, Iris Capital

Egypt

Basel Roshdy, Nile Capital

Levant

Lebanon • by Sami Beydoun & Elie Boujaoude, Berytech

Jordan • by Salwa Katkhuda, Oasis 500

Maghreb

William Fellows, Managing Principal, Lixia Capsia Gestionis

5

3rd Venture Capital in the Middle East & North Africa Report

9

United Arab EmiratesBy: Salam Saadeh - Managing Partner of Y+ Venture Partners and by Dr. Philip Boigner – Director of Technology Investment at Dubai Silicon Oasis Authority - Government of Dubai

In the past decade, the United Arab Emirates has emerged as one of the most economically prosperous countries in the world, with one of the highest GDP per capita and home to more than half of the global conglomerates. As the UAE moves forward, it is seeking to compete with the world’s leading nations by building a strong knowledge based economy as per its Vision 2021. As such, the UAE started developing policies and institutions to support its full transition towards that goal; evident by the fact that the United Arab Emir-ates is now home to number of government initiatives supporting private enterprises looking for capital and non-financial support. It has to be noted, however, that most of these offerings are only available to UAE nationals.

Khalifa FundKhalifa Fund for Enterprise Development is an independent body of the Abu Dhabi Government with a total capital investment of AED 2 billion. It is a part of the long-term vision of His Highness Sheikh Khalifa Bin Zayed Al Nahyan, President of the UAE and Ruler of Abu Dhabi, and is commit-ted to stimulate the country’s competitive economy and transform the Emir-ate of Abu Dhabi into a major investment and economic hub in the region.

The Fund aims to create a new generation of Emirati entrepreneurs by instill-ing and enriching the culture of investment amongst young people, as well as supporting and developing small to medium-sized investments in the Emir-ate. It offers a range of financing solutions geared to specific applicant’s pro-files, as well as a system of support services including training, development, data and consulting services and a number of marketing-focused initiatives to help develop applicants into successful entrepreneurs. In addition, Khalifa Fund also offers a number of social funding programmes and non-financial initiatives, targeted towards specific segments of the community, such as pro-viding opportunities for correctional inmates, widows, retirees, people with special needs. More: www.khalifafund.ae/en

Sheikh Mohammed Bin Rashid Establishment for Young Business Leaders (Dubai SME)

The Sheikh Mohammed Bin Rashid Establishment for Young Business Leaders (Dubai SME) was established by His Highness Sheikh Mohammed Bin Rashid Al Maktoum, UAE Vice President and Prime Minister and Ruler of Dubai, in 2002 and incorporated as an agency into the Department of Economic Devel-opment (DED). Its goal is to foster entrepreneurial culture in small and me-dium enterprises, with a focus on supporting and developing knowledge and innovation-based SMEs across all industry sectors.

Dubai SME offers a range of services and benefits designed to offer the much needed advice and support required to ensure the next generation of busi-ness leaders fulfill their potential, including advisory / consulting, funding facilities, business incubation. It primarily targets UAE Nationals but offers selected services to expats as well. More: www.sme.ae/en

3rd Venture Capital in the Middle East & North Africa Report

10

ICT Fund

The ICT Fund has a determined mission to provide targeted funding and advi-sory services to companies, organisations and individuals to empower them to develop the innovation and knowledge capital of the UAE ICT sector with their research, education and entrepreneurship. The Fund strives to promote a cul-ture of entrepreneurship in the UAE ICT sector and improve linkage between industry and academia to ultimately promote the involvement of UAE nation-als in the realm of scientific and technology research to foster self-reliance of the UAE in technology creation and development. More: www.ictfund.gov.ae

TwoFour54

Ibtikar, unit of TwoFour54 in Abu Dhabi, offers funding and support to young Arabs with great ideas. This includes seed funding, investment in content de-velopment guidance and planning. They help entrepreneurs get great ideas off the ground. This is all managed and delivered through their creative lab community where entrepreneurs can apply for funding, connect with other creative thinkers as well as get inspired and supported to bring their ideas to life. More: www.ibtikar.twofour54.com

in5

The in5 Innovation Hub is an environment that supports entrepreneurship and cultivates the development of the ICT and digital media start-up ecosystem in Dubai. It is part of TECOM. Their objective is to Support entrepreneurs from the early stage idea creation, through implementation, right up to the com-mercial launch of the product or service. In5 is targeted at entrepreneurs and start-ups with innovative ideas in information and communication technolo-gies, who are looking to create a thriving business concern. More: www.in5.ae

Silicon Oasis Founders

Silivon Oasis Founders (SOF) is a wholly owned entity of Dubai Silicon Oasis Authority (DSOA), a 100% owned entity by the Government of Dubai. SOF focuses on fostering local entrepreneurial talents in the promising mobile ap-plication space and related technologies. SOF’s expertise will help emerging entrepreneurs to refine their business proposals, and accelerate growth. SOF is open for all nationalities to apply. More: www.siliconOasisFounders.com

The above institutions together with many other popular common working spaces and incubators which popped up recently in the country are all try-ing to jump start the much needed entrepreneurial eco-system. We have wit-nessed during the past few years many interesting technology startups in the country, either started here or moved here from other neighboring countries to be close to their major clients, and the media. However, there are still major problems that such startups face on a regular basis, including:

High cost of setting up1-

Restrictive employment policies 2-

Limited access to smart funds3-

3rd Venture Capital in the Middle East & North Africa Report

11

Small steps by the government can easily solve the above problems and will contrib-ute heavily to the building of the knowledge economy everyone dreams of. Such steps include:

1. Provide a grace period for all startups

When it comes to their Setup Cost that can be funded through the free zones authorities by the government (a criteria can be enforced here). The Setup Cost includes registration, virtual office rental, and visas cost. Such grace period can be for [3] years, giving time for the startups to either make it or die.

2. Implement the Founder Visas policy

Where any startup that is supported by a UAE based VC or angel investor for up to at least [$200,000] can apply for [5] visas to get the initial team on board and increase the chance of making it.

3. Start a seeding program for VC funds

Where they can get up to [$5 million] from the government as seed capital, the VC managers will be vetted properly by an expert committee and will be required to spend at least 50% of their time in the country and invest all this money in UAE startups.

Small steps similar to the above suggested are believed to make a huge difference in a short period of time.

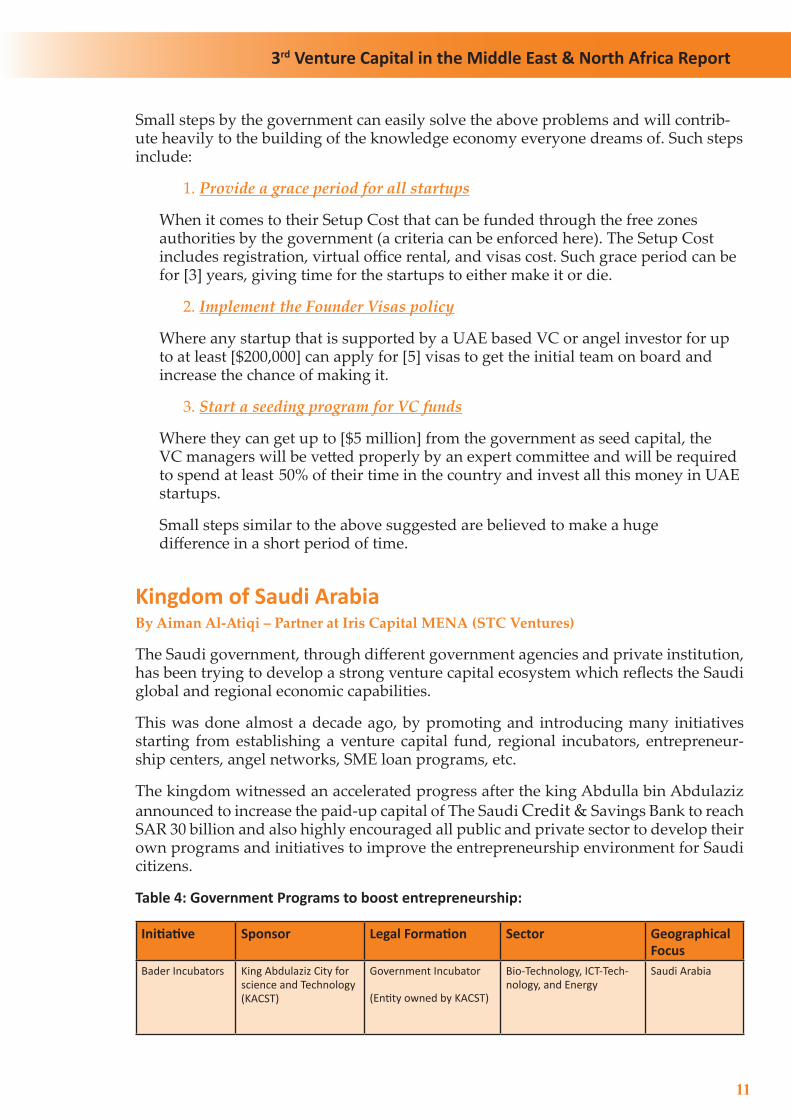

Kingdom of Saudi ArabiaBy Aiman Al-Atiqi – Partner at Iris Capital MENA (STC Ventures)

The Saudi government, through different government agencies and private institution, has been trying to develop a strong venture capital ecosystem which reflects the Saudi global and regional economic capabilities.

This was done almost a decade ago, by promoting and introducing many initiatives starting from establishing a venture capital fund, regional incubators, entrepreneur-ship centers, angel networks, SME loan programs, etc.

The kingdom witnessed an accelerated progress after the king Abdulla bin Abdulaziz announced to increase the paid-up capital of The Saudi Credit & Savings Bank to reach SAR 30 billion and also highly encouraged all public and private sector to develop their own programs and initiatives to improve the entrepreneurship environment for Saudi citizens.

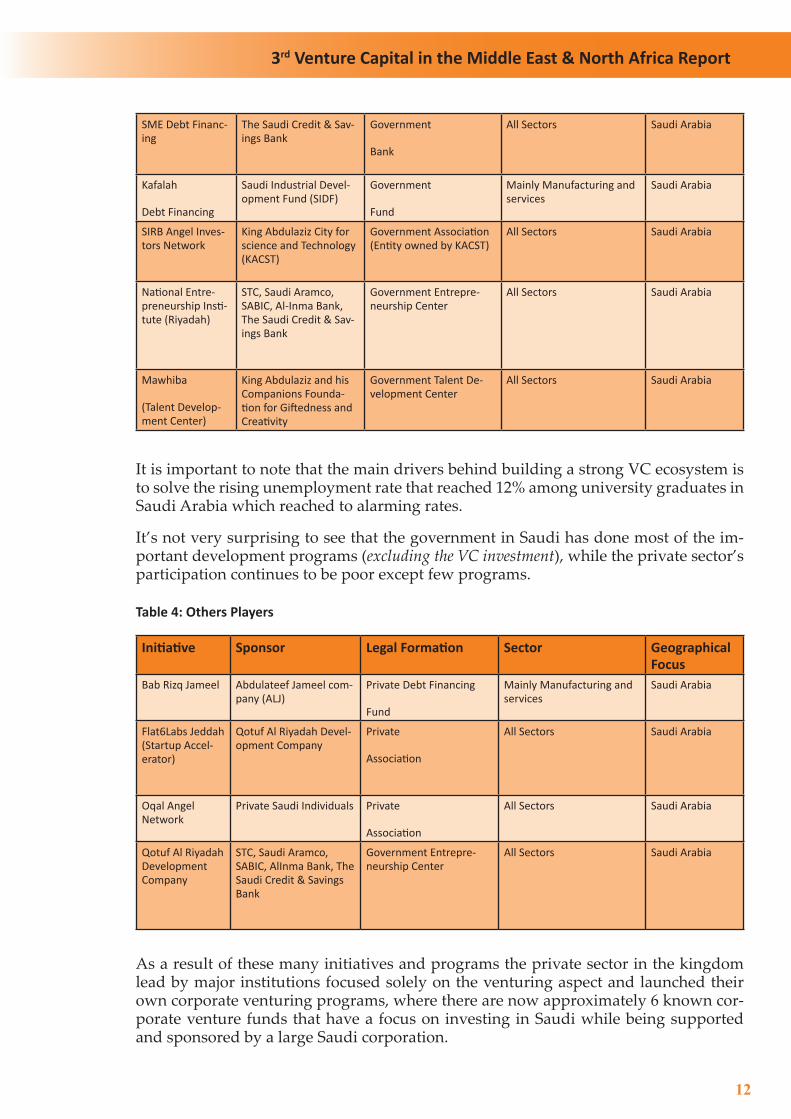

Table 4: Government Programs to boost entrepreneurship:

Initiative Sponsor Legal Formation Sector Geographical Focus

Bader Incubators King Abdulaziz City for science and Technology (KACST)

Government Incubator

(Entity owned by KACST)

Bio-Technology, ICT-Tech-nology, and Energy

Saudi Arabia

3rd Venture Capital in the Middle East & North Africa Report

12

SME Debt Financ-ing

The Saudi Credit & Sav-ings Bank

Government

Bank

All Sectors Saudi Arabia

Kafalah

Debt Financing

Saudi Industrial Devel-opment Fund (SIDF)

Government

Fund

Mainly Manufacturing and services

Saudi Arabia

SIRB Angel Inves-tors Network

King Abdulaziz City for science and Technology (KACST)

Government Association (Entity owned by KACST)

All Sectors Saudi Arabia

National Entre-preneurship Insti-tute (Riyadah)

STC, Saudi Aramco, SABIC, Al-Inma Bank, The Saudi Credit & Sav-ings Bank

Government Entrepre-neurship Center

All Sectors Saudi Arabia

Mawhiba

(Talent Develop-ment Center)

King Abdulaziz and his Companions Founda-tion for Giftedness and Creativity

Government Talent De-velopment Center

All Sectors Saudi Arabia

It is important to note that the main drivers behind building a strong VC ecosystem is to solve the rising unemployment rate that reached 12% among university graduates in Saudi Arabia which reached to alarming rates.

It’s not very surprising to see that the government in Saudi has done most of the im-portant development programs (excluding the VC investment), while the private sector’s participation continues to be poor except few programs.

Table 4: Others Players

Initiative Sponsor Legal Formation Sector Geographical Focus

Bab Rizq Jameel Abdulateef Jameel com-pany (ALJ)

Private Debt Financing

Fund

Mainly Manufacturing and services

Saudi Arabia

Flat6Labs Jeddah (Startup Accel-erator)

Qotuf Al Riyadah Devel-opment Company

Private

Association

All Sectors Saudi Arabia

Oqal Angel Network

Private Saudi Individuals Private

Association

All Sectors Saudi Arabia

Qotuf Al Riyadah Development Company

STC, Saudi Aramco, SABIC, AlInma Bank, The Saudi Credit & Savings Bank

Government Entrepre-neurship Center

All Sectors Saudi Arabia

As a result of these many initiatives and programs the private sector in the kingdom lead by major institutions focused solely on the venturing aspect and launched their own corporate venturing programs, where there are now approximately 6 known cor-porate venture funds that have a focus on investing in Saudi while being supported and sponsored by a large Saudi corporation.

3rd Venture Capital in the Middle East & North Africa Report

13

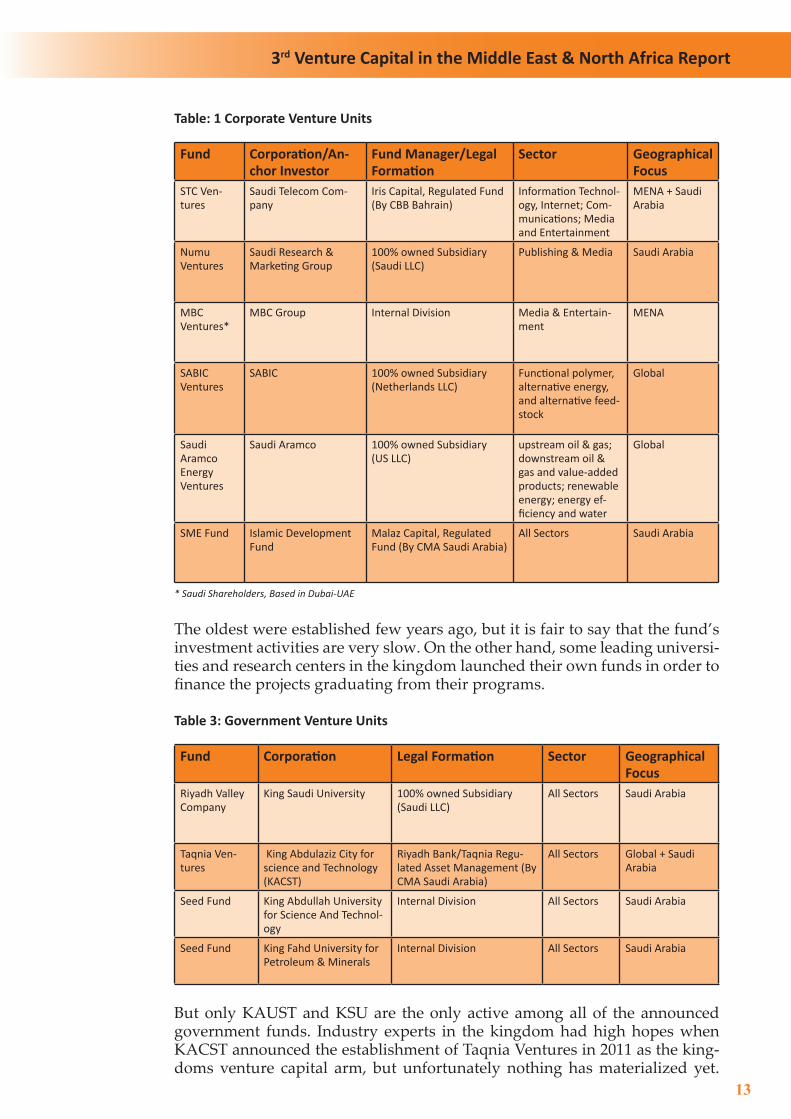

Table: 1 Corporate Venture Units

Fund Corporation/An-chor Investor

Fund Manager/Legal Formation

Sector Geographical Focus

STC Ven-tures

Saudi Telecom Com-pany

Iris Capital, Regulated Fund (By CBB Bahrain)

Information Technol-ogy, Internet; Com-munications; Media and Entertainment

MENA + Saudi Arabia

Numu Ventures

Saudi Research & Marketing Group

100% owned Subsidiary (Saudi LLC)

Publishing & Media Saudi Arabia

MBC Ventures*

MBC Group Internal Division Media & Entertain-ment

MENA

SABIC Ventures

SABIC 100% owned Subsidiary (Netherlands LLC)

Functional polymer, alternative energy, and alternative feed-stock

Global

Saudi Aramco Energy Ventures

Saudi Aramco 100% owned Subsidiary (US LLC)

upstream oil & gas; downstream oil & gas and value-added products; renewable energy; energy ef-ficiency and water

Global

SME Fund Islamic Development Fund

Malaz Capital, Regulated Fund (By CMA Saudi Arabia)

All Sectors Saudi Arabia

* Saudi Shareholders, Based in Dubai-UAE

The oldest were established few years ago, but it is fair to say that the fund’s investment activities are very slow. On the other hand, some leading universi-ties and research centers in the kingdom launched their own funds in order to finance the projects graduating from their programs.

Table 3: Government Venture Units

Fund Corporation Legal Formation Sector Geographical Focus

Riyadh Valley Company

King Saudi University 100% owned Subsidiary (Saudi LLC)

All Sectors Saudi Arabia

Taqnia Ven-tures

King Abdulaziz City for science and Technology (KACST)

Riyadh Bank/Taqnia Regu-lated Asset Management (By CMA Saudi Arabia)

All Sectors Global + Saudi Arabia

Seed Fund King Abdullah University for Science And Technol-ogy

Internal Division All Sectors Saudi Arabia

Seed Fund King Fahd University for Petroleum & Minerals

Internal Division All Sectors Saudi Arabia

But only KAUST and KSU are the only active among all of the announced government funds. Industry experts in the kingdom had high hopes when KACST announced the establishment of Taqnia Ventures in 2011 as the king-doms venture capital arm, but unfortunately nothing has materialized yet.

3rd Venture Capital in the Middle East & North Africa Report

14

Even though in Saudi it is very difficult to convince family groups and wealthy individuals to allocate part of their investment in venture capital investments in Saudi, we noticed few asset management firms launched SME funds to fo-cus on this type of investments but they have not been able to raise funds from private investors. This is due to the lucrative and high investment returns gen-erated from the real estate sector and the Saudi stock market.

Table 2: Venture Capital Fund

Fund Fund Manager Legal Formation Sector Geographical Focus

SME Fund(s)* Saudi Venture Capital Investment Company

Regulated Fund (By CMA Saudi Arabia)

All Sectors MENA

SME Fund Inma Bank/BlueVine Ventures

Regulated Fund (By CMA Saudi Arabia)

All Sectors Saudi Arabia

(*) Private Placement

Conclusion:

In principal Saudi Arabia is on the right track, but it still having many chal-lenges to overcome in order to create a strong VC ecosystem. The Saudi gov-ernment initiated all programs in order to have a comprehensive VC ecosys-tem. What is needed now is to improve the performance of these programs and pressure the management to deliver higher quality outcomes.

But going forward the Saudi government needs to improve or focus on the following:

Improve Business Environment:1)

According to the latest report of Doing Business (DB), Saudi Arabia ranked 13th globally and maintained its position in the first place in the region on the ease of doing business. However, businesses still face difficulties, enforce-ment of contracts and labor issues within the regulatory system in the coun-try.

Based on a Global Entrepreneurship Monitor (GEM) survey conducted from May to October 2009, among the factor-driven economies in the region, Saudi Arabia had the lowest total entrepreneurial activity (TEA) rate, only 4.7% of the adult population (18–64 years old) were actively involved in the start-up of a new business or owned a young business of less than three and half years old.

Also study by Michael Porter in 2008 noted that Saudi Arabia could have built a competitive economy and diversify beyond natural resources if it was will-ing to take a strategic approach, make multiple improvements in its business environment, truly open up competition and entrepreneurship in the private sector, and embark on a sustained effort to equip Saudi citizens with new skills, attitudes and mindsets.

3rd Venture Capital in the Middle East & North Africa Report

15

Creation of a government regulatory body for SME’s 2)

It has been one year and four months since the shoura councel approved (blessed) the creation of the Saudi small and medium enterprise commission. Without this we would continue to see many independent government and private sector lead initiatives being promoted without a unified country vi-sion.

Establishment of the Saudi SME stock exchange3)

The current structure of the Saudi Capital market and the financial services that operate under its regulations are not sufficient to support the growth of Saudi SMEs where VC and SME fund managers and investors find difficul-ties to exit their investment and realize their returns. It is very important for private equity markets to have clear and efficient “exit mechanisms” – the method by which investors and entrepreneurs (or a company’s management) “cash in” their investments and to increase the attractiveness of this segment.

Initiating Saudi PE/VC Fund of Fund’s Program:4)

I strongly believe that the Saudi government at this stage should introduce a private equity and venture capital Fund of funds program, A similar pro-gram was established in Turkey in 2007,the program was known as “ Istanbul Venture Capital Initiative (iVCi)”which was Turkey’s first dedicated Fund of Funds and co-investment program. The mission of iVCi is to provide access to finance to Turkish companies by being a catalyst for the development of the venture capital industry in Turkey through investments in independently-managed funds and co-investments. This builds on the vision that Istanbul shall become a crossroad location for the venture capital industry in South East Europe and Central Asia by the year 2020.

Similarly in our case for Saudi, The PE/VC Fund of Fund’s Program shall aim to invest in and co-invest with mainly three type of funds:

First Time Funds• : Funds that are managed by a team with no prior joint track record in managing a venture capital fund.

Established Funds• : Funds that are managed by a team with prior track record but no experience in Saudi Arabia, or a joint operation between a First Time Fund in Saudi Arabia and a team with previous track re-cord acquired abroad.

Experienced Funds• : Funds that are managed by a team with a prior joint track record in managing a venture capital fund in Saudi Arabia.

Through this strategy, the program will significantly help in the development of the venture capital industry in Saudi Arabia through investments in inde-pendently-managed funds and help to develop a new breed of Saudi venture capital professionals.

3rd Venture Capital in the Middle East & North Africa Report

16

Egypt VC Overview: Developments, Opportunities and ChallengesBy: Dr. Basel Roshdy – MD & CIO of Nile Capital & IT Ventures / Secretary General of Egyptian Private Equity Association (EPEA)

Ever since January 2011, when Egypt’s first revolution was ignited against the ruling political regime, the overall economical and business envi-ronment has been witnessing severe gyrations in general. Nevertheless, there has always been a very promising outlook based on a strong funda-mentals and growing efforts being invested to develop, support and im-prove entrepreneurship, job creation, innovation, governance, and a na-tion with a potentially superior landscape for venture capital investments.

Egypt has the largest population in the whole Arab World / MENA region with almost one third under the age of 25 years, a lot of natural and agricultural re-sources, diversified economic sectors, skilled and abundant labor force, and eagerness to develop new ideas and home-grown private businesses (some of which have turned into sizeable conglomerates and global companies over time).

With Egypt’s shifting political landscape come great opportunities for change. Post revolution youths have a renewed sense of patriotism and empowerment coupled with the assertion that they can cause real change. This has mainly taken form as new businesses sprout across the country, transforming our many social, economic and environmental issues into innovative business so-lutions. It is very exciting to see these budding entrepreneurs capitalize on their inherent talents as natural born entrepreneurs.

Over the past few years, there were and still are ongoing number of positive and dynamic developments in the ecosystem for VC and SMEs development, including more access to financing tools and facilities (such as leasing, factor-ing, micro-finance, mezzanine funding, soft loans, export credit facilities, etc. all in support of direct equity financing), SMEs banking development, profes-sional development and capacity building for improving technical and man-agement skills, corporate governance and audit training, some incentives for incorporating new businesses and SMEs as either companies or investment vehicles, and emergence of few more incubators and angel investors networks.

While most focus has been on ICT, a growing interest in industries such as energy, agriculture and manufacturing are now considered to be untapped potential with huge market opportunities. This has resulted in a growing emergence of sector-oriented startup businesses. Entrepreneurs are however hindered by several factors including bureaucratic hurdles in company regis-tration, a lack of a cohesive, supportive ecosystem, access to funding as well as a lack in basic training in business, marketing and technology integration.

However, Egypt still has a long and challenging path to go in order to improve and grow its VC ecosystem and increase the number and sizes of VC funds and SMEs-related investment tickets, as well as putting Egypt as a remark-able playing spot for regional and international players and various industrial partnerships and alliances.

3rd Venture Capital in the Middle East & North Africa Report

17

As of 2008, Egypt has ranked 67 globally in terms of VC ranking index, while in 2012 Egypt has ranked 56 – still within the current fluctuating and turbu-lent environment, based on weighted average assessment of key factors per-formance including: (1) economic activity; (2) depth of capital markets; (3) taxation; (4) investors protection and corporate governance; (5) human and social environment; and (6) entrepreneurial culture and deal opportunities. But still with different rankings across the last few years, Egypt occupies a mid-point position among major developing African and North Africa re-gion, as stated and sourced from the “Global Venture Capital and Private Equity Country Attractiveness Index Report” produced by Ernest & Young.

The General Authority for Investment & Free Zones (GAFI) has sponsored and launched last year the first sovereign SMEs fund (called Bedaya) with some focus on start-ups and VC investments, in partnership with some banks and financial institutions with committed capital of up to around EGP 200M in the first closing.

Recently a number of players have emerged and are becoming more active and booming in Egypt such as Sawari Ventures (ICT-focused VC fund and incubator with the famous Flat6 Lab platform for pioneering business cases competition), Ideavelopers and its managed Technology Development Fund has added some regional and global ICT investments and partnerships, Cairo Angel Network has been established as an integrated platform for profession-al angel investors, Smart Village has established technology incubators ser-vices and community, and more new initiatives and investment vehicles are on the way, such as the recently announced “Egypt-US Enterprise VC Fund”.

Innoventures – a leading company providing platform for seed stage start-ups and incubation services, specializing in the fields of clean-tech, ICT, electron-ics, media, market intelligence and inclusive businesses, through 6-month in-cubation program that offers seed funding, tailored business training, mentorship and access to partner networks, in return for a minority equity stake in each of the ventures incubated.

In addition, business NGOs and professional societies and academic institu-tions are developing and expanding entrepreneurial and VC-related activities and initiatives: Egyptian Junior Business Association (EJB), Endeavor Egypt, Al-Rowad, Middle East Council for Entrepreneurship & SMEs (MAKSABY now), American University in Cairo, German University in Cairo, Nile Uni-versity, Arab Science & Technology Academy, MIT business plan competi-tion, European and Euro-Mediterranean funded projects, and most recently and in growing actions the Egyptian Private Equity Association (EPEA) as a professional and specialized platform and industry-focused community and friendly organization for investment industry players and beneficiaries, and with a clear focus and direct target to develop further and flourish VC invest-ments and related capacity building and professional development services in Egypt and the MENA region. These are just examples, whereby there are other direct or indirect organizations, associations and professional bodies assisting in the process or ecosystem improvement such as Egyptian Banking Institute, GAFI, Ministry of Trade & Industry, Egyptian Credit & Risk Association, and many others to mention. Also, IFC, European Investment Bank (EIB), Euro-pean Bank for Reconstruction & Development (EBRD) and other international financial institutions have developed advisory and specialized programs for

3rd Venture Capital in the Middle East & North Africa Report

18

developing and empowering SMEs and potential VC investees to make them attractive and having more access to VC equity finance and partnerships.

Still, there are current challenges represented by the lack of and need for solid corporate governance and compliance systems, well-developed and im-proved laws for establishing and managing VC funds in Egypt. Of the many challenges, there is a growing need for:

1- Scientific, unbiased and thorough screening model

of the vast number of deal flow and prospect opportunities in the market.

2- More activation and development of capital markets and exit mechanisms

to facilitate exit strategies for VC investors and VC funds

3- Relaxed taxation regulations

4-Better enforcement of investors’ protection and conflict resolution.

5- Capacity building and regular training programs

to develop management and HR teams

6- Encouraging and improving innovation and scientific research

7- Increasing awareness about Entrepreneurship

through more seminars and conferences (including public and private ones and specialized and industrial roundtables with various stakeholders)

8- Encouraging and enhancing relevant debt financing

to match with VC equity funding,

9- National stability on both political and social security levels.

of course as an essential factor.

In summary, It is definitely evident that Egypt has all the prerequisites to un-leash a huge potential with its rich pool of ideas driven by a smart and edu-cated population, natural and industrial resources, diversified economy, hun-dreds of thousands of SMEs.

All it takes is a collective, focused effort with smart objectives and a reforming of mind-sets and regulations, in order to become the most attractive hub and a regional leader for VC funds, investments, and all related professional incuba-tion services and benefits for various stakeholders.

These efforts would eventually trickle down to the core in order to satisfy so-cial needs, job creation, quality enhancement and above all decent / attractive financial returns for investors.

3rd Venture Capital in the Middle East & North Africa Report

19

LebanonBy Sami Beydoun & Elie Boujaoude, Berytech fund

Q1: Entrepreneurship is not a very well understood concept. What in your opin-ion could be a common interpretation of “Entrepreneurship”?

An entrepreneur is someone who takes the initiative to create, assumes the risks, learns from his/her mistakes, and bounces back each time he/she fails. Entrepreneurship represents this overall attitude of individuals going through this process. In this sense, entrepreneurship does not necessarily im-ply leaving employment to start one’s own business. The process of initiat-ing creation, assuming the risk, learning and bouncing back can take place within the organization the so called entrepreneur works at. A smart organi-zation knows how to foster this spirit of entrepreneurship within its culture.

Entrepreneurship has a major influence and impact on the economy in terms of creating jobs, limiting brain drain and stimulating innovation. Entrepre-neurship is influenced by the existing ecosystem, which has a major role in stimulating and providing support to encourage enterprise creation and de-velopment, including:

Institutional level: political, environmental, regulatory framework•

Education: human capital, skills, universities, linkages with industries, •technology transfer

ICT: broadband, intellectual property, labs •

Business environment: infrastructure, ease of starting up a business, •competitiveness

Access to global markets: supply chain, diaspora, synergies on inter-•national level, business matching opportunities

Culture: trust, risk taking, ambition, social classes, collaboration•

Support: coaching, mentoring, networking, training, incubation, ac-•celeration

Money: capital markets, banks, regulations, funding opportunities, grants•

Key people: entrepreneurs, investors, decision makers, role models•

R&D: increased spending, technology transfer, linkages with industry, •research networks

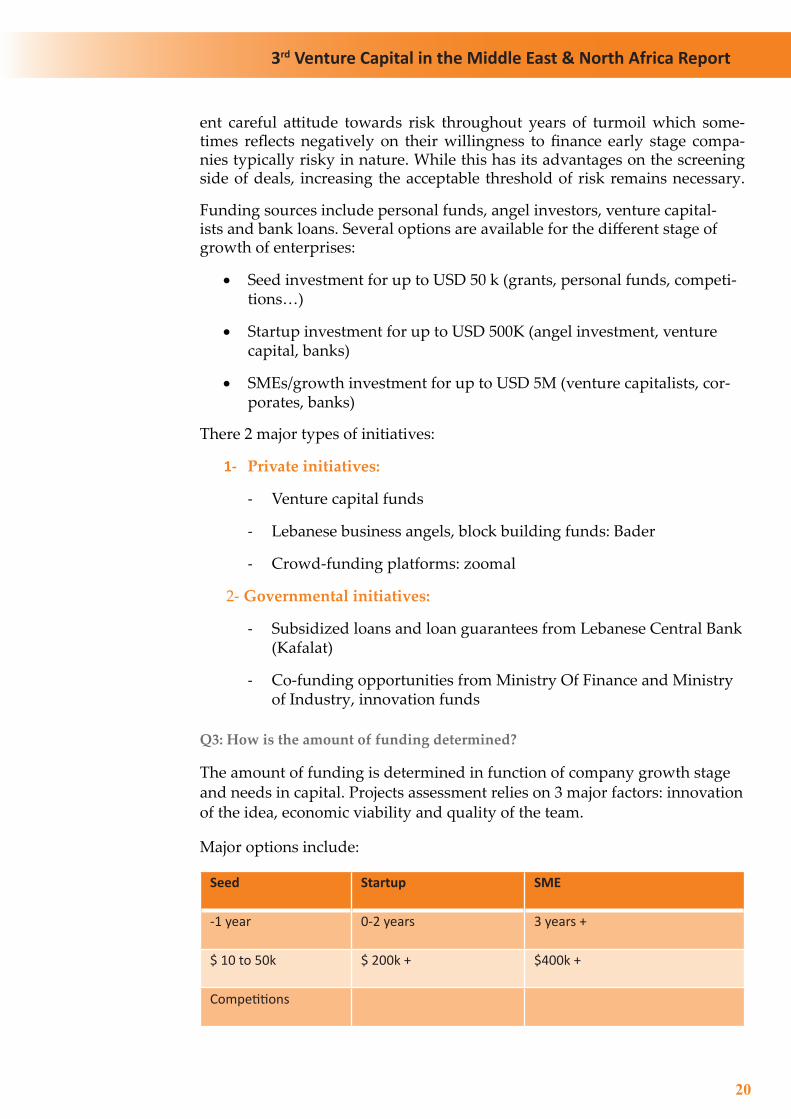

Q2: Has funding been easily accessible for Lebanese Entrepreneurs?

Overall the funds available to finance entrepreneurs in Lebanon whether in the form of equity or debt are more than enough to finance the current needs of entrepreneurs in Lebanon. This is partly due to a high market liquidity as well as the awareness of private and public institutions of the economic importance of entrepreneurship on one side, and the still limited but grow-ing deal flow of fruit bearing early stage enterprises on the other. Having said that, fund managers and lenders in Lebanon have developed an inher-

3rd Venture Capital in the Middle East & North Africa Report

20

ent careful attitude towards risk throughout years of turmoil which some-times reflects negatively on their willingness to finance early stage compa-nies typically risky in nature. While this has its advantages on the screening side of deals, increasing the acceptable threshold of risk remains necessary.

Funding sources include personal funds, angel investors, venture capital-ists and bank loans. Several options are available for the different stage of growth of enterprises:

Seed investment for up to • USD 50 k (grants, personal funds, competi-tions…)

Startup investment for up to • USD 500K (angel investment, venture capital, banks)

SMEs/growth investment for up to • USD 5M (venture capitalists, cor-porates, banks)

There 2 major types of initiatives:

Private initiatives: 1-

Venture capital funds-

Lebanese business angels, block building funds: Bader-

Crowd-funding platforms: zoomal-

2- Governmental initiatives:

Subsidized loans and loan guarantees from Lebanese Central Bank - (Kafalat)

Co-funding opportunities from Ministry Of Finance and Ministry - of Industry, innovation funds

Q3: How is the amount of funding determined?

The amount of funding is determined in function of company growth stage and needs in capital. Projects assessment relies on 3 major factors: innovation of the idea, economic viability and quality of the team.

Major options include:

Seed Startup SME

-1 year 0-2 years 3 years +

$ 10 to 50k $ 200k + $400k +

Competitions

3rd Venture Capital in the Middle East & North Africa Report

21

Zoomal.com Kafalat Kafalat

LBA Cedrus ventures, Wamda MEVP, Abraj, BBF, Capital trust

Berytech Fund Berytech Fund Berytech Fund

Q4: Who are the major VC players in Lebanon, the year of inception and how do they contribute to the overall ecosystem?

Major VC players in Lebanon include:

Berytech Fund

Cedrus Ventures

MEVP

Abraj Capital

Wamda

Capital Trust

They contribute to the entrepreneurship ecosystem by opening up investment and funding opportunities to entrepreneurs and stimulating enterprise cre-ation as well as supporting targeted programs such as business plan competi-tions, and pitch fests.

Other major players contribute to the ecosystem by enabling an encouraging platform to startup and develop companies, increasing deal flow for investors as per following:

Business Centers (Private Sector)•

Incuba-tor

Accelera-tor

Co-working Business Center & Hosting

Field

Berytechwww.berytech.org

X X X X Technology, multime-dia, Innovation

Beirut Digital District

www.beirutdigitaldis-trict.com

X X X Technology

Altcitywww.altcity.me

X X Social

Coworking+961

facebook.com/Cowork-ing961

X Business

Nabad

www.nabad.org

X Social

Cloud 5 X Business, Technology

3rd Venture Capital in the Middle East & North Africa Report

22

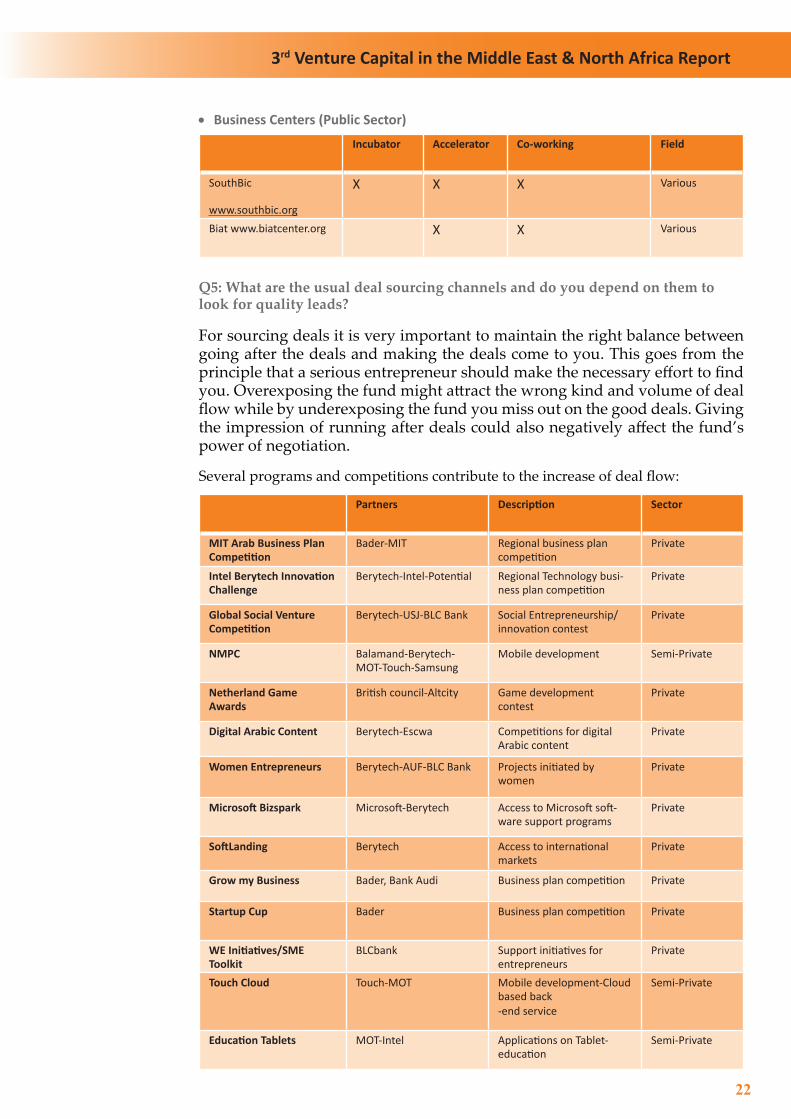

Business Centers (Public Sector)•

Incubator Accelerator Co-working Field

SouthBic

www.southbic.org

X X X Various

Biat www.biatcenter.org X X Various

Q5: What are the usual deal sourcing channels and do you depend on them to look for quality leads?

For sourcing deals it is very important to maintain the right balance between going after the deals and making the deals come to you. This goes from the principle that a serious entrepreneur should make the necessary effort to find you. Overexposing the fund might attract the wrong kind and volume of deal flow while by underexposing the fund you miss out on the good deals. Giving the impression of running after deals could also negatively affect the fund’s power of negotiation.

Several programs and competitions contribute to the increase of deal flow:

Partners Description Sector

MIT Arab Business Plan Competition

Bader-MIT Regional business plan competition

Private

Intel Berytech Innovation Challenge

Berytech-Intel-Potential Regional Technology busi-ness plan competition

Private

Global Social Venture Competition

Berytech-USJ-BLC Bank Social Entrepreneurship/innovation contest

Private

NMPC Balamand-Berytech-MOT-Touch-Samsung

Mobile development Semi-Private

Netherland Game Awards

British council-Altcity Game development contest

Private

Digital Arabic Content Berytech-Escwa Competitions for digital Arabic content

Private

Women Entrepreneurs Berytech-AUF-BLC Bank Projects initiated by women

Private

Microsoft Bizspark Microsoft-Berytech Access to Microsoft soft-ware support programs

Private

SoftLanding Berytech Access to international markets

Private

Grow my Business Bader, Bank Audi Business plan competition Private

Startup Cup Bader Business plan competition Private

WE Initiatives/SME Toolkit

BLCbank Support initiatives for entrepreneurs

Private

Touch Cloud Touch-MOT Mobile development-Cloud based back-end service

Semi-Private

Education Tablets MOT-Intel Applications on Tablet-education

Semi-Private

3rd Venture Capital in the Middle East & North Africa Report

23

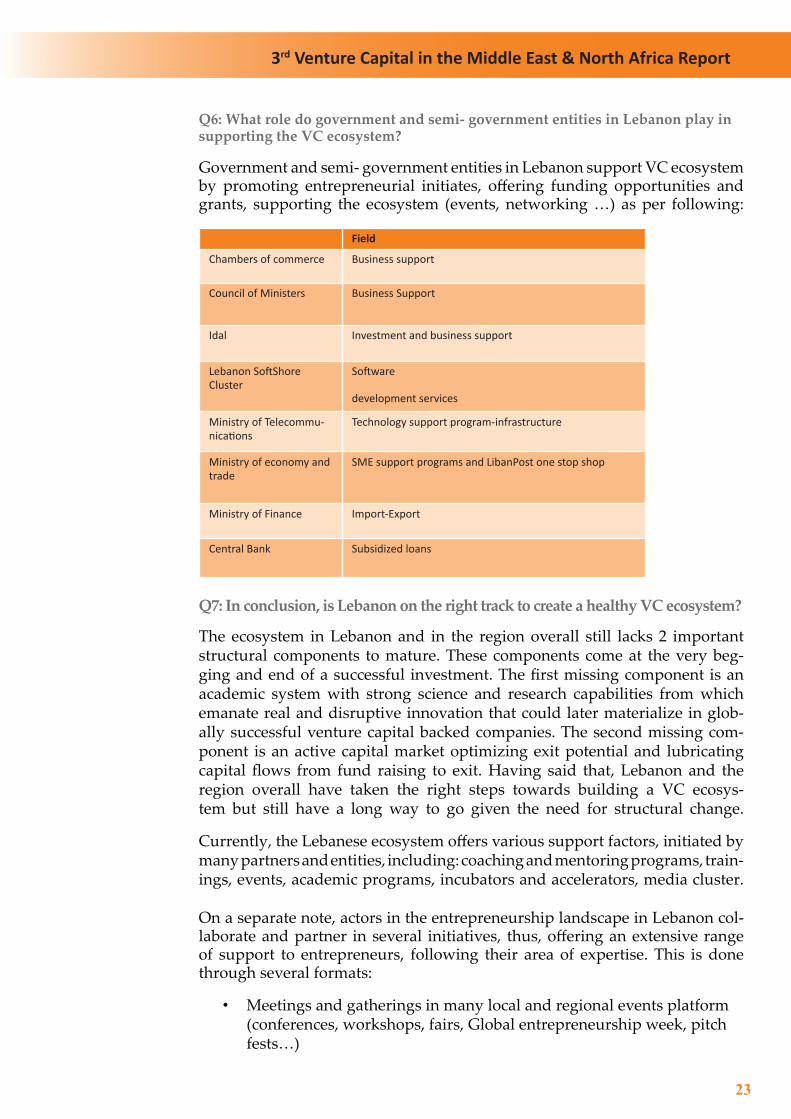

Q6: What role do government and semi- government entities in Lebanon play in supporting the VC ecosystem?

Government and semi- government entities in Lebanon support VC ecosystem by promoting entrepreneurial initiates, offering funding opportunities and grants, supporting the ecosystem (events, networking …) as per following:

Field

Chambers of commerce Business support

Council of Ministers Business Support

Idal Investment and business support

Lebanon SoftShore Cluster

Software

development services

Ministry of Telecommu-nications

Technology support program-infrastructure

Ministry of economy and trade

SME support programs and LibanPost one stop shop

Ministry of Finance Import-Export

Central Bank Subsidized loans

Q7: In conclusion, is Lebanon on the right track to create a healthy VC ecosystem?

The ecosystem in Lebanon and in the region overall still lacks 2 important structural components to mature. These components come at the very beg-ging and end of a successful investment. The first missing component is an academic system with strong science and research capabilities from which emanate real and disruptive innovation that could later materialize in glob-ally successful venture capital backed companies. The second missing com-ponent is an active capital market optimizing exit potential and lubricating capital flows from fund raising to exit. Having said that, Lebanon and the region overall have taken the right steps towards building a VC ecosys-tem but still have a long way to go given the need for structural change.

Currently, the Lebanese ecosystem offers various support factors, initiated by many partners and entities, including: coaching and mentoring programs, train-ings, events, academic programs, incubators and accelerators, media cluster.

On a separate note, actors in the entrepreneurship landscape in Lebanon col-laborate and partner in several initiatives, thus, offering an extensive range of support to entrepreneurs, following their area of expertise. This is done through several formats:

Meetings and gatherings in many local and regional events platform •(conferences, workshops, fairs, Global entrepreneurship week, pitch fests…)

3rd Venture Capital in the Middle East & North Africa Report

24

Competitions and support programs•

Online platforms and social media (directories, entrepreneurship sup-•port online, partners websites…)

Co-investment in potential startups and SMEs’ companies•

Jordan By Salwa Katkhude – Oasis 500

Q1: Entrepreneurship is not a very well understood concept in the MENA region. What in your opinion, could be a common interpretation of “Entre-preneurship”

Entrepreneurship is perceived in the region as taking risk, it remains an intimidating concept as there is a predominant fear of failure. Not hav-ing a stable job with a stable income is culturally looked down upon.

In the field of technology entrepreneurship, not enough success stories have come out of the region, so the confidence in technology entrepreneurship is still not very strong. In addition, not many failures are celebrated, which adds to the stigma that failure is a fundamentally bad thing. I am always reminded of one of the greatest entrepreneurs, Thomas Edison, when asked about how he failed 100 times before succeeding in inventing the light bulb. He said that he didn’t look at it that way; he viewed his “failures” as succeeding 100 times in how NOT to invent a light bulb. To me, this is the embodiment of the entrepreneurship spirit, and I believe this is the concept that is most widely misinterpreted in the region.

Q2: Has funding been easily accessible for Jordanian Entrepreneurs?

Entrepreneurship has been the focus of many governments in the region in the past 5 years. Several public funding initiatives have been established in Jordan with the help of donors to support entrepreneurial activities. In 2010 when there were very limited options for funding in Jordan, Oasis 500 was established against the backdrop of a dessert in early stage fund-ing, with an emphasis on training, mentorship and coaching to increase the chances of success. We got a very large number of applicants with very high demand for the acceleration program in Jordan. In only 3 years, Oa-sis 500 was able to invest in 60 teams and help establish their companies. In many cases, follow-on funding was secured from 3rd party investors.

In order to secure follow-on funding for these companies, Oasis 500 had to start its own regional angel network and hold several educational events to encourage investors to explore venture capital. As a result of these events, the first USD 1 million in Oasis 500 seed funding attracted USD 8 million in follow-on funding from 3rd parties.

A few venture capital funds were established in Jordan to invest and help build the entrepreneurial ecosystem as Jordan became a fertile ground for en-trepreneurs in the region. Although the funding climate for entrepreneurs has developed very quickly in Jordan (Amman has attracted the largest number of investments in startups in the Arab World in 2011 and 2012), there remains a problem with the accessibility of seed and early stage funding. Although there

3rd Venture Capital in the Middle East & North Africa Report

25

is ample funding in later stage companies whose business risk is relatively lower.

Angel investors are still not very comfortable with early stage investing, which is regarded as very risky, and prefer to stick to traditional investments like real estate because they understand it better as an asset class.

Q3 : How is the amount of funding determined?

For Oasis 500 we have 2 investment tracks; the first being the traditional startup track where each company is given USD 30K as a seed investment and enrolls in a 100-day acceleration program that involves intensive training, coaching, and mentorship. The funding is designed to last the company for 100 days and aims at reducing the risk of the company by getting some proof of concept in this period (whether it is traffic, revenue, user engagement, downloads beta release, demo, etc.), after which we help the company raise follow-on funding from angel investors, whom we vet, and later arrange for matchmaking and manage the investment process.

Companies who are more mature and are looking for larger amounts of growth capital can also apply to the Oasis 500 Growth Track, whereby if they qualify they can get an investment ranging from USD 50K-USD 500K from Oasis 500 with incubation mentorship and coaching support. The amount of funding depends on the need of the company and is governed by very specific milestones.

Q4 : Who are the major VC players in Jordan, the year of inception and how do they contribute to the overall ecosystem?

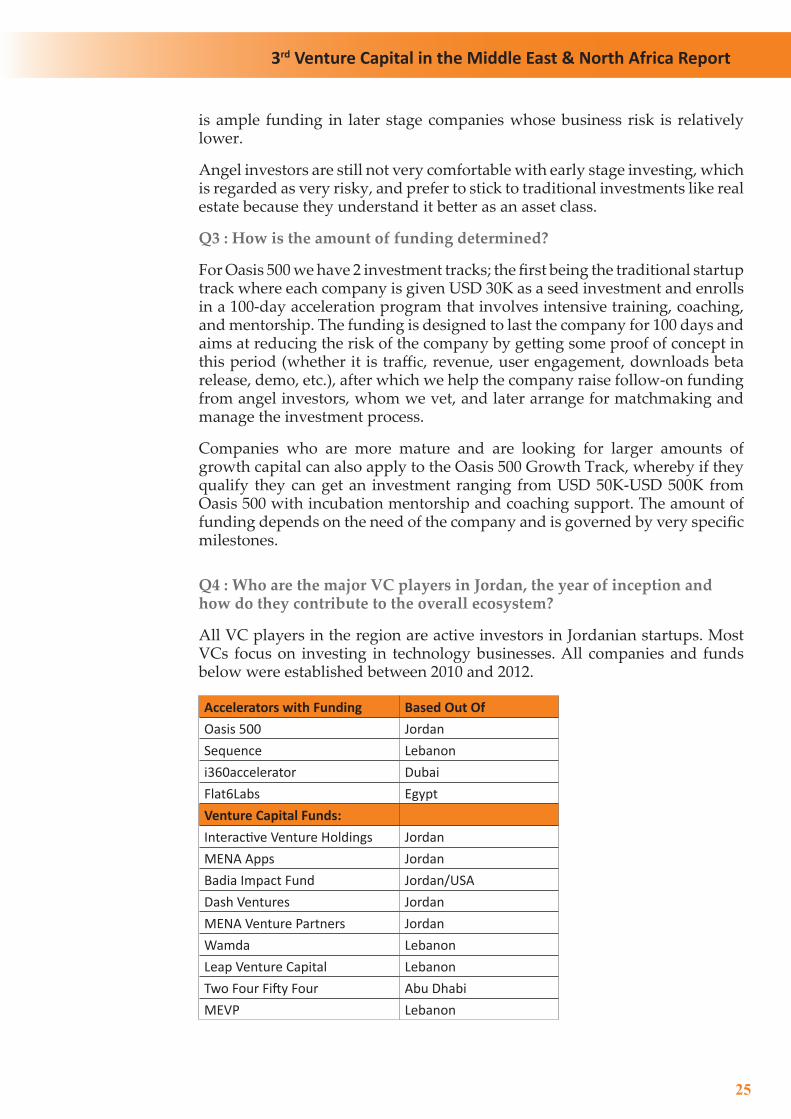

All VC players in the region are active investors in Jordanian startups. Most VCs focus on investing in technology businesses. All companies and funds below were established between 2010 and 2012.

Accelerators with Funding Based Out OfOasis 500 JordanSequence Lebanoni360accelerator DubaiFlat6Labs EgyptVenture Capital Funds:Interactive Venture Holdings JordanMENA Apps JordanBadia Impact Fund Jordan/USADash Ventures JordanMENA Venture Partners JordanWamda LebanonLeap Venture Capital LebanonTwo Four Fifty Four Abu DhabiMEVP Lebanon

3rd Venture Capital in the Middle East & North Africa Report

26

Q5 : What are the usual deal sourcing channels and do you depend on them to look for quality leads?

Oasis 500 started a non-for-profit capacity building company that focuses on training entrepreneurs on the important skills needed to start and grow a tech-nology business in order to secure and enhance its pipeline of deals. In many cases, for example, the entrepreneur has the right technical background but not the sales skills, or the right business background but limited knowledge on scaling in different markets. Many entrepreneurs also find it difficult to present to investors to get funding.

The Oasis 500 training program is a 6-day intensive workshop where the en-trepreneur gets immersed in training that covers a number of topics that were identified as critical for starting and growing a business. This training is the main pipeline for Oasis 500. We also seek to attend major regional entrepre-neurship competitions e.g. MIT Business Plan Competition, which we work with very closely for deal sourcing.

Q6: What role do government and semi- government entities in Jordan play in supporting the VC ecosystem?

JEDCO donor money that focuses on grants for startups and SMEs

King Abdulla Fund for Development: Focuses on capacity building programs in Jordan and was an anchor investor in Oasis 500.

Micro Finance institutions

All other VC funds and companies in the ecosystem are privately owned and run.

Q7: In conclusion, is Jordan on the right track to create a healthy VC ecosystem?

In 2011 and 2012, Jordan ranked #1 in the number of technology deals fund-ed in the Middle East and ranked #2 in the Middle East by amount of funds invested.

According to a Bloomberg study, Amman is the 10th best place to start a tech-nology company in the world. Jordan is also the top contributor among all Arab countries in terms of internet content, 75% of all Arabic online content originates from Jordan.

Jordan has ample talent and a hungry population and has become one of the most mature markets in the region for entrepreneurs and venture capital funds.

Oasis 500 alone has trained over 1,000 entrepreneurs seeking invest-ments, and invested in more than 60 companies in less than 3 years.

I would therefore conclude that Jordan is surely on the right track, but that doesn’t mean that there isn’t much work to be done. All parties, entre-preneurs and investors, need to increase their levels of maturity and ad-just their expectations as the dust settles and everyone sees the future a bit more clearly. I am very optimistic for Jordan and the region, but I realize that nothing worth building is built overnight and we all need to cooperate and move this critical industry forward because it offers the greatest hope in tackling the crippling outlook for unemployment in the MENA region.

3rd Venture Capital in the Middle East & North Africa Report

27

The Maghreb - Morocco By William Fellows, Lixia Capsia

Focus on High Impact Entrepreneurship & Venturing to Generate Sustainable Eco-nomic Growth & Employment

Across the MENA region venture investors (whether venture capital or private equity) face significant challenges with investment and business climates that are usually, as compared with peer regions and developed markets, rather challenging. For Venture investors globally, governments have typically fo-cused on taxation and fiscal incentives In the MENA region, although we face real issues in appropriate fiscal policy for venture investment, perhaps the key overriding challenge however is the business climate and a scarcity in the key raw resource: ambitious entrepreneurs. The specific components of the busi-ness climate challenges vary within the region – although commonalities like heavy red-tape, previously rational cultural aversion to risk taking, rigid and unreliable legal systems – crop up across many countries. Nevertheless, the comparative (to peer regions) lack of ambitious, new entrepreneurs emerging is a clear, undeniable challenge.

As the World Bank’s 2009 MENA business climate report, “From Privilege to Competition Unlocking Private-Led Growth in the Middle East and North Africa” noted, the region is characterized by firms that are much older than in oth-er parts of the world – indicating lack of innovation and competition – with the average age almost 10 years older than among peer regions. There are also fewer registered firms per capita as well, and with low relative exports, innovation, as compared to peers like China, the Republic of Korea, Malay-sia, or Turkey , all ample symptoms of a severe lack of sufficient ambitious entrepreneurial business creation relative to needs and relative to potential.

As venture investors can attest, potential entrepreneurs are there, but across the region the supporting environment in terms of tools, laws, rules and supporting programing for innovative, risk taking entrepreneurship – not only in high technology, but across all sectors (it is useful to remember FedEx came from and was one of the biggest VC wins in the US in the 70s)

- is severely lacking relative to the needs of the economy and society and the potential in the region.

Although over the past decade, entrepreneurship has been a buzzword in the MENA region with the various stakeholders beginning to take notice of the necessity for and potential of private entrepreneurs to generate economic growth and new employment opportunities, actual action has not been well targeted. Both MENA region governments, and in the lower income econo-mies of the region, International Development Agencies like the IFC, the American USAID and British DFID (etc.), have backed the emergence of a new set of SME and Entrepreneurship focused programs meant to promote small private business emergence. However, these have not been well-focused and have not grappled successfully with the environment challenge, nor in a fash-ion which truly enables venture investors and high-potential entrepreneurs to truly flourish.

As Josh Lerner, one of the world’s leading experts in venture capital and entrepreneurship development observed in his outstanding global survey,

3rd Venture Capital in the Middle East & North Africa Report

28

Boulevard of Broken Dreams: Why Public Efforts to Boost Entrepreneurship and Ven-ture Capital Have Failed-- and What to Do About It, that entrepreneurship and venture investment do not exist in a vacuum. As Lerner notes in observation doubly true in the MENA region, governments “neglect the importance of set-ting the table, or creating a favorable environment” tending to favor among the two policies that they employ to encourage venture capital and entrepre-neurial activities (“those that ensure that the economic environment is condu-cive to entrepreneurial activity and venture capital investments and those that directly invest in companies and funds”) the “fun” and visible one of direct investment either by creating government funds, seeding private funds, or providing other direct financing to firms.3

In the region, SME policy typically covers anything from a small Mom & Pop type shops and artisanal business to an established traditional family indus-trial firm to ambitious entrepreneurial firms seeking to grow and innovate in markets and management. Unfortunately, while it is often said that SMEs are a significant driver of economic growth, in fact in-depth data shows only a sub-set, the last category cited: innovative growth oriented SMEs & entrepreneurs. Recent in-depth studies are clear, whether from emerging or developed mar-kets, almost all net job growth attributed to SMEs broadly is in fact due to that subset of SMEs that are ambitious, entrepreneurial firms that are seeking to in-novate – meant broadly, not merely technology – and have growth ambitions.4

David Lingelbach, of Johns Hopkins University, Lynda de la Viña of Univer-sity of Texas and Paul Asel of the IFC found in their review of developing mar-ket entrepreneurs “new and growth-oriented firms are more likely to contribute to economic growth and provide important new sources of higher quality employment.”5

The OECD Working Group on SMEs found in a multinational survey of developed markets (France, Germany, Greece, Italy, Netherlands, Spain and Sweden and Quebec Province), “high-growth firms, … account for a significant share of jobs created and are key players in economic growth” not-ing as well that they account “ for a disproportionate share of gross job gains” particularly among young small firms, with 8-10% of SMEs, match-ing other findings, generating as much as 50% of net job growth6.

This subset of SMEs are also responsible for leading new innovation in busi-ness practices and technology and for a large portion of new exports. These SMEs are the exact focus of venture investors and there is a clear interest in effective public-private partnerships to enable more successful support.

However, what we typically see in MENA is venture investing policy lumped in with generic SME and even microfinance funding informal micro-enterpris-es. While well intended, not only do these vastly different types of enterprises with quite different needs –for funding and for business support – not ben-efit generally from efforts that are poorly suited all around, but governments miss the opportunity to have greater impact, and truly leverage venture in-vestment. The comparative lessons and data on entrepreneurship and venture show clearly that focusing on ambitious, innovative, growth oriented entrepre-neurs (in a wide sense, not only high tech), is needed. Thus, policy supporting SMEs should focus on addressing the particular challenges of ambitious, high growth oriented entrepreneurs and firms. This means addressing the business climate, to give them more tools to manage risk, to reduce uncertainty and to open doors to innovate and experiment (including failure and rebooting).

3rd Venture Capital in the Middle East & North Africa Report

29

The Moroccan example, where a comparatively substantial domestic venture investment sector has quietly emerged, is interesting for lessons, positive and negative. Largely encouraged not by explicit government policy for venture capital and private equity, but a useful combination of benign neglect of spe-cific VC policy with general liberty of locals and foreigners to invest equally as they saw fit and ongoing work on improving the general business climate. Morocco thus avoided (as Tunisian venture investors frequently point out) errors such as in Tunisia of hand-cuffing investors and fund managers with inappropriately prescriptive and restrictive investment rules and restrictions. However, the environment is still very challenging for new, ambitious entre-preneurs to emerge, although the lesson to derive from the Moroccan case is clear: Make starting and investing in businesses easier and liberal, remove restrictions that are not fundamentally and very clearly justified, and entre-preneurs and venture investors will push to emerge. And they will do better and more with greater flexibility. Taking the Moroccan experience as an exam-ple, the reforms effected by Morocco’s SME administration, the ANPME, have made the general SME business support program, Moussanda, much more market-friendly and -driven, although questions remain eligibility of earlier stage firms (given firm age requirements) and perhaps even a growth focus.

Practically, while the specific actions will vary by each country’s particulars like its legal and regulatory structure or business culture, a hard look is needed at “setting the table” for entrepreneurs, as Lerner calls the business climate for entrepreneurial ventures. Governments need to execute clear-eyed evaluation of how easy – or more often, not easy – it is in real practical terms and in com-parison with policies in countries or regions that lead in entrepreneurship. Governments also need to look at the effect of the whole environment rather than discrete parts. Any one barrier by itself often seems ‘not so bad.’ Collec-tively growth oriented entrepreneurs and venture investors suffer from the thous and cuts of “not so bad” barriers. Even where restrictions on business and investment may well be justified (notably in protecting employees from abuses or the environment), it is useful for governments to look at alternative models to find more market friendly or more generally efficient ways to implement.

As Lerner emphasizes in Boulevard of Broken Dreams, entrepreneurial activ-ity does not exist in a vacuum. There is a fundamental need for reforms to create a real positive environment for entrepreneurs based on a realistic as-sessment of practical challenges to launching new ventures. Fixing practical, lived issues in the business climate including the support ecosystem and le-gal tools available, business climate - ease and cost of starting business, be-yond the typical focus on “access to finance”, is crucial. One stop shops that are in reality 1 stop times 10, all too often the case in the region, are deadly.

Governments must also look particularly to ‘Best in Class’ global standards (and not merely familiar standards) for venturing and for business creation, not only to encourage foreign venture investors, but also to not disadvantage their domestic entrepreneurs. The availability of tools to balance risk between part-ners and investors, such as the ability to use flexible corporate structures and tools like preferred shares to balance incentives for success with governance concerns – easily, without doubt and excessive cost is key. The Moroccan case illustrates that while alternatives exist, if they’re hard (or expensive) to access or understand, this impedes unnecessarily entrepreneurs and venturing. Pol-icy makers frequently do not realize the importance of enabling the venture

3rd Venture Capital in the Middle East & North Africa Report

30

investors and entrepreneurs to come up with tailored solutions, particularly in the MENA region where cultural sensitivity about ownership percentages, and the stigma attached to failure, make balancing outside investors’ legitimate desires with entrepreneurs’ equally legitimate desires all the more difficult. Government support to this class of entrepreneurs and the venture invest-ment process by extension also needs to be holistic relative to the entrepre-neurial process. A frequent error is to focus purely on pre-money start-ups or one narrow segment, and expect all to fly within a single budget cycle; forgetting enterprises take many years to fully get up to speed. Further, gov-ernment policy in this area frequently ignore market capacity, focusing on promoting business creation and funding in industries or geographic areas that simply lack the infrastructure to be truly attractive to private invest-ment. Policy should also be broad in geography and in the conception of the entrepreneurs, within the rubric of Innovation and Ambition for Growth.

This later point is important to ensure that both venture investors and policy makers do not think too narrowly about opportunities. Policy has tended to push discussion of venture financing and entrepreneurship policy towards the specifically high-tech over the past 20 years. Arguably this is clouding our dis-cussions – and potentially clouding and distorting the development of effective government policy for the MENA region in promoting entrepreneurship and achievable innovation. Taking lessons from the early stages of American venture capital - illustratively take FedEx (or Aramex in region), an example of process and management innovation drawing on existing technology – and from other emerging markets and allowing for the rebooting and recycling first round inno-vation in supposedly ‘mature’ industries, as is often seen in the emerging Asian markets, has powerful potential in the region, but policy wise often is missed.In sum, governments should focus on aiding both venture investors and high growth potential entrepreneurs, as the generators of the key benefits attributed broadly to SMEs, via:

Focus business climate reforms with combined liberalizing investment 1. and business climate

Regulation focused on truly key protections, and benchmarked a. against best in class comparables from other regions;

Flexible business support and tools, such as easy ability to b. arrange tailored corporate governance, difference ownership categories and ownership rights;

Support business ecosystem where market gaps are observed, c. but via market based provision and providers to support pri-vate market emergence;

Informed and guided by market conditions and feedback2.

Entrepreneur focus on high potential, either in partnership a. with or informed by existing Venture investors for selection and funding;

Broad conception of innovation within innovative growth b. oriented focus, without undue restriction on private capital by sector or geography.

3rd Venture Capital in the Middle East & North Africa Report

31

Financing matched to or under private management with incentives 3. to make their return on investment success not passive asset manage-ment.

Notes

1“From Privilege to Competition Unlocking Private-Led Growth in the Middle East and North Africa” World Bank, 2009, p. 7-11.

2FedEx raised around USD 70 million from twenty of the USA’s leading risk venture investors, which made it the most largest new company VC financing in U.S. history at that time. See Wikipedia’s Federal Express entry, http://en.wikipedia.org/w/index.php?title=FedEx_Express&oldid=567638078

3Josh Lerner, “The Boulevard of Broken Dreams: Innovation Policy and Entrepreneurship” Harvard University and National Bureau of Economic Research, based on Boulevard of Broken Dreams: Why Public Efforts to Boost Entre-preneurship and Venture Capital Have Failed-- and What to Do About It, Princeton, Princeton University Press, 2009.

4See Erkko Autio Global Entrepreneurship Monitor, 2007 Global Report on High-Growth Entrepreneur-ship, p. 5; Rhett Morris, Global Entrepreneurship Monitor, 2011 High-Impact Entrepreneurship Global Report

5David Lingelbach, Lynda de la Viña, Paul Asel “What’s distinctive about growth-oriented entrepreneurship in developing countries?” p. 8, 2005.(http://papers.ssrn.com/sol3/papers.cfm?abstract_id=742605)

6See OECD Working Party on SMEs, “High-Growth SMEs and Employment” OECD Secretariat, 2002; Patrick Huot and Christine Carrington, “High-Growth SMEs” SME Financing Data Initiative, Government of Canada, May 2006; Also, for example results of UK survey “One In Ten SME Firms Hold Key To Driving Future Employment” Inside Business UK (http://www.insidebusiness.uk.com/business-news/item/261), April 2011. Also Antoinette Schoar, “The Divide between Subsistence and Transformational Entrepreneurship,” Innovation Policy and the Economy, 10 (2010) 57-81.

3rd Venture Capital in the Middle East & North Africa Report

32

MENA VC INVESTMENT DATA

KPMGNote: The data covers only structured VC funds that meet the MENA PE Association VC criteria. The data does not include direct investments, seed, incubation or invest-ment programs investing in VC. For more details on the data criteria, see Appendix 1. In addition, readers with an interest in the Maghreb can also refer to the AMIC (Morrocan PE Association) Reports, which cover Moroccan funds in detail, using dif-ferent criteria.

1. InvestmentsAs the MENA region continues to feel the impact of the global financial crisis together with the more recent political instability in some countries, available data suggests that the VC industry continues to experience an increase in deal activity. The medium to long term outlook for MENA’s VC industry remains positive as strong macro-fundamentals continue to drive the region’s economic recovery.

While the industry in general continues to invest cautiously, the upward trend in activity during the last three years is indicative of VC investment opportunities in the region and the industry’s growth despite geo-political challenges. This is a key achievement for the region’s VC industry which, arguably, remains fairly nascent and in the early phases of it’s develop-ment life cycle.

We note that, given the nature and size of VC investments, a significant portion are either not publically announced or, if they are announced, the value of the investment is not. For the purposes of our analysis be-low, we have focused on transaction volume as opposed to value.

During the last three years 119 VC transactions were completed compared to 56 during the three years 2007 to 2009. This upward trend has not been seen in MENA’s wider private equity industry where 234 private equity transactions were completed during the last three years, compared to 292 from 2007 to 2009.

Source: Zawya Private Equity Monitor

2006 2007 2008 2009 2010 2011 2012

10

0

10

20

30

40

50

60

13 13

3023

42

54

No.

of t

rans

actio

ns

Number of VC transactions since 2006

6

3rd Venture Capital in the Middle East & North Africa Report

33

The IT and software sectors continue to be the most popular amongst VC investors. Of the total transactions in the region’s VC industry since 2010, 47 percent were in the IT and software sectors. There have been 74 com-pleted IT and software transactions since 2006, of which 56 occurred dur-ing the period 2010 to 2012.

We note “others” primarily represents the energy, healthcare and transport sectors.

Source: Zawya Private Equity Monitor

Source: Zawya Private Equity Monitor

3rd Venture Capital in the Middle East & North Africa Report

34

Based on available data, Tunisia, Morocco and Lebanon lead the MENA re-gion in terms of the number of VC investments with 27, 26 and 25 transactions from 2010 to 2012, respectively. While the total number of VC deals in Egypt increased from 4 in 2007 to 2009 to 15 in 2010 to 2012, it remains politically volatile and saw a reduction in VC activity from 9 deals in 2011 to 6 in 2012.