Economic Impact Statement - Venture Capital in Queensland

52

QUEENSLAND ECONOMIC DEVELOPMENT THROUGH AN INCREASE IN VENTURE CAPITAL INVESTMENT - A REVIEW OF THE FAILINGS IN THE CURRENT INDUSTRY, HOW TO FIX THOSE FAILINGS AND SET THE STATE'S ECONOMY APART FROM IT'S COMPETITORS ECONOMIC IMPACT STATEMENT JULY 2012

Transcript of Economic Impact Statement - Venture Capital in Queensland

QUEENSLAND ECONOMIC DEVELOPMENT

THROUGH AN INCREASE IN VENTURE CAPITAL

INVESTMENT - A REVIEW OF THE FAILINGS IN

THE CURRENT INDUSTRY, HOW TO FIX THOSE

FAILINGS AND SET THE STATE'S ECONOMY

APART FROM IT'S COMPETITORS

ECONOMIC

IMPACT STATEMENT

JULY 2012

QUEENSLAND ECONOMIC DEVELOPMENT

THROUGH AN INCREASE IN VENTURE CAPITAL

INVESTMENT - A REVIEW OF THE FAILINGS IN

THE CURRENT INDUSTRY, HOW TO FIX THOSE

FAILINGS AND SET THE STATE'S ECONOMY

APART FROM IT'S COMPETITORS

ECONOMIC

IMPACT STATEMENT

Prepared by

Darren Lelliott MBA MFP BComm

in conjunction with

Professor George Earl Dip QS, Grad Dip (PD), MSc (PM), PhD (QUT), AAIQS, FAIB,

MRICS, MAIPM, MAPI, MPIA, MUDIA, MULI Director Bond University Institute of Sustainable

Development; Bond University; Queensland, Australia

CONTENTS 1 INTRODUCTION 1

2 VENTURE CAPITAL’S DUAL OUTCOMES 2

2.1 Future State & National Development 2

2.1.1 Enabling Entrepreneurial Drivers 2

2.1.2 High Impact Investment 4

2.1.3 Venture capital-backed companies fast growing 4

2.1.4 Venture capital backed companies high employers 5

2.1.5 Economic Multiplier 6

2.2 Limited Partner (Investor) Returns 6

2.2.1 Historic Investment Performance 6

2.2.2 Return Expectations 7

3 QUEENSLAND’S VENTURE CAPITAL INDUSTRY 9

3.1 Venture Capital in Queensland 9

4 ATTRACTING BUSINESS TO QUEENSLAND 11

4.1.1 Requirements to Increase Venture Gravity 11

4.1.2 Universities 12

4.1.3 Government policy 12

4.1.4 Venture Funding (Risk Capital) 14

5 MAKING VENTURE CAPITAL A SUSTAINABLE INDUSTRY 15

5.1 Is venture capital management an art or science 15

5.2 Asset Return Range 15

5.3 Economic Equilibrium 16

5.3.1 Disjoint in Investment Beneficiaries 16

5.3.2 Time Lags 16

5.3.3 Achieving Equilibrium 17

5.4 An Argument of Scale 17

5.5 Sustainable Venture Capital Model 17

6 ACHIEVING OPTIMAL INDUSTRY SCALE 19

6.1 Domestic Superannuation Funds 19

6.1.1 Investment Allocations 20

6.1.2 Willingness to Invest 21

6.2 Offshore Fund of Funds 22

7 CONCLUSION & RECOMMENDATONS 23

7.1 Conclusion 23

7.1.1 A sustainable Queensland venture capital industry 23

7.1.2 Queensland’s Economic Benefits 24

7.1.3 Queensland's Employment Benefits 25

7.1.4 Queensland’s Innovation Corridor 25

7.2 Recommendations 26

7.2.1 Expansion of local venture capital industry 26

7.2.2 Develop a strategy for the ‘SEQ innovation corridor’ 27

7.2.3 Sponsor further research 27

7.2.4 Promotion to foreign investors & fund-of-funds 27

Annexure 1. Economic Development Loss Through Lack of Local Venture

Capital Management 28

Annexure 2. Lelliott’s Sustainable Venture Capital Model 31

8 GLOSSARY 46

9 REFERENCES 47

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 1

1 INTRODUCTION BY PROF GEORGE EARL

In my many years of activity in business and academia I have been presented with many new innovations and technologies which I had hoped to see developed through to commercial success.

Unfortunately, like most Australians, I had come to believe that while Australia is particularly good at innovation we are terrible at supporting the commercialisation of such innovations and that there was little I could do about it. My expectation was that between government policy and an underperforming venture capital industry we had little prospect of changing the status quo.

As such when Lelliott first made me aware of his theories with regard to "Economic Development Loss Through a Lack of Local Venture Capital Management" and the "Sustainable Venture Capital

Model" I had a renewed sense of optimism and felt that his theories warranted further consideration.

Economic development requires continuous business renewal, the leading industries of today did not exist yesterday and will themselves be replaced tomorrow. Venture capital is just one part of ensuring that renewal process occurs consistently over time and as such it is time we started to view the function of venture capital as another necessary and mainstream component of the

economic environment. It results in accelerated business growth and employment. The economic benefits of venture capital investment are such that they should be considered part of the economic imperative.

All levels of government understand this and support, in principle, the growth and development of an Australian venture capital industry, and yet the Australian venture capital industry remains weak, indeed concerns have been expressed that its illness may be terminal. The theories put forward by Lelliott go a long way in demonstrating that historic government policy attempts were almost certain to fail because the macro principles of industry have not been understood and as such policies have not dealt with imbalances in the macro issues.

In conjunction with Lelliott's theories I have prepared this Economic Impact Statement to explore aspects of the venture capital industry nationally and at the state level. While Lelliott's theories are incomplete and have not been subjected to extensive analysis or peer review at this time I include them, and in some regards use them as the cornerstone of my arguments, as they review existing data and propose a complete model that not only succinctly explains what is wrong with the current industry, but precisely how to fix the problems and develop a sustainable venture capital industry.

The ‘Sustainable Venture Capital Model’ is potentially a groundbreaking model for managing the entire industry and as such it is being made available for the first time in this paper and exclusively for the benefit of Queensland.

With the power of this new industry model there would exist a rare opportunity for Queensland to capitalise on the current retarded industry before the growth begins.

Applying a fresh and optimistic eye (as becomes possible with the insight of the ‘Sustainable Venture Capital Model’) it is possible to review how to make SEQ a location to attract innovative businesses (i.e. increasing the ‘venture gravity’) and then demonstrate just how this can, and

should be done, not as a Silicon Valley but an Australian corridor of innovation with unique Queensland characteristics.

All of these objectives may be achieved in a reasonable timeframe and will require little state or local government investment.

I am so convinced of the benefits that will arise out of an improved venture capital industry in Queensland that in conjunction with Messrs Graham Hart AM, Glendon Young and Darren Lelliott

we have formed Elcano Capital for the purpose of establishing venture capital funds to operate in line with the Sustainable Venture Capital Model.

George Earl

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 2

2 VENTURE CAPITAL’S DUAL OUTCOMES

There are two types of return potentially arising out of venture capital and an effective national venture capital industry;

1. the economic development impact; and 2. the actual financial return to investors of specific funds.

Unfortunately the history of the Australian venture capital industry might lead to the conclusion that these two returns have a significant negative correlation as economic benefits are high whilst actual investor returns have historically been low.

Investor returns need to be appropriate or else investors will not make future investments, as has

been demonstrated with the year-on-year decline in investment commitments to venture capital in Australia.

As will be shown Lelliott suggests that research indicates that there may be a simple mathematical explanation as to the poor historic returns from the Australian venture capital industry and it is not the size of our economy, a lack of skills in venture capital management or our entrepreneurs, or a lack of investment opportunities.

2.1 Future State & National Development

There is much postulation about a post-resources Australia and more specifically Queensland and while this may not occur for some time it is acknowledged that forethought on this proposition needs to occur now.

At different times in Queensland’s economic history there have been three main economic drivers, agriculture, resources and to a lesser extent manufacturing. However, what have always been underlying factors in any economic development are:

entrepreneurial endeavours; risk taking; starting ventures for profit; and innovation in products and services (either as new, modified or enhanced).

When Queensland winds-down its current resources activities what will its economy look like? Will it revert to agriculture, will the manufacturing industry be reinvigorated, will it still be resources but of a different kind, will there be a new “super industry” or will it be a state of many SME businesses across a wide spectrum without significant “super industries”?

No one knows which but no matter which it shall always require those economic drivers listed above.

2.1.1 Enabling Entrepreneurial Drivers

There is a lot of discussion as to how to best enhance or stimulate entrepreneurism, the legislative environment formulating the environment to nurture the entrepreneurial spirit, whilst still providing consumer protection, education and network opportunities.

The creation of or enhancement of an overall environment for entrepreneurism is beyond the scope

of this paper, however, in assuming such activity will occur then businesses will be established or current ones will seek to expand and in doing so most will require external funds. Funds, for this purpose, can be either debt or equity, but the access to such funding remains on an inverse relationship with the businesses stage of development and its profitability.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 3

Figure 1: Profitability Vs Funding Relationship

The question of business funding is a well understood one and is best represented in the model represented below, Figure 2: Venture Capital Life Cycle. There are some variances to this model and the internet is starting to see some instances that vary from this model but those are exceptions and are a long way from representing a true change to the funding model.

This model is deceptive in that it appears to demonstrate that for each stage of the cycle there is funding available.

Figure 2: Venture Capital Life Cycle

As recently as late April 2012 Bill Shorten MP lead a trade mission to Israel to “attempt to understand how it is it that Israel-a country of 7.2 million people, a third of the size of Tasmania, sixty per cent desert, only sixty three years old, surrounded by enemies, with limited natural resources-produces more start-ups than large, peaceful and stable nations like Japan, India, Korea, Canada, the United Kingdom and Australia”i.

The head of the Productivity Commission, Gary Banks, has also spoken out as to the weakness of strategies to save employment through government hand-outs to the existing manufacturing sectorii; innovation is a key economic and performance driver for individual businesses. Australian Bureau of Statistics dataiii show that businesses that innovate are:

twice as likely to boost their productivity, 2½ times more likely to increase their contribution to their community,

2½ times more likely to put on staff, Four times more likely to increase the range of products or services they offer, and;

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 4

Five times more likely to target overseas markets.

Now more than ever, innovation is critical to lift productivity, economic growth, and employment through the creation of and invigoration of markets.

Venture capital is seen as crucial in innovation-driven economies as it provides significant funding for commercially high risk early-stage opportunities which may eventually redefine industries and sectors1, as has been identified as being an economic priority by the Liberal party with the Economic policyiv to “Enhance Australia’s venture capital market”.

2.1.2 High Impact Investment

The following is an internationally accepted definition of venture capital:

A venture capital fund provides more than just money to the company. Typically, the venture capital takes a seat on the board of directors and participates actively in company operations. This commitment often includes providing strategic counsel regarding development and production, making connections to aid sales and marketing efforts, and assisting in hiring key management. As part of this process, the venture capitalist also guides the company through multiple rounds of financing.

These elements – the patience, the hands on guidance, the willingness to take on risk and fail – make venture capital a unique asset class and may enable it to drive the Queensland economy faster and generate more jobs than other asset classes, as it does the U.S. economy. The significance of the U.S. venture capital industry has permitted it to historically set that economy apart from its international competitors.

Both the Canadian and U.S. governments use a measure of the number of billion dollar corporations per trillion dollars of GDP, as shown in Figure 3 below. On this scale Australia

presently rates well against Canada, both rate poorly against the U.S. However, in the last decade Canada has realised that without encouraging innovation, in part via substantial further venture capital investment, it stands to lose ground internationally, to the detriment of its economy. As such venture capital has been pursued as a national priority in Canada and the results are already extremely promising.

Figure 3: Firms with more than $1 billion market capitalisation per $ trillion GDP

Source: Elcano Capital; Australian figures are as per 2012 while US AND Canada are as per 2010; Bloomberg; Global Insight; McKinsey analysis.

2.1.3 Venture capital-backed companies fast growing

Over the past half century, venture-backed innovations have consistently spawned not only life-changing technologies but entire new industries. These include semiconductors, the internet, biotechnology, medical devices and clean technology, which in turn have spawned exciting

1 Allman K, Edler J, Georghiou L, Jones B, Miles I, Modivar O, Ramlogan R & Rigby J (2011) Measuring wider framework

conditions for successful innovation: A system’s review of UK and international innovation data, Index Report, NESTA, UK.

4

2^

2^

5

1

4

22

9

13

0 5 10 15 20 25

Total

Healthcare

Information Technology

US

Canada

Aust

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 5

subsectors of their own. Such evolutions create virtuous circles of innovation, job creation and revenue growth that benefit all Australians.

Venture-backed companies typically go on to fuel these new industries in terms of employment and revenue share. With their focus on innovation, high-growth potential and entrepreneurial spirit, these companies set themselves on a unique, positive trajectory that prevails long after the venture capitalist exits the investment.

Data gathered by the European Private Equity & Venture Capital Association2 shows that of the venture capital investees surveyed:

The post-investment period is characterised by large percentage increases in turnover; Most reporting companies reported an improved competitive position in terms of both market

share and profits;

Venture-backed companies deploy growth strategies to increase their sales in export markets; The venture capital investment enabled investee companies to create an average of 46 jobs

per company; Employees at all levels achieved higher levels of earnings and other forms of remuneration

following the investment; Almost three-quarters of seed/start-up companies could not have existed without venture

capital.

Anecdotal evidence in Australia indicates the same whereby because our venture capital industry is so weak by international standards so many of our innovative companies either fail or cease being Australian in order to survive.

2.1.4 Venture capital backed companies high employers

Evidence exists to suggest that venture capital backed companies are not only faster growing than their non-investee peers, but also that venture capital investment, at adequate levels, will result in almost 90% of investees increasing employee numbers.

For example while investment in venture-backed companies in the U.S. only equates to between 0.1% and 0.2% of U.S. GDP those companies employed 11% of the total U.S. private sector

workforce and generated revenue equal to 21% of U.S. GDP.

Looking forward, venture capital’s impact on the U.S. economy will likely grow even larger because

2 European Private Equity & Venture Capital Association (2002), Survey of the Economic and Social Impact of Venture Capital in Europe – Research Paper,

http://www.evca.eu/uploadedFiles/Home/Knowledge_Center/EVCA_Research/Economical_Impact/EconomicImpactofVentureCapital.pdf

could not have existed or

would have

developed more slowly

(94.5%)

would have developed in the same way

(4.7%)

would have developed

faster

(0.8%)

Without venture capital, my company.....

SOURCE: EVCA (2002)

Figure 4: Impact of the investment on the creation,

survival and growth of the company - all responding companies

Figure 5: Change in the total number of employees post

venture capital investment – all responding companies

Increase(89.70%)

Decrease(7.10%)

Same(3.10%)

SOURCE: EVCA (2002)

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 6

many of the fastest growing venture-backed companies in the U.S. today have yet to go public.

IHS Global Insightv research suggests that 92% of job growth for young companies occurs after their initial public offerings. This fact underscores the importance of IPO markets and of ensuring that our most innovative young companies can access the capital they need to grow.

Throughout its history, venture capital investment has built entire industry sectors by funding ground breaking innovations. From biotechnology to information technology to clean technology, thousands of start-ups have been brought to life, improving the way we live and work each day.

2.1.5 Economic Multiplier

Economic multipliers are difficult to determine and it would be even more difficult to accurately determine a multiplier effect from venture capital investment as such investment can be spread across a range of industries and at different stages in the growth of a business.

However, in the same manner that valuations of a business are impacted by its stage of business, i.e. the more advanced the business the higher its valuation per share, the effect of $1 of investment into a business in its ‘early stage’ will have far greater impact than the same $1 later, obviously this is demonstrated whereby $1M invested with Mark Zuckerberg when he was still in his dormitory at Harvard may have bought you 30% of his business then but only 1/100,000th% today.

Similarly your $1M may have been the difference between the survival of Mr Zuckerberg’s business and its resulting 1,500 employees then or not even paying for the CEO today.

For the purpose of this document the economic multiplier for an effective Australian venture capital industry investment is conservatively approximated to be 4 (assuming the innovation benefits outlined by the ABS and the EVCA data3).

As such the $120M of venture capital investment in 2010 should have a multiplied economic impact of no less than $480M.

2.2 Limited Partner (Investor) Returns

2.2.1 Historic Investment Performance

All over the world venture capital had its last set of ‘hey days’ in conjunction with the tech stock bubbles of 2001. Because the venture capital model got caught up in the tech bubble investment capital was easy, valuations were loose and the resulting losses were significant. It has taken the last ten years for those losses to work through the venture capital industry figures.

Table 16 is the last available recording of venture capital returns by AVCAL and demonstrates an industry average -5.4% IRR.

3 While ABS data demonstrates the employment, community contribution, productivity and export benefits of such innovative businesses it is difficult to determine a suitable macroeconomic or

partial multiplier3 for such investment (the ABS ceased production of Input-Output multipliers in its 98-99 publication3).

Table 16: Australian Private Equity Benchmarks - Cumulative Annualized IRR since

inception. Overall results as of June 30, 2008 for funds formed 1985-2007

Stage No. Avg Pooled Upper Median Lower DPI RVPI TVPI

Venture

Capital 37 -5.4 -1.4 3.3 -0.6 -14.8 0.29 0.66 0.95

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 7

Figure 6: Venture Capital Performance vs Investments: 1990-2008

Sources: National Venture Capital Association Yearbook 2009: Kauffman Foundation www.kauffman.org

Figure 6 and Figure 7 demonstrate the U.S. trend of venture capital investment performance against both investments made and committed capital. Note that due to the average 10 year cycle of venture capital funds and the escalation of investments up until the tech stock bubble bursting in 2001 many funds have not had to realise their investments or declare final IRRs until 2004

through to the present.

Figure 7: Venture Capital Performance vs. Committed Capital: 1990-2008 Sources: National Venture Capital Association Yearbook 2009: Kauffman Foundation www.kauffman.org

It is possible that by acknowledging the flaws of early venture capital investment strategies and having developed a relatively conservative investment strategy the industry may have already addressed those issues but will not see the result for several more years.

2.2.2 Return Expectations

The following table demonstrates expected investment returns across a sector. Returns are determined basically by the level of risk associated with that asset class.

Venture capital investment involves substantial risks due to many factors including, unproven products/services, unproven management, unproven markets for the product or service, the illiquid nature of the asset. As such it should have a commensurate return (within this graph as

represented by ‘Private equity’).

However, venture capital is not the same asset class as private equity as it involves a different investment strategy and generally invests at an earlier stage of investees than private equity and as such the expected return might better be represented at or above the emerging markets level of 14%.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 8

Figure 8: Returns by asset class

Of course if an asset class is not making its appropriate risk assessed level of averaged return funds will cease to flow to that asset class. This has been demonstrated in Australia’s decline in venture capital investment.

FY 2010 saw investment of $150m into 14 funds, while FY 2011 shows a drop to $120m investment but between only 3 funds. It is difficult to draw too many conclusion just on this data because the average may have been, 2010 = $10.7M/Fund, 2011 = $40M/Fund, it could have been that because fewer funds were seeking capital in 2011 less was raised (unfortunately the data is not broken down to a sufficient level of detail to be better informed).

What we do know is that funding in 2010 was raised primarily for latter stage venture capital funds while earlier stage increased; Seed @ $40m up 162%, Early Stage @ $80m up 41%. As much as 50% of the capital raised in 2011 may have come from the Innovation Investment Fund of the federal government.

It is arguable that except for the acknowledged benefits to the economy Australia’s venture capital industry would have ceased to exist as there is no economic substantiation as to why investors should still be investing into this asset class on the basis of historic returns alone.

0 4 8 12 16

S&P 500

Barclays Agg

Real estate

Distressed debt

Hedge funds

Private equity

Emerging markets

Returns by asset class (%)

Venture Capital

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 9

3 QUEENSLAND’S VENTURE CAPITAL INDUSTRY

3.1 Venture Capital in Queensland

In researching the state of innovation and supporting innovation in Australia, particularly with regard to venture capital investment, Brisbane and Queensland barely rate a mention. Recently a rating of start-up ecosystemsvi was reported with Sydney ranked 21st and Melbourne 22nd. While this is a poor showing for those two cities the article was completely silent with regard to Brisbane and the fact it did not even make the rankings.

Now it seems Brisbane stands to fall further behind with Perth expanding its financial services sector and surpassing Brisbanevii.

However, Queensland has been assessed by McKinsey consultants as having a high degree of innovation momentum but a lack of diversity. In McKinsey’s assessment it outperforms, for potential in innovation, both Sydney and Melbourne.

Figure 9: McKinsey; Mapping innovation clusters

Source: McKinsey Digital, http://whatmatters.mckinseydigital.com/flash/innovation_clusters/

Figure 10, demonstrates an assumption that Queensland should not have its equitable share of investment as the text attaching to this diagram stated “The over-representation of Victoria and Queensland can be explained thus:

- Victoria has historically had prominent industrial and IT sectors; and - Queensland’s share is partly a reflection of its ‘Smart State’ initiatives”

Yet the data shows that Queensland, at 22% of PE investment is only marginal above its GSP

(19%) contribution to GDP and no greater than NSW’s 35% against GSP (32%) contribution to GDP. However, this representation is distorted as it includes private equity whereas Figure 20: Percentage distribution across states, demontrates the volume of venture capital investment against each states GSP contribution to GDP.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 10

Figure 10: Private equity investment in Australia by state

SOURCE: PWC AVCAL (2006)

In order to capitalise on its innovation potential Queensland needs, among other things, access to venture capital investment.

Venture capital investment is low in Australia today but Queensland based innovative companies should expect to gain their share of this pool.

Lelliott argues, in his theory of "Economic Development Loss Through Lack of Local Venture Capital Management' Annexure 1, that Queensland isn't receiving it's fair entitlement for one very simple reason, that the amount of investment into a region has a strong correlation to the amount of venture capital management representation in that region.

As such it appears that because Queensland has low representation, while NSW and Victoria have high representation those states not only ensure they receive an adequate percentage of available venture capital investment but also receive that percentage that should otherwise have resided in under-represented states, such as Queensland.

The significance of his hypothesis is that it is not merely enough for a national effort to increase the amount of investment into venture capital where the current weighting of venture capital

management exists as this would simply mean that those states with the greater representation would assume even more investment funds and Queensland's investment deficit would become even greater. Therefore it is just as important to increase the percentage of venture capital management in Queensland as it is ensure greater amounts of venture capital investment.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 11

4 ATTRACTING BUSINESS TO QUEENSLAND

Venture gravity is that condition whereby a geographic location has such appeal that new and existing ventures gravitate to that area. Yes Silicon Valley has the most venture gravity in the world but thus far it has proven impossible to duplicate a Silicon Valley elsewhere. But that does

not mean that other locations don’t have venture gravity.

All of the state capitals already have a degree of venture gravity as entrepreneurs are drawn from their regional locations to these urban hubs. However, it is possible to further increase South East Queensland’s venture gravity.

By increasing South East Queensland’s venture gravity ventures first from regional NSW and then

major NSW regional centres, followed by Sydney and Melbourne will flow to Queensland.

This flow of ventures, along with the growth of Queensland originated ventures, would be significant given the employment impact of venture capital funded ventures and other economic multiples of investment into those ventures. Furthermore, if Queensland is able to increase its venture gravity to a reasonable extent then it should also result in an inflow of venture capital investment, so much so that Queensland should become a net importer of venture capital investment and not the current and historic net exporter of investment funds for the development

and benefit of NSW and Victoria.

4.1.1 Requirements to Increase Venture Gravity

Research shows that most innovation hubs (that being a location that has significant venture gravity to have attracted a number of innovation ventures) start with a steady flow of early stage innovations – often generated by scientists or entrepreneurs at top-flight research universities,

government laboratories or existing start-ups.

The presence of at least one established, innovative, venture-backed anchor company that draws talent to the area and spins out entrepreneurs also help seed the ecosystem.

In addition to capital, these entrepreneurs need ongoing counsel from lawyers, accountants and other business professionals to get their ideas off the ground. Such support networks build up over time and provide start-ups and venture capitals with specialised services such as intellectual

property protection, IPO registration compliance and human resources support.

Encouragement from state and local government in the forms of favourable tax and investment policies, common-sense regulatory structures and funding of basic research provide a third essential component. Healthy infrastructure, which includes a strong transportation network, affordable housing, high-quality schools and a robust cultural scene, completes the system.

By assembling and pursuing these elements smartly, states and regions can establish favourable environments for venture-backed companies to grow and contribute to the local economy in meaningful ways. Enough of these elements exist in SEQ already so that its venture gravity could increase dramatically with the inclusion of more venture capital funds and fund managers.

Turner (2012) claims those elements necessary to duplicate the successes of Silicon Valley are as follows:

1. Strong research driven Universities (with endowments); 2. Globally experienced repeat entrepreneurs; 3. Sophisticated risk capital; 4. Social capital; 5. Knowledge sharing; 6. Tolerance of risk taking; 7. Creative destruction;

8. Constructive failure; 9. Positive aggregate returns; and 10. Supportive government policy.

Treasury and the Productivity Commission have undertaken studies as to the cause of 'clusters'4 such as Silicon Valley and how to duplicate these. It has been noted that in spite of numerous

4 Australian Treasury, Venture capital in Australia, p7

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 12

attempts around the world, including within the U.S. comparisons have not come close. As such it is not constructive to focus on a duplication but rather on what exists within Queensland, in particular South East Queensland, and within our culture and maximise the opportunities with those present constraints in mind.

Cultural characteristics:

Knowledge sharing; Tolerance of risk taking; Creative destruction; and Constructive failure.

Other characteristics:

Globally experienced repeat entrepreneurs; and Positive aggregate returns.

Organisational characteristics:

Strong research driven Universities (with endowments); Sophisticated risk capital (DESI and MESI [incl venture capital],

Social capital is included in this item); and Supportive government policy.

Once Turner's characteristics are rearranged, as above, and a more optimistic view is taken of the Australian scenario and the more quantitative aspects of our venture capital industry are considered then it is possible to argue as follows:

Cultural Characteristics - the cultural aspects of Australia are what they are and are what make Australia what it is today. Whilst there may be benefits economically in modifying some attitudes in accordance with Turner’s arguments it is not realistic to consider changing such in an organised way or on a short timeframe. As such it is more pragmatic to be aware of what exists and formulate expectations and a framework for innovation development within that framework, this most likely will never result in another Silicon Valley but does not mean we cannot get a whole lot more efficient in supporting innovation.

Other Characteristics – it is arguable that these characteristics are presently available and that the claim of a lack of entrepreneurial experience is a cultural cringe, or perhaps misallocating the present deficiencies in innovation support. Many of the top examples of successful

commercialisation of innovations involves first time entrepreneurs that have been supplemented by experienced management available either locally or brought in from another region. Australia has management expertise functioning both at home and abroad with many professional expatriates stating a willingness to return to Australia if opportunities exist.

Organisational Characteristics – these three elements are arguably the only ones that can be directly controlled and for which strategies developed. As such these three areas also receive the

greatest percentage of the blame. However, a less sceptical review of these three areas is likely to demonstrate a different scenario.

4.1.2 Universities

In Australia we have many excellent universities of both research and teaching focus and that many of our universities have proactively engaged in teaching of entrepreneurship and have active commercialisation units, but that they have not been able to successfully commercialise

predominantly for reasons of a lack of necessary risk capital.

Bond University is one such university and being Australia’s only private university it places a heavy emphasis on entrepreneurship and commercialisation. In spite of this commercialisation has continued to be a problem for Bond because of the lack of risk capital in Australia, and South East Queensland more specifically. Not only is risk capital insufficient but because of the disjoint between DESI and MESI there is no cohesive way to fuddle through the varying levels of funding

requirements in a manner that is conducive to establishing and continuously operating a professional commercialisation unit within the university.

It is for this reason Bond University is party to this research and has entered into a research partner relationship with Elcano Capital.

4.1.3 Government policy

While there will always be areas for improvement there have been many attempts within government policy, at both state and federal level, to encourage commercialisation and incentivise

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 13

entrepreneurship. However, research indicates that where government becomes too embroiled in venture capital decision making the result is often failure and as such government involvement in this most commercial of ventures should be to set policy in support of the function and leave all operational elements to venture capital managers.

To date the last two attempts by federal governments to incentivise and grow venture capital investment have failed as follows:

1. Pooled Development Funds – whilst appearing to have good taxation benefits on complying investments they utilised an Australian specific (non-universal) design. They have also proved overly restrictive and too cumbersome to manage and were superseded as a result; and

2. Venture Capital Act based Early Stage Venture Capital Limited Partnerships (ESVCLPs) and

Venture Capital Limited Partnerships (VCLPs) – the change to these venture capital Act based programs did see a conversion to a more universally accepted and understood structure for venture capital investment (although the State based Partnership Act ‘Incorporated Limited Partnership’ is cumbersome and poorly understood). Initially the complete taxation exemption of ESVCLPs seems attractive but unfortunately the same type of government interference with investment selection and management has rendered this structure almost unusable for ordinary venture capital funds. Furthermore, an apparent oversight in structuring the legislation5 renders the supposed taxation incentives potentially detrimental to Australian superannuation funds6. VCLPs have no taxation incentive inherent to themselves7 and are only of potential taxation benefit to venture capital managers.

A far simpler incentive structure which will not be inclusive of the government interference that historically renders the structures unusable is a simple taxation benefit to super funds as follows;

Up to X% 0.5% to 1.0%) of a super fund assets invested into a venture capital fund operated by an Australian domiciled venture capital firm (such a firm being a registered member with the venture capital industry association AVCAL), such fund being specifically limited to making investments into Australian domiciled ventures, shall have that contribution taxed at a beneficial rate of 10% and all income from the investments of that complying X% of fund assets taxed at the beneficial rate of 10%.

This represents a 33% saving in the tax on those contributions and their earnings and while that

may not appear as attractive as a complete tax exemption it would retain the following taxation structure that is lost under ‘complete tax exemption’:

1. Dividend franking offsets; 2. The ability to claim management and other fees and costs of making the investment; and 3. The ability to offset capital losses against capital gains.

This structure would be simple to design, implement and manage. The industry self-regulation through AVCAL membership would give the federal government a single point with which to negotiate as and when it felt modifications might be required to avoid abuse of the structure.

Use of this self-regulation would also ensure the commerciality of investment structures and not the historic attempts at overregulation apparent in the PDFs, ESVCLPs and VCLPs. Furthermore, it may be possible to address some of the key limitations of venture capital as an asset class, transparency, valuation methodology, illiquidity, by negotiating ‘best practice methodology’ in

these areas for AVCAL members8.

It is not envisaged that all super funds would place the full 1% into venture capital investments but sufficient investment should flow as to sustain the optimal industry investment range of 0.075% to 0.125% of GDP. Should the flow of funds become too great the federal government would have the ability to adjust flow by simply adjusting the percent of assets gaining the

5 An oversight the regulators, ATO and AusIndustry, only became aware of after being notified by Elcano Capital almost 5 years after implementation of the structure. 6 This limitation is not expected to have the same negative impact with regard to the ‘direct early stage investor’ strategy. 7 Any claimed taxation benefit is only an entitlement to foreign investors that are otherwise

entitled to the taxation benefits in their own right, rendering the claimed benefits illusory. 8 AVCAL already requires some of these ‘best practice’ methodologies of its corporate members.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 14

entitlements.

4.1.4 Venture Funding (Risk Capital)

Venture financing refers to all forms of funding available to a venture in its early stages of development and operation but this research only with the ‘risk capital’ component, that being capital in exchange for an equitable interest in the venture.

In turn ‘risk capital’ is broken down to that ‘direct early stage investment’ (DESI) component and the ‘managed early stage investment’ (MESI) component.

While there are many variations to the norm DESI is provided earlier than MESI and serves a different function as MESI is expected to be inclusive of more guidance, introduction to networks, assistance with finding and selecting appropriate executives, etc.

4.1.4.1.1 Direct Early Stage Investment (DESI)

The private nature of the DESI market and the fact that because it has historically enjoyed no government assistance or incentive program means that data on this market is scarce and often unreliable. It also means that this market is difficult to find and inconsistent in its approach, quality and benefits.

An organised DESI market means investment networks, but being subscale results in poor quality of deal flow, and providing a fraction of the services claimed to be offered. This is not unique to Australia and Campbell (2003) states that as a result of UK angel networks being subscale “One well-known regional UK forum is described by one of its detractors as ‘infested with bankers, lawyers and accountants trying to sell their services’”. This description is anecdotally seen to be just as apt for the Australian market in businesses of ‘angel networks’ and most so-called ‘venture capital’ firms.

4.1.4.1.2 Managed Early Stage Investment (MESI)

This document is of course primarily dealing with MESI in the form of venture capital but it is worth reflecting here that whilst there are some levels of weakness in the other organisational characteristics necessary to create venture gravity the most significant fault lies in the near absence of MESI due to the low volume of investment into this sector and, as has been argued here, that even where there has been greater investment flow it may not have been adequate

from a pure mathematical balance of probabilities to sustain the industry.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 15

5 MAKING VENTURE CAPITAL A SUSTAINABLE INDUSTRY

5.1 Is venture capital management an art or science

The question as to whether venture capital management is more science or an art has long waged and is not unique to this industry or to investment management in general.

At stake is the question of the value of the management and its ability to demand high financial rewards.

Another way of describing this argument is:

Which will deliver the greater likelihood of investment outperformance (i.e. a return above that expected for the asset class or above the average of other managers of that asset class) astute investment management decisions based primarily on qualitative assessments, or can strategies be formulated through quantitative analysis.

Of course the answer always requires a combination of the two but it appears that the venture capital management industry may have historically relied too heavily on the former, qualitative or art based approach.

The argument that maximised outcomes for venture capital, or other Direct Early Stage

Investment must rely almost entirely on the quality of the investment decision maker and manager appears correct when considering a single transaction (micro level assessment) because of the following parameters of the investment type:

limited available information on any potential investment; illiquidity of investment; and lack of available industry wide data for benchmarking.

However, at the broader fund or industry levels (macro level analysis) this seems at odds with the evidence.

This issue is important because just as a fund is highly unlikely to return adequate investment returns to LPs when it has a poor quality and inexperienced management team so too will that fund suffer poor returns when the macro level dynamics are wrong at either, or both, the fund or

industry levels.

Arguably this is self-evident whereby the Australian and other venture capital markets internationally, have either consistently performed below what should be the appropriate rate of investment return or been unable to sustain a healthy rate of return.

Today there continues to be lot of discussion as to the failing of the Australian venture capital industry but with almost all of this discussion remaining focused on the qualitative aspects such as

claims that the failures arise primarily from a lack of experience in venture capital management and the need for more education and government funded investment pools from which trainees can gain experience.

There is little doubt that such proposals will be beneficial but without addressing the quantitative issues they will have little positive effect.

Fluctuations in both the venture capital industries (macro level) comparative performance and

resulting inflows to the industry must be strong indicators that it is unsustainable in its current form.

5.2 Asset Return Range

In simple terms venture capital investment requires an appropriate yield from that investment and what is an appropriate yield is determined by where it sits with regard to the level of risk the

investor holds, e.g. likelihood of loss to some or all of that investment. As stated above on this scale venture capital should return approximately 14% on the basis of its Risk: Reward.

Each asset class rate of return expectation is really an average of the return from all investments within that asset class. But the actual rates will be within a band for this asset class (excludes those outside a mean variance determinant for the asset class).

For example Figure 8: Returns by asset class, provides an indicative averaged return rate for real

estate of approximately 8% but the range might be 6.5% to 9%. Where a particular

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 16

investment/fund or investment product from this asset class sits within this range will result from, among other things, the capability of the investment manager.

As such it is within an asset class range whereby the qualitative aspects should have the greatest impact, not in the ability to even get to this range. If this assumption is correct then it is possible to conclude it is the macro (quantitative) factors that must be failing our Australian venture capital industry.

5.3 Economic Equilibrium

There is generally stability and sustainability within an asset class return range because of the weight of investments within that asset class and the effect of economic equilibrium on that asset class.

If, for example, there were a sudden decrease in the volume of funds invested in the real estate asset class (i.e. a shift in the weight of the real estate market) then investment performance will move outside this range as prices will have gone up and therefore returns would also go up beyond the upper end of the return range.

This change in price occurs because there is, or has historically been, a constant element affecting the real estate asset class, demand driven by growth (of population and the economy).

However, upon seeing the above average returns going to this asset class new investors would pour into the class increasing the supply of projects and pushing prices, and as such investment returns, down. This fluctuation of the market with changes in supply and demand will continue until the market is again in a relative state of equilibrium. It is only when a market is in relative equilibrium that it is also relatively sustainable (equilibrium = sustainability).

The Australian venture capital asset class has not historically performed in this way. Investment

has flowed in with a cyclical motion seemingly more associated with super fund investment manager sentiment towards overall economic conditions and when the latest internationally backed Superperformer venture capital backed project most recently listed on the NASDAQ (2012 should therefore see an uptick in venture capital investment on the back of the Facebook payout to its venture capital backers).

The underlying element of demand driven by growth of the economy is just as relevant for the

venture capital asset class and that growth results in the opportunities for new ventures, resulting in a demand for venture investment but in spite of this the same pressure is not present to get and keep this asset class at equilibrium. There are two reasons that the forces of market equilibrium have not occurred over the venture capital asset class:

1. Disjoint between the investment beneficiaries; and 2. Significant time lags in the asset class.

5.3.1 Disjoint in Investment Beneficiaries

As noted above in 2 above there are two effective beneficiaries from venture capital investment; the economy and Limited Partners (investors).

But with such poor historic investment returns most Australian LPs have not enjoyed the expected benefits. Thus leaving only the economic benefits but the recipients of these benefits largely don’t financially contribute back to venture capital investment.

Australian governments, as guardians and monitors of our economy, do invest into venture capital (in recent years the federal government has been by far the largest investor but this comes with many limitations and potential disadvantages9) but this contribution is not adequate of itself.

The disjoint in beneficiaries exists today, but only because venture capital investors are not directly receiving adequate investment returns as per expectations this is primarily the result of the asset

class not getting up to scale and being sustained at an adequate scale of investment.

5.3.2 Time Lags

venture capital investments are both illiquid and opaque by nature. The result is that time lags are considerable from the point of investment until the point of investment returns. While the AVCAL

9 See Lerner - Boulevard of Broken Dreams.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 17

valuation methodology goes some way to providing assurances of fair and reasonable progressive investment valuations the lack of transparency in the asset class and the lack of correlation between ongoing investment valuations against realisation values raises concerns that artificially inflated valuations cannot be relied upon during the life of a fund.

Therefore, it may be 10 years between making a venture capital investment and getting the investment feedback by way of declared dividends.

One way in which the issue of the transparency may be addressed is through a closer alignment between LPs and specific investments, such as by operating investment on a single investee basis. Elcano Capital has developed the unique capability of such direct alignment between one or more investors and a specific project through the tax incentivised federal government ESVCLP program and believes this will be better suited for the DESI strategy stated in 4.1.4 above.

5.3.3 Achieving Equilibrium

As stated above the available evidence, in conjunction with established economic theory, only leaves the conclusion that equilibrium has not yet been achieved as a balance of macro factors has not yet been achieved.

Surprisingly our research of existing international theory on macro level venture capital industry management has only demonstrated the lack of such theory.

5.4 An Argument of Scale

While this area still requires further research, both at the local and international levels, evidence indicates that scale plays an important role with regard to the likelihood of investment returns at the appropriate level.

Scale is relevant at all three levels of venture capital activity;

1. National Industry; 2. Manager and Fund; and 3. Transactions.

Due to the interrelationship between factors most likely to impact overall ratios of success or failure at all three levels, each level needs to achieve a minimum scale to be effective, i.e. have the greatest statistical likelihood of achieving overall success resulting in appropriate levels of investor returns.

From initial review of the available data (substantial further research is required before a conclusion could be made) it appears probable that in the same way that failing to achieve a minimum set of scales reduces the statistical likelihood of achieving appropriate rates of return so too does the rate of return reduce beyond a certain point, i.e. it appears that an optimal range

exists across all three levels described.

5.5 Sustainable Venture Capital Model

The 'Sustainable Venture Capital Model', Annexure 2, presents a model demonstrating the deficiencies with venture capital as a national industry and hypothesises that continuing the Australian venture capital industry as it has been is likely to not only destroy what there is of this vital industry but also hold Australia and Queensland back from performing at the economic levels they are capable of achieving.

It hypothesises that there is an optimal range at the three levels of venture capital:

1. Industry; 2. Fund; and 3. Transaction.

Where any one of these levels is outside the optimal range it has a destabilising effect which results in the asset class underperforming to such an extent as to threaten the ongoing existence of that asset class. The theory suggests that this is the current and historic position of the Australian and Queensland venture capital industries, but that by becoming aware of these issues we can start to modify policies and commitments to the sector for the purpose of making it self-sustaining.

By self-sustaining the model proposes that so long as the asset class is returning on investment

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 18

within an averaged range appropriate for its risk levels then this shall ensure a continuous flow of investment.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 19

6 ACHIEVING OPTIMAL INDUSTRY SCALE

The Sustainable Venture Capital Model does not concern itself with the source of venture capital investment just the impacts. In assuming, for want of an alternative macro model to achieve a sustainable Australian venture capital industry, that the Sustainable Venture Capital Model is

correct and that the hypothesised optimal levels need to be achieved considerations must now be given as to the availability and sourcing of at least $850M worth of annual investment.

The three sources are as follows:

1. Domestic Managed superannuation funds, government and corporate investment (short-term);

2. Offshore fund-of-funds investment (medium-term); and 3. Domestic self-managed-super-funds (long-term).

6.1 Domestic Superannuation Funds

61% of Venture Capital investment in Australia originates from resident corporate super funds (ABS: 5678.0 - Venture Capital and Later Stage Private Equity, Australia, 2010-11) with the remaining 39% spread across 7 investor types and none contributing greater than 10%.

Australia has the world’s 13th largest wealth fund in the Future Fund, and through the compulsory superannuation system, Australia has the fourth-largest pool of retirement funds in the world, currently at $1.3 trillion and projected to grow to $4 trillion in the next 10 years10.

Figure 11: Deloitte's projected total superannuation

assets

Figure 12: Deloitte projected net contributions

There are essentially two types of Super funds for our purposes, Self Managed Super Funds

(SMSFs) and Managed Super Funds (which includes Corporate funds, Industry funds, Public sector funds, Retail funds and Pooled superannuation trusts).

While SMSFs represent the fastest growing segment of the Super market it is also the most diffuse option (there being 458,561 as of Dec 2011) and is not considered to be a short-term option11 because:

(a) a single SMSF will have a relatively low balance by comparison to a Managed Super Fund; and

(b) it will increase the cost of marketing and time to market in pursuing a SMSF strategy.

The Managed Super Funds hold $1.3 trillion of investment funds (ABS: 5655.0 - Managed Funds, Australia, December 2011). Unfortunately available data does not break down these balances by States, however, using the population data and making an assumption that as the national GDP contribution from each state is approximately equivalent to those state population percentages (see Figure 20: Percentage distribution across states) then Figure 13: Value of superannuation assets by percentage of state contribution to population and GDP. can be extrapolated.

10 Deloitte Actuaries & Consultants, Dynamics of the Australian Superannuation System The next 20 years: 2009 – 2028, March 2009. 11 It is likely that SMSFs will become contributors to VC in the coming years and one of the proposals includes a strategy for attracting such investment in the longer term.

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 20

Figure 13: Value of superannuation assets by percentage of state contribution to population and GDP.

Source: Elcano Capital

Therefore it is assumed that the component of Managed Super Funds originating from Queensland is $254Bn. It is also known that NSW and Vic are overweight in financial services companies and as such a heavy percentage of these Queensland originated Super funds are managed outside the state.

Figure 14: Assumption of Queensland Super Assets Managed Outside Queensland’ gives some figures for different percentages of Queensland originated funds managed outside this state. If

that is 60% then $101Bn worth of managed super funds are managed within Queensland.

6.1.1 Investment Allocations

Most Super fund trustees are risk averse when it comes to investment allocation strategies and while those trustees do not generally determine investment allocations they do provide the strategy for the consulting asset allocation advisers. Asset allocation advisers will use a range of theories in formulating their advice but the main one is Modern Portfolio theory, as developed by

Nobel laureate Harry Markowitz. In essence this is a mathematical model for maximising portfolio return at an accepted level of risk by combining a variety of asset classes with known (or assumed) risk measures.

What comprises the ideal asset mix is ‘elastic’ and will vary between any two asset consultants but as a general rule of thumb it is suggested that a small percentage (on average 5%) of a portfolio should be made up of ‘alternate assets’. It is a small allocation because investments in this

category carry high risks and potential rewards.

‘Alternate Assets’, in its broadest sense, comprises any investment that is not the standard listed equities, cash, fixed interest, property. Some unconventional investments may fall into this category and over the last ten years a lot of this allocation was taken up with derivatives and options products (falling under what was the boutique category of hedge fund investments) but otherwise is largely filled with Private Equity and lastly a small allocation to Venture Capital investments.

Frontier Investment Consulting claims to allocate around 3%of their investments to Australian private equity. Of that 3%, about 20% is typically allocated to venture capital12, or more directly meaning 0.6% of assets allocated to venture capital investment. While Chant West claims to allocate 2.5% of assets held by growth funds to alternate assets with 61% - 80% of this to PE funds (no details given for venture capital allocations from this).

12 http://investordaily.com.au/archive/13508.xml

StateSuperannuation (pension)

funds ($A M)

NSW 406,083

VIC 312,698

QLD 254,685

WA 130,459

SA 92,129

TAS 28,389

ACT 20,316

NT 12,799

1,257,557

% mgd outside Qld Residual mgd in Qld ($A M)

40% 152,811

50% 127,343

60% 101,874

Figure 14: Assumption of Queensland Super Assets

Managed Outside Queensland

Source: Elcano Capital

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 21

Figure 15: Achieving Optimal Scale through Queensland Super Funds Contributions

Source: Elcano Capital.

Figure 15 is a calculation of the impact of a strategy of 3% of Queensland originated super funds being directed towards PE investment and 20% of that allocation going towards venture capital investment.

Under these assumptions it is estimated that Queensland should presently have $1.1Bn worth of venture capital investment already and that it should have $290M of new investment each year.

Figure 15 assumes investment only from the managed component of super funds, as such once SMSF starts making contributions it will have a further profound impact in this area.

If we apply the assumed economic multiplier of 4x it represents approximately $1.2Bn worth of new state development investment, generated from within the state and without requiring any new

State government investment into this area.

If the asset allocation of 0.6% of inflowing managed super funds ($1.46Bn p.a.) did flow to venture capital investment then it would exceed the minimum of the optimal range ($850M p.a.). As such the managed super fund industry alone has more than the capacity to get the Australian venture capital market to its optimal investment range and as such better protect the ability of those funds gaining the investment return appropriate for the asset class, without considering the

flow on economic benefits to the economy and their individual fund members from having a vibrant economy based on more than one overwhelming source of national income, resources.

6.1.2 Willingness to Invest

At this time it is not possible to know whether the Super Fund trustees will be willing to invest into venture capital again, certainly investment had almost ceased after the 2001 tech bubble but it did grow again until 2008 when the GFC again saw a large drop in venture capital investment (ABS:

5678.0 - Venture Capital and Later Stage Private Equity, Australia, 2010-11).

Queensland based Super Funds may have historically either:

(c) Been reluctant to invest into Queensland based venture capital funds because of the lack of credible funds; or

(d) Not been approached to make allocations into Queensland based venture capital funds.

Brad Holzberger, QSuper chief investment officer put it succinctly when he pointed out that13 ‘much of the current asset allocation had not changed over the past 20 years, and that was mainly the result of herd behaviour, as none of the funds had been willing to divert too much from the industry average out of fear of falling periodically short of their peers’.

Media coverage of the state of depressed listed equities, both domestically and internationally, along with strong indicators that the real estate market will remain depressed for some time has

lead to many commentators claiming these markets could remain low for another decade. The Australian Financial Review has recently quoted Deutsche Bank strategist Tim Baker as pointing out that super fund "Cash holdings are very high and the share of super sitting in cash and deposits is 15 percent, whereas it used to be less than 10 percent"14.

13 http://investordaily.com.au/archive/13943.xml 14 The Australian Financial Review, Super rolling in cash, p 10, Thursday 12 July 2012.

%Mgd: 70% No.FirmsQld 5

%PE 3%

%VC: 20%

Column1 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

$Billion 1,306 1,653 2,000 2,270 2,540 2,810 3,080 3,350 3,620 3,890 4,160

$Mgd 914 1,157 1,400 1,589 1,778 1,967 2,156 2,345 2,534 2,723 2,912

PE 27.42 34.71 42.00 47.67 53.34 59.01 64.68 70.35 76.02 81.69 87.36

VC 5.48 6.94 8.40 9.53 10.67 11.80 12.94 14.07 15.20 16.34 17.47

%Increase 27% 21% 14% 12% 11% 10% 9% 8% 7% 7%

$Increase 1.46 1.46 1.13 1.13 1.13 1.13 1.13 1.13 1.13 1.13

QldComponent 1.10 1.39 1.68 1.91 2.13 2.36 2.59 2.81 3.04 3.27 3.49

QldIncrease 0.29 0.29 0.23 0.23 0.23 0.23 0.23 0.23 0.23 0.23

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 22

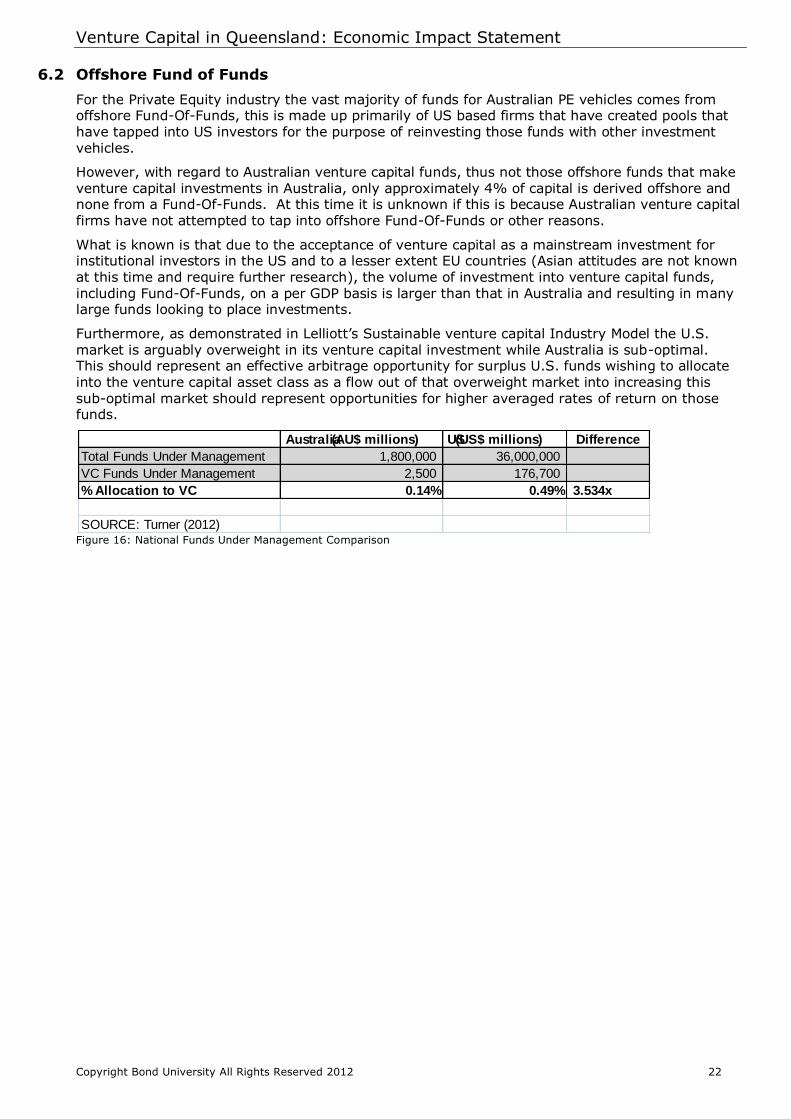

6.2 Offshore Fund of Funds

For the Private Equity industry the vast majority of funds for Australian PE vehicles comes from offshore Fund-Of-Funds, this is made up primarily of US based firms that have created pools that have tapped into US investors for the purpose of reinvesting those funds with other investment vehicles.

However, with regard to Australian venture capital funds, thus not those offshore funds that make venture capital investments in Australia, only approximately 4% of capital is derived offshore and none from a Fund-Of-Funds. At this time it is unknown if this is because Australian venture capital firms have not attempted to tap into offshore Fund-Of-Funds or other reasons.

What is known is that due to the acceptance of venture capital as a mainstream investment for institutional investors in the US and to a lesser extent EU countries (Asian attitudes are not known

at this time and require further research), the volume of investment into venture capital funds, including Fund-Of-Funds, on a per GDP basis is larger than that in Australia and resulting in many large funds looking to place investments.

Furthermore, as demonstrated in Lelliott’s Sustainable venture capital Industry Model the U.S. market is arguably overweight in its venture capital investment while Australia is sub-optimal. This should represent an effective arbitrage opportunity for surplus U.S. funds wishing to allocate

into the venture capital asset class as a flow out of that overweight market into increasing this sub-optimal market should represent opportunities for higher averaged rates of return on those funds.

Figure 16: National Funds Under Management Comparison

Australia(AU$ millions) US(US$ millions) Difference

Total Funds Under Management 1,800,000 36,000,000

VC Funds Under Management 2,500 176,700

% Allocation to VC 0.14% 0.49% 3.534x

SOURCE: Turner (2012)

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 23

7 CONCLUSION & RECOMMENDATONS

7.1 Conclusion

7.1.1 A sustainable Queensland venture capital industry

It is extraordinary to realise just how little comprehensive analysis has been conducted into

venture capital as an economic asset class. Little empirical data has been effectively compiled and analysed before now. Remarkable given just how significant an economic driver of wealth and employment this investment class is, or rather is known to be if operating effectively.

The Australian venture capital industry appears broken, it isn’t it is just poorly understood and therefore has historically been managed in ignorance. How can governments create effective policy to manage an industry it does not understand? How can investment managers create

effective investment management strategies over an asset class it only understands at the micro level? How can investors feel any reasonable certainty of investment returns? Of course the answer to all three questions is they cannot do so in ignorance and they have not as is self-evident.

Of course venture capital is not just an Australian phenomenon so how is it done differently in other markets? It appears there is little, if any, difference in the ignorance or its impact and that it

is most probable that those that have had better returns are doing so intuitively and just because of the sheer volume of available funds, as appears the case in the U.S.

But with an understanding and a useable industry model the veil of ignorance can be lifted and for the first time comparatively small markets, such as Australia, Queensland, Spain, Italy and others can establish national strategies and policies for their own industries. With this newly emerging post-information revolution economies will need to have strategies for constant renewal of its business base. Venture investment, including venture capital, is only a component of this but as has been seen historically in national case studies all over the world without effective access to venture investment nations renew their business base much slower, if at all and often follow developments made in other countries and don't lead such developments.

The ‘Sustainable Venture Capital Model’ may provide just such a model and has been made available exclusively to Queensland, at this time, as a blueprint so that this state can prepare itself by ensuring it has at least adequate venture capital management representation.

The opportunity exists because the model's developer, Lelliott, must conduct further data research, primary data collection, model development, testing and validation before being able to formally publish his ‘Sustainable Venture Capital Model’, which he expects to do as a doctoral thesis.

This model is intuitive in that when it is put forward the logic immediately strikes us. As it utilises economic principles substantiated in other contexts it reassures us of its relevance even before the

complete data set is available and testing is complete. In essence the simplicity of what Lelliott proposes may be summarised in the analogy that we need to 'prime-the-pump' before we will get an adequate flow of investment returns otherwise, as has been seen, no matter how we wind the motor little flow occurs.

With the ‘Sustainable Venture Capital Model’ for the first time getting this industry to sustainability may be relatively straight forward and is certainly achievable.

Straight forward because what the model states is required is to get and keep:

1. National venture capital investment within an optimal range - proposed as being 0.075% - 0.125% of GDP;

2. Each fund should be of an optimal size - proposed as being $100M to $300M; and 3. Fund average investment value in an optimal range - proposed as being $3.5M to $5.5M.

Achievable in Australia and Queensland because;

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 24

1. Domestic managed superannuation funds with a policy of 0.06% of assets to venture capital investment (5% to alternate assets incl 3% to PE & 20% of this to venture capital is 0.06% assets) = 0.125% GDP (Short-term strategy);

2. Offshore fund-of-funds redirecting investment out of overweight U.S. market & Israel to Australia should represent an arbitrage benefit until our local market achieves equilibrium (Medium-term strategy);

3. Self-managed-super-funds as Australia’s fastest growing asset pool may be encouraged to make small asset allocations to this asset class as suitable investment products become available (Long-term strategy).

It seems all of the indicators are there as to allow the reweighting towards venture capital, in accordance with the "Sustainable Venture Capital Model", over the next five years;

1. A macro model has been proposed which suggests that 'priming-the-pump' of this asset class will get it to a self-sustaining level;

2. The process of 'priming-the-pump' will take several years during which many aspects have to be better understood and managed. During that time it will take a leap of faith against what appears to be the evidence of a poor performing asset class. It would not be possible to take such a leap of faith during bouyant investment performances in mainstream asset classes; and

3. Due to poor investment performance in mainstream asset classes in recent years the percentage of funds in cash and deposits is high. As such it would be easier and less expensive for super funds to move a small allocation from cash to be available for venture capital investment.

7.1.2 Queensland’s Economic Benefits

Without venture capital funds based and managed in Queensland investment will continue to flow out of the state. Already NSW benefits not only from the super fund investments of Queensland but also from the venture capital investments it makes into NSW using Queensland originated super contributions. If the volume of national venture capital investment is to increase in accordance with the ‘Sustainable Venture Capital Model’ at the present level of state representation for venture capital managers Lelliott calculates the state would gain an estimated $22.29 Billion worth of economic benefit over the next ten years15.

15 Assumes 60% of Qld originated super contributions managed out of state as per Figure 14 and state increase in venture capital investment per Figure 15.

0.55

1.04 1.36

1.65 1.91

2.15 2.36

2.58 2.81

3.03 2.83

1.17

2.22

2.90

3.52

4.07

4.57

5.02

5.49

5.97

6.45

6.03

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Value Losing 53% out of state

Value all in state

$Billion

$47.42 Billion

$22.29 Billion

Queensland's Lost Economic Benefit from future Venture Capital investment

Venture Capital in Queensland: Economic Impact Statement

Copyright Bond University All Rights Reserved 2012 25

Figure 17: Impact of under representation at full investment. Source: Elcano Capital

However, as Figure 17 demonstrates it should have received $47.42 Billion worth of economic benefit over that time period, this $25.13 Billion in economic benefit will be lost with most of it being absorbed by NSW and Victoria.

Instead of being a net exporter of investment to NSW and Victoria Queensland could and should become a net importer of investments from those states.

7.1.3 Queensland's Employment Benefits

As per European Private Equity & Venture Capital Association research16 it is estimated that 90% of investees will increase employee numbers by an average of 46 jobs post-investment. The following table, Figure 18: Employment Impact17, demonstrates the increase in employment if

allocations are made to Queensland based venture capital management firms in accordance with Figure 15: Achieving Optimal Scale through Queensland Super Funds Contributions.

Figure 18: Employment Impact Source: Elcano Capital

Figure 19: Cumulative Employee Numbers

Source: Elcano Capital

However, the majority of job growth (92%) is expected to occur once an investee IPOs and such increase is not included in this table.

7.1.4 Queensland’s Innovation Corridor

Previous investigations as to the creation of an Australian Silicon Valley may have been flawed in their thinking because of the lack of understanding of the venture capital industry and in disregarding existing cultural aspects. It is neither possible nor necessary to duplicate Silicon Valley and Queensland should not attempt to do so.

What is possible is the creation, or expansion of, an innovation corridor in SEQ by combining existing characteristics and a developed SEQ based venture investment industry.

16 See 2.1.3 and 2.1.4. 17 As calculated by Lelliott 2012.

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

QldIncrease 0.29 0.29 0.23 0.23 0.23 0.23 0.23 0.23 0.23 0.23

No New Funds p.a. 3 3 2 2 2 2 2 2 2 2

New Investees 45 45 30 30 30 30 30 30 30 30

New Employees 1,863 1,863 1,242 1,242 1,242 1,242 1,242 1,242 1,242 1,242

Cumulative Employee No.s 1,863 3,726 4,968 6,210 7,452 8,694 9,936 11,178 12,420 13,662

13,662

6,955

0

2000

4000

6000

8000

10000

12000

14000

16000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Cumulative Employees -under-represented state