TOWARDS A GLOBAL MODEL OF VENTURE CAPITAL?

59

TOWARDS A GLOBAL MODEL OF VENTURE CAPITAL? William L. Megginson * The University of Oklahoma Current draft: December 31, 2001 * University of Oklahoma. This paper is based on Chapter 15, “Venture Capital and Private Equity,” of Scott B. Smart, William L. Megginson and Larry J. Gitman, Corporate Finance (South-Western Publishing Company, Cincinnati, 2003). Earlier versions of the material in this paper were presented at the Shanghai Seminar on Venture Capital Development, Fudan University, Shanghai, PRC in December 1999, at the Chinese University of Hong Kong in October 2000, and in various graduate and undergraduate classes in the engineering and business schools of the University of Oklahoma. I am very grateful to participants in these seminars and classes for their specific comments and recommendations. Please address correspondence to: William L. Megginson Professor & Rainbolt Chair in Finance Price College of Business 307 West Brooks, 205A Adams Hall The University of Oklahoma Norman, OK 73019-4005 Tel: (405) 325-2058; Fax: (405) 325-1957 e-mail: [email protected] website: http://faculty-staff.ou.edu/M/William.L.Megginson-1

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of TOWARDS A GLOBAL MODEL OF VENTURE CAPITAL?

TOWARDS A GLOBAL MODEL OF VENTURE CAPITAL?

William L. Megginson * The University of Oklahoma

Current draft: December 31, 2001

* University of Oklahoma. This paper is based on Chapter 15, “Venture Capital and Private Equity,” of Scott B. Smart, William L. Megginson and Larry J. Gitman, Corporate Finance (South-Western Publishing Company, Cincinnati, 2003). Earlier versions of the material in this paper were presented at the Shanghai Seminar on Venture Capital Development, Fudan University, Shanghai, PRC in December 1999, at the Chinese University of Hong Kong in October 2000, and in various graduate and undergraduate classes in the engineering and business schools of the University of Oklahoma. I am very grateful to participants in these seminars and classes for their specific comments and recommendations. Please address correspondence to:

William L. Megginson Professor & Rainbolt Chair in Finance Price College of Business 307 West Brooks, 205A Adams Hall The University of Oklahoma Norman, OK 73019-4005 Tel: (405) 325-2058; Fax: (405) 325-1957 e-mail: [email protected] website: http://faculty-staff.ou.edu/M/William.L.Megginson-1

TOWARDS A GLOBAL MODEL OF VENTURE CAPITAL?

Abstract

This paper examines whether a truly global market for venture capital and private equity is emerging or

whether the current situation of segmented national markets is likely to endure. We document phenomenal

growth in venture capital fund raising and investment over the past decade in the United States, western

Europe and in certain Asian countries, but not in Japan or in most developing countries. We compare

contracting practices, investment patterns and returns between the U.S. and Europe, and find that there has

been considerable convergence between these two large VC markets, particularly over the past four years.

This convergence is likely to continue. Nonetheless, we conclude that the major national markets will remain

effectively segmented and suggest that venture capital will continue to be much more important in common

law countries than in civil law countries for the foreseeable future.

TOWARDS A GLOBAL MODEL OF VENTURE CAPITAL?

Whenever someone or something has been the recipient of a great deal of favorable attention from

journalists and other commentators, one often says that they have had a “good press.” By any measure,

venture capital has enjoyed an extremely good press over the past decade. It has been embraced as a key tool

for economic and technological development by policy-makers, academics and business commentators alike,

and the U.S. venture capital industry is often held up as the model other nations should attempt to replicate.

However, very little research or commentary has been directed towards answering whether it is possible

(much less desirable) to mimic the American model of venture capital. This paper is a first crack at

addressing this issue.

Defined broadly, “venture capital” has been a fixture of western civilization for many centuries. In

this context, the decision by Spain’s Ferdinand and Isabella to finance Christopher Columbus’ voyage of

exploration can be considered one of history’s most profitable venture capital investments (at least for the

Spanish). However, modern venture capital--defined as a professionally managed pool of money raised for

the sole purpose of making actively-managed direct equity investments in rapidly-growing private companies,

and with a well-defined exit strategy--is a much more recent financial innovation, and one that has until very

recently been almost exclusively American.

There can be little doubt that the total volume of venture capital flowing through the financial

systems of almost all developed countries has risen very sharply over the past decade, and especially since

1995. While the U.S venture capital industry still represents about two-thirds of the world’s total, and is still

4-6 times the size of Western Europe’s, other countries have indeed been adopting many American

investment and fund-raising practices and at least a superficial case for convergence in venture capital

techniques can be made. On the other hand, striking differences remain between American and European

practices, and indeed between VC practices in different European markets. We therefore ask the question: “Is

a truly global, integrated market for venture capital and private equity investment now emerging, or will the

“global” venture capital industry continue to consist of segmented national markets with distinctive fund

raising and investment practices?” Much will ride on the answer to this question.

This paper is organized as follows. Section 1 discusses the economic impact of venture capital

investment and section 2 presents an overview of the global venture capital and private equity market in

2000. This section also examines whether the national differences are related to legal systems and/or

differences in the use of capital markets versus intermediated financing. Section 3 describes key features of

the world’s largest venture capital market, the United States. Section 4 describes Western Europe’s private

equity market, while section 5 discusses venture capital practices in other OECD countries (especially Japan

4

and Canada) and briefly surveys venture capital’s role in the developing countries of Latin America, Africa

and Asia. Section 6 summarizes and presents our conclusions about whether a global market is emerging and

about the transferability of America’s venture capital practices.

1. The Economic Impact of Venture Capital Investing

It is not hard to understand why policy-makers are so fond of venture capital (VC). Both academic

and practitioner-oriented research now clearly demonstrates that VC investing adds value. A recent study by

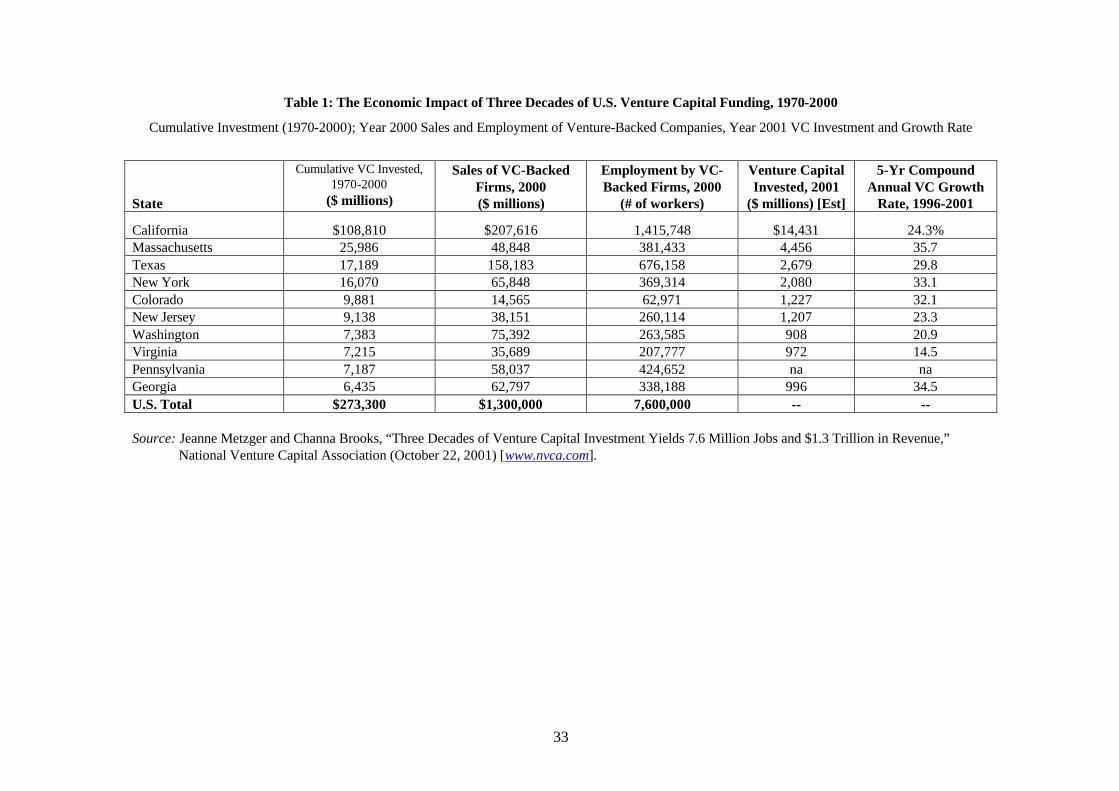

the National Venture Capital Association (NVCA) [www.nvca.com] documents the scale and economic

impact of 30 years of VC investment in the United States. Key details of this study are reproduced in Table 1.

Over the three decades 1970-2000, American venture capitalists invested no less than $273.3 billion into

companies in all 50 states. These firms now employ 7.6 million people and generate over $1.3 trillion in

annual sales revenue, representing 5.9% and 13.1% of the respective U.S. national totals. The NVCA study

finds that on average every $36,000 in VC investment creates one new job.

Similarly, A study by the European Private Equity and Venture Capital Association (EVCA)

[www.evca.com], entitled “The Economic Impact of Venture Capital in Europe,” found that VC-backed

European companies generated significantly higher growth rates in sales, research spending, exports and job

creation during the 1990-1995 period than did otherwise comparable non-VC-backed companies. Recent

updates of this study find that European VCs invested € 34.9 billion ($31.4 billion) in over 10,400

companies in 2000 and achieved similarly impressive results.

Though academic studies tend not to focus on the direct economic impact of VC investment, several

have examined how VCs help overcome the significant problems involved in funding entrepreneurial growth

companies. These firms have great difficult obtaining external financing both because they must invest in

risky growth options (intangible assets) and because there is pervasive informational asymmetry between

entrepreneur and financier. Early studies by Tybejee and Bruno (1984), Sahlman (1988, 1990) and Gorman

and Sahlman (1989), plus later studies by Admati and Pfleiderer (1994), Barry (1994), Lerner (1995) and

Hellmann (1998) all document significant value creation by VCs. Two recent papers also make important

contributions to our understanding of how VCs influence firm growth and development. Hellmann and Puri

(2000) show that “innovator firms” are much more likely to obtain VC funding than are “imitator firms” and

that the innovative companies are able to bring products to market much significantly faster than other

companies. Kaplan and Strömberg (2001b) find that VCs help overcome principal-agent contracting

problems through sophisticated contracting, pre-investment screening and post-investment monitoring and

advising. Commentators of the venture capital scene frequently encapsulate how VCs create value by saying

that they are active investors who bring much more than money to their portfolio companies.

5

2. An Overview of the Global Market for Venture Capital

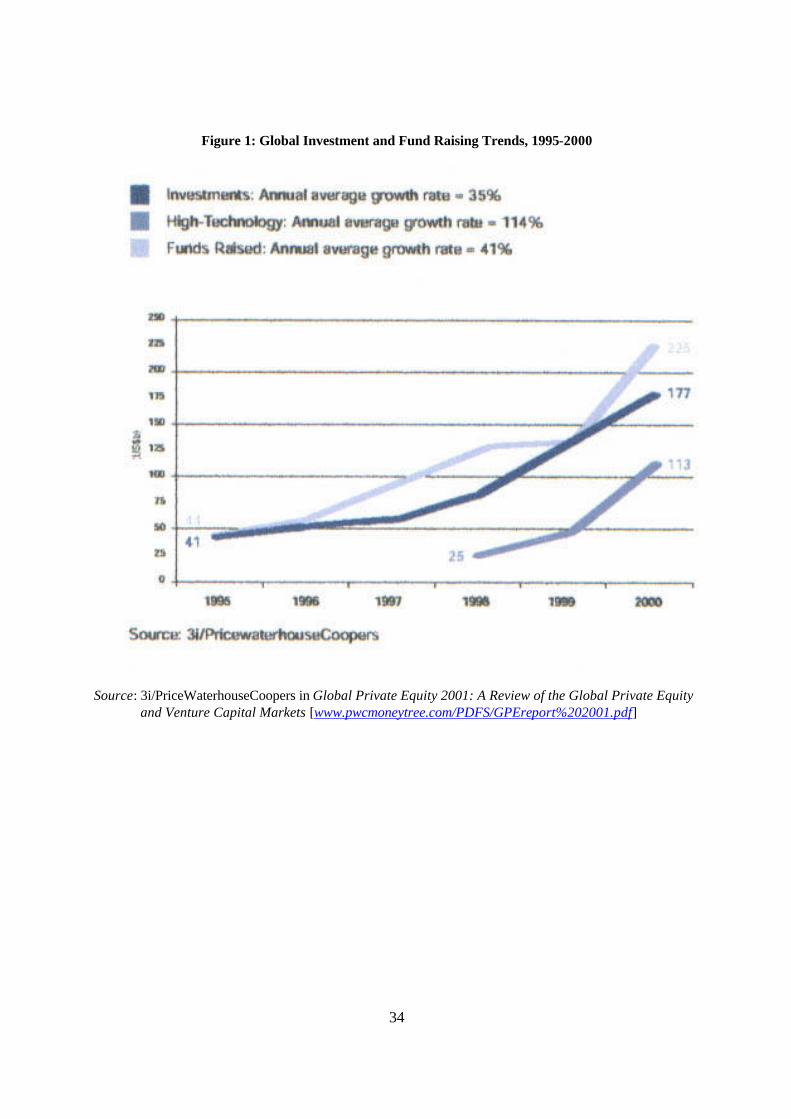

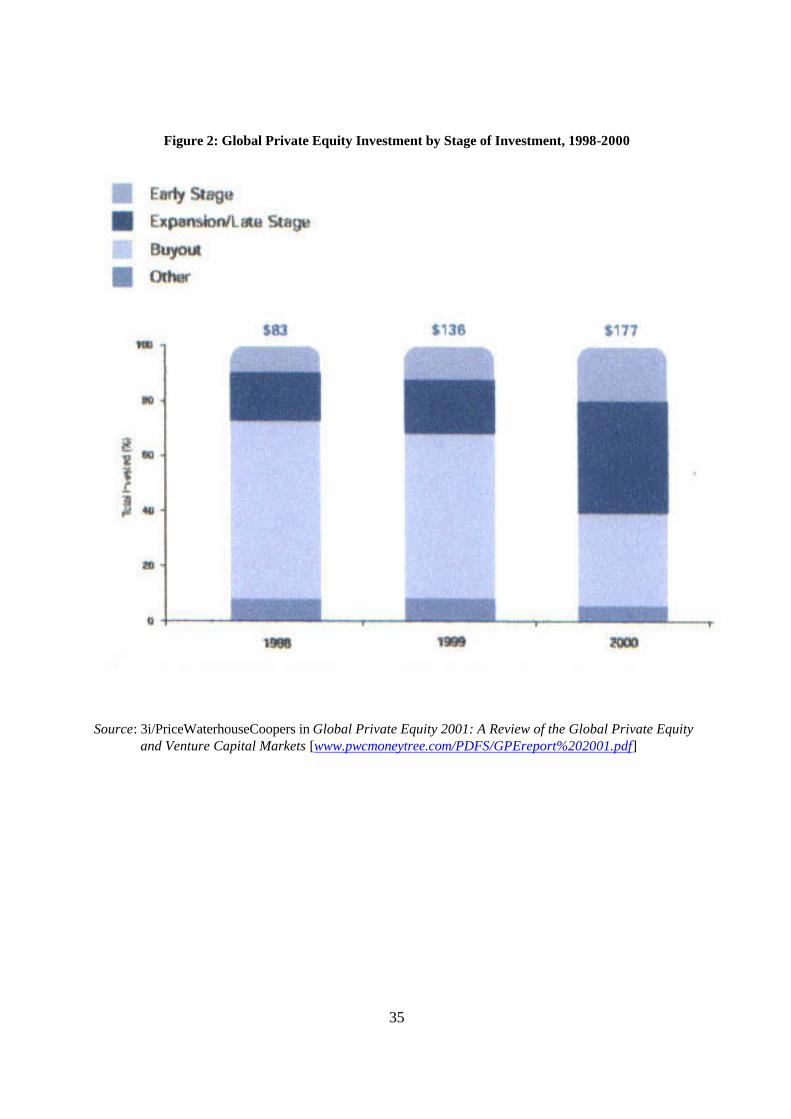

Trends in the global market are described in Figures 1 and 2. These show that the total value of

venture capital raised and invested worldwide grew very rapidly between 1995 and 2000. The fastest growing

sector has been high technology. Additionally, increasing fractions of the total were allocated to “true”

venture capital in 2000 than in 1998, as the fraction allocated to buyouts shrank while early state and

expansion stage investment increased. Furthermore, the amount of total investment allocated to high

technology worldwide increased from $25 billion in 1998 to $113 billion in 2000, which implies an average

annual growth rate of 114%!

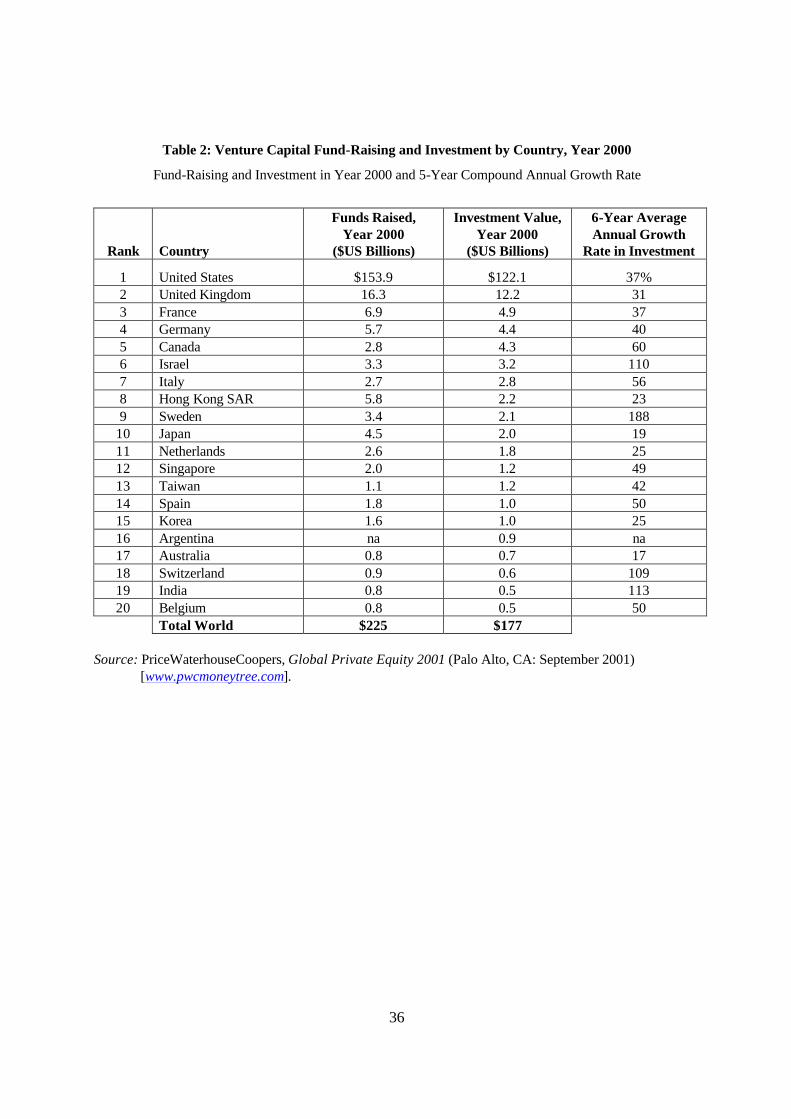

Table 2 describes the total amount of private equity raised and invested in the 20 top recipient

countries during the year 2000. This table also details the six-year average annual growth rate in investment.

Several trends are immediately apparent. First, the total amount of VC and private equity funding raised

globally in 2000 ($225 billion) exceeded total investment ($177 billion) by $48 billion, and this pattern held

for most individual countries as well as in the aggregate. While there is always a difference between the

amount of fund raising and investment, the difference in 200 was especially large. Second, VC investment

spending grew very rapidly in most of the large national markets over the five-year period 1995-2000. While

spending increased at a very respectable average annual rate of 37% per year in the U.S., spending surged by

more than 100% per year in Israel, Sweden, Switzerland and India. Finally, the two largest VC markets in

2000 were, as usual, the U.S. and Great Britain, followed by France, Germany, Canada and Israel. France

knocked Germany from third to fourth place for the first time in 2000.

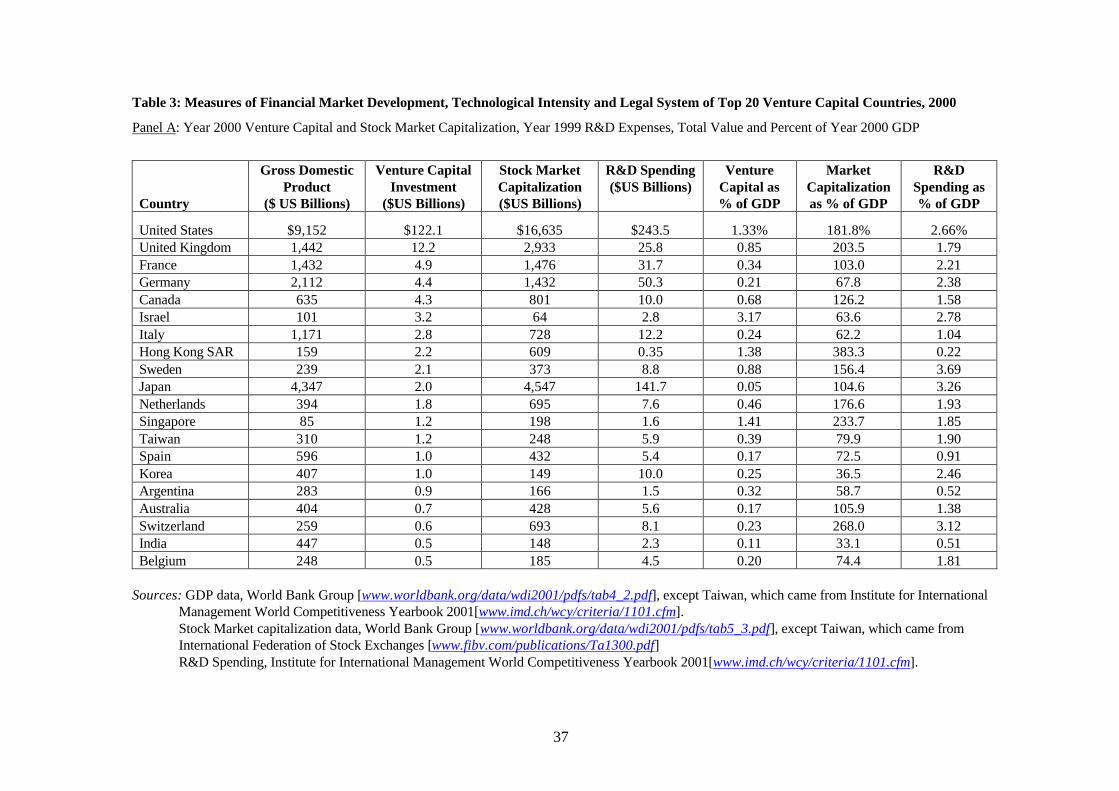

Absolute levels of VC fund raising and investment, though informative, do not really address the

relative importance of venture financing in different countries. Panel A of Table 3 attempts to do this by also

showing, for the top 20 recipient countries, the year 2000 levels of gross domestic product, year-end stock

market capitalization and national research and development spending in 1999 (the most recent year

available). The table then computes VC spending, stock market capitalization and R&D spending in terms of

percent of GDP. This table reveals dramatic variations in the relative importance of venture capital, stock

market valuations, and R&D spending among these twenty countries. Venture capital spending as a percent

of GDP ranges from a trivial 0.05% in Japan and 0.11% in India to 1.33% in the U.S, 1.38% in Hong Kong,

1.41% in Singapore and an amazing 3.17% of Israel’s GDP.1 Stock market capitalization as a percent of

GDP varies between lows of 33.1% in India and 36.5% in Korea to 181.8% in the United States and 203.5%,

233.7%, 268.0% and 383.3% in Britain, Singapore, Switzerland and Hong Kong, respectively. Finally,

1 Jeng and Wells (2000) present a case study analysis of the factors contributing to Israel’s success as a market

for venture capital fund raising and investment. Their study highlights the catalytic role government policy can play in promoting VC spending, though their analysis of Germany’s much less successful development program also points to the drawbacks of an active governmental role. As it happens, Dow Jones reported in early 2002 that Israel’s VC market contracted by over a third (about $1 billion) during 2001, so even successful venture capital innovators can be hit by global recession [Financial Times, January 3, 2002, p. 21].

6

research spending varies from lows of 0.22% , 0.51% and 0.52% of the GDPs of Hong Kong, India and

Argentina, respectively, to highs of 3.12%, 3.26%, and 3.69% for Switzerland, Japan and Sweden. America’s

R&D spending to GDP ratio is 2.66%.

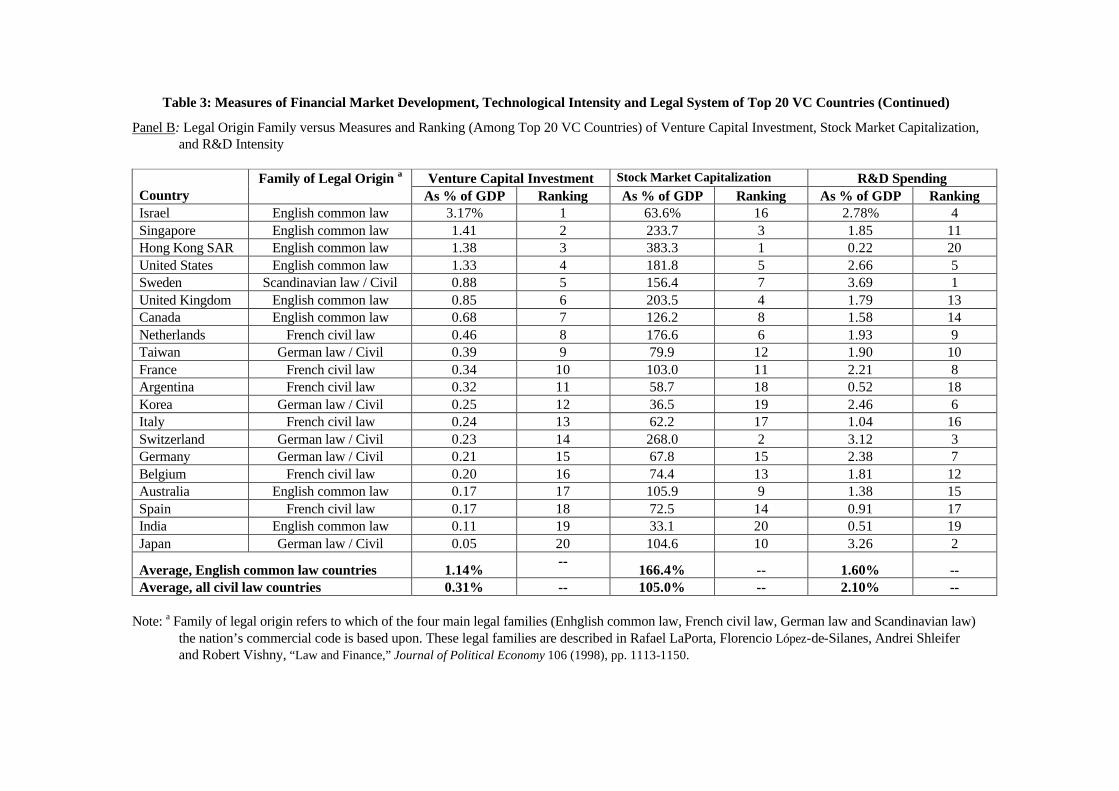

As a further step in analyzing the international differences in venture financing, Panel B of Table 3

ranks the top 20 recipient countries by VC funding as a percent of GDP, and also presents separate rankings

for market capitalization and R&D spending relative to national output. The key innovation of this table,

however, is to also present the legal family each country’s commercial code is based on. This listing comes

from the “Law and Finance” literature, pioneered by LaPorta, López-de-Silanes, Shleifer and Vishny (1997,

1998, 2000), which documents that countries with English common law codes offer greater protection to

investors and thus have much larger capital markets than do countries with commercial codes based on the

German, Scandinavian and French families of civil law (all of which are ultimately drawn from Roman law

and can be considered civil law countries). The results in Table 3 strongly support the importance of legal

family on both the relative importance of stock markets and, especially, venture capital funding. However,

there is no significant difference regarding R&D spending. The average venture capital spending to GDP

ratio for the eight English common law countries is 1.14%, almost three times the 0.31% ratio of the twelve

civil law countries. Likewise, the stock market capitalization to GDP ratios for the common law countries,

166.4%, is two-thirds higher than the 10.5.0% capitalization to GDP ratio for civil law nations. On the other

hand, R&D spending relative to GDP is actually higher in civil law (2.10%) than in common law (1.60%)

countries. This clearly suggests that civil and common law countries invest similar proportions of national

income in R&D as a way to create growth opportunities, but common law countries rely much more heavily

on financial markets in general, and venture capitalists in particular, to fund that research spending.

Two other academic studies examining international differences in venture capital usage, Black and

Gilson (1998) and Jeng and Wells (2000), find that venture capital is much more important in countries with

large domestic capital markets. Jeng and Wells show that later-stage VC funding levels are especially

sensitive to the health and size of that country’s IPO market. Their regression analyses also show that venture

financing is significantly less important in civil law than in common law countries.

3. Venture Capital Financing in the United States

Within the United States, the importance of a vibrant entrepreneurial sector has been steadily

growing during the 1990s. In fact, almost one-third of all the expansion in business activity since 1991 has

been accounted for by the growth of the high technology sector, which encompasses primarily information-

processing industries such as telecommunications and computer hardware and software. Furthermore, recent

research indicates both that American business is finally learning how to turn information-processing

technology into sustainable competitive advantage and that the profitability of such investment is now

significantly higher than more traditional investment spending.

7

As discussed in depth in Gompers and Lerner (2001), the formal birth of America’s venture capital

industry is usually traced to the American Research and Development Company that began operating in New

York City shortly after the end of World War II, though funds associated with wealthy families--such as the

fund established by the Rockefeller family, Venrock Associates--began operating many years earlier. From its

birth through the late 1970s, the total pool of venture capital was quite small and most of the active funds

were sponsored either by financial institutions (i.e., Citicorp Venture Capital) or non-financial corporations

such as Xerox. Most of the money raised by these funds came from their corporate backers and from wealthy

individuals or family trusts. While many of these features would soon be rendered anachronistic, there were

two features of early venture capital funds that remain equally applicable today: (1) most of the investments

made by these funds were intermediate-term, equity-related investments targeted at technology-based private

companies and (2) the venture capitalists played a unique role as active investors, contributing both capital

and expertise to portfolio companies while exercising real managerial oversight. Also, from the very start,

venture capitalists looked to invest in companies with the potential of going public or being acquired at a

premium within a reasonable time frame (3-7 years), and which offered investment returns of 25-50 percent

per year, depending upon the stage of company development.

A fundamental change in the U.S. venture capital market occurred during the late 1970s, and this can

be traced to two seemingly unrelated public policy innovations. First, Congress lowered the top personal

income tax rate on realized capital gains from 35 to 28 percent in 1978, thereby significantly increasing the

effective return to value-creating entrepreneurship. In 1979, the Labor Department relaxed its “Prudent Man

Rule,” thus effectively authorizing pension fund managers to allocate up to five percent of fund assets to

private equity investments. While neither of these changes appears revolutionary, the effect of their

implementation on venture capital funding was dramatic. Total funding increased from $68.2 million in 1977

to $978.1 million in 1978 (both figures are in 1987 dollars). A further capital gains tax reduction in 1981 saw

total venture capital funding grow from $961.4 million in 1980 to $5.1 billion in 1983. Funding then

remained in the $2-5 billion range for the rest of the 1980s. After falling to $1.3 billion in 1991, venture

capital funding began a steady climb to a record $106.8 billion in 2000, but then fell back to “only” $34.0

billion during the first three quarters of 2001. To put the recent surge into perspective, the peak second

quarter 2000 fund raising total of $31.7 billion (into 185 funds) was larger than any annual fund raising total

prior to 1999. Key patterns observed in VC investment are discussed in more depth in section 3.2 below.

3.1. Types of Venture Capital Funds

In discussing venture capital, one must carefully differentiate between institutional venture capital

funds and angel capitalists. Venture capitalists are formal business entities with full-time professionals

dedicated to seeking out and funding promising ventures, while angel capitalists (or business angels, as they

are sometimes called) are wealthy local businesspeople who make private equity investments on a more ad-

hoc basis and who do not generally operate as formal business entities. A vibrant market for this angel

8

capital exists and routinely provides over $50 billion per year in total equity investment to private businesses

in the United States.2 Until very recently, angel capitalists provided far more total investment to

entrepreneurial companies each year than did institutional venture capital firms. Nonetheless, we focus on the

latter group throughout this paper since these firms operate nationally and provide the performance

benchmark against which all private equity investment is compared.

There are four basic categories of institutional venture capital funds, as described in Pratt (1997).

First, Small Business Investment Companies (SBICs) are federally chartered corporations that were

established as a result of the Small Business Administration Act of 1958. Since then, SBICs have invested

over $14 billion in approximately 80,000 small firms.3 Historically, these venture capitalists have relied on

their unique ability to borrow money from the U.S. Treasury at very attractive rates. SBICs were thus the only

types of venture capitalist that preferred to structure their investments as debt rather than equity. This feature

seriously hampered their flexibility, but a revision of the law in 1992 has made it possible for SBICs to

obtain equity capital from the Treasury in the form of preferred equity interests, and also to organize

themselves as limited partnerships. The evidence thus far suggests that this change, by itself, will not be

enough for SBICs to regain venture capital market share.

Second, financial venture capital funds are subsidiaries of financial institutions, particularly

commercial banks. These are generally set up both to nurture portfolio companies that will ultimately become

profitable customers of the corporate parent and to earn high investment returns by leveraging the financial

expertise and contacts of existing corporate staff. Though many financial VC funds are organized as SBICs,

their orientation is sufficiently specialized that they are generally classified separately. Third, corporate

venture capital funds are subsidiaries or stand-alone firms established by non-financial corporations. These

are generally established by industrial firms eager to gain access to emerging technologies by making early-

stage investments in high-tech firms. Finally, venture capital limited partnerships are funds established by

professional venture capital firms, which act as the general partners organizing, investing, managing, and

ultimately liquidating the capital raised from the limited partners. While most venture capital limited

partnerships have a single-industry focus, the firms themselves are not associated with any single corporation

or group.

While all four types of venture capitalists are active, the industry has long been dominated by limited

partnerships, at least partly because these are the only group which do not bring a separate agenda to venture

2 The angel capital market is discussed in Freear (1994), Lerner (1998), Sohl (1999), Freear, Sohl and Wetzel (2000) and Wong (2001). Some of the pitfalls that can be encountered by entrepreneurs seeking funding are described in Gruner (1998), while Weisul (2001) lists several of the larger angel capital organizations active today. Finally, Campbell (2001a) cites a Global Entrepreneurship Monitor 2001 report suggesting that informal investors (angels) provide about $196 billion to start-up and early stage companies in 29 countries each year.

3 SBICs are discussed in more depth in Brewer and Genay (1994), Kinn and Zaff (1997) and Birnbaum (1999). A Federal Reserve Board study of SBIC investment behavior and the financial characteristics of the firms in which they invest is available at http://fedinprint.frbsf.org/cgi/dtbcgi.exe.

9

investments. The SBICs have been hampered both by their historical reliance on an inappropriate funding

sources for venture capital investing, and by the myriad regulations that go with being a government-

sponsored company. The financial and corporate funds tend to suffer because their ultimate loyalty is to the

interests of the corporate parents, rather than the portfolio companies, which often leads to conflicts of

interest between financier and entrepreneur and between the corporate funds and other venture capital

investors. Further, both financial and non-financial corporate funds have found it difficult to adopt

appropriate compensation packages for their venture capital professionals, since these contracts are both

more lucrative and more performance-based than is typical for professionals elsewhere in their parent

companies. For all these reasons, the venture capital limited partnerships now control over 75 percent of total

industry resources, and their sway over fund-raising seems to be increasing. Gompers and Lerner (2001)

provide a detailed history of the development of the U.S. venture capital industry and describe the key

comparative advantages of limited partnerships as organizational vehicles.

Before proceeding, we should point out one other important problem with corporate venture

investing. Both financial and non-financial corporate funds have histories of only intermittent commitment to

venture capital investing, and both have shown a tendency to cut back on funding during down cycles. While

corporate VC investment is clearly surging once again, many of these corporations are electing to make their

venture investments by participating as limited partners in VC funds rather than by establishing their own

funds. Additionally, non-financial corporations in many high-tech industries are opting for strategic

partnerships and joint ventures with start-up firms rather than making strictly financial investments in these

firms. This is often a highly synergistic arrangement, since the established company gains access to

promising new technologies, while the smaller firm gains access to the marketing and technological resources

of the larger company.4

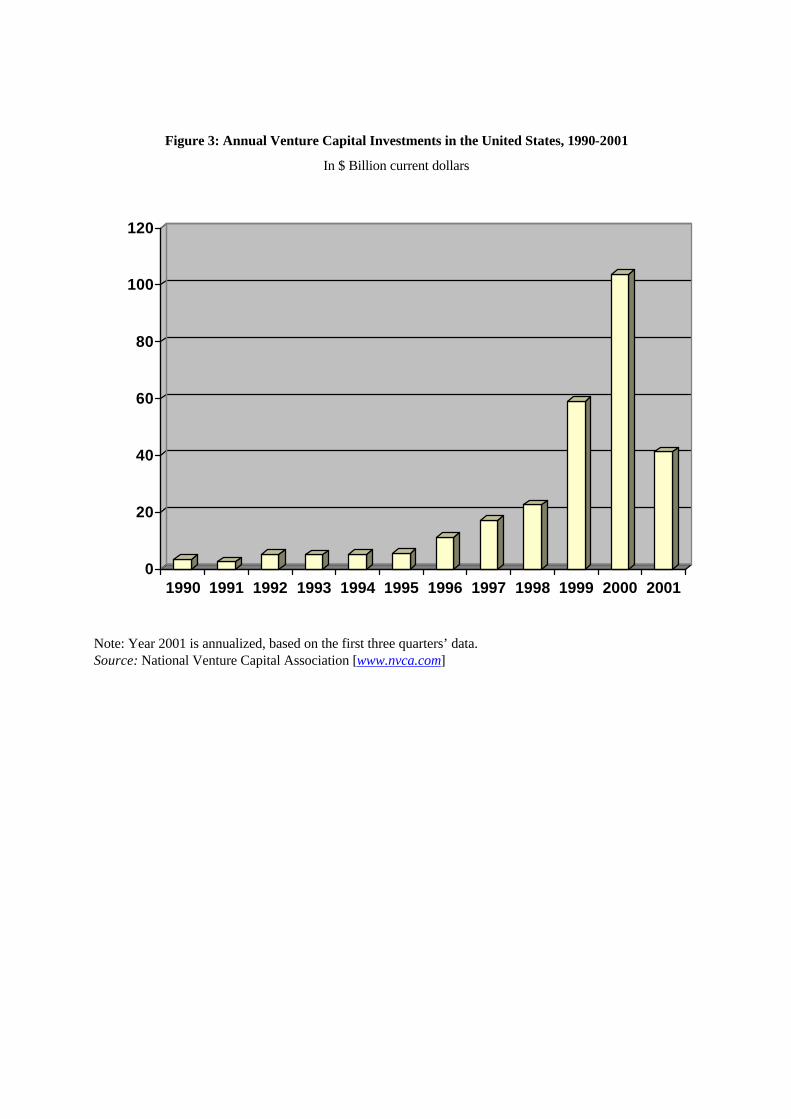

3.2. Investment Patterns of U.S. Venture Capital Firms

Given the amount of media and political attention lavished on venture capital in the United States,

most people are surprised to learn just how small the industry actually was before 1998. The total amount of

capital invested each year from 1989 through 2001 is detailed in Figure 3. Annual disbursements naturally

differ from total fund-raising since the total amount of money available for investment is the sum of realized

investment returns (from IPOs and mergers of portfolio companies) and new fund inflows from investors. As

Figure 3 makes clear, total investments by institutional venture capitalists never exceeded $6 billion per year

until 1996, but then total investment spending surged to an astonishing $106 billion spread over 5,606

companies in 2000. This average investment of $11.69 million per company was almost three times larger

than the $4.42 million average investment per company in 1995. Average investment per company grew

4 An early discussion of the failings of corporate VC investing is provided in Hardymon, DeNino and Salter

(1983), while the contemporary European corporate venture capital market is discussed in Campbell (2001b).

10

steadily between 1995 and 2001, but has declined to $11.69 million during the first three quarters of 2001.

Total VC spending peaked at $28.5 billion in the third quarter of 2000, and has declined every quarter since,

falling to $7.7 billion ($8.84 million per company) during 3Q2001. The full year 2001 investment figures

will probably come in around $40 billion. If so, this would represent a sharp fall, but from an exceptional

height, and 2001 would still represent the third highest annual level of investment ever. The true question is

whether total VC investment spending will again surge past $100 billion per year or will stabilize at half that

level—or even lower. This will not become clear until spending stabilizes and at least two up quarters are

registered.5

Whereas the bulk of venture capital funding once came either from corporate sponsors (in the case of

financial or corporate funds) or wealthy individuals, institutional investors have become by far the dominant

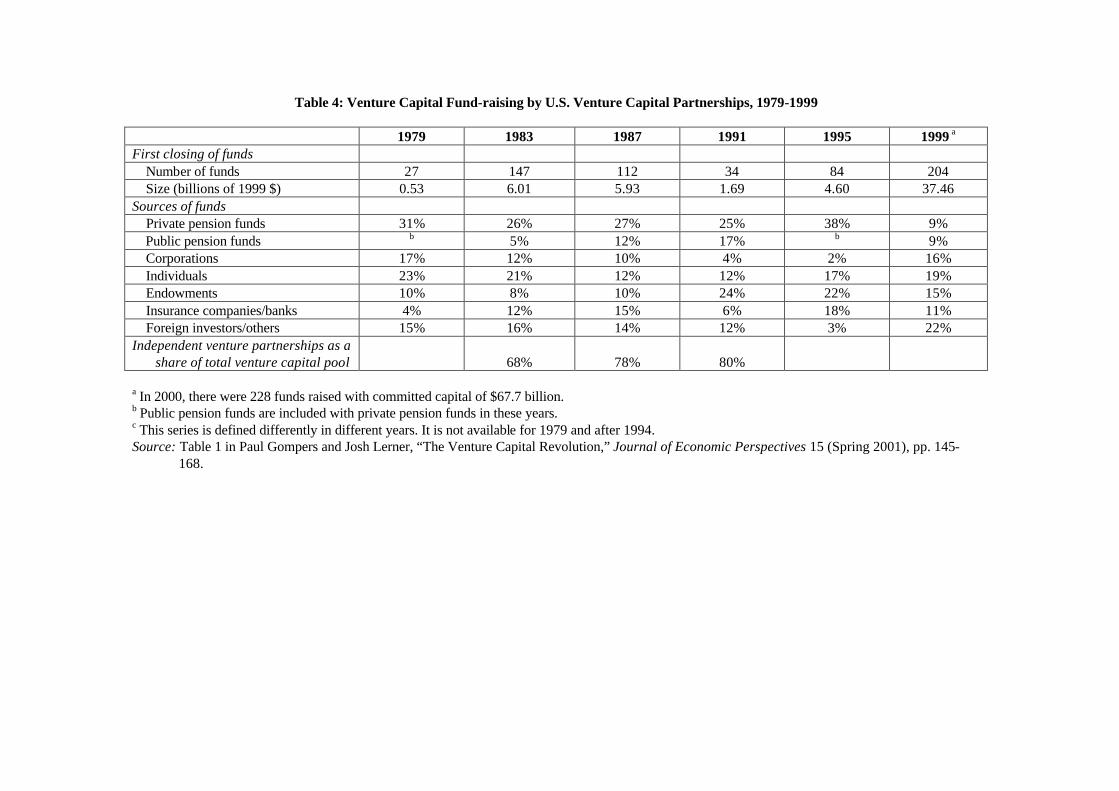

sources of funding today. As shown in table 4, pension funds alone typically account for 30-45% of all new

moneys raised by institutional venture capital firms, though their share in 1999 fell to only 18%, and these

investors are especially important for VC limited partnerships. In spite of the fact that few pension funds

allocate more than one or two percent of their total assets to private equity funding, their sheer size makes

them extremely important investors, and their long-term investment horizons make them ideal partners for

venture capital funds. Financial and non-financial corporations usually represent the second largest

contributors of capital to venture funds, accounting for 15-30 percent of the total. The corporate share of the

total was 20% in 1995, but rose to 27% in 1995. The recent surge in corporate funding seemingly represents

another cycle of corporate venture capital investing, so it remains to be seen whether the current phase will

prove any more lasting than previous ones. Foundations and endowments are the third important source of

venture capital funding, usually accounting for 10-25 percent of the total (22% in 1995 and 15% in 1999).

Foreign investors have become increasingly important recently, and (in combination with “other” investors)

accounted for 22% of 1999’s total funding. Individuals and family trusts are the final major group of venture

capital investors. While these two groups together generally contribute 10-25 percent of the total venture

capital funding (17% in 1995 and 19% in 1999), it should be noted that the absolute size of the pool of

capital under management is much larger than it was in early years when family money dominated the

industry.6

5 A number of academic studies have examined how various factors—especially the incidence and levels of personal and corporate taxation—influence the amount of money raised and invested by American venture capital funds each year. Gompers and Lerner (1998a) find that decreases in capital gains tax rates appear to have a positive and important impact on commitments to new venture capital funds. This is actually rather surprising, since the dominant investors in VC funds are untaxed pension funds. Gompers and Lerner conclude that the relationship between taxation and VC commitments is an induced one—in that reductions in tax rates cause more entrepreneurs to start companies and thus demand private equity financing. The findings of Gentry and Hubbard (2000) also suggest that the entrepreneurship entry decision is highly sensitive to tax rates.

6 One venture capital firm, Technology Funding (www.technlogyfunding.com), announced in 1997 that it was

launching a $100 million fund aimed at an unusual group of sponsors: small investors. As described in Weisul (1997), the firm planned to use the internet to raise capital over a two-year period, and accepted subscriptions as small as $1,000 (versus the $1,000,000 minimum typical in venture capital limited partnerships).

11

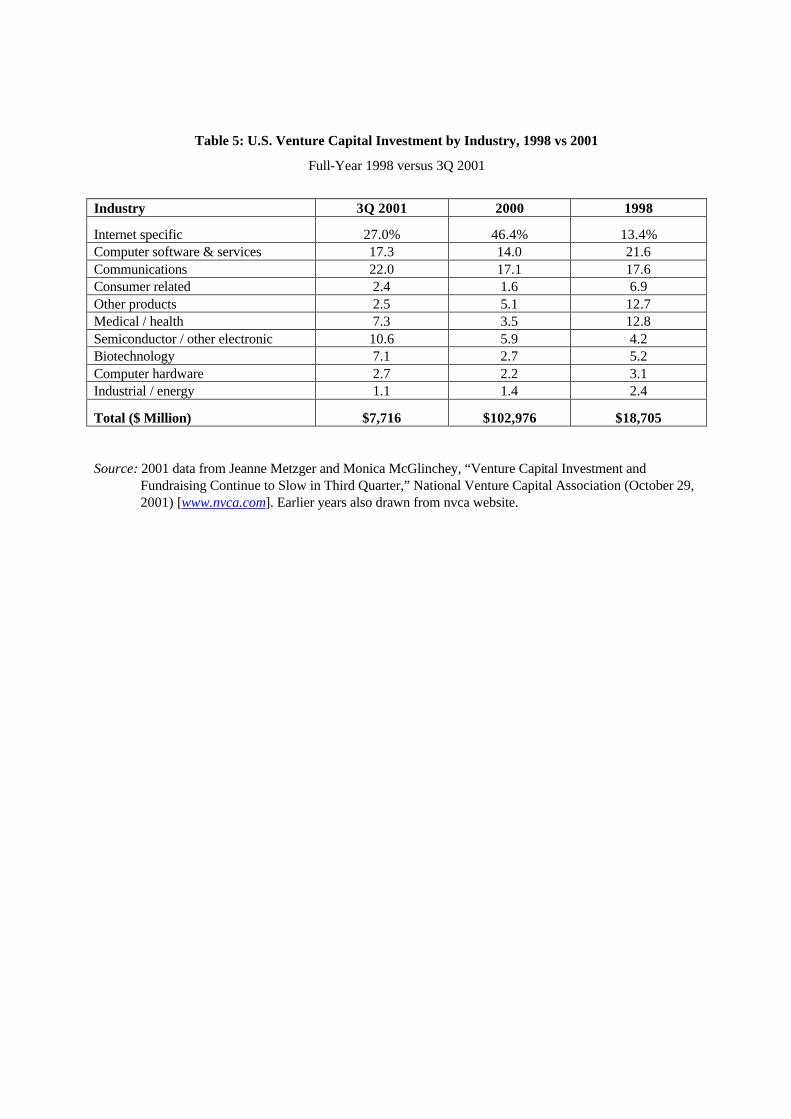

3.3. Industrial and Geographic Distribution of Venture Capital Investment

One reason why institutional venture capital investments have been so successful historically is that

these firms’ managers tend to invest only in those industries where they have some competitive advantage,

and where their brand of active involvement in portfolio company management can create real economic

value. Table 5 presents a listing of the industries that received the most venture capital funding in 1998, 2000

and the third quarter of 2001. As has been true for the past three years, over three-quarters of both third

quarter-2001’s (76.9%) and year-2000’s (83.4%) total investment went into the area of information

technology (communications and computers). Internet-specific investments alone accounted for 27.0% of

total investment in 3Q 2001, and a whopping 46.4% of year-2000’s total. The remaining fraction of VC

investment during 3Q 2001 and 2000 was divided roughly evenly between biotechnology and health care-

related companies (combined totals of 14.4% in 3Q 2001 and 6.2% in 2000) and consumer, industrial, and

other products and services (6.0% in 3Q 2001 and 8.1% in 2000).

Yet another striking regularity in venture capital investment patterns concerns the geographical

distribution of the companies receiving funding. As has been the case throughout the modern era, the state of

California was the single largest recipient of venture capital investment in the third quarter of 2001. Northern

California alone accounted for 30.5% of 3Q 2001’s total investment, and 32.5% of year-2000’s, while

Southern California accounted for an additional 8.1% and 8.4% of the respective period totals. The next three

largest recipients of VC financing during 3Q 2001 were New England (13.1%), the Southwest (9.5%) and the

greater New York area (8.7%). New York accounted for a larger share of the year-2000 total (11.8%), and

New England (10.2%) and the Southwest (6.2%) accounted for lower fractions, but the basic geographic

pattern of VC investment rarely varies much from year to year.

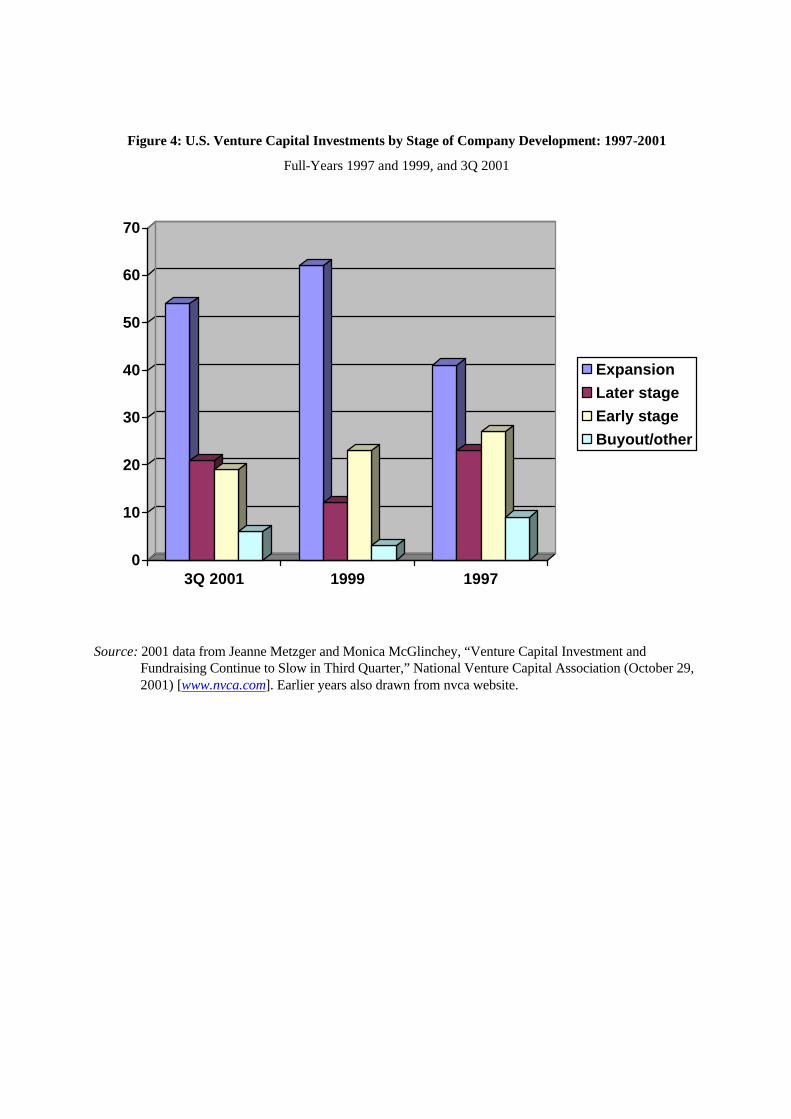

3.4. Venture Capital Investment by Stage of Company Development

The popular image of venture capitalists holds that they specialize in making investments in start-up

or very early-stage companies. This is only partly true. In fact, as Figure 4 documents, early stage financing

accounted for only 194% of total investment in the third quarter of 2001, down from 23% in 1999 and 26%

in 1997. Truly early stage (start-up and seed stage) financing represented a mere 0.96% of 3Q 2001

financing, and similarly small fractions were allocated in earlier years. On the other hand, if we broaden the

definition of early-stage to include a fraction of expansion spending, total early-stage investment would

probably fall in the range of 35-50 percent of venture capital disbursements each year. Being rational

investors, venture capitalists are as leery as anyone else of backing extremely risky new companies, and will

do so only if the entrepreneur/founder is well-known to the venture capitalists, the venture is extraordinarily

promising, or both. Late-stage investments in more mature private companies accounted for 20.9% of total

venture capital investment in 3Q 2001, 12% in 1999 and 23 percent in 1997, while 6-10% of venture capital

12

investment has been allocated to buyouts, acquisitions and other investments in recent years. Later-stage

investments cover funding for marketing programs, major production plant expansions, and financing made

in preparation for accessing the public capital markets. This has accounted for 12-23% of total investment

over the past four years.

While the actual distribution between early and later stage funding varies from year to year, one

principle of venture capital funding never changes: the earlier the development stage of the portfolio

company, the higher must be the expected return on the venture capitalist’s investment. Professional venture

capitalists typically demand compound annual investment returns in excess of 50 percent on start-up

investments, but are often willing to accept returns of 20-30 percent per year on later-stage deals, since the

risk of the investment is far lower in more established portfolio companies. As we will see when the

mechanics of venture investment pricing are discussed later in this section, the higher the required return, the

greater the fraction of his or her company an entrepreneur must surrender in order to obtain funding.

On the other hand, it is usually not a stark choice between early and late stage investments. Most

venture capital funds that invest in a company during its early years remain committed to the firm as it

develops, and will often participate in second, third, fourth, and higher-round financing as the portfolio

company matures. Each subsequent round is generally at a higher price, embodying a lower required return,

unless funding must be obtained under conditions of duress. In this sense, the most famous recent venture

capital backed U.S. company, Amazon.com, was somewhat unusual in that it received only one round of

venture capital funding from Kleiner Perkins Caulfield & Byers in July 1996, though this did bring the firm

no less than $8 million.7

3.5. Organization and Funding of Venture Capital Limited Partnerships

As mentioned earlier, venture capital limited partnerships have come to dominate the institutional

venture capital industry. This demonstrated survival value is based on several factors, two of which stand out

as especially important. First, these partnerships can focus totally on the financing and development of

portfolio companies as stand-alone ventures, unlike corporate and financial venture capital funds that must

balance the competing interests of the portfolio company and the corporate parent. Second, as described in

Gompers and Lerner (2001), the limited partnership has advantages of limited life and limited liability for

investors, as well as tax advantages, over the corporate form of organization. The fact that a relative handful

of funds dominate venture capital fund-raising every year suggests both the comparative advantage of limited

partnerships in general, and the value of experience and reputation in particular.

Most of the top venture capital firms are organized as general partnerships, and many of these are

7 These investments were funneled through two of KPCB’s funds, Kleiner Perkins Caulfield & Byers VIII and

KPCB Information Sciences Zaibatsu Fund II. In addition, L. John Doerr, who is easily the best known and most respected of the current generation of venture capitalists, became an Amazon.com director as part of the investment agreement (see Peltz (1996)).

13

concentrated in California’s Silicon Valley outside of San Francisco.8 These firms usually begin the venture

financing process by creating a distinct limited partnership fund, typically with a target amount of capital to

be raised and often with a dedicated investment target, such as funding internet start-ups. The year 1998

witnessed the successful launch of two mega-funds: Warburg, Pincus Equity Partners, L.P. and Hicks, Muse,

Tate & Furst Equity Fund IV, L.P. These two funds raised $5 billion and $4 billion, respectively. As the

Roman numeral after the Hicks, Muse fund name implies, this firm has launched many previous successful

funds, and both of the funds listed above were easily subscribed by investors (the companies were able to

raise the amounts intended). Even in the more challenging period of 2000-2001, Gupta (2001) reports that

J.P. Morgan Capital partners raised two funds with a combined total value of $13 billion.

While some of the largest venture funds are created by public offerings of limited partnership

interests (which can then be freely traded), most venture funds are organized and capitalized by private

negotiation between the fund’s sponsor and a well-established group of institutional investors.9 To say that a

fund is “capitalized” at its inception is something of a misnomer. In actual practice, the limited partners make

capital commitments, which the general partner then draws on over time as the fund becomes fully invested.

In addition to organizing the limited partnership, the sponsoring firm acts as the general partner (and has

unlimited liability) over the fund’s entire life, which is generally designed to be 7-10 years. As general

partner, the VC firm is responsible for (1) seeking out investment opportunities for the fund’s capital and

negotiating the terms upon which these investments will be made; (2) monitoring the performance of the

portfolio companies and providing additional funding and expertise as these private firms develop; (3)

finding an attractive exit opportunity, such as an IPO or a merger, that will allow the fund to liquidate its

investment in the portfolio companies; and (4) distributing the realized cash returns from these exit

opportunities to the limited partners and then terminating the fund’s existence. For its services, the sponsor

generally receives a percentage claim on the realized return (almost always 20 percent) as well as an annual

management fee equal to 1-3 percent (usually 2.5 percent) of the fund’s total committed capital.

Not surprisingly, the relationship between venture capitalists and investors is fraught with agency

problems. Investors must commit large amounts of money for long-term, illiquid, non-transparent

investments in private partnerships over which they can exercise no direct control without forfeiting their

limited liability. Venture capitalists have clear incentives to expropriate the limited partner’s wealth, and have

many opportunities to do so—including setting up new funds (that exclude the old limited partners) to finance

8 In particular, Sand Hill Road in the city of Menlo Park is considered venture capital’s Ground Zero. This

street is home to no less than 50 venture capital firms, as well as a large number of accounting, legal, and investment banking firms. In spite of this, Niedorf (1998) reports many VC firms prefer to set up in less expensive (and more private) digs elsewhere in the region.

9 Huemer (1992) presents a discussion of how regulation hampers the potential popularity of public VC funds, although two early empirical studies of venture capital performance [Martin and Petty (1983) and Brophy and Guthner (1988)] used data from public venture funds in their analyses.

14

the most promising companies and making side deals with the best portfolio companies. Reputational

considerations help control this problem, but numerous covenants are also inserted into the limited

partnership agreements between investors and VCs to control these agency conflicts. The covenants most

frequently inserted into VC investment agreements are described in Table 6.

Many senior partners at top venture capital firms have become legendary for their skill in finding,

nurturing, and bringing to market many famous high-tech companies. Examples include John Doerr of

Kleiner Perkins, Caulfield, and Byers, William Hambricht of Hambricht and Quist, and Sam Rosen of Rosen

Partners. While these industry leaders have become extraordinarily wealthy, even “ordinary” venture

capitalists have done quite well during the current boom.10 Partners and associates in venture capital firms

quite often are engineers or other technically trained professionals who themselves worked in high-tech

companies before becoming full-time venture capitalists. This experience gives them in-depth knowledge of

both the technological and business aspects of the industries they invest in, and this expertise, along with

capital and contacts, is what entrepreneurs look for when they approach a venture capitalist for funding. For

example, Mr. Doerr of Kleiner Perkins Caulfied & Byers has bachelors and masters degrees in electrical

engineering (plus an MBA from Harvard Business School), and worked for Intel Corporation for five years

before becoming a professional venture capitalist.

3.6. How Venture Capitalists Structure Their Investments

Although one should be careful in describing anything as idiosyncratic as a venture capital

investment contract as “standard,” numerous industry commentators have described regularities that are

observed in almost all real funding agreements between entrepreneurs and venture capitalists. Kaplan and

Strömberg (2001b) present what is probably the most comprehensive academic analysis of how VCs contract

with entrepreneurs to allocate cash flow and control rights between the firm and the VC fund. In the interest

of space, only the most important of these typical features are covered here. However, the real world of

finance offers few more interesting examples of sophisticated financial contracting.11

First and foremost, venture capital investment agreements are legal contracts that allocate risk,

return, and ownership rights between the entrepreneur (and other existing owners of a portfolio company) and

the venture capital fund making the financial investment. The actual distribution of rights and responsibilities

depends on (1) the experience and reputation of the entrepreneur; (2) the attractiveness of the portfolio

company as an investment opportunity; (3) the stage of the company’s development; (4) the negotiating skills

10 An academic examination of the determinants of venture capitalist compensation is provided in Gompers

and Lerner (1999a).

11 If one can only read a single academic article about how and why venture capital is invested as discussed here, the paper chosen must be Sahlman (1988). We also draw heavily on Testa (1988), Sahlman (1990), Gompers (1995) and Lerner (1995) in our discussion here.

15

of the contracting parties; and (5) the overall state of the venture capital market.12 If a respected and

experienced entrepreneur is approaching a venture capitalist with an opportunity to invest in an established

company with a promising technology, at a time (such as the late 1990s) when competition between venture

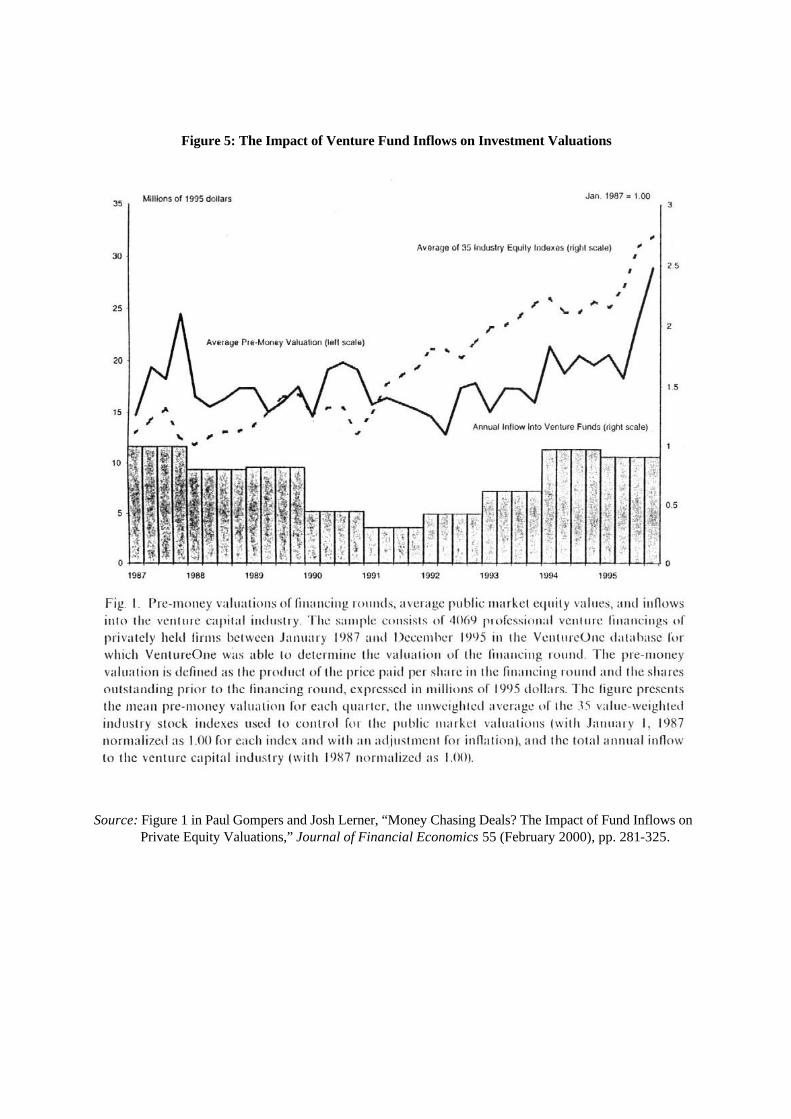

capital funds is fierce, the entrepreneur will be able to secure financing on very attractive terms. Gompers and

Lerner (2000) present striking evidence of the impact of unusually heavy cash inflows into the VC industry,

as Figure 5 makes clear. During the periods 1987-1990 and 1992-1995, large inflows significantly inflated

investee company valuations, and this impact was greatest in VC-intensive regions (especially California and

Boston) and for later stage companies that could profitably employ larger cash infusions. If, on the other

hand, an inexperienced entrepreneur asks for start-up funding at a time when little venture capital is being

raised (such as the early 1990s), the entrepreneur will have to accept fairly onerous contract terms if he or she

is able to attract funding at all.

The first step in any private equity financing is invariably for the parties to agree on a current

valuation for the portfolio company, prior to the venture capitalist’s investment. This will be based on the

company’s past R&D efforts, its current level of sales revenue and tangible assets, and the present value of

expected future profits if the company obtains new capital for growth. This valuation is also critical to

determining how much of the company the venture capital fund will receive in exchange for its investment.

Next, the parties must agree on the amount of new funding the venture capitalist will provide and the

required return on that investment.13 Naturally, the higher the perceived risk the higher the required return,

and this is usually inversely related to the stage of the portfolio company’s development. As mentioned

above, many venture capitalists demand a compound annual return of 50 percent or more on early-stage

investments, but are satisfied with half that on later-stage deals. The pricing of venture capital funding is

discussed more fully later in this section.

One key method of minimizing investment risk is to use staged financing. To illustrate how this

works, assume that a company expects to need $25 million in private funding in order to fully commercialize

a promising new technology. Rather than invest the entire amount at once, the venture capitalist is far more

likely to initially invest only enough (say, $5 million) to fund the company to its next development stage (i.e.,

to develop a working prototype), and to demand a very high required return on that initial investment tranche.

Once the company successfully achieves the promised outcome, the venture capitalist will provide funding for

12 The actual process of VC investment screening and decision-making is examined empirically in Kaplan and

Strömberg (2000), and they show that many factors—market size, business strategy, the firm’s technology and customer base and potential competition—all influence the investment decision. Kaplan and Strömberg also describe how the allocation of control rights between VC and entrepreneur is determined, while Baker and Gompers (2001) examine how board seats are allocated and Christopher (2001) describes several of the important legal hurdles VCs must confront when evaluating an investment opportunity.

13 Entrepreneurs wishing to determine how much capital they should try to obtain from VCs should read the

classic Harvard Business school article by Stancill (1987), “How Much Money Does your New Venture Need?”.

16

the next development stage, and since the risk has been reduced the funding will be provided at a higher per-

share price (a lower required return). Staged financing is not only a very efficient way to minimize risk for

the venture capitalist, it also gives the venture fund an extremely valuable option to deny or delay additional

funding. This cancellation option places the maximum feasible amount of financial risk onto the

entrepreneur, but in return allows him or her to obtain funding at a less onerous price than it would otherwise

be offered. Staged financing also provides tremendous incentives for the entrepreneur to create value, since at

each new funding stage capital will be provided on increasingly attractive terms.

Gompers (1995) provides two classic examples of how staged financing should work in the

development of private companies: Apple Computer and Federal Express. Apple received three rounds of

private equity funding. In the first round venture capitalists purchased stock at $0.09 per share, but this rose

to $0.28 per share in the second and then $0.97 per share in the third round. Needless to say, all of these

investments proved spectacularly profitable when Apple went public at $22 per share in 1980. On the other

hand, investors in Federal Express used staged financing with more telling effect during their three rounds of

private equity financing. The investors purchased stock for $204.17 per share in round one, but the firm’s

early performance was much poorer than anticipated. In the second round, shares were purchased for $7.34

each, but the company’s finances continued to deteriorate so a third financing round, at $0.63 per share was

required. As we know, Fedex eventually became a roaring success, and went public at $6 per share in 1978,

but staged financing allowed venture capitalists to intervene decisively during the firm’s problematic early

development.

A distinguishing characteristic of venture capital investment contracts is their extensive and very

sophisticated use of positive and negative covenants. These are contract clauses that mandate certain things

that the portfolio firm’s managers must do (positive covenants) and must not do (negative covenants). Some

of these covenants are found in many standard bond and loan financing contracts, such as covenants which

specify maximum acceptable leverage and dividend payout ratios, require the firm to carry certain types of

business insurance, and/or restrict the firm’s ability to acquire other firms or sell assets without prior investor

approval. Amazon.com provides an example of this; the firm’s bank required the company’s founder, Jeffry

Bezos, to personally guarantee all the company’s borrowing prior to its IPO. Other covenants, however, are

found only in private equity investment contracts. These include:

1. Ownership right agreements, which not only specify how equity ownership will be apportioned after

the initial venture investment is made, but also specify that the venture capital investment group will

be allocated a certain number of seats on the firm’s board of directors, and will enjoy pre-specified

voting rights. These often include the right to veto major corporate actions, and even remove the

management team if performance goals aren’t met. Cole and Sokol (1997) discuss the importance of

venture capitalist control rights. Since venture capitalists are active investors, they also demand

contract provisions ensuring their ongoing access to the firm’s accounts and facilities.

17

2. Ratchet provisions protect the venture group’s ownership rights in the event that the firm is forced to

sell new equity under duress. Generally, these provisions ensure that the venture capital group’s

share values will be adjusted so that the penalty of selling low-priced new stock is borne more by the

entrepreneur than by the venture capital funds. For example, if the venture fund purchased shares

initially valued at $1 each, and the firm is subsequently required to sell new stock at $0.50 per share,

a “full ratchet” provision mandates that the venture group be allocated one additional new share for

each one currently held to compensate them for the decline in stock value (a “partial ratchet” only

partially compensates the venture group). Obviously, not many rounds of such financing would be

required to completely wipe out a management team’s ownership stake, since they have no ratchet

protection.14 While Frederick Smith’s ownership stake in Federal Express was not wiped out by the

multiple rounds of distressed financing, it was much reduced.

3. Registration, participation, and repurchase rights preserve attractive exit opportunities for venture

capital investors. Although entrepreneurs are frequently content to remain private, if they can also

remain independent, this is anathema to venture capitalists. Demand registration rights give the

venture fund the right to force the firm to register shares with the SEC for a public offering--at the

firm’s expense. As an example, the venture capital investors in Amazon.com had such a demand

registration right. Participation rights ensure that the venture fund is able to participate in any

private sale of stock the firm’s managers arrange for themselves. The venture group will usually also

insist on a contract provision mandating that their ownership stake be repurchased by the firm if the

company is unable to execute an IPO or arrange a private sale within a specified time frame.

4. Stock option plans are typically provided for current and prospective managers. Venture capitalists

usually insist that a large pool of stock be set aside to compensate current managers for superior

performance and to attract talented new managers as the company grows. Setting stringent

performance targets for these options ensures that the interests of management and venture

capitalists are properly aligned. Once again, Amazon.com provides an example of this contracting

feature. At the time of the firm’s IPO, no less than 10.8 million shares were reserved under two

stock option plans, and over 4 million had already been allocated to the firm’s executives.

The listing of covenants typically found in venture capital investment contracts presented above is by

no means comprehensive. Other covenants lay out the terms under which additional funding will be provided

by the venture capital funds and further specify how ownership rights can be exercised by the contracting

parties. These include termination and golden parachute rights for the entrepreneur if he or she is forced out.

14 For a simple discussion of ratchet provisions, see Hoffman and Blakey (1987). The critical importance of the

lead venture capitalist being able to retain a proportionate share in multi-round financings is described theoretically in Admati and Pfleiderer (1994).

18

However, the most fascinating and distinguishing feature of venture capital investment contracts is

unquestionably their almost exclusive reliance on convertible securities (particularly convertible preferred

stock) as the investment vehicle of choice.

3.6.1. Why convertible securities are used in venture capital financing

Most people assume that, because venture capitalists are known as equity investors, they simply

purchase the common stock of the portfolio companies in which they decide to finance. In fact, venture

investments are almost never funded with common stock or with non-convertible preferred stock or debt.15

Instead, venture capitalists almost invariably fund their investment with either convertible debt or (much

more frequently) convertible preferred stock, for several reasons. First, since corporate law requires that all

shareholders be treated equally, venture capitalists would only be able to exercise effective voting control

with common stock if they were to purchase a majority of a firm’s common shares, and to purchase these at

the same price as other investors. This would be both extremely expensive and would place far more of the

firm’s business risk on the venture group than on the entrepreneur. Since convertible debt or preferred stock

is a separate class of security from common stock, contract terms and covenants specific to that issue can be

negotiated. Furthermore, since multiple classes of convertible debt or preferred stock can be created,

extremely complex and sophisticated contracting arrangements can be worked out between the firm and many

different investor groups [Gompers (1998)].16

A second reason why venture capitalists prefer convertible debt or preferred stock to common stock

as an investment vehicle is that this makes their claim senior to that of the entrepreneur and other existing

owners. Since this forces the entrepreneur to bear most of the firm’s business risk, the senior status of

convertible preferred stock or debt provides the maximum feasible protection for the venture group’s

investment. On the other hand, preferred stock or subordinated debt is a junior claim to debt, so funding a

company in this way also preserves its borrowing capacity, thus making it easier for the firm to arrange trade

credit or bank loans. The fact that the coupon rate on these convertible securities is typically set at zero (or a

very low percentage rate) clearly implies that venture capitalists are structuring their investments in this way

for contract flexibility reasons, rather than to earn a positive cash flow on their private company investments.

The primary rationale for using convertible securities is to give the venture capital group a claim on the

portfolio company’s earnings and market value in the event the firm is highly successful. In point of fact,

15 As mentioned earlier, SBICs have historically been an exception to this rule, since their funding patterns

dictated they structure their investments as loans. This will probably change, since they can now obtain their own funding via a security that is effectively preferred stock. Additionally, Wong (2001) shows that angel capitalists generally use only common stock in their investments.

16 Numerous theoretical studies have attempted to explain the use of convertibles by venture capitalists. These include Admati and Pfleiderer (1994), Hellmann (1998) Berglöf (1994) and, most recently, Bascha and Walz (2001). To our knowledge, however, Gompers (1997) is the only empirical academic study of convertible usage.

19

most convertible securities are converted into common stock before venture-backed companies execute initial

public offerings, partly to present an uncluttered balance sheet to prospective investors and partly to lock in

common equity stakes (and capital gains) before inviting in new stockholders.17

One final, and perhaps decisive, motivation for using convertible preferred stock as an investment

vehicle rather than any type of debt security is the fact that a creditor who attempts to exercise corporate

control with a debt security is exposed to significant potential legal liability. Creditors generally wish only to

lend a firm money and be repaid; they do not seek operational control of the firm, and if they are proven to be

exercising such control (through contract terms or through demands made upon management) they can held

legally accountable for the management’s actions and the firm can lose the tax-deductibility of its interest

payments. By structuring its investment as preferred stock, the venture capital group is able to avoid these

legal problems and retain the ability to exercise effective oversight without fear of legal challenges. For all of

these reasons, the venture capitalists backing Amazon.com structured their entire investment (in June 1996)

as convertible preferred stock, for which they paid $14.05 per share. Two of the firm’s directors, who

purchased convertible preferred stock in a much smaller financing round in early 1997, paid $40 per share.

3.7. The Pricing of Venture Capital Investments

As mentioned above, one of the critical factors to be determined in negotiations between

entrepreneur and venture capitalist is the pricing of the new investment funding. The pricing of VC

investments is discussed in several academic and practitioner articles.18 Unfortunately, there is no general

consensus as to specific methodology, so the material presented here should be taken as illustrative only.

Actual contract terms will be much more idiosyncratic. The impact of required return on the fraction of her

company an entrepreneur must exchange for a given dollar investment can be profound, as the following

example illustrates. Assume that the president and founder of the start-up company Internet Concepts

Corporation (ICC), approaches a technology-oriented venture capital fund for $5,000,000 in new funding to

support her firm’s rapid growth. After intense negotiations, the parties agree that ICC is currently (prior to

VC investment) worth $10,000,000 and that the risk of the firm is such that the venture capitalist is entitled

to a 50% compound annual (expected) return. Assume further that both parties agree that ICC should plan to

execute an IPO in five years, at which time the firm is expected to have net profits of $4,000,000 and to sell

at a price-to-earnings ratio of 20 times, which will value the company at $80,000,000. The promised value of

the venture capitalist’s stake in five years is calculated using basic future value computations, with an initial

17 Since most existing stockholders are prohibited by law (Rule 144) or by their investment bankers from

selling their shares during a firm’s IPO, and for up to two years thereafter, there is an additional reason to convert quasi-equity claims such as convertible debt and preferred stock into common stock well before the initial offering. Doing so starts the holding-period clock that much sooner.

18 This example is based on information presented in Schilit and Willig (1996b). Additional discussion of the pricing of VC investments is presented in Morris (1988) and Katz (1990).

20

investment amount (A) of $5 million, a required return (r) of 50 percent, and an investment horizon (n) of

five years:

FV = A (1 +r)n = $5,000,000 (1.50)5 = $5,000,000 (7.6) = $38,000,000 (Eq. 1)

To determine what fraction of the ICC’s equity (% Equity) that the venture capitalist will receive, this future

value (FV) is divided by ICC’s expected market valuation (Exp MV) at the time of the IPO:

% Equity = FV ÷ Exp MV = $38,000,000 ÷ $80,000,000 = 0.475 (Eq. 2)

This means that the venture capital fund will receive 47.5% of ICC’s equity in exchange for its $5

million investment. If the required return on investment had instead been established as 40%, rather than

fifty, the promised value of the venture capitalist’s share at the time of the IPO would have been $26.9

million and the fund would have claimed only one-third (33.6%) of ICC’s equity, rather than almost half.

From the venture capitalist’s point of view, one particularly attractive result of demanding a high required

return is that doing so will discourage entrepreneurs who really do not believe their own rosy sales and

earnings growth projections, since only the most confident entrepreneur will agree to a funding strategy that

promises to enrich the financier in full before any value is allocated to him or her.

3.8. The Profitability of Venture Capital Investments

By their very nature, as illiquid investments in rapidly growing private companies, venture capital –

backed companies are difficult to value prior to realization (through IPO, merger, or liquidation). It is thus

quite hard to make any sweeping generalizations about the profitability of these investments over time.

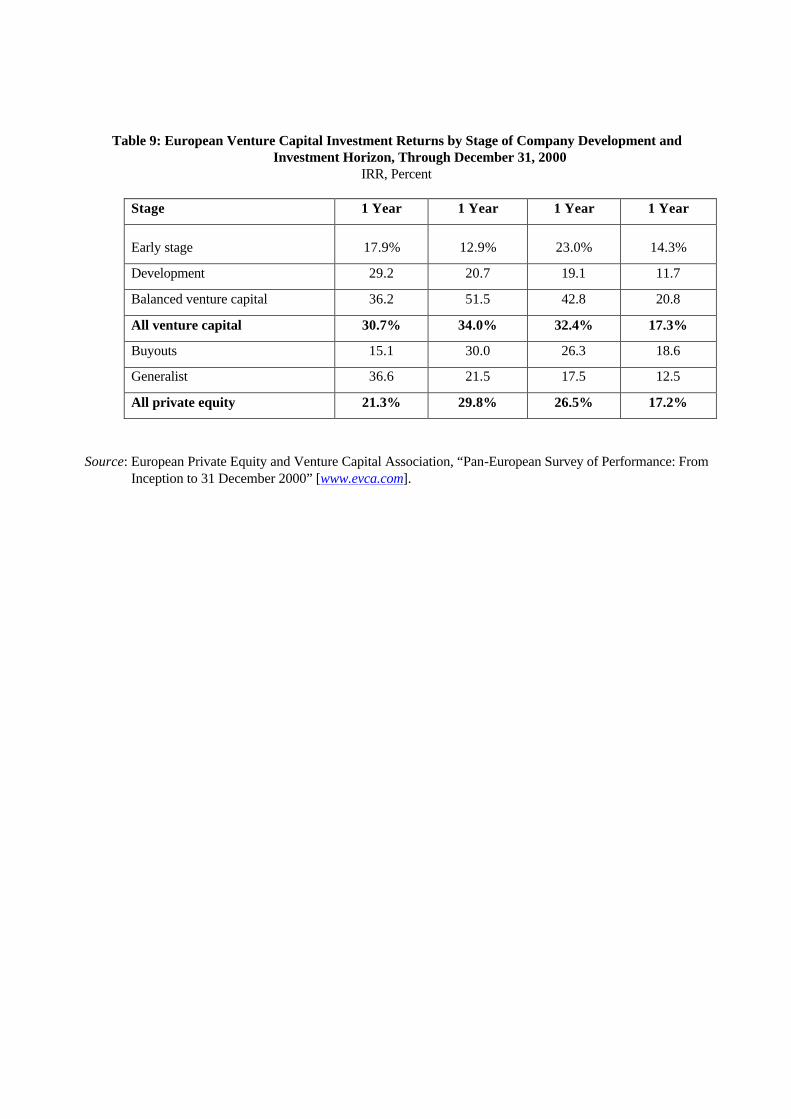

Nonetheless, it seems clear that investments made by venture capital funds during the middle 1990s, and

which matured during the 1999-2000 period, earned average compound annual returns of up to 30%.

Gompers and Lerner (2001) document repeated examples of boom and bust investment cycles, in which very

high realized returns prompt excessive new capital inflows into VC funds, which in turn cause returns to drop

sharply over the next harvest cycle. Although the 30% annual return was typical for venture capital funds

during the 1970s and early 1980s, Figure 6 makes clear that such a level of profitability was not achieved

even once from 1984 to 1996. Returns were again at target levels in 1995 and 1996, and then surged in 1999

and 2000. However, more recent returns following the collapse of the NASDAQ market in March 2000 have

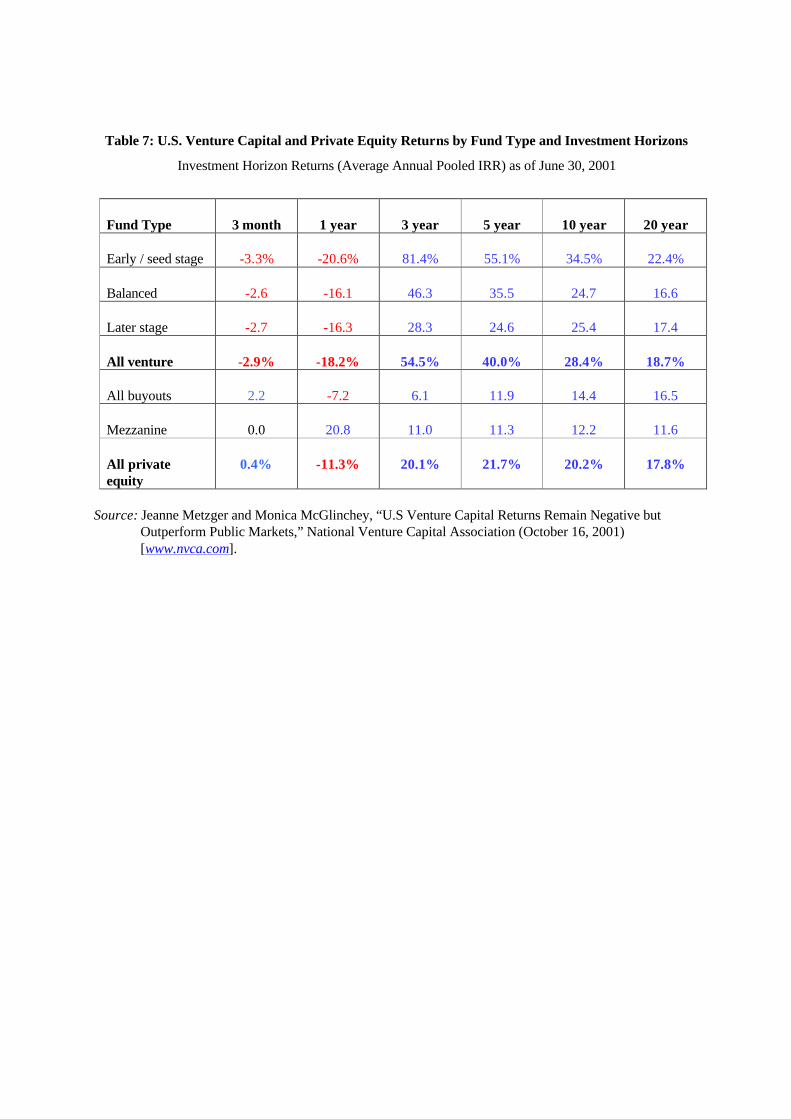

been uniformly negative, as Table 7 demonstrates. A key question is whether the massive influx of new

venture capital that occurred during the 1998-2000 period will have the same negative impact on returns over

the next five years.

On the other hand, there is a strongly positive correlation between venture returns and those on small

stock funds (not shown), which highlights the importance of a healthy public stock market for small stocks in

21

general and for initial public offerings in particular. Since IPOs are the preferred exit opportunity for venture

capital investors, and because the “recycling” of realized returns is an important source of new venture capital

funding, any decline in investor appetite for new issues has an immediate negative impact on the venture

capital industry.19

3.9. Exit Strategies Employed by Venture Capitalists

VCs are not long-term equity investors; their objective is to add value to a private company and then

to harvest their investment once the company is mature enough. There are three principal methods of exiting

an investment: (1) through an initial public offering (IPO) of shares to outside investors; (2) by selling the

portfolio company directly to another company [the merger, or M&A option]; and (3) by selling the company

back to the entrepreneur/founders [the redemption option, described in Fellers (2001a,b)]. IPOs are by far

the most profitable and prestigious option for the venture capitalists. It is also a very realistic option; during

the 1990-2000 period, 5,803 companies executed IPOs on American capital markets, and these issues raised

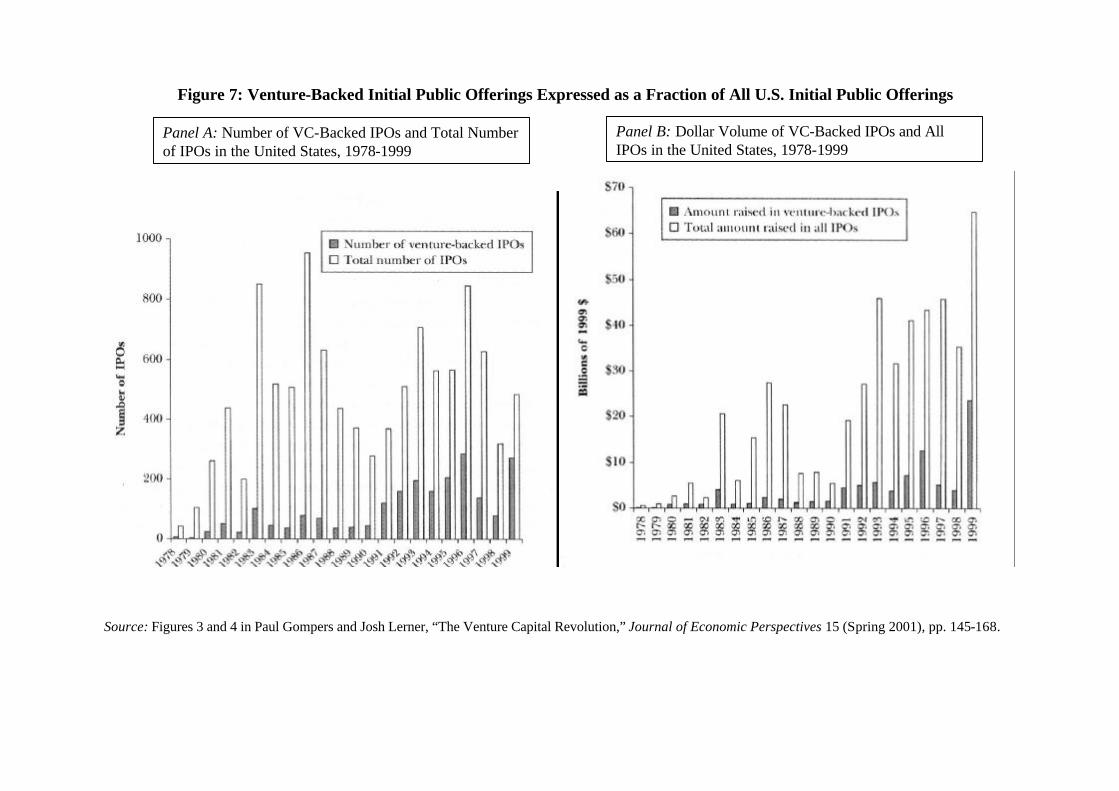

$419.5 billion. Figures 7 A&B demonstrate that the importance of venture capital-backed IPOs grew steadily

over the decade, to the point where well over half of all IPOs in 1999 were VC-backed, and these represented

almost half of the then-record $71.0 billion raised in that year. VCs also create value at the IPO, by attracting

prestigious underwriters and by certifying that all relevant information is being disclosed to investors. Barry,

et al (1990) and Megginson and Weiss (1991) find that VC backing reduced the level of underpricing in IPOs

during the 1980s, though Beatty and Welch (1996) find that this relationship is reversed during the 1990s.

Perhaps surprisingly, VCs do not exit at the time of an IPO. Instead they retain shares for several

months or even years and then typically distribute shares back to the limited partners. These distributions are

usually not anticipated by investors, so their announcement is a surprise. Figure 8 shows that distributions

typically occur after a period of sharply rising stock prices, and that the average stock price response to

distribution announcements is significantly negative. The studies by Gompers and Lerner (1998b) and

Bradley, Jordan, Yi and Roten (2001) both document this negative return.20

3.9. Government Support for Venture Capital in the United States

It is perhaps appropriate to end our discussion of American venture capital with a brief survey of

government-sponsored venture capital funding programs in the United States. As we have seen, the most

successful American private equity investment programs are those that are structured as limited partnerships

19 The role of venture capitalists in deciding when to take a portfolio company public is detailed in Lerner

(1994) and Gompers (1996), while the difficulties encountered by entrepreneur/founders of non-venture backed firms in trying to arrange an acquisition for their firms are described in Bianchi (1992).

20 According to an NVCA press release on October 16, 2001, the value of cash and stock distributed to limited partners by VCs grew from $1.88 billion during the first quarter of 1999 to an astounding $18.72 billion during the first quarter of 2000, but then fell steadily back to $2.10 billion during 2Q 2001.

22

and organized by professional venture capitalists. Since it would be difficult to imagine an environment more

alien to public-sector rules and regulations, it is tempting to conclude that governments have never been and

can never be valuable partners in sponsoring entrepreneurial investment. The truth, however, is much more

nuanced.

Economic historians document that the federal government has played a key direct or catalytic role in

developing many of the most important technologies that underpin modern industrial society--from aerospace

engineering to material science to computers (especially computers). Additionally, federally-chartered Small

Business Investment Companies accounted for two-thirds of all the venture capital funding allocated to

American business from the 1950s to 1969, and continued to play an important role even after private

partnerships rose to preeminence. Finally, Lerner (1999) documents that one of the most important and

visible federal programs, the Small Business Innovation Research (SBIR) grant program, has proven very

successful at fostering technological innovation and corporate growth. Firms which received SBIR grants

grew significantly faster than a matched set of non-awardees, suggesting that these grants allowed firms to

overcome financing constraints which otherwise would have proven binding. On the other hand, Lerner’s

finding that the positive effects of SBIR wards were confined to firms based in zip codes with substantial

private venture capital activity suggests that government programs are only effective when they supplement,

rather than attempt to supplant or promote, private fund-raising and investment.

4. The European Market for Venture Capital and Private Equity

Although “classic” venture capital investment by privately financed partnerships in early-stage

entrepreneurial growth companies has traditionally been a distinctly American phenomenon, private equity

financing has long been an established financial specialty in Western Europe. Since this continent is the

birthplace both of the industrial revolution and of modern capitalism, it is not surprising that a highly

sophisticated method of funneling growth capital to private (often family-owned) companies should be

observed. In fact, private equity fund-raising in Europe compared quite well with the United States in total

annual amounts raised and invested until 1997, and showed far less annual variability. The chief differences

between European and American venture capital lie in: (1) the principal sources of funds for venture capital

investing, (2) the organization of the venture funds themselves, (3) the development stage of the portfolio

companies able to attract venture financing, and (4) the principal method of harvesting venture capital

investments. As we will see, these differences are all related, and help explain why venture capital is widely

believed to be more successful in the United States than it is in Europe--both from the standpoint of

promoting rapid technological development and as a private investment vehicle for individual and

23

institutional investors.21

Before proceeding, we should point out a definitional difference between Europe and the United

States. Whereas American commentators tend to refer to all professionally managed, equity-based

investments in private, entrepreneurial growth companies as venture capital, European commentators tend to

sharply differentiate between venture capital and private equity investment. Where necessary, we will

maintain this distinction, but in general we will refer to both private equity and venture capital (high-tech)

investment simply as European venture capital.

4.1. European Venture Capital and Private Equity Fund Raising and Investment

As in the United States, VC fund raising and investment has grown rapidly since the mid-1990s.

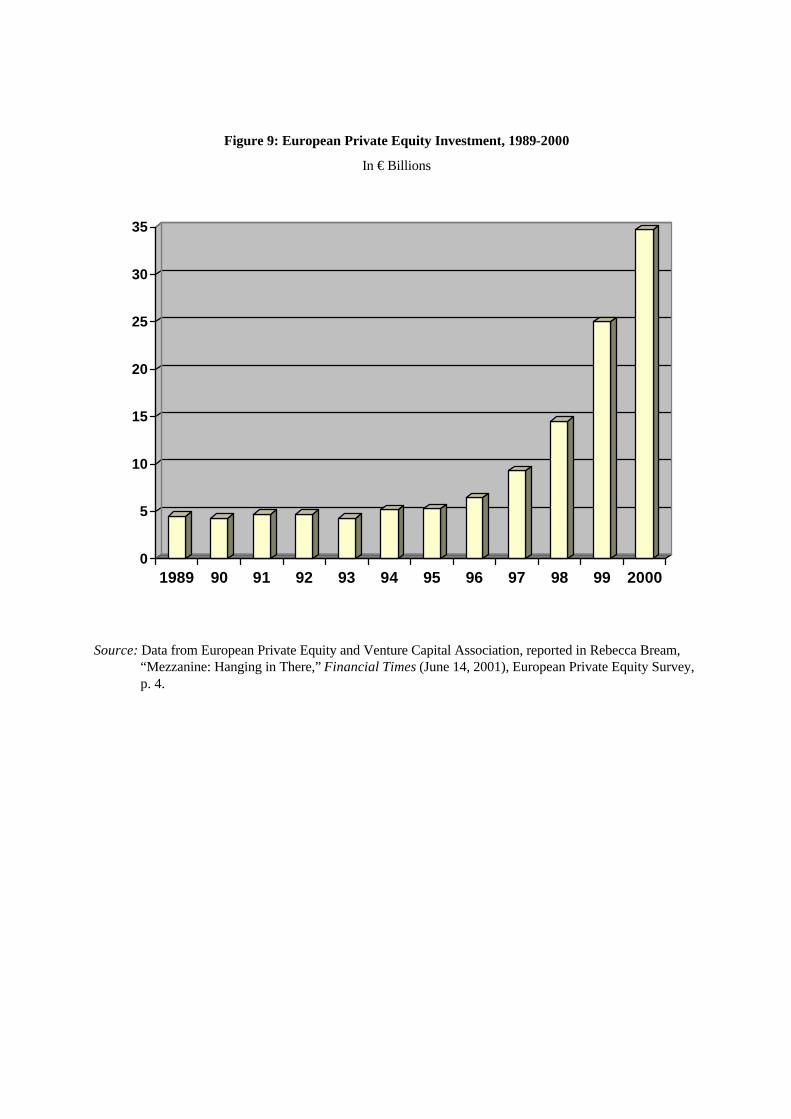

Figure 9 describes the growth in total VC investment over the period 1989-2000. According to data

published by the European Private Equity and Venture Capital Association (EVCA, www.evca.com), total

investment grew from a stable level of about € 5 billion per year during the 1989-1996 period to €25 billion

in 1999 and €34.9 billion (invested in some 10,440 companies) in 2000. Disbursements dropped somewhat

to €11.1 billion during the first half of 2001, but this annualized pace would still make 2001 the third highest

investment year ever. Fund raising grew even more dramatically over this period, rising from about €5 during

1995 to nearly €48 billion in 2000. Since the early 1980s, a cumulative total of more than €125 billion has

been raised for investment in European private equity.

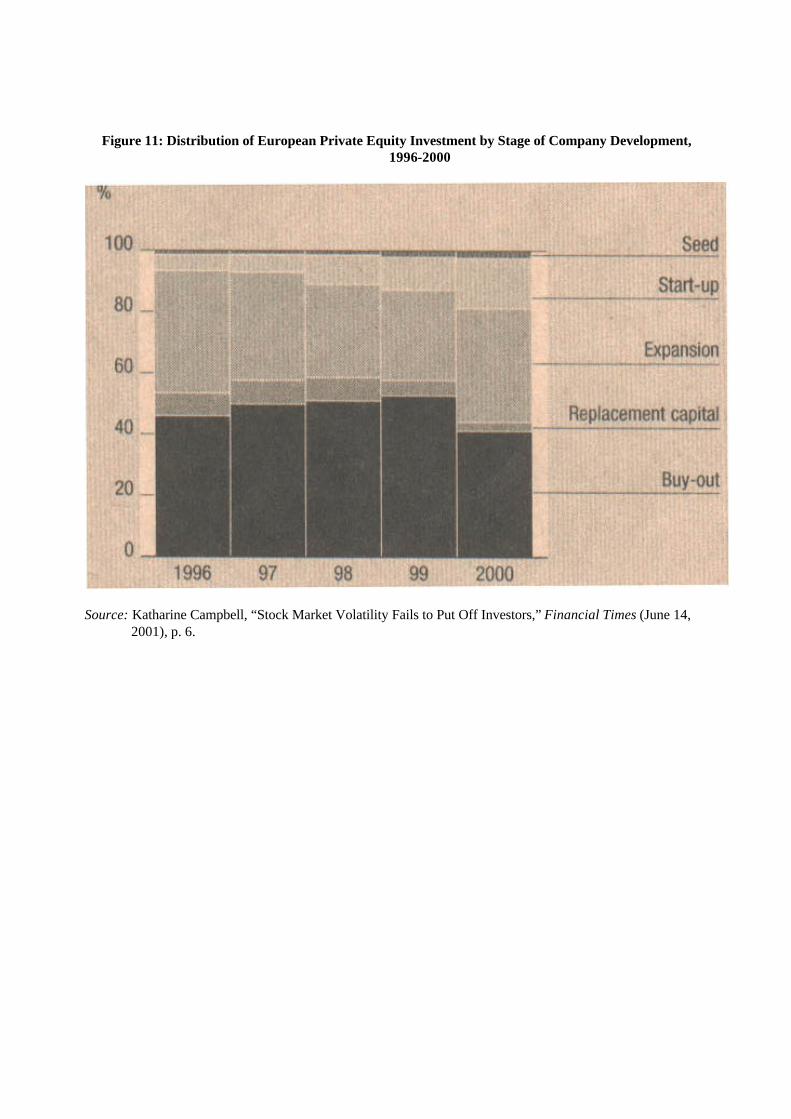

Historically, European VC has been funneled to different industries and different types of companies

than in the United States, though this has been changing of late. As recently as 1996, less than one-fourth of

European venture capital went into high technology investments; by 2000, the fraction allocated to high tech

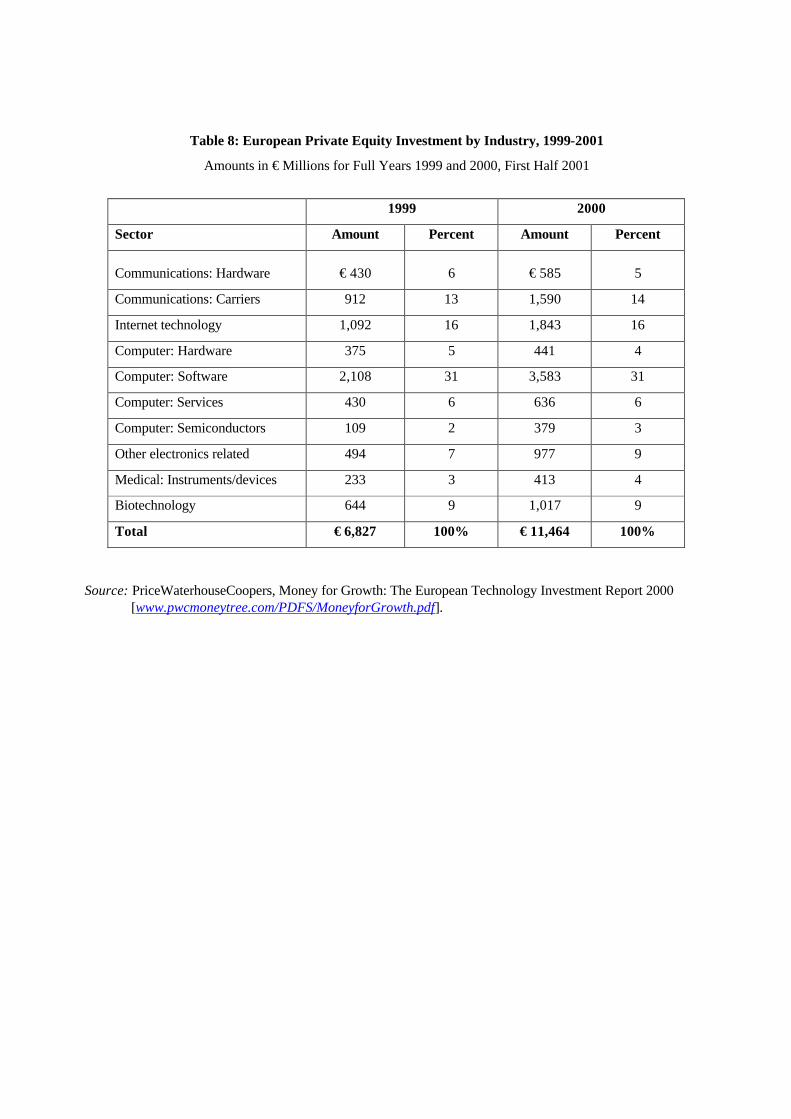

industries topped 54%. Table 8 describes the industry breakdown of European private equity investments in

technology for the years 1999 and 2000. As in the U.S., roughly 80% of European high tech VC investment

is funneled into computers and communications businesses.

In one important respect, venture capital funding patterns in Europe and America have long been

very similar in that both are highly concentrated geographically. Some 38% of year-2000’s total investment,

and no less than 45% percent of 1999’s total, was targeted at British companies. In 2000, France (15% of the

total) displaced Germany (14%) to become the second largest recipient of European VC investment, though

both countries experienced very strong growth in investment inflows. Italy accounted for an additional 8.8%

of the total, and small countries such as Sweden, the Netherlands, and Switzerland were disproportionately

well represented.

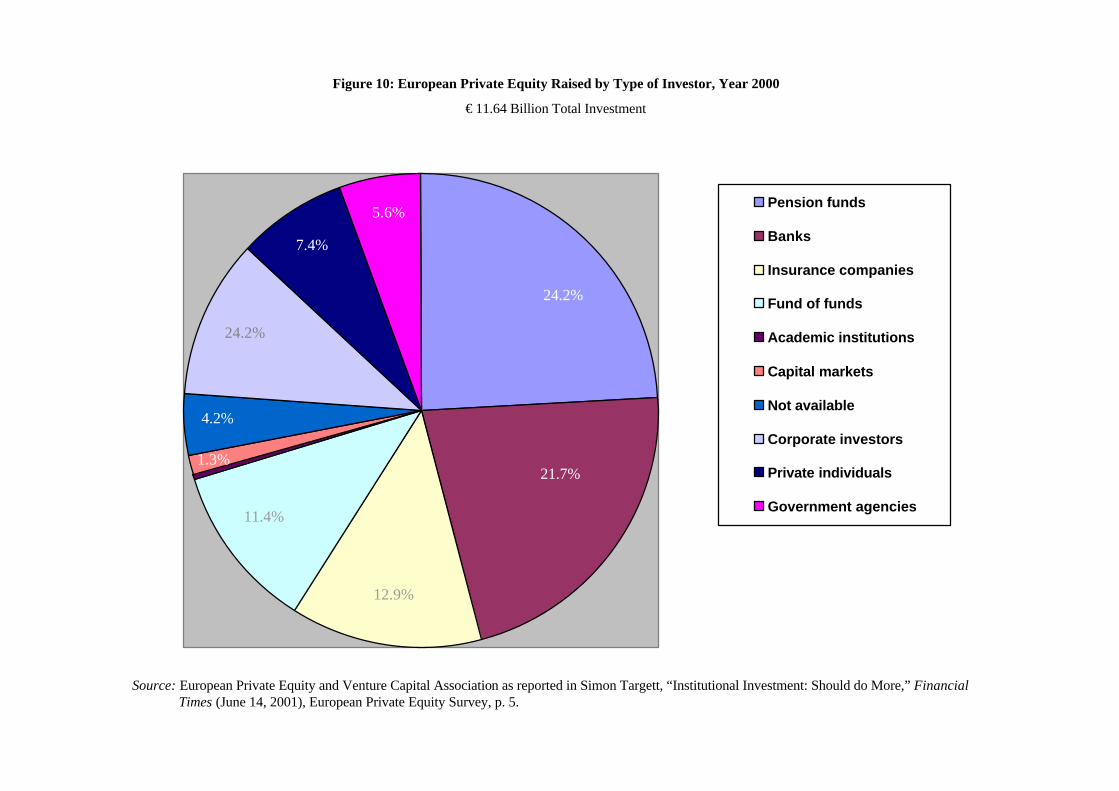

4.2. The Changing Source of Funding for European Venture Capital

21 The discussion in this section draws heavily on Black and Gilson (1998), Schilit and Willig (1996a), Jeng

and Wells (2000) and Arundale (2000).

24

The sourcing of European venture capital funds differs from their American counterparts primarily in

the Europe’s greater reliance on financial institutions (which tend to be very powerful in Europe) and lesser

reliance on pension funds, which generally play a much smaller role in the old world than in the new. Banks,