Lashed to the Mast? The Politics of NDC Pension Reform

50

IN THE FINAL DECADES OF THE TWENTIETH CENTURY , governments around the world began to dramatically change the form and function of old-age pension systems. These reforms were generally motivated by a combination of population aging, slowing eco- nomic growth, and tightening budget constraints; together these led both to rising pen- sion costs and to declining resources with which governments could finance old-age pension liabilities. 1 Many governments responded to these pressures by revising the parameters of tradi- tional defined benefit pay-as-you-go (PAYG) public pension systems with incremental changes to contribution or benefit rates, retirement age, or indexation rules to keep pen- sion systems in line with changing economic and demographic trends and state fiscal capacity. Other governments, however, opted for more fundamental, structural revisions of the design and objectives of old-age pension systems through the creation of mandatory individual, financial defined contribution (FDC) pension schemes, wherein pension bene- fits are based on individual contributions to a (typically) privately managed pension fund, and the market return to capital on those funds. Throughout the 1990s, the ideas and tech- nology behind funded pension schemes were disseminated broadly throughout the world. By the end of the decade, more than 20 countries, from South America to East Asia, Europe, and the Former Soviet Union had adopted funded, defined contribution pension schemes either as the dominant “pillar” in mandatory pension schemes, or as part of mul- tipillar structural reforms. 2 By the middle of the 1990s, however, a new model of structural pension reform—the non-financial (or notional) defined contribution (NDC) scheme—had also emerged. 3 The 345 Chapter 14 Lashed to the Mast? The Politics of NDC Pension Reform Sarah M. Brooks and R. Kent Weaver* * Sarah M. Brooks is assistant professor of political science at Ohio State University; R. Kent Weaver is professor of public policy and government at Georgetown University and a senior fellow in the Governance Studies Program at the Brookings Institution. The research reported herein was partially funded pursuant to a grant from the U.S. Social Security Administration (SSA) funded as part of the Retirement Research Consor- tium at Boston College. The opinions and conclusions are solely those of the authors and should not be construed as representing the opinions or policy of the SSA or any agency of the federal government. The authors would like to thank Daniele Franco, Agneta Kruse, and Edward Palmer for extensive and helpful comments on an earlier draft of this chapter.

Transcript of Lashed to the Mast? The Politics of NDC Pension Reform

IN THE FINAL DECADES OF THE TWENTIETH CENTURY, governments around the worldbegan to dramatically change the form and function of old-age pension systems. Thesereforms were generally motivated by a combination of population aging, slowing eco-nomic growth, and tightening budget constraints; together these led both to rising pen-sion costs and to declining resources with which governments could finance old-agepension liabilities.1

Many governments responded to these pressures by revising the parameters of tradi-tional defined benefit pay-as-you-go (PAYG) public pension systems with incrementalchanges to contribution or benefit rates, retirement age, or indexation rules to keep pen-sion systems in line with changing economic and demographic trends and state fiscalcapacity. Other governments, however, opted for more fundamental, structural revisionsof the design and objectives of old-age pension systems through the creation of mandatoryindividual, financial defined contribution (FDC) pension schemes, wherein pension bene-fits are based on individual contributions to a (typically) privately managed pension fund,and the market return to capital on those funds. Throughout the 1990s, the ideas and tech-nology behind funded pension schemes were disseminated broadly throughout the world.By the end of the decade, more than 20 countries, from South America to East Asia,Europe, and the Former Soviet Union had adopted funded, defined contribution pensionschemes either as the dominant “pillar” in mandatory pension schemes, or as part of mul-tipillar structural reforms.2

By the middle of the 1990s, however, a new model of structural pension reform—thenon-financial (or notional) defined contribution (NDC) scheme—had also emerged.3 The

345

Chapter 14

Lashed to the Mast? The Politics of NDC Pension Reform

Sarah M. Brooks and R. Kent Weaver*

* Sarah M. Brooks is assistant professor of political science at Ohio State University; R.Kent Weaver is professor of public policy and government at Georgetown University anda senior fellow in the Governance Studies Program at the Brookings Institution.

The research reported herein was partially funded pursuant to a grant from the U.S.Social Security Administration (SSA) funded as part of the Retirement Research Consor-tium at Boston College. The opinions and conclusions are solely those of the authors andshould not be construed as representing the opinions or policy of the SSA or any agencyof the federal government. The authors would like to thank Daniele Franco, AgnetaKruse, and Edward Palmer for extensive and helpful comments on an earlier draft of thischapter.

Pension_ch14.qxd 12/7/05 3:46 PM Page 345

NDC approach was the key feature of a national pension reform in Sweden that wasadopted as framework legislation in 1994 and as final legislation in 1998. Italy, Latvia, andPoland followed Sweden’s lead.

NDC pensions combine the PAYG financing that is characteristic of traditional definedbenefit (DB) schemes with the defined contribution (DC) structure of individual accounts.NDC schemes tie benefits closely to individual contribution history over an entire work-ing life, but credit those contributions with a notional interest rate tied to wage growth oroverall economic growth rather than providing a return on specific financial assets.Notional accounts contain no real capital that can be claimed at retirement as a lump sumor that can purchase an annuity in the private market. Instead, at the time of retirement,the government converts the notional account balance into an annuity on the basis ofcohort life expectancy, and finances this benefit on a PAYG basis.

Although NDC pension schemes represent an important departure from both the incre-mental reforms of DB schemes and from individual account, prefunded DC models, manyof the individual elements of the NDC scheme design that allow it to control costs are notnew; they have been utilized on an ad hoc and often temporary basis in incrementalreforms to PAYG-DB pension schemes. The originality of the NDC model lies primarily incombining those elements into a coherent package with a clear policy objective, and imbu-ing that package with presumed perpetuity.

A number of “good policy” arguments have been advanced for adopting NDC mea-sures. First, proponents cite the enhanced “fairness” associated with the DC formula overDB schemes that base retirement benefits on the last salary or last few years’ wages, whichtend to redistribute implicitly toward high-income workers with steeper earnings profiles.NDC schemes make any redistribution more explicit by removing it from the main NDCpillar of the pension scheme and creating a separate scheme with the objective of reducingpoverty. Second, supporters of NDC-based reforms argue that the tighter link betweencontributions and benefits signals to workers that it is important to work longer to securean adequate pension, thus enhancing system financing along with individual responsibil-ity and work effort. Third, NDC-based reforms ensure a long-term balance between pen-sion contributions and payouts. Fourth, NDC reforms do not expose individuals to short-and medium-term fluctuations in market returns and annuity prices that may arise in FDCindividual accounts. Fifth—and of particular importance to government finance min-istries—NDC pension reforms may provide a fiscally attractive alternative to funding thetransition to funded DC plans because they do not require government to finance benefitsfor a transitional generation as a country moves to a system of funded individualaccounts.

A final potential advantage offered by NDC reform is the perception of permanency,and hence credibility, that it imparts to the social security system. By reducing the need forgovernments to intervene regularly to adjust pension system parameters, the “politicalrisk” of policy change in response to political pressures associated with public pensionsystems is significantly reduced. Indeed, the repeated tinkering with rules of DB systemsin many countries has made those systems much less of a “defined benefit” in practicethan in theory, especially for future retirees whose benefits are most likely to be affected.The sense of ownership felt by workers who receive regular statements tracking their ris-ing notional account balances reinforces this sense of permanency of the NDC scheme. Theresulting sense of property rights may create a “lock-in” effect that deters politicians fromintervening to arbitrarily reduce or confiscate the notional capital accumulated in the NDCaccounts.

On the negative side, however, because NDC schemes accommodate increasinglongevity completely through benefit reductions, stabilizing pension contribution rates

346 PENSION REFORM: ISSUES AND PROSPECTS FOR NDC SCHEMES

Pension_ch14.qxd 12/7/05 3:46 PM Page 346

will lead to gradual erosion of pension values as populations age if workers do not post-pone their retirement.

This discussion of potential “lock in” and political risk suggests that political calcula-tions as well as policy advantages and disadvantages may play a very important role inpolicy makers’ calculations on NDC-based reforms. Indeed, the central working hypothe-sis in this chapter is that NDC-based pension systems offer important political advantagesto politicians in an era when credit-claiming opportunities in pension policy are few andblame-avoiding incentives are strong. In particular, NDC-based systems:

• Provide a “clean hands” mechanism that lowers replacement rates as the system isphased in while allowing politicians to avoid blame.

• Obfuscate the degree of future retrenchment because it is not known in advance, butrather depends on future economic and demographic developments.

• Avoid having to repeatedly deal with pension retrenchment and refinancing in thefuture.

In short, the complexity and automaticity of the NDC scheme creates important opportu-nities to limit traceability and blame for benefit retrenchment: automatic adjustment mech-anisms based on economic and demographic trends absolve politicians of responsibilityfor potential future benefit reductions. Like Ulysses in resisting the Sirens, governmentsmay be able to “lash themselves to mast” of a fixed contribution rate and automatic adjust-ment mechanisms, resisting temptations to pay unsustainable benefits to current andfuture retirees.

The adoption of NDC schemes may also generate new political risks, however, becausethey accommodate increased liabilities (such as those from unanticipated longevity gains)or revenue shortfalls (for example, those due to wage decline) by reducing benefits. To theextent that benefit values for younger birth cohorts fall short of public expectations aboutthe absolute and relative value of pensions, politicians may confront a powerful politicalbacklash as populations age. This may in turn lead to a “loosening of the lashes” on con-tribution rates and automatic adjustments, to contributions to the system from the generalgovernment budget, and/or to pressure for enhanced “social protection” pensions outsidethe NDC pillar.

The spread of NDC-based pension reforms thus raises important questions both forsocial science theory and for pension policy making. From the perspective of social sciencetheory, NDC-based pension reforms represent an important example of what Jon Elsterhas called “pre-commitment” or “self-binding” efforts to limit future options in a way thatfurthers their long-term interests. Indeed, Elster uses the Ulysses and the Sirens metaphorin much of his writing on precommitment (Elster 1979, 2000). NDC-based pension reformscan also be seen as a combination of several blame-avoiding strategies that allows politi-cians to reconcile their policy and political objectives by making politically risky decisionsthrough what Kent Weaver (1986, 1988) has called “automatic government” mechanismsrather than by requiring politicians to make those decisions openly. Thus NDC systems donot represent a departure from the common practice in PAYG-DB pension systems of mak-ing hard-to-detect revisions, such as revisions to indexation rates, in order to achieve fiscaland policy goals.

Examining the adoption and implementation of NDC-based pension reforms providesan opportunity to examine how agenda-limiting precommitment mechanisms areadopted and how they operate in practice. Two questions are addressed in this study.First, are NDC-based reforms more likely to get on the agenda and win adoption in somecountries than in others? If so, is it the characteristics of a country’s current pension sys-tem, the political ideology of elites, or the characteristics of the political system—or some

LASHED TO THE MAST? THE POLITICS OF NDC PENSION REFORM 347

Pension_ch14.qxd 12/7/05 3:46 PM Page 347

combination of these and other factors—that determines whether countries consider andadopt NDC-based reforms? Second, do NDC-based reforms actually succeed in de-politi-cizing painful and costly pension retrenchment decisions and limiting blame to incum-bent politicians, or do they have a tendency to spark resistance that undercuts theirintended effects?

In the first section of the chapter we briefly outline the characteristics of NDC pensionsystems, arguing that NDC pension schemes should be seen as a set of principles that maybe more or less closely followed in practice. The second section develops a framework foranalyzing why NDC pension systems have increasingly been on the agenda in recentyears and discusses conditions that facilitate considering and adopting NDC-basedreform, including the complex question of why there has been a stronger move towardadopting NDC in some countries and regions than others. The third section of the chapterexamines implementation challenges that may arise in NDC systems as they are adoptedand mature, as well as their political sustainability. The final section of the chapter assessesthe prospects for a further spread of NDC pension systems. In short, the chapter askswhether and under what conditions adoption of NDC pensions is likely to be an effectivemeans of allowing politicians to “lash themselves to the mast” of a stabilized contributionrate and depoliticize the process of pension retrenchment. This, in turn, plays into thebroader question of whether NDC-based reforms are likely to play a major role in address-ing the immense aging issue facing both developed and developing societies in comingdecades.

How NDC Works

Although the NDC system represents a synthesis of the PAYG-DB and FDC systems, itdiffers from these in the way it apportions risk and reward, and in its likely politicalconsequences. Although notional accounts share with FDC schemes a tight linkbetween pension benefits and individual contributions, NDC systems are by design notadvance funded.4 As noted above, NDC schemes also differ markedly from FDC sys-tems in their treatment of capital market risks. NDC systems diminish individuals’exposure to fluctuations in market rates of return and annuity prices associated withprivately managed funded-DC schemes by using a notional interest rate. Workers inNDC schemes continue to be exposed to significant demographic risks, however, suchas unanticipated gains in longevity during working life, and to sustained declines infertility around the time of retirement. By shrinking the overall contribution base to thepension system, such trends would cause declines in pension benefits to maintain over-all financial balance of the NDC system.5 At the same time, the annual indexation ofannuities to wage growth exposes retired workers to the risk of declines in benefits ifwages and productivity fall.

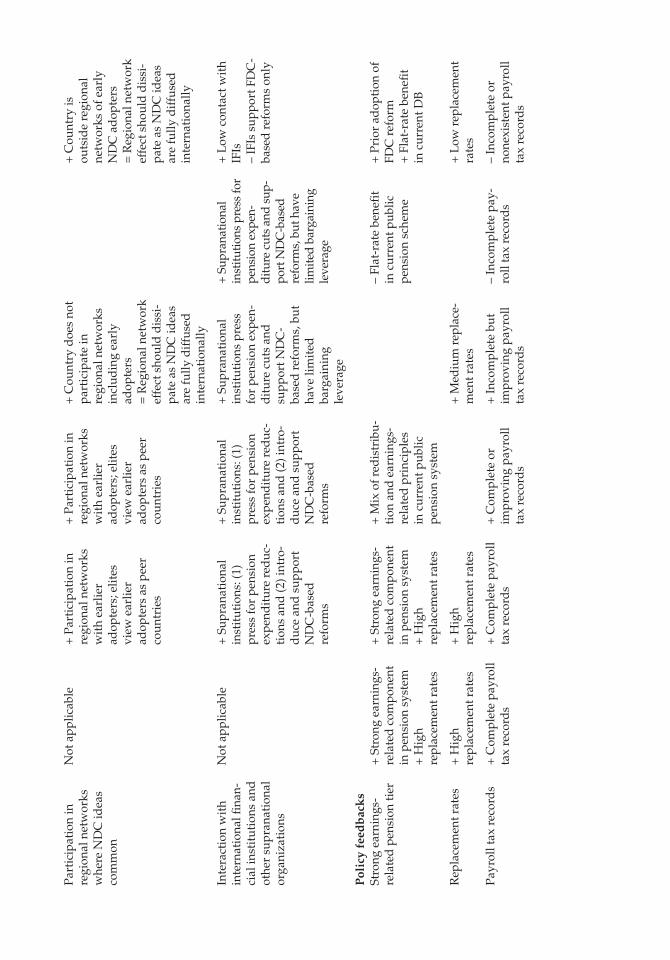

NDC systems also differ from traditional DB schemes in important ways, as shown inthe first and fourth columns of table 14,1, which show different gradations of DB and NDCpension schemes. But as the second and third columns of the table show, a number of“middle positions” between DB and NDC pension schemes are possible on many of thesekey elements of pension system design. Some elements associated with NDC pension sys-tems, such as life expectancy adjustments, have been enacted as ad hoc reforms of existingDB pension systems (column 2). And NDC-based systems sometimes take a “weak” or“partial” form, with one or more provisions that make them less than fully self-sustainingor inclusive (column 3). Table 14.1 divides these elements of pension system structure intofour categories: structural features, coverage, time horizon, and exclusivity.

348 PENSION REFORM: ISSUES AND PROSPECTS FOR NDC SCHEMES

Pension_ch14.qxd 12/7/05 3:46 PM Page 348

Tab

le 1

4.1.

Non

-fin

anci

al P

ensi

on P

rovi

sion

s A

s a

Con

tin

uu

m f

rom

Defi

ned

Ben

efit t

o D

efin

ed C

ontr

ibu

tion

Pro

visi

onD

efine

d be

nefit

Mid

dle

posi

tion

DB

ref

orm

s“W

eak”

or

“Par

tial

” N

DC

“Str

ong”

or

“ful

l” N

DC

Str

uct

ura

l fea

ture

sFu

ndin

g

Year

s of

ear

ning

s an

dco

ntri

buti

ons

inco

rpor

ated

in b

enefi

t rul

e

Lif

e ex

pect

ancy

at

reti

rem

ent

Ret

irem

ent a

ge

Ent

irel

y PA

YG

Can

incl

ude

anyt

hing

from

no w

ork

(but

res

iden

cy o

rna

tion

alit

y) r

equi

rem

ent t

osp

ecifi

ed y

ears

of c

ontr

ibu-

tion

s (i

nclu

din

g “b

est y

ears

”an

d “

final

sal

ary”

arr

ange

-m

ents

)

No

prov

isio

n in

ben

efit c

al-

cula

tion

Fixe

d s

tand

ard

ret

irem

ent

age

(may

incl

ude

actu

aria

lad

just

men

ts fo

r ea

rlie

r or

late

r re

tire

men

t; m

ay b

e ad

hoc

incr

ease

s in

ret

irem

ent

age

over

tim

e)

May

hav

e so

me

adva

nced

fund

ing,

usu

ally

for

liqui

d-

ity

purp

oses

Rep

lace

men

t rat

e ba

sed

on

num

ber

of y

ears

that

cor

re-

spon

ds

to th

e en

tire

wor

king

life

for

typi

cal w

orke

r

Incl

usio

n of

“d

emog

raph

icfa

ctor

” in

ben

efit c

alcu

lati

onto

fully

or

part

ially

com

pen-

sate

for

popu

lati

on a

ging

Flex

ible

ret

irem

ent a

gean

d/

or a

utom

atic

incr

ease

sin

ret

irem

ent a

ge to

fully

or

part

ially

com

pens

ate

for

long

evit

y in

crea

ses

Ent

irel

y PA

YG

May

incl

ude

som

eno

nfina

nced

cre

dit

s fo

r no

n-w

ork

acti

viti

es

Infr

eque

nt o

r in

com

plet

e(f

or e

xam

ple,

exc

lusi

on o

fpo

stre

tire

men

t) a

dju

stm

ent

for

incr

ease

s in

long

evit

y; n

oau

tom

atic

mec

hani

sm to

corr

ect f

or in

com

plet

ech

ange

s

Min

imum

age

to c

laim

ben

e-fit

, but

no

stan

dar

dre

tire

men

t age

. Ina

deq

uate

adju

stm

ent f

or e

arlie

r or

late

r re

tire

men

t

Res

erve

s bu

ilt u

p fo

r la

rge

dem

ogra

phic

coh

orts

, to

hold

tran

sfer

s fr

om g

ener

albu

dge

t and

for

long

-ter

msy

stem

bal

ance

Full

link

betw

een

cont

ribu

-ti

ons

and

ear

ning

s

Ben

efit l

evel

s ad

just

fully

(inc

lud

ing

curr

ent r

etir

ees)

and

aut

omat

ical

ly fo

rin

crea

ses

in lo

ngev

ity

Min

imum

age

to c

laim

ben

e-fit

, but

no

stan

dar

dre

tire

men

t age

. Par

tial

ret

ire-

men

t pos

sibl

e. F

ull a

ctua

rial

adju

stm

ent f

or e

arlie

r or

late

r an

d p

arti

al r

etir

emen

t

Pension_ch14.qxd 12/7/05 3:46 PM Page 349

Tab

le 1

4.1.

(con

tin

ued

)

Pro

visi

onD

efine

d be

nefit

Mid

dle

posi

tion

DB

ref

orm

s“W

eak”

or

“Par

tial

” N

DC

“Str

ong”

or

“ful

l” N

DC

Infl

atio

n an

d e

cono

mic

grow

th

Fina

ncin

g

Red

istr

ibut

ion

acro

ssge

nera

tion

s

Ben

efits

ad

just

ed fo

rin

flat

ion

and

/or

ear

ning

sin

crea

ses,

som

etim

es w

ith

ad h

oc c

hang

es to

res

trai

nco

sts

May

incl

ude

payr

oll t

axes

and

/or

gen

eral

rev

enue

s;re

venu

es a

dju

sted

to n

eed

sof

PA

YG

sys

tem

on

auto

mat

ic o

r ad

hoc

bas

is

Firs

t gen

erat

ions

gen

eral

lyw

inne

rs a

s in

“Po

nzi”

sche

me

Bene

fits

adju

sted

for

infla

tion

and/

or e

arni

ngs

incr

ease

s;in

dexa

tion

rule

inco

rpor

ates

brak

es fo

r po

or e

cono

mic

perf

orm

ance

and

hig

h in

fla-

tion,

whi

ch m

ay o

r m

ay n

otbe

follo

wed

in p

ract

ice

Payr

oll t

axes

fixe

d “

inth

eory

” at

max

imum

targ

etle

vel (

for

exam

ple,

bel

ow 1

0pe

rcen

t in

Can

ada,

20

perc

ent i

n G

erm

any)

but

may

be

revi

sed

in p

ract

ice

May

be

rest

rict

ed w

ithi

n D

B ti

ers

by lo

wer

ing

repl

acem

ent r

ates

and

tyin

gco

ntri

buti

on r

ates

to le

vel

need

ed to

be

self

-sus

tain

ing

over

long

term

Bene

fits

adju

sted

with

infla

-tio

n an

d/or

ear

ning

s. In

com

-pl

ete

brak

es fo

r po

orec

onom

ic p

erfo

rman

ce a

nd/

or g

over

nmen

t mak

es a

d ho

cad

just

men

ts in

bra

ke to

enha

nce

elec

tora

l pro

spec

ts

Payr

oll t

ax r

ate

wit

h pa

rt o

fco

ntri

buti

on r

ate

used

toco

ver

pens

ion

righ

ts g

rant

edbu

t not

cov

ered

by

ind

ivid

-ua

l’s o

wn

cont

ribu

tion

Cre

dit

s gi

ven

to s

ome

coho

rts

for

whi

ch n

o co

ntri

-bu

tion

s w

ere

mad

e; p

ossi

ble

gene

rati

onal

red

istr

ibut

ion

due

to s

hift

ing

labo

r m

arke

t

Ben

efits

ad

just

ed w

ith

the

inte

rnal

rat

e of

ret

urn,

whi

chis

tied

fully

to e

arni

ngs

grow

th

Fixe

d p

ayro

ll ta

x ra

te; a

llco

ntri

buti

ons

paid

giv

e an

ND

C a

ccou

nt v

alue

, and

all

nonc

ontr

ibut

ory

righ

ts a

refin

ance

d e

xter

nally

(for

exam

ple,

wit

h ge

nera

l rev

-en

ues)

Poss

ible

gen

erat

iona

l red

is-

trib

utio

n d

ue to

shi

ftin

gla

bor

mar

ket

Pension_ch14.qxd 12/7/05 3:46 PM Page 350

Sour

ce:C

ompi

led

by

auth

ors.

Red

istr

ibut

ion

wit

hin

gene

rati

ons

Cov

erag

e

Tim

e h

oriz

on

Exc

lusi

vity

Perm

itte

d w

ithi

n D

B ti

er,

base

d o

n lim

ited

num

ber

of“h

igh

year

s” o

n w

hich

ben

e-fit

s ar

e ba

sed

, hig

her

repl

acem

ent r

ates

for

low

earn

ers,

cre

dit

s gi

ven

for

whi

ch n

o co

ntri

buti

ons

have

been

mad

e

No

ND

C c

over

age

No

cove

rage

of N

DC

sys

tem

No

ND

C p

ensi

on ti

er

May

be

rest

rict

ed w

ithi

n D

Bti

ers

by in

crea

sing

num

ber

of y

ears

on

whi

ch b

enefi

tsar

e re

plac

ed, e

limin

atin

g or

red

ucin

g re

plac

emen

t rat

ed

iffe

rent

ials

and

lim

itin

gcr

edit

s fo

r no

nwag

e ac

tivi

ty

Not

app

licab

le

Lat

er c

ohor

ts o

f wor

kers

cove

red

by

“qua

si-N

DC

”re

form

s (f

or e

xam

ple,

life

-ex

pect

ancy

ad

just

men

ts to

bene

fits

or r

etir

emen

t age

)

Not

app

licab

le

Som

e cr

edit

s gi

ven

for

acti

v-it

ies

for

whi

ch n

o co

ntri

bu-

tion

s w

ere

mad

e

Onl

y so

me

sect

ors

(for

exam

ple,

pri

vate

sec

tor)

are

cove

red

by

ND

C s

yste

m

Onl

y so

me

coho

rts

(for

exam

ple,

new

labo

r m

arke

ten

tran

ts o

r th

ose

und

er a

ge50

) cov

ered

by

ND

C s

yste

m

ND

C-b

ased

pen

sion

is o

nly

one

of s

ever

al p

ublic

pens

ion

tier

s

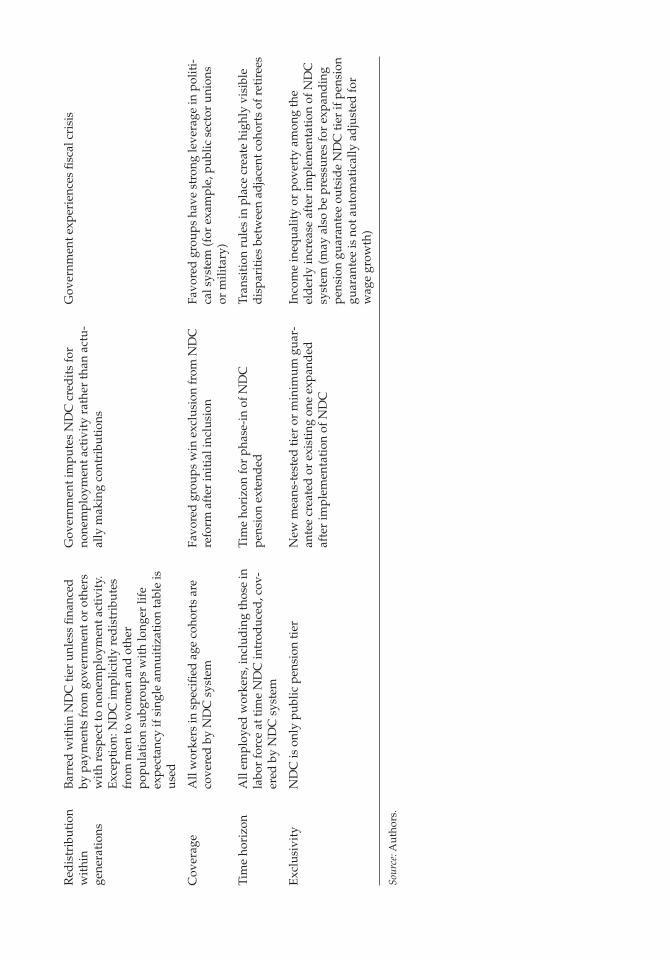

Bar

red

wit

hin

ND

C ti

erun

less

fina

nced

by

paym

ents

from

gov

ernm

ent o

r ot

hers

wit

h re

spec

t to

none

mpl

oy-

men

t act

ivit

y. E

xcep

tion

:N

DC

impl

icit

ly r

edis

trib

utes

from

men

to w

omen

and

othe

r po

pula

tion

sub

grou

psw

ith

long

er li

fe e

xpec

tanc

y if

sing

le a

nnui

tiza

tion

tabl

e is

used

All

wor

kers

in s

peci

fied

age

coho

rts

are

cove

red

by

ND

Csy

stem

All

empl

oyed

wor

kers

,in

clud

ing

thos

e in

labo

rfo

rce

at ti

me

ND

Cin

trod

uced

, cov

ered

by

ND

C s

yste

m

ND

C is

onl

y pu

blic

pen

sion

tier

Pension_ch14.qxd 12/7/05 3:46 PM Page 351

Structural FeaturesA wide range of variation is possible on multiple dimensions of the structural features ofpension systems (table 14.2). For example, while most non-financial DB pension schemesoperate solely on a PAYG basis, the Swedish NDC scheme incorporates “buffer funds” thatprefund some benefits and protect against small dips in contributions and demographicbulges in the population of retirees.6 Indeed, proponents of NDC argue that buffer fundsshould in principle be included in an NDC scheme (see Palmer 2006a).

352 PENSION REFORM: ISSUES AND PROSPECTS FOR NDC SCHEMES

Table 14.2. The NDC Pension Continuum in Practice

Sweden GermanyProvision (NDC initiator; full NDC) Poland (full NDC) (middle position DB)

Structuralfeatures

Advancedfunding

Life expectancyat retirement

Retirement age

Inflation andeconomicgrowth

Payroll tax rate

Redistributionacrossgenerations

Redistributionwithingenerations

PAYG plus buffer fundpartially accumulatedunder old pensionsystem

Unisex, account balancesand benefits adjustedboth before and afterretirement

Flexible, with NDC andFDC pensions drawableno earlier than age 61;partial withdrawal pos-sible

Account balances andbenefits adjusted forwage growth (initialbenefit is higher thanactuarial amount andadjusted for wagegrowth minus 1.6%)

Fixed at 16% for NDCtier and 2.5% for FDCtier

Eliminated once NDCsystem is fully phased in

In pension annuity, fromshorter-lived to longer-lived pensioners, andfrom men to women

PAYG plus buffer fund(surplus in 1st pillar +privatization revenue +1% temporary contribu-tion)

Unisex, but calculatedfor life expectancy at theage of retirement

minimum: 60 (women) 65 (men)

Accumulation is wagegrowth plus labor forcegrowth; annuitiesindexed to consumerprices, unless real wagesare falling, in which casethey are uprated in linewith nominal wages(that is, cut in real terms)

12.22% to NDC7.3% to FDC

Minimal, through mini-mum pension guarantee

In pension annuity, fromshorter-lived to longer-lived pensioners, andfrom men to women

PAYG with general rev-enues and “eco-tax” aswell as payroll tax;small “sustainabilityreserve”

Benefits adjust forchanges in systemdependency ratio

Normal retirement ageof 65; incentives forearly retirement beingreduced

Benefits adjusted forwage growth

Governmentcommitment to holdcontribution rate to nohigher than 20%through 2020 and 22%through 2030

Modest, through DBformula

In pension annuity, fromshorter-lived to longer-lived pensioners, andfrom men to women

Pension_ch14.qxd 12/7/05 3:46 PM Page 352

With respect to population aging—and in particular rising life expectancy at retire-ment—PAYG-DB schemes generally do not provide for automatic adjustments to thechanging demographic, social, and economic context in which the system is embedded.Thus, as populations age, the schemes may require periodic government intervention toadjust benefit levels or retirement ages. NDC schemes automatically accommodatechanges in life expectancy by calculating annuities on the basis of individual accumula-tions and life expectancy at the time of retirement. But such measures can also be includedin DB schemes to partially or fully adjust for population aging, for example the Kohl gov-ernment’s “demographic factor” enacted as part of a short-lived pension reform and the“sustainability factor” enacted by the Schröder government.7 Similarly, public PAYG-DBschemes generally include a fixed standard retirement age, usually with some sort ofadjustment (which varies greatly across countries in its actuarial accuracy) for earlier orlater retirement. A number of countries have raised the standard age in recent years inresponse to population aging. The Swedish NDC scheme, on the other hand, has replacedthe standard retirement age with flexible retirement age (pensions can be drawn no earlierthan age 61), no upward age at which pension rights can be earned, and with the benefitbased on the life expectancy of the retiree’s birth cohort at the time of retirement. ButNDC-like proposals have also been made for retirement age changes in public PAYG-DB,such as proposals in the United States that would raise the age for receipt of “full” socialsecurity entitlements as longevity increases.

Perhaps the most distinctive attribute of NDC pension systems is the fixing of a long-term contribution rate and the dependence of pension adjustments on the size of the wagebase. With this “lashing to the mast” of contribution rates, future adjustments to keep pen-sion systems sound must in theory be made on the benefit side. For DB pensions operatedon PAYG basis, on the other hand, payroll tax contribution rates and benefit levels are usu-

LASHED TO THE MAST? THE POLITICS OF NDC PENSION REFORM 353

Table 14.2. (continued)

Sweden GermanyProvision (NDC initiator; full NDC) Poland (full NDC) (middle position DB)

Coverage

Time horizon

Exclusivity

Universal

Persons born 1938–1953receive benefits partiallyin old system. Personsborn 1954 and laterreceive benefits entirelyin new system

No. Combined withsmaller FDC tier andinflation-indexed guar-antee pension for thosewith low lifetimeearnings

Universal

Phases in beginning in2005

No. Quasi-mandatoryprivate pillar and“zero-pillar” added

Source: Information on Poland is from Góra and Rutkowski (2000) and Chlon-Dominczak and Góra (2006);information on Germany is from Börsch-Supan and Wilke (2006); information on Sweden is from Sweden,National Social Insurance Board (2004).

Not universal; separateprograms for farmersand uniformed services

New system mandatoryfor all born beginning in1949; FDC mandatoryfor people born afterDecember 31, 1968

No. Combined with FDCsystem, plus tax-financedminimum pension sup-plement (for minimum25 years’ contributions)if NDC+FDC annuitiesare below minimum

Pension_ch14.qxd 12/7/05 3:46 PM Page 353

ally adjusted on an ad hoc basis as current funding needs change. A number of countriesalso use general revenues or some other form of revenue (for example, the German eco-tax) to finance part of their PAYG-DB pension system costs. Given increased longevity inmost countries and flagging employment growth in a number of countries, there has beenstrong upward pressure on DB pension contribution rates over the past 30 years.8

In response to this trend, many countries have in recent years tried to stabilize contri-bution rates to their DB pensions through a variety of mechanisms. In Canada, for exam-ple, the federal and provincial governments have pledged to keep payroll taxes under 10percent in the long term; if benefit costs are projected to exceed that target within a speci-fied projection period, a combination of benefit cuts and contribution rate increases isautomatically triggered.9 Germany, where pension contribution rates grew to over 20 per-cent of earnings in recent years, has also acted to try to stabilize contribution rates at nomore than 20 percent through the year 2020 and 22 percent through 2030.10 In the UnitedStates, congressional Republicans made it very clear at the time of the 1983 Social Securityrescue package that they would tolerate no further increases in contribution rates, andthere have been none.11 In short, even without the explicit “lashing to the mast” of contri-bution rates associated with NDC pension reforms, public non-financial DB systems canand have undertaken a number of actions to stabilize contribution rates.

Non-financial DB and NDC pension systems also differ significantly in their potentialfor intergenerational redistribution. DB pensions typically offer a much higher rate ofreturn on contributions to the first generations in the program, when the ratio of contribu-tors to beneficiaries is much higher than in later generations (especially as longevityincreases). NDC pensions, on the other hand, are intended to restrict intergenerationalredistribution. However, several PAYG-DB pension schemes, notably in Canada and theUnited States, have also moved to restrict intergenerational redistribution by making verylong term projections of contribution rates and benefit costs and developing contributionrates and benefit levels that are intended to be stable over that projection period with thesupport of reserve funds.12

In principle, NDC schemes treat all contributions to the system the same way in termsof accruing credits (with adjustments for wage or—as in Italy—GDP growth over time):only actual contributions accrue credits, and all credits result in equal payouts (actuariallyadjusted for life expectancy at retirement). If credits are granted for other reasons, theymust be accompanied by financing from general tax revenues, or the financial equilibriumof the system will be jeopardized. Even NDC systems may contain some elements of intra-generational redistribution in payout, however, notably in the use of gender-neutral annu-itization tables that do not reflect real gender differences in life expectancy.

Many PAYG-DB schemes include more complex patterns of intragenerational redistrib-ution. Some countries, notably the United States, offer higher replacement rates for thefirst dollars of earnings, effectively offering a higher replacement rate for low earners.Many PAYG-DB schemes also base benefits on a contributor’s highest or final number ofearnings years (for example, the highest three, fifteen, or twenty years). To the extent thatthe benefit formula is based on final salary or only the latest years’ earnings, it privilegesworkers with a steeper career-earnings profile. Such workers are typically the most afflu-ent and better educated in society. In recent years, public PAYG-DB pension systems inmany countries have been altered to limit redistribution within generations in some ways,for example by lengthening the number of contribution years used in calculating pensionentitlements or by flattening replacement rate differentials across earnings levels. Butthere has also been a widespread expansion in noncontributory credits given for care-giving in a number of countries.

354 PENSION REFORM: ISSUES AND PROSPECTS FOR NDC SCHEMES

Pension_ch14.qxd 12/7/05 3:46 PM Page 354

The use by NDC schemes of a benefit formula based on contributions over the entirecareer both diminishes the degree of regressive redistribution caused by final salary benefitformulas and at the same time eliminates the possibility for progressive redistribution ofpension benefits. The overall progressivity of an NDC-based retirement income systemthus depends critically on the existence of mechanisms within or outside the NDC compo-nent to progressively reapportion risk and benefits to those who are the least well off. Thiscan be done in either of two ways. First, contributions can be made for individuals thatincrease their benefit entitlement. In Sweden, for example, contributions are made into thesystem for periods spent in providing childcare, military service, unemployment, sicknessand disability covered by public social insurance, and for compensated parental leave andhigher education. The money to finance these credits is transferred from the general bud-get to the NDC reserve fund on a yearly basis. Partial NDC reforms have imputed creditswithout financing them immediately, but these elements require a future tax-based trans-fer burden to make the system sustainable. Second, changes may be made in other tiers ofthe retirement income system that add or “reinvent” existing redistributive elements, suchas by topping-up benefits to a minimally guaranteed level. To date, all countries introduc-ing NDC schemes have constructed a minimum benefit guarantee financed from generalrevenues. Indeed, without an adjustment of other pension tiers to ease the transition toNDC, the distributional change resulting from a change to NDC is likely to impose suchheavy costs on some groups that its chances of winning adoption and being sustained aresubstantially reduced.

Time HorizonPension reforms can also be distinguished by their phase-in periods. The U.S. increase ofretirement age from 65 to 67, for example, is being phased in over almost 40 years from thetime it was enacted to the time it will be fully in effect. To date, countries implementingNDC reforms also show great differences in the time horizon over which they phase intheir reforms. NDC reforms can be applied to rights acquired under the previous system,if adequate contribution records exist.13 In the Swedish reform legislated between 1994and 1998, for example, all workers born after 1953 are entirely in the new system; earliercohorts born between 1937 and 1953 are partially in the new system. In Italy, on the otherhand, only new entrants to the labor market will have their benefits fully calculated underthe new NDC rules. A longer phase-in period is likely to weaken opposition from the mostattentive publics—the elderly and the near-elderly—but it also lessens near-term bud-getary savings from reform.

CoverageCountries can also differ in the degree to which the NDC system will apply to all membersof the workforce when it is fully phased in. Excluding key sectors (for example, the mili-tary, or, as in Poland, farmers) from a shift to NDC may help governments manage the pol-itics of reform, although doing so clearly raises questions of equitable treatment. It willalso mean that career changes into a sector covered by NDC can entail losing benefit priv-ileges in the sector from which workers migrate.

ExclusivityMost countries have multipillar pension systems. Thus even when an NDC system is fullyphased in, it may not be the sole, or even the largest, source of public pension income. The1994 pension reform in Sweden, for example, created a multipillar pension scheme inwhich the average wage worker could expect to receive a retirement pension from an NDC

LASHED TO THE MAST? THE POLITICS OF NDC PENSION REFORM 355

Pension_ch14.qxd 12/7/05 3:46 PM Page 355

account and a mandatory individual financial DC account. There is also a garantipensionfinanced from general revenues for low-wage workers and workers with interrupted earn-ings histories, which tops up their accumulated pension accounts to a socially acceptableminimum. The NDC tier is dominant, however—financed by a 16 percent payroll contri-bution, compared with a contribution of 2.5 percent of covered wages into financial (thatis, funded) individual accounts. The Polish government similarly adopted a mixed NDCand funded-DC scheme, wherein 15 percent of covered wages are credited to the first(NDC) pillar and indexed with a notional interest rate equal to growth in the coveredwage bill. Nine percent of covered wages are transferred to the funded scheme in Poland,and invested according to market principles.14 The Latvian pension reform also combinesan NDC pillar with a financial DC scheme. The NDC pillar was financed with contribu-tions of 20 percent of covered wages from the outset. The individual financial accountscheme, which came into force in 2001, initially received 2 percent of covered wages, whilecontributions to the NDC component decreased to 18 percent. Following a transitionschedule specified in the law, the split will be 10 percent and 10 percent by 2010.15

Overall, the preceding discussion suggests that a political analysis of NDC pension sys-tems must recognize that the boundaries between and NDC and non-financial DB pen-sions are fuzzy rather than sharp. Not only have certain elements of NDC, such aslife-expectancy adjustments, been used since the mid-1990s on an ad hoc basis in incre-mental DB reforms, but also countries such as Italy have adopted partial NDC reforms inways that may be unstable in the medium or long terms. In the case of Italy, for example,the government imputes contributions to notional accounts for some groups higher thanthose that are actually made. At the same time, the Italian system does not have automaticstabilizers, nor does it automatically take into account pre- or postretirement increases inlongevity. Finally, Italy has established an inflexible rate of return on accumulated contri-butions, raising questions about the medium- to long-term stability of the system.16 Ifincomplete adoption of NDC is possible, so too, presumably, is an incomplete dismantling:thus an analysis of NDC politics must also include an assessment of the risks of an ad hocunraveling of NDC reforms.

Despite the tighter link between contributions and benefits, NDC schemes maynonetheless bear the heavy imprint of political values, objectives, and concessions to pow-erful domestic political groups. Governments may intervene in the accumulation phase ofthe NDC system, for instance, to credit socially valued activities that are not rewarded bymarkets, such as the provision of credits for child rearing, education, and military service.At the same time, powerful groups such as the military or specific industrial sectors mayclaim privileges within the NDC framework to the extent that governments credit notionalaccounts for workers in these sectors to finance special benefits such as early retirement.17

The use of unisex mortality tables likewise represents a political decision to redistributefrom men to women. At the same time, NDC systems usually redistribute credits of work-ers who die before retirement to other workers within the same cohort, rather than to theworkers’ surviving family members. This redistribution of credits represents a politicaljudgment in which the claim of survivors within the family is weighed against those ofworkers within the cohort, to whom such credits are apportioned.

The Politics of NDC Innovation, Diffusion, and Adoption

The discussion above suggests some important general propositions about the politics ofadopting NDC-focused pension reforms. First, it suggests that although NDC-basedreforms have some features that may be politically attractive for reelection oriented politi-

356 PENSION REFORM: ISSUES AND PROSPECTS FOR NDC SCHEMES

Pension_ch14.qxd 12/7/05 3:46 PM Page 356

cians—in particular, such reforms enhance the capacity for politicians to distance them-selves from long-term benefit and eligibility cuts—they are not without political draw-backs as well.

Second, it suggests that the attitudes of important actors in pension reform politics—notably finance ministries, trade unions, and groups representing retirees—are likely to beheavily influenced by what else is in the pension reform package, particularly by whatprotections are afforded to the aged through the provision of income-tested pensions orsupplemental DC pensions to compensate for any losses, and who is expected to pay forthe costs for those parts of the reform package.

Third, this analysis suggests that proponents of an NDC-based reform may be able toaffect the political prospects for reform through specific design features in the reform. Inparticular, the pace of transition strongly influences the degree and visibility of the mater-ial and distributive effects of NDC reforms, and thus the political viability of these mea-sures. If a reform is phased in quickly, the terms of the new scheme are not only morecostly and transparent, they are also at greater risk of political backlash. Other features ofNDC program design that are likely to affect a proposal’s political prospects include thespecific provisions of other pension tiers and how they compensate any losers from theshift to NDC (for example, the creation of new income-tested pensions), as well as whichgroups (for example, civil servants or the military), if any, are excluded from this shift.There may also be significant battles over whether and how much to provide credits fornon-wage-related benefits within an NDC pension scheme, as well as over the question ofwho should pay for those credits.

Finally, the politics of NDC adoption and rejection is likely to be a moving target. Howpoliticians perceive and react to NDC proposals is likely to evolve over time as the conceptis diffused more broadly among technocratic elites and as experience with implementingNDC-based pension regimes grows.

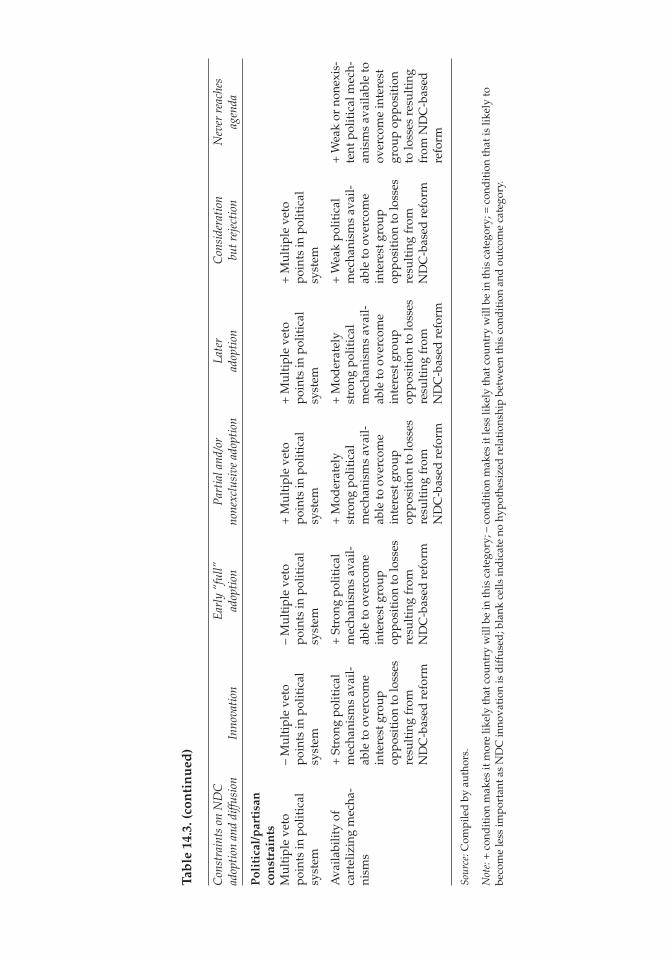

This very general overview of the calculus of key actors does not take us very far,however, toward understanding why NDC pension reforms are likely to get on the gov-ernment’s agenda and win adoption in some countries and not in others, let alonewhether an NDC-based reform will be sustained once it has been adopted. To under-stand these cross-national variations and how they are likely to evolve over time it isimportant first to introduce contextual factors that vary across countries, notably theseverity of the challenges that extant pension systems face, the weight of various socialactors, and the barriers that a political system imposes to instituting major reforms. Sec-ond, it is important to take a process-oriented approach, distinguishing between theforces that are critical at different stages of NDC politics: (1) initial development of theNDC idea and its first application, (2) diffusion of the concept to the agendas of othercountries, (3) adoption or rejection of the NDC idea once it is on a government’s agendain a specific country, and (4) sustaining an NDC reform once it is in place. Third, it isimportant to examine whether NDC is adopted fully or partially—that is, to examinethe structural features, coverage, time horizon, and exclusivity of NDC-based schemesin particular countries. Thus we can imagine a continuum of outcomes ranging fromearly “full” adoption of NDC-based reform to partial and/or later adoption, to consid-eration and rejection of NDC-based reforms, or to the issue never even making it ontothe agenda, as shown in table 14.3. (Of course, countries may shift over time betweencategories.) Since the NDC “innovation” is now well developed, we will focus on thediffusion of NDC-based reforms and their full or partial adoption or rejection.18 Sus-taining implementation of NDC-based reforms will be considered in the next section ofthe chapter.

LASHED TO THE MAST? THE POLITICS OF NDC PENSION REFORM 357

Pension_ch14.qxd 12/7/05 3:46 PM Page 357

Tab

le 1

4.3.

Pot

enti

al R

elat

ion

ship

s b

etw

een

Str

uct

ura

l Var

iab

les

and

ND

C C

hoi

ce

Con

stra

ints

on

ND

C

Ear

ly “

full”

Par

tial

and

/or

Late

rC

onsi

dera

tion

Nev

er r

each

esad

opti

on a

nd d

iffus

ion

Inno

vati

onad

opti

onno

nexc

lusi

ve a

dopt

ion

adop

tion

but r

ejec

tion

agen

da

Eco

nom

ic/

dem

ogra

ph

icco

nst

rain

tsA

ging

pre

ssur

e

Fisc

al p

ress

ure

Payr

oll t

ax r

ates

Idea

tion

al f

orce

sSt

reng

th o

f dom

es-

tic

forc

es fa

vori

ngm

arke

t-ba

sed

pen

-si

on r

efor

m

+ V

ery

stro

ngd

emog

raph

ic a

ging

pres

sure

s

+ V

ery

high

bud

get

defi

cits

and

deb

t/G

DP

rati

o

+ V

ery

high

pay

roll

tax

rate

s

+ P

olit

ical

forc

esfa

vori

ng s

tate

-fo

cuse

d p

ublic

pen

-si

on s

yste

m a

rest

rong

+ V

ery

stro

ngd

emog

raph

ic a

ging

pres

sure

s

+ H

igh

bud

get

defi

cits

and

deb

t/G

DP

rati

o

+ V

ery

high

pay

roll

tax

rate

s

– Fu

nded

DC

rath

er th

an N

DC

mor

e lik

ely

to b

ead

opte

d w

here

ide-

olog

ical

ly c

onse

rv-

ativ

e fo

rces

are

very

str

ong

+ S

tron

gd

emog

raph

ic a

ging

pres

sure

s

+ F

und

ed D

C li

kely

to p

lay

rela

tive

lyla

rger

rol

e th

anN

DC

in m

ulti

tier

syst

em w

here

bud

-ge

t defi

cits

and

deb

t/G

DP

rati

o ar

elo

w

+ H

igh

payr

oll t

axra

tes

+ F

und

ed D

C li

kely

to p

lay

rela

tive

lyla

rger

rol

e th

anN

DC

in m

ulti

tier

syst

em w

here

ideo

-lo

gica

lly c

onse

rva-

tive

forc

es a

re fa

irly

stro

ng

+ M

oder

ate

but

incr

easi

ngd

emog

raph

ic a

ging

pres

sure

s

+ M

oder

ate

but

incr

easi

ng b

udge

td

efici

ts a

ndd

ebt/

GD

Pra

tio

+ H

igh

or r

isin

gpa

yrol

l tax

rat

es

+ P

arti

es fa

vori

ngco

ntin

ued

sta

tefo

cus

in p

ublic

pen

-si

on s

yste

m g

ain

stre

ngth

aft

erpe

riod

of s

tale

mat

e

+ M

oder

ate

dem

o-gr

aphi

c ag

ing

pres

-su

res

+ D

eclin

ing

bud

get

pres

sure

and

deb

t/G

DP

rati

o

+ W

eak

dem

ogra

phic

agi

ngpr

essu

res

+ L

ow b

udge

td

efici

ts a

ndd

ebt/

GD

Pra

tio

– L

ow p

ayro

ll ta

xra

tes

or n

o pa

yrol

lta

x

+ F

und

ed D

Cra

ther

than

ND

Cm

ore

likel

y to

be

adop

ted

whe

re id

e-ol

ogic

ally

con

serv

-at

ive

forc

es a

reve

ry s

tron

g

Pension_ch14.qxd 12/7/05 3:46 PM Page 358

Part

icip

atio

n in

regi

onal

net

wor

ksw

here

ND

C id

eas

com

mon

Inte

ract

ion

wit

hin

tern

atio

nal fi

nan-

cial

inst

itut

ions

and

othe

r su

pran

atio

nal

orga

niza

tion

s

Pol

icy

feed

bac

ks

Stro

ng e

arni

ngs-

rela

ted

pen

sion

tier

Rep

lace

men

t rat

es

Payr

oll t

ax r

ecor

ds

Not

app

licab

le

Not

app

licab

le

+ S

tron

g ea

rnin

gs-

rela

ted

com

pone

ntin

pen

sion

sys

tem

+ H

igh

repl

acem

ent r

ates

+ H

igh

repl

acem

ent r

ates

+ C

ompl

ete

payr

oll

tax

reco

rds

+ P

arti

cipa

tion

inre

gion

al n

etw

orks

wit

h ea

rlie

rad

opte

rs; e

lites

view

ear

lier

adop

ters

as

peer

coun

trie

s

+ S

upra

nati

onal

inst

itut

ions

: (1)

pres

s fo

r pe

nsio

nex

pend

itur

e re

duc

-ti

ons

and

(2) i

ntro

-d

uce

and

sup

port

ND

C-b

ased

refo

rms

+ S

tron

g ea

rnin

gs-

rela

ted

com

pone

ntin

pen

sion

sys

tem

+ H

igh

repl

acem

ent r

ates

+ H

igh

repl

acem

ent r

ates

+ C

ompl

ete

payr

oll

tax

reco

rds

+ P

arti

cipa

tion

inre

gion

al n

etw

orks

wit

h ea

rlie

rad

opte

rs; e

lites

view

ear

lier

adop

ters

as

peer

coun

trie

s

+ S

upra

nati

onal

inst

itut

ions

: (1)

pres

s fo

r pe

nsio

nex

pend

itur

e re

duc

-ti

ons

and

(2) i

ntro

-d

uce

and

sup

port

ND

C-b

ased

refo

rms

+ M

ix o

f red

istr

ibu-

tion

and

ear

ning

s-re

late

d p

rinc

iple

sin

cur

rent

pub

licpe

nsio

n sy

stem

+ C

ompl

ete

orim

prov

ing

payr

oll

tax

reco

rds

+ C

ount

ry d

oes

not

part

icip

ate

inre

gion

al n

etw

orks

incl

udin

g ea

rly

adop

ters

= R

egio

nal n

etw

ork

effe

ct s

houl

d d

issi

-pa

te a

s N

DC

idea

sar

e fu

lly d

iffu

sed

inte

rnat

iona

lly

+ S

upra

nati

onal

inst

itut

ions

pre

ssfo

r pe

nsio

n ex

pen-

dit

ure

cuts

and

supp

ort N

DC

-ba

sed

ref

orm

s, b

utha

ve li

mit

edba

rgai

ning

leve

rage

+ M

ediu

m r

epla

ce-

men

t rat

es

+ In

com

plet

e bu

tim

prov

ing

payr

oll

tax

reco

rds

+ Su

pran

atio

nal

inst

itutio

ns p

ress

for

pens

ion

expe

n-di

ture

cut

s an

d su

p-po

rt N

DC

-bas

edre

form

s, b

ut h

ave

limite

d ba

rgai

ning

leve

rage

– Fl

at-r

ate

bene

fitin

cur

rent

pub

licpe

nsio

n sc

hem

e

– In

com

plet

e pa

y-ro

ll ta

x re

cord

s

+ C

ount

ry is

outs

ide

regi

onal

netw

orks

of e

arly

ND

C a

dop

ters

= R

egio

nal n

etw

ork

effe

ct s

houl

d d

issi

-pa

te a

s N

DC

idea

sar

e fu

lly d

iffu

sed

inte

rnat

iona

lly

+ L

ow c

onta

ct w

ith

IFIs

– IF

Is s

uppo

rt F

DC

-ba

sed

ref

orm

s on

ly

+ P

rior

ad

opti

on o

fFD

C r

efor

m+

Fla

t-ra

te b

enefi

tin

cur

rent

DB

+ L

ow r

epla

cem

ent

rate

s

– In

com

plet

e or

none

xist

ent p

ayro

llta

x re

cord

s

Pension_ch14.qxd 12/7/05 3:46 PM Page 359

Tab

le 1

4.3.

(con

tin

ued

)

Con

stra

ints

on

ND

C

Ear

ly “

full”

Par

tial

and

/or

Late

rC

onsi

dera

tion

Nev

er r

each

esad

opti

on a

nd d

iffus

ion

Inno

vati

onad

opti

onno

nexc

lusi

ve a

dopt

ion

adop

tion

but r

ejec

tion

agen

da

Pol

itic

al/p

arti

san

con

stra

ints

Mul

tipl

e ve

topo

ints

in p

olit

ical

syst

em

Ava

ilabi

lity

ofca

rtel

izin

g m

echa

-ni

sms

– M

ulti

ple

veto

poin

ts in

pol

itic

alsy

stem

+ S

tron

g po

litic

alm

echa

nism

s av

ail-

able

to o

verc

ome

inte

rest

gro

upop

posi

tion

to lo

sses

resu

ltin

g fr

omN

DC

-bas

ed r

efor

m

– M

ulti

ple

veto

poin

ts in

pol

itic

alsy

stem

+ S

tron

g po

litic

alm

echa

nism

s av

ail-

able

to o

verc

ome

inte

rest

gro

upop

posi

tion

to lo

sses

resu

ltin

g fr

omN

DC

-bas

ed r

efor

m

+ M

ulti

ple

veto

poin

ts in

pol

itic

alsy

stem

+ M

oder

atel

yst

rong

pol

itic

alm

echa

nism

s av

ail-

able

to o

verc

ome

inte

rest

gro

upop

posi

tion

to lo

sses

resu

ltin

g fr

omN

DC

-bas

ed r

efor

m

+ M

ulti

ple

veto

poin

ts in

pol

itic

alsy

stem

+ M

oder

atel

yst

rong

pol

itic

alm

echa

nism

s av

ail-

able

to o

verc

ome

inte

rest

gro

upop

posi

tion

to lo

sses

resu

ltin

g fr

omN

DC

-bas

ed r

efor

m

+ M

ulti

ple

veto

poin

ts in

pol

itic

alsy

stem

+ W

eak

polit

ical

mec

hani

sms

avai

l-ab

le to

ove

rcom

ein

tere

st g

roup

oppo

siti

on to

loss

esre

sult

ing

from

ND

C-b

ased

ref

orm

+ W

eak

or n

onex

is-

tent

pol

itic

al m

ech-

anis

ms

avai

labl

e to

over

com

e in

tere

stgr

oup

oppo

siti

onto

loss

es r

esul

ting

from

ND

C-b

ased

refo

rm

Sour

ce:C

ompi

led

by

auth

ors.

Not

e:+

con

dit

ion

mak

es it

mor

e lik

ely

that

cou

ntry

will

be

in th

is c

ateg

ory;

– c

ond

itio

n m

akes

it le

ss li

kely

that

cou

ntry

will

be

in th

is c

ateg

ory;

= c

ond

itio

n th

at is

like

ly to

beco

me

less

impo

rtan

t as

ND

C in

nova

tion

is d

iffu

sed

; bla

nk c

ells

ind

icat

e no

hyp

othe

size

d r

elat

ions

hip

betw

een

this

con

dit

ion

and

out

com

e ca

tego

ry.

Pension_ch14.qxd 12/7/05 3:46 PM Page 360

Agenda Setting and AdoptionA critical component of any policy reform process is formulating the policy problem insuch a way that the issue achieves agenda status. To Kingdon (1995), policy proposals arelikely to reach and remain on a government’s agenda only if they appear to be broadlycongruent with the values of policy makers and the public, as well as politically feasible,affordable, and likely to make some improvement in a perceived policy problem. Ofcourse, successful coupling of these dimensions is typically the work of a skilled policyentrepreneur. To Orenstein (2000), such “proposal actors” are critical in establishing the“intellectual agenda” of a reform. In addition to putting reform on the political agenda,proposal actors introduce new policy innovations and delimit the feasible range of policyoutcomes for the country.19 Examining structural pension reforms in Eastern Europe andCentral Asia, Orenstein found that where there are fewer, and more like-minded, proposalactors, the possibility for adopting an ambitious structural reform was greatly enhanced.Importantly, however, while incorporating a broader range of interests in the early stagesof reform (such as where disparate interest groups and government ministries advancereform proposals) tends to diminish the magnitude and pace of reform, to the extent thatbroad agreement (or “buy-in”) is achieved during the agenda-setting phase, both theimplementation and the longer-term prospects for sustainability are enhanced.20 Accord-ingly, we examine in the next sections the key factors shaping whether and to what extentcountries move toward NDC pension reform. These include (1) whether the problem orchallenge of structural pension reform is brought onto the national agenda and how theproblem is defined by key actors, (2) whether the specific policy alternative of NDC pensionreform is one of the options considered by policy makers, and (3) how policy feedbacks fromexisting pension regimes as well as (4) the structure of political institutions shape both thealternatives considered and the prospects for NDC adoption.

In examining the first factor, we look at the extent to which governments are pressed toreform state pension schemes by varying degrees of demographic change, budgetary con-straints, and macroeconomic pressures. Second, we discuss how exposure to, and henceadoption of, NDC ideas are influenced by the strength of various domestic ideologicalgroupings as well as countries’ interaction with supranational institutions such as theEuropean Union and the World Bank. In looking at the third factor, we examine how feed-backs from prior policy choices may make considering and adopting NDC-based reformsmore or less likely, such as by shaping how the problem and its feasible solutions are per-ceived, and by influencing the political coalitions that have developed around currentpolicies. Last, we examine how the structure of political institutions and political competi-tion affect both the political advantages and costs associated with NDC systems, andhence the likely barriers to policy change.21

Table 14.3 outlines hypothesized relationships between specific variables and severalpossible outcomes (for example, first innovation with NDC, early adoption, partial adop-tion, consideration and rejection of NDC, NDC never reaching agenda), while table 14.4develops an informal “scorecard” of the relationship between causes and outcomes.Specifically, the table highlights the hypothesized relationship between our key variablesand the outcomes achieved by several countries with respect to NDC reform (for example,with Sweden as innovator, Italy as a partial adopter of NDC, Uruguay as a country thatrejected NDC in favor of a mix of DB and DC, and the United States representing a coun-try where NDC has not yet reached the agenda).

Economic-Demographic Pressures for System ChangeThe wave of structural pension reforms that began in the 1980s and swelled in the 1990shas been widely attributed to significant demographic and economic changes, which

LASHED TO THE MAST? THE POLITICS OF NDC PENSION REFORM 361

Pension_ch14.qxd 12/7/05 3:46 PM Page 361

Tab

le 1

4.4.

Cou

ntr

y C

har

acte

rist

ics

and

ND

C R

efor

m O

utc

omes

Cou

ntry

Swed

enIt

aly

Ger

man

yU

rugu

ayU

nite

d St

ates

Out

com

e

Eco

nom

ic/d

emog

rap

hic

con

stra

ints

Agi

ng p

ress

ure

(% p

opul

atio

n 65

+in

par

enth

eses

)

Fisc

al p

ress

ure

Payr

oll t

ax r

ates

(tot

al p

ayro

ll ta

xra

tes

in p

aren

thes

es)

Idea

tion

al f

orce

sSt

reng

th o

f dom

esti

c fo

rces

favo

r-in

g m

arke

t-ba

sed

pen

sion

ref

orm

Inte

ract

ion

wit

h IF

Is a

nd o

ther

supr

anat

iona

l org

aniz

atio

ns

Part

icip

atio

n in

reg

iona

l net

wor

ksw

here

ND

C id

eas

are

com

mon

Pol

icy

feed

bac

ks

Stro

ng e

arni

ngs-

rela

ted

pen

sion

tier

Rep

lace

men

t rat

es

Com

plet

e pa

yrol

l tax

rec

ord

s

Pol

itic

al/p

arti

san

con

stra

ints

Mul

tipl

e ve

to p

oint

s in

pol

itic

alsy

stem

?

Mec

hani

sms

for

over

com

ing

pol-

icy

grid

lock

?

Full

ND

C s

yste

mad

opte

d

Ver

y hi

gh (1

7.4%

)

Ver

y st

rong

inea

rly

1990

s

Hig

h (2

6.09

%)

Wea

k

No

Bec

ame

hub

ofne

twor

k

Yes

Ver

y hi

gh

Yes

Wea

k

Stro

ng

Par

tial

ND

C s

yste

mad

opte

d w

ith

long

pha

se-i

n

Ver

y hi

gh (1

7.8%

)

Ver

y st

rong

Ver

y hi

gh (4

1.11

%)

Wea

k

No

inte

ract

ion

wit

h IF

Is,

but E

urop

ean

Uni

onpr

essu

re to

red

uce

pen-

sion

spe

ndin

g

Yes

Yes

Ver

y hi

gh

Yes

Stro

ng

Mix

ed

Ele

men

ts o

f ND

C a

dopt

ed,

retr

acte

d, a

nd r

eado

pted

Ver

y hi

gh (1

6.1%

)

Ver

y st

rong

Ver

y hi

gh (4

0.91

%)

Fair

ly w

eak

No

inte

ract

ion

wit

h IF

Is,

but E

urop

ean

Uni

onpr

essu

re to

red

uce

pen-

sion

spe

ndin

g

Yes

Yes

Ver

y hi

gh

Yes

Wea

k

Dec

linin

g

Mix

ed D

B-f

unde

d D

Cre

form

Hig

h (1

2.9%

)

Ver

y st

rong

Ver

y hi

gh (3

5.5%

)

Wea

k

Yes,

wit

h In

ter-

Am

eri-

can

Dev

elop

men

tB

ank,

whi

ch p

rese

nted

ND

C o

ptio

n in

199

2.

No

Yes

Hig

h

No

Stro

ng

Wea

k

ND

C n

ot o

n ag

enda

Hig

h (1

2.3%

)

Mod

erat

e

Mod

erat

e (2

2.7%

)

Stro

ng

No

No

Yes

Mod

erat

e

Yes

Stro

ng

Wea

k

Sour

ce:F

or d

ata

on a

ging

and

pay

roll

tax

rate

s: U

.S. S

ocia

l Sec

urit

y A

dm

inis

trat

ion,

Soc

ial S

ecur

ity

Pro

gram

s T

hrou

ghou

t the

Wor

ld, m