How Geographical Distances and Religiosity Determining Access to Baitul Maal wat Tamwil ?

16

How Geographical Distances and Risk Preference Determine Access to Islamic MFI Davy Hendri Lecturer of Islamic Economics at FEBI Dept. IAIN Imam Bonjol Padang, Researcher at POCIN Insitute of Economics [email protected] www.davyhendri.blogspot.com

-

Upload

independent -

Category

Documents

-

view

7 -

download

0

Transcript of How Geographical Distances and Religiosity Determining Access to Baitul Maal wat Tamwil ?

How Geographical Distances and Risk Preference Determine Access to Islamic MFI

Davy HendriLecturer of Islamic Economics at FEBI Dept. IAIN Imam Bonjol Padang,

Researcher at POCIN Insitute of [email protected]

www.davyhendri.blogspot.com

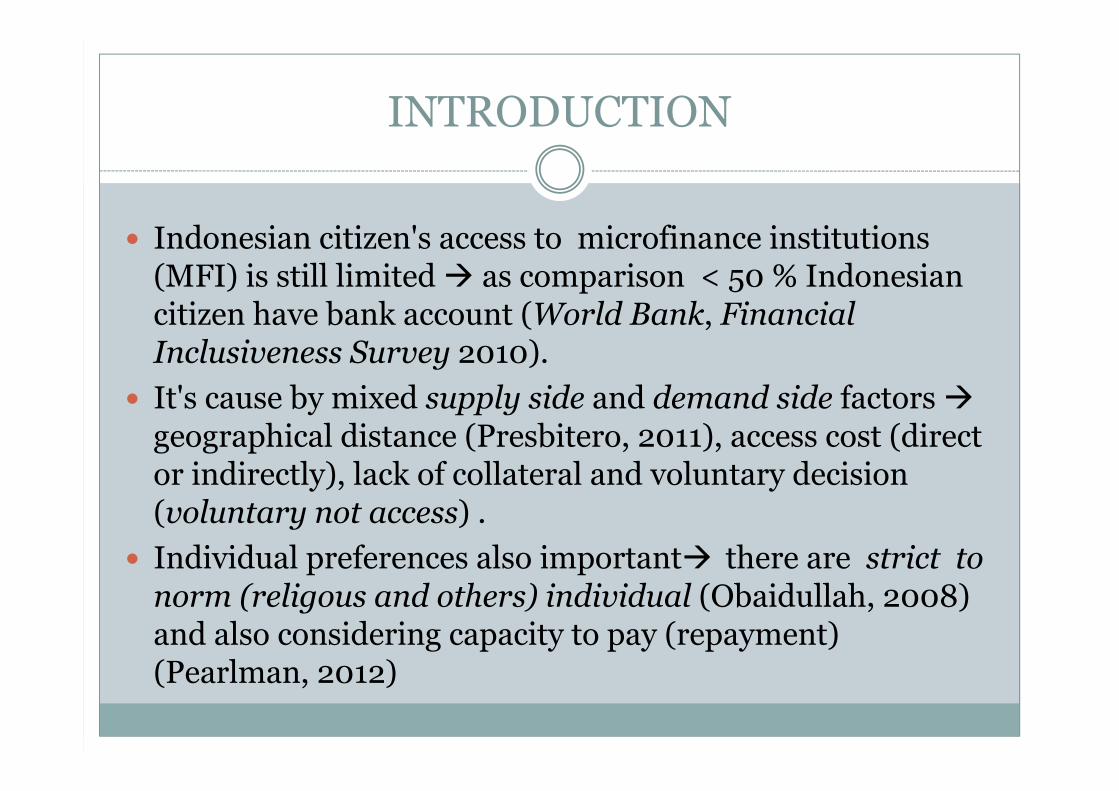

INTRODUCTION

Indonesian citizen's access to microfinance institutions (MFI) is still limited as comparison < 50 % Indonesian citizen have bank account (World Bank, Financial Inclusiveness Survey 2010).

It's cause by mixed supply side and demand side factors geographical distance (Presbitero, 2011), access cost (direct or indirectly), lack of collateral and voluntary decision (voluntary not access) .

Individual preferences also important there are strict to norm (religous and others) individual (Obaidullah, 2008) and also considering capacity to pay (repayment) (Pearlman, 2012)

Intro…Cont

With the special characteristics of Islamic microfinance contracts that do not charge interest on the loan expected to be of interest to individuals who are more religious

Financing (not loan) based on real asset suitable for risk-averse individaul

The fact shows that although being the majority of the population, but their access to Islamic MFI is still limited

Problem Formulation

If the distance constraints is a major factor then of religiosity factor will not be able to provide information on access variation. Meanwhile, if the factor of religiosity that the main constraint then wherever Islamic MFI’s location, all Muslims will have the same access to it. should be no need for Islamic MFI

Whether individual-based or group-based lending, religiosity is an important indicator of potential borrowers who are considered to be a proxy for social collateral (replaces physical collateral) as well as reduce the potential for moral hazard (Berggren, 2014) but if group consist heterogenous risk-preference individual tend to adverse risk-averse members

So, what is more dominant factors constrain access to this institution?

Research Questions

Do borrowers of Islamic MFI more religous than borrowers of conventional MFI ?

Do both borrower type revealed different risk-preference?

Do another socio-economics attribute matter in determining access decision to islamic MFI ?

Literature Review

Pearlman (2011) found that people who still face problem with his/her financial risk management if dampering by external shock tend not to access to MFI voluntary

Dunia (2013), in his master thesis which comparing Jordanian Islamic MFI vs conv't MFI found surprisingly result that borrower of Islamic MFI tend to risk-lovers

Research Method

The main dataset for analysis is the Indonesian Family Life Survey (IFLS)-IV 2007. Based on a sample representing 83% of Indonesia's population includes 29 060 adults in 12 688 households living in 312 communities in 13 provinces in Indonesia. In the book community characteristics and facilities (03 books section G) provided the question about people's habits communities (rural/urban villages) in saving/borrowing in Islamic MFI whose location is divided into two, namely in the community (access to) and outside the community (access to outside).

Meanwhile, in the books of individual and household characteristics are also available the question of religion and the status of individual religiosity in every community (book section 3A TR). Therefore, the status of access is only available at the community level, then the characteristic determinant on an individual level as religiusititas, risk preferences, social capital and the level of household characteristics such as the ownership of the business, with the exception of expenditure per capita, diaggregasi to the community level.

Estimation strategic

Data aggregation Aggregation into community level is done in 2 phases : First, add the data at the individual and household levels,

both in numerical and binary into a community level. Second, followed by making the proportion (ratio) by

dividing this figure by the number of population in the community. So that all relevant data is the data BMT consumer agencies such as the ratio of the proportion of the number of Muslims in a community (village / village), the proportion of Muslims are religious in a community and so on

Estimation strategic..contMeasurement of Risk-preference and Religiosity

Variabel risk-preference dikonstruk melalui serangkaian (1 set) pertanyaan khusus merujuk kepada kuisioner IFLS (Indonesian Family Live Survey). Dua pertanyaan preferensi risiko yang dianalisis adalah pertanyaan SI21 dan SI22 dalam modul individu/rumah tangga pada buku 2A. Jika pilihan responden dalm pertanyaan SI21 adalah C dan dilakukan uji konsistensi melalui cross-check jawaban dari pertanyaan SI22. Jika responden tadi kemudian juga menjawab C pada pertanyaan SI22 maka dia dianggap memiliko prefrensi menghindari resiko (risk-averse). Nilai 1 adalah kode untuk respon menghindari risiko, dan nilai-nilai dari 1 dikodekan untuk lainnya (biak risk-lover maupun risk-neutral).

Variabel religiusitas pada buku 3A seksi TR pada pertanyaan TR11, responden juga diminta untuk mengevaluasi religiusitas sendiri dari ukuran 4 skala negatif mulai dari ; "1. sangat taat", "2. taat", "3. agak taat" dan "4. tidak taat". Sesuai dengan tujuan penelitian ini maka hanya variasi religiusitas responden muslim yang akan menjadi regressors utama

Estimation strategic...cont

Data analyzed by using Probit regression :

The variable is the vector of aggregate characteristics of individuals in the community. While it is a vector of aggregate characteristics of households in the community. While it is a vector of variables at the level of the community itself. All variables on the right hand side (RHS) above model is the same for both models. The difference lies in the variable on the left side (LHS), the dependent variable.

In the first model, the access to BMT if located in a community that is worth 1 if yes and 0 if not. While the second model, the access to BMT if located outside of the community that is worth 1 if yes and 0 if not.

ihllihiii LHXP

iX

hiH

liL

Result and Discussion

Islamic MFI at glance distributed rather evenly in urban areas distributed rather evenly in the community

(samples) are relatively better off than the average total population

Result and Discussion

-.10

.1.2

.3.4

Pr(T

otka

ses)

.4 5.4 10.4 15.4 20.4 25.4 30.4 35.4 40.4 45.4jarak

Predictive Margins with 95% CIs

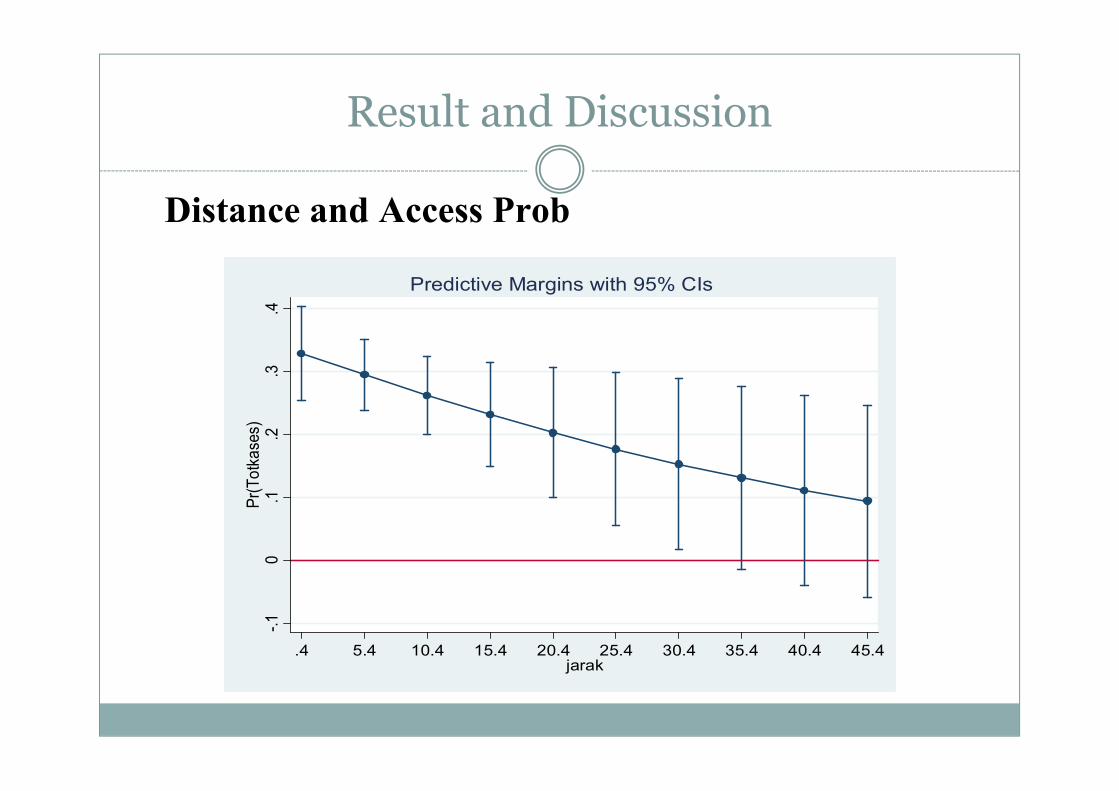

Distance and Access Prob

Result...cont

0.2

.4.6

.81

Pr(O

utak

ses)

.4 .45 .5 .55 .6 .65 .7 .75 .8 .85 .9 .95 1riskpop

Predictive Margins with 95% CIs

Risk-averse and Access Prob

Conclution

Community count more on MFI competition rather than geographical distance

There are ambiguity in relationship between risk preference and access type to Islamic MFI

There are positive and negative impact of their behaviour change

Religious status is very important to determine the status of access to BMT (religiousity is matters).

Policy Implication

Islamic MFI expansion strategy should refer to the findings of the substitution relationship between BMT access to social capital and the second pattern of relationships, substitute and complementary, between Islamic MFI with other conv't MFI.

Gov't can encourage all the stakeholders, namely BMT, communities and other MFI can do mutually beneficial partnership with the communities themselves in area where Islamic MFI located and with conv't MFI on blank-spot area, the location on where the financial institution is not available at all

TERIMAKASIH