HKEX Investor Presentation - HKEX Group

50

HKEX Investor Presentation Investor Relations Apr, 2021

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of HKEX Investor Presentation - HKEX Group

HKEX Investor Presentation

Investor Relations

Apr, 2021

Disclaimer

The information contained in this document is for general informational purposes only and does not constitute an offer, solicitation, invitation or

recommendation to subscribe for or purchase any securities, or other products or to provide any investment advice or service of any kind. This

document is solely intended for distribution to and use by professional investors. This document is not directed at, and is not intended for

distribution to or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or

which would subject Hong Kong Exchanges and Clearing Limited (“HKEX”) to any registration requirement within such jurisdiction or country.

This document contains forward-looking statements which are based on the current expectations, estimates, projections, beliefs and

assumptions of HKEX about the businesses and the markets in which it and its subsidiaries operate. These forward-looking statements are not

guarantees of future performance and are subject to market risk, uncertainties and factors beyond the control of HKEX. Therefore, actual

outcomes and returns may differ materially from the assumptions made and the statements contained in this document.

Where this document refers to Shanghai-Hong Kong Stock Connect and/or Shenzhen-Hong Kong Stock Connect (together, the “Stock Connect”

programs), please note that currently, access to northbound trading is only available to intermediaries licensed or regulated in Hong Kong;

southbound trading is only available to intermediaries licensed or regulated in Mainland China. Direct access to the Stock Connect is not

available outside Hong Kong and Mainland China.

Where this document refers to Bond Connect, please note that currently, access to northbound trading is only available to foreign investors that

are able to trade onshore bonds on the China Foreign Exchange Trade System & National Interbank Funding Centre.

Although the information contained in this document is obtained or compiled from sources believed to be reliable, HKEX does not guarantee the

accuracy, validity, timeliness or completeness of the information or data for any particular purpose, and shall not accept any responsibility for, or

be liable for, errors, omissions or other inaccuracies in the information or for the consequences thereof. The information set out in this document

is provided on an “as is” and “as available” basis and may be amended or changed. It is not a substitute for professional advice which takes

account of your specific circumstances and nothing in this document constitutes legal advice. HKEX shall not be responsible or liable for any loss

or damage, directly or indirectly, arising from the use of or reliance upon any information provided in this document.

Agenda

01 | Key Performance and Growth Drivers

02 | Group Financial Update

03 | Strategic Plan 2019-2021

04 | China Connectivity

05 | Appendix

HKEX – leading vertically integrated exchange group

Note: Figures for FY2020 (unless otherwise stated)

1. From 2009 to 2020

2. Corporate items accounted for 5% of total revenue in 2020 and are not shown on this slide.

HKEX GROUP

Leading diversified exchange group in the Asian Time Zone

HK’s only exchange group

World’s leading IPO venue – ranked #1 in 7 of the past 12 years1

Pioneer in Mainland capital markets connectivity

London Metal Exchange – globally leading base metals exchange

REVENUE:

HK$16.3bn

EBITDA:

HK$12.3bn

PAT:

HK$9.4bn

EPS:

HK$7.49

DPS:

HK$6.71(90% payout)

Cash EquitiesEquity & Financial

DerivativesCommodities

TechnologyPost Trade

Primary & Secondary Markets Post Trade Market Access

2020

Revenue

Share2

26% 17% 7%40%

5%

Market Data

FY2019

REVENUE:

HK$ 19.2bn

EBITDA:

HK$14.6bn

PAT:

HK$11.5bn

EPS:

HK$9.11

DPS:

HK$8.17(90% payout)

FY2020

Financials

4

Q1 2021 key highlights

1 | Financial Performance

• Record quarterly revenue and other income of HK$5,956mn (+49% YoY) with core

business revenue up by 35% YoY, driven by record headline ADT

• Record quarterly Stock Connect revenue and other income of HK$737mn (+82% YoY)

• Net investment income of HK$418mn (Q1 2020: HK$47mn loss)

• Profit attributable to shareholders at record quarterly high of HK$3,840mn (+70% YoY)

2 | Business and Strategy

• Strong IPO market – #3 globally by IPO funds raised (HK$137bn, more than 9x

Q1 2020)

• Published a consultation paper on proposals to enhance and streamline listing regime

for overseas issuers

• Strong Connect schemes performance – record high ADT across all platforms

• Ongoing market microstructure, technology enhancements and product launches

• Appointment of new CEO-designate, Nicolas Aguzin

• Published a consultation paper in April on proposed enhancements to the Corporate

Governance Code and related Listing Rules

5

21.830.0 33.9

25.216.4

36.6 40.151.6

17

110 122138 126

174

218183

154

0

50

100

150

200

250

0

20

40

60

80

100

120

2021

Core business well-positioned for organic and structural growth

Source: HKEX, Dealogic.

1. Shanghai-HK and Shenzhen-HK Stock Connect was launched in Nov 2014 and Dec 2016 respectively.

2. Buy + Sell ADT.

3. 2021 YTD as of Mar 2021.

Broad Product Ecosystem Attracting Diverse Mainland and International Investor Base

Transformational Growth from China’s Opening1IPOs Driving ADT Growth

Southbound Connect

Jumbo IPOs

Global Investors

Risk Management

Algo / Quant Investors

After-hours Trading

+10.8% +11.4%

Futures OptionsCAGR

CAGR

+72.3% +51.6%

Northbound ADT2

(RMB billion)

Southbound ADT2

(HK$ billion)

CAGR CAGR

Total IPO funds raised (US$ billion)

# of IPOs

New Economy Listing

Reforms

• Biotech

• WVR

• Secondary Listings

Strong Pipeline of

Mainland and

International Listings

Global fundraising rank Continuing Portfolio

Diversification

A-share Inclusion in

Global Benchmarks

SB Connect Limited by

Investor Eligibility Cap

Securities ADT

(HK$ billion)

Derivatives ADV

(’000 contracts)

A

B C

Focus on Revenue Growth and Cost DisciplineD

3 3

3 3

2016

2013

2018

2014

2017

2015

2019

Global fundraising rank

2020

3

63 69

106

6788

10787

129

2242015

2013

2020

2014

2019

2016

2017

2018

2021

2013

2014

2015

2016

2017

2018

2019

2020

2021

533 577

769 762870

1,2041,069

1,133

1,410

#3 #2 #1 #1 #3 #1 #1 #2 #3

6 5 1020

42

91

127

2018

2019

2017

2015

2021

2016

2020

3 410

13 11

24

61

2020

2019

2015

2016

2017

2018

2021

32

6

Diverse international investor base attracted to broad product ecosystem

1. HKEX signed a licence agreement with MSCI to introduce futures contracts on the MSCI China A Index, subject to regulatory approval and market conditions.

2. See next pages for details

A

Short

Selling

Stock

Options Stock

Futures

DWs

CBBCs

Index

Futures

OTC

ETPs Currency

Futures

Stock

Connect

Bond

Connect

A-share

Derivatives1

Stocks

Recent initiatives and future focus

Market microstructure enhancements: leading to better price

discovery and trade efficiency

Targeted marketing and client support: onboarding 10+ clients

each year

Incentives: driving increased volumes

Product cross-selling: creating arbitrage opportunities

Algo / Quant Participation in Cash Market

Due to…

• Presence of stamp duty

• Minimal high frequency trading

• Single market structure

Relatively low(circa. 10-20% of ADT)

Algo / Quant Participation in Derivatives Market

Relatively high(circa. 40-60% of ADV)

Driven by…

• No stamp duty

• Market maker participation

• Capital efficiency

Asia & EM

Index Futures2

7

New MSCI Suite – growing product ecosystem to connect global trades

1. All contracts denominated in USD unless otherwise specified

2. Started trading in HKEX since 2018

A

Key Dynamics

Expanding our product UNDERLYING

Licenced a suite of MSCI indexes in Asia and Emerging

Markets to introduce 40+ futures and options contracts

Broadening and deepening LIQUIDITY

Allow investors to Trade Asia, in Asia

Complement existing HSI and HSCEI index futures

Enhancing our COMPETITIVENESS

Better capital efficiency

Creating a competitive one-stop shop for China and Asian

exposures

Reinforces Hong Kong’s role as the leading global market in the Asian Time Zone, with the broadest suite of MSCI

derivatives products

NTRSingle country

Price ReturnSingle country

Options

MSCI Taiwan

MSCI Australia

MSCI China Free

MSCI Hong Kong

MSCI India

MSCI Indonesia

MSCI Japan

MSCI Japan (JPY)

MSCI Malaysia

MSCI New Zealand

MSCI Philippines

MSCI Singapore

MSCI Singapore Free

MSCI Taiwan

MSCI Taiwan 25/50

MSCI Thailand

MSCI Vietnam

Regional

MSCI AC Asia ex Japan2

MSCI EM Asia

MSCI EM Asia ex China

MSCI EM Asia ex Korea

MSCI EM EMEA

MSCI EM ex China

MSCI EM ex Korea

MSCI EM LatAm

MSCI Emerging Markets

MSCI Pacific

MSCI Pacific ex Japan

Regional

MSCI China Free

MSCI India

MSCI Indonesia

MSCI Japan (JPY)

MSCI Malaysia

MSCI Philippines

MSCI Taiwan 25/50

MSCI Thailand

MSCI Singapore Free

(SGD)

MSCI Taiwan

MSCI Vietnam

MSCI Emerging Markets

HKEX MSCI Product Suite1

MSCI China Free

8

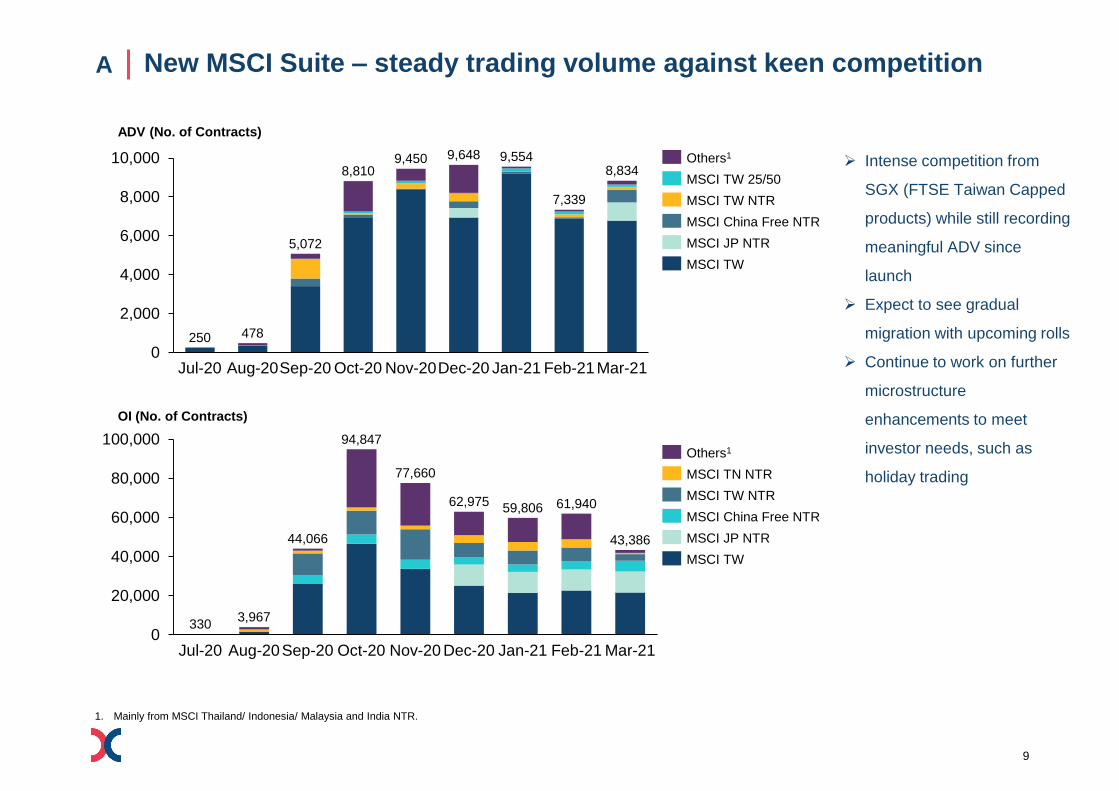

New MSCI Suite – steady trading volume against keen competitionA

0

2,000

4,000

6,000

8,000

10,000

Aug-20Jul-20

478250

Sep-20 Oct-20 Nov-20Dec-20 Jan-21

5,072

8,8109,450 9,648 9,554

8,834

Feb-21Mar-21

7,339

MSCI JP NTR

Others1

MSCI TW 25/50

MSCI TW NTR

MSCI China Free NTR

MSCI TW

0

20,000

40,000

60,000

80,000

100,000

330

Jul-20 Jan-21Aug-20 Nov-20Oct-20Sep-20 Dec-20

3,967

44,066

94,847

Mar-21

77,660

62,97559,806

Feb-21

61,940

43,386

Others1

MSCI TN NTR

MSCI JP NTR

MSCI TW NTR

MSCI China Free NTR

MSCI TW

ADV (No. of Contracts)

Intense competition from

SGX (FTSE Taiwan Capped

products) while still recording

meaningful ADV since

launch

Expect to see gradual

migration with upcoming rolls

Continue to work on further

microstructure

enhancements to meet

investor needs, such as

holiday trading

OI (No. of Contracts)

1. Mainly from MSCI Thailand/ Indonesia/ Malaysia and India NTR.

9

No. of IPO

– Total

– New Economy1

– Biotech2

IPO Funds Raised by Segments

Source: HKEX, as of Mar 2021.

1. Include Non-18A Biotech companies

2. Only include Chapter 18A Biotech companies

IPO Funds Raised

(HK$ bn)

2021 Jan – March Fundraising Summary

174 218 183

14 27 38

0 5 9

IPO Funds Raised

(#3 globally)18 New Economy

& Biotech Companies Listed…

…raising

HK$129.2bn

+846% YoY +3,061% YoY

HK$136.6bn

84.1 145.5 159.6 142.7

7.5

18.5 16.1 40.4

7.2

44.4

124.0 138.5

217.0

121.9

0

100

200

300

400

2017 2018 2019 2020 2021

Others Biotech New Economy

128.5

288.0

314.2

154

36

14

400.2

Strongly performing IPO market boosted by new economy issuers and

secondary listings

B

World’s second-largest fund raising hub for biotech

companies

HKEX was delighted to host its first ever Southeast Asia

Forum on 3 Dec 2020

Dialogues with the Biotech Community with PhiRDA -

attracted 292,000+ views

HKEX Biotech Summit 2020 (Virtual) – received

extensive interest from scientists, biotech entrepreneurs,

investors, technology experts and policymakers

Ongoing listing reforms

Shortening of IPO settlement cycle

Enhancing listing regime for overseas issuers

Enhancing the bookbuilding and price discovery aspects

of IPOs (cornerstone investors, pricing flexibility,

clawback mechanism)

136.6

32

15

3

10

% of respective ADT

% of single stock option ADV

Source: HKEX, as of Mar 2021. S – Secondary listings; W – Weighted Voting Rights; H – H shares

In 2021, 24% of cash ADT and 22% of stock option ADV is contributed by the top 31 IPOs since 2018

31 Jumbo IPOs > US$1bn (HK$7.8bn) since Jan 2018

Rank Company name IPO date IPO size

(HK$bn)

1 Alibaba Group - SW 26/11/2019 101.20

2 China Tower - H 08/08/2018 58.80

3 Kuaishou Technology - W 05/02/2021 48.30

4 Budweiser Brewing APAC 30/09/2019 45.08

5 Xiaomi Corporation - W 09/07/2018 42.61

6 JD.COM - SW 18/06/2020 34.56

7 Meituan Dianping - W 20/09/2018 33.14

8 JD Health International 08/12/2020 31.00

9 Netease - S 11/06/2020 24.26

10 Baidu - SW 23/03/2021 23.94

11 Bilibili - SW 29/03/2021 23.23

12 Yum China - S 10/09/2020 17.27

13 China Bohai Bank - H 16/07/2020 15.90

14 GDS - SW 02/11/2020 14.88

15 Evergrande Property 02/12/2020 14.27

16 ESR Cayman Ltd. 01/11/2019 14.06

17 Tigermed - H 07/08/2020 12.31

18 China Resources Mixc Lifestyle 09/12/2020 12.27

19 New Oriental - S 09/11/2020 11.65

20 Blue Moon Group Holdings Limited 16/12/2020 11.31

21 ZTO Express - SW 29/09/2020 11.28

22 Shimao Services 30/10/2020 9.95

23 Nongfu Spring - H 08/09/2020 9.60

24 Shenwan Hongyuan - H 26/04/2019 9.09

25 Hansoh Pharmaceutical Group 14/06/2019 9.04

26 Topsports International 10/10/2019 9.01

27 Ping An Healthcare and Technology 04/05/2018 8.77

28 Jiangxi Bank - H 26/06/2018 8.60

29 WuXi AppTec - H 13/12/2018 8.28

30 Smoore 10/07/2020 8.19

31 Sunac Service 19/11/2020 8.00

Rising contribution to volumes from Jumbo IPOs

3.0%

10.5%

7.3%

24.3%

15.6%

3.3

9.2

31.4

53.5

2018 2019 2020 2021 YTD

Cash Market ADT (HK$ bn) contributed

by the Jumbo IPOs and related Structured Products ADT

1.3%

3.0%

23.9%

21.5%

Jumbo IPOs contributing to increased trading activityB

11

Alibaba, NetEase and JD.com secondary listings contributed to ~6% of Hong Kong market’s ADT in Q1 2021, with a clear

trend of ADR conversion to HK shares

Source: HKEX, FactSet, as of 31 Mar 2021 (quarterly update)

Note: Alibaba is listed on NYSE, while NetEase and JD.com are listed on NASDAQ (figures as bold)

1. Based on total CCASS balance deducting the balance of main custodian bank as reference

ADT/ADV in HKEXAlibaba,

NetEase & JDMarket Total %

Equities + DWs + CBBCs

(HK$ bn)13.7 224.4 6.1

SSO

(Volume, ‘000)43.8 826.7 5.3

Strong Boost to HK Markets Trading

ADR conversion to HK shares

Number of Hong Kong (freely traded) shares as % of total issued shares globally

Alibaba NetEase JD.com

HKEX Trading Share – YTD Mar 2021

26/11/2019

(IPO)

31/03/2021

20.7%

2.5%

726%

11/06/2020

(IPO)

8.6%

31/03/2021

4.5%

90%

18/06/2020

(IPO)

31/03/2021

14.2%

5.1%

178%

Continuous trading volume migration and ADR conversion from

secondary listings

B

% of

TradingAlibaba NetEase JD.com

SEHK 18.3% 27.3% 20.8%

FINRA ADF 31.4% 21.8% 25.8%

NYSE 15.2% 1.2% 1.7%

NASDAQ 10.1% 29.0% 26.0%

NYSE Arca 8.0% 6.9% 8.3%

Other US

Exchanges17.1% 13.7% 17.4%

12

0

100

200

300

400

500

600

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Transformational growth from China’s opening

Source: HKEX, Bond Connect, ChinaBond, SCH;

1. Shanghai-HK and Shenzhen-HK Stock Connect was launched in Nov 2014 and Dec 2016 respectively.

2. Foreign participation in CIBM was first allowed in 2010 when the PBOC rolled out a Pilot Scheme to allow foreign financial institutions to invest in CIBM.

3. Data as of Mar 31st, 2021.

Benefiting from the increased capital flow into and out of Mainland China,

in particular inbound flows driven by international index inclusions

C

Stock Connect1 Bond Connect

+79.7%+78.7%

Northbound(RMB billion)

Southbound(HK$ billion)

Portfolio Value Portfolio Value

Total Foreign Participation in CIBM2

(RMB billion)

Bond Connect

launch

Foreign Holdings in Chinese Bonds

(US$ bn)

Foreign

Ownership (%)

US$547bn

3.4%

Continuing portfolio diversification by Mainland and

international investors

Inclusion of A shares into major global benchmarks

Increasing selection of new economy companies in

Southbound Stock Connect

Inclusion of Mainland bonds into global fixed income

indices

Easier access to the Mainland bond market via more

trading platforms

Increasing use of RMB globally and need to reinvest

into RMB assets

Investors

Onboarded

=2,450

YTD ADT

RMB25.3bn

CAGRCAGR

333

125 186

531668

1,429

2,340 2,360

2015

2021

2018

2017

2016

2019

2020

115

364

927789

1,138

2,097

2,550

2018

2015

2017

2016

2019

2020

2021

13

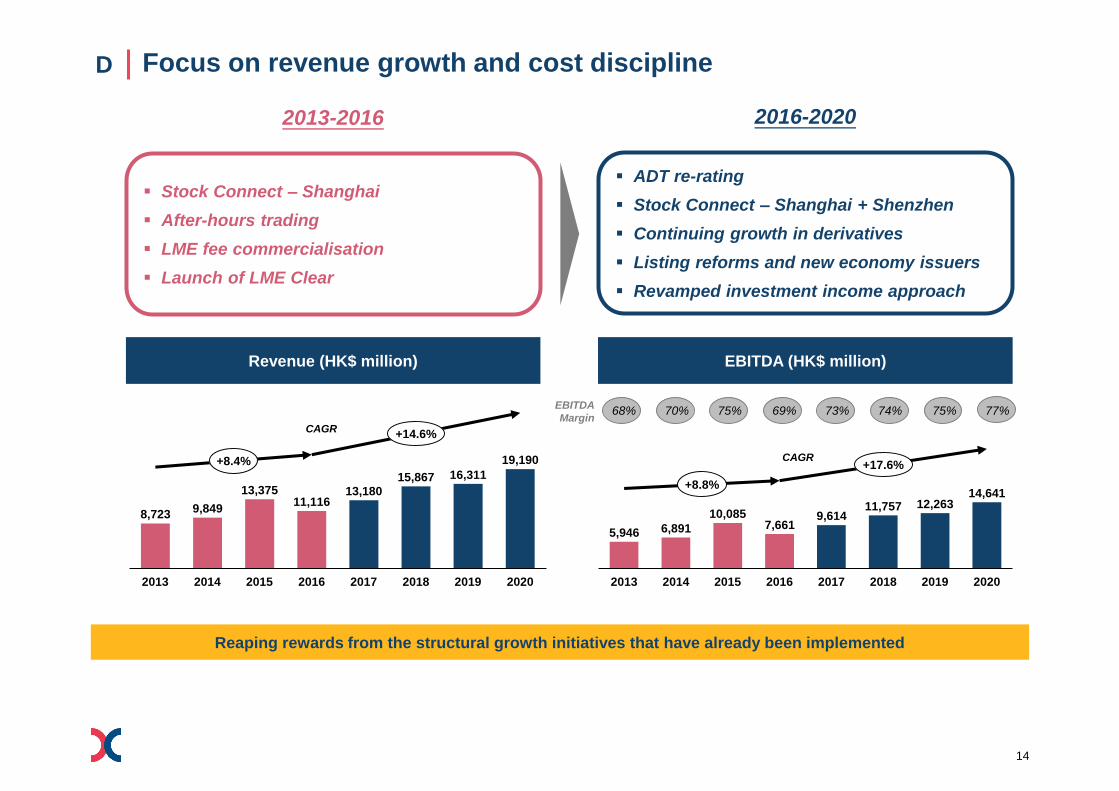

Focus on revenue growth and cost discipline

Reaping rewards from the structural growth initiatives that have already been implemented

D

Revenue (HK$ million) EBITDA (HK$ million)

2013-2016 2016-2020

Stock Connect – Shanghai

After-hours trading

LME fee commercialisation

Launch of LME Clear

ADT re-rating

Stock Connect – Shanghai + Shenzhen

Continuing growth in derivatives

Listing reforms and new economy issuers

Revamped investment income approach

CAGR

EBITDA

Margin

CAGR

8,7239,849

13,37511,116

13,18015,867 16,311

19,190

201820142013 201920162015 20202017

+8.4%

+14.6%

5,946 6,891

10,0857,661

9,61411,757 12,263

14,641

20192013 20172014 2015 2016 2018 2020

+8.8%

+17.6%

68% 70% 75% 69% 73% 74% 75% 77%

14

Focus on revenue growth and cost discipline

Increased operating leverage from revenue growth, delivered by structural drivers combined with opex discipline

D

Operating Expenses (HK$ million) Profit Attributable to Shareholders (HK$ million)

2013-2016 2016-2020

Investment in growth initiatives to capture

China opportunities

Upgrading core infrastructure to strengthen

technological foundation

Reaping rewards of past investments and

benefiting from operating leverage

Increased cost discipline

Investment in automation and operational

efficiency

CAGR

Net Profit

Margin

CAGR

2,777 2,9583,290 3,455 3,566

4,110 4,0484,549

20162013 2014 2015 2017 20192018 2020

+7.6%

+7.1%

4,552 5,165

7,9565,769

7,4049,312 9,391

11,505

2013 20172014 2015 20192016 2018 2020

+8.2%

+18.8%

1. If the impact of HKFRS 16 were excluded, 2019 Operating Expense would be HK$4,362 million and the 2016-2019 CAGR would be 8.1%.

52% 52% 59% 52% 56% 59% 58% 60%

1

15

Sustainability is at our core, and is business critical

Progressing our financial markets and communities for the benefit of all

OUR MARKETS

Swift COVID-19 response with timely disclosure &

AGM guidance and communications

Ongoing promotion of ESG standards with the

updated ESG Guide, new e-Learning series and

updated ESG guidance letter and active

involvement in global ESG standardisation

engagement

Promoting sustainable and green finance with the

launch of STAGE and the LME’s sustainability plan

Enhancing Corporate Governance Code -

published a consultation paper in April outlining

proposed enhancement to corporate governance

standards among listed issuers in Hong Kong,

specifically in the areas of director independence,

diversity and ESG

OUR PEOPLE

Official launch of HKEX Foundation with the

flagship $20m Charity Partnership Programme,

$10m COVID-19 emergency relief donations and

HKEX University Scholarship, as well as other

ongoing donations and e-volunteering activities for

the community

Supporting employees’ wellbeing across the

Group, especially during COVID-19

Championing workplace diversity through internal

training, advocacy and partnership with

professional groups, universities and NGOs

OUR OPERATIONS

Engaged the markets in adopting sustainable

business practices, e.g. e-IPO regime, LME

passport

Internal evaluations of board performance

Ongoing enhancement of employees’ awareness of

our legal and compliance obligations

Implementation of HKEX Future Workplace and

digitalisation of internal workflows to improve

efficiency and reduce paper consumption

TALENT ENGAGEMENTRISK CULTUREREPUTATION

Recognised as a sustainability leader with the constituent status in various sustainability indexes,

e.g., Dow Jones Sustainability Indexes, FTSE4Good, Hang Seng Corporate Sustainability Index series

16

Agenda

01 | Key Performance and Growth Drivers

02 | Group Financial Update

03 | Strategic Plan 2019-2021

04 | China Connectivity

05 | Appendix

Q1 2021: Record financial results

Revenue and profit at record quarterly highs

Higher investment income YoY, due to external portfolio gains

1. All percentage changes are computed based on amounts reported in financial statements.

2. Represents gross revenue and other income before deducting transaction-related expenses (Q1 2020: HK$17mn; Q1 2021: HK$45mn)

3. Core business revenue represents total revenue and other income, excluding net investment income and HKEX Foundation donation income (Q1 2020: HK$Nil; Q1 2021: HK$46mn).

4. EBITDA margin is calculated based on EBITDA divided by revenue and other income less transaction-related expenses.

EBITDA

+61%

Margin(4)

75% 81%

$3.0bn

Q1 2020

$4.8bn

Q1 2021

Core business revenue(3) Net investment income

+35% N/A

$4.1bn

Q1 2020

$5.5bn

Q1 2021

$(47)mn

Q1 2020

$418mn

Q1 2021

+49%

Total revenue & other income(2)

$4.0bn

Q1 2020

$6.0bn

Q1 2021

PAT

+70%

$2.3bn

Q1 2020

$3.8bn

Q1 2021

(HK$)

Basic earnings per share

+68%

$1.80

Q1 2020

$3.03

Q1 2021

18

Q1 2021 vs Q1 2020: Record quarterly revenue and profit due to record

headline ADT and strong Stock Connect trading volumes

1. Represents gross revenue and other income before deducting transaction-related expenses (Q1 2020: HK$17mn; Q1 2021: HK$45mn)

2. Excludes transaction-related expenses, depreciation and amortisation, finance costs, and share of results of joint ventures

3. For the purpose of this presentation, tax impact of NII is not considered when calculating the PAT attributable to NII.

4. EBITDA margin is calculated based on EBITDA divided by revenue and other income less transaction-related expenses.

5. From July 2020 onwards, the donation income from the Stock Code Balloting Charity Scheme was received by HKEX Foundation (HKEXFN), and then the amounts previously paid by issuers

directly to the Hong Kong Community Chest were paid by HKEX Foundation. As a result, HKEX records both donation income under revenue and other income, and HKEX Foundation

charitable donations under operating expenses.

Basic earnings per shareOperating

expenses(2) EBITDAProfit attributable to HKEX

shareholders(3)

Opex due to higher staff costs

and IT expenses

Foundation donations(5)

EBITDA margin 6% PAT % more than EBITDA

due to a one-off deferred tax

charge arising from UK tax

rate from 17% to 19% in Q1

2020, and lower % increase in

D&A

EPS % less than PAT due to

shares issued for scrip dividends

in April 2020

Revenue and

other income(1)

Trading & clearing fees from

record headline ADT and

Northbound ADT

Depository fees from e-IPO

and Stock Connect portfolio fees

Net investment income (NII) due

to HK$680mn from external

portfolio (Q1 2020: HK$521mn

losses; Q1 2021: HK$159mn gains)

partly offset by interest income

Core business4,056

Core business5,492

Core business1,007

Core business1,077

Core business3,032

Core business4,370

Core business2,310

Core business3,401

Core business1.84

Core business2.68

HKEXFN46

HKEXFN1

HKEXFN25

HKEXFN(1)

HKEXFN21

HKEXFN(1)

HKEXFN21

HKEXFN0.02

NII (47)

NII 418

NII (47)

NII 418

NII (47)

NII 418

NII (0.04)

NII 0.33

4,009

5,956

1,008 1,102

2,984

4,809

2,262

3,840

1.80

3.03

Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021

ADTMargin(4)75% 81%

HK$120.9bn +86% HK$224.4bn

Total

+70%

Core business

+47%

Core business

+44%

Total

+49%

Total

+61%

Core business

+35%

(HK$ mn)

Total

+68%

Core business

+46%

(HK$)

Total

+9%

Core business

+7%

19

Q1 2021 vs Q4 2020: PAT up 31% due to record headline ADT and lower

Opex, partly offset by decrease in net investment income

Revenue and other income(1)

Trading and clearing fees from record

headline ADT and Northbound ADT

Stock Exchange listing fees from in

newly listed DWs and CBBCs

Partly offset by:

NII due to HK$257mn gains from

external portfolio (Q4 2020: HK$416mn; Q1

2021: HK$159mn) and interest income

Operating expenses(2) EBITDAProfit attributable to

HKEX shareholders(3)

Staff costs due to special gratuity

payments in Q4 2020

Foundation donations

Remaining decrease due to seasonality

EBITDA margin 7% due to in

revenue and in opex

PAT % more than EBITDA due to

D&A

Core business4,282

Core business5,492

Core business1,246

Core business1,077

Core business2,996

Core business4,370

Core business2,163

Core business3,401

HKEXFN72

HKEXFN46

HKEXFN55

HKEXFN25

HKEXFN17

HKEXFN21

HKEXFN17

HKEXFN21

NII 745

NII 418

NII 745

NII 418

NII 745

NII 418

5,099

5,956

1,301 1,102

3,758

4,809

2,925

3,840

Q4 2020 Q1 2021 Q4 2020 Q1 2021 Q4 2020 Q1 2021 Q4 2020 Q1 2021

HK$224.4bnHK$141.0bnMargin(4) 81%74%

+59%

ADT

Total

+31%

Core business

+57%

Core business

+28%

Core business

+46%

Total

+17%

Total

+28%

(HK$ mn)

1. Represents gross revenue and other income before deducting transaction-related expenses (Q4 2020: HK$40mn; Q1 2021: HK$45mn).

2. Excludes transaction-related expenses, depreciation and amortisation, finance costs, and share of results of joint ventures

3. For the purpose of this presentation, tax impact of NII is not considered when calculating the PAT attributable to NII.

4. EBITDA margin is calculated based on EBITDA divided by revenue and other income less transaction-related expenses.

Core business

-14%

Total

-15%

20

Higher revenue for most segments

External portfolio saw gains of $159mn

Trading fees &

tariffs from

record ADT of

equity products

and Northbound

ADT

Trading fees &

tariffs from DWs,

CBBCs & warrants

from ADT

Trading fees from

futures and

options from

HKFE ADV, partly

offset by stock

options ADV

Listing fees due

to record newly

listed DWs and

CBBCs

Trading fees

from LME

chargeable ADV

Clearing fees

from ADT &

SIs, and record

Stock Connect

clearing revenue

Depository fees

from e-IPO fees

and Stock

Connect portfolio

fees

Investment income

due to interest

income from lower

interest rates

Network fees

due to usage

of the Orion

Central Gateway

& China Connect

Central Gateway,

and new

throttle fees

Net investment

income (NII)

from gains

from external

portfolio but partly

offset by interest

income

HKEX Foundation

donation income

$46m

(HK$ mn)

Change year-on-year

%

(42)

658113

496 36686

4,009

5,956

YTD Q1 2020 Cash Equity and FinancialDerivatives

Commodities Post Trade Technology Corporate Items YTD Q1 2021Q1 2020 Q1 2021

N/A+57% +13% -10% +28% +17% +49%

Segmental revenue

1. Headline ADT up 86% (Q1 2020: HK$120.9bn; Q1 2021: HK$224.4bn); ADT of equity products included under Cash segment up 91% (Q1 2020: HK$103.4bn; Q1 2021: HK$198.0bn); ADT of

DWs, CBBCs and warrants included under Equity and Financial Derivatives segment up 51% (Q1 2020: HK$17.5bn; Q1 2021: HK$26.4bn)

21

Higher EBITDA for all segments except for Commodities

1. EBITDA margin is calculated based on EBITDA divided by revenue and other income less transaction-related expenses.

EBITDA

1,027741 238

1,535

143

2,984

1,673

801197

2,009

180

4,809

Trading fees & tariffs

$646m from record ADT of

equity products and record

Stock Connect trading

revenue

Opex $12m due to staff

costs and IT costs

Trading fees & tariffs from DWs,

CBBCs & warrants $76m from

ADT

Trading fees from futures and options

$62m from HKFE ADV, partly

offset by stock options ADV

Listing fees $105m due to record

newly listed DWs and CBBCs

Transaction-related expenses

$19m due to MSCI license fees

Opex $34m due to allocated

costs of Listing Division from listing

fees from DWs and CBBCs, and MSCI

incentives

Trading fees $54m from

LME chargeable ADV

Clearing fees $482m from

record ADT, and record Stock

Connect clearing revenue

Depository fees $186m

from e-IPO service fees &

Stock Connect portfolio fees

Investment income $174m

due to interest return

Opex $13m due to staff

costs and IT costs

EBITDA margin 6%

Network fees $27m due to

usage of the Orion Central

Gateway & China Connect

Central Gateway, and new

throttle fees

+63% +8% -17% +31% +26% +61%

CashEquity & Financial

DerivativesCommodities Post Trade Technology

Group Total

(incl. Corp. Items)

Share of Group EBITDA (before Corporate Items)

%

28% 34%

EBITDA Margin

88% 92% 84% 82% 59% 55% 88% 90% 67% 73%

75% 81%

20% 17% 6% 4% 42% 41% 4% 4%

Q1 2020 Q1 2021

%

($ million)

100% 100%

Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021

(1)

22

Higher YoY net investment income due to gains from external portfolio

External portfolio – improved performance reflecting market

valuations

Internal funds – lower income from reduced interest rates, partly

offset by higher fund sizes

(HK$ mn)

Net investment income by category of investments

Debt

securities

Collective

investment

schemes

Cash &

bank

depositsFX

478

22

(521)

(26)

235

13159

11

Average fund size

15.7 22.8

146.8

186.2

29.4

34.0

Corporate Funds

Margin Funds

Clearing HouseFunds

Q1 2020 Q1 2021

191.9

243.0(HK$ bn)

(521)

101

340

33

159

60

193

6

Net investment income by funds

(HK$ mn)

Corporate Funds (External Portfolio)

Margin

Funds

Corporate Funds (Internal)

Clearing

House Funds

Q1

2020

Q1

2021

Q1

2020

Q1

2021Q1

2020

Q1

2021

Q1

2020

Q1

2021

Q1

2020

Q1

2021

Q1 2021: income of HK$418mn (Q1 2020: loss of HK$47mn)

Q1

2020

Q1

2021

Q1

2020

Q1

2021

Q1

2020

Q1

2021

23

Agenda

01 | Key Performance and Growth Drivers

02 | Group Financial Update

03 | Strategic Plan 2019-2021

04 | China Connectivity

05 | Appendix

The Global Markets Leader in the Asian Time Zone –

Connecting China, Connecting the World

Our 2019-2021 Strategic Vision

Global

Markets

Global

Liquidity

China

Markets

Global

Underlying

China

Liquidity

China

Underlying

Globally ConnectedChina Anchored Technology Empowered

Facilitating China’s

internationalisation and

investment diversification

Bringing global liquidity

to China and Asia Pacific

underlying

Leveraging new technology

for modernisation and

growth

25

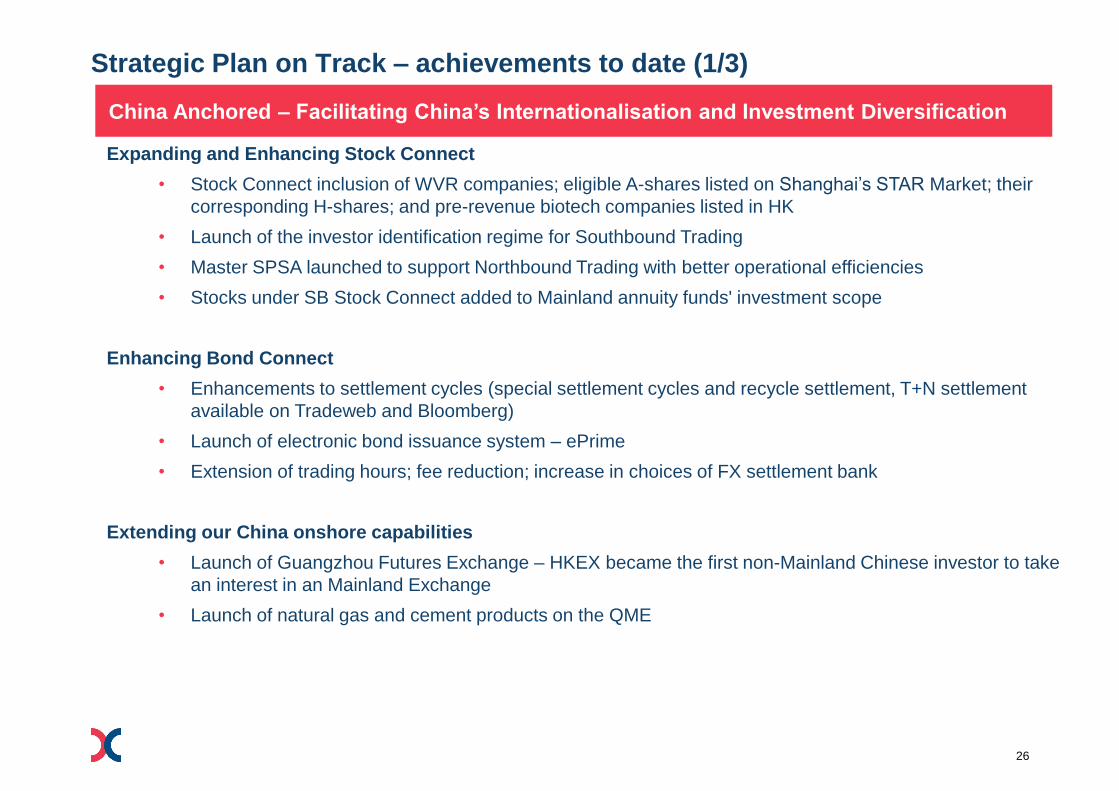

China Anchored – Facilitating China’s Internationalisation and Investment Diversification

Expanding and Enhancing Stock Connect

• Stock Connect inclusion of WVR companies; eligible A-shares listed on Shanghai’s STAR Market; their

corresponding H-shares; and pre-revenue biotech companies listed in HK

• Launch of the investor identification regime for Southbound Trading

• Master SPSA launched to support Northbound Trading with better operational efficiencies

• Stocks under SB Stock Connect added to Mainland annuity funds' investment scope

Enhancing Bond Connect

• Enhancements to settlement cycles (special settlement cycles and recycle settlement, T+N settlement

available on Tradeweb and Bloomberg)

• Launch of electronic bond issuance system – ePrime

• Extension of trading hours; fee reduction; increase in choices of FX settlement bank

Extending our China onshore capabilities

• Launch of Guangzhou Futures Exchange – HKEX became the first non-Mainland Chinese investor to take

an interest in an Mainland Exchange

• Launch of natural gas and cement products on the QME

Strategic Plan on Track – achievements to date (1/3)

26

3 | Strategic Plan on Track – 2020 HighlightsGlobally Connected – Bringing Global Liquidity to China and Asia Pacific Underlying

Enhancing our IPO regime

• New grandfather arrangements to enable qualifying issuers with Corporate WVR to seek secondary

listings in Hong Kong

• Shortening of the structured product listing cycle from five to three trading days

• Published a consultation paper on proposals to enhance and streamline the listing regime for

overseas issuers

Broadening our product ecosystem across asset classes

• MSCI suite of Asia and Emerging Markets Index Futures and Options

• Hang Seng TECH Index Futures and Options; Inline Warrants; Weekly Index options

• USD and CNH denominated Silver Futures; New cash-settled metals futures on LME

Developing into the ETF issuance and trading hub of the Asia time zone

• Welcomed new types of ETPs – active equity ETF, ESG China A shares ETF, commodity-based L&I

Product, HK – listed biotech companies focused ETF, ETF tracking the Shanghai’s STAR Market

• Launched the Hong Kong-Mainland ETF Cross-listing Scheme

• Introduced a new spread table and continuous quoting market making obligations to enhance

liquidity; cross-listing link with Euroclear; buy-in exemption

Improving market microstructure

• Enhanced Volatility Control Mechanism (VCM) and Pre-Opening Session (POS)

• Temporary migrated LME trading activities from the Ring to electronic pricing

• LME launched electronic warranting solution to replace paper warrants

Strategic Plan on Track – achievements to date (2/3)

Globally Connected – Bringing Global Liquidity to China and Asia Pacific Underlying

27

3 | Strategic Plan on Track – 2020 HighlightsTechnology Empowered – Leveraging New Technology for Modernisation and Growth

Modernising our systems

• FINI concept paper for shortening of IPO settlement cycle

• Relocation of the secondary data centre to become a Tier 3 data centre

• Completion of the derivatives system infrastructure upgrade

Leveraging new technology

• Announced launch of Synapse in Q1 2022 to automate and streamline post trade workflow for

Northbound Stock Connect

• Deployed new technologies (e.g., Robotic Process Automation, AI) across HKEX businesses

• Continued to scale up our Robotic Process Automation (RPA) programme and AI usage across our

businesses to improve operational efficiency

Expanding our horizons

• Launch of Fusion Bank, a new virtual bank in partnership with multiple leading HK businesses (HKEX

has minority shareholding)

• Minority investment in Huakong TsingJiao, which specialises data and multi-party computation

technologies

Strategic Plan on Track – achievements to date (3/3)

Technology Empowered – Leveraging New Technology for Modernisation and Growth

28

2019-2021 Strategy – FICC themes

FIXED INCOME AND CURRENCY COMMODITIES

Facilitate CNY access

Enhance Bond Connect

Expand suite of offshore rates / FX

derivatives on onshore underlying

Build post-trade infrastructure(custody, settlement, collateral management, FX)

Expand product suite

Market structure evolution

Asian Time Zone expansion

Commodity Connect

29

Key components of our FIC strategy

Expand Existing Platform

Capture CNY Opportunities

Invest in Post-Trade Infrastructure

Bond Connect enhancements

Listed bonds and derivatives

Southbound Bond Connect

CNY accessibility – repository, tracking and monitoring

IRS and repo + Derivatives Connect

CNY trading platform

Custody, settlement and collateral management

Trade repository and monitoring

International linkages

30

LME volume softened recently given pandemic battered global

economic activities…

Source: LME data as of Mar 2021

1. Excluding Admin Trades, 2021 YTD: 547,320 lots.

475

584 634

676 700

670 619 624

730 697

610 564

0

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021YTD

ADV (‘000 lots)6 Dec 2012

HKEX

acquisition

22 Sep 2014

LME Clear

Launch

Post-acquisition

integration and

LME Clear launch

Commercialisation

of the platform

with LP and new

trader programme

Strategic pathway, future

platform development and

revised fee structure

1

31

…while multiple enhancements are on track

• Continuing the success of the Strategic

Pathway, with new contracts continue to

build liquidity especially in ferrous suite

• 2020 prioritisation of electronic options

market to simplify and standardise areas of

its market structure

• Aim to provide feedback in Q2 2021 on

Market Structure Discussion Paper, based

on the market feedback received in Q1

Strategic Pathway

• Continued embedding of responsible sourcing requirements into the LME brand lists, ensuring that LME

brand listing is a clear indicator of good ethical standing

• Launch of 2020 sustainability strategy proposals to reflect market interest in broader sustainability story

with a focus on low carbon aluminium

Sustainability focus

• Significant investment in new trading

platform

• Supporting industry initiatives to enhance

security of off-warrant metal storage

• Investigating solutions to enable the spot

trading and sourcing of specific metal types

• Insourcing warrant depository to streamline

the warrant lodgement and withdrawal

process, and provide significant operational

efficiencies

Continued innovation

• Promoting the highest standards of fair and orderly trading on the LME’s market

• Delivery of off-warrant stock reporting to provide better industry-wide metals stock transparency

• Deliver a modern market structure by close collaboration with external and internal stakeholders

Market leadership

32

Market microstructure enhancements at HKEX

We have achieved 30+ enhancements in the last 2 years and will continue to ensure

competitiveness and efficiency of our markets

Areas of Focus Key Achievements so far Since 2019

Improve Ease

of Access

• Better client onboarding

• Participants system testing enhancements

• Northbound throttle expansion (Stock Connect)

Reduce Frictional

Trading Costs

• Expand Closing Auction Session (Cash)

• After-hours trading extension to 3am (Derivatives)

• New spread table, Market Making enhancements and stamp duty exemption on ETP

market

Improve

Capital Efficiency

• Better cash interest rebates to participants

• Flexibility in Clearing Participants (CP) setup in HK and Stock Connect markets

• Flexibility for Non-CPs in clearing arrangements

Enhance Risk

Management

& Market Integrity

• Revamp Pre-Opening Session and Volatility Control Mechanism (Cash)

• Self-Match Prevention (Derivatives)

• Holiday trading and trading hour enhancements for MSCI products

• Shorten IPO settlement cycle

• Pre-Trade Risk Management Enhancements

• Increase Position Limit for certain products

Selected Initiatives in the Pipeline

We aim to build a quality market and a sustainable ecosystem of policies, participants and products

33

Agenda

01 | Key Performance and Growth Drivers

02 | Group Financial Update

03 | Strategic Plan 2019-2021

04 | China Connectivity

05 | Appendix

The penetration level of equity market through Stock Connect

Source: Wind, HKEX

1. Data as of Mar 2021.

Stock Connect covers the majority of the market by market cap and turnover

Stock Connect Coverage(% of all Mainland & HK listed companies)

32%

37%

20%

% of domestic market included in Stock Connect

MUTUAL MARKET

80%

80%

80%

73%

75%

87%

By

Market

Cap

By

Turnover

By

Number

78%of total market cap

76%of total turnover

29%of total number of

companies

SSE

SSE

SSE

SZSE

SZSE

SZSE

519

587

885

35

24.6 30.3 21.4 21.6 37.1 31.6

56.2 48.1 74.2 75.7

62.5 21.1 26.6 21.4 23.9

47.944.8

75.2

63.3

92.8 88.7

69.0

7.5 6.8

6.3 6.9

12.910.6

13.9

14.1

35.2 33.4

22.3

4.3 3.8

3.6 4.3

8.7 8.8

13.2

13.6

34.6 38.0

24.6

6.4 6.0 8.6 10.9 13.5 17.9 21.6 30.6

43.6 37.8

32.0 34.4

57.4 67.5

52.8 56.8

106.795.8

158.5

139.1

236.8 235.8

178.4

1.7%2.3%

3.7% 3.9%4.8% 5.3% 5.7% 6.1%

6.8%6.1%

5.4% 4.8%5.8% 5.6%

6.4%7.3%

9.0% 8.5%9.6% 9.9%

14.2%15.3%

11.8%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0

50

100

150

200

250

300

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20 Q3 20 Q4 20 Jan 21 Feb 21 Mar 21

Stock Connect – trading trends

Stock Connect revenue continued to set record highs,

reaching 12% of the Group’s total revenue and other income in Q1 2021 (FY 2020 and Q1 2020: 10%)

Stock Connect generated record revenue of HK$737mn in Q1 2021, 82% higher than Q1 2020 (HK$404mn)

Stock Connect Northbound and Southbound Trading ADT reached RMB126.8bn and HK$60.8bn respectively in Q1 2021

Shanghai Northbound (1)

Shenzhen Northbound (1)

Shanghai Southbound

Total average daily trading volume

Percentage of Southbound turnover of Hong Kong Market

Stock Connect average daily trading volume (HK$ bn)

Source: HKEX, SSE and SZSE data

1. Northbound (NB) trading is conducted in RMB; the NB figures in the chart are converted to HKD based on the month-end exchange rate.

2. May not add up due to roundings

Shenzhen Southbound NB record of

RMB191.2bn on

7 Jul 2020

SB record

of HK$100.3bn

on 24 Feb 2021

36

Stock Connect (Northbound)

Portfolio Value

RMB billion

4.79.6

20.4

41.7

91.3

126.8

34.731.7

77.3

84.3

124.3MSCI

rebalancing

days

Average Daily Turnover

2018

2017

2019

RMB billion

20212,461 2,452

2,360

785

9511,033

1,050

9321,043

1,054

1,094

1,160

1,2211,264

1,429

601 576 566 592686 662 698 680 719

621 679 668

202 233 253 270 301347 366 404 437

491 502 530

1,437 1,439

1,298

1,450 1,518

1,687

1,9522,013

1,8921,950

2,089

2,340

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: HKEX

1. Data as of 31 Mar 2021.

2020

37

Source: HKEX, SGX, CFFEX, FIA

1. As of Mar 2021.

2. CSI 300 Index Futures was launched in Apr 2010.

3. Numbers in brackets represent the number of constituents within the underlying index.

* 2021 data as of Mar 2021.

Index futures on China underlying

ADV (’000 contracts)

Hang Seng Index Futures (52)3 HSCEI Futures (51)3

NOTIONAL VALUE1

US$180kNOTIONAL VALUE1

US$70k

FTSE China A50 Index Futures (SGX) (50)3 CSI 300 Index Futures (CFFEX) (300)3

NOTIONAL VALUE1

US$17kNOTIONAL VALUE1

US$233k

2

MAINLAND CHINA

Trading Fee: RMB36.93/contract, 0.0023% to notional value

Trading Fee: HK$3.50/contract, 0.0006% to notional value

Trading Fee: US$1.10/contract, 0.0061% to notional value

Trading Fee: HK$10.00/contract, 0.0007% to notional value

38%62%

WEIGHTING COMPOSITION1

OTHER

85 94 83 80 6986

131 127

234209

167 164

20162014 20192010 2013 20172011 2012 2015 2018 2020 2021*

5061 65

86 89

135 134117

152139 146

133

20152011 20202010 20172012 2013 2014 2016 2018 2019 2021*

2 1239

84

159

369

270 260

339

391 383412

2014 20182010 20172011 2012 201620152013 2019 2020 2021*

251 207

432

812884

1,136

17 17 3196 123 147

201720122010 20142011 20162013 2015 20202018 2019 2021*

38

Tapping into China’s vast bond market

Source: CBIRC (Feb 2021), PBOC, SSZ and SZSE (Mar 2021), BIS and IMF (Dec 2019 for the Bond vs GDP chart)

0

25

50

US China Japan UK FR

Bank Assets Equities Bonds

US$49tn

US$12tn

US$16tn

International

Investors

China’s Bond

Market

Key Policy Drivers

• Risk migration from banking sector to bond market

• Greater credit differentiation amid ongoing market

reforms

• Funding needs for economic transition and

infrastructure projects – e.g. Belt & Road; Panda

bonds

• Enhanced bond issuance and disclosure standards

Growing International Demand

• Yield differential against developed markets

• Inclusion in emerging market bond indexes

• Geographical and asset class diversification

• Growing convertibility of RMB / SDR inclusion

• More efficient access – Bond Connect

Outstanding,

US$ tn Relative to GDP

192%

99% 244%

173%222%

39

0

100

200

300

400

500

600

Pilot scheme

to access

CIBM

RQFII

investment

QFII

investment

Long-only

investment

Bond

Connect

launch

(1)0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Bond Connect has significantly grown foreign participation in China’s bond market

Source: ChinaBond + SCH, Bloomberg, BIS

1. Foreign participation in the CIBM data as of Mar 2021

2. BBGA is Bloomberg Barclay Global-Aggregate, GBI-EM is J.P. Morgan Government Bond Index-Emerging Markets series, WGBI is FTSE World Government Bond Index

Foreign participation in the CIBM increased by 322% since launch of Bond Connect in July 2017(1)

Number of Bond Connect participants has grown to 2,450 as of Mar 2021

Bond Connect Mar 2021 YTD ADT: RMB 25.3bn

68%64%

46%41% 39% 38%

29%

13%8%

~3%

DE FR AU UK IT CA US RU JP China

Growth DriversForeign Participation in the CIBM

Average: 38.5% 15%

Achievable

target

Foreign Ownership %

US$547bn

Foreign Holdings in Chinese Bonds

(US$ billion)

Foreign Ownership (%)Inclusion of Mainland bonds in global fixed income

indexes (BBGA, GBI-EM, WGBI)2

Greater adoption of RMB globally and

need to reinvest in RMB assets

Improving access to the Mainland bond market

3.4%

1

40

Agenda

01 | Key Performance and Growth Drivers

02 | Group Financial Update

03 | Strategic Plan 2019-2021

04 | China Connectivity

05 | Appendix

Financial highlights – Income Statement

(HK$ mn, unless stated otherwise) Q1 2021% of Revenue &

Other IncomeQ1 2020

% of Revenue &

Other IncomeYoY Change

Results

Revenue and other income 5,956 100% 4,009 100% 49%

Less: Transaction-related expenses (45) (1%) (17) (0%) 165%

Revenue and other income less transaction-related

expenses5,911 99% 3,992 100% 48%

Operating expenses (1,102) (19%) (1,008) (25%) 9%

EBITDA 4,809 81% 2,984 74% 61%

Depreciation and amortisation (327) (5%) (274) (7%) 19%

Operating profit 4,482 75% 2,710 68% 65%

Finance costs and share of results of joint ventures (23) (0%) (30) (1%) (23%)

Profit before taxation 4,459 75% 2,680 67% 66%

Taxation (632) (11%) (422) (11%) 50%

Loss attributable to non-controlling interests 13 0% 4 0% 225%

Profit attributable to HKEX shareholders 3,840 64% 2,262 56% 70%

Capex 331 216 53%

Basic earnings per share HK$3.03 HK$1.80 68%

Headline ADT on the Stock Exchange HK$224.4 bn HK$120.9 bn 86%

1. % does not add up due to roundings.

42

Performance by operating segment

HK$ mn Cash

Equity &

Financial

Derivatives

Commodities Post Trade TechnologyCorporate

Items

Group

Q1 2021

Group

Q1 2020

Revenue and other income 1,820 1,011 361 2,248 248 268 5,956 4,009

% of Group Total 31% 17% 6% 38% 4% 4% 100% 100%

Less: Transaction-related

expenses- (33) - (12) - - (45) (17)

Revenue and other income less

transaction-related expenses1,820 978 361 2,236 248 268 5,911 3,992

Operating expenses (147) (177) (164) (227) (68) (319) (1,102) (1,008)

EBITDA 1,673 801 197 2,009 180 (51) 4,809 2,984

% of Group Total 35% 16% 4% 42% 4% (1%) 100% 100%

EBITDA margin(1) 92% 82% 55% 90% 73% N/A 81% 75%

Depreciation and amortisation (327) (274)

Finance costs (39) (49)

Share of results of joint ventures 16 19

Profit before taxation 4,459 2,680

1. EBITDA margin is calculated based on EBITDA divided by revenue and other income less transaction-related expenses.

43

Operating expenses and depreciation & amortisation

Staff costs due to

payroll adjustments

due to

maintenance

expenses for new IT

systems and

network upgrades

Stable Professional fees

incurred for strategic

initiatives (e.g.

consulting fee for

HKATS review in

2020)

due to IT

systems rolled out

in 2020 (e.g. Orion

Risk Platform for

Cash Market)

Incentives

relating to MSCI

index futures

contracts

Total opex due to

staff costs, IT

costs and

Foundation

donations, partly

offset by

professional fees

1. Includes product marketing and promotion expenses

2. Excludes transaction-related expenses, depreciation and amortisation, finance costs, and share of results of joint ventures

(HK$ mn)

+ 10% - 3% - 41% + 9% + 19%+ 9%

89

703 765

152 167

29 28 34 20 1 2597

1,0081,102

274327

Staff costs and

related expenses

IT & computer

maintenance expPremises expenses Professional fees

Other operating

expenses (1) Total opex (2) Depreciation and

amortisation

Q1 2020 Q1 2021

+ 9%+ 2,400%

HKEX Foundation

charitable donations

2021 amount mainly

represents

donations made by

HKEX Foundation

to HK Community

Chest

Investment in talent and infrastructure

+ 7%Excl.

donations

Q1 2020 Q1 2021Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021 Q1 2020 Q1 2021

44

1,4321,553 1,543

1,241

1,716 1,777

2,0331,878

2,562 2,479 2,443

1,828

2,608 2,597

2,2071,979

2,262

2,971

3,347

2,925

3,840

2,751 2,879 2,848 2,6383,048

3,155 3,4543,523

4,150 4,044 4,1023,571

4,288 4,290

3,987

3,746

4,009

4,773

5,309 5,099

5,956

842 825 825 924823 869 877 957 920 971 1,012

1,153956 970 937

1,134 1,008 1,037 1,0931,301

1,102

1,897 2,045 2,014

1,705

2,2152,277

2,567 2,555

3,215 3,061 3,077

2,404

3,3183,307

3,038

2,600

2,984

3,722

4,177

3,758

4,809

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Profit attributable to shareholders

Revenue and other income

Operating expenses

EBITDA

Q1 2021 performance above historical trendline

HKEX saw a strong start to 2021 with record quarterly financial results driven by robust trading volumes in the Cash Market

1. Represents gross revenue and other income before deducting transaction-related expenses

2. Operating expenses exclude transaction-related expenses, depreciation and amortisation, finance costs, share of results of joint ventures, and costs arising from the proposed combination with

London Stock Exchange Group plc (LSEG).

3. Dotted trend lines are illustrative and do not constitute a forward forecast.

(2)

Quarterly performance

(HK$ mn)

(1)

2016 2017 2018 2019 2020 2021

45

Comparison of trading activity across global Exchanges

*Source: WFE and Bloomberg as of Mar 2021. Except NYSE and Cboe as of Dec 2020, B3, Euronext and DB as of Feb 2021, NSE as of Jan 2021.

1. ADT and turnover velocity takes into account both on-exchange and block trading. For Nasdaq, NYSE and Cboe, trades executed on their trading platforms include those listed on other US

exchanges, hence their turnover velocity covers the whole US market.

2. HKEX ADT includes equities only, excluding ETPs and structured products.

ADT & Velocity (1) of Major Global Exchanges (US$ billion)

= Last 6 months (Oct 20 - Mar 21) velocity*

= Last month (Mar 21) velocity

= ADT

176% 88% 51% 87% 195% 117% 61% 125% 362% 205% 78% 116% 330% 207% 76% 147% 41%

369% 223% 86%

287.5

112.4

68.3

8.8 6.217.4

9.7 8.3

73.9

56.2

19.631.1 26.8

10.94.7 9.3

1.0

NASDAQ Deutsche

Börse

B3CboeNYSE TMX ENXLSE

Group

SZSE SSE HKEX(2) ASXJPX KRX NSE TWSE SGX

46

21.83

6.63

10.79

9.17

10.61

1.410.98

0.57 0.41

CME Group ICE (incl.LIFFE)

SHFE DCE ZCE HKEXDerivatives

SGX LME CFFEX

ADV in million

2.57(5 tons equivalent)

No. of contracts

(in million)

% of volume in

commodities0.0%13.9% 56.6% 100.0% 100.0% 100.0% 0.05% 10.5% 100.0%

Global derivatives trading landscape

Source: Company website, data as of Mar 2021.

160(5 tons equivalent)

1,331 409 626 532 616 86 61 36 24

47

Northbound(1): RMB2,360bn; Southbound(2): HK$2,550bn

Stock Connect shareholding value

Northbound Top 25(3)

Rank Stock nameShare value in CCASS

(RMB million)

% of issued shares Venue

1 Kweichow Moutai Co.,Ltd. 192,750 7.63% SH

2 Midea Group Co., Ltd. 86,419 14.91% SZ

3 Ping An Insurance (Group) * 69,926 8.20% SH

4 China Merchants Bank Co.,Limited * 65,167 6.18% SH

5 Gree Electric Appliances,Inc. 62,098 16.46% SZ

6 Jiangsu Hengrui Medicine Co.,Ltd. 60,217 12.32% SH

7 Wuliangye Yibin Co.,Ltd. 57,223 5.50% SZ

8 China Tourism Group Duty Free 57,107 9.55% SH

9 Contemporary Amperex Technology 49,000 6.52% SZ

10 Ping An Bank Co., Ltd. 46,389 10.86% SZ

11 Longi Green Energy Technology Co., 31,330 9.43% SH

12 Foshan Haitian Flavouring And Food 31,244 6.03% SH

13 Inner Mongolia Yili Industrial Group 30,044 12.65% SH

14 Shenzhen Mindray Bio-Medical 28,291 5.83% SZ

15 Sany Heavy Industry Co.,Ltd 26,703 9.22% SH

16 China Yangtze Power Co.,Ltd. 26,276 5.38% SH

17 Nari Technology Co., Ltd. 19,639 13.73% SH

18 Wuxi Apptec Co., Ltd. * 19,464 9.40% SH

19 Wanhua Chemical Group Co.,Ltd. 19,381 12.89% SH

20 Beijing Oriental Yuhong Waterproof 19,257 16.03% SZ

21 China Vanke Co., Ltd. * 18,380 6.30% SZ

22 Anhui Conch Cement Company * 17,725 8.65% SH

23 Focus Media Information Technology 16,487 12.10% SZ

24 Aier Eye Hospital Group Co.,Ltd. 16,430 6.72% SZ

25 Hangzhou Tigermed Consulting 16,387 14.56% SZ

Southbound Top 25(3)

Rank Stock nameShare value in CCASS

(HK$ million)

% of issued shares

1 Tencent Holdings Limited 375,061 6.40%

2 China Construction Bank Corporation* 182,003 11.57%

3 Industrial And Commercial Bank Of China 143,997 29.73%

4 Meituan 111,553 6.34%

5 Hsbc Holdings Plc 89,385 9.46%

6 Xiaomi Corporation 81,566 12.56%

7 China Mobile Limited 79,585 7.62%

8 Cnooc Limited 44,665 12.30%

9 Hong Kong Exchanges And Clearing Limited 42,111 7.25%

10 Semiconductor Manufacturing International* 36,934 18.92%

11 Anta Sports Products Limited 34,512 10.06%

12 Wuxi Biologics (Cayman) Inc. 30,104 7.33%

13 China Resources Beer (Holdings) Company 29,615 14.97%

14 Sunny Optical Technology (Group) Company 28,081 14.44%

15 Sunac China Holdings Limited 25,743 16.54%

16 Agricultural Bank Of China Limited* 25,530 26.70%

17 Great Wall Motor Company Limited 25,300 37.87%

18 China Pacific Insurance (Group) Co. Ltd.* 23,290 27.37%

19 Smoore International Holdings Limited 22,829 0.00%

20 Country Garden Services Holdings Company 21,095 8.95%

21 Bank Of China Limited* 18,888 7.62%

22 Innovent Biologics, Inc. 18,017 15.69%

23 China Feihe Limited 17,989 9.14%

24 Kingsoft Corporation Limited 17,803 25.12%

25 Man Wah Holdings Limited 16,245 25.44%

Source: Bloomberg and HKEX as of Mar 2021 (* A&H shares), does not add up due to roundings.

1. Shanghai Northbound: RMB1,282bn; Shenzhen Northbound: RMB1,078bn

2. Shanghai Southbound: HK$1,503bn; Shenzhen Southbound: HK$1,046bn

3. Ranked by share value in CCASSS

48

Comparison of Exchanges – Top 10 stocks by turnover value(1)

Source: Bloomberg data as of Mar 2021

1. Ranked by YTD ADT (US$m).

* Dual class voting share

New economy stocks now account for significant portions of the turnover

Company(RED =

Chinese companies)

YTD ADT

A-Share YTD ADT

Mkt. Cap

Rank

TENCENT 2,285 - 1

MEITUAN-W 1,173 - 4

ALIBABA 1,059 - 2

XIAOMI-W 998 - 14

CHINA MOB 722 - 6

KUAISHOU 631 - 8

HKEX 552 - 12

BAIDU 502 - 17

BYD 461 1,302 56

SMIC 438 301 68

CompanyYTD ADT

NIO* 5,520

ALIBABA* 4,689

BAIDU* 3,596

FUTU* 1,556

PINDUODUO* 1,375

JD* 1,050

BILIBILI* 910

XPENG* 909

GSX TECHEDU* 713

TENCENT MUSIC* 693

CompanyYTD ADT

H-Share YTD ADT

Mkt. Cap

Rank

KWEICHOW MOUTAI

CO LTD-A1,557 - 1

LONGI GREEN ENERGY

TECHNOL-A1,334 - 16

PING AN INSURANCE

GROUP CO-A1,281 437 5

SANY HEAVY

INDUSTRY CO LTD-A807 - 24

TONGWEI CO LTD-A 776 - 46

ZIJIN MINING GROUP

CO LTD-A705 126 35

CHINA TOURISM

GROUP DUTY F-A694 - 9

CHINA MERCHANTS

BANK-A691 155 3

CHINA NORTHERN

RARE EARTH -A646 - 102

CITIC SECURITIES CO-

A618 76 25

CompanyYTDADT

H-Share YTD ADT

Mkt. Cap

Rank

EAST MONEY

INFORMATION CO-A1,453 - 15

BYD CO LTD -A 1,302 461 11

WULIANGYE YIBIN CO

LTD-A1,234 - 1

BOE TECHNOLOGY

GROUP CO LT-A1,104 - 20

CONTEMPORARY

AMPEREX TECHN-A1,076 - 2

TIANQI LITHIUM CORP-A 851 - 92

TCL TECHNOLOGY

GROUP CORP-A843 - 34

SUNGROW POWER

SUPPLY CO LT-A840 - 47

LUXSHARE PRECISION

INDUSTR-A737 - 18

GANFENG LITHIUM CO

LTD-A687 94 42

Top 10: 35% of Total ADT Top 10: 14% of Total ADT Top 10: 12% of Total ADT Top 10: 70% of Total ADT

HKEX SSE SZSEUS Listed

Chinese Stocks

49

86

166

101 72 70 63 67 64 74 78 93 107

146 107 92 86 101 95

77 77

121 114 141 141

246 234 198

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

-

50

100

150

200

250

300

350

400

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Q1 Q2 Q3 Q4 Jan Feb Mar

2015 2016 2017 2018 2019 2020 2021

394

868 499 377

215 184 193 221 201 195 231 203 227 173 129 134 260 260 186 168 313 240 400 299 448 408 345

303

712

428 537

323 342 309 296 242 247 277 250 246 232 171 187

332 325 272 273

518 400

609 475

609 529

442

698

1,579

927 914

537 526 502 517 443 442 508 453 474 405 300 321

593 585

459 440

831

640

1,009

774

1,058 937

787

0

1,000

2,000

3,000

4,000

5,000

6,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q Jan Feb Mar

2015 2016 2017 2018 2019 2020 2021

2020:-3%

Index

IndexADT RMB billion

ADT HK$ billion

SSE ADT (LHS) SZSE ADT (LHS) CSI 300 (RHS)

2015 :+6% 2016: -11%

2015: -7% 2016:+0.4%

2017: +22%

2017: +36%

HKEX ADT (LHS) Hang Seng Index (RHS)

2018: -25% 2019:+36%

2019:+9%2018: -14%

2020:+27%

Source: HKEX, SSE, SZSE & Bloomberg

Note: Data as of Mar.

1. SSE ADT excludes STAR companies.

2. Does not add up due to roundings.

2021:+4%

2021:-3%

Market activity in Mainland and Hong Kong markets

50