Grameenphone Limited - EBL Securities Ltd.

39

Analyst: Mohammad Asrarul Haque [email protected] Phone: +880 1753 509329 Grameenphone Limited Valuation Update (21 June,2021) DSE: GP; BLOOMBERG: GRAM:BD Current Market Price: BDT 343.1 Target Price: BDT 355.0 Rating: Accumulate Outlook: Neutral Sector: Telecommunication Upside Potential:3.5% Exp. Dividend Yield: 3.8% Exp. Total Return: 7.3% Page 1 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | 21 June 2021 N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report. Industry Telecommunication Market Cap (BDT mn) 463,287.9 Paid-up Capital (BDT mn) 13,503.0 Rating Validity December 2021 52W High-Low 238.8 - 391.0 Forward PE 13.0 Forward PB 7.6 Current no. of shares (mn) 1,350.3 Free float shares (mn) 135.0 2019A 2020A 2021E 2022E Financial Information (BDT mn): Net Sales 143,656 139,606 140,422 141,558 EBITDA 90,103 87,090 85,986 87,480 EBIT 66,652 63,440 61,075 63,504 Profit After Tax 34,517 37,187 33,874 35,307 Total Assets 148,734 148,184 147,154 147,585 Total Debt & Lease 23,768 21,716 20,476 20,476 Total Equity 38,347 52,108 50,223 51,773 Retained Earnings 16,988 30,750 28,866 30,416 Cash 13,761 2,599 (525) 5,464 Dividend (C/B)% 130% 275% 250% 260% Margin: OPEX to Sales 31.4% 31.3% 33.2% 32.9% EBITDA 62.7% 62.4% 61.2% 61.8% Operating Profit 46.4% 45.4% 43.5% 44.9% Net Profit 24.0% 26.6% 24.1% 24.9% Growth (YoY): Net Sales 8.1% -2.8% 0.6% 0.8% EBITDA 13.6% -3.3% -1.3% 1.7% EBIT 17.4% -4.8% -3.7% 4.0% Net Profit 3.5% 7.7% -8.9% 4.2% Total Asset 7.2% -0.4% -0.7% 0.3% Profitability: ROA 24.0% 25.0% 22.9% 24.0% ROE 91.8% 82.2% 66.2% 69.2% Payout Ratio 50.9% 50.8% 99.7% 99.4% Dividend Yield 4.5% 7.9% 7.0% 7.3% PEG ratio 3.2 1.6 (1.6) 3.2 Leverage: Debt Ratio 16.0% 14.7% 13.9% 13.9% Debt-Equity 62.0% 41.7% 40.8% 39.5% Times Int. Earned 26.4 168.5 28.2 30.2 Altman Z SCORE 4.1 5.0 5.0 5.1 Valuation: EPS (BDT) 25.6 27.5 25.1 26.1 NAVPS (BDT) 28.4 38.6 37.2 38.3 P/E (x) 11.2 12.6 14.2 13.6 P/NAV (x) 10.1 9.0 9.5 9.3 EV/EBITDA (x) 4.4 5.6 5.8 5.7 EV/Sales (x) 2.8 3.5 3.6 3.5 Price/Sales (x) 2.7 3.4 3.4 3.4 Price/OCF (x) 6.7 14.0 8.3 8.1 *SOURCE; COMPANY DISCLOSURES & EBLSL RESEARCH; ** KEY TERMINOLOGIES ARE PRESENTED AT THE END OF THE REPORT Grameenphone Limited (GP) is the largest telecommunication service provider in Bangladesh. The immediate parent of GP is Telenor Mobile Communications AS and the ultimate parent is Telenor ASA; both the companies were incorporated in Norway. Key Catalyst Efficiency in managing solid growth in subscriber acquisition, revenue and net profit with controlled OPEX even in challenging business environment. Strong brand image and active subscriber base have positioned the company ahead of its rivals. GP recently acquired 10.4 MHz new spectrum at a cost of $391.15 million and currently holds a total of 47.4 MHz spectrum, highest in the industry. Growing contribution from data indicates growth potential. Contribution of data revenue increased to 24.4% in 2020 from only 8.1% in 2015. Handsome dividend payout policy (nearly 100% each year). Risk Factor Higher OTT platform use and high voice call rates causing decline in voice call services usage and revenue (6.6%YoY revenue drop in 2020). Growing use of ISP/PSTN broadband internet services may negatively affect long term cellular data consumption. Failure to successfully diversify business in new and innovative segments may lead to long-term business downsizing. Regulatory pressures and ongoing tussles between the operator and the regulator reducing the market value of GP. Any unfavorable outcome of ongoing dispute may lead to massive financial burden for the company and can cause significant value erosion. Tougher business restrictions from the regulator may emerge anytime on the ground of being an operator with significant market power (SMP). Grameenphone experienced remarkable regulatory challenges in the history of Bangladesh telecommunication industry over the last couple of years that are yet to fully settle. The year 2020 started with the continuation of the tussle between GP and BTRC (telecom regulator) concerning BDT125 bn system audit claim. However, GP managed to mitigate the dispute since the second quarter after deposit of BDT 20.0 billion against the audit dispute, as instructed by the honorable Supreme Court. Besides, the regulator also implemented initial SMP restrictions during the year. Meanwhile, GP’s earnings during the year were in line with our expectations. As this point of time, we view GP’s stock as fairly valued with its current market prices and our estimated intrinsic value based on our assessment of the operator’s future business potential while keeping in mind significant uncertainties and contingencies. We have updated our valuation model based on recent disclosures, our assessment of recent company performance and expectation of future outlook, macro-economic and industry outlook etc. We are assigning ‘Accumulate’ rating on GP stock with a December 2021 estimated intrinsic value of BDT 355.0 per share and 130% expected interim dividend. Our intrinsic price can yield a total 7.3% on holding GP stock till December 2021.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Grameenphone Limited - EBL Securities Ltd.

Analyst: Mohammad Asrarul Haque

[email protected] Phone: +880 1753 509329

Grameenphone Limited

Valuation Update (21 June,2021) DSE: GP; BLOOMBERG: GRAM:BD

Current Market Price: BDT 343.1 Target Price: BDT 355.0 Rating: Accumulate Outlook: Neutral

Sector: Telecommunication Upside Potential:3.5%

Exp. Dividend Yield: 3.8%

Exp. Total Return: 7.3%

Page 1 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | 21 June 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

Industry Telecommunication Market Cap (BDT mn) 463,287.9 Paid-up Capital (BDT mn) 13,503.0 Rating Validity December 2021 52W High-Low 238.8 - 391.0 Forward PE 13.0 Forward PB 7.6 Current no. of shares (mn) 1,350.3 Free float shares (mn) 135.0

2019A 2020A 2021E 2022E

Financial Information (BDT mn):

Net Sales 143,656 139,606 140,422 141,558

EBITDA 90,103 87,090 85,986 87,480

EBIT 66,652 63,440 61,075 63,504

Profit After Tax 34,517 37,187 33,874 35,307

Total Assets 148,734 148,184 147,154 147,585

Total Debt & Lease 23,768 21,716 20,476 20,476

Total Equity 38,347 52,108 50,223 51,773

Retained Earnings 16,988 30,750 28,866 30,416

Cash 13,761 2,599 (525) 5,464

Dividend (C/B)% 130% 275% 250% 260%

Margin:

OPEX to Sales 31.4% 31.3% 33.2% 32.9%

EBITDA 62.7% 62.4% 61.2% 61.8%

Operating Profit 46.4% 45.4% 43.5% 44.9%

Net Profit 24.0% 26.6% 24.1% 24.9%

Growth (YoY):

Net Sales 8.1% -2.8% 0.6% 0.8%

EBITDA 13.6% -3.3% -1.3% 1.7%

EBIT 17.4% -4.8% -3.7% 4.0%

Net Profit 3.5% 7.7% -8.9% 4.2%

Total Asset 7.2% -0.4% -0.7% 0.3%

Profitability:

ROA 24.0% 25.0% 22.9% 24.0%

ROE 91.8% 82.2% 66.2% 69.2%

Payout Ratio 50.9% 50.8% 99.7% 99.4%

Dividend Yield 4.5% 7.9% 7.0% 7.3%

PEG ratio 3.2 1.6 (1.6) 3.2

Leverage:

Debt Ratio 16.0% 14.7% 13.9% 13.9%

Debt-Equity 62.0% 41.7% 40.8% 39.5%

Times Int. Earned 26.4 168.5 28.2 30.2

Altman Z SCORE 4.1 5.0 5.0 5.1

Valuation:

EPS (BDT) 25.6 27.5 25.1 26.1

NAVPS (BDT) 28.4 38.6 37.2 38.3

P/E (x) 11.2 12.6 14.2 13.6

P/NAV (x) 10.1 9.0 9.5 9.3

EV/EBITDA (x) 4.4 5.6 5.8 5.7

EV/Sales (x) 2.8 3.5 3.6 3.5

Price/Sales (x) 2.7 3.4 3.4 3.4

Price/OCF (x) 6.7 14.0 8.3 8.1

*SOURCE; COMPANY DISCLOSURES & EBLSL RESEARCH; ** KEY TERMINOLOGIES ARE PRESENTED AT THE END OF THE

REPORT

Grameenphone Limited (GP) is the largest telecommunication service provider in Bangladesh. The immediate parent of GP is Telenor Mobile Communications AS and the ultimate parent is Telenor ASA; both the companies were incorporated in Norway.

Key Catalyst

Efficiency in managing solid growth in subscriber acquisition, revenue and net profit with controlled OPEX even in challenging business environment.

Strong brand image and active subscriber base have positioned the company ahead of its rivals.

GP recently acquired 10.4 MHz new spectrum at a cost of $391.15 million and currently holds a total of 47.4 MHz spectrum, highest in the industry.

Growing contribution from data indicates growth potential. Contribution of data revenue increased to 24.4% in 2020 from only 8.1% in 2015.

Handsome dividend payout policy (nearly 100% each year).

Risk Factor

Higher OTT platform use and high voice call rates causing decline in voice call services usage and revenue (6.6%YoY revenue drop in 2020).

Growing use of ISP/PSTN broadband internet services may negatively affect long term cellular data consumption.

Failure to successfully diversify business in new and innovative segments may lead to long-term business downsizing.

Regulatory pressures and ongoing tussles between the operator and the regulator reducing the market value of GP.

Any unfavorable outcome of ongoing dispute may lead to massive financial burden for the company and can cause significant value erosion.

Tougher business restrictions from the regulator may emerge anytime on the ground of being an operator with significant market power (SMP).

Grameenphone experienced remarkable regulatory challenges in the history of Bangladesh telecommunication industry over the last couple of years that are yet to fully settle. The year 2020 started with the continuation of the tussle between GP and BTRC (telecom regulator) concerning BDT125 bn system audit claim. However, GP managed to mitigate the dispute since the second quarter after deposit of BDT 20.0 billion against the audit dispute, as instructed by the honorable Supreme Court. Besides, the regulator also implemented initial SMP restrictions during

the year.

Meanwhile, GP’s earnings during the year were in line with our expectations. As this point of time, we view GP’s stock as fairly valued with its current market prices and our estimated intrinsic value based on our assessment of the operator’s future business potential while keeping in mind significant uncertainties and

contingencies.

We have updated our valuation model based on recent disclosures, our assessment of recent company performance and expectation of future outlook, macro-economic and industry outlook etc. We are assigning ‘Accumulate’ rating on GP stock with a December 2021 estimated intrinsic value of BDT 355.0 per share and 130% expected interim dividend. Our intrinsic price can yield a total 7.3% on holding GP stock till December

2021.

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 2 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

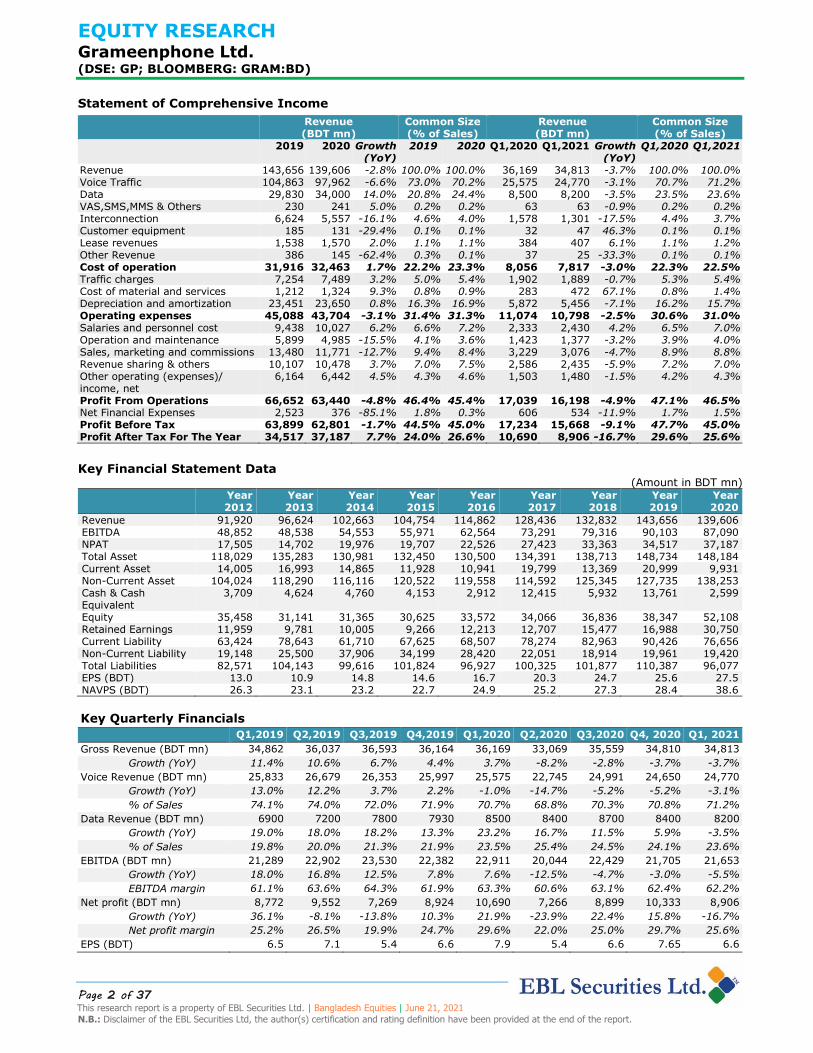

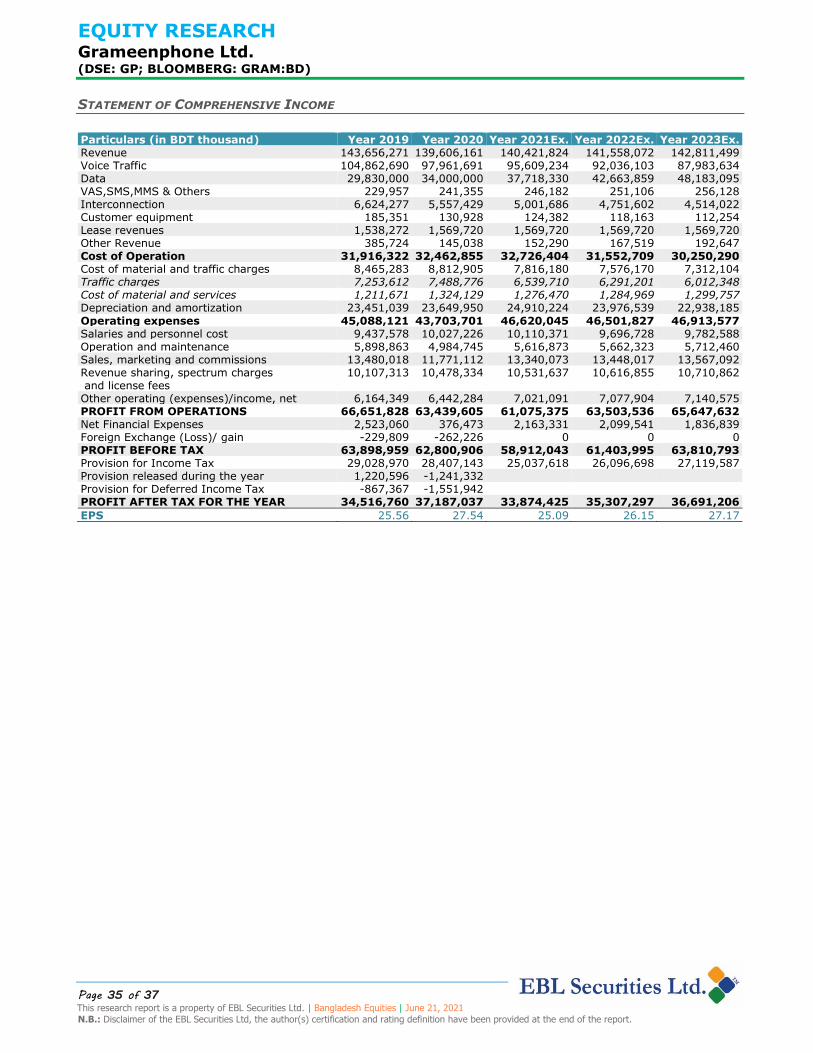

Statement of Comprehensive Income

Revenue (BDT mn)

Common Size (% of Sales)

Revenue (BDT mn)

Common Size (% of Sales)

2019 2020 Growth (YoY)

2019 2020 Q1,2020 Q1,2021 Growth (YoY)

Q1,2020 Q1,2021

Revenue 143,656 139,606 -2.8% 100.0% 100.0% 36,169 34,813 -3.7% 100.0% 100.0% Voice Traffic 104,863 97,962 -6.6% 73.0% 70.2% 25,575 24,770 -3.1% 70.7% 71.2% Data 29,830 34,000 14.0% 20.8% 24.4% 8,500 8,200 -3.5% 23.5% 23.6% VAS,SMS,MMS & Others 230 241 5.0% 0.2% 0.2% 63 63 -0.9% 0.2% 0.2% Interconnection 6,624 5,557 -16.1% 4.6% 4.0% 1,578 1,301 -17.5% 4.4% 3.7% Customer equipment 185 131 -29.4% 0.1% 0.1% 32 47 46.3% 0.1% 0.1% Lease revenues 1,538 1,570 2.0% 1.1% 1.1% 384 407 6.1% 1.1% 1.2% Other Revenue 386 145 -62.4% 0.3% 0.1% 37 25 -33.3% 0.1% 0.1% Cost of operation 31,916 32,463 1.7% 22.2% 23.3% 8,056 7,817 -3.0% 22.3% 22.5% Traffic charges 7,254 7,489 3.2% 5.0% 5.4% 1,902 1,889 -0.7% 5.3% 5.4% Cost of material and services 1,212 1,324 9.3% 0.8% 0.9% 283 472 67.1% 0.8% 1.4% Depreciation and amortization 23,451 23,650 0.8% 16.3% 16.9% 5,872 5,456 -7.1% 16.2% 15.7% Operating expenses 45,088 43,704 -3.1% 31.4% 31.3% 11,074 10,798 -2.5% 30.6% 31.0% Salaries and personnel cost 9,438 10,027 6.2% 6.6% 7.2% 2,333 2,430 4.2% 6.5% 7.0% Operation and maintenance 5,899 4,985 -15.5% 4.1% 3.6% 1,423 1,377 -3.2% 3.9% 4.0% Sales, marketing and commissions 13,480 11,771 -12.7% 9.4% 8.4% 3,229 3,076 -4.7% 8.9% 8.8% Revenue sharing & others 10,107 10,478 3.7% 7.0% 7.5% 2,586 2,435 -5.9% 7.2% 7.0% Other operating (expenses)/ income, net

6,164 6,442 4.5% 4.3% 4.6% 1,503 1,480 -1.5% 4.2% 4.3%

Profit From Operations 66,652 63,440 -4.8% 46.4% 45.4% 17,039 16,198 -4.9% 47.1% 46.5% Net Financial Expenses 2,523 376 -85.1% 1.8% 0.3% 606 534 -11.9% 1.7% 1.5% Profit Before Tax 63,899 62,801 -1.7% 44.5% 45.0% 17,234 15,668 -9.1% 47.7% 45.0% Profit After Tax For The Year 34,517 37,187 7.7% 24.0% 26.6% 10,690 8,906 -16.7% 29.6% 25.6%

Key Financial Statement Data (Amount in BDT mn)

Year 2012

Year 2013

Year 2014

Year 2015

Year 2016

Year 2017

Year 2018

Year 2019

Year 2020

Revenue 91,920 96,624 102,663 104,754 114,862 128,436 132,832 143,656 139,606 EBITDA 48,852 48,538 54,553 55,971 62,564 73,291 79,316 90,103 87,090 NPAT 17,505 14,702 19,976 19,707 22,526 27,423 33,363 34,517 37,187 Total Asset 118,029 135,283 130,981 132,450 130,500 134,391 138,713 148,734 148,184 Current Asset 14,005 16,993 14,865 11,928 10,941 19,799 13,369 20,999 9,931 Non-Current Asset 104,024 118,290 116,116 120,522 119,558 114,592 125,345 127,735 138,253 Cash & Cash Equivalent

3,709 4,624 4,760 4,153 2,912 12,415 5,932 13,761 2,599

Equity 35,458 31,141 31,365 30,625 33,572 34,066 36,836 38,347 52,108 Retained Earnings 11,959 9,781 10,005 9,266 12,213 12,707 15,477 16,988 30,750 Current Liability 63,424 78,643 61,710 67,625 68,507 78,274 82,963 90,426 76,656 Non-Current Liability 19,148 25,500 37,906 34,199 28,420 22,051 18,914 19,961 19,420 Total Liabilities 82,571 104,143 99,616 101,824 96,927 100,325 101,877 110,387 96,077 EPS (BDT) 13.0 10.9 14.8 14.6 16.7 20.3 24.7 25.6 27.5 NAVPS (BDT) 26.3 23.1 23.2 22.7 24.9 25.2 27.3 28.4 38.6

Key Quarterly Financials

Q1,2019 Q2,2019 Q3,2019 Q4,2019 Q1,2020 Q2,2020 Q3,2020 Q4, 2020 Q1, 2021

Gross Revenue (BDT mn) 34,862 36,037 36,593 36,164 36,169 33,069 35,559 34,810 34,813

Growth (YoY) 11.4% 10.6% 6.7% 4.4% 3.7% -8.2% -2.8% -3.7% -3.7%

Voice Revenue (BDT mn) 25,833 26,679 26,353 25,997 25,575 22,745 24,991 24,650 24,770

Growth (YoY) 13.0% 12.2% 3.7% 2.2% -1.0% -14.7% -5.2% -5.2% -3.1%

% of Sales 74.1% 74.0% 72.0% 71.9% 70.7% 68.8% 70.3% 70.8% 71.2%

Data Revenue (BDT mn) 6900 7200 7800 7930 8500 8400 8700 8400 8200

Growth (YoY) 19.0% 18.0% 18.2% 13.3% 23.2% 16.7% 11.5% 5.9% -3.5%

% of Sales 19.8% 20.0% 21.3% 21.9% 23.5% 25.4% 24.5% 24.1% 23.6%

EBITDA (BDT mn) 21,289 22,902 23,530 22,382 22,911 20,044 22,429 21,705 21,653

Growth (YoY) 18.0% 16.8% 12.5% 7.8% 7.6% -12.5% -4.7% -3.0% -5.5%

EBITDA margin 61.1% 63.6% 64.3% 61.9% 63.3% 60.6% 63.1% 62.4% 62.2%

Net profit (BDT mn) 8,772 9,552 7,269 8,924 10,690 7,266 8,899 10,333 8,906

Growth (YoY) 36.1% -8.1% -13.8% 10.3% 21.9% -23.9% 22.4% 15.8% -16.7%

Net profit margin 25.2% 26.5% 19.9% 24.7% 29.6% 22.0% 25.0% 29.7% 25.6%

EPS (BDT) 6.5 7.1 5.4 6.6 7.9 5.4 6.6 7.65 6.6

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 3 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

SYNOPSIS

Grameenphone Ltd. leads the telecommunication sector in Bangladesh with 46.5% subscriber market share. It has been leading the industry in almost every aspects such as subscription, revenue, cost leadership, profitability and innovation. The service portfolio of the operator mainly concentrated on voice and data segment only with almost 95% of total revenue contribution. The journey of Grameenphone as a telecom brand in Bangladesh started on 26th

March 1997 with an aim to empower the rural population of Bangladesh with network connectivity. It was the first telecom operator to launce pre-paid services in the country and the first telecom company to become listed with the capital market and has been maintaining highest market capitalization in DSE since its listing. Currently, Telenor Mobile Communications AS, Norway owns 55.8% ownership while Grameen Telecom, Bangladesh holds 34.2% ownership of the company.

The company grew at a rate of 5.9% over the last 5 years while its bottom-line also witnessed 13.5% CAGR during the same period. GP’s unique ability to control operating costs with higher efficiency led to significant improvement in profit margins that ultimately resulted into noticeable improvement in net profit margins. OPEX to sales reduced

to 31.3% in 2020 against 36.4% in 2015 and CAGR in net revenue during the same period was 13.5%. Efficiency in management of operating cost has been acting as the key catalyst for sound improvement in bottom-line over the years. Though ARPU experienced downtrend, stability in APPM and robust data consumption growth contributing towards improvement in EBITDA margin (53.4% in 2015 to 62.4% in 2020). GP’s unstoppable business growth is mostly supported by seasoned management expertise, brand loyalty, innovation in product and service offerings and growing reliance on technological solution in designing business strategy.

The company’s growing contribution from data indicates steady growth potential in near future. Contribution of data revenue increased to 24.4% in 2020 from only 8.1% in 2015 with 32% CAGR in data revenue against 5.9% CAGR in

total revenue. Data revenue growth in 2020 was driven by only 8% YoY growth in average data revenue per user per month (data ARPU) as a result of 52% data volume growth and 50% growth in Average Data usage per user per Months (AMBPU) despite 28% reduction in data prices (APPMB). Besides, accelerated drive on the expansion of 4G network capacity, along with the continued focus on 4G conversion also contributing towards higher data consumption. However, with higher use of over the top (OTT) calls in an environment of high voice call charges, revenue from voice calls may continue to decline, however, higher data revenue will partially offset the losses. GP recently acquired 10.4 MHz new spectrum at a cost of $391.15 million and currently holds a total of 47.4 MHz spectrum. GP is currently in a better position to offer better services with its highest spectrum holding in the industry and has recently converted all of its BTS (Base Transceiver Station) in to 4G.

Dispute on system audit claims by BTRC remains a concern but after initial deposit of BDT20.0 bn, the company’s relation with regulator and government has improved. Meanwhile, GP has been declared as an operator with Significant Market Power (SMP) and as per the SMP act, the regulator may time to time impose some business restrictions to restrict the operator from grabbing more market share.

As the local telecom industry is heading towards its maturity stage, with its conventional service offerings, GP is not also an exception. GP’s historical growth engine with steady operating performance is being challenged by slow-down

in average minutes of usages by consumers and lower revenue per user per months triggered by higher OTT platform dependency and significant decline in data prices. At present scenario, ignoring the regulatory tussles & pandemic impact, GP’s growth in next few years will be mostly driven by growth in data usage (AMBPU). However, as data price (APPMB) likely to decline further, data revenue growth will slow down. Currently, the country’s total internet penetration rate is 59.5% and internet penetration rate of GP is only 24%. So, we think that there is still room for growth in data subscription as well along with increase in average data consumption per user for the next few years. However, global telecom industry is taking a shift towards innovative product offerings, IOT and cloud based services, video streaming etc. if the company fails to diversify its business landscape with the changing trend in the industry, its future growth potential will become restricted. Meanwhile, the global pandemic, COVID-19 and its spread in Bangladesh and resultant country-wide shut-down/ lock-down also hampered the operational performance of the company and likely to affect the performance in 2021 as well due to persisting virus spread and future uncertainty.

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 4 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

Table of Contents

CONTENTS

SYNOPSIS............................................................................................................................................... 3

1.0 Investment Thesis .............................................................................................................................. 5

1.1 Valuation/ Determination of Intrinsic Value .......................................................................................... 5

1.2 Discounted Cash Flow Valuation: ....................................................................................................... 6

1.3 Relative Valuation ............................................................................................................................ 8

1.4 Peer Comparison ............................................................................................................................. 9

2.0 Business Description .......................................................................................................................... 13

2.1 Product & Services Offering .............................................................................................................. 13

3.0 Industry Review ................................................................................................................................ 14

3.1 The Industry in Focus ...................................................................................................................... 14

3.2 Market Competition Scenario ............................................................................................................ 15

3.3 Cellular Data Market Highlights ......................................................................................................... 17

3.4 Regulatory Landscape ...................................................................................................................... 18

3.4 Recent Developments in the Industry ................................................................................................. 18

3.5 Industry Outlook and Possible Future Developments ............................................................................ 19

4.0 Corporate Profile ............................................................................................................................... 21

Shareholding Pattern ............................................................................................................................ 21

5.0 Assessment of Corporate Governance ................................................................................................... 22

6.0 Core strengths, Challenges & Business Outlook of Grameenphone ............................................................ 23

7.0 Telecom Regulatory Environment for Grameenphone .............................................................................. 25

8.0 Analysis on Financial Performance ........................................................................................................ 27

9.0 Analysis on the Recent Financial and Operational Performance ................................................................. 31

9.1 Latest Q1,2021 Performance Review ................................................................................................. 31

Key Terminologies ................................................................................................................................... 34

Formulas Used ....................................................................................................................................... 34

Statement of Comprehensive Income......................................................................................................... 35

Statement of Financial Position ................................................................................................................. 36

Key Financial Indicators ........................................................................................................................... 37

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 5 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

1.0 INVESTMENT THESIS

1.1 Valuation/ Determination of Intrinsic Value

Fairly valued with moderate upside based on both DCF and

Relative Valuation Matrices

At the current market price of BDT 343.1 per share, GP’s shares have a P/E multiple of 13.0 for its Q1, 2021 annualized earnings as on 21 June 2021. Taking into consideration of a number of valuation multiples/ methods, intrinsic value for GP stands at BDT 355.0 per share, based on our estimate.

Grameenphone Ltd. appears to be fairly-valued at current market price based on absolute valuation based on projected cash flows and dividends and relative valuation methodologies calculated over 2012 to 2020 audited financial results and historical valuation multiples.

Determination of Fair Value Per Share

Valuation Methods Estimated Value Weights

Absolute Stock Valuation:

Terminal Cash Flow Method 339.2

50% Terminal EV/EBITDA Method 321.0

Dividend Discount Model 317.3

Residual Income Model 308.3

Average 321.5

Relative Valuation

Hist. Price to net revenue 347.3

50%

Hist. Price to cash flows 356.5

Hist. Price to earnings 427.2

Hist. Price to book value 414.9

Hist. EV/EBIT 392.1

Hist. EV/EBITDA 395.2

Average 388.9

Estimated Intrinsic Value 355.2

Current Price 343.1

Target Price 355.0

Expected Capital Gain 3.5%

Target Holding Period December 2021

Expected Dividend Yield 3.8%

Total Six Month's Return 7.3%

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 6 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

1.2 Discounted Cash Flow Valuation:

We have updated our DCF based valuation of Grameenphone Limited by forecasting Free Cash Flows up to 2030. To derive the intrinsic value, we estimated terminal value at the end of 2030 using- 1. Constant Growth Cash flow Method

2. EV/ EBITDA Exit Multiple Method Our DCF analysis with a discount rate of 11.14% & terminal growth rate of 3.5% and terminal EV/ EBITDA multiple of 6.5(x) gives us Enterprise Value of BDT 470.1 billion using the constant FCFF growth model and BDT 445.5 billion using Exit Multiple Method. The DCF based fair value using Constant Growth Cash Flow method stands at BDT 339.2 per share for the company and BDT 321.0 per share using Exit Multiple Method considering 1,350.3 million number of shares outstanding.

(Figures in BDT million) 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 DCF Valuation Based on Terminal Cash Flows Profit for the Year 33,874 35,307 36,691 37,410 37,113 37,966 38,171 37,650 37,054 36,646 Add: After Tax Interest Expenses 1,244 1,207 1,056 930 847 736 587 472 399 130 Add: Depreciation & Amortization 24,910 23,977 22,938 22,013 21,239 19,544 18,027 16,800 15,835 15,081 Less: Investment in NWC -1,383 1,216 18 429 1,040 557 942 1,271 1,159 1,035 Less: Capital Expenditures 26,809 17,553 17,553 17,553 17,553 12,000 12,000 12,000 12,000 12,000 Free Cash Flow to the Firm 34,603 41,721 43,114 42,371 40,605 45,689 43,843 41,651 40,129 38,822 Terminal value of FCF 525,872 Discount Factor 1.0000 0.8998 0.8096 0.7284 0.6554 0.5897 0.5306 0.4774 0.4296 0.3865 Present Value Adjusted Free Cash flow to the Firm

266,855

PV of Terminal value of FCF 203,245 Enterprise Value 470,100 Plus: Cash & cash equivalent 7,530 Less: Interest Debt 19,577 Equity Value 458,053 No. of Share Outstanding 1,350

Value per Share (BDT) 339.2

DCF Valuation Based on using Exit Multiple Method Terminal Value with assumed EV/ EBITDA 513,752 Free Cash Flow to the Firm 34,603 41,721 43,114 42,371 40,605 45,689 43,843 41,651 40,129 38,822 Discount Factor 1.0000 0.8997 0.8095 0.7284 0.6553 0.5896 0.5305 0.4773 0.4294 0.3864 Present Value of Explicit FCFF 266,855 Present Value of Terminal Value 178,657 Total Enterprise Value 445,512 Less: Debt 19,577 Add: Cash 7,530 Equity Value 433,465

Value per Share (BDT) 321.0

Residual Income Model

(Figures in BDT million) 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 Equity Charge 5,516 5,686 5,712 5,668 5,592 5,609 5,649 5,631 5,549 5,495 Residual Income 28,358 29,621 30,979 31,742 31,522 32,357 32,522 32,018 31,505 31,151 Terminal value of Residual Income

421,969

Beginning Book Value of Equity 52,107 Present Value of Residual Income

201,066

Present Value of Terminal Residual Income

163,088

Equity Value 416,120 Value Per Share 308.3

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 7 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

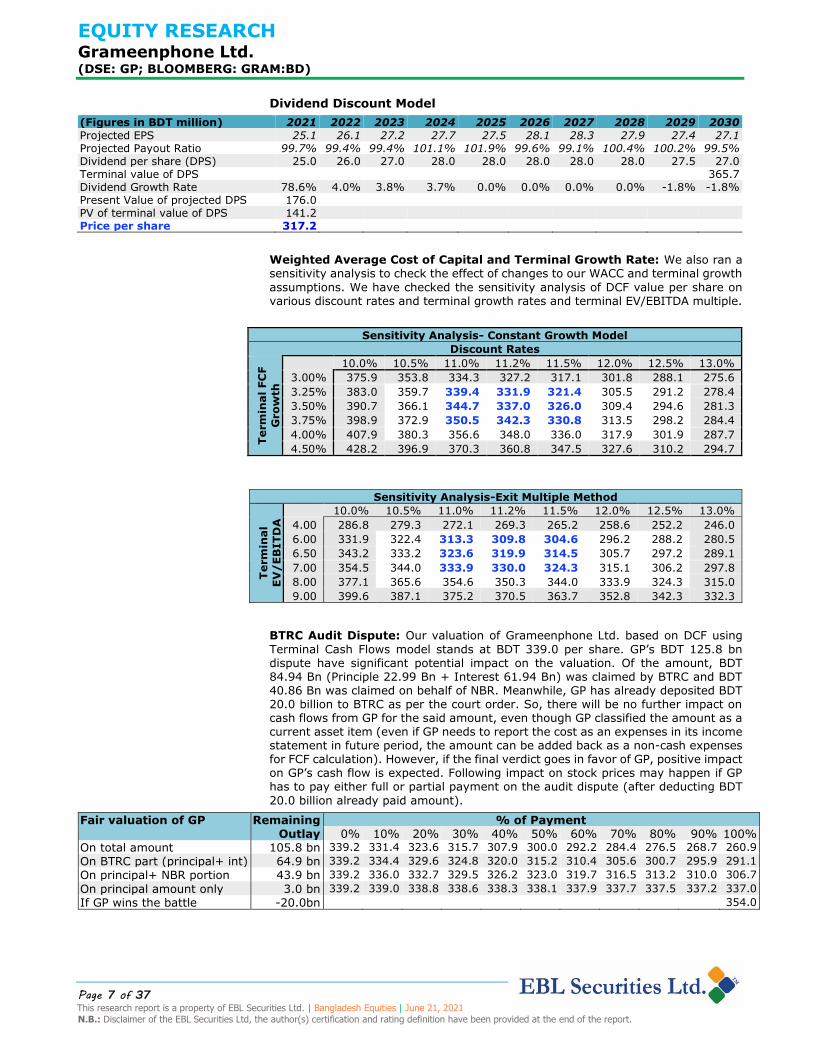

Dividend Discount Model

(Figures in BDT million) 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Projected EPS 25.1 26.1 27.2 27.7 27.5 28.1 28.3 27.9 27.4 27.1 Projected Payout Ratio 99.7% 99.4% 99.4% 101.1% 101.9% 99.6% 99.1% 100.4% 100.2% 99.5% Dividend per share (DPS) 25.0 26.0 27.0 28.0 28.0 28.0 28.0 28.0 27.5 27.0 Terminal value of DPS 365.7 Dividend Growth Rate 78.6% 4.0% 3.8% 3.7% 0.0% 0.0% 0.0% 0.0% -1.8% -1.8% Present Value of projected DPS 176.0 PV of terminal value of DPS 141.2 Price per share 317.2

Weighted Average Cost of Capital and Terminal Growth Rate: We also ran a sensitivity analysis to check the effect of changes to our WACC and terminal growth

assumptions. We have checked the sensitivity analysis of DCF value per share on various discount rates and terminal growth rates and terminal EV/EBITDA multiple.

Sensitivity Analysis- Constant Growth Model

Discount Rates

Term

inal FC

F

Gro

wth

10.0% 10.5% 11.0% 11.2% 11.5% 12.0% 12.5% 13.0%

3.00% 375.9 353.8 334.3 327.2 317.1 301.8 288.1 275.6

3.25% 383.0 359.7 339.4 331.9 321.4 305.5 291.2 278.4

3.50% 390.7 366.1 344.7 337.0 326.0 309.4 294.6 281.3

3.75% 398.9 372.9 350.5 342.3 330.8 313.5 298.2 284.4

4.00% 407.9 380.3 356.6 348.0 336.0 317.9 301.9 287.7

4.50% 428.2 396.9 370.3 360.8 347.5 327.6 310.2 294.7

Sensitivity Analysis-Exit Multiple Method

Term

inal

EV

/E

BITD

A 10.0% 10.5% 11.0% 11.2% 11.5% 12.0% 12.5% 13.0%

4.00 286.8 279.3 272.1 269.3 265.2 258.6 252.2 246.0

6.00 331.9 322.4 313.3 309.8 304.6 296.2 288.2 280.5

6.50 343.2 333.2 323.6 319.9 314.5 305.7 297.2 289.1

7.00 354.5 344.0 333.9 330.0 324.3 315.1 306.2 297.8

8.00 377.1 365.6 354.6 350.3 344.0 333.9 324.3 315.0

9.00 399.6 387.1 375.2 370.5 363.7 352.8 342.3 332.3

BTRC Audit Dispute: Our valuation of Grameenphone Ltd. based on DCF using

Terminal Cash Flows model stands at BDT 339.0 per share. GP’s BDT 125.8 bn dispute have significant potential impact on the valuation. Of the amount, BDT 84.94 Bn (Principle 22.99 Bn + Interest 61.94 Bn) was claimed by BTRC and BDT 40.86 Bn was claimed on behalf of NBR. Meanwhile, GP has already deposited BDT 20.0 billion to BTRC as per the court order. So, there will be no further impact on cash flows from GP for the said amount, even though GP classified the amount as a current asset item (even if GP needs to report the cost as an expenses in its income statement in future period, the amount can be added back as a non-cash expenses for FCF calculation). However, if the final verdict goes in favor of GP, positive impact on GP’s cash flow is expected. Following impact on stock prices may happen if GP has to pay either full or partial payment on the audit dispute (after deducting BDT

20.0 billion already paid amount).

Fair valuation of GP Remaining Outlay

% of Payment 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

On total amount 105.8 bn 339.2 331.4 323.6 315.7 307.9 300.0 292.2 284.4 276.5 268.7 260.9

On BTRC part (principal+ int) 64.9 bn 339.2 334.4 329.6 324.8 320.0 315.2 310.4 305.6 300.7 295.9 291.1

On principal+ NBR portion 43.9 bn 339.2 336.0 332.7 329.5 326.2 323.0 319.7 316.5 313.2 310.0 306.7

On principal amount only 3.0 bn 339.2 339.0 338.8 338.6 338.3 338.1 337.9 337.7 337.5 337.2 337.0

If GP wins the battle -20.0bn 354.0

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 8 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

1.3 Relative Valuation

We tried to compare the performance of Grameenphone Limited based on its

historical earnings multiple.

Earnings Based Valuation Comparable (Time Series Analysis):

(In BDT million*) 2012 2013 2014 2015 2016 2017 2018 2019 2020 CAGR 8 Years

A. Total assets 118,029 135,283 130,981 132,450 130,500 134,391 138,713 148,734 148,184 Asset growth 14.60% -3.20% 1.10% -1.50% 3.00% 3.20% 7.20% -0.40% 2.90% B. Net revenue 91,920 96,624 102,663 104,754 114,862 128,436 132,832 143,656 139,606 Net revenue growth 5.10% 6.30% 2.00% 9.60% 11.80% 3.40% 8.10% -2.80% 5.40% C. EBITDA 48,852 48,538 54,553 55,971 62,564 73,291 79,316 90,103 87,090 EBITDA growth -0.60% 12.40% 2.60% 11.80% 17.10% 8.20% 13.60% -3.30% 7.50% D. EBIT 33,675 33,199 36,896 36,964 41,566 49,954 56,777 66,652 63,440 EBIT growth -1.40% 11.10% 0.20% 12.50% 20.20% 13.70% 17.40% -4.80% 8.20% E. Net profit after tax 17,505 14,702 19,976 19,707 22,526 27,423 33,363 34,517 37,187 NPAT Growth -16.00% 35.90% -1.30% 14.30% 21.70% 21.70% 3.50% 7.70% 9.90% F. Net cash flow from operating activities

29,936 37,081 31,255 38,791 46,152 57,783 60,413 57,393 33,572

Cash flow growth 23.90% -15.70% 24.10% 19.00% 25.20% 4.60% -5.00% -41.50% 1.40%

G. Book value of equity 35,458 31,141 31,365 30,625 33,572 34,066 36,836 38,347 52,108 H. Enterprise value (EV) 245,952 291,406 517,343 371,620 407,458 642,456 503,395 395,923 487,806 I. No of shares outstanding 1,350 1,350 1,350 1,350 1,350 1,350 1,350 1,350 1,350 J. Price per share 175 200.9 361.9 253 284.1 470.8 367.3 285.8 347.1

Valuation Ratios

Median Price to net revenue 2.6 2.8 4.8 3.3 3.3 4.9 3.7 2.7 3.4 3.3 Price to cash flows 7.9 7.3 15.6 8.8 8.3 11.0 8.2 6.7 14.0 8.3 Price- earnings 13.5 18.5 24.5 17.3 17.0 23.2 14.9 11.2 12.6 17.0 Price- book value 6.7 8.7 15.6 11.2 11.4 18.7 13.5 10.1 9.0 11.2 EV/ EBIT 7.3 8.8 14.0 10.1 9.8 12.9 8.9 5.9 7.7 8.9 EV/ EBITDA 5.0 6.0 9.5 6.6 6.5 8.8 6.3 4.4 5.6 6.3

* All values are in BDT million except no of shares, growth rates & valuation multiples

Earnings & Book Value Based Valuation:

A. Historical Average Multiples(x) B. Exp. Values 2021 (BDT mn) C. Per share values

D. Price Per Share (A x C)

Price to net revenue 3.3 Net revenue 140,422 104.0 347.3 Price to cash flows 8.3 Cash Flows 57,905 42.9 356.5 Price to earnings 17.0 NPAT 33,874 25.1 427.2 Price to book value 11.2 Book Value 50,223 37.2 414.9

Average Value Per Share 386.5

Valuation based on Enterprise Value of the company

Based on Historical Enterprise Value Multiple EV/EBIT EV/ EBITDA Target Multiple 8.9 6.3 Bases (EBIT or EBITDA)- Est. 2021 61,075 85,986 Enterprise Value 541,506 545,724 Plus: Cash & cash equivalent 7,530 7,530 Less: Interest Debt 19,577 19,577 Equity Value 529,459 533,677 Value Per Share 392.1 395.2 Average Value per share 393.7

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 9 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

1.4 Peer Comparison Robi Axiata Limited (Robi) has recently been enlisted with Dhaka Stock Exchange and Chittagong Stock Exchange on 24 December, 2020. Key financial comparisons between the two companies are provided below.

ROBI Grameenphone Comparison

Key Fundamentals (As on 21 Jun 2021)

Market Cap (BDT mn) 230,993 463,288 2.0x

Enterprise Value (EV) (BDT mn) 279,914 482,405 1.7x

Stocks Price (BDT) 44.1 343.1 7.8x

Number of Shares Outstanding (mn) 5,238 1,350 0.3x

Annualized EPS (BDT) 0.28 26.38 94.2x

Last Audited EPS (BDT) 0.33 27.54 83.5x

Latest NAVPS (BDT) 12.7 45.19 3.6x

Year 2020 Year 2020

Balance Sheet Items (BDT mn) ROBI Grameenphone Comparison

Total Assets 199,465 148,184 0.7x

Current Assets 19,537 9,931 0.5x

Non-current Assets 179,928 138,253 0.8x

Total Equity 65,956 52,108 0.8x

Paid Up Capital 52,379 13,503 0.3x

Retained Earnings 6,914 30,750 4.4x

Cash & Cash Equivalent 9,833 2,599 0.3x

Total Debt (Excl. Lease) 24,337 1,240 0.1x

Total Lease 34,417 20,476 0.6x

Current Liabilities 73,800 76,656 1.0x

Non-current Liabilities 59,708 19,420 0.3x

Income Statement Items (BDT mn) ROBI Grameenphone Comparison

Revenue 75,643 139,606 1.8x

Cost of Operation 47,358 32,463 0.7x

Operating Cost 17,758 43,704 2.5x

EBITDA 31,917 87,090 2.7x

Operating Profit 10,526 63,440 6.0x

Finance Expenses 4,889 376 0.1x

Profit before tax 5,509 62,801 11.4x

Provision for tax 3,955 25,614 6.5x

Net Profit 1,553 37,187 23.9x

Ratios ROBI Grameenphone

ROA 0.8% 25.0%

ROE 2.4% 82.2%

Debt-Equity 89.1% 41.7%

Debt-Assets 29.5% 14.7%

EBITDA Margin 42.2% 62.4%

NPAT Margins 2.1% 26.6%

Pricing Based on Relative Valuation:

Particulars of GP Benchmark Multiple Exp. Value per share(BDT)

Peer Forward P/E An. EPS 2021: 26.38 156.43 4,127.1

Peer Forward P/NAVPS Latest NAPVPS: 45.19 3.46 156.3

Peer EV/EBIT EBIT: 63,440 mn 26.77 1,248.8

Peer EV/EBITDA EBITDA: 87,090 mn 8.72 553.5

Peer Price to Sales Sales per share:103.39 3.03 313.6

Peer Price to Cash Flow Cash Flow per share:24.86 9.01 224.1

Based on the above comparison, with most of the popular valuation methods, it appears that Grameenphone Limited

is currently undervalued compared to the valuation of Robi Axiata Ltd. However, in terms of the absolute valuation methodologies and relative valuation of Grameenphone based on its own historical multiples, we found that Grameenphone Limited is currently fairly priced with limited upside potential.

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 10 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

1.2 Key Valuation Assumptions/ Inputs

Based on prevailing industry perspective and our own assessment & expectation of

company performance, we have initiated some changes to our earlier projections. However, future projection is subject to enormous regulatory unpredictability. We tried to make the best possible forecast of GP’s financials based on available historical data, present industry insights and our own market observation.

Revenue: Grameenphone Ltd. achieved moderate 5.9% CAGR in its topline during the preceding five years (2015 to 2020). The growth in the recent period was mainly driven by increased contribution of data revenue. Even though Voice remained the core component of GP’s revenue pie, its contribution is on the decline. Contribution

from data revenue in 2020 stood at 24.4% against 20.8% in 2019.

Historical Projected

Particulars 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Voice ARPU 129.8 125.8 126.1 127.0 124.5 111.0 104.0 96.2 88.4 80.6 72.8 67.6 62.4 57.2 52.0 46.8

AMPU 244 258 256 234 217 210 200 185 170 155 140 130 120 110 100 90

APPM (Inc. Interconnect) 0.53 0.49 0.49 0.54 0.57 0.53 0.52 0.52 0.52 0.52 0.52 0.52 0.52 0.52 0.52 0.52

APPM (Voice Only) 0.46 0.44 0.45 0.50 0.54 0.50 0.49 0.49 0.49 0.49 0.49 0.49 0.49 0.49 0.49 0.49

Data ARPU+ 53 60 63 62 64 69 73 74 71 67 63 59 56 53 52 51

AMBPU 284 488 651 1059 1653 2472 3461 4499 5399 6209 6985 7683 8452 9297 10226 11249 APPGB 192.4 125.3 99.2 60.2 39.7 28.7 21.5 16.8 13.4 11.0 9.2 7.9 6.8 5.9 5.2 4.6

Blended ARPU 155 162 167 157 157 150 143 139 135 129 122 116 110 103 96 90

Blended APPM 0.64 0.63 0.65 0.67 0.72 0.71 0.72 0.75 0.79 0.83 0.87 0.90 0.92 0.93 0.96 1.00

Total BD Population (mn) 158.9 160.8 162.7 164.6 166.5 168.4 170.4 172.3 174.3 176.3 178.3 180.4 182.4 184.5 186.7 188.8

Total GP Subscriber (mn) 56.7 58.0 65.3 72.7 76.5 79.0 82.2 85.5 88.9 92.5 96.2 100.0 104.0 108.2 112.5 117.0

Industry Sub. Penetration 84.2% 78.6% 89.2% 95.4% 99.4% 101.0% 103.0% 105.0% 107.5% 110.0% 112.5% 115.0% 117.5% 120.0% 122.5% 125.0%

Growth in GP Subscriber 10.0% 2.2% 12.7% 11.3% 5.1% 3.4% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

GP Market Penetration 35.7% 36.0% 40.2% 44.2% 45.9% 46.9% 48.3% 49.6% 51.0% 52.4% 53.9% 55.4% 57.0% 58.6% 60.3% 62.0% GP Market Share 42.4% 45.9% 45.0% 46.3% 46.2% 46.5% 46.8% 47.2% 47.5% 47.7% 47.9% 48.2% 48.5% 48.8% 49.2% 49.6%

Mobile data Users (mn) 15.7 24.5 31.2 37.1 40.6 41.3 45.2 51.3 62.2 69.3 76.9 85.0 88.4 91.9 95.6 99.4

Net Addition (Data Subs. mn) 4.9 8.8 6.7 5.9 3.5 0.7 3.9 6.1 10.9 7.1 7.6 8.1 3.4 3.5 3.7 3.8

Growth in Data Subscription 45.4% 56.1% 27.3% 18.8% 9.5% 1.8% 9.5% 13.5% 21.3% 11.4% 10.9% 10.5% 4.0% 4.0% 4.0% 4.0%

Data Volume (Total) Growth 227.7% 168.1% 69.9% 93.2% 70.9% 52.2% 53.3% 47.5% 45.6% 28.1% 24.8% 21.6% 14.4% 14.4% 14.4% 14.4%

Data subscriber as

% of Total Users 27.7% 42.3% 47.8% 51.0% 53.1% 52.3% 55.0% 60.0% 70.0% 75.0% 80.0% 85.0% 85.0% 85.0% 85.0% 85.0% GP Data market penetration 9.9% 15.2% 19.2% 22.5% 24.4% 24.5% 26.5% 29.8% 35.7% 39.3% 43.1% 47.1% 48.5% 49.8% 51.2% 52.7%

Data Sources: Grameenphone Ltd, The World Factbook, CIA and EBLSL Own Estimate.

*Historical data as reported by the operator.

The key variables for voice revenue forecast are projected subscriber base and average voice revenue per user (ARPU). The subscriber base forecast is further

dependent on projected population of the country and expected industry subscriber penetration and expectation of GP’s market share within the industry. Meanwhile, projected average voice revenue per user (ARPU) also depends on expected average minutes of usage per subscriber (AMPU) and average price per minutes of voice calls (APPM). Likewise, our projection of future data revenue is also dependent on a number of variables including data market penetration, average data price (APPMB), data volume consumption (AMBPU) etc.

We have used following function to forecast the revenue of GP during our forecasted

horizon:

𝑅1 = 𝑆�� ∗ (𝑀 ∗ ��𝑚) + 𝑆𝐷 ∗ (𝑀𝐵 ∗ ��𝑚𝑏) + 𝑅𝑂

0 ∗ (1 + 𝑔𝑅𝑜)

Where,

𝑅1 = 𝑁𝑒𝑥𝑡 𝑝𝑒𝑟𝑖𝑜𝑑 𝑝𝑟𝑜𝑗𝑒𝑐𝑡𝑒𝑑 𝑟𝑒𝑣𝑒𝑛𝑢𝑒 𝑆�� = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑛𝑢𝑚𝑏𝑒𝑟 𝑜𝑓 𝑣𝑜𝑖𝑐𝑒 𝑠𝑢𝑏𝑠𝑐𝑟𝑖𝑝𝑡𝑖𝑜𝑛 𝑀 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑚𝑖𝑛𝑢𝑡𝑒𝑠 𝑜𝑓 𝑢𝑠𝑎𝑔𝑒 ��𝑚 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑚𝑖𝑛𝑢𝑡𝑒𝑠 𝑀 ∗ ��𝑚 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑣𝑜𝑖𝑐𝑒 𝑟𝑒𝑣𝑒𝑛𝑢𝑒 𝑝𝑒𝑟 𝑢𝑠𝑒𝑟, 𝑖𝑛𝑐𝑙𝑢𝑑𝑖𝑛𝑔 𝑖𝑛𝑡𝑒𝑟𝑐𝑜𝑛𝑛𝑒𝑐𝑡𝑖𝑜𝑛 (𝐴𝑅𝑃𝑈) 𝑆𝐷 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑛𝑢𝑚𝑏𝑒𝑟 𝑜𝑓 𝑑𝑎𝑡𝑎 𝑠𝑢𝑏𝑠𝑐𝑟𝑖𝑝𝑡𝑖𝑜𝑛 𝑀𝐵 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑀𝑒𝑔𝑎𝐵𝑦𝑡𝑒 𝑜𝑓 𝑢𝑠𝑎𝑔𝑒 ��𝑚𝑏 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑀𝑒𝑔𝑎𝐵𝑦𝑡𝑒 𝑀 ∗ ��𝑚 = 𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑑𝑎𝑡𝑎 𝑟𝑒𝑣𝑒𝑛𝑢𝑒 𝑝𝑒𝑟 𝑢𝑠𝑒𝑟 (𝐴𝑅𝑃𝑈) 𝑅𝑂

0 = 𝑙𝑎𝑠𝑡 𝑝𝑒𝑟𝑖𝑜𝑑 𝑟𝑒𝑣𝑒𝑛𝑢𝑒 𝑓𝑟𝑜𝑚 𝑜𝑡ℎ𝑒𝑟 𝑠𝑜𝑢𝑟𝑐𝑒𝑠 (𝐶𝑢𝑠𝑡𝑜𝑚𝑒𝑟 𝑒𝑞𝑢𝑖𝑝𝑚𝑒𝑛𝑡, 𝑉𝐴𝑆, 𝑆𝑀𝑆, 𝑀𝑀𝑆 & 𝑜𝑡ℎ𝑒𝑟𝑠) 𝑔𝑅𝑜

= 𝐺𝑟𝑜𝑤𝑡ℎ 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑣𝑒𝑛𝑢𝑒 𝑓𝑟𝑜𝑚 𝑜𝑡ℎ𝑒𝑟 𝑠𝑜𝑢𝑟𝑐𝑒𝑠

Our long term business forecast of Grameenphone is based on the continuation of existing service portfolio of the operator. However, if the operator can successfully position itself in any new business segment with notable revenue contribution, we will revise our projections and valuation accordingly.

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 11 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

Voice AMPU experienced steady decline over the past years and declined to 210 minutes per user per month in 2020 from 258 minutes of usage in 2016. We expect the usage of voice calls will continue to decline in future along with higher OTT (Over the top) service adoption. The downside of average voice call price per minute is protected by the regulation (minimum floor prices in the industry) and that may increase further for GP, if regulator imposes price specific SMP instructions in future.

Average Data Consumption Per User (AMBPU) Growth

Average Data Price (APPMB) Growth

Source: EBLSL Research & Estimates

We expect that revenue from voice traffic will be declining while data revenue will be growing. However, data revenue will be growing at a decreasing rate as the period of faster data penetration is almost over and with continued price reduction and faster ISP/PSTN broadband penetration, mobile data consumption will become less attractive in the long run. Furthermore, even though data consumption is forecasted to grow steadily, in line with industry competition and regulatory

pressure, data prices will experience a declining trend in future, hurting the data revenue of the operator. Despite, the forecasted decline in voice revenue, it will remain as a key revenue contributor to the company’s earnings.

Revenue Contribution of Grameenphone Ltd.

Historical Projected

Particulars 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Voice Traffic 70.3% 67.3% 65.9% 73.4% 73.0% 70.2% 68.1% 65.0% 61.6% 58.5% 56.0% 54.3% 52.8% 51.6% 49.8% 47.5%

Data 8.1% 12.5% 16.4% 19.2% 20.8% 24.4% 26.9% 30.1% 33.7% 36.9% 39.5% 41.2% 42.4% 43.3% 44.7% 46.6%

VAS,SMS,MMS & Others 7.3% 7.6% 7.3% 0.1% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2%

Interconnection 10.2% 8.0% 6.7% 5.8% 4.6% 4.0% 3.6% 3.4% 3.2% 3.0% 2.9% 2.9% 3.0% 3.1% 3.1% 3.2%

Customer equipment 2.0% 2.4% 1.9% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

Lease revenues 0.0% 0.0% 0.0% 1.2% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.2% 1.2% 1.2% 1.3%

Other revenue 2.2% 2.1% 1.7% 0.2% 0.3% 0.1% 0.1% 0.1% 0.1% 0.2% 0.2% 0.3% 0.4% 0.5% 0.8% 1.2%

Operating performance: Controlled cost of operation and operating expenditures

policy has resulted into increased operating profit margin. Higher revenue and operating efficiency contributing towards healthy EBITDA. GP has always focused in controlling its OPEX with efficient control measures, which resulted into growth in EBITDA as well as increased EBITDA margin over the years. EBITDA margin increased from 50.2% in 2013 to 62.4% in 2020. Analyzing the recent financials and observing the market scenario, we can expect that GP will continue to optimize its operating performance in line with revenue generation.

Following significant assumptions were applied to our projection of GP’s future financial performance. GP also shares 5.5% of its revenue as ‘revenue sharing’ and 1.0% of its revenue as ‘contribution to social obligation fund’ with BTRC as per licensing conditions. Licensing conditions also require the operator to pay annual fees and spectrum charges.

40.0

%

125.

4%

71.8

%

33.4

%

62.7

%

56.1

%

49.5

%

40.0

%

30.0

%

20.0

%

15.0

%

12.5

%

10.0

%

10.0

%

10.0

%

10.0

%

10.0

%-20.0%

0.0 %

20. 0%

40. 0%

60. 0%

80. 0%

100 .0%

120 .0%

140 .0%

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1E

2022

E

202

3E

202

4E

202

5E

202

6E

202

7E

202

8E

2029

E

203

0E

Growth in AMBPU Linear (Growth in AMBPU)

-31.

2%

-57.

2%

-34.

9%

-20.

8%

-39.

3%

-34.

1% -27.

7%

-25.

0%

-22.

0%

-20.

0%

-18.

0%

-16.

0%

-15.

0%

-14.

0%

-13.

0%

-12.

0%

-11.

0%

-70.0%

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0 %

2014

2015

2016

2017

2018

2019

2020

2021

E

2022

E

2023

E

2024

E

2025

E

2026

E

2027

E

2028

E

2029

E

2030

E

Growth in APPMB Linear (Growth in APPMB )

GP has most effective cost control mechanism in the industry

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 12 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

Cost Item Sources of Cost Historical Rates Forecast

2016 2017 2018 2019 2020 2021 to 2030

Traffic charges %of revenue from voice traffic & interconnection

6.62% 6.00% 5.75% 6.51% 7.23% 6.50%

Cost of material and services % of revenue from material and traffic charges

35.42% 33.54% 59.99% 51.80% 63.45% 61.00%

Salaries and personnel cost % of net sales 7.21% 6.87% 6.45% 6.57% 7.18% 7.20%

Operation and maintenance % of net sales 3.27% 3.12% 4.20% 4.11% 3.57% 4.00%

Sales, marketing and commissions % of net sales 10.88% 8.76% 10.60% 9.38% 8.43% 9.50%

Revenue sharing, spectrum charges, licence fees, & Contribution to Social Obligation Fund

% of net sales 7.75% 7.64% 7.21% 7.04% 7.51% 7.50%

Other operating income (expenses), net

% of net sales 7.14% 8.50% 6.32% 4.29% 4.61% 5.00%

Dividend history and projections: Like most other MNC’s, GP has a good track record of handsome cash dividend disbursements in the form of both interim and final payment. We expect that GP will continue to follow the same

payout policy, unless there arises any unforeseeable needs for retaining income.

Historical Dividend Payout 2012 2013 2014 2015 2016 2017 2018 2019 2020 Interim 90% 90% 95% 80% 85% 105% 125% 90% 130% Final 50% 50% 65% 60% 90% 100% 155% 40% 145% Total 140% 140% 160% 140% 175% 205% 280% 130% 275% DPS 14.0 14.0 16.0 14.0 17.5 20.5 28.0 13.0 27.5 EPS 13.0 10.9 14.8 14.6 16.7 20.3 24.7 25.6 27.5 Payout Ratio 108.0% 128.6% 108.2% 95.9% 104.9% 100.9% 113.3% 50.9% 99.9% Source: GP Annual Reports and EBLSL Research

Forecasted Dividend Payout

2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 Interim 130% 130% 140% 150% 150% 150% 150% 150% 150% 150% Final 120% 130% 130% 130% 130% 130% 130% 130% 125% 120% Total 250% 260% 270% 280% 280% 280% 280% 280% 275% 270% DPS 25.0 26.0 27.0 28.0 28.0 28.0 28.0 28.0 27.5 27.0 EPS 25.1 26.1 27.2 27.7 27.5 28.1 28.3 27.9 27.4 27.1 Payout Ratio 99.7% 99.4% 99.4% 101.1% 101.9% 99.6% 99.1% 100.4% 100.2% 99.5% Source: EBLSL Research Estimates

Potential Litigation Risk: Grameenphone experienced significant disruption in its operation in last couple of years caused by the regulatory tussles with BTRC, notably for BDT125.8 Bn information system audit claim from the operator. Of the amount, BDT 84.94 Bn (Principle 22.99 Bn + Interest 61.94 Bn) was claimed by BTRC and BDT 40.86 Bn was claimed on behalf of NBR. In 2011, BTRC conducted its first audit on Grameenphone Ltd. but the operator then disputed the audit process. Again another fresh audit was conducted in 2015 for the period of 1997 to 2014 but GP continued to deny the claim by questioning the validity and process of the audit.

Meanwhile, NOC’s for various services were also halted by the regulator to pile up pressure on the operator that has hampered the operating activities of the company significantly during the year 2019 and early 2020. The government was also preparing to appoint administrator at Grameenphone Ltd. However, as per the order of the Appellate Division of Supreme the court, GP has deposited BDT 20 billion to BTRC in first half of 2020. After the said deposit, GP’s relation with the regulator eased and several restrictions were withdrawn. The matter is now under the jurisdiction of the Court. Significant uncertainty still prevails there regarding the final settlement of the dispute. Any unfavorable verdict may cause large one time cash outlay from the operator’s book.

BTRC Audit dispute for BDT125.8 Bn

yet remain unresolved

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 13 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

2.0 BUSINESS DESCRIPTION

Grameenphone Ltd. operates a digital mobile telecommunications network based on the GSM standard in the 900 MHz, 1800 MHz and 2100 Mhz frequency bands, under the license granted by the Bangladesh Telecommunication Regulatory Commission (BTRC). The company was awarded with license of 4G/LTE cellular mobile phone services on 19 February 2018. Over the last decade, Grameenphone

has added 13,443 users per day on average.

In addition to existing 37 MHz spectrum, GP has acquired fresh 10.4 MHz spectrum in March 2021 at a combined cost of $378.75 million plus 15% VAT. Total spectrum holding of the company as on date stands at 47.4 MHz.

Mobile spectrum licenses held by Grameenphone Ltd. Spectrum Bandwidth (MHz) Expiry 900 MHz 2×7.4 2026

1800 MHz 2×7.2 + 2×7.4 2026 2x5 2033 2x0.4 2036

2100 MHz 2×10 2028 2x 10 2036

Grameenphone LTD: Key Statistics No of Subscribers 80.75 mn* Pre-paid user % of total 98.0% Mobile data Users 41.7 mn*

4G Subscriber 21.5 mn # of 4G sites 15,590 Geographic Coverage 96.3% Population Coverage 99.6% 4G Population Coverage 95.8% Smartphone Users having GP connection 28.4 mn *As on March 2021; in April No of Subscribers declined to 80.50 mn

2.1 Product & Services Offering

Until now 70% of the company’s revenue are generated for voice traffic service. Data service revenue is continuously increasing its share of pie while contribution from voice traffic service is declining due to robust growth in data revenue. Grameenphone is continuously diversifying its product offerings to retain its growing momentum in the digital marketplace. The operator has been focusing on simplification of its voice call offerings and in line with this, several of the Voice Call packages has been discontinued over the years. GP’s 98% of subscribers are prepaid package subscribers. Currently, in pre-paid segments only 4 packages are available.

Grameenphone Pre-paid Packages

Nishchinto (Attractive Flat Rate for All)

Bondhu (Highest F&F Numbers)

Djuice (Exclusive Community Rate)

Smile

Call Rate: 24 poisha/ 10 second FNF: N/A SMS: 50 poisha / SMS and 25 Poisha/ Bangla SMS Pulse: 10 second

Call Rate: 27.5 poisha/10 second FNF: 1 Super FnF (7.5 poisha/10 second) & 17 FnF (12 poisha/10 second) SMS: 50 poisha / SMS and 25 Poisha/ Bangla SMS Pulse: 10 second

Call Rate: 26 poisha/ 10 second FNF: 10 FnF (12 poisha/ 10 second) & 5 Super FnF (7.5 poisha/ 10 second) SMS: 50 poisha/SMS and 25 Poisha/ Bangla SMS Pulse: 10 second

Call Rate: 28 poisha/ 10 second FNF: 3 FnF (12 paisa/10 second) SMS: 50 poisha / SMS and 25 Poisha/ Bangla SMS Pulse: 10 second

Source: Grameenphone website & EBLSL Research; As on 09 May 2021.

Along with those voice packages, Grameenphone offers customer with more simplified & user-friendly services through customized bundle packs and flexi plans (where customers can make their chosen voice and data bundle with chosen duration of validity). GP has multiple data offerings ranging from 1 day to 30 days

GP provides all kinds of

telecommunication related services

available in the country with its largest network coverage

Voice traffic is the main service offering

of the company with 98% of the pre-

paid user base.

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 14 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

of validity and very small to large volume packs. Data price has been reduced over time in line with the market competition. Despite the reduction in data prices, the company has been able to achieve robust data service revenue growth due to large addition to data subscriber base and increased data usage per subscriber.

Besides voice traffic and data service offerings, the operator has also diversified its businesses in different VAS, GP online shop for selling mobile communication devices to end customers, financial services like GPAY and MobiCash along with several IoT & cloud based services including MyGP, WowBox and GP Music etc. app based digital services. Innovation in these digital services has the potential to reshape the business model of the operator in future even though nothing such services could have visible impact on the financials of the operator yet.

3.0 INDUSTRY REVIEW

Two major telecom service offerings in Bangladesh are “Voice Calls” and “Internet Data” services. Revenue from voice calls still dominate the industry while contribution from data revenue is growing exponentially since the launching of 3G

in Bangladesh. Meanwhile, introduction of 4G in 2018 has further uplifted the data service revenue even though the country is yet to reap the full potential of 4G.

However, voice revenue is expected to remain key revenue drivers over the next few years despite the declining trend over the last few years against increased data usage growth and increasing trend in OTT (Over the Top) usage.

The surge in Covid-19 pandemic in Bangladesh since the early 2020 has increased the adoption of digital lifestyle and working

culture has also become more digitalized and relevant regulatory barriers have been removed. Mobile telephone services has become a key players in today’s economic activities and other essential services. However, COVID-19 has triggered deepest recession globally since the last year and ultimate outcome is yet unknown. The pandemic is expected to trigger major contraction across countries and also could have lasting impact on the productivity and potential output. Likewise, the economy of Bangladesh also comprise of large number of daily wage earners and salaried persons, who lost their jobs all on a sudden. While the economic recovery from the slowdown will depend on multitude of factors, most of the

Asian countries including Bangladesh has shown faster recovery than expected.

3.1 The Industry in Focus:

Favorable macro-economic dynamics helping the industry growth: The growing MAC population, large number of young age population, increased

urbanization, and consistent GDP growth, digitalization of public and private services along with increased access to data connectivity are the key growth drivers for the industry. Young and middle-aged people are the major users of mobile communication devices and around 60% of the entire country belongs to these two groups. The country has a large population base with steadily increasing disposable income along with comparatively low penetration of internet connectivity. The country is now undergoing a transformation period towards getting more digital that will have a major contribution from

telecommunication industry and the industry is also expected to enjoy sound growth along with this transformation journey.

A multi-SIM market with growing subscriber base: The telecom sector is Bangladesh is expected to witness modest growth in terms of subscriber acquisition as unique subscriber penetration is lower and favorable macro-economic dynamics are expected to make positive contribution towards

Key Product/Service Portfolio

Source: Company disclosure

Bangladesh Telecom Industry Subscriptions (In Mn)

Source: BTRC data and EBLSL Projections; F=EBLSL forecast.

Bangladesh Age Distribution Structure

Source: CIA (US Central Intelligence Agency) World Fact Book 2020 est.

Voice Trafic, 70.2%

Data, 24.4%

Interconnection, 4.0%

Other Revenue, 1.5%

-

25.0

50.0

75.0

100.0

125.0

150.0

175.0

200.0

225.0

250.0

201

5

201

6

201

7

201

8

201

9

202

0

202

1F

202

2F

202

3F

202

4F

202

5F

202

6F

202

7F

202

8F

202

9F

203

0F

26.48%

18.56%

40.72%

7.41% 6.82%

0.0 0%

5.0 0%

10. 00%

15. 00%

20. 00%

25. 00%

30. 00%

35. 00%

40. 00%

45. 00%

0-14 years: 15-24years:

25-54years:

55-64years:

>65 years:

Revenue from voice calls dominate the industry

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 15 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

increased digitalization and higher adoption of telecom services. With current smartphone penetration of 38.76% of mobile users and 59.76% real SIM penetration in the country population, there remains significant room for growth.

The ‘Digital Bangladesh’ vision has accelerated the industry growth: The Digital Bangladesh Journey is gaining momentum with the increased collaboration between government and the telecom industry. The government of Bangladesh, through its 7th five year plan had reinforced its goals and objectives for digital Bangladesh with adoption of IT practices and tools on a wider scale to enable economic, cultural and social development and particular attention has also been given to greater adoption of e-Governance and e-Services solutions. The government is working towards digitalizing 90% of its services by 2021 and currently serving more than 60 million people through

6790 digital centers, setting up 39 IT parks and has already digitalized 600 public services and currently in the process of digitalizing 2800 more public services.

3.2 Market Competition Scenario

Due to increased competitiveness among few players, the industry has witnessed some major events in the past few years: With two mobile phone operators having been merged and another shutting down, a six-player market has turned out to be a four-player one. Robi (Axiata) got merged with Airtel (Bharti Airtel) to attain operational efficiency in 2016, which made them the second largest operator by number of connections. Meanwhile, Citycell, the country’s first telco left the battle after a long period of struggle to survive in the industry. BTRC has suspended its operating license due to nonpayment of dues in Q4, 2016. Banglalink, another leading operator in the industry has been operating with steady growth in the number of subscribers but its market share is continually on the wane. Teletalk, the only state-owned operator, failed to

attract users despite having significant government support in various issues. The only operator that has been continually outperforming the industry in terms of both subscriber acquisition as well as profitability is ‘Grameenphone’, a concern of Norway based ‘Telenor’.

Highly competitive market with major focus on value driven growth strategy: The competitive landscape in the local telecom industry can be identified based on price and value offerings. An estimated 70% of consumers

puts high value on the quality, coverage, service, security, differentiation and innovation while rest 30% of the consumers looks for mostly low price. Among the local market players, leading operator Grameenphone has successfully positioned itself as a premium brand with best network coverage and higher price. Meanwhile, Robi has been strategically executing dual brand (Robi & Airtel) proposition targeting specific user segments and value proposition for each segment.

VEON’s subsidiary Banglalink has positioned itself in low price and low network coverage segment for Value for Money user base. State-owned telecom brand Teletalk operates with poor

network coverage and mostly offers services at significantly lower prices.

The operators are also implementing their service upgradation in line with respective user segmentation. For example, while Robi pursued to gain 4G

leadership in the market after launch of 4G in the local market, actual service quality was compromised. GP expanded 4G coverage on a slow and steady basis

Telecom Market Positioning: Brand Perceptions

46%

30%

21%

3%

Telecom Industry Market Share

GP Robi Banglalink Teletalk

Top three players hold 97% of the

market share with leading position

seized by GP

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 16 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

with optimal utilization of their 2G and 3G networks based on geographical preferences and brought whole country under 4G coverage and achieved 4G leadership by 2021. GP always strived to maintain better quality data speed and uninterrupted service in their respective bandwidths.

Competitive Landscape

Operator Name Brand Name Major Shareholders Market Share Technology

Grameenphone Ltd. Grameenphone Telenor Norway, Grameen Telecom Trust

46.5% GSM

Robi Axiata Ltd. Robi/ Airtel Axiata Group Berhad 29.9% GSM

Banglalink Digital Communications Limited

Banglalink Veon Group Netherlands 20.7% GSM

Teletalk Bangladesh Ltd. Teletalk Govt. of Bangladesh 2.9% GSM

Source: BRTC & EBL Securities Ltd. Research

Grameenphone dominates the oligopoly market: The telecommunication

sector in Bangladesh is oligopolistic in nature where only few operators serving the market while nearly half of the industry subscribers belong to only a single operator. GP dominates the telecom industry with 46.5% of the total market share in terms of active mobile user as on March 2021. Banglalink was in the

second leading position before the merger of Robi with Airtel. However, 8.2 million subscribers from Airtel have been added to Robi’s subscriber base through this merger and that uplifted the operator (Robi) into the second-leading position.

Potential New Entry

Buyer Power

Supplier Power

Substitutes

Competitive Rivalry Intense completion among theexisting players in terms of price,market campaigns, bundle offers,subscriber acquisition etc.

Very Low potential of new entry due tohuge capital investment requirement,saturated industry, restricted entry intothe industry by the regulator

Easy to switch between operators, MultiSIM market, MNP facility etc enableshigh bargain power of buyers in theindustry. Buyers can go for the bestprices bundles and network availability.Allocation of Spectrum Frequency is

controlled by the government andpower of the government as supplieris very high IP telephony services, OTT platforms

are the cheapest availablesubstitutes for voice and messagingservices. Increased penetration ofISP/PSTN broadband services andWIFI connectivity are the low costalternatives with unlimited volume.

PORTER'S FIVE FORCES

Source: EBL Securities ltd. Research

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 17 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

High market competition posits downward pressure on ARPU: ARPU in telecom sector has been witnessing a downward trend owing to increased price competition mainly in terms of data service revenue. Even though prices of voice traffic services are protected from market competition with the introduction of floor price system in the industry, data usage getting momentum in the country and

correspondingly voice services experiencing down-trend in terms of volume of usage. More pricing power generated by Robi-Airtel merger: Even though Robi has become the second-largest market player in the industry with highest spectrum holding, it could not pose any significant threat to GP. Rather, the threat of a price war by Airtel has eroded due to reduced market competition and GP has successfully capitalized the opportunity with increase in the prices of its voice calls.

3.3 Cellular Data Market Highlights

Market for mobile internet is enjoying hefty growth driven by subscriber addition and increased penetration: Bangladesh has advanced significantly in terms of internet connectivity. Last 5 years CAGR in total number of internet subscribers in Bangladesh was 13.4% and that of mobile internet

was 12.6%. Contribution of data revenue to total revenue of the country’s leading mobile operator GP increased to 24.4% as on 2020 compared to meagre 3.4% in the year 2013, reflecting the overall industry scenario.

The total number of Internet Subscribers has reached 116.14 million at the end of March 2021. Of the total connections, 91.6% are through the mobile network snd 8.4% through the internet service providers (ISP & PSTN). Even though WiMAX services were getting popularity in the past, since the launching of 3G,

WiMAX service providers were experiencing de-growth in subscription and has lost the market completely in mid-2020. Qubee, Banglalion Communications and Ollo had been providing WiMAX connection in Bangladesh.

As of March 2021, there are around 106.33 million mobile internet connections in Bangladesh i.e., 60.9% of mobile users are now using internet with cellular phones. The country’s data penetration is still far below than other countries in the region. Mobile data subscription penetration in Bangladesh is around 62.5%, however, estimated unique data user penetration (headcount) is still at

around 35-40%. This significant deviation between mobile data connection penetration and mobile data user penetration is due to having multiple number of connections by the same users.

Industry Mobile Data Subscription Trend Bangladesh Mobile Internet Penetration

Source: BTRC & EBLSL Research

0.0%5.0%10.0%15.0%20.0%25.0%30.0%35.0%40.0%45.0%50.0%55.0%60.0%65.0%

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

2013 2014 2015 2016 2017 2018 2019 2020

Mobile Data User (mn)% of Industry sub. base

0.0%

22.1%26.9%

32.4%39.0%

46.1%52.0%

56.3%60.8%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mobile Internet Panetration

Linear (Mobile Internet Panetration)

012345

Competition inthe industry

Potential of newentrants into the

industry

Power ofsuppliers

Power ofcustomers

Threat ofsubstituteproducts

Porter's five forces analysis

Nil=0; Very Low=1; Low=2; Moderate=3; High=4; Very High=5

Contribution of data revenue to total revenue

of the mobile operators growing gradually

EQUITY RESEARCH Grameenphone Ltd. (DSE: GP; BLOOMBERG: GRAM:BD)

Page 18 of 37 This research report is a property of EBL Securities Ltd. | Bangladesh Equities | June 21, 2021

N.B.: Disclaimer of the EBL Securities Ltd, the author(s) certification and rating definition have been provided at the end of the report.

Increased broadband penetration to challenge cellular data growth: Last 5 years CAGR in ISP+PSTN connections were 25.0% against 12.6% CAGR in mobile internet subscription. This clearly indicates that even though contribution of broadband internet is still insignificant, it is getting momentum in Bangladesh. Currently 91.6% of the total internet connection is supported by mobile internet while rest of the connections are provided by ISP+PSTN operators.

3.4 Regulatory Landscape

The sector experiences rigid regulatory environment and high taxation: The telecom industry is highly regulated and highly taxed sector in Bangladesh.

Publicly traded/ listed corporations are imposed with a 40% income tax while unlisted telecom operators are exposed to a 45% income tax, a much higher rate compared to any other industry. Besides, 5.5% of the revenue sharing will remain unchanged up to 2032 as per the decision taken in a telecom operators’ meeting with Prime Minister’s ICT Affairs Adviser in 2017.

Besides, the Companies under telecom sector undergo very strict and unpredictable regulatory

environment which put its earnings into vulnerable position. Several unresolved and long pending regulatory issues remained a key concern for the company. The operators have various unresolved issues with Bangladesh Telecommunication Regulatory Commission (BTRC) and National

Board of Revenue (NBR) in the ground of illegal broadband internet services, audit, tax on replacement SIM, VAT rebate etc. which is currently on trial of

court.

The telecom service prices are controlled by the regulator: For regular voice calls, there is currently a BDT 2 ceiling and a floor price of BDT 0.25 for each minute, which the regulator fixed in 2008 after a cost modelling analysis

supported by the International Telecommunication Union (ITU). After a few years, the BTRC set the ceiling at BDT 0.50 for each local SMS and BDT 2 for international SMS. There is no lower price limit in this segment. At present, the data service prices are set by the operators, with the regulator having no benchmark to check the rationality of the pricing.

3.4 Recent Developments in the Industry

Robi, the second leading mobile operator of the country, became listed

in the capital market: The long-waited debut of the country’s second leading mobile operator, Robi Axiata has finally taken place in December 2020. The operator offloaded 10% of the shares (including ESPP) to raise about BDT5,237.9 million for network expansion at face value of BDT 10.0 each (at par). Of the total 523.8 million IPO shares, 387.8 million has been offered to the public and institutional investors in Bangladesh, while the remaining 136.1 million was set aside for employees and directors of Robi under the employee share purchase plan (ESPP). The operator formally launched its operation in Bangladesh with the brand name of Aktel in 1997 as Telekom Malaysia International (Bangladesh). After acquisition of its share by Axiata Group Berhad, a Malaysian telecommunications conglomerate, it was rebranded as Robi and changed its name to Robi Axiata Limited. Later got merged with Airtel

Bangladesh, the merged company, in November 2016.

Fresh development in regulatory landscape might bring changes in existing business operations of telecom operators: The government of Bangladesh and telecom regulatory body, BTRC is working to bring various new regulatory developments.

VAT, TAX and other Regulatory Charges for Telecom Industry Gross Revenue Sharing 5.5% of annual audited gross revenue Social Obligation Fund 1% of annual audited gross revenue SD on sale of new and replacement SIM 35% Supplementary duty (SD) 15% VAT inclusive of SD 5% on Mobile Internet

15% on Voice & other telecom services Surcharge 1% Income Tax 40% (For publicly traded companies)

45% (For non-listed companies) SIM Tax BDT 200 each Source: EBLSL Research

Broadband internet (ISP/PSTN) is gaining popularity in Bangladesh

Approved voice call charge ceiling & limit is BDT0.25 to BDT2.0 per minute

Robi offloaded 10% of its shares in the stock market in December 2020.