20November 2020_India_Daily - Kotak Securities

98

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. Contents Special Reports Initiating Coverage Divis Laboratories: New world order Strategy Strategy: A weaker week, but expected Daily Alerts Results Bharat Electronics: Excellent performance Sector alerts Automobiles & Components: State-wise demand trends in 2QFY21 Construction Materials: Cement prices stable, demand remains robust INDIA DAILY November 20, 2020 India 19-Nov 1-day 1-mo 3-mo Sensex 43,600 (1.3) 7.5 14.1 Nifty 12,772 (1.3) 7.4 12.9 Global/Regional indices Dow Jones 29,483 0.2 4.1 6.3 Nasdaq Composite 11,905 0.9 3.4 5.7 FTSE 6,334 (0.8) 7.6 5.3 Nikkei 25,515 (0.4) 8.3 11.5 Hang Seng 26,357 (0.7) 7.3 6.3 KOSPI 2,546 (0.0) 8.0 12.0 Value traded – India Cash (NSE+BSE) 811 637 609 Derivatives (NSE) 65,723 16,436 15,97 3 Deri. open interest 6,828 4,361 4,056 Forex/money market Change, basis points 19-Nov 1-day 1-mo 3-mo Rs/US$ 74.3 10 85 (74) 10yr govt bond, % 6.2 - (2) (8) Net investment (US$ mn) 18-Nov MTD CYTD FIIs 727 5,869 12,415 MFs (12) (2,148 ) (1,420) Top movers Change, % Best performers 19-Nov 1-day 1-mo 3-mo TTMT/A IN Equity 72 (5.1) 30.5 65.3 IIB IN Equity 818 (1.2) 30.8 59.3 AXSB IN Equity 612 (3.9) 23.8 40.6 TTMT IN Equity 168 (3.2) 29.5 38.0 KMB IN Equity 1,826 (0.2) 33.4 36.5 Worst performers BHEL IN Equity 29 2.5 1.7 (24.3) EDEL IN Equity 61 0.7 6.9 (19.6) UPLL IN Equity 417 (2.3) (8.7) (15.3) PNB IN Equity 30 (2.8) 9.7 (14.5) IHFL IN Equity 177 (2.8) 15.9 (13.3) [email protected] Contact: +91 22 6218 6427

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of 20November 2020_India_Daily - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Contents

Special Reports

Initiating Coverage

Divis Laboratories: New world order

Strategy

Strategy: A weaker week, but expected

Daily Alerts

Results

Bharat Electronics: Excellent performance

Sector alerts

Automobiles & Components: State-wise demand trends in 2QFY21

Construction Materials: Cement prices stable, demand remains robust

INDIA DAILY November 20, 2020 India 19-Nov 1-day 1-mo 3-mo

Sensex 43,600 (1.3) 7.5 14.1

Nifty 12,772 (1.3) 7.4 12.9

Global/Regional indices

Dow Jones 29,483 0.2 4.1 6.3

Nasdaq Composite 11,905 0.9 3.4 5.7

FTSE 6,334 (0.8) 7.6 5.3

Nikkei 25,515 (0.4) 8.3 11.5

Hang Seng 26,357 (0.7) 7.3 6.3

KOSPI 2,546 (0.0) 8.0 12.0

Value traded – India

Cash (NSE+BSE) 811 637 609

Derivatives (NSE) 65,723 16,436 15,97

3

Deri. open interest 6,828 4,361 4,056

Forex/money market

Change, basis points

19-Nov 1-day 1-mo 3-mo

Rs/US$ 74.3 10 85 (74)

10yr govt bond, % 6.2 - (2) (8)

Net investment (US$ mn)

18-Nov MTD CYTD

FIIs 727 5,869 12,415

MFs (12) (2,148

) (1,420)

Top movers

Change, %

Best performers 19-Nov 1-day 1-mo 3-mo

TTMT/A IN Equity 72 (5.1) 30.5 65.3

IIB IN Equity 818 (1.2) 30.8 59.3

AXSB IN Equity 612 (3.9) 23.8 40.6

TTMT IN Equity 168 (3.2) 29.5 38.0

KMB IN Equity 1,826 (0.2) 33.4 36.5

Worst performers

BHEL IN Equity 29 2.5 1.7 (24.3)

EDEL IN Equity 61 0.7 6.9 (19.6)

UPLL IN Equity 417 (2.3) (8.7) (15.3)

PNB IN Equity 30 (2.8) 9.7 (14.5)

IHFL IN Equity 177 (2.8) 15.9 (13.3)

[email protected]: +91 22 6218 6427

Company Report

For Private Circulation Only. In the US, this document may only be distributed to QIBs (qualified institutional buyers) as defined under rule 144A of the Securities Act of 1933. This document is not for public distribution

and has been furnished to you solely for your information and may not be reproduced or redistributed to any other person. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

Divis Laboratories (DIVI)

Pharmaceuticals

New world order. Divi’s has built a global leadership across its API portfolio, and we

expect it to benefit from a shift in global supply chains, driving 20% CAGR over

FY2020-23E. However, for the synthesis segment, our analysis of over >350 NCEs

suggests a steep and continued decline in peak tonnage requirements over time, with

the opportunity from new product introductions over CY2016-18 to be only US$450

mn, across 60 launches. At ~35X FY2023E EPS, we believe the stock fully captures

the generics growth, while ignoring the emerging headwinds to the higher valued

synthesis business. We initiate with REDUCE rating, and Fair Value of Rs3,000/share.

Best-in-class synthesis business, though headwinds emerging

Over the years, DIVI’s has emerged as a partner of choice for several of its key Big Pharma

customers for synthesis projects, with expertise in scaling up high tonnage products. Despite a

near-term benefit from fast-track development of certain customer projects, largely for Covid-

19 treatments, in our view, we see risks of a significant slowdown in growth over the longer

term. Our deep dive, bottom-up analysis of >350 NCEs launched post CY2000 indicates a

continued and steep decline in tonnage requirements, with the trend in particular accelerating

post CY2015. For example, CY2016-18 NCE launches are only likely to have a peak global API

requirement of 113 tons (average: 2 tons), a sharp decline compared to 5,192 tons for

CY2001-10 launches, thereby bringing down the addressable opportunity from new product

introductions to US$450 mn, with no product in the >US$25 mn opportunity bucket. Even as

we expect the segment to grow 15% CAGR over FY2020-23E, we expect the growth rate to

moderate to high-single digits from FY2023E, and expect contribution to decline to 38% of

revenues by FY2023E from 41% in FY2020, and down from peak of 51% in FY2016.

Generics API segment has significant runway for growth

Divi’s has emerged as a dominant, independent API provider globally, with leading market

shares globally for 11 APIs, and dominant market share in several high-volume products such

as naproxen, which now accounts for ~18% of consolidated revenues. We expect Divi’s to

benefit from a structural shift in global supply chains, which are likely to favor Indian API

companies, with significant scope for market share gains across products. We believe Divi’s

recent capacity additions will enable market share gains across its existing portfolio, with

potential for incremental Rs12-15 bn revenues from existing products, and further Rs5-6 bn

from new product introductions by FY2024-25, driving 20% revenue CAGR over FY2020-23E.

Expect 23% EPS CAGR over FY2020-23E; initiate with REDUCE

We initiate coverage on Divi’s with a REDUCE rating and Fair Value of Rs3,000/share, based on

32X Dec 2020 EPS, a ~50% premium to frontline peers, and at a ~30% discount to global

CDMOs. While Divi’s has an industry-leading API business that can further scale, we expect

synthesis to moderate over the medium term, given global industry shifts. Divi’s superior

business model is reflected in 22% RoACE at the peak of its capex cycle. However, at 25X

FY2023E EV/EBITDA, and 35X FY2023E P/E, valuations fully capture the superior growth in

generics APIs, while ignoring the increasing risks to the synthesis segment.

Company data and valuation summary

Company data Stock data High Low Price performance 1M 3M 12M

Rating: REDUCE 52-week range 3,499 1,626 Absolute (%) 11.0 8.7 98.2

Priced at close of: Rel. to BSE-30 (%) 3.0 (3.7) 84.0

Current price (Rs) Capitalisation Forecasts/valuation 2021 2022E 2023E

3,435 Market cap (Rs bn) 911 EPS (Rs) 70.9 85.8 97.0

Net debt/(cash) (Rs bn) (10.9) P/E (X) 48.4 40.0 35.4

Free float (%) 48.0 RoAE (%) 23.8 24.6 23.7

Shares outstanding (mn) 265 EV/EBITDA (X) 33.5 27.8 24.7

Source: Company, Kotak Institutional Equities estimates

19-Nov-20

REDUCE

November 19, 2020

INITIATING COVERAGE

Sector view: Attractive

CMP (`): 3,435

Fair Value (`): 3,000

BSE-30: 43,600

Chirag Talati, CFA

Kumar Gaurav

[email protected]: +91 22 6218 6427

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Divis Laboratories Pharmaceuticals

FINANCIAL SNAPSHOT

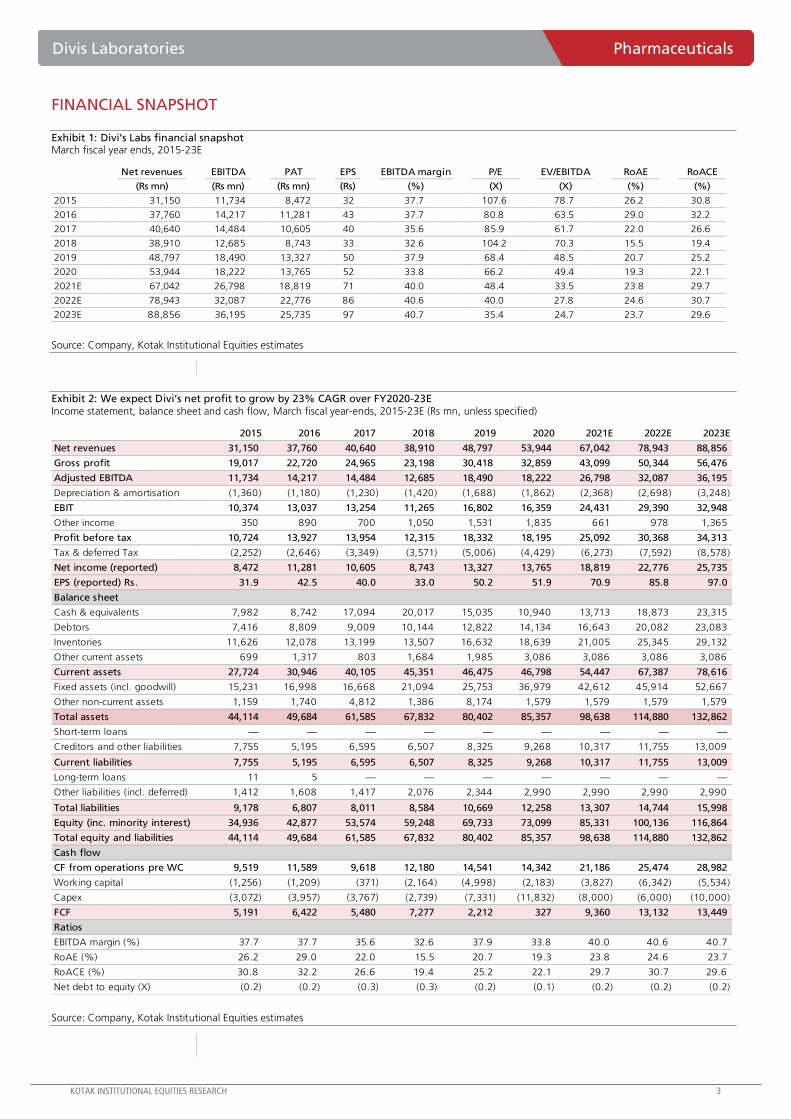

Exhibit 1: Divi’s Labs financial snapshot March fiscal year ends, 2015-23E

Net revenues EBITDA PAT EPS EBITDA margin P/E EV/EBITDA RoAE RoACE

(Rs mn) (Rs mn) (Rs mn) (Rs) (%) (X) (X) (%) (%)

2015 31,150 11,734 8,472 32 37.7 107.6 78.7 26.2 30.8

2016 37,760 14,217 11,281 43 37.7 80.8 63.5 29.0 32.2

2017 40,640 14,484 10,605 40 35.6 85.9 61.7 22.0 26.6

2018 38,910 12,685 8,743 33 32.6 104.2 70.3 15.5 19.4

2019 48,797 18,490 13,327 50 37.9 68.4 48.5 20.7 25.2

2020 53,944 18,222 13,765 52 33.8 66.2 49.4 19.3 22.1

2021E 67,042 26,798 18,819 71 40.0 48.4 33.5 23.8 29.7

2022E 78,943 32,087 22,776 86 40.6 40.0 27.8 24.6 30.7

2023E 88,856 36,195 25,735 97 40.7 35.4 24.7 23.7 29.6

Source: Company, Kotak Institutional Equities estimates

Exhibit 2: We expect Divi’s net profit to grow by 23% CAGR over FY2020-23E Income statement, balance sheet and cash flow, March fiscal year-ends, 2015-23E (Rs mn, unless specified)

2015 2016 2017 2018 2019 2020 2021E 2022E 2023E

Net revenues 31,150 37,760 40,640 38,910 48,797 53,944 67,042 78,943 88,856

Gross profit 19,017 22,720 24,965 23,198 30,418 32,859 43,099 50,344 56,476

Adjusted EBITDA 11,734 14,217 14,484 12,685 18,490 18,222 26,798 32,087 36,195

Depreciation & amortisation (1,360) (1,180) (1,230) (1,420) (1,688) (1,862) (2,368) (2,698) (3,248)

EBIT 10,374 13,037 13,254 11,265 16,802 16,359 24,431 29,390 32,948

Other income 350 890 700 1,050 1,531 1,835 661 978 1,365

Profit before tax 10,724 13,927 13,954 12,315 18,332 18,195 25,092 30,368 34,313

Tax & deferred Tax (2,252) (2,646) (3,349) (3,571) (5,006) (4,429) (6,273) (7,592) (8,578)

Net income (reported) 8,472 11,281 10,605 8,743 13,327 13,765 18,819 22,776 25,735

EPS (reported) Rs. 31.9 42.5 40.0 33.0 50.2 51.9 70.9 85.8 97.0

Balance sheet

Cash & equivalents 7,982 8,742 17,094 20,017 15,035 10,940 13,713 18,873 23,315

Debtors 7,416 8,809 9,009 10,144 12,822 14,134 16,643 20,082 23,083

Inventories 11,626 12,078 13,199 13,507 16,632 18,639 21,005 25,345 29,132

Other current assets 699 1,317 803 1,684 1,985 3,086 3,086 3,086 3,086

Current assets 27,724 30,946 40,105 45,351 46,475 46,798 54,447 67,387 78,616

Fixed assets (incl. goodwill) 15,231 16,998 16,668 21,094 25,753 36,979 42,612 45,914 52,667

Other non-current assets 1,159 1,740 4,812 1,386 8,174 1,579 1,579 1,579 1,579

Total assets 44,114 49,684 61,585 67,832 80,402 85,357 98,638 114,880 132,862

Short-term loans — — — — — — — — —

Creditors and other liabilities 7,755 5,195 6,595 6,507 8,325 9,268 10,317 11,755 13,009

Current liabilities 7,755 5,195 6,595 6,507 8,325 9,268 10,317 11,755 13,009

Long-term loans 11 5 — — — — — — —

Other liabilities (incl. deferred) 1,412 1,608 1,417 2,076 2,344 2,990 2,990 2,990 2,990

Total liabilities 9,178 6,807 8,011 8,584 10,669 12,258 13,307 14,744 15,998

Equity (inc. minority interest) 34,936 42,877 53,574 59,248 69,733 73,099 85,331 100,136 116,864

Total equity and liabilities 44,114 49,684 61,585 67,832 80,402 85,357 98,638 114,880 132,862

Cash flow

CF from operations pre WC 9,519 11,589 9,618 12,180 14,541 14,342 21,186 25,474 28,982

Working capital (1,256) (1,209) (371) (2,164) (4,998) (2,183) (3,827) (6,342) (5,534)

Capex (3,072) (3,957) (3,767) (2,739) (7,331) (11,832) (8,000) (6,000) (10,000)

FCF 5,191 6,422 5,480 7,277 2,212 327 9,360 13,132 13,449

Ratios

EBITDA margin (%) 37.7 37.7 35.6 32.6 37.9 33.8 40.0 40.6 40.7

RoAE (%) 26.2 29.0 22.0 15.5 20.7 19.3 23.8 24.6 23.7

RoACE (%) 30.8 32.2 26.6 19.4 25.2 22.1 29.7 30.7 29.6

Net debt to equity (X) (0.2) (0.2) (0.3) (0.3) (0.2) (0.1) (0.2) (0.2) (0.2)

Source: Company, Kotak Institutional Equities estimates

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

VALUATION: INITIATE COVERAGE WITH A REDUCE RATING

We initiate coverage on Divi’s with a REDUCE rating and Fair Value of Rs3,000/share, based on 32X Dec 2022

EPS, a ~50% premium to frontline peers, and at a ~30% discount to global CDMOs such as Wuxi and Samsung.

Even as Divi’s has an industry-leading API business that can further scale given its capacity expansion, as well

as emerging opportunities from dislocations in global supply chains, we expect synthesis to moderate over

the medium term, given global industry shifts. Divi’s superior business model is reflected in 22% RoACE at the

peak of its capex cycle. However, at 25X FY2023E EV/EBITDA, and 35X FY2023E P/E, valuations fully capture

the potential superior growth in generics APIs, while ignoring the medium-to-longer-term risks challenges to

the synthesis segment.

We initiate coverage with a REDUCE rating; Fair Value of Rs3,000

We initiate coverage on Divi’s with a REDUCE rating and a fair value of Rs3,000/share, based

on 32X Dec 2022 EPS, a 50% premium to frontline Indian generics peers, 25% premium to

its long-term average, and a discount to CDMO peers such as Wuxi and Samsung, though

these operate on in much different and higher barrier to entry markets for outsourcing,

warranting a discount. At current valuations of 25X FY2023E EV/EBITDA, and 35X FY2023E

EPS (premium to take-out multiples for Cambrex), valuations fully capture the potential

superior growth in generics APIs, and ignore the increasing capital intensity resulting from

declining synthesis contribution to the mix.

We believe the generics API business is a best-in-class business that is well-poised to

capitalize on global dislocations in the supply chain, given its dominance in its core API

portfolio. We expect Divi’s to gain share across its key API products, and expect new API

introductions over the medium term, providing visibility on its ability to generate mid-teens

revenue growth for the segment over FY2021-24E, on a high base, after taking into account

the superlative growth in FY2021.

Our argument for a discount is also underpinned by our analysis of the synthesis market

opportunity, where we believe reducing peak tonnage requirements means that growth

rates on a sustainable basis will likely decline to high single digits from FY2023E, once the

full benefit of recently announced capex (which we believe is partly for Covid-19 projects

being fast-tracked by partners) is fully in the base. We also see limited utility in extrapolating

the multiples of CDMOs like WuXi and Lonza, given their presence across the spectrum of

technologies, including small molecules (across tonnage, as well as formulations and API, as

well as cytotoxic and non-cytotoxic), biologics (substance and fill/finish), vaccines, as well as

newer technology platforms such as gene therapy and CAR-T.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Divis Laboratories Pharmaceuticals

Exhibit 3: Divi’s trading at 43X one-year forward P/E 1-year forward P/E multiple (X)

10

15

20

25

30

35

40

45

50

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Jan

-20

Source: Bloomberg

Exhibit 4: Divi’s trading at 30X one-year forward EV/EBITDA 1-year forward EV/EBIDTA multiple (X)

0

5

10

15

20

25

30

35

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Jan

-20

Source: Bloomberg

Exhibit 5: Divi’s trades at a premium to Indian peers Valuation summary, KIE coverage universe, March fiscal year ends, 2019-23E

Company Rating (Rs mn) (US$ mn) 2020 2021E 2022E 2023E 2020 2021E 2022E 2023E 2020 2021E 2022E 2023E 2020 2021E 2022E 2023E

Aurobindo Pharma 830 REDUCE 486,417 7,260 46.7 59.3 59.8 63.3 17.8 14.0 13.9 13.1 11.1 8.4 7.9 7.1 1.9 1.9 2.0 2.0

Biocon 423 SELL 507,300 7,572 6.1 7.8 9.9 11.3 69.7 54.2 42.6 37.3 36.3 25.0 19.7 17.1 9.2 6.5 5.5 5.0

Cipla 742 BUY 598,464 8,932 19.2 29.7 33.4 45.8 38.7 25.0 22.2 16.2 18.9 13.7 12.4 9.0 3.4 3.1 3.1 2.9

Dr. Reddy's 4,708 SELL 782,775 11,683 107.5 157.4 203.3 267.2 43.8 29.9 23.2 17.6 19.3 17.0 13.0 10.1 4.6 4.1 3.7 3.5

Laurus 269 REDUCE 143,915 2,148 23.9 17.3 18.6 22.5 11.2 15.6 14.5 11.9 27.4 11.0 9.7 7.5 4.7 2.9 2.7 2.3

Lupin 884 ADD 400,878 5,983 21.7 27.1 42.4 51.1 40.7 32.7 20.9 17.3 15.7 14.0 9.8 8.0 2.8 2.8 2.5 2.4

Sun Pharma 507 ADD 1,217,273 18,168 19.1 21.2 23.7 27.8 26.6 23.9 21.4 18.3 15.1 13.7 11.7 10.0 4.0 4.0 3.7 3.6

Torrent 2,635 REDUCE 445,832 6,654 54.9 72.0 89.0 104.7 48.0 36.6 29.6 25.2 21.5 18.6 15.8 13.9 5.3 5.0 4.7 4.4

Pharma 4,582,853 68,401 33.8 25.6 22.0 18.2 17.5 14.2 12.0 9.9 3.7 3.3 2.9 2.6

EV/EBITDA (X) EV/Sales (X)

Price (Rs)

Market cap. EPS (Rs) PER (X)

Source: Company, Kotak Institutional Equities estimates

Exhibit 6: Global CRAMS/CRO comparative valuation Valuation summary, calendar year ends, 2019-21E

Market cap.

Company (US$ mn) 2020 2021E 2022E 2023E 2020 2021E 2022E 2023E 2020 2021E 2022E 2023E 2020 2021E 2022E 2023E

Divi's 12,153 66.2 48.4 40.0 35.4 49.4 33.5 27.8 24.7 16.7 13.4 11.3 10.0 19.3 23.8 24.6 23.7

Catalent 17,150 89.8 41.5 35.9 29.5 29.7 21.5 19.2 16.9 6.4 5.3 4.9 4.4 10.6 12.9 13.2 14.7

Celltrion 34,896 122.2 66.7 55.3 49.1 71.8 42.2 35.4 31.0 34.2 21.2 17.4 14.9 17.1 18.6 19.2 18.1

Lonza 48,773 68.5 43.7 38.3 33.4 31.5 28.1 25.1 22.0 8.1 7.7 7.2 6.6 13.0 14.0 14.2 14.7

Samsung Biologics 46,282 228.5 210.6 136.9 103.5 346.5 124.1 95.7 77.6 95.1 48.4 39.4 33.3 5.5 5.8 9.0 10.9

Syngene 3,099 55.6 58.0 46.8 36.0 37.2 32.6 26.3 21.4 11.2 10.0 8.4 7.0 19.9 15.9 17.0 18.7

Wuxi Biologics 42,547 295.6 185.7 133.0 92.4 252.2 145.5 96.2 68.5 82.4 51.8 35.4 24.8 11.7 10.2 12.2 14.9

Average 132.3 93.5 69.5 54.2 116.9 61.1 46.5 37.4 36.3 22.5 17.7 14.4 13.9 14.4 15.6 16.5

Notes:

(1) March fiscal year-ends 2020-23 for Divi's, Syngene. Calendar year-ends 2019-22 for other companies

P/E ratio EV/EBITDA (X) EV/Sales (X) RoAE (%)

Source: Bloomberg

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

SYNTHESIS MARKET SET FOR A MAJOR DISRUPTION

Over the years, DIVI’s has emerged as a partner of choice for several of its key Big Pharma customers for

synthesis projects, with expertise in scaling up high tonnage products. Despite a near-term benefit from fast-

track development of certain customer projects, we see risks of a significant slowdown in growth over the

longer term, as our deep-dive analysis into all NCEs launched post CY2000 indicates a continued and steep

decline in tonnage requirements, with the trend accelerating post CY2015. We expect CY2016-18 NCE

launches to have a peak global API requirement of only 113 tons (average: 2 tons), a sharp decline compared

to 5,192 tons for CY2001-10 launches. While we expect the segment to grow at 15% CAGR over FY2020-23E,

we expect the growth rate to moderate to high-single digits from FY2023E.

Divi’s is a global leader in custom synthesis

We expect a stable near and medium-term outlook for the synthesis business, with

expectations of strong 15% CAGR over FY2020-2E, given its existing pipeline, with some

benefits of capacity debottlenecking, as well as near-term benefits from Rs4 bn dedicated

capex for a few unspecified Phase III projects that are getting fast-tracked by customers. We

suspect the capex is related to key intermediate manufacturing for molnupiravir, Merck’s

oral Covid-19 anti-viral project in development, which is currently in Phase III development,

with an EUA (emergency use authorization) filing expected in Dec 2020. In contrast to the

generic API segment, which will benefit from changing market dynamics, we discuss major

trends that will likely disrupt the custom synthesis market over the longer term.

Exhibit 7: Custom synthesis segment likely to see steady growth

until FY2023E Mach fiscal year-ends, 2015-23E (Rs bn)

15

19 21 20

24

27

31

35 35

-

5

10

15

20

25

30

35

40

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Source: Industry data, Kotak Institutional Equities estimates

Exhibit 8: Synthesis contribution has declined to ~41% of

revenues Mach fiscal year-ends, 2015-23E (% of revenues)

51 51

45 44 44 41

39 39 38

-

10

20

30

40

50

60

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Source: Industry data, Kotak Institutional Equities estimates

Divi’s strict adherence to IPR norms, proven delivery capability through the development

cycle, commercial supply track-record, and strong relationship with pharma majors marked

its transformation from an API player to a global leader in custom synthesis, and particularly,

in the US$16-20 bn CMO market for innovator APIs, with the segment contributing nearly

half of Divi’s revenues, with significantly superior profitability than API’s and neutraceuticals

segments. Divi’s has four R&D centres and two pilot plants, and through these, it has strong

presence in all stages of product development, starting from process development in labs to

all stages of pre-clinical and clinical trials, and more importantly, reliable commercial supplies

for the intermediate or API through the life cycle.

Recurring commercial

revenue streams

contribute >75% of

synthesis revenues

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Divis Laboratories Pharmaceuticals

Within the spectrum of opportunities, DIVI’s core competence lies in (1) chiral chemistry,

which has been the backbone of several successful NCE introductions (more than half of the

drugs currently in use are chiral compounds), and (2) difficult to scale high tonnage APIs,

where innovators need a reliable provider to scale the manufacturing over the development

and commercial stage, without material disruptions. We believe commercial supplies of such

large volume APIs contribute >75% of Divi’s custom synthesis revenues, making it critical for

Divi’s to have a steady stream of high-tonnage API launches to drive recurring business over

the longer term. DIVI’s historic track-record has helped it win repeat business from most of

its key Big Pharma customers, with customers spanning 6 of the top 10 global companies,

and preferred supplier relationship with several large pharma companies such as Merck

(losartan, sitagliptin intermediates), GSK (anti-virals including valacyclovir and dolutegravir),

Astra Zeneca (UCB (levetiracetam)), etc.

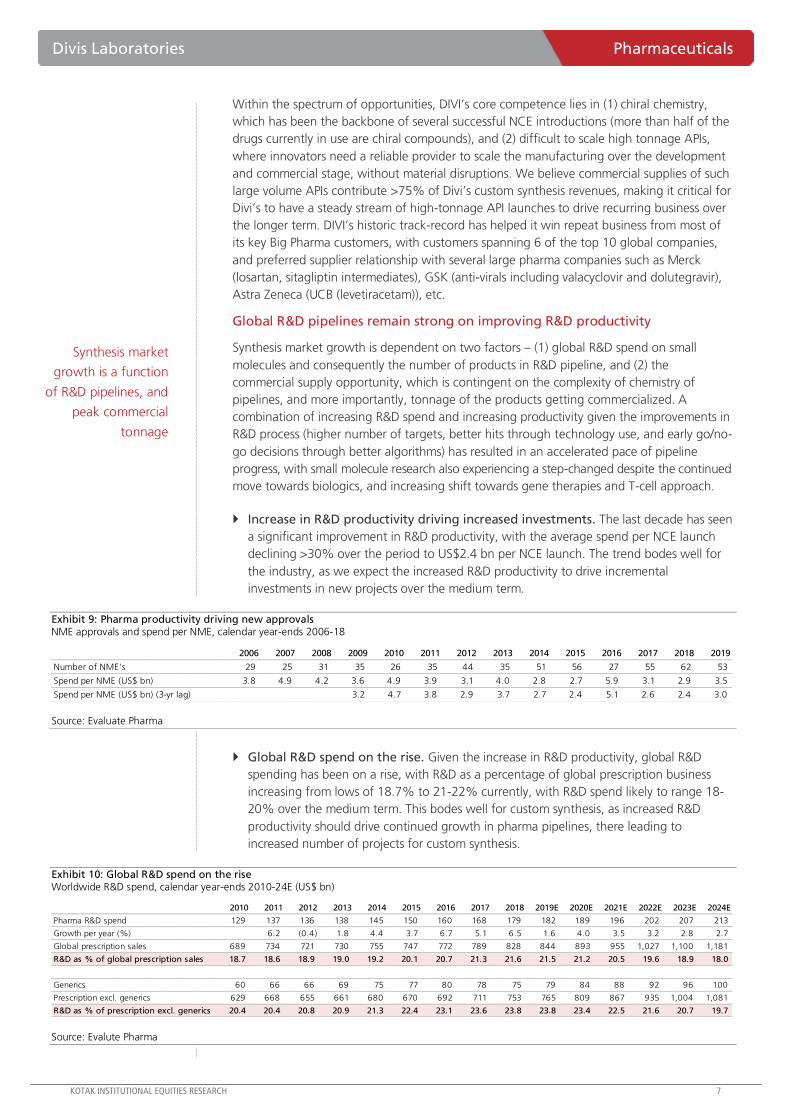

Global R&D pipelines remain strong on improving R&D productivity

Synthesis market growth is dependent on two factors – (1) global R&D spend on small

molecules and consequently the number of products in R&D pipeline, and (2) the

commercial supply opportunity, which is contingent on the complexity of chemistry of

pipelines, and more importantly, tonnage of the products getting commercialized. A

combination of increasing R&D spend and increasing productivity given the improvements in

R&D process (higher number of targets, better hits through technology use, and early go/no-

go decisions through better algorithms) has resulted in an accelerated pace of pipeline

progress, with small molecule research also experiencing a step-changed despite the continued

move towards biologics, and increasing shift towards gene therapies and T-cell approach.

Increase in R&D productivity driving increased investments. The last decade has seen

a significant improvement in R&D productivity, with the average spend per NCE launch

declining >30% over the period to US$2.4 bn per NCE launch. The trend bodes well for

the industry, as we expect the increased R&D productivity to drive incremental

investments in new projects over the medium term.

Exhibit 9: Pharma productivity driving new approvals NME approvals and spend per NME, calendar year-ends 2006-18

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Number of NME's 29 25 31 35 26 35 44 35 51 56 27 55 62 53

Spend per NME (US$ bn) 3.8 4.9 4.2 3.6 4.9 3.9 3.1 4.0 2.8 2.7 5.9 3.1 2.9 3.5

Spend per NME (US$ bn) (3-yr lag) 3.2 4.7 3.8 2.9 3.7 2.7 2.4 5.1 2.6 2.4 3.0

Source: Evaluate Pharma

Global R&D spend on the rise. Given the increase in R&D productivity, global R&D

spending has been on a rise, with R&D as a percentage of global prescription business

increasing from lows of 18.7% to 21-22% currently, with R&D spend likely to range 18-

20% over the medium term. This bodes well for custom synthesis, as increased R&D

productivity should drive continued growth in pharma pipelines, there leading to

increased number of projects for custom synthesis.

Exhibit 10: Global R&D spend on the rise Worldwide R&D spend, calendar year-ends 2010-24E (US$ bn)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019E 2020E 2021E 2022E 2023E 2024E

Pharma R&D spend 129 137 136 138 145 150 160 168 179 182 189 196 202 207 213

Growth per year (%) 6.2 (0.4) 1.8 4.4 3.7 6.7 5.1 6.5 1.6 4.0 3.5 3.2 2.8 2.7

Global prescription sales 689 734 721 730 755 747 772 789 828 844 893 955 1,027 1,100 1,181

R&D as % of global prescription sales 18.7 18.6 18.9 19.0 19.2 20.1 20.7 21.3 21.6 21.5 21.2 20.5 19.6 18.9 18.0

Generics 60 66 66 69 75 77 80 78 75 79 84 88 92 96 100

Prescription excl. generics 629 668 655 661 680 670 692 711 753 765 809 867 935 1,004 1,081

R&D as % of prescription excl. generics 20.4 20.4 20.8 20.9 21.3 22.4 23.1 23.6 23.8 23.8 23.4 22.5 21.6 20.7 19.7

Source: Evalute Pharma

Synthesis market

growth is a function

of R&D pipelines, and

peak commercial

tonnage

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

Increased productivity driving more products through the funnel. Given the

improvements in R&D productivity, and continued increase in R&D investments, the

number of R&D projects at every stage is exhibiting a steady increase from CY2010-17.

This, in turn, should drive a steady number of new approvals over the medium term.

Increasing projects in the pipeline should help drive early fee for service revenues for the

synthesis providers, and the development to approval lifecycle typically offer US$5-10 mn

revenue per product, though these are non-recurring revenues, and hence, the recurring

revenues from commercial supplies are critical to drive sustainable growth for the industry.

Exhibit 11: Research pipeline for NCEs remains robust Calendar year-ends, 1995-2017

Phase 1995 2005 2010 2011 2012 2013 2014 2015 2016 2017

Pre-clinical 1,446 2,054 2,195 2,178 2,461 2,467 2,369 2,834 2,953 3,077

Phase I 231 435 682 643 659 651 677 750 774 799

Phase II 383 481 749 746 754 735 762 825 830 835

Phase III 202 163 186 196 201 199 208 227 229 232

Pre-reg 78 46 26 34 30 38 41 40 42 44

Reg 33 10 7 10 8 14 19 15 16 18

Launched 959 1,249 1,377 1,387 1,423 1,450 1,478 1,523 1,539 1,579

Source: Evaluate Pharma

Small molecules likely to continue to dominate global pharma sales. Contrary to

expectations and despite a continued increase in number of biotechnology-led approvals,

small molecules have continued to dominate the market, and given the sharp increase in

small molecule-led approvals from CY2010-19, we expect small molecules to continue to

dominate the global market accounting for >2/3rd of global pharma market by CY2024.

Exhibit 12: Conventional chemical based drugs likely to account for substantial portion of the market % of world-wide drug sales from biotechnology vs conventional products, calendar year-ends, 2010-24E

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020E 2021E 2022E 2023E 2024E

Biotechnology 18 18 20 21 22 23 25 26 28 29 30 31 32 33 34

Conventional 82 82 80 79 78 77 75 74 72 71 70 69 68 67 66

Source: Evaluate Pharma

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Divis Laboratories Pharmaceuticals

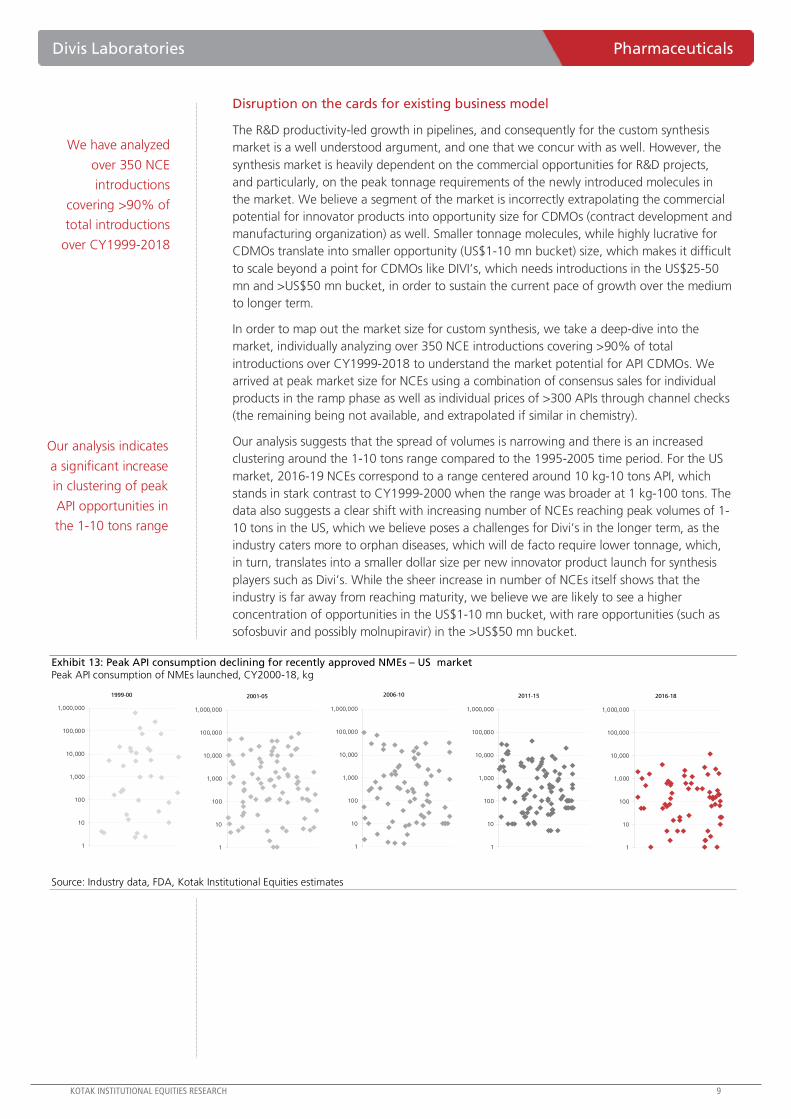

Disruption on the cards for existing business model

The R&D productivity-led growth in pipelines, and consequently for the custom synthesis

market is a well understood argument, and one that we concur with as well. However, the

synthesis market is heavily dependent on the commercial opportunities for R&D projects,

and particularly, on the peak tonnage requirements of the newly introduced molecules in

the market. We believe a segment of the market is incorrectly extrapolating the commercial

potential for innovator products into opportunity size for CDMOs (contract development and

manufacturing organization) as well. Smaller tonnage molecules, while highly lucrative for

CDMOs translate into smaller opportunity (US$1-10 mn bucket) size, which makes it difficult

to scale beyond a point for CDMOs like DIVI’s, which needs introductions in the US$25-50

mn and >US$50 mn bucket, in order to sustain the current pace of growth over the medium

to longer term.

In order to map out the market size for custom synthesis, we take a deep-dive into the

market, individually analyzing over 350 NCE introductions covering >90% of total

introductions over CY1999-2018 to understand the market potential for API CDMOs. We

arrived at peak market size for NCEs using a combination of consensus sales for individual

products in the ramp phase as well as individual prices of >300 APIs through channel checks

(the remaining being not available, and extrapolated if similar in chemistry).

Our analysis suggests that the spread of volumes is narrowing and there is an increased

clustering around the 1-10 tons range compared to the 1995-2005 time period. For the US

market, 2016-19 NCEs correspond to a range centered around 10 kg-10 tons API, which

stands in stark contrast to CY1999-2000 when the range was broader at 1 kg-100 tons. The

data also suggests a clear shift with increasing number of NCEs reaching peak volumes of 1-

10 tons in the US, which we believe poses a challenges for Divi’s in the longer term, as the

industry caters more to orphan diseases, which will de facto require lower tonnage, which,

in turn, translates into a smaller dollar size per new innovator product launch for synthesis

players such as Divi’s. While the sheer increase in number of NCEs itself shows that the

industry is far away from reaching maturity, we believe we are likely to see a higher

concentration of opportunities in the US$1-10 mn bucket, with rare opportunities (such as

sofosbuvir and possibly molnupiravir) in the >US$50 mn bucket.

Exhibit 13: Peak API consumption declining for recently approved NMEs – US market Peak API consumption of NMEs launched, CY2000-18, kg

1

10

100

1,000

10,000

100,000

1,000,000

1

10

100

1,000

10,000

100,000

1,000,000

1

10

100

1,000

10,000

100,000

1,000,000

1

10

100

1,000

10,000

100,000

1,000,000

2001-051999-00 2006-10 2011-15

1

10

100

1,000

10,000

100,000

1,000,000

2016-18

Source: Industry data, FDA, Kotak Institutional Equities estimates

We have analyzed

over 350 NCE

introductions

covering >90% of

total introductions

over CY1999-2018

Our analysis indicates

a significant increase

in clustering of peak

API opportunities in

the 1-10 tons range

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

US opportunity likely to decline steeper than anticipated

Our analysis shows a consistent decline in the opportunity size in terms of the peak tonnage

requirements of NCEs launched from CY1999-2018, with the trend particularly accelerating

post CY2015, with peak tonnage for launches from CY2016-18 at only 42 tons in the US.

To put this in perspective, the largest launch in CY1999 has an expected peak tonnage

requirement in the US of >700 tons. From CY1999-2015, the decline in tonnage

requirements was getting offset by higher pricing for newly launched APIs, with our analysis

indicating that average pricing increased from ~US$265/kg for products launched in

CY1999-2000 to an average or ~US$5,100/kg for products launched from CY2011-15. This

led to the market size for custom synthesis increasing from US$332 mn for products

launched in CY1999-2000 to US$1.4 bn for products launched from CY2011-15, though,

partially benefitting from sofosbuvir global launch, which we believe had a peak market size

of >US$300 mn. Excluding sofosbuvir, the CY2011-15 bucket saw a doubling in market size,

driven by a large number of new launches in the small molecule category.

In contrast, new product introductions post CY2015 are expected to see a steep decline in

the market opportunity given stable pricing with average pricing likely to grow only to

~US$5,500/kg, while the peak tonnage is likely to drop 80% from CY2011-15 levels,

resulting in a sharp contraction in the peak new product opportunity for CDMOs. We expect

this trend to continue as our analysis of pipeline indicates similar low tonnage launches from

CY2019-22 timeframe, with products such as molnupiravir being an exception. We expect

this trend to result in further drop in the new product opportunity, which we expect will

further bring down the medium to longer term growth for custom synthesis market, even as

the near-term outlook remains robust given that bulk of the peak opportunities for the

CY2006-10 and CY2011-15 buckets fall in the CY2018-24E timeframe.

Exhibit 14: Total peak API consumption for all NCE launches

from 1999-2018 – US market Calendar year-ends 1999-2018 (tons)

1,257

597

444

272

42

0

200

400

600

800

1,000

1,200

1,400

1999-00 2001-05 2006-10 2011-15 2016-18

Source: Industry data, Kotak Institutional Equities estimates

Exhibit 15: Opportunity bucket declining post surge in CY2011-

15 time frame – US market Peak market opportunity, calendar year-ends, 1999-2018 (US$ mn)

332409

521

1,361

239

0

200

400

600

800

1,000

1,200

1,400

1,600

1999-00 2001-05 2006-10 2011-15 2016-18

Source: Industry data, Kotak Institutional Equities estimates

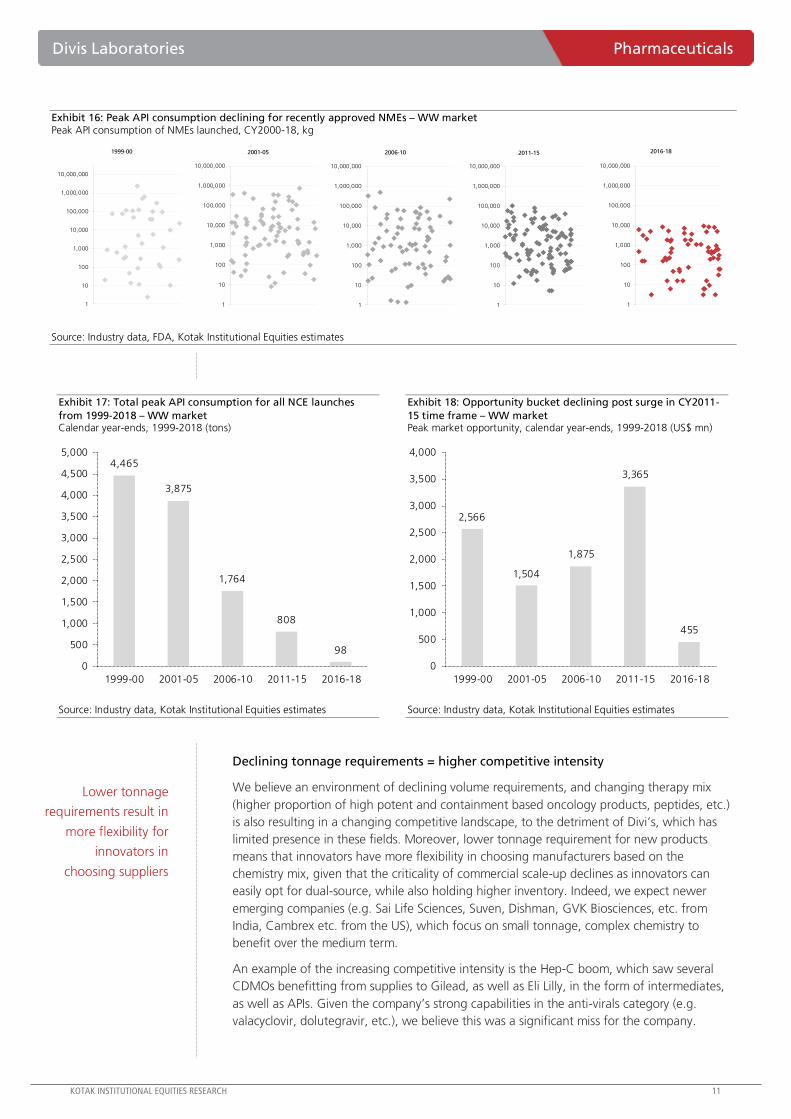

Ex-US likely to be critical given the higher patient volumes

We see this trend as universal, impacting both US as well as ex-US opportunities, though we

do see increased contribution from ex-US opportunities given our expectations of a decline

in the premium of API prices for the US over ex-US, particularly, as US sales are increasingly

more driven by formulation prices. This, in turn, should drive increased contribution from ex-

US, due to higher number of treated patients over time.

We see the trend of

declining peak

tonnage

requirements

accelerating post

CY2015

Combined peak

tonnage for launches

from CY2016-18 in

the US stands at only

42 tons

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Divis Laboratories Pharmaceuticals

Exhibit 16: Peak API consumption declining for recently approved NMEs – WW market Peak API consumption of NMEs launched, CY2000-18, kg

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

2001-051999-00 2006-10 2011-15

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

2016-18

Source: Industry data, FDA, Kotak Institutional Equities estimates

Exhibit 17: Total peak API consumption for all NCE launches

from 1999-2018 – WW market Calendar year-ends, 1999-2018 (tons)

4,465

3,875

1,764

808

98

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1999-00 2001-05 2006-10 2011-15 2016-18

Source: Industry data, Kotak Institutional Equities estimates

Exhibit 18: Opportunity bucket declining post surge in CY2011-

15 time frame – WW market Peak market opportunity, calendar year-ends, 1999-2018 (US$ mn)

2,566

1,504

1,875

3,365

455

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1999-00 2001-05 2006-10 2011-15 2016-18

Source: Industry data, Kotak Institutional Equities estimates

Declining tonnage requirements = higher competitive intensity

We believe an environment of declining volume requirements, and changing therapy mix

(higher proportion of high potent and containment based oncology products, peptides, etc.)

is also resulting in a changing competitive landscape, to the detriment of Divi’s, which has

limited presence in these fields. Moreover, lower tonnage requirement for new products

means that innovators have more flexibility in choosing manufacturers based on the

chemistry mix, given that the criticality of commercial scale-up declines as innovators can

easily opt for dual-source, while also holding higher inventory. Indeed, we expect newer

emerging companies (e.g. Sai Life Sciences, Suven, Dishman, GVK Biosciences, etc. from

India, Cambrex etc. from the US), which focus on small tonnage, complex chemistry to

benefit over the medium term.

An example of the increasing competitive intensity is the Hep-C boom, which saw several

CDMOs benefitting from supplies to Gilead, as well as Eli Lilly, in the form of intermediates,

as well as APIs. Given the company’s strong capabilities in the anti-virals category (e.g.

valacyclovir, dolutegravir, etc.), we believe this was a significant miss for the company.

Lower tonnage

requirements result in

more flexibility for

innovators in

choosing suppliers

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

DIVI’S COULD EMERGE AS BENEFICIARY OF AN EMERGING WORLD ORDER IN API’S

Divi’s has emerged as a dominant, independent API provider globally, with leading market shares globally for

11 APIs, with dominant market share in several high volume products such as naproxen, which now accounts

for ~18% of consolidated revenues. We expect Divi’s to benefit from a structural shift in global supply chains,

which are likely to favor Indian API companies, with significant scope for market share gains across products.

We believe Divi’s recent capacity additions will enable it to add significant market share across its top-11

products, with potential for incremental Rs12-15 bn revenues from existing products, and further Rs5-6 bn

from new product introductions by FY2024-25, driving 20% revenue CAGR over FY2020-23E.

Process improvement-led strategy for high tonnage APIs

Divi’s journey in the API segment from its inception to reaching ~Rs27 bn revenues started

with a focus on organic chemistry driven products, particularly, for chiral APIs, such as

naproxen, where Divi’s improved the process by eliminating solvent use, and thereby

creating a process that was not only low-cost, but could be scaled to thousands of tons.

Over time, Divi’s replicated the strategy to a number of products, with its strengths in chiral

chemistry and creating organic processes, by targeting high tonnage products, where it

created process that could be replicated on batch size in excess of 1 tons typically, which has

enabled it to emerge as one of the lowest cost producers for all of its key high tonnage APIs.

Smart product selection further enabled the company to significantly scale its existing

business, with its six of its key API products also falling in top-20 APIs by volumes globally.

This is meaningful, as we believe at least half of the remaining 14 products within the top-

20 products are largely commodity products with limited process advantage for any player

globally. More importantly, Divi’s product portfolio also consists of volume growth products,

with underlying volume for its top-10 products growing at ~7% CAGR from CY2013-19. A

combination of smart product selection, and process led large-batch size manufacturing

strategy has enabled Divi’s to emerge as the world leader in 18 of 26 APIs in its portfolio.

Exhibit 19: Volumes of top-10 products have grown at ~7%

CAGR from CY2013-19 Global market size, calendar year-ends, 2013-19

9,4

68

10

,28

7

11,3

66

12,4

05

13,0

69

13,5

06

13,9

44

7.0

8.7

10.5

9.1

5.4

3.3 3.2

0

2

4

6

8

10

12

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2013 2014 2015 2016 2017 2018 2019

Top-10 API's WW market (tons, LHS) Growth (%, RHS)

Source: Industry, Kotak Institutional Equities estimates

Exhibit 20: Naproxen sales doubled from FY2014-19 March fiscal year-ends, 2014-20

2,6

50

3,1

50

3,3

50

2,9

00

2,7

50

3,3

55

3,4

00

4,764

5,607

6,797 6,502 5,837

8,783

9,605

-

2,000

4,000

6,000

8,000

10,000

12,000

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2014 2015 2016 2017 2018 2019 2020

Volumes (tons, LHS) Revenues (Rs mn, RHS)

Source: Company, Kotak Institutional Equities estimates

Six of Divi’s key API

products fall in top-

20 APIs by volumes

globally

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Divis Laboratories Pharmaceuticals

Exhibit 21: Divi’s API portfolio focuses on high-tonnage chiral API’s Global market size, calendar year-end, 2019

3,964

2,612 2,371 2,101

1,184 733 605 140 120

116

8.5

2.5

12.5

4.8

1.3

12.4

8.1

-4.5

8.1

-7.8

(10)

(5)

-

5

10

15

-

900

1,800

2,700

3,600

4,500

Gab

apen

tin

Napro

xen

Leve

tira

ceta

m

Iop

amid

ol

Vals

art

an

Pre

gabalin

Vala

cycl

ovi

r

Dext

rom

eth

orp

han

Phenyl

eph

rine

Nabum

etone

Market size (tons) [LHS] CY2015-19 volume CAGR (%) [RHS]

Source: Industry, Kotak Institutional Equities estimates

Exhibit 22: Divi’s has globally leading market shares for its top APIs Global market size, calendar year-end, 2019

60 5855 55

49

2016 14 13

84

0

10

20

30

40

50

60

70

Napro

xen

Nabum

etone

Gab

apen

tin

Dext

rom

eth

orp

han

Carb

idop

a

Pre

gabalin

Phenyl

eph

rine

Vala

cycl

ovi

r

Leve

tira

ceta

m

Vals

art

an

Iop

amid

ol

Source: Industry, Kotak Institutional Equities estimates

Divi’s is a global

market leader in 18

of 26 APIs in its

portfolio

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

Focus on quality and economies of scale to help drive volumes

Divi’s currently has one facility in Hyderabad, and post the commissioning of Unit-3, two

facilities in Vizag. The two key facilities, Unit-1 and 2, are approved by most regulatory

authorities globally, including the US FDA and the EU GMP, etc. Unit-1 and 2 have

aggregate reactor volume of 9,659 KL, which is slated to increased to 15,580 KL with the

completion of debottlenecking and capacity enhancement projects, and should be sufficient

to manufacture between 7-10 K tons of API/intermediates.

Divi’s has historically had a stellar track record in regulatory audits, barring the unfortunate

incident in Dec 2017, that escalated into an import alert, though, there are few instances of

companies getting out of import alert within a year, which is a big testament to Divi’s focus

on cGMP, and more importantly, record keeping and data integrity, as we believe the

company was able to provide all the documentation, including retrospective analysis of all

the batches of naproxen, spanning five years, with a new testing method, in less than six

months. Moreover, we believe Divi’s focus on custom synthesis segments, and its ability to

win repeat, high-tonnage business is a testament to its quality focus. It is worth noting that

we have not come across of any material recalls for any of the finished dosage forms due to

impurity concerns for innovator companies or generic manufacturers that rely on Divi’s

intermediates or APIs. Post the US FDA issues, Divi’s has also expanded its quality focus by

employing 3-40 subject matter experts to further adopt best practices in key areas, and

strengthen its quality framework.

Exhibit 23: Existing and upcoming facilities for Divi’s

Unit Location

Land area

(acres)

# of

reactors

Existing

capacity (tons)

Post-expansion

(tons) Description Regulatory status

Unit I

Chotuppal

Mandan near

Hyderabad

500 362 2,670 6,350

Spread across 500 acres with production

blocks for API and intermediates. Additional 7

blocks capacity enhancement, with brownfield

expansion through SEZ unit. (DC-SEZ).

Last inspected in June'19 with

zero 483 observations.

Unit II

Chippada

Village near

Vizag

490 1,018 10,740 14,400

Spread across 490 acres with an EOU (8

blocks), an SEZ unit (Unit 9) and a DSN SEZ

(block 6), with capacity enhancement

through 7 new blocks at DCV-SEZ.

Last inspected in Nov'19 with

zero 483 observations.

Unit III Kakinada 500 Likely to require Rs6-8 bn capex.

Commissioning likely in FY2025

Unit IV Nellore 200 Likely to require Rs4-6 bn capex.

Commissioning likely in FY2025

N/A

N/A

Source: Company, Kotak Institutional Equities

Putting numbers to the capex plan

From FY2017-20, Divi’s has spent Rs14-15 bn in debottlenecking and capacity

enhancements at Units-1 and 2, as well as for setting up Unit-3, with the company

indicating further Rs10-15 bn capex over FY2021-24E for its Kakinada and Nellore projects.

This is the first major capacity expansion by Divi’s in over a decade, with the project leading

to excitement for the Street given Divi’s track record of efficiently deploying capital, which

has seen it earn superior return ratios compared to peers. We believe the capex plan will

help add significant capacities, and position Divi’s to gain share from competitors,

particularly, given the ongoing shifts away from China, owing to large-scale price

fluctuations, ranging from key starting materials to APIs, as mentioned earlier. We believe

the recent capex has potential to add Rs18-22 bn incremental generic API revenues for Divi’s

by FY2025 (11-13% CAGR from FY2021-25E).

Divi’s can likely add

Rs12-15 bn in

incremental revenues

from existing APIs

post recent capex

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Divis Laboratories Pharmaceuticals

Incremental Rs12-15 bn potential from existing APIs. We believe a large part of the

capex expansion is towards adding capacities for existing products and enhancing vertical

integration given that Divi’s has seen increase in demand for its core APIs from its existing

customers, as well as new inquiries, though, it has been unable to satisfy the demand due

to capacity constraints. We believe the incremental capacities will help add significant

revenues from products such as valsartan, where API remains in short supplies, with most

API producers using the API for captive consumption, and limited capacities available from

independent API proviers such as Divi’s. Over the past year, Divi’s customers have

launched the generic in the US, but more meaningfully from RoW markets, which are

sticky in nature. Given the underlying volume growth in other flagship products, such as

naproxen, gabapentin, iopamidol, dextromethorphan and pregabalin, we believe Divi’s

will be able to utilize the new capex over coming 3-4 years, with the volume and pricing

dynamics suggesting peak potential of Rs12-15 bn revenues (incremental 9-11% CAGR

over FY2021-24E), as depicted in Exhibits 23-24.

Exhibit 24: Capacity expansion at Vizag to add meaningful

capacities for existing products Existing and incremental capacities (tons)

2,700

1,250

300 270 150 90

810

375

300 200 150 270

-

1,000

2,000

3,000

4,000

Napro

xen

Gab

apen

tin

Leve

tira

ceta

m

Dext

rom

eth

orp

han

Pre

gabalin

Vals

art

an

Source: Company, Kotak Institutional Equities estimates

Exhibit 25: Capacity expansion will help DIVI target Rs10 bn

incremental revenues through market share gains Peak potential revenues from capacity expansion (Rs mn)

4,995

3,848

2,637

1,998

1,110

555 -

1,000

2,000

3,000

4,000

5,000

Vals

art

an

Dext

rom

eth

orp

han

Napro

xen

Leve

tira

ceta

m

Gab

apen

tin

Pre

gabalin

Source: Company, Kotak Institutional Equities estimates

Rs5-6 bn revenue potential from new APIs post capacity enhancements. A critique

of the Divi’s API model is its inability to add new products in the pipeline on a consistent

basis, in contrast to an emerging API business model by companies like MSN, which rely

on aggressive new launches (15-20 API scale-ups annually as compared to DIVI’s portfolio

of ~35 APIs) and targeting a mix of very low tonnage products to high tonnage new

product expirations. We believe Divi’s focus on high tonnage means that it has to be

selective in its APIs in order to create a global leadership. We believe the capacity

bottlenecks also played a role in its inability to introduce new products to the market over

the past 2-3 years, though, we believe, based on the capacity expansion plans, Divi’s can

easily add Rs5-6 bn in revenues from new product introductions (incremental 3-5%

CAGR over FY2021-24E), based on its recent new product offerings, as detailed in

Exhibits 25-26.

New launches can help

add Rs5 bn

incremental revenues

post recent capex

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

Exhibit 26: Capacity expansion to help target volumes for new

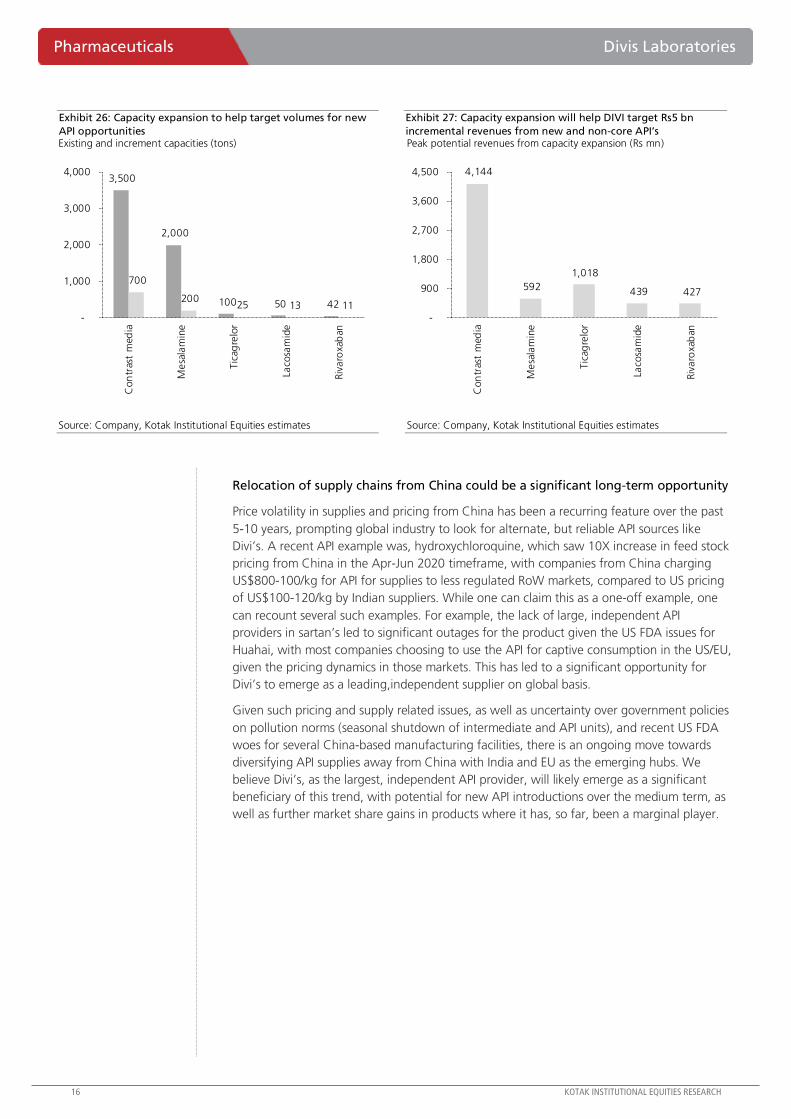

API opportunities Existing and increment capacities (tons)

3,500

2,000

100 50 42

700

200 25 13 11

-

1,000

2,000

3,000

4,000

Con

tras

t m

edia

Mesa

lam

ine

Tic

agre

lor

Laco

sam

ide

Riv

aro

xab

an

Source: Company, Kotak Institutional Equities estimates

Exhibit 27: Capacity expansion will help DIVI target Rs5 bn

incremental revenues from new and non-core API’s Peak potential revenues from capacity expansion (Rs mn)

4,144

592

1,018

439 427

-

900

1,800

2,700

3,600

4,500

Con

tras

t m

edia

Mesa

lam

ine

Tic

agre

lor

Laco

sam

ide

Riv

aro

xab

an

Source: Company, Kotak Institutional Equities estimates

Relocation of supply chains from China could be a significant long-term opportunity

Price volatility in supplies and pricing from China has been a recurring feature over the past

5-10 years, prompting global industry to look for alternate, but reliable API sources like

Divi’s. A recent API example was, hydroxychloroquine, which saw 10X increase in feed stock

pricing from China in the Apr-Jun 2020 timeframe, with companies from China charging

US$800-100/kg for API for supplies to less regulated RoW markets, compared to US pricing

of US$100-120/kg by Indian suppliers. While one can claim this as a one-off example, one

can recount several such examples. For example, the lack of large, independent API

providers in sartan’s led to significant outages for the product given the US FDA issues for

Huahai, with most companies choosing to use the API for captive consumption in the US/EU,

given the pricing dynamics in those markets. This has led to a significant opportunity for

Divi’s to emerge as a leading,independent supplier on global basis.

Given such pricing and supply related issues, as well as uncertainty over government policies

on pollution norms (seasonal shutdown of intermediate and API units), and recent US FDA

woes for several China-based manufacturing facilities, there is an ongoing move towards

diversifying API supplies away from China with India and EU as the emerging hubs. We

believe Divi’s, as the largest, independent API provider, will likely emerge as a significant

beneficiary of this trend, with potential for new API introductions over the medium term, as

well as further market share gains in products where it has, so far, been a marginal player.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

Divis Laboratories Pharmaceuticals

NEUTRACEUTICALS CONTRIBUTION UNLIKELY TO GO UP MATERIALLY

We see the neutraceutials business offering steady growth and expect 16% revenue CAGR from FY2020-23E,

benefitting from a post Covid-19 surge in the use of neutraceuticals, though, given the competitive landscape,

we believe, the segment is likely to remain a relatively smaller contributor for Divi’s, with existing players

such as BASF and DSM likely to continue to dominate the segment.

Divi’s also manufactures specialty ingredients for use in nutraceutical products. This segment

mainly consists of β-carotenoids and luteins (low end products), lycopene and analogue

compounds (high end products), as well as Vitamin-D derivatives. Carotenoids is a US$1.8

bn market and falls into Divi’s core strengths given (1) large volume requirements of ~1,800

tons, (2) well diversified geographic spread with the EU accounting for roughly half of the

global market, and the US accounting for only a quarter of the market, and (3) consistent 3-

4% volume growth. However, despite entering this segment in late mid-2000’s, DIVI has

had limited success in the segment, with sales still below the US$50 mn mark, and <5%

market share of global market, that has seen companies such as BASF and DSM continuing

to dominate. We expect the segment to remain a steady growth driver, delivering 16%

CAGR from CY2020-23E, though, we do not expect the segment to create a meaningful

impact on overall growth for Divi’s.

Exhibit 28: Neutraceuticals segment to post steady growth March fiscal year-ends, 2015-23E (Rs mn)

1.4 1.5 1.9

2.4 2.5

3.8

4.6

5.5

6.4 51

12

21

29

5

52

21 20

15

-

10

20

30

40

50

60

0

1

2

3

4

5

6

7

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Neutraceuticals (Rs mn) [LHS] % growth [RHS]

Source: Company, Kotak Institutional Equities estimates

Exhibit 29: Neutraceuticals likely to remain a small segment March fiscal year-ends, 2015-23E (% of sales)

4 4

5

6

5

7 7 7 7

-

1

2

3

4

5

6

7

8

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Source: Company, Kotak Institutional Equities estimates

Exhibit 30: Competitive benchmarking of key neutraceuticals competitors globally

DSM BASF Allied Divi's ZMC

Product portfolioComprehensive

portfolioSimilar to DSM Similar to DSM Inferior to DSM

More active in animal

feed

Backward

integration levels

Backward integrated to

crystal production

Backward integrated to

crystal production

Backward integrated to

crystal production

Backward integrated to

crystal production

Backward integrated to

crystal production

Focus

Focus across human

nutrition (~$40% of the

market), animal feed

(~45% of the market),

as well as dietary

supplements (~15% of

the market), and

cosmetics.

Higher focus on animal

feed (~45% of the

market), though, has

seen increased focus on

human nutrion over the

past few years

High focus on human

nutrition (~40% of the

market)

High focus on human

nutrition (~40% of the

market)

More active in animal

feed (~45% of the

market)

Source: Industry data, Kotak Institutional Equities

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

KEY RISKS

High reliance on naproxen sales, and potential market shifts such as ongoing shifts to pregabalin, gabapentin

enacarbil and brivaracetam, high customer concentration, sharper decline in custom synthesis opportunities,

regulatory risks on manufacturing and inability to scale up newly commissioned facilities are some of the key

risks for Divi’s.

Divi’s has high product concentration from top-5 products. We have discussed Divi’s

core strengths in products such as naproxen and the top-5 generic products in earlier

sections. While we do not anticipate any disruption to Divi’s generics business, particularly,

naproxen, given the economies of scale that Divi’s operates on, as well as its cost

advantages, any disruptions from new therapies, particularly for products such as

levetiracetam (from brivaracetam) and gabapentin (from gapabentin enacarbil) can impact

overall volumes and revenues of the generics segment over the longer term.

Inability to add meaningful new projects to custom synthesis segment. Divi’s has

maintained its preferred supplier relationship with 6 of top-10 Big Pharma companies

over the past decade or even longer. However, we also see a few gaps over the past few

years, such as its inability to participate in the Hep-C opportunity, which was a one of its

kind opportunity for custom synthesis (and even generics). This, along, with our analysis

on emerging therapies and declining tonnage requirements (detailed in synthesis segment)

mean that it is now critical for Divi’s to significantly broaden its basket of customers, as

well as its product basket to encompass more low tonnage products.

Exhibit 31: Product and customer concentration is a risk March fiscal year-ends, 2015-23E (% of revenues)

2015 2016 2017 2018 2019 2020 2021E 2022E 2023E

Top product 18 18 16 15 18 18 17 16 16

Top-5 products 44 43 43 46 47 47 46 46 46

Top-5 customers 43 38 41 42 37 36 — — —

Source: Kotak Institutional Equities estimates

Any issues with the US FDA or other regulatory agencies could hurt growth. Divi’s

has historically had a stellar track record in regulatory audits, barring the unfortunate

incident in Dec 2017, that escalated into an import alert, though, there are few instances

of companies getting out of import alert within a year, which is a big testament to Divi’s

focus on cGMP, and more importantly, record keeping and data integrity, as we believe

the company was able to provide all the documentation, including retrospective analysis

of over 2,000 batches of naproxen, spanning five years, with a new testing method, in

less than six months. Moreover, we believe Divi’s focus on custom synthesis segments,

and its ability to win repeat, high-tonnage business is a testament to its quality focus. It is

worth noting that we have not come across of any recalls for any of the finished dosage

forms for innovator companies that rely on Divi’s intermediates or APIs.

Recent case against the CFO for insider trading is a risk. The SEBI, in an order passed

in July 2020, had issued a penalty of Rs9.7 mn against L. Kishore Babu, the CFO of the

company, and his family members, as well as associates, in an insider trading case dating

back to CY2017, pertaining to the lifting of import alert for Unit-II. Following, the SEBI

order, Mr Kishore Babu went on a three-month leave. We understand he has now settled

the case with SEBI, and is back as the CFO of the company.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Divis Laboratories Pharmaceuticals

Top-heavy organization has been a strength, but could also pose a risk. Divi’s has a

well laid-out succession plan, as the second generation promoters, are now taking over

the mantle, with Kiran Divi now appointed as the CEO, and in-charge of the operations

of the company. He is supported by his sister, Nilima Motaparti, as well as Prakash Divi

(cousin), who looks after business development, and is now in charge of key client

relations. The second generation has stepped up well, and Mr Kiran Divi’s role was

particularly noteworthy during the import alert issue at Unit-II, which happened just when

he was taking up the operational roles (earlier he was looking after business development

as well).

Exhibit 32: Key management personnel and compensation March fiscal year-ends, 2015-20 (Rs mn)

Name Designation 2015 2016 2017 2018 2019 2020

Murali Divi Chairman & MD 354 450 465 402 588 524

NV Ramana Executive Director 182 230 242 206 299 269

Kiran Divi CEO 124 156 162 140 202 184

Kishore Babu L CFO 16 17 36 21 23 24

Nilima Motaparti Whole time Director — — — 5 7 50

Madhusudan Rao Divi Whole time Director 10 10 19 10 10 10

PV Lakshmi Rajani Company Secretary 2 3 3 2 3

Devendar Rao General Manager 13 14 29 17 18 20

Hemanth Kumar General Manager 13 14 29 17 18 20

Madhu Babu D Vice President — — — 10 11 13

Prasad YTS General Manager 13 14 29 17 18 20

Ramakrishna S General Manager 13 14 29 17 18 20

Ramana LV General Manager 8 10 21 12 14 15

Ramesh Babu L VP, Procurement 12 13 17 15 17 18

Ramesh Babu M General Manager 13 14 29 17 18

Satya Prakash Divi VP (Sales & Marketing) 16 17 19 21 23 24

Srinivasa Rao P General Manager 13 14 29 17 18 20

Subba Rao K Deputy General Manager — 6 13 — — 11

Sudhakar P Deputy General Manager — 6 13 — — —

Veeraiah Chowdary G Deputy General Manager — 6 13 — — —

Balaji Siripurapu Deputy General Manager — — 10 — — —

MNA Rao General Manager R&D — 10 11 — — —

Naga Sekhar Deputy General Manager — 6 13 — — —

Punna Rao AML Deputy General Manager — 6 11 — — —

Ramaiah Chowdary P General Manager 5 8 17 — — —

Salaries of key employees 805 1,039 1,256 947 1,307 1,238

Source: Company, Kotak Institutional Equities

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

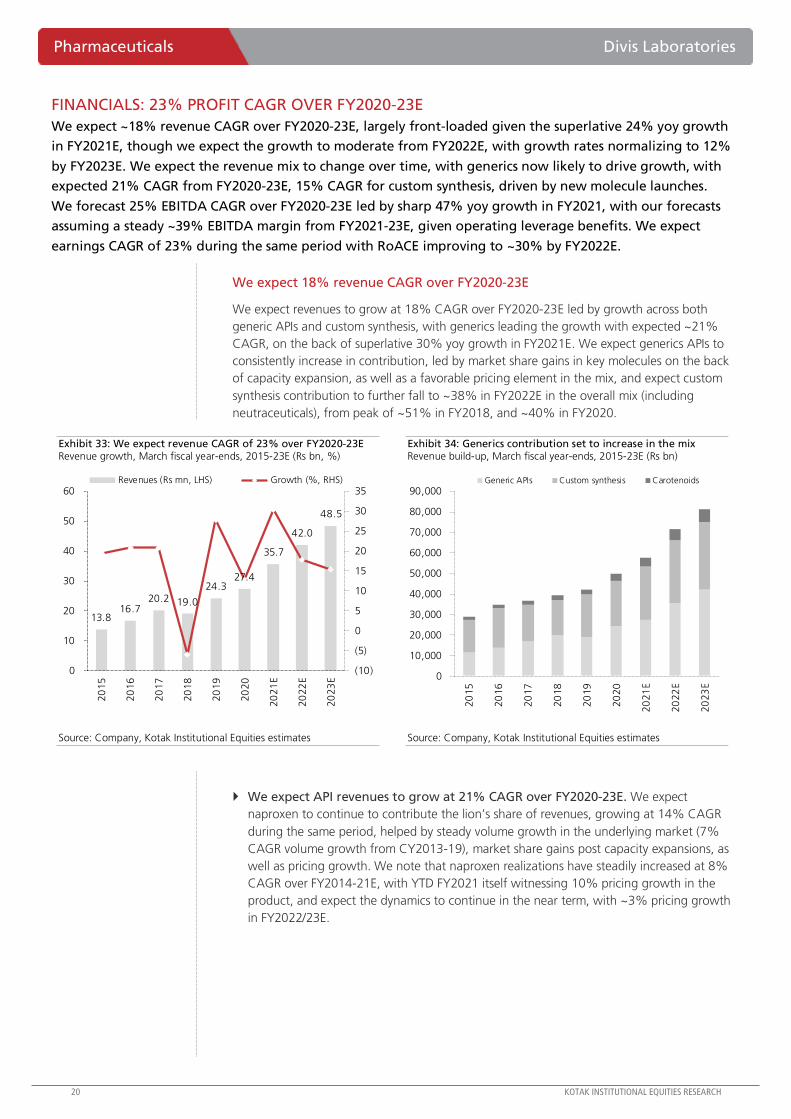

FINANCIALS: 23% PROFIT CAGR OVER FY2020-23E

We expect ~18% revenue CAGR over FY2020-23E, largely front-loaded given the superlative 24% yoy growth

in FY2021E, though we expect the growth to moderate from FY2022E, with growth rates normalizing to 12%

by FY2023E. We expect the revenue mix to change over time, with generics now likely to drive growth, with

expected 21% CAGR from FY2020-23E, 15% CAGR for custom synthesis, driven by new molecule launches.

We forecast 25% EBITDA CAGR over FY2020-23E led by sharp 47% yoy growth in FY2021, with our forecasts

assuming a steady ~39% EBITDA margin from FY2021-23E, given operating leverage benefits. We expect

earnings CAGR of 23% during the same period with RoACE improving to ~30% by FY2022E.

We expect 18% revenue CAGR over FY2020-23E

We expect revenues to grow at 18% CAGR over FY2020-23E led by growth across both

generic APIs and custom synthesis, with generics leading the growth with expected ~21%

CAGR, on the back of superlative 30% yoy growth in FY2021E. We expect generics APIs to

consistently increase in contribution, led by market share gains in key molecules on the back

of capacity expansion, as well as a favorable pricing element in the mix, and expect custom

synthesis contribution to further fall to ~38% in FY2022E in the overall mix (including

neutraceuticals), from peak of ~51% in FY2018, and ~40% in FY2020.

Exhibit 33: We expect revenue CAGR of 23% over FY2020-23E Revenue growth, March fiscal year-ends, 2015-23E (Rs bn, %)

13.816.7

20.2 19.0

24.327.4

35.7

42.0

48.5

(10)

(5)

0

5

10

15

20

25

30

35

0

10

20

30

40

50

60

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Revenues (Rs mn, LHS) Growth (%, RHS)

Source: Company, Kotak Institutional Equities estimates

Exhibit 34: Generics contribution set to increase in the mix Revenue build-up, March fiscal year-ends, 2015-23E (Rs bn)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Generic APIs Custom synthesis Carotenoids

Source: Company, Kotak Institutional Equities estimates

We expect API revenues to grow at 21% CAGR over FY2020-23E. We expect

naproxen to continue to contribute the lion’s share of revenues, growing at 14% CAGR

during the same period, helped by steady volume growth in the underlying market (7%

CAGR volume growth from CY2013-19), market share gains post capacity expansions, as

well as pricing growth. We note that naproxen realizations have steadily increased at 8%

CAGR over FY2014-21E, with YTD FY2021 itself witnessing 10% pricing growth in the

product, and expect the dynamics to continue in the near term, with ~3% pricing growth

in FY2022/23E.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Divis Laboratories Pharmaceuticals

We expect other existing APIs such as levetiracetam, gabapentin and pregabalin to

benefit from capacity additions and increasing levels of backward integration. We expect

losartan sales to continue growing on the back of market share gains for the innovator in

RoW markets, with the API likely to emerge as a top-3 product behind naproxen and

dextromethorphan, with top-3 APIs likely to cross US$100 mn sales each by FY2023E. We

also expect a meaningful increase in valsartan sales over the period with the product likely

to emerge as a top-5 largest product in Divi’s generics portfolio, behind naproxen,

dextromethorphan and gabapentin moving to >US$50 mn bucket by FY2022E. We also

expect Divi’s to partly retain (around a third) benefits of INR depreciation for products

where it has a dominant market leadership position.

Custom synthesis. We expect synthesis business to grow at ~15% CAGR from FY2020-

23E, helped by steady growth for the key underlying molecules, and benefitting from the

recently announced Rs4 bn capex, which, we suspect is largely towards a dedicated

capacity for Covid-19 anti-virals, possibly, Merck’s molnupiravir, where Phase III data is

likely in Dec 2020, followed by an emergency use authorization (EUA) in the same month.

Neutraceuticals. We expect neutraceuticals portfolio to grow at steady 16% CAGR from

FY2020-23E, though it is likely to remain a sub-10% revenue contributor to revenues.

Exhibit 35: We expect growth across both custom synthesis and generics Revenue break-up, March fiscal year-ends, 2015-23E

2015 2016 2017 2018 2019 2020 2021E 2022E 2023E

Revenues (Rs mn)

Generics 13,825 16,713 20,180 18,978 24,255 27,352 35,661 42,027 48,475

Custom synthesis 15,788 19,190 18,088 16,884 20,731 21,976 25,842 30,546 33,055

Neutraceuticals 1,370 1,536 1,857 2,390 2,510 3,810 4,616 5,540 6,371

Total 30,984 37,439 40,125 38,252 47,497 53,138 66,119 78,113 87,900

Revenue Mix (%)

Generics 45 45 50 50 51 51 54 54 55

Custom synthesis 51 51 45 44 44 41 39 39 38

Neutraceuticals 4 4 5 6 5 7 7 7 7

Total 100 100 100 100 100 100 100 100 100

Growth (%)

Generics 19 21 21 (6) 28 13 30 18 15

Custom synthesis 30 22 (6) (7) 23 6 18 18 8

Neutraceuticals 51 12 21 29 5 52 21 20 15

Total 26 21 7 (5) 24 12 24 18 13

Concentration data (% of sales)

Top product 18 18 16 15 18 18 17 16 16

Top-5 products 44 43 43 46 47 47 46 46 46

Top-5 customers 43 38 41 42 37 36 — — —

Source: Company, Kotak Institutional Equities estimates

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

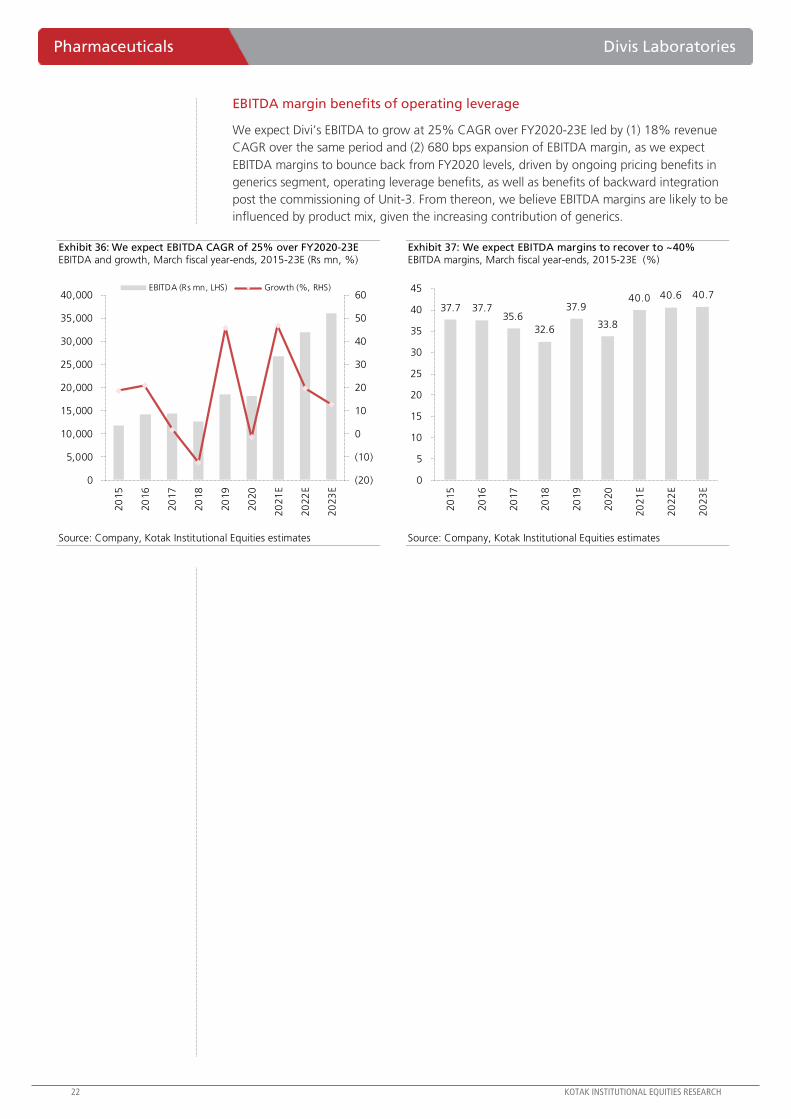

EBITDA margin benefits of operating leverage

We expect Divi’s EBITDA to grow at 25% CAGR over FY2020-23E led by (1) 18% revenue

CAGR over the same period and (2) 680 bps expansion of EBITDA margin, as we expect

EBITDA margins to bounce back from FY2020 levels, driven by ongoing pricing benefits in

generics segment, operating leverage benefits, as well as benefits of backward integration

post the commissioning of Unit-3. From thereon, we believe EBITDA margins are likely to be

influenced by product mix, given the increasing contribution of generics.

Exhibit 36: We expect EBITDA CAGR of 25% over FY2020-23E EBITDA and growth, March fiscal year-ends, 2015-23E (Rs mn, %)

(20)

(10)

0

10

20

30

40

50

60

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

EBITDA (Rs mn, LHS) Growth (%, RHS)

Source: Company, Kotak Institutional Equities estimates

Exhibit 37: We expect EBITDA margins to recover to ~40% EBITDA margins, March fiscal year-ends, 2015-23E (%)

37.7 37.735.6

32.6

37.9

33.8

40.0 40.6 40.7

0

5

10

15

20

25

30

35

40

45

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Source: Company, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Divis Laboratories Pharmaceuticals

Increasing profitabality to drive returns from FY2021/22E

Divi’s has a strong balance sheet and the company has remained debt free despite the capex

cycle over the past two years. While the incremental capex has resulted in a dilution in

return ratios in FY2019-20, we expect RoACE to jump sharply from FY2021 post the

commissioning of the new facility, and full benefits of capacity enhancements, with

FY2023E RoCE likely to move up back to ~30%, though, we expect the longer-trajectory to

trends downwards, given the increasing contribution of generics segment, which will cap

the asset turn to 1.6-1.8X over the medium term, with the company already indicating two

more rounds of capacity enhancements at Kakinada (Rs8-10 bn capex) and Nellore (Rs6-8 bn

capex).

Exhibit 38: We expect capex requirements to increase given

increasing generics contribution March fiscal year-ends, 2014-23E (Rs mn)

3,072 3,957 3,767

2,739

7,331

11,832

8,000

6,000

10,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Source: Company, Kotak Institutional Equities estimates

Exhibit 39: We expect sharp improvement in FCF from FY2021E March fiscal year-ends, 2014-23E (Rs mn)

5,191

6,422 5,480

7,277

2,212

327

9,360

13,132 13,449

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

20

15

20

16

20

17

20

18

20

19

20

20

20

21

E

20

22

E

20

23

E

Source: Company, Kotak Institutional Equities estimates

Exhibit 40: Return ratios to improve gradually as formulation business starts contributing Return ratios, March fiscal year-ends, 2012-23E (%)

27.1 26.0

27.4 26.2

29.0

22.0

15.5

20.7 19.3

23.8 24.6 23.7

30.2 30.131.4 30.8

32.2

26.6

19.4

25.2

22.1

29.730.7

29.6

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E 2023E

RoAE RoACE

Source: Company, Kotak Institutional Equities estimates

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Pharmaceuticals Divis Laboratories

Working capital to remain stable

Divi’s has historically had a longer cash conversion cycle due to high inventories, particularly,

for its generics API business, which is a function of its “make to stock” business model. The

company typically holds inventory of key APIs available throughout the year for partners,

thereby giving them flexibility to plan manufacturing batches, as typically, other API

companies have a lead time of 45-60 days of delivery for API. The strategy also enables Divi’s

to plan production seamlessly by minimizing capacity bottlenecks. We believe this strategy