![[Kotak] India Daily, July 25, 2017 - Kotak Securities](https://static.fdokumen.com/doc/165x107/63161b1a15106505030be7d5/kotak-india-daily-july-25-2017-kotak-securities.jpg)

22May 2017_India_Daily - Kotak Securities

153

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. Kotak Institutional Equities Research [email protected] . Mumbai: +91-22-4336-0000 Contents Special Reports Strategy Strategy: GST: The finishing line is finally here Daily Alerts Results State Bank of India: Standalone shines; subsidiaries weak Motherson Sumi Systems: Strong performance of SMP business Grasim Industries: In line; high costs affect VSF, but chemicals improve Tata Power: Down, but not out Muthoot Finance: Gets back on track Karur Vysya Bank: A quarter where profits take precedence DB Corp.: Weak print Jyothy Laboratories: Weaker-than-expected performance KEC International: Blockbuster end to a great year Kalpataru Power Transmission: Resilient performance Results, Change in Reco Bajaj Auto: Margins surprised negatively Cummins India: Attractiveness lessens Dhanuka Agritech: Downgrade to REDUCE on rich valuations TeamLease Services: 4QFY17 - staffing segment remains buoyant Company alerts Titan Company: Investor forum takeaways: upbeat revenue growth prognosis Sun TV Network: Multiple tailwinds PVR: GST - modest benefit versus high expectations Sector alerts Automobiles: GST rates to be neutral for the sector Insurance: A solid beginning INDIA DAILY May 22, 2017 India 19-May 1-day 1-mo 3-mo Sensex 30,465 0.1 3.7 5.5 Nifty 9,428 (0.0) 3.4 5.6 Global/Regional indices Dow Jones 20,805 0.7 1.3 0.1 Nasdaq Composite 6,084 0.5 2.9 3.8 FTSE 7,471 0.5 5.0 2.3 Nikkei 19,716 0.6 5.9 1.7 Hang Seng 25,175 0.2 4.7 4.0 KOSPI 2,297 0.4 6.1 9.0 Value traded – India Cash (NSE+BSE) 331 307 331 Derivatives (NSE) 6,464 5,207 5,317 Deri. open interest 3,464 3,327 3,321 Forex/money market Change, basis points 19-May 1-day 1-mo 3-mo Rs/US$ 64.6 (21) 6 (229) 10yr govt bond, % 7.2 - (2) (7) Net investment (US$ mn) 18-May MTD CYTD FIIs 56 386 2,903 MFs 36 1,058 6,955 Top movers Change, % Best performers 19-May 1-day 1-mo 3-mo DLFU IN Equity 207.6 (0.0) 13.2 42.1 BOI IN Equity 178.3 (0.5) 18.5 39.6 HDIL IN Equity 91.4 0.7 (0.5) 38.8 RECL IN Equity 217.0 (0.8) 5.9 37.3 FB IN Equity 112.4 1.1 21.7 33.3 Worst performers GNP IN Equity 659.2 (2.3) (27.0) (30.1) IDEA IN Equity 87.9 1.0 3.0 (21.9) UNSP IN Equity 1920.8 (6.1) 0.9 (19.9) DIVI IN Equity 611.0 (0.2) (3.1) (18.6) TECHM IN Equity 416.2 (1.5) (2.7) (18.1)

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 22May 2017_India_Daily - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Kotak Institutional Equities Research [email protected] . Mumbai: +91-22-4336-0000

Contents

Special Reports

Strategy

Strategy: GST: The finishing line is finally here

Daily Alerts

Results

State Bank of India: Standalone shines; subsidiaries weak

Motherson Sumi Systems: Strong performance of SMP business

Grasim Industries: In line; high costs affect VSF, but chemicals improve

Tata Power: Down, but not out

Muthoot Finance: Gets back on track

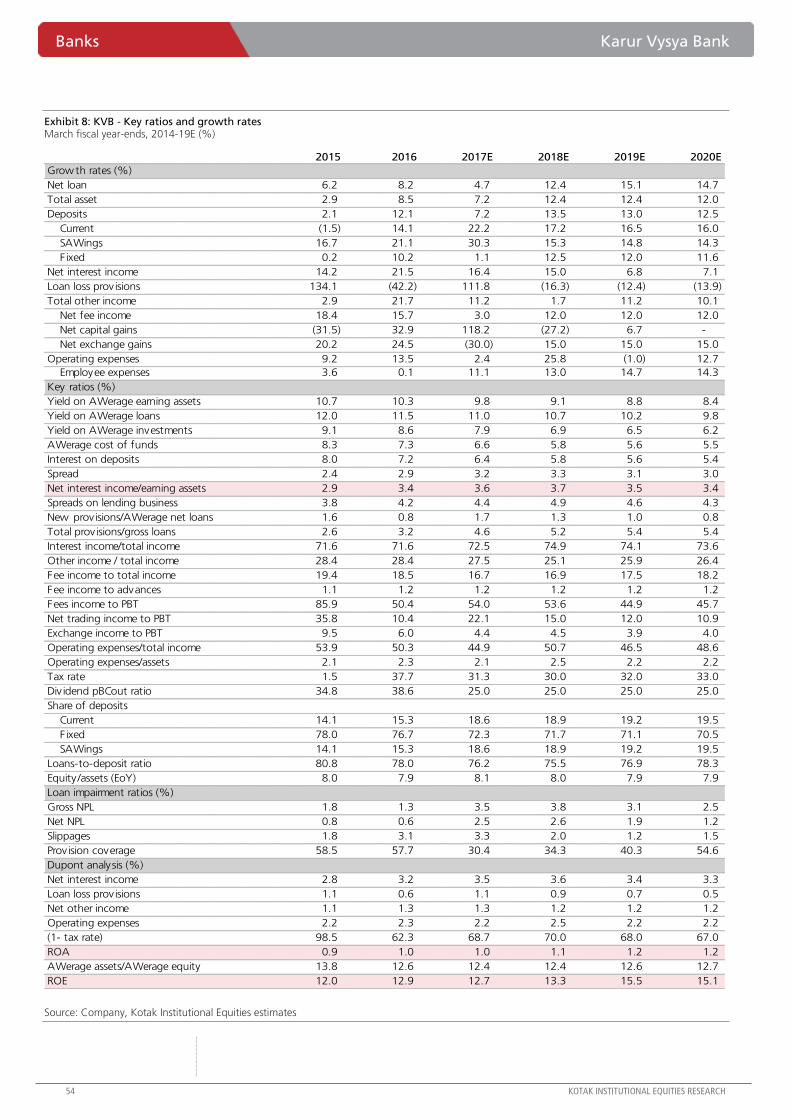

Karur Vysya Bank: A quarter where profits take precedence

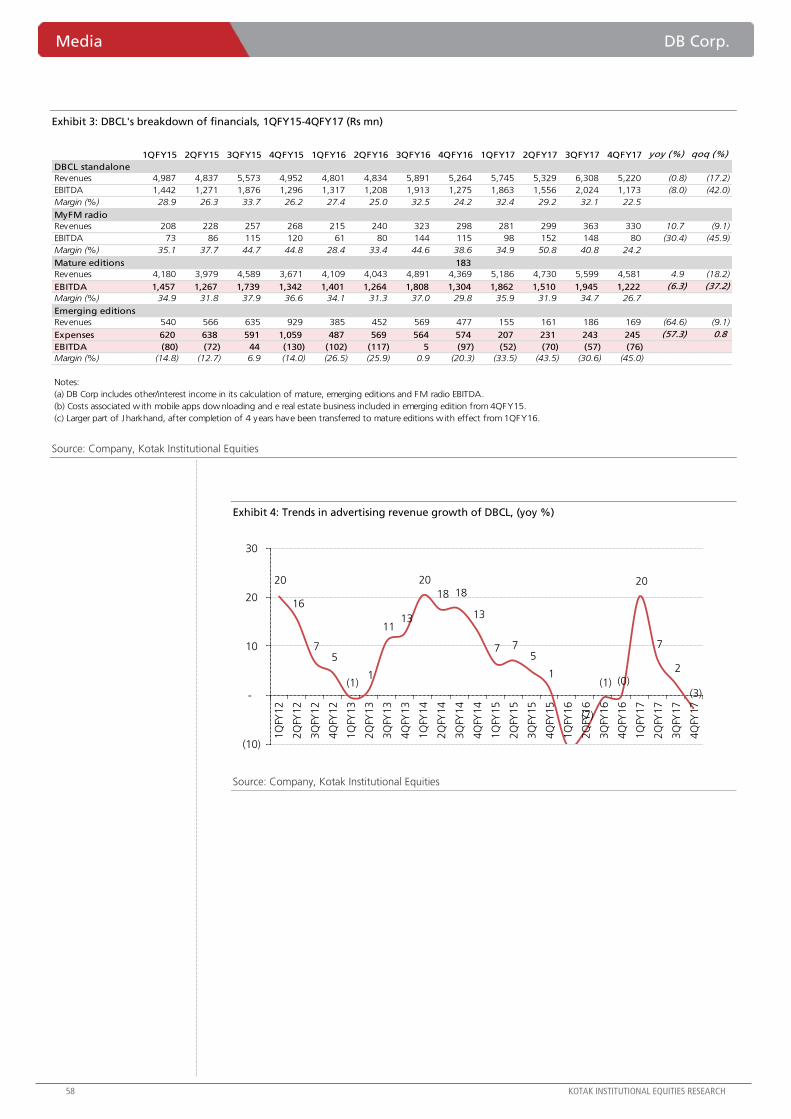

DB Corp.: Weak print

Jyothy Laboratories: Weaker-than-expected performance

KEC International: Blockbuster end to a great year

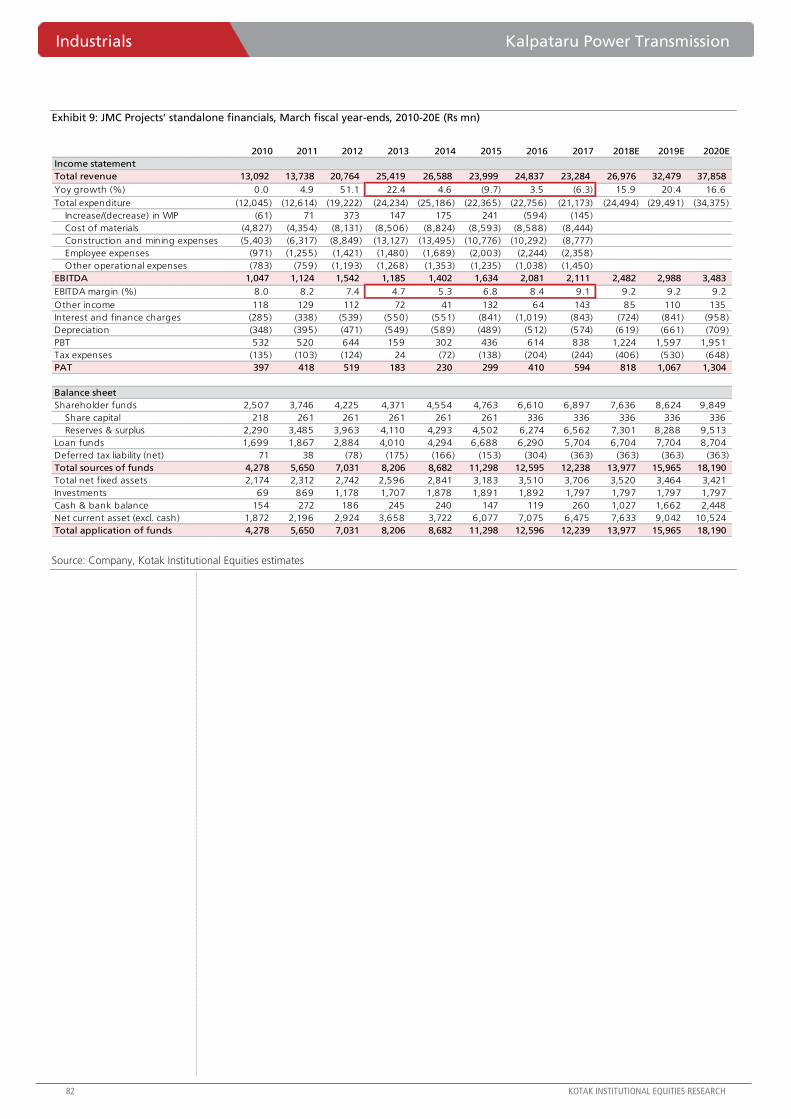

Kalpataru Power Transmission: Resilient performance

Results, Change in Reco

Bajaj Auto: Margins surprised negatively

Cummins India: Attractiveness lessens

Dhanuka Agritech: Downgrade to REDUCE on rich valuations

TeamLease Services: 4QFY17 - staffing segment remains buoyant

Company alerts

Titan Company: Investor forum takeaways: upbeat revenue growth prognosis

Sun TV Network: Multiple tailwinds

PVR: GST - modest benefit versus high expectations

Sector alerts

Automobiles: GST rates to be neutral for the sector

Insurance: A solid beginning

INDIA DAILY May 22, 2017 India 19-May 1-day 1-mo 3-mo

Sensex 30,465 0.1 3.7 5.5

Nifty 9,428 (0.0) 3.4 5.6

Global/Regional indices

Dow Jones 20,805 0.7 1.3 0.1

Nasdaq Composite 6,084 0.5 2.9 3.8

FTSE 7,471 0.5 5.0 2.3

Nikkei 19,716 0.6 5.9 1.7

Hang Seng 25,175 0.2 4.7 4.0

KOSPI 2,297 0.4 6.1 9.0

Value traded – India

Cash (NSE+BSE) 331 307 331

Derivatives (NSE) 6,464 5,207 5,317

Deri. open interest 3,464 3,327 3,321

Forex/money market

Change, basis points

19-May 1-day 1-mo 3-mo

Rs/US$ 64.6 (21) 6 (229)

10yr govt bond, % 7.2 - (2) (7)

Net investment (US$ mn)

18-May MTD CYTD

FIIs 56 386 2,903

MFs 36 1,058 6,955

Top movers

Change, %

Best performers 19-May 1-day 1-mo 3-mo

DLFU IN Equity 207.6 (0.0) 13.2 42.1

BOI IN Equity 178.3 (0.5) 18.5 39.6

HDIL IN Equity 91.4 0.7 (0.5) 38.8

RECL IN Equity 217.0 (0.8) 5.9 37.3

FB IN Equity 112.4 1.1 21.7 33.3

Worst performers

GNP IN Equity 659.2 (2.3) (27.0) (30.1)

IDEA IN Equity 87.9 1.0 3.0 (21.9)

UNSP IN Equity 1920.8 (6.1) 0.9 (19.9)

DIVI IN Equity 611.0 (0.2) (3.1) (18.6)

TECHM IN Equity 416.2 (1.5) (2.7) (18.1)

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Kotak Institutional Equities Research [email protected] Mumbai: +91-22-4336-0000

GST rate on most services at 18% versus the current 15%

Exhibit 1 gives the GST rates of various services broken down by key sectors and sub-sectors.

As can be seen, the government has put most services in the 18% category. As in the case of

goods, the government has exempt certain mass-consumption items (education, healthcare,

transportation on local and metro trains) from GST or kept the GST rate at 5% (transportation

in general). However, the 18% tax on communication is on the higher side, in our view. Also,

the GST rate of 28% on cinema tickets for multiplexes and 12-40% GST rate on F&B items

(blended 11% currently) will be negative for the listed multiplex stocks versus expectations.

GST rates on most goods in the range of 12-28%

Exhibit 2 shows the GST rates on various goods broken down by key sectors and sub-sectors.

We have already covered this in detail in our May 19 report. The government is yet to decide on

the rates for two important sectors—textiles (apart from branded garments at 18%; the

definition of branded garment is not clear since it can technically include private labels from the

unorganized sector too) and precious metals and jewelry. The government will decide on the

rates for these two categories of goods on June 3.

Limited impact on inflation as GST tax rates on common items are below current rates

We see limited impact on CPI inflation due to the changes to tax rates from July 1 following the

implementation of GST as the government has (1) exempt fresh food items completely from

GST, same as in the current taxation system, (2) kept the rates on edible oils and processed

foods items at 5-12% (with the exception of aerated waters), (3) exempt services such as

education and healthcare completely from GST, same as under the current system and (4) kept

the rate on transportation at 5% in general. The aforementioned goods and services account

for a large share of the CPI basket (see Exhibit 3).

Interesting to see how the government handles tax on gold, precious metals and jewelry

It would be interesting to see how the government handles the vexatious issue of tax on gold

and jewelry since (1) the industry vehemently opposes any changes to the taxation structure and

(2) gold imports have surged of late (see Exhibit 4). In our view, the government should

separate the two ‘roles’ of gold between savings and consumption and tax the ‘roles’ separately

to achieve its objectives of (1) higher disclosures on purchase and sale of gold and (2) higher

household financial savings. Accordingly it can (1) exempt ‘paper’ gold (gold bonds) completely

from tax as is the case for other financial savings products (other than any GST on transaction

fees), (2) tax bullion at a rate of 5% to discourage savings in the form of physical gold and

(3) tax jewelry overall at 12% GST or making charges (service) separately at 18% GST.

Strategy India

GST: The finishing line is finally here. We believe GST is all set to be implemented on

July 1, 2017 with (1) the GST Council finalizing the GST rates on almost all goods and

services and (2) 12 states passing the state GST laws; more will do so over the next few

weeks. The government has followed a multi-pronged approach to prepare for the

implementation of GST. However, we are less sure about the readiness of companies,

especially the smaller ones, to adopt GST in a smooth manner.

INDIA

MAY 22, 2017

UPDATE

BSE-30: 30,465

QUICK NUMBERS

7% of goods

exempt, 14% at 5%,

17% at 12%, 43%

at 18% and 19% at

28% GST rate

Most services to be

taxed at 18% versus

current rate of 15%

40% of CPI basket

exempt from GST

Sanjeev Prasad [email protected]

Mumbai: +91-22-4336-0830

Sunita Baldawa [email protected]

Mumbai: +91-22-4336-0896

Anindya Bhowmik [email protected]

Mumbai: +91-22-4336-0897

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Exhibit 1: GST rate on most services at 18% versus the current 15% Current service tax rates and GST rates on various services

Source: Government of India, Kotak Institutional Equities

Services Current rate GST rate Companies impacted

Communication

Broadband services 15 18

DTH& cable services 15 18 Dish TV

Telecom services 15 18 Airtel, Idea

Education

Elementary and secondary Nil Nil

Higher education & PG Nil Nil

Vocational education Nil Nil

Entertainment

Amusement parks 15% + E-tax 28

Gambling 15 28

Live sports 15% + E-tax 28

Movies ~30 blended 28 PVR

Theatre, drama, classical dance 15% + E-tax 18

Healthcare

Diagnostics Nil Nil Dr Lal Pathlabs

Hospitals, clinics Nil Nil Apollo Hospitals

Hospitality

Non-AC/alcohol serving restaurants 15 12

AC, alcohol serving restaurants 15% + VAT 18

Five star restaurants 15% + VAT 28

Hotels & lodging between Rs1,000 & Rs2,500/day 15 12

Hotels & lodging between Rs2,500 & Rs5,000/day 15% + VAT 18

Hotels & lodging above Rs5,000/day 15% + VAT 28

Transportation

Air transportation (economy) ~6 5

Air transportation (other than economy) ~9 12

Rail transportation (local & metro) Nil Nil

Rail transportation (AC & 1st class) ~5 5

Renting of metered cab, auto-rickshaw Nil Nil

Public transport (other than tourism) Nil Nil

Renting of cab, radio taxi ~5 5

India Strategy

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: GST rate on most goods in the range of 12-28% Central excise duty, state VAT and GST rates on goods

Source: Government of India, Kotak Institutional Equities

Central Current

Goods excise duty State VAT effective rate GST rate Companies impacted

Automobiles

Two-wheelers 12.5 12.5-14.5 24.3 28Bajaj Auto, Eicher Motors, Hero

Motocorp and TVS Motors

Three-wheelers 12.5 12.5-14.5 24.3 28

Small petrol cars/Compact SUVs 12.5 12.5-14.5 24.3 29 Maruti Suzuki

Small diesel cars/Compact SUVs 12.5 12.5-14.5 24.3 31 Maruti Suzuki

Mid-sized cars 24 12.5-14.5 32.3 43 Maruti Suzuki

Large cars 30 12.5-14.5 34.1 43 Maruti Suzuki

Large SUVs 27 12.5-14.5 35.9 43 M&M

Commercial vehicles 12.5 12.5-14.5 24.3 28Ashok Leyland, Bharat Forge, Eicher

Motors, Tata Motors and Wabco

Tractors 8.8 4-6 11.9 12 M&M

Cement

Cement

12.5% + Rs125/ton

(Chargeable on 30%

discount to MRP)

12.5-14.5 23-26 28UltraTech, ACC, Ambuja, Shree Cement

and other mid-cap names

Consumer durables

Air-conditioner, microwave oven, refrigerator, washing machines 12.5 12-5-14.5 26-30 28 Havells, Voltas, Whirlpool

Fans, water heaters, mixer juicer grinders 12.5 12-5-14.5 26-30 28 Crompton

Consumer staples

FMCG products (except those stated below) 12.55-12.5 (varies

across states)16-24 28 All FMCG companies

Bakery items

Bread Nil Nil Nil Nil

Pastries and cakes 6 5-12.5 11-18 18 Britannia

Rusks, toasted bread and similar toasted products Nil 5-12.5 5-12.5 5 Britannia

Beverages

Aerated waters containing added sugars 21 15 32-36 28

Fruit pulp or fruit juice-based drinks 6 5 11-12 12 Dabur, Manpasand Beverages

Mineral water 12.5 12.5 26-28 18

Tea and coffee Nil 5 4-6 5

Cigarettes

Cigarettes46 (blended; varies

based on stick's length)

27 (blended - varies

across states)40-70

28% + fixed cess +

ad valorem cessITC, VST, Godfrey Phillips

Dairy products

Butter and others fats (ghee, butter oil etc.) Nil 5-12.5 5-12.5 12 Britannia

Cheese Nil 12.5 12.5 12 Britannia

Fresh milk (ex-UHT), curd, butter milk, paneer Nil Nil Nil Nil

Milk powder/ UHT milk, skimmed milk, cream, yoghurt Nil 5 4-6 5 Nestle, Britannia

SMP, milk food for babies (ex-condensed milk) Nil Nil Nil 5 Nestle

Other food items

Chocolates, chewing gum 12.5 12.5 26-28 28 Nestle

Honey (branded) Nil 5 4-6 5 Dabur

Ice cream 6 12.5 16-20 18 HUVR

Namkeens 12.5 12.5 26-28 12

Pasta 6 12.5 18 18 Nestle, ITC

Sauce, soup and broths 12.5 12.5 26-28 18

Vegetable oils Nil 5 4-6 5 Marico, Agro Tech Foods

Personal care items

Coconut oil Nil 5 4-6 5 Marico, Dabur

Hair oils (excluding coconut oil), toothpaste, soaps 12.5 12.5 26-28 18 Marico, Dabur, Bajaj Corp., Emami

Perfumes, deodorants, shampoos, hair cream, hair dyes 12.5 12.5 26-28 28

Sanitary napkins Nil 5 4-6 12 P&G Hygiene

Building materials

Paints 12.5 12.5 26-28 28 All paint companies

Prepared glues and other prepared adhesives (under 1Kg) 12.5 12.5 26-28 18

Sanitaryware, faucets, tiles 12.5 7-12.5 18-24 28 Cera, HSIL, Kajaraia, Somany

Others

Apparel/garments 2 4-5 6-7 Not decidedArvind, Kewal Kiran, Nandan Denim and

Page Industries

Bullion/Jewelry 1 1 2 Not decided Titan, PC Jeweller

Notes:

(a) Excise duty and state VAT are charged on different ‘bases’ and hence , they are not additive.

(b) Swachh Bharat, Krishi Kalyan and Infrastructure cess to be subsumed in GST within one year of implementation.

(c) Small cars/mini SUVs includes vehicles <4 m in length and engine size less than 1,200 cc/1,500 cc for petrol/diesel vehicles

(d) Mid-sized cars/SUVs includes vehicles >4 m in length and engine size less than 1,500 cc

(e) Large SUVs/Cars includes vehicles with engine size greater than 1,500 cc

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Exhibit 3: Gold imports have surged recently Value of gold imports, March fiscal year-ends, 2014-17 (US$ bn)

Source: CEIC, Kotak Institutional Equities

Exhibit 4: GST-exempt items have 40% weight in CPI basket Weight of various food items in CPI basket (%)

Source: MOSPI, Kotak Institutional Equities

1.4 1.3

2.6

1.8 2.2

3.1

1.8 2.1

3.8 4.2

5.6

1.4 1.6

2.0

5.0

3.1

2.4 2.0

3.0

5.0

2.0 1.7

3.5 3.8

2.9

1.4 1.0

1.2 1.5

1.2 1.1 1.1

1.8

3.5

4.4

2.0 2.0

3.5

4.2 3.8

0

1

2

3

4

5

6

7

Jan

-14

Mar-

14

May-

14

Jul-1

4

Sep

-14

Nov-

14

Jan

-15

Mar-

15

May-

15

Jul-1

5

Sep

-15

Nov-

15

Jan

-16

Mar-

16

May-

16

Jul-1

6

Sep

-16

Nov-

16

Jan

-17

Mar-

17

Gold imports

Weight in CPI

Fresh food items 30.0

Edible oils and processed food items 15.2

Education 4.5

Healthcare 5.8

Transportation 2.5

Others 42.0

Total 100.0

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Kotak Institutional Equities Research [email protected] Mumbai: +91-22-4336-0000

Solid operating profit growth gives headroom to improve coverage

SBI reported a sharp rise in earnings, which was supported by solid growth in operating profits.

Revenue growth of 9% yoy was led by 18% yoy growth in NII despite loan growth being weak

at 8% yoy. NIM improved qoq by ~5 bps as the bank benefitted due to demonetization as well

as one-off interest on tax refunds. CASA ratio was stable qoq. Consolidated performance was

weak as the subsidiaries reported a huge loss ahead of the merger. There were higher

provisions for bad loans as well as retirement-related expenses.

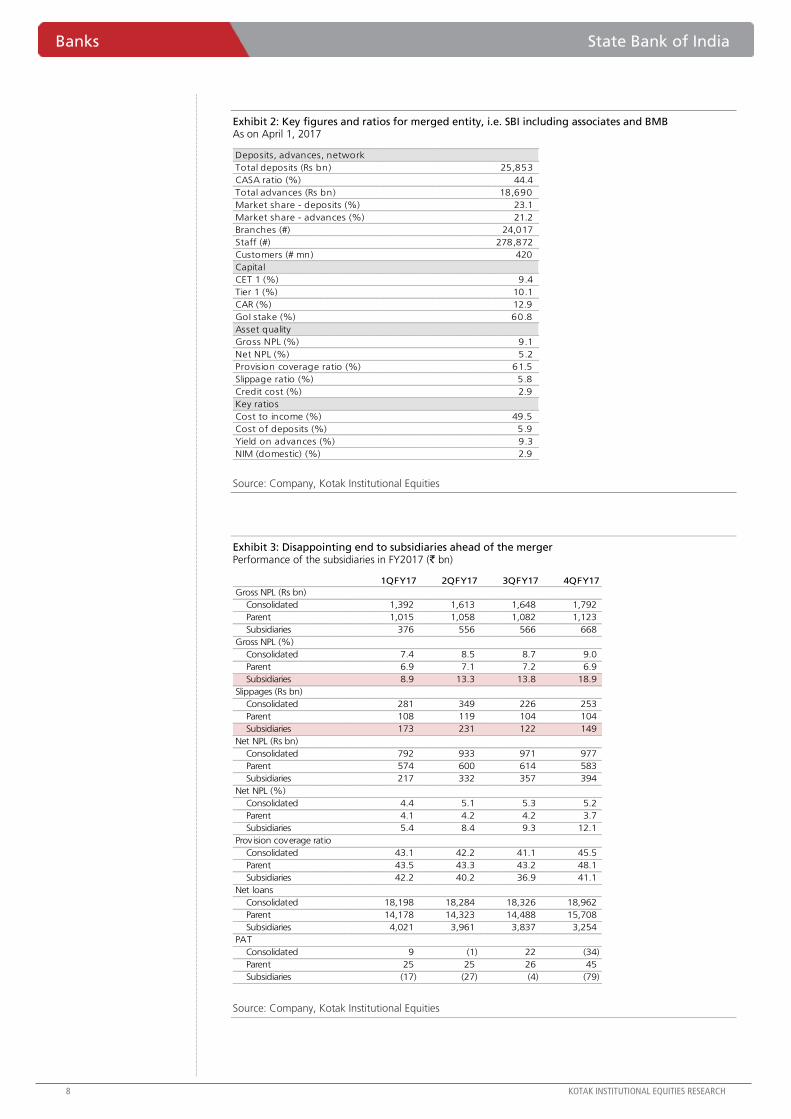

A weak end to subsidiaries; NPLs closer to any other mid-tier public bank

The banking subsidiaries reported a steep loss in 4QFY17 and FY2017 resulting in a big drag in

consolidated performance. The slippages were high at ~15% for the quarter/year resulting in

gross NPLs increasing closer to ~19%, similar to most mid-tier public banks. Net NPLs were at

12% yoy with overall coverage ratio stable yoy but improving qoq. These banks cut back lending,

ahead of the consolidation, resulting in loans declining ~20% yoy. The performance has been

quite disappointing though the management highlighted that such a performance is unlikely to

be repeated as the bank has taken full control over the operations in the past few months.

Maintain BUY: awaiting resolutions while merger-related pain seems to be complete

We maintain BUY rating on SBI with TP of ₹350 (from `360 earlier) with key changes to

estimates on credit costs and impairment outlook. At our TP, we value the bank at 1.5X book

(1X reported) and 10X FY2019E EPS for RoEs in the range of ~10% in the short term. Our

broad thesis on the bank remains unchanged as it remains our preferred idea in public banks.

We have seen one major rerating in the bank over the past year but any incremental return

from here is contingent on (1) pace of resolutions and (2) quantum of haircuts. Outcomes for

many of these large accounts are not quick and require lengthy approval process and consensus

from all banks and stakeholders. While we continue to see a fair amount of work done for

resolving these assets, we have not yet seen the conclusion making it difficult to understand the

full impact of these resolutions. On the other hand, the merger process seems to be going

smoothly and we are unlikely to see any major surprises in 1QFY18 results.

State Bank of India (SBIN) Banks

Standalone shines; subsidiaries weak. SBI reported a sharp improvement in operating

profit growth of 25% yoy giving headroom for higher provisions as slippages were

stable qoq. Revenue growth of 9% yoy was led by NII growth on the back of decline in

funding costs. Slippages declined to 2.6% and net NPL ratios declined qoq. The merger

is now complete and the only negative surprise was the performance of subsidiaries,

which was quite disappointing. We have moved to consolidated performance post-

merger with a broadly unchanged price. Maintain BUY as it remains our preferred idea

in PSU banks; TP ₹ 350 (from ₹ 360).

BUY

MAY 22, 2017

RESULT

Coverage view: Attractive

Price (`): 308

Target price (`): 350

BSE-30: 30,465

QUICK NUMBERS

NII grew 18% yoy;

earnings grew 2.2X

yoy

Gross NPLs at 6.9%;

restructured loans

at 2.3% of loans

Maintain BUY with

TP at ₹350 (from

`360 earlier)

M B Mahesh CFA [email protected]

Mumbai: +91-22-4336-0886

Nischint Chawathe [email protected]

Mumbai: +91-22-4336-0887

Abhijeet Sakhare [email protected]

Mumbai: +91-22-4336-0889

State Bank of India

Stock data Forecasts/Valuations 2017 2018E 2019E

52-week range (Rs) (high,low) EPS (Rs) 13.1 16.1 29.5

Market Cap. (Rs bn) EPS growth (%) 2.6 22.7 82.7

Shareholding pattern (%) P/E (X) 23.4 19.1 10.5

Promoters 60.2 NII (Rs bn) 618.6 815.1 950.0

FIIs 10.9 Net profits (Rs bn) 104.8 130.8 238.9

MFs 8.0 BVPS 131.1 158.4 197.1

Price performance (%) 1M 3M 12M P/B (X) 2.3 1.9 1.6

Absolute 8.4 14.3 78.3 ROE (%) 6.3 6.4 10.3

Rel. to BSE-30 4.4 6.9 48.7 Div. Yield (%) 0.8 0.9 1.0

Company data and valuation summary

315-166

2,497.8

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Exhibit 1: SBI quarterly results March fiscal year-ends, 4QFY16 - 4QFY17 (` mn)

Source: Company, Kotak Institutional Equities estimates

4QFY17 4QFY17E 4QFY16 3QFY17 4QFY17E 4QFY16 3QFY17 2017 2016 (% chg.) 2018E

Income earned 473,926 437,571 428,314 439,256 8 11 8 1,755,183 1,636,853 7 2,353,488

Income on advances 298,612 286,600 292,425 298,313 4 2 0 1,195,100 1,156,660 3 1,608,547

Income on investments 135,070 139,694 110,079 126,087 (3) 23 7 482,053 423,040 14 664,327

Interest on balance w ith RBI 40,244 11,277 25,810 14,857 257 56 171 78,029 57,153 37 80,614

Interest expense 293,219 282,744 275,406 291,741 4 6 1 1,136,580 1,068,039 6 1,538,352

Net interest income (NII) 180,707 154,826 152,908 147,515 17 18 23 618,603 568,815 9 815,136

Non-interest income 103,275 89,765 106,956 96,619 15 (3) 7 354,609 281,584 26 656,190

Fees, commission 60,780 51,417 57,940 40,110 18 5 52 178,030 144,160 23 267,045

Invt. income 17,660 10,170 14,160 39,690 74 25 (56) 107,490 51,688 108 132,490

Forex income 5,890 5,534 4,850 5,910 6 21 (0) 26,760 21,123 27 53,520

Other income excl. treasury 85,615 79,595 92,796 56,929 8 (8) 50 247,119 229,896 7 523,700

Total income 283,982 244,591 259,864 244,135 16 9 16 973,212 850,398 14 1,471,326

Operating expenses 106,688 120,211 117,945 118,702 (11) (10) (10) 464,728 417,824 11 879,448

Staff expenses 45,393 53,637 49,130 54,833 (15) (8) (17) 264,893 251,138 5 368,574

Other retirement contributions 17,030 15,225 20,300 16,540 12 (16) 3

Other operating expenses 61,295 51,349 48,517 47,329 19 26 30 199,835 166,685 20 510,874

Pre-provision operating profit 177,295 124,380 141,919 125,433 43 25 41 508,484 432,575 18 591,879

Provisions and extraordinaries 117,401 79,839 131,741 89,428 47 (11) 31 359,927 294,838 22 407,626

Loan loss provisions 109,929 72,717 121,392 72,446 51 (9) 52 351,152 302,907 16 400,864

Standard assets 2,890 6,820 9,960 13,640 NM (71) NM

Investment depreciation 780 196 (60) 100 299 (1,400) 680 2,080 1,496 39 -

Other provisions 3,802 107 449 3,243 3,463 747 17 6,696 (9,565) (170) 6,762

PBT 59,894 44,541 10,179 36,004 34 488 66 148,557 137,737 8 184,253

Less tax 14,716 14,573 (2,460) 9,904 1 (698) 49 43,711 38,234 14 53,433

Profit after tax 45,178 29,968 12,638 26,100 51 257 73 104,846 99,503 5 130,819

Fees to PBT (%) 101.5 569.2 111.4 119.8 104.7 144.9

Treasury income/PBT (%) 28.2 139.7 110.0 71.0 36.4 71.9

Cost income ratio (%) 37.6 45.4 48.6 47.8 49.1 59.8

Tax rate (%) 24.6 (24.2) 27.5 29.4 27.8 29.0

Key balance sheet data (Rs bn)

Advances gross 16,273 15,095 14,972 8 9

Advances net 15,711 14,637 14,478 7 9

Deposits 20,448 17,307 20,408 18 0

Investments 7,660 4,771 8,339 61 (8)

Yield management ratios (%)

Cost of deposits 5.8 6.2 5.9

Yield on advances 9.4 10.0 9.5

Net interest margin (Reported, Qtly ) 2.8 3.0 2.8

Asset quality details

Gross NPLs (Rs bn) 1,123 982 1,082 14 4

Gross NPLs (%) 6.9 6.5 7.2

Net NPLs (Rs bn) 583 558 614 4 (5)

Net NPLs (%) 3.7 3.8 4.2

Slippages 103.7 303.1 103.6

Provision coverage (%) 48.1 43.2 43.2

Provision coverage (tech w /o, %) 66.0 60.7 62.9

Standard restructured loans (Rs bn) 366 391 346 (6) 6

Standard restructured loans (%) 2.3 2.7 2.4

Capital adequacy details (%)

CAR 13.1 13.1 12.9

Tier I 10.4 9.9 10.0

(% chg.)

Banks State Bank of India

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Key figures and ratios for merged entity, i.e. SBI including associates and BMB As on April 1, 2017

Source: Company, Kotak Institutional Equities

Exhibit 3: Disappointing end to subsidiaries ahead of the merger Performance of the subsidiaries in FY2017 (` bn)

Source: Company, Kotak Institutional Equities

Deposits, advances, network

Total deposits (Rs bn) 25,853

CASA ratio (%) 44.4

Total advances (Rs bn) 18,690

Market share - deposits (%) 23.1

Market share - advances (%) 21.2

Branches (#) 24,017

Staff (#) 278,872

Customers (# mn) 420

Capital

CET 1 (%) 9.4

Tier 1 (%) 10.1

CAR (%) 12.9

GoI stake (%) 60.8

Asset quality

Gross NPL (%) 9.1

Net NPL (%) 5.2

Provision coverage ratio (%) 61.5

Slippage ratio (%) 5.8

Credit cost (%) 2.9

Key ratios

Cost to income (%) 49.5

Cost of deposits (%) 5.9

Yield on advances (%) 9.3

NIM (domestic) (%) 2.9

1QFY17 2QFY17 3QFY17 4QFY17

Gross NPL (Rs bn)

Consolidated 1,392 1,613 1,648 1,792

Parent 1,015 1,058 1,082 1,123

Subsidiaries 376 556 566 668

Gross NPL (%)

Consolidated 7.4 8.5 8.7 9.0

Parent 6.9 7.1 7.2 6.9

Subsidiaries 8.9 13.3 13.8 18.9

Slippages (Rs bn)

Consolidated 281 349 226 253

Parent 108 119 104 104

Subsidiaries 173 231 122 149

Net NPL (Rs bn)

Consolidated 792 933 971 977

Parent 574 600 614 583

Subsidiaries 217 332 357 394

Net NPL (%)

Consolidated 4.4 5.1 5.3 5.2

Parent 4.1 4.2 4.2 3.7

Subsidiaries 5.4 8.4 9.3 12.1

Provision coverage ratio

Consolidated 43.1 42.2 41.1 45.5

Parent 43.5 43.3 43.2 48.1

Subsidiaries 42.2 40.2 36.9 41.1

Net loans

Consolidated 18,198 18,284 18,326 18,962

Parent 14,178 14,323 14,488 15,708

Subsidiaries 4,021 3,961 3,837 3,254

PAT

Consolidated 9 (1) 22 (34)

Parent 25 25 26 45

Subsidiaries (17) (27) (4) (79)

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Fresh slippages decline; impairments including watchlist declines 70 bps to

~10%

High slippages, credit cost for standalone bank. Slippages remained high at 2.6%

(albeit ~30 bps lower qoq), with nearly 50% of slippages from watchlist accounts (iron &

steel, textiles and ‘others’). Total impaired loans (GNPL and restructured loans) declined

40 bps qoq to 9.2%, comprising 6.9% gross NPL and 2.3% restructured loans. Credit

cost for the quarter was 2.9%, up ~100 bps qoq.

Delayed AQR recognition impacts associates’ asset quality in FY2017. Asset quality

at the group level was much weaker with gross NPL of 9.1% and net NPL of 5.2%.

Slippage for the year was also much higher at 5.8% with credit cost of 2.9%. SBI

highlighted that uniform recognition of stress loans led to higher slippages as AQR-

related slippages identified by RBI were much lower for associate banks – these had to be

recognized in line with parent’s recognition standards.

Power exposure lead to a higher, revised watchlist. SBI has revised the watchlist

loans to `324 bn from `132 bn at the end of the year. `324 bn is spilt as `220 bn

corresponding to SBI while rest is from associate banks. Weak power exposures without

power purchase agreements (PPAs) were included in the watchlist – these were not

included earlier as they were under construction.

7% of power loans under watchlist. SBI has nearly `146 bn loans to power sector of

which 3% is already NPL and 17% is non-investment grade exposure. Of these 10%, SBI

has identified 7% as those exposure needs attention and hence have been included in

the watchlist exposures.

~40% coverage in top-50 NPLs. Top 50 NPL accounts comprise nearly 48% of total

gross NPLs, with coverage ratio of ~40%. As such, there is scope to further improve

coverage levels on these accounts. SBI’s overall standalone coverage ratio improved ~300

bps qoq to 66%, which is one of the highest among PSU banks. Including associate

banks, the coverage ratio was lower at ~62%.

Exhibit 4: Post-merger watchlist exposure is `324 bn Sector-wise watchlist exposure, March 2016-March 2017 (Rs bn)

Source: Company, Kotak Institutional Equities

Exhibit 5: Nearly 45% of FY2017 slippages were from watchlist accounts Break-up of slippages, March fiscal year-ends, 1QFY17-4QFY17 (Rs bn)

Source: Company, Kotak Institutional Equities

Mar-16 Sep-16 Dec-16 Mar-17 Post-merger

Construction, roads & engg. 87 41 19 18 31

Power 47 37 30 28 111

Iron & steel 43 27 19 - 35

Oil & gas 34 34 - - -

Textile 12 9 8 4 8

Telecom 8 8 8 8 32

Others 117 103 96 74 107

Total 348 260 180 132 324

1QFY17 2QFY17 3QFY17 4QFY17 FY2017

Total slippages 108 119 104 104 434

Corporate - watchlist 29 49 73 54 206

Corporate - non-watchlist 7 20 27 24 78

Others (retail, agri, SME) 71 50 3 26 150

Banks State Bank of India

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 6: 7% of the power sector exposure under watchlist, out of ~17% of non-investment grade

exposure Break-up of power sector exposure (approximate values), March 2017 (%)

Source: Company, Kotak Institutional Equities

Exhibit 7: NPLs increased in key portfolios like mid-corporate segment Sectoral break-up of NPLs, March fiscal year-ends, 2011-17 (%)

Notes: (a) Gross NPL has been calculated based on outstanding NPL in each category to the reported advances. These ratios differ from those reported by the bank (exposures have been reclassified between various segments).

Source: Company, Kotak Institutional Equities

Exhibit 8: Restructured loans as % of loans is one of the lowest among public banks Restructured loans, March fiscal year-ends, 2012-17

Source: Company, Kotak Institutional Equities

PSUs40%

Investment grade40%

Non-investment grade10%

Under watchlist7%

NPL3%

2011 2012 2013 2014 2015 2016 2017 2011 2012 2013 2014 2015 2016 2017

Corporate 4 5 10 24 15 207 331 0.2 0.3 0.6 1.0 0.5 6.3 9.7

Mid-corporate 60 127 184 263 230 415 470 3.8 7.4 9.0 11.5 10.6 17.1 19.3

International 23 25 28 38 26 78 68 2.1 1.9 1.7 1.8 1.1 2.9 2.4

SME 78 119 145 155 164 170 159 6.5 7.1 7.9 8.6 9.0 7.8 7.0

Agri 45 78 101 107 107 87 75 4.8 9.0 9.3 8.9 8.9 6.9 5.5

Retail 44 42 43 30 25 25 22 2.6 2.3 2.0 1.3 0.9 0.8 0.5

Total 253 397 512 616 567 982 1,123 3.3 4.4 4.8 5.0 4.3 6.5 6.9

Gross NPLs (Rs bn) Gross NPLs (%)

2012 2013 2014 2015 2016 2017 2012 2013 2014 2015 2016 2017

BOB 171 196 207 259 137 108 6.0 6.0 5.2 6.1 3.6 2.8

BoI 164 164 208 218 129 NA 6.5 5.6 5.5 5.3 3.4 NA

Canara 79 181 232 284 232 216 3.4 7.5 7.7 8.6 7.2 6.3

PNB 11 305 355 383 201 119 0.4 9.9 10.2 10.1 4.9 2.8

SBI 163 322 431 558 391 366 1.9 3.1 3.6 4.3 2.7 2.3

Union 91 116 154 181 176 162 4.1 4.2 5.3 5.2 3.1 1.9

Restructured loans (Rs bn) Restructured loans (% of loans)

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Exhibit 9: Gross NPLs inched up in the quarter as slippages remained high Movement of NPLs, March fiscal year-ends, 4QFY15-4QFY17 (` bn)

Source: Company, Kotak Institutional Equities

Exhibit 10: Asset quality stable in the quarter Gross NPLs, net NPLs and provision coverage ratio, March fiscal year-ends, 2007-17 (%)

Source: Company, Kotak Institutional Equities

4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

Opening 619.9 567.3 564.2 568.3 981.7 981.7 1,015.4 1,057.8 1,081.7

Addition 47.7 73.2 58.8 206.9 303.1 108.0 118.5 103.6 103.7

Cash recoveries 44.9 12.1 8.9 6.6 16.3 16.5 13.4 10.0 12.0

Upgradation 6.8 14.9 6.3 3.8 1.0 11.7 2.1 10.6 10.0

Write-off 48.7 49.2 39.4 37.0 32.1 46.1 60.6 59.1 39.9

Closing Gross NPL 567.3 564.2 568.3 981.7 981.7 1,015.4 1,057.8 1,081.7 1,123.4

Provision coverage (without w/off) 51.4 49.2 49.7 43.2 43.2 43.5 43.3 43.2 48.1

Provision coverage (reported) 69.1 69.5 70.5 65.2 60.7 61.6 62.1 62.9 66.0

Fresh impairment (%)

Slippages 1.5 2.3 1.8 9.1 8.3 3.0 3.3 2.9 2.6

Fresh restructuring 3.9 1.2 0.8 - - - - - -

Total 5.4 3.5 2.6 9.1 8.3 3.0 3.3 2.9 2.6

Outstanding (%)

Gross NPL 4.3 4.3 4.2 5.1 6.5 6.9 7.1 7.2 6.9

Restructured loans 4.3 4.4 4.0 2.7 2.7 2.6 2.6 2.4 2.3

Total 8.5 8.7 8.1 7.8 9.2 9.5 9.7 9.6 9.2

30

38

46

54

62

70

0.0

1.4

2.8

4.2

5.6

7.0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Gross NPLs (LHS) Net NPLs (RHS) Provision coverage (RHS)

Banks State Bank of India

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

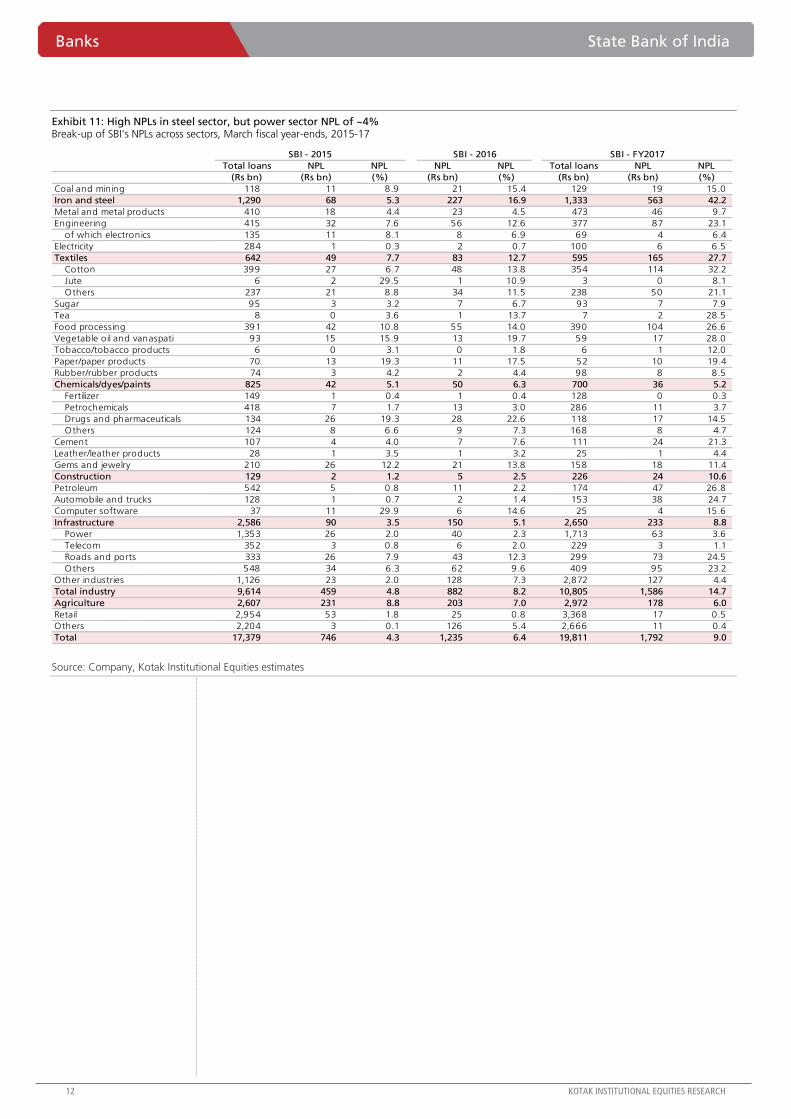

Exhibit 11: High NPLs in steel sector, but power sector NPL of ~4% Break-up of SBI's NPLs across sectors, March fiscal year-ends, 2015-17

Source: Company, Kotak Institutional Equities estimates

Total loans NPL NPL NPL NPL Total loans NPL NPL

(Rs bn) (Rs bn) (%) (Rs bn) (%) (Rs bn) (Rs bn) (%)

Coal and mining 118 11 8.9 21 15.4 129 19 15.0

Iron and steel 1,290 68 5.3 227 16.9 1,333 563 42.2

Metal and metal products 410 18 4.4 23 4.5 473 46 9.7

Engineering 415 32 7.6 56 12.6 377 87 23.1

of which electronics 135 11 8.1 8 6.9 69 4 6.4

Electricity 284 1 0.3 2 0.7 100 6 6.5

Textiles 642 49 7.7 83 12.7 595 165 27.7

Cotton 399 27 6.7 48 13.8 354 114 32.2

Jute 6 2 29.5 1 10.9 3 0 8.1

Others 237 21 8.8 34 11.5 238 50 21.1

Sugar 95 3 3.2 7 6.7 93 7 7.9

Tea 8 0 3.6 1 13.7 7 2 28.5

Food processing 391 42 10.8 55 14.0 390 104 26.6

Vegetable oil and vanaspati 93 15 15.9 13 19.7 59 17 28.0

Tobacco/tobacco products 6 0 3.1 0 1.8 6 1 12.0

Paper/paper products 70 13 19.3 11 17.5 52 10 19.4

Rubber/rubber products 74 3 4.2 2 4.4 98 8 8.5

Chemicals/dyes/paints 825 42 5.1 50 6.3 700 36 5.2

Fertilizer 149 1 0.4 1 0.4 128 0 0.3

Petrochemicals 418 7 1.7 13 3.0 286 11 3.7

Drugs and pharmaceuticals 134 26 19.3 28 22.6 118 17 14.5

Others 124 8 6.6 9 7.3 168 8 4.7

Cement 107 4 4.0 7 7.6 111 24 21.3

Leather/leather products 28 1 3.5 1 3.2 25 1 4.4

Gems and jewelry 210 26 12.2 21 13.8 158 18 11.4

Construction 129 2 1.2 5 2.5 226 24 10.6

Petroleum 542 5 0.8 11 2.2 174 47 26.8

Automobile and trucks 128 1 0.7 2 1.4 153 38 24.7

Computer software 37 11 29.9 6 14.6 25 4 15.6

Infrastructure 2,586 90 3.5 150 5.1 2,650 233 8.8

Power 1,353 26 2.0 40 2.3 1,713 63 3.6

Telecom 352 3 0.8 6 2.0 229 3 1.1

Roads and ports 333 26 7.9 43 12.3 299 73 24.5

Others 548 34 6.3 62 9.6 409 95 23.2

Other industries 1,126 23 2.0 128 7.3 2,872 127 4.4

Total industry 9,614 459 4.8 882 8.2 10,805 1,586 14.7

Agriculture 2,607 231 8.8 203 7.0 2,972 178 6.0

Retail 2,954 53 1.8 25 0.8 3,368 17 0.5

Others 2,204 3 0.1 126 5.4 2,666 11 0.4

Total 17,379 746 4.3 1,235 6.4 19,811 1,792 9.0

SBI - FY2017SBI - 2015 SBI - 2016

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Loan growth of 8% yoy; adjusted loan growth of 14% yoy

Headline loan growth of 8% yoy was better than system loan growth of ~5% yoy. Loan

growth adjusting for food credit, FCNR redemptions and credit substitutes (CP, NCD) was

much higher at 14% yoy.

Retail segment performed better with 21% yoy loan growth. SME (3% yoy growth), mid-

corporate (flat yoy) and large corporate (4% yoy) witnessed slower loan growth. Retail

segment constitutes ~25% of the loan book.

The bank remains cautious in lending to SME and the mid corporate portfolio after

witnessing high levels of stress from these segments. Within retail growth in the housing

loans remains strong at 17% yoy. Auto loans grew by 21% yoy. Gross NPL ratio in retail

segment is just ~0.5%.

We are lot more concerned on growth as we are witnessing headline growth for the

sector slowing to 5% levels. We are less confident that SBI would be able to grow at a

significant premium despite their advantage on cost of funds as the bank has a strong

portfolio of companies who can tap alternate markets to raise funds and make early

repayment.

While SBI is also participating in the CP/NCD market, these loans will entail lower

margins. We are noting banks appear to be a lot more comfortable in reducing their

spreads to maintain growth momentum, which could hurt margins if growth takes

precedence.

We are building loan growth at 10-12% in the medium term as we don’t think the

growth will be sufficient to replace the repayment cycle of the loans taken in the previous

capex cycle.

Exhibit 12: Loan growth of 14% yoy, adjusting for credit substitute, food credit and FCNR loans Credit growth, March fiscal year-ends, 2016-17 (Rs bn)

Source: Company, Kotak Institutional Equities

2016 2017 YoY (%)

Domestic advances 12,427 13,411 8

Food credit 216 46 (79)

Domestic advances (ex food credit) 12,211 13,365 9

Commercial paper 131 587 348

Corporate bonds 412 596 45

Domestic including credit substitutes 12,754 14,548 14

Overseas advances 2,668 2,862 7

FCNR-B advances 185 66 (64)

Foreign offices ex FCNR-B 2,483 2,796 13

Overall adjusted credit growth 15,237 17,344 14

Corporate advances 5,726 5,849 2

Credit substitute as % of domestic corporate loans 9 20

Banks State Bank of India

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 13: Share of SME and mid-corporate loans has been coming off, increased for retail and large corporate loans Loan growth and loan break-up, March fiscal year-ends, 2011-17 (%)

Source: Company, Kotak Institutional Equities

NIM improved marginally qoq to 2.8%

Reported NIM improved ~5 bps qoq to 2.8%. Reported cost of deposits declined by ~10 bps

qoq to 5.8% while yield on advances also declined ~5 bps qoq to 9.4%. Margin pressure

due to fall in MCLR rates will be partly offset by (1) repricing of associates deposits which are

priced higher than parent, (2) bank has an excess SLR of ~5% which can be deployed in the

form of loans or credit substitutes, (3) parent’s treasury yields are better than associates.

CASA ratio declined marginally to 46%. SA growth was strong at 28% yoy. Bank indicated

that it has retained around 60-70% of the demonetization-related deposit flows. Bank has

benefitted from higher average balances in savings accounts post demonetization, greater

traction in corporate salary packages and new current accounts.

Exhibit 14: Credit / Deposit ratio improved during the quarter March fiscal year-ends, 4QFY14-4QFY17 (%)

Source: Company, Kotak Institutional Equities

Exhibit 15: Margins improve qoq March fiscal year-ends, 4QFY14-4QFY17 (%)

Source: Company, Kotak Institutional Equities

2011 2012 2013 2014 2015 2016 2017 2011 2012 2013 2014 2015 2016 2017

Corporate and others 3.2 7.3 12.2 38.0 16.2 17.1 3.6 19.3 17.5 16.3 19.5 21.1 21.9 21.0

International 12.7 24.1 24.6 26.8 9.4 13.8 7.3 14.5 15.2 15.7 17.2 17.6 17.7 17.6

Mid-corporate 19.4 10.0 18.2 11.5 (4.7) 11.4 0.2 20.8 19.4 19.0 18.3 16.3 16.1 14.9

SME 22.8 41.3 8.9 (2.4) 0.9 20.0 3.5 15.8 18.9 17.1 14.4 13.6 14.4 13.8

Retail 22.2 10.8 14.9 13.3 14.6 20.0 21.2 21.7 20.4 19.4 19.1 20.4 21.7 24.3

Agriculture 21.2 (9.0) 25.8 10.7 (0.4) 4.7 7.4 12.5 9.7 10.1 9.7 9.0 8.3 8.3

Total 18.0 18.1 20.7 15.4 7.3 13.0 7.8

Loan growth (YoY %) Loan break-up (%)

87

84

82 8282

79

8283

85

79

77

71

77

70

74

78

82

86

90

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

3.2 3.3 3.2

3.2

3.4

3.0 3.0

3.2 3.2

2.9 2.8

2.7

3.1

2.5

2.7

3.0

3.2

3.5

3.7

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Exhibit 16: SBI has focused on growth while peers are consolidating balance sheets NII growth and loan growth, March fiscal year-ends, 4QFY15-4QFY17 (%)

Source: Company, Kotak Institutional Equities

Exhibit 17: MCLR rates have decline by 120 bps since April 2016

Source: Company, Kotak Institutional Equities

Exhibit 18: SBI has cut deposit rates in the last quarter Change in term deposit rates for deposits less than `10 mn (%)

Source: Company, Kotak Institutional Equities

4QFY16 1QFY17 2QFY17 3QFY17 4QFY17 4QFY16 1QFY17 2QFY17 3QFY17 4QFY17

BoB 14.8 (2.6) 5.6 15.9 7.6 (10.3) (11.2) (14.6) (8.9) (0.1)

BoI 12.0 (4.7) (9.9) 5.7 (4.1) (7.3) 0.5 (1.8) (2.7) 2.7

Canara (4.5) (8.3) (7.7) 8.4 14.1 (1.6) (0.9) 1.3 (0.1) 5.3

OBC 4.3 (9.3) (4.9) (17.4) (3.4) 3.8 2.6 (0.9) (2.6) 8.4

PNB (27.0) (9.8) (10.2) (9.4) 33.1 8.4 2.8 3.4 (1.8) 1.7

SBI 3.9 4.2 3.5 (3.5) 18.2 12.6 10.7 8.3 (1.1) 7.3

Union (1.7) (1.3) 8.4 7.0 14.5 5.7 5.1 9.6 5.5 8.6

Loan growth (%)NII growth (%)

Apr-16 May-16 Jun-16 Jul-16 Aug-16 Oct-16 Nov-16 Jan-17 Feb-17

Overnight 8.95 8.90 8.90 8.90 8.85 8.80 8.65 7.75 7.75

One month 9.05 9.00 9.00 9.00 8.95 8.90 8.75 7.85 7.85

Three month 9.10 9.05 9.05 9.05 9.00 8.95 8.80 7.90 7.90

Six month 9.15 9.10 9.10 9.10 9.05 9.00 8.85 7.95 7.95

One year 9.20 9.15 9.15 9.15 9.10 9.05 8.90 8.00 8.00

Two years 9.30 9.25 9.25 9.25 9.20 9.15 9.00 8.10 8.10

Three years 9.35 9.30 9.30 9.30 9.25 9.20 9.05 8.15 8.15

Jan-15 Oct-15 Nov-15 Oct-15 Mar-16 Oct-16 Nov-16 Dec-16 May-16

7-14 days 5.00 5.25 5.25 5.25 5.25 5.50 5.50 5.50 5.50

15-30days 5.00 5.25 5.25 5.25 5.25 5.50 5.50 5.50 5.50

31-45days 5.00 5.25 5.25 5.25 5.25 5.50 5.50 5.50 5.50

46 -90 days 7.00 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50

91-120days 7.00 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50

120-180 days 7.00 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50

181-270 days 7.25-7.5 6.75-7.0 6.75-7.0 6.75-7.0 6.75-7.0 6.75-7.0 6.75-7.0 6.50 6.50

271 days-1year 7.50 7.00 7.00 7.00 7.00 7.00 7.00 6.50 6.50

1 year-2year 8.50 7.25-7.5 7.25-7.5 7.25-7.5 7.25-7.5 7.05-7.1 7.05-7.10 6.9-6.75 6.9-6.75

2 year-3year 8.50 7.50 7.50 7.50 7.50 7.00 7.00 6.75 6.25

3 years-5 years 8.50 7.00 7.00 7.00 7.00 6.50 6.50 6.50 6.25

5 years-8 years 8.25 7.00 7.00 7.00 7.00 6.50 6.50 6.50 6.25

8years-10

years

8.25 7.00 7.00 7.00 7.00 6.50 6.50 6.50 6.25

Banks State Bank of India

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 19: SBI has cut base rates by 75 bps in the current cycle Change in base rate and PLR (%)

Source: Company, Kotak Institutional Equities

Exhibit 20: Strong traction in savings account CASA ratio break-up across banks, March fiscal year ends, 2007-17 (%)

Source: Company, Kotak Institutional Equities

Costs growth at 5% yoy; merger to drive cost efficiencies

Overall operating expenses growth was 5% yoy, led by 10% yoy decline in staff cost and

16% yoy growth in non-staff expenses. Higher non-staff cost reflects spend towards IT,

network and technology-related infrastructure. Staff cost decline is a result of wage gap

between those retiring and the fresh recruits, a trend that is likely to continue.

Bank is benefitting from retirements at the higher salary levels and fresh recruitments at

lower salaries. We think this would be a long term gains that they are likely to see

considering the declining age of the bank’s employee base. Retirement related expenses

declined by 17% yoy at the standalone level in 4QFY17. Retirement related expenses in

FY2017 were stable yoy. Nearly 35% of parent’s staff is under defined contribution

schemes as compared to 40% for the associate banks.

Date PLR Base rate

Oct-10 12.50 7.60

Jan-11 12.75 8.00

Feb-11 13.00 8.25

Apr-11 13.25 8.50

May-11 14.00 9.25

Jul-11 14.25 9.50

Aug-11 14.75 10.00

Sep-12 14.50 9.75

Jan-13 14.45 9.70

Sep-13 14.55 9.80

Nov-13 14.75 10.00

Apr-15 - 9.85

Jun-15 - 9.70

Oct-15 - 9.30

Jan-17 - 9.25

18.8 18.3 14.9 11.2 11.5 9.4 9.2 8.0 7.9 7.8 6.2

29.7 28.7 26.7 31.9 34.6

34.5 34.5 33.7 32.6 33.6 34.6

-

12

24

36

48

60

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Current Savings

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

We believe that the cost growth is a sustainable advantage for the bank. The

management has indicated that it would like to keep growth in physical and human

infrastructure at minimum levels. Further, it would look to reduce other non-staff costs

though it may not be as material as what we have seen recently. We expect <10% yoy

cost growth over FY2017-19E.

Merger to drive synergies over time. Cost synergies are imminent post-merger over the

medium term as the merged entity rationalizes its branch and ATM network,

redundancies are eliminated, IT, loan processing centers, treasury functions are

integrated. Staff redundancies will be addressed by redeployment into revenue-

generating functions such as sales, business development and new initiatives such as

wealth management.

Exhibit 21: Cost-to-income increased during the quarter Operating costs and cost-income ratio, March fiscal year-end, 4QFY14-4QFY17

Source: Company, Kotak Institutional Equities

Exhibit 22: Decline in share of retirement related cost Retirement costs and staff costs to total income, March fiscal year-end, 2010-4QFY17

Source: Company, Kotak Institutional Equities

Retail fee income growth at 11% yoy; non-interest income declines 2% yoy

Non-interest income declined 2% yoy as the base quarter had the benefit of FX gains on

repatriation. Growth across other categories such as fee income (5% yoy), treasury gains

(25% yoy), recovery in written-off accounts (22% yoy), FX income (21% yoy), dividend

(flat yoy) was healthy.

While overall fee income growth was 5% yoy, retail fee income was 11% yoy, reflecting

the pressure on corporate fees. Loan processing fees, comprising of ~18% of fees,

declined 8% yoy. Transaction fees, comprising ~30% of fees grew just 2% yoy.

Cross-sell can become an important driver of fee income going forward. This segment

comprises only 5% of fee income currently, despite nearly 40% CAGR over FY2013-17.

Bank is focusing on leveraging on data analytics on customized sales across nearly 420

mn strong customer franchise. Growth of the recently launched wealth management unit

will drive fee income.

45

50 53 51

47

51

50

39

45

49 51 49

44

30

38

46

54

62

70

0

25

50

75

100

125

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

Operating costs (LHS)

Cost-income (RHS)(Rs bn) (%)

16 26 20 16 23 18 19 25 23 29 17 24 23 27 -

7

14

21

28

35

15

20

25

30

35

40

2010

2011

2012

2013

2014

2015

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

Retirement costs to staff costs (RHS)Staff costs to income (LHS)

Banks State Bank of India

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 23: ~40% CAGR in cross-sell fee income Break-up of cross-sell fee income, March fiscal year-ends, 2013-17 (Rs mn)

Source: Company, Kotak Institutional Equities estimates

Other key highlights for the quarter

Capital. CAR and tier-1 of the standalone was 13.1% and 9.8% respectively. Post-

merger, this has declined marginally to 12.9% and 9.4%.

SBI Cards. SBI Cards reported PAT growth of 37% yoy to `3.9 bn in FY2017. It has a

credit cards market share of 15.3% (up 50 bps yoy) with spends market share of 13.1%

(up 120 bps yoy). SBI is in process to increase its combined stake in the two card entities

(front-end and back-end) to 74% from 55%. Business had RoE of ~30%.

SBI Fund Management. FY2017 PAT grew 36% yoy to `2.2 bn. AUM grew 47% yoy to

`1.57 tn with market share of 8.6%, up 70 bps yoy. Monthly SIP book has grown by

64% yoy. Business had RoE of ~30%.

SBI Capital Markets. FY2017 PAT declined ~10% yoy to `2.5 bn, with RoE of 20%. It

was ranked first (by no. of issues) and second (by issue amount) for FY2017 for overall

equity deals.

SBI General Insurance. General insurance business reported net profit in FY2017 after

loss for two consecutive years. RoE of ~14% has scope to improve further. Gross written

premium for FY2018 is projected to grow at 35% yoy.

Exhibit 24: SBI has stakes in several large companies which can be monetized SBI’s key investments and financial metrics, March fiscal year-ends, 2016

Source: Company, Kotak Institutional Equities

`

2013 2014 2015 2016 2017 CAGR (%)

Life 1,440 1,595 2,446 3,372 4,646 34

MF 339 281 700 623 1,811 52

General 233 409 566 731 1,070 46

Other 74 63 171 165 239 34

Total 2,086 2,348 3,883 4,891 7,766 39

SBI's stake FY2016 PAT FY2016 NW FY2016 RoE

Strategic investment (%) (Rs mn) (Rs mn) (%)

IL&FS 6 2,740 56,057 5

NSE 5 4,393 52,110 8

BSE 5 1,061 22,320 5

CDSL 10 634 3,581 18

UTI 18 2,321 15,475 15

CCIL 21 3,172 19,801 16

SIDBI 13 12,172 111,845 11

Central Warehousing Corporation 22 1,978 18,218 11

NSDL 5 820 4,109 20

ARCIL 20 143 15,200 1

NPCI 11 1,176 5,578 21

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Exhibit 25: SBI forecasts and valuation March fiscal year-ends, 2013-2019E

Notes:

1. ABVPS: Reported book value of the standalone business less net NPLs at 70%

2. Data from FY2018 is for the consolidated book. Note that the adjusted book value is reduced for

revaluation reserves

3. BVPS including banking subs: Adjusted book value of the standalone bank and net worth of banking

subsidiaries

Source: Company, Kotak Institutional Equities estimates

Exhibit 26: State Bank of India 1 year forward multiples

Rolling APBR (including banking subsidiaries), 2008 - 2017

Source: Company, Bloomberg, Kotak Institutional Equities estimates

Exhibit 27: SBI trading premium to peers has improved SBI trading premium to PSU Banks, 2008 – 2017

Source: Company, Bloomberg, Kotak Institutional Equities estimates

Net int.

income PAT EPS P/E ABVPS APBR RoE

(Rs bn) (Rs bn) (Rs) (X) (Rs) (X) (%)2013 443 141 21 14.7 115 2.6 15.4

2014 493 109 15 20.8 119 2.5 10.0

2015 550 131 18 17.3 134 2.2 10.6

2016 569 100 13 23.6 121 2.4 7.3

2017E 619 105 13 23.0 131 2.2 6.3

2018E 815 131 16 18.8 158 1.9 6.4

2019E 950 239 29 10.3 197 1.5 10.3

2020E 373 391 48 6.3 255 1.2 15.0

0

1

1

2

2

3

May-

08

May-

09

May-

10

May-

11

May-

12

May-

13

May-

14

May-

15

May-

16

May-

17

0.8

1.0

1.2

1.3

1.5

1.7

May-

08

May-

09

May-

10

May-

11

May-

12

May-

13

May-

14

May-

15

May-

16

May-

17

Banks State Bank of India

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

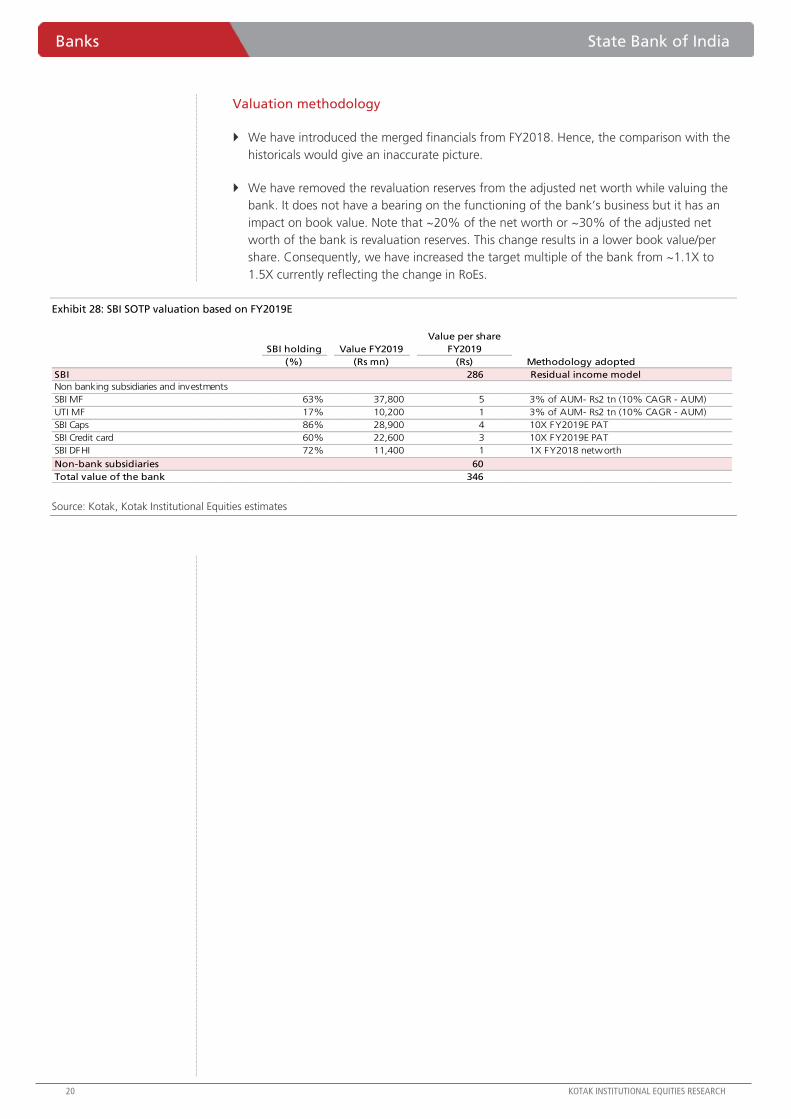

Valuation methodology

We have introduced the merged financials from FY2018. Hence, the comparison with the

historicals would give an inaccurate picture.

We have removed the revaluation reserves from the adjusted net worth while valuing the

bank. It does not have a bearing on the functioning of the bank’s business but it has an

impact on book value. Note that ~20% of the net worth or ~30% of the adjusted net

worth of the bank is revaluation reserves. This change results in a lower book value/per

share. Consequently, we have increased the target multiple of the bank from ~1.1X to

1.5X currently reflecting the change in RoEs.

Exhibit 28: SBI SOTP valuation based on FY2019E

Source: Kotak, Kotak Institutional Equities estimates

SBI holding Value FY2019

(%) (Rs mn) Methodology adopted

SBI 286 Residual income model

Non banking subsidiaries and investments

SBI MF 63% 37,800 5 3% of AUM- Rs2 tn (10% CAGR - AUM)

UTI MF 17% 10,200 1 3% of AUM- Rs2 tn (10% CAGR - AUM)

SBI Caps 86% 28,900 4 10X FY2019E PAT

SBI Credit card 60% 22,600 3 10X FY2019E PAT

SBI DFHI 72% 11,400 1 1X FY2018 networth

Non-bank subsidiaries 60

Total value of the bank 346

Value per share

FY2019

(Rs)

State Bank of India Banks

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Exhibit 29: SBI – growth rates and key ratios March fiscal year-ends, 2015-20E (%)

Notes:

(a) Data from FY2018 is the consolidated performance of the bank

Source: Company, Kotak Institutional Equities estimates

2015 2016 2017E 2018E 2019E 2020E

Growth rates (%)Net loan 7.5 12.6 7.3 32.0 11.7 12.2

Total Asset 14.3 10.3 19.8 30.4 11.9 12.6

Deposits 13.1 9.8 18.1 38.0 11.7 12.2

Current 10.0 12.2 5.2 36.1 13.3 13.8

Sav ings 8.7 13.4 24.3 30.4 12.1 12.5

F ixed 16.2 7.4 16.2 43.1 11.4 11.8

Net interest income 11.6 3.4 8.8 31.8 16.5 11.9

Loan loss provisions 29.8 50.7 15.9 14.2 (6.9) (27.5)

Total other income 21.7 24.7 25.9 85.0 10.5 9.0

Net fee income 4.5 9.4 23.5 50.0 12.0 12.0

Net capital gains 58.7 42.9 108.0 23.3 7.5 -

Net exchange gains 2.1 9.1 26.7 100.0 12.0 12.0

Operating expenses 8.3 8.0 11.2 89.2 9.0 6.9

Employee expenses 4.6 6.7 5.5 39.1 5.9 2.8

Key ratios (%)Yield on average earning assets 8.3 8.2 7.7 8.1 8.0 7.9

Yield on average loans 9.0 8.4 7.9 8.8 8.6 8.6

Yield on average investments 8.3 9.1 8.0 7.5 7.3 7.1

Average cost of funds 5.7 5.7 5.2 5.6 5.5 5.5

Interest on deposits 6.0 6.0 5.6 5.9 5.8 5.8

Difference 2.6 2.5 2.4 2.6 2.4 2.4

Net interest income/earning assets 3.0 2.8 2.7 2.8 2.7 2.7 New provisions/average net loans 1.6 2.2 2.3 2.2 1.7 1.1

Interest income/total income 70.9 66.9 63.6 55.4 56.7 57.4

Fee income to total income 17.0 17.0 18.3 18.1 17.9 18.1

Operating expenses/total income 49.8 49.1 47.8 59.8 57.2 55.3

Tax rate 32.2 27.8 29.4 29.0 29.0 29.0

Div idend payout ratio 20.2 20.3 19.8 17.4 10.2 6.6

Share of deposits

Current 7.9 8.1 7.2 7.1 7.2 7.3

F ixed 58.7 57.4 56.5 58.6 58.4 58.2

Sav ings 33.4 34.5 36.4 34.4 34.5 34.6

Loans-to-deposit ratio 82.4 84.6 76.8 73.5 73.5 73.5

Equity/assets (EoY) 6.3 6.4 7.0 6.3 6.2 6.3

Asset quality trends (%)Gross NPL (%) 4.3 6.5 6.8 8.1 7.0 6.0

Net NPL (%) 2.1 3.8 3.7 4.7 3.9 3.1

Slippages (%) 2.4 4.9 3.0 2.1 1.8 1.8

Provision coverage (%, ex write-off) 51.4 43.2 48.1 45.2 48.0 51.8

Dupont analysis (%)Net interest income 2.9 2.6 2.5 2.6 2.5 2.5

Loan loss provisions 1.0 1.4 1.4 1.3 1.0 0.6

Net other income 1.2 1.3 1.4 2.1 1.9 1.9

Operating expenses 2.0 1.9 1.9 2.8 2.6 2.5

Invt. depreciation (0.0) 0.0 0.0 - - -

(1- tax rate) 67.8 72.2 70.6 71.0 71.0 71.0

RoA 0.7 0.5 0.4 0.4 0.6 0.9

Average assets/average equity 15.6 15.8 14.9 15.2 16.1 16.1

RoE 10.6 7.3 6.3 6.4 10.3 15.0

Banks State Bank of India

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 30: SBI – P&L and balance sheet March fiscal year-ends, 2015-20E (` mn)

Notes:

(a) Data from FY2018 is the consolidated performance of the bank

Source: Company, Kotak Institutional Equities estimates

2015 2016 2017E 2018E 2019E 2020E

Income statementTotal interest income 1,523,971 1,636,853 1,755,183 2,353,488 2,786,484 3,127,160

Loans 1,123,439 1,156,660 1,195,100 1,608,547 1,892,830 2,123,694

Investments 353,536 423,040 482,053 664,327 791,836 888,171

Total interest expense 973,818 1,068,035 1,136,580 1,538,352 1,836,493 2,064,330

Net interest income 550,153 568,818 618,603 815,136 949,990 1,062,831

Loan loss provisions 201,017 302,907 351,152 400,864 373,123 270,365

Net interest income (after prov.) 349,136 265,911 267,451 414,273 576,867 792,466

Other income 225,759 281,584 354,609 656,190 724,971 790,400

Net fee income 131,728 144,160 178,030 267,045 299,090 334,981

Net capital gains 36,180 51,688 107,490 132,490 142,490 142,490

Net exchange gains 19,360 21,123 26,760 53,520 59,942 67,135

Operating expenses 386,776 417,824 464,728 879,448 958,463 1,024,782

Employee expenses 235,371 251,138 264,893 368,574 390,415 401,489

Depreciation on investments (5,901) 1,496 2,080 - - -

Other Provisions 880 (9,565) 6,696 6,762 6,830 6,898

Pretax income 193,140 137,741 148,557 184,253 336,545 551,185

Tax provisions 62,124 38,234 43,711 53,433 97,598 159,844

Net Profit 131,016 99,507 104,846 130,819 238,947 391,342 % growth 20.3 (24.0) 5.4 24.8 82.7 63.8

PBT - Treasury + Provisions 352,955 380,890 400,994 459,389 574,009 685,958

% growth 18.3 7.9 5.3 14.6 25.0 19.5

Balance sheetCash and bank balance 1,547,558 1,674,677 1,719,720 2,133,025 2,351,761 2,606,996

Cash 149,432 150,809 135,728 162,874 195,449 234,538

Balance w ith RBI 1,009,406 1,145,484 1,199,361 1,585,520 1,771,681 1,987,826

Balance w ith banks 24,338 31,239 37,487 37,487 37,487 37,487

Net value of investments 4,817,587 4,770,973 7,659,900 10,164,821 11,666,891 13,515,150

Govt. and other securities 3,776,542 3,603,989 6,492,916 9,096,596 10,598,666 12,446,926

Shares 43,365 43,279 43,279 43,279 43,279 43,279

Debentures and bonds 305,278 411,268 411,268 411,268 411,268 411,268

Net loans and advances 13,000,264 14,637,004 15,710,780 20,731,368 23,165,502 25,991,693

F ixed assets 93,292 103,893 429,190 648,846 575,689 502,558

Other assets 1,022,097 1,404,084 1,540,080 1,617,084 1,730,280 1,851,399

Total assets 20,480,798 22,590,630 27,059,670 35,295,144 39,490,122 44,467,796

Deposits 15,767,932 17,307,224 20,447,510 28,219,479 31,532,815 35,379,818

Current 1,245,723 1,398,070 1,471,230 2,002,216 2,268,835 2,581,013

F ixed 9,248,881 9,931,693 11,543,420 16,523,610 18,400,632 20,574,750

Savings 5,273,328 5,977,461 7,432,860 9,693,653 10,863,348 12,224,056

Borrow ings and bills payable 2,253,350 2,426,290 3,361,325 3,280,126 3,715,309 4,213,629

Other liabilities 1,175,133 1,414,371 1,367,965 1,573,160 1,809,134 2,080,504

Total liabilities 19,196,416 21,147,886 25,176,800 33,072,765 37,057,259 41,673,952

Total shareholders' equity 1,284,382 1,442,744 1,882,861 2,222,379 2,432,863 2,793,844

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Kotak Institutional Equities Research [email protected] Mumbai: +91-22-4336-0000

Strong 4QFY17 results led by improvement in performance of SMP business

Motherson Sumi has reported consolidated EBITDA of `12.4 bn (24.6% yoy), which was 6%

above our estimates due to (1) stronger-than-expected revenue growth in standalone and

SMP businesses and (2) better-than-expected profitability in the SMP business. Net profit

adjusted for one-off expenses was `5.4 bn (+27.8% yoy), which was 15% above our

estimates; higher outperformance at the net profit level was due to higher other income,

lower interest expenses and lower tax rate.

The company reported standalone EBITDA of `3.6 bn (+17.4% yoy), which was in line with

our estimates as stronger-than-expected revenue growth was offset by lower-than-expected

EBITDA margin. Revenues grew by 19% yoy led by strong growth in passenger vehicle

industry volumes and increase in market share due to presence in Maruti’s high-growth

models such as Baleno and Brezza. EBITDA margin came in 20.6% (down 20 bps and 60 bps

qoq), which was 100 bps below our estimates due to lower gross margins.

Revenues for SMR business were EUR420 mn (+15% yoy), which was in line with our

estimate. EBITDA margin came in at 12.9% (down 20 bps yoy and up 110 bps qoq) as

compared to our estimate of 12.5%. Revenues for SMP business were EUR810 mn (+21%

yoy), which was ahead of our estimate of 15% yoy growth. EBITDA margin came in at 6.8%

(up 160 bps yoy and up 90 bps qoq) as compared to our estimate of 6%.

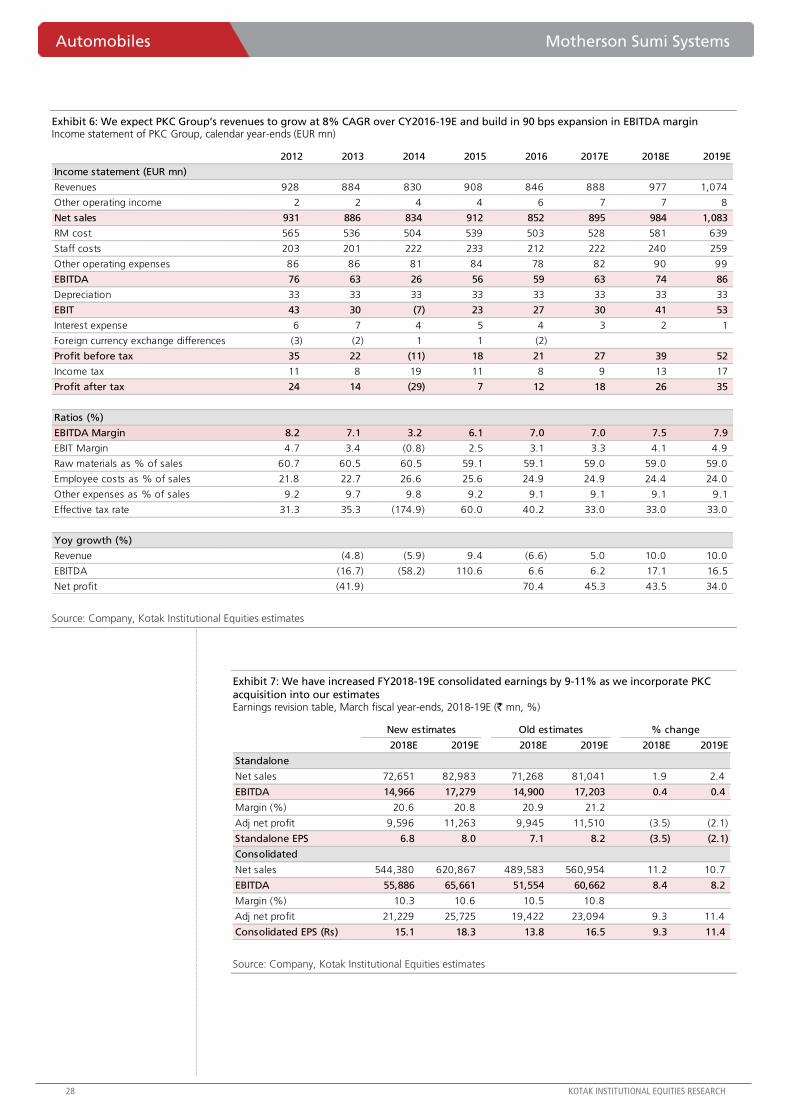

Increase our estimates as we build in PKC acquisition; maintain SELL with revised TP of `340

We have increased our FY2018-19E consolidated EPS estimates by 9-11% as we build in PKC

acquisition in our estimates. Our earnings estimates for standalone entity and SMRPBV business

remain largely unchanged. For PKC Group, we build in (1) 9% revenue CAGR over CY2016-19E

and (2) 90 bps expansion in EBITDA margin leading to 13%/40% EBITDA and EPS CAGR over

CY2016-19E. We have revised our SoTP-based target price to ₹340 (from ₹300 earlier) due to

(1) PKC acquisition and (2) rollover to March 2019E.

Motherson Sumi Systems (MSS) Automobiles

Strong performance of SMP business. Motherson reported strong 4QFY17 results

with 25% yoy growth in consolidated EBITDA, which was 6% above our estimates due

to stronger-than-expected revenue growth and profitability of SMP business. Standalone

business reported 17% yoy EBITDA growth (in line) led by order wins for Maruti’s

successful models. Going ahead, while we remain positive on the company’s growth

prospects, we believe valuations are expensive at 23X FY2019E EPS. We maintain our

SELL rating with revised target price of ₹340 (₹300 earlier) as we build in PKC

acquisition in our estimates and roll over to March 2019E.

SELL

MAY 22, 2017

RESULT

Coverage view: Cautious

Price (`): 424

Target price (`): 340

BSE-30: 30,465

Hitesh Goel [email protected]

Mumbai: +91-22-4336-0878

Nishit Jalan [email protected]

Mumbai: +91-22-4336-0877

Motherson Sumi Systems

Stock data Forecasts/Valuations 2017 2018E 2019E

52-week range (Rs) (high,low) EPS (Rs) 11.6 15.1 18.3

Market Cap. (Rs bn) EPS growth (%) 18.4 30.8 21.2

Shareholding pattern (%) P/E (X) 36.6 28.0 23.1

Promoters 63.1 Sales (Rs bn) 424.8 544.4 620.9

FIIs 19.7 Net profits (Rs bn) 16.2 21.2 25.7

MFs 6.5 EBITDA (Rs bn) 42.8 55.9 65.7

Price performance (%) 1M 3M 12M EV/EBITDA (X) 15.1 11.6 9.8

Absolute 12.8 21.1 56.2 ROE (%) 25.6 23.7 24.5

Rel. to BSE-30 8.6 13.2 30.2 Div. Yield (%) 0.5 1.1 1.3

Company data and valuation summary

429-255

594.5

Automobiles Motherson Sumi Systems

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Consolidated EBITDA 6% ahead of estimates

Motherson Sumi has reported consolidated EBITDA of `12.4 bn (+24.6% yoy), which was

6% above our estimates due to (1) stronger-than-expected revenue growth and (2) better-

than-expected profitability in the SMP business. Consolidated revenues increased by 14.5%

yoy (KIE 10.7%), which was led by (1) 19% yoy revenue growth in the standalone business

and (2) 19% yoy revenue growth in SMRPBV business in euro terms. We note that euro has

depreciated by 4.3% on yoy basis in 4QFY17, thus reported SMRPBV revenues in rupee

terms increased by 14% yoy in 4QFY17. Net profit adjusted for one-off expenses (details

below) was `5.4 bn (+27.8% yoy), which was 15% above our estimates; higher

outperformance at net profit level was due to (1) higher other income (`948 mn versus

estimate of `430 mn), (2) lower interest expenses (`0.84 bn versus estimate of `1.1 bn) and

(3) lower tax rate (22.4% versus estimate of 33%). One-off expenses include costs incurred

in connection with the acquisition of PKC Group.

For FY2017, the company has reported (1) consolidated revenue growth of 14% led by

double-digit revenue growth in India and SMRPBV business, (2) EBITDA growth of 21% led

by 60 bps expansion in EBITDA margin driven by standalone and SMP business and (3)

adjusted net profit growth of 26%. The company has recommend (1) bonus shares in the

ratio of 1:2 (1 bonus share for every 2 shares held) and (2) dividend of `2 per share for

FY2017.

Standalone business: Strong quarter led by 17% yoy revenue growth

The company reported revenues of ₹17.4 bn (+18.9% yoy), which was 4% above our

estimates. Revenue growth was led by strong growth in passenger vehicle industry

volumes and increase in market share due to presence in Maruti’s high-growth models

such as Baleno and Brezza.

The company reported 4QFY17 EBITDA of `3.6 bn (+17.4% yoy), which was in line with

our estimates as stronger-than-expected revenue growth was offset by lower-than-

expected EBITDA margin. EBITDA margin came in 20.6% (down 20 bps and 60 bps qoq),

which was 100 bps below our estimates due to lower gross margins.

Net profit came in at `2.7 bn, which was 18% above our estimates due to lower-than-

expected interest expenses and tax rate. Interest expense was negative in the quarter

(despite gross debt of `13 bn) due to forex gain on loans led by rupee appreciation. Tax

rate for the quarter was 25.2% versus our estimate of 31.5%.

SMRPBV business: SMP’s revenue growth and EBITDA margin surprise positively

SMR business. Revenues increased by 14.8% yoy to EUR420 mn while EBITDA margin

came in at 12.9% (down 20 bps yoy and up 110 bps qoq). We were building in 15% yoy

revenue growth and 12.5% EBITDA margin in our estimates. For FY2017, revenues are

up 13% in euro terms and EBITDA margin was 10.8% (10.5% in FY2016).

SMP business. Revenues increased by 21.1% yoy to EUR810 mn while EBITDA margin

came in at 6.8% (up 160 bps yoy and up 90 bps qoq). We note that reported EBITDA

margin is after start-up expenses of EUR11 mn during the quarter (130 bps impact on

EBITDA margin). We were building in 15% yoy revenue growth and 6% EBITDA margin

in our estimates; thus the profitability was better than our estimates. For FY2017,

revenues are up 14% in euro terms and EBITDA margin was 6.4% (5.7% in FY2016).

Order book situation. The company has won new orders worth EUR4 bn in FY2017 and

current outstanding order book stands at EUR12.9 bn.

Net debt. Consolidated net debt `54.7 bn as of March 2017 (`43 bn as of March 2016).

Standalone net debt was `11 bn as of March 2017 versus `4.7 bn as of March 2016.

Increase in consolidated net debt (from `25.4 bn in 3QFY17) has increased due to PKC

Group acquisition.

Motherson Sumi Systems Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Increase FY2018-19E EPS estimates by 9-11% due to PKC acquisition

We have increased our FY2018-19E consolidated EPS estimates by 9-11% as we build in

PKC acquisition in our estimates. Our earnings estimates for standalone entity and SMRPBV

business remain largely unchanged. For PKC Group, we build in (1) 9% revenue CAGR over

CY2016-19E and (2) 90 bps expansion in EBITDA margin leading to 13%/40% EBITDA and

EPS CAGR over CY2016-19E.

For the SMRPBV business, we build in 15% revenue CAGR over FY2017-20E and expect

EBITDA margin to increase to 9.2% by FY2020E from ~8% in FY2017.

Exhibit 1: 4QFY17 standalone EBITDA was in line; PAT was aided by lower interest expense (includes forex gain) and tax rate MSSL standalone 4QFY17 results, March fiscal year-ends (` mn)

Source: Company, Kotak Institutional Equities estimates

(%chg.)

4QFY17 4QFY17E 4QFY16 3QFY17 4QFY17E 4QFY16 3QFY17 FY2017 FY2016 % chg. FY2018E

Net sales from operations 16,912 16,401 14,321 14,983 3.1 18.1 12.9 61,417 51,656

Other operating income 478 300 299 681 59.4 60.0 (29.7) 1,711 1,173

Net sales 17,390 16,701 14,620 15,664 4.1 18.9 11.0 63,129 52,829 19.5 72,651

Raw materials (9,391) (8,852) (7,744) (8,347) 6.1 21.3 12.5 (33,845) (28,535) (38,919)

Staff costs (2,476) (2,100) (2,051) (2,082) 17.9 20.7 18.9 (8,560) (7,133) (9,758)

Other expenses (2,056) (2,150) (1,752) (2,087) (4.4) 17.4 (1.5) (8,313) (6,955) (9,008)

Exchange fluctuations 107 — (29) 170 349 101

Total expenses (13,816) (13,102) (11,575) (12,345) 5.5 19.4 11.9 (50,369) (42,522) (57,685)

EBITDA 3,574 3,600 3,044 3,318 (0.7) 17.4 7.7 12,760 10,307 23.8 14,966

Depreciation (507) (510) (506) (500) (0.6) 0.3 1.4 (1,977) (2,009) (2,084)

EBIT 3,067 3,090 2,539 2,818 (0.7) 20.8 8.8 10,783 8,298 29.9 12,882

Other income 457 400 376 401 1,069 1,709 1,265

Interest expense 124 (100) (73) (100) (124) (474) (439)

Profit before tax 3,648 3,390 2,842 3,120 7.6 28.4 16.9 11,728 9,532 23.0 13,709

Tax expense (921) (1,068) (454) (990) (13.8) 103.0 (7.0) (3,455) (2,346) (4,113)

Profit after tax 2,727 2,322 2,388 2,130 17.5 14.2 28.1 8,273 7,186 15.1 9,596

Adj PAT 2,727 2,322 2,388 2,130 17.5 14.2 28.1 8,273 6,887 20.1 9,596

# of shares 1,404 1,404 1,323 1,404 1,404 1,323 1,404

EPS (Rs/share) 1.9 1.7 1.8 1.5 17.5 7.6 28.1 5.9 5.2 6.8

Tax rate (%) 25.2 31.5 16.0 31.7 29.5 24.6 30.0

As a % of revenues

Raw material 54.0 53.0 53.0 53.3 53.6 54.0 53.6

Staff costs 14.2 12.6 14.0 13.3 13.6 13.5 13.4

Other expenses 11.8 12.9 12.0 13.3 13.2 13.2 12.4

EBITDA margin (%) 20.6 21.6 20.8 21.2 20.2 19.5 20.6

EBITDA margin (ex forex) 19.9 21.6 21.0 20.1 19.7 19.3 20.6

EBIT Margin 17.6 18.5 17.4 18.0 17.1 15.7 17.7

Automobiles Motherson Sumi Systems

26 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Standalone net sales growth was strong at 19% yoy in 4QFY17 Motherson Sumi's standalone net sales growth, March fiscal year-ends 2011-17 (%)

Source: Company, Kotak Institutional Equities

Exhibit 3: Standalone EBITDA margin (ex-forex gain) was largely flat on qoq basis Standalone quarterly ex-forex EBITDA margin trend, March fiscal year-ends, 2011-17 (%)

Source: Company, Kotak Institutional Equities

58

6770

55

34

17

9

41 41

2327

2 2

16

41

14 14 12

3 1

10

2

1318 17

2419

0

10

20

30

40

50

60

70

80

1Q

FY1

1

2Q

FY1

1

3Q

FY1

1

4Q

FY1

1

1Q

FY1

2

2Q

FY1

2

3Q

FY1

2

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

3Q

FY1

4

4Q

FY1

4

1Q

FY1

5

2Q

FY1

5

3Q

FY1

5

4Q

FY1

5

1Q

FY1

6

2Q

FY1

6

3Q

FY1

6

4Q

FY1

6

1Q

FY1

7

2Q

FY1

7

3Q

FY1

7

4Q

FY1

7

Yoy growth (%)

10

12

14

16

18

20

22

24

1Q

FY1

1

2Q

FY1

1

3Q

FY1

1

4Q

FY1

1

1Q

FY1

2

2Q

FY1

2

3Q

FY1

2

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

3Q

FY1

4

4Q

FY1

4

1Q

FY1

5

2Q

FY1

5

3Q

FY1

5

4Q

FY1

5

1Q

FY1

6

2Q

FY1

6

3Q

FY1

6

4Q

FY1

6

1Q

FY1

7

2Q

FY1

7

3Q

FY1

7

4Q

FY1

7

Ex forex EBITDA margin (%)

Motherson Sumi Systems Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

Exhibit 4: Consolidated EBITDA was 6% above estimates due to stronger revenue growth and profitability in SMP business MSSL consolidated 4QFY17 results, March fiscal year-ends (` mn)

Source: Company, Kotak Institutional Equities estimates

Exhibit 5: Consolidated net debt increased on qoq basis due to PKC acquisition MSSL consolidated net debt position, March fiscal year-ends, 2012-17 (` bn)

Source: Company, Kotak Institutional Equities

(%chg.)

4QFY17 4QFY17E 4QFY16 3QFY17 4QFY17E 4QFY16 3QFY17 FY2017 FY2016 % chg. FY2018E

Net sales from operations 111,000 96,634 105,138 14.9 5.6 419,842 365,803

Other operating income 1,839 1,916 903 (4.0) 103.6 4,911 6,360

Net sales 112,839 109,042 98,549 106,041 3.5 14.5 6.4 424,752 372,163 14.1 544,380

Raw materials (67,041) (57,593) (65,427) 16.4 2.5 (257,507) (224,093) (326,698)

Staff costs (21,748) (19,544) (19,964) 11.3 8.9 (80,909) (71,573) (106,672)

Other expenses (11,507) (11,426) (9,903) 0.7 16.2 (43,671) (40,710) (55,123)

Exchange fluctuations (138) (32) 346 182 (306) —

Total expenses (100,434) (88,595) (94,948) 13.4 5.8 (381,905) (336,681) (488,493)

EBITDA 12,405 11,764 9,954 11,093 5.5 24.6 11.8 42,847 35,482 20.8 55,886

Depreciation (2,707) (2,800) (3,362) (2,733) (3.3) (19.5) (0.9) (10,590) (10,872) (15,058)

EBIT 9,698 8,964 6,593 8,360 8.2 47.1 16.0 32,257 24,610 31.1 40,828

Other income 948 430 55 433 120.3 1,629.0 118.6 1,463 392 2,216

Interest expense (838) (1,100) (696) (1,084) (23.8) 20.4 (22.7) (3,749) (3,450) (4,207)

Profit before tax 9,808 8,294 5,951 7,710 18.3 64.8 27.2 29,971 21,552 39.1 38,837

Exceptional item (974) — — — (974)

Tax expense (2,198) (2,737) (528) (2,845) (19.7) 316.8 (22.7) (9,103) (5,193) (12,290)

Share of profit from associates 424 600 448 609 1,831 1,377 2,014

Minority interest 2,311 1,450 1,623 1,314 6,181 4,814 7,333

Profit after tax 4,748 4,707 4,249 4,159 0.9 11.7 14.2 15,543 12,922 20.3 21,229

Adj PAT 5,430 4,707 4,249 4,159 15.4 27.8 30.6 16,225 12,922 25.6 21,229

# of shares 1,404 1,404 1,323 1,404 1,404 1,323 1,404

EPS (Rs/share) 3.9 3.4 3.2 3.0 11.6 9.8 15.1

Tax rate (%) 22.4 33.0 8.9 36.9 30.4 24.1 31.6

As a % of revenues

Raw material 59.4 58.4 61.7 60.6 60.2 60.0

Staff costs 19.3 19.8 18.8 19.0 19.2 19.6

Other expenses 10.2 11.6 9.3 10.3 10.9 10.1

EBITDA margin (%) 11.0 10.8 10.1 10.5 10.1 9.5 10.3

EBITDA margin (ex forex) 11.1 10.8 10.1 10.1 10.0 9.6 10.3

EBIT Margin 8.6 8.2 6.7 7.9 7.6 6.6 7.5

41.544.4

42.8 43.1 43.142.4

45.744.4

39.342

48.3 47.1

31.3

35.9

45.647.5

43.046.3

21.825.4

54.7

0

10

20

30

40

50

60

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

3Q

FY1

4

4Q

FY1

4

1Q

FY1

5

2Q

FY1

5

3Q

FY1

5

4Q

FY1

5

1Q

FY1

6

2Q