India Daily, January 9, 2014 - Kotak Securities

72

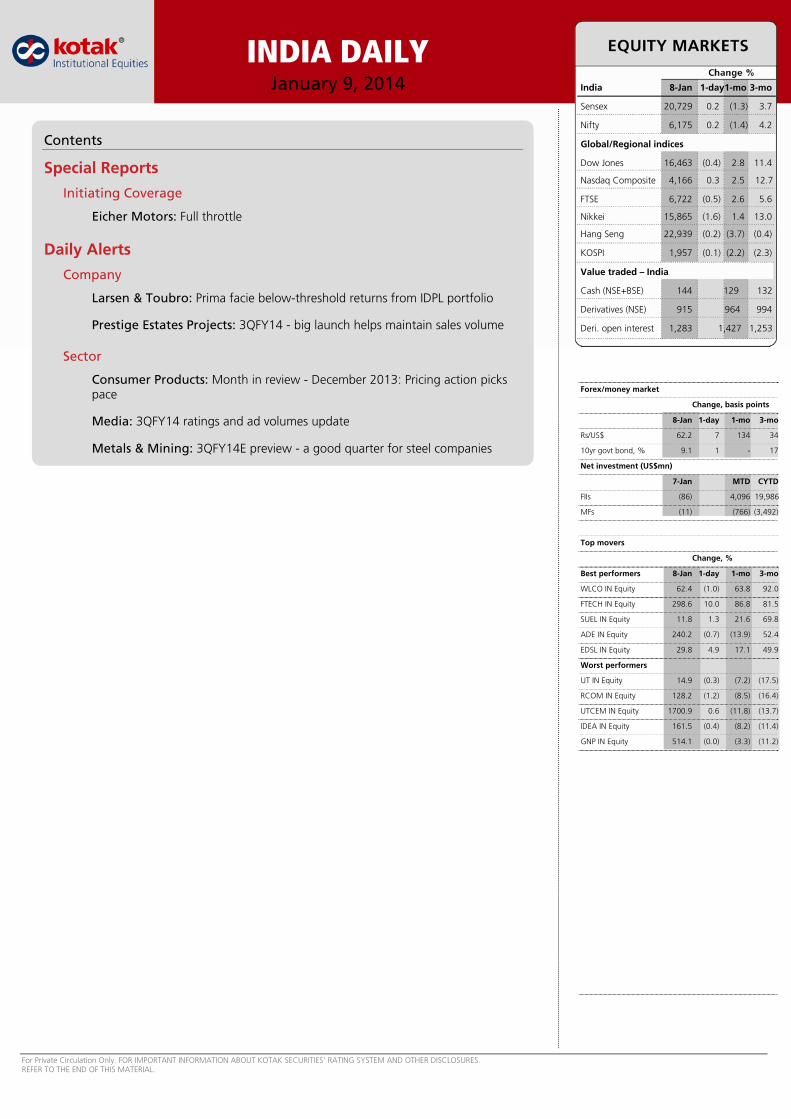

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. INDIA DAILY January 9, 2014 India 8-Jan 1-day1-mo 3-mo Sensex 20,729 0.2 (1.3) 3.7 Nifty 6,175 0.2 (1.4) 4.2 Global/Regional indices Dow Jones 16,463 (0.4) 2.8 11.4 Nasdaq Composite 4,166 0.3 2.5 12.7 FTSE 6,722 (0.5) 2.6 5.6 Nikkei 15,865 (1.6) 1.4 13.0 Hang Seng 22,939 (0.2) (3.7) (0.4) KOSPI 1,957 (0.1) (2.2) (2.3) Value traded – India Cash (NSE+BSE) 144 129 132 Derivatives (NSE) 915 964 994 Deri. open interest 1,283 1,427 1,253 Forex/money market Change, basis points 8-Jan 1-day 1-mo 3-mo Rs/US$ 62.2 7 134 34 10yr govt bond, % 9.1 1 - 17 Net investment (US$mn) 7-Jan MTD CYTD FIIs (86) 4,096 19,986 MFs (11) (766) (3,492) Top movers Change, % Best performers 8-Jan 1-day 1-mo 3-mo WLCO IN Equity 62.4 (1.0) 63.8 92.0 FTECH IN Equity 298.6 10.0 86.8 81.5 SUEL IN Equity 11.8 1.3 21.6 69.8 ADE IN Equity 240.2 (0.7) (13.9) 52.4 EDSL IN Equity 29.8 4.9 17.1 49.9 Worst performers UT IN Equity 14.9 (0.3) (7.2) (17.5) RCOM IN Equity 128.2 (1.2) (8.5) (16.4) UTCEM IN Equity 1700.9 0.6 (11.8) (13.7) IDEA IN Equity 161.5 (0.4) (8.2) (11.4) GNP IN Equity 514.1 (0.0) (3.3) (11.2) Contents Special Reports Initiating Coverage Eicher Motors: Full throttle Daily Alerts Company Larsen & Toubro: Prima facie below-threshold returns from IDPL portfolio Prestige Estates Projects: 3QFY14 - big launch helps maintain sales volume Sector Consumer Products: Month in review - December 2013: Pricing action picks pace Media: 3QFY14 ratings and ad volumes update Metals & Mining: 3QFY14E preview - a good quarter for steel companies

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of India Daily, January 9, 2014 - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

INDIA DAILYJanuary 9, 2014 India 8-Jan 1-day1-mo 3-mo

Sensex 20,729 0.2 (1.3) 3.7

Nifty 6,175 0.2 (1.4) 4.2

Global/Regional indices

Dow Jones 16,463 (0.4) 2.8 11.4

Nasdaq Composite 4,166 0.3 2.5 12.7

FTSE 6,722 (0.5) 2.6 5.6

Nikkei 15,865 (1.6) 1.4 13.0

Hang Seng 22,939 (0.2) (3.7) (0.4)

KOSPI 1,957 (0.1) (2.2) (2.3)

Value traded – India

Cash (NSE+BSE) 144 129 132

Derivatives (NSE) 915 964 994

Deri. open interest 1,283 1,427 1,253

Forex/money market

Change, basis points

8-Jan 1-day 1-mo 3-mo

Rs/US$ 62.2 7 134 34

10yr govt bond, % 9.1 1 - 17

Net investment (US$mn)

7-Jan MTD CYTD

FIIs (86) 4,096 19,986

MFs (11) (766) (3,492)

Top movers

Change, %

Best performers 8-Jan 1-day 1-mo 3-mo

WLCO IN Equity 62.4 (1.0) 63.8 92.0

FTECH IN Equity 298.6 10.0 86.8 81.5

SUEL IN Equity 11.8 1.3 21.6 69.8

ADE IN Equity 240.2 (0.7) (13.9) 52.4

EDSL IN Equity 29.8 4.9 17.1 49.9

Worst performers

UT IN Equity 14.9 (0.3) (7.2) (17.5)

RCOM IN Equity 128.2 (1.2) (8.5) (16.4)

UTCEM IN Equity 1700.9 0.6 (11.8) (13.7)

IDEA IN Equity 161.5 (0.4) (8.2) (11.4)

GNP IN Equity 514.1 (0.0) (3.3) (11.2)

Contents

Special Reports

Initiating Coverage

Eicher Motors: Full throttle

Daily Alerts

Company

Larsen & Toubro: Prima facie below-threshold returns from IDPL portfolio

Prestige Estates Projects: 3QFY14 - big launch helps maintain sales volume

Sector

Consumer Products: Month in review - December 2013: Pricing action picks pace

Media: 3QFY14 ratings and ad volumes update

Metals & Mining: 3QFY14E preview - a good quarter for steel companies

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

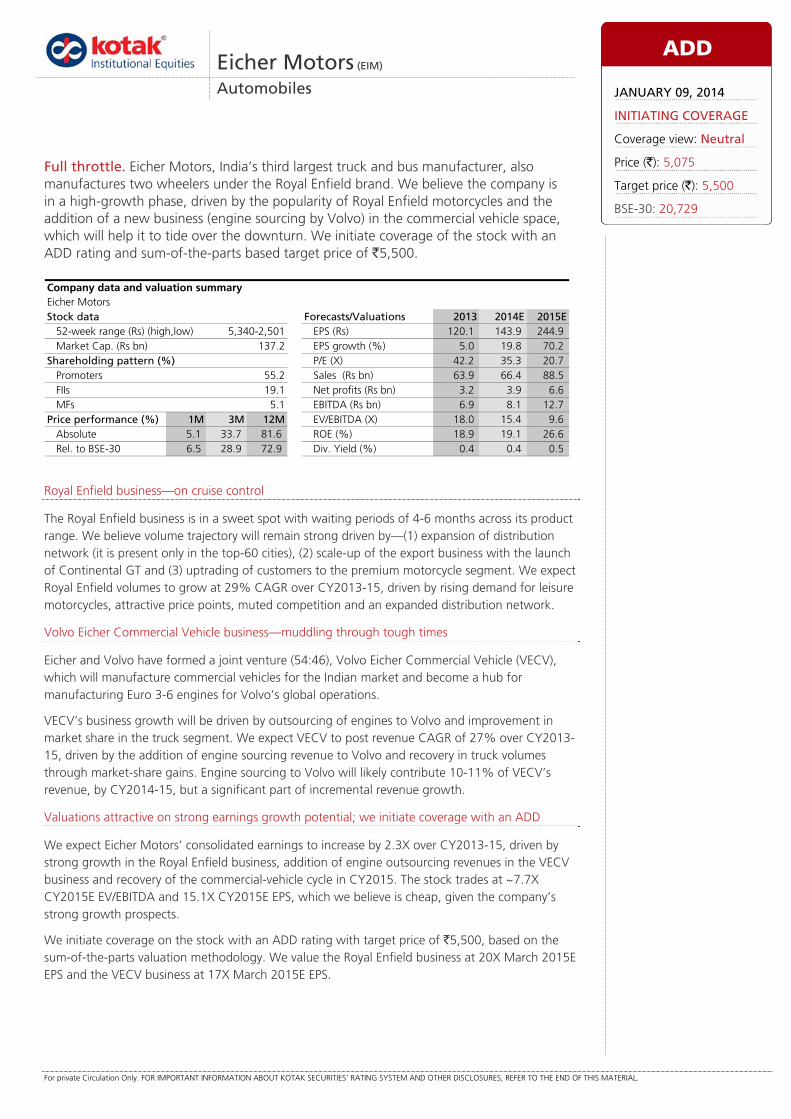

Royal Enfield business—on cruise control

The Royal Enfield business is in a sweet spot with waiting periods of 4-6 months across its product range. We believe volume trajectory will remain strong driven by—(1) expansion of distribution network (it is present only in the top-60 cities), (2) scale-up of the export business with the launch of Continental GT and (3) uptrading of customers to the premium motorcycle segment. We expect Royal Enfield volumes to grow at 29% CAGR over CY2013-15, driven by rising demand for leisure motorcycles, attractive price points, muted competition and an expanded distribution network.

Volvo Eicher Commercial Vehicle business—muddling through tough times

Eicher and Volvo have formed a joint venture (54:46), Volvo Eicher Commercial Vehicle (VECV), which will manufacture commercial vehicles for the Indian market and become a hub for manufacturing Euro 3-6 engines for Volvo’s global operations.

VECV’s business growth will be driven by outsourcing of engines to Volvo and improvement in market share in the truck segment. We expect VECV to post revenue CAGR of 27% over CY2013-15, driven by the addition of engine sourcing revenue to Volvo and recovery in truck volumes through market-share gains. Engine sourcing to Volvo will likely contribute 10-11% of VECV’s revenue, by CY2014-15, but a significant part of incremental revenue growth.

Valuations attractive on strong earnings growth potential; we initiate coverage with an ADD

We expect Eicher Motors’ consolidated earnings to increase by 2.3X over CY2013-15, driven by strong growth in the Royal Enfield business, addition of engine outsourcing revenues in the VECV business and recovery of the commercial-vehicle cycle in CY2015. The stock trades at ~7.7X CY2015E EV/EBITDA and 15.1X CY2015E EPS, which we believe is cheap, given the company’s strong growth prospects.

We initiate coverage on the stock with an ADD rating with target price of `5,500, based on the sum-of-the-parts valuation methodology. We value the Royal Enfield business at 20X March 2015E EPS and the VECV business at 17X March 2015E EPS.

Eicher Motors (EIM)

Automobiles

Full throttle. Eicher Motors, India’s third largest truck and bus manufacturer, also manufactures two wheelers under the Royal Enfield brand. We believe the company is in a high-growth phase, driven by the popularity of Royal Enfield motorcycles and the addition of a new business (engine sourcing by Volvo) in the commercial vehicle space, which will help it to tide over the downturn. We initiate coverage of the stock with an ADD rating and sum-of-the-parts based target price of `5,500.

Eicher MotorsStock data Forecasts/Valuations 2013 2014E 2015E

52-week range (Rs) (high,low) EPS (Rs) 120.1 143.9 244.9Market Cap. (Rs bn) 137.2 EPS growth (%) 5.0 19.8 70.2

Shareholding pattern (%) P/E (X) 42.2 35.3 20.7Promoters 55.2 Sales (Rs bn) 63.9 66.4 88.5FIIs 19.1 Net profits (Rs bn) 3.2 3.9 6.6MFs 5.1 EBITDA (Rs bn) 6.9 8.1 12.7

Price performance (%) 1M 3M 12M EV/EBITDA (X) 18.0 15.4 9.6Absolute 5.1 33.7 81.6 ROE (%) 18.9 19.1 26.6Rel. to BSE-30 6.5 28.9 72.9 Div. Yield (%) 0.4 0.4 0.5

Company data and valuation summary

5,340-2,501

ADD

JANUARY 09, 2014

INITIATING COVERAGE

Coverage view: Neutral

Price (`): 5,075

Target price (`): 5,500

BSE-30: 20,729

Eicher Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

FINANCIAL SNAPSHOT

Eicher Motors, consolidated forecasts and valuation, calendar year-ends, 2009-16E

Net sales EBITDA PAT EPS EV/EBITDA P/E RoCE RoE(Rs mn) (Rs mn) (Rs mn) (Rs) (X) (X) (%) (%)

2009 29,386 1,444 834 31 85.6 164.3 6.1 7.7 2010 43,971 3,569 1,889 70 33.9 72.5 17.8 16.1 2011 56,775 5,551 3,088 114 21.7 44.4 18.3 21.9 2012 63,899 5,490 3,243 120 22.4 42.2 12.6 18.9 2013E 66,438 6,153 3,884 144 20.2 35.3 10.1 19.1 2014E 88,487 10,443 6,610 245 11.7 20.7 15.2 26.6 2015E 110,554 14,919 9,068 336 7.7 15.1 19.1 28.5 2016E 132,967 17,076 10,669 395 6.2 12.8 19.5 26.2

Source: Company, Kotak Institutional Equities estimates

We expect earnings to more than double over CY2013-15E Eicher Motors consolidated profit & loss, balance sheet and cash flow statement, calendar year-ends, 2009-16E (` mn)

2009 2010 2011 2012 2013E 2014E 2015E 2016EProfit model (Rs mn)Net sales 29,386 43,971 56,775 63,899 66,438 88,487 110,554 132,967

EBITDA 1,444 3,569 5,551 5,490 6,153 10,443 14,919 17,076 Other income 1,054 1,276 1,768 1,366 1,943 2,284 2,905 3,693 Interest (87) (95) (77) (38) (23) (23) (23) (23)

Depreciaton (539) (573) (640) (822) (1,222) (1,650) (2,002) (2,282)

Profit before tax 1,873 4,177 6,602 5,997 6,850 11,054 15,799 18,464 Extraordinary income/(expenses) — — — — — — — —

Tax (578) (1,108) (1,628) (1,249) (1,882) (2,890) (4,186) (4,871) Minority interest (461) (1,179) (1,886) (1,506) (1,084) (1,553) (2,544) (2,924)

Net profit 834 1,889 3,088 3,243 3,884 6,610 9,068 10,669 Adjusted net profit 834 1,889 3,088 3,243 3,884 6,610 9,068 10,669 Adjusted diluted EPS (Rs) 31 70 114 120 144 245 336 395 Balance sheet (Rs mn)Equity 127 269 270 270 270 270 270 270

Reserves and surplus 10,564 12,052 14,661 17,279 20,468 26,289 34,410 44,131

Deferred tax liability 142 249 645 1,232 1,232 1,232 1,232 1,232 Minority interest 5,747 6,774 8,377 9,485 10,569 12,122 14,666 17,590

Total borrowings 1,264 956 504 389 389 389 389 389 Current liabilities 6,978 9,332 13,343 16,060 16,075 18,615 21,391 24,013

Total liabilities 24,820 29,633 37,799 44,715 49,003 58,917 72,359 87,626 Net fixed assets 3,758 4,513 8,991 14,962 20,439 25,190 27,588 29,505 Investments 2,941 4,586 5,126 6,385 12,385 15,385 21,885 30,385

Cash 11,707 12,457 11,973 8,035 707 269 324 633 Other current assets 6,415 8,043 11,528 15,271 15,410 18,011 22,500 27,040

Miscellaneous expenditure — 35 182 62 62 62 62 62

Total assets 24,820 29,633 37,799 44,715 49,003 58,917 72,359 87,626 Free cash flow (Rs mn)Operating cash flow excl. working capital 1,031 2,986 4,273 4,436 4,270 7,552 10,732 12,205

Working capital changes 2,654 374 (238) 389 (123) (62) (1,712) (1,919) Capital expenditure (701) (1,315) (4,173) (7,820) (6,700) (6,400) (4,400) (4,200)

Free cash flow (ex financing) 2,984 2,045 (138) (2,995) (2,553) 1,090 4,620 6,087 RatiosEBITDA margin (%) 4.9 8.1 9.8 8.6 9.3 11.8 13.5 12.8

Debt/equity (X) 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0 Net debt/equity (X) (1.2) (1.3) (1.1) (0.7) (0.6) (0.5) (0.6) (0.7)

Book value (Rs per share) 396 455 546 648 766 982 1,283 1,643 RoAE (%) 7.7 16.1 21.9 18.9 19.1 26.6 28.5 26.2

Source: Company, Kotak Institutional Equities estimates

Automobiles Eicher Motors

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

VALUATIONS—ATTRACTIVE DUE TO STRONG GROWTH PROSPECTS We initiate coverage on Eicher Motors with an ADD rating. We like the medium-term story with a ramp-up in

Royal Enfield volumes and market-share gains in the truck business. Sourcing of engines by Volvo for its

global operations is also likely to open new growth opportunities for the company. We value the company

through the sum-of-the-parts valuation methodology. We value the Royal Enfield business at

20X March 2015E EPS and the VECV business at 17X March 2015E EPS. Our one-year target price is `5,500.

Eicher Motors has two business verticals—the Royal Enfield (RE) business (two wheelers) and the Volvo Eicher Commercial Vehicle (VECV) business. We have valued the businesses separately as they have different growth profiles and return ratios. The RE business is an asset-light business with a superior margin profile and the VECV business has better long-term growth prospects but is asset heavy and has lower return ratios.

We value the RE business at 20X March 2015E EPS as we believe the business can post 15% CAGR over the next decade as we expect customers to uptrade to the premium segment with a rise in income levels. RE is also likely to convert 55% of its EBITDA into free cash and incremental capital invested is about 60%. We believe there is no direct comparison to the RE business due to its niche positioning but the Harley Davidson business has a similar customer profile and business model.

We expect RE to trade at a premium to Harley Davidson. RE and Harley Davidson operate in the leisure motorcycle segment with Harley Davidson focused mainly on developed markets and RE focused on India. Key reasons for our higher valuation for the RE business than the Harley Davidson business are as follows.

Both businesses have asset-light models but the RE business has superior asset turns (4-5X) compared with Harley Davidson (~2X) and RE’s operating margin profile is also superior as RE builds up scale. RE’s incremental RoIC is about 60% and Harley Davidson’s is ~20%.

RE’s growth prospects are much better than Harley Davidson’s as RE has a strong brand presence in an under-penetrated Indian market and Harley Davidson operates in developed markets (90% of its sales are in North America and Europe) where growth prospects are subdued. Emerging market consumers in India and Indonesia, the main markets that will drive growth in the premium motorcycle segment, prefer vehicles in the 250-650 cc range, which are affordable and more suited to the build of Indian and Indonesian men/women. Harley Davidson does not have a product below 800 cc and will need to invest in a product line in the 350-500 cc range to challenge RE.

RE’s customer profile is changing from a leisure user to a commuter. The management indicated that half its customers in India use the motorcycle for regular commutes and not for leisure. We believe this will help the company to improve volume growth as it can tap the commuter segment, as well.

In India, competition is muted in the premium motorcycle space, in which RE operates (350-500 cc) and given that RE’s price-value proposition is quite attractive, we do not see an immediate threat to the RE brand.

We value the VECV business at 17X March 2015E EPS as we expect VECV to post 15% CAGR over the next decade, higher than our industry forecast of commercial vehicle CAGR of 12%, driven by market-share gains. VECV will benefit from superior Volvo technology, which will be used in heavier tonnage trucks, which will result in class-leading fuel efficiency and low maintenance. The VECV business will also convert 30% of its EBITDA into free cash after capex expansion and generate a healthy 17-20% return on capital employed over a commercial cycle.

Eicher Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

We expect VECV to trade at a significant premium to Ashok Leyland, a comparable player in the commercial-vehicle segment. The reasons for ascribing a higher multiple to VECV are as follows.

The VECV business is likely to grow faster than Ashok Leyland’s in the commercial-vehicle business as it enters new product segments. It has a limited number of products in the market compared with Ashok Leyland.

Volvo is likely to use VECV as a sourcing base for engines for global sales (Euro 3 to 6 compliant engines) which will be far superior to Ashok Leyland’s engines. Eicher-Volvo will also use these engines for trucks to be sold in India. We believe this could lead to improved market share for Eicher in India as Volvo trucks are likely to be more fuel efficient and need lower maintenance than its peers’.

Ashok Leyland has invested heavily in joint ventures, which has led to a significant increase in debt whereas VECV does not have net debt on its balance sheet, making it less vulnerable to cyclical downturns.

We value Eicher Motors at `5,500 per share based on the SOTP methodology Sum-of-the-parts valuation table for Eicher Motors (`)

Multiple EPS EV(X) (Rs) (Rs/share)

StandaloneEquity value per share (Rs) based on March 2015 EPS 20.0 200 3,996 Eicher stake in VECVEquity value per share (Rs) based on March 2015 EPS 17.0 158 2,686 Eicher stake in VECV 54 Eicher equity value in VECV 1,461 Equity value 5,457 Target price 5,500

Source: Kotak Institutional Equities estimates

What does the current price imply?

We did a Reverse DCF exercise to determine what the current price implies for the RE and VECV businesses. We discuss the key findings of the Reverse DCF exercise.

Assumptions behind the Royal Enfield Reverse DCF value of `3,500

We forecast domestic two-wheeler penetration over CY2013-26. We expect penetration to saturate at 80% ownership (on a single-ownership basis per household) by CY2026. We expect domestic two-wheeler volume CAGR of 7% over CY2013-26 and domestic motorcycle volume CAGR of 6%.

China’s two-wheeler penetration is far higher than India’s at 17% per person versus 9% in India. China’s two-wheeler annual volumes are 24 mn against 14 mn units in India. Additionally, China sells 20 mn electric bikes every year. We believe China’s two-wheeler penetration is far from the peak as Southeast Asian countries like Indonesia and Thailand have penetration per person of 23-25%. The average price of a motorcycle in China is US$400 versus US$800 in India, which implies penetration in China is higher due to low prices. China’s per capita income on a PPP basis is 2.4X that of India. India’s per capita income (on a PPP basis) will reach US$8,600 by CY2026E assuming 7% growth in real income. Indian two-wheeler volumes will rise to 34 mn by CY2026E. At similar income levels, China sells 44 mn two wheelers a year, including electric bikes, but the price in China is half that in India.

Automobiles Eicher Motors

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Reverse DCF value of `3,500 for RE implies (1) volume CAGR of 11% over CY2013-26E and terminal volume growth of 2%, (2) 2.4% annual increase in ASPs during this period and (3) EBIT margin falling from 21% currently to 17% in CY2026. Harley Davidson operates at 15-16% EBIT margins and 90% of its revenue comes from developed markets. We believe RE’s EBIT margins could decline to these levels as competition intensifies.

For RE to achieve volume CAGR of 11% the following assumptions should play out. (1) The share of premium motorcycles should increase from 17% currently to 24% by CY2026 in the domestic motorcycle industry; (2) the share of the 250-500 cc segment should increase from 14% currently to 25% by CY2026 in the premium motorcycle segment and (3) RE’s market share in the 250-500 cc segment should decline from 95% currently to 68% by CY2026.

Assumptions behind the Reverse DCF value of `1,500 for VECV

The Reverse DCF value of `1,500 (for Eicher’s 54.4% stake) implies (1) volume CAGR of 11% over CY2014-30 and terminal growth of 3%, (2) gross annual average selling price increase of 2% over this period and (3) EBIT margins declining from 8% to 6% by CY2030.

Reverse DCF implies annual sales volume growth of 12% in the medium term and 10% in the long term DCF model for Royal Enfield, calendar year-ends, 2014-26E

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026EVolumes (units) 254,938 293,179 328,361 367,764 411,896 461,323 516,682 568,350 625,185 687,704 756,474 832,121 915,333Gross average price (Rs/vehicle) 105,347 110,614 115,039 117,340 119,687 122,080 124,522 127,012 129,553 132,144 134,786 137,482 140,232Gross vehicle revenues 26,857 32,430 37,774 43,153 49,298 56,318 64,338 72,187 80,994 90,876 101,962 114,402 128,359Spare part revenues 1,278 1,406 1,547 1,732 1,940 2,173 2,434 2,629 2,839 3,066 3,311 3,576 3,862Excise duty 3,376 4,060 4,719 5,178 5,916 6,758 7,721 8,662 9,719 10,905 12,235 13,728 15,403Net revenue 24,759 29,776 34,603 39,707 45,323 51,733 59,052 66,154 74,114 83,037 93,038 104,250 116,818EBIT 5,250 6,468 7,422 8,339 9,518 10,864 12,401 12,569 14,082 15,777 17,677 19,807 19,859EBIT (1-tax) 4,253 5,175 5,864 5,762 6,577 7,507 8,569 8,685 9,730 10,902 12,215 13,687 13,723Depreciation/amortisation 201 215 233 210 225 241 260 280 301 323 347 373 318(Increase)/decrease in working capital (116) (124) (209) 957 337 385 439 (559) 362 406 456 511 574Capital expenditure (200) (200) (300) (269) (307) (351) (401) (392) (440) (445) (499) (560) (419)Free cash flows 4,138 5,066 5,588 6,661 6,831 7,782 8,868 8,014 9,953 11,186 12,518 14,011 14,195Years discounted 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 10.0 11.0 12.0 13.0 Discount factor 0.9 0.8 0.7 0.6 0.6 0.5 0.5 0.4 0.4 0.3 0.3 0.3 0.2 Discounted cash flow 3,695 4,039 3,977 4,233 3,876 3,943 4,011 3,237 3,589 3,602 3,599 3,596 3,253Core PBT 5,250 6,468 7,422 8,339 9,518 10,864 12,401 12,569 14,082 15,777 17,677 19,807 19,859Tax expense 1,431 1,795 2,123 2,577 2,941 3,357 3,832 3,884 4,351 4,875 5,462 6,121 6,136Core PAT 3,819 4,673 5,298 5,762 6,577 7,507 8,569 8,685 9,730 10,902 12,215 13,687 13,723Core EPS (Rs) 141 173 196 213 244 278 317 322 360 404 452 507 508

Near-term volume growth (CY2017-20) 12.0 NPV CalcLong-term growth (CY2021-26) 10.0 Sum of free cash flow 48,650 WACC used (%) 12.0 Terminal value 33,183 Terminal growth rate (%) 2.0 Enterprise value 81,833 Capitalization rate (%) 10.0 Net cash 12,312 Terminal value calculation Net present value-equity 94,145 Cash flow in terminal year 14,195 Shares o/s (mn) 27 Terminal value 144,794 NPV /share(Rs) 3,487 Discounted value 33,183

Source: Kotak Institutional Equities estimates

Eicher Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Reverse DCF implies annual sales volume growth of 12% in the medium term and 10% in the long term Key assumptions behind the DCF model for Royal Enfield, calendar year-ends, 2014-26E

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026EKey assumptionsVolume growth (%) 45.0 15.0 12.0 12.0 12.0 12.0 12.0 10.0 10.0 10.0 10.0 10.0 10.0 Gross average price increase (%) 6.0 5.0 4.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 Spare parts revenue growth (%) 10.0 10.0 10.0 12.0 12.0 12.0 12.0 8.0 8.0 8.0 8.0 8.0 8.0 Two-wheeler penetration Number of households (mn) 254 263 266 271 278 283 287 291 293 295 297 299 301India's population (mn) 1,239 1,254 1,269 1,284 1,298 1,312 1,326 1,335 1,343 1,351 1,360 1,368 1,377 Domestic two-wheeler population (mn units) 105.8 116.1 126.2 135.8 145.5 156.7 168.5 180.5 192.6 204.6 216.6 226.9 240.9 Domestic two-wheeler volumes (mn units) 14.7 16.2 17.8 19.6 21.6 23.3 25.2 26.7 28.3 30.0 31.8 33.7 33.7 Penetration per person for two wheelers (%) 8.5 9.3 9.9 10.6 11.2 11.9 12.7 13.5 14.3 15.1 15.9 16.6 17.5 Penetration per household for two wheelers (%) 41.7 44.1 47.4 50.1 52.3 55.4 58.7 62.0 65.7 69.4 72.9 75.9 80.0 Domestic motorcycle volumes (mn units) 11.1 12.0 13.0 14.0 14.9 15.7 16.7 17.5 18.4 19.3 20.3 21.3 22.4 Premium motorcycle volumes (mn units) 1.9 2.0 2.3 2.5 2.8 3.0 3.3 3.5 3.9 4.1 4.5 4.9 5.4 Premium m/c as % of m/c vols 17.0 17.0 18.0 18.0 19.0 19.0 20.0 20.0 21.0 21.0 22.0 23.0 24.0 Share of 250-500cc segment in premium m/c 14.2 16.0 16.0 17.0 18.0 18.0 20.0 22.0 23.0 24.0 24.0 25.0 25.0 Royal enfield share in 250-500cc segment (%) 95.0 89.7 87.9 85.8 81.1 85.7 77.4 73.7 70.3 70.6 70.6 67.9 68.2 Key ratios (%)EBIT margin (%) 21.2 21.7 21.4 21.0 21.0 21.0 21.0 19.0 19.0 19.0 19.0 19.0 17.0 Effective tax rate (%) 19.0 20.0 21.0 30.9 30.9 30.9 30.9 30.9 30.9 30.9 30.9 30.9 30.9 Excise duty as percentage of domestic revenue 12.6 12.5 12.5 12.0 12.0 12.0 12.0 12.0 12.0 12.0 12.0 12.0 12.0 Capex as % of change in revenues 2.1 3.6 5.6 5.0 5.0 5.0 5.0 5.0 5.0 4.5 4.5 4.5 3.0 Depreciation as a percentage of avg. gross block 5.8 5.9 5.9 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 4.0 Year-end net WCap excl. cash (days of sales) (23.6) (18.2) (13.6) (20.0) (20.0) (20.0) (20.0) (15.0) (15.0) (15.0) (15.0) (15.0) (15.0) Gross block (incl. CWIP) 3,575 3,775 4,075 4,344 4,651 5,002 5,403 5,796 6,236 6,681 7,180 7,739 8,158 Year-end net WCap (excl. cash) (1,740) (1,616) (1,407) (2,365) (2,701) (3,086) (3,525) (2,967) (3,329) (3,735) (4,190) (4,701) (5,275)

Source: Kotak Institutional Equities estimates

Reverse DCF implies annual sales volume growth of 12% in the medium term and 8% in the long term DCF model for VECV, calendar year-ends, 2014-30E

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2026E 2027E 2028E 2029E 2030EVolumes (units) 47,736 59,289 73,724 82,571 92,480 103,577 116,006 184,088 198,815 214,720 231,897 250,449Gross average price (Rs/vehicle) 1,004,963 1,043,728 1,060,246 1,081,451 1,103,080 1,125,142 1,147,645 1,292,435 1,318,283 1,344,649 1,371,542 1,398,973Gross vehicle revenues 47,973 61,882 78,166 89,297 102,012 116,539 133,134 237,921 262,094 288,723 318,057 350,372Spare part revenues 14,070 14,050 14,234 15,657 17,223 18,945 20,839 33,069 35,715 38,572 41,658 44,991Engine revenues 8,211 13,164 16,379 16,871 17,377 17,898 18,435 22,012 22,673 23,353 24,054 24,775Excise duty 6,526 8,318 10,414 10,716 12,241 13,985 15,976 28,551 31,451 34,647 38,167 42,045Net revenue 63,728 80,778 98,365 111,109 124,370 139,397 156,432 264,452 289,030 316,001 345,602 378,093EBIT 3,543 6,449 7,372 8,889 9,950 11,152 12,515 18,512 20,232 22,120 24,192 22,686EBIT (1-tax) 2,083 4,058 4,624 6,151 6,885 7,717 8,660 12,810 14,001 15,307 16,741 15,698Depreciation/amortisation 1,449 1,787 2,050 2,163 2,327 2,514 2,728 4,047 4,301 4,580 4,888 4,719(Increase)/decrease in working capital 54 (1,588) (1,710) 1,988 (348) (398) (455) (481) (530) (584) (643) 2,172Capital expenditure (6,200) (4,200) (3,900) (2,783) (3,179) (3,632) (4,149) (4,389) (4,835) (5,326) (5,867) (5,170)Free cash flows (2,614) 57 1,065 7,519 5,684 6,201 6,784 11,987 12,937 13,978 15,119 17,419Years discounted 1.0 2.0 3.0 4.0 5.0 6.0 7.0 13.0 14.0 15.0 16.0 17.0 Discount factor 0.9 0.8 0.7 0.6 0.6 0.5 0.5 0.2 0.2 0.2 0.2 0.1 Discounted cash flow (2,334) 45 758 4,778 3,225 3,142 3,069 2,747 2,647 2,554 2,466 2,537 Core PBT 3,543 6,449 7,372 8,889 9,950 11,152 12,515 18,512 20,232 22,120 24,192 22,686 Tax expense 1,460 2,391 2,748 2,738 3,064 3,435 3,854 5,702 6,231 6,813 7,451 6,987 Core PAT 2,083 4,058 4,624 6,151 6,885 7,717 8,660 12,810 14,001 15,307 16,741 15,698 Core EPS (Rs) 77 150 171 228 255 286 321 474 519 567 620 581

Near-term volume growth (CY2017-20) 12.0 NPV CalcLong-term growth (CY2021-30) 8.0 Sum of free cash flow 41,978 WACC used (%) 12.0 Terminal value 29,034 Terminal growth rate (%) 3.0 Enterprise value 71,013 Capitalization rate (%) 9.0 Net cash 3,342 Terminal value calculation Net present value-equity 74,354 Cash flow in terminal year 17,419 Shares o/s (mn) 27 Terminal value 199,350 NPV /share(Rs) 2,754 Discounted value 29,034 Eicher share in VECV 1,498

Source: Kotak Institutional Equities estimates

Automobiles Eicher Motors

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Reverse DCF implies annual sales volume growth of 12% in the medium term and 8% in the long term Key assumptions behind the Reverse DCF model for VECV, calendar year-ends, 2014-30E

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2026E 2027E 2028E 2029E 2030EKey assumptionsVolume growth (%) 13.7 24.2 24.3 12.0 12.0 12.0 12.0 8.0 8.0 8.0 8.0 8.0 Gross average price increase (%) 2.7 3.9 1.6 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 2.0 Spare parts revenue growth (%) (1.7) (0.1) 1.3 10.0 10.0 10.0 10.0 8.0 8.0 8.0 8.0 8.0 Key ratios (%)EBIT margin (%) 5.6 8.0 7.5 8.0 8.0 8.0 8.0 7.0 7.0 7.0 7.0 6.0 Effective tax rate (%) 41.2 37.1 37.3 30.8 30.8 30.8 30.8 30.8 30.8 30.8 30.8 30.8 Excise duty as % of domestic revenue 13.6 13.4 13.3 12.0 12.0 12.0 12.0 12.0 12.0 12.0 12.0 12.0 Capex as % of change in revenues 89.8 30.2 23.9 25.0 25.0 25.0 25.0 20.0 20.0 20.0 20.0 16.0 Depreciation as a % of avg. gross block 5.4 5.6 5.7 5.5 5.5 5.5 5.5 5.5 5.5 5.5 5.5 5.0 Year-end net Wcap. excl. cash (days of sales) 8.6 16.1 20.7 10.0 10.0 10.0 10.0 8.0 8.0 8.0 8.0 5.0 Gross block (incl. CWIP) 29,829 34,029 37,929 40,711 43,890 47,522 51,671 75,774 80,609 85,935 91,801 96,972 Year-end net WCap (excl. cash) 1,137 2,725 4,434 2,446 2,795 3,193 3,648 5,215 5,745 6,328 6,971 4,800

Source: Kotak Institutional Equities estimates

We expect Royal Enfield’s strong growth to continue and VECV volumes to recover in CY2014 Eicher Motors sales volumes, calendar year-ends, 2009-16E (units)

2009 2010 2011 2012 2013E 2014E 2015E 2016ESales volumes (units)StandaloneTwo-wheelers 51,955 52,576 74,626 113,432 175,820 254,938 293,179 328,361 VECVDomestic5-14 ton 16,893 26,426 31,381 29,541 25,110 28,876 36,095 45,119 >16 ton 1,424 4,219 7,352 7,699 6,544 7,526 10,160 13,716 Buses 3,282 4,819 6,496 8,521 7,243 7,967 9,162 10,537 ExportsCargo 2,037 2,073 2,652 1,822 1,913 2,104 2,420 2,710 Buses 628 644 456 679 713 784 902 1,010 Volvo trucksVolvo trucks domestic 900 1,094 705 569 455 478 550 632 Total 25,164 39,275 49,042 48,831 41,978 47,736 59,289 73,724 Yoy change (%)StandaloneTwo-wheelers 1.2 41.9 52.0 55.0 45.0 15.0 12.0 VECVDomestic5-14 ton 56.4 18.8 (5.9) (15.0) 15.0 25.0 25.0 >16 ton 196.3 74.3 4.7 (15.0) 15.0 35.0 35.0 Buses 46.8 34.8 31.2 (15.0) 10.0 15.0 15.0 ExportsCargo 1.8 27.9 (31.3) 5.0 10.0 15.0 12.0 Buses 2.5 (29.2) 48.9 5.0 10.0 15.0 12.0 Volvo trucksVolvo trucks domestic 21.6 (35.6) (19.3) (20.0) 5.0 15.0 15.0 Total 56.1 24.9 (0.4) (14.0) 13.7 24.2 24.3

Source: Company, Kotak Institutional Equities estimates

Eicher Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Royal Enfield will continue to contribute a significant part of total EBITDA Revenue, EBITDA and PBT breakdown, Eicher Motors, calendar year-ends, 2009-16E (` mn, %)

2009 2010 2011 2012 2013E 2014E 2015E 2016ERevenue (Rs mn)Standalone 4,080 4,844 7,378 11,793 18,636 28,135 33,836 39,321 VECV (54.4% stake) 14,711 22,942 29,298 31,638 30,262 38,218 48,468 59,176 Total 18,791 27,786 36,676 43,431 48,898 66,353 82,304 98,497 Revenue mix (%)Standalone 21.7 17.4 20.1 27.2 38.1 42.4 41.1 39.9 VECV (54.4% stake) 78.3 82.6 79.9 72.8 61.9 57.6 58.9 60.1 Total 100 100 100 100 100 100 100 100 EBITDA (Rs mn)Standalone 250 416 765 1,454 2,996 5,451 6,683 7,654 VECV (54.4% stake) 650 1,715 2,603 2,196 1,717 2,715 4,480 5,126 Total 900 2,131 3,368 3,650 4,713 8,166 11,163 12,780 EBITDA mix (%)Standalone 27.8 19.5 22.7 39.8 63.6 66.7 59.9 59.9 VECV (54.4% stake) 72.2 80.5 77.3 60.2 36.4 33.3 40.1 40.1 Total 100 100 100 100 100 100 100 100 PBT (Rs mn)Standalone 466 866 1,418 1,738 3,754 6,503 8,159 9,651 VECV (54.4% stake) 765 1,801 2,820 2,317 1,848 2,647 4,336 4,983 Total 1,232 2,667 4,238 4,055 5,602 9,150 12,495 14,634 PBT mix (%)Standalone 37.9 32.5 33.5 42.9 67.0 71.1 65.3 65.9 VECV (54.4% stake) 62.1 67.5 66.5 57.1 33.0 28.9 34.7 34.1 Total 100 100 100 100 100 100 100 100

Source: Company, Kotak Institutional Equities estimates

Automobiles Eicher Motors

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

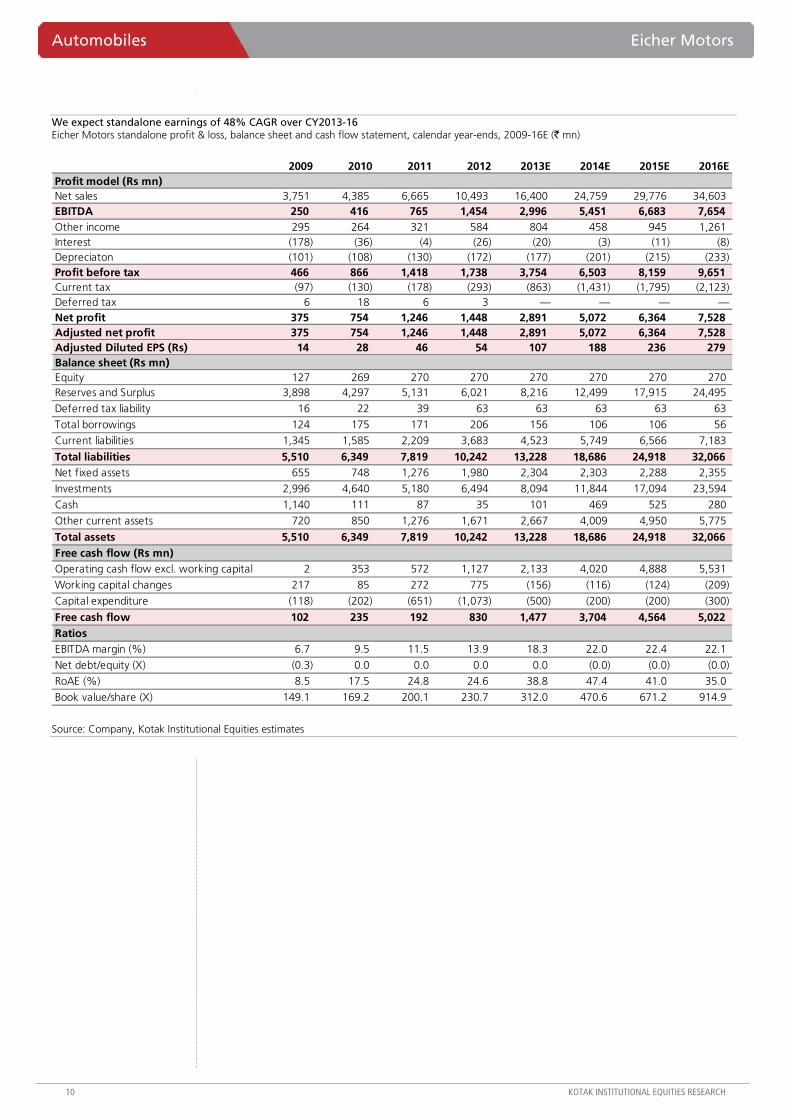

We expect standalone earnings of 48% CAGR over CY2013-16 Eicher Motors standalone profit & loss, balance sheet and cash flow statement, calendar year-ends, 2009-16E (` mn)

2009 2010 2011 2012 2013E 2014E 2015E 2016EProfit model (Rs mn)Net sales 3,751 4,385 6,665 10,493 16,400 24,759 29,776 34,603 EBITDA 250 416 765 1,454 2,996 5,451 6,683 7,654 Other income 295 264 321 584 804 458 945 1,261 Interest (178) (36) (4) (26) (20) (3) (11) (8) Depreciaton (101) (108) (130) (172) (177) (201) (215) (233) Profit before tax 466 866 1,418 1,738 3,754 6,503 8,159 9,651 Current tax (97) (130) (178) (293) (863) (1,431) (1,795) (2,123) Deferred tax 6 18 6 3 — — — —Net profit 375 754 1,246 1,448 2,891 5,072 6,364 7,528 Adjusted net profit 375 754 1,246 1,448 2,891 5,072 6,364 7,528 Adjusted Diluted EPS (Rs) 14 28 46 54 107 188 236 279 Balance sheet (Rs mn)Equity 127 269 270 270 270 270 270 270 Reserves and Surplus 3,898 4,297 5,131 6,021 8,216 12,499 17,915 24,495

Deferred tax liability 16 22 39 63 63 63 63 63

Total borrowings 124 175 171 206 156 106 106 56 Current liabilities 1,345 1,585 2,209 3,683 4,523 5,749 6,566 7,183

Total liabilities 5,510 6,349 7,819 10,242 13,228 18,686 24,918 32,066 Net fixed assets 655 748 1,276 1,980 2,304 2,303 2,288 2,355

Investments 2,996 4,640 5,180 6,494 8,094 11,844 17,094 23,594

Cash 1,140 111 87 35 101 469 525 280

Other current assets 720 850 1,276 1,671 2,667 4,009 4,950 5,775

Total assets 5,510 6,349 7,819 10,242 13,228 18,686 24,918 32,066 Free cash flow (Rs mn)Operating cash flow excl. working capital 2 353 572 1,127 2,133 4,020 4,888 5,531

Working capital changes 217 85 272 775 (156) (116) (124) (209)

Capital expenditure (118) (202) (651) (1,073) (500) (200) (200) (300)

Free cash flow 102 235 192 830 1,477 3,704 4,564 5,022 RatiosEBITDA margin (%) 6.7 9.5 11.5 13.9 18.3 22.0 22.4 22.1

Net debt/equity (X) (0.3) 0.0 0.0 0.0 0.0 (0.0) (0.0) (0.0)

RoAE (%) 8.5 17.5 24.8 24.6 38.8 47.4 41.0 35.0

Book value/share (X) 149.1 169.2 200.1 230.7 312.0 470.6 671.2 914.9

Source: Company, Kotak Institutional Equities estimates

Eicher Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

We expect 53% CAGR in consolidated net profit over CY2013-15 Eicher Motors consolidated profit & loss, balance sheet and cash flow statement, calendar year-ends, 2009-16E (` mn)

2009 2010 2011 2012 2013E 2014E 2015E 2016EProfit model (Rs mn)Net sales 29,386 43,971 56,775 63,899 66,438 88,487 110,554 132,967

EBITDA 1,444 3,569 5,551 5,490 6,153 10,443 14,919 17,076 Other income 1,054 1,276 1,768 1,366 1,943 2,284 2,905 3,693

Interest (87) (95) (77) (38) (23) (23) (23) (23)

Depreciaton (539) (573) (640) (822) (1,222) (1,650) (2,002) (2,282)

Profit before tax 1,873 4,177 6,602 5,997 6,850 11,054 15,799 18,464 Tax (578) (1,108) (1,628) (1,249) (1,882) (2,890) (4,186) (4,871)

Minority Interest (461) (1,179) (1,886) (1,506) (1,084) (1,553) (2,544) (2,924)

Net profit 834 1,889 3,088 3,243 3,884 6,610 9,068 10,669 Adjusted net profit 834 1,889 3,088 3,243 3,884 6,610 9,068 10,669 Adjusted Diluted EPS (Rs) 31 70 114 120 144 245 336 395 Balance sheet (Rs mn)Equity 127 269 270 270 270 270 270 270

Reserves and Surplus 10,564 12,052 14,661 17,279 20,468 26,289 34,410 44,131

Deferred tax liability 142 249 645 1,232 1,232 1,232 1,232 1,232

Minority Interest 5,747 6,774 8,377 9,485 10,569 12,122 14,666 17,590

Total borrowings 1,264 956 504 389 389 389 389 389

Current liabilities 6,978 9,332 13,343 16,060 16,075 18,615 21,391 24,013

Total liabilities 24,820 29,633 37,799 44,715 49,003 58,917 72,359 87,626 Net fixed assets 3,758 4,513 8,991 14,962 20,439 25,190 27,588 29,505

Investments 2,941 4,586 5,126 6,385 12,385 15,385 21,885 30,385

Cash 11,707 12,457 11,973 8,035 707 269 324 633

Other current assets 6,415 8,043 11,528 15,271 15,410 18,011 22,500 27,040

Miscellaneous expenditure - 35 182 62 62 62 62 62

Total assets 24,820 29,633 37,799 44,715 49,003 58,917 72,359 87,626 Free cash flow (Rs mn)Operating cash flow excl. working capital 1,031 2,986 4,273 4,436 4,270 7,552 10,732 12,205

Working capital changes 2,654 374 (238) 389 (123) (62) (1,712) (1,919)

Capital expenditure (701) (1,315) (4,173) (7,820) (6,700) (6,400) (4,400) (4,200)

Free cash flow (ex financing) 2,984 2,045 (138) (2,995) (2,553) 1,090 4,620 6,087 RatiosEBITDA margin (%) 4.9 8.1 9.8 8.6 9.3 11.8 13.5 12.8

Debt/equity (X) 0.1 0.1 0.0 0.0 0.0 0.0 0.0 0.0

Net debt/equity (X) (1.2) (1.3) (1.1) (0.7) (0.6) (0.5) (0.6) (0.7)

Book value (Rs per share) 396 455 546 648 766 982 1,283 1,643

ROAE (%) 7.7 16.1 21.9 18.9 19.1 26.6 28.5 26.2

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

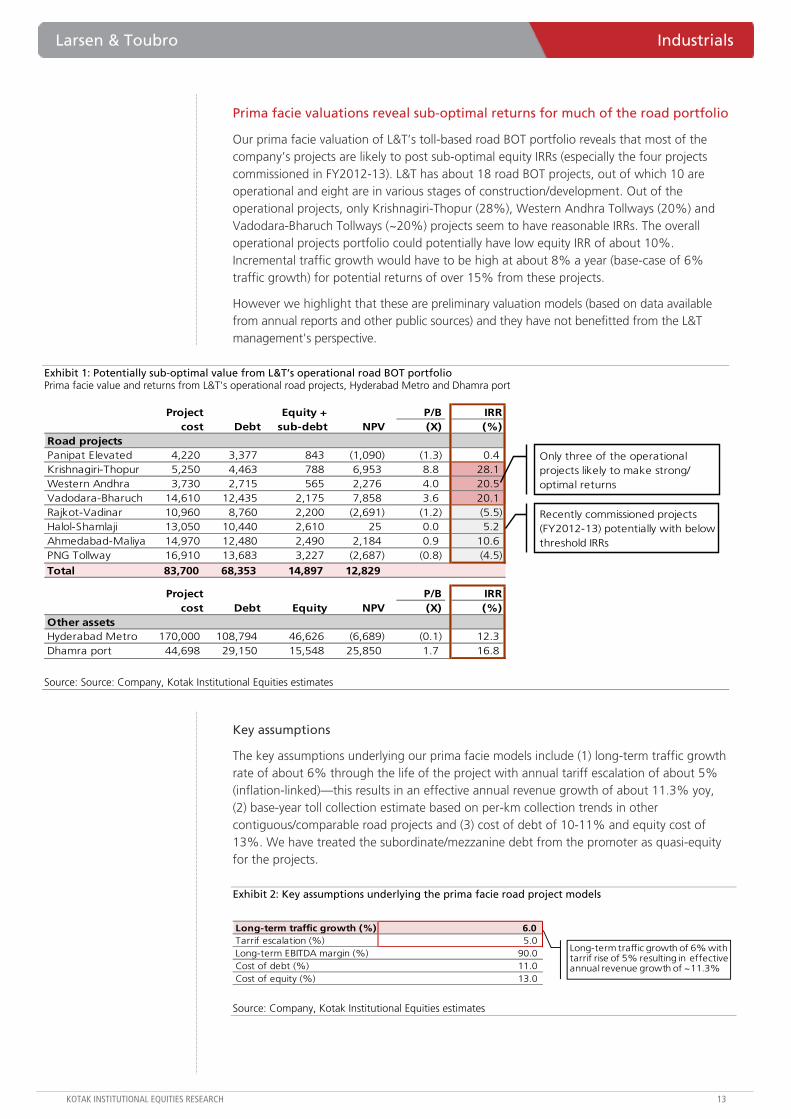

Prima facie valuations reveal below-threshold returns of about 10% for L&T’s road portfolio

Our prima facie valuation reveals that L&T’s operational toll-road portfolio may have sub-optimal equity IRR of 10% (returns especially low for the four recently commissioned projects in FY2012-13). This is due to sharp traffic disappointments (16% below estimates) partly on one-offs such as law & order issues and toll plaza bypass (though we note long-term disappointments in Vadodara-Bharuch, Panipat elevated corridor; four-year toll collection CAGR of only ~8%). Returns may be even lower for the under-construction portfolio as they were won during a period of stiffer competition (FY2011-12). Some limitations the of analysis include (1) done on weak FY2013 base, (2) no specific input for L&T, (3) no provision for project-specific opportunities and constraints.

May add to debt; Hyderabad Metro sub-optimal; Dhamra deal reasonable; execution an issue

The road portfolio may need cash support over the next few years adding to high debt (ex-finance consolidated debt of `355 bn at the end of FY2013, which can rise to `550 bn by the end of FY2015). Even the Hyderabad Metro (25% of development portfolio) may potentially post sub-optimal returns (12%) with large downside to base traffic, real estate monetization, project cost (equity IRR of 5-7% and a large negative NPV of `50-60 bn in a worst-case scenario). Dhamra port sale (`55 bn EV; 1.7X book; 16-17% equity IRR) seems reasonable given its long-term potential. Construction of three road projects (cost ~`60 bn) is yet to start (September 2013 NHAI data).

We retain estimates; reiterate REDUCE with a target price of `970 after sharp performance

Low returns may affect the value realization from monetization/induction of a strategic partner and take the sheen off the stock as a large share of capital (21% ex-finance) is deployed in the assets.

We believe our value of 1XP/B (FY2015E-end estimates book value) for L&T’s asset portfolio is reasonable. We retain REDUCE (TP: `970) on full valuations (post the recent outperformance) with risks related to margin pressure (commodities, competition) and large consolidated debt in a weak environment. We believe overall valuation levels will stay in check on low returns and low growth.

Larsen & Toubro (LT)

Industrials

Prima facie below-threshold returns from IDPL portfolio. Our prima facie analysis of operating road projects of L&T IDPL, shows the blended portfolio IRR of eight operational projects is ~10%. We believe under-construction projects can be even worse as competition was higher over FY2011-12 (large premium payments committed to NHAI). In a recent note we highlighted that Hyderabad Metro may post mediocre returns with large risks, related to traffic, cost and real estate absorption. Such returns can (1) affect the value realization from monetization/induction of a strategic partner and (2) take the sheen off the stock, as debt grows, and projects may need support from the parent.

Larsen & ToubroStock data Forecasts/Valuations 2014 2015E 2016E

52-week range (Rs) (high,low) EPS (Rs) 48.2 58.0 72.1Market Cap. (Rs bn) 924.5 EPS growth (%) (8.1) 20.5 24.3

Shareholding pattern (%) P/E (X) 20.7 17.2 13.8Promoters 0.0 Sales (Rs bn) 854.4 991.1 1,151.7FIIs 18.2 Net profits (Rs bn) 44.5 53.6 66.6MFs 7.5 EBITDA (Rs bn) 108.9 126.1 146.8

Price performance (%) 1M 3M 12M EV/EBITDA (X) 15.1 13.7 12.2Absolute (13.0) 18.1 (3.4) ROE (%) 12.2 13.0 14.2Rel. to BSE-30 (11.8) 13.9 (8.0) Div. Yield (%) 1.3 1.4 1.6

Company data and valuation summary

1,154-677

REDUCE

JANUARY 09, 2014

UPDATE

Coverage view: Cautious

Price (`): 998

Target price (`): 970

BSE-30: 20,729

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Prima facie valuations reveal sub-optimal returns for much of the road portfolio

Our prima facie valuation of L&T’s toll-based road BOT portfolio reveals that most of the company’s projects are likely to post sub-optimal equity IRRs (especially the four projects commissioned in FY2012-13). L&T has about 18 road BOT projects, out of which 10 are operational and eight are in various stages of construction/development. Out of the operational projects, only Krishnagiri-Thopur (28%), Western Andhra Tollways (20%) and Vadodara-Bharuch Tollways (~20%) projects seem to have reasonable IRRs. The overall operational projects portfolio could potentially have low equity IRR of about 10%. Incremental traffic growth would have to be high at about 8% a year (base-case of 6% traffic growth) for potential returns of over 15% from these projects.

However we highlight that these are preliminary valuation models (based on data available from annual reports and other public sources) and they have not benefitted from the L&T management's perspective.

Exhibit 1: Potentially sub-optimal value from L&T’s operational road BOT portfolio Prima facie value and returns from L&T's operational road projects, Hyderabad Metro and Dhamra port

Project Equity + P/B IRRcost Debt sub-debt NPV (X) (%)

Road projectsPanipat Elevated 4,220 3,377 843 (1,090) (1.3) 0.4 Krishnagiri-Thopur 5,250 4,463 788 6,953 8.8 28.1 Western Andhra 3,730 2,715 565 2,276 4.0 20.5 Vadodara-Bharuch 14,610 12,435 2,175 7,858 3.6 20.1 Rajkot-Vadinar 10,960 8,760 2,200 (2,691) (1.2) (5.5) Halol-Shamlaji 13,050 10,440 2,610 25 0.0 5.2 Ahmedabad-Maliya 14,970 12,480 2,490 2,184 0.9 10.6 PNG Tollway 16,910 13,683 3,227 (2,687) (0.8) (4.5)

Total 83,700 68,353 14,897 12,829

Project P/B IRRcost Debt Equity NPV (X) (%)

Other assetsHyderabad Metro 170,000 108,794 46,626 (6,689) (0.1) 12.3 Dhamra port 44,698 29,150 15,548 25,850 1.7 16.8

Recently commissioned projects (FY2012-13) potentially with below threshold IRRs

Only three of the operational projects likely to make strong/ optimal returns

Source: Source: Company, Kotak Institutional Equities estimates

Key assumptions

The key assumptions underlying our prima facie models include (1) long-term traffic growth rate of about 6% through the life of the project with annual tariff escalation of about 5% (inflation-linked)—this results in an effective annual revenue growth of about 11.3% yoy, (2) base-year toll collection estimate based on per-km collection trends in other contiguous/comparable road projects and (3) cost of debt of 10-11% and equity cost of 13%. We have treated the subordinate/mezzanine debt from the promoter as quasi-equity for the projects.

Exhibit 2: Key assumptions underlying the prima facie road project models

Long-term traffic growth (%) 6.0 Tarrif escalation (%) 5.0 Long-term EBITDA margin (%) 90.0 Cost of debt (%) 11.0 Cost of equity (%) 13.0

Long-term traffic growth of 6% with tarrif rise of 5% resulting in effective annual revenue growth of ~11.3%

Source: Company, Kotak Institutional Equities estimates

Industrials Larsen & Toubro

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

We have selected eight out of the 10 operational road projects for our analysis—not included (1) Coimbatore bypass project—won a long time ago (1997) and (2) Interstate-Palanpur project (annuity-based project; have restricted the analysis to toll-based projects). Exhibit 3 summarizes the details of the projects.

Exhibit 3: Key details of L&T’s operational BOT road projects (` mn)

Length Project CA(kms) cost Grant/ Premium CoD Period 2013 2014E 2015E 2013 2014E 2015E

Road projectsPanipat Elevated 10 4,220 Rs3.5 bn -ve grant over 10 yrs (post CoD) Jul-08 20 yrs 453 504 561 (372) (367) (565) Krishnagiri-Thopur 86 5,250 Rs3.6 bn -ve grant over 10 yrs (post CoD) Feb-09 20 yrs 1,212 1,348 1,501 (38) 87 251 Western Andhra 56 3,730 Rs450 mn positive grant Mar-09 20 yrs 481 535 596 (112) (95) (25) Vadodara-Bharuch 83 14,610 Rs4.7 bn upfront payment Jun-09 15 yrs 2,268 2,524 2,809 (405) 75 (59) Rajkot-Vadinar 132 10,960 12.95% rev. share increasing by 1% p.a. Feb-12 20 yrs 682 759 845 (1,135) (1,112) (1,064) Halol-Shamlaji 173 13,050 10.2% rev. share increasing by 1% p.a. Apr-12 20 yrs 933 1,131 1,259 (1,251) (1,059) (977) Ahmedabad-Maliya 180 14,970 12.13% rev. share increasing by 1% p.a. Apr-12 22 yrs 885 1,438 1,601 (843) (1,142) (1,041) PNG Tollway 60 16,910 6.2% rev. share increasing by 1% p.a. Oct-12 20 yrs 189 855 952 (376) (1,489) (1,418) Total 780 83,700 7,102 9,095 10,123 (4,531) (5,101) (4,900)

Revenues Net PAT

Source: Source: Company, Kotak Institutional Equities estimates

Exhibit 4: Financial structure (equity, promoter debt, external debt) of L&T’s operational road projects

Projectcost Total Capital Quasi-equity Total External Promoter Comments

Panipat Elevated 4,220 843 843 - 3,377 927 2,450 Rs2.45 bn non-convertible debentures from IDPLKrishnagiri-Thopur 5,250 788 788 - 4,463 4,011 452 Small L&A from Narmada InfraWestern Andhra 3,730 565 565 - 2,715 2,715 - No subordinate-debt from promoterVadodara-Bharuch 14,610 2,175 435 1,740 12,435 12,435 - Rs1.74 bn promoter subordinate-debt (quasi equity)Rajkot-Vadinar 10,960 2,200 1,100 1,100 8,760 8,760 - Rs1.1 bn promoter mezzanine debt (quasi-equity)Halol-Shamlaji 13,050 2,610 1,305 1,305 10,440 10,440 - Rs1.3 bn promoter mezzanine debt (quasi-equity)Ahmedabad-Maliya 14,970 2,490 1,490 1,000 12,480 12,480 - Rs1 bn promoter mezzanine debt (quasi-equity)PNG Tollway 16,910 3,227 1,691 1,536 13,683 13,683 - Rs1.5 bn promoter mezzanine debt (quasi-equity)Total 83,700 14,897 8,217 6,681 68,353 65,451 2,902

DebtEquity

Source: Source: Company, Kotak Institutional Equities estimates

Out of four recently won contracts only the Beawer project has begun construction, leading to execution disappointment

Apart from the operational portfolio, L&T has about eight road projects that are in various stages of construction (likely to be commissioned over the next 1-2 years). Based on the prima facie valuations of the operational projects, we believe the projects under construction could potentially post even lower returns as these projects were won in a relatively high competition environment (2011-12) with large premium commitments to NHAI. Three road projects (project cost of ~`60 bn) have not yet started construction as of September 2013 NHAI data—Deccan Tollways, Amravati Jalgaon and Jalgaon- Maharashtra Border.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Exhibit 5: Details of L&T’s under-construction BOT road projects (` mn)

Length Project Concession(kms) Cost Debt Equity Grant/ Premium CoD period

Under construction projectsDevihalli-Hassan 77 4,940 2,238 900 Rs1.8 bn positive grant Nov-13 30 yrsBeawar-Pali-Pindwara 244 24,720 18,540 6,180 Rs2.5 bn annual premium increasing at 5% p.a. Jun-14E 23 yrsSamakhiali-Gandhidham 56 13,000 10,400 2,600 Rs676 mn annual premium increasing at 5% p.a. Mar-14E 24 yrsChennai-Tada 43 8,480 6,784 1,696 17.07% revenue share increasing by 1% p.a. Mar-14E 15 yrsAmravati-Jalgaon 275 27,000 20,250 6,750 Rs1.3 bn annual premium increasing at 5% p.a. Mar-15E 19 yrsJalgaon-Gujarat/Mah border 209 21,000 15,750 5,250 Rs1.45 bn annual premium increasing at 5% p.a. Mar-15E 20 yrsDeccan Tollways 145 12,730 9,548 3,183 Rs810 mn annual premium increasing at 5% p.a. Sep-15E 25 yrs

1,049 111,870 83,510 26,559

Source: Source: Company, Kotak Institutional Equities

Large miss on toll attributed to stabilization phase; gap can increase

Toll collection for L&T’s roads portfolio was 16% below the company’s expectations in FY2013. The company attributed this largely to the initial stabilization phase with specific mention of teething issues in Gujarat projects such as (1) law and order problems, (2) temporary bypasses to evade toll check points and (3) the presence of a parallel road without a toll. L&T is trying to address these issues and hopes to recover the traffic trajectory. This is on top of a general slowdown in traffic seen across its road projects. Slower growth and commissioning of new projects would possibly increase the gap beyond the current 16%, versus projection over the next two years or so. Start of projects won more recently and in general against more aggressive competition could also increase the gap.

Exhibit 6: Large revenue miss in FY2013 at the portfolio level Per day gross toll collection for L&T's portfolio, March fiscal year-ends, 2010-14E (` mn)

13.3

16.8

23.3

32.7

36.8

0

8

16

24

32

40

2010 2011 2012 2013 2014E

(Rs mn per day)16% miss versus internal estimate

Source: Company, Kotak Institutional Equities

However, we note that traffic pick-up over the past four years, after the initial start, has remained low in assets like Vadodara-Bharuch and Panipat elevated corridor. Annual revenues have grown at a CAGR of 8-8.5% for the two projects; adjusted for a potential inflation-linked tariff escalation of 7-8% during this period, this would imply relatively flat/low traffic growth over FY2010-13.

Industrials Larsen & Toubro

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 7: Toll collections from Vadodara-Bharuch and Panipat Corridor projects, March fiscal year-ends, 2010-13 (` mn)

2010 2011 2012 2013 CAGR (%)Annualized revenuesVadodara-Bharuch 1,794 1,897 2,112 2,268 8.1 Panipat Elevated Corridor 355 387 420 453 8.4

Source: Company, Kotak Institutional Equities

Projects may require support over the next few years; debt may rise

L&T’s road portfolio may need some equity/cash-flow support over the next few years as low/disappointing traffic levels may lead to losses. This may result in potential debt at the parent level, increasing the high consolidated debt burden. We note this would be apart from the incremental equity requirements of under-construction/development projects in the company’s portfolio.

Exhibit 8: Operational projects may need equity support from the parent over the next few years Project-wise free cash flow to equity for L&T's operational road projects, March fiscal year-ends, 2014-20E (` mn)

2014E 2015E 2016E 2017E 2018E 2019E 2020EOperational projectsPanipat Elevated (195) (466) (790) (676) (458) (345) (286) Krishnagiri-Thopur 227 371 263 435 789 1,064 1,057 Western Andhra (132) (62) (108) 174 218 340 255 Vadodara-Bharuch 212 78 186 1,177 1,445 1,987 1,694 Rajkot-Vadinar (733) (685) (537) (1,019) (1,061) (472) (461) Halol-Shamlaji (537) (456) (331) (431) (914) (649) (165) Ahmedabad-Maliya (471) (370) (215) (391) (842) (638) (135) PNG Tollway (747) (677) (550) (465) (652) (1,264) (1,115)

Cumulative FCFE (2,376) (2,268) (2,081) (1,195) (1,476) 22 843

Source: Company, Kotak Institutional Equities estimates

Hyderabad Metro prima facie valuation implies below-threshold IRR

Our prima facie valuation for L&T’s Hyderabad Metro project reflects that the project could potentially have sub-optimal equity IRR of 12% (with a negative NPV of about –`6.7 bn). This is against a potential equity investment of `46 bn.

May have downside as traffic, real estate monetization estimates may disappoint

Key underlying assumptions include (1) base-year (FY2013) traffic of 1.5 mn passengers a day, (2) traffic growth of 4% over FY2013-21E tapering to 1%, (3) 35% EBITDA margin in the first year of operations, scaling up to a steady state of 60% and (4) 18.5 mn sq. ft of real estate monetization over 10 years (starting 2018E). Exhibit 9 summarizes the assumptions built into our prima facie model of the project.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

Exhibit 9: Key assumptions underlying our prima facie valuation of the Hyderabad Metro project

Financing structureProject cost (Rs mn) 170,000 Equity (Rs mn) 46,626 Debt (Rs mn) 108,794 Grant (Rs mn) 14,580

TimelinesConcession period 60 yrsExpected CoD Mar-17

Key operational assumptionsBase-year traffic (mn pax per day) 1.5 Initial traffic growth (%) 4.0 Tariff escalation (%) 5.0 Cost of debt (%) 11.0 Tax rate (%) 30.0 Cost of equity (%) 13.0

Real estate developmentTotal area to be developed 18.5 mn sq. ftTimeline to monetize entire area 10 yrsAverage rental in FY2013 (per month) Rs40-45 per sq. ft

Assuming small Rs5-6 bn escalation versus estimated project cost of Rs164 bn

Debt: equity of 70:30

Based on timelines shared by the company

Against Delhi Metro current traffic level of 2 mn pax

On lease basis

Based on current rental rates in Hyderabad

Source: Kotak Institutional Equities estimates

Our assumptions for the project are based mainly on the feasibility study/traffic forecast included in the Detailed Project Report (DPR) of the Hyderabad Metro and the established track record by Delhi Metro over the past few years.

We believe our valuation could face some potential downside on the following factors

Favorable base year traffic assumption. Our model builds base-year passenger traffic of about 1.5 mn passengers a day against present traffic levels of 2 mn for Delhi Metro (in FY2013); this is versus a population and metro network size of over 2X in Delhi. Hence our assumption could face some downside risk. We also note very sharp disappointment in the Delhi Metro project in terms of traffic projected versus actual initial ridership (actual ridership was only about a fourth of what was initially estimated).

Exhibit 10: Delhi Metro actual ridership only a fourth of initial projections Actual versus project traffic in the Delhi Metro project

Year Actual Estimated2006 493 2,497 19.7 2007 622 2,760 22.5 2008 768 3,049 25.2 2009 889 3,369 26.4

Actual as % of estimated

Ridership ('000 pax per day)

Source: CDM report on Delhi Metro, UNFCCC website

Real estate monetization of 1.5-2 mn sq. ft a year may not be easy in Hyderabad. Our model builds monetization of the 18.5 mn sq. ft of commercial real estate over 10 years (starting from FY2018)—an average of about 1.85 mn sq. ft a year. This may not be easy to achieve in Hyderabad with current levels of overall annual off-take levels of about 1-1.5 mn sq. ft. However we note that Hyderabad’s rental rates are relatively low (compared with those of Bangalore) and could potentially rise; this would positively impact the valuation, to some extent.

Industrials Larsen & Toubro

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Potential project cost escalations. The estimated capex of `170 bn for the project—about `2.4 bn per km of network, seems relatively low compared to costs of other metro projects (Delhi Metro Phase 3, Jaipur Metro, Mumbai Phase 1, Gurgaon Metro).

Exhibit 11: Comparison of capex in Hyderabad Metro and Delhi Metro projects

Hyderabad Jaipur Mumbai GurgaonMetro Phase-II Phase-III Metro Metro Ph 1 Metro

Approved route length (kms) 71 102 103 35 11 6 No. of stations 66 85 67 31 12 6 Estimated capex (Rs mn) 163,750 191,310 352,420 97,320 43,210 18,500 Capex per km (Rs mn) 2,301 1,871 3,420 2,767 3,903 3,136

Delhi Metro

Source: DMRC, JMRC, IL&FS, Industry, Hyderabad Metro website, Kotak Institutional Equities

No additional real estate capex included. We note that we have not assumed additional capex for the 18.5 mn sq. ft of real estate development involved in the project.

Value highly sensitive to traffic growth and base-traffic assumptions

We note that the valuation of the project is highly sensitive to the base-year traffic and growth assumptions. In case the base-year traffic (in FY2013) is assumed at about 1 mn passengers a day (versus our assumption of 1.5 mn) the project could have a large negative NPV of –`24 bn and low 10.9% equity IRR.

Exhibit 12: Sensitivity of NPV of Hyderabad Metro project at base traffic and traffic growth estimates

Base - 1% Base-case Base + 1% Base + 2% Base + 3%1.00 (27,920) (23,626) (18,311) (11,616) (3,012) 1.25 (20,501) (15,151) (8,510) (123) 10,655 1.50 (13,118) (6,689) 1,276 11,315 24,222 1.75 (5,760) 1,703 10,979 22,707 37,782 2.00 1,533 10,071 20,682 34,043 51,230

Traffic growth rate (%)

Base traffic (mn pax per

day)

Source: Kotak Institutional Equities estimates

Worst case—can have very large negative value considering the size of the project

Our worst-case scenario estimates potential negative potential NPV of –`62 bn and equity IRR of 7.7%. This assumes (1) base year traffic of 1 mn passengers a day (versus a base case of 1.5 mn), (2) about 10 mn sq. ft of real estate absorption over 12 years (against 18 mn sq. ft assumed in our base model) and (3) about 10% higher project cost of `187 bn (versus our base case assumption of `170 bn).

Dhamra port sale value seems fair for a reasonably attractive asset

News flows suggest the potential sale of the Dhamra port asset (a JV between L&T and Tata Steel) to Adani Ports & SEZ Ltd (APSEZ) for a likely enterprise value of about `55 bn. Against this, the project has been funded through (1) `29 bn of debt, (2) `6.5 bn of equity invested by L&T and Tata Steel (`3.24 bn each) and (3) `9 bn of subordinate debt/quasi-equity invested by L&T and Tata Steel (at the end of FY2013).

This transaction implies a price-to-book value (adjusted for the loan funds) of about 1.7X for L&T’s and Tata Steel’s historical investment in the port (share capital + quasi-equity). While this valuation may appear expensive on an EV/EBITDA basis currently (implies over 6X FY2013 EBITDA), we believe it may be reasonable given the long-term potential for growth and expansion at the port.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Exhibit 13: Sale implies 2X P/B value (on historically invested book) Implied valuation of Dhamra port acquisition by ADSEZ (` mn)

Rs mnTotal capital employed 44,698 Debt 29,150 Total equity 15,548

Share capital 6,480 Subordinate debt/ quasi-equity 9,068

Acquisition EV 55,000 Implied equity value (EV-debt) 25,850 Implied P/B (X) 1.7

Source: Company, Kotak Institutional Equities

Assuming `12.9 bn as positive cash inflow (sales realization of L&T’s stake) in FY2014E and equity investments/subordinate loans given to Dhamra Port over FY2006-13 (adjusting for interest received on subordinate loans), the deal may imply reasonable equity IRR of 16-17%.

Exhibit 14: Implied equity IRR on the sale of the Dhamra port asset, March fiscal year-ends, 2006-14E (` mn)

2006 2007 2008 2009 2010 2011 2012 2013 2014L&T's investment in Dhamra portEquity investmet 533 936 1,236 1,586 2,465 3,240 3,240 3,240 Subordinate loans - - - - - 1,401 3,677 4,534 Total investment 533 936 1,236 1,586 2,465 4,641 6,917 7,774 Change in equity/ L&AEquity investmet (annual) (533) (403) (300) (350) (879) (775) - - 12,925 Subordinate loans - - - - - (1,401) (2,275) (857) Add: Interest received on sub-loans - - - - - 7 270 416 Net cash flow (533) (403) (300) (350) (879) (2,169) (2,005) (441) 12,925 Equity IRR (%) 16.8

Source: Company, Kotak Institutional Equities estimates

Deal finalization closer post recent environment clearance for the second phase

News flows suggested that the Dhamra port asset sale was contingent on the project receiving land allocation and securing environment and coastal zone approvals for its next phase of expansion. In September 2013, the Expert Appraisal Committee (EAC) recommended the environment and coastal zone clearances for the second phase of expansion at Dhamra port. Land acquisition itself was contingent on environmental clearance. Hence we believe the company could be a step closer to finalization of the asset sale deal.

Dhamra port profile—27 mn ton bulk cargo port on the east coast of India

Dhamra Port (DPCL) is a 50:50 joint venture between L&T and Tata Steel. The port (phase 1) consists of two operational berths with a cumulative berth length of 700 mts (350 mts each) with a capacity to handle volumes of about 27 mn tons a year. Berth 1 is an import berth for handling coal and limestone cargo while berth 2 is an export berth for handling iron ore cargo. The port has a deep draft of about 18.5 mts and is capable of accepting capsize vessels. The project also has large scope for expansion with a total waterfront availability of over 4.5 kms and 742 acres of land. The master plan for the port involves eventual expansion to 13-15 berths with capacity to handle over 100 mn tons of cargo.

Recent operations—strong scale-up in Dhamra port volumes

We note a strong scale-up in cargo volumes handled at Dhamra port. The port recorded cargo volumes of 3.1 mn tons in 1QFY14, up 34% yoy (the port handled over 11 mn tons in FY2013E, up about 118% yoy, from 5.06 mn tons in FY2012).

Industrials Larsen & Toubro

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 15: Strong scale-up in volumes at Dhamra port Quarterly cargo volumes handled at Dhamra port, March fiscal year-ends, 2012-1QFY14

0.5

1.3 1.5

1.8

2.3 2.2

3.3 3.3 3.1

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1QFY12 2QFY12 3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14

(mn tons) Dhamra cargo volumes

Source: Company, Kotak Institutional Equities

The company expects the port to handle about 16 mn tons of cargo in FY2014 (up 44.5% yoy) and record positive cash profit (about `250 mn) in FY2014 against a cash loss of `1.94 bn reported in FY2013.

Exhibit 16: Operational highlights of Dhamra port, March fiscal year-ends, 2012-14E (` mn)

2012 2013 2014EVolumes (MMT) 5.1 11.1 16.0 Yoy growth (%) 118.8 44.5 Net revenues (incl. other income) 1,970 5,060 7,800 EBITDA (100) 2,070 4,160 EBITDA margin (%) (5.1) 40.9 53.3 Interest to banks (2,920) (3,190) (3,050) Interest payment on promoter loans (280) (820) (860) Cash profit/ (loss) (3,300) (1,940) 250 Depreciation (1,280) (1,460) (1,500) PBT (4,580) (3,400) (1,250) Tax expenses - - - Net PAT (4,580) (3,400) (1,250)

Source: Company, Kotak Institutional Equities estimates

Sub-optimal returns could potentially affect monetization

L&T recently announced it was considering a potential IPO and listing of select road projects in Singapore (as part of its plans to monetize its development assets in IDPL). The low potential value/sub-optimal returns of the underlying assets could slow progress on this envisaged transaction. Even if the company lists only a few select assets, the valuation of cherry-picked assets cannot be extended to the entire development portfolio. The transaction size itself may not make a significant difference given the large equity base of IDPL’s portfolio.

Large equity requirement of about `82 bn for L&T’s development portfolio

L&T envisages about `82 bn of incremental investment requirement (`20 bn in FY2014E) for projects including (1) `62 bn of existing commitments and (2) `20 bn of incremental projects (supported by `10 bn from project-specific partners in incremental projects). This is expected to be funded through (1) strategic investment of `20 bn (we believe 15-22% of stake sale may help to raise this amount, implying a valuation range of `90-130 bn), (2) Dhamra stake sale for `9 bn, (3) specific investor in metro, mezzanine equity of `13 bn and (4) `40 bn from portfolio churn, securitization, bonds and further dilution at IDPL level.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Exhibit 17: Incremental equity requirement and funding for IDPL's existing and new projects (` bn)

Total project cost 439Invested capital 42Equity requirement 82

DeploymentExisting projects 62New projects (net) 20Total 82SourcingStrategic investor 20Dhamra sale 9Investor for metro mezzan 13SecuritizationBonds/debtFurther dilutionTotal 82

40

Stake sale to fund new project capex

Source: Company, Kotak Institutional Equities

Potential for further increase in already high consolidated debt

L&T reported large consolidated debt of `620 bn at the end of FY2013 (against `472 bn at the end of FY2012). Adjusted for the finance subsidiaries L&T had consolidated debt of `355 bn at the end of FY2013, about a third of which resides in its infrastructure development subsidiaries.

We believe the consolidated debt of L&T is likely to rise over the next 2-3 years as the company makes progress on its under-construction/development projects in roads, metro and power. Prima facie, we believe L&T could potentially have consolidated ex-finance debt of about `550 bn by end-FY2015. This debt may become an overhang in an environment of lower-than-expected growth (gap versus expectations would continue to widen) and high capital cost

Exhibit 18: Large consolidated debt likely to further increase over the next 2-3 years Break up of L&T's consolidated debt between standalone and key subsidiary groups, March fiscal year-ends, 2012-16E (` mn)

2012 2013 2014E 2015E 2016EConsolidated debt 471,501 619,937 779,542 893,536 990,366 Standalone debt 98,958 88,342 128,342 128,342 118,342 Subsidiary debt 392,195 541,874 651,200 765,194 872,024

Financial Services 208,741 264,882 314,927 365,017 423,865 Developmental Projects 70,242 111,393 152,642 185,996 222,978 Power Development 21,035 38,526 50,400 67,200 67,200 Property Development 21,761 35,882 43,382 50,882 58,382 Ship building 22,174 27,537 33,537 38,537 41,037 Heavy Engineering 11,612 14,692 15,442 16,692 17,692 Power 15,673 23,668 23,668 23,668 23,668 Hydrocarbons 10,516 13,225 13,225 13,225 13,225 Corporate 2,154 1,082 1,082 1,082 1,082 Electrical & Automation 924 595 595 595 595 Infrastructure 3,235 6,781 IT & Technology 2,950 2,608 1,297 1,297 1,297 Machinery & Industrial Products 1,179 1,003 1,003 1,003 1,003

Debt drawn in infrastructure development SPVs

Mainly in L&T Finance & L&T Infrastructure Finance subs

Primarily Nabha Power

In boiler and turbine manufacturing JVs

Primarily in L&T Seawoods, CSJ Infra and L&T Realty

Source: Company, Kotak Institutional Equities estimates

Development projects related debt could increase by `40-45 bn each year over FY2014-16 (assuming no debt repayment in operational projects).

Industrials Larsen & Toubro

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 19: Development projects-related debt to rise over next 2-3 years Project-wise debt in L&T’s development portfolio, March fiscal year-ends, 2012-16E (` mn)

2012 2013 2014E 2015E 2016EIDPLL&T Infrastructure Development Projects 755 5,100 5,100 5,100 5,100 Road projectsL&T Panipat Elevated Corridor 3,252 3,165 3,165 3,165 3,165 L&T Krishnagiri Thopur Toll Road 7,076 6,592 6,592 6,592 6,592 L&T Western Andhra Tollway 2,642 2,642 2,642 2,642 2,642 L&T Transportation Infrastructure 1,325 1,099 1,099 1,099 1,099 L&T Interstate Road Corridor 4,236 4,158 4,158 4,158 4,158 L&T Vadodara Bharuch Tollway 13,339 12,503 12,503 12,503 12,503 L&T Rajkot-Vadinar Tollway 6,088 9,333 9,333 9,333 9,333 L&T Ahmedabad-Maliya Tollway 8,800 13,766 13,766 13,766 13,766 L&T Halol-Shamlaji Tollway 10,140 11,961 11,961 11,961 11,961 L&T Samakhiali Gandhidham Tollway 1,200 3,805 3,805 3,805 3,805 PNG Tollway 8,397 13,393 13,393 13,393 13,393

L&T Chennai-Tada Tollway 1,621 1,965 4,509 4,509 4,509 L&T Deccan Tollways - - 2,387 4,774 8,115 L&T BPP Tollway - 3,650 8,285 11,993 14,774 L&T Krishnagiri Walajahpet Tollway 357 3,898 7,494 7,494 7,494 L&T Devihalli Hassan Tollway 850 1,999 3,004 3,004 3,004 L&T East-West Tollway Ltd - - 3,038 7,088 13,163 L&T Great Eastern Highway Ltd - - 3,150 6,300 11,025 MetroL&T Metro Rail (Hyderabad) - 12,367 29,560 49,620 69,679 PowerNabha Power 18,535 34,826 50,400 67,200 67,200 Total infra debt 91,276 149,919 203,042 253,196 290,178

Debt drawn in development projects could increase by about Rs40-45 bn each year for the next three years as projects get completed

Source: Company, Kotak Institutional Equities

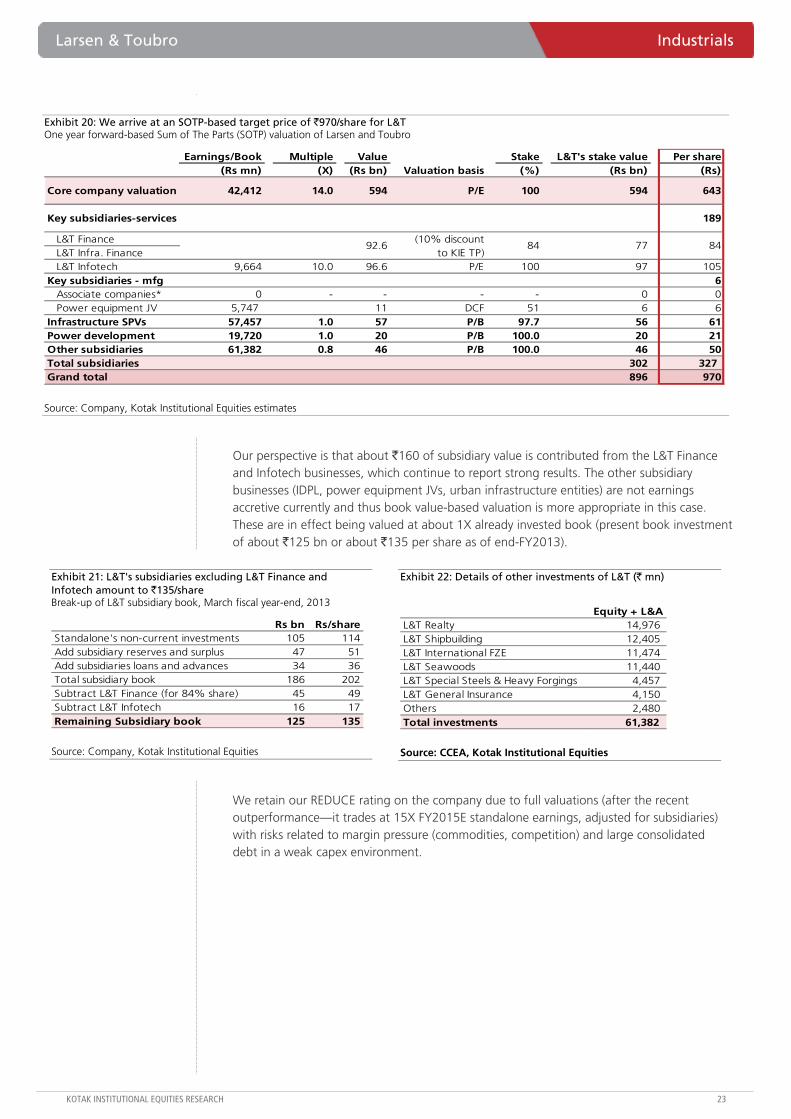

We retain estimates and target price of `970; reiterate REDUCE

We retain our standalone estimates of `51.5 and `54.7 and our consolidated estimates of `48.2 and `58 for FY2014E and FY2015E respectively.

Our SOTP-based target price of `970 comprises (1) `643/share from the core construction business based on 14X one-year forward earnings, (2) `84/share from the financial services subsidiaries (based on KIE target price), (3) `105/share from L&T Infotech (10X forward earnings), (4) `85/share from infrastructure development and power subsidiaries and (5) `50/share from other investments.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Exhibit 20: We arrive at an SOTP-based target price of `970/share for L&T One year forward-based Sum of The Parts (SOTP) valuation of Larsen and Toubro

Earnings/Book Multiple Value Stake L&T's stake value Per share (Rs mn) (X) (Rs bn) (%) (Rs bn) (Rs)

Core company valuation 42,412 14.0 594 P/E 100 594 643

Key subsidiaries-services 189

L&T FinanceL&T Infra. FinanceL&T Infotech 9,664 10.0 96.6 P/E 100 97 105

Key subsidiaries - mfg 6 Associate companies* 0 - - - - 0 0 Power equipment JV 5,747 11 DCF 51 6 6

Infrastructure SPVs 57,457 1.0 57 P/B 97.7 56 61 Power development 19,720 1.0 20 P/B 100.0 20 21 Other subsidiaries 61,382 0.8 46 P/B 100.0 46 50 Total subsidiaries 302 327 Grand total 896 970

84

Valuation basis

92.6 (10% discount

to KIE TP) 84 77

Source: Company, Kotak Institutional Equities estimates

Our perspective is that about `160 of subsidiary value is contributed from the L&T Finance and Infotech businesses, which continue to report strong results. The other subsidiary businesses (IDPL, power equipment JVs, urban infrastructure entities) are not earnings accretive currently and thus book value-based valuation is more appropriate in this case. These are in effect being valued at about 1X already invested book (present book investment of about `125 bn or about `135 per share as of end-FY2013).

Exhibit 21: L&T's subsidiaries excluding L&T Finance and Infotech amount to `135/share Break-up of L&T subsidiary book, March fiscal year-end, 2013

Rs bn Rs/shareStandalone's non-current investments 105 114Add subsidiary reserves and surplus 47 51Add subsidiaries loans and advances 34 36Total subsidiary book 186 202Subtract L&T Finance (for 84% share) 45 49Subtract L&T Infotech 16 17Remaining Subsidiary book 125 135

Source: Company, Kotak Institutional Equities

Exhibit 22: Details of other investments of L&T (` mn)

Equity + L&AL&T Realty 14,976 L&T Shipbuilding 12,405 L&T International FZE 11,474 L&T Seawoods 11,440 L&T Special Steels & Heavy Forgings 4,457 L&T General Insurance 4,150 Others 2,480 Total investments 61,382

Source: CCEA, Kotak Institutional Equities

We retain our REDUCE rating on the company due to full valuations (after the recent outperformance—it trades at 15X FY2015E standalone earnings, adjusted for subsidiaries) with risks related to margin pressure (commodities, competition) and large consolidated debt in a weak capex environment.

Industrials Larsen & Toubro

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 23: Standalone balance sheet and income statement of L&T, March fiscal year-ends, 2009-16E (` mn)

2009 2010 2011 2012 2013 2014E 2015E 2016EIncome statementNet operating revenues 339,385 370,348 439,049 531,705 608,733 679,986 781,209 894,267Cost of goods sold (300,164) (322,592) (382,685) (469,067) (544,798) (612,663) (705,629) (809,046)S, G & A (17,703) (14,627) (19,903) (22,230) (20,911) (24,480) (26,561) (29,511)Salaries & wages (19,745) (23,791) (28,845) (36,635) (44,363) (54,209) (62,871) (71,926)EBIDTA 39,222 47,756 56,364 62,639 63,935 67,323 75,580 85,220EBIDTA margin (%) 11.6 12.9 12.8 11.8 10.5 9.9 9.7 9.5Other income 7,398 9,502 11,811 13,383 18,509 17,852 16,599 16,969Interest (4,156) (5,053) (6,474) (6,661) (9,824) (10,563) (13,476) (12,951)Depreciation (3,073) (4,159) (6,003) (7,005) (8,194) (8,378) (8,865) (9,210)PBT 39,404 48,059 55,708 62,553 64,571 66,234 69,838 80,028Tax (12,312) (16,409) (19,459) (18,538) (18,005) (18,719) (19,383) (22,315)PAT 27,092 31,650 36,250 44,015 46,566 47,515 50,455 57,713Extraordinaries 7,725 12,105 3,329 550 2,541 0 0 0Reported PAT 34,817 43,755 39,579 44,565 49,107 47,515 50,455 57,713EPS (Rs) 30.8 35.0 39.7 47.9 50.4 51.5 54.7 62.5Balance sheetShareholders funds 124,351 182,884 218,241 252,019 291,427 326,283 363,344 405,675 Equity capital 1,171 1,204 1,218 1,225 1,231 1,846 1,846 1,846 Reserves & surplus 123,180 181,679 217,024 250,794 290,196 324,437 361,497 403,829 Total debt 65,560 68,008 71,611 98,958 88,342 128,342 128,342 118,342 Total sources of funds 190,157 251,125 290,074 351,188 379,769 454,626 491,686 524,017 Total fixed assets 50,538 62,231 72,370 82,255 87,101 90,722 96,858 97,648 Intangible assets 1,408 1,427 2,212 1,381 1,919 1,919 1,919 1,919 Investments 82,637 137,053 146,848 158,719 161,034 172,197 178,170 199,731 Net working capital (excl. cash) 48,303 36,869 53,975 91,110 117,191 172,446 189,645 207,052 Cash and bank balances 7,753 14,319 17,304 19,053 14,947 19,762 27,516 20,089 Total application of funds 190,157 251,125 290,074 351,188 379,769 454,626 491,686 524,017 Cash flow statementCash flow from operations (1,600) 47,522 26,996 12,383 29,625 638 42,121 49,515 Cash flow from investing activities (30,695) (69,191) (25,681) (27,120) (14,792) (23,163) (20,972) (31,562) Free cash flow (32,295) (21,668) 1,315 (14,737) 14,834 (22,526) 21,148 17,954 Cash flow from financing activities 31,688 29,330 2,711 17,109 (17,773) 27,341 (13,395) (25,381) Net cash (utilized)/ generated (608) 7,662 4,026 2,372 (2,939) 4,816 7,754 (7,427) Cash balance at start of the year 9,645 7,753 14,319 17,304 19,053 14,947 19,762 27,516 Cash balance at end of the year 7,753 14,319 17,304 19,053 14,947 19,762 27,516 20,089

Source: Company, Kotak Institutional Equities estimates

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Consolidated financials

Exhibit 24: Consolidated balance sheet and income statement of L&T, March fiscal year-ends, 2009-16E (` mn)

2009 2010 2011 2012 2013 2014E 2015E 2016EIncome statementRevenues 404,799 439,698 520,891 643,131 744,980 854,399 991,130 1,151,737 Expenditure (355,457) (376,001) (443,982) (555,711) (646,894) (745,533) (864,996) (1,004,967) EBITDA 49,342 63,697 76,910 87,420 98,087 108,866 126,134 146,770 EBITDA margin (%) 12.2 14.5 14.8 13.6 13.2 12.7 12.7 12.7 Other income 5,920 7,766 8,532 8,290 10,959 9,183 7,505 7,181 Interest & finance charges 4,620 6,919 8,309 11,019 20,950 27,332 30,954 32,567 Depreciation 7,038 9,273 12,432 15,523 15,865 20,016 20,840 22,176 PBT 43,603 55,271 64,701 69,167 72,231 70,700 81,845 99,209 Tax 14,249 20,374 23,479 22,826 23,855 26,223 28,264 32,611 PAT 29,355 34,897 41,222 46,342 48,375 44,478 53,581 66,598 EPS (Rs) 31.8 37.8 44.7 50.2 52.4 48.2 58.0 72.1 One-time items 8,537 19,611 3,339 568 4,149 - - - Reported PAT 37,891 54,507 44,562 46,910 52,524 44,478 53,581 66,598

Balance SheetShare holder's funds 161,046 231,658 260,766 311,402 365,126 410,073 461,479 524,120 Capital 1,171 1,204 1,218 1,225 1,231 1,846 1,846 1,846 Reserves and surplus 149,289 219,581 249,288 292,643 337,366 381,698 433,104 495,745 Minority interest 10,586 10,873 10,260 17,535 26,529 26,529 26,529 26,529 Loan funds 184,000 226,561 327,983 471,501 619,937 726,746 823,144 912,121 Deferred tax liability 1,308 1,530 3,101 818 1,837 2,349 2,349 2,349 Total sources of funds 346,354 459,749 591,850 783,721 986,900 1,112,640 1,260,444 1,412,062 Net block 155,892 189,789 279,865 343,135 417,400 460,039 506,634 520,990 Cash & bank balances 14,590 33,216 36,446 35,221 36,312 5,019 20,632 47,494 Investments 68,054 99,279 92,158 87,895 87,675 83,205 81,121 90,285 Net current assets 97,231 126,592 183,380 317,470 445,513 564,376 652,056 753,293 Total application of funds 346,354 459,749 591,850 783,721 986,900 1,112,640 1,260,444 1,412,062

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

3QFY14 sales performance: Buoyed by new launch in Bangalore

A big launch in Bangalore, ‘Prestige Lakeside Habitat’, helped Prestige garner sales of 1.55 mn sq. ft for `9.4 bn in 3QFY14. We assume around 63% of the sales achieved to be contributed by the new launch. New large-scale project launches have contributed 70-90% of quarterly sales (or in the immediate quarter thereafter), showing strong push of sales at new projects. Excluding the subsequent phases of the 3QFY14 launch, Prestige plans to launch over 18 mn sq. ft between 1QFY15E and 2QFY16E (we expect no new launch in 4QFY14E) across four cities.

Robust collections indicate strong construction progress

Prestige’s collections have been steadily increasing. Collections have increased from an average of `3.3 bn in FY2012 to `6 bn in FY2014, indicating strong construction progress at its residential projects, relegating the constant debtors to do with particular commercial and super-luxury residential sales only (given a separate business model followed for them). With an estimated collections order book of `55 bn at end-3QFY14 and plans to launch more projects in FY2015, we expect the collections run-rate to increase further in FY2015E to an average of `7 bn/quarter.

Prestige is the largest constructor in India; what next from here?

At end-1HFY14, Prestige had over 56 mn sq. ft of built-up area under construction, which we believe is the highest in India. Prestige has scaled up rapidly in Bangalore (the largest residential market in India by volumes) to take advantage of a buoyant market in the past 3 years. Its sales have increased from an average of 1.6 mn sq. ft/year during FY2006-11 to 5.7 mn sq. ft a year during FY2012-14E, a 3X jump. With a high base in Bangalore now, we would expect more launches from Prestige in other markets like Chennai and Hyderabad to see a consolidated volume jump.

What’s in store for 3QFY14E results?

We assume Prestige’s gross collections margin on its residential projects is around 40%, thus supporting a strong business development case. Prestige utilizes debt to fund its office buildings (annuity income projects) given a positive spread. While we expect debt to increase and remain comfortable about it, the quantum of increase depends on its business development expenditure.

Prestige Estates Projects (PEPL)

Real Estate

3QFY14—big launch helps maintain sales volume. Prestige’s 3QFY14 sales stood at 1.6 mn sq. ft for `9.4 bn. Prestige has achieved 80% of the FY2014 guidance of `43 bn of sales and collections of `23 bn. We expect the collections order book from sales to grow to `55 bn at end-3QFY14E, and expect it to increase to `7 bn/quarter in FY2015E. With a high base in Bangalore, we await management plans to further increase volumes through expansions elsewhere; maintain BUY with a target price of `200.

Prestige Estates ProjectsStock data Forecasts/Valuations 2013 2014E 2015E