india daily - Kotak Securities

152

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. Contents Special Reports Strategy Strategy: A good month for AlphaBet Strategy: Taking stock Theme Report Automobiles & Components: 2Ws - quest to conquer the world Daily Alerts Company alerts National Aluminium Co.: Cash burn to continue, growth projects to erode balance sheet Sector alerts Automobiles & Components: Honda launches H’Ness CB350 IT Services: Expect a robust quarter of growth Telecommunication Services: The VLR conundrum Economy alerts Economy: Borrowing target retained Economy: Trade-led BOP surplus INDIA DAILY October 1, 2020 India 30-Sep 1-day 1-mo 3-mo Sensex 38,068 0.2 (2.1) 7.5 Nifty 11,248 0.2 (1.9) 7.8 Global/Regional indices Dow Jones 27,782 1.2 (3.0) 8.0 Nasdaq Composite 11,168 0.7 (6.5) 10.0 FTSE 5,866 (0.5) 0.1 (4.7) Nikkei 23,185 (0.0) 0.2 4.8 Hang Seng 23,459 0.8 (6.9) (4.0) KOSPI 2,328 0.9 0.1 10.4 Value traded – India Cash (NSE+BSE) 518 585 625 Derivatives (NSE) 22,618 14,184 10,90 1 Deri. open interest 3,802 3,348 2,969 Forex/money market Change, basis points 30-Sep 1-day 1-mo 3-mo Rs/US$ 73.5 (26) 50 (192) 10yr govt bond, % 6.4 (2) (11) 12 Net investment (US$ mn) 29-Sep MTD CYTD FIIs (144) - 4,076 MFs (6) - 2,597 Top movers Change, % Best performers 30-Sep 1-day 1-mo 3-mo APHS IN Equity 2,148 3.0 28.6 62.8 AL IN Equity 74 (0.7) 8.1 54.4 TTMT/A IN Equity 63 4.6 23.9 53.4 HCLT IN Equity 812 (0.1) 17.7 47.1 JSTL IN Equity 278 (2.2) (3.2) 45.1 Worst performers YES IN Equity 13 (1.5) (10.2) (51.1) IHFL IN Equity 157 3.3 (23.6) (28.6) BHARTI IN Equity 421 (3.4) (22.9) (24.9) PNB IN Equity 29 (1.9) (17.7) (21.6) BOB IN Equity 41 (0.7) (13.7) (20.1) [email protected] Contact: +91 22 6218 6427

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of india daily - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Contents

Special Reports

Strategy

Strategy: A good month for AlphaBet

Strategy: Taking stock

Theme Report

Automobiles & Components: 2Ws - quest to conquer the world

Daily Alerts

Company alerts

National Aluminium Co.: Cash burn to continue, growth projects to erode balance sheet

Sector alerts

Automobiles & Components: Honda launches H’Ness CB350

IT Services: Expect a robust quarter of growth

Telecommunication Services: The VLR conundrum

Economy alerts

Economy: Borrowing target retained

Economy: Trade-led BOP surplus

INDIA DAILY October 1, 2020 India 30-Sep 1-day 1-mo 3-mo

Sensex 38,068 0.2 (2.1) 7.5

Nifty 11,248 0.2 (1.9) 7.8

Global/Regional indices

Dow Jones 27,782 1.2 (3.0) 8.0

Nasdaq Composite 11,168 0.7 (6.5) 10.0

FTSE 5,866 (0.5) 0.1 (4.7)

Nikkei 23,185 (0.0) 0.2 4.8

Hang Seng 23,459 0.8 (6.9) (4.0)

KOSPI 2,328 0.9 0.1 10.4

Value traded – India

Cash (NSE+BSE) 518 585 625

Derivatives (NSE) 22,618 14,184 10,90

1

Deri. open interest 3,802 3,348 2,969

Forex/money market

Change, basis points

30-Sep 1-day 1-mo 3-mo

Rs/US$ 73.5 (26) 50 (192)

10yr govt bond, % 6.4 (2) (11) 12

Net investment (US$ mn)

29-Sep MTD CYTD

FIIs (144) - 4,076

MFs (6) - 2,597

Top movers

Change, %

Best performers 30-Sep 1-day 1-mo 3-mo

APHS IN Equity 2,148 3.0 28.6 62.8

AL IN Equity 74 (0.7) 8.1 54.4

TTMT/A IN Equity 63 4.6 23.9 53.4

HCLT IN Equity 812 (0.1) 17.7 47.1

JSTL IN Equity 278 (2.2) (3.2) 45.1

Worst performers

YES IN Equity 13 (1.5) (10.2) (51.1)

IHFL IN Equity 157 3.3 (23.6) (28.6)

BHARTI IN Equity 421 (3.4) (22.9) (24.9)

PNB IN Equity 29 (1.9) (17.7) (21.6)

BOB IN Equity 41 (0.7) (13.7) (20.1)

[email protected]: +91 22 6218 6427

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Each single factor portfolio outperforms

After an August where none of the single factor portfolios beat the benchmark, September was

a kinder month for the AlphaBet suite. All four factors – momentum, fundamental, low-

volatility and sentiment – outperformed against the index. Momentum was the best performing

factor in September, which came as a relief after its horrid performance in CY2020 YTD.

Sentiment remains the best-performing factor YTD, delivering an outperformance of 47% over

the index.

All-Season benefits from pharma exposure

The outperformance of single factors also translated into the outperformance of the multi-

factor All-Season portfolio. It beat the benchmark by 8.6% in September, benefiting from

exposure to pharma (DRRD and CIPLA) and HCLT. On YTD basis, it is now up 15.9%, beating

the benchmark by 22.4%.

Higher volatility bad news for the anti-factor portfolio

Higher volatility was bad news for the anti-factor portfolio. The concentrated anti-factor

portfolio was down 5.3%, and the broad anti-factor portfolio was down 7.8%. The anti-factor

portfolio consists of stocks with the weakest fundamentals, poorest sentiment change, highest

volatility and the lowest momentum. Despite its underperformance in September, the anti-

factor portfolio is still up, and outperforming the benchmark, YTD.

October 2020 changes to the concentrated All-season portfolio

October 2020 concentrated All-Season portfolio consists of Hindustan Unilever (HUVR), Tata

Steel (TATA), Britannia Industries (BRIT), Dr Reddy’s Laboratories (DRRD) and Tata Consultancy

Services (TCS). TATA and TCS replace HCL Technologies (HCLT) and Cipla (CIPLA) in the

concentrated All-season portfolio. We show the factor scores of these stocks and their position

within the universe in Exhibits 4 – 7. The single factor portfolios are provided in Exhibits 8-17.

The anti-factor portfolio, which contains the stocks with the worst factor scores, has Tata

Motors (TTMT), Axis Bank (AXSB), ONGC (ONGC), IndusInd Bank (IIB) and Grasim Industries

(GRASIM). AlphaBet recommendations can differ from KIE analyst recommendations.

Strategy AlphaBet

A good month for AlphaBet. With the return of volatility, normal service resumed in

terms of factor performance. All the single factor portfolios in the AlphaBet suite

outperformed the index in September. The anti-factor portfolio, a collection of stocks

with the weakest fundamentals, lowest momentum, highest volatility and poorest

sentiment change, underperformed the benchmark by 4%. The multi-factor All-Season

portfolio beat the index by ~9%. We add TATA and TCS to the concentrated All-Season

portfolio, replacing CIPLA and HCLT.

INDIA

OCTOBER 01, 2020

UPDATE

BSE-30: 38,068

QUICK NUMBERS

Momentum the best

performing single-

factor in September

(4.4%)

Sentiment the best

performing factor

YTD (41%)

All-Season

outperformance

versus index (~9%

in September, 22%

YTD)

Anurag Singh

[email protected]: +91 22 6218 6427

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

PERFORMANCE UPDATE: A GOOD MONTH FOR ALPHABET

In our previous note dated September 1, we noted the outperformance of high-volatility

stocks in August, but cautioned against taking a position in these names. Our

recommendation was based on the expectation of return of volatility. These fears were

realized in September. After falling below 20 in August, India VIX remained elevated above

20 through most of September.

Realized volatility was also up in September, when compared to July and August. This was

not good news for the higher volatility names. A basket of the 10 highest volatility names in

Nifty Index, as of August 31, had an average return of -5.3% and a median return of -5.7%

over September. On the other hand, a similar basket of 10 lowest volatility names had an

average return of 1.7% and a median return of 0.9%. The index returned -1.2% during

September.

September was a good month for all single-factor portfolios. After enduring a rough

CY2020 till date, momentum was the best performing single factor. The concentrated

momentum portfolio, buffeted by its exposure to pharma sector and RIL, outperformed the

index by more than 5%.

The concentrated All-Season portfolio, which is a multi-factor portfolio of five stocks from

Nifty-50 Index with the best momentum, sentiment, volatility and fundamental

characteristics, beat the index by more than 8% in September. Exhibit 1 shows the

performance of the AlphaBet portfolios in the month of September.

The concentrated All-Season portfolio has now outperformed the benchmark by close to

22% from the start of 2020. While the benchmark’s total return in 2020 is close to -7%, the

concentrated All-Season portfolio has returned ~16%.

Exhibit 1: All single factor portfolios outperform against Nifty; concentrated All-Season portfolio beats the index by ~9% Performance of single factor and All-Season portfolios in September 2020

Source: Bloomberg, Kotak Institutional Equities

We also show the difference in the median of the returns of the best-performing 25 stocks

and the median of the returns of the worst-performing 25 stocks from the BSE-200 Index

each month. The higher the difference, the better the opportunities are for stock pickers.

The spread between the best performers and the worst performers had remained depressed

for close to 5 years before the Covid-19 pandemic. However, March to August had

performance spreads in the top quartile of historical performance spreads. The spread

reverted to a lower level in September (Exhibit 2).

September 2020 returns (%) YTD returns (%) Active September returns (%) Active YTD returns (%)

Nifty Index (1.2) (6.5) NA NA

Concentrated All-season 7.4 15.9 8.6 22.4

Broad All-Season 4.0 0.7 5.2 7.1

Concentrated fundamental (0.7) 3.2 0.5 9.7

Broad fundamental 1.7 4.1 2.9 10.6

Concentrated low volatility (0.1) (7.8) 1.1 (1.4)

Broad low volatility 2.0 1.6 3.2 8.0

Concentrated momentum 4.4 (24.6) 5.6 (18.2)

Broad momentum 3.1 (14.3) 4.3 (7.8)

Concentrated sentiment 2.1 41.0 3.3 47.4

Broad sentiment (1.3) (3.5) (0.1) 3.0

Concentrated anti-factor (5.3) 6.2 (4.1) 12.7

Broad anti-factor (7.8) 10.6 (6.6) 17.1

India Strategy

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Past few months were good for active stock pickers with higher dispersion between the returns of best-performers and the

worst-performers Dispersion of returns (in %), measured as the difference of (a) median of returns of best-performing 25 stocks in BSE-200 Index and (b) median of returns of worst-performing 25 stocks in BSE-200 Index, over each month

Source: Bloomberg, Kotak Institutional Equities

0

10

20

30

40

50

60

70

80

90

Dec-

05

May-

06

Oct

-06

Mar-

07

Aug

-07

Jan

-08

Jun-0

8

Nov-

08

Apr-

09

Sep

-09

Feb-1

0

Jul-1

0

Dec-

10

May-

11

Oct

-11

Mar-

12

Aug

-12

Jan

-13

Jun-1

3

Nov-

13

Apr-

14

Sep

-14

Feb-1

5

Jul-1

5

Dec-

15

May-

16

Oct

-16

Mar-

17

Aug

-17

Jan

-18

Jun-1

8

Nov-

18

Apr-

19

Sep

-19

Feb-2

0

Jul-2

0

Dispersion of returns 3-month moving average

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

OCTOBER 2020 PORTFOLIOS

The stocks selected in the concentrated All-Season portfolio for the October 2020 portfolio

are Hindustan Unilever (HUVR), Tata Steel (TATA), Britannia Industries (BRIT), Dr Reddy’s

Laboratories (DRRD) and Tata Consultancy Services (TCS). TCS and TATA replace HCLT and

CIPLA.

Exhibit 3 shows the top half of the Nifty50 Index, as sorted by the combined multi-factor

score. The tickers in red (top five) are a part of the concentrated All-Season portfolio.

Exhibit 3: TCS and TATA replace HCLT and CIPLA in the September All-Season portfolio Top half of Nifty50 Index, as sorted by combined factor score; stock names in red are part of the October 2020 concentrated All-Season portfolio

Source: Bloomberg, Kotak Institutional Equities

Exhibit 4 shows the volatility metrics of the five stocks, alongside the bar chart of the same

for the benchmark. The chart demarcates the four quartiles (color coded) for the three

metrics included in our volatility factor – price volatility, downside deviation and max

drawdown. We also show the relative position of our All-Season portfolio picks and which

quartile they fall into. We truncate the metrics by clipping the edges at both ends. That is, to

reduce the effect of outliers, we cap the metrics at 90th and 10th percentile, respectively.

We also show similar metrics for momentum, fundamental and sentiment scores (see

Exhibits 5-7).

Stock name Sentiment Fundamental Momentum Low volatility Multi-factor

Dr Reddy's Laboratories Ltd 3.0 (0.2) 0.4 0.7 1.0

Tata Consultancy Services Ltd 1.4 0.6 (0.4) 1.0 0.7

Tata Steel Ltd 2.4 (0.1) 0.7 (0.7) 0.6

Hindustan Unilever Ltd (0.6) 1.1 (0.0) 1.7 0.5

Britannia Industries Ltd 0.2 0.3 0.3 1.0 0.5

Reliance Industries Ltd 1.0 (0.3) 0.9 0.3 0.5

Asian Paints Ltd 0.1 0.4 (0.0) 1.4 0.5

Bajaj Auto Ltd 0.6 0.4 (0.2) 0.7 0.4

Nestle India Ltd (0.8) 0.5 0.1 1.4 0.3

Power Grid Corp of India Ltd (0.4) 0.4 (0.1) 1.3 0.3

Cipla Ltd/India (0.4) (0.2) 1.2 0.6 0.3

Eicher Motors Ltd 1.0 0.2 0.4 (0.5) 0.3

HCL Technologies Ltd 0.1 0.4 (0.1) 0.6 0.2

HDFC Bank Ltd (0.4) 0.8 (0.3) 0.9 0.2

Infosys Ltd (0.4) 0.8 (0.2) 0.7 0.2

ITC Ltd (0.4) 1.0 (0.4) 0.6 0.2

Shree Cements Ltd 0.0 (0.2) 0.3 0.6 0.2

Wipro Ltd 0.4 0.2 (0.6) 0.7 0.2

Maruti Suzuki India Ltd 1.1 (0.1) 0.1 (0.4) 0.2

Tech Mahindra Ltd (0.1) 0.4 (0.3) 0.6 0.2

UltraTech Cement Ltd 0.4 (0.2) (0.3) 0.6 0.1

SBI Life Insurance (0.2) 0.5 (0.1) 0.2 0.1

Hero MotoCorp Ltd (0.1) 0.3 0.0 (0.0) 0.0

Bharti Airtel Ltd 0.2 (1.7) 1.4 0.2 0.0

India Strategy

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 4: All stocks in conc. All-Season portfolio, except Tata Steel, have good volatility

characteristics Concentrated All-Season portfolio, relative to benchmark, on volatility metrics

Source: Bloomberg, Kotak Institutional Equities

Exhibit 5: None of the stocks in the conc. All-Season portfolio have outstanding momentum score Concentrated All-Season portfolio, relative to benchmark, on momentum metrics

Source: Bloomberg, Kotak Institutional Equities

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Exhibit 6: HUVR has good operating performance, high stability and not-very-expensive valuation Concentrated All-Season portfolio, relative to benchmark, on fundamental metrics

Source: Bloomberg, Kotak Institutional Equities

Exhibit 7: DRRD and TATA have excellent sentiment score, while HUVR’s sentiment score is below

average Concentrated All-Season portfolio, relative to benchmark, on sentiment metrics

Source: Bloomberg, Kotak Institutional Equities

We also show the portfolio for the broad and concentrated All-Season portfolio, along with

the different single factor portfolios in Exhibits 8-17.

India Strategy

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 8: TATA and TCS enter the concentrated All-Season portfolio The concentrated All-Season portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Exhibit 9: Broader sector representation in the broad All-Season portfolio The broad All-Season portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Exhibit 10: Reliance and Pharma make a large chunk of concentrated momentum portfolio The concentrated momentum portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 30.0% ADD

Britannia Industries Ltd 21.7% ADD

Tata Consultancy Services Ltd 21.2% REDUCE

Dr Reddy's Laboratories Ltd 17.5% SELL

Tata Steel Ltd 9.6% BUY

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 13.4% ADD

Asian Paints Ltd 9.6% REDUCE

Power Grid Corp of India Ltd 8.5% BUY

Cipla Ltd/India 7.7% BUY

Britannia Industries Ltd 6.9% ADD

Tata Consultancy Services Ltd 6.8% REDUCE

HDFC Bank Ltd 6.7% ADD

Bajaj Auto Ltd 6.5% BUY

ITC Ltd 6.5% BUY

HCL Technologies Ltd 5.8% ADD

Dr Reddy's Laboratories Ltd 5.6% SELL

Infosys Ltd 5.1% BUY

Reliance Industries Ltd 4.6% ADD

Eicher Motors Ltd 3.3% REDUCE

Tata Steel Ltd 3.1% BUY

Stock name Portfolio Weight KIE analyst recommendation

Cipla Ltd/India 28.7% BUY

Bharti Airtel Ltd 20.2% BUY

Divi's Laboratories 19.4% NA

Reliance Industries Ltd 17.0% ADD

Sun Pharmaceutical Industries Ltd 14.6% REDUCE

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Exhibit 11: Broad momentum portfolio is relatively diversified across sectors The broad momentum portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Exhibit 12: BRIT replaces INFO in the concentrated low-volatility portfolio The concentrated low volatility portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Exhibit 13: The broad low-volatility portfolio has a defensive tilt The broad low volatility portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 15.8% ADD

Nestle India Ltd 11.7% REDUCE

Cipla Ltd/India 9.0% BUY

Britannia Industries Ltd 8.1% ADD

HCL Technologies Ltd 6.8% ADD

Shree Cements Ltd 6.6% SELL

Dr Reddy's Laboratories Ltd 6.6% SELL

Bharti Airtel Ltd 6.4% BUY

Divi's Laboratories 6.1% NA

Reliance Industries Ltd 5.4% ADD

Sun Pharmaceutical Industries Ltd 4.6% REDUCE

Eicher Motors Ltd 3.9% REDUCE

Tata Steel Ltd 3.6% BUY

JSW Steel Ltd 3.5% ADD

Tata Motors Ltd 2.0% SELL

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 27.7% ADD

Nestle India Ltd 20.5% REDUCE

Asian Paints Ltd 19.8% REDUCE

Power Grid Corp of India Ltd 17.6% BUY

Britannia Industries Ltd 14.3% ADD

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 12.4% ADD

Nestle India Ltd 9.2% REDUCE

Asian Paints Ltd 8.9% REDUCE

Power Grid Corp of India Ltd 7.9% BUY

Britannia Industries Ltd 6.4% ADD

Tata Consultancy Services Ltd 6.3% REDUCE

Wipro Ltd 6.2% ADD

HDFC Bank Ltd 6.2% ADD

Bajaj Auto Ltd 6.0% BUY

NTPC Ltd 5.4% BUY

HCL Technologies Ltd 5.3% ADD

Shree Cements Ltd 5.2% SELL

Dr Reddy's Laboratories Ltd 5.2% SELL

Divi's Laboratories 4.8% NA

Infosys Ltd 4.7% BUY

India Strategy

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 14: Sentiment revision highest for TATA over the past one month The concentrated sentiment portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Exhibit 15: IT and staples are the highest allocation in the broad sentiment portfolio The broad sentiment portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Exhibit 16: HDFCB replaces TCS in the concentrated fundamental portfolio The concentrated sentiment portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Stock name Portfolio Weight KIE analyst recommendation

Tata Consultancy Services Ltd 30.0% REDUCE

Dr Reddy's Laboratories Ltd 24.9% SELL

Maruti Suzuki India Ltd 16.5% SELL

Eicher Motors Ltd 14.9% REDUCE

Tata Steel Ltd 13.6% BUY

Stock name Portfolio Weight KIE analyst recommendation

Asian Paints Ltd 11.8% REDUCE

Britannia Industries Ltd 8.5% ADD

Tata Consultancy Services Ltd 8.3% REDUCE

Wipro Ltd 8.3% ADD

Bajaj Auto Ltd 8.0% BUY

UltraTech Cement Ltd 7.2% BUY

HCL Technologies Ltd 7.1% ADD

Dr Reddy's Laboratories Ltd 6.9% SELL

Divi's Laboratories 6.4% NA

Housing Development Finance Corp Ltd 5.8% NR

Reliance Industries Ltd 5.6% ADD

Maruti Suzuki India Ltd 4.6% SELL

Eicher Motors Ltd 4.1% REDUCE

Tata Steel Ltd 3.8% BUY

JSW Steel Ltd 3.7% ADD

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 30.0% ADD

HDFC Bank Ltd 20.9% ADD

ITC Ltd 20.4% BUY

Infosys Ltd 15.9% BUY

Coal India Ltd 12.9% BUY

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Exhibit 17: A bouquet of sectors in the broad fundamental portfolio The broad sentiment portfolio, as of September 30, 2020

Source: Bloomberg, Kotak Institutional Equities

Stock name Portfolio Weight KIE analyst recommendation

Hindustan Unilever Ltd 13.2% ADD

Asian Paints Ltd 9.5% REDUCE

Power Grid Corp of India Ltd 8.4% BUY

Britannia Industries Ltd 6.8% ADD

Tata Consultancy Services Ltd 6.7% REDUCE

HDFC Bank Ltd 6.6% ADD

Bajaj Auto Ltd 6.4% BUY

ITC Ltd 6.4% BUY

Hero MotoCorp Ltd 5.7% REDUCE

HCL Technologies Ltd 5.7% ADD

Tech Mahindra Ltd 5.7% BUY

Larsen & Toubro Ltd 5.4% BUY

Infosys Ltd 5.0% BUY

Reliance Industries Ltd 4.5% ADD

Coal India Ltd 4.0% BUY

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Recovery still a work in progress

Electricity consumption nosedived in the aftermath of the lockdown. On an adjusted yoy

basis, by end of March, electricity consumption was down 40%. It has slowly recovered

since, with a couple of minor setbacks, and is now up 14% yoy (Exhibit 34).

Lockdown took its toll on movement of goods as well. E-waybill generation fell from 1.7

million per day (FY2020 average) to 0.3 million per day (April 2020). It has steadily improved

since then, and the daily average in the fourth week of September was 2.0 million e-waybills

per day (Exhibit 7). Railway freight volumes were also adversely impacted. April freight

volume was down 36% yoy. It has now recovered and is up 15% yoy in September (Exhibit

8). Port volumes remain depressed though with almost all major ports showing a yoy drop in

volumes in August (Exhibit 10).

Digital transactions benefitted from lockdown. UPI and IMPS transactions did fall in the

aftermath of lockdowns, but now they are much higher than FY2020 averages. NETC

FASTag transactions are also at an all-time high (Exhibit 29-30).

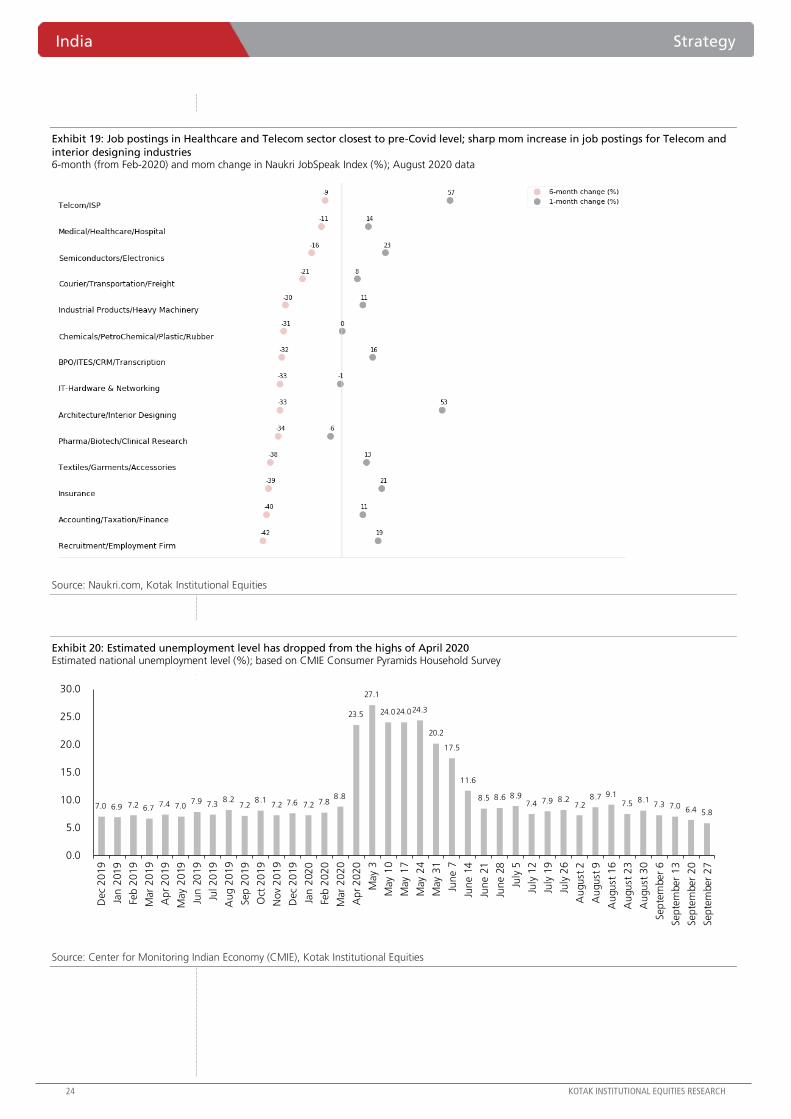

Job postings dried up when lockdowns were announced. Retail and hospitality sectors were

the worst affected. Most industries have recovered to some extent, but new job postings in

August were still down ~40% from Feb 2020 level (Exhibits 18-19). The consumption of

petroleum products is still some way off from normal levels. Petrol consumption was down

8% and diesel consumption was down 21% yoy in August (Exhibits 32-33). A cross-country

comparison of Google mobility data (Exhibits 27-28) over a select set of countries shows that

the recovery in India lags behind recovery in most countries. In terms of excess time spent at

residence and visits to workplaces, India’s recovery to normalcy is behind every other country

except Philippines.

Some positive news on Covid front

The number of new cases declined further this week (Exhibit 46) and this was not on account of

lower testing (Exhibits 49, 51). This coupled with higher recoveries meant a further reduction in

number of active cases. The case fatality rate has remained at 1.6% for more than a week now

(Exhibit 63).

Strategy KIE Covid-19 Tracker

Taking stock. More than six months have elapsed since the announcement of the first

lockdown. We take stock of the recovery in some of the key economic indicators.

Electricity consumption, e-waybill generation and NETC FASTag transactions are back to

pre-Covid level. Railway freight volumes are also up yoy. However, other indicators like

petroleum product consumption, job postings, port volumes and civil aviation are still well

below their pre-Covid level. Time spent at residences and visits to workplaces, per Google

mobility reports, are also significantly lower than the pre-Covid benchmark.

INDIA

OCTOBER 01, 2020

UPDATE

BSE-30: 38,068

QUICK NUMBERS

India consumed

14% more

electricity in the

past week,

compared to a

similar period in the

previous year

Railway freight

volume up 15% yoy

in September

Test positivity rate

declines to 7.5%

Anurag Singh

[email protected]: +91 22 6218 6427

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

FURTHER PROGRESS IN RECOVERY

KIE’s Covid-19 Tracker examines the impact of Covid-19 on the economy through several sets of factors

contributing to economic activity. We find that (1) electricity consumption over the past seven days was 14%

higher when compared to a similar period over the previous year; (2) UPI and IMPS transaction values

continue to be strong in fourth week of September, (3) daily average import duty collection in September is

higher than that of August, and (4) railway freight volume was up both mom and yoy in September.

Steady improvement in most indicators

We track a set of indicators as a proxy for economic activity.

Road traffic. Road traffic remains lower than 2019 levels. This data is available for four

Indian cities – Mumbai, New Delhi, Bengaluru and Pune (Exhibits 2-5). While road traffic

is up from the extreme lows of April 2020, the week-on-week change in congestion level

was divergent across cities. The level of congestion remained flat to slightly positive,

compared to the previous week, in Mumbai, New Delhi and Pune while it increased in

Bengaluru (Exhibit 7). We also track the number of e-waybills generated. This is available

on a weekly basis and is a proxy for the movement of goods across the country. The daily

average of e-waybills generated over the fourth week of September was higher than the

daily average in August and of the first three weeks of September.

Civil aviation data. We track the number of domestic departures and the passengers

carried (Exhibit 6). The number of daily domestic departures has increased to over 1430

now. For comparison, the pre-Covid daily average was close to 4,000. The pace of

improvement has quickened over the past two weeks. The number of passengers on

these flights is now close to 135,000, as against pre-Covid figure of 400,000. Since the

re-start of domestic aviation, both the number of domestic departures and number of

passengers have tripled.

Electricity consumption. Covid-19 forced a prolonged lockdown and temporary

shutting down of factories. This, in turn, led to lower electricity consumption. We show

the daily electricity consumption of major states (Exhibits 34-45) in India and compare this

with consumption in the same week of CY2019. Electricity consumption in India, over the

seven day period ending September 29, was the 14% higher than the electricity

consumption in the similar period in 2019. For comparison, electricity consumption in

CY2020 for the week ending September 22 was 7% higher than that in CY2019. Seven

out of ten states we track saw higher electricity consumption in the past week compared

to a similar period the previous year. We do note however that the state-level electricity

consumption gaps are quite volatile and may change dramatically from one week to the

next.

Payment data. We use payment data released by RBI and National Payment Corporation

of India (NPCI). Specifically, we track UPI, IMPS and NETC FASTag transaction values. Daily

average UPI and IMPS transaction values have recorded an all-time high in September.

NETC transactions are at pre-Covid levels (Exhibits 29-30). We continue to see UPI and

IMPS payments peaking in the first week of month and then falling from there (Exhibit 31).

Also, we note that some of the UPI/IMPS transactions may be in lieu of cash payments (as

people avoid handling cash used by others) and may not reflect more total spending by

consumers. NETC FASTag transactions have continued to increase week-on-week.

Real estate and vehicle purchases. We track the number of property sales registered in

Maharashtra and the daily number of vehicles registered in Regional Transport Offices

under the Vahan4 umbrella (Exhibits 14-17). The daily average of property registrations in

Maharashtra in September is much higher than the daily average of March 2020. In terms

of vehicle registrations, number of cars and two-wheeler registrations increased mom in

August.

India Strategy

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Railway/Ports data. We show daily average metric tons of freight carried by Indian

railways as a proxy of goods movement in India. We also show the year-on-year change

in the freight load for major commodities (Exhibits 8-9). Railway freight volume is up

sequentially in September. Also, on a yoy basis, the railway freight volume is higher in

September. We also show the volume of traffic at major ports and the change in volume

for major commodities (Exhibits 10-13). Container volume increased on a month-on-

month basis at JNPT; however it was well below the pre-Covid level. The volume at

Paradip port also declined. The ports on the western coast of India (Mumbai, Kandla and

JNPT) saw an increase in the yoy decline of port traffic. On the other hand, yoy decline in

volume moderated for the ports located on the eastern coast of India (Paradip, Kolkata

and Vishakhapattnam).

Employment and business sentiment. Covid-19 has led to hiring freezes as well as

involuntary attrition in certain industries. We show the change in the number of new job

postings since March 2020, and the change in new job postings in the most recent

month, on Naukri.com (Exhibits 18 and 19). The hospitality industry continues to remain

the worst affected industry as of August end. Pharma and healthcare industry has been

the least affected. Most industries saw an increase in the number of new job postings in

August, when compared to July. We also show estimated nation-wide unemployment

level based on CMIE survey (Exhibit 20). The unemployment level estimated by CMIE is

close to 8%. Finally, we show the number of new companies registered with the Ministry

of Corporate Affairs each month (Exhibit 21). The number of new companies registered

in August was similar to the number of companies registered in July.

Movement of people. We use Google mobility reports to track the change in the time

spent by people at their residences and number of visits to their workplaces compared

against the pre-Covid baseline (Exhibits 23-28). After falling for several weeks, the excess

time spent at residences increased this week across the country. Also, the recovery in

metro cities lagged the wider recovery for excess time spent at residential areas and

excess visits to workplaces. We also compare recovery in mobility in India to the same in a

select set of countries. India’s recovery towards normalcy is slower and behind many

other countries. Google has temporarily suspended updates to a few categories like

retail/recreation and grocery stores. Therefore, we have removed those exhibits from our

tracker. We will add them back once Google starts updating them once again.

Import duty collection. We also monitor external trade by comparing the import duty

collected in the current period against the import duty collected during the same period

in FY2020 (Exhibit 22). Daily average import duty collected was higher in September after

declining in August.

Petroleum product consumption. Petroleum consumption is another proxy of

economic activity. We track this using data released by Petroleum Planning and Analysis

Cell (PPAC). Monthly data (Exhibits 32-33) shows that consumption of motor spirit

(petroleum) in June was already back to March 2020 consumption level. Petrol

consumption increased marginally in August, compared to July. However, diesel

consumption declined again in August, and diesel consumption in August was lower than

the consumption in May.

Most of the indicators above show that economic activity is still below the pre-Covid period

(Exhibit 1). As evidence from other countries suggests, the road to recovery will not be a

straight line, especially as long as the daily case count continues to increase.

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Exhibit 1: Most economic indicators improving Economic indicators tracked by KIE

Source: Kotak Institutional Equities

Exhibits 2 to 5 show vehicular congestion data for four major cities – Mumbai, New Delhi,

Bengaluru and Pune. Current congestion data is compared to day-of-week adjusted

historical average.

Exhibit 2: The congestion levels in Mumbai remained unchanged from previous week Daily traffic congestion data (Mumbai), relative to historical average (%) as estimated on Oct 1

Source: TomTom.com, Kotak Institutional Equities

Indicator Direction Comments

MovementLow, but

improving

Road traffic was flat on a week-on-week basis. Railway freight

data increased sequentially in September. Google mobility

report also flat week-on-week. Daily average e-waybills

continue to increase.

New vehicle

registration

Low, but

improving

Cars and two-wheeler registrations are now close to two-thirds

of pre-Covid level, but the registrations growth has flattened.

Agri-vehicles less affected.

Electricity

consumptionNormal

Electricity consumption gap negative, meaning India consumed

more electricity in past week, compared to a similar period in

2019.

Property sales Normal

Property sale registrations in Maharashtra were much higher in

September as compared to April 2020. They are also higher

than March 2020 daily average.

New job postingsLow, but

improving

Most industries saw an increase in the number of new job

postings in August, when compared to July. The Naukri

JobSpeak index increased by 11%.

Import duty

collection

Low, and

improvingDaily import duty collection increased in September

Petrochem

consumption

Low, and

stagnant

While petrol consumption increased marginally in August,

diesel consumption saw another mom decline in August.

India Strategy

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 3: Road congestion in New Delhi was flat week on week Daily traffic congestion data (New Delhi), relative to historical average (%) as estimated on Oct 1

Source: TomTom.com, Kotak Institutional Equities

Exhibit 4: Bengaluru traffic congestion nudged up over the past week Daily traffic congestion data (Bengaluru), relative to historical average (%) as estimated on Oct 1

Source: TomTom.com, Kotak Institutional Equities

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

Exhibit 5: Traffic congestion in Pune was flat, compared to previous week Daily traffic congestion data (Pune), relative to historical average (%) as estimated on Oct 1

Source: TomTom.com, Kotak Institutional Equities

Exhibit 6 shows the number of domestic flights and the passengers carried. This compares

with a daily average of ~3,000 domestic flights per day and ~400,000 daily domestic

passengers in pre-Covid period.

Exhibit 6: Number of departures averages around 1430 per day Daily domestic departures (#) and passengers carried (#)

Source: Ministry of Civil Aviation, Kotak Institutional Equities

Exhibit 7 shows the daily average e-waybills generated. E-waybills are needed to transport

goods of value over Rs 50,000. For the months prior to June 2020, we divide the number of

monthly e-waybills generated by 30 to estimate the average daily number of e-waybills

generated. From June 2020, we divide the weekly data by 7 to get the average daily e-

waybills generated for the week.

The number of average daily e-waybills generated fell slightly in March 2020, and sharply in

April 2020 demonstrating the effect of lockdown. With the relaxations in lockdown effective

from May 4, we see that the average daily e-waybills generated have been rising on a week-

on-week basis.

0

200

400

600

800

1,000

1,200

1,400

1,600

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

25

-May

29

-May

2-J

un

6-J

un

10

-Ju

n1

4-J

un

18

-Ju

n2

2-J

un

26

-Ju

n3

0-J

un

4-J

ul

8-J

ul

12

-Ju

l1

6-J

ul

20

-Ju

l2

4-J

ul

28

-Ju

l1

-Au

g5

-Au

g9

-Au

g1

3-A

ug

17

-Au

g2

1-A

ug

25

-Au

g2

9-A

ug

2-S

ep

6-S

ep

10

-Sep

14

-Sep

18

-Sep

22

-Sep

26

-Sep

Passengers Departures (rhs)

India Strategy

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 7: Number of daily e-waybills generated continues to increase Daily average e-waybills generated (mn)

Source: GST Network, Kotak Institutional Equities

Similarly, railway freight data (Exhibits 8 and 9) shows that there was a sharp decline in

railway freight movement in March and April.

Exhibit 8: Railway freight remains sequentially higher in September Daily average freight traffic (mn tons)

Source: Indian Railways, Kotak Institutional Equities

0.9

1.2

1.6 1.5

1.6 1.6

1.8

1.5 1.7 1.7 1.7

1.8 1.8 1.8

1.7 1.7 1.7 1.7 1.8 1.8

1.8 1.9 1.9

1.4

0.3

0.8

1.4 1.6 1.6

1.7 1.8 1.9

2.0

0.0

0.5

1.0

1.5

2.0

2.5

Ap

r-1

8

May-

18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

Oct

-18

No

v-1

8

Dec-

18

Jan

-19

Feb

-19

Mar-

19

Ap

r-1

9

May-

19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

Sep

1 -

Sep

6

Sep

7 -

Sep

13

Sep

14

- Sep

20

Sep

21

- S

ep

26

3.7

3.3

2.2

2.7

3.1 3.1 3.0

3.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Ap

r-1

8

May-

18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

Oct

-18

No

v-1

8

Dec-

18

Jan

-19

Feb

-19

Mar-

19

Ap

r-1

9

May-

19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Exhibit 9: Freight volume up yoy for all categories in September Yoy change (%) for different freight categories

Source: Indian Railways, Kotak Institutional Equities

Apart from rail and road, we also show the impact of Covid-19 and lockdown on port

volumes. Exhibit 10 shows that all major ports saw a yoy drop in volume, when compared to

April and May 2019. The commodities which were most affected were coal and containers

(Exhibit 11). Jawaharlal Nehru Port Trust (JNPT) which handles a significant amount of India’s

container volumes saw a large decline in container volume in April and May (Exhibit 12).

Similarly, Paradip port trust, which handles a significant portion of India’s coal and iron ore

volumes, saw decline in April and May, with the largest drop in volume coming in coal

volumes (Exhibit 13).

Exhibit 10: Western coast ports saw an increase in yoy decline, while eastern coast ports saw a moderation in yoy decline in August Yoy change (%) in total volume handled

Source: Indian Ports Association, Kotak Institutional Equities

9% 19%

100%

13% 7% 2% 14% 15%

(150%)

(100%)

(50%)

0%

50%

100%

150%

Coal/coke Cement/clinker Food Fertilizer Container Petroleum/gases Others Total

Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

(32%)

(13%) (13%)

(27%)

(33%)

(18%)(19%)

(1%)

(7%)

(15%)

(28%)

(22%)(23%)

(10%)(13%)

(9%)

(16%)

(8%)

(14%)

(9%)

12%

(17%) (17%)

(9%)

(40%)(35%)(30%)(25%)(20%)(15%)(10%)(5%)0%5%

10%15%

Ko

lkata

Para

dip

Vis

hakh

ap

att

nam

Mu

mb

ai

JNPT

Deen

dayal (K

an

dla

)

Apr & May yoy change June yoy change July yoy change August yoy change

India Strategy

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 11: Container volume data better in August, compared to previous months Yoy change (%) in selected commodities across major ports

Source: Indian Ports Association, Kotak Institutional Equities

Exhibit 12: Container traffic increased in August at JNPT; though still well below pre-Covid levels Monthly container traffic (‘000s TEUs) at JNPT

Source: Jawaharlal Nehru Port Trust (JNPT), Kotak Institutional Equities

(15%)

(36%)

14%

(14%)

34%

(36%)

(24%)

(36%)

(19%)(15%) (12%)

26%

(11%)

22%

(32%)(37%)

(24%)

10%

(26%)

5%

40% 34%

17%

(8%)

(44%)

(15%)(6%)

(22%)

(3%)

38%

16%

55%

1%

(30%)

(13%) (14%)

(60%)

(40%)

(20%)

0%

20%

40%

60%

PO

L

Oth

er

liquid

s

Iro

n o

re

Fert

ilizers

fin

ish

ed

Fert

lizers

raw

Co

al -

therm

al an

dst

eam

Co

al -

cokin

g a

nd

oth

ers

Co

nta

iners

(TEU

s)

Oth

ers

Apr & May yoy change June yoy change July yoy change August yoy change

448 449

410 431 434

400 403 384

418 426 417 410

284 275 289

344 353

0

50

100

150

200

250

300

350

400

450

500

Ap

r-1

9

May-

19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Exhibit 13: August saw yet another decline in volumes at Paradip port; iron ore volume was higher

though Commodity traffic handled (‘000s MTs) at Paradip port

Source: Paradip Port Trust, Kotak Institutional Equities

We split the vehicle registration data into 4 categories – car registrations (Exhibit 14), two-

wheelers registration (Exhibit 15), goods vehicles registrations and agri-vehicles registration

(Exhibit 16). We see that agri-vehicle registrations were least impacted and have recovered

the quickest. Goods vehicle registrations remain extremely low.

Exhibit 14: Number of car registrations in the second half of August were strong; mom improvement

continues Daily average car registrations (as reported by Vahan)

Source: Ministry of Road Transport and Highways, Kotak Institutional Equities

3,206 3,531 3,091 3,304 3,418 3,023 3,042 2,981 2,360

3,176 2,047 2,122

2,795 2,579 2,173

1,062 1,054

966 638 1,176 1,550 1,410 1,321

1,466

1,483

979 1,316

1,711 1,357 1,671

3,642 3,451

2,720 2,690 2,411 2,344

3,579 3,670 3,566

3,686

3,707 1,996

2,665 2,597

2,234

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

POL Iron Ore Coal

0

2,000

4,000

6,000

8,000

10,000

Cars

FY2020 April 2020 May 2020 June 2020 July 2020 August 2020

India Strategy

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 15: Two-wheeler registrations increases only slightly in August Daily two-wheeler registration (as reported by Vahan)

Source: Ministry of Road Transport and Highways, Kotak Institutional Equities

Exhibit 16: Goods vehicle registrations still much below FY2020 average; however mom recovery

continues Daily goods vehicles and agri-vehicles registration (as reported by Vahan)

Source: Ministry of Road Transport and Highways, Kotak Institutional Equities

The number of property sale registrations in Maharashtra (Exhibit 17) was extremely low in

April 2020 (this was also on account of registration offices being closed).

0

10,000

20,000

30,000

40,000

50,000

Two-wheelers

FY2020 April 2020 May 2020 June 2020 July 2020 August 2020

0

500

1,000

1,500

2,000

2,500

Goods vehicles Agri-vehicles

FY2020 April 2020 May 2020 June 2020 July 2020 August 2020

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Exhibit 17: Daily average Maharashtra property registrations have increased sharply in September Average daily registration of property sales in Maharashtra (#)

Source: Department of Registration and Stamps (Maharashtra), Kotak Institutional Equities

Naukri JobSpeak Index measures the number of new job postings in each industry on a

monthly basis. We show the industries where the number of new job postings decreased

the least (Exhibit 18) and industries where the number of new job postings decreased the

most (Exhibit 19).

Center for monitoring Indian economy (CMIE) estimates unemployment rate in India

through surveys (Exhibit 20).

Exhibit 18: Hospitality and retail continues to be the worst affected sectors; however, a large mom increase in job postings in retail sector 6-month (from Feb-2020) and mom change in Naukri JobSpeak Index (%); August 2020 data

Source: Naukri.com, Kotak Institutional Equities

3,195

3,685

4,248

3,492

4,160

3,811 3,731

3,217

2,678 2,663

3,348

3,662 3,886

3,598

2,832

26

972

2,702 2,503

2,646

3,936

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Jan

-19

Feb

-19

Mar-

19

Ap

r-1

9

May-

19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

India Strategy

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 19: Job postings in Healthcare and Telecom sector closest to pre-Covid level; sharp mom increase in job postings for Telecom and

interior designing industries 6-month (from Feb-2020) and mom change in Naukri JobSpeak Index (%); August 2020 data

Source: Naukri.com, Kotak Institutional Equities

Exhibit 20: Estimated unemployment level has dropped from the highs of April 2020 Estimated national unemployment level (%); based on CMIE Consumer Pyramids Household Survey

Source: Center for Monitoring Indian Economy (CMIE), Kotak Institutional Equities

7.0 6.9 7.2 6.7 7.4 7.0

7.9 7.3 8.2

7.2 8.1

7.2 7.6 7.2 7.8 8.8

23.5

27.1

24.0 24.0 24.3

20.2

17.5

11.6

8.5 8.6 8.9 7.4 7.9 8 .2

7.2 8.7 9.1

7.5 8.1 7.3 7.0

6.4 5.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Dec

20

19

Jan

201

9

Feb

20

19

Mar

20

19

Ap

r 2

01

9

May

20

19

Jun

20

19

Jul 2

01

9

Au

g 2

01

9

Sep

20

19

Oct

20

19

No

v 2

01

9

Dec

20

19

Jan

202

0

Feb

20

20

Mar

20

20

Ap

r 2

02

0

May

3

May

10

May

17

May

24

May

31

Jun

e 7

Jun

e 1

4

Jun

e 2

1

Jun

e 2

8

July

5

July

12

July

19

July

26

Au

gu

st 2

Au

gu

st 9

Au

gu

st 1

6

Au

gu

st 2

3

Au

gu

st 3

0

Sep

tem

ber

6

Sep

tem

ber

13

Sep

tem

ber

20

Sep

tem

ber

27

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Exhibit 21: Company registrations remained high in August Number of private and public companies registered with Ministry of Corporate Affairs during a month

Source: Ministry of Corporate Affairs, Kotak Institutional Equities

We also show the daily import duty collected and compare it against the daily average of

import duty collected for same period in FY2020 (Exhibit 22). The import duty collection in

April 2020 was extremely low. Since then, import duty collections have improved but they

still remain some distance below the FY2020 average.

Exhibit 22: Import duty collection continues to be strong in September Daily import duty collection (Rs bn)

Source: Central Board of Indirect Taxes and Customs, Kotak Institutional Equities

We also use Google mobility reports to show that track time spent at residences (Exhibit 23)

and excess visits to workplaces (Exhibit 24). Google has temporarily suspended updates to

categories like ‘retail/recreational’ and ‘grocery/pharmaceutical’. Therefore, we have

removed those exhibits from our report.

Google mobility reports use the location data from Android phones. These reports note the

time spent in locations classified as ‘residence’, and visits to ‘workplace’ and then compare it

against the time spent/visits to these locations during pre-Covid baseline period.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Mar-

20

18

Ap

r-2

01

8

May-

201

8

Jun

e-2

01

8

July

-20

18

Au

g-2

01

8

Sep

t-20

18

Oct

-20

18

No

v-2

01

8

Dec-

20

18

Jan

-20

19

Feb

-20

19

Mar-

20

19

Ap

r-2

01

9

May-

201

9

Jun

e-2

01

9

July

-20

19

Au

g-2

01

9

Sep

t-20

19

Oct

-20

19

No

v-2

01

9

Dec-

20

19

Jan

-20

20

Feb

-20

20

Mar-

20

20

Ap

r-2

02

0

May-

202

0

Jun

e-2

02

0

July

-20

20

Au

g-2

02

0

8.1

5.7

7.5 7.3

9.3 8.8

10.1 10.9

0

2

4

6

8

10

12

FY2

02

1,

YTD

Ap

ril 2

02

0

May

20

20

Jun

e 2

02

0

July

20

20

Au

gu

st 2

02

0

Sep

tem

ber

20

20

FY2

02

0,

sam

e p

eri

od

India Strategy

26 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 23: An increase in excess time spent at residences over the past ten days, reversing the trend towards normalcy Change, from pre-Covid baseline, in time spent in residential areas (%); and its seven-day moving average for India and a select group of metros

Source: Google mobility report, Kotak Institutional Equities

Exhibit 24: There is a significant gap between the recovery in non-metro districts and metro cities in visits to workplaces Change, from pre-Covid baseline, in visit to workplaces (%); and its seven-day moving average for India and a select group of metros

Source: Google mobility report, Kotak Institutional Equities

We also show the change in time spent at residential and visits to workplaces for major

Indian states (Exhibits 27-28) and compare it to previous week. Finally, we compare the

recovery in these metrics in India, versus a select group of countries (Exhibits 29 - 30).

-5

0

5

10

15

20

25

30

35

40

15

-Feb

22

-Feb

29

-Feb

7-M

ar

14

-Mar

21

-Mar

28

-Mar

4-A

pr

11

-Ap

r

18

-Ap

r

25

-Ap

r

2-M

ay

9-M

ay

16

-May

23

-May

30

-May

6-J

un

13

-Ju

n

20

-Ju

n

27

-Ju

n

4-J

ul

11

-Ju

l

18

-Ju

l

25

-Ju

l

1-A

ug

8-A

ug

15

-Au

g

22

-Au

g

29

-Au

g

5-S

ep

12

-Sep

19

-Sep

India Metro India (7-day MA) Metros (7-day MA)

-100

-80

-60

-40

-20

0

20

15

-Feb

22

-Feb

29

-Feb

7-M

ar

14

-Mar

21

-Mar

28

-Mar

4-A

pr

11

-Ap

r

18

-Ap

r

25

-Ap

r

2-M

ay

9-M

ay

16

-May

23

-May

30

-May

6-J

un

13

-Ju

n

20

-Ju

n

27

-Ju

n

4-J

ul

11

-Ju

l

18

-Ju

l

25

-Ju

l

1-A

ug

8-A

ug

15

-Au

g

22

-Au

g

29

-Au

g

5-S

ep

12

-Sep

19

-Sep

India Metro India (7-day MA) Metros (7-day MA)

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

Exhibit 25: Many states saw the time spent at residences increase Change, from pre-Covid baseline, in time spent at residential areas (%), same figure for previous week; states with significant increase highlighted

Source: Google mobility report, Kotak Institutional Equities

Exhibit 26: Number of visits to workplaces did not change meaningfully for most states Change, from pre-Covid baseline, in number of visits to workplaces (%), same figure for previous week; states with significant decrease highlighted

Source: Google mobility report, Kotak Institutional Equities

Excess time spent at residence (current) Excess time spent at residence (1 week back)

India 14.9 13.0

Andhra Pradesh 15.9 14.7

Bihar 10.1 6.9

Delhi 12.4 12.4

Gujarat 13.1 11.4

Haryana 11.9 10.1

Jharkhand 13.6 11.4

Karnataka 15.1 14.0

Kerala 20.0 15.4

Madhya Pradesh 15.1 12.3

Maharashtra 19.9 18.1

Odisha 15.6 11.6

Punjab 11.4 8.9

Rajasthan 11.4 8.3

Tamil Nadu 14.9 12.9

Telangana 15.6 15.1

Uttar Pradesh 12.7 11.0

Uttarakhand 12.7 10.9

West Bengal 14.9 12.9

Excess visits to workplace (current) Excess visits to workplace (1 week back)

India (31.1) (32.0)

Andhra Pradesh (25.0) (27.9)

Bihar (18.9) (18.7)

Delhi (36.6) (38.1)

Gujarat (25.6) (27.0)

Haryana (28.9) (30.1)

Jharkhand (23.0) (25.1)

Karnataka (37.3) (39.4)

Kerala (28.6) (27.6)

Madhya Pradesh (25.4) (26.4)

Maharashtra (42.3) (43.1)

Odisha (30.1) (31.6)

Punjab (31.4) (30.3)

Rajasthan (24.4) (25.4)

Tamil Nadu (30.3) (32.0)

Telangana (37.4) (39.3)

Uttar Pradesh (25.0) (26.3)

India Strategy

28 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 27: Only Philippines, from a select group of countries, is above India in excess time spent in residential areas Change from pre-Covid baseline, in time spent in residential areas (%) for select group of countries; on first day of each month and the last available date

Source: Google mobility report, Kotak Institutional Equities

Exhibit 28: Similarly, only Philippines lags India in terms of number of excess visits to workplaces, Change from pre-Covid baseline, in visits to workplaces (%) for select group of countries; on first day of each month and the last available date

Source: Google mobility report, Kotak Institutional Equities

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 29

Payment statistics by National Payments Corporation of India (NPCI) shows that UPI and

IMPS payments have rebounded sharply after their precipitous drop in April 2020 (Exhibits

29-31).

Exhibit 29: UPI & IMPS transaction values in September are much higher than in previous months Daily average UPI and IMPS transaction values (in Rs bn)

Source: National Payments Corporation of India, Reserve Bank of India, Kotak Institutional Equities

Exhibit 30: NETC FASTag transactions have increased slowly over the past three months; September daily average slightly higher than

Feb-2020 daily average Daily average NETC FASTag transaction values (in Rs bn)

Source: National Payments Corporation of India, Kotak Institutional Equities

47 51 49 49 52 54

64 63 68

72 74 69

50

73

87 94 96

108

56 60 58

61 63 61

71 68 70 72 72

67

40

56

69 73

76 82

0

20

40

60

80

100

120

UPI IMPS

0.2 0.2 0.2 0.2 0.2 0.2

0.2 0.3

0.4

0.5

0.6

0.5

0.1

0.4

0.5 0.5

0.6

0.6

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

India Strategy

30 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 31: NETC FASTag transactions continue to increase week-on-week Daily average UPI and IMPS (in Rs bn) and NETC transaction values (in Rs crores)

Source: National Payments Corporation of India, Kotak Institutional Equities

We also show the consumption data for petro-products – motor spirits (petrol) and high

speed diesel (Exhibits 32 and 33).

Exhibit 32: Petrol consumption increased marginally in August; still lower than August 2019 Monthly petrol consumption (‘000s metric tons) and year-on-year change in consumption (%)

Source: Petroleum Planning and Analysis Cell, Kotak Institutional Equities

93

74

48

84

65

52

102

82

52

86

65

52

100

83

51

90

71

55

123

91

63

99

76

64

0

20

40

60

80

100

120

140

UPI IMPS NETC FASTag

June W1 June W2 June W3 June W4 July W1 July W2 July W3 July W4

Aug W1 Aug W2 Aug W3 Aug W4 Sep W1 Sep W2 Sep W3 Sep W4

2,459

2,737 2,639

2,523 2,575

2,372 2,539 2,535 2,473 2,456 2,511

2,156

973

1,769

2,281 2,263 2,381

-70

-60

-50

-40

-30

-20

-10

0

0

500

1,000

1,500

2,000

2,500

3,000

Ap

r-1

9

May-

19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

Petrol consumption yoy change (rhs)

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 31

Exhibit 33: Diesel consumption dropped again in August Monthly high speed diesel consumption (‘000s metric tons) and year-on-year change in consumption (%)

Source: Petroleum Planning and Analysis Cell, Kotak Institutional Equities

We also track electricity consumption (Exhibits 34 to 45) for a few major states –

Maharashtra, New Delhi, Andhra Pradesh, Karnataka, Gujarat, Tamil Nadu, Telangana,

Madhya Pradesh, Uttar Pradesh and Haryana. We show daily electricity consumption

compared to the same week in the calendar year prior (CY2019). The horizontal axis shows

the week of the year. Rather than comparing to recent 1-month or 3-month figures, we

compare against same week from the previous calendar year to isolate any effect of the

weather.

Exhibit 34: India consumed more electricity in the past week, compared to a similar period in the

previous year Reduction in electricity consumption (%) compared to same period last calendar year for India over past seven days

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

7,323 7,788

7,451

6,841

6,117 5,837

6,510

7,571 7,387 6,942 7,160

5,651

3,250

5,495

6,302

5,524

4,849

-60

-50

-40

-30

-20

-10

0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Ap

r-1

9

May-

19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-2

0

May-

20

Jun

-20

Jul-

20

Au

g-2

0

Diesel consumption yoy change (rhs)

(50.0%)

(40.0%)

(30.0%)

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

7-M

ar

14

-Mar

21

-Mar

28

-Mar

4-A

pr

11

-Ap

r

18

-Ap

r

25

-Ap

r

2-M

ay

9-M

ay

16

-May

23

-May

30

-May

6-J

un

13

-Ju

n

20

-Ju

n

27

-Ju

n

4-J

ul

11

-Ju

l

18

-Ju

l

25

-Ju

l

1-A

ug

8-A

ug

15

-Au

g

22

-Au

g

29

-Au

g

5-S

ep

12

-Sep

19

-Sep

26

-Sep

India Strategy

32 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 35: Seven states consumed more electricity this week than a similar period last year Reduction in average electricity consumption (%) compared to same period last calendar year

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

Exhibit 36: Maharashtra consumed less electricity in the past week compared to similar period last

year Electricity consumption (mn kWh) in Maharashtra compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

Karn

ata

ka

Tela

ng

an

a

Mah

ara

shtr

a

An

dh

ra P

rad

esh

Tam

il N

adu

Guja

rat

Hary

an

a

Delh

i

Mad

hya

Pra

desh

Utt

ar

Pra

desh

Week ending Sep 29, 2020 Week ending Sep 22, 2020

405 380

0

100

200

300

400

500

600

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Maharashtra 2019 Maharashtra 2020

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 33

Exhibit 37: Delhi used more electricity over the previous week, compared to similar period last year Electricity consumption (mn kWh) in Delhi compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

Exhibit 38: Gap in consumption in Andhra Pradesh narrowed Electricity consumption (mn kWh) in Andhra Pradesh compared to the same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

80

106

0

20

40

60

80

100

120

140

160

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Delhi 2019 Delhi 2020

168

147

0

50

100

150

200

250

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Andhra Pradesh 2019 Andhra Pradesh 2020

India Strategy

34 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 39: The electricity consumption gap decreased for Karnataka Electricity consumption (mn kWh) in Karnataka compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

Exhibit 40: Tamil Nadu’s electricity consumption gap was higher, compared to similar period last

calendar year Electricity consumption (mn kWh) in Tamil Nadu compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

157 149

0

50

100

150

200

250

300

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Karnataka 2019 Karnataka 2020

271

307

0

50

100

150

200

250

300

350

400

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Tamil Nadu 2019 Tamil Nadu 2020

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 35

Exhibit 41: Telangana electricity consumption continues to be lower than the consumption in

CY2020 Electricity consumption (mn kWh) in Telangana compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

Exhibit 42: Gujarat used more electricity over the past seven days, compared to similar period last

year Electricity consumption (mn kWh) in Gujarat compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

167

133

0

50

100

150

200

250

300

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Telangana 2019 Telangana 2020

275

326

0

50

100

150

200

250

300

350

400

450

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Gujarat 2019 Gujarat 2020

India Strategy

36 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 43: MP consumed more electricity in the past week, compared to similar period last year Electricity consumption (mn kWh) in Madhya Pradesh compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

Exhibit 44: Extremely volatile consumption gap continues in Uttar Pradesh Electricity consumption (mn kWh) in Uttar Pradesh compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

154

205

0

50

100

150

200

250

300

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

MP 2019 MP 2020

281

398

0

100

200

300

400

500

600

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

UP 2019 UP 2020

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 37

Exhibit 45: Haryana’s electricity consumption gap was negative Electricity consumption (mn kWh) in Haryana compared to same week last calendar year (Jan 24 – Sep 29)

Source: Central Electricity Regulatory Commission, Kotak Institutional Equities

145

190

0

50

100

150

200

250

300

Week 5 Week 9 Week 13 Week 17 Week 21 Week 25 Week 29 Week 33 Week 37

Haryana 2019 Haryana 2020

India Strategy

38 KOTAK INSTITUTIONAL EQUITIES RESEARCH

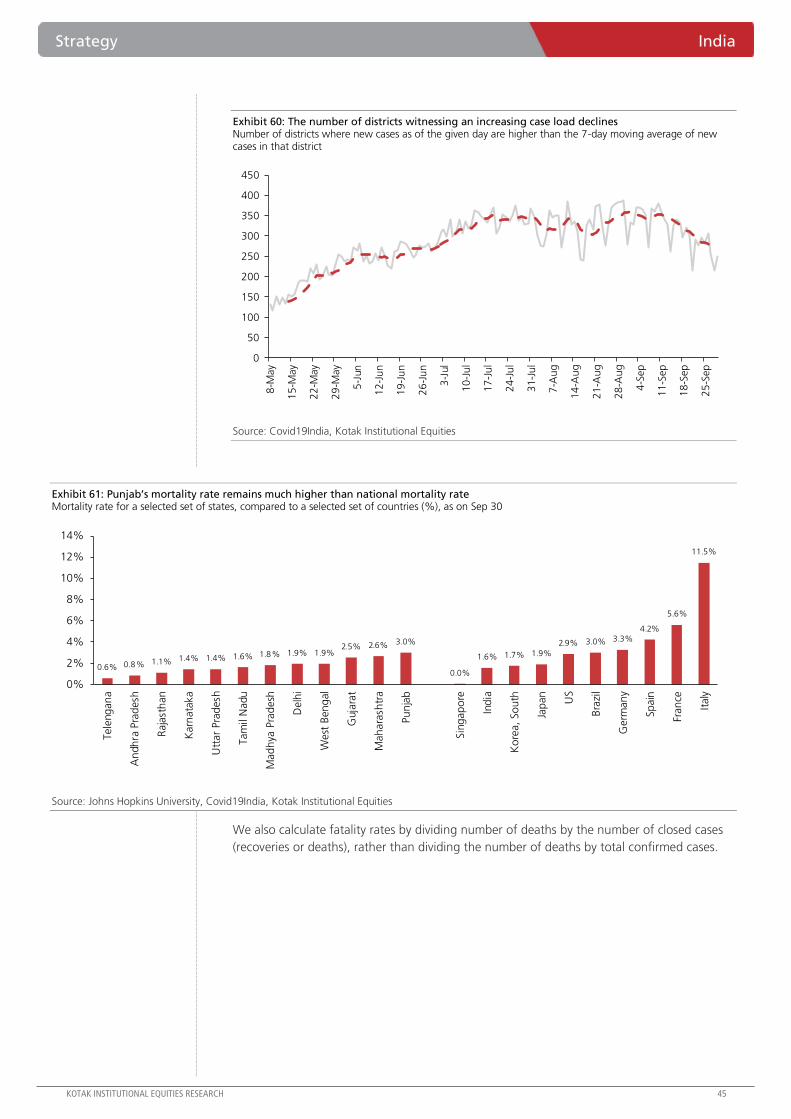

Covid-19 case updates

We continue to see an increase in the number of new confirmed cases. However, recoveries

also continue to rise (Exhibit 46).

Exhibit 46: The number of new cases was consistently lower over the past week Number of recovered cases, deaths, active cases (LHS) and new confirmed cases (RHS), as on Sep 30

Source: Johns Hopkins University, Kotak Institutional Equities

We also show the three-day moving average of new cases (Exhibit 47) and the seven day

moving average of change in active cases (Exhibit 48).

Exhibit 47: Three-day moving average of new cases fell to 80,000 Daily new confirmed cases and their three-day moving average, as on Sep 30

Source: Johns Hopkins University, Kotak Institutional Equities

0

12,000

24,000

36,000

48,000

60,000

72,000

84,000

96,000

108,000

0

600,000

1,200,000

1,800,000

2,400,000

3,000,000

3,600,000

4,200,000

4,800,000

5,400,000

6,000,000

6,600,000

Number of recovered cases Number of deaths

Number of active cases Number of new confirmed cases (RHS)

0

15,000

30,000

45,000

60,000

75,000

90,000

105,000

4-M

ar

11

-Mar

18

-Mar

25

-Mar

1-A

pr

8-A

pr

15

-Ap

r

22

-Ap

r

29

-Ap

r

6-M

ay

13

-May

20

-May

27

-May

3-J

un

10

-Ju

n

17

-Ju

n

24

-Ju

n

1-J

ul

8-J

ul

15

-Ju

l

22

-Ju

l

29

-Ju

l

5-A

ug

12

-Au

g

19

-Au

g

26

-Au

g

2-S

ep

9-S

ep

16

-Sep

23

-Sep

New confirmed cases 3-day moving average

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 39

Exhibit 48: Fewer new cases and more recoveries meant that number of active cases decreased in the past two weeks Daily change in active cases and their seven-day moving average, as on Sep 30

Source: Johns Hopkins University, Kotak Institutional Equities

Exhibit 49: After a week of low testing, the number of tests were almost back to normal this week Seven-day moving average of daily samples tested (#)

Source: Covid19India, Kotak Institutional Equities

The seven-day compounded growth rate of confirmed cases has been broadly falling since the

announcement of lockdown (Exhibit 50). However, at this juncture, we believe that absolute

numbers are a better metric to track than growth rates.

(40,000)

(30,000)

(20,000)

(10,000)

0

10,000

20,000

30,000

1-A

pr

8-A

pr

15

-Ap

r

22

-Ap

r

29

-Ap

r

6-M

ay

13

-May

20

-May

27

-May

3-J

un

10

-Ju

n

17

-Ju

n

24

-Ju

n

1-J

ul

8-J

ul

15

-Ju

l

22

-Ju

l

29

-Ju

l

5-A

ug

12

-Au

g

19

-Au

g

26

-Au

g

2-S

ep

9-S

ep

16

-Sep

23

-Sep

New active cases 7-day moving average

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

India Strategy

40 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 50: India's seven-day CDGR continues to decline Long-term compounded daily growth rate (CDGR) of cases, since the day number of cases crossed 30, and seven-day CDGR, as on Sep 30

Source: Johns Hopkins University, Kotak Institutional Equities

Several restrictions were relaxed in lockdown 4.0. From June 1 onwards, there have been a

further graded relaxations. We show that the positive sample rate trended downward in

lockdown 1.0, stabilized at around 4% in lockdown 2.0, increased slightly in lockdown 3.0

and sharply in lockdown 4.0 (Exhibit 51).

Exhibit 51: Lower number of cases, with testing almost back to usual numbers, implies a lower

positive rate Seven-day moving average of new cases divided by seven-day moving average of incremental samples tested; different phases of lockdown are shaded differently

Source: Covid19India, ICMR, Kotak Institutional Equities