15July 2020_India_Daily - Kotak Securities

89

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. Contents Special Reports Theme Report Reliance Industries: The virtuous cycle On the forefront of digital ecosystem in India targeting 4Cs of the business model We now ascribe US$62 bn of EV to the offline retail footprint and digital commerce foray Reiterate BUY with revised FV of Rs2,150, noting several catalysts in the medium term Daily Alerts Result Mindtree: A quarter that could have been worse but for top client Revenues from travel, hospitality decline 54.6% qoq, top client concentration increases to 30% Thoughts on top client concentration and future of travel and transportation vertical Marginal cut in revenue estimates with broadly unchanged EPS estimates Results, Change in Reco Wipro: Upgrade to ADD on inexpensive valuations Wipro reports sharp revenue contraction; EBIT margin increase sharply led by cost management Focus of CEO Thierry Delaporte to be on profitable growth Challenges aplenty but all in the price; upside from moderate improvement in performance Change in Reco Shree Cement: Efficient but expensive FY2020 reports record margins, retains leadership in cost efficiency Strong operating performance improves FCF yield and balance sheet strength Growth to sustain, expansions on track and low utilization provide headroom Downgrade to SELL on expensive valuations post the recent rally INDIA DAILY July 15, 2020 India 14-Jul 1-day 1-mo 3-mo Sensex 36,033 (1.8) 8.4 18.6 Nifty 10,607 (1.8) 8.1 18.8 Global/Regional indices Dow Jones 26,643 2.1 3.4 13.4 Nasdaq Composite 10,489 0.9 7.8 25.0 FTSE 6,180 0.1 1.9 10.4 Nikkei 22,902 1.4 6.4 17.1 Hang Seng 25,478 (1.1) 7.2 5.5 KOSPI 2,205 1.0 8.6 18.7 Value traded – India Cash (NSE+BSE) 572 632 598 Derivatives (NSE) 15,160 11,314 6,270 Deri. open interest 3,664 2,930 1,912 Forex/money market Change, basis points 14-Jul 1-day 1-mo 3-mo Rs/US$ 75.3 0 (53) (112) 10yr govt bond, % 6.1 - (17) (81) Net investment (US$ mn) 13-Jul MTD CYTD FIIs (11) (169) (2,610) MFs (107) (377) 4,481 Top movers Change, % Best performers 14-Jul 1-day 1-mo 3-mo IHFL IN Equity 223 (6.3) 45.6 143.5 BHEL IN Equity 39 (8.7) 33.7 81.4 RIL IN Equity 1,917 (0.9) 18.7 68.3 EDEL IN Equity 57 (0.4) 30.3 63.6 ARBP IN Equity 809 (0.0) 5.3 57.2 Worst performers YES IN Equity 21 (5.0) (27.8) (14.5) COAL IN Equity 128 (1.7) (2.9) (12.7) HUVR IN Equity 2,235 (1.3) 7.2 (10.2) DIVI IN Equity 2,218 (0.8) (5.0) (7.4) PIDI IN Equity 1,381 (1.1) (3.6) (6.4) [email protected] Contact: +91 22 6218 6427

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 15July 2020_India_Daily - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Contents

Special Reports

Theme Report

Reliance Industries: The virtuous cycle

On the forefront of digital ecosystem in India targeting 4Cs of the business

model

We now ascribe US$62 bn of EV to the offline retail footprint and digital

commerce foray

Reiterate BUY with revised FV of Rs2,150, noting several catalysts in the

medium term

Daily Alerts

Result

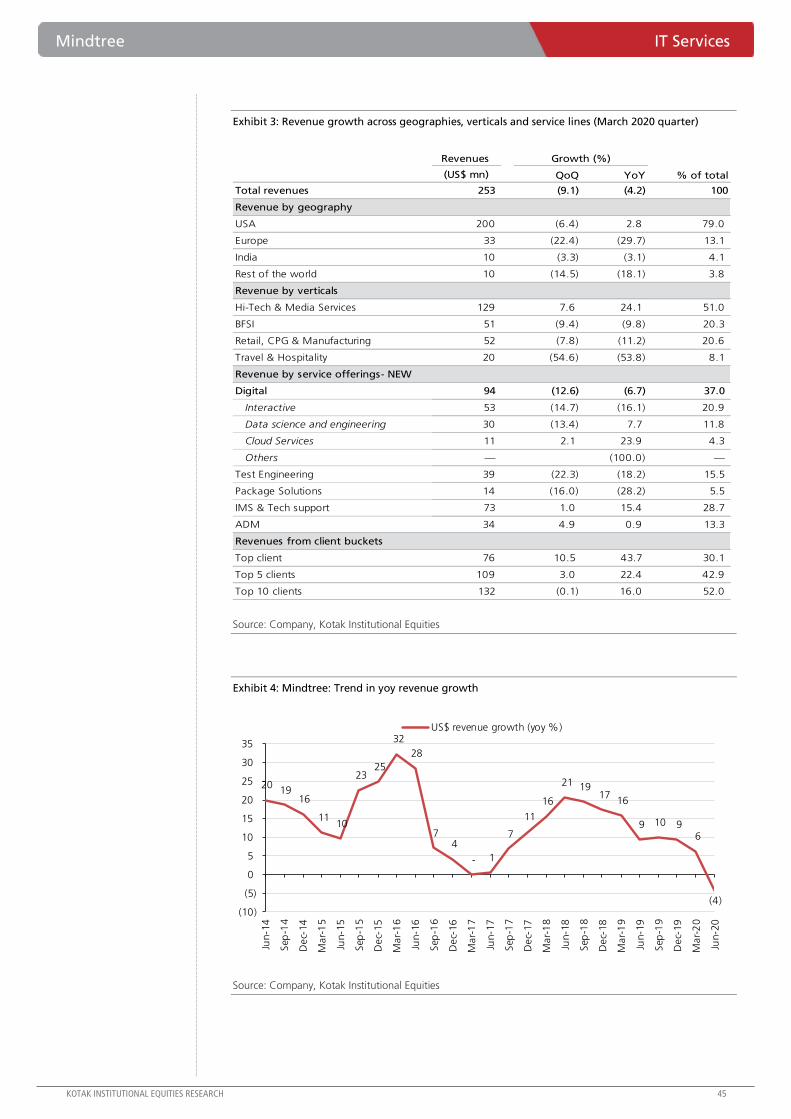

Mindtree: A quarter that could have been worse but for top client

Revenues from travel, hospitality decline 54.6% qoq, top client

concentration increases to 30%

Thoughts on top client concentration and future of travel and

transportation vertical

Marginal cut in revenue estimates with broadly unchanged EPS estimates

Results, Change in Reco

Wipro: Upgrade to ADD on inexpensive valuations

Wipro reports sharp revenue contraction; EBIT margin increase sharply led

by cost management

Focus of CEO Thierry Delaporte to be on profitable growth

Challenges aplenty but all in the price; upside from moderate improvement

in performance

Change in Reco

Shree Cement: Efficient but expensive

FY2020 reports record margins, retains leadership in cost efficiency

Strong operating performance improves FCF yield and balance sheet

strength

Growth to sustain, expansions on track and low utilization provide

headroom

Downgrade to SELL on expensive valuations post the recent rally

INDIA DAILY July 15, 2020 India 14-Jul 1-day 1-mo 3-mo

Sensex 36,033 (1.8) 8.4 18.6

Nifty 10,607 (1.8) 8.1 18.8

Global/Regional indices

Dow Jones 26,643 2.1 3.4 13.4

Nasdaq Composite 10,489 0.9 7.8 25.0

FTSE 6,180 0.1 1.9 10.4

Nikkei 22,902 1.4 6.4 17.1

Hang Seng 25,478 (1.1) 7.2 5.5

KOSPI 2,205 1.0 8.6 18.7

Value traded – India

Cash (NSE+BSE) 572 632 598

Derivatives (NSE) 15,160 11,314 6,270

Deri. open interest 3,664 2,930 1,912

Forex/money market

Change, basis points

14-Jul 1-day 1-mo 3-mo

Rs/US$ 75.3 0 (53) (112)

10yr govt bond, % 6.1 - (17) (81)

Net investment (US$ mn)

13-Jul MTD CYTD

FIIs (11) (169) (2,610)

MFs (107) (377) 4,481

Top movers

Change, %

Best performers 14-Jul 1-day 1-mo 3-mo

IHFL IN Equity 223 (6.3) 45.6 143.5

BHEL IN Equity 39 (8.7) 33.7 81.4

RIL IN Equity 1,917 (0.9) 18.7 68.3

EDEL IN Equity 57 (0.4) 30.3 63.6

ARBP IN Equity 809 (0.0) 5.3 57.2

Worst performers

YES IN Equity 21 (5.0) (27.8) (14.5)

COAL IN Equity 128 (1.7) (2.9) (12.7)

HUVR IN Equity 2,235 (1.3) 7.2 (10.2)

DIVI IN Equity 2,218 (0.8) (5.0) (7.4)

PIDI IN Equity 1,381 (1.1) (3.6) (6.4)

[email protected]: +91 22 6218 6427

Company Report

For Private Circulation Only. In the US, this document may only be distributed to QIBs (qualified institutional buyers) as defined under rule 144A of the Securities Act of 1933. This document is not for public distribution and has been furnished to you solely for your information and may not be reproduced or redistributed to any other person. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

Reliance Industries (RIL)

Oil, Gas & Consumable Fuels

The virtuous cycle. RIL’s leadership in connectivity and retail businesses and recent

strategic partnership with Facebook will enable it to further expand its presence in

India’s digital ecosystem, which can create significant value in the long run. We expect

the foray in digital commerce business to be the next big driver of RIL stock, with the

valuation of legacy O2C and digital services segments broadly established in a

reasonable range for now. We retain BUY rating on the stock, raising our SoTP-based

Fair Value to Rs2,150 and valuing the overall retail business at an EV of US$62 bn.

On the forefront of digital ecosystem in India targeting 4Cs of the business model

RIL’s well-established connectivity business under Jio Platforms, formidable offline retail

footprint under Reliance Retail, proposed foray in the digital commerce segment under JioMart

and recent strategic partnership with Facebook, have propelled it to the forefront of consumer-

facing digital ecosystem opportunity in India. We believe RIL’s ever-expanding portfolio of

products and services to target the 4Cs of the digital ecosystem—connectivity, commerce,

content and currency—will enable it to leverage the sizeable traffic across its consumer-facing

verticals, generate new revenue streams and create significant value in the long run.

We now ascribe US$62 bn of EV to the offline retail footprint and digital commerce foray

Our analysis of the overall retail business opportunity in this report suggests that Reliance

Retail can potentially double its revenues to over US$26 bn from core segments in next four

years, while achieving an incremental GMV of US$12 bn from its foray in India’s e-commerce

market, which is all set to treble to US$100 bn by FY2025. We ascribe US$62 bn of EV to RIL’s

retail business, (1) ascribing 25X EV/EBITDA multiple to core retail segment versus 20X earlier

and (2) factoring incremental contribution of US$17 bn (~Rs1.3 tn) from the digital commerce

business based on probability-weighted scenarios that may evolve for e-commerce in India by

FY2030. (1) RIL’s proven track record of execution, (2) large customer base of Jio and retail

segments, (3) strategic tie-up with WhatsApp, (4) unmatched portfolio of private labels and

exclusive brand tie-ups, (5) India’s domestic-centric policies and (6) possible inorganic ventures,

will enable the company to overcome the head-start achieved by other e-commerce players.

Reiterate BUY with revised FV of Rs2,150, noting several catalysts in the medium term

We reiterate BUY on RIL, while raising our SoTP-based FV to Rs2,150 from Rs1,750 earlier,

ascribing higher value to the retail business and rolling forward to September 2021; our

estimates remain largely unchanged as we incorporate the recent transactions and FY2020 AR.

Progress on digital commerce business, monetization of incremental ecosystem opportunities,

increase in telecom tariffs and recovery in O2C business environment are the key catalysts to

watch out for. Potential closure of transactions related to O2C and fiber-InvIT, and further

strategic partnerships in digital services and retail business can be positive triggers as well.

Company data and valuation summary

BUY

July 15, 2020

THEME

Sector view: Attractive

CMP (`): 1,917

Fair Value (`): 2,150

BSE-30: 36,033

INSIDE

RIL has established

leadership in offline retail

.................. .pg12

Fast growing multi-

category retailer with a

formidable footprint

.................. .pg16

Aspirations to tap India’s

e-commerce

opportunity..pg22

Tarun Lakhotia

Garima Mishra

Hemang Khanna

Shubhangi Nigam

Reliance Industries

Stock data Forecasts/valuations 2020 2021E 2022E

52-week range (Rs) (high,low) EPS (Rs) 66.7 69.8 93.3

Mcap (bn) (Rs/US$) EPS growth (%) 1.2 4.6 33.7

ADTV-3M (mn) (Rs/US$) P/E (X) 28.7 27.5 20.5

Shareholding pattern (%) P/B (X) 2.5 2.3 2.0

Promoters 48.9 EV/EBITDA (X) 16.7 13.9 9.5

FIIs 25.9 RoE (%) 9.4 8.6 10.7

MFs/BFIs Div. yield (%) 0.3 0.4 0.4

Price performance (%) 1M 3M 12M Sales (Rs bn) 5,967 5,093 6,453

Absolute 21 63 51 EBITDA (Rs bn) 831 893 1,204

Rel. to BSE-30 13 39 62 Net profits (Rs bn) 396 414 593

1,948-867

11,363/150.7

5.3/6.2

35,427/470

[email protected]: +91 22 6218 6427

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Reliance Industries Oil, Gas & Consumable Fuels

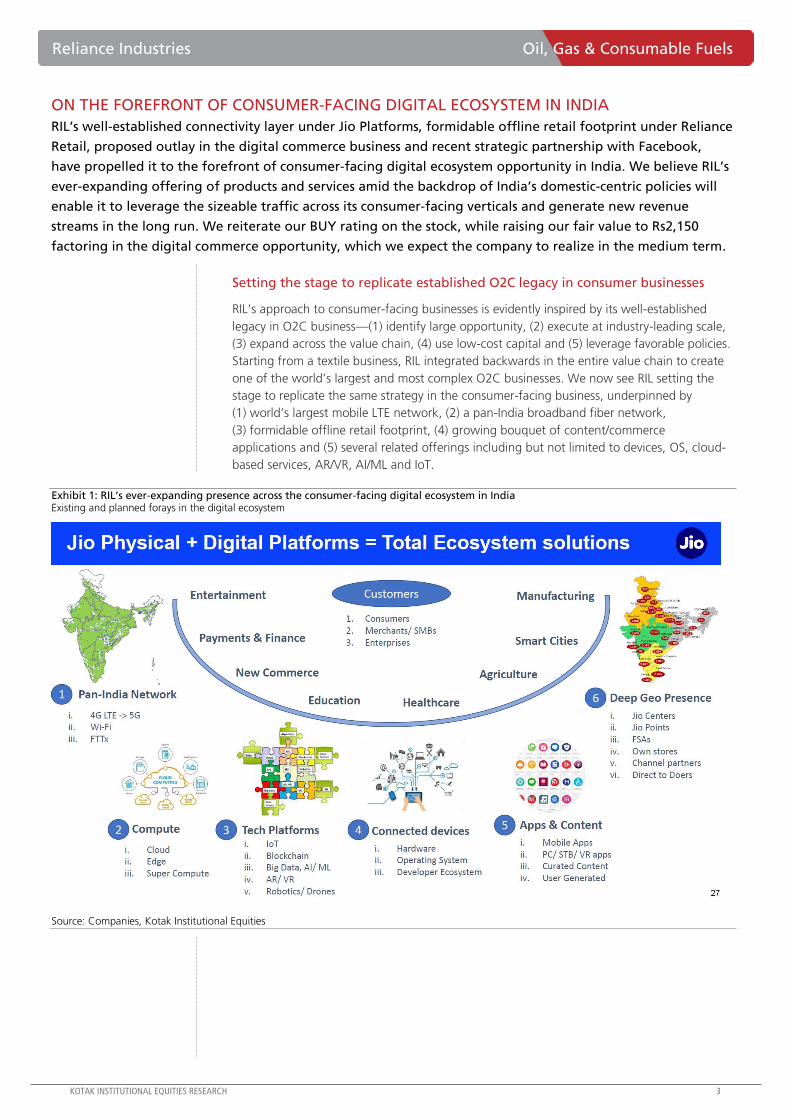

ON THE FOREFRONT OF CONSUMER-FACING DIGITAL ECOSYSTEM IN INDIA

RIL’s well-established connectivity layer under Jio Platforms, formidable offline retail footprint under Reliance

Retail, proposed outlay in the digital commerce business and recent strategic partnership with Facebook,

have propelled it to the forefront of consumer-facing digital ecosystem opportunity in India. We believe RIL’s

ever-expanding offering of products and services amid the backdrop of India’s domestic-centric policies will

enable it to leverage the sizeable traffic across its consumer-facing verticals and generate new revenue

streams in the long run. We reiterate our BUY rating on the stock, while raising our fair value to Rs2,150

factoring in the digital commerce opportunity, which we expect the company to realize in the medium term.

Setting the stage to replicate established O2C legacy in consumer businesses

RIL's approach to consumer-facing businesses is evidently inspired by its well-established

legacy in O2C business—(1) identify large opportunity, (2) execute at industry-leading scale,

(3) expand across the value chain, (4) use low-cost capital and (5) leverage favorable policies.

Starting from a textile business, RIL integrated backwards in the entire value chain to create

one of the world’s largest and most complex O2C businesses. We now see RIL setting the

stage to replicate the same strategy in the consumer-facing business, underpinned by

(1) world’s largest mobile LTE network, (2) a pan-India broadband fiber network,

(3) formidable offline retail footprint, (4) growing bouquet of content/commerce

applications and (5) several related offerings including but not limited to devices, OS, cloud-

based services, AR/VR, AI/ML and IoT.

Exhibit 1: RIL’s ever-expanding presence across the consumer-facing digital ecosystem in India Existing and planned forays in the digital ecosystem

Source: Companies, Kotak Institutional Equities

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

RIL targeting the 4Cs of the digital ecosystem business model

Well-established digital ecosystem companies across the world have exhibited a few

common traits and strategies—(1) a robust scalable technology backbone connecting a large

base of consumers on a best-in-class digital interface, that acts as a hook, (2) offering of

incremental layers to fulfill the customers’ requirements of products, services or content

within their own ecosystem or through an open marketplace, (3) providing transactional

capability through an integrated payments mechanism and (4) generating revenues and

profits through a combination of advertising, commissions and subscription.

We believe RIL has chartered its path in a similar way to service the entire spectrum of the

digital ecosystem in India—(1) connectivity through mobile/fiber-to-the-home/enterprise

services, (2) commerce through offline retail, online foray and digitizing large unorganized

segment, (3) content through its bouquet of media and entertainment apps and related

business verticals and (4) currency through transaction capabilities. RIL’s recent strategic tie-

up with Facebook/WhatsApp may enable it to enhance its powerful digital ecosystem

offering by connecting to customers through integrated user-friendly interfaces to meet

most, if not all, of their requirements in the digital world.

Exhibit 2: Jio Platforms + Reliance Retail can evolve into large revenue generating companies akin to their Chinese counterparts Comparison of product offerings of Jio Platforms + Reliance Retail with Alibaba and Tencent

Reliance Retail + Jio Platforms Alibaba group Tencent

B2C commerce

(1) Retail own brands: Fresh, Smart, Market, Ajio

etc. (2) Textile own brands (3) In-Store brands:

John Players, Snactac, avaasa (Ethnic

Indianwear), GoodLife (Full range grocery brand)

and LYF smartphones (4G mobile devices)

Taobao is B2C/C2C focused, enabling small

businesses and individuals to open online stores.

Tmall offers a wide selection of branded products

oriented towards China's growing middle class.

Partnered with JD.com in 2014. JD.com features

prominently on WeChat.

B2B commerceReliance Market and JioMart can evolve as a

large B2B national supplier

Alibaba B2B is a trading platform, connecting

manufacturers from countries such as China, India,

US and Thailand with international buyers.

Local commerceJioMart enabled O2O connecting offline

customers with online B2C/B2B platforms

Ele.me (connects local shops to consumers), Didi

Kuaidi (cab aggregator)Didi Kuaidi (cab aggregator)

Payment and fintech JioMoney/JioPayAlipay: online third-party payments platform,

providing transaction and escrow services. Weixin Pay, QQ Wallet, LiCaiTong, WeSure, Weiliadai

Logistics Grab (acquired in 2019)Cainiao Logistics - provides logistics support to all

of Alibaba's operations

Social media and

messagingFB, Instagram, Whatsapp, JioChat, JioCall Influencing and personal content on Taobao QQ IM, Weixin and WeChat (Free service)

Digital content JioMovies, JioTV, JioSaavn, JioNews Relevant digital content on B2C websitesAdvanced Casual Games ACGs, Mobile games,

Massively Multiplayer Online Games MMOGs

MarketingFacebook and Instagram Platforms, JioAds Cross-

device Marketing Technology Platform.

Online advertising. Alimama is an online marketing

platform that provides sellers on Alibaba Group's

marketplaces a range of marketing and advertising

services. Advertisers can choose between pay-for-

performance and display marketing. These ads are

the primary means through which Alibaba makes

money from Taobao.

Online advertising. (1) Media. Includes news, video

and music properties, e.g. Tencent News app;

QQ.com and verticals; regional portals; QQ Music

etc. (2) Social and others. Includes social properties,

app store, browser and ad networks, e.g. Qzone, QQ,

Weixin Official Accounts, Weixin Moments, Mini

Programs, QQ Browser, Mobile Ad Network,

YingYongBao etc.

Online infrastructure

JioCloud Store and Access your files from

anywhere. JioBrowser Fast, Safe & Light weight

browser. JioSecurity Protect phone, secure data

Aliyun Alibaba Cloud. Develops platforms for cloud

computing and data management, ensuring that

Alibaba's e-commerce portals can handle its

massive traffic and transaction volumes.

Utilities & Infrastructure (Cloud services, Browser)

Offline retail

Network of ~12,000 stores with US$12 bn of

core revenues across grocery, consumer

electronics and fashion & lifestyle

Hema Supermarket, Intime Retail, Suning Vipshop

Source: Companies, Kotak Institutional Equities

We look at the growth profile of Tencent, which transformed itself from being the provider

of only a messenger service to offering multiple products in the communications, social

networking, gaming, media, fintech, cloud segments for users and enterprises (refer

Appendix 1 for more details). In the subsequent sections, we evaluate RIL’s existing offline

retail business and online B2C and B2B commerce opportunities and how we expect it to

unfold over the next few years.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Reliance Industries Oil, Gas & Consumable Fuels

We ascribe fair value of US$62 bn for RIL’s retail segment

We compute fair value of US$62 bn for retail business attributable to RIL for its 94.38%

stake, while ascribing (1) US$48 bn to existing offline retail segment at 25X EBITDA of core

retail business and 10X EBITDA on fuel and recharges based on our September 2022

estimates and (2) US$17 bn to digital commerce opportunity based on probability-weighted

scenario analysis of the industry evolution by FY2030, discounted back to September 2021.

We see further potential upside from incremental revenue-generating opportunities as RIL

capitalizes on its leadership in the retail ecosystem.

RIL’s digital commerce business comprises JioMart’s online B2C business and the kirana

digitization program. We believe the digitized kiranas will be key enablers of RR’s online

business and hence, we see limited merit in valuing the B2B distribution business separately.

We acknowledge that valuation of digital commerce businesses remains subjective for now;

that said, we remain confident that the vast under-penetration of organized retail, the huge

user base garnered by Jio, execution capabilities of RIL group and domestic-centric policies in

India can together drive significant scale-up of these new businesses in a quick time.

Valuing existing offline retail at US$48 bn

We value RR’s offline core retail business segment at US$45 bn based on 25X EV/EBITDA

multiple on September 2022 estimates, in line with our DCF-implied target multiple for

Avenue Supermarts. We include incremental value of US$3 bn for fuel and recharges

segment, valuing it at 10X EV/EBITDA multiple on September 2022 estimates.

Exhibit 3: Retail companies command higher valuation multiples given large untapped opportunity Peer valuation of retail companies in India, March fiscal year-ends, 2020-22E

2020 2021E 2022E 2020 2021E 2022E

Food and grocery retailers

Avenue Supermarts Ltd 71.4 71.9 41.7 6.1 5.5 3.9

Future Retail Ltd 8.4 5.9 5.2 0.5 0.4 0.4

Average 39.9 38.9 23.5 3.3 3.0 2.1

Apparel, footwear, jewelry retailers

Aditya Birla Fashion & Retail 9.0 11.7 7.0 1.2 1.4 1.1

Bata 44.8 34.9 22.1 8.8 7.6 4.9

Future Lifestyle Fashions Lt 4.0 4.0 3.0 0.6 0.6 0.4

Shoppers Stop Ltd 7.0 11.0 8.0 1.0 1.2 1.0

TCNS Clothing Co Ltd 13.9 18.7 9.7 2.3 2.6 1.9

Trent Ltd 40.0 55.0 33.0 6.5 7.3 5.0

Titan 36.0 53.0 30.3 4.2 5.1 3.7

Vmart Retail Ltd 16.0 25.0 15.0 2.1 2.1 1.3

Average 21.3 26.7 16.0 3.3 3.5 2.4

EV/EBITDA (X) EV/Revenue (X)

Notes: (a) KIE estimates used for Avenue Supermarts, ABFRL and TCNS Clothing.

Source: Bloomberg, Kotak Institutional Equities estimates

Valuing digital commerce business at equity valuation of US$17 bn

In our attempt to value RR’s e-commerce business, we create three plausible scenarios by

envisaging, (1) duopoly market with top-2 players commanding 80% market share, (2) an

oligopolistic market with three large players including RR commanding 80% market share

and (3) a hyper-competitive and fragmented market with several large players. We assign 40%

probability each to the first two scenarios and 20% probability to the third scenario.

Based on our FY2030 e-commerce industry GMV estimate of US$225 bn and reasonable

assumptions on market share and margins for RR in the respective scenarios, we compute

probability-weighted equity value of US$17 bn, discounted back to September 2021.

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 4: We compute US$17 bn of equity value based on probability-weighted valuation scenario for RR’s digital commerce segment Valuation scenario for digital commerce business, March fiscal year-end, 2030 (US$ bn)

Scenario A - Duopoly Scenario B - Oligopoly Scenario C - Intense competition

DescriptionTop-2 players command 80% in the e-

commerce market

Top-3 players commanding 80%

market share

All the players continue fighting for

market share

Gross Merchandise Value

(GMV, US$ bn)225 225 225

Market share of RR's e-

commerce segment (%)40 30 20

GMV of RR's e-commerce

segment (US$ bn)90 67 45

Explanation Limited discounting by top-2 players Limited discounting by top-3 playersDiscounting continues to attract new

customers and retain old ones

Operating profit / EBITDA

margin (%)8.0 7.0 (10.0)

EBITDA of RR's e-commerce

segment (US$ bn)7.2 4.7 (4.5)

EV/EBITDA valuation multiple

(X)12.0 12.0 NA

ExplanationStable cash flow generating business

will command a high valuation multiple

Unstable cash flows and hence a low

valuation multiple

Continues to burn cash; accumulated

EBITDA loss included in CAC

EV of RR's e-commerce

segment (US$ bn)86.3 56.6 —

Initial investment in customer

acquisition costs (US$ bn)18.0 20.2 22.5

Equity value of RR's e-

commerce segment (US$ bn)68.3 36.4 (22.5)

Equity value discounted to

Sep-2021 (US$ bn)31.2 16.6 (10.3)

Probability 0.4 0.4 0.2

Probability-weighted equity

value (US$ bn)17.1

Source: Kotak Institutional Equities estimates

With RR having only begun its digital commerce business (JioMart’s online grocery delivery

business and the kirana B2B distribution business), we believe value creation from this

business will happen only over the medium term (next decade or so). Our optimism for this

business segment for RR stems from various factors—(1) initial-phase development of e-

commerce market has already happened in India, (2) Jio has already brought a large

population online (nearly 400 mn subscribers); low buyer penetration implies large growth

opportunity, (3) RR’s large physical store presence and associated infrastructure provides it

with competitive advantage and (4) regulatory advantage of having the ability to store and

sell own inventory as opposed to restrictions on majority foreign-owned competitors

(Amazon and Flipkart). Overall, we think RR is best positioned amongst its peers as it has a

presence across the entire value chain of offline B2C retail, B2B retail and kirana network

which can all feed the online business.

We concede that e-commerce business model in India is marked by high competitive

intensity, which may keep customer acquisition costs elevated for some time. We also

acknowledge that RIL is presently one of the several players in the Indian e-commerce

market and ramp-up of digital commerce foray will not be without challenges. We further

see that while supply-side constraints have been addressed by retailers, demand aggregation

remains a challenge and typically results in high customer acquisition costs. It is here that

RIL’s partnership with WhatsApp may hold it in good stead. In this context, we believe a

probability-weighted model is a reasonable way to value RR’s digital commerce business.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Reliance Industries Oil, Gas & Consumable Fuels

Raise fair value to Rs2,150 factoring in the digital commerce opportunity

We raise our SoTP-based fair value of RIL to Rs2,150 from Rs1,750 earlier, ascribing higher

value to existing core retail business at 25X EV/EBITDA multiple versus 20X earlier,

incrementally factoring in Rs1.3 tn (~US$17 bn) of fair value from the digital commerce

business, which we expect the company to realize in the medium term and rolling forward

to September 2021. We have also updated our model for recent transactions related to Jio

Platform and rights issue and details from subsidiary annual reports; we have not

incorporated digital commerce business in our estimates for retail business for now.

Exhibit 5: Our SoTP valuation of Reliance is Rs2,150 per share Sum-of-the-parts valuation, September 2021E (Rs)

EBITDA EV/EBITDA EV Valuation

(Rs bn) (X) (Rs bn) (US$ bn) (Rs/share)

Energy 4,774 63 752

Petrochemicals 322 7.5 2,419 32 381

Refining and marketing 259 7.5 1,944 26 306

Upstream 46 9.0 412 5 65

Digital services 4,489 59 707

Base case 519 10.0 5,190 69 817

Telecom option value 654 9 103

Minority interest (1,355) (18) (213)

Retail 4,708 62 741

Core retail 137 25.0 3,424 45 539

Fuel and recharges 24 10.0 240 3 38

Digital commerce 1,299 17 205

Minority interest (256) (3) (40)

Total enterprise value 13,971 185 2,201

Real estate projects / others 126 2 20

Outstanding receipts from rights issue 398 5 63

Consolidated net debt 844 11 133

Fair value 13,651 181 2,150

Notes:

(a) We use 6.349 bn shares including rights issue but excluding 412.8 mn treasury shares.

Source: Kotak Institutional Equities estimates

Exhibit 6: We ascribe option value of Rs654 bn (US$9 bn) for telecom business Calculation of option value for Jio in a two-private player market structure (Rs bn)

Incremental revenues assuming Jio garners 50% share of VIL 268

Incremental EBITDA at 60% margins 161

EV/EBITDA (X) 10.0

Incremental EV 1,608

Incremental capex to support higher market share (300)

Net equity value accretion 1,308

Option value assuming 50% probability 654

Source: Kotak Institutional Equities estimates

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 7: Financial model of Reliance Retail, March fiscal year-ends, 2016-25E (Rs bn)

2016 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Profit model

Revenues (gross) 209 333 622 1,166 1,465 1,691 2,232 2,628 2,966 3,326

Core retail 189 255 362 735 928 946 1,307 1,559 1,770 2,000

Jio and fuel 22 83 330 570 702 866 1,091 1,256 1,406 1,560

EBITDA 9 12 25 62 97 93 143 179 212 249

Core retail 9 11 22 52 83 75 121 153 183 217

Jio and fuel (0) 1 4 10 14 18 22 26 29 32

EBIT 5 8 21 55 83 74 116 146 175 208

Net income 3 5 13 33 57 54 83 105 128 155

Contribution to RIL's EPS (Rs) 0 1 2 5 9 9 12 16 19 23

Balance sheet

Net-worth 55 69 92 128 184 238 321 426 554 709

Net debt 11 (3) 32 120 28 179 200 183 125 33

Invested capital 67 66 124 248 212 417 522 609 679 743

Operating metrics (%)

Revenue growth 20.0 59.3 86.7 87.4 25.6 15.4 32.0 17.7 12.8 12.2

Core retail 34.9 42.3 102.9 26.2 1.9 38.2 19.3 13.5 13.0

Jio and fuel 277.6 296.9 73.1 23.0 23.4 26.0 15.2 11.9 11.0

EBITDA margins 4.3 3.5 4.1 5.3 6.6 5.5 6.4 6.8 7.1 7.5

Core retail 4.2 6.0 7.0 8.9 7.9 9.2 9.8 10.4 10.9

Jio and fuel 1.3 1.1 1.8 2.0 2.1 2.0 2.0 2.0 2.0

EBIT margins 2.4 2.4 3.3 4.8 5.6 4.4 5.2 5.6 5.9 6.3

RoAE 5.2 8.5 16.5 30.0 36.6 25.5 29.8 28.1 26.1 24.6

RoACE 5.0 7.8 14.2 19.4 26.7 17.4 18.4 19.2 20.2 21.8

Source: Company, Kotak Institutional Equities estimates

Exhibit 8: Financial model of Reliance Jio, March fiscal year-ends, 2018-25E (Rs bn)

2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Assumptions

Wireless subscriber base at end-period (mn) 187 307 388 432 452 471 489 509

Wireless subscriber market share (%) 17 28 34 37 38 38 39 40

Wireless ARPU (Rs/month) 102 131 130 147 165 178 186 195

Broadband subscriber base at end-period (mn) 1 1 4 7 11 15 18

Broadband ARPU (Rs/month) — — 702 720 730 740 747

Overall EBITDA margins (%) 33 39 40 46 49 51 53 55

Profit model

Revenues 202 388 543 739 920 1,063 1,189 1,318

EBITDA 67 151 216 340 452 541 630 723

Net income 7 30 56 158 234 307 387 474

Contribution to RIL's EPS (Rs) 1 5 10 20 28 36 46 56

Balance sheet

Net-worth 1,029 404 1,710 1,868 2,101 2,408 2,795 3,269

Effective net debt 1,400 1,456 495 475 237 (122) (546) (1,045)

Invested capital 2,278 1,760 2,144 2,408 2,544 2,645 2,770 2,914

Cash flow

Operating cash flow (20) 50 99 261 358 433 500 565

Working capital (29) (75) (37) 16 15 12 10 11

Capital expenditure (358) (438) (518) (240) (220) (242) (168) (189)

Free cash flow (407) (464) (455) 37 153 203 342 387

Returns (%)

RoAE 0.8 4.1 5.3 8.8 11.8 13.6 14.9 15.6

RoACE 0.9 2.6 5.2 8.0 11.0 13.7 16.6 19.6

CRoCI 2.5 6.9 8.4 11.6 14.3 16.6 19.0 21.3

Adjusted CRoCI 2.5 6.9 8.8 12.0 15.1 18.7 24.5 33.2

Source: Company, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Reliance Industries Oil, Gas & Consumable Fuels

Exhibit 9: We expect consumer-facing businesses to drive robust growth in EBITDA over the next few years Consolidated segment-wise break-up of EBITDA, March fiscal year-ends, 2016-23E (Rs bn)

2016 2017 2018 2019 2020 2021E 2022E 2023E

EBITDA

Petrochemicals 137 165 243 379 309 260 320 325

Refining and marketing 268 286 306 261 245 186 249 269

Oil and gas 69 13 17 16 4 5 30 62

Organized retail 9 12 25 62 97 93 143 179

Digital services — (0) 68 153 225 355 472 566

Others (65) (13) (17) (32) (48) (6) (9) (12)

Total 417 462 642 839 831 893 1,204 1,389

Source: Company, Kotak Institutional Equities estimates

Exhibit 10: RIL's earnings are leveraged to several business drivers Sensitivity of consolidated EBITDA, EPS and SoTP to key assumptions, March fiscal year-end, 2022

Change (Rs bn) (%) (Rs bn) (%) (Rs/share) (%)

Refining margins +US$1/bbl 39 3% 4.6 5% 46 2%

Refining operating cost+US$0.5/bbl (20) -2% (2.3) -2% (23) -1%

Petchem margins +US$25/ton 39 3% 4.6 5% 46 2%

Retail EBITDA margins +50 bps 11 1% 1.3 1% 44 2%

Jio wireless ARPU +Rs10/month 40 3% 4.7 5% 63 3%

Jio wireless subscriber +25 mn 28 2% 3.3 4% 45 2%

Exchange rate Rs1/US$ 11 1% 1.3 1% 13 1%

Base case 1,204 93 2,150

EBITDA EPS SoTP valuation

Source: Kotak Institutional Equities estimates

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 11: Consolidated profit model, balance sheet and cash flow statement for RIL, March fiscal year-ends, 2016-23E (Rs bn)

2016 2017 2018 2019 2020 2021E 2022E 2023E

Profit model (Rs bn)

Net sales 2,740 3,054 3,917 5,671 5,967 5,093 6,453 6,963

EBITDA 417 462 642 839 831 893 1,204 1,389

Other income 75 94 89 81 140 196 205 224

Finance cost (37) (38) (81) (165) (220) (216) (195) (173)

DD&A expense (116) (116) (167) (209) (222) (272) (332) (387)

Pretax profits 339 401 483 546 528 601 882 1,053

Minority interest/share of associates 2 (0) 1 (1) (4) (43) (64) (83)

Extraordinary items 46 — 11 5 (2) — — —

Effective tax (89) (102) (133) (154) (128) (144) (226) (270)

Net profits 299 299 361 396 394 414 593 699

Adjusted net profits 253 299 350 391 396 414 593 699

Adjusted EPS (Rs) 43 51 59 66 67 70 93 110

Balance sheet (Rs bn)

Total equity 2,316 2,637 2,935 3,871 4,533 5,040 5,993 6,643

Deferred tax liability 205 212 245 451 512 544 592 642

Minority interest 34 29 35 83 80 1,299 1,363 1,446

Total borrowings 1,807 1,966 2,188 2,875 2,914 2,450 1,937 1,930

Other liabilities 1,629 2,224 2,709 2,696 3,590 3,428 3,456 3,327

Total liabilities and equity 5,990 7,068 8,113 9,976 11,630 12,761 13,341 13,988

Cash 110 30 43 75 309 1,119 1,324 1,708

Loans and advances 29 37 50 74 224 224 224 224

Other assets 917 1,032 1,341 1,814 2,014 2,001 2,201 2,320

Total fixed assets 4,094 5,185 5,851 5,658 6,315 6,650 6,824 6,968

Investments 840 784 829 2,355 2,768 2,768 2,768 2,768

Total assets 5,990 7,068 8,113 9,976 11,630 12,761 13,341 13,988

Effective net debt 1,663 2,237 2,349 2,335 2,487 1,023 111 (469)

Free cash flow (Rs bn)

Operating cash flow, excl. working capital 211 212 353 475 504 556 829 995

Working capital 78 155 185 (251) 192 42 21 (58)

Capital expenditure (469) (781) (740) (936) (765) (788) (697) (719)

Other income 37 15 23 16 22 196 205 224

Free cash flow (143) (400) (178) (697) (47) 5 358 441

Ratios (%)

Debt/equity 78.0 74.6 74.5 74.3 64.3 48.6 32.3 29.1

Net debt/equity 71.8 84.8 80.0 60.3 54.9 20.3 1.9 (7.1)

RoAE 11.2 12.1 12.6 11.5 9.4 8.6 10.7 11.1

RoACE 6.8 6.9 7.7 7.8 7.2 7.0 8.1 8.7

Adjusted RoACE 12.3 13.3 12.3 11.8 9.9 8.3 10.7 11.9

CRoCI 6.6 6.2 7.4 7.5 7.3 7.9 9.6 10.5

Adjusted CRoCI 11.8 12.2 10.2 12.4 10.3 11.3 14.2 15.9

Source: Company, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Reliance Industries Oil, Gas & Consumable Fuels

SETTING THE STAGE TO COMMAND LEADERSHIP IN THE COMMERCE BUSINESS

RIL’s accelerated expansion in the offline retail business over the past few years followed by its recent foray

into digital commerce via JioMart sets the stage for it to command leadership in the entire retail value chain.

The strategic commercial partnership with Facebook/WhatsApp can enable it to reach out to customers with

user-friendly interfaces to enable online shopping, payments and cross-sell other digital services, while

domestic-centric policies may allow it to overcome the head-start achieved by other e-commerce players.

Long runway of growth for organized retailers in India

India’s retail market is highly unorganized and while penetration of organized retail has been

on the rise, several categories such as food and grocery and apparel offer a long runway of

growth to organized retailers.

Exhibit 12: Food and grocery is the largest category but the least penetrated by organized retail Snapshot of India’s retail market, March fiscal year-ends, 2017-25E (US$ bn)

2020-25E CAGR

2017 2020E 2025E (%)

Nominal GDP 2,464 3,555 6,265 12

Private consumption 1,454 2,062 3,634 12

Private consumption as proportion of GDP (%) 59 58 58

Merchandise retail 710 990 1,708 12

Merchandise retail as proportion of private consumption (%) 49 48 47 (0)

Organized retail 67 119 256 17

Organized retail as proportion of retail (%) 9 12 15 5

Category-wise size of retail

Food and grocery 474 659 1,126 11

Apparel and accessories 56 79 139 12

Jewelry and watches 55 77 136 12

Consumer electronics 42 59 104 12

Home and living 31 44 77 12

Others 23 32 57 12

Pharmacy and wellness 21 30 52 12

Foot apparel 8 10 18 12

Total 710 990 1,708 12

Category-wise contribution to overall retail (%)

Food and grocery 67 67 66

Apparel and accessories 8 8 8

Jewelry and watches 8 8 8

Consumer electronics 6 6 6

Home and living 4 4 4

Others 3 3 3

Pharmacy and wellness 3 3 3

Foot apparel 1 1 1

Total 100 100 100

Penetration of organized retail (%)

Food and grocery 3 4

Apparel and accessories 24 36

Jewelry and watches 28 35

Consumer electronics 27 34

Home and living 11 13

Others 13 15

Pharmacy and wellness 11 20

Foot apparel 27 34

Source: Technopak, Kotak Institutional Equities estimates

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

RIL has established leadership in India’s offline retail business

Reliance Retail (RR) has gradually metamorphosed from a network of standalone stores into

a behemoth achieving core retail revenues of US$13 bn in FY2020 underpinned by an

offline presence of ~11,800 outlets across 7,000+ cities and towns. It has steadily cemented

its leadership presence in India’s organized retail space by increasing its touch-points at a

pace of 48% over FY2017-20 and adding retail trading area at a CAGR of 28%, which led

to revenues growing at a robust CAGR of 54% in the given period. In India’s largely

fragmented as well as unorganized merchandise retail landscape, RR now commands a

market-share of ~1.4% (excluding recharges and fuel retail), and is the largest retailer in

terms of presence as well as revenues.

Exhibit 13: Multi-category retailer with presence across key consumption baskets RR’s various retail categories with revenue and proportion contribution, March fiscal year-end, 2020

Source: Company, Kotak Institutional Equities

Exhibit 14: RR is a leader in India’s fragmented retail market RR’s estimated market-share in key retail categories, March fiscal year-end, 2020

Reliance Retail Overall India market RR's market-share

(US$ bn) (US$ bn) (%)

Grocery retail 5 659 0.7

Fashion and lifestyle retail 2 166 1.1

Electronics retail 6 59 10.1

Total 12 884 1.4

Source: Company, Kotak Institutional Equities estimates

F&G

F&L

CE

JR

PR

Reliance Retail

Consumer electronics

(US$6 bn, 27%)

Fashion and lifestyle

(US$2 bn, 8%)

Connectivity

(US$7 bn, 34%)

Food and grocery

(US$5 bn, 21%)

Petroleum retail

(US$2 bn, 9%)

Reliance TrendsReliance Fresh

Reliance JewelsReliance Smart

Trends FootwearSmart Point

Project EveReliance Market

AJIO.comJioMart

Reliance Digital

Jio Point

RESQ

Brand Partnerships

Digital commerce portal

Offline store format

Business segmentRelianceDigital

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Reliance Industries Oil, Gas & Consumable Fuels

Exhibit 15: Formidable presence across the country Segment-wise presence across the country

Source: Company, Kotak Institutional Equities

Online retail market in India expected to increase to US$225 bn by FY2030

We believe Indian online retail market GMV could treble from US$30 bn (in FY2020) to

reach US$100 bn by FY2025 and increase further to US$225 bn by FY2030, providing a fair

amount of growth runway for RR. This growth in online retail will be driven by rising internet

penetration, improving buyer penetration and higher online spends per shopper as online

merchandise assortment improves and the propensity to shop online (for reasons such as

ease of purchase, return, payment) continues to improve.

Exhibit 16: We expect India to be a US$2.9 tn merchandise retail market by FY2030 Consumption and retail metrics of India, March fiscal year-ends, 2017-30E

2017 2020 2025E 2030E 2020-25E 2025-30E

Nominal GDP 2,464 3,555 6,265 10,557 12 11

Private consumption 1,454 2,062 3,634 6,123 12 11

Private consumption as proportion of GDP (%) 59 58 58 58

Merchandise retail 710 990 1,708 2,878 12 11

Merchandise retail as proportion of private consumption (%) 49 48 47 47

Organized retail 67 119 256 547 17 16

Organized retail as proportion of retail (%) 9 12 15 19

CAGR (%)

Source: Technopak, Kotak Institutional Equities estimates

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 17: Number of online shoppers significantly lag internet users and can rise substantially Categorization of the Indian online user by use case, December calendar year-end, 2020E

Source: Flipkart, Bain & Company, Kotak Institutional Equities

Exhibit 18: Improving buyer penetration and spends will drive e-commerce market size to US$225 bn by FY2030 Estimated size of e-commerce market, March fiscal year-ends, 2015-30E

2020-25 CAGR 2025-30 CAGR

2015 2016 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025E 2030E (%) (%)

Population (mn) 1,257 1,269 1,281 1,293 1,305 1,318 1,330 1,343 1,354 1,367 1,380 1,422 0.9 0.6

Internet penetration (%) 24 27 33 38 49 55 60 64 67 70 73 78

Internet population (mn) 302 343 422 494 637 725 798 859 907 957 1,007 1,109 6.8 1.9

Number of online shoppers (mn) 30 40 50 69 96 120 144 168 196 226 258 372 16.5 7.6

Buyer penetration (%) 10 12 12 14 15 17 18 20 22 24 26 34

Online money spent (Rs) 8,015 11,307 12,437 14,303 16,448 18,093 19,903 21,893 24,082 26,490 29,139 45,247 10.0 9.2

Yoy increase in online spend (%) 148 41 10 15 15 10 10 10 10 10 10 9

Total e-commerce market size (Rs bn) 240 452 623 980 1,579 2,173 2,870 3,683 4,713 5,975 7,506 16,846 28 18

Total e-commerce market size (US$ bn) 4 7 9 15 23 31 38 49 63 80 100 225 26.7 17.5

Yoy growth (%) 76 34 64 49 36 25 28 28 27 26

Source: IAMAI, Census 2011, TRAI, Kotak Institutional Equities estimates

The Indian online retail landscape is dominated by online marketplaces such as Flipkart and

Amazon India – both majority foreign-held and hence cannot carry out B2C retail operations.

We believe this will be a key differentiator between RR’s model and the others – being an

Indian entity, RR will have the flexibility to sell its own inventory, private labels and the like,

unlike most extant players who can only be aggregators.

RIL is getting ready to tap O2O and B2B opportunities

Alongside Facebook’s strategic investment in Jio Platforms, Reliance Retail and WhatsApp

have entered into a commercial partnership agreement to further accelerate Reliance Retail’s

digital commerce business through its JioMart platform and to support digital

transformation of small and medium-sized businesses using integration with WhatsApp.

We believe RR’s arrangement with WhatsApp can enable access to a huge untapped

opportunity to play for a bigger share of the pie in India’s huge retail market, ~98% of

which is still offline. This can give RR a higher pool of ‘transacting users’ as opposed to only

‘online users’ enabling superior user monetization in the future.

We reckon RR may look at multiple monetization streams—(1) O2O offering to end-

customers serviced by a combination of local kirana networks and RR’s own offline presence,

(2) commission-based revenues by transforming India’s retail distribution network by

aggregating distribution requirements of large clusters of kirana stores and (3) transactional

revenues by enabling transactions on ‘JioPay’.

625

360

303

180

105

- 100 200 300 400 500 600 700

Internet users

Chatting and social media

Video content

Service transactions

Product transactors

Number of users (mn)

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Reliance Industries Oil, Gas & Consumable Fuels

Apart from the offline business, RIL is attempting new models to further boost its presence

in India’s fast growing organized retail space: it is partnering with small kirana stores by

digitizing them through JioPoS offering and attempting to increase its distribution reach,

and has also launched its online grocery portal, JioMart, which already has a presence in

~200 cities.

JioMart provides an interesting play by straddling both offline retail (the large but

unorganized network of kirana stores that it seeks to integrate, as well as RIL’s offline stores)

and online retail (WhatsApp enabled e-commerce which could potentially interlink with

other plays such as AJIO).

In the following sections we focus separately on Reliance Retail’s offline and online

operations, value proposition to the end-customers, new business initiatives and a

framework to value the business in the medium term.

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

FAST GROWING MULTI-CATEGORY RETAILER WITH A FORMIDABLE FOOTPRINT

RR has posted strong 54% CAGR in revenues of its core retail operations over FY2017-20. This has been driven

by a healthy pace of store additions (48% CAGR) as well as strong SSSG. We believe RR will continue to invest

in its offline network to maintain its dominance as well as to complement its online offering. Leveraging its

relationship with Jio’s other apps as well as WhatsApp, RR can transform into a multi-channel retail

behemoth with a large O2O play.

RR’s existing offline business comprises two broad categories: core retail (comprising food

and grocery, fashion & lifestyle and consumer electronics businesses) and others (comprising

revenues from Jio recharges and fuel retail).

Existing retail revenues to more than double in four years

We model existing offline retail revenues to more than double in FY2020-24 growing by a

robust 19% CAGR over the next four years, assuming similar growth trajectory for core

retail and Jio and fuel segments. We expect margins of core retail business to expand by

~150 bps to 10.4% in FY2024 and that of other segments to remain stable around 2%,

which will cumulatively enhance overall margins to 7.1% in FY2024 from 6.6% in FY2020.

We have assumed weaker numbers for FY2021 factoring in anticipated impact on consumer

discretionary spends amid ongoing lockdowns and bleak economic outlook.

Exhibit 19: We expect offline retail business revenues to double in four years Financial model of Reliance Retail, March fiscal year-ends, 2016-25E (Rs bn)

2016 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Profit model

Revenues (gross) 209 333 622 1,166 1,465 1,691 2,232 2,628 2,966 3,326

Core retail 189 255 362 735 928 946 1,307 1,559 1,770 2,000

Jio and fuel 22 83 330 570 702 866 1,091 1,256 1,406 1,560

EBITDA 9 12 25 62 97 93 143 179 212 249

Core retail 9 11 22 52 83 75 121 153 183 217

Jio and fuel (0) 1 4 10 14 18 22 26 29 32

EBIT 5 8 21 55 83 74 116 146 175 208

Net income 3 5 13 33 57 54 83 105 128 155

Contribution to RIL's EPS (Rs) 0 1 2 5 9 9 12 16 19 23

Balance sheet

Net-worth 55 69 92 128 184 238 321 426 554 709

Net debt 11 (3) 32 120 28 179 200 183 125 33

Invested capital 67 66 124 248 212 417 522 609 679 743

Operating metrics (%)

Revenue growth 20.0 59.3 86.7 87.4 25.6 15.4 32.0 17.7 12.8 12.2

Core retail 34.9 42.3 102.9 26.2 1.9 38.2 19.3 13.5 13.0

Jio and fuel 277.6 296.9 73.1 23.0 23.4 26.0 15.2 11.9 11.0

EBITDA margins 4.3 3.5 4.1 5.3 6.6 5.5 6.4 6.8 7.1 7.5

Core retail 4.2 6.0 7.0 8.9 7.9 9.2 9.8 10.4 10.9

Jio and fuel 1.3 1.1 1.8 2.0 2.1 2.0 2.0 2.0 2.0

EBIT margins 2.4 2.4 3.3 4.8 5.6 4.4 5.2 5.6 5.9 6.3

RoAE 5.2 8.5 16.5 30.0 36.6 25.5 29.8 28.1 26.1 24.6

RoACE 5.0 7.8 14.2 19.4 26.7 17.4 18.4 19.2 20.2 21.8

Source: Company, Kotak Institutional Equities estimates

Robust growth in offline retail driven by store additions and rising throughput

RR’s core retail revenues (excluding fuel and telecom) have increased at an impressive ~54%

CAGR over FY2017-20. Reported profitability (EBITDA) from the same has also increased at a

CAGR of 74% over the same period. RR is present across key verticals such as food and

grocery, general merchandise, apparel and footwear, jewelry, electronics and toys. Besides,

RR also operates several stores in partnership with several international brands.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

Reliance Industries Oil, Gas & Consumable Fuels

Exhibit 20: RR's healthy revenue growth has been driven by increase in store count and throughput Details of RR's category-wise store count and revenues, March fiscal year-ends, 2017-20

2017-20 CAGR

2017 2018 2019 2020 (%)

Store count (#)

Grocery 447 537 605 797 21

Consumer electronics 266 287 357 400 15

Jio Points 1,645 5,381 7,684 8,201 71

Fashion and lifestyle 1,258 1,368 1,769 2,386 24

Total 3,616 7,573 10,415 11,784 48

Total excluding Jio points 1,971 2,192 2,731 3,583 22

Segment-wise revenues (Rs bn)

Grocery 108 140 234 346 47

Consumer electronics 95 152 392 446 67

Fashion and lifestyle 51 71 110 136 39

Total core revenues 254 363 735 928 54

Break-up of core retail revenues (%)

Grocery 43 39 32 37

Consumer electronics 38 42 53 48

Fashion and lifestyle 20 20 15 15

Source: Company, Kotak Institutional Equities

Store addition data reveals that RR has been most aggressive in adding stores in the fashion

and lifestyle formats. RR has consciously developed multiple formats to serve a diverse set of

customers.

Exhibit 21: RR operates multiple formats under its key segments of grocery, apparel and electronics Snapshot of RR’s various store formats

Grocery

Reliance Fresh Neighbourhood store offering fresh produce, grocery and other daily need items

Reliance Smart Supermarket store dealing in fresh foods, staples, home & personal care items, apparel and general merchandise

Reliance Market Cash and carry chain serving B2B customers

Smart PointSmaller version of Reliance Smart serving everyday needs of customers in the grocery and pharmacy categories.

Also offers assisted e-commerce.

Apparel

Trends Flagship chain catering to value focused customer. Large variety of own brands.

Reliance Footprint Offers wide range of products across footwear, luggage, handbags & accessories

Reliance Jewels Retailer of fine and precious jewelry

Project Eve Experiential store catering to women's apparel needs

AjioOnline portal offering curated fashion from over 500 national and international brands. Also retails its own

private label.

Consumer electronics

Reliance Digital Big box electronics retailer stocking 200+ national and international brands

Jio store Smaller stores focused on offering mobility & communication devices and bouquet of Jio services

Reliance Resq Dedicated service arm offering end-to-end product lifecycle support

Source: Company, Kotak Institutional Equities

RR’s core retail revenues also include sales of Jio-related devices such as JioPhone on which

the company possibly earns a small margin. Sale of these devices has driven a large increase

in revenues from electronics retail from FY2019 onwards.

RR has not consistently shared format-wise margins; however recent margin disclosures

reveal that RR’s margins compare favorably with its better performing peers such as Avenue

Supermarts in grocery, Trent in apparel retail and Croma in electronics retail.

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 22: Margin expansion across formats has driven a strong increase in EBITDA Segment-wise margin profile of Reliance Retail, March fiscal year-ends, 2017-20

2017-20 CAGR

2017 2018 2019 2020 (%)

Segment-wise revenues (Rs bn)

Grocery 108 140 234 346 47

Consumer electronics 95 152 392 446 67

Fashion and lifestyle 51 71 110 136 39

Total core revenues 254 363 735 928 54

Segment-wise EBITDA (Rs bn)

Grocery 11 23

Consumer electronics 19 28

Fashion and lifestyle 22 32

Total EBITDA 11 22 52 83 98

Segment-wise EBITDA margins (%)

Grocery 4.9 6.5

Consumer electronics 4.7 6.2

Fashion and lifestyle 19.9 23.9

Overall 4.2 6.0 7.0 8.9

Source: Company, Kotak Institutional Equities

While certain metrics such as format-wise retail trading area are not available, we try and

benchmark RR’s various formats with relevant peers.

Food and grocery – large growth runway

RIL’s food and grocery business comprise of its Reliance Market, Reliance Smart, and

Reliance Fresh formats. RR had 765 stores altogether under these formats as of March 2020.

Reliance Smart is the large hypermarket format retailing food and grocery, FMCG products

and general merchandise. Reliance Fresh is the smaller fresh food and grocery format.

Margins for different grocers vary on account of store ownership: Dmart, for instance, owns

its stores and hence pays very little rent. RR predominantly operates on a rental model and

hence margins are comparable more with peers such as Future Retail, Star Bazaar (Trent

Hypermarket) and Spencer’s.

The comparison below shows that RIL’s grocery retail business is notching decent margins,

despite the segment being intensely competitive. Management has attributed the margin

expansion in FY2020 to improved SSSG as well as positive impact from Ind-AS 116 adoption.

Exhibit 23: RR is one of the few profitable food and grocery retailers in India Operating metrics of Indian food and grocery retailers, March fiscal year-ends, 2019-20 (Rs mn)

2019 2020 2018 2019 2019 2020 2019 2020 2018 2019

No. of stores (#) 176 214 285 292 605 765 156 160 35 39

Revenues (Rs mn) 200,045 248,702 184,793 201,649 233,713 346,010 21,872 23,733 9,396 10,005

EBITDA (Rs mn) 16,333 21,283 8,371 10,369 11,370 22,530 139 793 (1,035) (802)

EBITDA margin (%) 8% 9% 5% 5% 5% 7% 1% 3% -11% -8%

Trent

Hypermarket Spencer's RetailAvenue Supermarts Future Retail Reliance Retail

Source: Companies, Kotak Institutional Equities

We believe RIL’s offline food and grocery retail network will play a critical role in enabling

the company’s recent online offering JioMart.

Apparel – Reliance Trends rapidly gaining scale

Reliance Trends is RR’s flagship apparel retail format, with 1,400+ stores currently. Besides

Trends, RR has various other retail formats to cater to a wide set of customers.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Reliance Industries Oil, Gas & Consumable Fuels

Exhibit 24: RR has apparel formats spanning all customer segments Various apparel retail formats of RR

Apparel segment Reliance format

Luxury International partner brands, Ajio Gold

Mid-segment Ajio, M&S, Project Eve, Reliance Jewels

Value fashion Trends, Trends Woman, Trends Man, Trends Footwear, Payless, Vision Express

Value Reliance Market, SMART

Source: Company, Kotak Institutional Equities

Indian retailers have been adding the maximum number of stores in the urban mass market

family format stores such as Pantaloons (ABFRL) and Westside/Zudio (Trent). These stores

have registered impressive SSSG in FY2019-20 boosted by improved merchandising, sharper

price-quality proposition as well as focus on private label (60% for Pantaloons and 90% for

Westside). From a store count perspective, Reliance Trends is the largest and fastest growing

chain in the value fashion category.

Exhibit 25: Reliance Trends is one of the fastest growing affordable fashion retail chain Net store additions of Indian apparel retailers, March fiscal year-ends, 2015-20

2015 2016 2017 2018 2019 2020

Store count

ABFRL-Lifestyle brands 1,735 1,877 1,761 1,813 1,980 2,253

ABFRL-Pantaloons 134 163 209 275 308 342

FBB 46 51 54 61 94 95

FLFL 358 369 372 332 339 354

Reliance Trends 271 344 458 670 1,400

Trent-Westside 85 93 111 125 150 173

Vmart 108 123 141 171 214 266

Net store additions

ABFRL-Lifestyle brands 194 142 (116) 52 167 273

ABFRL-Pantaloons 27 29 46 66 33 34

FBB — 5 3 7 33 1

FLFL 31 11 3 (40) 7 15

Reliance Trends — — 73 114 212 730

Trent-Westside 5 8 18 14 25 23

Vmart 19 15 18 30 43 52 Notes: (a) FY2020 results of FLFL and Future Retail are yet to be published and hence store count is as of 9MFY20.

Source: Companies, Kotak Institutional Equities

RR has surprised us with consistently high margin metrics for its fashion and lifestyle

segment (which includes apparel, luxury brands, jewelry businesses). A comparison with

peers also indicates that RR’s segment margins are significantly superior to its peers. This

may be a function of better store economics of Reliance Trends particularly in Tier II/III cities

and higher throughput. The jump in FY2020 EBITDA margin was in part due to Ind-AS 116

implementation.

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 26: RR has reported robust operating metrics for its Fashion and Lifestyle segment Operating metrics of Indian apparel and jewelry retailers, March fiscal year-ends, 2019-20 (Rs mn)

2018 2019 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020

No. of stores (#) 372 332 308 342 1,769 2,400 264 293 287 327 150 170

Revenues (Rs mn) 42,192 53,774 31,940 35,135 109,675 135,520 34,813 33,810 160,296 167,382 25,317 31,777

EBITDA (Rs mn) 3,885 4,632 2,310 2,220 21,830 32,420 2,533 5,494 21,472 24,177 2,365 5,632

EBITDA margin (%) 9% 9% 7% 6% 20% 24% 7% 16% 13% 14% 9% 18%

Tanishq (Titan)Pantaloons (ABFRL) Westside (Trent)

Reliance Retail

(Fashion and Lifestyle) Shoppers' Stop

Future Lifestyle and

Fashion

Notes: (a) Financials for FY2019 are pre IndAS-116 and are not comparable with FY2020; Pantaloons EBITDA for FY2019 and FY2020 is pre IndAS-116.

Source: Companies, Kotak Institutional Equities s

Other formats in the lifestyle segment include Reliance Gems and Reliance Footwear. RR also

has partnership with brands such as M&S, Mothercare, and luxury brands such as Armani,

Michael Kors and Steve Madden.

E-commerce players ramping up their offline investments; RR in driver’s seat

Large global e-commerce companies may have emerged first as online-only platforms,

however, they have also been investing into offline assets, highlighting the importance of

having presence across channels. RIL, with its large offline network has a first-mover

advantage and can capitalize on this network as it seeks to expand its online offering.

E-commerce players such as Amazon and Flipkart are working on their offline retail

strategies in India. Globally, similar strategies are being followed by Amazon and Alibaba to

fine-tune their O2O (online-to-offline) strategy.

Amazon India – picking up stakes in Indian retailers

Amazon India has picked up stakes in three offline retailers, Future Group, More Retail

and Shoppers Stop. We believe Amazon has done this with a view to improve its offline

supply chain and to get exclusive access to products of these chains to offer online. Further,

Amazon also wants to utilize the offline footprint of these stores to push its own private

labels: AmazonBasics — products include ACs, HDMI cables, batteries and cables, home

necessities, and general merchandise and apparel labels—Prowl and Just F. Amazon may use

these stores to retail its grocery brands as well.

Apart from this, recently launched ‘Local Shops on Amazon’ initiative is to enable offline

stores to do more business through their platform. It has already signed up over 5,000

offline shops, including large retailers such as Tata’s Croma, as sellers on its platform. Offline

stores will be allowed to ship orders themselves, ship it through third-party logistics or even

through Amazon’s fulfillment channel.

Smart Stores launched by Amazon Pay allows customers to scan QR codes to explore

products within offline stores and pay for them using various payment instruments. It will

provide own credit facility under the ‘buy now, pay later’ scheme. Smart Stores will also

expose product listings on the app, allowing customers to see their details and reviews.

Flipkart: partnering with local stores to ramp up its grocery sales

Flipkart has partnered with 37,000 kirana stores to leverage their network and help them

turn around as convenience stores. Flipkart has also recently partnered with retail chains like

Spencer’s and Vishal Mega Mart to enable hyperlocal deliveries of groceries and essentials

in various cities.

It has partnered with Authentic Brands to license and distribute fashion brand Nautica in

India. As a part of the agreement, Flipkart will manage Nautica’s online and offline

businesses in the country through a network of franchisees. Nautica currently has more than

40 retail stores in India.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Reliance Industries Oil, Gas & Consumable Fuels

Alibaba: rapidly developing its offline network in China

Alibaba has a majority stake in brick-and-mortar retailer Intime. It has also invested in

Hema, a 150-unit grocery chain in 21 Chinese cities. Hema seamlessly integrates physical

store conveniences with digital tools, Hema has been called ‘the most futuristic retailer’ in

the world. Hema offers free 30-minute deliveries of fresh produces within a radius of 3

kilometers from stores. Hema is the only Chinese supermarket chain operating both online

and offline channels; it virtually dominates Chinese online grocery scene. Its business has

been gaining steam during the Covid-19 crisis, with its sales more than tripling.

Alibaba Group also has acquired 36% of Sun Art Retail Group, which operate nearly 400

hypermarkets under the Auchan and RT-Mart banners. Per the agreement, Alibaba would

share its Digital commerce technology and insights of consumer trends with RT Mart to

expedite its digitization, sync its online and offline operations, improve its in-store layout and

increase efficiencies in the grocer’s inventory management.

As part the digital makeover, RT-Mart gains access to Alibaba’s customer insights, supply-

chain management, retail technologies and electronic payments via Alipay.

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

ASPIRATIONS TO TAP INDIA’S E-COMMERCE OPPORTUNITY

Reliance Retail is all set to tap India’s burgeoning e-commerce opportunity by leveraging its widespread

offline presence across consumption categories and benefiting from domestic-centric policies, which may

allow it to overcome the headstart by other e-commerce players. The company’s approach to target the

lowest common-denominator for consumer, food and grocery, through its JioMart platform, and its recent

strategic tie-up with WhatsApp, may allow it to expand the universe of online transactors in India. This

coupled with enhancement and expansion of existing online offerings such as AJIO and RelianceDigital may

propel it to the pole position in e-commerce business as well in the medium term.

From grocery to other categories: RIL can amass US$12 bn GMV by FY2025

RIL already has the online apparel property AJIO, which has evolved into a fashion

marketplace retailing Reliance Trend’s private label, RR’s partner luxury brands as well as

third-party brands. With RIL already targeting apparel and grocery, the two large

components of retail (76% of overall retail in FY2020), we believe it can steadily foray into

other categories such as jewelry, home and living, consumer electronics and others. It

already has offline formats offering this merchandise and hence it would be only a matter of

time before it readies its comprehensive online merchandise offering.

A steady foray into digital commerce backed by its own merchandise, partnership with a

variety of brands, pan-India network and widespread customer reach via WhatsApp and

other popular apps, and regulations favoring Indian companies can drive RIL to steadily ramp

up its share in the Indian digital commerce market. We believe it can achieve digital

commerce GMV of US$12 bn by FY2025, implying a 12% share in the e-commerce market.

Exhibit 27: RIL can achieve digital commerce GMV of US$12 bn by FY2025 RIL's estimated online GMV, March fiscal year-ends, 2020-25E (US$ bn)

2020 2021E 2022E 2023E 2024E 2025E

Estimated e-commerce market size (US$ bn) 31 38 49 63 80 100

Incremental annual GMV (US$ bn) 8 11 14 17 20

Base case

RIL's share in incremental GMV (%) 2 8 15 22 28

RIL's cumulative GMV (US$ bn) 0 1 3 7 12

Source: Kotak Institutional Equities estimates

Grocery to be JioMart’s biggest bet; to steadily ramp-up other segments

We believe online commerce provides RIL the opportunity to monetize its Jio customer

better, especially since it already has a large offline presence and a variety of merchandise is

being sold via Reliance Retail’s store network. RR already has e-commerce websites called

AJIO.com for sale of apparel and RelianceDigital.in for sale of electronics products.

The recent large-scale launch of JioMart gives it footprint in grocery as well. Grocery is

particularly attractive as it is currently highly unorganized and RR has the opportunity to

seize a sizeable first-mover advantage. Note that other e-commerce players such as Amazon

and Flipkart have been relatively late entrants to this category and we believe their

operations in the food and grocery category are not very sizeable yet.

RR has been tactical in focusing on the food and grocery segment via JioMart, instead of

traditional large e-commerce categories. We believe this may be deliberate as: (1) large initial

focus on electronics has led to a plateauing of user base of other competitors such as

Amazon and Flipkart and is now forcing them to look towards grocery, and (2) unlike

Amazon and Flipkart, JioMart’s access to 380 mn+ telecom subscribers and its tie-up with

WhatsApp can allow it to sell grocery to a much larger customer base.

As highlighted above, food and grocery is the largest retail category in India, and also the

highest frequency purchase item. It is also highly fragmented and unorganized, and thus

presents an opportunity for large retailers to garner a share in the business. Further, as

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Reliance Industries Oil, Gas & Consumable Fuels

incomes increase, spends in this category can continue to increase at least the rate of

growth of real GDP. We believe it is this market size and customer reach that RIL intends to

tap into.

RR may benefit from regulations favoring domestic retailers

Unlike its other foreign owned peers, RIL does not have to contend with restrictions of multi-

brand retail in its B2C business. Regulations have tended to become stricter for foreign-

owned e-commerce players, as local sellers have protested against large, company-owned

sellers being active on marketplaces, effectively accusing marketplaces of buying and selling

products.

A case in point is that of Flipkart, which was recently denied permission by the DPIIT

(Department for Promotion of Industry and Internal Trade) to undertake a food retail

business in India citing violation of marketplace model. Per DPIIT, a foreign-owned

marketplace cannot be a seller on its own platform. However, rival Amazon already operates

in the space through subsidiary Amazon Retail India (ARIPL); this may also be reviewed by

DPIIT.

In April 2020, the government tweaked FDI policy, banning fresh investments from China

through the automatic route. Chinese e-commerce companies such as Alibaba are large

investors in Indian startups like BigBasket. The change in policy makes it mandatory for all

Chinese investors to seek government approval before investing in Indian firms, which may

affect further funding rounds in startups by Chinese investors.

Exhibit 28: Government has restricted foreign investment in inventory led e-commerce and multi-brand retail Details of permitted foreign investment in Indian retail

Foreign

investment cap

(%) Government approval Comments

Sale of products (other than food)

manufactured in India by the manufacturer100 Automatic Retail sale via e-commerce is allowed.

Sale of food products manufactured in

India100 Government approval Retail sale via e-commerce is allowed.

Cash and carry/wholesale trading

including B2B e-commerce100 Automatic

Wholesale/cash and carry trader can also undertake single brand retail trading.

Such traders will be mandated to maintain separate books of accounts for

these two arms of the business and duly audited by the statutory auditors.

Government regulations have to be separately complied with by the respective

business arms.

B2B e-commerce 100 Automatic

Such companies would engage only in B2B e-commerce and not in retail trading,

thus implying that existing restrictions on FDI in domestic trading would be

applicable to ecommerce as well.

Market place model of e-commerce 100 Automatic

Marketplace model of e-commerce means providing of an IT platform by an e-

commerce entity on a digital & electronic network to act as a facilitator between

buyer and seller.

An e-commerce entity will not permit more than 25% of the sales value

generated on its marketplace from one vendor or their group companies.

Inventory model of e-commerce Not allowed Foreign investment is not permitted in inventory-based model of e-commerce.

Single brand product retail trading 100

Automatic up to 49%;

government approval

beyond this

For foreign investment beyond 51%, sourcing of 30% of the value of goods

purchased be done from India preferably from MSMEs, in all sectors. The

quantum of domestic sourcing will be self-certified by the company, to be

subsequently checked by statutory auditors. The procurement requirement is to

be met in the first instance as an average five years total value of goods

purchased beginning April 1 of the year of the commencement of the business.

Thereafter it shall be met on an annual basis.

Multi brand retail trading 51 Government approval Minimum amount to be brought in as foreign investment is US$100 mn.

At least 50% of the total foreign investment brought in the first tranche of

US$100 mn shall be invested in 'back-end infrastructure' within three years.

Source: DPIIT, Kotak Institutional Equities

The presence of a large offline network will give RR an edge that its other competitors such

as BigBasket and Grofers do not have. RR can benefit from an established supply chain

(sourcing, warehousing, store inventory), something which its competitors will take a while

to establish when entering into new cities.

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Oil, Gas & Consumable Fuels Reliance Industries

Exhibit 29: BigBasket and Grofers command a small share of the grocery market Standalone financials of BigBasket and Grofers, March fiscal year-ends, 2015-19 (Rs mn)

2014 2015 2016 2017 2018 2019

Revenues

BigBasket 751 1,837 5,275 10,905 15,832 27,526

Grofers — — 80 132 298 701

EBITDA

BigBasket (23) (77) (941) (1,778) (3,070) (5,580)

Grofers — — (2,279) (2,809) (2,661) (4,484)

PBT

BigBasket (23) (76) (1,034) (1,918) (3,103) (5,627)

Grofers — — (2,251) (2,683) (2,583) (4,480)

Notes: (a) Grofers reports gross commission as revenue as it does not own inventory. Its revenue figures are thus notcomparable with those of BigBasket.

Source: Tofler, MCA, Kotak Institutional Equities

Industry discussions reveal that the two specialist grocery delivery companies clocked

~US$1.5-2 bn of GMV in FY2020, implying a minuscule 0.2-0.3% share of online grocery in

the overall food and grocery pie. This is also much lower than higher shares that e-

commerce has managed to achieve in certain other categories such as electronics and

apparel. We believe grocery has been a much tougher nut to crack for most companies

given: (1) inherently low margins in the business, (2) low ATV (average transaction value)

compared to categories such as apparel and electronics, (3) demand for quick turnaround

times and deliveries, (4) high number of SKUs demanded per order, and (5) high competition

from offline channel.

JioMart: B2C model may undergo several iterations

JioMart has commenced its online grocery delivery business on a pan-India basis by

connecting local kirana shops to customers. JioMart’s model involves forming a local

network of kirana stores so as to have their entire inventory online, allocating incoming

orders to stores based on product availability and proximity, and facilitating delivery to the

customer by its own network. The grocery shop shares a certain margin with JioMart for

every order originated by JioMart. Per RIL, JioMart intends to act as a centralized

procurement and delivery platform between manufacturers and merchant partners. JioMart

will enable digitization of merchants through Jio PoS at the backend and JioMart app at the

front-end.

The local store aggregation model has not met with much success in the past as local stores

may not carry very large assortment of products resulting in a mismatch between product

shown on JioMart’s website and actual product delivered to the customer. Control of

customer experience will thus be key for JioMart to succeed in the business. We believe

these can be addressed by: (1) control of the back-end of these stores by JioMart, (2) very

localized inventory view offered by JioMart on its website, and (3) efficient delivery logistics

(either by store or JioMart).

RIL’s opportunity size in this business extends to Indian food and grocery retail market,

estimated at US$660 bn for FY2020. Grocery is a low margin category and hence revenue

opportunity will be smaller at 7-10% of GMV opportunity at US$46-66 bn.

JioMart’s kirana digitization strategy to supplement digital commerce

We believe RR’s JioMart seeks to not only become a meaningful grocery retailer by providing

customers the convenience of shopping online, it also seeks a slice of the large B2B market,

which hitherto has been driven by traditional distributors. While the proportion of modern

trade has been on the rise, we believe RIL would want to integrate its Reliance Market

offering with its network of kirana stores, thereby disintermediating the existing value chain

(company – distributor – wholesaler – stockist – retailer). We believe this business can be an

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Reliance Industries Oil, Gas & Consumable Fuels

important feeder to the digital commerce business and can significantly aid supply

aggregation in a fragmented market.

RR’s intent to launch its distribution service on a large scale can help it amass sizeable

revenues. RR will need to establish a virtuous cycle by offering consistently low-priced

products to shops, the widest variety while at the same time negotiating for best prices with

FMCG companies and other large producers. As discussed above, RR has several private

labels in its grocery retail business. It can push these private labels on a large scale through

this channel and ultimately to customers ordering products online. This business is currently

in a trial phase and we expect it to be gradually ramped up, in sync with JioMart online.

JioMart: B2B operations launched but execution will be key

After piloting its operations in parts of Mumbai, RIL commenced operations of JioMart, its

online groceries delivery portal. Besides B2C operations, RR has also sought to build a