![[Kotak] India Daily, April 2, 2019 - Kotak Securities](https://static.fdokumen.com/doc/165x107/63265a4f5c2c3bbfa803a474/kotak-india-daily-april-2-2019-kotak-securities.jpg)

India Daily, May 24, 2016 - Kotak Securities

55

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. Contents Daily Alerts Results Britannia Industries: Still a good bet Torrent Pharmaceuticals: Better late than never WABCO India: Continues to outpace industry growth DishTV: Steady subscriber growth story with comfort on margins City Union Bank: Stable performance Jyothy Laboratories: Operationally in-line quarter Company alerts Just Dial: Slow path to recovery Sector alerts Metals & Mining: Steel imports - a sharp fall in April 2016 KIE COMMUNICATION We are dropping coverage on Aban Offshore, given the lack of visibility on contracts, which makes it difficult to forecast earnings. We had suspended rating and target price in May 2012. INDIA DAILY May 24, 2016 India 23-May 1-day 1-mo 3-mo Sensex 25,230 (0.3) (2.4) 9.3 Nifty 7,731 (0.2) (2.1) 10.1 Global/Regional indices Dow Jones 17,493 (0.0) (2.8) 6.1 Nasdaq Composite 4,766 (0.1) (2.9) 4.9 FTSE 6,136 (0.3) (2.8) 4.6 Nikkei 16,562 (0.6) (5.8) 4.1 Hang Seng 19,809 (0.2) (7.7) 3.2 KOSPI 1,947 (0.4) (3.4) 1.8 Value traded – India Cash (NSE+BSE) 165 195 197 Derivatives (NSE) 4,015 2,963 4,578 Deri. open interest 2,552 2,403 2,557 Forex/money market Change, basis points 23-May 1-day 1-mo 3-mo Rs/US$ 67.5 2 77 (98) 10yr govt bond, % 7.8 1 (2) (37) Net investment (US$ mn) 20-May MTD CYTD FIIs (103) 168 1,967 MFs 156 507 906 Top movers Change, % Best performers 23-May 1-day 1-mo 3-mo HDIL IN Equity 94.0 0.1 13.0 55.7 UPLL IN Equity 570.7 (1.0) 9.1 50.7 MMFS IN Equity 294.4 (0.4) 6.8 44.6 DLFU IN Equity 121.3 (1.2) (1.1) 42.6 YES IN Equity 978.1 0.0 11.7 41.6 Worst performers LPC IN Equity 1465.1 (2.6) (6.0) (16.8) JPA IN Equity 6.1 (3.2) (25.8) (13.6) HCLT IN Equity 733.6 (0.4) (13.2) (9.6) ADSEZ IN Equity 181.1 1.8 (21.3) (9.5) UBBL IN Equity 715.5 (2.2) (5.2) (9.3)

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of India Daily, May 24, 2016 - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Contents

Daily Alerts

Results

Britannia Industries: Still a good bet

Torrent Pharmaceuticals: Better late than never

WABCO India: Continues to outpace industry growth

DishTV: Steady subscriber growth story with comfort on margins

City Union Bank: Stable performance

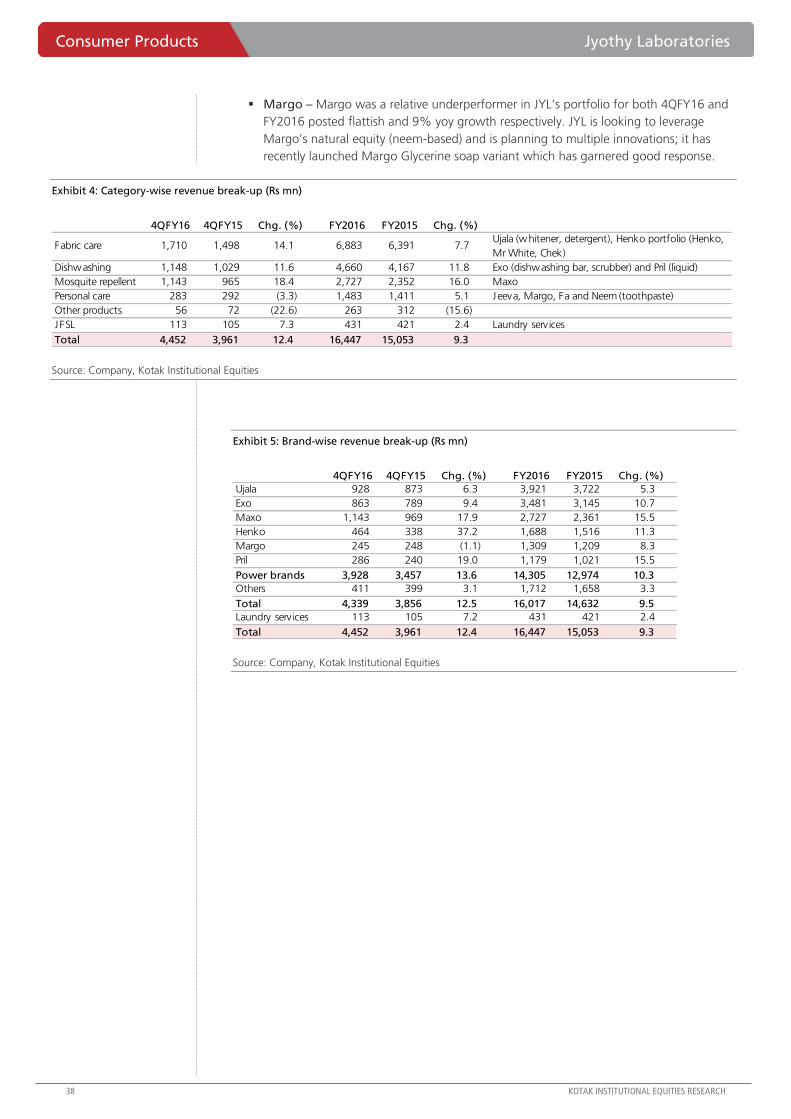

Jyothy Laboratories: Operationally in-line quarter

Company alerts

Just Dial: Slow path to recovery

Sector alerts

Metals & Mining: Steel imports - a sharp fall in April 2016

KIE COMMUNICATION

We are dropping coverage on Aban Offshore, given the lack of visibility on contracts,

which makes it difficult to forecast earnings. We had suspended rating and target price

in May 2012.

INDIA DAILY May 24, 2016 India 23-May 1-day 1-mo 3-mo

Sensex 25,230 (0.3) (2.4) 9.3

Nifty 7,731 (0.2) (2.1) 10.1

Global/Regional indices

Dow Jones 17,493 (0.0) (2.8) 6.1

Nasdaq Composite 4,766 (0.1) (2.9) 4.9

FTSE 6,136 (0.3) (2.8) 4.6

Nikkei 16,562 (0.6) (5.8) 4.1

Hang Seng 19,809 (0.2) (7.7) 3.2

KOSPI 1,947 (0.4) (3.4) 1.8

Value traded – India

Cash (NSE+BSE) 165 195 197

Derivatives (NSE) 4,015 2,963 4,578

Deri. open interest 2,552 2,403 2,557

Forex/money market

Change, basis points

23-May 1-day 1-mo 3-mo

Rs/US$ 67.5 2 77 (98)

10yr govt bond, % 7.8 1 (2) (37)

Net investment (US$ mn)

20-May MTD CYTD

FIIs (103) 168 1,967

MFs 156 507 906

Top movers

Change, %

Best performers 23-May 1-day 1-mo 3-mo

HDIL IN Equity 94.0 0.1 13.0 55.7

UPLL IN Equity 570.7 (1.0) 9.1 50.7

MMFS IN Equity 294.4 (0.4) 6.8 44.6

DLFU IN Equity 121.3 (1.2) (1.1) 42.6

YES IN Equity 978.1 0.0 11.7 41.6

Worst performers

LPC IN Equity 1465.1 (2.6) (6.0) (16.8)

JPA IN Equity 6.1 (3.2) (25.8) (13.6)

HCLT IN Equity 733.6 (0.4) (13.2) (9.6)

ADSEZ IN Equity 181.1 1.8 (21.3) (9.5)

UBBL IN Equity 715.5 (2.2) (5.2) (9.3)

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Weak end to an otherwise solid year; volume growth rates remain robust in double digits

After many quarters of outperformance and strong earnings delivery, Britannia (BRIT) reported a

miss in 4QFY16 driven by weaker-than-expected revenues, drop in other income and sharp

jump in ETR – consolidated net operating revenues grew 7% yoy to `22.1 bn (KIE: `23 bn),

EBITDA grew 15% yoy to `2.91 bn (KIE: `3.36 bn) and recurring PAT grew 14% yoy to `1.9 bn

(KIE: `2.3 bn) – its weakest quarterly performance over the past three years. Volume growth

during the quarter remained robust at 10% (despite material deceleration in category growth

rates) indicating further market share gains for BRIT.

Consolidated EBITDA margins for the quarter expanded 80 bps yoy (150 bps below our

estimates largely due to weaker leverage) to 13.3%; we note BRIT managed input cost inflation

well (GMs contracted 35 bps yoy, in line with our estimates) and cost-control efficiencies

continued to aid margins (A&SP went up 3% yoy, conversion charges were down 9% yoy and

other expenses increased 5% yoy in absolute terms). For FY2016, BRIT delivered consolidated

net revenues, EBITDA and recurring PAT growth of 10% (led by volume growth of 10-11%),

42% and 42% respectively; recurring EPS stood at `68. EBITDA margin expanded 320 bps yoy

to 14.3% aided by 210 bps expansion in GMs and cost-control efficiencies.

Cut EPS estimate by 9-11%; risk-reward favorable post correction – retain BUY

Even though BRIT’s performance was weak relative to high expectations that the company has

set (and surpassed for many quarters), absolute growth rates have remained robust and ahead-

of-market. We believe the company is well-poised to tackle both demand and margin

challenges. Risk-reward remains favorable post sharp correction in the stock on account of

weak 4QFY16 results; the stock is trading at 28X FY2018E revised EPS versus sector average

multiple (ex-ITC) of 32X. We note the company’s internals in terms of RoCE, FCF generation

and FCF conversion are healthier versus several peers trading at relatively expensive valuations.

Weak 4QFY16 drives 9-11% cut in our FY2017-18 EPS estimates led by 3-5% cut in revenues

and 80-90 bps cut in EBITDA margin (led by surge in input costs); retain BUY with a revised TP

of `3,100 (from `3,300) as we roll over to March 2018E (based on 32X target P/E multiple).

Britannia Industries (BRIT) Consumer Products

Still a good bet. Britannia’s (BRIT) 4QFY16 performance was clearly a miss on all

counts and drives 9-11% cut in our EPS estimates for FY2017-18. Near-term weak

demand conditions notwithstanding, we believe BRIT is well-poised to continue its

double-digit revenue growth momentum (though construct of volume-price will

change) led by distribution expansion, market share gains in the Hindi belt and strong

innovation funnel. Price hikes and cost-efficiency initiatives should help sustain margins

despite RM headwinds. Post correction, risk-reward has become favorable – retain BUY

with a revised TP of `3,100 (from `3,300) as we roll over to March 2018E.

BUY

MAY 24, 2016

RESULT

Coverage view: Cautious

Price (`): 2,683

Target price (`): 3,100

BSE-30: 25,230

Anand Shah

Rohit Chordia

Abhas Gupta

Britannia Industries

Stock data Forecasts/Valuations 2016 2017E 2018E

52-week range (Rs) (high,low) EPS (Rs) 68.0 79.6 97.6

Market Cap. (Rs bn) EPS growth (%) 50.4 17.0 22.7

Shareholding pattern (%) P/E (X) 39.4 33.7 27.5

Promoters 50.7 Sales (Rs bn) 86.8 98.2 113.5

FIIs 18.8 Net profits (Rs bn) 8.2 9.5 11.7

MFs 5.9 EBITDA (Rs bn) 12.3 14.2 17.2

Price performance (%) 1M 3M 12M EV/EBITDA (X) 25.9 22.2 18.0

Absolute (5.0) (4.3) 10.4 ROE (%) 54.1 46.2 42.8

Rel. to BSE-30 (2.7) (11.2) 22.3 Div. Yield (%) 0.7 0.9 1.1

Company data and valuation summary

3,434-2,421

321.8

Britannia Industries Consumer Products

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Exhibit 1: Key changes to consolidated estimates, Britannia Industries, March fiscal year-ends,

2017-18E

Source: Company, Kotak Institutional Equities estimates

Exhibit 2: Interim consolidated results of Britannia Industries, March fiscal year-ends (Rs mn)

Source: Company, Kotak Institutional Equities

2017E 2018E 2017E 2018E 2017E 2018E

Net operating revenues (Rs mn) 98,212 113,516 101,246 118,867 (3.0) (4.5)

EBITDA (Rs mn) 14,188 17,200 15,430 19,053 (8.1) (9.7)

EBITDA margin (%) 14.4 15.2 15.2 16.0 -80 bps -88 bps

Net income (Rs mn) 9,551 11,716 10,496 13,083 (9.0) (10.4)

EPS (Rs/share) 79.6 97.6 87.5 109.1 (9.0) (10.5)

Other assumptions

Gross margin (%) 41.9 42.2 42.5 42.9 -65 bps -68 bps

Volume growth - Biscuits (%) 8.0 10.0 10.5 11.5 -250 bps -150 bps

Realisation growth - Biscuts (%) 4.0 5.0 3.5 5.0 50 bps -1 bps

Revised Earlier Change (%)

4QFY16 4QFY16E 4QFY15 3QFY16 KIE Est yoy qoq FY2016 FY2015 (% chg.) FY2017E

Net sales 21,898 22,635 20,318 22,236 (3) 8 (2) 86,071 77,751 11 97,351

Other operating income 216 378 318 166 (43) (32) 30 718 833 (14) 861

Net operating income 22,114 23,013 20,636 22,402 (4) 7 (1) 86,789 78,584 10 98,212

Material cost (12,810) (13,324) (11,883) (12,924) (4) 8 (1) (49,989) (46,918) 7 (57,060)

Gross profit 9,304 9,689 8,753 9,478 (4) 6 (2) 36,799 31,666 16 41,152

Gross margin (%) 42.1 42.1 42.4 42.3 -4 bps -35 bps -24 bps 42.4 40.3 210 bps 41.9

Employee cost (869) (875) (764) (860) (1) 14 1 (3,365) (2,823) 19 (3,846)

Advertising and promotion (2,087) (1,979) (2,029) (1,839) 5 3 13 (7,378) (6,517) 13 (8,134)

Conversion and other charges (1,073) (1,165) (1,179) (1,275) (8) (9) (16) (4,735) (4,881) (3) (5,016)

Other expenditure (2,363) (2,314) (2,253) (2,285) 2 5 3 (9,056) (8,824) 3 (9,968)

Total expenditure (19,202) (19,656) (18,107) (19,183) (2) 6 0 (74,523) (69,962) 7 (84,025)

EBITDA 2,912 3,357 2,530 3,219 (13) 15 (10) 12,265 8,622 42 14,188

OPM (%) 13.3 14.8 12.4 14.5 -154 bps 84 bps -118 bps 14.3 11.1 316 bps 14.6

Other income 243 309 283 275 (21) (14) (12) 1,000 880 14 1,184

Interest (15) (7) (8) (12) 118 83 25 (49) (39) 26 (42)

Depreciation (308) (295) (494) (281) 5 (38) 10 (1,134) (1,445) (22) (1,399)

Pretax profits 2,832 3,365 2,311 3,202 (16) 23 (12) 12,082 8,018 51 13,930

Tax (929) (1,061) (637) (1,024) (12) 46 (9) (3,920) (2,252) 74 (4,381)

PAT 1,903 2,303 1,674 2,178 (17) 14 (13) 8,163 5,766 42 9,549

Minority interest/share of associates (0) (1) (1) 1 2 2 2

Recurring PAT 1,902 2,303 1,673 2,179 (17) 14 (13) 8,164 5,768 42 9,551

Extraordinary items — — — (103) (103) 1,119 -

Net profit (reported) 1,902 2,303 1,673 2,076 (17) 14 (8) 8,061 6,887 17 9,551

Recurring EPS (Rs) 15.9 19.2 14.0 18.2 (17) 14 (13) 68.0 48.1 41 79.6

Income tax rate (%) 32.8 31.5 27.6 32.0 127 bps 524 bps 83 bps 32.4 28.1 435 bps 31.4

Costs as a percentage of sales

Material cost 57.9 57.9 57.6 57.7 3 bps 34 bps 23 bps 57.6 59.7 -211 bps 58.1

Employee cost 3.9 3.8 3.7 3.8 12 bps 22 bps 9 bps 3.9 3.6 28 bps 3.9

Advertising and promotion 9.4 8.6 9.8 8.2 83 bps -40 bps 122 bps 8.5 8.3 20 bps 8.3

Conversion and other charges 4.9 5.1 5.7 5.7 -22 bps -87 bps -85 bps 5.5 6.2 -76 bps 5.1

Other expenditure 10.7 10.1 10.9 10.2 63 bps -24 bps 48 bps 10.4 11.2 -80 bps 10.1

(% chg.)

Consumer Products Britannia Industries

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 3: Interim standalone results of Britannia Industries, March fiscal year-ends (Rs mn)

Source: Company, Kotak Institutional Equities

Key takeaways from management concall

Overall demand environment challenging. Overall demand environment remains

challenging across FMCG categories including biscuits. Management shared a chart in its

presentation, which indicates that biscuits category has witnessed material slowdown in

4QFY16 and month on month deceleration over July 2015 to March 2016 (refer to

Exhibit 4). Management also indicated – (1) premium products have exhibited a lot more

resilience and continue to grow in double digits while value segment of biscuit category

posted flattish-to-negative growth and (2) while BRIT will continue to chase

ahead-of-market growth rates, it will not chase growth at the cost of profitability as it

expects demand recovery to be gradual.

BRIT continues to outperform driven by strong growth rates in weaker states.

While rural growth has slowed down across categories, Britannia’s rural growth continues

to outpace urban growth due to distribution-led expansion in rural markets (especially

weaker states/Hindi belt). Management highlighted – (1) states like Gujarat, MP and

Rajasthan witnessed strong 15%+ growth yoy in FY2016 while UP registered 9% yoy

growth (parts of UP growing faster; BRIT is looking to break up UP in different parts to

improve its growth trajectory), (2) BRIT has gained market share across these 4 regions

and (3) overall BRIT has gained 150 bps value market share and has grown at almost 2X

category growth rates in volume terms in FY2016. Refer to Exhibit 5 for details.

4QFY16 4QFY16E 4QFY15 3QFY16 KIE Est yoy qoq FY2016 FY2015 (% chg.) FY2017E

Net sales 19,938 20,630 18,466 20,315 (3) 8 (2) 78,689 71,005 11 88,987

Other operating income 243 324 255 182 (25) (4) 34 790 755 5 886

Net operating income 20,181 20,953 18,720 20,497 (4) 8 (2) 79,479 71,760 11 89,873

Material cost (11,829) (12,244) (10,922) (11,908) (3) 8 (1) (46,223) (43,168) 7 (52,748)

Gross profit 8,352 8,710 7,798 8,589 (4) 7 (3) 33,256 28,592 16 37,125

Gross margin (%) 41.4 41.6 41.7 41.9 -19 bps -28 bps -52 bps 41.8 39.8 199 bps 41.3

Employee cost (530) (545) (470) (531) (3) 13 (0) (2,092) (1,785) 17 (2,411)

Advertising and promotion (1,710) (1,654) (1,695) (1,515) 3 1 13 (6,154) (5,507) 12 (6,779)

Conversion and other charges (1,409) (1,460) (1,470) (1,606) (3) (4) (12) (5,988) (6,018) (1) (6,501)

Other expenditure (2,025) (1,997) (1,951) (1,919) 1 4 6 (7,707) (7,585) 2 (8,445)

Total expenditure (17,503) (17,900) (16,508) (17,480) (2) 6 0 (68,165) (64,063) 6 (76,885)

EBITDA 2,678 3,054 2,212 3,018 (12) 21 (11) 11,315 7,697 47 12,988

OPM (%) 13.3 14.6 11.8 14.7 -131 bps 145 bps -146 bps 14.2 10.7 351 bps 14.5

Other income 243 318 290 260 (24) (16) (7) 986 876 13 1,167

Interest (3) (3) (3) (3) 19 19 (9) (13) (12) 3 (10)

Depreciation (241) (222) (421) (213) 9 (43) 13 (869) (1,173) (26) (1,108)

Pretax profits 2,677 3,148 2,079 3,062 (15) 29 (13) 11,419 7,388 55 13,038

Tax (835) (1,053) (628) (1,024) (21) 33 (18) (3,825) (2,243) 71 (4,368)

PAT 1,842 2,095 1,450 2,038 (12) 27 (10) 7,594 5,145 48 8,670

Extraordinary items — — (40) (103) (103) 1,079 -

Net profit (reported) 1,842 2,095 1,410 1,935 (12) 31 (5) 7,491 6,224 20 8,670

Recurring EPS (Rs) 15.4 17.5 12.1 17.0 (12) 27 (10) 63.3 42.9 48 72.3

Income tax rate (%) 31.2 33.4 30.2 33.4 -226 bps 97 bps -225 bps 33.5 30.4 313 bps 33.5

Costs as a percentage of sales

Material cost 58.6 58.5 58.3 58.1 11 bps 27 bps 51 bps 58.2 60.2 -200 bps 58.7

Employee cost 2.6 2.6 2.5 2.6 6 bps 11 bps 3 bps 2.6 2.5 14 bps 2.7

Advertising and promotion 8.5 7.8 9.1 7.4 64 bps -59 bps 108 bps 7.7 7.7 6 bps 7.5

Converstion and other charges 7.0 7.6 7.9 7.8 -62 bps -88 bps -86 bps 7.5 8.4 -86 bps 7.2

Other expenditure 10.0 9.8 10.4 9.4 18 bps -39 bps 67 bps 9.7 10.6 -88 bps 9.4

(% chg.)

Britannia Industries Consumer Products

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Exhibit 4: Biscuits growth has slowed down mom and grew in low-single digits over last few months Biscuits category growth rates, yoy (%)

Source: Company, Nielsen, Kotak Institutional Equities

Exhibit 5: BRIT continues to gain market share driven by strong growth in weaker states (Hindi belt)

Source: Company, Nielsen, Kotak Institutional Equities

Innovation to remain a key growth driver. BRIT will continue to focus on innovation

agenda in both premium and value end – (1) it has recently launched new variants under

NutriChoice oats and premium variant in Good Day called Nuts Cookie, (2) Deuce remains

under test market phase (launched in Bangalore) and will be rolled out pan-India in

2HFY17, (3) it has relaunched multiple parts of its portfolio including breads, Tiger

Kreamz, Milk Bikis and 50-50 over the last 3-6 months and has received good response.

Consumer Products Britannia Industries

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Continue to focus on expanding distribution reach. Management highlighted that

distribution gap between BRIT (at 4.6 mn outlets) and category universe (7.6 mn outlets)

offers significant headroom for growth; management highlighted three key distribution

expansion levers – (1) direct reach expansion; BRIT has doubled its direct reach from over

last three years to 1.3 mn outlets in FY2016 (has narrowed the gap with Parle to 1.2 mn

outlets), (2) rural reach expansion; BRIT continues to expand its rural reach via hub and

spoke model (not directly controlled via BRIT; it currently has 8,000 rural distributors and

(3) distribution expansion in Hindi belt; this remains a key focus area as BRIT’s gap in

Hindi belt versus competitors is much larger.

Dairy expansion plans under works. Management highlighted that dairy business

growth was weak in FY2016. However, it is working on a blueprint for expansion of dairy

business (likely to roll out in 3-4 months) with key focus on establishing a fully integrated

supply chain. In terms of product focus, BRIT will initially start with focus on existing

products like cheese (including variants), milk powder, condensed milk and whey powder

and will look to expand in other products like desserts and drinks at a later stage.

Other takeaways. (1) Capex – management has revised its capex guidance downwards

as it expects demand recovery to be gradual; it has now guided for `4 bn capex in

FY2017 and spent `2.1 bn in FY2016 (its earlier guidance was `9 bn+ capex for FY2016-

17), (2) input cost inflation – it expects 5% inflation in its input cost basket and the

company will look to negate this via price hikes (both absolute and removal of

promotional grammage) and (3) short-term loans and advances (consolidated) at

March 2016-end jumped to `6.1 bn (up from `4.65 bn); this largely included `3.25 inter-

corporate deposits in March 2015-end (bulk of this is to group entities) – management

indicated that ICDs to group entities inched up further by `0.5 bn.

Exhibit 6: BRIT delivered another strong quarter with 10% volume growth

Source: Company, Kotak Institutional Equities estimates

3.5

2.0

5.5

4.0 5.0

4.0 3.5

2.5

10.0

6.0

8.0 8.0

10.0

12.0 11.0

10.0

0

2

4

6

8

10

12

14

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

Britannia Industries Consumer Products

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Exhibit 7: Price/mix-led growth turned negative partly impacted by excise hike

Source: Company, Kotak Institutional Equities estimates

7.3 6.7

11.3 9.5 9.9 9.7

7.6

6.5

5.3

7.0

5.6 6.0

3.0

(0.1) (0.2)

(2.0)

(4)

(2)

0

2

4

6

8

10

12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

Consumer Products Britannia Industries

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 8: Key revenue growth assumptions, March fiscal year-ends, 2013-19E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

2013 2014 2015 2016 2017E 2018E 2019E

Standalone Revenue breakup

Product-wise revenue (Rs mn)

Biscuits and high protein food 46,758 53,145 60,520 66,975 75,227 86,887 98,968

Bread 6,018 6,774 7,637 8,805 10,121 11,507 13,027

Cake and rusk 3,108 3,043 4,022 5,067 6,119 7,510 9,129

Others 613 517 515 545 578 613 650

Total gross revenue 56,497 63,479 72,693 81,393 92,045 106,516 121,774

Growth yoy (%)

Biscuits and high protein food 11.5 13.7 13.9 10.7 12.3 15.5 13.9

Bread 21.5 12.6 12.7 15.3 15.0 13.7 13.2

Cake and rusk 14.5 (2.1) 32.2 26.0 20.8 22.7 21.6

Others 31.4 (15.8) (0.4) 6.0 6.0 6.0 6.0

Total gross revenue 12.9 12.4 14.5 12.0 13.1 15.7 14.3

Product-wise volumes (MT)

Biscuits and high protein food 628,617 653,762 709,331 787,358 850,347 935,381 1,019,566

Bread 145,661 151,487 162,091 179,111 197,022 214,754 233,545

Cake and rusk 26,034 24,732 29,678 35,614 40,956 47,919 55,586

Total product volumes 800,311 829,981 901,101 1,002,083 1,088,325 1,198,054 1,308,696

Growth yoy (%)

Biscuits and high protein food 5.0 4.0 8.5 11.0 8.0 10.0 9.0

Bread 9.0 4.0 7.0 10.5 10.0 9.0 8.7

Cake and rusk 12.0 (5.0) 20.0 20.0 15.0 17.0 16.0

Total product volumes 5.9 3.7 8.6 11.2 8.6 10.1 9.2

Product-wise realisation (Rs/MT)

Biscuits and high protein food 74,382 81,291 85,319 85,063 88,466 92,889 97,069

Bread 41,312 44,719 47,115 49,160 51,372 53,581 55,778

Cake and rusk 119,376 123,031 135,506 142,282 149,396 156,716 164,238

Total realisation 69,827 75,860 80,100 80,679 84,044 88,396 92,553

Growth yoy (%)

Biscuits and high protein food 6.2 9.3 5.0 (0.3) 4.0 5.0 4.5

Bread 11.5 8.2 5.4 4.3 4.5 4.3 4.1

Cake and rusk 2.3 3.1 10.1 5.0 5.0 4.9 4.8

Total realisation 6.4 8.6 5.6 0.7 4.2 5.2 4.7

Subsidiary revenue breakup (Rs mn)

Britannia Dairy 3,095 3,043 3,334 3,456 3,902 4,419 4,946

Daily Bread 233 201 158 142 135 129 122

Strategic Food International 2,323 2,722 3,379 3,852 4,391 5,050 5,782

Al Sallan (65%) 1,254 1,356 1,637 1,866 2,127 2,446 2,807

Total subsidiary revenue 6,904 7,323 8,508 9,316 10,556 12,044 13,657

Less: Intersegmental (1,182) (1,346) (1,759) (1,931) (2,188) (2,497) (2,831)

Consolidated gross revenues (Rs mn) 62,218 69,455 79,442 88,778 100,412 116,063 132,600

Growth yoy (%)

Britannia Dairy 5.4 (1.7) 9.5 3.7 12.9 13.3 11.9

Daily Bread (3.3) (13.8) (21.2) (10.0) (5.0) (5.0) (5.0)

Strategic Food International 23.3 17.2 24.1 14.0 14.0 15.0 14.5

Al Sallan (65%) 16.8 8.2 20.7 14.0 14.0 15.0 14.8

Total subsidiary revenue 12.6 6.1 16.2 9.5 13.3 14.1 13.4

Consolidated revenues 12.7 11.6 14.4 11.8 13.1 15.6 14.2

Britannia Industries Consumer Products

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

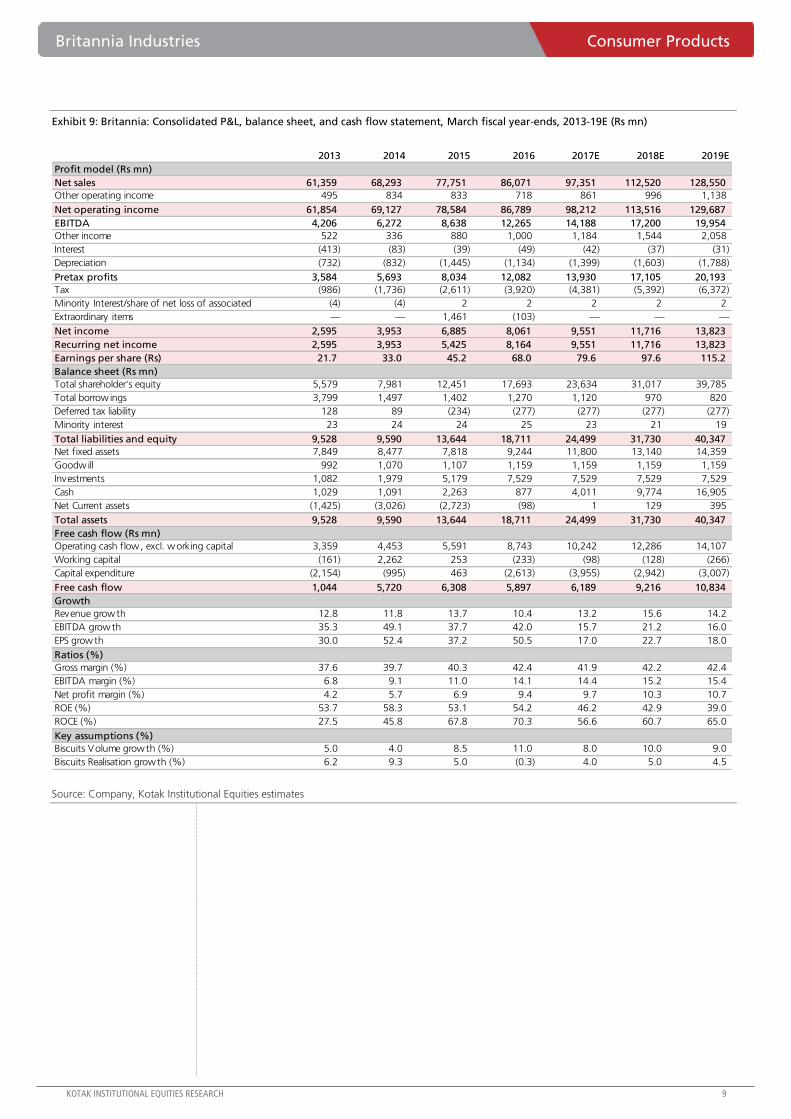

Exhibit 9: Britannia: Consolidated P&L, balance sheet, and cash flow statement, March fiscal year-ends, 2013-19E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

2013 2014 2015 2016 2017E 2018E 2019E

Profit model (Rs mn)

Net sales 61,359 68,293 77,751 86,071 97,351 112,520 128,550

Other operating income 495 834 833 718 861 996 1,138

Net operating income 61,854 69,127 78,584 86,789 98,212 113,516 129,687

EBITDA 4,206 6,272 8,638 12,265 14,188 17,200 19,954

Other income 522 336 880 1,000 1,184 1,544 2,058

Interest (413) (83) (39) (49) (42) (37) (31)

Depreciation (732) (832) (1,445) (1,134) (1,399) (1,603) (1,788)

Pretax profits 3,584 5,693 8,034 12,082 13,930 17,105 20,193

Tax (986) (1,736) (2,611) (3,920) (4,381) (5,392) (6,372)

Minority Interest/share of net loss of associated (4) (4) 2 2 2 2 2

Extraordinary items — — 1,461 (103) — — —

Net income 2,595 3,953 6,885 8,061 9,551 11,716 13,823

Recurring net income 2,595 3,953 5,425 8,164 9,551 11,716 13,823

Earnings per share (Rs) 21.7 33.0 45.2 68.0 79.6 97.6 115.2

Balance sheet (Rs mn)

Total shareholder's equity 5,579 7,981 12,451 17,693 23,634 31,017 39,785

Total borrow ings 3,799 1,497 1,402 1,270 1,120 970 820

Deferred tax liability 128 89 (234) (277) (277) (277) (277)

Minority interest 23 24 24 25 23 21 19

Total liabilities and equity 9,528 9,590 13,644 18,711 24,499 31,730 40,347

Net fixed assets 7,849 8,477 7,818 9,244 11,800 13,140 14,359

Goodwill 992 1,070 1,107 1,159 1,159 1,159 1,159

Investments 1,082 1,979 5,179 7,529 7,529 7,529 7,529

Cash 1,029 1,091 2,263 877 4,011 9,774 16,905

Net Current assets (1,425) (3,026) (2,723) (98) 1 129 395

Total assets 9,528 9,590 13,644 18,711 24,499 31,730 40,347

Free cash flow (Rs mn)

Operating cash flow, excl. working capital 3,359 4,453 5,591 8,743 10,242 12,286 14,107

Working capital (161) 2,262 253 (233) (98) (128) (266)

Capital expenditure (2,154) (995) 463 (2,613) (3,955) (2,942) (3,007)

Free cash flow 1,044 5,720 6,308 5,897 6,189 9,216 10,834

Growth

Revenue growth 12.8 11.8 13.7 10.4 13.2 15.6 14.2

EBITDA growth 35.3 49.1 37.7 42.0 15.7 21.2 16.0

EPS growth 30.0 52.4 37.2 50.5 17.0 22.7 18.0

Ratios (%)

Gross margin (%) 37.6 39.7 40.3 42.4 41.9 42.2 42.4

EBITDA margin (%) 6.8 9.1 11.0 14.1 14.4 15.2 15.4

Net profit margin (%) 4.2 5.7 6.9 9.4 9.7 10.3 10.7

ROE (%) 53.7 58.3 53.1 54.2 46.2 42.9 39.0

ROCE (%) 27.5 45.8 67.8 70.3 56.6 60.7 65.0

Key assumptions (%)

Biscuits Volume growth (%) 5.0 4.0 8.5 11.0 8.0 10.0 9.0

Biscuits Realisation growth (%) 6.2 9.3 5.0 (0.3) 4.0 5.0 4.5

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Abilify drives EBITDA outperformance

TRP delivered a good quarter with revenues largely in line with our expectations, as the domestic

business division showed signs of revival after two quarters of subpar growth, delivering 13%

yoy growth. The management guided to ahead-of-the-market growth in FY2017 as price

increases in Chelcal/Chymoral are expected to help offset ~100 bps impact from expansion of

the NLEM basket. Brazil and RoW revenues too were weak, declining by ~16% and ~19%

respectively, impacted by cross-currency headwinds. The US business reported revenues of

US$76 mn, US$10 mn higher than our expectations, largely on account of Abilify. We expect

this to sharply decline in the coming quarters with incremental competition. EBITDA exceeded

our estimates by ~8%, largely due to the Abilify boost.

US scale-up benefits from Abilify—mending the fractured model

On our estimates, TRP booked ~US$25 mn Abilify sales in 4QFY16 and ~US$220 mn in FY2016.

Ex-Abilify, we believe TRP’s US base quarterly run-rate has moved up to ~US$50 mn in 4QFY16

(US$36 mn in 4QFY15). However, competitive dynamics for Abilify are sharply deteriorating,

and we expect FY2017 to be a weak year for launches as well. TRP filed less than five ANDAs in

FY2016, and now has only 20 ANDAs pending approval in the US. TRP guided to R&D costs

doubling to 8% of revenues in FY2018 as it intensifies efforts to build its US pipeline. Despite

the near-term pressure on earnings, we believe this is a step in the right direction. Among TRP’s

pending pipeline, only Renvela/Renagel are likely to be material contributors, though given the

FDA guidelines on characterization and lack of vertical integration, we believe TRP’s launch will

be in the second wave in 2HFY18. However, we believe the new wave of filings will not

materialize until FY2019, as we expect filing momentum to improve only from 2HFY17.

Expect pressures on profitability from FY2017; REDUCE

We expect Torrent’s FY2017/18 growth to come under pressure, with cross-currency headwinds

(Brazilian real) also adding to growth concerns. Torrent’s shares are currently trading at ~25X

and ~20X FY2017/18E EPS respectively. We cut our FY2017/18E EPS by ~12% and ~7%

respectively largely on account of higher R&D spend. We value TRP at 19X FY2018E EPS at a

discount to frontline peers. We retain REDUCE with a TP of ₹1,260 (from ₹1,320 earlier).

Torrent Pharmaceuticals (TRP) Pharmaceuticals

Better late than never. TRP had a good quarter with sales in line with our expectations,

although EBITDA beat our estimates by ~8%, helped by Abilify with other divisions

performing largely in line with expectations. Following years of neglect on organic R&D

efforts, TRP is now guiding to a doubling of R&D costs to ~₹5 bn (8% of sales) in

FY2017, which we see as a step in the right direction. However, we expect the current

R&D efforts to have a visible impact only from FY2019. We cut our FY2017/18E EPS by

~6% each. REDUCE with a revised TP of ₹1,260 (from ₹1,320).

REDUCE

MAY 24, 2016

RESULT

Coverage view: Cautious

Price (`): 1,330

Target price (`): 1,260

BSE-30: 25,230

Chirag Talati, CFA

Kumar Gaurav

Torrent Pharmaceuticals

Stock data Forecasts/Valuations 2016 2017E 2018E

52-week range (Rs) (high,low) EPS (Rs) 101.8 57.5 66.0

Market Cap. (Rs bn) EPS growth (%) 129.3 (43.5) 14.8

Shareholding pattern (%) P/E (X) 13.1 23.1 20.1

Promoters 71.3 Sales (Rs bn) 66.8 63.2 71.5

FIIs 12.2 Net profits (Rs bn) 17.2 9.7 11.2

MFs 5.7 EBITDA (Rs bn) 27.2 15.3 17.4

Price performance (%) 1M 3M 12M EV/EBITDA (X) 8.4 15.2 13.2

Absolute (9.0) 2.8 8.6 ROE (%) 58.6 25.9 24.5

Rel. to BSE-30 (6.8) (4.6) 20.3 Div. Yield (%) 3.0 1.0 1.1

Company data and valuation summary

1,698-1,155

225.0

Torrent Pharmaceuticals Pharmaceuticals

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Exhibit 1: Torrent Pharma interim results March fiscal year-ends (Rs mn)

Source: Company, Kotak Institutional Equities estimates

Other key takeaways from the conference call

US FDA inspection at Indrad facility was conducted in May 2016, which was mainly

related to two filed products. 2-3 observations were noted, however, according to

management, observations were minor in nature. Indore dermatology facility was also

inspected in April 2016.

Torrent currently has 20 ANDA pending approval (including 6 tentative approval) in the

US. The company intends to file 15-20 additional ANDAs in FY2017 (including 4-5

products in dermatology segment). Torrent has guided for R&D spend to be ~8% of

FY2017 sales. Number of scientists has doubled starting 1QFY16 and the full impact of

increase in scientists is not captured in FY2016.

Nexium has witnessed a slow ramp-up for Torrent and the company is targeting for 5-7%

market share during FY2017. Management expects 2 additional players to enter Abilify

market in the coming quarter. 10 products are slated to be launched in US during

FY2017 of which Crestor will be the largest product by brand sales. Management expects

growth in US to be driven by commissioning of Dahej facility (1.8bn tablet capacity) while

freed up capacity at Indrad plant will be used for incremental supply to UK and Germany.

Number of medical representatives in India declined to 2,720 and has driven significant

improvement in field force productivity. Torrent sees 1-1.2% impact in sales due to NLEM

which the company intends to offset by new product launches. The company took a price

hike in Elder portfolio in 3QFY16 and expects improvement in domestic segment growth

rate to be driven by new product launches and full impact of price hike in Elder portfolio.

(% chg.) yoy

4QFY16 4QFY16E 4QFY15 3QFY16 4QFY16E 4QFY15 3QFY16 FY2016 FY2015 (% chg.) FY2017E

Sales 14,990 15,050 11,540 15,390 (0.4) 29.9 (2.6) 66,760 46,534 43.5 63,074

Raw material (4,110) (4,594) (3,610) (3,720) (10.5) 13.9 10.5 (15,770) (14,148) 11.5 (19,431)

Employee expenses (2,300) (2,242) (2,350) (2,060) 2.6 (2.1) 11.7 (8,560) (8,418) 1.7 (9,844)

R&D expenses (660) (602) (519) (600) 9.6 27.1 10.0 (2,460) (1,910) 28.8 (5,046)

Other expenses (3,080) (3,149) (3,441) (2,880) (2.2) (10.5) 6.9 (12,770) (11,856) 7.7 (14,302)

EBITDA 4,840 4,463 1,620 6,130 8.4 198.8 (21.0) 27,200 10,201 166.6 14,450

Other income 240 600 1,000 (1,420) 760 2,856 1,300

Interest (380) (420) (470) (420) (1,860) (1,752) (1,044)

Depreciation (650) (620) (600) (610) (2,460) (1,907) (3,056)

Pretax profits 4,050 4,023 1,550 3,680 0.7 161.3 10.1 23,640 9,398 151.5 11,650

Tax (480) (887) (250) (200) (6,420) (1,888) (2,563)

Minority interest - - - - - (0) -

Net income - reported 3,570 3,135 1,300 3,480 13.9 174.6 2.6 17,220 7,510 129.3 9,087

Net income - adjusted 3,570 3,135 1,300 3,480 13.9 174.6 2.6 17,220 7,510 129.3 9,087

Adjusted EPS (Rs) 21.1 18.6 7.7 20.6 13.9 174.6 2.6 101.8 44.4 129.3 53.7

Tax rate (%) 11.9 22.1 16.1 5.4 27.2 20.1 22.0

Segment wise sales

Domestic Formulation 4,470 4,421 3,960 4,460 1.1 12.9 0.2 18,250 16,090 13.4 20,905

US 5,140 4,424 2,250 5,580 16.2 128.4 (7.9) 26,720 8,320 221.2 26,720

Brazil 1,190 1,201 1,410 1,180 (0.9) (15.6) 0.8 5,060 6,060 (16.5) 5,060

Other branded 770 809 950 760 (4.8) (18.9) 1.3 3,020 3,430 (12.0) 3,020

Other generics 1,900 2,305 1,760 1,950 (17.6) 8.0 (2.6) 7,730 7,510 2.9 7,730

CRAMS 1,520 1,890 1,210 1,460 (19.6) 25.6 4.1 5,990 5,120 17.0 5,990

Total 14,990 15,050 11,540 15,390 (0.4) 29.9 (2.6) 66,760 46,534 43.5 63,074

% margin

Raw material (27.4) (30.5) (31.3) (24.2) (23.6) (30.4) (30.8)

Staff cost (15.3) (14.9) (20.4) (13.4) (12.8) (18.1) (15.6)

R&D expenses (4.4) (4.0) (4.5) (3.9) (3.7) (4.1) (8.0)

Other expenditure (20.5) (20.9) (29.8) (18.7) (19.1) (25.5) (22.7)

EBITDA 32.3 29.7 14.0 39.8 40.7 21.9 22.9

Pharmaceuticals Torrent Pharmaceuticals

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Torrent Pharma - change in earnings estimates March fiscal year-ends (Rs mn)

Source: Company, Kotak Institutional Equities estimates

Exhibit 3: Abilify erosion set to hurt US business in FY2017/18 March fiscal year-ends, 2011-18E (US$ mn)

Source: Company, Kotak Institutional Equities estimates

2017E 2018E 2017E 2018E 2017E 2018E

Sales 61,176 68,205 63,188 71,543 3.3 4.9

Gross profits 43,724 48,375 44,228 50,110 1.2 3.6

EBITDA 16,340 17,835 15,282 17,394 (6.5) (2.5)

PBT 13,249 15,154 12,482 14,325 (5.8) (5.5)

Tax (2,915) (3,324) (2,746) (3,152) (5.8) (5.2)

PAT 10,334 11,820 9,736 11,174 (5.8) (5.5)

EPS 61.1 69.9 57.5 66.0 (5.8) (5.5)

Old Estimates New estimates Changes %

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Limited competition/P-IV's/FTF's 0 0 32 47 19 265 78 68 71

TRP base business 29 45 32 74 120 147 185 233 302

Total sales 29 45 64 121 139 412 263 301 373

growth % 19.0 53.7 42.2 89.2 14.5 196.9 (36.1) 14.2 24.2

Limited competition/P-IV's/FTF's as % of Sales 0.0 0.0 50.6 39.1 13.6 64.3 29.5 22.5 19.0

Torrent Pharmaceuticals Pharmaceuticals

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Exhibit 4: Torrent Pharma - profit and loss, balance sheet, cash model March fiscal year-ends, 2011-19E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Profit and loss statement

Net sales 22,330 27,975 31,696 41,847 46,534 66,760 63,074 72,111 83,531

COGS (7,916) (9,829) (10,505) (13,886) (14,148) (15,770) (19,431) (22,165) (25,764)

Staff cost (3,895) (5,337) (6,549) (7,834) (8,418) (8,560) (9,844) (11,075) (12,570)

SG&A (4,974) (5,257) (6,975) (8,071) (11,856) (12,770) (14,302) (15,864) (17,959)

R&D (1,388) (1,320) (1,111) (1,700) (1,910) (2,460) (5,046) (5,769) (7,100)

EBITDA 4,157 6,232 6,556 10,356 10,201 27,200 14,450 17,238 20,138

Pretax profits 3,427 4,602 5,817 8,438 9,398 23,640 11,650 14,156 17,381

Tax (739) (730) (1,476) (1,833) (1,888) (6,420) (2,563) (3,114) (3,824)

Adjusted net profit 2,702 3,879 4,350 6,637 7,510 17,220 9,087 11,042 13,557

Shares outstanding (mn) 169 169 169 169 169 169 169 169 169

Adjusted EPS (Rs) 16.0 22.9 25.7 39.2 44.4 101.8 53.7 65.3 80.1

Balance sheet

Current assets 15,944 19,872 25,598 34,046 40,587 46,610 48,682 50,894 56,324

Net block 8,155 8,918 10,825 13,808 15,999 21,262 25,043 28,583 31,923

Goodwill and intangibles — 239 226 286 17,804 15,968 14,132 12,296 10,460

Fixed assets 9,414 10,607 11,919 15,995 38,524 41,720 43,664 45,369 46,873

Total assets 25,358 30,479 37,517 50,041 79,111 88,330 92,346 96,263 103,197

Current liabilities 7,484 10,359 12,287 16,239 18,277 22,600 24,363 27,466 31,578

Debt 6,588 6,490 9,355 12,951 31,885 27,080 22,080 14,080 6,080

Other long-term liabilities 1,062 1,692 1,656 1,827 4,038 4,760 5,016 5,328 5,710

Total liabilities 15,134 18,541 23,298 31,017 54,201 54,440 51,459 46,874 43,368

Shareholders' equity 10,224 11,938 14,219 19,024 24,910 33,890 40,887 49,389 59,828

Total liabilities and equity 25,358 30,479 37,517 50,041 79,111 88,330 92,346 96,263 103,197

Cash flow

Profit before taxes 3,423 3,586 5,817 8,438 9,398 23,640 11,650 14,156 17,381

Depreciation and amortisation 626 817 827 870 1,907 2,460 3,056 3,296 3,496

Change in working capital 619 1,518 (4,218) (1,197) (4,094) 7,678 (8,345) (4,036) (4,494)

Other adjustements (718) (848) (891) (2,119) 890 (4,526) (2,307) (2,803) (3,442)

Total operational cash flow 3,950 5,073 1,536 5,993 8,102 29,253 4,055 10,613 12,942

Investment cash flow

Investment in fixed assets (2,650) (1,703) (2,929) (4,001) (2,426) (5,919) (5,000) (5,000) (5,000)

Acquisitions 19 11 85 19 (19,539) — — — —

Total investment cash flow (2,326) (1,459) (2,417) (3,653) (21,623) (5,919) (5,000) (5,000) (5,000)

Total financing cash flow (676) (1,920) 197 864 12,123 (15,574) (5,090) (8,540) (9,118)

Net cash flow 943 1,560 (733) 3,197 (1,393) 7,760 (6,035) (2,927) (1,176)

Free cash flow 1,319 3,382 (1,309) 2,011 (13,862) 23,334 (945) 5,613 7,942

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Strong revenue growth led by introduction of ABS; EBITDA margin impacted by one-offs

Wabco India reported revenues of ₹5.7 bn (+48% yoy) in 4QFY16 which was 8% ahead of our

estimates. The domestic OEM segment’s revenues increased by 76% yoy driven by the

introduction of ABS in trucks from October 2015 and strong volume growth in the MHCV

industry. Revenues related to ABS were around ₹800 mn during the quarter; excluding ABS, the

OEM segment’s revenues grew by 38% yoy in 4QFY16 (+25% yoy for FY2016) as compared to

25% yoy in MHCV production volumes in 4QFY16 (27% yoy in FY2016). Export revenues

increased by 30% yoy to ₹1.5 bn; the capacity utilization of the new export plant is 40-45%

which should improve next year. The company reported 8% yoy growth in aftermarket segment

revenues. EBITDA at ₹0.8 bn (+43% yoy) was 4% below our estimates due to lower-than-

expected gross margin. Gross margin deteriorated by 160bps qoq (KIE 20bps qoq decline); as

per the company, this was due to weaker product mix within the OEM segment and could vary

across quarters. Other expenses (+54% yoy) include non-recurring items of ₹140 mn (2.5%

margin impact) related to provision for bad debts and write-offs related to duty drawback.

Overall, the company reported EBITDA margin of 14.2% (KIE 16%). Reported PAT at ₹573 mn

(+88% yoy) was 5% ahead of our estimates due to higher other income and lower tax rate.

Growth outlook remains strong; expect Wabco to deliver 22% EPS CAGR over FY2016-19E

We expect Wabco to deliver 20% revenue CAGR over FY2016-19E led by (1) full year revenues

of ABS in FY2017, (2) continued strong growth in exports due to the parent’s target to increase

sourcing from low cost countries and (3) double-digit growth in domestic CV industry. We

expect EBITDA margin to improve to 17%/17.5% in FY2017E/18E led by (1) improvement in

gross margin due to the increase in localization of content in ABS to 90-95% by 3QFY17 from

60% currently and (2) normalization of one-off expenses which impacted 4QFY16.

Lower FY2017-18E EPS estimate by 1-4%; maintain BUY with revised target price of ₹6,500

We cut our FY2017-18E EPS estimates by 1-4% due to 40-90 bps cut in our EBITDA margin

assumptions. Consequently, we lower our DCF-based target price to ₹6,500 (from ₹6,600) but

maintain BUY rating. Slower-than-expected ramp-up in the adoption of AMT technology and

weakness in MHCV industry volumes are key risks to our investment thesis.

WABCO India (WIL) Automobiles

Continues to outpace industry growth. Wabco India reported strong 4QFY16 results

with 48% yoy revenue growth led by the introduction of ABS in trucks. EBITDA margin

in this quarter was impacted by weaker product mix and some non-recurring items. We

expect EBITDA margin to improve with increase in localization of ABS. Growth outlook

remains strong due to significant scope of increase in content per vehicle in trucks in

India; we expect the company to deliver 22% EPS CAGR over FY2016-19E. Maintain

BUY with a revised TP of ₹6,500 (from ₹6,600 earlier).

BUY

MAY 24, 2016

RESULT

Coverage view: Attractive

Price (`): 5,793

Target price (`): 6,500

BSE-30: 25,230

Hitesh Goel

Nishit Jalan

WABCO India

Stock data Forecasts/Valuations 2016 2017E 2018E

52-week range (Rs) (high,low) EPS (Rs) 107.9 145.7 170.1

Market Cap. (Rs bn) EPS growth (%) 69.6 35.1 16.7

Shareholding pattern (%) P/E (X) 53.7 39.8 34.1

Promoters 75.0 Sales (Rs bn) 18.4 24.0 27.4

FIIs 2.3 Net profits (Rs bn) 2.0 2.8 3.2

MFs 8.2 EBITDA (Rs bn) 2.9 4.1 4.8

Price performance (%) 1M 3M 12M EV/EBITDA (X) 36.0 25.6 21.4

Absolute (1.8) 4.6 3.4 ROE (%) 21.3 23.4 22.3

Rel. to BSE-30 0.6 (2.9) 14.6 Div. Yield (%) 0.1 0.2 0.2

Company data and valuation summary

7,450-5,166

109.9

WABCO India Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Exhibit 1: Wabco India reported strong 4QFY16 results; revenue increased by 48% yoy albeit gross margin declined by 160bps qoq Wabco India 4QFY16 result summary, March fiscal year-ends (₹ mn)

Source: Company, Kotak Institutional Equities estimates

4QFY16 4QFY16E 4QFY15 3QFY16 4QFY16E 4QFY15 3QFY16 FY2016 FY2015 Yoy chg.(%) FY2017E

Segment wise

OEM 3,180 2,826 1,805 2,355 12.5 76.2 35.0 9,244 6,056 13,720

Aftermarket 740 768 686 626 (3.7) 7.9 18.2 2,608 2,324 2,563

Exports 1,469 1,400 1,132 1,339 4.9 29.8 9.7 5,542 4,336 6,631

Other operating income 272 260 209 258 4.5 30.3 5.3 984 764 1,087

Net sales 5,665 5,254 3,832 4,578 7.8 47.8 23.7 18,382 13,480 36.4 24,001

Raw materials (3,480) (3,153) (2,280) (2,739) 10.4 52.6 27.0 (10,997) (7,929) (14,392)

Staff costs (467) (480) (394) (453) (2.7) 18.5 3.0 (1,738) (1,434) (2,085)

Other expenses (913) (780) (594) (609) 17.1 53.7 50.0 (2,718) (2,082) (3,438)

Total expenses (4,860) (4,413) (3,268) (3,801) 10.1 48.7 27.8 (15,453) (11,446) (19,915)

EBITDA 805 842 564 777 (4.3) 42.8 3.7 2,929 2,035 44.0 4,086

Depreciation (147) (145) (121) (142) 1.2 21.2 3.3 (562) (467) (607)

EBIT 659 697 443 635 (5.4) 48.7 3.8 2,367 1,568 50.9 3,479

Other income 102 60 59 61 70.2 73.0 68.5 346 203 360

Interest expense (2) — (2) — (2) (4) —

Profit before tax 759 757 500 695 0.4 51.9 9.2 2,712 1,767 53.5 3,839

Tax expense (186) (212) (196) (180) (12.0) (4.9) 3.6 (666) (559) (1,075)

Profit after tax 573 545 304 515 5.2 88.4 11.2 2,046 1,208 69.4 2,764

# of shares 19 19 19 19 19 19 19

EPS (Rs/ share) 30.2 28.7 16.0 27.2 107.9 63.7 145.7

Tax rate (%) 24.6 28.0 39.2 25.9 24.6 31.6 28.0

As % of net revenues

Raw material 61.4 60.0 59.5 59.8 59.8 58.8 60.0

Staff costs 8.2 9.1 10.3 9.9 9.5 10.6 8.7

Other expenses 16.1 14.8 15.5 13.3 14.8 15.4 14.3

EBITDA margin 14.2 16.0 14.7 17.0 15.9 15.1 17.0

EBIT margin 11.6 13.3 11.6 13.9 12.9 11.6 14.5

change (%)

Automobiles WABCO India

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Our DCF-based target price for Wabco India is ₹6,500 Wabco India DCF valuation methodology, March fiscal year-ends, 2015-30E (₹ mn)

Source: Company, Kotak Institutional Equities estimates

Exhibit 3: We cut our FY2017-18E EPS estimates by 1-4% due to lower EBITDA margin assumptions Earnings revision table of Wabco India, March fiscal year-ends, 2016-18E (₹ mn)

Source: Company, Kotak Institutional Equities estimates

2015 2016E 2017E 2018E 2019E 2020E 2023E 2027E 2028E 2029E 2030E

Net revenue 13,480 18,383 24,001 27,370 31,138 40,450 69,346 120,713 138,833 158,175 179,863

EBIT 1,770 2,713 3,839 4,480 4,982 6,472 11,095 19,314 22,213 25,308 28,778

EBIT (1-tax) 1,209 2,047 2,764 3,226 3,587 4,660 7,989 13,906 15,994 18,222 20,720

Depreciation / Amortisation 467 562 607 697 737 872 1,445 2,629 2,993 3,409 3,810

(Inc)/Dec in working capital (277) 184 (936) (990) (619) (1,531) (2,104) (2,563) (2,979) (3,179) (2,087)

Capital expenditure (725) (881) (1,000) (1,000) (1,557) (1,820) (3,121) (4,225) (4,859) (5,536) (4,497)

Free cash flows 674 1,913 1,436 1,933 2,148 2,181 4,209 9,747 11,149 12,915 17,947

Discounted cash flow — — 1,933 1,926 1,754 2,442 3,659 3,754 3,900 4,861

WACC (%) 11.5 NPV calculation

Terminal growth rate 5.0 Sum of free cash flow 38,675

Capitalization rate (%) 6.5 Terminal value 78,517

Date 31-Mar-18 Enterprise value 117,191

Terminal value Calculation Net debt (6,359)

Cash flow in terminal year 17,947 Net present value-equity 123,551

Terminal value 289,908 Shares o/s (mn) 19

Discounted terminal value 78,517 NPV /share (Rs) 6,514

Key assumptions

Revenue build-up

Air assist and full air actuation system 5,835 7,717 9,260 10,372 11,616 13,010 17,952 26,284 28,912 31,225 33,098

yoy growth (%) 40.1 32.3 20.0 12.0 12.0 12.0 10.0 10.0 10.0 8.0 6.0

Spares 1,990 2,229 2,563 2,948 3,390 3,899 5,624 8,692 9,561 10,326 10,945

yoy growth (%) 10.6 12.0 15.0 15.0 15.0 15.0 12.0 10.0 10.0 8.0 6.0

Exports of automotive systems 4,317 5,526 6,631 7,625 8,769 10,084 14,032 20,545 22,599 24,181 25,390

yoy growth (%) 3.4 28.0 20.0 15.0 15.0 15.0 10.0 10.0 10.0 7.0 5.0

ABS (OEM) 574 1,800 4,200 4,620 5,082 5,590 7,441 10,894 11,983 12,942 13,718

yoy growth (%) 81.4 213.8 133.3 12.0 10.0 10.0 10.0 10.0 10.0 8.0 6.0

ABS (Replacement) 4,200 9,790 14,334 15,767 17,344 19,078

yoy growth (%) 92.6 10.0 10.0 10.0 10.0

Automated manual transmission (OEM) 127 160 436 775 1,313 5,923 15,660 19,294 23,536 29,662

yoy growth (%) — 26.0 173.1 77.6 69.3 32.8 24.7 23.2 22.0 26.0

Automated manual transmission (Replacement) — — — — 697 6,459 21,415 27,595 35,250 44,396

yoy growth (%) 54.7 29.9 28.9 27.7 25.9

Others 764 984 1,187 1,369 1,506 1,656 2,125 2,891 3,122 3,372 3,574

yoy growth (%) 17.8 28.8 20.6 15.3 10.0 10.0 8.0 8.0 8.0 8.0 6.0

Total 13,480 18,383 24,001 27,370 31,138 40,450 69,346 120,713 138,833 158,175 179,863

EBIT margin (%) 13.1 14.8 16.0 16.4 16.0 16.0 16.0 16.0 16.0 16.0 16.0

Tax rate (%) 31.7 24.5 28.0 28.0 28.0 28.0 28.0 28.0 28.0 28.0 28.0

Capex as % of revenues 5.4 4.8 4.2 5.0 5.0 4.5 4.5 3.5 3.5 3.5 2.5

Content per truck (US $) 446 525 645 660 675 693 778 855 875 900 924

YoY chg (%) 17.8 22.9 2.3 2.3 2.7 2.2 2.4 2.4 2.9 2.6

2017E 2018E 2017E 2018E 2017E 2018E

Net sales 24,001 27,370 24,223 27,451 (0.9) (0.3)

EBITDA 4,086 4,797 4,324 4,926 (5.5) (2.6)

Margin (%) 17.0 17.5 17.9 17.9

Net Profit 2,764 3,226 2,874 3,246 (3.8) (0.6)

EPS (Rs/share) 145.7 170.1 151.5 171.1 (3.8) (0.6)

New estimates Old estimates Yoy chg (%)

WABCO India Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

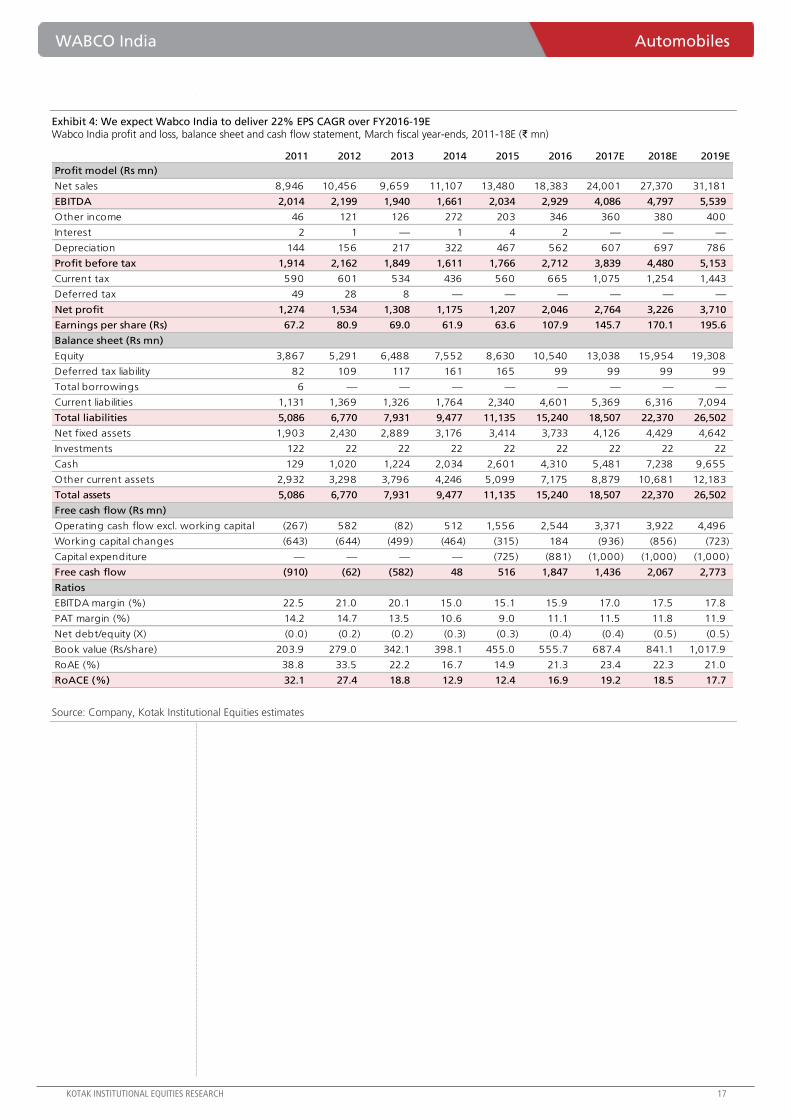

Exhibit 4: We expect Wabco India to deliver 22% EPS CAGR over FY2016-19E Wabco India profit and loss, balance sheet and cash flow statement, March fiscal year-ends, 2011-18E (₹ mn)

Source: Company, Kotak Institutional Equities estimates

2011 2012 2013 2014 2015 2016 2017E 2018E 2019E

Profit model (Rs mn)

Net sales 8,946 10,456 9,659 11,107 13,480 18,383 24,001 27,370 31,181

EBITDA 2,014 2,199 1,940 1,661 2,034 2,929 4,086 4,797 5,539

Other income 46 121 126 272 203 346 360 380 400

Interest 2 1 — 1 4 2 — — —

Depreciation 144 156 217 322 467 562 607 697 786

Profit before tax 1,914 2,162 1,849 1,611 1,766 2,712 3,839 4,480 5,153

Current tax 590 601 534 436 560 665 1,075 1,254 1,443

Deferred tax 49 28 8 — — — — — —

Net profit 1,274 1,534 1,308 1,175 1,207 2,046 2,764 3,226 3,710

Earnings per share (Rs) 67.2 80.9 69.0 61.9 63.6 107.9 145.7 170.1 195.6

Balance sheet (Rs mn)

Equity 3,867 5,291 6,488 7,552 8,630 10,540 13,038 15,954 19,308

Deferred tax liability 82 109 117 161 165 99 99 99 99

Total borrowings 6 — — — — — — — —

Current liabilities 1,131 1,369 1,326 1,764 2,340 4,601 5,369 6,316 7,094

Total liabilities 5,086 6,770 7,931 9,477 11,135 15,240 18,507 22,370 26,502

Net fixed assets 1,903 2,430 2,889 3,176 3,414 3,733 4,126 4,429 4,642

Investments 122 22 22 22 22 22 22 22 22

Cash 129 1,020 1,224 2,034 2,601 4,310 5,481 7,238 9,655

Other current assets 2,932 3,298 3,796 4,246 5,099 7,175 8,879 10,681 12,183

Total assets 5,086 6,770 7,931 9,477 11,135 15,240 18,507 22,370 26,502

Free cash flow (Rs mn)

Operating cash flow excl. working capital (267) 582 (82) 512 1,556 2,544 3,371 3,922 4,496

Working capital changes (643) (644) (499) (464) (315) 184 (936) (856) (723)

Capital expenditure — — — — (725) (881) (1,000) (1,000) (1,000)

Free cash flow (910) (62) (582) 48 516 1,847 1,436 2,067 2,773

Ratios

EBITDA margin (%) 22.5 21.0 20.1 15.0 15.1 15.9 17.0 17.5 17.8

PAT margin (%) 14.2 14.7 13.5 10.6 9.0 11.1 11.5 11.8 11.9

Net debt/equity (X) (0.0) (0.2) (0.2) (0.3) (0.3) (0.4) (0.4) (0.5) (0.5)

Book value (Rs/share) 203.9 279.0 342.1 398.1 455.0 555.7 687.4 841.1 1,017.9

RoAE (%) 38.8 33.5 22.2 16.7 14.9 21.3 23.4 22.3 21.0

RoACE (%) 32.1 27.4 18.8 12.9 12.4 16.9 19.2 18.5 17.7

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Kotak Institutional Equities Research [email protected] Mumbai: +91-22-4336-0000

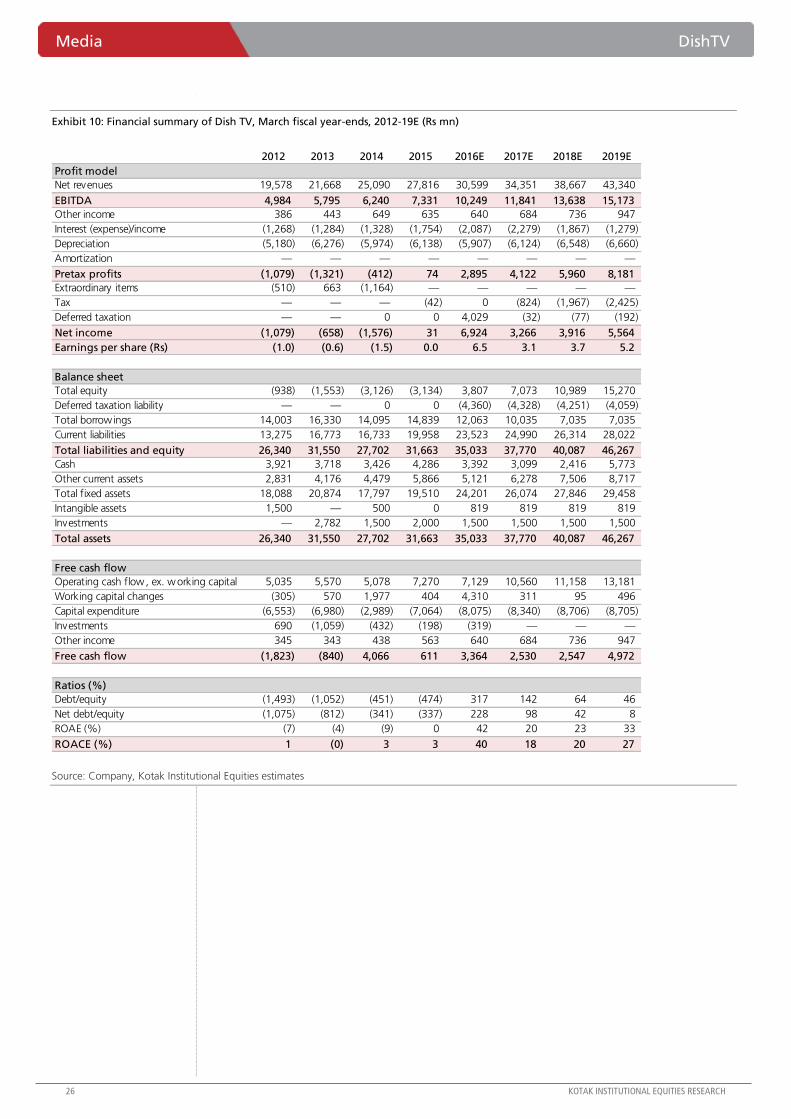

4QFY16— Sub adds and ARPU tracking well, content costs disappoint

Dish TV’s EBITDA of `2.61 bn was 6% below our estimate. The negative surprise was due to

higher content costs (up 12% qoq). Content costs increased 7% yoy in FY2016, higher than

the run-rate of 5% yoy in 9MFY15, but within a guided range of 5-7%. Net sub adds at 508K

(KIE 475K) were up 60% qoq and 25% yoy driven by (1) robust demand in view of phase III

digitization activity in select markets and T20 cricket world cup, and (3) launch of low-ARPU

pack, Dish99 (tariff of `174/month versus `270/month for SD base pack). ARPU increased ~1%

qoq to `174 from `172; higher activation income in a quarter having strong sub adds boosts

ARPU while higher contribution of low-ARPU packs drags it down. Net profit of `4.8 bn

included deferred tax expense of `4.36 bn. Net debt increased by `800 mn to `6.4 bn.

Pros and cons of changing subscriber mix

Low-ARPU packs Dish99 (launched in Dec 2015) and Zing (launched in March 2014) with

monthly tariff of about `175-200 (versus `270 for SD base pack) contributed 30% and 20% to

sub adds in 4Q. These packs have better margins due to lower content costs as a proportion of

revenue. However, it drags ARPU growth. Additionally, although margin accretive, likely higher

subsidy on low-ARPU packs and lower absolute EBITDA/sub negatively impacted Free cash flow

conversion at the margin. Dish TV has upped the ante on marketing to push more HD sales

(20% of sub adds at present), a lever to drive ARPU growth. Dish TV’s guidance of 3% ARPU

growth in FY2017 despite likely annual price increase of about 7-8%+ factors in changing subs

mix. The flip side of this change in subs mix is that Dish’s subscriber base will be less vulnerable

to churn in the event of any disruptive cable + broadband offering by Reliance Jio.

Inexpensive valuations; steady 14-15% EBITDA growth ahead; Maintain BUY

Dish TV is trading at inexpensive valuation of 7.1X FY2018 EV/EBITDA. It is well-placed to deliver

about 12% CAGR in revenues (~9% from subs growth and 3% from ARPU) and about 15%

CAGR in EBITDA over the next 2-3 years. The ongoing consultative process to bring parity in

pricing between different distribution platforms augur well for DTH and will help DTH players

become more efficient from a content cost perspective. Upside from digitization, if

implemented, will pose upside risk to our estimates. We value Dish TV at 10X FY2018

EV/EBITDA and we partially factor in the risk of adverse verdict in the ongoing license fees case

(~`6 impact on fair value assuming 50% possibility of ~`11.5 bn liability materializing).

DishTV (DITV) Media

Steady subscriber growth story with comfort on margins. Dish TV reported strong

508K net sub adds and 1.2% qoq increase in ARPU but EBITDA at `2.6 bn (-2% qoq;

+18% yoy) missed our estimate by 6% due to high content costs. The management has

guided 1.5 mn net sub adds, 3% ARPU growth, 7-10% increase in content cost and

35% EBITDA margin for FY2017. Subscriber addition can exceed guidance on effective

implementation of digitization; margin guidance is comforting. We tweak estimates, roll

over to FY2018 and maintain TP of `115 valuing Dish TV at 10X EV/EBITDA.

BUY

MAY 24, 2016

RESULT

Coverage view: Neutral

Price (`): 88

Target price (`): 115

BSE-30: 25,230

Jaykumar Doshi

DishTV

Stock data Forecasts/Valuations 2016 2017E 2018E

52-week range (Rs) (high,low) EPS (Rs) 6.5 3.1 3.7

Market Cap. (Rs bn) EPS growth (%) ###### (52.8) 19.9

Shareholding pattern (%) P/E (X) 13.6 28.8 24.0

Promoters 64.4 Sales (Rs bn) 30.6 34.4 38.7

FIIs 8.7 Net profits (Rs bn) 6.9 3.3 3.9

MFs 5.8 EBITDA (Rs bn) 10.2 11.8 13.6

Price performance (%) 1M 3M 12M EV/EBITDA (X) 9.8 8.3 7.1

Absolute (0.6) 25.6 7.5 ROE (%) 41.5 19.6 23.5

Rel. to BSE-30 1.8 16.6 19.1 Div. Yield (%) 0.0 0.0 0.0

Company data and valuation summary

122-65

94.1

DishTV Media

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

A roundup of FY2016 and like-to-like comparison with FY2015

Dish TV’s subscription revenues grew 15.4% yoy led by 12% yoy growth in net subscribers

(up 1.55 mn to 14.5 mn) and about 3.5% growth in ARPU; adjusted for service tax increase

ARPU growth would be about 4.5-5% yoy (like-to-like). EBITDA increased 40% yoy to

`10.25 bn led by 620 bps expansion in EBITDA margin to 33.5%. We note that about 300

bps expansion in margin is attributable to lower license fees provisioning following the

transfer of non-core activities to Dish Infra subsidiary. In the absence of this restructuring,

License fees would have been higher by about `900 mn, EBITDA lower by the same amount,

EBITDA growth would have been 28% yoy and EBITDA margin 30.5%. Content costs

increased 7% yoy, significantly lower than revenue growth and content cost as a proportion

of revenues declined 180 bps to 28%. Net debt decreased `3.4 bn during the year to `6.4

bn

Guidance on content cost inflation and margins is comforting

Following renegotiation of its large content deals in 2014, Dish TV’s content cost as a

proportion of subscription revenues has reduced by about 400 bps to 30.3% over FY2014-

16. A resetting of content contracts at higher rate upon upcoming renewals with Star and

Zee in Sep 2016 was a key concern of several investors. We believe Dish TV’s prevailing

content costs as a percentage of revenues is a function of efficient negotiations; we were

not expecting any material headwind to margins. TRAI’s ongoing consultative process

following TDSAT judgment ordering non-discriminatory pricing between broadcasters and all

distributors (cable as well as DTH platforms) has strengthened DTH’s negotiating power, at

the margin. Dish TV management has guided for 7-10% increase on content costs in

FY2017, marginally below our below-consensus content cost inflation estimate. We are

building 10% and 12.5% increase in content costs for FY2017E and FY2018E. FY2017

EBITDA margin guidance is at 35%.

Brand-building efforts encouraging, robust HD sales imperative for ARPU

growth

HD accounts for 10% of net subscriber base and 20% of subscriber additions. Dish TV’s HD

subs and penetration is lower than some of its peers, partly due to the difference in

positioning of various players and slightly lower focus of Dish TV on HD. The management

has stepped up brand-building and it is visible in the increase in advertising across mediums

(advertising expense increased to `250 mn from `140 mn in the previous quarter). Brand-

building exercise is encouraging. Pick-up in HD sales from current levels is required for

steady growth in ARPU and to partly offset the drag of low-ARPU packs on overall ARPU.

We note that HD tarriff is about `190-250 higher than a SD pack while Dish99 and Zing are

about `70-100 below SD base pack.

Strict and timely implementation of digitization (low probability event) present

upside to subscriber growth expectations

Dish TV has guided for 1.5 mn net subscriber additions in FY2017E, below our and street’s

expectations of about 1.65-2 mn. Dish has not built any benefit from digitization given

uncertainty around implementation timelines in view of pending court cases. In the event of

acceleration in digitization activity, sub adds could be higher. As per the management,

about 6-7 mn subscribers in phase III markets are yet to be digitized while 14 mn STBs have

been seeded (total STB requirement for phase III was about 20 mn).

Media DishTV

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

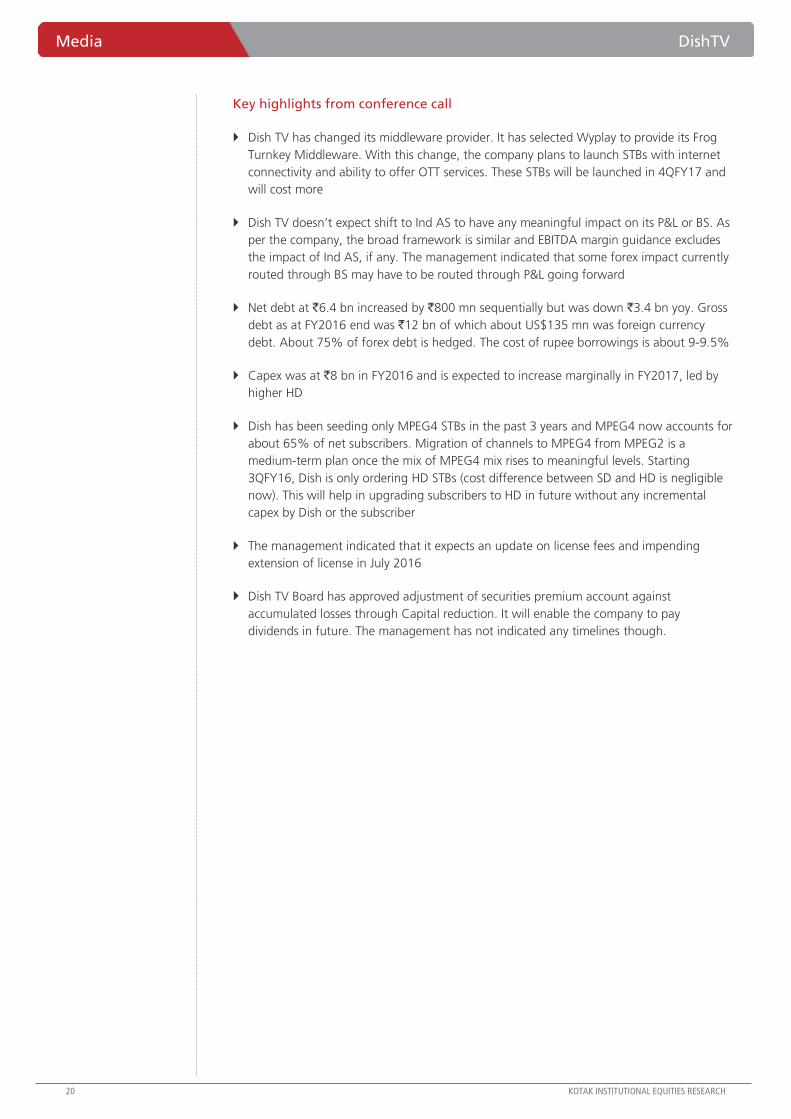

Key highlights from conference call

Dish TV has changed its middleware provider. It has selected Wyplay to provide its Frog

Turnkey Middleware. With this change, the company plans to launch STBs with internet

connectivity and ability to offer OTT services. These STBs will be launched in 4QFY17 and

will cost more

Dish TV doesn’t expect shift to Ind AS to have any meaningful impact on its P&L or BS. As

per the company, the broad framework is similar and EBITDA margin guidance excludes

the impact of Ind AS, if any. The management indicated that some forex impact currently

routed through BS may have to be routed through P&L going forward

Net debt at `6.4 bn increased by `800 mn sequentially but was down `3.4 bn yoy. Gross

debt as at FY2016 end was `12 bn of which about US$135 mn was foreign currency

debt. About 75% of forex debt is hedged. The cost of rupee borrowings is about 9-9.5%

Capex was at `8 bn in FY2016 and is expected to increase marginally in FY2017, led by

higher HD

Dish has been seeding only MPEG4 STBs in the past 3 years and MPEG4 now accounts for

about 65% of net subscribers. Migration of channels to MPEG4 from MPEG2 is a

medium-term plan once the mix of MPEG4 mix rises to meaningful levels. Starting

3QFY16, Dish is only ordering HD STBs (cost difference between SD and HD is negligible

now). This will help in upgrading subscribers to HD in future without any incremental

capex by Dish or the subscriber

The management indicated that it expects an update on license fees and impending

extension of license in July 2016

Dish TV Board has approved adjustment of securities premium account against

accumulated losses through Capital reduction. It will enable the company to pay

dividends in future. The management has not indicated any timelines though.

DishTV Media

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Exhibit 1: Interim results of Dish TV India (DITV), March fiscal year-ends (Rs mn)

Source: Company, Kotak Institutional Equities

(b) chg (%) (b)

4QFY16 4QFY16E 4QFY15 3QFY16 4QFY16E 4QFY15 3QFY16 FY2016 FY2015 chg (%)

Total revenues 7,994 7,973 7,299 7,715 0 10 4 30,599 26,880 14

DTH serv ice revenues 7,480 7,438 6,751 7,211 1 11 4 28,675 25,302 13

Subscription revenues 7,410 7,328 6,581 7,111 1 13 4 28,275 24,502 15

Lease rental income 70 110 170 100 (36) (59) (30) 400 800 (50)

Bandwidth/Advertising revenues 420 435 430 410 (3) (2) 2 1,545 1,230 26

Other operating revenues 94 100 119 94 (6) (22) (0) 379 350 8

Total expenditure (5,385) (5,200) (5,090) (5,060) 4 6 6 (20,350) (19,548) 4

Direct operating costs (3,816) (3,750) (3,681) (3,695) 2 4 3 (14,780) (14,010) 5

--Content and other cost (2,315) (2,125) (2,076) (2,073) 9 12 12 (8,555) (8,008) 7

--License fees (551) (550) (543) (782) 0 1 (30) (2,175) (2,888) (25)

--Other direct cost (950) (1,075) (1,062) (840) (12) (11) 13 (4,051) (3,114) 30

Selling and distribution expenses (812) (750) (833) (679) 8 (3) 20 (2,835) (3,186) (11)

Employee expenses (298) (300) (248) (289) (1) 20 3 (1,229) (1,018) 21

Overhead expenses (459) (400) (328) (397) 15 40 16 (1,506) (1,334) 13

EBITDA 2,609 2,773 2,209 2,655 (6) 18 (2) 10,249 7,331 40

EBITDA Margin (%) 32.6 34.8 30.3 34.4 33.5 27.3

Other income 218 100 160 42 118 36 419 640 635 1

Interest expense (512) (500) (456) (549) 2 12 (7) (2,087) (1,754) 19

Depreciation (1,516) (1,550) (1,550) (1,463) (2) (2) 4 (5,907) (6,138) (4)

Pretax profits 799 823 363 686 (3) 120 17 2,895 74

Extraordinaries — — — — — —

Tax provision 4,029 — (14) — 4,029 (42)

Minority interest — — — — — —

Net income 4,828 823 350 686 486 1,282 604 6,924 31 NA

EPS 4.5 0.8 0.3 0.6 6.5 0.0

Operational metrics

Net subscriber additions ('000s) 508 475 404 317 6.9 25.7 60.3 1.55 1.53

Net paying subscribers (mn) 14.5 14.4 12.9 14.0 0.2 12.0 3.6 14.5 12.92

Subs ARPU (Rs/month/sub) 174 172 179 172 1.2 (2.8) 1.2 175 172

Annualized churn rate (%) 8.4 7.7 8.4 8.4 8 (0) (1)

Notes:

(a) Starting 1QFY16, Dish TV has started netting-off certain collection fees (commisions) paid to its trade partners from its revenues

and costs. This change is EBITDA neutral.

(b) 4QFY15 and FY2015 financials restated for like-to-like comparison.

Media DishTV

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Revised estimates for DITV, FY2017E-18E (Rs mn)

Source: Company, Kotak Institutional Equities

Exhibit 3: Trends in Dish TV's net ARPU, 1QFY12-4QFY16 (Rs/sub/month)

Source: Company, Kotak Institutional Equities

Revised Previous Change (%)

2017E 2018E 2017E 2018E 2017E 2018E

Subscription revenues 32,183 36,339 32,454 37,061 (0.8) (1.9)

Other revenues 2,169 2,329 2,089 2,171 3.8 7.3

Total revenues 34,351 38,667 34,543 39,232 (0.6) (1.4)

Operating cost (16,151) (18,046) (16,282) (18,403) (0.8) (1.9)

Other expenses (6,360) (6,983) (6,380) (6,962) (0.3) 0.3

Total expenditure (22,511) (25,029) (22,662) (25,365) (0.7) (1.3)

EBITDA 11,841 13,638 11,881 13,867 (0.3) (1.7)

D&A expenses (6,124) (6,548) (6,380) (6,598) (4.0) (0.8)

EBIT 5,717 7,091 5,501 7,269 3.9 (2.5)

PAT 3,266 3,916 3,876 4,847 (15.7) (19.2)

EPS (Rs/share) 3.1 3.7 3.6 4.5 (15.7) (19.2)

EBITDA margin (%) 34.5 35.3 34.4 35.3

Key assumptions

Net subscribers yr-end (mn) 15.9 17.4 16.0 17.6

Net subscriber additions (mn) 1.48 1.47 1.63 1.55

ARPU (Rs/month/sub) 177 182 178 184

ARPU growth (yoy %) 2.5 2.9 3.0 3.4

Source: Company data, Kotak Institutional Equit ies

Notes.

(a) ARPU boosted by change in accouting policy start ing 1QFY15.

(b) ARPU suppressed by change in accouting policy start ing 1QFY16.

150 152 152 151

156

159 160 158

165 165 166

163

170 173

177 179

174 171 172

174

140

150

160

170

180

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

DishTV Media

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Exhibit 4: Strong pick-up in net subscriber additions in 4Q

Source: Company, Kotak Institutional Equities

Exhibit 5: Churn rate remains stable at 8.4% (annualized)

Source: Company, Kotak Institutional Equities

0

150

300

450

600

3.0

6.0

9.0

12.0

15.0

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

Net subscribers (LHS, mn) Net subscriber additions (RHS, '000s)

5

8

11

14

17

20

-

100

200

300

400

500

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

Churn (LHS, '000s) Annualised churn (RHS, %)

Media DishTV

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 6: Content costs growth likely to be in high-single digits in FY2017E

Source: Company, Kotak Institutional Equities

Exhibit 7: Trends in EBITDA margins and content inflation

Source: Company, Kotak Institutional Equities

(5)

5

15

25

35

500

1,000

1,500

2,000

2,500

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

Content costs (LHS, Rs mn) Growth (RHS, yoy %)

18

21

24

27

30

33

36

(10)

-

10

20

30

40

50

1Q

FY12

2Q

FY12

3Q

FY12

4Q

FY12

1Q

FY13

2Q

FY13

3Q

FY13

4Q

FY13

1Q

FY14

2Q

FY14

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

Content inflation (LHS, yoy %) EBITDA margin (RHS, %)

DishTV Media

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

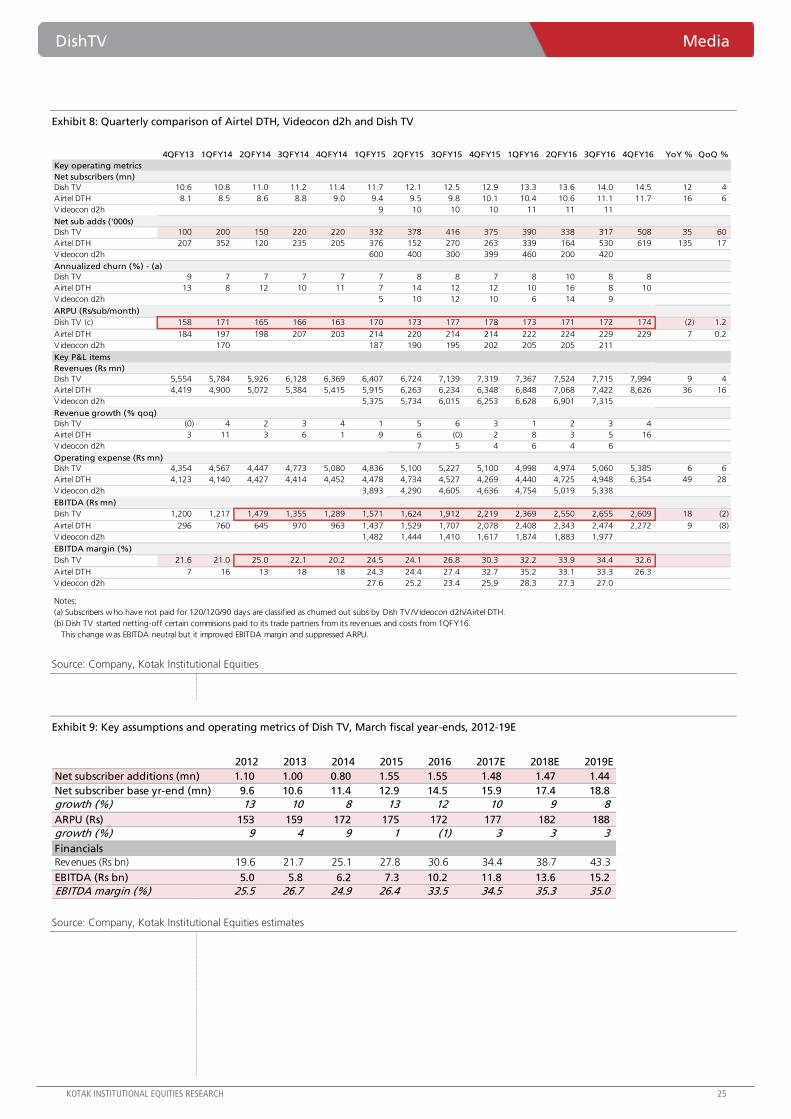

Exhibit 8: Quarterly comparison of Airtel DTH, Videocon d2h and Dish TV

Source: Company, Kotak Institutional Equities

Exhibit 9: Key assumptions and operating metrics of Dish TV, March fiscal year-ends, 2012-19E

Source: Company, Kotak Institutional Equities estimates

4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 YoY % QoQ %

Key operating metrics

Net subscribers (mn)

Dish TV 10.6 10.8 11.0 11.2 11.4 11.7 12.1 12.5 12.9 13.3 13.6 14.0 14.5 12 4

Airtel DTH 8.1 8.5 8.6 8.8 9.0 9.4 9.5 9.8 10.1 10.4 10.6 11.1 11.7 16 6

Videocon d2h 9 10 10 10 11 11 11

Net sub adds ('000s)

Dish TV 100 200 150 220 220 332 378 416 375 390 338 317 508 35 60

Airtel DTH 207 352 120 235 205 376 152 270 263 339 164 530 619 135 17

Videocon d2h 600 400 300 399 460 200 420

Annualized churn (%) - (a)

Dish TV 9 7 7 7 7 7 8 8 7 8 10 8 8

Airtel DTH 13 8 12 10 11 7 14 12 12 10 16 8 10

Videocon d2h 5 10 12 10 6 14 9

ARPU (Rs/sub/month)

Dish TV (c) 158 171 165 166 163 170 173 177 178 173 171 172 174 (2) 1.2

Airtel DTH 184 197 198 207 203 214 220 214 214 222 224 229 229 7 0.2

Videocon d2h 170 187 190 195 202 205 205 211

Key P&L items

Revenues (Rs mn)

Dish TV 5,554 5,784 5,926 6,128 6,369 6,407 6,724 7,139 7,319 7,367 7,524 7,715 7,994 9 4

Airtel DTH 4,419 4,900 5,072 5,384 5,415 5,915 6,263 6,234 6,348 6,848 7,068 7,422 8,626 36 16

Videocon d2h 5,375 5,734 6,015 6,253 6,628 6,901 7,315

Revenue growth (% qoq)

Dish TV (0) 4 2 3 4 1 5 6 3 1 2 3 4

Airtel DTH 3 11 3 6 1 9 6 (0) 2 8 3 5 16

Videocon d2h 7 5 4 6 4 6

Operating expense (Rs mn)

Dish TV 4,354 4,567 4,447 4,773 5,080 4,836 5,100 5,227 5,100 4,998 4,974 5,060 5,385 6 6

Airtel DTH 4,123 4,140 4,427 4,414 4,452 4,478 4,734 4,527 4,269 4,440 4,725 4,948 6,354 49 28

Videocon d2h 3,893 4,290 4,605 4,636 4,754 5,019 5,338

EBITDA (Rs mn)

Dish TV 1,200 1,217 1,479 1,355 1,289 1,571 1,624 1,912 2,219 2,369 2,550 2,655 2,609 18 (2)

Airtel DTH 296 760 645 970 963 1,437 1,529 1,707 2,078 2,408 2,343 2,474 2,272 9 (8)

V ideocon d2h 1,482 1,444 1,410 1,617 1,874 1,883 1,977

EBITDA margin (%)

Dish TV 21.6 21.0 25.0 22.1 20.2 24.5 24.1 26.8 30.3 32.2 33.9 34.4 32.6

Airtel DTH 7 16 13 18 18 24.3 24.4 27.4 32.7 35.2 33.1 33.3 26.3

V ideocon d2h 27.6 25.2 23.4 25.9 28.3 27.3 27.0

Notes:

(a) Subscribers who have not paid for 120/120/90 days are classified as churned out subs by Dish TV/V ideocon d2h/Airtel DTH.

(b) Dish TV started netting-off certain commisions paid to its trade partners from its revenues and costs from 1QFY16.

This change was EBITDA neutral but it improved EBITDA margin and suppressed ARPU.

2012 2013 2014 2015 2016 2017E 2018E 2019E

Net subscriber additions (mn) 1.10 1.00 0.80 1.55 1.55 1.48 1.47 1.44

Net subscriber base yr-end (mn) 9.6 10.6 11.4 12.9 14.5 15.9 17.4 18.8

growth (%) 13 10 8 13 12 10 9 8

ARPU (Rs) 153 159 172 175 172 177 182 188

growth (%) 9 4 9 1 (1) 3 3 3

Financials

Revenues (Rs bn) 19.6 21.7 25.1 27.8 30.6 34.4 38.7 43.3

EBITDA (Rs bn) 5.0 5.8 6.2 7.3 10.2 11.8 13.6 15.2

EBITDA margin (%) 25.5 26.7 24.9 26.4 33.5 34.5 35.3 35.0

Media DishTV

26 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 10: Financial summary of Dish TV, March fiscal year-ends, 2012-19E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

2012 2013 2014 2015 2016E 2017E 2018E 2019E

Profit model

Net revenues 19,578 21,668 25,090 27,816 30,599 34,351 38,667 43,340

EBITDA 4,984 5,795 6,240 7,331 10,249 11,841 13,638 15,173

Other income 386 443 649 635 640 684 736 947

Interest (expense)/income (1,268) (1,284) (1,328) (1,754) (2,087) (2,279) (1,867) (1,279)

Depreciation (5,180) (6,276) (5,974) (6,138) (5,907) (6,124) (6,548) (6,660)

Amortization — — — — — — — —

Pretax profits (1,079) (1,321) (412) 74 2,895 4,122 5,960 8,181

Extraordinary items (510) 663 (1,164) — — — — —

Tax — — — (42) 0 (824) (1,967) (2,425)

Deferred taxation — — 0 0 4,029 (32) (77) (192)

Net income (1,079) (658) (1,576) 31 6,924 3,266 3,916 5,564

Earnings per share (Rs) (1.0) (0.6) (1.5) 0.0 6.5 3.1 3.7 5.2

Balance sheet

Total equity (938) (1,553) (3,126) (3,134) 3,807 7,073 10,989 15,270

Deferred taxation liability — — 0 0 (4,360) (4,328) (4,251) (4,059)

Total borrow ings 14,003 16,330 14,095 14,839 12,063 10,035 7,035 7,035

Current liabilities 13,275 16,773 16,733 19,958 23,523 24,990 26,314 28,022

Total liabilities and equity 26,340 31,550 27,702 31,663 35,033 37,770 40,087 46,267

Cash 3,921 3,718 3,426 4,286 3,392 3,099 2,416 5,773

Other current assets 2,831 4,176 4,479 5,866 5,121 6,278 7,506 8,717

Total fixed assets 18,088 20,874 17,797 19,510 24,201 26,074 27,846 29,458

Intangible assets 1,500 — 500 0 819 819 819 819

Investments — 2,782 1,500 2,000 1,500 1,500 1,500 1,500

Total assets 26,340 31,550 27,702 31,663 35,033 37,770 40,087 46,267

Free cash flow

Operating cash flow, ex. working capital 5,035 5,570 5,078 7,270 7,129 10,560 11,158 13,181

Working capital changes (305) 570 1,977 404 4,310 311 95 496

Capital expenditure (6,553) (6,980) (2,989) (7,064) (8,075) (8,340) (8,706) (8,705)

Investments 690 (1,059) (432) (198) (319) — — —

Other income 345 343 438 563 640 684 736 947

Free cash flow (1,823) (840) 4,066 611 3,364 2,530 2,547 4,972

Ratios (%)

Debt/equity (1,493) (1,052) (451) (474) 317 142 64 46

Net debt/equity (1,075) (812) (341) (337) 228 98 42 8

ROAE (%) (7) (4) (9) 0 42 20 23 33

ROACE (%) 1 (0) 3 3 40 18 20 27

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

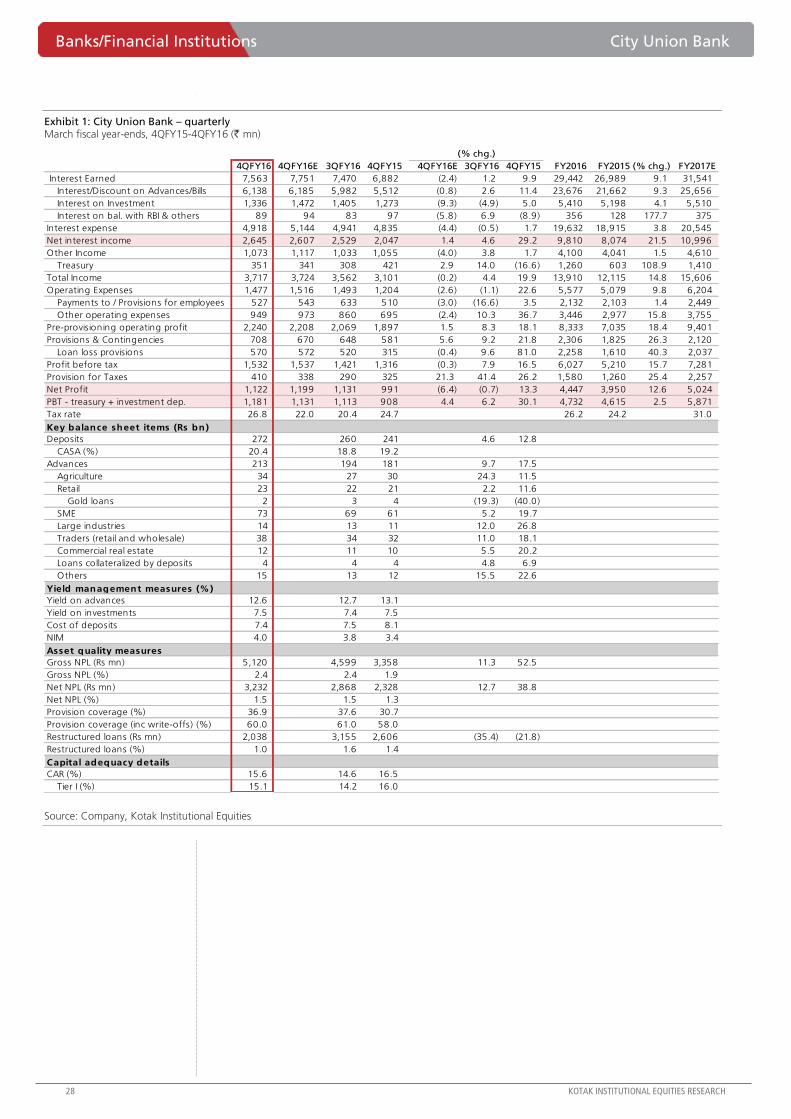

Steady performance driven by NIM expansion and loan growth

CUBK delivered in-line PBT growth of 16% yoy (13% yoy PAT growth on higher tax rate), as

17% yoy loan growth and NIM expansion (~50 bps yoy and ~15 bps qoq) drove 29% NII

growth. Other income growth was muted at 2% yoy as treasury income declined sharply by

17% yoy, while core fee growth was soft at 2% yoy. Operating expense growth was 23% yoy

(on a lower base), driven by non-staff costs. Credit costs increased 22% yoy, with the ratio

increasing by ~10 bps qoq to 1.2%. Ex-gold loan growth of 23% yoy was driven by segments

across the board, and SME/traders segment more specifically. CASA ratio improvement of ~150

bps to 20% and growth of ~20% yoy need more quarters of growth to establish as a trend.

Gross NPL unchanged qoq at 2.4%; slippages in steel along expected lines

CUBK reported stable qoq gross NPL ratio at 2.4%. Slippages increased 10 bps qoq to 1.2% as

one steel account, previously highlighted as weak, slipped from standard restructured loans

(~50% of slippage in the quarter). As such, total impaired loans declined ~60 bps qoq to 3.4%.

Consequently, SMA-2 outstanding declined ~100 bps qoq to 4.4% of loans. The bank did not

sell any loans to ARC in the year and the current SR book is about 1.7% of loans. The bank has

guided slippages of 1.75-2.0% for FY2017E. Recovery/upgrade was weak in the quarter due to

delay in sale/closure, with higher write-offs leading to stable GNPL ratio. We estimate gradual

decline in slippages from 2.3% in FY2016 to 1.9% by FY2019E, leading to decline in credit

costs from 1.2% to 0.7% during this period.

Maintain BUY with TP of `120

We maintain our BUY rating on the stock with TP at ₹120 (from ₹110). At our TP, we value the

bank at 1.9X book and 12X FY2018E EPS for RoEs in the range of ~15-16% and ~15% CAGR

in the medium term. While the bank has clearly outperformed other regional banks, current

valuation of ~1.6X FY2018E book is attractive to own this franchise that is predominantly based

in southern India and has seen relatively lower impairment trends than the sector. The bank is

well-capitalized with tier-1 ratio of 15%. The key risk for the bank would be to deliver earnings

growth given the expected decline in NIM and expense growth, without being too aggressive