India Daily, April 25, 2012 - Kotak Securities

59

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL. INDIA DAILY April 25, 2012 India 24-Apr 1-day1-mo 3-mo Sensex 17,207 0.6 (0.9) 0.8 Nifty 5,223 0.4 (1.1) 1.2 Global/Regional indices Dow Jones 13,002 0.6 (0.6) 1.9 Nasdaq Composite 2,962 (0.3) (3.5) 5.1 FTSE 5,709 0.8 (2.5) (0.2) Nikkie 9,535 0.7 (4.8) 7.3 Hang Seng 20,702 0.1 0.2 2.9 KOSPI 1,969 0.3 (2.9) 0.8 Value traded – India Cash (NSE+BSE) 141 138 163 Derivatives (NSE) 1,501 1,698 2,053 Deri. open interest 1,283 1,476 1,435 Forex/money market Change, basis points 24-Apr 1-day 1-mo 3-mo Rs/US$ 52.5 (16) 148 229 10yr govt bond, % 8.6 4 16 30 Net investment (US$mn) 23-Apr MTD CYTD FIIs (65) 109 8,975 MFs (19) (79) (282) Top movers -3mo basis Change, % Best performers 24-Apr 1-day 1-mo 3-mo TTMT IN Equity 311.9 0.7 14.4 35.0 TGBL IN Equity 118.5 0.9 5.1 24.4 APNT IN Equity 3462.0 (0.3) 11.3 21.5 HCLT IN Equity 510.2 3.0 5.2 21.2 ITC IN Equity 245.1 0.1 10.2 18.9 Worst performers ADE IN Equity 278.9 0.2 (3.4) (30.3) ESOIL IN Equity 51.4 (0.5) (5.9) (17.6) SUEL IN Equity 22.7 0.2 (18.9) (16.7) RCOM IN Equity 80.4 (1.4) (10.1) (16.4) UNTP IN Equity 120.0 (6.1) (9.7) (16.3) Contents Daily Alerts Results Sesa Goa: Quarterly numbers muted, but in line Coromandel International: Higher sales into channel inventories mean weak 1HFY13 Rallis India: Disappointing results Polaris Financial Technology: No saving grace Results, Change in Reco Petronet LNG: Weak results Change in Reco Larsen & Toubro: Risk-reward in fair balance after sharp correction; upgrade to ADD Company Reliance Industries: Lessons from disappointments Sector Infrastructure: West coast container capacity delay to benefit Mundra/Pipavav; upgrade ADSEZ News Round-up COAL IN. Power producers (including NTPC) have refused to sign the new Fuel Supply Agreement with Coal India, saying that the proposed contract is biased and absolves the state-owned companies of all obligations. (ECNT) COAL IN. Coal India said it has fixed a production target of 468.74 MT for the current FY. (BSTD) RPWR IN. The Asian Development Bank (ADB) agreed to lend a further USD 103mn to a solar power project owned by Reliance Power in Rajasthan. (THBL) PLNG IN. Petronet LNG may get strategic partner to buy Asian Development Bank's (ADB) stake in the company. The bank is planning to sell its 5.2% stake in Petronet LNG. (THBL) STLT IN / SESA IN. The Competition Commission of India has approved the merger of Sterlite Industries & Sesa Goa that was announced by parent company Vedanta Resources on February 25th. (BSTD) BHFC IN. Alstom-Bharat Forge said it has bagged a USD 302mn order for supplying power equipment to state-run NTPC's power plants. (BSTD) UNBK IN / CRPBK IN. Union Bank of India and Corporation Bank has slashed their benchmark lending rate by 15bps. (ECNT) AXSB IN. Axis Bank’s proposed acquisition of Enam Securities’ businesses has received final approval from the RBI. The bank now aims to integrate these operations by the end of 3rd quarter of this FY. (BSTD) Source: ECNT= Economic Times, BSTD = Business Standard, FNLE = Financial Express, THBL = Business Line.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of India Daily, April 25, 2012 - Kotak Securities

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

INDIA DAILYApril 25, 2012 India 24-Apr 1-day1-mo 3-mo

Sensex 17,207 0.6 (0.9) 0.8

Nifty 5,223 0.4 (1.1) 1.2

Global/Regional indices

Dow Jones 13,002 0.6 (0.6) 1.9

Nasdaq Composite 2,962 (0.3) (3.5) 5.1

FTSE 5,709 0.8 (2.5) (0.2)

Nikkie 9,535 0.7 (4.8) 7.3

Hang Seng 20,702 0.1 0.2 2.9

KOSPI 1,969 0.3 (2.9) 0.8

Value traded – India

Cash (NSE+BSE) 141 138 163

Derivatives (NSE) 1,501 1,698 2,053

Deri. open interest 1,283 1,476 1,435

Forex/money market

Change, basis points

24-Apr 1-day 1-mo 3-mo

Rs/US$ 52.5 (16) 148 229

10yr govt bond, % 8.6 4 16 30

Net investment (US$mn)

23-Apr MTD CYTD

FIIs (65) 109 8,975

MFs (19) (79) (282)

Top movers -3mo basis

Change, %

Best performers 24-Apr 1-day 1-mo 3-mo

TTMT IN Equity 311.9 0.7 14.4 35.0

TGBL IN Equity 118.5 0.9 5.1 24.4

APNT IN Equity 3462.0 (0.3) 11.3 21.5

HCLT IN Equity 510.2 3.0 5.2 21.2

ITC IN Equity 245.1 0.1 10.2 18.9

Worst performers

ADE IN Equity 278.9 0.2 (3.4) (30.3)

ESOIL IN Equity 51.4 (0.5) (5.9) (17.6)

SUEL IN Equity 22.7 0.2 (18.9) (16.7)

RCOM IN Equity 80.4 (1.4) (10.1) (16.4)

UNTP IN Equity 120.0 (6.1) (9.7) (16.3)

Contents

Daily Alerts

Results

Sesa Goa: Quarterly numbers muted, but in line

Coromandel International: Higher sales into channel inventories mean weak 1HFY13

Rallis India: Disappointing results

Polaris Financial Technology: No saving grace

Results, Change in Reco

Petronet LNG: Weak results

Change in Reco

Larsen & Toubro: Risk-reward in fair balance after sharp correction; upgrade to ADD

Company

Reliance Industries: Lessons from disappointments

Sector

Infrastructure: West coast container capacity delay to benefit Mundra/Pipavav; upgrade ADSEZ

News Round-up

COAL IN. Power producers (including NTPC) have refused to sign the new Fuel Supply Agreement with Coal India, saying that the proposed contract is biased and absolves the state-owned companies of all obligations. (ECNT)

COAL IN. Coal India said it has fixed a production target of 468.74 MT for the current FY. (BSTD)

RPWR IN. The Asian Development Bank (ADB) agreed to lend a further USD 103mn to a solar power project owned by Reliance Power in Rajasthan. (THBL)

PLNG IN. Petronet LNG may get strategic partner to buy Asian Development Bank's (ADB) stake in the company. The bank is planning to sell its 5.2% stake in Petronet LNG. (THBL)

STLT IN / SESA IN. The Competition Commission of India has approved the merger of Sterlite Industries & Sesa Goa that was announced by parent company Vedanta Resources on February 25th. (BSTD)

BHFC IN. Alstom-Bharat Forge said it has bagged a USD 302mn order for supplying power equipment to state-run NTPC's power plants. (BSTD)

UNBK IN / CRPBK IN. Union Bank of India and Corporation Bank has slashed their benchmark lending rate by 15bps. (ECNT)

AXSB IN. Axis Bank’s proposed acquisition of Enam Securities’ businesses has received final approval from the RBI. The bank now aims to integrate these operations by the end of 3rd quarter of this FY. (BSTD)

Source: ECNT= Economic Times, BSTD = Business Standard, FNLE = Financial Express, THBL = Business Line.

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

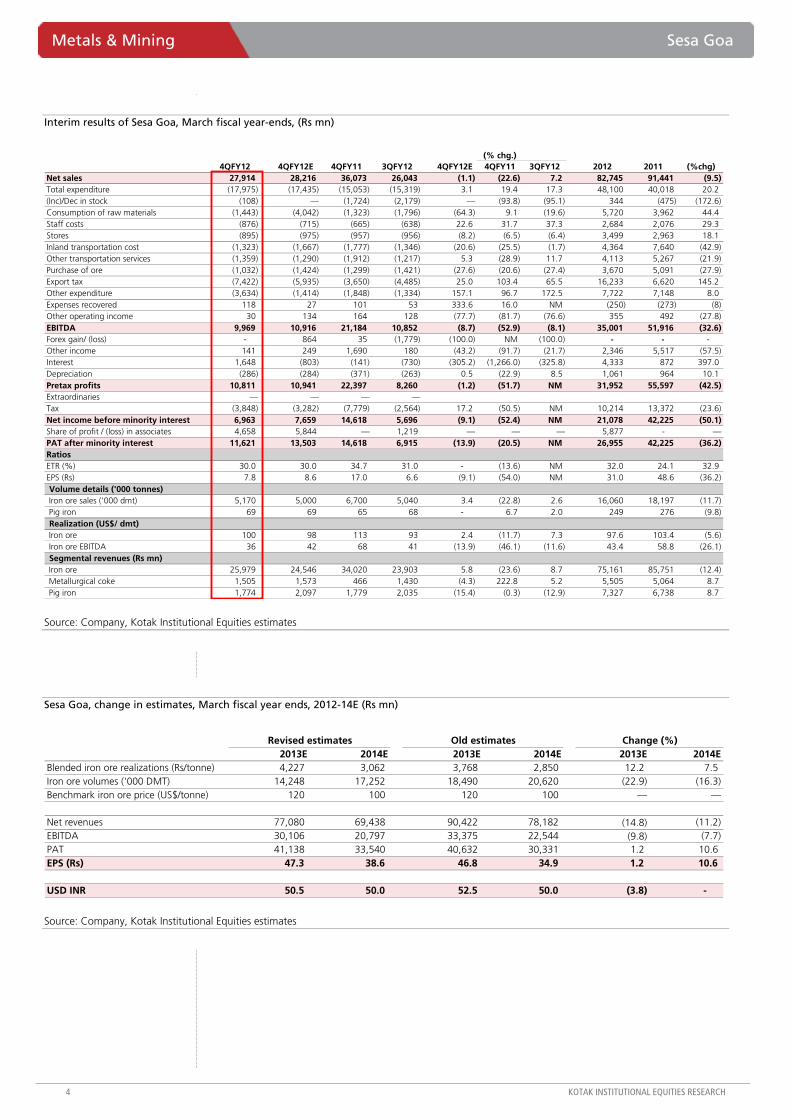

Quarterly performance muted, but in line

Sesa reported EBITDA of Rs9.97 bn, down 52.9% yoy. EBITDA performance was impacted by (1) an increase in exports tax to 30% and (2) lower volumes due to logistics constraints in Goa and continuation of the mining ban in Karnataka. Adjusting for a forex loss of Rs1.5 bn, reported in other expenses, EBITDA was 5.1% ahead of our estimate. Iron ore realization of US$100/tonne increased 7.3% qoq and declined 11.7 % yoy. Net income of Rs11.6 bn was in line with our estimates and includes Rs4.66 bn from consolidation of share of earnings in Cairn India.

Iron ore shipments in 4QFY12, of 5.2 mn tones, declined 22.8 % yoy. In FY2012 iron ore shipments declined 7.2% to 16 mn tonnes—a reflection of logistics constraints in Goa, a mining ban in Karnataka and termination of a mining lease agreement with a third party in Orissa due to unfavorable contractual terms.

Volumes may decline in FY2013E

Sesa’s Karnataka iron ore mine has been classified in Category B in the CEC report that was submitted to the Supreme Court. Category B comprises mining leases with moderate violations. CEC recommended restart of mining only after a comprehensive set of measures is implemented. The Supreme Court of India has refrained from giving specific direction on the restart of mining by Category B mines. Restart of mining in Karnataka, as a result, remains uncertain for Sesa. Mines in Goa have been impacted by logistics constraints and trucking restrictions. Therefore, we cut FY2013E and FY2014E volumes by 23% and 16% to 14.2 mn and 17.2 mn tonnes respectively.

Consolidated operations matter for valuation; iron ore is one of the many segments

After group restructuring, all assets owned by Vedanta Resources, except Konkola Copper Mines, will be consolidated into a single entity, Sesa Sterlite. Valuations, as a result, will be influenced by performance of assets/companies operating in verticals such as energy, zinc, aluminium, power and other businesses. We value the Sesa Sterlite business at Rs220, based on SOTP valuation for different business segments. We retain our ADD rating on the stock due to inexpensive valuations. Our fair value is based on conservative assumptions.

Sesa Goa (SESA)

Metals & Mining

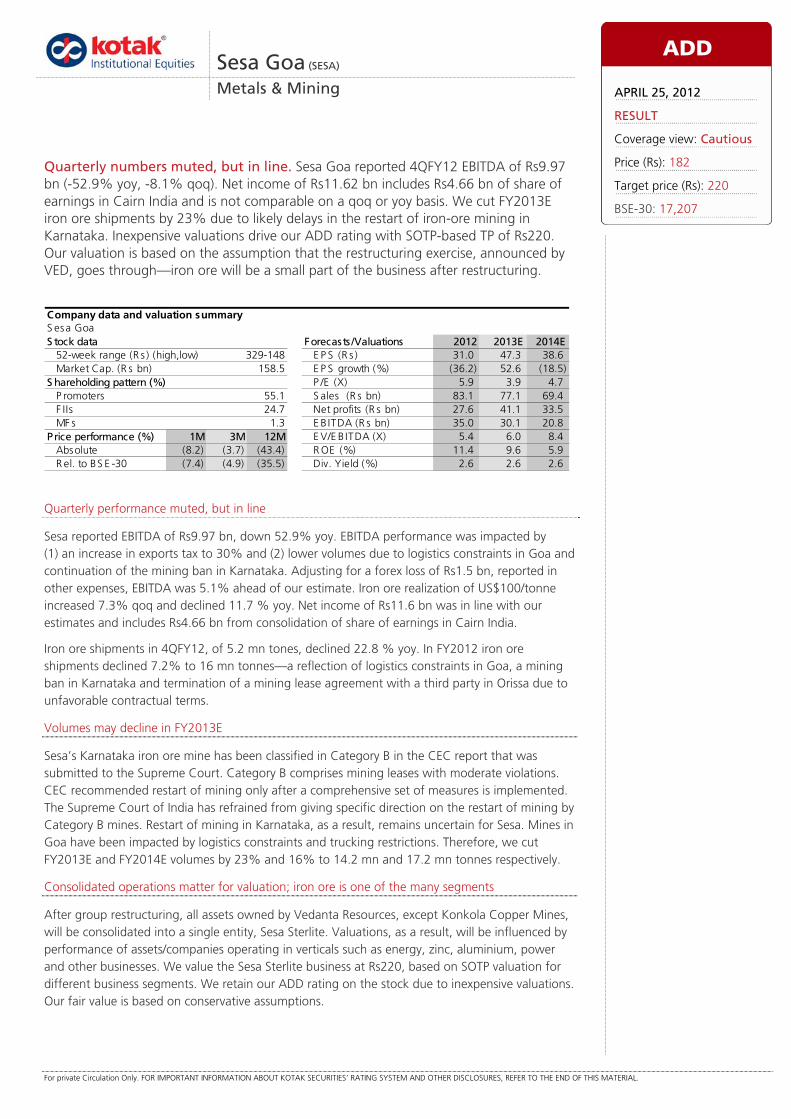

Quarterly numbers muted, but in line. Sesa Goa reported 4QFY12 EBITDA of Rs9.97 bn (-52.9% yoy, -8.1% qoq). Net income of Rs11.62 bn includes Rs4.66 bn of share of earnings in Cairn India and is not comparable on a qoq or yoy basis. We cut FY2013E iron ore shipments by 23% due to likely delays in the restart of iron-ore mining in Karnataka. Inexpensive valuations drive our ADD rating with SOTP-based TP of Rs220. Our valuation is based on the assumption that the restructuring exercise, announced by VED, goes through—iron ore will be a small part of the business after restructuring.

S esa GoaS tock data Forecasts /Valuations 2012 2013E 2014E

52-week range (R s ) (high,low) E P S (R s ) 31.0 47.3 38.6Market Cap. (R s bn) 158.5 E P S growth (%) (36.2) 52.6 (18.5)

S hareholding pattern (%) P /E (X) 5.9 3.9 4.7P romoters 55.1 S ales (R s bn) 83.1 77.1 69.4F IIs 24.7 Net profits (R s bn) 27.6 41.1 33.5MF s 1.3 E B ITDA (R s bn) 35.0 30.1 20.8

Price performance (%) 1M 3M 12M E V/E B ITDA (X) 5.4 6.0 8.4Absolute (8.2) (3.7) (43.4) R OE (%) 11.4 9.6 5.9R el. to BS E -30 (7.4) (4.9) (35.5) Div. Yield (%) 2.6 2.6 2.6

Company data and valuation summary

329-148

ADD

APRIL 25, 2012

RESULT

Coverage view: Cautious

Price (Rs): 182

Target price (Rs): 220

BSE-30: 17,207

Sesa Goa Metals & Mining

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Announcement of addition to reserves and resources, a positive

Sesa announced net accretion of 68 mn tonnes to reserves and resources, taking the total number to 374 mn tonnes. A press release indicates that R&R has been reviewed and certified as per JORC standards. Cut off Fe grade used to assess R&R is consistent with earlier years. R&R of 306 mn tonnes as at FY 2011 was divided into A Narrain mine in Karnataka with R&R of 51.4 mn tonnes and various mines in Goa accounting for the balance R&R. Average Fe grade of R&R in FY2011 was ~52%.

Accretion to reserves is a positive, though the challenge is to get approval to restart mining in Karnataka and investment in logistics, and EC clearance to step-up exports from Goa.

We value iron ore business at Rs30/share post restructure; Rs90 pre-restructure

We expect iron ore prices to remain in a narrow band in 2012 before declining in 2013 and beyond. Slowdown in China would have hurt but for continued iron ore supply issues in India. Production step-up from major and junior miners in Australia and likely easing of logistics constraints in Brazil will lead to steady easing of iron ore prices. Our estimates for the iron ore business are based on benchmark iron price assumptions of US$120 and US$100/tonne for FY2013E and FY2014E, respectively.

We value the iron ore business at Rs87/share based on near-term iron ore price, as indicated above, and long-term iron ore price assumption of US$85/tonne. We assume mining operations in Karnataka will restart in FY2014 and assume R&R accretion of 10 mn tonnes in DCF-based fair value for the business.

Other details

Sesa has declared final dividend of Rs2/share, taking the total dividend payout to Rs4/share in FY2012.

4QFY12 results included one-off charge of Rs661 mn for the Cairn India acquisition.

Sesa has reclassified reporting of forex losses between the other expenses line (above EBITDA) and finance cost. Forex gain was Rs800 mn in 4QFY12. Sesa partly adjusted forex loss of 9MFY12 in the other expenses line in 4QFY12.

Sesa reported cash and cash equivalents of Rs5.9 bn and debt of Rs37.3 bn at the end of March 2012.

Metals & Mining Sesa Goa

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Interim results of Sesa Goa, March fiscal year-ends, (Rs mn)

(% chg.)4QFY12 4QFY12E 4QFY11 3QFY12 4QFY12E 4QFY11 3QFY12 2012 2011 (%chg)

Net sales 27,914 28,216 36,073 26,043 (1.1) (22.6) 7.2 82,745 91,441 (9.5) Total expenditure (17,975) (17,435) (15,053) (15,319) 3.1 19.4 17.3 48,100 40,018 20.2 (Inc)/Dec in stock (108) — (1,724) (2,179) — (93.8) (95.1) 344 (475) (172.6) Consumption of raw materials (1,443) (4,042) (1,323) (1,796) (64.3) 9.1 (19.6) 5,720 3,962 44.4 Staff costs (876) (715) (665) (638) 22.6 31.7 37.3 2,684 2,076 29.3 Stores (895) (975) (957) (956) (8.2) (6.5) (6.4) 3,499 2,963 18.1 Inland transportation cost (1,323) (1,667) (1,777) (1,346) (20.6) (25.5) (1.7) 4,364 7,640 (42.9) Other transportation services (1,359) (1,290) (1,912) (1,217) 5.3 (28.9) 11.7 4,113 5,267 (21.9) Purchase of ore (1,032) (1,424) (1,299) (1,421) (27.6) (20.6) (27.4) 3,670 5,091 (27.9) Export tax (7,422) (5,935) (3,650) (4,485) 25.0 103.4 65.5 16,233 6,620 145.2 Other expenditure (3,634) (1,414) (1,848) (1,334) 157.1 96.7 172.5 7,722 7,148 8.0 Expenses recovered 118 27 101 53 333.6 16.0 NM (250) (273) (8) Other operating income 30 134 164 128 (77.7) (81.7) (76.6) 355 492 (27.8) EBITDA 9,969 10,916 21,184 10,852 (8.7) (52.9) (8.1) 35,001 51,916 (32.6) Forex gain/ (loss) - 864 35 (1,779) (100.0) NM (100.0) - - - Other income 141 249 1,690 180 (43.2) (91.7) (21.7) 2,346 5,517 (57.5) Interest 1,648 (803) (141) (730) (305.2) (1,266.0) (325.8) 4,333 872 397.0 Depreciation (286) (284) (371) (263) 0.5 (22.9) 8.5 1,061 964 10.1 Pretax profits 10,811 10,941 22,397 8,260 (1.2) (51.7) NM 31,952 55,597 (42.5) Extraordinaries — — — —Tax (3,848) (3,282) (7,779) (2,564) 17.2 (50.5) NM 10,214 13,372 (23.6) Net income before minority interest 6,963 7,659 14,618 5,696 (9.1) (52.4) NM 21,078 42,225 (50.1) Share of profit / (loss) in associates 4,658 5,844 — 1,219 — — — 5,877 - —PAT after minority interest 11,621 13,503 14,618 6,915 (13.9) (20.5) NM 26,955 42,225 (36.2) RatiosETR (%) 30.0 30.0 34.7 31.0 - (13.6) NM 32.0 24.1 32.9 EPS (Rs) 7.8 8.6 17.0 6.6 (9.1) (54.0) NM 31.0 48.6 (36.2) Volume details ('000 tonnes)Iron ore sales ('000 dmt) 5,170 5,000 6,700 5,040 3.4 (22.8) 2.6 16,060 18,197 (11.7) Pig iron 69 69 65 68 - 6.7 2.0 249 276 (9.8) Realization (US$/ dmt)Iron ore 100 98 113 93 2.4 (11.7) 7.3 97.6 103.4 (5.6) Iron ore EBITDA 36 42 68 41 (13.9) (46.1) (11.6) 43.4 58.8 (26.1) Segmental revenues (Rs mn)Iron ore 25,979 24,546 34,020 23,903 5.8 (23.6) 8.7 75,161 85,751 (12.4) Metallurgical coke 1,505 1,573 466 1,430 (4.3) 222.8 5.2 5,505 5,064 8.7 Pig iron 1,774 2,097 1,779 2,035 (15.4) (0.3) (12.9) 7,327 6,738 8.7

Source: Company, Kotak Institutional Equities estimates

Sesa Goa, change in estimates, March fiscal year ends, 2012-14E (Rs mn)

Revised estimates Old estimates Change (%)2013E 2014E 2013E 2014E 2013E 2014E

Blended iron ore realizations (Rs/tonne) 4,227 3,062 3,768 2,850 12.2 7.5 Iron ore volumes ('000 DMT) 14,248 17,252 18,490 20,620 (22.9) (16.3) Benchmark iron ore price (US$/tonne) 120 100 120 100 — —

Net revenues 77,080 69,438 90,422 78,182 (14.8) (11.2) EBITDA 30,106 20,797 33,375 22,544 (9.8) (7.7) PAT 41,138 33,540 40,632 30,331 1.2 10.6 EPS (Rs) 47.3 38.6 46.8 34.9 1.2 10.6

USD INR 50.5 50.0 52.5 50.0 (3.8) -

Source: Company, Kotak Institutional Equities estimates

Sesa Goa Metals & Mining

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

SOTP-based target price of Sesa Sterlite

EBITDA Multiple EV Net debtImplied M Cap

Sterlite's stake

Attributable M Cap Contribution

(Rs bn) (X) (Rs bn) (Rs bn) (Rs bn) (%) (Rs bn) Rs/ share

BALCO 7 6.3 46 44.8 0.9 51.0 0 0 VAL 15 6.5 97 220.9 (123.5) 100.0 (124) (42) Copper business

Copper smelting business 10 6.0 63 (8) 70.9 100.0 71 24 Copper mining 2

Zinc businessHindustan Zinc 67 5.5 370 (220) 590 64.9 383 129 Zinc International 15 3.5 54 21 75 100.0 75 25

Sesa Goa (iron ore mining) 30 Cairn India (fair value assumed at the current market price) 133 Debt transferred for Cairn India acquisition (97) Synergies and other businesses 16 Target price (Rs/ share) 221

Source: Kotak Institutional Equities estimates

Sesa Goa, key assumptions, March fiscal year-ends, 2010-14E, (Rs mn)

2010 2011 2012E 2013E 2014E

Tonnages ('000 dmt)

Iron ore production 11,543 10,952 9,021 9,472 11,840

Iron ore purchases 5,185 4,029 1,595 1,595 1,595

Iron ore sales 15,177 14,368 12,820 11,067 13,435

Metallurgical coke sales 263 266 251 392 420

Pig Iron sales 270 266 251 375 500

Tonnages ('000 dmt) (consolidated)

Iron ore production 12,633 13,162 10,789 11,240 13,961

Iron ore purchases 7,445 5,794 3,008 3,008 3,290

Iron ore sales 19,434 18,256 16,000 14,248 17,252

Metallurgical coke sales 263 266 251 392 420

Pig Iron sales 270 266 251 375 500

Realizations

Average ore realization (US$/tonne) 53 93 91 84 61

Metallurgical coke prices (Rs/tonne) 13,545 17,731 22,782 21,329 19,714

Source: Company, Kotak Institutional Equities estimates

Metals & Mining Sesa Goa

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Sesa Sterlite, key assumptions, March fiscal year ends, 2010-14E (Rs mn)

2010 2011 2012E 2013E 2014EVolumes (tonnes)Aluminium metal 267,802 247,412 267,453 268,770 268,770 Copper 333,244 303,327 335,619 335,605 335,584 Iron ore ('000 dmt) 19,434 18,256 16,000 14,248 17,252 Lead 64,391 57,229 83,250 125,800 125,800 Power (mn units) — — 5,990 12,495 14,664 Refined silver 139 147 200 351 396 Zinc 577,685 712,603 769,125 804,285 835,050 Zinc International 427 442 452 453 Average realization (Rs/tonne)Aluminium ingots 96,607 118,384 122,071 135,730 137,500 Copper cathode 303,652 398,148 433,996 419,556 383,804 Iron ore (Rs/tonne) 2,909 4,665 4,453 4,227 3,062 Lead 105,922 114,877 112,210 114,235 124,571 Power (Rs/unit) 3.5 3.5 3.5 Silver (Rs mn/tonne) 25 37 46 44 45 Zinc 99,421 106,469 104,178 108,439 119,864 LME assumptions (US$/tonne)Zinc 1,936 2,186 2,050 2,025 2,300 Lead 1,990 2,244 2,150 2,100 2,350 Copper 6,500 8,138 8,300 7,450 7,150 Aluminium 1,900 2,257 2,225 2,350 2,450

Source: Company, Kotak Institutional Equities estimates

Sesa Goa Metals & Mining

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Earnings and valuation impact from Vedanta group restructuring (Rs mn)

Sterlite Sesa Goa Sesa-Sterlite2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E

EBITDA (attributable)Hindustan Zinc 39,391 43,649 53,083 39,391 43,649 53,083 Sterlite Industries- ex Hindustan Zinc 28,712 33,726 39,663 28,712 33,726 39,663 Sterlite Industries (consolidated) 68,103 77,375 92,745 68,103 77,375 92,745 Sesa Goa 35,001 30,106 20,797 35,001 30,106 20,797 Cairn India 59,216 81,460 69,783 VAL 4,425 14,971 15,272 Consolidated attributable EBITDA 68,103 77,375 92,745 35,001 30,106 20,797 166,744 203,912 198,598

Net debt (attributable)Hindustan Zinc (116,494) (142,842) (180,385) (116,494) (142,842) (180,385) Sterlite + subs- ex-HZ 44,308 36,364 2,125 44,308 36,364 2,125 Sterlite (72,186) (106,477) (178,259) (72,186) (106,477) (178,259) Cairn India (39,869) (59,105) (89,890) Sesa 31,325 21,897 15,202 31,325 21,897 15,202 VAL (excluding loans by Sterlite) 200,860 220,860 240,860 Cairn India acquisition debt pushdown 287,965 287,965 287,965 Attributable debt (72,186) (106,477) (178,259) 31,325 21,897 15,202 408,094 365,139 275,877

Shares outstanding (mn) 3,361 3,361 3,361 869 869 869 2,965 2,965 2,965 Stock price 107 107 107 186 186 186 181 181 181 Market capitalization 357,968 357,968 357,968 161,827 161,827 161,827 536,614 536,614 536,614 Value of Cairn India's stake (without holdco discount) 137,016 137,016 137,016 Enterprise value 285,781 251,491 179,708 56,135 46,708 40,013 944,708 901,754 812,491 EV/EBITDA (X) 4.2 3.3 1.9 1.6 1.6 1.9 5.7 4.4 4.1

Earnings impact (Rs mn)Hindustan Zinc 35,864 38,352 45,780 35,864 38,352 45,780 Sterlite-ex HZ 16,461 13,315 18,148 16,461 13,315 18,148 Sterlite - consolidated (excluding VAL) 52,325 51,668 63,928 52,325 51,668 63,928 Sesa Goa 14,088 12,944 8,392 21,078 17,891 11,868 Cairn India 51,002 65,162 54,882 VAL (assuming no capitalization of interest) (6,942) (2,002) (1,914) (23,533) (10,437) (10,429) Cairn India debt (14,974) (14,974) (14,974) Total 45,383 49,665 62,015 14,088 12,944 8,392 85,898 109,309 105,275

EPS 13.5 14.8 18.5 16.2 14.9 9.7 29.0 36.9 35.5 P/E (X) 7.9 7.2 5.8 11.5 12.5 19.3 6.2 4.9 5.1

Source: Kotak Institutional Equities estimates

Metals & Mining Sesa Goa

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Sesa Goa (consolidated), profit model, balance sheet and cash-flow model, March fiscal year-ends, 2009-2014E (Rs mn)

2010 2011 2012E 2013E 2014EProfit model (Rs mn)Net sales 58,583 92,051 83,101 77,080 69,438 EBITDA 31,448 51,543 35,001 30,106 20,797 Other income 4,260 5,399 2,346 698 1,222 Interes t (517) (381) (4,333) (3,239) (3,239) Depreciaiton (745) (964) (1,061) (1,080) (1,212) Profit before tax 34,446 55,597 31,952 26,484 17,568 Taxes (8,056) (13,372) (10,214) (8,593) (5,700) Net profit 26,390 42,225 21,078 17,891 11,868 Income from associates — — 5,877 23,247 21,672 PAT 26,291 42,225 26,955 41,138 33,540 Earnings per share (Rs) 29.4 48.6 31.0 47.3 38.6

Balance sheet (Rs mn)E quity 79,177 128,104 151,182 188,271 217,761 Deferred tax liability 750 682 1,046 1,046 1,046 Total Borrowings 19,606 9,995 37,342 37,342 37,342 Minority interes t 433 — — — —Current liabilities 12,400 17,256 14,442 10,815 9,977 Total liabilities 112,366 156,037 204,011 237,473 266,125 Net fixed assets 22,557 31,443 41,443 44,388 47,385 Inves tments 45,649 87,998 136,626 159,874 181,546 Cash 23,918 8,970 6,017 15,445 22,140 Other current as sets 20,242 27,626 19,925 17,767 15,054 Miscellaneous expenditure (0) — — — —Total assets 112,366 156,037 204,011 237,473 266,125 Free cash flow (Rs mn)Operating cash flow excl. working capital 23,922 38,372 19,793 18,274 11,858 Working capital changes 1,791 (3,037) 4,886 (1,469) 1,875 Capital expenditure (1,316) (8,330) (8,050) (4,025) (4,210) Free cash flow 24,397 27,005 16,629 12,780 9,524 RatiosDebt/equity (%) 0.2 0.1 0.2 0.2 0.2 Net debt/equity (%) (0.8) (0.8) 0.1 0.1 0.0 R oAE (%) 36.1 36.8 11.4 9.6 5.9 RoACE (%) 31.6 32.6 11.6 8.8 5.9

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

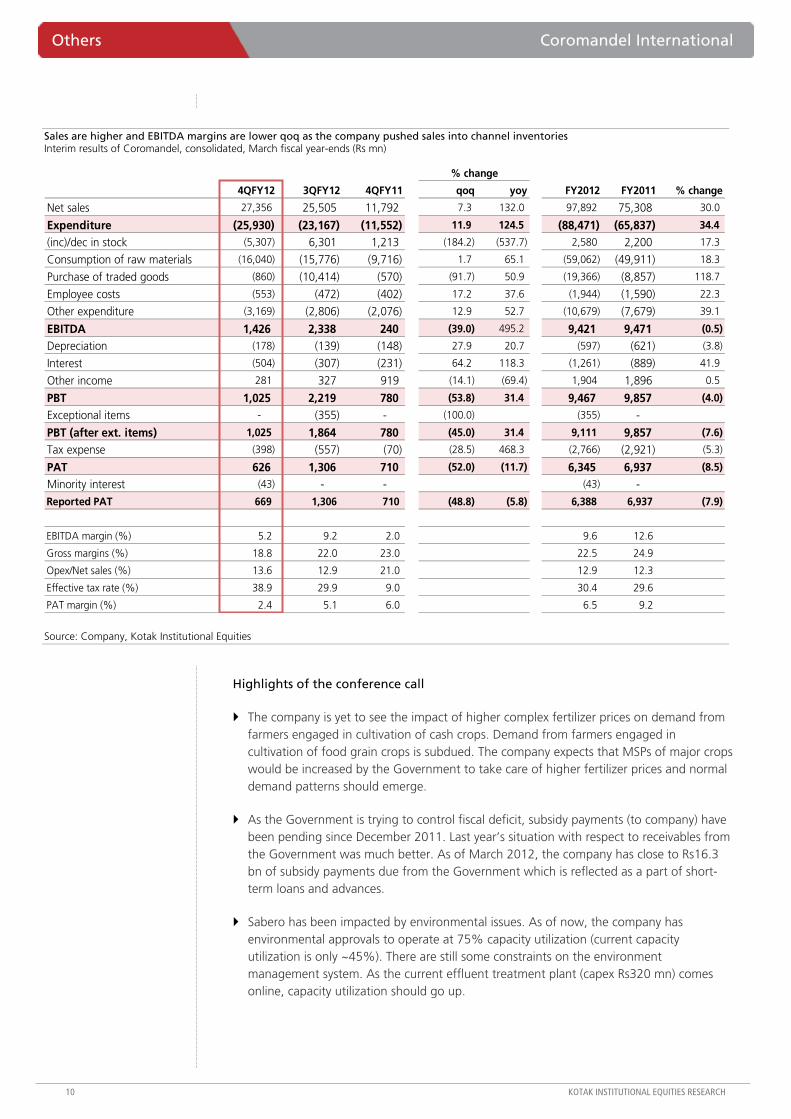

EBITDA margins weak – inventories pushed into sales channel

Coromandel reported net sales at Rs27.4 bn (+7.3% qoq, +132% yoy), significantly higher than our estimates. Reported EBITDA at Rs1.4 bn was in line with our estimates. The company reported 4QFY12 EBITDA margins at 5.2%, lower versus 9.2% in 3QFY12, even as sales moved higher qoq from Rs25.5 bn in 3QFY12. 4Q is a seasonally weaker quarter and higher sales qoq mean that the company has pushed inventories into the sales channel (dealer level) ahead of lower subsidy rates in FY2013. The fact that EBITDA margins have moved lower qoq means that the company has given discounts/other incentives in order to push sales.

As per the company, dip in EBITDA margins in 4QFY12 is a one-off and the margins should normalize going forward.

Working capital has increased

Working capital levels have increased substantially versus FY2011. Working capital stood at Rs24 bn in March 2012 versus Rs13 bn in March 2011 even as it declined from Rs27 bn in September 2011. Net current assets increased from Rs43 bn in 2QFY12 to Rs50 bn in 4QFY12 led by higher inventories (Rs19.2 bn in 4QFY12 versus Rs15 bn in 2QFY12) and higher debtors (Rs9.6 bn in 4QFY12 versus Rs4 bn in 2QFY12) even as advances declined from Rs23.6 bn in 2QFY12 to Rs21 bn in 4QFY12.

Excess inventories of ~3 mn tons in the sales channel – 1HFY13 sales could be subdued

As per the company, there are excess inventories of ~3 mn tons of complex fertilizers in the sales channel which could depress sales in 1HFY13. In case imports reduce going forward, recovery in domestic sales could be faster.

We retain our estimates and SELL rating

We retain our estimates and SELL rating on the company with an unchanged target price of Rs260/share.

Coromandel International (CRIN)

Others

Higher sales into channel inventories mean weak 1HFY13. Coromandel’s 4QFY12 results were in line with estimates. EBITDA margins declined to 5.2% (versus 9.2% in 3QFY12) even as sales increased to Rs27.4 bn (versus Rs25.5 bn in 3QFY12) with the company pushing inventory in the sales channel ahead of a cut in subsidy rates in FY2013. Hence, net current assets increased from Rs43 bn in 2QFY12 to Rs50 bn in 4QFY12 even as working capital reduced from Rs27 bn in 2QFY12 to Rs24 bn in 4QFY12.

Coromandel InternationalStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 22.5 22.7 24.6Market Cap. (Rs bn) 79.8 EPS growth (%) (8.5) 0.9 8.5

Shareholding pattern (%) P/E (X) 12.6 12.5 11.5Promoters 64.0 Sales (Rs bn) 97.9 95.4 104.4FIIs 7.7 Net profits (Rs bn) 6.4 6.4 7.0MFs 5.3 EBITDA (Rs bn) 9.4 10.3 10.8

Price performance (%) 1M 3M 12M EV/EBITDA (X) 10.3 8.9 8.2Absolute (2.3) 3.5 (11.1) ROE (%) 27.5 23.3 21.9Rel. to BSE-30 (1.4) 2.3 1.3 Div. Yield (%) 2.6 2.7 2.9

Company data and valuation summary

376-251

SELL

APRIL 24, 2012

RESULT

Coverage view:

Price (Rs): 283

Target price (Rs): 260

BSE-30: 17,207

Others Coromandel International

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Sales are higher and EBITDA margins are lower qoq as the company pushed sales into channel inventories Interim results of Coromandel, consolidated, March fiscal year-ends (Rs mn)

4QFY12 3QFY12 4QFY11 qoq yoy FY2012 FY2011 % change

Net sales 27,356 25,505 11,792 7.3 132.0 97,892 75,308 30.0

Expenditure (25,930) (23,167) (11,552) 11.9 124.5 (88,471) (65,837) 34.4

(inc)/dec in stock (5,307) 6,301 1,213 (184.2) (537.7) 2,580 2,200 17.3

Consumption of raw materials (16,040) (15,776) (9,716) 1.7 65.1 (59,062) (49,911) 18.3

Purchase of traded goods (860) (10,414) (570) (91.7) 50.9 (19,366) (8,857) 118.7

Employee costs (553) (472) (402) 17.2 37.6 (1,944) (1,590) 22.3

Other expenditure (3,169) (2,806) (2,076) 12.9 52.7 (10,679) (7,679) 39.1

EBITDA 1,426 2,338 240 (39.0) 495.2 9,421 9,471 (0.5)

Depreciation (178) (139) (148) 27.9 20.7 (597) (621) (3.8)

Interest (504) (307) (231) 64.2 118.3 (1,261) (889) 41.9

Other income 281 327 919 (14.1) (69.4) 1,904 1,896 0.5

PBT 1,025 2,219 780 (53.8) 31.4 9,467 9,857 (4.0)

Exceptional items - (355) - (100.0) (355) -

PBT (after ext. items) 1,025 1,864 780 (45.0) 31.4 9,111 9,857 (7.6)

Tax expense (398) (557) (70) (28.5) 468.3 (2,766) (2,921) (5.3)

PAT 626 1,306 710 (52.0) (11.7) 6,345 6,937 (8.5)

Minority interest (43) - - (43) - Reported PAT 669 1,306 710 (48.8) (5.8) 6,388 6,937 (7.9)

EBITDA margin (%) 5.2 9.2 2.0 9.6 12.6

Gross margins (%) 18.8 22.0 23.0 22.5 24.9

Opex/Net sales (%) 13.6 12.9 21.0 12.9 12.3

Effective tax rate (%) 38.9 29.9 9.0 30.4 29.6

PAT margin (%) 2.4 5.1 6.0 6.5 9.2

% change

Source: Company, Kotak Institutional Equities

Highlights of the conference call

The company is yet to see the impact of higher complex fertilizer prices on demand from farmers engaged in cultivation of cash crops. Demand from farmers engaged in cultivation of food grain crops is subdued. The company expects that MSPs of major crops would be increased by the Government to take care of higher fertilizer prices and normal demand patterns should emerge.

As the Government is trying to control fiscal deficit, subsidy payments (to company) have been pending since December 2011. Last year’s situation with respect to receivables from the Government was much better. As of March 2012, the company has close to Rs16.3 bn of subsidy payments due from the Government which is reflected as a part of short-term loans and advances.

Sabero has been impacted by environmental issues. As of now, the company has environmental approvals to operate at 75% capacity utilization (current capacity utilization is only ~45%). There are still some constraints on the environment management system. As the current effluent treatment plant (capex Rs320 mn) comes online, capacity utilization should go up.

Coromandel International Others

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Inventory of Rs19 bn includes Rs9.2 bn of finished good inventories most of which are in the sales channel and hence subsidy rates of FY2012 would be applicable. Hence, the company won’t be affected by the lower subsidy rates fixed by the Government in FY2013E.

Current assets increased, led by higher debtors and inventories Balance sheet of Coromandel, consolidated, March fiscal year-ends (Rs mn)

4QFY12 2QFY12 4QFY11

Liabilities

Share capital 283 282 282

Reserves and surplus 23,721 23,926 19,286

Shareholder's funds 24,003 24,209 19,567

Minority interest 158

Deferred tax liability 675 715 815

Total debt 28,760 23,193 15,478

Liabilities 24,553 14,682 18,110

Provisions 1,502 1,250 1,321

Total liabilities 79,651 64,048 55,292

Assets

Fixed assets 14,756 12,449 11,041

Goodwill on consolidation 3,470 - -

Investments 1,495 2,857 1,706

Current assets

Cash 9,847 5,634 9,605

Trade receivables 9,579 3,971 2,024

Inventories 19,218 15,477 15,139

Loand and advances 21,160 23,661 11,396

Other current assets 126 - 4,381

Total current assets 59,930 48,742 42,544

Total assets 79,651 64,048 55,292

Current assets 50,083 43,109 32,939

Working capital 24,027 27,176 13,507

Source: Company, Kotak Institutional Equities

Others Coromandel International

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Financial summary: Coromandel International Profit model, balance sheet and cash flow statement of Coromandel International, March fiscal year-ends (Rs mn)

2007 2008 2009 2010 2011 2012 2013E 2014EProfit model (Rs mn)Income 20,665 37,573 93,750 63,947 75,279 97,892 95,352 104,392EBITDA 1,994 4,128 6,521 7,100 9,450 9,420 10,302 10,804Other income 160 432 2,066 1,362 1,896 1,904 1,478 1,369Interest (320) (699) (876) (782) (868) (1,261) (1,564) (1,065)Depreciation (399) (522) (562) (594) (621) (597) (736) (826)Profit before tax 1,435 3,339 7,149 7,086 9,857 9,467 9,480 10,283Tax expense (457) (1,238) (3,140) (2,409) (2,921) (2,766) (3,076) (3,336)Exceptional items 189 — 1,586 — — (355) — —Reported PAT 1,167 2,101 5,595 4,677 6,937 6,345 6,404 6,946Minority interest (43) (43) (43)Reported PAT 1,167 2,101 5,595 4,677 6,937 6,388 6,447 6,989Adjusted PAT 916 1,829 3,256 3,778 5,603 5,353 5,406 6,021EPS 4.1 7.4 19.8 16.6 24.6 22.6 22.8 24.8Balance sheet (Rs mn)Equity 5,511 7,955 12,120 15,015 19,567 24,004 27,856 32,124Total borrowings 5,493 10,431 17,708 20,470 16,638 28,760 19,377 13,377Deferred tax liability/minority interest 713 825 795 855 815 833 833 833Current liabilities and provisions 5,985 8,359 17,626 10,031 18,391 26,055 18,250 19,935Total liabilites 17,702 27,570 48,248 46,370 55,411 79,651 66,316 66,269Net fixed assets 3,873 7,402 7,966 9,576 11,430 14,756 14,520 15,953Investments and goodwill 2,115 718 2,208 1,693 1,705 4,965 4,965 4,965Cash 1,695 1,072 4,253 9,605 9,605 9,847 6,467 2,999Other current assets 10,019 18,377 33,821 25,497 32,671 50,083 40,364 42,353Total assets 17,702 27,570 48,248 46,370 55,411 79,651 66,316 66,269RatiosEBITDA margin (%) 9.6 11.0 7.0 11.1 12.6 9.6 10.8 10.3Net debt/equity (X) 0.69 1.18 1.11 0.72 0.36 0.79 0.46 0.32Book value (Rs/share) 19.5 28.2 42.9 53.2 69.3 85.1 98.7 113.8ROAE (%) 27.9 24.4 26.3 26.3 30.9 23.7 20.2 19.5ROACE (%) 10.2 14.7 13.4 12.8 16.9 13.8 12.7 14.3

Source: Company, Kotak Institutional Equities

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

EBITDA margins lowest in past three years – gross margins intact

Rallis reported 4QFY12 standalone (SA) sales at Rs1.99 bn (-36% qoq, -12% yoy) which were lower than our estimates. Reported 4QFY12 (SA) EBITDA at Rs132 mn (-77% qoq, -55% yoy) was lower than our estimates led by lower margins at 6.6% (lowest in the past three years). Pricing was intact in the market as is evident from 4QFY12 (SA) gross margins at 39% (-80 bps yoy, -163 bps qoq) which were stable. EBITDA margins were hit as sales declined (-12% yoy) even as expenses (excluding raw materials) were up 5% yoy. Reported PAT (SA) at Rs118 mn was boosted by write-back of cessation costs (Thane plant) of Rs71 mn and other income of Rs71 mn.

Net working capital declines led by lower debtors

Net working capital of the company (consolidated) declined from Rs1.39 bn in September 2011 to Rs1.07 bn in March 2012 led by lower debtors (declined from Rs1.99 bn in September 2011 to Rs1.04 bn in March 2012). In our view, the company’s decision not to push sales in an environment of depressed demand is judicious and the balance sheet is much more efficient, as a result.

Reasons for poor performance

The management attributed the poor performance to the following: (1) Poor farm economics which led to lower usage of pesticides and also usage of lower value products, (2) erratic rains in Andhra, Maharashtra, Karnataka and West Bengal (45% of the pesticide industry in India) also led to lower usage, (3) paddy, pulses and oil seed acreages fell yoy, and (4) the company has moved out of red triangle (environmentally hazardous) products which used to contribute 6-7% of sales.

As per the management, increase in MSPs by the Government should improve farm economics and hence, improve demand conditions for agri-inputs going forward.

Metahelix reports encouraging numbers for the year

Metahelix reported sales and net profit of Rs814 mn and Rs5.5 mn in FY2012 versus sales and net loss of Rs424 mn and Rs149 mn in FY2011. The company is creating a hybrid seed for the BT cotton market (biggest seed market by value in India), which should take another 2-3 years.

Rallis India (RALI)

Others

Disappointing results. Rallis’ 4QFY12 results were below estimates led by 12% decline in standalone sales which clearly indicates subdued demand on account of pressure on farm profitability. Pricing was maintained in the market which is evident in stable gross margins. EBITDA margins at 6.6% (lowest in the past three years) took a hit as expenses (excluding raw materials) increased 5% yoy. We have cut our PAT estimates by 6% and 7% for FY2013E and FY2014E respectively. Retain BUY with a revised target price of Rs145 (Rs160 earlier) at 16.5X September 2013 EPS.

Rallis IndiaStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 5.1 8.2 9.4Market Cap. (Rs bn) 23.8 EPS growth (%) (21.6) 60.9 14.7

Shareholding pattern (%) P/E (X) 24.0 14.9 13.0Promoters 51.0 Sales (Rs bn) 12.7 14.6 16.0FIIs 8.7 Net profits (Rs bn) 1.0 1.6 1.8MFs 14.5 EBITDA (Rs bn) 2.1 2.6 2.9

Price performance (%) 1M 3M 12M EV/EBITDA (X) 11.7 9.2 7.9Absolute 0.9 (0.4) (14.6) ROE (%) 21.6 25.1 23.4Rel. to BSE-30 1.8 (1.6) (2.8) Div. Yield (%) 1.6 1.6 1.6

Company data and valuation summary

187-113

BUY

APRIL 24, 2012

RESULT

Coverage view:

Price (Rs): 122

Target price (Rs): 145

BSE-30: 17,207

Others Rallis India

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Sales declined yoy which led to decline in EBITDA margins even as gross margins are intact Interim results of Rallis, consolidated, March fiscal year-ends (Rs mn)

4QFY12 3QFY12 4QFY11 qoq yoy FY2012 FY2011 % change

Sales 2,160 3,261 2,457 (34) (12) 12,749 10,863 17

Raw material cost (1,253) (1,888) (1,415) (34) (11) (7,428) (6,336) 17

Employee cost (207) (236) (176) (12) 18 (902) (729) 24

Other expenses (577) (575) (563) 0 2 (2,292) (1,883) 22

EBITDA 124 563 302 (78) (59) 2,126 1,915 11

Other income/forex gain/(loss) 70 (83) 67 (185) 5 (28) 138 (120)

Depreciation and amortization (87) (72) (52) 20 69 (287) (171) 68

Interest cost (28) (41) (24) (33) 17 (146) (37) 291

Extraordinaries 71 (242) - (129) (172) -

Profit before tax 150 124 294 21 (49) 1,494 1,845 (19)

Tax (net) (57) (57) (102) 0 (44) (487) (581) (16)

Net income 93 67 192 38 (52) 1,007 1,264 (20)

Minority interest (6) (10) 4 (35) (259) 15 4 287

Adjusted net income 99 77 188 29 (47) 992 1,260 (21)

Margins (%)

Gross margins 42 42 42 42 42

EBITDA 5.7 17.3 12.3 16.7 17.6

% change

Source: Company, Kotak Institutional Equities

Decline in sales led to EBITDA margins at 6.6%, lowest in the past three years Interim results of Rallis, standalone, March fiscal year-ends (Rs mn)

1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12 3QFY12 4QFY12 qoq yoy

Net sales from operations 1,960 3,631 2,681 2,195 2,327 4,270 3,028 1,895 (37) (14)

Other operating income 72 49 32 72 55 95 70 100 42 38

Total income 2,033 3,680 2,712 2,267 2,382 4,365 3,098 1,994 (36) (12)

Raw material cost (1,219) (2,110) (1,593) (1,361) (1,434) (2,607) (1,835) (1,214) (34) (11)

Employee cost (184) (184) (185) (143) (202) (194) (208) (177) (15) 23

Other expenditure (399) (504) (420) (473) (433) (484) (484) (472) (2) (0)

EBITDA 231 883 515 290 312 1,081 570 132 (77) (55)

Depreciation (36) (40) (44) (52) (51) (70) (69) (82) 19 56

Other income/forex gain/(loss) 12 11 19 65 2 (68) (62) 71 (214) 9

Interest (net) 9 1 (11) (17) (20) (29) (29) (16) (44) (6)

Exceptional items - - - - - - (242) 71 (129)

PBT 216 855 480 285 243 914 168 175 4 (39)

Tax (68) (268) (143) (95) (78) (295) (57) (57) 0 (40)

PAT 148 587 337 190 166 619 111 118 6 (38)

Gross margin (%) 40.0 42.7 41.3 40.0 39.8 40.3 40.8 39.1

EBITDA margin (%) 11.4 24.0 19.0 12.8 13.1 24.8 18.4 6.6

% change

Source: Company, Kotak Institutional Equities

Rallis India Others

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Net working capital declined, led by lower debtors Interim balance sheet of Rallis, consolidated, March fiscal year-ends (Rs mn)

4QFY12 2QFY12 4QFY11

Liabilities

Share capital 195 195 195

Reserves and surplus 5,336 5,435 4,855

Shareholder's funds 5,530 5,630 5,049

Minority interest 15 33 22

Deferred tax liability 131 125 32

Total debt 1,506 1,652 1,148

Liabilities 3,423 3,898 3,330

Provisions 622 651 586

Total liabilities 11,226 11,988 10,167

Assets

Fixed assets 4,236 4,108 3,834

Goodwill on consolidation 1,533 1,481 1,236

Investments 227 246 256

Current assets

Cash 112 216 146

Trade receivables 1,035 1,988 1,064

Inventories 2,717 2,729 2,289

Loand and advances 1,358 1,207 1,329

Other current assets 8 12 13

Total current assets 5,230 6,153 4,841

Total assets 11,226 11,988 10,167

Current assets 5,118 5,936 4,695

Net working capital 1,073 1,388 779

Source: Company, Kotak Institutional Equities

Change in estimates

We have reduced our PAT estimates for FY2013E and FY2014E by 6% and 7% respectively. We maintain our BU Y rating with a reduced target price of Rs145 (Rs160 earlier) at 16.5X September 2013 EPS.

Change in estimates for Rallis, consolidated, March fiscal year-ends

New Old % change New Old % changeRevenue (Rs mn) 14,618 15,285 (4.4) 16,025 17,392 (7.9) EBITDA (Rs mn) 2,645 2,770 (4.5) 2,914 3,171 (8.1) Net income (Rs mn) 1,596 1,689 (5.5) 1,830 1,975 (7.3)

FY2013E FY2014E

Source: Company, Kotak Institutional Equities

Others Rallis India

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Financial summary: Rallis Profit model, balance sheet and cash flow statement, consolidated, March fiscal year-ends (Rs mn)

2008 2009 2010 2011 2012 2013E 2014EProfit model (Rs mn)Sales 6,957 8,562 9,005 10,934 12,749 14,618 16,025EBITDA 802 1,303 1,667 1,991 2,126 2,645 2,914Other income 906 33 70 69 (28) 116 172Interest (43) (34) (27) (40) (146) (65) (23)Depreciation (201) (229) (183) (175) (287) (309) (324)Extraordinardy items — — — — (172) 0 0Profit before tax 1,464 1,072 1,527 1,845 1,494 2,387 2,739Tax expense (211) (352) (512) (580) (487) (774) (889)Minority interest — — — — 15 16 20Extraordinardy items — — — — — — — PAT 1,253 720 1,015 1,264 992 1,596 1,830EPS 6.4 3.7 5.2 6.5 5.1 8.2 9.4Balance sheet (Rs mn)Equity 2,198 2,617 4,245 5,049 5,530 6,696 8,113Preference capital 880 880 — — — — — Total borrowings 466 825 81 1,172 1,506 862 — Deferred tax liability/minority interest (132) (102) (53) 54 145 129 109Current liabilities and provisions 2,011 2,608 3,041 3,891 4,045 5,068 5,515Total liabilites 5,423 6,828 7,314 10,167 11,226 12,755 13,737Net fixed assets 1,479 1,877 2,648 4,009 4,236 4,676 4,661Goodwill — — — 1,236 1,533 1,533 1,533Investments 555 1,362 1,402 256 227 227 227Cash 84 82 119 146 112 18 529Other current assets and miscellaneous 3,305 3,509 3,145 4,520 5,118 6,301 6,786Total assets 5,423 6,828 7,314 10,167 11,226 12,755 13,737RatiosEBITDA margin (%) 11.5 15.2 18.5 18.2 16.7 18.1 18.2Net debt/equity (X) 0.17 0.28 (0.01) 0.20 0.25 0.13 (0.07)Book value (Rs/share) 11.3 13.5 21.8 26.0 28.4 34.4 41.7ROAE (%) 36.4 29.0 28.2 26.2 21.6 25.1 23.4ROACE (%) 8.9 18.9 23.2 23.6 18.4 21.2 22.0

Source: Company, Kotak Institutional Equities

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

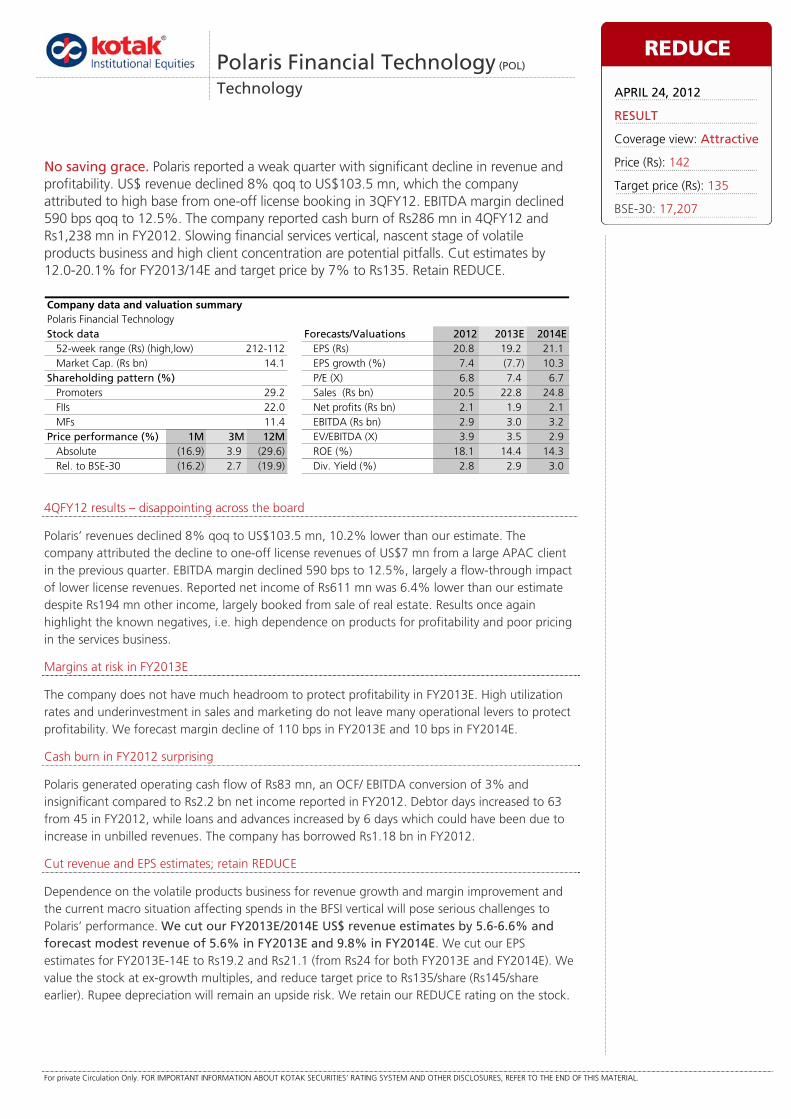

4QFY12 results – disappointing across the board

Polaris’ revenues declined 8% qoq to US$103.5 mn, 10.2% lower than our estimate. The company attributed the decline to one-off license revenues of US$7 mn from a large APAC client in the previous quarter. EBITDA margin declined 590 bps to 12.5%, largely a flow-through impact of lower license revenues. Reported net income of Rs611 mn was 6.4% lower than our estimate despite Rs194 mn other income, largely booked from sale of real estate. Results once again highlight the known negatives, i.e. high dependence on products for profitability and poor pricing in the services business.

Margins at risk in FY2013E

The company does not have much headroom to protect profitability in FY2013E. High utilization rates and underinvestment in sales and marketing do not leave many operational levers to protect profitability. We forecast margin decline of 110 bps in FY2013E and 10 bps in FY2014E.

Cash burn in FY2012 surprising

Polaris generated operating cash flow of Rs83 mn, an OCF/ EBITDA conversion of 3% and insignificant compared to Rs2.2 bn net income reported in FY2012. Debtor days increased to 63 from 45 in FY2012, while loans and advances increased by 6 days which could have been due to increase in unbilled revenues. The company has borrowed Rs1.18 bn in FY2012.

Cut revenue and EPS estimates; retain REDUCE

Dependence on the volatile products business for revenue growth and margin improvement and the current macro situation affecting spends in the BFSI vertical will pose serious challenges to Polaris’ performance. We cut our FY2013E/2014E US$ revenue estimates by 5.6-6.6% and forecast modest revenue of 5.6% in FY2013E and 9.8% in FY2014E. We cut our EPS estimates for FY2013E-14E to Rs19.2 and Rs21.1 (from Rs24 for both FY2013E and FY2014E). We value the stock at ex-growth multiples, and reduce target price to Rs135/share (Rs145/share earlier). Rupee depreciation will remain an upside risk. We retain our REDUCE rating on the stock.

Polaris Financial Technology (POL)

Technology

No saving grace. Polaris reported a weak quarter with significant decline in revenue and profitability. US$ revenue declined 8% qoq to US$103.5 mn, which the company attributed to high base from one-off license booking in 3QFY12. EBITDA margin declined 590 bps qoq to 12.5%. The company reported cash burn of Rs286 mn in 4QFY12 and Rs1,238 mn in FY2012. Slowing financial services vertical, nascent stage of volatile products business and high client concentration are potential pitfalls. Cut estimates by 12.0-20.1% for FY2013/14E and target price by 7% to Rs135. Retain REDUCE.

Polaris Financial TechnologyStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 20.8 19.2 21.1Market Cap. (Rs bn) 14.1 EPS growth (%) 7.4 (7.7) 10.3

Shareholding pattern (%) P/E (X) 6.8 7.4 6.7Promoters 29.2 Sales (Rs bn) 20.5 22.8 24.8FIIs 22.0 Net profits (Rs bn) 2.1 1.9 2.1MFs 11.4 EBITDA (Rs bn) 2.9 3.0 3.2

Price performance (%) 1M 3M 12M EV/EBITDA (X) 3.9 3.5 2.9Absolute (16.9) 3.9 (29.6) ROE (%) 18.1 14.4 14.3Rel. to BSE-30 (16.2) 2.7 (19.9) Div. Yield (%) 2.8 2.9 3.0

Company data and valuation summary

212-112

REDUCE

APRIL 24, 2012

RESULT

Coverage view: Attractive

Price (Rs): 142

Target price (Rs): 135

BSE-30: 17,207

Technology Polaris Financial Technology

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Other results and earnings call highlights

The management guided to FY2013E revenues of Rs24.0-24.6 bn, at an average Re/US$ rate of 50. This translates into US$480-492 mn of revenues, a growth of 12-15%. The guidance is aggressive in our view.

The consolidated headcount was 12,886 with 4QFY12 net addition of 382.

The outstanding hedge book stood at $218 mn spread over FY2013-15E, at an average Re/US$ rate of 50.26.

Polaris announced 11 wins in Intellect. Intellect contributed US$108 mn out of FY2012 revenue of US$428 mn.

DSO days increased sharply to 63 days from 56 days at the end of 3QFY12.

Attrition was down to 15.6% from 18% at the end of the previous quarter.

Exhibit 1: Polaris Software Interim Results - 4QFY12 (Rs mn)

qoq yoy4QFY11 3QFY12 4QFY12 % chg. % chg. KIE

Revenues (US$ mn) 96.7 112.5 103.5 (8.0) 7.1 115.3 (10.2) Total Revenues 4,375 5,725 5,203 (9.1) 18.9 5,752 (9.6) Cost of Revenues (3,022) (3,766) (3,567) (5.3) 18.0 (3,918) (9.0) Gross Profit 1,354 1,959 1,636 (16.5) 20.9 1,834 (10.8) SG&A Expenses (827) (904) (985) 9.0 19.2 (965) 2.1 EBITDA 527 1,055 651 (38.3) 23.5 870 (25.2) Other income 133 (124) 194 (256.7) 46.2 25 690.1 Interest expense (4) (8) (10) (8) EBDT 656 923 835 (9.6) 27.3 886 (5.8) Depreciation (87) (131) (134) 2.8 54.6 (135) (0.6) Minority interest 1 1 - Pretax profits 569 793 701 (11.6) 23.2 751 (6.6) Provision for Tax (90) (183) (165) (9.6) 84.4 (198) (16.6) Net Profit 480 611 536 (12.2) 11.8 553 (3.1) Extraordinaries 96 1 75 100 Net Profit reported 576 612 611 (0.0) 6.2 653 (6.4)

EPS - recurring (Rs) 4.8 6.1 5.4 (12.2) 11.8 5.5 Margins (%)Gross margin 30.9 34.2 31.4 31.9 SG&A expenses 18.9 15.8 18.9 16.8 EBITDA margin 12.0 18.4 12.5 15.1 EBIT margin 10.1 16.2 9.9 12.8 Net profit margin 13.2 10.7 11.8 11.4 Tax rate 18.7 23.0 23.5 26.4

% Deviation

Source: Company, Kotak Institutional Equities estimates

Polaris Financial Technology Technology

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

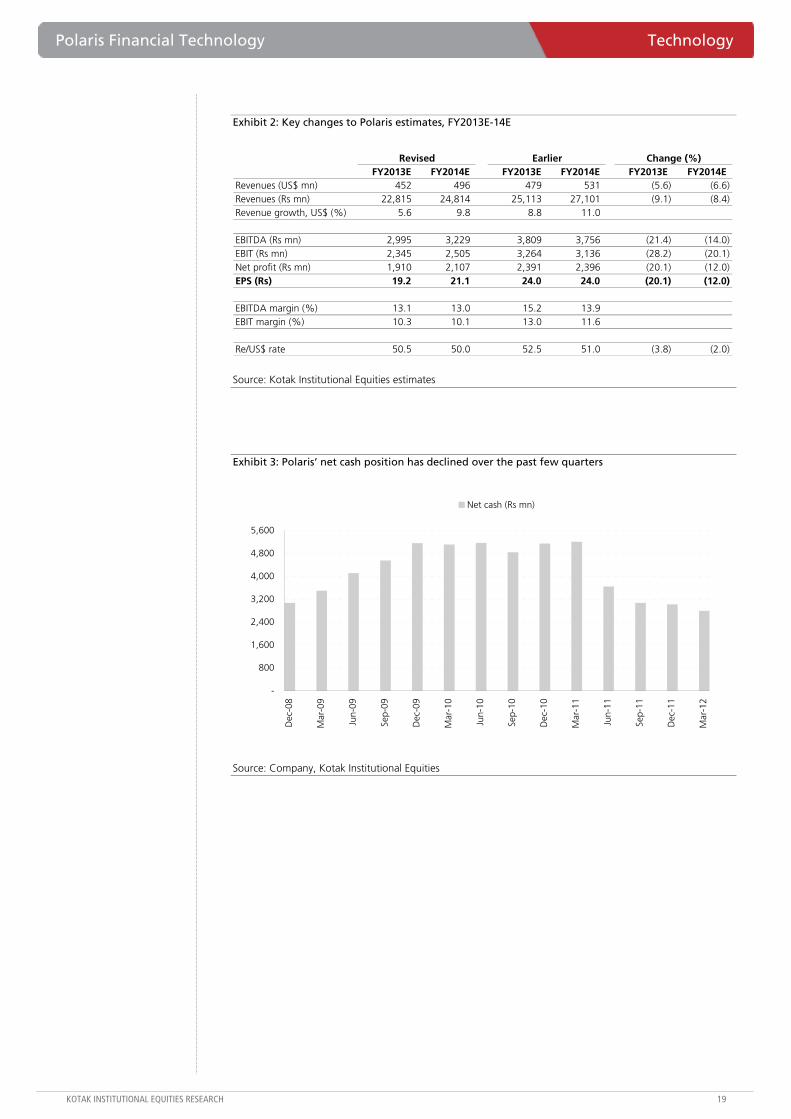

Exhibit 2: Key changes to Polaris estimates, FY2013E-14E

FY2013E FY2014E FY2013E FY2014E FY2013E FY2014ERevenues (US$ mn) 452 496 479 531 (5.6) (6.6) Revenues (Rs mn) 22,815 24,814 25,113 27,101 (9.1) (8.4) Revenue growth, US$ (%) 5.6 9.8 8.8 11.0

EBITDA (Rs mn) 2,995 3,229 3,809 3,756 (21.4) (14.0) EBIT (Rs mn) 2,345 2,505 3,264 3,136 (28.2) (20.1) Net profit (Rs mn) 1,910 2,107 2,391 2,396 (20.1) (12.0) EPS (Rs) 19.2 21.1 24.0 24.0 (20.1) (12.0)

EBITDA margin (%) 13.1 13.0 15.2 13.9 EBIT margin (%) 10.3 10.1 13.0 11.6

Re/US$ rate 50.5 50.0 52.5 51.0 (3.8) (2.0)

Revised Earlier Change (%)

Source: Kotak Institutional Equities estimates

Exhibit 3: Polaris’ net cash position has declined over the past few quarters

-

800

1,600

2,400

3,200

4,000

4,800

5,600

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Net cash (Rs mn)

Source: Company, Kotak Institutional Equities

Technology Polaris Financial Technology

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 4: Condensed consolidated financials for Polaris, March fiscal year-ends, 2010-14E (Rs mn)

FY2010 FY2011 FY2012 FY2013E FY2014EProfit & Loss ModelRevenues 13,538 15,863 20,527 22,815 24,814 EBITDA 2,220 2,139 2,906 2,995 3,229 Depreciation (350) (337) (472) (650) (724) EBIT 1,870 1,802 2,434 2,345 2,505 Other Income (73) 494 369 272 399 PBT 1,788 2,285 2,775 2,576 2,863 Tax (255) (359) (706) (666) (756) Net Profit 1,533 1,926 2,069 1,910 2,107 Balance Sheet (Rs mn)Total Equity 8,725 10,325 12,525 13,956 15,562 Borrowings 25 83 1,260 1,260 1,260 Total capital 8,749 10,408 13,785 15,217 16,822 Net fixed Assets 2,271 2,937 3,987 4,442 4,543 Investments 3,897 3,843 1,803 1,803 1,803 Goodwill 506 644 1,994 1,994 1,994 Working Capital 2,041 2,891 5,961 6,937 8,442 - Cash 1,237 1,423 2,224 3,096 4,333 - Current Assets 3,830 5,274 8,209 8,812 9,482 - Current Liabilities 3,026 3,805 4,473 4,971 5,373 Total assets 8,749 10,408 13,785 15,217 16,822 Free Cash Flow (Rs mn)Cash generated from operations 2,163 2,085 2,634 1,934 2,906 Working Capital Changes 871 (914) (1,854) (309) (268) Capital expenditure (429) (941) (1,476) (901) (825) Tax (290) (359) (706) (666) (756) Free Cash Flow 2,315 (129) (1,402) 59 1,057

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Results marred by decline in volumes and lower tariffs

PLNG reported net income of `2.45 bn (-17% qoq and +18.8% yoy), 19% below our expected `3 bn. PLNG’s EBITDA declined 15.9% qoq to `4.2 bn, led by (1) a decline in re-gasification volumes to 135 tn BTU (-6.9% qoq and +7.4% yoy) and (2) lower implied re-gasification tariffs of `36.6/mn BTU (-6.1% qoq and +11.7% yoy). We note that the company reported a foreign exchange fluctuation gain of `575.3 mn, which it passed on to consumers and has been adjusted while computing blended re-gasification tariffs.

Potential regulation of marketing margins on spot LNG volumes to impact earnings

We see downside risks to PLNG’s earnings from potential regulation of marketing margins on imported natural gas. We highlight that PLNG’s profitability has improved significantly in FY2012, led by high marketing margins on spot LNG cargoes. We compute implied marketing margins of `32.3/mn BTU on spot volumes for FY2012 (see Exhibit 1), which seems very high compared to actual re-gasification tariffs of `33.8/mn BTU during the same period.

Revise rating to REDUCE with a target price of `140

We revise our rating on PLNG stock to REDUCE from SELL previously with an unchanged 12-month DCF-based target price of `140. We have assumed full capacity utilization at PLNG’s Dahej and Kochi terminals in the long term. We model higher re-gasification tariffs for Kochi terminal at `42.5/mn BTU versus current tariff of `35.02/mn BTU for Dahej terminal. We expect PLNG’s re-gasification tariff to increase by 5% yoy in FY2013-14 and remain flat thereafter. We note that higher re-gasification tariffs may be sustained in the near term in the absence of regulations.

Revise earnings to reflect higher re-gasification tariffs for Kochi

We revise our EPS estimates for FY2013-15 to `14.3, `13.3 and `17.6 from `13.6, `11.8 and `16.5 respectively, to reflect (1) higher re-gasification tariffs for the Kochi terminal, (2) revised Rupee exchange rate assumptions, (3) higher LNG price assumptions, reflecting higher crude prices and (4) other minor changes.

Petronet LNG (PLNG)

Energy

Weak results. PLNG reported 4QFY12 net income at 2̀.45 bn (-17% qoq), sharply lower than our estimate of `3 bn, led by (1) lower-than-expected re-gasification volumes of 135 tn BTU (-6.9% qoq) and (2) lower implied re-gasification tariffs of `36.6/mn BTU (-6.1% qoq). We revise our rating on PLNG to REDUCE from SELL previously. Our 12-month target price remains unchanged at `140. Downside risks exist from (1) potential regulatory interventions in LNG business and (2) lower-than-expected volumes.

Petronet LNGStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 14.1 14.3 13.3Market Cap. (Rs bn) 110.1 EPS growth (%) 74.0 1.5 (7.2)

Shareholding pattern (%) P/E (X) 10.4 10.3 11.0Promoters 50.0 Sales (Rs bn) 226.6 318.2 429.6FIIs 14.5 Net profits (Rs bn) 10.6 10.7 10.0MFs 7.9 EBITDA (Rs bn) 18.3 18.9 21.7

Price performance (%) 1M 3M 12M EV/EBITDA (X) 7.1 7.6 6.7Absolute (10.4) (8.2) 7.6 ROE (%) 29.7 23.8 18.0Rel. to BSE-30 (9.5) (9.3) 22.6 Div. Yield (%) 1.7 1.7 1.7

Company data and valuation summary

186-125

REDUCE

APRIL 24, 2012

RESULT, CHANGE IN RECO.

Coverage view: Neutral

Price (Rs): 147

Target price (Rs): 140

BSE-30: 17,207

QUICK NUMBERS

• 135 tn BTU of re-gasification volumes

• `36.6/mn BTU implied tariff

• `32/mn BTU of implied marketing margins on spot volumes for FY2012

Energy Petronet LNG

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

PLNG has earned significantly higher tariffs on spot cargoes Calculation of tariffs based on FY2012 results of PLNG (` mn)

Volumes (tn BTU)Contracted volumes 372.1 Tolling volumes 72.7 Spot volumes 103.6 Total volumes 548.4 Tariffs (Rs/mn BTU)Actual re-gasification tariffs 33.8 Implied tariff 37.8 Computation of marketing marginsTotal contribution 20,712 Contribution from contracted volumes 12,564 Contribution from tolling volumes 2,456 Estimated loss due to internal consumption 1,156 Implied contribution from spot cargoes 6,848 Implied marketing margins for spot cargoes (Rs/mn BTU) 32.3

Source: Company, Kotak Institutional Equities estimates

Key highlights from 4QFY12 results

Exhibit 2 gives the details of PLNG’s 4QFY12 results and compares them with 3QFY12 and 4QFY11 results.

Interim results of Petronet LNG, March fiscal year-ends (` mn)

(% chg.) yoy4QFY12 4QFY12E 4QFY11 3QFY12 4QFY12E 4QFY11 3QFY12 FY2012 FY2011 (% chg.)

Net sales 64,330 72,701 39,860 62,653 (11.5) 61.4 2.7 226,579 131,973 71.7Total expenditure (60,100) (67,640) (36,347) (57,620) (11.1) 65.4 4.3 (208,287) (119,810) 73.8Raw material (59,393) (66,980) (35,743) (57,006) (11.3) 66.2 4.2 (205,867) (118,012) 74.4Staff cost (108) (128) (122) (64) (15.8) (11.6) 68.5 (298) (306) (2.6)Other expenditure (599) (532) (482) (550) 12.6 24.3 8.8 (2,122) (1,493) 42.1EBITDA 4,230 5,061 3,513 5,032 (16.4) 20.4 (15.9) 18,292 12,163 50.4Other income 221 275 204 164 (19.5) 8.6 34.8 849 570 49.0Depreciation (458) (476) (455) (463) (3.8) 0.8 (1.0) (1,842) (1,847) (0.3)Interest (342) (370) (431) (345) (7.6) (20.7) (0.8) (1,774) (1,931) (8.1)Profit before tax 3,651 4,489 2,831 4,389 (18.7) 29.0 (16.8) 15,525 8,954 73.4Extraordinary/prior period items — — 110 — — 110Current tax (1,180) (1,221) (900) (1,360) (4,800) (2,650)Deferred tax liabilities/assets (20) (241) 22 (75) (150) (218)Profit after tax 2,451 3,027 2,063 2,954 (19.0) 18.8 (17.0) 10,575 6,196 70.7Adj Profit after tax 2,451 3,027 1,953 2,954 (19.0) 25.5 (17.0) 10,575 6,086 73.8EPS (Rs) 3.3 4.0 2.6 3.9 14.1 8.1 Tax rate (%) 32.9 32.6 31.0 32.7 31.9 32.0

Total volumes (tn BTU) 135.0 144.0 125.8 144.9 (6.3) 7.4 (6.9) 548.4 440.4 24.5Implied re-gasification tariff (Rs/mn BTU) 36.6 39.7 32.7 39.0 (7.9) 11.7 (6.1) 37.8 31.7 19.1

Notes:(a) The re-gasification tariff computed here is different from actual tariffs due to inclusion of direct re-gasification and associated costs.

Source: Company, Kotak Institutional Equities estimates

Implied tariffs decline qoq. We compute implied tariffs at `36.6/mn BTU in 4QFY12 versus `39/mn BTU in 3QFY12 and `32.7/mn BTU in 4QFY11. The qoq decline in implied tariffs despite a 5% increase in base re-gasification tariffs reflects presumably lower marketing margins on spot LNG cargoes.

Petronet LNG Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

LNG volumes decline qoq. PLNG reported 6.9% qoq decline in re-gasification volumes to 135 tn BTU versus 144.9 tn BTU in 3QFY12, led by (1) lower contracted volumes of 93.5 tn BTU in 4QFY12 (-4.9 tn BTU qoq) and (2) lower tolling volumes of 15 tn BTU (-6.8 tn BTU qoq). Spot LNG volumes increased modestly to 26.5 tn BTU from 24.7 tn BTU in 3QFY12.

Increase in other expenditure. PLNG’s other expenditure increased to `599 mn in 4QFY12 from `550 mn in 3QFY12 and `482 mn in 4QFY11.

Increase in other income. Other income increased to `221 mn for 4QFY12 from `164 mn in 3QFY12 and `204 mn in 4QFY11.

Key assumptions behind our earnings model

We discuss the key assumptions underlying our earnings model below (see Exhibit 3).

We model Petronet's volumes to ramp-up to 17 mtpa by FY2015E Key volume/price assumptions for Petronet LNG, March fiscal year-ends, 2007-15E

2008 2009 2010 2011 2012E 2013E 2014E 2015E Volume assumptions (mn tons)Contract LNG volumes 4.8 4.8 7.1 7.5 7.3 8.4 10.5 13.8 Spot LNG volumes 1.5 1.5 0.4 0.6 2.0 1.7 1.5 1.5 Tolling volumes — — 0.3 0.6 1.4 1.6 1.6 1.6 Total volumes 6.3 6.3 7.9 8.7 10.8 11.6 13.5 16.8 Price assumptions (US$/mn BTU)LNG purchase price (FOB) 3.7 4.2 4.6 5.6 8.1 10.2 11.9 12.9 Landed cost (incl. import tariff) 4.2 4.7 5.2 6.3 9.0 11.1 13.0 14.0 Re-gasification charges for Dahej 0.69 0.64 0.65 0.71 0.70 0.68 0.73 0.77 Re-gasification charges for Dahej (Rs/mn BTU) 27.8 29.2 30.6 32.2 33.8 35.5 37.2 38.6 Re-gasification charges for Kochi 0.82 0.84 0.89 Re-gasification charges for Kochi (Rs/mn BTU) 42.5 43.0 44.6 Escalation in re-gasification charges (%) 5.0 5.0 5.0 5.0 5.0 5.0 5.0 3.7 Sales price (US$/mn BTU) 4.9 5.4 5.8 7.0 9.7 11.8 13.7 14.8 Other assumptionsRupee/US dollar exchange rate 40.1 45.8 47.4 45.6 47.9 52.0 51.0 50.0

Source: Company, Kotak Institutional Equities estimates

Volumes. We model contract LNG volumes of 8.4 mn tons, 10.5 mn tons and 13.8 mn tons in FY2013E, FY2014E and FY2015E respectively. We model spot LNG imports (including tolling) of 3.2 mn tons in FY2013E, 3 mn tons in FY2014E and 3 mn tons in FY2015E versus 3.5 mn tons in FY2012.

Re-gasification tariffs. We model PLNG’s re-gasification tariffs to increase by 5% in each year over FY2013-14 and remain flat thereafter until FY2022, the terminal year of our DCF model (see Exhibit 4). We have assumed higher re-gasification tariff of `42.5/mn BTU for Kochi terminal versus current tariff of `35.02/mn BTU for Dahej terminal.

Exchange rate. We assume an exchange rate for FY2013E, FY2014E and FY2015E of `52/US$, `51/US$ and `50/US$ respectively, versus `52.5/US$, `51/US$ and `50/US$ previously.

Energy Petronet LNG

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Our DCF-based fair value for PLNG is `140 Calculation of equity value of PLNG using discounted cash flow analysis (` mn)

2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E EBITDA 18,881 21,738 26,603 29,768 33,757 35,862 36,021 35,860 35,689 35,506 35,506 35,506Adjusted tax expense (3,826) (3,839) (5,834) (6,203) (7,649) (8,901) (9,658) (10,425) (11,146) (11,825)Change in working capital (4,959) (1,895) (2,569) (1,334) (1,737) (656) (8) (506) (591) (696)Operating cash flow 10,096 16,004 18,199 22,231 24,370 26,305 26,355 24,929 23,951 22,985Capital expenditure (20,896) (11,450) (12,000) (6,500) (1,000) (1,000) (1,000) (1,000) (1,000) (5,335)Free cash flow (10,800) 4,554 6,199 15,731 23,370 25,305 25,355 23,929 22,951 17,650 17,650 17,650Discounted cash flow-now (9,675) 3,626 4,388 9,894 13,065 12,575 11,200 9,393 8,008 5,474Discounted cash flow-1 year forward 4,080 4,936 11,134 14,698 14,147 12,600 10,570 9,009 6,158 5,474Discounted cash flow-2 year forward 5,553 12,526 16,541 15,915 14,175 11,892 10,138 6,928 6,158 5,474

Now + 1-year + 2-yearsDiscount rate (%) 12.5% 12.5% 12.5%Total PV of free cash flow 67,948 92,807 105,301Terminal value assumptionGrowth in perpetuity 0.0% 0.0% 0.0%FCF in 2022E 17,650 17,650 17,650Exit FCF multiple (X) 8.0 8.0 8.0 141 -1.0% -0.5% 0.0% 1.0% 1.5%Exit EV/EBITDA multiple (X) 4.0 4.0 4.0 11.5% 152 155 158 165 170Terminal value 141,202 141,202 141,202 12.0% 143 146 149 155 159PV of terminal value 43,792 43,792 43,792 12.5% 136 138 141 146 150Total company value 111,741 136,600 149,093 13.0% 129 131 133 138 141

13.5% 122 124 126 131 133Net debt 19,096 34,330 34,499Equity value 92,644 102,270 114,594 Shares outstanding (mn) 750 750 750 Equity value of regasification business (Rs) 124 136 153 Equity value of 26% stake in Dahej Port (Rs) 4 4 4 Fair value of PLNG (Rs) 128 141 157

Fiscal Year end (March 31, XXXX) March-13 March-14 March-15 March-16 March-17 March-18 March-19 March-20 March-21 March-22 March-23 March-24Today 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12 24-Apr-12Days left 341 706 1,071 1,437 1,802 2,167 2,532 2,898 3,263 3,628 3,993 4,359 Years left 0.93 1.93 2.93 3.94 4.94 5.94 6.94 7.94 8.94 9.94 10.94 11.94 Discount factor at WACC 0.90 0.80 0.71 0.63 0.56 0.50 0.44 0.39 0.35 0.31 0.28 0.24

Sensitivity of 12-month fair value to WACC and perpetual growthPerpetual growth (%)

WA

CC

(%

)

Source: Kotak Institutional Equities estimates

Petronet LNG Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Petronet LNG: Profit model, balance sheet, cash model March fiscal year-ends, 2008-15E (` mn)

2008 2009 2010 2011 2012 2013E 2014E 2015EProfit model (Rs mn)Net sales 65,553 84,287 106,491 131,973 226,579 318,196 429,591 580,775EBITDA 8,661 9,013 8,465 12,163 18,292 18,881 21,738 26,603Other income 536 765 978 563 849 723 419 462Interest (1,024) (1,012) (1,839) (1,931) (1,774) (1,090) (2,853) (2,710)Depreciation (1,022) (1,025) (1,609) (1,847) (1,842) (2,622) (4,551) (4,854)Extraordinary items — — — 117 — — — —Pretax profits 7,152 7,740 5,995 9,064 15,525 15,892 14,753 19,500Tax (2,185) (2,526) (1,410) (2,650) (4,800) (3,581) (3,217) (5,122)Deferred taxation (220) (30) (540) (218) (150) (1,576) (1,570) (1,204)Net profits 4,747 5,184 4,045 6,196 10,575 10,736 9,967 13,173Earnings per share (Rs) 6.3 6.9 5.4 8.1 14.1 14.3 13.3 17.6

Balance sheet (Rs mn)Total equity 16,185 19,834 22,349 26,802 35,198 43,755 51,542 60,357Deferred taxation liability 2,692 2,722 3,262 3,480 3,630 5,206 6,776 7,980Total borrowings 15,776 22,817 24,998 32,161 30,340 39,342 40,342 41,342Currrent liabilities 8,588 8,922 9,006 12,134 22,943 24,564 32,112 42,285Total liabilities and equity 43,242 54,295 59,614 74,577 92,110 112,866 130,771 151,964Cash 3,586 6,578 3,405 1,540 9,845 3,613 4,444 4,783Current assets 7,890 11,519 8,811 12,334 22,758 29,338 38,780 51,523Total fixed assets 26,293 33,156 42,012 49,053 58,109 78,516 86,148 94,259Investments 5,473 3,043 5,386 11,649 1,399 1,399 1,399 1,399Total assets 43,242 54,295 59,614 74,577 92,110 112,866 130,771 151,964

Free cash flow (Rs mn)Operating cash flow, excl. working capital 6,982 5,378 5,513 8,348 10,445 12,078 14,935 17,805Working capital 1,589 (3,384) 3,026 (1,079) 386 (4,959) (1,895) (2,569)Capital expenditure (263) (27) (15,757) (8,889) (9,625) (20,896) (11,450) (12,000)Investments (2,780) 2,462 (2,339) (6,263) 10,250 — — —Free cash flow 5,528 4,429 (9,556) (7,882) 11,457 (13,778) 1,591 3,236Other income (414) 695 452 386 849 723 419 462

Ratios (%)Debt/equity 84 101 98 106 78 80 69 60 Net debt/equity 65 72 84 101 53 73 62 53 RoAE 27.8 25.0 16.8 22.2 30.6 24.5 18.6 20.8RoACE 30.7 33.2 20.1 25.5 41.1 21.7 14.9 18.0 Adjusted CROCI 32.0 28.5 17.7 25.1 34.7 15.7 16.3 18.8

Key assumptions (US$/mn BTU)Contract LNG volumes (mn tons) 4.8 4.8 7.1 7.5 7.3 8.4 10.5 13.8Total LNG volumes (mn tons) 6.3 6.3 7.9 8.7 10.8 11.6 13.5 16.8LNG purchase price (FOB) 3.7 4.2 4.6 5.6 8.1 10.2 11.9 12.9Base re-gasification charges 0.69 0.64 0.65 0.71 0.70 0.68 0.73 0.77Sales price 4.9 5.4 5.8 7.0 9.7 11.8 13.7 14.8Rupee/US dollar exchange rate 40.1 45.8 47.4 45.6 47.9 52.0 51.0 50.0

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Inflows: Rs709 bn in FY2013E; Rs700 bn+ inflow possible on segmental/geographical diversity

Annual inflow traction of Rs700 bn+ may be possible on (1) diverse presence across segments, (2) strong activity in certain sectors (T&D, roads, urban infrastructure) and (3) widening international opportunities. We build Rs709 bn inflows in FY2013 (a 4% decline over Rs735 bn in FY12E) led by (1) Rs331 bn from infrastructure (buildings, roads, railways and water), (2) Rs144 bn from power (mostly T&D; negligible inflows from generation), (3) Rs161 bn from process and O&G and (4) Rs74 bn from other segments. Strong backlog of Rs1.45 tn provides confidence to our EPC execution of Rs529 bn in FY2013E (14% yoy growth) and Rs587 bn in FY2014E (up 11% yoy).

Margin: Some decline already panned out, build further dip in FY2013E; level not exorbitant vs peers

L&T’s margins are likely to contract about 100 bps in FY2012. We build a further 50-75 bps margin contraction over FY2012-14E. Thus downside risk on margins is potentially low even with order inflow focused on roads, T&D and buildings. Even in absolute terms, L&T’s EBITDA margin do not seem high versus peers (KEC, Kalpataru) even as percentage overheads seem lower.

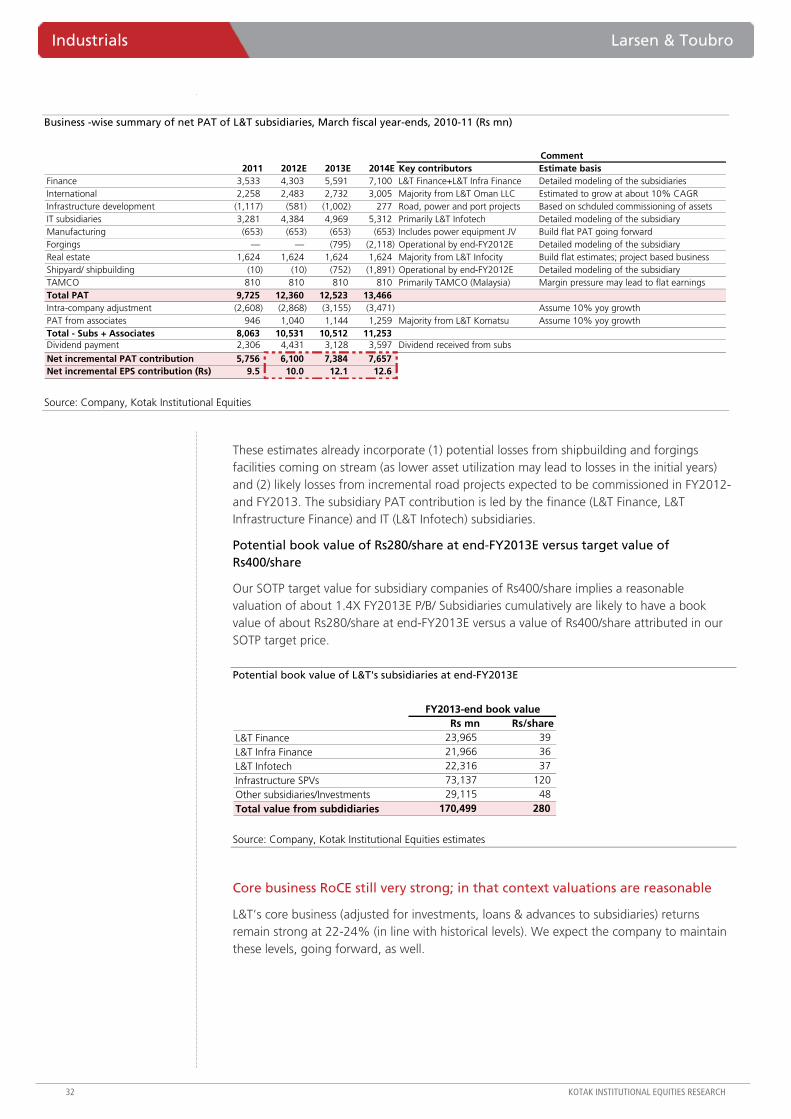

Subsidiaries: Rs400 value is 1.3X P/B; fear of losses exaggerated as Rs13 incremental EPS possible

L&T’s subsidiaries could contribute a net incremental EPS of about Rs13 to consolidated EPS for FY2013 and FY2014. Fear of losses from forgings, shipbuilding and power subsidiaries is likely exaggerated and near-term focused, as these can be large opportunities over the medium-term. We value subsidiaries at Rs400/share and this valuation is essentially about 1.3X P/B on FY2013E.

Significant correction, strong RoCEs, limited downside to estimates; upgrade to ADD

We upgrade L&T to ADD (from REDUCE) with TP of Rs1,350 (Rs1,380 earlier) as (1) significant time and price correction offers better risk-reward, (2) limited incremental downside to inflow, revenue and margin estimates, (3) strong core business RoCE of 20-22% despite building lower margins and higher working capital, (4) reasonable core business valuations (of 12.4X FY2013E and 11.5X FY2014E P/E); after adj. for subsidiaries at 1.3X FY2013E P/B and are below 10-year lows as well, (5) much more diversified and strong positioning versus its infrastructure/capital goods peers.

Larsen & Toubro (LT)

Industrials

Risk-reward in fair balance after sharp correction; upgrade to ADD. We upgrade L&T to ADD (from REDUCE) on limited downside to estimates and valuations (2.1X P/B, 12.4X adj. P/E on FY2013E) well below the 10-year average. Downside to estimates limited on (1) revenues, on large backlog, (2) margins, absolute margins not high versus peers and build 200 bps decline from peak, (3) inflows, very diverse segmental/ geographical presence (Rs700 bn in FY13E), (4) strong standalone adj. RoCEs of 20-22% support valuations and (5) subsidiary valuation (Rs400) reasonable based on P/B (1.3X FY2013E).

Larsen & ToubroStock data Forecasts/Valuations 2012 2013E 2014E

52-week range (Rs) (high,low) EPS (Rs) 78.1 82.4 91.5Market Cap. (Rs bn) 741.9 EPS growth (%) 15.4 5.4 11.0

Shareholding pattern (%) P/E (X) 15.6 14.8 13.3Promoters 0.0 Sales (Rs bn) 641.1 734.6 821.0FIIs 17.0 Net profits (Rs bn) 47.6 50.2 55.7MFs 5.5 EBITDA (Rs bn) 100.2 113.9 127.2

Price performance (%) 1M 3M 12M EV/EBITDA (X) 11.0 10.1 9.3Absolute (6.3) (9.9) (28.6) ROE (%) 16.5 14.8 14.3Rel. to BSE-30 (5.5) (11.0) (18.7) Div. Yield (%) 1.1 1.1 1.1

Company data and valuation summary

1,868-969

ADD

APRIL 24, 2012

CHANGE IN RECO.

Coverage view: Cautious

Price (Rs): 1,219

Target price (Rs): 1,350

BSE-30: 17,207

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

Rs700 bn+ a year inflow traction possible on segmental/geographical diversity

We build an order inflow decline of 4% in FY2013E to Rs700-710 bn (post expected inflow decline of about 8% in FY2012 to Rs735 bn). Our FY2013 inflow estimate is based on:

Rs331 bn of inflows from the infrastructure segment. This is likely to be led by commercial buildings and road projects. We believe roads segment could potentially contribute about Rs95 bn of inflows in FY2013 based on 800-900 km worth of road projects from in-house development project wins, other developer orders and other agencies such as states (apart from NHAI). Additionally industrial and commercial buildings segment may contribute about Rs120 bn of orders (based on historical track record). Other potential contributors to this segment include railways (about Rs50 bn led by opportunities from DFCC, orders from ongoing Hyderabad metro, other urban infra projects) and water (Rs50 bn based on track record and typically originating from city level municipal corporations).

Rs143 bn from the power segment. This is mainly from the T&D segment with no significant contribution from the generation segment. T&D may contribute Rs125 bn worth of orders in FY2012 and we expect that T&D can contribute Rs115 bn worth of orders in FY2013. Note that more than half of FY2012E T&D inflows were from international markets and about 40-45% was domestic. We do not expect meaningful contribution from the generation segment.

Rs161 bn from process and oil & gas segments. This includes platforms, pipelines, mineral and metals, refineries and petrochemicals. International markets could potentially contribute Rs70-80 bn of inflows (about Rs50 bn in FY2012E) on back of increasing focus as well as near-shore presence with fabrication facilities (yard in Oman) and the remaining Rs80-90 bn from the domestic market (brown-field investments and pending order decisions in projects underway).

Rs67 bn from others segments. This includes mainly product orders from segments such as machinery and industrial products and electrical and electronics products.

Industrials Larsen & Toubro

28 KOTAK INSTITUTIONAL EQUITIES RESEARCH

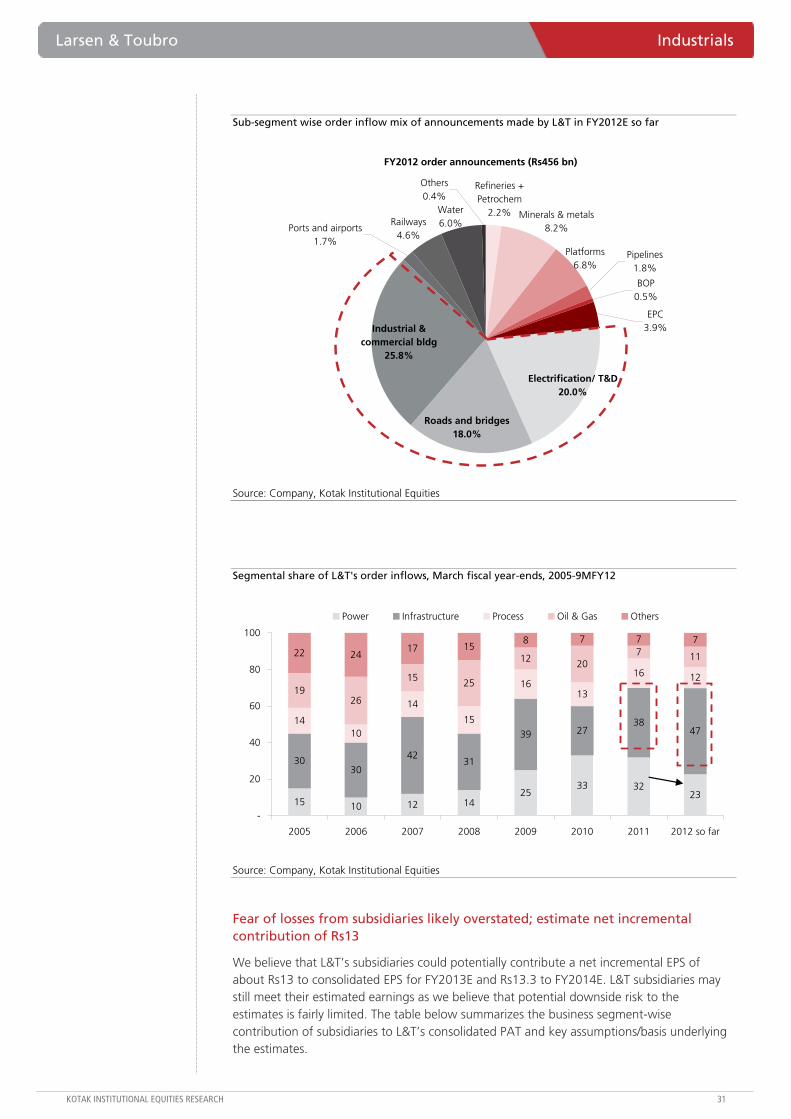

Rough break-up of sector-wise order inflows of L&T

Segment 2008 2009 2010 2011 9M Rep. + 4Q Ann. KIE Est. 2013EProcess + Oil & Gas 168 (137) 144 (140) 230 (168) 183 (139) 141 (87) 161 161

Refineries 38 37 21 12 —Petrochemicals 3 8 30 — 10 25 Minerals & metals 54 80 43 99 38 80

Steel sector 50 59 10 93 21 Bulk material handling — — — 4 —Platforms 42 — 74 18 31 45 Pipelines — 15 — 6 8 15

Power 59 (35) 129 (80) 230 (217) 255 (200) 140 (111) 160 144 BOP 5 20 45 46 2 10 EPC — — 103 93 18 25 Equipment — 16 24 28 — —

Electrification/ T&D 30 45 45 32 91 125 115 Domestic 8 26 17 14 34 International 23 19 28 18 57

Infrastructure 130 (100) 201 (185) 188 (112) 303 (220) 291 (256) 349 331 Roads and bridges 3 43 — 33 82 125 95

Ports and airports 55 — — 22 8 10 15 Railways 3 28 8 70 21 25 50

Industrial & commercial bldg 33 92 92 72 118 145 120

Residential 17 14 32 53 61 Water 6 23 13 23 27 45 50

Others 63 (7) 41 (5) 49 (10) 56 (5) 46 (2) 67 74 Total 420 (280) 516 (410) 696 (507) 798 (565) 618 736 709

Note: Figures in brackets represent quantum of orders announced (versus the reported number)

FY2012E

25

Source: Company, Kotak Institutional Equities estimates

We believe annual order inflow traction of Rs700 bn+ may be possible for L&T based on (1) a meaningful presence across a diverse set of sectors, (2) potential strong activity in sectors such as roads, T&D and urban infrastructure segment (witnessed in strong ordering activity of PGCIL, NHAI etc.), and (3) improved traction in overseas geographies across segments providing relatively large opportunities.

L&T announced inflows of about Rs124 bn in 4QFY12, led by infrastructure (roads, buildings), power (T&D) and process (metals) segments. Adding this to the Rs494 bn of inflows reported in 9MFY12, it implies full-year inflows of about Rs618 bn for L&T. This is versus our estimate of Rs735 bn and management guidance of 0-5% growth (Rs800 bn).

However L&T had announced only about 75% of its total recorded inflows in 9MFY12 and hence actual inflows in 4QFY12E are likely to be higher and may thus reach our estimate of Rs735 bn for the full year. Note that L&T has emerged as the lowest bidder for two NHAI projects (bids opened on March 30, 2012) in Maharashtra, with a cumulative project cost of about Rs45 bn (Amravati-Jalgaon and Jalgaon-Gujarat/Maharashtra border projects).

Loss of large opportunities

L&T missed some potentially large opportunities in FY2012: (1) it did not win orders from the NTPC bulk tenders and (2) it did not qualify to bid for a US$4 bn contract for the construction of the new Abu Dhabi Airport.

Larsen & Toubro Industrials

KOTAK INSTITUTIONAL EQUITIES RESEARCH 29

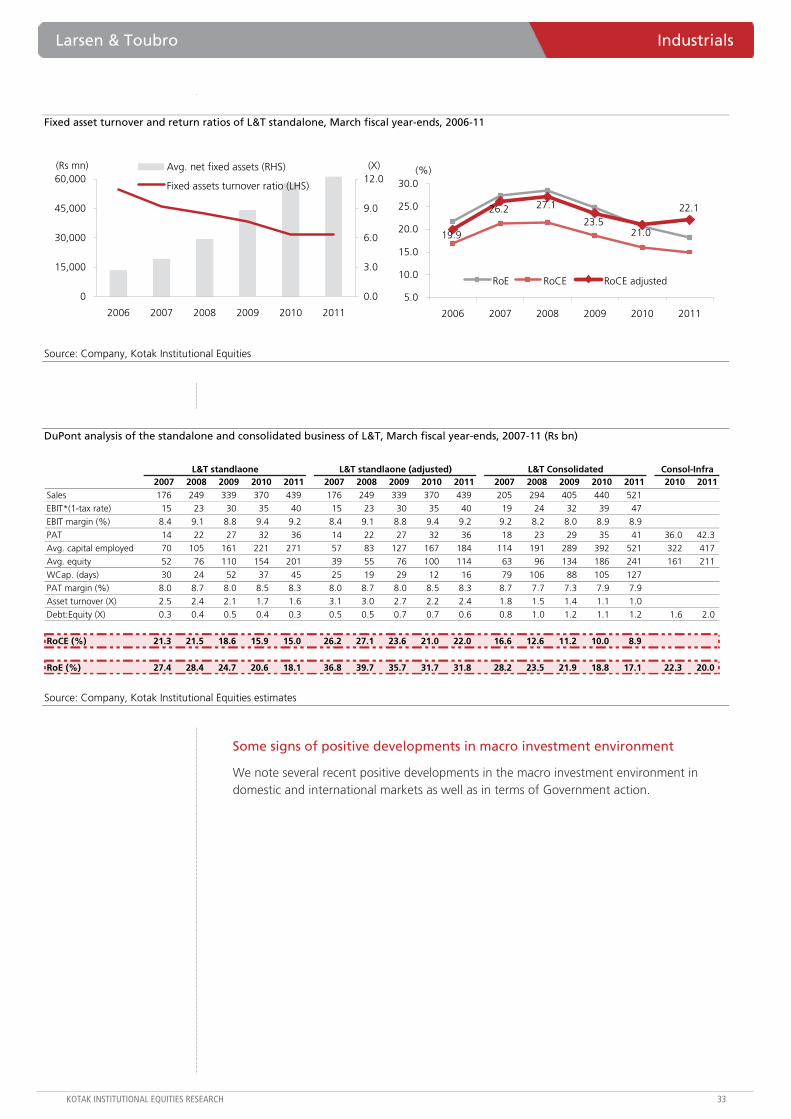

Margin contraction built in; levels not exorbitant (comparable to peers)

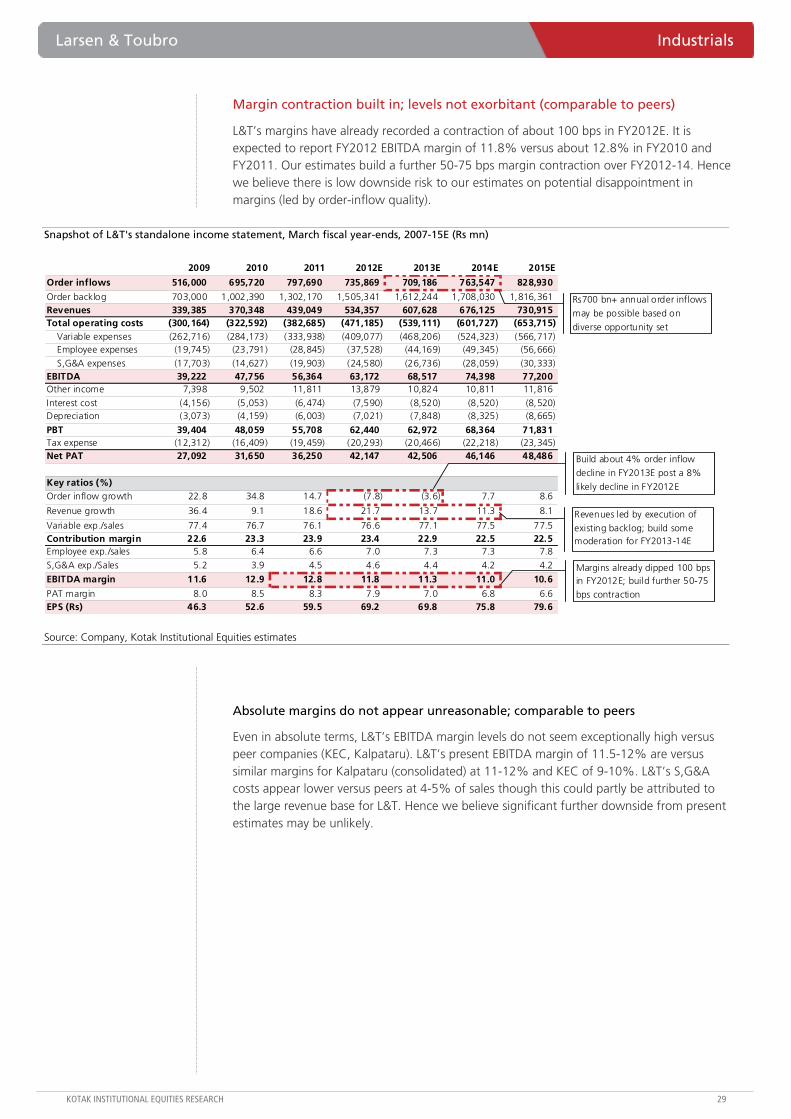

L&T’s margins have already recorded a contraction of about 100 bps in FY2012E. It is expected to report FY2012 EBITDA margin of 11.8% versus about 12.8% in FY2010 and FY2011. Our estimates build a further 50-75 bps margin contraction over FY2012-14. Hence we believe there is low downside risk to our estimates on potential disappointment in margins (led by order-inflow quality).

Snapshot of L&T's standalone income statement, March fiscal year-ends, 2007-15E (Rs mn)

2009 2010 2011 2012E 2013E 2014E 2015E

Order inflows 516,000 695,720 797,690 735,869 709,186 763,547 828,930

Order backlog 703,000 1,002,390 1,302,170 1,505,341 1,612,244 1,708,030 1,816,361 Revenues 339,385 370,348 439,049 534,357 607,628 676,125 730,915 Total operating costs (300,164) (322,592) (382,685) (471,185) (539,111) (601,727) (653,715)

Variable expenses (262,716) (284,173) (333,938) (409,077) (468,206) (524,323) (566,717) Employee expenses (19,745) (23,791) (28,845) (37,528) (44,169) (49,345) (56,666)

S,G&A expenses (17,703) (14,627) (19,903) (24,580) (26,736) (28,059) (30,333) EBITDA 39,222 47,756 56,364 63,172 68,517 74,398 77,200 Other income 7,398 9,502 11,811 13,879 10,824 10,811 11,816

Interest cost (4,156) (5,053) (6,474) (7,590) (8,520) (8,520) (8,520) Depreciation (3,073) (4,159) (6,003) (7,021) (7,848) (8,325) (8,665)

PBT 39,404 48,059 55,708 62,440 62,972 68,364 71,831 Tax expense (12,312) (16,409) (19,459) (20,293) (20,466) (22,218) (23,345) Net PAT 27,092 31,650 36,250 42,147 42,506 46,146 48,486

Key ratios (%)Order inflow growth 22.8 34.8 14.7 (7.8) (3.6) 7.7 8.6

Revenue growth 36.4 9.1 18.6 21.7 13.7 11.3 8.1

Variable exp./sales 77.4 76.7 76.1 76.6 77.1 77.5 77.5 Contribution margin 22.6 23.3 23.9 23.4 22.9 22.5 22.5 Employee exp./sales 5.8 6.4 6.6 7.0 7.3 7.3 7.8

S,G&A exp./Sales 5.2 3.9 4.5 4.6 4.4 4.2 4.2

EBITDA margin 11.6 12.9 12.8 11.8 11.3 11.0 10.6

PAT margin 8.0 8.5 8.3 7.9 7.0 6.8 6.6 EPS (Rs) 46.3 52.6 59.5 69.2 69.8 75.8 79.6

Build about 4% order inflow

decline in FY2013E post a 8%

likely decline in FY2012E

Revenues led by execution of

existing backlog; build some moderation for FY2013-14E

Margins already dipped 100 bps in FY2012E; build further 50-75 bps contraction

Rs700 bn+ annual order inflows

may be possible based on

diverse opportunity set

Source: Company, Kotak Institutional Equities estimates

Absolute margins do not appear unreasonable; comparable to peers

Even in absolute terms, L&T’s EBITDA margin levels do not seem exceptionally high versus peer companies (KEC, Kalpataru). L&T’s present EBITDA margin of 11.5-12% are versus similar margins for Kalpataru (consolidated) at 11-12% and KEC of 9-10%. L&T’s S,G&A costs appear lower versus peers at 4-5% of sales though this could partly be attributed to the large revenue base for L&T. Hence we believe significant further downside from present estimates may be unlikely.

Industrials Larsen & Toubro

30 KOTAK INSTITUTIONAL EQUITIES RESEARCH

EBITDA margin of L&T (standalone) versus peer companies, March fiscal year-ends, 2009-13E (Rs mn)

2009 2010 2011 9MFY12 2012E 2013EL&T (standalone)Revenues 339,385 370,348 439,049 347,264 534,357 607,628 Total operating costs (300,164) (322,592) (382,685) (310,828) (471,185) (539,111) EBITDA 39,222 47,756 56,364 36,436 63,172 68,517

Key ratios (%)Variable exp./sales 77.4 76.7 76.1 76.9 76.6 77.1 Contribution margin 22.6 23.3 23.9 23.1 23.4 22.9 Employee exp./sales 5.8 6.4 6.6 7.9 7.0 7.3 S,G&A, other exp./Sales 5.2 3.9 4.5 4.6 4.6 4.4

EBITDA margin 11.6 12.9 12.8 10.5 11.8 11.3

Kalapataru Power (consolidated)Revenues 18,824 26,316 28,741 19,588

Total operating costs (16,603) (22,989) (25,098) (17,404) EBITDA 2,221 3,327 3,643 2,184 Key ratios (%)Variable exp./sales 76.7 75.8 74.9 72.7 Contribution margin 23.3 24.2 25.1 27.3 Employee exp./sales 5.8 5.9 6.7 6.4 S,G&A, other exp./Sales 5.7 5.7 5.7 9.8

EBITDA margin 11.8 12.6 12.7 11.2

KEC InternationalRevenues 34,288 39,072 44,742 37,458 54,074 58,445 Total operating costs (31,278) (35,014) (40,116) (34,469) (49,466) (53,145) EBITDA 3,010 4,059 4,626 2,989 4,609 5,300

Key ratios (%)Variable exp./sales 74.4 76.0 72.3 72.3 72.3 72.0