CABLES & WIRES - Yes Securities

41

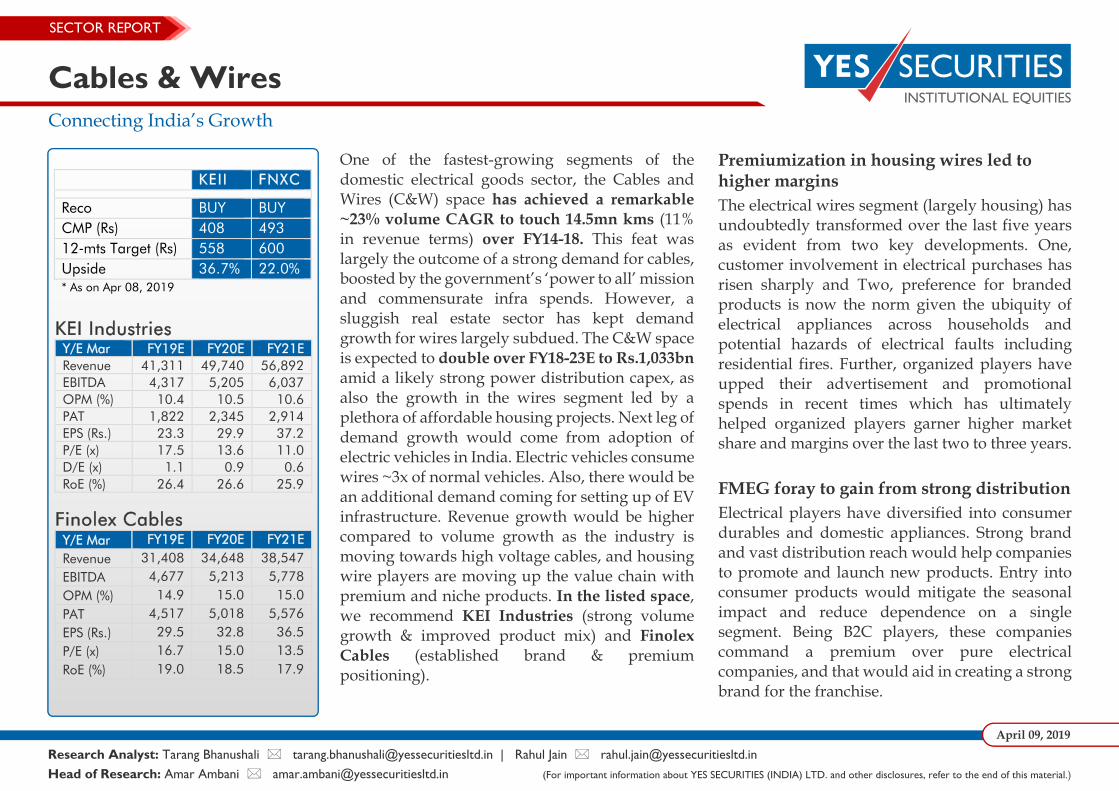

CABLES & WIRES Connecting India’s Growth

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of CABLES & WIRES - Yes Securities

CABLES & WIRES

Connecting India’s Growth

Research Analyst: Tarang Bhanushali [email protected] | Rahul Jain [email protected] Head of Research: Amar Ambani [email protected] (For important information about YES SECURITIES (INDIA) LTD. and other disclosures, refer to the end of this material.)

Cables & Wires Connecting India’s Growth

SECTOR REPORT

April 09, 2019

KEII FNXC

Reco BUY BUY CMP (Rs) 408 493 12‐mts Target (Rs) 558 600 Upside 36.7% 22.0% * As on Apr 08, 2019

KEI Industries Y/E Mar FY19E FY20E FY21E Revenue 41,311 49,740 56,892 EBITDA 4,317 5,205 6,037 OPM (%) 10.4 10.5 10.6 PAT 1,822 2,345 2,914 EPS (Rs.) 23.3 29.9 37.2 P/E (x) 17.5 13.6 11.0 D/E (x) 1.1 0.9 0.6 RoE (%) 26.4 26.6 25.9

Finolex Cables Y/E Mar FY19E FY20E FY21E Revenue 31,408 34,648 38,547 EBITDA 4,677 5,213 5,778 OPM (%) 14.9 15.0 15.0 PAT 4,517 5,018 5,576 EPS (Rs.) 29.5 32.8 36.5 P/E (x) 16.7 15.0 13.5 RoE (%) 19.0 18.5 17.9

One of the fastest-growing segments of the domestic electrical goods sector, the Cables and Wires (C&W) space has achieved a remarkable ~23% volume CAGR to touch 14.5mn kms (11% in revenue terms) over FY14-18. This feat was largely the outcome of a strong demand for cables, boosted by the government’s ‘power to all’ mission and commensurate infra spends. However, a sluggish real estate sector has kept demand growth for wires largely subdued. The C&W space is expected to double over FY18-23E to Rs.1,033bn amid a likely strong power distribution capex, as also the growth in the wires segment led by a plethora of affordable housing projects. Next leg of demand growth would come from adoption of electric vehicles in India. Electric vehicles consume wires ~3x of normal vehicles. Also, there would be an additional demand coming for setting up of EV infrastructure. Revenue growth would be higher compared to volume growth as the industry is moving towards high voltage cables, and housing wire players are moving up the value chain with premium and niche products. In the listed space, we recommend KEI Industries (strong volume growth & improved product mix) and Finolex Cables (established brand & premium positioning).

Premiumization in housing wires led to higher margins The electrical wires segment (largely housing) has undoubtedly transformed over the last five years as evident from two key developments. One, customer involvement in electrical purchases has risen sharply and Two, preference for branded products is now the norm given the ubiquity of electrical appliances across households and potential hazards of electrical faults including residential fires. Further, organized players have upped their advertisement and promotional spends in recent times which has ultimately helped organized players garner higher market share and margins over the last two to three years. FMEG foray to gain from strong distribution Electrical players have diversified into consumer durables and domestic appliances. Strong brand and vast distribution reach would help companies to promote and launch new products. Entry into consumer products would mitigate the seasonal impact and reduce dependence on a single segment. Being B2C players, these companies command a premium over pure electrical companies, and that would aid in creating a strong brand for the franchise.

Cables & Wires

2

KEI Industries: Retail penetration to drive growth KEI has emerged as the fastest growing cables and wires company in the listed space over the past five years. Strong demand from the power distribution sector and increasing share of housing wires has propelled KEI’s growth. Increasing domestic market reach and improved brand visibility through media spends has helped doubling of revenues through dealer network over FY14-18, at Rs.9.8bn (28.2% of revenue). The company has also doubled its institutional sales on the back of strong demand from infra & power distribution sectors and KEI’s comprehensive range in its cables portfolio. On the back of capacity expansion, EHV & EPC order execution, and strong demand from power distribution sector, we expect KEI to witness a 18% revenue CAGR over FY18-21. Increase in share of higher margin segments (470bps) should bring about an 83bps expansion in operating margins over FY18-21. We believe the company would witness some rerating given a likely 26.4% PAT CAGR over FY18-21, RoE of +25% and D/E trending lower to 0.6x. We initiate with a Buy rating for a target price of Rs.558 (15x FY21E P/E). Exhibit 1: Consumer Electricals sector valuation snapshot

Finolex cables: A Pure Premium play Finolex Cables is a leading player in the domestic cables and wires industry. It has a vast distribution network across India and commands a notable premium over its peers. The company has ramped up its communication cables business and has diversified into higher margin consumer electric products. Remarkably enough, Finolex has maintained its premium brand image despite the weak growth in electrical C&W segment, with no compromise whatsoever on margins and working capital cycle even during this tough phase. With green shoots visible in 9M FY19, we believe growth over the next two years would be led by new product introduction, strong demand for optic fibre and growing FMEG contribution. Increased promotional expenses coupled with expansion of dealer network should help FMEG product revenues double over FY18-21. We expect a revenue CAGR of 11% over FY18-21E with OPM of ~15%, and we believe that the valuation gap between Finolex and its peers in the electrical industry will narrow as it continues to deliver superior margins and increase the share of FMEG products. We value the company at 20x standalone FY21E P/E (higher than its 3-yr average of 19x) and initiate coverage with a Buy rating for a target price of Rs.600.

Company Mcap CAGR (FY18-

21E) (%) EBITDA margin (%) RoE (%) RoCE (%) P/E (x)

Rs. mn Rev PAT FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E Finolex Cabl 75,404 11.0 19.1 15.7 14.9 15.0 15.0 14.4 17.2 16.6 16.0 20.9 19.0 18.5 17.9 22.8 16.7 15.0 13.5 KEI Ind. 31,971 18.0 26.4 9.8 10.4 10.5 10.6 27.1 26.4 26.6 25.9 23.8 26.1 27.9 28.9 22.2 17.5 13.6 11.0 Havells 474,451 15.4 19.0 13.9 13.5 14.3 14.9 20.0 20.9 22.5 23.0 26.9 28.3 30.5 31.4 66.6 56.8 46.4 39.6 Vguard 94,074 13.4 23.5 8.2 8.1 9.5 10.2 19.5 18.7 22.1 23.4 26.1 25.1 29.4 31.1 69.7 62.5 45.9 37.0 Crompton 141,657 11.6 18.1 13.0 13.0 13.6 14.2 49.5 40.8 39.0 37.1 42.9 40.2 44.8 50.6 43.7 38.6 31.8 26.6 Symphony 94,922 17.9 11.7 27.5 21.8 23.0 24.0 35.8 26.2 27.0 25.4 46.8 35.4 36.6 34.8 49.3 52.9 41.3 35.4 Orient Elect 33,313 13.9 26.7 8.5 9.0 9.4 9.5 40.3 29.6 29.5 27.4 46.9 35.5 36.9 36.1 52.0 37.6 29.8 25.6

Source: Company, Bloomberg, YES Sec – Research, * As on Apr 08, 2019

Cables & Wires

3

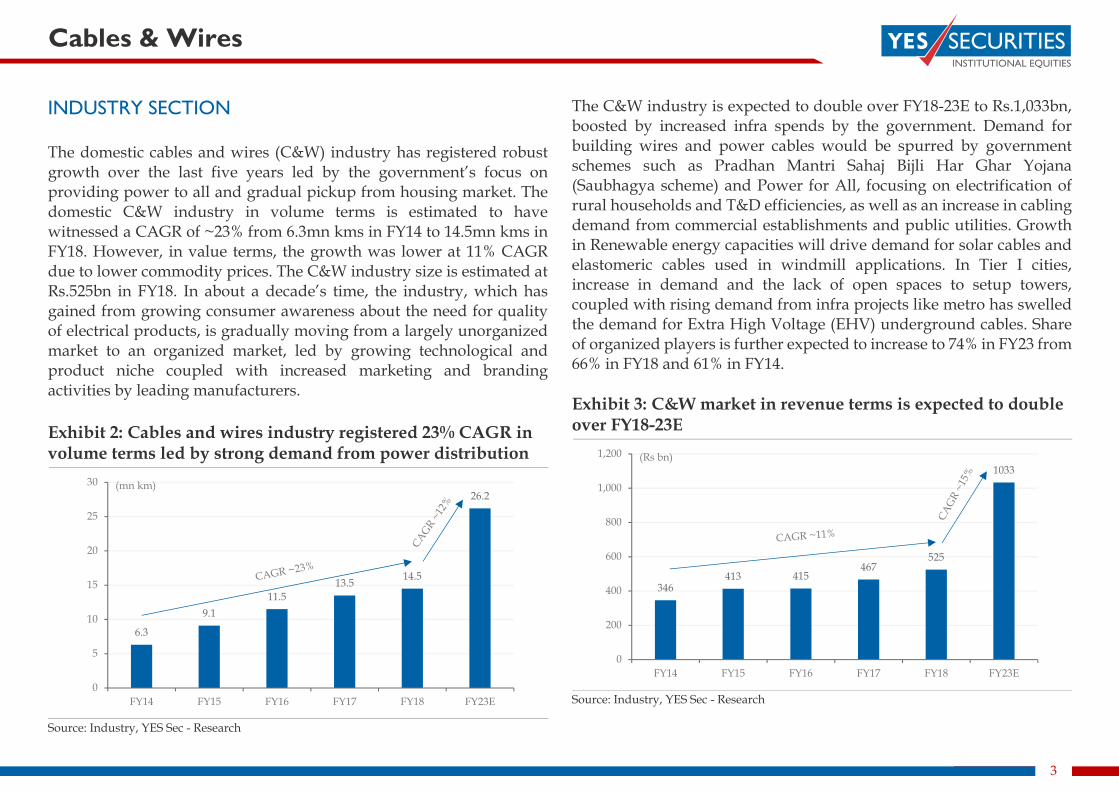

INDUSTRY SECTION The domestic cables and wires (C&W) industry has registered robust growth over the last five years led by the government’s focus on providing power to all and gradual pickup from housing market. The domestic C&W industry in volume terms is estimated to have witnessed a CAGR of ~23% from 6.3mn kms in FY14 to 14.5mn kms in FY18. However, in value terms, the growth was lower at 11% CAGR due to lower commodity prices. The C&W industry size is estimated at Rs.525bn in FY18. In about a decade’s time, the industry, which has gained from growing consumer awareness about the need for quality of electrical products, is gradually moving from a largely unorganized market to an organized market, led by growing technological and product niche coupled with increased marketing and branding activities by leading manufacturers. Exhibit 2: Cables and wires industry registered 23% CAGR in volume terms led by strong demand from power distribution

Source: Industry, YES Sec - Research

The C&W industry is expected to double over FY18-23E to Rs.1,033bn, boosted by increased infra spends by the government. Demand for building wires and power cables would be spurred by government schemes such as Pradhan Mantri Sahaj Bijli Har Ghar Yojana (Saubhagya scheme) and Power for All, focusing on electrification of rural households and T&D efficiencies, as well as an increase in cabling demand from commercial establishments and public utilities. Growth in Renewable energy capacities will drive demand for solar cables and elastomeric cables used in windmill applications. In Tier I cities, increase in demand and the lack of open spaces to setup towers, coupled with rising demand from infra projects like metro has swelled the demand for Extra High Voltage (EHV) underground cables. Share of organized players is further expected to increase to 74% in FY23 from 66% in FY18 and 61% in FY14. Exhibit 3: C&W market in revenue terms is expected to double over FY18-23E

Source: Industry, YES Sec - Research

6.3

9.111.5

13.5 14.5

26.2

0

5

10

15

20

25

30

FY14 FY15 FY16 FY17 FY18 FY23E

(mn km)

346413 415

467525

1033

0

200

400

600

800

1,000

1,200

FY14 FY15 FY16 FY17 FY18 FY23E

(Rs bn)

Cables & Wires

4

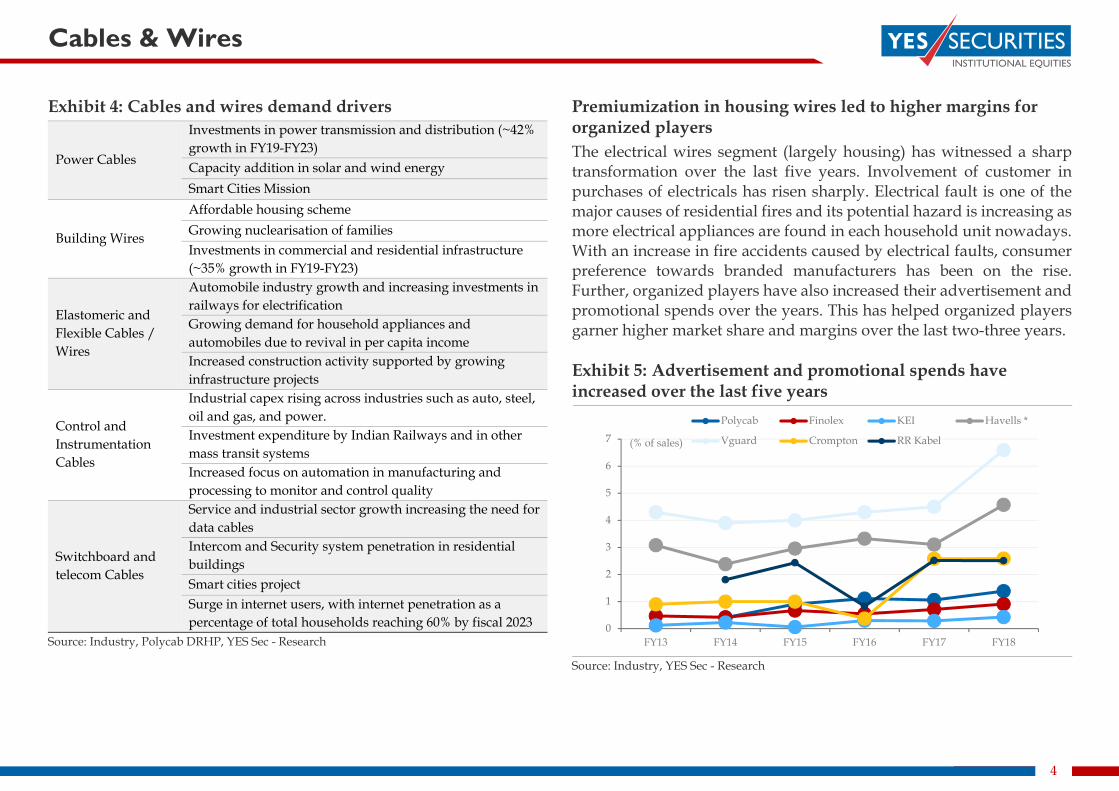

Exhibit 4: Cables and wires demand drivers

Power Cables

Investments in power transmission and distribution (~42% growth in FY19-FY23) Capacity addition in solar and wind energy Smart Cities Mission

Building Wires

Affordable housing scheme Growing nuclearisation of families Investments in commercial and residential infrastructure (~35% growth in FY19-FY23)

Elastomeric and Flexible Cables / Wires

Automobile industry growth and increasing investments in railways for electrification Growing demand for household appliances and automobiles due to revival in per capita income Increased construction activity supported by growing infrastructure projects

Control and Instrumentation Cables

Industrial capex rising across industries such as auto, steel, oil and gas, and power. Investment expenditure by Indian Railways and in other mass transit systems Increased focus on automation in manufacturing and processing to monitor and control quality

Switchboard and telecom Cables

Service and industrial sector growth increasing the need for data cables Intercom and Security system penetration in residential buildings Smart cities project Surge in internet users, with internet penetration as a percentage of total households reaching 60% by fiscal 2023

Source: Industry, Polycab DRHP, YES Sec - Research

Premiumization in housing wires led to higher margins for organized players The electrical wires segment (largely housing) has witnessed a sharp transformation over the last five years. Involvement of customer in purchases of electricals has risen sharply. Electrical fault is one of the major causes of residential fires and its potential hazard is increasing as more electrical appliances are found in each household unit nowadays. With an increase in fire accidents caused by electrical faults, consumer preference towards branded manufacturers has been on the rise. Further, organized players have also increased their advertisement and promotional spends over the years. This has helped organized players garner higher market share and margins over the last two-three years. Exhibit 5: Advertisement and promotional spends have increased over the last five years

Source: Industry, YES Sec - Research

0

1

2

3

4

5

6

7

FY13 FY14 FY15 FY16 FY17 FY18

(% of sales)

Polycab Finolex KEI Havells *

Vguard Crompton RR Kabel

Cables & Wires

5

Exhibit 6: Campaigns of cables & wires players in the industry Company Campaigns

Finolex Cables

Suraksha, Behtar ElectriKAL ke liye

KEI Industries

Jodey Dilon Ke Taar

Syska

Kyunki, wires less nahi, wires more

V-Guard

Bringing home a better tomorrow

Company Campaigns

Havells

Wires That Don’t Catch Fire

Polycab

Connection Bachat Ka, Connection Zindagi ka

RR Kabel

Akalmand Bano Sahi Chuno

Anchor by Panasonic

Naye India ke badhte load ke liye

Source: Companies, YES Sec - Research

Cables & Wires

6

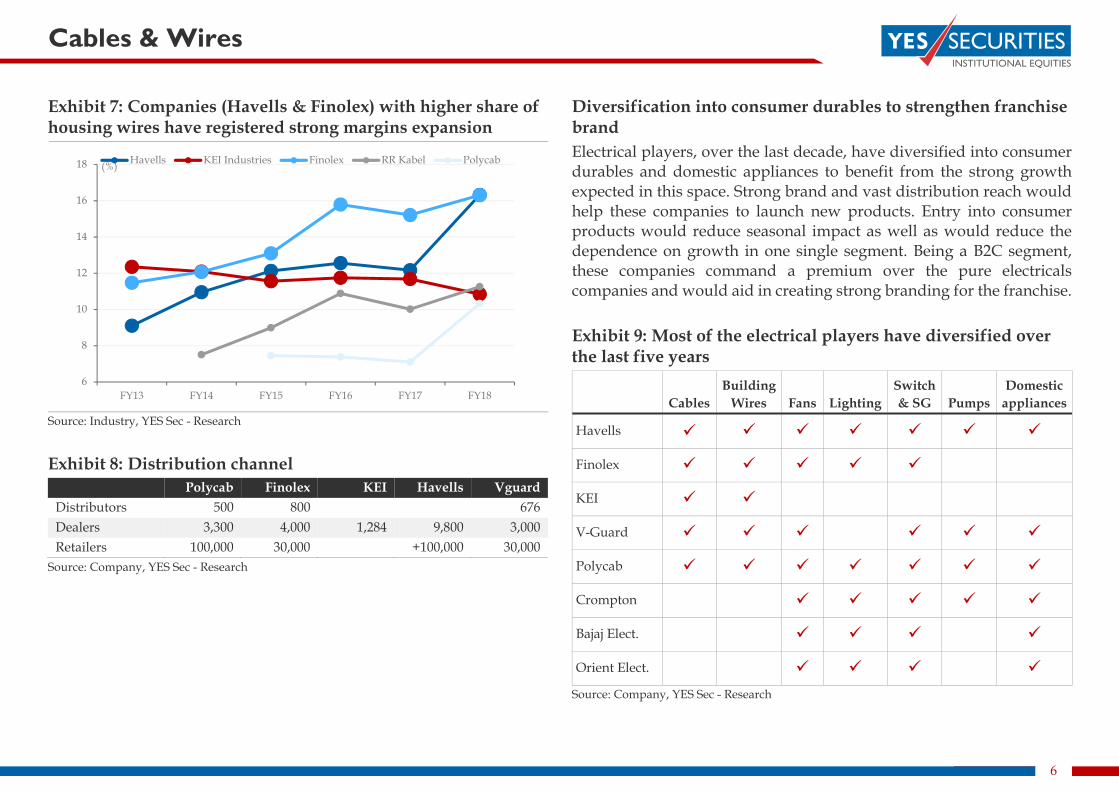

Exhibit 7: Companies (Havells & Finolex) with higher share of housing wires have registered strong margins expansion

Source: Industry, YES Sec - Research Exhibit 8: Distribution channel

Polycab Finolex KEI Havells Vguard Distributors 500 800 676 Dealers 3,300 4,000 1,284 9,800 3,000 Retailers 100,000 30,000 +100,000 30,000

Source: Company, YES Sec - Research

Diversification into consumer durables to strengthen franchise brand Electrical players, over the last decade, have diversified into consumer durables and domestic appliances to benefit from the strong growth expected in this space. Strong brand and vast distribution reach would help these companies to launch new products. Entry into consumer products would reduce seasonal impact as well as would reduce the dependence on growth in one single segment. Being a B2C segment, these companies command a premium over the pure electricals companies and would aid in creating strong branding for the franchise. Exhibit 9: Most of the electrical players have diversified over the last five years

Cables Building

Wires Fans Lighting Switch & SG Pumps

Domestic appliances

Havells

Finolex

KEI

V-Guard

Polycab

Crompton

Bajaj Elect.

Orient Elect.

Source: Company, YES Sec - Research

6

8

10

12

14

16

18

FY13 FY14 FY15 FY16 FY17 FY18

(%) Havells KEI Industries Finolex RR Kabel Polycab

Cables & Wires

7

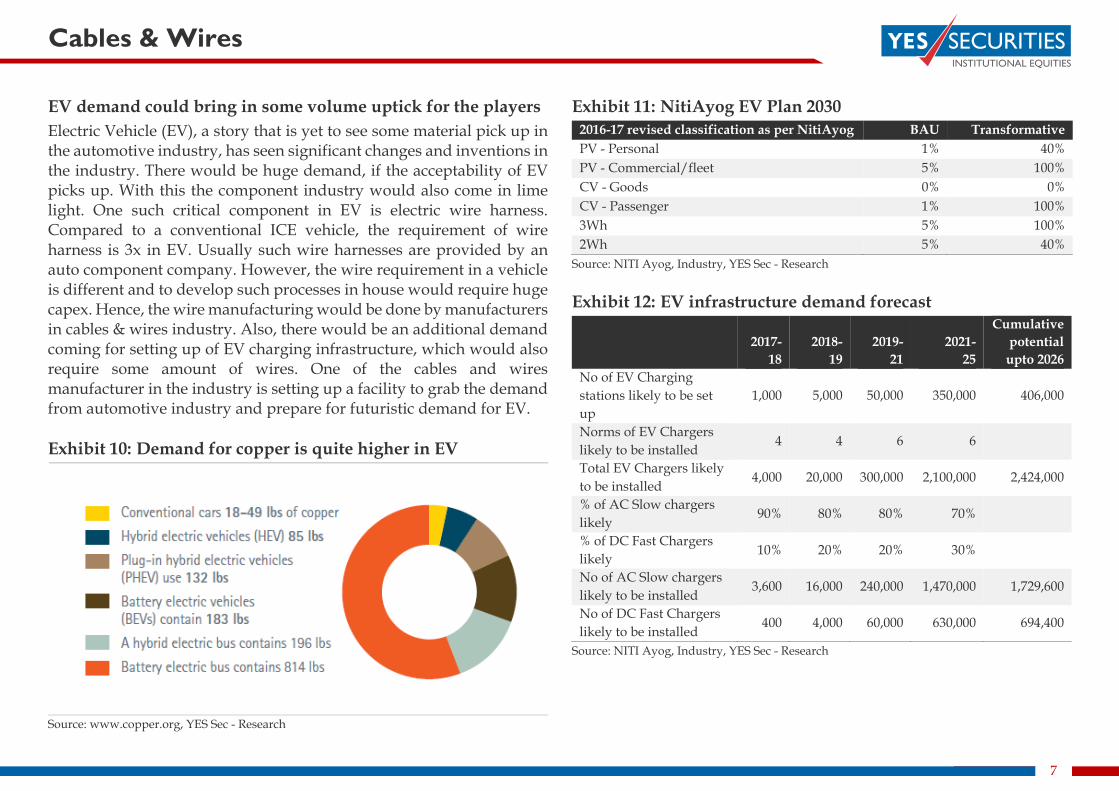

EV demand could bring in some volume uptick for the players Electric Vehicle (EV), a story that is yet to see some material pick up in the automotive industry, has seen significant changes and inventions in the industry. There would be huge demand, if the acceptability of EV picks up. With this the component industry would also come in lime light. One such critical component in EV is electric wire harness. Compared to a conventional ICE vehicle, the requirement of wire harness is 3x in EV. Usually such wire harnesses are provided by an auto component company. However, the wire requirement in a vehicle is different and to develop such processes in house would require huge capex. Hence, the wire manufacturing would be done by manufacturers in cables & wires industry. Also, there would be an additional demand coming for setting up of EV charging infrastructure, which would also require some amount of wires. One of the cables and wires manufacturer in the industry is setting up a facility to grab the demand from automotive industry and prepare for futuristic demand for EV. Exhibit 10: Demand for copper is quite higher in EV

Source: www.copper.org, YES Sec - Research

Exhibit 11: NitiAyog EV Plan 2030 2016-17 revised classification as per NitiAyog BAU Transformative PV - Personal 1% 40% PV - Commercial/fleet 5% 100% CV - Goods 0% 0% CV - Passenger 1% 100% 3Wh 5% 100% 2Wh 5% 40%

Source: NITI Ayog, Industry, YES Sec - Research Exhibit 12: EV infrastructure demand forecast

2017-18

2018- 19

2019- 21

2021- 25

Cumulative potential

upto 2026 No of EV Charging stations likely to be set up

1,000 5,000 50,000 350,000 406,000

Norms of EV Chargers likely to be installed

4 4 6 6

Total EV Chargers likely to be installed

4,000 20,000 300,000 2,100,000 2,424,000

% of AC Slow chargers likely

90% 80% 80% 70%

% of DC Fast Chargers likely

10% 20% 20% 30%

No of AC Slow chargers likely to be installed

3,600 16,000 240,000 1,470,000 1,729,600

No of DC Fast Chargers likely to be installed

400 4,000 60,000 630,000 694,400

Source: NITI Ayog, Industry, YES Sec - Research

Cables & Wires

8

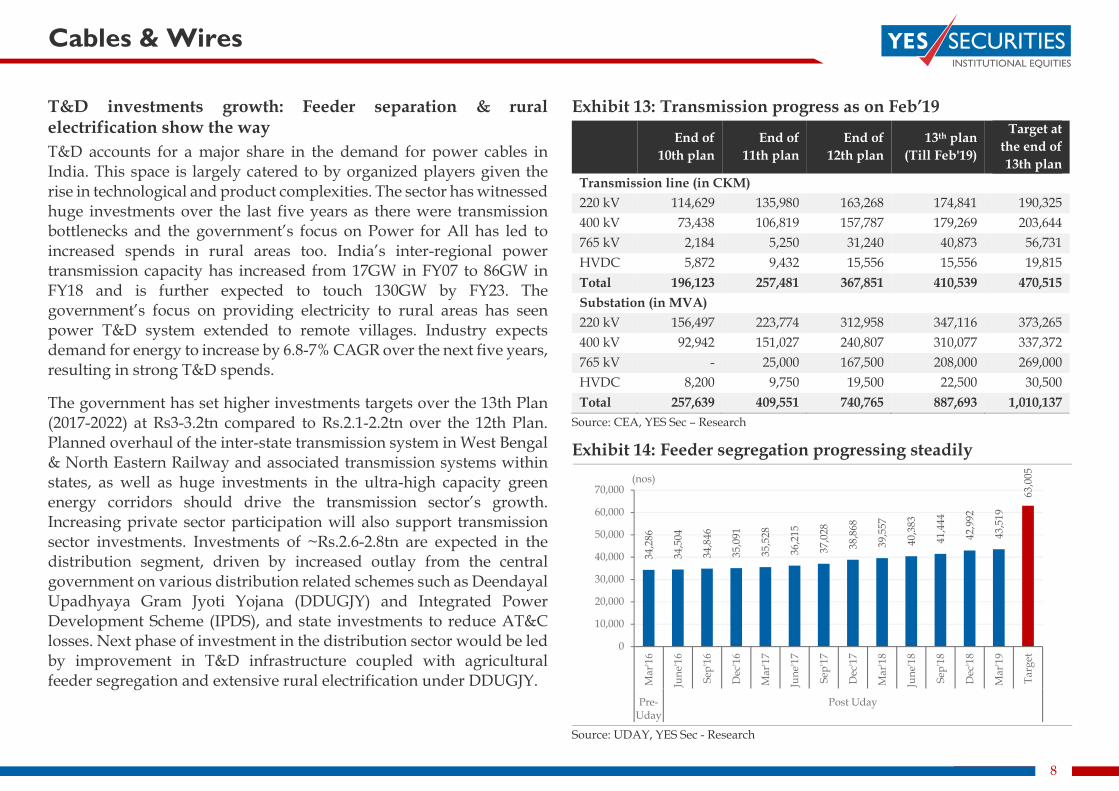

T&D investments growth: Feeder separation & rural electrification show the way T&D accounts for a major share in the demand for power cables in India. This space is largely catered to by organized players given the rise in technological and product complexities. The sector has witnessed huge investments over the last five years as there were transmission bottlenecks and the government’s focus on Power for All has led to increased spends in rural areas too. India’s inter-regional power transmission capacity has increased from 17GW in FY07 to 86GW in FY18 and is further expected to touch 130GW by FY23. The government’s focus on providing electricity to rural areas has seen power T&D system extended to remote villages. Industry expects demand for energy to increase by 6.8-7% CAGR over the next five years, resulting in strong T&D spends.

The government has set higher investments targets over the 13th Plan (2017-2022) at Rs3-3.2tn compared to Rs.2.1-2.2tn over the 12th Plan. Planned overhaul of the inter-state transmission system in West Bengal & North Eastern Railway and associated transmission systems within states, as well as huge investments in the ultra-high capacity green energy corridors should drive the transmission sector’s growth. Increasing private sector participation will also support transmission sector investments. Investments of ~Rs.2.6-2.8tn are expected in the distribution segment, driven by increased outlay from the central government on various distribution related schemes such as Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY) and Integrated Power Development Scheme (IPDS), and state investments to reduce AT&C losses. Next phase of investment in the distribution sector would be led by improvement in T&D infrastructure coupled with agricultural feeder segregation and extensive rural electrification under DDUGJY.

Exhibit 13: Transmission progress as on Feb’19

End of 10th plan

End of 11th plan

End of 12th plan

13th plan (Till Feb'19)

Target at the end of 13th plan

Transmission line (in CKM) 220 kV 114,629 135,980 163,268 174,841 190,325 400 kV 73,438 106,819 157,787 179,269 203,644 765 kV 2,184 5,250 31,240 40,873 56,731 HVDC 5,872 9,432 15,556 15,556 19,815 Total 196,123 257,481 367,851 410,539 470,515 Substation (in MVA) 220 kV 156,497 223,774 312,958 347,116 373,265 400 kV 92,942 151,027 240,807 310,077 337,372 765 kV - 25,000 167,500 208,000 269,000 HVDC 8,200 9,750 19,500 22,500 30,500 Total 257,639 409,551 740,765 887,693 1,010,137

Source: CEA, YES Sec – Research

Exhibit 14: Feeder segregation progressing steadily

Source: UDAY, YES Sec - Research

34,2

86

34,5

04

34,8

46

35,0

91

35,5

28

36,2

15

37,0

28

38,8

68

39,5

57

40,3

83

41,4

44

42,9

92

43,5

19

63,0

05

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Mar

'16

June

'16

Sep'

16

Dec

'16

Mar

'17

June

'17

Sep'

17

Dec

'17

Mar

'18

June

'18

Sep'

18

Dec

'18

Mar

'19

Targ

et

Pre-Uday

Post Uday

(nos)

Cables & Wires

9

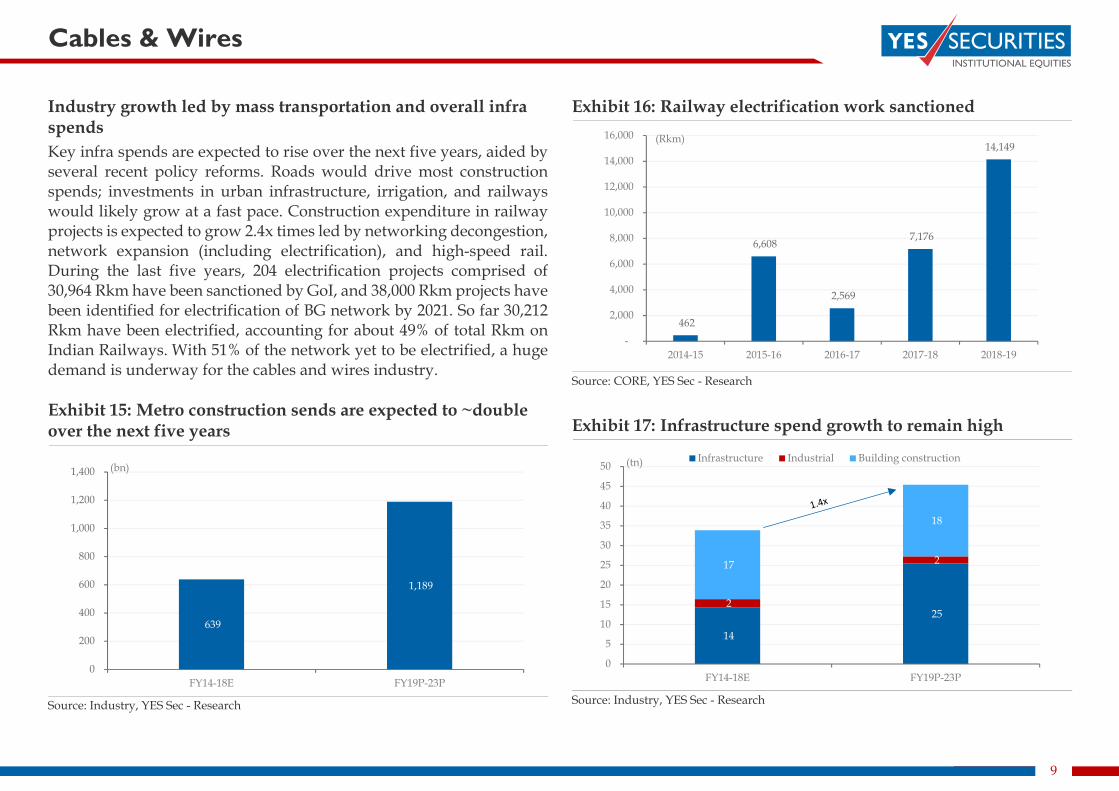

Industry growth led by mass transportation and overall infra spends Key infra spends are expected to rise over the next five years, aided by several recent policy reforms. Roads would drive most construction spends; investments in urban infrastructure, irrigation, and railways would likely grow at a fast pace. Construction expenditure in railway projects is expected to grow 2.4x times led by networking decongestion, network expansion (including electrification), and high-speed rail. During the last five years, 204 electrification projects comprised of 30,964 Rkm have been sanctioned by GoI, and 38,000 Rkm projects have been identified for electrification of BG network by 2021. So far 30,212 Rkm have been electrified, accounting for about 49% of total Rkm on Indian Railways. With 51% of the network yet to be electrified, a huge demand is underway for the cables and wires industry. Exhibit 15: Metro construction sends are expected to ~double over the next five years

Source: Industry, YES Sec - Research

Exhibit 16: Railway electrification work sanctioned

Source: CORE, YES Sec - Research

Exhibit 17: Infrastructure spend growth to remain high

Source: Industry, YES Sec - Research

639

1,189

0

200

400

600

800

1,000

1,200

1,400

FY14-18E FY19P-23P

(bn)

462

6,608

2,569

7,176

14,149

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2014-15 2015-16 2016-17 2017-18 2018-19

(Rkm)

14

25 2

2 17

18

0

5

10

15

20

25

30

35

40

45

50

FY14-18E FY19P-23P

(tn) Infrastructure Industrial Building construction

Cables & Wires

10

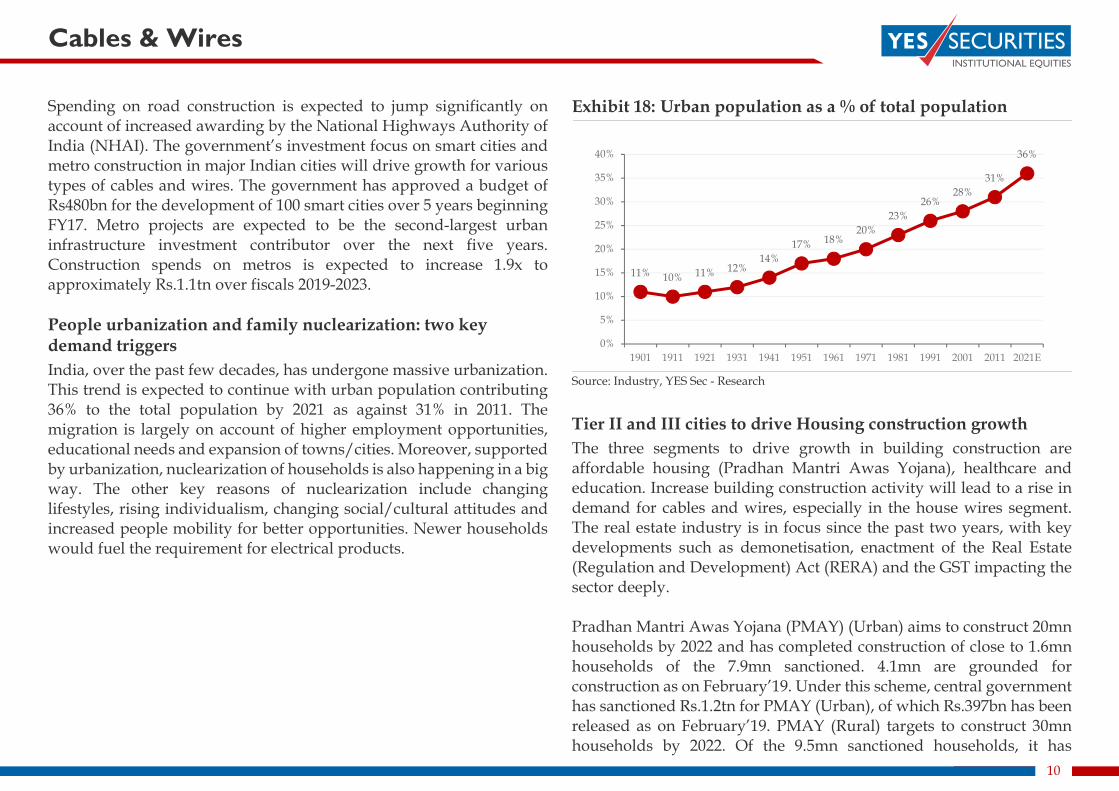

Spending on road construction is expected to jump significantly on account of increased awarding by the National Highways Authority of India (NHAI). The government’s investment focus on smart cities and metro construction in major Indian cities will drive growth for various types of cables and wires. The government has approved a budget of Rs480bn for the development of 100 smart cities over 5 years beginning FY17. Metro projects are expected to be the second-largest urban infrastructure investment contributor over the next five years. Construction spends on metros is expected to increase 1.9x to approximately Rs.1.1tn over fiscals 2019-2023. People urbanization and family nuclearization: two key demand triggers India, over the past few decades, has undergone massive urbanization. This trend is expected to continue with urban population contributing 36% to the total population by 2021 as against 31% in 2011. The migration is largely on account of higher employment opportunities, educational needs and expansion of towns/cities. Moreover, supported by urbanization, nuclearization of households is also happening in a big way. The other key reasons of nuclearization include changing lifestyles, rising individualism, changing social/cultural attitudes and increased people mobility for better opportunities. Newer households would fuel the requirement for electrical products.

Exhibit 18: Urban population as a % of total population

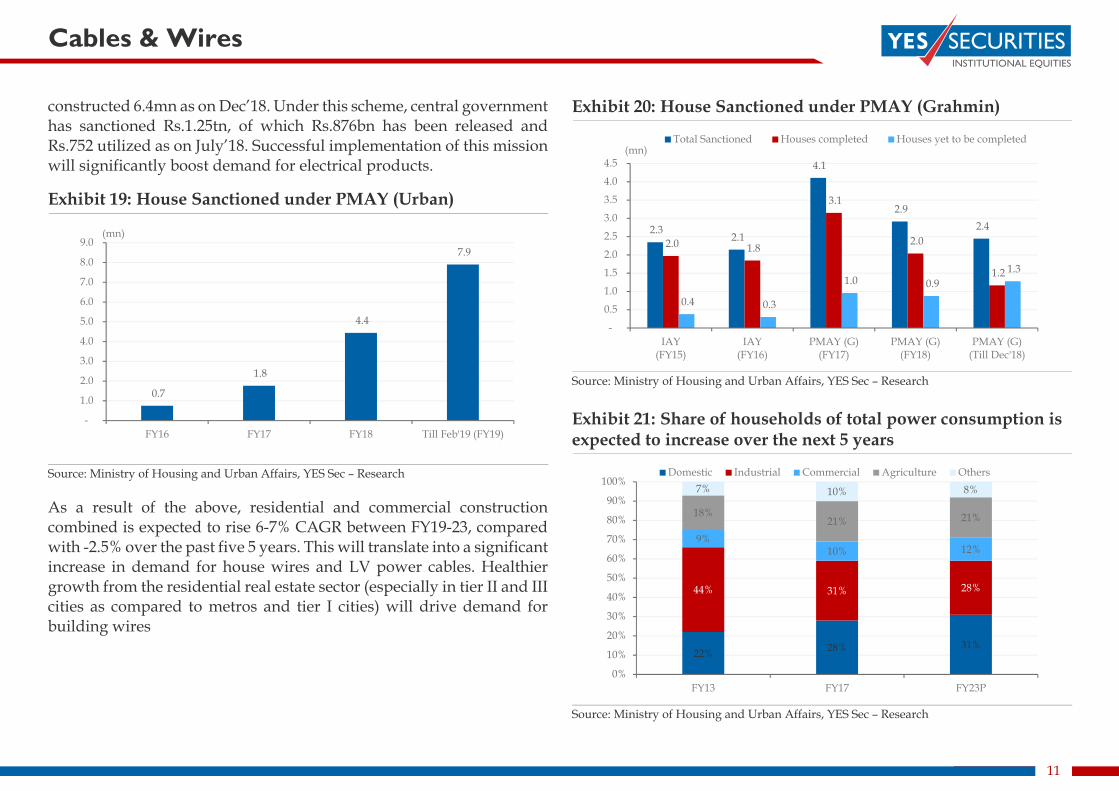

Source: Industry, YES Sec - Research Tier II and III cities to drive Housing construction growth The three segments to drive growth in building construction are affordable housing (Pradhan Mantri Awas Yojana), healthcare and education. Increase building construction activity will lead to a rise in demand for cables and wires, especially in the house wires segment. The real estate industry is in focus since the past two years, with key developments such as demonetisation, enactment of the Real Estate (Regulation and Development) Act (RERA) and the GST impacting the sector deeply. Pradhan Mantri Awas Yojana (PMAY) (Urban) aims to construct 20mn households by 2022 and has completed construction of close to 1.6mn households of the 7.9mn sanctioned. 4.1mn are grounded for construction as on February’19. Under this scheme, central government has sanctioned Rs.1.2tn for PMAY (Urban), of which Rs.397bn has been released as on February’19. PMAY (Rural) targets to construct 30mn households by 2022. Of the 9.5mn sanctioned households, it has

11% 10% 11% 12%14%

17% 18%20%

23%26%

28%31%

36%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1901 1911 1921 1931 1941 1951 1961 1971 1981 1991 2001 2011 2021E

Cables & Wires

11

constructed 6.4mn as on Dec’18. Under this scheme, central government has sanctioned Rs.1.25tn, of which Rs.876bn has been released and Rs.752 utilized as on July’18. Successful implementation of this mission will significantly boost demand for electrical products.

Exhibit 19: House Sanctioned under PMAY (Urban)

Source: Ministry of Housing and Urban Affairs, YES Sec – Research As a result of the above, residential and commercial construction combined is expected to rise 6-7% CAGR between FY19-23, compared with -2.5% over the past five 5 years. This will translate into a significant increase in demand for house wires and LV power cables. Healthier growth from the residential real estate sector (especially in tier II and III cities as compared to metros and tier I cities) will drive demand for building wires

Exhibit 20: House Sanctioned under PMAY (Grahmin)

Source: Ministry of Housing and Urban Affairs, YES Sec – Research Exhibit 21: Share of households of total power consumption is expected to increase over the next 5 years

Source: Ministry of Housing and Urban Affairs, YES Sec – Research

0.7

1.8

4.4

7.9

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

FY16 FY17 FY18 Till Feb'19 (FY19)

(mn) 2.3 2.1

4.1

2.9 2.4

2.0 1.8

3.1

2.0

1.2

0.4 0.3

1.0 0.9 1.3

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

IAY(FY15)

IAY(FY16)

PMAY (G)(FY17)

PMAY (G)(FY18)

PMAY (G)(Till Dec'18)

(mn)Total Sanctioned Houses completed Houses yet to be completed

22% 28% 31%

44% 31% 28%

9%10% 12%

18%21% 21%

7% 10% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY17 FY23P

Domestic Industrial Commercial Agriculture Others

Cables & Wires

12

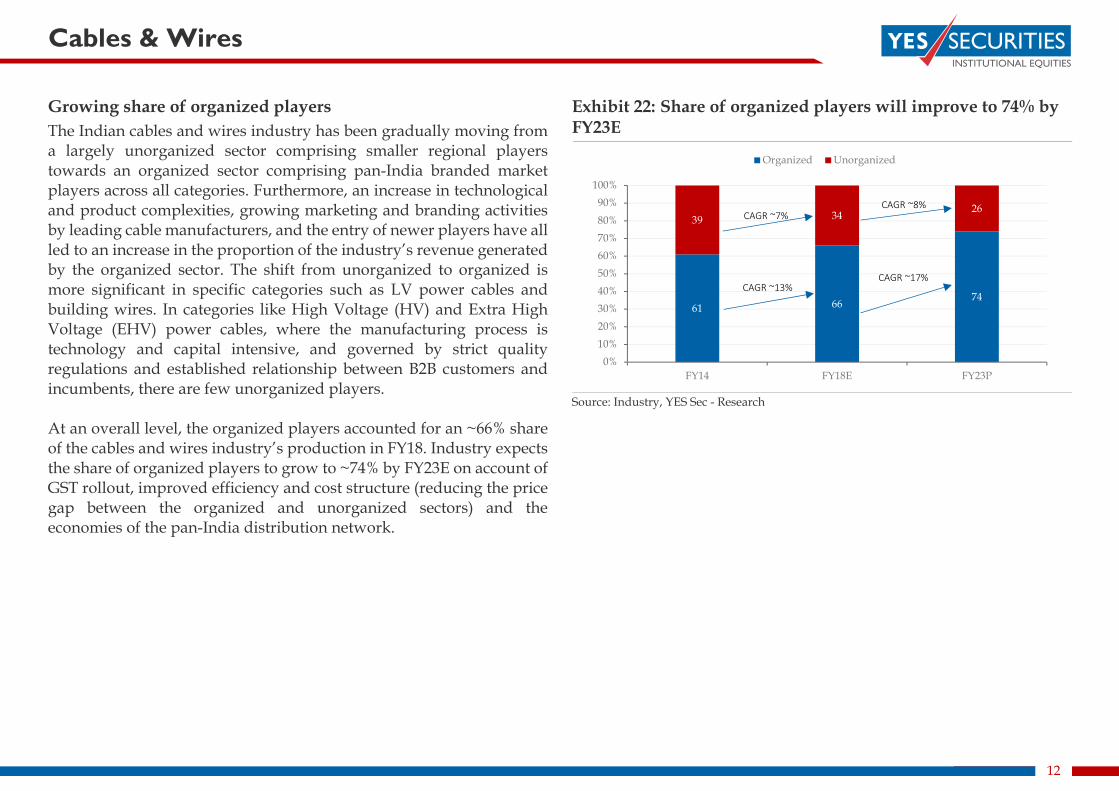

Growing share of organized players The Indian cables and wires industry has been gradually moving from a largely unorganized sector comprising smaller regional players towards an organized sector comprising pan-India branded market players across all categories. Furthermore, an increase in technological and product complexities, growing marketing and branding activities by leading cable manufacturers, and the entry of newer players have all led to an increase in the proportion of the industry’s revenue generated by the organized sector. The shift from unorganized to organized is more significant in specific categories such as LV power cables and building wires. In categories like High Voltage (HV) and Extra High Voltage (EHV) power cables, where the manufacturing process is technology and capital intensive, and governed by strict quality regulations and established relationship between B2B customers and incumbents, there are few unorganized players. At an overall level, the organized players accounted for an ~66% share of the cables and wires industry’s production in FY18. Industry expects the share of organized players to grow to ~74% by FY23E on account of GST rollout, improved efficiency and cost structure (reducing the price gap between the organized and unorganized sectors) and the economies of the pan-India distribution network.

Exhibit 22: Share of organized players will improve to 74% by FY23E

Source: Industry, YES Sec - Research

61 66 74

39 34 26

0%10%20%30%40%50%60%70%80%90%

100%

FY14 FY18E FY23P

Organized Unorganized

CAGR ~13%

CAGR ~7%CAGR ~8%

CAGR ~17%

COMPANY SECTION

Research Analyst: Tarang Bhanushali [email protected] | Rahul Jain [email protected] Head of Research: Amar Ambani [email protected] (For important information about YES SECURITIES (INDIA) LTD. and other disclosures, refer to the end of this material.)

KEI Industries Ltd - BUY Retail penetration to drive growth

COMPANY REPORT

April 09, 2019

CMP (Rs) (As on Apr 08, 2019) 408 Sector: Consumer Electricals

12‐mts Target (Rs) 558 Market cap (Rs mn) 31,971

Upside 36.7% Enterprise value (Rs mn) 39,609

Exhibit 23: Financial summary Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Revenue 26,281 34,650 41,311 49,740 56,892 yoy growth (%) 11.8 31.8 19.2 20.4 14.4 Operating profit 2,687 3,388 4,317 5,205 6,037 OPM (%) 10.2 9.8 10.4 10.5 10.6 Reported PAT 937 1,443 1,822 2,345 2,914 yoy growth (%) 49.8 54.1 26.3 28.7 24.3 EPS (Rs) 12.0 18.4 23.3 29.9 37.2 P/E (x) 33.9 22.2 17.5 13.6 11.0 EV/EBITDA (x) 14.5 11.7 9.2 7.8 6.6 Debt/Equity (x) 1.6 1.4 1.1 0.9 0.6 RoE (%) 22.6 27.1 26.4 26.6 25.9 RoCE (%) 24.1 23.8 26.1 27.9 28.9

Source: Company, YES Sec - Research

KEI has emerged as the fastest growing cables and wires company inthe listed space over the past five years. Strong demand from thepower distribution sector and increasing share of housing wires haspropelled KEI’s growth. Increasing reach in the domestic market andimproving brand visibility via various media spends, has led to thecompany doubling its revenue through dealer network over FY14-18to Rs.9.8bn (28.2% of revenue). The company has also managed todouble its institutional sales on the back of strong demand frominfrastructure & power distribution sector and KEI’s comprehensiverange in its cables portfolio. On the back of capacity expansion,execution of orders in EHV & EPC and strong demand from powerdistribution sector, we expect KEI to witness 18% revenue CAGRover FY18-21. Increase in share of higher margin segments (470bps)would lead to an expansion of 83bps in operating margin over FY18-21. We believe the company would continue to witness some reratingas it is expected to report 26.4% PAT CAGR over FY18-21, RoE wouldstay +25% and D/E would trend lower to 0.6x. We initiate with a Buyrating for a target price of Rs.558 (15x FY21E P/E).

Housing wires to propel growth In 9M FY19, sales through dealer network grew ~50% on a yoy basisand increased its revenue share to 33.4% from 26% in FY14. Since thissegment is largely B2C, margins are higher by 100-150bps and workingcapital requirement is lower compared to institutional business. OverFY13-19, KEI has more than doubled its dealers to 1,400 and hasincreased its advertisement spends 10x. Higher sales through channelfinancing will reduce working capital requirements. We expect dealerbusiness revenue to more than double over FY18-21 to Rs.20bn led bygrowing reach and focused spends on advertisements.

Re-rating to continue; Initiate with Buy KEI has witnessed valuation re-rating on the back of strong earningsgrowth, while keeping leverage under check and improving RoE sharply from 11% in FY15 to 27.1% in FY18. We believe the companywould continue to witness valuation re-rating as earnings growthremains robust on a large base, D/E declines and RoE would stay +25%levels.

KEI Industries Ltd

14

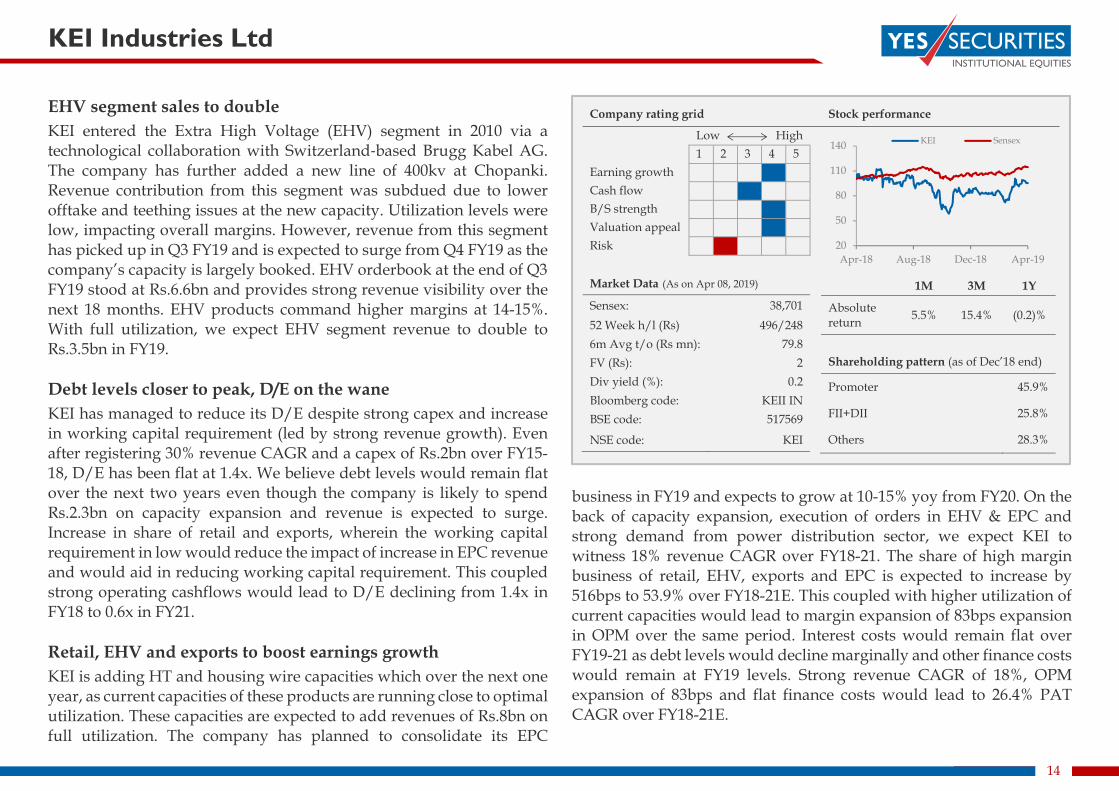

EHV segment sales to double KEI entered the Extra High Voltage (EHV) segment in 2010 via a technological collaboration with Switzerland‐based Brugg Kabel AG. The company has further added a new line of 400kv at Chopanki. Revenue contribution from this segment was subdued due to lower offtake and teething issues at the new capacity. Utilization levels were low, impacting overall margins. However, revenue from this segment has picked up in Q3 FY19 and is expected to surge from Q4 FY19 as the company’s capacity is largely booked. EHV orderbook at the end of Q3 FY19 stood at Rs.6.6bn and provides strong revenue visibility over the next 18 months. EHV products command higher margins at 14-15%. With full utilization, we expect EHV segment revenue to double to Rs.3.5bn in FY19. Debt levels closer to peak, D/E on the wane KEI has managed to reduce its D/E despite strong capex and increase in working capital requirement (led by strong revenue growth). Even after registering 30% revenue CAGR and a capex of Rs.2bn over FY15-18, D/E has been flat at 1.4x. We believe debt levels would remain flat over the next two years even though the company is likely to spend Rs.2.3bn on capacity expansion and revenue is expected to surge. Increase in share of retail and exports, wherein the working capital requirement in low would reduce the impact of increase in EPC revenue and would aid in reducing working capital requirement. This coupled strong operating cashflows would lead to D/E declining from 1.4x in FY18 to 0.6x in FY21. Retail, EHV and exports to boost earnings growth KEI is adding HT and housing wire capacities which over the next one year, as current capacities of these products are running close to optimal utilization. These capacities are expected to add revenues of Rs.8bn on full utilization. The company has planned to consolidate its EPC

business in FY19 and expects to grow at 10-15% yoy from FY20. On the back of capacity expansion, execution of orders in EHV & EPC and strong demand from power distribution sector, we expect KEI to witness 18% revenue CAGR over FY18-21. The share of high margin business of retail, EHV, exports and EPC is expected to increase by 516bps to 53.9% over FY18-21E. This coupled with higher utilization of current capacities would lead to margin expansion of 83bps expansion in OPM over the same period. Interest costs would remain flat over FY19-21 as debt levels would decline marginally and other finance costs would remain at FY19 levels. Strong revenue CAGR of 18%, OPM expansion of 83bps and flat finance costs would lead to 26.4% PAT CAGR over FY18-21E.

Company rating grid Stock performance Low High 1 2 3 4 5 Earning growth Cash flow B/S strength Valuation appeal Risk

Market Data (As on Apr 08, 2019) 1M 3M 1Y

Absolute return 5.5% 15.4% (0.2)%

Shareholding pattern (as of Dec’18 end)

Promoter 45.9%

FII+DII 25.8%

Others 28.3%

Sensex: 38,701 52 Week h/l (Rs) 496/248 6m Avg t/o (Rs mn): 79.8 FV (Rs): 2 Div yield (%): 0.2 Bloomberg code: KEII IN BSE code: 517569 NSE code: KEI

20

50

80

110

140

Apr-18 Aug-18 Dec-18 Apr-19

KEI Sensex

KEI Industries Ltd

15

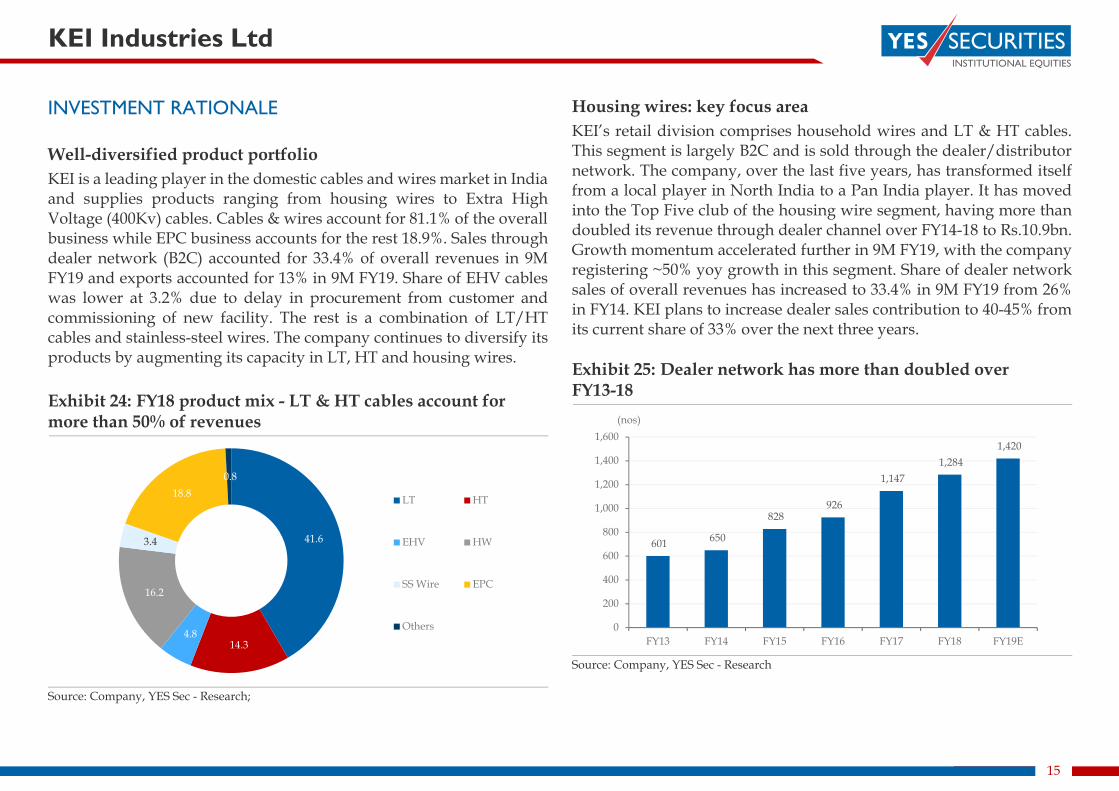

INVESTMENT RATIONALE Well-diversified product portfolio KEI is a leading player in the domestic cables and wires market in India and supplies products ranging from housing wires to Extra High Voltage (400Kv) cables. Cables & wires account for 81.1% of the overall business while EPC business accounts for the rest 18.9%. Sales through dealer network (B2C) accounted for 33.4% of overall revenues in 9M FY19 and exports accounted for 13% in 9M FY19. Share of EHV cables was lower at 3.2% due to delay in procurement from customer and commissioning of new facility. The rest is a combination of LT/HT cables and stainless-steel wires. The company continues to diversify its products by augmenting its capacity in LT, HT and housing wires. Exhibit 24: FY18 product mix - LT & HT cables account for more than 50% of revenues

Source: Company, YES Sec - Research;

Housing wires: key focus area KEI’s retail division comprises household wires and LT & HT cables. This segment is largely B2C and is sold through the dealer/distributor network. The company, over the last five years, has transformed itself from a local player in North India to a Pan India player. It has moved into the Top Five club of the housing wire segment, having more than doubled its revenue through dealer channel over FY14-18 to Rs.10.9bn. Growth momentum accelerated further in 9M FY19, with the company registering ~50% yoy growth in this segment. Share of dealer network sales of overall revenues has increased to 33.4% in 9M FY19 from 26% in FY14. KEI plans to increase dealer sales contribution to 40-45% from its current share of 33% over the next three years. Exhibit 25: Dealer network has more than doubled over FY13-18

Source: Company, YES Sec - Research

41.6

14.3 4.8

16.2

3.4

18.8 0.8

LT HT

EHV HW

SS Wire EPC

Others

601 650

828 926

1,147 1,284

1,420

0

200

400

600

800

1,000

1,200

1,400

1,600

FY13 FY14 FY15 FY16 FY17 FY18 FY19E

(nos)

KEI Industries Ltd

16

Exhibit 26: Ad spends have jumped over last 3 years as company’s focus has been on branding and increasing retail market share

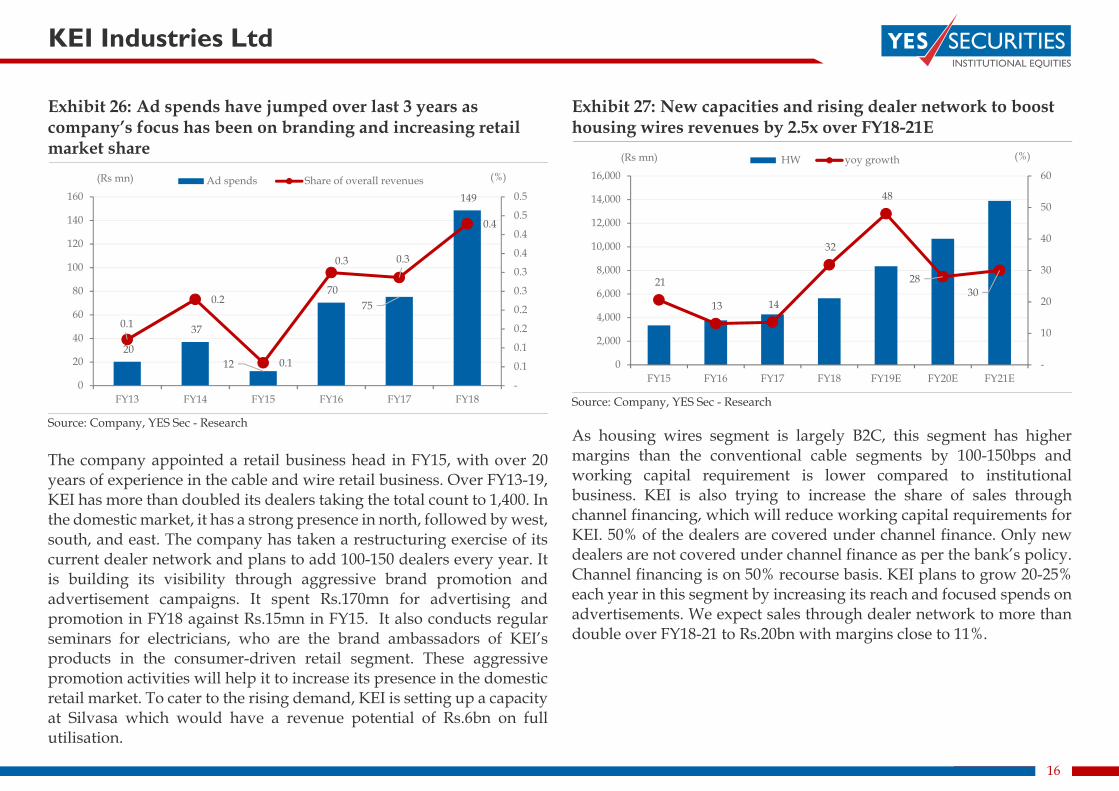

Source: Company, YES Sec - Research The company appointed a retail business head in FY15, with over 20 years of experience in the cable and wire retail business. Over FY13-19, KEI has more than doubled its dealers taking the total count to 1,400. In the domestic market, it has a strong presence in north, followed by west, south, and east. The company has taken a restructuring exercise of its current dealer network and plans to add 100-150 dealers every year. It is building its visibility through aggressive brand promotion and advertisement campaigns. It spent Rs.170mn for advertising and promotion in FY18 against Rs.15mn in FY15. It also conducts regular seminars for electricians, who are the brand ambassadors of KEI’s products in the consumer-driven retail segment. These aggressive promotion activities will help it to increase its presence in the domestic retail market. To cater to the rising demand, KEI is setting up a capacity at Silvasa which would have a revenue potential of Rs.6bn on full utilisation.

Exhibit 27: New capacities and rising dealer network to boost housing wires revenues by 2.5x over FY18-21E

Source: Company, YES Sec - Research As housing wires segment is largely B2C, this segment has higher margins than the conventional cable segments by 100-150bps and working capital requirement is lower compared to institutional business. KEI is also trying to increase the share of sales through channel financing, which will reduce working capital requirements for KEI. 50% of the dealers are covered under channel finance. Only new dealers are not covered under channel finance as per the bank’s policy. Channel financing is on 50% recourse basis. KEI plans to grow 20-25% each year in this segment by increasing its reach and focused spends on advertisements. We expect sales through dealer network to more than double over FY18-21 to Rs.20bn with margins close to 11%.

20

37

12

70 75

149

0.1

0.2

0.1

0.3 0.3

0.4

-

0.1

0.1

0.2

0.2

0.3

0.3

0.4

0.4

0.5

0.5

0

20

40

60

80

100

120

140

160

FY13 FY14 FY15 FY16 FY17 FY18

(%)(Rs mn) Ad spends Share of overall revenues

21

13 14

32

48

28 30

-

10

20

30

40

50

60

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) HW yoy growth

KEI Industries Ltd

17

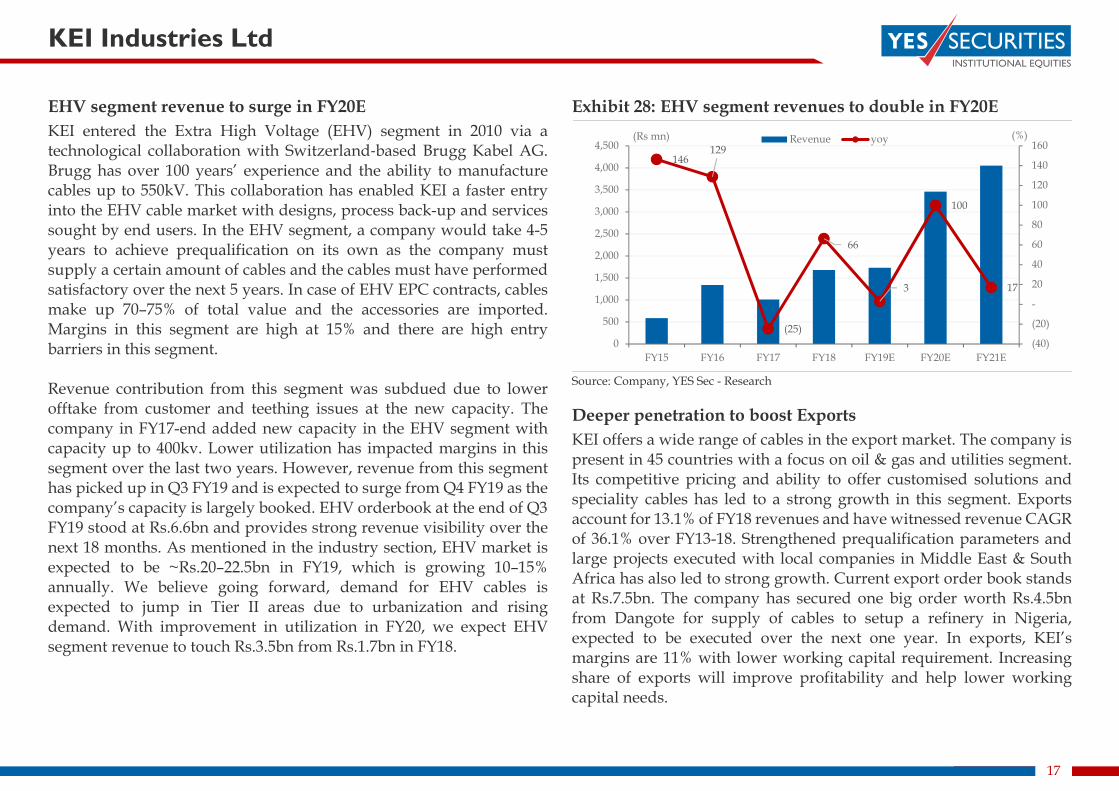

EHV segment revenue to surge in FY20E KEI entered the Extra High Voltage (EHV) segment in 2010 via a technological collaboration with Switzerland‐based Brugg Kabel AG. Brugg has over 100 years’ experience and the ability to manufacture cables up to 550kV. This collaboration has enabled KEI a faster entry into the EHV cable market with designs, process back-up and services sought by end users. In the EHV segment, a company would take 4-5 years to achieve prequalification on its own as the company must supply a certain amount of cables and the cables must have performed satisfactory over the next 5 years. In case of EHV EPC contracts, cables make up 70–75% of total value and the accessories are imported. Margins in this segment are high at 15% and there are high entry barriers in this segment. Revenue contribution from this segment was subdued due to lower offtake from customer and teething issues at the new capacity. The company in FY17-end added new capacity in the EHV segment with capacity up to 400kv. Lower utilization has impacted margins in this segment over the last two years. However, revenue from this segment has picked up in Q3 FY19 and is expected to surge from Q4 FY19 as the company’s capacity is largely booked. EHV orderbook at the end of Q3 FY19 stood at Rs.6.6bn and provides strong revenue visibility over the next 18 months. As mentioned in the industry section, EHV market is expected to be ~Rs.20–22.5bn in FY19, which is growing 10–15% annually. We believe going forward, demand for EHV cables is expected to jump in Tier II areas due to urbanization and rising demand. With improvement in utilization in FY20, we expect EHV segment revenue to touch Rs.3.5bn from Rs.1.7bn in FY18.

Exhibit 28: EHV segment revenues to double in FY20E

Source: Company, YES Sec - Research Deeper penetration to boost Exports KEI offers a wide range of cables in the export market. The company is present in 45 countries with a focus on oil & gas and utilities segment. Its competitive pricing and ability to offer customised solutions and speciality cables has led to a strong growth in this segment. Exports account for 13.1% of FY18 revenues and have witnessed revenue CAGR of 36.1% over FY13-18. Strengthened prequalification parameters and large projects executed with local companies in Middle East & South Africa has also led to strong growth. Current export order book stands at Rs.7.5bn. The company has secured one big order worth Rs.4.5bn from Dangote for supply of cables to setup a refinery in Nigeria, expected to be executed over the next one year. In exports, KEI’s margins are 11% with lower working capital requirement. Increasing share of exports will improve profitability and help lower working capital needs.

146 129

(25)

66

3

100

17

(40)

(20)

-

20

40

60

80

100

120

140

160

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) Revenue yoy

KEI Industries Ltd

18

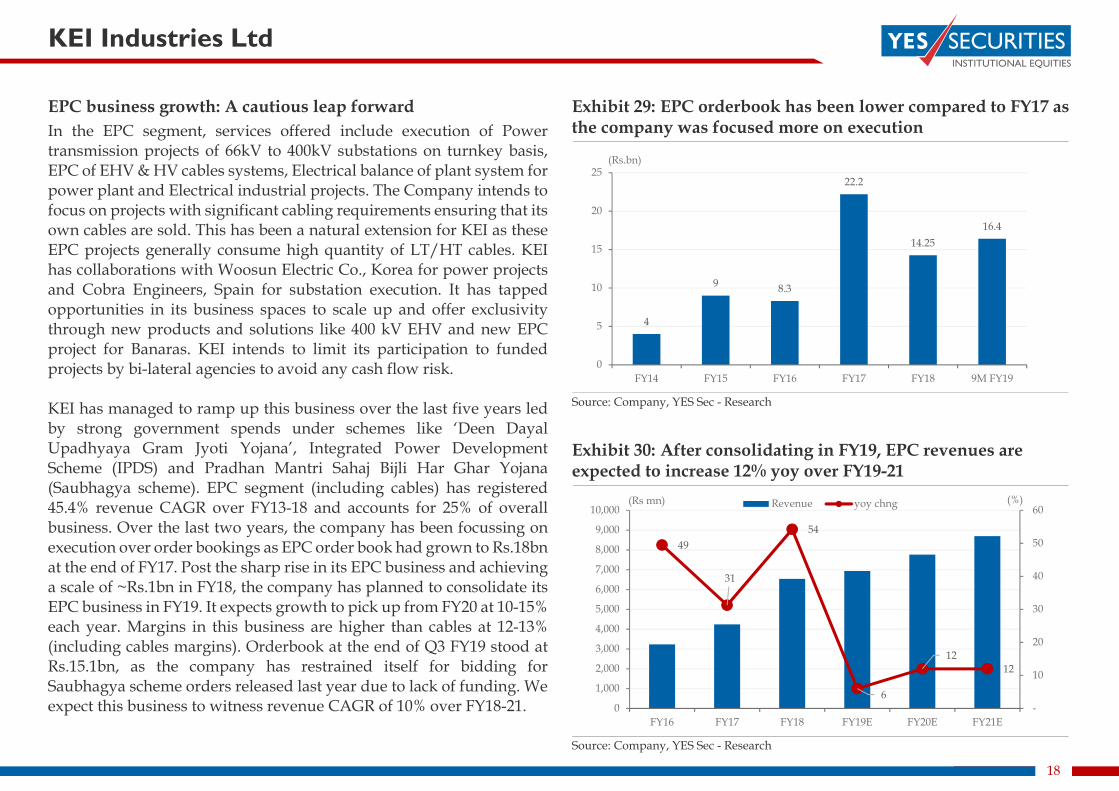

EPC business growth: A cautious leap forward In the EPC segment, services offered include execution of Power transmission projects of 66kV to 400kV substations on turnkey basis, EPC of EHV & HV cables systems, Electrical balance of plant system for power plant and Electrical industrial projects. The Company intends to focus on projects with significant cabling requirements ensuring that its own cables are sold. This has been a natural extension for KEI as these EPC projects generally consume high quantity of LT/HT cables. KEI has collaborations with Woosun Electric Co., Korea for power projects and Cobra Engineers, Spain for substation execution. It has tapped opportunities in its business spaces to scale up and offer exclusivity through new products and solutions like 400 kV EHV and new EPC project for Banaras. KEI intends to limit its participation to funded projects by bi-lateral agencies to avoid any cash flow risk. KEI has managed to ramp up this business over the last five years led by strong government spends under schemes like ‘Deen Dayal Upadhyaya Gram Jyoti Yojana’, Integrated Power Development Scheme (IPDS) and Pradhan Mantri Sahaj Bijli Har Ghar Yojana (Saubhagya scheme). EPC segment (including cables) has registered 45.4% revenue CAGR over FY13-18 and accounts for 25% of overall business. Over the last two years, the company has been focussing on execution over order bookings as EPC order book had grown to Rs.18bn at the end of FY17. Post the sharp rise in its EPC business and achieving a scale of ~Rs.1bn in FY18, the company has planned to consolidate its EPC business in FY19. It expects growth to pick up from FY20 at 10-15% each year. Margins in this business are higher than cables at 12-13% (including cables margins). Orderbook at the end of Q3 FY19 stood at Rs.15.1bn, as the company has restrained itself for bidding for Saubhagya scheme orders released last year due to lack of funding. We expect this business to witness revenue CAGR of 10% over FY18-21.

Exhibit 29: EPC orderbook has been lower compared to FY17 as the company was focused more on execution

Source: Company, YES Sec - Research

Exhibit 30: After consolidating in FY19, EPC revenues are expected to increase 12% yoy over FY19-21

Source: Company, YES Sec - Research

4

9 8.3

22.2

14.2516.4

0

5

10

15

20

25

FY14 FY15 FY16 FY17 FY18 9M FY19

(Rs.bn)

49

31

54

6

12 12

-

10

20

30

40

50

60

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) Revenue yoy chng

KEI Industries Ltd

19

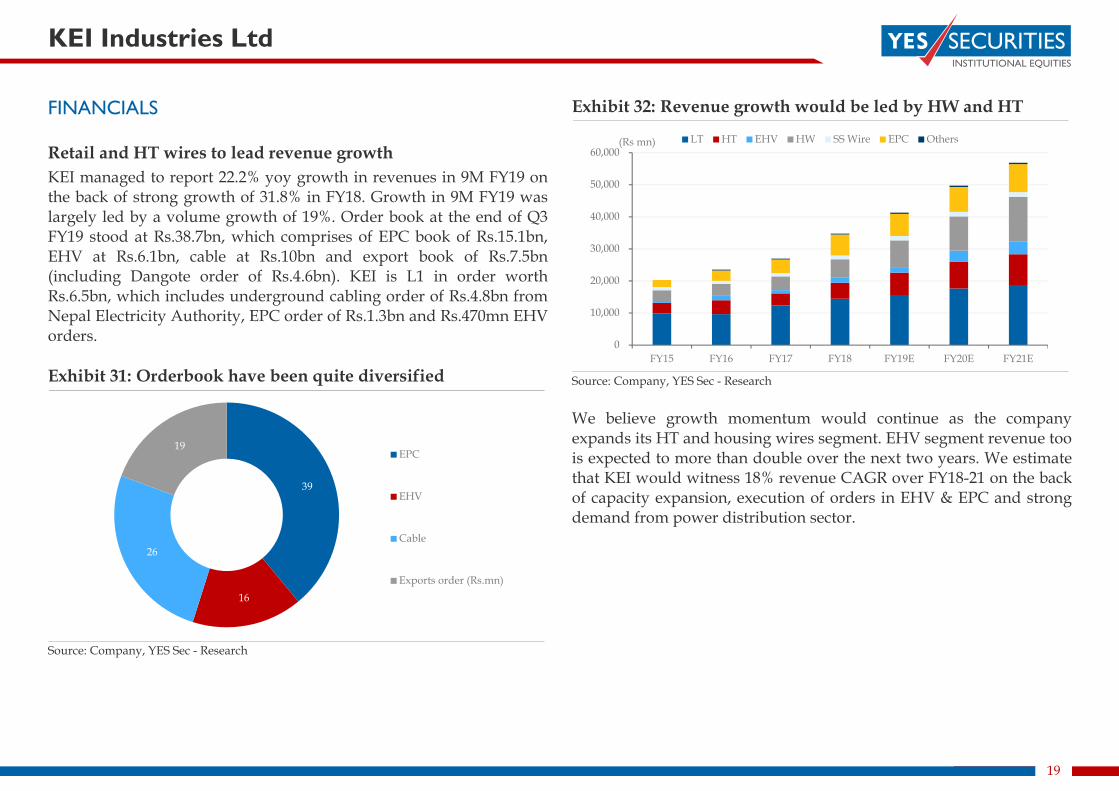

FINANCIALS Retail and HT wires to lead revenue growth KEI managed to report 22.2% yoy growth in revenues in 9M FY19 on the back of strong growth of 31.8% in FY18. Growth in 9M FY19 was largely led by a volume growth of 19%. Order book at the end of Q3 FY19 stood at Rs.38.7bn, which comprises of EPC book of Rs.15.1bn, EHV at Rs.6.1bn, cable at Rs.10bn and export book of Rs.7.5bn (including Dangote order of Rs.4.6bn). KEI is L1 in order worth Rs.6.5bn, which includes underground cabling order of Rs.4.8bn from Nepal Electricity Authority, EPC order of Rs.1.3bn and Rs.470mn EHV orders. Exhibit 31: Orderbook have been quite diversified

Source: Company, YES Sec - Research

Exhibit 32: Revenue growth would be led by HW and HT

Source: Company, YES Sec - Research We believe growth momentum would continue as the company expands its HT and housing wires segment. EHV segment revenue too is expected to more than double over the next two years. We estimate that KEI would witness 18% revenue CAGR over FY18-21 on the back of capacity expansion, execution of orders in EHV & EPC and strong demand from power distribution sector.

39

16

26

19 EPC

EHV

Cable

Exports order (Rs.mn)

0

10,000

20,000

30,000

40,000

50,000

60,000

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(Rs mn) LT HT EHV HW SS Wire EPC Others

KEI Industries Ltd

20

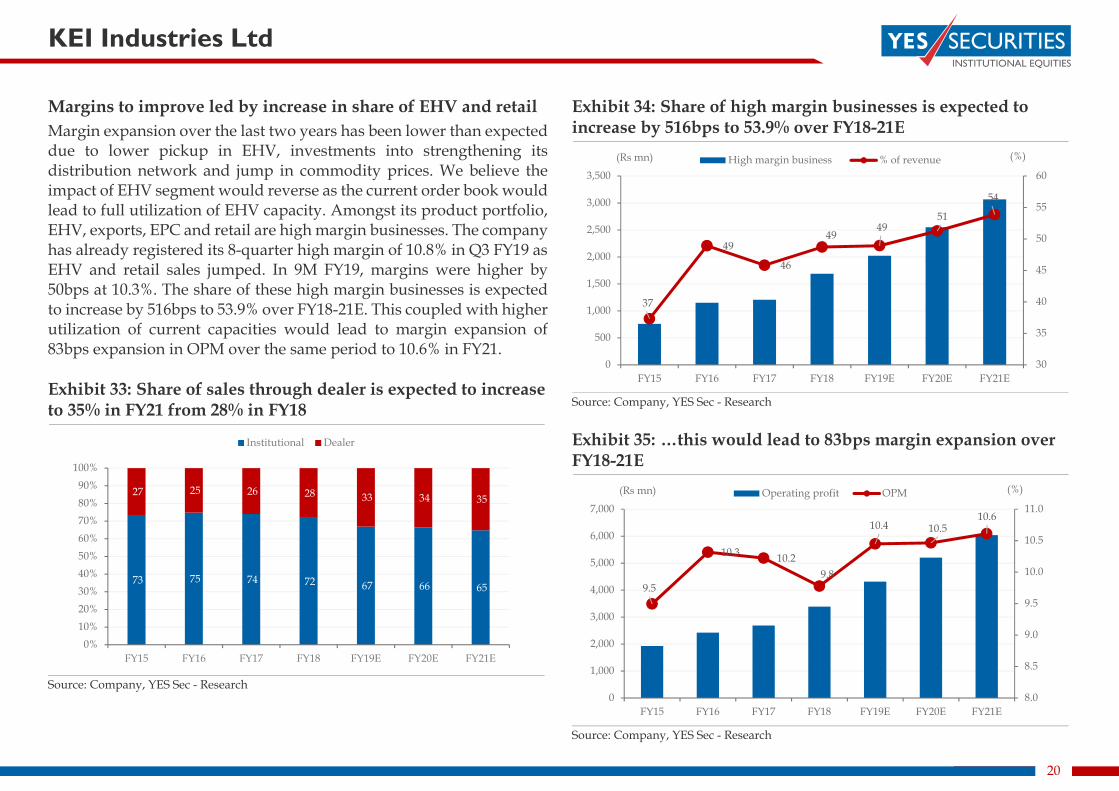

Margins to improve led by increase in share of EHV and retail Margin expansion over the last two years has been lower than expected due to lower pickup in EHV, investments into strengthening its distribution network and jump in commodity prices. We believe the impact of EHV segment would reverse as the current order book would lead to full utilization of EHV capacity. Amongst its product portfolio, EHV, exports, EPC and retail are high margin businesses. The company has already registered its 8-quarter high margin of 10.8% in Q3 FY19 as EHV and retail sales jumped. In 9M FY19, margins were higher by 50bps at 10.3%. The share of these high margin businesses is expected to increase by 516bps to 53.9% over FY18-21E. This coupled with higher utilization of current capacities would lead to margin expansion of 83bps expansion in OPM over the same period to 10.6% in FY21. Exhibit 33: Share of sales through dealer is expected to increase to 35% in FY21 from 28% in FY18

Source: Company, YES Sec - Research

Exhibit 34: Share of high margin businesses is expected to increase by 516bps to 53.9% over FY18-21E

Source: Company, YES Sec - Research Exhibit 35: …this would lead to 83bps margin expansion over FY18-21E

Source: Company, YES Sec - Research

73 75 74 72 67 66 65

27 25 26 28 33 34 35

0%10%20%30%40%50%60%70%80%90%

100%

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Institutional Dealer

37

49

46

49 49

51

54

30

35

40

45

50

55

60

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) High margin business % of revenue

9.5

10.3 10.2 9.8

10.4 10.5 10.6

8.0

8.5

9.0

9.5

10.0

10.5

11.0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) Operating profit OPM

KEI Industries Ltd

21

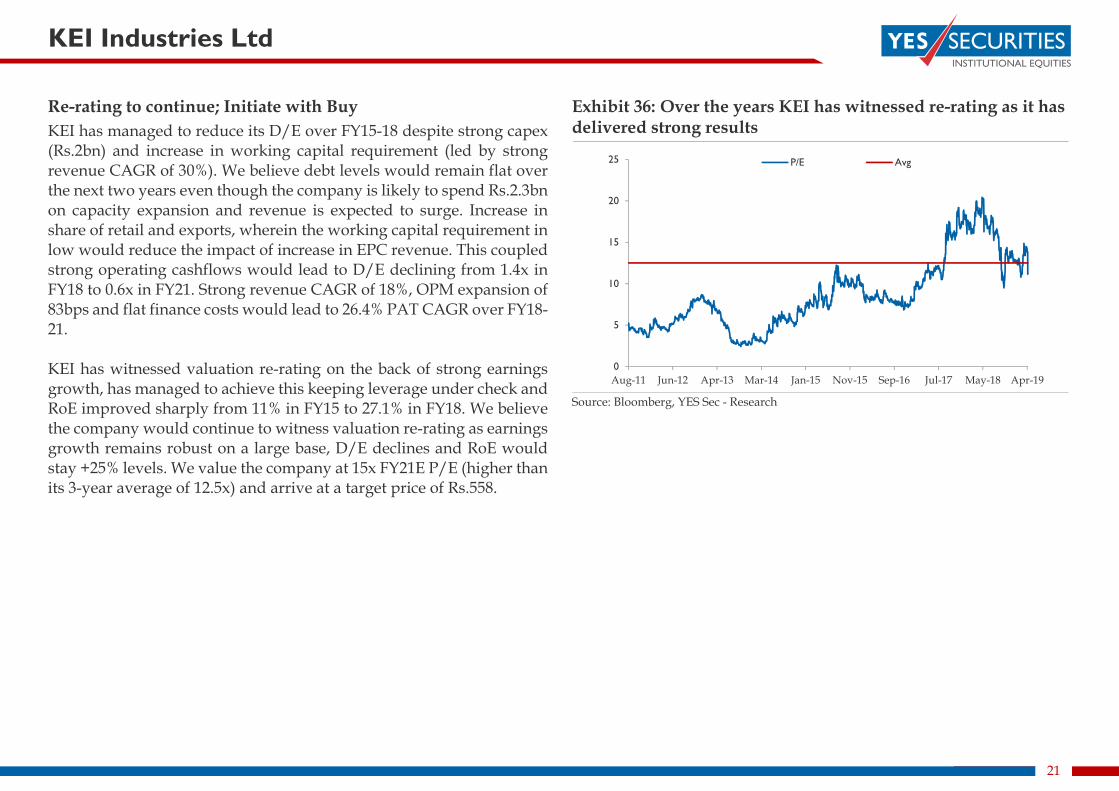

Re-rating to continue; Initiate with Buy KEI has managed to reduce its D/E over FY15-18 despite strong capex (Rs.2bn) and increase in working capital requirement (led by strong revenue CAGR of 30%). We believe debt levels would remain flat over the next two years even though the company is likely to spend Rs.2.3bn on capacity expansion and revenue is expected to surge. Increase in share of retail and exports, wherein the working capital requirement in low would reduce the impact of increase in EPC revenue. This coupled strong operating cashflows would lead to D/E declining from 1.4x in FY18 to 0.6x in FY21. Strong revenue CAGR of 18%, OPM expansion of 83bps and flat finance costs would lead to 26.4% PAT CAGR over FY18-21. KEI has witnessed valuation re-rating on the back of strong earnings growth, has managed to achieve this keeping leverage under check and RoE improved sharply from 11% in FY15 to 27.1% in FY18. We believe the company would continue to witness valuation re-rating as earnings growth remains robust on a large base, D/E declines and RoE would stay +25% levels. We value the company at 15x FY21E P/E (higher than its 3-year average of 12.5x) and arrive at a target price of Rs.558.

Exhibit 36: Over the years KEI has witnessed re-rating as it has delivered strong results

Source: Bloomberg, YES Sec - Research

0

5

10

15

20

25

Aug-11 Jun-12 Apr-13 Mar-14 Jan-15 Nov-15 Sep-16 Jul-17 May-18 Apr-19

P/E Avg

KEI Industries Ltd

22

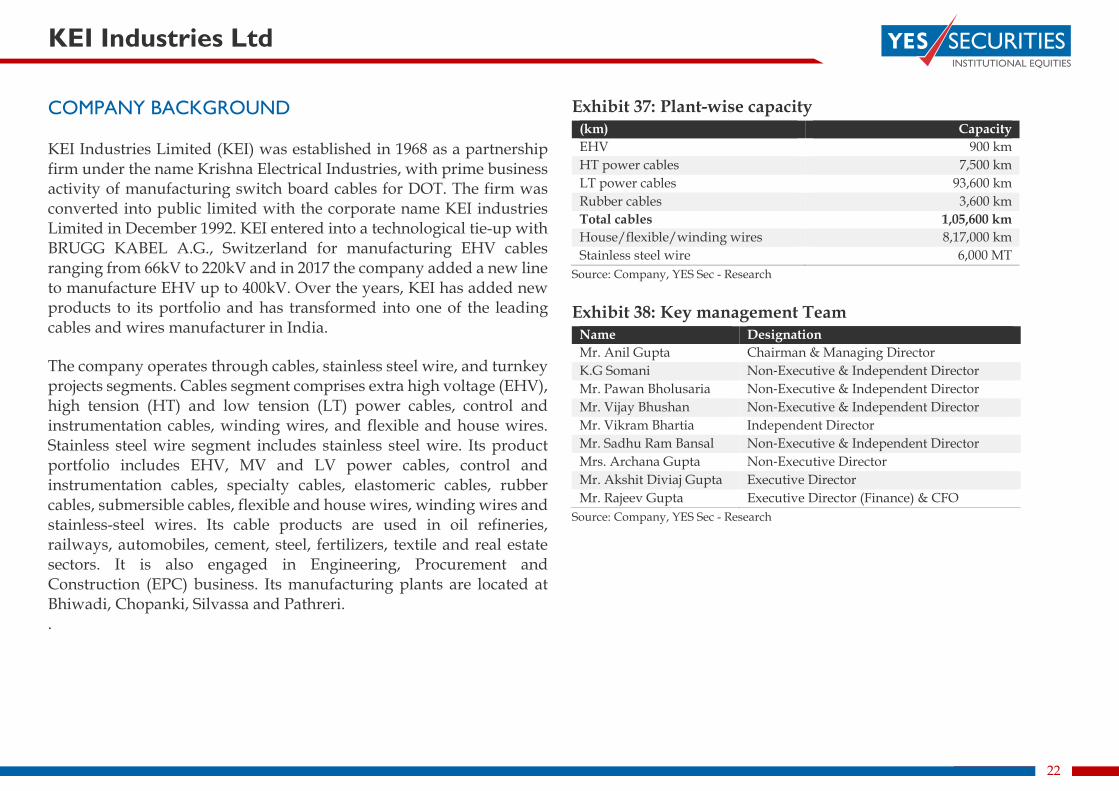

COMPANY BACKGROUND KEI Industries Limited (KEI) was established in 1968 as a partnership firm under the name Krishna Electrical Industries, with prime business activity of manufacturing switch board cables for DOT. The firm was converted into public limited with the corporate name KEI industries Limited in December 1992. KEI entered into a technological tie-up with BRUGG KABEL A.G., Switzerland for manufacturing EHV cables ranging from 66kV to 220kV and in 2017 the company added a new line to manufacture EHV up to 400kV. Over the years, KEI has added new products to its portfolio and has transformed into one of the leading cables and wires manufacturer in India. The company operates through cables, stainless steel wire, and turnkey projects segments. Cables segment comprises extra high voltage (EHV), high tension (HT) and low tension (LT) power cables, control and instrumentation cables, winding wires, and flexible and house wires. Stainless steel wire segment includes stainless steel wire. Its product portfolio includes EHV, MV and LV power cables, control and instrumentation cables, specialty cables, elastomeric cables, rubber cables, submersible cables, flexible and house wires, winding wires and stainless-steel wires. Its cable products are used in oil refineries, railways, automobiles, cement, steel, fertilizers, textile and real estate sectors. It is also engaged in Engineering, Procurement and Construction (EPC) business. Its manufacturing plants are located at Bhiwadi, Chopanki, Silvassa and Pathreri. .

Exhibit 37: Plant-wise capacity (km) Capacity EHV 900 km HT power cables 7,500 km LT power cables 93,600 km Rubber cables 3,600 km Total cables 1,05,600 km House/flexible/winding wires 8,17,000 km Stainless steel wire 6,000 MT

Source: Company, YES Sec - Research Exhibit 38: Key management Team

Name Designation Mr. Anil Gupta Chairman & Managing Director K.G Somani Non‐Executive & Independent Director Mr. Pawan Bholusaria Non‐Executive & Independent Director Mr. Vijay Bhushan Non‐Executive & Independent Director Mr. Vikram Bhartia Independent Director Mr. Sadhu Ram Bansal Non‐Executive & Independent Director Mrs. Archana Gupta Non‐Executive Director Mr. Akshit Diviaj Gupta Executive Director Mr. Rajeev Gupta Executive Director (Finance) & CFO

Source: Company, YES Sec - Research

KEI Industries Ltd

23

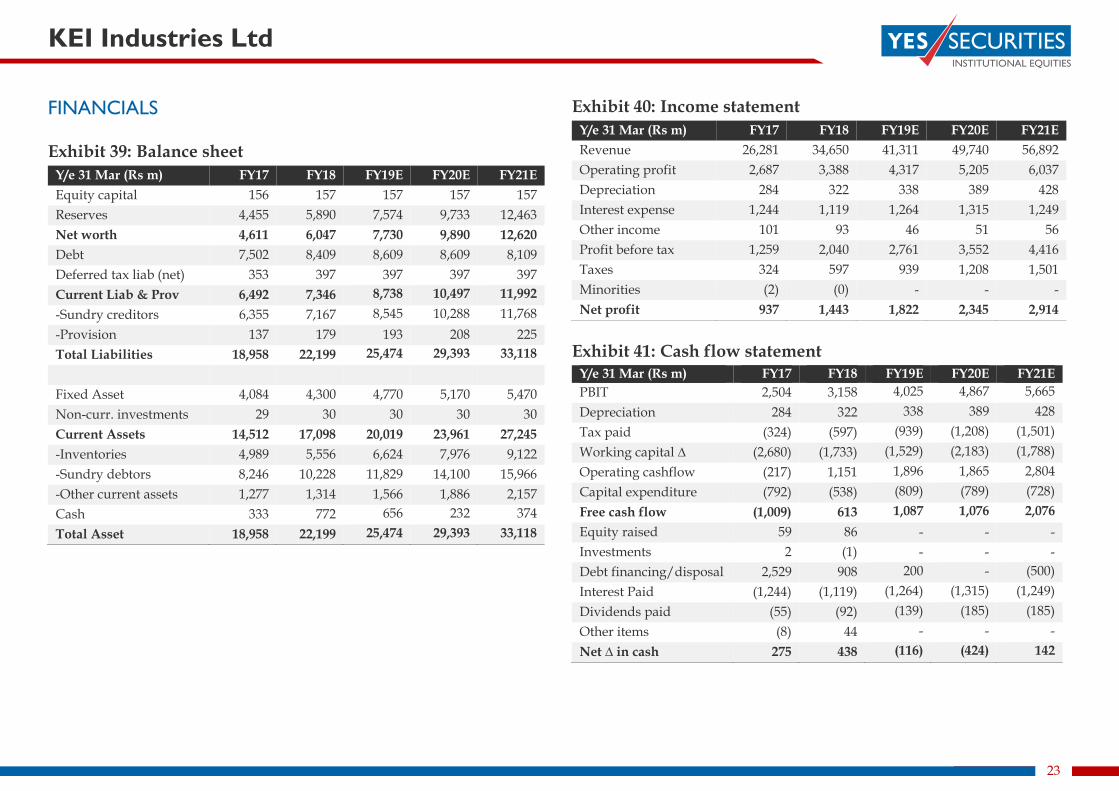

FINANCIALS Exhibit 39: Balance sheet

Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Equity capital 156 157 157 157 157 Reserves 4,455 5,890 7,574 9,733 12,463 Net worth 4,611 6,047 7,730 9,890 12,620 Debt 7,502 8,409 8,609 8,609 8,109 Deferred tax liab (net) 353 397 397 397 397 Current Liab & Prov 6,492 7,346 8,738 10,497 11,992 -Sundry creditors 6,355 7,167 8,545 10,288 11,768 -Provision 137 179 193 208 225 Total Liabilities 18,958 22,199 25,474 29,393 33,118

Fixed Asset 4,084 4,300 4,770 5,170 5,470 Non-curr. investments 29 30 30 30 30 Current Assets 14,512 17,098 20,019 23,961 27,245 -Inventories 4,989 5,556 6,624 7,976 9,122 -Sundry debtors 8,246 10,228 11,829 14,100 15,966 -Other current assets 1,277 1,314 1,566 1,886 2,157 Cash 333 772 656 232 374 Total Asset 18,958 22,199 25,474 29,393 33,118

Exhibit 40: Income statement Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Revenue 26,281 34,650 41,311 49,740 56,892 Operating profit 2,687 3,388 4,317 5,205 6,037 Depreciation 284 322 338 389 428 Interest expense 1,244 1,119 1,264 1,315 1,249 Other income 101 93 46 51 56 Profit before tax 1,259 2,040 2,761 3,552 4,416 Taxes 324 597 939 1,208 1,501 Minorities (2) (0) - - - Net profit 937 1,443 1,822 2,345 2,914

Exhibit 41: Cash flow statement

Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E PBIT 2,504 3,158 4,025 4,867 5,665 Depreciation 284 322 338 389 428 Tax paid (324) (597) (939) (1,208) (1,501) Working capital ∆ (2,680) (1,733) (1,529) (2,183) (1,788) Operating cashflow (217) 1,151 1,896 1,865 2,804 Capital expenditure (792) (538) (809) (789) (728) Free cash flow (1,009) 613 1,087 1,076 2,076 Equity raised 59 86 - - - Investments 2 (1) - - - Debt financing/disposal 2,529 908 200 - (500) Interest Paid (1,244) (1,119) (1,264) (1,315) (1,249) Dividends paid (55) (92) (139) (185) (185) Other items (8) 44 - - - Net ∆ in cash 275 438 (116) (424) 142

KEI Industries Ltd

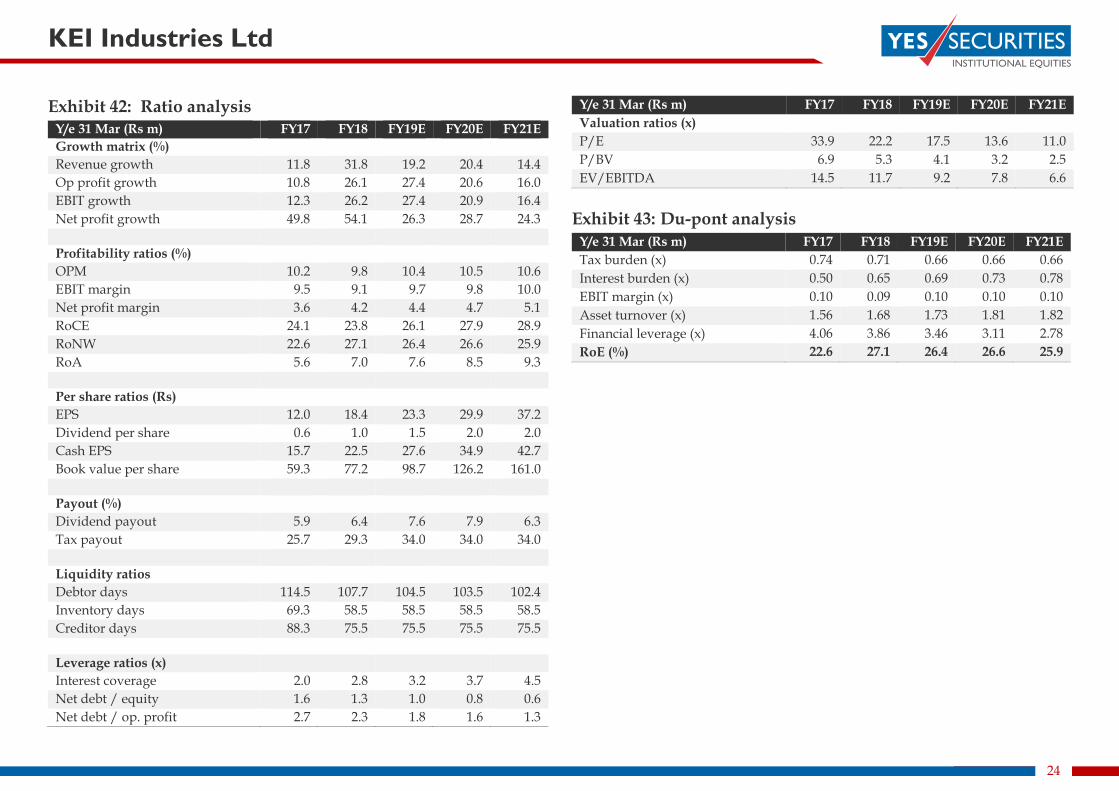

24

Exhibit 42: Ratio analysis Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Growth matrix (%) Revenue growth 11.8 31.8 19.2 20.4 14.4 Op profit growth 10.8 26.1 27.4 20.6 16.0 EBIT growth 12.3 26.2 27.4 20.9 16.4 Net profit growth 49.8 54.1 26.3 28.7 24.3 Profitability ratios (%) OPM 10.2 9.8 10.4 10.5 10.6 EBIT margin 9.5 9.1 9.7 9.8 10.0 Net profit margin 3.6 4.2 4.4 4.7 5.1 RoCE 24.1 23.8 26.1 27.9 28.9 RoNW 22.6 27.1 26.4 26.6 25.9 RoA 5.6 7.0 7.6 8.5 9.3 Per share ratios (Rs) EPS 12.0 18.4 23.3 29.9 37.2 Dividend per share 0.6 1.0 1.5 2.0 2.0 Cash EPS 15.7 22.5 27.6 34.9 42.7 Book value per share 59.3 77.2 98.7 126.2 161.0 Payout (%) Dividend payout 5.9 6.4 7.6 7.9 6.3 Tax payout 25.7 29.3 34.0 34.0 34.0 Liquidity ratios Debtor days 114.5 107.7 104.5 103.5 102.4 Inventory days 69.3 58.5 58.5 58.5 58.5 Creditor days 88.3 75.5 75.5 75.5 75.5 Leverage ratios (x) Interest coverage 2.0 2.8 3.2 3.7 4.5 Net debt / equity 1.6 1.3 1.0 0.8 0.6 Net debt / op. profit 2.7 2.3 1.8 1.6 1.3

Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Valuation ratios (x) P/E 33.9 22.2 17.5 13.6 11.0 P/BV 6.9 5.3 4.1 3.2 2.5 EV/EBITDA 14.5 11.7 9.2 7.8 6.6

Exhibit 43: Du-pont analysis

Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Tax burden (x) 0.74 0.71 0.66 0.66 0.66 Interest burden (x) 0.50 0.65 0.69 0.73 0.78 EBIT margin (x) 0.10 0.09 0.10 0.10 0.10 Asset turnover (x) 1.56 1.68 1.73 1.81 1.82 Financial leverage (x) 4.06 3.86 3.46 3.11 2.78 RoE (%) 22.6 27.1 26.4 26.6 25.9

Research Analyst: Tarang Bhanushali [email protected] | Rahul Jain [email protected] Head of Research: Amar Ambani [email protected] (For important information about YES SECURITIES (INDIA) LTD. and other disclosures, refer to the end of this material.)

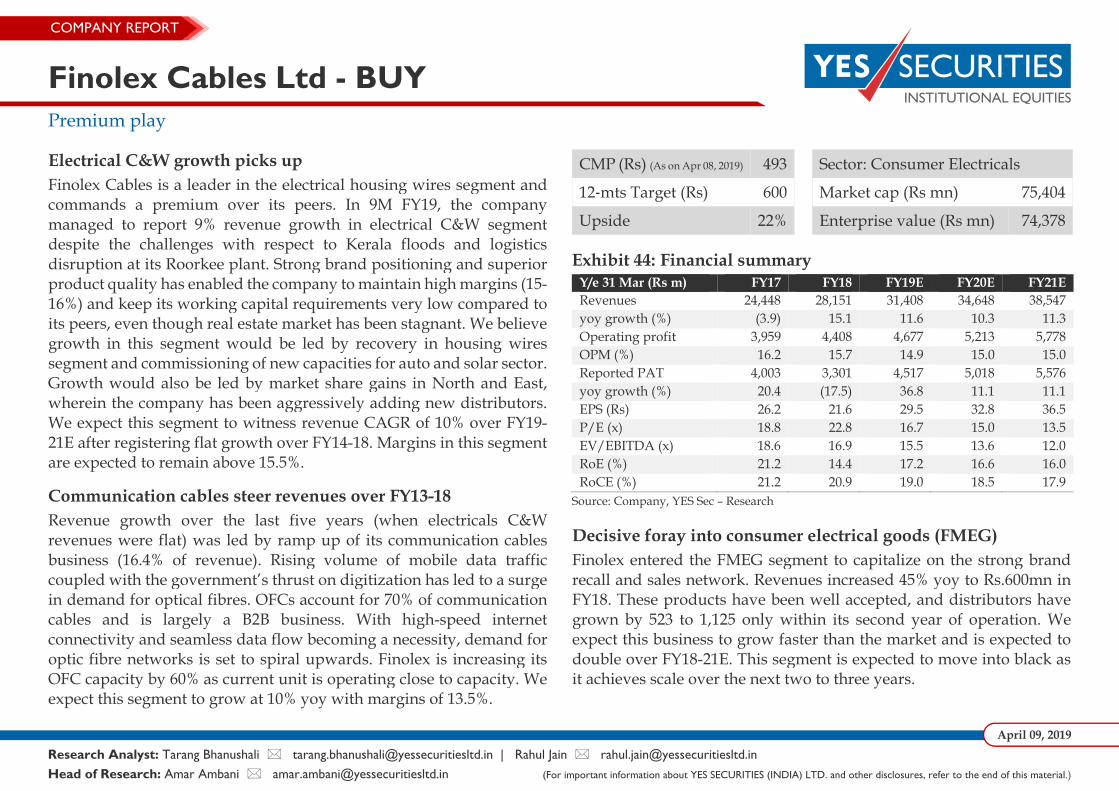

Finolex Cables Ltd - BUY Premium play

COMPANY REPORT

April 09, 2019

CMP (Rs) (As on Apr 08, 2019) 493 Sector: Consumer Electricals

12‐mts Target (Rs) 600 Market cap (Rs mn) 75,404

Upside 22% Enterprise value (Rs mn) 74,378

Exhibit 44: Financial summary Y/e 31 Mar (Rs m) FY17 FY18 FY19E FY20E FY21E Revenues 24,448 28,151 31,408 34,648 38,547 yoy growth (%) (3.9) 15.1 11.6 10.3 11.3 Operating profit 3,959 4,408 4,677 5,213 5,778 OPM (%) 16.2 15.7 14.9 15.0 15.0 Reported PAT 4,003 3,301 4,517 5,018 5,576 yoy growth (%) 20.4 (17.5) 36.8 11.1 11.1 EPS (Rs) 26.2 21.6 29.5 32.8 36.5 P/E (x) 18.8 22.8 16.7 15.0 13.5 EV/EBITDA (x) 18.6 16.9 15.5 13.6 12.0 RoE (%) 21.2 14.4 17.2 16.6 16.0 RoCE (%) 21.2 20.9 19.0 18.5 17.9

Source: Company, YES Sec – Research

Electrical C&W growth picks up Finolex Cables is a leader in the electrical housing wires segment andcommands a premium over its peers. In 9M FY19, the companymanaged to report 9% revenue growth in electrical C&W segmentdespite the challenges with respect to Kerala floods and logisticsdisruption at its Roorkee plant. Strong brand positioning and superiorproduct quality has enabled the company to maintain high margins (15-16%) and keep its working capital requirements very low compared toits peers, even though real estate market has been stagnant. We believegrowth in this segment would be led by recovery in housing wiressegment and commissioning of new capacities for auto and solar sector.Growth would also be led by market share gains in North and East,wherein the company has been aggressively adding new distributors.We expect this segment to witness revenue CAGR of 10% over FY19-21E after registering flat growth over FY14-18. Margins in this segmentare expected to remain above 15.5%.

Communication cables steer revenues over FY13-18 Revenue growth over the last five years (when electricals C&Wrevenues were flat) was led by ramp up of its communication cablesbusiness (16.4% of revenue). Rising volume of mobile data trafficcoupled with the government’s thrust on digitization has led to a surgein demand for optical fibres. OFCs account for 70% of communicationcables and is largely a B2B business. With high-speed internetconnectivity and seamless data flow becoming a necessity, demand foroptic fibre networks is set to spiral upwards. Finolex is increasing itsOFC capacity by 60% as current unit is operating close to capacity. Weexpect this segment to grow at 10% yoy with margins of 13.5%.

Decisive foray into consumer electrical goods (FMEG) Finolex entered the FMEG segment to capitalize on the strong brandrecall and sales network. Revenues increased 45% yoy to Rs.600mn inFY18. These products have been well accepted, and distributors have grown by 523 to 1,125 only within its second year of operation. Weexpect this business to grow faster than the market and is expected to double over FY18-21E. This segment is expected to move into black asit achieves scale over the next two to three years.

Finolex Cables Ltd

26

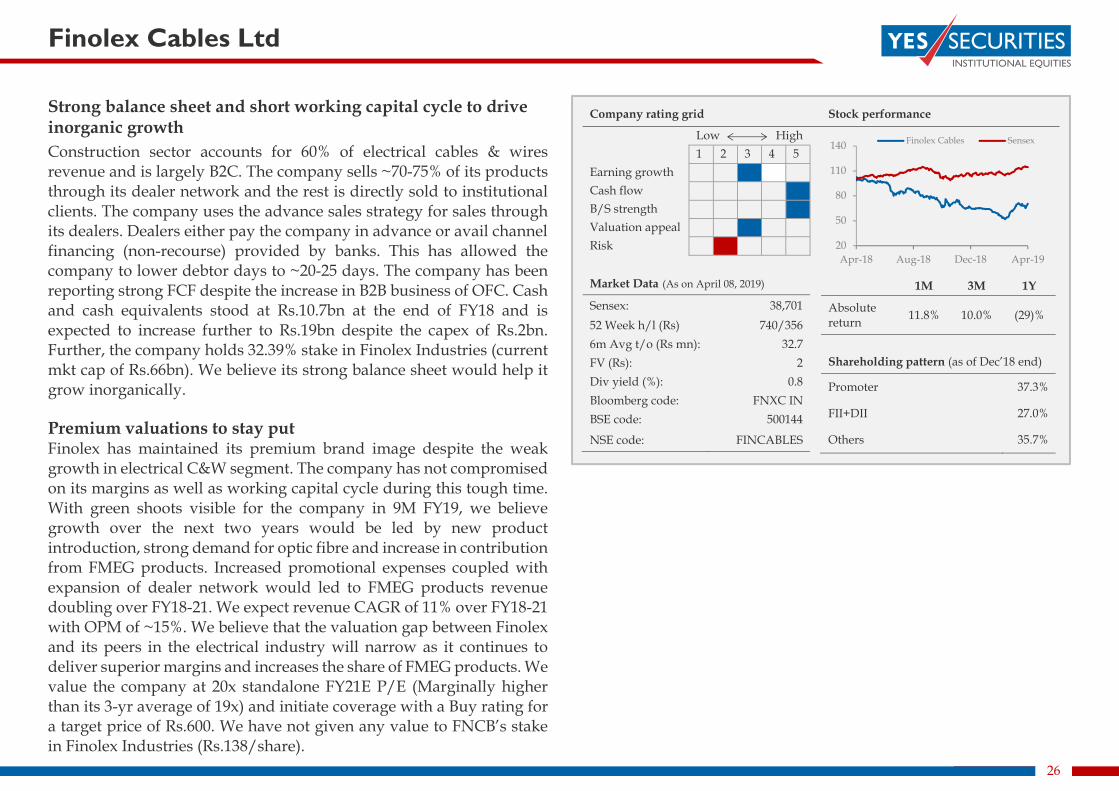

Strong balance sheet and short working capital cycle to drive inorganic growth Construction sector accounts for 60% of electrical cables & wires revenue and is largely B2C. The company sells ~70-75% of its products through its dealer network and the rest is directly sold to institutional clients. The company uses the advance sales strategy for sales through its dealers. Dealers either pay the company in advance or avail channel financing (non-recourse) provided by banks. This has allowed the company to lower debtor days to ~20-25 days. The company has been reporting strong FCF despite the increase in B2B business of OFC. Cash and cash equivalents stood at Rs.10.7bn at the end of FY18 and is expected to increase further to Rs.19bn despite the capex of Rs.2bn. Further, the company holds 32.39% stake in Finolex Industries (current mkt cap of Rs.66bn). We believe its strong balance sheet would help it grow inorganically. Premium valuations to stay put Finolex has maintained its premium brand image despite the weak growth in electrical C&W segment. The company has not compromised on its margins as well as working capital cycle during this tough time. With green shoots visible for the company in 9M FY19, we believe growth over the next two years would be led by new product introduction, strong demand for optic fibre and increase in contribution from FMEG products. Increased promotional expenses coupled with expansion of dealer network would led to FMEG products revenue doubling over FY18-21. We expect revenue CAGR of 11% over FY18-21 with OPM of ~15%. We believe that the valuation gap between Finolex and its peers in the electrical industry will narrow as it continues to deliver superior margins and increases the share of FMEG products. We value the company at 20x standalone FY21E P/E (Marginally higher than its 3-yr average of 19x) and initiate coverage with a Buy rating for a target price of Rs.600. We have not given any value to FNCB’s stake in Finolex Industries (Rs.138/share).

Company rating grid Stock performance Low High 1 2 3 4 5 Earning growth Cash flow B/S strength Valuation appeal Risk

Market Data (As on April 08, 2019) 1M 3M 1Y

Absolute return 11.8% 10.0% (29)%

Shareholding pattern (as of Dec’18 end)

Promoter 37.3%

FII+DII 27.0%

Others 35.7%

Sensex: 38,701 52 Week h/l (Rs) 740/356 6m Avg t/o (Rs mn): 32.7 FV (Rs): 2 Div yield (%): 0.8 Bloomberg code: FNXC IN BSE code: 500144 NSE code: FINCABLES

20

50

80

110

140

Apr-18 Aug-18 Dec-18 Apr-19

Finolex Cables Sensex

Finolex Cables Ltd

27

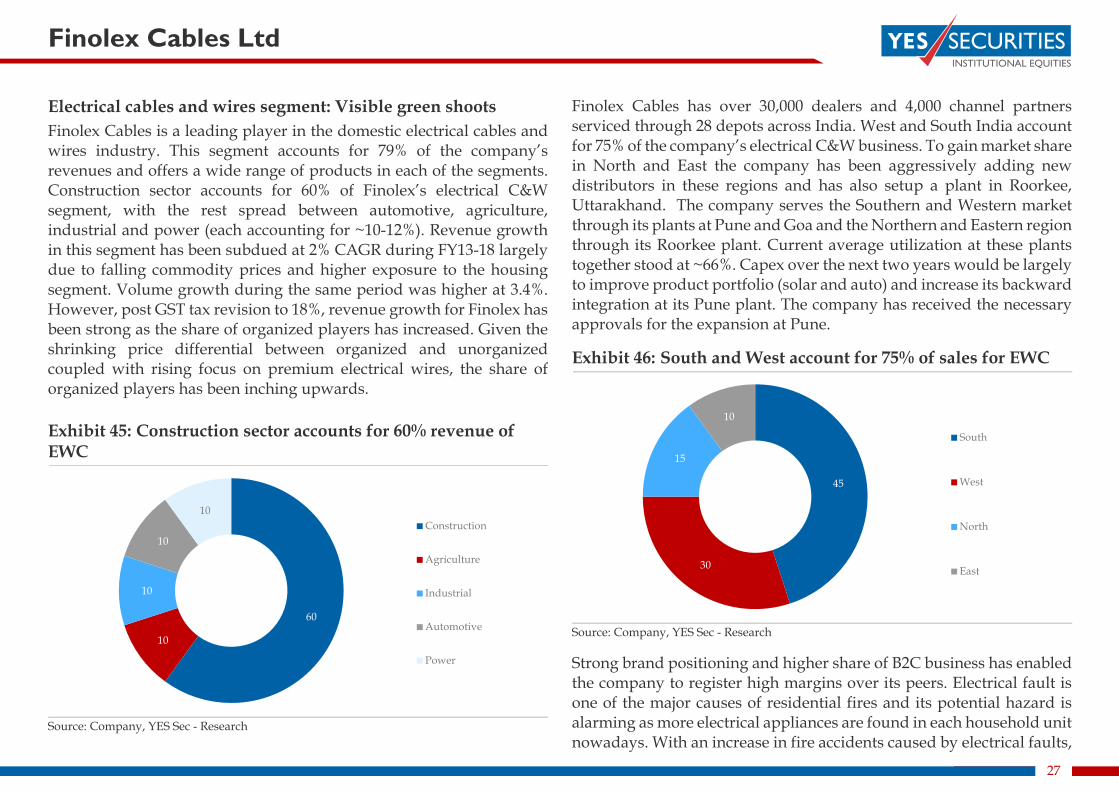

Electrical cables and wires segment: Visible green shoots Finolex Cables is a leading player in the domestic electrical cables and wires industry. This segment accounts for 79% of the company’s revenues and offers a wide range of products in each of the segments. Construction sector accounts for 60% of Finolex’s electrical C&W segment, with the rest spread between automotive, agriculture, industrial and power (each accounting for ~10-12%). Revenue growth in this segment has been subdued at 2% CAGR during FY13-18 largely due to falling commodity prices and higher exposure to the housing segment. Volume growth during the same period was higher at 3.4%. However, post GST tax revision to 18%, revenue growth for Finolex has been strong as the share of organized players has increased. Given the shrinking price differential between organized and unorganized coupled with rising focus on premium electrical wires, the share of organized players has been inching upwards. Exhibit 45: Construction sector accounts for 60% revenue of EWC

Source: Company, YES Sec - Research

Finolex Cables has over 30,000 dealers and 4,000 channel partners serviced through 28 depots across India. West and South India account for 75% of the company’s electrical C&W business. To gain market share in North and East the company has been aggressively adding new distributors in these regions and has also setup a plant in Roorkee, Uttarakhand. The company serves the Southern and Western market through its plants at Pune and Goa and the Northern and Eastern region through its Roorkee plant. Current average utilization at these plants together stood at ~66%. Capex over the next two years would be largely to improve product portfolio (solar and auto) and increase its backward integration at its Pune plant. The company has received the necessary approvals for the expansion at Pune.

Exhibit 46: South and West account for 75% of sales for EWC

Source: Company, YES Sec - Research

Strong brand positioning and higher share of B2C business has enabled the company to register high margins over its peers. Electrical fault is one of the major causes of residential fires and its potential hazard is alarming as more electrical appliances are found in each household unit nowadays. With an increase in fire accidents caused by electrical faults,

60

10

10

10

10Construction

Agriculture

Industrial

Automotive

Power

45

30

15

10

South

West

North

East

Finolex Cables Ltd

28

consumer preference towards branded manufacturers has been on the rise. This has led to companies like Finolex to garner higher margins over the last 2-3 years. The company expects to maintain its margins around 15-16% going forward.

Exhibit 47: EWC revenue growth expected to be ~10% yoy

Source: Company, YES Sec - Research

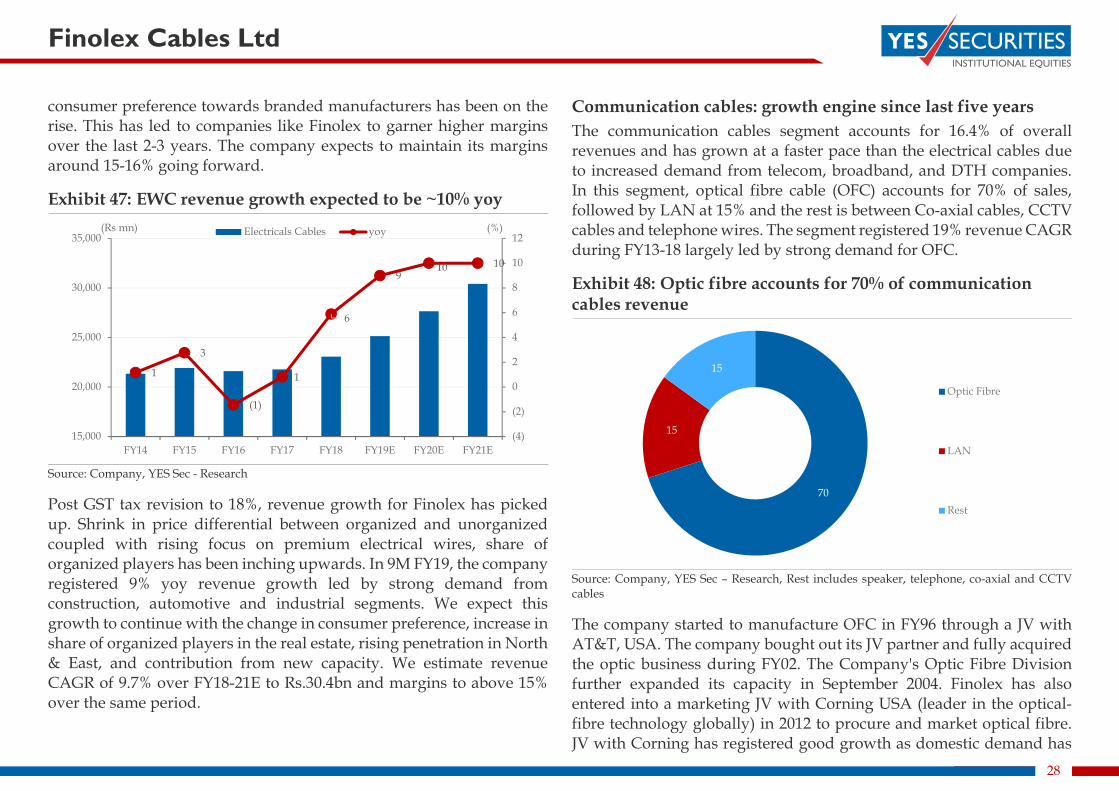

Post GST tax revision to 18%, revenue growth for Finolex has picked up. Shrink in price differential between organized and unorganized coupled with rising focus on premium electrical wires, share of organized players has been inching upwards. In 9M FY19, the company registered 9% yoy revenue growth led by strong demand from construction, automotive and industrial segments. We expect this growth to continue with the change in consumer preference, increase in share of organized players in the real estate, rising penetration in North & East, and contribution from new capacity. We estimate revenue CAGR of 9.7% over FY18-21E to Rs.30.4bn and margins to above 15% over the same period.

Communication cables: growth engine since last five years The communication cables segment accounts for 16.4% of overall revenues and has grown at a faster pace than the electrical cables due to increased demand from telecom, broadband, and DTH companies. In this segment, optical fibre cable (OFC) accounts for 70% of sales, followed by LAN at 15% and the rest is between Co-axial cables, CCTV cables and telephone wires. The segment registered 19% revenue CAGR during FY13-18 largely led by strong demand for OFC.

Exhibit 48: Optic fibre accounts for 70% of communication cables revenue

Source: Company, YES Sec – Research, Rest includes speaker, telephone, co-axial and CCTV cables

The company started to manufacture OFC in FY96 through a JV with AT&T, USA. The company bought out its JV partner and fully acquired the optic business during FY02. The Company's Optic Fibre Division further expanded its capacity in September 2004. Finolex has also entered into a marketing JV with Corning USA (leader in the optical-fibre technology globally) in 2012 to procure and market optical fibre. JV with Corning has registered good growth as domestic demand has

1

3

(1)

1

6

9 10 10

(4)

(2)

0

2

4

6

8

10

12

15,000

20,000

25,000

30,000

35,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) Electricals Cables yoy

70

15

15

Optic Fibre

LAN

Rest

Finolex Cables Ltd

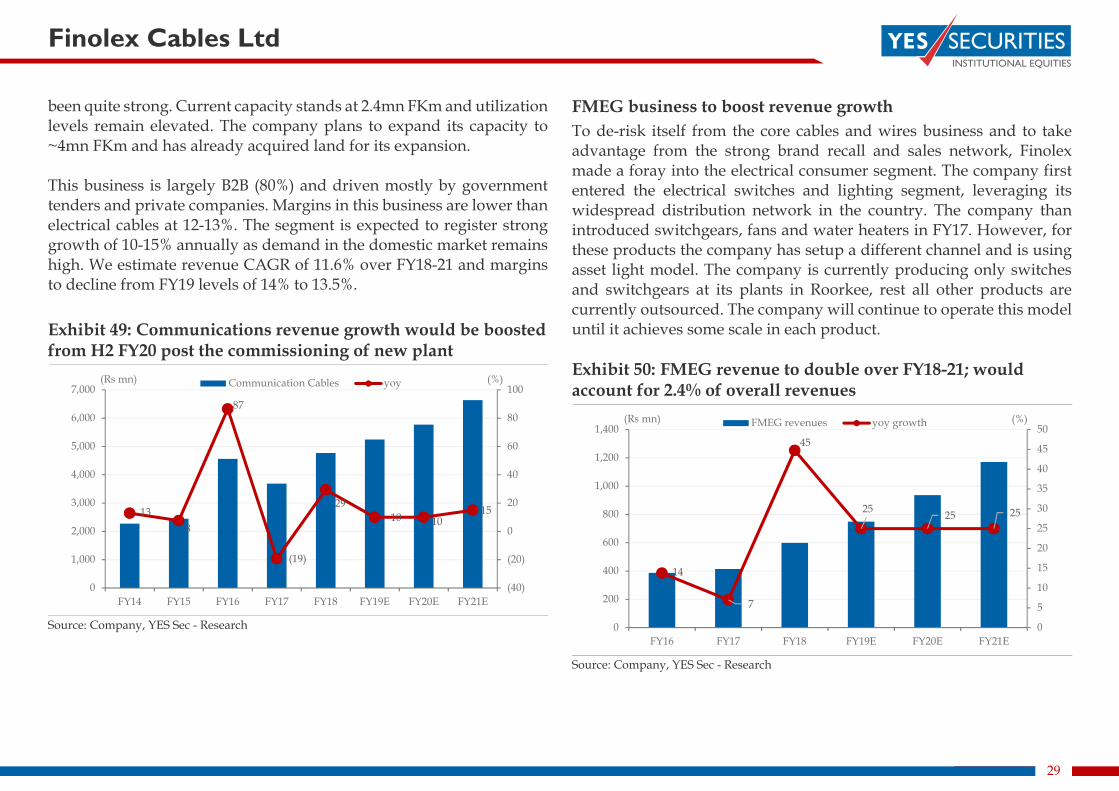

29

been quite strong. Current capacity stands at 2.4mn FKm and utilization levels remain elevated. The company plans to expand its capacity to ~4mn FKm and has already acquired land for its expansion. This business is largely B2B (80%) and driven mostly by government tenders and private companies. Margins in this business are lower than electrical cables at 12-13%. The segment is expected to register strong growth of 10-15% annually as demand in the domestic market remains high. We estimate revenue CAGR of 11.6% over FY18-21 and margins to decline from FY19 levels of 14% to 13.5%. Exhibit 49: Communications revenue growth would be boosted from H2 FY20 post the commissioning of new plant

Source: Company, YES Sec - Research

FMEG business to boost revenue growth To de-risk itself from the core cables and wires business and to take advantage from the strong brand recall and sales network, Finolex made a foray into the electrical consumer segment. The company first entered the electrical switches and lighting segment, leveraging its widespread distribution network in the country. The company than introduced switchgears, fans and water heaters in FY17. However, for these products the company has setup a different channel and is using asset light model. The company is currently producing only switches and switchgears at its plants in Roorkee, rest all other products are currently outsourced. The company will continue to operate this model until it achieves some scale in each product. Exhibit 50: FMEG revenue to double over FY18-21; would account for 2.4% of overall revenues

Source: Company, YES Sec - Research

13 8

87

(19)

29 10 10

15

(40)

(20)

0

20

40

60

80

100

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) Communication Cables yoy

14

7

45

25 25 25

0

5

10

15

20

25

30

35

40

45

50

0

200

400

600

800

1,000

1,200

1,400

FY16 FY17 FY18 FY19E FY20E FY21E

(%)(Rs mn) FMEG revenues yoy growth

Finolex Cables Ltd

30

These products have been well-accepted in the market and within its second year the number of distributors stocking it have grown by 523 to 1,125. Revenue from these products improved to Rs.600mn in FY18 from Rs.414mn in FY17. Currently most of the products have positive contribution, however, with the high advertising and promotion costs, the segment is reporting loss at operating level. We expect this business to grow faster than the market and would drive overall growth for the company. Increased promotional expenses coupled with expansion of dealer network would led to FMEG products revenue doubling over FY18-21E. This segment is expected to move into black over the next 2-3 years as the company achieves some scale. Copper rods biz to stay subdued To support its requirement of Copper Rods, the company entered a JV with Essex Group Inc, USA for manufacture of copper rods. The plant was set up at Goa with a capacity of 60,000tpa. Later in the year FY01, Finolex bought out the JV from its American partner. It used to sell surplus copper rods to third parties (Rs.1.2bn in FY14); sales dropped in recent years due to the falling premium to cathode. The company may look at increasing sales to third parties when situation is favourable.

JV performance to look up Over the years Finolex has formed JV with companies which are global leaders in technology and products. Currently, Finolex has two operational JVs, one with Sumitomo Electric Industries of Japan and another with Corning SAS. JV with Sumitomo was entered in 2007 to set up an extra-high-voltage (EHV) cable plant to manufacture cables above 33kV. Performance of this JV has been below par as the JV obtained final certification for its 400kV-EHV cables in December ’17, after 10 years of setting up the JV. Till date, the company have invested Rs.1.6bn in the JV and will continue to support for the next 1.5-2 years. Under full utilization, the company would be able to supply 325km thereby clocking Rs.5bn turnover from Rs.750-800mn expected to be registered in FY19. Demand for EHV wires has been on the high as power distributors are converting overhead transmission wires to underground. Demand growth is also led by an increase in demand from Metro operators. Currently, half of EHV demand is met through imports and hence domestic EHV producers have huge scope in this segment. The management expects the business to break even over the next two years as execution picks up. In 2012, Finolex entered into a JV with Corning USA (leader in the optical-fibre technology globally) to procure and market optical fibre. Finolex also employed Corning’s technology to augment its capacity from 1.2mn FKm to 2mn FKm at their existing plant at Pune. As per the JV agreement, all further requirements of OFC beyond the company’s capacity would be met through purchases from Corning. JV with Corning has registered good growth as domestic demand has been quite strong.

Finolex Cables Ltd

31

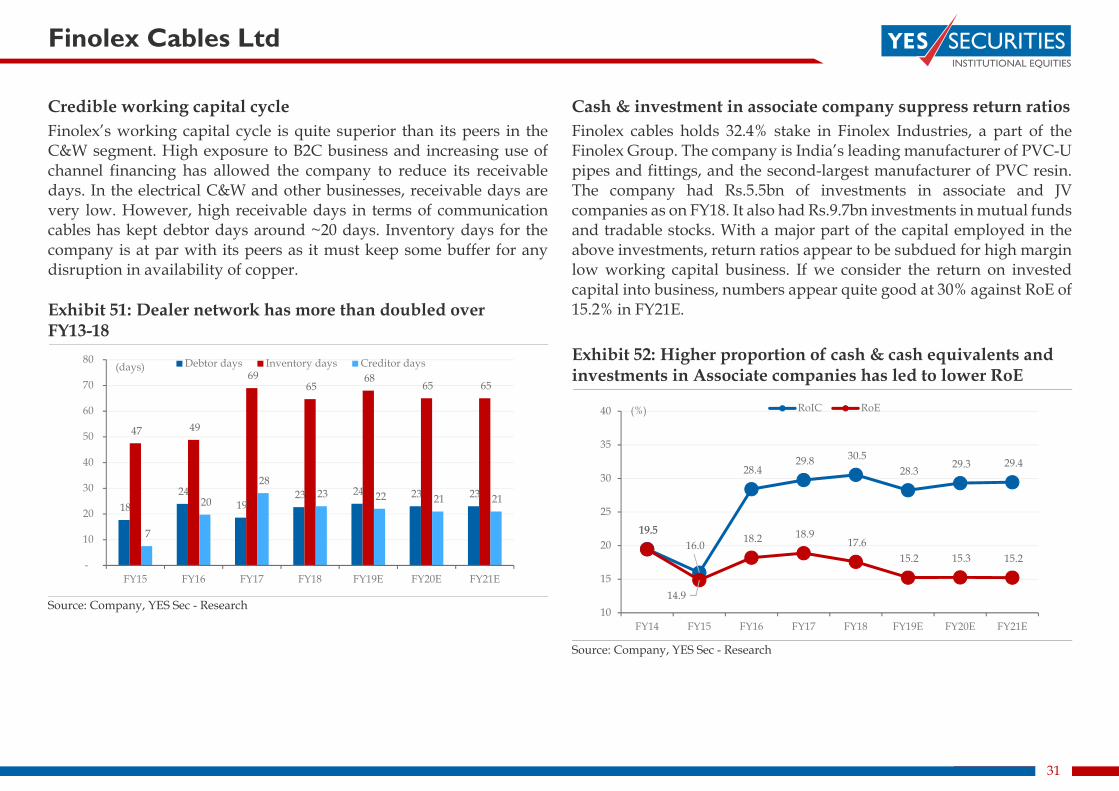

Credible working capital cycle Finolex’s working capital cycle is quite superior than its peers in the C&W segment. High exposure to B2C business and increasing use of channel financing has allowed the company to reduce its receivable days. In the electrical C&W and other businesses, receivable days are very low. However, high receivable days in terms of communication cables has kept debtor days around ~20 days. Inventory days for the company is at par with its peers as it must keep some buffer for any disruption in availability of copper. Exhibit 51: Dealer network has more than doubled over FY13-18

Source: Company, YES Sec - Research

Cash & investment in associate company suppress return ratios Finolex cables holds 32.4% stake in Finolex Industries, a part of the Finolex Group. The company is India’s leading manufacturer of PVC-U pipes and fittings, and the second-largest manufacturer of PVC resin. The company had Rs.5.5bn of investments in associate and JV companies as on FY18. It also had Rs.9.7bn investments in mutual funds and tradable stocks. With a major part of the capital employed in the above investments, return ratios appear to be subdued for high margin low working capital business. If we consider the return on invested capital into business, numbers appear quite good at 30% against RoE of 15.2% in FY21E. Exhibit 52: Higher proportion of cash & cash equivalents and investments in Associate companies has led to lower RoE

Source: Company, YES Sec - Research

18 24

19 23 24 23 23

47 49

69 65

68 65 65

7

20

28 23 22 21 21

-

10

20

30

40

50

60

70

80

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(days) Debtor days Inventory days Creditor days

19.5 16.0

28.4 29.8 30.5

28.3 29.3 29.4

19.5

14.9

18.2 18.9 17.6

15.2 15.3 15.2

10

15

20

25

30

35

40

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%) RoIC RoE

Finolex Cables Ltd

32

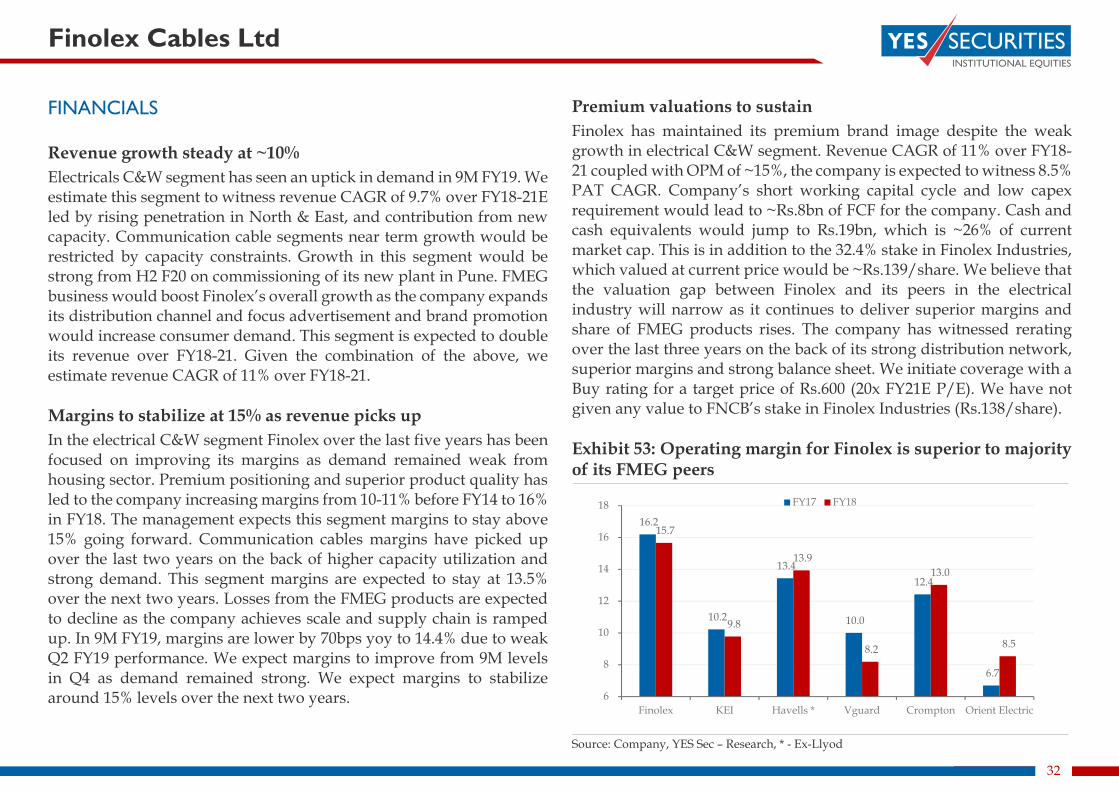

FINANCIALS Revenue growth steady at ~10% Electricals C&W segment has seen an uptick in demand in 9M FY19. We estimate this segment to witness revenue CAGR of 9.7% over FY18-21E led by rising penetration in North & East, and contribution from new capacity. Communication cable segments near term growth would be restricted by capacity constraints. Growth in this segment would be strong from H2 F20 on commissioning of its new plant in Pune. FMEG business would boost Finolex’s overall growth as the company expands its distribution channel and focus advertisement and brand promotion would increase consumer demand. This segment is expected to double its revenue over FY18-21. Given the combination of the above, we estimate revenue CAGR of 11% over FY18-21. Margins to stabilize at 15% as revenue picks up In the electrical C&W segment Finolex over the last five years has been focused on improving its margins as demand remained weak from housing sector. Premium positioning and superior product quality has led to the company increasing margins from 10-11% before FY14 to 16% in FY18. The management expects this segment margins to stay above 15% going forward. Communication cables margins have picked up over the last two years on the back of higher capacity utilization and strong demand. This segment margins are expected to stay at 13.5% over the next two years. Losses from the FMEG products are expected to decline as the company achieves scale and supply chain is ramped up. In 9M FY19, margins are lower by 70bps yoy to 14.4% due to weak Q2 FY19 performance. We expect margins to improve from 9M levels in Q4 as demand remained strong. We expect margins to stabilize around 15% levels over the next two years.

Premium valuations to sustain Finolex has maintained its premium brand image despite the weak growth in electrical C&W segment. Revenue CAGR of 11% over FY18-21 coupled with OPM of ~15%, the company is expected to witness 8.5% PAT CAGR. Company’s short working capital cycle and low capex requirement would lead to ~Rs.8bn of FCF for the company. Cash and cash equivalents would jump to Rs.19bn, which is ~26% of current market cap. This is in addition to the 32.4% stake in Finolex Industries, which valued at current price would be ~Rs.139/share. We believe that the valuation gap between Finolex and its peers in the electrical industry will narrow as it continues to deliver superior margins and share of FMEG products rises. The company has witnessed rerating over the last three years on the back of its strong distribution network, superior margins and strong balance sheet. We initiate coverage with a Buy rating for a target price of Rs.600 (20x FY21E P/E). We have not given any value to FNCB’s stake in Finolex Industries (Rs.138/share). Exhibit 53: Operating margin for Finolex is superior to majority of its FMEG peers

Source: Company, YES Sec – Research, * - Ex-Llyod

16.2

10.2

13.4

10.0

12.4

6.7

15.7

9.8

13.9

8.2

13.0

8.5

6

8

10

12

14

16

18

Finolex KEI Havells * Vguard Crompton Orient Electric

FY17 FY18

Finolex Cables Ltd

33

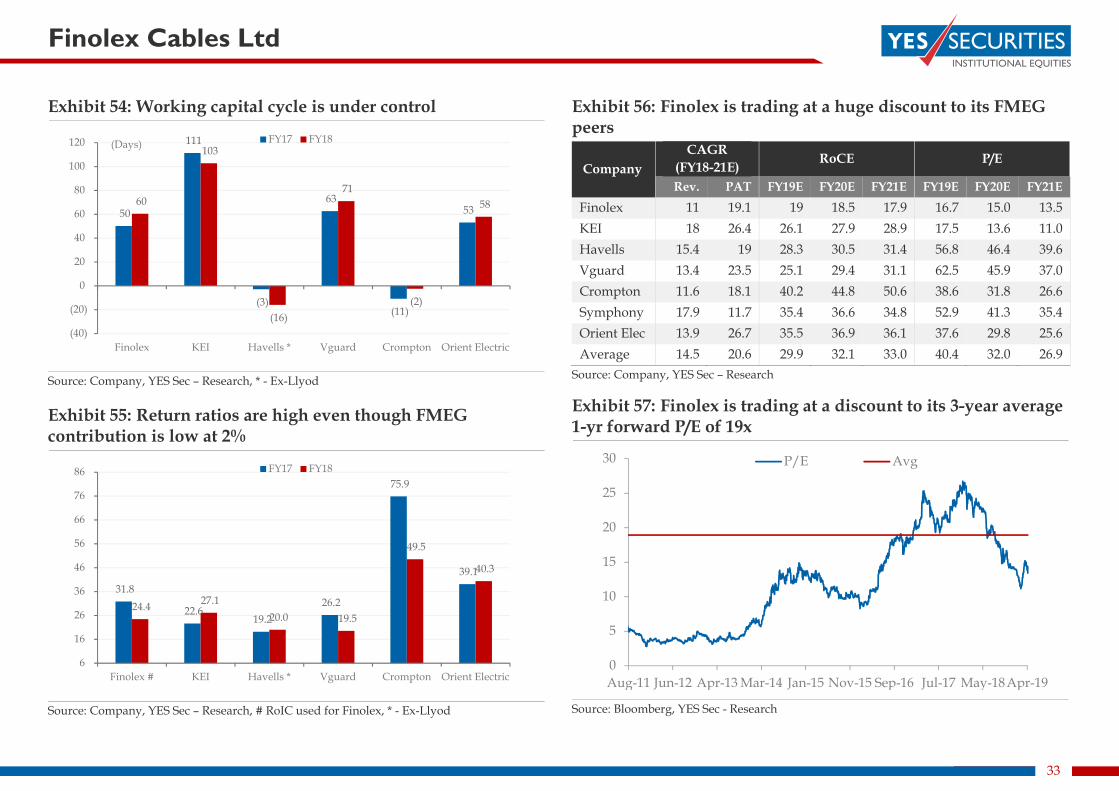

Exhibit 54: Working capital cycle is under control

Source: Company, YES Sec – Research, * - Ex-Llyod Exhibit 55: Return ratios are high even though FMEG contribution is low at 2%

Source: Company, YES Sec – Research, # RoIC used for Finolex, * - Ex-Llyod

Exhibit 56: Finolex is trading at a huge discount to its FMEG peers

Company CAGR

(FY18-21E) RoCE P/E

Rev. PAT FY19E FY20E FY21E FY19E FY20E FY21E Finolex 11 19.1 19 18.5 17.9 16.7 15.0 13.5 KEI 18 26.4 26.1 27.9 28.9 17.5 13.6 11.0 Havells 15.4 19 28.3 30.5 31.4 56.8 46.4 39.6 Vguard 13.4 23.5 25.1 29.4 31.1 62.5 45.9 37.0 Crompton 11.6 18.1 40.2 44.8 50.6 38.6 31.8 26.6 Symphony 17.9 11.7 35.4 36.6 34.8 52.9 41.3 35.4 Orient Elec 13.9 26.7 35.5 36.9 36.1 37.6 29.8 25.6 Average 14.5 20.6 29.9 32.1 33.0 40.4 32.0 26.9

Source: Company, YES Sec – Research

Exhibit 57: Finolex is trading at a discount to its 3-year average 1-yr forward P/E of 19x

Source: Bloomberg, YES Sec - Research

50

111

(3)

63

(11)

53 60

103

(16)

71

(2)

58

(40)

(20)

0

20

40

60

80

100

120

Finolex KEI Havells * Vguard Crompton Orient Electric

(Days) FY17 FY18

31.8

22.6 19.2

26.2

75.9

39.1

24.4 27.1 20.0 19.5

49.5

40.3

6

16

26

36

46

56

66

76

86

Finolex # KEI Havells * Vguard Crompton Orient Electric

FY17 FY18

0

5

10

15

20

25

30

Aug-11 Jun-12 Apr-13 Mar-14 Jan-15 Nov-15 Sep-16 Jul-17 May-18Apr-19

P/E Avg

Finolex Cables Ltd

34