Nuvoco Vistas Corporation Ltd. - Ventura Securities

32

1 | Page (03 rd Nov 21) For any further query, please email us on [email protected] Nuvoco Vistas Corporation Ltd. Fifth largest cement player with multiple triggers for value unlocking

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Nuvoco Vistas Corporation Ltd. - Ventura Securities

1 | P a g e ( 0 3 r d N o v 2 1 )

For any further query, please email us on [email protected]

TABLE OF CONTENTS

Nuvoco Vistas Corporation Ltd.

Fifth largest cement player with multiple triggers for value

unlocking

2 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

TABLE OF CONTENTS

Summary 3

Valuation and Peer Comparison 4

Financial Analysis & Projections 7

Journey and Plant Location with Capacity 8

Key Growth Drivers 9

Industry wide growth opportunity 9

Leadership position especially in east India region 11

Strategically located cement production facilities 18

Business Quality Score 23

Annual Report Takeaways 24

Key Management Personnel 26

Risk & Concerns 26

Quarterly Financials 29

Summary of Management Commentary on Quarterly Performance 30

Financial Statement Analysis & Projections 31

Disclaimer 32

3 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Nuvoco Vistas Corp. Ltd. (Nuvoco) promoted by Dr. Karsanbhai K. Patel (Nirma

Group) is one of the largest cement company and concrete manufacturers in East

India. Over FY14-21 Nuvoco has aggressively expanded capacity at 15% CAGR to 22.32

MMTPA (primarily through acquisitions of Lafarge in 2016 and Emami in FY21) to

emerge as the 5th largest cement company in India.

Being primarily located in East India (75% capacity) and the North, Nuvoco is well

placed to benefit from the cement demand due to higher infrastructural growth, rural

housing aided by PMAY-G, and increasing budgetary allocations for various

government schemes. We forecast average utilization levels to remain over 80%+

leading to a revenue growth of 17.1% CAGR to INR 12,039.3 crore (volume CAGR of

11.9% to 23.75 MTPA, average realization CAGR of 5% to INR 5069/ton) over the

period FY21-24.

Coupled with the higher utilizations and significant cost rationalization initiatives (like

reworking logistics and focusing on captive power) EBIDTA/tonne is expected to be

enhanced by ~INR 250 by FY23. With the implementation of these measure, we

believe Nuvoco would be better placed (than peers) to tide over the headwinds of

input cost inflation. In addition, the paring of debt from the IPO proceeds has

significantly helped in deleveraging the balance sheet.

At the CMP of INR 549.2, Nuvoco is valued at $105.2 FY24E EV/T. This is at a significant

discount to that of its peers operating in the eastern geography. We believe that the

valuation discount is unjustified and expect the stock to get re-rated once the market

starts taking cognizance of (i) the size of its operations (5th largest cement company

in India) (ii) operating leverage from the high utilization levels and cost saving

initiatives, and (iii) de-levered balance sheet.

We initiate coverage with a BUY for a 24-month price target of INR 680 (8.9x

FY24EV/ EBIDTA, $130 FY24E EV/T), representing an upside of 24.2% from the CMP

of INR 547.3.

Key Financial Data (INR Cr, unless specified)

Revenue EBITDA

Net Profit

EBITDA (%)

Net Profit

(%) EPS (₹)

BVPS (₹)

RoE (%)

RoIC (%)

P/E (X) P/BV

(X)

EV/ EBITDA

(X)

FY20 6,793.2 1,297.1 249.3 19.1 3.7 7.9 167.5 4.7 5.6 69.4 3.3 17.5

FY21 7,488.8 1,460.5 (25.9) 19.5 (0.3) (0.8) 232.4 (0.4) (3.6) (667.6) 2.4 16.9

FY22E 8,975.2 1,682.6 209.7 18.7 2.3 5.9 252.9 2.3 4.7 93.5 2.2 13.5

FY23E 10,784.6 2,371.4 769.0 22.0 7.1 21.5 274.5 7.8 8.6 25.5 2.0 9.1

FY24E 12,039.3 2,727.2 1,109.9 22.7 9.2 31.1 303.0 10.3 10.8 17.7 1.8 7.2

BUY @ CMP INR 547 Target: INR 680 in 24 months Upside Potential: 24%

Fifth largest cement player with multiple triggers for value unlocking

Industry Cement

Scrip Details

Face Value (INR) 10.0

Market Cap (INR Cr) 19,547

Price (INR) 547.3

No of Shares O/S (Cr) 35.7

3M Avg Vol (000) 104

52W High/Low (INR) 578/471

Dividend Yield (%) 0

Shareholding (%) Sept 2021

Promoter 71.03

Institution 23.66

Public 5.31

TOTAL 100.0

Price Chart

52000

54000

56000

58000

60000

62000

64000

460

480

500

520

540

560

580A

ug, 2

1

Sep

, 21

Oct

, 21

Nuvoco (LHS) SENSEX (RHS)

Nuvoco Vistas Corporation Ltd.

4 | P a g e ( 0 3 r d N o v 2 1 )

For any further query, please email us on [email protected]

Valuation and Comparable Metric of Domestic and Global Cement Manufacturing Companies

Source: Ventura Research & Bloomberg

PEG

Company Name Mkt Cap Price 2024 2022 2023 2024 2022 2023 2024 2022 2023 2024 2022 2023 2024 2022 2023 2024 2022 2023 2024 2022 2023 2024

(fig in INR Crores)

Nuvoco Vistas 19,613 549.2 0.3 89.7 24.5 16.9 13.0 8.8 6.9 2.3 7.8 10.3 5.3 9.4 12.3 8,975 10,785 12,039 18.7 22.0 22.7 2.3 7.1 9.2

Ultratech Cement 2,22,784 7,709.7 1.0 31.7 26.4 22.3 17.1 14.9 12.4 14.0 14.8 15.3 20.1 21.5 25.2 53,026 58,995 63,552 25.0 25.4 27.0 13.2 14.3 15.7

Dalmia Bharat 37,863 2,023.5 1.5 32.5 26.0 21.0 13.2 11.3 9.8 8.5 9.7 10.7 11.0 12.6 14.3 12,175 14,022 15,783 24.6 24.9 25.2 9.6 10.4 11.4

Shree Cement 1,04,446 28,948.0 1.6 38.9 33.3 28.0 23.3 20.3 15.0 15.1 15.2 15.3 17.4 17.8 53.2 15,945 18,252 20,375 28.1 28.2 28.8 16.9 17.2 18.3

ACC 45,003 2,396.5 2.6 20.6 18.4 18.2 11.0 9.4 NA 13.6 13.6 13.1 30.7 34.4 NA 18,187 19,742 21,236 18.9 19.3 19.5 12.0 12.4 11.7

Ambuja Cement 81,014 408.0 1.5 22.1 20.5 17.8 9.0 7.7 6.3 12.9 12.4 12.5 43.3 48.5 32.4 33,399 36,069 39,638 22.2 22.6 23.4 11.0 11.0 11.5

Star Cement 4,126 100.0 1.5 14.2 10.7 NA 9.0 7.3 NA 14.7 17.3 NA NA NA NA 2,173 2,487 NA 20.6 22.2 NA 14.8 17.1 NA

Net Margin (%)P/E (x) EV/EBIDTA (x) RoE (%) RoIC (%) Sales EBITDA Margin (%)

Company North West South East Central

ACC 18 12 31 23 17

Ambuja Cement 41 28 0 24 7

Birla Corp 21 29 0 15 35

Dalmia Bharat 0 10 40 51 0

Nuvoco 22 0 0 78 0

Shree Cement 61 0 7 32 0

Star Cement 0 0 0 100 0

The Ramco Cement 0 0 84 16 0

Ultratech Cement 21 25 18 14 21

Regions wise capacity share (%)

For any further query, please email us on [email protected]

5 | P a g e ( 0 3 r d N o v 2 1 )

For any further query, please email us on [email protected]

More than 20% ROIC and significant room for margin expansion are potential re-rating factors

Source: Ventura Research, ACE Equity & Bloomberg

Ultratech Cement

Dalmia Bharat

Shree Cement

Ambuja Cement

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

6.0 7.0 8.0 9.0 10.0 11.0 12.0 13.0 14.0 15.0 16.0

FY24

Ro

IC (

%)

FY24 EV/EBIDTA (x)

Nuvoco Vistas

Ultratech Cement

Dalmia Bharat

Shree Cement

ACCAmbuja Cement

5

7

9

11

13

15

17

19

21

18 20 22 24 26 28 30 32

FY24

Re

ven

ue

CA

GR

(%

)

FY24 EBIDTA Margin (%)

6 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Our Bull and Bear Case Scenarios

We have prepared a Bull and Bear case scenario based on Nuvoco’s FY24 sales, EBIDTA, and

EV/EBIDTA.

• Bull Case: We have assumed Rs.12,039.3 cr of sales in FY24E (CAGR of 17.1%), EBIDTA

Margin of 22.7%, along with the marginal re-rating to 9.7X FY24E EV/EBITDA, which

will result in a Bull Case price target of INR 740 per share (upside of 35.2% from CMP).

• Bear Case: We have assumed Rs.10,521.3 cr of sales in FY24 (CAGR of 12.0%), EBIDTA

Margin of 20.7% along with 7.7X FY24E EV/EBITDA, which will result in a Bear Case

price target of INR 472 per share (downside of 13.8% from CMP).

Bull & Bear Case Scenario

Bull Case Price

INR 740 per share

Target Price

INR 680 per share

Bear Case Price

INR 472 per share

Current Price

INR 547.3 per share

Sales of Rs.12,039.3 cr in FY24 (CAGR

of 17.1%) and 9.7x FY24E EV/EBIDTA.

Sales of Rs.10,521.3 cr in FY24 (CAGR

of 12.0%) and 7.7x FY24E EV/EBIDTA.

7 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Financial Analysis and Projections

With all the key drivers in place, we expect Nuvoco’s sales volumes and revenues to grow at a

CAGR of 11.9% to 23.75 MTPA and 17.1% to INR 12,039.3 cr over FY21-24E respectively.

Premium product launches, cost rationalization and the captive power generation will help to

improve profitability. EBITDA is estimated to grow at a CAGR of 23.1% to INR 2,727.2 cr, while

EBITDA/T is expected to improve to INR 1,148/T by FY24E. The company aims to be net debt-

free by FY25, which would lead to faster growth in PAT (from the loss of INR 25.9 cr to a profit

of INR 1,109.9 cr by FY24E). Subsequently, RoE and RoIC are expected to improve to 10.3%

(+1061bps) and 12.3% (+1619bps), respectively, by FY24E.

Nuvoco’s Financial Summary

Source: Company Reports & Ventura Research

Figures in INR Crores FY19 FY20 FY21 FY22E FY23E FY24E

Sales Volume (MTPA) 15.8 14.6 17.0 18.7 21.7 23.8

YoY Growth (%) (7.5) 15.9 10.2 16.1 9.4

Capacity Utilization (%) 93.1 90.3 77.6 78.5 86.7 94.9

NSR (Rs./T) 4,457.0 4,639.4 4,412.9 4,801.2 4,969.2 5,068.6

Revenue 7,052.1 6,793.2 7,488.8 8,975.2 10,784.6 12,039.3

YoY Growth (%) (3.7) 10.2 19.8 20.2 11.6

Raw Material cost 1,444.7 1,230.0 1,206.8 1,265.5 1,553.0 1,793.9

Raw Material cost (Rs./T) 913.0 840.0 711.1 677.0 715.6 755.2

Power & Fuel 1,374.1 1,225.6 1,356.3 1,903.8 1,945.0 1,915.8

Power & Fuel cost (Rs./T) 868.5 837.0 799.2 1,018.4 896.2 806.6

Freight and forwarding charges 1,983.2 1,776.1 2,029.4 2,463.7 2,933.4 3,310.8

Freight and forwarding cost (Rs./T) 1,564.0 1,407.4 1,172.2 1,317.9 1,351.6 1,393.9

Employee Cost 381.1 404.6 482.0 573.6 676.9 798.7

Employee Cost (Rs./T) 240.9 276.3 284.0 306.9 311.9 336.3

Other Expenses 951.3 859.7 953.8 1,086.0 1,304.9 1,492.9

Other Expenses (Rs./T) 601.2 587.1 562.0 580.9 601.3 628.5

EBIDTA 917.7 1,297.1 1,460.5 1,682.6 2,371.4 2,727.2

EBIDTA Margin (%) 13.0 19.1 19.5 18.7 22.0 22.7

EBIDTA (Rs./T) 580.0 885.9 860.6 900.1 1,092.7 1,148.2

PAT (26.5) 249.3 (25.9) 209.7 769.0 1,109.9

PAT Margin (%) (0.4) 3.7 (0.3) 2.3 7.1 9.2

PAT (Rs./T) (16.7) 170.2 (15.3) 112.2 354.3 467.3

Net Worth 4,988.3 5,279.3 7,323.7 9,033.4 9,802.4 10,823.0

Return on Equity (%) (0.5) 4.7 (0.4) 2.3 7.8 10.3

Invested Capital 7,783.4 8,410.5 12,320.4 12,110.0 11,852.2 10,942.6

Return on Invested Capital (%) (8.6) 5.9 (3.8) 5.3 9.4 12.3

Cash Flow from Operations 860.1 1,024.8 1,717.4 1,428.0 2,316.7 2,862.3

Cash Flow from Investing (148.6) (310.1) (2,924.1) (447.3) (883.5) (553.7)

Cash Flow from Financing (646.8) (559.1) 1,419.7 (473.2) (1,823.2) (1,940.2)

Net Cash Flow 64.7 155.6 213.0 507.5 (390.1) 368.5

Free Cash Flow 279.3 455.3 1,165.7 901.0 1,716.7 2,762.3

YoY Growth (%) 63.0 156.0 (22.7) 90.5 60.9

Total Debt 3,375.4 3,642.1 5,908.7 4,538.2 3,214.2 1,716.9

Net Debt 2,795.1 3,131.2 4,996.7 3,076.6 2,049.8 119.6

Net Debt to Equity (x) 0.6 0.6 0.7 0.3 0.2 0.0

Net Debt to EBITDA (x) 3.0 2.4 3.4 1.8 0.9 0.0

8 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Journey of the company

Source: RHP, Company Reports & Ventura Research

Plant locations and capacity

Capacity (MTPA)

Region/States FY19 FY20 FY21 FY22E FY23E

East India Production 8.7 9.1 17.4 18.9 20.1

Arasmeta 1.9 1.9 1.9 1.9 1.9

Sonadih 0.6 0.6 0.7 0.7 0.7

Jojobera 4.6 5.0 5.0 6.5 6.5

Mejia 1.7 1.7 1.7 1.7 1.7

Risda 0.0 0.0 3.0 3.0 3.0

Panagarh 0.0 0.0 2.5 2.5 2.5

Bhabua 0.0 0.0 0.8 0.8 2.0

Jajpur 0.0 0.0 2.0 2.0 2.0

North India Production 4.9 4.9 4.9 4.9 4.9

Chittorgarh 2.1 2.1 2.1 2.1 2.1

Nimbol 2.3 2.3 2.3 2.3 2.3

Bhiwani 0.5 0.5 0.5 0.5 0.5

Total Cement capacity 13.6 14.0 22.3 23.8 25.0

Source: Company Reports & Ventura Research

Year Events

1999Commencement of operations in India with acquisition of cement business of Tata Iron & Steel Company Ltd. in Jharkhand

incuding Jojobera and Sonadih Cement Plants.

2000 Acquisition of the cement business of Raymond Ltd, Chhattisgarh including the Arasmeta Cement Plant.

2008 Acquisition of ready-mix concrete business of Larsen & Toubro Limited.

2009 Commissioning of the Mejia grinding unit in West Bengal. Commissioning of a new clicnker line at the Sonadih Cement Plant.

2012 Inauguration of Construction Development and Innovation Centre (CDIC) in Mumbai.

2013 Commissioning of operations at Chittorgarh Cement Plant, Rajasthan.

2014Nirma Group entered the cement business through a greenfield cement plant in Nimbol. Commissioning of operations at

Bhiwani Cement Plant, Haryana.

2016 Acquisition of all Equity shares held by Lafarge to Nirchem Cement Limited (erstwhile wholly-owned subsidiary of Nirma Ltd.).

2017 Amalgamation of Nirchem Cement Limited with Nuvoco Vistas Corp. Ltd.

2019 Commissioning of first Captive Power Plant and Waste Heat Recovery in Chittorgarh Cement Plant

2020Amalgamation with Nimbol Cement Plant, Rajasthan of Nirma Ltd. Acquisition of NU Vista Limited (formerly Emami Cement Ltd.)

as a wholly-owned subsidiary

9 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Key Growth Drivers

Industry-wide growth opportunity

India is the second largest cement producer in the world. The Indian cement industry is a vital

part of its economy and provides employment, directly or indirectly, to more than a million

people. According to the Budget of FY22, the Indian Cement Industry has an installed capacity

of approximately 545 million tonnes comprising over 250 large cement plants. The share of the

top 5 players in the industry has grown to ~50.5% led by consolidation and higher organic

growth by large players. Driven by its foray into value-added products such as RMC and white

cement, the industry has diversified a little.

Sectoral Mix and growth

Source: RHP, Company Reports & Ventura Research

6223

15

63

27

10

Sectoral Mix (%)

Housing Infrastructure Commercial & Industrial

FY21

FY26E 5.5

7.55.0

6.0

8.5

8.5

8.0

7.0

Demand growth segmentation (%)

Housing Infrastructure Commercial & Industrial Overall

FY21

FY26E

10 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Regional Capacity Breakup

23

23

16

9

7

22

Northern region capacity breakup (%)

Ultratech Cement Shree Cement Lafarge Holcim

JK Cement JK Lakshmi Rest

17

16

1615

11

26

Eastern region capacity breakup (%)

Nuvoco Lafarge Holcim Dalmia Bharat

Ultratech Cement Shree Cement Rest

41

21

63

3

26

Western region capacity breakup (%)

Ultratech Cement Lafarge Holcim Sanghi Industries

JK Lakshmi JSW Cement Rest11

9

7

7

7

59

Southern region capacity breakup (%)

Ultratech Cement Ramco Chettinad

India Cement Dalmia Bharat Rest

34

1312

10

9

22

Central region capacity breakup (%)

Ultratech Cement Birla Corporation Jaypee Group

Prism Cement Lafarge Holcim Rest

11 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

State-wise cement demand State-wise cement capacity Zone FY21E FY26E CAGR (%) Zone FY21E FY26E CAGR (%) Jharkhand East 9.1 14.5 10 Bihar East 9.0 15.5 11 Odisha East 14.5 23.0 10 Odisha East 20.0 34.0 11 Bihar East 17.5 26.5 9 West Bengal East 27.5 35.0 5 West Bengal East 21.5 31.0 8 Jharkhand East 15.5 18.5 4 Chhattisgarh East 9.8 13.5 7 Punjab North 5.5 6.5 3 Gujarat West 23.0 30.5 6 Chhattisgarh East 26.5 30.5 3 Rajasthan North 22.8 30.0 6 Rajasthan North 79.0 90.5 3 Punjab North 9.1 10.5 3 Gujarat West 35.0 37.0 1

Source: RHP, Company Reports & Ventura Research

In order to develop the country's infrastructure, the Indian government has undertaken several

projects related to the construction of roads and highways, both in the rural and urban areas,

along with the development of industrial hubs in different parts of the country. These schemes

and initiatives are together expected to drive the growth of the Indian cement industry, since

it is one of the primary materials for the successful execution of such projects.

The Pradhan Mantri Awas Yojana aims to provide affordable housing for all by 2022 in over

4000 towns across India. This is likely to provide the necessary push to the affordable housing

segment and boost the growth of the construction sector, which would lead to an increase in

demand for cement, hence helping it grow further. In the Union Budget FY 2021-22, the

Government of India has extended benefits, under Section 80-IBA of the Income Tax Act, until

March 31, 2022, to promote affordable rental housing in India.

The allocation of INR. 13,750 crores and INR. 12,294 cr for Urban Rejuvenation Mission:

AMRUT and the Smart Cities Mission and Swachh Bharat Mission, respectively and Rs. 27,500

cr in the Union Budget under Pradhan Mantri Awas Yojana.

Leadership position especially in east India region

The company is the largest cement manufacturer in East India and the fifth largest cement

manufacturer in India in terms of capacity. Nuvoco’s capacity share was approximately 17% in

terms of consolidated capacity in East India, ~4.7% in terms of consolidated capacity in North

India and consolidated capacity was 22.32 MMTPA as on FY21, ~4.2% of the industry’s installed

capacity in India as of December 2020. The company grew at a fast pace, owing to mega

acquisition of Lafarge Holcim in 2016 and NU Vista (formerly Emami Cement Ltd) in 2020. With

a consolidated cement capacity of 23.8 MTPA currently (end of 1QFY22), Nuvoco has become

the fifth largest cement company in India.

In the northern region, Nuvoco has an integrated plant in Chittogargh, a split blending unit in

Haryana and an integrated unit in Nimbol (transferred from Nirma to NVCL in fiscal 2020).

These units will benefit from synergies, including rationalisation of the marketing network and

cost savings because of ramp-up in scale of operations.

India has over 20 large and medium cement manufacturers and more than 50 smaller

producers. Cement brands are largely classified into three brands - Category A, B and C brands

12 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

(“CAT A, B and C” respectively). CAT A producers are considered to be premium cement brands,

whereas CAT B and CAT C producers sell at par or below the price of the base brand of a CAT

A player. This leads to a huge variation in cement prices with the difference between the

Premiums brand of CAT A companies and that of CAT C brand in the same market. Premium

brands like Nuvoco Vistas Concreto and Duraguard MF, Ultratech Weatherplus and ACC Gold

are market leaders in prices and usually enjoy a premium of Rs 100-150/ bag over CAT C Brand

in the same market.

Leadership position with dominant position at East India region

Source: RHP, Company Reports & Ventura Research

13 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Pan-India capacity

Source: RHP, Company Reports & Ventura Research

14 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Fifth largest cement player with region-wise revenue share

Source: RHP, Company Reports & Ventura Research

Diversified range of revenue stream

The company offer a range of over 50 products across cement, RMX and modern building

materials.

Cement

As a part of its cement portfolio, Nuvoco has leading brands with multiple products under each

brand including Concreto, Duraguard, Premium Slag Cement, Nirmax, Double Bull, Infracem

and Procem. The company’s key brands include Concreto, Concreto Green, Duraguard,

Duraguard Microfiber, Duraguard Waterseal, Duraguard Silver, Duraguard Rapidx Xtra,

Premium Slag Cement, Nirmax Cement, Infracem Cement, Double Bull Cement, Procem

Cement, Double Bull Master and Double Bull Subh. After being launched in 2004 Concreto has

been one of the best-selling brands, while Concreto and Duraguard are market leaders in terms

of cement prices in the respective segment as well as regions.

Nuvoco has 79% contribution to turnover coming from the trade segment and this is 800bps

higher than its peers. The trade segment has better realisations which lead to higher

profitability.

Ready Mix Concrete (RMC)

Nuvoco’s brand portfolio in the ready-mix concrete business includes Concreto, Instamix,

Artiste and X-Con range of products. This portfolio includes products such as self-compacting

concrete, decorative concrete, ready-to-use concrete, crack-resistant concrete, concrete with

steel fibers, and lean concrete, as well as concrete with varied characteristics for specialty uses.

Nuvoco had scaled down its RMC business in FY21 as it exited various non-profitable markets.

116.8

66.0

43.430.8

22.3

0

20

40

60

80

100

120

140

Ult

rate

ch

Lafa

rge

Ho

lcim

gro

up

Shre

e C

emen

t

Dal

mia

Nu

voco

Cement capacity (MTPA) as on FY21

75

20

5

Region-wise revenue share (%)

East North Central

15 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

RMC region wise capacity

Source: RHP, Company Reports & Ventura Research

Modern Building Materials

The company’s modern building material products are a key differentiator. Nuvoco’s suite of

products under this category include a range of construction chemicals, tile adhesives, wall

putty, dry plaster, cover blocks and ready-mix dry concrete. Its modern building material

products are marketed and sold under the “Zero M” and “Instamix” brands.

The company has a dedicated Construction Development and Innovation Centre (CDIC) located

in Mumbai and 17,500 sq. feet, NABL1-accredited facility serving as an incubation centre for

innovative products.

33

25

24

18

Nuvoco’s RMC plants are spread across India (FY21) (%)

West North South East

16 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Nuvoco’s Product Portfolio

Source: RHP, Company Reports & Ventura Research

Cement

Source: RHP, Company Reports & Ventura Research

Ready-Mix Concrete (RMX) Modern Building Materials

Source: RHP, Company Reports & Ventura Research

17 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Innovative Products

Source: RHP, Company Reports & Ventura Research

Double digit growth with strong realization

Source: Bloomberg, Company Reports & Ventura Research

15.814.6

17.018.7

21.7

23.8

4457

4639

4413

4801

4969

5069

4,000

4,200

4,400

4,600

4,800

5,000

5,200

0

5

10

15

20

25

FY19 FY20 FY21 FY22E FY23E FY24E

Sales Vol. & NSR

Sales Vol. (MTPA) NSR (Rs./T) (RHS) 93% 90%

78% 78%

87%

95%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY19 FY20 FY21 FY22E FY23E FY24E

Total Cement Utilization (%)

100

105

110

115

120

125

130

Ap

r-1

2

No

v-12

Jun

-13

Jan

-14

Aug

-14

Mar

-15

Oct

-15

May

-16

Dec

-16

Jul-

17

Feb

-18

Sep

-18

Ap

r-1

9

No

v-19

Jun

-20

Jan

-21

Aug

-21

India cement prices WPI

250

260

270

280

290

300

310

320

330

340

350

FY17 FY18 FY19 FY20 FY21 H1FY22

Cement Price (Rs./Bag)

North East

18 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Strategically located cement production facilities that are in close proximity to

raw materials and key markets

Nuvoco’s plants are spread across different states in the eastern region, so that flyash is largely

available at less than 150kms. Its Jojobera (Jharkhand) and Mejia (West Bengal) grinding units

are at less than 2kms distance from thermal power plants. Its Panagarh (West Bengal) plant

also has less than 50km lead distance for flyash sourcing. In the north, Nuvoco’s flyash lead

distance ranges between 120-600kms. Most of the slag cement manufacturing plants can

source slag requirements at less than 180km. It has a ~20 years supply arrangement for ~2.1mn

MT at a pre-determined rate (lower than spot market price) and another 0.5mn MT at market

price, adding further to its cost competitiveness.

The company has strong distribution capabilities in the eastern region. Nuvoco also has railway

connectivity across six out of its 11 plants, which is helping for movement of raw material, fuel

and cement. The business integration & synergy of Nu Vista with Nuvoco will help to bring

down its overall lead distance. Through the synergy of NU Vista, Nuvoco intends to bring down

the overall lead distance from ~390km to ~350km through cross manufacturing of brands at

its various factories. Nuvoco is also reorganising clinker logistics for its grinding units in the

east, thus lowering its clinker movement cost.

The company has five integrated plants across Rajasthan and Chhattisgarh. In the past two

years, it has added thermal and WHRS capacities across these five locations, leading to 105MW

of CPP and 45MW of WHRS. Total power capacity of Nuvoco reach to 196 MW.

The company has a long-term tie-up with Tata Steel in the state of Jharkhand for the Jojobera

plant. A 20-year contract starting February 2019 to 2039.

Production Mix

Source: RHP, Brokers report, Ventura Research

60

26

14

Production Mix (%)

PPC Slag cement OPC

1.8 1.7 1.81.9

2.12.2

0.0

0.5

1.0

1.5

2.0

2.5

FY19 FY20 FY21 FY22E FY23E FY24E

Cement to clinker ratio

(x)

19 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Strategic locational benefits

Locations Plant Type

FY21 Cement Capacity (MTPA)

Limestone Lead distance

(km)

Clinker lead Distance

(km)

Flyash lead Distance

(km)

Slag lead Distance

(km)

Railway sidings

Nimbol (Rajasthan) IU 2.3 4-10

300-480 NA No Chittorgarh (Rajasthan) IU 2.1 0.5-6

120-600 NA Yes

Sonadih (Chhattisgarh) IU 0.65 2-2.5

70-150 NA Yes Arasmeta (Chhattisgarh) IU 1.89 3-45

45-100 NA Yes

Risda (Chhattisgarh) IU 3 2

110-150 120 No

Mejia (West Bengal) GU 1.65

620-690 1-2 NA Yes Panagarh (West Bengal) GU 2.5

800 30-65 32-180 Yes

Jojobera (Jharkhand) GU 4.95

450-530 1-2 10-350 Yes

Bhabua (Bihar) GU 0.8

600 115-220 NA No Jajpur (Odisha) GU 2

600 NA 12-180 No

Bhiwani (Haryana) BU 0.5

450-550 Nearby NA No

IU: Integrated Unit, GU: Grinding Unit, BU: Blending Unit

Source: RHP, Brokers report, Ventura Research

Limestone reserves

Operational Mines

Mine Name Location Reserves Date of Certification of Mining

Plan Arasmeta Chhattisgarh 25.0 12-Feb-21 Chilhati Chhattisgarh 150.0 11-Dec-19 Kirari Chhattisgarh 25.3 12-Feb-21 Sonadih Chhattisgarh 23.1 10-Dec-20 Sinla Rajasthan 14.7 05-Apr-21 Digrana Rajasthan 14.1 05-Apr-21 Sita Ram Ji ka Khera Rajasthan 66.0 26-Mar-18 Arniya Joshi Rajasthan 63.9 24-Jan-20 Chittapur Karnataka 221.2 20-Apr-18 Risda Chhattisgarh 222.1 18-Jan-20 Total 821.5 Non-Operational Mines

Mine Name Location Reserves Date of Certification of Mining

Plan Arasmeta Chhattisgarh 14.2 28-Oct-20 Sonadih Chhattisgarh 156.8 03-Oct-16 Dhandhani Chhattisgarh 15.8 06-Jan-21 Nagaur Rajasthan 127.0 24-Jul-19 Nagaur Rajasthan 168.8 24-Jul-19 Tengada Andhra Pradesh 391.8 21-Oct-14 Total 874.3

Source: RHP, Ventura Research

20 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Upcoming capacities & various projects to fuel further profitable growth

The cement plants are located at various strategic locations in East and North India. These

locations allow the company to effectively sell and market their products in East and North

India as well as access to select key markets in Central India. It has three integrated units and

five grinding units located in East India, and two integrated units, and one blending unit located

in North India.

Nuvoco has 30+ years of limestone reserves across all its plant locations in the north and east

regions. At its Nimbol plants, the current limestone capacity can last for the next 12 years.

However, the company intends to participate in upcoming auctions of new mines in the region

to augment its limestone capacity.

The company is to set up captive power plants in all integrated units and at the Jojobera

grinding unit. The Arasmeta plant as well as the Jojobera plant is expected to start generating

electricity by Q3FY22. By Q3FY22, the company would have completed all power projects and

with that will have 150 megawatts of Captive Power Plants, 45 megawatts of Waste Heat

Recovery systems and 1.5 megawatts of solar plants. All these projects combined are expected

to meet ~65-70% of the total power requierments of the company by FY24E. The company is

among the best in the industry in terms of installed capacity of WHR per million tonne of

cement capacity.

The company is implementing clinker rerouting, where the clinker from the Risda Cement Plant

will be moved via Sonadih Cement Plant railhead to grinding unit, which will eliminate

additional handling charges and reduce overall cost and increased profitability of the business.

Lowering external power dependency

Source: Company Reports & Ventura Research

The company is debottlenecking its cement grinding capacity by 2.7MTPA – all in the east. It

completed its Jharkhand grinding unit expansion (1.5 MTPA) at the end of Q1FY22 and expects

0%

20%

40%

60%

80%

100%

120%

FY19 FY20 FY21

Power requierment

Grid WHR CPP Solar

0

1

1

2

2

3

3

4

4

5

5

0

200

400

600

800

1,000

1,200

Power cost/T (Rs.) FY21 WHRS / Cement (MW/MT)

21 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

to commission the Bihar grinding expansion (1.2MTPA) by H1FY23. It is also debottlenecking

its clinker capacity by 0.9 MTPA (across three plant locations – 0.3mn MT each at Nimbol in

Rajasthan, and Sonadih and Risda in Chhattisgarh) by FY23E. Other greenfield projects are

Gulburge and Maharashtra yet to announce size. The company is embarking on clinker

debottlenecking in three of its kilns, out of which the company has already started work on

two kilns; one in the Nimbol plant in the North and the other in the Risda plant in the East and

Nuvoco is expecting to commission the debottlenecking by FY23. The company is looking at a

capex of over close to Rs.1,000 cr in FY22 and FY23.

In the northern region, the company has launched the Double Bull brand in the trade segment

under a separate channel. The company has also launched its Concreto brand in Odisha from

the NU Vista plant. These moves will increase Nuvuco’s blended cement sales and share of

trade sales as well, thereby improving its cement realization.

After completion of all the projects, the company is targetting cost savings of ~INR 250 till

FY23E. It will fuel profitable growth for the company as well as improve margins significantly.

Unit cost analysis

Particular FY19 FY20 FY21 FY22E FY23E FY24E NSR (Rs./T) 4,457.0 4,639.4 4,412.9 4,801.2 4,969.2 5,068.6 YoY Growth (%) 4.1 (4.9) 8.8 3.5 2.0 Raw Material cost (Rs./T) 913.0 840.0 711.1 677.0 715.6 755.2 YoY Growth (%) (8.0) (15.3) (4.8) 5.7 5.5 Power & Fuel cost (Rs./T) 868.5 837.0 799.2 1,018.4 896.2 806.6 YoY Growth (%) (3.6) (4.5) 27.4 (12.0) (10.0) Employee Cost (Rs./T) 240.9 276.3 284.0 306.9 311.9 336.3 YoY Growth (%) 14.7 2.8 8.0 1.6 7.8 Freight and forwarding (Rs./T) 1,564.0 1,407.4 1,172.2 1,317.9 1,351.6 1,393.9 YoY Growth (%) (10.0) (16.7) 12.4 2.6 3.1 Other Expenses (Rs./T) 601.2 587.1 562.0 580.9 601.3 628.5 YoY Growth (%) (2.3) (4.3) 3.4 3.5 4.5 EBIDTA (Rs./T) 580.0 885.9 860.6 900.1 1,092.7 1,148.2 YoY Growth (%) 52.7 (2.9) 4.6 21.4 5.1

Source: Company Reports & Ventura Research

Improvement in financial position

Financials of the company have remained stressed due to serial acquitions made by Nuvoco.

The recent IPO has helped with fuel of Rs.1500 cr and other Rs.500 cr through equity

conversion of debt from Kotak Special Situation Fund in FY21, which has reduced balance sheet

stress.

22 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Gaining financial strength

Source: Company Reports & Ventura Research

-5

0

5

10

15

20

25

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY19 FY20 FY21 FY22E FY23E FY24E

Revenue to improve on capacities addition with better realizations

Total Revenue YoY growth

-10

-5

0

5

10

15

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY19 FY20 FY21 FY22E FY23E FY24E

Higher profitability and debt repayment to improve return ratios

Net Worth Invested Capital

ROIC (RHS) ROE (RHS)

-5

0

5

10

15

20

25

-500

0

500

1,000

1,500

2,000

2,500

3,000

FY19 FY20 FY21 FY22E FY23E FY24E

Cost reduction to drive profitability

EBITDA PAT

EBITDA Margin (RHS) PAT Margin (RHS)

0

5

10

15

20

25

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY19 FY20 FY21 FY22E FY23E FY24E

Improvement in margins accelerate cash flow generation

CFO FCFF Net Working Capital Days (RHS)

0

1

2

3

4

5

6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY19 FY20 FY21 FY22E FY23E FY24E

Operating cash flow would be utilized towards faster debt repayments

Total Debt Net Debt

Net Debt to Equity Net Debt to EBITDA

Interest Coverage Ratio

1

1

1

1

1

1

1

1

1

2

FY19 FY20 FY21 FY22E FY23E FY24E

Strong volume growth with better realizations drive assets utilization

INR Cr %

INR Cr %

INR Cr %

INR Cr Days

INR Cr (x)

(x)

23 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Business Quality Score

Key Criteria Score Risk Comments

Management & Leadership

Management Quality 8 Low The management is of decent quality. It has been able to deliver growth by taking calculated risks.

Promoters Holding Pledge 10 Low The promoter holding is 71.03% and there is no promoter pledging as of Sept 2021.

Board of Directors Profile 7 Low The average experience of directors is >20 years with significant experience in cement, RMX, manufacturing, FMCG, accounts/finance, strategic planning and operations

Industry Consideration

Industry Growth 7 Low Cement industry is key to development of infrastructure and housing. The government’s thrust is towards infrastructure creation & development, road & highway construction, and boost in affordable housing.

Regulatory Environment or Risk 7 Low

The company operates in the domestic market and is therefore not exposed to international regulations. But the company is exposed to a range of environmental laws & regulations, ban or restriction in usage of few raw material

Entry Barriers / Competition 8 Low

Entry of a new company in the cement industry would require a strong capital base and a huge investment. There are 30+ large, mid and small cement manufacturers available in the country. Larger players get the benefits of consolidation and gaining market share.

Business Prospects

New Business / Client Potential 8 Low The company has a leading market share in the eastern India region which is expected to grow at a higher rate compared to other regions.

Business Diversification 4 High

Cement is a regional specific industry and the growth of regions will drive the growth of businesses in the industry. Nuvoco has premium cement products which command a premium price in the industry. RMX and other business segments contribute to lower revenue to the company.

Market Share Potential 8 Low Nuvoco is the fifth largest and dominant east India player in India.

Margin Expansion Potential 7 Low Cost rationalization, captive power plant helps to Nuvoco to improve its profitability and financial strength.

Earnings Growth 8 Low Higher east India growth and new capacity will lead volume growth and margin expansion

Valuation and Risk

Balance Sheet Strength 7 Low Higher debt on the balance sheet drags down its strength but IPO funds and improvement in operating cash flows on account of better margins and decent volume growth will lead to strengthening balance sheet.

Debt Profile 7 Low With the increase in CFO due to reducing capex, we expected that Nuvoco can become net debt-free by FY24.

FCF Generation 7 Low With all the key drivers in place, we are expecting positive FCF generation.

Dividend Policy 1 High The company has never paid a dividend in the past 6 years.

Total Score

Ventura Score (%)

104

70 Moderate

The overall risk profile of the company is good and we consider it as a Moderate risk company for investments

Source: Company Reports & Ventura Research

24 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Annual Report Takeaways

We analyzed the FY21 annual report of Nuvoco and our key observations are as follows:

Key Takeaways

• Reduction in power cost & Freight cost: For cement operations, the power and fuel

costs of the company have decreased by 13% from Rs.990/T in FY20 to Rs.858/T in

FY21. Power cost has reduced mainly due to the commissioning of CPP at the Sonadih

Cement Plant, a ramp up of existing WHRs and CPP commissioned in FY 2019-20 and a

reduction in the electricity tariff rate.

For cement operations, the freight and forwarding cost decreased by 10%, from

Rs.1,324/T in FY20 to Rs.1,197/T in FY21 due to an increase in direct dispatches and a

reduction in road freight costs in the North, partially offset by an increase in diesel

prices.

• Rights issue: The Company has allotted 54,545,455 and 18,181,819 fully paid-up equity

shares, having a face value of Rs.10/- each of the Company to Niyogi Enterprise Private

Limited (the “Holding Company”) on a Rights basis on June 8, 2020 and July 22, 2020,

respectively. This resulted in an increase in the issued, subscribed and paid-up share

capital of the Company to Rs.3,150,890,610; divided into 315,089,061 equity shares

having face value of Rs.10/- each.

• New Product Development: Cement - During FY21, the company launched Duraguard

Silver (premium composite cement). With reduced porosity and lesser chances of

thermal cracks, Duraguard Silver helps in preventing any damage caused by seepage

or temperature changes. Its high resistance to chloride makes it a better alternative

than regular PPC providing increased protection to the TMT bars.

RMX – the company launched four products namely, InstaMix Xpress (pre-mixed,

ready-to-use, bagged, dry concrete), Artiste Signature (a special and collaborative

collection designed by Gauri Khan Designs and International Designs available

exclusively for Nuvoco’s customers), Concreto Permadure (a water-and-

cracksresistant concrete) and Concreto Ecodure (controls thermal cracks in mass

concrete foundation and improves durability).

Modern Building Materials (MBM) - During FY21, Nuvoco launched ‘Zero M Type 3

Premium Cover Blocks’.

Pay Grades

The remuneration growth of Vice Chairman & MD and CFO has significantly outpaced the

median remuneration growth of the company in the past 5 years. Further, it has also outpaced

the CAGR growth in revenue, EBITDA and PAT over the same period.

25 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Remuneration in the last 5 years

Source: Company Reports & Ventura Research

Management & Leadership Team Turnover

Details on Board of Director and KMPs

Source: Company Reports

Auditor qualifications & significant notes to accounts

MSKA & Associates is the auditor and there were no qualifications/emphasis of matters

highlighted by them in the FY21 Annual Report.

Parameter (Fig in INR Cr) FY17 FY18 FY19 FY20 FY21 CAGR%

Vice Chairman & MD 7.4 6.6 9.5 4.7 5.2 (8.5)

Share in Total Employee Cost (%) 2.6 2.1 2.5 1.2 1.1

Chief Financial Officer 3.0 0.7 1.7 2.2 2.7 (3.0)

Share in Total Employee Cost (%) 1.0 0.2 0.5 0.5 0.6

Remuneration of SVP/VP/GM 0.5 0.6 0.9 0.8 0.9 12.6

Share in Total Employee Cost (%) 0.2 0.2 0.2 0.2 0.2

Employee Cost 290.0 317.5 381.1 404.6 482.0 13.5

Employee Cost as % of Revenue (%) 5.0 5.0 5.4 6.0 6.4

Board of Director & KMP FY17 FY18 FY19 FY20 FY21

Hiren Patel CM CM CM

Jayakumar Krishnaswamy MD MD MD

Ujjwal Batria MD MD

Berjis Desai ID ID ID ID ID

Bhavna Doshi ID ID ID ID ID

Achal Bakeri ID

Kaushikbhai Patel ID ID NED

Shruta Sanghavi CS CS CS

Ajay Pratap Singh CS CS

Suketu Shah NED NED NED NED

Sharad Shrimali NED

Mr. Maneesh Agrawal CFO CFO CFO CFO

CM-Chairman NED-Non Executive Director

MD-Managing Director ID-Independent Director

CFO-Chief Financial Officer CS-Company Secretary

26 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Major Related Party Transactions with promoters and KMPs

In FY19 and FY20, related party transactions are higher due to intercorporate deposit.

Related Party Transactions are relatively low

Source: Company Reports & Ventura Research

Contingent Liabilities

Contingent liabilities are very high compared to the net worth and revenue. These are mostly

from disputes on Income Tax.

Contingent Liabilities are reasonably high

Source: Company Reports & Ventura Research

Management Team

Source: Company Reports

Key Risks & Concerns

• COVID-19 pandemic led slowdown

Since late 2019, the outbreak of COVID-19 has resulted in a global health crisis and

triggered a global economic downturn and contraction. Due to a production halt

during the lockdown period, the company continued to incur fixed and semi-variable

costs, which adversely impacted its profitability for FY21.

Parameter (Fig in INR Cr) FY17 FY18 FY19 FY20 FY21

Related Party Trans 44.5 154.2 484.4 814.5 33.2

Compensation to KMP 12.4 6.8 0.9 8.8 3.2

Transactions as % of Revenue (%) 1.0 2.6 6.9 12.1 0.5

Parameter (Fig in INR Cr) FY17 FY18 FY19 FY20 FY21

Claims against the company not acknowledged 517.1 658.2 494.7 621.0 641.6

Transactions as % of Revenue (%) 8.9 10.5 7.0 9.1 8.6

Transactions as % of Net Worth (%) 13.6 16.6 9.9 11.8 8.8

Key Person Designation Details

Mr. Hiren PatelChairman & Non-

executive Director

He holds a bachelor’s degree in engineering from Stevens Institute of Technology, New Jersey,

USA and a master’s degree in business administration from Drexel University, Pennsylvania,

USA. He has been associated with the Nirma group since the year 1997. He has experience in the

cement, consumer goods, chemicals and health care industry.

Mr. Jayakumar Krishnaswamy MD

He holds a bachelor’s degree in engineering (mechanical) from University of Delhi. He has

experience across FMCG, paint, and coating industry. He has previously been associated with

Hindustan Unilever Limited and Akzo Nobel India Limited.

Mr. Maneesh Agrawal Chief Financial Officer

He holds a bachelor’s degree in commerce from Hansraj College, University of Delhi. He is a

qualified chartered accountant. He has over two decades of experience primarily in cement,

RMX and paper businesses. He has previously been associated with Dalmia Bharat Limited and

Ballarpur Industries Limited.

27 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

In addition, throughout March, April and May 2021, due to an increase in the number

of daily COVID-19 cases, several state governments in India re-imposed lockdowns,

curfews and other restrictions to curb the spread of the virus. The detection of new

strains and subsequent waves of COVID-19 infections in several states in India as well

as throughout various parts of the world, which has adversely affected business

operations.

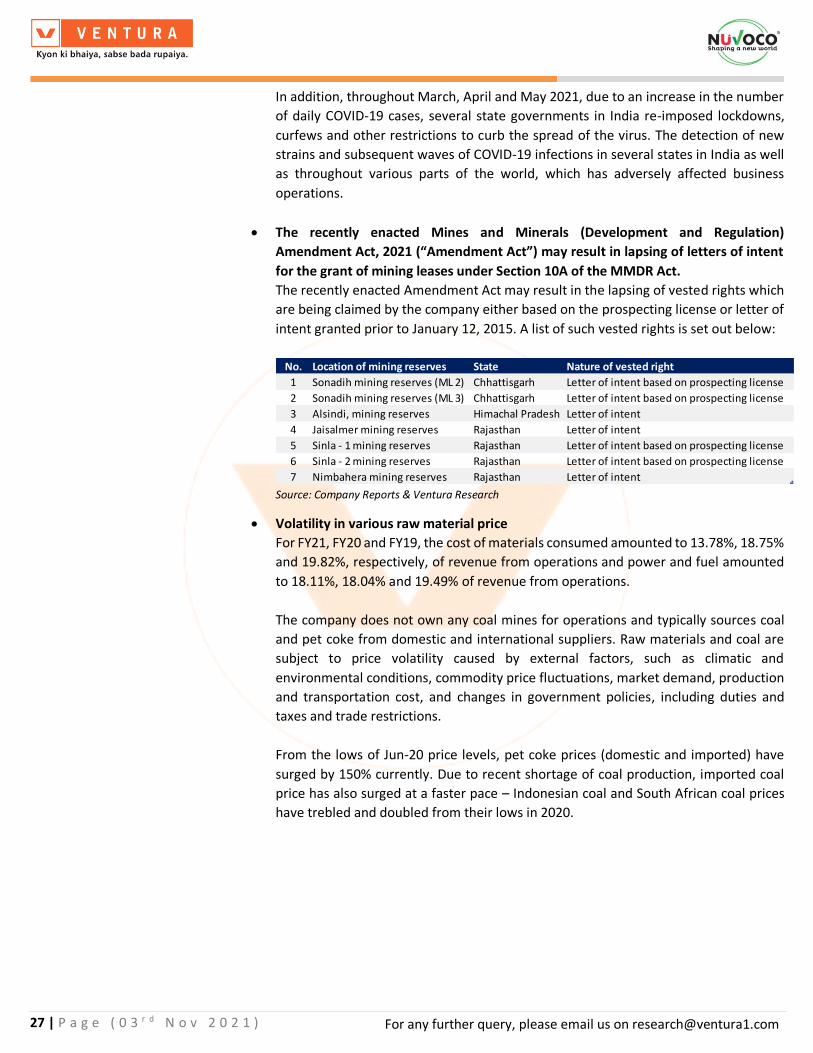

• The recently enacted Mines and Minerals (Development and Regulation)

Amendment Act, 2021 (“Amendment Act”) may result in lapsing of letters of intent

for the grant of mining leases under Section 10A of the MMDR Act.

The recently enacted Amendment Act may result in the lapsing of vested rights which

are being claimed by the company either based on the prospecting license or letter of

intent granted prior to January 12, 2015. A list of such vested rights is set out below:

Source: Company Reports & Ventura Research

• Volatility in various raw material price

For FY21, FY20 and FY19, the cost of materials consumed amounted to 13.78%, 18.75%

and 19.82%, respectively, of revenue from operations and power and fuel amounted

to 18.11%, 18.04% and 19.49% of revenue from operations.

The company does not own any coal mines for operations and typically sources coal

and pet coke from domestic and international suppliers. Raw materials and coal are

subject to price volatility caused by external factors, such as climatic and

environmental conditions, commodity price fluctuations, market demand, production

and transportation cost, and changes in government policies, including duties and

taxes and trade restrictions.

From the lows of Jun-20 price levels, pet coke prices (domestic and imported) have

surged by 150% currently. Due to recent shortage of coal production, imported coal

price has also surged at a faster pace – Indonesian coal and South African coal prices

have trebled and doubled from their lows in 2020.

No. Location of mining reserves State Nature of vested right

1 Sonadih mining reserves (ML 2) Chhattisgarh Letter of intent based on prospecting license

2 Sonadih mining reserves (ML 3) Chhattisgarh Letter of intent based on prospecting license

3 Alsindi, mining reserves Himachal Pradesh Letter of intent

4 Jaisalmer mining reserves Rajasthan Letter of intent

5 Sinla - 1 mining reserves Rajasthan Letter of intent based on prospecting license

6 Sinla - 2 mining reserves Rajasthan Letter of intent based on prospecting license

7 Nimbahera mining reserves Rajasthan Letter of intent

28 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Raw material price surging

Source: Index Mundi, Bloomberg, Company Reports

• Dependency on eastern and northern region

A majority of cement operations are concentrated in the eastern and northern region

of India, such as Jojobera (in Jharkhand), Bhabua (in Bihar), Jajpur (in Orissa), Mejia

and Panagarh (in West Bengal), Sonadih, Arasmeta and Risda (in Chhattisgarh), Nimbol

and Chittorgarh (in Rajasthan) and Bhiwani (in Haryana). For FY21, 81% of the total

sales volume was in East India (covering the states such as West Bengal, Chhattisgarh,

Jharkhand, Bihar, Odisha and Assam) and 19% of the total sales volume was in North

India (covering the states such as Rajasthan, Haryana, Delhi and Punjab). Nuvoco faces

the risk of regional concentration and presence in over supply markets, which may

result in lower than peer valuations.

• Any change in incentives and subsidies applicable to the company or a delay in

disbursement of benefits

In FY21, FY20 and FY19, the company availed incentives and subsidies amounting to

Rs.77 cr, Rs.47 cr and Rs.81 cr, respectively. This does not include power subsidies,

which are adjusted against Nuvoco’s monthly power bills. Any delay or changes in

schemes by state governments can affect the financial performance of the company.

0

50

100

150

200

250

55

60

65

70

75

80

85

90

95

100

105

Jan

-18

Apr

-18

Jul-

18

Oct

-18

Jan

-19

Apr

-19

Jul-

19

Oct

-19

Jan

-20

Apr

-20

Jul-

20

Oct

-20

Jan

-21

Apr

-21

Jul-

21

Oct

-21

Diesel Price (Rs./Ltr) Pet Coke Price (Rs.) (RHS)

25

75

125

175

225

275

Oct

-16

Feb

-17

Jun

-17

Oct

-17

Feb

-18

Jun

-18

Oct

-18

Feb

-19

Jun

-19

Oct

-19

Feb

-20

Jun

-20

Oct

-20

Feb

-21

Jun

-21

Coal prices ($)

Indonesia coal prices Australia coal prices

29 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Quarterly and Annual Performance

Source: Company Reports & Ventura Research

Figures in INR Crores FY20 Q1FY21 Q4FY21 FY21 Q1FY22 FY22E FY23E FY24E

Sales Volume (MTPA) 14.6 1.8 5.6 17.0 4.2 18.7 21.7 23.8

YoY Growth (%) 15.9 141.7 10.2 16.1 9.4

Capacity Utilization (%) 90.3 77.6 78.5 86.7 94.9

NSR (Rs./T) 4,639.4 4,808.7 4,699.3 4,412.9 5,208.0 4,801.2 4,969.2 5,068.6

Revenue 6,793.2 841.5 2,631.6 7,488.8 2,203.0 8,975.2 10,784.6 12,039.3

YoY Growth (%) 10.2 161.8 19.8 20.2 11.6

Raw Material cost 1,230.0 181.0 494.7 1,206.8 249.5 1,265.5 1,553.0 1,793.9

Raw Material cost (Rs./T) 840.0 1,034.5 883.4 711.1 589.7 677.0 715.6 755.2

Power & Fuel 1,225.6 134.1 440.8 1,356.3 429.5 1,903.8 1,945.0 1,915.8

Power & Fuel (Rs./T) 837.0 766.4 787.2 799.2 1,015.3 1,018.4 896.2 806.6

Freight and forwarding charges 1,776.1 207.3 718.4 2,029.4 591.7 2,463.7 2,933.4 3,310.8

Freight and forwarding (Rs./T) 1,213.0 1,184.5 1,282.8 1,195.9 1,398.9 1,317.9 1,351.6 1,393.9

Employee Cost 404.6 98.8 131.9 482.0 140.7 573.6 676.9 798.7

Employee Cost (Rs./T) 276.3 564.6 235.6 284.0 332.6 306.9 311.9 336.3

Other Expenses 859.7 97.4 321.7 953.8 277.3 1,086.0 1,304.9 1,492.9

Other Expenses (Rs./T) 587.1 556.5 574.5 562.0 655.6 580.9 601.3 628.5

EBIDTA 1,297.1 123.0 524.0 1,460.5 514.0 1,682.6 2,371.4 2,727.2

EBIDTA Margin (%) 19.1 14.6 19.9 19.5 23.3 18.7 22.0 22.7

EBIDTA (Rs./T) 885.9 702.9 935.7 860.6 1,215.1 900.1 1,092.7 1,148.2

PAT 249.3 (91.0) (91.0) (25.9) 114.0 209.7 769.0 1,109.9

PAT Margin (%) 3.7 (10.8) (3.5) (0.3) 5.2 2.3 7.1 9.2

PAT (Rs./T) 170.2 (520.0) (162.5) (15.3) 269.5 112.2 354.3 467.3

Adjusted EPS (Rs) 7.9 (3.1) (3.1) (0.8) 3.6 5.9 21.5 31.1

P/E Ratio 69.2 (665.3) 93.2 25.4 17.6

Enterprise Value 22,678.4 24,543.9 22,623.7 21,597.0 19,666.8

EV/EBITDA 17.5 16.8 13.4 9.1 7.2

Net Worth 5,279.3 7,323.7 9,033.4 9,802.4 10,823.0

Return on Equity (%) 4.7 (0.4) 2.3 7.8 10.3

Invested Capital 8,410.5 12,320.4 13,571.6 13,016.6 12,539.9

Return on Invested Capital (%) 5.9 (3.8) 5.3 9.4 12.3

Cash Flow from Operations 1,024.8 1,717.4 1,428.0 2,316.7 2,862.3

Cash Flow from Investing (310.1) (2,924.1) (447.3) (883.5) (553.7)

Cash Flow from Financing (559.1) 1,419.7 (473.2) (1,823.2) (1,940.2)

Net Cash Flow 155.6 213.0 507.5 (390.1) 368.5

Total Debt 3,642.1 5,908.7 4,538.2 3,214.2 1,716.9

Net Debt 3,131.2 4,996.7 3,076.6 2,049.8 119.6

Net Debt to Equity (x) 0.6 0.7 0.3 0.2 0.0

Net Debt to EBITDA (x) 2.4 3.4 1.8 0.9 0.0

30 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Summary of Management Commentary and Quarterly Performance over last few quarters

Key Criteria View Comments Q1FY22

Business Performance POSITIVE

Sales volume up by 141.7% YoY to 4.2 MTPA and capacity utilization was 76.0%

Revenues up 161.8% YoY to INR 2203 cr, EBITDA up 317.9% to INR 514 cr (EBITDA/T of INR 1215), PAT of INR 114 cr (PAT/T of INR 270) against loss of INR 91 cr in Q1FY21.

Healthy pricing across eastern & northern region has help to improve realisation.

An increase in capacity utilization and cost efficiencies from Aichi Steel along with strong metal prices, compared to Q1FY21, improved the overall performance.

Outlook & Strategy POSITIVE

Arasmeta plant as well as the Jojobera plant is expected to start generating electricity by Q3FY22. By Q3FY22, the company would have completed all power projects and with that will have 150 megawatt of Captive Power Plants and 45 megawatts of Waste Heat Recovery systems.

Sales volume guidance for FY22: 18 – 18.7 MTPA.

EBITDA/tn guidance for FY22: INR 840-879.

Source: Company Reports & Ventura Research

31 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Financial Analysis & Projections

Figures in INR Crores FY20 FY21 FY22E FY23E FY24E Figures in INR Crores FY20 FY21 FY22E FY23E FY24E

Income Statement Per Share Data & Yield

Revenue 6,793.2 7,488.8 8,975.2 10,784.6 12,039.3 Adjusted EPS (Rs) 7.9 (0.8) 5.9 21.5 31.1

YoY Growth (%) (3.7) 10.2 19.8 20.2 11.6 Adjusted CEPS (Rs) 24.7 24.4 32.8 46.2 56.9

Raw Material Cost 1,230.0 1,206.8 1,265.5 1,553.0 1,793.9 Adjusted BVPS (Rs) 167.5 232.4 252.9 274.5 303.0

YoY Growth (%) (14.9) (1.9) 4.9 22.7 15.5 FCF per share (Rs) 14.2 (5.0) 21.2 34.9 59.8

Power & Fuel Cost 1,225.6 1,356.3 1,903.8 1,945.0 1,915.8 FCF Yield (%) 2.6 (0.9) 3.9 6.4 10.9

YoY Growth (%) (10.8) 10.7 40.4 2.2 (1.5) CFO per share (Rs) 32.5 54.5 40.0 64.9 80.1

Employee Cost 404.6 482.0 573.6 676.9 798.7 CFO Yield (%) 5.9 9.9 7.3 11.8 14.6

YoY Growth (%) 6.2 19.1 19.0 18.0 18.0

Freight Cost 1,776.1 2,029.4 2,463.7 2,933.4 3,310.8 Sovency Ratio (X)

YoY Growth (%) (10.4) 14.3 21.4 19.1 12.9 Total Debt to Equity 0.7 0.8 0.5 0.3 0.2

Other Expenses 859.7 953.8 1,086.0 1,304.9 1,492.9 Net Debt to Equity 0.6 0.7 0.3 0.2 0.0

YoY Growth (%) (9.6) 10.9 13.9 20.2 14.4 Net Debt to EBITDA 2.4 3.4 1.8 0.9 0.0

EBITDA 1,297.1 1,460.5 1,682.6 2,371.4 2,727.2 Interest Coverage Ratio 1.8 1.0 1.4 3.0 5.1

YoY Growth (%) 41.4 12.6 15.2 40.9 15.0

Margin (%) 19.1 19.5 18.7 22.0 22.7 Return Ratios (%)

Depreciation & Amortization 527.9 793.8 824.6 881.0 921.7 Return on Equity 4.7 (0.4) 2.3 7.8 10.3

EBIT 769.3 666.7 858.0 1,490.4 1,805.5 Return on Capital Employed 5.6 (3.6) 4.7 8.6 10.8

YoY Growth (%) 83.3 (13.3) 28.7 73.7 21.1 Return on Invested Capital 5.9 (3.8) 5.3 9.4 12.3

Margin (%) 11.3 8.9 9.6 13.8 15.0

Other Income 36.7 33.9 25.0 36.5 31.2 Working Capital Ratios

Finance Cost 419.2 664.0 602.7 499.2 353.6 Receivable Days 27 22 24 26 26

Exceptional Item 0.0 0.0 0.0 0.0 0.0 Inventory Days 32 35 37 36 35

PBT 386.8 36.5 280.2 1,027.7 1,483.2 Payable Days 42 44 43 42 42

YoY Growth (%) 2,229.7 (90.6) 667.0 266.7 44.3 Net Working Capital Days 18 13 18 20 19

Margin (%) 5.7 0.5 3.1 9.5 12.3 Net Working Capital to Sales (%) 0.3 0.2 0.2 0.2 0.2

Reported Tax 137.5 62.5 70.5 258.7 373.3

Tax Rate (%) 35.6 170.9 25.2 25.2 25.2 Valuation (X)

PAT 249.3 (25.9) 209.7 769.0 1,109.9 P/E Ratio 69.4 (667.6) 93.5 25.5 17.7

YoY Growth (%) - - - 266.7 44.3 P/BV Ratio 3.3 2.4 2.2 2.0 1.8

Margin (%) 3.7 (0.3) 2.3 7.1 9.2 EV/EBITDA 17.5 16.9 13.5 9.1 7.2

EV/Sales 3.3 3.3 2.5 2.0 1.6

Balance Sheet

Share Capital 242.4 315.1 357.2 357.2 357.2 Cash Flow Statement

Total Reserves 5,036.9 7,008.6 8,676.3 9,445.3 10,465.8 Profit Before Tax 386.8 36.5 280.2 1,027.7 1,483.2

Shareholders' Fund 5,279.3 7,323.7 9,033.4 9,802.4 10,823.0 Add: Depreciation 527.9 793.8 824.6 881.0 921.7

Long Term Borrowings 2,931.3 5,561.2 4,161.2 2,761.2 1,211.2 Add: Finance Cost 419.2 664.0 602.7 499.2 353.6

Long Term Lease Liabilities 33.6 89.1 107.7 129.4 144.5 Change in Other Assets & Liabilities (163.3) 216.1 (25.2) 315.8 513.0

Other Financial Liabilities 52.8 62.5 74.9 90.1 100.5 Change in Working Capital (8.3) 69.4 (183.9) (148.3) (35.8)

Long Term Provisions 70.3 81.4 96.9 114.3 134.9 Less: Tax Paid (137.5) (62.5) (70.5) (258.7) (373.3)

Other Non Current Liabilities 0.0 2.1 2.6 3.1 3.4 Cash Flow from Operations 1,024.8 1,717.4 1,428.0 2,316.7 2,862.3

Deferred Tax Liabilities 1,441.9 1,881.0 1,839.9 2,210.8 2,468.1 Net Capital Expenditure (569.5) (547.3) (527.0) (600.0) (100.0)

Total Liabilities 9,809.1 15,001.1 15,316.6 15,111.3 14,885.6 Change in Investments 259.3 (2,376.8) 79.7 (283.5) (453.7)

Net Block 6,220.8 9,324.2 9,226.9 9,176.7 8,607.1 Cash Flow from Investing (310.1) (2,924.1) (447.3) (883.5) (553.7)

Capital WIP 647.0 1,235.8 617.9 247.2 247.2 Proceeds from issue of equity capital 0.0 1,600.0 1,500.0 0.0 0.0

Right of Use Assets 101.7 329.3 282.6 235.6 179.6 Payment of Lease Liabilities (20.1) (63.2) 29.9 36.2 25.1

Invesment Properties 1.2 0.5 0.6 0.8 0.8 Change in LT Borrowings (220.0) 8.8 (1,400.0) (1,400.0) (1,550.0)

Goodwill 2,443.9 3,278.5 3,278.5 3,278.5 3,278.5 Change in ST Borrowings 0.0 74.4 (0.3) 39.8 27.6

Other Intangible Assets 1,202.6 2,109.0 2,493.6 2,963.9 3,221.5 Proceeds from issue of Debentures 0.0 500.0 0.0 0.0 0.0

Intangible Assets under development 0.0 4.4 4.4 4.4 4.4 Share issue expenses (0.9) (49.7) 0.0 0.0 0.0

Investments 0.1 0.1 0.1 0.1 0.1 Less: Finance Cost (419.2) (664.0) (602.7) (499.2) (353.6)

Loans 0.2 1.5 1.8 2.2 2.4 Change in Other Liabilities 101.2 13.5 0.0 0.0 0.0

Other LT Financial Assets 579.1 787.5 943.8 1,134.0 1,266.0 Cash Flow from Financing (559.1) 1,419.7 (473.2) (1,823.2) (1,940.2)

Income Tax Assets 133.9 133.2 146.5 153.9 161.6 Net Cash Flow 155.6 213.0 507.5 (390.1) 368.5

Other Non Current Assets 107.1 191.3 229.2 275.5 307.5 Opening Balance of Cash 98.3 253.9 493.1 1,000.6 610.5

Net Current Asset (1,628.4) (2,394.2) (1,909.2) (2,361.2) (2,390.9) Addition through business combination 0.0 26.3 0.0 0.0 0.0

Total Assets 9,809.1 15,001.1 15,316.6 15,111.3 14,885.6 Closing Balance of Cash 253.9 493.1 1,000.6 610.5 979.0

32 | P a g e ( 0 3 r d N o v 2 0 2 1 )

For any further query, please email us on [email protected]

Disclosures and Disclaimer

Ventura Securities Limited (VSL) is a SEBI registered intermediary offering broking, depository and portfolio management services to clients. VSL is member of BSE, NSE

and MCX-SX. VSL is a depository participant of NSDL. VSL states that no disciplinary action whatsoever has been taken by SEBI against it in last five years except

administrative warning issued in connection with technical and venial lapses observed while inspection of books of accounts and records. Ventura Commodities Limited,

Ventura Guaranty Limited, Ventura Insurance Brokers Limited and Ventura Allied Services Private Limited are associates of VSL. Research Anal yst (RA) involved in the

preparation of this research report and VSL disclose that neither RA nor VSL nor its associates (i) have any financial interest in the company which is the subject matter

of this research report (ii) holds ownership of one percent or more in the securities of subject company (iii) have any material conflict of interest at the time of

publication of this research report (iv) have received any compensation from the subject company in the past twelve months (v) have managed or co-managed public

offering of securities for the subject company in past twelve months (vi) have received any compensation for investment banking merchant banking or brokerage

services from the subject company in the past twelve months (vii) have received any compensation for product or services from the subject company in the past twelve

months (viii) have received any compensation or other benefits from the subject company or third party in connection with the research report. RA involved in the

preparation of this research report discloses that he / she has not served as an officer, director or employee of the subject company. RA involved in the preparation of

this research report and VSL discloses that they have not been engaged in the market making activity for the subject company. Our sales people, dealers, traders and

other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed

herein. We may have earlier issued or may issue in future reports on the companies covered herein with recommendations/ information inconsistent or different those

made in this report. In reviewing this document, you should be aware that any or all of the foregoing, among other things, may give rise to or potential conflicts of

interest. We may rely on information barriers, such as "Chinese Walls" to control the flow of information contained in one or more areas within us, or other areas, units,

groups or affiliates of VSL. This report is for information purposes only and this document/material should not be construed as an offer to sell or the solicitation of an

offer to buy, purchase or subscribe to any securities, and neither this document nor anything contained herein shall form the basis of or be relied upon in connection

with any contract or commitment whatsoever. This document does not solicit any action based on the material contained herein. It is for the general information of the

clients / prospective clients of VSL. VSL will not treat recipients as clients by virtue of their receiving this report. It does not constitute a personal recommendation or

take into account the particular investment objectives, financial situations, or needs of clients / prospective clients. Similarly, this document does not have regard to

the specific investment objectives, financial situation/circumstances and the particular needs of any specific person who may receive this document. The securities

discussed in this report may not be suitable for all investors. The appropriateness of a particular investment or strategy wi ll depend on an investor's individual

circumstances and objectives. Persons who may receive this document should consider and independently evaluate whether it is suitable for his/ her/their particular

circumstances and, if necessary, seek professional/financial advice. And such person shall be responsible for conducting his/her/their own investigation and analysis of

the information contained or referred to in this document and of evaluating the merits and risks involved in the securities forming the subject matter of this document.

The projections and forecasts described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties

and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections

and forecasts were based will not materialize or will vary significantly from actual results, and such variances will likely increase over time. All projections and forecasts

described in this report have been prepared solely by the authors of this report independently of the Company. These projections and forecasts were not prepared with

a view toward compliance with published guidelines or generally accepted accounting principles. No independent accountants have expressed an opinion or any other

form of assurance on these projections or forecasts. You should not regard the inclusion of the projections and forecasts des cribed herein as a representation or

warranty by VSL, its associates, the authors of this report or any other person that these projections or forecasts or their underlying assumptions will be achieved. For

these reasons, you should only consider the projections and forecasts described in this report after carefully evaluating all of the information in this report, including

the assumptions underlying such projections and forecasts. The price and value of the investments referred to in this document/material and the income from them

may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance. Future returns are not

guaranteed and a loss of original capital may occur. Actual results may differ materially from those set forth in projections . Forward-looking statements are not

predictions and may be subject to change without notice. We do not provide tax advice to our clients, and all investors are s trongly advised to consult regarding any

potential investment. VSL, the RA involved in the preparation of this research report and its associates accept no liabilities for any loss or damage of any kind arising out

of the use of this report. This report/document has been prepared by VSL, based upon information available to the public and sources, believed to be reliable. No

representation or warranty, express or implied is made that it is accurate or complete. VSL has reviewed the report and, in so far as it includes current or historical

information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. The opinions expressed in this document/material are subject

to change without notice and have no obligation to tell you when opinions or information in this report change. This report or recommendations or information

contained herein do/does not constitute or purport to constitute investment advice in publicly accessible media and should not be reproduced, transmitted or published

by the recipient. The report is for the use and consumption of the recipient only. This publication may not be distributed to the public used by the public media without

the express written consent of VSL. This report or any portion hereof may not be printed, sold or distributed without the wri tten consent of VSL. This document does

not constitute an offer or invitation to subscribe for or purchase or deal in any securities and neither this document nor anything contained herein shall form the basis

of any contract or commitment whatsoever. This document is strictly confidential and is being furnished to you solely for your information, may not be distributed to

the press or other media and may not be reproduced or redistributed to any other person. The opinions and projections express ed herein are entirely those of the

author and are given as part of the normal research activity of VSL and are given as of this date and are subject to change without notice. Any opinion estimate or

projection herein constitutes a view as of the date of this report and there can be no assurance that future results or events will be consistent with any such opinions,

estimate or projection. This document has not been prepared by or in conjunction with or on behalf of or at the instigation of, or by arrangement with the company or

any of its directors or any other person. Information in this document must not be relied upon as having been authorized or approved by the company or its directors

or any other person. Any opinions and projections contained herein are entirely those of the authors. None of the company or its directors or any other person accepts

any liability whatsoever for any loss arising from any use of this document or its contents or otherwise arising in connection therewith. The information contained herein

is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this

communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives

Segments” as prescribed by Securities and Exchange Board of India before investing in Securities Market.

Ventura Securities Limited - SEBI Registration No.: INH000001634

Corporate Office: I-Think Techno Campus, 8th Floor, ‘B’ Wing, Off Pokhran Road No 2, Eastern Express Highway, Thane (W) – 400608