Adani group - Ventura Securities

250

1

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Adani group - Ventura Securities

1

( 0 9 t h D e c 2 1 )

For any further query, please email us on [email protected]

TABLE OF CONTENTS

Significant wealth creators 03

Adani Green Energy 06

Adani Ports & Special Economic Zone 50

Adani Transmission 117

Adani Total Gas 161

Adani Enterprises 195

Disclaimer 250

22

( 0 9 t h D e c 2 1 )

For any further query, please email us on [email protected]

Significant wealth creators

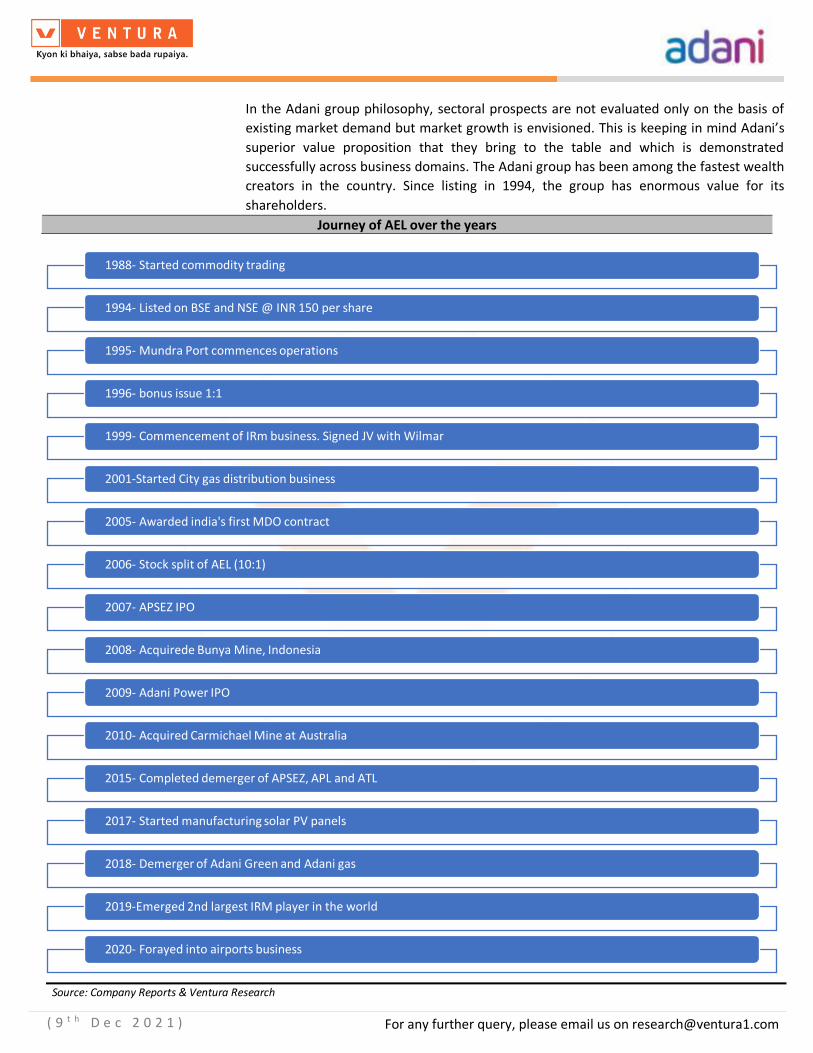

From humble origins with the listing of Adani Enterprises Ltd, today the group has spawned

into a multi national diversified conglomerate with a cumulative market cap of 133.25 bn $

comprising 6 listed entities namely

• Adani Enterprises Ltd (AEL) -m.cap 25.6 bn $)

• Adani Ports and SEZ Ltd (APSEZ) -m.cap 21.2 bn $)

• Adani Transmission Ltd (ATL) -m.cap 28.1 bn $)

• Adani Green Energy Ltd (AGEL) -m.cap 29.4 bn $)

• Adani Total gas Ltd (ATGL) -m.cap 26.1 bn $)

• Adani Power Ltd -m.cap 5.4 bn $)

Intergenerational promoters with a large stake bring long term focus to the business

Today Gautam Adani, family and next generation with their vision of “Courage, Commitment

and Trust” have built one of the most vibrant and dynamic business groups. With significant

stake in the listed entities in their individual capacities, they bring to the business stability and

long term focus which has contributed to significant wealth creation.

Strategic partnerships with domain experts have added value to the business entities

Value creation has been the single most important focus that has aided the Adani group.

Wherever essential they have entered into strategic partnerships/JV’s with international

domain leaders to bring best practices to the existing businesses. They roped in

• The Total Energies SE, a French group, for their foray into City Gas Distribution (CGD)

business of Adani Total Gas Ltd (ATGL) and the renewable energy business of Adani

Green Energy Ltd (AGEL). Today, not only is ATGL India’s largest CGD company but

AGEL has gone a step further to emerge as the world’s largest solar energy player by

2025 and the world’s largest renewable energy producer by 2030.

• Adani Wilmar Limited (AWL) an equal JV started in 1999 is today one of India’s largest

agribusiness company which is slated to IPO in the not too distant future. The JV

partner Wilmar group is Asia’s leading agri business group and has scripted the success

story of Adani Wilmar. The edible oil brand Fortune is the leader in its category with

~17% market share.

• When Adani Transmission Limited (ATL) acquired the power distribution business for

the Mumbai geography, they roped in Qatar Investment Authority as a strategic

financial investor in their step down subsidiary Adani Electricity Mumbai Ltd (AEML).

• For its data centre business, Adani Enterprises Ltd (AEL) has entered into a JV with

EdgeConneX, a company with a decade’s experience of serving global cloud service

providers in mature markets.

33

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

• In the Airport vertical, AEL is scouting for domain experts who will beef up the growth

of the airports business. In addition, it is also looking at tieing up with business partners

to develop non aero revenue streams.

Secret sauce of the success of the Adani group

1. Executions Skill- The group believes in a time bound execution philosophy with clear

deliverables in place.

2. Capital Management- The group redesigns the capital structure of the asset & has

access to pool of best global investors.

3. Multi fold growth- The business is scaled up to match industry leading practices along

with significant focus on revenue expansion.

4. Value creation- Once the revenue expansion is done, focus turns to earning industry

leading margins via large operating scale.

ESG

The group’s future investment is aligned to sustainable growth with focus on preserving

environment. Adani group has publicly disclosed various ESG goals and is among the few

groups to have ESG committee in place across all its listed companies.

We initiate coverage on the listed entities of the Adani group as follows:

Adani Enterprises Ltd- AEL stands among the few listed company to have generated >30%

CAGR in wealth for its investors Over the years, AEL has incubated various businesses of the

group like transmission, renewable energy, city gas distribution etc which have themselves

gone on to become big business themselves. In its 2nd phase, AEL is currently incubating

several new businesses like airports, data centres, solar manufacturing, roads, defence & green

businesses. Adani Wilmar a JV company is on the verge of unlocking value through its proposed

IPO.

Adani Ports and SEZ Ltd- In a post-covid scenario, where the world is distancing itself from its

over dependance on China, India has emerged as a reliable, responsible and geopolitically

viable option for global manufacturing. Further, favourable policies like Atmanirbhar Bharat,

Make in India Make for World, PLI schemes, etc., have helped create a launch pad for resurgent

Company name Rating CMP INR PT INR

Upside

%

M.cap

INR cr

Revenue

CAGR

FY21-24

%

EBITDA

CAGR

FY21-24

%

PAT

CAGR

FY21-24

%

FY24 RoE

%

FY24 RoIC

%

AEL

Buy for long

term 1,723 1,889 10 189,519 20.6 54.5 10.0 5.8 8.6

APSEZ Buy 770 1,697 121 157,133 24.3 24.8 20.1 18.6 19.0

ATL Buy 1,854 2,797 51 203,921 17.0 20.3 31.2 18.1 10.8

AGEL Buy 1,390 2,810 102 217,343 72.3 78.7 146.9 40.2 11.5

ATGL Buy 1,685 2,012 19 185,356 45.6 33.8 40.1 28.7 28.8

44

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

EXIM volumes, which are expected to scale to 1790-2570 MMT by FY30 from 971 MMT clocked

in FY21. Adani Ports & Special Economic Zone Ltd (APSEZ) with its portfolio of 13 ports

(installed capacity of 560 MMT & 28.6% EXIM volume share), is well positioned to expand its

market share to 38.9% from this surge in EXIM trade.

Adani Transmission Ltd- Adani Transmission Ltd (ATL) is India’s leading private sector

transmission player with a 35% market share. ~INR 3 trillion of TBCB projects are expected to

be allocated to the private players over FY21-30. ATL with its superior execution and O&M

skills, demonstrated high ‘total availability factor’, best in class EBIDTA margins of 92% and

capital management excellence is best placed to benefit from this. The 35-year TBCB contracts

provide for long term visibility. Over FY21-24, we expect a 33.4%/26.1% CAGR in the

operational asset base and revenues to INR 41,560 crore /INR 6,257 crore respectively.

Adani Green Energy Ltd- Adani Green Energy Limited (AGEL) is one of the largest renewable

companies in India, with a current project portfolio of 13,990 MW and 20,284 of MW locked-

in growth (from under construction assets). The company has aspirations to up its installed

capacity to 25 GW / 45 GW by 2025 / 2030 respectively making it the world’s largest renewable

company by capacity. With India’s stated intent of procuring 450 GW from renewable energy

by 2030, AGEL is well placed to benefit from this megatrend. Currently the company has a

~5.3% of share in India’s renewable installed capacity, which is set to grow to ~10% by 2030.

Adani Total Gas Ltd- ATGL, a JV (equal stake of 37.4%) between Adani Group and French

energy major Total Energies (TOTAL), is India’s largest private-sector city gas distributor (CGD),

with 19 standalone operational geographical areas (GAs). In addition, ATGLs equal stake JV

with Indian Oil Corporation (IOC) – IOAGPL houses another 19 GA thus enabling ATGL to

emerge as a true pan India CGD player. Both JV partners, Total (which has operations in 108

countries) and IOC (parent of Petronet LNG), bring rich experience in sourcing LNG at

competitive prices besides ensuring availability.

55

( 0 9 t h D e c 2 1 )

For any further query, please email us on [email protected]

TABLE OF CONTENTS

Adani Green Energy Ltd.

Parabolic growth trajectory while significantly de-risked

66

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Adani Green Energy Limited (AGEL) is one of the largest renewable companies in

India, with a current project portfolio of 13,990 MW and 20,284 of MW locked-in

growth (from under construction assets). The company has aspirations to up its

installed capacity to 25 GW / 45 GW by 2025 / 2030 respectively making it the world’s

largest renewable company by capacity. With India’s stated intent of procuring 450

GW from renewable energy by 2030, AGEL is well placed to benefit from this

megatrend. Currently the company has a ~5.3% of share in India’s renewable installed

capacity, which is set to grow to ~10% by 2030.

AGEL’s strong execution skills, land procurement strategy and superlative capital

management have ensured that project implementation is done before time, leading

to a shorter payback period and faster cash flow generation. Further, the fact that

Adani Green is able to dispatch its entire capacity at a 10% discount to the current

market clearing price (of the relevant state) and still deliver returns ensures that AGEL

has the highest possible efficiency and return on investment.

Risk mitigation through long term PPAs, pervasive use of technology, roping in Total

Energy as a strategic partner, and matching debt mature profile to the life-cycle of

the PPA contracts is an added advantage.

Marquee global investors have subscribed to its Investment Grade long term Green

Bonds and consortium of 18 international bankers provide for construction finance

on revolving credit. This is a testimony of AGEL’s inherent strengths in attracting

global capital, which is so vital for sustaining the blitzkrieg pace of growth. On ESG

compliance too, AGEL has left no stone unturned to deploy best global practices.

Despite the fact that AGEL has seen a sharp spurt in its stock price (outperforming the

broader index and its peers by a wide margin), we believe that there exists significant

room for further upside. We initiate coverage on AGEL with a BUY and FY24 based

target price of INR 2,810 per share, implying 102% upside over the next 24 months.

Key Financial Data (INR Cr, unless specified)

Revenue EBITDA

Net Profit

EBITDA (%)

Net Profit

(%) EPS (₹)

BVPS (₹)

RoE (%)

RoIC (%)

P/E (X) P/BV

(X)

EV/ EBITDA

(X)

FY20 2,549 1,450 (23) 56.9 (0.9) (0.1) 14.8 (1.0) 6.6 (9,371.4) 93.3 158.0

FY21 3,124 2,235 210 71.5 6.7 1.3 13.6 9.5 7.0 1,026.4 101.4 106.6

FY22E 6,224 4,767 1,084 76.6 17.4 6.9 20.5 33.0 10.1 198.8 67.1 52.4

FY23E 9,129 7,294 1,414 79.9 15.5 9.0 29.6 30.1 10.1 152.5 46.6 36.7

FY24E 15,978 12,750 3,162 79.8 19.8 20.2 49.8 40.2 11.5 68.2 27.7 23.3

BUY @ CMP INR 1,390 Target: INR 2,810 in 24 months Upside Potential: 102%

Parabolic growth trajectory while significantly de-risked

Industry Power

Scrip Details

Face Value (INR) 10.0

Market Cap (INR Cr) 2,17,343

Price (INR) 1,390

No of Shares O/S (Cr) 156

3M Avg Vol (000) 52.2

52W High/Low (INR) 1428/860

Dividend Yield (%) 0

Shareholding (%) Sept 2021

Promoter 60.14

Institution 18.15

Public 21.71

TOTAL 100.0

Price Chart

20,000

30,000

40,000

50,000

60,000

70,000

10

510

1,010

1,510

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

AGEL (LHS) SENSEX (RHS)

Adani Green Energy Ltd.

77

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Source: Company Reports & Ventura Research

0

500

1,000

1,500

2,000

Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

1 year forward EV/EBITDA band chart

EV per sh 52.07x 58.57x

65.07x 71.57x 78.07x

-50

0

50

100

150

200

250

300

Apr

-20

Jun

-20

Aug

-20

Oct

-20

Dec

-20

Feb

-21

Apr

-21

Jun

-21

Aug

-21

Oct

-21

EV/EBITDA & Std Deviation

EV/EBIDTA Average Upper SD 1

Upper SD 2 Lower SD 1 Lower SD 2

Strong growth visibility drives price

88

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Valuation

Adani Green Energy Limited (AGEL) is one of the largest renewable energy companies in India,

with a current project portfolio of 13,990 MW with locked-in growth of 20,284 MW.

We have used the DCF model to value AGEL since it has signed PPAs that throw up significant

cash over the next 25 years (typical life of a renewable PPA contract). While AGEL’s stated

intent is to build capacities of 45GW by 2030, the confirmed PPAs on hand are for 20.3 GW by

2025 and cash flows from these projects would be available at least till FY50. We have modeled

25 GW of capacity by FY25 and over the period FY25-FY55, we have conservatively modeled

1000 MW per annum. Any further confirmed PPA’s signed would be over and above our

estimates. We have also built-in conservative assumptions with regards to CUF & margin

assumptions and we would want to see “proof of the pudding” before we incorporate the same

in our financial model.

India, in its bid to achieve net zero emissions by 2070, would have to rely heavily on renewable

energy and enhance its total capacity 14.5X to 5630 GW (bulk of which would be from

renewable sources). As demonstrated across all business units of the Adani Group, they intend

to achieve significant scale and size and hence, our 1000 MW per annum capacity addition

post 2025 is an extremely conservative estimate.

We have discounted back the future cash flows to FY24 and value the company at INR 2,810

per share, presenting an upside of 102% from the CMP of INR 1,390.

99

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

DCF Valuation

Source: Company Reports & Ventura Research

FY22E FY23E FY24E FY25E FY26E FY27E FY28E FY29E FY30E FY40E FY45E FY50E FY55ETotal Installed capacity (MW) 7,954 11,234 18,300 25,000 26,000 27,000 28,000 29,000 30,000 40,000 45,000 50,000 55,000

Solar capacity (MW) 5,163 6,793 13,409 20,109 21,109 22,109 23,109 24,109 25,109 35,109 40,109 45,109 50,109

Wind capacity (MW) 1,101 1,701 2,151 2,151 2,151 2,151 2,151 2,151 2,151 2,151 2,151 2,151 2,151

Hybrid capacity (MW) 1,690 2,740 2,740 2,740 2,740 2,740 2,740 2,740 2,740 2,740 2,740 2,740 2,740

Solar CUF (%) 25.0 25.3 25.4 25.4 25.4 25.4 25.4 25.4 25.4 25.4 25.4 25.4 25.4

Wind CUF (%) 36.8 38.6 38.6 38.6 38.6 38.6 38.6 38.6 38.6 38.6 38.6 38.6 38.6

Hybrid CUF (%) 40.0 46.0 46.0 46.0 46.0 46.0 46.0 46.0 46.0 46.0 46.0 46.0 46.0

Solar Revenue (Rs.Cr.) 4,318 5,080 10,771 21,344 23,808 24,705 25,584 26,411 27,230 34,701 38,026 41,114 43,967

Wind Revenue (Rs.Cr.) 774 1,463 2,134 2,134 2,134 2,133 2,133 2,133 2,133 2,133 2,133 2,133 2,133

Hybrid Revenue (Rs.Cr.) 426 2,556 3,043 3,043 3,043 3,043 3,043 3,043 3,043 3,043 3,043 3,043 3,043

EBIDTA (Rs.Cr.) 4,767 7,294 12,750 21,188 23,155 23,900 24,603 25,265 25,919 31,851 34,506 36,972 39,250

EBIDTA Margin (%) 76.6 79.9 79.8 79.8 79.8 79.9 79.9 79.9 79.9 79.8 79.8 79.8 79.8

Long Term Market Return 11.0%

Risk Free Rate 6.4%

Cost of Equity 6.7%

Interest Rate 10.5%

Tax Rate 25.2%

Cost of Debt 7.9%

WACC 7.1%

Terminal Value Growth 3.0%

Terminal Value 6,11,329

FY24E FY25E FY26E FY27E FY28E FY29E FY30E FY40E FY45E FY50E FY55E

FCFF (20,855) (19,032) 4,296 13,556 14,126 14,611 15,147 19,164 21,131 22,224 24,194

Discount Factor from FY24 0.93 0.87 0.81 0.76 0.71 0.66 0.62 0.31 0.22 0.16 0.11

Discounted FCFF from FY24 (19,477) (16,600) 3,499 10,313 10,036 9,694 9,386 5,994 4,695 3,508 2,713

Total of Discounted FCFF FY24 1,42,870

FY24 Present Value of Terminal Value 3,78,808

FY24 Value of Operations 5,21,678

FY24 Net Debt 82,153

FY24 Value of Equity 4,39,525

FY24 Value of Equity per share 2,810

1010

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Our Bull and Bear Case Scenarios

We have prepared a Bull and Bear case scenario based on AGEL’s terminal growth.

• Bull Case: With the ambitious capacity expansion plan to become the world’s largest

renewable energy generation company. AGEL has a significant opportunity to grow its

business in the coming years. We have assumed a terminal growth of 4%, which will

result in a Bull case price target of INR 3,629 (upside of 161% from the CMP).

• Bear Case: We have assumed a terminal growth of 1%, which will result in a Bear case

price target of INR 1,982 (upside of 43% from the CMP). Our base case implies a

significant margin of safety for buying at the current price.

Bull & Bear Case Scenario

Source: Ventura Research

Investment Triggers

• Strong growth potential of the industry

• De-risking strategies that provide long term revenue visibility and strong cashflow generation.

Catalysts

• Need for adoption of renewable energy sources

• Rapid urbanization, rural electrification, adoption of EVs, raising consumer durable penetration, growth in GDP & per capita income, Make in India and China+1 are likely to increase power consumption in India.

Bull Case Price

INR 3,629 per share

Target Price

INR 2,810 per share

Bear Case Price

INR 1,982 per share

Current Price

INR 1,390 per share

4% terminal value growth

3% terminal value growth

1% terminal value growth

1111

( 0 9 t h D e c 2 1 )

For any further query, please email us on [email protected]

Valuation and Comparable Metric of Domestic and Global Renewable energy Companies

Source: Ventura Research & Bloomberg

AGEL is a pureplay renewable IPP

NTPC & Tata Power are energy companies with a mix bag of thermal, renewable, manufacturing etc.

Sterling & Wilson is primarily an EPC company.

Azure & Renew Power are Indian corporates listed in US

For any further query, please email us on [email protected] 1212

( 0 9 t h D e c 2 1 )

For any further query, please email us on [email protected]

Strong EBIDTA growth and significant room for margin sustainability are potential re-rating factors

Source: Ventura Research, ACE Equity & Bloomberg

Adani Green

Tata PowerNTPC Ltd.

JSW Energy

Enphase Energy

Darling Ingredients

Brookfield Renewable

Clearway Energy

First Solar

NextEra Energy

SolarEdge Tech

Orsted A/S

Siemens Gamesa

Enel

Azure Power

-2.0

8.0

18.0

28.0

38.0

48.0

58.0

68.0

78.0

88.0

5.5 10.5 15.5 20.5 25.5 30.5 35.5 40.5

FY24

EB

IDT

A C

AG

R (

%)

FY24 EV/EBIDTA (x)

Adani Green

Tata Power

NTPC Ltd.

10

20

30

40

50

60

70

80

90

100

110

4 14 24 34 44 54 64 74 84 94

FY24

Rev

en

ue

CA

GR

(%

)

FY24 EBIDTA Margin (%)

1313

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Financial Analysis and Projections

We expect AGEL’s overall revenues to grow at a CAGR of 72.3% to INR 15,978.0 cr over FY21-

24E as 18,300 MW of renewable capacity is operationalized. This blitzkrieg growth is

supported by

• 65% CAGR in solar installation capacity to 13.4 GW, resulting in 86% CAGR volume

growth to 31,424 Mn Units, and 68% CAGR revenue growth to INR 10,771 cr.

• wind power generation capacity is expected to grow at 84% CAGR to 2 GW leading to

a 132% CAGR volume growth to 7,412 Mn Units, and 122% CAGR revenue growth to

INR 2,134 cr.

• hybrid generation is expected to clock a 27% CAGR to 2.7 GW triggering a 96% CAGR

volume growth to 11,041 Mn Units, and 93% CAGR revenue growth to INR 3,043 cr.

EBITDA is estimated to grow at a CAGR of 78.7% to INR 12,750.4 cr. PAT is estimated to grow

at a CAGR of 146.9% to INR 3,162.4 cr. Subsequently, RoE and RoIC are expected to improve

to 40.2% (+3,069bps) and 11.5% (+445bps), respectively, by FY24E.

1414

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

AGEL’s Financial Summary

Source: Company Reports & Ventura Research

1515

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

AGEL’s story in charts

0

50

100

150

200

250

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Strong revene growth on the cards

Solar power Wind power Hybrid power

EPC Traded Goods YoY Growth (%)

(%)INR Cr.

0

20

40

60

80

100

120

FY19 FY20 FY21 FY22E FY23E FY24E

Solar projects to remain the mainstay of the renewable energy source

Solar power Wind power Hybrid power

EPC Traded Goods

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY19 FY20 FY21 FY22E FY23E FY24E FY25E

Growing energy units sale

Total Units sale Blended Average Tariff (Rs./Unit)

Mn Units Rs.

0

1

2

3

4

5

6

0

5,000

10,000

15,000

20,000

25,000

30,000

FY19 FY20 FY21 FY22E FY23E FY24E

Growing units sales across sources

Solar Units sale Wind Units sale

Hybrid Units sale Solar Tariff (Rs./Units)

Wind Tariff (Rs./Units) Hybrid Tariff (Rs./Units)

Mn Units Rs.

(40)

(20)

0

20

40

60

80

100

(2,000)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Improving profitability

EBITDA Net Profit

EBITDA Margin (%) Net Margin (%)(%)

INR Cr

(30)

(20)

(10)

0

10

20

30

40

50

0

20,000

40,000

60,000

80,000

1,00,000

FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Improving return ratio despite ongoing capex

Net Worth Invested Capital

RoE (%) RoIC (%)

(%)INR Cr

1616

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Source: Company Reports & Ventura Research

0

2

4

6

8

10

12

0

20,000

40,000

60,000

80,000

1,00,000

FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Higher debt due to huge capex plans

Total Debt Net Debt

Net Debt to Equity (X) Net Debt to EBITDA (X)

(X)INR Cr

(4,000)

(2,000)

0

2,000

4,000

6,000

8,000

10,000

(25,000)

(20,000)

(15,000)

(10,000)

(5,000)

0

5,000

10,000

FY17 FY18 FY19 FY20 FY21 FY22E FY23E FY24E

High capex to be a drag on FCF generation

CFO FCF

CFO to EBITDA (%) FCF to Net Profit (%)

(%)INR Cr

1717

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Company overview

With a portfolio of 13,990 MW of installed capacity and secured PPAs of 20,284 MW, Adani

Green Energy Limited (AGEL), part of the Adani group, is one of the largest renewable energy

companies in India. The electricity generated is supplied to sovereign and sub sovereign

promoted entities on the back of 25-year long-term Power Purchase Agreements (PPAs). With

a portfolio of 54 operational projects and 12 projects under construction, AGEL is driving India

on its renewable energy journey.

Source wise Capacity Breakup (in MW)

Source: Company Reports & Ventura Research

By 2030, AGEL aspires to emerge as the world’s largest renewable energy company scaling its

renewable generation capacities to 25GW by 2025 and further to 45GW by 2030.

AGEL is the first Indian renewable energy developer to issue a 20-year amortizing project

finance type structure - the USD Green Bond of USD 362.5 mn. This provides foreign investors

an opportunity to participate in the Indian renewable energy space via investment-grade

bonds.

AGEL past performance – launchpad for its aggressive growth trajectory

In the past 5 years, while leading peers have struggled to grow, AGEL has successfully

onboarded significant capacity driven by

• strong pipeline of greenfield capacities

• fully funded capex

• harnessing inorganic growth opportunities

However, margins of the company remained volatile in the past 5 years.

4763

647

15393

2151

2740

Solar Wind Hybrid

5,410 MW operational

20,284 MW Locked-in Growth

1818

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

AGEL posted profitable growth

Source: Company Reports & Ventura Research

Particulars FY17 FY18 FY19 FY20 FY21 CAGR (%) Min (%) Max (%) FY17 FY18 FY19 FY20 FY21

Adani Green 1716.9 195.1 39.0 23.9 22.6 58.0 22.6 1716.9 80.4 56.3 74.1 56.9 71.5

TATA Power -6.5 -2.7 11.3 -2.5 11.4 4.2 -6.5 11.4 20.0 9.0 10.0 18.0 18.0

SW Solar 19.9 -32.3 -8.9 -9.6 -32.3 19.9 8.0 8.0 6.0 -7.0

Websol Energy 5.9 -38.1 -62.6 185.2 -21.5 -15.1 -62.6 185.2 10.0 9.0 -36.0 1.0 22.0

NTPC 11.8 7.4 13.9 9.2 1.9 8.0 1.9 13.9 26.0 26.0 23.0 29.0 31.0

Borosil Renewable 34.3 13.6 20.4 25.0 85.0 -2.6 13.6 85.0 11.0 14.0 14.0 14.0 39.0

JSW Energy -15.9 -2.6 13.5 -9.5 -16.3 -15.1 -16.3 13.5 40.0 34.0 31.0 43.0 42.0

KPI Global -6.0 23.0 9.0 72.0 73.0 40.7 -6.0 73.0 68.0 59.0 45.0 46.0 57.0

India Macro Factors

Power Consumption Growth (%) 4.1 6.1 5.2 1.3 -1.1 3.1 -1.1 6.1

GDP Growth - Nominal (%) 11.8 11.0 10.5 7.8 -3.0 7.5 -3.0 11.8

GDP Growth - Real (%) 8.3 6.8 6.5 4.0 -7.3 3.5 -7.3 8.3

Core Sector Growth (%) 5.3 4.5 5.8 -8.6 12.6 0.0 -8.6 12.6

Revenue Growth (%) EBITDA Margin (%)5 yrs Revenue Performance

1919

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Key growth drivers

Gargantuan growth opportunity for the renewable energy sector

The coming together of multiple factors has resulted in the renewable energy sector offering

growth potential which is expected to sustain for decades. These factors are enumerated

below

Low per capita electricity consumption cannot last for very long

Today, India is the third-largest energy-consuming country globally, and yet it has one of the

lowest per capita consumption. In our opinion, this dichotomy cannot last for very long and

the per capita consumption is only set to explode.

World Per capital energy consumption (kWh)

Source: Ministry of power, World data, Company Reports & Ventura Research

As per an independent think-tank Council on Energy, Environment and Water (CEEW), for net

zero emissions by 2070 India would need to put up 5630 GW of renewable power (or ~14.5X

the current installed capacity of 388 GW). The reasons for this surge in renewable power

demand are enumerated below

• India’s population to overtake China by 2027

It is expected that by 2027, India will become the most populous country, overtaking

China.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0

200

400

600

800

1,000

1,200

India Per capita electricity (kWh)

5% CAGR 2010-18

2020

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Population growth -

Source: Statista, Company Reports & Ventura Research

With its median age of 29 (compared to 38 for USA and China), India has the largest youthful

population in the world. This will ensure that the growth in consumption will sustain over

decades.

India’s youthful population to sustain power consumption growth for decades -

Source: Statista, Company Reports & Ventura Research

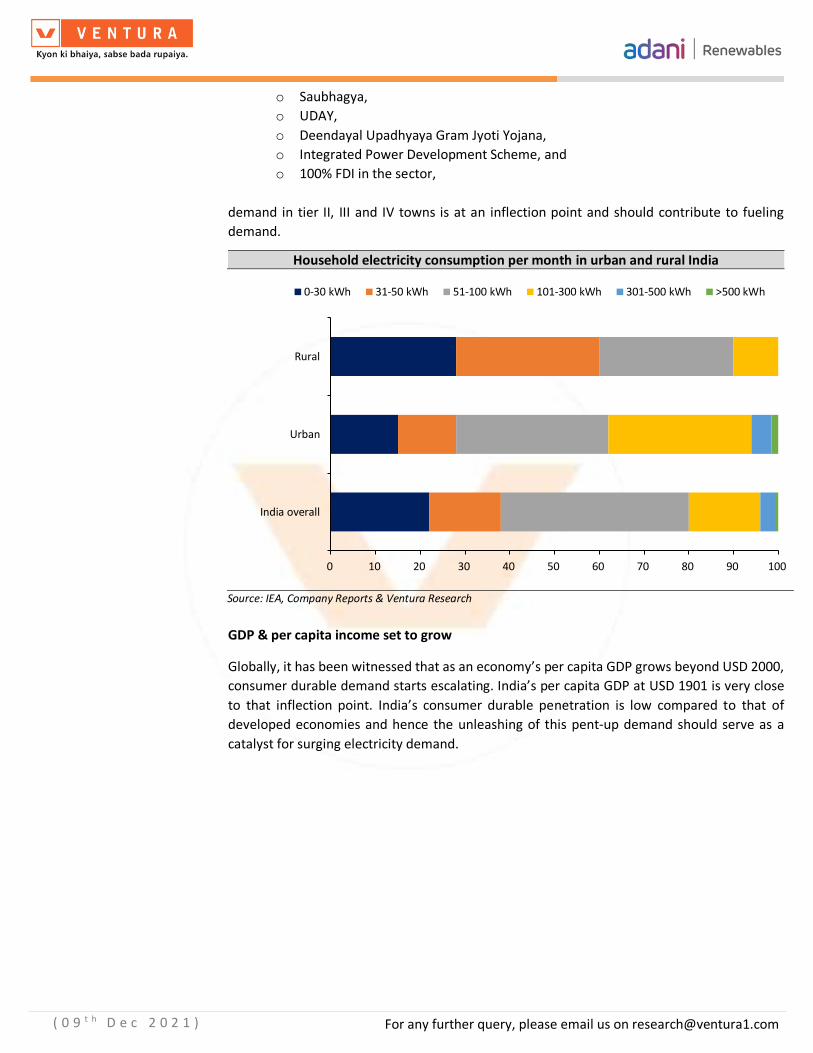

• Electricity demand in Tier II, III and IV towns set for a long-term upward trajectory

Over 65.5% of India’s electricity demand is concentrated among the cosmopolitan

centres and large cities. With the success of the reform schemes like

o 24*7 power for all,

150

350

550

750

950

1,150

1,350

1,550

1,750

China India USA Indonesia Pakistan Brazil

Population of countries (in Mn.) 2021 Population of countries (in Mn.) 2030

Population of countries (in Mn.) 2050

15

20

25

30

35

40

45

50

India China USA Brazil Japan

2121

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

o Saubhagya,

o UDAY,

o Deendayal Upadhyaya Gram Jyoti Yojana,

o Integrated Power Development Scheme, and

o 100% FDI in the sector,

demand in tier II, III and IV towns is at an inflection point and should contribute to fueling

demand.

Household electricity consumption per month in urban and rural India -

Source: IEA, Company Reports & Ventura Research

GDP & per capita income set to grow

Globally, it has been witnessed that as an economy’s per capita GDP grows beyond USD 2000,

consumer durable demand starts escalating. India’s per capita GDP at USD 1901 is very close

to that inflection point. India’s consumer durable penetration is low compared to that of

developed economies and hence the unleashing of this pent-up demand should serve as a

catalyst for surging electricity demand.

0 10 20 30 40 50 60 70 80 90 100

India overall

Urban

Rural

0-30 kWh 31-50 kWh 51-100 kWh 101-300 kWh 301-500 kWh >500 kWh

2222

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Under penetration of consumer durables demand sets the tone for exponential growth in electricity consumption

Source: Havells presentation, Company Reports & Ventura Research

Appliance ownership in India has been growing and diversifying. In 1990, the only appliance

that most households had was a ceiling fan. By 2019, television had also become quite

commonplace, and the number of refrigerators was steadily increasing.

By 2040, air conditioners, personal computers, and washing machines are expected to become

much more common, particularly in urban areas.

Indian household’s appliance ownership is set to explode

Source: IEA, Company Reports & Ventura Research

An illustration of how the demand explosion is expected to occur can be better visualized

taking into consideration demand for air conditioning. Air conditioner stock is expected to

zoom to 670 million units by 2040 from a paltry 30+ million units presently. As a result, India’s

3

23

43

63

83

103

123

India China USA

10 10

15

11

5

7

9

11

13

15

17

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

WashingMachines

Refrigerator Room AirConditioner

ColorTelevision

2019 2025E CAGR (%)

INR Cr

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1990 2000 2010 2019 2030 2040

Room Air Conditioner Color Television Refrigerator

Personal computer Washing Machines Dishwasher

Dryer

2323

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

consumption of electricity for cooling will grow six-fold to reach 650 TWh by 2040. Around

two‐thirds of this demand will come from the residential sector, with the remainder stemming

from a steady rise in office buildings, retail, education, hotels, and hospitals, etc.

Present-day lifestyle of always being connected to fuel incremental demand

The present-day lifestyle of always being connected, would mean that the demand on the

existing energy capacities would only multiply.

Connected lifestyle

Source: Company Reports & Ventura Research

Action on climate change to lead to an irreversible change for renewable energy sources

With climate change and global warming being a pressing issue, alternate sources of non-

polluting fossil fuel-based energy resources would have to be speedily inducted into the energy

mix. Solar and wind are infinite sources of this non-polluting energy.

India, in keeping with its pledge at the Paris convention and COP26, has undertaken to enhance

the renewable energy generation from the current 175 GW to 450 GW by 2030.

During the COP 26 summit, the Indian PM has taken a pledge to meet 50 percent of the

country’s energy requirements from renewable energy (RE) by 2030.

2424

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Power generation growth & capacity break-up -

Source: Ministry of power, Company Reports & Ventura Research

Installed Capacity Mix 2030

Source: CEA, Company Reports & Ventura Research

India has abundant untapped sources of renewable energy

The National Institute of Solar Energy has assessed India’s solar potential at 748 GW (assuming

3% wasteland coverage by solar PV modules). The assessed wind energy potential, as per the

National Institute of Wind Energy, is estimated at 302.25 GW at 100 meters above ground

level.

(5)

0

5

10

15

20

0200400600800

1,0001,2001,4001,600

Power Generation (Bn Units)

Fossil Fuel Generation Grw (%)

Non-Fossil Fuel Generation Grw (%)

Power Generation Grw (%)

Bn Units (%)

Power generation sources break-up (%)

Coal Other Fosil fuel

Hydro Wind, Solar & Other RE

Nuclear

Fossil Fuels Non-Fossil Fuels

2525

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

State wise potential of renewable energy generation

Source: karenvis, Company Reports & Ventura Research

These represent adequate sources of renewable energy to meet India’s total energy

requirements.

Current solar and wind capacity installation suggest significant growth opportunities still to be tapped

Source: CEA, Company Reports & Ventura Research

161

120 110 111 81

469

0

50

100

150

200

250

300

350

400

450

500

Rajasthan Gujarat Maharashtra Jammu &Kashmir

Karnataka Others

Wind Energy (GW) Solar Energy (GW) Total Renewable potential (GW)

0

2

4

6

8

10

12

14

16

Solar Wind

2626

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Solar & wind share of total annual generation in India's renewables-rich states -

Source: CEA, Company Reports & Ventura Research

Need for electric mobility solutions

The global drive to embrace electric mobility itself would mean that power requirements

would surge dramatically.

The subsidy programs Faster Adoption and Manufacturing of Electric Vehicles (FAME) 2015

and the second phase of the policy, FAME‐II 2019 (with a budget of $1.4 billion for three years)

provided the much-needed initial encouragement for the growth of EVs in India. The incentives

included were not only for the purchase of electric and hybrid vehicles but also for the

deployment of charging stations.

It is estimated that ~7 million electric cars will ply on Indian roads by 2030 and 27 million by

2040. A more significant opportunity for electrification exists in the form of 2W & 3W EVs.

From 1.8 million 2W & 3W in 2019, it is estimated that this number will gallop to 55 million by

2030 and 160 million by 2040.

0

5

10

15

20

25

30

35

Solar Wind

2727

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

EV Penetration (%)

Source: KPMG, Company Reports & Ventura Research

Fuel inflation will get contained in a renewable energy regime

Fossil fuel inflation has been a cash guzzler for Indian households. On the other hand,

renewable energy contracts are typically long-term in nature and the recent downtrend in

price discovery has proven that declining prices of renewable energy (lower than fossil fuels)

supplies are possible. This, in our opinion, is one of the single largest attributes of renewable

energy that can accelerate EV adoption and replace IC vehicles.

AGEL leveraging the large renewable energy opportunity

Adani Green Energy Limited (AGEL), capitalizing on the large renewable energy opportunity,

has been quick to establish one of the largest Indian renewable companies. Today, it has an

operational portfolio of 5.4 GW out of the 20.4 GW of PPA contracts, offering a 4x locked-in

growth.

The portfolio also includes an inorganic acquisition of 5 GW renewable assets of SB Energy

India. This portfolio holds 1,700 MW of operational renewable assets, 2,554 MW of assets

under construction and 700 MW of assets near construction. Solar capacity accounts for 84%

of the portfolio (4,180 MW), wind-solar hybrid capacity accounts for 9% (450 MW) and wind

capacity accounts for 7% (324 MW).

The total renewable portfolio of AGEL of around ~20.4 GW makes the company the largest

renewable power developer in India today. By 2030, AGEL aspires to build a renewable energy

capacity of 45 GW. In the process, AGEL by 2025 would become the world’s largest solar power

company and the largest renewable power company by 2030. Currently the company has a

~5.3% share in India’s renewable installed capacity, which is set to grow to ~10% by 2030.

Segment Sub-segment EV Penetration (%)

2025 2030

2W Scooters 15-25 50-70 B2B 40-60 60-80 B2C 13-18 40-60 Motorcycles 1-2 10-20 Overall 7-10 25-35

3W Overall 35-45 65-75

4W-PV Personal 1-3 10-15 Commercial 5-10 20-30

Buses STUs 15-25 25-40

2828

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

AGEL’s aspirations defying gravity

Source: Company Reports & Ventura Research

AGEL has been successful in de-risking all aspects of capacity creation that has ensured speed

in scaling up

AGEL’s speed in building capacity has been nothing less than extraordinary. They have been

able to scale their capacities given their

- strong project management and execution skills,

- in-house EPC and O&M, which is a low-cost enabler,

- a speedy implementation which results in lower payback and early cashflow generation,

- leveraging global capital at competitive costs & elongated maturities that help in sustaining

cashflow

- ability to tie-up long term fixed price PPAs with low counterparty risk providing for project

viability and revenue visibility

Strong project management and execution skills

Land acquisition experience and ability to secure right-of-way

Land acquisition and securing the ‘right-of-way’ are the biggest challenges to the timely

completion of the projects. Adani Group has rich experience in pan-Indian land identification

and pricing as well as liaisoning with local and state-level officials for securing the right of way.

As a result of which, it has a head start compared to its peers.

The Adani Group has been proactive in identifying ~2 lac acres of land at 85+ locations pan-

India having good renewable energy potential. It has already secured the purchase of 1 lac

acres with its philosophy of resource planning 3 years in advance.

1.9 2.0 2.5 3.5

8.2

12.3

18.3

25.0

45.0

1.0

6.0

11.0

16.0

21.0

26.0

31.0

36.0

41.0

46.0

51.0

FY18 FY19 FY20 FY21 FY22E FY23E FY24E FY25E FY30E

2929

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Where ever possible AGEL has introduced a combination of bi-facial & mono-facial PV modules

to maximize “sun capture”, thereby lowering its land footprint per MW to 3.2 acres per MW

(from the earlier 5 acres per MW).

Project implementation initiated only post securing 100% transmission connectivity

Further, the company ensures 100% transmission connectivity before any project

implementation is initiated. This helps in mitigating any unforeseen risks before

implementation of any projects.

Centralized and digitally-enabled Project Management & O&M teams ensure smooth

operational sustenance

For project implementation, it has well-established standardized SOPs for execution and O&M.

All project implementation is centrally managed by a Project Management and Assurance

Group (PMAG) and 125 strong Energy Network Operation Center (ENOC) . The digitally-

enabled ENOC provides real-time data monitoring with regards to electricity generation,

locations of plant faults, and rectification.

The capable of fault monitoring has been refined right down to the module level of 315 watts i.e.

0.000315 MW and at each WTG level for the wind farms. Further at the inception stage itself, we ensure

plants design is configured to generate such a granular level of data. AGEL’s IoT and Cloud-Based

Analytics Platform at the ENOC enables analytics driven real time monitoring of renewable plants

across 12 states in India thereby ensuring high plant availability of 99% (Solar) and significantly

high power supply EBITDA of over 90%.

As a second layer of performance assurance process of integrating and using automated drones for

thermography of solar modules for identifying module-level faults and waer & tear of WTGs is a;lso

being taken up.

Thus, remote management of all sites from a single location leads to rapid scale-up of capacity.

For O&M, AGEL deploys ~3-4 employees for a 250 MW plant. Further, outsourced contract

labour is deployed on a fortnightly basis and nearly ~20% of the company’s plants undertake

robotic cleaning of the PV modules. For training of filed engineers modern technologies like

AR & VR are being experimented with.

This wholistic technology-driven approach and in-depth data analytic has enabled AGEL benchmark

energy generation near P50 level generation (for solar) and P75 level (for wind) which is at par with the

highest global thresholds.

Assured & timely equipment supply from global vendors ensures timely project execution

The scale at which the company operates, assured supply chain becomes important. AGEL has

strong relationship with global vendors which results in timely supply at cheapest of costs

without compromising on quality.

The vibrancy of this supply chain was tested during the pandemic when AGEL was able to

commission 571 MW of capacity without any material delays.

3030

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

It also leverages existing relationships with over 200,000 vendors on a pan-India basis which

helps in successful and timely implementation of its projects.

All these measures taken to de-risk project implementation have ensured that capacities are

commenced well ahead of stipulated timelines leading to earlier payback and cashflow

generation.

Advance de-risking for potential pipeline with focus on most critical resource

Source: Company Reports & Ventura Research

Energy network operation center

Source: Company Reports & Ventura Research

3131

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Adequate financing with long tenure and lowest cost ensures project viability and revenue

visibility

The capital requirements for a renewable energy project ranges between INR 4-6 crore per

MW. Considering the aspirations of AGEL, needless to say, there is a huge demand for capital.

To shore up its equity base, AGEL roped in global major Total Energy as a strategic partner.

Total not only invested INR 3707 cr for a 50% stake in 3 SPVs (with a cumulative 2.35 GW of

capacity) but also sourced a 20% stake at the holdco level from the promoters for a sum of

USD 2.5 Bn. For this consideration, Total has one board representative who brings project

execution experience to the table.

AGEL’s Capital Management Program enables de-risking at both the construction and

operation stage while optimizing the stakeholder returns with well-established access to

international capital markets through a revolving construction facility and placement of green

bonds.

Total Energy investment

Source: Company Reports & Ventura Research

Matching funding with the PPA tenure

As 75% of the project capex is funded through debt, AGEL’s ability to tie-up debt at the SPVs

remains a key monitorable.

- The company has issued Green bonds worth USD 750 mn at the holdco level to meet

the equity funding needs of the SPVs. It is also in the process of tying up another USD

950 mn. Moody’s has done credit assessments for a total of USD 1.7 bn.

- AGEL has further secured a revolving Construction Framework Agreement for USD

1.35 bn with participation from 18 international banks to fully fund the construction

pipeline.

Once a project is commissioned and power generation stabilized (within the first three-to-six

months), the construction finance debt is refinanced with the help of long tenure Green bonds.

For this purpose, the company has issued

- ‘BB+‘ rated USD 500 mn Green Bonds of 5 years tenure and 10.5% cost issued for

refinancing 930 MW Restricted Group 1 (RG 1),

- ‘BBB-‘ IG rated USD 362.5 mn Green Bonds of 20 years tenure and 9.5% cost issued for

refinancing 570 MW Restricted Group 2 (RG 2).

3232

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

All in all, the company has a total limit of Rs.13000 cr of bond issuance already approved.

Going forward, AGEL is looking to raise long term funding to match the tenures of PPAs,

thereby de-risking any kind of asset liability mismatch.

Funding hierarchy

Source: Company Reports & Ventura Research

Long-term PPA contracts and low counterparty risk

Most of the PPA contracts (88%) secured by AGEL are with sovereign or sub-sovereign counter

parties (NTPC, NHPC, Adani power and SECI). This helps negate the counter party risk of default

or any delays in receipts.

Also, with all of the future power generation being pre-sold, all revenue related uncertainties

are eliminated, leading to long-term asset viability and revenue visibility.

As of today, only ~3% of revenue from Tamil Nadu State Electricity Board (TNEB) are delayed.

This delay has led to a penal interest liability of ~INR 500 cr, which is also receivables.

Low counterparty risk

Source: Company Reports & Ventura Research

Sovereign / Sovereign equivalent rated Others

3333

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Strong revenue visibility on the cards

The company has spread its power generation resources across 12 states which reduces

dependency on any one state as well as weather and state specific risks.

AGEL pan-India presence

Source: Company Reports & Ventura Research

During the period FY21-24E, we expect the solar capacity to grow at 65% CAGR to 13.4 GW

which will resulting in 86% CAGR volume growth to 31,424 Mn Units, and 68% CAGR revenue

growth to INR 10,771 cr.

3434

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

During the period FY21-24E, we expect the wind capacity to grow at 84% CAGR to 2 GW which

will resulting in 132% CAGR volume growth to 7,412 Mn Units, and 122% CAGR revenue growth

to INR 2,134 cr.

During the period FY22E-24E, we expect the hybrid capacity to grow at 27% CAGR to 2.7 GW

which will result in 96% CAGR volume growth to 11,041 Mn Units, and 93% CAGR revenue

growth to INR 3,043 cr.

With all the key drivers in place, we expect AGEL’s overall revenues to grow at a CAGR of 72.3%

to INR 15,978.0 cr over FY21-24E. EBITDA is estimated to grow at a CAGR of 78.7% to INR

12,750.4 cr. PAT is estimated to grow at a CAGR of 146.9% to INR 3,162.4 cr. Subsequently,

RoE and RoIC are expected to improve to 40.2% (+3,069bps) and 11.5% (+445bps),

respectively, by FY24E.

The company is targeting ~17% of equity IRR from any projects and projects IRR of ~12-13%.

The company has ~20-25% of equity IRR for some projects.

Power supply capacity and revenue mix

Source: Company Reports & Ventura Research

1,970 2,319 3,320

7,954 11,234

18,300

25,000 26,000

27,000 28,000

29,000 30,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Average Installed Capacity (MW)

Solar (MW) Wind (MW)

Hybrid (MW) Installed capacity (MW)

1,913 2,065 2,419

6,065

9,676

16,586

28,410

0

5,000

10,000

15,000

20,000

25,000

30,000

FY19 FY20 FY21 FY22E FY23E FY24E FY25E

Power supply revenue mix (Rs.Cr.)

Solar (Rs.Cr.) Wind (Rs.Cr.) Hybrid (Rs.Cr.) Revenue (Rs. Cr)

3535

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Renewable energy portfolio performance

Source: Company Reports & Ventura Research

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

1,500

11,500

21,500

31,500

41,500

51,500

61,500

71,500

FY19 FY20 FY21 FY22E FY23E FY24E FY25E

Solar Units sale (mn units) Average Tariff (Rs./Unit)

2.0

2.5

3.0

3.5

4.0

4.5

20

1,020

2,020

3,020

4,020

5,020

6,020

7,020

8,020

FY19 FY20 FY21 FY22E FY23E FY24E FY25E

Wind Units sale (mn units) Average Tariff (Rs./Unit)

2.7

2.7

2.8

2.8

2.9

2.9

3.0

800

2,800

4,800

6,800

8,800

10,800

12,800

FY22E FY23E FY24E FY25E

Hybrid Units sale (mn units) Average Tariff (Rs./Unit)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY19 FY20 FY21 FY22E FY23E FY24E FY25E

Total Units sale Blended Average Tariff (Rs./Unit)

(40)

(20)

0

20

40

60

80

100

(2,000)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Improving profitability

EBITDA Net Profit

EBITDA Margin (%) Net Margin (%)(%)

INR Cr

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1,00,000

FY19 FY20 FY21 FY22E FY23E FY24E

Growing CFO but higher capex needs more debt

CFO (RHS) Total Debt (LHS)

3636

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Strong organizational commitment to adopting best in class ESG initiatives

AGEL has a strong commitment to emerge

• in the Top 10 global companies for ESG benchmarking for the electric utility sector by

FY25

• to become a Single use Plastic Free ( SuPF ) company by FY24

• to become Zero Waste to Landfill (ZWL) company by FY25

• to become net water neutral for all its plants (with more than 200 MW generation

capacity) by FY25

AGEL has further adopted strong ESG practices and recently scored 66 out of 100 in DJSI-S&P

Global’s Corporate Sustainability Assessment significantly ahead of global Electric Utility sector

average of 38. Also, it has been assigned MSCI ESG rating of ‘A’.

ESG philosophy

Source: Ministry of power, Company Reports & Ventura Research

3737

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Environmental philosophy

Source: Ministry of power, Company Reports & Ventura Research

Social philosophy

Source: Ministry of power, Company Reports & Ventura Research

3838

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Governance philosophy

Source: Ministry of power, Company Reports & Ventura Research

3939

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Business Quality Score

Key Criteria Score Risk Comments

Management & Leadership

Management Quality 8 Low The management is of decent quality. It has been able to deliver growth while taking calculated risks.

Promoters Holding Pledge 5 Moderate The promoter holding is 60.14% and there is 1.1% of promoter pledging as of Sept 2021.

Board of Directors Profile 7 Low The average experience of directors is >20 years with significant experience in industry. Also, many of the board members are working since inception.

Industry Consideration

Industry Growth 7 Low Renewable energy is the need of the hour for tackling climate change. Further, India's per capita electricity consumption which is abysmally low (when compared to developed nations) is set to explode.

Regulatory Environment or Risk 7 Low The company has locked in growth for 25 GW of renewable capacity. In addition, the 25 years of PPAs provides strong revenue visibility.

Entry Barriers / Competition 6 Moderate High capex and long gestation period provide for high entry barriers. Competitive environment is low since there is enough room for growth spanning decades.

Business Prospects

New Business / Client Potential 8 Low India’s power requirements are set to explode and renewable energy is expected to replace conventional fossil fuels. As such there is no dearth of business potential.

Business Diversification 6 Moderate The company is into the renewable power generation business which has limited scope for diversification.

Market Share Potential 8 Low AGEL is the largest renewable energy generator company in India.

Margin Expansion Potential 7 Low Cost rationalization, improving utilization of under constructed assets will helps to AGEL to improve its profitability.

Earnings Growth 8 Low Higher electricity demand and needs for renewable energy generation will drive growth.

Valuation and Risk

Balance Sheet Strength 4 High

Elevated debt levels and capex hungry growth will mean that the balance sheet will remain leveraged. However, the innovated financial engineering has helped lower stress on the balance sheet by extending the debt tenure and addressing any potential asset-liability mismatch.

Debt Profile 4 High Higher debt on the balance sheet and aggressive capex plans will not go towards reducing the debt burden.

FCF Generation 6 Moderate Higher capex plans will result in a negative FCF for the next few years.

Dividend Policy 4 High Aggressive growth plans shun the possibility of any dividend payout in the short to medium term.

Total Score

Ventura Score (%)

95

65 Moderate

The overall risk profile of the company is moderate and we consider it as a Moderate risk company for investments

Source: Company Reports & Ventura Research

4040

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Annual Report Takeaways

We analyzed the FY21 annual report of AGEL and our key observations are as follows:

Key Takeaways

• Scale: The company believes that the vastness of the opportunity is among the largest

in the world. It is servicing the growing needs of a nation where the per capita

electricity consumption is a fraction of the corresponding consumption in developed

economies, representing decades of prospective growth. India’s primary energy

demand is expected to grow at a CAGR of 4.2% between 2017 and 2040, faster than

any major economy.

• Low-cost bidder: AGEL is also the lowest (L1) bidder in 4.5 GW solar tenders from

Andhra Pradesh Green Energy Corporation. The total renewable portfolio of AGEL of

around ~19 GW makes the company the largest renewable power developer in India

today.

• Investment of Total Energy: An important development at AGEL was the expansion of

its partnership with French energy major TOTAL SA. The latter acquired 20% equity in

the company in addition to holding 50% in 2,353 MW of operational solar assets. This

respect enhancing equity ownership is a validation of AGEL’s capability in building

quality assets, O&M excellence and governance practices.

• Strong pipeline: AGEL’s consolidated portfolio and pipeline were a sizable ~19 GW as

on 31st March, 2021, with considerable optimism of achieving its stated aspiration of

25 GW in renewable energy capacity by 2025.

• Funding pipeline: The company diversified its funding source from conventional Indian

debt providers to the global Green Bond market. Global funding access holds out twin

advantages of predictable long-term costs on the one hand, and an extended

repayment tenure on the other, graduating what is essentially a debt instrument to

quasi-equity. AGEL mobilized a USD 1.35 Billion revolving construction facility that will

keep financing the long under-construction pipeline. This is one of the largest revolving

project financing deals in Asia’s renewable energy sector.

Pay Grades

The remuneration growth of KMP is in line with the performance of the company. The

Chairman has not taken any hike in remuneration in the last four years.

Remuneration in the last 4 years

Source: Company Reports & Ventura Research

Parameter (Fig in INR Cr) FY18 FY19 FY20 FY21 CAGR%

Chairman 0.0 0.0 0.0 0.0 NA

Share in Total Employee Cost (%) NA NA NA NA

Chief Financial Officer 1.4 2.3 1.4 0.0 NA

Share in Total Employee Cost (%) 3.3 3.9 1.3 NA

Remuneration of SVP/VP/GM 0.0 4.2 6.3 7.7 760.0

Share in Total Employee Cost (%) 0.0 7.1 5.9 20.2

Employee Cost 43.7 59.7 107.0 38.0 (4.5)

Employee Cost as % of Revenue (%) 2.9 2.9 4.2 1.2

4141

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Management & Leadership Team Turnover

Details on Board of Director and KMPs

Source: Company Reports

Auditor qualifications & significant notes to accounts

BSR & Co. LLP & Dharmesh Parikh & Co. LLP are the auditors and there were no

qualifications/emphasis of matters highlighted by them in the FY21 Annual Report.

Major Related Party Transactions with promoters and KMPs

Over the last four years, related party transactions continue to remain elevated. These

transactions are mainly due to Unsecured Perpetual Debt & Loans and Advances given to

various parties.

Related Party Transactions are relatively higher

Source: Company Reports & Ventura Research

Board of Director & KMP FY18 FY19 FY20 FY21

Gautam S Adani CM CM CM CM

Vneet S Jaain MD & CEO

Jayant Parimal CEO CEO CEO

Rajesh S Adani NED NED NED NED

Dinesh Kanabar NED NED

Raminder Singh Gujral NED NED

Sandeep Singhi ID ID ID ID

Poornima Advani ID ID ID

Jose Ignacio Sanz Saiz ID ID

Sagar R Adani ED ED ED

Pragnesh S Darji CS CS CS CS

Raaj Kumar Sah ID ID

Jay Shah ID

Sushama Oza ID

CM-Chairman NED-Non Executive Director

MD-Managing Director ID-Independent Director

CFO-Chief Financial Officer CS-Company Secretary

WTD-Whole Time Director ED-Executive Director

Parameter (Fig in INR Cr) FY18 FY19 FY20 FY21

Related Party Trans 8,444.9 2,681.5 2,470.0 5,339.0

Compensation to KMP 1.4 6.6 0.0 3.0

Transactions as % of Revenue (%) 570.6 130.6 96.9 171.0

4242

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Contingent Liabilities

Contingent liabilities are well within range.

Contingent Liabilities are lower

Source: Company Reports & Ventura Research

Management Team

Source: Company Reports

Parameter (Fig in INR Cr) FY18 FY19 FY20 FY21

Claims against the company not acknowledged 30.9 52.6 60.0 66.0

Contingent Lia. as % of Revenue (%) 2.1 2.6 2.4 2.1

Contingent Lia. as % of Net Worth (%) 2.3 2.7 2.5 3.0

Key Person Designation Details

Mr. Gautam Adani Chairman & MD

Mr. Gautam Adani has over 36 years of business experience. Under his

leadership, the Adani Group has emerged as a global integrated infrastructure

player with interests across resources, logistics and energy verticals.

Mr. Rajesh Adani Non-Executive Director

Mr. Rajesh Adani has been associated with Adani Group since its inception.

He is in-charge of the operations of the Group and is responsible for

developing its business relationships.

Mr. Sagar R. Adani Executive Director

He aims to build the Group’s identity around an integrated business model,

backed by his sound understanding of new processes, systems, and

macroeconomic issues, coupled with his growing experience. He holds a

degree in Economics from Brown University, USA.

Mr. Vneet Jaain CEO

He has been associated with Adani Group for over 15 years. During his

association, he has been spearheaded on Group’s strategy for its energy and

infrastructure business and has been instrumental growing various

businesses from conceptualisation to operation - renewable, power

CA Kaushal Shah CFO

He has held various leadership positions in Adani Group during his total 29

years of experience. Kaushal is a Chartered Accountant of 1993 batch and

holds a Bachelor of commerce from Gujarat University, India and degree of

PGDISA from Institute of Chartered Accountants of India.

4343

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Key Risks & Concerns

• Land availability risk

Renewable energy projects require a huge land parcel, 4 acres of land for a 1 MW

power generation unit. So, for the total under construction pipeline of 20 GW of

project execution, the company requires ~80,000 acres of land. Also, for ongoing capex

further requires a land of ~1,80,000 acre of land. Any unavailability of land or delay in

land acquisition will adversely impact the performance of the company.

• Higher leverage on the balance sheet

Majority of growth of the company is debt funded growth so any adverse situation or

inability to repay debt will impact business and performance adversely. Higher debt

will increase the interest burden and any adverse business scenario will hamper future

growth. Higher ongoing and future capex will require higher borrowing in future also.

However, the company’s renewable capacity installed in the past started throwing

decent cash flows, which will definitely support balance sheet strength.

Debt laden balance sheet

Source: Company Reports & Ventura Research

• Promoters stake pledge

This was at disconcerting levels in FY21 but has subsequently reduced to being less of

an issue

0

2

4

6

8

10

12

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1,00,000

FY17 FY18 FY19 FY20 FY21 FY22E FY23E FY24E

Total Debt Net Debt Net Debt to Equity (X) Net Debt to EBITDA (X)

4444

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Pledge as a % of total Shares held by Promoters

Source: Company Reports & Ventura Research

• The renewable energy sites are vulnerable to the hostile impact of cyclone and other

adverse weather conditions.

0

5

10

15

20

25

30

35

40

45

4545

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Quarterly and Annual Performance

Source: Company Reports & Ventura Research

4646

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Summary of Management Commentary and Quarterly Performance over last few quarters

Key Criteria View Comments

Q2FY21

Business Performance POSITIVE Revenues up 1% YoY to INR 718 cr, Revenue from power supply up 15% to INR 530 cr, Power supply EBITDA up 19% to INR 490 cr.

Solar energy units up 22% to 1,187 Mn units, CUF of 20.7%, Wind energy units up 11% to 162 Mn units, CUF of 30.3%

Q3FY21

Business Performance POSITIVE

Revenues up 61% YoY to INR 843 cr, Revenue from power supply up 31% to INR 591 cr, Power supply EBITDA up 34% to INR 532 cr. Solar energy units up 27% to 1,200 Mn units, CUF of 20.8%, Wind energy units up 106% to 103 Mn units, CUF of 18.9%

Q4FY21

Business Performance POSITIVE

Revenues up 51% YoY to INR 1,082 cr, Revenue from power supply up 15% to INR 690 cr, Power supply EBITDA up 15% to INR 626 cr. Solar energy units up 24% to 1,482 Mn units, CUF of 24.3%, Wind energy units up 20% to 132 Mn units, CUF of 22.2%

Q1FY22

Business Performance POSITIVE

Revenues up 23% YoY to INR 1,079 cr, Revenue from power supply up 39% to INR 848 cr, Power supply EBITDA up 41% to INR 789 cr. Solar energy units up 39% to 1,650 Mn units, CUF of 25%, Wind energy units up 103% to 404 Mn units, CUF of 38.5%

Outlook & Strategy POSITIVE

150 MW wind plant commissioned in Gujarat

50 MW solar plant commissioned in Uttar Pradesh

Signed definitive agreements for 100% acquisition of SB Energy Holdings Limited. It houses 4,954 MW of renewable assets in India. The target portfolio consists of 84% solar capacity (4,180 MW), 9% wind-solar hybrid capacity (450 MW) and 7% wind capacity (324 MW).

Q2FY22

Business Performance POSITIVE Revenues up 112% YoY to INR 1,295 cr, Revenue from power supply up 58% to INR 834 cr, Power supply EBITDA up 61% to INR 787 cr. Solar energy units up 41% to 1,430 Mn units, CUF of 21.4%, Wind energy units up 185% to 471 Mn units, CUF of 42.9%

Outlook & Strategy POSITIVE

PPA signing commenced with SECI towards Letter of Award previously received for manufacturing linked solar project of 8 GW with signing of PPAs for 867 MW in Oct 2021. Awarded 450 MW Wind project from SECI in Oct 2021

Capacity guidance for FY25: 25000 MW (including inorganic acquisition).

Run-rate EBITDA guidance for FY25: ~INR 20,000 cr.

Source: Company Reports & Ventura Research

4747

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Financial Analysis & Projections

Source: Company Reports & Ventura Research

4848

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

This page left intentionally blank

4949

( 0 9 t h D e c 2 1 )

For any further query, please email us on [email protected]

TABLE OF CONTENTS

Adani Ports & Special

Economic Zone Ltd.

The largest port and integrated logistics player

5050

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

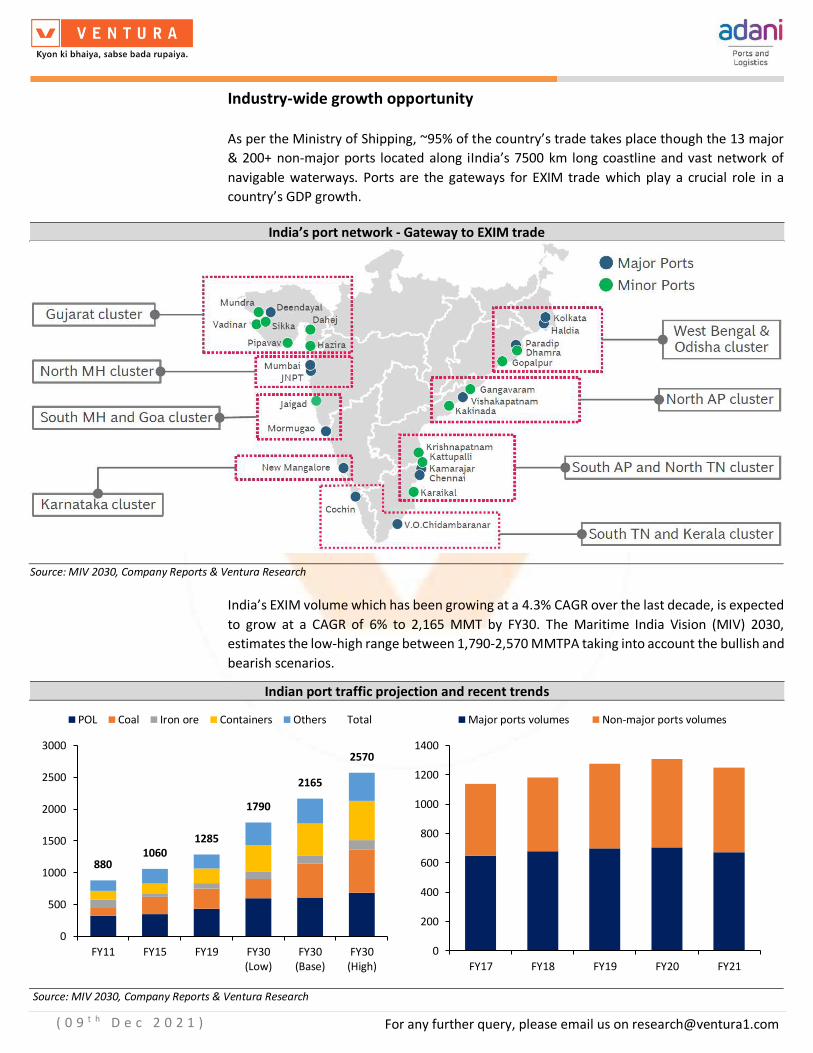

In a post-covid scenario, where the world is distancing itself from its over dependance

on China, India has emerged as a reliable, responsible and geopolitically viable option

for global manufacturing. Further, favourable policies like Atmanirbhar Bharat, Make

in India Make for World, PLI schemes, etc., have helped create a launch pad for

resurgent EXIM volumes, which are expected to scale to 1790-2570 MMT by FY30

from 971 MMT clocked in FY21. Adani Ports & Special Economic Zone Ltd (APSEZ)

with its portfolio of 13 ports (installed capacity of 560 MMT & 28.6% EXIM volume

share), is well positioned to expand its market share to 38.9% from this surge in EXIM

trade.

Another growth driver of APSEZ is its foray into the highly fragmented USD 160 bn

(growing at 10% CAGR) logistic infrastructure vertical through its wholly owned

subsidiary Adani Logistics Limited (ALL). ALL has fast established itself as a leading

player in the container handling, bulk goods, agri-logistics and warehousing verticals.

PM Modi’s “Gati Shakti” in combination with the National Logistic Policy and

digitization is expected to be a game-changer as it aims to lower the logistic cost from

the present 14% of GDP to 7-8% over the next 5-6 years and boost economic

development. Given the Adani group’s global scale of operations, execution

excellence and capital raising capability, we expect APSEZ to emerge as the largest

transport utility.

We expect a 20.4% CAGR volume growth to 432 MMT and 52.2% growth from

logistics leading to a 24.3% /24.8% /20.1% CAGR growth in revenue / EBIDTA / PAT to

INR 24,106.2 cr/ INR 15,515.4 cr/ INR 8,769.9 cr by FY24. Despite continuing

investments, we believe that peak debt is behind us and strong cashflow generation

should enable APSEZ to achieve lower balance sheet leverage. We initiate coverage

with a BUY for a DCF based price objective of INR 1,697, representing an upside of

120% over the next 24 months. Concor is a strategic fit for APSEZ and a winning bid

would lead to a major re-rating of the stock.

Omicron breakout and slowdown in global trade are risks to our estimates.

Key Financial Data (INR Cr, unless specified)

Revenue EBITDA

Net Profit

EBITDA (%)

Net Profit

(%) EPS (₹)

BVPS (₹)

RoE (%)

RoIC (%)

P/E (X) P/BV

(X)

EV/ EBITDA

(X)

FY20 11,439 5,505 3,763 48.1 32.9 17.5 120.2 14.7 7.9 41.5 6.0 32.5

FY21 12,550 7,983 4,994 63.6 39.8 23.2 149.3 16.3 9.8 31.2 4.9 23.2

FY22E 16,917 10,848 5,592 64.1 33.1 26.0 170.0 15.9 13.2 27.9 4.3 16.9

FY23E 19,955 12,912 6,762 64.7 33.9 31.5 194.5 16.8 15.8 23.1 3.7 13.9

FY24E 24,106 15,515 8,770 64.4 36.4 40.8 225.9 18.6 19.0 17.8 3.2 11.2

BUY @ CMP INR 770 Target: INR 1,697 in 24 months Upside Potential: 120%

The largest port and integrated logistics player

Industry Ports

Scrip Details

Face Value (INR) 2.0

Market Cap (INR Cr) 1,52,049

Price (INR) 770

No of Shares O/S (Cr) 204

3M Avg Vol (000) 267

52W High/Low (INR) 901/428

Dividend Yield (%) 0.69

Shareholding (%) Sept 2021

Promoter 63.83

Institution 31.15

Public 5.02

TOTAL 100.0

Price Chart

20000

30000

40000

50000

60000

70000

120.00

320.00

520.00

720.00

920.00

APSEZ SENSEX

Adani Ports & Special Economic

Zone Ltd.

5151

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Source: Company Reports & Ventura Research

0

200

400

600

800

1,000

1,200

Apr

-14

Jul-

14O

ct-1

4Ja

n-1

5A

pr-1

5Ju

l-15

Oct

-15

Jan

-16

Apr

-16

Jul-

16O

ct-1

6Ja

n-1

7A

pr-1

7Ju

l-17

Oct

-17

Jan

-18

Apr

-18

Jul-

18O

ct-1

8Ja

n-1

9A

pr-1

9Ju

l-19

Oct

-19

Jan

-20

Apr

-20

Jul-

20O

ct-2

0Ja

n-2

1A

pr-2

1Ju

l-21

1 year forward EV/EBITDA band chart

EV per sh 7.76x 12.11x

16.46x 20.81x 25.16x

0

5

10

15

20

25

30

01-A

pr-

14

01-S

ep-1

4

01-F

eb-1

5

01-J

ul-

15

01-D

ec-1

5

01-M

ay-1

6

01-O

ct-1

6

01-M

ar-1

7

01-A

ug-

17

01-J

an-1

8

01-J

un

-18

01-N

ov-1

8

01-A

pr-

19

01-S

ep-1

9

01-F

eb-2

0

01-J

ul-

20

01-D

ec-2

0

01-M

ay-2

1

EV/EBITDA & Std Deviation

EV/EBIDTA Average Upper SD 1

Upper SD 2 Lower SD 1 Lower SD 2

30.00

130.00

230.00

330.00

430.00

530.00

630.00

730.00

830.00

930.00

02-Apr-18 02-Apr-19 02-Apr-20 02-Apr-21

Peer group price performance

APSEZ CONCOR Gujarat Pipavav GDL

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

10-Apr-18 10-Apr-19 10-Apr-20 10-Apr-21

APSEZ commands slightly premium valuation to CONCOR, which has significantly expanded in

the past 1 year

Strong business potential deserves re-rating

5252

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Valuation

We have used the DCF model to value APSEZ. We have discounted back the future cash flows

to FY24 and value the company at INR 1,697 per share, presenting an upside of 120% from the

CMP of INR 770.

DCF Valuation

Source: Company Reports & Ventura Research

Long Term Market Return 11%

Risk Free Rate 6.3%

Cost of Equity 9.6%

Interest Rate 9.0%

Tax Rate 22.0%

Cost of Debt 6.9%

WACC 8.4%

Terminal Value Growth 3.0%

Terminal Value 5,56,877

FY24E FY25E FY26E FY27E FY28E FY29E FY30E FY31EFCFF 8237 10090 12539 14795 17605 20441 24791 29124

Discount Factor from FY24 0.92 0.85 0.79 0.72 0.67 0.62 0.57 0.53

Discounted FCFF from FY24 7,600 8,589 9,847 10,720 11,770 12,608 14,108 15,291

Total of Discounted FCFF FY24 90,533

FY24 Present Value of Terminal Value 2,92,380

FY24 Value of Operations 3,82,913

FY24 Net Debt 18,223

FY24 Value of Equity 3,64,690

FY24 Value of Equity per share 1,697

5353

( 0 9 t h D e c 2 0 2 1 )

For any further query, please email us on [email protected]

Our Bull and Bear Case Scenarios

We have prepared a Bull and Bear case scenario based on APSEZ’s terminal growth.

• Bull Case: As the largest integrated port and logistics company in India, APSEZ has a

significant opportunity to grow its business in the coming years. We have assumed a

terminal growth of 4%, which will result in a Bull case price target of INR 1,931 (upside

of 151% from the CMP).

• Bear Case: We have assumed a terminal growth of 1%, which will result in a Bear case