Gati Ltd. - HDFC securities

20

Gati Ltd. 1 Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, vel illum dolore eu feugiat nulla ▪ Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, ▪ quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, ▪ vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi. et iusto odio dignissim qui blandit praesent luptatum zzril delenit Initiating Coverage Gati Ltd. 21-June-2021

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Gati Ltd. - HDFC securities

Gati Ltd.

1

Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, vel illum dolore eu feugiat nulla

▪ Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy

nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam,

▪ quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat,

▪ vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi. et iusto odio dignissim qui blandit praesent luptatum zzril delenit

Initiating Coverage

Gati Ltd. 21-June-2021

Gati Ltd.

2

Industry LTP Recommendation Base Case Fair Value Bull Case Fair Value Time Horizon

Logistics Rs. 145.9 Buy on dips to Rs.136.5 & add more on dips to Rs 118.5 Rs. 157 Rs. 187 2 quarters

Our take Gati Ltd. (Gati) offers a wide range of services, viz. express distribution, supply chain management solution, e-commerce logistics, managed value-added transportation services (MVATS) and fuel stations. In 2020, Allcargo Logistics Ltd. (ALL) had acquired a stake of 46.86% from the erstwhile promoter, open offer, preferential allotment and open market purchases and became a promoter in the company. Gati will derive benefits and synergies from the strong parentage of Allcargo and would be able to offer end-to-end services across the value chain.

Post-acquisition, ALL has initiated a restructuring with a clear focus on becoming asset light, which will enhance efficiency and profitability and deleverage the balance sheet. The company has exited the asset-heavy cold chain business (sold the entire 70% stake to existing shareholder Mandala Capital AG Ltd), discontinued other lossmaking trading/ freight forwarding businesses (GEITL) and disposed its non-core assets (land and buildings). Also, the divestment of the low-margin fuel station business (five petrol pumps) that it has planned should be over by FY22.

Express distribution & supply chain segment contributes 78% to revenue, while fuel station contributes 18% and other business segments contribute the balance. The company has an extensive pan-India presence that covers 735 out of the total of 739 districts in the country, operating on more than 1,900+ scheduled routes with 1,500 fleet, 5,000+ trucks and 600+ operating centres, and 7,000 business partners. Gati aims to enhance its SME segment revenue share from the current 26% to 50% in the next two years, given its differentiated service offerings with strong digital initiatives such as chatbot, AP integrations and automation.

We expect the company’s revenue to be hit in the near term by a COVID-led economic slowdown. The industry is highly dependent on the manufacturing sector and government support, which are expected to slow down along with the economy. However, post the reopening of the economy, the business of Gati should bounce back sharply.

Valuation and recommendation We expect the company to gain from (1) its longstanding experience in the logistics sector, (2) Allcargo as its new promoter, (3) diversification of customer base, and (4) revenue offering from different segments. Also, Allcargo’s focus on restructuring the business will improve return ratios and financials and transform the business to an asset-light model.

HDFC Scrip Code GATLTDEQNR

BSE Code 532345

NSE Code GATI

Bloomberg GTIC:IN

CMP June 18, 2021 145.9

Equity Capital (cr) 24.4

Face Value (Rs) 2

Eq- Share O/S(cr) 12.2

Market Cap(Rscr) 1899

Book Value (Rs) 48

Avg.52 Wk Volume 1298144

52 Week High 157.70

52 Week Low 41.50

Share holding Pattern % (March, 2021)

Promoters 51.90

Institutions 1.57

Non Institutions 46.53

Total 100.0

Fundamental Research Analyst Jimit Zaveri [email protected]

Gati Ltd.

3

Further, it is pertinent to note that the logistics sector is highly underpenetrated and has a high share of unorganized players (~95%). We believe this presents a structural growth opportunity that can be harnessed with limited investment. Huge opportunity size (large unorganized market), long operating experience in a stable industry, and improving return ratios with new promoters provides comfort. ALL has a longstanding relationship with customers across the globe and, with the acquisition of Gati, it would be well-placed in the domestic express distribution segment to offer a wide range of logistic solutions to its international customers. With the increasing share of rail in the EXIM container trade and relatively better positioning of stronger players in the organized sector, road transporters like Gati stand to benefit. This benefit could sustain and increase with the arrival of Dedicated Freight Corridor (DFC). The COVID-led slowdown has adversely impacted the year FY21 and could partly impact FY22E as utilization has gone down and there is a sharp fall in manufacturing activities of various sectors, which could lead to the company reporting 10% topline CAGR over FY21P-23E. The stock is currently trading at 24.7x FY23E PE, 14.5x FY23E EV/EBITDA. We believe the base case fair value of the stock is Rs.157 (26.5x FY23E PE) and in the bull case the fair value of the stock is Rs.187 (31.5x FY23E PE). Investors willing to take some risk can buy on dips at Rs.136.5 (23x FY23E PE) and add more on dips to Rs.118.5 (20x FY23E PE).

Financial Summary Particulars (Rs cr) Q4FY21 Q4FY20 YoY-% Q3FY21 QoQ-% FY19 FY20 FY21P FY22E FY23E

Total Operating Income 407 370 10% 401 1% 1,863 1,712 1,314 1,653 1,588

EBITDA 8 -19 LP 25 -68% 94 36 27 89 120

APAT -164 -63 LL -25 LL 18 -62 -228 45 77

Diluted EPS (Rs) -13.48 -5.66 LL -2.1 LL 1 -5 -18 3 6

RoE-% 3 -8 -36 8 13

P/E (x) 103.4 NA NA 41.8 24.7

EV/EBITDA 18.3 48.5 63.7 19.4 14.5 (Source: Company, HDFC sec)

Gati Ltd.

4

Q4FY21 result update Revenue of the company grew by 10% YoY to Rs.407 cr. EBITDA came in at Rs.8 cr vis-à-vis loss of Rs.19 cr in the same quarter in the

previous year (loss to profit YoY).

Segment-wise Revenue of the express distribution & SCM segment has grown 20% YoY to Rs.336 cr while EBIT posted a lower loss YoY and came in

at Rs.0.37 cr. Revenue of surface express distribution was Rs.300 cr (+5% QoQ) and volume was 250,318 MT (+5% QoQ); revenue of air express came in at Rs.12 cr (flat QoQ) while volume of the same was 1,496 MT (-0.4% QoQ). Revenue of e-commerce logistics was Rs.4 cr (-60% QoQ) and volume was 3,754 MT (-59% QoQ). Revenue of SCM was Rs.12 cr (-20% QoQ) and revenue of other segment Rs.8 cr (-14% QoQ) in Q4FY21.

Revenue of the fuel station segment has grown 12% YoY to Rs.71 cr while EBIT has grown 15% YoY to Rs.16 cr. Gati provided for exceptional items in Q4FY21 of Rs.204.9 cr cleaning up the past issues as under: a) Diminution amounting to Rs.171.03 cr in the present fair value of the assets sold during the year and proposed to be sold which is disclosed as “Assets held for Sale”. b) Overdue advances amounting to Rs.18.46 cr given to few parties in previous years have been fully provided in the current quarter. c) Past receivable of Rs.4.10 cr from Air India remains sub-judice before Hon`ble High Court of New Delhi. Same has been provided for during the quarter. d) The wholly owned subsidiary i.e., Gati Asia Pacific Pte Ltd (GAP) and it's two step down subsidiaries ceased to be a subsidiary with effect from August 16, 2020 after the transfer of investment to AllCargo Belgium N.V & Wingdom APAC Ltd, Hongkong, loss of which is Rs.11.27 cr. Long-term triggers Promoter change will help grow with efficiency In 2020, Allcargo Logistics Ltd acquired a stake of 46.86% from the erstwhile promoters, public open offer (in March 2020 @Rs.75 per

share), Preferential allotment (@Rs.75) and open market purchases and became a promoter of the company. Post the completion of the

acquisition, Mr Shashi Kiran Shetty was appointed as Chairman and Managing Director of Gati Ltd. The Board of Gati has approved

Gati Ltd.

5

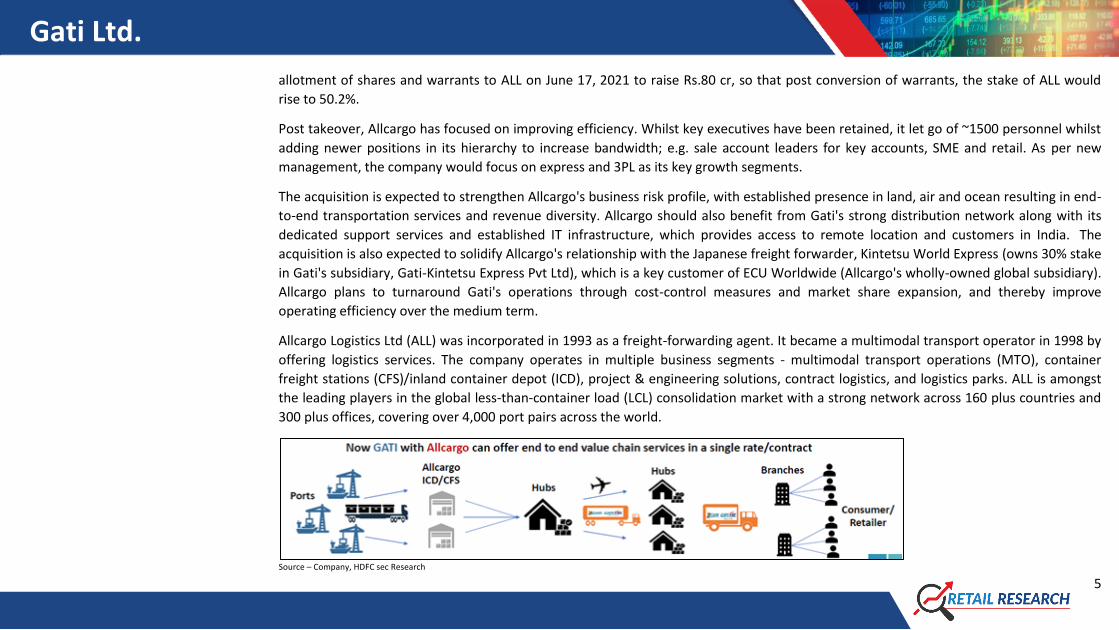

allotment of shares and warrants to ALL on June 17, 2021 to raise Rs.80 cr, so that post conversion of warrants, the stake of ALL would

rise to 50.2%.

Post takeover, Allcargo has focused on improving efficiency. Whilst key executives have been retained, it let go of ~1500 personnel whilst

adding newer positions in its hierarchy to increase bandwidth; e.g. sale account leaders for key accounts, SME and retail. As per new

management, the company would focus on express and 3PL as its key growth segments.

The acquisition is expected to strengthen Allcargo's business risk profile, with established presence in land, air and ocean resulting in end-

to-end transportation services and revenue diversity. Allcargo should also benefit from Gati's strong distribution network along with its

dedicated support services and established IT infrastructure, which provides access to remote location and customers in India. The

acquisition is also expected to solidify Allcargo's relationship with the Japanese freight forwarder, Kintetsu World Express (owns 30% stake

in Gati's subsidiary, Gati-Kintetsu Express Pvt Ltd), which is a key customer of ECU Worldwide (Allcargo's wholly-owned global subsidiary).

Allcargo plans to turnaround Gati's operations through cost-control measures and market share expansion, and thereby improve

operating efficiency over the medium term.

Allcargo Logistics Ltd (ALL) was incorporated in 1993 as a freight-forwarding agent. It became a multimodal transport operator in 1998 by

offering logistics services. The company operates in multiple business segments - multimodal transport operations (MTO), container

freight stations (CFS)/inland container depot (ICD), project & engineering solutions, contract logistics, and logistics parks. ALL is amongst

the leading players in the global less-than-container load (LCL) consolidation market with a strong network across 160 plus countries and

300 plus offices, covering over 4,000 port pairs across the world.

Source – Company, HDFC sec Research

Gati Ltd.

6

The company has started deriving benefits and synergies from Allcargo. In FY21, Gati received 28 leads on the express business side.

Different service offering Gati-KWE’s express distribution brings multi-modal deliveries which cover over 99% of the country’s districts. Customers can choose and

customize distribution services based on needs. Whether there is a need to move parcels, freight or special cargo, the company has cost-

effective and time-sensitive services to offer. It has a strong presence in the Asia Pacific region and SAARC countries, along with an

extensive network across India, offering services to 19,800 pin codes, covering 735 out of 739 districts in India, operating in more than

1,900+ scheduled routes with 1500 fleets, 5000+ trucks and 600+ operating centres, and 7,000 business partners.

Express Plus – A unique service that offers faster delivery than any average surface movement service.

Express – A cost-effective surface cargo movement for shipments with a time-definite delivery schedule.

Premium Plus – Specially-designed service that promises delivery within 12 hours or before noon the next day across all major ports in

India.

Premium – A cost-effective service that assures delivery within 24 hours, 48 hours and more than 48 hours through our multi-modal

network across metros and non-metros in India.

Gati E-Connect – It is a dedicated e-commerce logistics vertical, which is India’s first integrated e-commerce logistics solutions provider.

Backed by express distribution, Gati E-Connect can reach over 99% of India’s districts to offer seamless last-mile delivery solutions.

Air Freight – Gati Air brings a dedicated air freight service built on over 30 years of logistics and supply chain experience, and a

commitment to moving cargo across India's metros and non-metro cities alike. Experience combined with network and tie-up with IndiGo

Airlines, India's largest airline, gives it an edge in terms of safely and efficiently moving cargo across the country.

Supply Chain Management Solutions (SCM) – Supply chain management solutions feature over 65 warehouses across the country,

including 3 e-fulfilment centers that cater to sectors like e-commerce, hospitality, healthcare and electronics, among others. Each

warehouse is designed and built to meet global standards. The company has ~4.1 mn sq ft of warehousing space across multiple locations

and 31 hubs to serve transportation.

Gati Ltd.

7

Source – Company, HDFC sec Research

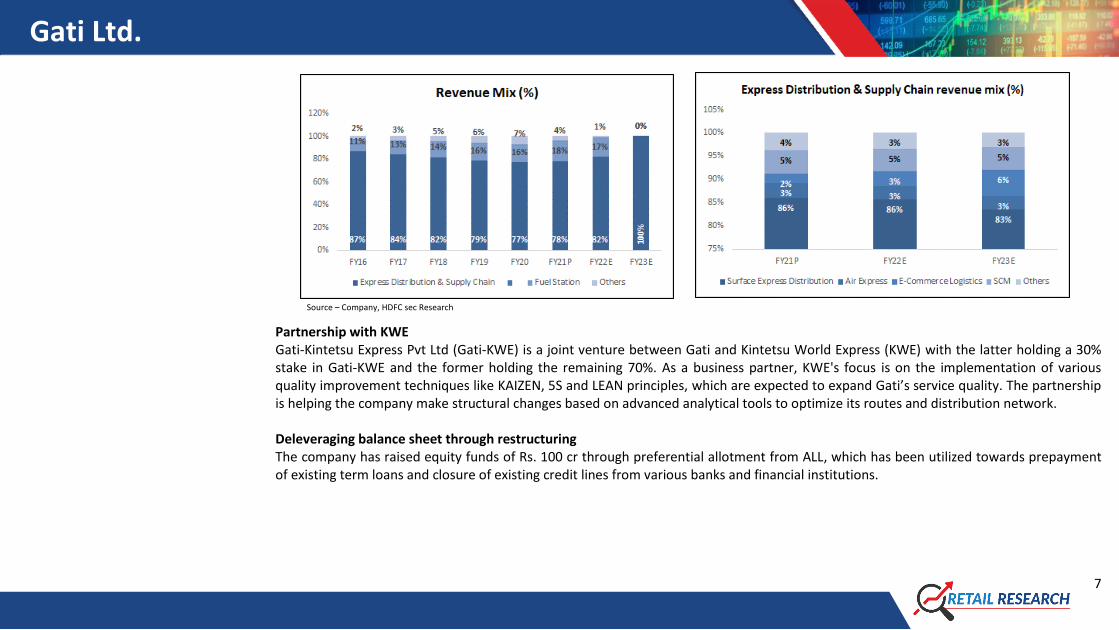

Partnership with KWE Gati-Kintetsu Express Pvt Ltd (Gati-KWE) is a joint venture between Gati and Kintetsu World Express (KWE) with the latter holding a 30% stake in Gati-KWE and the former holding the remaining 70%. As a business partner, KWE's focus is on the implementation of various quality improvement techniques like KAIZEN, 5S and LEAN principles, which are expected to expand Gati’s service quality. The partnership is helping the company make structural changes based on advanced analytical tools to optimize its routes and distribution network. Deleveraging balance sheet through restructuring The company has raised equity funds of Rs. 100 cr through preferential allotment from ALL, which has been utilized towards prepayment of existing term loans and closure of existing credit lines from various banks and financial institutions.

Gati Ltd.

8

Source – Company, HDFC sec Research

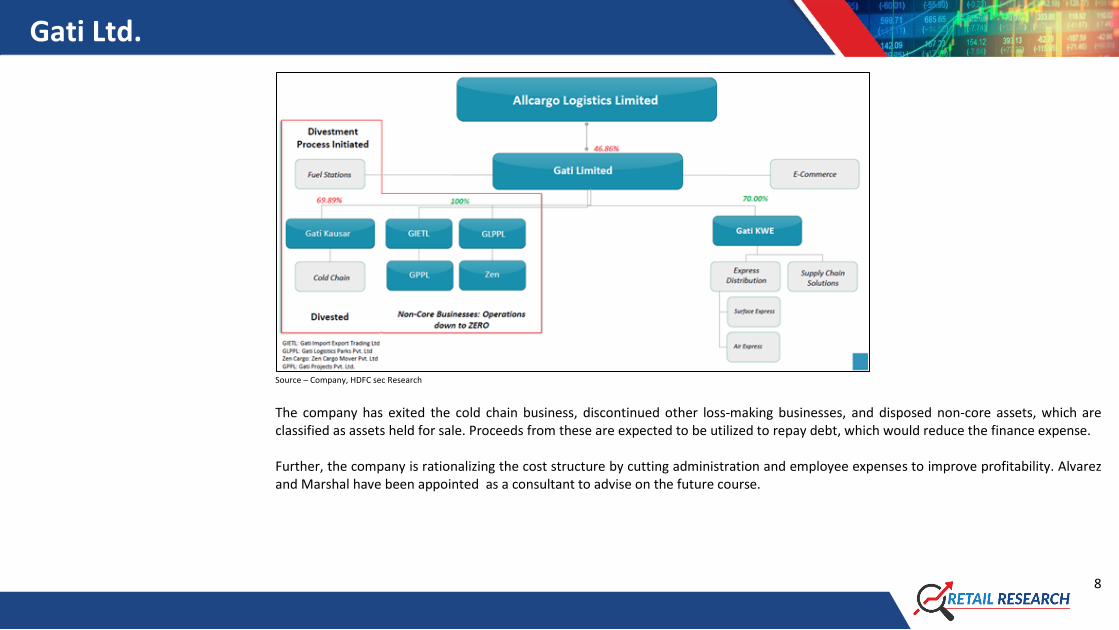

The company has exited the cold chain business, discontinued other loss-making businesses, and disposed non-core assets, which are classified as assets held for sale. Proceeds from these are expected to be utilized to repay debt, which would reduce the finance expense. Further, the company is rationalizing the cost structure by cutting administration and employee expenses to improve profitability. Alvarez and Marshal have been appointed as a consultant to advise on the future course.

Gati Ltd.

9

Growth aspirations & targets:

Source – Company, HDFC sec Research

Gati Ltd.

10

The company has decided to divest the fuel station business by FY22. New management has focused on the core business (express

logistics and SCM) and turning around the business.

Diversified clientele

Gati has a diversified client base which helps mitigate the risk of revenue concentration from few clients. A diversified client base from

different sectors can help reduce the impact of a slowdown in any one sector.

KEA = Key Enterprise Accounts

Gati Ltd.

11

Source – Company, HDFC sec Research

Gati and Allcargo partnership adds a new level of strength to the former’s offerings owing to the latter’s expertise and leadership in

various logistics verticals like NVOCC, container freight station and inland container depot operations, contract logistics, project logistics

and warehousing. Gati’s customers can now explore all of these. In addition, its customers also stand to benefit from the opportunity to

tap into Allcargo’s global network that operates through more than 300 offices in over 160 countries.

Gati Ltd.

12

Launch of project “Avvashya”

Project Avvashya is the transformation project which aspires to ‘Redefine Gati’ by channelizing the team’s spirit to drive growth and

efficiency, and thereby optimise sales, operations, and processes. These efforts are expected to help the company consolidate its position

as India’s premier express distribution company and grow into a digitally-enabled, customer-focused, futuristic organisation working on an

asset-light business model.

What could go wrong? Internal challenges (change of ownership and management of Gati):

Post takeover by Allcargo logistics in 2020 remains to be seen how growth and margin expansion pan out over medium term. Strong

network scale could allow correction of past errors without ceding market share.

Weak balance sheet Gati has lower interest coverage with a below-average return ratio. Also, the company has lower profitability; if this continues, the balance sheet would remain weak, going ahead.

Gati Ltd.

13

Source – Company, HDFC sec Research

Delay in divestment of fuel business The company has decided to divest the fuel station business by FY22E. If there is any delay in sale proceeds receipts, the debt repayment schedule could be disturbed. COVID-led slowdown hampers revenue Political disturbances and CAA protests created problems for the company in pre-COVID times and post-COVID, lockdowns and economic slowdown have impacted its revenue adversely. The second wave of COVID-19 has again disturbed the movements of goods, which has an adverse impact on revenue. The economic slowdown has affected the company’s growth and its capacity utilization, which is a key factor to improve profitability and hike prices since lower capacity utilization reduces both profitability and price realization.

The company may find it difficult to maintain the current return ratios after it incurs the capex it has planned, if it is unable to scale up revenue and profitability to the same or larger extent.

Even within the organized space, the company faces competition from existing players and PE-backed new players.

Gati Ltd.

14

Inability to invest in future technology/analytics may imply weakening competitive positioning. Company would have to hire more professional talent in order to be ahead of the curve. Client concentration: Since the company is into e-commerce logistics, majority of the revenue generated is from a couple of major e-commerce players. During FY20 Amazon alone has contributed around 32.50% as against 29.05% in FY19. Top 8 players contribute around 73% of the total revenue from express distribution.

About the company Gati Ltd (Gati) was established in 1989 by Mr Mahendra Agrawal; it offers a wide range of services like express distribution, supply chain management solution, e-commerce logistics, managed value-added transportation services (MVATS), freight forwarding and fuel station. The express distribution and supply chain (EDSC) division, which was operated by Gati earlier, has been transferred to Gati Kintetsu Express Pvt Ltd (GKEPL), which is a joint venture between Gati and Kintetsu World Express Inc - Japan’s leading logistics provider - with an equity contribution in the ratio of 70:30 respectively. In 2020, Allcargo Logistics Ltd acquired a stake and became a promoter of the company.

Gati Ltd.

15

Industry The Indian logistics industry is highly fragmented, characterized by the presence of numerous unorganized or regional players, who account for ~90% of it. This industry’s size is ~Rs.25,000 cr (as of FY19), which is expected to grow at ~10% CAGR every year until 2025.

Source – Deloitte, HDFC sec Research

Surface logistics continues to grow vis-a-vis air logistics due to the difference in the cost of booking shipment through the two. Air logistics

is 4-5 times more expensive than surface logistics. The cost of the bulkier shipment is higher in air transport than in surface transport,

which further makes the latter more attractive. State and central governments have made robust investments in schemes such as

Bharatmala to upgrade road networks. This would improve the growth of surface logistics. Also, major value-added services such as door-

to-door delivery of shipments in a time-sensitive manner with real-time shipment tracking facilities fuel the growth of the Indian logistics

industry.

Gati Ltd.

16

Source – Company, HDFC sec Research

Large players have a key advantage over regional players as they have pan-India networks of sorting centers and branches and better

infrastructures with better technologies. Also, it is expected that large national players would gain market share from the regional players

over time.

The elimination of inter-state check-posts under the GST norms has improved the average truck speed, productivity, demand for grade-A

warehouses, and demand for value-added services. This should further reduce the turnaround time for surface logistics players. All

consignments worth over Rs 50,000 require e-way bills, which have increased the compliance burden for the unorganized players. The

government has already granted infrastructure status to the logistics industry and created a separate division for it within the ministry of

commerce. This move is expected to ease access to financing for logistics companies.

The recent Union Budget witnessed the allocation of Rs.1.7 lakh cr towards transport infrastructure, promising to monetize 12 highways,

spread over 6,000 kilometers, by 2024. This is likely to further benefit freight movement and transportation costs.

Gati Ltd.

17

B2B express is a proxy to manufacturing growth. With increased focus on domestic manufacturing through Atmanirbhar Bharat, PLI

schemes, etc. B2B express, which forms about half of express industry, could grow 14-15% CAGR over FY20-25E, perhaps up to FY30. This

is due to higher formalization/manufacturing given reduced tax rate/PLI schemes. B2C express growth will follow ecommerce and may

post 28-30% CAGR over FY20-25E as mobile penetration increases from present one third and ecommerce rises further in tier 2/3 cities.

With existing hub-and-spoke model, SME share can be increased further through branch expansion.

In B2B express, majority of clients are involved in manufacturing and engineering. Some key industries include electronics, auto

components, textiles and pharma.

The top 5 players (all with national presence) to have 50-55% market share in B2B express logistics and these have have significant

advantages of network scale and pricing. Having said this there exists a longer tail of regional players across national routes.

B2B express is driven more by network presence and relationships. New entrants would have to incur significant capex in the short run

possibly with suitable discounts to build sufficient volumes; spend higher upfront capex (especially towards processes/technologies). All

this would lead to significantly lower return profile.

Peer comparison as per FY21P financial Company CMP (As on 18-06-2021) Mcap (Rs. Cr.) NPM% RoE% RoCE% D/E(x) TTM P/E (x)

Gati 146 1899 -19 -36 0 0 NA

TCI Express 1446 5553 12 26 34 0 55

Blue Dart Express 5589 13246 3 22 20 2 113

Mahindra Logistics 574 4116 1 5 9 0 137

*Bloomberg estimate, NA=Not Availab

Sales (Rs. Cr) EBIDTA Margin (%) PAT (Rs. Cr)

FY20 FY21E FY22E FY23E FY20 FY21E FY22E FY23E FY20 FY21E FY22E FY23E

Gati 1712 1314 1653 1588 2 2 5 8 -62 -228 45 77

TCI Express 1032 844 1105 1220 12 16 14 14 89 101 110 122

Blue Dart Express* 3175 3288 3707 4160 15 21 21 21 -42 102 193 268

Mahindra Logistics 3471 3264 3849 4599 5 4 5 5 55 30 68 103

Gati Ltd.

18

Financials Income Statement Balance Sheet

(Rs Cr) FY18 FY19 FY20 FY21P FY22E FY23E As at March FY18 FY19 FY20 FY21P FY22E FY23E

Net Revenue 1736 1863 1712 1314 1653 1588 SOURCE OF FUNDS

Growth (%) 2.7 7.3 -8.1 -23.2 25.8 -3.9 Share Capital 21.7 21.7 24.4 24.4 24.6 26.0

Operating Expenses 1659 1769 1676 1287 1564 1469 Reserves 707 703 719 501 530 644

EBITDA 77 94 36 27 89 120 Minority Interest 114 122 104 85 85 85

Growth (%) -19.6 22.3 -62.2 -23.8 228.0 34.2 Shareholders' Funds 843 846 847 610 640 755

EBITDA Margin (%) 4.4 5.1 2.1 2.1 5.4 7.5 Lease Liabilities 69 60 57 57

Other Income 77.9 16.0 13.3 10.4 11.0 15.0 Long Term Debt 216 169 97 26 26 26

Depreciation 30.0 29.5 43.7 40.1 35.6 36.1 Long Term Provisions & Others 13 15 9 11 0 0

EBIT 125 81 5 -3 64 98 Total Source of Funds 1071 1030 1022 708 723 839

Interest 47.0 45.3 53.6 45.1 29.8 24.0 APPLICATION OF FUNDS

Exceptional Items -23.6 0.0 0.0 204.9 0.0 0.0 Net Block 996 1001 1023 648 648 618

PBT 102 35 -48 -253 35 74 Non-Current Investments 4 2 0 0 0 0

Tax 15.3 12.4 35.8 -6.6 8.7 18.7 Deferred Tax Assets (net) 3 4 6 24 24 24

RPAT 86 23 -84 -246 26 56 Long Term Loans & Advances 83 104 104 92 96 104

Minority Int. -5 5 -22 -18 -19 -21 Total Non Current Assets 1086 1112 1134 764 768 746

APAT 91 18 -62 -228 45 77 Current Investments 0 0 78 0 0 0

Growth (%) 287.5 -79.9 -439.2 LL LP 69.5 Inventories 9 12 10 4 9 9

EPS 7.0 1.4 -4.8 -17.5 3.5 5.9 Trade Receivables 243 239 205 195 235 213

Short term Loans & Advances 69 71 69 20 22 24

Cash & Equivalents 42 48 49 56 67 172

Other Current Assets 7 8 40 197 178 210

Total Current Assets 370 377 450 473 511 628

Short-Term Borrowings 105 114 154 145 134 96

Trade Payables 124 149 116 89 120 113

Other Current Liab & Provisions 155 194 255 269 274 296

Short-Term Provisions 1 2 37 26 29 30

Total Current Liabilities 385 459 563 530 556 535

Net Current Assets -15 -82 -112 -56 -45 93

Total Application of Funds 1071 1030 1022 708 723 839

Gati Ltd.

19

Cash Flow Statement Key Ratios (Rs Cr) FY18 FY19 FY20 FY21P FY22E FY23E FY18 FY19 FY20 FY21P FY22E FY23E

Reported PBT 54 35 -48 -253 35 74 Profitability (%)

Adjustment 32 67 108 298 54 45 EBITDA Margin 4.4 5.1 2.1 2.1 5.4 7.5

Working Capital Change 38 20 -4 12 30 -40 EBIT Margin 7.2 4.3 0.3 -0.2 3.9 6.2

Tax Paid 0 -24 -27 -8 -9 -19 APAT Margin 5.0 1.2 -4.9 -18.7 1.6 3.5

OPERATING CASH FLOW ( a ) 125 98 28 49 111 61 RoE 13.4 2.5 -8.5 -35.9 8.4 12.6

Capex -25 -36 -26 -187 0 30 RoCE 10.7 7.2 0.5 -0.3 8.1 11.2

Free Cash Flow 100 62 3 -138 111 91 Solvency Ratio

Investments 7 -8 -60 -242 -4 -8 D/E 0.4 0.4 0.3 0.3 0.3 0.2

Non-operating income 2 2 2 164 11 15 Interest Coverage 2.7 1.8 0.1 -0.1 2.2 4.1

INVESTING CASH FLOW ( b ) -15 -42 -83 -265 7 37 PER SHARE DATA

Debt Issuance / (Repaid) -43 5 34 -515 -11 0 EPS 44.6 1.7 -5.7 -21.0 4.2 7.1

Interest Expenses -47 -45 -46 -317 -30 -24 CEPS 11.2 4.4 -1.5 -15.4 6.6 8.7

FCFE 10 22 -9 -970 70 67 BV 67 67 61 48 51 62

Share Capital Issuance 0 1 100 74 0 1 Dividend 1.0 0.8 0.9 0.8 0.5 0.8

Dividend 0 0 0 -10 -6 -10 Turnover Ratios (days)

FINANCING CASH FLOW ( c ) -90 -39 88 -769 -47 -33 Debtor days 51 47 44 54 52 49

NET CASH FLOW (a+b+c) 19 18 33 -985 71 65 Inventory days 2 2 2 2 2 2

Creditors days 22 28 29 29 28 28

Working Capital Days 31 21 17 27 26 23

VALUATION

P/E 20.8 103.4 NA NA 41.8 24.7

P/BV 2.2 2.2 2.4 3.0 2.9 2.4

EV/EBITDA 22.4 18.3 48.5 63.7 19.4 14.5

Dividend Yield 0.7 0.5 0.6 0.5 0.3 0.5

Dividend Payout 2.2 56.7 NA NA 14.3 13.5

(Source: Company, HDFC sec)

One Year Price Chart

Gati Ltd.

20

Disclosure: I, Jimit Zaveri, (MBA - Finance), authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of

publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Research Analyst or his relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month

immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest.

Any holding in stock – No

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith fro m sources believed to be reliable.

Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information

purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction,

availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or

indirectly, for any purposes or in any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced

by foreign currencies effectively assume currency risk.

It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or

other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company( ies) or may have any other potential conflict of interests with respect to any recommendation and other related

information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds,

changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities

of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or

merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business.

HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of

publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment b anking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information

presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in

connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066

Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600

HDFC Securities Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA Corporate Agent License No.: CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN -

U67120MH2000PLC152193

Mutual Funds Investments are subject to market risk. Please read the offer and scheme related documents carefully before investing.