HDFC BANK LTD. - Ashika Group

84

Market Overview Prominent Headlines September 2019 Q&A with CIO Mutual Fund Overview Stock Picks Monthly Insight Performance Valuation at a Glance Crude oil update Sector - Automobile Economy Review Economy Chart Book Management Meet Note Technical View Market Diary Commodity monthly round-up Book Review World Economic Calendar IN SIGHT October 2019 HDFC BANK LTD. | SIEMENS INDIA LTD. | INDIAN HOTELS COMPANY LTD. Q&A WITH Mr. Sachin Relekar, Chief Investment Officer - Equity, LIC Mutual Fund ReforMS galore

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of HDFC BANK LTD. - Ashika Group

Market OverviewProminent Headlines September 2019Q&A with CIOMutual Fund OverviewStock Picks

Monthly Insight PerformanceValuation at a GlanceCrude oil updateSector - Automobile

Economy ReviewEconomy Chart BookManagement Meet NoteTechnical View

Market DiaryCommodity monthly round-upBook ReviewWorld Economic Calendar

INSIGHTOctober 2019

HDFC BANK LTD. | SIEMENS INDIA LTD. | INDIAN HOTELS COMPANY LTD.

Q&A WITH Mr. Sachin Relekar,

Chief Investment Officer - Equity, LIC Mutual Fund

ReforMS galore

Marketoverview1 41 Economy

review

6 Q&A Mr. Sachin Relekar, Chief Investment Officer - Equity, LIC Mutual Fund

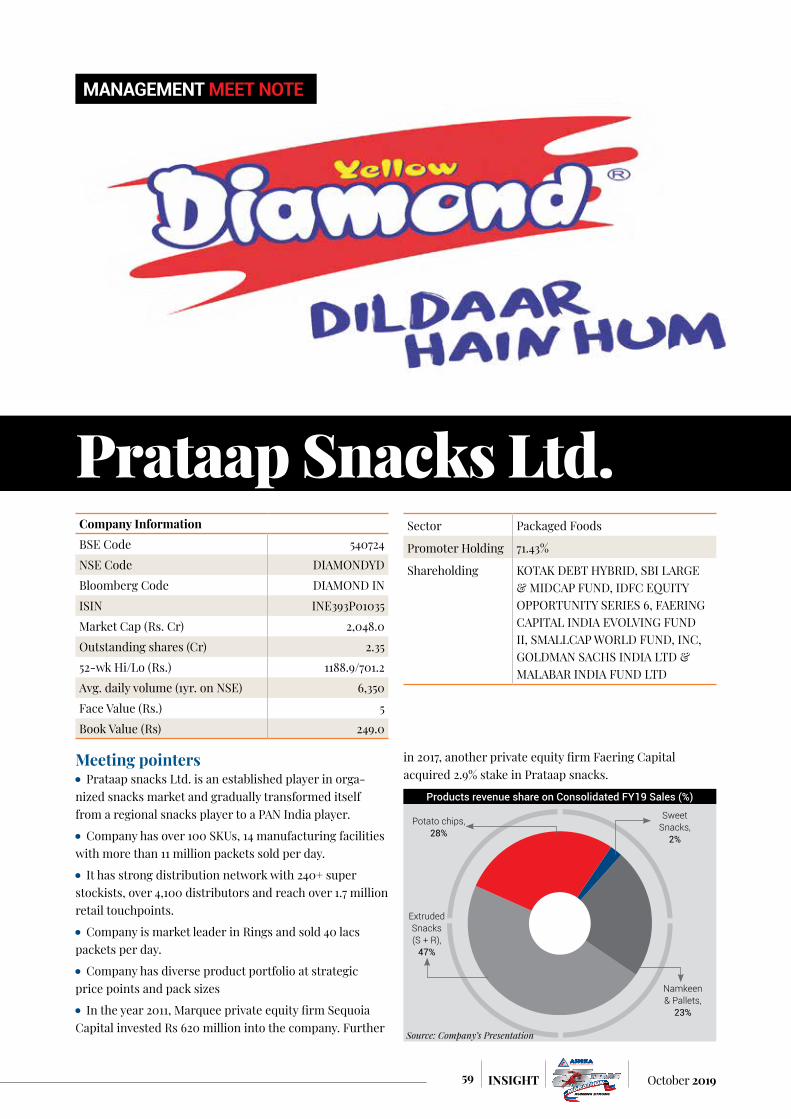

59 Managementmeet note• Prataap Snacks Ltd.

15 Stockpicks• HDFC Bank Ltd.• Siemens India Ltd.• Indian Hotels Company

Ltd.

28 Valuationat a glance

70 Marketdiary

74 Book review - Subscribed by Tien Tzuo

Economychart book 48

Mutualfund overview 10 Technical

view 63

Monthlyinsight performance 24

Crude oil update 30

Commoditymonthly

round-up 71

Worldeconomic calendar 78

Sector -Automobile 34

Prominent headlines September 2019 4PROMINENT

HEADLINES

INSIDE THIS ISSUE

MarketOVERVIEW

1 October 2019INSIGHT

...the government came out with a surprise package, a surgical strike on bears as the government announced a reduction in the corporate tax rate from ~34% to 25.17% (inclusive of surcharge & cess). Domestic corporates now have an option to pay tax at 22% if they give up all the exemptions. This is a massive trigger to revive the animal spirits more importantly, resurrecting sentiments that were down in the dump yard.

Subdued corporate earnings growth, shortfall in GST collections, low IIP/GDP growth numbers, continuous

FPI outflows (from equities) and steep

decline in broader stock indices were continuously hitting the headlines. Negative rhetoric surrounded every part of the economy as domestic concerns from low demand to job

losses have been hogging limelight and urging for urgent government intervention. Not to mention, there were risks associated with chances of global recession, a fall out of trade

2October 2019 INSIGHT

wars. Taking chances on the soft sensitive situation (over job losses), industries like auto & FMCG have been urging the government to reduce GST rates. However, reduction of GST, in the face of already diminishing GST collections, would have implied drastic divergence from fiscal consolidation, fearing rating downgrade. Besides, it was quite evident, that if the government went forward with GST reduction in one industry, others will follow suit, thus the government needed to find a solution which would be impartial and universal thus benefitting all. This is after economists and experts have constantly blamed the government for demonetization and following it up with implementation of GST and failing to create adequate employment. The final nail in the coffin came in the form of liquidity crisis engulfing the NBFC sector and thus slowing down consumption particularly for the auto and consumer durables sector. The government was taking baby steps with a series of announcements made by Finance minister (FM) every week to address the issues plaguing the economy. For the last month or so, the FM announced withdrawal of surcharge on capital gains on super rich & FPIs, an upfront Rs.70,000 crore equity infusion into public sector banks (PSBs) to boost lending,

sops for export sector and Rs 20,000 crore fund for housing sector, mega merger of PSBs. However, these steps although important, but failed to make any significant boost to the sentiments as well to the corporate earnings. Prompting to come out something big, the government came out with a surprise package, a surgical strike on bears as the government announced a reduction in the corporate tax rate from ~34% to 25.17% (inclusive of surcharge & cess). Domestic corporates now have an option to pay tax at 22% if they give up all the exemptions. This is a massive trigger to revive the animal spirits more importantly, resurrecting sentiments that were down in the dump yard. To provide fillip to private investment and government’s ‘Make in India’ initiative, another new provision has been inserted in the Income Tax Act with effect from FY20, which allows any new domestic company incorporated on or after October 1, 2019 to make fresh investment in manufacturing, an option to pay income tax at 15%. This benefit is available to companies that do not avail any exemption/incentive and commences their production on or before March 31, 2023. The effective tax rate for these companies shall be 17.01% inclusive of surcharge & cess. This is a master stroke from the government being impartial to all

industries and all major shortcoming haunting the economic growth has been addressed with a single move. According to CRISIL, the reduction in tax rate could help the top 1000 listed companies save Rs 37,000 crore this fiscal year. Thus, there is a straightaway gain at the bottomline, resulting in improving their return on equities (ROE) of all companies. This incremental cashflows to the corporate is at the discretion of the management if they want to pass it on to customers or channelize to debt reduction or put into incremental investments to increase capacity. Other announcements included removal of FPI surcharge on derivatives, removal of 20% tax on buybacks for listed companies for announcements were made before July 15, 2019. For those continuing to opt for exemptions, Minimum Alternative Tax (MAT) has been reduced to 15% from existing 18.5%. Based on the government estimates, the revenue shortfall for the government could be ~Rs 1.45tn, that needs to be filled up by divestment, most probably. Thus, the fiscal stimulus pegged at ~0.8% of GDP is well thought of to address multiple issues. After the tax cut, India has come at one of the lowest taxed nation (22%) and certainly lowest for new companies (15%).

How Corporate India will be taxed (in %)

How Corporate India will be taxed (in %)

New mfg cos.

Existing companies Min. Alternate Tax

Without exemptions & deductions at

new rates

With exemptions and deductions at existing rates

Cos. with turnover <Rs 400 crores in FY17-18

Others New rate Old rate

Corporate tax rate 15.00 22.00 25.00 30.00 15.00 18.50

After surcharge

Total income Rs 1-10 core16.50 24.20

26.75 32.10 16.05 19.80

Total income> Rs 10 crore 28.00 33.60 16.80 20.72

After health & education cess

Total income< Rs 1 crore

17.16 25.17

26.00 31.20 15.60 19.24

Total income Rs 1-10 core 27.82 33.38 16.69 20.59

Total income> Rs 10 crore 29.12 34.94 17.47 21.55Source: Hindubusinessline, rates are applicable for domestic companies

3 October 2019INSIGHT

With just one stroke, the government has (a) upgraded earnings for corporates (b) given impetus to private capex (c) made India globally attractive, with the lowest taxed nation (for new investments) which will attract FDI (d) a fillip to ‘Make in India’ initiative by the government. However, the move will not result in immediate demand revival, for that to happen, government needed to lower personal income taxes or may be a GST cut (considering that it is fully passed on by manufacturers). However, research shows that consumption backed by investment growth is a lot more sustainable than consumption fueled by credit amid falling investment & savings. Essentially, during the last five to six years, India’s consumption was driven by credit, and this jinx was broken after the liquidity crisis hit prominent NBFCs. Thus, the revival of consumption will be a long-drawn process however will be sustainable if backed by higher capex, higher job generation and thus translating into higher demand. This is where the government needs to keep on improving the ease of doing business in India with reforms on

land & labour apart from land and labour reform, agricultural reforms, infrastructure reforms, direct tax code (DTC), financial sector reforms and the simplification of GST will be clear agendas for Modi 2.0. In an recent International event Modi has wooed investors and promised for further tax and market reforms to make India even more competitive. The low interest environment will also help fuel demand for project loans, thus the credit growth has every chance of improvement from here on. This is where the whole focus will shift towards the next monetary policy by RBI. So far, the RBI has already done its part and cut rates four times this year, by a cumulative 110 basis points, to spur growth. However, the big stimulus by the government also comes with added risks of fiscal slippage, which might push the bond yields higher. Rupee might well come under pressure after the exuberance in the stock markets dies down. However, if FPIs make a comeback, this could very well result in some appreciation. The RBI might very well wait on the sideline and watch out how the rates are transmitted by the banks after RBI’s strong mandate to

the banks to link floating rate loans to external benchmarks. Besides, there will be some clarity from the government until next monetary policy meet, with regards to the fiscal position or the counter moves to address the shortfall together with the bond yields & INR. The government might very well cut down on public expenditure to consolidate its fiscal balances which again will be growth inhibitive. For instance, the fiscal boost in 2008–09 proved to be quite effective in lifting aggregate demand. It was led by both tax cuts together with expenditure ramp-up; backed by massive monetary easing which was also concurrent with global fiscal stimulus which lifted capital inflows. We could be very well moving to period of easy global liquidity as US central bank has reduced rates twice this year, European central bank has lowered interest rates to their lowest ever level of -0.5% and announced stimulus of €20 billion of bonds every month from November onwards. Meanwhile inversion in yields is a common phenomenon now in developed economies which leaves the policymakers much to ponder over.

Paras BothraPresident - Equity ResearchEmail - [email protected]: 022 6611 1704 / 1786Mobile: 98203 97061

Country-wise effective corporate tax rate for 2019 (%)India (New Companies) * 15%Hong Kong SAR 17%Singapore 17%Switzerland 18%UK 19%Russia 20%Taiwan 20%Thailand 20%Vietnam 20%Sweden 21%India* 22%Malaysia 24%China 25%Indonesia 25%South Korea 25%US 27%Germany 30%Japan 31%France 31%Brazil 34%

Source: Media articles, KPMG

If you want to invest in a market where there is scale, come

to India. If you want to invest in a market where the latest trends and features are appre-ciated, come to India. If you want to invest in start-ups with a huge market, come to India. If you want to invest in one of the world’s largest infrastructure ecosystem, come to India - Narendra Modi, Prime Minister

To make the econ-omy stronger, the government

has taken all measures and I want to say that the fundamentals of the country’s economy are strong. We are not in any crisis. Some reactions from non-banking financial companies (NBFCs) are there. But we are addressing all issues - Prakash Javadekar, Union Minister

We are looking at 100 billion dollar investment

by Saudi Arabia in the infrastructure sector - Amit Kumar Ghosh, Joint Secretary for Highways

Huge export potential exists in chemical and

allied sector and it should make a combined effort to set higher goals and aspire for extraordinary results - Piyush Goyal, Commerce and Industry Minister

We need to think what kind of innovation we

need to undertake to attain a high trajectory growth. The government is active, the fundamen-tals of Indian economy is intact and we will continue to do whatever it required to take India back to high trajectory growth rate - Amitabh Kant, Niti Aagoy CEO

From a valuation point of view, market is reason-

ably cheap in small and mid-caps, fairly valued in large caps and expensive in super-large caps. However, the confidence on earnings growth is not coming through because of variety of issues - Nilesh Shah, managing director at Kotak Mahin-dra Asset Management Company

In spectrum auctions, for sub-1GHz, it is possible that someone

might want to pick up some spectrum for 4G but 5G pricing is still the main challenge. Our members have indicated that at the current prices, it does not make sense to invest this kind of money - Rajan Mathews, Cellular Oper-ators’ Association of India (COAI) Director-General

In the digital sphere itself, we are keen to make India a $1 trillion

economy. India is emerg-ing as a big center for electronic manufacturing. From just two mobile fac-tories in 2014, India now has 269 mobile factories in 2019 - Ravi Shankar Prasad, Union minister

Indicators are suggest-ing that stocks have bottomed out, partic-

ularly midcaps, and this is a good time to invest. We have a much better monsoon this year. Banks are flushed with funds. Bank credit will grow by 15% and we have come out of NPA cycles. We are seeing the beginning of a turnaround, but it will be slow - Rakesh Jhunjhun-wala, ACE investor

We are most bullish on the Indian market

because of the Modi reform, but also because of the incredible growth potential of over a billion people being lifted out of poverty. The consumer market in India will be growing rapidly and drive economic growth in years to come - Mark Mobius, founder of Mobius Capital Partners LLP

India’s move to cut corporate tax rate will push growth to higher

levels. It is going to give a boost to companies in India and also companies that want to invest in India. This will definitely attract capital but more importantly I believe it will boost the economic growth in the country because with more investments, you are going to get more growth - Mark Mobius, founder, Mobius Capital Partners

PROMINENT HEADLINES SEPTEMBER 2019

4October 2019 INSIGHT

We are not a member of the Nuclear

Suppliers Group and due to this we dont really have the ability to get the necessary fuel supply for producing nuclear energy and if India gets a solu-tion on this front, then the country could be a model in this area for the rest of the world - Naren-dra Modi, Prime Minister

It is a very bold measure, and it is a highly positive

step. India’s corporate tax now becomes very competitive compared to other emerging market economies in ASEAN and other parts of Asia. So far as international investors are concerned, so far as FDI is concerned, I think India stands definitely in a very competitive posi-tion, and would be able to attract higher invest-ments - Shaktikanta Das, RBI Governor

From the latest eco-nomic numbers, we can see the growth

is slowing down. India has many other attributes but the primary thing that attracts foreign money is growth - Mark Matthews, MD, Julius Baer

There are no plans to revise the fiscal deficit target for

the current fiscal at the moment and a decision in this regard will be taken before the annual Budget - Nirmala Sitharaman, Finance Minister

The Rs 1.45-lakh crore tax giveaway is unlikely to widen

the fiscal deficit much, as the shortfall will be met through increased tax collections due to higher growth. Direct and indirect tax revenues are expected to go up with growth picking up after these tax cuts - Rajiv Kumar, Niti Aayog Vice Chairman

When you don’t understand the #GRAVITY of

the economic slowdown, the words stumble and reasoning becomes feeble. If someone thinks that maths doesn’t help understanding gravity and economics, then it’s a sign that you are hiding the actual statistical data. Newton must be smiling - Raghuram Rajan, former RBI governor

Midcap and smallcaps have turned attractive

on a standalone basis and even if you were to drastically reduce your assumptions on growth there are good number of pockets of mid and small-caps that are reflecting value and that is what the market is starting to realise - Taher Badshah, chief investment officer for equities at Invesco Mutual Fund

The credit from banks must grow by 12 per cent every year to meet the Centre’s target to achieve a $5-trillion economy within the next five years and the step taken for mergers of the PSBs is in the right direction to meet the goal - Dinesh Kumar Khara, SBI MD

The move to reduce the corporate tax rate a “big revolutionary step” for investment, and was called as a historic move by businesses. This is just the beginning, there’s more to come. It’s a golden opportunity to partner India … The government of India respects wealth creation - Narendra Modi, Prime Minister of India

5 October 2019INSIGHT

6October 2019 INSIGHT

With the recent incident in Saudi Arabia and volatility in crude price, how do you read this whole situation and what will be the impact here in India? Crude supply side shocks is something which the economy doesn’t want at this point of time and this is the last thing which anybody will prefer because as such there are lot of macro headwinds both globally and domestically. We are also going through a cyclical domestic slowdown while globally there are trade talks which is kind of not settling down quickly. We have also seen Europe going through quite a slow pace. So, at this point in time this is the most negative event which can happen but at the same time what we have to understand is that the extent and the period for things to normalize considering that the world is quiet well supplied with the oil. Now this shock, the spike which is there could be a temporary thing or this could be a longer-term thing also. The

question is not about technically restoring production to the same level. The bigger question is about the risk perception regarding the safety of oil supply and logistics over a longer period of time.

Overall, on the longer term our expectation on oil prices are quite benign just because if you look at the portion of EVs which are likely to rise over a period of time in the automobile sector. Therefore, we believe structurally oil prices will remain favourable from India’s perspective but these kind of phases will happen and this is something one has to take into account. One should look at is not just about the short term impact but the longer term impact. If there is actually a spike in the risk perception about the safety of oil, logistics and supply issues then this could be major issues but otherwise the kind of noises or kind of comment made by Saudi, US and what other global media is reporting we are not overly concerned about it.

So, u meant to say that this oil prices hike which has happen or the sharp spike in oil price is going to be quiet temporary in nature? And EV is going to be the real thing in the long term?The role of oil in the global economy is anyway declining and that will decline even faster as EV becomes cheaper and the production increases. This will obviously reduce the role of oil supply in the global economy plus shale oil production is now actually stabilizing. In fact, US has become a net exporter of crude products. Before this event, Saudi has taken a voluntary cut of 1.2 mbpd to support oil price. So, there is already an excess of oil supply in the world. However, because of geopolitical issues if the risk perception about the safety of logistics and continuity of supply changes then a risk premium could be added to the oil price.

Do you perceive that EVs are going to be a big challenge for the automobile industry and what is your take on massive slowdown in the automobile sector? Globally EV is a disruptive force, everybody is talking about it, OEMs are investing hugely behind getting this stabilized in the portfolio. But in terms of its share fleet size, and it is still not that mainstream anywhere in the world. There is a lot of talk and lot of investment which is happening behind it and companies are trying to adopt that technology because eventually the infrastructure for supporting the EVs will also come in place. In India government is giving a lot of push and supporting it in ways such as GST rate on EV are less, interest rate subvention etc. From economy point of view reliance on the crude oil import goes down and in longer term it is far better option because EVs will have lower cost of ownership as number of parts are less. However, before it becomes the mainstream it also has to become affordable and has to be supported with volumes. The other aspect of it is, let’s assume that EVs have become mainstream, the demand for crude oil transportation fuel will go down. That means it will become cheaper and if it becomes so cheap to a point that even then the EVs become unaffordable,

Q&A WITH CIO

Mr. Sachin Relekar - Chief Investment Officer - Equity, LIC Mutual Fund

7 October 2019INSIGHT

so there is always a competition between the two. Some of the global analyst reports saying that the sales of EVs will take over the sales of IC engine vehicle maybe somewhere in between 2024-25. These are only blue paper as of now which have been made some long-term projection. So, we are quite far away from that point as of now and companies will get time in adopting the new technology. But one thing is very clear, the investment requirement to adopt to EV or migrate to EV platform is going to be huge and therefore the players with scale i.e. companies having larger balance sheet and with investment capability will be able to adopt to the transition phase better. The smaller or marginal players will have bigger challenges in migrating to that. I think in terms of two wheelers, and scooters that the transition will be much faster because already we are seeing prototype concepts are working very fine and as prices come down adoption will also be faster. For passenger vehicles India might take a little longer because our infrastructure will also take time to come into place but as it becomes a mass phenomenon then adoption will become faster. But this is all subject to lot of other variables and factors which should be play out. It’s not that EVs has been invented now. Even in early 1920s there was the concept of EV, however it was not being adopted because the infrastructure for IC in terms of fuel availability came up, infrastructure for EV didn’t came up. But the technology now is much more refined, prices are falling so convenience level has improved but one must be watchful about it.

Crude oil prices also plays a major role in EV taking off, so you have any understanding about the fact that what is the crude oil range likely to be, taking into account the availability of shell gas?In case of shale gas / oil a marginal cost of production is important. What in the initial phases the shale gas production was on a lower scale so marginal cost of production was higher. However, gradually marginal cost of production has come down as the technology improved. In case of EVs also it’s too early to say that. EVs technology is becoming competitive

gradually. It is improving as not only the cost of battery is coming down but also the range (Km travelled per charge) has been improving. The technology is improving rapidly. Therefore, the breakeven point at which EV becomes competitive for a crude oil price would be shifting downward much faster.

So, it is all going to be a match of crude oil prices coming down and EV volume rising.Like I said at the beginning, some of the global analysts and blue papers suggested that incremental sales from EVs taking over IC engine sales globally will come somewhere in 2024-25 though IC engines will be in play and it will not go away completely because there will be some vehicle which will be more affordable in IC engine range v/s EV, both can co-exist.

Do you think the traditional Indian automobile companies are well equipped to transition themselves or realign their business model?We are talking more of PVs and 2 wheelers; CVs is a different ball game it will take little longer also for the OEMs. All PV players as such has some investment into the EVs and there is enough time for them for transition and they will transition that won’t be a challenge, the question is how much investment you would require and will that be making sense from a return on capital point of view for a longer period of time.

RBI has slashed interest rates by 110 bps this year and probably there are one or two more in the anvil, however the transmission didn’t happen as smoothly. How do you see and interpret the recent mandate to link floating rates to external benchmarks in this regard? Transmission has already happened for few segments, for instance, home loans are available cheaper at around 8%, probably the lowest in last 10 years. Housing loan has large shares of retail loans and is the most significant. However, unsecured loans will not get cheaper due to inherent risks involved as the risk premium takes care of the asset quality issues. In terms of transmission, the real concern would be the velocity or the

credit offtake and not just about the rates. Now, credit offtake is slower because of slower investment cycle. That’s, a real concern. For a good quality borrower decent interest rates are available. As of now, interest rates are more reflected into capital market asset prices, wherein some of these are at very high premium compared to historic levels.

However, low interest rates are not benefitting the economy because of the slowness of the investment cycle. We have gone through lot of transition in the last 2-3 years which cannot be ignored such as the demonetization, followed by GST. It had their impact on the broader economy. As these effects fade off, then the momentum will gradually come back. As the GST compliance improves, the GST revenues will also improve, aiding government finances and driving investment cycle and that’s where the impact of low interest regime will be pronounced as this will drive government capex. As government finances improve, they will have more funds to implement projects on a larger scale and the private capex will eventually come in to play. Low interest rates alone will be less effective if the fiscal position is tight. The impact will also be evident in the form of weaker currency. Therefore, the in direct tax buoyancy needs to pick up to make the fiscal position strong. However, the GST system is still young with lot of things getting implemented like that of the E-way bill and a lot of compliance work is going on. GST is a technology led platform. Besides, there is always a part for technology enablement and making the system more transparent in terms of refunds, timelines etc.

Coming back to interest rate transmission, interest rates for all segments cannot come down altogether since risk premium is dependent on consumer to consumer. For instance, microfinance rates won’t come down drastically, this is a high-risk segment and so these loans will be priced higher because of the risks involved. Credit card interest rates, two-wheeler loans, these products are designed in such a way that the rates will not come down to very low levels considering risk.

8October 2019 INSIGHT

However, for corporates with strong credit rating, they will be beneficiary of lower interest rates. Till now, banks were reluctant to lower deposit rates but it is now coming down, thus transmission will now happen however it is also dependent on the risk premium.

Although the general feeling is that NPAs have peaked out, however new NPAs crop up every now and then for the corporate facing banks. How do you see the NPA cycle now?There is no new wave of NPAs. Large ticket size NPAs are either in NCLT or undergoing through resolution stage. Besides, large ticket size NPAs happened in two or three sectors - metals & mining, power and road & construction. Some of these are all identified and stressed loans for banks actually peaked out in 2018-19 and these have been recognized and provided for, thus resulting in losses for banks. The entire pain went for eight quarters. Post which we are going through a slower kind of economic phase so there are these NPAs which are cropping up. However, incremental issues in loans are not very large, and these are taken care of in the provisions for banks. Some credit costs are part of business of banks and it will not come down to zero. At the same time, some of the mid-corporate entities which are slipping as NPAs, the quantum is certainly not very large and they are either having problems to dispose of assets or going through a cash crunch because of the slow state of the economy. However, it depends on the size of the bank, for a small bank these NPAs as a percentage could still have a major impact but for a large bank, this not very concerning. Also, some of this is seasonal in nature (agri loans) and will get addressed as we move on.

Post Altico incident, how do you see the NBFC space panning out. Is asset/liability mismatch issue still haunting the NBFC space/housing finance companies (HFC)?Asset liability mismatch is one thing. Bigger problem is if your loan becomes non performing. If you are building a long-term asset book based on short term funding (like CPs), the mismatch is in the public domain.

However, that adjustment is going on particularly for those HFCs/NBFCs which have access to the capital markets. Some of them who were not able to rebalance their books had to run down their asset book. However, it could impact asset quality itself.

The residential housing products which are priced reasonably there is decent demand for it. The issue is with the premium products in relation to specific micro markets. On the other hand, commercial real estate is doing relatively better. Post RERA and GST, there is a migration towards brands and some of the companies which are listed, better corporate houses have witnessed an increase in sales volumes. Some of the builders or developers who were not able to attract buyers on their own are getting into joint development agreement with better established brands. There is a formalization and consolidation of the market which is good from the longer-term point of view as this will bring in more transparency. So, the NBFC problem especially, asset-liability mismatch problems have been recognized. However, there could be incremental challenges ahead but any issues of large scale are unlikely to recur.

So, you say that whole of the NBFC issue is in public domain and nothing major is going to come up?Surprises will happen, I mean good thing is like we have gone through huge kind of churn in this but it has not led to a contagion which says a lot about the stability and the sturdiness about our regulation also. Besides, the way the entire exposure has been fixed so we have seen very large companies running down the entire book but we didn’t see the shocks spreading massively into the system which is actually a good thing to happen otherwise that could have been a different kind of problem altogether.

Coming down to the income level of the people and the consumption now has sharply slowed down so how do you see this consumption basket, the income level of the people and the unemployment talks?Unemployment is a very different subject. Consumption constitutes a

very large ~70% of GDP. Obviously, when there is economic slowdown the discretionary consumption will get affected. However, I am not too much worried from longer time frame because I believe that consumption will sort itself out. Consumer discretionary is also a very mixed picture. It’s basically a case to case where we are witnessing some consumer durable companies are growing with double digit volume. AC sales are up 40% in last quarter. There are categories which are under penetrated which are doing very well, and there are categories which are saturated like automobiles. Modern retail business in growing fast. FMCG is growing at slower pace which is also to do with the base effect they grew very fast after demonetization and the benefit of GST which came through. Personal income level is a matter of concern because there is inequality, also some section is actually going better and some are falling behind but that needs to be seen in terms of way the technology is playing role in this new economy which is lot more subject to disruption, lot more subject to so called mixed economy, that is something of a long term phenomena. India is a very young demography, will remain young for around 2040, so there will be a propensity for consumption and saving. Our income levels will keep growing higher, our productivity will improve once as some of the larger things like fiscal deficit starts improving , public infrastructure will get built up, technology will play a much bigger role , efficiency in the system will go up and the efficiency will lead to higher disposal income. For longer term our per capita GDP will actually improve, so once it crosses the threshold of $2000 per capita income which we are very close to then the demand for discretionary will actually pick up faster.

The upcoming festive season needs to be watched closely because if this consumption slowdown is a cyclical kind of thing it will compensate in the upcoming festive season.Possibly. Except auto or the large ticket size kind of consumption otherwise things are expected to stabilize. There are certain categories

9 October 2019INSIGHT

which are in the right side of disruption, certain companies which are adopting the technology faster they are actually getting the market share and are growing much faster.

Media reports highlighted that Amazon and Flipkart are saying there is no recession kind of thing and there are not sign of any slowdown?E-commerce or modern trade is where the value migration is happening and consumers are finding convenience. So overall consumption is growing at slower pace, but these e-commerce companies are growing at much higher pace, logistics for consumer companies is growing very fast. We are seeing food delivery aggregators are growing at a very fast pace as technology is on their side. Opportunity are more in the micro than the macro.

When we say that structurally consumption is going to be the key theme over the next many years then do you see that valuation premium which many of the companies enjoy will sustain?It differs from company to company. If for your company whose competitive advantage period comes to an end, we will see derating. We have seen some of the very prime companies in consumption space getting de-rated very sharply when growth came down. For each company, each business needs to be looked at separately and there is a framework for looking at it. We are very clear that we will not get into the company having corporate governance and sustainability issues. We are are looking to buy companies having capital efficiency, competitive advantage and scalability. We are basically aligning our portfolio towards that. We look to pay reasonable price for that.

While we are saying that consumption is a very big opportunity in India we also need a company which is properly aligned to that and capable in terms of executing that with the proper competitive advantage. Otherwise we could have company in a big industry without any

competitive advantage or very sub optimal kind of capital efficiency. It might not able to create wealth.

Some of the categories for the future which you think will grow?Services, is going to be a big profit pool creation. Within that if globally you look at which are the sectors where profit pools are much higher compared to in India, some of the sectors which are at the nascent stage and probably there the profit pool will be much higher.

So, two things which we are focusing on is one is the GST compliance driving formalization and technology. There you will find value migration from unorganized to organized which is a large thing. Technology is playing big role in all the businesses, business which are adopting to that will gain. Consumer and financial services will benefit from this. Govt. services will also be a big winner. Globally if you look at in the developed market, there profit pool from these sectors are very large and is disproportionately high. Within financial services, capital market intermediaries has very large relevance in terms of profit pool.

How do you see the midcap & small cap story panning out from here on? What would be the strategy?Investment approach doesn’t change, it be a large cap or a midcap or a small cap. There is a five-point framework which is very well articulated. There are risk parameters which are clearly identified with corporate governance as well as the management quality being one of the top filters. Second is the business sustainability for instance if you are in a business which is subjected to a technology risk or to environmental risk or any sort of regulation & all which kind of blurs the visibility beyond three years, we will not take exposure to those businesses. Having screened out companies based on these parameters; the first thing we look out for companies with optimal capital efficiency so that they can fund their growth. Second is competitive advantage and third is scalability of the business. These parameters don’t change with the

size of the company. We need to be certain about these aspects so as to stay invested in these companies and see them moving to higher market capitalization. Business might go through difficult times and cycles, however companies qualifying these parameters would see through the difficult times and would come out strong over a longer period of time.

What is the advice you want to give to retail investors, how should they position themselves in the current market situation?Our advice for retail is consistent. Retail investors should focus on asset allocation. Mutual funds are enablers for long term financial goals. There should be clarity with regards to financial goal or investment horizon. If the same is longer term in nature of 5-7 years. Historical data shows that the probability is near zero to lose the money in equities. If you have a long-term investment horizon of 5 years and above, one should allocate more to equity as an asset class. Thus, it depends on the asset allocation and being realistic about return expectations. It is advisable to have conservative expectations somewhere around the nominal GDP growth over longer period of time.

What’s your take on the recent massive corporate tax cuts by the government? We believe this is a very big reform. It is very simple idea of a single tax rate and there have not been any caveats put in and lot of people will migrate to it. The quality companies which have a competitive advantage will be benefited in terms of higher earnings and higher capital efficiency. Secondly, the industries which have significant share of unorganized and non-compliant competition, market consolidation will happen towards organized and compliant players. These are the two near term impacts which will likely play out in next one year or so. In the medium to long term, deep reforms will also be followed up with some other regulatory improvements like land & labour reforms, which will eventually lead to pick up in the investment cycle.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

10October 2019 INSIGHT

Investment ObjectiveThe scheme aspires to generate long term capital appre-ciation by investing substantially in a portfolio of equity and equity linked instruments of large cap and midcap companies. Suitable for investors with moderate risk appetite and investment horizon of more than 3 years.

Investment StrategyThe Fund is focused to generate long-term capital appreciation by investing mainly in equity and equity related instruments of Large & Mid-cap companies. It may also invest a certain portion of its corpus in debt and money market securities. Mid-size companies offer attractive long-term growth opportunities than relatively large-cap companies. while they tend to be more volatile and less liquid than large-cap companies in general.

Investment framework of the fund is based on 5 parameters

Strong & sustainable earnings growth in the long term

Scalability of business

Quality management & governance

Capital efficiency

Competitive advantage

As per SEBI mandate, large & mid cap schemes must invest a minimum 35 per cent of their corpus in large cap companies, and another 35 per cent in mid cap companies. The large and mid-cap category makes sense because of the strict investment mandate imposed by SEBI for

every mutual fund category. Since a large and mid-cap fund invests in both large and mid-cap stocks, it can give higher returns than purely large cap funds and less risky than pure small cap schemes.

The scheme has registered an impressive performance over the recent years. The scheme has outperformed its benchmark during both the short and long term periods. It is a relatively aggressive scheme which holds more of sectors, like banking and finance, the growth of which is dependent on the economic growth of the country. It is the right scheme for investors who wish to earn potentially high returns for relatively high-risk levels.

Mutual Fund Overview LIC MF LARGE & MID CAP FUND

Important Information

NAV (G) (Rs.) 15.4

NAV (D) (Rs.) 13.6

Inception Date February 25, 2015

Fund size (Rs. Cr.) 509.4

Fund Manager Sachin Relekar

Entry load N.A

Exit Load For units in excess of 12% of the investment,1% will be charged for

redemption within 365 days

Benchmark NIFTY Large Midcap 250 TRI

Min Investment (Rs.) 5000

Min SIP Investment (Rs.) 1000Note: All data are as on August 31, 2019; NAV are as on September 24, 2019Source: Factsheet, Value Research

11 October 2019INSIGHT

Key RatiosBeta (x) 0.99Standard deviation (%) 14.62Sharpe Ratio 0.25Alpha (%) 0.80R Squared 0.79Expense ratio (%) 2.77Portfolio Turnover ratio (%) 134.00Avg Market cap (Rs. Cr.) 59,568

Month of Recom

Fund Name Benchmark NAV as on 23.08.2019

1 Year Return

(%)

3 Year Return (%)

5 Year Return

(%)

Aug-18 Franklin India Equity Saving Fund S&P BSE Small Cap 10.0 -- -- --

Sep-18 Sundaram Services Fund S&P BSE 200 10.6 -- -- --

Oct-18 Reliance Balanced Advantage Fund CRISIL Hybrid 35+65 Aggressive 88.7 0.5 8.4 8.1

Nov-18 Kotak Emerging Equity Scheme NIFTY Midcap 100 35.2 -11.0 4.6 11.9

Jan-19 Tata Hybrid Equity Fund CRISIL Hybrid 25+75 Aggressive 203.4 -4.27 3.41 7.75

Feb-19 Invesco India Contra Fund S&P BSE 500 43.8 -12.13 8.78 10.94

Mar-19 Mirae Asset Large Cap Fund NIFTY 200 48.13 -4.4 10.02 11.26

Apr-19 SBI Focused Equity Fund S&P BSE 500 133.31 -4.12 8.85 11.13

May-19 Invesco India Small Cap Fund S&P BSE 250 SmallCap TRI 9.24 - - -

Jun-19 ICICI Prudential Multi Asset Fund Nifty 50 Total Return (70) 255.19 -1.28 7.36 7.97

Jul-19 ICICI Prudential Asset Allocator Fund CRISIL Hybrid 50+50 Moderate Index

55.19 5.03 9.49 9.37

Aug-19 Reliance MultiCap Fund S&P BSE 500 86.62 -9.4 4.95 6.7

Note: All data are as on August 31, 2019; NAV are as on September 24, 2019Source: Factsheet, Value Research

Ashika Mutual Fund Recommendation Alpha Generation

Performance of the Fund alongwith Benchmark (as on Sep 20, 2019) 1 month 3 months 6 months 1 year 3 Years 5 Years Since Inception

Fund (%) 4.12 0.72 2.77 1.80 9.61 9.30Benchmark (%) 3.19 -3.39 -0.97 -0.78 9.32

Asset Allocation

Equity Debt Cash

85.59% 0.00% 14.41%

37.6

9.4

7.6

6.7

6.6

5.1

3.7

2.7

2.0

2.0

0 10 20 30 40

Financial

Chemicals

Services

Technology

FMCG

Healthcare

Automobile

Energy

Construction

Cons Durable

% SECTOR ALLOCATION

Portfolio as on Aug 31, 2019Stocks % of Net assetsBajaj Finance 5.9HDFC Bank 5.3City Union Bank 4.8ICICI Bank 4.7HDFC 3.9Cholamandalam Invest. & 3.6Tata Consultancy Services 3.5Bajaj Finserv 3.4Avenue Supermarts 3.3Infosys 3.2

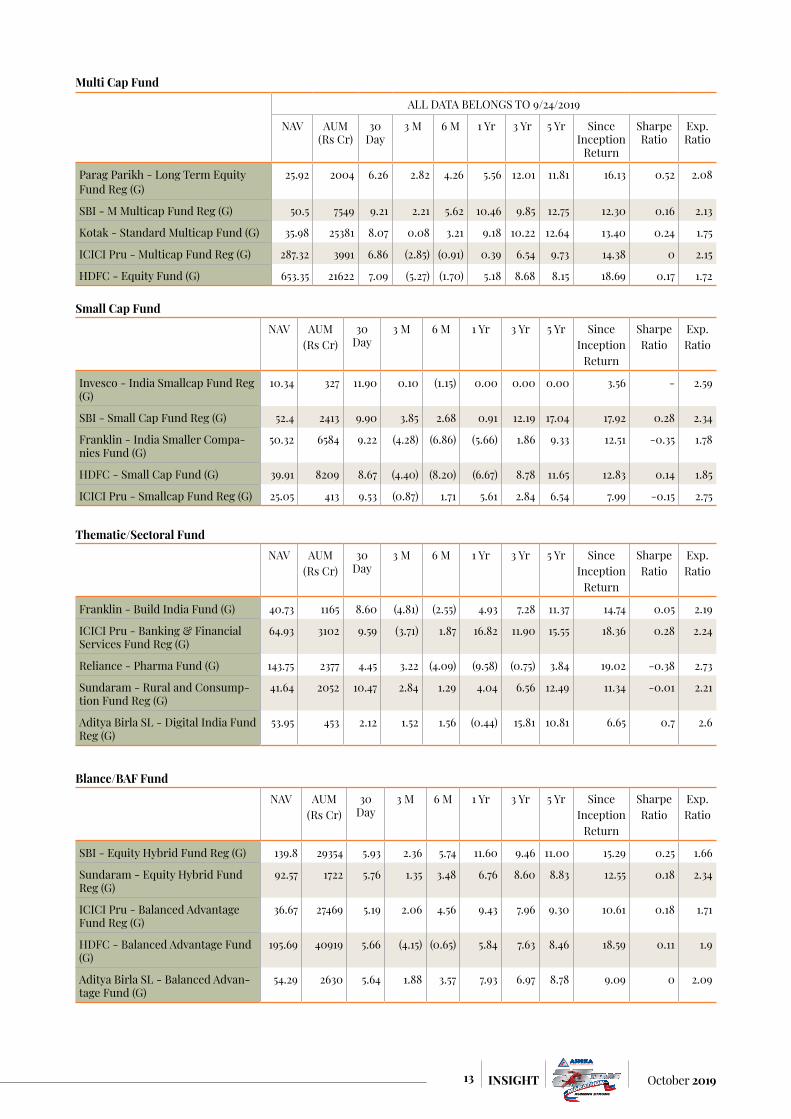

12October 2019 INSIGHT

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

SBI - Contra Fund Reg (G) 103.52 1309 9.74 (2.77) (4.62) (2.03) 2.04 5.84 17.46 -0.31 2.36

HDFC - Capital Builder Value Fund (G)

281.66 4257 7.97 (2.26) (5.06) (2.75) 7.27 9.43 13.89 0.05 1.96

Reliance - Value Fund (G) 73.58 2902 10.09 (0.68) 1.16 6.10 7.59 9.94 14.96 0.01 2.02

Kotak - India EQ Contra Fund (G) 53.11 819 7.42 0.70 2.15 5.22 11.18 10.51 12.51 0.32 2.58

Invesco - India Contra Fund (G) 47.17 3992 7.82 (1.13) (1.19) 2.14 10.45 11.67 13.26 0.26 2.01

Value Fund

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Axis - Focused 25 (G) 29.43 7841 9.41 4.44 10.31 8.68 13.69 13.67 15.96 0.39 2.03

Mirae - Asset Focused Fund Reg (G) 11.18 1381 9.56 5.41 0.00 0.00 0.00 0.00 30.32 - 2.08

SBI - Focused Equity Fund Reg (G) 144.68 5127 8.53 1.68 5.30 10.58 10.67 12.36 19.38 0.24 2.11

HDFC - Focused 30 Fund (G) 77 454 11.25 (2.31) (0.53) 2.69 5.22 6.47 14.58 -0.16 2.55

Sundaram - Select Focus Reg (G) 184.31 973 6.53 0.67 4.36 8.07 11.89 8.95 18.47 0.37 2.48

Focus Fund

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Mirae - Asset Tax Saver Fund Reg (G)

18.03 2306 7.79 1.10 3.90 9.11 14.05 0.00 17.06 0.54 1.9

Kotak - Tax Saver Scheme (G) 44.72 896 7.70 (0.47) 3.74 8.84 8.79 11.34 11.42 0.12 2.4

Invesco - India Tax Plan (G) 51.26 859 8.12 0.75 1.73 3.53 9.12 10.60 13.70 0.16 2.42

Sundaram - Diversified Equity (G) 99.58 2439 8.42 (1.97) (0.16) 2.22 5.25 8.87 12.27 -0.09 2.13

SBI - M Tax Gain Reg (G) 139.08 6683 7.68 (1.64) (2.11) 1.79 4.24 6.57 15.31 -0.18 1.99

ELSS Fund

ALL DATA BELONGS TO 9/24/2019

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

SBI - Large & Midcap Fund Reg (G) 221.98 2493 9.48 0.78 1.84 5.96 7.49 10.68 13.83 0.02 2.25

Mirae - Asset Emerging Bluechip Fund Reg (G)

54.29 7759 7.62 1.23 3.62 10.90 12.82 16.99 19.85 0.41 1.88

ICICI Pru - Large & Mid Cap Fund Reg (G)

320.62 3457 7.34 (1.57) 0.44 1.01 5.59 7.11 17.75 -0.09 1.99

LIC - Large & Mid Cap Fund - Reg (G)

15.44 509 8.97 4.47 6.28 8.35 10.08 0.00 9.95 0.25 2.77

Sundaram - Large and Mid Cap Fund (G

35.28 721 9.72 1.99 4.21 8.20 11.98 12.12 10.56 0.30 2.65

Large & Mid Cap Fund

13 October 2019INSIGHT

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Invesco - India Smallcap Fund Reg (G)

10.34 327 11.90 0.10 (1.15) 0.00 0.00 0.00 3.56 - 2.59

SBI - Small Cap Fund Reg (G) 52.4 2413 9.90 3.85 2.68 0.91 12.19 17.04 17.92 0.28 2.34

Franklin - India Smaller Compa-nies Fund (G)

50.32 6584 9.22 (4.28) (6.86) (5.66) 1.86 9.33 12.51 -0.35 1.78

HDFC - Small Cap Fund (G) 39.91 8209 8.67 (4.40) (8.20) (6.67) 8.78 11.65 12.83 0.14 1.85

ICICI Pru - Smallcap Fund Reg (G) 25.05 413 9.53 (0.87) 1.71 5.61 2.84 6.54 7.99 -0.15 2.75

Small Cap Fund

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Franklin - Build India Fund (G) 40.73 1165 8.60 (4.81) (2.55) 4.93 7.28 11.37 14.74 0.05 2.19

ICICI Pru - Banking & Financial Services Fund Reg (G)

64.93 3102 9.59 (3.71) 1.87 16.82 11.90 15.55 18.36 0.28 2.24

Reliance - Pharma Fund (G) 143.75 2377 4.45 3.22 (4.09) (9.58) (0.75) 3.84 19.02 -0.38 2.73

Sundaram - Rural and Consump-tion Fund Reg (G)

41.64 2052 10.47 2.84 1.29 4.04 6.56 12.49 11.34 -0.01 2.21

Aditya Birla SL - Digital India Fund Reg (G)

53.95 453 2.12 1.52 1.56 (0.44) 15.81 10.81 6.65 0.7 2.6

Thematic/Sectoral Fund

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

SBI - Equity Hybrid Fund Reg (G) 139.8 29354 5.93 2.36 5.74 11.60 9.46 11.00 15.29 0.25 1.66

Sundaram - Equity Hybrid Fund Reg (G)

92.57 1722 5.76 1.35 3.48 6.76 8.60 8.83 12.55 0.18 2.34

ICICI Pru - Balanced Advantage Fund Reg (G)

36.67 27469 5.19 2.06 4.56 9.43 7.96 9.30 10.61 0.18 1.71

HDFC - Balanced Advantage Fund (G)

195.69 40919 5.66 (4.15) (0.65) 5.84 7.63 8.46 18.59 0.11 1.9

Aditya Birla SL - Balanced Advan-tage Fund (G)

54.29 2630 5.64 1.88 3.57 7.93 6.97 8.78 9.09 0 2.09

Blance/BAF Fund

ALL DATA BELONGS TO 9/24/2019

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Parag Parikh - Long Term Equity Fund Reg (G)

25.92 2004 6.26 2.82 4.26 5.56 12.01 11.81 16.13 0.52 2.08

SBI - M Multicap Fund Reg (G) 50.5 7549 9.21 2.21 5.62 10.46 9.85 12.75 12.30 0.16 2.13

Kotak - Standard Multicap Fund (G) 35.98 25381 8.07 0.08 3.21 9.18 10.22 12.64 13.40 0.24 1.75

ICICI Pru - Multicap Fund Reg (G) 287.32 3991 6.86 (2.85) (0.91) 0.39 6.54 9.73 14.38 0 2.15

HDFC - Equity Fund (G) 653.35 21622 7.09 (5.27) (1.70) 5.18 8.68 8.15 18.69 0.17 1.72

Multi Cap Fund

14October 2019 INSIGHT

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Aditya Birla SL - Equity Savings Fund Reg (G)

13.63 843 3.41 4.85 0.96 3.57 5.09 4.74 6.56 -0.21 2.34

HDFC - Equity Savings Fund (G) 36.93 4910 1.59 2.77 (0.71) 1.11 4.36 6.92 9.10 0.14 1.93

ICICI Pru - Equity Savings Fund (G)

14.19 1617 1.43 2.53 1.43 3.73 8.40 6.82 7.61 0.39 1.36

Kotak - Equity Savings Fund Reg (G)

14.52 2003 2.09 2.60 1.28 2.91 5.79 7.31 7.70 0.24 2.16

Reliance - Equity Savings Fund Reg (G)

11.97 1124 (1.23) (0.20) (4.99) (5.93) (4.76) 2.94 4.24 -0.41 2.19

SBI - Equity Savings Fund Reg (G) 13.29 1759 2.95 4.28 1.96 3.74 6.68 5.41 6.72 -0.23 1.69

Equity Savings

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Aditya Birla SL - Arbitrage Fund Reg (G)

19.53 4308 0.11 0.32 1.45 3.35 6.38 6.04 6.80 0.01 0.84

HDFC - Arbitrage Fund WP (G) 22.61 4825 0.08 0.28 1.38 3.15 6.10 5.78 7.08 -0.46 0.75

ICICI Pru - Equity Arbitrage Fund Reg (G)

25.15 12243 0.05 0.27 1.38 3.25 6.24 6.03 7.51 0.07 0.95

Kotak - Equity Arbitrage Fund (G) 27.2 15629 0.09 0.30 1.41 3.28 6.31 6.18 7.42 0.35 0.97

Reliance - Arbitrage Fund (G) 19.53 8937 0.07 0.25 1.39 3.27 6.35 6.27 7.71 0.47 1.04

SBI - Arbitrage Opp Fund Reg (G) 24.8 4237 0.07 0.27 1.46 3.43 6.36 6.05 7.30 0.02 0.88

Arbitrage Fund

ALL DATA BELONGS TO 9/24/2019

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Invesco - India Dynamic Equity Fund (G)

29.49 908 0.16

26.45 (26/10/2018)

0.00% 0.89 3.22 5.51 2.55 0.09 2.22

ICICI Pru - Asset Allocator Fund (G)

57.02 3041 1.10

52.2208 (09/10/2018)

0.00% 1.74 4.20 8.77 8.17 0.66 1.41

ICICI Pru - Multi-Asset Fund (G)

265.98 10942 0.37

243.8023 (14/02/2019)

0.00% (1.55) 0.47 2.71 4.96 0.17 1.93

SBI - Dynamic Asset Alloca-tion Fund (G)

13.43 683 0.08

12.7887 (26/10/2018)

0.00% 0.49 0.96 2.48 5.46 0.06 2.19

Dynamic/ Multi Assets

NAV AUM (Rs Cr)

30 Day

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

ICICI Pru - Retirement Fund Pure Debt Plan (G)

10.65 196 - 10 (27/02/2019)

3.16% 2.38 5.68 0.00 0.00 - 2.02

Aditya Birla SL - Retirement Fund 30s Plan (G)

9.94 93 - 9.061 (22/08/2019)

0.00% 0.79 (0.80) 0.00 0.00 - 2.68

HDFC - Retirement Savings Fund Hybrid Equity Reg (G)

16.8 313 - 15.077 (26/10/2018)

0.00% (0.34) 1.30 6.96 5.69 - 2.44

Aditya Birla SL - Bal Bhav-ishya Yojna Wealth Plan (G)

10.33 161 - 9.45 (22/08/2019)

0.00% 0.78 (0.96) 0.00 0.00 - 2.64

ICICI Pru - Child Care Gift Plan Reg

138.37 612 (0.15)

126.8 (26/10/2018)

0.00% (2.54) (1.76) 2.64 5.29 -0.08 2.55

Solution Fund

15 October 2019INSIGHT

HDFC Bank Ltd.

STOCK PICKS

CMP: Rs 1230 Rating: BUY Target: Rs 1395

Investment RationaleDominant market positionHDFC Bank is the fastest growing large bank, accounting for 7% of market share among all banks and 27% among private sector banks (as of Dec 2018) with strong customer base of over 49 million. It is a comprehensive bank with a balanced presence across retail, SME and corporate segments through significant reach (more than 5000 branches pan India), brand value

and wide range of product offering. HDFC Bank has a balanced presence (branches) in metro, urban, semi-urban and rural areas at 28%, 19%, 31% and 22% respectively, as of March 2019. The bank started 5 to 6 years back in expanding its presence in semi urban and rural regions and now accounts for 53% of branches. In the private banking space, HDFC bank is the largest and most profitable bank, with total asset of Rs 12.4 trillion and net profit of Rs 210

billion as of FY19. It has continued its dominance in both retail and wholesale with ratio of 54:46 for its loan book. Over the years, HDFC bank has built one of the strongest liability franchise, aided by wide presence, superior technology offerings and comprehensive product packages in transaction banking. HDFC Bank is also the market leader in credit cards driven by cross selling to existing customers (~65% of credit card portfolio) while existing customers

Company InformationBSE Code 500180NSE Code HDFCBANKBloomberg Code HDFCB INISIN INE040A01034Market Cap (Rs. Cr) 678211Outstanding shares(Cr) 546.652-wk Hi/Lo (Rs.) 1282.7 / 942.5Avg. daily volume (1yr. on NSE) 3439586Face Value(Rs.) 1Book Value (Rs) 273.9

Promoter 26.3%

DII 17.1%

FII 38.6%

Share holding pattern as on June 2019

Others 18.0%

16October 2019 INSIGHT

account for ~50% of the personal loan segment. Expansion in rural regions will enable the bank to earn strong fee income thus supporting robust other income growth (which accounts ~27% of net revenues in FY19). Its dominance in private banking space, deep reach to customers and wide range of financial products make HDFC bank different from other financial institutions. .

Low funding costs entail healthy marginsHDFC bank is amongst the lowest deposit costs bank in the industry. In past 3-4 years, the bank witnessed decline in its cost of deposits from 5.91% in FY16 to 4.82% in FY18, due to demonetization drive by government. Cost of deposits has only slightly inched up to 5.03% in FY19, despite tight liquidity environment. Low cost deposit is due to bank’s healthy proportion of CASA deposits which has been in the range of 43% to 48% in last 3-4 years. Low cost funds coupled with stable interest rate cycle helped the bank to maintain healthy NIMs over the years. For the last 3 years, bank has maintained average NIMs of 4.3-4.4%. Higher yield from assets on account of higher proportion & product mix of retail loans also supported its stable NIMs. Rising competition and intent on higher profitability led to shift from corporate to retail segment with

contribution increasing from 47% in FY15 to 53% in FY19. Besides, within the retail, high yielding unsecured book (personal loans & credit cards) has increased from ~24% in FY15 to ~33% in FY19, thus fueled better than industry advances growth of 22% during the same period for the bank. The bank’s strong ability to maintain healthy proportion of CASA deposits together with focus on high yield retail loan would keep its NIMs stable over the years.

Strong asset quality & robust return on assetsOver the years, HDFC bank is one of the best banks in maintaining healthy asset quality in the industry. As of FY19, bank has maintained a very high specific provision cover at 71% of NPAs with total coverage ratio (including general & floating provisions) at 117%. Focus on high yielding retail loan (accounting for 54% of loan portfolio) and being very selective in project finance, is the primary factor behind superior asset quality performance since existence. Management has always maintained that capacity utilization above 80% will be the indication for beginning of investment cycle (currently capacity utilization ~76%) which looks to be a few quarters away. The pickup in the investment cycle is required for large ticket project finance. For last 3 years the bank has maintained

average gross NPA and net NPA of 1.24% and 0.37% respectively, which is commendable in the industry. Although, in last 3 years asset quality has marginally deteriorated on account of cyclical trends in its agriculture loan portfolio due to the volatile monsoon season and frequent farm loan waivers announced by various state governments. The crisis in NBFC and HFCs sector has also not deterred its portfolio. The bank management has reviewed its existing NBFC portfolio and believes that the portfolio is well-positioned, and it does not see an immediate concern on any exposure as the bank has always lent to high-rated NBFCs based on an internal risk assessment. One of the key strengths of the bank has been its ability to reduce operating expenses and thus compensated for higher provisioning expenses. There has been consistent decline in cost to income (C/I) ratio every year after peaking at 49.7% in FY12. For the last three years, C/I declined from 43.4% in FY17 to 39.7% in FY19 and the management has targeted for further reduction. HDFC bank’s strong operating efficiencies and stable asset quality led to steady rise in return on assets (RoA). The management has maintained RoA between 1.9% to 2% since FY13. The most notable thing is that strong RoA growth has come without compromising on asset quality and margins. It is expected that improvement in RoA over the next 3 years should be driven more by operating synergies coming out of digital banking initiatives and lower branch additions and recruits, thereby boosting productivity ratios.

Recent updates On business: During Q1FY20, HDFC

Bank showed a mild moderation in business growth as well as on asset quality. Credit growth came in lower at 17% while provisions was higher due to increased rate of provisions on agri book & on unsecured book and auto loans. Given the heavy reliance of the unsecured loans (~18% of loan book) and auto (11% of loan book), a rise in credit costs is inevitable, however a lot of this is cyclical in nature, besides the management

HDFC Bank Ltd. Price Chart

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 20,000

500

600

700

800

900

1000

1100

1200

1300

Sep-

16

Dec

-16

Mar

-17

Jun-

17

Sep-

17

Dec

-17

Mar

-18

Jun-

18

Sep-

18

Dec

-18

Mar

-19

Jun-

19

Sep-

19

Volume (000's) (RHS) HDFC Bank

17 October 2019INSIGHT

opines that it is still not even close to budgeted credit cost in any product segment. The bank expects to sustain credit cost within 80–100bps. Upbeat on festive season: HDFC

Bank still sees good prospects ahead of festive season in the next couple of months driven by aggressive marketing campaigns and tie-ups with brands and partners and therefore in a position to offer cashbacks and discounts. The bank wants to leverage its unparalleled distribution network and sense a good opportunity to capture market share at the expense of competitors. Cost optimization: Management

has guided to reduce cost to income ratio over next three years to 35% from ~40% currently as digitalization scales up. Five-pronged strategy for growth:

(a) The bank plans to expand its branch network, adding another 600-700 branches per year, and it plans to double its new customer acquisition to 6mn customers in FY20. (b) It will leverage on the 600k CSCs (common service centres) to scale up business and expects 100k feet-on-street by June 2020 (c) Use VRMs (virtual relationship managers) to cater to 6m customers and eventually to ensure that profitability per customer from this segment matches profitability per customer from 3mn customers who have dedicated RMs (generating 50% of retail earnings) (d) Despite being loss making, HDFC Bank wants to increase merchant acquisition from 1mn in FY19 to 4mn by FY21. This would also aid in cross-selling of asset & liability products (e) The bank will leverage on digital banking and use its API-based platform more actively and integrate it well with

e-commerce players. In the process it will bring down its cost to income ratio too. On Fund raising: The recent

relaxation in risk-weights (RW) for retail book pushed up Tier1 by 90bps to 15.8%. HDFC Bank doesn’t see any fund raise in coming few quarters unless the credit demand requires additional capital. As of 1QFY20, total CAR stood at 16.9% On separate listing of HDB

Financial services: HDFC Bank may consider separate listing of its subsidiary to raise fund, when credit environment revives. As of 1QFY20, HDB financial services has total loan book of Rs 56,287 crore and the Bank held 95.5% stake. Repo rate linked loans – not much

impact on margins: HDFC Bank’s retail loans are largely fixed rate in nature and doesn’t see any short-term impact on the NIMs. Currently SA rate is 3.5% and TD rates are at 7.1% and the bank has slashed the TD rates recently. Nevertheless, the management is confident to maintain the NIMs in the range of 4.1%-4.4%. Corporate tax cut: The Government

has announced downward revision in corporate tax rate from existing 30% to 22% from FY20 onwards, which would lower effective tax rate to 25.17% at higher end from the current level of 34.95%. HDFC bank’s effective tax rate stood at 34.5% for FY19 and is expected to provide a jump of ~14% to the bottomline in FY20.

Key Risks Higher inflation may prompt RBI

to hike the interest rate, which could result in higher cost of funds and lower margins for bank Slowdown in economy and higher

unemployment could increase NPA for the bank as weak economic growth would hurt the earnings of corporate and individuals

ValuationHDFC Bank has built a robust retail franchisee over the years and has been growing consistently thus gaining market share across retail products. On account of a strong CASA franchisee, it has been able to earn consistently strong NIMs of 4.3% and being a retail bank hasn’t been subjected to asset quality hiccups and has maintained adequate capitalization levels and healthy return ratios. It’s expansion into the rural & semi-urban areas and cross-selling to existing customers ensures plenty of room to grow and thus generating healthy interest income as well as fee income. We believe HDFC Bank will sustain its best in class track record on asset quality despite minor blemishes given its focus on internal customers, strict adherence to strong cash flow based lending and firm focus on risk management. HDFC bank has formulated a five-pronged strategy to drive the next leg of growth driven by digitization initiatives. In the process, the management expects to reduce cost to income ratio over next three years to 35% from ~40%. Despite minor hiccups on asset quality over the last three years, The management has maintained its ROA driven by operating leverage and remains one of the best compounding machines in the sector. Thus, we recommend our investors to BUY the scrip with target of Rs 1395, from 12 to 18 months investment perspective. Currently, the bank is valued at P/BV of 3.36x on FY21E BVPS of Rs 369.3.

Particulars (in Rs Cr) FY18 FY19 FY20E FY21E

Net interest Income 40,095 48,243 58,209 69,329

NIM (%) 4.4% 4.4% 4.3% 4.2%

Operating Profit 32,625 39,750 48,326 57,938

PAT 17,487 21,078 29,042 36,232

EPS (Rs) 33.69 38.70 53.14 66.29

BV (Rs) 204.8 273.9 315.8 369.3

GNPA (%) 1.3% 1.4% 1.7% 1.7%Source: Ace equity & Ashika Research

18October 2019 INSIGHT

Siemens India Ltd.CMP: Rs 1515 Rating: BUY Target: Rs 1700

Company overviewSiemens India Ltd. (SIL) is a 75% subsidiary of Siemens AG, Germany, which has presence in more than 200 countries. SIEM offers diverse products and services solutions in power generation, transmission and distribution, automation and

drives, industrial and digital solution. Siemens has 22 factories located across the country, 8 Centres of Competence, 11 R&D centres and a nationwide sales and service network. The factories in India mainly aim at manufacturing steam turbines, motors, switchgears,

generators, transformers, relay and smart grid systems etc. The strategic business unit in India can be divided into divisions namely: Power and Gas, Energy Management, Building Technologies, Mobility, Digital Factory, Process Industries and Drives. Siemens has its associations

Company InformationBSE Code 500550NSE Code SIEMENSBloomberg Code SIEM INISIN INE003A01024Market Cap (Rs. Cr) 51370Outstanding shares(Cr) 35.652-wk Hi/Lo (Rs.) 1493.8 / 850.25Avg. daily volume (1yr. on NSE) 563,519Face Value(Rs.) 2Book Value 240.1

Promoter 75.0%

DII 11.8%

FII 2.1%

Share holding pattern as on June 2019

Others 11.1%

STOCK PICKS

19 October 2019INSIGHT

with the Indian Railways for more than six decades and has been a preferred technology and customized solution provider since then.

Investment RationaleDigitalization a long-term growth driverUnder its digitalization/automation drive, SIL continue to bring digitalization across its business spectrum (Energy, Infrastructure, Discrete & Process Industries, Mobility) to provide customers with advantages such as quick uptime, speed, flexibility, quality, efficiency and security (Plant security, network security and System Integrity). This has become reality due to its key technical capabilities (Internet of Things (IOT), Artificial Intelligence (AI), Digital Twin, Mindsphere). There is huge potential of digitalization adoption in the Indian context given the government’s focus on increasing the share of manufacturing from the current 17% to 25%. This would mean an incremental annual manufacturing output of ~USD 500-600trn requiring a capex of USD 1.3-1.5trn and therefore, in order to compete globally, the need to adopt digital technologies is of utmost importance. The group has invested over USD 10bn in software acquisitions since 2017 and is amongst the top 10 players in the world. The other business, which has seen significant traction, includes

the mobility/railways business. Large capex has been earmarked with major projects including metro projects. It expects opportunities from metro projects and railway signaling order activities to start in next few quarters. The Company is expecting limited traction in power generation and construction space. In Oil & Gas space, while capex has reduced, the opex has increased. With focus on profitability, SIL continues to remain selective in taking new orders. Digitalization as a business has shown tremendous growth in recent times and will continue to be a huge growth driver for the company.

New business structure to bring synergiesSiemens, in line with its Parent’s Vision 2020+, has re-organized business verticals to four vs. five earlier. The intent is to achieve business synergies and improve product/services delivery to clients. Siemens’ new segmental organization groups the offerings by end-market applications into five verticals namely Gas & Power (35% share), Smart Infrastructure (29% share), Digital Industries (20% share), Mobility segment (8% share) and Portfolio of Companies (9% share). Smart Infrastructure and Digital Industries will cumulatively contribute 49% of revenues, larger than 35% share for Gas and Power segment. Smart Infrastructure requires lower import content and greater share of solutions over product offerings. Digital industries, on the other hand, provide an opportunity to improve service revenues through analytics on top of the Mindsphere platform licensed out to customers by the parent Siemens AG. Such renewed focus would help win new businesses as both public and private sector clients defer ordering and execution.

Innovation Day: New OfferingsSiemens recently organized its 2nd innovation day, to showcased technologies related to IoT, AI and Next47, apart from additional applications/proof of concepts under MindSphere and Digital Twin. While MindSphere is a cloud-based IoT operating system, Digital Twin provides virtual representation of products and production process. Under Next47, the company is investing in startups with strategic interest. SIL’s existing client engagement and capabilities to extend offering from the initial product designing/development stage to final servicing/maintenance enables the company to better engage with customers. Additionally, the vast repository of data across verticals coupled with analytical technology will help the company enhance productivity of its customers.

Siemens India Ltd. Price Chart

0

500

1,000

1,500

2,000

2,500

850

950

1050

1150

1250

1350

1450

1550

Sep-

16

Dec-

16

Mar

-17

Jun-

17

Sep-

17

Dec-

17

Mar

-18

Jun-

18

Sep-

18

Dec-

18

Mar

-19

Jun-

19

Sep-

19

Volume (000's) (RHS) Siemens

There is huge potential of digitalization adoption in the Indian context given the government’s focus on increasing the share of manufacturing from the current 17% to 25%.

20October 2019 INSIGHT

Healthy orders inflowOrder inflow during the quarter was up 6.4% YoY at Rs. 30.2 bn, this was mainly on account of two large orders received in Energy management segment. For 9MSY19, order inflow was up 12% YoY at Rs. 100 bn, mainly led by healthy short cycle orders (below Rs1 bn) which was up 14% YoY. Order back log at the end of 9MSY19 at Rs. 130 bn (Book/Bill at 1.1x). The company has completed 66% of execution for HVDC order and expected to fully execute in next 18 months-time frame. SIL expect order inflow momentum to continue from Metro, Captive Power Plant, F&B, Chemicals, Water etc. The management continues to focus on driving its short term and digitalization businesses with a clear focus on profitable growth and working capital management.

Capex to bear fruit Siemens has the most diversified product portfolio, catering to wide end-markets. The company has gone through significant capacity build-up over the past decade, while many of its businesses witnessed demand headwinds, leading to significant capacity under-utilisation. Going forward, Siemens is likely to experience faster sales growth, with

lower capex. It turns out to be most cyclical among its MNC peers and could witness a meaningful uptick in profit margins. Siemens has the best working capital cycle among peers, which is an additional positive for upside growth and return ratios.

Key Risks Slowdown in key infra verticals

including Government capex and private investments

Slowdown in key export markets including INR depreciation

Any adverse corporate action by Parent’s for business verticals

ValuationSiemens is one of the most diversified industrial product/solutions companies in India with exposure to a wide range of industries. Over the past three-four years, the company has simplified its business structure, apart from reducing operating margin volatility. It is expected that the company to continue on its margin improvement trajectory led by buoyancy in gross margin and continued cost cutting measures. Siemens continues its focus on the areas of electrification, automation and digitalization which appears to be more profitable on the margins front.

Siemens is well placed to monetize its strength in digitalization across its business spectrum which is gaining momentum. Management is seeing traction of customers for the digital portfolio which Siemens offers and is expected to be a huge growth driver for the company. Going ahead, sectors which are expected to drive growth are Food & Beverage, Chemicals, Water, Smart Infrastructures (Data centers, Hospitals, Commercial offices and Airports), Captive Power and Railways. Siemens is emerging as a much more scalable business for the long term given its focus on smart solutions, which entail lower capital intensity, providing scope for profitability and margin improvement. We expect Siemens to benefit from its strong focus on Digitalization/Automation opportunity due to very low penetration and industry’s drive to improve efficiency along with access to parent’s robust global product portfolio and a favourable transformation in domestic industrial capex. Hence, we hold positive view on the scrip and recommend BUY with a target price of Rs 1700 from 12 - 18 months investment perspective. Currently, the scrip is valued at P/E multiple of 42.6x on FY21E Bloomberg consensus EPS of Rs 34.8.

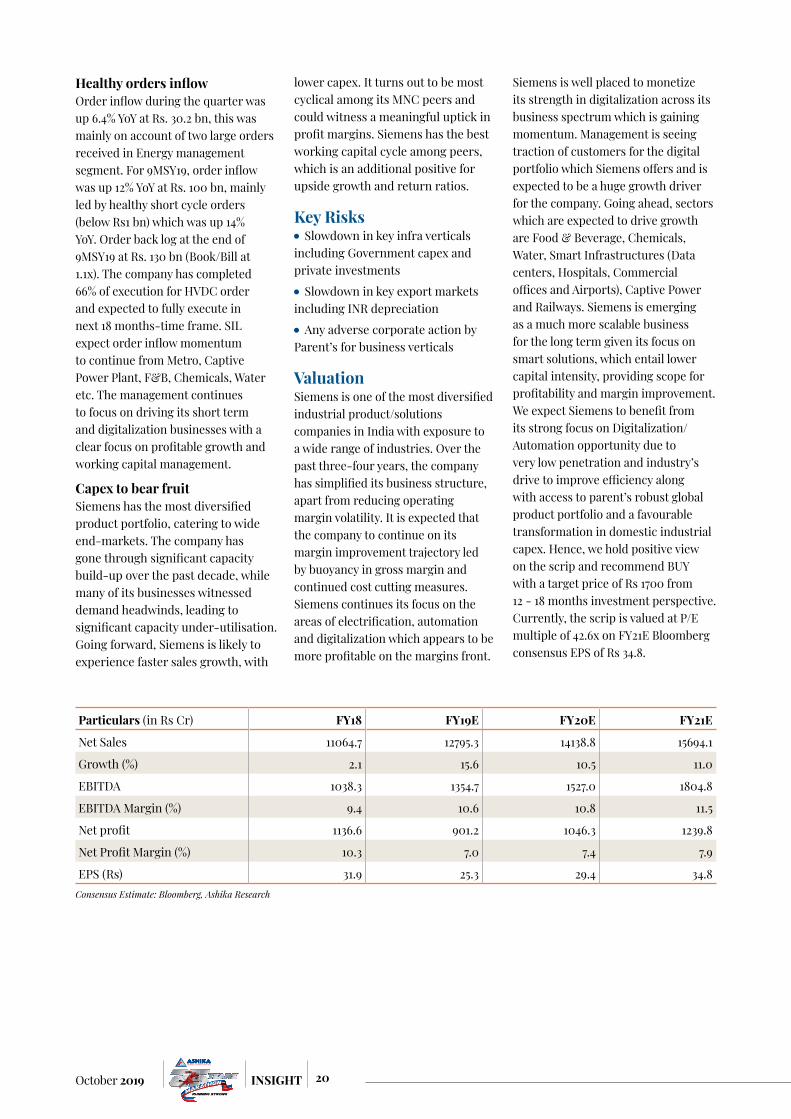

Particulars (in Rs Cr) FY18 FY19E FY20E FY21E

Net Sales 11064.7 12795.3 14138.8 15694.1

Growth (%) 2.1 15.6 10.5 11.0

EBITDA 1038.3 1354.7 1527.0 1804.8

EBITDA Margin (%) 9.4 10.6 10.8 11.5

Net profit 1136.6 901.2 1046.3 1239.8

Net Profit Margin (%) 10.3 7.0 7.4 7.9

EPS (Rs) 31.9 25.3 29.4 34.8Consensus Estimate: Bloomberg, Ashika Research

21 October 2019INSIGHT

Indian Hotels Company Ltd.

CMP: Rs 159 Rating: BUY Target: Rs 185

Company overviewIndian Hotel Company ltd. (IHCL), a Tata Group company is South Asia’s largest hospitality company. Incorporated in 1899, IHCL has increased its total number of hotels

to 151 with 18,217 rooms inventory, including international properties in US, UK and Middle East countries. Apart from hotel, it also offers ancillary services like restaurants, spas, catering services and clubs.

With ‘Aspiration 2022’, company intent to achieve higher scale and sustain profitability. In order to expand its operation and stay ahead of competition, management is committed to add 15 new properties

Company InformationBSE Code 500850NSE Code INDHOTELBloomberg Code IH INISIN INE053A01029Market Cap (Rs. Cr) 18,992.5 Outstanding shares (Cr) 118.93 52-wk Hi/Lo (Rs.) 164.3/110.0Avg. daily volume (1yr. on NSE) 1,080,860 Face Value (Rs.) 1Book Value (Rs) 37.9

Promoter 39.1%

Others 19.8%

DII 41.1%

Share holding pattern as on June 2019

STOCK PICKS

22October 2019 INSIGHT

every year. Further, corporate tax rate cut and reduction of GST rate on room tariff are the two positive triggers for Indian hotel industry.

Investment RationaleGST & Corporate tax rate cut to boost hotel industry growthIndian hotel industry got double tax relief by way of corporate tax rate cut and reduction in GST rate on room tariff. The GST Council reduced GST for hotel accommodation with tariffs of up to Rs 7,500 per night to 12% from 18% earlier and on room tariff of above Rs 7,500 to 18% from 28%. There will be no GST on room tariffs of below Rs 1,000 per night. With the lower GST rates, room rates will become cheaper and will push occupancy level of the hotels, thereby improving the Average Room Rates (ARR) for hotel industry and also become attractive and competitive as a tourist destination globally. The expected uptick in the occupancy rate augurs well in terms of pricing for the hotel sector, which is already witnessing a favorable demand-supply scenario. The demand for hotel rooms is rising by 5-6%, while the room inventory is increasing less than 4%, thus turning favorable demand-supply scenario. During 1QFY20, occupancy rate for hotel industry declined by two percentage points at about 65-66% due to low business travels and weak consumption sentiment. Thus, GST rate cut before the start of the peak season starting from October to March should help hotels to fare better. The hotel industry earn nearly 70% of their profit from October to March season, thus this period is seasonally strong period for the industry. With the new GST rates, the tax gap between luxury

and mid-segment hotels has narrowed and that would help organized hotel players to gain market share from unorganized players. Besides, lower corporate tax rate is expected to improve the demand of corporate travelers. The corporate segment account a large share of the hotel’s revenue pie. Government bold move by reducing corporate tax rate from 34.9% to 25.17% has benefited many sectors, especially hotel industry as most of the major hotels faced effective tax rates of over 33% as against new rate. In listed hotel space, IHCL faced higher effective tax rate of 39% in FY19 as against new rate of 25.17%, thus there could be a gain of nearly 13% in net profit. Further, lower GST rate on room tariffs will help in improving IHCL’s occupancy rate and ARR in coming quarters.

Strongly positioned in domestic marketIHCL, with its 151 hotels in domestic markets, covers all major cities and caters to the increasing demand of