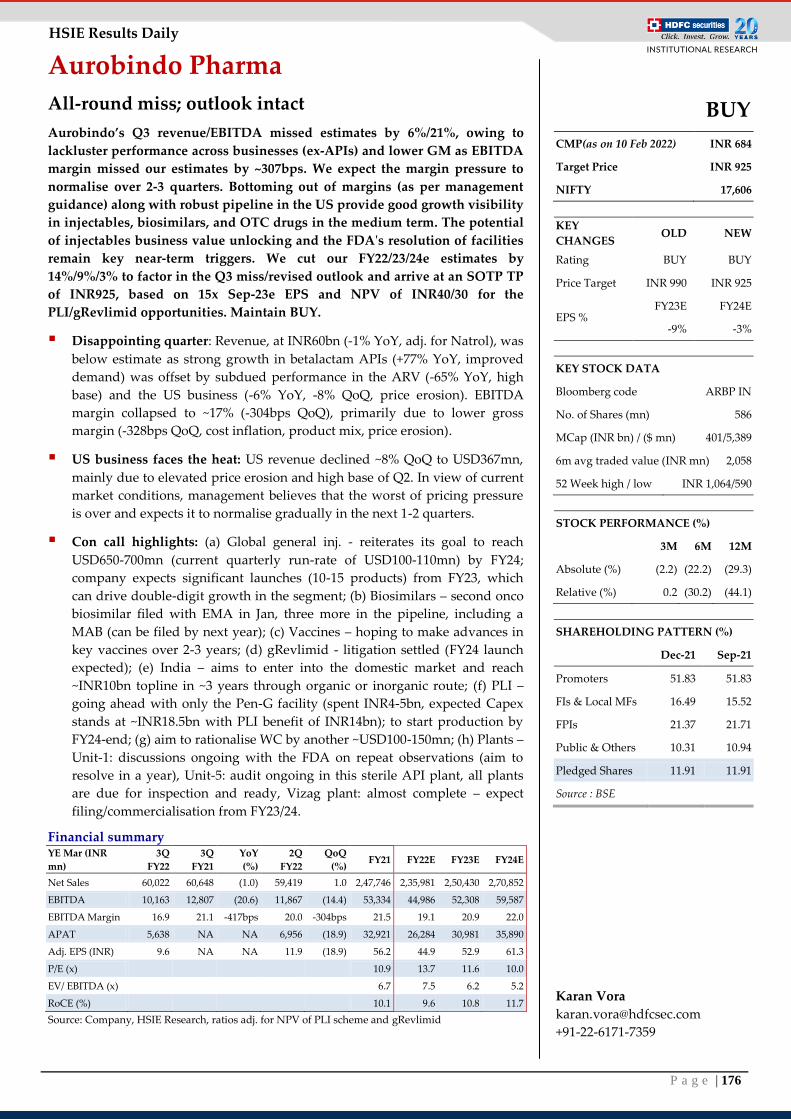

Quarterly flipbook - HDFC securities

205

India Equity Strategy Quarterly flipbook Quarterly flipbook:Q3FY22–Demand recovery sustaining but input cost inflation gets more pronounced, impacting profitability Q3FY22 earnings season saw an overall in-line performance with divergences across sectors and companies. Aggregate revenue/PAT grew by 29.7%/24.8% YoY across the HSIE coverage universe (~200 stocks), while they had a two-year CAGR of 13.5%/21.3%. Our coverage universe saw strong growth in the segments of energy, metals, chemicals, consumer discretionary, insurance & capital markets and large banks, while industrials, cements and pharmaceuticals were a disappointment. IT continued its steady growth. A common thread connecting most of the management commentaries was that industries are facing unprecedented input cost inflation and pricing actions are being implemented in order to protect margins. However, price hikes are being taken in a calibrated manner, to prevent the momentum in demand recovery from being derailed. Rising crude oil poses an additional threat to already elevated raw material prices. Varun Lohchab [email protected] +91-22-6171-7334 Amit Kumar,CFA [email protected] +91-22-6171-7354 Atishray Malhan [email protected] +91-22-6171-7363

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Quarterly flipbook - HDFC securities

India Equity Strategy

Quarterly flipbook

Quarterly flipbook:Q3FY22–Demand recovery sustaining but

input cost inflation gets more pronounced, impacting

profitability

Q3FY22 earnings season saw an overall in-line performance with divergences across

sectors and companies. Aggregate revenue/PAT grew by 29.7%/24.8% YoY across the

HSIE coverage universe (~200 stocks), while they had a two-year CAGR of

13.5%/21.3%. Our coverage universe saw strong growth in the segments of energy,

metals, chemicals, consumer discretionary, insurance & capital markets and large

banks, while industrials, cements and pharmaceuticals were a disappointment. IT

continued its steady growth. A common thread connecting most of the management

commentaries was that industries are facing unprecedented input cost inflation and

pricing actions are being implemented in order to protect margins. However, price

hikes are being taken in a calibrated manner, to prevent the momentum in demand

recovery from being derailed. Rising crude oil poses an additional threat to already

elevated raw material prices.

Varun Lohchab [email protected]

+91-22-6171-7334

Amit Kumar,CFA [email protected]

+91-22-6171-7354

Atishray Malhan [email protected]

+91-22-6171-7363

25 February 2022 Strategy

India Equity Strategy

d

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

Quarterly flipbook:Q3FY22–Demand recovery sustaining but input

cost inflation gets more pronounced, impacting profitability

Q3FY22 earnings season saw an overall in-line performance with divergences

across sectors and companies. Aggregate revenue/PAT grew by 29.7%/24.8% YoY

across the HSIE coverage universe (~200 stocks), while they had a two-year CAGR

of 13.5%/21.3%. Our coverage universe saw strong growth in the segments of

energy, metals, chemicals, consumer discretionary, insurance & capital markets

and large banks, while industrials, cements and pharmaceuticals were a

disappointment. IT continued its steady growth. A common thread connecting

most of the management commentaries was that industries are facing

unprecedented input cost inflation and pricing actions are being implemented in

order to protect margins. However, price hikes are being taken in a calibrated

manner, to prevent the momentum in demand recovery from being derailed.

Rising crude oil poses an additional threat to already elevated raw material prices.

~48% of our coverage stocks have beaten earnings estimates (vs. ~57% in Q2FY22).

Overall, the slight beat for the coverage universe (2.7%) was led by energy and

metal sectors, given their high combined weightages (~35%) in the aggregate

profit pool. Acknowledging the ground reality that input price inflation may take

longer than desired to subside, most of the sectors witnessed earning cuts with the

exception of large banks, technology, chemicals, energy, metal, insurance, and

capital markets. Consequently, overall earnings estimates were largely

maintained. Earnings upgrades were led by commodities and energy while

consumption faced margin headwinds. For the HSIE coverage universe, FY22/FY23

earnings growth stands at 31.7%/21.2%, leading to doubling of earnings over FY20-

23, post 28% YoY earnings growth in FY21. However, FY23 earnings could be at

risk, as we feel the stronger earnings momentum expected in FY23 has advanced

to FY22. Furthermore, Nifty consensus FY22 EPS remains largely unchanged. Nifty

is trading at ~22.9x FY22 EPS and ~20.6x FY23 EPS.

Sector highlights: Consumer staples demand remained muted due to subdued rural

recovery and witnessed price-led revenue growth. Consumer discretionary revival,

on the other hand, continued, given the wedding season and opening up of

shopping centres (after the unlock). Most large banks demonstrated asset quality

improvements, lower slippages, and higher recoveries that led to impressive PPOP

growth. Consequently, lending accelerated, resulting in promising credit growth.

Technology companies sustained their ride on cloud migration and digital adoption

wave, but unprecedented attrition persisted. Product price erosion in developed

markets impacted growth of pharma, while chemicals grew, led by higher price

realisations. Higher crude realisations helped growth of upstream oil & gas

companies, but city gas companies faced headwinds due to higher spot gas prices.

Higher presales growth and reducing leverage of realty companies adds to the

optimism prevailing in the housing and building materials sector. However, cement

companies faced difficulty in passing costs to consumers due to moderate demand in

the quarter. Infrastructure order books remained healthy. Power and auto sectors

continued their green journey with increased focus on renewable and EV.

Our preferred sectors continue to be large cap banks and IT, industrial & real

estate, insurance, and capital markets, while we remain underweight on

consumption (staples, discretionary, and autos), NBFCs, and small banks.

Q3FY22 results snapshot: Overall, it was an encouraging quarter, indicating a

sustained earnings momentum. In terms of stocks, notable earnings upgrades were

visible in CAMS, Apollo Hospitals, Navin Fluorine, V-mart, Kotak Bank, Dr Reddy’s

Lab, Dalmia Bharat, Jubilant Foodworks, Cadila, Shree Cement, and Tata Power.

Model portfolio: We maintain bias towards economy-facing and value sectors.

Stocks added/weight increased Stocks removed/weight reduced

Axis Bank, Cipla, ITC, Cummins India Radico Khaitan, CDSL, Ajanta Pharma

Q3FY22 deviation in estimates in comparison

to previews

Sector Revenue PAT

Autos -0.5% -3.5%

Banks and NBFCs 0.6% 5.1%

Insurance -3.0% -0.7%

Capital Markets -4.2% -3.9%

Consumer- Staples 6.8% 1.6%

Consumer Discretionary

(ex-Autos) -0.1% -6.7%

Industrials (Infrastructure+

Cap Goods+ Logistics) 0.3% -11.7%

Real Estate 3.2% 46.5%

IT and Exchanges 1.1% -0.4%

Energy (Oil & Gas) 2.3% 6.2%

Cement and Building

Materials -0.9% -19.0%

Chemicals 14.1% 44.4%

Pharma -2.4% 3.4%

Power/Utilities 4.9% 2.0%

Aviation 33.0% 45.5%

Metal 4.0% 3.6%

Total 1.9% 2.7%

Source: Bloomberg & HSIE Research

Sectoral Change in PAT Estimates in

comparison to Q2FY22

Sector FY22E FY23E

Autos -20.3% -3.6%

Banks and NBFCs 4.4% 1.8%

Insurance 5.8% 0.6%

Capital Markets 6.5% -0.2%

Consumer- Staples -0.6% -0.1%

Consumer Discretionary

(ex-Autos) -0.8% 1.2%

Industrials (Infrastructure+

Cap Goods+ Logistics) -5.1% -5.1%

Real Estate -0.2% 0.6%

IT and Exchanges 1.5% 1.4%

Energy (Oil & Gas) 0.8% -2.6%

Cement and Building

Materials -8.1% -6.5%

Chemicals 10.8% 2.4%

Power -0.5% -0.2%

Pharma -1.4% -2.3%

Aviation 14.3% -2.7%

Metal 4.4% 4.0%

Total 0.6% -0.4%

Source: HSIE Research

Varun Lohchab

+91-22-6171-7334

Amit Kumar,CFA

+91-22-6171-7354

Atishray Malhan

+91-22-6171-7363

P a g e | 2

Strategy

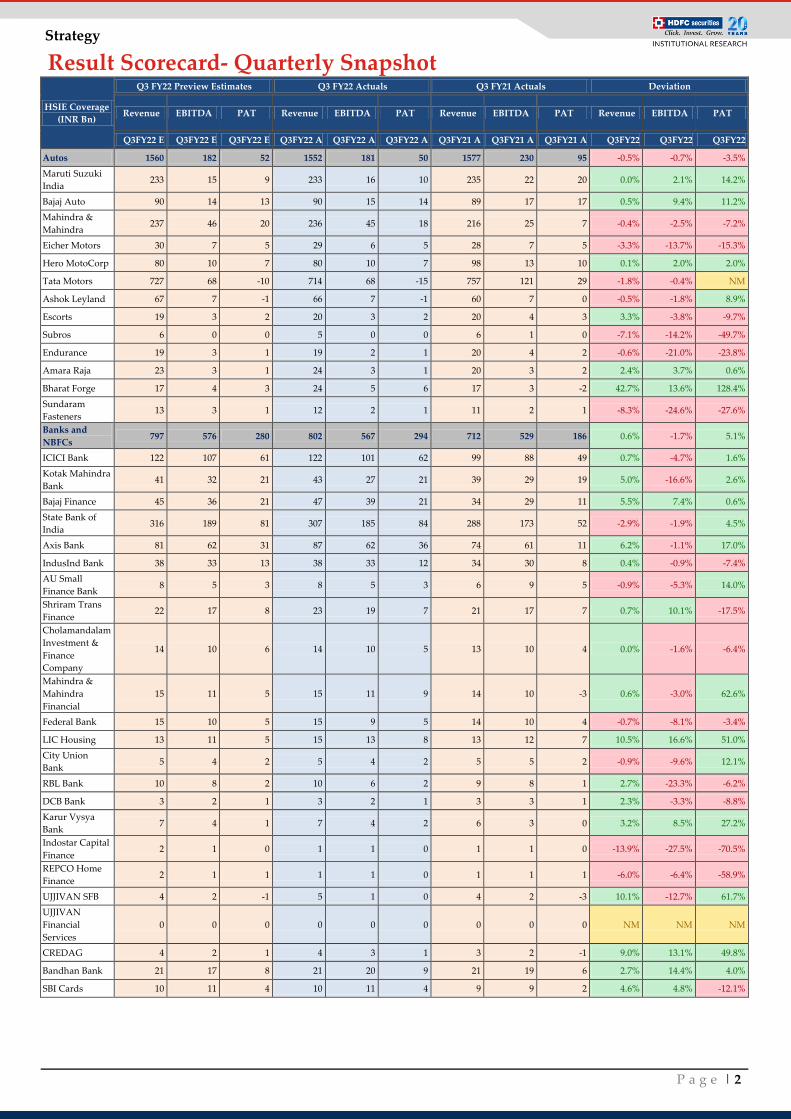

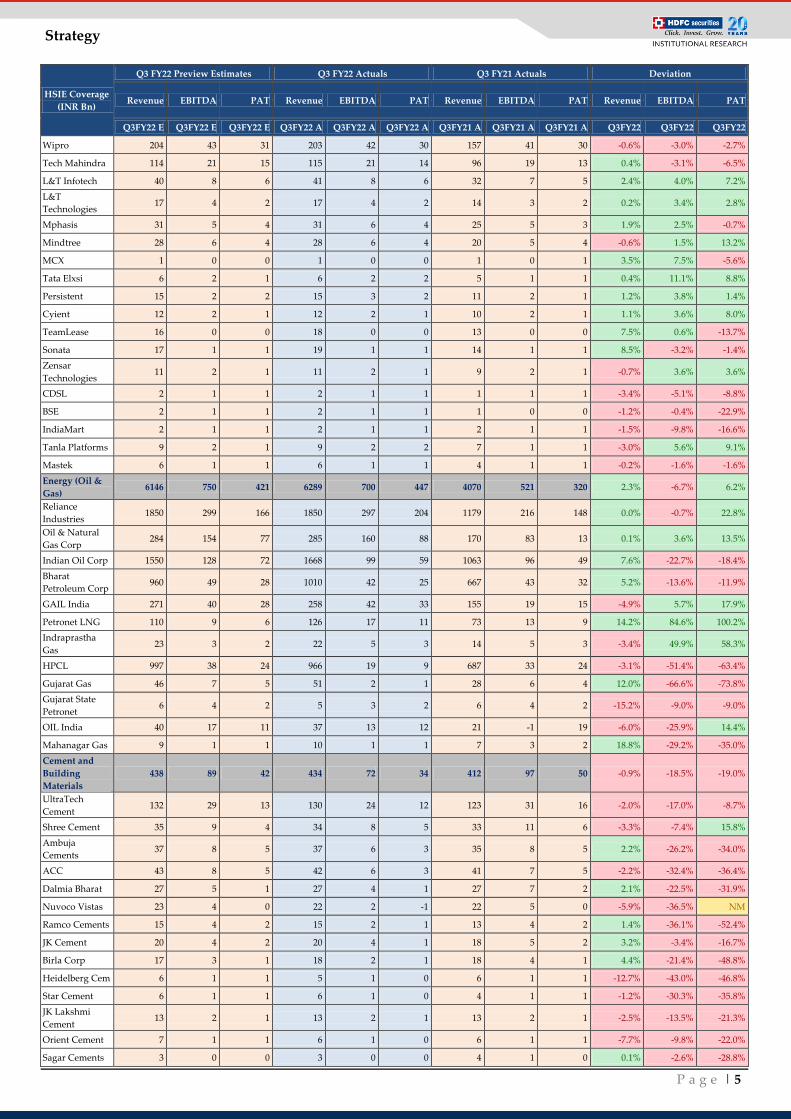

Result Scorecard- Quarterly Snapshot

HSIE Coverage

(INR Bn)

Q3 FY22 Preview Estimates Q3 FY22 Actuals Q3 FY21 Actuals Deviation

Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT

Q3FY22 E Q3FY22 E Q3FY22 E Q3FY22 A Q3FY22 A Q3FY22 A Q3FY21 A Q3FY21 A Q3FY21 A Q3FY22 Q3FY22 Q3FY22

Autos 1560 182 52 1552 181 50 1577 230 95 -0.5% -0.7% -3.5%

Maruti Suzuki

India 233 15 9 233 16 10 235 22 20 0.0% 2.1% 14.2%

Bajaj Auto 90 14 13 90 15 14 89 17 17 0.5% 9.4% 11.2%

Mahindra &

Mahindra 237 46 20 236 45 18 216 25 7 -0.4% -2.5% -7.2%

Eicher Motors 30 7 5 29 6 5 28 7 5 -3.3% -13.7% -15.3%

Hero MotoCorp 80 10 7 80 10 7 98 13 10 0.1% 2.0% 2.0%

Tata Motors 727 68 -10 714 68 -15 757 121 29 -1.8% -0.4% NM

Ashok Leyland 67 7 -1 66 7 -1 60 7 0 -0.5% -1.8% 8.9%

Escorts 19 3 2 20 3 2 20 4 3 3.3% -3.8% -9.7%

Subros 6 0 0 5 0 0 6 1 0 -7.1% -14.2% -49.7%

Endurance 19 3 1 19 2 1 20 4 2 -0.6% -21.0% -23.8%

Amara Raja 23 3 1 24 3 1 20 3 2 2.4% 3.7% 0.6%

Bharat Forge 17 4 3 24 5 6 17 3 -2 42.7% 13.6% 128.4%

Sundaram

Fasteners 13 3 1 12 2 1 11 2 1 -8.3% -24.6% -27.6%

Banks and

NBFCs 797 576 280 802 567 294 712 529 186 0.6% -1.7% 5.1%

ICICI Bank 122 107 61 122 101 62 99 88 49 0.7% -4.7% 1.6%

Kotak Mahindra

Bank 41 32 21 43 27 21 39 29 19 5.0% -16.6% 2.6%

Bajaj Finance 45 36 21 47 39 21 34 29 11 5.5% 7.4% 0.6%

State Bank of

India 316 189 81 307 185 84 288 173 52 -2.9% -1.9% 4.5%

Axis Bank 81 62 31 87 62 36 74 61 11 6.2% -1.1% 17.0%

IndusInd Bank 38 33 13 38 33 12 34 30 8 0.4% -0.9% -7.4%

AU Small

Finance Bank 8 5 3 8 5 3 6 9 5 -0.9% -5.3% 14.0%

Shriram Trans

Finance 22 17 8 23 19 7 21 17 7 0.7% 10.1% -17.5%

Cholamandalam

Investment &

Finance

Company

14 10 6 14 10 5 13 10 4 0.0% -1.6% -6.4%

Mahindra &

Mahindra

Financial

15 11 5 15 11 9 14 10 -3 0.6% -3.0% 62.6%

Federal Bank 15 10 5 15 9 5 14 10 4 -0.7% -8.1% -3.4%

LIC Housing 13 11 5 15 13 8 13 12 7 10.5% 16.6% 51.0%

City Union

Bank 5 4 2 5 4 2 5 5 2 -0.9% -9.6% 12.1%

RBL Bank 10 8 2 10 6 2 9 8 1 2.7% -23.3% -6.2%

DCB Bank 3 2 1 3 2 1 3 3 1 2.3% -3.3% -8.8%

Karur Vysya

Bank 7 4 1 7 4 2 6 3 0 3.2% 8.5% 27.2%

Indostar Capital

Finance 2 1 0 1 1 0 1 1 0 -13.9% -27.5% -70.5%

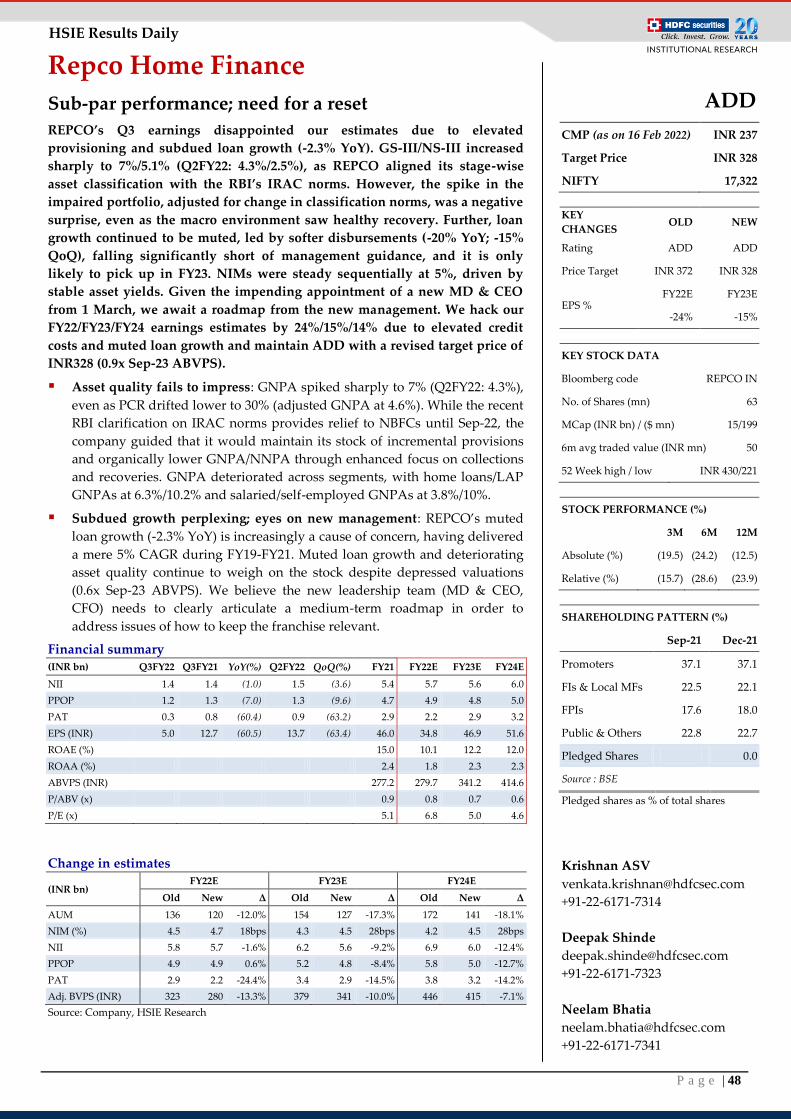

REPCO Home

Finance 2 1 1 1 1 0 1 1 1 -6.0% -6.4% -58.9%

UJJIVAN SFB 4 2 -1 5 1 0 4 2 -3 10.1% -12.7% 61.7%

UJJIVAN

Financial

Services

0 0 0 0 0 0 0 0 0 NM NM NM

CREDAG 4 2 1 4 3 1 3 2 -1 9.0% 13.1% 49.8%

Bandhan Bank 21 17 8 21 20 9 21 19 6 2.7% 14.4% 4.0%

SBI Cards 10 11 4 10 11 4 9 9 2 4.6% 4.8% -12.1%

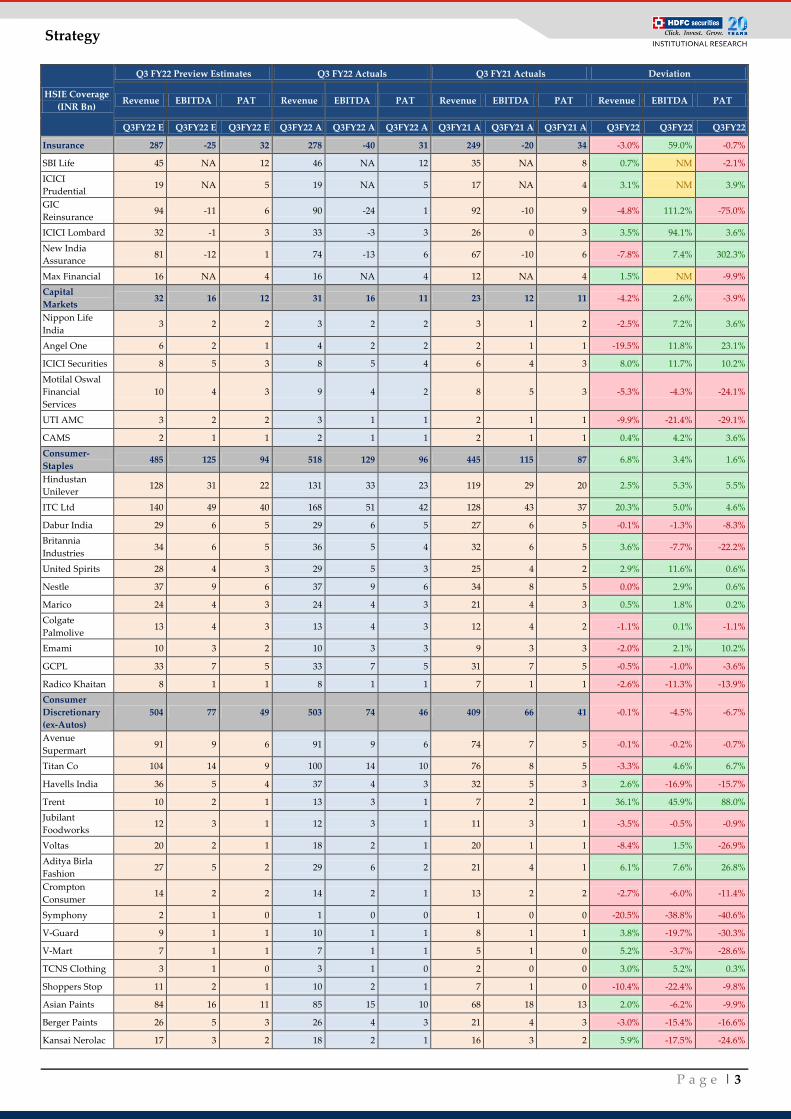

P a g e | 3

Strategy

HSIE Coverage

(INR Bn)

Q3 FY22 Preview Estimates Q3 FY22 Actuals Q3 FY21 Actuals Deviation

Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT

Q3FY22 E Q3FY22 E Q3FY22 E Q3FY22 A Q3FY22 A Q3FY22 A Q3FY21 A Q3FY21 A Q3FY21 A Q3FY22 Q3FY22 Q3FY22

Insurance 287 -25 32 278 -40 31 249 -20 34 -3.0% 59.0% -0.7%

SBI Life 45 NA 12 46 NA 12 35 NA 8 0.7% NM -2.1%

ICICI

Prudential 19 NA 5 19 NA 5 17 NA 4 3.1% NM 3.9%

GIC

Reinsurance 94 -11 6 90 -24 1 92 -10 9 -4.8% 111.2% -75.0%

ICICI Lombard 32 -1 3 33 -3 3 26 0 3 3.5% 94.1% 3.6%

New India

Assurance 81 -12 1 74 -13 6 67 -10 6 -7.8% 7.4% 302.3%

Max Financial 16 NA 4 16 NA 4 12 NA 4 1.5% NM -9.9%

Capital

Markets 32 16 12 31 16 11 23 12 11 -4.2% 2.6% -3.9%

Nippon Life

India 3 2 2 3 2 2 3 1 2 -2.5% 7.2% 3.6%

Angel One 6 2 1 4 2 2 2 1 1 -19.5% 11.8% 23.1%

ICICI Securities 8 5 3 8 5 4 6 4 3 8.0% 11.7% 10.2%

Motilal Oswal

Financial

Services

10 4 3 9 4 2 8 5 3 -5.3% -4.3% -24.1%

UTI AMC 3 2 2 3 1 1 2 1 1 -9.9% -21.4% -29.1%

CAMS 2 1 1 2 1 1 2 1 1 0.4% 4.2% 3.6%

Consumer-

Staples 485 125 94 518 129 96 445 115 87 6.8% 3.4% 1.6%

Hindustan

Unilever 128 31 22 131 33 23 119 29 20 2.5% 5.3% 5.5%

ITC Ltd 140 49 40 168 51 42 128 43 37 20.3% 5.0% 4.6%

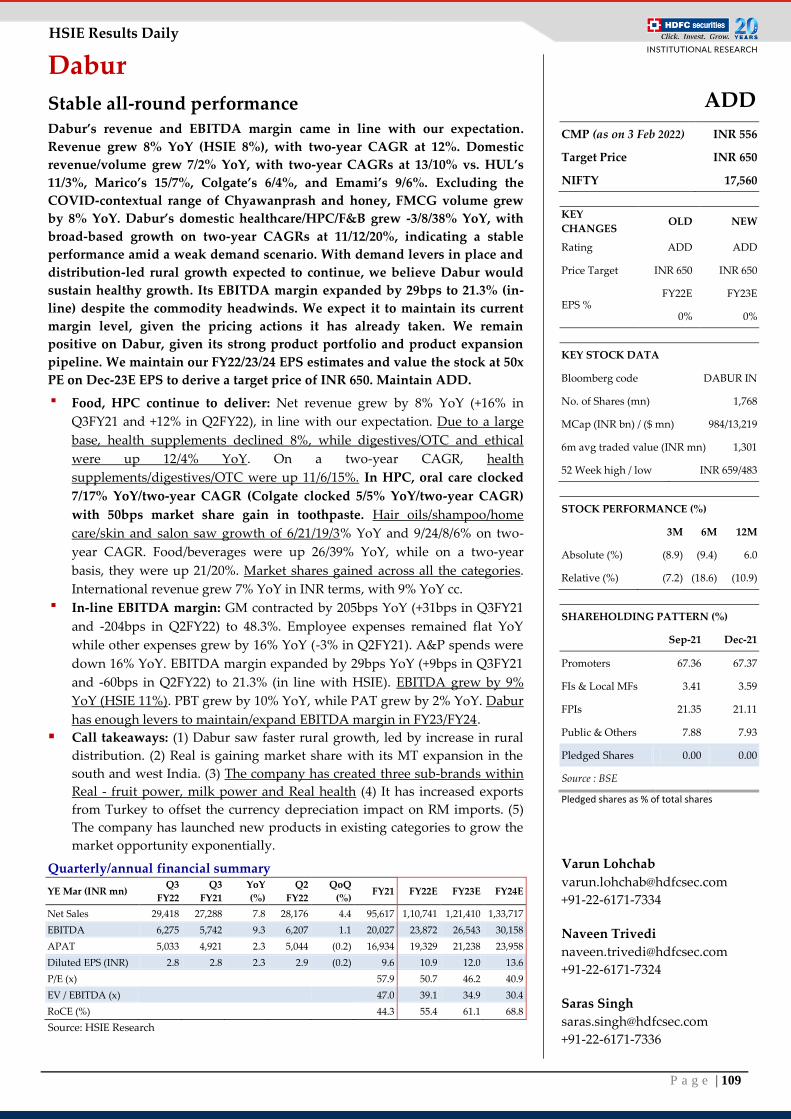

Dabur India 29 6 5 29 6 5 27 6 5 -0.1% -1.3% -8.3%

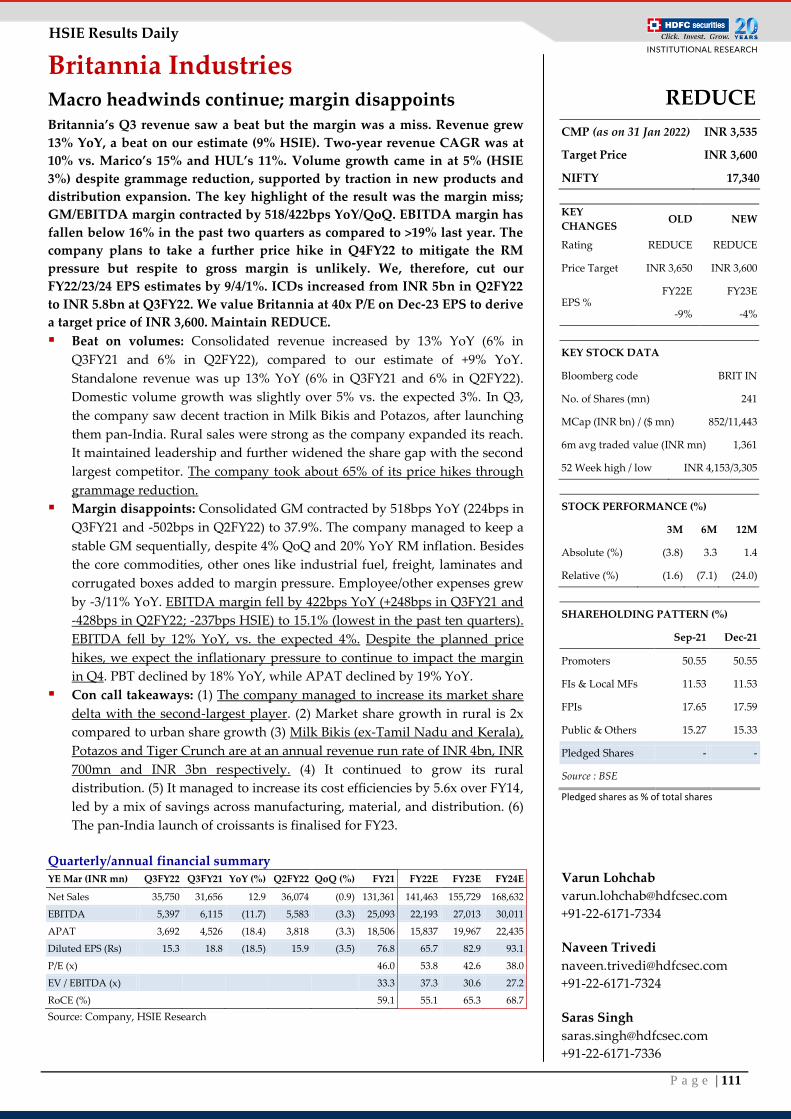

Britannia

Industries 34 6 5 36 5 4 32 6 5 3.6% -7.7% -22.2%

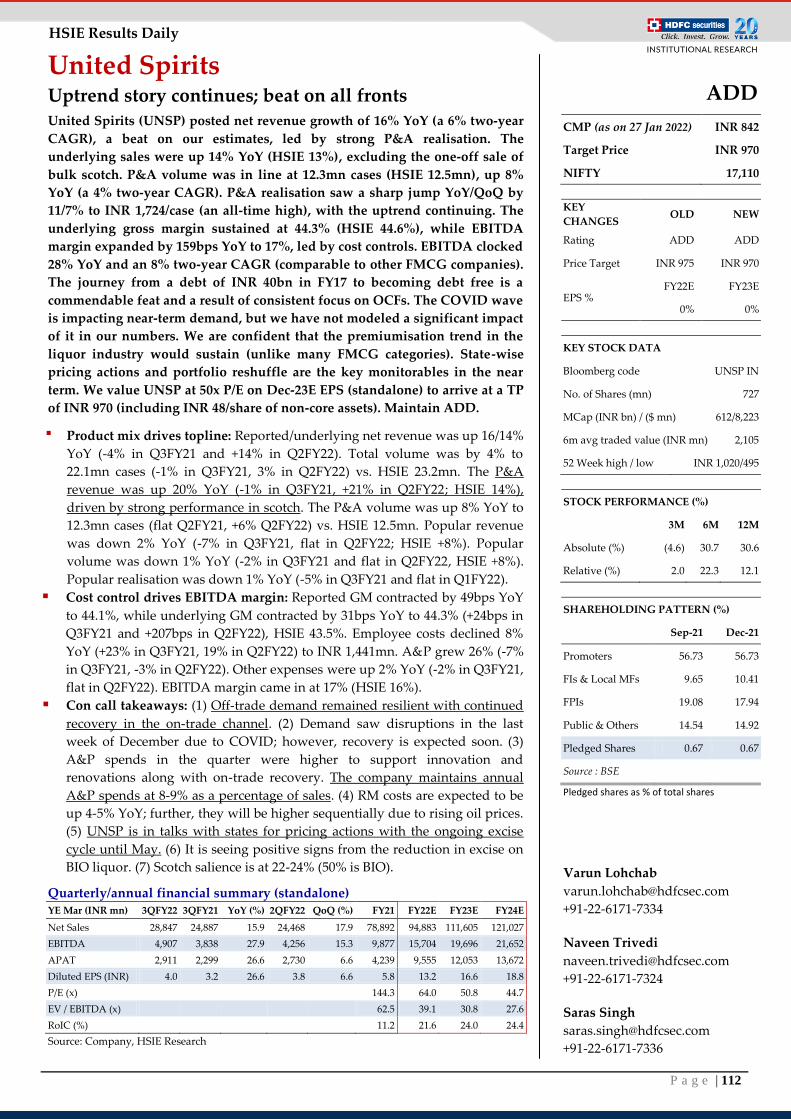

United Spirits 28 4 3 29 5 3 25 4 2 2.9% 11.6% 0.6%

Nestle 37 9 6 37 9 6 34 8 5 0.0% 2.9% 0.6%

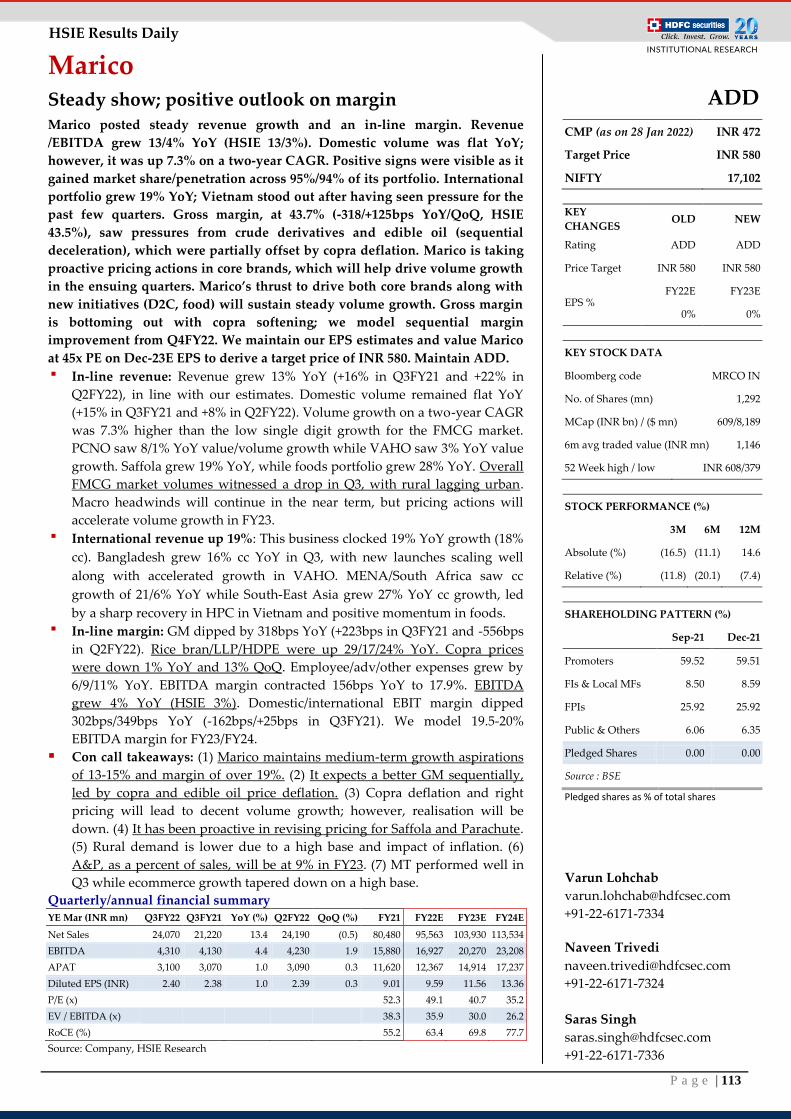

Marico 24 4 3 24 4 3 21 4 3 0.5% 1.8% 0.2%

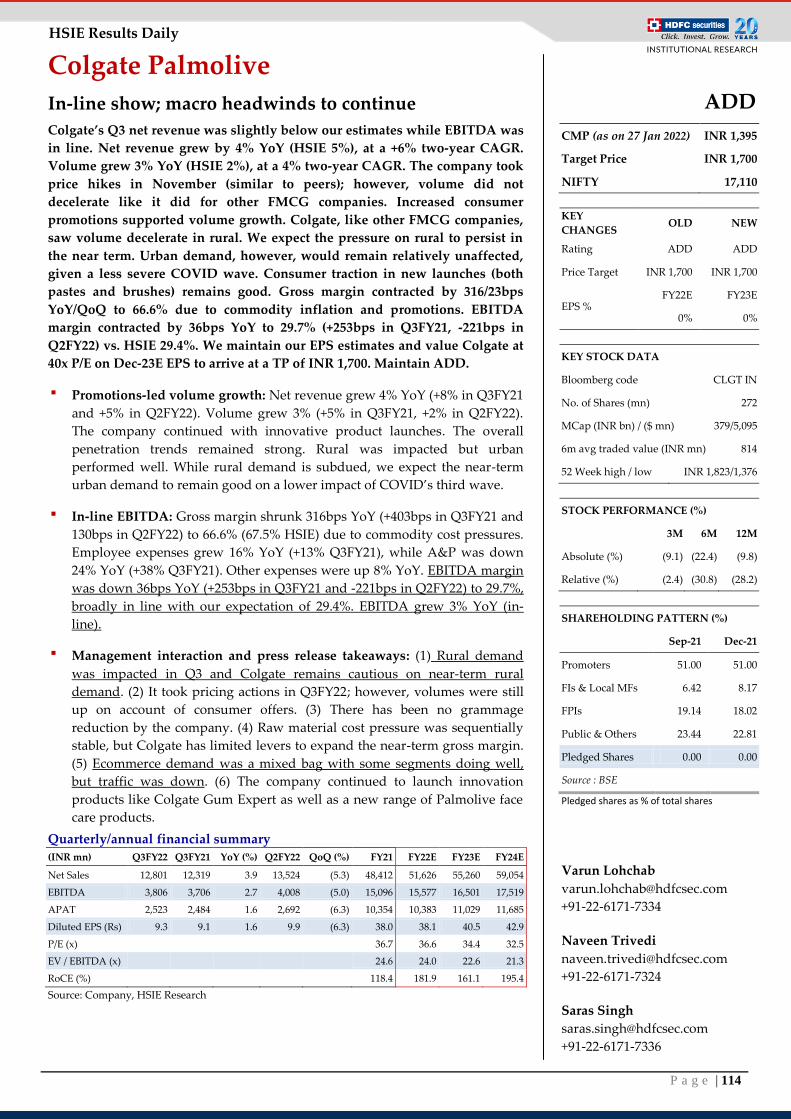

Colgate

Palmolive 13 4 3 13 4 3 12 4 2 -1.1% 0.1% -1.1%

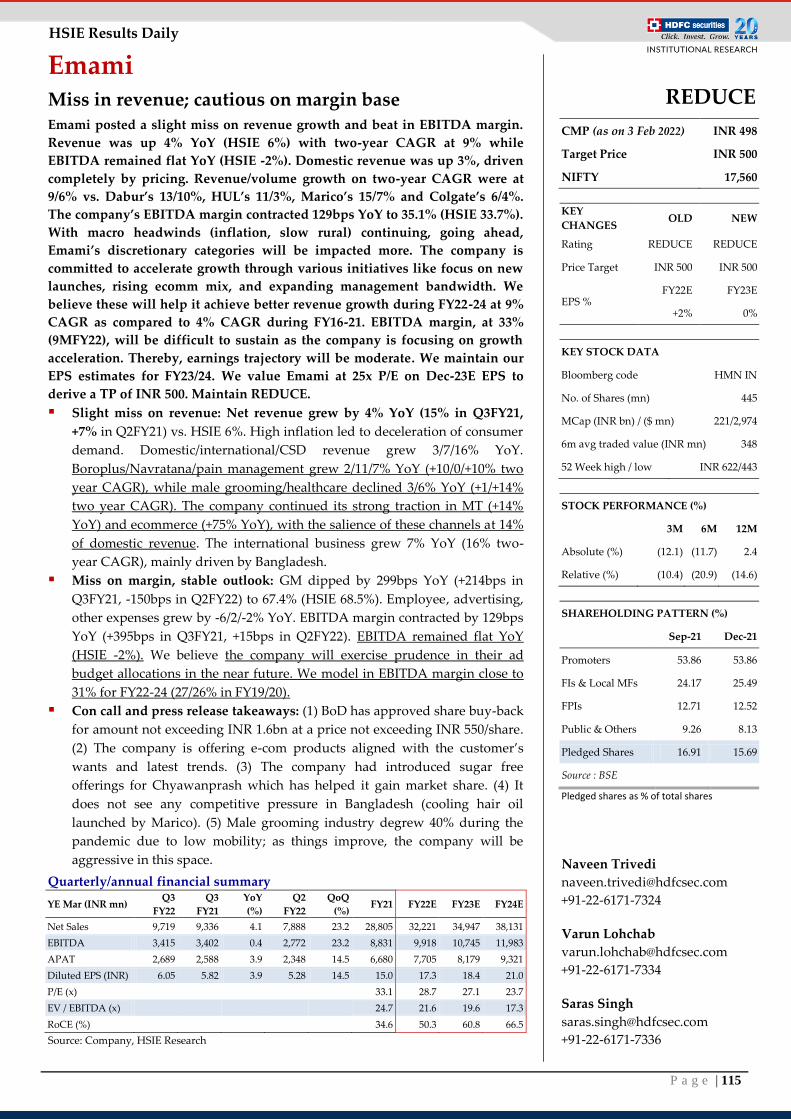

Emami 10 3 2 10 3 3 9 3 3 -2.0% 2.1% 10.2%

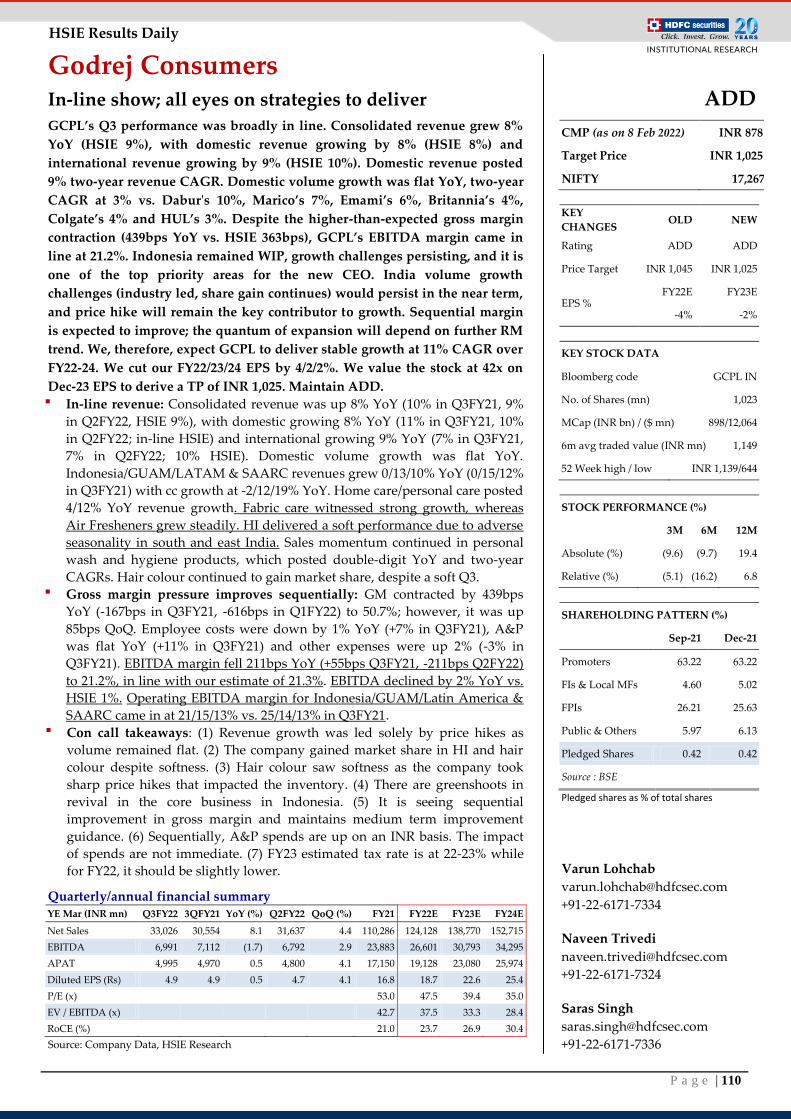

GCPL 33 7 5 33 7 5 31 7 5 -0.5% -1.0% -3.6%

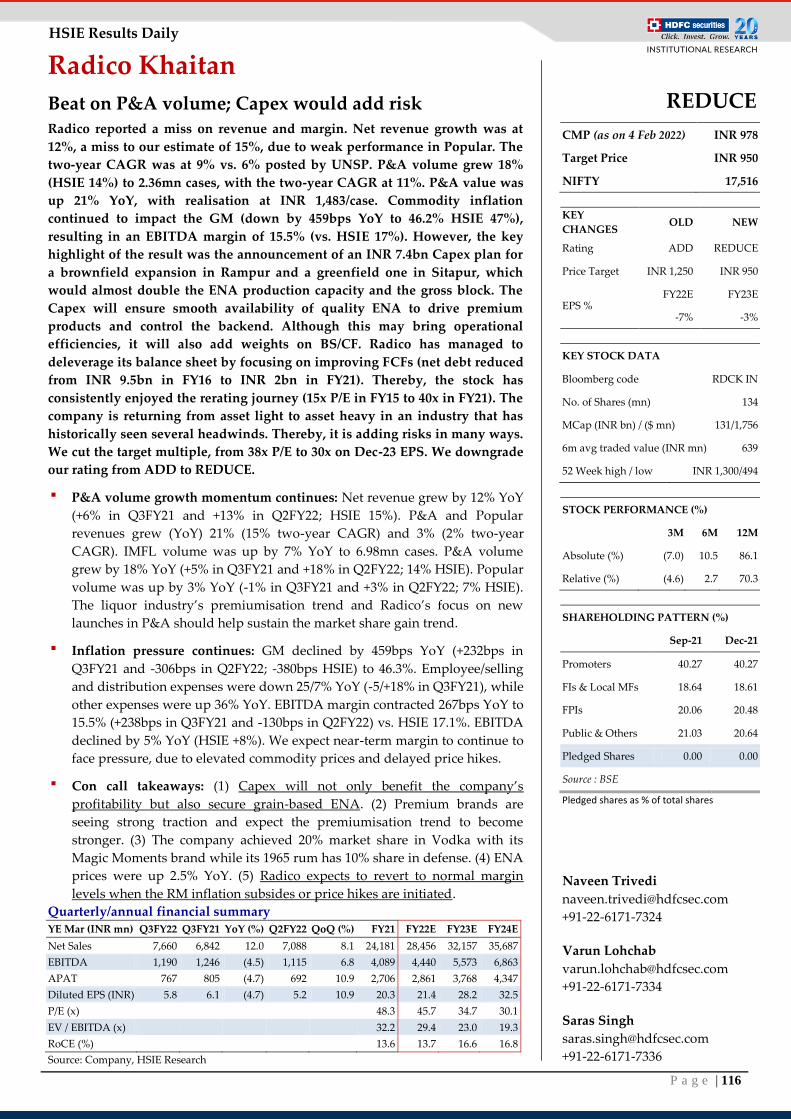

Radico Khaitan 8 1 1 8 1 1 7 1 1 -2.6% -11.3% -13.9%

Consumer

Discretionary

(ex-Autos)

504 77 49 503 74 46 409 66 41 -0.1% -4.5% -6.7%

Avenue

Supermart 91 9 6 91 9 6 74 7 5 -0.1% -0.2% -0.7%

Titan Co 104 14 9 100 14 10 76 8 5 -3.3% 4.6% 6.7%

Havells India 36 5 4 37 4 3 32 5 3 2.6% -16.9% -15.7%

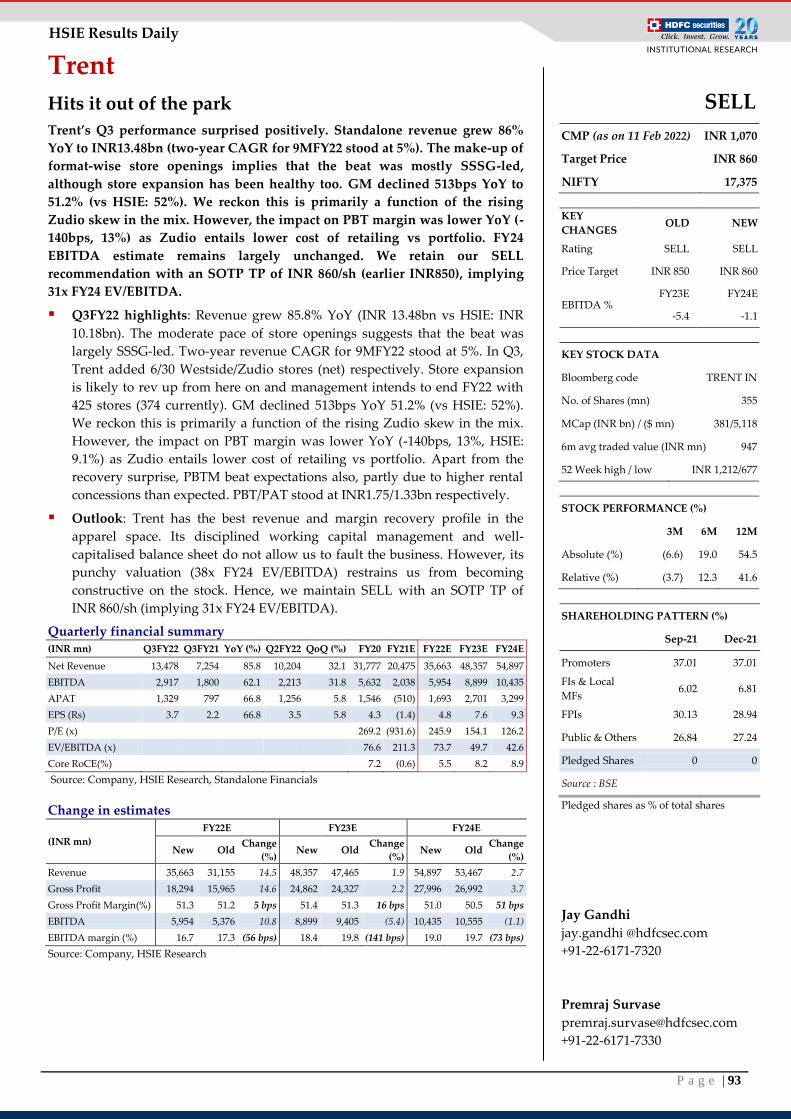

Trent 10 2 1 13 3 1 7 2 1 36.1% 45.9% 88.0%

Jubilant

Foodworks 12 3 1 12 3 1 11 3 1 -3.5% -0.5% -0.9%

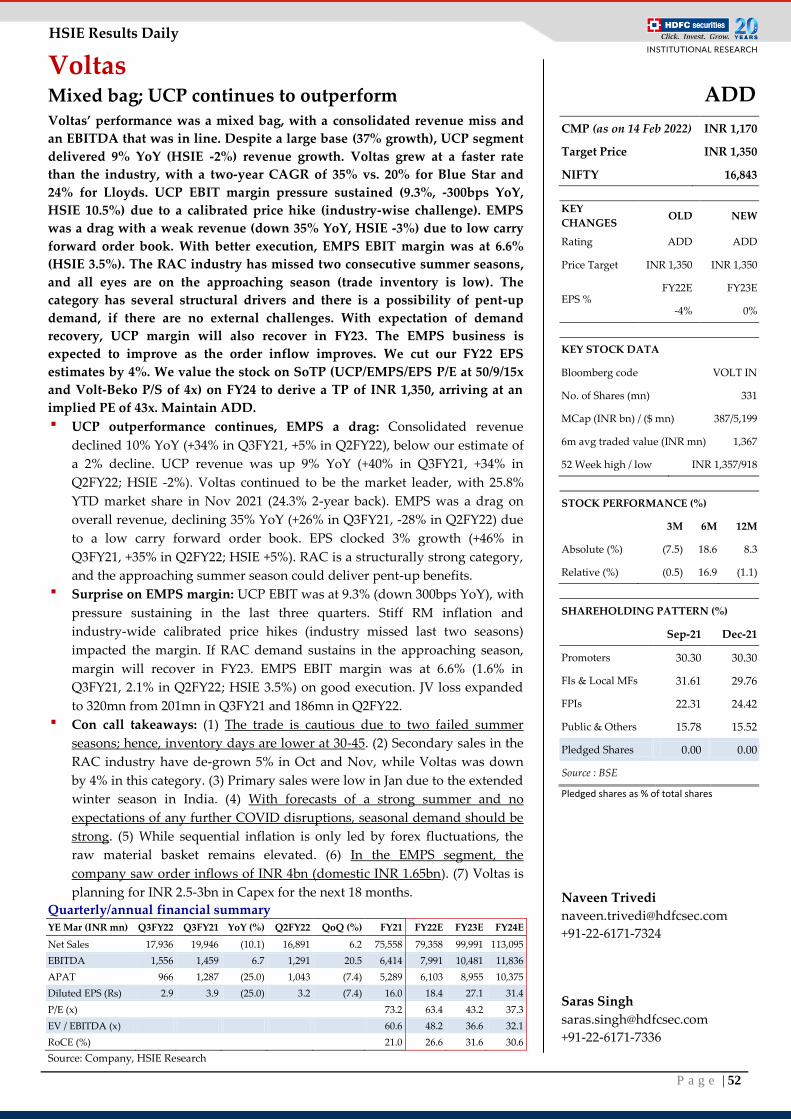

Voltas 20 2 1 18 2 1 20 1 1 -8.4% 1.5% -26.9%

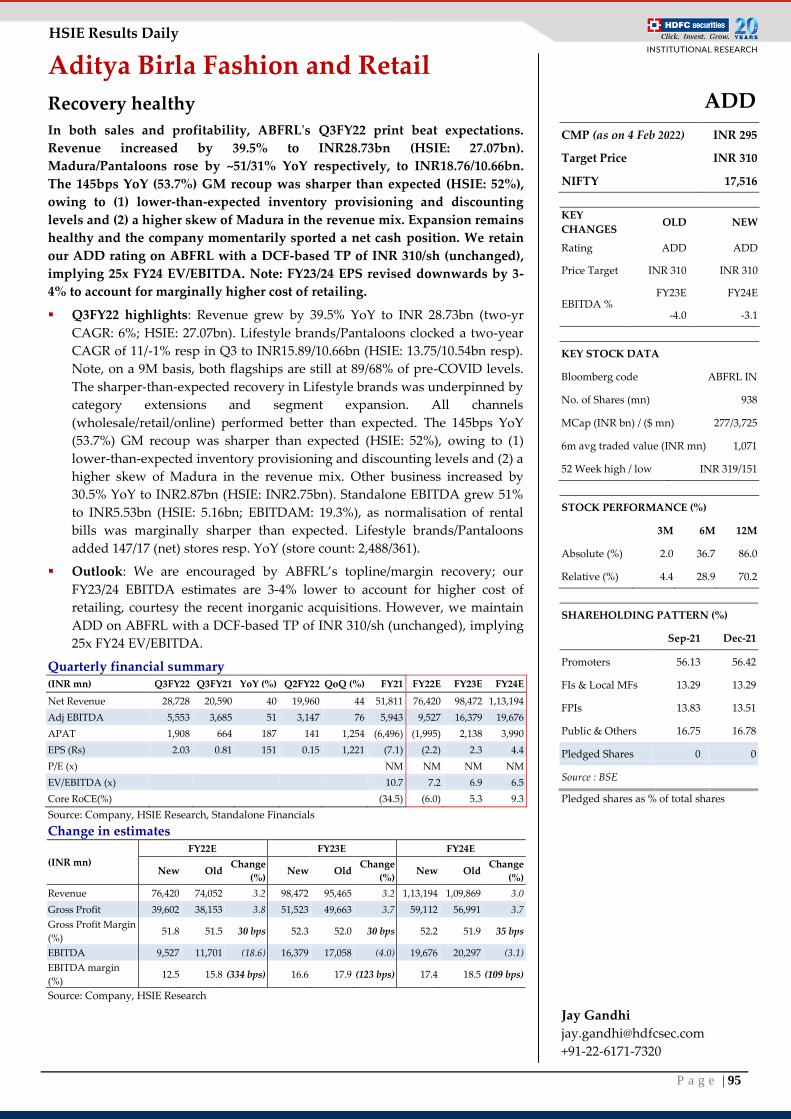

Aditya Birla

Fashion 27 5 2 29 6 2 21 4 1 6.1% 7.6% 26.8%

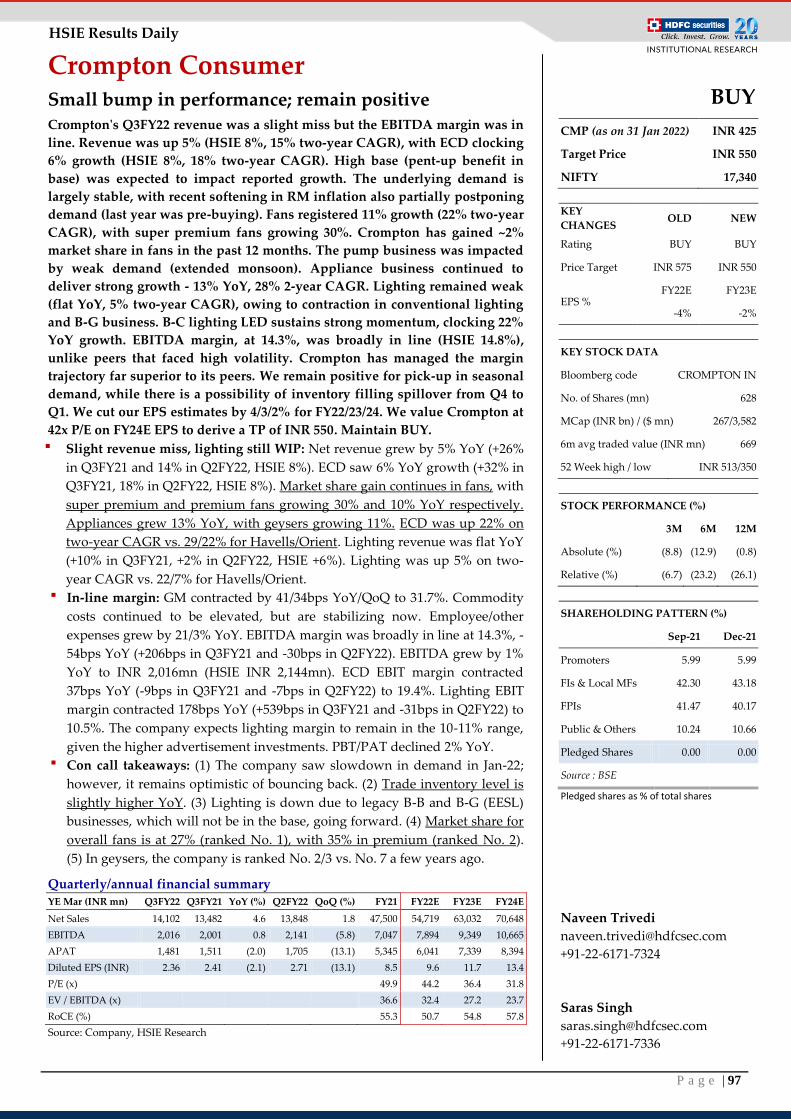

Crompton

Consumer 14 2 2 14 2 1 13 2 2 -2.7% -6.0% -11.4%

Symphony 2 1 0 1 0 0 1 0 0 -20.5% -38.8% -40.6%

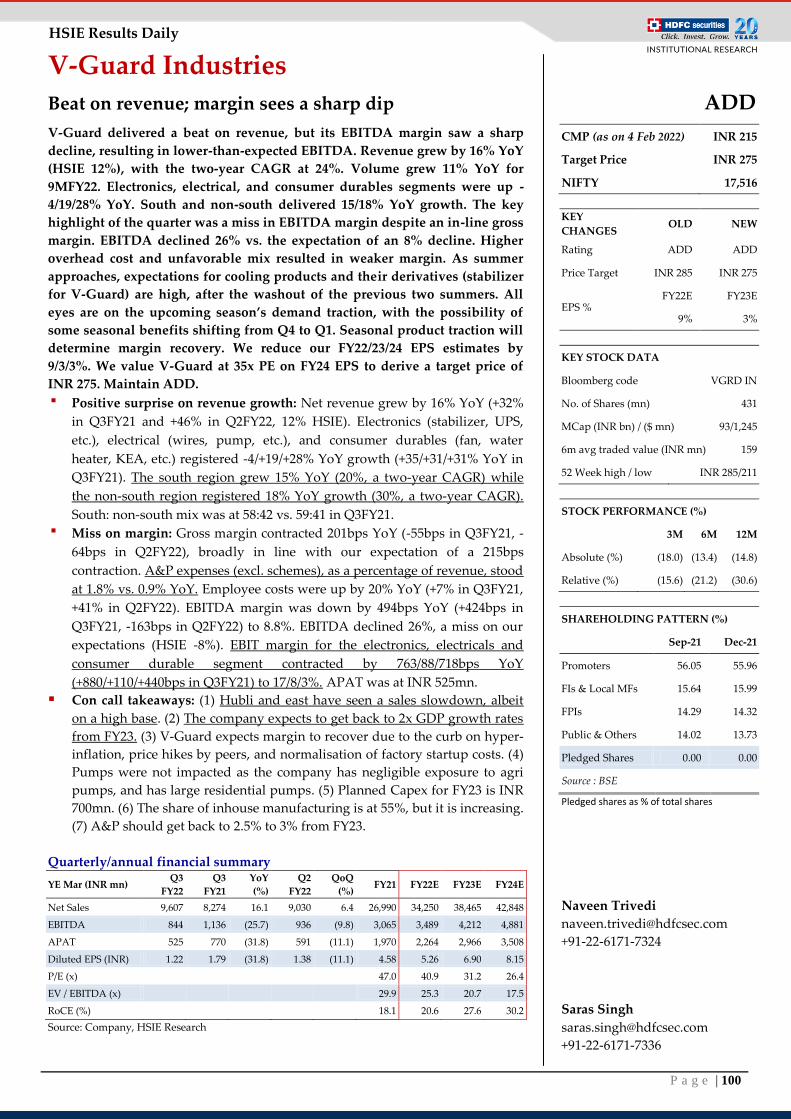

V-Guard 9 1 1 10 1 1 8 1 1 3.8% -19.7% -30.3%

V-Mart 7 1 1 7 1 1 5 1 0 5.2% -3.7% -28.6%

TCNS Clothing 3 1 0 3 1 0 2 0 0 3.0% 5.2% 0.3%

Shoppers Stop 11 2 1 10 2 1 7 1 0 -10.4% -22.4% -9.8%

Asian Paints 84 16 11 85 15 10 68 18 13 2.0% -6.2% -9.9%

Berger Paints 26 5 3 26 4 3 21 4 3 -3.0% -15.4% -16.6%

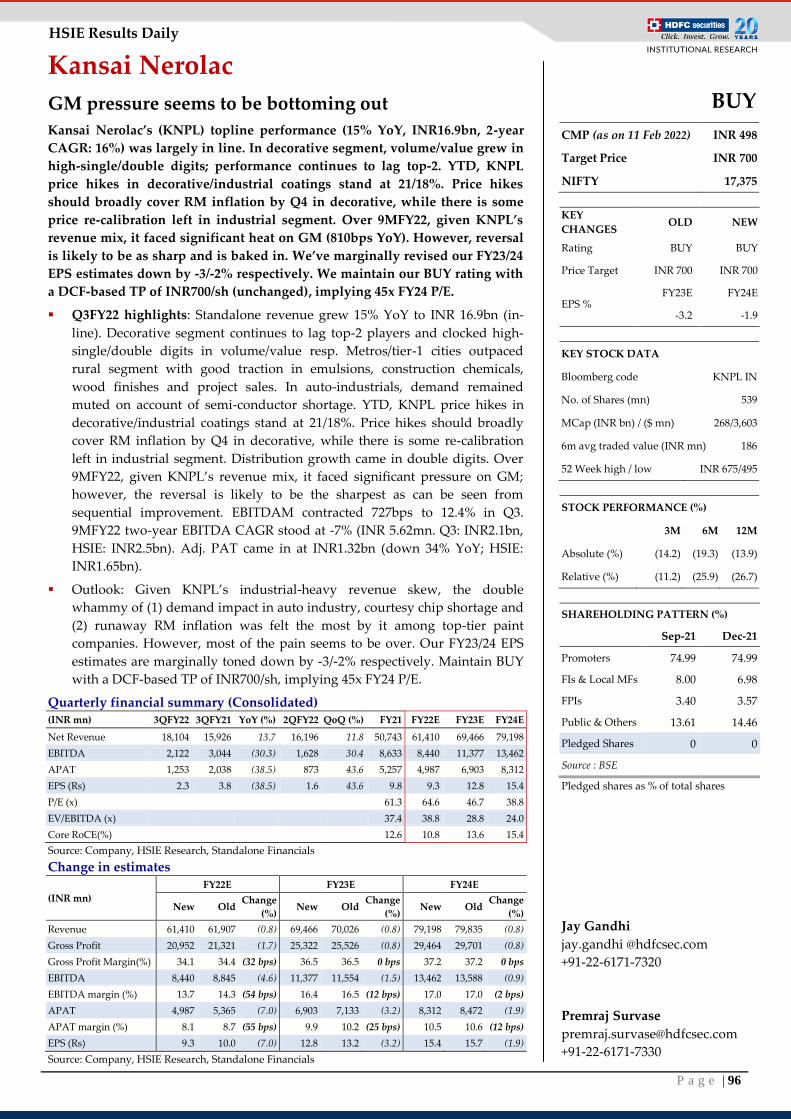

Kansai Nerolac 17 3 2 18 2 1 16 3 2 5.9% -17.5% -24.6%

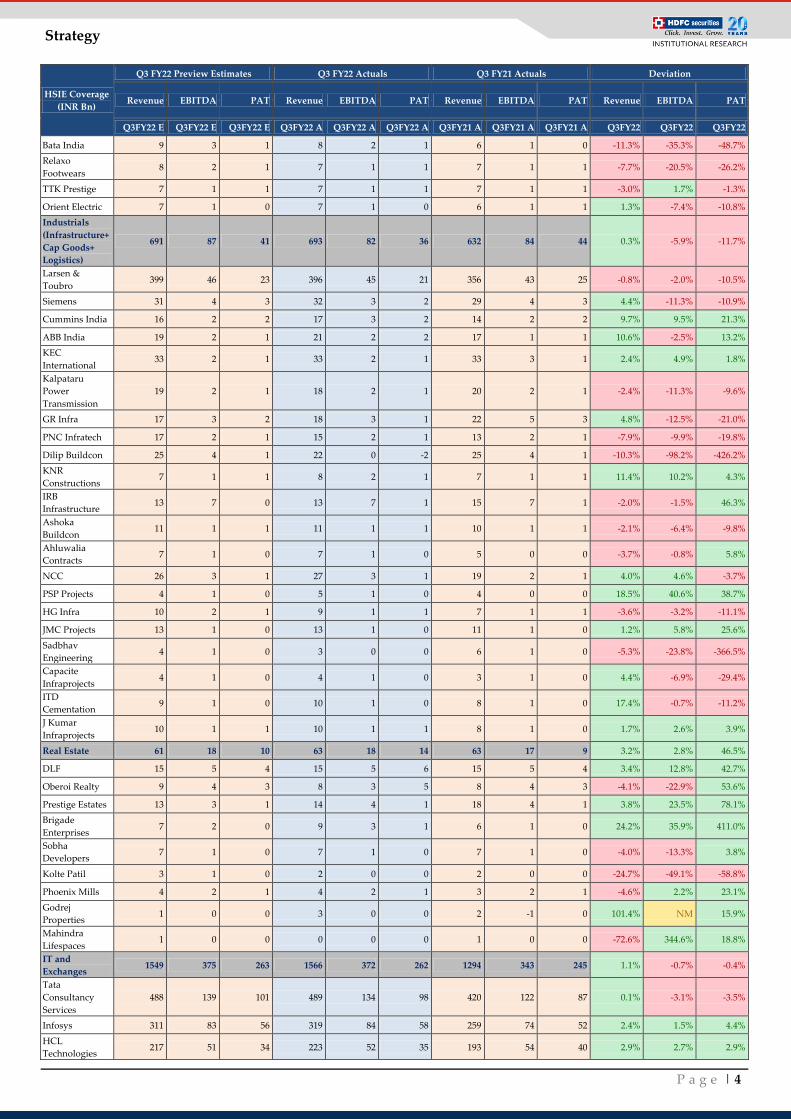

P a g e | 4

Strategy

HSIE Coverage

(INR Bn)

Q3 FY22 Preview Estimates Q3 FY22 Actuals Q3 FY21 Actuals Deviation

Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT

Q3FY22 E Q3FY22 E Q3FY22 E Q3FY22 A Q3FY22 A Q3FY22 A Q3FY21 A Q3FY21 A Q3FY21 A Q3FY22 Q3FY22 Q3FY22

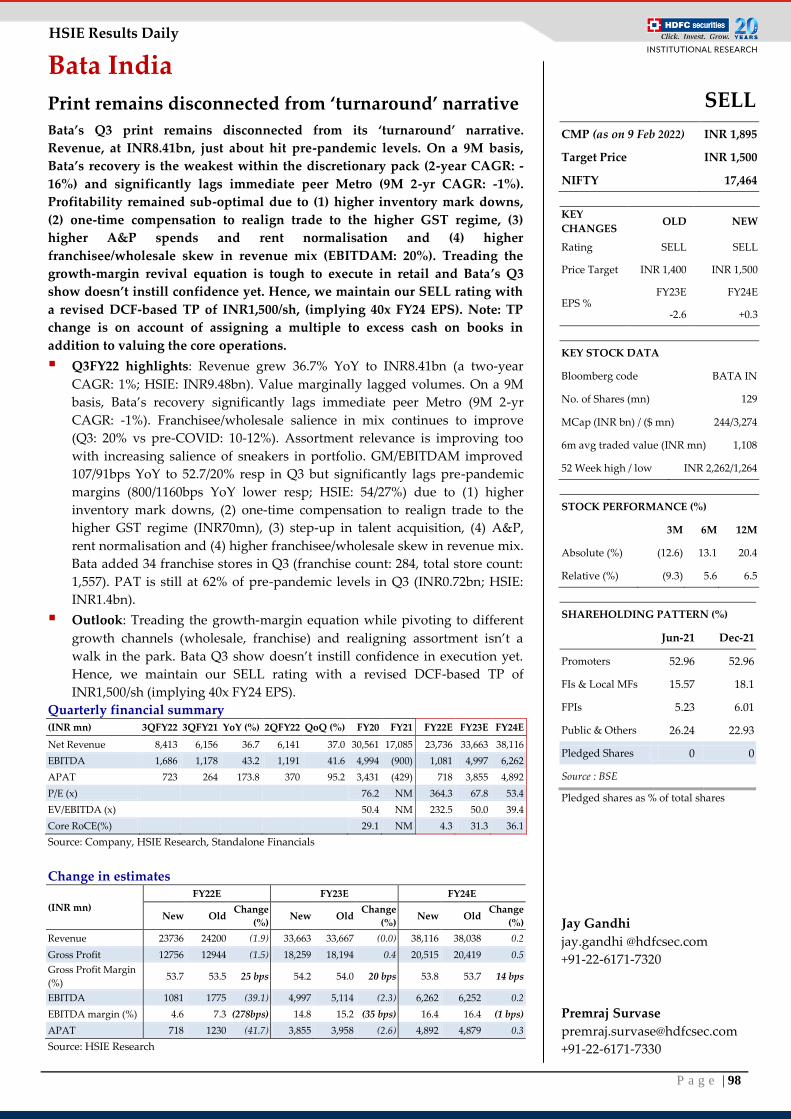

Bata India 9 3 1 8 2 1 6 1 0 -11.3% -35.3% -48.7%

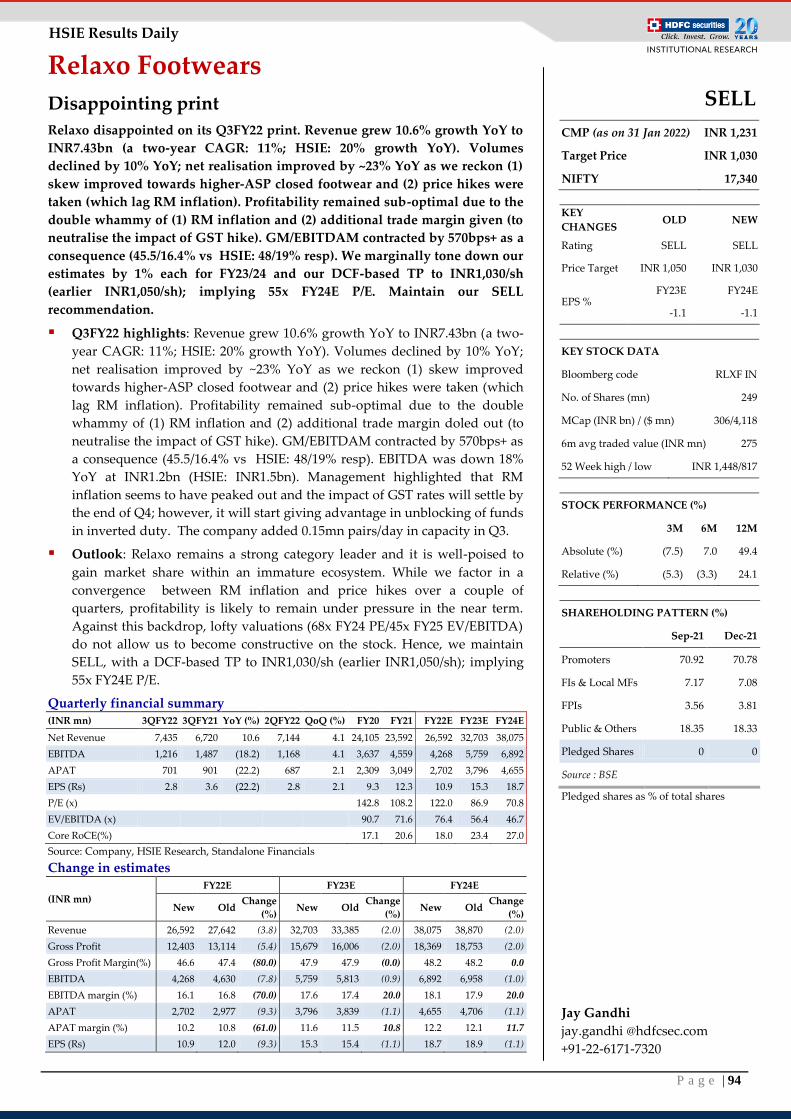

Relaxo

Footwears 8 2 1 7 1 1 7 1 1 -7.7% -20.5% -26.2%

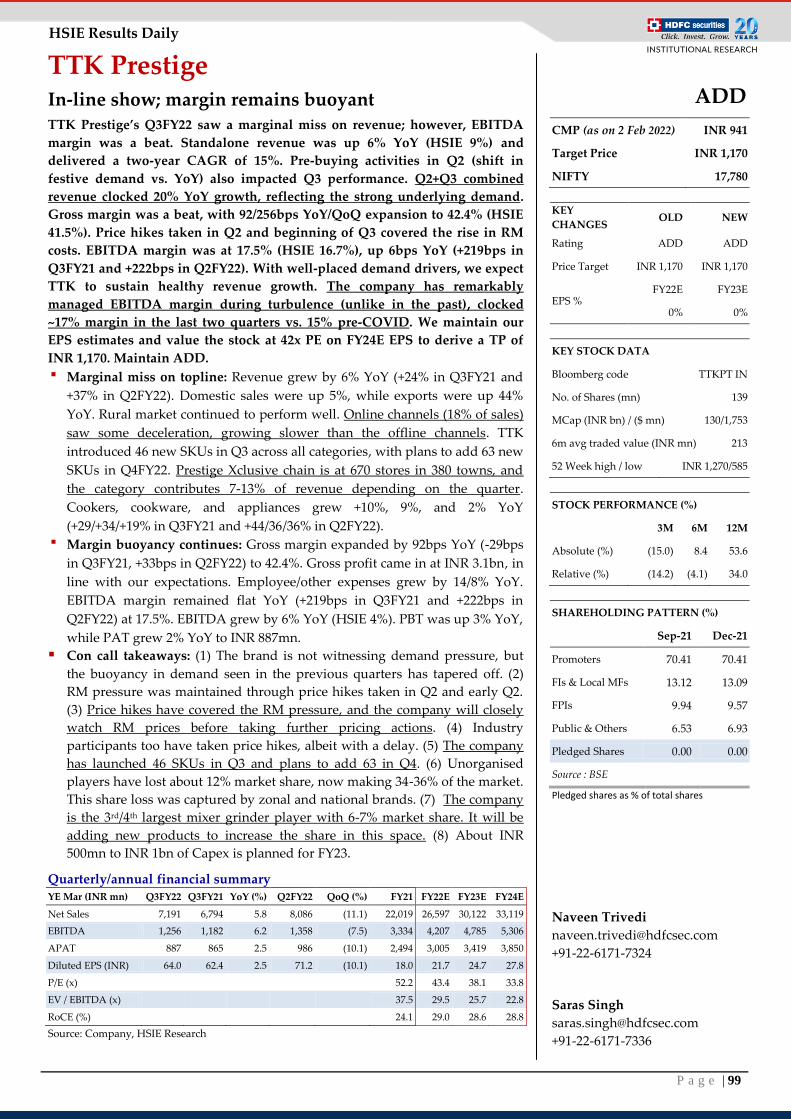

TTK Prestige 7 1 1 7 1 1 7 1 1 -3.0% 1.7% -1.3%

Orient Electric 7 1 0 7 1 0 6 1 1 1.3% -7.4% -10.8%

Industrials

(Infrastructure+

Cap Goods+

Logistics)

691 87 41 693 82 36 632 84 44 0.3% -5.9% -11.7%

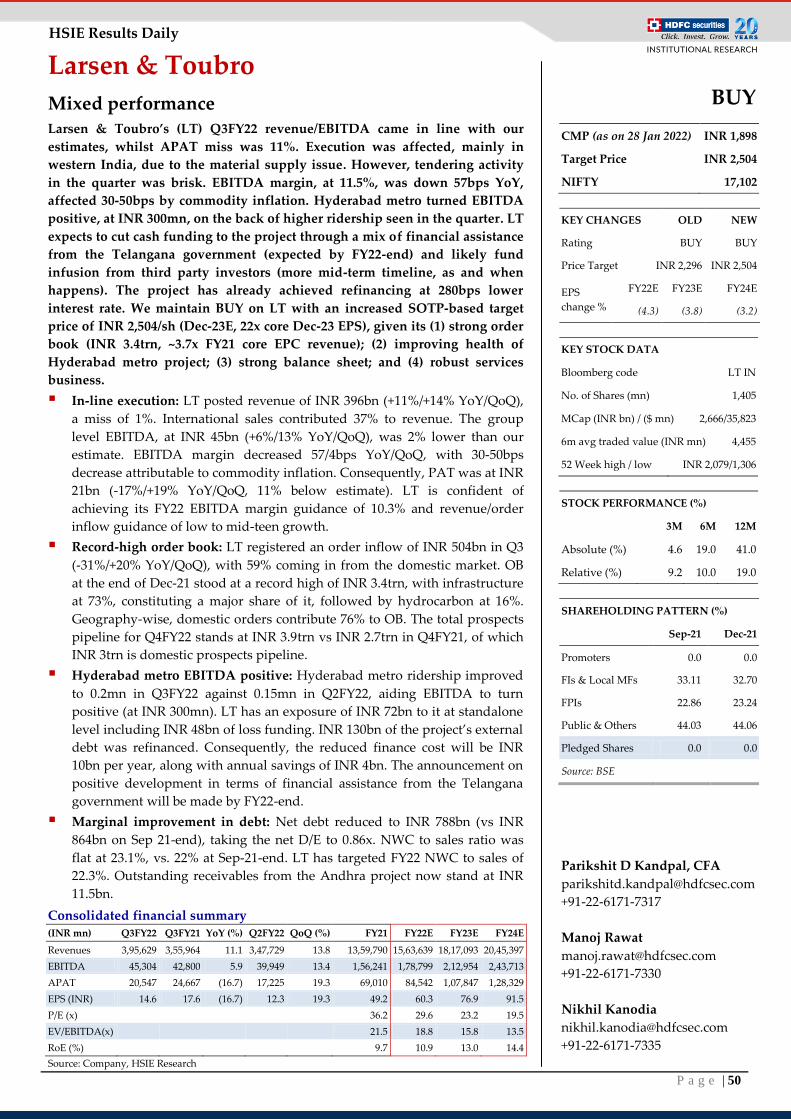

Larsen &

Toubro 399 46 23 396 45 21 356 43 25 -0.8% -2.0% -10.5%

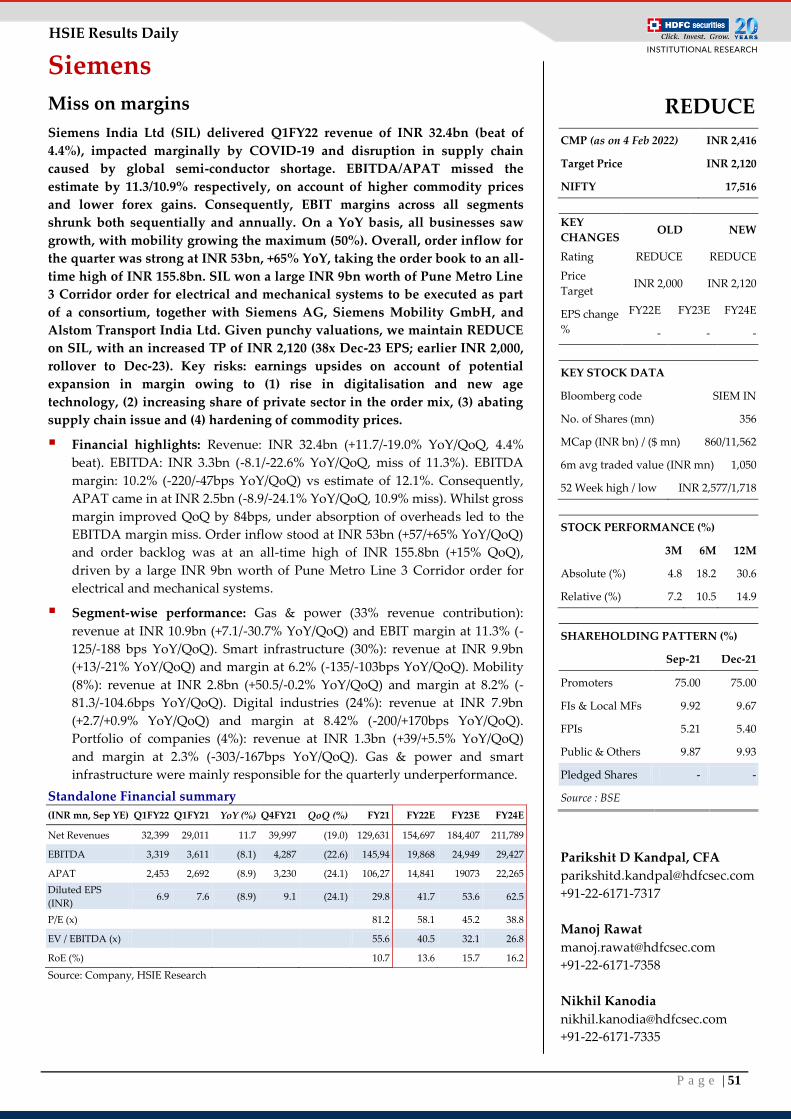

Siemens 31 4 3 32 3 2 29 4 3 4.4% -11.3% -10.9%

Cummins India 16 2 2 17 3 2 14 2 2 9.7% 9.5% 21.3%

ABB India 19 2 1 21 2 2 17 1 1 10.6% -2.5% 13.2%

KEC

International 33 2 1 33 2 1 33 3 1 2.4% 4.9% 1.8%

Kalpataru

Power

Transmission

19 2 1 18 2 1 20 2 1 -2.4% -11.3% -9.6%

GR Infra 17 3 2 18 3 1 22 5 3 4.8% -12.5% -21.0%

PNC Infratech 17 2 1 15 2 1 13 2 1 -7.9% -9.9% -19.8%

Dilip Buildcon 25 4 1 22 0 -2 25 4 1 -10.3% -98.2% -426.2%

KNR

Constructions 7 1 1 8 2 1 7 1 1 11.4% 10.2% 4.3%

IRB

Infrastructure 13 7 0 13 7 1 15 7 1 -2.0% -1.5% 46.3%

Ashoka

Buildcon 11 1 1 11 1 1 10 1 1 -2.1% -6.4% -9.8%

Ahluwalia

Contracts 7 1 0 7 1 0 5 0 0 -3.7% -0.8% 5.8%

NCC 26 3 1 27 3 1 19 2 1 4.0% 4.6% -3.7%

PSP Projects 4 1 0 5 1 0 4 0 0 18.5% 40.6% 38.7%

HG Infra 10 2 1 9 1 1 7 1 1 -3.6% -3.2% -11.1%

JMC Projects 13 1 0 13 1 0 11 1 0 1.2% 5.8% 25.6%

Sadbhav

Engineering 4 1 0 3 0 0 6 1 0 -5.3% -23.8% -366.5%

Capacite

Infraprojects 4 1 0 4 1 0 3 1 0 4.4% -6.9% -29.4%

ITD

Cementation 9 1 0 10 1 0 8 1 0 17.4% -0.7% -11.2%

J Kumar

Infraprojects 10 1 1 10 1 1 8 1 0 1.7% 2.6% 3.9%

Real Estate 61 18 10 63 18 14 63 17 9 3.2% 2.8% 46.5%

DLF 15 5 4 15 5 6 15 5 4 3.4% 12.8% 42.7%

Oberoi Realty 9 4 3 8 3 5 8 4 3 -4.1% -22.9% 53.6%

Prestige Estates 13 3 1 14 4 1 18 4 1 3.8% 23.5% 78.1%

Brigade

Enterprises 7 2 0 9 3 1 6 1 0 24.2% 35.9% 411.0%

Sobha

Developers 7 1 0 7 1 0 7 1 0 -4.0% -13.3% 3.8%

Kolte Patil 3 1 0 2 0 0 2 0 0 -24.7% -49.1% -58.8%

Phoenix Mills 4 2 1 4 2 1 3 2 1 -4.6% 2.2% 23.1%

Godrej

Properties 1 0 0 3 0 0 2 -1 0 101.4% NM 15.9%

Mahindra

Lifespaces 1 0 0 0 0 0 1 0 0 -72.6% 344.6% 18.8%

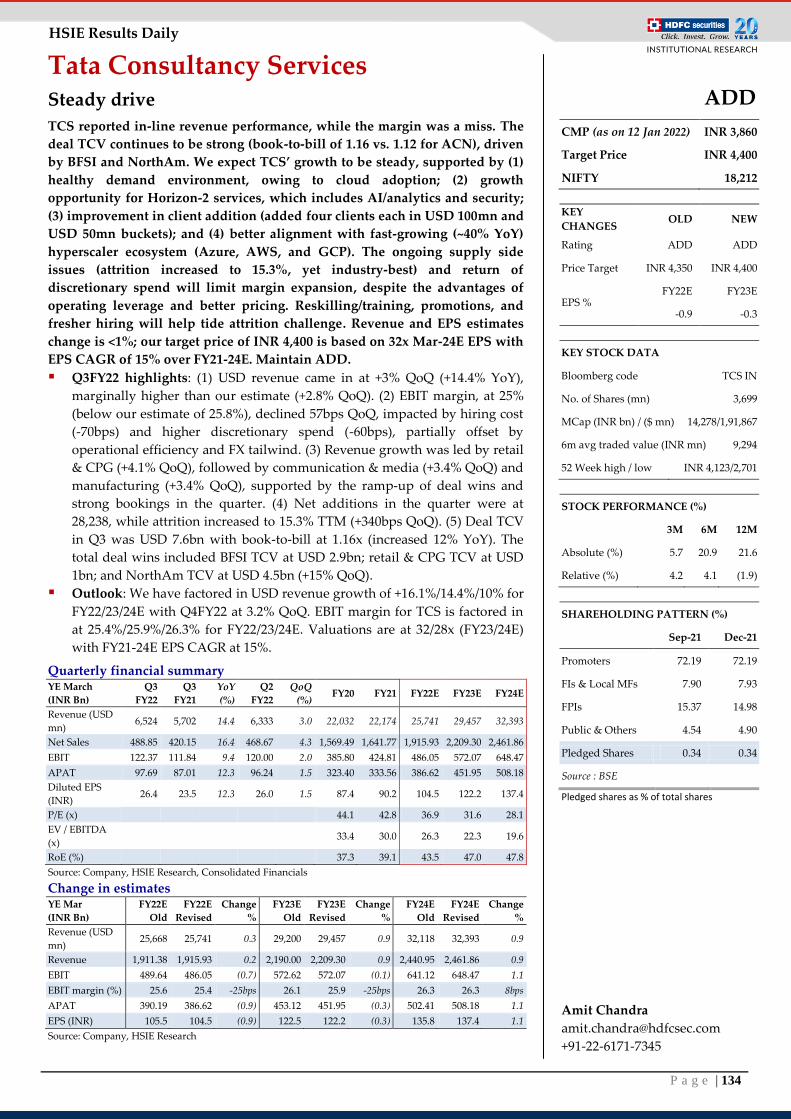

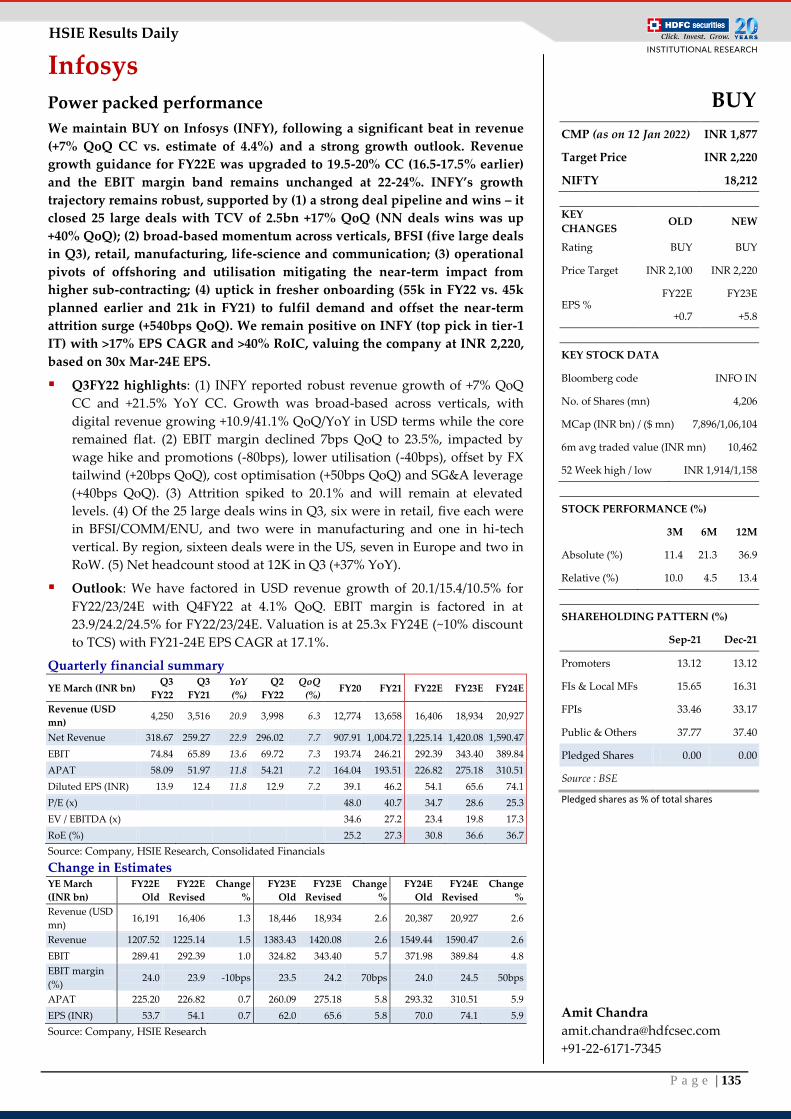

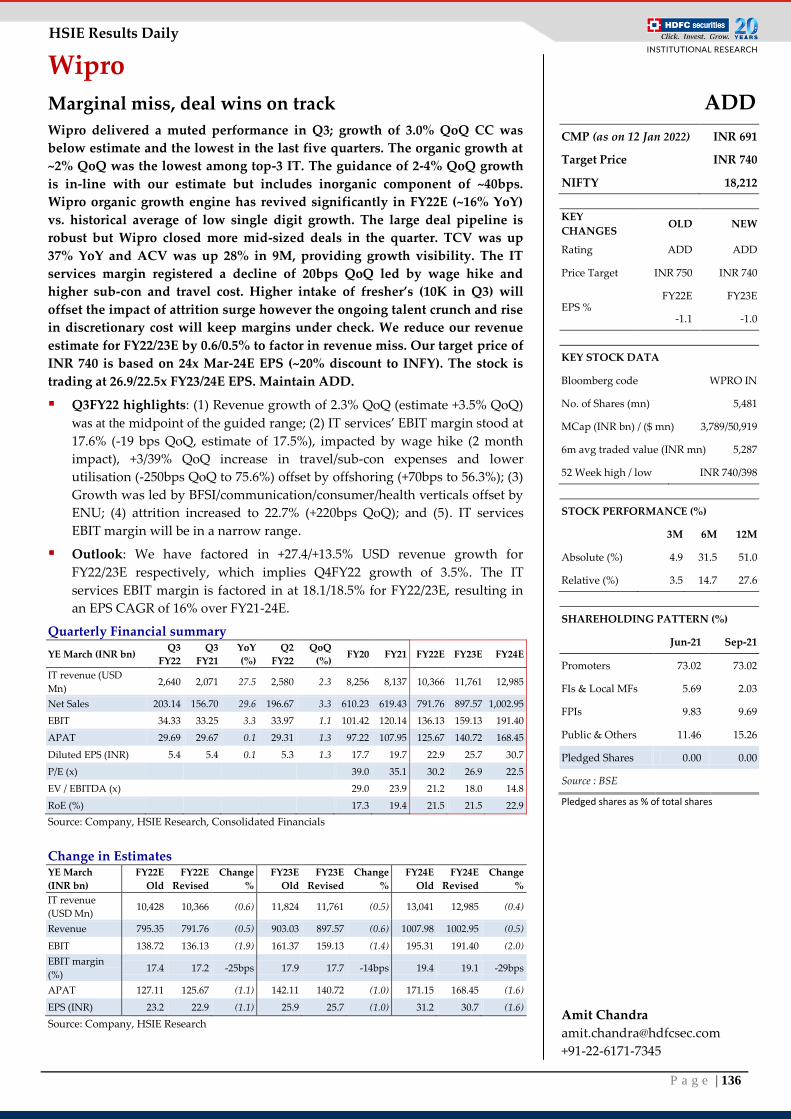

IT and

Exchanges 1549 375 263 1566 372 262 1294 343 245 1.1% -0.7% -0.4%

Tata

Consultancy

Services

488 139 101 489 134 98 420 122 87 0.1% -3.1% -3.5%

Infosys 311 83 56 319 84 58 259 74 52 2.4% 1.5% 4.4%

HCL

Technologies 217 51 34 223 52 35 193 54 40 2.9% 2.7% 2.9%

P a g e | 5

Strategy

HSIE Coverage

(INR Bn)

Q3 FY22 Preview Estimates Q3 FY22 Actuals Q3 FY21 Actuals Deviation

Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT

Q3FY22 E Q3FY22 E Q3FY22 E Q3FY22 A Q3FY22 A Q3FY22 A Q3FY21 A Q3FY21 A Q3FY21 A Q3FY22 Q3FY22 Q3FY22

Wipro 204 43 31 203 42 30 157 41 30 -0.6% -3.0% -2.7%

Tech Mahindra 114 21 15 115 21 14 96 19 13 0.4% -3.1% -6.5%

L&T Infotech 40 8 6 41 8 6 32 7 5 2.4% 4.0% 7.2%

L&T

Technologies 17 4 2 17 4 2 14 3 2 0.2% 3.4% 2.8%

Mphasis 31 5 4 31 6 4 25 5 3 1.9% 2.5% -0.7%

Mindtree 28 6 4 28 6 4 20 5 4 -0.6% 1.5% 13.2%

MCX 1 0 0 1 0 0 1 0 1 3.5% 7.5% -5.6%

Tata Elxsi 6 2 1 6 2 2 5 1 1 0.4% 11.1% 8.8%

Persistent 15 2 2 15 3 2 11 2 1 1.2% 3.8% 1.4%

Cyient 12 2 1 12 2 1 10 2 1 1.1% 3.6% 8.0%

TeamLease 16 0 0 18 0 0 13 0 0 7.5% 0.6% -13.7%

Sonata 17 1 1 19 1 1 14 1 1 8.5% -3.2% -1.4%

Zensar

Technologies 11 2 1 11 2 1 9 2 1 -0.7% 3.6% 3.6%

CDSL 2 1 1 2 1 1 1 1 1 -3.4% -5.1% -8.8%

BSE 2 1 1 2 1 1 1 0 0 -1.2% -0.4% -22.9%

IndiaMart 2 1 1 2 1 1 2 1 1 -1.5% -9.8% -16.6%

Tanla Platforms 9 2 1 9 2 2 7 1 1 -3.0% 5.6% 9.1%

Mastek 6 1 1 6 1 1 4 1 1 -0.2% -1.6% -1.6%

Energy (Oil &

Gas) 6146 750 421 6289 700 447 4070 521 320 2.3% -6.7% 6.2%

Reliance

Industries 1850 299 166 1850 297 204 1179 216 148 0.0% -0.7% 22.8%

Oil & Natural

Gas Corp 284 154 77 285 160 88 170 83 13 0.1% 3.6% 13.5%

Indian Oil Corp 1550 128 72 1668 99 59 1063 96 49 7.6% -22.7% -18.4%

Bharat

Petroleum Corp 960 49 28 1010 42 25 667 43 32 5.2% -13.6% -11.9%

GAIL India 271 40 28 258 42 33 155 19 15 -4.9% 5.7% 17.9%

Petronet LNG 110 9 6 126 17 11 73 13 9 14.2% 84.6% 100.2%

Indraprastha

Gas 23 3 2 22 5 3 14 5 3 -3.4% 49.9% 58.3%

HPCL 997 38 24 966 19 9 687 33 24 -3.1% -51.4% -63.4%

Gujarat Gas 46 7 5 51 2 1 28 6 4 12.0% -66.6% -73.8%

Gujarat State

Petronet 6 4 2 5 3 2 6 4 2 -15.2% -9.0% -9.0%

OIL India 40 17 11 37 13 12 21 -1 19 -6.0% -25.9% 14.4%

Mahanagar Gas 9 1 1 10 1 1 7 3 2 18.8% -29.2% -35.0%

Cement and

Building

Materials

438 89 42 434 72 34 412 97 50 -0.9% -18.5% -19.0%

UltraTech

Cement 132 29 13 130 24 12 123 31 16 -2.0% -17.0% -8.7%

Shree Cement 35 9 4 34 8 5 33 11 6 -3.3% -7.4% 15.8%

Ambuja

Cements 37 8 5 37 6 3 35 8 5 2.2% -26.2% -34.0%

ACC 43 8 5 42 6 3 41 7 5 -2.2% -32.4% -36.4%

Dalmia Bharat 27 5 1 27 4 1 27 7 2 2.1% -22.5% -31.9%

Nuvoco Vistas 23 4 0 22 2 -1 22 5 0 -5.9% -36.5% NM

Ramco Cements 15 4 2 15 2 1 13 4 2 1.4% -36.1% -52.4%

JK Cement 20 4 2 20 4 1 18 5 2 3.2% -3.4% -16.7%

Birla Corp 17 3 1 18 2 1 18 4 1 4.4% -21.4% -48.8%

Heidelberg Cem 6 1 1 5 1 0 6 1 1 -12.7% -43.0% -46.8%

Star Cement 6 1 1 6 1 0 4 1 1 -1.2% -30.3% -35.8%

JK Lakshmi

Cement 13 2 1 13 2 1 13 2 1 -2.5% -13.5% -21.3%

Orient Cement 7 1 1 6 1 0 6 1 1 -7.7% -9.8% -22.0%

Sagar Cements 3 0 0 3 0 0 4 1 0 0.1% -2.6% -28.8%

P a g e | 6

Strategy

HSIE Coverage

(INR Bn)

Q3 FY22 Preview Estimates Q3 FY22 Actuals Q3 FY21 Actuals Deviation

Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT

Q3FY22 E Q3FY22 E Q3FY22 E Q3FY22 A Q3FY22 A Q3FY22 A Q3FY21 A Q3FY21 A Q3FY21 A Q3FY22 Q3FY22 Q3FY22

Deccan

Cements 2 0 0 2 0 0 2 0 0 8.4% 59.1% 75.9%

Supreme

Industries 21 4 3 19 3 2 18 4 3 -7.4% -11.6% -11.4%

Astral Limited 10 2 1 11 2 1 9 2 1 11.8% 5.6% 10.4%

Prince Pipe

Limited 6 1 1 7 1 1 5 1 1 9.9% 12.2% 14.5%

Kajaria

Ceramics 10 2 1 11 2 1 8 2 1 4.9% -9.1% -8.0%

Somany

Ceramics 6 1 0 6 1 0 5 1 0 -2.0% -15.9% -15.9%

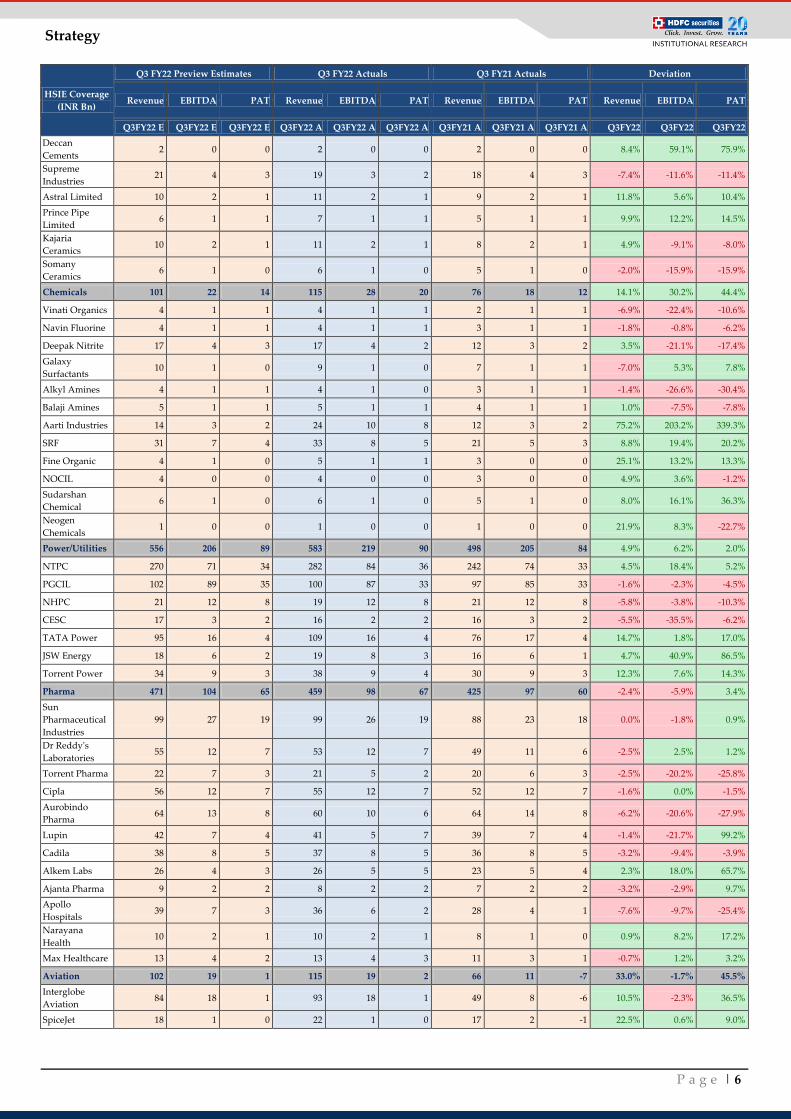

Chemicals 101 22 14 115 28 20 76 18 12 14.1% 30.2% 44.4%

Vinati Organics 4 1 1 4 1 1 2 1 1 -6.9% -22.4% -10.6%

Navin Fluorine 4 1 1 4 1 1 3 1 1 -1.8% -0.8% -6.2%

Deepak Nitrite 17 4 3 17 4 2 12 3 2 3.5% -21.1% -17.4%

Galaxy

Surfactants 10 1 0 9 1 0 7 1 1 -7.0% 5.3% 7.8%

Alkyl Amines 4 1 1 4 1 0 3 1 1 -1.4% -26.6% -30.4%

Balaji Amines 5 1 1 5 1 1 4 1 1 1.0% -7.5% -7.8%

Aarti Industries 14 3 2 24 10 8 12 3 2 75.2% 203.2% 339.3%

SRF 31 7 4 33 8 5 21 5 3 8.8% 19.4% 20.2%

Fine Organic 4 1 0 5 1 1 3 0 0 25.1% 13.2% 13.3%

NOCIL 4 0 0 4 0 0 3 0 0 4.9% 3.6% -1.2%

Sudarshan

Chemical 6 1 0 6 1 0 5 1 0 8.0% 16.1% 36.3%

Neogen

Chemicals 1 0 0 1 0 0 1 0 0 21.9% 8.3% -22.7%

Power/Utilities 556 206 89 583 219 90 498 205 84 4.9% 6.2% 2.0%

NTPC 270 71 34 282 84 36 242 74 33 4.5% 18.4% 5.2%

PGCIL 102 89 35 100 87 33 97 85 33 -1.6% -2.3% -4.5%

NHPC 21 12 8 19 12 8 21 12 8 -5.8% -3.8% -10.3%

CESC 17 3 2 16 2 2 16 3 2 -5.5% -35.5% -6.2%

TATA Power 95 16 4 109 16 4 76 17 4 14.7% 1.8% 17.0%

JSW Energy 18 6 2 19 8 3 16 6 1 4.7% 40.9% 86.5%

Torrent Power 34 9 3 38 9 4 30 9 3 12.3% 7.6% 14.3%

Pharma 471 104 65 459 98 67 425 97 60 -2.4% -5.9% 3.4%

Sun

Pharmaceutical

Industries

99 27 19 99 26 19 88 23 18 0.0% -1.8% 0.9%

Dr Reddy's

Laboratories 55 12 7 53 12 7 49 11 6 -2.5% 2.5% 1.2%

Torrent Pharma 22 7 3 21 5 2 20 6 3 -2.5% -20.2% -25.8%

Cipla 56 12 7 55 12 7 52 12 7 -1.6% 0.0% -1.5%

Aurobindo

Pharma 64 13 8 60 10 6 64 14 8 -6.2% -20.6% -27.9%

Lupin 42 7 4 41 5 7 39 7 4 -1.4% -21.7% 99.2%

Cadila 38 8 5 37 8 5 36 8 5 -3.2% -9.4% -3.9%

Alkem Labs 26 4 3 26 5 5 23 5 4 2.3% 18.0% 65.7%

Ajanta Pharma 9 2 2 8 2 2 7 2 2 -3.2% -2.9% 9.7%

Apollo

Hospitals 39 7 3 36 6 2 28 4 1 -7.6% -9.7% -25.4%

Narayana

Health 10 2 1 10 2 1 8 1 0 0.9% 8.2% 17.2%

Max Healthcare 13 4 2 13 4 3 11 3 1 -0.7% 1.2% 3.2%

Aviation 102 19 1 115 19 2 66 11 -7 33.0% -1.7% 45.5%

Interglobe

Aviation 84 18 1 93 18 1 49 8 -6 10.5% -2.3% 36.5%

SpiceJet 18 1 0 22 1 0 17 2 -1 22.5% 0.6% 9.0%

P a g e | 7

Strategy

HSIE Coverage

(INR Bn)

Q3 FY22 Preview Estimates Q3 FY22 Actuals Q3 FY21 Actuals Deviation

Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT Revenue EBITDA PAT

Q3FY22 E Q3FY22 E Q3FY22 E Q3FY22 A Q3FY22 A Q3FY22 A Q3FY21 A Q3FY21 A Q3FY21 A Q3FY22 Q3FY22 Q3FY22

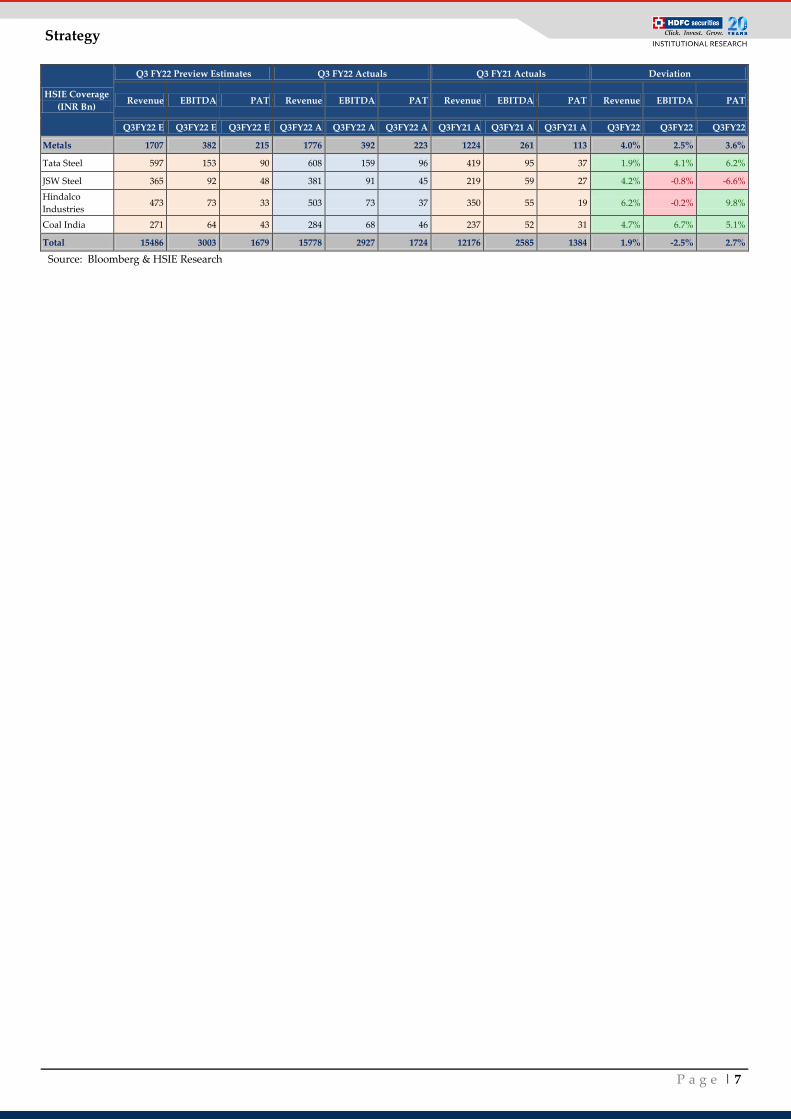

Metals 1707 382 215 1776 392 223 1224 261 113 4.0% 2.5% 3.6%

Tata Steel 597 153 90 608 159 96 419 95 37 1.9% 4.1% 6.2%

JSW Steel 365 92 48 381 91 45 219 59 27 4.2% -0.8% -6.6%

Hindalco

Industries 473 73 33 503 73 37 350 55 19 6.2% -0.2% 9.8%

Coal India 271 64 43 284 68 46 237 52 31 4.7% 6.7% 5.1%

Total 15486 3003 1679 15778 2927 1724 12176 2585 1384 1.9% -2.5% 2.7%

Source: Bloomberg & HSIE Research

P a g e | 8

Strategy

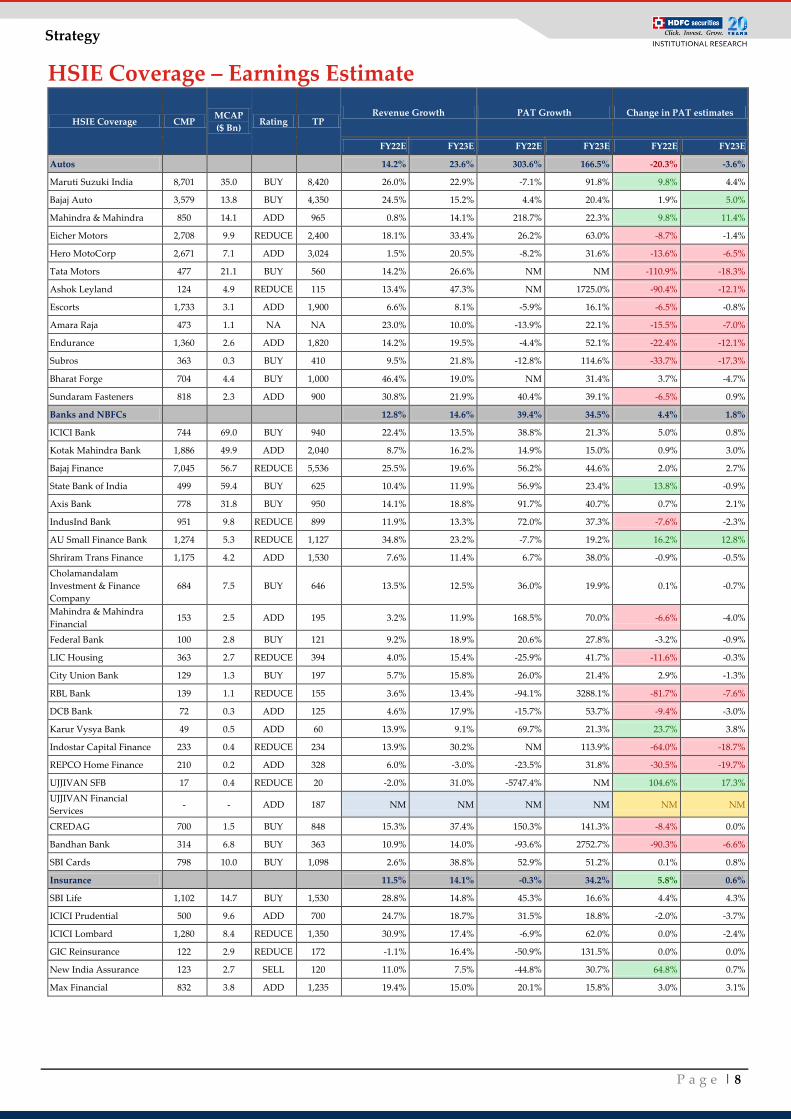

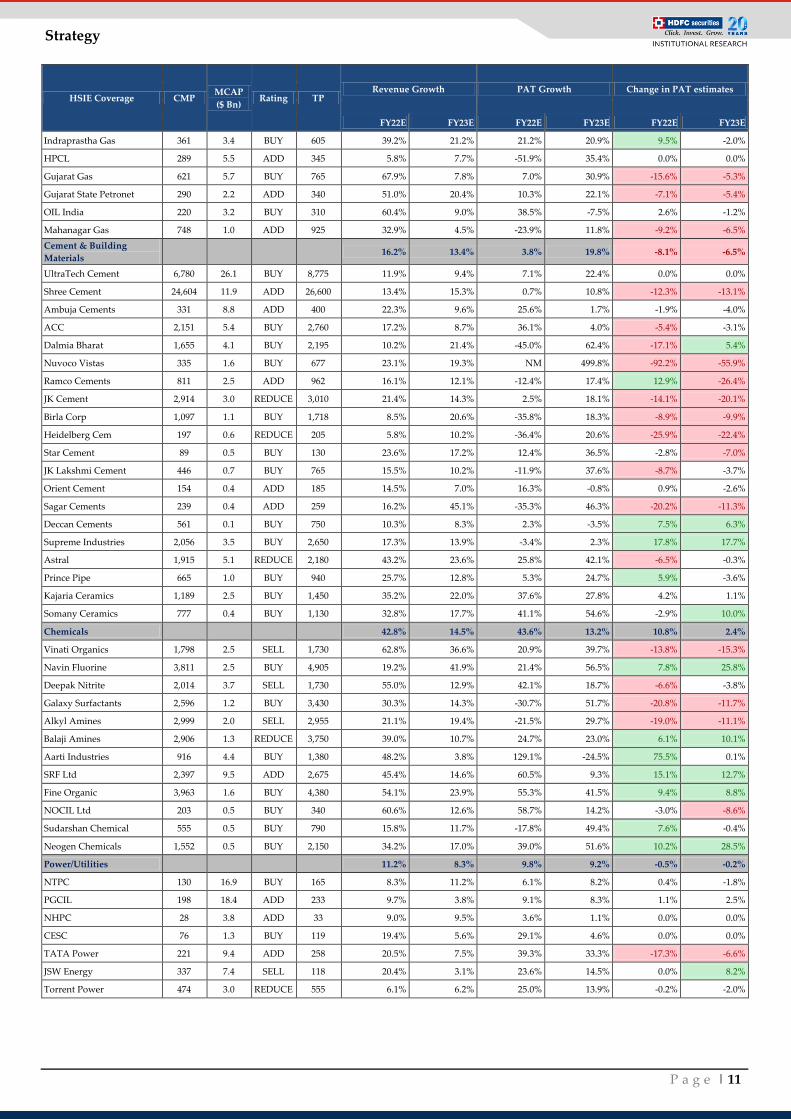

HSIE Coverage – Earnings Estimate

HSIE Coverage CMP MCAP

($ Bn) Rating TP

Revenue Growth PAT Growth Change in PAT estimates

FY22E FY23E FY22E FY23E FY22E FY23E

Autos

14.2% 23.6% 303.6% 166.5% -20.3% -3.6%

Maruti Suzuki India 8,701 35.0 BUY 8,420 26.0% 22.9% -7.1% 91.8% 9.8% 4.4%

Bajaj Auto 3,579 13.8 BUY 4,350 24.5% 15.2% 4.4% 20.4% 1.9% 5.0%

Mahindra & Mahindra 850 14.1 ADD 965 0.8% 14.1% 218.7% 22.3% 9.8% 11.4%

Eicher Motors 2,708 9.9 REDUCE 2,400 18.1% 33.4% 26.2% 63.0% -8.7% -1.4%

Hero MotoCorp 2,671 7.1 ADD 3,024 1.5% 20.5% -8.2% 31.6% -13.6% -6.5%

Tata Motors 477 21.1 BUY 560 14.2% 26.6% NM NM -110.9% -18.3%

Ashok Leyland 124 4.9 REDUCE 115 13.4% 47.3% NM 1725.0% -90.4% -12.1%

Escorts 1,733 3.1 ADD 1,900 6.6% 8.1% -5.9% 16.1% -6.5% -0.8%

Amara Raja 473 1.1 NA NA 23.0% 10.0% -13.9% 22.1% -15.5% -7.0%

Endurance 1,360 2.6 ADD 1,820 14.2% 19.5% -4.4% 52.1% -22.4% -12.1%

Subros 363 0.3 BUY 410 9.5% 21.8% -12.8% 114.6% -33.7% -17.3%

Bharat Forge 704 4.4 BUY 1,000 46.4% 19.0% NM 31.4% 3.7% -4.7%

Sundaram Fasteners 818 2.3 ADD 900 30.8% 21.9% 40.4% 39.1% -6.5% 0.9%

Banks and NBFCs

12.8% 14.6% 39.4% 34.5% 4.4% 1.8%

ICICI Bank 744 69.0 BUY 940 22.4% 13.5% 38.8% 21.3% 5.0% 0.8%

Kotak Mahindra Bank 1,886 49.9 ADD 2,040 8.7% 16.2% 14.9% 15.0% 0.9% 3.0%

Bajaj Finance 7,045 56.7 REDUCE 5,536 25.5% 19.6% 56.2% 44.6% 2.0% 2.7%

State Bank of India 499 59.4 BUY 625 10.4% 11.9% 56.9% 23.4% 13.8% -0.9%

Axis Bank 778 31.8 BUY 950 14.1% 18.8% 91.7% 40.7% 0.7% 2.1%

IndusInd Bank 951 9.8 REDUCE 899 11.9% 13.3% 72.0% 37.3% -7.6% -2.3%

AU Small Finance Bank 1,274 5.3 REDUCE 1,127 34.8% 23.2% -7.7% 19.2% 16.2% 12.8%

Shriram Trans Finance 1,175 4.2 ADD 1,530 7.6% 11.4% 6.7% 38.0% -0.9% -0.5%

Cholamandalam

Investment & Finance

Company

684 7.5 BUY 646 13.5% 12.5% 36.0% 19.9% 0.1% -0.7%

Mahindra & Mahindra

Financial 153 2.5 ADD 195 3.2% 11.9% 168.5% 70.0% -6.6% -4.0%

Federal Bank 100 2.8 BUY 121 9.2% 18.9% 20.6% 27.8% -3.2% -0.9%

LIC Housing 363 2.7 REDUCE 394 4.0% 15.4% -25.9% 41.7% -11.6% -0.3%

City Union Bank 129 1.3 BUY 197 5.7% 15.8% 26.0% 21.4% 2.9% -1.3%

RBL Bank 139 1.1 REDUCE 155 3.6% 13.4% -94.1% 3288.1% -81.7% -7.6%

DCB Bank 72 0.3 ADD 125 4.6% 17.9% -15.7% 53.7% -9.4% -3.0%

Karur Vysya Bank 49 0.5 ADD 60 13.9% 9.1% 69.7% 21.3% 23.7% 3.8%

Indostar Capital Finance 233 0.4 REDUCE 234 13.9% 30.2% NM 113.9% -64.0% -18.7%

REPCO Home Finance 210 0.2 ADD 328 6.0% -3.0% -23.5% 31.8% -30.5% -19.7%

UJJIVAN SFB 17 0.4 REDUCE 20 -2.0% 31.0% -5747.4% NM 104.6% 17.3%

UJJIVAN Financial

Services - - ADD 187 NM NM NM NM NM NM

CREDAG 700 1.5 BUY 848 15.3% 37.4% 150.3% 141.3% -8.4% 0.0%

Bandhan Bank 314 6.8 BUY 363 10.9% 14.0% -93.6% 2752.7% -90.3% -6.6%

SBI Cards 798 10.0 BUY 1,098 2.6% 38.8% 52.9% 51.2% 0.1% 0.8%

Insurance

11.5% 14.1% -0.3% 34.2% 5.8% 0.6%

SBI Life 1,102 14.7 BUY 1,530 28.8% 14.8% 45.3% 16.6% 4.4% 4.3%

ICICI Prudential 500 9.6 ADD 700 24.7% 18.7% 31.5% 18.8% -2.0% -3.7%

ICICI Lombard 1,280 8.4 REDUCE 1,350 30.9% 17.4% -6.9% 62.0% 0.0% -2.4%

GIC Reinsurance 122 2.9 REDUCE 172 -1.1% 16.4% -50.9% 131.5% 0.0% 0.0%

New India Assurance 123 2.7 SELL 120 11.0% 7.5% -44.8% 30.7% 64.8% 0.7%

Max Financial 832 3.8 ADD 1,235 19.4% 15.0% 20.1% 15.8% 3.0% 3.1%

P a g e | 9

Strategy

HSIE Coverage CMP MCAP

($ Bn) Rating TP

Revenue Growth PAT Growth Change in PAT estimates

FY22E FY23E FY22E FY23E FY22E FY23E

Capital Markets

26.7% -1.5% 21.6% -10.4% 6.5% -0.2%

Nippon Life India 312 2.6 ADD 425 22.3% 11.0% 11.1% 7.9% 1.6% -3.1%

Angel One 1,324 1.5 BUY 1,870 81.0% 15.8% 91.3% 17.5% NA NA

ICICI Securities 651 2.8 ADD 920 30.1% -13.5% 33.6% -21.9% 10.1% -1.4%

Motilal Oswal Financial

Services 889 1.7 ADD 1,000 5.2% -8.8% -6.0% -27.5% 9.1% 8.9%

UTI AMC 802 1.4 BUY 1,215 38.7% 3.8% 27.2% -12.2% 1.6% -6.1%

CAMS 2,312 1.5 ADD 2,885 27.4% 10.4% 37.4% 12.9% 3.7% 1.3%

Consumer- Staples

14.9% 9.5% 14.0% 12.3% -0.6% -0.1%

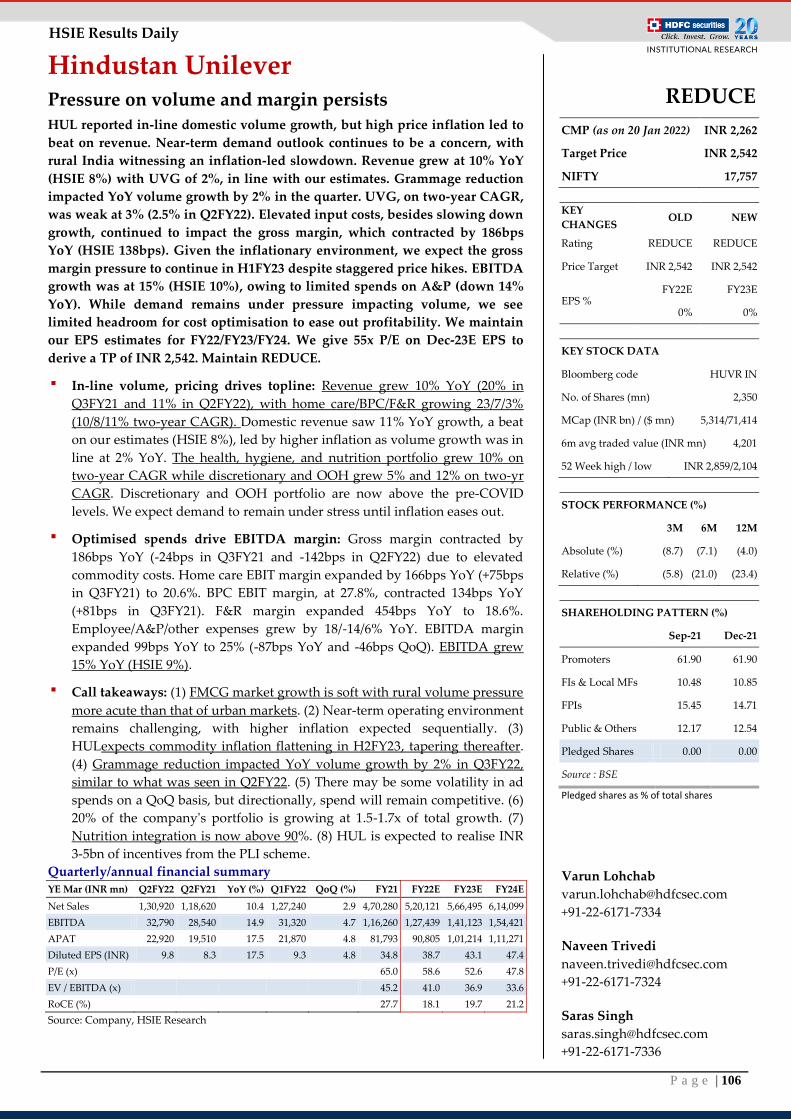

Hindustan Unilever 2,261 70.8 REDUCE 2,542 10.6% 8.9% 11.0% 11.5% 0.2% 0.3%

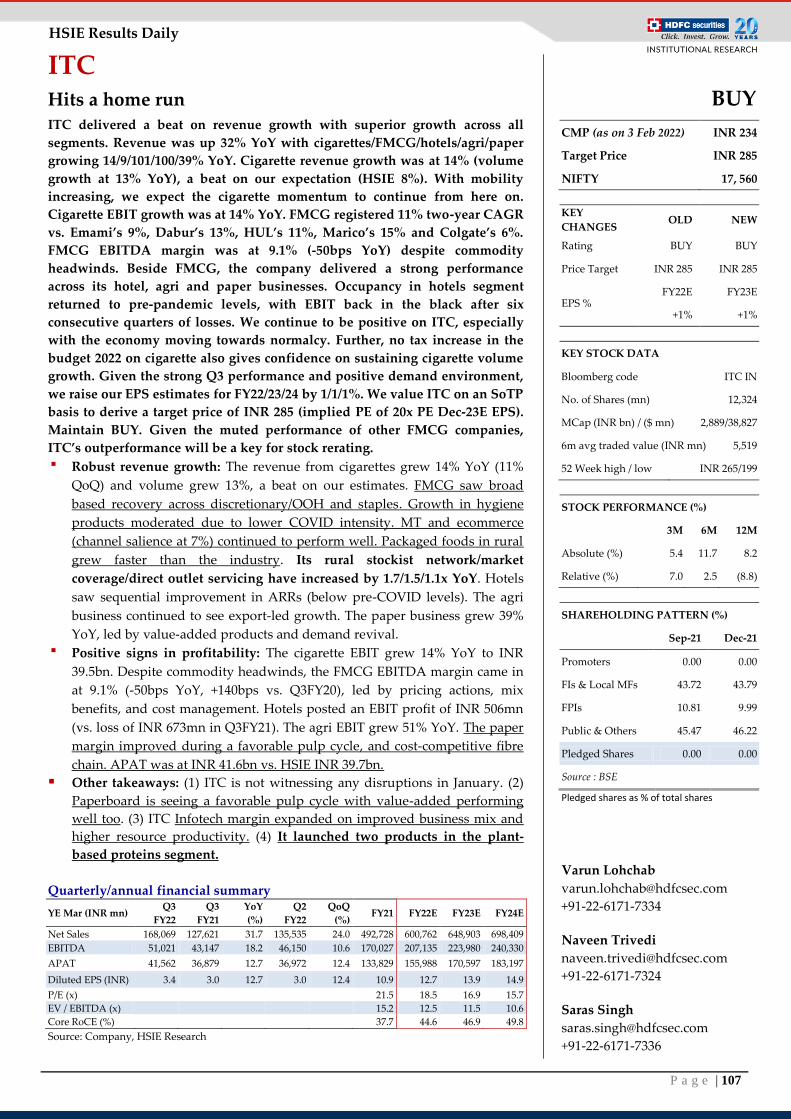

ITC 216 35.5 BUY 285 21.9% 8.0% 16.6% 9.4% 0.3% 0.7%

Dabur India 543 12.8 ADD 650 15.8% 9.6% 14.1% 9.9% 0.5% -1.3%

Britannia Industries 3,511 11.3 REDUCE 3,600 7.7% 10.1% -14.4% 26.1% -9.7% -3.7%

United Spirits 857 8.3 ADD 970 20.3% 17.6% 125.4% 26.1% 1.8% 1.5%

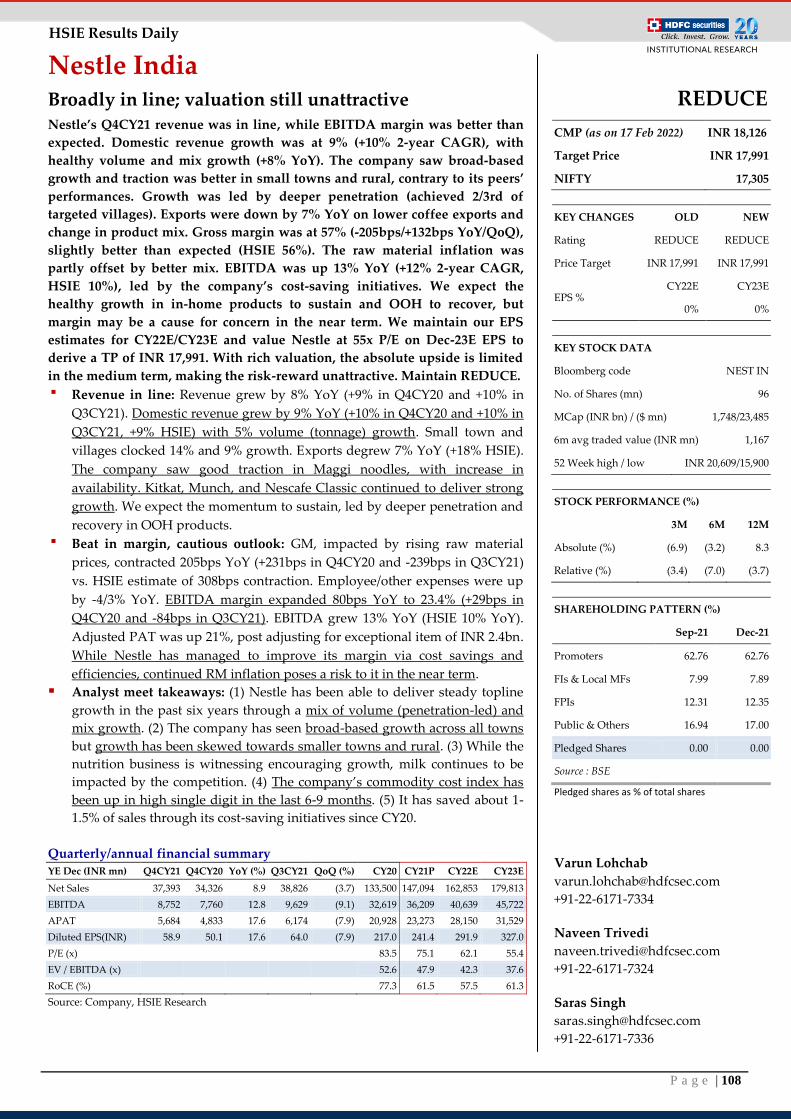

Nestle 17,927 23.0 REDUCE 17,991 10.7% 10.4% 21.0% 12.0% -0.8% -0.3%

Marico 501 8.6 ADD 600 18.7% 8.8% 12.2% 22.4% 0.0% 0.0%

Colgate Palmolive 1,432 5.2 ADD 1,700 6.6% 7.0% 0.3% 6.2% -0.6% -2.0%

Emami 481 2.8 REDUCE 500 11.9% 8.5% 15.3% 6.2% 1.8% 0.3%

GCPL 804 11.0 ADD 1,025 12.6% 11.8% 11.5% 20.7% -4.5% -2.2%

Radico Khaitan 911 1.6 REDUCE 950 17.7% 13.0% 5.7% 31.7% -7.9% -3.8%

Consumer Discretionary

(ex-Autos) 29.1% 22.8% 40.0% 39.6% -0.8% 1.2%

Avenue Supermart 4,193 36.2 SELL 2,800 28.2% 43.3% 41.3% 57.3% 1.3% -0.2%

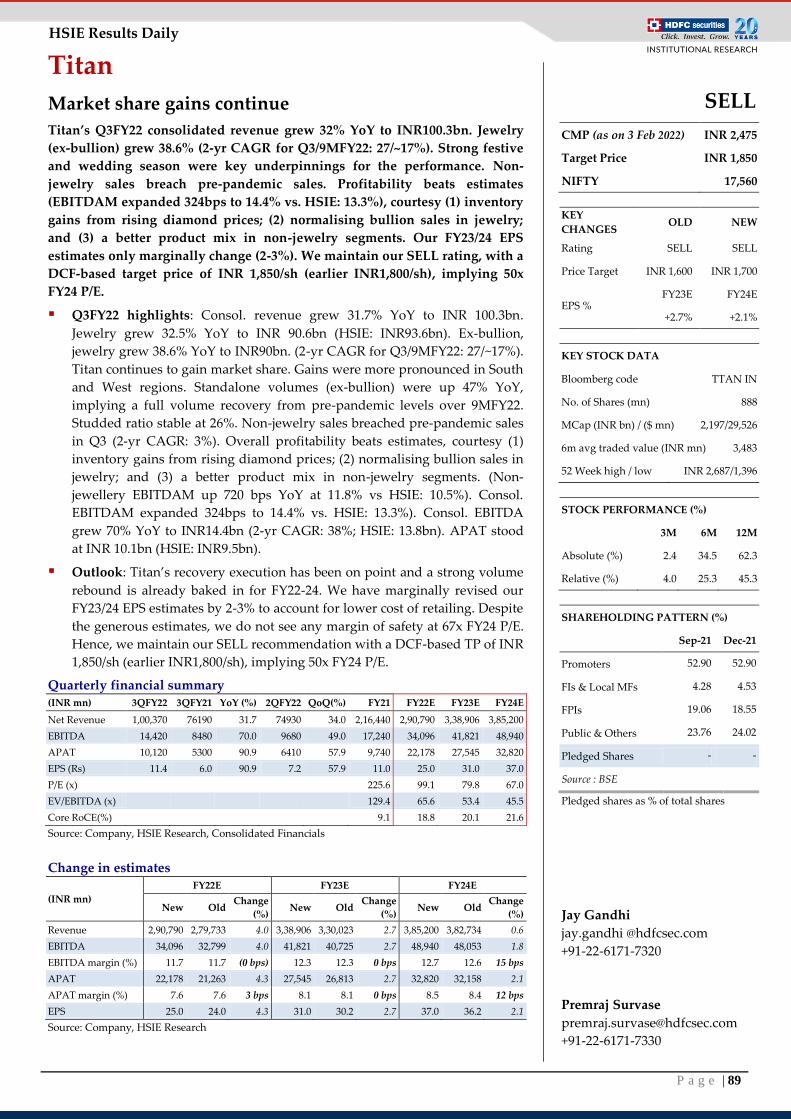

Titan Co 2,496 29.6 SELL 1,850 34.4% 16.5% 127.7% 24.2% 8.2% 5.6%

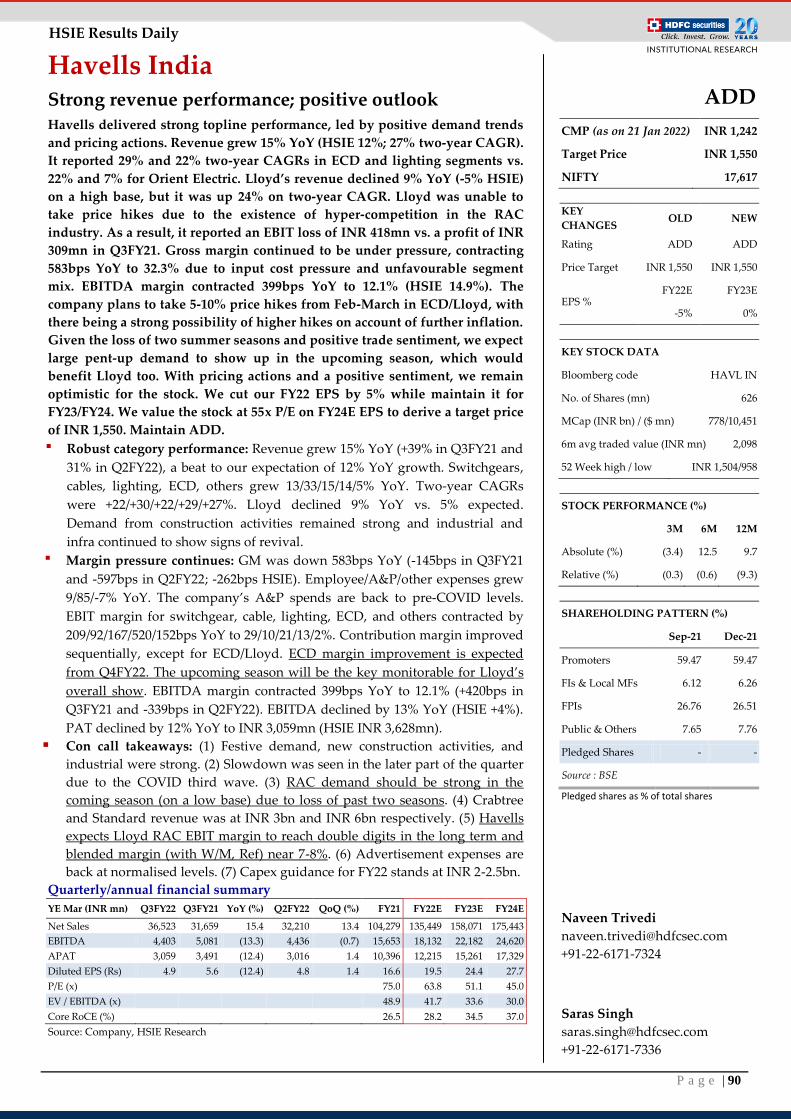

Havells India 1,202 10.0 ADD 1,550 29.9% 16.7% 17.5% 24.9% -5.9% -1.4%

Trent 1,054 5.0 SELL 860 74.2% 35.6% NM 59.5% 38.7% -11.5%

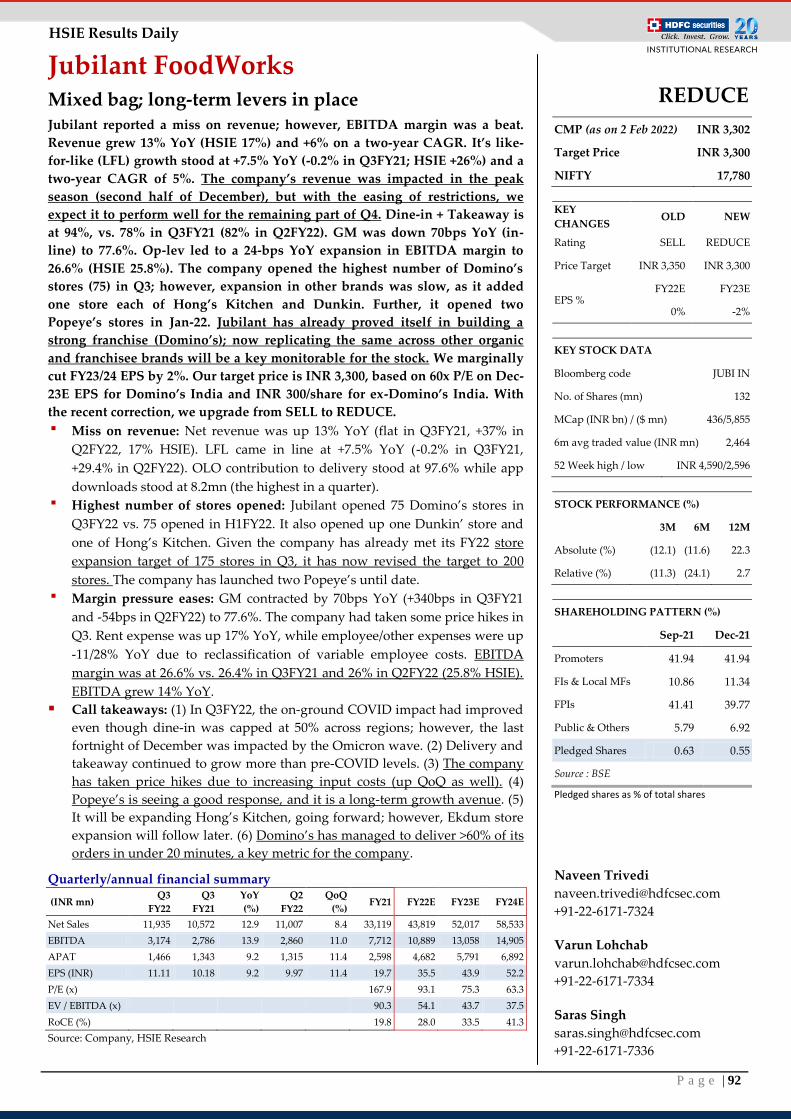

Jubilant Foodworks 3,030 5.3 REDUCE 3,300 32.3% 18.7% 80.3% 23.7% 0.9% -2.2%

Voltas 1,239 5.5 ADD 1,350 5.0% 26.0% 15.4% 46.7% -10.8% -3.4%

Aditya Birla Fashion 269 3.4 ADD 310 47.5% 28.9% 91.1% NM 0.0% -21.8%

Crompton Consumer 408 3.4 BUY 550 15.2% 15.2% 13.0% 21.5% -4.5% -2.5%

Symphony 966 0.9 ADD 1,200 22.4% 18.3% 34.1% 41.5% -23.8% -8.9%

V-Guard 197 1.1 ADD 275 26.9% 12.3% 14.9% 31.0% -11.3% -4.0%

V-Mart 3,397 0.9 ADD 3,700 55.1% 63.7% 22.7% 335.9% -54.0% -8.9%

TCNS Clothing 676 0.6 SELL 575 42.0% 44.0% NM 3491.8% -72.8% 6.2%

Shoppers Stop 337 0.5 SELL 230 61.0% 29.2% 65.5% NM 0.0% 0.0%

Asian Paints 3,237 41.4 SELL 2,700 27.5% 11.3% -4.1% 29.1% 1.0% -0.8%

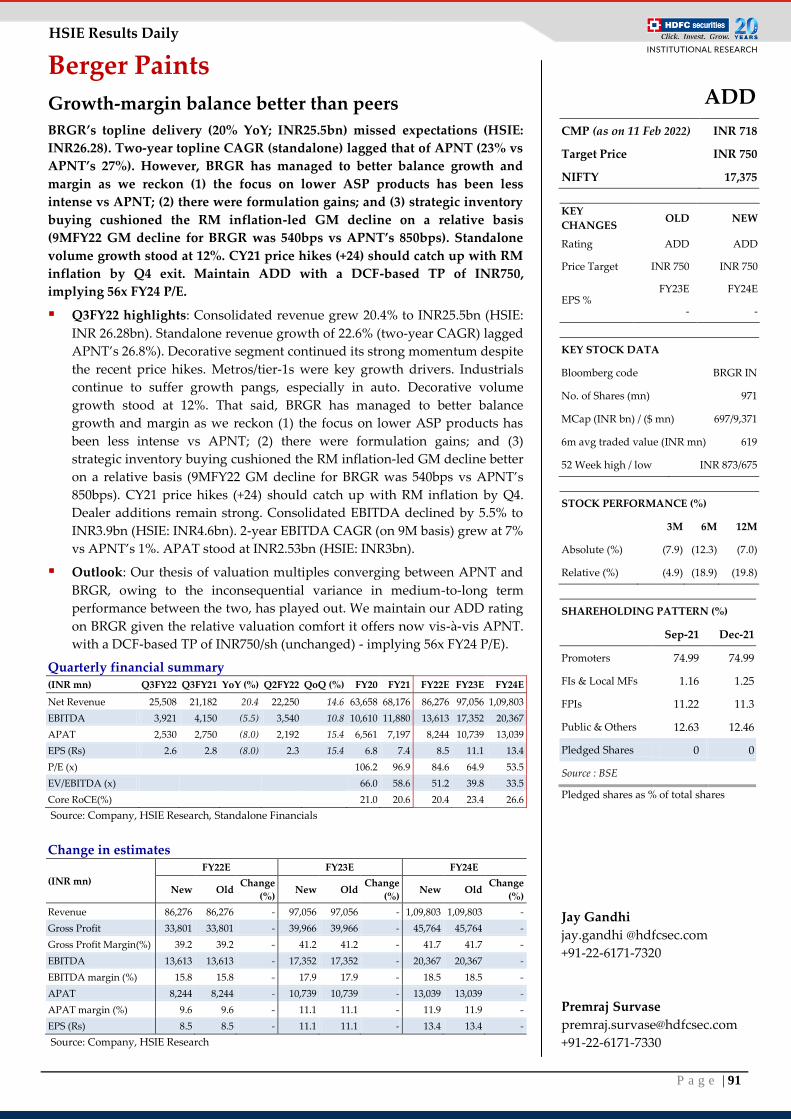

Berger Paints 730 9.5 ADD 750 26.5% 12.5% 14.5% 30.3% -10.6% -5.4%

Kansai Nerolac 464 3.3 BUY 700 22.0% 12.2% 2.0% 29.0% 4.0% 0.0%

Bata India 1,868 3.2 SELL 1,500 41.6% 39.1% -267.2% 436.2% NA NA

Relaxo Footwears 1,231 4.1 SELL 1,030 12.7% 23.0% -8.5% 36.2% NA NA

TTK Prestige 804 1.5 ADD 1,170 20.8% 13.3% 20.5% 13.8% -0.6% -0.5%

Orient Electric 324 0.9 BUY 400 27.5% 15.5% 18.2% 31.5% -0.1% 0.0%

Industrials

(Infrastructure+ Cap

Goods+ Logistics)

16.5% 16.2% 24.5% 34.1% -5.1% -5.1%

Larsen & Toubro 1,821 34.1 BUY 2,504 15.0% 16.2% 22.5% 27.6% -4.3% -3.8%

Siemens 2,396 11.4 REDUCE 2,120 19.3% 19.2% 39.7% 28.5% 0.0% 0.0%

Cummins India 966 3.6 BUY 1,253 42.0% 8.9% 27.3% 38.1% -25.2% -25.8%

ABB India 2,098 5.9 REDUCE 1,815 19.1% 23.6% 280.9% 1.1% 67.2% 1.7%

KEC International 451 1.5 BUY 578 7.1% 15.1% -29.9% 89.4% -32.5% -11.5%

Kalpataru Power

Transmission 401 0.8 BUY 559 -5.0% 11.9% -16.5% 21.8% -6.0% -7.5%

GR Infra 1,397 1.8 BUY 2,358 13.1% 18.5% 8.3% 42.0% 0.0% 0.0%

PNC Infratech 273 0.9 BUY 412 22.8% 12.7% 32.6% 18.8% 2.0% -3.4%

P a g e | 10

Strategy

HSIE Coverage CMP MCAP

($ Bn) Rating TP

Revenue Growth PAT Growth Change in PAT estimates

FY22E FY23E FY22E FY23E FY22E FY23E

Dilip Buildcon 268 0.5 BUY 490 -0.6% 9.5% -146.0% -277.6% -182.4% -45.1%

KNR Constructions 305 1.1 BUY 360 17.0% 15.3% 37.6% 25.0% 0.4% 2.1%

IRB Infrastructure 236 1.9 ADD 302 11.0% 11.0% 189.3% 44.6% 76.9% 76.4%

Ashoka Buildcon 92 0.3 BUY 162 15.0% 11.7% -29.4% 46.2% 0.0% 0.0%

Ahluwalia Contracts 381 0.3 BUY 522 37.8% 15.0% 107.6% 43.0% -32.5% -18.3%

NCC 61 0.5 BUY 122 38.8% 23.1% 51.6% 66.5% 2.8% -0.9%

PSP Projects 513 0.2 BUY 671 37.1% 20.1% 73.6% 8.7% 15.1% 2.8%

HG Infra 594 0.5 BUY 988 42.2% 14.5% 61.4% 5.8% 11.4% 4.8%

JMC Projects 90 0.2 BUY 162 40.2% 11.9% 37.0% 108.5% -22.0% 0.4%

Sadbhav Engineering 32 0.1 ADD 50 5.3% 22.6% NM 193.5% -19.3% -47.6%

Capacite Infraprojects 131 0.1 BUY 232 56.7% 44.6% 2574.0% 147.3% -41.5% -21.1%

ITD Cementation 69 0.2 BUY 125 37.0% 18.0% 512.6% 70.8% -2.1% -14.3%

J Kumar Infraprojects 166 0.2 BUY 279 35.0% 16.5% 211.7% 30.4% 21.4% 2.7%

Real Estate

14.2% 18.1% 83.5% 36.9% -0.2% 0.6%

DLF 345 11.4 BUY 460 11.0% 10.5% 41.4% 30.7% 0.0% 0.0%

Oberoi Realty 932 4.5 ADD 1,060 34.0% 9.9% 69.2% -2.2% 9.6% 27.4%

Prestige Estates 450 2.4 ADD 540 -17.7% 19.3% 11.9% 50.5% -28.7% -5.0%

Brigade Enterprises 498 1.5 ADD 530 53.5% 8.2% 505.1% -29.2% 161.8% -6.6%

Sobha Developers 768 1.0 ADD 964 28.4% 19.2% 109.1% 120.9% -16.4% -6.9%

Kolte Patil 278 0.3 BUY 377 52.4% 22.8% NM 114.5% -45.0% -11.2%

Phoenix Mills 951 2.3 BUY 1,360 38.1% 41.0% 242.0% 184.0% 0.0% 0.1%

Godrej Properties 1,597 5.9 REDUCE 1,800 64.1% 25.0% 1061.7% 62.9% -8.4% -16.0%

Mahindra Lifespaces 303 0.6 BUY 379 87.6% 145.7% NM 351.5% NM -0.1%

IT and Exchanges

20.0% 15.9% 16.8% 17.2% 1.5% 1.4%

Tata Consultancy Services 3,563 175.7 ADD 4400 16.7% 15.3% 15.9% 16.9% 0.8% 1.0%

Infosys 1,743 97.7 BUY 2220 21.9% 15.9% 17.2% 21.3% 3.7% 7.4%

HCL Technologies 1,153 41.7 BUY 1485 13.8% 14.3% 7.7% 13.1% 0.7% -5.8%

Wipro 567 41.4 ADD 740 27.8% 13.4% 16.4% 12.0% 2.9% 3.1%

Tech Mahindra 1,413 18.3 BUY 2050 17.2% 16.6% 23.1% 16.0% -2.1% -1.1%

L&T Infotech 5,912 13.8 ADD 7675 26.9% 21.8% 19.9% 20.4% 1.3% -1.0%

L&T Technologies 4,455 6.3 ADD 5750 20.4% 19.6% 51.8% 18.1% -2.3% -5.6%

Mphasis 3,108 7.8 BUY 3800 22.9% 21.0% 18.2% 23.4% -1.4% -2.0%

Mindtree 3,802 8.4 ADD 5060 32.1% 21.0% 35.0% 20.7% 5.5% 4.8%

MCX 1,294 0.9 BUY 2,150 -10.3% 28.6% -31.6% 64.2% -22.0% -17.5%

Tata Elxsi 6,604 5.5 REDUCE 5900 34.5% 27.3% 46.3% 24.6% 6.2% 4.4%

Persistent 3,960 4.0 ADD 4900 35.0% 26.7% 49.8% 29.2% 0.1% 5.4%

Cyient 831 1.2 BUY 1285 10.5% 14.7% 32.2% 14.2% -1.0% -6.8%

TeamLease 3,957 0.9 BUY 5,260 33.5% 25.6% 49.8% 37.8% 0.1% -0.3%

Sonata 729 1.0 BUY 1085 29.5% 21.5% 50.0% 17.6% 2.8% -1.1%

Zensar Technologies 343 1.0 BUY 600 15.9% 16.0% 12.2% 7.7% -5.8% -15.3%

CDSL Ltd 1,383 1.9 BUY 1,800 66.1% 18.4% 59.5% 22.1% -3.3% 0.2%

BSE 2,078 1.2 BUY 2,260 44.6% 12.4% 72.5% 24.9% 4.6% 10.7%

IndiaMart 4,822 2.0 BUY 8,000 12.3% 28.8% 10.9% 13.7% -3.6% -3.0%

Tanla Platforms 1,553 2.8 BUY 1,880 37.9% 20.5% 52.7% 16.4% NA NA

Mastek 2,688 1.1 BUY 3365 26.6% 18.1% 38.7% 15.1% 7.7% 0.9%

Energy (Oil & Gas)

35.7% 9.7% 10.6% 18.4% 0.8% -2.6%

Reliance Industries 2,374 214.2 ADD 2,820 72.5% 15.0% 16.6% 36.0% -3.4% -4.0%

Oil & Natural Gas Corp 161 27.0 BUY 208 17.9% 7.2% 97.5% 19.0% -0.2% -0.6%

Indian Oil Corp 117 14.7 ADD 140 10.4% 4.2% -36.0% -5.6% 7.9% -5.8%

Bharat Petroleum Corp 357 10.3 ADD 435 47.4% 7.9% -34.5% 1.6% 6.8% -7.7%

GAIL India 139 8.2 BUY 215 51.7% 12.5% 67.1% -5.0% 13.9% 8.4%

Petronet LNG 205 4.1 REDUCE 230 66.7% 3.4% -4.8% -17.3% 5.9% -4.2%

P a g e | 11

Strategy

HSIE Coverage CMP MCAP

($ Bn) Rating TP

Revenue Growth PAT Growth Change in PAT estimates

FY22E FY23E FY22E FY23E FY22E FY23E

Indraprastha Gas 361 3.4 BUY 605 39.2% 21.2% 21.2% 20.9% 9.5% -2.0%

HPCL 289 5.5 ADD 345 5.8% 7.7% -51.9% 35.4% 0.0% 0.0%

Gujarat Gas 621 5.7 BUY 765 67.9% 7.8% 7.0% 30.9% -15.6% -5.3%

Gujarat State Petronet 290 2.2 ADD 340 51.0% 20.4% 10.3% 22.1% -7.1% -5.4%

OIL India 220 3.2 BUY 310 60.4% 9.0% 38.5% -7.5% 2.6% -1.2%

Mahanagar Gas 748 1.0 ADD 925 32.9% 4.5% -23.9% 11.8% -9.2% -6.5%

Cement & Building

Materials 16.2% 13.4% 3.8% 19.8% -8.1% -6.5%

UltraTech Cement 6,780 26.1 BUY 8,775 11.9% 9.4% 7.1% 22.4% 0.0% 0.0%

Shree Cement 24,604 11.9 ADD 26,600 13.4% 15.3% 0.7% 10.8% -12.3% -13.1%

Ambuja Cements 331 8.8 ADD 400 22.3% 9.6% 25.6% 1.7% -1.9% -4.0%

ACC 2,151 5.4 BUY 2,760 17.2% 8.7% 36.1% 4.0% -5.4% -3.1%

Dalmia Bharat 1,655 4.1 BUY 2,195 10.2% 21.4% -45.0% 62.4% -17.1% 5.4%

Nuvoco Vistas 335 1.6 BUY 677 23.1% 19.3% NM 499.8% -92.2% -55.9%

Ramco Cements 811 2.5 ADD 962 16.1% 12.1% -12.4% 17.4% 12.9% -26.4%

JK Cement 2,914 3.0 REDUCE 3,010 21.4% 14.3% 2.5% 18.1% -14.1% -20.1%

Birla Corp 1,097 1.1 BUY 1,718 8.5% 20.6% -35.8% 18.3% -8.9% -9.9%

Heidelberg Cem 197 0.6 REDUCE 205 5.8% 10.2% -36.4% 20.6% -25.9% -22.4%

Star Cement 89 0.5 BUY 130 23.6% 17.2% 12.4% 36.5% -2.8% -7.0%

JK Lakshmi Cement 446 0.7 BUY 765 15.5% 10.2% -11.9% 37.6% -8.7% -3.7%

Orient Cement 154 0.4 ADD 185 14.5% 7.0% 16.3% -0.8% 0.9% -2.6%

Sagar Cements 239 0.4 ADD 259 16.2% 45.1% -35.3% 46.3% -20.2% -11.3%

Deccan Cements 561 0.1 BUY 750 10.3% 8.3% 2.3% -3.5% 7.5% 6.3%

Supreme Industries 2,056 3.5 BUY 2,650 17.3% 13.9% -3.4% 2.3% 17.8% 17.7%

Astral 1,915 5.1 REDUCE 2,180 43.2% 23.6% 25.8% 42.1% -6.5% -0.3%

Prince Pipe 665 1.0 BUY 940 25.7% 12.8% 5.3% 24.7% 5.9% -3.6%

Kajaria Ceramics 1,189 2.5 BUY 1,450 35.2% 22.0% 37.6% 27.8% 4.2% 1.1%

Somany Ceramics 777 0.4 BUY 1,130 32.8% 17.7% 41.1% 54.6% -2.9% 10.0%

Chemicals

42.8% 14.5% 43.6% 13.2% 10.8% 2.4%

Vinati Organics 1,798 2.5 SELL 1,730 62.8% 36.6% 20.9% 39.7% -13.8% -15.3%

Navin Fluorine 3,811 2.5 BUY 4,905 19.2% 41.9% 21.4% 56.5% 7.8% 25.8%

Deepak Nitrite 2,014 3.7 SELL 1,730 55.0% 12.9% 42.1% 18.7% -6.6% -3.8%

Galaxy Surfactants 2,596 1.2 BUY 3,430 30.3% 14.3% -30.7% 51.7% -20.8% -11.7%

Alkyl Amines 2,999 2.0 SELL 2,955 21.1% 19.4% -21.5% 29.7% -19.0% -11.1%

Balaji Amines 2,906 1.3 REDUCE 3,750 39.0% 10.7% 24.7% 23.0% 6.1% 10.1%

Aarti Industries 916 4.4 BUY 1,380 48.2% 3.8% 129.1% -24.5% 75.5% 0.1%

SRF Ltd 2,397 9.5 ADD 2,675 45.4% 14.6% 60.5% 9.3% 15.1% 12.7%

Fine Organic 3,963 1.6 BUY 4,380 54.1% 23.9% 55.3% 41.5% 9.4% 8.8%

NOCIL Ltd 203 0.5 BUY 340 60.6% 12.6% 58.7% 14.2% -3.0% -8.6%

Sudarshan Chemical 555 0.5 BUY 790 15.8% 11.7% -17.8% 49.4% 7.6% -0.4%

Neogen Chemicals 1,552 0.5 BUY 2,150 34.2% 17.0% 39.0% 51.6% 10.2% 28.5%

Power/Utilities

11.2% 8.3% 9.8% 9.2% -0.5% -0.2%

NTPC 130 16.9 BUY 165 8.3% 11.2% 6.1% 8.2% 0.4% -1.8%

PGCIL 198 18.4 ADD 233 9.7% 3.8% 9.1% 8.3% 1.1% 2.5%

NHPC 28 3.8 ADD 33 9.0% 9.5% 3.6% 1.1% 0.0% 0.0%

CESC 76 1.3 BUY 119 19.4% 5.6% 29.1% 4.6% 0.0% 0.0%

TATA Power 221 9.4 ADD 258 20.5% 7.5% 39.3% 33.3% -17.3% -6.6%

JSW Energy 337 7.4 SELL 118 20.4% 3.1% 23.6% 14.5% 0.0% 8.2%

Torrent Power 474 3.0 REDUCE 555 6.1% 6.2% 25.0% 13.9% -0.2% -2.0%

P a g e | 12

Strategy

HSIE Coverage CMP MCAP

($ Bn) Rating TP

Revenue Growth PAT Growth Change in PAT estimates

FY22E FY23E FY22E FY23E FY22E FY23E

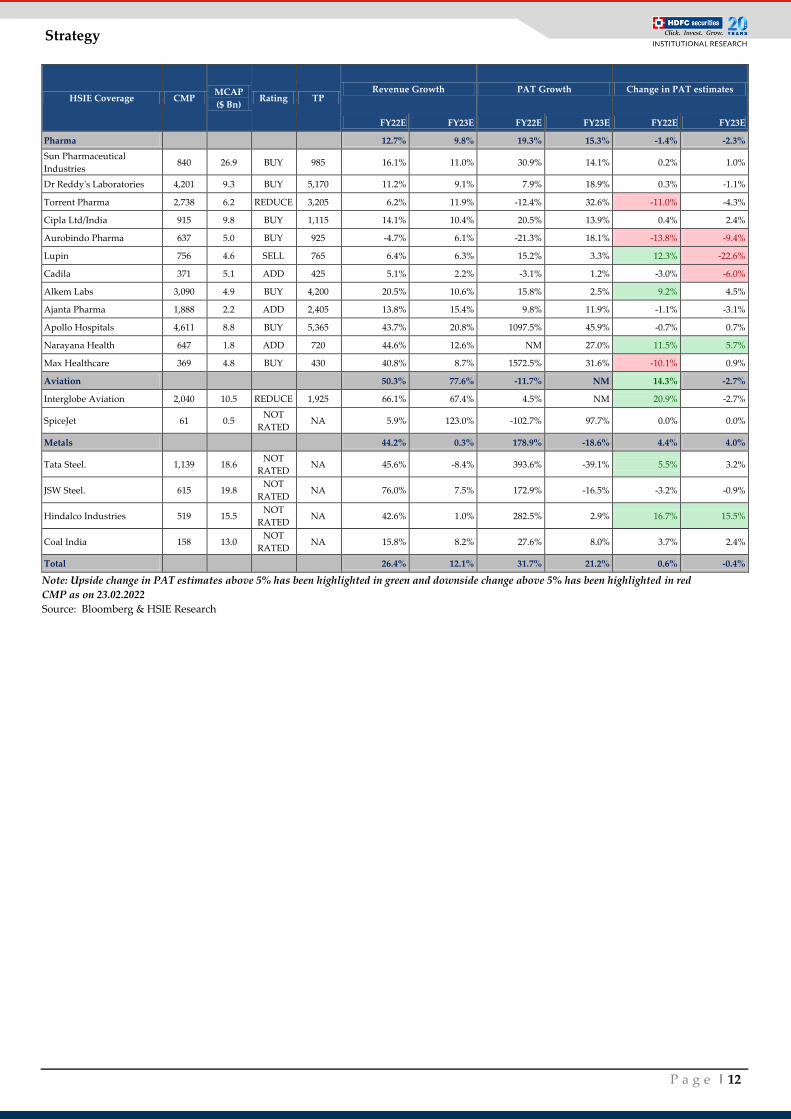

Pharma

12.7% 9.8% 19.3% 15.3% -1.4% -2.3%

Sun Pharmaceutical

Industries 840 26.9 BUY 985 16.1% 11.0% 30.9% 14.1% 0.2% 1.0%

Dr Reddy's Laboratories 4,201 9.3 BUY 5,170 11.2% 9.1% 7.9% 18.9% 0.3% -1.1%

Torrent Pharma 2,738 6.2 REDUCE 3,205 6.2% 11.9% -12.4% 32.6% -11.0% -4.3%

Cipla Ltd/India 915 9.8 BUY 1,115 14.1% 10.4% 20.5% 13.9% 0.4% 2.4%

Aurobindo Pharma 637 5.0 BUY 925 -4.7% 6.1% -21.3% 18.1% -13.8% -9.4%

Lupin 756 4.6 SELL 765 6.4% 6.3% 15.2% 3.3% 12.3% -22.6%

Cadila 371 5.1 ADD 425 5.1% 2.2% -3.1% 1.2% -3.0% -6.0%

Alkem Labs 3,090 4.9 BUY 4,200 20.5% 10.6% 15.8% 2.5% 9.2% 4.5%

Ajanta Pharma 1,888 2.2 ADD 2,405 13.8% 15.4% 9.8% 11.9% -1.1% -3.1%

Apollo Hospitals 4,611 8.8 BUY 5,365 43.7% 20.8% 1097.5% 45.9% -0.7% 0.7%

Narayana Health 647 1.8 ADD 720 44.6% 12.6% NM 27.0% 11.5% 5.7%

Max Healthcare 369 4.8 BUY 430 40.8% 8.7% 1572.5% 31.6% -10.1% 0.9%

Aviation

50.3% 77.6% -11.7% NM 14.3% -2.7%

Interglobe Aviation 2,040 10.5 REDUCE 1,925 66.1% 67.4% 4.5% NM 20.9% -2.7%

SpiceJet 61 0.5 NOT

RATED NA 5.9% 123.0% -102.7% 97.7% 0.0% 0.0%

Metals

44.2% 0.3% 178.9% -18.6% 4.4% 4.0%

Tata Steel. 1,139 18.6 NOT

RATED NA 45.6% -8.4% 393.6% -39.1% 5.5% 3.2%

JSW Steel. 615 19.8 NOT

RATED NA 76.0% 7.5% 172.9% -16.5% -3.2% -0.9%

Hindalco Industries 519 15.5 NOT

RATED NA 42.6% 1.0% 282.5% 2.9% 16.7% 15.5%

Coal India 158 13.0 NOT

RATED NA 15.8% 8.2% 27.6% 8.0% 3.7% 2.4%

Total

26.4% 12.1% 31.7% 21.2% 0.6% -0.4%

Note: Upside change in PAT estimates above 5% has been highlighted in green and downside change above 5% has been highlighted in red

CMP as on 23.02.2022

Source: Bloomberg & HSIE Research

P a g e | 13

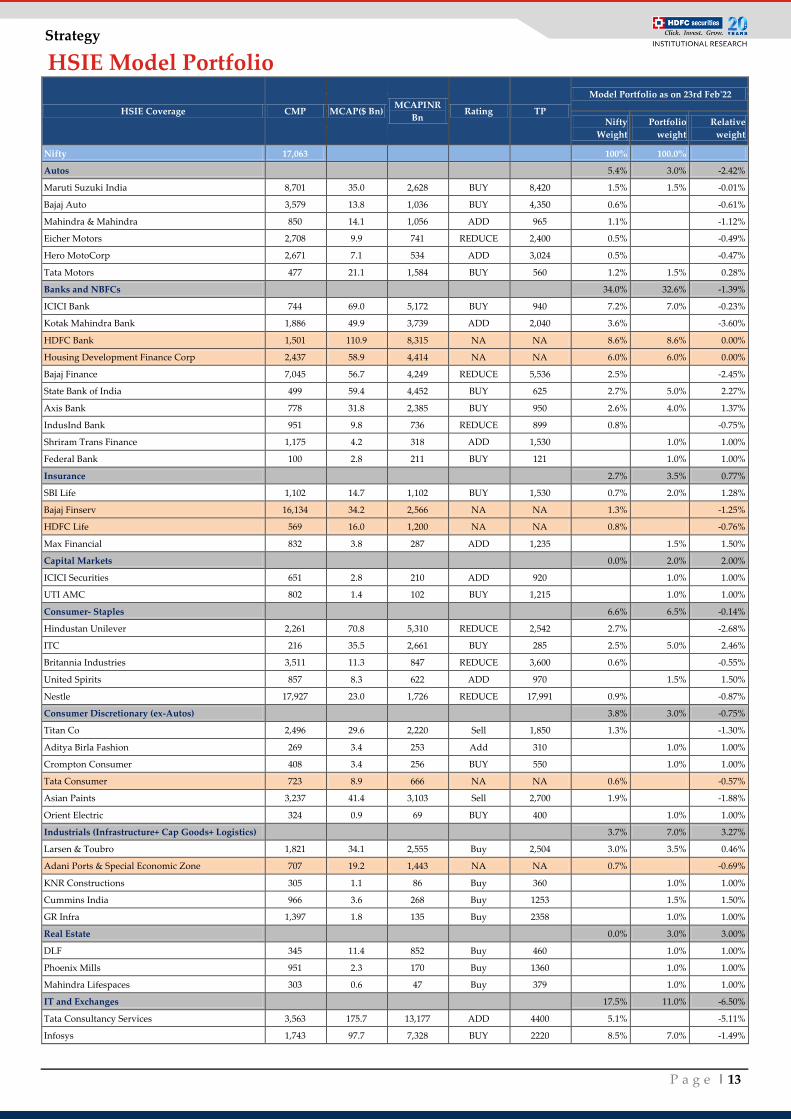

Strategy

HSIE Model Portfolio

HSIE Coverage CMP MCAP($ Bn) MCAPINR

Bn Rating TP

Model Portfolio as on 23rd Feb'22

Nifty

Weight

Portfolio

weight

Relative

weight

Nifty 17,063

100% 100.0%

Autos

5.4% 3.0% -2.42%

Maruti Suzuki India 8,701 35.0 2,628 BUY 8,420 1.5% 1.5% -0.01%

Bajaj Auto 3,579 13.8 1,036 BUY 4,350 0.6% -0.61%

Mahindra & Mahindra 850 14.1 1,056 ADD 965 1.1% -1.12%

Eicher Motors 2,708 9.9 741 REDUCE 2,400 0.5% -0.49%

Hero MotoCorp 2,671 7.1 534 ADD 3,024 0.5% -0.47%

Tata Motors 477 21.1 1,584 BUY 560 1.2% 1.5% 0.28%

Banks and NBFCs

34.0% 32.6% -1.39%

ICICI Bank 744 69.0 5,172 BUY 940 7.2% 7.0% -0.23%

Kotak Mahindra Bank 1,886 49.9 3,739 ADD 2,040 3.6% -3.60%

HDFC Bank 1,501 110.9 8,315 NA NA 8.6% 8.6% 0.00%

Housing Development Finance Corp 2,437 58.9 4,414 NA NA 6.0% 6.0% 0.00%

Bajaj Finance 7,045 56.7 4,249 REDUCE 5,536 2.5% -2.45%

State Bank of India 499 59.4 4,452 BUY 625 2.7% 5.0% 2.27%

Axis Bank 778 31.8 2,385 BUY 950 2.6% 4.0% 1.37%

IndusInd Bank 951 9.8 736 REDUCE 899 0.8% -0.75%

Shriram Trans Finance 1,175 4.2 318 ADD 1,530 1.0% 1.00%

Federal Bank 100 2.8 211 BUY 121 1.0% 1.00%

Insurance

2.7% 3.5% 0.77%

SBI Life 1,102 14.7 1,102 BUY 1,530 0.7% 2.0% 1.28%

Bajaj Finserv 16,134 34.2 2,566 NA NA 1.3% -1.25%

HDFC Life 569 16.0 1,200 NA NA 0.8% -0.76%

Max Financial 832 3.8 287 ADD 1,235 1.5% 1.50%

Capital Markets

0.0% 2.0% 2.00%

ICICI Securities 651 2.8 210 ADD 920 1.0% 1.00%

UTI AMC 802 1.4 102 BUY 1,215 1.0% 1.00%

Consumer- Staples

6.6% 6.5% -0.14%

Hindustan Unilever 2,261 70.8 5,310 REDUCE 2,542 2.7% -2.68%

ITC 216 35.5 2,661 BUY 285 2.5% 5.0% 2.46%

Britannia Industries 3,511 11.3 847 REDUCE 3,600 0.6% -0.55%

United Spirits 857 8.3 622 ADD 970 1.5% 1.50%

Nestle 17,927 23.0 1,726 REDUCE 17,991 0.9% -0.87%

Consumer Discretionary (ex-Autos)

3.8% 3.0% -0.75%

Titan Co 2,496 29.6 2,220 Sell 1,850 1.3% -1.30%

Aditya Birla Fashion 269 3.4 253 Add 310 1.0% 1.00%

Crompton Consumer 408 3.4 256 BUY 550 1.0% 1.00%

Tata Consumer 723 8.9 666 NA NA 0.6% -0.57%

Asian Paints 3,237 41.4 3,103 Sell 2,700 1.9% -1.88%

Orient Electric 324 0.9 69 BUY 400 1.0% 1.00%

Industrials (Infrastructure+ Cap Goods+ Logistics)

3.7% 7.0% 3.27%

Larsen & Toubro 1,821 34.1 2,555 Buy 2,504 3.0% 3.5% 0.46%

Adani Ports & Special Economic Zone 707 19.2 1,443 NA NA 0.7% -0.69%

KNR Constructions 305 1.1 86 Buy 360 1.0% 1.00%

Cummins India 966 3.6 268 Buy 1253 1.5% 1.50%

GR Infra 1,397 1.8 135 Buy 2358 1.0% 1.00%

Real Estate

0.0% 3.0% 3.00%

DLF 345 11.4 852 Buy 460 1.0% 1.00%

Phoenix Mills 951 2.3 170 Buy 1360 1.0% 1.00%

Mahindra Lifespaces 303 0.6 47 Buy 379 1.0% 1.00%

IT and Exchanges

17.5% 11.0% -6.50%

Tata Consultancy Services 3,563 175.7 13,177 ADD 4400 5.1% -5.11%

Infosys 1,743 97.7 7,328 BUY 2220 8.5% 7.0% -1.49%

P a g e | 14

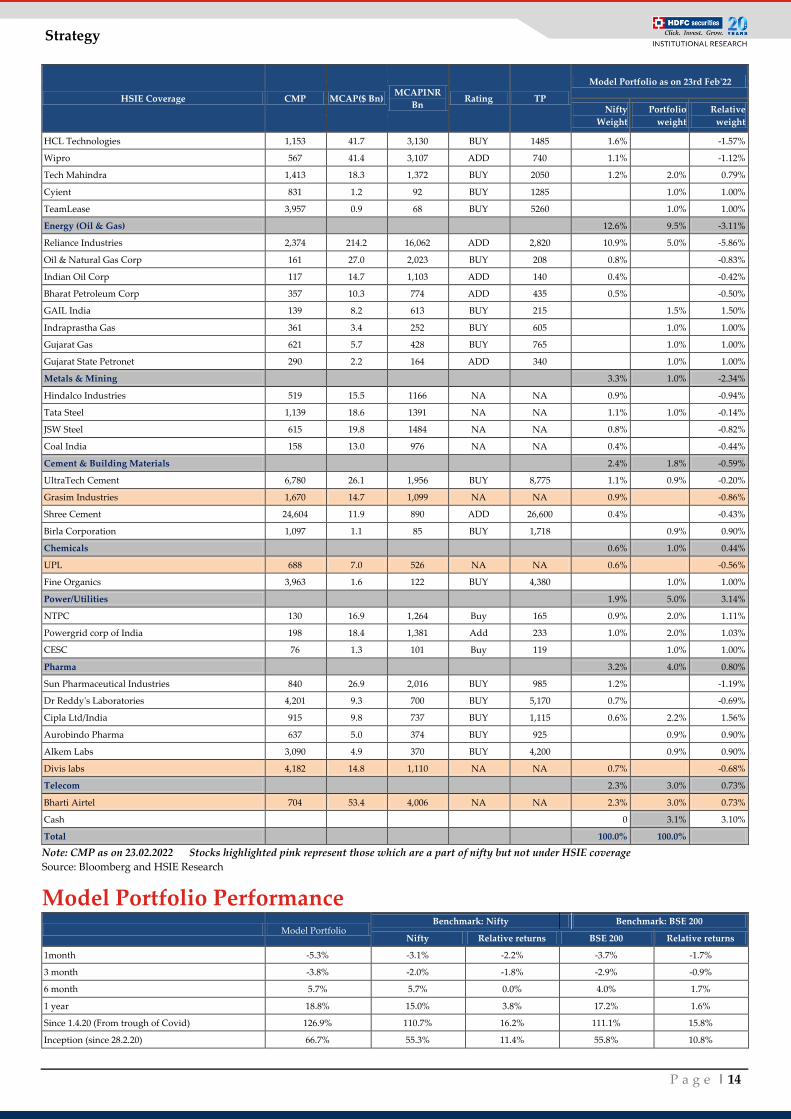

Strategy

HSIE Coverage CMP MCAP($ Bn) MCAPINR

Bn Rating TP

Model Portfolio as on 23rd Feb'22

Nifty

Weight

Portfolio

weight

Relative

weight

HCL Technologies 1,153 41.7 3,130 BUY 1485 1.6% -1.57%

Wipro 567 41.4 3,107 ADD 740 1.1% -1.12%

Tech Mahindra 1,413 18.3 1,372 BUY 2050 1.2% 2.0% 0.79%

Cyient 831 1.2 92 BUY 1285 1.0% 1.00%

TeamLease 3,957 0.9 68 BUY 5260 1.0% 1.00%

Energy (Oil & Gas) 12.6% 9.5% -3.11%

Reliance Industries 2,374 214.2 16,062 ADD 2,820 10.9% 5.0% -5.86%

Oil & Natural Gas Corp 161 27.0 2,023 BUY 208 0.8% -0.83%

Indian Oil Corp 117 14.7 1,103 ADD 140 0.4% -0.42%

Bharat Petroleum Corp 357 10.3 774 ADD 435 0.5% -0.50%

GAIL India 139 8.2 613 BUY 215 1.5% 1.50%

Indraprastha Gas 361 3.4 252 BUY 605 1.0% 1.00%

Gujarat Gas 621 5.7 428 BUY 765 1.0% 1.00%

Gujarat State Petronet 290 2.2 164 ADD 340 1.0% 1.00%

Metals & Mining 3.3% 1.0% -2.34%

Hindalco Industries 519 15.5 1166 NA NA 0.9% -0.94%

Tata Steel 1,139 18.6 1391 NA NA 1.1% 1.0% -0.14%

JSW Steel 615 19.8 1484 NA NA 0.8% -0.82%

Coal India 158 13.0 976 NA NA 0.4% -0.44%

Cement & Building Materials 2.4% 1.8% -0.59%

UltraTech Cement 6,780 26.1 1,956 BUY 8,775 1.1% 0.9% -0.20%

Grasim Industries 1,670 14.7 1,099 NA NA 0.9% -0.86%

Shree Cement 24,604 11.9 890 ADD 26,600 0.4% -0.43%

Birla Corporation 1,097 1.1 85 BUY 1,718 0.9% 0.90%

Chemicals 0.6% 1.0% 0.44%

UPL 688 7.0 526 NA NA 0.6% -0.56%

Fine Organics 3,963 1.6 122 BUY 4,380 1.0% 1.00%

Power/Utilities 1.9% 5.0% 3.14%

NTPC 130 16.9 1,264 Buy 165 0.9% 2.0% 1.11%

Powergrid corp of India 198 18.4 1,381 Add 233 1.0% 2.0% 1.03%

CESC 76 1.3 101 Buy 119 1.0% 1.00%

Pharma 3.2% 4.0% 0.80%

Sun Pharmaceutical Industries 840 26.9 2,016 BUY 985 1.2% -1.19%

Dr Reddy's Laboratories 4,201 9.3 700 BUY 5,170 0.7% -0.69%

Cipla Ltd/India 915 9.8 737 BUY 1,115 0.6% 2.2% 1.56%

Aurobindo Pharma 637 5.0 374 BUY 925 0.9% 0.90%

Alkem Labs 3,090 4.9 370 BUY 4,200 0.9% 0.90%

Divis labs 4,182 14.8 1,110 NA NA 0.7% -0.68%

Telecom 2.3% 3.0% 0.73%

Bharti Airtel 704 53.4 4,006 NA NA 2.3% 3.0% 0.73%

Cash 0 3.1% 3.10%

Total 100.0% 100.0%

Note: CMP as on 23.02.2022 Stocks highlighted pink represent those which are a part of nifty but not under HSIE coverage

Source: Bloomberg and HSIE Research

Model Portfolio Performance Model Portfolio

Benchmark: Nifty Benchmark: BSE 200

Nifty Relative returns BSE 200 Relative returns

1month -5.3% -3.1% -2.2% -3.7% -1.7%

3 month -3.8% -2.0% -1.8% -2.9% -0.9%

6 month 5.7% 5.7% 0.0% 4.0% 1.7%

1 year 18.8% 15.0% 3.8% 17.2% 1.6%

Since 1.4.20 (From trough of Covid) 126.9% 110.7% 16.2% 111.1% 15.8%

Inception (since 28.2.20) 66.7% 55.3% 11.4% 55.8% 10.8%

P a g e | 15

Strategy

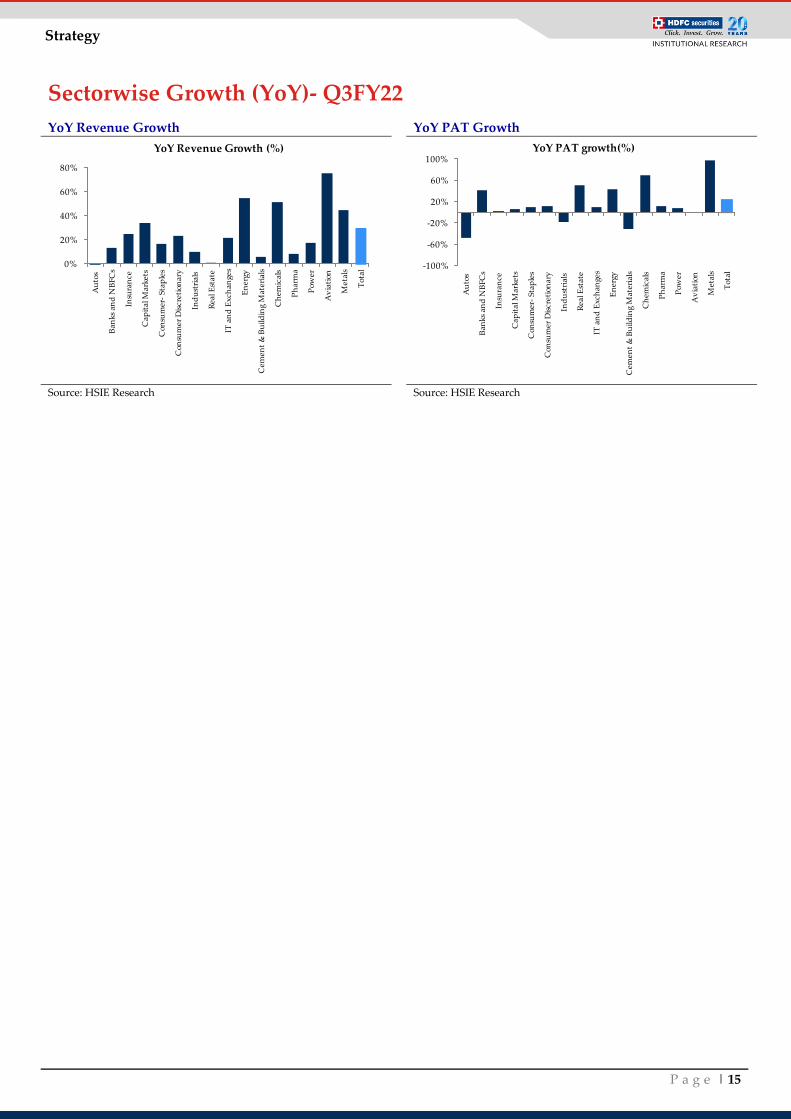

Sectorwise Growth (YoY)- Q3FY22

YoY Revenue Growth YoY PAT Growth

Source: HSIE Research Source: HSIE Research

0%

20%

40%

60%

80%

Au

tos

Ban

ks a

nd

NB

FCs

Insu

ran

ce

Cap

ital

Mar

kets

Con

sum

er-

Stap

les

Con

sum

er D

iscr

etio

nar

y

Ind

ust

rial

s

Rea

l Est

ate

IT a

nd

Exc

han

ges

En

ergy

Cem

ent

& B

uild

ing

Mat

eria

ls

Ch

emic

als

Ph

arm

a

Pow

er

Av

iati

on

Met

als

Tot

al

YoY Revenue Growth (%)

-100%

-60%

-20%

20%

60%

100%

Au

tos

Ban

ks a

nd

NB

FCs

Insu

ran

ce

Cap

ital

Mar

kets

Con

sum

er-

Stap

les

Con

sum

er D

iscr

etio

nar

y

Ind

ust

rial

s

Rea

l Est

ate

IT a

nd

Exc

han

ges

En

ergy

Cem

ent

& B

uild

ing

Mat

eria

ls

Ch

emic

als

Ph

arm

a

Pow

er

Av

iati

on

Met

als

Tot

al

YoY PAT growth(%)

P a g e | 16

HSIE Results Daily

BFSI

P a g e | 17

HSIE Results Daily

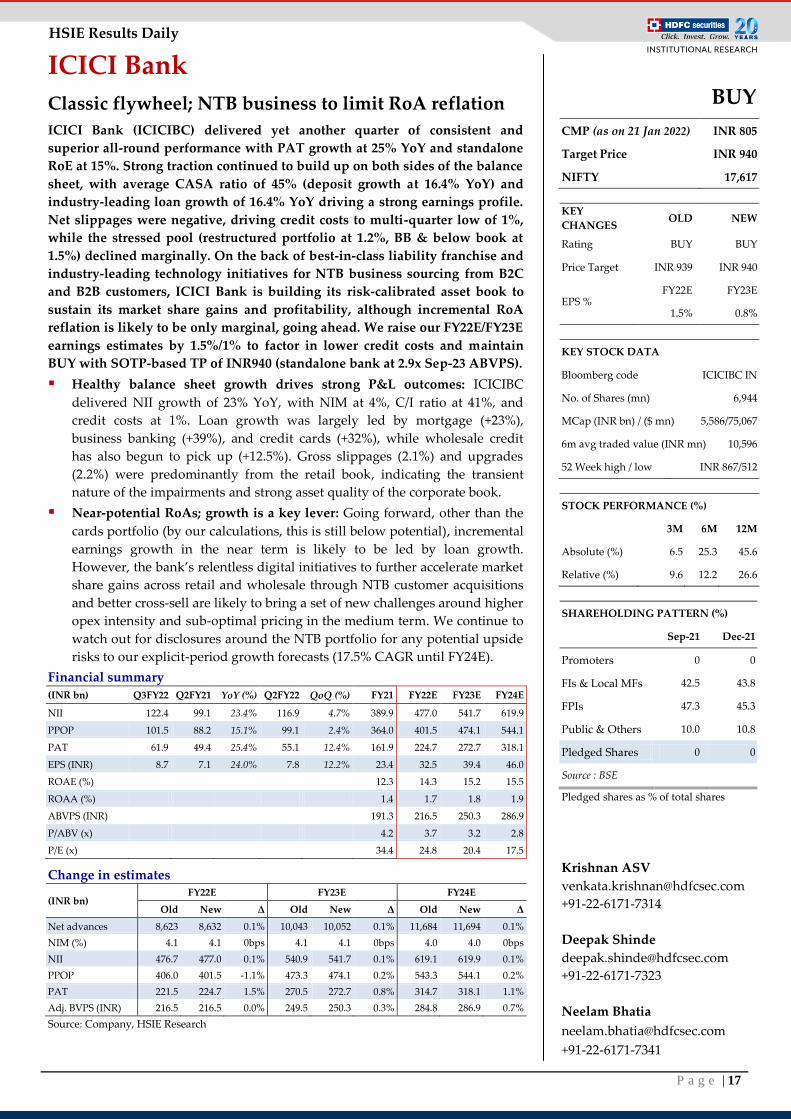

ICICI Bank

Classic flywheel; NTB business to limit RoA reflation

ICICI Bank (ICICIBC) delivered yet another quarter of consistent and

superior all-round performance with PAT growth at 25% YoY and standalone

RoE at 15%. Strong traction continued to build up on both sides of the balance

sheet, with average CASA ratio of 45% (deposit growth at 16.4% YoY) and

industry-leading loan growth of 16.4% YoY driving a strong earnings profile.

Net slippages were negative, driving credit costs to multi-quarter low of 1%,

while the stressed pool (restructured portfolio at 1.2%, BB & below book at

1.5%) declined marginally. On the back of best-in-class liability franchise and

industry-leading technology initiatives for NTB business sourcing from B2C

and B2B customers, ICICI Bank is building its risk-calibrated asset book to

sustain its market share gains and profitability, although incremental RoA

reflation is likely to be only marginal, going ahead. We raise our FY22E/FY23E

earnings estimates by 1.5%/1% to factor in lower credit costs and maintain

BUY with SOTP-based TP of INR940 (standalone bank at 2.9x Sep-23 ABVPS).

Healthy balance sheet growth drives strong P&L outcomes: ICICIBC

delivered NII growth of 23% YoY, with NIM at 4%, C/I ratio at 41%, and

credit costs at 1%. Loan growth was largely led by mortgage (+23%),

business banking (+39%), and credit cards (+32%), while wholesale credit

has also begun to pick up (+12.5%). Gross slippages (2.1%) and upgrades

(2.2%) were predominantly from the retail book, indicating the transient

nature of the impairments and strong asset quality of the corporate book.

Near-potential RoAs; growth is a key lever: Going forward, other than the

cards portfolio (by our calculations, this is still below potential), incremental

earnings growth in the near term is likely to be led by loan growth.

However, the bank’s relentless digital initiatives to further accelerate market

share gains across retail and wholesale through NTB customer acquisitions

and better cross-sell are likely to bring a set of new challenges around higher

opex intensity and sub-optimal pricing in the medium term. We continue to

watch out for disclosures around the NTB portfolio for any potential upside

risks to our explicit-period growth forecasts (17.5% CAGR until FY24E).

Financial summary

(INR bn) Q3FY22 Q2FY21 YoY (%) Q2FY22 QoQ (%) FY21 FY22E FY23E FY24E

NII 122.4 99.1 23.4% 116.9 4.7% 389.9 477.0 541.7 619.9

PPOP 101.5 88.2 15.1% 99.1 2.4% 364.0 401.5 474.1 544.1

PAT 61.9 49.4 25.4% 55.1 12.4% 161.9 224.7 272.7 318.1

EPS (INR) 8.7 7.1 24.0% 7.8 12.2% 23.4 32.5 39.4 46.0

ROAE (%) 12.3 14.3 15.2 15.5

ROAA (%) 1.4 1.7 1.8 1.9

ABVPS (INR) 191.3 216.5 250.3 286.9

P/ABV (x) 4.2 3.7 3.2 2.8

P/E (x) 34.4 24.8 20.4 17.5

Change in estimates

(INR bn) FY22E FY23E FY24E

Old New Δ Old New Δ Old New Δ

Net advances 8,623 8,632 0.1% 10,043 10,052 0.1% 11,684 11,694 0.1%

NIM (%) 4.1 4.1 0bps 4.1 4.1 0bps 4.0 4.0 0bps

NII 476.7 477.0 0.1% 540.9 541.7 0.1% 619.1 619.9 0.1%

PPOP 406.0 401.5 -1.1% 473.3 474.1 0.2% 543.3 544.1 0.2%

PAT 221.5 224.7 1.5% 270.5 272.7 0.8% 314.7 318.1 1.1%

Adj. BVPS (INR) 216.5 216.5 0.0% 249.5 250.3 0.3% 284.8 286.9 0.7%

Source: Company, HSIE Research

BUY

CMP (as on 21 Jan 2022) INR 805

Target Price INR 940

NIFTY 17,617

KEY

CHANGES OLD NEW

Rating BUY BUY

Price Target INR 939 INR 940

EPS % FY22E FY23E

1.5% 0.8%

KEY STOCK DATA

Bloomberg code ICICIBC IN

No. of Shares (mn) 6,944

MCap (INR bn) / ($ mn) 5,586/75,067

6m avg traded value (INR mn) 10,596

52 Week high / low INR 867/512

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) 6.5 25.3 45.6

Relative (%) 9.6 12.2 26.6

SHAREHOLDING PATTERN (%)

Sep-21 Dec-21

Promoters 0 0

FIs & Local MFs 42.5 43.8

FPIs 47.3 45.3

Public & Others 10.0 10.8

Pledged Shares 0 0

Source : BSE

Pledged shares as % of total shares

Krishnan ASV

+91-22-6171-7314

Deepak Shinde

+91-22-6171-7323

Neelam Bhatia

+91-22-6171-7341

P a g e | 18

HSIE Results Daily

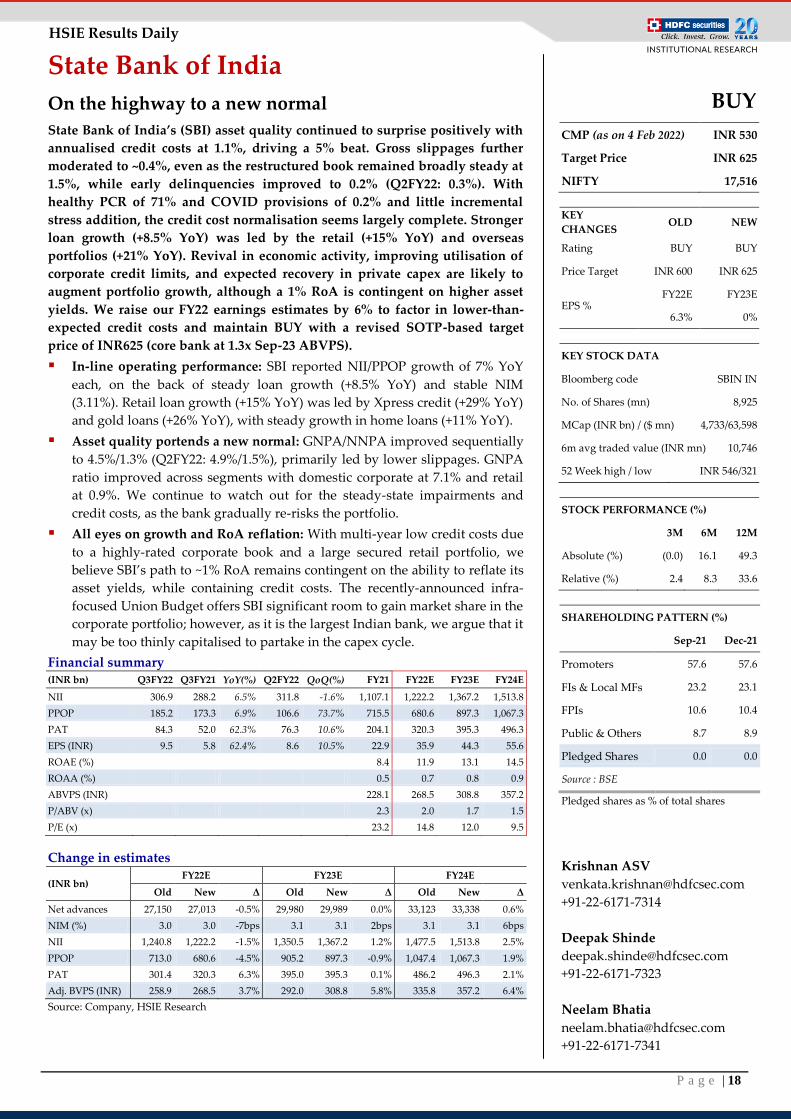

State Bank of India

On the highway to a new normal

State Bank of India’s (SBI) asset quality continued to surprise positively with

annualised credit costs at 1.1%, driving a 5% beat. Gross slippages further

moderated to ~0.4%, even as the restructured book remained broadly steady at

1.5%, while early delinquencies improved to 0.2% (Q2FY22: 0.3%). With

healthy PCR of 71% and COVID provisions of 0.2% and little incremental

stress addition, the credit cost normalisation seems largely complete. Stronger

loan growth (+8.5% YoY) was led by the retail (+15% YoY) and overseas

portfolios (+21% YoY). Revival in economic activity, improving utilisation of

corporate credit limits, and expected recovery in private capex are likely to

augment portfolio growth, although a 1% RoA is contingent on higher asset

yields. We raise our FY22 earnings estimates by 6% to factor in lower-than-

expected credit costs and maintain BUY with a revised SOTP-based target

price of INR625 (core bank at 1.3x Sep-23 ABVPS).

In-line operating performance: SBI reported NII/PPOP growth of 7% YoY

each, on the back of steady loan growth (+8.5% YoY) and stable NIM

(3.11%). Retail loan growth (+15% YoY) was led by Xpress credit (+29% YoY)

and gold loans (+26% YoY), with steady growth in home loans (+11% YoY).

Asset quality portends a new normal: GNPA/NNPA improved sequentially

to 4.5%/1.3% (Q2FY22: 4.9%/1.5%), primarily led by lower slippages. GNPA

ratio improved across segments with domestic corporate at 7.1% and retail

at 0.9%. We continue to watch out for the steady-state impairments and

credit costs, as the bank gradually re-risks the portfolio.

All eyes on growth and RoA reflation: With multi-year low credit costs due

to a highly-rated corporate book and a large secured retail portfolio, we

believe SBI’s path to ~1% RoA remains contingent on the ability to reflate its

asset yields, while containing credit costs. The recently-announced infra-

focused Union Budget offers SBI significant room to gain market share in the

corporate portfolio; however, as it is the largest Indian bank, we argue that it

may be too thinly capitalised to partake in the capex cycle.

Financial summary (INR bn) Q3FY22 Q3FY21 YoY(%) Q2FY22 QoQ(%) FY21 FY22E FY23E FY24E

NII 306.9 288.2 6.5% 311.8 -1.6% 1,107.1 1,222.2 1,367.2 1,513.8

PPOP 185.2 173.3 6.9% 106.6 73.7% 715.5 680.6 897.3 1,067.3

PAT 84.3 52.0 62.3% 76.3 10.6% 204.1 320.3 395.3 496.3

EPS (INR) 9.5 5.8 62.4% 8.6 10.5% 22.9 35.9 44.3 55.6

ROAE (%) 8.4 11.9 13.1 14.5

ROAA (%) 0.5 0.7 0.8 0.9

ABVPS (INR) 228.1 268.5 308.8 357.2

P/ABV (x) 2.3 2.0 1.7 1.5

P/E (x) 23.2 14.8 12.0 9.5

Change in estimates

(INR bn) FY22E FY23E FY24E

Old New Δ Old New Δ Old New Δ

Net advances 27,150 27,013 -0.5% 29,980 29,989 0.0% 33,123 33,338 0.6%

NIM (%) 3.0 3.0 -7bps 3.1 3.1 2bps 3.1 3.1 6bps

NII 1,240.8 1,222.2 -1.5% 1,350.5 1,367.2 1.2% 1,477.5 1,513.8 2.5%

PPOP 713.0 680.6 -4.5% 905.2 897.3 -0.9% 1,047.4 1,067.3 1.9%

PAT 301.4 320.3 6.3% 395.0 395.3 0.1% 486.2 496.3 2.1%

Adj. BVPS (INR) 258.9 268.5 3.7% 292.0 308.8 5.8% 335.8 357.2 6.4%

Source: Company, HSIE Research

BUY

CMP (as on 4 Feb 2022) INR 530

Target Price INR 625

NIFTY 17,516

KEY

CHANGES OLD NEW

Rating BUY BUY

Price Target INR 600 INR 625

EPS % FY22E FY23E

6.3% 0%

KEY STOCK DATA

Bloomberg code SBIN IN

No. of Shares (mn) 8,925

MCap (INR bn) / ($ mn) 4,733/63,598

6m avg traded value (INR mn) 10,746

52 Week high / low INR 546/321

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) (0.0) 16.1 49.3

Relative (%) 2.4 8.3 33.6

SHAREHOLDING PATTERN (%)

Sep-21 Dec-21

Promoters 57.6 57.6

FIs & Local MFs 23.2 23.1

FPIs 10.6 10.4

Public & Others 8.7 8.9

Pledged Shares 0.0 0.0

Source : BSE

Pledged shares as % of total shares

Krishnan ASV

+91-22-6171-7314

Deepak Shinde

+91-22-6171-7323

Neelam Bhatia

+91-22-6171-7341

P a g e | 19

HSIE Results Daily

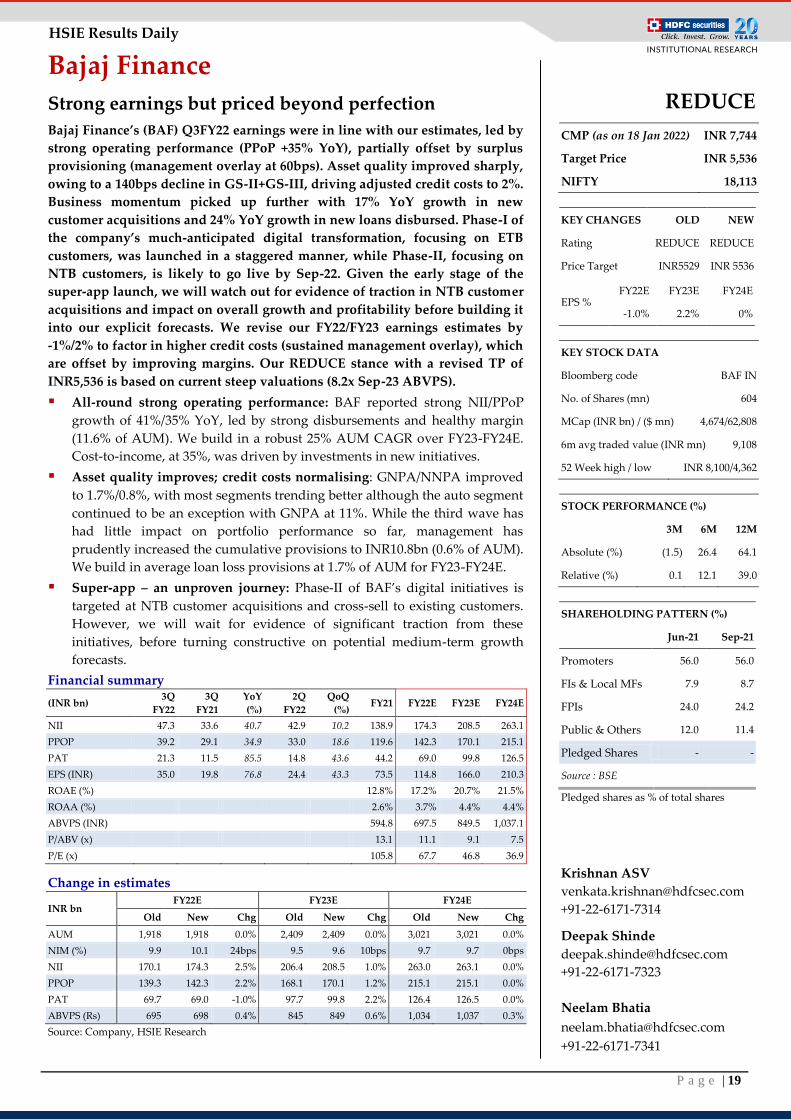

Bajaj Finance

Strong earnings but priced beyond perfection

Bajaj Finance’s (BAF) Q3FY22 earnings were in line with our estimates, led by

strong operating performance (PPoP +35% YoY), partially offset by surplus

provisioning (management overlay at 60bps). Asset quality improved sharply,

owing to a 140bps decline in GS-II+GS-III, driving adjusted credit costs to 2%.

Business momentum picked up further with 17% YoY growth in new

customer acquisitions and 24% YoY growth in new loans disbursed. Phase-I of

the company’s much-anticipated digital transformation, focusing on ETB

customers, was launched in a staggered manner, while Phase-II, focusing on

NTB customers, is likely to go live by Sep-22. Given the early stage of the

super-app launch, we will watch out for evidence of traction in NTB customer

acquisitions and impact on overall growth and profitability before building it

into our explicit forecasts. We revise our FY22/FY23 earnings estimates by

-1%/2% to factor in higher credit costs (sustained management overlay), which

are offset by improving margins. Our REDUCE stance with a revised TP of

INR5,536 is based on current steep valuations (8.2x Sep-23 ABVPS).

All-round strong operating performance: BAF reported strong NII/PPoP

growth of 41%/35% YoY, led by strong disbursements and healthy margin

(11.6% of AUM). We build in a robust 25% AUM CAGR over FY23-FY24E.

Cost-to-income, at 35%, was driven by investments in new initiatives.

Asset quality improves; credit costs normalising: GNPA/NNPA improved

to 1.7%/0.8%, with most segments trending better although the auto segment

continued to be an exception with GNPA at 11%. While the third wave has

had little impact on portfolio performance so far, management has

prudently increased the cumulative provisions to INR10.8bn (0.6% of AUM).

We build in average loan loss provisions at 1.7% of AUM for FY23-FY24E.

Super-app – an unproven journey: Phase-II of BAF’s digital initiatives is

targeted at NTB customer acquisitions and cross-sell to existing customers.

However, we will wait for evidence of significant traction from these

initiatives, before turning constructive on potential medium-term growth

forecasts.

Financial summary

(INR bn) 3Q

FY22

3Q

FY21

YoY

(%)

2Q

FY22

QoQ

(%) FY21 FY22E FY23E FY24E

NII 47.3 33.6 40.7 42.9 10.2 138.9 174.3 208.5 263.1

PPOP 39.2 29.1 34.9 33.0 18.6 119.6 142.3 170.1 215.1

PAT 21.3 11.5 85.5 14.8 43.6 44.2 69.0 99.8 126.5

EPS (INR) 35.0 19.8 76.8 24.4 43.3 73.5 114.8 166.0 210.3

ROAE (%) 12.8% 17.2% 20.7% 21.5%

ROAA (%) 2.6% 3.7% 4.4% 4.4%

ABVPS (INR) 594.8 697.5 849.5 1,037.1

P/ABV (x) 13.1 11.1 9.1 7.5

P/E (x) 105.8 67.7 46.8 36.9

Change in estimates

INR bn FY22E FY23E FY24E

Old New Chg Old New Chg Old New Chg

AUM 1,918 1,918 0.0% 2,409 2,409 0.0% 3,021 3,021 0.0%

NIM (%) 9.9 10.1 24bps 9.5 9.6 10bps 9.7 9.7 0bps

NII 170.1 174.3 2.5% 206.4 208.5 1.0% 263.0 263.1 0.0%

PPOP 139.3 142.3 2.2% 168.1 170.1 1.2% 215.1 215.1 0.0%

PAT 69.7 69.0 -1.0% 97.7 99.8 2.2% 126.4 126.5 0.0%

ABVPS (Rs) 695 698 0.4% 845 849 0.6% 1,034 1,037 0.3%

Source: Company, HSIE Research

REDUCE

CMP (as on 18 Jan 2022) INR 7,744

Target Price INR 5,536

NIFTY 18,113

KEY CHANGES OLD NEW

Rating REDUCE REDUCE

Price Target INR5529 INR 5536

EPS % FY22E FY23E FY24E

-1.0% 2.2% 0%

KEY STOCK DATA

Bloomberg code BAF IN

No. of Shares (mn) 604

MCap (INR bn) / ($ mn) 4,674/62,808

6m avg traded value (INR mn) 9,108

52 Week high / low INR 8,100/4,362

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) (1.5) 26.4 64.1

Relative (%) 0.1 12.1 39.0

SHAREHOLDING PATTERN (%)

Jun-21 Sep-21

Promoters 56.0 56.0

FIs & Local MFs 7.9 8.7

FPIs 24.0 24.2

Public & Others 12.0 11.4

Pledged Shares - -

Source : BSE

Pledged shares as % of total shares

Krishnan ASV

+91-22-6171-7314

Deepak Shinde

+91-22-6171-7323

Neelam Bhatia

+91-22-6171-7341

P a g e | 20

HSIE Results Daily

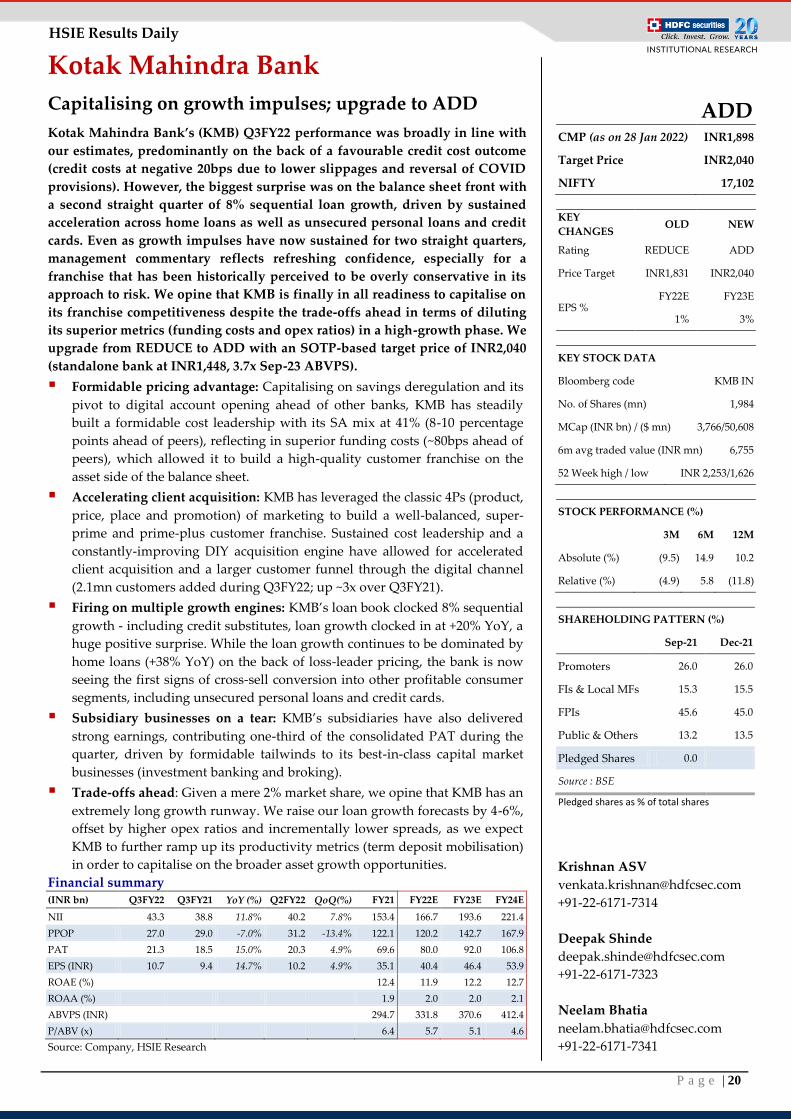

Kotak Mahindra Bank

Capitalising on growth impulses; upgrade to ADD

Kotak Mahindra Bank’s (KMB) Q3FY22 performance was broadly in line with

our estimates, predominantly on the back of a favourable credit cost outcome

(credit costs at negative 20bps due to lower slippages and reversal of COVID

provisions). However, the biggest surprise was on the balance sheet front with

a second straight quarter of 8% sequential loan growth, driven by sustained

acceleration across home loans as well as unsecured personal loans and credit

cards. Even as growth impulses have now sustained for two straight quarters,

management commentary reflects refreshing confidence, especially for a

franchise that has been historically perceived to be overly conservative in its

approach to risk. We opine that KMB is finally in all readiness to capitalise on

its franchise competitiveness despite the trade-offs ahead in terms of diluting

its superior metrics (funding costs and opex ratios) in a high-growth phase. We

upgrade from REDUCE to ADD with an SOTP-based target price of INR2,040

(standalone bank at INR1,448, 3.7x Sep-23 ABVPS).

Formidable pricing advantage: Capitalising on savings deregulation and its

pivot to digital account opening ahead of other banks, KMB has steadily

built a formidable cost leadership with its SA mix at 41% (8-10 percentage

points ahead of peers), reflecting in superior funding costs (~80bps ahead of

peers), which allowed it to build a high-quality customer franchise on the

asset side of the balance sheet.

Accelerating client acquisition: KMB has leveraged the classic 4Ps (product,

price, place and promotion) of marketing to build a well-balanced, super-

prime and prime-plus customer franchise. Sustained cost leadership and a

constantly-improving DIY acquisition engine have allowed for accelerated

client acquisition and a larger customer funnel through the digital channel

(2.1mn customers added during Q3FY22; up ~3x over Q3FY21).

Firing on multiple growth engines: KMB’s loan book clocked 8% sequential

growth - including credit substitutes, loan growth clocked in at +20% YoY, a

huge positive surprise. While the loan growth continues to be dominated by

home loans (+38% YoY) on the back of loss-leader pricing, the bank is now

seeing the first signs of cross-sell conversion into other profitable consumer

segments, including unsecured personal loans and credit cards.

Subsidiary businesses on a tear: KMB’s subsidiaries have also delivered

strong earnings, contributing one-third of the consolidated PAT during the

quarter, driven by formidable tailwinds to its best-in-class capital market

businesses (investment banking and broking).

Trade-offs ahead: Given a mere 2% market share, we opine that KMB has an

extremely long growth runway. We raise our loan growth forecasts by 4-6%,

offset by higher opex ratios and incrementally lower spreads, as we expect

KMB to further ramp up its productivity metrics (term deposit mobilisation)

in order to capitalise on the broader asset growth opportunities.

Financial summary (INR bn) Q3FY22 Q3FY21 YoY (%) Q2FY22 QoQ(%) FY21 FY22E FY23E FY24E

NII 43.3 38.8 11.8% 40.2 7.8% 153.4 166.7 193.6 221.4

PPOP 27.0 29.0 -7.0% 31.2 -13.4% 122.1 120.2 142.7 167.9

PAT 21.3 18.5 15.0% 20.3 4.9% 69.6 80.0 92.0 106.8

EPS (INR) 10.7 9.4 14.7% 10.2 4.9% 35.1 40.4 46.4 53.9

ROAE (%) 12.4 11.9 12.2 12.7

ROAA (%) 1.9 2.0 2.0 2.1

ABVPS (INR) 294.7 331.8 370.6 412.4

P/ABV (x) 6.4 5.7 5.1 4.6

Source: Company, HSIE Research

ADD CMP (as on 28 Jan 2022) INR1,898

Target Price INR2,040

NIFTY 17,102

KEY

CHANGES OLD NEW

Rating REDUCE ADD

Price Target INR1,831 INR2,040

EPS % FY22E FY23E

1% 3%

KEY STOCK DATA

Bloomberg code KMB IN

No. of Shares (mn) 1,984

MCap (INR bn) / ($ mn) 3,766/50,608

6m avg traded value (INR mn) 6,755

52 Week high / low INR 2,253/1,626

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) (9.5) 14.9 10.2

Relative (%) (4.9) 5.8 (11.8)

SHAREHOLDING PATTERN (%)

Sep-21 Dec-21

Promoters 26.0 26.0

FIs & Local MFs 15.3 15.5

FPIs 45.6 45.0

Public & Others 13.2 13.5

Pledged Shares 0.0

Source : BSE

Pledged shares as % of total shares

Krishnan ASV

+91-22-6171-7314

Deepak Shinde

+91-22-6171-7323

Neelam Bhatia

+91-22-6171-7341

P a g e | 21

HSIE Results Daily

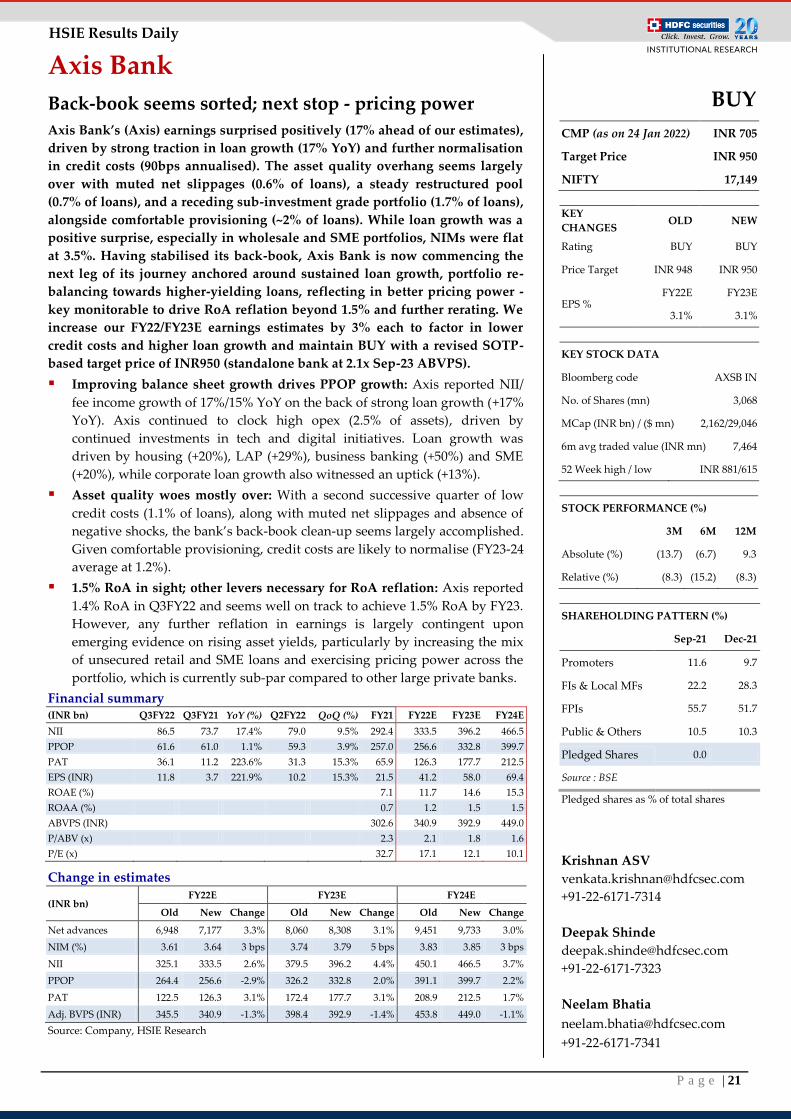

Axis Bank

Back-book seems sorted; next stop - pricing power

Axis Bank’s (Axis) earnings surprised positively (17% ahead of our estimates),

driven by strong traction in loan growth (17% YoY) and further normalisation

in credit costs (90bps annualised). The asset quality overhang seems largely

over with muted net slippages (0.6% of loans), a steady restructured pool

(0.7% of loans), and a receding sub-investment grade portfolio (1.7% of loans),

alongside comfortable provisioning (~2% of loans). While loan growth was a

positive surprise, especially in wholesale and SME portfolios, NIMs were flat

at 3.5%. Having stabilised its back-book, Axis Bank is now commencing the

next leg of its journey anchored around sustained loan growth, portfolio re-

balancing towards higher-yielding loans, reflecting in better pricing power -

key monitorable to drive RoA reflation beyond 1.5% and further rerating. We

increase our FY22/FY23E earnings estimates by 3% each to factor in lower

credit costs and higher loan growth and maintain BUY with a revised SOTP-

based target price of INR950 (standalone bank at 2.1x Sep-23 ABVPS).

Improving balance sheet growth drives PPOP growth: Axis reported NII/

fee income growth of 17%/15% YoY on the back of strong loan growth (+17%

YoY). Axis continued to clock high opex (2.5% of assets), driven by

continued investments in tech and digital initiatives. Loan growth was

driven by housing (+20%), LAP (+29%), business banking (+50%) and SME

(+20%), while corporate loan growth also witnessed an uptick (+13%).

Asset quality woes mostly over: With a second successive quarter of low

credit costs (1.1% of loans), along with muted net slippages and absence of

negative shocks, the bank’s back-book clean-up seems largely accomplished.

Given comfortable provisioning, credit costs are likely to normalise (FY23-24

average at 1.2%).

1.5% RoA in sight; other levers necessary for RoA reflation: Axis reported

1.4% RoA in Q3FY22 and seems well on track to achieve 1.5% RoA by FY23.

However, any further reflation in earnings is largely contingent upon

emerging evidence on rising asset yields, particularly by increasing the mix

of unsecured retail and SME loans and exercising pricing power across the

portfolio, which is currently sub-par compared to other large private banks.

Financial summary (INR bn) Q3FY22 Q3FY21 YoY (%) Q2FY22 QoQ (%) FY21 FY22E FY23E FY24E

NII 86.5 73.7 17.4% 79.0 9.5% 292.4 333.5 396.2 466.5

PPOP 61.6 61.0 1.1% 59.3 3.9% 257.0 256.6 332.8 399.7

PAT 36.1 11.2 223.6% 31.3 15.3% 65.9 126.3 177.7 212.5

EPS (INR) 11.8 3.7 221.9% 10.2 15.3% 21.5 41.2 58.0 69.4

ROAE (%) 7.1 11.7 14.6 15.3

ROAA (%) 0.7 1.2 1.5 1.5

ABVPS (INR) 302.6 340.9 392.9 449.0

P/ABV (x) 2.3 2.1 1.8 1.6

P/E (x) 32.7 17.1 12.1 10.1

Change in estimates

(INR bn) FY22E FY23E FY24E

Old New Change Old New Change Old New Change

Net advances 6,948 7,177 3.3% 8,060 8,308 3.1% 9,451 9,733 3.0%

NIM (%) 3.61 3.64 3 bps 3.74 3.79 5 bps 3.83 3.85 3 bps

NII 325.1 333.5 2.6% 379.5 396.2 4.4% 450.1 466.5 3.7%

PPOP 264.4 256.6 -2.9% 326.2 332.8 2.0% 391.1 399.7 2.2%

PAT 122.5 126.3 3.1% 172.4 177.7 3.1% 208.9 212.5 1.7%

Adj. BVPS (INR) 345.5 340.9 -1.3% 398.4 392.9 -1.4% 453.8 449.0 -1.1%

Source: Company, HSIE Research

BUY

CMP (as on 24 Jan 2022) INR 705

Target Price INR 950

NIFTY 17,149

KEY

CHANGES OLD NEW

Rating BUY BUY

Price Target INR 948 INR 950

EPS % FY22E FY23E

3.1% 3.1%

KEY STOCK DATA

Bloomberg code AXSB IN

No. of Shares (mn) 3,068

MCap (INR bn) / ($ mn) 2,162/29,046

6m avg traded value (INR mn) 7,464

52 Week high / low INR 881/615

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) (13.7) (6.7) 9.3

Relative (%) (8.3) (15.2) (8.3)

SHAREHOLDING PATTERN (%)

Sep-21 Dec-21

Promoters 11.6 9.7

FIs & Local MFs 22.2 28.3

FPIs 55.7 51.7

Public & Others 10.5 10.3

Pledged Shares 0.0

Source : BSE

Pledged shares as % of total shares

Krishnan ASV

+91-22-6171-7314

Deepak Shinde

+91-22-6171-7323

Neelam Bhatia

+91-22-6171-7341

P a g e | 22

HSIE Results Daily

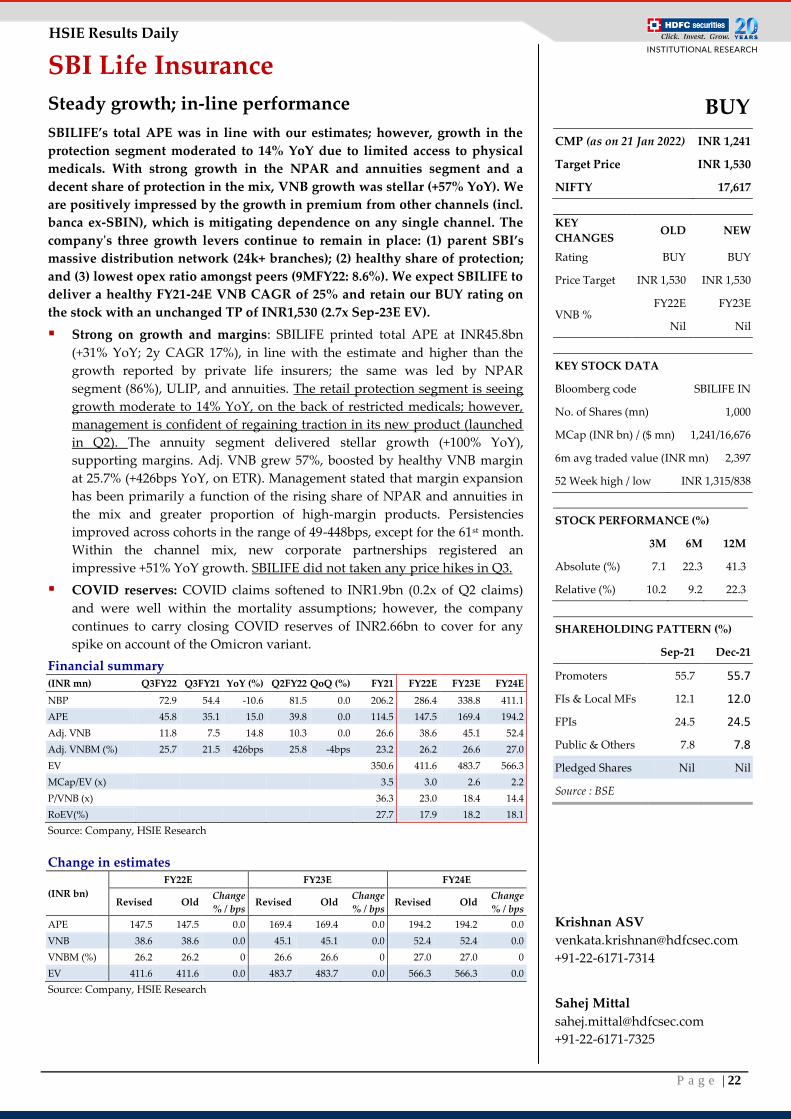

SBI Life Insurance

Steady growth; in-line performance SBILIFE’s total APE was in line with our estimates; however, growth in the

protection segment moderated to 14% YoY due to limited access to physical

medicals. With strong growth in the NPAR and annuities segment and a

decent share of protection in the mix, VNB growth was stellar (+57% YoY). We

are positively impressed by the growth in premium from other channels (incl.

banca ex-SBIN), which is mitigating dependence on any single channel. The

company's three growth levers continue to remain in place: (1) parent SBI’s

massive distribution network (24k+ branches); (2) healthy share of protection;

and (3) lowest opex ratio amongst peers (9MFY22: 8.6%). We expect SBILIFE to

deliver a healthy FY21-24E VNB CAGR of 25% and retain our BUY rating on

the stock with an unchanged TP of INR1,530 (2.7x Sep-23E EV).

Strong on growth and margins: SBILIFE printed total APE at INR45.8bn

(+31% YoY; 2y CAGR 17%), in line with the estimate and higher than the

growth reported by private life insurers; the same was led by NPAR

segment (86%), ULIP, and annuities. The retail protection segment is seeing

growth moderate to 14% YoY, on the back of restricted medicals; however,

management is confident of regaining traction in its new product (launched

in Q2). The annuity segment delivered stellar growth (+100% YoY),

supporting margins. Adj. VNB grew 57%, boosted by healthy VNB margin

at 25.7% (+426bps YoY, on ETR). Management stated that margin expansion

has been primarily a function of the rising share of NPAR and annuities in

the mix and greater proportion of high-margin products. Persistencies

improved across cohorts in the range of 49-448bps, except for the 61st month.

Within the channel mix, new corporate partnerships registered an

impressive +51% YoY growth. SBILIFE did not taken any price hikes in Q3.

COVID reserves: COVID claims softened to INR1.9bn (0.2x of Q2 claims)

and were well within the mortality assumptions; however, the company

continues to carry closing COVID reserves of INR2.66bn to cover for any

spike on account of the Omicron variant.

Financial summary (INR mn) Q3FY22 Q3FY21 YoY (%) Q2FY22 QoQ (%) FY21 FY22E FY23E FY24E

NBP 72.9 54.4 -10.6 81.5 0.0 206.2 286.4 338.8 411.1

APE 45.8 35.1 15.0 39.8 0.0 114.5 147.5 169.4 194.2

Adj. VNB 11.8 7.5 14.8 10.3 0.0 26.6 38.6 45.1 52.4

Adj. VNBM (%) 25.7 21.5 426bps 25.8 -4bps 23.2 26.2 26.6 27.0

EV

350.6 411.6 483.7 566.3

MCap/EV (x)

3.5 3.0 2.6 2.2

P/VNB (x)

36.3 23.0 18.4 14.4

RoEV(%)

27.7 17.9 18.2 18.1

Source: Company, HSIE Research

Change in estimates

(INR bn)

FY22E FY23E FY24E

Revised Old Change

% / bps Revised Old

Change

% / bps Revised Old

Change

% / bps

APE 147.5 147.5 0.0 169.4 169.4 0.0 194.2 194.2 0.0

VNB 38.6 38.6 0.0 45.1 45.1 0.0 52.4 52.4 0.0

VNBM (%) 26.2 26.2 0 26.6 26.6 0 27.0 27.0 0

EV 411.6 411.6 0.0 483.7 483.7 0.0 566.3 566.3 0.0

Source: Company, HSIE Research

BUY

CMP (as on 21 Jan 2022) INR 1,241

Target Price INR 1,530

NIFTY 17,617

KEY

CHANGES OLD NEW

Rating BUY BUY

Price Target INR 1,530 INR 1,530

VNB % FY22E FY23E

Nil Nil

KEY STOCK DATA

Bloomberg code SBILIFE IN

No. of Shares (mn) 1,000

MCap (INR bn) / ($ mn) 1,241/16,676

6m avg traded value (INR mn) 2,397

52 Week high / low INR 1,315/838

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) 7.1 22.3 41.3

Relative (%) 10.2 9.2 22.3

SHAREHOLDING PATTERN (%)

Sep-21 Dec-21

Promoters 55.7 55.7

FIs & Local MFs 12.1 12.0

FPIs 24.5 24.5

Public & Others 7.8 7.8

Pledged Shares Nil Nil

Source : BSE

Krishnan ASV

+91-22-6171-7314

Sahej Mittal

+91-22-6171-7325

P a g e | 23

HSIE Results Daily

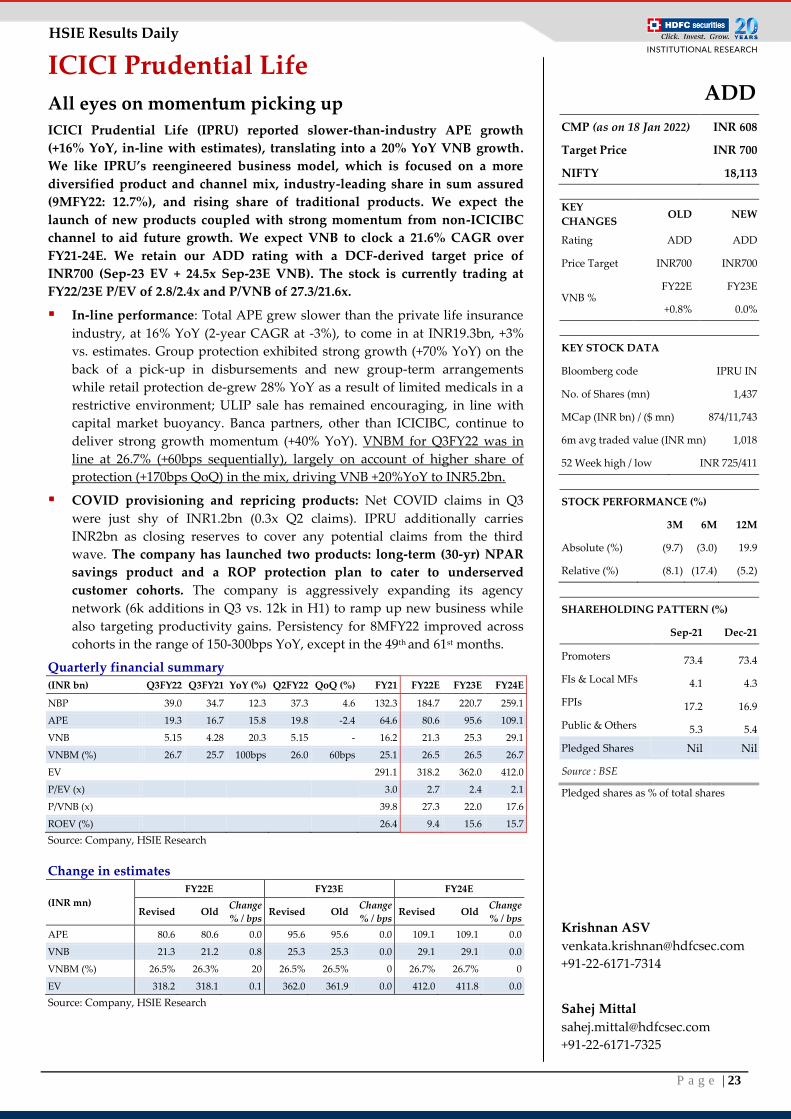

ICICI Prudential Life

All eyes on momentum picking up

ICICI Prudential Life (IPRU) reported slower-than-industry APE growth

(+16% YoY, in-line with estimates), translating into a 20% YoY VNB growth.

We like IPRU’s reengineered business model, which is focused on a more

diversified product and channel mix, industry-leading share in sum assured

(9MFY22: 12.7%), and rising share of traditional products. We expect the

launch of new products coupled with strong momentum from non-ICICIBC

channel to aid future growth. We expect VNB to clock a 21.6% CAGR over

FY21-24E. We retain our ADD rating with a DCF-derived target price of

INR700 (Sep-23 EV + 24.5x Sep-23E VNB). The stock is currently trading at

FY22/23E P/EV of 2.8/2.4x and P/VNB of 27.3/21.6x.

In-line performance: Total APE grew slower than the private life insurance

industry, at 16% YoY (2-year CAGR at -3%), to come in at INR19.3bn, +3%

vs. estimates. Group protection exhibited strong growth (+70% YoY) on the

back of a pick-up in disbursements and new group-term arrangements

while retail protection de-grew 28% YoY as a result of limited medicals in a

restrictive environment; ULIP sale has remained encouraging, in line with

capital market buoyancy. Banca partners, other than ICICIBC, continue to

deliver strong growth momentum (+40% YoY). VNBM for Q3FY22 was in

line at 26.7% (+60bps sequentially), largely on account of higher share of

protection (+170bps QoQ) in the mix, driving VNB +20%YoY to INR5.2bn.

COVID provisioning and repricing products: Net COVID claims in Q3

were just shy of INR1.2bn (0.3x Q2 claims). IPRU additionally carries

INR2bn as closing reserves to cover any potential claims from the third

wave. The company has launched two products: long-term (30-yr) NPAR

savings product and a ROP protection plan to cater to underserved

customer cohorts. The company is aggressively expanding its agency

network (6k additions in Q3 vs. 12k in H1) to ramp up new business while

also targeting productivity gains. Persistency for 8MFY22 improved across

cohorts in the range of 150-300bps YoY, except in the 49th and 61st months.

Quarterly financial summary

(INR bn) Q3FY22 Q3FY21 YoY (%) Q2FY22 QoQ (%) FY21 FY22E FY23E FY24E

NBP 39.0 34.7 12.3 37.3 4.6 132.3 184.7 220.7 259.1

APE 19.3 16.7 15.8 19.8 -2.4 64.6 80.6 95.6 109.1

VNB 5.15 4.28 20.3 5.15 - 16.2 21.3 25.3 29.1

VNBM (%) 26.7 25.7 100bps 26.0 60bps 25.1 26.5 26.5 26.7

EV

291.1 318.2 362.0 412.0

P/EV (x)

3.0 2.7 2.4 2.1

P/VNB (x)

39.8 27.3 22.0 17.6

ROEV (%)

26.4 9.4 15.6 15.7

Source: Company, HSIE Research

Change in estimates

(INR mn)

FY22E FY23E FY24E

Revised Old Change

% / bps Revised Old

Change

% / bps Revised Old

Change

% / bps

APE 80.6 80.6 0.0 95.6 95.6 0.0 109.1 109.1 0.0

VNB 21.3 21.2 0.8 25.3 25.3 0.0 29.1 29.1 0.0