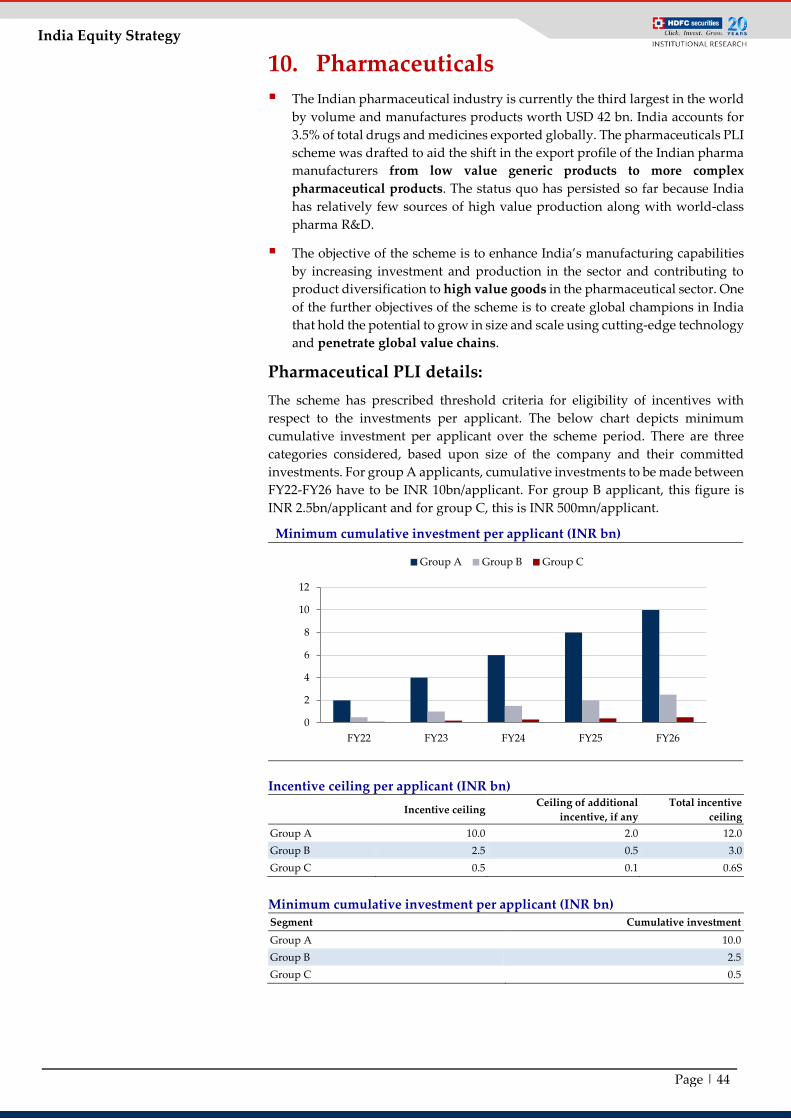

India Equity Strategy - HDFC securities

64

India Equity Strategy PLI: Spearheading India’s manufacturing push

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of India Equity Strategy - HDFC securities

India Equity Strategy

PLI: Spearheading India’s manufacturing push

India Equity Strategy

While India’s nominal GDP increase of ~49% in the last five years is anencouraging development, it is worth highlighting that this growth has come atthe expense of growing reliance on Chinese imports. India’s imports fromChina have grown from USD 61bn in FY17 to USD 93bn in FY22, accounting for16% of overall imports on average over this period. Currently, the key goodsimported from China are mainly electronic goods, mechanical appliances, andchemicals. In the wake of pandemic-led global supply chain disruptions, Indiahas realised the importance of reducing its dependence on China and creating aself-sustaining manufacturing ecosystem. The Production Linked Incentive(PLI) is the government’s flagship fiscal response to the country’s rising importdependence, which aims to boost the country’s manufacturing sector from 15-17% of the total GDP at present to a target of 25%.

Varun [email protected]+91-22-6171-7334

Amit Kumar, [email protected]+91-22-6171-7354

Atishray [email protected]+91-22-6171-7363

13 April 2022 Strategy

India Equity Strategy

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

PLI: Spearheading India’s manufacturing push While India’s nominal GDP increase of ~49% in the last five years is an encouraging development, it is worth highlighting that this growth has come at the expense of growing reliance on Chinese imports. India’s imports from China have grown from USD 61bn in FY17 to USD 93bn in FY22, accounting for 16% of overall imports on average over this period. Currently, the key goods imported from China are mainly electronic goods, mechanical appliances, and chemicals. In the wake of pandemic-led global supply chain disruptions, India has realised the importance of reducing its dependence on China and creating a self-sustaining manufacturing ecosystem. The Production Linked Incentive (PLI) is the government’s flagship fiscal response to the country’s rising import dependence, which aims to boost the country’s manufacturing sector from 15-17% of the total GDP at present to a target of 25%. With a total incentive outlay of ~USD 35 bn during the life of all 15 announced PLI schemes, we estimate total incremental sales to be in the range of USD 470-500 bn, attracting a total investment of ~USD 62 bn and directly generating ~3.1 mn jobs. The schemes cover a multitude of sectors, with each one having reached a different level of manufacturing and technological maturity in India so far. Based on the underlying themes, these 15 PLI schemes can be divided into three categories:

Sunrise sectors: Schemes targeting industries and goods that are in their nascentstages of development or manufacturing; semiconductors, ACC battery,advanced automobiles and drones.

Import substitution: Schemes targeting to strengthen the domesticmanufacturing ecosystem in industries and goods that have prominent domesticdemand, which is primarily being met by imports; telecom & networkingproducts, solar PV modules, pharma APIs, medical devices, IT hardware andspecialty steel.

Export focus: Schemes targeting industries where the government aims to makeIndia a global manufacturing hub and an export leader; large-scale electronicsmanufacturing, white goods, textiles, food processing, pharmaceutical drugs.

Based on our analysis, we expect the large-scale electronics, telecom & networking products, and textile product PLI schemes to outperform due to factors like a presently conducive domestic ecosystem, lucrative economics of the PLI schemes, and ancillary government support. Correspondingly, the semiconductor, IT hardware, medical devices, and drones PLI schemes are expected to be slow starters due to certain supply chain bottlenecks, unfavorable domestic factors, and insufficient R&D expenditure. We believe that continued government dialogue with industry participants will help bring modifications in the schemes to overcome these challenges and ensure the success of these PLI schemes. Explicit supply chain gaps: Based on our analysis, the printed circuit board assembly (PCBA) and key battery raw material such as lithium and cobalt are the key input materials on which the success of six out of 15 schemes hinges upon. PCBA constitutes ~40% of Bill of Material (BoM) of electronic goods, while battery cells account for 25% of the total cost of an electric vehicle. India is grossly dependent on foreign imports of these materials. Securing indigenous manufacturing of these materials will be a key driver in ensuring high domestic value addition and unleashing the full potential of the respective PLI schemes. We estimate that the 15 PLI schemes would scale up from FY23 onwards and contribute total incremental sales of ~USD 157 bn and GDP addition of ~USD 53 bn (1.1% of GDP) in FY27, resulting in a blended manufacturing GVA of ~34%.

PLI: Scheme-wise incentive outlay

PLI Scheme Govt Outlay (INR Bn)

Semiconductor 760

Electronics 386

IT hardware 73

White goods 62

Automobiles 259

ACC Battery 181

Telecom 122

Solar modules 240

Pharma APIs 69

Pharma drugs 150

Medical devices 32

Food products 109

Specialty steel 63

Textile 107

Drones 1

Total 2,616

Varun Lohchab [email protected] +91-22-6171-7334

Amit Kumar, CFA [email protected] +91-22-6171-7354

Atishray Malhan [email protected] +91-22-6171-7363

Page | 2

India Equity Strategy PLI Overall Snapshot

Sr. No

Targeted Industry

Committed Govt

Incentive (INR bn)

Projected Increase

in CAPEX (INR bn)

Incremental sales of

companies over scheme tenure (INR

bn)

Tenure of Scheme

Scheme Status Expected

direct Job creation

1 Semiconductor 760 1,700 5,000* FY23-27 Applications phase 450,000

2 Large Scale Electronics Manufacturing 386 110 10,500 FY21-26 Production started

in H2 FY21 200,000

3 IT Hardware(Laptop/Tab) 73 25 1,600 FY21-26 Production started

in FY22 36,000

4 White Goods (ACs & LED) 62 46 810 FY 21-29 Production started

in FY22 44,000

5 Automobiles & Auto Components 259 425 2,300 FY23-28 Capex phase 750,000 6 Advance Chemistry Cell (ACC) Battery 181 450 920 FY23-29 Capex phase 200,000

7 Telecom & Networking Products 122 33 1,820

FY21-27 Production started

In FY22 40,000

8 High-Efficiency Solar PV Modules 240 910 500 FY22-27 2nd round

application ongoing

160,000

9 (KSMs)/DIs and pharma APIs 69 54 420 FY21-30 Production started

in FY22 12,000

10 Manufacturing of Pharmaceutical Drugs 150 180 1,800 FY21-29 Capex phase 100,000 11 Mfg of Medical Devices 32 10 650 FY21-28 Capex phase 18,000 12 Food Products 109 61 1,200* FY21-27 Capex phase 250,000

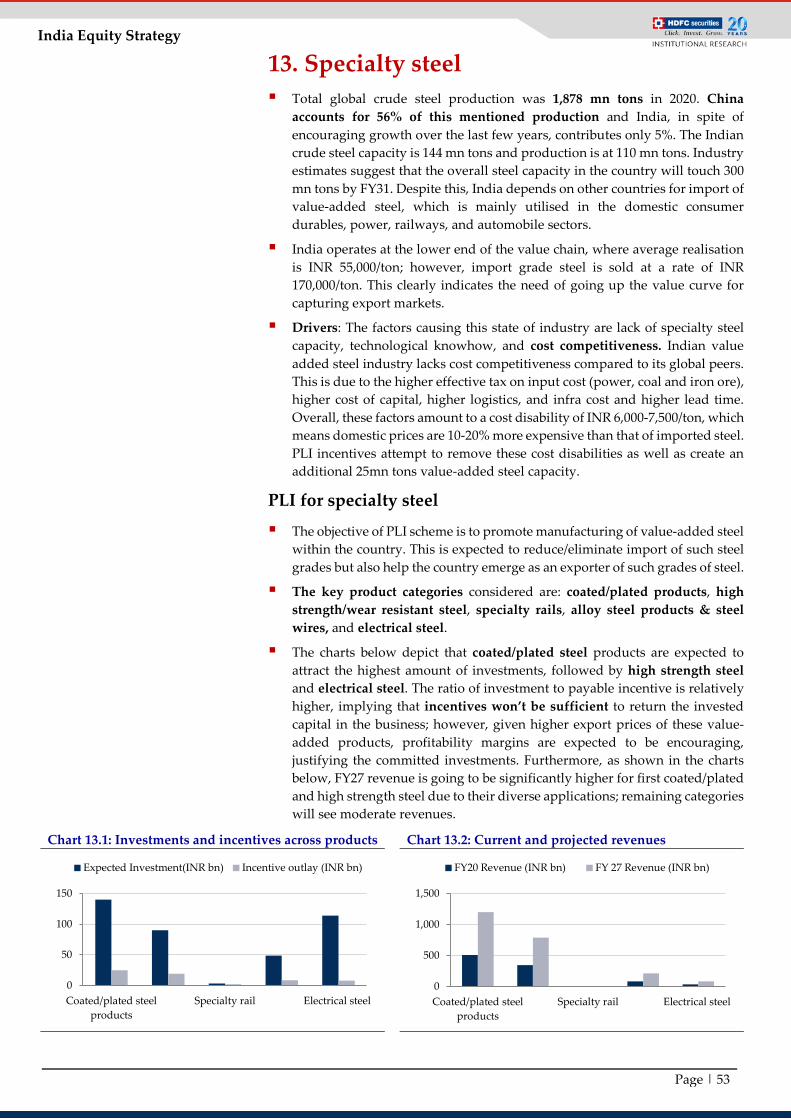

13 Specialty Steel 63 396 5,600* FY23-31 Application phase 68,000

14 Textile Products 107 190 3,000 FY23-30 Approvals

Pending 750,000

15 Drones and Components 1 50 15 FY22-25 Application phase 10,000 Total Sum 2,616 4,641 36,135 3,088,000

*HSIE estimates based on government disclosures The table above reflects the government’s estimated incentive outlay, investment, incremental sales, and direct job creation estimates for all 15 schemes over the tenure of their schemes. Considering a typical production tenure of 5 years, the average annual asset turnover of the PLI schemes is ~2x. The largest government outlay is for the semiconductors PLI scheme, accounting for ~29% of the total incentive outlay, highlighting the need for a massive fiscal push to kick-start India’s semiconductor chip manufacturing. The largest incremental sales are expected to come from the large scale electronics manufacturing scheme (mobile phones), accounting for ~29% of total incremental sales, accenting the government’s push towards achieving USD 126 bn of domestic mobile phone sales and USD 300 bn of electronics goods manufacturing by FY26.

Page | 3

India Equity Strategy PLI: Incentives vs Investments for a participating company

Sr. No

Targeted Industry

Min. Inv amount per

company (INR bn)

Incentive per company based on

estimated sales (INR bn)

Investment recoverable from

incentive (%)

Adequacy level

1 Semiconductor 200 80* 40% Medium

2 Large Scale Electronics

Manufacturing 10 37.2 372% Very high

3 IT Hardware(Laptop/Tab) 5 4.15 83% Medium

4 White Goods (ACs &

LED) 6 4.80 80% Medium

5 Automobiles & Auto

Components 20 20 100% High

6 Advance Chemistry Cell

(ACC) Battery NA( incentive depends upon multiple factor along with production

7 Telecom & Networking

Products 1 2** 200% Very high

8 High-Efficiency Solar PV

Modules NA( incentive depends upon multiple factor along with

production)

9 (KSMs)/DIs and pharma

APIs NA( API specific)

10 Manufacturing of

Pharmaceutical Drugs 10 12 120% High

11 Mfg of Medical Devices 1.8 1.21 67% Medium 12 Food Products 1 1.50 150% High 13 Specialty Steel NA (Depends upon future steel prices) 14 Textile Products 3 2 67% Medium 15 Drones and Components 0.4 12.5 <5% Very Low

*Average amount chosen based on the three incentivized node size. Incentives for semiconductor PLI to be given on total project cost ** The reported minimum and maximum incentive as a % of invested capital is 48% and 348% respectively. Based on the Year 1 on-the-ground performance of the telecom PLI scheme, we estimate on average The table above highlights our estimates regarding the incentives each applicant can earn on average based on the minimum incremental investment required. It is important to note that many schemes have different segments and categories of applicants based on the product and company size; we have chosen to highlight the largest segments by revenue addition to be representatives of their respective schemes. As seen in the table, the incentives relative to investment vary from scheme to scheme. We have found that schemes such as large scale electronics manufacturing and telecom & networking products have garnered immense attention from industry participants because applicants can comfortably recover their entire cost of investment over the tenure of the schemes. Schemes such as IT hardware and medical devices, servicing the domestic industries that are already plagued with cost disabilities in comparison to global peers, have had a much more tepid response because the incentives offered are not lucrative enough to make additional production more feasible.

In the forthcoming sections of this report, we will analyze each PLI scheme and their respective targeted industries, highlighting the individual strengths, opportunities, and challenges that need to be overcome.

Page | 4

India Equity Strategy

Contents Semiconductors ................................................................................................ 5 Large-scale electronics ................................................................................... 10 IT hardware ..................................................................................................... 16 White goods .................................................................................................... 20 Automobile and auto components .............................................................. 24 Advanced chemistry cells (ACC) battery ................................................... 30 Telecom and networking products .............................................................. 35 High efficiency solar PV modules ............................................................... 38 Active pharmaceuticals ingredients (API).................................................. 41 Pharmaceuticals.............................................................................................. 44 Medical devices .............................................................................................. 47 Food processing .............................................................................................. 50 Specialty steel.................................................................................................. 53 Textiles ............................................................................................................. 56 Drones and components ............................................................................... 59

Page | 5

India Equity Strategy 1. Semiconductors Semiconductor chips are the brains behind the smooth functioning of modern day electronic devices such as smart phones, smart TVs, laptops, washing machines, advanced vehicles, etc. They are indispensable in our daily lives, thus making it imperative to understand the global semiconductor ecosystem.

The semiconductor chip industry is a market worth USD 556bn globally. It is growing at an impressive 9% per year rate, driven by consumer electronics, 5G implementations, and automotive innovations. China has grown to be the largest consumer of semiconductor chips in the world, mirroring the growth in its consumer electronics, telecom, and automobile sectors over the last two decades. Chart 1.1 shows the consumption market share trend of various countries over the years; China’s extraordinary growth is evident:

Chart 1.1: Semiconductor consumption share trend across countries

Source: The McLean Report, HSIE Research Having understood the consumption patterns across countries, the next part of the puzzle is to understand the various steps involved in semiconductor manufacturing and the countries that play important roles in the process. Chart 1.2 below explains the key processes involved: research, design, manufacturing, assembly, testing, marking & packaging (ATMP), and distribution.

Chart 1.2: Semiconductor value chain

Source: Semiconductor Industry Association, HSIE Research

19% 20% 25% 29% 35% 40% 43% 42% 47% 53% 56% 57% 59% 61%

0%

20%

40%

60%

80%

100%20

03

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2019

China America Europe Japan Rest of the world

Page | 6

India Equity Strategy

Research & development: This involves pre-production work to improve processing capability and speed at a reduced cost. This step is capital intensive and accounts for ~25% of final sales value.

Design: This step is highly skill intensive and involves design software and electronic design automation (EDA); it decides the design of electronic circuit to be printed on wafers for specific end uses.

Manufacturing/fabrication: This process starts with making polysilicon, which is a purified form of Silicon (99.9999999% pure i.e., 9 Nines). It is melted at 1,500 degree Celsius and p or n type conducting elements are added for imparting electrical properties to form ingots. These ingots are cut into thin slices to form wafers. Photolithography machines are then used for optically printing electronic circuits (as per electronic designs) on to a silicon wafer covered with light sensitive photo resist material. It produces a printed wafer.

Image 1.1: Polysilicon Image 1.2: Silicon Image 1.3: Wafers cut from Ingots

Image 1.4: Printed wafer

Source: OCI Source: Sumco Corporation Source: Sumco Corporation Source: Samsung

Assembly & testing: This is a labour-intensive process. The printed wafer is cut along scribed lines to separate each die, which is later connected electrically to produce final chip. It is tested for performance.

Image 1.5: Die getting separated

Image 1.6: Standalone Chip

Image 1.7: Assembled Chip

Source: TSMC Source: TSMC Source: TSMC

Distribution: Finished semiconductors are sold to OEMs for use in electronic goods etc.

Leading companies: There are two models of manufacturing semiconductors:

Integrated device model: Under this model, design and manufacturing both are carried out by the same company. Leading examples are Intel, Samsung, and Texas Instruments.

Fab-foundry model: This is a more prevalent model, under which design and fabrication are done by separate companies. Design companies outsource manufacturing & assembly works to contract manufacturers. Companies involved in various processes are mentioned below:

Fabless (chip designing) - AMD (USA), Qualcomm (USA)

Page | 7

India Equity Strategy Foundry (contract manufacturing)- TSMC (Taiwan), SMIC (China),

Samsung (S Korea)

Assembly, test, packaging - Amkor (S Korea), SPIL (Taiwan)

Contribution of various countries in global value chain Chart 1.3 reflects the percentage of global sales done by various countries across the semiconductor value chain:

Chart 1.3: % of Global sales by various countries

Source: McKinsey, HSIE Research

Key findings from the above chart can be summarised as below:

Equipment and chip designing domains are dominated by the US. Taiwan has the lion’s share in foundry as well as assembly & testing, making it a country of strategic significance.

In spite of being the largest consumer of semiconductors (~60%), China has a miniscule share in the overall value chain of production. It only has minor shares in fabless, foundry and assembly. In most of the value chain segments, China is dependent on imports from other countries, which pushes its trade deficit higher and makes it vulnerable to supply chain fluctuations.

It is evident that the value chain is heavily concentrated in favour of a few countries; the U.S. controls design and Taiwan controls foundry and assembly of chips. Furthermore, the key equipment lithography machine is 67% controlled by ASML (Netherlands), other suppliers being Kodak (Japan) and Nikon (Japan) and Ultratech (US). Furthermore, all these suppliers make Deep Ultraviolet lithography (DUV) machine, which can take 193 nm wavelengths of lasers for printing of electronic circuits. ASML is the only company in the world that makes EUV or extreme ultraviolet lithography machine, which uses 13 nm wavelength of laser to improve chip density by 3x. This means three times more circuits can be printed in the same-sized wafer, thereby improving processing capacity and enabling reduction in size and cost of electronic devices that use these chips. An EUV costs approximately USD 150 mn. ASML enjoys dominance in the semiconductor world due to its exclusivity vis-à-vis EUV lithography machine production. The biggest foundry in the world which belongs to Taiwan semiconductor manufacturing company (TSMC), also depends on ASML for supply of these machines. Hence, it won’t be an exaggeration to say that the semiconductor value chain revolves around ASML.

4528

63 58 4711 11

120

1 182 71

4920

3014

19 4

10

31 1

1

16

1

11

1534 40

65

17 440

425

0%20%40%60%80%

100%

Equi

pmen

t

Mat

eria

ls (N

onw

afer

s) Waf

er

Elec

tron

icde

sign

auto

mat

ion

Fabl

ess

Inte

grat

edde

vice

Mfg

Foun

dary

Ass

embl

y &

test

ing

USA Taiwan Europe China Others

Page | 8

India Equity Strategy Due to heavy concentration in this value chain, countries with specific

product abilities can exert dominance on other competing countries by denying them to use their products or facilities. Interestingly, the Dutch company ASML denied selling EUV machines to China in 2019 and this policy has been continued till date. Reportedly, the US administration lobbied with the Dutch government to make them decline requests of China amidst the ongoing trade war. Hence, this advanced micro-processing capability remained inaccessible to China and it became dependent on other countries for buying chips. This can partially explain China’s recent increased interest over Taiwan. Its import of semiconductor has grown at 23% to reach USD 350 bn approximately in 2020; China spends more on semiconductor chip imports than it does on importing oil. China’s crude oil trade deficit was USD 185bn in 2020 while it was USD 233Bn for semiconductor chips in the same year. Building its own EUV lithography machine will be an uphill battle for China as it would take roughly 10 years along with support of US based machine component suppliers, coupled with billions of dollars.

Therefore, it can be summarised that semiconductor foundries, equipments and materials have the potential to be used as tools of geopolitical dominance.

Indian context

Annual consumption of semiconductors was $15bn in 2020, most of which was made available through imports.

Most of the major semiconductor companies (TI, Broadcom, Intel, Qualcomm, Samsung, and Huawei) have their fabless IP & chip design houses in India, employing 30,000 Indian engineers for designing 3,000 chips.

India has a cost advantage vis-à-vis western countries due to lower salaries of design staff; however, higher power and capital costs remain impediments to development of the ecosystem.

Vibrant IC design ecosystem: global design houses based in India added value worth USD 33bn in 2020.

India has a limited presence in assembly & test, where the leading companies are SPEL, ChipTest, and Tessolve.

Raw material and other enablers required are large quantities of pure water, uninterrupted power, ultra pure sand with high silicon content and a pollution-free environment. Even an impurity of micro meter diameter can disrupt the circuit. Purity at nano meter scale is expected.

The supply of high precision lithography machine; heavy Capex requirement (>USD 10 bn), steep expensive learning curve with technology access and risk of low capacity utilisation remain key factors to success.

Page | 9

India Equity Strategy Semiconductors - PLI scheme highlights

Silicon semiconductor fab: Minimum investment required is INR 200 bn; capital support offered by scheme is 30-50% of the project cost, as per the node size of the fab.

Display fab: Minimum investment required is INR 100bn; capital support offered by the scheme is up to 50% of the project cost (maximum allowed per beneficiary: INR 120bn).

Compound semi-conductors/silicon photonics/sensors fab: Minimum investment required is INR 1 bn and capital support offered is 30% of the Capex amount.

Semiconductor assembly, testing, marketing, and packaging: Minimum investment required is INR 500 mn and capital support offered is 30% of the Capex amount.

Additionally, semiconductor design for integrated circuits:

Design-linked incentive: Reimbursement of 50% of expenditure to a ceiling of INR 150 mn/applicant.

Deployment-linked incentive: Incentive of 4-6% of net sales over five years, up to INR 300 mn/applicant.

Scheme envisages selecting two candidates each for semiconductor fabs and displaying fabs.

Current applicants

Semiconductor fabs (two to be approved): Vedanta in JV with Foxconn, IGSS Ventures, Singapore, ISMC Analog (with Tower semiconductor Israel) (investments - USD13.6bn; government support sought - USD 5.6bn).

Display fabs (two to be approved): Vedanta & Elest (investments - USD 6.7bn; government support sought - USD 2.7 bn).

Our opinion: Although this PLI scheme has the right intentions, its success will depend not only on government support but also on technological prowess of manufacturing companies, heavy Capex, availability of large chip fabrication orders to ascertain high capacity utilisation and ensure low cost per chip, availability of EUV lithography machine, pure raw material, pollution-free environment and uninterrupted power supply. In the absence of any such experienced company and environment enablers, the visibility of success of scheme is currently low. We need to track its progress and ground level execution periodically.

Page | 10

India Equity Strategy 2. Large-scale electronics

Manufacturing background of mobile phones:

Domestic mobile phone manufacturing has come a long way; India manufactured mobile phones worth USD 30 bn in FY21, a ten-fold increase from FY15 production value of USD 3bn. At the start of 2014, India boasted only three mobile phone manufacturing units - Nokia’s Chennai factory, Samsung’s Noida factory, and LG’s Pune factory. After the Nokia factory shut down due to tax disputes, the country was left with only two mobile phone manufacturing sites. Fast forward to 2019, and the company had a total of 268 mobile phone manufacturing units. From having a trade deficit of ~USD 8 bn in FY15, India became a net mobile phone exporter in FY20 (Chart 2.1), mainly due to a massive domestic manufacturing push by the government.

Recognising the importance of the electronic manufacturing sector, India created a favorable environment, adopting several crucial policies over the past 7-8 years. India designed National Policy on Electronics, 2012, to create a globally competitive Electronics System Design and Manufacturing (ESDM) industry, serving both the budding domestic demand and a possible export opportunity. Manufacturing mobiles domestically was further made attractive by the central government’s flagship programme ‘Make in India’ in 2014. The government supplemented ‘Make in India’ with the Digital India Programme in 2015. Several initiatives launched under the programme helped boost the domestic demand for mobile phones and facilitated the expansion of domestic mobile phone manufacturing.

The real game changer for the industry came in the FY16 Union Budget in the form of the Phased Manufacturing Programme (PMP), which was designed to encourage domestic production of mobile handsets through offering a differential excise duty for domestic mobile manufacturers. A countervailing duty (CVT) on imports at 12.5% and excise duty at 1% without input tax credit (or 12.5% with input tax credit) were implemented. The government first announced a duty of 10% on mobile phones in July 2017, which was subsequently raised to 15% in December 2017. The Union Budget of 2018-19 further raised the customs duties on mobile phones from 15% to 20% to encourage domestic manufacturing of mobile phones. All the aforementioned reasons led to a massive influx of foreign manufacturers, especially Chinese firms, into India.

Starting with OPPO in August 2015, companies such as Xiaomi, HTC, Asus, Motorola, and Gionee followed suit shortly after and set up their own manufacturing units in India. Simultaneously, the demand for mobile phones in the country picked up rapidly. Increasing digital adoption and globalisation, a rising Indian middle class, and enhancement of smartphone importance in day-to-day life kick-started the domestic mobile phone market. The key catalyst came in 2016 with the launch of Jio, ushering India into the world of dirt-cheap data prices, making it much easier for the masses to afford and use mobile phones. The resultant effect of these factors was the doubling of domestic mobile phone consumption from ~USD 14 bn in FY16 to ~USD 28 bn in FY21. Growth in mobile phone production can be seen below in chart 2.2.

Page | 11

India Equity Strategy

Chart 2.1: Mobile Phone Balance of Trade (USD Bn) Chart 2.2: Mobile Phone Production in India (Mn)

Source: MEITY, HSIE Research Source: MEITY, HSIE Research

Mobile phones have a huge part to play in the government’s aim to reach a total electronics manufacturing value of USD 300 billion in FY26 from USD 74 bn in FY21 (table 2.1). As of 2021, the estimated global mobile phone market size was USD 540 bn, with India accounting for a mere 6-7% of it. The government holds an ambition of achieving total mobile phone production value of USD 126 bn by FY26. PLI for large scale electronics is an impetus to industry in order to achieve this goal. It would mean that India’s market share in the mobile phone world market, which is estimated to reach USD 650 bn by 2026, would be in the range of 19-20%. India currently exports ~10% of the USD 30 billion worth of mobile phones manufactured. The government anticipates the share of exports to increase massively to 60% by FY26 as a result of incremental production from the PLI scheme.

Table 2.1: Roadmap to USD 300 bn electronics manufacturing Product segment FY21 FY26(E) IT hardware (laptops, tablets) 3 25 Mobile Phones 30 126 Consumer electronics (TV and audio) 9.5 23 Strategic electronics 4 12 Industrial electronics 10.5 25 Wearables and hearables - 8 PCBA 0.5 12 Auto electronics 6 23 LED lighting 2.2 16 Telecom equipment - 12 Electronic components 9 18 Total 74.7 300 Source: ICEA, HSIE Research

-7.7

-5.8

-3.6 -3.3

0.0

2.8

0.9

2.7

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22*

58

110

175

225

290330

300321

2014 2015 2016 2017 2018 2019 2020 2021

Page | 12

India Equity Strategy Large-scale electronics PLI details: The eligibility criteria for first round of PLI for large-scale electronics are given below:

Segment Proposed incentive rate (%)

Incremental investment over base year

Incremental sales of manufactured goods over base year

Mobile (Invoice value>INR 15000)

Year 1: 6% Year 2: 6% Year 3: 5% Year 4: 5% Year 5: 4%

INR 10 bn over 4 years Year 1: 2.5 Year 2: 5.0 Year 3: 7.5 Year 4: 10.0

Year 1: INR 40 bn Year 2: INR 80 bn Year 3: INR 150 bn Year 4: INR 200 bn Year 5: INR 250 bn

Mobile-domestic INR 2 bn over 4 years Year 1: 0.5 Year 2: 1.0 Year 3: 1.5 Year 4: 2.0

Year 1: INR 5 bn Year 2: INR 10 bn Year 3: INR 20 bn Year 4: INR 35 bn Year 5: INR 50 bn

Specified electronic components

INR 1 bn over 4 years Year 1: 0.25 Year 2: 0.5 Year 3: 0.75 Year 4: 1.0

Year 1: INR 1 bn Year 2: INR 2 bn Year 3: INR 3 bn Year 4: INR 4.5 bn Year 5: INR 6 bn

With success in the first round, a second round was rolled out. The eligibility criteria for the second round of PLI are:

Segment Proposed incentive rate

Incremental investment over base year

Incremental sales of manufactured goods over base year

Specified electronic components

Year 1:5% Year 2: 4% Year 3: 4% Year 4: 3%

INR 250 mn over 4 years Cumulative minimum at the end of Year 1: INR 50 mn Year 2: INR 110 mn Year 3: INR 180 mn Year 4: INR 250 mn

Year 1: INR 150 mn Year 2: INR 350 mn Year 3: INR 600 mn Year 4: INR 1 bn

Specified electronic components considered are: transistors, diodes, resistors, capacitors, PCB, PCB printing inks, sensors, transducers, actuators, assembly, testing, packaging, etc.

The incentives ranges from 3-6% of sales, based on the year of production, provided companies fulfill the incremental investment and revenue over base year requirements. A total of 16 companies have been approved for the large-scale electronics PLI:

Mobile phones (invoice value of INR 15,000 and above): Foxconn, Samsung, Pegatron, Rising Star, and Wistron.

Mobile phones (domestic companies): Lava, Micromax, Optiemus, Padget (Dixon), United Telelinks Neolyncs.

Specified electronic components: AT&S, Neolync, Sahasra Electronics, Ascent Circuits, Silicon Power.

The scheme is designed in a way to attract manufacturers by comfortably covering their total cost of investment and, in most cases, providing incentives worth more than the project cost itself. The following table shows the annual incentive that can be earned by manufacturers under the ‘mobile phones (invoice value of INR 15,000 and above)’ category, if they achieve the minimum incremental sales figures over a minimum committed investment of INR 10 bn:

Page | 13

India Equity Strategy

Year of Production Minimum Incremental Sales (INR bn) Incentive Rate (%) Annual Incentive (INR

bn) FY22 40 6 2.4 FY23 80 6 4.8 FY24 150 5 7.5 FY25 200 5 10.0 FY26 250 4 10.0 Total 34.7

As seen in the table above, a total incentive of INR 34.7 bn can be earned on a cumulative investment of INR 10 bn over the tenure of the scheme. It becomes evident as to why the scheme is a lucrative one for manufacturers. It is imperative to note that the incentive per company is capped in each category by an annual ceiling. For example, since there are five approved applicants in the ‘mobile phones (invoice value of INR 15,000 and above)’ segment, the year-wise incentive ceiling is capped at 1/5th of the annual outlay for the segment.

The FY22 production from the PLI schemes has been encouraging. Based on the production trajectory, total domestic production under the scheme is expected to overshoot government estimates of USD 6 bn. Samsung, Wistron, and Pegatron alone are expected to account for USD 5 bn of production under the scheme in FY22, with Foxconn and Bharat FIH (Rising Star) expected to start production in Q1FY23.

The PLI scheme, coupled with other incentives, aims to offset India’s overall cost disadvantage when compared to its global competitors; India had an estimated 7.5-9.8% cost disability differential compared to Vietnam and ~17.3-19% compared to China in 2018. The disability gap has certainly narrowed since then as China faces its own issues in areas such as power. India as well has seen marginal cost improvements.

According to the ICEA estimates, if USD 100 is the cost of producing a phone without subsidies, after adding all the incentives and subsidies provided by each respective country, China can manufacture it for ~USD80 while Vietnam can manufacture it for ~USD89. The PLI helps bridge some of the cost discrepancy and after factoring in the PLI and other incentives, the average cost of manufacturing in India comes to ~USD92.

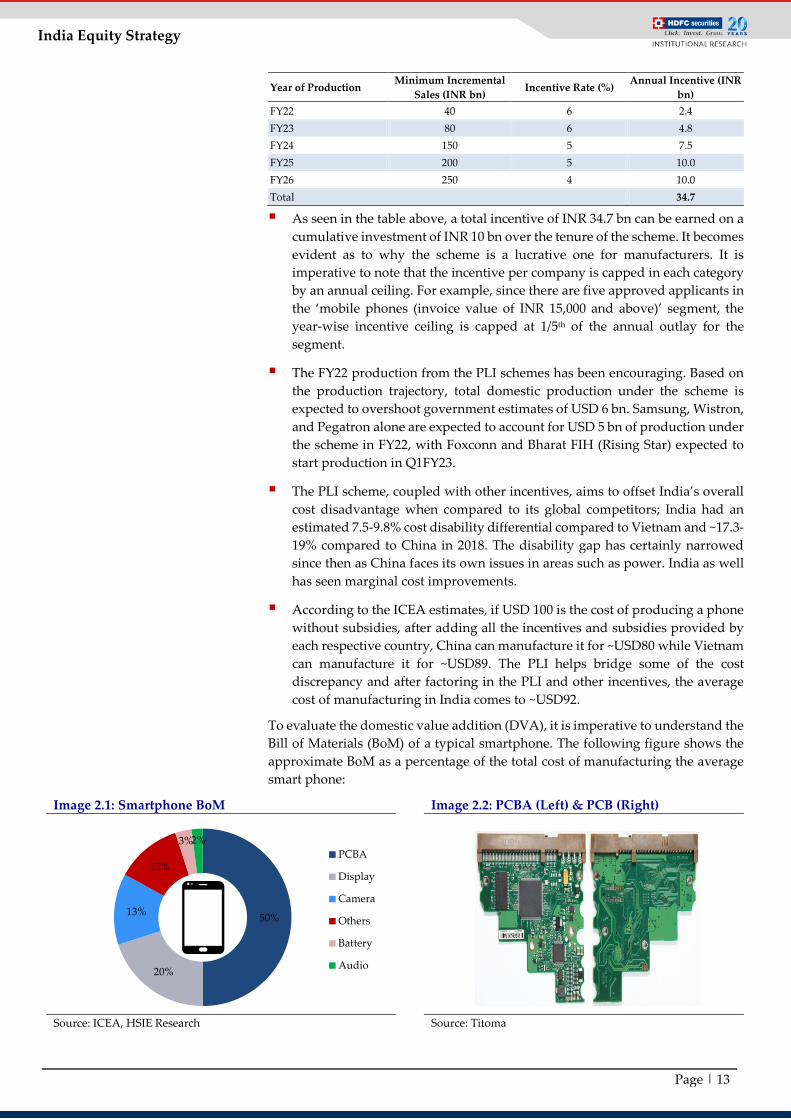

To evaluate the domestic value addition (DVA), it is imperative to understand the Bill of Materials (BoM) of a typical smartphone. The following figure shows the approximate BoM as a percentage of the total cost of manufacturing the average smart phone:

Image 2.1: Smartphone BoM Image 2.2: PCBA (Left) & PCB (Right)

Source: ICEA, HSIE Research Source: Titoma

50%

20%

13%

12%

3%2%PCBA

Display

Camera

Others

Battery

Audio

Page | 14

India Equity Strategy

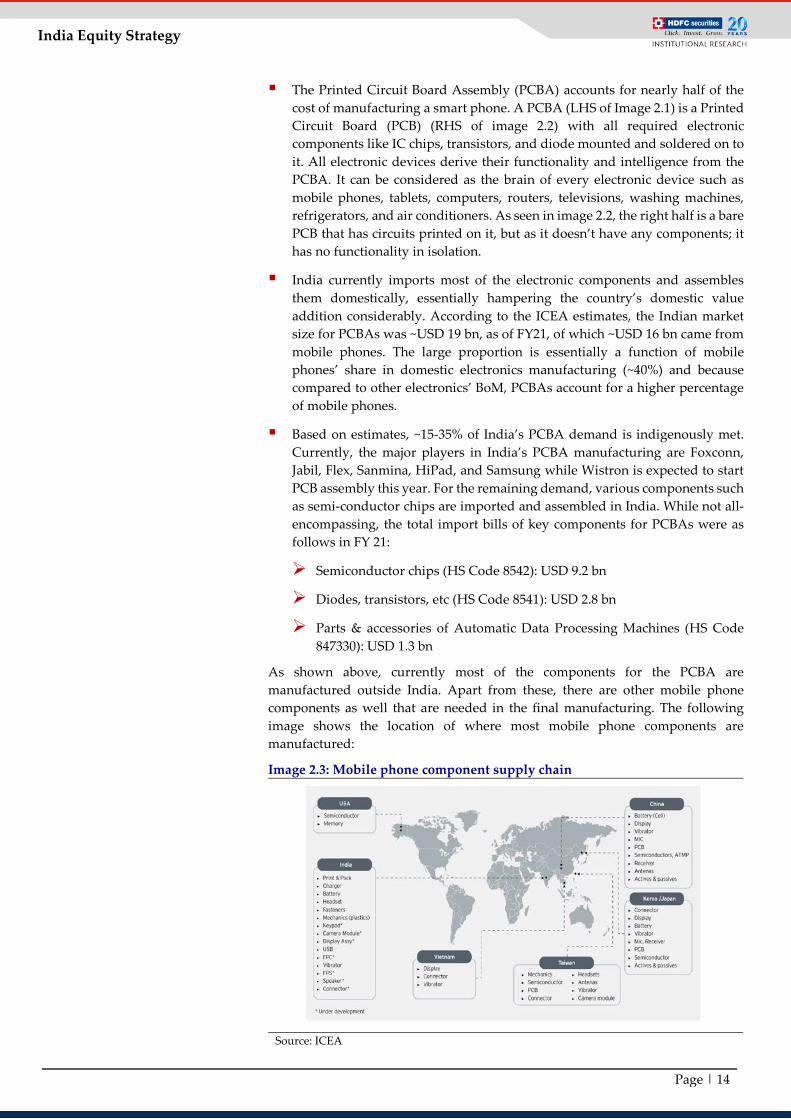

The Printed Circuit Board Assembly (PCBA) accounts for nearly half of the cost of manufacturing a smart phone. A PCBA (LHS of Image 2.1) is a Printed Circuit Board (PCB) (RHS of image 2.2) with all required electronic components like IC chips, transistors, and diode mounted and soldered on to it. All electronic devices derive their functionality and intelligence from the PCBA. It can be considered as the brain of every electronic device such as mobile phones, tablets, computers, routers, televisions, washing machines, refrigerators, and air conditioners. As seen in image 2.2, the right half is a bare PCB that has circuits printed on it, but as it doesn’t have any components; it has no functionality in isolation.

India currently imports most of the electronic components and assembles them domestically, essentially hampering the country’s domestic value addition considerably. According to the ICEA estimates, the Indian market size for PCBAs was ~USD 19 bn, as of FY21, of which ~USD 16 bn came from mobile phones. The large proportion is essentially a function of mobile phones’ share in domestic electronics manufacturing (~40%) and because compared to other electronics’ BoM, PCBAs account for a higher percentage of mobile phones.

Based on estimates, ~15-35% of India’s PCBA demand is indigenously met. Currently, the major players in India’s PCBA manufacturing are Foxconn, Jabil, Flex, Sanmina, HiPad, and Samsung while Wistron is expected to start PCB assembly this year. For the remaining demand, various components such as semi-conductor chips are imported and assembled in India. While not all-encompassing, the total import bills of key components for PCBAs were as follows in FY 21:

Semiconductor chips (HS Code 8542): USD 9.2 bn

Diodes, transistors, etc (HS Code 8541): USD 2.8 bn

Parts & accessories of Automatic Data Processing Machines (HS Code 847330): USD 1.3 bn

As shown above, currently most of the components for the PCBA are manufactured outside India. Apart from these, there are other mobile phone components as well that are needed in the final manufacturing. The following image shows the location of where most mobile phone components are manufactured:

Image 2.3: Mobile phone component supply chain

Source: ICEA

Page | 15

India Equity Strategy

As seen in the map above, India currently manufactures the battery pack, phone vibrator, and key plastics needed to make mobile phones. Based on the BoM breakdown provided earlier, an optimistic figure for the percentage of total manufacturing cost from domestic manufacturing would be in the range of 10-15%. Assuming a 5% operating profit margin, which is the industry average, the Domestic Value Addition (DVA) comes up to be 14-19%, broadly in line with the government’s current DVA calculation of 15-20%. Other critical components besides the PCBA, namely the display and the camera, are imported from Vietnam, China, Taiwan, Korea, and Japan.

The government has estimated that the domestic value addition of mobile phone manufacturing can increase from the current 15-20% to 35-40%. For reference, China currently has a DVA of 25-40% across different product categories in electronics manufacturing despite its immense size of USD 1 trillion worth electronic products. One of the key reasons for China’s success is that the localisation of components used is ~70%.

The Indian government’s DVA figure seems to be optimistic, given India's dependence on imports for key mobile components such as semi-conductor chips. While the semi-conductor PLI aims to curb this dependence and the electronics PLI has a small outlay dedicated to specific mobile phone components, the proposed cumulative production is not enough to compensate for the import dependency.

While the electronics manufacturing PLI is a step in the right direction for India, to truly extract the maximum value addition from the budding mobile phone manufacturing ecosystem in India, it is imperative to invest more in the ‘n-1’ electronic components. Even a partial success in production of semiconductor, diode, transistor, or PCB will pave the way for significantly improving DVA for mobile manufacturers.

Our opinion: The PLI scheme further strengthens the government’s ambitious plan of making the mobile phone segment contribute significantly and attaining electronics manufacturing worth USD 300 bn by FY26. However, the government’s estimated DVA expansion of mobile phone manufacturing from the current 15-20% to 35-40% seems optimistic. In order to achieve DVA ambitions, the industry needs to invest more in production of electronic components, viz. semiconductor chips, diodes, and PCB. Nevertheless, we expect the manufacturing of finished mobile phones to do very well on the back of a budding and rapidly growing domestic manufacturing ecosystem, and even possibly outperform the government’s expectations.

Page | 16

India Equity Strategy 3. IT hardware

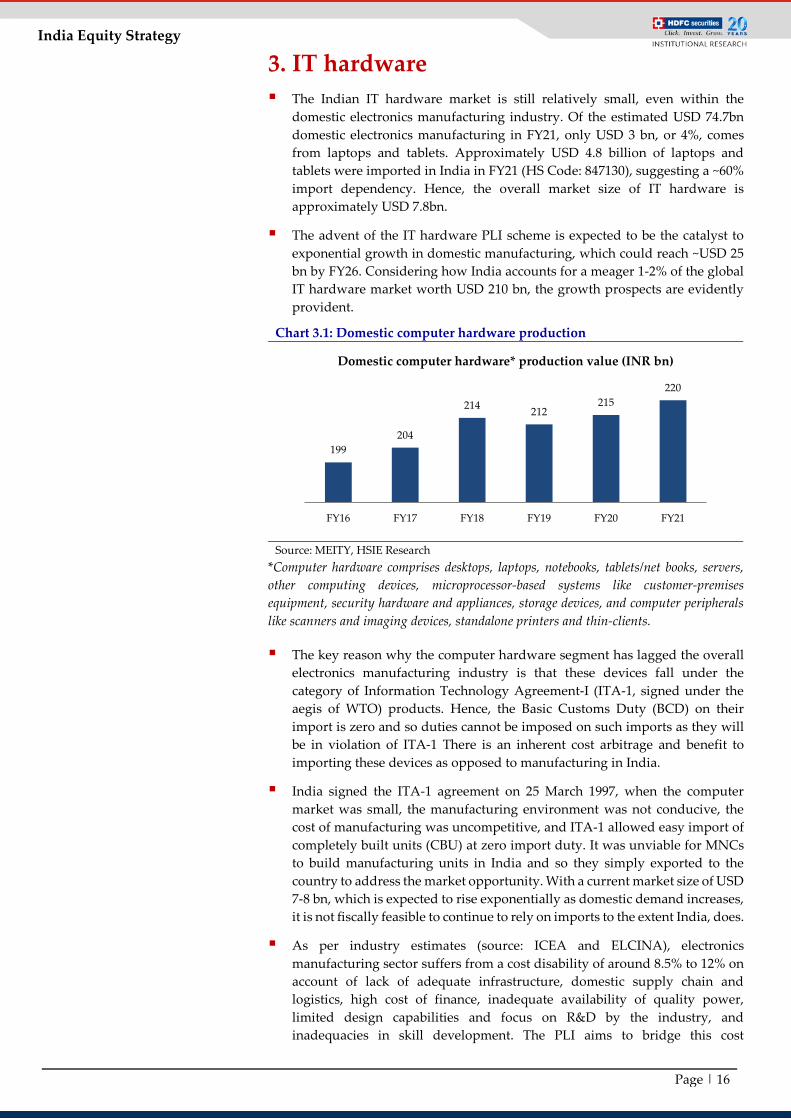

The Indian IT hardware market is still relatively small, even within the domestic electronics manufacturing industry. Of the estimated USD 74.7bn domestic electronics manufacturing in FY21, only USD 3 bn, or 4%, comes from laptops and tablets. Approximately USD 4.8 billion of laptops and tablets were imported in India in FY21 (HS Code: 847130), suggesting a ~60% import dependency. Hence, the overall market size of IT hardware is approximately USD 7.8bn.

The advent of the IT hardware PLI scheme is expected to be the catalyst to exponential growth in domestic manufacturing, which could reach ~USD 25 bn by FY26. Considering how India accounts for a meager 1-2% of the global IT hardware market worth USD 210 bn, the growth prospects are evidently provident.

Chart 3.1: Domestic computer hardware production

Source: MEITY, HSIE Research

*Computer hardware comprises desktops, laptops, notebooks, tablets/net books, servers, other computing devices, microprocessor-based systems like customer-premises equipment, security hardware and appliances, storage devices, and computer peripherals like scanners and imaging devices, standalone printers and thin-clients.

The key reason why the computer hardware segment has lagged the overall electronics manufacturing industry is that these devices fall under the category of Information Technology Agreement-I (ITA-1, signed under the aegis of WTO) products. Hence, the Basic Customs Duty (BCD) on their import is zero and so duties cannot be imposed on such imports as they will be in violation of ITA-1 There is an inherent cost arbitrage and benefit to importing these devices as opposed to manufacturing in India.

India signed the ITA-1 agreement on 25 March 1997, when the computer market was small, the manufacturing environment was not conducive, the cost of manufacturing was uncompetitive, and ITA-1 allowed easy import of completely built units (CBU) at zero import duty. It was unviable for MNCs to build manufacturing units in India and so they simply exported to the country to address the market opportunity. With a current market size of USD 7-8 bn, which is expected to rise exponentially as domestic demand increases, it is not fiscally feasible to continue to rely on imports to the extent India, does.

As per industry estimates (source: ICEA and ELCINA), electronics manufacturing sector suffers from a cost disability of around 8.5% to 12% on account of lack of adequate infrastructure, domestic supply chain and logistics, high cost of finance, inadequate availability of quality power, limited design capabilities and focus on R&D by the industry, and inadequacies in skill development. The PLI aims to bridge this cost

199204

214 212215

220

FY16 FY17 FY18 FY19 FY20 FY21

Domestic computer hardware* production value (INR bn)

Page | 17

India Equity Strategy discrepancy and make it economically viable to manufacture tablets and laptops in India.

To determine the factors that hinder the creation of a sizable and sustainable manufacturing ecosystem in India, it is imperative to analyse the disabilities faced by Indian manufacturers compared to those in China and Vietnam. The following table shows the breakdown of factors that lead to the aforementioned cost disability. It is evident that, as Vietnam and China support their products so aggressively, India also needs to support its producers with fiscal incentives. The PLI attempts to address this requirement.

Factors resulting in cost reduction India Vietnam China Corporate income tax exemption/reductions 0.73% - 0.95% 1.5% - 2% 2% Subsidy for machinery and equipment Nil 0.2% 3% State subsidies in India for capital investments 0.6% - 1.2% NA NA Cost of power 0% 1% 1% Interest subvention on working capital 0% 1.5% - 2% 3% - 3.5% R&D Subsidy 0.15% 0.4% - 1% 2% Incentive for supporting industry 0% 0.5% - 1% 0% Manufacturing incentives - 0% 1% - 2% Exemption/reduction of land rental 0% 0.5% 0.6% Industrial land development support 0.4% 0.5% 0.6% Building (or plug and play) Negligible 0.3% 1% Labor subsidy Negligible 0.5% 2% Logistics 0% 0.5% 1% Factors assisting ‘Ease of Doing Business’ - 1.5% - 2.5% 2% - 3% Duty-free imports for creating fixed assets, and of inputs not available domestically

0% 0.5% -

Total 1.88% - 2.7% 9.4% - 12.5% 19.2% - 21.7% Cost disability differential for India vs others - 7.5% - 9.8% 17.3% - 19% Source: ICEA, HSIE Research

PLI scheme details The below table reflects sales and investments-related eligibility criteria for applicants, after achieving which, they will be considered for incentives. Overall, the government outlay is INR 73.25bn.

Eligibility threshold criteria (INR bn)

Segment Proposed incentive rate Incremental Investment over Base Year (FY21)

Incremental sales of Manufactured Goods over Base

Year (FY21) IT Hardware Companies 1. Laptops (Invoice value

of INR 30,000 & above) 2. Tablets (Invoice value

of INR 15,000 & above) 3. All-in-one PCs 4. Servers

Year 1: 4% Year 2:3% Year 3: 2%

Year 4: 2%/1%

INR 5 bn over 4 years with a cumulative minimum of:

Year 1: INR 0.5 bn Year 2: INR 1.5 bn Year 3: INR 3.0 bn Year 4: INR 5.0 bn

Year 1: INR 10 bn Year 2: INR 25 bn Year 3: INR 50 bn

Year 4: INR 100 bn

Domestic Companies 1. Laptops 2. Tablets 3. All-in-one PCs 4. Servers

INR 200 mn over 4 years with a cumulative minimum of:

Year 1: INR 40 mn Year 2: INR 80 mn Year 3: INR 140 mn Year 4: INR 200 mn

Year 1: INR 0.5 bn Year 2: INR 1.0 bn Year 3: INR 2.0 bn Year 4: INR 3.0 bn

Page | 18

India Equity Strategy

Expected government incentive outlay Annual ceiling on net incremental sales Financial year Total incentive (INR bn)

FY22 7.20

FY23 13.05

FY24 18.20

FY25 34.80

Total 73.25

Financial year IT Hardware

companies (INR bn)

Domestic companies (INR

bn) FY22 30.0 3.0

FY23 75.0 6.0

FY24 150.0 16.0

FY25 300.0 24.0

Total 555.0 49.0

The incentives range from 1-4%, based on the year of production, provided companies fulfill the incremental investment and revenue over base year requirements. The companies that have been selected under the scheme are as follows:

IT hardware companies: Dell, ICT (Wistron), Flextronics, and Rising Stars Hi-Tech (Foxconn).

Domestic companies: Lava International Ltd, Dixon Technologies (India) Ltd, Infopower Technologies (JV of Sahasra and MiTAC), Bhagwati (Micromax) Neolync, Optiemus, Netweb, Smile Electronics, VVDN, and Panache Digilife.

Of the total estimated production of INR 1.6 trillion over the scheme period, the approved companies under IT Hardware category have proposed a production of INR 847bn. Also, the approved companies under the Domestic Companies category have proposed a production of INR 760bn. The IT Hardware PLI is expected to add total incremental sales of ~USD 21 bn from FY22 to FY25, and aid India’s IT hardware market to grow to an estimated size of ~USD 25 bn by FY26.

The following table shows the annual incentive that can be earned by manufacturers under the ‘IT Hardware Companies’ category, if they achieve the minimum incremental sales figures over a minimum committed investment of INR 5 bn:

Year of production Minimum incremental sales (INR bn) Incentive rate (%) Annual incentive

(INR bn) FY22 10 4 0.4 FY23 25 3 0.75 FY24 50 2 1.0 FY25 100 1 / 2 1.0 / 2.0 Total 3.15 / 4.15

As seen in the above table, the incentives earned over minimum incremental sales and the minimum cumulative investment does not cover the total project cost. For earning higher incentives, companies need to achieve higher sales amounts, which will help them recover their entire initial investments. Further, earlier, when the government had announced the scheme, estimated production of up to INR 3.26 trillion was assumed to be plausible, but, later, seeing the industry’s muted response, production target was reduced to INR 1.6 trillion.

IT hardware manufacturers blamed this on the low incentive structure which works out to an average of 2-2.5% over a four-year period, figures that do not justify the relocation of units from China or Vietnam, especially for hardware products where import duties are nil. Industry executives believe that the ideal incentive structure for IT hardware should be roughly 7% - 8%. As is the issue with the PLI scheme for mobile phones, the PCB bottleneck is one that is standing in the way of maximising value unlocking. PCBAs account for

Page | 19

India Equity Strategy ~40% of the total bill of materials (BoM) for tablets and laptops, and the individual components are primarily being imported into the country.

For stepping up efforts to manufacture these components domestically and hence improving domestic value addition in final electronic products, the government has been diligently strategising. It launched Scheme for Promotion of Manufacturing of Electronic Components & Semiconductors (SPECS) in 2020.

The scheme provides financial incentive of 25% on capital expenditure for the identified list of electronic goods that comprise downstream value chain of electronic products, i.e., electronic components, semiconductor/display fabrication units, ATMP units, specialised sub-assemblies and capital goods for manufacture of aforesaid goods, all of which involve high value-added manufacturing.

As of Jan 2022, the government has approved proposals of 20 companies under SPECS, with an estimated investment of INR 200bn. While this is definitely a step in the right direction, the government will need to expand the range and size of incentives it provides to intermediary electronic component manufacturers in order to achieve its DVA ambitions of 25-30%, from the current 10-15% in IT hardware manufacturing.

Our opinion: The government will need to expand the range and size of the incentives it provides to intermediary electronic component manufacturers in order to achieve its DVA ambitions of 25-30%, from the current 10-15% in IT hardware manufacturing. The incentive rates provided in the PLI scheme should also be increased to make India more cost competitive (compared to peers). The scheme has been under-subscribed for this very reason, as industry executives feel that the ideal incentive structure for IT hardware should be in the range of 7-8%. Based on the current scheme structure, we expect the IT hardware scheme to face difficulties in meeting the government’s expectations.

Page | 20

India Equity Strategy 4. White goods

The Indian AC industry was sized at ~USD 2.7 bn in FY20. With an estimated import value of USD 1.2 bn, India’s import dependency was pegged at nearly 50%. The white goods PLI aims to address this discrepancy and make India a net exporter of AC and AC components. It highlights the government’s plan to reduce imports completely, 70% of which come from China and Thailand.

The white goods PLI targets key AC components that are used to manufacture ACs, when combined together. Currently, a total value of USD 1.8 bn worth of key AC components (HS Code 8414), including compressors and vacuum pumps, are imported in India, hampering the domestic value add potential.

The PLI aims to address these shortcomings, as they come under the targeted goods in the ‘high value AC intermediates’ and ‘low value AC intermediate’ segments. With a total government outlay of INR 63.4bn, the government intends to add a total incremental production value of AC components of USD 11 bn during FY22-FY28, and consequently a total of AC production value of USD13 Bn.

The LED segment in the scheme is imperative to have, considering the massive amount of imports into the company for these targeted components. The estimated FY22 total imports for LEDs, excluding solar cells, are estimated to be ~USD1.5 bn (HS code: 8541). Trends of trade balances of key AC components and LEDs over the years can be seen in the chart 4.1 below. The PLI attempts to counter these prevalent trade deficits.

The incremental total sales from FY22-28 led by the PLI scheme are expected to be around USD 2-3 bn.

Chart 4.1: AC components trade balance

*FY22 (Apr – Jan) Source: Ministry of Commerce & Industry, HSIE Research

*FY22 (Apr – Jan) Source: Ministry of Commerce & Industry, HSIE Research

0.8 0.7 0.6 0.8 0.8 0.8 0.9 1.01.5 1.4 1.4 1.6 1.8 1.9 1.7 1.8

-0.8 -0.7 -0.7 -0.8 -1.0 -1.0 -0.8 -0.8

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22*

Trade balance of key AC components HS Code: 8414 (USD bn)

Export Import Trade Balance

0.2 0.2 0.1 0.2 0.2 0.3 0.2 0.21.53.1 4.0 4.7 3.2 2.7 2.8

4.8

-1.3-2.9 -3.9 -4.6 -3.0 -2.4 -2.6

-4.6

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22*

Trade balance of LEDs HS code: 8541 (USD bn)

Export Import Trade Balance

Page | 21

India Equity Strategy PLI scheme details:

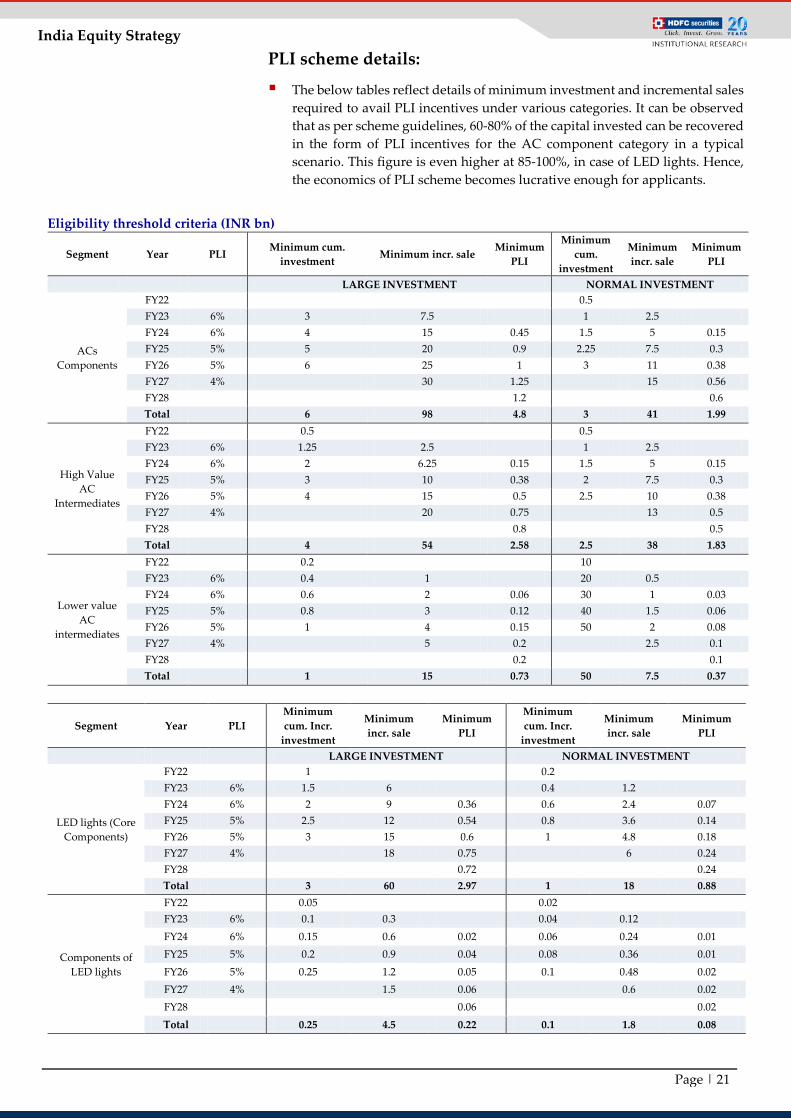

The below tables reflect details of minimum investment and incremental sales required to avail PLI incentives under various categories. It can be observed that as per scheme guidelines, 60-80% of the capital invested can be recovered in the form of PLI incentives for the AC component category in a typical scenario. This figure is even higher at 85-100%, in case of LED lights. Hence, the economics of PLI scheme becomes lucrative enough for applicants.

Eligibility threshold criteria (INR bn)

Segment Year PLI Minimum cum. investment Minimum incr. sale Minimum

PLI

Minimum cum.

investment

Minimum incr. sale

Minimum PLI

LARGE INVESTMENT NORMAL INVESTMENT

ACs Components

FY22 0.5 FY23 6% 3 7.5 1 2.5 FY24 6% 4 15 0.45 1.5 5 0.15 FY25 5% 5 20 0.9 2.25 7.5 0.3 FY26 5% 6 25 1 3 11 0.38 FY27 4% 30 1.25 15 0.56 FY28 1.2 0.6 Total 6 98 4.8 3 41 1.99

High Value AC

Intermediates

FY22 0.5 0.5 FY23 6% 1.25 2.5 1 2.5 FY24 6% 2 6.25 0.15 1.5 5 0.15 FY25 5% 3 10 0.38 2 7.5 0.3 FY26 5% 4 15 0.5 2.5 10 0.38 FY27 4% 20 0.75 13 0.5 FY28 0.8 0.5 Total 4 54 2.58 2.5 38 1.83

Lower value AC

intermediates

FY22 0.2 10 FY23 6% 0.4 1 20 0.5 FY24 6% 0.6 2 0.06 30 1 0.03 FY25 5% 0.8 3 0.12 40 1.5 0.06 FY26 5% 1 4 0.15 50 2 0.08 FY27 4% 5 0.2 2.5 0.1 FY28 0.2 0.1 Total 1 15 0.73 50 7.5 0.37

Segment Year PLI Minimum cum. Incr.

investment

Minimum incr. sale

Minimum PLI

Minimum cum. Incr.

investment

Minimum incr. sale

Minimum PLI

LARGE INVESTMENT NORMAL INVESTMENT

LED lights (Core Components)

FY22 1 0.2 FY23 6% 1.5 6 0.4 1.2 FY24 6% 2 9 0.36 0.6 2.4 0.07 FY25 5% 2.5 12 0.54 0.8 3.6 0.14 FY26 5% 3 15 0.6 1 4.8 0.18 FY27 4% 18 0.75 6 0.24 FY28 0.72 0.24 Total 3 60 2.97 1 18 0.88

Components of LED lights

FY22 0.05 0.02 FY23 6% 0.1 0.3 0.04 0.12 FY24 6% 0.15 0.6 0.02 0.06 0.24 0.01 FY25 5% 0.2 0.9 0.04 0.08 0.36 0.01 FY26 5% 0.25 1.2 0.05 0.1 0.48 0.02 FY27 4% 1.5 0.06 0.6 0.02 FY28 0.06 0.02 Total 0.25 4.5 0.22 0.1 1.8 0.08

Page | 22

India Equity Strategy In the first round of the PLI application, a total of 42 companies were

approved for both the AC and LED segments. INR 39bn investment was committed by 26 companies in the AC segment while INR 7.1bn was committed by 16 companies in the LED segment. The government has opened the second round of applications from 10 March 2022 to 25 April 2022 to fulfill the remaining outlay.

As mentioned earlier, the PLI scheme is not for finished goods but rather for the key components that are then assembled by OEMs to make the finished goods, which in this case are ACs. It is, hence, imperative to have a look at a typical AC bill of material (BoM). Compressor, heat exchanger, and PCB contribute majorly towards the cost of a typical inverter AC. Most of these components are covered under the PLI scheme.

Chart 4.2: Inverter AC component cost break-up

Source: HSIE Research Image 4.1: Compressor Image 4.2: Heat exchanger Image 4.3: Fan

Motor

Source: LG Source: Amber Enterprises Source: Daikin

Key products and approved applicants The below table lists key products that selected applicants have committed to invest and build capacities in.

Applicant Eligible product Committed investment (INR bn)

Hindalco Industries Copper tubes, aluminium for heat exchanger 5.39 Diakin AC Compressor, control assembly, motor, heat exchanger 5.39 Amber Enterprises control assembly, motor, heat exchanger 4.60 HI-Volt Enterprises Compressor, motor 3.54

PG Technoplast Compressor, control Assy, motor, heat exchanger, plastic moulding

3.21

Mettube India Copper tube 3.0

EPAC Durables Display, control assembly, heat exchanger, plastic moulding, fan

3.0

Midea India Compressor 2.5

Syska LED LED driver, printed circuit board, LED light management systems

1.5

Dixon Tech LED engine, LED module, LED light management systems

1.0

Total 46.14

Compressor (ODU), 23%

Heat Exchanger (ODU), 11%

Sheet Metal, 9%

Fan Blade (ODU), 3%Fan Motor

(ODU), 4%

Refrigerant (ODU), 4%

Others, 16%

Heat Exchanger (IDU), 8%

Fan Motor (IDU), 4%

PCB (ODU), 18%

Page | 23

India Equity Strategy

The PLI scheme essentially targets most of the costs associated with an AC’s BoM; ~80% of the total cost, to be precise. The government boasts an expected domestic value addition increase from 25% to 75% as a direct result of the PLI scheme. Based on the estimated revenue generation of USD 11 billion over the tenure of the scheme, the expectation is that India will become largely self-reliant in the manufacturing of ACs. This in turn is likely to help the country reduce its import dependence for ACs and eventually become a net exporter. The quantum of incremental sales and the targeted components make DVA expansion plausible.

The white goods PLI scheme also targets the LED lights segment. As shown in the figure above, India’s imports of LEDs, excluding solar cells, are expected to touch USD 1.5 bn in FY22, clearly indicating the need to incentivise and push domestic manufacturing in the industry. LEDs have a wide variety of applications; they are used in smart phones, digital watches, cameras, automotive heat lamps, aviation lighting, digital computers, and calculators. This versatile usage of LED lights has led to its inclusion in the PLI scheme.

Through this scheme, India is planning to promote efficient lighting technologies. LED lights due to their energy efficiencies are expected to gradually replace high-power-consuming lighting sources and incandescent bulbs.

The LED segment of the PLI also targets key components and aims to make the country self-reliant in LED supply chain, as opposed to simply assembling LEDs in the country. The scheme targets key components such as LED drivers and LED chips, which are primarily being imported from China currently. While the intention behind the scheme is a step in the right direction, the size of the scheme is simply not enough to make a meaningful impact.

Domestic LED lights manufacturing is estimated to be USD 2.2bn while imports excluding solar cell LEDs account for USD 1.5 bn, pegging the current domestic demand at ~USD 3.7 bn. With the advent of Government of India’s UJALA scheme and the increased adoption of LED lights, the industry is expected to ramp up significantly in the coming years, requiring a larger and more sustainable LED component ecosystem in the country.

So far, the committed investment by applicants has only been to the tune of INR 7.2bn by 16 companies, nowhere near the investment required for the country to be self-reliant. The economies of scale achieved by Chinese companies in LED components have made it unviable for most domestic countries to operate in the space. Further, even with the presence of custom duties, it is still cheaper for OEMs to import components from China. The quantum of incentives provided to LED component manufacturers needs to be larger to invite a higher level of committed investments to increase the scale of domestic production.

Our opinion: Based on the key components of AC targeted by the government through the scheme, the DVA expansion from 25% to 75% seems plausible. Furthermore, the estimated revenue generation of USD 10-11 bn is likely to make India a net exporter of ACs by the end of the scheme’s tenure. Also, given increasing demand of LED lights, trade deficits are increasing in this segment. At present, the committed investments under the scheme are far from enough. Incentives offered should be much higher to attract more players to participate in this scheme. . We expect the white goods scheme to largely perform in line with the government’s expectations.

Source: Designua

Page | 24

India Equity Strategy 5. Automobile and auto components The automotive industry is a major economic contributor in India. The sector, a key growth driver, is responsible for 35% of manufacturing GDP of India. The PLI scheme for this sector proposes financial incentives to boost domestic manufacturing of advanced automotive technology products and attract investments in the automotive manufacturing value chain.

The most prevalent automotive technology is electric vehicles and, hence, it becomes imperative to understand its constitution and key components.

Electric vehicles (four-wheelers) As shown in the below diagram, an electric vehicle (EV) is much different from an internal combustion engine (ICE) as it does not have any fuel tank, combustion mechanism, or exhaust pipe. Hence, it doesn’t contribute to pollution. Given the world’s increasing focus on sustainability, pollution control and environment protection, an EV is expected to rapidly replace ICE across geographies. EVs use battery packs as their energy source for driving. Electric traction motor and power electronics controller are the other important components:

Image 5.1: Electric 4 wheeler (4W EV)

Source: U.S. Department of Energy

The list below provides a break-up of various components required to make an electric four wheeler. It suggests that 42% of the overall bill of material (BOM) is import dependent. It includes battery cell, electric traction motor, semiconductors and other power electronics controller. Chassis, drive train and battery management system are domestically manufactured. It is worth mentioning that the key component battery cell has been considered as a part of another PLI scheme for reducing dependence on expensive imports (PLI scheme for ACC battery).

Table 5.1: Cost break-up of a four-wheeler electric vehicle Component % Cost Sourcing Battery cell 24% Import Battery mgt system 11% Domestic Electric traction motor 10% Import Semiconductors 4% Import Rest of power electronics controller 4% Import Chassis & body 20% Domestic Drive train 7% Domestic Other 20% domestic Total 100%

Page | 25

India Equity Strategy Key component of EV- battery A battery, which consists of battery cells and battery management system, accounts for approximately 35% of the overall cost of a 4W EV. It is the most important component of the vehicle as it drives its function. The most popular advanced chemistries are lithium ferrum phosphate (LFP) or nickel cobalt aluminum (NCA) batteries. In both of these cases, the key fundamental element is a battery cell (image 5.2). It consists of a cathode, anode, electrolyte, and separator. Cathode and anode help in electron movement through the electrolyte resuting in current flow, while a separator ensures that cathode and anode remain insulated from each other. If the separator malfunctions, it could cause a short circuit and battery could burn up in flames. Separators are made of polyolefin, which is composed of polyethylene, polypropylene, or the lamination of one over another. The desired quality of a separator is to withstand high temprature; otherwise, it may dissolve in the high temperature environment, resulting in a short circuit.

In a typical battery, 74 such wired cells are connected parallelly to form a group. Eight such groups are connected electrically in series to form a module (Image 2.3). Battery pack is formed by connecting 16 such modules in a series arrangement. Battery pack entails two rows of seven modules each in the flat section, while two other modules are stacked in the front (image 2.4, 2.5, and 2.6). Hence, overall 9,472 cells are required to form a typical battery pack for a 4W EV.

Image 5.2: Battery cell Image 5.3: Battery module

Source: Lesics Engineers Pvt Ltd Source: Lesics Engineers Pvt Ltd

Images 5.4, 5.5 & 5.6: Battery modules arranged to form battery pack and fitted in vehicle ‘

Source: Lesics Engineers Pvt Ltd Source: U.S. Department of Energy Source: “Car” Magazine UK

Page | 26

India Equity Strategy Electric vehicles - key raw material and supply locations

Image 5.7: Key raw materials found in South Africa, China, Indonesia & Congo

Image 5.8: Lithium ion battery raw materials reserves across countries

Source: Niti Aayog Source: Niti Aayog

The above two images (image 5.7 & 5.8) reflect the geographical locations where key raw materials for both the popular battery chemistries are available.

It can be observed in image 5.7 that cobalt, manganese, nickel and graphite, key to NMC chemistry, are found mainly in South Africa, Congo, Indonesia, and China. Furthermore, image 2.8 indicates that the key material lithium for LFP chemistry is found in China, Bolivia, Chile, and Australia. Remarkably, Australia has the greatest availability of key material for li-ion battery manufacturing.

Having understood the saliency of lithium, it is worthwhile to know its global sources. Table 5.2 reflects that Bolivia has the largest lithium reserves (21 mn tonnes) in the world. In spite of this, it isn’t the largest producer as most of its reserves are available at steep elevation, where it is difficult to extract.

Bolivia, Chile, and Argentina account for ~56% of global lithium reserves of 89 mn tons and are collectively called the lithium-triangle. Chinese firms have already received mining concessions in this region and hence, are pioneers in battery production.

Table 5.2: Lithium reserves across countries

Country Lithium reserves (Mn Tonnes) (Mn tonnes)

Bolivia 21 Argentina 19 Chile 9.8 Australia 7.3 China 5.1 Congo 3 Source: U.S. Geological Survey, HSIE Research

Australia, Chile, and China are the leading lithium producing countries. The below table underscores lithium production by countries in 2021:

Page | 27

India Equity Strategy Lithium production across countries (2020)

Country 2020 Lithium production (Tonnes) (Mn tonnes) % of World total

Australia 55,000 52.4% Chile 26,000 24.8% China 14,000 13.3% Argentina 6,200 5.9% Others 4,600 4.4% Total 105,000 100% Source: U.S. Geological Survey, HSIE Research

Indian efforts: So far, India has been lagging in securing substantial lithium or other key battery material reserves. The geological survey of India has been exploring lithium reserves in Arunachal Pradesh, Chhattisgarh, Rajasthan, J&K, Jharkhand, and Andhra Pradesh. Preliminary findings suggest a very small reserve of 1,600 tonnes in Karnataka.

Khanij Bidesh Nigam Ltd (KABIL) is a JV between NALCO, Mineral Exploration Corporation Ltd (MECL), and Hindustan Copper (HCL). Through this, India is working on acquiring mines of strategic minerals such as lithium and cobalt in producing countries like Australia, Argentina, Bolivia, and Chile.

Hence, India has remained dependent on imported lithium so far. We need to track progress on acquisition of mines by Indian companies.

Electric Vehicle – two-wheelers (E2W) components break-up

As shown in image 5.9, battery cells and motor and electronic control units are imported for manufacturing an electric two-wheeler. This means that approximately 53% of the cost of overall raw material is import dependent. Hence, price of E2W will be a function of import prices of these key components. And, hence, the price of E2W is at the mercy of global supply & pricing of these key components.

Image 5.9: Cost breakup of an electric 2 wheeler (E2W)

Source: Goldman Sachs, HSIE Research

Page | 28

India Equity Strategy

Policy support: Government has extended support by way of FAME-II policy (faster adoption of manufacturing of hybrid & electric vehicles). It is a budgetary support of INR 100bn to generate demand by way of supporting 7,000 e-buses, 5 lakh e-3 wheelers, 55,000 four-wheeler EVs and 1 mn electric two-wheelers. So far, it has supported sales of more than 3 lakh vehicles and spent INR 11 bn on incentives. It is valid until 31 Mar 2024. For a E2W buyer, policy offers a subsidy of INR 15,000 per KWH of vehicle up to a ceiling of 40% of the vehicle cost. This typically means a support of INR 45-50K for an E2W costing INR 150,000. This is leading to faster adoption of E2W and its growing sales.

In our view, the cost of the vehicle needs to come down by way of securing raw material supplies, battery innovations, and economy of scale. FAME-II support can take industry to only a small extent further; however, for real growth and development of industry, E2W prices need to come at par with conventional petrol two wheeler prices without subsidy.

Automobile and auto components - PLI scheme highlights

Scheme has two parts - Champion OEM and component champion incentive scheme.

Eligibility: Investments to be done for approved products with 50% value addition.

Cumulative new domestic investment (INR bn)

Champion OEM (Except

2W/3W)

Champion OEM (2W/3W)

Component champion

New non-auto investor(OEM)

New non auto investor

(component)

Upto FY23 3 1.5 0.4 3 0.8 Up to FY24 8 4 1 8 2 Up to FY25 14 7 1.75 14 3.5 Up to FY26 17.5 8.75 2.2 17.5 4.4 Up to FY27 (Total Investment) 20 10 2.5 20 5

Champion OEM & OEM investor: Minimum INR 1.25 bn sales in first year and 10% YoY growth

Determined sales value (INR bn)

<20 20-30 30-40 >40 Additional 2% incentive if cumulative sales >100 bn over 5 years

Incentives (% of sales) Base yr-FY20

13% 14% 15% 16%

Component champion & component investor: Minimum INR 0.25 bn sales in first year and 10% YoY growth

Determined sales value (INR bn)

<2.5 2.5-5 5-7.5 >7.5 Additional 2% incentive if cumulative sales >12.5 bn over 5 years 5% more for BEV & hydrogen fuel components

Incentives (% of sales) Base year-FY20

8% 9% 10% 11%

Page | 29

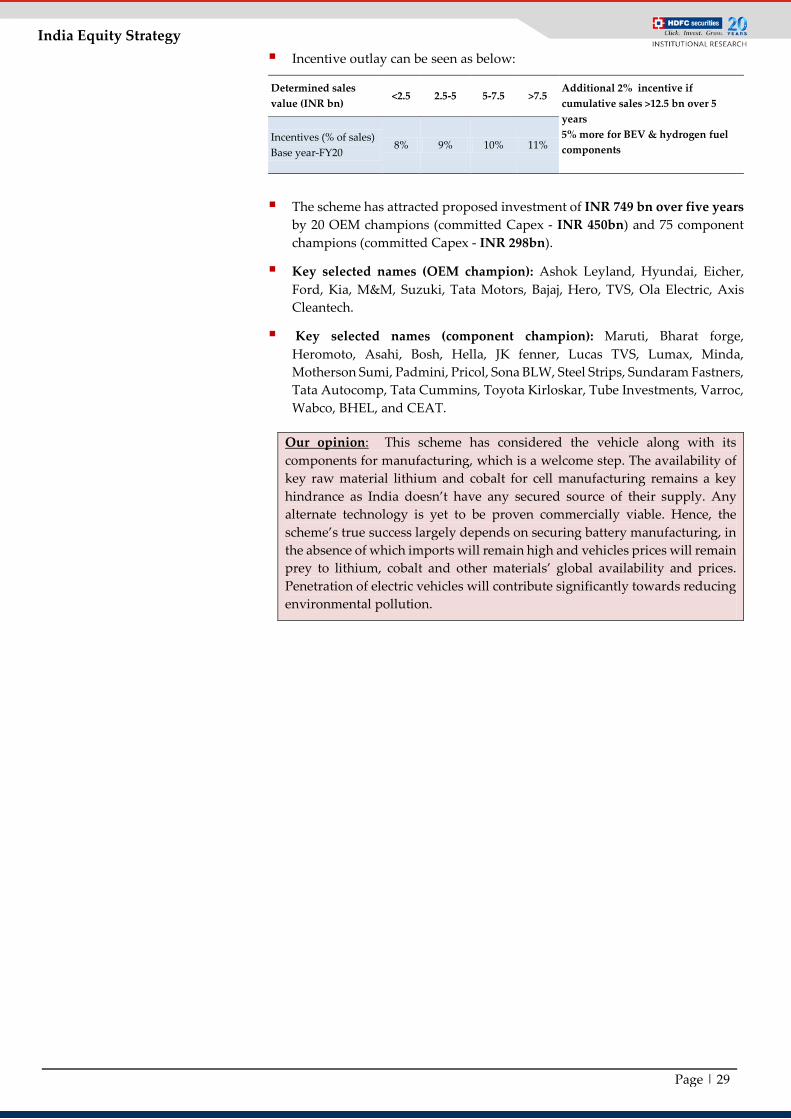

India Equity Strategy Incentive outlay can be seen as below:

Determined sales value (INR bn)

<2.5 2.5-5 5-7.5 >7.5 Additional 2% incentive if cumulative sales >12.5 bn over 5 years 5% more for BEV & hydrogen fuel components

Incentives (% of sales) Base year-FY20

8% 9% 10% 11%

The scheme has attracted proposed investment of INR 749 bn over five years by 20 OEM champions (committed Capex - INR 450bn) and 75 component champions (committed Capex - INR 298bn).

Key selected names (OEM champion): Ashok Leyland, Hyundai, Eicher, Ford, Kia, M&M, Suzuki, Tata Motors, Bajaj, Hero, TVS, Ola Electric, Axis Cleantech.

Key selected names (component champion): Maruti, Bharat forge, Heromoto, Asahi, Bosh, Hella, JK fenner, Lucas TVS, Lumax, Minda, Motherson Sumi, Padmini, Pricol, Sona BLW, Steel Strips, Sundaram Fastners, Tata Autocomp, Tata Cummins, Toyota Kirloskar, Tube Investments, Varroc, Wabco, BHEL, and CEAT.

Our opinion: This scheme has considered the vehicle along with its components for manufacturing, which is a welcome step. The availability of key raw material lithium and cobalt for cell manufacturing remains a key hindrance as India doesn’t have any secured source of their supply. Any alternate technology is yet to be proven commercially viable. Hence, the scheme’s true success largely depends on securing battery manufacturing, in the absence of which imports will remain high and vehicles prices will remain prey to lithium, cobalt and other materials’ global availability and prices. Penetration of electric vehicles will contribute significantly towards reducing environmental pollution.

Page | 30

India Equity Strategy 6. Advanced chemistry cells (ACC) battery Advanced chemistry cells (ACCs) are advanced energy storage technologies

that can store electric energy either as electrochemical or chemical energy and convert it back to electrical energy as and when required.

Integrated battery value can be divided into battery pack assembly and ACCs. A few companies in the country have already started investing in battery pack assembly, although the current overall capacity is miniscule as compared to global capacity. Investments in ACCs manufacturing and overall value addition is negligible. Hence, entire domestic demand of ACCs is met only through imports.

Through the PLI scheme for ACCs, government intends to optimally incentivize potential investors to set up mega scale ACC manufacturing facilities with emphasis on maximum value addition, quality output, and achieving a pre-committed capacity. No incentive is being offered to conventional battery pack technology as it is already being manufactured in India currently.

Various ACC battery technologies being researched in the country are li-ion battery, hydrogen as fuel solid state batteries, and sodium ion batteries.

Lithium-ion batteries

Current capability of India along with lithium ion battery (LiB) manufacturing value chain is explained in the table below. It can be observed that most of the Indian companies are present in the battery pack assembly segment and current focus on cell manufacturing capacity creation is very low. Hence, there is widespread dependence on imported battery cells.

Table 6.1: LiB value chain

Si. No. Stage of Value chain Description Current status

1 Material sourcing Virgin raw material sourced after mining

Negligible reserves in India; Lithium, cobalt, controlled by few countries

2 Material manufacturing

Manufacturing of cathode, anode, electrode, casing, separator , terminals

“Epsilon carbon” is manufacturing synthetic graphite anode. copper aluminum layer mfg also being done by few companies.

3 Cell manufacturing Mfg of cell from materials Cell mfg being done by Suzuki Denso Toshiba JV, Godi energy & Log 9 materials

4 Cell to Pack conversion

Cell to pack assembly with Battery mgt system (BMS), Dependent on Chinese imported cells

Cell to pack conversion being done by many companies viz. Exide-Leclanche, Waree, Ipower, Trontek, Ather, Ola electric, Amara Raja

Out of total cost of LiB, cells account for 65%, battery pack accounts for 15%, battery management system (BMS) accounts for 15% and the outer box accounts for the remaining 5%:

Battery pack - Key components are copper harness, non reactive glue and outer casing. All of these are produced locally; thermal pads are imported.

BMS – Pre-printed protection circuit board is imported from China and printing is done in India.

Outer box - It is locally produced and, hence, no imports are necessary.

LiB cell- Imported (77% of overall cost is on account of raw material; it is entirely imported).

Page | 31

India Equity Strategy Currently li-ion battery costs around USD 132/KWH; it has fallen from USD

1220/KWH in 2010, mainly driven by achieved economies of scale by Chinese battery producers.

ACC battery KWH required: A typical two-wheeler vehicle may require 2.5-3KWH battery, while a four-wheeler EV will require approximately 35KWH as battery storage. Battery storage requirement may vary with different models of cars; for example, a BMW requires 85 KWH batteries and offers a higher drive range in a charge. Also, electric buses require a 250KWH battery.

Two of the common li-Ion cell chemistries are lithium ferrous phosphate (LFP) and nickel manganese cobalt (NMC).

LFP Vs NMC:

LFP can operate in a temperature range of -4 degrees to 70 degrees, while for NMC, the optimum operating temperature range is from -20 degrees to +55 degree Celsius. Due to this reason, NMC may catch fire in high temperature geographies.

LFP requires more space than NMC so it is suitable for larger vehicles (3W/4W/fleet).

LFP uses phosphorus as cathode, which is less expensive than cobalt used in NMC.

LFP has a long lifecycle of cell (3,000 charge/discharge) and, hence, it lasts 5-7 years while NMC has a lower lifecycle of cells (750 charge/discharge cycle) and lasts only 2-3 years.

Given the benefits, the overall LFP chemistry is the optimum choice for four-wheeler electric vehicles.

Planned investments in battery space and cell manufacturing

Globally, li-ion battery capacity has grown from 250 GWH in 2018 to 700 GWH in 2021 (75% in China); battery prices have reduced from USD 185/KWH to USD 132/KWH during the same period.

The projected global capacity of li-ion is expected to grow to 2,250 GWH by 2025 (country-wise break-up of the same is expected to be China-55%, EU-20%, US-10%). The US and Europe are committing large investments to manufacture large capacities, while China continues its investment journey.

Table 6.2 lists down the ongoing projects in the development of battery ecosystem. Many companies are exploring these projects even without PLI support, indicating their conviction on future growth of industry and projected growth in demand.

Table 6.2: Battery ecosystem development Company Description Location Amara Raja USD 1 bn investment in battery mfg in next 5 yrs Tirupati Log 9 materials Developed high power cell, fast charging and long life, planning to implement in 2W/3W Bengaluru Exide-Leclanche Invested INR 25 bn for 1.5GWH battery assembly facility Ahmedabad Suzuki denso Toshiba INR 50 bn invested for manufacturing 30 mn cells (1GWH capacity) Ahmedabad

Adani group Plans to invest in li-ion battery manufacturing complex; USD 20 bn allocated for renewable space in next decade

Ahmedabad

Reliance Battery manufacturing complex to be set up. Giga factory to be part of INR 750 bn Investment Jamnagar Tata Chemicals Giga facility. 2 GWH (INR 8bn) in phase-1 & 10GWH (INR 40Bn in phase-2) Dholera C4V 5GWH capacity with investments of INR 40 bn Karnataka Godi Energy 5GWH capacity of cell manufacturing in the next five years Hyderabad Epsilon advanced 1 lakh tonne of synthetic graphite anode Bangalore Greenko energy Plan of setting up gigafactory (5GWH) by investing USD 1 bn Telangana Lucas TVS Initial investment of INR 25 bn; plan of having 10GWH facility in two phases Chennai

Page | 32

India Equity Strategy Alternate battery technologies