first quarter 2018 results - Grupo Aeroportuario del Centro Norte

40

FIRST QUARTER 2018 RESULTS INVESTOR PRESENTATION

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of first quarter 2018 results - Grupo Aeroportuario del Centro Norte

FIRST QUARTER

2018 RESULTS

INVESTOR

PRESENTATION

This presentation may contain forward-looking information and statements. Forward-looking statements are statements that are

not historical facts. These statements are only predictions based on our current information and expectations and projections

about future events. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,” “target,”

“estimate,” or similar expressions. While OMA's management believes that the expectations reflected in such forward-looking

statements are reasonable, investors are cautioned that forward-looking information and statements are subject to various risks

and uncertainties, many of which are difficult to predict and are generally beyond the control of OMA, that could cause actual

results and developments to differ materially from those expressed in, or implied or projected by, the forward-looking

information and statements. These risks and uncertainties include, but are not limited to, those discussed in our most recent

annual report filed on Form 20-F under the caption “Risk Factors.” OMA undertakes no obligation to update publicly its forward-

looking statements, whether as a result of new information, future events, or otherwise.

2

A b o u t t h e C o m p a n y

Our businesses

13 Airports in the central-north region of Mexico, serving 20 million

passengers in LTM 1Q18.

2 Hotels; NH Collection Hotel in Terminal 2 of the Mexico City

Airport, and Hilton Garden Inn at Monterrey Airport

1 Industrial Park at Monterrey Airport

Who we are

More than 1,000 employees committed to providing aeronautical,

commercial and real state services of excellence to our

passengers and clients.

Listed in BMV and NASDAQ since 2006

Part of the main index of the BMV (IPC)

3

Company

Overview

Aeronautical

Business

Non-

Aeronautical

Business

Financial

Results

MDP &

Maximum

Rates

Outlook and

Industry

Value Proposal

Historical Performance

Shareholder Structure

Board of Directors and

Management Team

Operations &

Sustainability

Connectivity &

New Routes

Passenger Traffic

Airline Participation

AR 2Q17

Commercial Strategy

Diversification Strategy

NAR 2Q17

Historical NAR Growth

2Q17 Highlights

Cost & Efficiency

Balance Sheet

Profitability Indicators

Value Distribution

Investments 2016-2020

New Terminals

Maximum Rates

Industry Trends

Airline Fleets: Orders

and Expected

Load Factor1Q18

1Q18

1Q18

Value Proposal

Company

Overv iew

1

Historical Performance

Shareholder Structure

2

3

Board of Directors and

Management Team4

Operations & Sustainability5

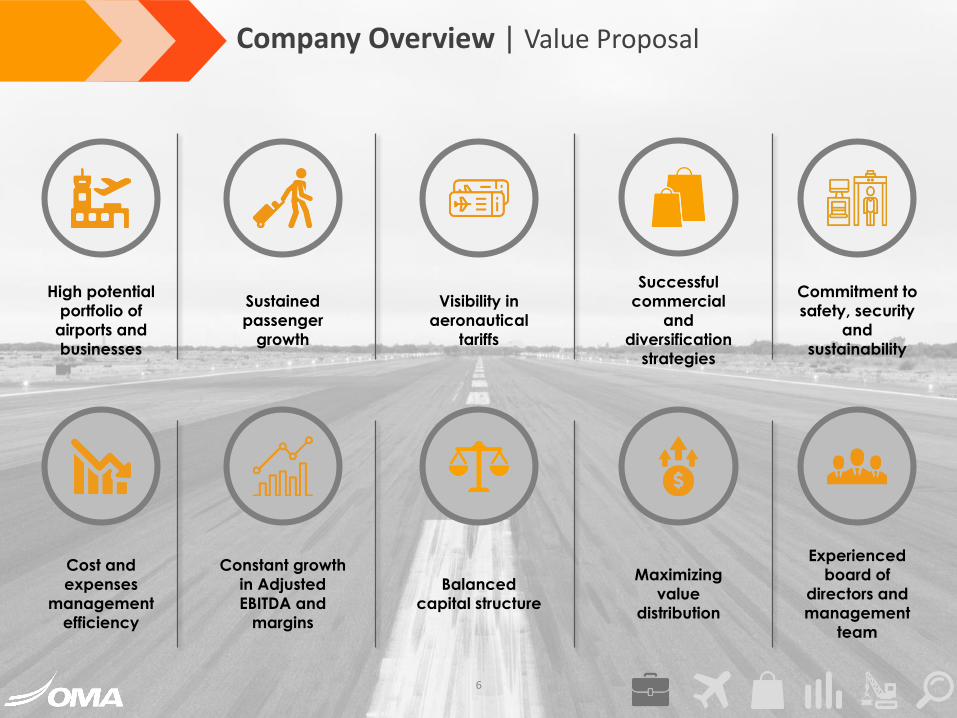

Company Overview | Value Proposal

High potential

portfolio of

airports and

businesses

Maximizing

value

distribution

Constant growth

in Adjusted

EBITDA and

margins

Balanced

capital structure

Cost and

expenses

management

efficiency

Commitment to

safety, security

and

sustainability

Sustained

passenger

growth

Visibility in

aeronautical

tariffs

Successful

commercial

and

diversification

strategies

Experienced

board of

directors and

management

team

6

81% 81% 81% 82% 81% 81% 77% 76%76%

74%74% 73%

19% 19% 19%18%

19%19%

23%24%

24%

26%

26%27%

1,897 1,988 1,896 2,144

2,459 2,820

3,065 3,422

4,145

5,205

5,803 6,031

14.2 14.1

11.5 11.6 11.8

12.6 13.3

14.7

16.9

18.8 19.7

20.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

-

2,000

4,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 LTM Mar18

Aeronautical Revenues Non-Aeronautical Revenues Passenger Traffic (million)

Company Overview | Historical Performance

% Adj.

EBITDA2

Sustained positive trends through economic and business cycles

Note: From 2010 to LTM Mar18 figures expressed under IFRS; 2001 - 2009 figures expressed under MFRS.1 Represents the sum of aeronautical and non-aeronautical revenues (excludes construction). 2 Adjusted EBITDA Margin = Adjusted EBITDA / (Aeronautical + Non-Aeronautical Revenues). Adjusted EBITDA = Operating income + Depreciation and Amortization + Maintenance Provision.3 Passenger traffic as of March 31, 2018

7

• PAX 7.9%

• Revenues 13.7%

• Adjusted EBITDA 18.2%

CAGR 2011-LTM Mar18

3

56% 53% 51% 44% 51% 54% 55% 55% 59% 64% 66% 67%

Company Overview | Shareholder Structure

8

SETA1 – BB shares

12.6%

1.9%

CONOISA1 – B shares

Public Float2 - B Shares

85.5%

Market Cap3.

Ps. Bn. $34.9 / USD Bn. $1.9

1 Servicios de Tecnología Aeroportuaria, S.A. de C.V. (SETA) and Controladora de Operaciones de Infraestructura, S.A. de C.V. (CONOISA) are wholly owned subsidiaries of Empresas ICA ,S.A.B. de C.V.2 Float includes repurchased shares

³ BM V Price Ps.88.65 as of M arch 31, 2018. Exchange rate used: 18.3445

Note: Share holding information as of M arch 31, 2018

CORPORATE GOVERNANCE

5 of 11 Directors are independentmembers

Board Audit and Corporate PracticesCommitees are 100% independent

Company Overview | Board of Directors & Management Team

9

EXPERIENCED MANAGEMENT TEAM(Average time with OMA: 12 years)

Porfirio GonzálezChief Executive OfficerWith the Company since 1998

Ruffo Pérez PliegoChief Financial OfficerWith the Company since 2018

Alfredo DomínguezGeneral CounselWith the Company since 2004

Héctor CortésChief Commercial OfficerWith the Company since 2001

Enrique NavarroAirport Operations ManagerWith the Company since 2004

Roberto OntiverosInfraestructure and Maintenance ManagerWith the Company since 2008

Company Overview | Operations & Sustainability

10

Always striving to meet international standards.

Environment

Social Responsibility

SustainabilityPerformance

OccupationalHealth and Safety

Quality and Customer Service

CULIACÁN AIRPORT MAZATLÁN AIRPORT

AerodromeCertification

Connectivity &

New Routes

Aero na u t ica l

Bus iness

1

Passenger Traffic

Airline Participation

2

3

Aeronautical Revenues 1Q184

4 4 n e w d i r e c t r o u t e s i n 2 0 1 7

Aeronautical Business | Connectivity & New Routes

+ 4 . 8 %

P A X i n 2 0 1 7

+5.8%

1

1

International Routes

6

6

3

2

Domestic Routes

2 Other

+ 8 . 0 %

P A X i n 1 Q 1 8Seats added in 1Q18

5

4

5

International Routes

11

5

5

3

Domestic Routes

6 Other

Other+2.0%Seats added in 2017

2 1 n e w d i r e c t r o u t e s i n 1Q18

MTY

Aeronautical Business | Passenger Traffic

CUU

CJS

CUL

MZT

DGO

TRC

ZCLSLP

TAM

REX

ZIH

ACA

At Monterrey Airport• Aeromexico regional hub

• VivaAerobus main base

• Volaris secondary base

• Interjet secondary base

Passenger Traffic

13

Note: Percentages in graphs represent Passenger share by type of airport.

Passenger Traffic1Q18

Total Pax: 4.9 million (+8%)

85% Domestic: 4.2 million (+8.4%)

15% International: 0.7 million (+5.8%)

Metropolitan

46%

Regional

31%

Tourist

15%

Border

Cities

8%

(%) YoY 3M18 Passenger Growth +2%

+14%

+27%

+5%

+4%

-19%

+14%+8%

-1%

-2%

-1%

88% Domestic: 17.2 million (+5.1%)

12% International: 2.4 million (+2.8%)

Total Pax: 19.7 million (+4.8%)

2017

+9%+1%

United 21% (-0.6%)

American 21% (+7.3%)

Aeroméxico 17%

(+13.6%)

Delta 10% (-2%)

Volaris 8% (-1.3%)

Interjet 6% (+10.8%)

Charters 6% (+0.2%)

Alaska 5% (-18.4%) Other 6%

(-6.9%)

Aeronautical Business | Airline Participation LTM18

14

85% DomesticPassengers

15% InternationalPassengers

VivaAerobus 28%

(+22%)

Aeroméxico 27%

(-1.5%)

Volaris 20%

(-2.7%)

Interjet 17%

(+0.4%)

Magnicharter 3% (+14.8%)

Other 5%

(+2.7%)

Note: Percentages in graphs represent 1) Passenger share by category and 2) % change LTM Mar18 v s LTM Mar17

Aeronautical Business | Aeronautical Revenues 1Q18

Domestic Passenger Charges

InternationalPassenger Charges

AirportServices

Aeronautical

Revenues

* Total Revenues excluding Construction Revenues

15

Ps.734+25.2%

61% of

Aeronautical

Revenue

Ps.301+9%

25% of

Aeronautical

Revenue

mm

mm Ps.169+11%

14% of

Aeronautical

Revenue

mm

+18.7%

76% of Total

Revenue*

Ps. 245.6 / PAX

Ps.1,204mm

Commercial Strategy

Non -

Aero na u t ica l

Bus iness

1

Diversification Strategy

NAR 1Q18

2

3

Historical NAR Growth4

Non-Aeronautical Business | Commercial Strategy

10 Commercial Initiatives Implemented in 1Q18Airport Type QuantityMonterrey Car rental 4Culiacán and San Luis Potosí Hotel promotion 2

Monterrey and Zacatecas Retailer 2

Monterrey Advertising 1

Durango Bank services 1

17

Maximize commercial

areas

Balance between

internationalfranchises & local brands

Develop premium

offerings & loyalty

programs

Addinnovativeadvertising

Non-Aeronautical Business | Diversification Strategy

17.4% of NAR | 287 Rooms

Avg. Room Rate:Ps.2,226 per night (+5.1% yoy)

Occupancy Rate: 88% | EBITDA Margin: 38.3%

6.1% of NAR | 134 Rooms

Avg. Room Rate: Ps.2,023 per night (+3.

Occupancy Rate: 73% | EBITDA Margin: 38.4%

NH Collection Hotel at Mexico City Airport Hilton Garden Inn Hotel in MTY

OMA Carga Real Estate Industrial Park In MTY

3 warehouses leased | 3 warehouses signed in 4Q17 and 1Q18; revenue starts in 2Q18 and 3Q18 | 1 warehouse under construction for

commercialization

18

36.3%

Ps.2,053 per night

79% 39.8%

| +13.3% revenues in 1Q1810.4.0% of NAR

revenues in 1Q181,650m2 | New ground cargo facility

started operations on February 16, 2017

17.1% of NAR | 287 Rooms 6.3% of NAR | 134 Rooms

Ps.2,342 per night

86%

| +5.9%1.0% of NAR | Ps.5.61.5% of NAR million

Non-Aeronautical Business | 1Q18

Commercial Activities

Diversification Activities

Complementary Activities

Non-

Aeronautical

Revenues

* Total Revenues excluding Construction Revenues

19

46% of NAR

+13.8%

Ps.174

Ps.138+5.9%

37% of NAR

Ps.376mm+11.3%

24% of Total Rev.*Ps. 76.7 / PAX

mm mm

mm

Ps.64+17.0%

17% of NAR

Non-Aeronautical Business | Historical NAR Growth

Non-Aeronautical Revenues (NAR) have increased faster than

passenger traffic as a result of commercial initiatives and

diversification projects

20

67% 64% 56% 53%53%

51%49% 48% 48%

25%

28% 28%29%

28%

31%

35%

36% 36%

8%

7%

16%

19%

19%

17%

16%

16%16%

42

50

55

60

61

66

71

74 75

90

140

190

240

290

340

390

440

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2011 2012 2013 2014 2015 2016 2017 LTM Mar18

NAR - Commercial/PAX NAR - Diversification/PAX NAR Complementary/PAX NAR PAX

+204%

+73%

• PAX +7.9%• NAR +14.9%• NAR/PAX +7.3%

CAGR 2011 - LTM Mar18

1Q18 Highlights1

Cost & Efficiency

Balance Sheet

2

3

Profitability Indicators4

F inanc ia l

Resu l t s

Value Distribution5

Financial Results | 1Q18 Highlights

Revenues*Cost of Services and

G&AAdjusted EBITDA**

Consolidated Net

Income

* Total Revenues excluding Construction Revenues** Adjusted EBITDA Margin = Adjusted EBITDA / (Aeronautical + Non-Aeronautical Revenues). Adjusted EBITDA = Operating income + Depreciation and Amortization + Maintenance Provision.22

+16.8%

Ps. 1,580

Ps. 322.3 / PAX (+8.2%)

Aeronautical +18.7%

Non-Aero. +11.3%

Ps. 1,072

+23.1%Ps. 218.8 / PAX (+14%)

1Q18 Margin 67.9%

Ps. 610+44%

Ps. 124.5 / PAX (+33.4%)

mm

mm

mm

mmPs. 394

+3.1%Ps. 80.4 / PAX (-4.5%)

2011 2012 2013 2014 2015 2016 2017 LTM Mar18

Financial Results | Cost & Efficiency

23

Costs and expenses control

has contributed to the

generation of EBITDA

Aj EBITDA / PAX

AR+NAR / PAX

Total Operating Costs and Expenses1/ PAX

Distribution of Operating Costs and

Expenses*

• Economies of scale• Generation and purchase of renewable energy• Development a culture of savings• Improvement of operational systems• Development of human capital

Cost Control Strategy

38%

24%

13%

12%

7%6%

Cost of Services

Administrative Expenses

Depreciation & Amortization

Concession taxes

Major Maintenance Provision

Technical Assistance Fee

CAGR2011 - LTM Mar18

10.6%

5.9%

-0.2%

*As of March 31, 2018. Excluding construction cost and other expenses (revenues).

MXN 97%

USD 3%

75% 67% 56% 56% 59% 60% 63%

25% 33% 44% 44% 41% 40% 37%

2012 2013 2014 2015 2016 2017 LTM

Mar18

Financial Results | Balance Sheet

Total Debt | Shareholders’ Equity (Book Value)

Debt Profile*

Strong Financial Position* Low LeveragePs.Million Net Debt / Adjusted EBITDA

Capital Structure Evolution

24

4,612 2,666

1,946

Total Debt Cash Net Debt

Long Term

99%

Short Term

1%

0.6

0.9 1.0

0.8

0.5 0.5 0.5

2012 2013 2014 2015 2016 2017 LTM

Mar18

6.6 8.2

10.9

8.3 9.9

13.8 15.1 15.6

10.1

12.8

18.8 16.8

20.8

28.0 29.6 29.3

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2011 2012 2013 2014 2015 2016 2017 LTM Mar18

Financial Results | Profitability Indicators

ROA / ROEPercentage

Earnings per SharePesos

25

1.5 2.1

3.0 2.6

3.1

4.8 5.4

5.9

2011 2012 2013 2014 2015 2016 2017 LTM Mar18

CAGR 2011 - LTM Mar18

• ROA +13.0%

• ROE +16.4%

• EPS +21.1%

Financial Results | Value Distribution

Dividend or Capital

Reimbursement

Dividend Yield / Payout Ratio

Ps. Million

Percentage

Dividend Yield was calculated with the stock price at the end of each year.

Percentage

26

Note: The amounts shown were paid in the following year, after the annual shareholder meeting.1 The payment was made on May 16, 20. 17

500

1,200 1,200 1,200

1,400

1,600 1,600

2011 2012 2013 2014 2015 2016 2017

81

147

100

117 113

85 75

5.7

8.6

6.9

4.4 4.2

4.5

3.9

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

-

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017

Investments 2016-20201

New Terminals

Maximum Rates

2

3

MDP &

Max imum

Ra te s

MDP & Maximum Rates | Investments 2016-2020

Visibility of capital expenditure requirements through 2020

Total Committed Investment Ps.5,443mmpesos of Dec. 31, 2017

28

1,5861,522

1,157

711

466452

1,428

2,377

711

466

8%

26%

44%

13%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1,000

1,500

2,000

2,500

2016 2017 2018e 2019e 2020e

Committed

Actual / Expected

Monterrey

28%

Acapulco

13%

Chihuahua

10%

San Luis

Potosí9%

Reynosa

8%

Zihuatanejo

7%

Tampico

6%

Culiacán

4%

Ciudad Juárez,

4%

Durango, 3%

Torreón, 3%

Mazatlán, 3%

Zacatecas, 2%

MDP & Maximum Rates | Investments 2016-2020

0%0%0%0%0%0%

Other

ICAO Certification

Operational

Infrastructure

Expansion

Major

Maintenance

Security, Safety

& IT Equipment

Terminal

Expansion

& Remodeling

Most Important Projects

Terminal Expansion

• Monterrey• Ciudad Juárez

New Terminals• Acapulco• Reynosa

Operational Infrastructure• Monterrey• Culiacán• Durango

• Chihuahua• San Luis Potosí• Tampico

Total Committed Investment Ps.5,443mmpesos of Dec. 31, 2017

29

+ Expected Strategic Investment 2018

Ps.100 mm

49%

16%

11%

11%

7%6%

MDP & Maximum Rates | New Terminals

Ps.589 mm

Investment

Total PAX mm1.1 1.3, +18%

Capacity Comfort

April 17, 2018

Start of Operations

Acapulco Airport

30

13,534 m2 15,326 m2*

Total Area

Terminal building, m2 +13%Commercial spaces, m2 +42%

3 levels plus a mezzanine

* New terminal net surface

m2

MDP & Maximum Rates | New Terminals

Ps.327 mm

Investment

Total PAX mm0.3 0.9, +200%

Capacity

2 levels

Comfort

2,608 m2 7,590 m2*

Total Area

4Q 2018**

Start of Operations

Reynosa Airport

31

Terminal building, m2 +191%Commercial spaces, m2 +213%

** Expected* New terminal net surface

MDP & Maximum Rates | Expansion & Remodeling Terminals

Ps.366 mm

Investment

Total PAX mm0.5 1.3, +160%

Capacity

3,832 m2 10,398 m2*

Total Area

1Q 2019**

Start of Operations

** Expected32

Terminal building, m2 +171%Commercial spaces, m2 +116%

* Net surface after remodeling and expansion

San Luis Potosí Airport

7,951 m2 13,074 m2*

MDP & Maximum Rates | Expansion & Remodeling Terminals

33** Expected* Net surface after remodeling and expansion

Ps.322 mm

Investment

Total PAX mm0.9 1.6, +78%

Capacity

4Q 2018**

Start of Operations

Terminal building, m2 +64%Commercial spaces, m2 +30%

Total Area

Chihuahua Airport

87 m2 502 m2*

MDP & Maximum Rates | Expansion & Remodeling Terminals

34** Expected* Net surface after remodeling and expansion

Ps.125 mm

Investment

Total PAX mm2.3 3.2, +39%

Capacity

2Q 2018**

Start of Operations

Terminal building, m2 +477%Commercial spaces, m2 +12%

Total Area

Monterrey Airport – Regional Boarding Area

Visibility on Aeronautical Revenues Through 2020

• Maximum rate (Regulated revenue per workload unit) increased in each airport

• The maximum rate for each succeeding year through 2020 will be adjusted by inflation and an

efficiency factor of 0.70%

MDP & Maximum Rates | Maximum Rates

1 Weighted average using passenger traffic for each period and expressed in constant MXN of December 31, 2017 considering efficiency factor effect 2 MXN of December 31, 2017

2018 (2)

13 Airports MT

Maximum288

(ACA)

Minimum186(SLP)

Weighted average(1) 247

Weighted average

rate increase(3)

+9.4% Domestic Passenger Charges+6.3% International Passenger Charges

+6.3% in SAEs

35

99.4%

93.7%94.5%

98.0%

2015 2016 2017 2018e

MT Compliance

3 Increased on January 31, 2018.

Industry Trends1

Airline Fleets: Orders and

Expected2

Out lo o k and

I ndus t ry

3 Load Factor

Outlook and Industry | Industry Trends

Air Industry Low

Penetration in Mexico

Projected Domestic

Passenger Traffic CAGR

2016-2036

Source: World Bank. Latest information available of 2016 Source: Airbus. (Global Market Forecast 2017-2036)

37

0.30.4 0.5

0.9

2.4

2.5

Argentina Mexico Brazil Chile Canada United

States

2.0%

2.3%

3.5%

4.4%

4.8% 4.8%

5.1%

United

States

Canada Russia Mexico Brazil Brazil Central

America

117

45 44

19

0

124

51 50

19

3

125

56 56

21

8

133

70 69

21

10

131

78

71

24

10

130

78

70

24

10

Historical Airline Fleets and Available SeatsAirplanes

Outlook and Industry | Airline Fleets: Orders and Expected

Source: Airlines latest fleet information available. Estimated seats, based on fleet.

38

2013 2014 2015 2016 2017 1Q18

Fle

et

Ava

ilab

le S

ea

ts

13,321 14,944 15,335

16,723 18,268 17,846

6,222 6,594 7,917

8,722

10,698 10,698

7,230 8,160

9,296

12,282 12,574 12,400

2,812 2,972 3,472 3,600

4,512 4,512

-

150

400

500 500 500

Outlook and Industry | Airline Fleets: Orders and Expected

Source: DGAC, Airlines. Latest information available.

Airline Expansion Orders

(2013 – 2022)

39

100

80

5547

Aeromexico Interjet Vivaaerobus Volaris

G r u p o A e r o p o r t u a r i o d e l C e n t r o N o r t e , S . A . B . , d e C . V.

Chief Financial OfficerRuffo Pérez Pliego | [email protected] | +52.81.8625.4300

Investor RelationsEmmanuel Camacho | [email protected] | +52.81.8625.4308