What is an appropriate VAT rate in Afghanistan?

22

University of Central Asia Graduate School of Development Institute of Public Policy and Administration Certificate in Policy Analysis (What is the Appropriate Value Added Tax (VAT) Rate in Afghanistan?) Mohammad Aqeel Tahery

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of What is an appropriate VAT rate in Afghanistan?

University of Central Asia

Graduate School of Development

Institute of Public Policy and Administration

Certificate in Policy Analysis

(What is the Appropriate Value Added Tax (VAT) Rate inAfghanistan?)

Mohammad Aqeel Tahery

Kabul 2015

Table of Content

1. Introduction …………………………………………………………………………………...1

2. Problem description ………………………………………………..…………………………3

2.1Problem statement...………………………………………………………………………3

2.2 Symptoms of the Problem………………………………………………………………..3

2.3Scope of the problem...……………………………………………………………...…….3

2.4External factors...……………………………………………………………………….....4

2.5Stake holders…………………………………………..……………………………….….4

2.6 Problem Evaluation need………………………..………………………………….…….5

3. Policy Alternatives……………….……………………...…………………………………….6

4. Recommendation……………………………………………………………………………....8

5. Evaluation ……………………………………………………………………………………..9

5. Limitations…………………………………………………………………………………....10

6. Conclusion……………………………………………………………………………………10

References

Tables

Table 1……………………………………………………………….…………………….5

Abstract:

Economic instability of Afghanistan and its reliability on foreign aids caused the

government decide to seek new revenue sources, one of them application of VAT in the

country which subsequently issues of its different aspects raised; VAT rate as most

significant ones which caused that government post pond VAT application twice for two

years to find the most appropriate VAT rate combination (including zero rate and

exemptions) that could be acceptable to all stake holders. This paper is intended to

provide general background and recommendation for VAT rate in Afghanistan that

could be acceptable to all stakeholders, first section describes the main features and

aspects of VAT rate issue, section II focuses on alternatives for current VAT rate in

context of three options (Option 1: Reducing Standard VAT rate Option 2: Increasing

standard VAT rate Option 3: Multi VAT rate system), section III recommends Multi VAT

rates system option for the issue of VAT rate, section IV summarizes the main

conclusions and evaluation of the alternative.

1. Introduction:

The economy of Afghanistan has improved significantly since 2002

due to the infusion of multi-billion US dollars in international

assistance and investments, as well as remittances from experts.

It is also due to dramatic improvements in agricultural

production. However, Afghanistan still remains poor for now and

highly dependent on foreign aid.

Afghan government must consider ways to raise their revenue by

consider new sources of revenue to solve revenue and expenses gap

in national budget, in addition, it is a significant and growing

problem across Afghanistan that undermines security, development,

state and democracy-building.

Considering the economic and trading situation of Afghanistan

along security issues which caused that government seek new

revenue sources to increase national annual revenues, government

has intended to apply VAT as a tax revenue and as one of the main

conditions of IMF for supporting Afghanistan, so issues raised

along the process of implementation that the main one can be

considered that: what can be an appropriate combination of VAT

rates in economic context of Afghanistan?

Value added tax as a source of tax revenue for government and the

main effects of its rate on national budget and businesses in

Afghanistan along effect of VAT rate on specific goods and

services elasticity and cross border trades, need public and

businesses support on VAT rate which is going to be implemented

in Afghanistan so there must be a rate which can be accept able

for public and be profitable for government.

Middle Asian and south Asian countries neighbor to Afghanistan

all has applied VAT, considering it as a main source of revenue

(e.g. India) by different VAT rate relative to their economic

situation and the combination of global spread of VAT and the

rapid globalization of economic activity which has resulted in an

interaction between VAT systems, along with increasing VAT rate

have raised the profile of VAT as a significant issue in cross

border trades as a great source of revenue for countries which

shows the importance of VAT implementation in low revenue

countries like Afghanistan.

There is no agreed framework for application of VAT in cross

border trade in the region so the absence of such framework has

increased the uncertainty and complexity of VAT application in

Afghanistan, raising several issues including appropriate VAT

rate combination for goods and services.

An overview of obstacles and opportunities ahead of VAT

application and decision for the right VAT combination rate along

exemptions and public and businesses feedback to it as affected

ones will be helpful for Ministry of Finance as the government

body for its application and controller in Afghanistan which has

been in struggle of application of VAT in past recent years.

2. Problem description:

2.1 Problem statement: VAT is a direct revenue source to

government like an indirect tax to people that on each

transaction of goods and services VAT is charged and passed to

buyer that at last the consumer will pay so its rate will have

significant impact on people. VAT rate one of the main issues

that caused VAT application being post pond has raised tensions

between the stakeholders about the most appropriate rates that

can be applied which has both support and incentive of the public

and for the businesses in the country along being congruent

enough with the regional VAT rates.

2.2 Symptoms of the Problem: Lack of reliable information

regarding public trends and high corruption in government that

caused unreliability of public from government and unstable

trading system in Afghanistan were the main obstacles against

choosing an appropriate VAT rate Combination.

2.3 Scope of the Problem: Middle Asian and south Asian

countries neighbor to Afghanistan all has applied VAT,

considering it as a main source of revenue (e.g. India) by

different VAT rate relative to their economic situation and the

combination of global spread of VAT and the rapid globalization

of economic activity which has resulted in an interaction between

VAT systems. As VAT is going to be applied on businesses that

have more than 200 million Afghani year turnover the 500

businesses which VAT is going to apply on will have less burden

except more paper works and the public as the main payers of

taxes which is being determined by VAT rate and Ministry of

Finance as its applier and controller will be involved in

struggling with the issue. So an appropriate VAT rate in matrix

of mentioned perspectives of the issue is needed to be chosen.

2.4 External factors: Along economic situation of

Afghanistan which is highly unstable and relied on foreign aids

and unfair political competitions of neighboring countries which

always want Afghanistan as a weak country beside them and

regional trading systems, all had their effects on VAT rate in

Afghanistan.

Pre mentioned factors have been used as leverage from outside

over weakness of government for choosing an appropriate VAT rate

in the country so their negative effects were somehow

supplemented of current issue.

2.5 Stakeholders: People of Afghanistan as the one of burden

suffering groups on this issue like other people of the world are

not interested in having new tax along other ones that are paying

and for sure their feedbacks by its nature will have great impact

on application of VAT chosen rate by government as the main

stakeholder.

Businesses that are the main economic chains of the country are

the ones who have to manage the prices in market that they can

survive their businesses, sell their goods and services along

doing the challenging paper works so regarding their number and

amount of money they do work with will not be interested in

having all mentioned problems ahead of their businesses when

there be an absence of appropriate VAT rate.

Ministry of Finance as the planner and controller of VAT rate in

one aspects will generate more revenue for government by choosing

high rate but in other aspect gaining public support and keeping

businesses on their track along balancing trading attractiveness

of country for businesses will have lots to do and the power to

positive and negative influence on the issue.

Media and government survey publications along meetings with

regional public representatives and business associations for

having their opinions and level of acceptance of the issue will

be good ways of involving all stakeholders.

2.6 Problem Evaluation need: Regional integration is now

forcing countries to harmonize their taxation system in order to

avoid competitive distortions across countries. This means that,

without special measures, goods will be taxed twice if they are

exported from one country that does have different VAT rate to

another country or has sales tax instead. Vice versa, goods that

are imported from a VAT-free country into another country with

VAT will result in no sales tax and only a fraction of the usual

VAT. There are also significant differences in taxation for goods

that are being imported / exported between countries with

different rate of VAT.

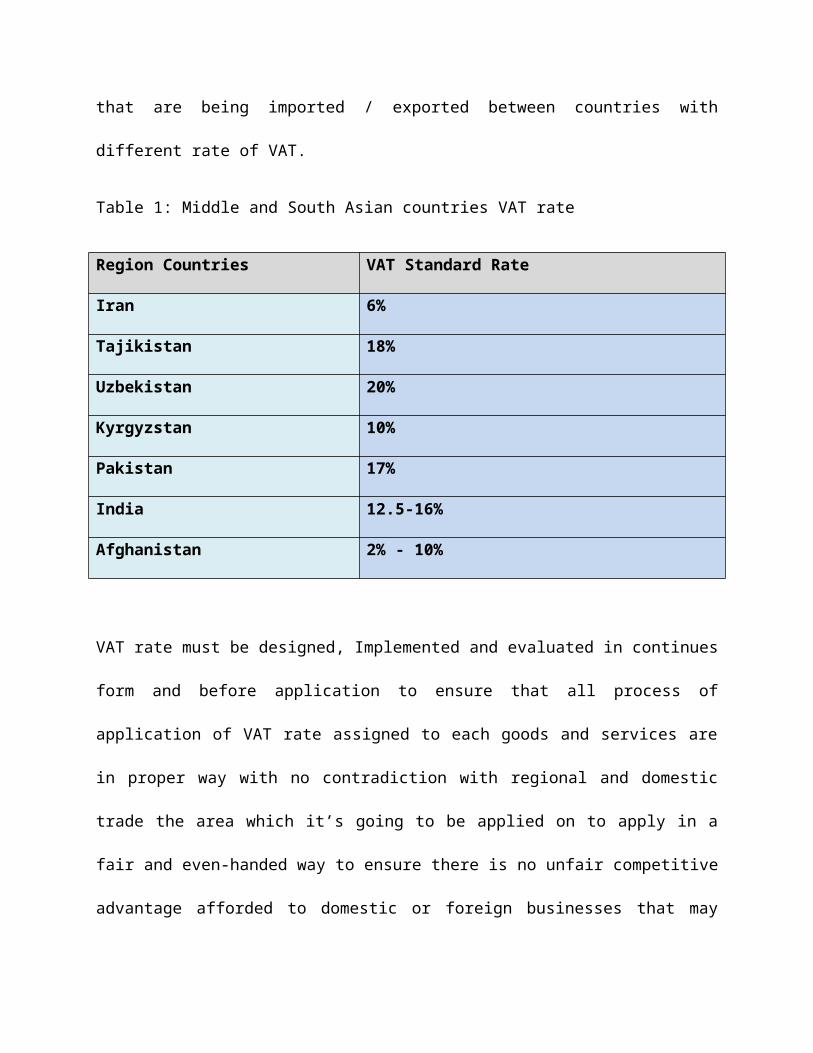

Table 1: Middle and South Asian countries VAT rate

Region Countries VAT Standard Rate

Iran 6%

Tajikistan 18%

Uzbekistan 20%

Kyrgyzstan 10%

Pakistan 17%

India 12.5-16%

Afghanistan 2% - 10%

VAT rate must be designed, Implemented and evaluated in continues

form and before application to ensure that all process of

application of VAT rate assigned to each goods and services are

in proper way with no contradiction with regional and domestic

trade the area which it’s going to be applied on to apply in a

fair and even-handed way to ensure there is no unfair competitive

advantage afforded to domestic or foreign businesses that may

otherwise distort international trade and limit consumer choices

and buying ability.

3. Policy alternatives:

Taking all aspects of the issue into consideration the following

are four options for the issue of appropriateness of the VAT

rate:

Option 1: Reducing Standard VAT rate

Option 2: Increasing standard VAT rate

Option 3: Multi VAT rates system

Afghan Government by Considering the economic situation of

Afghanistan which is highly unstable and mostly depended to

foreign aids specially in security sectors and the need of

development projects for tackling the fiscal problems that

Afghans are facing, has chosen multiple revenue generating

sources and systems to be developed, implemented and used that

VAT was the second chosen one.

As Afghan government policies have sat VAT as one of revenue

sources to fill the gap of losing foreign aids in national

budget, government revenues from this tax system must be proper

to be relied on, so as much the VAT rate are high government

revenues will be more at the customs also in domestic

transactions.

Increasing VAT rate from its current 8 % rate politically and

economically will be a solution to part of current fiscal crisis

in Afghanistan as government revenues will increase along that

and from jurisdictional perspective since there is high VAT rate

in region will make less impact to regional trade and businesses

with Afghanistan and in other hand higher VAT rate than 8 % will

make Afghanistan VAT rate closer to balanced VAT rate in the

region which makes easier feasibility and more efficient

application of VAT rate but Experience has shown that when a VAT

rate is increased, some retailers use this Opportunity to further

increase prices above Budget day increase, which would add to the

effect On inflation. The higher VAT rate makes the VAT

politically unacceptable and will put upward pressure on

inflation.

Reducing VAT standard rate which is 8% for now can be considered

as an incentives for more private sector and foreign investments

when there is less tax over there transactions and imports

specially when there is high VAT tax rate in neighboring

countries also the real burden suffering group which is the

public will show less resistance to the tax implementation which

is a huge privilege to government, its impact over trade and

regional businesses will be there however.

Reducing VAT rate will provide more flexibility for businesses

and public over there decisions with lower taxes which a more

efficient VAT rate therefore could reduce the VAT finally paid by

the citizens.

Using multiple VAT rate for transactions and imports is one of

the most time burdening and hard works in VAT from perspective of

its administrative feasibility and jurisdictional case which is a

big problem for Afghan government at the current situation and

needs expertise that could assign different rate for different

goods properly but when there is multiple rate for different

goods and services from one side it will keep peoples buying

ability high for inelastic goods and services and from other side

it will be revenue generating engine for government, at the same

time less disincentives will be made for businesses and

transactions; Multiple VAT rate will bring equity of tax paying

for different public levels.

4. Recommendation:

Each option above had implications for the implementation, cost,

effectiveness, political, economic and jurisdiction perspective

so based on detailed analysis of above options it is recommended

that Ministry of Finance consider the third option, Multiple VAT

rate System.

Although the VAT may become a “money machine,” as usually

acclaimed, but only if it is coherent in rate structuring and

broad-based. The practical advice is that the VAT rate structure

be designed as coherent as possible, preferably with multiple

standard rates, few exemptions, and zero rating being exclusively

granted to exports. Broadening base, in general sense, reduces

deadweight loss and provides an opportunity for lowering the rate

for inelastic goods and thereby, increasing compliance, from a

theoretical point of view there is no presumption that a single

VAT rate will minimize economic distortions, multiple rate may,

however, offer a greater opportunity to fit the VAT to various

social and political ends (Gillis, 1990: 12). If so designed, the

VAT is effective and efficient.

All registered businesses are obligated by law to issue VAT

invoices when conducting transactions with other VAT registered

businesses. When conducting business with unregistered

businesses and the final consumer, sellers are obligated to issue

a sales receipt showing the cost of the item and the amount of

VAT paid by the unregistered person.

Invoice based VAT rate show the price of buying and selling so

need high level of record keeping and accounting and severe

administrative capacity when there is more than one rate; the

problem is already solved for ministry of finance by national tax

controlling, monitoring and administer database.

Multiple rate structure is inherently complex, but yet it is

argue able for it on both efficiency and equity grounds. The

rule specifies that to overcome the issue the followings are

recommendations to Ministry of Finance:

Tax rate on a good should be set inversely proportional to

the good’s own demand elasticity.

It implies that the rate should be differentiated across

different groups of goods and services of various demand

elasticity. Lower rate must be applied to the goods and

services consumed primarily by the poor.

The possibility of VAT differentiation for different goods

and services has been raised.

The intention is to influence consumer demand for goods

which represents negative or positive effects in production,

by using high and low VAT rate, respectively.

Lower VAT rate on labor intensive services have also been

suggested as a means to promote employment.

5. Evaluation:

The evaluation purpose is to apply a practical, implementable and

comprehensive VAT rates combination in the country to achieve the

desired outcome after implementation of the recommendations so

based on ministry vision to have reliable, creditable and public

supported VAT rate, evaluation framework involves all

stakeholders and legislative authorities that could gain their

support and be politically and financially acceptable.

The costs for the evaluation will be determined according the

procurement sources and the selected approaches but estimably it

will be around 100000 AF for the process.

6. Limitations:

Budgetary: There will be less budgetary limits for

implementation of the recommended VAT rate due Ministry of

Finance as VAT applier and controller has a coherent system which

is used for all taxes in Afghanistan including databases for

registration, invoices printing and creation and tax collection

that can be considered as a pre provided base for VAT rate.

Time: Thinking of fiscal crisis and foreign aids reduction

along transition phase that Afghanistan is passing through

applying the recommended VAT rate is essential as soon as

possible for overcoming the low revenue issue as part.

Resources: As ministry of Finance already has the mentioned

coherent revenue system there will be no limits for equipment but

in case of qualified personnel there will be needs of experts in

the field however of experienced taxing staff.

7. Conclusion:

Considering economic situation of afghan people along that the

fiscal crisis which government is struggling with, two different

scope which effects the VAT rate in Afghanistan which shows that

VAT rate must be as low as possible to lower the pressure over

the public with low economic level and at the same time be used

as a source of revenue for government so the rate which can be

fit to both circumstances, along considering interests of

stakeholders has to gain the public trust who have to burden the

tax rate.

Reducing and increasing current VAT rate will only fulfill one

aspect of the issue, the government needs or public desire of low

taxes and interests of multiple stakeholders along different VAT

rates of regional countries over trading goods with Afghanistan

will not be all considered with mentioned alternatives of current

VAT rate.

Multiple VAT rates over goods and services creditably

differentiated according to their elasticity for people and

ongoing trading situation of country can be the best option for

addressing all perspectives of the issue.

Afghan government along all budgetary and resources limitations

and the shortage of time to over comes the issue must have a

well-planned, budgeted and realistic evaluation process prior

considering implementation of the changes in the VAT rate when

applying recommended multi rate VAT.

References:

Afghanistan Revenue Department (VAT Overview Booklets)

Afghanistan Revenue Department (VAT Brochures)

Andrew M C Smith, Ainul Islam & M. Moniruzzaman(2011) “

Consumption Taxes In Developing Countries” Victoria University Of Wellington.

Working Paper No. 82

Bird, R.M & Gendron, P-P (2006) “Is VAT Best Way To Impose

General Consumption Tax In Developing Countries?” International

Studies Program, Working Paper 06-17

Bird, R.M & Gendron, P-P (2010) “What Do (And Don’t) We Know

About the Value Added Tax?” Challenges from Globalization Ii

OECD (2014) “International VAT/GST Guidelines” Global Forum on VAT

OECD (2014) “Consumption Tax Trends 2014” OECS Publishing.

Http://Dx.Doi.Org/10.1787/Ctt-2014-En

Richard M. Bird (2005) “Value-Added Taxes in Developing and

Transitional Countries: Lessons and Questions” International Tax Program

Sternlieb, S (2014) “Inadequate Revenue Threatens Afghanistan’s

Stability” International Journal of Security & Development.

Http://Dx.Doi.Org/10.5334/Sta.Dl

Tuan Minh Le (2003) “Value Added Taxation: Mechanism, Design, and

Policy Issues” World Bank