The role of commercial banks in financing small, medium and ...

THE INFLUENCE OF CREDIT RISK MANAGEMENT ON FINANCIAL PERFORMANCE

OF COMMERCIAL BANKS IN KENYA

OYUGI FREDRICK OTIENO

STUDENT REG.NO.HD 433-C004-1681/2013

DBA 4112 FINANCE SEMINAR

ABSTRACT

Financial risk in a banking organization is possibility that the

outcome of an action or event could bring up adverse impacts.

Such outcomes could either result in a direct loss of earnings or

capital or may result in imposition of constraints on bank’s

ability to meet its business objectives. This study evaluates the

influence of credit risk management on financial performance of

Commercial Banks in Kenya.

Descriptive, correlation and regression techniques were used in

the analysis. The findings revealed that credit management has a

significant impact on the financial performance of Kenyan banks.

i

Therefore, it is recommended that Commercial Banks need to be

cautious in setting up a credit policy that might not negatively

affect their financial performance.

ii

TABLE OF CONTENTS

ABSTRACT.......................................................i

CHAPTER ONE....................................................11.0 INTRODUCION................................................11.1 Statement of the problem...................................21.2 General Objective..........................................3

1.2.1 Specific Objectives....................................31.3 Research Questions.........................................41.4 Research Scope.............................................4

CHAPTER TWO....................................................5LITERATURE REVIEW..............................................52.1 Credit Risk Management Strategies..........................52.2 Theoretical Review.........................................9

2.2.1 Portfolio theory.......................................92.2.2 Arbitrage Pricing Theory (APT)........................102.2.3 Information Theory....................................10

2.3 Conceptual Framework……………………………………………………………………..…………………………………………….10

2.3 Empirical Review..........................................11

CHAPTER THREE.................................................14THE METHODOLOGY...............................................14

CHAPTER FOUR..................................................15RESULTS AND FINDINGS..........................................154.1 Credit guarantee..........................................154.2 Credit monitoring.........................................15

iii

4.3 Loan Security.............................................164.4 Credit approval process...................................164.5 Credit appraisal analysis.................................164.6 Credit risk scoring.......................................174.7 Conclusion and Recommendations............................17REFERENCES....................................................19

APPENDIX 1:LIST OF COMMERCIAL BANKS...........................22

iv

CHAPTER ONE

1.0 INTRODUCION

Lending is an integral element of banking business; it is itself

at the heart of an economy’s financial architecture. It therefore

behoves policy makers to continually review the credit market to

minimize inefficiencies that hinder faster economic growth.

Credit risk is the current and prospective risk earnings or

capital arising from an obligor’s failure to meet the terms of

any contract with the bank or otherwise to perform as agreed

(Kargi, 2011). Credit risk management is a structured approach to

managing uncertainties through risk assessment developing

strategies to manage it, and mitigation of risk using managerial

resources. The strategies include transferring to another party,

avoiding the risk, reducing the negative effects of the risk and

accepting some or all of the consequences of a particular risk.

Credit risk management is very important to banks as it is an

integral part of the loan process. It maximizes bank risk,

adjusted risk rate of return by maintaining credit risk exposure

with view to shielding the bank from the adverse effects of

credit risk

When banks grant loans, they expect the customers to repay the

principal and interest on an agreed date. A credit facility is

said to be performing if payment of both principal and interest

are up to date in accordance with agreed repayment terms. The

non-performing loans (NPLs) represent credits which the banks

perceive as possible loss of funds due to loan defaults. They are

1

further classified into substandard, doubtful or lost. Bank

credit in lost category hinders bank from achieving their set

target (Kolapo et al., 2012).

Financial performance is company’s ability to generate new

resources, from day- to- day operations, over a given period of

time; performance is gauged by net income and cash from

operations. A bank is a commercial or state institution that

provides financial services, including issuing money in various

forms, receiving deposits of money, lending money and processing

transactions and the creating of credit (Campel, et. al., 1993).

Credit risk management models include the systems, procedures and

control which a company has in place to ensure the efficient

collection of customer payments and minimize the risk of non-

payment. The high level of non-performing loans is a challenge to

many commercial banks in Kenya, which is evidence that commercial

banks are faced by a big risk of their credit. Commercial banks

are vital institutional framework for national development

because they contribute about 50 percent of the Gross Domestic

Product. Lending in commercial banks is the main source of making

profit hence need for efficient credit risk management practices

within the industry.

Financial institutions are exposed to a variety of risks among

them; interest rate risk, foreign exchange risk, political risk,

market risk, liquidity risk, operational risk and credit risk

(Yusuf, 2003; Cooperman, Gardener and Mills, 2000). In some

2

instances, commercial banks and other financial institutions have

approved decisions that are not vetted; there have been cases of

loan defaults and non-performing loans, massive extension of

credit and directed lending. Policies to minimize on the negative

effects have focused on mergers in banks and NBFIs, better

banking practices but stringent lending, review of laws to be in

line with the global standards, well capitalized banks which are

expected to be profitable, liquid banks that are able to meet the

demands of their depositors, and maintenance of required cash

levels with the central bank which

means less cash is available for lending (Central Bank Annual

Report, 2004). This has led to reduced interest income for the

commercial banks and other financial institutions and by

extension reduction in profits (De Young et al, 2001). Banks are

investing a lot of funds in credit risk management modeling. The

case in point is the Basel 11 accord.

1.1 Statement of the problem

The Banking sector is currently facing pressure from both the

Government and the Public to lower the interest rates on loans.

On the other hand Banks are facing various challenges like non-

performing loans, stagnant interest rates, mobile money transfer

services which have greatly affected their profitability.

Hence Commercial Banks in their efforts to reduce the impact of

non-performing loans and mobile money transfer, have adopted new

Credit Risk Management techniques and Agency Banking.

3

According to Besis (2005) Risk management is important to Bank

management because banks are ‘risk machines’ they take risks;

they transform them and embed them to banking products and

services. Risks are uncertainties resulting in adverse

variations of profitability or in losses.

Various risks faced by commercial banks include credit risk,

market risks, interest rates risk, liquidity risk and operational

risk. (Shubhasis,2005).

A surge in bad debts and flat growth in interest income has

slowed down Equity Banks profitability.The banks are feeling the

heat of a new Central Bank of Kenya directive on the treatment of

non-performing loans which has inflated their bad debts book and

forced them to set aside additional cash as provision for

defaulters. (Business Daily dated 24th February 2014).

Locally Ndung’u (2003) in his study on the determinants of

profitability of quoted Commercial Banks in Kenya finds that

sound asset and liability management had a significant influence

on profitability.

Ngumi (2013) found that Bank innovations namely automated teller

machines, debit and credit cards, interest Banking, mobile

banking, electronic funds transfer and point of sale terminals

had statistically significant influence on financial performance

of Commercial Banks in Kenya.

4

Based on these studies performed and risk of non-performing loans

and competition faced by Banks in Kenya, there is need to conduct

a study to evaluate the influence of Credit Risk Management on

Financial Performance of Commercial Banks in Kenya.

1.2 General Objective

The study will seek to establish the effects of Credit risk

management on Financial Performance of Commercial Banks in Kenya.

1.2.1 Specific Objectives

i) To determine the effect credit guarantees have on financial

performance of commercial banks in Kenya.

ii) To determine the effect of loan security on financial

Performance of commercial banks in Kenya.

iii) To determine the effect of credit risk scoring on financial

performance of commercial banks in Kenya

iv) To determine the effect of credit appraisal analysis on

financial performance of commercial banks in Kenya.

v) To determine the effect of credit approval process and

sanctions on financial performance of commercial banks.

vi) To establish the moderating effect of Central Bank of Kenya

regulations.

vii) To establish the moderating effect of Government Regulations

1.3 Research Questions

i) What is the effect of credit guarantees on the financial

performance of Kenyan commercial banks

5

ii) What is the effect of loan security on the financial

performance of commercial banks in Kenya?

iii) Does credit risk scoring impact on the financial

performance of banks in Kenya?

iv) What is the effect of credit appraisal analysis on the

financial performance of Kenyan banks?

v) Does credit approval process and sanctions impact on a

bank’s financial performance

vi) What is the moderating effect of central bank of Kenya’s

regulations?

vii) What is the moderating effect of government regulations?

1.4 Scope

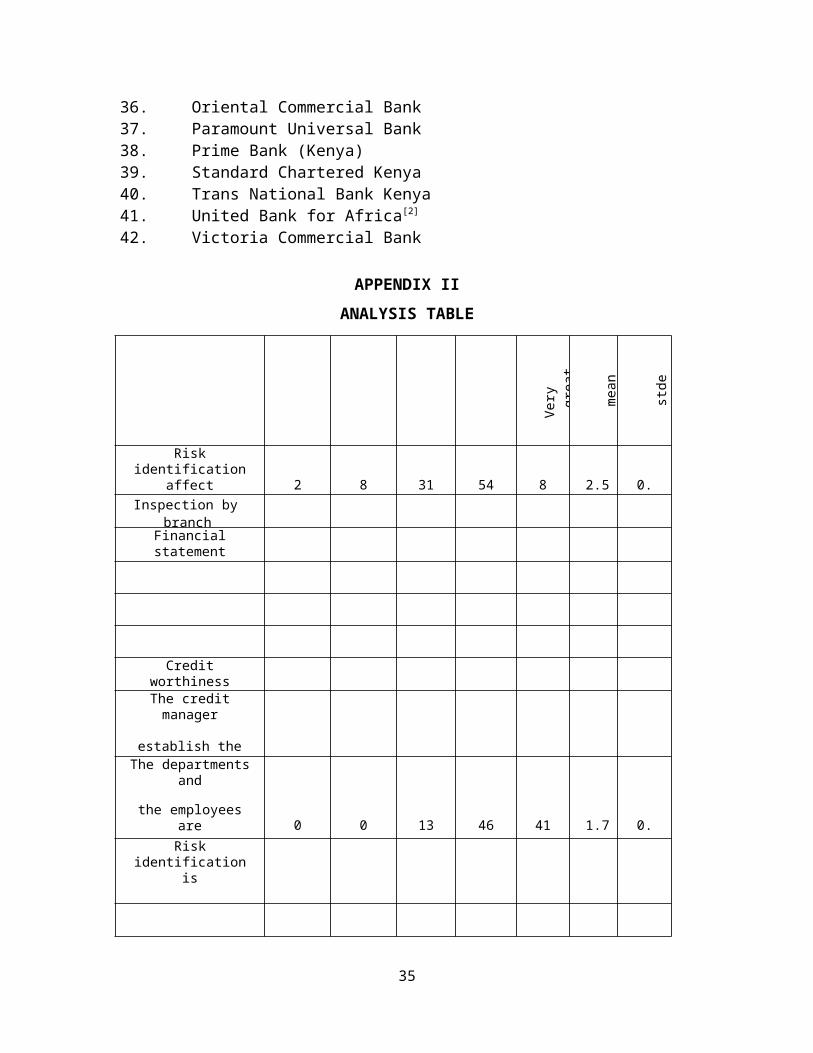

The study covered 42 commercial banks licenced by the CentralBank of Kenya. The commercial banks that formed the units of analysis are those that were in operation by close of business on 31st December, 2013.

6

CHAPTER TWO

2.0 LITERATURE REVIEW

A bank exists not only to accept deposits but also to grant

credit facilities, therefore inevitably exposed to credit risk.

Credit risk is by far the most significant risk faced by banks

and the success of their business depends on accurate measurement

and efficient management of this risk to a greater extent than

any other risks (Gieseche, 2004). According to Chen and Pan

(2012), credit risk is the degree of value fluctuations in debt

instruments and derivatives due to changes in the underlying

credit quality of borrowers and counterparties. Coyle (2000)

defines credit risk as losses from the refusal or inability of

credit customers to pay what is owed in full and on time. Credit

risk is the exposure faced by banks when a borrower (customer)

defaults in honoring debt obligations on due date or at maturity.

This risk interchangeably called ‘counterparty risk’ is capable

of putting the bank in distress if not adequately managed. Credit

risk management maximizes bank’s risk adjusted rate of return by

maintaining credit risk exposure within acceptable limit in order

to provide framework for understanding the impact of credit risk

management on banks’ profitability (Kargi, 2011). Demirguc-Kunt

and Huzinga (1999) opined that credit risk management is in two-

fold which includes, the realization that after losses have

occurred, the losses becomes unbearable and the developments in

the field of financing commercial paper, securitization, and

7

other non-bank competition which pushed banks to find viable loan

borrowers.

The main source of credit risk include, limited institutional

capacity, inappropriate credit policies, volatile interest rates,

poor management, inappropriate laws, low capital and liquidity

levels, direct lending, massive licensing of banks, poor loan

underwriting, laxity in credit assessment, poor lending

practices, government interference and inadequate supervision by

the central bank (Kithinji, 2010).An increase in bank credit risk

gradually leads to liquidity and solvency problems. Credit risk

may increase if the bank lends to borrowers it does not have

adequate knowledge about.

2.1 Credit Risk Management Strategies

The credit risk management strategies are measures employed by

banks to avoid or minimize the adverse effect of credit risk. A

sound credit risk management framework is crucial for banks so as

to enhance profitability guarantee survival. According to

Lindergren (1987), the key principles in credit risk management

process are sequenced as follows; establishment of a clear

structure, allocation of responsibility, processes have to be

prioritized and disciplined, responsibilities should be clearly

communicated and accountability assigned. The strategies for

hedging credit risk include but not limited to these;

i. Credit Derivatives: This provides banks with an approach which

does not require them to adjust their loan portfolio. Credit

8

derivatives provide banks with a new source of fee income and

offer banks the opportunity to reduce their regulatory capital

(Shao and Yeager, 2007). The commonest type of credit derivative

is credit default swap whereby a seller agrees to shift the

credit risk of a loan to the protection buyer. Frank Partnoy and

David Skeel in Financial Times of 17 July, 2006 said that “credit

derivatives encourage banks to lend more than they would, at

lower rates, to riskier borrowers”. Recent innovations in credit

derivatives markets have improved lenders’ abilities to transfer

credit risk to other institutions while maintaining relationship

with borrowers (Marsh, 2008).

ii. Credit Securitization: It is the transfer of credit risk to a

factor or insurance firm and this relieves the bank from

monitoring the borrower and fear of the hazardous effect of

classified assets. This approach insures the lending activity of

banks. The growing popularity of credit risk securitization can

be put down to the fact that banks typically use the instrument

of securitization to diversify concentrated credit risk exposures

and to explore an alternative source of funding by realizing

regulatory arbitrage and liquidity improvements when selling

securitization transactions (Michalak and Uhde,2009). A cash

collateralized loan obligation is a form of securitization in

which assets (bank loans) are removed from a bank’s balance sheet

and packaged (tranched) into marketable securities that are sold

on to investors via a special purpose vehicle (SPV) (Marsh,2008).

9

iii. Compliance to Basel Accord: The Basel Accord are

international principles and regulations guiding the operations

of banks to ensure soundness and stability. The Accord was

introduced in 1988 in Switzerland. Compliance with the Accord

means being able to identify, generate, track and report on risk-

related data in an integrated manner, with full auditability and

transparency and creates the opportunity to improve the risk

management processes of banks. The New Basel Capital Accord

places explicitly the onus on banks to adopt sound internal

credit risk management practices to assess their capital adequacy

requirements (Chen and Pan, 2012).

iv. Adoption of a sound internal lending policy: The lending

policy guides banks in disbursing loans to customers. Strict

adherence to the lending policy is by far the cheapest and

easiest method of credit risk management. The lending policy

should be in line with the overall bank strategy and the factors

considered in designing a lending policy should include; the

existing credit policy, industry norms, general economic

conditions of the country and the prevailing economic climate

(Kithinji,2010).

v. Credit Bureau: This is an institution which compiles

information and sells this information to banks as regards the

lending profile of a borrower. The bureau awards credit score

called statistical odd to the borrower which makes it easy for

banks to make instantaneous lending decision. Example of a credit

10

bureau is the Credit Risk Management System (CRMS) of the Central

Bank of Kenya (CBK)

11

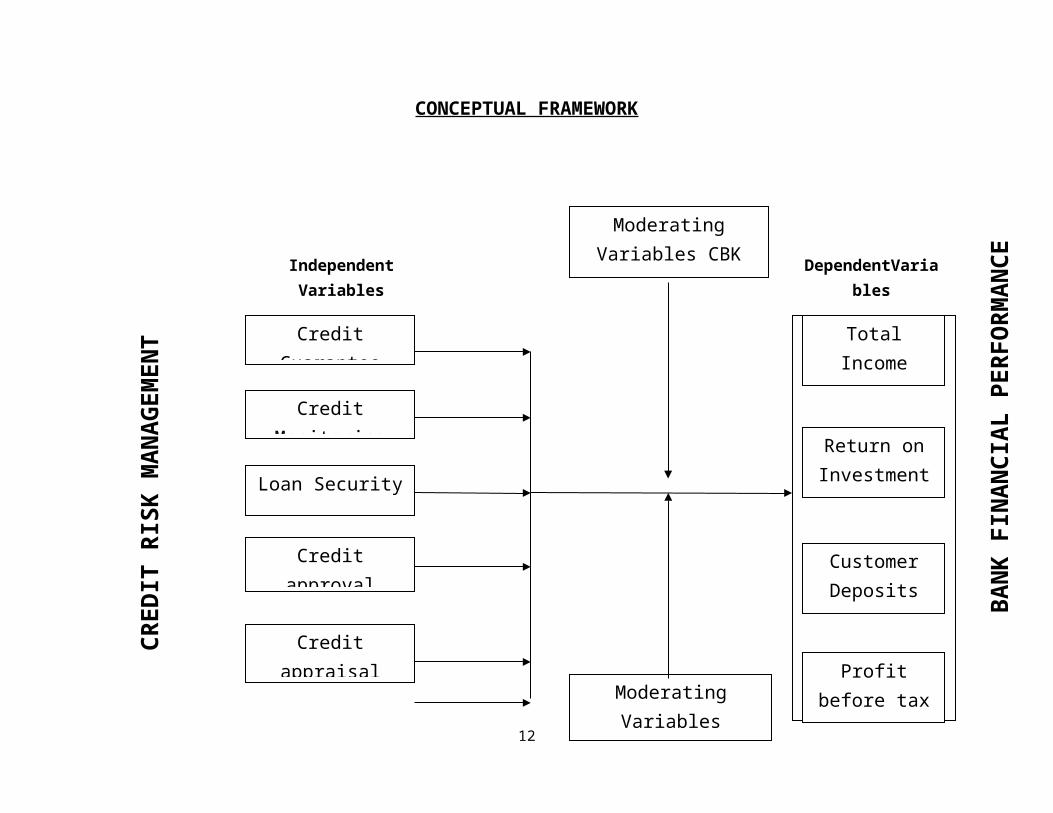

CONCEPTUAL FRAMEWORK

12

ModeratingVariables CBKRegulations

DependentVariables

TotalIncome

ModeratingVariablesGovernment

Profitbefore tax

CustomerDeposits

Return onInvestment

s

CRED

IT R

ISK

MANA

GEME

NT

IndependentVariables

CreditGuarantee

Creditapproval

Creditappraisal

BANK

FIN

ANCI

AL P

ERFO

RMANCE

Loan Security

CreditMonitoring

13

Credit riskscoring

2.2 Theoretical Review

2.2.1 Portfolio theory

Since the 1980s, companies have successfully applied modern

portfolio theory to market risk. Many companies are now using

value at risk models to manage their interest rate and market

risk exposures. Unfortunately, however, even though credit risk

remains the largest risk facing most companies, the practice of

applying modern portfolio theory to credit risk has lagged

(Margrabe, 2007)

Companies recognize how credit concentrations can adversely

impact financial performance. As a result, a number of

institutions are actively pursuing quantitative approach to

credit risk measurement. This industry is also making significant

progress toward developing tools that measure credit risk in

portfolio context. They are also using credit derivatives to

transfer risk efficiently while preserving customer

relationships. Portfolio quality ratios and productivity

indicators have been adapted (Kairu 2009). The combination of

these developments has vastly accelerated progress in managing

credit risk in a portfolio context.

Traditionally, organizations have taken an asset-by-asset

approach to credit risk management. While each company’s method

varies, in general this approach involves periodically evaluating

the quality of credit exposures, applying a credit risk rating,

14

and aggregating the results of this analysis to identify a

portfolio’s expected losses. The foundation of the asset-by-asset

approach is a sound credit review and internal credit risk rating

system. This system enables management to identify changes in

individual credits, or portfolio trends in a timely manner. Based

on the changes identified, credit identification, credit review,

and credit risk rating system management can make necessary

modifications to portfolio strategies or increase the supervision

of credits in a timely manner. While the asset-by-asset approach

is a critical component to managing credit risk, it does not

provide a complete view of portfolio credit risk, where the term

risk refers to the possibility that actual losses exceed expected

losses. Therefore, to gain greater insight into credit risk,

companies increasingly look to complement the asset-by-asset

approach with a quantitative portfolio review using a credit

model (Mason and Roger, 1998). Companies increasingly attempt to

address the inability of the asset-by-asset approach to measure

unexpected losses sufficiently by pursuing a portfolio approach.

One weakness with the asset-by-asset approach is that it has

difficulty identifying and measuring concentration. Concentration

risk refers to additional portfolio risk resulting from increased

exposure to credit extension, or to a group of correlated

creditors (Richardson, 2002).

2.2.2 Arbitrage Pricing Theory (APT)

A more interesting alternative was the Arbitrage Pricing Theory

(APT) of Ross (1976). Stephen Ross's APT approach moved away from15

the risk vs. return logic of the CAPM, and exploited the notion

of pricing by arbitrage to its fullest possible extent. As Ross

himself has noted, arbitrage-theoretic reasoning is not unique to

his particular theory but is in fact the underlying logic and

methodology of virtually all of finance theory. This theory

subscribes to the fact that an estimate of the benefits of

diversification would require that practitioners calculate the

covariance of returns between every pair of assets. In their

Capital Asset Pricing Model (CAPM), Morris (2001) solved this

practical difficulty by demonstrating that one could achieve the

same result merely by calculating the covariance of every asset

with respect to a general market index. With the necessary

calculating power reduced to computing these far fewer terms

(betas), optimal portfolio selection became computationally

feasible.

2.2.3 Information Theory

Derban, Binner and Mullineux (2005) recommended that borrowers

should be screened especially by banking institutions in form of

credit assessment. Collection of reliable information from

prospective borrowers becomes critical in accomplishing effective

screening as indicated by symmetric information theory.

Qualitative and quantitative techniques can be used in assessing

the borrowers although one major challenge of using qualitative

models is their subjective nature. However according to Derban,

Binner and Mullineux (2005), borrowers attributes assessed

through qualitative models can be assigned numbers with the sum16

of the values compared to a threshold. This technique minimizes

processing costs, reduces subjective judgments and possible

biases. The rating systems will be important if it indicates

changes in expected level of credit loan loss. Brown Bridge

(1998, pp.173-89) concluded that quantitative models make it

possible to numerically establish which factors are important in

explaining default risk, evaluating the relative degree of

importance of the factors, improving the pricing of default risk,

screening out bad loan applicants and calculating any reserve

needed to meet expected future loan losses.

2.3 Empirical Review

There have been debate and controversies on the impact of credit

risk management andbank’s financial performance. Some scholars

e.g., (Li Yuqi 2007; Naceur and Kandil 2006; Kinthinji 2010;

Kolapo, Ayeni and Ojo 2012; Kargi 2011;) amongst others have

carried out extensive studies on this topic and produced mixed

results; while some found that credit risk management impact

positively on banks financial performance, some found negative

relationship and others suggest that other factors apart from

credit risk management impacts on bank’s performance.

Specifically, Kargi (2011) found in a study of Nigeria banks from

2004 to 2008 that there is a significant relationship between

banks performance and credit risk management. He found that loans

and advances and non-performing loans are major variables that

determine asset quality of a bank.

17

Kolapo, Ayeni and Ojo (2012) using panel data regression for the

period 2000 to 2010 found that the effect of credit risk on

bank’s performance measured by the Return on Asset (ROA) of banks

is cross sectionally invariant. They concluded that the nature

and managerial pattern of individual firms do not determine the

impact. Also, Hosna, Manzura and Juanjuan (2009) reemphasized the

effect of credit risk management on profitability level of banks.

They concluded that higher capital requirement contributes

positively to bank’s profitability. Muhammed, Shahid, Munir and

Ahad (2012) used descriptive, correlation and regression

techniques to study whether credit risk affect banks performance

in Nigeria from 2004 to 2008. They also found that credit risk

management has a significant impact on profitability of Nigerian

banks.

Boahene, Dasah and Agyei (2012) used regression analysis to

determine whether there is a significant relationship between

credit risk and profitability of Ghanain banks. They followed the

line of Hosna, Manzura and Juanjuan (2009) by using Return of

Equity as a measure of bank’s performance and a ratio of non-

performing loans to total asset as proxy for credit risk

management. They found empirically that there is an effect of

credit risk management on profitability level of Ghaninian banks.

The study also suggests that higher capital requirement

contributes positively to bank’s profitability. Li yuqi (2007)

examined the determinants of bank’s profitability and its

implications on risk management practices in the United Kingdom.

18

The study employed regression analysis on a time series data

between 1999 and 2006. Six measures of determinants of bank’s

profitability were employed. Theyproxied Liquidity,credit and

capital as internal determinants of bank’s performance. GDP

growth rate, interest rate and inflation ratewere used as

external determinants of banks profitability. The six variables

were combined into one overall composite index of bank’s

profitability. Return on Asset (ROA) was used as an indicator of

bank’s performance. It was found that liquidity and credit risk

have negative impact on bank’s profitability.

Poudel (2012) appraised the impact of the credit risk management

in bank’s financial performance in Nepal using time series data

from 2001 to 2011. The result of the study indicates that credit

risk management is an important predictor of bank’s financial

performance. Fredrick

(2010) demonstrated that credit risk management has a strong

impact on bank’s financial performance in Kenya. Meanwhile,

Jackson (2011) towed the line of Fredrick (2010) by using CAMEL

indicators as independent variables and return on Equity as a

proxy for banks performance. His findings were also in line with

that of Fredrick who also concluded that CAMEL model can be used

as proxy for credit risk management. Musyoki and Kadubo (2011)

also found that credit risk management is an important predictor

of bank’s financial performance; they concluded that banks

success depends on credit risk management.

19

Onaolapo (2012), while analyzing the credit risk management

efficiency in Nigerian commercial banking sector from 2004

through 2009 provides some further insight into credit risk as

profit enhancing mechanism. They used regression analysis and

found rather an interesting result that there is a minimal

causation between deposit exposure and bank’s performance.

Kithinji (2010) analyzed the effect of credit risk management

(measured by the ratio of loans and advances on total assets and

the ratio of non-performing loans to total loans and advances on

return on total asset in Kenyan banks between 2004 to 2008). The

study found that the bulk of the profits of commercial banks is

not influenced by the amount of credit and non-performing loans.

The implication is that other variables apart from credit and

non-performing loans impact on banks’ profit. Kithinji (2010)

result provides the rationale to consider other variables that

could impact on bank’s performance.

The Basel Committee on Banking Supervision(1999) asserts that

loans are the largest and most obvious source of credit risk,

while others are found on the various activities that the bank

involve itself with. Therefore, it is a requirement for every

bank worldwide to be aware of the need to identify measure,

monitor and control credit risk while also determining how credit

risk could be lowered. This means that a bank should hold

adequate capital against these risks and that they are adequately

compensated for risk incurred. This is stipulated in Basel II,

which regulates banks about how much capita they need to put

20

aside against these types of financial and operational risks they

face.

In response to this, commercial banks have almost universally

embarked upon an upgrading of their risk management and control

systems. Also, it is in the realization of the consequence of

deteriorating loan quality on profitability of the banking sector

and the economy at large that this work is motivated.

21

CHAPTER THREE

THE METHODOLOGY

The study used descriptive research design. The target population

of this study was management staff working in commercial banks of

the top, middle and low level management ranks. The sample size

was about 440 respondents. The data collection instruments were

questionnaires. Qualitative datacollected was analyzed by

descriptive statistics using SPSS and presented through

percentages,means, standard deviations and frequencies. For this

study, the researcher was interested inmeasuring the effect of

credit risk management on the financial performance of commercial

banks in Kenya. The factors are β (independent variables) and

dependent variable isY.

The study adapted a model similar to that used by Gakure, R. W.,

Ngugi, J. K., Ndwiga, P. M., &Waithaka, S. M. (2012). Which

studied the effect of credit risk management techniques on the

performance of unsecured bank loan employed by commercial banks

in Kenya?

Y= β0+ β1X1+β2X2+ β3X3+ β4X4+ β5X5+ β6X6 +α

Where;

Y =Bank performance (Profit before tax)22

β0=Regression coefficientβ1, β2, β3, β4, β5= Slopes of regression equation.

X1 = Credit guarantee

X2 =Credit monitoring

X3=Loan security

X4=Credit approval process

X5 =Credit appraisal analysis

X6 =Credit risk scoring

α= Error term (assumed to be zero)

The equation was solved by the use of statistical model applying SPSS.

CHAPTER FOUR

RESULTS AND FINDINGS

4.1 Credit guarantee

From the findings, it was observed that credit guarantee affects

financial performance of commercial banks to a moderate extent as

indicated by a mean of 2.7. This is because most of the customers

wishing to take up banks services like loans do not have

sufficient guarantee hence most of them would rather not take up

the service. This is lost business opportunity for the bank hence

low profits.

23

4.2 Credit monitoring

From the findings, the respondents indicated that risk monitoring

moderately affected bank’s performance as indicated by a mean of

2.4. The respondents indicated that controls in place and

responses in place affected the bank’s profitability to a great

extent as indicated by a mean of 2.6, the respondents indicated

that reporting and review affected the performance to a moderate

extent as indicated by a mean of 2.5 and Internal control

affected the performance as indicated by a mean of 2.4. Results

indicate that credit approval guidelines and monitoring of

borrowers affect the profitability to a great extent as indicated

by a mean of 1.8 and that Clear established process affect the

performance of the bank to a great extent as indicated by a mean

of 1.5.

According to the findings, the respondents strongly agreed that

frequent contact with borrowers, creating an environment that the

bank can be seen as a solver of problems and trusted adviser and

that monitoring the flow of borrower's business through the

bank's account affect banks performance as indicated by a mean of

2.6, the respondents strongly agreed that developing the culture

of being supportive to borrowers whenever they are recognized to

be in difficulties and are striving to deal with the situation

affect the performance as indicated by a mean of 2.5, the

respondents agreed that Regular review of the borrower's reports

as well as an on-site visit affect the performance of the bank as

indicated by a mean of 2.1 and the respondents agreed that

24

updating borrowers credit files and periodically reviewing the

borrowers rating assigned at the time the credit was granted

affect the banks financial performance as indicated by a mean of

2.0 and 1.9 respectively.

4.3 Loan Security

Respondents indicated that loan security affect financial

performance of a bank moderately as indicated by a mean of 2.5

since it is an issue already known that for anyone to get a loan

from a bank then they must have a form of security. The findings

indicated that suppose there was no security then banks would

have had more customers but not necessarily improved

profitability since the default rate would also be high.

4.4 Credit approval process

Respondents indicated that credit approval guidelines and

monitoring of borrowers affect the banks performance to a great

extent as indicated by a mean of 1.8 and that Clear established

process affect the performance of the bank to a great extent as

indicated by a mean of 1.5. From the findings, the respondents

strongly agreed that clear established process for approving new

credits and extending the existing credits has been observed to

be very important while managing Credit Risks in banks and banks

must have in place written guidelines on the credit approval

process and the approval authorities of individuals or committees

as well as the basis of those decisions affect the performance of

25

the bank as indicated by a mean of 2.0, the respondents agreed

that monitoring of borrowers is very important as current and

potential exposures change with both the passage of time and the

movements in the underlying variables affect the performance of

bank as indicated by a mean of 1.9, the respondents agreed that

prudent credit practice requires that persons empowered with the

credit approval authority should not also have the customer

relationship responsibility, some approval authorities will be

reserved for the credit committee in view of the size and

complexity of the credit transaction and that credits to related

parties should be closely analyzed and monitored so that no

senior individual in the institution is able to override the

established credit granting process affected bank performance as

indicated by a mean of 1.8.

4.5 Credit appraisal analysis

From the findings, the respondents indicated that credit

appraisal affect the performance of banks to a moderate extent as

indicated by a mean of 2.5, Classification affect customer

deposits to a great extent as indicated by a mean of 2.2, Risk

evaluation affect the profitability of bank to a great extent as

indicated by a mean of 1.9, Risk estimation affect bank

performance to a great extent as indicated by a mean of 1.7 and

determining risk reduction measures affected the financial

performance to a great extent as indicated by a mean 1.6.

Respondents strongly agreed that risk analysis and assessment

comprises identification of the outcomes as indicated by a mean

26

of 2.2, the respondents strongly agreed that risk analysis and

assessment comprises estimation the magnitude of the consequences

as indicated by a mean of 1.9, the respondents agreed that risk

analysis and assessment comprises the probability of those

outcomes as indicated by a mean of 1.6.

4.6 Credit risk scoring

From the study, it was observed that risk scoring affects banks

financialperformance to a moderate extent as indicated by a mean

of 2.5; Inspection by branch managers affected the performance to

a great extent as indicated by a mean of 2.3; financial statement

analysis also affected the performance to a great extent as

indicated by a mean of 2.1; Establishing standards affected the

performance banks to a great extent as indicated by a mean of

1.7, Credit scoring affected the performance of banks to a great

extent as indicated by a mean of 1.6, Risk rating and collateral

and Credit worthiness analysis affected the performance of banks

to a great extent as indicated by a mean of 1.5. The study

revealed that the credit manager established the crucial

observation areas inside and outside the bank as indicated by a

mean of 2.5, that the departments and the employees are assigned

with responsibilities to identify specific risks as indicated by

a mean of 1.7, and that risk identification is positively

significant to influence risk management practices as indicated

by a mean of 1.6.

27

4.7 Conclusion and Recommendations

The study investigated the influence of credit risk management on

financial performance of commercial banks in Kenya. From the

findings it is concluded that banks financial performance is

inversely influenced by level of loans and advances, non-

performing loans and deposits thereby exposing them to great risk

of liquidity and distress. Therefore, management need to be

cautious in setting up a credit policy that will not negatively

affect profitability and also they need to know how credit policy

affects the operation of their banks to ensure judicious

utilization of deposits and maximization of profit. Improper

credit risk management reduce the bank’s profitability, affects

the quality of its assets and increase loan losses and non-

performing loan which may eventually lead to financial distress.

Central bank of Kenya for policy purpose should regularly assess

the lending attitudes of financial institutions. One direct way

is to assess the degree of credit crunch by isolating the impact

of supply side of loan from demand side taking into consideration

the opinion of the firms about bank’s lending attitude. Finally,

strengthening the securities market will have positive impact on

the overall development of the banking sector by increasing

competitiveness in the financial sector. When the range of

portfolio selection is wide, people can compare the return and

security of their investment among the banks and the securities

market operators. As a result banks remain under some pressure to

improve their financial soundness.

28

REFERENCES

Adeleye, B. C., Annansingh, F., &Nunes, M. B. (2004). Risk management practices in IS outsourcing: an investigation into commercial banks in Nigeria. International Journal of Information Management, 24(2), 167-180.

29

Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D. (2008).Bank-specific, industry-specific and macroeconomic determinants of bank profitability.Journal of international financial Markets, Institutions and Money, 18(2), 121-136.

Ayo, C. K., Adewoye, J. O., & Oni, A. A. (2010). The state of e-banking implementation in Nigeria: A post-consolidation review. Journal of emerging trends in economics and management sciences, 1(1), 37-45.

Barth, J. R., Caprio, G., & Levine, R. (2000).Banking systems around the globe: do regulation and ownership affect performance and stability?(Vol. 15).World Bank Publications.

Basel, I. I. (2004). International convergence of capital measurement and capital standards: a revised framework. Bank for international settlements.

Basle Committee on Banking Supervision.(1995). International convergence of capital measurement and capital standards.Basle Committee on Banking Supervision.

Brownbridge, M. (1998, March).The causes of financial distress inlocal banks in Africa and implications for prudential policy.United Nations Conference on Trade and Development.

Claessens, S., Demirgüç-Kunt, A., & Huizinga, H. (2001). How doesforeign entry affect domestic banking markets?.Journal of Banking & Finance, 25(5), 891-911.

Ezeoha, A. E. (2011). Banking consolidation, credit crisis and asset quality in a fragile banking system: Some evidence from Nigerian data. Journal of Financial Regulation and Compliance, 19(1), 33-44.

Flamini, V., Schumacher, L., & McDonald, C. A. (2009).The determinants of commercial bank profitability in Sub-Saharan Africa.InternationalMonetary Fund.

30

Framework, A. R. (2006).International Convergence of Capital Measurement and Capital Standards.

Gakure, R. W., Ngugi, J. K., Ndwiga, P. M., &Waithaka, S. M. (2012). Effect 0f Credit Risk Management Techniques 0n The Performance 0f Unsecured Bank Loans Employed Commercial Banks In Kenya. International Journal of Business and Social Research, 2(4), 221-236.

Gordy, M. B. (2003). A risk-factor model foundation for ratings-based bank capital rules.Journal of financial intermediation, 12(3), 199-232.

Huizinga, H. (2000). Financial structure and bank profitability (Vol. 2430).World Bank Publications.

Ikhide, S. I., &Alawode, A. A. (2001).Financial sector reforms, macroeconomic instability and the order of economic liberalization: The evidence from Nigeria (Vol. 112). African Economic Research Consortium.

Kargi, H. S. (2011). Credit Risk and the Performance of Nigerian Banks.AhmaduBello University, Zaria.

Khrawish, H. A. (2011). Determinants of commercial banks performance: evidence from Jordan. International Research Journal of Finance and Economics, 81, 148-159.

Kithinji, A. M. (2010). Credit risk management and profitability of Commercial banks in kenya. School of Business, University of Nairobi, Nairobi.

Kolapo, T. F., Ayeni, R. K., &Oke, M. O. (2012). Credit risk and commercial banks’ performance in Nigeria: A panel model approach.Australian Journal of Business and Management Research, 2(2), 31-38.

Kosmidou, K. (2008). The determinants of banks' profits in Greeceduring the period of EU financial integration.Managerial Finance, 34(3), 146-159.

Kosmidou, K., &Pasiouras, F. (2005). The Determinants of Profits and Margins in the Greek Commercial Banking Industry: evidence

31

from the period 1990-2002. Financial Engineering Laboratory, Department of Production Engineering and Management, Technical University of Crete Working Paper.

Kosmidou, K., Pasiouras, F., &Tsaklanganos, A. (2007). Domestic and multinational determinants of foreign bank profits: The case of Greek banks operating abroad. Journal of Multinational Financial Management, 17(1), 1-15.

Kosmidou, K., Tanna, S., &Pasiouras, F. (2005). Determinants of profitability of domestic UK commercial banks: panel evidence from the period 1995-2002. In Money Macro and Finance (MMF) Research Group Conference (Vol. 45).

Lozano-Vivas, A., &Pasiouras, F. (2010). The impact of non-traditional activities on the estimation of bank efficiency: international evidence. Journal of Banking & Finance, 34(7), 1436-1449.

Mathuva, D. M. (2009). Capital Adequacy, Cost Income Ratio and the Performance of Commercial Banks: The Kenyan Scenario. International Journal of Applied Economics & Finance, 3(2).

Morris, J. (2001). Risk diversification in the credit portfolio: an overview of country practices. International Monetary Fund.Olweny, T., &Shipho, T. M. (2011).Effects of banking sectoral factors on the profitability of commercial banks in Kenya.Economics and Finance Review, 1(5), 1-30.

Ongore, V. O., &Kusa, G. B. (2013).Determinants of Financial Performance of Commercial Banks in Kenya.International Journal of Economics & Financial Issues (IJEFI), 3(1).

Owojori, A. A., Akintoye, I. R., &Adidu, F. A. (2011). The challenge of risk management in Nigerian banks in the post consolidation era. Journal of Accounting and Taxation, 3(2), 23-31.

Pasiouras, F., &Kosmidou, K. (2007).Factors influencing the profitability of domestic and foreign commercial banks in the

32

European Union.Research in International Business and Finance, 21(2), 222-237.

Richard, E., Chijoriga, M., Kaijage, E., Peterson, C., &Bohman, H. (2008).Credit risk management system of a commercial bank in Tanzania.International Journal of Emerging Markets, 3(3), 323-332.

Reengineering Factors on Organizational Performance of Nigerian banks: Information Technology Capability as the Moderating Factor.International Journal of Business and Social Science, 2(13), 198-201.

Sacerdoti, E. (2005). Access to bank credit in sub-Saharan Africa: key issues and reform strategies. International Monetary Fund.

Santomero, A. M. (1997). Commercial bank risk management: an analysis of the process. Journal of Financial Services Research, 12(2-3), 83-115.

Valencia, F. (2012).Systemic banking crises: a new database (Vol. 12). International Monetary Fund.

Waweru, N. M., &Kalani, V. M. (2009). Commercial Banking Crises in Kenya: causes and Remedies. African Journal of Accounting, Economics, Finance & Banking Research, 4(4).

Wenner, M., Navajas, S., Trivelli, C., &Tarazona, A. (2007). Managing credit risk in rural financial institutions in Latin America (No. 34819). Inter-American Development Bank.

Whymark, J. (1998). Benchmarking and credit risk management in financial services. Benchmarking for Quality Management & Technology, 5(2), 126-137.

Zeller, M. (1998). Determinants of repayment performance in credit groups: The role of program design, intragroup risk pooling, and social cohesion. Economic Development and Cultural Change, 46(3), 599-620.

33

APPENDIX 1

LIST OF COMMERCIAL BANKS

1. ABC Bank (Kenya)2. Bank of Africa3. Bank of Baroda4. Bank of India5. Barclays Bank (Kenya)6. CFC Stanbic Bank7. Chase Bank (Kenya)8. Citibank9. Commercial Bank of Africa10. Consolidated Bank of Kenya11. Cooperative Bank of Kenya12. Credit Bank13. Development Bank of Kenya14. Diamond Trust Bank15. Dubai Bank Kenya16. Ecobank17. Equatorial Commercial Bank18. Equity Bank19. Family Bank20. Fidelity Commercial Bank Limited21. First Community Bank22. Giro Commercial Bank23. Guaranty Trust Bank24. Guardian Bank25. Gulf African Bank26. Habib Bank27. Habib Bank AG Zurich28. I&M Bank29. Imperial Bank Kenya30. Jamii Bora Bank31. Kenya Commercial Bank32. K-Rep Bank33. Middle East Bank Kenya34. National Bank of Kenya35. NIC Bank

34

36. Oriental Commercial Bank37. Paramount Universal Bank38. Prime Bank (Kenya)39. Standard Chartered Kenya40. Trans National Bank Kenya41. United Bank for Africa[2]

42. Victoria Commercial Bank

APPENDIX IIANALYSIS TABLE

Very

gr

eat

mean

stde v

Riskidentification

affect 2 8 31 54 8 2.5 0.5Inspection by

branch Financialstatement

CreditworthinessThe creditmanager

establish thecrucialThe departments

and

the employeesare 0 0 13 46 41 1.7 0.

7Riskidentification

is

35

Determine riskreduction

36

Copyright © 2022 FDOKUMEN