Determinants of Commercial Banks Profitability in Nigeria: A case study of selected banks

PROJECT REPORT SUBMITTED TOWARDS THE

PARTIAL FULFILLMENT OF POST GRADUATE

DEGREE IN INTERNATIONAL BUSINESS

GHAN SHYAM RATHI

MBA-IB (2012-2014)

ROLL NO: A1802012051

FACULTY GUIDE

DR. AJIT MITTAL

AMITY INTERNATIONAL BUSINESS SCHOOL

NOIDA

AMITY UNIVERSITY-UTTAR PRADESH

DISSERTATION REPORT

ON

Financial services to the rural population:

A study on the role of commercial banks in

India

1 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

CERTIFICATE OF ORIGIN

This is to certify that Mr. Ghan Shyam Rathi, student of MBA-

International Business has worked upon a project titled “Financial

services to the rural population: A study on the role of commercial

banks in India” submitted to Dr. Ajit Mittal, Department of

International Business, Amity International Business School, Amity

University Uttar Pradesh, Noida.

I hereby certify it is an original contribution with existing knowledge

and faithful record of work carried out by them under my guidance and

supervision.

Signature Signature

(Faculty Guide) (Student)

2 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

ACKNOWLEDGEMENT

I express my sincere gratitude to my faculty guide Dr. Ajit Mittal of

AMITY INTERNATIONAL BUSINESS SCHOOL, for his able

guidance, continuous support and cooperation throughout my project,

without which the present work would not have been possible.

Also, I am thankful to my institute, for giving me an opportunity to

broaden my knowledge on the Indian Commercial Banks and rural

development by providing me the topic for dissertation “Financial

services to the rural population: A study on the role of commercial

banks in India”.

.

GHAN SHYAM RATHI

3 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

Table of Index

S.NO PARTICULARS PG.NO

1 Abstract 4

2

Chapter-1: Introduction

1.1 Background

1.2 Need for the Study

1.3 Objectives of the Study

5

3 Chapter-2: Critical Review of the Literature 7

4

Chapter-3: Research Methodology

3.1 Data Collection Sources

3.2 Data Collection Method

3.3 Limitation of the Study

10

5

Chapter-4: Data Analysis & Presentation

4.1 Introduction

4.2 Guidelines of RBI on Financial Inclusion

4.2.1 Guidelines

4.2.2 What has been achieved so far?

4.2.3 Cost & Consequences of Financial Exclusion

4.3 Study of Current Networking System & Future Potential of

Commercial Banks Operation in Rural India

4.4 Study of various Financial Services Provided by Commercial

Banks In India

4.5 Findings of the Study

12

6 Conclusion 31

7 References 32

4 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

Abstract

Inclusive growth is possible only through proper mechanism which channelizes all the resources

from top to bottom. Financial inclusion is an innovative concept which makes alternative

techniques to promote the banking habits of the rural people because, India is considered as

largest rural people consist in the world. Financial inclusion is aimed at providing banking and

financial services to all people in a fair, transparent and equitable manner at affordable cost.

Households with low income often lack access to bank account and have to spend time and

money for multiple visits to avail the banking services, be it opening a savings bank account or

availing a loan, these families find it more difficult to save and to plan financially for the future.

This paper is an attempt to discuss the role of RBI and commercial banks in providing financial

services to rural India.

5 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

CHAPTER-1: Introduction

Finance is a panacea for all the ills of weaker and poor section. Commercial banks in India since

nationalization, is providing finance to weaker section under priority sector lending (PSL). In

this system banks have some targets and sub targets of deploying fund and credit to preferred and

desired section and sectors of the economy, basically the rural.

1.1 Background

“The soul of India lives in its villages" - Mahatma Gandhi

This famous observation made by Mahatma Gandhi many years ago, still holds true. The rural

population comprises the core of Indian society and also represents the real India.

India lives in numerous villages, scattered throughout the country. Rural areas are form to nearly

70 percent of India’s population and have historically accounted for more than half of Indian

consumption. Even with increasing urbanization and migration, it is estimated that 63 percent of

India’s population will continue to live in rural areas by 2025. In terms of economic output, rural

India accounts for 48 percent of the country’s economy and the rural markets have the potential

to reach $500 billion by 2020. Thus rural areas will continue to remain vitally important to the

Indian economy.

The rural population in India comprises the core of Indian society and represents the real India.

According to the 2011 census, there are 6,40,867 villages in India and about 83.3 crores of

Indian population lives in these villages among 121 crores of total population.

Finance is one of the important keys to success. Finance is a panacea for all the ills of weaker

and poor section. Commercial banks in India since nationalization, providing finance to weaker

section under priority sector lending (PSL). In this system banks have some targets and sub

targets of deploying fund and credit to preferred and desired section and sectors of the economy.

Preferred and desire section is weaker section and sectors are agriculture, small scale industries,

small business man, education, housing and micro finance. In India GDP rate is decreasing and

now ranging about 5%. This growth rate is still satisfactory in comparison to Europe and other

world. We need inclusive growth where all sectors and sections of the economy grow, not to

exclude anyone. Banks have progressed remarkably and achieved its targets and sub targets set

under PSL. Microfinance has reduced the role of money lenders in rural India. The overall effect

of bank finance on the economy of weaker section is positive and banks are truly helping in

poverty alleviation. Despite various qualities and goodness in the scheme of priority sector

lending, it is not free from problems.

6 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

The rural population in India suffers from a great deal of indebtness and is subject to

exploitation to the credit market due to high interest and lack of convenient access to credit.

Rural household needs credit for investing in agriculture and strengthening out seasonable

fluctuation in earnings. Since cash flows and savings in rural areas for the majority of households

are small, rural households typically tend to rely on credit for other consumption needs like

education, health, food etc. Rural households need access to financial institutions that can

provide them with credit at lower rates and at reasonable terms than the traditional money

lenders and thereby help them avoid debt-traps that are common in rural India.

1.2 Need for the Study

India’s 70% of the population lives in villages. However a significant proportion of 6,40,867

villages does not have a single bank branch leading to the financial exclusion of rural population.

As India’s development, to a large extent, depends on this segment’s economic growth, so, it is

imperative to bring the unbanked population within the ambit of banking. Invariably financially

excluded people depend on money lenders even for their day to day needs, borrowing at

exorbitant rates to finally get caught in a debt trap. On the other hand, these people are

completely ignorant of financial products like insurance, which may protect them in adverse

circumstances. Moreover, the rural poor suffer from financial impediments due to their seasonal

income, irregularity of work and job related migration. In the light of such issue, the need of the

hour is a financial ecosystem built to meet their living standards ensuring the growth of the

economy as a whole.

1.3 Objectives of the Report

The research intends to meet the following objectives during the study:

- To study the guidelines of RBI for financial inclusion

- To study the current networking system and future potential growth of different banks

operational in rural India.

- To analyze the various financial services provided by the commercial banks to the

rural population

7 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

CHAPTER-2: Critical Review of Literature

Financial inclusion, of late, has become the buzzword in academic research, public policy

meetings and seminars drawing wider attention in view of its important role in aiding economic

development of the resource poor developing economies. In the Indian scenario, the term

‘financial inclusion’ is popular in financial circles, especially after the Reserve Bank of India

(RBI) announced a series of measures in its credit policy for 2006-07 to include many of the

hitherto excluded groups in the banking net.

Rangarajan Committee (2008) on financial inclusion stated that: “Financial inclusion may be

defined as the process of ensuring access to financial services and timely and adequate credit

where needed by vulnerable groups such as weaker sections and low income groups at an

affordable cost.” The financial services include the entire gamut of savings, loans, insurance,

credit, payments, etc. The financial system is expected to provide its function of transferring

resources from surplus to deficit units, but both deficit and surplus units are those with low

incomes, poor background, etc. By providing these services, the aim is to help them come out of

poverty.

The approach to financial inclusion in India encompasses concentrating on vast majority who are

excluded (Thorat, 2007, Sharma, 2008, Subbarao, 2009, RBI, 2009). Financial Inclusion can

be monitored in two ways, one; exclusion from payments system, i.e. not having access to a bank

account. The second type of exclusion is from formal credit markets, requiring the excluded to

approach informal and exploitative markets. Through nationalization of banks in 1969, it was

envisaged to extend coverage of banks in unbanked areas, thus increasing the scope of covering

larger population. Recently the focus has been concentrated on providing affordable basic

banking services.

Indian Institute of Banking & Finance (IIBF) opines, “Financial inclusion is delivery of

banking services at an affordable cost (‘no frills’ accounts,) to the vast sections of disadvantaged

and low income group. Unrestrained access to public goods and services is the sine qua non of an

open and efficient society”.

Empirical evidence time and again emphasizes the relationship between finance and growth.

According to the works of King and Levine (1993) and Levine and Zervos (1998), at the

cross-country level, evidence indicates that various measures of financial development

(including assets of the financial intermediaries, liquid liabilities of financial institutions,

domestic credit to private sector, stock and bond market capitalization) are robustly and

positively related to economic growth. Other studies also establish a positive relationship

between financial development and growth at the industry level, like the one by Rajan and

Zingales (1998). The topical endogenous growth literature structured on ‘learning by doing’

processes, allocates a special role to finance (Aghion and Hewitt, 1998 and 2005). The

researchers so far have not only looked at how finance facilitates economic activity, but also

social aspects like poverty, hunger, etc. The consensus is that finance promotes economic

growth, but the magnitude of impact differs.

8 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

As banking services are in the nature of public good, it is essential that availability of banking

and payment services to the entire population without discrimination is the prime objective of the

public policy. In India the focus of financial inclusion at present is confined to ensuring a bare

minimum access to a savings bank account. The international definitions of financial inclusion

have been viewed in much wider perspective (Leeladhar, 2005)

Roshny Unnikrishnan et. al (2012), analysed in their study “Enabling Financial Inclusion at

the bottom of the Economic Pyramid”, the importance of financial inclusion in economic

empowerment. This study identified the variables in enabling financial inclusion, analyzed the

barriers to effective financial inclusion and the prerogative steps to be taken to overcome the

barriers and enable inclusive growth. The study concluded by identifying the variables that

empower the masses financially and stating the importance of social inclusion in relation to

financial inclusion and also by reinforcing the importance of self-sustenance at the bottom of the

economic pyramid.

Hemavathy Ramasubbian and Ganesan Duraiswamy (2012) suggested, in their article The

Aid of Banking Sectors in Supporting Financial Inclusion - An Implementation Perspective

from Tamil Nadu State, India, that though over the past six years the FI strategy had improved

the life style of BPL, but missing focus on savings and credit improvement strategies degrades

the benefits of FI. This paper surveys analyzes the issues pertaining to implementation of

financial inclusion in economically down trodden districts of Tamil Nadu, India.

Rama Pal and Rupayan Pal (June 2012) analyzed in their article Income Related

Inequality in Financial Inclusion and Role of Banks: Evidence on Financial Exclusion in

India, income related inequality in financial inclusion in India using a representative household

level survey data, linked to State-level factors. This paper also provides estimates of the effects

of various socio, economic and demographic characteristics of households on propensity of a

household to use formal financial services, and compare that for rural and urban sectors. A

notable result is that greater availability of banking services fosters financial inclusion,

particularly among the poor.

Chattopadhyay, Sadhan Kumar (2011) conducted a study titled Financial Inclusion in

India: A case-study of West Bengal. An index of financial inclusion (IFI) has been developed

in the study using data on three dimensions of financial inclusion. It is revealed from the index

that Kolkata district leads with the highest value of IFI, while rest of the districts show a very

low level of financial inclusion. A survey was also conducted in the state in order to gauge the

financial inclusion in rural Bengal and the results reveal that around 38 per cent of the

respondents do not have sufficient income to open a savings account in the bank.

9 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

Reddy K. Sriharsha (2011) in his article, A Study on Extent of Financial Inclusion among

Small Borrowers in Andhra Pradesh, studied the flow of credit to small borrowers with the

objective to evaluate the extent of financial Inclusion based on credit to small borrowers with

special reference to agricultural credit in Andhra Pradesh. This paper attempted to fill this gap by

evaluating the extent of financial inclusion in Andhra Pradesh based on the penetration of credit

to small borrowers.

Vijay Kelkar (2010) analysed in his article Financial Inclusion for Inclusive Growth that

enhanced financial inclusion will drastically reduce the farmers’ indebtedness, which is one of

the main causes of farmers’ suicides. The second important benefit is that it will lead to more

rapid modernization of Indian agriculture.

Dr. Vigneswara Swamy and Dr. Vijayalakshmi (2009) conducted the study on Role of

Financial Inclusion for Inclusive Growth in India - Issues & Challenges and concluded that

Financial Inclusion has far reaching consequences, which can help many people come out of

abject poverty conditions. Financial inclusion provides formal identity, access to payments

system & deposit insurance. The objective of financial inclusion is to extend the scope of

activities of the organized financial system to include within its ambit people with low incomes.

Through graduated credit, the attempt must be to lift the poor from one level to another so that

they come out of poverty.

10 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

CHAPTER-3: Research Methodology

The report is based on an exploratory research. The study is based on secondary data.

3.1 Data Collection Sources

Relevant data are availed from the sources have been considered and analyzed:

Annual Report of:

- Reserve Bank of India(RBI),

- State Bank of India(SBI),

- ICICI Bank

- HDFC Bank

- Union Bank of India(UNI)

Microfinance gate way

Report of Steering Committee

Research papers

- Indian Journal of Research

- B.V. Rural Institute

- International Journal of Research in IT & Management

- International Journal of Scientific Research

- IBS, Hyderabad

International Finance Corporation-World Bank Group

RBI annual publications (2010-2013)

Newspapers

- The Hindu

- Economic Times

- Business Standard

- Reddif mail

3.2 Data Collection Method

Analysis has been done on the basis of well proven financial inclusion indicators namely:

1. Banking system penetration

2. Size and depth of financial market

3. Bank savings penetration

4. Development of financial system

5. Number of basic accounts and

6. Implementation of financial inclusion initiatives

11 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

3.3 Limitation of the Study

The study is based on secondary data. Only the websites and newspapers have been studied for

conducting the study. No primary data has been collected i.e. no respondents has been taken nor

any questioner has been made. Hence, actual information related to banking penetration and its

services to rural population hasn’t been known.

12 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

CHAPTER-4: Data Presentation & Analysis

4.1 Introduction

This chapter presents the findings of the secondary research carried out for this dissertation.

This research was employed to guide data collection. Data collected from the various sources

have been presented in this chapter for the mentioned objectives.

Analysis has also been done for the data presented in the form of bar graphs.

Findings have been mentioned for the given study after presenting and analyzing the data for the

study.

.

4.2 Guidelines of RBI on Financial Inclusion

Under this objective of the study, financial inclusion guidelines issued by RBI along with

studying the achievements of RBI on context of financial inclusion in regard to the cost and

consequences of financial exclusion will be presented.

4.2.1 Guidelines

(a) Reach

i. Branch expansion in rural areas

Branch authorization has been relaxed to the extent that banks do not require prior

permission to open branches in centers with population less than 1 lakh, which is subject

to reporting. To further step up the opening of branches in rural areas, banks have been

mandated to open at least 25 per cent of their new branches in unbanked rural centres.

In the Annual Policy Statement for 2013-14, banks have been advised to consider

frontloading (prioritizing) the opening of branches in unbanked rural centres over a three

year cycle co-terminus with their FIPs. This is expected to facilitate the branch expansion

in unbanked rural centres.

ii. Agent Banking - Business Correspondent/ Business Facilitator Model

In January 2006, the Reserve Bank permitted banks to utilise the services of

intermediaries in providing banking services through the use of business facilitators and

business correspondents. The BC model allows banks to do ‘cash in - cash out’

transactions at a location much closer to the rural population, thus addressing the last

mile problem.

13 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

iii. Combination of Branch and BC Structure to deliver Financial Inclusion

The idea is to have a combination of physical branch network and BCs for extending

financial inclusion, especially in geographically dispersed areas. To ensure increased

banking penetration and control over operations of BCs, banks have been advised to

establish low cost branches in the form of intermediate brick and mortar structures in

rural centres between the present base branch and BC locations, so as to provide support

to a cluster of BCs (about 8-10 BCs) at a reasonable distance of about 3-4 kilometers.

(b) Access

i. Relaxed KYC norms

o Know Your Customer (KYC) requirements have been simplified to such an

extent that small accounts can be opened with self-certification in the presence

of bank officials.

o RBI has allowed ‘Aadhaar’ to be used as one of the eligible documents for

meeting the KYC requirement for opening a bank account.

ii. Roadmap for Banking Services in unbanked Villages

- In the first phase, banks were advised to draw up a roadmap for providing

banking services in every village having a population of over 2,000 by March

2010. Banks have successfully met this target and have covered 74398

unbanked villages.

- In the second phase, Roadmap has been prepared for covering remaining

unbanked villages i.e. with population less than 2000 in a time bound manner.

About 4,90,000 unbanked villages with less than 2000 population across the

country have been identified and allotted to various banks. The idea behind

allocating villages to banks was to ensure availability of at least one banking

outlet in each village.

(c) Products

i. Bouquet of Financial services

In order to ensure that all the financial needs of the customers are met, RBI

advised banks to offer a minimum of four basic products, viz.

A savings cum overdraft account

A pure savings account, ideally a recurring or variable recurring

deposit

A remittance product to facilitate EBT and other remittances, and

Entrepreneurial credit products like a General Purpose Credit Card

(GCC) or a Kisan Credit Card (KCC)

14 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

ii. Basic Savings Bank Deposit Account (BSBDA)

The account should be considered a normal banking service available to all. This

account shall not require any minimum balance. The account will provide an ATM

card or ATM-cum-debit card. Services will include deposit and withdrawal of cash at

bank branches as well as ATMs; receipt/ credit of money through electronic payment

channels or by means of deposit/ collection of cheques drawn by central/ state

government agencies and departments; and While there will be no limit on the

number of deposits that can be made in a month, account holders will be allowed a

maximum of four withdrawals in a month, including ATM withdrawals.

These facilities will be provided without any charges. Also, no charge will be levied

for non-operation/ activation of an inoperative BSBDA

(d) Transactions

i. Direct Benefit Transfer

The recent introduction of direct benefit transfer, leveraging the Aadhaar platform,

will help facilitate delivery of social welfare benefits by direct credit to the bank

accounts of beneficiaries. The government, in future, has plans to route all social

security payments through the banking network, using the Aadhaar based platform as

a unique identifier of beneficiaries. In order to ensure smooth roll out of the

Government’s Direct Benefit Transfer (DBT) initiative, banks have been advised to:

Open accounts of all eligible individuals in camp mode with the support of

local Government authorities.

Seed the existing and new accounts with Aadhaar numbers.

Put in place an effective mechanism to monitor and review the progress in

implementation of DBT.

4.2.2. What has been achieved so far?

1. Banking outlets in villages have increased to nearly 2, 68,000 in March 2013 compared to

67,694 outlets in March 2010.

2. About 7,400 rural branches have been opened during this 3-year period compared with a

reduction of about 1300 rural branches during the last two decades.

3. Nearly 109 million Basic Savings Bank Deposit Accounts (BSBDAs) have been added,

taking the total number of BSBDA to 182 million. The share of ICT-based accounts has

increased substantially. The percentage of ICT accounts to total BSBDAs increased from

25 per cent in March 2010 to 45 per cent in March 2013.

4. With the addition of nearly 9.48 million farm sector households during this period, 33.8

million households have been provided with small entrepreneurial credit as at the end of

March 2013.

15 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

5. With the addition of nearly 2.25 million non-farm sector households during this period,

3.6 million households have been provided with small entrepreneurial credit as at the end

of March 2013.

6. About 4904 lakh transactions have been carried out in ICT based accounts through BCs

during the three year period

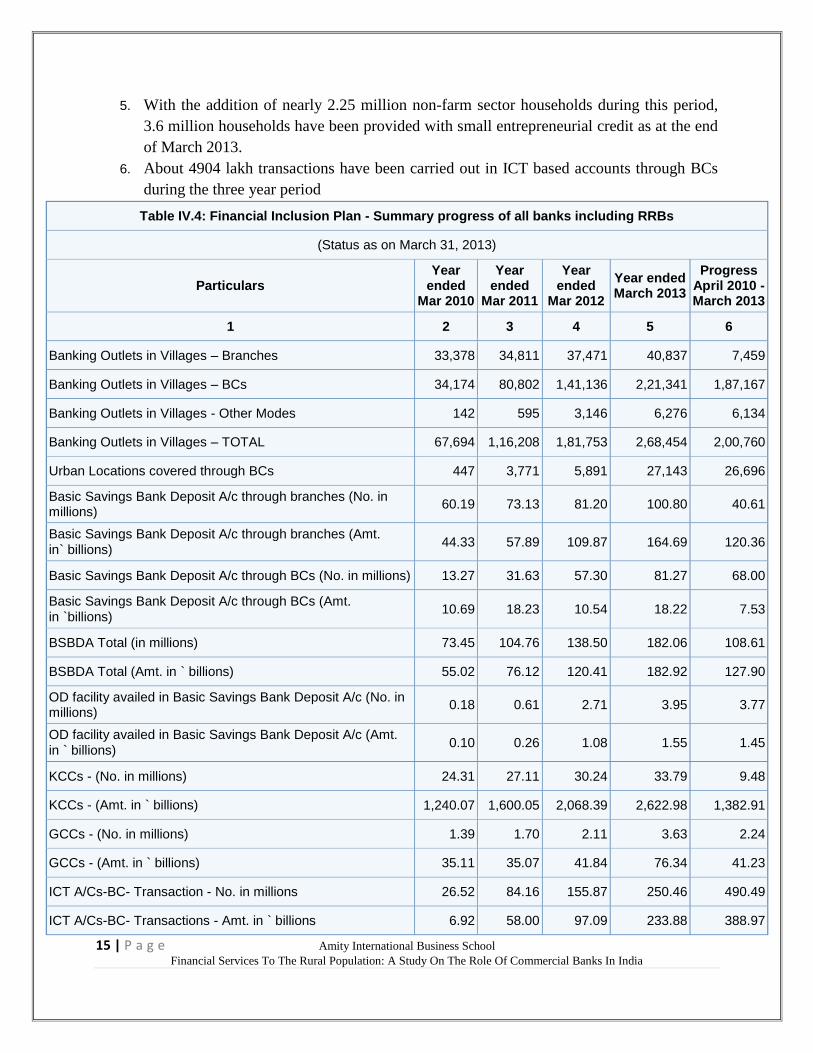

Table IV.4: Financial Inclusion Plan - Summary progress of all banks including RRBs

(Status as on March 31, 2013)

Particulars Year

ended Mar 2010

Year ended

Mar 2011

Year ended

Mar 2012

Year ended March 2013

Progress April 2010 - March 2013

1 2 3 4 5 6

Banking Outlets in Villages – Branches 33,378 34,811 37,471 40,837 7,459

Banking Outlets in Villages – BCs 34,174 80,802 1,41,136 2,21,341 1,87,167

Banking Outlets in Villages - Other Modes 142 595 3,146 6,276 6,134

Banking Outlets in Villages – TOTAL 67,694 1,16,208 1,81,753 2,68,454 2,00,760

Urban Locations covered through BCs 447 3,771 5,891 27,143 26,696

Basic Savings Bank Deposit A/c through branches (No. in millions)

60.19 73.13 81.20 100.80 40.61

Basic Savings Bank Deposit A/c through branches (Amt.

in` billions) 44.33 57.89 109.87 164.69 120.36

Basic Savings Bank Deposit A/c through BCs (No. in millions) 13.27 31.63 57.30 81.27 68.00

Basic Savings Bank Deposit A/c through BCs (Amt.

in `billions) 10.69 18.23 10.54 18.22 7.53

BSBDA Total (in millions) 73.45 104.76 138.50 182.06 108.61

BSBDA Total (Amt. in ` billions) 55.02 76.12 120.41 182.92 127.90

OD facility availed in Basic Savings Bank Deposit A/c (No. in millions)

0.18 0.61 2.71 3.95 3.77

OD facility availed in Basic Savings Bank Deposit A/c (Amt.

in ` billions) 0.10 0.26 1.08 1.55 1.45

KCCs - (No. in millions) 24.31 27.11 30.24 33.79 9.48

KCCs - (Amt. in ` billions) 1,240.07 1,600.05 2,068.39 2,622.98 1,382.91

GCCs - (No. in millions) 1.39 1.70 2.11 3.63 2.24

GCCs - (Amt. in ` billions) 35.11 35.07 41.84 76.34 41.23

ICT A/Cs-BC- Transaction - No. in millions 26.52 84.16 155.87 250.46 490.49

ICT A/Cs-BC- Transactions - Amt. in ` billions 6.92 58.00 97.09 233.88 388.97

16 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

SOURCE: RBI ANNUAL REPORT PUBLICATION 2013

4.2.3 Cost & Consequences of Financial Exclusion

1. The more tangible outcomes of financial exclusion include cost and security issues in

managing cash flow and payments, compromised standard of living resulting from lack

of access to short-term credit, higher costs associated with using informal credit,

increased exposure to unethical, predatory and unregulated providers, vulnerability to

uninsured risks, and long-term or extended dependence on welfare as opposed to savings.

2. Financial exclusion can impose significant costs on individuals, families and society as a

whole. These include (i) barriers to employment as employers may require wages to be

paid into a bank account; (ii) opportunities to save and borrow can be difficult to access;

(iii) owning or obtaining assets can be difficult; (iv) difficulty in smoothening income to

cope with shocks; and (v) exclusion from mainstream society.

3. In terms of cost to the individuals, financial exclusion leads to higher charges for basic

financial transactions like money transfer and expensive credit, besides all round

impediments in basic/ minimum transactions involved in earning livelihood and day to

day living. It could also lead to denial of access to better products or services that may

require a bank account. It exposes the individual to the inherent risk in holding and

storing money – operating solely on a cash basis increases vulnerability to loss or theft.

4. Another cost of financial exclusion is the loss of business opportunity for banks,

particularly in the medium-term. Banks often avoid extending their services to lower

income groups because of initial cost of expanding the coverage which may sometimes

exceed the revenue generated from such operations

17 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

4.3 To study the current networking system and future potential growth of

different banks operational in rural India.

To study the current networking system and future potential growth of different banks

operational in rural India. In order of achieving these objectives, following banks’ data have been

used:

ICICI Bank

HDFC Bank

SBI Bank

Union Bank

Current working system and future growth of banks in financing rural India

Following is a list of 4 banks (2 public bank, 2 private bank) explaining their achievement of

financial inclusion till 2013 and their growth prospect.

1. ICICI Bank:

Financial Inclusion (as of March 2013):

Working with over 25 Business Correspondents (BCs) who have a network of over 7,500

Customer Service Points (CSPs), covering more than 13,500 villages across India.

Established 152 rural branches(including 127 low cost branches in unbanked

villages), representing over 40% of its total branch additions during 2013

At March 31, 2013, about 14.9 million financial inclusion accounts with over 13,500

villages under the coverage of its financial inclusion plan

Vodafone India-ICICI Bank partnership launched its mobile money transfer and payment

service 'M-Pesa'

The Bank’s micro savings products include micro savings accounts, fixed deposits,

recurring deposits, insurance and electronic benefit transfer of different Government

Subsidies and payments.

Around 47% of the Bank’s branches are in rural and semi-urban areas

launched 308 gramin branches to provide basic banking services in unbanked villages

and plan to scale it up to 500 by 2013 (the bank has nearly 17 per cent or 560 branches in

the state, out of which 103 are in rural areas, including 43 gramin branches in unbanked

villages across 10 districts. The bank operates 308 gramin branches.)

Provider of Kisan Credit Cards

18 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

2. SBI Bank

Financial Inclusion (as of March 2013):

Bank has rolled out 38,480 Business Correspondent Customer Service Points through

alliances both at the national and regional level. Transactions volume through BC

channel has grown 2.4 times during FY12-13 at `13,033 crores over FY 11-12.

As at 31.03.13, out of total 14,816 branches, 66% (9851branches) are in Rural and Semi-

urban areas.

A new tractor loan scheme with relaxations in eligibility, margin, security, interest &

upfront fee was launched. Also a revised KCC scheme was rolled out for the benefit of

farmers. Relaxed collateral security norms for all agri loans upto `1lac was introduced

Opened 2.03 crores small accounts with simplified KYC.

Offering various technological-enabled products, through Business Correspondents (BC)

channel, such as, Savings Bank, RD, STDR, remittances & OD facilities.

Bank has covered 12,931 FI villages (population>2000) and 7,600 FIP villages

(population <2000).

Direct Benefit Transfer (DBT) Scheme successfully rolled out. SBI has Lead

responsibility in 28 out of 121 DBT pilot districts. SBI has successfully completed

1.31ac transactions amounting to ` 8.77 crores a Sponsoring Bank, in addition to handling

0.41 lac transactions amounting to ` 7.08 crores as Receiving Bank.

Around 99% households covered & 9.85 lac accounts linked with Aadhaar in 43 pilot

districts.

5.45 lac SHGs were credit linked with credit deployment of ` 5,600 crores.

The Bank has disbursed loans aggregating `63,936 crores in FY’13 surpassing the annual

GOI target of `60,000 crores and 11.89 lakh new famers were brought into the bank’s

fold during the year.

Special campaigns were launched to accelerate agribusiness growth:

‘Swarna Dhara Campaigns’ for agri-gold loans was continued, with quarterly

competitions and garnered ` 14,345 crores business. ‘Tractor Carnival’ launched

from 1st Sep’ 12 to regain the market share, resulted in a business growth of ` 328

crores (8083 tractor loans).

Special interest concessions ranging from 1.5% to 3.5% were extended to

promote loan growth in high value agriculture activities like horticulture, minor

irrigation, seed processing, warehousing, rural godowns, fishery, dairy, poultry,

dealers in agri inputs, farm machinery etc.

Relaxed collateral security norms up to `1.00 lac for all agri loans and `3.00 lac

for loans with recovery tie up arrangements have been leveraged to improve

quality Agri-Business.

19 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

launched Dynamic Insurance products catering to different customer segments,

initiated online term plans with – “E-Shield” the first significant foray into online

distribution and “Grameen Bima” catering to the micro insurance sector aimed at

financial inclusion.

3. HDFC Bank

“Bharat and India must converge and Bharat should not be left behind”.

Financial Inclusion (as of March 2013):

Achieved the milestone of disbursing loans to 20 lakh borrowers under the 'Sustainable

Livelihood Initiative' or SLI, the bank's flagship financial inclusion programme.

The bank has reached 7,900 villages across 24 states and plans to reach all the states in

the coming months.

Along with providing loans, it also provides training to the farmers and other people

providing weavings, harvesting etc.

successfully open 48,000 micro-recurring and fixed deposits and have supported over

600,000 of its low-income microfinance clients with life insurance coverage

Across India, 56% of all branches in HDFC Bank's network are located in semi-urban

and rural areas

760,000 No-Frills Savings Accounts opened

4. Union Bank of India

Financial Inclusion (as of March 2013):

ATM enabled Kisan Credit Card was introduced

Provided banking services to 3,506 government allotted villages each with a population

greater than 2,000.

Established banking services in 19,208 villages

5.8 million no frills banking accounts opened in FY 2013 (13.3 million no frills accounts)

Extended “Pragati”—microloan product to 39,410 customers

Micro-Remittance facility for migrants extended through BC model, now available for

interbank using NEFT platform

Opened 9 Financial Literacy centers counseling 11,610= people

Micro Finance Linkage:

134,640 Self Help Groups have borrowed 7.98 billion rupees

Launching Women Self Help Groups through partner NGO.

20 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

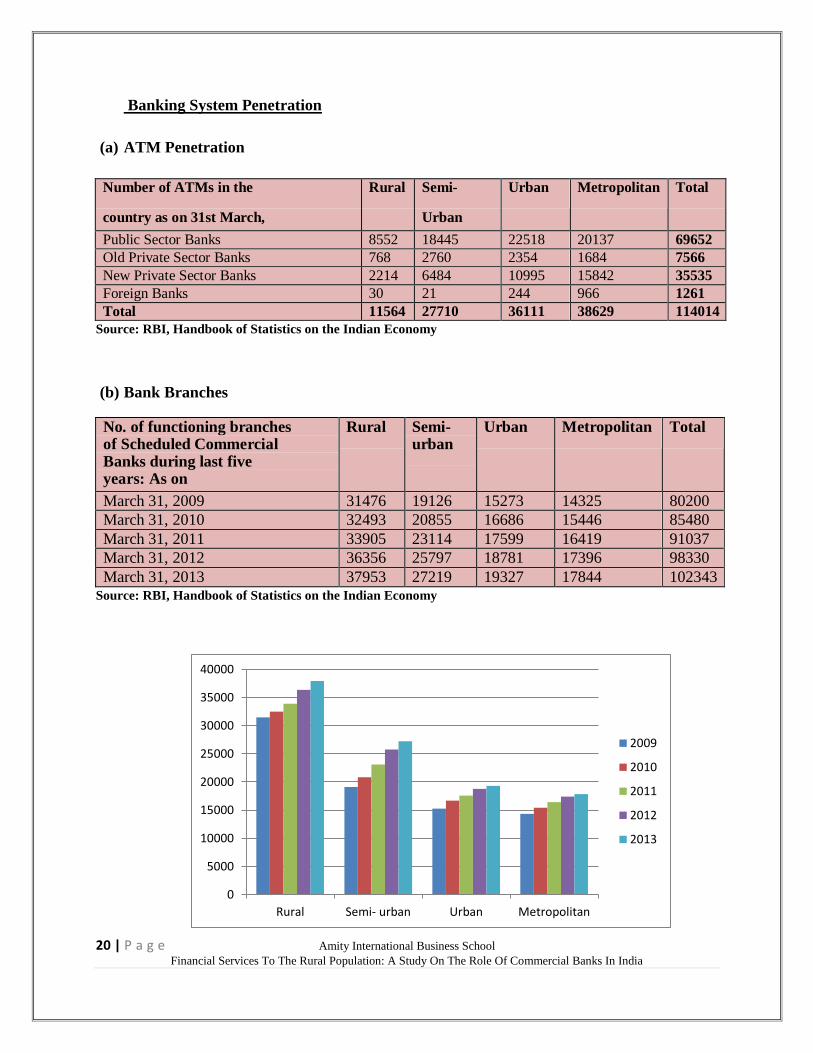

Banking System Penetration

(a) ATM Penetration

Source: RBI, Handbook of Statistics on the Indian Economy

(b) Bank Branches

No. of functioning branches of Scheduled Commercial Banks during last five years: As on

Rural Semi- urban

Urban Metropolitan Total

March 31, 2009 31476 19126 15273 14325 80200 March 31, 2010 32493 20855 16686 15446 85480 March 31, 2011 33905 23114 17599 16419 91037 March 31, 2012 36356 25797 18781 17396 98330 March 31, 2013 37953 27219 19327 17844 102343

Source: RBI, Handbook of Statistics on the Indian Economy

0

5000

10000

15000

20000

25000

30000

35000

40000

Rural Semi- urban Urban Metropolitan

2009

2010

2011

2012

2013

Number of ATMs in the

country as on 31st March,

2013 Rural

Rural Semi-

Urban

Urban Metropolitan Total

Public Sector Banks 8552 18445 22518 20137 69652 Old Private Sector Banks 768 2760 2354 1684 7566 New Private Sector Banks 2214 6484 10995 15842 35535 Foreign Banks 30 21 244 966 1261 Total 11564 27710 36111 38629 114014

21 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

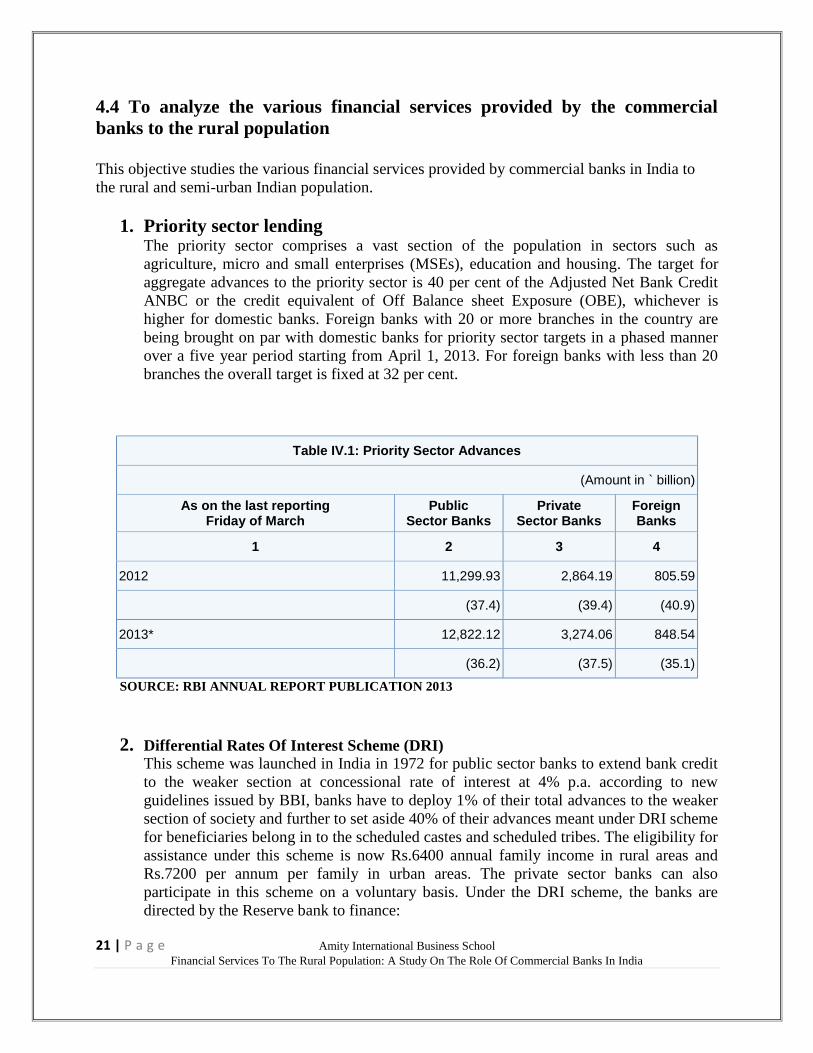

4.4 To analyze the various financial services provided by the commercial

banks to the rural population

This objective studies the various financial services provided by commercial banks in India to

the rural and semi-urban Indian population.

1. Priority sector lending The priority sector comprises a vast section of the population in sectors such as

agriculture, micro and small enterprises (MSEs), education and housing. The target for

aggregate advances to the priority sector is 40 per cent of the Adjusted Net Bank Credit

ANBC or the credit equivalent of Off Balance sheet Exposure (OBE), whichever is

higher for domestic banks. Foreign banks with 20 or more branches in the country are

being brought on par with domestic banks for priority sector targets in a phased manner

over a five year period starting from April 1, 2013. For foreign banks with less than 20

branches the overall target is fixed at 32 per cent.

Table IV.1: Priority Sector Advances

(Amount in ` billion)

As on the last reporting Friday of March

Public Sector Banks

Private Sector Banks

Foreign Banks

1 2 3 4

2012 11,299.93 2,864.19 805.59

(37.4) (39.4) (40.9)

2013* 12,822.12 3,274.06 848.54

(36.2) (37.5) (35.1)

SOURCE: RBI ANNUAL REPORT PUBLICATION 2013

2. Differential Rates Of Interest Scheme (DRI) This scheme was launched in India in 1972 for public sector banks to extend bank credit

to the weaker section at concessional rate of interest at 4% p.a. according to new

guidelines issued by BBI, banks have to deploy 1% of their total advances to the weaker

section of society and further to set aside 40% of their advances meant under DRI scheme

for beneficiaries belong in to the scheduled castes and scheduled tribes. The eligibility for

assistance under this scheme is now Rs.6400 annual family income in rural areas and

Rs.7200 per annum per family in urban areas. The private sector banks can also

participate in this scheme on a voluntary basis. Under the DRI scheme, the banks are

directed by the Reserve bank to finance:

22 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

Scheduled castes and scheduled tribes and other engaged on the modest scale in

agriculture and allied activities.

The physically-handicapped people on the modest scale by offering loans for cottage and

rural industries and vocations like sewing garments, making reasonably cheap edibles,

running way side tea stalls, basket-making etc.

People engaged in elementary processing of forest products.

Village artisans in the decentralized sector.

3. Loans for Tenant Farmers

Regarding lending to tenants and oral sharecroppers, RBI has already advised banks to

accept certificates provided by local administration/ Panchayati Raj Institutions to testify

their status and identity. The Internal Working Group suggests that banks may consider

taking, as an alternative, an affidavit explaining their identity and status for loans up to a

certain amount (say, Rs. 50,000/-), where field visits and local enquiries do indicate that

the tenant/sharecropper has a right to the usufruct of the land. It further recommends that

banks may encourage such farmers to form Self-Help Groups (SHGs) to create social

capital that could instead be used as collateral for purposes of giving crop loan.

With banks and financial institutions shying away from lending to tenant farmers, the

Andhra Pradesh Government has begun a drive to identify eligible farmers and share the

list with banks in the vicinity. To begin with, it plans to issue a loan eligibility card to

about 5.55 lakh „Licensed Cultivators'. The banks will not seek any security or guarantee

for loans up to Rs. 50,000.

With five high security features (such as watermarks which can be seen only under ultra

violet light), these cards would be valid for one year and would assign no right on land to

tenant farmers. After one year, they will have to renew it or get a new one.

Apart from making them eligible for loans, these cards would help tenant farmers get

access to input subsidies and insurance claims which generally go to landowners.

4. Indira Awas Yojana (IAY)

IAY is one of the major flagship programmes of the Rural Development Ministry. It aims

at construction of houses for the Below the Poverty Line (BPL) population in the

villages. Under the scheme, financial assistance worth Rs. 45,000 in plain areas and Rs.

48,500 in difficult areas is provided for construction of houses. In addition, RBI has

advised all banks to lend up to Rs.. 20,000 per IAY house at a differential interest rate of

4 per cent. The houses are allotted in the name of the woman or jointly between husband

and wife. The construction of the houses is the sole responsibility of the beneficiary and

engagement of contractors is strictly prohibited. Sanitary latrines are required to be

constructed along with each IAY house for which additional financial assistance is

provided from Total Sanitation Campaign. Smokeless chullah are also a requirement and

23 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

additional financial assistance towards this end is provided from the Rajiv Gandhi

Grameen Vidyutikaran Yojana.

5. No frills accounts

No frills accounts have to have a zero or a very low balance requirement with limited

transaction facilities. For instance, take the State Bank of India’s (SBI) no-frills account.

To open a no-frills account with SBI, you must be at least 18 years or age and earning a

gross income of Rs.5000 per month or less. You have to make an initial deposit of just

Rs. 50 and you are not required to maintain any minimum balance while operating the

account. Your account can hold a maximum of Rs.10, 000 as the total value of business

connections of the account holder, including other deposit accounts. You receive a

passbook, an ATM-cum-Debit card free of cost and you are also able to avail of the

cheques facility.

6. Loan:

Loans from banks tend to be more standardised across India. If a particular bank is

offering a specific type of loan from a branch in a village in Bihar, it will usually offer

the same product from its branches in Maharashtra or any other state. As per Reserve

Bank of India guidelines, for loans up to Rs. 25000 per borrower, no margin money or

collateral security or third party guarantee will be insisted upon by the financing banks

except hypothecation of assets created out of the loans. The rate of interest chargeable to

the beneficiaries or banks will be those as may be especially declared by the Reserve

Bank of India / NABARD from time to time. Repayable may be subject to the cash flow

of the scheme, the loan repayment period will be between 3 to 10 years with a

moratorium of 6 to 12 months.

Types of loans those are available

(a) Bank of India

Name of the loan: Star Mahila Gold

The purpose of Star Mahila Gold Loan Scheme is for purchase of gold ornaments,

preferably hallmarked, from reputed jewellers and/or gold coins from the Bank of

India. This scheme mainly targets Indian women, between 18 year and 60 years of

age. They may be working or non-working.

(b) Central Bank of India

Name of the loan: Cent Kalyani

This scheme was launched to benefit women entrepreneurs and women professionals.

It offers financial assistance to women who wish to start business or pursue careers in

industry, agricultural and allied activities or follow any profession. The bank, with a

24 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

network of branches spread throughout the country, welcomes women entrepreneurs

to avail financial assistance for pursuing careers of their choice.

(c) Karur Vysya Bank

Name of the loan: KVB Mahila Swarna Loan

Karur Vysya Bank offers instalment loans to working women within the age of 18-50

years for purchase of gold, diamond ornaments and silver wares. These women must

be permanently employed in central/state government offices, public sector

undertakings, reputed public and private companies, teachers, lecturers, professors

and employees of schools, colleges and universities and other reputed institutions. A

guarantee may be given by the husband of the borrower. In case the husband is not

there, a guarantee from the father or any other earning member of the family or third

party guarantee can be obtained. In case of fully secured loans, the guarantee may be

waived.

(d) UCO Bank

Name of the loan: Nari Sakthi

This scheme was started to provide financial assistance to salaried women.

Concessions are offered on interest and the repayment can be made in 5years, in

equated monthly instalments. The lady should be either a permanent employee or

should have completed 3 years of service, among other conditions.

(e) Vijaya Bank

Name of the loan: Assistance to Rural Women in Non-Farm Development

(ARWIND)

Assistance to Rural Women in Non-Farm Development (ARWIND) was introduced

to support their economic activities of rural women in the non-farm sector on a cluster

or group basis. This scheme has two components- the credit component (wherein a

recognised self-help or voluntary group can take loans to help women) and the

promotional component (where the women entrepreneur or professional herself is

given a loan).

Name of the loan: Assistance for Marketing of Non-Farm Products of Rural

Women (MAHIMA)

Assistance for Marketing of Non-Farm Products of Rural Women (MAHIMA)

scheme envisages providing loans and also assistance in grant to Registered

Voluntary Agencies (VA), Non-Governmental Organisations (NGOs) and other

promotional organisations engaged in marketing the products of rural women. Such

25 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

organisations should have been working for at least 3 years with proven track record

and experience in production or marketing of rural products and should satisfy the

norms of the financing banks and NABARD prescribed from time to time.

7. Credit Requirements for Farmers

There are a number of loans that are available specifically for farmers. The most popular

amongst these are Kisan Credit Cards and various crop loans for farmers.

(a) Kisan Credit Card The Kisan Credit Card is an innovative form of providing adequate and timely credit

to farmers with flexible and simplified procedures. It has a single window clearance

and is broad based – it meets the short-term, medium term and long term credit needs

of the borrowers for agriculture and allied activities and a reasonable component for

consumption needs.

Farmers covered under the scheme are issued a credit card and a pass book or a credit

card-cum-pass book which contains their name, address, particulars of land holding,

borrowing limit, validity period, a passport size photograph of holder etc. This serves

both as an identity card and facilitates regular recording of transactions. It is valid for

3 to 5 years subject to annual review. The security, margins, rate of interest, etc. on

the card is set as per RBI norms.

The farmers are required to produce their card-cum-pass book whenever they operate

the account – i.e. withdraw money or repay their loans. The card can be operated

through issuing branches or PACS in the case of Cooperative Banks or through other

designated branches at the discretion of bank.

Farmers can use the card to make a number of withdrawals and repayments, as long

as they remain within their credit limit. The credit limit is fixed on the basis of their

land holding, cropping pattern and scale of finance that they require. Within the

overall limit, there are sub limits which cover short term, medium term as well as

term credit. These are fixed at the discretion of the issuing banks.

Farmers are given the flexibility to reschedule their loans in case of damage to crops

due to natural calamities.

(b) Crop Loans for Farmers

A crop loan consists of short term credit and is generally obtained from primary credit

co-op societies of a village or from a commercial bank. The period of the loan is

about one year, except for sugarcane for which the period is 18 months. Crop loans

are given to farmers either on the basis of the gross value of the crop or on the basis

of the cost of cultivation. The farmer has to offer his land as a security against which

the loan is given.

26 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

There is a three tier structure providing crop-loans through co-operative institutions.

An apex bank or state co-operative bank forwards such loans to a district central co-

operative bank. The district co-operative bank, in turn forwards it to the village co-

operative credit society. If a farmer takes such a loan from a commercial bank, it is

available at a nearby branch. As a result, farmers can get such loans in the village

itself.

Since a crop loan is for one season, it is to be repaid in one instalment after the

harvest of the crop. A crop loan is an annual requirement and a farmer has to take a

fresh loan for every new crop season. Therefore, he has to repay the earlier loan with

interest within stipulated time. Further, since such loans are required every

season/every year, the procedure of getting such loans is simple and convenient.

8. Longer term credit needs of farmers

Beyond loans for cropping and farm maintenance, for farmers to increase their scale of

operation, they require very long term credit. This could involve taking loans with terms

of anywhere between 5 to 20 years or even more, in some special cases. Some activities

that may require long term loans include creation of a sinking well, land levelling,

fencing and permanent improvements on land, purchase of large machinery like tractors

with attachments such as trolleys, establishment of fruit orchard (such as mango, cashew,

coconut, sapota (chiku), orange, pomegranate, fig, guava, etc. Such activities may require

very large investments and may not give returns for a period of even 4-5 years. However,

they are required if the farmer wants to increase his scale of operations.

9. Direct Finance’ for Agricultural Purposes

Direct Agricultural advances denote advances given by banks directly to farmers for

agricultural purposes. These include short-term loans for raising crops i.e. for crop loans.

In addition, advances upto Rs. 5 lakh to farmers against pledge/hypothecation of

agricultural produce (including warehouse receipts) for a period not exceeding 12

months, where the farmers were given crop loans for raising the produce, provided the

borrowers draw credit from one bank.

Direct finance also includes medium and long-term loans (Provided directly to farmers

for financing production and development needs) such as Purchase of agricultural

implements and machinery, Development of irrigation potential, Reclamation and Land

Development Schemes, Construction of farm buildings and structures, etc. Other types of

direct finance to farmers includes loans to plantations, development of allied activities

such as fishery, poultry etc and also establishment of bio-gas plants, purchase of land for

agricultural purposes by small and marginal farmers and loans to agri-clinics and agri-

business centres.

27 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

10. ‘Indirect Finance’ to Agriculture

Indirect finance denotes to finance provided by banks to farmers indirectly, i.e., through

other agencies. Important items included under indirect finance to agriculture are as

under:

Credit for financing the distribution of fertilizers, pesticides, seeds, etc.

Loans upto Rs. 25 lakhs granted for financing distribution of inputs for the allied

activities such as, cattle feed, poultry feed, etc

Loans to Electricity Boards for reimbursing the expenditure already incurred by

them for providing low tension connection from step-down point to individual

farmer for energizing their wells.

Loans to State Electricity Boards for Systems Improvement Scheme under

Special Project Agriculture (SI-SPA).

Loans to Arthias (commission agents in rural/semi-urban areas) for meeting their

Working capital requirements on account of credit extended to farmers for supply

of inputs.

Lending to Non-Banking Financial Companies (NBFCs) for on-lending to

agriculture.

28 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

4.5 Findings of the Study

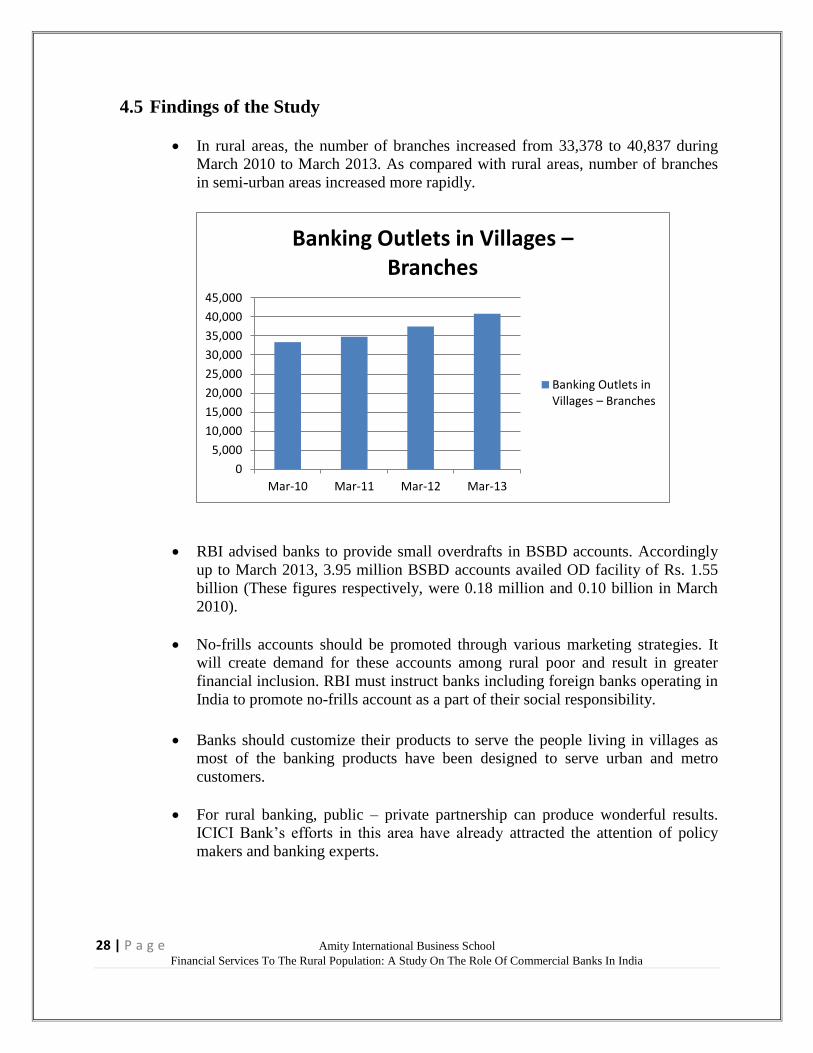

In rural areas, the number of branches increased from 33,378 to 40,837 during

March 2010 to March 2013. As compared with rural areas, number of branches

in semi-urban areas increased more rapidly.

RBI advised banks to provide small overdrafts in BSBD accounts. Accordingly

up to March 2013, 3.95 million BSBD accounts availed OD facility of Rs. 1.55

billion (These figures respectively, were 0.18 million and 0.10 billion in March

2010).

No-frills accounts should be promoted through various marketing strategies. It

will create demand for these accounts among rural poor and result in greater

financial inclusion. RBI must instruct banks including foreign banks operating in

India to promote no-frills account as a part of their social responsibility.

Banks should customize their products to serve the people living in villages as

most of the banking products have been designed to serve urban and metro

customers.

For rural banking, public – private partnership can produce wonderful results.

ICICI Bank’s efforts in this area have already attracted the attention of policy

makers and banking experts.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Mar-10 Mar-11 Mar-12 Mar-13

Banking Outlets in Villages – Branches

Banking Outlets in Villages – Branches

29 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

The number of BSBD accounts opened increased from 73.45 million in March

2010 to 182.06 million in March 2013

Banks have been advised to issue KCCs to small farmers for meeting their credit

requirements. Up to March 2013, the total number of KCCs issued to farmers

remained at 33.79 million with a total outstanding credit of Rs.2622.98 billion

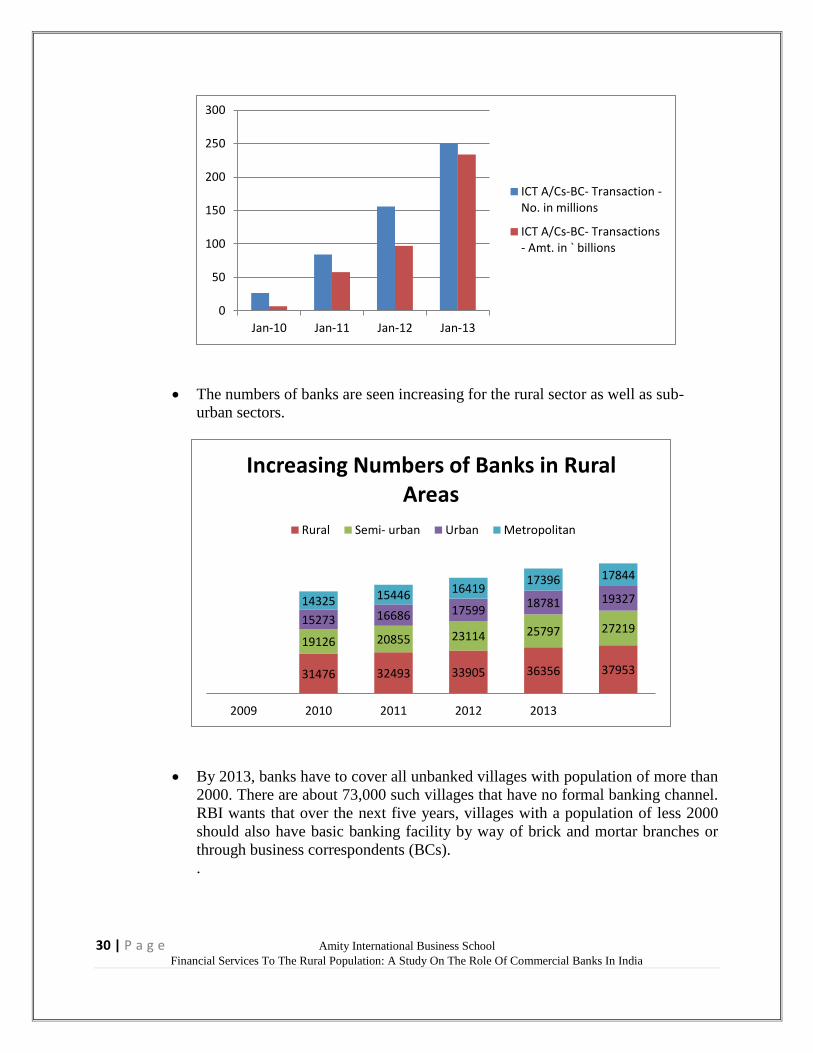

The number of ICT-based transactions through BCs increased from 26.52 million

in March 2010 to 250.46 million in March 2013, while transactions amount

increased steadily from Rs.6.92 billion to Rs.233.88billion during the same

period.

0

50

100

150

200

Jan-10 Jan-11 Jan-12 Jan-13

BSBDA Total (in millions)

BSBDA Total (in millions)

0

5

10

15

20

25

30

35

40

Jan-10 Jan-11 Jan-12 Jan-13

KCCs - (No. in millions)

KCCs - (No. in millions)

30 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

The numbers of banks are seen increasing for the rural sector as well as sub-

urban sectors.

By 2013, banks have to cover all unbanked villages with population of more than

2000. There are about 73,000 such villages that have no formal banking channel.

RBI wants that over the next five years, villages with a population of less 2000

should also have basic banking facility by way of brick and mortar branches or

through business correspondents (BCs).

.

0

50

100

150

200

250

300

Jan-10 Jan-11 Jan-12 Jan-13

ICT A/Cs-BC- Transaction -No. in millions

ICT A/Cs-BC- Transactions- Amt. in ` billions

31476 32493 33905 36356 37953

19126 20855 23114 25797 27219 15273 16686 17599

18781 19327 14325 15446 16419 17396 17844

2009 2010 2011 2012 2013

Increasing Numbers of Banks in Rural Areas

Rural Semi- urban Urban Metropolitan

31 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

Conclusion

Financing the rural, in reality, is far reaching positive consequences which can help resource

poor people to access the formal financial services in order to pull themselves out of abject

poverty. The focus on the common man is particularly imperative in India as he is the more often

ignored one in the process of economic development. Indeed, with the process of financial

inclusion, the attempt should be to lift the resource poor from poverty through coordinated action

amongst the banks, the government and other related institutions in order to facilitate access to

bank accounts and other related services.

Access to financial services such as savings, insurance and remittances are extremely importance

for poverty alleviation and development. The issue of financial inclusion has received large

importance in India during the recent years. India had invested considerable amount of resources

in expanding its banking network with the objective of reaching to the people. During the last 40

years huge infrastructure has been created in the banking sector. However, this large

infrastructure that has penetrated even remote rural areas has been able to serve only a small part

of the potential customers. While India is on a very high growth path, majority of the people are

out of the growth process. This is neither desirable nor sustainable for the nation. We also know

that one of most important driving forces of growth is institutional finance. Therefore, it is now

realized that unless all the people of the society are brought under the ambit of institutional

finance, the benefit of high growth will not percolate down and by that process majority of the

population will be deprived of the benefits of high growth.

Financial inclusion is the road which India needs to travel towards becoming a global player. An

inclusive growth will act as a source of empowerment and allow people to participate more

effectively in the economic and social process. Banks that have global ambitions must meet local

aspirations. Financial access will also attract global market players to our country that will result

in increasing employment and business opportunities. Banks should, therefore, take extra care to

ensure that the poor are not driven away from banking because the technology interface is

unfriendly. This requires training the banks’ frontline staff and managers as well as Business

Correspondents on the human side of banking. Sufficient provisions should be in built in the

business model to take care of customer grievances. It can be summarized that the “The future

lies with those who see the poor as their customers” as commerce for the poor is more viable

than the rich.

32 | P a g e Amity International Business School

Financial Services To The Rural Population: A Study On The Role Of Commercial Banks In India

References

1. Mohan Rakesh (2006), Economic Growth, Financial Deepening and Financial Inclusion,

Address by Rakesh Mohan, Deputy Governor, Reserve Bank of India at the Annual

Bankers’ Conference 2006, November 3, Hyderabad.

2. Rajan R G and Zingales L (1998), “Financial Dependence and Growth”, American

Economic Review, Vol. 88, No. 3, pp. 559-586.

3. Rajan R G and Zingales L (2003), Saving Capitalism from Capitalists, Crown Business,

New York.

4. Rangarajan Committee (2008), “Report of the Committee on Financial Inclusion”, Final,

January

5. The Hindu Business Line (2008), “Commercial Banks Should Address Inclusion Issue”,

Tuesday, September 16.

6. Agarwal Amol (2008), “The Need for Financial Inclusion with an Indian

Perspective”,Economic Research, March 3, IDBI Gilts, India. Financial Reports of RBI.

7. Oya Pinar Ardic Maximilien Heimann Nataliya Mylenko. (2011). Access to Financial

Services and the Financial Inclusion Agenda Around the World, The World Bank, pp 1

17.

8. Santanu Dutta and Pinky Dutta. (2009). The effect of literacy and bank penetration on

Financial Inclusion in India: A statistical analysis. Tezpur University, pp 1-4.

9. Mandira Sarma and Jesim Pais. (2008). Financial Inclusion and Development: A Cross

Country Analysis, Indian Council for Research on International Economic Relations, pp

1-28.

10. Handbook of Statistics on the Indian Economy, RBI 2012-13, 2011-2012

11. Mithani, D.M. Money, Banking, ‘International, Trade And public Finance’ – Himalaya

Publishing House Bombay.

12. Niranjana. S, and Anubumani,V 2002 ‘Social Objectives And Priority Sector Lending,

Banking And Financial Sector Reform In India’, Deep And Deep Publications, PP-231.

13. RBI Annual Report Publication, 2013

14. SBI Annual Report Publication, 2013

15. ICICI Bank Annual Report Publication, 2013

16. The Business Standard (2012), “Banking the Unbanked Rural India”, Tuesday, December

24

7. Economic Times (2013), “Implementation of financial inclusion initiatives”, achievement

of HDFC Bank, Sunday, November 15

17. Satya R. Chakravarty and Rupayan Pal, Measuring Financial Inclusion: An Axiomatic

Approach, Indira Gandhi Institute of Development Research publication, (WP– 2010

003).

18. Chakrabarty, K.C.(2011), “Financial Inclusion”, Presentation at St. Xavier’s College,

Mumbai on September 7, 2011

Copyright © 2022 FDOKUMEN